Training Report

71

A Study on Rural Insurance in IDBI By – Devanshu Divya Roll no. 2012105 IMT-Nagpur Company Guide Faculty Guide C.Shanthi Prof. Hanish Rajpal Asst Branch Head. IMT, Nagpur IDBI Federal Life Date 14-06-2013 1

-

Upload

independent -

Category

Documents

-

view

2 -

download

0

Transcript of Training Report

A Study on Rural Insurance in IDBI

By – Devanshu Divya

Roll no. 2012105

IMT-Nagpur

Company Guide Faculty

GuideC.Shanthi Prof. Hanish

Rajpal

Asst Branch Head.

IMT, Nagpur

IDBI Federal Life

Date 14-06-2013

1

AcknowledgementI would like to express my sincere gratitude to my company

guide Mrs. C. Shanthi Yagyanath, Asst Branch Head, IDBI

Federal Life Insurance Co. Ltd., Coimbatore for guiding and

helping me complete my Project Report. Her encouragement, time

and effort are greatly appreciated.

I would then like to thank my faculty guide, Prof. Hanish

Rajpal, for all his valuable inputs and constant support

towards me and providing me an opportunity to learn outside

the class room. Till now, it has been a truly wonderful

learning experience.

I would like to thank all my friends who are doing their SIP

from IDBI Federal Life Insurance Co. Ltd. for their valuable

suggestions and support. Last but not the least I would like

to thank all the respondents who are offering their opinions

and suggestions and sometimes critical views, which is helping

me to constantly update myself and come out with a successful

project report.

Devanshu Divya

2

Table of ContentsS. No. Title Page no.

1. Executive summary 4-6

2. Introduction 7-18

3 Objective of the study 19

4 Description of model studied 20-21

5 IDBI profile 22-24

3

6 Research Methodology 25-27

7 Tabulation and Results 28-40

8 Interpretations and conclusion 28-40

9 Recommendations 41-45

10 Limitation of study 46

11 Scope for future improvements 47-48

12 Bibliography 49

Executive summary IDBI Federal entered into Microinsurance as a condition for

acquiring a license to sell insurance in India. Unlike many

other insurance companies, IDBI Federal immediately saw the

benefits of microinsurance. These included fulfilment of

corporate social responsibility; use of the microinsurance to

get the brand into a new market (today’s micro clients may be

tomorrow’s high premium clients); and as a means of developing

a good relationship with the Indian insurance regulator. The

Insurance Regulatory and Development Authority (IRDA) feels

strongly about the importance of microinsurance and the need

4

for private insurers to play a role in serving the rural and

social sectors. Company realised that microinsurance would

require innovative thinking because insurance products for

low-income households was not just normal insurance with lower

premiums and benefits. In particular, company also realised

that selling micro insurance would require a new distribution

mechanism.

Rural market of India is one of the most unexplored markets so

far. A huge customer base of rural market is opening new

dimensions of marketing. IDBI has also entered into rural

market with insurance coverage named Microsurance. This plan

is extremely useful to Micro Finance Institutions, Self Help

Groups and NGOs to insure the lives of their group members and

thus provide security to the group members’ families. The plan

can also be used for providing loan protection to the group

members’ families. This project will aim to gather more

information about rural market and try to find new insurance

plan. Also a SWOT analysis can be done for IDBI in rural

market. An attempt for better plan for rural market can also

be developed or some significant changes can be bought in

rural insurance sector.

First we discuss the roadmap how we are exploring market for

IDBI here. The objective of the study is decided and it

followed up by research. A proper research design is farmed

for it and research methodology is followed up. The research

methodology followed here is survey method. The survey is

conducted by the help of questionnaire; this survey is

conducted in villages nearby to Patna and in Hindi language.

5

Later the questionnaire is updated in English to carry out the

analysis part. The analysis will include key findings about

insurance in rural sector and answers to objectives targeted.

The distribution costs, product designing to the needs of the

rural people, the viability of opening offices in rural areas

are preventing major life insurance companies to opt out of

this market. In this thesis an effort is made to study the

rural life insurance market and try to identify the major

factors inhibiting the insurance companies leading to ignore

this market. The techniques that are being adopted by the top

5 insurance companies in the rural market , the limitations of

their techniques and specific recommendations of marketing

techniques for wide spread insurance coverage etc are

discussed. The study is based on the analysis of the data

collected from at least 200 individual policy holders having

insurance policies in one or more number of insurance

companies and also from two hundred agents.

Rural India is where the next ‘big’ opportunity is. Indian

rural market constitutes approximately 72% of total Indian

population even as of date. The diverse customers spread

through 638,635 villages across the states and union

territories of India present a great untapped opportunity.

More than half of the Indian population residing in these

areas has seasonal income while the other part of the

population draws irregular income.

Majority of rural population is involved in farming sector

either directly or indirectly (farming, marginal farming, and

marginal land labourers etc.) and the balance of the large

6

population comprises of skilled labourers; artisans which

includes carpenters, masons etc.; and small scale shop owners

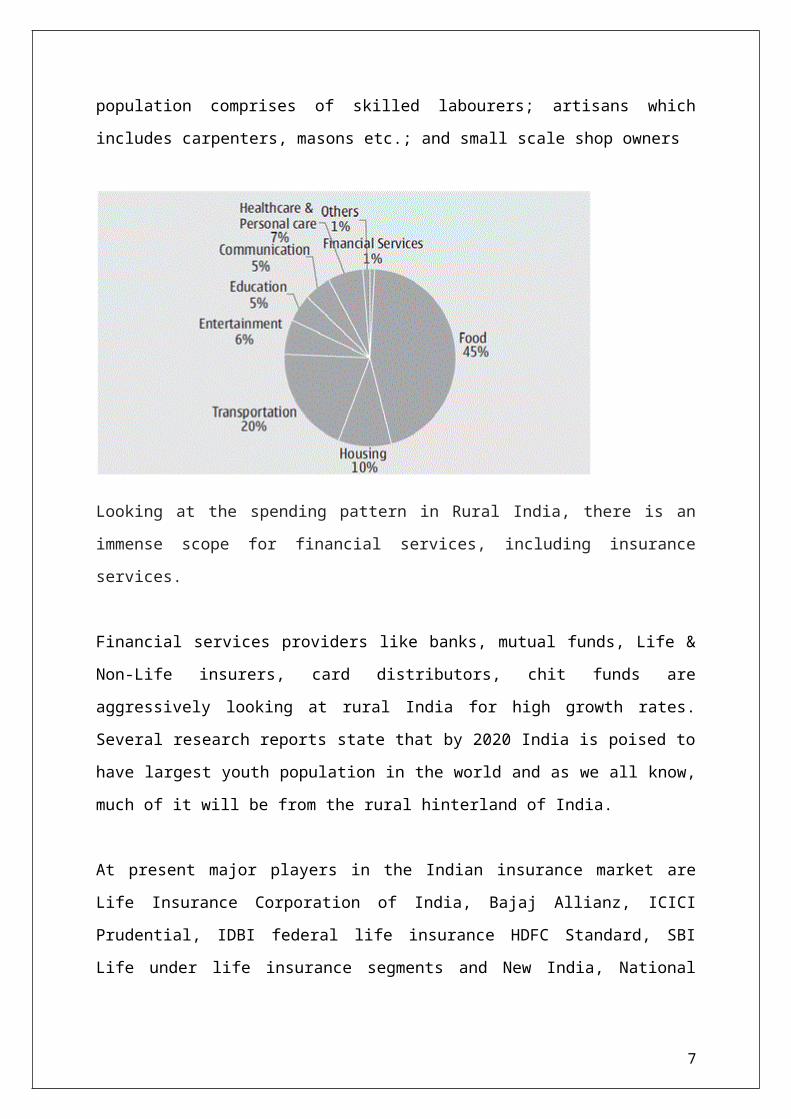

Looking at the spending pattern in Rural India, there is an

immense scope for financial services, including insurance

services.

Financial services providers like banks, mutual funds, Life &

Non-Life insurers, card distributors, chit funds are

aggressively looking at rural India for high growth rates.

Several research reports state that by 2020 India is poised to

have largest youth population in the world and as we all know,

much of it will be from the rural hinterland of India.

At present major players in the Indian insurance market are

Life Insurance Corporation of India, Bajaj Allianz, ICICI

Prudential, IDBI federal life insurance HDFC Standard, SBI

Life under life insurance segments and New India, National

7

Insurance, Oriental, United India, ICICI Lombard under non-

life insurance segments etc.

In the year 2000 when the insurance regulator came into being

and the sector was opened up for private sector participation,

the insurance penetration (total premium as a percentage of

GDP) in India was just 2.1 per cent and the coverage was

largely concentrated among the well-off. The Authority, which

has been vested with developmental responsibilities apart from

its regulatory functions, therefore sought to not only expands

coverage but also to correct the imbalances in

availability/distribution of insurance across geographic

locations and economic classes

An attempt is made to find the lacuna in the existing

marketing techniques adopted by different life insurance

companies and suggestions based on the data collected and

analysis are provided to develop tailor made techniques

suiting the rural poor.

8

Introduction

Apraaptasya praapanam yoga; Praaptsya rakhanam kshema”

Thus says Shankara in his commentary on Bhagavadgita (Geetha

Bhashyam). Yoga means getting the things one has not got and

Kshema means protection of things one has got. The sum and

substance of the two are the essence of insurance. Life

insurance is a social security tool. This is more pronounced

in rural areas that promote and sustain the life links of the

economy. The various programs of the government promoting

agriculture and tiny industries, the scientific agricultural

practices, the agrarian reforms, the empowerment of village

panchayats and such other activities have created reasonable

disposable incomes in the hands of the rural folk. At the same

time we find the rural economy dependent on vagaries of

monsoons. The existence of Below Poverty Line (BPL) families,

the stark illiteracy, and the low levels of awareness are the

major stumbling blocks to protect themselves against risks.

The life insurance penetration in rural areas as percentage of

Gross Domestic Product (GDP) is around 2.8% as at 2005 and

9

again the so called penetration is catering to the needs of

rural rich.

India’s insurance industry, private and public, has its roots

in the 19th century. The British government set up state-run

social protection schemes for its colonial officials, many of

which evolved into today’s schemes. The first private

insurance company was the Oriental Life Insurance Company,

which started in Calcutta in 1818. Under British rule, many

insurers operated in India. In 1938, the British passed the

Insurance Act, comprehensive insurance legislation, which

remains the cornerstone of the insurance industry today.

Regulated insurers are divided into two categories: life and

general insurance. Life insurance includes products like

endowments policies and retirement annuities. General

insurance covers all other types of insurance. In 1956, the

Indian government nationalized the life insurance industry.

The reasons given at the time were high levels of fraud in the

industry and a desire to spread insurance more widely, as

Nehru noted at time in parliament, “we require life insurance

to spread rapidly all over the country and to bring a measure

of security to our people.” The government combined 154

insurance providers and formed the Life Insurance Corporation

(LIC) of India. General insurance remained in private hands

until 1973 when it too was nationalized. Prior to

nationalization, 68 Indian and 45 non-Indian entities sold

insurance. All of these were absorbed into one giant

corporation, the General Insurance Corporation (GIC) with its

four subsidiaries: Oriental Insurance Company Limited, New

10

India Assurance Company Limited, National Insurance Company

Limited, United India Insurance Company Limited. Despite

Nehru’s desires, in the decades following nationalization,

insurance products were designed primarily for those with

regular income streams, i.e., those in formal employment.

