Transition from back-arc rifting to oceanic arc associated Kuroko formation in late Cenozoic NE...

119

Report on Financial Analysis of Omni Services Incorporated

-

Upload

independent -

Category

Documents

-

view

1 -

download

0

Transcript of Transition from back-arc rifting to oceanic arc associated Kuroko formation in late Cenozoic NE...

Report on

Financial Analysis of Omni

Services Incorporated

Financial Analysis of Omni Services

Incorporated

Prepared for:M. Sadiqul Islam, Ph.D.

Course instructor

F-307: Analysis of Security Investment

Lecturer

Department of finance

University of Dhaka

Prepared by:

Zarin Tasnim 17-009

Tamanna Nigar

17-031

Fatema-Tuj-Johora Shorna

17-119

Samanta Haque

17-191

Date of Submission: February 18, 2014

Department of Finance

Faculty of Business StudiesUniversity of Dhaka

Acknowledgement

In the preparation of this report, we constantly meet many

stumbling blocks. However, the presence of various people helped

to simplify matters and hence made the completion of this report

possible.

Firstly, we would like to thank our course instructor, M. Sadiqul

Islam, Ph.D. (Professor of department of finance), who’s constant

presence and words of encouragement inspired us to do our very

best. Without his guidance and availability, this report would

not have been possible and gave the directions we needed to

prepare this report.

Secondly, we would also like to take this opportunity to

acknowledge the help provided to us by some personals of those we

surveyed for giving us time from their busy schedule, providing

us with information that was required to complete the report.

Finally, we would like to thank each individual group member and

the numerous people who offered us help and kindly answered all

the questions in our survey and gave advice and suggestions to

ensure that we provide an in-depth report on the analysis of

business environment of cement industry and its cost behavior.

18th February, 2014

M. Sadiqul Islam, Ph.D.

Professor

Department of Finance

Faculty of Business Studies

University of Dhaka

Subject: Submission of group report on “ Financial Analysis of Omni

Services Incorporated ”

Dear Sir:

Here is the group report on the “Financial Analysis of Omni

Services Incorporated” that you asked us to prepare as a part of

requirement of our BBA Program Analysis of Security Investment

course F-307. In presenting this report, we have tried our level

best to include all the relevant information and the examples to

make the report informative and comprehensive.

This report was assigned to us with a view to scrutinizing our

skill and flamboyance when it comes to banking know-how.

Moreover, the purpose of this term paper was to extract our inner

ability & enhance our banking related potentials.

The information of this paper is directly collected from thecase manuscript provided to us & our course textbook & should notgo beyond the norm.

We hope you will find the report in appropriate manner. Lookingforward to know your feedback.

Sincerely yours,

………………………….

Samanta Haque

(On behalf of the group)

B.B.A. 17th Batch

University of Dhaka

Executive summaryAs a course requirement for Analysis of Security Investment

course, F-307 the report is on a “Financial Analysis of Omni

Services Incorporated”, which is assigned to us by our honorable

course teacher, M. Sadiqul Islam, Ph.D., Professor, Department of

Finance, University of Dhaka.

The report deals with the study, and research we have done on thecase that was given to by our honorable course instructor. Thecase is on Omni Services Incorporation which is traditionallyconsidered to be a part of industrial laundry business but nowknown as textile lessors.

As Omni Services INC is an USA company at first the economicanalysis of the country is portrayed. After portraying theeconomic analysis company analysis is included following by anelaborate description of the company in question Omni ServicesINC. To understand the company better ratio analysis isincluded. The information was available in the case for ratioanalysis. We have done Dupont analysis to get a broader picture fthe return earned by the company. Then the SWOT analysis isprovided with the help of the industry analysis which we havedone in the earlier part.

We have prepared problem statement which is the most importantpart of the report. after studying the case thoroughly we came todetermine the problem faced by Omni Services INC. the problem wasto determine whether the company should go for merger with astrong French company also in rental linen business The SocieteGenerale de Location et Services Textiles (Textiles).

We have figured out the best possible solution for this problemby using valuation methods such as FCFF (free cash flow to firm),

FCFE ( free cash flow to equity) and DDM ( dividend discountmodel) to determine the price per share of Omni via the valuationof the firm. Income statement, balance sheet was given from theyear 1973 to 1979. But we had to calculate the price per share of1985 so we have prepared forecasted income statement, balancesheet from 1980 to 1985. We have assumed growth rate fromhistorical trends.

After describing elaborately the solution of the problems andalternative course of action we have given a recommendation forthe merger decision which according to us will benefit both theparties. We have come to the decision by calculating the shareprice of Omni.

In the recommendation we have provided the merger price for bothyear 1980 and 1985. And have calculated the prices of the totalshares. And justified our recommendation with proper explanation.

Table of Contents1. Introduction......................................................21.1. Origin of the Report...........................................2

1.2. Objective of the Report........................................21.3. Scope of the Report:...........................................3

1.4. Methodology:...................................................31.5. Limitations:...................................................3

2. Economic analysis of USA:.........................................6Trade & Investment:.................................................7

Unemployment:.......................................................8Inflation:..........................................................9

2.1. Financial industry crisis:.....................................92.2. Political fallout:............................................12

3. Company overview:................................................153.1. Management body of Omni:......................................15

3.2. Omni’s products and services:.................................153.3. Areas served by Omni Services INC:............................15

3.4. Location of Omni Subsidiaries:................................163.5. Specialty of Omni Services INC:...............................16

4. Industry analysis:...............................................184.1. Market characteristics:.......................................18

4.2. Porter five forces Model......................................194.3. PESTEL analysis:..............................................21

4.4. Key Players:..................................................244.5. Competitive Advantage:........................................26

5. Ratio Analysis...................................................285.1. Liquidity ratio:..............................................28

5.2. Solvency Ratio:...............................................30

9 | P a g e

5.3. Profitability Indicator Ratio:................................335.4. Debt Ratios:..................................................36

5.5. Operating Performance Ratios:.................................395.6. Cash-Flow Indicator Ratios:...................................41

5.7. DuPont Analysis...............................................425.8. SWOT Analysis of Omni Services:...............................43

6. Comparison of Omni Services INC with industry:...................477. Problem Statement:...............................................62

8. Solution to problem no 1:........................................658.1. Finding out the value of the firm:............................65

8.2. Finding out the value of Stock:...............................669. Solution to problem using FCFF ( Free cash flow to firm):........69

9.1. Finding out the value of the firm:............................6910. Alternative method (Using FCFE Method):........................74

11. Alternative method (Using Dividend Discount Model):............7712. Recommendations:...............................................79

13. Conclusion:....................................................8214. References:....................................................83

10 | P a g e

Chapter 1Introduction of report

Origin of the report

Objection of the report

Scope of the report

Methodology

Limitation

1 | P a g e

Financial Analysis of OmniServices Incorporated

1. IntroductionThe report attempts to explain the problems faced by Omni

Services Incorporated which is trying to survive the competitivemarket of industrial laundry business now known as textile lessors.

To survive this competitive market the company needs to implement some

strategies. There are some problems that Omni Services have faced and

our report requirement is to give solution for those problems

1.1. Origin of the ReportAs a course requirement for Analysis of Security Investment

course, F-307 the report is on the empirical analysis of Omni

Services INC. which is assigned to us by our honorable course

instructor, M. Sadiqul Islam, Ph.d. Professor, Department of

Finance, and University of Dhaka.

1.2. Objective of the ReportThe report deals with the study, and research we have done on the

case that was given to by our honorable course instructor. The

case is on Omni Services Incorporation which is traditionally

considered to be a part of industrial laundry business but now

known as textile lessors. We, the group members, are trying our

level best to obtain the precise and related facts. The

subsequent group report was assigned as a part of mandatory

2 | P a g e

requirement for F-307 course. Some more definite objectives of

the report were to:

To analyze the background and main features of

To depict an industry analysis to understand the position of

Omni Service in the industry

To point out the problems faced by the company in current

situations and giving solutions to the problems.

To provide sufficient data either in support of merging or

against with a French company called “the Societe Generale

de Location et Services Textiles”

To give an overall overview of the company’s position in

comparison with its competitors.

1.3. Scope of the Report:The report mainly examines the current financial position of Omni

Services Incorporation and gives solution to the problems faced

by the company.

1.4. Methodology:This report has been completed by taking information from

different relevant sources. However, this report also consists of

a significant amount of data obtained from both primary and

secondary sources. We have collected the data mainly from two

sources. These sources are given below:

i. Primary Data Source:

3 | P a g e

The case was given to us by our honorable course instructor M.

