Citigroup Mortgage Loan Trust 2021-INV1 - S&P Global

25

Presale: Citigroup Mortgage Loan Trust 2021-INV1 June 28, 2021 Preliminary Ratings Class Preliminary ratings(i) Amount ($) Initial interest rate (%) Credit enhancement (%) Class type A-1 AAA (sf) 126,325,000 2.000(ii) 15.00 Super senior/initial exchangeable A-1-IO1 AAA (sf) 126,325,000(iii) 0.500(iv) -- Senior/interest only/initial exchangeable A-1-IO2 AAA (sf) 126,325,000(iii) 0.100(v) -- Senior/interest only/initial exchangeable A-1-IOX AAA (sf) 126,325,000(iii) 0.109(vi) -- Senior/interest only/initial exchangeable A-1A AAA (sf) 126,325,000 2.500(vii) 15.00 Super senior/exchangeable A-1-IO3 AAA (sf) 126,325,000(iii) 0.600(viii) -- Senior/interest only/exchangeable A-1-IO1W AAA (sf) 126,325,000(iii) 0.209(ix) -- Senior/interest only/exchangeable A-1-IO2W AAA (sf) 126,325,000(iii) 0.709(x) -- Senior/interest only/exchangeable A-1W AAA (sf) 126,325,000 2.709(xi) 15.00 Super senior/exchangeable A-2 AAA (sf) 52,635,000 2.000(ii) 15.00 Super senior/initial exchangeable A-2-IO1 AAA (sf) 52,635,000(iii) 0.500(iv) -- Senior/interest only/initial exchangeable A-2-IO2 AAA (sf) 52,635,000(iii) 0.100(v) -- Senior/interest only/initial exchangeable A-2-IOX AAA (sf) 52,635,000(iii) 0.109(vi) -- Senior/interest only/initial exchangeable A-2A AAA (sf) 52,635,000 2.500(vii) 15.00 Super senior/exchangeable A-2-IO3 AAA (sf) 52,635,000(iii) 0.600(viii) -- Senior/interest only/exchangeable A-2-IO1W AAA (sf) 52,635,000(iii) 0.209(ix) -- Senior/interest only/exchangeable A-2-IO2W AAA (sf) 52,635,000(iii) 0.709(x) -- Senior/interest only/exchangeable A-2W AAA (sf) 52,635,000 2.709(xi) 15.00 Super senior/exchangeable A-3 AAA (sf) 210,535,000 2.000(ii) 15.00 Senior/exchangeable A-3-IO1 AAA (sf) 210,535,000(iii) 0.500(iv) -- Senior/interest only/exchangeable A-3-IO2 AAA (sf) 210,535,000(iii) 0.100(v) -- Senior/interest only/exchangeable Presale: Citigroup Mortgage Loan Trust 2021-INV1 June 28, 2021 PRIMARY CREDIT ANALYSTS Alicia Clarke New York + 1 (212) 438 8805 alicia.clarke @spglobal.com Terry G Osterweil New York + 1 (212) 438 2567 terry.osterweil @spglobal.com SECONDARY CONTACTS Marcio Rocha New York + 1 (212) 438 6223 marcio.rocha @spglobal.com Adam J Odland Centennial + 1 (303) 721 4664 adam.odland @spglobal.com SURVEILLANCE CREDIT ANALYST Truc T Bui San Francisco + 1 (415) 371 5065 truc.bui @spglobal.com ANALYTICAL MANAGER Vanessa Purwin New York + 1 (212) 438 0455 vanessa.purwin @spglobal.com www.standardandpoors.com June 28, 2021 1 © S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimer on the last page. 2680378

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Citigroup Mortgage Loan Trust 2021-INV1 - S&P Global

Presale:

Citigroup Mortgage Loan Trust 2021-INV1June 28, 2021

Preliminary Ratings

ClassPreliminaryratings(i) Amount ($)

Initialinterest rate

(%)Credit

enhancement (%) Class type

A-1 AAA (sf) 126,325,000 2.000(ii) 15.00 Super senior/initial exchangeable

A-1-IO1 AAA (sf) 126,325,000(iii) 0.500(iv) -- Senior/interest only/initialexchangeable

A-1-IO2 AAA (sf) 126,325,000(iii) 0.100(v) -- Senior/interest only/initialexchangeable

A-1-IOX AAA (sf) 126,325,000(iii) 0.109(vi) -- Senior/interest only/initialexchangeable

A-1A AAA (sf) 126,325,000 2.500(vii) 15.00 Super senior/exchangeable

A-1-IO3 AAA (sf) 126,325,000(iii) 0.600(viii) -- Senior/interest only/exchangeable

A-1-IO1W AAA (sf) 126,325,000(iii) 0.209(ix) -- Senior/interest only/exchangeable

A-1-IO2W AAA (sf) 126,325,000(iii) 0.709(x) -- Senior/interest only/exchangeable

A-1W AAA (sf) 126,325,000 2.709(xi) 15.00 Super senior/exchangeable

A-2 AAA (sf) 52,635,000 2.000(ii) 15.00 Super senior/initial exchangeable

A-2-IO1 AAA (sf) 52,635,000(iii) 0.500(iv) -- Senior/interest only/initialexchangeable

A-2-IO2 AAA (sf) 52,635,000(iii) 0.100(v) -- Senior/interest only/initialexchangeable

A-2-IOX AAA (sf) 52,635,000(iii) 0.109(vi) -- Senior/interest only/initialexchangeable

A-2A AAA (sf) 52,635,000 2.500(vii) 15.00 Super senior/exchangeable

A-2-IO3 AAA (sf) 52,635,000(iii) 0.600(viii) -- Senior/interest only/exchangeable

A-2-IO1W AAA (sf) 52,635,000(iii) 0.209(ix) -- Senior/interest only/exchangeable

A-2-IO2W AAA (sf) 52,635,000(iii) 0.709(x) -- Senior/interest only/exchangeable

A-2W AAA (sf) 52,635,000 2.709(xi) 15.00 Super senior/exchangeable

A-3 AAA (sf) 210,535,000 2.000(ii) 15.00 Senior/exchangeable

A-3-IO1 AAA (sf) 210,535,000(iii) 0.500(iv) -- Senior/interest only/exchangeable

A-3-IO2 AAA (sf) 210,535,000(iii) 0.100(v) -- Senior/interest only/exchangeable

Presale:

Citigroup Mortgage Loan Trust 2021-INV1June 28, 2021

PRIMARY CREDIT ANALYSTS

Alicia Clarke

New York

+ 1 (212) 438 8805

Terry G Osterweil

New York

+ 1 (212) 438 2567

SECONDARY CONTACTS

Marcio Rocha

New York

+ 1 (212) 438 6223

Adam J Odland

Centennial

+ 1 (303) 721 4664

SURVEILLANCE CREDIT ANALYST

Truc T Bui

San Francisco

+ 1 (415) 371 5065

ANALYTICAL MANAGER

Vanessa Purwin

New York

+ 1 (212) 438 0455

www.standardandpoors.com June 28, 2021 1

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2680378

Preliminary Ratings (cont.)

ClassPreliminaryratings(i) Amount ($)

Initialinterest rate

(%)Credit

enhancement (%) Class type

A-3-IOX AAA (sf) 210,535,000(iii) 0.109(vi) -- Senior/interest only/exchangeable

A-3A AAA (sf) 210,535,000 2.500(vii) 15.00 Senior/exchangeable

A-3-IO3 AAA (sf) 210,535,000(iii) 0.600(viii) -- Senior/interest only/exchangeable

A-3-IO1W AAA (sf) 210,535,000(iii) 0.209(ix) -- Senior/interest only/exchangeable

A-3-IO2W AAA (sf) 210,535,000(iii) 0.709(x) -- Senior/interest only/exchangeable

A-3W AAA (sf) 210,535,000 2.709(xi) 15.00 Senior/exchangeable

A-4 AAA (sf) 19,318,000 2.000(ii) 7.20 Senior support/initialexchangeable

A-4-IO1 AAA (sf) 19,318,000(iii) 0.500(iv) -- Senior/interest only/initialexchangeable

A-4-IO2 AAA (sf) 19,318,000(iii) 0.100(v) -- Senior/interest only/initialexchangeable

A-4-IOX AAA (sf) 19,318,000(iii) 0.109(vi) -- Senior/interest only/initialexchangeable

A-4A AAA (sf) 19,318,000 2.500(vii) 7.20 Senior/exchangeable

A-4-IO3 AAA (sf) 19,318,000(iii) 0.600(viii) -- Senior/interest only/exchangeable

A-4-IO1W AAA (sf) 19,318,000(iii) 0.209(ix) -- Senior/interest only/exchangeable

A-4-IO2W AAA (sf) 19,318,000(iii) 0.709(x) -- Senior/interest only/exchangeable

A-4W AAA (sf) 19,318,000 2.709(xi) 7.20 Senior/exchangeable

A-5 AAA (sf) 229,853,000 2.000(ii) 7.20 Senior/exchangeable

A-5-IO1 AAA (sf) 229,853,000(iii) 0.500(iv) -- Senior/interest only/exchangeable

A-5-IO2 AAA (sf) 229,853,000(iii) 0.100(v) -- Senior/interest only/exchangeable

A-5-IOX AAA (sf) 229,853,000(iii) 0.109(vi) -- Senior/interest only/exchangeable

A-5A AAA (sf) 229,853,000 2.500(vii) 7.20 Senior/exchangeable

A-5-IO3 AAA (sf) 229,853,000(iii) 0.600(viii) -- Senior/interest only/exchangeable