These were overwhelmingly men in urban areas. The poor,

working mostly in agriculture, were largely overlooked by

these new companies. When the ideological winds of change blew

in the early the early 1990s, the Indian government set about

liberalizing its insurance markets. It set up a commission of

enquiry under the chairmanship of R N Malhotra. The central

outcome of the commission was the establishment of the

Insurance Regulatory and Development Authority (IRDA) that in

turn laid the framework for the entry of private (including

foreign) insurance companies.

Under the provisions of sections 32–B and 32–C of the

Insurance Act, 1938, insurance companies are obliged to

provide such percentages of business as may be specified by

the IRDA, for persons in the rural sector or social sector,

workers in the unorganised or informal sector, for

economically vulnerable or backward classes of the society and

other categories of persons, as may be specified by the IRDA.

The IRDA has, in pursuance of the provisions of the above two

sections of the Insurance Act, issued the (Obligations of

Insurers to Rural or Social Sectors) Regulations, 2000, which

lays down that every insurer transacting general insurance

business, shall underwrite business in the rural sector, to

the extent of at least 2% of total gross premium in the first

11

financial year, at least 3% of gross premium in the second

financial year and 5% of the gross premium in the third and

further financial years. The obligations include insurance for

crops. The Rural sector has been defined as any place which,

as per the last census, has a population of not more than

5000, density of population of not more than 400 per square

kilometre, and at least 75% of the male working population

engaged in agriculture. The Government of India has launched

various programmes for the benefit of small farmers, marginal

farmers, agricultural labourers, etc. Since 1980, all these

programmes have been integrated into Integrated Rural

Development Programme (IRDP) which is funded by the Central

and State governments on 50:50 basis. The objective of the

programme is to provide, to the target group of rural

families, a package of assistance comprising of income

generating assets, working capital, etc. through subsidy,

institutional credit, etc. Special insurance schemes are

framed to protect the beneficiaries of IRDP projects. Under

these policies, the rates of premium are lower and claims

procedure is simplified. Whenever, the word ‘scheme’ is used

hereafter, it refers to these special policies. Insurers will

evolve appropriate strategies and plans to meet these

obligations.

The Life Insurance Corporation of India identified the need of

rural life insurance and the very first objectives of the LIC

of India is to ―spread life insurance much more widely and in

particular to the rural areas and to the socially and

12

economically backward classes with a view to reaching all

insurable persons in the country and providing them adequate

financial cover against death at a reasonable cost‖. (Central

office, LIC of India: Corporate Policies published in1984)

In spite of the above laudable objective, the concept of

marketing entered in to life insurance industry very lately

and the rural focus is still nascent.

Challenges in rural market

Consumers are scattered and spread over a vast area.

Exposure to print media is very low.

Variations to dialect and life styles abound.

Message comprehension poor.

Non-conventional media more expensive and cumbersome.

Awareness and distribution channels not available

particularly for insurance.

The general insurance industry in India, prior to

nationalization concentrated its efforts in the urban

organized sector to the relative neglect of the vast

population in the rural areas. After nationalization, the

approach of the general insurance industry towards the rural

market has changed considerably. The insurers have broken

their old shell of big cities and large business houses. They

have made sincere efforts in reaching their service to the

remotest village and satisfying insurance need of the rural

population which are very different from the traditional urban

market. Many need based covers have been designed, especially

13

for the rural market, keeping in view the needs of economic

activity in rural areas. By opening offices in smaller towns

and appointing Development officers and agents, specially

catering to rural areas, we 57 have also tried to make the

services available as near to the clients as possible. Through

our innovative publicity and advertising efforts in local

languages through media which are easily accessible to the

rural population, we have also attempted to reach the message

of insurance to the rural population.

Shirodkar, S.M says, ―Insurance industry in other parts of the

world has also been somewhat slow in adopting marketing

concepts and it is natural that our country is not an

exception to this general trend .......... It is now becoming

increasingly evident that a new stage of societal orientation

is being ushered in. Insurance industry must take due

cognizance of this shift in emphasis and recognize the truth

of 'the old order changeth, yielding place to new'. An

increasing marketing orientation will alone usher in long term

success based on consumer satisfaction and loyalty. Some signs

of this change are visible in the shape of LIC's new pension

plans (Jeevan Dhara and Jeevan Akshay) as well as its entering

in to the mutual fund and housing finance fields to satisfy

customer needs in these areas. The decentralizations of

servicing functions and authority to the first line (branch)

offices and use of microprocessors to improve customer service

14

are other steps taken towards this end‖. ―New Horizons in

Planning: Path to Progress‖ published by the LIC of India

(1990) says as follows

Till then the market has been broadly divided into urban and

rural. Till then the market has been broadly divided into

urban and rural. However it was felt that this broad

classification did not give sufficient knowledge as regards

the extent of market exploitation and potential availability.

It was felt a detailed planning; segment wise on the following

pattern will lead to better results. Basic segments on the

basis of occupations (to be recorded in proposal papers)

1. Segment I: Professional and managerial group (professional,

technical, executive and managerial workers)

2. Segment II: Regular income group (clerical and sales

workers).

3. Segment III: Self-employed group (farmers, fisher men,

cultivators and other related workers).

4. Agricultural labourers.

Thus segmental planning with rural focus started after the OIC

(Organization Improvement Cell) set up of decentralization of

the LIC of India in early 80s. ―Corporate Policies‖ published

by LIC Central Office (1994) elaborates the objectives and

goals of its marketing policy as follows: Objectives:

15

As a national organization LIC should provide optimal

financial security through life insurance, as extensively as

possible, to diverse populations in urban and rural areas:

with different occupations and sources of income and

economic value; and

in high, middle and low income levels and more especially

those whose income is not regular and the economically

weaker sections; having in mind

The changing socio-economic environment of the

country;

The organization's prime concern with customer

satisfaction;

The need to provide cover at the minimum

possible price;

The need for mobilizing an increasing volume of

savings; and

The economic viability of operations to ensure

stability and growth of LIC.

For achieving the above- stated objectives, the goals are

spelt out as follows:

Bringing about a marketing approach in the various tiers

of the organizational hierarchy.

Better penetration into rural areas and market segments –

urban& rural -hitherto not adequately explored.

Offering adequate range of products suitable for

different segments of people.

Improving customer satisfaction.

16

Developing a dynamic field organization.

Improving cost effectiveness.

The techniques adopted are:

Planning and performance budgeting.

Product development.

Product mix.

Competent and productive agency organization.

Adequate training of the sales force.

Reward system to agents.

Incentives to the development officers.

Introduction of group schemes.

Consumer education.

PR & Publicity.

Philip Kotler has dealt the subject of marketing with reference

to life insurance industry in USA which is worth relevant and

significant. He says thus:

―Marketing entered into the consciousness of different

industries at different times --- Marketing spread most

rapidly in consumer packaged goods companies, consumer durable

companies, and industrial equipment companies in that order –

Bankers initially showed great resistance to marketing but in

the end embraced it enthusiastically.

“Marketing has begun to attract interest in the insurance industry and the

stock brokerage industry although marketing is still poorly understood in

these industries”.

17

Mc Kinsey & Company, a global Management consulting firm

published its report on Indian life insurance in 2007 and it

says, ―By 2012 about 10.3 million household with income

greater than Rs 2 lakh will control more than 22 per cent of

rural consumption. Further more rural India will not be one

market. Pockets of attractive rural market will emerge in

certain parts of India. Players will need to understand their

needs, design products to match them and create distribution

models to reach a highly fragmented consumer base cost

effectively‖. It further says, ―Though private sector players

are dwarfed by LIC's presence some private insurers have

reached a meaningful scale. Significantly, these players are

entering second and third tier towns and even rural areas.

D.K. Mehrotra, MD of LIC in his address to Indian Merchants

Chamber, Mumbai says that a noticeable aspect of the Indian

market is its rural blend. The Indian population is largely

rural and a welcome feature in terms of prospects is that the

affluence in our country is on the increase in rural India. It

is encouraging to see life insurance companies getting

proactive in rural markets. With the momentum building up,

most of them are lining up new micro products that exclusively

cater to rural clientele. Given the pace of business,

estimates suggest that rural sales are likely to account for

over 22-25% of the total sales revenue over the next few

months.

Belying the general perception that it is expensive to do

business in rural areas and that insurers just stick to

18

mandatory numbers as per rules, it is cheering news for rural

India that many private life insurers are putting in place

exclusive marketing initiatives to take on rural business as a

vibrant business proposition. And why not, rural is profitable

business! Market surveys have indicated that the rural savings

to income ratio is around 30%, which is higher than the urban

population. Given the vast potential for insurance products in

rural India, different techniques are likely to emerge.

Segmentation of the rural market, new approaches to leverage

extensive rural banking services or savings oriented insurance

products to provide flexibility in premium payment could be

techniques to tap the vast rural potential. Rural India is

going rapid transformation and various markets are awakening

to the realization of the potential that exists in the rural

and semi urban areas. The distinction between urban, semi

urban and rural areas is getting blurred. It is no longer

correct to presume that whatever is not urban is rural.

However despite such an open market, around 68% of the rural

economy still lies untapped due to lack of perceived

opportunities by the investors'. Indian insurance market issuddenly agog with activity. Several universally renowned players

have entered into tie up with Indian companies for a fruitful

alliance. This has led to the emergence of a vibrant market with

the hitherto monopolistic public sector players joining the race

with renewed fervour. Whether all this is going to be

translated into a victory for the customer is the million

dollar question, especially in low thrust areas like rural

19

insurance, pension product etc. The new insurers variously

need the government to:

Liberalize distribution.

Lift foreign ownership restrictions.

Provide access to the attractive parts of the pensions

market.

Issue longer dated securities.

Deregulate non-life tariffs.

A dissertation on comparative and competitive analysis of

private life insurance companies in India since their entry‖

says that LIC is an undoubted leader in the field of average

number of policies per year in the last five years. It is seen

that private insurance companies are gaining momentum and are

trying to defeat LIC in case of new insurances. Main reason

behind LIC for having such a large number of policies is the

trust of the common man. LIC being a government agency has got

a faith of Indian mass. People are not yet prepared to give

their savings in the hands of private players.

World Insurance Report, 2008 by Capgemini, while dealing with

Indian life insurance, observes that despite recent growth,

there is still tremendous untapped potential in the Indian

insurance sector. India accounts for 16% of the world

population, but accounted for only 1.68% of the world life

insurance market in 2006. India is also far behind world

averages in terms of insurance penetration, and insurance

density. A mere 20% of the insurable population aged 20 to 60

years is currently covered by life insurance.

20

Dr Vinayagara Murthy, in his research article, ―Indian

Insurance: Modern Marketing Approach‖, says,‖ Marketing

strategies for insurance in the emerging scenario could be

understood in terms of the following

Steps:

R>>>>>>STP>>>>>MM>>I>>>>C.

