CEPAL Review No. 72

198

CEPAL Review is prepared by the Secretariat of the Economic Commission for Latin America and the Caribbean. The views expressed in the signed articles, including the contributions of Secretariat staff members, however, represent the personal opinion of the authors and do not necessarily reflect the views of the Organization. The designations employed and the presentation of material in this publication do not imply the expression of any opinion whatsoever on the part of the Secretariat concerning the legal status of any country, territory, city or area or its authorities, or concerning the delimitation of its frontiers or boundaries. CEPAL Review is published in Spanish and English versions three times a year. Annual subscription costs for 2000 are US$ 30 for the Spanish version and US$ 35 for the English version. The price of single issues is US$ 15 in both cases. The cost of a two-year subscription (2000-2001) is US$ 50 for the Spanish-language version and US$ 60 for English. A subscription application form may be found just before the section “Recent ECLAC Publications”. Applications for the right to reproduce this work or parts thereof are welcomed and should be sent to the Secretary of the Publications Board, United Nations Headquarters, New York, N.Y. 10017, U.S.A. Member States and their governmental institutions may reproduce this work without application, but are requested to mention the source and inform the United Nations of such reproduction. Copyright © United Nations 2000 All rights reserved Printed in Chile LC/G.2120-P — December 2000 United Nations Publication ISSN 0251 - 2920 / ISBN 92-1-121306-1

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of CEPAL Review No. 72

CEPAL Review is prepared by the Secretariat of the Economic Commission for Latin America and theCaribbean. The views expressed in the signed articles, including the contributions of Secretariat staff members, however, represent the personal opinion of the authors and do not necessarily reflect the views of theOrganization. The designations employed and the presentation of material in this publication do not implythe expression of any opinion whatsoever on the part of the Secretariat concerning the legal status of anycountry, territory, city or area or its authorities, or concerning the delimitation of its frontiers or boundaries.

CEPAL Review is published in Spanish and English versions three times a year.Annual subscription costs for 2000 are US$ 30 for the Spanish version and US$ 35 for the English version.The price of single issues is US$ 15 in both cases.The cost of a two-year subscription (2000-2001) is US$ 50 for the Spanish-language version and US$ 60 forEnglish.A subscription application form may be found just before the section “Recent ECLAC Publications”.

Applications for the right to reproduce this work or parts thereof are welcomed and should be sent to theSecretary of the Publications Board, United Nations Headquarters, New York, N.Y. 10017, U.S.A. MemberStates and their governmental institutions may reproduce this work without application, but are requested tomention the source and inform the United Nations of such reproduction.

Copyright © United Nations 2000All rights reserved

Printed in Chile

LC/G.2120-P — December 2000

United Nations Publication

ISSN 0251 - 2920 / ISBN 92-1-121306-1

CEPAL REVIE W 72

United Nations

ECLAC

JOSE ANTONIO OCAMPOJOSE ANTONIO OCAMPOJOSE ANTONIO OCAMPOJOSE ANTONIO OCAMPOJOSE ANTONIO OCAMPOExecutive Secretary

REYNALDO BAJRAJREYNALDO BAJRAJREYNALDO BAJRAJREYNALDO BAJRAJREYNALDO BAJRAJDeputy Executive Secretary

CEPAL REVIE W 72

CEPALCEPALCEPALCEPALCEPALRRRRREVIEWEVIE WEVIE WEVIE WEVIE W

OSCAR ALOSCAR ALOSCAR ALOSCAR ALOSCAR ALTIMIRTIMIRTIMIRTIMIRTIMIRDirector of the Review

EUGENIO LAHERAEUGENIO LAHERAEUGENIO LAHERAEUGENIO LAHERAEUGENIO LAHERATechnical Secretary

UNITED NATIONS

Notes and explanation of symbolsThe following symbols are used in tables in the Review:

(…) Three dots indicate that data are not available or are not separately reported.

(—) A dash indicates that the amount is nil or negligible.

A blank space in a table means that the item in question is not applicable.

(–) A minus sign indicates a deficit or decrease, unless otherwise specified.

(.) A point is used to indicate decimals.

(/) A slash indicates a crop year or fiscal year, e.g., 1970/1971.

(-) Use of a hyphen between years, e.g., 1971-1973, indicates reference to the complete number ofcalendar years involved, including the beginning and end years.

References to “tons” mean metric tons, and to “dollars”, United States dollars, unless otherwise stated.Unless otherwise stated, references to annual rates of growth or variation signify compound annual rates.Individual figures and percentages in tables do not necessarily add up to the corresponding totals, becauseof rounding.

Guidelines for contributorsto CEPAL Review

The editorial board of the Review are always interested in encouraging the publication of articleswhich analyse the economic and social development of Latin America and the Caribbean. With this inmind, and in order to facilitate the presentation, consideration and publication of papers, they haveprepared the following information and suggestions to serve as a guide to future contributors.—The submission of an article assumes an undertaking by the author not to submit it simultaneouslyto other periodical publications.—Papers should be submitted in Spanish, English, French or Portuguese. They will be translated intothe appropriate language by ECLAC.—Every article must be accompanied by a short summary (of about 300 words) giving a brief descrip-tion of its subject matter and main conclusions. This summary will also be published on the ECLACHome Page on the Internet.—Papers should not be longer than 10,000 words, including the summary, notes and bibliography, ifapplicable, but shorter articles will also be considered.—One copy of the original text should be submitted, accompanied by a copy on diskette (Word forWindows 95 format), to CEPAL Review, casilla 179-D, Santiago, Chile. In the absence of the copy ondiskette, two printed or typed copies should be provided. Texts may also be sent by e-mail to:[email protected].—All contributions should be accompanied by a note clearly indicating the title of the paper, the name ofthe author, the institution he belongs to, his nationality, his fax and telephone numbers, and his e-mailaddress.—Footnotes should be kept to the minimum, as should the number of tables and figures, whichshould not duplicate information given in the text.—Special attention should be paid to the bibliography, which should not be excessively long. All thenecessary information must be correctly stated in each case (name of the author or authors, completetitle (including any subtitle), publisher, city, month and year of publication and, in the case of a series,the title and corresponding volume number or part, etc.).—The editorial board of the Review reserve the right to make any necessary revision or editorialchanges in the articles, including their titles.—Authors will receive a one-year courtesy subscription to the Review, plus 30 offprints of theirarticle, both in Spanish and in English, at the time of publication in each language.

C E P A L R E V I E W 7 2

D E C E M B E R 2 0 0 0

C O N T E N T S

Social stratification under tension in a globalized era 7Emilio Klein and Víctor Tokman

Employment trends in Latin America and the Caribbeanduring the 1990s 31Jürgen Weller

The labour market and income distribution in Colombiain the 1990s 53José Antonio Ocampo, Fabio Sánchez and Camilo Ernesto Tovar

New challenges for equity in Uruguay 79Rubén Kaztman, Fernando Filgueira and Magdalena Furtado

The adjustment strategies of Mexican ejidatarios in the faceof neoliberal reform 99Benjamin Davis

Population ageing and pension systemsin Latin America 119Jorge Bravo

Expert opinion as an instrument for assessinginvestment in primary education 143Ernesto Schiefelbein, Laurence Wolff and Paulina Schiefelbein

What schools teach us about educatingpoor children in Chile? 159Beverley A. Carlson

Static and dynamic effects of Mercosur.The case of the footwear sector 179Marta Bekerman and Pablo Sirlin

Recent ECLAC publications 199

7

SOCIAL STRATIF ICATION UNDER TENSION IN A GLOBALIZED ERA • EMIL IO KLEIN AND VICTOR TOKMAN

C E P A L R E V I E W 7 2 • D E C E M B E R 2 0 0 0C E P A L R E V I E W 7 2

DECEMBER 2000

Social stratificationunder tension in a

globalized era

Emilio Klein

Sociologist, MultidisciplinaryTechnical Team,International LabourOrganization (ILO),Santiago, [email protected]

Víctor Tokman

Regional Director forthe Americas,ILO, Santiago, [email protected]

The objective of this paper is to explore the effects of glo-balization on the labour market and social stratification. Itis generally held that globalization will bring about progressfor nations and people. This, however, is far from clear, sincethe experience of almost two decades has been raising in-creasing doubts about the potential net gains and, particu-larly, the distribution of such gains. Clearly, there are win-ners and losers among both countries and people. We willconcentrate on the effects upon people within countries andrefer only to one region: Latin America. Our aim is to iden-tify winners and losers in the globalization process and, par-ticularly, the impact on social stratification. Is globalizationleading towards greater social integration within nations, oris social disintegration the result (because only some groupsare being integrated, while a majority is progressively ex-cluded)? To analyse this issue, the paper is structured intofour parts. The first looks at globalization as an integral partof a policy compact, since it is necessary to consider theimpact of the whole package rather than trying to isolatepartial effects. The second concentrates on the effects onemployment, incomes and equity. The third explores changesin the social structure associated with some of the main pro-cesses accompanying globalization. Lastly, we draw someconclusions about the social structure of Latin America dur-ing the reform period.

C E P A L R E V I E W 7 2 • D E C E M B E R 2 0 0 08

SOCIAL STRATIF ICATION UNDER TENSION IN A GLOBALIZED ERA • EMIL IO KLEIN AND VICTOR TOKMAN

IGlobalization as partof a policy compact

Globalization in a restricted sense refers to majorchanges in trade, finance and information that havetaken place in the international economy. This processhas not happened in isolation, but as an integral part ofa policy package combining internal adjustment mea-sures with changes in the way countries relate to theinternational economy. Three main processes charac-terize the emerging situation: globalization,privatization and deregulation (Tokman, 1997). Thepolicy compact followed by most countries, at least inLatin America, came to be known after 1989 as the“Washington Consensus” (Williamson, 1990).

