The Aftermath of a Recession: Citigroup Inc.

67

Running Head: The Aftermath of a Recession: Citigroup Inc. The Aftermath of a Recession: Citigroup Inc. Jessica L. Grimes Shashank R. Ganugupati Pragga M. Liza University of West Florida

Transcript of The Aftermath of a Recession: Citigroup Inc.

Running Head: The Aftermath of a Recession: Citigroup Inc.

The Aftermath of a Recession: Citigroup Inc.

Jessica L. Grimes

Shashank R. Ganugupati

Pragga M. Liza

University of West Florida

2THE AFTERMATH OF A RECESSION: CITIGROUP INC.

Table of Contents

I. Abstract

4

II. Introduction

5

III. Historical Overview

5

IV. Citigroup during the Financial Crisis

6

A. High-risk, High-growth Strategy 6

B. Federal Bailout Assistance 7

C. Systemic Risk 7

V. Citigroup’s Competencies

7

VI. Citigroup’s Competition

8

3THE AFTERMATH OF A RECESSION: CITIGROUP INC.

VII. Major Competitors

8

A. Wells Fargo 8

B. JPMorgan 9

C. Bank of America 9

VIII. Market Segment and Trends

10

A. Competitive Landscape 10

B. Industry Life Cycle 12

C. Market Segmentation 12

D. Products and Services Segmentation 17

E. Capital Intensity 18

F. Technology 18

G. Revenue Volatility 19

IX. Citigroup’s World

20

X. Citigroup’s Vision, Mission, and Strategic Objectives

20

4THE AFTERMATH OF A RECESSION: CITIGROUP INC.

XI. Universal Banking Model

21

XII. Organizational Structure

22

XIII. Citigroup’s Performance

23

A. Environmental Performance 22

B. Social Performance 24

C. Financial Performance 25

a. Stock Performance 25

b. Key Financial Data 26

XIV. Citigroup’s Challenges

27

A. A Tarnished Reputation 27

B. Diseconomies of Scale 28

C. Pending Litigations 29

D. Citigroup Culture 30

E. Increased Regulations 31

5THE AFTERMATH OF A RECESSION: CITIGROUP INC.

F. Failure of Federal Stress Tests 31

G. Downsizing 32

H. Debt Reduction Efforts 32

XV. Analysis Question

32

XVI. References

34

XVII. Appendix

39

6THE AFTERMATH OF A RECESSION: CITIGROUP INC.

Abstract

This paper explores Citigroup Inc.’s managerial decisions

and the consequences that followed. From its humble beginning in

New York to the market giant it is today, Citigroup has squared

off with major competitors and encountered many environmental

changes along the way. In the late 2000s, Citigroup struggled

during a financial recession, and survived only due to government

support. Although the firm survived the downturn, it needed to

learn from its mistakes and implement major changes. Citigroup’s

environmental, social, and financial performance are also

discussed. In the aftermath of the recession Citigroup faced

mounting obstacles, including a soiled reputation, diseconomies

of scale, lawsuits, cultural clashes, governmental interference,

and downsizings. The good news is that the firm survived, but the

bad news is that it now faces a multitude of problems.

7THE AFTERMATH OF A RECESSION: CITIGROUP INC.

A delicious slice of pepperoni pizza in bustling New York

City. An instant download of the latest number one rock song on

iTunes. A scrumptious junior cheeseburger from Wendy’s. A quarter

of a gallon of gasoline in beautiful California. A scratch-off

lottery ticket potentially worth millions of dollars. What common

thread connected each of these products? In 2012, consumers paid

only one dollar for each of these items (Krasny, Floro, & Lubin,

2012).

Similarly, in March 2009, shareholders could have purchased

one particular share of stock for only 97 cents. Surely, this

penny stock belonged to some risky venture firm, or some

8THE AFTERMATH OF A RECESSION: CITIGROUP INC.floundering company that lacked adequate resources. Perhaps,

consumers would have been surprised to learn that this stock

actually belonged to the third largest financial institution in

the United States. For the globally present, highly influential,

financial conglomerate, Citigroup Inc., this historical event was

a precursor of years of despair. This paper carefully explores

the environment and circumstances surrounding Citigroup’s unusual

stock price on that day.

Historical Overview

In 1812 Samuel Osgood, an advocate of foreign trade,

founded City Bank of New York. In 1829, the bank merged with

Farmer’s Loan and Trust, and became America’s first trust

company. A few years later, City Bank purchased substantial

interest in Lackawanna Iron and Steel Company. Finally, in 1866

City Bank president, Moses Taylor, invested in the telegraph firm

that eventually created the transatlantic cable (Citigroup Inc.,

2015).

Throughout the 20th century, the firm expanded its global

operations, and eventually, the firm became known as Citicorp

(Citigroup Inc., 2015). The most significant expansion occurred

9THE AFTERMATH OF A RECESSION: CITIGROUP INC.in 1998, when Citicorp merged with Travelers Insurance, and

formed Citigroup Inc. During the early 2000s, Citigroup

aggressively pursued a high-growth, high-risk strategy and

engaged in a series of rapid mergers and acquisitions (Wilmarth,

2014).

A major acquisition occurred in 2008, when Citigroup

purchased Wachovia’s retail operations, wealth management

business, and investment bank. As part of the negotiation,

Citigroup inherited $53 billion of senior and subordinated debt.

In addition, Citigroup absorbed $42 billion in losses due to

Wachovia’s high number of toxic, adjustable rate mortgages

(Citigroup-Wachovia, 2008).

Citigroup during the Financial Crisis

In the mid-2000s, housing prices soared to new

heights. Bankers, with their eyes fixed securely on streams of

dollar signs, eagerly extended mortgages to practically anybody

with a pulse. Bankers paid little regard to applicants’ job

stability or credit rating, and instead focused on the valuable

collateral that would, in theory, suffice for any defaults.

Eventually, the economy revealed that speculations were

10THE AFTERMATH OF A RECESSION: CITIGROUP INC.incorrect. Bankers scrutinized their balance sheets with horror,

to find themselves buried in toxic assets. An entire failing

industry had been mistaken, and was now in such dire straits that

it desperately beckoned the Federal Government to help. Any

innovations and expansions of previous eras paled in comparison

to the quagmire that the industry faced.

As Citigroup’s internal control mechanisms failed,

shareholders sold their stocks in droves. The market became

saturated, and Citigroup’s stock price plummeted to a lowly 97

cents. When stock prices became so undervalued that a raider

could have purchased the company for a price less than its book

value, there was risk of a hostile takeover (Dess, Lumpkin,

Eisner, & McNamara, 2014).

High-risk, High-growth Strategy

Citigroup’s strategy during this era was twofold. First, the

firm rapidly expanded its operations, both globally and

domestically. Citigroup’s outstretched arms lured countries in

Asia, Europe, the Middle East, Africa, Latin America, and North

America (Citigroup Inc., 2015). Prior to the recession, Citigroup

believed that its global presence created a competitive

11THE AFTERMATH OF A RECESSION: CITIGROUP INC.advantage. Second, the bank extended as many loans as possible,

with an utter disregard for applicants’ qualifications. This

dangerous combination of high-risk and high-growth proved to be

seriously flawed.

Federal Bailout Assistance

Armed with the knowledge of just how dangerous the situation

was, the Federal government implemented the Troubled Assets

Relief Program (TARP). This program was created to allow the Fed

to purchase troubled assets and equity from select financial

institutions.

Systemic Risk

America’s financial system was such an integrated component

of the global economy that the failures of certain banks were

believed to be detrimental to overall economic health (Haider,

2014). This belief led to the coinage of a term, too-big-to fail,

which was frequently used to describe the United States’ four

largest banks. Many consumers argued that instead of too-big-to-fail,

a more appropriate term was too-big-to-manage-effectively. Many too-big-

to-fail financial institutions, including Citigroup, restructured

via spin-off divisions and sales of some segments (Roe, 2014).

12THE AFTERMATH OF A RECESSION: CITIGROUP INC.

Citigroup’s Competencies (after change)

Citigroup demonstrated three primary competencies. First,

the firm’s domestic and global presence created a platform that

produced steady growth. Second, the firm’s technological and

organizational restructuring generated cost efficiencies.

Finally, Citigroup’s improved financial position provided

protection against adverse market conditions (Citigroup Inc.,

2015). These three competencies were invaluable in such a

competitive market.

