printmgr file - Nomura Now

675

FINAL OFFER DOCUMENT Dated March 27, 2019 Book Built Issue Embassy Office Parks REIT (Registered in the Republic of India as an irrevocable trust under the Indian Trusts Act, 1882 and as a real estate investment trust under the Securities and Exchange Board of India (Real Estate Investment Trusts) Regulations, 2014, on August 3, 2017 at Bengaluru having registration number IN/REIT/17-18/0001) Principal Place of Business: Royal Oaks, Embassy Golf Links Business Park, Off Intermediate Ring Road, Bengaluru 560 071, Karnataka, India Tel: +91 80 3322 0000/ 2222; Fax: +91 80 4903 0046; Compliance Officer: Ramesh Periasamy E-mail: [email protected]; Website: www.embassyofficeparks.com TRUSTEE MANAGER EMBASSY SPONSOR BLACKSTONE SPONSOR AXIS TRUSTEE Axis Trustee Services Limited Embassy Office Parks Management Services Private Limited Embassy Property Developments Private Limited BRE/ Mauritius Investments Embassy Office Parks REIT (“Embassy REIT”) is issuing 158,333,200* Units (as defined herein) for cash at a price of `300 per Unit aggregating `47,499.96* million (the “Issue”). * Subject to finalization of Basis of Allotment INITIAL PUBLIC ISSUE IN RELIANCE UPON REGULATION 14(1) OF THE SECURITIES AND EXCHANGE BOARD OF INDIA (REAL ESTATE INVESTMENT TRUSTS) REGULATIONS, 2014, AS AMENDED (THE “REIT REGULATIONS”) The Units of the Embassy REIT are proposed to be listed on the National Stock Exchange of India Limited (the “NSE”) and BSE Limited (the “BSE”, together with the NSE, the “Stock Exchanges”). The Embassy REIT has received in-principle approvals from the NSE and the BSE for listing of the Units pursuant to letters dated October 11, 2018 and October 9, 2018, respectively. NSE is the Designated Stock Exchange for this Issue. This Issue will constitute 20.52%* of the issued and paid-up Units on a post-Issue basis in accordance with Regulation 14(2A) of the REIT Regulations. * Subject to finalization of Basis of Allotment The Price Band and the Minimum Bid Size (as determined by the Manager in consultation with the Lead Managers) was announced on the websites of the Embassy REIT, the Embassy Sponsor, the Manager and the Stock Exchanges as well as advertised in all editions of the Financial Express (a widely circulated English national daily newspaper), all editions of Jansatta (a widely circulated Hindi national daily newspaper) and in all editions of Vishwavani (a Kannada daily newspaper with wide circulation in Karnataka) at least two Working Days prior to the Bid/ Issue Opening Date. The announcement/ advertisement contained relevant financial ratios computed for both the upper and lower end of the Price Band. For further information, see “Basis for Issue Price” on page 434. This Issue is being made through the Book Building Process and in compliance with the REIT Regulations and the SEBI Guidelines, wherein not more than 75% of the Issue (excluding the Strategic Investor Portion) was available for allocation on a proportionate basis to Institutional Investors. The Manager in consultation with the Lead Managers, allocated up to 60% of the Institutional Investor Portion to Anchor Investors on a discretionary basis in accordance with the REIT Regulations and the SEBI Guidelines. Further, not less than 25% of the Issue (excluding the Strategic Investor Portion) was available for allocation on a proportionate basis to Non-Institutional Investors, in accordance with the REIT Regulations and the SEBI Guidelines, subject to valid Bids being received at or above the Issue Price. The Issue also includes participation by Strategic Investors (as defined hereafter) in accordance with the SEBI Guidelines. For details, see “Issue Information” on page 404. RISKS IN RELATION TO THE FIRST ISSUE This being the first issue of Units by the Embassy REIT, there has been no formal market for the Units of the Embassy REIT. No assurance can be given regarding the active or sustained trading in Units or regarding the price at which the Units will be traded after listing. GENERAL RISKS Investments in Units involve a degree of risk and investors should not invest any funds in the Issue unless they can afford to take the risk of losing their entire investment. For taking an investment decision, investors must rely on their own examination of the Embassy REIT and the Issue. Prospective Investors are advised to read “Risk Factors” on page 22 before making an investment decision relating to the Issue. Each prospective investor is advised to consult its own advisors in respect of the consequences of an investment in the Units being issued pursuant to the Offer Document and this Final Offer Document. This Final Offer Document has been prepared by the Manager solely for providing information in connection with the Issue. The Securities and Exchange Board of India (“SEBI”) and the Stock Exchanges assume no responsibility for or guarantee the correctness or accuracy of any statements made, opinions expressed or reports contained herein. Admission of the Units to be issued pursuant to the Issue for trading on the Stock Exchanges should not be taken as an indication of the merits of the Embassy REIT or of the Units. A copy of this Final Offer Document has been delivered to the SEBI and the Stock Exchanges. MANAGER’S AND SPONSORS’ ABSOLUTE RESPONSIBILITY The Manager having made all reasonable inquiries, accepts responsibility for and confirms that this Final Offer Document contains all information with regard to the Embassy REIT and the Issue, which is material in the context of the Issue, that the information contained in this Final Offer Document is true and correct in all material aspects and is not misleading in any material respect, that the opinions and intentions expressed herein are honestly held and that there are no other facts, the omission of which makes this Final Offer Document as a whole or any of such information or the expression of any such opinions or intentions misleading in any material respect. Each Sponsor, severally and not jointly, accepts responsibility for and confirms only the statements specifically confirmed or undertaken by such Sponsor in this Final Offer Document, to the extent of the information specifically pertaining to such Sponsor. GLOBAL COORDINATORS AND BOOK RUNNING LEAD MANAGERS REGISTRAR TO THE ISSUE Morgan Stanley India Company Private Limited 18F, Tower 2, One Indiabulls Centre 841, Senapati Bapat Marg Mumbai 400 013 Maharashtra, India Tel: +91 22 6118 1000 Fax: +91 22 6118 1040 E-mail: [email protected] Investor grievance e-mail: [email protected] Website: www.morganstanley.com Contact Person: Prakhar Jaju SEBI Registration No.: INM000011203 Kotak Mahindra Capital Company Limited 1 st Floor, 27 BKC Plot No. C - 27, “G” Block Bandra Kurla Complex Bandra (East), Mumbai 400 051 Maharashtra, India Tel: +91 22 4336 0000 Fax: + 91 22 6713 2447 E-mail: [email protected] Investor grievance e-mail: [email protected] Website: www.investmentbank.kotak.com Contact Person: Ganesh Rane SEBI Registration No.: INM000008704 J.P. Morgan India Private Limited J.P. Morgan Tower Off. C.S.T. Road Kalina, Santacruz (East) Mumbai 400 098 Maharashtra, India Tel: +91 22 6157 3000 Fax: +91 22 6157 3911 E-mail: [email protected] Investor grievance e-mail: [email protected] Website: www.jpmipl.com Contact Person: Saarthak K Soni SEBI Registration No.: INM000002970 DSP Merrill Lynch Limited Ground Floor, “A” Wing One BKC, “G” Block Bandra Kurla Complex Bandra (East), Mumbai 400 051 Maharashtra, India Tel: +91 22 6632 8000 Fax: +91 22 2204 8518 E-mail: [email protected] Investor grievance e-mail: [email protected] Website: www.ml-india.com Contact Person: Karthik S. Prabhakaran SEBI Registration No.: INM000011625 Karvy Fintech Private Limited (formerly KCPL Advisory Services Private Limited) Karvy Selenium Tower B Plot 31-32, Gachibowli, Financial District, Nanakramguda, Hyderabad 500 032 Telangana, India Tel: +91 40 6716 2222 Fax: +91 40 2343 1551 E-mail: [email protected] Investor grievance e-mail: [email protected] Website: http://www.karvyfintech.com Contact Person: Mr. M Murali Krishna SEBI Registration No.: INR000000221 ## BOOK RUNNING LEAD MANAGERS Axis Capital Limited 1 st Floor, Axis House C-2 Wadia International Centre P.B. Marg, Worli Mumbai 400 025 Maharashtra, India Tel: +91 22 4325 2183 Fax: +91 22 4325 3000 E-mail: [email protected] Investor grievance e-mail: [email protected] Website: www.axiscapital.co.in Contact Person: Mayuri Arya SEBI Registration No.: INM000012029 Credit Suisse Securities (India) Private Limited 9F/10F, Ceejay House Plot “F” Dr. Annie Besant Road Worli, Mumbai 400 018 Maharashtra, India Tel: +91 22 6777 3885 Fax: +91 22 6777 3820 E-mail: list.embassyreit@credit- suisse.com Investor grievance e-mail: list.igcellmer-bnkg@credit- suisse.com Website: www.credit- suisse.com Contact Person: Anand Bang SEBI Registration No.: INM000011161 Deutsche Equities India Private Limited The Capital, 14 th floor C-70, “G” Block Bandra Kurla Complex Mumbai 400 051 Maharashtra, India Tel: +91 22 7180 4444 Fax: +91 22 7180 4199 E-mail: [email protected] Investor grievance e-mail: [email protected] Website: www.db.com/India Contact Person: Viren Jairath SEBI Registration No.: INM000010833 Goldman Sachs (India) Securities Private Limited Rational House 951-A, Appasaheb Marathe Marg Prabhadevi Mumbai 400 025 Maharashtra, India Tel: +91 22 6616 9000 Fax: +91 22 6616 9001 E-mail: gs- embassyofficeparks- [email protected] Investor grievance e-mail: [email protected] Website: www.goldmansachs.com Contact Person: Mrinalini Baral SEBI Registration No.: INM000011054 HSBC Securities and Capital Markets (India) Private Limited 52/60, Mahatma Gandhi Road Fort, Mumbai 400 001 Maharashtra, India Tel: +91 22 2268 5555 Fax: +91 22 2263 1284 E-mail: [email protected] Investor grievance e-mail: investorgrievance@hsbc. co.in Website: www.hsbc.co.in/ 1/2/corporate/ equitiesglobalinvestment banking Contact Person: Shreye Mirani/ Vaibhav Grewal SEBI Registration No.: INM000010353 IIFL Holdings Limited IIFL Centre, 10th Floor Kamala City, Senapati Bapat Marg Lower Parel (West) Mumbai 400 013 Maharashtra, India Tel: +91 22 4646 4600 Fax: +91 22 2493 1073 E-mail: [email protected] Investor grievance e-mail: [email protected] Website: www.iiflcap.com Contact Person: Devendra Maydeo/ Aditya Agarwal SEBI Registration No.: INM000010940 JM Financial Limited 7 th Floor, Cnergy Appasaheb Marathe Marg Prabhadevi Mumbai 400 025 Maharashtra, India Tel: +91 22 6630 3030 Fax: +91 22 6630 3330 E-mail: [email protected] Investor grievance e-mail: [email protected] Website: www.jmfl.com Contact Person: Prachee Dhuri SEBI Registration No.: INM000010361 Nomura Financial Advisory and Securities (India) Private Limited Ceejay House, Level 11 Plot “F” Shivsagar Estate Dr. Annie Besant Road Worli Mumbai 400 018 Maharashtra, India Tel: +91 22 4037 4037 Fax: +91 22 4037 4111 E-mail: [email protected] Investor grievance e-mail: investorgrievances-in @nomura.com Website: www.nomuraholdings.com /company/group/asia/india/ index.html Contact Person: Manish Agarwal/ Vishal Kanjani SEBI Registration No.: INM000011419 BID/ISSUE PROGRAM # BID/ ISSUE OPENED ON: March 18, 2019* BID/ ISSUE CLOSED ON: March 20, 2019 * The Anchor Investor Bid/Issue Period was March 15, 2019 # The Issue also includes participation by Strategic Investors in accordance with the SEBI Guidelines ## The registration is currently under the name of Karvy Computershare Private Limited. Karvy Fintech Private Limited has filed an application with the SEBI for registration under its new name, which is currently pending

