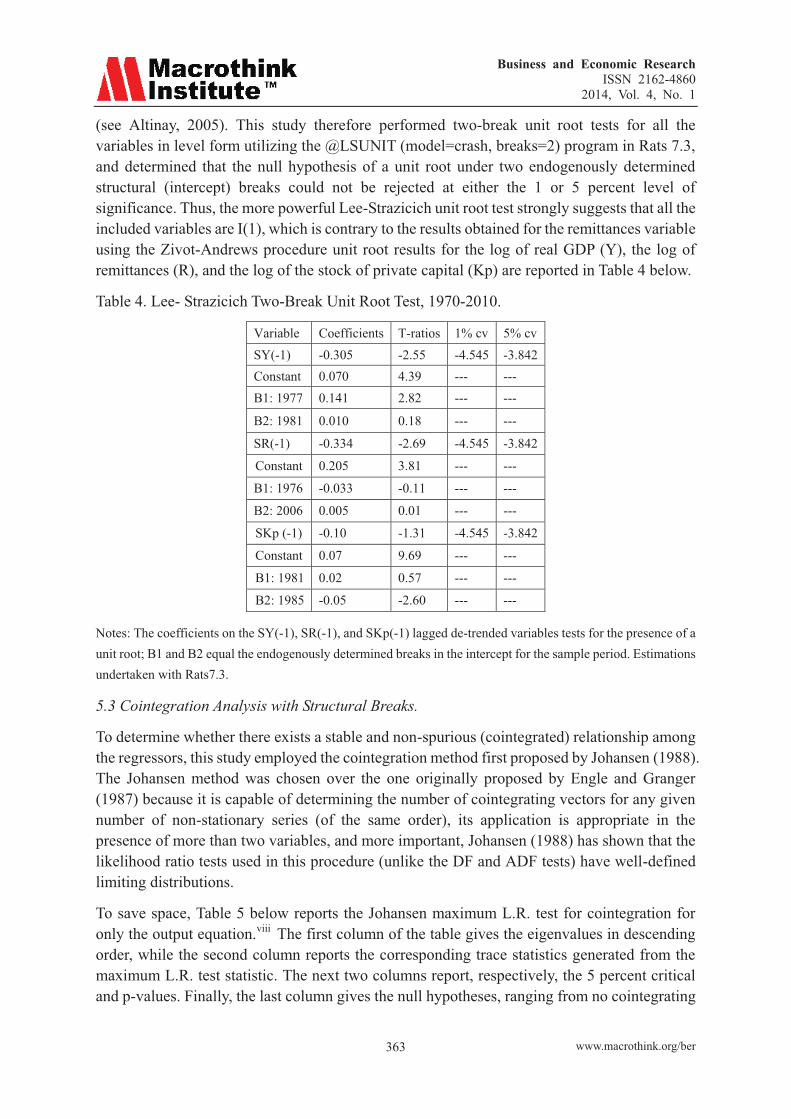

BER: Vol. 4, No.1, June 2014, published

380

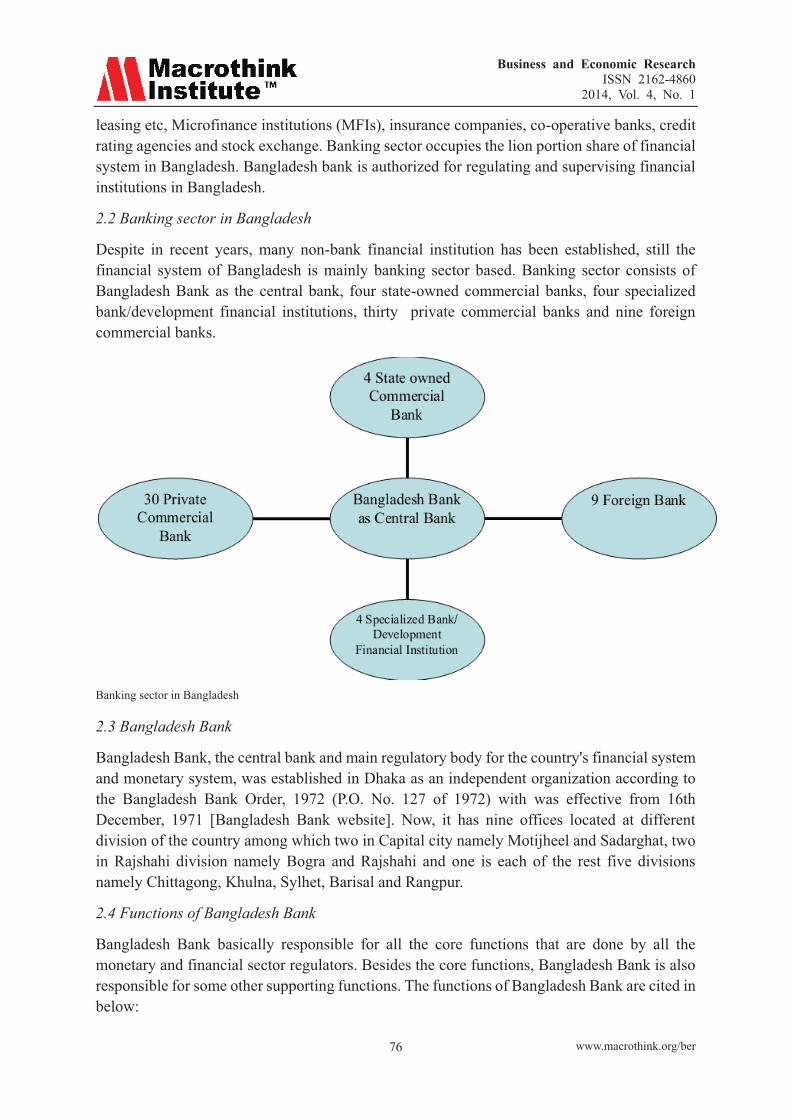

-

Upload

macrothink -

Category

Documents

-

view

0 -

download

0

Transcript of BER: Vol. 4, No.1, June 2014, published

Business and Economic Research ISSN 2162-4860

2014, Vol.4, No. 1

http://ber.macrothink.org

Editorial Team

Editor-in-Chief

Dr. Sahar Bahmani, University of Wisconsin at Parkside, United States

Editorial Assistant

Daisy Young, Macrothink Institute, United States

Associate Editors

Dr Angela Wright, CIT, Ireland

Dr. Manuel Alejandro Cardenete, University Loyola Andalusia, Spain

Dr. Judy Li, Lincoln University, New Zealand

Editorial Board

Ajmer Singh, Kurukshetra University, India

Alunica V. MORARIU, Faculty of Economics and Public Administration, "Stefan cel Mare" University of Suceava, ROMANIA

Angel Espiniella-Menendez, University of Oviedo, Spain

Annamaria Fiore, Regional Innovation and Technology Agency (ARTI), Italy

Antonio Ruiz-Porras, University of Guadalajara, CUCEA, Mexico

Dr. Armin J. Kammel, Danube University Krems, Austria

Bilal Khalaf Sakarneh, Isra University, Jordan

Bratu (Simionescu) Mihaela, Faculty of Cybernetics, Statistics and Economic Informatics, Romania

Cosimo Magazzino, Roma Tre University/LUSPIO University, Italy

Prof Dr Eddie John Fisher, Universidad de Oriente, Santiago de Cuba, Cuba Univerzita Palackeho, Olomouc, Czech Republic, United Kingdom

Dr. Ewa J. Kleczyk, TargetRx, Inc, United States

Eyup Dogan, Clemson University, United States

Business and Economic Research ISSN 2162-4860

2014, Vol.4, No. 1

http://ber.macrothink.org

Fahmi Shaaban Fararah, Malaysia

Frantisek Svoboda, Masaryk University, Czech Republic

Grigorios L Kyriakopoulos, National Technical University of Athens (NTUA), Greece

Hazem Ali Marashdeh, Alhosn University, Jordan

Associate Professor Hengky Sumisto Halim, Universiti Utara Malaysia, Malaysia

Dr Mohd Rizal Muwazir, University of Malaya, Malaysia

Dr. Mohammad Nurul Huda Mazumder, Multimedia University, Malaysia

Mohammad Reza Noruzi, Tarbiat Modarres University, Policy Making in Public Sector Management, Iran

DR Motsomi Marobela, Department of Management, University of Botswana, Botswana

Dr Olubukunola Ranti Uwuigbe, Dept of Accounting, School of Business, Covenant University, Nigeria

Dr. Piotr Siemiątkowski, Nicolaus Copernicus University, Poland

Professor Pacha Malyadri, Principal Government Degree College, Osmania University INDIA, India

Dr. Ramil Maano Perez, Eastern Visayas State University, Philippines

Dr. Said Jaouadi, College of business and administration, Jazan University, Saudi Arabia

Mr. Sandip Sarker, MBA candidate, Management & Business Administration School, Khulna University, Bangladesh

Dr Santosh Banadahally Manjegowda, Chinmayi Research and Consulting, India

Prof. Shyamkumar D. Kalpande, MET's Institute of Engineering, BKC- Nashik, Pune University, India

Dr. Socrates Ogalesco Ballais, Eastern Visayas State University, Philippines

Dr Uwalomwa Uwuigbe, Dept of Accounting, Covenant University

Business and Economic Research ISSN 2162-4860

2014, Vol. 4, No. 1

http://ber.macrothink.org I

Contents

Strategy and Structure: A Learning Perspective and Analysis

Eric W. Ford, Rebecca Wells, Terrie C. Reeves 1-13

A Quantitative and Theoretical Analysis of Ghana’s Internal Migration, Economic Growth and poverty Reduction: A Disaggregated Approach, from 1980 to 2012*

Nicholas Awuse, Patrick Tandoh Offin 14-22

What factors Influence Internal migration and Wage Growth? an Empirical Analysis of Private Formal Sector in Bolgatanga-Ghana

