Winning the Retirement Game by Doug Moore 5 30 12 update - mobile 770-608-8711

40

1

-

Upload

independent -

Category

Documents

-

view

4 -

download

0

Transcript of Winning the Retirement Game by Doug Moore 5 30 12 update - mobile 770-608-8711

1

2

Winning the Retirement Game

1. The New Bubble Economy – Are Bonds and Gold

Next? Don’t Let This One Explode Your Wealth!

How to Earn Respectable Returns With Out Worrying About Stock, Bond and Gold Bubbles

2. Tired of the Roller-Coaster? – Want to get off?

How to Reach Retirement and Actually Stay Retired by Avoiding the Coming American Income Crisis

3. The Market is UP…Mainly to Here!

A Lesson from Mad Magazine on How to Read and Interpret Misleading Market Advertising and News

4. Are These Risks in YOUR Portfolio?

Hidden Risks That Ruin Retirement Life-styles

5. The Buffets Were Right!

…Both Jimmy and Warren.

6. To Vary or Not to Vary –

Why Leading Experts Love to Hate Variable Annuities

3

The New Bubble Economy… Don’t Let This One Explode Your Wealth

Money talks, it says, “Good-bye”. I came across a book by that title when doing research for another book. I have listened to countless clients over the years and studied countless more reports and analysis and it’s a truth retirees have been experiencing in shockingly large numbers. In fact, the new norm is low to no growth and lots of head-aches and needless losses.

My goal in writing this is to help my readers have the opposite experience: have their money say, “Hello”, to them for a life-time. I studied Greek philosophy as part of my BA studies and the Greek language for part of my Masters. A concept the Greeks had was, “Arête”, or balance. The balanced life is not free from stress but has a healthy dose of stress that stretches them: body, mind, soul, and spirit. People need to balance their money between risk and safety: too much safety can mean zero returns after taxes and low rates. Too much risk can mean total loss of one’s nest egg is today’s bubble economy. Believe me you don’t want this to happen. If this has already happened to you, I am sorry for your misfortune. You were misinformed and this book will show you why and help give you tools to avoid the same mistakes when the next bubble bursts. That’s “when” not “if”.

There is healthy stress (like exercising) and then there is unhealthy, unnecessary stress (like losing nest-egg money). Are you the type of person that likes to feel like you are in control of your life and finances? Probably, or you wouldn’t be reading this! Most people feel great stress when they feel like they are out of control. When their portfolios crash and their brokers don’t call them, they feel let down. When their on-line accounts suddenly crash without warning due to events out of their control, they feel stress. They feel out of control when their bank account interest rates aren’t keeping up with inflation. I address how to avoid these types of stressors and more in this publication.

Clients are smart to consider the impact of running out of money before running out of life. This is the biggest worry that most people face as they retire or live in retirement. I provide a game plan in this publication that keeps you in control with a strategy that puts you in the winner’s circle.

4

Winning the Retirement Game requires one thing: understanding the game and then implementing the strategies in this publication.

Americans who are approaching retirement age or are already in retirement have many reasons to worry about their savings. The questions and considerations for planning winning retirements include addressing the following points:

Will I have a sufficient income? Should I risk more losses in the market?

The devaluation of my biggest asset - my home. Housing prices plummeted – should I rent, buy a smaller home or get a Reverse Mortgage?

No Cost of Living increase for Social Security & there may not be one next year either. Govt. SSI is Bankrupt – can I rely on this?

Lowest interest rates seen in many years.

Depleted Investments from the worst recession and market crashes in in decades – Can I afford to lose more?

Starting in 2015, Social Security payouts will begin to exceed more than what is paid in via payroll taxes. Odds are the government will raise taxes, and/or cut benefits in order to bring the system into balance. Is my retirement plan both Tax efficient and Stock Market Proof?

Military personnel have had their pension checks reduced. Will they further reduce pensions again next year?

Corporate Pensions: Chrysler defaulted on their pension plans – Is my pension safe and am I 100% sure it will be there for me in the future?

The market has not been friendly to retirees in the new Millennium. Nor has housing and banking. We have all hoped for strong recovery after the huge tax payer bail-outs and quantitative easing (that is – printing money) but for over 10 years the records show that returns have been negligible. This is why some call it the “Lost Decade”: no real profits in exchange for a nerve wracking decade on a financial roller-coaster (see: Tired of the Roller-Coaster?). Another year of waiting for the market to recover could prove disastrous to your financial health. For all the grief investors went through and trillions in bail-outs, 2011 closed with a whimper. It has offered up only losses or tepid returns for all their pain-staking tenacity and top minds in the industry are casting a wary eye on current trends.

5

Karlan Tucker, ranked as one of Denver’s top financial advisors, states, “the S&P 500 is close to where it was in January of 2000. Seldom does it post a 10% gain for a year, and on average there have been no years with a 10% gain. Maybe they meant the NASDAQ? Well, the math doesn’t work there either since it’s down 50% from 2000.” He fully endorses the strategies I reveal below. Tucker continues: “I wonder why anyone ever listens to stock analysts given that more than 90% of the time their recommendations are either buy or hold. Their bias is so strong that it becomes laughable. This year, American Airlines announced they were in financial trouble and that bankruptcy was a possibility. Did the analysts who follow their stock see it coming? Was it their job to see it coming? If not, what does an analyst do? The week before American Airlines filed bankruptcy, Barclays, Deutsche Bank and Morgan Stanley, as well as EVERY company who tracked the stock, had a buy or hold rating on the stock”. No wonder so many people feel like they have been losing the retirement game. The “coaches” don’t seem to know which end is up…or when to get their clients out of a losing game that can ruin not only a season but a life. A huge reason Americans have been losing out is that they are given buy signals or entry points by brokers but they give no exit signals. I reveal why in a later chapter.

Even with January & February’s market up-tick, the market is still nowhere near where it was predicted to be (see “The Market is Up…Mainly to Here”). Could we be hitting another ceiling that is ready to slam the market back down? Fund Manager John Hussman thinks so. He and other fund managers are wary that, “market conditions like today's almost always lead to sharp pullbacks over the next six months” (Yahoo Finance, Feb 2012).

Jason Zweig, in his Intelligent Investor column, asks the question that in the light of yesterday’s record drop in the market after a run up (2/10/12 -- the biggest drop of for 2012), “Why is it so hard for investors to regard such short term hot streaks with the cold eye they deserve?” He cites analysts at Decision Research and studies led by neuroscientist Paul Glimcher of New York University who have proven that because of the way human brains are wired, the vast majority of people make bad investment decisions over and over again. He concludes by stating, “Thus, after a decade of mostly dismal returns, even a month or two of out-performance might prompt you into an impulsive plunge back toward

6

stocks. Some investors seem to have learned how to resist this tendency, and you should, too” (WSJ).

Proof of the retiree income crisis can be found in a recent Wall Street Journal article: “More Elderly Find They Can’t Afford Not to Work.” They cite one elderly lady who lost half her life savings to recent market crashes. She now has to work at age 78. The millionaire CPA, or I should say, former millionaire, had the same story. Due to market losses he lost his million dollar home; so did the oil-engineer’s wife who told me her brokers kept on telling her, “they are only paper losses”. These are stories I hear on a monthly basis. The numbers don’t lie: “As of December (2011) 1,310,000 Americans age 75 and older were working, a 25% jump from 1.05 million in 2005, according to the Bureau of Labor Statistics” (WSJ Jan 21-22, p.1). What the brokers aren’t saying is that the paper losses they have generated for clients are translating into retirement life-style losses: loss of comforts, freedoms, travel plans, vacations and fun that had been planned. The real crisis that retirees are facing then is an Income Crisis and some are just a “bubble away” from losing their dreams.

A new series of bubbles are about to blow according to the September 2011 issue of Smart Money. They see serious bubbles not only

in stocks but also in Gold, Oil & Bonds: “If even one of these trends catches fire, the

interest people collect on bonds they currently own will be less valuable – and the

bonds’ prices will plummet. Contrary to popular belief, says Tom Atteberry, manager of the $3.7 Billion FPA New Income fund, ‘the bond market is the high risk place’” (see Article Addendums). It’s not a matter of “if” but “when”. “What” bubble will burst first is debatable however. “Who” in their right mind wants to be in one is the over-riding question. Certainly nest-egg money should be bubble proof.

In this report I will show you how to get off the “bubble band-wagon” and solve today’s Baby Boomer Income Crisis. Boomers are becoming more cautious and are looking for solutions. “If there’s one thing we know from 2007and 2008, investor psychology has changed and people don’t want to chase what they think is a bubble”, states Matthew Lloyd, Chief Investment Strategist at Advisors Asset Managers, who have 7.2 billion in assets under management (WSJ 2/2/12 C1).

7

Harnessing the sector outlined in this publication the proper way, you can earn respectable returns in up markets AND protect your assets and annual gains in down markets.

Many leading experts are saying the recent “pops” in the market are not the full explosion we have yet to hear…and it will rival the 50% declines of 2007-2008. Hopefully you will act on some of the following strategies and save yourself from seeing your hard earned money disappear in the flames of the next major crash. Remember, bonds can get bubbles too.