Sadiqul Islam, Ph.d, which is used as primary source. This case

deals with a textile lessors company named Omni Services,

Incorporated. The theoretical segments were mainly ascertained

from the textbooks suggested under this course.

ii. Secondary Data Source:

In addition to the aforementioned two sources of data, different

websites and related articles were taken into consideration for

preparing the report.

1.5. Limitations:The most important factor constraining our study was the

difficulty regarding getting the face to face data exclusive to

the risk factor. That’s why, despite our utmost efforts possible;

we couldn’t come up with satisfactory level of different data.

On the other hand Research work is very much comprehensive. It is

an accumulation of both information and estimation of different

factors. It requires a great effort and long sound planning to

make this report. It is true that we got help from many

responsible people. But still we faced some problem. Because of

some unavoidable reasons; we, sometime, face problem in some

portion of the report. But we tried our level best to overcome

this. The report was on financial planning of Omni Services INC.

we have prepared an elaborate company overview, industry overview

4 | P a g e

for this report. In this respect there may be some lacking in the

report because of our knowledge limitation. We tried to write the

report in a sequential way but there may be some problems in the

sequence of the report. But all these errors are totally

unintentional. At the end we are very happy to present this

report to the readers and its success will depend on the positive

response of the readers.

5 | P a g e

Chapter 2 Analysis of

Economy: USA

6 | P a g e

2. Economic analysis of USA: The economy of the United States is the world's largest singlenational economy. Its GDP at purchasing power parity is also thelargest of any single country in the world, approximately a fifthof the global total. The United States has a mixed economy and hasmaintained a stable overall GDP growth rate, a moderateunemployment rate, and high levels of research and capitalinvestment. Its five largest trading partners are Canada, China,Mexico, Japan, and Germany.

The recession which occurred in the early 1980's was the mostsevere and the most significant in terms of economic policy ofthe post-World War II recessions.

The economic upheaval of the 1970s had important politicalconsequences. The American people expressed their discontent withfederal policies by turning out Carter in 1980 and electingformer Hollywood actor and California governor Ronald Reagan aspresident.

The early 1980s recession was a severe recession in the UnitedStates which began in July 1981 and ended in November. Theprimary cause of the recession was a contractionary monetarypolicy established by the Federal Reserve System to control highinflation. The wake of the 1973 oil crisis and the 1979 energycrisis, stagflation began to afflict the economy of the UnitedStates

The real GDP from 1980 onward was fluctuating up and down and onaverage not trending in either direction. It is perhaps best torefer to this condition as an economic malaise rather than arecession because the economy was in difficulty more than a yearbefore it was officially an economic recession.

7 | P a g e

The immediate cause of the Great Depression of the 1930's was thecatastrophic collapse of investment purchases. There were priorcauses, such as the real interest rate stemming from restrictivemonetary policy, but it is in investment purchases that thesefactors have their effect.

The profile for mid-1981 to 1982 was especially disturbing. It isthe classic picture of a catastrophic collapse in progress.

What the GDP statistics show is that prior to 1979 the GDP hadbeen growing by about fifty to a hundred billion dollars perquarter. In 1979 the growth continues but at a slower rate, aboutthirty billion per quarter. Then after the second quarter of 1980there is an actual fall in GDP of about five billion and thenanother fall of nine billion in the next quarter. The economythen recovers in the fourth quarter of 1980 and adds a hundredbillion and another hundred billion in the first quarter of 1981.The economy then falls in the second quarter only to rise in thethird and fall in the fourth. The erratic pattern continues in1982 but in 1983 the economy commences to grow again.

Only part of the period would fit the notion of recession as aperiod of decline in GDP and even less of it would fit the strictdefinition of a recession as a period in which the GDP declinedfor two quarters or more. But clearly the whole period of 1980-82is one of an economic malaise and represents an episode ofeconomic difficulty. Although recessions are defined in terms ofoutput (GDP) they are felt in terms of the unemployment rate.

There was a perceptible rise in the unemployment rate in 1980.The unemployment rate rose as the period of no growth in outputpersisted while the labor force grew. The peak unemployment ratespersisted after the economy began to grow again in 1983 becauseof the backlog of unemployed workers that had accumulated duringthe period of no growth. Perhaps most important, after the

8 | P a g e

recovery of growth the unemployment rate stayed at a higher levelthan it had been at before the recession.

So far there has been no mention of the cause of the recession ormalaise or whatever one wants to call it. The cause clearly wasPaul Volcker's tight money policy which the Fed carried out tokill the chronic inflation that had developed in the U.S. economyduring the 1970's. The real interest rate is the key variablebecause it determines the level of investment. However, the levelof investment is an accumulation of work on past initiatedinvestment projects as well as the current ones so the level ofinvestment has a lagged response to the real interest rate.

A subsidiary issue is the impact of the Reagan administration'sfiscal policy. Some taxes were cut, government expenditures insome fields were also cut and the net impact has to be evaluated.There were record high levels of deficits, but macroeconomicanalysis indicates that governmental actions attempting tostimulate the economy will not be effective unless there aredeficits.

There was also a trade deficit that worried politicians. Thetrade deficit was an effect of the high value of the dollarrelative to other currencies and this in turn was the result ofthe high real interest rates in the U.S. compared to othercountries.

Trade & Investment:The key variable affected by the high real interest rates was thelevel of investment purchases. Investment purchases started todrop in the third quarter of 1979, the quarter in which thepolicy of more severe constraint on monetary growth wasannounced, and continued downward to the third quarter of 1980.From then there was a partial recovery until the third quarter of1981. Thereafter investment purchases turned downward andcontinued downward until the fourth quarter of 1982. By that

9 | P a g e

quarter investment purchases were off the previous peak of thesecond quarter of 1979 by almost $61 billion. Had there been nocompensating increases in the other components of aggregatedemand the GDP would have been down almost $134 billion. Thiswould have led to an unemployment rate of about 10.4 percentinstead of the 8 percent rate that prevailed.

Had there been no compensating increases in the other componentsof aggregate demand the levels of investment and GDP would havecontinued downward and there would have been a full blowndepression. But there were compensating changes. The mostpublicized was the Reagan Tax Cut. There were cuts in some fieldsof Federal government purchases but increases, notably indefense, in others.

The tax cut was justified in terms of Supply-side Economics butequally well could have been justified in terms of demand-sidestimulation of the economy. The increase in government purchasesalong with the tax cut led one economist to characterize theeconomic policy of the Reagan administration as being"Keynesianism on steroids." Regardless of how the policies werepublicized and characterized the end result is that they kept theanti-inflation policy of the Volcker Fed from recreating theconditions of 1929-1930 when the Fed precipitated the GreatDepression. For more on the role of Fed policies in creating theGreat Depression see Depression Money.

It is to be noted that the deficits of the Federal Government didnot "crowd out" private investment. On the contrary, theexpectations of economic recovery and growth induced higherlevels of investment purchases. In other words, private borrowingwas enticed in. Where did the funds come from for businesses toborrow? They came from the increased savings generated by therecovery of the economy. It is also to be noted that theincreased deficits of the Federal government did not lead toincreased inflation. On the contrary during the time of the

10 | P a g e

increased deficits the chronic inflation of the 1970's collapsedand did not re-emerge

The nation endured a deep recession throughout 1982. Businessbankruptcies rose 50 percent over the previous year. Farmers wereespecially hard hit, as agricultural exports declined, cropprices fell, and interest rates rose. But while the medicine of asharp slowdown was hard to swallow, it did break the destructivecycle in which the economy had been caught. By 1983, inflationhad eased, the economy had rebounded, and the United States begana sustained period of economic growth. The annual inflation rateremained under 5 percent throughout most of the 1980s and intothe 1990s.

Unemployment:Unemployment had risen from 5.1% in January 1974 to a high of9.0% in May 1975. Although it had gradually declined to 5.6% byMay 1979, unemployment began rising again thereafter. It jumpedsharply to 6.9% in April 1980 and to 7.5% in May 1980. A mildrecession from January to July 1980 kept unemployment high, butdespite economic recovery unemployment remained at historicallyhigh levels (about 7.5%) through the end of 1981. In mid-1982,Rockford, Illinois had the highest unemployment of all Metroareas with 25%. In September 1982, Michigan led the nation with14.5%. Alabama was second with 14.3% and West Virginia was thirdwith 14.0%. The Youngstown–Warren Metropolitan Area had an 18.7%rate, the highest of all Metro areas. Stamford, Connecticut hadthe lowest with 3.5% unemployment.