Here, R = Market Research STP = Segmentation, targeting and

positioning. MM = Marketing Mix I = Implementation C = Control

Having done market research and finalizing on segmentation,

targeting and positioning the strategy would focus on the

marketing mix. While determining the implementation

methodology, the four characteristics viz., intangibility,

inseparability, perishability and variability give rise to

certain unique requirements that deserve careful attention

while formulating the marketing strategy for insurance. After

implementation, the insurers should concentrate on the

effective control that would enhance their business. The

agents, by using various strategies sell the product by

convincing the customers. Moreover, they push policies with

highest premium to pocket a higher commission. The

consultative approach to selling is the modern approach, which

helps customers to buy. The four step process includes:

1. Need discovery,

2. Selection of product‘

3. Need satisfaction presentation, and

4. Servicing the sale

This approach to selling requires understanding of concepts

and principles borrowed from the fields of psychology,

21

communications, and sociology and needs a lot of personal

commitments and self-discipline from the seller.

―Low penetration of insurance in India, as elsewhere, has

varied explanations, economic and sociological. One basic

factor that puts a brake on growth is low propensity to

consume: low propensity for life insurance, not necessarily

because of considerations of affordability nor because of

inadequate range of insurance products and services. The major

determining factor is lack of awareness of life insurance per

se. And this phenomenon is not confined to rural and semi-

rural segments of society: it pervades urban populace as well.

Surprising isn‘t it, but true.

In Oracle White Paper on insurance, Chuk Johnston says, ‗the

question for today‘s insurance carriers and providers is this:

how adaptable are your IT systems and what impact can adaptive

systems have on your business? Having adaptive systems can

help you to identify and remove constraints that impede your

ability to prepare for and respond to an ever-changing market.

By using adaptive systems that provide a solid foundation

along with process flexibility, data elasticity, and

information access, you can open the dam that is holding back

the potential of your business, and seize new opportunities‘.

The feedback obtained from existing bank assurance customers

showed that 13% of the customers did not know the details of

the policy they have purchased and its future usage or

benefits, 19% customers felt they have not got sufficient

cover for insurance needs of their family, 96% of customers

rated LIC as the best financially stable insurance company and

22

17% of customers felt private insurers can better service the

claims than PSU insurers but rest 83% considered PSU insurers

as better in claim paying ability and systems.

The report published by Celent says that India‘s life

insurance market is booming and the market has grown at a

healthy CAGR of 24% over the past 5 years. Most of this growth

is from the urban areas. The increase in competition is

forcing insurance providers to look beyond urban centres and

take their trade to the more challenging rural hinterlands of

the country, where only 3% of the population of more than 720

million people have any form of life insurance coverage.

Understanding rural life insurance and assumptions: The discussion on rural marketing and life insurance rural

marketing led to the idea that rural life insurance marketing

encompasses the whole gamut of activities which include the

following:

There is availability of much untapped rural potential

with regard to life insurance.

Lack of proven marketing techniques and lack of will for

penetration from the private players.

Inadequate market research of the needs of rural

customers with regard to life insurance.

Inadequate use of new techniques for tapping the rural

market.

Viewing rural coverage more of regulatory obligation than

social obligation by the private players.

One size fits all strategy in designing products.

23

The following points emerged from the review of literature

with regard to techniques for the spread of insurance coverage

in rural areas.

The identification of rural needs and necessities.

Designing the products suiting to the needs.

Devising innovative methods to price the insurance

products suiting the needs.

Positioning the product around the rural horizon.

Selection of opinion makers as advisers and also buyers

of insurance products to infuse trust towards the

companies.

Creating the innovative distribution channels and

strengthening the existing channels.

Advertising products understandable to rural folk.

Aiming at inclusive growth.

More business orientation and not a charity. And also

fulfilling a social obligation.

Scientific management and collection mechanism with rural

focus.

The following points emerged from the review of

literature: The rural market is fast growing and rural customers are

market savvy as do the urbanites.

The awareness levels of rural people with regard to life

insurance are less.

The needs and necessities of rural people have certain

special features.

24

The purchase decisions are broadly decided on special

parameters.

The commitment of the individual insurance companies towards

social objectives can enhance the rural life insurance

coverage.

Insurance companies are using yesterday‘s techniques to

today‘s markets.

Insurance penetration in the rural areas is very low. The

private players have no definite and exclusive marketing

techniques for this sector. The large untapped potential in

rural hinterlands is known to all insurers but their marketing

techniques are prosaic. Every author talks of devising

innovative marketing techniques but there is less research as

to what techniques fit in to spectrum at micro level. Based on

this research gap and literature review, the problem of

designing meaningful marketing techniques gains importance.

The research problem therefore is identified as identifying

and determining the specific marketing techniques for wider

insurance coverage. Therefore this study gains relevance for

analysing the existing rural life insurance market, the

existing marketing techniques and suggest suitable methods for

a wider insurance coverage as a total social protection.

Further the review has focused on important issues such as:

Lack of adequate life insurance awareness.

Lack of proven marketing techniques by the private

players.

Low spread of Insurance message.

Heterogeneity of rural landscape.

The gap between the potential available and tapped.

25

The research gap in terms of rural expectations and rural

coverage.

Rural and Social Sector ObligationsThere are two central regulations that have shaped

microinsurance in India. The first is a set of regulations

published in 2002 entitled the “Obligations of Insurers to

Rural Social Sectors.” This is essentially a quota system. It

compels insurers to sell a percentage of their policies to de

facto low-income clients. It was imposed directly on insurers

that entered after the market was liberalised. The old public

insurance monopolies have no specified quotas, but have to

ensure that the amount of business done with the specified

sectors was not “less than what has been recorded by them for

the accounting year ended 31st March, 2002.”

Rural areas are all locations outside of officially classified

urban areas. Life insurers must sell 7% of total policies by

number (not value) in the first year, with increasing amount

of up to 16% in Year 5. With general insurance, 2% of gross

premium income must come from rural areas in the first year,

3% in Year 2, and 5% thereafter.

The regulations for the rural sector do not specify the income

levels of clients directly. They specify that the clients must

come from rural areas. With the great majority of poverty in

India located in rural areas, the effect of such a stipulation

is to ensure that poor clients are sold policies.

At present, the rural quotas are relatively low, so it is

possible for many insurers to meet their rural sector targets

26

by selling high value policies to wealthier residents of rural

areas, but the quota rises each year. The targets for life

insurance are likely to be easier to hit than for general

insurance. Consider, for example, how many insurance policies

covering huts need to be sold to equal 5% of the premium of a

$100,000 house in Bangalore.

This regulation has generated massive pressure on insurers to

sell microinsurance. Without selling microinsurance, they

cannot sell their more profitable products. To date the IRDA

has fined a number of insurers for failing to meet their

targets. Continued non-compliance to the rural and social

obligations could result in suspension of license to operate.

The social sector includes low-income groups consisting of

unorganised workers and economically vulnerable or backward

classes in urban and rural areas, for example Dalit’s or

untouchables. Insurers must cover a specified number of new

lives each year from these groups, from 5000 policies in Year

1, up to 20,000 policies in Year 5.

It is difficult to assess the costs and benefits of the

regulation without further research. On the one hand, the

regulation has created a frenzy of interest by regulated

insurers to enter into microinsurance. The regulation has also

been the motor for important innovation. To date, much of the

innovation in other countries has derived from donors,

academics or MFIs working on the issue. In India, in their

drive to meet their rural and social sector targets, regulated

insurers are developing innovative new products and delivery

27

channels. They bring their considerable resources to this

task.

The impact of the quota is of course not all positive. There

have been unverified reports that some insurers are dumping

poorly serviced products on clients solely to meet their

targets. As soon as they have met their targets, some have

immediately stopped selling microinsurance.

This practice is difficult to regulate, as it is harder to

police the quality of insurance sold and serviced to the poor

than its quantity. It would certainly be socially unfortunate

if the regulation resulted in a mass of poorly serviced

products sold at a loss, to enable insurers to concentrate on

their more profitable products. This situation would not

result in meaningful sustainable financial deepening, but more

akin to charity, forced on insurers to allow them to do

business in India.

28

Objective of study

I. To understand the potential of the rural insurance

sector

II. To develop a plan for exploring new market or less

explored market.

III. To study the market penetration in rural sector by

IDBI.

IV. To analyse the competition in rural insurance market

i.e. IDBI VS other leading insurance companies.

V. To develop a plan for increasing customer base in

existing rural insurance market.

VI. To develop new insurance plan according to their

needs and requirements.

VII. To improve the presence of IDBI in rural insurance

sector.

Insurance sector in India is very much explained by urban

population. However companies are now showing inclination

towards rural India also. Many companies have launched their

rural project.

29

Our objective aims to study the rural insurance in every

possible aspect. Questions are raised for every issues and a

survey is conducted to find solution of every query.

Questionnaire is generated to arrive at conclusion of our

objectives.

We will try to study the whole insurance sector also whether

they really show interest in rural market or they have entered

in rural market just for completion purpose.

We would also find the answers effectiveness of advertisement

and other promotional activities of life insurance companies.

Description of concept usedAs rural security is vital for the growth of the economy, the

most serious problem confronting the rural security is

inadequate life insurance coverage and inadequate coverage of

all their liabilities. Inclusive growth demands inclusive

insurance coverage for a tension free life. Creating assets

without the provision of an insurance umbrella prove to be a

30

futile exercise in the long run. Lack of market research with

regard to specific life insurance needs and lack of societal

marketing have inhibited the growth of life insurance

penetration in the rural areas. The present study aims at

studying the rural life insurance market in all angles – rural

aspirations and expectations, the insurance awareness, present

marketing techniques, the deficiencies in the light of low

levels of rural penetration and offering some suggestions for

improvement in profitability of the companies coupled with

wider rural coverage.

The present research is intended to study the rural life

insurance market and the rural centric marketing techniques

and the expectations of the rural customers which are

specified in objectives. The research design selected is,

therefore, exploratory or formulative research and the major

emphasis is on the discovery of ideas and insights. A critical

pre requisite to this study is to know the marketing

strategies which is the domain of the top management and may

not be revealed officially. Since the researcher himself is a

person from the life insurance industry for nearly 3 decades

and having worked in 2 major life insurers and having seen the

techniques from inside the offices, the personal observation

over the years at work situation is brought in for the study.

The reliance on the observation is only to the extent of

ensuring the objectivity of the data gathered and is not

central to the study. The known details are explained and

deficiencies are identified to suggest suitable suggestions at

the end of the thesis. Still, since the marketing techniques

31

are dynamic and ever changing and are the domain of the top

management, the research design is aimed at to see what is

there than to predict, to interpret what is distinct and

visible rather than to visualize and finally suggest viable

marketing techniques for wider rural coverage.

The objectives of the study are made use of to formulate

hypothesis and primary data is utilized to check the

hypotheses. The works of other writers on insurance also

provided insights for formulating hypotheses.

Hypotheses for study: Based on the objectives of the study and the points emerged

from the survey of literature, the following hypotheses are

made for testing:

For studying the awareness levels of rural people with regard to life insurance and

their perception of private companies with regard to safety aspects:

Majority of the customers believe that SBI Life Insurance

Company is a government company.

The rural policy holders perceive that investment in

private life insurance companies is safe.

IRDA is considered as a guaranteeing authority of

investments in the minds of rural people‘.

For studying the expectations of the rural customers with regard to type of products

and frequency of payment of premiums:

Direct sale strategy with cheaper premiums is preferred

in rural areas.

32

People in rural areas prefer insurance coverage on

liabilities.

People in rural areas prefer pension plans.

The daily pygmy collection of premium is inversely

proportional to yearly income‘.

For studying the rural centric marketing management techniques adopted by the life

insurance companies and also the deficiencies vis-à-vis expectations of the

customers.

