TAP/Southern Corridor and Greece: National and Regional Implications

12

TAP/SOUTHERN CORRIDOR AND GREECE: NATIONAL AND REGIONAL IMPLICATIONS THANOS DOKOS DIRECTOR, HELLENIC FOUNDATION FOR EUROPEAN & FOREIGN POLICY (ELIAMEP) THEODORE TSAKIRIS HEAD, THE ENERGY PROGRAMME ELIAMEP ASSISTANT PROFESSOR FOR GEOPOLITICS & HYDROCARBONS, UNIVERSITY OF NICOSIA 102 THANOS DOKOS, THEODORE TSAKIRIS

-

Upload

independent -

Category

Documents

-

view

5 -

download

0

Transcript of TAP/Southern Corridor and Greece: National and Regional Implications

TAP/SOUTHERN CORRIDOR AND GREECE:

NATIONAL AND REGIONAL IMPLICATIONS

THANOS DOKOS

DIRECTOR, HELLENIC FOUNDATION FOR EUROPEAN & FOREIGN POLICY (ELIAMEP)

THEODORE TSAKIRIS

HEAD, THE ENERGY PROGRAMME ELIAMEP ASSISTANT PROFESSOR FOR GEOPOLITICS & HYDROCARBONS,

UNIVERSITY OF NICOSIA

102

THAN

OS D

OKOS

, TH

EODO

RE T

SAKI

RIS

The Trans Adriatic Pipeline (TAP), which will transport natural gas from Azerbaijan

to Italy via Greece and Albania, will contribute to European energy security.

The global energy landscape is changing, shaped by shifting pat-terns of demand, new reserves entering the production stage (in-cluding, of course, the “shale gas revolution” in the U.S.), new players, alignments and evolving rules. Natu-ral and man-made disasters (such as Fukushima), the EU economic crisis and geopolitical crises in Ukraine, Libya, Nigeria and Iraq also continue to influence the energy sector and the global economy in key ways.

The question of European energy security and the need to diversify Europe’s natural gas suppliers fo-cused attention on the strategic sig-nificance of Southeastern Europe as a transport hub for natural gas from the Caspian region, and potentially the Eastern Mediterranean. In or-der to meet increasing natural gas demand and reduce East and South East Europe’s high levels of energy dependency on a single exporter, namely Russia, European authori-ties have been keen to promote pro-jects that contribute to supply diver-sification.1

In this context, the Southern Gas Corridor has an important role. The

Trans Adriatic Pipeline (TAP), which will transport natural gas from Azer-baijan to Italy via Greece and Albania, will contribute to European energy security as well as providing a major boost for Greece’s economy, regional standing and ability to emerge as a leading transit hub on a Southern-Northern Axis. The combination of TAP with a series of interconnecting pipelines linking the Aegean with the Baltic Sea, starting with Inter-connector Greece-Bulgaria (IGB), will be key.

Europe’s Southern Gas Corridor Strategy is based on the need to maximize imports of non-Russian gas via non-Russian controlled terri-tory, so as to establish a third, follow-ing Russia, Norway and Northern Af-rica (Algeria, Libya, Egypt), route of supply diversification. As potential sources of supply for the Southern Gas Corridor, the European Com-mission has recognised not only Caspian (Azerbaijan) and Central Asian gas (Uzbekistan, Kazakhstan and primarily Turkmenistan) but also Middle Eastern gas from Iraq’s future production as well as from the potential expansion of Egyptian net exports, although the political

1. EU’s primary energy security goals should be to reduce the strategic dependence of individual Member-States on single external suppliers and to ensure that energy markets are liquid, open and functioning according to stable market rules rather than power logics. Of course, energy security needs also needs to be balanced against environmental and economic competitiveness concerns. (Dreyer & Stang, EU-ISS, p. 5)

103

CASPIAN REPORT, FALL 2014

instability which has plagued Iraq, Syria and Egypt has suspended their export potential in the short to me-dium-term.2

Any discussion of the TAP (which won the tender to transport Azerbai-jani gas to Europe via Turkey) and Trans Anatolian Natural Gas Pipe-line (TANAP) requires an analysis of the geopolitical environment which

