Baron Funds® - Quarterly Report - printmgr file

186

September 30, 2021 Baron Funds ® Quarterly Report Seems like everybody has got a side hustle these days. Even Ron was considering going back to his roots as an ice cream truck driver (Summer 1963…True Story!). “There is no better run company than SpaceX. They attract the most amazing talent. No one can compete.” Jared Isaacman. Civilian astronaut commander SpaceX Inspiration4. Founder. Shift4 Payments. September 15, 2021. The principal mission of Elon Musk’s Space Exploration Technologies Corp. (“SpaceX”) is to provide low-cost commercial and government access to space. This is being accomplished through what Elon calls RRR, rapid rocket reusability. Other defense aerospace businesses that make profits by selling extraordinarily expensive rockets, well in excess of $100 million to $200 million each, and using them only once, thought this an impossible task. Perhaps because they would sell fewer rockets if the rocket ships could be used multiple times rather than just once? Elon has often commented, “Think how expensive it would be to fly from New York to London if you used a 747 once and then scrapped the plane?” Most government aerospace contracts are on a cost-plus basis. This means that the more expensive the award, the larger the guaranteed profit to the provider. Elon’s SpaceX bids for contracts and attempts to “do the most for the least… better service at lower price is the goal.” SpaceX has accomplished the incredibly difficult goal of making rockets reusable in order to get to space at a lower cost. It is now preparing a massive 390-foot tall Starship, designed as a general-purpose transport to anywhere in the solar system. The Starship rocket architecture is expected to support cheaper orbital launches, space refueling, Moon landing, and hopefully, by mid-decade, a Mars mission. We expect SpaceX to soon commercialize Starlink, ultimately a 40,000 satellite, low earth orbit constellation. Among its services, which we believe will be numerous, Starlink will provide satellite broadband to a material portion of planet Earth’s population where it is uneconomic to provide fast internet by fiber or cable. Starlink will also provide complimentary communications services to existing providers, which could, in many instances, reduce their costs and boost their opportunities. Jared Isaacman was the Commander for the first all-civilian astronaut orbital space flight. This space mission was launched from Kennedy Space Center in Florida on September 15, 2021. The spaceship and its crew were in orbit for three days. Real orbit. Real space. 365 miles from Earth’s surface. Not a thrill ride when passengers like Captain Kirk got to look at our planet for a few minutes from an altitude of 60 miles, the edge of space, and then fall back to Earth. SpaceX scientific and technological oriented missions are profound and actually take place in space. Jared chose his crew for his civilian mission and was responsible for melding them into a functioning unit. Jared believes it is difficult to create a problem-solving culture like that of SpaceX’s, which is oriented to First Principles. For example, when Jared learned to fly a fighter jet as a civilian several years ago, he was required to memorize 100 pages of instructions. As the commander of this mission, he was required to study and learn 3,000 pages of instructions and undergo three FRRs, “flight readiness reviews.” All were chaired by Elon. The first lasted 18 hours, the second 10 hours, and the final 3 hours. The objective was for the space crew to “do things a certain way, every time.” Day-to-day tasks were all documented, reduced to a checklist, and embedded in operational training. Everything references a procedure. Check 405, for example, if a light bulb is not turned on. Everything is intended to preserve mindshare so that your brainpower can be focused on what hasn’t been considered. No “going rogue” by this crew. OK. Competition. Jeff Bezos’ Blue Origin was founded in September 2000. SpaceX in May 2002. Blue Origin has not yet been to orbit. Blue Origin has not yet demonstrated reusability. SpaceX has accomplished both in the past five years. Blue Origin and SpaceX both bid for a Lunar Lander contract from the government. Normally, government contracts are granted to two parties. SpaceX was the sole winner of the Lunar Lander contract awarded in April 2021. SpaceX had bid TABLE OF CONTENTS Letter from Ron 1 Letter from Linda 7 Baron Funds Performance 24 Baron Asset Fund 31 Baron Growth Fund 35 Baron Small Cap Fund 42 Baron Opportunity Fund 48 Baron Partners Fund 55 Baron Fifth Avenue Growth Fund 61 Baron Focused Growth Fund 67 Baron International Growth Fund 74 Baron Real Estate Fund 79 Baron Emerging Markets Fund 90 Baron Global Advantage Fund 95 Baron Discovery Fund 102 Baron Durable Advantage Fund 107 Baron Real Estate Income Fund 112 Baron WealthBuilder Fund 122 Baron Health Care Fund 129 Baron FinTech Fund 134 Portfolio Holdings 154 $2.9 billion. Blue Origin bid $5.9 billion. Blue Origin is now suing NASA believing it was not treated fairly. This is a meaningful win for SpaceX, making it clear that Blue Origin is far behind SpaceX. BARON FUNDS

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Baron Funds® - Quarterly Report - printmgr file

September 30, 2021

Baron Funds®

Quarterly Report

Seems like everybody has got a side hustle these days.Even Ron was considering going back to his roots as an ice

cream truck driver (Summer 1963…True Story!).

“There is no better run company thanSpaceX. They attract the most amazingtalent. No one can compete.” Jared Isaacman.Civilian astronaut commander SpaceXInspiration4. Founder. Shift4 Payments.September 15, 2021.

The principal mission of Elon Musk’s SpaceExploration Technologies Corp. (“SpaceX”) is toprovide low-cost commercial and governmentaccess to space. This is being accomplishedthrough what Elon calls RRR, rapid rocketreusability. Other defense aerospace businessesthat make profits by selling extraordinarilyexpensive rockets, well in excess of $100 millionto $200 million each, and using them only once,thought this an impossible task. Perhaps becausethey would sell fewer rockets if the rocket shipscould be used multiple times rather than justonce? Elon has often commented, “Think howexpensive it would be to fly from New York toLondon if you used a 747 once and then scrappedthe plane?” Most government aerospace contractsare on a cost-plus basis. This means that the moreexpensive the award, the larger the guaranteedprofit to the provider. Elon’s SpaceX bids forcontracts and attempts to “do the most for theleast… better service at lower price is the goal.”

SpaceX has accomplished the incredibly difficultgoal of making rockets reusable in order to get tospace at a lower cost. It is now preparing amassive 390-foot tall Starship, designed as ageneral-purpose transport to anywhere in the solarsystem. The Starship rocket architecture isexpected to support cheaper orbital launches,space refueling, Moon landing, and hopefully, bymid-decade, a Mars mission. We expect SpaceX tosoon commercialize Starlink, ultimately a 40,000satellite, low earth orbit constellation. Among itsservices, which we believe will be numerous,Starlink will provide satellite broadband to amaterial portion of planet Earth’s populationwhere it is uneconomic to provide fast internet byfiber or cable. Starlink will also providecomplimentary communications services toexisting providers, which could, in many instances,reduce their costs and boost their opportunities.

Jared Isaacman was the Commander for the firstall-civilian astronaut orbital space flight. Thisspace mission was launched from KennedySpace Center in Florida on September 15, 2021.The spaceship and its crew were in orbit forthree days. Real orbit. Real space. 365 miles

from Earth’s surface. Not a thrill ride when passengerslike Captain Kirk got to look at our planet for a fewminutes from an altitude of 60 miles, the edge of space,and then fall back to Earth. SpaceX scientific andtechnological oriented missions are profound andactually take place in space.

Jared chose his crew for his civilian mission and wasresponsible for melding them into a functioning unit.Jared believes it is difficult to create a problem-solvingculture like that of SpaceX’s, which is oriented to FirstPrinciples. For example, when Jared learned to fly afighter jet as a civilian several years ago, he was requiredto memorize 100 pages of instructions. As the

commander of this mission, he was required tostudy and learn 3,000 pages of instructions andundergo three FRRs, “flight readiness reviews.”All were chaired by Elon. The first lasted 18hours, the second 10 hours, and the final 3hours. The objective was for the space crew to“do things a certain way, every time.”Day-to-day tasks were all documented, reducedto a checklist, and embedded in operationaltraining. Everything references a procedure.Check 405, for example, if a light bulb is notturned on. Everything is intended to preservemindshare so that your brainpower can befocused on what hasn’t been considered. No“going rogue” by this crew.

OK. Competition. Jeff Bezos’ Blue Origin wasfounded in September 2000. SpaceX in May 2002.Blue Origin has not yet been to orbit. Blue Originhas not yet demonstrated reusability. SpaceX hasaccomplished both in the past five years. BlueOrigin and SpaceX both bid for a Lunar Landercontract from the government. Normally,government contracts are granted to two parties.SpaceX was the sole winner of the Lunar Landercontract awarded in April 2021. SpaceX had bid

TABLE OF CONTENTSLetter from Ron 1Letter from Linda 7Baron Funds Performance 24Baron Asset Fund 31Baron Growth Fund 35Baron Small Cap Fund 42Baron Opportunity Fund 48Baron Partners Fund 55Baron Fifth Avenue Growth Fund 61Baron Focused Growth Fund 67Baron International Growth Fund 74Baron Real Estate Fund 79Baron Emerging Markets Fund 90Baron Global Advantage Fund 95Baron Discovery Fund 102Baron Durable Advantage Fund 107Baron Real Estate Income Fund 112Baron WealthBuilder Fund 122Baron Health Care Fund 129Baron FinTech Fund 134Portfolio Holdings 154

$2.9 billion. Blue Origin bid $5.9billion. Blue Origin is now suingNASA believing it was nottreated fairly. This is ameaningful win for SpaceX,making it clear that Blue Originis far behind SpaceX.

BARONF U N D S

Letter from Ron

Boeing and SpaceX were awarded crewed flightsby NASA in 2014. Boeing’s award was for $4.2billion and SpaceX’s for $2.6 billion. Bothcontracts were for identical services. SpaceXexecuted its first crewed flight in May 2020.Boeing needs to first rerun an unmanned demoflight. Its first one failed. NASA announced inOctober it had shifted two astronauts from aBoeing mission to a SpaceX flight.