Globalization means that national economies arenow more integrated with the international economyand that goods, capital and communications, and alsopeople, are closer together today than ever before inthe past. This has been the result both of the openingup of economies and of rapid technological change.Trade and financial liberalization has come aboutthrough reductions in tariff and non-tariff barriers re-sulting from i) multilateral agreements in the GeneralAgreement on Tariffs and Trade (GATT) and the cre-ation of its successor, the World Trade Organization(WTO); ii) new or reactivated integration schemes, suchas the North American Free Trade Agreement (NAFTA)and the South American free trade association knownas Mercosur; iii) an explosion of bilateral trade agree-ments during recent years; and, most importantly,iv) unilateral tariff reductions as a key component ofthe adjustment policy package. Latin American tariffsdecreased from an average of between 35% and 100%(minimum and maximum rates) in 1985 to between14% and 22% in the early 1990s. Diversification of thetariff structure has also been greatly reduced, and isnow limited in most countries to three or fewer tariffcategories (Tokman, 1999).

Globalization opens up new opportunities forgrowth and job creation, but at the same time affectsthe determinants of employment and wages and requiresregulation to prevent unfair international competition.

A preliminary version of this paper was prepared at the requestof UNDP as a contribution to the Human Development Report, 1999.

For example, given the differences in factor endow-ment, it is expected that trade from developing to de-veloped countries will largely consist of goods whoseproduction involves intensive use of unskilled labour.This could increase the demand for workers of this typeand decrease the gap between the wages of skilled andunskilled labour.

If this came about, though, it could combine withthe differences in remuneration and labour regulationsthat obtain between countries to generate trade expan-sion based on unfair labour practices or increased ex-ploitation of workers. The prospect has sparked an in-ternational discussion about how this outcome can beavoided and whether there is a need for additional regu-lation. While there has been no general agreement onhow to proceed, it is clear that nobody postulates theequalization of wages between countries, since thiswould affect the competitive position of developingcountries. Nor is it accepted that trade expansion shouldbe based on labour exploitation. Trade sanctions forthose who do not comply with minimum internationallabour standards have been mooted, but so far the ideahas been ruled out because of the danger of their beingmisused as an instrument of trade protection. There is,however, more general agreement about the need fornational and international monitoring to ascertainwhether economic progress is being accompanied bysocial progress and, particularly, by compliance withbasic labour standards among all trading partners. Thishas been incorporated into the International LabourOrganization (ILO) Declaration on Fundamental Prin-ciples and Rights at Work and its Follow-up, adoptedby the International Labour Conference on 18 June1998.

Globalization also affects the determinants of jobcreation and wages because in open economies the abil-ity to compete becomes a major factor and places con-straints on wage adjustments. There now has to be acloser link between wages and productivity than therewas in the old economic environment. In closed econo-mies, wage increases in excess of productivity growthcan be transferred to prices, resulting in inflation; inopen economies, the outcome is a reduced capacity to

9

SOCIAL STRATIF ICATION UNDER TENSION IN A GLOBALIZED ERA • EMIL IO KLEIN AND VICTOR TOKMAN

C E P A L R E V I E W 7 2 • D E C E M B E R 2 0 0 0

compete. In addition, demand fluctuations mean thatcompanies have to be able to adapt faster and showgreater flexibility in production and labour processes.

Privatization is the second feature of the new eco-nomic environment. Privatization reduces the size andfunctions of government and increases the importanceof the private sector and markets in the managementand allocation of resources. Public-sector employmentnaturally falls, rationalization by the new owners re-duces total employment and public-sector enterprisesare transferred to national or international capitalists,the main motive being the need to reduce budget defi-cits during adjustment. Increasingly, furthermore, re-sponsibility for investment is transferred to the privatesector and public investment is limited to basic infra-structure and social sectors, with growing private-sec-tor involvement in the execution and management ofthese.

Deregulation is the third process in this new envi-ronment. This has meant reducing protection and gov-ernment intervention in trade, finance and labour mar-kets. As was mentioned earlier, trade and financialliberalization are leading to increased globalization,while product and labour market protection is beingreduced in order to increase economic efficiency andenable markets to play a greater role in the allocationof resources. The deregulation process has in part beendriven by substantial legal reforms, but there has alsobeen a considerable de facto increase in flexibilitybrought about by the unfettered operation of markets.

The threefold process of globalization,privatization and deregulation is occurring in an inter-national environment characterized by “universaliza-tion” of economic and social problems and by increasedideological homogeneity. Today, employment problemsand social exclusion are no longer to be found solely indeveloping countries, but constitute a major challengeeven in the more developed economies of the world.Unemployment in some of the industrialized countriesof the Organisation for Economic Co-operation andDevelopment (OECD) is stubbornly high; more than 30million people are officially classified as unemployed,while a further 10 million are no longer actively seek-ing work (OECD, 1994 and ILO, 1996). The average rateof unemployment exceeds 10% and in the case of somevulnerable groups, like young people, one in five isjobless in many countries. The end of the Cold Warbroke down ideological barriers, and today’s conflictsare caused less by ideological divergence and more bylocal interests or by a natural reaction against the so-cial cost of adjustment.

The three processes are interrelated in both practi-cal and analytical terms. On the analytical side, global-ization could not have advanced had it not been accom-panied by the other components of adjustment thatreduced trade protection, as well as by financial liberal-ization and privatization with all the opportunities theseopened up for increased trade, capital flows and foreigndirect investment. All these policies contributed to theattainment of macroeconomic balance, but they were alsonecessary conditions for integration into the worldeconomy. These sets of policies were fully incorporatedinto the Washington Consensus, together with instru-ments designed to help secure fiscal discipline. The lat-ter were included with the main objective of ensuringprice stability, but they also play an important role increating incentives for capital inflows in a framework ofgreater stability. Indeed, the one thing that has not beenliberalized is the movement of unskilled workers. Someretrospective policies regularizing illegal migration havebeen introduced, but closed borders, or at least tight regu-lation of flows, continue to be the rule.

The recent economic history of Latin Americancountries shows that, in practice, globalization has beenaccompanied by privatization and deregulation. Thetiming and policy mix has varied according to countryand it is perhaps premature to evaluate the results. Onlyfive countries –Brazil, Chile, Colombia, Costa Rica andUruguay– have attained a per capita income level higherthan in the pre-crisis period. Even fewer have achieveda high and sustained rate of growth, Chile and Colom-bia being the only countries that have been able to ex-pand at more than 5% a year for four consecutive years.Growth rates have been erratic and stop-go cycles havebeen the norm. In addition, other factors have influ-enced performance. Initial conditions were different ineach country: some started the reform process early,others only in the late 1980s or early 1990s. The policymix at each stage was also different.

In spite of the differences, after a decade and ahalf of adjustment it can be concluded that all LatinAmerican countries have been involved in the global-ization and adjustment process, and that privatizationand deregulation have been an integral part of the policycompact. The results are still unclear and policy instru-ments are continually evolving, but it is plain that theregion is today more open and integrated into the worldeconomy, more privatized and less regulated than it wasbefore 1980. All these things have happened simulta-neously; hence, any analysis of results should take ac-count of the context. This is what we shall do in therest of this paper.

C E P A L R E V I E W 7 2 • D E C E M B E R 2 0 0 010

SOCIAL STRATIF ICATION UNDER TENSION IN A GLOBALIZED ERA • EMIL IO KLEIN AND VICTOR TOKMAN

IIEmployment, incomes and equity under globalization

2. The results in practice

a) Productivity gains and international competitive-ness

The first of the expected outcomes that is actually ob-served in most countries is productivity growth in trad-able sectors, particularly manufacturing industry. Aswill be seen below, this outcome is associated with areduction in the employment level of the sector. Duringthe 1990s, productivity per employee expanded at an-nual rates of between 5% and 7% in Argentina, Brazil,Mexico and Peru, while the rate was about 3% in Chile.

The effects on international competitiveness varydepending on the country studied and the indicatorsused to measure labour costs. It is usually argued thatoverpriced labour can affect access to internationalmarkets, and in a more competitive environment costsdo indeed matter. Overpriced labour can be the resultof higher wages or high non-wage labour costs or both.The situation in most Latin American countries doesnot seem to justify the priority given to this issue (ex-cept for some necessary adjustments).

Although they have recently recovered somewhat,wages in most Latin American countries are still lowerthan in 1980. Minimum wages were 26% lower on av-erage in 1999 than in 1980, but wages in manufactur-ing industry rose by 2.9% in the same period. Non-wage labour costs vary from country to country, rangingfrom 38% to 64% of wages. In the case of Chile andArgentina, non-wage labour costs are higher than inKorea, similar to those of the United States, and muchlower than those prevailing in European OECD coun-tries. Hourly labour costs in Latin American manufac-turing industry range from US$ 2.10 to US$ 6.50; thisis between one third and one eighth of the United Stateslevel and less even than in the South-East Asian coun-tries. Labour cost differences per unit of output aresmaller due to higher productivity in competingcountries (table 1). This shows what a high priority hasto be given to raising productivity, as opposed to merelycutting costs, if competitiveness is to be improved(Tokman and Martínez, 1999).

The fact that relative labour costs are not high doesnot mean there is no scope for making adjustments tothe labour cost structure to reduce them further and,

1. The effects anticipated

Globalization is expected to have two main effects onlabour and incomes. Firstly, productivity gains, particu-larly in tradable sectors, should result in increased em-ployment and lower prices in those sectors. The lattershould also result in improved real incomes and wel-fare for the population. Secondly, increased wages inexport sectors, assumed to be more intensive in un-skilled labour, should result in a reduction of wage dif-ferentials by skill level and, hence, in increased equity.

The reduction or elimination of tariffs and non-tariff barriers should lead to a fall in the relative pricesof tradable goods. This would result, on the productionside, in factors being reallocated to export sectors and,on the consumption side, to expenditure being reallo-cated to imported goods and services. Consequently,there should be a positive effect on employment result-ing from export growth, while reductions in the rela-tive prices of importable goods should lead to an in-crease in real incomes. Trade liberalization shouldtherefore result in increased welfare.