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of printmgr file - Nomura Now

FINAL OFFER DOCUMENTDated March 27, 2019

Book Built Issue

Embassy Office Parks REIT(Registered in the Republic of India as an irrevocable trust under the Indian Trusts Act, 1882 and as a real estate investment trust under the Securities and Exchange Board of India (Real Estate Investment

Trusts) Regulations, 2014, on August 3, 2017 at Bengaluru having registration number IN/REIT/17-18/0001)Principal Place of Business: Royal Oaks, Embassy Golf Links Business Park, Off Intermediate Ring Road, Bengaluru 560 071, Karnataka, India

Tel: +91 80 3322 0000/ 2222; Fax: +91 80 4903 0046; Compliance Officer: Ramesh PeriasamyE-mail: [email protected]; Website: www.embassyofficeparks.com

TRUSTEE MANAGER EMBASSY SPONSOR BLACKSTONE SPONSOR

AXIS TRUSTEE

Axis Trustee Services Limited Embassy Office Parks ManagementServices Private Limited

Embassy Property DevelopmentsPrivate Limited

BRE/ Mauritius Investments

Embassy Office Parks REIT (“Embassy REIT”) is issuing 158,333,200* Units (as defined herein) for cash at a price of `300 per Unit aggregating `47,499.96* million (the “Issue”).* Subject to finalization of Basis of Allotment

INITIAL PUBLIC ISSUE IN RELIANCE UPON REGULATION 14(1) OF THE SECURITIES AND EXCHANGE BOARD OF INDIA (REAL ESTATE INVESTMENT TRUSTS) REGULATIONS, 2014, ASAMENDED (THE “REIT REGULATIONS”)

The Units of the Embassy REIT are proposed to be listed on the National Stock Exchange of India Limited (the “NSE”) and BSE Limited (the “BSE”, together with the NSE, the “Stock Exchanges”). The Embassy REIT has received in-principleapprovals from the NSE and the BSE for listing of the Units pursuant to letters dated October 11, 2018 and October 9, 2018, respectively. NSE is the Designated Stock Exchange for this Issue. This Issue will constitute 20.52%* of the issued andpaid-up Units on a post-Issue basis in accordance with Regulation 14(2A) of the REIT Regulations.

* Subject to finalization of Basis of Allotment

The Price Band and the Minimum Bid Size (as determined by the Manager in consultation with the Lead Managers) was announced on the websites of the Embassy REIT, the Embassy Sponsor, the Manager and the Stock Exchanges as well asadvertised in all editions of the Financial Express (a widely circulated English national daily newspaper), all editions of Jansatta (a widely circulated Hindi national daily newspaper) and in all editions of Vishwavani (a Kannada daily newspaper withwide circulation in Karnataka) at least two Working Days prior to the Bid/ Issue Opening Date. The announcement/ advertisement contained relevant financial ratios computed for both the upper and lower end of the Price Band. For further information,see “Basis for Issue Price” on page 434.

This Issue is being made through the Book Building Process and in compliance with the REIT Regulations and the SEBI Guidelines, wherein not more than 75% of the Issue (excluding the Strategic Investor Portion) was available for allocation on aproportionate basis to Institutional Investors. The Manager in consultation with the Lead Managers, allocated up to 60% of the Institutional Investor Portion to Anchor Investors on a discretionary basis in accordance with the REIT Regulations and theSEBI Guidelines. Further, not less than 25% of the Issue (excluding the Strategic Investor Portion) was available for allocation on a proportionate basis to Non-Institutional Investors, in accordance with the REIT Regulations and the SEBI Guidelines,subject to valid Bids being received at or above the Issue Price. The Issue also includes participation by Strategic Investors (as defined hereafter) in accordance with the SEBI Guidelines. For details, see “Issue Information” on page 404.

RISKS IN RELATION TO THE FIRST ISSUE

This being the first issue of Units by the Embassy REIT, there has been no formal market for the Units of the Embassy REIT. No assurance can be given regarding the active or sustained trading in Units or regarding the price at which the Units will betraded after listing.

GENERAL RISKS

Investments in Units involve a degree of risk and investors should not invest any funds in the Issue unless they can afford to take the risk of losing their entire investment. For taking an investment decision, investors must rely on their own examinationof the Embassy REIT and the Issue. Prospective Investors are advised to read “Risk Factors” on page 22 before making an investment decision relating to the Issue. Each prospective investor is advised to consult its own advisors in respect of theconsequences of an investment in the Units being issued pursuant to the Offer Document and this Final Offer Document. This Final Offer Document has been prepared by the Manager solely for providing information in connection with the Issue. TheSecurities and Exchange Board of India (“SEBI”) and the Stock Exchanges assume no responsibility for or guarantee the correctness or accuracy of any statements made, opinions expressed or reports contained herein. Admission of the Units to beissued pursuant to the Issue for trading on the Stock Exchanges should not be taken as an indication of the merits of the Embassy REIT or of the Units. A copy of this Final Offer Document has been delivered to the SEBI and the Stock Exchanges.

MANAGER’S AND SPONSORS’ ABSOLUTE RESPONSIBILITY

The Manager having made all reasonable inquiries, accepts responsibility for and confirms that this Final Offer Document contains all information with regard to the Embassy REIT and the Issue, which is material in the context of the Issue, that theinformation contained in this Final Offer Document is true and correct in all material aspects and is not misleading in any material respect, that the opinions and intentions expressed herein are honestly held and that there are no other facts, the omissionof which makes this Final Offer Document as a whole or any of such information or the expression of any such opinions or intentions misleading in any material respect. Each Sponsor, severally and not jointly, accepts responsibility for and confirmsonly the statements specifically confirmed or undertaken by such Sponsor in this Final Offer Document, to the extent of the information specifically pertaining to such Sponsor.

GLOBAL COORDINATORS AND BOOK RUNNING LEAD MANAGERS REGISTRAR TO THE ISSUE

Morgan Stanley India Company PrivateLimited18F, Tower 2, One Indiabulls Centre841, Senapati Bapat MargMumbai 400 013Maharashtra, IndiaTel: +91 22 6118 1000Fax: +91 22 6118 1040E-mail: [email protected] grievance e-mail:[email protected]: www.morganstanley.comContact Person: Prakhar JajuSEBI Registration No.: INM000011203

Kotak Mahindra Capital Company Limited1st Floor, 27 BKCPlot No. C - 27, “G” BlockBandra Kurla ComplexBandra (East), Mumbai 400 051Maharashtra, IndiaTel: +91 22 4336 0000Fax: + 91 22 6713 2447E-mail: [email protected] grievance e-mail:[email protected]: www.investmentbank.kotak.comContact Person: Ganesh RaneSEBI Registration No.: INM000008704

J.P. Morgan India Private LimitedJ.P. Morgan TowerOff. C.S.T. RoadKalina, Santacruz (East)Mumbai 400 098Maharashtra, IndiaTel: +91 22 6157 3000Fax: +91 22 6157 3911E-mail: [email protected] grievance e-mail:[email protected]: www.jpmipl.comContact Person: Saarthak K SoniSEBI Registration No.: INM000002970

DSP Merrill Lynch LimitedGround Floor, “A” WingOne BKC, “G” BlockBandra Kurla ComplexBandra (East), Mumbai 400 051Maharashtra, IndiaTel: +91 22 6632 8000Fax: +91 22 2204 8518E-mail: [email protected] grievance e-mail:[email protected]: www.ml-india.comContact Person: Karthik S. PrabhakaranSEBI Registration No.: INM000011625

Karvy Fintech Private Limited(formerly KCPL Advisory ServicesPrivate Limited)Karvy Selenium Tower BPlot 31-32, Gachibowli,Financial District, Nanakramguda,Hyderabad 500 032Telangana, IndiaTel: +91 40 6716 2222Fax: +91 40 2343 1551E-mail: [email protected] grievance e-mail:[email protected]: http://www.karvyfintech.comContact Person: Mr. M Murali KrishnaSEBI Registration No.: INR000000221##

BOOK RUNNING LEAD MANAGERS

Axis Capital Limited1st Floor, Axis HouseC-2 Wadia InternationalCentreP.B. Marg, WorliMumbai 400 025Maharashtra, IndiaTel: +91 22 4325 2183Fax: +91 22 4325 3000E-mail:[email protected] grievance e-mail:[email protected]:www.axiscapital.co.inContact Person: Mayuri AryaSEBI Registration No.:INM000012029

Credit Suisse Securities(India) Private Limited9F/10F, Ceejay HousePlot “F”Dr. Annie Besant RoadWorli, Mumbai 400 018Maharashtra, IndiaTel: +91 22 6777 3885Fax: +91 22 6777 3820E-mail:[email protected] grievance e-mail:[email protected]: www.credit-suisse.comContact Person: Anand BangSEBI Registration No.:INM000011161