A-5-IO1W AAA (sf) 229,853,000(iii) 0.209(ix) -- Senior/interest only/exchangeable

A-5-IO2W AAA (sf) 229,853,000(iii) 0.709(x) -- Senior/interest only/exchangeable

A-5W AAA (sf) 229,853,000 2.709(xi) 7.20 Senior/exchangeable

A-6 AAA (sf) 31,575,000 2.000(ii) 15.00 Super senior/initial exchangeable

A-6-IO1 AAA (sf) 31,575,000(iii) 0.500(iv) -- Senior/interest only/initialexchangeable

A-6-IO2 AAA (sf) 31,575,000(iii) 0.100(v) -- Senior/interest only/initialexchangeable

A-6-IOX AAA (sf) 31,575,000(iii) 0.109(vi) -- Senior/interest only/initialexchangeable

A-6A AAA (sf) 31,575,000 2.500(vii) 15.00 Super senior/exchangeable

A-6-IO3 AAA (sf) 31,575,000(iii) 0.600(viii) -- Senior/interest only/exchangeable

A-6-IO1W AAA (sf) 31,575,000(iii) 0.209(ix) -- Senior/interest only/exchangeable

www.standardandpoors.com June 28, 2021 2

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2680378

Presale: Citigroup Mortgage Loan Trust 2021-INV1

Preliminary Ratings (cont.)

ClassPreliminaryratings(i) Amount ($)

Initialinterest rate

(%)Credit

enhancement (%) Class type

A-6-IO2W AAA (sf) 31,575,000(iii) 0.709(x) -- Senior/interest only/exchangeable

A-6W AAA (sf) 31,575,000 2.709(xi) 15.00 Super senior/exchangeable

A-7 AAA (sf) 157,900,000 2.000(ii) 15.00 Super senior/exchangeable

A-7-IO1 AAA (sf) 157,900,000(iii) 0.500(iv) -- Senior/interest only/exchangeable

A-7-IO2 AAA (sf) 157,900,000(iii) 0.100(v) -- Senior/interest only/exchangeable

A-7-IOX AAA (sf) 157,900,000(iii) 0.109(vi) -- Senior/interest only/exchangeable

A-7A AAA (sf) 157,900,000 2.500(vii) 15.00 Super senior/exchangeable

A-7-IO3 AAA (sf) 157,900,000(iii) 0.600(viii) -- Senior/interest only/exchangeable

A-7-IO1W AAA (sf) 157,900,000(iii) 0.209(ix) -- Senior/interest only/exchangeable

A-7-IO2W AAA (sf) 157,900,000(iii) 0.709(x) -- Senior/interest only/exchangeable

A-7W AAA (sf) 157,900,000 2.709(xi) 15.00 Super senior/exchangeable

A-8 AAA (sf) 84,210,000 2.000(ii) 15.00 Super senior/exchangeable

A-8-IO1 AAA (sf) 84,210,000(iii) 0.500(iv) -- Senior/interest only/exchangeable

A-8-IO2 AAA (sf) 84,210,000(iii) 0.100(v) -- Senior/interest only/exchangeable

A-8-IOX AAA (sf) 84,210,000(iii) 0.109(vi) -- Senior/interest only/exchangeable

A-8A AAA (sf) 84,210,000 2.500(vii) 15.00 Super senior/exchangeable

A-8-IO3 AAA (sf) 84,210,000(iii) 0.600(viii) -- Senior/interest only/exchangeable

A-8-IO1W AAA (sf) 84,210,000(iii) 0.209(ix) -- Senior/interest only/exchangeable

A-8-IO2W AAA (sf) 84,210,000(iii) 0.709(x) -- Senior/interest only/exchangeable

A-8W AAA (sf) 84,210,000 2.709(xi) 15.00 Super senior/exchangeable

A-11 AAA (sf) 8,421,400 0.66(xii) 15.00 Super senior/floater/exchangeable

A-11-IO AAA (sf) 8,421,400(iii) 4.34(xiii) -- Senior/interest only/inversefloater/exchangeable

A-11-A AAA (sf) 42,107,000 5.660(xiv) 15.00 Super senior/floater/exchangeable

A-11-AIO AAA (sf) 42,107,000(iii) 4.340(xv) Senior/interest only/inversefloater/exchangeable

A-12 AAA (sf) 8,421,400 5.000(xvi) 15.00 Super senior/exchangeable

B-1 AA (sf) 7,182,000 2.000(xvii) 4.30 Subordinate/initial exchangeable

B-1-IO AA (sf) 7,182,000(iii) 0.500(xviii) -- Subordinate/interest only/initialexchangeable

B-1-IOX AA (sf) 7,182,000(iii) 0.209(xix) -- Subordinate/interest only/initialexchangeable

B-1-IOW AA (sf) 7,182,000(iii) 0.709(xx) -- Subordinate/interestonly/exchangeable

B-1W AA (sf) 7,182,000 2.709(xi) 4.30 Subordinate/exchangeable

B-2 A (sf) 4,830,000 2.000(xvii) 2.35 Subordinate/initial exchangeable

www.standardandpoors.com June 28, 2021 3

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2680378

Presale: Citigroup Mortgage Loan Trust 2021-INV1

Preliminary Ratings (cont.)

ClassPreliminaryratings(i) Amount ($)

Initialinterest rate

(%)Credit

enhancement (%) Class type

B-2-IO A (sf) 4,830,000(iii) 0.500(xviii) -- Subordinate/interest only/initialexchangeable

B-2-IOX A (sf) 4,830,000(iii) 0.209(xix) -- Subordinate/interest only/initialexchangeable

B-2-IOW A (sf) 4,830,000(iii) 0.709(xx) -- Subordinate/interestonly/exchangeable

B-2W A (sf) 4,830,000 2.709(xi) 2.35 Subordinate/exchangeable

B-3 BBB (sf) 2,353,000 2.000(xvii) 1.40 Subordinate/initial exchangeable

B-3-IO BBB (sf) 2,353,000(iii) 0.500(xviii) -- Subordinate/interest only/initialexchangeable

B-3-IOX BBB (sf) 2,353,000(iii) 0.209(xix) -- Subordinate/interest only/initialexchangeable

B-3-IOW BBB (sf) 2,353,000(iii) 0.709(xx) -- Subordinate/interestonly/exchangeable

B-3W BBB (sf) 2,353,000 2.709(xi) 1.40 Subordinate/exchangeable

B-4 BB (sf) 1,486,000 2.709(xi) 0.80 Subordinate/initial exchangeable

B-5 B (sf) 867,000 2.709(xi) 0.45 Subordinate/initial exchangeable

B-6 NR 1,115,470 2.709(xi) 0.00 Subordinate/initial exchangeable

PT NR 247,686,470(iii) 2.709(xi) 0.00 Exchangeable

R NR N/A N/A N/A Residual

Note: This presale report is based on information as of June 28, 2021. The ratings shown are preliminary. This report does not constitute arecommendation to buy, hold, or sell securities. Subsequent information may result in the assignment of final ratings that differ from thepreliminary ratings. (i)The collateral and structural information in this report reflect the term sheet dated June 25, 2021. (ii)The lesser of 2.00%and the product of the net WAC divided by 2.60% and 2.00%. (iii)Notional balance. (iv)The lesser of 0.50% and the product of the net WACdivided by 2.60% and 0.50%. (v)The lesser of 0.10% and the product of the net WAC divided by 2.60% and 0.10%. (vi)The greater of the excess ofthe net WAC over 2.60% and zero. (vii)The lesser of 2.50% and the product of the net WAC divided by 2.60% and 2.50%. (viii)The lesser of 0.60%and the product of the net WAC divided by 2.60% and 0.60%. (ix)The annual rate equal to the sum of the excess, if any, of the net WAC over2.60% and the lesser of 0.10% and the product of the net WAC divided by 2.60% and 0.10%. (x)The annual rate equal to the sum of the excess, ifany, of the net WAC over 2.60% and the lesser of 0.60% and the product of the net WAC divided by 2.60% and 0.60%. (xi)The net WAC. (xii)Thelesser of the related benchmark for the accrual period plus 0.65%, 5.00%, and the class A-11 net WAC cap. (xiii)The annual rate equal to theexcess, if any, of the lesser of 5.00% and the product of the net WAC divided by 2.60%; and 5.00% over the pass-through rate for the class A-11certificates for the distribution date. (xiv)The lesser of the related benchmark for the accrual period plus 0.65%, 5.00% and the class A-11A netWAC cap. (xv) The annual rate equal to the excess, if any, of the lesser of 5.00% and the product of the net WAC divided by 2.60% and 5.00%over the pass-through rate for the class A-11A certificates for the distribution date. (xvi)The lesser of 5.00% and the product of the net WACdivided by 2.60% and 5.00%. (xvii)The lesser of 2.00% and the net WAC. (xviii)The lesser of 0.50% and the greater of the excess of the net WACover 2.00% and zero. (xix)The greater of the excess of the net WAC over 2.50% and zero. (xx)The greater of the excess of the net WAC over 2.00%and zero. WAC--Weighted average coupon. IO--Interest only. NR--Not rated. N/A--Not applicable.

Profile

Expected closing date July 8, 2021.

Cutoff date June 1, 2021.

First payment date July 26, 2021.