“The ability to learn rapidly and translatethat into experimentation and action.” RichLesser. CEO. Boston Consulting Group. “ACEO Who Advises Other CEOs” The New YorkTimes. Corner Office. September 2021.

That was the response by Boston ConsultingGroup’s CEO to the question, “What were thecommon characteristics of CEOs who did wellover the past eighteen months?”

Elon Musk, with his focus on First Principles,which means stripping away everything but corefoundation principles and starting over, is theCEO of both Tesla, Inc. and SpaceX. Baron hassignificant investments in each of these twodistinct businesses. Elon also happens to be oneof the greatest CEO students of businesses andhuman behavior…with an unusual, probablyunique, ability to translate what he has learnedinto experimentation and action. As well as toattract exceptionally talented engineers to workwith him to realize his vision.

When Elon was a child, his mom nicknamed him“Encyclopedia.” That was because he read theencyclopedia, sort of the way the rest of us readbooks. This was both because he has alwaysbeen intellectually curious…and because itprobably enabled Elon to escape into anotherworld from a childhood that was not anespecially happy one. As a result, Elon as a youthcould answer almost any question posed by hismom or anyone else. …which is not a lotdifferent from Elon’s current efforts to learn by“questioning everything”…and to implementlogical solutions quickly based on what he haslearned. “Why does it have to be that way?” iswhat Elon most often asks, or some variation ofthat comment, according to many who workmost closely with him.

CNBC, Bloomberg, and Reuters have reportedthat Volkswagen’s CEO, Herbert Diess, invitedElon Musk as a “surprise guest” to address VW’s200-person executive team last week! Diess ischallenging Volkswagen to pivot faster frominternal combustion engine cars to electricvehicles. In a recent newspaper interview, Eloncalled Volkswagen an “icon” and Tesla’s“greatest challenger.” Diess returned the

compliment and felt his executives could learnto be more agile and fast moving from the CEOof the business Diess admires and believes isVW’s strongest competitor!

Nearly all car companies have reduced theirautomobile production dramatically in recentmonths. This is due to a shortage of computerchips. This has not been the case for Tesla, whichis currently producing electric cars at anannualized rate nearly double its production in2020. Diess first asked Elon how Teslaaccomplished this. Elon responded that he is firstan engineer focused on supply chains, logistics,and production. That skill enabled Tesla to bebetter prepared and more nimble than its rivals.When other car companies cancelled chip ordersat the beginning of COVID, Elon increasedTesla’s orders. Further, Diess told his fellow VWexecutives it took Tesla only two weeks for itsengineers to rewrite software that allowed it toswitch from one microchip vendor to another!That feat was regarded as astounding by manyVW engineering executives who listened to thepresentation. Elon, we believe, embodies thecharacteristics of a CEO whom BCG’s RichLesser described as performing best duringCOVID.

Marvelle Sullivan Berchtold is an independenttrustee of Baron Funds and the former head ofmergers and acquisitions of Europeanpharmaceutical giant Novartis. Marvelle recentlytold me, “You are a learning machine.” Marvellewas then helping me understand how thecovalent bonds in the material used for a glassand plastic vial patented for biotechnology drugswould provide important benefits for theindustry. Plastic makes the vial un-breakable andglass makes the vial impenetrable. Glassprevents inorganic impurities in plastic fromleaching into biotech drugs within the vial.

George Blumenthal, Founder and CEO,International Cellular Communications, told mein 2001 that, “Your business didn’t fail in thecrash of communications businesses when the“internet bubble” burst in 2000. That wasbecause you tried to understand how businesseswork and the implications of their CEO’s actions.You dissemble businesses in your head and try toput them together again the same way. Yourcuriosity and questioning about how things workmakes you a better investor and less likely tomake mistakes.” That is what we teach ouranalysts. They need to be certain theyunderstand as much as possible about how thingswork so they will be able to assess the likelihoodof businesses and individuals being successful.

When I spoke with Kristin Kulik-Peters, our newChief Marketing Officer, she remarked that I hadbuilt a research and management organizationbased on the premise of “questioningeverything.” That with the purpose ofdiscovering long-term investment opportunitiesin competitively advantaged growth companiesrun by exceptional people. All this in order toenable our clients’ savings to grow faster thanthe economy and protect our clients frominflation. “Your steadily growing staff of 38investment professionals with whom you workhave adopted your beliefs and are nowadvocates. We now need to curate our contentand amplify that message on social media.”“That is a great plan,” I responded. “Your job, asthe Nike saying goes, is to ‘Just Do It!’” “Anddon’t forget to give credit to the 133 otheroutstanding individuals who are spending theircareers at Baron,” I added.

“The Blink of an Eye.” Rabbi Elliott J.Cosgrove. Park Avenue Synagogue. RoshHashanah. Jewish New Year. 5782.September 7, 2021.

On Rosh Hashanah, the Jewish New Year 5782,the Rabbi of New York City’s Park AvenueSynagogue where many of my friends aremembers, delivered a “who shall live, who shalldie” sermon several thought I should read. Thesermon encompassed two chilling stories thatillustrate the fragility of life and make you ask“Why?” and “What if?”

In the first story, a rising college senior andmember of that congregation was in a caraccident in Chicago. The accident was so serioushe had to be taken from his vehicle with the“jaws of life.” Miraculously, the young studentescaped with only bruises! Regardless, he wastaken to a nearby hospital for an MRI to becertain there was no concussion, which provedto be the case. However, the MRI, unexpectedly,detected a rapidly growing brain tumor thatwould have soon become inoperable threateningthat young man’s chances to survive. Thestudent was operated upon and was in theRabbi’s congregation in September. If thestudent had not been in the accident, it isunlikely he would still be alive.

In the second story, two weeks after theaccident in the first story, a rising college junior,also in Chicago, was in his car driving when hewas hit by a stray bullet. The bullet severed hisspinal cord from which there could be norecovery. Three days later that young studentlay paralyzed in a hospital bed, unable to breathewithout a ventilator and able to communicate

2

September 30, 2021 Letter from Ron

“yes” or “no” only by blinking his eyesresponding to an alphabet board. With his familyand friends at his bedside, he signaled his momby blinking that he was ready to die.

The Rabbi then told his congregation that it washard to understand the meaning of theserandom events for which only seconds meantthe difference between life and death. In the firstinstance, were it not for the accident, the tumorwould not have been discovered, and thestudent probably would have died. In the second,if the student had taken an extra second to tiehis shoelace, fumbled for his keys, or taken a callon his cell phone, he would still be alive!

“Play every match like it may be your last,” washow Novak Djokovic, perhaps the greatest tennisplayer ever, noted in an interview this year atthe U.S. Open in New York City. “The blink of aneye” is what the Rabbi tells us is the differencebetween life and death. Novak tells us not howwe want to die but how we want to live.

My life’s story is a series of “What ifs?”…butcertainly nothing as illustrative as the fragility oflife in the Rabbi’s stories. The role “luck” hasplayed in my life is startling.…as is the role luckplays in everyone else’s lives as well. Mine wouldlikely have been vastly different if I hadn’t triedto sell Fuller Brushes door to door in a D.C.apartment building in the summer of 1966 tomake spending money. At the time, I had abiochemistry teaching fellowship at GeorgetownUniversity. The fellowship stipend was $1,600per year! Since I couldn’t afford an apartmentwith windows, I was living in a basement in RockCreek Park desperate to earn gasoline money formy motorcycle…and spending money to takedates somewhere…anywhere… When I knockedon a door in that building, a well-dressed manonly a few years older than I was, answered.When he and his wife invited me to show themmy Fuller brushes, I first asked why he wasn’t inVietnam? He told me he was earning $11,000per year in a “critical skills, Vietnam draft-deferred” patent examiner job in the U.S. PatentOffice, and he was attending law school in theevenings on scholarship. “Wow,” I thought. “Igotta do that.” He changed my life! It makes yourealize how many decisions you make and howsuch a large part of success is good luck andbeing agile.

Among the most satisfying elements of my careeras an analyst, portfolio manager, CEO, andbusiness Founder are the “thank yous” I get nearlyevery day. They come from people saying “hello”and “thank you” in restaurants…e-mails…phonecalls...letters…and when I am just walking on the

streets of New York or East Hampton….Atsummer’s end 2021, Judy and I were crossingMain Street in East Hampton. A car cut us off andthe front passenger’s window rolled down. “Hi,Ron,” the passenger hollered, startling us. “We’reFred and Selma. Thanks for the returns. We loveyour annual meetings. Thanks for them, too.”When we returned to New York City that Sundayevening I was dispatched to find dinner. I walkedup Madison Avenue looking for a deli. I wasstopped by “Larry and Harriet.” They told me theyare friends of Jeff Kolitch’s parents. Jeff is thePortfolio Manager of Baron Real Estate Fund andBaron Real Estate Income Fund. “Thank you forwhat you do for us. We really enjoyed the bookyou mentioned in one of your letters that Judytold you to read. Does Judy have any morerecommendations?” I replied, “That book washistorical fiction about Nikola Tesla, ThomasEdison (not a very nice person), GeorgeWestinghouse, JP Morgan, Thomas Cravath, andAlexander Graham Bell. The title was ‘The LastDays of Night.’ If Judy gives me another readingassignment I will pass it on.”

A few weeks later, I received an e-mail fromGregg Lorberbaum. Gregg has represented ourbusiness for more than 30 years negotiatingcommercial property leases. We have paid himmillions of dollars in fees over that period andhave never once had a written contract. All on ahandshake. Gregg’s note of congratulations wasfor me being included on the Forbes list again. “Iknow you do what you do because you love itbut it’s nice to see ’the good guys win.’ WhatForbes doesn’t consider is how much wealth youhave created for others! That is where the truecongrats lay.”