Citigroup’s Competition

Traditional banking systems generally catered to the

needs of middle and upper income individuals. As a result, banks

tended to withdraw from less advantaged communities, leaving a

niche market available for fringe banks. Individuals in these

low-income communities relied on substitute products, such as

payday loans, check cashing services, money wiring companies,

pawn shops, title loans, rent-to-own retailers, and tax refund

loans. These substitute products often charged higher fees than

comparable services at traditional banks. A disproportionate

13THE AFTERMATH OF A RECESSION: CITIGROUP INC.amount of fringe banks’ customers were racial and ethnic

minorities. (Fowler, Cover, & Kleit, 2014).

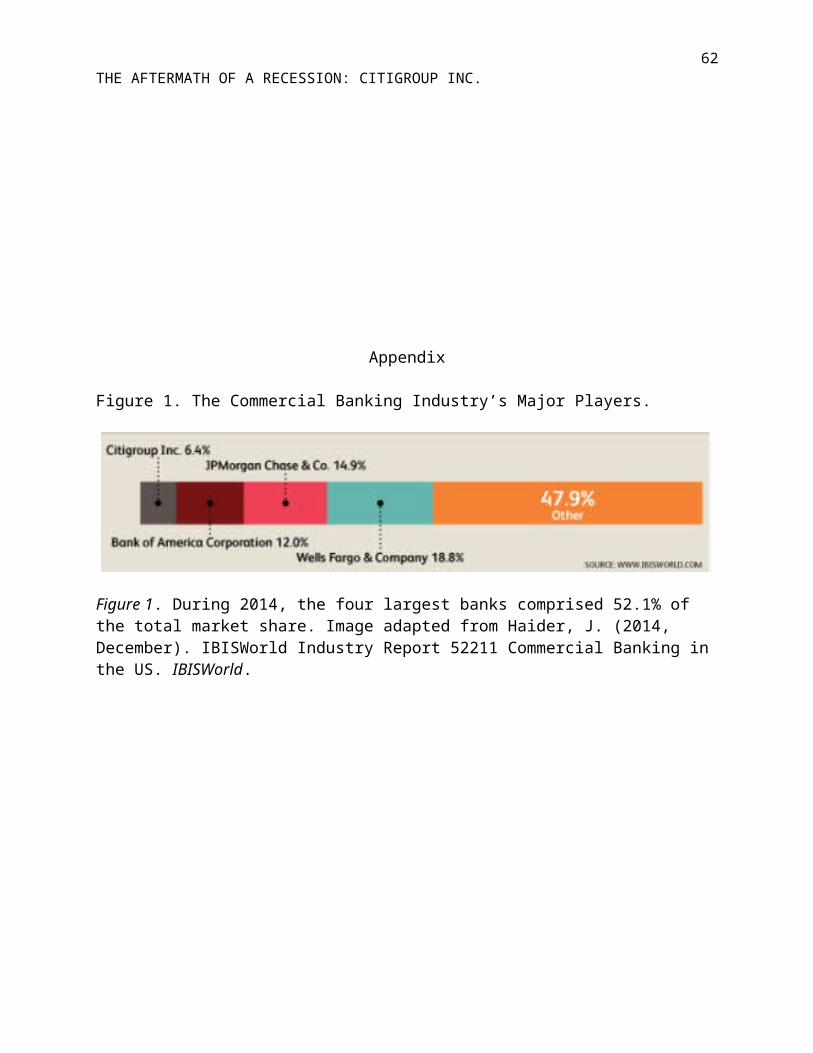

Major Competitors

Over the last decade, growth through mergers and

acquisitions played a critical role in the success of major

commercial banks. These activities created a landscape that was

highly concentrated, and formed an oligopoly. As displayed in

Figure 1, Citigroup’s major competitors were Wells Fargo,

JPMorgan, and Bank of America. Collaboratively, these four firms

controlled 52.1% of total industry revenue in 2014 (Haider,

2014).

Wells Fargo

Wells Fargo, founded in 1852, operated 9,000 retail

branches, over 12,000 ATMs, and employed a staff of 269,200. The

firm’s three major segments included community banking, wholesale

banking, and wealth, brokerage and retirement services. Wells

Fargo acquired segments of Wachovia for $15.1 billion, a move

that generated $65 billion in revenue and marked a 111.8%

increase in 2009. Figure 2 presents the annual revenue for each

of Citigroup’s major competitors during 2009. Additionally, Wells

14THE AFTERMATH OF A RECESSION: CITIGROUP INC.Fargo became the United States’ largest mortgage lender. It

controlled 18.8% of the total commercial banking sector, and

reported a consolidated net profit of $19 billion (Haider, 2014).

JPMorgan

JPMorgan, the largest bank in terms of assets in the United

States, owned assets worth $2.2 trillion. It acquired Washington

Mutual for $1.9 billion in 2009, which caused its retail banking

to expand westward and increased the firm’s profitability.

JPMorgan was also the leading US credit card issuer, with 64.5

million customer accounts. Its loans were valued at $128 billion.

The bank’s domestic network spanned 5,614 branches, 18,699 ATMs,

and 25,000 employees. Due to its strong financial position,

JPMorgan became one of the first financial institutions to repay

its $25 billion debt, associated with the Troubled Asset Relief

Program (TARP). During 2014, JPMorgan generated $63.6 billion in

revenue and controlled 14.9% of the total commercial banking

sector (Haider, 2014).

Bank of America

Another fierce competitor, Bank of America, was recognized

as the world’s largest holding-backed company in terms of

15THE AFTERMATH OF A RECESSION: CITIGROUP INC.revenue. It claimed 12% of total industry revenue and served

approximately 53 million consumers in the US alone. Bank of

America’s products included retail banking, investments, and

asset management services. The firm operated 5,500 retail-banking

centers, 16,300 ATMs, and an online banking system with 30

million users. In 2008, Bank of America acquired Merrill Lynch.

Due to increased regulatory and restructuring costs, its net

income decreased by $4.5 billion, to a net loss of $1.2 billion.

From 2008-2013, Bank of America recorded net losses and saw a

considerable drop in total revenue. At its most vulnerable point,

Bank of America received two bailouts, totaling $45 billion, from

the government’s relief program (Haider, 2014).

Market Segment and Trends

Competitive Landscape

Citigroup played major roles in both commercial and

investment banking in US. The competitive landscapes in these two

different sectors were analyzed independently. The subprime

mortgage crisis caused large-scale merger and acquisition

activity in both banking sectors. Within the banking sector, four

of the top five commercial banks engaged in either merger or

16THE AFTERMATH OF A RECESSION: CITIGROUP INC.acquisition activities during the crisis. Although the market

shares of the top four banks have grown, major losses by

Citigroup and Bank of America have weakened their individual

market shares (Haider, 2014).

Commercial banking was a highly competitive industry.

Generally, firms in this industry competed with banks, thrifts,

credit unions, government agencies, mortgage brokers and other

nonbank organizations that offered financial services. These

firms also competed with non-regulated banks and thrifts owned by

varying corporations. These entities offered financial services

through alternative delivery channels like the internet. The

basis of competition hinged on customer service, interest rates,

product quality, breadth of products and services, lending

limits, and customer convenience, such as branch locations.

(Haider, 2014).

The investment banking and securities dealing industry

operated with a medium level of market share concentration. The

top five companies, JPMorgan, Bank of America, Morgan Stanley,

Citigroup and Goldman Sachs, accounted for an estimated 47.8% of

total market share. The top four companies accounted for 40% of

17THE AFTERMATH OF A RECESSION: CITIGROUP INC.industry revenue in 2014. Similar to commercial banking, there

was rapid consolidation of firms in the investment banking

industry (Hoopes, 2014).

Cost structures throughout the industry varied considerably

among firms. They depended extensively on the financial

activities industry operators chose to engage in. As the industry

consolidated and the range of services broadened into those

traditionally offered by other industries, the size and

geographic reach of industry players increased (Haider, 2014).

Competitive conditions intensified as merger activities

produced larger, better-capitalized, and more geographically

diverse companies. Conglomerate firms were able to offer wider

arrays of financial products and at more competitive prices.

Additionally, as technology progressed, the need for depository

institutions to act as intermediaries for bank transactions

diminished.

