SBI CARDS AND PAYMENT SERVICES LIMITED - Nomura ...

485

PROSPECTUS March 6, 2020 Please read Section 32 of the Companies Act, 2013 100% Book Built Offer SBI CARDS AND PAYMENT SERVICES LIMITED Our Company was incorporated as “SBI Cards and Payment Services Private Limited” on May 15, 1998, as a private limited company under the Companies Act, 1956, at New Delhi, with a certificate of incorporation granted by the Registrar of Companies, National Capital Territory of Delhi and Haryana at New Delhi (“RoC”). On the conversion of our Company to a public limited company pursuant to a special resolution passed by our shareholders on August 2, 2019, our name was changed to “SBI Cards and Payment Services Limited” and a fresh certificate of incorporation dated August 20, 2019 was issued by the RoC. For details of the change in the registered office of our Company, see “History and Certain Corporate Matters” on page 168. Corporate Identity Number: U65999DL1998PLC093849 Registered Office: Unit 401 & 402, 4 th Floor, Aggarwal Millennium Tower E-1,2,3, Netaji Subhash Place, Wazirpur, New Delhi 110 034, India; Tel: +91 (11) 6126 8100 Corporate Office: 2 nd Floor, Tower-B, Infinity Towers, DLF Cyber City, Block 2 Building 3, DLF Phase 2, Gurugram, Haryana 122 002, India; Tel: +91 (124) 458 9803 Contact Person: Ms. Payal Mittal Chhabra, Company Secretary and Compliance Officer; Tel: +91 (124) 458 9803 E-mail: [email protected]; Website: www.sbicard.com OUR PROMOTER: STATE BANK OF INDIA INITIAL PUBLIC OFFERING OF 137,149,314 * EQUITY SHARES OF FACE VALUE OF ₹ 10 EACH (“EQUITY SHARES”) OF SBI CARDS AND PAYMENT SERVICES LIMITED (OUR “COMPANY” OR THE “COMPANY” OR THE “ISSUER”) FOR CASH AT A PRICE OF ₹ 755 ** PER EQUITY SHARE (INCLUDING A SHARE PREMIUM OF ₹ 745 PER EQUITY SHARE) (THE “OFFER PRICE”) AGGREGATING TO ₹ 103,407.88 * MILLION, COMPRISING A FRESH ISSUE OF 6,622,516 * EQUITY SHARES BY OUR COMPANY AGGREGATING TO ₹ 4,993.25 MILLION (“FRESH ISSUE”) AND AN OFFER FOR SALE OF 130,526,798 * EQUITY SHARES (THE “OFFERED SHARES”) AGGREGATING TO ₹ 98,414.64 * MILLION, INCLUDING 37,293,371 * EQUITY SHARES AGGREGATING TO ₹ 28,118.47 * MILLION BY STATE BANK OF INDIA (“SBI”) (“PROMOTER SELLING SHAREHOLDER”) AND 93,233,427 * EQUITY SHARES AGGREGATING TO ₹ 70,296.17 * MILLION BY CA ROVER HOLDINGS (“CA ROVER”) (“INVESTOR SELLING SHAREHOLDER” AND TOGETHER WITH THE PROMOTER SELLING SHAREHOLDER, THE “SELLING SHAREHOLDERS” AND SUCH OFFER, THE “OFFER FOR SALE” AND TOGETHER WITH THE FRESH ISSUE, THE “OFFER”). THE OFFER INCLUDED A RESERVATION OF 1,864,669 ** EQUITY SHARES, FOR SUBSCRIPTION BY ELIGIBLE EMPLOYEES (AS DEFINED HEREINAFTER) (THE “EMPLOYEE RESERVATION PORTION”) AND A RESERVATION OF 13,052,680 * EQUITY SHARES, FOR SUBSCRIPTION BY SBI SHAREHOLDERS (AS DEFINED HEREINAFTER) (THE “SBI SHAREHOLDERS RESERVATION PORTION”). THE OFFER LESS THE EMPLOYEE RESERVATION PORTION AND THE SBI SHAREHOLDERS RESERVATION PORTION IS HEREINAFTER REFERRED TO AS THE “NET OFFER”, AGGREGATING TO 122,231,965 * EQUITY SHARES. THE OFFER AND THE NET OFFER CONSTITUTES 14.61 * % AND 13.02 * % OF THE POST-OFFER PAID UP EQUITY SHARE CAPITAL OF OUR COMPANY, RESPECTIVELY. *Subject to finalisation of Basis of Allotment **Our Company and the Selling Shareholders in consultation with the BRLMs, have offered a discount of ₹ 75 per Equity Share to Eligible Employees bidding in the Employee Reservation Portion THE FACE VALUE OF THE EQUITY SHARES IS ₹ 10 EACH AND THE OFFER PRICE IS 75.5 TIMES THE FACE VALUE OF THE EQUITY SHARES The Offer has been made in terms of Rule 19(2)(b) of the Securities Contracts (Regulation) Rules, 1957, as amended, (the “SCRR”) read with Regulation 31 of the Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2018, as amended (“SEBI ICDR Regulations”). The Offer was made through the Book Building Process, in compliance with Regulation 6(1) of the SEBI ICDR Regulations, where not more than 50% of the Net Offer will be Allotted on a proportionate basis to Qualified Institutional Buyers (“QIBs”) (the “QIB Category”), provided that our Company and the Selling Shareholders in consultation with the BRLMs, has allocated up to 60% of the QIB Category to Anchor Investors, on a discretionary basis (the “Anchor Investor Portion”), of which one-third was reserved for domestic Mutual Funds, subject to valid Bids being received from domestic Mutual Funds at or above the price at which Equity Shares were allocated to Anchor Investors. Further, 5% of the QIB Category (excluding the Anchor Investor Portion) was made available for allocation on a proportionate basis to Mutual Funds only and the remainder of the QIB Category was made available for allocation on a proportionate basis to all QIBs (other than Anchor Investors), including Mutual Funds, subject to valid Bids being received at or above the Offer Price. Further, not less than 15% of the Net Offer was made available for allocation on a proportionate basis to Non-Institutional Investors and not less than 35% of the Net Offer was made available for allocation to Retail Individual Investors, in accordance with the SEBI ICDR Regulations, subject to valid Bids being received at or above the Offer Price. All Bidders (other than Anchor Investors) were mandatorily required to participate in this Offer through the Application Supported by Block Amount (“ASBA”) process, and were required to provide details of their respective bank account (including UPI ID for Retail Individual Investors using UPI Mechanism) in which the Bid Amount will be blocked by the SCSBs or the Sponsor Bank, as the case may be. Anchor Investors were not permitted to participate in the Anchor Investor Portion through the ASBA process. For details, see, “Offer Procedure” on page 404. RISKS IN RELATION TO THE FIRST OFFER This being the first public issue of the Equity Shares of our Company, there has been no formal market for the Equity Shares. The face value of the Equity Shares is ₹ 10 and the Offer Price is 75.5 times the face value of the Equity Shares. The Offer Price (as decided by our Company and the Selling Shareholders, in consultation with the BRLMs) in accordance with the SEBI ICDR Regulations, and as stated in “Basis for Offer Price” on page 97, should not be taken to be indicative of the market price of the Equity Shares after the Equity Shares are listed. No assurance can be given regarding an active and/or sustained trading in the Equity Shares or regarding the price at which the Equity Shares will be traded after listing. GENERAL RISKS Investments in equity and equity-related securities involve a degree of risk and investors should not invest any funds in this Offer unless they can afford to take the risk of losing their investment. Investors are advised to read the Risk Factors carefully before taking an investment decision in this Offer. For taking an investment decision, investors must rely on their own examination of our Company and the Offer, including the risks involved. The Equity Shares have not been recommended or approved by the Securities and Exchange Board of India (“SEBI”), nor does SEBI guarantee the accuracy or adequacy of the contents of this Prospectus. Specific attention of the investors is invited to “Risk Factors” on page 28. ISSUER’S AND SELLING SHAREHOLDERS’ ABSOLUTE RESPONSIBILITY Our Company, having made all reasonable inquiries, accepts responsibility for and confirms that this Prospectus contains all information with regard to our Company and the Offer, which is material in the context of the Offer, that the information contained in this Prospectus is true and correct in all material aspects and is not misleading in any material respect, that the opinions and intentions expressed herein are honestly held and that there are no other facts, the omission of which makes this Prospectus as a whole or any of such information or the expression of any such opinions or intentions, misleading in any material respect. Further, each of the Selling Shareholders, severally and not jointly, accept responsibility for only such statements confirmed or undertaken by such Selling Shareholders in this Prospectus to the extent such statements pertain to such Selling Shareholder and/or its portion of the Offered Shares and confirms that such statements are true and correct in all material respects and are not misleading in any material respect. However, each Selling Shareholder, severally and not jointly, does not assume any responsibility for any other statements, including without limitation, any and all of the statements made by or in relation to our Company or the other Selling Shareholders in this Prospectus. LISTING The Equity Shares offered through the Red Herring Prospectus are proposed to be listed on the BSE and NSE. We have received in-principle approvals from the BSE and NSE for the listing of the Equity Shares pursuant to letters dated December 6, 2019 and December 16, 2019, respectively. For the purpose of this Offer, BSE is the Designated Stock Exchange. A signed copy of the Red Herring Prospectus has been and this Prospectus shall be filed with the RoC in accordance with Section 26(4) of the Companies Act, 2013. For details of the material contracts and documents that were available for inspection from the date of the Red Herring Prospectus up to the Bid/Offer Closing Date, see “Material Contracts and Documents for Inspection” on page 478. BOOK RUNNING LEAD MANAGERS Kotak Mahindra Capital Company Limited 1 st Floor, 27 BKC, Plot No. C – 27 "G" Block, Bandra Kurla Complex Bandra (East), Mumbai 400 051 Maharashtra, India Telephone: +91 22 4336 0000 E-mail: [email protected] Investor Grievance E-mail: [email protected] Website: www.investmentbank.kotak.com Contact Person: Mr. Ganesh Rane SEBI Registration No.: INM000008704 Axis Capital Limited Axis House, Level 1 C-2 Wadia International Centre P. B. Marg, Worli, Mumbai 400 025 Maharashtra, India India Telephone: +91 22 4325 2183 E-mail: [email protected] Investor Grievance E-mail: [email protected] Website: www.axiscapital.co.in Contact Person: Ms. Simran Gadh SEBI Registration No.: INM000012029 DSP Merrill Lynch Limited Ground Floor, “A” Wing One BKC, “G” Block Bandra Kurla Complex Bandra (East), Mumbai 400 051 Maharashtra, India Telephone: +91 22 6632 8000 E-mail: [email protected] Investor Grievance E-mail: [email protected] Website: www.ml-india.com Contact Person: Mr. Ahmed Kolsawala SEBI Registration No.: INM000011625 HSBC Securities and Capital Markets (India) Private Limited 52/60, Mahatma Gandhi Road, Fort, Mumbai 400 001 Maharashtra, India Telephone: +91 22 2268 5555 E-mail: [email protected] Investor Grievance E-mail: [email protected] Website: https://www.business.hsbc.co.in/en- gb/in/generic/ipo-open-offer-and-buyback Contact Person: Ms. Sanjana Maniar SEBI Registration No.: INM000010353 BOOK RUNNING LEAD MANAGERS REGISTRAR TO THE OFFER Nomura Financial Advisory and Securities (India) Private Limited Ceejay House, Level 11, Plot F Shivsagar Estate Dr. Annie Besant Road, Worli Mumbai 400 018, Maharashtra, India Telephone: +91 22 4037 4037 Email: [email protected] Investor grievance e-mail: [email protected] Website:www.nomuraholdings.com/company/group/asia/india/index.html Contact person: Mr. Vishal Kanjani/Mr. Sandeep Baid SEBI Registration No.: INM000011419 SBI Capital Markets Limited* 202, Market Tower ‘E’ Cuffe Parade, Mumbai 400 005 Maharashtra, India Telephone: +91 22 2217 8300 E-mail: [email protected] Investor Grievance E-mail: [email protected] Website: www.sbicaps.com Contact Person: Mr. Sambit Rath/ Mr. Karan Savardekar SEBI Registration No.: INM000003531 Link Intime India Private Limited C-101, 1 st Floor, 247 Park Lal Bahadur Shastri Marg, Vikhroli (West) Mumbai – 400 083 Maharashtra, India Telephone: +91 22 4918 6200 Email: [email protected] Website: www.linkintime.co.in Contact Person: Shanti Gopalkrishnan SEBI Registration No: INR000004058 BID/OFFER PERIOD BID/OFFER OPENED ON** March 2, 2020 BID/OFFER CLOSED ON (QIB BIDDERS) March 4, 2020 BID/OFFER CLOSED ON March 5, 2020 * SBI participated as a Selling Shareholder in the Offer for Sale. SBI Capital Markets Limited (“SBICAP”) has signed the due diligence certificate and has been disclosed as a BRLM for the Offer. SBI and SBICAP are associates in terms of the Securities and Exchange Board of India (Merchant Bankers) Regulations, 1992, as amended (the “SEBI Merchant Bankers Regulations”). Accordingly, in compliance with the proviso to Regulation 21A of the SEBI Merchant Bankers Regulations and Regulation 23(3) of the SEBI ICDR Regulations, SBICAP was involved only in the marketing of the Offer. ** The Anchor Investor Bidding Date was one Working Day prior to the Bid/Offer Opening Date i.e February 28, 2020.