This made me think how lucky for me…andothers…that I didn’t get into medical school allthose years ago. The summer before my senioryear in college, in addition to working days as alifeguard in Asbury Park, I worked 11 PM to 7 AMin a hospital emergency room holding dyingindividuals who had been shot or stabbed on agurney…cleaning bed pans…and wrappingbodies from the ICU after patients died andputting them in a freezer. This was enough forme.

Bobby, an individual with whom I was friendly inhigh school, recently called our office and askedto speak with me by zoom. My last conversationwith Bobby was in 1961 at our graduation fromAsbury Park High School! After a few minutes ofpleasantries he told me, “I’m calling because I’dlike to invest with you for my daughter. How doI do that?” I recommended that he purchaseBaron WealthBuilder Fund. Baron WealthBuilder

Fund owns only Baron mutual funds, all but oneof which have outperformed their respectivebenchmarks since inception. BaronWealthBuilder Fund’s operating expenses arecapped at just 5 basis points and the Funddoesn’t charge a management fee. Further,Baron WealthBuilder Fund’s 16 top-performingunderlying funds charge institutionalmanagement fees and expenses…which are lessthan “retail” management fees and expenses.This is whether you invest $2,000 or millionswith us. Baron WealthBuilder Fund was foundedDecember 29, 2017 and is the number oneperforming equity asset allocation fund since itsinception. I then asked Bobby what made himcall me. “I’ve been reading about you for a longtime, “ he said. “You also helped me with math inhomeroom,” he continued. “That’s why.”

“If your younger selves confronted youtoday, would they like you?” “Would they beproud of the person you’ve become…of thelives you’ve lived?” Rabbi Ari Lorge. CentralSynagogue. New York City. September 21,2018.

Judy and I have three grandsons. Leo is 9 1⁄2years old, Ari is 7 1⁄2, and Levi, whose birth datewas June 30 (Quarter End 2021), is just 90 daysold. Ari loves basketball. I love to play basketballwith him. A few weeks ago, Ari told me,“Gran’pa, I think I could play basketball virtuallyall day long if someone brought me water andfood.” Hint, hint. Last summer, once a week, a6’8” basketball player, who as a college juniorwas the starting forward for the University ofPittsburgh and will likely soon be drafted in theNBA, came to our home to coach Ari. Thatathlete, a super talented and incredibly niceyoung man, is the most sought after teacher ofyoung basketball players on Long Island.

At summers end, I was shooting hoops with Ariwhen we stopped playing for a few minutes. “Ari,when you grow up and graduate college, do youthink you’d like to work at Baron Capital withyour Dad and Uncle Michael just like Daddy andUncle Michael work with me?” “No, Gran’pa, Iwant to play in the NBA.” “Ari, you’re 3’8” tall,you’re Jewish, and you can’t jump,” I responded.“But I’m really fast, Gran’pa,” he replied as he ranaround me, stole the ball, and dribbled for aperfect layup. “Ari, how about this? There are noreally old basketball players, except LeBron, sohow about after you graduate from college youplay in the NBA for a few years and then joinDaddy and Uncle Michael at Baron?” He pausedfor a moment before answering, “That’s a goodidea, Gran’pa.” I obviously believe it’s never tooearly to plant the seeds…

3

Letter from Ron

In Spring 2018, I wrote you that CentralSynagogue’s Rabbi Lorge began his Yom Kippur“Day of Atonement” sermon by asking us, “Doyou think if your younger selves confronted youtoday, would they like you?” The Rabbi thenspoke of a U.K. documentary whose narratorsbegan in 1964 to interview seven year oldchildren and continued to film those interviewsat seven year intervals through today. “Wouldyour younger self be proud of how you havelived your life, the person you have become?”were the questions those interviewers asked theindividuals who today are 64 years old.

My grandson Ari is now about the same age asthe subject individuals when they began toparticipate in that U.K. documentary almost 60years ago. I am pretty certain that Ari, and Leotoo, are proud of their family, our business andits impact on so many who rely upon it today,and who have become financially securebecause of our efforts.

Of course, I hope what I regard as our familybusiness will endure. On March 12, 2082, 60years from now, Baron Capital will be onehundred years old!!! It is important to me and toour family that in 60 years Ari, Leo, and Levi canlook back on their lives and know that theiryounger selves would be proud of the lives theyhave led and the individuals they have become.The moral of this story is that it is never toosoon to teach the values of hard work, kindness,

and charity, Tzedakah, which my faith regards asa moral and ethical obligation, and L’dor v’dor,passing traditions from one generation to thenext. If our grandchildren, just like our sonsDavid and Michael, also have unquenchablecuriosity and love of learning, characteristicsthat I believe are important to becomingsuccessful investors like our two sons, andhappy, productive individuals, I will regard Judyand my jobs as parents and grandparents welldone.

We will continue to provide you withinformation about Baron Funds that wewould like to have if our roles werereversed. Thank you for your confidence injoining us as investors in Baron Funds.

Respectfully,

Ronald BaronCEO and Portfolio ManagerSeptember 30, 2021

P.S. Baron mutual funds are highly ranked byMorningstar from their Inceptions throughSeptember 30, 2021. It is not common formutual funds to outperform their benchmark

indexes. That is the reason low cost index fundshave become so popular.

As of 9/30/2021, 16 of 17 Baron Funds,representing 98.3% of Baron Funds’ assetsunder management (“AUM”), haveoutperformed their respective passivebenchmarks since their inceptions. In addition,14 of those funds, representing 98.0% of BaronFunds’ AUM, rank in the top 17% of theirrespective Morningstar categories; and 11 funds,representing 72.7% of AUM, rank in the top 8%.(This includes Baron Partners Fund that is theNumber One mutual fund of 2,193 mutualfunds since 1992!)*

My recommendation? Buy Baron WealthBuilderFund for a diversified fund that ownstop-performing Baron mutual funds.

P.P.S. Don’t forget. Baron Capital wasfounded March 12, 1982…

So…we will be celebrating our business’ 40thAnniversary in 2022…and we haven’t heldour annual conference either this year or lastdue to COVID…and, this is the RoaringTwenties…

So…if I were you I wouldn’t miss our 29thAnnual Baron Investment Conference onNovember 4, 2022 at the Metropolitan OperaHouse, Lincoln Center, New York City…justsayin’…

*This is a hypothetical ranking created by Baron Capital using Morningstar data and is as of 9/30/2021. There were 2,193 share classes in these nineMorningstar Categories for the period from 4/30/2003 to 9/30/2021.

Note, the peer group used for these analyses includes all U.S. equity share classes in Morningstar Direct domiciled in the U.S., including obsolete funds, indexfunds, and ETFs. The individual Morningstar Categories used for this analysis are the Morningstar Large Blend, Large Growth, Large Value, Mid-Cap Blend,Mid-Cap Growth, Mid-Cap Value, Small Blend, Small Growth, and Small Value Categories.

The Morningstar Large Growth Category consisted of 1,235, 1,024, and 762 share classes for the 1-, 5-, and 10-year periods. Morningstar rankedBaron Partners Fund in the 1st, 1st, 1st, and 1st percentiles for the 1-, 5-, 10-year, and since conversion periods, respectively. The Fund converted intoa mutual Fund 4/30/2003, and the category consisted of 417 share classes.

Investors should consider the investment objectives, risks, and charges and expenses of the investment carefully before investing. The prospectus and summaryprospectuses contain this and other information about the Funds. You may obtain them from the Funds’ distributor, Baron Capital, Inc., by calling1-800-99BARON or visiting www.BaronFunds.com. Please read them carefully before investing.

4

September 30, 2021 Letter from Ron

Baron Funds (Institutional Shares) and Benchmark Performance 9/30/2021

AnnualizedReturn

Since FundInception

AnnualizedBenchmark

ReturnSince FundInception

InceptionDate

Average Annualized Returns Annual ExpenseRatioFund Primary Benchmark 1-Year 3-Year 5-Year 10-Year Net Assets

SMALL CAP

Baron Growth Fund Russell 2000 Growth Index 14.25% 8.89% 12/31/1994 36.55% 19.75% 21.16% 17.64% 1.04%(3) $9.20 billion

Baron Small Cap Fund Russell 2000 Growth Index 11.58% 7.32% 9/30/1997 30.11% 17.86% 20.29% 17.15% 1.05%(3) $5.32 billion

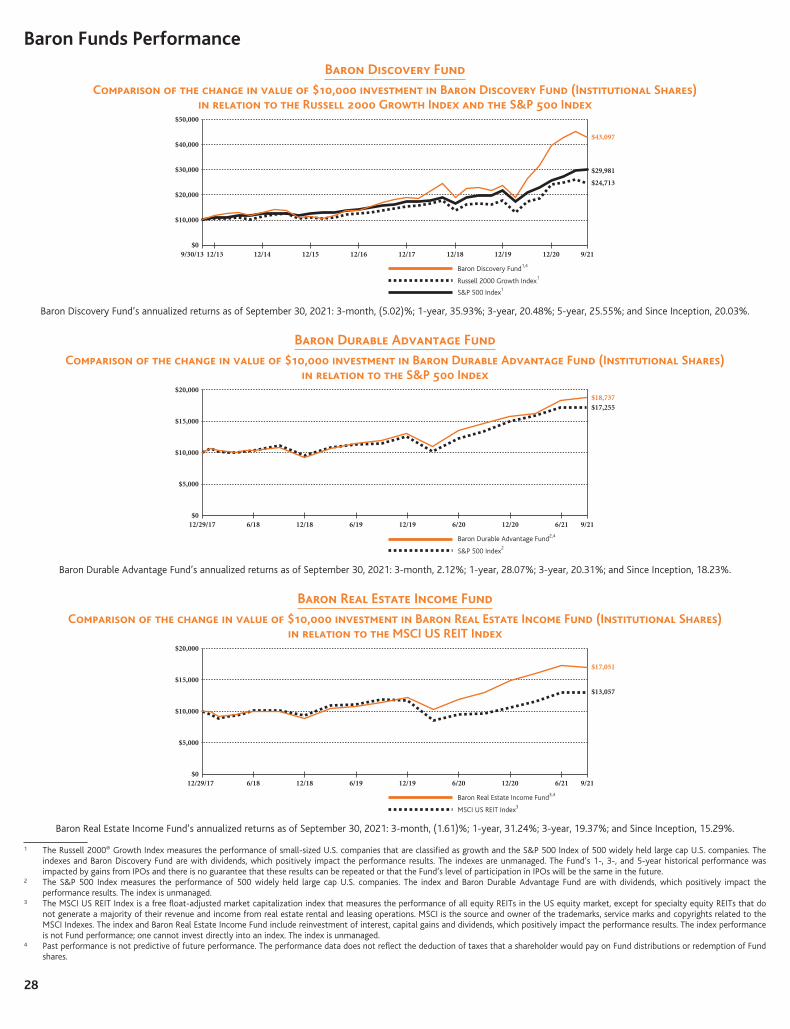

Baron Discovery Fund† Russell 2000 Growth Index 20.03% 11.97% 9/30/2013 35.93% 20.48% 25.55% N/A 1.08%(3) $2.03 billion

