Adapting business practices to the SAI’s environment: towards a new Performance Measurement...

36

ISSN 1831-449X European Court of Auditors 2013 MAY N o 05 MAI JOURNAL Cour des comptes européenne

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of Adapting business practices to the SAI’s environment: towards a new Performance Measurement...

ISS

N 1831-449X

European Court of Auditors

2013

MAY

No 05

MA I

JOURNALCour des comptes européenne

Tous les numéros de notre Journal se trouvent sur les sites / The Journal can be found on : INTERNET : http://eca.europa.eu/portal/page/portal/publications/JournalEU bookshop : http://bookshop.europa.eu/

PRODUCTIONRédacteur en chef / Editor in Chief : Rosmarie Carotti Tél. / tel.: 00352 4398 - 45506 - e-mail : [email protected] en page, diffusion / Layout, distribution : Direction de la Présidence - Directorate of the Presidency Photos : Reproduction interdite / Reproduction prohibited

THE CONTENTS OF THE INTERVIEWS AND THE ARTICLES ARE THE SOLE RESPONSIBILITY OF THE INTERVIEWEES AND AUTHORS

AND DO NOT NECESSARILY REFLECT THE OPINION OF THE EUROPEAN COURT OF AUDITORS

Copyright

1

SOMMAIREPages

02 ADAPTING BUSINESS PRACTICES TO THE SAI’S ENVIRONMENT: TOWARDS A NEW PERFORMANCE MEASUREMENT FRAMEWORK By Dr Georgia KONTOGEORGA, Auditor in the Hellenic Court of Auditors – Trainee in the Private O� ce of Mr Ioannis SARMAS

05 SPECIAL REPORT 1/2013 “HAS THE EU SUPPORT TO THE FOOD-PROCESSING INDUSTRY BEEN EFFECTIVE AND EFFICIENT IN ADDING VALUE TO AGRICULTURAL PRODUCTS?” The report was produced by Chamber I. Jan KINŠT was the reporting Member, Michael BAIN the Head of the NR4 - Performance Unit B, and Klaus STERN the team-leader for this audit By Rosmarie CAROTTI

07 SPECIAL REPORT 23/2012 "LES ACTIONS STRUCTURELLES DE L’UE ONT-ELLES CONTRIBUÉ AVEC SUCCÈS À LA RÉGÉNÉRATION DE FRICHES INDUSTRIELLES ET MILITAIRES?" Le rapport a été établi par la Chambre II et présenté à la presse le 18 avril 2012 par M. Henri GRETHEN, Membre rapporteur de la Cour et par M. Alain VANSILLIETTE, Chef d'unité ENV Par Rosmarie CAROTTI

09 MR MILAN MARTIN CVIKL, MEMBER OF THE COURT PRESENTS THE ECA'S WORK IN SLOVENIA - Presentation of the SR 22/2012: Do the European Integration Fund and European Refugee Fund contribute eª ectively to the integration of the third-country nationals? - Lectures at the universities of Maribor and Ljubljana - Presentation of AR 2011 in the National Council and meeting with President - Presentation of AR 2011 to Slovene Government stakeholders By the Private O� ce of Mr Milan Martin CVIKL 11 GROWTH‐ENHANCING EXPENDITURE IN EU COHESION SPENDING FROM 2007 TO 2013 A study presented on 9 April 2013 by the Centre for European Economic Research (ZEW) in Mannheim in the framework of an ECA’s Chamber II seminar organised by Dr. Harald NOACK, Member of the Court By Rosmarie CAROTTI 14 MR LADISLAV BALKO, MEMBER OF THE ECA, REPRESENTED THE ECA AT THE SEMINAR AND FESTIVE PROGRAMME MARKING THE 20TH ANNIVERSARY OF THE SUPREME AUDIT OFFICE OF THE SLOVAK REPUBLIC By Branislav URBANIČ, Head of Private O� ce of Mr Ladislav BALKO

15 TWENTY YEARS OF INDEPENDENT AUDIT IN THE SLOVAK REPUBLIC Interview with the Supreme Audit O� ce of the Slovak Republic President Ján JASOVSKÝ

18 BOOK REVIEW: “THE EUROPEAN COURT OF AUDITORS IN THE MULTI-LEVEL CONTROL SYSTEM” BY DOMENICO SICLARI By Andrea MONORCHIO, Professor of State Accounting, economist and former General Accountant of Italy 20 CINQUANTIÈME ANNIVERSAIRE DU TRAITÉ DE L’ÉLYSÉ FRANCE / ALLEMAGNE : IDENTITÉS OU MODÈLES ÉCONOMIQUES ? Débat organisé par l’Institut Pierre Werner et l’Institut la Banque européenne d’Investissement Intervenants : Guillaume DUVAl, rédacteur en chef de la revue Alternatives économiques, Alfred STEINHERR, ancien chef économiste à la BEI, professeur à la Sacred Heart University (Lux.), M. Frank ENGEL, député européen, chef de la délégation luxembourgeoise du Parti populaire européen By Rosmarie CAROTTI

22 FOCUS : Brief summary of the ¹ nancial crisis in Cyprus leading up to the recent events By Andreas ANTONIADES, Private O� ce Attaché 23 A BRIEF LIST OF MISUSED ENGLISH TERMINOLOGY IN EU PUBLICATIONS This is an update of the list published in the Journal in February 2012 and March 2012 By Jeremy GARDNER, translator 32 HELLO TO / GOODBYE TO

CONTENTS

Couverture/Cover:- ECA’s Chamber II seminar organised by Dr. Harald Noack, Member of the Court- Mr Ladislav Balko, Member of the ECA, represented the ECA at the seminar and festive programme marking the 20th Anniversary of the Supreme Audit Office of the Slovak Republic

Couverture/Cover:- ECA’s Chamber II seminar organised by Dr. Harald Noack, Member of the Court

p.11

p.02

p.05

p.07

p.09

p.14

p.15

p.18

p.20

p.23

2

ADAPTING BUSINESS PRACTICES TO THE SAI’S ENVIRONMENT: TOWARDS A NEW PERFORMANCE MEASUREMENT FRAMEWORK

By Dr Georgia KONTOGEORGA, Auditor in the Hellenic Court of Auditors – Trainee in the Private O� ce of Mr Ioannis SARMAS

It is generally agreed that in a democratic society public expenditure should be founded on an efficient financial management and control system (Vallés, 2005, Forward, p. xi).

Supreme Audit Institutions play a key role in this regard. Firstly, their audit reports propose measures for improving administration and help the executive to make optimum use of public money. At the same time, they ensure that the political objectives of the expenditure are achieved at the lowest possible cost and that the accounts are drawn up in a transparent manner. Secondly, the publication of audit findings familiarises citizens with the activities of the government and its representatives. They are also the only institutions that are in a position to deliver an independent opinion as to the quality of the management of the public sector and the extent to which the bureaucracy operates in accordance with pre-defined principles (INTOSAI, 2001, Final Task Force Report, Preamble).

From as early as the industrial revolution, as a result of the increased size of enterprises and the separation of ownership and management, audit began to “supervise” and ensure that management made proper use of available funds to the extent of the set objectives.

Correspondingly in the public sector, bearing in mind audit’s customary activity of verifying compliance with financial legislation, this activity gradually started to focus on supervising public management. This change resulted in the emergence of a new trend in the 1970s, mainly in the United Kingdom, Australia and New Zealand, termed new public management or NPM) (García Crespo, 2005, p. 9).

This new type of public management proposes abandoning bureaucracy and adopting innovative practices applied in the private sector, i.e. basically that public organisations change their focus from procedures to the results of those procedures (Hood, 1995). Such a change inevitably affects the nature of the audit as well, in that it moves its focus from accountability and legality (traditional audit) to economy, efficiency and effectiveness (the three ‘E’s). However, performance audit is not considered to be a “creation” of NPM (Barzelay, 1996, p. 24, Pollitt et al., 1999, p. 56).

SAIs have now largely adopted practices and conditions that have applied for years in the field of private enterprise: they clearly establish their vision and mission, set their strategic course, build up their capacities, and evaluate and make public their productivity, in accordance with the requirements of the international standards of SAIs developed by INTOSAI. Those standards (ISSAIs) essentially adapt the International Federation of Accountants’ (IFAC) private-sector accounting standards to the financial environment. In general, financial audit largely involves integrating private-sector audit standards into the public domain (Sarmas, 2006, pages 95 and 96).

In order to evaluate their capacity and effectiveness, SAIs employ various devices, including reports on their activities and development, evaluations vis-à-vis the ISSAI framework, and national or internationally developed performance indicators.

If an SAI is to evaluate its operation objectively, it should point out the positive points, shortcomings, gaps and constraints it encounters and then draw up a capacity building programme. Factors limiting an SAI’s capacity may be lack of resources, the low skills level of staff, lack of independence and, in the domestic context, under-developed management of the system of public finances (e.g. inadequate accounting systems, financial statements with limitations, limited or complete absence of internal control, lack of familiarity with international accounting and audit standards, etc.).