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of SBI CARDS AND PAYMENT SERVICES LIMITED - Nomura ...

PROSPECTUS

March 6, 2020

Please read Section 32 of the Companies Act, 2013

100% Book Built Offer

SBI CARDS AND PAYMENT SERVICES LIMITED

Our Company was incorporated as “SBI Cards and Payment Services Private Limited” on May 15, 1998, as a private limited company under the Companies Act, 1956, at New Delhi, with a certificate of incorporation granted by the

Registrar of Companies, National Capital Territory of Delhi and Haryana at New Delhi (“RoC”). On the conversion of our Company to a public limited company pursuant to a special resolution passed by our shareholders on August 2,

2019, our name was changed to “SBI Cards and Payment Services Limited” and a fresh certificate of incorporation dated August 20, 2019 was issued by the RoC. For details of the change in the registered office of our Company, see

“History and Certain Corporate Matters” on page 168.

Corporate Identity Number: U65999DL1998PLC093849

Registered Office: Unit 401 & 402, 4th Floor, Aggarwal Millennium Tower E-1,2,3, Netaji Subhash Place, Wazirpur, New Delhi 110 034, India; Tel: +91 (11) 6126 8100

Corporate Office: 2nd Floor, Tower-B, Infinity Towers, DLF Cyber City, Block 2 Building 3, DLF Phase 2, Gurugram, Haryana 122 002, India; Tel: +91 (124) 458 9803

Contact Person: Ms. Payal Mittal Chhabra, Company Secretary and Compliance Officer; Tel: +91 (124) 458 9803

E-mail: [email protected]; Website: www.sbicard.com

OUR PROMOTER: STATE BANK OF INDIA

INITIAL PUBLIC OFFERING OF 137,149,314* EQUITY SHARES OF FACE VALUE OF ₹ 10 EACH (“EQUITY SHARES”) OF SBI CARDS AND PAYMENT SERVICES LIMITED (OUR “COMPANY” OR THE “COMPANY” OR

THE “ISSUER”) FOR CASH AT A PRICE OF ₹ 755**

PER EQUITY SHARE (INCLUDING A SHARE PREMIUM OF ₹ 745 PER EQUITY SHARE) (THE “OFFER PRICE”) AGGREGATING TO ₹ 103,407.88* MILLION, COMPRISING

A FRESH ISSUE OF 6,622,516* EQUITY SHARES BY OUR COMPANY AGGREGATING TO ₹ 4,993.25 MILLION (“FRESH ISSUE”) AND AN OFFER FOR SALE OF 130,526,798

* EQUITY SHARES (THE “OFFERED SHARES”)

AGGREGATING TO ₹ 98,414.64* MILLION, INCLUDING 37,293,371

* EQUITY SHARES AGGREGATING TO ₹ 28,118.47

* MILLION BY STATE BANK OF INDIA (“SBI”) (“PROMOTER SELLING SHAREHOLDER”) AND

93,233,427* EQUITY SHARES AGGREGATING TO ₹ 70,296.17

* MILLION BY CA ROVER HOLDINGS (“CA ROVER”) (“INVESTOR SELLING SHAREHOLDER” AND TOGETHER WITH THE PROMOTER SELLING

SHAREHOLDER, THE “SELLING SHAREHOLDERS” AND SUCH OFFER, THE “OFFER FOR SALE” AND TOGETHER WITH THE FRESH ISSUE, THE “OFFER”).

THE OFFER INCLUDED A RESERVATION OF 1,864,669**

EQUITY SHARES, FOR SUBSCRIPTION BY ELIGIBLE EMPLOYEES (AS DEFINED HEREINAFTER) (THE “EMPLOYEE RESERVATION PORTION”) AND A

RESERVATION OF 13,052,680* EQUITY SHARES, FOR SUBSCRIPTION BY SBI SHAREHOLDERS (AS DEFINED HEREINAFTER) (THE “SBI SHAREHOLDERS RESERVATION PORTION”). THE OFFER LESS THE

EMPLOYEE RESERVATION PORTION AND THE SBI SHAREHOLDERS RESERVATION PORTION IS HEREINAFTER REFERRED TO AS THE “NET OFFER”, AGGREGATING TO 122,231,965* EQUITY SHARES. THE

OFFER AND THE NET OFFER CONSTITUTES 14.61*% AND 13.02

*% OF THE POST-OFFER PAID UP EQUITY SHARE CAPITAL OF OUR COMPANY, RESPECTIVELY.