In the short run, however, the employment growthresulting from increased exports could be offset by adecrease in employment in sectors that compete withimports. Increased competition in these sectors forcesenterprises to increase productivity, generally at the ex-pense of employment. The net employment effect ofeconomic opening will depend on the demand forlabour in both tradable and non-tradable sectors andon labour supply dynamics. This, in turn, will affectaverage wages in each sector.

Another anticipated result of trade liberalizationis that it will lead to a rise in the relative prices of de-veloping country goods whose production involves in-tensive use of unskilled labour. This would lead to anincrease in the demand for unskilled workers and a risein their relative wages. As a consequence, wage dis-persion would diminish.1

1 For a discussion of the theoretical foundations of this expecta-tion and its empirical validity in developed countries see, amongothers, Bhagwati and Dehejia (1993), Lawrence and Slaughter(1993), Wood (1994), ILO (1995) and Sachs and Shatz (1994).

11

SOCIAL STRATIF ICATION UNDER TENSION IN A GLOBALIZED ERA • EMIL IO KLEIN AND VICTOR TOKMAN

C E P A L R E V I E W 7 2 • D E C E M B E R 2 0 0 0

particularly, to lower the cost of unskilled labour. Taxeson unskilled workers tend to reduce employment, whilesome of the existing taxes on the wage bill would bemore efficient if they were transferred to other sourcesof revenue, particularly those that go to finance housingor other investments.

The evolution of labour costs in the 1990s alsothrows up other policy issues for consideration. Labourcosts deflated by consumer prices have not increasedahead of productivity, for instance, in Argentina, Bra-zil, Mexico or Peru, and have thus been no impedi-ment to increased access to international markets. How-ever, when expressed in dollars rather than localcurrency, or when observed in relation to producerprices, the gains are slighter, and in most cases com-petitiveness has declined (table 1). This is due to theeffects of macroeconomic policy during the period, asin most countries this involved national currenciesbeing kept overvalued owing to the need to reduce in-flation and to the liberalization of capital flows. Part ofthe decline is explained by delays in adjusting theexchange rate.

Meanwhile, domestic prices adapt at differingspeeds to a more competitive economic environment:prices for traded goods, generally included in producerprices, adjust relatively quickly, while those for consumergoods, which are more influenced by non-traded goodsand services, tend to be slower in adjusting. The result isthat while labour costs expressed in consumer price termsdid not rise, they actually increased very fast in relationto producer prices. This change in relative prices, while

it lies outside the labour market sphere, does influencethe dynamics of wage determination because it leads tothe outlook of workers (based on the purchasing powerof wages) diverging from that of those who operate busi-nesses (based on profit margins).

Furthermore, as the situation after mid-1997 clearlyillustrates, competitiveness is also dependent on devel-opments in other countries. Despite a rise of between0.4% and 10% in the competitiveness of Latin Ameri-can countries, their ability to compete with goods fromthe Asian countries deteriorated. Competitiveness gainsin these countries were about 50% –ranging from 20%in Thailand to 60% in Malaysia– while among LatinAmerican countries the largest increase, in Colombia,was about 10%.

To sum up, productivity grew, as expected, as a con-sequence of the reform process, but some adjustmentsare still needed. Firstly, if international competitivenessis to be maintained, non-wage labour costs need to beexamined. Secondly, macroeconomic policies, particu-larly overvalued exchange rates and relative prices,should be reviewed. Lastly, productivity gains have beeninsufficient to close the gap with competitors.

b) Job creation

A second effect of globalization has been inadequatejob creation in relation to the rapid increase in the eco-nomically active population (EAP). On average, the non-agricultural EAP has grown by over 3% a year, partly asa result of increasing female participation in the wageeconomy (table 2). Job creation has lagged due to slow

TABLE 1

Selected countries: Labour costs and international competitivenessa

Hourly Non-wage Hourly cost Labour costs Annual changes 1990-1995wage labour costs of labour per unit of Labour Produc- Competitivenessb

(dollars) as % of wages (dollars) output costs tivity(United States = 100) A B A B C

Argentina 4.6 42.5 6.5 55 -2.0 13.1 7.0 9.2 -6.1 3.7Brazil 3.7 58.2 5.9 60 2.9 8.5 7.5 4.5 -0.9 4.3Chile 2.5 38.0 3.5 43 4.3 9.4 3.2 -1.1 -5.7 5.9Mexico 1.9 42.0 2.8 47 1.2 1.5 5.2 4.0 3.6 naPeru 1.3 64.3 2.1 43 5.1 11.6 6.6 1.4 -4.5 0.3United States 12.6 40.3 17.7 100 2.6 3.8 -1.2 naGermany 16.1 78.5 28.7 150 2.1 1.8 -0.3 naRepublic of Korea 6.8 21.9 8.2 60 3.6 11.9 8.0 50.0

Source: Tokman and Martínez (1999), ILO (1998) and updating by authors.

a Manufacturing industry, circa 1997. Competitiveness is defined as the difference between changes in productivity and labour costs.b A = Changes in local currency at constant prices, deflated by consumer price index (1990-1995).

B = Changes in dollars (1990-1995).C = Changes in dollars between July 1997 and June 1998.

C E P A L R E V I E W 7 2 • D E C E M B E R 2 0 0 012

SOCIAL STRATIF ICATION UNDER TENSION IN A GLOBALIZED ERA • EMIL IO KLEIN AND VICTOR TOKMAN

and erratic economic growth. The result has been ris-ing unemployment.

The average unemployment rate in Latin Americarose from 6% in 1980 to 8.7% in 1983, i.e., during thefirst phase of adjustment. Unemployment fell from 1983to 1992, but never returned to its 1980 level. After 1992unemployment grew continuously, reaching 8.8% in1999. These developments reveal not only the limitedcapacity of the region’s economies to bring down un-employment, but also increased vulnerability, since con-tinuous adjustments entail a return to previous higherlevels of unemployment. By 1999, Latin American un-employment had returned to the high levels of the mid-1980s.

Four aspects should be taken into account in evalu-ating the way unemployment affects the people of LatinAmerica. The first is that it can be misleading simplyto compare the unemployment level with, for instance,the rates of over 10% prevailing in some OECD coun-tries. Most countries lack unemployment insurance, andprotection is generally occupation-linked. Joblessnessmeans no income and no protection, and this is one ofthe main sources of social exclusion. Secondly, unem-

ployment disproportionately affects women and youngpeople. While the female unemployment rate is about30% higher than the average, rates for young peopleare usually double the national figure. Unsurprisingly,women and young people account for a large propor-tion of the excluded. Thirdly, there are also large re-gional variations within countries. Adjustment tends tohave a disproportionate effect on places where key sec-tors in need of restructuring are located. These activi-ties generally constitute the main source of employ-ment and production, and restructuring affects thewhole region.

The situation also differs from country to country.Size, the degree of modernization attained and the stagereached in the reform process are determining factorsin unemployment. Small, open economies are more vul-nerable to external fluctuations and tend to have higherand more erratic unemployment rates than larger, moreclosed economies (where internal demand plays thebiggest role and provides more autonomy). Again, incountries that have reached an advanced stage of ur-banization and modernization, labour markets mainlyadjust through unemployment, while in those with a

TABLE 2

Latin America: Economic activity, employment, wages and poverty(Annual growth rates and index)

Indicator

Economic activityGNPa

GNP per capitaa

Inflationa

Population and employmentPopulationa

Total EAPa

Urban EAP (%)Non-agricultural employmenta

Open unemployment rateInformal employment (%)b

Public-sector employment (%)c

Wagesd

Real manufacturing wagesReal minimum wages

PovertyPercentage of households in poverty (%)Urbanization of poverty (%)

Source: ILO, on the basis of national statistics.

a Annual growth rates. d Index 1980 = 100.b Percentage of urban employment. e 1997 figure.c Percentage of total EAP.

1980 1985 1990 1995 1999

… 0.6 1.9 2.9 0.0… -1.6 -0.1 1.1 -1.8… 134.8 487.5 287.5 9.8

… 2.1 1.9 1.8 1.8… 3.5 3.1 2.6 2.666.9 70.0 72.8 75.3 76.6… 3.5 4.4 3.0 2.86.7 10.1 8.0 7.2 8.840.2 47.0 44.4 46.5 48.515.7 16.6 15.5 13.4 13.0

100.0 93.1 86.6 92.9 102.9100.0 86.4 68.4 70.8 73.8

35.0 37.0 41.0 38.0 36.071.4 … 85.4 84.2 83.3e

13

SOCIAL STRATIF ICATION UNDER TENSION IN A GLOBALIZED ERA • EMIL IO KLEIN AND VICTOR TOKMAN

C E P A L R E V I E W 7 2 • D E C E M B E R 2 0 0 0

large agricultural population or small formal sector, un-deremployment is the main adjustment variable. Lastly,the stage reached in the reform process also matters.Early reformers have been the most successful in re-ducing unemployment, while latecomers –particularlythose that are now in the early phases of adjustment–tend to have higher and rising unemployment.

c) Changes in the employment structure

In addition to a higher unemployment rate, reform hasbrought about profound changes in the structure of em-ployment. Four main interrelated processes can be iden-tified: privatization, the shift from goods-producing sec-tors to services, the increase in informal working, andthe loss of job security. These processes can be seen tohave taken place in the 1990s, when most countrieswere already beyond or well advanced in the adjust-ment process.

Privatization introduced a major change in patternsof job creation in Latin America, owing to the role tra-ditionally played by the public sector as the employerof last resort (something that will be discussed in thenext section) and an important contributor to the de-velopment of the middle classes. Government did notdirectly contribute to employment growth in the 1990s.On the contrary, its share of urban employment fell inthe region as a whole, from 15.5% in 1990 to 13.0% in1999. This decrease does not include falls in public-sector employment that took place in earlier periods,as in Chile. This movement from public- to private-sector employment occurred in all countries, while insome –including Argentina, Costa Rica and Panama–the decline amounted to as much as five to ten percent-age points.