Once these challenges have been identified, the SAI is able to develop an appropriate capacity building strategy that will be based on its strong points and address the shortcomings, gaps and constraints impeding its effectiveness (INTOSAI, CBC, 2007, p. 10).

3

ADAPTING BUSINESS PRACTICES TO THE SAI’S ENVIRONMENT: TOWARDS A NEW PERFORMANCE MEASUREMENT FRAMEWORK

The efficiency of SAIs can also be evaluated using generic models/tools that have been developed and used to evaluate enterprises (e.g. SWOT analysis, balanced scorecard, etc.). However, owing to the specificity involved in evaluating an SAI’s performance, more specialised evaluation models have been developed for this purpose by either international development organisations (donor agencies) or the SAIs themselves. The first category includes tools used to evaluate the systems for managing a country’s public finances (Public Financial Management or PFM systems) before development loans are granted, and thereby to ascertain whether the donors may rely on the audits of a country’s SAI to ensure that their development money is used properly (e.g. PEFA Framework, World Bank CFAA, etc.). The models concerned evaluate an SAI in the context of a country’s broader system of financial management (Public Financial Management or PFM).

The second category contains models that have been developed by the actual SAIs (e.g. PASAI Capability Model, AFROSAI-E Capability Model, NAO Maturity Model, GAO Accountability Organisation Maturity Model, CBNA Framework, etc.) on the basis of international standards – which are also influenced by the corresponding private sector standards – that are used both to evaluate their capabilities and as development models. For example, the NAO Maturity Model evaluation criteria are based on the INTOSAI standards, best practices and the European Foundation for Quality Management’s (EFQM) entrepreneurial excellence model. The GAO’s Accountability Organisation Maturity Model is pyramidal, has six hierarchical levels and is based on Maslow’s pyramid of satisfaction and hierarchy of needs, while the conceptual basis of the PASAI Capability Model draws on the Humphrey Capability Maturity Model® or CMM®, which is a tool that has been used extensively in avionics software, but also generally to evaluate government projects worldwide.

At international level the SAIs are organisations with various different characteristics and to date there has not been an internationally accepted model, nor have there been absolute standards of excellence on whose basis they could be judged overall (DFID, 2005).

Twenty existing tools and models were evaluated on the basis of 12 selected criteria by the Working Group on the Value and Benefits of SAIs – WGVBS) at the 4th meeting held in Jamaica in 2011. It was found that none of the existing models meets all 12 criteria, which is why it is necessary to develop a model that is universally applicable to all SAIs, irrespective of their structure and geographical location.

The New SAI Performance Measurement Framework (New SAI PMF) will provide an overview of the seven most important performance areas of an SAI using 22 indicators (SAI 1-22), and a descriptive performance report (SAI Performance Report or PR). According to the preliminary draft of the new model, the seven sectors are as follows:

1) heading Α: SAI Performance (SAI indicators 1 to 5)

2) heading Β: Independence & Legal Framework (SAI indicators 6 to 8)

3) heading C: Strategy for Organizational Development (SAI indicator 9)

4) heading D: Audit Standards & Methodology (SAI indicators 10 to 14)

5) heading Ε: Management & Support Structures (SAI indicators 15 and 16)

6) heading F: Human Resources (SAI indicators 17 to 19)

7) heading G: Communication & Stakeholder Management (SAI indicators 20 to 22).

The new model that is due to be presented at XXI INCOSAI in China the end of 2013 will be able to be used for each type of assessment (self assessment, peer assessment, external assessment and performance audit assessment) on an optional basis and will include as many of the strong points of existing models as possible (INTOSAI, WGVBS, 2012). The indicators will be rated on a scale of one to four, in line with the practice established in the AFROSAI-E Capability Model, with the dimensions of each indicator being assessed on the basis of the PEFA Framework.

4

ADAPTING BUSINESS PRACTICES TO THE SAI’S ENVIRONMENT: TOWARDS A NEW PERFORMANCE MEASUREMENT FRAMEWORK

Attainment of performance level 3 will be equivalent to compliance with the ISSAIs and other internationally accepted good practices. Levels 1 and 2 represent increased divergence from the ISSAIs, while a fourth performance level has also been envisaged, one that indicates that the SAI not only meets the related criteria of the ISSAIs, but also further defined characteristics that would enhance the value and benefits expected to result from its operation.

In the current context of economic recession, the need for accountability on the part of public officials, transparency in the making available of public money and reinforcement of financial management systems is all the more urgent. The standards, principles and practices of private enterprises, adapted as necessary, may prove useful to the SAIs, which should not view developments from the sideline, but play a leading role and monitor the trends in the ever-changing environment in which they operate.

According to the assessment model developed by the Government Accountability Office (GAO), every SAI is in a unique position and, given its reputation for independence, professionalism and reliability, its ultimate mission (corresponding to the apex of the pyramidal hierarchy) should be to provide policy makers with a picture of the future and notify them of the emerging trends and future challenges. By encouraging early action on matters that can still be managed, the SAIs can help their governments to take earlier and more knowledge-based action to avoid crises.

This new mission should be added to every SAI’s portfolio of capacities and supplement traditional audit responsibilities (fighting fraud, improving transparency, increasing accountability, etc.) (Walker, 2007).

BIBLIOGRAPHICAL REFERENCES

Barzelay, M. (1996). Performance auditing and the new public management: changing roles and strategies of central audit institutions. In: OECD, Performance audit and the modernization of government. Paris: PUMA/OECD, 15-56.

DFID (Department for International Development) (2005). How to note: “Working with Supreme Audit Institutions”. Part of the Policy Division Info series. Ref. No: PD Info 079, July.

García Crespo, Μ. (2005). Public Control: A General View, in Milagros García Crespo (eds). Public Expenditure Control in Europe: Coordinating Audit Functions in the European Union. Edward Elgar, 3-29.

Hood, C. (1995). The New Public Management in the 1980s: Variations on a Theme. Accounting, Organizations and Society, 20(2/3), 93-109.

INTOSAI (2001). Independence of SAIs Project, Final Task Force Report, March 31, 2001.

INTOSAI Capacity Building Committee (CBC) (2007). Building Capacity in Supreme Audit Institutions: A Guide. UK National Audit Office, November 2007, DG Ref: 7509RB.

INTOSAI Donor Secretariat for the WGVBS (2012). SAI Performance Measurement Framework: Concept Note (Draft 8.9.12). INTOSAI, IDI.

Pollitt, C., Girre, X., Lonsdale, J., Mul, R., Summa, H. & Waerness, M. (1999). Performance or Compliance? Performance Audit and Public Management in Five Countries. Oxford University Press.

Walker, D.M. (2007). Enhancing Performance, Accountability, and Foresight. US GAO Presentation by Comptroller General of the United States, speech before the Caribbean Organization of Supreme Audit Institutions (CAROSAI), GAO-07-165CG.

Vallés, J.M.F. (2005). Foreword in Milagros García Crespo (eds). Public Expenditure Control in Europe: Coordinating Audit Functions in the European Union. Edward Elgar.

Sarmas, D.I. (2006). Καλύτερο Κράτος: Η Σπατάλη, η Διαφθορά και ο Σύγχρονος Δημοσιονομικός Έλεγχος (A Better State: Waste, Corruption and Modern State Audit). Athens-Komotini: A. Sakkoulas editions (in Greek).

5

SPECIAL REPORT 1/2013“HAS THE EU SUPPORT TO THE FOOD-PROCESSING INDUSTRY BEEN EFFECTIVE AND EFFICIENT IN ADDING VALUE TO AGRICULTURAL PRODUCTS?”By Rosmarie Carotti

The report was produced by Chamber I. Jan KINŠT was the reporting Member, Michael BAIN the Head of the NR4 - Performance Unit B, and Klaus STERN the team-leader for this audit

As part of the Rural Development Policy, the EU made available € 5.6 billion for the period 2007-2013 to fund investment by enterprises that process and market agricultural and forestry products. These investments should add value to those products and thus improve the marketing opportunities, with the ultimate objective of increasing the competitiveness of agriculture. This funding is complemented by national spending, which brings the total public funding to € 9 billion.

All this public money is channelled through a measure called “Adding value to agriculture and forestry products”, known also as “Measure 123”. It is used principally to give grants that cover between 20% and 50% of the companies’ total eligible investment costs. The investments financed are made by start-ups or existing businesses for new or improved plant or machinery, or for the construction of new facilities to process and market agricultural products.

This spending falls under shared management between the Commission and the Member States; while the Commission has an ultimate responsibility for an effective use of EU funds, the actual operational and financial management of the measure is carried out by the Member States.

