world-economic-and-social-survey-2003.pdf - the United ...

318

In 2002, the world economy did not recover from its slowdown of the previous year, and exhibited another weak performance. Unemployment increased in many countries. International trade lacked dynamism. Capital flows to developing countries declined owing to the difficult economic and political environment that characterized much of the year and that persisted into early 2003. As part one of the World Economic and Social Survey 2003 shows, the world economy remains some distance away from achieving the fast and sustained economic growth needed to confront poverty and other challenges. Part two of the Survey examines the effects on poverty of growth-enhancing economic policies. When Governments draw up fis- cal and monetary policies, or seek to enhance trade and agricultural productivity, or, in the case of a number of countries, make the transi- tion from a planned economy to the market, they should carefully assess the effects of these policies on the poor—especially in light of the com- mitment they have made to reduce, by the year 2015, the proportion of people living on less than a dollar a day and the proportion of those who suffer from hunger. The Survey argues that while long-term eco- nomic growth is a powerful force behind poverty reduction, it is neces- sary and possible to tailor policies in order to achieve even greater reductions. The global target of the Millennium Development Goal for the eradication of poverty is bold but achievable. At the global level, many millions of people have been rescued from poverty, in particular because of progress in the world’s most populous countries, China and India. However, the results there tend to obscure setbacks or stagnation PREFACE W O R L D E C O N O M I C A N D S O C I A L S U R V E Y 2 0 0 3 III

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of world-economic-and-social-survey-2003.pdf - the United ...

In 2002, the world economy did not recover from its slowdown

of the previous year, and exhibited another weak performance.

Unemployment increased in many countries. International trade lacked

dynamism. Capital flows to developing countries declined owing to the

difficult economic and political environment that characterized much of

the year and that persisted into early 2003. As part one of the World

Economic and Social Survey 2003 shows, the world economy remains

some distance away from achieving the fast and sustained economic

growth needed to confront poverty and other challenges.

Part two of the Survey examines the effects on poverty of

growth-enhancing economic policies. When Governments draw up fis-

cal and monetary policies, or seek to enhance trade and agricultural

productivity, or, in the case of a number of countries, make the transi-

tion from a planned economy to the market, they should carefully assess

the effects of these policies on the poor—especially in light of the com-

mitment they have made to reduce, by the year 2015, the proportion of

people living on less than a dollar a day and the proportion of those

who suffer from hunger. The Survey argues that while long-term eco-

nomic growth is a powerful force behind poverty reduction, it is neces-

sary and possible to tailor policies in order to achieve even greater

reductions.

The global target of the Millennium Development Goal for the

eradication of poverty is bold but achievable. At the global level, many

millions of people have been rescued from poverty, in particular

because of progress in the world’s most populous countries, China and

India. However, the results there tend to obscure setbacks or stagnation

PREFACE

W O R L D E C O N O M I C A N D S O C I A L S U R V E Y 2 0 0 3 III

elsewhere—for example, in many of the least developed countries, par-

ticularly in Africa, where the number of poor people is expected to rise.

Governments therefore need to pursue the reforms that will ensure sus-

tainable growth, and the international community must provide the

assistance that can enable these policies to succeed.

Indeed, in a world where economies are increasingly more inte-

grated, the importance of international cooperation cannot be overem-

phasized. The international community has forged consensus on devel-

opment priorities and actions, as defined in the outcomes of the meet-

ings in Doha, Monterrey, Mexico, and Johannesburg, South Africa, and

has pledged to move forward on the basis of shared responsibilities and

mutual commitments. This Survey is intended not just as a source of

information and analysis, but also as a spur to action. I commend it to

the widest possible audience.

W O R L D E C O N O M I C A N D S O C I A L S U R V E Y 2 0 0 3IV

KOFI A. ANNANSecretary-General

After being delayed through increasing geopolitical tensions andother economic uncertainties, faster economic growth is expected toreturn to the world economy in the second half of 2003. Some signshave been already evident in the United States of America, a countrythat once again will be instrumental in launching the global recovery.Nonetheless, the sustainability of the recovery will depend upon howfast the positive impulses that originated in the United States are spreadvia trade and investment throughout the world and are picked up andmaintained by the other economies. Part one of the World Economicand Social Survey 2003 examines the factors that have shaped therecent economic performance of the global economy and analyses theforces that will likely determine its course in the near term.

The negative effects of the past boom in equity markets and capitalspending continued to constrain economic activity in 2002 and early2003, as overcapacity in several sectors discouraged new investmentwhile growing unemployment constrained consumption. Increasinguncertainty brought about by geopolitical tensions and corporate gover-nance failures compounded the problem. Sluggish global economicgrowth, with its accompanying weak trade and reduced capital flows,resulted in depressed commodity prices and fewer resources for devel-oping countries. Growth suffered as a result, particularly in those devel-oping countries that were also facing constraints on adopting counter-cyclical policies.

The invasion of Iraq took a heavy toll on human life and economicactivity in the region. Another non-economic shock, a severe and high-ly contagious respiratory disease (severe acute respiratory syndrome(SARS)), clouded economic prospects in several countries in early 2003but appears now to have been contained. Additionally, several positivefactors remain in place to facilitate a recovery. Macroeconomic policyis supportive in several countries and interest rates continue to be lowin many developed countries while cyclical inventory adjustment willalso contribute to recovery.

It is likely, however, that the recovery’s strength will not be as pro-nounced as in past cyclical upturns. The increase in longer-term unem-ployment, for instance, will continue to contain demand for some time.Furthermore, the depreciation of the United States dollar will moderateimport demand by the United States, thus weakening a powerful stimu-lus to the world economy. Finally, this short-term economic outlook issurrounded by a number of uncertainties and risks, which are discussedfurther in part one of the Survey.

FOREWORD

W O R L D E C O N O M I C A N D S O C I A L S U R V E Y 2 0 0 3 V

Part two of the Survey examines the relationships between recenteconomic policies and poverty reduction. The commitment by MemberStates to the achievement of the Millennium Development Goals has putpoverty reduction at the top of the global agenda. MillenniumDevelopment Goal 1 is for a reduction in absolute poverty, but there isstill widespread poverty throughout the developing countries and insome of the transition economies and still considerable pockets ofpoverty even in the richest of the developed countries. Thus, all groupsof countries are trying to devise policies to eradicate poverty.

Sustained economic growth is an effective means to reduce poverty.Historical experience has shown that growth has always lifted a numberof people out of poverty. Often the income distribution within a countryhas worsened while growth has accelerated, but it is unknown for thepoor to lose ground in absolute (as compared with relative) terms dur-ing a period of long-term growth. As their incomes expand, the rich willalways demand better goods and services from the poor and will havethe ability to pay for them. The lifting of millions of human beings outof absolute poverty in China and India since their pro-growth and mar-ket-friendly reforms raised their growth rates has been one of the mostsignificant and encouraging developments in the global economy at thebeginning of the new millennium. It is to be hoped that their successwill be emulated in other regions of the world where rapid growth hasnot yet been achieved.

The Survey looks at policies that countries adopt to promotegrowth—fiscal and monetary policies, trade and agricultural policiesand the replacement of central planning by a market-based economy. Itasks whether and how they can be attuned and, where necessary, com-plemented in order to achieve even greater reductions in poverty. Therenewed national and international concern regarding poverty has led tothe collection of much better data and to greater efforts to listen to thevoices of the poor which will help policy makers in their task. PovertyReduction Strategy Papers are now required for all World Bank andInternational Monetary Fund lending to low-income countries.

Chapter IV sets the stage for the subsequent discussion by examiningin depth the growth-poverty nexus. While growth benefits the poor inincome terms, periods of growth have not always seen improvements inother indicators of poverty, such as health and educational achieve-ments. Moreover, in the short term, economic growth might affect somegroups adversely. The analysis of a policy’s effects on poverty cannot

W O R L D E C O N O M I C A N D S O C I A L S U R V E Y 2 0 0 3VI

be unidimensional and confined to a simple headcount. It must addresssuch matters as the time dimension and also the many different groupsthat can be affected, including women and vulnerable minorities,regions within a country, and urban and rural dwellers.

Chapter V looks at how monetary and fiscal policy, by achievingmacroeconomic stability, assist in ensuring growth and poverty reduc-tion. However, stability is particularly important, as periods of stop-gocan be harmful to the poor who do not have the cushions to protectthemselves during a downturn. For this reason, during economic expan-sion and prosperity, it would be wise for Governments to put in placethose social protection schemes that will be needed if and when theeconomy falters. Many programmes, though, are designed to reachthose in the formal sector, which leaves the informal sector unprotectedand unattended after being hit by recession. Governments should, then,explore other forms of social assistance, based on grass-roots involve-ment, that reach the poor in the informal sector.

The effects of trade liberalization on the poor are examined in chapterVI. Trade reform is normally not undertaken with any specific intentionof benefiting the poor. Rather, by expanding the choice of goods avail-able to all consumers and increasing the competition between domesticand foreign suppliers, trade liberalization should benefit the poor bymaking their limited budgets stretch further. Trade liberalization can alsospur economic dynamism and growth and, as growth reduces poverty,lead to a reduction in poverty. It is on the demand for labour that muchconcern is concentrated—concern that trade liberalization would dis-place the poor employed in domestic industries that cannot compete withimports, or that the need to attract foreign direct investment wouldinduce countries to lower their labour standards. The Survey examinesthese possible negative effects of liberalization, and argues that, wherenecessary, these concerns can be addressed by specific policy interven-tions. They do not detract from the overall efficacy of trade and invest-ment liberalization in helping everyone, including the poor.

Another area where liberalization has been pursued has been in agri-culture, which is analysed in chapter VII. As with trade, the basic ratio-nale of market liberalization is to make available to consumers a widervariety of goods at cheaper prices. This should benefit the poor as con-sumers of food. However, the rural poor are also producers of foodstuffsand this aspect must be taken into account in any programme of reform.In many cases, corrective measures will have to be taken as reforms are

W O R L D E C O N O M I C A N D S O C I A L S U R V E Y 2 0 0 3 VII

implemented. Market-based land reform, where a willing seller sells toa willing buyer, is another policy now being increasingly pursued. Thechapter argues that this can lead to greater economic efficiency andmore equitable patterns in rural growth.

The last chapter reviews the impact on poverty of the change from acentrally planned system to a market system. In the economies in tran-sition, this could be brought about only through an initial recession—whose length and depth varied widely across countries—as industriesthat had been overmanned or otherwise not viable in a market economywere forced to shed labour or to close down. As social benefits wereoften provided by the place of work, those who lost their jobs were hitespecially hard, through losing both their income and their social pro-tection. What is now increasingly apparent in the transition economiesis that, although the return to economic growth will lift out of povertythose whose situation was caused by their losing their jobs, there is stilla large class of the chronically poor who will not benefit so easily fromrenewed growth. Carefully targeted interventions are necessary toaddress the causes of their poverty.

Part two of the Survey, then, presents a nuanced picture of the possi-bilities of reducing poverty. It balances the optimistic assessment thatthe Millennium Development Goal is achievable at the global level,with the realization that, unless strong measures are taken nationallyand internationally, many countries will fail to reduce the number of theabsolute poor and many regions and groups of people will not escapeavoidable poverty. These strong measures do not imply an abandonmentof those macroeconomic policies that have been seen to result in sus-tainable economic growth, but rather their refinement and the enactmentof complementary policies to ensure that the resulting economic growthwill bring about an even greater reduction in poverty.