The existing rural policies of different companies are

need based.

Life insurance agents are influenced by extra rewards for

promoting rural policies‘.

Life Insurance companies are really interested in rural

businesses.

Satisfaction of customer influences repeat businesses.

Group insurance is preferred than the individual business

by the agents for rural people‘.

Life insurance awareness has an effect on the business

volumes of companies‘.

The caste/ religion of the agent have effect on sale of

insurance policies.

Company ProfileAbout IDBI Federal Life Insurance

33

IDBI Federal Life Insurance Co Ltd is a joint-venture of IDBI

Bank, India’s premier development and commercial bank, Federal

Bank, one of India’s leading private sector banks and Ageas, a

multinational insurance giant based out of Europe. In this

venture, IDBI Bank owns 48% equity while Federal Bank and

Ageas own 26% equity each. Having started in March 2008, in

just five months of inception, IDBI Federal became one of the

fastest growing new insurance companies to garner Rs 100 Cr in

premiums. The company offers its services through a vast

nationwide network of 2137 partner bank branches of IDBI Bank

and Federal Bank in addition to a sizeable network of advisors

and partners. As on 28th February 2013, the company has issued

over 8.65 lakh policies with a sum assured of over Rs. 26,591

Cr. They have been awarded the PMAA Awards (2009) for best

Dealer/Sales force Activity, EFFIE Award (2011) for effective

advertising, and conferred with the status of ‘Master Brand

2012-13’ by the CMO Council USA and CMO Asia.

About the sponsors of IDBI Federal Life Insurance Co

Ltd

IDBI Bank Ltd. continues to be, since its inception, India’s

premier industrial development bank. It came into being as on

July 01, 1964 (under the Companies Act, 1956) to support

India’s industrial backbone. Today, it is amongst India’s

foremost commercial banks, with a wide range of innovative

products and services, serving retail and corporate customers

34

in all corners of the country from 1077 branches and 1702

ATMs.

Federal Bank is one of India’s leading private sector banks,

with a dominant presence in the state of Kerala. It has a

strong network of over 1060 branches and 1158 ATMs spread

across India. The bank provides over four million retail

customers with a wide variety of financial products. Federal

Bank is one of the first large Indian banks to have an

entirely automated and interconnected branch network.

Ageas is an international insurance group with a heritage

spanning more than 180 years. Ranked among the top 20

insurance companies in Europe, Ageas has chosen to concentrate

its business activities in Europe and Asia, which together

make up the largest share of the global insurance market.

These are grouped around four segments: Belgium, United

Kingdom, Continental Europe and Asia.

Product Range

INCOMESURANCE

Incomesurance not only gives you unmatched transparency and

flexibility but there are lots of other features which are

inbuilt in the product like convenient premium payment

options, Tax benefits and double advantage of Endowment and

Money Back plan.

35

Incomesurance combines Endowment and Money Back benefits into

one plan. You can get periodic payments as in Money Back or

get a lump sum at maturity as in Endowment. You can make it

into an Endowment plan or Money Back plan, as you wish.

WEALTHSURANCE

The Wealthsurance Foundation Plan enables you to save and

build wealth to meet your financial goals. However, unlike

other investment alternatives, it also enables you to achieve

your wealth goals even in the event of unexpected death,

accidents, disablement or serious illness.

The Wealthsurance Foundation Plan can ensure that your plans

for wealth creation are achieved by protecting that plan with

insurance benefits.

With Wealthsurance Foundation Plan, you can:

Save into the Plan as much money as you want whether at

one time, at regular intervals or as per your

convenience.

Build your wealth by choosing the investments your

savings go into and change them from time to time as you

wish.

Get adequate life insurance cover with a unique built-in

terminal illness benefit, so that the financial security

of your loved ones is assured and your plans are always

realized.

36

RETIRESURANCE

The IDBI Federal Retiresurance Pension Plan is a Unit Linked

Insurance Plan that helps you accumulate your funds for your

retirement. The plan is tailor-made for the ever changing

investment environment, with built-in flexibilities to manage

your investment mix. On retirement, you can use the maturity

proceeds to buy an annuity so that you have a monthly pay

check for life, even after you stop earning your regular

income.

HOMESURANCE

The Homesurance Protection Plan is a reducing term plan, which

provides insurance cover equal to the outstanding balance of

your home loan. In the unfortunate event of death of the home

loan borrower, the insurance cover enables repayment of the

home loan liability.

A home loan is usually a large liability and if the breadwinner

who would repay the loan were not to be there, it could become

a serious burden to the family. The Homesurance Protection Plan

protects against this liability.

BONDSURANCE

Bondsurance is a single premium plan which allows you to make

a one-time investment and get a guaranteed amount on maturity.

37

You can choose a maturity period of 5 or 10 years for your

investment. At the end of the chosen period, you will receive

a guaranteed maturity amount.

Besides the guaranteed maturity amount, Bondsurance also provides a life insurance cover. In case of death before the maturity date, a Death Benefit which is also guaranteed will bepaid. Thus you can get life insurance cover, while earning an assured return on your investment.

Research Methodology Materials and methods which are used in conducting the studyare presented under the following headings:

Research location. Sampling design. Collection of data. Analysis of data.

Research location: Life Insurance marketing in rural areas is spread throughoutthe country extending more than the six lakh villages. Thesocial security and life insurance needs are felt in all thesevillages. All these villages fall under the category of eitherpure rural or semi urban. Two such districts of Bihar, namely,Hajipur (pure rural) and Patna rural district (rural and semiurban characteristics) are selected for the study. The surveyfor doing this research was conducted in these 2 districts of

38

Bihar viz, Hajipur rural and Patna rural districts. Theoffices of all private insurance companies are located inPatna and hence Patna rural district is selected. Forselecting the other district, the following criteria areconsidered:

Exposure to all private players. Contribution of primary sector,

The rationale for selecting Hajipur and Patna (rural) beingtheir proximity to the capital city, Patna where the branchesof all private life insurance companies are present and thecustomers are exposed to all private players in one way orother. The population of Patna is nearly 24 lakhs and population ofHajipur is 7 lakhs including rural population. However therural population is not known.

Sampling design: For collecting the responses from the customers, clustersampling technique followed by simple random sampling isadopted to ensure the representation of the data for the wholepopulation. Cluster sampling means random selection ofsampling units consisting of population elements. Then fromeach selecting unit, a sample of population elements is drawnby either simple random selection or stratified randomselection.

A survey for questionnaire is conducted in these two villages.Their response is entered by surveyor as many of respondentswere not able to understand English.

The category to which they belongs

1. Landless agricultural labourers. 2. Farmers who own lands. 3. Salaried professionals such as teachers, doctors, nurses,

anganwadi workers and such other people. 4. Artisans, petty shop owners, hoteliers, cobblers,

potters, bidi workers, weavers etc.

39

5.People engaged in service sector like agents (post andinsurance), pigmy collectors, vegetable dealers,suppliers and distributors of products.

Data collection

Primary data:The primary data is collected through questionnaires. The questionnaires contain both open ended and close ended questions that are simple and easy to understand. The questionnaires administered to customers have close ended questions which include dichotomous (Yes or No answers) and multiple choice questions to the tune of 5 (selecting from 5 given alternative answers). Open ended questions are asked where diverse information is required giving scope for the customers to air their views

Questions aimed at eliciting life insurance awareness levels like whether they know the existence of private players, whether investing in private companies is safe as per their perception, whether they recognize SBI Life Insurance Company as a government owned company, knowledge of IRDA, what prompted them to take policy ( agent pressure/ savings/ to meet future expenses/ to meet contingencies) etc.

Questions aimed at eliciting information with regard to satisfaction/ dissatisfaction levels like whether they received policy bonds and premium notices on time, whether claims are settled on time, whether they have gone for repeat sales etc.

Questions aimed at eliciting the life insurance product knowledge like – whether they are aware of rural insurance. Are they aware of IDBI Federal insurance company and are they aware of Microinsurance.

The primary data is collected from respondents of two village. This Experience Survey from the people having experience with the problem under study is felt necessary

40

since the objective of the research is to obtain insight in to the new ideas relating to the research problem. The questions are both open ended (seven) and close ended (fourteen). Questions are also asked with regard to their suggestions for spreading the message of life insurance in rural areas. The questions are designed to elicit the following information: The questions aimed at eliciting information whether in

their view the different life insurance companies have plans to suit the needs of rural people, whether there isa necessity to design cost effective policies, whether the life insurance companies, in their opinion, are really interested in social security etc.

The questions aimed at eliciting information as to the real difficulties in selling the rural policies, what type of policies they suggest for rural folk, suggestionsfor popularizing insurance plans in rural areas etc.

The questions aimed at eliciting information whether the customers, in their view, believe that the investment in private companies are safe, whether the investment decisions are swayed by caste and religious considerations, whether opinion makers have any say in investment decisions etc.

The questions aimed at eliciting information whether theyexpect more incentives/ commissions for popularizing insurance in rural areas.

Secondary Data:The secondary data is collected through the annual reports of LICof India and other life insurance companies, the journals of IRDA, the internal magazine of LIC, viz., Yogakshema, the publications of Information & Broad Casting dept, viz, Yojana, India Year Books, the web sites of LIC of India and other privatecompanies, the lead bank reports of the selected districts under study etc. The brochures, pamphlets and advertisement material are collected from across the branches of different life insurance companies.

Tools of analysis of data:

Primary Data Analysis

41

To test the reliability of the questionnaire meant for the customers, the questionnaire was initially administered to 30 policy holders each for Patna and Hajpur respondents as a pilot study. On analysing the answers of the customers, suitable changes are effected to the main questionnaire and administered to 200 respondents from Patna and Hajipur rural areas.

Secondary data analysis

The secondary data collected is analysed by tabulation, histograms, pie charts, line diagrams and graphs.

42

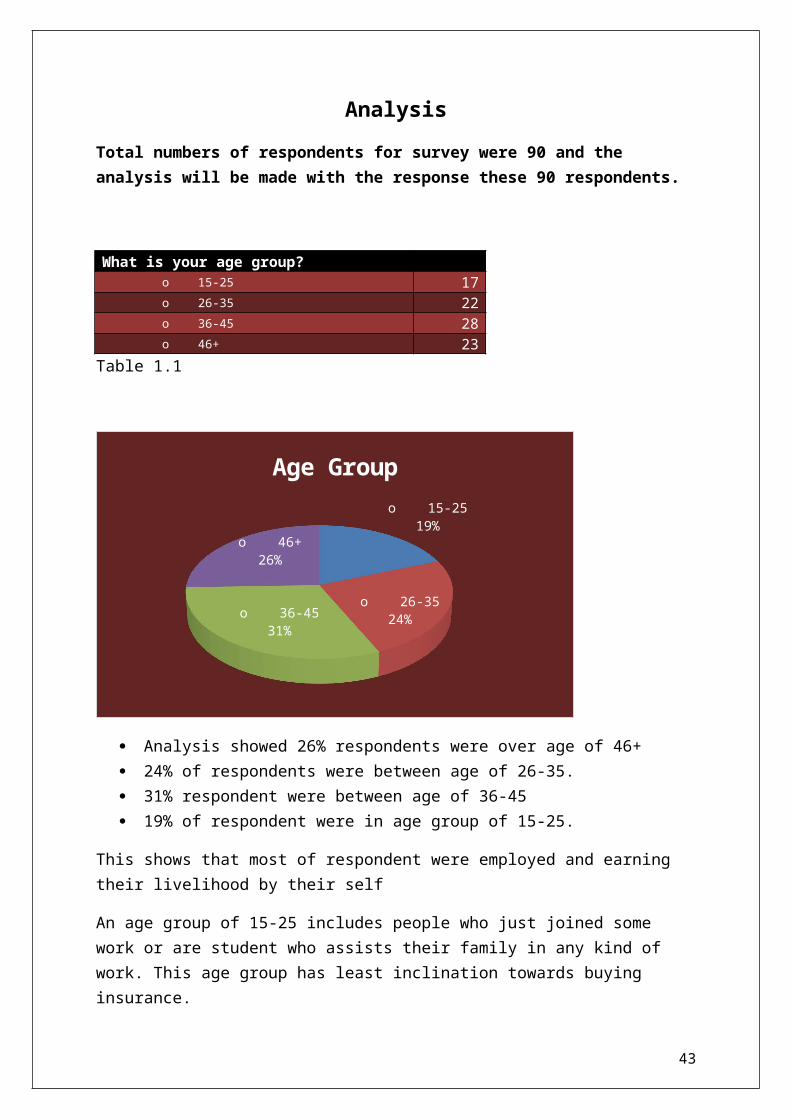

AnalysisTotal numbers of respondents for survey were 90 and the analysis will be made with the response these 90 respondents.