The peak of the recession was in November and December 1982, whenthe nationwide unemployment rate was 10.8%, highest since TheGreat Depression. As of 2013, it is still the highest since the1930s. In November, West Virginia and Michigan had the highestunemployment with 16.4%. Alabama was in third with 15.3%. SouthDakota had the lowest unemployment rate in the nation, with 5.6%.

11 | P a g e

Flint, Michigan had the highest unemployment rate of all Metroareas with 23.4%. In March 1983, West Virginia's unemploymentrate hit 20.1%. In the Spring of 1983, thirty states had doubledigit unemployment rates. When Reagan won re-election in 1984,the latest unemployment numbers (August 1984) showed WestVirginia still had the highest in the nation, 13.6%, withMississippi in second with 11.1%, and Alabama in third with10.9%.

Inflation:Inflation, which had averaged 3.2% annually in the post-warperiod, had more than doubled after the 1973 oil shock to a 7.7%annual rate. Inflation reached 9.1% in 1975, the highest ratesince 1947. Inflation declined to 5.8% the following year, butthen edged higher. By 1979, inflation reached a startling 11.3%and in 1980 soared to 13.5%. A brief recession occurred in 1980.Several key industries—including housing, steel manufacturing andautomobile production—experienced a downturn from which they didnot recover through the end of the next recession. Many of theeconomic sectors that supplied these basic industries were alsohard-hit. Each period of high unemployment was caused by theFederal Reserve, as it substantially increased interest rates toreduce high inflation; each time, once inflation fell andinterest rates were lowered, unemployment slowly fell.

Determined to wring inflation out of the economy, Federal Reservechairman Paul Volcker slowed the rate of growth of the moneysupply and raised interest rates. The federal funds rate, whichwas about 11% in 1979, rose to 20% by June 1981. The primeinterest rate, a highly important economic measure, eventuallyreached 21.5% in June 1982.

2.1. Financial industry crisis:

12 | P a g e

The recession had a severe effect on financial institutions suchas savings and loans and banks.

Banks:The recession came at a particularly bad time for banks due to arecent wave of deregulation. The Depository InstitutionsDeregulation and Monetary Control Act of 1980 had phased out anumber of restrictions on banks' financial practices, broadenedtheir lending powers, and raised the deposit insurance limit from$40,000 to $100,000 (raising the problem of moral hazard). Banksrushed into real estate lending, speculative lending, and otherventures just as the economy soured. By mid-1982, the number ofbank failures was rising steadily. Bank failures reached a post-depression high of 42 as the recession and high interest ratestook their toll. By the end of the year, the Federal DepositInsurance Corporation (FDIC) had spent $870 million to purchasebad loans in an effort to keep various banks afloat.In July 1982, Congress enacted the Garn–St. Germain DepositoryInstitutions Act of 1982 (Garn–St. Germain), which furtherderegulated banks as well as deregulating savings and loans. TheGarn–St. Germain act authorized banks to begin offering moneymarket accounts in an attempt to encourage deposit in-flows,removed additional statutory restrictions in real estate lending,and relaxed loans-to-one-borrower limits. The legislationencouraged a rapid expansion in real estate lending at a timewhen the real estate market was collapsing, increased theunhealthy competition between banks and savings and loans, andencouraged overbuilding of branches. The recession affected thebanking industry long after the economic downturn technicallyended in November 1982. In 1983, another 50 banks failed—easilybeating the Great Depression record of 43 failures set in 1940.The Federal Deposit Insurance Corporation (FDIC) listed another540 banks as "problem banks" on the verge of failure.

13 | P a g e

In 1984, the Continental Illinois National Bank and TrustCompany, the nation's seventh-largest bank (with $45 billion inassets), failed. The FDIC had long known of Continental Illinois'problems. The bank had first approached failure in July 1982 whenthe Penn Square Bank, which had partnered with ContinentalIllinois in a number of high-risk lending ventures, collapsed.But federal regulators were reassured by Continental Illinoisexecutives that steps were being taken to ensure the bank'sfinancial security. After Continental Illinois' collapse, federalregulators were willing to let the bank fail in order to reducemoral hazard and encourage other banks to rein in some of theirmore risky lending practices. But members of Congress and thepress felt Continental Illinois was "too big to fail." In May1984, federal banking regulators were forced to offer a $4.5billion rescue package to Continental Illinois.

Continental Illinois may not have been "too big to fail," but itscollapse could have caused the failure of some of the biggestbanks in the United States. The American banking system had beensignificantly weakened by the severe recession and the effects ofderegulation. Had other banks been forced to write off loans toContinental Illinois, institutions such as Manufacturers HanoverTrust Company, Bank of America and perhaps Citicorp would havebeen insolvent?

The S&L crisis:The recession also significantly worsened a crisis in the savingsand loan industry. In 1980, there were approximately 4,590 state-and federally chartered savings and loan institutions (S&Ls) withtotal assets of $616 billion. Beginning in 1979, S&Ls beganlosing money due to spiraling interest rates. Net S&L income,which totaled $781 million in 1980, fell to a loss of $4.6billion in 1981 and a loss of $4.1 billion in 1982. Tangible networth for the entire S&L industry was virtually zero. The FederalHome Loan Bank Board (FHLBB) regulated and inspected S&Ls, and

14 | P a g e

administered the Federal Savings and Loan Insurance Corporation(FSLIC), which insured deposits at S&Ls. But the FHLBB'senforcement practices were significantly weaker than those ofother federal banking agencies. Until the 1980s, savings andloans had limited lending powers. The FHLBB was, therefore, arelatively small agency overseeing a quiet, stable industry.Accordingly, the FHLBB's procedures and staff were inadequate tosupervise S&Ls after deregulation gave the financial institutionsa broad array of new lending powers. Additionally, the FHLBB wasunable to add to its staff because of stringent limits on thenumber of personnel it could hire and the level of compensationit could offer. These limitations were placed on the agency bythe Office of Management and Budget, and were routinely subjectto the political whims of that agency and political appointees inthe Executive Office of the President. In financial circles, theFHLBB and FSLIC were called "the doormats of financialregulation.

Because of its weak enforcement powers, the FHLBB and FSLICrarely forced S&Ls to correct poor financial practices. The FHLBBrelied heavily on its persuasive powers and the states to enforcebanking regulations. With only five enforcement lawyers, theFHLBB was in a poor position to enforce the law even had itwanted to.

One consequence of the FHLBB's lack of enforcement abilities wasthe promotion of deregulation and aggressive, expanded lending toforestall insolvency. In November 1980, the FHLBB lowered networth requirements for federally insured S&Ls from 5% of depositsto 4%. The FHLBB further lowered net worth requirements to 3% inJanuary 1982. Additionally, the agency only required S&Ls to meetthese requirements over a 20-year period. This phase-in rulemeant that S&Ls less than 20 years old had practically no capitalreserve requirements. This encouraged extensive chartering of new

15 | P a g e

S&Ls, because a $2 million investment could be leveraged into$1.3 billion in lending.

Congressional deregulation worsened the S&L crisis. The EconomicRecovery Tax Act of 1981 encouraged a boom in commercial realestate building projects. The passage of DIDMCA and the Garn–St.Germaine act expanded the authority of federally chartered S&Lsto make acquisition, development, and construction real estateloans and eliminated the statutory limit on loan-to-value ratios.These changes allowed S&Ls to make high-risk loans to developers.Beginning in 1982, many S&Ls rapidly shifted away fromtraditional home mortgage financing and into new, high-riskinvestment activities such as casinos, fast-food franchises, skiresorts, junk bonds, arbitrage schemes, and derivativeinstruments.

Federal deregulation also encouraged state legislatures toderegulate state-chartered S&Ls. Unfortunately; many of thestates which deregulated S&Ls were also soft on supervision andenforcement. In some cases, state-chartered S&Ls had closepolitical ties to elected officials and state regulators, whichfurther weakened oversight.

As the risk exposure of S&Ls expanded, the economy slid into therecession. Soon, hundreds of S&Ls were insolvent. Between 1980and 1983, 118 S&Ls with $43 billion in assets failed. The FederalSavings and Loan Insurance Corporation (FSLIC), the federalagency which insured the deposits of S&Ls, spent $3.5 billion tomake depositors whole again. The FSLIC pushed mergers as a way toavoid insolvency. From 1980 to 1982, there were 493 voluntarymergers and 259 forced mergers of savings and loans overseen bythe agency. Despite these failures and mergers, there were still415 S&Ls at the end of 1982 that were insolvent.