W O R L D E C O N O M I C A N D S O C I A L S U R V E Y 2 0 0 3VIII

Nitin DesaiUnder-Secretary-Generalfor Economic and Social Affairs

CONTENTS

Preface . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .IIIForeword . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .VExplanatory notes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .XV

PART ONE. STATE OF THE WORLD ECONOMY

Chapter Page

I. THE WORLD ECONOMY IN 2003 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .3Delayed recovery . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .4A lacklustre international economic environment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .7Policy responses to slow growth . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .9Regional performance and prospects . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .10

Developed countries: recovery derailed . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .10Economies in transition: limited deceleration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .12Developing countries: continuing underachievement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .12

Short-term uncertainties and risks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .14Delivering on the new development commitment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .17

Securing progress on the trade agenda . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .18Addressing external debt . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .19Reviving concessional financial flows . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .20

II. INTERNATIONAL TRADE AND FINANCE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .23International trade . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .24Commodity prices and markets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .29

World oil market: recent developments and prospects . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .29Non-fuel commodities: excess supplies and weak demand . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .32

Trade policy developments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .37Financial flows to developing countries and economies in transition . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .41

Private capital flows . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .42Official flows . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .45

Continuing reform of the international financial architecture . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .50Crisis prevention activities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .50Approaches to crisis resolution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .57

III. THE CURRENT SITUATION IN THE WORLD’S ECONOMIES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .63Developed economies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .64

North America: recovery under way . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .64Developed Asia and the Pacific: subdued growth in Japan and vigour elsewhere . . . . . . . . . . . . . . . . . . . . . . . . . . .70Western Europe: upturn faces negative headwinds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .72

W O R L D E C O N O M I C A N D S O C I A L S U R V E Y 2 0 0 3 IX

Chapter Page

Economies in transition . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .76Central and Eastern Europe: withstanding the global slowdown . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .76The Baltic countries: the world’s fastest growing region . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .81Commonwealth of Independent States (CIS): sustaining robust growth . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .82

Developing economies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .87Africa: the challenge of poverty reduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .87East Asia: dealing with shocks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .93South Asia: moving towards a more balanced growth . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .97Western Asia: caught between war and volatile oil prices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .98Latin America and the Caribbean: slowly emerging from recession . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .101

PART TWO. ECONOMIC POLICY AND POVERTY

OVERVIEW . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .111

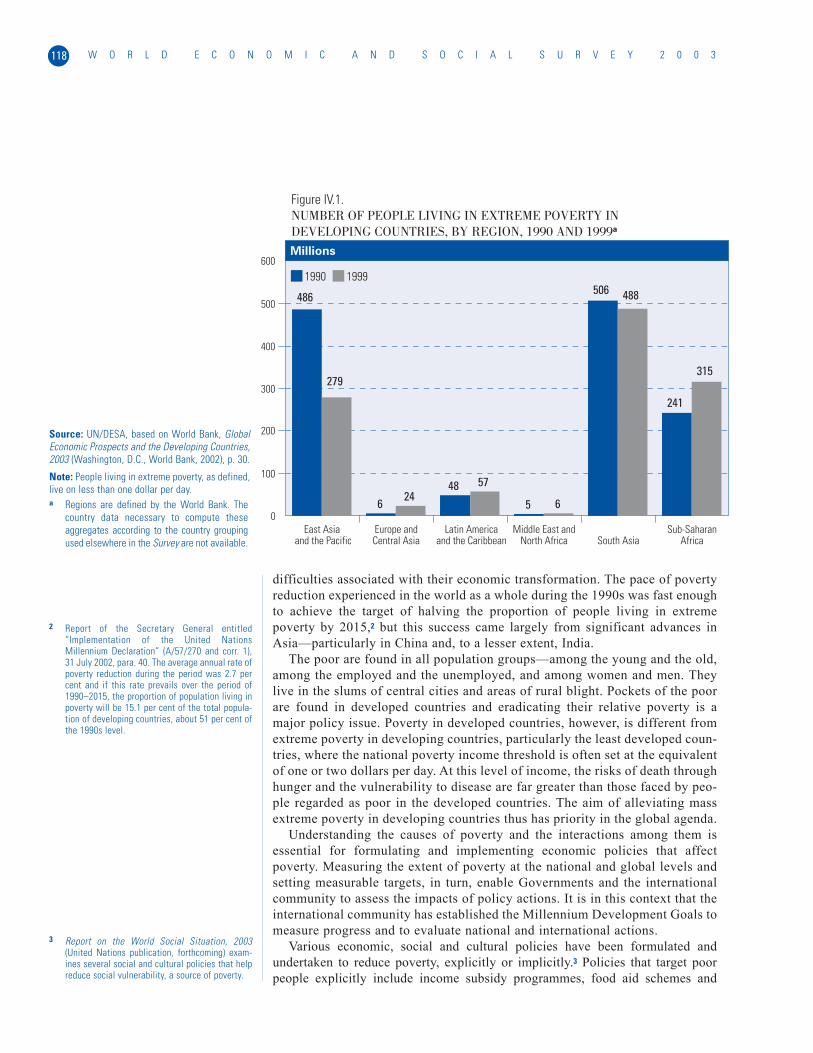

IV. GROWTH AND POVERTY: A FRAMEWORK FOR EVALUATING POLICY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .117Relationships between development, policy and poverty . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .120Average relationships between growth and poverty . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .123

General relationship between growth and poverty in the long run . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .124Looking behind the regional average . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .135

Deviation from averages . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .135Mobility in and out of poverty . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .136Evolution of poverty in the short run . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .138

Concluding remarks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .141

V. MACROECONOMIC POLICY AND POVERTY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .143Monetary policy and poverty . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .144Fiscal policy and poverty . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .145Macroeconomic policy in times of crisis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .148

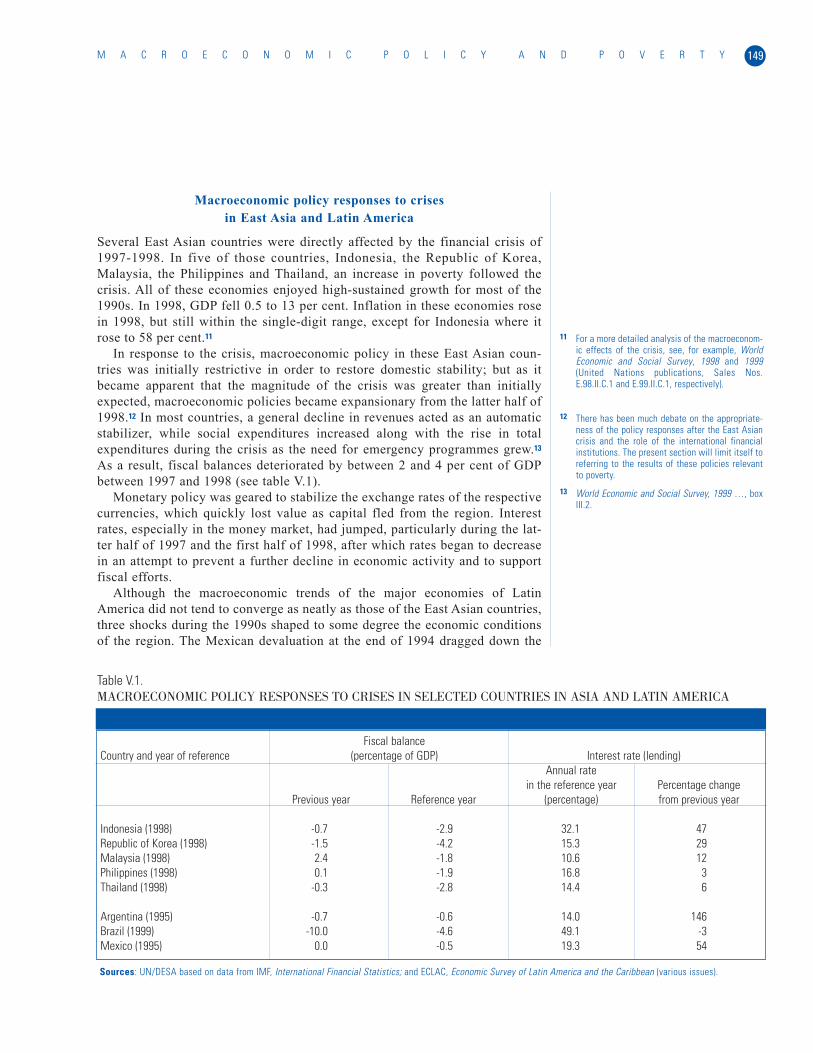

Macroeconomic policy responses to crises in East Asia and Latin America . . . . . . . . . . . . . . . . . . . . . . . . .149Comparing policy responses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .151

Poverty after the crises . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .152Direct measures to address urban poverty . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .154Policy implications and recommendations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .159