Deutsche Equities IndiaPrivate LimitedThe Capital, 14th floorC-70, “G” BlockBandra Kurla ComplexMumbai 400 051Maharashtra, IndiaTel: +91 22 7180 4444Fax: +91 22 7180 4199E-mail:[email protected] grievance e-mail:[email protected]:www.db.com/IndiaContact Person: Viren JairathSEBI Registration No.:INM000010833

Goldman Sachs (India)Securities Private LimitedRational House951-A, Appasaheb MaratheMargPrabhadeviMumbai 400 025Maharashtra, IndiaTel: +91 22 6616 9000Fax: +91 22 6616 9001E-mail: [email protected] grievance e-mail:[email protected]:www.goldmansachs.comContact Person: MrinaliniBaralSEBI Registration No.:INM000011054

HSBC Securities andCapital Markets (India)Private Limited52/60, Mahatma GandhiRoadFort, Mumbai 400 001Maharashtra, IndiaTel: +91 22 2268 5555Fax: +91 22 2263 1284E-mail:[email protected] grievance e-mail:[email protected]: www.hsbc.co.in/1/2/corporate/equitiesglobalinvestmentbankingContact Person: ShreyeMirani/ Vaibhav GrewalSEBI Registration No.:INM000010353

IIFL Holdings LimitedIIFL Centre, 10th FloorKamala City, SenapatiBapat MargLower Parel (West)Mumbai 400 013Maharashtra, IndiaTel: +91 22 4646 4600Fax: +91 22 2493 1073E-mail:[email protected] grievance e-mail:[email protected]:www.iiflcap.comContact Person:Devendra Maydeo/Aditya AgarwalSEBI Registration No.:INM000010940

JM Financial Limited7th Floor, CnergyAppasaheb Marathe MargPrabhadeviMumbai 400 025Maharashtra, IndiaTel: +91 22 6630 3030Fax: +91 22 6630 3330E-mail:[email protected] grievance e-mail:[email protected]: www.jmfl.comContact Person: PracheeDhuriSEBI Registration No.:INM000010361

Nomura Financial Advisoryand Securities (India)Private LimitedCeejay House, Level 11Plot “F” Shivsagar EstateDr. Annie Besant RoadWorli Mumbai 400 018Maharashtra, IndiaTel: +91 22 4037 4037Fax: +91 22 4037 4111E-mail:[email protected] grievance e-mail:[email protected]:www.nomuraholdings.com/company/group/asia/india/index.htmlContact Person: ManishAgarwal/ Vishal KanjaniSEBI Registration No.:INM000011419

BID/ISSUE PROGRAM#

BID/ ISSUE OPENED ON: March 18, 2019* BID/ ISSUE CLOSED ON: March 20, 2019* The Anchor Investor Bid/Issue Period was March 15, 2019# The Issue also includes participation by Strategic Investors in accordance with the SEBI Guidelines## The registration is currently under the name of Karvy Computershare Private Limited. Karvy Fintech Private Limited has filed an application with the SEBI for registration under its new name, which is currently pending

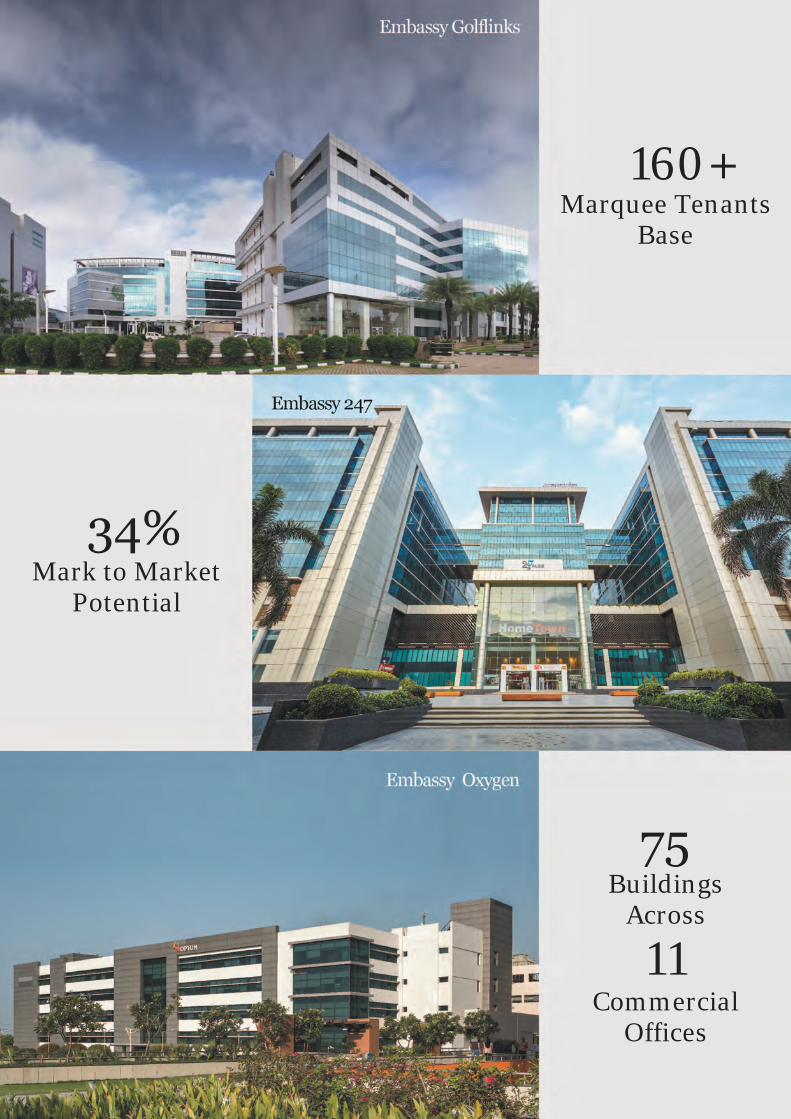

33 msf Leasable Area

4 Gateway Cities

95% Occupancy

No

Note: As of December 31, 2018

maheshwh

Stamp

160+ Marquee Tenants

Base

Mark to Market Potential

75 Buildings

Across

11 Commercial

Offices

34%

TABLE OF CONTENTS

I. GENERAL . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

NOTICE TO INVESTORS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3PRESENTATION OF FINANCIAL DATA AND OTHER INFORMATION . . . . . . . . . . . . . . . . . . 7FORWARD-LOOKING STATEMENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

II. EXECUTIVE SUMMARY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

III. RISK FACTORS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

IV. ABOUT THE EMBASSY REIT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 61

BACKGROUND OF THE EMBASSY REIT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 61INDUSTRY OVERVIEW . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64OUR BUSINESS AND PROPERTIES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 131THE SPONSORS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 216THE MANAGER . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 220THE TRUSTEE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 227CORPORATE GOVERNANCE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 230RELATED PARTY TRANSACTIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 243MANAGEMENT FRAMEWORK . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 247OTHER PARTIES INVOLVED IN THE EMBASSY REIT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 257

V. FORMATION TRANSACTIONS IN RELATION TO THE EMBASSY REIT . . . . . . . . . . . . . 261

VI. FINANCIAL INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 275

SUMMARY FINANCIALS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 275MANAGEMENT’S DISCUSSION AND ANALYSIS OF FACTORS AFFECTING THEFINANCIAL CONDITION AND RESULTS OF OPERATIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . 278PROJECTIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 320DISTRIBUTION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 356LEVERAGE AND CAPITALIZATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 359FINANCIAL INDEBTEDNESS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 372

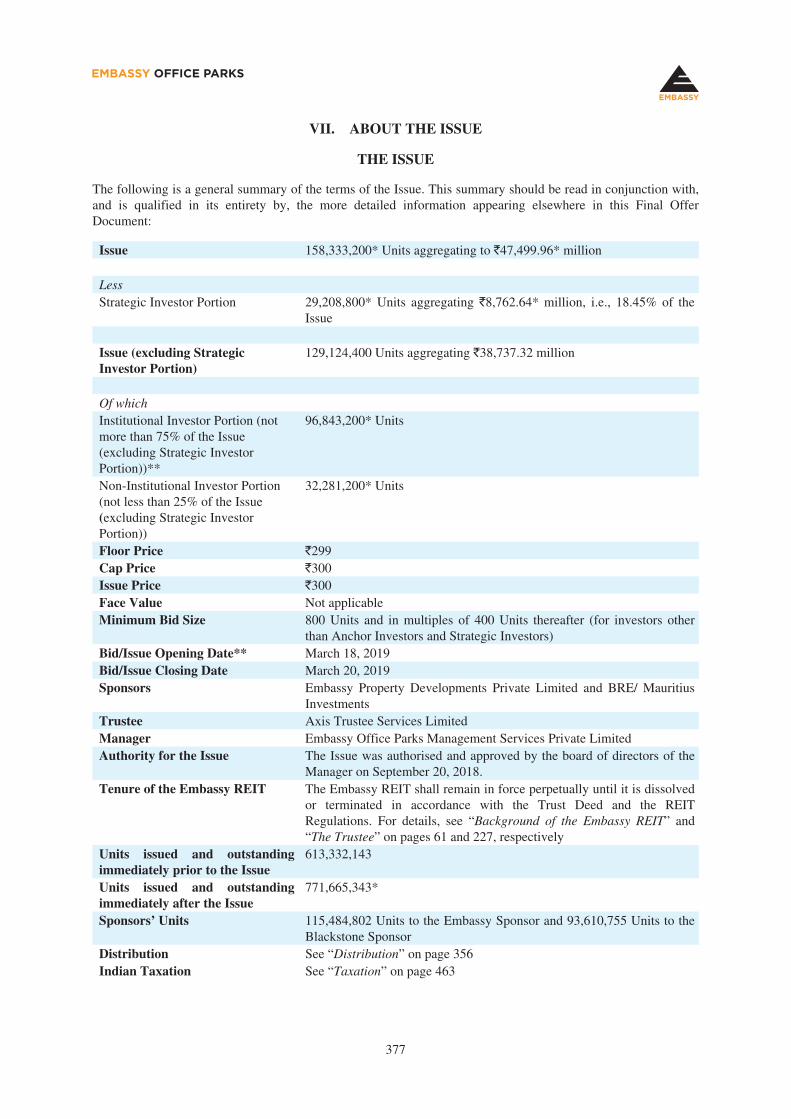

VII. ABOUT THE ISSUE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 377

THE ISSUE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 377USE OF PROCEEDS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 380ISSUE STRUCTURE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 399INFORMATION CONCERNING THE UNITS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 402ISSUE INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 404BASIS FOR ISSUE PRICE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 434RIGHTS OF UNITHOLDERS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 436