Final scheduled paymentdate

May 25, 2051.

Certificates' amount,including unrated classes

$247.7 million in aggregate.

www.standardandpoors.com June 28, 2021 4

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2680378

Presale: Citigroup Mortgage Loan Trust 2021-INV1

Profile (cont.)

Collateral type First-lien, fixed-rate, fully amortizing residential mortgage loans secured by one- tofour-family residential properties, planned-unit developments, and condominiums to primeborrowers. The pool consists of 758 investor ability-to-repay exempt mortgage loans.

Collateral U.S. residential mortgage loans.

Credit enhancement Subordination of the certificates that are lower in the payment priority provides creditenhancement for each class or rated certificate.

Participants

Issuer Citigroup Mortgage Loan Trust2021-INV1.

Sponsor and mortgage loan seller Citigroup Global Markets Realty Corp.

Depositor Citigroup Mortgage Loan Trust Inc.

Trust administrator, paying agent, exchange trustee, certificate registrar, andbackup advancing party

U.S. Bank N.A.

Servicer PennyMac Corp.

Trustee U.S. Bank Trust N.A.

Custodian Deutsche Bank National Trust Co.

Initial loan seller PennyMac Corp.

Rationale

The preliminary ratings assigned to Citigroup Mortgage Loan Trust 2021-INV1's (CMLTI2021-INV1's) mortgage pass-through certificates reflect our view of:

- The high-quality collateral in the pool (see the Collateral Summary section below);

- The transaction's credit enhancement;

- The transaction's associated structural mechanics;

- The transaction's representation and warranty (R&W);

- PennyMac Loan Services LLC, which provides fulfillment services to PennyMac Corp.;

- The geographic concentration;

- The 100% due diligence results consistent with the represented loan characteristics; and

- The impact that the economic stress brought on by COVID-19 pandemic will likely have on theperformance of the mortgage borrowers in the pool (for additional information see "EconomicOutlook U.S. Q2 2021: Let The Good Times Roll," published March 24, 2021) and liquidityavailable in the transaction.

Environmental, Social, And Governance (ESG)

Our rating analysis considers a transaction's potential exposure to ESG credit factors. For RMBS,we view the exposure to environmental credit factors as average, social credit factors as above

www.standardandpoors.com June 28, 2021 5

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2680378

Presale: Citigroup Mortgage Loan Trust 2021-INV1

average, and governance credit factors as below average (see " ESG Industry Report Card:Residential Mortgage-Backed Securities," March 31, 2021). Social credit factors are generallyconsidered above average because housing is viewed as one of the most basic human needs andconduct risk presents a direct social exposure for lenders and servicers, particularly as regulatorsare increasingly focused on ensuring fair treatment of borrowers. For RMBS, social risk isgenerally factored into our base-case assumptions. In our view, the transaction's exposure to ESGcredit factors is in line with our sector benchmark. We have not identified any material ESG creditfactors in our analysis. Therefore, ESG credit factors do not influence our assessment of thetransaction's credit quality.

Noteworthy Features

100% investment property loans

Each of the loans in the pool is secured by an investment property that was underwritten based onthe borrower's debt-to income (DTI) rather than the investment property cash flow. These loansare exempt from the ATR rules.

100% government-sponsored enterprise (GSE) eligible loans

We applied a neutral documentation type adjustment factor to 100% of the loans in the poolbecause we believe these loans have similar risk profiles to the loans that meet our criteria for fulldocumentation as they are GSE-eligible mortgages.

No loans currently in forbearance at closing

On March 27, 2020, the CARES Act enacted COVID-19-related relief for borrowers withgovernment-backed mortgage loans in the form of a temporary forbearance of up to 12 months ofscheduled payments. The updates we made on April 17, 2020, to our mortgage outlook andcorresponding archetypal foreclosure frequency levels account for a portion of the borrowersentering COVID-19-related temporary forbearance plans and their impact to the overall creditquality of collateralized pools (see "Guidance: Methodology And Assumptions For Rating U.S.RMBS Issued 2009 And Later," published Dec. 8, 2020). To the extent a securitization pool exhibitsgrowth levels in forbearance over time beyond those otherwise expected, additional adjustmentsmay be applied.

As of the June 1, 2021, cutoff date, none of the mortgage loans in the pool had borrowers who hadrequested or entered into a COVID-19-related forbearance plan or exited from a prior forbearanceplan. Any loan that enters a forbearance plan between the cutoff and the closing dates will remainin the pool. As of June 23, 2021, we are aware no mortgage loans were granted forbearance sincethe cutoff date.

While we recognize that temporary forbearance related to the COVID-19 pandemic could begranted at some level in the pool going forward, we decided not to apply an additional pool-levelloss adjustment factor because none of the mortgage loans were in an active forbearance plan asof June 23, 2021, and the collateral quality of the pool is strong.

We will continue to monitor the credit behavior related to temporary forbearance as the situationevolves and more performance information becomes available and may adjust our loss coveragelevels accordingly, which could impact the ratings.

www.standardandpoors.com June 28, 2021 6

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2680378

Presale: Citigroup Mortgage Loan Trust 2021-INV1

Principal and interest (P&I) advances

PennyMac Corp., as servicer, will advance monthly P&I payments through liquidation ondelinquent loans. If the servicer fails in its obligation to fund any required advance, the trustadministrator, U.S. Bank N.A., will be obligated to fund the required advance.

COVID-19-related deferrals of forborne amounts

Although general delinquency and forbearance levels amid the COVID-19 pandemic have fallensince their peak last summer, our credit analysis considers how COVID-19-related deferrals offorborne amounts could impact the transaction. Although the transaction does not have anyCOVID-19-related forbearance loans as of the cutoff date, we focused on how those amountswould be handled within the transaction if subsequent forbearance resulted in a deferral ofprincipal, interest, taxes, and/or insurance payments.

If the servicer were to perform COVID-19-related deferrals during the forbearance period (i.e.,applicable principal, interest, taxes, and insurance amounts), the deferred advances would beconsidered principal deferred amounts. Furthermore, the deferred advances would be reimbursedto the servicer (or trust administrator when applicable) at the time of deferral or modificationwhere the servicer adds those advanced amounts to the principal balance of the loan (but onlyfrom principal collections) rather than at the time of loan payoff or liquidation.

According to the payment waterfall, if this occurs, the principal distribution amount to thecertificates will be reduced by the principal deferred amounts, starting with the subordinateprincipal distribution amount and then the senior principal distribution amount (if the subordinateprincipal distribution amount is insufficient). Because the reimbursement of servicer advances ina given period reduces the amount of funds available for distribution, the exclusion of thoseamounts only from principal payments to the certificates for the given period prevents potentialinterest shortfalls to the certificates. Principal deferred amounts are treated as a realized loss atthe time of deferral or modification, which coincides with the reduction in principal, and as asubsequent recovery within the waterfall if or when those amounts are paid (e.g., at loan maturity,prepayment, liquidation). The additional realized loss due to those COVID-19-related deferrals isaccounted for by the revision to our 'B' (base-case) projected foreclosure frequency assumptionfor an archetypal loan to 3.25% from 2.50% (for additional information, see "Guidance:Methodology And Assumptions For Rating U.S. RMBS Issued 2009 And Later," published April 17,2020).

Preliminary ratings on class B-4 and B-5 certificates are capped by minimumcredit enhancement levels

The preliminary rated classes passed rating stress scenarios commensurate with their assignedpreliminary ratings in our cash flow analysis. Although the class B-4 and B-5 certificates passedour 'BB+' and 'B+' rating level stresses, respectively, the credit enhancements at those ratinglevels were lower than the minimum credit enhancement levels as specified in our criteria.Consequently, we assigned the 'BB (sf)' and 'B (sf)' preliminary ratings to the class B-4 and B-5certificates, respectively, based on our criteria.

www.standardandpoors.com June 28, 2021 7

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2680378

Presale: Citigroup Mortgage Loan Trust 2021-INV1

Collateral Summary

CMLTI 2021-INV1 is an RMBS transaction backed by a collateral pool that consists of GSE-eligibleinvestor mortgage loans made to prime borrowers. The mortgage pool comprises 758 mortgageloans with a principal balance of approximately $247.7 million as of the cutoff date.

The mortgage pool consists of loans to borrowers with high credit quality (weighted average FICOscore of 774) and considerable home equity, as demonstrated by the pool's weighted averageoriginal and current combined loan-to-value (LTV) ratios of approximately 60.8% and 60.5%,respectively.

The weighted average seasoning is approximately three months, and the average loan balance is$326,763. The mortgage loans are all ATR exempt loans.

Approximately 45.0% of the pool is concentrated in California, with the next largestconcentrations in Washington (9.2%), New Jersey (5.3%), Virginia (4.6%), and Florida (3.8%). Theremaining concentrations are dispersed throughout 29 states and the District of Columbia.

The collateral pool is generally in line with our expectations of a prime residential mortgage pool(see table 1). The pool's 'AAA' loss coverage requirement was determined to be 4.70%. In ouranalysis, we considered the following mortgage loan characteristics to be weaker than ourarchetypal pool:

- Occupancy status (investor property),

- Self-employed borrowers, and

- Loan purpose (cash-out refinances).

Per our criteria ("Methodology And Assumptions For Rating U.S. RMBS Issued 2009 And Later,"published Feb. 22, 2018), we applied a neutral documentation type adjustment factor to 100% ofthe loans in the pool because we believe these loans have similar risk profiles to the loans thatmeet our criteria for full documentation.