Federal action initially caused this problem by allowing theseinstitutions to get involved in creating wealth through unhealthy

16 | P a g e

fractional reserve practices, a.k.a. lending out much more moneythan they could ever afford to pay back out to customers if theycame to withdraw their money. This ultimately led to S&Lsfailure. Later, the government’s inaction worsened the industry'sproblems. Responsibility for handling the S&L crisis lay with theCabinet Council on Economic Affairs (CCEA), an intergovernmentalcouncil located within the Executive Office of the President. Atthe time, the CCEA was chaired by Treasury Secretary DonaldRegan. The CCEA pushed the FHLBB to refrain from re-regulatingthe S&L industry, and adamantly opposed any governmentalexpenditure to resolve the S&L problem. Furthermore, the Reaganadministration did not want to alarm the public by closing alarge number of S&Ls. These actions significantly worsened theS&L crisis.

The S&L crisis lasted well beyond the end of the economicdownturn. The crisis was finally quelled by passage of theFinancial Institutions Reform, Recovery and Enforcement Act of1989. The estimated total cost of resolving the S&L crisis wasmore than $160 billion.

2.2. Political fallout:The recession was nearly a year old before President RonaldReagan stated on October 18, 1981, that the economy was in a"slight recession". The recession, which has been termed the"Reagan recession’ coupled with budget cuts (which were enactedin 1981 but began to take effect in 1982), led many voters tobelieve that Reagan was insensitive to the needs of averagecitizens. In January 1983, Reagan's popularity rating fell to 35%—approaching levels experienced by Richard Nixon and Jimmy Carterat their most unpopular. Although his approval rating did notfall as low as Nixon's during the Watergate scandal, Reagan'sreelection seemed unlikely.

17 | P a g e

Pressured to counteract the increased deficit caused by therecession, Reagan agreed to a corporate tax increase in 1982.However, he refused to raise income taxes or cut defensespending. The Tax Equity and Fiscal Responsibility Act of 1982instituted a three-year, $100 billion tax hike—the largest taxincrease since World War II.

The 1982 mid-term Congressional elections were largely viewed asa referendum on Reagan and his economic policies. The electionresults proved to be a setback for Reagan and the Republicans.The Democrats gained 26 House seats, which at the time was themost for the party in any election since the "Watergate year" of1974. However, the net balance of power in the Senate wasunchanged.

The Size of the Government:The central theme of Reagan's national agenda, however, was hisbelief that the federal government had become too big andintrusive. In the early 1980s, while he was cutting taxes, Reaganwas also slashing social programs. Reagan also undertook acampaign throughout his tenure to reduce or eliminate governmentregulations affecting the consumer, the workplace, and theenvironment. At the same time, however, he feared that the UnitedStates had neglected its military in the wake of the Vietnam War,so he successfully pushed for big increases in defense spending.

The combination of tax cuts and higher military spendingoverwhelmed more modest reductions in spending on domesticprograms. As a result, the federal budget deficit swelled evenbeyond the levels it had reached during the recession of theearly 1980s. From $74,000 million in 1980, the federal budgetdeficit rose to $221,000 million in 1986. It fell back to$150,000 million in 1987, but then started growing again. Someeconomists worried that heavy spending and borrowing by thefederal government would re-ignite inflation, but the Federal

18 | P a g e

Reserve remained vigilant about controlling price increases,moving quickly to raise interest rates any time it seemed athreat. Under Chairman Paul Volcker and his successor, AlanGreenspan, the Federal Reserve retained the central role ofeconomic traffic cop, eclipsing Congress and the president inguiding the nation's economy.

19 | P a g e

Chapter 3 Company Overview: Omni Services Incorporation

Management body of Omni Omni’s products and services

Areas served by Omni Services INC

Location of Omni Subsidiaries

Specialty of Omni Services INC

20 | P a g e

3. Company overview:OMNI Services Inc. was a holding company for 12 companies. Eachof the subsidiaries was called Rental Uniform Service and waslocated in the eastern United States. Mr. Martin had learnedabout the business while working for an industrial laundry inCincinnati, Ohio. In 1954, he went into partnership with hisfather-in-law to operate a small uniform rental business inRoanoke, Virginia. In partnership with his father-in-law heopened the Culpeper plant in 1959, and Mr. Martin moved toCulpeper to operate it. It was quickly successful, and sales hadgrown at a rate of 20% almost every year since its founding. Theonly thing that seemed to stem growth of that operation had beenplan fire in 1974.

By 1968, Mr. Martin had started new operation in Hanover,Pennsylvania, and Morgantown, West Virginia. The three plants,each called Rental Uniform Service (RUS), were separatelyincorporated. Even though the shareholders and board members werevirtually identical, the internal Revenue Service had treatedthem as separate entities, and the combined taxes were thussomewhat lower. By 1972, nine RUSs had been added, the separateincorporation tax advantages had disappeared, and the 11 separateoperations had become subsidiaries of the newly formed OmniServices Inc.

3.1. Management body of Omni: Omni had a total of 48 investors, although three were of primaryimportance: N.B. Martin, the founder, president, and chairman ofthe board, with 56% of the stock; T.Y. Martin, N.B.’s brother,Omni’s secretary treasurer, and president of the Culpeper RUS,who held 23%, and the Omni ESOP with 12.5%.

3.2. Omni’s products and services:

21 | P a g e

Omni supplied industrial uniforms to 75000 people. Four days aweek, a total of 150 trucks left the plants operated by Omni’s 12rental uniform services. Each day every truck had an establishedroute in a nearby metropolitan area. The driver stopped at suchplaces as service stations, garages, and automobile dealershipsto deliver six packaged shirts and trousers delivered were thesame as those that the driver had picked up the previous week.The employees’ names, and often the names of the companies, werestitched on the shirts. The soiled uniforms were returned to theplant for washing or dry cleaning and mending. In addition, Omniprovided executive garments for office and management personnel,shop towels, walk mats, fender covers, and linen roll towels.

3.3. Areas served by Omni Services INC:Most of Omni’s business was located in large metropolitan areas,and 11 of its 12 subsidiaries were located on the fringes ofthose areas. The largest and oldest operation, the plant inCulpeper, served the Washington, D.C area as well as several lesspopulated areas- Culpeper, Charlottesville, and Lynchburg,Virginia.

3.4. Location of Omni Subsidiaries:OMNI Services Inc. was a holding company for 12 companies. Each of the subsidiaries was called Rental Uniform Service and was located in the eastern United States. The location of Omni Services Incorporated is given below:

State college

Allentown

Alliance

Hanover

Morgantown

Cumberland

22 | P a g e

Culpeper

Calhoun

Griffin

Birmingham

Auburn

Albany

3.5. Specialty of Omni Services INC:Omni was the first firm of any size in Virginia to offer anemployee stock ownership plan ( ESOP) a kind of profit sharingplan in which Omni stock was purchased and held in trust for eachemployee. None of Omni’s 600 employees belonged to a union.

23 | P a g e

Chapter 4 Analysis of

Industry: Textile lessor

Industry

24 | P a g e

4. Industry analysis:Firms like Omni were traditionally considered to be part of theindustrial laundry business, but the industry had recently becomeknown as textile lessors.

4.1. Market characteristics:In the case which was given to us by our course instructor the name of five Rental Uniform Service firms was highlighted. as we were instructed to fins the solution for the problem only with the help of case and not from any other sources the 5 Rental Uniform Service firms along with Omni Services INC was regarded as industry. We have studied the information available to us and have prepared “ market at a glance” diagram. The diagram is drawnbelow:

Market at a glance

Market at a glance

25 | P a g e

5.5 %

4.2. Porter five forces ModelThis model identifies and analyzes 5 competitive forces thatshape every industry, and helps determine an industry'sweaknesses and strengths. According to model the 5 forces thatshape our service industry is described below:

Figure: Porter’s Five Forces model26 | P a g e

Market at a

Threat of new entrants:

Threat of new entrants is high. More new companies may enter inthis market and imitate the products of Omni’s. Successfulbusiness ideas are imitated a lot. And the sales volume of theindustry is high so new companies can enter the market.

Bargaining power of suppliers:

Bargaining power of suppliers is high as thesuppliers are incorporated. Suppliers caninfluence the quality and price of the goodsand services.