*Subject to finalisation of Basis of Allotment

**Our Company and the Selling Shareholders in consultation with the BRLMs, have offered a discount of ₹ 75 per Equity Share to Eligible Employees bidding in the Employee Reservation Portion

THE FACE VALUE OF THE EQUITY SHARES IS ₹ 10 EACH AND THE OFFER PRICE IS 75.5 TIMES THE FACE VALUE OF THE EQUITY SHARES

The Offer has been made in terms of Rule 19(2)(b) of the Securities Contracts (Regulation) Rules, 1957, as amended, (the “SCRR”) read with Regulation 31 of the Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2018, as amended (“SEBI ICDR Regulations”). The Offer was made through the Book Building Process, in compliance with Regulation 6(1) of the SEBI ICDR Regulations, where not more than 50% of the Net Offer will be Allotted on a

proportionate basis to Qualified Institutional Buyers (“QIBs”) (the “QIB Category”), provided that our Company and the Selling Shareholders in consultation with the BRLMs, has allocated up to 60% of the QIB Category to Anchor Investors, on a

discretionary basis (the “Anchor Investor Portion”), of which one-third was reserved for domestic Mutual Funds, subject to valid Bids being received from domestic Mutual Funds at or above the price at which Equity Shares were allocated to Anchor Investors. Further, 5% of the QIB Category (excluding the Anchor Investor Portion) was made available for allocation on a proportionate basis to Mutual Funds only and the remainder of the QIB Category was made available for allocation on a

proportionate basis to all QIBs (other than Anchor Investors), including Mutual Funds, subject to valid Bids being received at or above the Offer Price. Further, not less than 15% of the Net Offer was made available for allocation on a proportionate basis

to Non-Institutional Investors and not less than 35% of the Net Offer was made available for allocation to Retail Individual Investors, in accordance with the SEBI ICDR Regulations, subject to valid Bids being received at or above the Offer Price. All Bidders (other than Anchor Investors) were mandatorily required to participate in this Offer through the Application Supported by Block Amount (“ASBA”) process, and were required to provide details of their respective bank account (including UPI ID

for Retail Individual Investors using UPI Mechanism) in which the Bid Amount will be blocked by the SCSBs or the Sponsor Bank, as the case may be. Anchor Investors were not permitted to participate in the Anchor Investor Portion through the ASBA

process. For details, see, “Offer Procedure” on page 404.

RISKS IN RELATION TO THE FIRST OFFER

This being the first public issue of the Equity Shares of our Company, there has been no formal market for the Equity Shares. The face value of the Equity Shares is ₹ 10 and the Offer Price is 75.5 times the face value of the Equity Shares. The Offer Price

(as decided by our Company and the Selling Shareholders, in consultation with the BRLMs) in accordance with the SEBI ICDR Regulations, and as stated in “Basis for Offer Price” on page 97, should not be taken to be indicative of the market price of

the Equity Shares after the Equity Shares are listed. No assurance can be given regarding an active and/or sustained trading in the Equity Shares or regarding the price at which the Equity Shares will be traded after listing.

GENERAL RISKS

Investments in equity and equity-related securities involve a degree of risk and investors should not invest any funds in this Offer unless they can afford to take the risk of losing their investment. Investors are advised to read the Risk Factors carefully before taking an investment decision in this Offer. For taking an investment decision, investors must rely on their own examination of our Company and the Offer, including the risks involved. The Equity Shares have not been recommended or approved

by the Securities and Exchange Board of India (“SEBI”), nor does SEBI guarantee the accuracy or adequacy of the contents of this Prospectus. Specific attention of the investors is invited to “Risk Factors” on page 28.

ISSUER’S AND SELLING SHAREHOLDERS’ ABSOLUTE RESPONSIBILITY

Our Company, having made all reasonable inquiries, accepts responsibility for and confirms that this Prospectus contains all information with regard to our Company and the Offer, which is material in the context of the Offer, that the information contained in this Prospectus is true and correct in all material aspects and is not misleading in any material respect, that the opinions and intentions expressed herein are honestly held and that there are no other facts, the omission of which makes this Prospectus as

a whole or any of such information or the expression of any such opinions or intentions, misleading in any material respect. Further, each of the Selling Shareholders, severally and not jointly, accept responsibility for only such statements confirmed or

undertaken by such Selling Shareholders in this Prospectus to the extent such statements pertain to such Selling Shareholder and/or its portion of the Offered Shares and confirms that such statements are true and correct in all material respects and are not

misleading in any material respect. However, each Selling Shareholder, severally and not jointly, does not assume any responsibility for any other statements, including without limitation, any and all of the statements made by or in relation to our Company or the other Selling Shareholders in this Prospectus.

LISTING

The Equity Shares offered through the Red Herring Prospectus are proposed to be listed on the BSE and NSE. We have received in-principle approvals from the BSE and NSE for the listing of the Equity Shares pursuant to letters dated December 6, 2019

and December 16, 2019, respectively. For the purpose of this Offer, BSE is the Designated Stock Exchange. A signed copy of the Red Herring Prospectus has been and this Prospectus shall be filed with the RoC in accordance with Section 26(4) of the Companies Act, 2013. For details of the material contracts and documents that were available for inspection from the date of the Red Herring Prospectus up to the Bid/Offer Closing Date, see “Material Contracts and Documents for Inspection” on page

478.

BOOK RUNNING LEAD MANAGERS

Kotak Mahindra Capital Company Limited 1

st Floor, 27 BKC, Plot No. C – 27

"G" Block, Bandra Kurla Complex

Bandra (East), Mumbai 400 051

Maharashtra, India Telephone: +91 22 4336 0000

E-mail: [email protected]

Investor Grievance E-mail: [email protected] Website: www.investmentbank.kotak.com

Contact Person: Mr. Ganesh Rane

SEBI Registration No.: INM000008704

Axis Capital Limited Axis House, Level 1

C-2 Wadia International Centre

P. B. Marg, Worli, Mumbai 400 025

Maharashtra, India India

Telephone: +91 22 4325 2183

E-mail: [email protected] Investor Grievance E-mail: [email protected]

Website: www.axiscapital.co.in

Contact Person: Ms. Simran Gadh

SEBI Registration No.: INM000012029

DSP Merrill Lynch Limited Ground Floor, “A” Wing

One BKC, “G” Block

Bandra Kurla Complex

Bandra (East), Mumbai 400 051 Maharashtra, India

Telephone: +91 22 6632 8000

E-mail: [email protected] Investor Grievance E-mail:

Website: www.ml-india.com

Contact Person: Mr. Ahmed Kolsawala SEBI Registration No.: INM000011625

HSBC Securities and Capital Markets (India) Private

Limited

52/60, Mahatma Gandhi Road, Fort, Mumbai 400 001

Maharashtra, India

Telephone: +91 22 2268 5555

E-mail: [email protected]

Investor Grievance E-mail: [email protected]

Website: https://www.business.hsbc.co.in/en-gb/in/generic/ipo-open-offer-and-buyback

Contact Person: Ms. Sanjana Maniar

SEBI Registration No.: INM000010353

BOOK RUNNING LEAD MANAGERS REGISTRAR TO THE OFFER

Nomura Financial Advisory and Securities (India) Private Limited

Ceejay House, Level 11, Plot F Shivsagar Estate Dr. Annie Besant Road, Worli

Mumbai 400 018, Maharashtra, India

Telephone: +91 22 4037 4037

Email: [email protected] Investor grievance e-mail: [email protected]

Website:www.nomuraholdings.com/company/group/asia/india/index.html

Contact person: Mr. Vishal Kanjani/Mr. Sandeep Baid SEBI Registration No.: INM000011419

SBI Capital Markets Limited*

202, Market Tower ‘E’ Cuffe Parade, Mumbai 400 005

Maharashtra, India

Telephone: +91 22 2217 8300

E-mail: [email protected] Investor Grievance E-mail: [email protected]

Website: www.sbicaps.com

Contact Person: Mr. Sambit Rath/ Mr. Karan Savardekar SEBI Registration No.: INM000003531

Link Intime India Private Limited C-101, 1

st Floor, 247 Park

Lal Bahadur Shastri Marg, Vikhroli (West)

Mumbai – 400 083

Maharashtra, India

Telephone: +91 22 4918 6200 Email: [email protected]