The consolidation of the investment banking industry also

increased the movement of senior staff between firms. The

government had imposed restrictions on the compensation of senior

staff at some banks due to the TARP. Citigroup and others

18THE AFTERMATH OF A RECESSION: CITIGROUP INC.complained that these regulations created a competitive

disadvantage due to the increasing difficulty of attracting and

retaining personnel (Hoopes, 2014).

Citigroup identified three global trends that affected the

banking industry. The first trend, globalization, described how

economies, markets, and nations have become increasingly

connected across the globe. The second trend, urbanization,

identified the concentration of people and consumption around

cities. The third trend, digitalization, described how technology

transformed industries. Banks that kept these trends in mind

generated greater efficiencies, and reaped higher profits.

Industry Life Cycle

The commercial banking industry’s life cycle is described as

mature, and is evident by merger and acquisition activities,

increased regulations, and increased product competition. The

benefits stemming from consolidation increased after the subprime

mortgage crisis. The number of commercial banks declined

substantially, especially among smaller banks that found it

difficult to compete. The growing availability of the Internet

19THE AFTERMATH OF A RECESSION: CITIGROUP INC.generated price competition and, as a result, profits declined.

However, successful launches of mobile and online banking

platforms were seen as an indication of new revenue

opportunities, and growth projections over the next five years

seemed promising (Haider, 2014).

Market Segmentation

By the year 2050, the Earth’s elderly population will

outnumber children for the first time in history (Balestra &

Dottori, 2011). These baby boomers reside throughout the globe and

influence many industries, including banking. The implications of

an aging population’s influence on the economy are enormous.

Financial institutions were the main channel for capital

distribution to a variety of businesses. Due to their realm of

influence, banks needed to be strong and vibrant to facilitate

positive changes in the environment (Brennant & Ritch, 2010). As

the population ages, the government will spend an increasing

percentage of gross domestic product (GDP) on Medicare, Medicaid,

and Social Security. The United States must facilitate economic

growth with increases in savings, investments, and exports, and

20THE AFTERMATH OF A RECESSION: CITIGROUP INC.reductions in spending, consumption, and imports in order to

maintain a balanced economy (Ferguson, 2013).

Most Generation Y shoppers have had the displeasure of

standing in line behind the little old lady who insists on paying

for her groceries with a check. Of course, she must carefully

balance her checking account before leaving the counter. She has

had the same account for 40 years and is perfectly satisfied. In

contrast, the Generation Y individual quickly swipes his choice

of credit card, grabs his groceries, and dashes out the door. All

the while, the little old lady is still reviewing her cash

register receipt.

Although on the surface it seems that checks are obsolete

and technology savvy payment methods are trending, commercial

banks must be careful to consider the demands of their most

important customers. Not only do baby boomers outnumber any other

generation, they also have much deeper pockets. If baby boomers

still want a free toaster, then banks should stock their supply

closets full of toasters! Save the credit cards, mobile apps,

and online banking for the young whippersnappers. The aging of

the population will result in a massive transfer of wealth in the

21THE AFTERMATH OF A RECESSION: CITIGROUP INC.near future, and banks with the most satisfied baby boomers will

greatly benefit from their affluence (Teller Vision, 2014).

Banks that promoted products that appealed to baby boomers

offered retirement planning and advice, wealth transfer planning,

and platforms through which this generation could learn new

technology like mobile apps (Yu & Ray, 2014). Citigroup’s

personal wealth management teams were comprised of trust and

estate attorneys, wealth planning analysts, tax specialists,

business valuation specialists, and investment analysts. The firm

has claimed “We are uniquely qualified to help with the complex

financial planning needs of the baby boomer generation

(Citigroup, 2015).”

A more detailed analysis of the baby boomer segment revealed

that this segment could be further divided into subgroups. These

groups were labeled as traditionalists, balancers, elite, and unhappy and

unmoving segments. Each segment was defined by its members’ common

behaviors and characteristics, including similar product demands

(Global Consumer Banking Survey, 2014).

Traditionalists were less educated, less wealthy, had the

lowest remote channel usage, and were frequent ATM users. They

22THE AFTERMATH OF A RECESSION: CITIGROUP INC.typically used the fewest services, but were willing try new

products. This group especially valued loyalty rewards. Fifty-

three percent of this group were college graduates, but their

median income was only $16,358, due to the fact that most were

retired. Banks profited from this group through ATM fees, rewards

programs, and digital demonstrations that increased the ease of

learning new technology (Global Consumer Banking Survey, 2014).

Balancers were comfortable with remote channels, but valued

their banking relationship. They emphasized fee transparency and

customer service, and generally kept accounts open for lengthy

periods. Fifty-nine percent of this group were college graduates,

and their median income was $41,429. Banks attracted this segment

through strong customer relationships, built on honest

communication and a willingness to provide assistance (Global

Consumer Banking Survey, 2014).

Elites were among the oldest of the baby boomers. They were

highly educated and had large incomes and assets. They reported a

need for advocacy and trust, and showed were willing to increase

their business with banks that helped them achieve their

23THE AFTERMATH OF A RECESSION: CITIGROUP INC.financial goals. Elites were heavy users of online channels and

valued self-service financial management tools. Seventy percent

of this group were college graduates, and their median income was

$43,667. Banks appealed to this segment through self-service

financial management tools and financial advice (Global Consumer

Banking Survey, 2014).

The unhappy and unmoving group criticized their primary

financial service provider and the industry overall, but were

unlikely to move due to their belief that all providers are the

same. They complained frequently about unexpected fees and

difficulty solving problems. They seldom used branch or remote

channels. This segment was comprised of older individuals. They

were the least educated and had low household incomes and few

assets. Only 47% of this group were college graduates, and their

median income was $25,000. Banks that maintained business in this

segment increased satisfaction and trust by improving problem

resolution and reassuring customers of that their personal

information was protected (Global Consumer Banking Survey, 2014).

24THE AFTERMATH OF A RECESSION: CITIGROUP INC.

Consumers have faced significant financial strains due to a

deteriorating job market and dwindling asset values, but they

have still embraced new technologies, such as video, and adopted

online behaviors at an astonishing rate. These trends were

particularly true for Gen Y consumers, also known as millennials, and

Gen X consumers (Global Consumer Banking Survey, 2014).

The Generation X & Y customers were grouped into four global

segments, upwardly mobiles, new world adapters, safety seekers,

and the self-sufficient. Each segment was defined by its members’

common behaviors and characteristics, including similar product

and service preferences. These segments varied by size, assets

and willingness to pay premiums for key benefits (Global Consumer

Banking Survey, 2014).

Upwardly mobiles were the smallest segment. They were young

and highly educated, with high household incomes and significant

investable assets. They owned the most products, but were prone

to leave because they viewed banks as relatively interchangeable.

This group valued financial advice and was most likely to

experience problems that required assistance. Most customers in

25THE AFTERMATH OF A RECESSION: CITIGROUP INC.this segment were 18-34 years old. Eighty percent were college

graduates, with a median income of $48,571. Bank attracted this

group with specialized financial advice across multiple channels

(Global Consumer Banking Survey, 2014).

New world adopters were younger, highly educated, and had

significant savings relative to their modest incomes. They were

heavy users of technology and were receptive to new market

entrants offering substitute products. They frequently opened and

closed accounts, and viewed banks as relatively undifferentiated.

Seventy-five percent of this group were college graduates, with a

median income of $29,584. Banks profited from these customers

through the use of data analytics and new technology developments

(Global Consumer Banking Survey, 2014).

The largest segment of the population, safety seekers were

relatively younger, less educated and more limited in their cash

flow and savings. Safety seekers were likely to trust and

advocate for their provider. They strongly preferred using

branches for most services, but they had relatively small

portfolios. This group valued fee transparency and protection of

26THE AFTERMATH OF A RECESSION: CITIGROUP INC.personal information safe. Fifty-three percent of this group were

college graduates, with a median income of $18,667. Banks that

recommended simple products that saved customers money appealed

to this group (Global Consumer Banking Survey, 2014).

The self-sufficient group was older, less educated, and more

limited financially. They had low levels of trust and rarely

opened and closed accounts. This group valued convenience and

preferred to use self-service tools rather than consult a

financial advisor. Fifty-one percent were college graduates, with

a median income of $29,922. Banks that empowered this group to

make decisions, by providing insights about their financial

status and behaviors attracted the most customers (Global

Consumer Banking Survey, 2014).