What is your age group?o 15-25 17o 26-35 22o 36-45 28o 46+ 23

Table 1.1

o 15-2519%

o 26-3524%o 36-45

31%

o 46+26%

Age Group

Analysis showed 26% respondents were over age of 46+ 24% of respondents were between age of 26-35. 31% respondent were between age of 36-45 19% of respondent were in age group of 15-25.

This shows that most of respondent were employed and earning their livelihood by their self

An age group of 15-25 includes people who just joined some work or are student who assists their family in any kind of work. This age group has least inclination towards buying insurance.

43

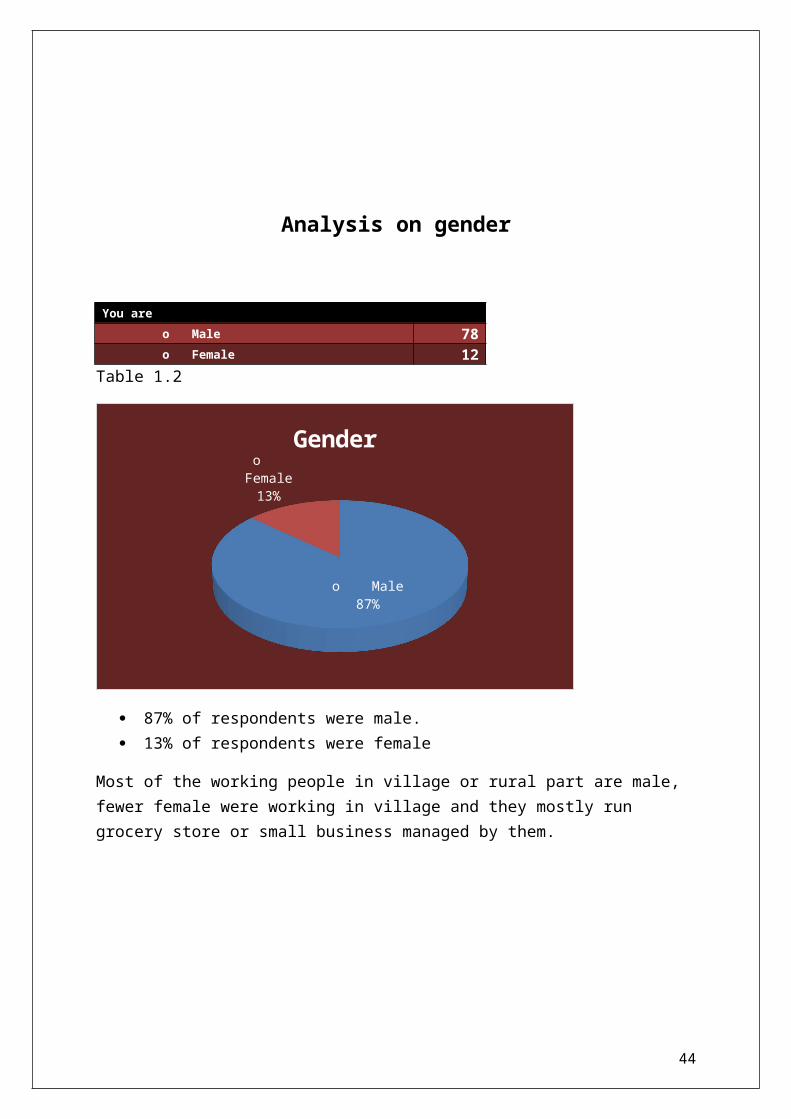

Analysis on gender

You areo Male 78o Female 12

Table 1.2

o Male87%

o Female13%

Gender

87% of respondents were male. 13% of respondents were female

Most of the working people in village or rural part are male, fewer female were working in village and they mostly run grocery store or small business managed by them.

44

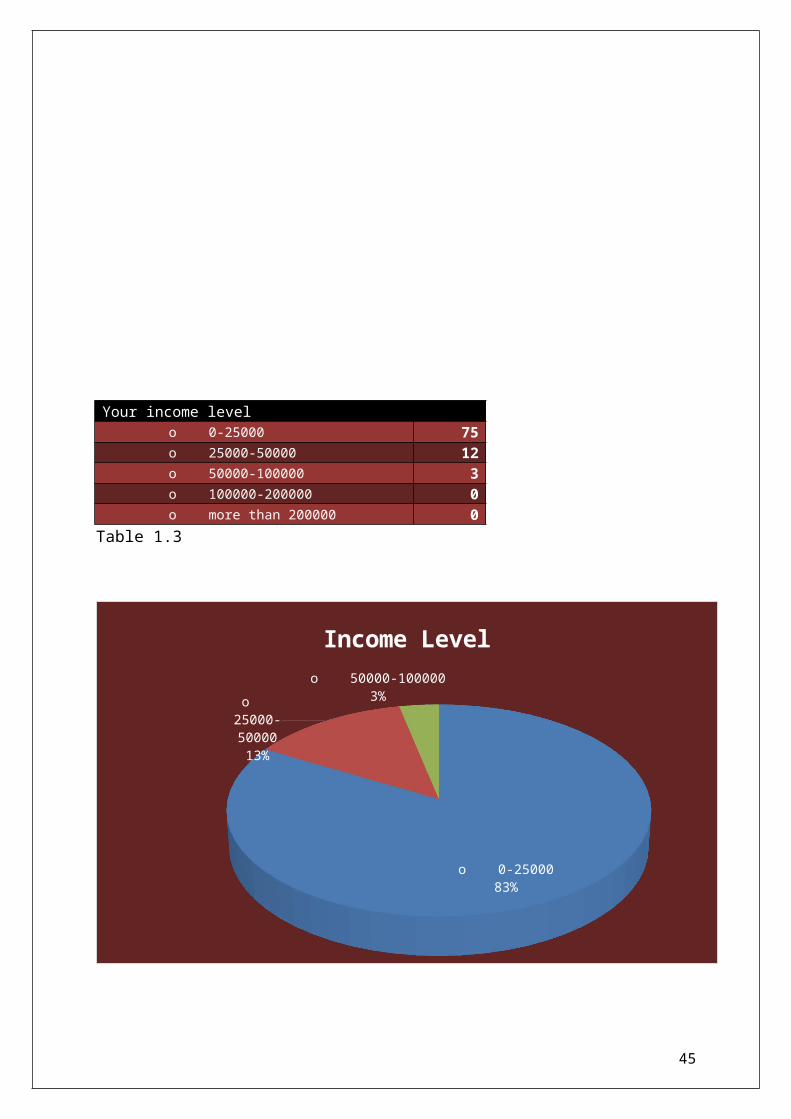

Your income levelo 0-25000 75o 25000-50000 12o 50000-100000 3o 100000-200000 0o more than 200000 0

Table 1.3

o 0-2500083%

o 25000-5000013%

o 50000-1000003%

Income Level

45

Income level suggested that around 83% of people were having income under Rs. 25,000.

Around 14% of respondent has income level of 25,000-50,000

3% of respondent reported income level 50,000-100,000 No respondent reported income over 200000

We can conclude that there less per capita income in villages so insurance with low premium will be more popular in villages.

However the purchasing power of these income groups can’t be doubted

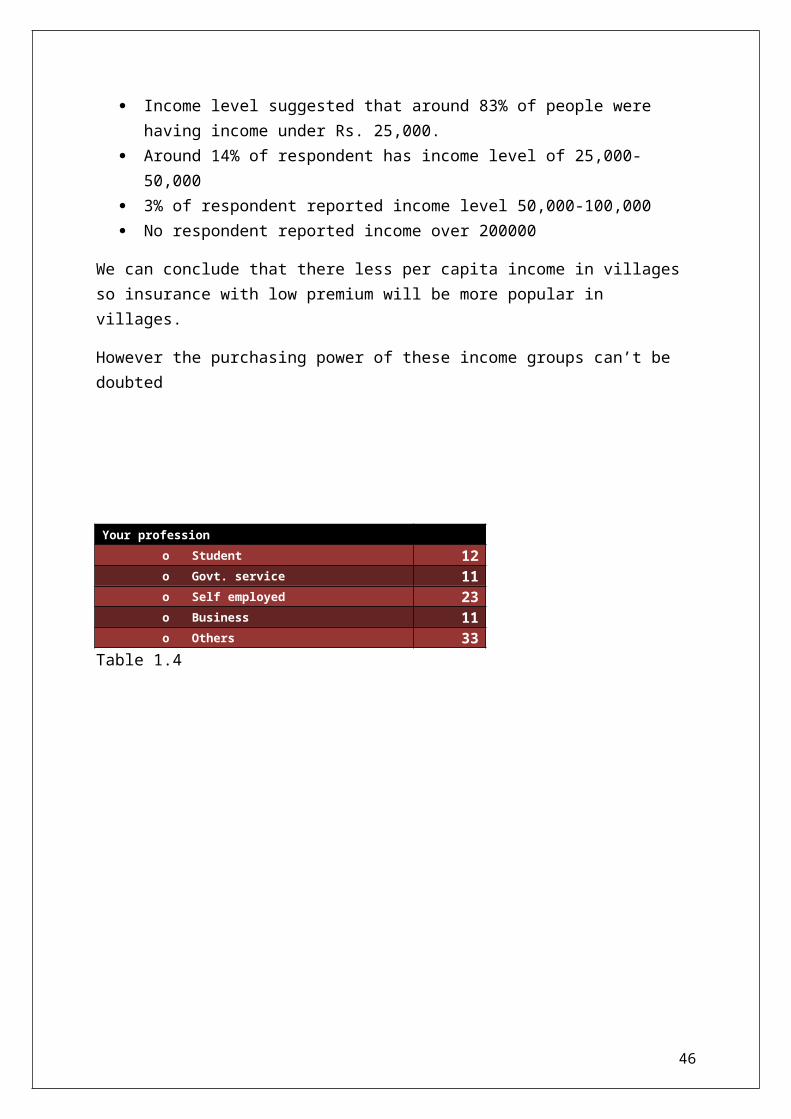

Your professiono Student 12o Govt. service 11o Self employed 23o Business 11o Others 33

Table 1.4

46

o Student13%

o Govt. service12%

o Self employed

26%

o Business12%

o Others37%

Profession

Analysis shows 13% of respondent were student 12% were public servant 12% owed some business 25% of respondent were self employed 37% had vivid way of earning livelihood

The interpretation which can be drawn here is that most of therespondent earned their livelihood by depending on farming, running small business, owned shop etc.