Nicholas Awuse, Patrick Tandoh Offin 23-31

Assessment of Internal Migration Policies in Developing Countries: Evidence from Tanzania

Robert Ebihart Msigwa, Kembo M. Bwana 32-47

The Business Competitiveness of Thailand in the ASEAN Region

Abdullah Kaid Al-Swidi, Arfan Shahzad 48-69

Performance Evaluation of the Banking Sector in Bangladesh: A Comparative Analysis

Md. Ariful Islam, Mahmudul Hasan Siddiqui, Kh. Fahim Hossain, Luthful Karim 70-107

Convertibility of Capital Account: A Comparative Analysis

Md. Ariful Islam, Md. Rayhan Islam, Mahmudul Hasan Siddiqui, Luthful Karim 108-132

Analysis of Quality Leadership in Reviving Economies and Politics in Muslim Countries

Mahfuzur Rahman, Md. Arphan Ali, Hasanul Banna, Md. Saifur Rahman 133-146

Personal Attributes and Motivation of Female Micro-Entrepreneurs in Ghana: A Case of Fishmongers in Central Region

CHRISTINA BOATENG 147-160

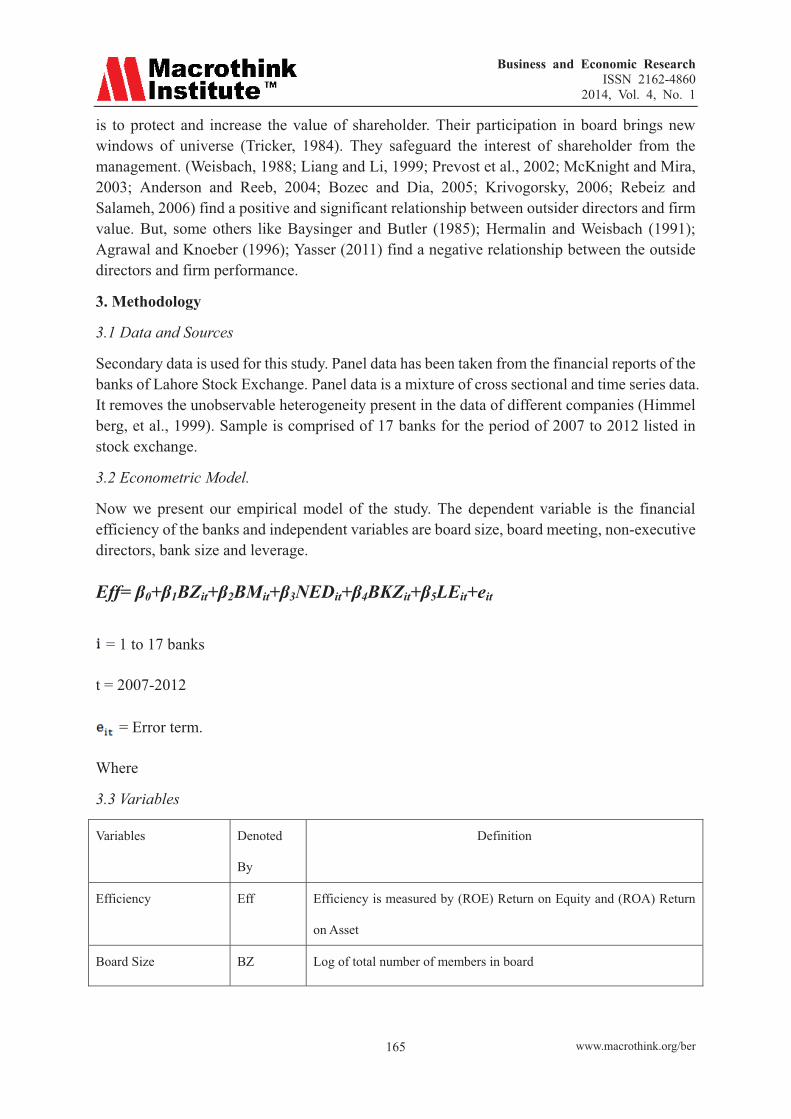

Theory and Empirical Evidence on Corporate Governance from Banking Sector of Pakistan

Waqas Tariq, Imran Ali, Muhammad Ibrahim, Muhammad Asim, Naeem Ur Rehman 161-172

Globalization to a Developing Economy: a Pain or a Gain

Roseline Oluwatoyin Oluitan 173-187

The Theory of Justice and Profit Maximization

Gennady Bilych 188-210

Enhancing International Performance of Exporting Firms through E-Business Integration

Mehmet Ali Ekemen, Pelin Bayram 211-229

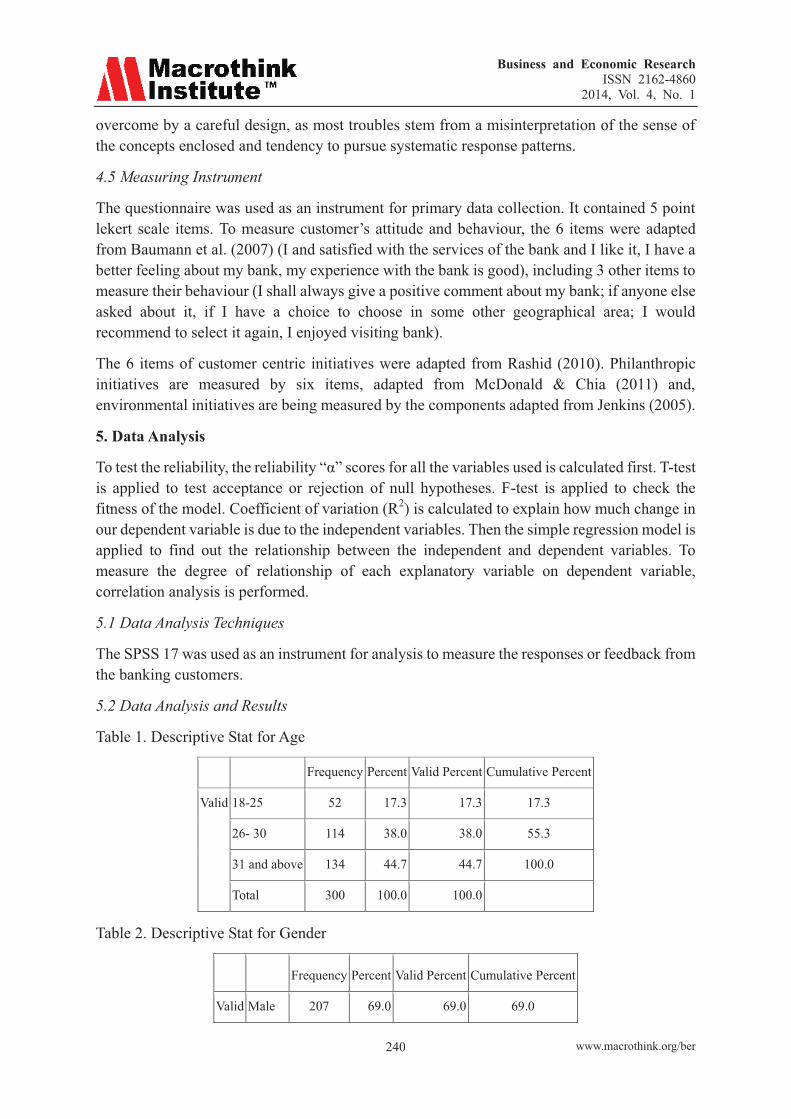

Do Corporate Social Responsibility Initiatives Favorable for Banks? Customer’s Perceptions

Shahbaz Khan, Nida Baig, Aon Waqas Awan, Muhammad Imdad Ullah 230-247

The Impact of Economic Crisis in Greece: Key Facts and an Overview of the Banking Sector

Fotios V. Mitsakis 248-265

Cultural Awareness, a Form of Risk Management in International Business: Case Study of China

Fadun Solomon Olajide 266-288

Business and Economic Research ISSN 2162-4860

2014, Vol. 4, No. 1

http://ber.macrothink.org II

Welfare Effects of Social Cash Transfers in Chipata and Kazungula Districts of Zambia

Gelson Tembo, Bernadette Chimai, Nicholas Freeland, Brian P. Mulenga 289-298

Effectiveness of Loan Portfolio Management in Rural SACCOS: Evidence from Tanzania

Joseph John Magali 299-318

Factors that Determines the Success of Business Demon Value Added Management

Albert Irawan 319-350

Remittances and Economic Growth in Mexico: An Empirical Study with Structural Breaks, 1970-2010

Miguel D. Ramirez 351-373

Reviewer Acknowledgements

Daisy Young 374

Business and Economic Research ISSN 2162-4860

2014, Vol. 4, No. 1

1

Strategy and Structure: A Learning Perspective and

Analysis

Eric W. Ford, Ph.D., MPH (Corresponding Author)

Chief Science Officer

Complex Task Assessment Solutions and Information Technology, LLC

& Pedagogue, University of North Carolina Greensboro

12 Winterberry Ct. Greensboro, NC 27455; USA

Tel: 806-787-3267 E-mail: [email protected]

Rebecca Wells, Ph.D.

Professor, Texas A&M University, College Station, TX

Tel: 979-458-2246 E-mail: [email protected]

Terrie C. Reeves, MBA, Ph.D.

Research Advisor, Digital Frontiers Consulting, Columbus, OH

E-mail: [email protected]

Received: November 23, 2013 Accepted: December 14, 2013

doi:10.5296/ber.v4i1.4602 URL: http://dx.doi.org/10.5296/ber.v4i1.4602

Abstract This paper integrates the strategy and structure constructs using organizational learning theory. Learning theory is refined by arraying strategic and structure constructs along a path dependent, concatenated, continuum that is congruent with the original model of strategy and structure originally proposed by Chandler. The model also enhances methodological rigor by increasing congruence between theory and statistic application. Findings indicate that a single construct of strategy and structure can be employed effectively in management research.