Website: www.linkintime.co.in

Contact Person: Shanti Gopalkrishnan SEBI Registration No: INR000004058

BID/OFFER PERIOD

BID/OFFER OPENED ON** March 2, 2020 BID/OFFER CLOSED ON (QIB BIDDERS) March 4, 2020

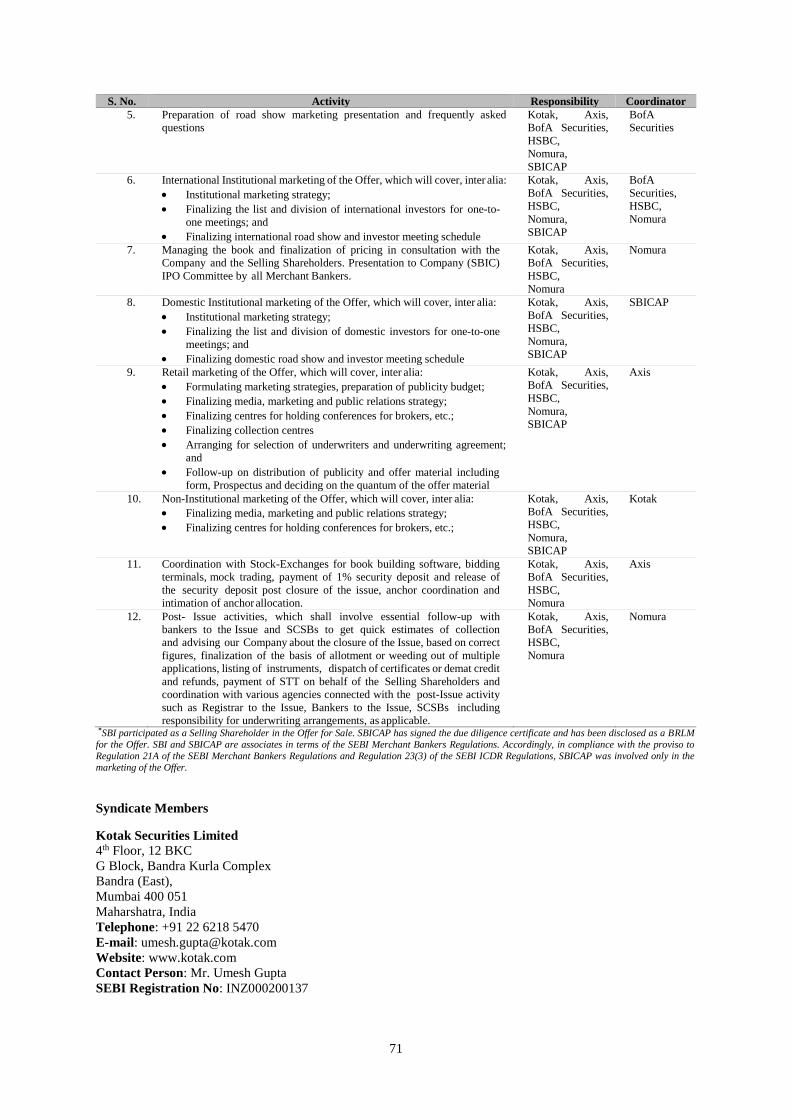

BID/OFFER CLOSED ON March 5, 2020 * SBI participated as a Selling Shareholder in the Offer for Sale. SBI Capital Markets Limited (“SBICAP”) has signed the due diligence certificate and has been disclosed as a BRLM for the Offer. SBI and SBICAP are associates in

terms of the Securities and Exchange Board of India (Merchant Bankers) Regulations, 1992, as amended (the “SEBI Merchant Bankers Regulations”). Accordingly, in compliance with the proviso to Regulation 21A of the SEBI

Merchant Bankers Regulations and Regulation 23(3) of the SEBI ICDR Regulations, SBICAP was involved only in the marketing of the Offer. **The Anchor Investor Bidding Date was one Working Day prior to the Bid/Offer Opening Date i.e February 28, 2020.

(This page is intentionally left blank)

TABLE OF CONTENTS

SECTION I – GENERAL .................................................................................................................................... 1

DEFINITIONS AND ABBREVIATIONS ..................................................................................................... 1 CERTAIN CONVENTIONS, USE OF FINANCIAL INFORMATION AND MARKET DATA AND

CURRENCY OF PRESENTATION ............................................................................................................ 15 FORWARD-LOOKING STATEMENTS ................................................................................................... 18 NOTICE TO PROSPECTIVE INVESTORS IN THE UNITED STATES .............................................. 20 SUMMARY OF THE OFFER DOCUMENT ............................................................................................. 21

SECTION II - RISK FACTORS ....................................................................................................................... 28

SECTION III – INTRODUCTION ................................................................................................................... 59

THE OFFER .................................................................................................................................................. 59 SUMMARY OF FINANCIAL INFORMATION ....................................................................................... 61 GENERAL INFORMATION ....................................................................................................................... 68 CAPITAL STRUCTURE .............................................................................................................................. 79 OBJECTS OF THE OFFER ......................................................................................................................... 93 BASIS FOR OFFER PRICE ........................................................................................................................ 97 STATEMENT OF SPECIAL TAX BENEFITS.......................................................................................... 99

SECTION IV- ABOUT OUR COMPANY ..................................................................................................... 103

INDUSTRY OVERVIEW ........................................................................................................................... 103 OUR BUSINESS .......................................................................................................................................... 131 KEY REGULATIONS AND POLICIES IN INDIA................................................................................. 157 HISTORY AND CERTAIN CORPORATE MATTERS ......................................................................... 168 OUR MANAGEMENT ............................................................................................................................... 175 OUR PROMOTER AND PROMOTER GROUP ..................................................................................... 194 OUR GROUP COMPANIES ...................................................................................................................... 200 DIVIDEND POLICY ................................................................................................................................... 206

SECTION V- FINANCIAL INFORMATION ............................................................................................... 207

FINANCIAL STATEMENTS..................................................................................................................... 207 OTHER FINANCIAL INFORMATION ................................................................................................... 319 CAPITALISATION STATEMENT ........................................................................................................... 320 FINANCIAL INDEBTEDNESS ................................................................................................................. 321 MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS

OF OPERATIONS ...................................................................................................................................... 323

SECTION VI – LEGAL AND OTHER INFORMATION ........................................................................... 360

OUTSTANDING LITIGATION AND MATERIAL DEVELOPMENTS ............................................. 360 GOVERNMENT AND OTHER APPROVALS ........................................................................................ 374 OTHER REGULATORY AND STATUTORY DISCLOSURES ........................................................... 377

SECTION VII – OFFER RELATED INFORMATION ............................................................................... 396

TERMS OF THE OFFER ........................................................................................................................... 396 OFFER STRUCTURE ................................................................................................................................ 400 OFFER PROCEDURE................................................................................................................................ 404 RESTRICTIONS ON FOREIGN OWNERSHIP OF INDIAN SECURITIES ...................................... 421

SECTION VIII – MAIN PROVISIONS OF THE ARTICLES OF ASSOCIATION ................................ 422

SECTION IX – OTHER INFORMATION .................................................................................................... 478

MATERIAL CONTRACTS AND DOCUMENTS FOR INSPECTION ................................................ 478 DECLARATION ......................................................................................................................................... 480

1

SECTION I – GENERAL

DEFINITIONS AND ABBREVIATIONS

Unless the context otherwise indicates or implies or unless otherwise specified, the following terms and

abbreviations have the following meanings in this Prospectus, and references to any statute or rules or guidelines

or regulations or circulars or notifications or policies will include any amendments, clarifications, modifications,

replacements or re-enactments thereto, from time to time. In case of any inconsistency between the definitions

given below and the definitions contained in the General Information Document (as defined below), the definitions

given below shall prevail.

The words and expressions used in this Prospectus, but not defined herein shall have the meaning ascribed to

such terms under the SEBI ICDR Regulations, the Companies Act, the SCRA, and the Depositories Act and the

rules and regulations made thereunder.

Company Related Terms

Term Description

“the Company”, “our

Company” or “the Issuer”

SBI Cards and Payment Services Limited, a public limited company incorporated

in India under the Companies Act, 1956 with its registered office at Unit 401 &

402, 4th Floor, Aggarwal Millennium Tower E-1,2,3, Netaji Subhash Place,

Wazirpur, New Delhi 110 034, India

“we”, “us” or “our” Unless the context otherwise indicates or implies, refers to our Company

AoA/ Articles of

Association/ Articles

The articles of association of our Company, as amended

Audit Committee The audit committee of our Board, as described in “Our Management” on page

175

Auditors/ Statutory Auditors The statutory auditors of our Company, being S. Ramanand Aiyar & Co.

Bank Distribution Agreement Agreement dated October 26, 2013, and amendment to such agreement dated

November 20, 2019 executed amongst SBI and our Company

Board/ Board of Directors The board of directors of our Company, or a duly constituted committee thereof

Cash Management Services

Agreement

Agreement for cash management services dated June 27, 2018, executed amongst

SBI and our Company, whose term has been extended by way of an agreement

dated May 24, 2019

CA Rover CA Rover Holdings, which is an entity ultimately controlled by the Carlyle group

Chairman Chairman of our Company

Chief Financial Officer/ CFO Chief financial officer of our Company

Compliance Officer The compliance officer of our Company in relation to the Offer

Corporate Office The corporate office of our Company, situated at 2nd Floor, Tower-B, Infinity

Towers, DLF Cyber City, Block 2 Building 3, DLF Phase 2, Gurugram,

Haryana 122 002, India

CSP MoU Memorandum of understanding dated March 16, 2016, executed amongst SBI

and our Company

CSR Committee The Corporate Social Responsibility committee of our Board, as described in

“Our Management” on page 175

Director(s) The director(s) on our Board of Directors

Equity Shares The equity shares of our Company of face value of ₹ 10 each

Electronic Transfer Agreement Memorandum of agreement for electronic transfer between SBI and our

Company dated March 29, 2017 and the terms extended by way of an addendum

agreement dated March 8, 2018

GE Capital GE Capital Mauritius Overseas Investments

Group Companies In terms of SEBI ICDR Regulations, the term “group companies” includes

companies (other than our Promoter) with which there were related party

transactions as disclosed in the Restated Financial Statements as covered under

the applicable accounting standards, and any other companies as considered

material by our Board, in accordance with the Materiality Policy, as described in

“Our Group Companies” on page 200

Independent Director Independent director(s) on our Board and eligible to be appointed as independent

directors under the provisions of the Companies Act and the SEBI Listing

2

Term Description

Regulations. For details of the Independent Directors, see “Our Management”

on page 175

Investor Selling Shareholder CA Rover

IPO Committee The IPO committee of our Board constituted to facilitate the process of the

Offer

KMP/ Key Managerial

Personnel

Key managerial personnel of our Company in terms of Regulation 2(1)(bb) of the

SEBI ICDR Regulations and as described in “Our Management” on page 175

Licensing Agreement Licencing agreement dated September 7, 2009 executed amongst SBI and our