SMALL/MID CAP

Baron Focused Growth Fund(1) Russell 2500 Growth Index 14.54% 9.33% 5/31/1996 42.30% 40.46% 32.52% 21.40% 1.07%(4) $745.08 million

MID CAP

Baron Asset Fund Russell Midcap Growth Index 12.46% 11.08%(2) 6/12/1987 25.29% 18.72% 20.45% 18.00% 1.05%(3) $6.17 billion

LARGE CAP

Baron Fifth Avenue GrowthFund Russell 1000 Growth Index 11.98% 12.31% 4/30/2004 19.44% 22.93% 24.52% 20.65% 0.78%/0.75%(3)(6) $837.21 million

Baron Durable Advantage Fund S&P 500 Index 18.23% 15.66% 12/29/2017 28.07% 20.31% N/A N/A 2.40%/0.70%(3)(7) $41.16 million

ALL CAP

Baron Partners Fund(1) Russell Midcap Growth Index 16.45% 10.90% 1/31/1992 57.43% 49.25% 38.93% 27.63% 1.30%(4)(5) $7.15 billion

Baron Opportunity Fund† Russell 3000 Growth Index 10.77% 6.96% 2/29/2000 33.91% 34.26% 32.95% 21.52% 1.08%(3) $1.61 billion

INTERNATIONAL

Baron Emerging Markets Fund MSCI EM Index 6.41% 3.25% 12/31/2010 17.95% 12.17% 9.61% 8.90% 1.09%(4) $9.52 billion

Baron Global Advantage Fund† MSCI ACWI Index 19.81% 10.67% 4/30/2012 22.56% 32.66% 29.58% N/A 0.92%/0.90%(4)(8) $2.77 billion

Baron International GrowthFund MSCI ACWI ex USA Index 12.75% 8.07% 12/31/2008 30.30% 16.32% 14.55% 12.13% 1.01%/0.95%(4)(9) $743.70 million

SECTOR

Baron Real Estate Fund MSCI USA IMI Extended RealEstate Index 16.88% 12.72% 12/31/2009 33.50% 25.89% 19.56% 19.05% 1.08%(4) $1.82 billion

Baron Real Estate Income Fund MSCI US REIT Index 15.29% 7.37% 12/29/2017 31.24% 19.37% N/A N/A 3.45%/0.80%(4)(10) $85.20 million

Baron Health Care Fund Russell 3000 Health CareIndex 25.35% 16.62% 4/30/2018 32.78% 23.11% N/A N/A 1.45%/0.85%(4)(11) $211.61 million

Baron FinTech Fund S&P 500 Index 37.32% 19.83% 12/31/2019 34.52% N/A N/A N/A 2.43%/0.95%(12) $77.04 million

EQUITY ALLOCATION

Baron WealthBuilder Fund S&P 500 Index 24.71% 15.66% 12/29/2017 35.42% 26.94% N/A N/A 1.22%/1.11%(4)(13) $481.86 million

(1) Reflects the actual fees and expenses that were charged when the Funds were partnerships. The predecessor partnerships charged a 20% performance fee (Baron PartnersFund) or a 15% performance fee (Baron Focused Growth Fund) after reaching a certain performance benchmark. If the annual returns for the Funds did not reflect theperformance fee for the years the predecessor partnerships charged a performance fee, returns would be higher. The Funds’ shareholders are not charged a performance fee.

(2) For the period June 30, 1987 to September 30, 2021.(3) As of 9/30/2020.(4) As of 12/31/2020.(5) Comprised of operating expenses of 1.05% and interest expenses of 0.25%.(6) Annual expense ratio was 0.78%, but the net annual expense ratio was 0.75% (net of Adviser’s fee waivers).(7) Annual expense ratio was 2.40%, but the net annual expense ratio was 0.70% (net of Adviser’s fee waivers).(8) Annual expense ratio was 0.92%, but the net annual expense ratio was 0.90% (net of Adviser’s fee waivers).(9) Annual expense ratio was 1.01%, but the net annual expense ratio was 0.95% (net of Adviser’s fee waivers).(10) Annual expense ratio was 3.45%, but the net annual expense ratio was 0.80% (net of Adviser’s fee waivers).(11) Annual expense ratio was 1.45%, but the net annual expense ratio was 0.85% (net of Adviser’s fee waivers).(12) Annual expense ratio was 2.43%, but the net annual expense ratio was 0.95% (net of Adviser’s fee waivers).(13) Annual expense ratio was 1.22%, but the net annual expense ratio was 1.11% (includes acquired fund fees and expenses, net of the Adviser’s fee waivers).† The Fund’s historical performance was impacted by gains from IPOs. There is no guarantee that these results can be repeated or that the Fund’s level of participation in

IPOs will be the same in the future.

The performance data quoted represents past performance. Past performance is no guarantee of future results. The investment return and principal value of aninvestment will fluctuate; an investor’s shares, when redeemed, may be worth more or less than their original cost. The Adviser reimburses certain Baron Fundexpenses pursuant to a contract expiring on August 29, 2032, unless renewed for another 11-year term and the Fund’s transfer agency expenses may bereduced by expense offsets from an unaffiliated transfer agent, without which performance would have been lower. Current performance may be lower orhigher than the performance data quoted. For performance information current to the most recent month end, visit www.BaronFunds.com or call1-800-99BARON.

5

Letter from Ron

Performance for the Institutional Shares prior to 5/29/2009 is based on the performance of the Retail Shares, which have a distribution fee. The InstitutionalShares do not have a distribution fee. If the annual returns for the Institutional Shares prior to 5/29/2009 did not reflect this fee, the returns would be higher.

Asset Fund’s 3Q 2021, Discovery Fund’s YTD, 1-, 3- and 5-year, Fifth Avenue Growth Fund’s 3Q 2021, FinTech Fund’s 3Q 2021, Global AdvantageFund’s YTD, 3- and 5-year, Opportunity Fund’s 3Q 2021, 3-, 5- and 10-year, and Small Cap Fund’s 3Q 2021 historical performance were impacted by gainsfrom IPOs and there is no guarantee that these results can be repeated or that the Funds’ level of participation in IPOs will be the same in the future.

Risks: All investments are subject to risk and may lose value.

Portfolio holdings as a percentage of net assets as of September 30, 2021 for securities mentioned are as follows: Tesla, Inc. – Baron Opportunity Fund (3.3%),Baron Partners Fund (40.5%*), Baron Focused Growth Fund (33.4%); Space Exploration Technologies Corp. – Baron Asset Fund (0.7%), Baron OpportunityFund (0.8%), Baron Partners Fund (4.2%*), Baron Fifth Avenue Growth Fund (0.2%), Baron Focused Growth Fund (3.6%), Baron Global Advantage Fund(0.4%).* % of Long Positions.

Portfolio holdings are subject to change. Current and future portfolio holdings are subject to risk.

Ranking information provided is calculated for the Retail Share Class and is as of 9/30/2021. The number of share classes in each category may vary dependingon the date that Baron downloaded information from Morningstar Direct. Morningstar calculates its category average performance and rankings using itsFractional Weighting methodology. Morningstar rankings are based on total returns and do not include sales charges. Total returns account formanagement, administrative, and 12b-1 fees and other costs automatically deducted from fund assets. The Morningstar Large Growth Categoryconsisted of 1,235, 1,024, and 762 share classes for the 1-, 5-, and 10-year periods. Morningstar ranked Baron Opportunity Fund in the 9th, 3rd, 7th, and 4th