1. Introduction The management literature has not used great precision in defining many common terms-particularly with respect to ‘strategic management’ (Ford, Ginter, & Duncan, 2000; Leontiades, 1982; Ronda-Pupo & Guerras-Martin, 2012). Often, strategic management is considered to have two parts-strategy and structure. Strategy is the activities that surround the determination of “basic long-term goals…and the allocation of resources necessary for carrying out these goals” (Chandler, 1962, p. 13). Structure variables encompass organizational

Business and Economic Research ISSN 2162-4860

2014, Vol. 4, No. 1

2

design characteristics that are critical to pursuing different strategies. Therefore, strategy and structure measures are both integral to a common latent construct. Further, there is empirical evidence they should be treated as a single metric because: 1) there is their relationship is reciprocal or interdependent in nature (Fredrickson, 1986) and 2) although the concepts are intellectually distinct, they behave as a single construct with variables describing each aspect intermingled.

The current study models learning in a path dependent continuum using Miller’s typology of six learning modes and learning theory. Specific variables were drawn from Miller and Friesen’s (1984) previous work on organizational configurations, later reflected in his(1996) learning typology. Item response theory (IRT) is used to analyze data from seventy-seven organizations’ performance on the configuration variables. Both the organizations and the variables are arrayed along a common single dimension that reflects a learning continuum.

The study makes a unique contribution to strategy literature by putting both strategy and structure variables onto a continuous array that indicates a capability path. Capability development is inherently a learning exercise and is consistent with the organizational learning perspective (Schiller, 2014). Therefore, for strategy researchers, the ability to array strategy and structure measures along a single continuum is important as it simplifies many analyses. For practitioners, the results provide a defined path to assess and develop strategic capabilities in a learning fashion.

2. Organizational Learning: Methodical and Emergent Constructs Organizational learning theory has been popular in management research because of the intuitive appeal of the concept that organizations, like people, can use information to change their behavior, and by so doing, may enjoy a longer, more productive existence. The analogies of organizational to individual learning may include the necessity of mastering one set of competencies before progressing to others that build on the foundation skills (Kusunoki, Nonaka, & Nagata, 1998). Thus, learning is posited to be a combinative achievement (Kogut & Zander, 1992), in which organizations master capabilities that are more fundamental before acquiring more complex strategic capacity.. Further, learning is the developmental process of modifying an organization’s “cognitive map” (Friedlander, 1983: 194) using organizational capabilities, thereby expanding the range of potential strategic responses to an ever-changing environment (Fiol, 1996; Huber, 1991).

It is important to note that in order for learning to take place in organizations elements of both strategy and structure are required. First, organizations need structures and processes to consolidate knowledge that would otherwise remain inside the minds of individuals (Argote, 1999). Second, organizations rely upon shared norms, ideally a shared strategic vision, that facilitates the exchange of information and its incorporation into collective strategies. Popper and Lipshitz (2000: 183) describe both structural and cultural factors as organizational learning mechanisms, which they define as “institutionalized structural and procedural arrangements that allow organizations to systematically collect, analyze, store, disseminate, and use information relevant to the performance of the organization and its members.” Sorensen (2002: 73) emphasizes the impact of learned organizational culture on organizational routines, but admits the possibility “that strong-culture firms may be better (or worse) at choosing appropriate strategies” (original parentheses). In contrast, this paper explores the organizational learning associated with successful strategizing. Although both culture and routines may be components of some strategic capabilities, the development of higher-level strategic capacity requires learning far beyond both. Understanding strategic capacity as a learning phenomenon allows us to probe its path dependent evolution based on previous work

Business and Economic Research ISSN 2162-4860

2014, Vol. 4, No. 1

3

in both the organizational strategy and individual development fields.

Strategic capacity in term of organizational learning theory has been characterized as either “methodical” or “emergent” (Miller, 1996). Formalized strategy mechanisms and structures for focusing on specific goals and objectives within existing paradigms are methodical in nature (Steiner, 1997), while incremental approaches to strategy, like emergent learning, rely on more subtle normative considerations (Miller, 1996). Despite the proliferation of conceptual, theoretical, and empirical studies on strategy-environmental fit, debate continues to surround a key question: how do firms learn the strategic capabilities they need to succeed financially in their prevailing environments (Chan, Yung, & Burns, 2000; Morgan & Hunt, 2002)?

2.1 Methodical Learning Modes Methodical learning employs rational analysis of data to make performance-optimizing decisions-an example being TQM. This is the model assumed by scientific management theory (Taylor, 1911) and is akin to “single loop” learning (Argyris & Schon, 1996; Ashby, 1960).

2.1.1 Structural Learning-Consciousness of Analysis and Adaptive Behaviour

The first, most constrained mode of methodical learning Miller (1996: 494) identified was Structural, which he described as being “one of the most pervasive forms of methodical learning.” Routines codify processes, enabling organizations to repeat sequences with a minimum of errors or effort. Such routines also encode values that guide how organizations learn. Thus, structural learning shapes both what organizations absorb and what is filtered out.

Two capabilities from Miller and Friesen’s (1984) previous work best reflect structural learning-Consciousness of Analysis and Adaptation. Consciousness of Analysis is the beginning of all planning and entails reflection on both problems and arrays of potential solutions. In this sense, it is the precursor of all other strategic actions, even incremental adaptations. Adaptive behavior may then be build on analysis by responding appropriately to environmental conditions whose implications have been considered. In turn, appropriate patterns of adaptation may precede the ability to conduct and learn from experiments.

2.1.2 Experimental Learning-Scanning and Control

The second mode of methodical thought and action Miller (1996) described was Experimental, portrayed as learning through problem-driven searches for better solutions. Experimentation is central to Total Quality Improvement, which assumes that organizations increase their efficiencies through a continuous cycle of incremental, data-driven trials (Deming, 1982). Like Structural Learning, Experimental Learning builds on assumptions of rationality and planned change. However, in this mode there is more action as new ideas are provisionally implemented.

The two activities that best illustrate experimental learning are Scanning, or the exploration of the firm’s environment for problems and opportunities, and Control, the mechanisms through which organizations learn about how well their existing routines are working (Miller & Friesen, 1984). Methodical use of Scanning and Control reduces the “cognitive burdens of top managers” (Miller, 1996: 493) and does not require long-term planning in the way more complex forms of organizational learning do. In fact, learning how to experiment on a small scale may be a precondition for predicting future consequences of larger decisions.

2.1.3 Analytic Learning-Futurity of Planning The third and least restrictive mode of methodical learning is Analytic, the deliberate, systematic assessment of current decisions on the future of the organization. Miller (1996)

Business and Economic Research ISSN 2162-4860

2014, Vol. 4, No. 1

4

specifically pointed to the type of strategic, ‘long-range,’ planning promulgated by Allison, Ansoff, and Steiner (1971; 1965; 1997, respectively) as characterizing this mode. According to Steiner, (1997: 14), Futurity is “the essence of strategic planning.” Miller (1996) portrays the Analytic mode as the highest in voluntarism. Another implication is that this mode is the most challenging among the methodical modes, and builds upon Structural and Experimental competencies. Moreover, all three methodical modes set the stage for the more spontaneous, creative emergent strategy development. Such a progression would be consistent with Brews and Hunt’s (1999: 903) findings that “formal specific planning may be a necessary precursor to successful…emergent strategy (Kusunoki et al.).”

2.2 Emergent Learning Modes Emergent or “double loop” learning, in contrast to methodical learning, is more intuitive, unstructured, and global in nature, and entails questioning underlying assumptions (Argyris & Schon, 1996).

2.2.1 Institutional Learning-Technocratization and Innovation

The most constrained emergent mode, Institutional, is a form of organizational learning in which members respond to the normative and symbolic logics of their contexts (DiMaggio & Powell, 1983). Such influences may become more powerful within organizations when higher proportions of members have professional identities and thus a common, profession-based ethos for action. As a critical mass of professional employees coalesces to shape strategic decisions, the process is described as Technocratization (Miller & Friesen, 1984). Technocratization can facilitate Innovation as professionals look to their peers at other organizations for guidance about emerging strategic options.

2.2.2 Interactive Learning-Integration and Risk taking

The second emergent thinking mode, Interactive, occurs when organizations discover new opportunities from the conflicting objectives of their members (Miller, 1996). Two factors indicate Interactive Learning capabilities. The first is Integration of Decisions, which occurs when units across the organization complement and support other units. The second is the Risk Taking necessary to effect larger changes in organizational strategy implied by paradigm shifts. Together, these complementary factors make it possible for organizations to learn from new perspectives, even when they conflict with the existing patterns of voluntary behavior. Further, when Interactive Learning becomes the norm it may facilitate the mode posited to be the most challenging of all, Synthetic Learning.

2.2.3 Synthetic Learning-Communication, Strategic Reappraisal, and Decentralization of Strategy-Making Authority The final, least restrictive mode of emergent thinking, Synthetic, is the intuitive, holistic incorporation of new elements into models for action (Nonaka, 1995). Synthetic Learning is the hardest learning mode because it requires the ability to discern patterns among seemingly unrelated phenomena. Although Miller (1996: 492) asserts that “synthesis is normally the product of a single creative mind,” in fact, the complexity of organizations’ internal and external contexts is arguably too great for even a small group to understand fully. The first element of Synthesis is the Communication flow throughout the organization necessary to transcend individual understanding and develop collective intelligence. At its highest level, this reaches the level of dialogue, a deeply attentive exchange “all but lost to the modern world” (Senge, 1990: 239). Dialogue may take the participants in completely unplanned directions as each voice builds on and responds to previous voices (Bakhtin, 1986). The purpose is to go beyond any one individual so that members can find new, shared meanings,

Business and Economic Research ISSN 2162-4860

2014, Vol. 4, No. 1

5

rather than simply defend their initial positions. Senge (1990: 239) describes the benefit of such dialogue: “collectively, we can be more insightful, more intelligent than we can possibly be individually.”