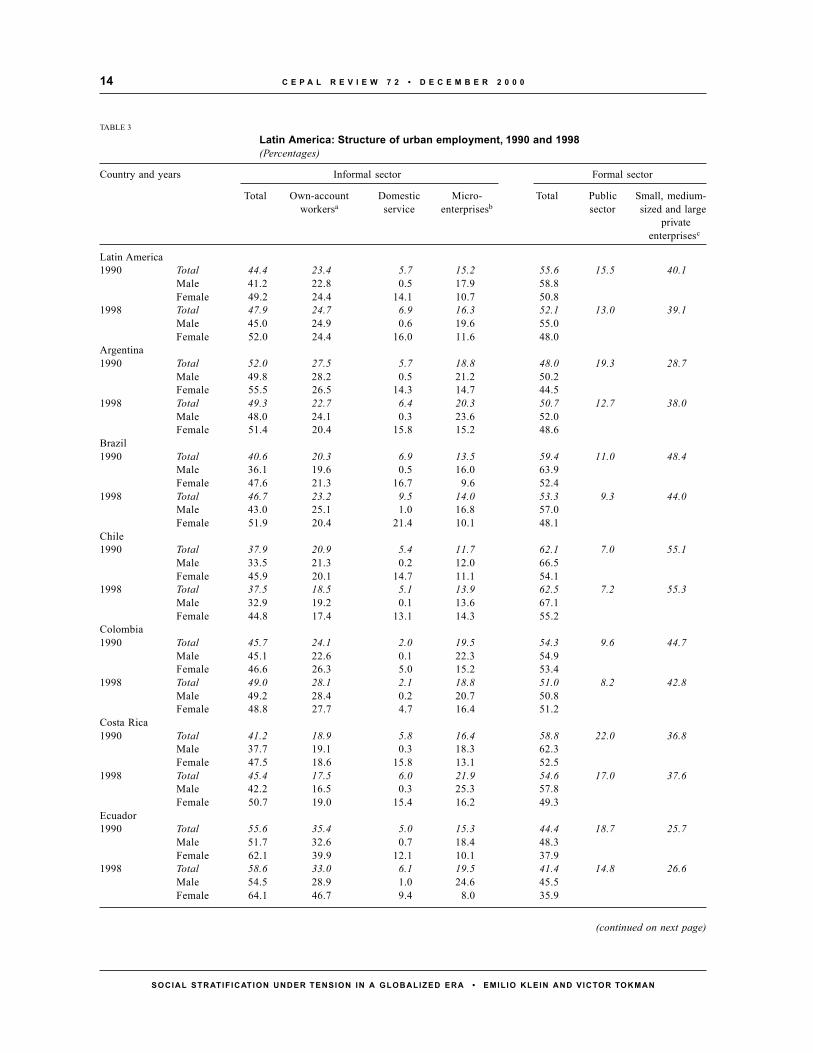

The employment shift from the public to the pri-vate sector was a direct consequence of the privatizationand deregulation processes accompanying globaliza-tion. State enterprises were transferred to the privatesector and government functions were reduced. It wasalso one of the main results of fiscal discipline, an im-portant component of stabilization policy. Budget defi-cits were generally reduced by cutting public expendi-ture, mostly the payroll, through a series of wage andemployment cuts (table 3).

Generally speaking, however, the transfer of jobswas not towards larger private companies. Their shareof total employment also declined over the same pe-riod, although at a slower pace than government em-ployment. Between 1990 and 1998, the employmentshare accounted for by such companies fell from 40%

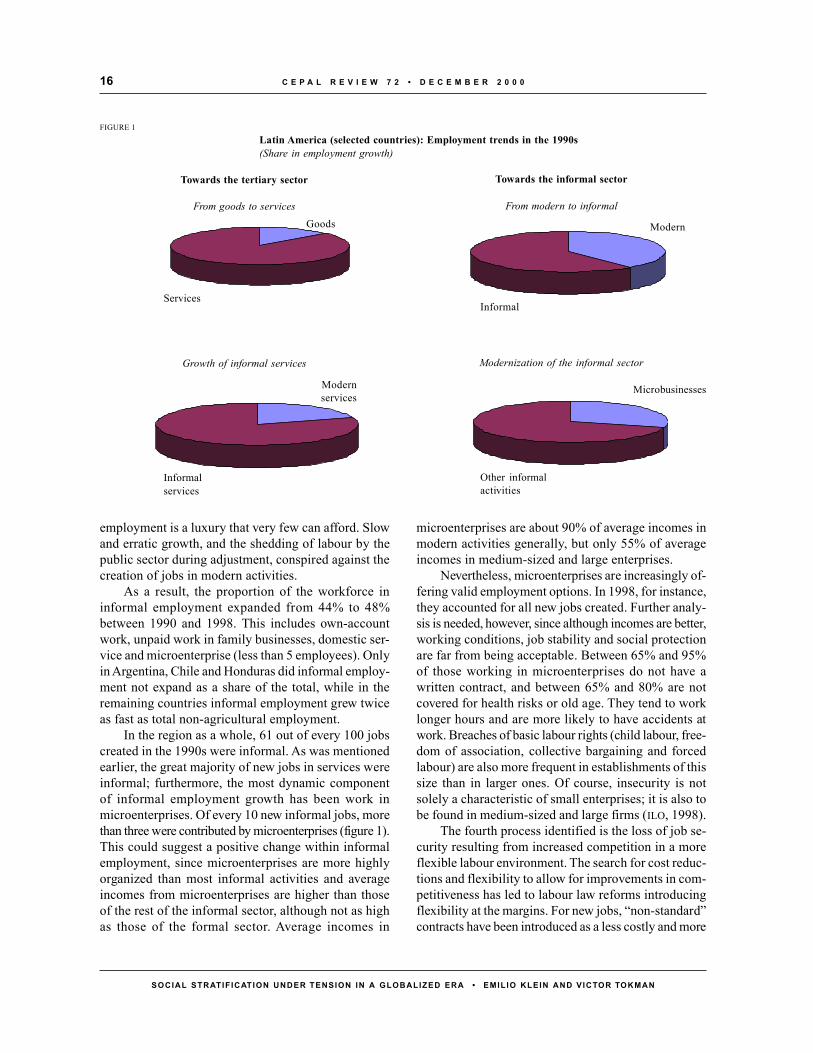

to 39%, the bulk of this decline taking place in coun-tries such as Brazil, Colombia and Venezuela. If smallenterprises are excluded, furthermore, the declineamounts to two percentage points (ILO, 1998). Largeenterprises (more than 100 employees) were the mostaffected by trade liberalization and the need to increaseproductivity (mostly through employment reduction).Only 17 out of every 100 new jobs created during the1990s were contributed by such companies. Increasedlabour flexibility facilitated adjustment, but at the costof a more erratic employment level, as is clearly illus-trated by the 1% decline in employment in large andmedium-sized enterprises in 1998, when these firmshad to adjust to increased competition from Asian prod-ucts (figure 1).

The second of the processes referred to, the shiftin employment from goods-producing sectors to ser-vices, was rapid in countries such as Bolivia, Costa Rica,Ecuador, Peru and Uruguay, where the share of manu-facturing employment fell by between four and six per-centage points during the 1990s.

In other countries the process was slower becauserestructuring was at a more mature stage (Chile) or agradual approach was followed (Brazil and Colombia)or, in cases like Panama, because the economy wassmall and already open.

The new structural conditions resulting from theadjustment process have left these sectors more vul-nerable to changes in competition. Manufacturing in-dustry contracted in 1998 as a result of increased com-petition from Asian products. This contraction of outputand employment was particularly large in food process-ing, textiles and clothing, shoes and machinery andequipment.

The shift of employment from manufacturing toservices is partly the result of increased competition ina more open economy. Falling employment has beenaccompanied by rising productivity which, particularlyin the short run, can only be achieved by cutting jobs.The effect has mainly been felt in urban employment,since agriculture, fishing and mining tend to contrib-ute to employment growth during the liberalizationprocess.

It cannot automatically be assumed that employ-ment growth in the service sector means a shift towardslow-productivity jobs. Some of the jobs created in thesector are in services that are integral to the modern-ization and globalization processes, such as finance,communications and trade. The productivity of thesesectors is usually higher than that of manufacturing andcan grow more rapidly. Unfortunately, this has not been

C E P A L R E V I E W 7 2 • D E C E M B E R 2 0 0 014

SOCIAL STRATIF ICATION UNDER TENSION IN A GLOBALIZED ERA • EMIL IO KLEIN AND VICTOR TOKMAN

TABLE 3

Latin America: Structure of urban employment, 1990 and 1998(Percentages)

