An Empirical Investigation of the True and Fair Override

49

Rock Center for Corporate Governance Stanford University Working Paper Series No. 44 London Business School Accounting Subject Area Working Paper No. ACCT031 Cass Business School Research Paper An Empirical Investigation of the True and Fair Override Gilad Livne City University London - Sir John Cass Business School Maureen F. McNichols Stanford University

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of An Empirical Investigation of the True and Fair Override

Rock Center for Corporate Governance

Stanford University Working Paper Series No. 44

London Business School

Accounting Subject Area Working Paper No. ACCT031

Cass Business School Research Paper

An Empirical Investigation of the True

and Fair Override

Gilad Livne

City University London - Sir John Cass Business School

Maureen F. McNichols Stanford University

An Empirical Investigation of the True and Fair Override

in the United Kingdom

Gilad Livne

Cass Business School

106 Bunhill Row

London EC1Y 8TZ

T +44 (0) 20 7040 5192

Maureen McNichols*

Graduate School of Business

Stanford University

Stanford CA 94305

650-723-0833

fmcnich@ stanford.edu

Current draft: July 23, 2008

*Corresponding author

We thank an anonymous referee, Stefan Ost, Sanjay Pareek, David Parkington, Amit Shanker

and Mike Staunton of London Share Price Database for their help with data collection, and

Qintao Fan and Yulin Long for their excellent research assistance. We also thank Mary Barth,

Bill Beaver, Robert Bushman, Elroy Dimson, Chris Higson, Steve Monahan, Dennis Oswald,

Peter Pope, L. Shivakumar, Martin Walker (the Editor), Terry Warfield, as well as seminar

participants at the American Accounting Association 2002 Annual Meeting, 2nd ESRC/CAIR

Conference Manchester University, HKUST Summer Symposium, INSEAD, London Business

School, Summer Camp of Stanford University, Tel Aviv University, University of California, at

Berkeley, University of Wisconsin, Madison and Warwick University, for many helpful

comments. Gilad Livne gratefully acknowledges the financial support of the Leverhulme Trust,

UK, and the London Business School, and the Accounting faculty of Stanford University for

their kind hospitality during summer of 2002. Maureen McNichols gratefully acknowledges the

support of the Stanford Graduate School of Business.

ABSTRACT

The True and Fair View concept requires companies to depart from GAAP or the law if

necessary to present a true and fair view of the corporation‟s financial affairs. We analyze UK

public companies invoking a true and fair override to assess whether overrides are associated

with weakened performance, earnings quality and informativeness. We find quantified overrides

increase income and equity significantly, and firms that invoke more costly overrides report

weaker performance. We also find that firms invoking the most costly overrides have less

informative financial statements than control firms, and lower earnings quality. In contrast,

firms invoking less costly overrides do not exhibit weaker performance, less informative

financial statements or weaker earnings quality. These findings are relevant for the debate on

principle- vs. rules-based accounting.

Keywords: principles- vs. rules-based accounting, earnings quality, informativeness of financial

statements, true and fair override.

JEL Classification Codes: M41

1

1. Introduction

This paper provides evidence on the use of the true and fair view (hereafter TFV)

override by UK companies. UK rules, the first International Accounting Standards (IAS 1,

2003) and legal requirements in the European Union require that public companies provide a true

and fair view of their financial affairs in the financial statements. Conceptually the notion of

TFV goes beyond conformity with GAAP in that it provides a reporting entity the option to

depart from the letter of the law or a promulgated accounting standard in certain circumstances.

Availing this option to firms entails the risk that increasing the set of accounting reporting

choices applied reduces the comparability and quality of corporate financial reports. On the

other hand, this option could enhance financial reporting if application of existing rules leads to

misleading financial reports. The use of broad principles to grant managers considerable

reporting flexibility has been advocated by some as superior to the philosophy of creating a

dense web of rigid and highly detailed reporting requirements. However, not all agree with that

view, especially US regulators and standard setters.

The debate on principle-based vs. rules-based accounting systems has come recently to

the fore in the wake of Enron and other well-known accounting scandals. Against this

background, the FASB and the SEC studied the issue of principles vs. rules-based reporting.

(e.g., FASB, 2002). The SEC has long questioned overrides of accounting standards, as is

evident from its policy to “challenge the basis on which such an override has been used and the

basis on which the auditors have given an unqualified report” in the case of UK firms listed in

the US (see SEC 2001). The SEC objects to the possibility of an override due to the concern that

2

the override requirement may lead to reduced comparability and transparency, and may be used

to mask poor financial performance or deteriorating asset quality.1

Our study provides evidence pertaining to this debate because it examines the nature of

overrides in a more principles-based accounting system, the UK. We postulate that invoking an

override is a result of cost-benefit analysis carried out by managers of reporting entities.

Specifically, we argue that there may be costs associated with an override, which are increasing

in the authoritative support for the accounting treatment subject to override. For example, a

departure from UK GAAP likely involves considerable costs because it increases the probability

of conflict with auditors and directors, potential intervention of regulatory bodies, and litigation

as well as criticism by various market participants (e.g., Jack, 1994, Brandt et al., 1997, and

Hines et al., 2001). The benefits to reporting managers may include attaining certain reporting

objectives, such as satisfying debt covenants. Therefore, overrides of GAAP are likely to be

invoked only when the resulting net benefits are sufficiently high.

We use data from the UK to examine this issue, given its long history with the true and

fair view requirement and the influence of UK standard-setters on shaping IAS. We find that the

vast majority of our sample involves overrides of lesser authoritative rules, such as an override of

the Companies Act to invoke GAAP. However, 19% of our sample observations involve an

override of UK GAAP. This relatively small number of cases suggests that either UK firms are

discouraged to override principles with more authoritative support, that circumstances giving rise

to GAAP overrides that are solely aimed at providing better information to investors are rare,

and/or that UK GAAP already provides sufficient flexibility.

Our primary goal is to investigate whether more costly overrides are associated with

weaker financial performance. We find that firms invoking what we hypothesize are more costly

1 See SEC Concept Release: International Accounting Standards 34-42430, Section IV.A.2 (dated 2/18/2000).

3

overrides tend to exhibit weaker financial performance and lower interest coverage. Moreover,

firms overriding GAAP exhibit a decline in performance in the first year of the override. If

overrides are invoked to present a true and fair view, one would expect them to be invoked by

successful firms as well as firms experiencing financial difficulties. These findings suggest that

the more costly overrides are not consistent with the spirit of true and fair presentation. On the

other hand, for firms invoking more “mechanical” and less costly overrides, such as non-

depreciation of investment properties we do not find evidence of weaker earnings or greater debt.

A secondary goal of this paper is to assess the valuation implications of earnings and

book values of override firms. Prior research (e.g., Ohlson, 1995) suggests that greater earnings

persistence should lead to higher coefficients on earnings and lower coefficients on book value

of equity in valuation models. If overrides represent manipulations that are transitory in nature,

we would expect to find lower (higher) coefficients on earnings (book value) for override firms

than control firms. We provide evidence that the earnings persistence of override firms is lower

than that of control firms for some costly overrides. We also find that companies that choose to

override GAAP with the most costly overrides provide less informative financial statements.

Taken as a whole, the evidence provided in this paper indicates that UK companies have

used the TFV override in well-defined circumstances. However, overrides that require

considerable managerial discretion tend to be invoked in less favorable circumstances,

suggesting the possibility that some firms invoke an override to mask weaker financial

performance. Consistent with this, the earnings of override firms are not more persistent than the

earnings of control firms.

The plan of the paper is as follows. Section 2 provides some background information on

the practice of true and fair override in the UK and European Union that is useful for the debate

4

about its admissibility. Section 3 develops the theory and main hypotheses examined in the

paper. Section 4 describes the data and procedures used in data collection. Section 5 reports the

main empirical findings and Section 6 concludes.

2. Background to the Debate on the True and Fair Override

The concept of true and fair view first appeared in the United Kingdom in the Joint Stock

Companies Registration and Regulation Act of 1844 (McGregor, 1992).2 The UK Companies

Act (1985) requires that financial statements „give a true and fair view.‟ Specifically, the

Companies Act (1985) requires that if, owing to special circumstances, compliance with the Act

would prevent compliance with true and fair presentation, the directors shall depart from the

requirement of the Act and quantify the effect of the departure.3

The concept of true and fair also shows up in a number of professional pronouncements.

At the broadest level, the ASB‟s (1993) Forward to Accounting Standards states that „the Board

envisages that only in exceptional circumstances will departure from the requirements of an

accounting standard be necessary in order for financial statements to give a true and fair view.‟

The specific disclosure requirements first appeared in UITF Abstract 7 (ASB, 1992) and later

incorporated into FRS 18 (ASB, 2000). In contrast to the Act, FRS 18 allows for the possibility

that some departures cannot be quantified.

While there is ambiguity regarding the exact meaning of the words „true‟ and „fair‟, the

legal view is that

the courts will treat compliance with accepted accounting principles as prima facie

evidence that the accounts are true and fair. Equally, deviation from accepted principles

will be prima facie evidence that they are not. Accounts which depart from the standard

2 Given that the UK is a common law country, it is quite plausible that this concept was used in practice well before

it was incorporated into this Act. 3 Nobes and Parker (1991) document that most of their sample directors were willing to depart from the details of

the law or a standard. This requirement also exists, or used to exist, in Australia, New Zealand and Singapore, as

well as in EU nations.

5

without adequate justification or explanation may be held not to be true and fair‟ (Lord

Justice Hoffmann (1983) and Hon. Mrs. Justice Arden (1984), as cited by Davies et al.

(1999) p. 8).

IAS 1, issued by the International Accounting Standards Board and amended in

December 2003, contains similar requirements for an override to those in the UK, though it

requires that financial statements “present fairly” a company‟s financial position, financial

performance and cash flows (paragraph 13). The Financial Reporting Council (the UK regulator

overseeing the ASB) has confirmed that following the adoption of IAS and “fair presentation” in

the EU, the concept of “true and fair view” remains a cornerstone of financial reporting and

auditing in the UK (FRC, 2005).

3. Theory and Hypotheses Development

3.1 FLEXIBLE VS. RIGID REPORTING REQUIREMENTS

Generally, a more flexible accounting system may be superior to a system in which the

set of accounting procedures is restricted if managers use the flexibility to provide better

information to investors or to improve contracting. For example, allowing non-GAAP reporting

can increase the value of the firm while reducing contract-negotiating and duplicate bookkeeping

costs (Leftwich, 1983). On the other hand, a flexible approach may be abused by self-interested

managers, resulting in dead-weight costs (Watts and Zimmerman, 1990). In particular, allowing

flexibility may allow opportunistic managers to portray the firm‟s financial performance as

stronger than would be shown with less flexible reporting, leading to lower earnings quality and

lessened informativeness of the financial statements.