percentiles for the 1-, 5-, 10-year, and since inception periods, respectively. The Fund launched 2/29/2000, and the category consisted of 265 share classes.Morningstar ranked Baron Partners Fund in the 1st, 1st, 1st, and 1st percentiles for the 1-, 5-, 10-year, and since conversion periods, respectively. The Fundconverted into a mutual Fund 4/30/2003, and the category consisted of 417 share classes. The Morningstar Mid-Cap Growth Category consisted of 584,495, and 386 share classes for the 1-, 5-, and 10-year periods. Morningstar ranked Baron Asset Fund in the 85th, 30th, 26th and 17th percentiles for the 1-, 5-,10-year, and since inception periods, respectively. The Fund launched 6/12/1987, and the category consisted of 19 share classes. Morningstar ranked BaronGrowth Fund in the 27th, 26th, 34th, and 8th percentiles for the 1-, 5-, 10-year, and since inception periods, respectively. The Fund launched 12/31/1994, and thecategory consisted of 54 share classes. Morningstar ranked Baron Focused Growth Fund in the 13th, 2nd, 2nd, and 4th percentiles for the 1-, 5-, 10-year, and sinceconversion periods, respectively. The Fund converted into a mutual Fund 6/30/2008, and the category consisted of 316 share classes. The Morningstar SmallGrowth Category consisted of 611, 506, and 381 share classes for the 1-, 5-, and 10-year time periods. Morningstar ranked Baron Small Cap Fund in the 86th,35th, 43rd, and 14th percentiles for the 1-, 5-, 10-year, and since inception periods, respectively. The Fund launched 9/30/1997, and the category consisted of91 share classes. Morningstar ranked Baron Discovery Fund in the 63rd, 7th, and 2nd percentiles for the 1-, 5-year, and since inception periods, respectively. TheFund launched 9/30/2013, and the category consisted of 430 share classes. The Morningstar Real Estate Category consisted of 246, 199, and 147 shareclasses for the 1-, 5-, and 10-year time periods. Morningstar ranked Baron Real Estate Fund in the 51st, 1st, 1st, and 1st percentiles for the 1-, 5-, 10-year, andsince inception periods, respectively. The Fund launched 12/31/2009, and the category consisted of 128 share classes. Morningstar ranked Baron Real EstateIncome Fund in the 74th and 3rd percentiles for the 1-year and since inception periods, respectively. The Fund launched 12/29/2017, and the category consistedof 221 share classes. The Morningstar Foreign Large Growth Category consisted of 439, 322, 221, and 197 share classes for the 1-, 5-, 10-year, and sinceinception (12/31/2008) periods. Morningstar ranked Baron International Growth Fund in the 4th, 17th, 20th, and 12th percentiles, respectively. The MorningstarDiversified Emerging Markets Category consisted of 784, 598, 317, and 279 share classes for the 1-, 5-, 10-year, and since inception (12/31/2010) periods.Morningstar ranked Baron Emerging Markets Fund in the 64th, 37th, 12th, and 4th percentiles, respectively. The Morningstar World Large-Stock GrowthCategory consisted of 352, 263, and 167 share classes for the 1-, 5-year, and since inception (4/30/2012) periods. Morningstar ranked Baron Global AdvantageFund in the 74th, 2nd, and 2nd percentiles, respectively. The Morningstar Health Category consisted of 167 and 138 share classes for the 1-year and sinceinception (4/30/2018) periods. Morningstar ranked Baron Health Care Fund in the 8th and 5th percentiles, respectively. The Morningstar Allocation—85%+Equity Category consisted of 166 and 153 share classes for the 1-year and since inception (12/29/2017) periods. Morningstar ranked Baron WealthBuilderFund in the 10th and 2nd percentiles, respectively.

© 2021 Morningstar. All Rights Reserved. The Morningstar information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) maynot be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for anydamages or losses arising from any use of this information. Past performance is no guarantee of future results.

The discussions of the companies herein are not intended as advice to any person regarding the advisability of investing in any particular security. The viewsexpressed in this report reflect those of the respective portfolio managers only through the end of the period stated in this report. The portfolio manager’sviews are not intended as recommendations or investment advice to any person reading this report and are subject to change at any time based on marketand other conditions and Baron has no obligation to update them.

Diversification cannot guarantee a profit or protect against loss.

BAMCO, Inc. is an investment adviser registered with the U.S. Securities and Exchange Commission (SEC). Baron Capital, Inc. is a limited purpose broker/dealerregistered with the SEC and member of the Financial Industry Regulatory Authority, Inc. (FINRA).

6

September 30, 2021 Letter from Linda

LINDA MARTINSON

CHAIRMAN, PRESIDENT AND COO

Every day for the past 18 months has been overly charged with uncertainty.The social and economic aftermath of the pandemic has been extraordinary,but the response and adaptability demonstrated by people and businessesaround the world have been remarkable. The pandemic is not yet in therear-view mirror, and we continue to face major challenges, including healthcare overloads, disruptions for employers and employees, and widespreadsupply chain issues. Nonetheless, we have become better at coping with thevolatility and changes caused by COVID. No one knows what lies ahead, yetthe efforts and recovery progress we see every day – in meetings andconversations with the companies we invest in and through generaleconomic and business data – makes us feel optimistic about the future.

We recognize that many things are different after such massive globalshock, and we anticipate some changes may be lasting. Yet, our main long-term investment premise remains unchanged – we expect, with noguarantees, that economies around the world will continue to grow at asolid pace over the coming decades, and equity markets will continue topresent attractive investment opportunities. The latest data from theInternational Monetary Fund supports our premise. As shown in the chartsbelow, developed and developing economies are expected to grow at amoderate to strong pace, and emerging economies are expected to increasetheir share of global GDP over the next five years, continuing the trend ofthe past 30 years.

World GDP Is Expected to Grow at A Solid Pace…Expected GDP Growth

Developed ex. U.S.

Emerging

World

U.S.

2%

3%

4%

5%

6%

7%

8%

2022 2023 2024 2025 2026

…Driven By Developing EconomiesShare of World GDP

United States

Developed Countries

ex. USA

China

India

Emerging Countriesex. China and India

Frontier/StandaloneRest of World

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

E20

22E

2024

E20

26E

Sources: GDP data from the International Monetary Fund, World Economic OutlookDatabase, April 2021. Country classifications from MSCI.

For over a decade, Baron has applied our long-term investment approach tonon-U.S. equities. Until recently, we had three mutual funds dedicated tonon-U.S./global equity investing. In July, we launched our fourth product,Baron New Asia Fund, a diversified portfolio which invests primarily incompanies with significant growth potential in Asia.

Our commitment to our non-U.S. products is driven by our strong belief thatthere are attractive investments outside the U.S. While many U.S. companiesare operating in non-U.S. markets, we believe that U.S. equities are not fullycapturing the dynamics and secular growth trends in other economies.

Investors tend to fall prey to home bias, a tendency to overinvest in theirhome country equities, which may result in missing out on the bestinvestment opportunities across the world. U.S. investors are not anexception. According to research by J.P. Morgan, the average U.S. investorhas about 78% of his or her equity allocation invested in U.S. stocks. At thesame time, U.S. stocks represent less than half of the total value of all globalpublic equities, and the U.S. represents less than 25% of global GDP, asshown on the next page.

7

Letter from Linda

U.S. Equity Investors Have a Home Bias

U.S. Investors

Average Equity Allocationby Geography

Global Equity Market

Market Cap Distribution

as of 9/30/2021

World GDP Estimates

GDP Percent Share

U.S. Equities

78%

Non-U.S.

Equities22%

U.S. Equities

43%Non-U.S. Equities

57%

$118 Tn

U.S.24.2%

Other Countries

75.8%

Sources: U.S. investors average equity allocation data from J.P. Morgan (published 9/30/2021); market capitalization data from FactSet as of 9/30/2021;

2021 GDP estimates data from the International Monetary Fund, World Economic Outlook Database, April 2021.

In the past, higher transaction costs and inaccessibility made non-U.S.equity investing difficult and inefficient. Nowadays, these hurdles have beenminimized, and investors have plenty of options to gain direct exposure tonon-U.S. markets.

One of the key advantages of investing globally is diversification. Companiesin different countries are positively or negatively affected by local changesand trends, independently of other developments around the world.

When stock prices are declining in the U.S., non-U.S. equities may move in adifferent direction or by a different magnitude, serving as potential offsetagainst the impact of the U.S. market.

Diversification helps investors mitigate the volatility of the returns of theirportfolios. Lower levels of correlations across markets provide a goodindicator of diversification opportunities. The chart below shows thecorrelation of returns of U.S. and non-U.S. equities over the past three, five,and 10 years. According to the data, the correlation between U.S. andemerging markets equities has been about 0.70 – 0.75, indicating amoderate tendency of the two to move similarly, which can providediversification benefits. The correlation with developed equity markets hasbeen slightly larger but still suggests diversification potential*.

Non-U.S. Equities Have Historically Offered DiversificationHistorical 3-, 5-, and 10-Year Correlations of U.S. Equities vs. Non-U.S. Equitiesas of 9/30/2021

0.97

0.82

0.74

0.97

0.81

0.70

0.96

0.81

0.69

0.50

0.75

1.00

World Equities

Non-U.S.Developed

EquityMarkets

Non-U.S.Emerging

EquityMarkets

3-Year

5-Year

10-Year

Sources: FactSet, Baron Capital.

World Equities are represented by the MSCI ACWI Index, Non-U.S. Developed Equity Markets are represented by the MSCI EAFE Index; Non-U.S. Emerging Equity Markets arerepresented by the MSCI Emerging Markets Index.

Note: A correlation of zero implies no relationship, while correlations close to 1 or -1 imply a strong positive or negative relationship, respectively. Correlations between 0.50 and0.70 are generally considered moderate. Correlation does not imply there is a causal relationship.

* Please note that diversification cannot guarantee a profit or protect against loss.

8

September 30, 2021 Letter from Linda

Historically, the relationship between the performance of U.S. and non-U.S.equities has moved in cycles. As shown on the charts below, periods ofbetter performance of U.S. stocks have been followed by periods of betterperformance of non-U.S. stocks. Over the past 10 years, the S&P 500 Indexhas outperformed both developed and emerging market equities. Althoughthis period of outperformance is longer than typical, it is not unprecedented(e.g., emerging markets outperformed U.S. stocks for about a decade, from2001 to 2012), and we believe that this cyclical pattern will remain.

The Performance of U.S. and Non-U.S. Equities Has BeenCyclical

Rolling 3-Year Differences in Annualized Returns

S&P 500 Index vs. (Developed MSCI EAFE Index)

-40%

-30%

-20%

-10%

0%

10%

20%

30%

Dec

-72

Dec

-74

Dec

-76

Dec

-78

Dec

-80

Dec

-82

Dec

-84

Dec

-86

Dec

-88

Dec

-90

Dec

-92

Dec

-94

Dec

-96

Dec

-98

Dec

-00

Dec

-02

Dec

-04

Dec

-06

Dec

-08

Dec

-10

Dec

-12

Dec

-14

Dec

-16

Dec

-18

Dec

-20

S&P 500 Index Outperformed

MSCI EAFE Index Outperformed

S&P 500 Index vs. (Emerging MSCI EM Index)

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

Dec

-72

Dec

-74

Dec

-76

Dec

-78

Dec

-80

Dec

-82

Dec

-84

Dec

-86

Dec

-88

Dec

-90

Dec

-92

Dec

-94

Dec

-96

Dec

-98

Dec

-00

Dec

-02

Dec

-04

Dec

-06

Dec

-08

Dec

-10

Dec

-12

Dec

-14

Dec

-16

Dec

-18

Dec

-20

S&P 500 Index Outperformed

MSCI EM Index Outperformed

Sources: FactSet, Baron Capital.