Country and years Informal sector Formal sector

Total Own-account Domestic Micro- Total Public Small, medium-workersa service enterprisesb sector sized and large

privateenterprisesc

Latin America1990 Total 44.4 23.4 5.7 15.2 55.6 15.5 40.1

Male 41.2 22.8 0.5 17.9 58.8Female 49.2 24.4 14.1 10.7 50.8

1998 Total 47.9 24.7 6.9 16.3 52.1 13.0 39.1Male 45.0 24.9 0.6 19.6 55.0Female 52.0 24.4 16.0 11.6 48.0

Argentina1990 Total 52.0 27.5 5.7 18.8 48.0 19.3 28.7

Male 49.8 28.2 0.5 21.2 50.2Female 55.5 26.5 14.3 14.7 44.5

1998 Total 49.3 22.7 6.4 20.3 50.7 12.7 38.0Male 48.0 24.1 0.3 23.6 52.0Female 51.4 20.4 15.8 15.2 48.6

Brazil1990 Total 40.6 20.3 6.9 13.5 59.4 11.0 48.4

Male 36.1 19.6 0.5 16.0 63.9Female 47.6 21.3 16.7 9.6 52.4

1998 Total 46.7 23.2 9.5 14.0 53.3 9.3 44.0Male 43.0 25.1 1.0 16.8 57.0Female 51.9 20.4 21.4 10.1 48.1

Chile1990 Total 37.9 20.9 5.4 11.7 62.1 7.0 55.1

Male 33.5 21.3 0.2 12.0 66.5Female 45.9 20.1 14.7 11.1 54.1

1998 Total 37.5 18.5 5.1 13.9 62.5 7.2 55.3Male 32.9 19.2 0.1 13.6 67.1Female 44.8 17.4 13.1 14.3 55.2

Colombia1990 Total 45.7 24.1 2.0 19.5 54.3 9.6 44.7

Male 45.1 22.6 0.1 22.3 54.9Female 46.6 26.3 5.0 15.2 53.4

1998 Total 49.0 28.1 2.1 18.8 51.0 8.2 42.8Male 49.2 28.4 0.2 20.7 50.8Female 48.8 27.7 4.7 16.4 51.2

Costa Rica1990 Total 41.2 18.9 5.8 16.4 58.8 22.0 36.8

Male 37.7 19.1 0.3 18.3 62.3Female 47.5 18.6 15.8 13.1 52.5

1998 Total 45.4 17.5 6.0 21.9 54.6 17.0 37.6Male 42.2 16.5 0.3 25.3 57.8Female 50.7 19.0 15.4 16.2 49.3

Ecuador1990 Total 55.6 35.4 5.0 15.3 44.4 18.7 25.7

Male 51.7 32.6 0.7 18.4 48.3Female 62.1 39.9 12.1 10.1 37.9

1998 Total 58.6 33.0 6.1 19.5 41.4 14.8 26.6Male 54.5 28.9 1.0 24.6 45.5Female 64.1 46.7 9.4 8.0 35.9

(continued on next page)

15

SOCIAL STRATIF ICATION UNDER TENSION IN A GLOBALIZED ERA • EMIL IO KLEIN AND VICTOR TOKMAN

C E P A L R E V I E W 7 2 • D E C E M B E R 2 0 0 0

Table 3 (continued)

Country and years Informal sector Formal sector

Total Own-account Domestic Micro- Total Public Small, medium-workersa service enterprisesb sector sized and large

privateenterprisesc

Honduras1990 Total 57.6 37.3 7.1 13.3 42.4 14.9 27.5

Male 45.1 25.7 0.5 18.9 54.9Female 72.0 50.5 14.6 6.9 28.0

1998 Total 57.9 37.0 5.0 15.9 42.1 10.3 31.8Male 52.0 27.9 0.9 23.2 48.0Female 64.1 46.7 9.4 8.0 35.9

Mexico1990 Total 47.5 25.0 5.1 17.3 52.5 25.0 27.5

Male 46.6 25.1 0.8 20.7 53.4Female 48.8 24.6 13.4 10.8 51.2

1998 Total 49.6 24.9 4.8 19.8 50.4 21.7 28.7Male 48.1 23.7 0.2 24.2 51.9Female 51.8 26.8 12.9 12.1 8.2

Panama1990 Total 36.0 19.8 7.9 8.3 64.0 32.0 32.0

Male 34.6 23.8 1.0 9.7 65.4Female 38.0 14.0 17.8 6.3 62.0

1998 Total 38.5 21.5 6.9 10.1 61.5 21.8 39.7Male 35.9 22.8 1.3 11.9 64.1Female 42.3 19.5 15.4 7.4 57.7

Perud

1990 Total 52.7 33.4 4.9 14.5 47.3 11.6 35.7Male 46.3 28.9 0.6 16.9 53.7Female 62.9 40.4 11.6 10.8 37.1

1998 Total 53.7 30.2 5.5 18.0 46.3 7.2 39.1Male 45.3 23.8 0.5 21.0 54.7Female 64.6 38.7 11.9 14.0 35.4

Uruguaye

1990 Total 39.1 18.6 6.8 13.7 60.9 20.1 40.8Male 33.7 18.6 0.2 15.0 66.3Femae 46.6 18.5 16.2 11.8 53.4

1998 Total 41.2 20.1 7.5 13.6 58.8 16.8 42.0Male 37.3 22.1 0.2 15.0 62.7Female 46.4 17.5 17.2 11.7 53.6

Venezuela1990 Total 38.6 22.3 3.9 12.4 61.4 22.3 39.1

Male 38.3 22.0 0.4 15.9 61.7Female 39.3 22.8 10.4 6.1 60.7

1998 Total 43.0 28.9 4.7 9.4 57.0 19.0 38.0Male 43.3 27.8 0.2 15.3 56.7Female 46.6 28.4 11.4 6.8 53.4

Source: ILO estimates, based on country household surveys and other official sources (revised series).a Includes own-account workers (other than professional and technical workers) and unpaid family workers.b Employed in establishments of up to five workers.c Enterprises with six or more workers.d Metropolitan Lima.e Montevideo.

the situation in Latin America in the recent past. Nineout of every ten new jobs created in the 1990s were inservices, but 70% of these were in low-productivityservices, chiefly personal, retail trade and transporta-tion services in the informal sector. Under these cir-cumstances, the shift to services means a decline inemployment quality.

The third major change in the employment struc-ture in the 1990s was the shift from formal to informalemployment. As was mentioned earlier, the limited jobcreation capacity of the formal economy, both publicand private, left increasing numbers of people with noalternative but to find or create their own occupationsin the informal sector; in the absence of insurance, un-

C E P A L R E V I E W 7 2 • D E C E M B E R 2 0 0 016

SOCIAL STRATIF ICATION UNDER TENSION IN A GLOBALIZED ERA • EMIL IO KLEIN AND VICTOR TOKMAN

employment is a luxury that very few can afford. Slowand erratic growth, and the shedding of labour by thepublic sector during adjustment, conspired against thecreation of jobs in modern activities.

As a result, the proportion of the workforce ininformal employment expanded from 44% to 48%between 1990 and 1998. This includes own-accountwork, unpaid work in family businesses, domestic ser-vice and microenterprise (less than 5 employees). Onlyin Argentina, Chile and Honduras did informal employ-ment not expand as a share of the total, while in theremaining countries informal employment grew twiceas fast as total non-agricultural employment.

In the region as a whole, 61 out of every 100 jobscreated in the 1990s were informal. As was mentionedearlier, the great majority of new jobs in services wereinformal; furthermore, the most dynamic componentof informal employment growth has been work inmicroenterprises. Of every 10 new informal jobs, morethan three were contributed by microenterprises (figure 1).This could suggest a positive change within informalemployment, since microenterprises are more highlyorganized than most informal activities and averageincomes from microenterprises are higher than thoseof the rest of the informal sector, although not as highas those of the formal sector. Average incomes in

microenterprises are about 90% of average incomes inmodern activities generally, but only 55% of averageincomes in medium-sized and large enterprises.

Nevertheless, microenterprises are increasingly of-fering valid employment options. In 1998, for instance,they accounted for all new jobs created. Further analy-sis is needed, however, since although incomes are better,working conditions, job stability and social protectionare far from being acceptable. Between 65% and 95%of those working in microenterprises do not have awritten contract, and between 65% and 80% are notcovered for health risks or old age. They tend to worklonger hours and are more likely to have accidents atwork. Breaches of basic labour rights (child labour, free-dom of association, collective bargaining and forcedlabour) are also more frequent in establishments of thissize than in larger ones. Of course, insecurity is notsolely a characteristic of small enterprises; it is also tobe found in medium-sized and large firms (ILO, 1998).

The fourth process identified is the loss of job se-curity resulting from increased competition in a moreflexible labour environment. The search for cost reduc-tions and flexibility to allow for improvements in com-petitiveness has led to labour law reforms introducingflexibility at the margins. For new jobs, “non-standard”contracts have been introduced as a less costly and more

FIGURE 1

Latin America (selected countries): Employment trends in the 1990s(Share in employment growth)

Towards the tertiary sector

From goods to servicesGoods

Services

Growth of informal services

Modernservices

Informalservices

Towards the informal sector

From modern to informal

Modern

Informal

Modernization of the informal sector

Microbusinesses

Other informalactivities

17

SOCIAL STRATIF ICATION UNDER TENSION IN A GLOBALIZED ERA • EMILIO KLEIN AND VICTOR TOKMAN

C E P A L R E V I E W 7 2 • D E C E M B E R 2 0 0 0

flexible alternative to the open-ended contracts thatwere once the norm. The resultant increase in flexibil-ity and reduction in labour costs were expected to leadto growth in the number of waged jobs created.

In the 1990s waged employment did indeed in-crease more rapidly than total employment, suggest-ing that the reform produced incentives to hiring. How-ever, the social cost involved was increasing insecurityof employment. The introduction of “non-standard”labour contracts was accompanied by an increase inthe number of workers without any written employ-ment contract at all. It should be noted that neither non-standard contracts nor the lack of any written legal con-tract automatically entail lower labour protection thanstandard contracts. Only the reform in Argentina madeallowance for this reduction in temporary contracts, theexistence of an employment relationship being subjectto proof in the absence of a written contract. However,inspection and control become more difficult with tem-porary contracts. In the case of workers without con-tracts, many are unofficial and work for cash, so thattheir conditions of employment are almost impossibleto check. This development, furthermore, has comeabout in a situation where labour inspection is gener-ally weak, and because it is rigid contracts that are le-gally recognized as standard ones, the reform has meantthat powers of guidance have been diminished.