Product and Services Segmentation

Citigroup catered to the diverse needs of individual

customers, corporations, governments and businesses. Its

27THE AFTERMATH OF A RECESSION: CITIGROUP INC.financial products and services included consumer banking and

credit, corporate and investment banking, securities brokerage,

transaction services and wealth management. Through its custody,

asset, and securities services, Citigroup’s custodial banks and

brokerage firms provided trust, fiduciary and custody services to

its customers. Citigroup’s investment banking and securities

dealings provided a range of services, including wealth

management, proprietary trading, securities underwriting, and

corporate financial services (Hoopes, 2014).

Commercial banks provided financial services to retail and

business clients in the form of commercial, industrial and

consumer loans. Banks offered a variety of products, including

auto loans, mortgage loans, business loans, student loans, and

others. They accepted deposits from customers, and used these

funds for loans. Other services included depository services,

like checking and savings accounts, and credit cards. Commercial

banks were regulated by the Federal Government (Haider, 2014).

Banks offered many types of credit cards, through which they

provided the funds required for consumer purchases in return for

a scheduled repayment. Customers opted to pay the full or partial

28THE AFTERMATH OF A RECESSION: CITIGROUP INC.balance, and customers that failed to pay on time or paid only

part of the balance paid the banks interest and fees. US credit

cards were not issued directly by Visa, MasterCard or any other

payment solution organization. Instead, these firms and other

similar corporations provided the infrastructure to process the

payments (Imbruglia, 2015).

Citigroup recently added commodity-based mutual funds and

alternative investments for its Asia-Pacific customers. The firm

introduced smart-beta strategies to broaden the exposure of Asian

portfolios. The Asia-Pacific region was the largest platform for

mutual funds, and generated over half of open-ended fund sales

globally. In addition, retail bank accounts located in the Asia-

Pacific region constituted 30% of Citigroup’s revenues worldwide

(Distributors, 2014). Product offerings in the Asia-Pacific

regions were extremely important to Citigroup’s global

operations.

Capital Intensity

A changing landscape encouraged banks to focus extensively

on vast ATM networks and improved technology in order to reduce

costs, establish global presence, and maintain customer

29THE AFTERMATH OF A RECESSION: CITIGROUP INC.satisfaction. The banking industry experienced a high level of

capital intensity, a ratio that compared the dollars spent on

plants, machinery, and equipment to dollars spent on labor.

Capital intensity has steadily increased since 2009, because

technology has become increasingly important (Haider, 2014).

Citigroup continued to invest considerable funds in technology

and communication infrastructure, and these expenses totaled $6.1

billion in 2013, a $5.1 billion increase since 2011 (Annual

Report, 2013).

Technology

In his 2014 keynote speech at the Mobile World Congress,

Corbat predicted that digital and mobile technologies would

create a $350 billion shift in market share over the next three

years. With such high stakes, Citigroup dedicated many resources

to technological innovations (Citigroup, 2015). In fact, these

innovations have become one of the firm’s greatest strengths.

Citigroup introduced a global financial technology

initiative that challenged technology developers to transform the

digital banking platform. The firm awarded top innovators $20,000

each, and selected multiple winners. Last year’s winners included

30THE AFTERMATH OF A RECESSION: CITIGROUP INC.names such as “Citi Wallet for Small Businesses,” “Concierge

App,” “Mobile Withdrawal,” “Piggi,” “PopMoney on Android Wear,”

and “Swift Banking. (Citigroup, 2015).” The depth of

participation in this initiative highlighted the increasing

importance of mobile technology. Citigroup has also developed new

digital technology that generated performance feedback from its

customers. The technology measured important aspects, such as

whether or not their customers would recommend the bank to others

(Distributors, 2014).

The rapid strides made in the information and communication

technology arena significantly influenced the banking industry

through IT applications in risk management and marketing of

financial products. The technological advancement and the growth

of e-commerce increased overall productivity in terms of improved

quality and a variety of banking services. Therefore, banks were

able to persuade consumers to continue to use their services,

while at the same time reducing operating costs. Major banks were

dedicated to improving technology and digital presence in order

to improve the ease and timeliness of their banking procedures.

31THE AFTERMATH OF A RECESSION: CITIGROUP INC.

In addition to these cost efficiencies, Citigroup enhanced

its brand image by actively participating in (Social Networking)

Facebook, Twitter, LinkedIn, and YouTube (Citigroup, 2015). In

2012, Citigroup introduced tablets and smartphone versions of

Citi VelocitySM and CitiDirect BESM, which allowed its clients to

have easy access to capital markets intelligence and services

across all product lines (Annual Report, 2013). Overall, major

participants competed through providing the best customer

experience at lowest price and using technology to reduce costs

(Haider, 2014).

In 2011, JPMorgan, introduced QuickDeposit, one of the first

fully integrated online check deposit and banking solutions, and

Chase QuickPay that allowed customers to transfer, receive, or

request money by using tablets, computers, and smartphones

(Haider, 2014). Other major companies such as Wells Fargo and

Bank of America also contributed to the development of banking

applications. In 2014, Bank of America surpassed 15 million

active mobile banking customers, and the bank introduced a new

mobile application to meet the growing demands (Bank of America,

2014).

32THE AFTERMATH OF A RECESSION: CITIGROUP INC.Revenue Volatility

Seventy percent of banks’ revenue from operations was

derived from interest income. Fluctuations in interest rates

significantly affected industry revenue, market value, and the

amount of financial intermediation (Scannella & Bennardo, 2013).

Banks that charged higher than average interest rates on loans

created a dilemma. The higher rates were offset because they

essentially reduced the demand for credit, and subsequently,

reduced lending growth.

General economic conditions also affected the industry.

Revenue volatility stayed around 12% during the five years to

2014, and was only exacerbated by the collapse of the financial

system and the contracting economy. However, the economy

continued to recover, and revenue volatility was anticipated to

subside from 2014 to 2019 (Haider, 2014).

Citigroup’s World

Citigroup’s Vision, Mission, and Strategic Objectives

The Citi never sleeps. This thought-provoking vision conjured up

the image of a firm that worked tirelessly around the clock. It

implied that long after the sun had set, competitors were asleep,

33THE AFTERMATH OF A RECESSION: CITIGROUP INC.and most businesses closed, Citigroup was still hard at work.

Globally present firms like Citigroup recognized that darkness

never had the opportunity to cover the entirety of their vast

operations.

Mission statements generally revealed an organization’s

purpose, scope of operations, and the foundation of its

competitive advantage (Dess, Lumpkin, Eisner, & McNamara, 2014).

Citigroup’s mission statement was:

“Citi works tirelessly to serve individuals, communities,

institutions and

nations. With 200 years of experience meeting the world's

toughest challenges

and seizing its greatest opportunities, we strive to create

the best outcomes

for our clients and customers with financial solutions that

are simple, creative

and responsible. An institution connecting over 1,000

cities, 160 countries and

millions of people, we are your global bank; we are Citi

(Citigroup, 2015).”

34THE AFTERMATH OF A RECESSION: CITIGROUP INC.Through this statement, Citigroup proclaimed that its main

purpose was service, and the scope of its operations reached far.

The bank pursued every type of customer, and offered a huge

variety of products. Citigroup believed that the basis of its

competitive advantage was its global presence. The firm amassed a

global footprint that no other financial institution had matched.

Strategic objectives were the means by which organizations

operationalized their mission statement (Dess, Lumpkin, Eisner, &

McNamara, 2014). Citigroup claimed to pursue four main strategic

objectives, which emphasized common purpose, responsible finance,

ingenuity, and leadership. The firm described its common purpose

objective as the solidarity of its employees, united together to

focus on client and stakeholder service. Citigroup’s responsible

finance objective claimed that the firm’s conduct was transparent,

dependable, and prudent. An ingenuity objective emphasized the use

of innovation, information, global presence, and quality

products. Finally, Citigroup’s leadership objective meant that the

firm promoted and trained its most talented employees (Citigroup,

2015).

Universal Banking Model

35THE AFTERMATH OF A RECESSION: CITIGROUP INC. As a conglomerate, Citigroup designed a new blueprint

for financial institutions. This combination of commercial

banking services, securities, and insurance services at one

location was a new concept, known as universal banking. Bankers

believed that this design created synergy and economies of scale

through improved customer satisfaction, lowered costs, increased

profitability and diversification, and a greater ability to

compete globally (Wilmarth, 2014).