Table 1

Collateral Characteristics

CMLTI2021-INV1

JPMMT2020-INV2(i)

CMLTI2021-J1

JPMMT2021-5

PSMC2021-2

PSMC2021-1

CMLTI2020-EXP2

Archetypalpool(ii)

Closing pool balance (mil.$)

248 342 318 361 357 426 311 N/A

Closing loan count (no.) 758 1014 373 388 432 514 644 N/A

Avg. loan balance ($) 326,763 337,145 852,808 929,466 826,393 829,589 482,735 N/A

WA original CLTV (%) 60.84 67.00 63.90 70.95 66.50 67.13 68.46 75.00

WA current CLTV (%) 60.47 66.30 63.50 70.63 67.10 66.50 56.06 75.00

WA FICO score 774 764 780 781 66.5 787 766 725

WA current rate (%) 3.00 4.50 2.91 2.95 782.00 3.12 3.93 N/A

WA original term (mos.) 354 360 360 360 360 360 343 360

WA seasoning (mos.)(iii) 3 6 3 3 5 5 55 0-6

WA debt-to-income (%) 34.95 36.00 28.69 31.60 29.60 30.12 31.45 36.00

WA DSCR (non-zero) N/A N/A N/A NA NA N/A N/A

www.standardandpoors.com June 28, 2021 8

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2680378

Presale: Citigroup Mortgage Loan Trust 2021-INV1

Table 1

Collateral Characteristics (cont.)

CMLTI2021-INV1

JPMMT2020-INV2(i)

CMLTI2021-J1

JPMMT2021-5

PSMC2021-2

PSMC2021-1

CMLTI2020-EXP2

Archetypalpool(ii)

Owner occupied (%) 0.00 0.00 97.07 93.34 96.60 98.38 76.15 100.00

Single-family (includingunattached and attachedPUD) (%)

68.79 62.10 98.48 90.63 96.90 95.87 83.55 100.00

Adjustable-rate loans (%) 0.00 0.00 0.00 0.00 0.00 18.43 0.00

Loans with IO payments(%)

0.00 0.20 0.00 0.00 0.00 4.02 0.00

Purchase (%) 24.14 40.60 18.47 54.63 23.90 29.75 38.74 100.00

Cash-out refinancing (%) 14.97 37.00 10.20 3.21 1.50 1.92 16.80 0.00

Full documentation (%) 100.00 100.00 100.00 100.00 100.00 100.00 100.00 100.00

Alternative documentation(%)

0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Other/assetdepletion/DSCRdocumentation (%)

0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Self-employed borrowers(%)

18.14 24.90 17.94 9.66 31.70 29.99 30.89 0.00

Loans with coborrowers(%)

47.42 45.90 61.98 66.45 63.10 69.76 59.30 0.00

Loans to borrowers withmultiple mortgages (%)(iv)

13.21 5.46 0.00 0.00 0.00 0.35 3.00 N/A

Loans to foreign borrowers(%) (foreign national andnon-permanent residentaliens)

2.63 1.03 0.87 2.00 2.00 0.00 0.65 0.00

Modified loans (%)(v) 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

PCEs (%)(v) 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Current (%) 100.00 100.00 100.00 100.00 100.00 100.00 100.00 100.00

30+ day delinquent (%) 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Length of P&I advancing(mos.)(vi)

Full Full Full Full Full Full Full Full

Pool-level adjustments (multiplicative factors)

Geographicconcentration

1.01 1.02 1.00 1.02 1.00 1.01 1.00 1.00

Mortgage operationalassessment

0.95 0.95 1.00 0.95 0.95 0.95 1.00 1.00

Representations andwarranties

1.00 1.00 1.00 1.00 1.00 1.00 1.03 1.00

Other (i.e., loanmodification/PCE/duediligence)

1.00 1.00 1.00 1.00 1.00 1.00 1.00 1.00

Combined pool-leveladjustments(vii)

0.96 0.97 1.00 0.97 0.95 0.96 1.03 1.00

www.standardandpoors.com June 28, 2021 9

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2680378

Presale: Citigroup Mortgage Loan Trust 2021-INV1

Table 1

Collateral Characteristics (cont.)

CMLTI2021-INV1

JPMMT2020-INV2(i)

CMLTI2021-J1

JPMMT2021-5

PSMC2021-2

PSMC2021-1

CMLTI2020-EXP2

Archetypalpool(ii)

Loss estimation(viii)

'AAA' loss coverage (%) 4.70 9.60 2.65 3.60 2.90 2.70 4.05 7.50

'AAA' foreclosurefrequency (%)

11.03 18.13 6.01 7.49 6.58 6.05 8.28 15.00

'AAA' loss severity (%) 42.65 52.95 44.09 48.06 44.07 44.63 48.91 50.00

'BBB' loss coverage(%)

1.15 2.85 0.75 0.85 0.65 0.60 1.25 1.92

'BBB' foreclosurefrequency (%)

4.82 8.93 2.70 2.89 2.56 2.31 3.93 6.41

'BBB' loss severity (%) 23.86 31.91 27.80 29.41 25.39 25.97 31.82 30.00

'B' loss coverage (%) 0.35 0.85 0.30 0.35 0.25 0.20 0.40 0.65

'B' foreclosurefrequency (%)

2.38 3.94 1.59 1.62 1.42 1.31 1.92 3.25

'B' loss severity (%) 14.71 21.57 18.84 21.60 17.61 15.27 20.79 20.00

(i)The loss estimates for JPMMT 2020-INV2 do not reflect updated base-case scenario. (ii)As defined in our Feb. 22, 2018, criteria article.(iii)Measured from the loan origination date. (iv)Limited to borrowers who have multiple mortgage loans or properties included in thesecuritized pool. (v)Limited to modified and PCE loans considered in our analysis. (vi)Months of P&I advancing on a delinquent mortgage loanto the extent such advances are deemed recoverable. (vii)The combined pool-level adjustments are the product of each pool-level adjustmentlisted above. (viii)The guidance document published April 17, 2020, reflects a revision to our 'B' (base-case) projected foreclosure frequencyassumption for an archetypal loan to 3.25% from 2.50%. CMLTI--Citigroup Mortgage Loan Trust. JPMMT--J.P. Morgan Mortgage Trust.PSMC--Pearl Street Mortgage Co. WA--Weighted average. CLTV--Combined loan-to-value ratio. DSCR--Debt service coverage ratio.PUD--Planned-unit development. IO--Interest-only. PCE--Prior credit event. P&I--Principal and interest. N/A--Not applicable.

Table 2 shows a breakdown of the pool by borrower FICO score.

Table 2

Updated Credit Score Statistics

FICO score Current balance (%) No. of loans Average current balance (000s $)

750+ 85.07 645 326.7

725-749 10.30 76 335.8

700-724 3.18 24 328.2

675-699 1.09 9 301.1

650-674 0.29 3 240.1

625-649 0.06 1 150.4

600-624 -- -- --

575-599 -- -- --

550-574 -- -- --

Below 500 -- -- --

Total 100.00 758 327.0

www.standardandpoors.com June 28, 2021 10

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2680378

Presale: Citigroup Mortgage Loan Trust 2021-INV1

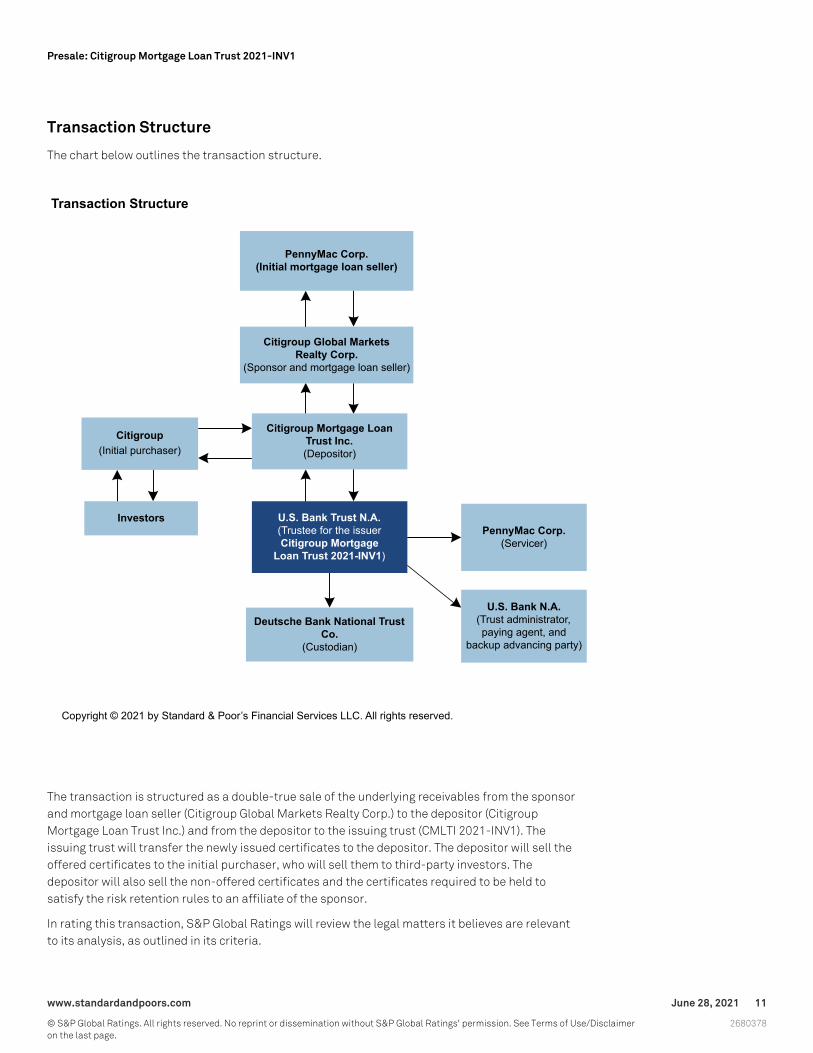

Transaction Structure

The chart below outlines the transaction structure.