In 1996, workers without contracts or with “non-standard” contracts accounted for 30% of all workersin Chile, 40% in Argentina and Colombia and 74% inPeru. Most worked in microenterprises: 50% in Chile,65-70% in Argentina and Colombia and 80% in Peru.However, medium-sized and large enterprises recordedthe largest proportion of “non-standard” contracts andsignificant percentages of workers without contracts:6% in Chile, 11% in Peru and 32% in Argentina andColombia. In the case of microenterprises, informalworking and lack of employment security have a cleartendency to overlap, since both are mainly the result ofinability to pay the costs of labour protection. Withlarger enterprises, the number of unregistered workersis an indication that the law is being circumvented(Tokman and Martínez, eds., 1999).

Not only is the proportion of workers potentiallyor actually exposed to insecure employment conditionshigh, but in most countries insecure employment ac-counts for all job growth in the 1990s. Of the four coun-tries analysed, only in Colombia was there an increasein open-ended employment; in Argentina, Chile andPeru there was a fall in the absolute numbers of suchcontracts. The exact nature of the transition from per-

manent to temporary employment differed from coun-try to country. In Argentina, the decline in the numberof open-ended contracts was entirely offset by growthin the number of workers without contracts, mainly inlarger enterprises. In Peru, the decline in open-endedemployment was compensated for in equal proportionsby workers with temporary contracts and workers with-out contracts, mostly in microenterprises. In Chile, mostnew jobs were provided by larger enterprises under tem-porary contracts.

The four processes described resulted in a declinein the quality of labour protection in the 1990s.Privatization, which could have been a positive devel-opment, was not so because of the inadequacy of jobcreation in modern private-sector companies. A shifttowards tertiary employment is also a priori neutral,since good jobs in services could make up for a declinein available manufacturing employment. However, mostof the new jobs in services were of low productivity.Increased informal working and insecure employmentconditions clearly resulted in lower job quality, althoughthis was somewhat offset by the rapid expansion ofemployment in microenterprises.

The changes in the employment structure can bemore clearly identified if looked at from a longer-termperspective. As can be seen in figure 2,2 during the threedecades prior to adjustment (1950-1980) an average of

2 Owing to the nature of the available data, in the case of somecountries the informal sector as defined for the purposes of figure2 includes microbusinesses with up to 10 employees, and its em-ployment share relates to urban employment. The revised series,in which the informal sector includes microbusinesses with up tofive employees and is related to urban employment, does not per-mit of long-term comparison.

FIGURE 2Latin America (selected countries): Sectoralcontribution to job creation, 1950-1996(Number of jobs contributed out of every 10 new jobs)

1950-1980

1980-1990

1990-1996

Micro-business

Own-accountworking

Publicsector

Modernsector

Domesticservices

C E P A L R E V I E W 7 2 • D E C E M B E R 2 0 0 018

SOCIAL STRATIF ICATION UNDER TENSION IN A GLOBALIZED ERA • EMILIO KLEIN AND VICTOR TOKMAN

60% of new jobs in Latin America were created by theformal sectors of the economy, with government ac-counting for 15% and medium-sized and large private-sector companies for 45%. The informal sector con-tributed 40% of new jobs, of which only 10% were inmicroenterprises (ILO, 1996).

A substantial change in the employment structureoccurred during the adjustment decade of the 1980s.The contribution made by employment in modern in-dustries fell to two out of every ten new jobs, this de-cline being most pronounced in modern private-sectorcompanies that had to adjust to a more open economy.The informal sector acted as a buffer: it doubled itscontribution to job creation, mostly in microenterprises,where it more than tripled. The 1990s saw a recoveryin labour absorption in larger private-sector companiesand continuing growth in informal employment.

To sum up, privatization has meant that public-sector employment is no longer contributing to labourabsorption. Larger enterprises, while they have beenrecovering from the adjustment decade, are still wellbelow the pre-adjustment level, and technologicalchange and decentralization of production and employ-ment mean that they are unlikely to be able to return toit. Indeed, business of all sizes account for the same5.5 out of every 10 new jobs as they did in the pre-adjustment period. The difference is that the main con-tributors now are microenterprises (including smallenterprises). This being the case, and informal and in-secure employment still being the norm in the sector,this employment shift has led to a decline in jobquality.

d) Wage trends and differentials

The adjustment process was expected to have two ef-fects on wages. It was predicted that wage levels wouldincrease as productivity grew, while wage differentialsby skill level would narrow as the demand for unskilledlabour increased because of the expansion of tradebased on labour-intensive sectors.

In 1990, both industrial and minimum wage lev-els were lower in real terms than they had been in1980. In both cases, though, there was a recoveryduring the 1990s. This was mainly due to success inreducing inflation, which declined from three digitsto less than 10% on average across Latin America.Latterly, productivity growth also contributed, particu-larly in the industrial sector. Nonetheless, as table 2shows, minimum wages are still substantially lowerthan in 1980.

Wage differentials have behaved in an unexpectedmanner, with the gaps between minimum and indus-trial wages and differences by skill or educational leveltending to widen. Industrial wages grew by 1.4% a yearbetween 1990 and 1997, while minimum wages in-creased by only 0.3%. Across Latin America, incomedifferentials between professional and technical work-ers and those employed in low-productivity sectors in-creased from 40% to 60% on average between 1990and 1994. This was the result of substantial growth inthe real incomes of high-skilled workers in modern ac-tivities and slow increases or even declines in the wagesof unskilled labour in low-productivity sectors. In eightout of ten countries for which data were available, thewage gap by skill level widened (ECLAC, 1997a). Thesame can also be seen when the wages of skilled work-ers are compared with those of blue-collar workers since1988 (IDB, 1998).

As wage gaps in Latin America widened over thisperiod, exactly the opposite trend was being seen inthe South-East Asian countries, despite the fact that in1980 wage gaps in Latin America were already the larg-est in the world. By 1997, the wage gap in LatinAmerica was 1.9 times as high as in developed coun-tries and the South-East Asian countries.

A number of explanations can be put forward forthis unexpected development. The effect of capital lib-eralization on the prices of capital goods could havebrought about an increase in investment and a concomi-tant demand for skilled labour. The expansion of im-ports from countries like China with an even greaterabundance of unskilled labour than Latin America, andcurrency appreciation, which favoured growth in moreskill-intensive non-tradable goods, are other factors(Lustig, 1998).

In addition, studies done on Brazil, Chile and Peru(Meller and Tokman, 1996; Paes de Barros and others,1996 and Saavedra, 1996) suggest that the maturity andcharacteristics of the trade liberalization process influ-ence the evolution of wage differentials. In Chile, wherethe liberalization process was at a more mature stage,large enterprises were able to expand employment af-ter 1984; in Brazil and Peru (two late starters in theprocess), large enterprises reduced employment in orderto raise productivity and competitiveness, while mostlabour absorption took place in small enterprises andmicroenterprises. In Chile demand for skilled labourgrew, while in the other two countries there was a shiftof labour from higher- to lower-productivity enterprisesand sectors, a process that was accompanied by net em-ployment growth in Peru but a net contraction in Brazil.

19

SOCIAL STRATIF ICATION UNDER TENSION IN A GLOBALIZED ERA • EMILIO KLEIN AND VICTOR TOKMAN

C E P A L R E V I E W 7 2 • D E C E M B E R 2 0 0 0

In both cases, however, wages for unskilled labour de-clined, either as a result of this employment shift or be-cause of the introduction of lower levels of labour pro-tection. Workers in microenterprises earn an averageof 30% to 50% less than those in larger establishments(ILO, 1997a), and the figure is still 20% even when per-sonal characteristics are homogenized (IDB, 1998).However, large companies replacing workers on long-term contracts with temporary ones reduce wages bybetween 35% and 40%, and by an additional 15% to30% if no written contract is drawn up (table 4). It ismainly unskilled workers who are switched to employmentcontracts of this type, and this practice has neutralizedany demand effect that may have resulted from tradeliberalization (ILO, 1998).

e) Poverty and equity

Poverty and inequality have increased during the reformprocess. Today, on average, there are more poor peopleand income differences are larger in Latin America thanbefore. The trend has not been a continuous one. Duringthe 1990s, when several countries had already completedthe stabilization and trade liberalization phases, povertyfell in most of the countries for which data are available.Only in Argentina and Venezuela did the level of pov-erty rise, while in Mexico it remained constant. In the13 remaining countries for which there are data, reportedpoverty fell (ECLAC, 1999).

The level of poverty is still higher today than in1980, and there has been no improvement in equity.On the contrary, income concentration has increasedsubstantially since the early 1980s, so that the Ginicoefficient is now at a level similar to that seen in1970 (0.52). This is because the income share of thepoorest quintile has declined while that of the highest

quintile has risen continuously, a rise that was inter-rupted only between 1980 and 1983. The intermediatequintiles, while performing better than the poorest, havestill not recovered the income shares they had at the be-ginning of the 1980s. In fact, of the two countries (Chileand Uruguay) that can show a significant decrease inpoverty, only in Uruguay has equity increased at the sametime.

Income concentration in Latin America has his-torically been the highest in the world. At present, theincome share of the top 5% is double that of the samegroup in industrialized countries, and more than 60%higher than in South-East Asian countries. At the otherextreme, the income share of the poorest 30%, at 7.5%,is the lowest in the world, being just 60% of the equiva-lent level in industrialized and Asian countries (IDB,1998). When a successful performer like Chile is com-pared to the United States, it is found that the incomeshares of the bottom 20% are similar (about 4.5%).However, to find a time when the shares of the upper20% were comparable, we have to go back as far as1929. If the Gini coefficient is calculated for 90% ofthe Latin American population (excluding the upper10%) it is found to average 0.36, which is similar tothe level seen in the United States, while in six of thecountries it is actually lower than in the United States(IDB, 1998). This clearly shows that greater incomeconcentration among the highest groups is a key ex-planatory factor.