– to a large extent - determined its eventual selection. The examination of the geopolitical underpinnings of TAP and its sister project TANAP

along with their impact on the re-gional balance of power is important for three principal reasons:

i. The region these pipelines will have to cross in order to connect the upstream producer (currently Azerbaijan, and in the longer term Iraq and/or Turkmenistan) with the main transit states (Georgia and Turkey) and finally the consumers in South East and Central Europe suf-fers from endemic instability. The attendant threat primarily relates to the possibility of disrupting the flow of natural gas through these pipe-lines after they are constructed. For instance, this affected Azerbaijani

exports to Turkey during the 2008 Russian-Georgian War.3

ii. The region’s net energy export-ers attribute an important geopo-litical significance to their oil and gas exports. These exports not only represent an important financial transaction which accounts for a major component of their respec-tive GDPs and budgetary revenues;4 they also represent a declaration of diplomatic intent, a marker geopo-litical orientation and an extension of its foreign policy. For Azerbaijan, the principal (if not sole) arbiter of the Southern Gas Corridor Strategy, energy export policy is “a means of consolidating its sovereignty”, ac-cording to Dr. Elhur Soltanov of Azerbaijan’s Diplomatic Academy.5

iii: The geopolitical notion of ener-gy trade as a component of foreign policy and national empowerment is not exclusive to the producing or ex-porting states. Several of the poten-tial transiting states, namely Georgia, Turkey, Greece, and even Albania, do not only want to secure stable and affordable natural gas supplies. They want to see diplomatic gains through the transit of these supplies through their own territory, for rea-sons that go beyond their immediate energy needs. In the case of Albania, for instance, those needs are practi-cally non-existent since the coun-try’s natural gas consumption is ex-tremely low.

THE GEOPOLITICAL NOTION OF ENERGY TRADE

AS A COMPONENT OF FOREIGN POLICY AND

NATIONAL EMPOWERMENT IS NOT EXCLUSIVE TO

THE PRODUCING OR EXPORTING STATES.

2. See inter alia, Gulmira Rzayeva & Theodoros Tsakiris, Strategic Imperative: Azerbaijani Gas Strategy and the EU’s Southern Corridor, SAM Center for Strategic Studies under the President of Azerbaijan, SAM Review #5, (Baku: June 2012), pp.6-13.

3. The flow of gas continued through the Turkish component of the South Caucasus Gas Pipeline that links Baku and Erzurum via Tbilisi. “BP: Gas Still Flowing on the Turkish Side of the South Caucasus Pipe”, DowJones, 12/08/2008.

4. In 2010, oil & gas exports amounted to 90% of Azeri exports that according to the CIA World Fact Book (updated to 12/07/2011) amounted to approximately $28,07 billion compared to a state budget of $28,83 billion in 2010. https://www.cia.gov/library/publications/the-world-factbook/geos/aj.html

5. Elhur Soltanov, Azerbaijan’s Energy Policy: Balancing North and East, Going West, paper presented at IENE’s 5th South East Europe Energy Dialogue, (Thessaloniki: 2-3 June 2011), p.2.

104

THAN

OS D

OKOS

, TH

EODO

RE T

SAKI

RIS

GREECE’S NATURAL GAS MARKET: FINANCIAL AND STRATEGIC CONSIDERATIONS

In order to understand the impact of TAP for the Greek energy strategy, it is necessary to first summarise the main challenges and characteristics of the domestic natural gas mar-ket, its main players and the way in which TAP connects to the country’s broader foreign energy policy of Greece, and in particular its ambi-tious “pipeline diplomacy.”

Greece is one of Europe’s most im-port dependent countries, with virtually no domestic oil or natural gas production. Although oil (52%) and gas (12%) correspond to almost 2/3 of the country’s Total Primary Energy Supply (TPES), oil and gas imports cover around 99% of final demand.6

Despite significant reserves of coal/lignite, which support the bulk of

national electricity production, there has not been any substantial new investment in increasing do-mestic reserves. This is no accident. Pushed by successive EU Environ-mental Regulations and Directives including the ECTS (European Car-bon Trading System) since the mid-1990s, Greece has been forced to move away from its most abundant, affordable and readily available do-mestic energy resource.