The universal banking model consisted of several separate,

essentially unrelated, businesses that operated independently of

one another, but reported to a common parent company. Citigroup

soon recognized that universal banking introduced a new set of

problems, including vast cultural differences, increased risk of

previously low-risk products, and unfulfilled stakeholder

expectations (Tuckey, 2005). Although Citigroup eventually

divested itself of Travelers’ in a spin-off, the many firms

continued to utilize the universal banking model.

Organizational Structure

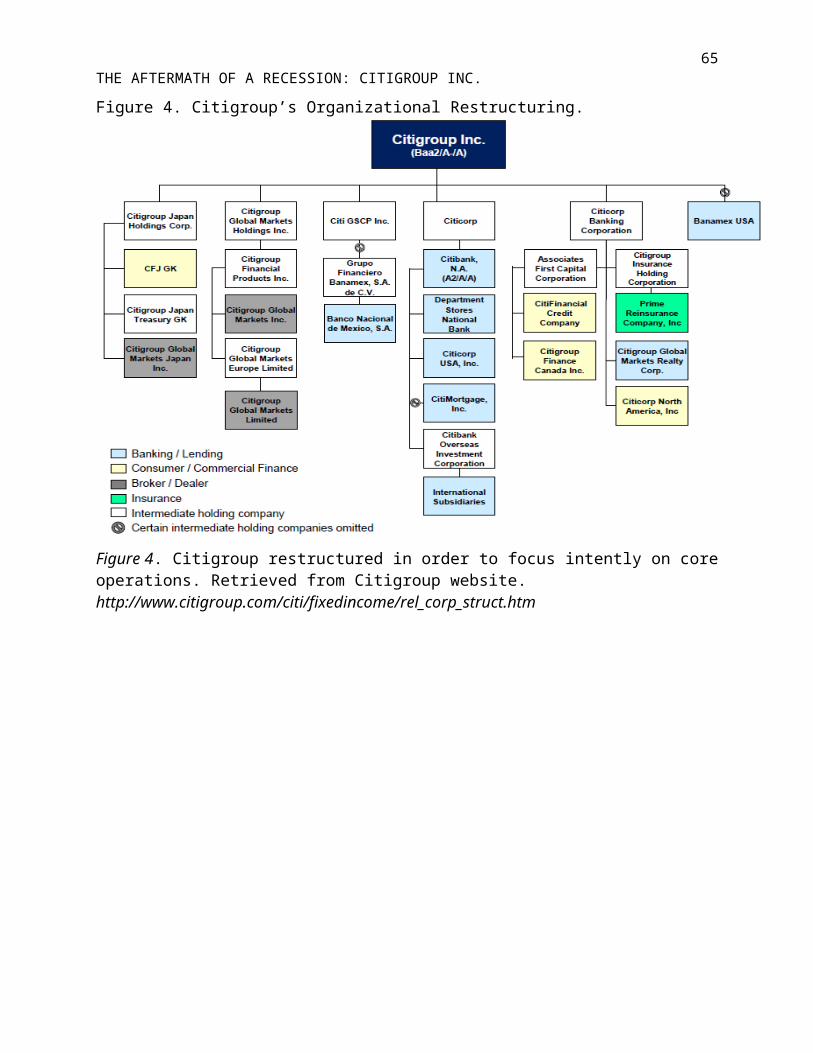

The aftermath of the recession revealed a desperate need for

Citigroup to restructure its organization. Former CEO, Vikram

36THE AFTERMATH OF A RECESSION: CITIGROUP INC.Pandit, drew a clear line in the sand between businesses that

would stay and businesses that would go. As displayed in Figure

4, the new organizational structure consisted of two main

segments, Citicorp and Citi Holdings (Wikipedia, 2015). Pandit

shifted focus to the company’s core operations, and made plans to

eliminate everything else.

Citigroup’s commercial banking operations, Citibank, was

considered a core business under the Citicorp umbrella (Citigroup

Inc., 2015). The Citi Holdings segment was created to hold toxic

assets until the firm could sell them. This new structure

resulted in a good bank and bad bank division of balance sheet items

(Aspan, 2012).

Pandit emphasized that Citi Holdings wasn’t necessarily just

a holding firm for toxic assets. The segment also included

promising businesses that Citigroup simply chose to no longer

pursue. Pandit planned to sell Citi Holdings’ businesses when the

appropriate market price was reached (Landy, 2009).

Businesses under the Citi Holdings umbrella included

mortgage portfolios, auto loans, student loans, foreign consumer

lending operations, a Mexican retirement fund administrator, a

37THE AFTERMATH OF A RECESSION: CITIGROUP INC.Japanese call center, commercial credit card operations, and

approximately $200 billion worth of toxic assets (Landy, 2009).

Pandit’s plan to separate these businesses from Citigroup’s core

businesses was aligned with new governmental regulations that

sought to reduce risk and increase liquidity.

Citigroup’s Performance

Traditional banking was typically concerned with providing

financial services that facilitated savings, improved the

efficiencies of resource allocation, and protected consumers from

risk. Recently, however, the government has intervened to ensure

that banks behave ethically and responsibly (Chiu, 2014). Banks

that chose to measure performance based on a triple bottom line

approach considered the firm’s financial, social and

environmental components of performance.

Environmental Performance

Citigroup developed initiatives, both domestically and

abroad, to preserve and sustain the environment. Its

Environmental and Social Policy Review Committee, comprised of

senior managers from varying business units, provided guidance

for the firm’s environmental sustainability issues. Citigroup’s

38THE AFTERMATH OF A RECESSION: CITIGROUP INC.2015 environmental goals, which were established in 2005,

included a 25% reduction in absolute GHG emissions, a 40%

reduction in the amount of waste dumped in landfills, a 20%

reduction in water consumption, LEED certification of 15% of its

real estate portfolio, and a 20% improvement in energy efficiency

(Citigroup Global Citizenship Report, 2013).

Citigroup emphasized its concern for foreign regions as

well. Since 2009, Citigroup has supported a Brazilian startup

company that generated renewable, wind powered energy. The firm

became a market leader in Latin America, and by 2013 had 225

employees. Citigroup also provided financing to KickStart, a

program whose mission was to release Africans from poverty by

supporting small scale farmers in Kenya (Citigroup Global

Citizenship Report, 2013).

Social Performance

The measure of Citigroup’s social performance included

the macroeconomic issue of non-discriminatory lending practices.

Inadequate funding in less developed regions was considered an

obstacle to economic prosperity. Citigroup faced a lot of

criticism for its role in the subprime mortgage crisis and its

39THE AFTERMATH OF A RECESSION: CITIGROUP INC.lack of “integrity, fairness, professionalism, and diligence”

(Chiu, 2014).

Banks that were once hesitant to extend loans to low-income

and minority individuals eagerly targeted these same individuals

during the subprime mortgage speculations. Some researchers

claimed that extensive empirical evidence that linked subprime

lending to applicants’ race and gender has been largely ignored.

Women and minorities tended to have less job security, fewer

assets, dimmer prospects, and higher overall risk than their

white, male counterparts (Dymski, Hernandez, & Mohanty, 2013).

In 2013, Corbat implemented a comprehensive training

program that emphasized the institution’s values in an effort to

combat fraud and improve Citigroup’s reputation (Citigroup Annual

Reports, 2013). The firm cited it diverse workforce as a

competitive advantage, due to its global presence. Citigroup

claimed that its corporate culture embraced diversity, which

facilitated better service in foreign markets. It designed

programs and policies that recruited and supported employees that

differed in cultural backgrounds, gender, race, ethnicity, age,

sexual orientation, sexual identity, disabilities, and veteran

40THE AFTERMATH OF A RECESSION: CITIGROUP INC.status. In 2013, Citigroup chose to emphasize the development and

retention of female and minority employees (Citi Diversity Annual

Report, 2013).

Financial Performance

Recently, Citigroup’s net income declined from $13.7 billion

in 2011 to $7.3 billion in 2014, despite relatively consistent

revenues. These decline was in spite of the fact that Citigroup’s

investment bank no longer participated in the toxic activities

that jeopardized the firm’s financial health in the past.

Citigroup also had substantially higher levels of capital. This

improvement in liquidity reflected the bank’s ability to better

absorb losses (Eavis, 2015).