DOW/S&P gains for 2011 have been wiped off the books and we’ve seen the worst crash since 2008. Investors lost 1 TRILLION DOLLARS on August 8th, 2011 alone. The indices on August 8th were as follows: the Dow 10,809.85 -634.76 -5.55% Nasdaq

2,357.69 -174.72 -6.90% S&P 500 1,119.46 -79.92 -6.66% Treasuries 2.34 -0.22 -8.56%. On August 14th a major paper headlined with “Market Madness Unnerves” citing a Morgan Stanley Smith Barney statement calling the week of the 8th – 12th, “The Wildest Week in Wall Street History.” Here’s what we are talking about: Monday, August 8th, market dives 634.76 points; Tuesday: up 429.92; Wed: down 519.83; Thursday: up 423.37; Friday: Up 125.71. Yes, for over a Decade the stock market has taken investors on a wild ride to nowhere. The market closed on 8/19/2011 at 10817.65 with Wall Street Journal stating: “Stocks End Week on a Sour Note.” The wildest week has turned into the “wildest month” with the market down even further at 10,638 on 9/22/11.

Mark Hulbert, quoted in Financial Advisor magazine, states, “’don’t let your financial advisor excuse his poor performance with reference to the so-called lost decade,’ he writes. ‘A good advisor could have prevented that decade from leading to your loss, too’.”

That’s exactly what I did for my clients who followed my advice: prevented losses and created guaranteed growth and income. I am not bragging. I just get tired of investors being misinformed.

Financial Advisor Journal heralds the insights of Rob Arnott in Fundamental Index newsletter, “the problem with the 2000s was overconfidence in the equity markets, which he compares to the overconfidence about the infallibility of the Titanic in 1912. The unshakeable faith in the equity risk premium”, he writes, “caused the $8 trillion U.S. pension supertanker to charge ahead with massive equity allocations into a decade that did not reward equity investors.”

8

Arnott says it was the worst decade in history for U.S. equity investors, worse than the 1850s and 1930s. In the first decade of the 21st century, the S&P 500 compounded at negative 1.0% per year, which was 3.6% below inflation. In the 1850s, it compounded by a positive 0.5% and in the 1930s by a negative 0.1%.” Warren Buffet offers an Investment 101 course. Its purpose is to throw doubt on the premises of the pension funds to assume they can make 8% a year. “He attacks with cynicism those CEO’s who present themselves as able to report higher earnings per share and thus promote their stock prices if they assume an 8% return on the corporate pension plan. In other words, it’s another make believe game by corporate executives whose concern is to ‘juice earnings’” (Forbes.com). Robert Lenzer writes, “The DOW Jones industrial average made a marvelous ascent in the 20th century from the impossible to recall level of 66 in 1900 to 11,497 at the eve of the new century – a compound rate of only 5.3%. Not 8%. Not 10%. Not 15%, that magic target many professional money managers believe they can hit. Croesus repeats – your return in the 20th century was 5.3% annualized before dividends and before inflation. Here’s the real downer, we are nowhere near that today” (R. Lenzer, Forbes.com). Buffet drives this point home in his annual meeting with shareholders. Lenzer cites Buffet’s address to shareholders stating, “You’re unlikely to make anything like 5.3% for the next 92 years. Swallow hard and read on. To achieve 5.3% this century would mean a Dow climbing from roughly 13,000 today to (gulp!) 2 million. As Warren opines: ‘We are now eight years into this century, and we have racked up less than 2,000 of the 1,988,000 Dow points the market needed to travel in this hundred years to equal the 5.3% of the last.’ Don’t expect the 5.3% in the 21st century. That’s the bottom line. Indeed, in the first seven years of this new century, we’ve made just 1,366 points – or less that 12% -- about 1.7% per

year. And for those of you who think you’ll make 10% -- or 8% from price appreciation and 2% from dividends, dream on. Because, as Buffet puts it so succinctly, you are implicitly forecasting a level of about 24,000,000 on the Dow by 2100’”.

Buffet likens investment advisers who promise such a performance to the Queen in Alice in Wonderland – and warns, ‘beware the glib

9

helper who fills your head with fantasies while he fills his pockets with fees’” (Forbes.com, The Croesus Chronicles Buffet: New Advice From On High, Robert Lenzer 4.30.08 – also see the article in this publication: The Buffets Were Right…).

Buffet ads, “If you are not going to be in the market for 10 years then you should not be in it for 10 minutes!” Why? Because the volatile nature

of the market can steal your initial investment early in the investment cycle thus requiring years to recapture the initial investment before seeing any gains. And remember, paper gains don’t count. You don’t realize gains in the market until you sell shares.

Needless to say, there is a lot of uncertainty in America and globally. But, one thing is for certain: Americans are still going to eat and they are still going to want a roof over their heads and a safe place for their money. This last

point is why I am providing this periodical to clients. You’ve got to have money in order to guarantee the ability to buy food and shelter. Therefore, your money had better have guarantees on it!

When my Grandpa Moore’s bank in Nebraska went under during the Great Depression, they gave him a house to compensate for all the money they lost in his account. He owned and operated Moore’s Modern Market, a grocery store serving the remote farm community that generations of Moores had lived in not far from the Pony Express trail. He and Grandma lived in that house from that day forward (the Great Depression) and throughout their over 60 years of marriage (Grandma taught Children’s Sunday-School at the same Church for over 50 years). Their grocery-store never closed because, people are going to buy food. People may let their phone go, they may have to let their cable TV and internet go, they may buy less clothes and take less vacations, but they are going to shop for groceries, they are going to want a safe place to sleep…and they will want safe place to keep their money.

Warren Buffet knows this and owns assets in the following sectors:

1. Food -- People will always buy food and drink and pay to have it transported to them: he owns shares of Coca-Cola, Sees Candy, Mars,

10

Wrigley and all of one Railroad (Railroads get food and building supplies to Americans. Rail is much cheaper than over the road haulers and Buffet is making an all-in bet that Americans will not give up the basic needs of life and will pay his company to transport those goods for a long time).

2. Housing – People want a roof over their heads -- he owns the suppliers that provide housing and the things that go in houses: He owns Shaw Carpet, Furniture Mart, a mobile home manufacturer, and part of a huge battery manufacturer (in China), and he recently bought a picture frame company in Atlanta.

3. Money -- He owns insurance companies. These include Geico (insures vehicles & and a has a green Gecko spokes “person”) and General Re (a re-insurance company). Insurance Companies are the sole provider of Annuities. They use Re-insurance companies to insure their policy-holders’ money. This 3rd point is probably the most interesting. Buffet’s daughter wrote a book about her dad and in it she stated: “If you want to get rich like my dad, buy an insurance company.” If you can’t buy an insurance company, you can still benefit from their strong returns and safety by making deposits in them. These deposits are not called shares but policies. Insurance companies keep much larger amounts of assets on hand than banks. He is also the biggest shareholder in Wells Fargo Bank.

Babe Ruth used the asset class we recommend in this publication during the Great Depression: it was the only major holding that he didn’t lose money in and the Insurance Industry was the only major employer to keep hiring in the Depression. And in the recent Great Recession; guess what? They were still hiring and clients got to keep all their gains and principal deposits.

Some pundits claim we are coming out of the Great Recession (and others say we are going into a 2nd Great Depression). Knowing this, we need to be pro-active, not reactive. As I will prove in this publication, what worked in the past works today...and better yet, improvements have been made due to new technology. We just experienced the biggest market crash (2007-08) and the highest volatility (Aug 2011) since the Depression and my clients did not lose a penny of their safe money. And, thanks to the “Annual Re-set Strategy”, they were able to keep annual gains earned via market participation strategies that they banked leading up to the 2008 Crash. Furthermore, when the markets rebounded, their accounts didn’t have to rebuild from 50% losses, they caught

11

some of the updraft of the markets from a zero-loss position (see Chart showing an actual client statement on page 37 of Article Addendums). You can buy in to this annual re-set strategy by owning certain types of FDIC Insured CD’s or Fixed Index Annuities (FIA’s). Remember, Buffet’s 3rd major asset class is Insurance and he’s been an owner of Insurance companies (he owns 100% of a couple of insurers) since his early days and recently got into banking in a smaller way owning about 6% of Wells Fargo (it was the best performing bank of 2011 losing only 6% in share value and Warren is the biggest shareholder according to Forbes, Feb 13, 2012). When investors lost 50% in the stock market crash of 2007-2008, how much do they have to make to get back to even -- 50%; 75% percent? No, a 50% loss in the market requires a 100% gain just to break even! Sadly, our government has seen fit to burden tax payers by bailing out the brokerages and banks that created the mess in the first place. We now sit on over 14 Trillion in debt due to bail-outs and 100 Trillion in unfunded liabilities. QE 1 and QE 2 didn’t get us back to even. And, according to Jim Rogers, “We already have QE 3. They are just lying to us about it. The Federal Reserve is still in the market spending huge amounts of money” (Financial Intelligence Report, p.3). QE, or Quantitative Easing, is a bubble causing “trick” that the White House is using to keep interest rates low by buying huge amounts of government bonds, “because the money supply numbers are going through the roof” (Rogers, p.3). Greed and fiscal irresponsibility are not just American problems. Socialistic Greece (who “cooked” their books) and other countries are breaking the back of the Eurozone…and if the Eurozone cracks, as some fear it will, we all get egg on our face. Quantitative Easing is a “program” the Fed called “Operation Twist” wherein

the Federal Reserve to prints money out of thin air in order to buy long term

bonds while selling short term bonds (see WSJ 3/14/12 A1&2). Pulling money out

of thin air certainly is “twisted” and will twist money out of your pockets for

generations to come. The program can temporarily contain inflation but then in

turn lead to more inflation. American citizens were given no choice. While

QE1&2 did help stem a total Wall Street meltdown, some economists fear it only

delayed a future crash. I think they are correct. The Fed basically, “Robbed Peter

to Pay Paul”. This was “Robin Hood in reverse”: Instead of robbing from the rich

12

to help the poor, they robbed from tax payers to keep Brokerages and Bankers in

the money. Future generations are being left with a tab they can’t pay and

shouldn’t have to.