The second dimension of Synthesis is the Strategic Reappraisal necessary to engage in “double-loop” learning. Unless organizational members are willing to rethink both their strategies and the means of attaining them, they will be limited to improving performance within old paradigms like strong culture organizations who perform routines reliably, but cannot easily change routines (Sorensen, 2002). Synthesis-developing new meanings out of information-requires the ability to rethink old frameworks.

The final dimension posited to indicate Synthetic capacities is Decentralization of Strategy-Making Power. Once relevant information is disseminated throughout the organization and members become accustomed to questioning existing strategies, the highest level of learning can be attained. In decentralized organizations, strategic decision-making power is distributed throughout the organization rather than reserved for top management.

The developmental logic of methodical and emergent strategic capabilities in this framework suggests that a model of organizational learning should have path dependent characteristics. Therefore, the following hypothesis is made about the model’s constructs:

Hypothesis 1: Methodical and emergent strategic capabilities fall along a single, unidimensional pathway.

3. Research Design Concomitant with the development of a new strategy-environment fit model is the need for a method to empirically test its propositions while maintaining congruency between methods and vocabulary (Venkatraman, 1989). In trying to meet this need, this study employed two distinct steps and an appropriate empirical analysis was matched to each step. First was an examination of the developmental pathways of health service organizations’ strategic capacities, using a set of latent trait analysis algorithms called Rasch analysis.

3.1 Sample and Data Health care organizations were studied for three reasons. First, researchers studying the U.S. health system are beginning to call for and apply learning theory in studying both markets and management practices (Committee on Quality of Health Care in America, 2001; Kohn, Corrigan, & Donaldson, 2000). This study answers those calls. Second, because the healthcare industry’s environment is unstable due to rapid technological change, dramatic government interventions, and increasing competition (Gould, 1988), strategies and structures are under significant pressure to learn. Therefore, any learning pathway identified across organizations is indicative of the larger learning paradigm taking place. Finally, Ketchen et al., (1997) found that single industry studies produced greater effect sizes on variables related to strategy.

Study data were obtained from two types of sources: (a) Forms 10-K, prospectuses, and other forms filed with the Securities and Exchange Commission (SEC) and annual reports in the case of for-profit health services organizations, and (b) strategic management cases about health services organizations found in the following textbooks, Case Research Journal for the years 1990 through mid-1995; Harvard Business School 1994-1995 Catalog of Teaching Materials; Preferred Individualized Case (PIC) Catalog; the European Clearinghouse Catalog of cases; the Western Ontario Business School Teaching Materials Catalog; and finally the Darden Graduate School of Business Catalog of cases. All cases contained reference to most of the study’s variables of interest. Organizations to be studied using SEC documents were chosen in

Business and Economic Research ISSN 2162-4860

2014, Vol. 4, No. 1

6

the following manner. Based on the Standard Industrial Classification (SIC) codes for publicly traded health services organizations obtained from a national broker, a list of all other health services organizations with the same SIC codes was compiled. SEC documentation was gathered for those organizations about whom information was available in Standard and Poor’s Corporate and Municipal Ratings, in Moody’s Bond Record, or in Value Line, and whose major source of revenue appeared to be direct patient care. Raters were directed to pay special attention to descriptive sections about the external environment and strategies intended to deal with the environment. Raters looked for organizational responses to competitors, regulations, reimbursement mechanisms, or other external factors, and for internal mechanism that might facilitate responses. They were also instructed to read auditors notes to financial statements for clues about operating system such as new technological or computer systems, quality program, human resource practices. Fifty-seven usable sets of SEC documents were obtained. The others were unsuitable because the major source of revenue was not patient care related or data on all variables was unavailable. The final sample consisted of 20 cases and 57 sets of SEC documentation.

3.2 Measures and Scoring Three sets of measures were developed to test the hypothesized relationship. First, a single measure of each organization’s position on the strategic capacity continuum was calculated. Using variables operationalized in previous research (Miller & Friesen, 1984), the strategic capacity measures used herein are based on the methodical and emergent organizational learning paradigms suggested by Miller (1996). Variables that failed to differentiate organizations in previous research or that did not have a direct counterpart in the learning paradigm descriptions were eliminated (See Appendix 1 for variable descriptions). In addition, the cues to scorers were modified for this study to reflect the health service context.

The variables were scored on a Likert scale with values ranging from one to seven. A value of one indicated that an organization lacked, or possessed very low amounts of a characteristic and a value of seven indicated that the organization had a significant amount of the capability. After extensive training sessions, multiple raters scored each organization’s documents. All raters rated 43 percent of organizations studied. On 99.4 percent of those organizations’ scores, evaluations varied by less than 2 between raters. Given this high level of agreement, scores were recorded as the average of the raters’ scores in the few instances when the raters’ scores differed.

Using a Rasch algorithm, a strategic capacity measure that Venkatraman (1989) would classify as using the ‘fit as profile deviation’ (p. 433) approach was developed. Here, differing levels of strategic capacity have been hypothesized as better suited for particular environmental conditions when better organizational performance is to be expected. Further, the concept of fit as profile deviation suggests that the degree of adherence to such a one-dimensional profile is related positively to performance. However, this study extended this analytical approach by using ipsative-scaling techniques to measure strategic capacity constructs. Ipsative scales’ (similar to Guttman scaling) major characteristics are as follows: they are hierarchically cumulative (i.e., firms posses all of the strategic capabilities scoring at and below their score); they can detect small shifts in value; the scores are ordinal; they measure one dimension; and items are ordered in difficulty or complexity so that getting to one item implies success with the preceding item. In demanding an ordered array of items, ipsative scales are more rigorous than mere point estimates of associations because they define the entire range of ability not merely one level. As Brews and Hunt (1999, p. 890) describe, “These more sophisticated methodologies (see for example Fredrickson, 1984; Wood & LaForge, 1979, 1981) have in

Business and Economic Research ISSN 2162-4860

2014, Vol. 4, No. 1

7

general produced stronger planning/performance relationships than earlier work (Priem, Rasheed, & Kotulic, 1995).” Further, by profiling all of the organizations together, rather than using a hold-out sample of successful organizations as Venktraman and Prescott (1990) did, the measure has more generalizability. The derived strategic capacity measure for each organization was then incorporated into interaction variables used in the second phase of the analyses related to hypotheses three through eight (a more detailed description of the algorithm is provided in the Analytic Approaches section).

3.3 Analytic Approaches The analytic approaches used in this study contributed to theoretical and statistical correspondence in two ways. First, using expert raters to score variables on a Likert-like scale helps to overcome possible unequal scalar qualities among the concepts being rated. Second, Latent Trait Analysis (LTA) including Rasch models, is a family of procedures used to estimate a measure’s dimensionality and the interval of ordinal-scaled items along a single dimension. First developed in the early 1960s for use in education and psychology, Rasch analysis models have been used to infer a person’s position along a series of hierarchical items.

Rasch analysis can also identify items, such as strategy and structure measures, that are redundant and those that do not fit the model. In order to create an interval scale, Rasch analysis estimates both abilities (an organization’s level of successful performance on a variable or capability) and item difficulty (level of resistance to successful performance) for a set of variables. The basic assumption is that the probability of an individual’s or organization’s success or failure on a particular item depends on both ability and the difficulty of the item.

The Rasch algorithm estimates item difficulty on a logistic scale in ‘logits’ (the log odds transformation of the probability of a correct response) and creates an interval scale. This technique can also identify characteristics or strategic capabilities that are redundant or that do not fit the presumed organizational learning pathway. The standardized infit (a weighted fit statistic) and outfit (an outlier sensitive fit statistic) statistics identify redundant items, noise, and outliers. Rasch users “routinely pay more attention to infit scores than outfit scores” (Bond & Fox, 2001, p. 43). Items with very low infit scores may be redundant. Items with unusually high infit scores indicate an unusual response pattern across items. For example, organizations with very high strategic capacity may lack an “easy,” lower level capability. Such items can either be removed, if they are captured by another measure, or be retained if they are theoretically essential.