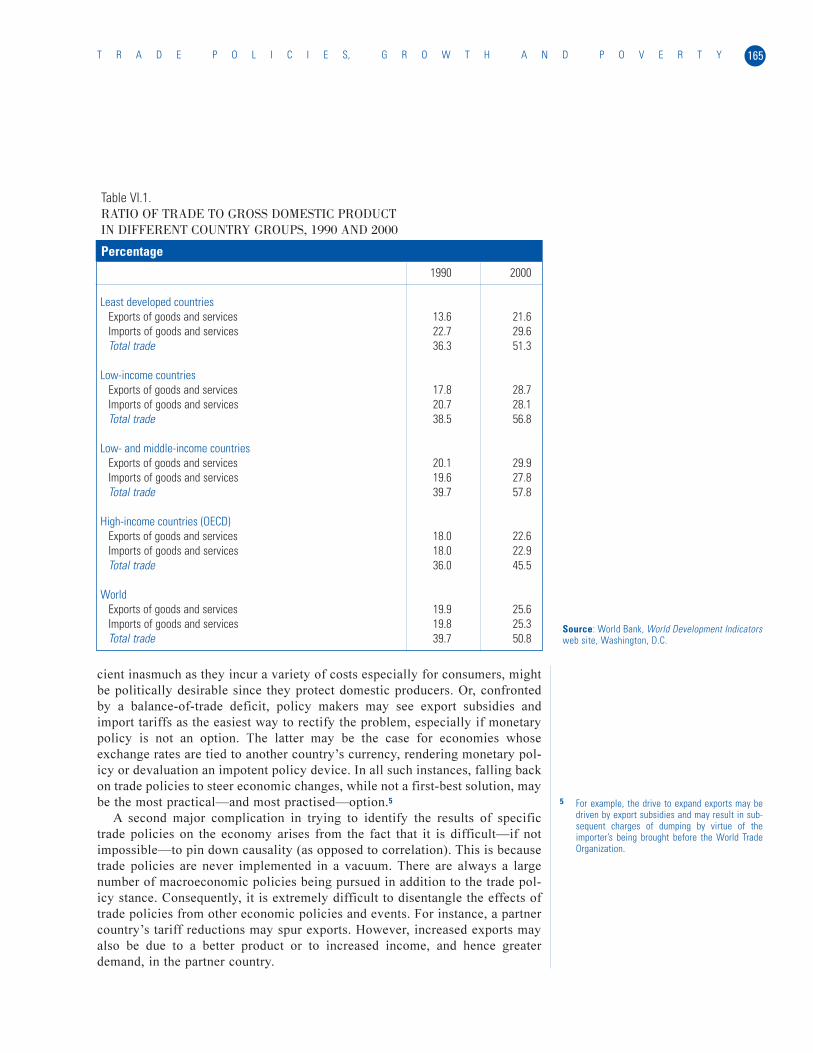

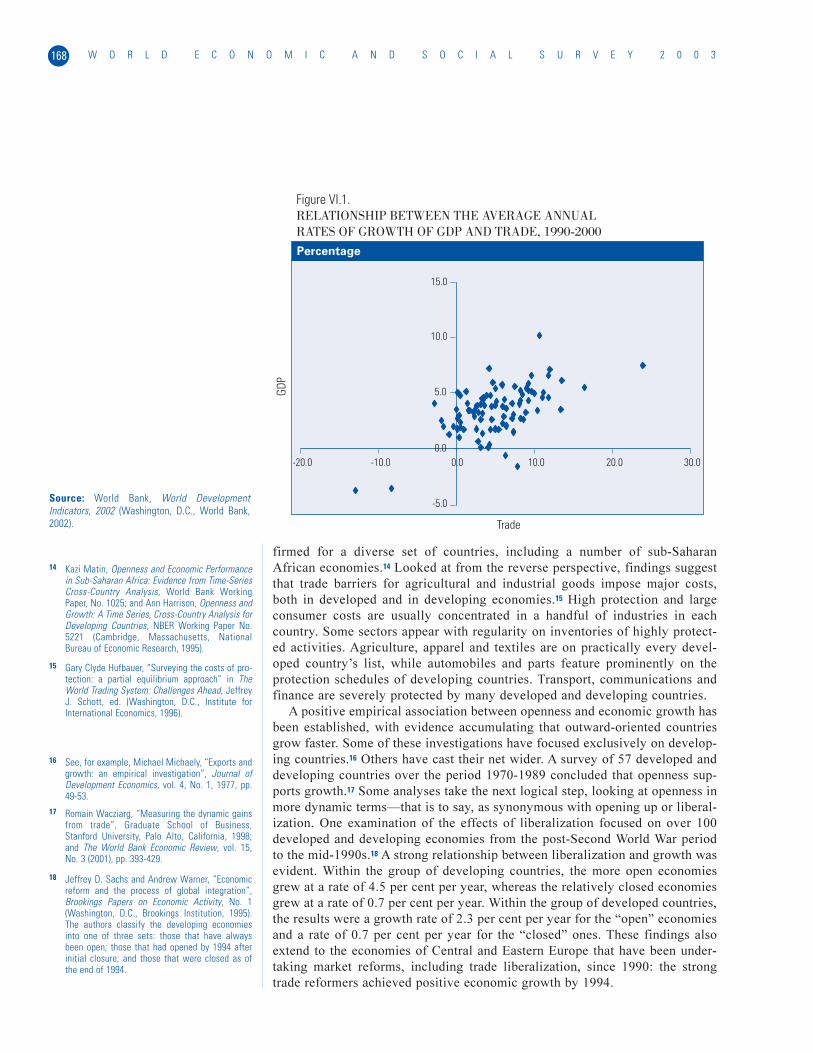

VI. TRADE POLICIES, GROWTH AND POVERTY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .163Trade and the economy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .164Trade and growth . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .167

Liberalization and growth in theory and practice . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .167Caveats concerning the trade-poverty link . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .169

Assessing the evidence . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .170

X T A B L E O F C O N T E N T S

Chapter Page

Adjustment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .171The channels for assuring the welfare of the poor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .172

Prices and availability of goods and services . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .172Labour markets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .174Investment and innovation: capital inflows and direct foreign investment . . . . . . . . . . . . . . . . . . . . . . . . . .176Government revenue . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .177The distribution of income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .179

The role of the international community . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .180Conclusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .185

VII. MARKET-BASED APPROACHES TO RURAL DEVELOPMENT IN SUB-SAHARAN AFRICA . . . . . . . . . . . . . . . .187Rural development and poverty reduction in sub-Saharan Africa . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .188

The need for greater emphasis on rural poverty reduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .188Focusing on sub-Saharan Africa . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .189

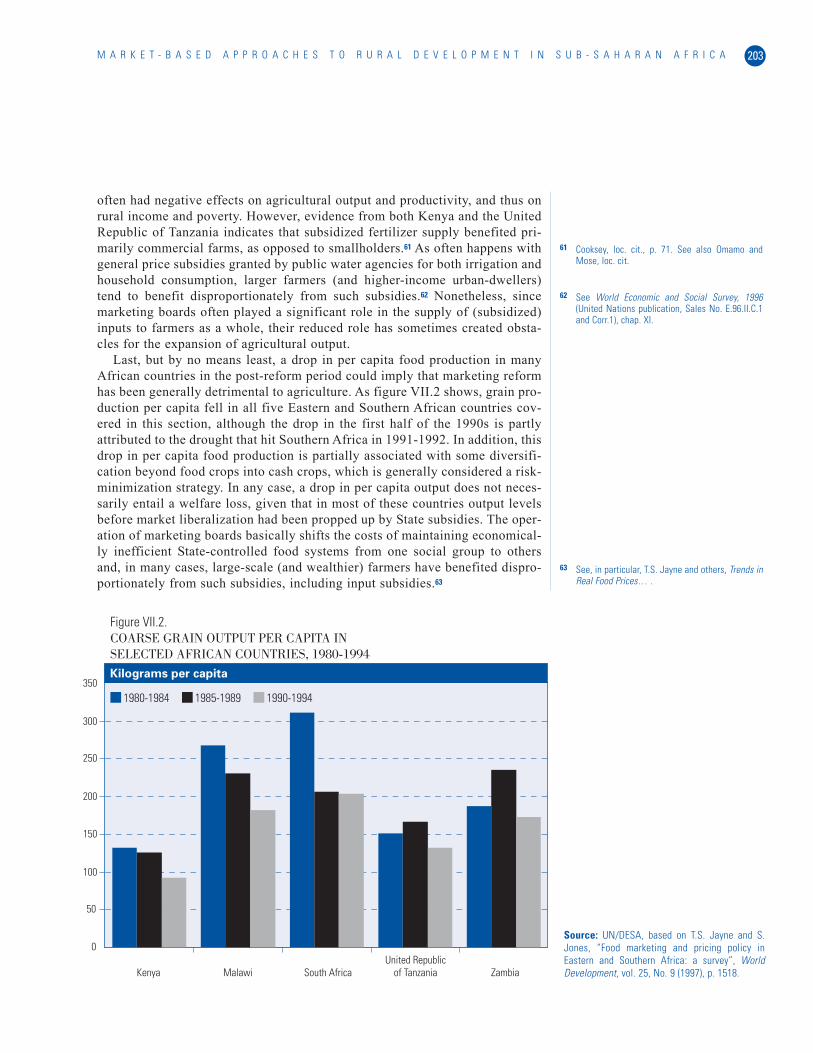

Food marketing reform in sub-Saharan Africa . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .192The role of food markets in rural poverty alleviation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .192Food marketing reform in selected African countries . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .194An assessment of food marketing reform in Africa . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .201

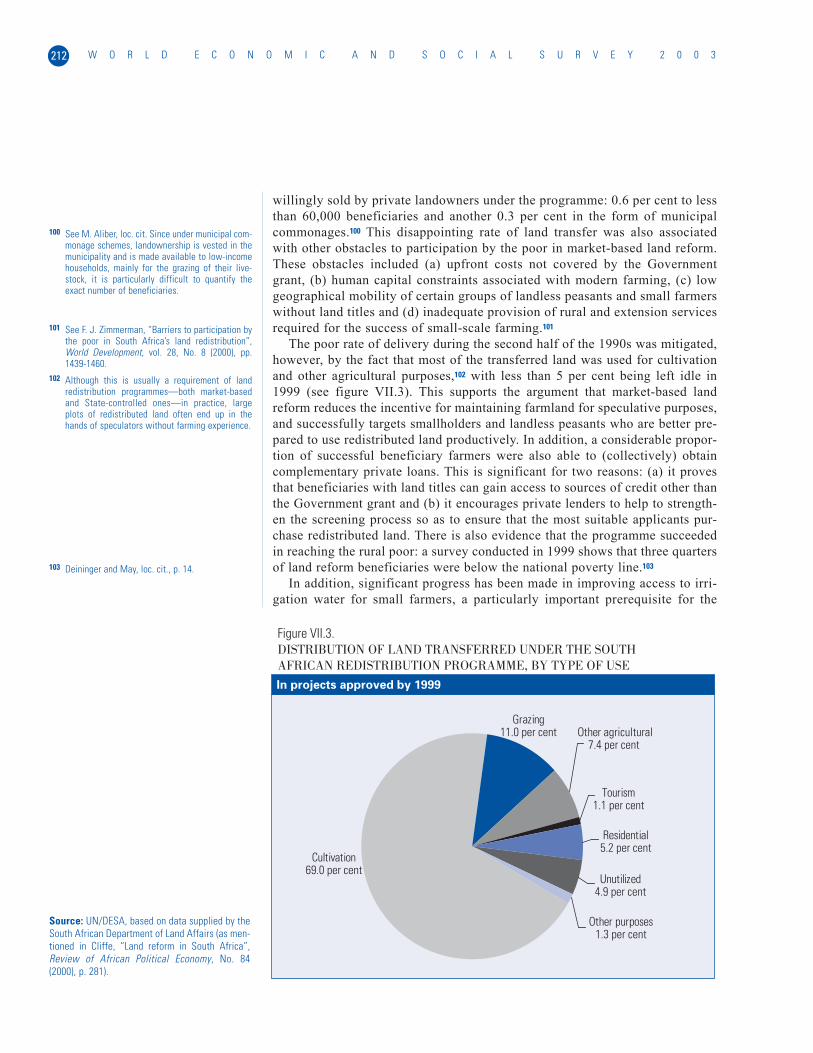

A market-based approach to land reform . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .205The central role of land reform in rural poverty alleviation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .205The case for market-based land reform . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .207Market-based land reform in South Africa . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .210An assessment of market-based land reform . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .215

Concluding remarks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .216

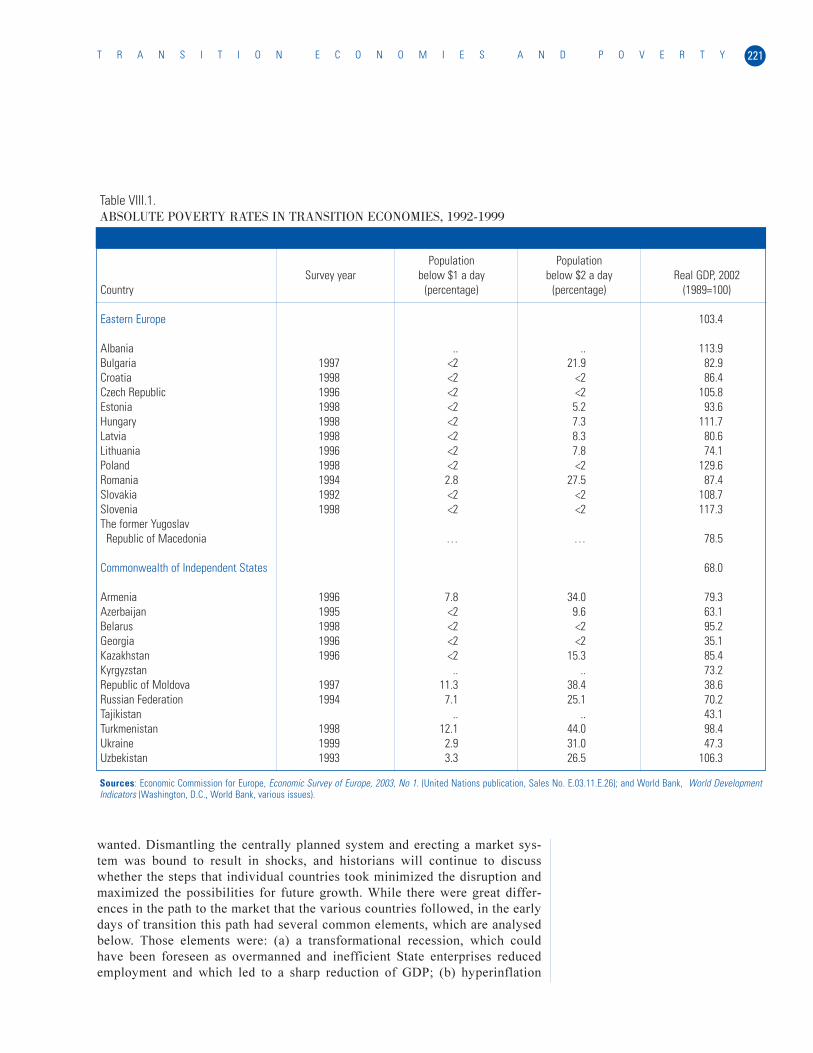

VIII. TRANSITION ECONOMIES AND POVERTY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .219The macroeconomic background . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .223

The transformational recession . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .223Inflation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .224Private sector investment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .225Income distribution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .225Fiscal policy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .226Trade and foreign exchange policy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .227