Wouldn’t it be nice to actually make money for a change and never have it run out?! Well we have just the strategy to help you grow your money and guarantee life-time income, plus, you keep control. Furthermore, Bank Investment Consultant states that our time tested, state regulated, needed no bail-out, life-time income product, is now being used in Banks because, “Indexed Annuities could be a godsend for bank investment reps”. FIA’s, “offer customers some upside potential with full downside protection”.

Tired of the Roller-Coaster? (Want to get off?)

The truth of the matter is that retirees and those trying to make plans to retire have been experiencing a chaotic, nauseous ride to nowhere on a very expensive roller-coaster called… “The Stock Market.” The market in itself isn’t evil and most of the companies don’t stink. Problem one is that the current way of harnessing the power of the market isn’t working. People retiring today need life-time income and want to eliminate risk…and need to before their income generating assets disappear in an explosion of risk and flames of uncontrolled government spending and international market and societal meltdowns and violence. Another problem that has created this roller-coaster of market risk and investor losses, according to Barrons, is poor ethics (for more on this read Pirates of Manhattan and famed economist Milton Friedman’s, Money Mischief). How many brokers were honest enough to suggest to their clients that they put a stop loss under their money in stocks? Why didn’t they? Some experts suggest it’s because they would have lost their trail commissions. This is probably true and an inherent problem in trusting a broker’s opinion about whether to stay in the market or not. They CANNOT give you an unbiased opinion.

How Much Do You Want to Lose? Most investors have an entrance point

but no exit strategy. The most important questions I believe an investor must ask himself about his money in the stock market are: “How much am I willing to lose? What is my sell point? At what point will my losses cause me to lose sleep?” So,

13

how much do you want to lose? What is your sell point? Would you lose sleep if you lost 20% of your portfolio tonight? Then your stop loss should be set in stone with your broker or in your online trading account at 20%. You alone know what your mental sell point is. Have you lost enough already? Are you tired of the roller-coaster? Then now is the time to sell from a psychological and naturally, financial, standpoint. I call this the, “Sleep at Night” principle. If you are going to lose sleep at night over an investment turned sour, get out now. If you think it’s going to turn sour and you will be mad at yourself if you don’t move out, move now. You don’t have to give up decent returns when you give up risk. Retirement is not a time to be worrying about losing money or about having to go out and find work again to make ends meet. It is the wise investor who can take his or her emotions out of the equation, know what their sell point is, and then set their stop losses either online or with their broker to “get out while the getting is good.” When people are approaching or in retirement, they need to move from asset accumulation strategies (via stocks, bonds and mutual funds) to Asset Preservation and Distribution accounts found in various types of fixed annuities (Immediate Annuities, CD type annuities, and Fixed Indexed Annuities or FIA’s). Research shows that most investors buy high and sell low due to emotions. This was proven by the Dalbar study which showed that even in up years in the market investor returns still only got around 3% returns at best. Our strategy takes emotions out of the picture and lets client accounts grow on auto-pilot with no losses in down years (see chart in addendums). Warren Buffet dedicated an article to the topic titled, “The Psychology of Investing.” Markets are not rational. They follow the emotions of the times and when times are bad, people flee for the doors…and the last ones out lose the biggest. Market pros are usually the first ones out leaving mom and pop investors holding the “bag”. Much like the captain who recently jumped off the giant cruise ship in Italy leaving passengers behind, Wall Street pros not only jump-ship first, they get bonuses for doing so! Facebook IPO investors have lost 24% to date (5 29 2012 WSJ). Unfortunately, another risk now lurks in the market and it has bitten into the effectiveness of placing stop loss orders on holdings. The new menaces now swimming around the shark tank of the market are called “flash crashes” and

14

many people had their portfolios shredded by these technologically induced crashes...even with stop losses set in place! Computer generated high-speed stock trading at certain hedge funds have been blamed for the flash crashes and most people doubt that this danger is able to be fixed. Barron’s May 2nd, 2011, (pages 28 & 29) states that middle-class American stock market investors are really “Anchovies in the Shark Tank”. They cite author Jim McTague’s new book Crap Shoot Investing and his revelation that the SEC’s implementation of Reg NMS and how it has led to “Flash Crashes” (with more to come). Furthermore, McTague reveals professional traders Arnuk and Suluzzi blew the whistle (to no avail) on their finding that “fairness and trust” no longer exist on Wall Street. The big guys win, the consumer loses. I strongly feel that every time one of our clients does business with us, we are doing them a favor. Most people don’t plan to fail, they just fail to plan. Others plan but they plan with the wrong set of information. Most financial advisors worth their salt know that clients wanting to create life-time income should never be told to take out more than 4% of their annual retirement savings. Now, when you consider that the market has returned a measly .2% annually for the past 12 years, it means most retirees have had to dig in to their retirement nest-eggs and remove nearly 40% of their “eggs” that they actually wanted and needed to keep to generate income. With inflation going up and their nest-eggs going down, naturally, they are worried and losing sleep. Well, we offer sleep insurance. “Sleep” does NOT mean boring! You trust insurance companies to insure your home; you trust insurance companies to insure your cars; you trust insurance companies to insure your valuables and your life. Why not trust insurance companies to protect your money and guarantee your life-time income too? In the article, “Don’t Scramble Your Nest Egg”, the Wall Street Journal states it’s the smart thing to do in approaching retirement. Annuities ensure that you never run out of money. And only annuity companies offer this life-time income guaranteed insurance. That is what they are designed to do. Life insurance protects you against living too short; Annuities insure you against living long…and we are all living longer. The brother of Dr. Christian Bernard, the inventor of the artificial heart who did the world’s first heart surgery is a financial professional who worked for an insurance company. He stated, “The problem today is not that we dying, the

15

problem today is that we are living longer.” Mortality tables have recently been re-set to age 120. Annuity owners get income for life, however long that may be, should they choose life-time income pay-outs. “Longevity Insurance” is the new catch-phrase. And those life-time income rider payments can go up! America’s most famous CPA, Ed Slot, writes: “Annuity experts say not to be lulled into believing that your only option with a fixed-rate indexed annuity is to accept inflation risk. Remember, investment and retirement planning is all about what’s right for you. As I wrote earlier, my mother had a fixed annuity and yet her checks would go up at times. How could this be? The answer is that a fixed annuity can be indexed to offer a degree of inflation protection, regardless of whether it’s an immediate or deferred type of annuity” (Ed Slott, CPA, Stay Rich for Life, pg. 119). Not only is Ed Slott’s educational documentary featured on PBS but Financial Advisor Journal says of him: “Ed Slott was named "The Best" source for IRA advice by The Wall Street Journal and called "America's IRA Expert" by Mutual Funds Magazine. He is a widely recognized professional speaker and educator specializing in retirement distribution planning, teaching both financial advisors and consumers how to best take advantage of our complicated tax code” (24 Jan 2012 e-version). I think it is safe to assume if professional Financial Advisors turn to Ed Slott for advice, you can trust when he infers in his book, “If fixed index annuities are good enough for me to recommend to my mom, they’re good enough to recommend to your clients.”

The question we should be asking ourselves as we approach retirement should not be: what’s the next hot sector, stock (May 2012’s Facebook “Faceplant” saw

investors lose 18% in the 1st 2 days of trading with the IPO!), or fund, but, how can I avoid an income crisis? What the media and glossy financial magazines tend to miss is that the real crisis is an income crisis amongst Baby Boomers and other groups brought about by a host of Market, Economic and Political Crisis. The Income Crisis is easily addressed by using annuities that do not crash with Wall Street and Banking cycles. Americans entering retirement have in mind enjoying their hard earned money and not having it become a source of worry, or worse, pain. The following Roller Coaster chart shows the gut wrenching range of emotions people invested in the market have faced and are facing as they try to find a solution to their income crisis (also see Market Cycles chart in the Addendums section, page 36).

16

All this begs the question: “With the market still at 2007 levels around

13,000 isn’t it time to look for a better plan?”

The good news: the Fixed Index Annuity strategy IS a better plan for your safe money (your Income Money) because it takes the guess work out of when to buy and when to sell while still harnessing the horse-power of the market. It does all this while also guaranteeing life-time income and guaranteed growth on income account riders.

17

On August 14th (2011) a major paper headlined with “Market Madness Unnerves” citing a Morgan Stanley Smith Barney statement calling the week of the 8th – 12th

,

“The Wildest Week in Wall Street History.” Here’s what we are talking

about: Monday, August 8th, market dives 634.76 points; Tuesday up 429.92; Wed. down 519.83; Thursday: up 423.37; Friday: Up 125.71. Yes, for over a Decade the stock market has taken investors on a wild ride to nowhere. Many people have come to agree with Mark Twain who wrote: “October: This is one of the peculiarly dangerous months to speculate in stocks. The others are July, January, September, April, November, May, March, June, December, August and February.” But, many have played it too safe by just parking in Money Market and Certificates of Depreciation (aka CD’s) at banks.

The “Annual Re-set Strategy” in Fixed Index Annuities (see Article Addendums) has become a popular way to harness the power of the market without risk of losses to principal amounts deposited. One or our carriers took in $5,000,000,000.00 last year alone due to favorable consumer reaction. Another carrier has over 1 Trillion in assets and owns Bill Gross’s PIMCO Fund! These are not “small potato” institutions we are talking about – they know how to grow your money AND keep it safe at the same time. The annual re-set strategy is used in a host of FIA’s from various carriers with A-Excellent ratings. Get Performance and Safety on the Same Dollar. Why hasn’t your broker told you about FIA’s? He or she either has not heard about them, doesn’t understand them, isn’t allowed by his brokerage to sell them, or doesn’t like the fact that most of them don’t pay life-time trail commissions to the broker.