The transaction is structured as a double-true sale of the underlying receivables from the sponsorand mortgage loan seller (Citigroup Global Markets Realty Corp.) to the depositor (CitigroupMortgage Loan Trust Inc.) and from the depositor to the issuing trust (CMLTI 2021-INV1). Theissuing trust will transfer the newly issued certificates to the depositor. The depositor will sell theoffered certificates to the initial purchaser, who will sell them to third-party investors. Thedepositor will also sell the non-offered certificates and the certificates required to be held tosatisfy the risk retention rules to an affiliate of the sponsor.

In rating this transaction, S&P Global Ratings will review the legal matters it believes are relevantto its analysis, as outlined in its criteria.

www.standardandpoors.com June 28, 2021 11

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2680378

Presale: Citigroup Mortgage Loan Trust 2021-INV1

Strengths And Weaknesses

We believe the following characteristics strengthen the CMLTI 2021-INV1 transaction:

- The mortgage pool consists of prime loans to borrowers with high credit quality (weightedaverage FICO score of 774) with considerable home equity, as demonstrated by the pool'sweighted average original and current combined LTV ratios of approximately 60.8% and 60.5%,respectively.

- Approximately 47% of the loans have two or more borrowers. As a result, we applied a pool level0.88x adjustment factor to our loss estimates.

- The weighted average DTI ratio for the pool is approximately 35.0%

- All of loans in this transaction were sold by PennyMac Corp. PennyMac Loan Services LLCprovides fulfillment services in connection with the mortgage loans PennyMac Corp. purchasedor acquired under its correspondent lending program. We applied a 0.95x adjustment to ourloss coverage estimates to account for our view of the loans' origination.

- AMC Diligence LLC, which is on our list of reviewed third-party due diligence providers,performed due diligence on 100.0% of the pool for regulatory compliance, credit, and propertyvaluation.

- The senior classes benefit from a credit support floor, in which the principal allocation to thesubordinate classes falls to zero on any distribution date where the subordinate certificates'aggregate balance is less than or equal to 1.00% of the cutoff collateral balance or 7.20% of thecurrent collateral balance. The subordinate classes benefit from a separate credit support floorequal to 1.00% of the cutoff collateral balance.

- During the initial five years, the subordinate certificates will be locked out of unscheduledprincipal allocation, limiting credit enhancement erosion for more senior certificates.

- As of June 1, 2021, none of the borrowers in the pool had requested or received any form ofCOVID-19-related payment assistance.

We believe the following factors weaken the CMLTI 2021-INV1 transaction:

- Approximately 18.1% of the pool by balance were made to self-employed borrowers. Weapplied a 1.02x adjustment factor to our loss estimates for these loans.

- Cash-out loans comprise approximately 15.0% of the pool by balance. We applied a 1.04xadjustment factor to our loss estimates for these loans.

QM and ATR standards

The Consumer Financial Protection Bureau issued final regulations for mortgage loans withapplications submitted on or after Jan. 10, 2014, specifying the standards for a QM. The rule doesnot apply to the mortgage loans included in this securitization because they are investor propertyloans.

Under the ATR rule, the originator and any assignee are jointly and severally liable for certaindamages that may be incurred from noncompliance with the rule (for more details, see Appendix Iof our criteria "Methodology And Assumptions For Rating U.S. RMBS Issued 2009 And Later,"published Feb. 22, 2018). Since each loan in the pool is not subject to the rule, we applied our

www.standardandpoors.com June 28, 2021 12

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2680378

Presale: Citigroup Mortgage Loan Trust 2021-INV1

criteria and determined that no additional credit enhancement was needed.

Advancing obligations

PennyMac Corp., the servicer, will be obligated to advance monthly principal and P&I paymentsthrough liquidation on delinquent loans. If the servicer fails in its obligation to fund any requiredadvance, the trust administrator, U.S. Bank N.A., will be obligated to fund the required advance.These advanced amounts are expected to be reimbursed to the servicer (or the trustadministrator, when applicable) from proceeds realized upon liquidation or if the advances aredeemed to be nonrecoverable. Therefore, the interest advance amounts are reflected in our lossseverity estimate.

Structural Features

The transaction has a typical shifting-interest structure with a five-year lockout period. Thesubordinate certificates are available as credit support for the senior certificates as long as theyare outstanding. To the extent the subordinate certificates are written down, the senior-supportcertificates will absorb losses and then any remaining losses will be applied to the super-seniorcertificates.

P&I collections are comingled and distributed to the senior and subordinate certificates,according to the payment priority. The paying agent will make monthly distributions from themonthly available distribution amounts (see tables 3-4). This generally includes all P&I theservicer collects from the borrowers, reduced by the following:

- Servicer, custodian, trust administrator, trustee, and backup P&I advance provider fees;

- Servicer reimbursements allowed under the deal documents;

- Extraordinary expense reimbursements (i.e., trustee, paying agent, exchange trustee, Rule17g-5 information provider, trust administrator, custodian, backup P&I advance provider,certificate registrar, reviewer, and arbitrator fees);

- Mortgage loan seller reimbursements; and

- Reimbursement for deposit errors.

Extraordinary expense payments are capped annually at $375,000. Because these expenses arepassed through as reduced contractual interest due to certificateholders, there was no impact onour assessment of the transaction's credit enhancement. However, we consider the extraordinaryexpenses when analyzing projected interest reduction amounts, as described further in theImputed Promises Analysis section below. In addition, monthly available distribution amounts willinclude insurance and liquidation proceeds, subsequent recoveries, full and partial prepayments,repurchase amounts and any clean-up call amounts paid.

Table 3

Payment Waterfall (Before The Credit Support Depletion Date)(i)

Priority Payment(ii)

1 Interest due (including any accrued unpaid interest shortfall), pro rata, to the senior class A-1, A-1-IO1,A-1-IO2, A-1-IOX, A-6, A-6-IO1, A-6-IO2, A-6-IOX, A-2, A-2-IO1, A-2-IO2, A-2-IOX, A-4, A-4-IO1, A-4-IO2, andA-4-IOX certificates.

www.standardandpoors.com June 28, 2021 13

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2680378

Presale: Citigroup Mortgage Loan Trust 2021-INV1

Table 3

Payment Waterfall (Before The Credit Support Depletion Date)(i) (cont.)

Priority Payment(ii)

2 The senior principal distribution amount (PDA)(iii) is divided proportionally into super senior and seniorsupport portions. The super senior portion is allocated sequentially to the class A-1, A-6, and A-2certificates, in that order. Concurrently, the senior support portion is allocated to the class A-4 certificates.

3 Interest due (including any accrued unpaid interest shortfall) to subordinate classes B-1, B-1-IO, andB-1-IOX followed by class B-1's subordinate PDA; then interest due (including any accrued unpaid interestshortfall) to subordinate classes B-2, B-2-IO, and B-2-IOX followed by class B-2's subordinate PDA(iii);then interest due (including any accrued unpaid interest shortfall) to subordinate classes B-3, B-3-IO, andB-3-IOX followed by class B-3's subordinate PDA(iii); and then sequentially to classes B-4, B-5, and B-6, inthat order. Interest and principal are paid to a class before payments to the next class IPIP.

4 To reimburse previously allocated realized losses and certificate write-down amounts in order of paymentpriority until fully reimbursed.

5 To pay any remaining unpaid trust expenses.

6 To pay any remainder to the residual interest holders.

(i)The first date on which the subordinate certificates' balances have been reduced to zero. (ii)MACRs that were exchanged for initial MACRsshall be entitled to a proportionate share of the interest and principal payments otherwise allocated to the initial MACRs. (iii)The senior PDA isgenerally the senior percentage of the scheduled principal amounts on the mortgage loans plus the senior prepayment percentage of theunscheduled principal collections on the mortgage loans. PDA--Principal distribution amount. MACR--Modifiable and exchangeable certificate.IPIP--Interest principal interest principal.

Table 4

Payment Waterfall (On Or After The Credit Support Depletion Date)(i)

Priority Payment(i)

1 Interest due (including any accrued unpaid interest shortfall), pro rata, to the senior classA-1, A-1-IO1, A-1-IO2, A-1-IOX, A-6, A-6-IO1, A-6-IO2, A-6-IOX, A-2, A-2-IO1, A-2-IO2,A-2-IOX, A-4, A-4-IO1, A-4-IO2, and A-4-IOX certificates.

2 Principal, pro rata, to the class A-1, A-6, A-2, and A-4 certificates.

3 Reimbursement for prior realized losses and certificate write-down amounts to the classA-1, A-6, and A-2 certificates, pro rata; and then reimbursement for prior realized lossesand certificate write-down amounts to the class A-4 certificates.