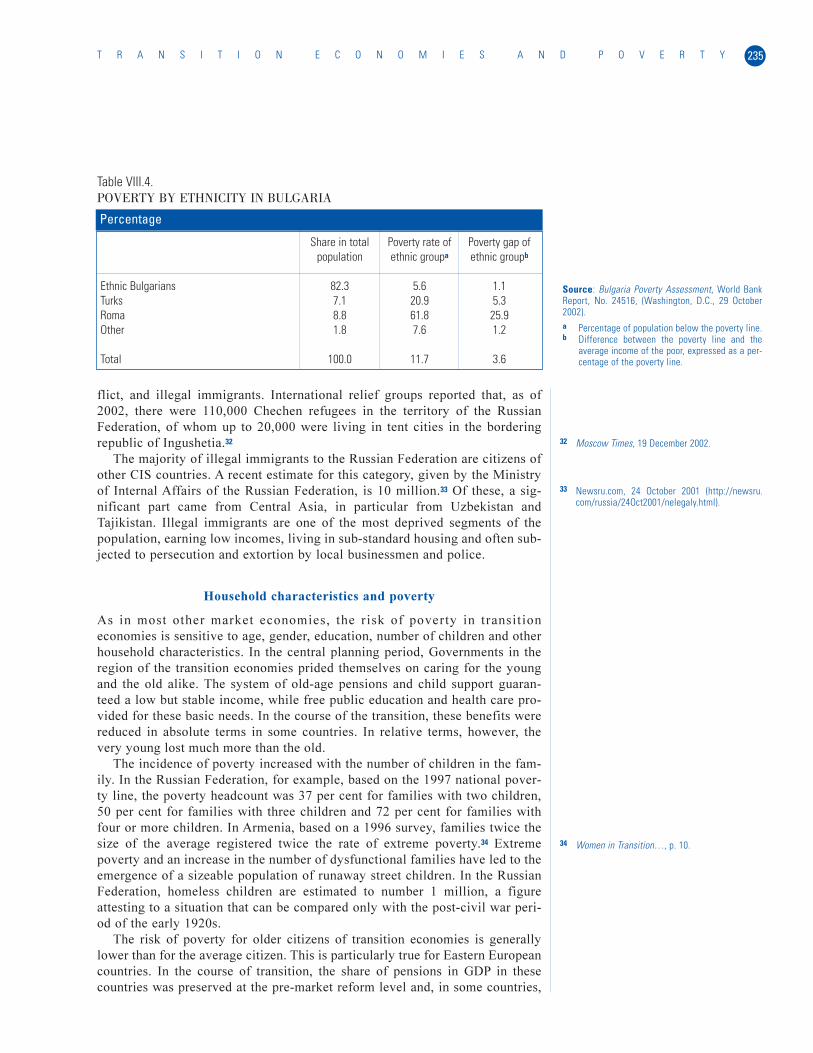

Transient versus chronic poverty . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .229The emergence of chronic poverty . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .229Sectoral and geographical differentiation of incomes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .231Conflicts and poverty . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .234Ethnic-specific poverty . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .234Household characteristics and poverty . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .235

W O R L D E C O N O M I C A N D S O C I A L S U R V E Y 2 0 0 3 XI

Chapter Page

Employment, unemployment and poverty . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .236Unemployment benefits and the minimum wage . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .238

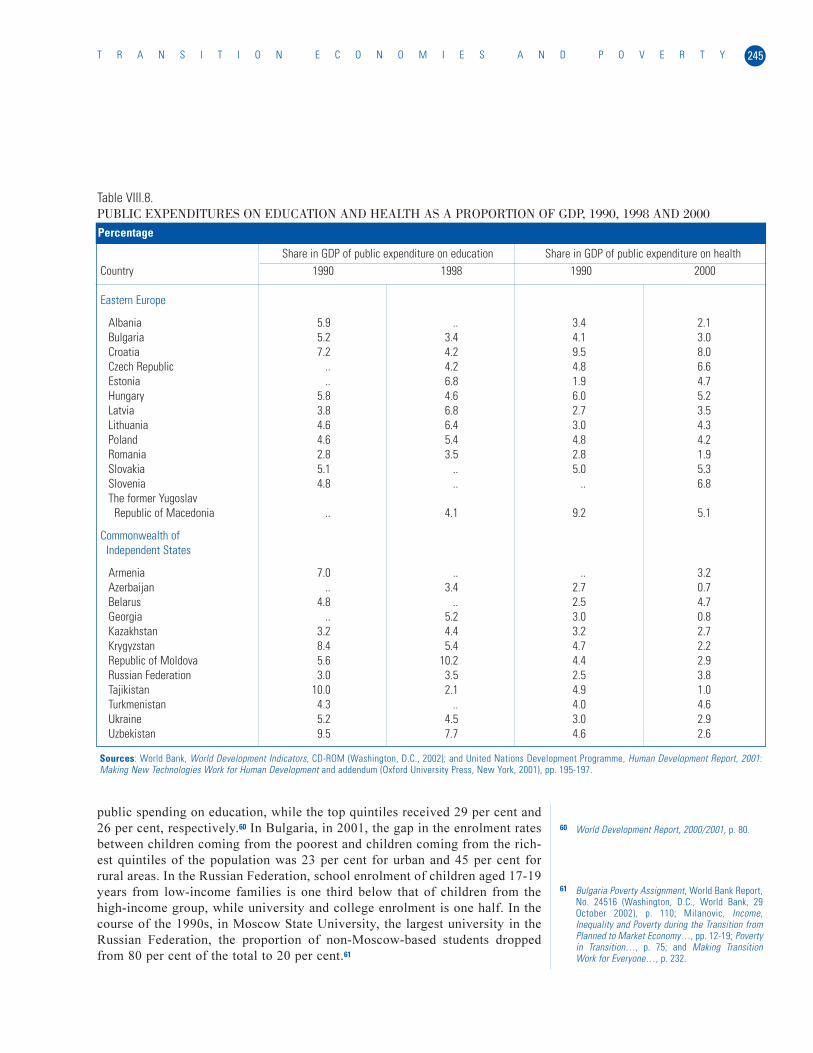

Coping with poverty: the government’s response . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .240Pensions reform . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .240Targeted social protection . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .242Untargeted subsidies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .243Public spending on education and health . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .244

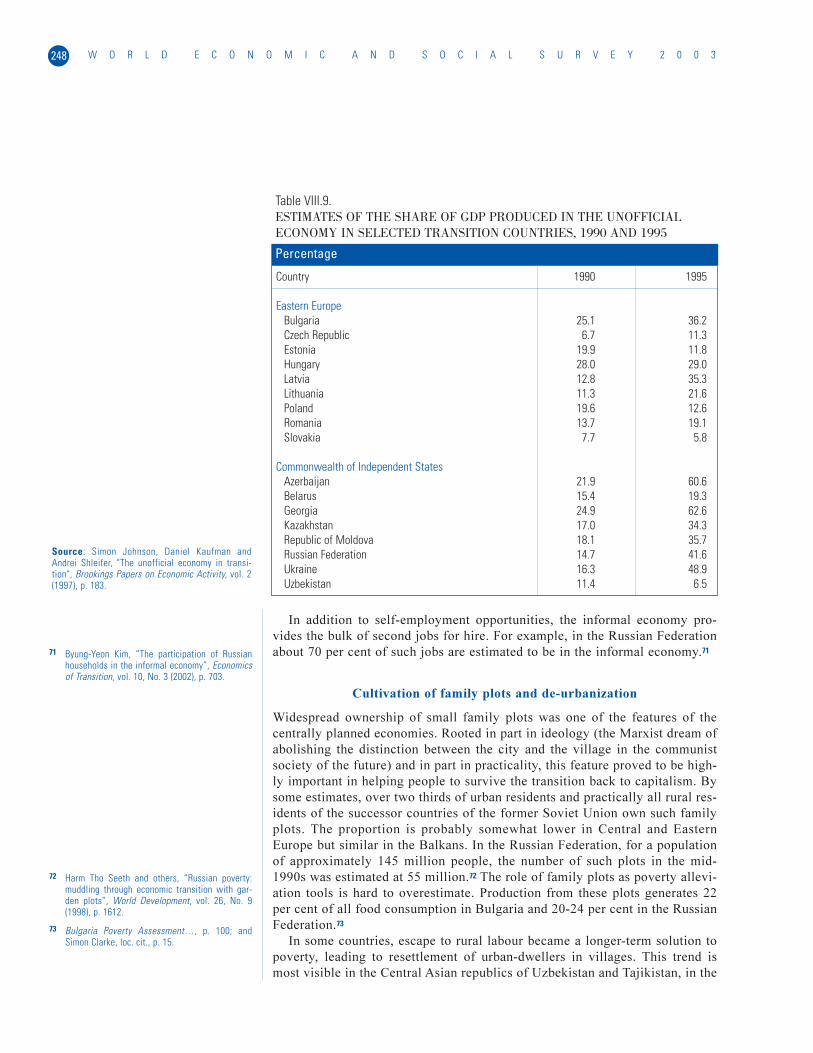

Coping with poverty: the private response . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .247Self-employment and the growth of the informal economy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .247Cultivation of family plots and de-urbanization . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .248Migration and emigration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .249The role of intra-framily transfers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .249

Conclusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .250

ANNEX

STATISTICAL TABLES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .253

BOXES

I.1. Economic implications of the depreciation of the United States dollar . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .15III.1. CIS-7 Initiative to Promote Poverty Reduction, Growth and Debt Sustainability

in the Low-income Countries of the Commonwealth of Independent States . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .84III.2. Elections and economic stability in Africa . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .89III.3. Ecuador and El Salvador: a tale of two dollarizations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .103IV.1. Equality, growth and poverty: are there trade-offs? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .126IV.2. Drawing the poverty line . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .130IV.3. Growth and relative poverty . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .132V.1. Participation of civil society in strengthening poverty reduction strategies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .147

VI.1. Beyond agriculture: furniture manufacturing in Ghana . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .182VI.2. Beyond agriculture: clothing and textile manufacturing in Lesotho . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .183VIII.1. Poverty in Armenia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .222VIII.2. The Russian Federation: land of billionaires? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .227VIII.3. Measurement of poverty in transition economies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .230VIII.4. The Russian defence industry: the case of a shrinking giant . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .232

XII T A B L E O F C O N T E N T S

Page

FIGURES

II.1. World trade: value of monthly exports, January 2001-February 2003 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .24II.2. Selected developed economies: growth of imports of goods and services,

seasonally adjusted, first quarter 2001-first quarter 2003 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .25II.3. Oil prices, January 2000-April 2003 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .30II.4. World oil supply and demand and OPEC production, first quarter 2000-fourth quarter 2003 . . . . . . . . . . . . . . . . . . . . . .31II.5. Non-fuel commodity prices, 1994-2003 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .33II.6. Yield spreads on emerging market bonds, 2 January 2002-30 April 2003 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .43III.1. Consumer confidence in the major economies, 1998-2003 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .65III.2. Industrial production, excluding construction, 1999-2003 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .66III.3. Unemployment rates in the EU-15, Japan and the United States, 1999-2003 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .68III.4. Euro zone: selected price indices, January 1999-April 2003 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .73III.5. Latin America, selected countries: industrial production index, seasonally adjusted, January 2001-February 2003 . . .102IV.1. Number of people living in extreme poverty in developing countries, by region, 1990 and 1999 . . . . . . . . . . . . . . . . . .118IV.2. Per capita income and extreme poverty in the 1990s . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .125IV.3. Growth and the evolution of extreme poverty, 1990-1999 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .134IV.4. Growth and the evolution of nationally defined poverty during the 1980s and 1990s . . . . . . . . . . . . . . . . . . . . . . . . . .135IV.5. Short-term evolution of poverty, first quarter 1996-third quarter 1999, Indonesia . . . . . . . . . . . . . . . . . . . . . . . . . . . . .140VI.1. Relationship between the average annual rates of growth of GDP and trade, 1990-2000 . . . . . . . . . . . . . . . . . . . . . . .168VII.1. Share of developing-country regions in world extreme poverty, 1999 and 2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .190VII.2. Coarse grain output per capita in selected African countries, 1980-1994 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .203VII.3. Distribution of land transferred under the South African redistribution programme,

by type of use (in projects approved by 1999) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .212