As a result, the country remained a net importer of electricity for around 3.5% of its needs in 2012, although imports dramatically in-creased during the first 7 months of 2014 in comparison to the same period the previous year. In July 2014, imports covered around 20% of Greece’s electricity demand. Ac-cording to ADMIE, the Independ-ent Transmission System Operator (TSO), the rise in imports replaced a sharp decline in lignite production

6. All energy graphs have been created based on data from the latest IEA Review of Greece’s energy policy. International Energy Agency, Energy Policies of IEA Countries: Greece 2011 Review, Paris (OECD: 2011).

105

CASPIAN REPORT, FALL 2014

that now covers around 50% of the electricity mix, down from 54% in 2012.7

Natural gas has been a relative late-comer to the Greek energy supply mix. It was not until 1995 it was introduced as a means of reducing the negative environmental impact of lignite-based electricity genera-tion and to replace the use of fuel oil for domestic and industrial heating. The “gasification” of Greece’s econ-omy, household energy consump-tion and industrial production has progressed rapidly since the early 2000s, with demand almost dou-bling from 2.4 billion cubic meters (bcm) in 2003 to an all time high of 4.4 bcm in 2011.8 The rise in natural gas imports displaced oil consump-tion significantly and constitutes the main reason behind the reduction of oil’s share in Greece’s TPES, from around 60% in 2004 to around 50% today.

In late 1995, natural gas made up just 0.6% of TPES, but now covers 12%. In 2004 its share of the domes-tic energy “pie” was limited to 6.8%. Gas demand increased by 10% an-nually from 2002-2008, driven by electricity generation that accounts for 64% of consumption. Electric-ity will remain the main driver of demand, equal to 68% of consump-tion in 2015 and 61% in 2020, as an increasing number of older PPC-owned lignite-fired electric-ity generation stations (i.e. Aliveri, Megalopoli) are retrofitted to run on natural gas while a number of new gas-fired stations are constructed

primarily by Independent (private) Power Producers (IPPs). These in-clude Protergia (Mytilineos Group), TERNA and the ELPEdison joint ven-ture between Edison and Hellenic Petroleum.9

Together with the economic reces-sion from 2010, the introduction of higher natural gas taxes has cur-tailed demand. It dropped to a low of 3.6 bcm in 2013, a 11.5% reduction compared to 2012. Projections of fu-ture demand vary between market participants but the general con-sensus is that the gradual recovery of the domestic economy combined with the continued pressure to move away from lignite will create condi-tions or relative demand inelasticity for natural gas in the medium-term. This translates to a mean projected demand of approximately 7 bcm by 2020. The 2012 projection by DEPA (the Greek Public Gas Company) of a 9,3 bcm consumption level in 2020 seems to be inflated, and is not shared by other market participants or the country’s Regulatory Author-ity for Energy (RAE). In its latest annual report to the European Com-mission (October 2013), RAE’s esti-mates are closer to DESFA’s revised projection of a final demand rate of 5.88 bcm in 2020, which is consider-ably more realistic.10

In spite of the increasing impor-tance of natural gas for the country’s energy security and the absence of domestic production, Greek energy policy has been relatively success-ful in consolidating the diversifica-tion of its import dependency. As

7. http://www.energia.gr/article.asp?art_id=84558. According to Greece’s RAE net electricity imports in 2012 accounted for merely 3,5% of demand with coal/lignite covering for 54% of electricity generation. Regulatory Authority for Energy/RAE, 2013 National Report to the European Commission, (Athens: October 2013), p.70

8. BP Statistical Review of World Energy 2014, p.23.

9. IEA, Greece Energy Review 2011, ibid, p.111-113. PPC or DEH in Greek is the largest quasi-monopolistic electricity producer of Greece that is largely controlled by the Greek state.

10. Regulatory Authority for Energy/RAE, 2013 National Report to the European Commission, (Athens: October 2013), pp.86-87.