The performance data quoted represents past performance. Past performance is noguarantee of future results. The index performance is not fund performance; onecannot invest directly into an index.

We cannot predict if or when the outperformance cycle may reverse. Itcould take a week, a year, or longer until it changes. As we have discussedmany times in the past, we believe market timing is not a good and durableinvestment strategy. We do believe, however, that having a balancedinvestment in global equities allows investors to capture opportunities asthey arise.

One reason to think the relative performance cycle may turn sooner thanlater is current relative valuations. As the charts below show, both developedand emerging market equities are valued significantly below U.S. equities. Itis hard to imagine that these discounts could become larger before somereversion to the historical average occurs.

Non-U.S. Equity Valuations Are Attractive

Forward P/E Ratio of Developed Foreign Equities

as Percent of U.S. Equities

76%

Historical Average

90%

40%

50%

60%

70%

80%

90%

100%

110%

Sep-

01

Sep-

02

Sep-

03

Sep-

04

Sep-

05

Sep-

06

Sep-

07

Sep-

08

Sep-

09

Sep-

10

Sep-

11

Sep-

12

Sep-

13

Sep-

14

Sep-

15

Sep-

16

Sep-

17

Sep-

18

Sep-

19

Sep-

20

Sep-

21

Forward P/E Ratio of Emerging Foreign Equities

as Percent of U.S. Equities

63%

Historical Average

74%

40%

50%

60%

70%

80%

90%

100%

110%

Sep-

01

Sep-

02

Sep-

03

Sep-

04

Sep-

05

Sep-

06

Sep-

07

Sep-

08

Sep-

09

Sep-

10

Sep-

11

Sep-

12

Sep-

13

Sep-

14

Sep-

15

Sep-

16

Sep-

17

Sep-

18

Sep-

19

Sep-

20

Sep-

21

Sources: FactSet, Baron Capital.

Note: Forward P/E Ratio is the next 12-month price-to-earnings ratio, based onFactSet estimates.

U.S. Equities are represented by the S&P 500 Index; Developed Foreign Equities arerepresented by the MSCI EAFE Index; Emerging Foreign Equities are represented by theMSCI EM Index.

9

Letter from Linda

The lasting underperformance of non-U.S. developed and emerging marketequity indexes does not mean that there haven’t been lucrativeopportunities in those markets. The performance of the popular indexes is amarket-cap weighted average outcome and does not provide informationabout the dispersion of the returns of the underlying index constituents.

The chart below illustrates the range of returns, or dispersion, of the stocksin the U.S. and non-U.S. equity markets over the past 10 years, as well asthe average stock returns in those markets. For example, in the U.S., thestock(s) that ranked in the 10th percentile by performance returned around

35% annualized, while the stock(s) that ranked in the 90th percentile lostaround 40% of their value on an annualized basis. (Our analysis is based onthe 10th and 90th percentiles to mitigate the effects of outliers.) Theaverage stock return in the U.S. was approximately 5.8% per year. Similarly,in China, stock performance ranged between 47% and -31%, with anaverage of 5.3% per year. This information suggests at least two things:(i) judging by the average returns, both the U.S. and China were good placesto invest, and (ii) the performance of the companies in both countries variedsignificantly.

Stocks In Different Markets Have Generated Attractive Spreads of ReturnsDispersion of Returns by Markets9/30/2011 – 9/30/2021, annualized

90th percentile

10th percentile

average

-60%

-45%

-30%

-15%

0%

15%

30%

U.S. E

quities

Emer

ging

Mar

kets

Develo

ped e

x. U.S.

United K

ingd

om

Fran

ce

Germ

any

Israe

l

Japan

Nether

lands

Spain

Switz

erlan

dKore

a

China

India

Brazil

Russia

60%

45%

Source: FactSet, Baron Capital.

U.S. Equities are represented by the Russell 3000 Index; Emerging Markets – by the MSCI EM Index; Developed ex. U.S. – by the MSCI EAFE Index; individual countries arerepresented by the stocks in the MSCI ACWI ex USA Index classified in the respective country. Dispersion is measured as the difference between the returns at the 10th and 90th

percentiles. The performance data quoted represents past performance. Past performance is no guarantee of future results. The index performance is not fund performance; onecannot invest directly into an index.

The average returns of U.S. and Chinese stocks were moderately good butcertainly not great. Since both markets experienced large dispersion, a skilledactive manager who is picking specific stocks could have producedsignificantly better results.

This conclusion is supported by an additional analysis, which also shows thatnot only were there great stocks in non-U.S. markets over the past decade,but also that there were plenty of them. According to the data shown

below, around 30% of the companies in the MSCI EAFE Index (developedmarkets equities) and the MSCI EM Index (emerging markets equities)outperformed the U.S. stock market in a typical calendar year. This result isdespite the lasting poor relative performance of both indexes versus U.S.equities. This result has been consistent in the first nine months of 2021 – asubstantial number of non-U.S. stocks have delivered higher returns than theS&P 500 Index despite the underperformance of both the MSCI EAFE Indexand the MSCI EM Index.

There are Always Good Opportunities in Non-U.S. Equity Markets

Index Returns and Outperformance Rates of Non-U.S. Stocks by Calendar Year*YTD 9/30/21 CY 2020 CY 2019 CY 2018 CY 2017 CY 2016 CY 2015 CY 2014 CY 2013 CY 2012 CY 2011

S&P 500 Index – Return 15.92% 18.40% 31.49% –4.38% 21.83% 11.96% 1.38% 13.69% 32.39% 16.00% 2.11%MSCI EAFE Index –Return 8.35% 7.82% 22.01% –13.79% 25.03% 1.00% –0.81% –4.90% 22.78% 17.32% –12.14%MSCI EM Index – Return –1.25% 18.31% 18.42% –14.58% 37.28% 11.19% –14.92% –2.19% –2.60% 18.22% –18.42%

% of Stocks in MSCIEAFE IndexOutperforming the S&P500 Index

32% 31% 32% 30% 57% 29% 51% 21% 35% 52% 25%

% of Stocks in MSCI EMIndex Outperforming theS&P 500 Index

30% 37% 28% 35% 55% 38% 23% 32% 11% 56% 19%

Source: FactSet, Baron Capital.

* Except for YTD 9/30/21, which is the period from 12/31/20 to 9/30/21. The performance data quoted represents past performance, including dividends. Past performance is noguarantee of future results. The index performance is not fund performance; one cannot invest directly into an index.

10

September 30, 2021 Letter from Linda

Performing the same analysis over rolling three-year periods shows similar results: typically, 20%-30% of non-U.S. stocks outperformed the S&P 500 Index.

Index Returns and Outperformance Rates of Non-U.S. Stocks by Rolling Three-Year PeriodsFor the 3 Years Ended:

9/30/21 12/31/20 12/31/19 12/31/18 12/31/17 12/31/16 12/31/15 12/31/14 12/31/13

S&P 500 Index – Return 56.07% 48.85% 53.17% 30.42% 38.29% 29.05% 52.59% 74.60% 56.82%

MSCI EAFE Index – Return 24.66% 13.41% 31.52% 8.87% 25.26% –4.73% 15.81% 36.98% 26.55%

MSCI EM Index – Return 28.03% 19.69% 38.89% 30.40% 29.87% –7.47% –18.94% 12.63% –6.07%

% of Stocks in MSCI EAFE IndexOutperforming the S&P 500 Index

12% 20% 27% 29% 42% 22% 27% 24% 24%

% of Stocks in MSCI EM IndexOutperforming the S&P 500 Index

20% 19% 26% 41% 30% 16% 9% 18% 11%

Source: FactSet, Baron Capital. The performance data quoted represents past performance, including dividends.Past performance is no guarantee of future results. The index performance is not fund performance; one cannot invest directly into an index.

There are two significant takeaways from the above data:

(i) Non-U.S. developed and emerging markets equities havecontinuously offered attractive investment opportunities; and

(ii) The MSCI EAFE Index and the MSCI EM Index haveunderperformed the S&P 500 Index most of the time over thepast decade, which indicates their construction has not enabledthem to capture the attractive investment opportunities in anoptimal way.

While the popular non-U.S. equity indexes can serve as a rough proxy forthe potential benefits of non-U.S. investing, in our view indexes have manydesign flaws to serve as models for actual investments.

One of the biggest drawbacks of such indexes is overdiversification due tothe inclusion of many stocks. As of 9/30/2021, the MSCI EAFE Index had845 constituents, and the MSCI EM Index had 1,418 constituents. After ahundred or so investments, the marginal diversification benefits of eachadditional holding become close to zero and turn mostly into redundancies.

In addition, many popular indexes are constructed to give more weight tostocks that have done best in the past, rather than the ones with higherfuture growth opportunities. This exposes investors in passive products thattrack these indexes to unmanaged momentum risk, among other risks.

Furthermore, indexes cannot account for a variety of risks and developmentsthat are important but hard to quantify or evaluate. These include politicalrisks, corruption, structural reforms, secular growth trends, demographicchanges, and many more. The nature and variety of these risks makes beingflexible and forward looking an essential prerequisite, particularly wheninvesting in less efficient markets.