Kinglinger’s Personal Finance magazine revealed that, “some planner’s anti-annuity bias may be partially based on self-interest. Money that is used to purchase an annuity is no longer an asset that can be counted toward an adviser’s management fee”(Kiplingers 10/01).

THE NEXT RIDE DOWN COULD BE THE WORST YET: Dent predicts that the Dow could trade as low as 3300 in a worst-case scenario. "Bubbles go back to where they started or a little lower," he says. "The stock market bubble started at (Dow) 3800 in late 1994."

While Dent predicts the Dow's crash will play out over several years, he sees clear and present danger in gold, silver, oil and other commodities. "All investors

18

should lighten up on or sell oil, silver, and gold as the U.S. dollar looks like it has bottomed and should rise ahead," he writes in the March issue of HS Dent Forecast…In sum, he believes efforts by global central bankers to fight inflation — with the notable exception of the Fed -- will hurt growth in emerging markets as well as demand for many commodities”.

As for the Fed, they are "checkmated," Dent says, suggesting the Ben Bernanke & Co. are damned if they do QE3 -- because the bond market will freak out -- and damned if they don't -- because the economy and financial markets are so dependent on easy money. Harry wrote this prediction months before the August 2010 crash.

We also have an answer for growth of income accounts even in a flat market using Income Riders (see pages 38 & 39 for details).

You trust your house, car, valuables, life and health to insurance companies, why not your money? No one has ever lost a penny of principal investment to market “explosions” using fixed and fixed index annuities. By “Fixed” the industry means that your principal is set in place and cannot fluctuate in principal premium deposit value like a Mutual Fund, Stock, or Variable Annuity.

As you can tell, I am a firm believer in diversifying and placing assets in fixed annuities for Life-time Income. Most accounts let you take up to 10% per year or even 100% after one year with some annuities if the policy owner so chooses. Being able to take out 10% per year offers more liquidity than most people need or should take out and they are wiser if they let their assets grow in guaranteed growth income accounts until they are ready to trigger life-time income. The surrender charges for taking out more than 10% free annual withdrawals are voluntary unlike stock and mutual fund surrender charges that occur due to market crashes and resultant investor flight out of funds. Generally, the longer the annuity contract value, the more a client can expect to make since the insurer can better afford to pay higher returns since they know they will have a longer time to put client money to work. The Real Surrender Charges of Mutual Funds: If a Mutual Fund or stock account holder needs 100% of his or her money back after a 50% market crash, they end up paying a 50% INVOLUNTARY SURRENDER CHARGE! Whereas, liquidity charges on annuities are voluntary and they are there to protect you, the consumer. FIA

19

policy owners suffer no losses to their principal investment during violent market down-turns and can take 10% out per year with no liquidity charges. Why There Have Been No Runs on Insurance Company Client Accounts: History proves that during the last Great Depression there were runs on the Banks and Brokerage houses. Bank accounts didn’t pay much interest then (or now) and didn’t have any surrender charges so Americans ran to their banks and emptied their accounts. Mr. Market emptied most investor accounts before they could even make that particular “run”. On the other hand, annuity account holders didn’t

experience a “run on the insurance company” either in the Great Depression or going into the Great Recession of 2008 because policy holders buy annuities for safety and life-time pay-out and want the security of knowing that the accounts won’t be shut down easily, thus protecting each policy-holder. Most insurance companies have $100 dollars is assets for every $100 on deposit whereas banks are only insured for about $25 for every $100 on deposit (source FDIC annual report). Remember, the advantage of FIA’s are their ability to both grow your money safely, get at it annually if you need to, and, most importantly, trigger life-time income payments that can go up in strong market conditions and these payments are guaranteed for as long as you live (by the way, a spouse passing away does not stop life-time payments if the policy is set up the right way – schedule a review with us to make sure yours is set up correctly. PLUS if there is money left in the accumulation account then the surviving spouse or children get that money if they are listed as beneficiaries – see us today to review your beneficiary arrangements).

The Market is Up, Mainly to Here…A Lesson from Mad Magazine

As a teen-ager, I went to California to visit relatives. My cousin loaned me his Mad Magazine. The cover had the grinning face of Mad’s poster boy with a big advertisement stating: “We’ve lowered our prices…mainly to here!!!” A big arrow pointed down from the top right corner to the middle right hand-side of the magazine where they had relocated the price tag. The price was the same but only its price-tag location was lowered! They were poking fun at false advertising. We see the same kind of advertising daily in the Investment columns and ads today: “The market is up”, but they leave off the, “mainly to here”: the reality is that the market is still struggling from where it was on January 3rd, 2000. Read on: The best market calls of the past 2 decades came from economist Harry Dent Jr., author of, The Great Depression Ahead. He predicted both the booming 90’s and the 3 horrendous crashes of 99, 2002 and 2007 through March 2009. He

20

predicts ANOTHER CRASH IS COMING after the DOW reaches around 13,200 that could see the DOW go as low as 3,000 DOW (stocks, gold and oil included). Should you participate in brinksmanship and try to ride to the crest of the wave before the next crash? I hope Dent is wrong but if he’s right,

AGAIN, do you want to be left with another 30 to 50% loss to your portfolio? If your goal is guaranteed life-time income with inheritance options, then a Fixed Index Annuity is the only way to reach that goal. In the opinion of many, advertising deception is practiced on a grand scale by mutual funds, brokerage houses and paid for articles in glossy financial publications. The public is getting tired too: case in point – Schwab has been sued 750 million dollars for reportedly misleading investors on the lack of safety of their money market accounts. The list of companies gets bigger every month as firms are sued in national cases. One pro athlete just got back a million dollars from another brokerage last week (not listed above) because they concealed the risks of investing in stocks. He had the money to sue: most people don’t. The prospectuses today are so nebulous in nature and long that often the fine print is buried at the back in other fine print that you need to read with a microscope! Was it Shakespeare who wrote: “The large print giveth, the fine print taketh away”? Probably not, but it’s often true. The Flaw of Averages -- Another major Wall Street advertising deception: Averages. When you hear a broker say, “Well, the AVERAGE RETURN on this fund is….on this stock is…”, RUN! Sam Savage, a Sr. Research Associate at Stanford University, writes, “If you count on the stock market’s average return to support you in retirement, you could wind up penniless”. He goes on to expose the fallacy of “averages” by stating, “Plans based on the assumption that average conditions will occur are usually wrong. A humorous example involves the statistician who drowned while fording a river that was, on average, only three feet deep.”

21

I don’t make market predictions but I do predict you will benefit from a free consultation to see how you can get income for life that will not blow up in the next market bubble. Who cares if the market makes it back up to 13,000 or even 14,000? I do! And FIA owners like my-self actually hope the market runs up, but if it runs down, we don’t lose principal or annual gains. The important point to remember is that Baby Boomers have got to do a paradigm shift mentally from Asset Accumulation to Asset Protection and Life-time Income Generation. As you plan your future retirement or try to improve your current retirement, your goal should be to never run out of money: you need a Spending Plan that includes life-time income guarantees. This is sheer logic.

Nor should you “lose money safely”. By “saving” at the bank at 0.5% to

1.5% when inflation is at around 3% you are really “losing” money safely. When you consider that real inflation is at least 6% (Jim Rogers) on up to 10% (Dr. Mark Skousen) then alarm bells should be going off! Plus you are needlessly taxed on non-IRA accounts via annual 1099’s. On top of that fact, another one is particularly shocking: 19% of Georgia’s Banks failed and had to close. Many big banks only survived thanks to your tax money bailing them out. In all, 67 Banking Institutions had failed in Georgia alone since mid-2008 (AJC 8/14/11 D2) and another 2 in Georgia were seized Labor Day Week-end 2011.

22

Banks can’t pay high rates when they are busy trying to survive (see

Addendum C). So who is paying high rates? Insurance Companies offering Annuities! How? Because they didn’t fail; they continued to pay high rates because they didn’t have junk loans and they weren’t trying to inflate their profits like CitiBank and others who were loaning out as much as $30,000 for every 1,000 they took in! The banks just make more money on CD’s and checking accounts. Can you blame them for not openly offering annuities? Annuity companies don’t build

branches on every corner so they can pass on the savings to consumers. While our advisors can write FDIC insured CD’s, in most cases we find better alternatives at Insurance Institutions work out better for clients. Food for thought: the minute you open a CD at a bank, you start losing money…safely. You get compounding LOW interest rates that don’t keep up with inflation,

THEN you get a 1099 on the interest earnings (unless you are in an IRA). Whereas, with a tax-deferred CD Annuity, you get TRIPLE COMPOUNDING: 1/ you get superior interest rates on the Principal Deposit, 2/ you make interest on the money you don’t have to now pay to the IRS (if you move out of a bank cd), 3/ and, you make interest on the interest if you keep letting it grow.