VIII. LEGAL AND REGULATORY MATTERS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 439

LEGAL AND OTHER INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 439REGULATIONS AND POLICIES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 451REGULATORY APPROVALS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 456TAXATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 463CERTAIN ERISA CONSIDERATIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 471MATERIAL CONTRACTS AND DOCUMENTS FOR INSPECTION . . . . . . . . . . . . . . . . . . . . . . 474

IX. OTHER INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 478

GENERAL INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 478DEFINITIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 487DECLARATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 505

X. ANNEXURES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 523

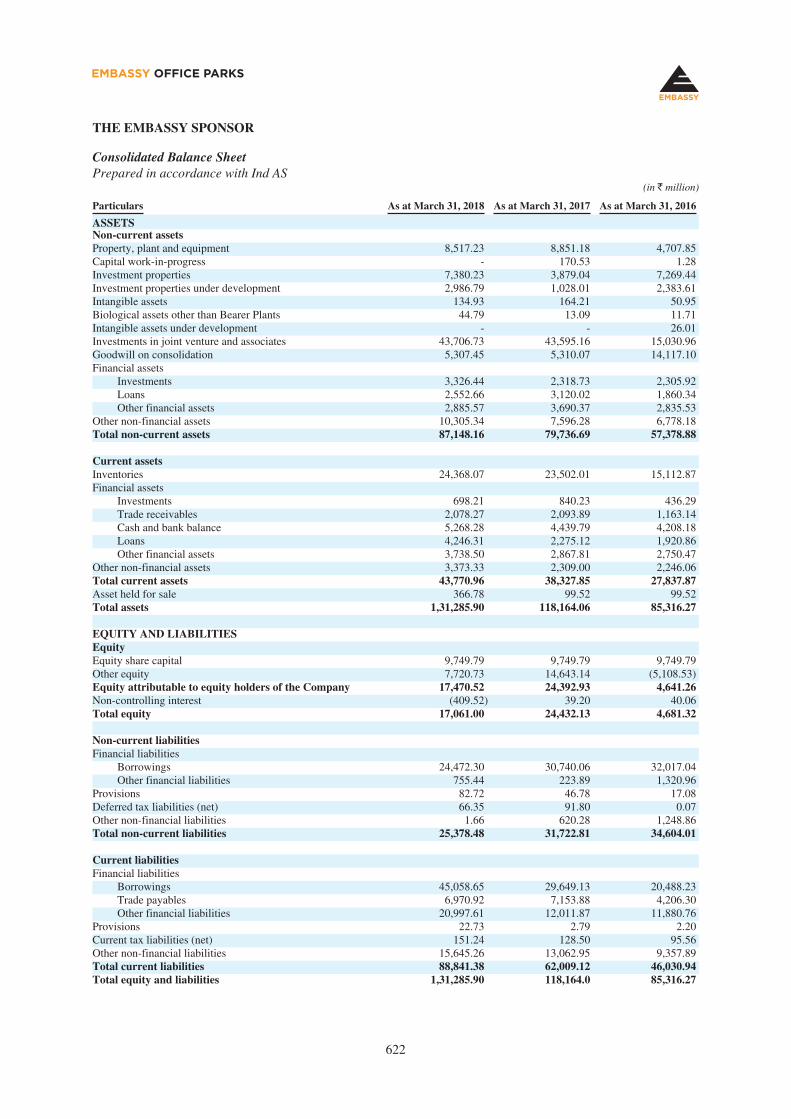

FINANCIAL INFORMATION OF THE EMBASSY REIT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 523FINANCIAL INFORMATION OF THE SPONSORS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 620FINANCIAL INFORMATION OF THE MANAGER . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 624SUMMARY VALUATION REPORT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 626CALCULATION OF UNITHOLDING PERCENTAGE IN RELATION TO THE FORMATIONTRANSACTIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 665ALTERNATIVE INVESTMENT FUND MANAGERS DIRECTIVE SUPPLEMENT . . . . . . . . . . 669

I. GENERAL

NOTICE TO INVESTORS

The statements contained in this Final Offer Document relating to the Embassy REIT and the Units are, in allmaterial respects, true, accurate and not misleading, and the opinions and intentions expressed in this Final OfferDocument with regard to the Embassy REIT and the Units are honestly held, have been reached after consideringall relevant circumstances and are based on reasonable assumptions and information presently available to theTrustee and the Manager. There are no other facts in relation to the Embassy REIT and the Units, the omission ofwhich would, in the context of the Issue, make any statement in this Final Offer Document misleading in anymaterial respect. Further, the Manager, the Embassy Sponsor and the Blackstone Sponsor have made allreasonable enquiries to ascertain such facts and to verify the accuracy of all such information and statements.

Investors acknowledge that they have not relied on the Lead Managers or any of their respective shareholders,employees, counsel, officers, directors, representatives, agents or affiliates in connection with such person’sinvestigation of the accuracy of such information or such person’s investment decision, and each such personmust rely on his/ her own examination of the Embassy REIT and the merits and risks involved in investing in theUnits. Investors should not construe the contents of this Final Offer Document as legal, business, tax, accountingor investment advice.

No person is authorized to give any information or to make any representation not contained in this Final OfferDocument and any information or representation not so contained must not be relied upon as having beenauthorized by or on behalf of the Embassy REIT or by or on behalf of the Lead Managers.

Notice to Prospective Investors in the United States

The Units have not been recommended by any U.S. federal or state securities commission or regulatory authority.Furthermore, the foregoing authorities have not confirmed the accuracy or determined the adequacy of this FinalOffer Document or approved or disapproved the Units. Any representation to the contrary is a criminal offence inthe United States. In making an investment decision investors must rely on their own examination of theEmbassy REIT and the terms of the Issue, including the merits and risks involved. The Units have not been andwill not be registered under the U.S. Securities Act of 1933, as amended (“Securities Act”) or any otherapplicable law of the United States and, unless so registered, may not be offered or sold within the United Statesexcept pursuant to an exemption from, or in a transaction not subject to, the registration requirements of theSecurities Act and applicable state securities laws. Accordingly, the Units are being offered and sold (a) in theUnited States only to persons reasonably believed to be “qualified institutional buyers” (as defined in Rule 144Aunder the Securities Act and referred to in this Final Offer Document as “U.S. QIBs”. For the avoidance of doubt,the term U.S. QIBs does not refer to a category of institutional investor defined under applicable Indianregulations and referred to in this Final Offer Document as “QIBs”) in transactions exempt from the registrationrequirements of the Securities Act; and (b) outside the United States in compliance with Regulation S under theSecurities Act and the applicable laws of the jurisdiction where those offers and sales occur.

Notice to Prospective Investors in the European Economic Area

This Final Offer Document has been prepared on the basis that all offers of the Units will be made pursuant to anexemption under the Prospectus Directive, as implemented in Member States of the European Economic Area(“EEA”), from the requirement to produce a prospectus for offers of Units. The expression “ProspectusDirective” means Directive 2003/71/EC of the European Parliament and Council EC (and amendments thereto,including the 2010 PD Amending Directive) and includes any relevant implementing measure in each RelevantMember State (as defined below). Accordingly, any person making or intending to make an offer within the EEAof Units which are the subject of the placement contemplated in this Final Offer Document should only do so incircumstances in which no obligation arises for the Embassy REIT or any of the Lead Managers to produce aprospectus for such offer. None of the Embassy REIT and the Lead Managers have authorized, nor do theyauthorize, the making of any offer of the Units through any financial intermediary, other than the offers made bythe Lead Managers which constitute the final placement of the Units contemplated in this Final Offer Document.

THE EMBASSY REIT WILL CONSTITUTE AN ALTERNATIVE INVESTMENT FUND FOR THEPURPOSE OF THE EUROPEAN UNION DIRECTIVE ON ALTERNATIVE INVESTMENT FUND

3

MANAGERS (DIRECTIVE 2011/61/EU) (“AIFMD”). THE ALTERNATIVE INVESTMENT FUNDMANAGER (“AIFM”) OF THE EMBASSY REIT WILL BE THE MANAGER.

UNITS MAY ONLY BE MARKETED TO PROSPECTIVE INVESTORS WHICH ARE RESIDENT,DOMICILED OR HAVE A REGISTERED OFFICE IN A EUROPEAN ECONOMIC AREA (“EEA”)MEMBER STATE (“EEA MEMBER STATE”) IN WHICH THE MARKETING OF UNITS HAS BEENREGISTERED OR AUTHORIZED (AS APPLICABLE) UNDER THE RELEVANT NATIONALIMPLEMENTATION OF ARTICLE 42 OF AIFMD, AND IN SUCH CASES, ONLY TO EEA PERSONSWHICH ARE “PROFESSIONAL INVESTORS” OR ANY OTHER CATEGORY OF PERSON TO WHICHSUCH MARKETING IS PERMITTED UNDER THE NATIONAL LAWS OF SUCH EUROPEANECONOMIC AREA MEMBER STATE (EACH AN “EEA PERSON”). THIS FINAL OFFER DOCUMENT ISNOT INTENDED FOR, SHOULD NOT BE RELIED ON BY AND SHOULD NOT BE CONSTRUED AS ANOFFER (OR ANY OTHER FORM OF MARKETING) TO ANY OTHER EEA PERSON.

A “PROFESSIONAL INVESTOR” FOR THE PURPOSES OF AIFMD IS AN INVESTOR WHO ISCONSIDERED TO BE A PROFESSIONAL CLIENT OR WHICH MAY, ON REQUEST, BE TREATED AS APROFESSIONAL CLIENT WITHIN THE RELEVANT NATIONAL IMPLEMENTATION OF ANNEX II OFDIRECTIVE 2004/39/EC (MARKETS IN FINANCIAL INSTRUMENTS DIRECTIVE).

A LIST OF JURISDICTIONS IN WHICH THE MANAGER AND/OR THE EMBASSY REIT HAVE BEENREGISTERED OR AUTHORIZED (AS APPLICABLE) UNDER ARTICLE 42 OF AIFMD IS AVAILABLEFROM THE MANAGER ON REQUEST. IF THE MANAGER HAS NOT BEEN REGISTERED ORAPPROVED IN A PARTICULAR EEA MEMBER STATE TO MARKET UNITS, THEN THE EMBASSYREIT IS NOT BEING MARKETED TO ANY EEA PERSON AT SUCH DATE IN THAT EEA MEMBERSTATE. TO THE EXTENT THAT AN AFFILIATE OF THE INVESTMENT MANAGER PROMOTES THETRUST IN AN EEA MEMBER STATE, THEN SUCH PROMOTION IS BEING UNDERTAKEN FOR ANDON BEHALF OF THE MANAGER IN SUCH CAPACITY.