In our view, skilled active non-U.S. equity managers can build and manage well-balanced portfolios without the deficiencies of an index and, as a result,potentially deliver significantly better returns. The scorecard below shows thatactive non-U.S. equity managers tend to outperform their Morningstar categorybenchmark a significant percentage of the time, delivering strong excess returns,particularly over longer investment periods. Their outperformance rates tend tobe stronger than those of active U.S. equity managers. The results from our high-level analysis include all active managers, good and bad.

A Significant Portion of Active Non-U.S. Equity Managers Have OutperformedHistorical Track Record of Active Managers in Select Equity Categoriesas of 9/30/2021

ForeignLarge Blend

ForeignLarge Growth

ForeignLarge Value

DiversifiedEmerging Markets

WorldStock*

AllForeign Funds

AllU.S. Funds**

Based on 1-YrExcess Returns

% Active Funds Outperforming 58% 77% 36% 60% 52% 59% 52%

Average Excess Return – All Active Funds 0.58% 3.60% –2.17% 3.06% 0.32% 1.98% 1.01%

Average Excess Return – Outperforming Funds 4.38% 6.01% 6.40% 8.34% 6.50% 7.18% 7.32%

Based on 3-YrExcess Returns

% Active Funds Outperforming 48% 63% 79% 62% 45% 58% 35%

Average Excess Return – All Active Funds –0.11% 1.46% 1.30% 2.43% –0.10% 1.22% –0.81%

Average Excess Return – Outperforming Funds 2.26% 3.59% 1.92% 4.96% 3.74% 3.86% 3.51%

Based on 5-YrExcess Returns

% Active Funds Outperforming 44% 68% 55% 44% 44% 51% 37%

Average Excess Return – All Active Funds –0.45% 1.25% 0.21% 0.38% –0.33% 0.37% –0.72%

Average Excess Return – Outperforming Funds 1.32% 2.64% 1.21% 2.89% 2.67% 2.61% 2.57%

Based on 10-YrExcess Returns

% Active Funds Outperforming 77% 76% 87% 57% 49% 68% 26%

Average Excess Return – All Active Funds 0.83% 1.35% 1.21% 0.68% –0.17% 0.82% –1.10%

Average Excess Return – Outperforming Funds 1.32% 1.98% 1.51% 1.95% 1.75% 1.88% 1.37%

Source: Morningstar Direct, Baron Capital. Note: The calculations are based on excess returns of each fund’s oldest share class vs. the category benchmark of the Morningstarcategory in which the fund was classified as of 9/30/2021. * Includes all funds classified in the following categories: US Fund World Large-Stock Blend, US Fund World Large-StockGrowth, US Fund World Large-Stock Value, US Fund World Small/Mid Stock. ** Includes all U.S. equity funds classified in Morningstar’s nine traditional style boxes. Theperformance data quoted represents past performance. Past performance is no guarantee of future results.

11

Letter from Linda

In our view, the meaningful outperformance rates and excess returns of active non-U.S. equity managers make a strong case for active over passive investing.Yet, flows in passive products continue to prevail, with those investors getting rewarded with only average market returns and missing a significantopportunity to outperform by a large margin.

Baron’s Approach to Non-U.S. Equity Investing

For over a decade, non-U.S. equity markets have been a significant source for investment ideas at Baron. Just as in the U.S., we are focused on innovation,durable, long-term growth opportunities, competitive advantages, and strong management teams. Currently, we have six investment professionals dedicatedto non-U.S. equity research, and many of our other research team members often contribute their industry expertise and global perspectives.

As of September 30, 2021, Baron Capital had over $14 billion invested in non-U.S. equities across all portfolios we manage. This represented approximately26% of our assets under management. Most of these assets were invested in our Global, International, and Emerging Markets Strategies.

Baron Has Significant Investments in Non-U.S. EquitiesBaron Capital – Breakdown of Total Assets Under Management,

as of 9/30/2021

U.S. Equities72.9%

Foreign -Emerging Markets18.5%

Foreign -Developed

Markets

Other 1.2%

7.2%

Total AssetsUnder

Management$54.6 Bn

Source: Morningstar Direct, Baron Capital.

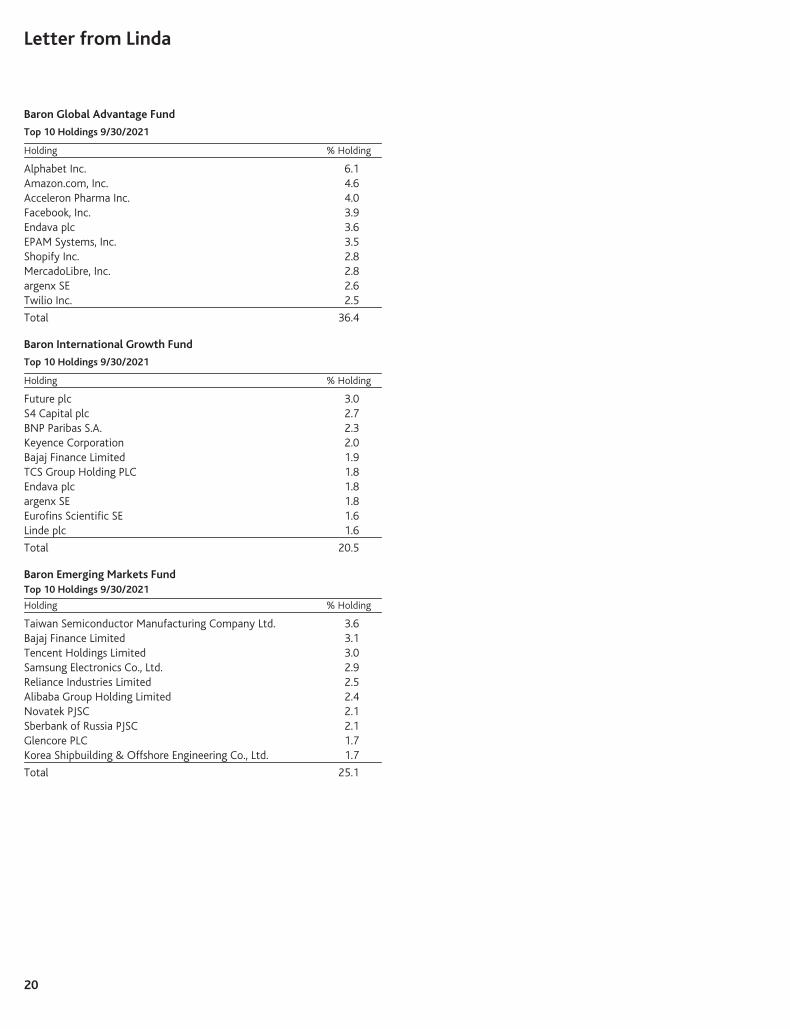

Our top 10 largest mutual fund investments in non-U.S. equities had a combined value of $2.8 billion as of 9/30/2021. As shown in the table below, Baron’scost for these investments was $1.6 billion, and over time they have generated $1.4 billion in realized and unrealized gains for our shareholders. For moreinformation about these companies, please see the appendix to this letter for business descriptions and our investment premises.

Baron’s Top Non-U.S. Holdings Have Generated Significant ReturnsBaron Funds – Top 10 Largest Non-U.S. Positions (Currently Held)

as of 9/30/2021

Security Cumulative Excess Return vs.

Security Name

AggregateBaron Funds

Cost($ millions)

AggregateBaron Funds

Gains($ millions)

AggregateBaron FundsInvestment

Value($ millions)

AggregateBaron Funds

% of NetAssets

# ofYearsHeld

SecurityCumulativeTotal Return

Russell 3000Growth Index

MSCI ACWIex USA Index

MSCI EMIndex

Bajaj Finance Ltd $ 191 $ 162 $ 367.5 0.76% 2.9 229.0% 128.1% 188.8% 186.8%

Taiwan Semiconductor Manufacturing Company Ltd. $ 182 $ 226 $ 345.7 0.72% 8.3 669.0% 364.4% 597.2% 604.4%

Endava plc $ 77 $ 230 $ 299.0 0.62% 3.2 439.1% 351.5% 413.6% 414.3%

Alibaba Group Holding Ltd $ 269 $ 46 $ 281.8 0.58% 7.0 57.7% –157.1% 10.8% 14.6%

Tencent Holdings Ltd. $ 181 $ 111 $ 280.5 0.58% 7.4 356.1% 116.5% 308.8% 307.3%

Samsung Electronics Co., Ltd. $ 166 $ 134 $ 272.4 0.56% 7.9 169.3% –89.6% 114.9% 118.0%

Adyen N.V. $ 84 $ 172 $ 255.4 0.53% 3.3 422.5% 332.8% 398.1% 401.4%

Wix.com Ltd. $ 128 $ 247 $ 240.5 0.50% 4.8 351.0% 183.9% 290.8% 283.3%

Reliance Industries Ltd. $ 147 $ 83 $ 236.8 0.49% 2.6 78.9% –7.3% 47.3% 50.8%

Spotify Technology S.A. $ 217 –$ 5 $ 215.0 0.44% 1.7 46.0% –3.1% 25.9% 25.4%

Total: $1,642 $ 1,407 $2,795 5.8%

Source: FactSet, Baron Capital.

The performance data quoted represents past performance. Past performance is no guarantee of future results. Portfolio holdings are subject to change. Current and futureportfolio holdings are subject to risk.

These 10 stocks are not only our largest non-U.S. investments; some of them are also among our longest-held investments. All 10 stocks have delivered significantabsolute returns over time, and all 10 have outperformed the MSCI EM Index and MSCI ACWI ex USA Index. Furthermore, despite the decade-long outperformanceof U.S. equities, six of these investments have significantly outperformed the Russell 3000 Index, and another two performed almost as well as the index.

12

September 30, 2021 Letter from Linda

Currently, Baron has four mutual funds dedicated to non-U.S./global equity investing:

- Baron Global Advantage Fund, which invests in growth companies around the world; and- Baron International Growth Fund, which invests mainly in non-U.S. growth companies in developed countries; and- Baron Emerging Markets Fund, which invests mainly in emerging market growth companies; and- Baron New Asia Fund, which invests primarily in growth companies located in Asia.