TABLES

I.1. Growth of world output and trade, 1994-2004 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .5I.2. Indicators of the international economic environment, 1998-2002 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .7I.3. Frequency of high and low growth of per capita output, 2000-2002 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .11II.1. Net transfer of financial resources to developing economies and economies in transition, 1994-2002 . . . . . . . . . . . . . .42II.2. Net financial flows to developing economies and economies in transition, 1992-2002 . . . . . . . . . . . . . . . . . . . . . . . . . .43II.3. Official development assistance of member countries of the Development Assistance Committee, 2002 . . . . . . . . . . .47III.1. Major industrialized countries: quarterly indicators, 2001-2002 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .67III.2. Economies in transition: quarterly indicators, 2001-2002 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .79III.3. Major developing countries: quarterly indicators, 2001-2002 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .94IV.1. Evolution of standard poverty measures in selected sub-Saharan countries . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .121IV.2. Proportion of households in chronic and transitory poverty, various countries . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .138V.1. Macroeconomic policy responses to crises in selected countries in Asia and Latin America . . . . . . . . . . . . . . . . . . . . . .149V.2. Effects of economic crises in selected countries in Asia and Latin America . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .153

W O R L D E C O N O M I C A N D S O C I A L S U R V E Y 2 0 0 3 XIII

Page

V.3. Social policy responses to economic crises . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .155VI.1. Ratio of trade to gross domestic product in different country groups, 1990 and 2000 . . . . . . . . . . . . . . . . . . . . . . . . . .165VII.1. Poverty in South Africa, 1995 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .210VII.2. Land distribution in South Africa: sliding scale of grants and personal contributions . . . . . . . . . . . . . . . . . . . . . . . . . . .214VIII.1. Absolute poverty rates in transition economies, 1992-1999 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .221VIII.2. Gini coefficients in transition economies, 1987-1998 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .226VIII.3. Transient and chronic poverty: Hungary, Poland and the Russian Federation, 1994-1996 . . . . . . . . . . . . . . . . . . . . . . . .231VIII.4. Poverty by ethnicity in Bulgaria . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .235VIII.5. Output, unemployment, and real wages in selected transition economies, 1991-2001 . . . . . . . . . . . . . . . . . . . . . . . . .237VIII.6. Public expenditures on pensions, 1994-2000 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .241VIII.7. Targeting of cash benefits in transition economies, 1996-1997 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .243VIII.8. Public expenditures on education and health as a proportion of GDP, 1990, 1998 and 2000 . . . . . . . . . . . . . . . . . . . . .245VIII.9. Estimates of the share of GDP produced in the unofficial economy

in selected transition countries, 1990 and 1995 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .248

XIV T A B L E O F C O N T E N T S

EXPLANATORY NOTES

The following symbols have been used in the tablesthroughout the report:

.. Two dots indicate that data are not available or are notseparately reported.

– A dash indicates that the amount is nil or negligible.

- A hyphen (-) indicates that the item is not applicable.

- A minus sign (-) indicates deficit or decrease, except as indicated.

. A full stop (.) is used to indicate decimals.

/ A slash (/) between years indicates a crop year or financial year, for example, 1990/91.

- Use of a hyphen (-) between years, for example, 1990-1991,signifies the full period involved, including the beginning and end years.

Reference to “tons” indicates metric tons and to “dollars” ($) United States dollars, unless otherwise stated.

Annual rates of growth or change, unless otherwise stated, refer to annual compound rates.

In most cases, the growth rate forecasts for 2003 and 2004 arerounded to the nearest quarter of a percentage point.

Details and percentages in tables do not necessarily add tototals, because of rounding.

The following abbreviations have been used:

AGOA African Growth and Opportunity Act (United States)

AIDS acquired immunodeficiency syndromeAPEC Asia-Pacific Economic CooperationASEAN Association of Southeast Asian Nationsbpd barrels per daybps basis pointsCAC collective action clauseCACM Central American Common MarketCAP Common Agricultural Policy (EU)

CCFF Compensatory and Contingency Financing Facility (IMF)

CDI Commitment to Development IndexCEFTA Central European Free Trade AgreementCFA Communauté financière africaineCFF Compensatory Financing Facility (IMF)CIS Commonwealth of Independent StatesCOMTRADE United Nations External Trade Statistics DatabaseDAC Development Assistance Committee (of OECD)EAP Enhanced Access Policy (IMF)EBRD European Bank for Reconstruction

and DevelopmentECA Economic Commission for AfricaECB European Central BankECE Economic Commission for EuropeECLAC Economic Commission for Latin America and

the CaribbeanEFF Extended Fund Facility (IMF)EMBI+ Emerging Markets Bond Index PlusEMU European Economic and Monetary UnionEPZ export processing zoneESAF Enhanced Structural Adjustment Facility (IMF)ESCAP Economic and Social Commission for Asia

and the PacificEU European UnionEURIBOR Euro Interbank Offered RateFDI foreign direct investmentf.o.b. free on boardFTAA Free Trade Area of the AmericasGATT General Agreement on Tariffs and TradeGDP gross domestic productGNI gross national incomeGNP gross national productGSP Generalized System of PreferencesGSTP Global System of Trade Preferences among

Developing CountriesGWP gross world productHICP Harmonized Index of Consumer PricesHIPC heavily indebted poor countriesHIV human immunodeficiency virusIADB Inter-American Development BankIBRD International Bank for Reconstruction and

DevelopmentICO International Coffee Organization

W O R L D E C O N O M I C A N D S O C I A L S U R V E Y 2 0 0 3 XV

XVI E X P L A N A T O R Y N O T E S

ICP International Comparison ProgrammeICT information and communication technologiesICTSD International Centre for Trade and Sustainable

DevelopmentIDA International Development AssociationIEA International Energy AgencyIFAD International Fund for Agricultural DevelopmentIFC International Finance CorporationIFI international financial institutionIMF International Monetary FundINTRASTAT system of data collection for intra-EU tradeITRO International Tripartite Rubber OrganisationLIBOR London Interbank Offered Ratembd millions of barrels per dayMERCOSUR Mercado Común del Sur (Southern

Common Market)NAFTA North American Free Trade AgreementNATO North Atlantic Treaty OrganizationNBER National Bureau of Economic Research

(Cambridge, Massachusetts)NEPAD New Partnership for Africa's DevelopmentNIPA National Income and Product AccountsNPL non-performing loanNPV net present valueODA official development assistanceOECD Organisation for Economic Cooperation

and DevelopmentOPEC Organization of the Petroleum Exporting Countriespb per barrelppp purchasing power parityPRGF Poverty Reduction and Growth Facility (IMF)

Project LINK international collaborative research group for econometric modelling, coordinated jointly by the Economic Monitoring and Assessment Unitof the United Nations Secretariat, and the

University of TorontoPRSP Poverty Reduction Strategy Paper

(IMF and World Bank)R&D research and developmentRTA regional trade agreementSADC Southern African Development CommunitySAF Structural Adjustment Facility (IMF)SARS severe acute respiratory syndromeSDRs special drawing rights (IMF)SDT special and differential treatmentSFF Supplementary Financing Facility (IMF)SITC Standard International Trade ClassificationSMEs small and medium-sized enterprisesSRF Supplemental Reserve Facility (IMF)STF Systemic Transformation Facility (IMF)TRIPs trade-related intellectual property rightsUNAIDS Joint United Nations Programme on Human

Immunodeficiency Virus/Acquired Immunodeficiency Syndrome (HIV/AIDS)

UNCTAD United Nations Conference on Trade and Development

UN/DESA Department of Economic and Social Affairs of the United Nations Secretariat

UNU United Nations UniversityVAT value-added taxWIDER World Institute for Development Economics

Research

The designations employed and the presentation of the material in this publication do not imply the expression of any opinion whatsoeveron the part of the United Nations Secretariat concerning the legal status of any country, territory, city or area or of its authorities, or con-cerning the delimitation of its frontiers or boundaries.

The term "country" as used in the text of this report also refers, as appropriate, to territories or areas.

a Names and composition of geographical areas follow those of "Standard country orarea codes for statistical use" (ST/ESA/STAT/SER.M/49/Rev.3), with one exception,namely, Western Asia, which in the Survey includes the Islamic Republic of Iran(owing to the large role of the petroleum sector in its economy) and excludes thetransition economies of the region. Also, "Eastern Europe", as used in this Survey,is a contraction of "Central and Eastern Europe"; thus the composition of the regiondesignated by the term differs from that of the strictly geographical grouping.

b As of 4 February 2003, the official name of “Federal Republic of Yugoslavia” hasbeen changed to “Serbia and Montenegro”.

For analytical purposes, the following country groupingsand subgroupings have been used:a

Developed economies (developed market economies):Europe, excluding the European transition economiesCanada and the United States of AmericaJapan, Australia and New Zealand.

Major developed economies (the Group of Seven):Canada, France, Germany, Italy, Japan, United Kingdom of Great Britain and Northern Ireland, United States of America.

European Union:Austria, Belgium, Denmark, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, Netherlands, Portugal, Spain, Sweden, United Kingdom of Great Britain and Northern Ireland.

Economies in transition:Central and Eastern European transition economies (CEETEs, sometimes contracted to “Eastern Europe”):

Albania, Bulgaria, Czech Republic, Hungary, Poland, Romania, Slovakia and successor States of the Socialist Federal Republic of Yugoslavia, namely, Bosnia and Herzegovina, Croatia, Slovenia, the former Yugoslav Republic of Macedonia, Yugoslavia.b

Baltic StatesEstonia, Latvia and Lithuania.

Commonwealth of Independent States (CIS)Armenia, Azerbaijan, Belarus, Georgia, Kazakhstan, Kyrgyzstan, Republic of Moldova, Russian Federation, Tajikistan, Turkmenistan, Ukraine, Uzbekistan.

Developing economies:AfricaAsia and the Pacific (excluding Japan, Australia, New Zealand and the member States of CIS in Asia) Latin America and the Caribbean.

Subgroupings of Asia and the Pacific:Western Asia plus Islamic Republic of Iran (commonly contracted to “Western Asia”):

Bahrain, Cyprus, Iran (Islamic Republic of), Iraq, Israel, Jordan, Kuwait, Lebanon, Oman, Qatar, Saudi Arabia, Syrian Arab Republic, Turkey, United Arab Emirates, Yemen.

Eastern and Southern Asia:All other developing economies in Asia and the Pacific (including China, unless listed separately). This group has in some cases been subdivided into:

ChinaSouth Asia: Bangladesh, India, Nepal, Pakistan, Sri LankaEast Asia: all other developing economies in Asia and the Pacific.

Subgrouping of Africa:Sub-Saharan Africa, excluding Nigeria and South Africa (commonly contracted to "sub-Saharan Africa"):

All of Africa except Algeria, Egypt, Libyan Arab Jamahiriya, Morocco, Nigeria, South Africa, Tunisia.

For particular analyses, developing countries have beensubdivided into the following groups:

Net-creditor countries:Brunei Darussalam, Kuwait, Libyan Arab Jamahiriya, Oman, Qatar, Saudi Arabia, Singapore, Taiwan Province of China, United Arab Emirates.

Net-debtor countries:All other developing countries.

Fuel-exporting countries:Algeria, Angola, Bahrain, Bolivia, Brunei Darussalam, Cameroon, Colombia, Congo, Ecuador, Egypt, Gabon, Indonesia, Iran (Islamic Republic of), Iraq, Kuwait, Libyan Arab Jamahiriya, Mexico, Nigeria, Oman, Qatar, Saudi Arabia, Syrian Arab Republic, Trinidad and Tobago, United Arab Emirates, Venezuela, Viet Nam.