4 Interest (including any accrued unpaid interest shortfalls), sequentially to the subordinatecertificates.

5 Principal sequentially to the subordinate certificates.

6 Reimburse previously allocated realized losses and certificate write-down amounts to thesubordinate certificates in order of payment priority until fully reimbursed.

7 Pay any remaining unpaid trust expenses without regard to the respective caps.

8 Any remainder to the residual interest holders.

(i)The terms used in this tableare used in the same capacityas in table 3.

The following classes serve as initial exchangeable (base or depositable) certificates: class A-1,A-1-IO1, A-1-IO2, A-1-IOX, A-2, A-2-IO1, A-2-IO2, A-2-IOX, A-4, A-4-IO1, A-4-IO2, A-4-IOX, A-6,A-6-IO1, A-6-IO2, A-6-IOX, B-1, B-1-IO, B-1-IOX, B-2, B-2-IO, B-2-IOX, B-3, B-3-IO, B-3-IOX, B-4,B-5, and B-6. The certificateholders can exchange the base or depositable certificates for severalcombinations of exchangeable certificates, including some interest-only (IO) classes, and viceversa, as specified in the offering documents. If an exchange is made, the exchanged certificates

www.standardandpoors.com June 28, 2021 14

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2680378

Presale: Citigroup Mortgage Loan Trust 2021-INV1

will receive a proportionate share of the P&I payments otherwise allocable to the classes of initialexchangeable certificates.

The senior percentage of scheduled principal collections and, for the first five years, 100% ofunscheduled principal collections on the mortgage loans will be allocated to the seniorcertificates, excluding the IO certificates. After five years, the portion of unscheduled principalcollections allocated to the senior certificates (excluding the IO certificates) will graduallydecrease (see table 5).

Table 5

Senior Prepayment Principal Distributions

Distribution date occurring in the following period Senior prepayment

July 2021-June 2026 100%.

July 2026–June 2027 The senior percentage plus 70% of the subordinate percentage.

July 2027-June 2028 The senior percentage plus 60% of the subordinate percentage.

July 2028-June 2029 The senior percentage plus 40% of the subordinate percentage.

July 2029-June 2030 The senior percentage plus 20% of the subordinate percentage.

July 2030 and thereafter The senior percentage.

However, if the step-down test is not satisfied, the senior allocation of unscheduled principalcollections on the mortgage loans will not decrease. The step-down test will be satisfied on anydistribution date if:

- The six-month average principal balance of all loans 60 days or more delinquent, as well asloans (without duplication) that are subject to a servicing modification within the previous 12months, is less than 50.0% of the principal balance of the subordinate certificates; and

- Cumulative realized losses on the mortgage loans do not exceed the levels listed in table 6.

Except in certain circumstances, scheduled principal payments will be distributed pro ratabetween senior certificates and subordinate certificates. These payments to the subordinatetranches will reduce the absolute level of credit enhancement to the senior certificates andrequire additional initial subordination above the expected loss in a given rating scenario.

Table 6

Step-Down Test

Distribution date occurring in the followingperiods

Cumulative realized losses as a % of the original aggregate subordinateclass principal amounts

July 2026-June 2027 20

July 2027-June 2028 25

July 2028-June 2029 30

July 2029-June 2030 35

July 2030 and thereafter 40

Principal distributions to subordinate certificates will be directed to more-senior classes if theratio of the sum of the balances of a particular subordinate class and all the classes lower than itin the capital structure to all of the certificates' total outstanding balance falls below theapplicable credit support percentage for that class at issuance (see table 7).

www.standardandpoors.com June 28, 2021 15

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2680378

Presale: Citigroup Mortgage Loan Trust 2021-INV1

Table 7

Applicable Credit Support At Issuance

Class (%)

B-1 7.20

B-2 4.30

B-3 2.35

B-4 1.40

B-5 0.80

B-6 0.45

In addition, the transaction structure includes a subordination floor that protects senior classesfrom tail risk as the pool pays down. If the aggregate class balance of the subordinate certificatesis less than or equal to 1.00% of the closing pool balance or less than or equal to 7.20% of thecurrent pool balance, all principal collections will be paid to the senior certificates. Thetransaction also has a separate 1.00% floor that benefits the subordinate certificateholders,locking out principal payments to subordinate certificates with lower payment priorities (see theLarge Loans And Tail Risk Considerations section).

Realized losses will be applied in reverse sequential order until each class' principal balance isreduced to zero: first to class B-6, then class B-5, then class B-4, then class B-3, then class B-2,and then class B-1 until all subordinate certificates are reduced to zero. If no subordinatecertificates are outstanding, realized losses will be applied to the senior-support certificates andthen pro rata to the super-senior certificates.

Geographic Concentration

S&P Global Ratings analyzes the pool's geographic concentration risk based on theconcentrations of loans in each of the core-based statistical areas (CBSAs), as defined by the U.S.Office of Management and Budget (see Appendix II of "Methodology And Assumptions For RatingU.S. RMBS Issued 2009 And Later," published Feb. 22, 2018). In this transaction, the top fiveCBSAs account for approximately 35.2% of the aggregate pool (see table 8). We applied ageographic concentration adjustment factor of 1.01x to our base loss coverage estimate becauseas the pool is geographically diversified.

Table 8

Geographic Concentration

CBSAcode(i) CBSA State

% bybalance

31084 Los Angeles-Long Beach-Glendale California 9.92

42644 Seattle-Bellevue-Kent Washington 7.14

41740 San Diego-Chula Vista-Carlsbad California 6.99

41940 San Jose-Sunnyvale-Santa Clara California 5.77

47894 Washington-Arlington-Alexandria District of Columbia-Virginia-Maryland-WestVirginia

5.40

www.standardandpoors.com June 28, 2021 16

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2680378

Presale: Citigroup Mortgage Loan Trust 2021-INV1

Table 8

Geographic Concentration (cont.)

CBSAcode(i) CBSA State

% bybalance

Top fiveCBSAs

-- -- 35.22

(i)The CBSA code refers to the metropolitan division code, if available. CBSA--Core-based statistical area (includes metropolitan statisticalareas and metropolitan divisions where defined, as well as micropolitan statistical areas).

Large Loans And Tail Risk Considerations

To address mortgage pools that contain large-balance loans, which may result in lessdiversification, we also perform a top concentration test when we assign an initial rating. For thisanalysis, we compare the loss coverage projection from our LEVELS analysis (in conjunction withany qualitative overlays) at each applicable rating level with minimum loss coverage projections asoutlined in our criteria, based on the closing collateral pool balances. In our loss coverage analysisfor this collateral pool, the large loan analysis was not a driver for the loss coverage at any ratinglevels.

Furthermore, with respect to tail risk, fast prepayments on shifting-interest structures typicallybenefit the senior certificates because unscheduled principal is applied to them disproportionallyearly in the transaction's life. However, as the number of loans in the transaction decreases, theeffect of a single loan's losses becomes greater. If conditional prepayment rates are slow andcollateral pool losses are not realized until later in a transaction's life (back-loaded losses), prorata pay mechanisms can then leave the senior certificates exposed to event risk later in thetransaction's life (for more information on tail risk in RMBS transactions, see "Older RMBSTransactions Face Increased Tail Risk As Their Pools Shrink," published Aug. 9, 2012). To mitigatethis risk, the transaction documents provide for a credit enhancement floor, specifying principalpayments will not be made to subordinate classes if the credit support available to the seniorclasses is less than or equal to 1.00% of the pool's original principal balance or 7.20% of thecurrent principal balance.

The transaction structure also has a "push-down" floor that protects the more-senior subordinatecertificates from tail risk by locking out the more-junior subordinate classes and redirecting theirsubordinate principal payments to the relatively more-senior classes. This floor becomes effectivewhen the aggregate balance of a subordinate class (other than the then-outstanding subordinateclass with the lowest numerical designation) and all other classes with a lower distribution priorityis less than or equal to 1.00% of the closing pool balance.

To gauge the appropriateness of this credit enhancement floor, instead of focusing on the largestloans by balance at issuance, we weigh the risk of the loans in the transaction by focusing onthose loans with the largest expected loss exposure, assuming default. Because the risk ofsubstantial hard credit support erosion to the senior certificates can take years, and given thelockout period, we estimate this risk by amortizing the loans through the lockout expiration at theend of year nine, when the transaction begins paying all principal pro rata.

After considering loan amortization, we believe that a 1.00% credit enhancement floor will besufficient to protect the senior certificates from tail risk as the transaction seasons. We alsobelieve that a separate 1.00% push-down floor will be sufficient to protect the more seniorsubordinate certificates, locking out principal payments to subordinate classes with lower

www.standardandpoors.com June 28, 2021 17

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2680378

Presale: Citigroup Mortgage Loan Trust 2021-INV1

payment priorities.

Mortgage Operational Assessment (MOA) Review

All loans in this transaction were sold by PennyMac Corp. PennyMac Loan Services LLC providesfulfillment services in connection with the mortgage loans purchased or acquired by PennyMacCorp. under PennyMac Corp.'s correspondent lending program. Therefore, we focused our MOAanalysis on PennyMac Loan Services LLC's platform.

S&P Global Ratings' overall MOA ranking on PennyMac Loan Services LLC, after reviewing itsorigination process for all residential mortgage loans, is AVERAGE. The overall ranking reflects anAVERAGE qualitative subranking and a AVERAGE quantitative subranking. Based on the results ofour MOA, we determined that the loss coverage adjustment factor for PennyMac is 0.95x.