Company as amended by Amendment to Licensing Agreement dated July 21,

2017 and Amendment Agreement to Licensing Agreement dated November 19,

2019

Managing Director and Chief

Executive Officer

Managing director and chief executive officer of our Company

Materiality Policy The policy adopted by our Board on November 11, 2019 and as amended on

February 12, 2020, for identification of Group Companies, material outstanding

litigation and outstanding dues to material creditors, in accordance with the

disclosure requirements under the SEBI ICDR Regulations

MoA/ Memorandum

of Association

The memorandum of association of our Company, as amended

NCDs Non-convertible debentures issued by our Company from time to time

Nomination and

Remuneration

Committee

The nomination and remuneration committee of our Board, as described in “Our

Management” on page 175

Promoter Group The persons and entities constituting the promoter group of our Company in terms

of Regulation 2(1)(pp) of the SEBI ICDR Regulations, as described in “Our

Promoter and Promoter Group” on page 194

Promoter/

Promoter Selling

Shareholder

Promoter of our Company, being, SBI

Registered Office The registered office of our Company, situated at Unit 401 & 402, 4th Floor,

Aggarwal Millennium Tower E-1,2,3, Netaji Subhash Place, Wazirpur, New

Delhi 110 034, India

Restated Financial Statements The restated financial statement of our Company as of and for the nine months

period ended December 31, 2019 and December 31, 2018 and as of and for the

financial years ended March 31, 2019, March 31, 2018 and March 31, 2017,

and the related notes, schedules and annexures thereto, prepared in accordance

with applicable provisions of the Companies Act, 2013 and restated in

accordance with the SEBI ICDR Regulations and included in “Financial

Statements” on page 207

Risk Management Committee The risk management committee of our Board, as described in “Our

Management” on page 175

RoC/ Registrar of Companies Registrar of Companies, National Capital Territory of Delhi and Haryana at New

Delhi

SBI State Bank of India

SBI UPI Agreement Agreement dated September 14, 2017, executed amongst SBI and our Company

SBIBPMSL SBI Business Process and Management Services Limited, previously known as

GE Capital Business Process Management Services Private Limited, which

amalgamated with our Company pursuant to the Scheme of Amalgamation

SBIC ESOP Scheme SBI Card Employee Stock Option Plan, 2019, approved by a resolution of our

Board dated January 16, 2019 and a special resolution of our Shareholders

adopted at the meeting held on February 22, 2019

Scheme of Amalgamation Scheme of amalgamation under sections 230 and 232 of the Companies Act,

2013 which provided for amalgamation of SBIBPMSL with our Company, as

approved by our Board on July 31, 2018

Selling Shareholders Together, the Promoter Selling Shareholder and the Investor Selling Shareholder

Shareholders The holders of the Equity Shares from time to time

Shareholders’ Agreement/

SHA

Shareholders agreement dated July 21, 2017, executed amongst our Company,

SBI, CA Rover and SBIBPMSL, amended by way of amendment letters dated

March 4, 2019 and August 2, 2019, respectively

3

Term Description

Stakeholders’

Relationship

Committee

The stakeholders’ relationship committee of our Board, as described in “Our

Management” on page 175

Offer Related Terms

Term Description

Acknowledgment Slip The slip or document issued by the respective Designated Intermediary(ies) to

a Bidder as proof of registration of the Bid cum Application Form

Allot/ Allotment/ Allotted Unless the context otherwise requires, allotment of Equity Shares pursuant to the

Fresh Issue and transfer of Equity Shares offered by the Selling Shareholders

pursuant to the Offer for Sale to successful Bidders

Allotment Advice The note or advice or intimation of Allotment, sent to each successful Bidder who

has been or is to be Allotted the Equity Shares after approval of the Basis of

Allotment by the Designated Stock Exchange

Allottee A successful Bidder to whom the Equity Shares are Allotted

Anchor Investor A QIB, who applied under the Anchor Investor Portion in accordance with the

requirements specified in the SEBI ICDR Regulations and the Red Herring

Prospectus

Anchor Investor

Allocation Price

₹ 755 per Equity Share

Anchor Investor Bidding

Date

One Working Day prior to the Bid/Offer Opening Date, on which Bids by

Anchor Investors were submitted, prior to and after which BRLMs did not

accept any Bids from Anchor Investors and allocation to the Anchor Investors

was completed, in this case being Feburary 28, 2020.

Anchor Investor Offer Price The final price at which Equity Shares will be Allotted to Anchor Investors in

terms of the Red Herring Prospectus and this Prospectus, which is a price equal

to or higher than the Offer Price but not higher than the Cap Price, in this case

being ₹ 755 per Equity Share. The Anchor Investor Offer Price has been decided

by our Company and the Selling Shareholders in consultation with the BRLMs

Anchor Investor Portion Up to 60% of the QIB Category which was allocated by our Company and the

Selling Shareholders in consultation with the BRLMs, to Anchor Investors, on

a discretionary basis in accordance with the SEBI ICDR Regulations. One third

of the Anchor Investor Portion was reserved for domestic Mutual Funds, subject

to valid Bids being received from domestic Mutual Funds at or above the price

at which allocation is made to Anchor Investors, which price was determined

by the Company and the Selling Shareholders in consultation with the BRLMs

Application Supported by

Blocked Amount/ ASBA

An application (whether physical or electronic) by a Bidder (other than Anchor

Investors) to make a Bid authorizing the relevant SCSB to block the Bid Amount

in the relevant ASBA Account and includes application made by RIIs using UPI,

where the Bid Amount was blocked upon acceptance of UPI Mandate Request

by RIIs

ASBA Account A bank account maintained with an SCSB and specified in the Bid cum

Application Form which has been blocked by such SCSB to the extent of the

appropriate Bid Amount in relation to a Bid by a Bidder (other than a Bid by an

Anchor Investor) and includes a bank account maintained by a Retail Individual

Investor linked to a UPI ID, which has been blocked in relation to a Bid by a

Retail Individual Investor Bidding through the UPI Mechanism

ASBA Bidder(s) All Bidders except Anchor Investors

ASBA Form An application form, whether physical or electronic, used by ASBA Bidders

bidding through the ASBA process, which was considered as the application for

Allotment in terms of the Red Herring Prospectus and this Prospectus

Axis Axis Capital Limited

Banker(s) to the Offer Collectively, the Escrow Collection Bank(s), Refund Bank(s), Public Offer

Account Bank(s) and the Sponsor Bank

Basis of Allotment The basis on which the Equity Shares will be Allotted to successful Bidders under

the Offer, as described in “Offer Procedure” on page 404

4

Term Description

Bid An indication to make an offer during the Bid/Offer Period by an ASBA Bidder,

or on the Anchor Investor Bidding Date by an Anchor Investor pursuant to

submission of a Bid cum Application Form, to subscribe to or purchase our Equity

Shares at a price within the Price Band, including all revisions and modifications

thereto, to the extent permissible under SEBI ICDR Regulations and in terms of

the Red Herring Prospectus and the Bid cum Application Form. The term

‘Bidding’ shall be construed accordingly

Bid Amount The highest value of the Bids indicated in the Bid cum Application Form and

payable by the Bidder or as blocked in the ASBA Account of the Bidder, as the

case may be, upon submission of the Bid in the Offer.

However, Eligible Employees applying in the Employee Reservation Portion

could apply at the Cut-off Price and the Bid amount was Cap Price net of

Employee Discount, multiplied by the number of Equity Shares Bid for by

such Eligible Employee and mentioned in the Bid cum Application Form

Bid cum Application Form The form in terms of which the Bidder was required to make a Bid, including an

ASBA Form, and which was considered as the application for the Allotment of

Equity Shares pursuant to the terms of the Red Herring Prospectus and this

Prospectus

Bid Lot 19 Equity Shares and in multiples of 19 Equity Shares thereafter

Bid/Offer Closing Date March 5, 2020, except in relation to any Bids received from the Anchor

Investors. The Bid/Offer Period for QIBs closed on March 4, 2020

Bid/Offer Opening Date March 2, 2020, except in relation to any Bids received from the Anchor

Investors

Bid/Offer Period Except in relation to Bids received from the Anchor Investors, the period

between the Bid/Offer Opening Date and the Bid/Offer Closing Date, inclusive

of both days during which the Bidders (excluding Anchor Investors) submitted

their Bids, in accordance with the SEBI ICDR Regulations and the terms of the

Red Herring Prospectus

Bidder Any investor who made a Bid pursuant to the terms of the Red Herring Prospectus

and the Bid cum Application Form and unless otherwise stated or implied,

includes an Anchor Investor

Bidding Centres Centres at which the Designated Intermediaries accepted the Bid cum Application

Forms, being the Designated SCSB Branch for SCSBs, Specified Locations for

the Syndicate, Broker Centres for Registered Brokers, Designated RTA Locations

for RTAs and Designated CDP Locations for CDPs

BofA Securities DSP Merrill Lynch Limited

Book Building Process The book building process as described in Part A of Schedule XIII of the SEBI

ICDR Regulations, in terms of which the Offer was made

Book Running Lead

Managers/ BRLMs

The book running lead managers to the Offer, in this case being Kotak, Axis, BofA

Securities, Nomura, HSBC and SBICAP.

SBI participated as a Selling Shareholder in the Offer for Sale. SBICAP has signed

the due diligence certificate and has been disclosed as a BRLM for the Offer. SBI

and SBICAP are associates in terms of the SEBI Merchant Bankers Regulations.