106

THAN

OS D

OKOS

, TH

EODO

RE T

SAKI

RIS

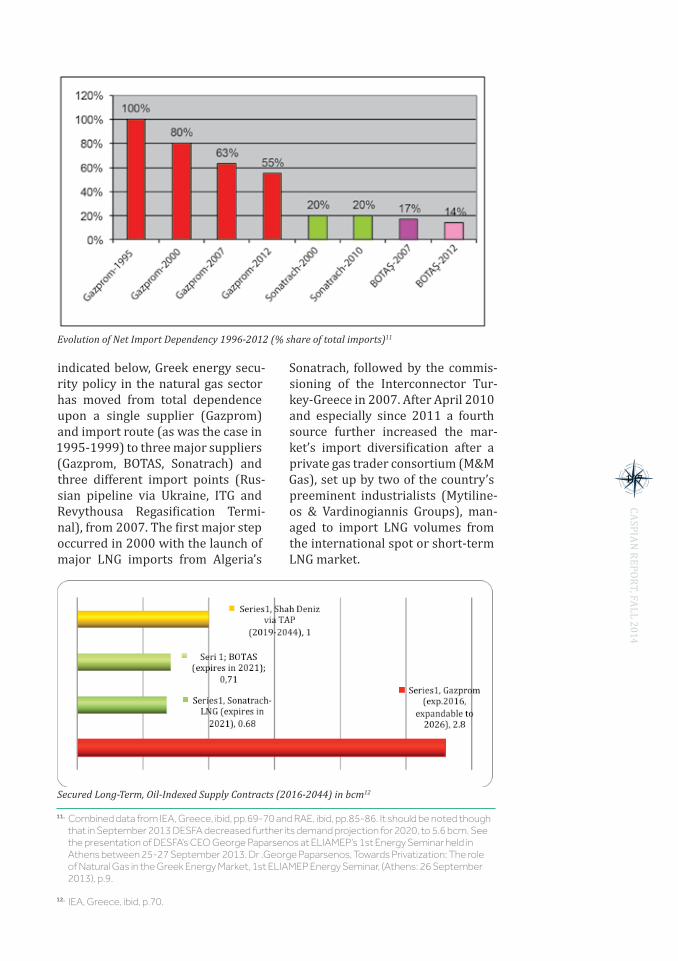

indicated below, Greek energy secu-rity policy in the natural gas sector has moved from total dependence upon a single supplier (Gazprom) and import route (as was the case in 1995-1999) to three major suppliers (Gazprom, BOTAS, Sonatrach) and three different import points (Rus-sian pipeline via Ukraine, ITG and Revythousa Regasification Termi-nal), from 2007. The first major step occurred in 2000 with the launch of major LNG imports from Algeria’s

Sonatrach, followed by the commis-sioning of the Interconnector Tur-key-Greece in 2007. After April 2010 and especially since 2011 a fourth source further increased the mar-ket’s import diversification after a private gas trader consortium (M&M Gas), set up by two of the country’s preeminent industrialists (Mytiline-os & Vardinogiannis Groups), man-aged to import LNG volumes from the international spot or short-term LNG market.

11. Combined data from IEA, Greece, ibid, pp.69-70 and RAE, ibid, pp.85-86. It should be noted though that in September 2013 DESFA decreased further its demand projection for 2020, to 5.6 bcm. See the presentation of DESFA’s CEO George Paparsenos at ELIAMEP’s 1st Energy Seminar held in Athens between 25-27 September 2013. Dr .George Paparsenos, Towards Privatization: The role of Natural Gas in the Greek Energy Market, 1st ELIAMEP Energy Seminar, (Athens: 26 September 2013), p.9.