6

3.2 DETERRENTS TO THE ABUSE OF FLEXIBLE REPORTING RULES

Three forces can deter managers from abusing reporting flexibility available to them.

First, anticipating potential abuse on the part of managers, shareholders and other contracting

parties can include clauses that impose penalties for invoking undesired TFV overrides.

However, such contracts may not be available in firms where management can set self-serving

terms in the contracts (Bebchuk, et al., 2002), and contract terms may be incomplete because it is

not possible to anticipate all possibilities for self-serving behavior (Watts and Zimmerman,

1990).

Second, a country‟s enforcement mechanisms and legal framework can deter

opportunistic reporting. Flexible accounting coupled with incomplete contracts may result in

many disputes between the reporting entity and third parties being referred to regulators or a

court of law. However, to paraphrase La Porta, et al. (1998, p. 1121), in an environment of

perfect judicial enforcement, reporting flexibility may be advantageous to investors because they

can appeal to a court if they fear being misled by managers. In contrast, when the courts have

limited discretion and enforcement power or litigation is costly, simple and restrictive sets of

rules also known as bright-line rules, for which violations are easy to judge, may be superior.

Third, the firm‟s governance system, including its directors and auditors, can deter

managers from abusing reporting rules. In the presence of strong oversight by the audit

committee and a professional body of auditors, managers face the requirement that any departure

from GAAP or the Act is either required or approved by the external auditor. An override may

be required if the auditor believes that following form will contrast with the need to follow

substance. Alternatively, in cases where the management-initiated override is not warranted, the

directors and auditors should deter managers from misreporting.

7

In summary, when recognition or disclosure rules are very flexible and deterrence

mechanisms are weak, opportunistic reporting can emerge. On the other hand, if rules are too

rigid and deviation from promulgated rules is very costly, firms may be unwilling to depart from

rules to provide financial statements that give a true and fair view.

3.3 SPECIFIC COSTS ASSOCIATED WITH TFV OVERRIDES IN THE UNITED KINGDOM

When a company invokes an override, it is likely to draw attention from various

interested parties, which in turn may involve costs. In particular, the company may be

investigated by the Financial Reporting Review Panel (FRRP), an affiliate of the ASB, which has

statutory powers to investigate whether annual reports comply with the Companies Act and

GAAP.4 It has been widely perceived in the UK that the FRRP has been an effective deterrent

mechanism against unreasonable violations of GAAP and the CA.5 Benston, et al. (2006) report

that about 20-30 per cent of cases before the FRRP arose from a TFV override, and that the

majority of these overrides were rejected because they were not compelling. Additional costs

may involve conflicts with auditors, scrutiny by analysts and institutional investors. It is

important to note, however, that such costs may not be present in other jurisdictions.6

In what follows we develop and order four categories of TFV overrides according to the

relation between the type of override and potential costs that the TFV firm may incur. The four

categories are as follows:

4 Peasnell, et al. (2001) find that 43 firms judged by the Panel during 1990-1999 to have issued defective statements

tend to exhibit weaker performance than size- industry- and time-matched control. They suggest that this may be

attributable to the higher likelihood that weak firms are referred to the Panel by disaffected shareholders. 5 For example, see Sykes, as quoted by Quick (2001), and Alexander and Archer (2003).

6 In Australia and New Zealand, it was felt that the override was used to avoid complying with GAAP. As a result,

the ability to invoke an override in these countries was removed in the 1990s (see McGregor, 1992, and Kirk, 2006,

for a review of the TFV override in these countries). The recent case of Societe Generale in France raises this

question as well. Hughes (2008)

8

1. Accounting standards, or similar pronouncements, prescribe one method, which

contradicts the Companies Act (CA) and thus require an override.

2. Accounting standards, or similar pronouncements, allow some choice but effectively

prefer a particular method in most cases. The preferred choice is consistent with the

CA. Thus, not following the preferred method also contradicts the CA, and hence

requires an override.

3. Accounting standards, or similar pronouncements, are silent on a particular issue, but

not the CA. Not following the CA requires an override. Note that in the absence of a

promulgated standard, the CA may be regarded as GAAP.

4. Accounting standards or similar pronouncements require a certain method, which is

overridden.

All else equal, the first category is expected to occur most frequently, because the

presumed superiority of GAAP triggers a “mechanical” override of the Companies Act,

suggesting little cost to invoking the override. In fact, due to the presumed supremacy of GAAP

over the CA, mechanical overrides may be costly to avoid.

The fourth category regards departures from generally accepted accounting rules. Under

the maintained presumption that following accounting standards is consistent with TFV, any

departure from GAAP is likely to be regarded as the most costly. This is particularly true if the

override is opportunistic and hence less defensible. Thus, a departure under this category is

expected to occur in a small number of cases in which managers deem the benefits from the

departure to be quite high and in excess of costs.

9

We expect that the second and third categories have greater cost than the first category

and less than the fourth category but their relative ordering is ambiguous. Thus, our numbering

of these categories is for convenience in reference and is not ordinal. The second category

involves situations where an accounting standard offers a choice, but expresses some preference

for one choice over the others. If not following the preferred option given in the standard

involves some kind of penalty, or unwarranted exposure, firms may be hesitant to depart from

the preferred choice unless the benefits outweigh the costs.

The third category involves cases where there are no specific rules except those required

by the CA. In the absence of promulgated standards, one can argue that the CA effectively

becomes GAAP. We do not expect this to occur at a high rate because accounting standards are

more comprehensive than the CA. Furthermore, to the extent that the CA is regarded as

authoritative, firms are less likely to depart from its requirements for opportunistic purposes due

to potential cost.7

3.4 HYPOTHESIS DEVELOPMENT

Our primary hypothesis is motivated by the previous discussion of costs and benefits of

invoking an override. Experience with the TFV override in Australia and New Zealand suggests

that management may exploit greater flexibility in financial reporting to influence the

perceptions of various parties as to the firms‟ status and performance. Relatedly, firms

experiencing weaker financial performance may be more likely to use the TFV override option to

avoid covenant violations, as suggested by the debt covenant hypothesis.8 Thus, in a reporting

system featuring an override, firms may exercise this discretion to improve reported performance

7 It is possible that matters that are not covered by UK GAAP are covered by IAS or US GAAP thus providing

support for the override. However, TFV firms in our sample do not typically make reference to other GAAP. (We

thank Mary Barth for pointing this out to us.) 8 See Dichev and Skinner (2002) for evidence from private lending in the U. S. that firms manipulate earnings to

avoid violating debt covenants.

10

and thereby avoid violating debt covenants. A competing alternative, which represents the view

in the UK Cook (1997), is that firms are motivated to override, and auditors provide approval, to

achieve better accounting treatment (e.g., the override is „corrective‟).9 Implicit in this view is

the high regard paid to specific UK institutions, such as the FRRP and the audit profession. Such

institutions may have played a smaller role in other jurisdictions with the resulting abuse of the

TFV requirement. In such a case, we would not expect weaker performance for UK override

firms. We expect that our ability to discriminate between these hypotheses is greatest for the

most costly overrides, where the offsetting benefits are the greatest. However, the extent to

which institutional forces deter firms from invoking an override to avoid a valid standard is an

empirical question, so our first hypothesis is two-sided. Stated in null form:

Hypothesis 1: Firms that invoke more costly overrides experience similar financial performance

and debt contracts to otherwise similar firms that do not invoke an override.

We supplement our primary investigation with evidence on the valuation implications of

overrides. While it is possible that an override is invoked solely to increase reported income or

influence contract outcomes, such as violation of debt covenants, it is not clear how the exercise

of such discretion will affect earnings quality. Moreover, firms may want to use an override as a

means of providing better information absent any other motivation. For example, an override

may result in greater earnings persistence (i.e., greater quality).10

Managers may be motivated to

do so because of the beneficial effect on the firm‟s cost of capital (Botosan, 1997).

Alternatively, depending on the principle adopted, an override could result in less information to

9 Relatedly, Oswald (2007) finds evidence consistent with this view in the context of R&D. In contrast, Feltham et

al. (2007) examine the relation between leverage and accounting choice and show that firms with poorer

performance have incentives to lower the precision of accounting earnings to avoid violation of debt covenants and

detection of bias. 10

Prior literature has viewed earnings persistence as an important aspect of earnings quality (e.g., Dechow and

Schrand, 2004)

11

investors, as some regulators fear and consistent with Ewert and Wagenhofer (2005). Similar to

our first hypothesis, the second hypothesis is two-sided. Stated in null form:

Hypothesis 2: The financial statements of TFV firms are as informative as the financial

statements of otherwise similar firms that do not invoke an override.