Accordingly, in compliance with the proviso to Regulation 21A of the SEBI

Merchant Bankers Regulations and Regulation 23(3) of the SEBI ICDR

Regulations, SBICAP was involved only in the marketing of the Offer

Broker Centres Broker centres of the Registered Brokers where Bidders (other than Anchor

Investors) could submit the ASBA Forms (in case of RIIs only ASBA Forms

under UPI) to a Registered Broker. The details of such broker centres, along

with the names and contact details of the Registered Brokers, are available on

the respective websites of the Stock Exchanges (www.bseindia.com and

www.nseindia.com)

CAN/Confirmation of

Allocation Note

Notice or intimation of allocation of the Equity Shares sent to Anchor Investors,

who have been allocated the Equity Shares, on or after the Anchor Investor

Bidding Date

Cap Price ₹ 755 per Equity Share

Circulars on Streamlining of

Public Issues

Circular no. CIR/CFD/POLICYCELL/11/2015 dated November 10, 2015 issued

by SEBI, as amended by circular (SEBI/HO/CED/DIL/CIR/2016/26) dated

5

Term Description

January 21, 2016 and circular (SEBI/HO/CFD/DIL2/CIR/P/2018/138) dated

November 1, 2018 as amended or modified by SEBI from time to time,

including circular (SEBI/HO/CFD/DIL2/CIR/P/2019/50) dated April 3, 2019,

circular (SEBI/HO/CFD/DIL2/CIR/P/2019/76) dated June 28, 2019, circular

(SEBI/HO/CFD/DIL2/CIR/P/2019/85) dated July 26, 2019, circular

(SEBI/HO/CFD/DCR2/CIR/P/2019/133) dated November 8, 2019 and any

other circulars issued by SEBI or any other governmental authority in relation

thereto from time to time

Client ID Client identification number of the Bidder’s beneficiary account

Collecting Depository

Participants/ CDPs

A depository participant, as defined under the Depositories Act, registered with

SEBI and who is eligible to procure Bids at the Designated CDP Locations in

terms of circular no. CIR/CFD/POLICYCELL/11/2015 dated November 10, 2015

issued by SEBI

CRISIL CRISIL Limited

CRISIL Research A division of CRISIL

Cut-off Price The Offer Price, finalized by our Company and the Selling Shareholders in

consultation with the BRLMs, in this case being ₹ 755 per Equity Share. Only

Retail Individual Bidders, Eligible Employees under the Employee Reservation

Portion and SBI Shareholders Bidding under the SBI Shareholders Reservation

Portion (subject to the Bid Amount being up to ₹ 200,000) were entitled to Bid at

the Cut-off Price. SBI Shareholders applying for the Bid Amount above ₹ 200,000

under the SBI Shareholders Reservation Portion, respectively, and QIBs

(including Anchor Investors) and Non-Institutional Investors, were not entitled to

Bid at the Cut-off Price.

Demographic Details The details of the Bidders including the Bidder’s address, name of the Bidder’s

father/husband, investor status, occupation, and bank account details and UPI ID,

as applicable

Designated CDP Locations Such locations of the Collecting Depository Participants where Bidders (except

Anchor Investors) could submit the ASBA Forms (in case of RIIs only ASBA

Forms under UPI). The details of such Designated CDP Locations, along with the

names and contact details of the CDPs are available on the respective websites of

the Stock Exchanges and updated from time to time

Designated Date The date on which the funds from the Escrow Account are transferred to the

Public Offer Account or the Refund Account, as appropriate, and the relevant

amounts blocked in the ASBA Accounts are transferred to the Public Offer

Account(s) and /or are unblocked, as applicable, in terms of the Red Herring

Prospectus and this Prospectus, after finalization of the Basis of Allotment in

consultation with the Designated Stock Exchange, following which the Board of

Directors may Allot Equity Shares to successful Bidders in the Offer

Designated Intermediaries In relation to ASBA Forms submitted by RIIs authorising an SCSB to block the

Bid Amount in the ASBA Account, Designated Intermediaries shall mean

SCSBs.

In relation to ASBA Forms submitted by RIIs where the Bid Amount will be

blocked upon acceptance of UPI Mandate Request by such RII using the UPI

Mechanism, Designated Intermediaries shall mean Syndicate, sub-syndicate,

Registered Brokers, CDPs and RTAs.

In relation to ASBA Forms submitted by QIBs NIIs, Eligible Employees, SBI

Shareholders Bidding under the SBI Shareholders Reservation Portion,

Designated Intermediaries shall mean SCSBs, Syndicate, sub-syndicate,

Registered Brokers, CDPs and RTAs

Designated RTA Locations Such centres of the RTAs where Bidders (except Anchor Investors) could submit

the ASBA Forms (in case of RIIs only ASBA Forms under UPI). The details of

such Designated RTA Locations, along with the names and contact details of the

RTAs are available on the respective websites of the Stock Exchanges

(www.nseindia.com and www.bseindia.com) and updated from time to time

Designated SCSB Branches Such branches of the SCSBs which shall collect the ASBA Forms, a list of which

is available on the website of SEBI at

6

Term Description

https://www.sebi.gov.in/sebiweb/other/OtherAction.do?doRecognised=yes or at

such other website as may be prescribed by SEBI from time to time

Designated Stock Exchange BSE Limited

Distributor A firm that offers and/or recommends investment products and services to

clients, as defined by the MiFID II Product Governance Requirements.

Draft Red Herring

Prospectus/ DRHP

The draft red herring prospectus dated November 26, 2019 filed with the SEBI

and Stock Exchanges and issued in accordance with the SEBI ICDR

Regulations, which did not contain complete particulars of the price at which

our Equity Shares are offered and the size of the Offer.

Eligible Employees All or any of the following:

(a) a permanent employee of our Company or our Promoter (SBI), working in

India or outside India, (excluding such employees who are not eligible to invest

in the Offer under applicable laws) as of the date of filing of the Red Herring

Prospectus with the RoC and who continued to be a permanent employee of our

Company or our Promoter (SBI), until the submission of the Bid cum

Application Form; and

(b) a Director of our Company, whether whole time or not, who is eligible to

apply under the Employee Reservation Portion under applicable law as on the

date of filing of the Red Herring Prospectus with the RoC and who continued to

be a Director of our Company, until the submission of the Bid cum Application

Form, but not including Directors who either themselves or through their

relatives or through any body corporate, directly or indirectly, hold more than

10% of the outstanding Equity Shares of our Company.

The maximum Bid Amount under the Employee Reservation Portion by an

Eligible Employee could not exceed ₹ 500,000. However, the initial Allotment

to an Eligible Employee in the Employee Reservation Portion shall not exceed

₹ 200,000. Only in the event of under-subscription in the Employee Reservation

Portion, the unsubscribed portion will be available for allocation and Allotment,

proportionately to all Eligible Employees who have Bid in excess of ₹ 200,000,

subject to the maximum value of Allotment made to such Eligible Employee

not exceeding ₹ 500,000

Eligible FPIs FPIs that are eligible to participate in this Offer in terms of applicable laws,

other than individuals, corporate bodies and family offices

Eligible NRI(s) A non-resident Indian, resident in a jurisdiction outside India where it is not

unlawful to make an offer or invitation under the Offer and in relation to whom

the Red Herring Prospectus and the Bid Cum Application Form constituted an

invitation to subscribe or purchase for the Equity Shares

Employee Discount Our Company and the Selling Shareholders in consultation with the BRLMs,

have offered a discount of ₹ 75 per Equity Share to Eligible Employees

Employee Reservation

Portion

The portion of the Offer being 1,864,669* Equity Shares, available for

allocation to Eligible Employees, on a proportionate basis

*Subject to finalisation of Basis of Allotment

Escrow Account(s) Account(s) opened with the Escrow Collection Bank for the Offer and in whose

favour the Anchor Investors will transfer money through direct credit or NEFT or

RTGS or NACH in respect of the Bid Amount when submitting a Bid

Escrow and Sponsor Bank

Agreement

The agreement dated February 18, 2020 entered into amongst our Company, the

Selling Shareholders, the Registrar to the Offer, the BRLMs, and Banker(s) to the

Offer for collection of the Bid Amounts from Anchor Investors and where

applicable remitting refunds, if any, to such Bidders, on the terms and conditions

thereof

Escrow Collection Bank A bank, which is a clearing member and registered with SEBI as a banker to an

issue under the SEBI BTI Regulations and with whom the Escrow Account has

been opened, in this case being State Bank of India.