Notice to Prospective Investors in Canada

The offer and sale of the Units in Canada will only be made under exemptions from the requirement to file aprospectus in the relevant province or territory and will be made only by a dealer duly registered under theapplicable securities laws of the relevant province or in accordance with an exemption from the applicableregistered dealer requirements. The Units may be sold only to purchasers purchasing, or deemed to bepurchasing, as principal that are accredited investors, as defined in National Instrument 45-106 ProspectusExemptions or subsection 73.3(1) of the Securities Act (Ontario), and are permitted clients, as defined inNational Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Obligations. Anyresale of the Units must be made in accordance with an exemption from, or in a transaction not subject to, theprospectus requirements of applicable securities laws.

Securities legislation in certain provinces or territories of Canada may provide a purchaser with remedies forrescission or damages if this Final Offer Document (including any amendment thereto) contains amisrepresentation, provided that the remedies for rescission or damages are exercised by the purchaser within thetime limit prescribed by the securities legislation of the purchaser’s province or territory. The purchaser shouldrefer to any applicable provisions of the securities legislation of the purchaser’s province or territory forparticulars of these rights or consult with a legal advisor.

Pursuant to section 3A.3 of National Instrument 33-105 Underwriting Conflicts (“NI 33-105”), the LeadManagers are not required to comply with the disclosure requirements of NI 33-105 regarding underwriterconflicts of interest in connection with this offering.

We hereby notify prospective Canadian purchasers that: (a) we may be required to provide personal informationpertaining to the purchaser as required to be disclosed in Schedule I of Form 45-106F1 under NI 45-106(including its name, address, telephone number and the aggregate purchase price of any Units purchased)(“personal information”), which Form 45-106F1 may be required to be filed by us under NI 45-106, (b) suchpersonal information may be delivered to the Ontario Securities Commission (the “OSC”) in accordance withNI 45-106, (c) such personal information is collected indirectly by the OSC under the authority granted to itunder the securities legislation of Ontario, (d) such personal information is collected for the purposes of the

4

administration and enforcement of the securities legislation of Ontario, and (e) the public official in Ontario whocan answer questions about the OSC’s indirect collection of such personal information is the AdministrativeSupport Clerk at the OSC, Suite 1903, Box 55, 20 Queen Street West, Toronto, Ontario M5H 3S8, Telephone:(416) 593-3684. Each prospective Canadian purchaser that purchases Units in this offering will be deemed tohave authorized the indirect collection of the personal information by the OSC, and to have acknowledged andconsented to its name, address, telephone number and other specified information, including the aggregatepurchase price paid by the purchaser, being disclosed to other Canadian securities regulatory authorities, and tohave acknowledged that such information may become available to the public in accordance with requirements ofapplicable Canadian laws.

Upon receipt of this Final Offer Document, each Canadian purchaser hereby confirms that it has expresslyrequested that all documents evidencing or relating in any way to the sale of the securities described herein(including for greater certainty any purchase confirmation or any notice) be drawn up in the English languageonly. Par la authorizi de ce document, chaque acheteur canadien confirme par les présentes qu’il a expressémentexigé que tous les documents faisant foi ou se rapportant de quelque manière que ce soit à la vente des authorimobilières décrites aux présentes (incluant, pour plus de certitude, toute confirmation d’achat ou tout avis) soientrédigés en anglais seulement.

Notice to Investors in certain other jurisdictions

The distribution of this Final Offer Document and the issue of the Units in certain jurisdictions may be restrictedby law. As such, this Final Offer Document does not constitute, and may not be used for or in connection with,an offer or solicitation by anyone in any jurisdiction in which such offer or solicitation is not authorised or to anyperson to whom it is unlawful to make such offer or solicitation. In particular, no action has been taken by theManager or the Lead Managers which would permit an Issue of the Units or distribution of this Final OfferDocument in any jurisdiction, other than India. Accordingly, the Units may not be offered or sold, directly orindirectly, and neither this Final Offer Document nor any Issue materials in connection with the Units may bedistributed or published in or from any country or jurisdiction that would require registration of the Units in suchcountry or jurisdiction.

Disclaimer

This Final Offer Document does not, directly or indirectly, relate to any invitation, offer or sale of any securities,instruments or loans (including listed non-convertible debentures or bonds, if any) that may be issued by theEmbassy REIT after the listing of the Units. Any person or entity investing in such issue or transaction by theEmbassy REIT should consult its own advisors. Neither the Lead Managers, nor their associates or affiliates haveany responsibility or liability for such issue or transaction by the Embassy REIT.

SEBI Disclaimer

It is to be distinctly understood that submission of the Draft Offer Document, the Offer Document or the FinalOffer Document to SEBI should not in any way be deemed or construed that the same has been cleared orapproved by SEBI. SEBI does not take any responsibility either for the financial soundness of any scheme or theproject for which the Issue is proposed to be made or for the correctness of the statements made or opinionsexpressed in the Draft Offer Document, the Offer Document or the Final Offer Document.

NSE Disclaimer

As required, a copy of the Offer Document has been submitted to National Stock Exchange of India Limited(hereinafter referred to as NSE). NSE has given vide its letter Ref.: NSE/LIST/63187 dated October 11, 2018permission to the Issuer to use the Exchange’s name in the Offer Document as one of the stock exchanges onwhich this Issuer’s units are proposed to be listed. The Exchange has scrutinized this draft offer document for itslimited internal purpose of deciding on the matter granting the aforesaid permission to this Issuer. It is to bedistinctly understood that the aforesaid permission given by NSE should not in any way be deemed or construedthat the offer document has been cleared or approved by NSE of been cleared or approved by NSE; nor does it inany manner warrant, certify or endorse the correctness or completeness of any of the contents of this offerdocument; nor does it warrant that this Issuer’s units will be listed or will continue to be listed on the Exchange;nor does it take any granting the aforesaid permission to this Issuer. It is to be distinctly understood that the

5

aforesaid permission given by NSE should not in any way be deemed or construed that the offer document hasresponsibility for the financial or other soundness of this REIT, its Sponsor, its Investment Manager or anyproject of this REIT.

Every person who desires to apply for or otherwise acquire any units of this REIT may do so pursuant toindependent inquiry, investigation and analysis and shall not have any claim against the Exchange whatsoever byreason of any loss which may be suffered by such person consequent to or in connection with such subscription /acquisition whether by reason of anything stated or omitted to be stated herein or any other reason whatsoever.

BSE Disclaimer

BSE Limited (the “Exchange”) has given vide its letter dated October 09, 2018 permission to this Trust to use theExchange’s name in this offer document as one of the stock exchanges on which this Units of this Trust areproposed to be listed. The Exchange has scrutinized this offer document for its limited internal purpose ofdeciding on the matter of granting the aforesaid permission to this Trust. The Exchange does not in any manner:-

a) warrant, certify or endorse the correctness or completeness of any of the contents of this offerdocument; or

b) warrant that this Trust Units will be listed or will continue to be listed on the Exchange; or

c) take any responsibility for the financial or other soundness of this Trust, its Investment Manager, itsSponsor(s), its Trustee or Project Manager(s);

and it should not for any reason be deemed or constructed that this offer document has been cleared or approvedby the Exchange. Every person who desires to apply for or otherwise acquires the Units of this Trust may do sopursuant to independent inquiry, investigation and analysis and shall not have any claim against the Exchangewhatsoever by reason of any loss which may be suffered by such person consequent to or in connection with suchsubscription/acquisition whether by reason of anything stated or omitted to be stated herein or for any otherreason whatsoever.

6

PRESENTATION OF FINANCIAL DATA AND OTHER INFORMATION

Certain Conventions

All references in this Final Offer Document to “India” are to the Republic of India.

Unless stated otherwise, all references to page numbers in this Final Offer Document are to the page numbers ofthis Final Offer Document.

Financial Data

Unless stated otherwise, the financial information included in this Final Offer Document in relation to theEmbassy REIT is derived from the Condensed Combined Financial Statements which have been prepared inaccordance with Ind AS, the REIT Regulations and the SEBI Guidelines for the purposes of this Issue, and inaccordance with the basis of preparation as set out in ‘Notes to Accounts – Note 2.1’ to the Condensed CombinedFinancial Statements. See “Financial Information of the Embassy REIT” on page 523.

Further, this Final Offer Document includes Projections for the Projection Years 2021, 2020 and 2019, preparedin accordance with the REIT Regulations and the SEBI Guidelines. See “Projections” on page 320.

The Embassy REIT, through the Holdco holds 50% of the equity shares of GLSP, which is a company that holdscompleted and rent generating properties and derives more than 75% of its operating income from real estateactivity as per the audited financial statements of GLSP for Fiscal 2018. However, since GLSP does not meet therequirements of an SPV as per the REIT Regulations, it is considered an investment of the Embassy REIT underRegulation 18(5) of the REIT Regulations. Since the Embassy REIT holds 50% of GLSP, it has not beenconsolidated in the Condensed Combined Financial Statements and has been initially recognized as aninvestment at cost which includes transaction costs. Subsequent to initial recognition, the investment in GLSPhas been measured in the Condensed Combined Financial Statements using the equity method, and accordinglythe share of profit or loss of GLSP, including other comprehensive income and other equity, has been included.However, the fair value of such investment has been disclosed in the statement of net assets at fair value in theCondensed Combined Financial Statements. Further, the carved out financial statements of EODPL for the ninemonths ended December 31, 2018, nine months ended December 31, 2017 and Fiscals 2018, 2017 and 2016 havebeen prepared in accordance with the Guidance Note on Combined and Carve-Out Financial Statements issuedby the ICAI. See “Financial Information of the Embassy REIT” on page 523.

Further, this Final Offer Document includes summary financial statements of the (i) Embassy Sponsor, as of andfor the Fiscals 2018, 2017 and 2016 from the consolidated audited financial statements of the Embassy Sponsor,of which the consolidated audited financial statements for the Fiscals 2018 and 2017 were prepared inaccordance with Ind AS and the Companies Act, and the consolidated audited financial statements for Fiscal2016 were prepared in accordance with Indian GAAP and the Companies Act; (ii) the Blackstone Sponsor, as ofand for the financial years ended December 31, 2017, 2016 and 2015, derived from the audited financialstatements of the Blackstone Sponsor which were prepared in accordance with IFRS; and (iii) the Manager, as ofand for the Fiscals 2018, 2017 and 2016 from the standalone audited financial statements of the Manager,prepared in accordance with Ind AS and the Companies Act. For further details, see “Financial Information ofthe Sponsors” and “Financial Information of the Manager” on pages 620 and 624, respectively.