4. Data

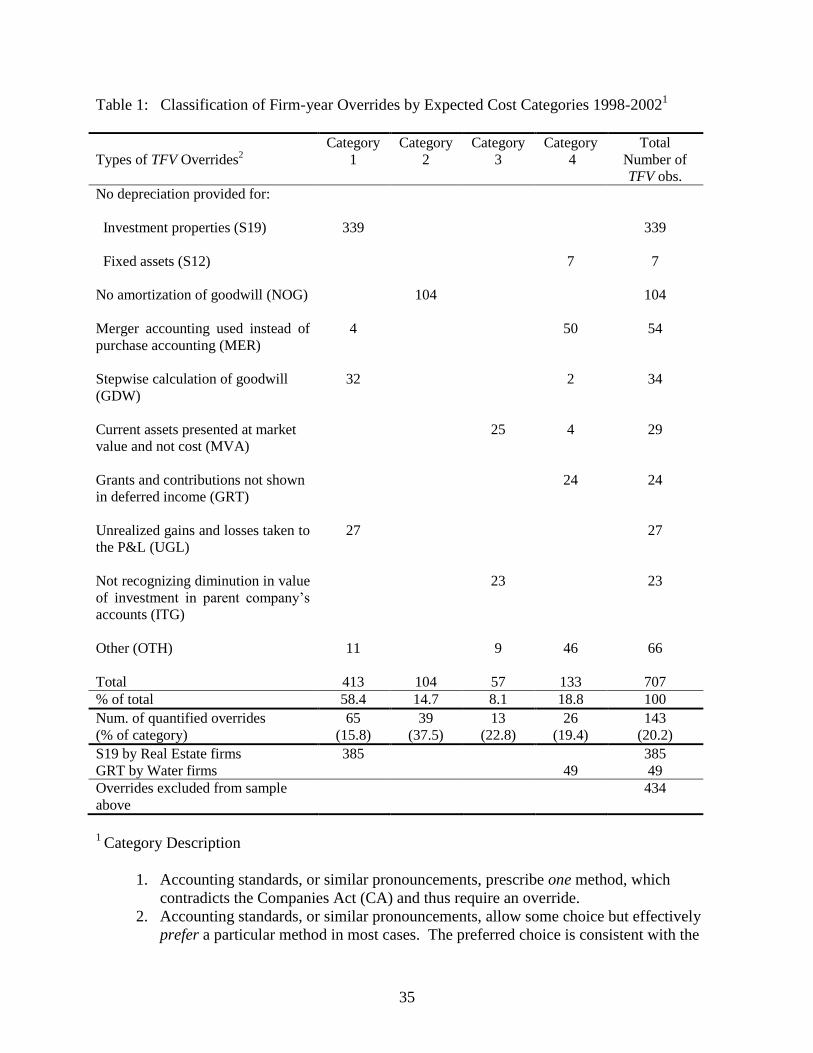

To identify firms invoking an override during the 1998-2002 period, we searched the

Lexis-Nexis UK annual reports database using key words “true and fair view,” “override” and

“departure.”11

As reported in Table 1, this search resulted in a sample of 1,141 firm-year

observations over the five years. Since in any given year, multiple overrides can be invoked by a

single company, we include in Table 1 only the highest override category in any given year. As

discussed below, we exclude 434 observations because they represent industry-wide practice,

which prevents us from finding a suitable control sample. The final sample thus involves 707

firm-year observations that represent overrides invoked by 307 firms.

Financial data were obtained from Datastream whereas share price data and market

values of equity were obtained from the London Share Price Database (LSPD). Auditor identity

and auditor‟s opinion were collected from Worldscope. We collected a control sample of

industry and size-matched firms for all override firms except those in the real estate and water

industries invoking industry-wide overrides. That is, the sample of 707 firm-year observations

excludes 434 overrides that are industry-wide practice (e.g., depreciation in the real-estate

industry) and hence no matched sample could be constructed. More specifically, we matched

each TFV firm with the firm from the same three digit SIC code with the closest market value at

11

One limitation of this search procedure is that it is possible that an override occurred but the reporting company

did not formulate it as such in the annual report (i.e., does not explicitly use any of the above terms). However, we

take some assurance that our search was effective from the fact that we identified a large number of overrides that

were separately provided to us by David Tonkin of Company Reporting.

12

the beginning of the TFV firm‟s fiscal year. Whenever the closest market value differed by more

than 20%, a new search was conducted at the two digit SIC code and, if necessary, at the one

digit SIC code. A control firm is used only for one TFV firm in any given year.12

We also require availability of share price data in the fourth month after the end of the

fiscal year because public firms are required to file preliminary reports with the London Stock

Exchange within 120 days from the fiscal year-end and many file the full report within three

months. To verify the adequacy of the matching procedure, we verified that the difference in the

mean and median market value is not significantly different from zero. The use of a matched

sample provides assurance that our comparisons are not affected by cross-sectional variations in

industry-specific factors or firm size, which may capture political cost considerations or other

factors that are not central to our analysis. In addition, within-industry matching works to

mitigate the possibility that a TFV firm and a control firm face fundamentally different

circumstances, which prompt one company to invoke an override because existing rules are

inappropriate for these circumstances.13

5. Empirical procedures and findings

5.1 TYPES OF OVERRIDES

All the override disclosures identified in our search were carefully read and analyzed and

then classified into nine major types of overrides according to the underlying accounting

12

An alternative matching procedure could involve identification of control firms facing similar circumstances that

can potentially give rise to a specific override (e.g., acquisitions of subsidiaries involving recognition of similar

goodwill). The primary reason we did not follow this procedure is that the heterogeneity of override types in the

sample would require substantial judgment on the part of the researcher to identify similar circumstances for control

firms. Second, matching beyond industry and market cap is likely to greatly constrain the size of the control sample. 13

Relatedly, the IASB now employs in IAS 1 the (rebuttable) presumption that compliance with GAAP would not

be misleading if other firms in similar circumstances follow GAAP. In this context, firms within the same industry

as the overriding firm may be presumed to be facing similar circumstances.

13

treatment affected by the override. We then further assign each of the override types to one of the

four cost categories discussed above. Table 1 presents these override types, classified by cost

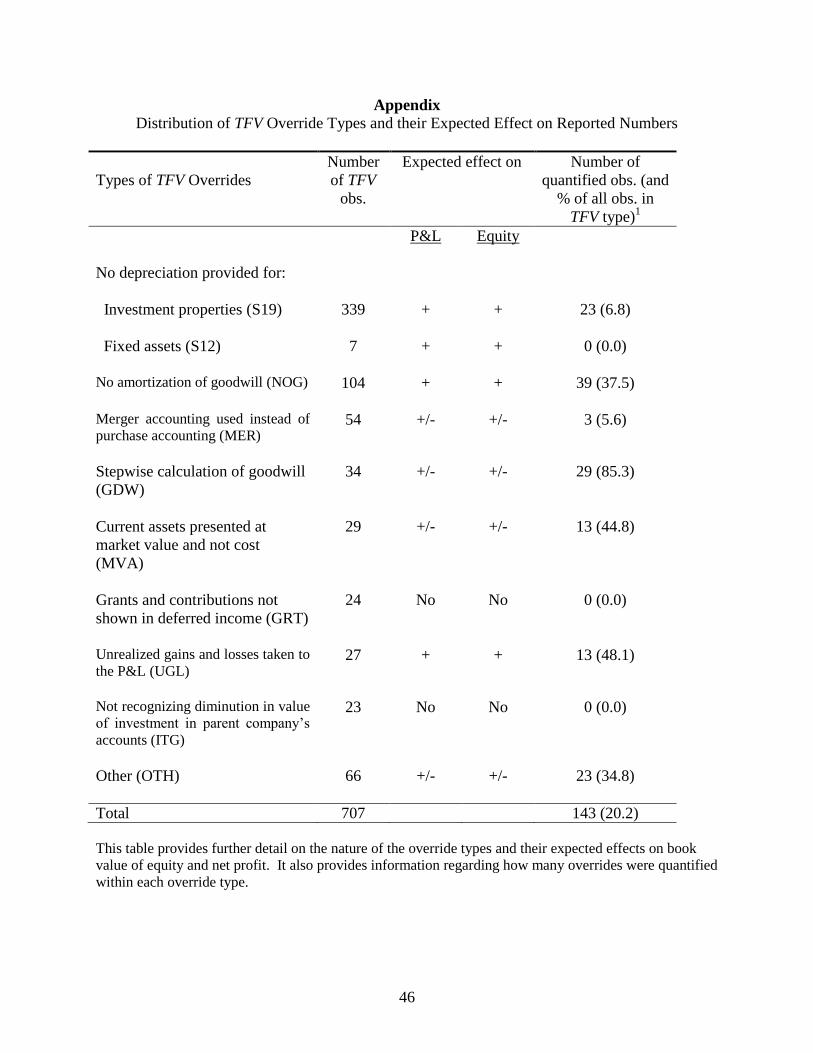

category, in descending order of frequency. It also shows how many overrides were quantified

in each cost category. The appendix presents further details regarding the expected effect of

each override type on the financial statements. As can be seen from Table 1, Category 1

overrides comprise the majority of the sample, and the rate of occurrence is substantially lower

for Category 4 than for Category 1. Also, the total number of overrides under Categories 2 and 3

(161 observations) is lower than that under Category 1, but higher than that for Category 4. The

most common override type is non-depreciation of investment properties, which is required by

GAAP but disallowed by the Companies Act. Hence this type is a Category 1 override. The

second most frequent override type is non-amortization of goodwill. While UK GAAP allows

for non-amortization, the relevant standard (FRS 10, ASB 1997) does not favor it and,

furthermore, requires annual impairment reviews that have been perceived as costly.14

As non-

amortization of goodwill also stands in contrast to the CA, it is classified as Category 2.

As Table 1 indicates, seemingly similar override types may relate to more than one

category. This is because each case is individually analyzed to determine the rule that was

departed from. Thus, for example, in the case of piecemeal calculation of goodwill, two cases

were found to violate GAAP while the other 32 cases were consistent with GAAP, but

inconsistent with the CA.

The findings in Table 1 show that Category 1 overrides are the most common, and

Category 4 overrides (outright departures from UK GAAP) are much less common. However,

14

The intention of the ASB might have been to encourage non-amortization, but as Davies et al. (1999, p. 769)

comment, “The implication of the ASB‟s definition [of goodwill] encourages the view that the life is normally

indefinite, and not just in exceptional cases….In practice, the impairment test has been seen to be very onerous, and

this has been a powerful disincentive for companies to argue that the life of the goodwill will exceed 20 years.”

14

Category 4 includes 133 firm-year observations invoked by 68 firms in our 5-year sample period,

suggesting that overriding GAAP is a non-negligible phenomenon.

5.2 FIRM PERFORMANCE BY TYPE OF OVERRIDE

In this section, we describe several analyses that provide evidence on whether firms that

invoke TFV overrides are doing so to report more favorable performance (Hypothesis 1). If

firms invoke overrides solely because they want to increase their reported income, or avoid

violation of debt covenants, we would expect to see significant differences in pre-override

performance or debt-related financial indicators between override and control sample firms. On

the other hand, if firms invoke overrides to increase the informativeness of their financial

statements, we would not expect TFV firms to exhibit weaker indicators before the effect of the

override.