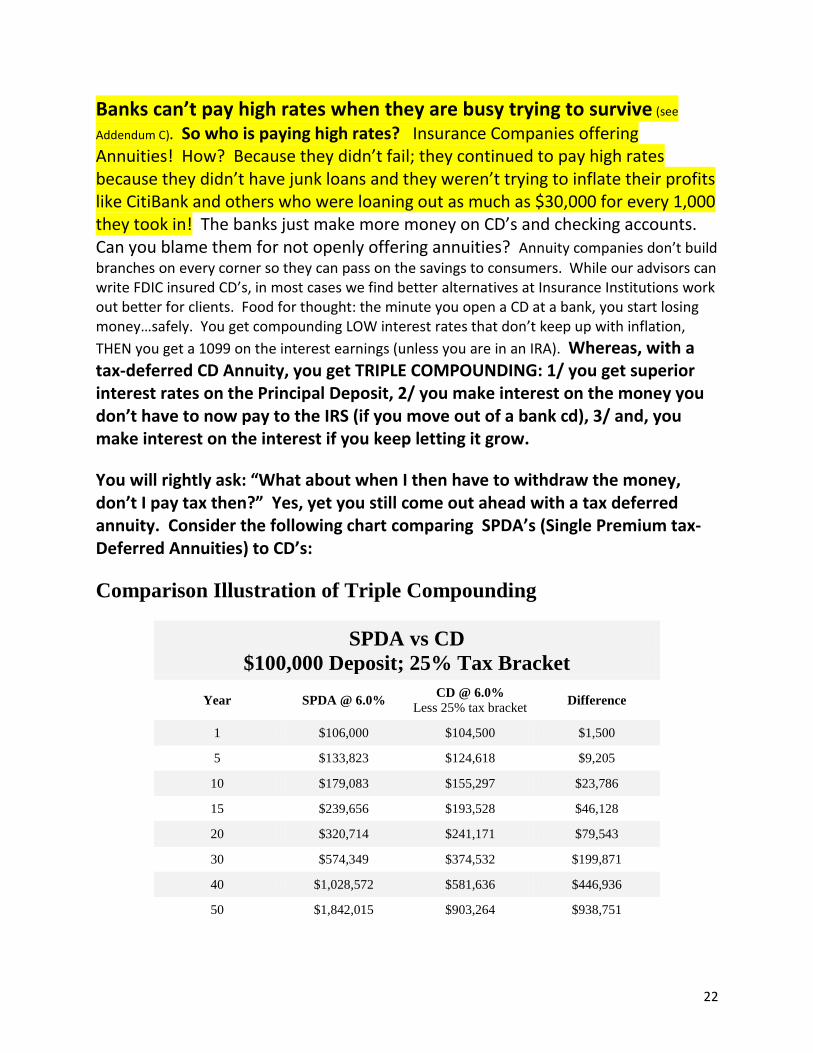

You will rightly ask: “What about when I then have to withdraw the money, don’t I pay tax then?” Yes, yet you still come out ahead with a tax deferred annuity. Consider the following chart comparing SPDA’s (Single Premium tax-Deferred Annuities) to CD’s:

Comparison Illustration of Triple Compounding

SPDA vs CD

$100,000 Deposit; 25% Tax Bracket

Year SPDA @ 6.0% CD @ 6.0%

Less 25% tax bracket Difference

1 $106,000 $104,500 $1,500

5 $133,823 $124,618 $9,205

10 $179,083 $155,297 $23,786

15 $239,656 $193,528 $46,128

20 $320,714 $241,171 $79,543

30 $574,349 $374,532 $199,871

40 $1,028,572 $581,636 $446,936

50 $1,842,015 $903,264 $938,751

23

One final step would be to consider the tax on the SPDA if surrendered for its full cash value. In

year 30, the gain in the SPDA is $474,349. At a 25% tax rate, the tax would be $118,587.

Subtracting the tax from the total cash value leaves the SPDA with a net value of $455,762;

which is still $81,230 more than the CD. The magic of "Triple Compounding"! (***see add.).

By moving money over from the Bank Building to the Insurance Building, you can get a guaranteed return of 15% over 5 years (5 years

times 3% = 15%; rates effective as of this writing 5/24/2012 – call for current rates) in a walk-away 5 year CD style Annuity for your short term money from an A-Excellent company! Why settle for .5 to 1.5%? And with FIA’s you have the potential to make even more. This is double what most banks are paying according to BankRate.com. What could you pay for with double the interest rate? Take that vacation; save more; give more?

The purpose of your money should determine where you should put it. Does it really make sense to put money in stocks for your emergency fund or life-time income accounts when they can implode? Use bank checking accounts for short term

emergency needs; use longer term fixed annuities to get more growth and life-time income; lastly, experts say, use stocks, commodities and mutual funds only for assets you can afford to lose in the next bubble. Do not make investment decisions based only on reading these articles or television or radio commentary. Each client should consider his or her time horizon, cash-flow needs and other variables before making investment decisions, Bank deposits or Annuity purchases.

Are These Risks in YOUR Portfolio?

1. Market Risk: Is Retirement a good time to lose your Nest-Egg? Retirees

need a strategy that offers growth without losing 52% to risk…like it did

from 2008-2009. The smarter way is to harness the power of the market without

ever putting your Nest-egg at risk. Even smarter is to capture the gains on an annual

basis too. Want your money to work smarter without risk?

2. Longevity Risk: Is your number-one fear the same as most retirees; the

fear of out-living their nest-egg dollars? Is there really a way to guarantee

that you never run out of money?

3. Safety risk: did you ever think that you could lose money safely? If your

CD return is 1.45% and inflation is 3% then you are losing money safely. To

24

add insult to injury, did your bank ever warn you that your real return

after 1099 taxes is not 1.45% but really closer to 1%?

4. Tax Risk: Why pay taxes on money you are not even using?

5. Inertia Risk: Did you ever think about inertia as risk? Is it not true that if a

person sits their money in the market waiting for it to improve, that waiting

is a risk since the market may crash while waiting?

6. International Terrorism Risk: When the Twin Towers were destroyed by terrorists

the market dropped 20%; when terrorists struck again in Spain, the Market in America

dropped again. Wouldn’t you agree that your retirement dollars need to be

terrorist-free from losses?

7. Flat Market Risk: A/ Where was the market in January 3, 2000? B/ Where is it today? C/ What if you could get a guaranteed growth in your income account of 5 or 7% no matter what the market does and higher when the market does better? According to many economists we may be entering into the same economic cycle that Japan has been in for nearly 30 years! Japan experienced a crash followed by a slowly downward spiraling market and economy that has never gotten back to its glory days. While still a strong country, the market has lost its sheen.

Would you be impressed if you knew America’s most influential CPA endorses

this strategy and his family actually owns it? Read Ed Slott’s endorsement by

clicking on the “Win” tab at www.WinningTheRetirementGame.com. Ed will

show you why he chose an FIA for his own mother!

How would it feel to have all the above risks to your principal eliminated by

using our Annual Reset and Income Rider strategy?

If you are even thinking about owning an annuity with a guaranteed living withdrawal benefit call us for a comparison. We have a hidden gem that has sealed the deal on some income cases that have been in the works for a while. Check this guaranteed lifetime income out:

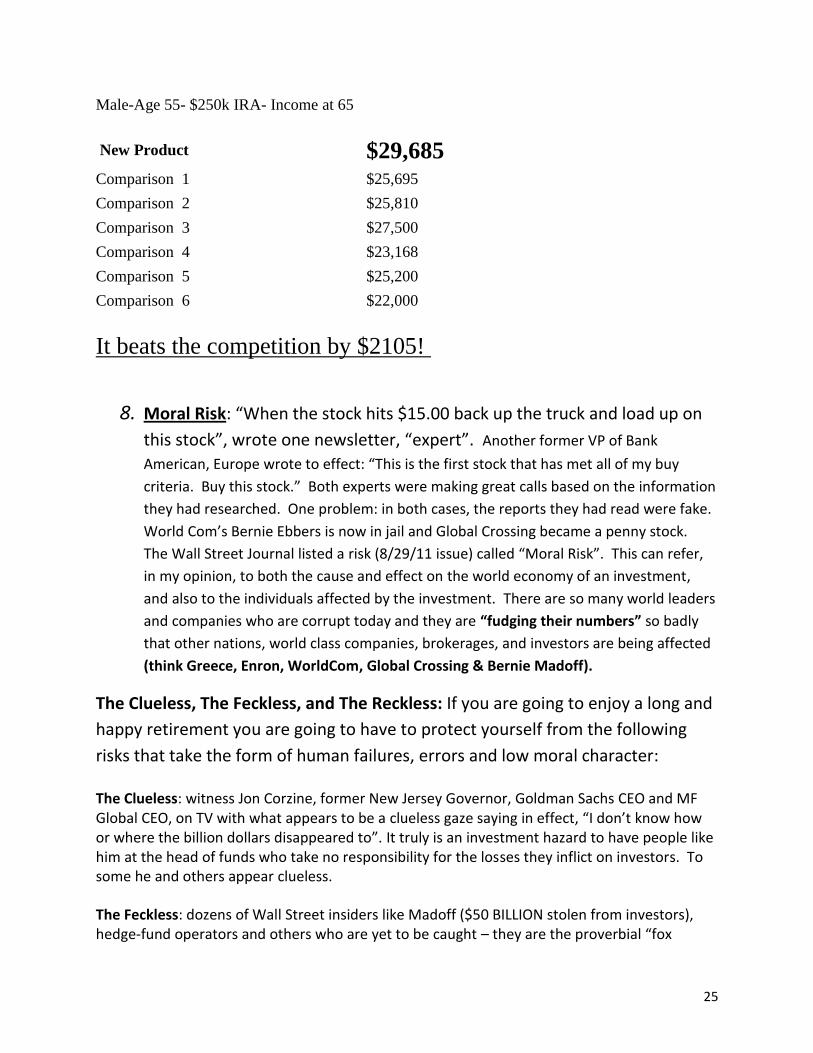

25

Male-Age 55- $250k IRA- Income at 65

New Product $29,685

Comparison 1 $25,695

Comparison 2 $25,810

Comparison 3 $27,500

Comparison 4 $23,168

Comparison 5 $25,200

Comparison 6 $22,000

It beats the competition by $2105!