Citigroup’s investment bank, had $1.06 trillion of assets at

the end of last year, a 12% increase from 2010. Over the same

period, the value of Goldman Sach’s assets dropped 6% while

JPMorgan’s investment and commercial banking divisions increased

by 4%. The fact that the values of some assets rose while others

declined was partially related to massive branch closures.

Stock Performance

41THE AFTERMATH OF A RECESSION: CITIGROUP INC.

Citigroup’s stock price was a roller coaster ride so nerve-

racking that everyone wanted off the ride. It was too fast, too

unpredictable, and far too dangerous. On Dec. 31, 2006, one share

of Citigroup’s stock cost a whopping $501.64 (Yahoo Finance,

2015). This peak marked that split second on the ride when the

view was spectacular and everything seemed perfect. However, the

coaster had accumulated enough momentum to thrust its passengers

quickly downward. In an instant, a trough appeared, and on a

March day in 2009 the stock price plummeted to 97 cents.

Since that time, the ride has not ended. It has fluctuated,

but no longer to such extremes. On Dec. 31, 2010, Citigroup’s

stock price was $47.11. Then on Dec. 31, 2011, it dropped to

$26.23. On the last days of 2012, 2013, and 2014 respectively,

the price climbed from $39.49 to $52.06 to $54.10 (Yahoo Finance,

2015).

Key Financial Data

Table 1 displays some of Citigroup’s key financial data.

Citigroup’s return on assets and return on equity have fluctuated

over the past five years. Since these ratios are affected by

annual earnings, total assets, and shareholder equity these

42THE AFTERMATH OF A RECESSION: CITIGROUP INC.fluctuations made sense in the aftermath of a recession.

Citigroup’s annual earnings were impacted by changes in interest

rates, pending litigations and regulatory costs, which were

sometimes unforeseen.

The firm’s net interest margin increased every year from

2011 (66.66%) to 2014 (77.81%). Low interest rates typically

reduced the net profit margin, so this increase was a positive

trend for Citigroup. The firm’s loss ratio has also trended

upward, which was a negative trend, and likely stemmed in part

from its mounting litigations. In 2010, this ratio was 35.95%,

and by 2014 it had reached 37.96%.

Citigroup’s reduction in its debt-to-equity ratio, from 2.33

in 2010 to 1.06 in 2014, was likely an indication that the firm

had shed some of its former debt. This reduction aligned with the

firm’s restructuring efforts. Total asset turnover remained

stable, at 0.05 over four of the past five years, possibly an

indication that the firm neither bought nor sold major assets in

recently.

Citigroup’s book value per share increased steadily, from

$56.26 in 2010 to $69.92 in 2014. This increase was positive, and

43THE AFTERMATH OF A RECESSION: CITIGROUP INC.possibly indicated that stockholders perceived the firm as more

valuable than during previous years. The costs associated with

one of Citigroup’s core competencies, technology and

communication, also increased over the past five consecutive

years. In 2010, these expenses totaled $4.9 billion and by 2014,

they totaled $6.4 billion.

Citigroup’s Challenges

A Tarnished Reputation

A positive reputation is a valuable and intangible

resource. It can draw prospective customers, generate interest in

investment opportunities, improve financial performance, attract

the attention of top employee talent, increase return on assets,

create competitive advantages, and generate positive feedback

from analysts (Weber, Erickson, & Stone, 2011). Banks must be

especially careful to maintain a positive image due to the

psychological and economic implications of consumer behavior. For

example, the widespread panic among consumers during the Great

44THE AFTERMATH OF A RECESSION: CITIGROUP INC.Depression led to bank runs that only exacerbated the country’s

problems.

One of the factors that influenced reputation during

the crisis was whether stakeholders believed that the

organization’s actions created the crisis. The media quickly

exposed Citigroup’s poor management decisions in a flurry of

negative publicity. As a result, Citigroup’s stakeholders

recognized the firm’s role in risky activities and reckless

behaviors.

Another influential factor was the firm’s past behaviors.

Although Citigroup had never before seen such substantial

financial losses, it was no stranger to losses or sanctions.

Citigroup had previously been involved in a plethora of scandals,

corruption, and unethical actions, including allegations of money

laundering and theft from consumer accounts. The firm was

involved in Enron, WorldCom, and Global Crossing scandals that

led to bankruptcies. Citigroup faced controversy over conflicts

of interest in investment research, a bond trading scandal,

numerous lawsuits, questionable bonus practices, and three

45THE AFTERMATH OF A RECESSION: CITIGROUP INC.government bailouts (Wikipedia, 2015). All of these factors

drastically harmed Citigroup’s reputation.

Shareholders rejected the firm’s executive compensation

plan, and the government loomed nearby with power to restructure

or liquidate the firm. Citigroup was even disciplined by the

Federal Reserve for inadequate risk-management procedures (Weber,

Erickson, & Stone, 2011). Citigroup’s managerial opportunism had

been protected with the use of golden parachutes and poison

pills.

Citigroup tried numerous tactics to defend its reputation

and divert the negative attention. The firm blamed the economy,

called media reports inaccurate, attempted to convince

stakeholders that Citigroup’s good outweighed its bad, and

praised its employees (Weber, Erickson, & Stone, 2011). It seemed

reasonable that Citigroup would have taken measures to repair its

image after so many stains, but did the firm really care?

In 2015, Citigroup allowed foreign and domestic retail

customers to engage in high-risk world currency trading with

leverage of up to 50:1. Last month, the firm’s trading desk lost

$150 million when Switzerland’s central bank eliminated the cap

46THE AFTERMATH OF A RECESSION: CITIGROUP INC.on the Swiss Franc’s peg to the Euro. Further, Citigroup didn’t

even demand a correction or a retraction. These activities

attracted high-risk gamblers, and only amplified Citigroup’s

reputation of risk (Martens & Martens, 2015).

One positive area of Citigroup’s reputation had remained

intact throughout the recession. Citigroup was renowned for its

position as the leading global bank. In January 2015, Citigroup

announced that it would reduce retail banking operations around

the globe and cited an inadequate number of branches as the

reason (Crews, 2015). This decision, aimed at reducing costs,

undermined what was perhaps the most stable part of the firm’s

reputation.

Diseconomies of Scale

Economies of scale refers to the reduced costs associated

with spreading of costs over an increased number of units. In

the banking industry, economies of scale often include the spread

of investments over more output, the consolidation of functions,

funding mix, and advertising (Larson, 2010). Economies of scale

often create synergy and leverage.

47THE AFTERMATH OF A RECESSION: CITIGROUP INC.

However, businesses that have merged may encounter

diseconomies of scale in the form of layoffs and downsizing,

structural problems, cultural clashes, and declining consumer

trust. (Aspen, 2012). It is difficult for the management of

supersize banks to oversee many different business lines

simultaneously. Supersize banks that stick to core operations,

like Wells Fargo, tended to perform better than their

counterparts (Bair, 2012).

In addition to economies of scale, banks often benefited

from economies of scope. For example, Citigroup’s ability to

offer investment banking, commercial banking, and insurance

services increased its business with large corporations, due to

the convenience of the variety of its product line. This

diversification also provided some protection to Citigroup during

the recession (Larson, 2010).

Pending Litigations

In spring of 2008, Citigroup faced numerous lawsuits from

claimants stating that the firm’s stock price was overstated due

to poor disclosure of risks. These lawsuits included eleven

derivative actions and four class action lawsuits regarding

48THE AFTERMATH OF A RECESSION: CITIGROUP INC.securities fraud. In addition, numerous former employees sued

Citigroup over retirement accounts (Shvartsman, 2008).

In 2013, Citigroup paid $3.5 billion to the US Federal

Housing Finance Agency for misrepresentation of the mortgage-

backed securities sold to Fannie Mae and Freddie Mac. These two

agencies were regulated by the FHA (Citi, 2013). Also in 2013,

Citigroup agreed to pay $730 million to the Arkansas Teacher

Retirement System and the Louisiana Sheriffs’ Pension and Relief

Fund for similar reasons (Giardina, 2013).

In August of 2014, Citigroup and the US Department of

Justice agreed to $7 billion for the settlement of a federal

investigation regarding Citigroup’s misrepresentation of toxic

financial products prior to the recession. Citigroup paid these

penalties and fees to the US Department of Justice, State

Attorneys, the Federal Deposit Insurance Corporation (FDIC), and

funds established for the purpose of aiding struggling consumers

(Compliance Reporter, 2014).