First, we examine the annual effect of overrides on income and the cumulative effect on

equity for the subsample of firms that disclose these amounts. The Companies Act and UK

GAAP require that firms invoking a TFV override disclose the particulars of any departure, the

reasons for it and its effect, where the effect is quantified if possible. As reported in Table 1,

only a small number of companies actually quantify the effect of their override. In some cases,

this occurs because a firm would not be able to characterize what number it would have reported,

as in the case of adopting merger (pooling) accounting instead of purchase accounting in

acquisition of a subsidiary In other cases, such as non-depreciation of investment properties,

quantification would require that the firm calculate the depreciation amount it would have

recorded, which is arbitrary if the firm views the asset as having an indefinite life.15

We expect

15 This view is questioned by Company Reporting, a leading UK publication that critically focuses on reporting

practices by listed companies:

Claiming that the effect of an override is not quantifiable is common practice amongst companies

not depreciating investment properties; although we have some difficulty in understanding why

15

that the median income and equity effects of an override are significantly positive if firms invoke

overrides opportunistically. If overrides are not income and equity-increasing, on average, it

seems less likely that they are invoked for opportunistic reasons. However, we note that because

only a fraction of firms quantify their override effects, the median for the sample as a whole may

differ from the median for the sample that disclosed the magnitude of the effects on income and

equity. Furthermore, our tests that the median effect is positive are less powerful than they

would be if based on a larger sample.

Second, we compare the characteristics of TFV firms to a control sample of industry and

size-matched firms. We test whether firms that invoke overrides are less profitable and

financially weaker than firms that do not. It should be noted that to the extent an override is

successful in masking poor performance or financial position, we are less likely to find evidence

supporting opportunistic behavior in measures based on net income. To mitigate potential

effects of overrides on profits, assets and equity, we use two measures to assess underlying

performance before the effect of an override: OPINC, the ratio of operating income before

depreciation and amortization to sales, and CFOTOS, the ratio of cash from operations to sales.

In addition, to assess the tightness of debt covenants before the effect of overrides, we use

DETOFIX, debt to gross book value of tangible fixed assets, and INTCV, the interest coverage

ratio. 16

Note that if contracts regularly contain clauses to undo the effect of overrides, we would

not expect to find an association between debt levels and the occurrence of overrides. Thus,

they are unable to calculate something like two per cent of the carrying value. In contrast, the

remaining … companies tend to state the accounting treatment adopted and why, but often neglect

to mention the requirement from which they are departing or the quantitative effect of that

departure. (Company Reporting, 2000)

16

Beneish and Press (1993) demonstrate that technical violation of accounting-based debt covenants is costly. In

addition, most of the violations in their sample are with respect to tangible net worth. Our focus on fixed tangible

assets in the calculation of DETOFIX thus captures lenders‟ preference for using tangible assets in debt covenants.

16

finding such an association would suggest either contracting parties agree not to undo overrides

or did not originally anticipate them.

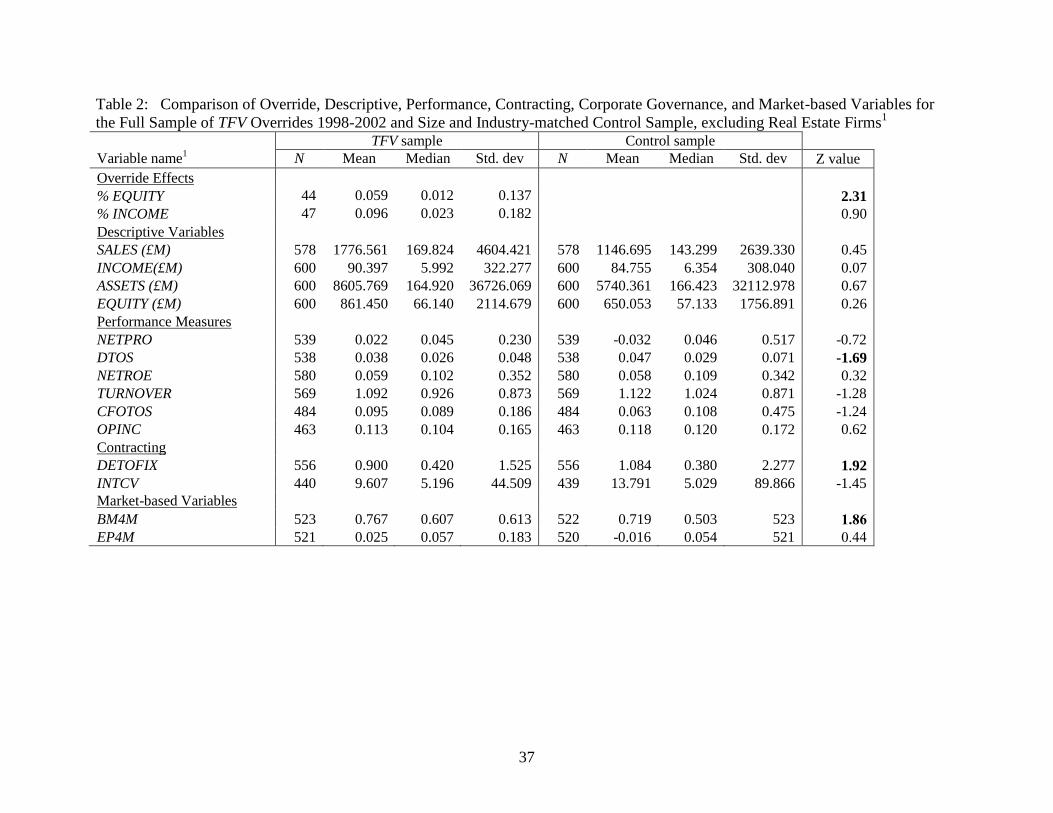

To give a comprehensive overview of the results of these tests, we begin by presenting

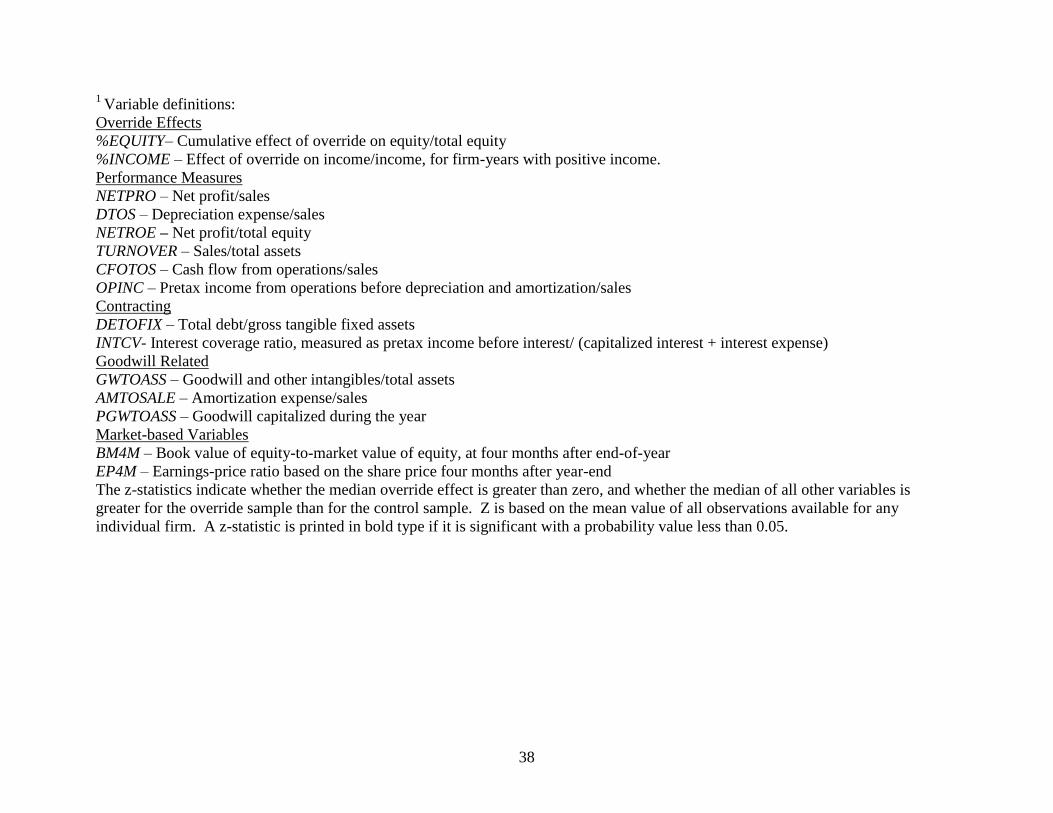

the findings for the entire sample of firm-years invoking any category of override. Table 2

presents descriptive statistics on several variables for both the TFV and the control samples.17

We calculate the Wilcoxon matched pair signed rank Z-statistic for the median difference in the

firm-specific means of the TFV and control samples, and report the results under the Z heading.

The advantage of this approach is that it is less susceptible to cross-sectional dependence in the

TFV sample. It also mitigates the influence of outliers.

Consistent with the theoretical considerations discussed earlier in the paper, we group the

variables into five categories: override effects, descriptive measures, performance measures, debt

contracting and market-related variables.18

The first category includes the override effects on

equity and income, on a percentage basis, for the subsample of firm-years in which the amount

of the effect was disclosed.19

The mean (median) increase in equity is 5.9% (1.2%) and the mean

(median) effect on income is 9.6% (2.3%). However, only the median effect for equity is

significantly positive with probability value less than 0.001. These findings thus provide some

support for the notion that firms invoking overrides tend to adopt income- and equity-increasing

accounting choices.

The second category includes descriptive measures, and indicates that TFV firms report

SALES (total turnover), INCOME (net income), ASSETS (total assets) and EQUITY (total

17

To ensure that the means reported are not unduly influenced by extreme observations, we exclude observations

with ratios greater than the 99th

percentile or less than the 1st percentile.

18 We also looked at corporate governance variables, such as the number of external directors and the size of the

board. However, we did not find significant differences between TFV firms and control firms. Thus, for brevity, we

do not tabulate the findings of these analyses. 19

The number of quantification observations in Table 2 is fewer than in Table1 due to lack of availability of profit

or equity data or negative values for these amounts.

17

shareholders‟ funds) that are not significantly greater than those of the control group. Turning to

performance measures, we observe that the net profit margin, NETPRO, is not significantly

different for the TFV and control samples. However, TFV firms have significantly lower

depreciation to sales, DTOS, which is not surprising given the large frequency of overrides that

result in non-depreciation of investment properties. The difference in the two measures of pre-

override profitability, CFOTOS and OPINC, are insignificant.

Under the hypothesis that TFV firms are motivated to override accounting rules to avoid

violating a debt covenant, one might expect DETOFIX to be higher for TFV firms. We find that

the median debt to gross fixed assets is indeed greater for TFV firms, suggesting that for the

sample as a whole, concern over leverage ratios may have motivated them to override asset-

reducing standards. Because we measure DETOFIX using gross fixed assets, this measure is not

affected by non-depreciation overrides. Alternatively, INTCV likely reflects the effects of any

income-increasing overrides and here we do not find a significant difference between TFV and

control firms for the entire sample.