The food processing industry generates an annual turnover of about € 950 billion and direct employment for over 4 million people. The ECA examined whether the measure was designed and implemented in a way that provided for the efficient funding of projects addressing clearly identified needs and whether the measure was monitored and evaluated in a way that allowed its results to be demonstrated.

The audit comprised a review of six rural development programmes in Spain, Italy, France, Lithuania, Poland and Romania. The ECA examined their management systems and visited 24 completed food-processing projects. The six Member States were not selected on a risk-based analysis but can be considered quite representative. Five of them were the highest spenders within Measure 123 and the ECA also aimed at a reasonable geographical coverage.

The key observations derived from the ECA’s audit work were:

The Member States did not clearly demonstrate the need for the measure in their spending plans and set very general objectives for the related support. The ECA would have expected the Commission to request the Member States to be more specific.

Mr Jan Kinšt, Member of the Court

6

SPECIAL REPORT 1/2013

Secondly, Member States do not select the projects with the highest potential benefits. The report presents cases of such inadequate selection.

Another important finding was that Member States do not ensure an efficient use of EU and national budget since they do not assess whether the beneficiary actually needs the support to undertake the investment (the so-called deadweight effect), or whether the supported investment is improving the situation of the beneficiary enterprise at the expense of a competitor (the so-called displacement effect).

The ECA observed that applications showing a high rate of return on the investment were given priority and that funds were granted for already completed projects.

The shortcomings described above were corroborated by the Court’s analysis of 24 funded projects. Only two of them met all criteria and only ten were considered to be satisfactory.

Finally, the ECA found that Member States do not monitor the results of the projects effectively and that mid-term evaluations are still a tool of limited use. This is an important issue since Member States must decide whether to include a similar measure in the next programming period from 2014.

On the basis of these observations, the ECA makes the following recommendations:

Firstly, Member States should clearly identify the need for funding and set objectives that are meaningful and measurable. The Commission should only approve programmes that do so.

Secondly, selection criteria should be defined that enable the most effective projects to be identified. These criteria should be rigorously applied.

Thirdly, the Commission and Member States should promote the adoption of best practices to mitigate the risk that companies that do not need the subsidy are supported.

Finally, the monitoring and evaluation applicable to the projects financed should be improved for the forthcoming programming period.

To conclude, the Commission has a unique opportunity when defining the measure and approving the rural programmes of Member States to insist that they submit programmes that are based on a clear analysis of needs. The selection of the projects falls under the sole responsibility of the Member States, but in terms of the design of the system there is shared responsibility of both the Commission and the Member States. And the Commission has a responsibility at the programming stage.

7

Cet audit de performance a été effectué entre mars et décembre 2011 à la Commission ainsi que dans les cinq États membres représentant la plus grande part des dépenses liées aux actions structurelles, à savoir : l’Allemagne, le Royaume-Uni, la Hongrie, la Pologne et la République tchèque. L’audit avait pour objet les 5,7 milliards d’euro provenant du Fonds européen développement régional et du Fonds de cohésion dépensés pour la régénération de friches au cours des périodes de programmation 2000-2006 et 2007-2013.

Les sites auparavant dédiés à un usage industriel ou militaire sont fréquemment appelés « friches ». Ces sites sont souvent contaminés par des polluants industriels et il est absolument essentiel qu’ils soient nettoyés.

Pour ce rapport, la Cour a examiné un échantillon de 27 projets de régénération dans les cinq États membres. Depuis l’an 2000, l’UE a investi 231 millions d’euros dans ces projets.

Les constatations et les recommandations de la Cour s’articulent autour de trois questions principales :

- la réalisation des objectifs en matière de régénération de friches,

- le ciblage des aides,

- le coût des résultats obtenus.

La réalisation des objectifs

La plupart des projets ont atteint leurs objectifs physiques ; par contre, l’occupation escomptée des parcelles ou des bâtiments après leur reconversion est moins importante que ce qui était prévu au départ. Avec leurs activités économiques, ces sites ont également générés moins d’emplois qu’espéré.

SPECIAL REPORT 23/2012"LES ACTIONS STRUCTURELLES DE L’UE ONT-ELLES CONTRIBUÉ AVEC SUCCÈS À LA RÉGÉNÉRATION DE FRICHES INDUSTRIELLES ET MILITAIRES?"

Par Rosmarie Carotti

Le rapport a été établi par la Chambre II et présenté à la presse le 18 avril 2012.M. Henri GRETHEN, Membre rapporteur de la Cour, a présenté les principales conclusions du rapport, tandis que M. Alain VANSILLIETTE, Chef d'unité ENV, a expliqué les constatations d’audit et les recommandations de la Cour

De gauche à droite: Mme Maria Del Carmen, teamleader; M. Alain Vansilliette, chef d'unité; M. Henri Grethen, Membre de la Cour; M. Marc Hostert, chef de cabinet; Mme Ildiko Preiss, attaché de cabinet

8

Les projets ont généralement été conçus suivant de bonnes pratiques et devraient avoir une incidence durable. Un grand nombre de ces sites ont dû faire l’objet d’assainissement et dans 50 % des cas cet assainissement n’a pas été accompagné de certification par des autorités indépendantes.

La Cour recommande tout d’abord, au niveau de la Commission, d’intégrer davantage ces projets dans un plan de développement global. Ensuite, la Commission devrait définir des standards communs qui permettent de déterminer quand un site est considéré comme danger pour la santé humaine et l’environnement, et jusqu’à quel niveau d’assainissement il faut descendre en fonction de l’usage prévu.

Au niveau des États membres, il faudrait davantage porter son attention aux études de marché au moment de choisir le futur usage des friches.

Le ciblage des aides

La deuxième question concerne le ciblage des aides. Les États membres disposent tous d’une politique de régénération des friches industrielles ; cependant, il y a une absence de registres recensant tous les sites et les sites contaminés pour sélectionner les friches les plus urgentes à traiter.

Les États membres disposent de stratégies mais pas de quantification des objectifs à atteindre. La Cour recommande d’avoir des stratégies accompagnées d’objectifs clairs et de continuer les efforts pour privilégier la régénération des anciens sites plutôt que d’utiliser des sites vierges. Il y a encore un certain nombre de friches problématiques appartenant à des propriétaires privés.

Le coût des résultats obtenus

En ce qui concerne la question de savoir si l’on pouvait obtenir davantage avec l’argent dépensé, beaucoup d’argent public a été dépensé sans que les pollueurs ne soient intervenus suffisamment.

La technique financière appelée déficit de financement (financing gap), qui permet de déterminer le subside nécessaire, n’a pas été appliquée dans une dizaine de cas. Il s’en suit que les besoins en matière d’aide publique n’ont pas toujours été évalués comme il se doit. Des insuffisances méthodologiques ont affecté les calculs.

Les autorités connaissent le principe du pollueur-payeur, mais dans aucun cas le pollueur n’a eu à supporter le coût total de la décontamination. Les possibilités de récupérer les aides publiques dans le cas où les projets génèrent davantage de recettes que prévu, sont limités. Ces projets sont souvent de nature à générer des recettes à long terme, 15 à 20 ans mais aucun mécanisme n’est prévu pour cela. La Cour signale également qu’en matière d’aides d’État certaines règles n’ont pas été correctement appliquées. En conséquence, trop a été payé par rapport à ce qui était nécessaire.

La Cour recommande à la Commission de développer des approches qui permettraient de tenir les pollueurs historiques davantage responsables et de mieux développer le concept de déficit de financement.

Aux États membres, la Cour recommande d’appliquer le principe du pollueur-payeur de manière plus rigoureuse, de bien évaluer toute la mesure dans laquelle on peut l’appliquer. La Cour leur recommande aussi d’apprécier de manière plus rigoureuse le déficit de financement et de tenir compte davantage des projets pour lesquels les promoteurs ont pu obtenir, par des conventions bilatérales, des réductions sur les prix d’achat. Ensuite, la Cour recommande d’introduire une méthode permettant le remboursement des aides au bénéfice de l’action publique sur une durée qui correspond à la vie du projet.

SPECIAL REPORT 23/2012

9

In March 2013 Milan Martin Cvikl presented the Special Report on the integration of third-country nationals (SR 22/2012) to the Slovene authorities responsible for SOLID1 programme, i.e. Ministry of the Interior. Following a brief introduction of the Court’s work, the main ¹ ndings of the report were presented. They were that although most of the individual projects were successful, their impact on the integration of third-country nationals could not be measured. Also the design of the SOLID programme hampered eª ectiveness and there was inadequate coordination with other EU funds.