The degree to which the financial information included in this Final Offer Document will provide meaningfulinformation is entirely dependent on the reader’s level of familiarity with Indian accounting policies andpractices, the Companies Act, the Indian GAAP, Ind AS, IFRS, the REIT Regulations and the SEBI Guidelines.Any reliance by persons not familiar with the accounting policies and practices on the financial disclosurespresented in this Final Offer Document should accordingly be limited.

The Fiscal for the Embassy REIT, the Manager and the Embassy Sponsor commences on April 1 and ends onMarch 31 of the next year and the Fiscal for the Blackstone Sponsor commences on January 1 and ends onDecember 31 of the same year. Accordingly, all references to a particular Fiscal, (unless stated otherwise or withrespect to the Blackstone Sponsor), are to the 12 month period ended on March 31 of that year.

In this Final Offer Document, any discrepancies in any table between the total and the sums of the amounts listedare due to rounding off.

7

Certain Non-GAAP Financial Metrics

The body of generally accepted accounting principles is commonly referred to as “GAAP.” Our managementbelieves that the presentation of certain non-GAAP measures provides additional useful information to investorsregarding our performance and trends related to our results of operations. Accordingly, we believe that whennon-GAAP financial information is viewed with GAAP or Ind AS financial information, investors are providedwith a more meaningful understanding of our ongoing operating performance and financial results. For thisreason, we are including in this Final Offer Document information regarding our EBITDA, EBITDA Margin, NetDistributable Cash Flow, Net Operating Income, and certain other metrics based on or derived from thesemetrics.

However, these financial measures are not measures determined based on GAAP, Ind AS or any otherinternationally accepted accounting principles, and you should not consider such items as an alternative to thehistorical financial results or other indicators of our cash flow based on Ind AS or IFRS. These non-GAAPfinancial measures, as defined by us, may not be comparable to similarly-titled measures as presented by othercompanies due to differences in the way non-GAAP financial measures are calculated. The non-GAAP financialinformation contained in this offering memorandum is not intended to comply with the reporting requirements ofthe United States Securities and Exchange Commission (the “SEC”) and will not be subject to review by theSEC. Even though the non-GAAP financial measures are used by management to assess our financial position,financial results and liquidity and these types of measures are commonly used by investors, they have importantlimitations as analytical tools, and you should not consider them in isolation or as substitutes for analysis of ourfinancial position or results of operations as reported under Ind AS or IFRS.

EBITDA and EBITDA Margin

We present EBITDA and EBITDA Margin for both historical and projection periods in this Final OfferDocument. For historical periods, we have elected to present EBITDA as a separate line item on the face of ourstatement of profit and loss, which forms a part of our Condensed Combined Financial Statements. In itsmeasurement, we do not include depreciation and amortization expense, finance costs and tax expense.

EBITDA does not have a standardized definition under Ind AS or IFRS, and our method of calculating EBITDAmay be different from the method used by most other companies to calculate EBITDA. We cannot assure youthat our EBITDA calculation will always be comparable with similarly named measures presented by othercompanies.

EBITDA and EBITDA margin have been calculated on the same basis as historical EBITDA and EBITDAmargin, subject to the inherent limitations generally involved in presenting Projection figures, as well as theassumptions set forth in this report. Such assumptions and inherent limitations may distort comparability acrosshistorical and Projection period. EBITDA and EBITDA margin are not recognized measures under Ind AS orIFRS. EBITDA and EBITDA margin should not be considered by themselves or as substitutes for net income,operating income or cash flow from operations or related margins or other measures of operating performance,liquidity or ability to pay dividends. For the projections period, we do not present a reconciliation of EBITDA toprofit after tax (EBITDA’s most comparable GAAP measure), as we have not included the projections ofadditional expense items required to arrive at the projected profit after tax. Further, we do not present profit aftertax in equal or greater prominence as EBITDA as would have been required under an offering registered with theUnited States Securities and Exchange Commission. For more information, see “Projections” on page 320 of thisFinal Offer Document.

Net Operating Income (NOI)

We present NOI in this Final Offer Document. We calculate NOI for our segments as the revenue fromoperations from the segment, less direct operating expenses of the segment (for a detailed calculation, please see“Management’s Discussion and Analysis of Factors Affecting Financial Conditions and Results of Operations—Non-GAAP Measures—Net Operating Income (“NOI”)) on page 316.

NOI as calculated by us is a primary driver of our managerial assessments and decision-making process. Wetherefore consider NOI to be a meaningful supplemental financial measure of our performance when consideredwith the Condensed Combined Financial Statements determined in accordance with Ind AS. We believe NOI is

8

helpful to investors in understanding the performance of our Commercial Offices, the Hilton at EmbassyGolflinks and Embassy Energy because it provides a direct measure of the operating results of our corebusinesses.

NOI does not have a standardized meaning, nor is it a recognized measure under Ind AS or IFRS, and may not becomparable with measures with similar names presented by other companies. NOI should not be considered byitself or as a substitute for comparable measures under Ind AS or IFRS or other measures of operatingperformance, liquidity or ability to pay dividends. Our NOI may not be comparable to the NOI of othercompanies/REITs due to the fact that not all companies/REITs use the same definition of NOI. Accordingly,there can be no assurance that our basis for computing this non-GAAP measure is comparable with that of othercompanies/REITs.

Further, for the projections period, we do not present a reconciliation of Net Operating Income to profit after tax(Net Operating Income’s most directly comparable Ind AS measure), as we have not included the projections ofadditional expense items required to arrive at the projected profit after tax. Further, we do not present profit aftertax in equal or greater prominence as Net Operating Income as would have been required under an offeringregistered with the United States Securities and Exchange Commission. For more information, see“Management’s Discussion and Analysis of Factors Affecting Financial Conditions and Results of Operations—Non-GAAP Measures—Net Operating Income (“NOI”)” and “Projections” on pages 316 and 320 respectively.

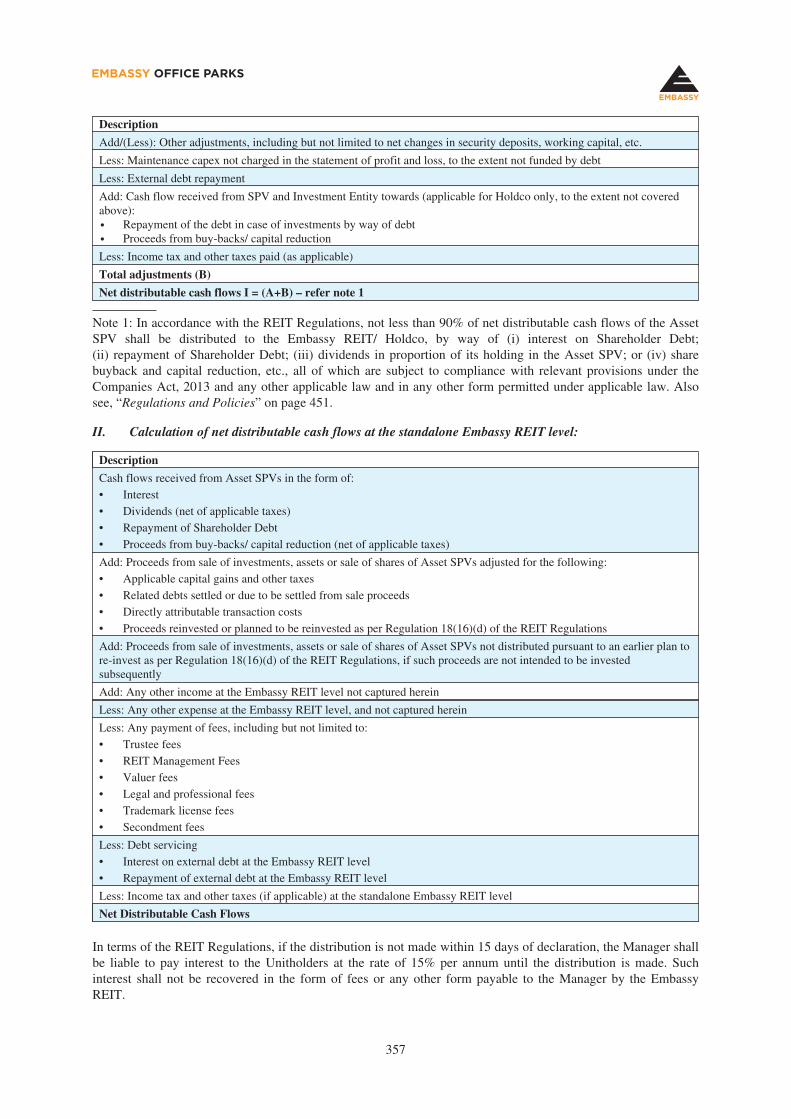

Net Distributable Cash Flow (NDCF)

We present NDCF in this Final Offer Document. We calculate NDCF in the manner specified in “Projections—Annexure D: NDCF framework for the Embassy REIT”. NDCF is a significant performance metric, theframework for which is adopted by the Manager in line with the Securities and Exchange Board of India (RealEstate Investment Trusts) Regulations, 2014 issued by SEBI on September 26, 2014, as amended from time totime and any circulars and guidelines issued thereunder. The Manager believes this metric serves as a usefulindicator of the REIT’s expected ability to provide a cash return on investment. NDCF does not have astandardized meaning and is not a recognized measure under Ind AS or IFRS, and may not be comparable withmeasures with similar names presented by other companies. NDCF should not be considered by itself or as asubstitute for net income, operating income or cash flow from operating activities or related margins or othermeasures of operating performance, liquidity or ability to pay dividends. For more information, see “Projections”on page 320.

Currency and Units of Presentation

All references to:

• “Rupees” or “`” or “INR” or “Rs.” are to Indian Rupee, the official currency of the Republic of India; and

• “USD” or “US$” are to United States Dollar, the official currency of the United States.

Except otherwise specified, we have presented certain numerical information in this Final Offer Document in“million” or “billion” units. One million represents 1,000,000 and one billion represents 1,000,000,000.