12. IEA, Greece, ibid, p.70.

Evolution of Net Import Dependency 1996-2012 (% share of total imports)11

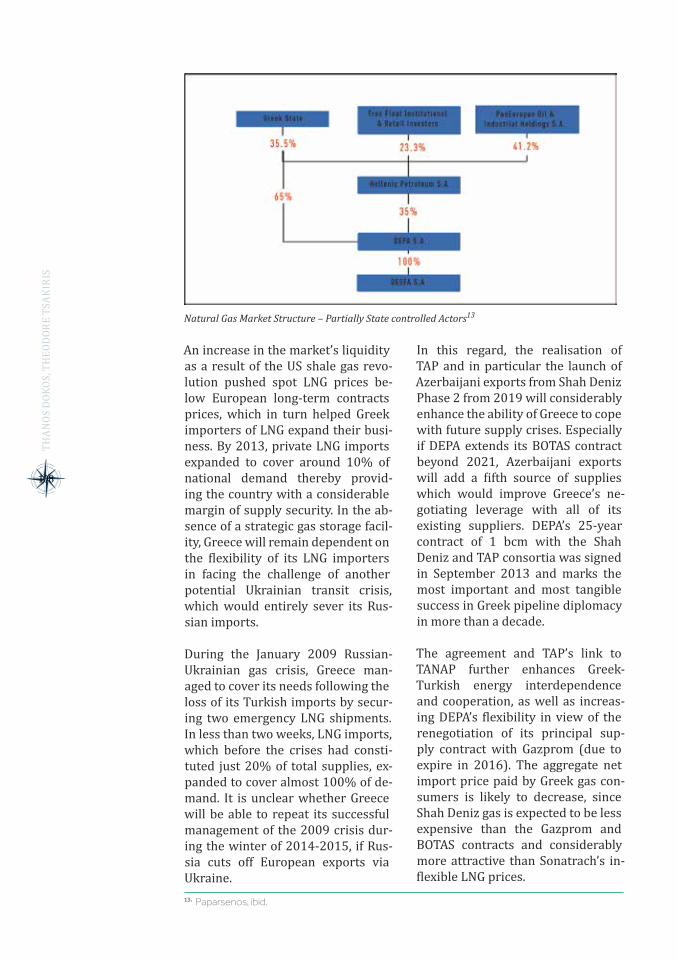

Secured Long-Term, Oil-Indexed Supply Contracts (2016-2044) in bcm12

107

CASPIAN REPORT, FALL 2014

An increase in the market’s liquidity as a result of the US shale gas revo-lution pushed spot LNG prices be-low European long-term contracts prices, which in turn helped Greek importers of LNG expand their busi-ness. By 2013, private LNG imports expanded to cover around 10% of national demand thereby provid-ing the country with a considerable margin of supply security. In the ab-sence of a strategic gas storage facil-ity, Greece will remain dependent on the flexibility of its LNG importers in facing the challenge of another potential Ukrainian transit crisis, which would entirely sever its Rus-sian imports.

During the January 2009 Russian-Ukrainian gas crisis, Greece man-aged to cover its needs following the loss of its Turkish imports by secur-ing two emergency LNG shipments. In less than two weeks, LNG imports, which before the crises had consti-tuted just 20% of total supplies, ex-panded to cover almost 100% of de-mand. It is unclear whether Greece will be able to repeat its successful management of the 2009 crisis dur-ing the winter of 2014-2015, if Rus-sia cuts off European exports via Ukraine.

In this regard, the realisation of TAP and in particular the launch of Azerbaijani exports from Shah Deniz Phase 2 from 2019 will considerably enhance the ability of Greece to cope with future supply crises. Especially if DEPA extends its BOTAS contract beyond 2021, Azerbaijani exports will add a fifth source of supplies which would improve Greece’s ne-gotiating leverage with all of its existing suppliers. DEPA’s 25-year contract of 1 bcm with the Shah Deniz and TAP consortia was signed in September 2013 and marks the most important and most tangible success in Greek pipeline diplomacy in more than a decade.

The agreement and TAP’s link to TANAP further enhances Greek-Turkish energy interdependence and cooperation, as well as increas-ing DEPA’s flexibility in view of the renegotiation of its principal sup-ply contract with Gazprom (due to expire in 2016). The aggregate net import price paid by Greek gas con-sumers is likely to decrease, since Shah Deniz gas is expected to be less expensive than the Gazprom and BOTAS contracts and considerably more attractive than Sonatrach’s in-flexible LNG prices.