Like every Baron product, all four Funds invest with a long-term view, and their primary objective is to generate excess returns driven by positive stockselection. However, each Fund’s strategy for achieving this objective is different. The chart on the left below shows each Fund’s equity investments by country.There are distinct differences among the Funds and versus a popular global equity index. The chart on the right shows the end market exposures of theportfolio companies, as it reflects the geographic source of their revenues.

The Baron Non-U.S./Global Equity Funds Are Distinctly DifferentBaron International Funds – Weights by Region/Country

as of 9/30/2021

61.1%58.6%

19.3%

67.7%

5.8% 6.5%

29.4%

10.4%

11.6%

32.6%

8.5%

6.7%3.4%8.4%

29.4%

48.9%

5.8% 9.8%

31.7% 34.4%

3.7%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

China

India

Baron Global Advantage Fund

Baron International Growth Fund

Baron Emerging Markets F

und

Baron New Asia Fund

MSCI ACWI IMI In

dex

Other Emerging

Other Developed

USA

Source: FactSet, Baron Capital.

Calculations exclude cash held in the portfolios. Revenue Exposure is estimated usingFactSet’s geographical revenue data as of 9/30/2021.

Baron International Funds – Revenue Exposure by Region/Country,

as of 9/30/2021

22.4%

9.3% 5.1% 5.2%

27.4%

27.9%

31.4%

8.5% 10.7%

34.2%

20.1%

23.4%

32.1%20.4%

20.4%3.6%4.5%

6.7%

7.5%

3.8%26.0% 31.4%

47.6%56.2%

14.2%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Baron Global Advantage Fund

Baron International Growth Fund

Baron Emerging Markets F

und

Baron New Asia Fund

MSCI ACWI IMI In

dex

Baron Global Advantage Fund has been managed by Alex Umansky since its inception in April 2012. Typically, the Fund has around 45 – 55 investments, farfewer than its primary benchmark, the MSCI ACWI Index (~3,000 holdings). As of 9/30/2021, its top 10 holdings represented over 36% of the portfolio,reflecting the high conviction of the manager. Yet, the Fund is well diversified across market capitalization, industries, geographies, and end markets. The chartsbelow show the Fund’s absolute and relative exposures by sector and geography.

Alex focuses on businesses that are driving or benefitting from disruptive change. To find such companies, Alex looks for the agents and/or beneficiaries ofdisruptive change in areas such as digitization, big data, cloud computing, machine learning, and autonomous driving.

He finds platform companies to be particularly well positioned to potentially benefit from disruptive change, as they can capitalize on scalable network effectsand large and diverse global addressable markets. Alex focuses on platform businesses with meaningful barriers to entry that have the ability to create aneco-system around their businesses that incentivizes partners to co-create value, benefit from network effects, which increases moats over time, and earn highmarginal profits (as the platform increases in value). In addition to the above criteria, Alex favors companies that have secular organic growth, strong free cashflows, higher/rising returns on invested capital, and low capital intensity. Our latest Baron Investor piece on Baron Global Advantage Fund, available on ourwebsite1, offers greater detail about the Fund and how Alex finds investment ideas.

1 https://www.baronfunds.com/investment-insights

13

Letter from Linda

Baron Global Advantage Fund is Differentfrom its BenchmarkBaron Global Advantage Fund vs. MSCI ACWI Indexas of 9/30/2021

SectorPortfolio Weight

Overweight/Underweight

16.4%%8.83Information Technology%9.7%6.91Health Care

%2.5%5.41Communication Services%6.4%0.71Consumer Discretionary

%2.1-%4.1Real Estate%6.2---Utilities

%5.3---Energy%0.4-%7.0Materials

Consumer Staples -- -6.8%%2.8-%5.1Industrials

%2.01-%1.4Financials

CountriesPortfolio Weight

Overweight/Underweight

%8.4%0.5Israel%0.4%3.5Netherlands

%5.3%6.3Argentina%4.2%3.5Canada

%9.1%3.3India%7.1%7.5China%6.1%6.1Uruguay%3.1%5.1Indonesia%2.1%7.1Brazil%9.0%4.06United States%6.0%7.0Poland

%1.0%4.0Mexico%1.0-%6.3KingdomUnited%9.0-%7.0Korea

Other Emerging -- -3.9%Other Developed -- -20.5%

Sources: FactSet, Baron Capital, MSCI.

Baron International Growth Fund has been managed by Michael Kasssince its inception in December 2008. The Fund usually invests in fewer than100 companies, far below the number of constituents in its primarybenchmark, the MSCI ACWI ex USA Index (~2,300 holdings). As of9/30/2021, its top 10 holdings represented over 20% of the portfolio.Michael takes significant active positions across individual companies,industries, and markets, which makes Baron International Growth Fundnotably different from its benchmark. The charts below show the Fund’sabsolute and relative exposures by sector and geography.

Michael has been combining investment themes and fundamental bottom-upstock picking to manage Baron International Growth Fund. Themes may bedriven by developments such as regulatory, political, or technologicalchanges; vertical integration in an industry; or changes in the financial oreconomic environment. They may be industry-specific (e.g., industrialautomation & robotics), country- and regional-specific (e.g., capital marketand credit expansion), or global in scope (e.g., intellectual capital,best-in-class). In international markets, we emphasize entrepreneurialmanagement, founders with significant ownership stakes, leaders withstrategic vision and financial sophistication, and management that thinks andacts like an “owner.” Our latest Baron Investor piece on Baron InternationalGrowth Fund, available on our website1, offers greater detail about the Fundand describes how Michael combines secular growth themes and bottom-upinvesting to find attractive investments outside the U.S.

Baron International Growth Fund is Differentfrom its BenchmarkBaron International Growth Fund vs. MSCI ACWI ex USA Indexas of 9/30/2021

SectorPortfolio Weight

Overweight/Underweight

%3.4%6.01Communication Services

%1.2%6.11CareHealth

%9.1%1.51Information Technology

%8.0%8.8Materials

%4.0-%8.11Industrials

%2.1EstateReal -1.4%

%9.2Energy -2.0%

Consumer Discretionary 10.3% -2.4%

--Utilities -3.0%

%5.41Financials -4.8%

Consumer Staples 2.8% -5.7%

CountriesPortfolio Weight

Overweight/Underweight

%4.8%5.71KingdomUnited

%9.3%5.7India

%7.2%9.3Russia

%3.2%7.2Israel

%3.2%3.2StatesUnited

%1.2%2.5Netherlands

%6.1%0.3Brazil

%6.1%1.3Spain

%6.0%8.0Poland

%2.0%6.0Norway

%30.0-%5.0Mexico

%2.0-%1.2Sweden

%4.0-%7.6France

%5.0-%0.1Italy

%6.0-%0.1Denmark

%0.1-%8.0KongHong

%3.1-%8.8China

%6.1-%4.4Switzerland

%8.1-%0.4Germany

%6.2-%1.1Korea

Other Developed -- -2.8%

%7.3-%7.0Australia

%1.5-%0.2Canada

%2.6-%2.9Japan

Other Emerging -- -8.9%

Sources: FactSet, Baron Capital, MSCI.

Baron Emerging Markets Fund has also been managed by Michael Kass sinceits inception in December 2010. The Fund usually invests in fewer than 100companies, significantly below the number of constituents in its primarybenchmark, the MSCI EM Index (~1,400 holdings). As of 9/30/2021, its top 10holdings represented over 25% of the portfolio. Michael takes significant activepositions across individual companies, industries, and markets, which makesBaron Emerging Markets Fund notably different from its benchmark. The chartsbelow show the Fund’s absolute and relative exposures by sector and geography.

Similar to Baron International Growth Fund, Michael has been combininginvestment themes and fundamental bottom-up stock picking to manage BaronEmerging Markets Fund. He looks for global economic, financial, and politicaldevelopments that will drive inflection points or trends. According to Michael,trends yield long-term value creation around which he constructs investablethemes. Some examples of current themes include: digitization, where the

1 https://www.baronfunds.com/investment-insights

14

September 30, 2021 Letter from Linda

primary beneficiaries include e-commerce platforms, data center operators, andmobile gaming & advertising companies; and India financialization, where theprimary beneficiaries include asset/mutual fund managers, wealth managers,and life insurers. In addition, Michael emphasizes entrepreneurial management,capital efficiency, and shareholder-friendly governance. Our latest Baron Investorpiece on Baron Emerging Markets Fund, available on our website1, offers greaterdetail about the Fund and describes how Michael finds attractive investmentopportunities in the complex world of emerging markets.

Baron Emerging Markets Fund is Differentfrom its BenchmarkBaron Emerging Markets Fund vs. MSCI EM Indexas of 9/30/2021

SectorPortfolio Weight

Overweight/Underweight

%5.5%4.01Industrials

%8.3%8.8Health Care

%3.0-%8.1Real Estate

Consumer Staples 5.3% -0.7%

%8.0-%0.5Energy

%3.1-%4.7Materials

%3.1-%1.81Financials

Consumer Discretionary 12.5% -2.2%

%3.2---Utilities

Communication Services 6.4% -3.9%

Information Technology 15.4% -5.5%

CountriesPortfolio Weight

Overweight/Underweight

%6.41%8.62India

%9.3%8.7Russia

%2.2%2.2Hong Kong

%7.1%2.6Brazil

%7.1%7.1United Kingdom

%1.1%1.1Japan

%0.1%2.1Hungary

%6.0%2.1Philippines

%4.0%4.0Norway

%4.0%4.0United States

%2.0%4.0Peru

%2.0%9.0Poland

%10.0%9.1Mexico

United Arab Emirates 0.3% -0.5%

%1.5-%9.82China

%5.7-%1.5Korea

%1.01-%6.4Taiwan

Other Emerging -- -13.6%