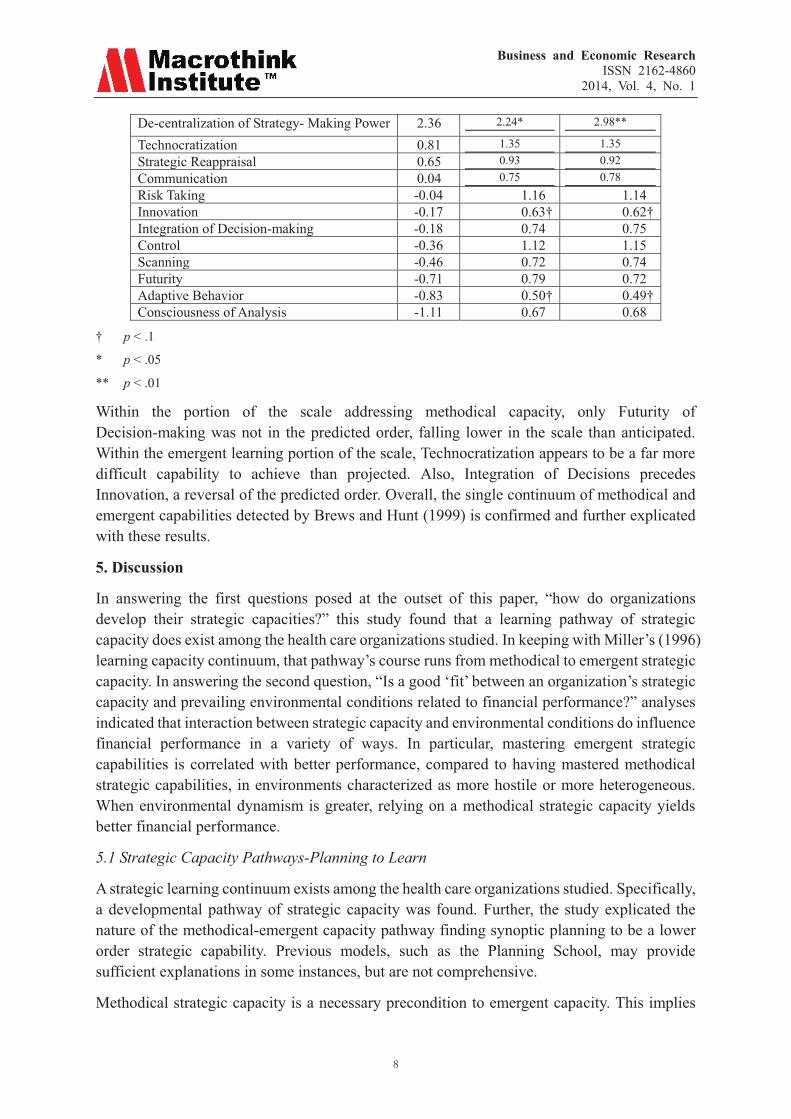

4. Results Results of the Rasch procedure are presented in Table 1. The twelve-item model had overall infit and outfit scores of 0.96 (p < 0.1) and 1.03 (p < 0.3) respectively with an item reliability of 0.71 (Cronbach’s alpha). These measures indicate a good model fit. This finding supports hypothesis 1 that Miller’s (1996) learning typology can be used to map strategic capacities along a single, unidemensional scale. Three of the items, Decentralization of Strategy-making, Innovation, and Adaptability / Proactivity were a significant distance from the central axis of the developmental pathway. Examining the points along the scale within each item, Decentralization of Strategy-making would have a better fit if it were reverse scored to measure centralization, thus putting it in the lower portion of the capacity scale. The other 11 strategic capacity measures were arrayed correctly, although two did not fit the model particularly well.

Table 1. Developmental Pathway Model of Strategic Management Dimensions and Diagnostics

Item Measure Infit Outfit

Business and Economic Research ISSN 2162-4860

2014, Vol. 4, No. 1

8

De-centralization of Strategy- Making Power 2.36 2.24* 2.98**

Technocratization 0.81 1.35 1.35 Strategic Reappraisal 0.65 0.93 0.92 Communication 0.04 0.75 0.78 Risk Taking -0.04 1.16 1.14 Innovation -0.17 0.63† 0.62† Integration of Decision-making -0.18 0.74 0.75 Control -0.36 1.12 1.15 Scanning -0.46 0.72 0.74 Futurity -0.71 0.79 0.72 Adaptive Behavior -0.83 0.50† 0.49† Consciousness of Analysis -1.11 0.67 0.68

† p < .1

* p < .05

** p < .01

Within the portion of the scale addressing methodical capacity, only Futurity of Decision-making was not in the predicted order, falling lower in the scale than anticipated. Within the emergent learning portion of the scale, Technocratization appears to be a far more difficult capability to achieve than projected. Also, Integration of Decisions precedes Innovation, a reversal of the predicted order. Overall, the single continuum of methodical and emergent capabilities detected by Brews and Hunt (1999) is confirmed and further explicated with these results.

5. Discussion

In answering the first questions posed at the outset of this paper, “how do organizations develop their strategic capacities?” this study found that a learning pathway of strategic capacity does exist among the health care organizations studied. In keeping with Miller’s (1996) learning capacity continuum, that pathway’s course runs from methodical to emergent strategic capacity. In answering the second question, “Is a good ‘fit’ between an organization’s strategic capacity and prevailing environmental conditions related to financial performance?” analyses indicated that interaction between strategic capacity and environmental conditions do influence financial performance in a variety of ways. In particular, mastering emergent strategic capabilities is correlated with better performance, compared to having mastered methodical strategic capabilities, in environments characterized as more hostile or more heterogeneous. When environmental dynamism is greater, relying on a methodical strategic capacity yields better financial performance.

5.1 Strategic Capacity Pathways-Planning to Learn

A strategic learning continuum exists among the health care organizations studied. Specifically, a developmental pathway of strategic capacity was found. Further, the study explicated the nature of the methodical-emergent capacity pathway finding synoptic planning to be a lower order strategic capability. Previous models, such as the Planning School, may provide sufficient explanations in some instances, but are not comprehensive.

Methodical strategic capacity is a necessary precondition to emergent capacity. This implies

Business and Economic Research ISSN 2162-4860

2013, Vol. 3, No. 2

www.macrothink.org/ber 9

that firms must learn methodical capabilities before they can learn emergent capabilities, and that methodical capacity is the more easily acquired. A further implication is that organizations, having mastered all capabilities, may then be able to draw upon appropriate ones depending upon the situation. However, not every methodical or emergent capability fell as closely along the pathway as anticipated. Decentralization of Strategic Planning, Adaptive Behavior, and Innovation did not fit the model well. One possible explanation for this anomaly relates to a firm’s place in the organizational life cycle. Constructs that are characteristic of entrepreneurial behaviors like these are found in young firms. Firms just starting out may not have had the time to develop methodical skills nor the history to engage in the sensemaking indicative of emergent strategies. Alternatively, it may be that entrepreneurial organizations must develop capacity all along the continuum quickly in order to survive; or perhaps entrepreneurial organizations must develop some strategic capabilities simultaneously with others. Another possible explanation is that these misfit capabilities are characteristics of prospector organizations. While Shortell and Zajac (1990) have shown that not all health services organizations are prospectors, due to rapid changes in the health services sector in recent years, more rapid acquisition of strategic capacities may be required for all health services organizations that survive. Forced into rapid strategic capacity acquisition, health services organizations have haphazardly acquired strategic capabilities, or for prospector firms, a separate pathway may exist that has innovation and adaptive behaviors as key stepping-stones. Nevertheless, even considering these deviations, the pathway described by the Rasch analysis closely matched the hypothesized ordering.

5.2 Limitations

Although the study strongly suggests both a path-dependent continuum of strategic capacity and significant implications of such capacity for financial performance in different environmental conditions, the cross-sectional nature of these data did not capture potential long-term financial performance benefits of adopting either more methodical or more emergent strategies under various environmental conditions. For instance, although greater emergent strategic capacity was negatively associated with financial performance, this begs the question of what the lagged effects might be. Does dynamism generally punish more innovative and organic strategic learning?-or are emergent learners rewarded later for investments that have negative affects now.? Similar issues arise relative to the other environmental dimensions examined. What are the long-term implications of investing in and learning more or fewer emergent capabilities in more and less heterogeneous and hostile environments over the long run? Longitudinal data will be necessary to determine how effects of different strategic learning levels relate to organizational performance over time. In addition, although health service providers constitute a diverse industry, the sample in this study included only direct service providers. There may be differences both in the progression of strategic capacity and its performance implications for firms in other service industries and for manufacturers.

5.3 Areas of Future Research

Based on this study, there appears to be a strong possibility that strategic capacity and environmental conditions interact in a variety of ways that affect financial performance. In

Business and Economic Research ISSN 2162-4860

2013, Vol. 3, No. 2

www.macrothink.org/ber 10

particular, the relationship of environmental dynamism, strategic capacity level, and organizational financial performance. However, using longitudinal data, the dynamic developmental effects of increasing strategic capacity could be examined. This study sets the stage for such future work.

A second avenue for future research is an examination of the relative importance of each of the six modes of strategic capacity in organizational performance under varying environmental conditions. Based on this study, it appears that strategic capacities must be developed in a distinct order. For example, scanning the environment might be less valuable to organizations that have a marginally developed consciousness of analyses capability. It is analogous to being in a conversation where you can hear the other person, but do not speak the language. Equally interesting would be analysis of the importance of the strategic capacity level for different types of organizations: it may be that differences exist among organizations of different ages or of different sizes. Determining those differences would be of great benefit for practitioners.

Finally, this study looked at health care organizations whose major business is in the United States. Health services organizations doing business in other parts of the world may find that strategic capacity must be developed in a different order for better performance, or that a certain capacity interacts with environmental conditions differently. A study of differences between U.S. organizations and organizations from other countries would advance over-all understanding of strategic capacity’s interaction with the environment around the world.

References

Allison, Graham T. (1971). Essence of Decision: Explaining the Cuban Missile Crisis. Boston: Brown Little.

Ansoff, H. Igor. (1965). Corporate Strategy: An Analytic Approach to Business Policy for Growth and Expansion. New York: McGraw-Hill.

Argote, Linda. (1999). Organizational learning: Creating, retaining and transferring knowledge. Boston: Kluwer Academic Publishers.

Argyris, Chris, & Schon, Donald A. (1996). Organizational Learning II. New York: Addison-Wesley Publishing Company.

Arthur, Michael B. (1996). Careers in City Politics: The Case for Urban Democracy. Administrative Science Quarterly, 41(4), 726-728. http://dx.doi.org/10.2307/2393875

Ashby, William Ross. (1960). Design for a brain : The origin of adaptive behavior. New York: Wiley.

Bakhtin, M. M. (1986). Speech Genres and Other Late Essays (V. W. McGee, Trans.). Austin, TX: University of Texas Press.

Bond, Trevor G., & Fox, Christine M. (2001). Applying the Rasch Model: Fundamental Measurement in the Human Sciences. Mahwah, N.J.: Lawrence Erlbaum Associates.

Chan, Joseph W.K., Yung, K.L., & Burns, N.D. (2000). Environment-strategy fit: a study of

Business and Economic Research ISSN 2162-4860

2013, Vol. 3, No. 2

www.macrothink.org/ber 11

Hong Kong manufacturing logistics. Logistics Information Management, 13(5), 286. http://dx.doi.org/10.1108/09576050010378513

Chandler, Alfred D., Jr. (1962). Strategy and structure: Chapters in the history of the American industrial enterprise. Cambridge, MA: MIT Press.