In a lively exchange of views the participants from departments of the ministry provided their views on our ¹ ndings and shared their experience and activities in the ¹ eld of integration of third-country nationals in Slovenia. They con¹ rmed that funds obtained through EIF and ERF are crucial for implementation of the integration programmes and activities oª ered to the third-country nationals. Among other activities, a special webpage www.infotujci.si has been created providing third-country nationals with important information for integration into Slovene society. Participants stated that, in practice, the level of implementation of the external borders fund is higher (a topic of one of the next special reports to be prepared by Chamber IV) compared to integration activities also for the reasons mentioned in our report. In the Member’s view for example in Slovenia, registration of applicants for foreign language courses is done via strict, formal administration procedure at the level of regional administrative units, while in some other countries it is done via NGOs. However, EU value added has been observed as for the ¹ rst time since Slovene independence a much wider set of activities on truly integrating third country nationals has been developed.

The exchange of views and experience was thus very useful. It indicated that the ¹ ndings in the special report were corroborated by major stakeholders also in Slovenia. The event not only publicised the Court’s activities and outputs but also raised awareness of the Court’s mission to promote sound ¹ nancial management. Our recommendations on the simpli¹ cation of the programme design, the need to ¹ nd synergies among the diª erent funds and creation of an appropriate fund(s) structure were in principle agreed by the Slovene managing authorities of EU integration programmes and funds. They will serve as solid basis for the programming and implementation of Slovenian and other Member States national programmes within the future Multiannual Financial Framework for the period 2014-2020.

1 SOLID programme aims to improve management of migratory Í ows at the level of the European Union and to strengthen solidarity between Member States. The programme is composed of four Funds: the External Borders Fund, the European Return Fund, the European Refugee Fund and the European Fund for the Integration of third-country nationals.

Mr MILAN MARTIN CVIKL, MEMBER OF THE COURT PRESENTSTHE ECA'S WORK IN SLOVENIABy the Private O� ce of Mr Milan Martin CVIKL

Presentation of the SR 22/2012: Do the European Integration Fund and European Refugee Fund contribute e¤ ectively to the integration of the third-country nationals?

Mr Milan Martin Cvikl at the Ministry of Interior

10

Lectures at the universities of Maribor and Ljubljana

In the last two months Mr. Cvikl held two lectures at Slovene universities. The subject was a general introduction to the Court of Auditors which included details of the mission, role, tasks and products of the Court and the role in the context of the European Union. Around 130 students, postgraduates and undergraduates in the ¹ elds of accounting, audit, banking and ¹ nance attended lectures at Maribor University and Ljubljana University. The lectures emphasised our mission and tasks, inter alia, to safeguard the ¹ nancial interests of the citizens of the European Union by verifying the reliability of accounts and legality and regularity of the transactions underlying the accounts. Also the Court promotes sound ¹ nancial management by making recommendations to diª erent stakeholders managing the EU funds.

In addition to presenting the cycle of audit work, the standards and legislation the Court follows to prepare the Declaration d’assurance (DAS) were explained as well. Mr Cvikl also spoke about the work and traineeship opportunities available at the Court. The audience gave much positive feedback. As a result we plan to continue with these lectures on an annual basis.

Presentation of AR 2011 in the National Council and meeting with President

In line with letter and spirit of Protocol 1 to the Lisbon Treaty the Court’s Annual Report is presented to as broad range of public stakeholders in Slovenia as possible. In February 2013 Mr Cvikl presented the Annual Report 2011 to the Members of the Slovene National Council.

According to the Constitution of the Republic of Slovenia the National Council is the representative body for social, economic, professional and local interests. It may exercise, among other responsibilities, the power of veto over laws. This requires that the National Assembly decides again on a law prior to its promulgation. It was therefore important to inform National Council about our ¹ ndings to enable them to be proactive when it comes to the EU budget matters. The National Council representatives raised a number of questions. They were about general EU issues, on VAT collection, on the remuneration of EU o� cials and the response of EU institutions to ¹ nancial crisis. There were also questions about practical issues on the funding of projects by EU funds, there were concerns about the long time gap between initiating a project and actually receiving EU funds and there were concerns about projects where the bene¹ ciaries were facing liquidity pressures.

The discussion con¹ rmed that the Members of National Council are not only interested in the EU matters but are, as representatives of local interests, employers, craftsmen, employees and other segments of society, actually closely involved with projects co-¹ nanced by EU funds.

Mr Cvikl also had a separate meeting with newly appointed President of National Council, Mr Bervar providing him with information on the Court, the mission and the importance of our work. Both emphasised that they would like to maintain and further develop the excellent relationship between Court and National Council of Slovenia.

Presentation of AR 2011 to Slovene Government stakeholders

Another event took place at the Centre of Excellence in Finance, which was established by the Government of Slovenia in cooperation with regional ministries of ¹ nances and the IMF, World Bank and others in 2001 following an earlier initiative by Mr Cvikl. In a meeting the AR 2011 was presented to several representatives from diª erent ministries and agencies managing or supervising the EU funds in Slovenia. The participants were professionals in the ¹ eld and discussion and exchange of experience and views was very interesting and bene¹ cial.

Presentation of AR 2011 in the National Council and meeting with President

MR MILAN MARTIN CVIKL, MEMBER OF THE COURT PRESENTSTHE ECA'S WORK IN SLOVENIA

11

The study “Growth-Enhancing Expenditure in EU Cohesion Spending from 2007 to 2013”, which aims at identifying the investment share of regional expenditure and its contribution to long-run growth, was introduced by Dr. Harald Noack and presented by Ph. D. Florian Misch, Deputy head of research on company taxation and public finance from the Centre for European Economic Research (ZEW).

Dr. Harald Noack invited Ph. D. Florian Mischer to present this study which was considered of particular interest because of the approach applied by the ZEW.

While the ECA’s financial audit follows a traditional approach, and its performance audit is oriented to the three “E’s” (economy, efficiency, effectiveness), this study had raised Dr. Noack’s interest because it "approaches the evaluation of regional spending from a new perspective which is complementary to existing ones. It develops a classification which aims at identifying the investment share or regional expenditure and its contribution to long-run growth”.

Ph. D. Florian Mischer explained that the study had been commissioned by the German Ministry of Finance in the political context of the budget negotiations from a German perspective. It was undertaken in August 2012 and was completed within few weeks with the contribution of five people. The study's conclusions were rather pessimistic about the effects of the EU Regional Policy.

ZEW is not part of the Regional Policy “evaluation” industry and was itself subject to criticism. In particular, the European Commission did not agree with the results of the study having been divulged in the German paper FAZ (Frankfurter Allgemeine Zeitung).

By value, Cohesion Policy is the second largest spending category in the EU budget. Altogether, its three main funds, namely the European Regional Development Fund (ERDF), the European Social Fund (ESF) and the Cohesion Fund (CF), account for approximately 38% of the EU budget in the current programming period (2007 – 2013).

One of the central objectives of EU Cohesion Policy is to offset economic, social and territorial disparities across Member States.

GROWTH‐ENHANCING EXPENDITURE IN EU COHESION SPENDINGFROM 2007 TO 2013

A study presented on 9 April 2013 by the Centre for European Economic Research (ZEW) in Mannheim, in the framework of an ECA’s Chamber II seminar organised by Dr. Harald NOACK, Member of the Court

By Rosmarie Carotti

From left to right: Mr Gabriele Cipriani, Director of Chamber II; Mr Lazaros S. Lazarou, Member of the Court; Dr. Harald Noack, Member of the Court; Ph. D. Florian Misch, Centre for European Economic Research (ZEW)

12

The ZEW study

The ZEW study focused exclusively on the long-run growth effects, and did not consider any other benefits. Up to 63% of cohesion spending showed to have no growth effects, although it is important to note that the study focuses primarily on ERDF and CF expenditure, with only marginal coverage of the Social Fund.

ZEW proposed a new methodology. In order to come up with a workable definition of the investment share, it made use of the fact that it would be misleading to equate capital expenditure with growth-enhancing expenditure. Public spending is neither a necessary nor a sufficient condition for impact on growth. ZEW, therefore, additionally developed a classification which assigned projects to different categories.

As ZEW based its classification on insights from empirical growth literature, an element of arbitrariness was unavoidable. In order to account for this fact, a distinction was made between “optimistic” and “pessimistic” scenarios.

A further difficulty resulted from the fact that EU Cohesion Policy funds a plethora of different types of projects in different areas with different types of beneficiaries. In addition project information was poor and lacked a common standard.

ZEW made use of detailed project lists from several regions as its central data source. Very heterogeneous regions and countries with respect to wealth and regional policy instruments were included in the sample. For the purpose of the analysis, 3 600 projects from the financial framework 2007 – 20013 were chosen and categorised.

The conclusion of the ZEW was the following: “ In budgetary debates, EU Cohesion Policy often appears sacrosanct as it, allegedly, is indispensable for stimulating long-run growth. While academic research has already expressed doubts about this view, our analysis provides further evidence along these lines”.

According to the ZEW, conceptually, there are three preconditions for growth effects:

1. Public spending must have productive effects;

2. Productive effects must exceed costs;

3. Consideration of O-ring theory (tasks of production must be executed proficiently together in order for any of them to be of high value).