Since most of them were earning livelihood by their self they may need insurance in some part of their life. This analysis confirms the tremendous potential hidden inside rural sector.

Insurance may also be a part of this business.

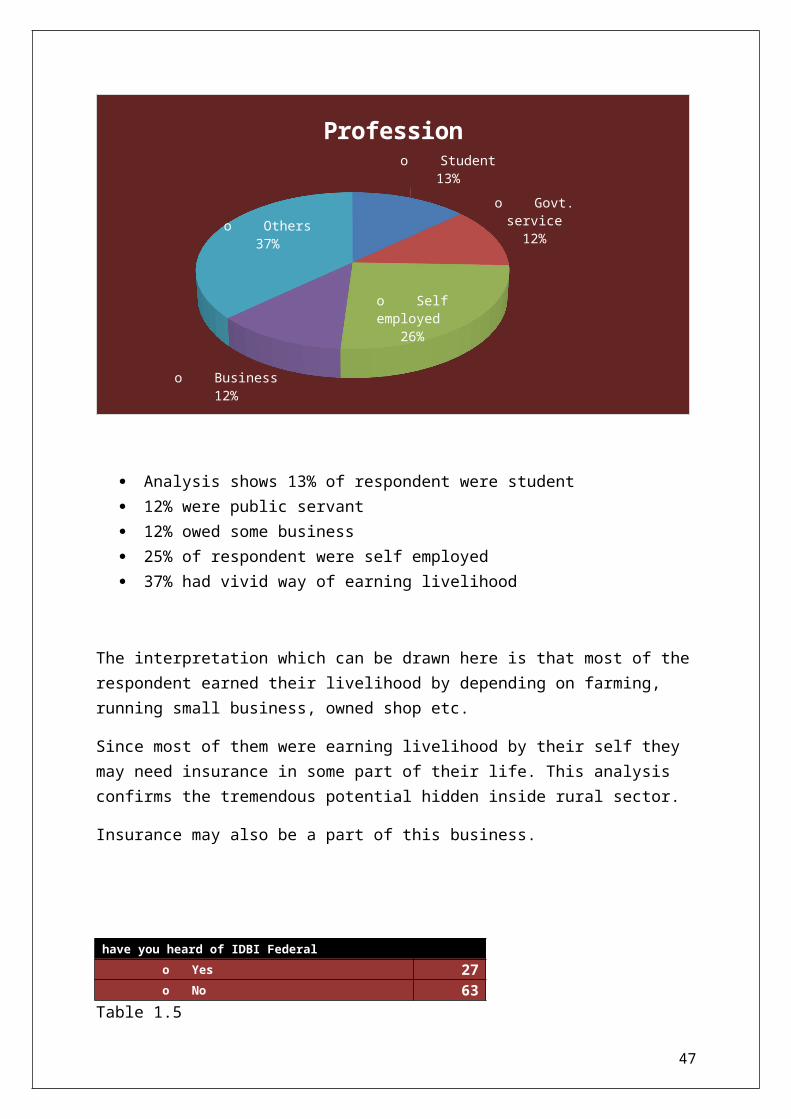

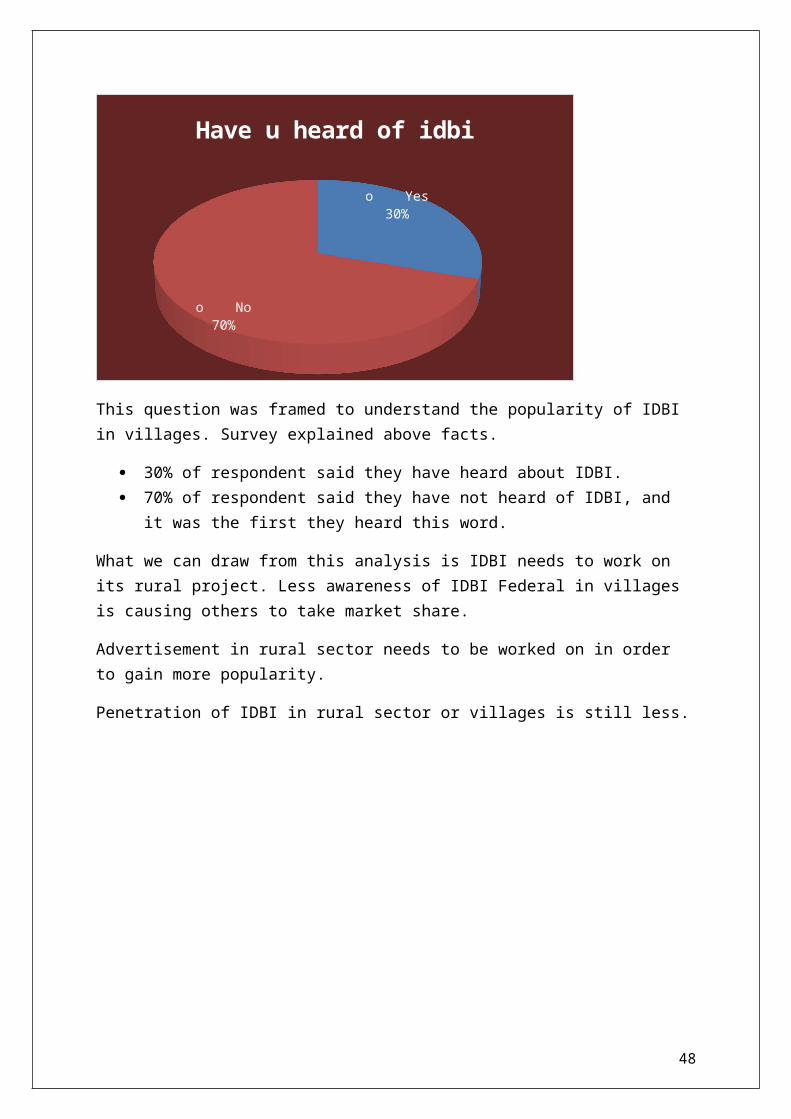

have you heard of IDBI Federalo Yes 27o No 63

Table 1.5

47

o Yes30%

o No70%

Have u heard of idbi

This question was framed to understand the popularity of IDBI in villages. Survey explained above facts.

30% of respondent said they have heard about IDBI. 70% of respondent said they have not heard of IDBI, and

it was the first they heard this word.

What we can draw from this analysis is IDBI needs to work on its rural project. Less awareness of IDBI Federal in villages is causing others to take market share.

Advertisement in rural sector needs to be worked on in order to gain more popularity.

Penetration of IDBI in rural sector or villages is still less.

48

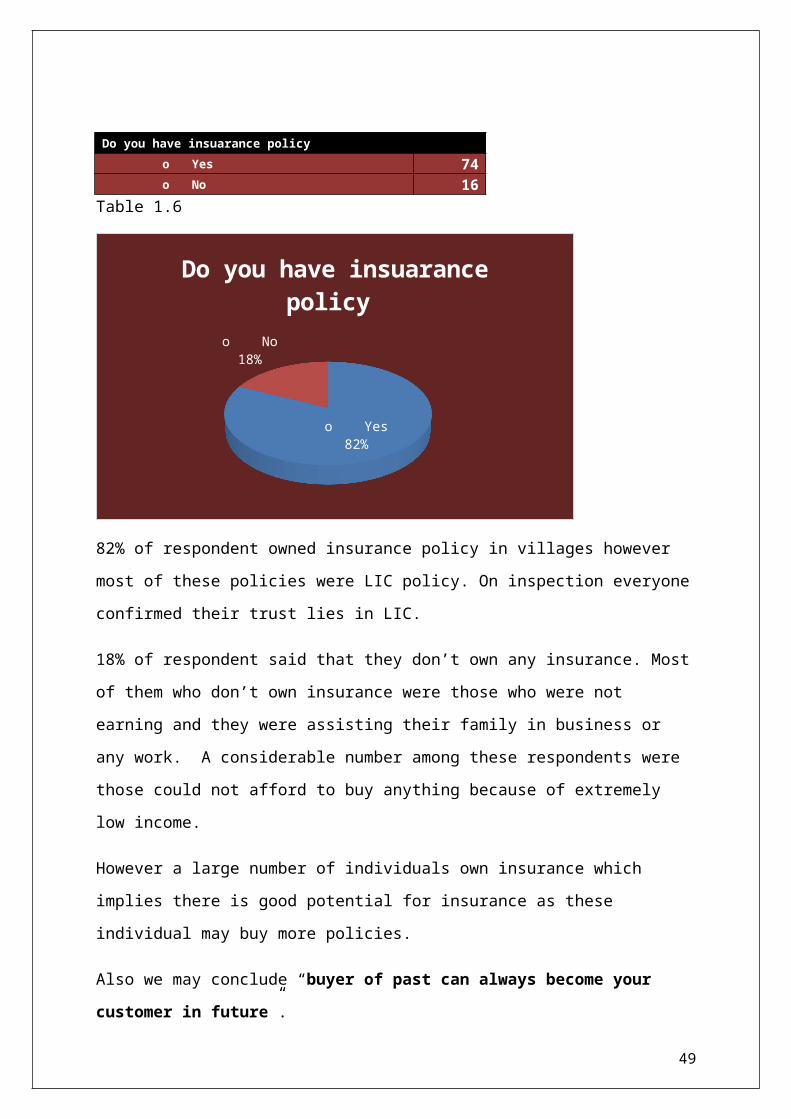

Do you have insuarance policyo Yes 74o No 16

Table 1.6

o Yes82%

o No18%

Do you have insuarance policy

82% of respondent owned insurance policy in villages however

most of these policies were LIC policy. On inspection everyone

confirmed their trust lies in LIC.

18% of respondent said that they don’t own any insurance. Most

of them who don’t own insurance were those who were not

earning and they were assisting their family in business or

any work. A considerable number among these respondents were

those could not afford to buy anything because of extremely

low income.

However a large number of individuals own insurance which

implies there is good potential for insurance as these

individual may buy more policies.

Also we may conclude “buyer of past can always become your

customer in future”.

49

would you like to buy insurance policyo Yes 57o No 33

Table 1.7

o Yes63%

o No37%

would you like to buy insurance policy

82% of respondent said they own policy and now 63% of

individual confirmed that they would like to buy policy.