Market-based variables comprise the final category of variables in Table 2. The ratio of

book to market value as measured four months after fiscal year-end, BM4M, is significantly

greater for override firms. The ratio of earnings to price, again measured four months after fiscal

year-end, EP4M, is not significantly different. These findings suggest that the market discounts

the equity of TFV firms relative to that of control firms and therefore that investors at least

partially adjust for the financial statement effects of the override.20

In summary, we do not find a significant difference between the pre-override profitability

of TFV firms and those of a size- and industry-matched sample. This may be due, at least in part,

20

It is interesting to note that the mean and median market-to-book ratios of override firms are closer to 1, which

one would expect if their accounting more fully captured their value.

18

to the fact that most of the overrides in Table 2 are mechanical. Nonetheless, we do find that

TFV firms have higher debt to fixed assets, suggesting that a motive for override may be related

to debt contracts.

It is important to recognize that the findings presented in Table 2 reflect the aggregation

of diverse override types. We therefore examine three subsamples, with an aim to understanding

whether differences in performance and debt contracting are observed where the overrides

involve the greatest discretion and are most costly.

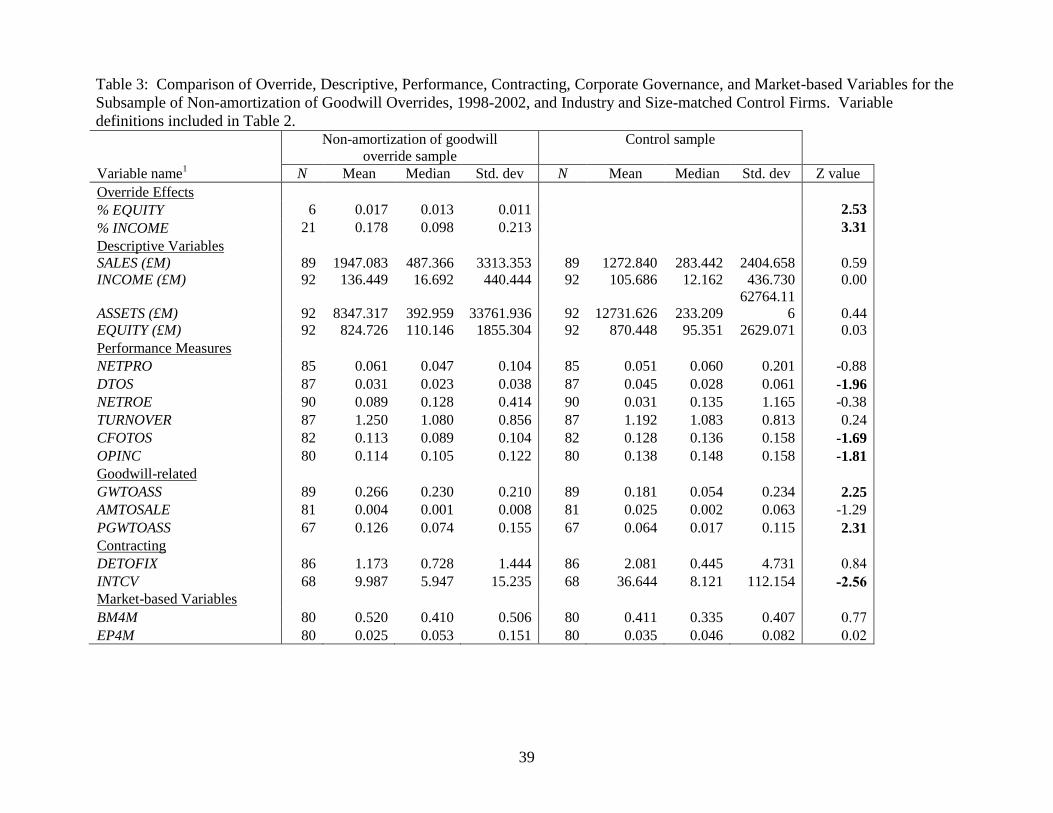

The first subsample we examine is that of firms invoking an override to avoid amortizing

goodwill, which we also refer to as the nonamortization of goodwill (NOG) subsample. This

override is conjectured to be costly because it is not the preferred method in FRS 10 and its

implementation involves real costs to review for impairment. As such, it is a Category 2

override, implying that we expect differences in financial performance or position to be more

pronounced than the overall sample. Put differently, firms overriding the principle of amortizing

goodwill may be exercising greater discretion than firms who override the depreciation of

investment property, as FRS 10 indicates that goodwill may have an indefinite useful life in

exceptional cases.

The second subsample we examine is category 4 overrides, firms that override UK

GAAP, which we refer to as the true GAAP override sample. We expect these to be the most

costly overrides and to involve the greatest discretion. The third subsample we examine, the S19

subsample, includes Category 1 overrides of the Companies Act requirement that all fixed assets

of finite life be depreciated, in order to follow the UK GAAP (SSAP 19) requirement that

investment assets be carried at fair value. Because the override is invoked to follow a more

19

authoritative standard, we would not expect to see differences in performance, debt contracts or

governance between firms invoking this override and the control sample.

The results for the non-amortization of goodwill subsample, reported in Table 3, indicate

that firms quantifying the magnitude of their override significantly increase reported income and

shareholders‟ equity by not amortizing goodwill. They also exhibit weaker performance than

that of industry- and size-matched control sample firms. Specifically, OPINC, the ratio of

operating income before depreciation and amortization to sales, and CFOTOS, the ratio of cash

from operations to sales are significantly lower for non-amortizing TFV firms than for control

firms. However, reported net income, net margin, return on equity and return on assets are not

significantly lower, consistent with the income-increasing effect of the override. Second, these

TFV firms have recognized significantly more goodwill than control firms, and due to the

override, report lower amortization as a percent of sales than control firms. This is clearly

reflected in the ratio of ending balance of goodwill and intangible assets to total assets,

GWTOASS, and in new goodwill capitalized during the year, PGWTOASS.21

The picture that

emerges for firms not amortizing goodwill is that they experience profitability before the

override that is lower than the control sample, and which may further deteriorate in the future

should they amortize the large amount of newly recognized goodwill. Third, these firms have a

significantly lower interest coverage ratio. Bearing in mind the lower cash generation, this

suggests that potential concern for violating debt covenants may have motivated the choice not to

amortize goodwill. Finally, investors do not appear to discount the book value or earnings of

these firms relative to the control sample, suggesting that investors view the reported numbers as

comparable to those of firms that did not invoke an override.

21

This finding is consistent with Aboody et al. (2000) who find that acquiring firms‟ tendency to use pooling

methods increases in the step-ups to targets‟ net assets.

20

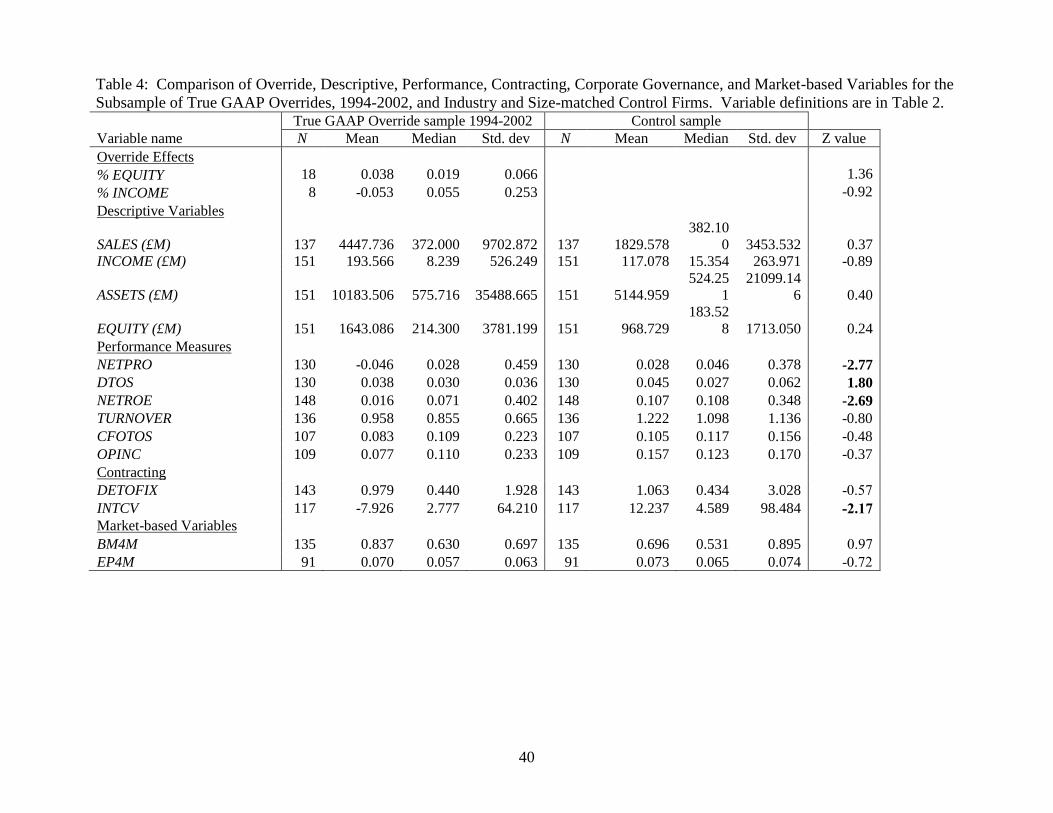

Our third analysis focuses on overrides of GAAP (Category 4), which we hypothesize

involve the highest cost. We expect to see significant differences in performance relative to

control firms if the higher cost of these departures is offset by greater benefits from reporting the

alternative financial statement amounts. As noted in Table 1, during 1998-2002 we find 133

firm-year observations of GAAP overrides. Given the considerable concern that the SEC and

various commentators have expressed regarding granting managers the ability to depart from

GAAP as well as the lack of sufficient evidence on such departures, we augmented our search to

encompass the nine-year period of 1994-2002. This procedure gives us a larger sample and

longer time series to examine factors associated with GAAP overrides: the resulting subsample

has 203 firm-years.22

Table 4 provides the comparison that pertains to the augmented subsample of GAAP

overrides. Due to limits on data availability, the number of observations for variables other than

override effects varies from 91 to 151 depending on the specific variable. For the subset of firms

that quantified the effect of their override, we find that the equity and income effects are not

significantly different from zero. Firms overriding GAAP are significantly less profitable after

the override than their respective control firms, as reflected in lower net margin and return on

equity, though cash from operations to sales and operating income to sales are not significantly

lower. Consistent with the lower level of reported profitability, interest coverage is also

significantly lower. However, we do not find a higher level of debt to fixed assets for TFV firms.