ZEW applied a combination of micro- and macro-evaluation (but did not estimate growth effects statistically) and made use of secondary information based on academic literature. It also assigned each project type growth effects based on the assumption of whether the project fulfilled preconditions 1 and 2.

There was an analysis of public goods versus private goods and the description of a pessimistic and optimistic scenario was meant to reflect the uncertainty of the information.

ZEW considered the data of the DG Regio project database, a centralised database of major projects, as not being representative. For the budgetary data, it considered the level of disaggregation too low or the sectoral classification did not match the one of the ZEW. For the purpose of its study, the best suited data source was therefore the list of beneficiaries, but unfortunately the project-level information is not standardized. It differs significantly not only when compared between countries,

GROWTH‐ENHANCING EXPENDITURE IN EU COHESION SPENDING FROM 2007 TO 2013

13

but also within regions of the same country. In the opinion of the ZEW, the reason is that DG Regio does not provide a unified template with unified criteria and quality standards to compile these lists. For ZEW, transparency about projects is absolutely critical.

At the end of the presentation, Dr. Noack opened the general debate. He referred to the Lisbon strategy by which the European Commission and the Member States want to develop Europe as the most competitive area globally. In the end, competition means to reach economic results - to reach growth.

Growth is not everything, but without growth Europe will not reach the Lisbon objective. Without growth, money may be spent as a subsidy but will not contribute to reaching the objective in the Lisbon strategy.

A wide range of issues was discussed in the general debate. Assumptions are critical to results, and some assumptions made by ZEW were put in doubt.

In connection with the result of the study that the Regional Policy had not contributed towards modernisation of administration, the question was raised if this was actually the role Regional Policy.

ZEW had concluded that microevaluation of impact for infrastructure projects was not possible. How was this to be understood, as the Commission’s answer to the financial crisis in the European economic recovery programme is the construction of large infrastructure.

It was identified that the ZEW study was more like a mapping of a project; the evaluation of long-run growth was ex ante and not ex post. The question was raised whether Cohesion Policy spending should apply to wealthier regions.

It is clear, the work of the ECA and the ZEW study derive from different needs. ECA’s performance audit aims at improving the management of EU funds; the ZEW study aims at giving the political leaders, the political stakeholders, the basis for decisions about the appropriate allocation of public spending.

To conclude with the words of Dr. Noack “We are living in a world which needs both models: the management side and the political side. In that respect, to work and think in a complementary way is a good idea.”

GROWTH‐ENHANCING EXPENDITURE IN EU COHESION SPENDING FROM 2007 TO 2013

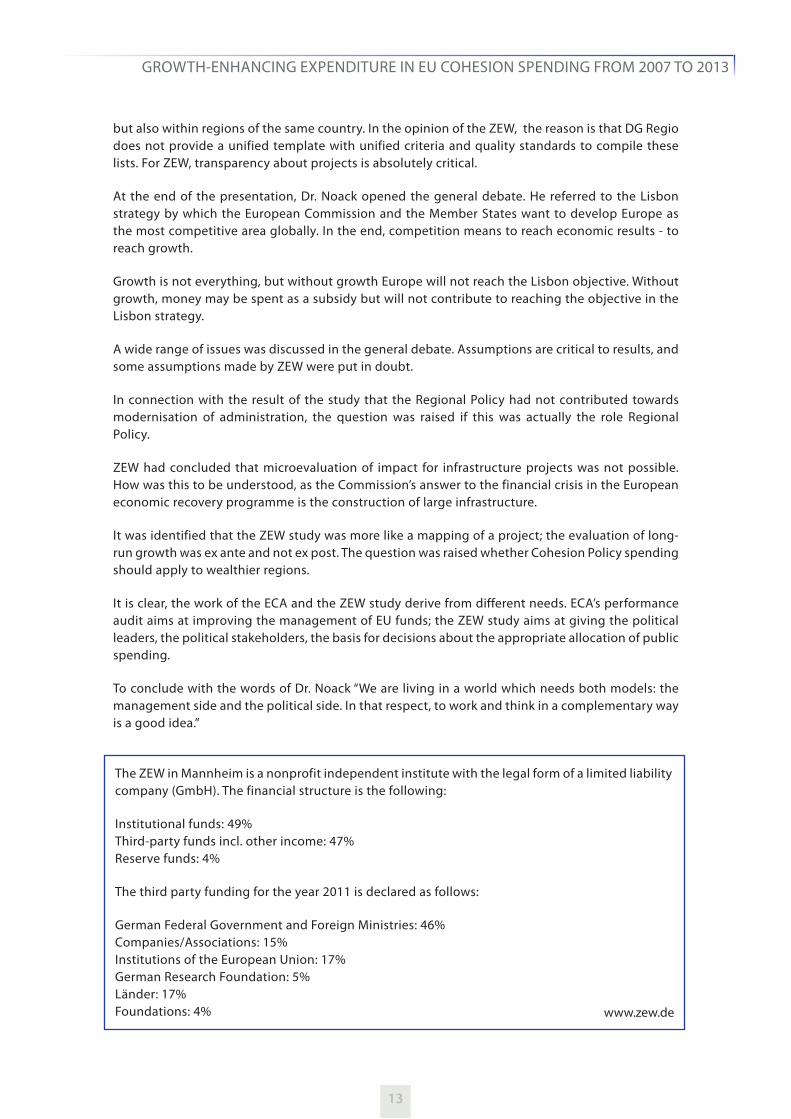

The ZEW in Mannheim is a nonprofit independent institute with the legal form of a limited liability company (GmbH). The financial structure is the following:

Institutional funds: 49%Third-party funds incl. other income: 47%Reserve funds: 4%

The third party funding for the year 2011 is declared as follows:

German Federal Government and Foreign Ministries: 46%Companies/Associations: 15%Institutions of the European Union: 17%German Research Foundation: 5%Länder: 17%Foundations: 4% www.zew.de

14

MR LADISLAV BALKO, MEMBER OF THE ECA, REPRESENTED THE ECA AT THE SEMINAR AND FESTIVE PROGRAMME MARKING THE 20TH ANNIVERSARY OF THE SUPREME AUDIT OFFICE OF THE SLOVAK REPUBLICBy Branislav URBANIČ, Head of Private O� ce of Mr Ladislav BALKO

With the coming into existence of the independent Slovak Republic on 1 January 1993, among other State institutions and bodies, the Supreme Audit Office of the Slovak Republic (SAO SR) was established. Its organisation, role and powers were in detail regulated in one of the very first laws of the new State – by the Act No. 39/1993 Coll..

Twenty years later, on 4 April 2013, the member of the European Court of Auditors from the EU Member State Slovak Republic, on behalf of the President of the Court Mr Vítor Caldeira, represented the Court at the seminar and festive programme held in Bratislava to mark the 20th Anniversary of the establishment of SAO SR.

The morning part of the event was devoted to a seminar on “The role of supreme audit institutions in the environment of changing socio-economic conditions”, which was introduced by the SAO SR President Mr Ján Jasovský and officially opened by the Speaker of the National Council of the Slovak Republic (Parliament) Mr Pavol Paška. Further prominent speakers included the Prime Minister of the Slovak Republic Mr Robert Fico and several highest representatives of European partner SAIs. Many interesting ideas resounded, for example that the SAIs should use the powers of their mandates wisely and that performance audits are an efficient tool to support change1, or that there is a certain harmony between the level of democracy and the level of public audit in a society2. Before closing the seminar, the SAO SR President Mr Ján Jasovský awarded a SAO SR medal to the representatives of the European partner SAIs, including the ECA.

The afternoon part consisted of a festive programme with addresses by further prominent guests, including the President of the Slovak Republic Mr Ivan Gašparovič, and further highest representatives of European partner SAIs and their international organisations, including the ECA. In his address, Mr Balko congratulated the current as well as the former Presidents of SAO SR and its entire staff to this important anniversary. He acknowledged the many achievements which the SAO SR made during the 20 years, and appreciated the excellent cooperation between the SAO SR and the ECA. To mark this acknowledgement and appreciation, Mr Balko presented Court medals both to the SAO SR as institution and to Mr Jasovský as its President.

1 Mrs Giedrė Švedienė, Auditor General of the Republic of Lithuania2 Mr Kurt Grüter, President of the Swiss Federal Audit O� ce

An interview on the occasion of the 20th anniversary of SAO SR was given by SAO SR President Mr Ján Jasovský. The ECA Journal is pleased to publish it.

Mr Balko presents Court medals both to the SAO SR as institution and to Mr Jasovský as its President

15

SAO SR President Mr Ján Jasovský presents a SAO SR medal to the Speaker of Parliament Mr Pavol Paška

The Supreme Audit Office of the Slovak Republic (SAO SR) is relatively young if compared to other Supreme Audit Institutions in Europe or world - it just had celebrated its twentieth anniversary.