Unless specified otherwise, any percentage amounts, as set forth in this Final Offer Document, have beencalculated on the basis of the Condensed Combined Financial Statements, and the summary financial statementsof the Embassy Sponsor on a consolidated basis, the Blackstone Sponsor on a standalone basis and the Manageron a standalone basis.

Historically, the audited standalone financial statements of the Asset SPVs and the Investment Entity have beenprepared in accordance with Indian GAAP and the Companies Act and audited by the statutory auditors of therespective Asset SPV and the Investment Entity. However, for the purposes of this Final Offer Document, theCondensed Combined Financial Statements, have been prepared in accordance with Ind AS. The date oftransition for the purpose of Ind AS for the Condensed Combined Financial Statements has been considered asApril 1, 2015.

Areas have been represented in square feet, square metres, acres and guntas.

9

Exchange Rates

This Final Offer Document contains conversion of certain other currency amounts into Indian Rupees. Theseconversions should not be construed as a representation that these currency amounts could have been, or can beconverted into Indian Rupees, at any particular rate.

The following table sets forth, for the dates indicated, information with respect to the exchange rate between theRupee and the US$ (in Rupees per US$):

Currency

As on (in `)

December 31, 2018 March 28, 2018* March 31, 2017 March 31, 2016

1 US$ 69.79 65.04 64.84 66.33

Source: www.rbi.org.in and www.fbil.org.in*The reference rate is not available for March 31, 2018, March 30, 2018 and March 29, 2018, being a Saturday and public holidays,respectively

Industry and Market Data

Unless stated otherwise, industry and market data used in this Final Offer Document has been obtained orderived from “Real Estate Market Report” dated September 18, 2018 issued by CBRE and “Hotel MarketReport” dated September 18, 2018 issued by Crowe Horwath HTL Consultants Pvt. Ltd. (“CHHTL”).

Industry publications generally state that the information contained in such publications has been obtained frompublicly available documents from various sources believed to be reliable but their accuracy and completenessare not guaranteed and their reliability cannot be assured. Accordingly, no investment decisions should be basedon such information. Although the Manager believes that the industry and market data used in this Final OfferDocument is reliable, it has not been independently verified by the Manager, the Embassy Sponsor, theBlackstone Sponsor, the Trustee or the Lead Managers, or any of their associates, affiliates or advisors. The dataused in these sources may have been re-classified by us for the purposes of presentation. Data from these sourcesmay also not be comparable. Such data involves risks, uncertainties and numerous assumptions and is subject tochange based on various factors, including those disclosed in “Risk Factors” on page 22 of this Final OfferDocument. Accordingly, investment decisions should not be based solely on such information.

The extent to which the market and industry data used in this Final Offer Document is meaningful depends on thereader’s familiarity with and understanding of the methodologies used in compiling such data. There are nostandard data gathering methodologies in the industry in which business of the Embassy REIT is conducted, andmethodologies and assumptions may vary widely among different industry sources.

In this regard, CHHTL has issued the following disclaimer:

“Crowe Horwath HTL Consultants Pvt. Ltd. (CHHTL) does not accept any liability arising out of reliance by anyperson or entity (apart from the Manager, the Embassy REIT, the Embassy Sponsor, the Blackstone Sponsor, theLead Managers or their respective affiliates) on its report or any errors or omissions in its report. The HotelMarket Report does not purport to provide all of the information a recipient may require in order to arrive at adecision. In no event shall CHHTL or its directors or personnel be liable to any party for any damage, loss, cost,expense, injury or other liability that arises out of or in connection with this report including, without limitation,any indirect, special, incidental, punitive or consequential loss, liability or damage of any kind.

CHHTL’s opinions are based on information available to us at the time of preparation of the report andeconomic, market and other conditions prevailing at the date of this report. Such conditions may changesignificantly over relatively short periods of time. Should circumstances change significantly, or additionalinformation become available, after the issuance of this report, the conclusions and opinions expressed hereinmay require revision. There is no requirement for CHHTL to update this report in any such circumstances. Thestatements and opinions expressed in this report are made in good faith and in the belief that such statements andopinions are not false or misleading.

10

Forward-looking statements

The Hotel Market Report contains estimates/ projections/ outlook and statements that may be regarded asforward-looking statements. These statements are based on a number of assumptions, expectations and estimateswhich, while considered by us to be reasonable, are inherently subject to significant uncertainties andcontingencies many of which are beyond the control of ourselves or the Manager (on whose behalf this report hasbeen prepared) or which may reflect future business decisions which are subject to change. Recipients of thisinformation are advised that the estimates/ projections/ outlook may be regarded as inherently tentative. Due tothe subjective judgments and inherent uncertainties of statements about future events, there can be no assurancethat the future results, or subsequent estimates/ projections/ outlook will not vary significantly from theestimates/ projections/ outlook and other statements set out in the Hotel Market Report”.

In this regard, CBRE has issued the following disclaimer:

“The “Real Estate Market Report”, prepared by CBRE (the “CBRE Report”) has been prepared based oninformation as of specific dates, which may no longer be current or reflect current trends and opinions and whichmay be based on estimates, projections, forecasts and assumptions that may prove to be incorrect. Users/Readersare advised to read the entire Report and also conduct their own due diligence before relying on the CBREReport. Any person’s reliance on the CBRE Report will be on an as is where is basis with no specificrepresentations or warranties and no party including the Sponsor, the Manager, the Trustee, any of the BRLMs,CBRE, or any other person connected with this Issue owes any party/person any liability for their reliance on theCBRE Report.”

Valuation data

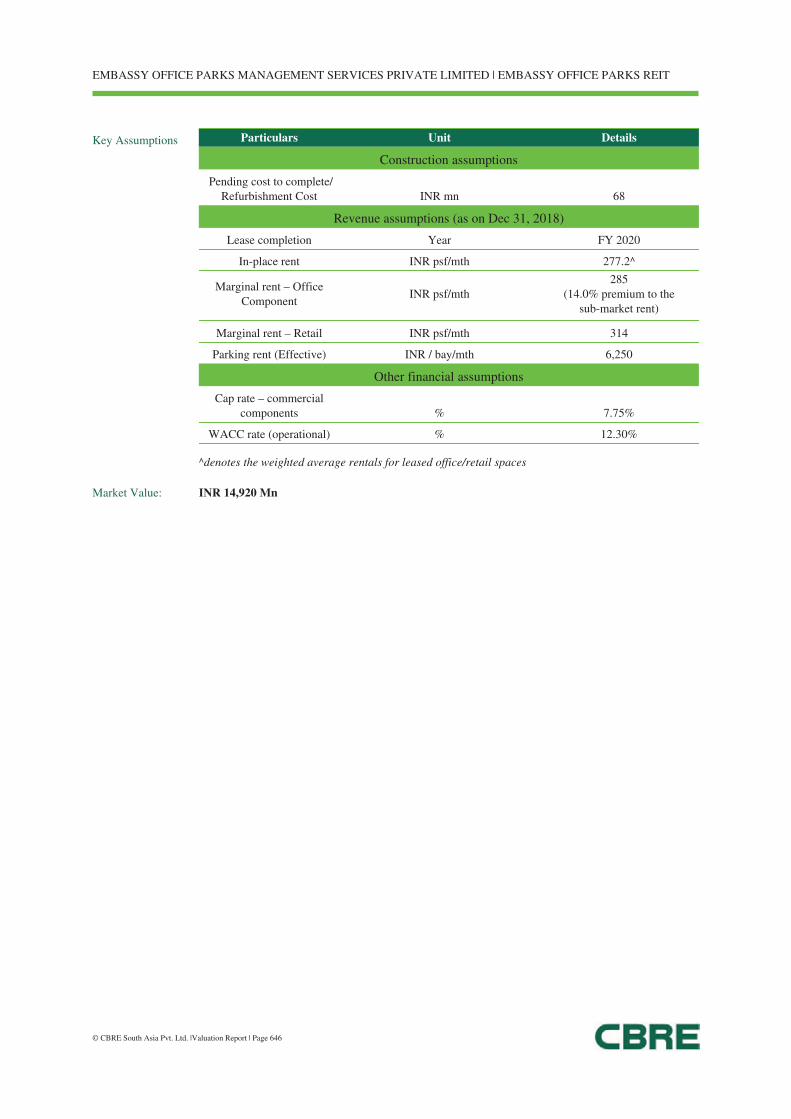

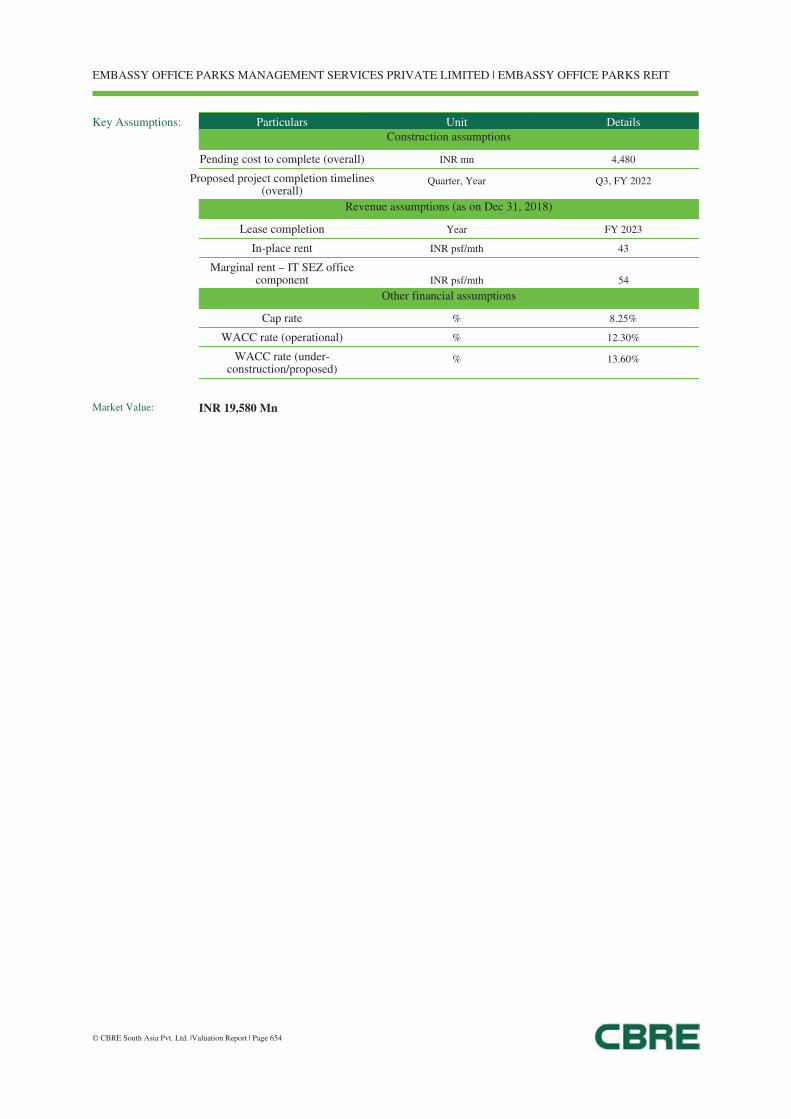

Unless stated otherwise, the summary valuation included in this Final Offer Document is a summary of the“Valuation Report” dated February 28, 2019, issued by CBRE. For details, see “Summary Valuation Report” onpage 626.