These findings provide support for the hypothesis that firms overriding GAAP are experiencing

weaker performance or have a greater incentive to raise earnings for debt contracts.

22

The main override types here are as follows: 57 overrides concern violation of requirements of FRS 6 merger

accounting (MER), 21 departures from the requirements of SSAP 4 (GRT), 16 departure from the requirement of

SSAP 12 to depreciate fixed assets (S12), 14 depart from FRS 9 accounting for associates and joint ventures, 13

overrides of SSAP 9 GAAP concerning current assets (MVA), 13 depart from GAAP concerning presentation

matters, 12 of FRS 4, accounting of capital instruments and 10 of FRS 1 presentation of the cash flow statement.

21

In our next subsample analysis, we examine overrides that can be regarded as

“mechanical” in that they represent an accounting treatment that is consistent with GAAP but is

in contrast to the requirements of the Companies Act (i.e., Category 1). This subsample

comprises non-depreciation of investment properties (by non real-estate firms) and is presented

in Table 5. We are interested in this subsample as a benchmark to the analysis of the more costly

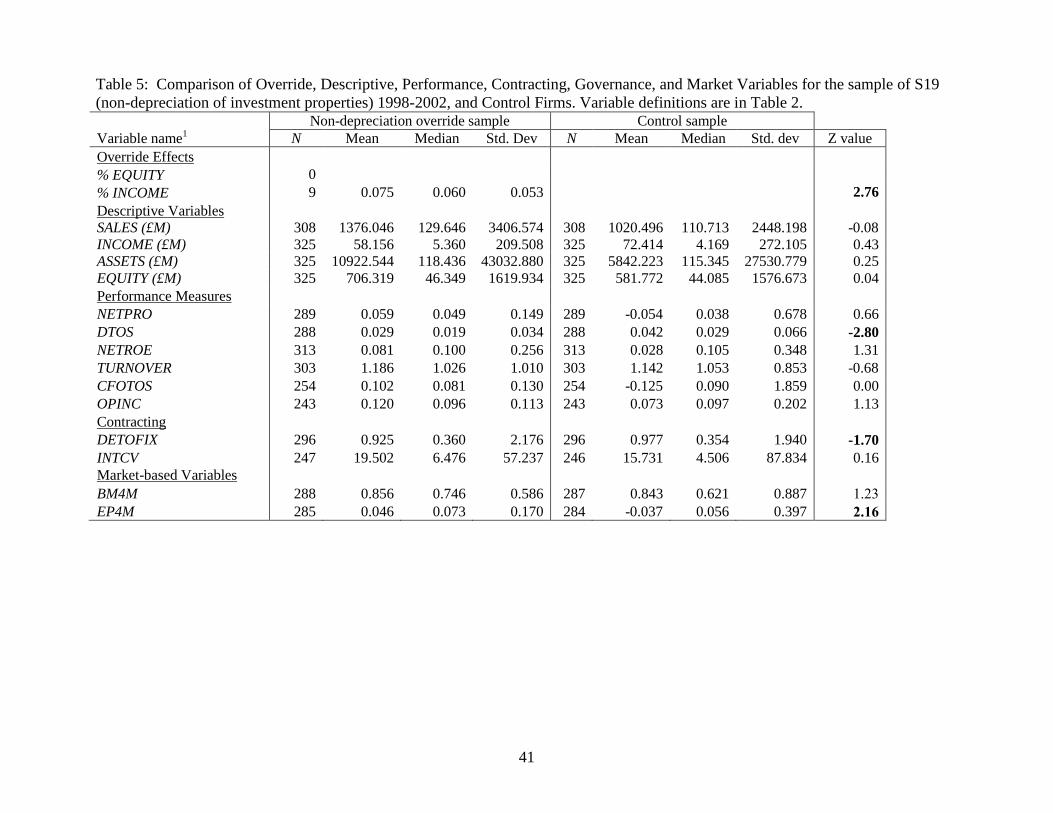

overrides, since we do not expect to find significant differences for mechanical overrides. The

median income effect of this override is significantly positive for the subset of firms that

quantified their effects, though none of these overriding firms quantified the equity effect.

However, the net profit margin for TFV firms is not greater than that of control firms. Consistent

with the override, TFV firms report significantly lower depreciation to sales relative to control

firms. Adjusting for depreciation however, the profitability of TFV and control firms seems to

be similar, as OPINC and CFOTOS are not significantly different between TFV and control

firms. The interest coverage ratio is insignificantly different for TFV firms and the debt to fixed

assets ratio, DETOFIX, is significantly lower, suggesting that debt covenants are not tighter for

TFV firms. Lastly, earnings to price, EP4M, is significantly higher for the override sample than

the control sample, indicating that the market at least partially adjusts for the difference in

depreciation and its implications for reported income and book value of equity. The overall

evidence thus seems to support the claim that non-depreciation of investment properties is

mechanical in nature and not an opportunistic accounting choice, consistent with our prediction

for a Category 1 override.23

The previously reported tests are based on a comparison of the TFV firms to industry and

size-matched control firms. The next set of tests examines the change in performance of TFV

23

Note that while the override itself is “mechanical” (all investment properties should not be depreciated under

GAAP), managers‟ identification of certain assets as investment properties may be opportunistic.

22

firms in the year they first adopted an override relative to the prior year. To the extent that

overrides are undertaken to increase income or equity, we would expect to find first-time

adoptions associated with worsening financial conditions. We therefore use the TFV firm in the

year prior to the first override as the control. We present results on the descriptive and

performance-related variables for the sample as a whole, and for the subsample of GAAP

overrides.

The left side of Table 6 presents the findings for the overrides for which we could

identify the first year of the override from the firm‟s financial statements and collect relevant

data for the prior year. The findings indicate that the changes in sales, assets and equity,

SALES, ASSETS and EQUITY, respectively, are all significantly positive, whereas the

change in income, INCOME, is not significantly positive. Consistent with this, the change in

scaled profitability measures, NETPRO, NETROE, and TURNOVER are all significantly

negative. However, the change in our measures of profitability before the effect of the override,

CFOTOS and OPINC, are not significantly negative. The debt contracting variables indicate

a marginally significant increase in debt to fixed assets and a statistically insignificant decline in

interest coverage. Finally, the change in the book-to-market and earnings to price ratios are

significantly positive, consistent with investors discounting book value of equity and earnings,

respectively, in the year of the override, relative to the prior year.

The right side of Table 6 presents the findings for the GAAP override subsample.

Similar to the sample as a whole, the change in scaled profitability measures, NETPRO, and

TURNOVER are significantly negative. In contrast to the entire sample, however, CFOTOS

and OPINC are negative, though CFOTOS is marginally significant. The changes in the debt

contracting variables and the market-based variables are not significantly different from zero.

23

Taken along with the findings in Table 4, the findings suggest that eroding performance may

have contributed to the decision to override GAAP.

Taken as a whole, the findings thus far suggest that firms invoking the more costly

overrides are experiencing weaker profitability. Firms invoking an override to avoid amortizing

goodwill have significantly lower pre-override profitability. Firms invoking an override of UK

GAAP have lower post-override profitability and experienced a significant decline in

profitability in the year of adoption.24

Such firms may also be concerned about violating debt

covenants, such as those based on interest coverage. An interpretation of these results is that in

the UK‟s environment, which is characterized by principle-based rules coupled with significant

deterrents to abuse, some companies would nevertheless be motivated to take advantage of the

TFV requirement. However, this in itself does not imply that with more rigid requirements (i.e.,

a rules-based environment) the frequency and magnitude of accounting manipulations in the UK

would have been lower.

5.3 IMPLICATIONS OF OVERRIDES FOR EARNINGS QUALITY AND INFORMATIVENESS

Our next analysis examines whether investors view TFV firms‟ financial statements as

less informative than those of control firms (Hypothesis 2). In the first set of tests, we focus on

one dimension of informativeness, the explanatory power of reported book value and earnings

per share for share prices. Following Joos and Lang (1994), we assess informativeness by the

adjusted R2 from the regression of share price on reported book value and earnings per share.

25

24

Peasnell, et al. (2005) find that the likelihood of UK managers making income-increasing abnormal accruals

during 1993-1996 to avoid reporting losses and earnings reductions is negatively related to the proportion of

outsiders on the board. 25

Following Barth and Clinch (2001), we examine the sensitivity of our findings to level and deflated regressions.

The untabulated findings are consistent with the estimation results for the deflated regressions we report.

24

Our tests use Ohlson‟s (1995) model relating stock prices to earnings and book values.26

He notes that his model can be interpreted as a weighted average of earnings and book value-

based valuation models. In his model, lower persistence of earnings will be captured by a lower

coefficient on income and a higher coefficient on book value of equity. We separately examine

this relation for positive and negative earnings, given the prior evidence by Hayn (1995) that

negative earnings are of lower persistence.

The estimation equation is

0 1 2 3 4P BV BV NI NI

(1)

where P is the stock price per share measured 4 months after fiscal yearend; BV is the book value

of equity per share; BV is the book value of equity per share times an indicator variable equal to

1 (0) if net earnings per share are negative (non-negative), NI is reported net earnings per share,

and NI is reported net earnings per share times an indicator variable equal to 1 (0) if net earnings

per share are negative (non-negative). We include BVandNI

because the coefficient on net

income is likely lower for reported losses, and the coefficient on book value of equity is likely

higher.27

We expect that 1 > 0, 2 > 0, 3 > 0 and 4 < 0. We estimate equation (1) for the

override and control samples separately, and test for differences in the R2

of the two

subsamples.28

26

For a related empirical application, see Ghosh, et al. (2005). 27

We also estimated a specification permitting a different slope coefficient on book value of equity for loss vs.

profitable firms. Although the coefficient on book value of equity changes, the overall explanatory power remains

similar and the pattern of explanatory power across subsamples is unaffected. We therefore tabulate the simpler

model. 28

Brown, et al. (1999) argue that scale effects in levels regressions increase R2, and this effect increases in the scale

factor‟s coefficient of variation. As a result, comparing R2 across samples is invalid unless the scale effect is

accounted for. They propose calculating the regression coefficient of variation to assess the potential impact of

scale effects. Because the control sample firms are matched to the TFV firms based on size and industry, we control

directly for scale. However, to ensure that these controls are effective, we examine the coefficients of variation to

draw inferences from R2s that are robust to the scale effect. We also applied the approach recommended by Gu

(2002) and find that none of our conclusions are affected.