Twenty years of an audit institution can be taken as relatively short time. Those years were unbelievably fast and dynamic times in the Slovak society. The important contribution to this era was the evolution of the SAO SR position and its rights that allow SAO SR act as an independent organ of audit and control in the entire field of public finance. Significant widening of the SAO SR rights occurred mainly in the last decade. But I can say with a little bit of grain of salt that there are even younger supreme audit institutions in the world. Our historical context is not only the last twenty years. The history of audit and financial control exceeds 250 years in Slovakia.

Could you shortly mention the important milestones in the twenty years of the SAO SR history?

SAO SR is an independent state organ that duly fulfils its position anchored in the Constitution of the Slovak Republic and international treaties. In its twenty years, SAO SR evolved gradually reflecting the most significant changes that happened in the society like the Slovakia’s accession to the European Union or the Slovak economy and public administration decentralisation. And in the last years, it was the effects of the global crisis in economy and finance. Every and each of the mentioned events meant new challenge for the SAO SR and SAO SR had to react by elevating the quality of its work and its employees. The accession to the European Union brought a duty to establish an organisational unit for audit of the EU funds use and adaptation of its audit activities methodology to the European standards as well as harmonisation of the SAO SR with other audit institutions. The public administration decentralisation in Slovakia and widening the SAO SR audit mandate to all public funds (including regional) meant complete reconstruction of the SAO SR from within and use of rationalisation, organisational, economic and motivation tools with a goal to manage its new position.

What comparison of the SAO SR work is the most visible when taking into account the situation in 1993 when the Slovak Republic was created and today?

The environment we live in changes rapidly and is more and more demanding in quality and transparency; today the access to information is extraordinary, almost unimaginable in time the SAO SR was established. At our web site, we, almost in real time, publish all the information and reports on audit results. The impulses and suggestions about the economic activities of the public entities come daily. Here it is where I see one important activity by the audit and control institution: to supplement the public with unbiased information on the results of the audited entities activities even if the information is not pleasant to the given organisation. Such situation was unimaginable in the time of the SAO SR establishment.

The SAO SR managed to build local respect and esteem not only by its mandate derived from the Constitution and Act on SAO SR but more by its independent and expert approach.

The important task of a supreme audit institution is transfer of good practice among individual entities of the public administration. Our auditors are confronted by varied approaches to an

TWENTY YEARS OF INDEPENDENT AUDIT IN THE SLOVAK REPUBLIC

Interview with the Supreme Audit O� ce of theSlovak Republic President Ján JASOVSKÝ

16

organisation management, various ways how to manage the property or financial means and they are able to assess that in adequate and expert manner. They are those who can offer the best solutions approved by practice, they can advice and be a partner to the audited subject. Our ultimate task is not to find mistakes or shortcomings in law observation although it is sometimes expected. There are many activities that on one hand observe the law (or they do not break it) but it doesn’t mean that they are sufficiently effective, economic and achieve the needed efficiency. The value is also represented by giving the correct information and conclusions from our audits in time and in the extent most possible.

The international esteem SAO SR enjoys is great despite its short existence in the context of other supreme audit offices.

We are pleased that during the recent celebrations organised at the occasion of the SAO SR 20th anniversary many our partners from abroad took part at our expert seminar The role of the supreme audit institutions in the environment of changing socio-economic conditions. Among them it was also Ladislav Balko, the Member of the European Court of Auditors representing the Slovak Republic. That had pleased us. If it wasn’t for the chance to tap into the deep knowledge and rich experience from all around the world that is concentrated in the working groups, seminars, INTOSAI, EUROSAI

and Contact Committee of the Heads of the Supreme Audit Offices of the EU Member states documents we wouldn’t achieve such results.

Not even then when, at our beginnings, our colleagues from the supreme audit institutions did offered unselfish help. We have received lot of knowledge and experience form our colleagues from Norway, Hungary, Austria, Czech Republic, Great Britain, Sweden, Denmark, Estonia, Slovenia or Poland. They have sent us their experts who thought us performance and finance audit. Some supreme audit institutions even allowed for a secondment at their home institutions. The Polish and Russian colleagues offered us their knowledge on possibilities of the information systems. I appreciate a lot the chance to cooperate with the excellent experts from Switzerland especially in the field of the audit on information systems and their safety.

How would you evaluate the cooperation with the European Court of Auditors?

The cooperation with European Court of Auditors (ECA) inherently had belonged to our international activities. The cooperation of the SOA SR and ECA had already begun in 2001 when the SAO SR mandate was widened to audit the EU funds and other means from abroad. The SAO SR have been gaining the experience from the ECA methods during the ECA audit missions to Slovakia when SAO SR accompanied the ECA audit teams and, on the other hand, the SAO SR auditors passed onto the ECA auditors their experience from the national audit environment. The excellent cooperation with Mr. Balko is on very friendly base and I value that a lot.

SAO SR has to have quality employees as the future lies chiefly in the performance audit.

We can be pleased that the quality of our activities stems from the internationally accepted standards and quality management systems. Just their knowledge, their incorporation into the internal norms represents the quality of the future activities. Incorporation of the new harmonised audit standards INTOSAI is foreseen for this year; also the CAF – The Common Assessment Framework – underwent its improvement. Daily we are confronted by increasingly faster development of the new norms, procedures, techniques and methods. No value can be created without bettering the processes of the internal activities, application of the new progressive knowledge, and, of course, without elevating the quality of the SAO SR or those who create the SAO SR results, our own employees.

ECA Member Mr Ladislav Balko speaks during the SAO SR festive programme

TWENTY YEARS OF INDEPENDENT AUDIT IN THE SLOVAK REPUBLIC

17

The future of any company or organisation is tied with its flexibility and ability to survive in ever changing environment. The appraisal of our present employees and those who were with the SAO SR in previous years was also the part of our meeting organised on the occasion of the 20th anniversary celebration.

At the present time the SAO SR celebrates, what lies for it in the future?

To increase the quality, to assess the preformed audit activities and to evaluate and measure the performance of the supreme audit institutions are the most important topics the whole international audit institutions community is engaged in today. That, I think, also foresees our future – future that is targeting the activities improvement based on permanent and continuous assessment. The pressure to discharge performance audits is already coming from the external environment for several years. The citizens, non-profit organisations, expert associations – they do not know to use the right terminology but we can see in their demands endeavour to look not only for the legality of conduct but also if the conduct or action was necessary at all and if it brought effect, if any. Our chief perspective is to look continuously for ways to improve the audit effect or its value. There is lot of possibilities how this value can be created. It could be done extensive way through the number of audited entities. It also can be done by more effective assessment of the issues where the audit contribution is high while taking into account the amount of the resources used and their anticipated low efficiency.

International guests at the SAO SR seminar

TWENTY YEARS OF INDEPENDENT AUDIT IN THE SLOVAK REPUBLIC

18

The research carried out in the excellent new publication “The European Court of Auditors in the multi-level control system” is, without doubt, unique in the field of European accounting and administrative law. The work describes, in summary form, the European Court of Auditors’ institutional structure, composition, organisation, procedures and audit methodology.

The author begins with a fundamental insight by a renowned expert on Italian administrative law, Professor Massimo Severo Giannini: “When an organisation manages public funds, (…) it is in everyone’s interest to know how such funds are used: this is the logic underpinning the oversight of public organisations”.

Taking this argument as a basis, the author embarks upon his own research, starting with the creation of the European Court of Auditors in 1975 and its operational beginnings in October 1977 in Luxembourg, where it is currently based. However, it was only with the Treaty of Maastricht in 1992 that the Court acquired EU-institution status, when a legislative requirement was introduced to publish an annual statement concerning the reliability and regularity of the Union’s accounts. The Treaty of Amsterdam extended the Court’s audit remit to external policy and joint security, justice and internal affairs. Of particular significance was the power to call upon the Court of Justice of the European Communities to safeguard its prerogatives vis-à-vis the other EU institutions. The Treaty of Nice and the European Constitution later established the composition of the Court, confirming its powers as laid down in the previous treaties.

The author must certainly be credited with covering the Court’s composition and general operating rules in a single, manageable volume and in a sequential, thorough and coherent manner.

From a cognitive perspective, the section dealing with the Court’s structure and organisation is also important. However, I believe particular emphasis should be placed on the pages devoted to the Court’s scrutiny of the financial legitimacy of the EU budget: the institution’s role is to improve the EU’s financial management and report to the European Parliament on the EU’s use of public funds.

The European Court of Auditors was created with this goal in mind, and the nature of its work has evolved with the extension of the European Parliament’s powers of budgetary oversight and with the full funding of the budget under the “Own Resources” system.