Bargaining power of customers:

For a stable market bargaining power ofcustomers needs to be low. If the number ofcompetition is lower, customers might not haveany option but buy the particular product at ahigh price. Omni is not the only company in themarket. It has five more similar productproviding competitors. So if the switching cost is lower,customers will buy products from Omni’s competitors.

Threat of substitute:

Threat of substitute is high. There are five similar rentaluniform service firms in the market. The price is one of the mostimportant determining factors. If Omni charges the same or only abit higher than its competitors, customers will buy thesubstitute products.

Industry rivalry among the existingfirms:

27 | P a g e

There are five rental union service firms other than Omni in the market. These are: Unitog, Rentex, Means services, Servisco and National service industries. So the rivalry among them is high.

4.3. PESTEL analysis: A PESTEL analysis is a framework or tool used by marketers toanalyze and monitor the macro-environmental (external marketingenvironment) factors that have an impact on an organization. Theresult of which is used to identify threats and weaknesses whichis used in a SWOT analysis.

PESTEL stands for: P – Political E – Economic S – Social T – Technological E – Environmental L – Legal

28 | P a g e

Figure: The PESTEL Model

All the external environmental factors (PESTEL factors):

The external environmental factors of Textile lessor industrypreviously known as industrial laundry business are describedbelow:

Political Factors

These are all about how and to what degree a governmentintervenes in the economy. This can include – government policy,

29 | P a g e

EconomicSocialTechnologicalEnvironmentalLegalPolitical

political stability or instability in overseas markets, foreigntrade policy, tax policy, labor law, environmental law, traderestrictions and so on. It is clear from the list above thatpolitical factors often have an impact on organizations and howthey do business. Organizations need to be able to respond to thecurrent and anticipated future legislation, and adjust theirmarketing policy accordingly. Political and regulatory changes inboth USA & France will affect the decision of merger.

Economic Factors

Economic factors have a significant impact on how an organizationdoes business and also how profitable they are. Factors include –economic growth, interest rates, exchange rates, inflation,disposable income of consumers and businesses and so on. Thesefactors can further be broken down into macro-economical andmicro-economical factors. Macro-economical factors deal with themanagement of demand in any given economy. Governments useinterest rate control, taxation policy and government expenditureas their main mechanisms they use for this. Micro-economicfactors are all about the way people spend their incomes. In ourcase, two countries are involved, USA & France. Omni services incof USA and textile of France are interested in merger. So anyeconomical change in either country will affect the merger.

Social Factors

Also known as socio-cultural factors are the areas that involvethe shared belief and attitudes of the population. These factorsinclude – population growth, age distribution, healthconsciousness, and career attitudes and so on. These factors areof particular interest as they have a direct effect on howmarketers understand customers and what drives them. Textilewants to spread their business in USA. So they want to merger

30 | P a g e

with Omni. If the merger happens, customers of Omni will beaffected too.

Technological Factors

We all know how fast the technological landscape changes and howthis impacts the way we market our products. Technologicalfactors affect marketing and the management thereof in threedistinct ways:

New ways of producing goods and services

New ways of distributing goods and services

New ways of communicating with target markets

Both the companies will be able to use each other’s resources tomake good products.

Environmental Factors

These factors have only really come to the forefront in the lastfifteen years or so. They have become important due to theincreasing scarcity of raw materials, pollution targets, doingbusiness as an ethical and sustainable company, carbon footprinttargets set by governments (this is a good example were onefactor could be classes as political and environmental at thesame time). These are just some of the issues marketers arefacing within this factor. More and more consumers are demandingthat the products they buy are sourced ethically and if possiblefrom a sustainable source.

Legal Factors

Legal factors include - health and safety, equal opportunities,advertising standards, consumer rights and laws, product labelingand product safety. It is clear that companies need to know whatis and what is not legal in order to trade successfully. If anorganization trades globally this becomes a very tricky area to

31 | P a g e

get right as each country has its own set of rules andregulations.

4.4. Key Players: The company we are focusing on is Omni Services INC. we havelearned from the previous section that Omni Services INC is inindustrial laundry business. The industrial laundry business isfragmented. Now the industry is known as textile lessors. Asmultidivisional firms like Omni Services were in directcompetition with local businesses that bought their uniforms andserviced their customers in a limited geographical area. Many ofOmni’s major competition were closely held, and a littlefinancial information was available about those operations. Themajor competitors of Omni Services INC were:

32 | P a g e

A brief description of these companies is given below: Rentex:

Rentex provided laundry and rental services, linen-supplyservices and dust control services thought nine facilities.Rentals comprised 100 percent of revenues. There were 640stockholders and 950 employees. Headquarters in Philadelphia,Pennsylvania.

Servisco:Servisco manufactured, rented and laundered work clothes anduniforms, machine wiping clothes, fender covers and linens. Italso provides contract building maintenance, housekeepingconsultant services and guard security services. Its main officeas in Hillside, New Jersey and it operated through 27 full

33 | P a g e

Key Player 2ServiscoKey Player 3Means ServicesKey Player 4NSIKey Player 5Unitog

service panel plants. There were 1501 stockholders and 6300employees.

Means Services:Means Services provided textile maintenance services by rental to

businesses in mid western states, with a concentration on

providing work garments, industrial wiping clothes, dust control

textiles, bed and table linens, towels, aprons uniforms and

continuous towel cabinets. The rental business was 100 percent of

its revenues. It has 25 processing plants, 2718 stockholders and

3900 employees. Headquarters in Chicago, Illinois.

National Service Industries ( NSI):NSI obtained 26 percent of revenues from renting table linens,

bed linen, operating room packs, towels, uniforms and dust

control materials, but lighting equipment and chemical products

were also manufactured. NSI was further diversified into

insulation service, men’s apparel, envelopes, furniture marketing

services, safety products, furniture leasing and amusement parks.

NSI headquarters were in Atlanta, Georgia and it had 10,994

employees.

Unitog:Unitog manufactured, rented and sold heavy duty, soil resistant

uniforms for service station employees, route drivers and

salesme. Rental business operated out of nine locations and

comprised 38 percent of revenues. Headquarters in Kansas city

Missouri. Approximately 420 stockholders and 2189 employees.

34 | P a g e

4.5. Competitive Advantage:Despite this strong competition, Omni Services INC provides

superior value to its clients because of its competitive

advantage. The following include competitive advantage:

Superior service to clients:

35 | P a g e

Omni provides superior services to their clients. That is thereason Omni Services INC’s profit was almost double of industryaverage profit before taxes.

employee stock ownership plan:

Omni was the first firm of any size in Virginia to offer anemployee stock ownership plan ( ESOP) a kind of profit sharingplan in which Omni stock was purchased and held in trust for eachemployee. None of Omni’s 600 employees belonged to a union. Thisis the second competitive advantage of Omni Services.

Attracting dependable and productive employees:

Omni’s major shareholder Mr. Martin always believed that theirlocations allowed them to attract employees that were moredependable and productive than the transient and high paid cityworker. Omni’s Success ca from the edge loyal employees gave thefirm.

36 | P a g e

37 | P a g e

Chapter 5

Ratio AnalysisSWOT Analysis

5. Ratio AnalysisRatio Analysis is a form of Financial Statement Analysis that isused to obtain a quick indication of a firm's financialperformance in several key areas. So using the Balance Sheet andIncome statement information of Omni Services the Ratio Analysisis done as follows:

5.1. Liquidity ratio:Liquidity ratio’s measure your company’s ability to cover itsexpenses. The two most common liquidity ratios are the currentratio and the quick ratio. Both are based on balance sheet items.

Current Ratio:

The current ratio is a reflection of financial strength. It isthe number of times a company’s current assets exceed its currentliabilities, which is an indication of the solvency of thebusiness.

Here is the formula to compute the current ratio:

Current Ratio = Total current assets / Total currentliabilities.

The Current ratio of Omni services Inc. from the year 1973 -1979is shown in the table below and then graphically represented:

1973 1974 1975 1976 1977 1978 1979Current Ratio

1.721195

2.337458

1.622449

1.626731

1.605442

1.445102

1.475243

38 | P a g e

1972 1973 1974 1975 1976 1977 1978 1979 19800

0.5

1

1.5

2

2.5

Current Ratio

Current Ratio

Quick Ratio:

The quick ratio is also called the “acid test” ratio. That’sbecause the quick ratio looks only at a company’s most liquidassets and compares them to current liabilities. The quick ratiotests whether a business can meet its obligations even if adverseconditions occur.