50

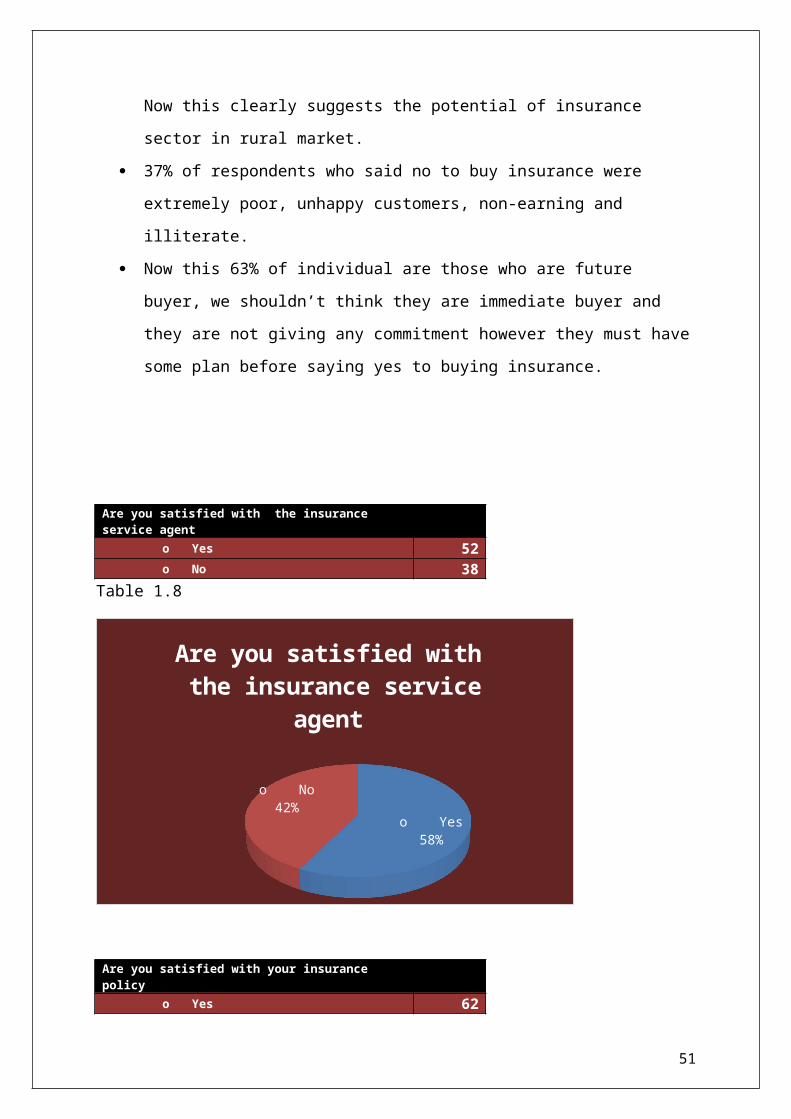

Now this clearly suggests the potential of insurance

sector in rural market.

37% of respondents who said no to buy insurance were

extremely poor, unhappy customers, non-earning and

illiterate.

Now this 63% of individual are those who are future

buyer, we shouldn’t think they are immediate buyer and

they are not giving any commitment however they must have

some plan before saying yes to buying insurance.

Are you satisfied with the insurance service agent

o Yes 52o No 38

Table 1.8

o Yes58%

o No42%

Are you satisfied with the insurance service

agent

Are you satisfied with your insurance policy

o Yes 62

51

o No 28Table 1.9

o Yes69%

o No31%

Are you satisfied with your insurance policy

58% of respondent said that they were satisfied with

their insurance service agent. The satisfaction level

according to them is the way they were explained about

the details of insurance, ways of paying premium,

benefits of buying insurance, convincing the buyer. Many

other reasons were given but they on individual view. We

omit them.

Individual who were not satisfied with their policies

because of blurred explanations by their agent. They were

not properly briefed about the kind of policies they were

buying and the benefits they were covered under.

52

When asked about the satisfaction level with their

policies around 70% of respondent said they were very

much satisfied with their policy. The reasons of their

satisfaction being the kind of policy under which they

were covered, hassle free way of paying premium, premium

based on their choice and dependent on their income.

Around 30% of respondent said that they were not happy

with their policy they own. They quoted various reasons

for being unsatisfied, frequent of them were payment of

premium, they were not properly informed about their

policies. Some of them did not even know the plan into

which they were.

A better implementation of plans in rural sector may

fetch customers from other insurance company and can also

help in consumer retention. A market study said that

around 30% of business comes from the existing consumer.

Thus a better service provided may help in building brand

and making better penetration in any market.

53

Did any insurance agent ever approached you?

o Yes 82o No 8

Table 1.10

o Yes91%

o No9%

Did any insurance agent ever approached you?

This question was asked in survey in order to know the

overall penetration of the insurance sector in rural

market. This will give a clear picture to understand the

efficiency of insurance agents in rural market.

91% of respondent agreed that they were approached by

insurance agent. This shows insurance agent penetrated

the rural market, however this survey is done near to

state capital village and because of presence of almost

all insurance companies agents were able to reach the

rural market. However many villages which are remotely

located the reach of insurance company is questionable.

However no confirm or exact statement can be made in this

question.

54

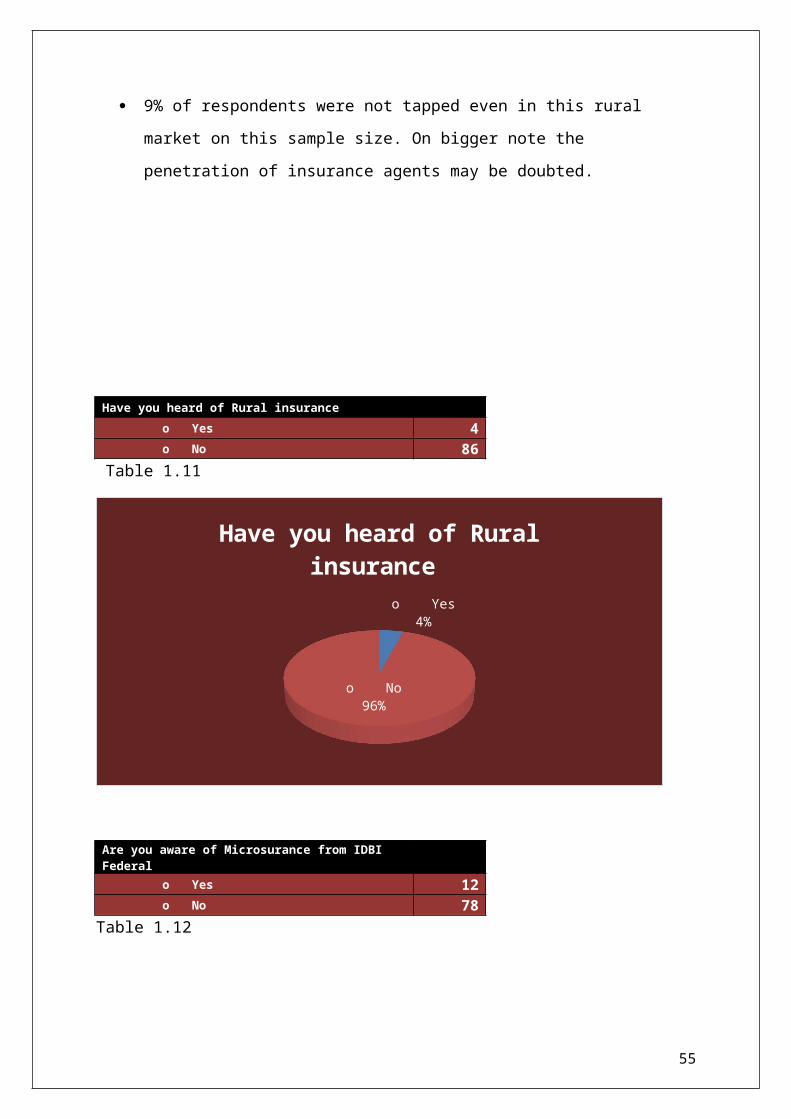

9% of respondents were not tapped even in this rural

market on this sample size. On bigger note the

penetration of insurance agents may be doubted.

Have you heard of Rural insuranceo Yes 4o No 86

Table 1.11

o Yes4%

o No96%

Have you heard of Rural insurance

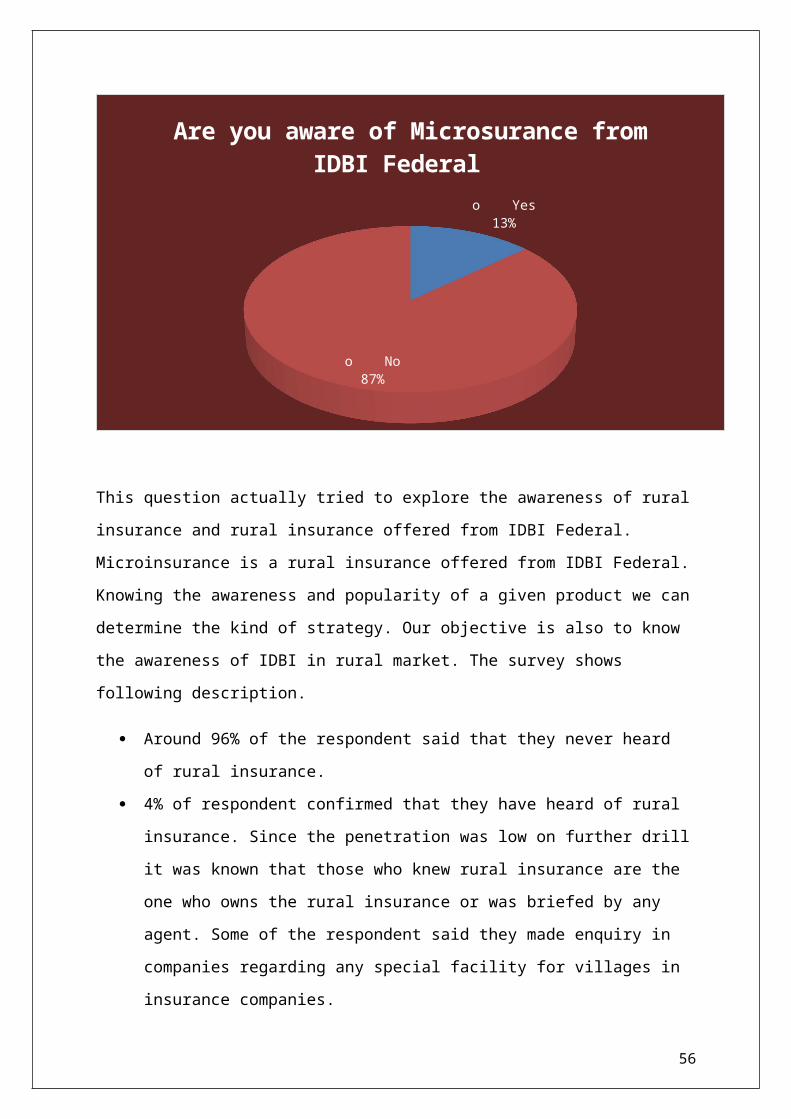

Are you aware of Microsurance from IDBI Federal

o Yes 12o No 78

Table 1.12

55

o Yes13%

o No87%

Are you aware of Microsurance from IDBI Federal

This question actually tried to explore the awareness of rural

insurance and rural insurance offered from IDBI Federal.

Microinsurance is a rural insurance offered from IDBI Federal.

Knowing the awareness and popularity of a given product we can

determine the kind of strategy. Our objective is also to know

the awareness of IDBI in rural market. The survey shows

following description.

Around 96% of the respondent said that they never heard

of rural insurance.

4% of respondent confirmed that they have heard of rural

insurance. Since the penetration was low on further drill

it was known that those who knew rural insurance are the

one who owns the rural insurance or was briefed by any

agent. Some of the respondent said they made enquiry in

companies regarding any special facility for villages in

insurance companies.

56

Microsurance

There were several policy holder of IDBI Federal however

they did not know what is the meaning of rural insurance

but they owned rural insurance.