During the last quarter of 2014, Corbat boosted Citigroup’s

efficiency through restructuring, but spent $800 million in the

process. He also effectively increased return on equity through

49THE AFTERMATH OF A RECESSION: CITIGROUP INC.elimination of some international segments. At the same time,

Citi Holding’s legal expenses totaled $2.7 million. These

combined expenses undermined Corbat’s efforts, and Citigroup only

saw a marginally profitable quarter (Gara, 2014).

Exorbitant legal fees followed Citigroup for years after the

recession. These expenses were a huge part of the reason that a

restructuring of the organization was necessary. Citi Holdings

was primarily created to separate these unfortunate expenses from

the improvements in core operations. These events further

contributed to the good bank, bad bank images of Citicorp and Citi

Holdings.

Citigroup Culture

Citigroup had experienced cultural clashes within its

organization for decades. At least part of the problem originated

from the acquisition of an investment bank, Salomon Brothers, in

1998. Citigroup differed in the incentives that it offered to

investment bankers versus commercial bankers, and these

differences often resulted in conflicts of interest (Authers,

2013).

50THE AFTERMATH OF A RECESSION: CITIGROUP INC.

Traders expected bonuses, and often accepted risky terms in

order to obtain them. In contrast, commercial bankers were

reluctant to extend loans to customers with poor credit. As a

one-stop-shop, the investment segment’s risky culture eventually

infiltrated the commercial banking arena. It became increasingly

difficult for employees to reject risky transactions, due to the

impact that it would have on their co-workers’ pay (Authers,

2013).

Many politicians believed that that the resulting riskiness

was a major contributor to the financial crisis and have

attempted to reintroduce the separation of investment and

commercial activities. John Reed, former CEO of Citicorp,

recently announced that he supported reinstatement of the Glass-

Steagall Act, which called for separation of banking segments,

and described the logic behind its repeal as flawed (Authers,

2013).

Increased Regulations

Besides increased legal expenses, Citigroup also battled

increased regulation expenses. These government regulations,

aimed at preventing future crises, focused on bank capital,

51THE AFTERMATH OF A RECESSION: CITIGROUP INC.liquidity, compensation, and corporate structure (Dermine, 2013).

The Credit Card Act of 2009, the Volcker Rule, Dodd-Frank, and

Basel III were a few examples. Although firms have complained

about the negative impact on revenues, most are in a more

financially stable condition as a result.

Failure of Federal Stress Tests

Since the financial crisis in 2008-2009, the Fed implemented

stress tests to determine if major banks were able to survive and

continue operations during extremely stressful periods. The

tests, which measured capital planning and procedures, carefully

evaluated banks’ risk management. The Fed conducted these stress

tests annually, beginning in 2011. Only banks with assets in

excess of $50 billion were forced to comply (Blanc, 2015).

Citigroup failed the government’s stress tests in 2012 and

2014. Last year’s failure was attributed to insufficient

internal controls, and the Fed cited Citigroup’s glaring

inability to predict revenues and losses as a major cause of the

failure (Blanc, 2015). These tests were part of the Dodd-Frank

Act, which President Obama signed into law in 2010. Corbat’s

predecessor, Vikram Pandit, resigned after the Fed rejected

52THE AFTERMATH OF A RECESSION: CITIGROUP INC.Citigroup’s capital plan in 2012. Last year, Citigroup’s stock

price fell by 5% after the Fed announced that the firm had failed

the test (Blanc, 2015).

In March 2015, the jobs of Citigroup’s three top executives

depended upon the results of the stress test. Investors created

intense pressure for Mike Corbat (CEO), John Gerspach (CFO), and

Brian Leach (Head of Risk) to pass this year’s test. Each

executive was asked to resign pending failure of the 2015 test.

Downsizing

In 2011, Citigroup employed 266 million individuals.

This figure has decreased every year since that time, consistent

with the downsizings portrayed by the media. By 2014, Citigroup

had reduced its staff to 241 million. In December of 2012,

Citigroup announced that it would eliminate 11,000 jobs.

Interestingly, over half of these layoffs were in global

operations. Similar announcements have occurred throughout the

industry.

Corbat, who historically boasted about Citigroup’s

advantages based on global presence, articulated a different

message. “I’m not sure that the idea of spreading yourself thin

53THE AFTERMATH OF A RECESSION: CITIGROUP INC.across the globe is necessarily a good strategy anymore.” These

reductions left some investors wondering if Citigroup was cutting

the very source of its advantage, its global presence (Horwitz &

Aspan, 2012).

Debt Reduction Efforts

After 2009, Citigroup made extensive balance sheet

changes in an attempt to reduce risk. At least 25% of Citigroup’s

balance sheets were comprised of cash, government securities, or

other liquid assets. Citigroup also had a small mortgage

portfolio relative to its size. The overall industry experienced

a slowdown due to economic woes and sluggish growth. These

factors, coupled with increasing governmental regulations led to

reduced profits. However, Citigroup’s remaining global presence

positioned it in a great location for emerging market growth

(Serwer, 2011).

Analysis Question

1. What would you recommend to Citigroup’s CEO, Michael Corbat,and his executive management team, as a long-term strategic plan in order to ensure Citigroup’s success despite the numerous challenges it faces? How should this plan be implemented?

54THE AFTERMATH OF A RECESSION: CITIGROUP INC.

References

Annual Report Citi. (2013). Citigroup. Retrieved March 7, 2015 from

http://www.citigroup.com/citi/investor/quarterly/2014/

annual-report/

55THE AFTERMATH OF A RECESSION: CITIGROUP INC.Aspan, M. (2012). Big-bank critics have a point, JPM alum says.

American Banker, 177 (F337), 6.

Aspan, M. (2012). Bad-bank 'holdings' unit continues to squeeze

Citi. American Banker, 177 (159), 2.

Authers, J. (2013, Sep. 8). Culture clash means banks must split,

says former Citi chief. The Financial Times Limited. Retrieved

from http://www.ft.com/intl/cms/s/0/2cfa6f18-1575- 11e3-950a-

00144feabdc0.html#axzz3UNNRmaqS

Bair, S. (2012). Why it’s time to break up the ‘too big to fail’

banks. Fortune, 165(2), 56.

Balestra, C., & Dottori, D. (2012). Aging society, health and the

environment. Journal of Population Economics, 25(3), 1045-1076.

doi:10.1007/s00148-011-0380-x

Bank of America: trends in consumer mobility report. (2014).

Newsroom. Retrieved March 10, 2015 from

http://newsroom.bankofamerica.com/sites/bankofamerica.

newshq.businesswire.com/files/press_kit/additional/

2014_BAC_Trends_in_Consumer_Mobility.pdf

Blanc, M. (2015, March 2). What happens ifs Citigroup Inc. fails

the fed’s stress test again? Bidness ETC. Retrieved from

56THE AFTERMATH OF A RECESSION: CITIGROUP INC.http://www.bidnessetc.com/35903-what-happens-if- citigroup-inc-

fails-the-feds-stress-test-again/2/

Brennant, C., & Ritch, E. (2010). Capturing the voice of older

consumers in relation to financial products and services.

International Journal of Consumer Studies, 34(2), 212-218. Retrieved

from doi:10.1111/j.1470-6431.2009.00831.x

Chiu, T. (2014). Putting responsible finance to work for Citi

microfinance. Journal of Business Ethics, 119(2), 219-234. Retrieved

from doi:10.1007/s10551-013-1626-

Choi, B., Shin, H. Lee, S. & Hur, T. (2006). Life cycle

assessment of a personal computer. LCA case studies. Retrieved

December 7, 2014 from ABI/Inform Global.

Citigroup reaches $7B mortgage bond settlement. (2014). Compliance

Reporter, 13.

Citi settles MBS lawsuit with FHA. (2013). Total Securitization & Credit

Investment, 42.

Citigroup-Wachovia: the details. (2008). Euroweek, (1074), 64.

Customer satisfaction with banks soars, but midsize institutions

face challenges. (2014). Teller Vision, (1443), 1-2.