Committee on Quality of Health Care in America. (2001). Crossing the Quality Chasm: A New Health System for the 21st Century. Washington, D.C.: National Academy Press.

Covin, J. G., & Slevin, D. P. (1989). Strategic management of small firms in hostile and benign environments. Strategic Management Journal, 10(1), 75-87. http://dx.doi.org/10.1002/smj.4250100107

Deming, W. Edwards. (1982). Out of the crisis. Cambridge, MA: MIT Center for Advanced Educational Services.

Dess, Gregory G., & Beard, Donald W. (1984). Dimensions of organizational task environments. Administrative Science Quarterly, 29, 52-73. http://dx.doi.org/10.2307/2393080

DiMaggio, Paul J., & Powell, Walter W. (1983). The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields. American Sociology Review, 48(2), 147-160. http://dx.doi.org/10.2307/2095101

Fiegenbaum, A., & Thomas, H. (1990). Strategic groups and performance - the United States insurance industry, 1970-84. Strategic Management Journal, 11(3), 197-215. http://dx.doi.org/10.1002/smj.4250110303

Fiol, C. Marlene. (1996). Consensus, Diversity, and Learning in Organizations. In J. R. Meindl, C. Stubbart & J. F. Porac (Eds.), Cognition within and Between Organizations (pp. 173-206). Thousand Oaks, CA: Sage.

Ford, Eric W., Ginter, Peter, M., & Duncan, W. Jack. (2000). The confusing words of strategy: Improving teaching and research. Paper presented at the Southwest Academy of Management, San Antonio, TX.

Fredrickson, J. W. (1984). The comprehensiveness of strategic decision processes: Extensions, observations, future directions. Academy of Management Journal, 27(3), 445-466. http://dx.doi.org/10.2307/256039

Fredrickson, J. W. (1986). The strategic decision process and organizational structure. Academy of Management Review, 11(2), 280-298.

Friedlander, F. (1983). Patterns of Individual and Organizational Learning. In S. Srivastva (Ed.), The Executive Mind. San Francisco: Jossey-Bass.

Goll, I., & Rasheed, A. M. A. (1997). Rational decision-making and firm performance: The moderating role of environment. Strategic Management Journal, 18(7), 583-591. http://dx.doi.org/10.1002/(SICI)1097-0266(199708)18:7<583::AID-SMJ907>3.0.CO;2-Z

Gould, Stephen J. (1988). Macrodynamic Trends in Health Care: A Distribution and Retailing

Business and Economic Research ISSN 2162-4860

2013, Vol. 3, No. 2

www.macrothink.org/ber 12

Perspective. Health Care Management Review, 13(2), 15.

Huber, George P. (1991). Organizational learning: An examination of thecontributing processes and the literatures. Organizational Science, 2, 88-115. http://dx.doi.org/10.1287/orsc.2.1.88

Kogut, Bruce, & Zander, Udo. (1992). Knowledge of the firm, combinative capabilities, and the replication of technology. Organization Science, 3(3), 383-397. http://dx.doi.org/10.1287/orsc.3.3.383

Kohn, Linda T., Corrigan, Janet M., & Donaldson, Molla S (Eds.). (2000). To Err is Human: Building a Safer Health System. Washington, D.C.: National Academy Press.

Kusunoki, Ken, Nonaka, Ikujiro, & Nagata, Akiya. (1998). Organizational capabilities in product development of Japanese firms: A conceptual framework and empirical findings. Organization Science, 9(6), 699-718. http://dx.doi.org/10.1287/orsc.9.6.699

Leontiades, Milton. (1982). The confusing words of business policy. Academy of Management Review, 7, 45-48.

Miller, Danny, & Friesen, Peter H. (1984). Organizations: A quantum view. Englewood Cliffs, NJ: Prentice-Hall.

Miller, Danny. (1996). A preliminary typology of organizational learning: Synthesizing the literature. Journal of Management, 22(3), 485-505. http://dx.doi.org/10.1287/orsc.9.6.699

Morgan, Robert E, & Hunt, Shelby D. (2002). Determining marketing strategy: A cybernetic systems approach to scenario planning. European Journal of Marketing, 36(4), 450. http://dx.doi.org/10.1108/03090560210417264

Nonaka, Ikujiro. (1995). The knowledge-creating company: How Japanese companies create dynamic of innovation. New York: Oxford University Press.

Popper, M., & Lipshitz, R. (2000). Organizational learning: Mechanisms, culture, and feasibility. Management Learning, 31(2), 181-196. http://dx.doi.org/10.1177/1350507600312003

Priem, Richard L., Rasheed, Abdul M., & Kotulic, A. G. (1995). Rationality in strategic decision processes, environmental dynamism and firm performance. Journal of Management, 21(5), 913-929. http://dx.doi.org/10.1177/014920639502100506

Ronda-Pupo, Guillermo Armando, & Guerras-Martin, Luis Ángel. (2012). Dynamics of the evolution of the strategy concept 1962–2008: a co-word analysis. Strategic Management Journal, 33(2), 162-188. http://dx.doi.org/10.1002/smj.948

Schiller, Stefan. (2014). Financial Information Related to Dynamic Capabilities: The Corporate Innovation Platform. Research in Business and Management, 1(1), 2-27. http://dx.doi.org/10.5296/rbm.v1i1.4496

Senge, Peter M. (1990). The Fifth Discipline: The Art and Practice of the Learning

Business and Economic Research ISSN 2162-4860

2013, Vol. 3, No. 2

www.macrothink.org/ber 13

Organization. New York: Doubleday Currency.

Sorensen, Jesper B. (2002). The strength if corporate culture and the reliability of firm performance. Administrative Science Quarterly, 47, 70-91. http://dx.doi.org/10.2307/3094891

Steiner, George A. (1997). Strategic Planning: What Every Manager Must Know. New York: Free Press.

Taylor, Frederick Winslow. (1911). The principles of scientific management (3rd ed.). New York: Harper and Brothers.

Venkatraman, N. (1989). The concept of fit in strategy research: Toward verbal and statistical correspondence. Academy of Management Review, 14(3), 423-444.

Wood, D. R. Jr., & LaForge, R. L. (1979). The impact of comprehensive planning on financial performance. Academy of Management Journal, 22(3), 516-526. http://dx.doi.org/10.2307/255741

Wood, D. R. Jr., & LaForge, R. L. (1981). Toward the development of a planning scale: An example from the banking industry. Strategic Management Journal, 2(2), 209-216. http://dx.doi.org/10.1002/smj.4250020209

Copyright Disclaimer

Copyright reserved by the author(s).

This article is an open-access article distributed under the terms and conditions of the Creative Commons Attribution license (http://creativecommons.org/licenses/by/3.0/).

Business and Economic Research ISSN 2162-4860

2014, Vol. 4, No. 1

www.macrothink.org/ber 14

A Quantitative and Theoretical Analysis of Ghana’s Internal Migration, Economic Growth and poverty

Reduction: A Disaggregated Approach, from 1980 to 2012*

Nicholas Awuse (Corresponding author)

Bolgatanga Polytechnic

P. O. Box 767, Sumbrungu, Bolgatanga, Ghana

Tel: 233-243-924-839 E-mail: [email protected]

Patrick Tandoh-Offin (PhD)

Ghana Institute of Management and Public Administration (GIMPA)

P. O. Box AH-50, Achimota-Accra, Ghana

Tel: 233-247-450-433 E-mail: [email protected]

Received: October 10, 2013 Accepted: November 1, 2013

doi:10.5296/ber.v4i1.4972 URL: http://dx.doi.org/10.5296/ber.v4i1.4972

Abstract

The study here was meant to examine the consequence of Ghana’s government spending on economic growth, internal migration and poverty reduction in Ghana using a disaggregated approach. It reveals that intensifying government outflow has not yielded any meaningful development in Ghana. Many researches had been conducted on the actual link connecting government expenditure, internal migration, economic growth and poverty reduction. Many of the studies until today have used the aggregate approach which has not yielded the desired results hence there is the need to vary the methodology.

This study made use of the data for the period (1980 - 2012). The findings from the study shows that Government total capital expenses (GTE), total recurrent outflows (GOF), Government cost on education (GCE) and power (POW) on the contrary, impacts negatively on economic growth and was significant. On the other hand, increasing Government spending on transport and communication (GCTC), and health (GDH) leads to an increase in economic

Business and Economic Research ISSN 2162-4860

2014, Vol. 4, No. 1

www.macrothink.org/ber 15

growth. From the results above, the authors advised that there should be public private participation in critical sectors of the Ghanaian economy in the areas of power and transport in order to accelerate the rate of development in Ghana. In addition to this recommendation, government should be more transparent and accountable in her spending.

Keywords: Government expenditure, Economic growth, Poverty reduction, Power, Health, Transport, Communication

1. Introduction

There is a serious argument among scholars around the world about the relationship between government spending, internal migration and its influence on economic growth. Governments over the world have two basic functions namely, protection (security) and provision of certain essential public goods, Nurudeen and Usman (2010). The protection function consists of the maintenance of rule of law and the enforcement of property rights. These have the potential to reduce the risks of criminality; protect life, property, and defend the nation from foreign attacks. The provisions of public goods such as defense, roads, education, health, and power, to mention a few are very important for any nation’s development.

Development specialists are of the view that if government spending on socio-economic and physical infrastructure equally across the country increases, it will encourage economic growth; reduce internal migration, and reduce (add) poverty. A typical example is government expenditure on health and education which are vital, and increases the productivity of labour which raises the growth of national output. In the same vein, expenditure on infrastructure such as roads, communications, power, etc, reduces production costs, increases private sector investment and profitability of firms, thus nurturing economic growth. Low educational attainment is known to be a major factor underlying the exclusion of the poor from the opportunities that come with economic growth ( Awuse et al 2014) Ravallion and Datt, 2003).