13% of the respondent confirmed that have heard of

Microsurance as they own or they know someone who are

owning this policy. They had little knowledge about what

it is or any details. The low penetration is a positive

sign for developing a new market base in many rural

sectors.

87% of the respondent said that never had heard of

Microsurance so any further drill to this survey was not

required.

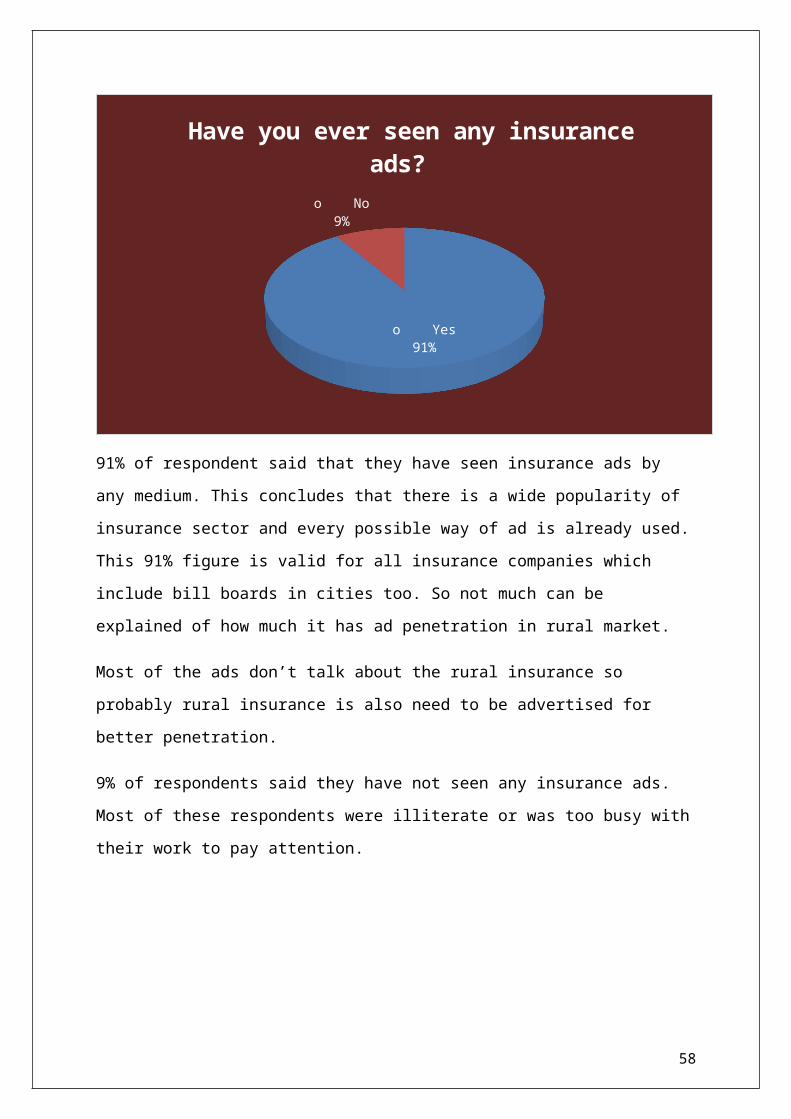

Have you ever seen any insurance ads?o Yes 82o No 8

Table 1.13

57

o Yes91%

o No9%

Have you ever seen any insurance ads?

91% of respondent said that they have seen insurance ads by

any medium. This concludes that there is a wide popularity of

insurance sector and every possible way of ad is already used.

This 91% figure is valid for all insurance companies which

include bill boards in cities too. So not much can be

explained of how much it has ad penetration in rural market.

Most of the ads don’t talk about the rural insurance so

probably rural insurance is also need to be advertised for

better penetration.

9% of respondents said they have not seen any insurance ads.

Most of these respondents were illiterate or was too busy with

their work to pay attention.

58

Recommendations

1.Recommendations aiming at generating life

insurance awareness in rural areas The low levels of life insurance awareness are evident

from the analysis of the primary and secondary data. With

a view to educate the customers and raising the awareness

levels, apart from the existing techniques such as mobile

publicity vans and publicity in print and electronic

media, The industry can create a consortium of life

insurance companies with the involvement of IRDA for

educating the rural people on a mass scale. Social

marketing technique is to be used to market the idea of

insurance before the individual life insurance company

steps in to the business. This consortium has to organize

exhibitions, slide shows, short films and such other

activities in the village markets frequently.

2.Recommendations aiming at generating awareness

program of the regulatory body (IRDA)The primary data has revealed that majority of the people

in the rural areas are not aware of the regulatory body,

i.e., IRDA and with the result averse to invest in

private companies perceiving them to be unsafe. It is

therefore recommended to print in all brochures,

pamphlets and policy bonds of all life insurance

59

companies the Grievance Redress Mechanism and highlight

the role of IRDA. This strategy is aimed at creating

trust in the mind sets of the rural customers. The

consortium of life insurance companies can also enlighten

the role of the regulating authority to the rural people.

3. Recommendations for suitable techniques aimed at

customer satisfactionFrom the primary data it is deduced that increased

customer satisfaction lead to repeat sales. Programs

aiming at customer satisfaction are felt more important

by private players to show demonstrative effect that they

mean business.

In order to maximize customer service, the life insurance

companies need to introduce employee appraisal linked

branch service index meters in all branches where each

and every service activity is measured according to scale

by the robust IT department monitoring from the head

office. The Service areas relate to issue of flawless

policy bond, change of address, sending premium notice,

mode correction, registering nominations & assignments,

settling survival benefits before date, loan sanctioning,

fund switching , claim settlement, free look

cancellation, courteous response to queries, disciplinary

actions against mis selling and a host of service related

things. Printing policy bond in regional language and

communicating in regional language avoiding insurance

jargons create right chord to relate the company to the

rural customer.

60

4.Recommendations for techniques aiming at

designing need based productsWe found that there is dearth of products suiting to

rural psyche. Except a few products of a few companies,

the general product design of all companies has no

exclusive rural orientation with a unique selling

proposition. The primary data also suggest that lack of

need based products as one of the reasons for low levels

of rural coverage. In order to design need based

products, insurance companies are advised to survey the

rural market thoroughly to assess the needs. A family

policy covering all members of the family can be launched

in order to cover maximum people at a stroke.

5.Recommendations with regard to recruitment of

rural agents aiming at more rural coverageWith a view to spread the message of life insurance on a

wider scale in each and every village, the life insurance

companies need to prepare branch socio economic profile

of each branch office with all details of caste /

religion/ income/ occupation composition of all villagers

and try to appoint agents from each stratum to tap the

business from each group. The Black Spot villages (where

there is no agent of any company) need to be identified

and agents are to be appointed in such villages. Since

opinion leaders play an important role in purchase

decisions, companies need to enlist the opinion leaders

as their Sales Force.

61

6.Recommendations for wider rural coverage through

low cost pension productsSince the incomes of the lower income groups in rural

areas could not be spared to purchase high premium

policies, the companies need to develop low cost group

insurance pension products on the lines of YS Abhaya

Hastham pension plan launched by AP government and

administered by LIC of India.

7.Recommendations for wider rural coverage by

insuring the liabilitiesThe liabilities of the rural people are not insured and

therefore the dependents of the bereaved families are

inheriting the debt. With an aim to provide social

security, the insurance companies can launch individual

plans, group plans and term plans to cover each and every

loan taken by the poor people. The life insurance

companies should educate the cooperative societies for

getting formal approval by cooperative members for the

mandatory insurance scheme for all loans sanctioned by

them. The commission can be paid to co-operative

societies.

8.Recommendations aiming at a marketing strategy of

daily pigmy collection of premiums for

agricultural labourersHaving analysed the expectations of the low income

agricultural labour group from the primary data, it was

62

discussed that daily wage earners can spare a few rupees

daily but find it difficult to pay a bulk premium at a

time. Insurance companies need to design policies with

daily pigmy collection mechanism and position the

products to agricultural labours.

9.Recommendations aiming at a marketing strategy of

rewarding the repeat purchasers to sustain

eternal relationshipInsurance companies should start giving reward points for

each repeat purchase and for each recycling of maturity

claim which can be redeemed when the last policy results

in to claim by way of maturity or death. This model may

be christened ‘Generations Relationship Rewards Scheme

(GRRS)’. This ensures loyalty on the part of the customer

towards the company at no extra expense. Preparing and

perfecting a unique customer ID for a policy holder with

various policies is a pre requisite for the success of

this model.

10. Recommendations for flexible and rural

centric premium collection mechanismsThe alternate premium collection mechanisms, viz, ECS,

Internet payment, Salary Saving Schemes may not work with

un bankable and financially exclusive population.

Insurance companies through consortium of all insurers

collect premiums through mobile vans at the village

markets and through ‘Collecting Banks’.

63

11. Recommendations aiming at increasing the bank

assurance potential in wider rural coverageIn India only 2% of the captive customers of the banks

are given insurance through bank assurance against the

global bench mark of 50 to 60%. Having analyzed the

reasons for low performance it is recommended for the

life insurance companies to have tie up with all regional

and cooperative banks and apart from paying commission to

banks, the insurance companies should float business

competitions to individual bank branch managers and

reward them without which they have no incentive to work

and bank assurance would be another portfolio to the

already existing jobs in the bank. Insurance companies

should also launch easy to understand bank assurance

specific exclusive products for facilitating the bank

managers to push the sales in an easy fashion.

12. Recommendations aiming at creation of Rural

Vertical department at the corporate offices of

the life insurance companiesThe IRDA stipulations of rural coverage are viewed by the

private life insurance companies more as on obligation

than as a commitment towards wider social coverage. To

unleash the rich untapped potential of the rural areas it

is recommended that the insurance companies establish a

Rural Vertical department at the corporate office for

planning, organizing and implementing rural social

objectives without losing sight on profits.

64

Entrepreneurship on a massive scale is need of the hour

and the life insurance companies explore the world of

rural markets through a separate set of agents

specialized in rural markets.

13. Recommendations aiming at advanced

professional training to rural agents for meeting

the rising expectations of the rural peopleRural India is a mixture of opposites. We witness raising

affluence of some and at the same time financially

excluded lot of people on the other side. We need

insurance advisors who are ambidextrous enough to cater

to the rural rich and also rural poor. The rural agent

has to equip himself with the subject of wealth creation

as well as social insurance coverage. It is therefore

recommended for all the insurance companies to form a

consortium and establish a National Insurance Academy for

training the agents of rural areas on the lines of NIA,

Pune and for initiating an exclusive training activity

and devise curriculum to rural agents across India. The

trainers of life insurance to the agents at the branch

offices need to be trained in this Academy.

14. Recommendations for robust IT initiatives for

rural life insurance coverage The IT initiatives presently practiced by the life

insurance companies are inadequate to rural life

insurance coverage. Recommendations for robust IT

initiatives for rural life insurance coverage:

65

The IT initiatives presently practiced by the life

insurance companies are inadequate to rural life

insurance coverage. This model where the company

representative chat with the villagers and personally

explain the features of the new products. Companies can

issue credit cards to rural policyholders and provision

can be made for paying premiums through credit cards.

Life Insurance companies are recommended to develop data

ware housing for each village of all districts comprising

the income, caste, religion and occupation details and

make use of the data for recruitment of agents from