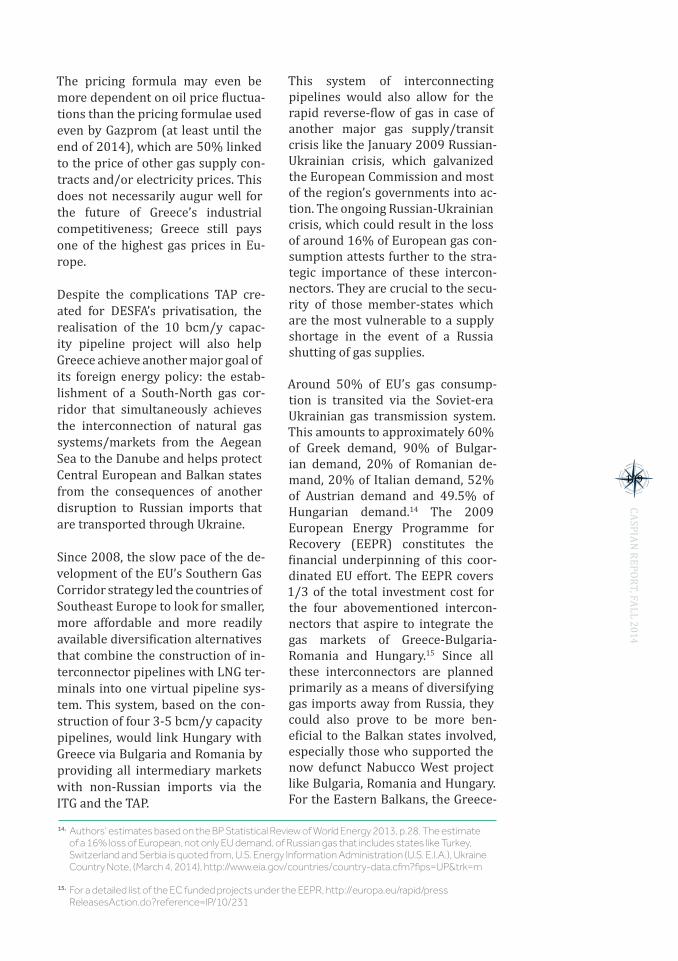

Natural Gas Market Structure – Partially State controlled Actors13

13. Paparsenos, ibid.

108

THAN

OS D

OKOS

, TH

EODO

RE T

SAKI

RIS

The pricing formula may even be more dependent on oil price fluctua-tions than the pricing formulae used even by Gazprom (at least until the end of 2014), which are 50% linked to the price of other gas supply con-tracts and/or electricity prices. This does not necessarily augur well for the future of Greece’s industrial competitiveness; Greece still pays one of the highest gas prices in Eu-rope.

Despite the complications TAP cre-ated for DESFA’s privatisation, the realisation of the 10 bcm/y capac-ity pipeline project will also help Greece achieve another major goal of its foreign energy policy: the estab-lishment of a South-North gas cor-ridor that simultaneously achieves the interconnection of natural gas systems/markets from the Aegean Sea to the Danube and helps protect Central European and Balkan states from the consequences of another disruption to Russian imports that are transported through Ukraine.

Since 2008, the slow pace of the de-velopment of the EU’s Southern Gas Corridor strategy led the countries of Southeast Europe to look for smaller, more affordable and more readily available diversification alternatives that combine the construction of in-terconnector pipelines with LNG ter-minals into one virtual pipeline sys-tem. This system, based on the con-struction of four 3-5 bcm/y capacity pipelines, would link Hungary with Greece via Bulgaria and Romania by providing all intermediary markets with non-Russian imports via the ITG and the TAP.

This system of interconnecting pipelines would also allow for the rapid reverse-flow of gas in case of another major gas supply/transit crisis like the January 2009 Russian-Ukrainian crisis, which galvanized the European Commission and most of the region’s governments into ac-tion. The ongoing Russian-Ukrainian crisis, which could result in the loss of around 16% of European gas con-sumption attests further to the stra-tegic importance of these intercon-nectors. They are crucial to the secu-rity of those member-states which are the most vulnerable to a supply shortage in the event of a Russia shutting of gas supplies.

Around 50% of EU’s gas consump-tion is transited via the Soviet-era Ukrainian gas transmission system. This amounts to approximately 60% of Greek demand, 90% of Bulgar-ian demand, 20% of Romanian de-mand, 20% of Italian demand, 52% of Austrian demand and 49.5% of Hungarian demand.14 The 2009 European Energy Programme for Recovery (EEPR) constitutes the financial underpinning of this coor-dinated EU effort. The EEPR covers 1/3 of the total investment cost for the four abovementioned intercon-nectors that aspire to integrate the gas markets of Greece-Bulgaria-Romania and Hungary.15 Since all these interconnectors are planned primarily as a means of diversifying gas imports away from Russia, they could also prove to be more ben-eficial to the Balkan states involved, especially those who supported the now defunct Nabucco West project like Bulgaria, Romania and Hungary. For the Eastern Balkans, the Greece-