On the other hand, a number of experts hold a different view and maintain that mounting government spending supports economic growth and ultimately reduces poverty. As an alternative, they call attention to higher government expenditure may contract the overall performance of the economy. For instance, in an effort to increase expenditure, government may raise taxes and/or borrow and crowds out private investment. If there are superior income taxes, it discourages individuals from working for long hours, applying for promotions in the case of regressive tax or even searching for jobs which have the potential to reduce income and aggregate demand. Nevertheless, more profit tax tends to add to production costs and reduce investment expenditure as well as profitability of firms. In Ghana, government disbursement has continued to rise as a result of massive receipts from production and sales of crude oil, and better demand for public goods like roads, communication, and power, Education, Health and Water. Moreover, there is a need to make available both interior and external safety measures for the people and the nation.

Available figures show that government machinery and total spending have continued to go up in the last three decades. In a similar manner, the total government continuous expenditure shows that expenditure on defense, internal security, education, health, agriculture,

Business and Economic Research ISSN 2162-4860

2014, Vol. 4, No. 1

www.macrothink.org/ber 16

construction, transport and communication increased during the period under review. In addition, the various components of capital expenditure that is, defense, agriculture, transport and communication, education, power, and health also show a rising development between 1980 and 2012.

2. Problem Statement

In Ghana, public outflow has a tremendous role to play in reducing regional inequalities, developing social overheads, establishing infrastructure for economic growth in the form of transport and communication conveniences, education and training, growth of capital goods, industries, research and development, were fundamental (Sinha, 2007). A public cost on infrastructure plays a basic role in this economy. According to Dickey and Fuller (1979), the appliance in which government expenses on public infrastructure was anticipated to affect the efficiency of economic growth and minimize poverty depends largely upon the accurate form and size of total public expenditure billed to economic and social development projects in the economy (Guest, 2003). When communal expenditure was incurred, by itself it may be directed to meticulous investments or to bring about re-allocation of the investible resources in the private sector of the economy.

This effect, therefore, was principally in the nature of rearrangement of resources from less to more desirable lines of investment. A vital way in which public expenditure can speed up the pace of economic growth was by tightening down the difference between social and private marginal productivity of confident investment. At this juncture, public expenditure on social and economic infrastructure like education, health, transport, communication, waste disposal, electricity, water and sanitation can make a payment to the show of the economy and hence reducing poverty and internal migration in Ghana. Murphy (2002) notes that internal migration has made major contributions to development, by accelerating economic growth, building up cities and establishing rural–urban linkages and return flows.

3. Literature Review

According to Laudau (2003), the share of government consumption to GDP reduces economic growth was consistent with the pro-market view that the growth in government constrains overall economic growth. These findings were significant to varying the sample periods, weighing them by population and a mix of both developed and developing countries (104 countries). Also Ram (1986) makes a rigorous attempt to incorporate a theoretical basis for tracing the impacts of government expenditure to growth through the use of production functions specified for both public and private sectors. The data spanned 115 countries to derive broad generalizations for the market economic investigated. It was discovered that government expenditure has significant positive externality effects on growth particular in the less developed countries (LDC) sample, but total government spending had a negative effect on growth. Lin (1994) uses a sample of 62 countries (1960 – 1985) and found that non- productive spending had no effect in growth in the advance countries but a positive impact in LDCs. In Ghana, government expenditure does not necessarily lead to economic growth; reduce internal migration and promote development.

Business and Economic Research ISSN 2162-4860

2014, Vol. 4, No. 1

www.macrothink.org/ber 17

Again, many Ghanaians are still experiencing poverty and more than 50 percent of them cannot make ends meet as defined by the United Nation. More so, poor infrastructure generally in Ghana has contributed partly to the falling down of many industries, thus increasing the rate of unemployment. Apart from the above, macroeconomic indicators have not also perform well over the years. It does well only in theory but in practice, it does reflect in the lives of Ghanaian. Therefore, the primary aim of this study is to explore the consequence of government expenditure on economic growth in Ghana. The study concerns itself with some fundamental questions below.

Firstly, does government expenditure have a significant influence on economic growth, internal migration and poverty reduction in Ghana? Secondly what policy measures must be adopted to improve management of government expenditure? Hence, the following hypotheses were formulated to guide the study.

H01: Government total capital expenditure does not have significant influence on economic growth and poverty reduction in Ghana.

H02: Government total capital expenditure has significant influence on economic growth and poverty reduction in Ghana.

H03: Government expenditure on transport and communication does not have significant influence on economic growth and poverty reduction.

H04: Government expenditure on transport and communication has significant influence on economic growth and poverty reduction.

4. Research Method

This lesson adopts graphic research design. As a result, the investigative tool used was the single equation, concerning the use of the ordinary least squares (OLS) multiple regression techniques. The government expenditure and the agencies work well to determining economic growth and poverty reduction. The model of this study therefore expresses economic growth (GRY) as a function of various levels and components of government expenditure which include Total Capital Expenditure (GTE), Poverty Reduction (PR) as a function of education and health, Total Recurrent Expenditure (GRE), Expenditures on Defense (ED), Agriculture (AGRE), Transport and Communication (ETC), Education (GEED), Power (POW) and Health (GEH). Thus, the growth model and poverty reduction is specified as follows and all the variables are equally well defined for clarity and analytical purposes:

GRY= β0 + β1 GTE + β2 GRE + β3 ED + β4 AGRE + β5 GEED + β6 GEH + β7 GETC +

β8POW + μ

GRY= - 0.745 + 0.004 + 0.030 - 0.767 – 0.052 + 0.112 + 0.121 + 0.420 + 0.056

Economic growth refers to the changes in real GDP. Real GDP in turn is obtained by dividing GDP at current market price by the consumer Price Index (CPI). According to experts, poverty reduction was to have access to essential needs as Education, Health and food, GRE was measured as total recurrent expenditure divided by the CPI. GTE is captured by the total capital

Business and Economic Research ISSN 2162-4860

2014, Vol. 4, No. 1

www.macrothink.org/ber 18

expenditure divided by CPI. AGRE is captured by government expenditure on agriculture divided by CPI. GEH is measured as government expenditure on health divided by CPI. GEED is captured by government expenditure on education divided by CPI. GETC is measured as government expenditure on transport and communication divided by CPI. POW is captured by government expenditure on power divided by CPI. Thus, we assumed the expenditure items to be actual expenditures. Prior estimation of the growth model above, standard econometric tests like stationary test and co-integration test was conducted in order to avoid the generation of spurious regression results.

5. Results and Discussion

In this equation we regressed all the explanatory variables on growth and poverty reduction model. The regression results showed that the explanatory variables jointly account for approximately 55 percentage changes in economic growth. The results showed that only health (GEH) and transport and communication (GETC) were correctly signed in support of the prior expectation, the other explanatory variables were negatively signed against a priori expectation.

The constant term which was the autonomous expenditure, that is government expenditure when all other explanatory variables were fixed was 15.9 percent. The estimation results also show that-total capital expenditure (GET), recurrent expenditure (GRE), expenditures on transport and communication (GETC), education (GEED), and health (GEH), were statistically significant in explaining the changes in economic growth. However, expenditures on defense (ED), power (POW) and agriculture (AGRE) were not significant in explaining economic growth. The Durbin Watson Statistic (2.10) shows the absence of auto correlation. The results also showed that 1 percentage increase in total capital expenditure in the previous two years causes economic growth to decline by 0.004 percentages.

On the other hand, a 1 percentage increase in total recurrent expenditure in the previous one year leads to 0.004 percentage decrease in economic growth. These findings were consistent with the research reported by Laudau (2003), that government expenditure may slowdown economic growth. The misallocation, mismanagement and diversion of public funds may have accounted for the negative impact of total capital and recurrent expenditures by government officials and political appointees. Also, one (1) percent increase on government expenditure on transport and communication in the previous one year results to an increased in economic growth by approximately 0.420 percentage. Thus, higher government expenditure on transport and communication creates an enabling environment for businesses to strive through reduced cost of production. Besides, the estimation shows that a one percentage increase in government expenditure on education in the previous one year causes economic growth to decline by approximately 0.112 percent. This was not surprising because funds meant for the development of the education sector have not been properly utilized and in most cases embezzled, thus precipitating the incessant strike by University Teachers Association of Ghana (UTAG), Polytechnic Teachers Association of Ghana (POTAG), Colleges of Education Teachers Association of Ghana (CETAG), Ghana National Association of Teachers (GNAT). Moreover, the estimated results indicated that a 1 percent increase in expenditure on health in the previous

Business and Economic Research ISSN 2162-4860

2014, Vol. 4, No. 1

www.macrothink.org/ber 19

one year leads to approximately 0.121percent increase in economic growth.

The government expenditure on health improves the health status and productivity of people, thereby promoting economic growth. The regression results also illustrated that a 1percentage change in expenditure on power in the previous year results to approximately 0.56 percentage decreases in economic growth. This is not surprising given the fact that in the last twenty decades before 1999, the power sector lacked gross neglect.

Also the billions of dollars spent between 1990s and 2010 by the administration of Presidents Mobutu Sese Seko of then Zaire, and Sani Abacha and Olusegun Obasanjo of Nigeria could not be accounted for. This has resulted in the poor performance of the power industry and the economy at large given the critical role of the power sector in economic development.

5.1 Data Discussion

Data availability is a major problem confronting African Countries including Ghana. Two major factors account for the scarcity of data on government expenditure and economic growth. The first is the unwillingness of governments to be open about the true cost of their expenditure on the various sectors of their economies. Some governments generally regard this information as an official state secret and are wary of revealing it. For African states, as for many other developing countries, withholding information on defense for example has three main attractions. One is to avoid criticism from within the country about the extent of the resources committed to defense in relation to other sectors, especially health and education. This is particularly true of states whose resources are meager. A second is the belief that making such information available will be tantamount to opening up the defenses of the state to others, especially neighboring countries - that knowledge of a country’s strength will make it vulnerable. The third is that defense, with all the secrecy associated with it, and is a fertile source of corruption for those directly in charge of the portfolio.