Fuel-importing countries:All other developing countries.

Least developed countries:Afghanistan, Angola, Bangladesh, Benin, Bhutan, Burkina Faso, Burundi, Cambodia, Cape Verde, Central African Republic, Chad, Comoros, Democratic Republic of the Congo (formerly Zaire), Djibouti, Equatorial Guinea, Eritrea, Ethiopia, Gambia, Guinea, Guinea-Bissau, Haiti, Kiribati, Lao People’s Democratic Republic, Lesotho, Liberia, Madagascar, Malawi, Maldives, Mali, Mauritania, Mozambique, Myanmar, Nepal, Niger, Rwanda, Samoa, Sao Tome and Principe, Senegal, Sierra Leone, Solomon Islands, Somalia, Sudan, Togo, Tuvalu, Uganda, United Republic of Tanzania, Vanuatu, Yemen, Zambia.

The designation of country groups in the text and the tables isintended solely for statistical or analytical convenience and doesnot necessarily express a judgement about the stage reached by aparticular country or area in the development process.

W O R L D E C O N O M I C A N D S O C I A L S U R V E Y 2 0 0 3 XVII

PART ONE STATEOF THEWORLDECONOMY

The world economy has not yet recovered from its slowdown in 2001.Gross world product (GWP) increased by less than 2 per cent in 2002,marking a second consecutive year of growth substantially below potential.China and India, together with a number of economies in transition, werenotable exceptions to the sub-par performance that characterized themajority of the world’s economies. More generally, as in 2001, a substan-tial number of developing countries, as well as a few developed countriesand economies in transition, experienced a decline in output per capita.Overall, the first few years of the new millennium have been a develop-ment disappointment for the majority of developing countries and anabsolute setback for a number of them.

A global recovery is now forecast for the second half of 2003, with GWPexpected to increase by 2 per cent for the year as a whole, accelerating toslightly above 3 per cent for 2004. The developed countries, most notablythe United States of America, are expected to lead the recovery and to pro-vide a stimulus to the rest of the world. However, world trade and inter-national financial flows will continue to be sluggish by the standards of the1990s, with exports growing by less than 4 per cent in 2003. Moreover, thestimulus provided by the United States will be reduced for many countriesif the recent depreciation of the dollar against their currencies persists.Under these circumstances, few developing countries are expected toreturn to their desirable longer-term rates of growth before the end of2004. The economies in transition, in contrast, have been relativelyresilient in the face of this slowdown and are expected to remain so.

The world economy was beset by heightened geopolitical uncertaintiesin late 2002 and early 2003. Such factors continue to pose a downside riskto global economic growth, but this risk diminished substantially in thesecond quarter of 2003. A new non-economic shock—severe acute respira-tory syndrome (SARS)—jolted economic activity in some countries inearly 2003 but appears to have been largely contained. On the other hand,there remain some well-identified economic risks that could pose a threatto short-term global growth. The most important is linked to the nature ofthe inevitable adjustment of the United States external deficit, a processthat appears to have started with the depreciation of the dollar. A second,related challenge is the possibility of deflation in a growing number ofcountries. In addressing these immediate threats, policy makers should notneglect the agenda that they have established to address longer-term glob-al development issues.

ITHE WORLDECONOMYIN 2003

3T H E W O R L D E C O N O M Y I N 2 0 0 3

DELAYED RECOVERY

It was expected that a recovery from the global economic slowdown of 2001would begin in the United States in the second half of 2002 and graduallyaccelerate and spread throughout the world economy. There was a tentativerecovery in 2002, but it quickly faded, largely because of the geopoliticaluncertainties associated with the looming confrontation with Iraq.

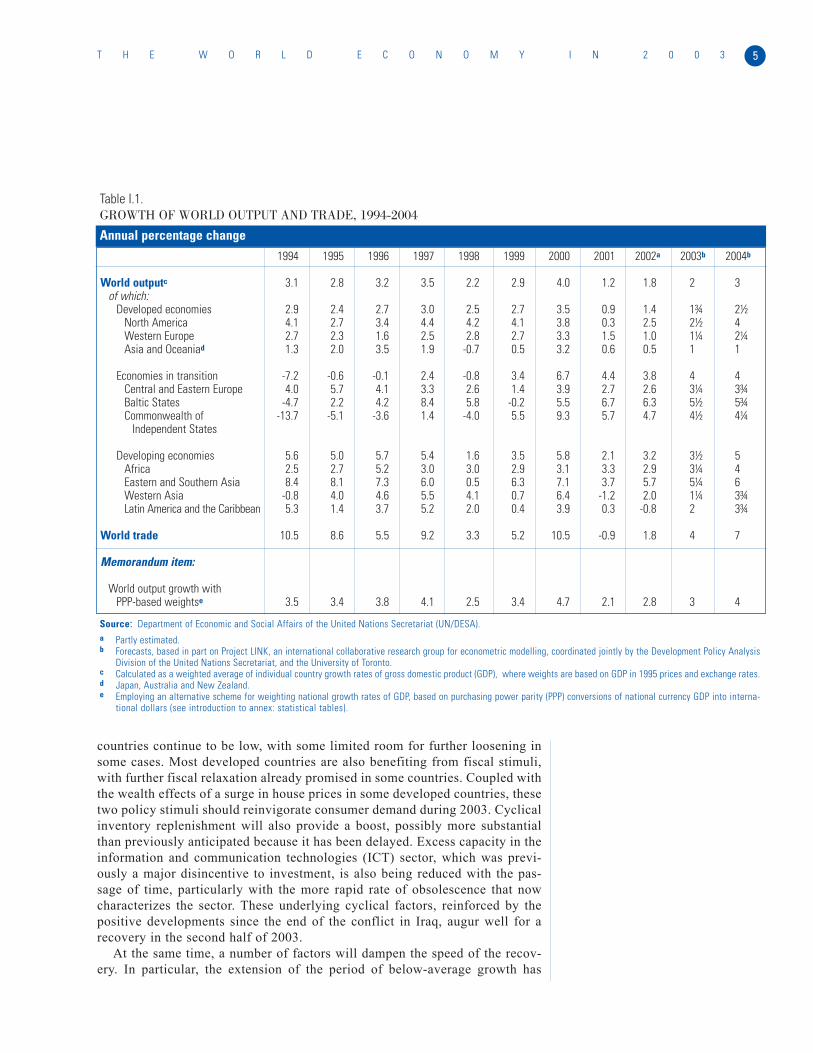

The heightened geopolitical uncertainties and perceived risks that arosebefore the invasion of Iraq permeated the world economy through a number ofchannels. The fear that conflict might disrupt oil supplies raised the prices ofoil far higher than warranted by economic fundamentals; higher oil prices werethemselves a global economic shock that dampened aggregate demand andimposed additional price pressures in oil-importing countries. Global politicaltensions caused most equity markets to plummet, aggravating the global assetprice deflation that had been in effect since 2000. In several countries, con-sumer and business confidence fell to their lowest levels in a decade. Businesscapital spending declined in many developed economies. Economically, theoverall effect of the stand-off with Iraq was reduced activity in late 2002 andearly 2003, with the setback being most pronounced in the developed countries(see table I.1). Instead of recovering as anticipated, growth in these countriesin the first quarter of 2003 was generally lower than a year earlier.

With the exception of Western Asia, the developing countries andeconomies in transition were less directly affected by the geopolitical uncer-tainties surrounding the issue of Iraq. Nevertheless, indirectly, the delayedrecovery in the developed countries itself had negative consequences. In somecases, most notably in Latin America, these were aggravated by domestic dif-ficulties. To a greater extent, however, domestic economic circumstances indeveloping countries and particularly in the economies in transition served asa buffer against the weak external environment. China and India offered themost pronounced examples of this but most of the economies in transition alsodemonstrated an important degree of domestically led growth. To a lesserextent, sub-Saharan Africa displayed similar signs of resilience, althoughgrowth remained modest.

The invasion of Iraq took a heavy toll on human life and economic activi-ty in the region. Nevertheless, the military action was briefer, less costly inhuman life, less extensive and less disruptive of global economic activity thanhad been feared, with the result that several of the earlier negative manifesta-tions of the previous geopolitical uncertainty were quickly and measurablyreduced. Oil prices retreated and are expected to fall further as global oil pro-duction recovers, with beneficial effects on global growth and on inflationarypressure in oil-importing countries. Equity prices rebounded in the post-inva-sion period, reflecting and contributing to increased optimism regarding eco-nomic prospects. There was also a post-conflict recovery in the indices of bothconsumer and business confidence. Most of the negative consequences of theearlier geopolitical uncertainties are expected to dissipate by the third quarterof 2003.

In addition, a number of the positive factors that were expected to prompt arecovery in 2002 remain in effect. The most important are the continuing stim-ulative effects of macroeconomic policy. Policy interest rates in the developed

W O R L D E C O N O M I C A N D S O C I A L S U R V E Y 2 0 0 34

countries continue to be low, with some limited room for further loosening insome cases. Most developed countries are also benefiting from fiscal stimuli,with further fiscal relaxation already promised in some countries. Coupled withthe wealth effects of a surge in house prices in some developed countries, thesetwo policy stimuli should reinvigorate consumer demand during 2003. Cyclicalinventory replenishment will also provide a boost, possibly more substantialthan previously anticipated because it has been delayed. Excess capacity in theinformation and communication technologies (ICT) sector, which was previ-ously a major disincentive to investment, is also being reduced with the pas-sage of time, particularly with the more rapid rate of obsolescence that nowcharacterizes the sector. These underlying cyclical factors, reinforced by thepositive developments since the end of the conflict in Iraq, augur well for arecovery in the second half of 2003.

At the same time, a number of factors will dampen the speed of the recov-ery. In particular, the extension of the period of below-average growth has

5T H E W O R L D E C O N O M Y I N 2 0 0 3

Table I.1.GROWTH OF WORLD OUTPUT AND TRADE, 1994-2004

1994 1995 1996 1997 1998 1999 2000 2001 2002a 2003b 2004b

World outputc 3.1 2.8 3.2 3.5 2.2 2.9 4.0 1.2 1.8 2 3of which:

Developed economies 2.9 2.4 2.7 3.0 2.5 2.7 3.5 0.9 1.4 1¾ 2½North America 4.1 2.7 3.4 4.4 4.2 4.1 3.8 0.3 2.5 2½ 4Western Europe 2.7 2.3 1.6 2.5 2.8 2.7 3.3 1.5 1.0 1¼ 2¼Asia and Oceaniad 1.3 2.0 3.5 1.9 -0.7 0.5 3.2 0.6 0.5 1 1

Economies in transition -7.2 -0.6 -0.1 2.4 -0.8 3.4 6.7 4.4 3.8 4 4Central and Eastern Europe 4.0 5.7 4.1 3.3 2.6 1.4 3.9 2.7 2.6 3¼ 3¾Baltic States -4.7 2.2 4.2 8.4 5.8 -0.2 5.5 6.7 6.3 5½ 5¾Commonwealth of -13.7 -5.1 -3.6 1.4 -4.0 5.5 9.3 5.7 4.7 4½ 4¼

Independent States

Developing economies 5.6 5.0 5.7 5.4 1.6 3.5 5.8 2.1 3.2 3½ 5Africa 2.5 2.7 5.2 3.0 3.0 2.9 3.1 3.3 2.9 3¼ 4Eastern and Southern Asia 8.4 8.1 7.3 6.0 0.5 6.3 7.1 3.7 5.7 5¼ 6Western Asia -0.8 4.0 4.6 5.5 4.1 0.7 6.4 -1.2 2.0 1¼ 3¾Latin America and the Caribbean 5.3 1.4 3.7 5.2 2.0 0.4 3.9 0.3 -0.8 2 3¾

World trade 10.5 8.6 5.5 9.2 3.3 5.2 10.5 -0.9 1.8 4 7

Memorandum item:

World output growth withPPP-based weightse 3.5 3.4 3.8 4.1 2.5 3.4 4.7 2.1 2.8 3 4

Source:: Department of Economic and Social Affairs of the United Nations Secretariat (UN/DESA).a Partly estimated.b Forecasts, based in part on Project LINK, an international collaborative research group for econometric modelling, coordinated jointly by the Development Policy Analysis

Division of the United Nations Secretariat, and the University of Toronto.c Calculated as a weighted average of individual country growth rates of gross domestic product (GDP), where weights are based on GDP in 1995 prices and exchange rates. d Japan, Australia and New Zealand.e Employing an alternative scheme for weighting national growth rates of GDP, based on purchasing power parity (PPP) conversions of national currency GDP into interna-

tional dollars (see introduction to annex: statistical tables).