25

We examine whether more costly overrides (NOG and GAAP) involve a loss of

informativeness. We compare these results to those of the “mechanical override” subsample, for

which we would not expect less informative financial statements. The bottom two rows of Table

7 show the R2 for the override and control subsamples. For the full sample of overrides from

1998-2002, the R2 is 0.65 for the TFV firms, in contrast to 0.47 for the control firms. These

findings indicate that earnings and book value do not have less explanatory power for the share

prices of override firms than for those of control firms. In addition, the untabulated coefficient

of variation is higher for the control sample, so the higher R2

is not due to scale. For the NOG

subsample, we find that both the TFV and control sample regressions have R2‟s of 0.67. Because

the coefficient of variation for the control sample is higher, these findings suggest that the

explanatory power of book value of equity and income for share prices of the override sample is

not less than for the control sample.

The results of the market-based tests for the GAAP overrides subsample are in contrast to

the previous findings. They indicate that the explanatory power of the book value of equity and

income for variation in GAAP override firm share prices is lower than for the control sample.

The coefficient of variation is higher for the override sample however, so the scale effect is not

inducing this finding. Given the findings in Tables 4 and 6, this is also consistent with the view

that GAAP overrides are invoked to mask deteriorating performance in the financial statements.

Finally, we estimate equation (1) for the subsample of firms that do not depreciate

investment properties, a treatment that is consistent with GAAP but inconsistent with the

Companies Act. To the extent that these are merely mechanical overrides, we do not expect to

find similar results to GAAP overrides. Indeed, for this sample, the R2 comparison suggests that

the book value of equity and income reported by override firms have greater explanatory power

26

for share prices than those reported by control firms. The coefficient of variation is greater for

the control sample, again indicating that scale bias is not inducing this result. This finding may

be explained, at least in part, by the fact that firms invoking S19 also annually revalue their

investment properties. Prior literature (e.g., Aboody et al., 1999) suggests that revaluations are

informative, implying that our results may reflect the greater informativeness of revalued

properties.

Our second set of tests of H2 focus on the coefficients on earnings and book values, to

examine whether TFV firms‟ earnings are perceived by investors as less persistent than those of

control firms. This test pools the control and TFV samples, but allows the coefficients to vary

between control and TFV firms. Specifically, we estimate an augmented version of Equation 1:

0 1 1 2 3 4 5 6

7 8

* *

* *

P TFV BV BV N I N I BV TFV BV TFV

N I TFV N I TFV

(2)

where TFV is an indicator variable assuming the value of one if the observation is for a TFV

firm, and zero otherwise.29

We test whether the persistence of earnings, as reflected in stock

prices, differs between TFV firms and control firms. Specifically, if the earnings of TFV firms

are artificially increased by the override and therefore are less persistent, we would expect 7 < 0

and 5 >0. By introducing the interaction variable NI *TFV in (2), we can also examine whether

investors perceive differences in the persistence of negative income, and whether investors

perceive differences in such persistence between TFV and control firms.

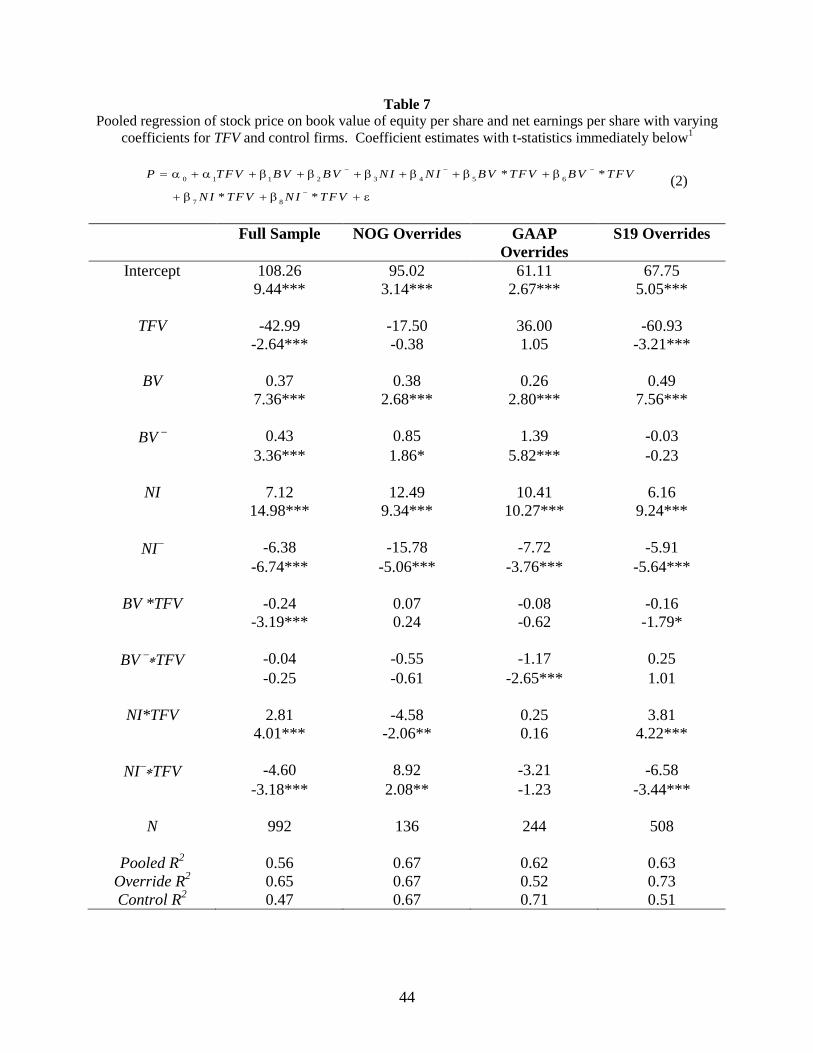

The results of this analysis are reported in Table 7. For the entire sample, the evidence

indicates differential weights on income and book value of equity between profit and loss firms.

Consistent with the prediction that losses are less persistent, the incremental coefficient on N I

29

The coefficients for this model are equivalent to those obtained in equation (1) but this specification allows for

direct tests of the difference in coefficients in earnings and book value between the override and control samples.

27

is negative and statistically significant (4 = -6.38, t = -6.74) and the incremental coefficient on

B V E , book value of equity for loss firms, is positive and statistically significant (2 = 0.43, t =

3.36). This finding also largely holds for the coefficients on the three subsamples: the coefficient

on negative net income is negative and significant for all three subsamples and the coefficient on

book value for negative income firms is positive and significant for the NOG and GAAP

override samples, though not for the S19 overrides.

As for the persistence of TFV firm earnings, we find that for profitable firms, the

incremental coefficient on TFV earnings, 7, is positive and statistically significant (7 = 2.81, t =

4.01). This finding indicates that investors perceive these firms to have greater earnings quality

than profitable control firms. Consistent with this, the incremental coefficient on book value of

equity of TFV firms, 5, is negative and significant (5 = -0.24, t = -3.19), indicating a lower

weight on equity in the valuation of TFV firms. For loss firms, the findings indicate an

insignificant incremental coefficient on the book value of equity of TFV firms, (5 = -0.04, t = -

0.25) and a significantly lower coefficient on the earnings of TFV loss firms, consistent with

these TFV firms having less earnings persistence. A substantially similar pattern is observed for

the S19 subsample as well.

In the GAAP override subsample, the findings do not indicate any difference in the

persistence of profit between control and TFV firms. However, 6, the coefficient on book value

for loss firms, BV-, is significantly smaller for override firms than control firms, consistent with

their financial statements being less informative overall. In addition, the coefficient on earnings

for loss firms is marginally significantly negative, suggesting less persistent earnings for loss

firms. These findings suggest that the lesser informativeness of GAAP override firms observed

in the R2 test is due to the firms earning losses.

28

In contrast to the findings for the GAAP override sample, the NOG subsample exhibits

offsetting effects on the persistence of profit and loss override firms, consistent with the finding

of similar R2 „s overall for both the NOG and control samples. For the S19 sample, as mentioned

above, we obtain qualitatively similar findings to those for the sample as a whole.

To summarize, the stock price-based tests indicate that the financial statements of firms

invoking the most costly overrides, the GAAP overrides, have lower explanatory power than

those of their control sample. This finding is in contrast to the findings for firms invoking the

NOG or S19 overrides, and for the override sample as a whole. The coefficient estimates

indicate that the weaker explanatory power of GAAP override firms is due to the market

discounting both the book value and earnings of GAAP override firms with losses. Our findings

therefore suggest investors at least partially discount earnings and book value of the override

firms where strategic use of overrides is most likely. In contrast, for the S19 sample, consistent

with our finding little support that firms invoke these opportunistically, investors view their

earnings as more persistent.

6. Conclusions and TFV under IAS so far

The true and fair view (TFV) concept allows companies to depart from the letter of the

law or a promulgated accounting standard in certain circumstances. The true and fair override

provides a rich and unexplored context for studying how firms exercise discretion over

accounting principles and their motives for exercising this discretion. In addition, this context

allows one to test whether such flexibility is informative and potentially provide insights into the

decades-long debate regarding trade-offs between flexible and rigid accounting rules.

29

We postulate that the incidence of a particular override is negatively related to the

strength of the authoritative support for the principle from which the reporting firm departs. This

is because the greater the support for the standard, the larger the cost of the departure. Our

findings are consistent with this conjecture in that overrides hypothesized to be costly are less

frequent than those hypothesized to be less costly.

We find that firms overriding principles with greater authoritative standing to avoid

amortizing goodwill have experienced weaker performance than industry and size-matched

firms. We find that firms overriding UK GAAP exhibit weaker profitability and experienced a

decline in pre-override profitability in the year the override was first adopted. The finding that

more costly overrides are invoked by firms with weaker financial performance suggests that UK

managers have used the flexibility available to them for reasons not intended by the rules.

Additional evidence suggests firms invoking an override of GAAP provide less informative

financial statements.

In conclusion, this paper contributes to the literature along several dimensions. The

paper‟s analysis helps to assess whether UK companies have taken advantage of the TFV

override to mask unfavorable performance or financial position. This evidence may be useful in

the current debate on whether accounting rules in the US should be more flexible. It also

provides evidence that may be useful to the ongoing deliberations by the SEC as to whether to

allow US firms to follow IAS, and to international accounting researchers who are interested in

the issue of harmonization and the effects of IAS.