First Bidder The Bidder whose name appears first in the Bid cum Application Form or the

Revision Form and in case of joint Bids, whose name appears as the first holder

of the beneficiary account held in joint names

Floor Price ₹ 750 per Equity Share

7

Term Description

Fresh Issue Fresh issue of 6,622,516* Equity Shares by our Company aggregating to ₹

4,993.25 million to be issued by our Company as part of the Offer, in terms of

the Red Herring Prospectus and this Prospectus

*Subject to finalisation of Basis of Allotment

General Information

Document or GID

The General Information Document for investing in public issues, prepared and

issued in accordance with the circular (CIR/CFD/DIL/12/2013) dated October

23, 2013 notified by SEBI, suitably modified and updated pursuant to, among

others, the circular (CIR/CFD/POLICYCELL/11/2015) dated November 10,

2015, the circular (CIR/CFD/DIL/1/2016) dated January 1, 2016, the circular

(SEBI/HO/CFD/DIL/CIR/P/2016/26) dated January 21, 2016, the circular

(SEBI/HO/CFD/DIL2/CIR/P/2018/22) dated February 15, 2018, the circular

(SEBI/HO/CFD/DIL2/CIR/P/2018/138) dated November 1, 2018, the circular

(SEBI/HO/CFD/DIL2/CIR/P/2019/50) dated April 3, 2019, the circular

(SEBI/HO/CFD/DIL2/CIR/P/2019/76) dated June 28, 2019 the circular

(SEBI/HO/CFD/DIL2/CIR/P/2019/85) dated July 26, 2019 and the circular

(SEBI/HO/CFD/DCR2/CIR/P/2019/133) dated November 8, 2019, included in

“Offer Procedure” on page 404

HSBC HSBC Securities and Capital Markets (India) Private Limited

Kantar IMRB Kantar IMRB

Kotak Kotak Mahindra Capital Company Limited

Maximum RII Allottees The maximum number of Retail Individual Investors who can be allotted the

minimum Bid Lot. This is computed by dividing the total number of Equity

Shares available for Allotment to Retail Individual Investors by the minimum

Bid Lot

Member State A member state of the EEA

MiFID II EU Directive 2014/65/EU on markets in financial instruments, as amended

MiFID II Product Governance

Requirements

Collectively, MiFID II, Articles 9 and 10 of Commission Delegated Directive

(EU) 2017/593 supplementing MiFID II, and any local implementing measures.

Monitoring Agency Central Bank of India

Mutual Fund Portion 5% of the QIB Category (excluding the Anchor Investor Portion) or 1,222,320*

Equity Shares which were made available for allocation to Mutual Funds only,

on a proportionate basis, subject to valid Bids being received at or above the

Offer Price

*Subject to finalisation of Basis of Allotment

Net Offer The Offer less the Employee Reservation Portion and the SBI Shareholders

Reservation Portion aggregating to 122,231,965* Equity Shares

*Subject to finalisation of Basis of Allotment

Net Proceeds Proceeds of the Offer that will be available to our Company, i.e., gross proceeds

of the Fresh Issue, less Offer Expenses to the extent applicable to the Fresh Issue.

For further details, see “Objects of the Offer” on page 93

Nomura Nomura Financial Advisory and Securities (India) Private Limited

Non-Institutional Category The portion of the Net Offer, being not less than 15% of the Net Offer or

18,334,795* Equity Shares, which was made available for allocation on a

proportionate basis to Non-Institutional Investors subject to valid Bids being

received at or above the Offer Price

*Subject to finalisation of Basis of Allotment

Non-Institutional

Investors/NIIs

All Bidders that are not QIBs (including Anchor Investors) or Retail Individual

Investors, who have Bid for Equity Shares for an amount of more than ₹ 200,000

(but not including NRIs other than Eligible NRIs)

Offer The public issue of 137,149,314* Equity Shares of face value of ₹ 10 each for

cash at a price of ₹ 755 each, aggregating to ₹ 103,407.88* million comprising

the Fresh Issue and the Offer for Sale. The Offer comprises the Net Offer,

Employee Reservation Portion and the SBI Shareholders Reservation Portion

*Subject to finalisation of Basis of Allotment

8

Term Description

Offer Agreement The agreement dated November 26, 2019 entered into amongst our Company,

the Selling Shareholders and the BRLMs, pursuant to which certain

arrangements are agreed to in relation to the Offer

Offer Price The final price at which Equity Shares will be Allotted to the successful Bidders

(except Anchor Investors), being ₹ 755 per Equity Share, as determined in

accordance with the Book Building Process by our Company and the Selling

Shareholders in consultation with the BRLMs in terms of the Red Herring

Prospectus on the Pricing Date. Equity Shares will be Allotted to Anchor

Investors at the Anchor Investor Offer Price in terms of the Red Herring

Prospectus.

A discount of ₹ 75 per Equity Share has been offered to Eligible Employees

bidding in the Employee Reservation Portion. This Employee Discount has been

decided by our Company and the Selling Shareholders in consultation with the

BRLMs

Offered Shares 130,526,798* Equity Shares offered as part of the Offer for Sale, including

37,293,371* Equity Shares by the Promoter Selling Shareholder and 93,233,427*

Equity Shares by the Investor Selling Shareholder

*Subject to finalisation of Basis of Allotment

OFS/ Offer for Sale The offer for sale of 130,526,798* Equity Shares aggregating to ₹ 98,414.64

million by the Selling Shareholders

*Subject to finalisation of Basis of Allotment

Price Band Price band ranging from a Floor Price of ₹ 750 per Equity Share to a Cap Price

of ₹ 755 per Equity Share

Pricing Date The date on which our Company and the Selling Shareholders in consultation

with the BRLMs, finalized the Offer Price

Prospectus This prospectus, dated March 6, 2020, to be filed with the RoC on or after the

Pricing Date in accordance with the provisions of Sections 26 and 32 of the

Companies Act 2013 and the SEBI ICDR Regulations, containing the Offer

Price, the size of the Offer and certain other information including any addenda

or corrigenda thereto

Prospectus Regulation Regulation (EU) 2017/1129 of the European Parliament and Council EC (and

any amendments thereto)

Public Offer Account The bank account opened with the Public Offer Account Bank under Section

40(3) of the Companies Act 2013 to receive monies from the Escrow Account(s)

and the ASBA Accounts on the Designated Date

Public Offer Account Bank The bank with whom the Public Offer Account is opened for collection of Bid

Amounts from the Escrow Account(s) and ASBA Accounts on the Designated

Date, in this case being State Bank of India, Capital Market Branch

QIB Category The portion of the Net Offer, being not more than 50% of the Net Offer, or

61,115,982* Equity Shares, which shall be Allotted to QIBs on a proportionate

basis, including the Anchor Investor Portion (in which allocation shall be on a

discretionary basis, as determined by our Company and the Selling Shareholders

in consultation with the BRLMs), subject to valid Bids being received at or

above the Offer Price

*Subject to finalisation of Basis of Allotment

Qualified Institutional

Buyers/ QIBs

A qualified institutional buyer as defined under Regulation 2(1)(ss) of the SEBI

ICDR Regulations

Red Herring Prospectus/ RHP The red herring prospectus dated February 18, 2020 issued in accordance with

Section 32 of the Companies Act 2013 and the SEBI ICDR Regulations which

did not have complete particulars of the price at which the Equity Shares shall

be Allotted and which was filed with the RoC at least three Working Days

before the Bid/Offer Opening Date, read with the corrigendum and clarification

to the red herring prospectus dated February 27, 2020

Refund Account The account opened with the Refund Bank from which refunds, if any, of the

whole or part of the Bid Amount shall be made to Anchor Investors

9

Term Description

Refund Bank The bank which is a clearing member registered with SEBI under the SEBI BTI

Regulations, with whom the Refund Account was opened, in this case being

State Bank of India, Capital Market Branch

Registered Brokers Stock brokers registered with the stock exchanges having nationwide terminals,

other than the members of the Syndicate and eligible to procure Bids in terms

of circular number CIR/CFD/14/2012 dated October 4, 2012, issued by SEBI

Registrar Agreement

The agreement dated November 26, 2019, entered into between our Company,

the Selling Shareholders and the Registrar to the Offer in relation to the

responsibilities and obligations of the Registrar to the Offer pertaining to the

Offer

Registrar and Share Transfer

Agents/ RTAs

Registrar and share transfer agents registered with SEBI and eligible to procure

Bids at the Designated RTA Locations in terms of circular no.

CIR/CFD/POLICYCELL/11/2015 dated November 10, 2015 issued by SEBI

Registrar to the Offer/

Registrar

Link Intime India Private Limited

Retail Category The portion of the Net Offer, being not less than 35% of the Net Offer, or

42,781,188* Equity Shares, that was available for allocation to Retail Individual

Investors, in accordance with the SEBI ICDR Regulations, subject to valid Bids

being received at or above the Offer Price

*Subject to finalisation of Basis of Allotment

Retail Individual Investors/

RIIs

Individual Bidders whose Bid Amount for Equity Shares in the Offer was not

more than ₹ 200,000 in any of the bidding options in the Offer (including HUFs

applying through their karta and Eligible NRIs and does not include NRIs other

than Eligible NRIs)

Revision Form The form used by the Bidders to modify the quantity of Equity Shares or the Bid

Amount in any of their Bid cum Application Forms or any previous Revision

Form(s), as applicable. QIBs bidding in the QIB category and Non-Institutional

Investors bidding in the Non-Institutional category were not permitted to

withdraw their Bid(s) or lower the size of their Bid(s) (in terms of quantity of

Equity Shares or the Bid Amount) at any stage. Retail Individual Investors could

revise their Bids during Bid/ Offer period and withdraw their Bids until Bid/ Offer

Closing Date

SBICAP SBI Capital Markets Limited

SBI Shareholders Individuals and HUFs who were the public equity shareholders of SBI, being our