Here is the formula for the quick ratio:

Quick Ratio = (Total Current Assets - Total Inventory) /Total Current Liabilities

The Quick ratio of Omni services Inc. from the year 1973 -1979 isshown in the table below and then graphically represented:

1973 1974 1975 1976 1977 1978 1979Quick Ratio

1.072546

1.791901

1.281341

1.128809

1.244218

1.012379

1.16165

39 | P a g e

1972 1973 1974 1975 1976 1977 1978 1979 19800

0.20.40.60.81

1.21.41.61.82

Quick Ratio

Quick Ratio

5.2. Solvency Ratio:Solvency ratios measure the stability of a company and itsability to repay debt. These ratios are of particular interest tobank loan officers. They should be of interest to us, too, sincesolvency ratios give a strong indication of the financial healthand viability of business. Some of the solvency ratio of OmniServices Inc. is analyzed below:

Debt-to-Worth ratio:

The Debt-to-Worth Ratio (or Leverage Ratio) is a measure of howdependent a company is on debt financing as compared to owner’s

40 | P a g e

equity. It shows how much of a business is owned and how much isowed.

The Debt-to-Worth Ratio is computed as follows:

Debt-to-Worth Ratio = Total Liabilities / Net Worth

The debt to worth ratio of Omni Services Inc. from the year 1973-1979 is listed and then presented graphically below:

1973 1974 1975 1976 1977 1978 1979 1973DebttoworthRatio 0.93 0.85 0.76 0.91 0.77 0.65 $0.69 0.93

1972 1973 1974 1975 1976 1977 1978 1979 1980$0.00 $0.10 $0.20 $0.30 $0.40 $0.50 $0.60 $0.70 $0.80 $0.90 $1.00

Debt to worth Ratio

Debt to worth Ratio

Working Capital:

Working capital is a measure of cash flow and is not a realratio. It represents the amount of capital invested in resourcesthat are subject to relatively rapid turnover (such as cash,

41 | P a g e

accounts receivable and inventories) less the amount provided byshort-term creditors.

Working capital should always be a positive number. Lenders useit to evaluate a company’s ability to weather hard times. Loanagreements often specify that the borrower must maintain aspecified level of working capital.

Working capital is computed as follows:

Working Capital = Total Current Assets - Total CurrentLiabilities

The working capital of Omni Services shows the following positionfrom the year 1973-1979:

1973 1974 1975 1976 1977 1978 1979WorkingCapital 507 1189 854 905 890 827 979

1973 1974 1975 1976 1977 1978 19790

200

400

600

800

1000

1200

1400

Working Capital

Working Capital

42 | P a g e

Net Sales to Working Capital:

The relationship between Net Sales and Working Capital is ameasurement of the efficiency in the way working capital is beingused by the business. It shows how working capital is supportingsales.

It is computed as follows:

Net Sales to Working Capital Ratio = Net Sales/Net WorkingCapital

The Omni Services Inc. possesses the following Net Sales toWorking Capital Position:

1973 1974 1975 1976 1977 1978 1979NetSalestoworkingCapital $13.90 $7.05 $12.00 $13.78 $16.86 $20.30 $20.61

43 | P a g e

1972 1973 1974 1975 1976 1977 1978 1979 1980$0.00

$5.00

$10.00

$15.00

$20.00

$25.00

Net sales to working capital

Net sales to working capital

5.3. Profitability Indicator Ratio:The profitability Indicator Ratio discusses the differentmeasures of corporate profitability and financial performance.These ratios, much like the operational performance ratios, giveus a good understanding of how well the company utilized itsresources in generating profit and shareholder value.

Operating profit Margin:

The objective of margin analysis is to detect consistency orpositive/negative trends in a company's earnings. Positive profitmargin analysis translates into positive investment quality. To alarge degree, it is the quality, and growth, of a company'searnings that drive its stock price. It is calculated as:

Operating Profit Margin = Operating profit / Net sales(revenue)

44 | P a g e

The operating profit margin of Omni Services shows the followingposition:

1973 1974 1975 1976 1977 1978 1979operating profitmargin $5.87 $8.89 $6.86 $8.12 $7.55 $7.56 $8.73

1972 1973 1974 1975 1976 1977 1978 1979 1980$0.00 $1.00 $2.00 $3.00 $4.00 $5.00 $6.00 $7.00 $8.00 $9.00

$10.00

Operating profit margin

Operating profit margin

Return on Equity:

This ratio indicates how profitable a company is by comparing itsnet income to its average shareholders' equity. The return onequity ratio (ROE) measures how much the shareholders earned fortheir investment in the company. The higher the ratio percentage,the more efficient management is in utilizing its equity base andthe better return is to investors.

It is calculated as follows:

45 | P a g e

Return on Equity = Net Income/ Average Shareholders’Equity

1973 1974 1975 1976 1977 1978 1979Returnon Equity 0.22 0.13 0.24 0.20 0.22 0.19 0.19

The ROE of Omni Service Inc From the 1973 to 1979 isfound to be in the following position:

1972 1973 1974 1975 1976 1977 1978 1979 1980$0.00

$0.05

$0.10

$0.15

$0.20

$0.25

Return on equity

Return on equity

Return on Assets:

This ratio indicates how profitable a company is relative to itstotal assets. The return on assets (ROA) ratio illustrates how

46 | P a g e

well management is employing the company's total assets to make aprofit. The higher the return, the more efficient management isin utilizing its asset base. The ROA ratio is calculated bycomparing net income to average total assets, and is expressed asa percentage.

Here is the Formula to calculate ROA:

Return On Assets (ROA) = Net Income/Average totalassets

The ROA position of Omni service from the year 1973 to 1979 is asfollows:

1973 1974 1975 1976 1977 1978 1979Return on Assets 0.22 0.12 0.23 0.18 0.20 0.21 0.18

1972 1973 1974 1975 1976 1977 1978 1979 1980$0.00

$0.05

$0.10

$0.15

$0.20

$0.25

Return on Assets

Return on Assets

47 | P a g e

5.4. Debt Ratios:These ratios give users a general idea of the company's overalldebt load as well as its mix of equity and debt. Debt ratios canbe used to determine the overall level of financial risk acompany and its shareholders face. In general, the greater theamount of debt held by a company the greater the financial riskof bankruptcy.

Debt Ratio:

The debt ratio compares a company's total debt to its totalassets, which is used to gain a general idea as to the amount ofleverage being used by a company. A low percentage means that thecompany is less dependent on leverage, i.e., money borrowed fromand/or owed to others. The lower the percentage, the lessleverage a company is using and the stronger its equity position.In general, the higher the ratio, the more risk that company isconsidered to have taken on.

It is calculated using the following formula:

Debt Ratio = Total liabilities / Total assets

The Debt ratio of Omni services Inc is as follows:

1973 1974 1975 1976 1977 1978 1979Debt Ratio 0.48 0.46 0.43 0.48 0.44 0.39 0.41

48 | P a g e

1972 1973 1974 1975 1976 1977 1978 1979 1980$0.00

$0.10

$0.20

$0.30

$0.40

$0.50

$0.60

Debt ratio

Debt ratio

Debt-Equity Ratio:

The debt-equity ratio is another leverage ratio that compares acompany's total liabilities to its total shareholders' equity.This is a measurement of how much suppliers, lenders, creditorsand obligors have committed to the company versus what theshareholders have committed.

It is calculated by the following formula:

Debt-Equity Ratio = Total Liabilities / ShareholdersEquity

The Debt -Equity Ratio of Omni services Inc. is asfollows:

1973 1974 1975 1976 1977 1978 1979Debt-EquityRatio

0.934276

0.853338

0.762311

0.908827

0.773414

0.649051

0.682208

49 | P a g e

1972 1973 1974 1975 1976 1977 1978 1979 19800

0.10.20.30.40.50.60.70.80.91

Debt equity Ratio

Debt equity Ratio

Capitalization Ratio:

The capitalization ratio measures the debt component of acompany's capital structure, or capitalization (i.e., the sum oflong-term debt liabilities and shareholders' equity) to support acompany's operations and growth.

Here is the formula:

Capitalization Ratio = Long-term Debt/Long-term debt +Shareholders’ Equity

The capitalization Ratio of Omni Services is as follows

50 | P a g e

1973 1974 1975 1976 1977 1978 1979Capitalization Ratio

0.399633

0.338898

0.25698

0.348511

0.311278

0.236684

0.262611

1972 1973 1974 1975 1976 1977 1978 1979 19800

0.050.1

0.150.2

0.250.3

0.350.4

0.45

Capitalization ratio

Capitalization ratio

5.5. Operating Performance Ratios:These ratios have differing inputs and measure different segmentsof a company's overall operational performance, but the ratios dogive users insight into the company's performance and managementduring the period being measured.