Of no less importance is the question of why glo-balization, and the adjustment package that accompa-nied it, did not help to bring Latin American equitylevels closer to those of the rest of the world. Conven-tional wisdom, based on the pioneering studies ofKuznets, would lead one to expect that, after a period

TABLE 4

Argentina, Chile, Colombia and Peru: Insecure employment

Waged workersa Hourly cost of labourb Composition of changes in waged employmentc

On Without Total With Without With Open-ended Temporary Without Total changetemporary contracts temporary contracts open contracts contracts contracts in wagedcontracts contracts -ended employment

contracts

Argentina 12.7 33.0 35.7 3.5 2.8 6.1 -652.7 25.7 726.9 100.0Chile 14.7 15.6 30.3 1.4 1.0 2.1 -89.9 138.9 51.0 100.0Colombia 8.3 31.0 39.3 1.9 1.6 3.3 81.9 13.3 4.8 100.0Peru 32.6 41.1 73.7 1.4 1.1 2.1 -19.3 56.8 62.6 100.0

Source: Tokman and Martínez (eds.) (1999) and ILO (1998).

a As percentages of total waged employment.b In dollars.c As percentages of changes in waged employment between 1990 and 1996.

C E P A L R E V I E W 7 2 • D E C E M B E R 2 0 0 020

SOCIAL STRATIF ICATION UNDER TENSION IN A GLOBALIZED ERA • EMILIO KLEIN AND VICTOR TOKMAN

of increased income concentration in the early stage ofdevelopment, equity would improve. This conventionalwisdom does not seem to hold today, even for devel-oped countries. The trend towards greater equity hasbeen cut short or, at best, suspended. Inequality hasincreased in the United States since the end of the 1960s,while in the United Kingdom it increased from 1979 to1989, and it likewise rose in Sweden after 1988(Atkinson, 1996 and Krugman, 1995). This suggeststhat Latin American countries may be following a uni-versal path as a result of policy homogenization, with-out having passed through the stage of increased eq-uity seen earlier in those countries.

Several factors can help explain why globalizationhas not improved equity in Latin America. They relateto population dynamics, the distribution of opportuni-ties and the workings of labour markets during the ad-justment process.

Rapid population growth has resulted, particularlyin poor households, in larger household size (50% moremembers in the lowest quintile than in the highest),higher dependency rates (almost treble) and lower par-ticipation rates (60%) (ECLAC, 1997a).

Access to opportunities, and particularly to edu-cation, is also unequal. Although the time people spendin education has increased on average (albeit moreslowly than in South-East Asian countries), it tendsto be unequally distributed. There is a high drop-outrate among poor households. While 94% of poor chil-

dren in educationally advanced countries are enrolledin the first year of school, the figure is only 76% inthe less advanced countries. Enrolment rates decreaseto 63% and 32% by the fifth year, and to 15% and 6%by the ninth year. Entry rates are similar for poor chil-dren and children from higher-income families, butthe latter remain at school for longer periods. By thefifth year, the rates are 93% and 83%, while by theninth year they are 58% and 49% (IDB, 1998). Inequal-ity of access is reinforced by higher rates of educa-tion to university level among higher-income fami-lies and by differences in education quality. Academicattainments (in mathematics and science) are on av-erage 50% higher in private schools, which are at-tended only by children from higher-income families,than in State schools, which 90% of the children ofthe poor attend.

A significant proportion of income differences,more than 55%, is explained by labour market out-comes. As argued above, increased unemployment,employment shifts towards less productive, more un-stable jobs and increased wage differentials tend towiden income inequalities since they affect poor house-holds disproportionately. Unemployment rates arehigher in poor households (in Chile the rate for thepoorest quintile was 2.7 times that for the richestquintile in 1996). In addition, job allocation is seg-mented. High-quality, well-paid jobs are largely heldby members of higher-income families, while low-qual-

TABLE 5

Latin America (nine countries): Indicators of employment transformation,informal working and average income growth by income groupa

(Percentages and annual growth rates)

Country Period Employmentb Informal workingc Average incomeof the employedd

Total Low Medium High Total Low Medium High Total Low Medium High

Argentina (1990-96) 0.5 1.0 1.2 -1.3 66 79 77 ... 4.5 3.5 4.2 6.4Brazil (1992-95) 3.5 5.8 2.2 3.5 81 66 85 95 1.3 1.3 1.2 1.5Chile (1990-96) 3.1 3.8 2.7 2.9 29 14 30 42 5.6 4.1 5.8 5.9Colombia (1992-96) 1.8 1.2 1.9 2.6 37 ... 66 22 3.6 2.5 3.3 3.9Costa Rica (1990-95) 4.4 3.7 3.5 7.0 51 70 48 42 1.9 -0.6 1.4 2.7Mexico (1990-95) 6.4 7.8 6.0 5.5 58 87 54 18 -2.1 -3.8 -2.1 0.2Panama (1989-95) 6.8 6.3 7.2 6.8 38 45 35 31 1.4 2.6 0.6 2.2Peru (1991-95) 5.1 6.3 4.2 5.4 69 97 51 32 3.0 2.7 -0.2 3.0Venezuela (1990-96) 2.6 2.3 2.2 3.8 77 100 87 31 -10.3 -11.5 -9.8 -9.1

Source: ILO, on the basis of household surveys in Argentina (Greater Buenos Aires), Brazil (urban area), Chile (urban area), Colombia (10 metropoli-tan areas), Costa Rica (urban area), Mexico (39 cities), Panama (metropolitan area), Peru (metropolitan Lima) and Venezuela (urban area).a Data refer to those employed in urban areas, excluding the agricultural and mining sectors. Workers have been grouped according to

income levels as determined by per capita household income quintiles. The income levels are: low (quintile I + quintile II), medium(quintile III + quintile IV) and high (quintile V). All indicators relate to the period shown for each country.

b Annual rate of employment growth (average for the period shown for each country).c Percentage of new jobs in informal activities during the period shown for each country.d Annual rate of average income growth for those in work, measured in constant prices (average for the period shown for each country).

21

SOCIAL STRATIF ICATION UNDER TENSION IN A GLOBALIZED ERA • EMILIO KLEIN AND VICTOR TOKMAN

C E P A L R E V I E W 7 2 • D E C E M B E R 2 0 0 0

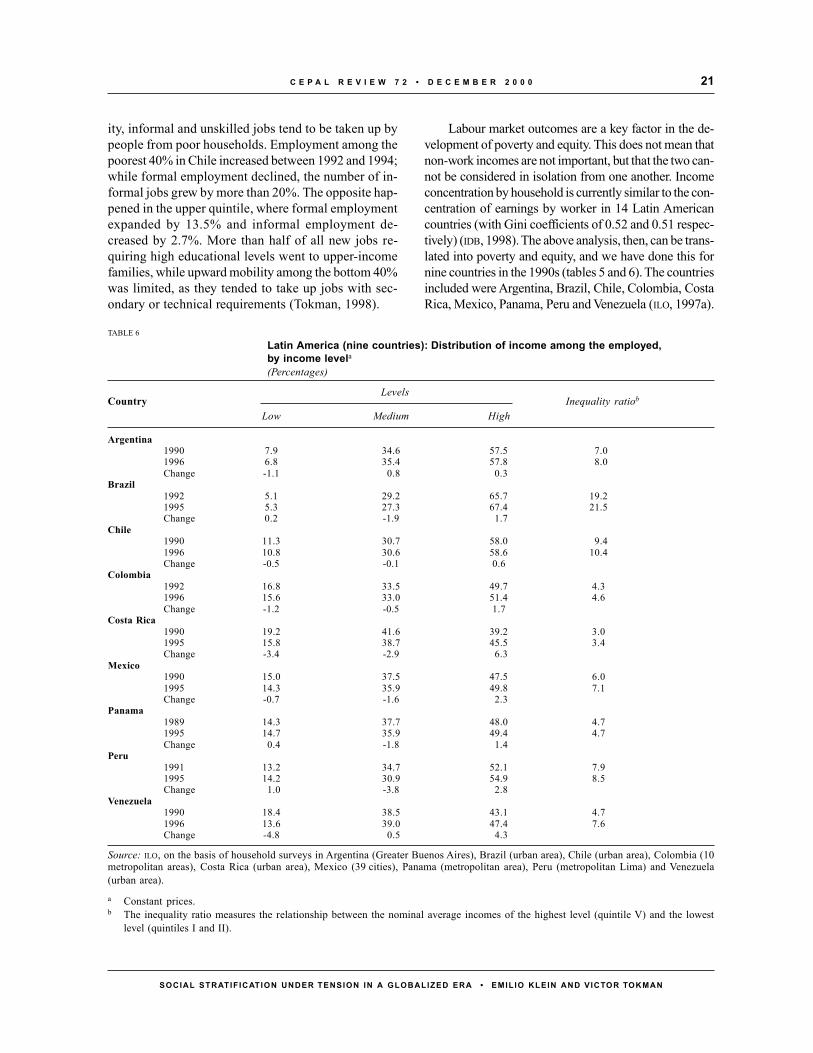

ity, informal and unskilled jobs tend to be taken up bypeople from poor households. Employment among thepoorest 40% in Chile increased between 1992 and 1994;while formal employment declined, the number of in-formal jobs grew by more than 20%. The opposite hap-pened in the upper quintile, where formal employmentexpanded by 13.5% and informal employment de-creased by 2.7%. More than half of all new jobs re-quiring high educational levels went to upper-incomefamilies, while upward mobility among the bottom 40%was limited, as they tended to take up jobs with sec-ondary or technical requirements (Tokman, 1998).

Labour market outcomes are a key factor in the de-velopment of poverty and equity. This does not mean thatnon-work incomes are not important, but that the two can-not be considered in isolation from one another. Incomeconcentration by household is currently similar to the con-centration of earnings by worker in 14 Latin Americancountries (with Gini coefficients of 0.52 and 0.51 respec-tively) (IDB, 1998). The above analysis, then, can be trans-lated into poverty and equity, and we have done this fornine countries in the 1990s (tables 5 and 6). The countriesincluded were Argentina, Brazil, Chile, Colombia, CostaRica, Mexico, Panama, Peru and Venezuela (ILO, 1997a).