Annual percentage change

aggravated some earlier weaknesses. For example, the further increase inunemployment, particularly, the increase in longer-term unemployment, is like-ly to constrain the growth of consumer demand. Similarly, the hostile interna-tional political environment had a particularly adverse effect on some specificsectors, notably international tourism and airlines, which had not recoveredfrom the fallout of the terrorist attacks of 11 September 2001. Some of thesesectors are not expected to recover fully for some time; meanwhile, their weak-ened positions, including bankruptcies, are likely to have negative effects ongrowth more generally. These negative factors are likely to reduce the acceler-ation in growth to levels below those usually seen in cyclical upturns.

Among the developed countries, the United States was the most adverselyaffected by the heightened geopolitical uncertainties and, correspondingly, isbenefiting the most from the return to normalcy. As in 2002, therefore, theUnited States is expected to lead the global economic recovery. No other majoreconomy appears to be in a position to assume this role in the near future.Japan, for example, continues to face difficulties in extricating itself from itsslow growth path while Germany appears to have entered a recession in early2003. Most countries are explicitly looking for improved growth in the UnitedStates to act as a catalyst in revitalizing their own economies.

Recovery in the United States is expected to materialize in the second halfof 2003 and to provide a stimulus to growth elsewhere. The depreciation of thedollar in early 2003, if sustained, will reinforce this recovery in the UnitedStates but will reduce the extent of the stimulus that United States growth pro-vides to the rest of the world. Nevertheless, there will be an acceleration in thegrowth of world trade, to the benefit of all countries. Many developing coun-tries are also benefiting from improved, albeit still historically low, commodi-ty prices and some have the advantage of lower interest rates in internationalcapital markets.

A widespread recovery is necessary because, while they may launch arecovery, the present positive forces in the developed countries, particularlythe United States, are unlikely to be sufficient on their own to sustain a recov-ery throughout 2004. Business investment has been particularly sluggish overthe past two years and will need to revive in order to sustain the momentum.The decline in excess capacity should increase the demand for new capital,while improved equity prices and higher profits as a result of the revival ofconsumer demand should ease its financing. Although low interest rates havenot stimulated business investment to date, they should facilitate increasedinvestment if other conditions improve. However, there is also a need for amore positive international environment, comprising improved internationaltrade and a revival of international capital flows, in order to induce increasedbusiness spending.

A better external environment will enable the economies in transition tobuild upon their recent domestic strength. In the developing countries, improv-ing external demand in the second half of 2003 and 2004 is expected to buttressrecovery in Latin America and to provide additional support to steady but lim-ited growth in Africa. Partially because of the effect of SARS in the early partof the year, growth will moderate in Southern and Eastern Asia in 2003 but willrebound in 2004. Similarly, the situation in Iraq will cause a slowdown inWestern Asia before the recovery forecast for 2004.

W O R L D E C O N O M I C A N D S O C I A L S U R V E Y 2 0 0 36

A LACKLUSTRE INTERNATIONAL ECONOMIC ENVIRONMENT

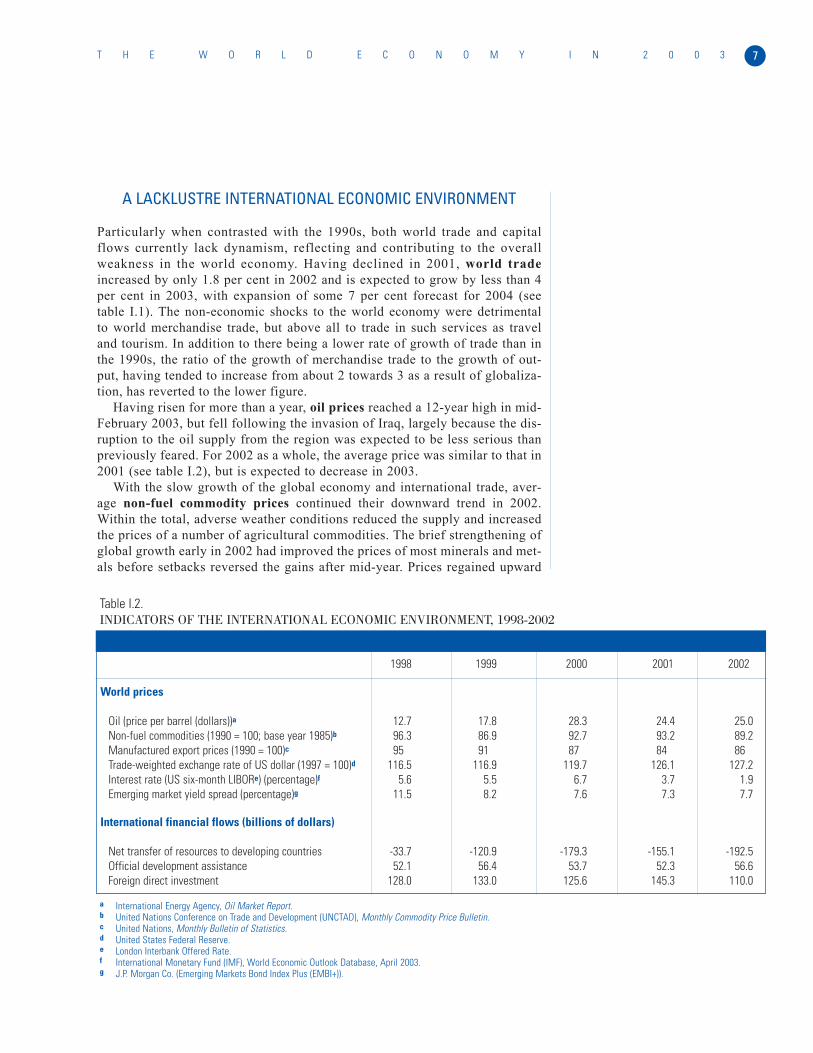

Particularly when contrasted with the 1990s, both world trade and capitalflows currently lack dynamism, reflecting and contributing to the overallweakness in the world economy. Having declined in 2001, world tradeincreased by only 1.8 per cent in 2002 and is expected to grow by less than 4per cent in 2003, with expansion of some 7 per cent forecast for 2004 (seetable I.1). The non-economic shocks to the world economy were detrimentalto world merchandise trade, but above all to trade in such services as traveland tourism. In addition to there being a lower rate of growth of trade than inthe 1990s, the ratio of the growth of merchandise trade to the growth of out-put, having tended to increase from about 2 towards 3 as a result of globaliza-tion, has reverted to the lower figure.

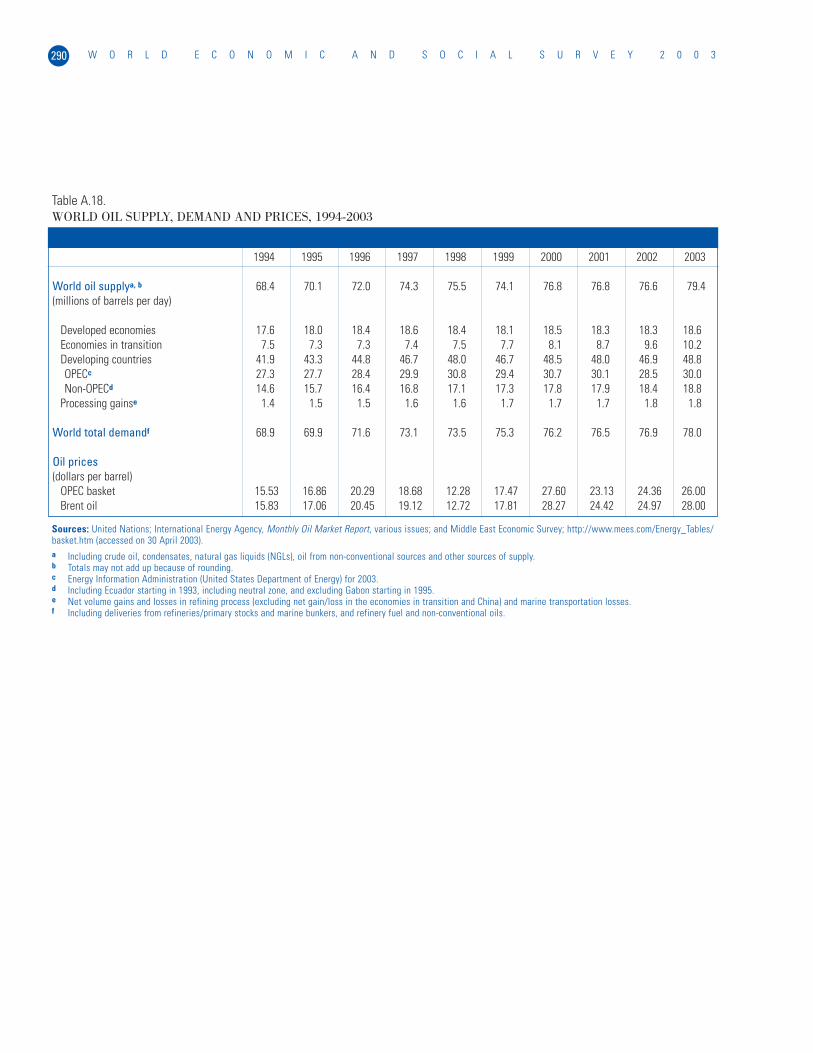

Having risen for more than a year, oil prices reached a 12-year high in mid-February 2003, but fell following the invasion of Iraq, largely because the dis-ruption to the oil supply from the region was expected to be less serious thanpreviously feared. For 2002 as a whole, the average price was similar to that in2001 (see table I.2), but is expected to decrease in 2003.

With the slow growth of the global economy and international trade, aver-age non-fuel commodity prices continued their downward trend in 2002.Within the total, adverse weather conditions reduced the supply and increasedthe prices of a number of agricultural commodities. The brief strengthening ofglobal growth early in 2002 had improved the prices of most minerals and met-als before setbacks reversed the gains after mid-year. Prices regained upward

7T H E W O R L D E C O N O M Y I N 2 0 0 3

Table I.2.INDICATORS OF THE INTERNATIONAL ECONOMIC ENVIRONMENT, 1998-2002

1998 1999 2000 2001 2002

World prices

Oil (price per barrel (dollars))a 12.7 17.8 28.3 24.4 25.0Non-fuel commodities (1990 = 100; base year 1985)b 96.3 86.9 92.7 93.2 89.2Manufactured export prices (1990 = 100)c 95 91 87 84 86Trade-weighted exchange rate of US dollar (1997 = 100)d 116.5 116.9 119.7 126.1 127.2Interest rate (US six-month LIBORe) (percentage)f 5.6 5.5 6.7 3.7 1.9Emerging market yield spread (percentage)g 11.5 8.2 7.6 7.3 7.7

International financial flows (billions of dollars)

Net transfer of resources to developing countries -33.7 -120.9 -179.3 -155.1 -192.5Official development assistance 52.1 56.4 53.7 52.3 56.6Foreign direct investment 128.0 133.0 125.6 145.3 110.0

a International Energy Agency, Oil Market Report.b United Nations Conference on Trade and Development (UNCTAD), Monthly Commodity Price Bulletin.c United Nations, Monthly Bulletin of Statistics.d United States Federal Reserve.e London Interbank Offered Rate.f International Monetary Fund (IMF), World Economic Outlook Database, April 2003.g J.P. Morgan Co. (Emerging Markets Bond Index Plus (EMBI+)).

momentum towards the end of 2002. With the global economic recovery gain-ing momentum and with the weakening of the dollar, most non-fuel commodi-ty prices are expected to strengthen during 2003 as a whole and in 2004.