51 | P a g e

Fixed Assets Turnover Ratio:

This ratio is a rough measure of the productivity of a company'sfixed assets (property, plant and equipment or PP&E) with respectto generating sales.

Here is the formula:

Fixed Asset Turnover = Revenue / Property, Plant and Equipment

The fixed Asset Turnover of Omni Services Inc .for the years1973-1979 is as follows:

1973 1974 1975 1976 1977 1978 1979Fixed Asset Turnover 2.29 3.19 2.97 2.44 2.44 2.48 2.43

1972 1973 1974 1975 1976 1977 1978 1979 1980$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

Fixed asset turnover ratio

Fixed asset turnover ratio

52 | P a g e

Sales/Revenue per employee:

As a gauge of personnel productivity, this indicator simplymeasures the amount of dollar sales, or revenue, generated peremployee.

It is calculated using the following formula:

Sales/Revenue per employee = Revenue / Number ofEmployees (average)

1973 1974 1975 1976 1977 1978 1979Sales / Revenue per employee 11.75 13.97 17.08 20.78 25.01 27.98 33.63

1972 1973 1974 1975 1976 1977 1978 1979 1980$0.00

$5.00

$10.00

$15.00

$20.00

$25.00

$30.00

$35.00

$40.00

sales/revenue per employee

sales/revenue per employee

53 | P a g e

5.6. Cash-Flow Indicator Ratios: These ratios are cash flow indicators, which focus on the cashbeing generated in terms of how much is being generated and thesafety net that it provides to the company. These ratios can giveusers another look at the financial health and performance of acompany.

Dividend payout Ratio:

This ratio identifies the percentage of earnings (net income) percommon share allocated to paying cash dividends to shareholders.The dividend payout ratio is an indicator of how well earningssupport the dividend payment.

It is calculated as follows:

Dividend Payout Ratio = Dividend per Common share /Earnings pershare

The Dividend payout Ratio of Omni Services is as follows:

1973 1974 1975 1976 1977 1978 1979Dividend PayoutRatio 0.16 0.26 0.18 0.19 0.15 0.16 0.16

54 | P a g e

1972 1973 1974 1975 1976 1977 1978 1979 1980$0.00

$0.05

$0.10

$0.15

$0.20

$0.25

$0.30

Dividend payout ratio

Dividend payout ratio

These are the key ratio analysis of Omni services which gives usa clearer view of their financial strength ability and position.

5.7. DuPont AnalysisDuPont analysis is an extended analysis of a company's return onequity. DuPont equation provides a broader picture of the returnthe company is earning on its equity. It tells where a company'sstrength lies and where there is a room for improvement. Itconcludes that a company can earn a high return on equity if:

It earns a high net profit margin; It uses its assets effectively to generate more sales;

and/or It has a high financial leverage

According to DuPont analysis:Return on Equity = Net Profit Margin × Asset Turnover × Financial Leverage

Return on Net Sales Total

55 | P a g e

Equity = Income

× × Assets

Sales TotalAssets

TotalEquity

The DuPont Analysis of Omni Services Inc. from the year 1973-1979the following results:

1973 1974 1975 1976 1977 1978 1979ROE 0.22277

40.12798

30.21463

10.18524

80.19738

20.17957

90.17864

9

When graphically represented it is as follows:

1972 1973 1974 1975 1976 1977 1978 1979 19800

0.05

0.1

0.15

0.2

0.25

ROE

ROE

5.8. SWOT Analysis of Omni Services:SWOT stands for Strengths, Weaknesses, Opportunities and Threats,and is an important tool often used to highlight where a businessor organization is, and where it could be in the future. It looksat internal factors, the strengths and weaknesses of a business,and external factors, the opportunities and threats facing thebusiness. The process can give you on overview of where the

56 | P a g e

business, and the environment it operates in, is strategically.This is an important, yet too simple to understand tool used bymany students, businesses and organizations for analysis.

The analysis shows Omni Services Inc. Strengths, Weaknesses,Opportunities and Threats. The SWOT analysis will give us a clearpicture of the business environment Oni services In. is operatingin.

Strengths:

The strengths of a business or organization are positive elements, something they do well and is under their control. The strengths of a company or group add value to it, and can be what gives it the edge in some areas over the competitors. The following section will outline main strengths of Omni services Inc. are:

Highly experienced owner-operator Very high gross margin A very loyal employee base Operates business in large Metropolitan areas Located on the fringes of large metropolitan areas Locations attracted employees that were more dependable and

productive than higher paid city worker First firm in Virginia to offer employee stock ownership

plan (ESOP) Innovative in managing employees

Weaknesses:

Weaknesses of a company or organization are things that need to be improved or performed better, which are under their control. Weaknesses are also things that place it behind competitors, or stop it from being able to meet objectives. The weaknesses of Omni services Inc. are:

57 | P a g e

Not located in the large metropolitan cities High transportation costs Very little flexibility in pricing Increased transportation time

Opportunities:

Opportunities are external changes, trends or needs that couldenhance the business or organization’s strategic position, orwhich could be of a benefit to them. This section will outlineopportunities that Omni services Inc was facing.. Theopportunities are:

Ability to develop additional RUS’s Affiliate relationships with vendors Development of proprietary products Development in expertise of linen towel sales Sale of a business for a significant P/E

Threats:

Threats are factors which may restrict damage or put areas of thebusiness or organization at risk. They are factors which areoutside of the company's control. Being aware of the threats andbeing able to prepare for them makes this section valuable whenconsidering contingency plans and strategies. This section willoutline main threats our Omni services Inc.

The increasing competition in industry The fragmented nature of industry Increase in the labor costs of the fringed areas New entrance in the uniform rental business that locate in

the Metropolitan areas Changes in regulations can impact the business

58 | P a g e

Financial Risks:

Financial Risks is the possibility that shareholders will losemoney when they invest in a company that has debt, if thecompany's cash flow proves inadequate to meet its financialobligations. Omni services inc. has a moderate level of businessrisk. These are the factors that may be considered to be risky infuture for Omni services Inc.

General economic factors may adversely affect theirfinancial performance.

Increased competition could adversely affect our financialperformance.

Risks associated with the suppliers from whom their productsare sourced could adversely affect their results ofoperations.

An inability to open new, cost effective operatingfacilities may adversely affect their expansion efforts.

Compliance with environmental laws and regulations couldresult in significant costs that adversely affect theirresults of operations.

Business Risk:

Business Risk is the possibility that a company will have lowerthan anticipated profits, or that it will experience a lossrather than a profit. Business risk is influenced by numerousfactors, including sales volume, per-unit price, input costs,competition, and overall economic climate and governmentregulations. In this case Omni services Inc. has a lower businessrisk because its sales growth are growing very significantly. Forexample the industry profit before taxes was about 5.5 percent,while Omni’s was almost double. Analyzing the financial

59 | P a g e

statements also gives evidence that Omni services Inc. is facinga lower level of business risk than the industry and competitors.

60 | P a g e

Chapter 6 Omni Service INC.