The author’s introductory remarks on the subject of EU budgetary control are important and significant. The EU’s total budget is approximately € 120 billion, or about 1% of the gross national income (GNI) of the 27 Member States: a modest figure when compared with national budgets. However, for some Member States, EU funds play an important role in funding public activities and the total amount is near or equivalent to some Member States’ GNI. EU revenue comes mainly from Member State contributions based on GNI, and on an amount related to the VAT collected at national level. Customs duties and agricultural levies (known as traditional own resources) also

BOOK REVIEW: “THE EUROPEAN COURT OF AUDITORS IN THE MULTI-LEVEL CONTROL SYSTEM” BY DOMENICO SICLARIBy Andrea Monorchio

Domenico Siclari is Director of the “G. Silvestri” Research Center in legal / economic and social sciences University for Foreigners "Dante Alighieri" REGGIO CALABRIA. He is Professor of Public Law and Researcher of Public Law and Administrative Law at the same University.

Andrea Monorchio is Professor of State Accounting and a respected Italian economist. He was General Accountant of Italy

19

account for a significant proportion of revenue. The make-up of the budget has changed over the years: today, most expenditure is on agriculture a nd cohesion policies.

Against a distressing backdrop of public disregard for systems of oversight, the book devotes in-depth and incisive attention to what is a fundamental part of the Court’s work. The author singles out the special features of the scrutiny of EU public expenditure which differ considerably from the work of the Court’s national counterparts.

Rather than favouring centralised bureaucratic operating structures, the audit model depicted in the book opts for working methods characterised by greater flexibility in terms of decision-making and operational responsibilities.

To ensure that EU taxpayers’ money is put to the best possible use (and so guarantees that the public derives maximum benefit from the way its money is spent), the Court is empowered to audit any person or organisation that manages EU funds: to this end, the author notes that the Court often carries out targeted, on-the-spot checks, the findings of which are set out in written reports that are sent to the Commission and Member State governments.

For this purpose, the Court examines all EU revenue and expenditure, as well as that of the EU’s various bodies, from the perspective of their legality and regularity, and ensures that the financial management has been sound. It produces an annual Statement of Assurance concerning the accounts (known by its French acronym “DAS”), but can publish special reports on specific topics at any time. In the Statement of Assurance, as well as reporting on the legality and regularity of the EU’s accounts, the Court also evaluates the economy, efficiency and effectiveness of EU expenditure: Was the minimum amount of funding used to achieve a given objective? Were resources put to the best possible use? Were pre-established objectives achieved? This is known as the audit of sound financial management.

The Court is consulted about proposals for measures to combat tax fraud and financial irregularities, and also assists the European Parliament and the Council in overseeing the implementation of the EU budget. Although the Court has no judicial powers and its opinions are not binding, this in no way detracts from the vital importance of its work.

Accounting policies and standards are based on the standards established by INTOSAI (the international organisation of supreme audit institutions) and IFAC (the international federation of accountants). When, either as a result of its own audit work or information provided by third parties, the Court learns of a potential case of fraud or corruption, it immediately passes the information on to the European Anti-Fraud Office (OLAF), which is responsible for conducting detailed investigations and taking appropriate action.

The Court has no judicial powers of its own. If its auditors discover cases of fraud or irregularities, it informs OLAF, the European Anti-Fraud Office.

One of the Court’s fundamental tasks is to present the European Parliament and the Council with an Annual Report on the previous financial year (known as the annual discharge”). The Parliament examines the Court’s report in detail before deciding whether or not to approve the Commission’s management of the budget.

The Court also issues opinions on the EU’s financial legislation and on anti-fraud regulations.The author has produced a comprehensive and exhaustive publication, which concludes with

a description of the ECA’s latest tasks and new areas of responsibility, and proposes it be given new judicial powers to complement its traditional audit activities.

The author should be congratulated on an admirable study. The result is excellent: his work will be useful not only for academic purposes but also for anyone who wishes to learn more about auditing at EU level.

TWENTY YEARS OF INDEPENDENT AUDIT IN THE SLOVAK REPUBLIC

20

Les commémorations du cinquantenaire du Traité de l’Élysée ont été une occasion d’explorer les relations entre la France et l’Allemagne dans une perspective européenne. Deux économistes de renom, Alfred Steinherr et Guillaume Duval, ont présenté les paysages économiques français et allemand et se sont interrogés sur leur valeur comme modèles européens. Frank Engel député européen a ouvert la discussion et participé au débat qui a été modéré par Christophe Langenbrink journaliste au quotidien Luxemburger Wort.

CINQUANTIÈME ANNIVERSAIRE DU TRAITÉ DE L’ÉLYSÉEFRANCE / ALLEMAGNE : IDENTITÉS OU MODÈLES ÉCONOMIQUES ?

Intervenants

Débat organisé par l’Institut Pierre Werner et l’Institut la Banque européenne d’Investissement

21 mars 2013

M. Frank Engel, député européen, chef de la délégation luxembourgeoise du Parti populaire européen

Guillaume Duval, rédacteur en chef de la revue Alternatives économiques

Alfred Steinherr, ancien chef économiste à la BEI, professeur à la Sacred Heart University (Luxembourg)

By Rosmarie Carotti

Loin d’être une célébration du cinquantenaire de l’amitié franco-allemande, le débat était une confrontation très critique avec la politique allemande et son modèle économique et de gestion des deniers publiques.

Si jusqu’ à récemment on avait l’impression au Luxembourg, que pour le cinquantenaire il y aurait en Allemagne et en France une entente sur la politique et l’économie européenne, cela ne semble plus être le cas aujourd’hui, affirme M. Engel. Il y aurait en France et en Allemagne une prise de conscience que les deux pays ne sont pas si similaires que la célébration des 50 ans d’amitié ne voudrait le laisser croire. Il ne s’agit pas d’un divorce entre France et Allemagne mais d’une divergence croissante d’opinion sur les choix, par exemple sur la nécessité d’une politique des changes pour l’euro. Donc, pas de convergence des modèles à l’heure actuelle mais plutôt affirmation de modèles qui ne sont pas les mêmes.

M. Duval insiste sur ce qui pourrait se passer si on cherchait à faire en sorte que tous les pays ressemblaient à l’Allemagne au sein de l’Europe et adoptaient des mesures du type de celles choisies dans le cadre des réformes menées par M. Schroeder.

La France est un pays qui va mal et qui a pris comme référence le modèle allemand à plusieurs reprises. Dans le passé cette référence avait le sens exactement contraire de celui d’ aujourd’hui. On préconisait d’aller dans le sens d’un modèle allemand qui laissait plus de place aux marchés financiers, à un pouvoir des salariés très important dans les entreprises, à des accords de branches très poussés. La référence au modèle allemand servait à l’époque à contrer les tentations très fortes de libéralisation du marché du travail dans les débats publics français.

Dans le débat actuel, en France mais aussi en Europe, la référence au modèle allemand a pris exactement le sens contraire. Elle est censée expliquer les raisons pour lesquelles il faudrait aujourd’hui libéraliser le marché du travail, à baisser les dépenses publiques, diminuer les impôts etc.. L’industrie allemande serait presque la seule à résister en Europe dans la crise actuelle grâce aux réformes Schroeder.

Cette thèse est fausse, selon M. Duval. Ce n’est pas grâce aux réformes Schroeder que l’Allemagne va mieux, c’est plutôt malgré les réformes Schroeder. Schroeder a réduit la cohésion sociale du pays et cela se payera dans le futur. Il a trop limité les dépenses et l’investissement publics. L’Allemagne est le seul pays européen de l’OCDE qui soit depuis les années 2000 en situation d’investissements publics faibles au point de ne pas compenser l’usure existante.

21

Si l’Allemagne s’en sort mieux que les autres aujourd’hui c’est qu’elle bénéficie d’une démographie très négative. La France, par contre, a une démographie relativement dynamique, qui engendre beaucoup de dépenses publiques et privées supplémentaires. Cela a joué de manière importante, en particulier sur l’immobilier. Sous la pression démographique la France a connu une bulle immobilière et une hausse importante des prix immobiliers, en Allemagne les prix de l’immobilier sont restés stables.

Deuxièmement, l’économie allemande a été la grande gagnante de la chute du mur de Berlin parce que le pays a su réintégrer très rapidement dans son système productif les pays d’Europe centrale et orientale où le coût du travail est cinq à dix fois inférieur à celui de la France.

En troisième lieu, l’Allemagne bénéficie d’une spécialisation très particulière dans le secteur des machines et des biens d’équipements.