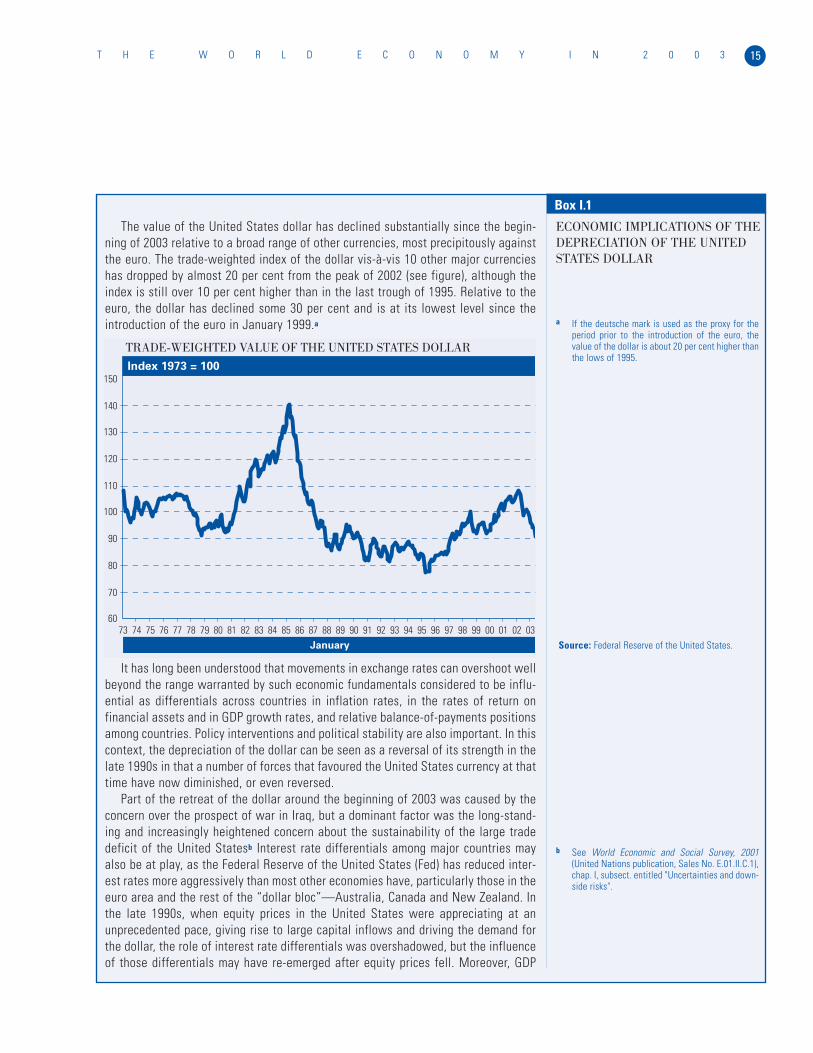

There was a substantial movement in the exchange rates among the majorcurrencies in mid-2002 and in the first few months of 2003, most notably adecline in the value of the United States dollar against the euro and, to a less-er extent, other major currencies. If this depreciation of the dollar is sustained,it will have major implications for global economic prospects (see below).

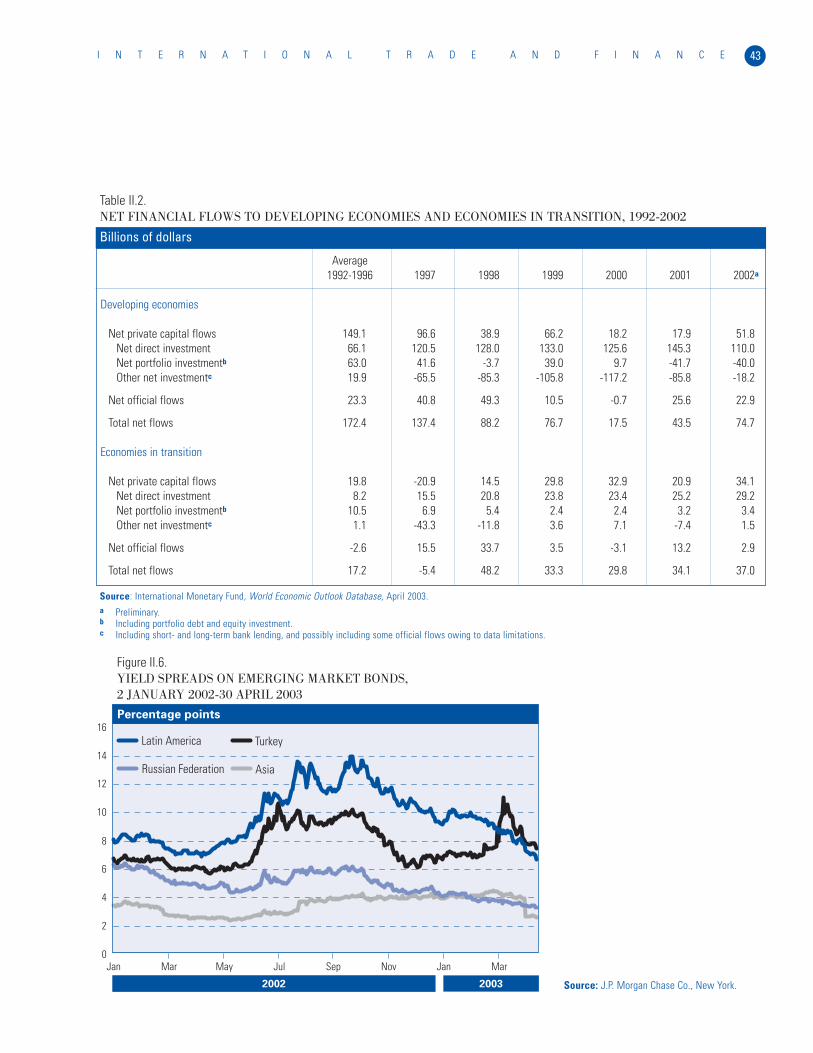

Net official financial flows to developing countries remained substantial in2002 but this was mostly because of large International Monetary Fund (IMF)loans to a few countries facing financial pressures. More encouragingly, offi-cial development assistance (ODA) increased in 2002, not only in absoluteterms but also, marginally, as a proportion of the gross national income (GNI)of donor countries. There were also pledges during the year of future increas-es in ODA, hopefully marking a turnaround in the downward trend that hascharacterized recent years.

Private international financial flows continued to be lacklustre in 2002and no major improvement is expected in the short term. Among the developedcountries, the global economic slowdown and the bursting of the bubble inequity markets have created a lull in international financial transactions,notably large cross-border mergers and acquisitions between companies.

For developing countries, official and private capital outflows and paymentsabroad associated with earlier inflows not only exceeded the correspondingreceipts for the sixth consecutive year in 2002 but did so by a record amount.This net financial transfer has exacerbated the negative effects for develop-ing countries of the slow growth in the real sectors of the developed countries.

Foreign direct investment (FDI) flows to developing countries initiallywithstood the global economic slowdown of 2001, possibly because of the lagbetween investment decisions and implementation. In 2002, however, globaleconomic conditions and the slowdown in privatizations resulted in a fall inFDI flows to developing countries, with the notable exception of China. Amajor resurgence in these flows seems unlikely in the short term. FDI flows toEastern European economies, on the other hand, continue to be robust, prompt-ed not only by cost considerations but also by the prospect of their entry intothe European Union (EU); these flows are expected to be sustained.

Reflecting their largely pro-cyclical nature as well as the poor geopoliticalclimate, other private capital flows to developing countries continued to beweak in 2002 and were exceeded by outflows. For those developing countriesthat are able to participate in international capital markets, the cost of interna-tional borrowing has tended to fall as lower interest rates in the developedcountries have been coupled with lower “spreads” for borrowing developingcountries, particularly since the invasion of Iraq. Private financial flows todeveloping countries may increase as the global geopolitical environmentimproves and the world economy gains momentum. However, these samedevelopments are likely to prompt a recovery in financial markets in developedcountries, which may reduce the present incentive to channel funds to devel-oping countries.

W O R L D E C O N O M I C A N D S O C I A L S U R V E Y 2 0 0 38

POLICY RESPONSES TO SLOW GROWTH

The extent of the initial economic slowdown, while severe, was reduced bythe counter-cyclical policy measures, including those of an automatic nature,adopted by many countries. There were, however, variations in the extent towhich countries were able or willing to adopt expansionary measures, par-ticularly as the period of slow growth lengthened. The continued sluggish-ness suggests the need for more stimuli, but the policy framework in a largenumber of economies is constraining many authorities from adopting suchmeasures.

The immediate reaction to the economic slowdown in 2000-2001 was sub-stantial reductions in policy interest rates in developed countries. Althoughenergy and, in some countries, housing prices rose in 2002, inflation was notseen as a major threat in the majority of developed countries and low interestrates were maintained in most countries throughout the year and into early2003. Some central banks, notably the Federal Reserve of the United States(Fed), reduced interest rates further in this period, bringing them to unusuallylow levels in many cases. The inflation-targeting rule followed by theEuropean Central Bank (ECB) until early 2003 gave it less room for manoeu-vre and delayed its cuts in policy interest rates until March 2003. At the sametime, it changed its inflation objective of 2 per cent from a ceiling to a target,allowing greater flexibility in its monetary policy. The possibility of deflationhas encouraged a number of central banks to indicate that they would considerthe possibility of further monetary easing if necessary. In several countries inEastern Europe, interest rates were reduced in 2002, primarily to dampen anyappreciation of the exchange rate so as to maintain competitiveness.

Most countries have had less scope for expansionary fiscal policies becausethe size of their fiscal deficits has made them subject to either a self-imposedbudgetary rule or a possible adverse reaction from global financial markets orthe international financial institutions. A major exception has been the UnitedStates where increased central government expenditures and reduced taxationin 2002 combined to produce a sizeable fiscal stimulus and a growing fiscaldeficit. In Western Europe, fiscal policy was slightly expansionary in 2002, butFrance, Germany and Italy are under pressure to consolidate their budgetarypositions in order to meet the 3 per cent deficit ceiling embodied in theStability and Growth Pact. Although it has no such policy rule, the Governmentof Japan is already in a difficult financial position and any further sizeable fis-cal stimulus would aggravate the risk of a further downgrade in its sovereigndebt by international rating agencies, further damaging economic confidence.

Many developing countries and some economies in transition improvedtheir fiscal positions in the 1990s but deficits remain a problem, aggravatedsince 2001 by reduced government receipts and, in some cases, increasedexpenditures to offset the economic slowdown. However, there is a broaddichotomy between developing countries with relatively sustainable macro-economic positions and those with macroeconomic disequilibria and/or other,often external, constraints. China and most economies in East Asia have beenable to use monetary and fiscal instruments in the appropriate counter-cycli-cal manner during the present period of slow growth. In contrast, mosteconomies in Latin America and Africa have had to give priority to address-

9T H E W O R L D E C O N O M Y I N 2 0 0 3

ing their macroeconomic imbalances; this has usually required using theirmacroeconomic policy instruments in a restrictive, currently pro-cyclicalmanner, rather than as a means of offsetting the present sluggish conditions.This dichotomy is likely to continue in 2003 and will contribute to a continu-ation of the divergent growth outcomes, and hence widening income dispari-ties, across regions and countries.

REGIONAL PERFORMANCE AND PROSPECTS

Because they have faster rates of population growth, developing countriesneed to grow faster than developed countries if they are to achieve a year-to-year improvement in the well-being of their average citizen. If they are tomake meaningful progress towards reducing the number of people living inpoverty, developing countries have to maintain a high growth rate continuous-ly for an extended period of time. The current period of sub-par growth hascompromised both these objectives.