Our qualitative review focused on three primary areas regarding PennyMac's residential loanorigination:

- Management and organization, including risk management and financial position;

- Origination process and underwriting, including the property valuation process; and

- Internal controls, encompassing third-party management, prefunding data quality,post-funding quality control, and regulatory compliance.

For our quantitative analysis, we reviewed acquisition volume, loan characteristics, and loanperformance history, including delinquencies and early payment defaults.

The AVERAGE qualitative subranking reflects our assessment of the following strengths andweaknesses.

Strengths and weaknesses

PennyMac's strength as an originator includes the following:

- The management team is highly experienced and knowledgeable,

- The company retains servicing on most of its loans,

- The company closely monitors its operating structure, with external and strengthened internalquality control checks,

- The company's thorough correspondent seller approval process, and

- The company's strong appraisal valuation practices.

PennyMac's weaknesses as an originator includes the following:

- Its aggressive growth strategy.

Our AVERAGE quantitative subranking reflects PennyMac's limited and mixed loan performancedata. We evaluated performance data for the company's origination from a combination of internaland external sources. PennyMac Loan Services LLC has limited performance history, particularlyno originations and performance data during the pre-2008 downturn in the housing cycle. As aresult, we weighted the quantitative review somewhat less in our overall MOA ranking.

www.standardandpoors.com June 28, 2021 18

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2680378

Presale: Citigroup Mortgage Loan Trust 2021-INV1

Third-Party Due Diligence Review

AMC Diligence LLC, which is on our list of reviewed third-party due diligence providers, performeddue diligence on 100% of the loans in the transaction. The scope of the loan review encompassedregulatory compliance, credit (underwriting) compliance, property valuation, and data integrity. Allbusiness-purpose loans are exempt from Regulation Z and the TILA-RESPA Integrated Disclosure(TRID) rule.

Highlights of the findings include:

Five loans were graded "C" for property valuation because the secondary valuation was outside ofthe negative 10% tolerance. For these loans, we made upward adjustments to the estimated losscoverage of 1.3x.

All loans received a grade "A" or "B" for credit and compliance.

We applied a pool level rounded due diligence adjustment factor of 1.00x.

R&Ws

Our review of the R&Ws focuses on whether the representations made by the mortgage loan seller(sponsor) are substantially consistent with the set of representations we published as part of ourcriteria (see Appendix IV of "Methodology And Assumptions For Rating U.S. RMBS Issued 2009 AndLater," published Feb. 22, 2018). Our assessment of the R&W framework accounts for automaticreview triggers, knowledge qualifiers, gap periods, sunset provisions, and enforcementmechanisms. We evaluate the strength of the R&W framework and consider whether any breachcould have a materially adverse impact on the certificateholders' interests. If the R&Ws and theframework do not address the components in our published R&W methodology, we determinewhether it is appropriate to assess additional credit enhancement. We also consider the R&Wprovider's ability to fulfill its obligations in the event of a breach.

The sponsor, Citigroup Global Markets Realty Corp., acquired the loans in this transaction fromPennyMac Corp., and is making the R&Ws related to the mortgage loans. In our view, the R&Wframework is generally similar to other R&W frameworks in comparable rated prime collateraltransactions. In this transaction, a breach review of a mortgage loan by an independentthird-party is automatically triggered if a loan becomes at least 120 days delinquent or isliquidated with a realized loss. As seen in other prime collateral transactions, a seriousdelinquency is a trigger for automatic review, which will be done by an independent third party.The R&W trigger event definition has certain carve-out language (trigger event preemptive factor)that does not cover mortgage loans subject to a forbearance plan or other loss mitigation measuredue to a hardship resulting from a pandemic or national emergency.

The R&Ws are generally consistent with our published criteria for U.S. RMBS issued in 2009 andlater, and they will remain in effect for the transaction's life without any sunsets. The R&Ws aresubject to knowledge qualifiers that are mitigated by curative language. A breach of therepresentation will occur if it is discovered that the circumstances regarding the mortgage loanare not accurately reflected in the representation, notwithstanding the mortgage loan seller'sactual knowledge or lack of knowledge.

The mortgage loan seller generally has 60 days to remedy a breach review trigger before a reviewcommences. If the trust administrator is unable to engage an independent reviewer after twoattempts, the controlling holder (who cannot be an affiliate of the mortgage loan seller) may waivethe review. The mortgage loan seller is generally required to remedy a breach identified by the

www.standardandpoors.com June 28, 2021 19

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2680378

Presale: Citigroup Mortgage Loan Trust 2021-INV1

reviewer if the breach materially and adversely affects the value of the mortgage loan or thecertificateholders' interests, or if it is related to certain missing loan documents. Review findingdisputes are subject to arbitration, which is final and binding. If the arbitration processdetermines that there has been a breach of one or more mortgage loan representations, thearbitration fees, expenses, and indemnification claims will be paid by the mortgage loan seller.However, if it determines that no breach of representation has occurred, the fees and expenseswill be paid by the trust.

In CMLTI 2021-INV1, if a borrower of a mortgage loan (excluding loans subject to a forbearanceplan) fails to make any of the first three monthly payments due after the origination date and failsto cure by the next month, the loan will be considered an early payment default (EPD) mortgageloan and the seller must purchase the loan at the repurchase price within 90 days. However, norepurchase will be required if the mortgage loan became an EPD mortgage loan due to the failureto properly credit a scheduled payment in connection with a servicing transfer, or if no scheduledpayment on the mortgage loan is 30 or more days delinquent as of the date the repurchase pricewould be payable by the seller.

Overall, we applied a 1.00x R&W adjustment to the loss coverage that takes into account theoverall R&W framework, the assets' strong credit quality, and the third-party due diligenceperformed on every loan to mitigate the risk.

Cash Flow And Scenario Analysis

We reviewed the transaction structure and performed a cash flow analysis to simulate variousrating stress scenarios to determine the preliminary ratings for each class, consistent with ourcriteria and accounting for the available credit enhancement (see table 9). We analyzed a variety ofscenarios for each rating category, including combinations of:

- Front- and back-loaded default timing curves,

- Two-year recovery lag assumptions, and

- Fast and slow prepayment assumptions.

For further detail on our cash flow stresses, see our criteria "Methodology And Assumptions ForRating U.S. RMBS Issued 2009 And Later," published Feb. 22, 2018.

Table 9

Cash Flow Assumptions

Scenario

AAA AA A BBB BB B

Recovery lag (mos.) 24 24 24 24 24 24

Prepayments (%)(i)

Low CPR 1.00 2.00 3.00 4.00 5.00 6.00

High CPR 20.00 20.00 20.00 20.00 20.00 20.00

Servicer stop advance (%) N/A N/A N/A N/A N/A N/A

Foreclosure frequency (%) 11.02 8.82 6.92 4.82 3.69 2.38

Loss severity (%) 42.65 37.98 28.90 23.86 18.97 14.71

Loss coverage (%) 4.70 3.35 2.00 1.15 0.70 0.35

(i)Using a standard prepayment convention. CPR--Conditional prepayment rate. N/A--Not applicable.

www.standardandpoors.com June 28, 2021 20

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2680378

Presale: Citigroup Mortgage Loan Trust 2021-INV1

We applied the foreclosure frequencies, loss severities, and combinations of the stresses notedabove in our cash flow runs, and the results show that each class in the transaction is enhanced toa degree consistent with its assigned preliminary rating.

The preliminary rated classes passed the rating stress scenarios commensurate with theirassigned preliminary ratings in our cash flow analysis. Although the class B-4 and B-5 certificatespassed our 'BB+' and 'B+' rating level stresses, respectively, the credit enhancements at thoserating levels were lower than the minimum credit enhancement levels as specified in our criteria.Consequently, we assigned our 'BB (sf)' and 'B (sf)' preliminary ratings to the class B-4 and B-5certificates, respectively.

Servicer stop advance stresses

The pool consists of prime collateral, and the servicer is contractually obligated to advancemonthly P&I payments through liquidation (or earlier, if the advance would be deemednon-recoverable) on delinquent loans. Therefore, we did not apply any servicer stop advancestresses due to the prime nature of the collateral and structural features that protect againstpotential liquidity issues. Although the current COVID-19 pandemic may cause some mortgageloans to enter forbearance, we decided not to apply an additional liquidity stress to cash flows,considering the servicer is obligated to provide full P&I advancing on mortgage loans that enter aCOVID-19-related payment assistance plan throughout the payment assistance period.

Weighted average coupon (WAC) deterioration stress

The pool is relatively homogenous in its distribution of coupons and the securities are netWAC-capped pass-throughs. Therefore, we did not apply WAC deterioration stresses.

Interest stresses

The certificates all have coupons subject to the net WAC rate cap, similar to most of the post-2009RMBS transactions that we have rated. If the net WAC rate decreases below the cap, the interestdue to the certificates will decrease by a similar amount. We have generally seen two forms of netWAC rate definitions in transactions that we have rated since 2009. In some transactions, the netWAC rate is defined generally as the current net mortgage rate of the outstanding loans in theprevious period (minus servicing fees, trustee fees, etc.). In these cases, extraordinary expensepayments will reduce the available distribution amount and cash flow to the certificateholders,thereby potentially limiting the cash available to pay interest or principal to the subordinatetranches.