Comparison with Industry

61 | P a g e

6. Comparison of Omni Services INC withindustry:

In exhibit 3 some financial information regarding these 5companies are given. we have assumed that industrial laundrybusiness industry is comprised of these six companies. We usedthe financial information available to for calculating industryaverage and then we have posted the items in graphs for comparingOmni Services INS with the same of industry. We compared OmniServices ratio with Industry average to overlook how Omni isdoing in the relevant industry. These 5 are the major competitorsof Omni Services and with the financial information available tous we have done a comparison. The bases of the comparisons are:

5- Year Growth in After-Tax Net Profit

5- year growth in Revenues

Current ratio

1978-1979 Growth in net worth

Net Profit on sales

Debt to common Equity

EPS ( Earning per share)

Dividend Payout Ratio

Average Yield

Book value per share

Return on Common equity

Sales ( in millions):

P/E Ratio

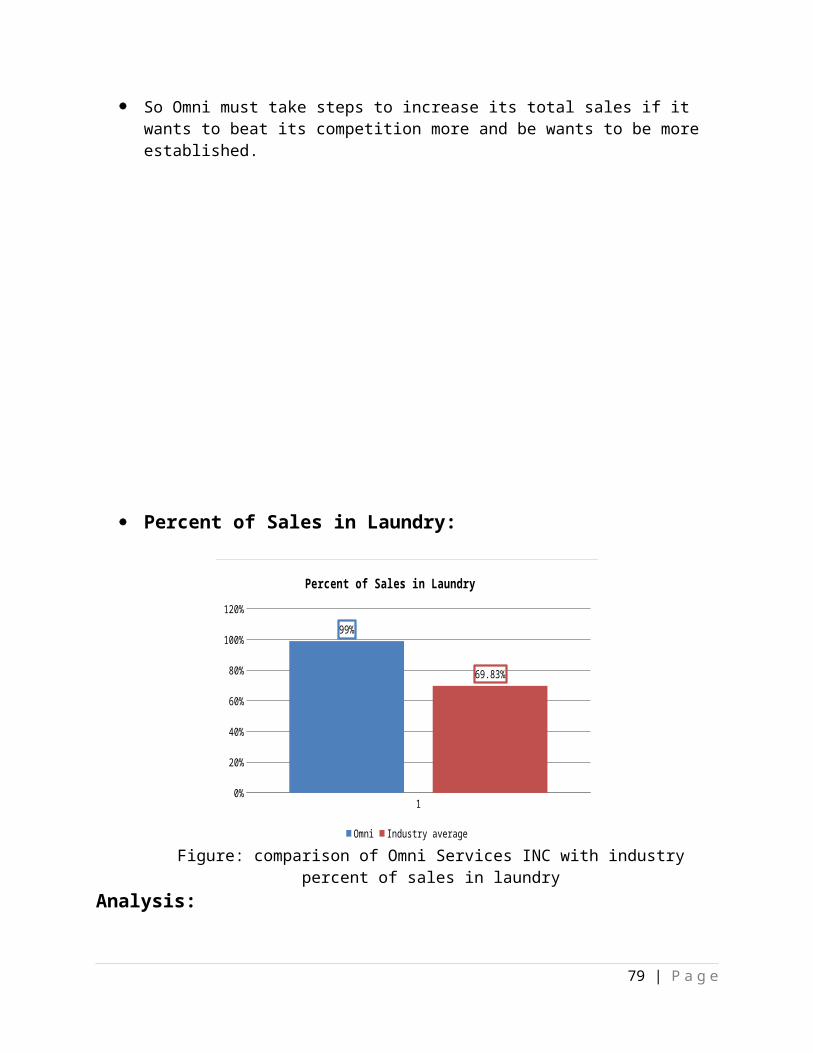

Percent of Sales in Laundry

62 | P a g e

Now Omni Services performance in the industry is evaluated incomparison with the industry. Omni services information withIndustry average is plotted n graphs are the results are comparedto see the position Omni Services INC holds in the industry.

5- Year Growth in After-Tax Net Profit:

Net Profit After tax is a more accurate look at operatingefficiency for leveraged companies. It does not include the taxsavings many companies get because they have existing debt. Inthe following graph we have plotted the data of Omni’s 5 yeargrowth in after tax Net profit against the industry growth inafter tax net profit.

Net Profit After tax = Operating Income x (1 - Tax Rate)

63 | P a g e

10.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00% 27.20%

12.23%

5 year growth in after tax Net Profit

Omni Industry average

Figure: comparison of Omni Services INC with industry

Analysis:

Growth in after tax net profit of Omni Services is higher

than industry by more than double, which is good that means

Omni Services will strive in the industry in the long run

There are many scopes of Omni Service’s in the future.

5- year growth in Revenues:Revenue growth illustrates sales increases/decreases over time.It is used to measure how fast a business is expanding. Morevaluable than a snapshot of revenue, revenue growth helps

64 | P a g e

investors identify trends in order to gauge revenue growth overtime.

Revenue Growth= (Revenue in Year 10 - Revenue in Year 1)/ Revenuein Year 1

10.00%

5.00%

10.00%

15.00%

20.00%

25.00%

19.20%

10.30%

5- year growth in Revenues

Omni Industry average

Figure: comparison of Omni Services INC with industry revenuegrowth

Analysis: Growth in revenue should be higher if one wishes to see

growth.

The industry growth rate is 10% as industrial laundry

service is a mature industry the growth is less than Omni

Service though Omni has started early it still has not

exhausted all its resources

The 5 year growth in revenue shows potential for Omni

Services.

65 | P a g e

For the revenue level ever so increasing Omni wants to

undertake a five year dividend growth plan.

Current ratio:The "current ratio' indicates the ability of a company to pay itscurrent liabilities from current assets, and, thus shows thestrength of a company's working capital position. The currentratio is significant to both short and long term creditors. Shortterm creditors are particularly interested in the current in thecurrent ratio since the conversion of inventories and accountsreceivable into cash is the primary source which the companyobtains the cash to pay short-term credits. Long-term creditorsare interested in the current ratio because a company that isunable to pay short term debts may be forced into bankruptcy.

Current ratio = Current assets ÷ Current liabilities

10.00

0.50

1.00

1.50

2.00

2.50

1.50

2.37

Current Ratio

Omni Industry average

66 | P a g e

Figure: comparison of Omni Services INC with industry Currentratio

Analysis: Generally, a current ratio of 2:1 is acceptable for most

firms Normally 1.5 is essential for industrial companies. So Omni

Services barely fits the marks. If we see industry averageit is higher than 2 which are moderately good.

This current ratio is capable of attracting long-termcreditors. So Omni should improve its Current Ratio.

1978-1979 Growth in net worth:The amount by which assets exceed liabilities. Net worth is a

concept applicable to individuals and businesses as a key measure

of how much an entity is worth. A consistent increase in net

worth indicates good financial health; conversely, net worth may

be depleted by annual operating losses or a substantial decrease

in asset values relative to liabilities. In the business context,

net worth is also known as book value or shareholders' equity.

Net Worth = Total Assets - Total Liabilities

67 | P a g e

10.00%2.00%4.00%6.00%8.00%

10.00%12.00%14.00%16.00%18.00%20.00% 17.80%

10.10%

1978-1979 Growth in net worth

Omni Industry average

Figure: Comparison of Omni Services INC with industry Net growthin 1978-1979

Analysis: As the growth in net worth of Omni Service is higher than

industry average it means the performance of Omni Service is

good.

In the graph the data used is for 1978-1979. This year’s

Omni’s total asset was greater than total liabilities which

are a good sign for the business and it increases industry

average which means the performance of the company exceeds

industry.

Net Profit on sales:

68 | P a g e

This ratio measures the ability of the revenue to sustain

expenses and give a positive net income. It is helpful in

identifying the proportion of sales units that remain after the

expenses.

Net Profit to net sales = Net Profit ÷ Net sales

10.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%6.10%

4.13%

Net Profit on sales

Omni Industry average

Figure: comparison of Omni Services INC with industry Net Profiton sales

Analysis: A higher ratio indicates a more profitable company that has

better control over its costs compared to its competitors.

as we can see from the graph that Omni Service’s Net Profit

on sales ratio is higher than industry average meaning

Omni’s control over its cost compared to its competitors is

higher.

69 | P a g e

From the graph it can be easily depicted that Omni is a

profitable company as its net profit on sales is higher than

its competitors.

Debt to common Equity:The debt to equity ratio expresses the relative equities ofowners and creditors of a company. This ratio is important tocreditors because it shows how much more the stockholders havecontributed to the company than the creditors themselves.

Equity to debt ratio = Equity ÷ Total Debt

10.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00% 35.60%

28.45%

Debt to common Equity

Omni Industry average

Figure: comparison of Omni Services INC with industry Debt tocommon equity

70 | P a g e

Analysis: Purpose is measurement of company financial leverage

as this ratio decreases , the company seems more attractive

to the creditors

Omni’s debt to common equity ratio seems to be greater than

the industry debt to equity ratios which means Omni must

take some steps to decrease its debt to equity ratios.

EPS ( Earning Per Share):EPS is the amount of net income per share of the company'soutstanding common stock .This is the most widely used index fora company's operations and is very important for both thepotential and the existing shareholders.

EPS = Earnings available to stockholders ÷ Average No.of shares outstanding

71 | P a g e

1$1.95

$2.00

$2.05

$2.10

$2.15

$2.20

$2.25

$2.30

$2.05

2.24

EPS

Omni Industry average

Figure: comparison of Omni Services INC with industry EPS

Analysis: EPS a popular measurement of profitability. As we can see