8. Moral Risk: “When the stock hits $15.00 back up the truck and load up on

this stock”, wrote one newsletter, “expert”. Another former VP of Bank

American, Europe wrote to effect: “This is the first stock that has met all of my buy

criteria. Buy this stock.” Both experts were making great calls based on the information

they had researched. One problem: in both cases, the reports they had read were fake.

World Com’s Bernie Ebbers is now in jail and Global Crossing became a penny stock.

The Wall Street Journal listed a risk (8/29/11 issue) called “Moral Risk”. This can refer,

in my opinion, to both the cause and effect on the world economy of an investment,

and also to the individuals affected by the investment. There are so many world leaders

and companies who are corrupt today and they are “fudging their numbers” so badly

that other nations, world class companies, brokerages, and investors are being affected

(think Greece, Enron, WorldCom, Global Crossing & Bernie Madoff).

The Clueless, The Feckless, and The Reckless: If you are going to enjoy a long and

happy retirement you are going to have to protect yourself from the following

risks that take the form of human failures, errors and low moral character:

The Clueless: witness Jon Corzine, former New Jersey Governor, Goldman Sachs CEO and MF Global CEO, on TV with what appears to be a clueless gaze saying in effect, “I don’t know how or where the billion dollars disappeared to”. It truly is an investment hazard to have people like him at the head of funds who take no responsibility for the losses they inflict on investors. To some he and others appear clueless.

The Feckless: dozens of Wall Street insiders like Madoff ($50 BILLION stolen from investors), hedge-fund operators and others who are yet to be caught – they are the proverbial “fox

26

guarding the hen-house” where your nest egg dollars can end up (watch the TV series American Greed; it will shock you that our economy can survive White collar Wall Street Crime at this rate).

The Reckless: With over 100 Trillion in unfunded liabilities like Social Security, we truly are on a collision course with our economy and the train conductors who got us to this point are escaping out the back door with Congressional, Federal and Corporate pensions with no repercussions while your children and grandchildren will be left with a bill they won’t be able to

pay and pensions they will never get. “Bail out Ben” Bernanke has proven to be the most socialistic Fed Reserve Chairman in history “spreading around” others’ wealth thereby creating economic havoc and laying the ground-work for more severe economic bubbles in the near future (Feb 2012 Forbes and Bloomberg/Business Week). I think many investors can identify with Bob Dylan’s song: Stuck In the Middle With You when he writes: “Stuck in the middle with you; and I’m wondering what it is I should do...Clowns to the left of me, jokers to the right, here I am, stuck in the middle with you.” Thankfully there are honest people in this world and good people in our country trying to fix the messes caused by the relatively few bad apples in our society. Not one of the institutions we work with needed bail outs for their Annuity Accounts. This is because the accounting standards for insurance companies are much tighter and stricter than for bankers or brokers. In

order to go into business in any state and in order to qualify for the re-insurance accounts purchased to insure annuity owner money insurers must prove that their money is safe and sound in order to pay life-time payments to clients. You can’t find even 5 Insurance companies folding in the past 5 years versus hundreds of banks (see Addendums). Insurance Companies didn’t need to go to the Federal Deposit Insurance Company because they ARE insurance companies just like the FDIC is an insurance company! They are stable in design as opposed to other financial institutions and trading operations.

The Buffets Were Right...

Both Jimmy and Warren!

Depending on which Buffet you listen to you may feel like your portfolio has either been “Wasting Away in Margaritaville” or it has been treading water…for the past 12 years.

As mentioned earlier, Warren Buffet, the Oracle of Omaha, stated in a Forbes article in 2006 that the best we can hope for out of the market for the New

27

Millennium is 5% per year. He wrote that when his best case scenario prophecy and the DOW was around 13,000. It is still under 13,000 6 years later!!! Warren’s

Best case hope: 45% return over 9 years: Best case scenario is a negative 9 year return ...ouch! It doesn’t have to be that way. CNN Money’s Jan/Feb 2012 Issue states that, “For most people, trading turns out to be just a reliable way to ERODE returns over time….researchers at Morningstar found that the typical investor captured a 0.2% return.” Buy and Hold doesn’t work anymore and according to research, you have a financial death wish if you try to day-trade. Why has the market changed? Retirees are pulling money out the market to spend on retirement not adding money for retirement. The market depends on mom and pop investors staying IN the market. But with millions of Baby Boomers retiring and wary of the 3 large crashes in the past 10 years, they want a spending plan they can never outlive…and the stock market can’t promise that. Also, our economy and market depends on consumer consumption to drive it onward and upward and Boomers are doing just the opposite: they are down-sizing and spending less on cars and clothes as they prepare to try to make their money last through an unknown length of years in retirement. They are smart and know they are heading into uncharted waters. European investors are so fearful of a PENDING CRASH that they are rushing in to German Bonds that PAY A NEGATIVE .12% return (WSJ, Jan 2012). They are willing to LOSE a relatively small amount MONEY just to find a place of safety that won’t lose them a lot of money like they have been losing in both the European, American and Japanese markets. Pharmaceutical giant CEO Andrew Witty dropped a bomb-shell in Wall Street Journal (Feb 8, 12 B1) stating, “We don’t leave any cash in European countries. We sweep all our cash raised during the day and send it to banks in the UK which we think are robust and secure. We’ve been doing this since early last year and we will continue doing so. There was a period last year where every day you were getting a phone call about Bank A, B or C which was perceived as about to go.” Guess what? One of my top five favorite FIA companies is based in England and has been in business for over 300 years! They have a huge operational base in the USA too. Americans who have bought Fixed Indexed Annuities (FIA’s) over the past 15 years have made significant returns and the new FIA’s are even better: they protect not only against Market Crashes but also against Flat Market Risk. Depending of which FIA they choose, clients can link to multiple Indexes such as the DOW, S&P500, Bonds, Gold, and Global Indexes at the same time with no down side risk. There is no fee or tax consequence to change Indexes annually. Advisors recommending the FIA strategy make half of what they would make recommending mutual

funds…so most don’t recommend them (FIA’s pay advisors the equivalent of ½% per year

or less over 20 years versus about 2% per year compensation for Mutual Funds and VA’s – & no commissions are taken out of client assets for FIA purchases. In fact many FIA’s pay a deposit

or premium bonus on 100% of the initial assets placed into the FIA). The geniuses who invented these financial instruments have added what is called Life Time Income Benefit riders that grow the income generating part of the

28

accounts even when the market is flat or negative. Some FIA’s also have Inheritance Rider options that allow clients to choose guaranteed rates to be paid out to heirs. Furthermore, one company also doubles the life-time income paid out to annuity owners should they need to go to a nursing home due to being able to not perform 2 “ADL’s” or Activities of Daily Living (no underwriting is needed to own this feature – even those already using canes or in wheel chairs can benefit).

Retirement is no time to let your life savings waste away in Margaritaville, market doldrums, market crashes or low bank interest rate CD’s (Certificates of Depreciation). A lot of people, “haven’t a clue” how

their portfolios got to where they are today and many institutions hope their clients stay “clueless” about the benefits of fixed index annuities. Now you are clued in: your job is not to bolster bank profits by accepting low rates; your job is not to make sure your broker’s trail commissions stay on target; your concern should be to take care of you.

To Vary Or Not To Vary? That’s the Question Why Experts Love to Hate Variable Annuities

OK, so you are clued in, you start the transfer process over to a winning strategy some type of fixed annuity or a blend of fixed annuities…then you get a call: “Oh, Mr. and Mrs. Investor, I see you’re moving to an Annuity. Well, we have those!” Your response may be: “Really? Well, why didn’t you tell me about them before I lost so much money or before I treaded water for 10 years?” You may also ask, “What type do you have?” Normally the answer will be, “Variable Annuities”. Variable Annuities are basically mutual funds wrapped around an annuity. And they have hidden risks and “take-backs” that have left investors perplexed at the losses they incurred in what they thought were “safe” products. I took the required course-work to allow me to offer Variable Annuities but after deeper analysis I couldn’t quite figure out why I would want to offer them. They don’t look client friendly; they have so many “smoke and mirror clauses” that you

29

have to take weeks to figure out the hundred plus pages of disclaimers, and even then, they are so complicated and the fees so high that I couldn’t in good conscience sell them. And a host of experts agree with my opinion on this…including two former top designers of Variable Annuities (VA’s). Their article, “Indexed Annuities May Be the Perfect Product”, gives in depth insight into why they, after being at the pinnacle of professional position & authority in the field, became huge proponents of FIA’s (see the Win tab at www.WinningTheRetirementGame.com). Jim Ellison, another Variable Annuity expert, provides the following chart:

According to a research

study from York

University in Canada and

Goldman Sachs, the

insurance fees that are

embedded in variable

annuities are way out of

proportion to their actual worth. A typical charge is 1.25% which would work out to an annual cost of $2,500

on a $200,000 annuity! (This does not include other charges discussed below). Keep in mind what truly is the death benefit that the insurance company is on the hook for, and what is yours already…the contract value”, writes Ellison. In other words, if you need your cash, you won’t have much if the market crashes and you need to surrender a part (or all) of your contract. One disgruntled VA owner told me, “My VA is of no use to me. It’s only valuable when I’m dead because it’s lost so much due to market crashes.” FIA’s offer gains, loss protection AND inheritance benefits.