57THE AFTERMATH OF A RECESSION: CITIGROUP INC.Crews, E. (2015, January 14). Citigroup can’t compete is shutting

down consumer division. The American Genius. Retrieved from

http://agbeat.com/business-news/citigroup-cant-c

compete-shutting-consumer-division/

Dermine, J. (2013). Bank regulations after the global financial

crisis: good intentions and unintended Evil. European Financial

Management, 19(4), 658-674. doi:10.1111/j.1468-

036X.2013.12017.x

Dess, Lumpkin, Eisner, & McNamara. (2014). Strategic management.

(7 Ed.) New York: NY

Distributors: Citi's wealth business making more use of tech.

(2014). FinanceAsia, 1.

Ferguson Jr, R., W. (2013). The road ahead: the graying of

America and its implications for finance and the economy.

Business Economics, 48(2), 1081 12.

doi:http://dx.doi.org/10.1057/be.2013.8

Fowler, C. S., Cover, J. K., & Kleit, R. G. (2014). The geography

of fringe banking. Journal of Regional Science, 54(4), 688-710.

doi:10.1111/jors.12144

58THE AFTERMATH OF A RECESSION: CITIGROUP INC.Dymski, G., Hernandez, J., & Mohanty, L. (2013). Race, gender,

power, and the US subprime mortgage and foreclosure: ameso

analysis. Feminist Economics, 19(3), 124-151.

doi:10.1080/13545701.2013.791401

Gara, A. (2014). Citigroup shares tumble from post-crisis high on

forecast of $2.7 billion fourth quarter charge. Forbes.Com, 5.

Giardina, M. (2013). Citigroup settles $730M price tag with

investors. Investment Management Mandate Pipeline, 3.

Global consumer banking survey 2014: Know your 8 customer

segments. (2014, January 1). Retrieved March 11, 2015,

fromhttp://www.ey.com/GL/en/Industries/Financial-

Services/Banking---Capital-Markets/Global-consumer-banking-

survey-2014--Know- your-8-customer-segments

Goddard, L. (2014, December). IBIS World Industry Report 52211

custody, assets and securities services in the US. IBIS World.

Retrieved March 2, 2015 from IBIS World.

Eavis, P. (2015, March 10). Citigroup’s roaring revival on Wall

Street. Retrieved March 11, 2015, from

http://www.nytimes.com/2015/03/11/business/dealbook/citigroups-

roaring- revival-on-wall-street.html?_r=0

59THE AFTERMATH OF A RECESSION: CITIGROUP INC.Haider, Z. (2014, December). IBIS World Industry Report 52211

Commercial banking in the US. IBIS World. Retrieved March 2,

2015 from IBIS World.

Hoopes, S. (2014, November). IBIS World Industry Report 52211

Investment banking and securities dealing in the US. IBIS World.

Retrieved March 2, 2015 from IBIS World.

Horwitz, J., & Aspan, M. (2012). Citi's latest cuts target its

international identity. American Banker, 177(186), 6.

Imbruglia, M. (2015, March). IBIS World Industry Report 52211

Credit card issuing in the US. IBIS World. Retrieved March 2,

2015 from IBIS World.

Industry Life Cycle. (n.d.). Inc. Retrieved December 7, 2014

from http://www.inc.com/encyclopedia/industry-life-

cycle.html

Javers, E. (2011). Citigroup tops list of banks who received

Federal aid. CNBC. Retrieved from

http://www.cnbc.com/id/42099554#.

Krasny, J., Floro, Z., & Lubin, G. (2012, July 28). 40 things you

can buy for a dollar. Business Insider. Retrieved from

60THE AFTERMATH OF A RECESSION: CITIGROUP INC.http://www.businessinsider.com/40-things-you-can-buy-for-a-

dollar-2012-7?op=1

Larson, R. (2010). Not too BIG enough. (Cover story). Dollars &

Sense, (288), 11-16.

Martens, P. & Martens, R. (2015, Jan. 20). Citigroup’s $150

million in currency losses deserve a closer look. Wall Street on

Parade. Retrieved from http://wallstreetonparade.com

/2015/01/citigroups-150-million-in-currency-losses-deserve-

a-closer-look/

Scannella, E. & Bennardo, D. (2013, May 10). Interest rate risk

in banking: a theoretical and empirical investigation

through a systemic approach (Asset & Liability Management).

Business Systems Review. Retrieved from www.business-systems-

review.org

Serwer, A. (2011). How Citi is coping in a trying time. Fortune,

164(7), 65-66.

Shvartsman, L. (2008). Citigroup faces more than a dozen subprime

related lawsuits. Total Securitization & Credit Investment, 22.

Tuckey, S. (2005). Citigroup failure undermines synergy claims.

National Underwriter / P&C, 109(10), 12-14.

61THE AFTERMATH OF A RECESSION: CITIGROUP INC.Weber, M., Erickson, S. L., & Stone, M. (2011). Corporate

reputation management: Citibank’s use of image restoration

strategies during the U.S. banking crisis. Journal of

Organizational Culture, Communications & Conflict, 15(2), 35-55

Wilmarth, A. E. (2014). Citigroup's unfortunate history of

managerial and regulatory failures. Journal of Banking Regulation,

15(3/4), 235-265. doi:10.1057/jbr.2014.16

Yahoo Finance. Historical prices - Citigroup Inc. Retrieved from

http://finance.yahoo.com/q/hp?

s=C&a=11&b=31&c=2005&d=11&e=31&f=2005&g=d

Yu, D., & Ray, J. (2014). Baby boomers put more money than trust

in banks. Gallup Poll Briefing, 4.

62THE AFTERMATH OF A RECESSION: CITIGROUP INC.

Appendix

Figure 1. The Commercial Banking Industry’s Major Players.

Figure 1. During 2014, the four largest banks comprised 52.1% of the total market share. Image adapted from Haider, J. (2014, December). IBISWorld Industry Report 52211 Commercial Banking in the US. IBISWorld.

63THE AFTERMATH OF A RECESSION: CITIGROUP INC.Figure 2. Industry Revenue (2000-2014)

Figure 2. Industry revenue initially declined after the recession, but have trended upward since 2011. Data adapted from Haider, J. (2014, December). IBISWorld Industry Report 52211 Commercial Banking in the US. IBISWorld.

Figure 3. Commercial Banking: Industry Life Cycle.

64THE AFTERMATH OF A RECESSION: CITIGROUP INC.

Figure 3. Commercial banking is a mature industry. Figure retrievedfrom IBIS World Industry Report 52211 Commercial Banking in the US. IBIS World.

65THE AFTERMATH OF A RECESSION: CITIGROUP INC.Figure 4. Citigroup’s Organizational Restructuring.

Figure 4. Citigroup restructured in order to focus intently on coreoperations. Retrieved from Citigroup website. http://www.citigroup.com/citi/fixedincome/rel_corp_struct.htm

66THE AFTERMATH OF A RECESSION: CITIGROUP INC.

Table 1. Citigroup’s Key Financial Ratios.

12/31/2014

12/31/2013

12/31/2012

12/31/2011

12/31/2010

Net Return on Assets (%)

0.39 0.73 0.40 0.58 0.56

Net Return on Equity (%)

3.53 6.95 4.10 6.49 6.71

Net Interest Margin (%)

77.81 74.31 69.86 66.66 68.73

Loss Ratio (%) 37.96 36.40 35.82 36.72 35.95

Calculated Tax Rate (%)

47.79 30.09 0.34 24.08 16.94

Revenue per Employee $375,817

$368,697

$349,267

$385,665

$428,712

Loans to Deposits 0.70 0.67 0.68 0.71 0.72

Total Debt to Equity 1.06 1.08 1.27 1.82 2.33

Total Asset Turnover 0.05 0.05 0.05 0.05 0.06

Cash & Equivalents Turnover

0.50 0.55 0.05 0.05 0.06

Cash Flow per Share 14.99 18.91 4.86 15.38 12.40

Book Value per Share 69.92 67.46 62.42 60.81 56.26

Citigroup’s key financial ratios reflected the firm’s recovery efforts and the counter effects of increased costs. The firm gradually realized increased profits, post-recession. Data retrieved from Mergent online company financials.

67THE AFTERMATH OF A RECESSION: CITIGROUP INC.

![Repensando a crítica do sistema penal no tempo da Great Recession [2015]](https://static.fdokumen.com/doc/165x107/6337ae416f78ac31240eb230/repensando-a-critica-do-sistema-penal-no-tempo-da-great-recession-2015.jpg)