In assessing the strength of our results and their applicability to other contexts, four

caveats are in order. First, one should bear in mind that departures from UK GAAP may not be

the same departures US firms or firms from any other country would take. Second, the reporting

30

practices that result in any country are a consequence of their standards, legal environment and

the manner in which standards are enforced, as the Australian experience demonstrated. Given

that the UK is at the high end of the range of enforcement of accounting standards, override

behavior in other countries might differ significantly from the behavior documented in the UK.

Third, only a small fraction of the overrides in our sample are quantified. It is possible that with

greater disclosures one could assess more accurately the effect on revenues, expenses, assets and

liabilities. It remains an open question whether the effect we have documented is representative.

If invoking firms tend to withhold information when the effect is large, our analysis may

underestimate the average impact. Fourth and finally, since 2005, UK companies report under

IAS rules. To the best of our knowledge, the TFV override has been used in only three cases,

two involving an override of pension accounting and the third involving recognition of trading

losses. It remains to be seen whether overrides of IAS GAAP will occur with any frequency, and

if so, whether similar factors to those documented here will motivate them.

31

REFERENCES

Aboody, D., M. Barth and R. Kasznik (1999), „Revaluations of Fixed Assets and Future Firm

Performance: Evidence from the UK‟. Journal of Accounting and Economics, Vol.26, Nos.1-3

(January), pp. 149-178.

Aboody, D., R. Kasznik and M. Williams (2000), „Purchase versus Pooling in Stock-for-Stock

Acquisitions: Why Do Firms Care?‟, Journal of Accounting and Economics, Vol.29, No.3

(June), pp. 261-286.

Accounting Standard Board (ASB) (1992), True and Fair Override Disclosures. UITF Abstract

7. London: ASB.

Accounting Standard Board (ASB) (1993), Forward to Accounting Standards. London: ASB.

Accounting Standard Board (ASB) (1997), Goodwill and Intangible Assets. FRS 10. London:

ASB.

Accounting Standard Board (ASB) (2000), Accounting Policies. FRS 18. London: ASB.

Alexander, D., and S. Archer (2003), “On Economic Reality, Representational Faithfulness and

the „True and Fair Override‟”. Accounting and Business Research, Vol.33, No.1, pp. 3-17.

Barth, M., and G. Clinch (2001), ‟Scale Effects in Capital Markets-Based Accounting Research.‟

Working Paper (Graduate School of Business, Stanford University).

Bebchuk, L. A., J. M. Fried and D. I. Walker (2002), „Managerial Power and Rent Extraction in

the Design of Executive Compensation‟. The University of Chicago Law Review, Vol.69, No.3

(Summer), pp. 751-846.

Beneish, M. D. and E. Press (1993), „Cost of Technical Violation of Accounting-Based Debt

Covenants‟. The Accounting Review, Vol.68, No.2 (April), pp. 233-257.

Benston, G., M. Bromwich and A. Wagenhofer (2006), „Principles- Versus Rules-Based

Accounting Standards: The FASB‟s Standard Setting Strategy‟. Abacus, Vol.42, No.2 (June), pp.

165-188.

Botosan, C. (1997), „Disclosure Level and the Cost of Equity Capital‟. The Accounting Review,

Vol.72, No.3 (July), pp. 323-349.

Brandt. R., S. Fearnley, T. Hines and V. Beattie (1997), „The Financial Reporting Review Panel:

An Analysis of its Activities‟. ICAEW, Financial Reporting Today: Current and Emerging

Issues, 1998. (London: Accountancy Books).

32

Brown, S., K. Lo, and T. Lys (1999), „Use of R2 in Accounting Research: Measuring Changes in

Value Relevance over the Last Four Decades‟. Journal of Accounting and Economics, Vol.28,

No.2 (December), pp. 83-115.

Company Reporting (2000), „Issue of the Month: The True and Fair Override‟. Company

Reporting, Vol.121, pp. 3-32.

Cook, A. (1997), „Requirement for a True and Fair View – a UK Standard-setter‟s Perspective‟.

The European Accounting Review, Vol.6, No. 4 (December), pp. 693-709.

Davies, M., R. Paterson and A. Wilson (1999), in Butterworths Tolley and Ernst & Young (eds.),

UK GAAP (sixth edition) (Croydon, Surrey: Tolley Publishing Co. Ltd).

Dechow, P. M. and C. M. Schrand (2004), „Earnings Quality’. (United States: Research

Foundation of CFA Institute)..

Dichev, I., and D. Skinner (2002), „Large-sample Evidence on the Debt Covenant Hypothesis‟.

Journal of Accounting Research, Vol.40, No.4 (September), pp. 1091-1123.

Ewert, R, and A. Wagenhofer (2005), „Economic Effects of Tightening Accounting Standards to

Restrict Earnings Management‟. The Accounting Review, Vol.80, No.4 (October), pp. 1101-

1124.

Feltham, G., S. Robb and P. Zhang (2007), „Precision in Accounting Information, Financial

Leverage and the Value of Equity.‟ Journal of Business Finance & Accounting, Vol.34, Nos.7 &

8 (September/October), pp. 1099-1122.

Financial Accounting Standards Board (FASB) (2002), „Proposal for a Principles-Based

Approach to U.S. Standard Setting‟. No. 1125-001, (October 21, 2002).

Financial Reporting Council (2005), „The Implications of New Accounting and Auditing

Standards For The “True and Fair View” and Auditors’ Responsibilities.‟ FRN PN 119 (August

9, 2005).

Ghosh, A., Z. Gu and P. C. Jain (2005), „Sustained Earnings and Revenue Growth, Earnings

Quality, and Earnings Response Coefficients‟. Review of Accounting Studies, Vol.10, No.1

(March), pp. 33-57.

Gu, Z. (2007), „Across-sample Incomparability of R2‟s and Additional Evidence on Value

Relevance Changes Over Time‟. Journal of Business Finance and Accounting, Vol.34, Nos.7-8

(September/October), pp. 1073-1098.

Hayn, C. (1995), „The Information Content of Losses‟. Journal of Accounting and Economics,

Vol.20, No. 2 (September), pp. 123-153.

33

Hines, T., K. McBride, S. Fearnley and R. Brandt (2001), „We‟re Off to See the Wizard: An

Evaluation of Directors‟ and Auditors‟ Experiences with the Financial Reporting Review Panel‟.

Accounting, Auditing and Accountability Journal, Vol.14, No.1, pp. 53-84.

Hughes, J. (2008), „SocGen Accounting Prompts Queries‟. Financial Times [London (UK)], 11

March 2008, p. 22.

International Accounting Standard 1 (2003), Presentation of Financial Statements, (London:

International Accounting Standard Board).

Jack, A. (1994), „A Review of the New Financial Reporting Structures” in L. Skerratand D.

Tonkin (eds.), Financial Reporting 1993-1994: A Survey of U.K. Reporting Practice (London:

Institute of Chartered Accountants in England and Wales), pp. 33-51.

Joos, P. and L. Lang (1994), „The Effects of Accounting Diversity: Evidence from the European

Union.‟. Journal of Accounting Research, Vol.32, No.3 (Supplement), pp. 141-168. Kirk, N.

(2006), „Perceptions of the True and Fair View Concept: An Empirical Investigation‟. Abacus,

Vol.42, No.2 (June), pp. 205-235.

La Porta, R., F. Lopez-de-Silanes and A. Shleifer(1998), „Law and Finance‟. Journal of Political

Economy, Vol.106, No.6 (December), pp. 1113-1155.

Leftwich, R. (1983), „Accounting Information in Private Markets: Evidence from Private

Lending Agreements‟. The Accounting Review, Vol.58, No.1 (January), pp. 23-42.

McGregor, W. (1992), „True and Fair View – An Accounting Anachronism‟. Australian

Accountant, Vol.62, No.1 (February), pp. 68-71.

Nobes, C. W. and R. H. Parker (1991), “„True and Fair‟: A Survey of UK Financial Directors”.

Journal of Business Finance and Accounting, Vol.18, No.3 (April), pp. 359-375.

Ohlson, J. A. (1995), „Earnings, Book Values, and Dividends in Equity Valuation‟.

Contemporary Accounting Research, Vol.11, No.2 (Spring), pp. 661-687.

Oswald, D. R. (2008), „The Determinants and Value Relevance of the Choice of Accounting for

Research and Development Expenditures in the United Kingdom‟. Journal of Business Finance

& Accounting, Vol.35, Nos.1-2 (January/March), pp.1-24.

Peasnell, K., P. Pope and S. Young (2001), „The Characteristics of Firms Subject to Adverse

Rulings by the Financial Reporting Review Panel‟. Accounting and Business Research, Vol.31,

No.4 (Autumn), pp. 291-311.

Peasnell, K., P. Pope and S. Young (2005), „Board Monitoring and Earnings Management: Do

Outside Directors Influence Abnormal Accruals?‟. Journal of Business, Finance and Accounting,

Vol.32, No.32 (September/October), pp. 1311-1346.

34

Quick, C. (2001), „Is Big Brother Watching You?‟. The Times (London), 15 March 2001.

U. S. Securities and Exchange Commission (2000), „Concept Release: International Accounting

Standards‟. Release No. 34-42430, Section IV.A.2, 18 February 2000, p. 7.

U. S. Securities and Exchange Commission. (2001), „Division of Corporation Finance:

International Financial Reporting and Disclosure Issues’. 1 May 2001.

http://www.sec.gov/divisions/corpfin/internatl/issues0501.htm

Watts, R. and J.L. Zimmerman (1990), „Positive Accounting Theory: A Ten Year Perspective‟.

The Accounting Review, Vol.65, No.1 (January), pp. 131-156.

35

Table 1: Classification of Firm-year Overrides by Expected Cost Categories 1998-20021

Types of TFV Overrides2

Category

1

Category

2

Category

3

Category

4

Total

Number of

TFV obs.

No depreciation provided for:

Investment properties (S19) 339 339

Fixed assets (S12) 7 7

No amortization of goodwill (NOG) 104 104

Merger accounting used instead of

purchase accounting (MER)

4 50 54

Stepwise calculation of goodwill

(GDW)

32 2 34

Current assets presented at market

value and not cost (MVA)

25 4 29

Grants and contributions not shown

in deferred income (GRT)