Ellison goes on to point out the high cost of ‘small’ fees: “According to Morningstar, the average variable annuity passes along total expenses of 2.2% of the assets per year. From MetLife’s (#1 variable annuity leader) Series XC prospectus, we find the following fees: mortality expense charge 1.30%, administration charge .25%, death benefit step up rider .80%, lifetime withdraw guarantee 1.50%, and portfolio expenses of .53%. What effect will a total of 4.38%

30

fees have on a $200,000 account? Would you believe a drain of $8,760 per year? How can this account survive in a turbulent market? On May 3rd, 1999 the Dow was at 11,031. Eleven and a half years later on November 23rd, 2010 it was at 11,036. With no gains and $8,760 annual fees, $96,360.00 vanishes from your pocket. Your fees are not that high you say? Cut them in half and you still give up over $48,000.00. That’s even before you tap it for income!” You may want to think twice about involving your money with a VA. In fact, it was announced today that Hartford, the 200 year old leader in Variable Annuity products, is getting out of the business of offering Variable Annuities (WSJ 3 22 2012) due to the head-aches associated with them both for consumers and the company.

Other experts writing against Variable Annuities include internationally acclaimed author and columnist Jane Bryant Quinn. She exposes the pitfalls of VA’s in her

Newsweek column: “You will rarely find me so deeply angry at a common investment product that I dream of blowing it to smithereens. Especially the ones sold by America’s leading

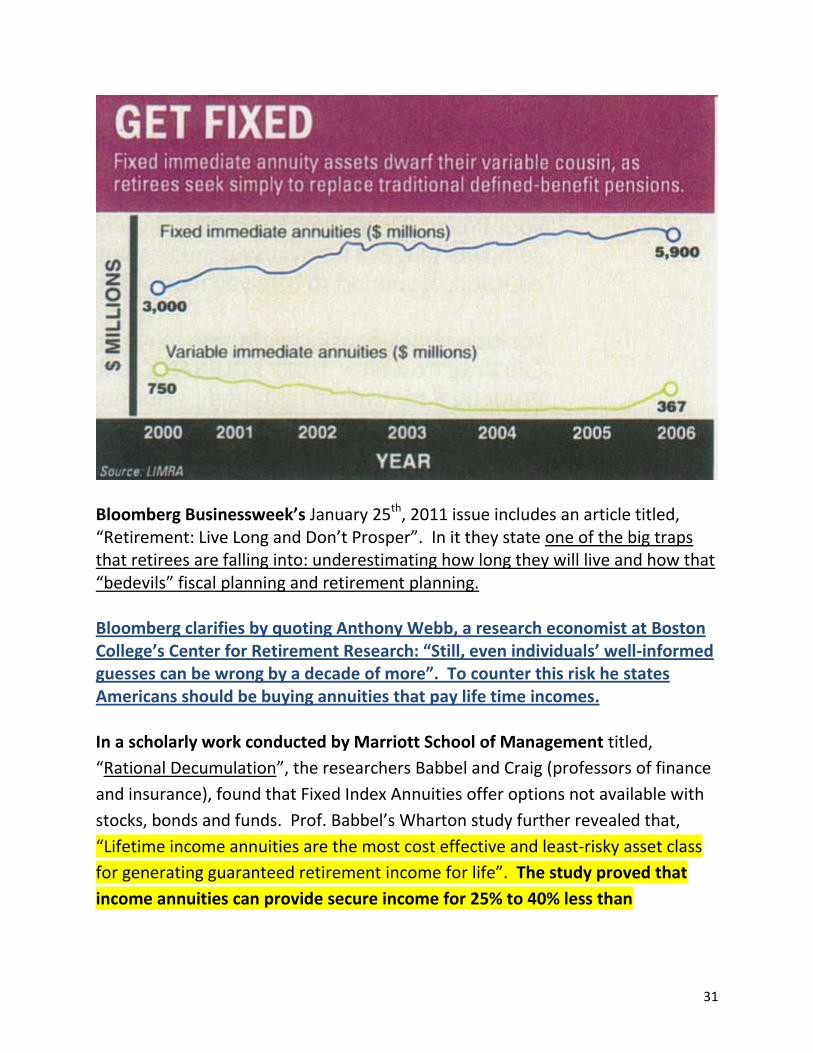

financial institutions.” She cites John Biggs, former chair of TIAA-CREF pension funds who states, “I cannot imagine a situation where I’d recommend a VA as a good idea” (Newseek, Aug 30, 2004). Jane Bryant Quinn also concurs with me when she writes, “Before going forward, let me define the battlefield. I am not dissing tax-deductible retirement annuities…nor ‘fixed annuities’ that pay a set rate of interest. Nor ‘immediate annuities’ that pay you a monthly income for life.” Bank Investment Consultant journal, in an article titled, “Immediate Annuities: Retirement’s Silver Bullet?” admonishes advisors to “Get Fixed (Annuities)” for their clients not Variable, “Fixed immediate annuity assets dwarf their variable cousin, as retirees seek simply to replace traditional defined-benefit pensions”. Here’s the chart they include to prove their point:

31

Bloomberg Businessweek’s January 25th, 2011 issue includes an article titled, “Retirement: Live Long and Don’t Prosper”. In it they state one of the big traps that retirees are falling into: underestimating how long they will live and how that “bedevils” fiscal planning and retirement planning. Bloomberg clarifies by quoting Anthony Webb, a research economist at Boston College’s Center for Retirement Research: “Still, even individuals’ well-informed guesses can be wrong by a decade of more”. To counter this risk he states Americans should be buying annuities that pay life time incomes. In a scholarly work conducted by Marriott School of Management titled,

“Rational Decumulation”, the researchers Babbel and Craig (professors of finance

and insurance), found that Fixed Index Annuities offer options not available with

stocks, bonds and funds. Prof. Babbel’s Wharton study further revealed that,

“Lifetime income annuities are the most cost effective and least-risky asset class

for generating guaranteed retirement income for life”. The study proved that

income annuities can provide secure income for 25% to 40% less than

32

traditional strategies due to an insurer's ability to spread risk across large

numbers of people. You absolutely owe it to yourself to look into this option.

Bank Investment Consultant Journal further elaborates on Professors Babbel and Craig’s research by writing: “They argue that the flexibility of today’s products makes criticism of annuities’ cost & performance obsolete, in part because

immediate annuities trump retirement income asset allocation strategies.” In fact, many of the top FIA’s have little or no costs and some even waive fees if

the market stays flat or goes negative, all while protecting annual gains that have been “re-set” or “swept” into holding accounts that cannot lose value once they have reached their annual or bi-annual anniversaries. The FIA studied returned 8% per year over the period the Dr. Babbel studied them and mirrored the best funds…only with no risk to the initial investment or annual gains! In turn, immediate annuity pay-outs while strong are often smaller than income stream pay-outs from distributions gained via Life Time Income Riders found in Fixed Index Annuities. Our proprietary software compares all top companies to find which Institutions are paying the highest at any given month. Life-time income streams differ depending on which company is used at what age and how long the income is deferred before being taken so it is important to get our quote engine charts before making a decision. Some companies even offer income doubling options if there is a need for a nursing home stay (and there is no under-writing for this rider! See Life Time Income & Win tabs for full details). There are also riders on some accounts for Home Health Care.

To close this section on Variable Annuity “Death Traps” let’s return to Jim Ellison’s insightful study and find out how to rescue your money from further decline and keep the death benefit: “Millions of variable annuity (referred to as VA) owners are beyond perplexed with the realization that their ‘safe’ variable annuity has lost 30-50% over the last 10 years. They feel trapped to hold on even while watching

their money fade away. What holds them? When they purchased their VA it came with a death benefit for an added cost (later disclosed). Now, many are struck with the reality that what started as an ‘investment vehicle’ has quickly turned into a life insurance contract due to

significantly higher death benefit (high water mark) than contract value (walk away value). So, early gains in the contract that have now been lost to market declines, have left the VA stripped of cash value and the annuity owner worth more dead than alive.

33

Ellison calls VA’s, “A dangerous trap with a high cost. The real issue: How do you protect from further losses and keep your death benefit? If you believe, as Warren Buffet does, that the stock market will only average no more than 5% per year for the long future; then annual fees of 3-5%, coupled with another market crash will destroy your dollars in a variable annuity. A little known secret could save those dollars from this point forward. Some variable annuities allow for the contact owner to make a tax free transfer out of the annuity and still maintain the death benefit amount. Usually, a minimum of $1,000 must be left in the variable annuity to keep the account open. So, in the example below the difference from the highest value ($253,000) and 2010 present value ($203,000) is $50,000. By keeping $1,000 in the contract value (inside the VA’s fixed account), you could transfer $202,000 to a safe alternative without taxation, keep the $50,000 as a death benefit, and assure you will never again have that sinking feeling when the stock market plummets.” Additionally, the product we use for this rescue credits a 10% bonus to your account on day one.

34

Don’t expect the person who sold you the variable annuity to tell you about this. You are presently exactly where they want you…in a fee generating machine! Warning: don’t try this on your own. Not all variable annuities offer this ‘bail out’ feature. Entrust this research and ‘leg work’ to us. If you have lost substantial assets inside your variable annuity, is it not worth investigating the possibility never to lose another dime? It’s your money, let us show you how to rescue it and make it grow”.

You now have information that you can use to win the retirement game. Act upon it to secure a rich and rewarding retirement. Take the first step and call our offices to see what a customized plan will look like based on your goals, risk tolerance, and time line.

To Your Successful Retirement!