However, in this transaction, extraordinary trust expense payments reduce the net WAC rate,which effectively allocates the extraordinary trust expenses pro rata across all senior andsubordinate certificateholders by reducing their interest payments by the amount of theextraordinary trust expenses paid (subject to the annual cap). Because subordination does notabsorb these expense amounts, our trust expense analysis does not have an impact on thetransaction's credit enhancement.

Imputed Promises Analysis

As noted above, our extraordinary trust expense analysis does not have an impact on thetransaction's credit enhancement. However, we impute the interest owed to the security holderswhen rating U.S. RMBS transactions where credit-related events can reduce interest owed to the

www.standardandpoors.com June 28, 2021 21

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2680378

Presale: Citigroup Mortgage Loan Trust 2021-INV1

tranches across the capital structure rather than an allocation of such credit-related loss to theavailable credit support, based on our criteria "Methodology And Assumptions For Rating U.S.RMBS Issued 2009 And Later," published Feb. 22, 2018, and associated guidance "Guidance:Methodology And Assumptions For Rating U.S. RMBS Issued 2009 And Later," published April 17,2020. WAC deterioration that occurs because of defaults, repurchases, or prepayments is notconsidered credit-related, and we therefore do not consider it in this analysis.

The transaction provides for credit-related loan modifications and extraordinary trust expenses toreduce the net WAC, at which the transaction's certificate coupons are capped. Therefore, weassessed the maximum potential rating (MPR) that could apply, based on our projected interestreduction amount (PIRA). We did not account for any cumulative interest reduction amountbecause this is a new issue transaction.

We assumed that 50.00% of the loans projected to default would be modified, consistent with ourcriteria. We also assumed that 75.00% of the projected modifications are interest ratemodifications, with an interest rate reduction of 2.00%. When added to the extraordinary trustexpenses, this resulted in a maximum PIRA on the rated certificates that is significantly below the4.50% threshold. We stressed extraordinary trust expenses by the relevant extraordinary expenseapplication factor, as documented in our criteria. Based on the results of our analysis, there wasno impact on the securities' MPR.

Historically, we have observed that extraordinary trust expenses have been minimal when theyoccur and extremely limited in pre-2009 RMBS transactions. We continue to expect their actualoccurrence in post-2009 transactions to be rare.

Operational Risk Assessment

Our criteria article "Global Framework For Assessing Operational Risk In Structured FinanceTransactions," published Oct. 9, 2014, presents our methodology and assumptions for assessingcertain operational risks (severity, portability, and disruption risks) associated with asset typesand key transaction parties (KTPs) that provide an essential service to a structured finance issuer.According to the criteria, we cap the ratings on a transaction if we believe operational risk couldlead to credit instability and affect the ratings.

As provided in the operational risk criteria, for severity risk and portability risk, there are threepossible rankings: high, moderate, or low. For disruption risk, there are four possible rankings:very high, high, moderate, or low.

According to our criteria, we rank both severity and portability risk for prime residential mortgagecollateral as low. In accordance with our criteria, if severity and portability risk are each assessedas being low, then the maximum potential rating typically would not be constrained and adisruption risk assessment is not necessary. The transaction's subservicer, PennyMac LoanServices LLC, is the KTP. Given these risk assessments, our operational risk criteria do not cap theratings on this transaction.

Related Criteria

- Criteria | Structured Finance | General: Global Framework For Payment Structure And CashFlow Analysis Of Structured Finance Securities, Dec. 22, 2020

- Criteria | Structured Finance | Legal: U.S. Structured Finance Asset Isolation AndSpecial-Purpose Entity Criteria, May 15, 2019

www.standardandpoors.com June 28, 2021 22

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2680378

Presale: Citigroup Mortgage Loan Trust 2021-INV1

- Criteria | Structured Finance | General: Counterparty Risk Framework: Methodology AndAssumptions, March 8, 2019

- Criteria | Structured Finance | General: Incorporating Sovereign Risk In Rating StructuredFinance Securities: Methodology And Assumptions, Jan. 30, 2019

- Criteria | Structured Finance | RMBS: Assumptions Supplement For Methodology AndAssumptions For Rating U.S. RMBS Issued 2009 And Later, Feb. 22, 2018

- Criteria | Structured Finance | RMBS: Methodology And Assumptions For Rating U.S. RMBSIssued 2009 And Later, Feb. 22, 2018

- Criteria | Structured Finance | RMBS: U.S. Residential Mortgage Operational AssessmentRanking Criteria, Feb. 22, 2018

- General Criteria: Methodology For Linking Long-Term And Short-Term Ratings, April 7, 2017

- Criteria | Structured Finance | RMBS: Methodology For Assessing Mortgage Insurance AndSimilar Guarantees And Supports In Structured And Public Sector Finance And Covered Bonds,Dec. 7, 2014

- Criteria | Structured Finance | General: Global Framework For Assessing Operational Risk InStructured Finance Transactions, Oct. 9, 2014

- General Criteria: Global Investment Criteria For Temporary Investments In TransactionAccounts, May 31, 2012

- General Criteria: Principles Of Credit Ratings, Feb. 16, 2011

- Criteria | Structured Finance | General: Global Methodology For Rating Interest-Only Securities,April 15, 2010

- Criteria | Structured Finance | General: Methodology For Servicer Risk Assessment, May 28,2009

Related Research

- S&P Global Ratings Publishes List of Third-Party Due Diligence Firms Reviewed For U.S. RMBSAs Of June 10, 2021, June 10, 2021

- Select Servicer List, June 3, 2021

- S&P Global Ratings Publishes List Of Third-Party Due Diligence Firms Reviewed For U.S. RMBSAs Of May 12, 2021, May 12, 2021

- ESG Industry Report Card: Residential Mortgage-Backed Securities, March 31, 2021

- Economic Outlook U.S. Q2 2021: Let The Good Times Roll, March 24, 2021

- U.S. Residential Mortgage Operational Assessment Rankings (As Of March 19, 2021), March 19,2021

- S&P Global Ratings Definitions, Jan. 5, 2021

- Can COVID-19 Cause A Cash Crunch For Certain U.S. RMBS, Aug. 21, 2020

- S&P Global Ratings Is Assessing The Impact Of COVID-19 On Mortgage Market Outlooks ForGlobal RMBS, April 17, 2020

- U.S. Residential Mortgage Input File Format For LEVELS, March 6, 2020

www.standardandpoors.com June 28, 2021 23

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2680378

Presale: Citigroup Mortgage Loan Trust 2021-INV1

- Servicer Evaluation: PennyMac Loan Services LLC, Feb. 6, 2020

- Credit Rating Model: LEVELS Model For U.S. Residential Mortgage Loans, Aug. 5, 2019

- Credit Rating Model: Intex RMBS Cash Flow Model, April 7, 2017

- Global Structured Finance Scenario and Sensitivity Analysis 2016: The Effects of The Top FiveMacroeconomic Factors, Dec. 16, 2016

- Standard & Poor's Comfortable With SFIG Draft Proposal Regarding TRID Due Diligence, April25, 2016

- Mortgage Originator Review: PennyMac Loan Services LLC, Aug. 15, 2016

- Older RMBS Transactions Face Increased Tail Risk As Their Pools Shrink, Aug. 9, 2012

www.standardandpoors.com June 28, 2021 24

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2680378

Presale: Citigroup Mortgage Loan Trust 2021-INV1

S&P may receive compensation for its ratings and certain credit-related analyses, normally from issuers or underwriters of securities or from obligors.S&P reserves the right to disseminate its opinions and analyses. S&P's public ratings and analyses are made available on its Web sites,www.standardandpoors.com (free of charge), and www.ratingsdirect.com and www.globalcreditportal.com (subscription), and may be distributedthrough other means, including via S&P publications and third-party redistributors. Additional information about our ratings fees is available atwww.standardandpoors.com/usratingsfees.

S&P keeps certain activities of its business units separate from each other in order to preserve the independence and objectivity of their respectiveactivities. As a result, certain business units of S&P may have information that is not available to other S&P business units. S&P has establishedpolicies and procedures to maintain the confidentiality of certain non-public information received in connection with each analytical process.

Credit-related and other analyses, including ratings, and statements in the Content are statements of opinion as of the date they are expressed andnot statements of fact. S&P's opinions, analyses and rating acknowledgment decisions (described below) are not recommendations to purchase,hold, or sell any securities or to make any investment decisions, and do not address the suitability of any security. S&P assumes no obligation toupdate the Content following publication in any form or format. The Content should not be relied on and is not a substitute for the skill, judgment andexperience of the user, its management, employees, advisors and/or clients when making investment and other business decisions. S&P does not actas a fiduciary or an investment advisor except where registered as such. While S&P has obtained information from sources it believes to be reliable,S&P does not perform an audit and undertakes no duty of due diligence or independent verification of any information it receives. Rating-relatedpublications may be published for a variety of reasons that are not necessarily dependent on action by rating committees, including, but not limitedto, the publication of a periodic update on a credit rating and related analyses.

To the extent that regulatory authorities allow a rating agency to acknowledge in one jurisdiction a rating issued in another jurisdiction for certainregulatory purposes, S&P reserves the right to assign, withdraw or suspend such acknowledgment at any time and in its sole discretion. S&P Partiesdisclaim any duty whatsoever arising out of the assignment, withdrawal or suspension of an acknowledgment as well as any liability for any damagealleged to have been suffered on account thereof.

Copyright © 2021 Standard & Poor's Financial Services LLC. All rights reserved.