Promoter (excluding such other persons not eligible under applicable laws, rules,

regulations and guidelines and depository receipt holders of SBI) as on the date of

the Red Herring Prospectus

SBI Shareholders

Reservation Portion

Reservation of 13,052,680* Equity Shares, that was available for allocation to

SBI Shareholders, on a proportionate basis

*Subject to finalisation of Basis of Allotment

Securities Act United States Securities Act of 1933

Self Certified Syndicate

Banks or SCSBs

(i) The banks registered with SEBI, offering services in relation to ASBA (other

than through UPI Mechanism), a list of which is available on the website of SEBI

at

https://www.sebi.gov.in/sebiweb/other/OtherAction.do?doRecognisedFpi=yes&i

ntmId=34 or

https://www.sebi.gov.in/sebiweb/other/OtherAction.do?doRecognisedFpi=yes&i

ntmId=35, as applicable, or such other website as updated from time to time, and

(ii) The banks registered with SEBI, enabled for UPI Mechanism, a list of which

is available on the website of SEBI at

https://www.sebi.gov.in/sebiweb/other/OtherAction.do?doRecognisedFpi=yes&i

ntmId=40

Share Escrow Agent The share escrow agent appointed pursuant to the Share Escrow Agreement

namely, Link Intime India Private Limited

Share Escrow Agreement The agreement dated February 18, 2020 entered into by and among the Selling

Shareholders, our Company and the Share Escrow Agent in connection with the

transfer of the respective portion of the Offered Shares by each Selling

10

Term Description

Shareholder and credit of such Equity Shares to the demat account of the

Allottees

Specified Locations Bidding centres where the Syndicate could accept Bid cum Application Forms, a

list of which was included in the Bid cum Application Form

Sponsor Bank The Banker to the Offer registered with SEBI, which was appointed by our

Company to act as a conduit between the Stock Exchanges and NPCI in order

to push the UPI Mandate Request by an RII in accordance with the UPI

Mechanism in terms of the SEBI circular bearing number

SEBI/HO/CFD/DIL2/CIR/P/2018/138) dated November 1, 2018, in this case

being HDFC Bank Limited

Stock Exchanges Together, the BSE and NSE

Syndicate Agreement The agreement dated February 18, 2020 entered into amongst the members of the

Syndicate, our Company, the Selling Shareholders and the Registrar to the Offer

in relation to the collection of Bids cum Application Forms by the Syndicate

Syndicate Members Intermediaries registered with the SEBI and permitted to carry out activities as

an underwriter, in this case being Kotak Securities Limited and SBICAP

Securities Limited

Syndicate or members of the

Syndicate

Collectively, the BRLMs and the Syndicate Members

Target Market Assessment A product approval process, which has determined that the Equity Shares are:

(i) compatible with an end target market of retail investors and investors who

meet the criteria of professional clients and eligible counterparties, each as

defined in MiFID II; and (ii) eligible for distribution through all distribution

channels as are permitted by MiFID II.

Underwriters The Book Running Lead Managers and the Syndicate Members

Underwriting Agreement The agreement dated March 6, 2020, entered into among our Company, the

Selling Shareholders, Registrar to the Offer and the Underwriters

UPI Unified Payments Interface which is an instant payment mechanism, developed

by NPCI

UPI ID ID created on the UPI for single-window mobile payment system developed by

the NPCI

UPI Mandate Request A request (intimating the Retail Individual Investors, by way of a notification

on the UPI application and by way of a SMS directing the Retail Individual

Investors to such UPI application) to the Retail Individual Investors using the

UPI Mechanism initiated by the Sponsor Bank to authorise blocking of funds

equivalent to the Bid Amount in the relevant ASBA Account through the UPI,

and the subsequent debit of funds in case of Allotment

UPI Mechanism The Bidding mechanism that may be used by Retail Individual Investors to

make Bids in the Offer in accordance with circular

(SEBI/HO/CFD/DIL2/CIR/P/2018/138) dated November 1, 2018, circular

(SEBI/HO/CFD/DIL2/CIR/P/2019/50 dated April 3, 2019, circular

(SEBI/HO/CFD/DIL2/CIR/P/2019/76) dated June 28, 2019, circular

(SEBI/HO/CFD/DIL2/CIR/P/2019/85) dated July 26, 2019, circular

(SEBI/HO/CFD/DCR2/CIR/P/2019/133) dated November 8, 2019 and any

other circulars issued by SEBI or any other governmental authority in relation

thereto from time to time

UPI PIN Password to authenticate UPI transaction

Working Day(s) All days on which commercial banks in Mumbai, India are open for business,

provided however, for the purpose of announcement of the Price Band and the

Bid/ Offer Period , “Working Day” shall mean all days, excluding all Saturdays,

Sundays and public holidays on which commercial banks in Mumbai, India are

open for business and the time period between the Bid/Offer Closing Date and

listing of the Equity Shares on the Stock Exchanges, “Working Day” shall mean

all trading days of the Stock Exchanges excluding Sundays and bank holidays

in India in accordance with Circulars on Streamlining of Public Issues

11

Conventional and General Terms and Abbreviations

Term Description

AIF(s) Alternative Investment Funds as defined in and registered with SEBI under the

SEBI AIF Regulations

BSE BSE Limited

CAGR Compounded Annual Growth Rate

CARO Companies (Auditor’s Report) Order, 2016

CDSL Central Depository Services (India) Limited

CIBIL Credit Information Bureau (India) Limited

CIN Corporate Identity Number

Companies Act 2013 The Companies Act, 2013, read with the rules, regulations, clarifications and

modifications thereunder

Consolidated FDI Policy The Consolidated FDI Policy, effective from August 28, 2017, issued by the

DPIIT, and any modifications thereto or substitutions thereof, issued from time to

time

Contract Labour Act Contract Labour (Regulation and Abolition) Act, 1970

Depositories Act Depositories Act, 1996, read with the rules, regulations, clarifications and

modifications thereunder

Depository A depository registered with the SEBI under the Securities and Exchange Board of

India (Depositories and Participants) Regulations, 1996

Depository Participant A depository participant as defined under the Depositories Act

DIN Director Identification Number

DoT Department of Telecommunication

DP ID Depository Participant’s identity number

DPIIT Department for Promotion of Industry and Internal Trade, Ministry of Commerce

and Industry (formerly Department of Industrial Policy and Promotion), GoI

EBITDA Earnings Before Interest, Tax, Depreciation and Amortization

EEA European Economic Area

EPF Act Employees’ Provident Fund and Miscellaneous Provisions Act, 1952

EPF Employees’ Provident Fund

EPS Earnings per share

ESI Act Employees’ State Insurance Act, 1948

ESI Employees’ State Insurance

FCNR-B Foreign Currency Non-Resident (Bank)

FDI Foreign direct investment

FEMA Foreign Exchange Management Act, 1999 read with rules and regulations

thereunder

FEMA Rules Foreign Exchange Management (Non-debt Instruments) Rules, 2019

Financial Year/fiscal/ Fiscal

Year/ FY/ F.Y.

The period of 12 months commencing on April 1 of the immediately preceding

calendar year and ending on March 31 of that particular calendar year

FPIs A foreign portfolio investor who has been registered pursuant to the SEBI FPI

Regulations

FVCI Foreign Venture Capital Investors (as defined under the Securities and Exchange

Board of India (Foreign Venture Capital Investors) Regulations, 2000) registered

with the SEBI

GDP Gross Domestic Product

GoI/ Central Government The Government of India

GST Goods and services tax

HUF(s) Hindu undivided family(ies)

ICAI The Institute of Chartered Accountants of India

IFRS International Financial Reporting Standards

IFSC Indian Financial System Code

Income Tax Act Income Tax Act, 1961

Ind AS The Indian Accounting Standards notified under Section 133 of the Companies

Act 2013 and referred to in the Ind AS Rules

Ind AS 24 Indian Accounting Standard 24 on Related Party Disclosure issued by the MCA

12

Term Description

Ind AS Rules Companies (Indian Accounting Standards) Rules, 2015 and the Companies (Indian

Accounting Standards) Amendment Rules, 2016, as amended

Indian GAAP Generally Accepted Accounting Principles in India notified under Section 133 of

the Companies Act 2013 and read together with paragraph 7 of the Companies

(Accounts) Rules, 2014 and Companies (Accounting Standards) Amendment

Rules, 2016

INR or Rupee or ₹ or Rs. Indian Rupee, the official currency of the Republic of India

IRDAI Insurance Regulatory and Development Authority of India

KYC Know Your Customer

LIBOR London Interbank Offered Rate

MCA The Ministry of Corporate Affairs, Government of India

MCLR Marginal Cost of Funds based Lending Rate

Master Directions Master Direction – Non-Banking Financial Company - Systemically Important

Non-Deposit taking Company and Deposit taking Company (Reserve Bank)

Directions, 2016, as updated

Mutual Funds Mutual funds registered with the SEBI under the SEBI (Mutual Funds) Regulations,

1996

NACH National Automated Clearing House

NAV Net asset value

NBFC Non-banking Financial Company

NBFC – ND - SI Systemically Important Non-Deposit Taking NBFC

NBFC - SI Systemically important non-banking financial company, as covered under

Regulation 2(1)(ss)(xiii) of the SEBI ICDR Regulations

NCR National Capital Region

NEFT National Electronic Fund Transfer

N.M. Not meaningful

NPCI National Payments Corporation of India

NR/ Non-resident A person resident outside India, as defined under the FEMA and includes a Non-

Resident Indian

NRI Non-Resident Indian

NSDL National Securities Depository Limited

NSE The National Stock Exchange of India Limited

OCB/ Overseas Corporate

Body

A company, partnership, society or other corporate body owned directly or