For Illustration Requests Email [email protected], or call: 770-608-8711

Addendums to Articles -- (*most articles mentioned in this publication can be found by clicking on the Win tab at www.WinningTheRetirementGame.com **see Win tab for full details and illustrations on Income Riders ). A. Smart Money: September 2011

issue states in regards to BOND BUBBLE: “MENTION A BUBBLE and most people

think of outrageous price tags – the $2 million Miami condo, the $600-a-share tech stock. But Jeff Rosenberg, chief fixed-income strategist for Bank of America Merrill Lynch, has another definition: “greater and greater risk for less and less compensation.” … As the economic recovery accelerates, inflation may well speed up. Whether it does or not, policy makers might increase interest rates to keep it in check. If lenders lose confidence in the U.S. government’s ability to curb its debt, they could easily demand higher yields on Treasuries. If even one of these trends catches fire, the interest people collect on bonds they currently own will be less valuable – and the bond’s prices will plummet. Contrary to popular belief, says Tom Atteberry, manager of the $3.7 Billion FPA New Income fund, ‘the bond market is the high risk place.’ B. Beware the Bond Bubble. Bond bears: The rush to Treasuries could make a bad bond market even worse (By JONNELLE MARTE -- Smart Money, Aug. 24

th, A Wall Street Journal publication): Spooked by stocks and unfazed by

the recent downgrade of U.S. debt, investors have turned to Treasuries as a safe haven. But are their moves inflating the risks in the broader bond market? The latest Treasury rally has done little to quiet year-long

concerns that bonds are in a bubble. Last week, investors flocked to government bonds, pushing yields on the 10-year Treasury below 2% for the first time in at least 50 years. That's also down from the 2.6% yield pre-downgrade, and below the 2.8% threshold first hit last October, when many took the view that the bond market was headed for a pop. Now bond bears say the latest rally is setting up the bond market for an even bigger crash once interest rates start to rise again. "You could potentially get whipsawed," says Elaine Stokes, co-manager of the $21 billion Loomis Sayles Bond fund” (excerpts).

35

C . Dr. M. Weiss: “This is precisely what I’ve been warning you about...Bank of America reported a whopping

$9.1 billion loss for the second quarter of 2011, with $8.5 billion of that shortfall coming from a settlement with investors over bad mortgage bonds. Overall, the results were worse than analysts had expected, and it’s worth noting that revenues declined in nearly ALL of the bank’s business units.

“And it isn’t just Bank of America that’s blowing up. Goldman Sachs also posted a pitiful earnings report, missing analysts’ estimates by a country mile! Excluding one-time costs, the company’s profits tanked 38% ... and revenue was also much less than anticipated. Still, I have to tell you: Things are only going to get WORSE for our nation’s banks from here! It explains why our nation’s entire financial system is on the brink of collapse ... how this terrible debt crisis could destroy the lives of millions of Americans ... and what steps you can take right now to protect your own family from the fallout” (Weiss Research excerpts).

D. Economist Harry Dent (cnn money): “Major Crash” Coming”: The first quarter comes to a close today with major averages at or near multi-year highs (end of March). Expect "substantial" further gains for stocks before a "major top" occurs in late summer, says noted forecaster Harry Dent, founder of HS Dent and The Dent Method. The good news, for those long, is Dent predicts the Dow will trade as high as 13,200 by mid-summer and the S&P 500 as high as 1430, or more-than 7% above current levels. The bad news is "then we could see another major crash," Dent says, forecasting the Dow could trade as low as 3300 in a worst-case scenario. "Bubbles go back to where they started ora little lower," he says. "The stock market bubble started at (Dow) 3800 in late 1994."

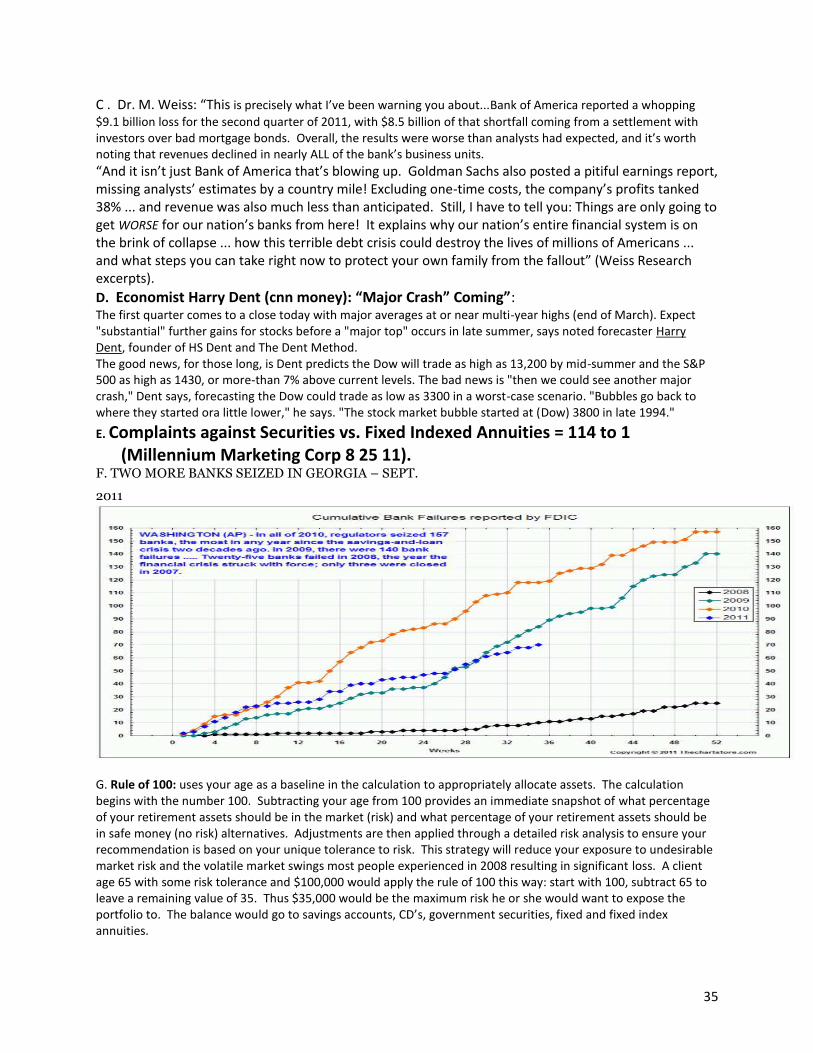

E. Complaints against Securities vs. Fixed Indexed Annuities = 114 to 1 (Millennium Marketing Corp 8 25 11). F. TWO MORE BANKS SEIZED IN GEORGIA – SEPT.

2011d

G. Rule of 100: uses your age as a baseline in the calculation to appropriately allocate assets. The calculation begins with the number 100. Subtracting your age from 100 provides an immediate snapshot of what percentage of your retirement assets should be in the market (risk) and what percentage of your retirement assets should be in safe money (no risk) alternatives. Adjustments are then applied through a detailed risk analysis to ensure your recommendation is based on your unique tolerance to risk. This strategy will reduce your exposure to undesirable market risk and the volatile market swings most people experienced in 2008 resulting in significant loss. A client age 65 with some risk tolerance and $100,000 would apply the rule of 100 this way: start with 100, subtract 65 to leave a remaining value of 35. Thus $35,000 would be the maximum risk he or she would want to expose the portfolio to. The balance would go to savings accounts, CD’s, government securities, fixed and fixed index annuities.

36

*** (from pages 22&23). Chart is for illustrative purposes only. Chart is to assist understanding the effect of compound interest without withdrawal to pay current income taxes. Taxes on the SPDA would have to be paid at some point. Illustrated rates are hypothetical and not guaranteed. This chart is for comparison only. 5 year CD rates are around 1.7% where-as CD type Annuity rates are averaging 2.8% at time of this writing 5/14/2012).

The Annual Reset strategy in a Fixed Index Annuity can help investors

capture healthy gains in the market while never experiencing a loss of

principal investment due to market volatility.

Life Time Income Benefit riders further enhance client income by

guaranteeing growth of the income account even in flat or negative markets. The chart on the next page is for illustration purposes only and the company may not be the right

choice for you as a client since, depending on your age, time-line to retirement and other factors,

there may be more suitable annuities and blends of other products. We also track over 20

companies every month to find which ones provide the best performance and riders. Many more

charts, articles and videos are posted online at www.WinningTheRetirementGame.com under

various tabs including the “Win” tab. Past gains do not guarantee future results but with FIA

Income Riders, Inheritance riders and other available riders offered by various companies these

riders can off-set the current low returns of CD’s and volatility of Stock portfolios.

37

year and even 5 year re-set strategies that may be more suitable for some retirees. s,

Immediate Annuities plus Stocks, Bonds and Real Estate may be desirable.

38

39

40

About the Author

Doug has been helping retirees and advising families and individuals since 1981. Dr. Moore earned membership in the coveted National Ethics Bureau which is closed to advisors with blemishes on their records. Many advisors do not qualify for membership due to failing background checks.

Doug’s primary focus is to help clients get opportunity and growth on the same dollar using safe, time proven, tax efficient strategies that are both state regulated and company guaranteed. Doug and his co-advisors have at their disposal the full universe of investment vehicles to best serve their clients’ needs based on their time line, risk tolerance, income and estate planning goals.

Having spent 19 years living in England, Scotland, Germany, Austria, Indonesia, the Philippine Islands and India, Doug has a unique perspective on the International economy. His volunteer work as a board member for Good News India, a rescue mission for over 2500 at risk children, plus two City of Mercy leper colonies, takes him back to India every few years (see, www.GoodNewsIndia.org).