It follows that, unless they were compelled to do so or unless there were reasons beyond their control, many African states were not willing to make such information available. The second reason for lack of information in the defense sector was the lack of capacity to report exact expenditure on the military. Over the years this capacity has diminished in many African states because they have lost highly qualified professionals from the government service to the better-paid private sector, including several donor projects.

Other professionals have migrated abroad within the context of the widely reported brain drain, leaving less qualified and usually less competent officers behind. Where highly qualified individuals are still left they are often too few and far between to make any appreciable impact on the budget process. In such states, the political leaders can then exploit this weakness to siphon off resources by diverting significant amounts of state money to defense, knowing full well that they will not be obliged to account for it.

5.1.1 The Reliability of the Data

Not only are expenditure data on defense, power, health and education scarce, but the quality of the data that are available is also very low. The problem of the reliability of the available data

Business and Economic Research ISSN 2162-4860

2014, Vol. 4, No. 1

www.macrothink.org/ber 20

emanates from three factors. The first is the unwillingness of governments to be open about the true cost of their expenditure establishments; in particular, they hide the actual cost of their investment in arms procurement. Such information is regarded as a state secret. The second is the dearth of qualified staff mentioned above, and the third was the reasons for which data are collected and provided.

This study argues that the nature of the reason that motivates a state to provide military expenditure data largely dictates the quality of the data, and hence their reliability. If Ghana Government is compelled by external actors to provide information will be more inclined to give misleading data than one which provides the data as part of routine government work. A large number of African states are now compelled to publish their expenditure, either as a result of demands by donors who provide budget support and want evidence of proper accounting or as a result of strong local demand by critical segments of their societies. Others publish the data purely as part of a routine government accounting procedure, and such data are likely to be of better quality, although reduced state capacity may still take its toll.

Reliability alone does not guarantee the validity of data if valid data are taken to be data that truly capture the whole of a country’s spending. A piece of data may be reliable without being valid. The fact that data emanate from government cannot guarantee their validity, since a government could doctor the data to suit its purposes. The problem of constant changes to the heading under which defense, power, health expenditures are budgeted or reported also arises here. A particular item might be listed in one budget under the ministry of defense or otherwise, in another under a ministry for the health, education and in yet another under the ministry for security. Sometimes the change will amount to no more than a change in nomenclature; at other times it could involve a significant impact on the composition of the budget.

This can greatly affect the validity of data, especially in longitudinal studies. If the composition of data changes repeatedly during the period being studied, a study may not be able to measure adequately what it purports to measure.

Data were derived from secondary sources. Pools of data were extracted from publications of the State of the Ghanaian Economy, Ghana Government Budget and Economic Policy Statement for Various Years, Ghana Statistical Service Yearly Report, The world Economic out Look 2006-2009, ISSER and CEPA annual reports. The sample data contain all the six sectors in which government carried out expenditure. The sample data used cover the period 1980 to 2012; and the sectors covered are six in number namely: defense (ED), agriculture (AGRE), transport and communication (GETC), education (GEED), power (POW) and health (GEH). The Regression Analysis was run by Econometric Stata.

5.1.2 Policy Direction

Facilitating government expenditure and economic growth in Ghana can minimize the level of internal migration and encourage even development in every aspect of Ghana. This will reduce inequalities in resource allocation and views every sector as important contributing to overall development of Ghana. Ghana government can make it a policy for every sector to submit data to the statistical service as a quarterly or monthly requirements, this will make the data more

Business and Economic Research ISSN 2162-4860

2014, Vol. 4, No. 1

www.macrothink.org/ber 21

reliable than to wait for donor agencies to demand data from them before they start generating fake data for them. But managing government expenditure to promote economic growth and reduce internal movement of people to seek for greener pastures will minimize in order to maximise the benefits economic growth while reducing costs and risks requires effective partnerships between governments, civil society, private sector organisations and donors.

6. Conclusion and Recommendations

The study aims at examining the consequence of government spending on economic growth, discouraging internal migration by ensuring even distribution of resources to all the regions and reduces poverty in Ghana using a disaggregated approach. The experimental results revealed that the negative total current expenditure significantly influences economic growth in Ghana. Although, the negative total capital expenditure significantly influences the economic growth in Ghana, yet the impact of government expenditure on transport and communication on economic growth was positive and significant. On these foundations, the following recommendations are proffered:

(1) Government should not play politics with expenditure on public goods just to win cheap popularity.

(2) The capital expenditure of government which spurs economic growth is presently at about 30 percent of total government expenditure, against recurrent expenditure of 0.004 percent. This trend, if reversed quickly would guarantee economic growth and reduce poverty.

(3) Government should keep an eye on the contract awarding process of capital projects closely, to prevent over estimation of implementation cost. This will bring about significant impact of public investment spending on economic growth.

(4) There should be successful channeling of public funds to productive activities, which will have a significant collision on economic growth.

(5) Government utilization spending should be well harmonized by all arms of government to prevent “Crowding out” effect on government investment.

References

Central Bank of Ghana (2007). Annual Report and Statement of Account. December 31, pp.23

Central Bank of Ghana (2008). Annual Report and Statement of Account. December 31, pp. 28

Central Bank of Ghana (2009). Annual Report and Statement of Account. December 31, pp. 35

Deloitte (2010). National Health Insurance Authority: Revenue and Expenditure Account for the Year Ended December 31, 2008, Accra.

Dickey, D. A., & Fuller, W. A. (1979). Distributions of the Estimators for Autoregressive Time Series with a Unit Root, Journal of the American Statistical Association, 74, 427-431.

Ecorys Macro Group (2010). Republic of Ghana Public Expenditure and Financial Accountability 2009. Public Financial Management Performance Assessment Report, Volume

Business and Economic Research ISSN 2162-4860

2014, Vol. 4, No. 1

www.macrothink.org/ber 22

I: Central Government, Accra.

Global Partnership for Education (2010). Mid-Term Evaluation of the EFA Fast Track Initiative, Washington D.C.

Guest, P. (2003). Bridging the Gap: Internal Migration in Asia, Population Council Thailand, paper prepared for the Conference on African Migration in Comparative Perspective, Johannesburg, South Africa, 4-7 June.

International Monetary Fund (2011). Ghana: Financial System Stability Assessment Update, Country Report 11/31, June, Washington D.C.

Laudau D. (2003). Testing Wagner’s Law for Turkey, 1960-2000. Review of Middle East Economics and Finance, 1(12), 129-140.

Lin, W. (1994). A Re-examination of Wager’s Law for Ten Countries Based on Co-integration and Error Correction Modeling Technique. Applied Financial Economics, 14, 577-589.

Murphy, R. (2002) How Migrant Labour is Changing Rural China, Cambridge: Cambridge

Nigerian Stock Exchange Fact Book (2001). 2005 and 2010 Editions, Published by Pathways Communications Ltd, Lagos State.

Nurudeen A. & A. Usman (2010). Government Expenditure and Economic Growth in Nigeria, 1979-2008: A Disaggregated analysis. Business and Economics Journal, 4, 1-11.

Ram, A. (1986). Causality between Income and Public Expenditure: A Broad International Perspective. Public Finance, 41(1), 393-414.

Ravallion, M., & Datt, G. (2003). Is India’s Economic Growth Leaving the Poor Behind? World Bank Policy Research Working Paper No 2846, Washington, DC: World Bank.

Sinha, D. (2007). Does the Wagner’s Law Hold for Thailand? A Time Series Study, Available online at http://mpra.ub.uni-muenchen.de/2560/

World Bank (2010b). Republic of Ghana: Improving the Targeting of Social Programs, Washington D.C.

World Bank (2011a). Republic of Ghana: Tackling Poverty in Northern Ghana, Washington D.C.

World Bank (2011b). Republic of Ghana: Improving Equity, Efficiency and Accountability of Education Service Delivery, Washington D.C.

Copyright Disclaimer

Copyright reserved by the author(s).

This article is an open-access article distributed under the terms and conditions of the Creative Commons Attribution license (http://creativecommons.org/licenses/by/3.0/).

Business and Economic Research ISSN 2162-4860

2014, Vol. 4, No. 1

www.macrothink.org/ber 23

What factors Influence Internal migration and Wage Growth? an Empirical Analysis of Private Formal

Sector in Bolgatanga-Ghana

Nicholas Awuse (Corresponding author)

Bolgatanga Polytechnic

P. O. Box 767, Sumbrungu, Bolgatanga, Ghana

Tel: 233-243-924-839 E-mail: [email protected]

Patrick Tandoh-Offin (PhD)

Ghana Institute of Management and Public Administration (GIMPA)

P. O. Box AH-50, Achimota-Accra, Ghana

Tel: 233-247-450-433 E-mail: [email protected]

Received: November 3, 2013 Accepted: November 25, 2013

doi:10.5296/ber.v4i1.4973 URL: http://dx.doi.org/10.5296/ber.v4i1.4973

Abstract

The primary aim of this study is to explore the determinants of wage growth velocity in personal formal sector of Bolgatanga Municipality. A primary data collection technique was used and sample size of 345 individuals interviewed using a well structured interview schedule and questionnaire by convenient sampling. Ordinary least square method was applied to study the dependency of growth rate of wage on different variables in Bolgatanga Municipality. Findings reveal that education, gender, experience, household area and marital status of the respondents absolutely affect growth of wages at less than 1% level of significance.

Keywords: Wage Growth, Private Formal, Bolgatanga, Education, Gender, Experience, internal migration, Household area, Marital Status, Ghana.

1. Introduction

Conventionally high wages were linked to high education. According to the theorists of human capital wages were intended to reward workers in progress and future revenues, graduates with advanced levels of education should be paid more than graduates with lower levels of

Business and Economic Research ISSN 2162-4860

2014, Vol. 4, No. 1

www.macrothink.org/ber 24