L’économie allemande a profité de la crise car le marché du travail allemand a été beaucoup moins flexible qu’en France. Les taux d’intérêts ont baissé en Allemagne, ce qui a permis à l’État d’économiser sur la dette publique. Ce qui est plus important encore, c’est que la crise a été aussi une aubaine pour les acteurs privés. Ce qui avait tué l’industrie française, espagnole, portugaise etc. dans les 10 premières années de l’euro c’était la montée de l’euro par rapport au dollar. La seule bonne nouvelle de la crise c’est que l’euro a baissé. Grâce à la baisse de l’euro par rapport au dollar l’Allemagne a réussi à compenser en gain d’exportations hors de la zone euro ce qu’elle a perdu sur la zone euro du fait de la crise. Sur tous ces aspects l’Allemagne a été gagnante de la crise des autres pays de la zone euro. Pour cela la pression est très faible en Allemagne pour trouver une vraie solution à la crise de la zone euro.

Pour conclure, M. Duval cite Joschka Fischer ancien-ministre des affaires étrangères « Il serait à la fois tragique et ironique que l’Allemagne réunifiée provoque pour la troisième fois par les moyens pacifiques cette fois avec les meilleurs intentions du monde, la ruine de l’ordre européen ».

M. Steinherr pense qu’on ne devrait pas chercher un modèle chez le voisin et que, si on veut faire une comparaison des systèmes, il faut une vue à long terme car les systèmes se développent sur de très longues périodes. À un certain moment, par exemple dans les années 60 et 80, l’économie française avait fonctionné mieux que l’économie allemande, si l’on prend comme indicateur le PIB par tête. Ce n’est que dans les années 90, grâce à l’unification allemande, que la croissance était supérieure en Allemagne. De 2000 à 2007, jusqu’au début de la crise, elle était supérieure en France et depuis 2007, elle est supérieure en Allemagne.

C’est le long terme qui est important. La spécialisation allemande est de longue date et M. Steinherr est de l’avis que l’Allemagne profite encore de sa période glorieuse autour de 1900 dans la recherche appliquée et fondamentale. L’Allemagne a énormément perdu après la deuxième guerre mondiale mais a su perfectionner les technologies dont elle disposait. Le pays réalise chaque année des surplus d’exportation. On peut utiliser l’épargne nationale de trois façons : pour l’investissement domestique, pour le financement du déficit du gouvernement ou pour les investissements étrangers. Or le surplus est un investissement net à l’étranger. Chaque année l’Allemagne consomme moins et donne le reste au monde, les Américains font le contraire et s’endettent comme beaucoup de pays européens aimeraient en faire autant.

L’investissement national, en Allemagne n’est que de 12% en moyenne des dernières années. Cela est très peu pour préparer l’avenir. Les français épargnent plus que les allemands. La différence est que le secteur public absorbe moins qu’en France et que les entreprises allemandes ont été plus rentables, ce qui leur a permis d’épargner plus que les entreprises françaises.

Pour résoudre la crise actuelle et pour rétablir la confiance dans le système, M. Steinherr propose une déflation dans les pays du nord qui aiderait à baisser la valeur réelle de la dette publique et va même jusqu’à proposer la sortie de l’Allemagne de l’Europe.

CINQUANTIÈME ANNIVERSAIRE DU TRAITÉ DE L’ÉLYSÉE

22

FOCUSEA

Autumn 2011 Cyprus public sector lost access to the ¹ nancial markets

24/12/2011 Emergency loan agreement with Russian Federation to cover the budget de¹ cit and to re-¹ nance maturing debt, amounting € 2.5 bn (5 years maturity)

21/2/2012 Eurogroup decision for the private sector involvement (PSI) in the the write down of sovereign debt of Greece - loss of € 4.5 bn for Cyprus banks (mainly for the two largest ones)

25/6/2012 Request of a bailout from the European Financial Stability Facility/ European Stability Mechanism, citing di� culties in supporting of the Cyprus banking sector

30/11/2012 Initial agreement between Troika and the previous Cyprus Government (memorandum of understanding on speci¹ c economic policy conditionality) on the bailout terms

2/2/2013

Submission from the private ¹ rm appointed by the Steering Committee of the report establishing the bank capitalisation needs (worst case scenario: EUR 10,1 bn, resulting together with the budget de¹ cits and the maturing debt re-¹ nance to a funding requirement of around € 18 bn - around 100% of the country's GDP)

24/2/2013 Election of Mr Nicos Anastasiades as new President of the Republic of Cyprus, taking o� ce on 1/3/2013

16/3/2013Eurogroup decision for the provision of a ¹ nancial assistance up to € 10 bn from the EU-IMF to Cyprus, in combination with a one-oª bank deposit levy of 6.7% for deposits up to €100 000 and 9.9% for higher deposits (estimated levy of € 5.8 bn)

19/3/2013 Rejection of the deal by the Cyprus House of Representatives

22/3/2013 Approval by the Cyprus House of Representatives of a plan to restructure Laiki Bank (second largest bank), by creating a "bad " and a "good" bank.

25/3/2013

Eurogroup decision for the provision of a ¹ nancial assistance up to € 10 bn from the EU-IMF to Cyprus, by preserving all deposits up to € 100 000, in combination with shutting down Laiki Bank (bad bank) and levying all its uninsured deposits, after transferring all of its remaining good assets and insured deposits below € 100 000 to Bank of Cyprus (largest bank), but levying, as well, the given percentage of uninsured deposits in Bank of Cyprus needed, in order to reach the aim of 9% tier 1 capital ratio for the new bank to be formed.

2/4/2013 Provisional agreement between Troika and the new Cyprus Government (memorandum of understanding on speci¹ c economic policy conditionality) on the bailout and the loan facility terms

8/4/2013 Agreement of the Russian Federation to restructure the loan of € 2,5 bn provided to the Republic of Cyprus on 24/12/2011

BRIEF SUMMARY OF THE FINANCIAL CRISIS IN CYPRUS LEADING UP TO THE RECENT EVENTS

(All developments until 8/4/2013)

By Andreas ANTONIADES, Private O� ce Attaché

23

A BRIEF LIST OF MISUSED ENGLISH TERMINOLOGY IN EU PUBLICATIONSBy Jeremy Gardner, translator

Introduction

Over the years, the European institutions have developed a vocabulary that differs from that of any recognised form of English. It includes words that do not exist or are relatively unknown to native English speakers outside the EU institutions and often even to standard spellcheckers/grammar checkers (‘planification’, ‘to precise’ or ‘telematics’ for example) and words that are used with a meaning, often derived from other languages, that is not usually found in English dictionaries (‘coherent’ being a case in point). Some words are used with more or less the correct meaning, but in contexts where they would not be used by native speakers (‘homogenise’, for example). Finally, there is a group of words, many relating to modern technology, where users (often even native speakers) ‘prefer’ a local term (often an English word or acronym) to the one normally used in English-speaking countries, which they may not actually know, even passively (‘GPS’ or ‘navigator’ for ‘satnav’, ‘SMS’ for ‘text’, ‘to send an SMS to’ for ‘to text’, ‘GSM’ or even ‘Handy’ for ‘mobile’ or ‘cell phone’, internet ‘key’, ‘pen’ or ‘stick’ for ‘dongle’, ‘recharge’ for ‘top-up/top up’ etc). The words in this last list have not been included because they belong mostly to the spoken language.

What do we mean by English?

English is the most widely-spoken language in the world1 and is currently an official language in 88 sovereign states and territories; it therefore follows that it has many different versions and standards (British, Irish, American, Australian, Canadian, Indian, Jamaican, Singapore etc.). However, our publications should be comprehensible for their target audience, which is largely British and Irish, and should therefore follow a standard that reflects usage in the United Kingdom and Ireland. This is not a value judgment on the various varieties of English, merely recognition of the need to communicate in the language that our readers understand best. Arguments that “agent” or “externalise”, for example, are used with different meanings in the United States, Singapore or Australia miss the point, as does the view that we should accept the EU usage of, say, ‘prescription’ because it can be found with the same meaning in a handful of countries and states that have a civil law tradition, like Scotland, or historical links with France, like Quebec, the State of Louisiana and Vanuatu.

Who cares?

A common reaction to this situation is that it does not matter as, internally, we all know what ‘informatics’ are (is?), what happens if we ‘transpose’ a Directive’ or ‘go on mission’ and that, when our ‘agents’ are on a contract, they are not actually going to kill anyone2. Indeed, internally, it may often be easier to communicate with these terms than with the correct ones (it is reasonable to suppose that fewer EU officials know ‘outsource’ than ‘externalise’, for example). However, the European institutions also need to communicate with the outside world and our documents need to be translated – both tasks that are not facilitated by the use of terminology that is unknown to native speakers and either does not appear in dictionaries or is shown in them with a different meaning. Finally, it is worth remembering that, whereas EU staff should be able to understand ‘real’ English, we cannot expect the general public to be au fait with the EU variety.

‘But the Commission uses the same terminology!’

A further objection that is often put forward is that we must use the same terminology as other institutions (the Commission in particular). That is to say, if the Commission uses the verb

This is an update of the list published in the Journal in February 2012 and March 2012

24

A BRIEF LIST OF MISUSED ENGLISH TERMINOLOGY IN EU PUBLICATIONS