TABLE 6

Latin America (nine countries): Distribution of income among the employed,by income levela(Percentages)

CountryLevels

Inequality ratiob

Low Medium High

Argentina1990 7.9 34.6 57.5 7.01996 6.8 35.4 57.8 8.0Change -1.1 0.8 0.3

Brazil1992 5.1 29.2 65.7 19.21995 5.3 27.3 67.4 21.5Change 0.2 -1.9 1.7

Chile1990 11.3 30.7 58.0 9.41996 10.8 30.6 58.6 10.4Change -0.5 -0.1 0.6

Colombia1992 16.8 33.5 49.7 4.31996 15.6 33.0 51.4 4.6Change -1.2 -0.5 1.7

Costa Rica1990 19.2 41.6 39.2 3.01995 15.8 38.7 45.5 3.4Change -3.4 -2.9 6.3

Mexico1990 15.0 37.5 47.5 6.01995 14.3 35.9 49.8 7.1Change -0.7 -1.6 2.3

Panama1989 14.3 37.7 48.0 4.71995 14.7 35.9 49.4 4.7Change 0.4 -1.8 1.4

Peru1991 13.2 34.7 52.1 7.91995 14.2 30.9 54.9 8.5Change 1.0 -3.8 2.8

Venezuela1990 18.4 38.5 43.1 4.71996 13.6 39.0 47.4 7.6Change -4.8 0.5 4.3

Source: ILO, on the basis of household surveys in Argentina (Greater Buenos Aires), Brazil (urban area), Chile (urban area), Colombia (10metropolitan areas), Costa Rica (urban area), Mexico (39 cities), Panama (metropolitan area), Peru (metropolitan Lima) and Venezuela(urban area).

a Constant prices.b The inequality ratio measures the relationship between the nominal average incomes of the highest level (quintile V) and the lowest

level (quintiles I and II).

C E P A L R E V I E W 7 2 • D E C E M B E R 2 0 0 022

SOCIAL STRATIF ICATION UNDER TENSION IN A GLOBALIZED ERA • EMILIO KLEIN AND VICTOR TOKMAN

On average, in the nine countries included, bothemployment and income per worker increased in the1990s, but the distribution of income favoured the up-per 20% of families. Employment grew fastest in poorhouseholds, followed by households in the upper 20%of income. Middle-income groups benefited the least(figure 3). Average income, however, grew most rap-idly in the higher income group, less rapidly in themiddle and most slowly among poor households. Thisis a consequence of segmented access to jobs by dif-ferent income groups. The poor, lacking in human capi-tal, tend to get access to informal jobs, while higher-income families tend to take up better jobs. About 70out of every 100 new jobs taken up by the poorest 40%were informal, while in the case of the middle 40% theratio was 52 out of every 100 new jobs. As a result,income concentration, as measured by the income dif-ference between the top 20% and the bottom 40%, in-creased in all the countries considered. Both the poorand the intermediate groups saw their share of totalincome diminish, the upper 20% being the only gain-ers. It seems likely, however, that relative poverty de-creased. Growth in employment and in earnings perworker, plus an increase in the number of family mem-bers at work, resulted in higher incomes for the poorand lower poverty in most countries during this period,the exceptions being Mexico and Venezuela.

The situation is fairly homogeneous across all thecountries. Incomes per worker grew fastest in theupper-income group in all the nine countries consid-ered, and employment did so in six of them. The situa-tion as regards developments in the poor and middlegroups is more diverse. In most countries, employmentgrew more rapidly for the poorest 40% than for themiddle 40%. However, income per worker grew fasterfor the middle-income group than for the low-incomegroup in six of the nine countries studied. As notedearlier, this was the result of differentiated access tojobs. Income differentials between the top 20% and thebottom 40% increased in all cases, with the cost beingborne by the poor and middle groups. In half thecountries the poor lost more ground than the middlegroup, while in the remainder the reverse was true.

FIGURE 3

Latin America (selected countries): Employmentand income growth by income level, 1990-1996(Percentages)

EmploymentAnnual growth rates

Low Medium HighIncome levels

Modern sector Informal sector

0123456

Average real incomeAnnual growth rates

01122

0

10

20

30

40

50

60

Low Medium High

1990 1996

Low Medium HighIncome levels

Low Medium High

Income distribution among those in work

Income levels

23

SOCIAL STRATIF ICATION UNDER TENSION IN A GLOBALIZED ERA • EMILIO KLEIN AND VICTOR TOKMAN

C E P A L R E V I E W 7 2 • D E C E M B E R 2 0 0 0

IIIAdjustment, global economies and

social stratification

Both the adjustment process in national economiesand the subsequent integration of these into the in-ternational economy have had a significant impacton the social stratification system. This is becausethat system is mainly based on an occupational struc-ture that has changed to reflect the transformationswrought in the labour market by economic restruc-turing. Some of the changes that have taken place,and the sociological consequences of these, will beanalysed below, with particular attention being paidto four aspects. The first is the relationship betweenthe transformation of public employment and middleclass impoverishment. The second is the wayprivatization generates increased social heterogene-ity, as a result of both involuntary labour mobilityand the growth of outsourcing. The third is the in-fluence of transnationalization on labour relationsystems. Lastly, we shall look at the increased dif-ferentiation emerging in employment growth areas,like microenterprise and agriculture.

1. Public-sector employment and the middle class

The first important issue is the new role of the Stateand its impact on the labour market. This transforma-tion has had two main effects. In the first instance, public-sector employment has declined in virtually all thecountries of the region. On average, public-sector em-ployment has decreased from 16% of the economicallyactive population at the beginning of the 1980s to 13%today, a fall of almost 20%. This average masks par-ticularly steep drops in some countries. For example,between 1990 and 1997 public-sector employment de-creased by 32% in Argentina, 33% in Bolivia, 22% inCosta Rica and 28% in Panama. This process has had alarge influence on social stratification in Latin America.It is a well documented fact that the origins and devel-opment of the middle class in Latin America wereclosely associated with the role of the State in promot-ing social and economic development during this cen-tury. In some countries this process began in the earlydecades of the century, in others it took place after theSecond World War, and in others again it is still going

on, but it is a feature of the entire region. This roleencompassed the creation of public employment andthe hiring of administrative staff to implement the de-velopment policies of the State, including health, edu-cation, public works and housing. The State was in-volved in creating employment in public enterprises ofall kinds, but essentially in those sectors deemed to beof national strategic importance (utilities, key naturalresources and basic industries). One illustration of theimportance of public-sector employment to the devel-opment of the middle class is the observation(Echeverría, 1985) that, in the 1970s, 60% of all LatinAmerican professionals were civil servants.

The occupational status of civil servants who havelost their jobs as a result of the decline in public-sectoremployment is unclear, and probably varies betweenand within countries. In some instances former civilservants have been eligible to receive compensationpayments, with which they have been able to start theirown businesses, usually as independent contractors oras micro-entrepreneurs. In many of these cases theirposition may have improved. In other cases, these re-dundancies have led to downward mobility. The fact isthat, in some countries, people discharged from the civilservice and public-sector enterprises have experiencedimpoverishment and loss of status, especially those whowere not professionals and whose status was based noton their educational attainments but on the occupationalpositions they held.

Again, those who have remained in public employ-ment have also lost status. With the economic adjust-ment measures that have been taken, the importance ofState administration has been reduced. At the same time,the prevailing ideological standpoint plays down therole of the State in society, and public functions do nothave the same prestige as before. One indication of thisis the reduced remuneration now given to civil servants;during the 1980s, the salaries of public employees fellby an average of 30% (ILO, 1992).

Of course, civil servants still enjoy considerableemployment stability, coupled with a certain amountof social protection and safety nets that, even thoughthey are far from satisfactory, provide some security

C E P A L R E V I E W 7 2 • D E C E M B E R 2 0 0 024

SOCIAL STRATIF ICATION UNDER TENSION IN A GLOBALIZED ERA • EMILIO KLEIN AND VICTOR TOKMAN

from the most pronounced of the negative trends oper-ating in today’s labour market. Furthermore, not all theremaining civil servants have seen their position worsen.One group, albeit small, have improved their incomesand status because they have been given increased re-sponsibilities and because demand from the privatesector for their type of specialization is high. This isparticularly true of those working for essential institu-tions in the new economic system, such as those incharge of overseeing and collecting tax revenues orcustoms duties. It is also true of those with a regulatoryrole in different areas of the financial system such asbanking, insurance and stock markets, and in the insti-tutions created to regulate privatized social securityactivities and utilities. As a result, wage and status dif-ferentials have widened in what used to be a very ho-mogeneous sector. The increasingly heterogeneouscharacter of the sector is not necessarily a negative fea-ture. Indeed, it may lead to greater economic efficiencyin the public sector if incentives related to labour pro-ductivity are introduced, as in fact is happening in ar-eas like education and health. Furthermore, if a highlyskilled labour force can be retained in the civil serviceby keeping wages and working conditions competitivewith the private sector, then the quality of the productwill improve. Creating opportunities for social mobil-ity and higher status for some of those working in thepublic sector by allowing wage differentials to increasecan result in improvements to the overall performanceof the sector.

2. Social heterogeneity and privatization ofpublic enterprises

The second feature of the changed role of the State isthe privatization of public-sector enterprises that hastaken place throughout Latin America. Privatization hashad a major impact on the way the labour market works,particularly where certain of its institutional character-istics are concerned. Labour market flexibility has beenachieved by various means. The first is greater scopeto dismiss workers. In almost all public enterprises thathave been privatized, a proportion of the labour forcehas been made redundant, the result in the first instancebeing an increase in open unemployment. This process,of course, is similar to the one seen in the private sec-tor. Some of these workers have not been able to findstable work and have become downwardly mobile, al-ternating between periods of underemployment andunemployment. Others have found employment simi-lar to the work they did for the public-sector enterprises