The valuation has been undertaken to ascertain the market value of the respective properties of the EmbassyREIT given the prevalent market conditions. In consideration of the same, a detailed assessment of the site andsurroundings has been undertaken with respect to the prevalent activities, change in dynamics impacting thevalues and the optimal use of the respective properties vis-à-vis their surrounding sub-market, etc. The valuationsare based on asset specific information provided by the Manager. The same has been assumed to be correct andhas been used for valuation exercise. Where it is stated in the report that another party has supplied informationto CBRE, this information is believed to be reliable but CBRE can accept no responsibility if this should provenot to be so.

A primary and secondary research exercise has been carried out in the catchment areas for the respective assets toascertain the transaction activity of commercial, retail and hospitality developments. This has been achievedthrough interactions with various market players such as developers, real estate brokers, key office tenants,hospitality occupiers, etc. The valuation exercise is based on prevailing market dynamics as on the date ofvaluation and does not take into account any unforeseeable developments which could impact the same in thefuture. Assumptions are a necessary part of undertaking valuations. CBRE adopts assumptions for the purpose ofproviding valuation advice because some matters are not capable of accurate calculation or fall outside the scopeof CBRE’s expertise, or CBRE’s instructions. The reader accepts that the valuation contains certain specificassumptions and acknowledges and accepts the risk that if any of the assumptions adopted in the valuation areincorrect, then this may have an effect on the valuation.

Although the Manager believes that the industry and market data used by CBRE for the valuation as part of thisFinal Offer Document is reliable, it has not been independently verified by the Manager, the Embassy Sponsor,the Blackstone Sponsor, the Trustee or the Lead Managers, or any of their associates, affiliates or advisors. Datafrom these sources may also not be comparable. Such data involves risks, uncertainties and numerousassumptions and is subject to change based on various factors, including those disclosed in “Risk Factors” onpage 22 of the Final Offer Document. Accordingly, investment decisions should not be based solely on suchinformation.

The extent to which the valuation assumptions used by CBRE in their summary valuation report as highlighted inthis Final Offer Document is meaningful depends on the reader’s familiarity with and understanding of themethodologies used in undertaking valuations.

11

Four Seasons Group related data

Four Seasons Hotels and Resorts Asia Pacific Pte Ltd and its affiliates (“Four Seasons Group”) is not related to,affiliated or associated with, or a partner in the business of, the Parties to the Embassy REIT, and norepresentation, warranty or guarantee is made or implied by the Four Seasons Group in respect of any statementor information made or contained in this Final Offer Document. No member of the Four Seasons Group nor anyof their respective shareholders, directors, officers, employees or agents has or will have any responsibility orliability arising out of, or related to, this Final Offer Document or the transactions contemplated by this FinalOffer Document, including any liability or responsibility for any statement or information made or contained inthis Final Offer Document.

Websites

The information contained on our websites, the websites of the Manager, the Trustee, the Embassy Sponsor, theLead Managers or the other websites referenced in this Final Offer Document or that can be accessed through ourwebsites or such other websites, neither constitutes part of this Final Offer Document, nor is it incorporated byreference therein and should not form the basis of any investment decision. For details of the websites of theManager, Trustee, Embassy Sponsor and Lead Managers, see “General Information” on page 478.

As of the date of this Final Offer Document, the Blackstone Sponsor does not have a website.

12

FORWARD-LOOKING STATEMENTS

Certain statements contained in this Final Offer Document that are not statements of historical fact constitute“forward-looking statements”. Bidders can generally identify forward-looking statements by terminology such as“aim”, “anticipate”, “believe”, “continue”, “can”, “could”, “estimate”, “expect”, “intend”, “may”, “objective”,“plan”, “potential”, “project”, “pursue”, “seek to”, “shall”, “should”, “will”, “would”, or other words or phrasesof similar import. Similarly, statements that describe the strategies, objectives, plans or goals of the EmbassyREIT and the Projections are also forward-looking statements. However, these are not the exclusive means ofidentifying forward-looking statements.

All statements regarding the expected financial conditions, results of operations, business plans and prospects ofthe Embassy REIT including the Projections are forward-looking statements. These forward-looking statementsinclude statements as to the business strategy, revenue, EBITDA, cash flow from operating activities, netdistributable cash flows, net operating income and profitability (including, without limitation, any financial oroperating data, projections or forecasts), new business and other matters in relation to the Embassy REITdiscussed in this Final Offer Document that are not historical facts. Further, please note that the Projectionsincluded in this Final Offer Document are based on a number of assumptions. For further details, see“Projections” on page 320.

The Summary Valuation Report included in this Final Offer Document is based on certain projections and shouldbe read together with assumptions and notes thereto.

Actual results may differ materially from those suggested by the forward-looking statements or financialprojections due to certain known or unknown risks or uncertainties associated with the Manager’s expectationswith respect to, but not limited to, the actual growth in the real estate sector, the Manager’s ability to successfullyimplement the strategy, growth and expansion plans, technological changes, cash flow projections, the outcomeof any legal or regulatory proceedings and the future impact of new accounting standards, regulatory changespertaining to the real estate sector in India and our ability to respond to them, and general economic and politicalconditions in India which have an impact on our business activities or investments, changes in competition andthe Manager’s ability to operate and maintain the Portfolio Assets. By their nature, certain of the market riskdisclosures are only estimates and could be materially different from what actually occurs in the future. As aresult, actual future gains, losses or impact on net interest income and net income could materially differ fromthose that have been estimated.

Factors that could cause actual results, performance or achievements of the Embassy REIT to differ materiallyinclude, but are not limited to, those discussed under “Risk Factors”, “Industry Overview”, “Our Business andProperties” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations”, onpages 22, 64, 131 and 278, respectively. Some of the factors that could cause the actual results, performance orachievements of the Embassy REIT to differ materially from those in the forward-looking statements andfinancial information include, but are not limited to, the following:

• We have assumed existing liabilities in relation to the Portfolio, which liabilities if realized may impact thetrading price of our Units, our profitability and ability to make distributions.

• We intend to obtain external debt financing to repay a portion of the debt of the Portfolio and to finance thePortfolio’s business and financing requirements after the completion of the Issue and the listing of the Units.The terms of this financing may limit our ability to make distributions to the Unitholders.

• We may utilize a significant amount of debt in the operation of our business, and our cash flows andoperating results could be adversely affected by required repayments or related interest and other risks of ourdebt financing. Our inability to service debt may impact our distributions to Unitholders

• The REIT Regulations impose restrictions on the investments made by us and require us to adhere to certaininvestment conditions, which may limit our ability to acquire and/ or dispose of assets or explore newopportunities. Further, the regulatory framework governing real estate investment trusts in India is new anduntested.

• The proposed holding and financing structure of the Portfolio may not be tax efficient.

13

• Our business is dependent on the Indian economy and financial stability in Indian markets, and anyslowdown in the Indian economy or in Indian financial markets could have a material adverse effect on ourbusiness.

• We have a limited operating history and may not be able to operate our business successfully or generatesufficient cash flows to make or sustain distributions.

• A significant portion of our revenues are derived from a limited number of large tenants, tenants in thetechnology sector and from a few integrated office parks. Any conditions that impact these tenants, thetechnology sector or parks may adversely affect our business, revenue from operations and financialcondition.

• Tenant leases across our Portfolio are subject to the risk of non-renewal, non-replacement or earlytermination. Further, vacant properties could be difficult to lease, which could adversely affect our revenues.

• Our business and profitability are dependent on the performance of the commercial real estate market inIndia, generally and any fluctuations in market conditions may have an adverse impact on our financialcondition.

• We may be required to record significant charges to earnings in the future when we review our Portfolio forpotential impairment.

• Our contingent liability could adversely affect our financial condition, results of operations and cash flows.

• We rely on third party operators to successfully operate and manage certain Portfolio Assets. Our results ofoperations may be adversely affected if we fail to effectively oversee the functioning of third-partyoperators.

• Compliance with, and changes in, environmental laws and regulations could adversely affect thedevelopment of our properties and our financial condition.

• If we are unable to maintain relationships with other stakeholders in our Portfolio, our financial conditionsand results of operation may be adversely affected.

• We are exposed to a variety of risks associated with safety, security and crisis management.

• We may be unable to successfully grow our business in new markets in India, which may adversely affectour growth, business prospects, results of operations and financial condition.

• We may be adversely affected if the Asset SPVs and Investment Entity are unable to obtain, maintain orrenew all regulatory approvals that are required for their respective business.

• If we are required to make any indemnity payments to the Lead Managers resulting from certain liabilitiesincurred in connection with the Issue under the indemnity that we have provided to them in the IssueAgreement and any Underwriting Agreement (if entered into), our ability to make distributions to theUnitholders may be adversely affected.

Forward-looking statements and financial projections reflect current views as of the date of this Final OfferDocument and are not a guarantee of future performance or returns to investors. There can be no assurance thatthe expectations reflected in the forward-looking statements and financial information will prove to be correct.These statements and projections are based on certain beliefs and assumptions, which in turn are based oncurrently available information. In accordance with the REIT Regulations, the calculations and assumptionsunderlying the Projections have been certified by the Manager and the Auditors. The Projections have beenprepared for inclusion in this Final Offer Document for the purposes of this Issue, using a set of assumptions thatinclude hypothetical assumptions about future events and management’s actions that are not necessarily expectedto occur, and have been approved by the board of directors of the Manager. Consequently, Bidders are cautionedthat the Projections may not be appropriate for purposes other than that described above. Given theseuncertainties, investors are cautioned not to place undue reliance on such forward-looking statements andProjections. In any event, these statements speak only as of the date of this Final Offer Document or therespective

14