14. Authors’ estimates based on the BP Statistical Review of World Energy 2013, p.28. The estimate of a 16% loss of European, not only EU demand, of Russian gas that includes states like Turkey, Switzerland and Serbia is quoted from, U.S. Energy Information Administration (U.S. E.I.A.), Ukraine Country Note, (March 4, 2014), http://www.eia.gov/countries/country-data.cfm?fips=UP&trk=m

15. For a detailed list of the EC funded projects under the EEPR, http://europa.eu/rapid/press ReleasesAction.do?reference=IP/10/231

109

CASPIAN REPORT, FALL 2014

Bulgaria Gas Interconnector (IGB) constitutes the first and most crucial link of this network.

The IGB would run for around 20-25 km in Greece, connecting the north-western city of Komotini with Bulgaria’s central city of Stara Zagora. The EEPR has earmarked €45 million for this project, which could be completed within 18-24 months from the beginning of its construction (originally scheduled to start in March 2012. Bulgaria’s state-controlled Bulgargaz signed a 1 bcm control with the Shan Deniz partners in September 2013; TAP may serve as a catalyst for the IGB, which has been plagued by the pro-crastination of the former Bulgarian government.

It is through IGB and its connection with TAP that Greece can also start offer its north-eastern European neighbours the transit security that Nabucco failed to deliver. As of mid-2014, the only missing parts of the puzzle were Bulgaria’s interconnec-tors with Romania (IBR) and Greece

(IGB), although the IBR was finally constructed in March 2014. The pipeline was expected to be commis-sioned in June 2014. The selection of TAP over Nabucco in June 2013 fa-cilitated the completion of Greece’s Eastern Balkans pipeline strategy, by creating a major impetus for Bul-garia to complete IGB by 2016, three years after its original timetable. As of August 2014, work on IGB has not even started, but DEPA believes that the pipeline will be commissioned within 2016.16

GREEK FOREIGN POLICY AND ENERGY

Even before the current crisis, Greece was consistently punching below its weight on most foreign and security policy issues, allow-ing itself to lose some of its regional influence in Southeastern Europe and letting its active role inside the European Union to atrophy. An in-ward looking and passive foreign policy led to very few foreign policy initiatives. The government failed to take advantage of opportunities for

16. “Bulgaria-Romania Gas Grid Interconnection to Become Functional in June”, Sofia News Agency, 26/03/2014, http://www.novinite.com/articles/159264

110

THAN

OS D

OKOS

, TH

EODO

RE T

SAKI

RIS

multilateral initiatives or to estab-lish tactical and strategic alliances. Now Greek foreign policy needs to recalibrate in response to a chang-ing regional and global security and economic environment, and sup-port to the national effort to re-build the economy; furthermore it must achieve that goal with limited re-sources and under time pressure.

Energy-related projects can be in-strumental in Greece’s effort to re-pair its image, regain a leading role in the region, increase its influence, accumulate ‘diplomatic capital’, and boost economic growth in the me-dium- to long-term. In addition to TAP, Greece should try to enlarge its footprint in the energy map through other projects, including South Stream, as well as the exploitation of potential hydrocarbons deposits in various parts of the country, notably in Western Greece and the maritime areas to the southeast of Crete.

While Greece should intensify its diplomatic efforts toward the de-limitation of its exclusive economic zone (EEZ) and other maritime zones with neighbouring countries according to the provisions of the United Nations Convention on the Law of the Sea UNCLOS, this should not unduly delay efforts to exploit natural resources in the aforemen-tioned areas. In the context of its deep economic and political crisis, Greece went through a phase of hy-drocarbon hysteria, where the Greek people, exhausted by the austerity policies, were looking for a magic formula, an easy way out of the eco-nomic crisis: energy resources fit the description perfectly.

There are now more realistic pub-lic expectations and the Greek gov-ernment has taken the necessary preliminary steps for research and exploitation of hydrocarbons by ten-

dering exploration and production licenses in three areas in Western Greece (February 2012 - July 2013). It is preparing to issue a mega-ten-der for 20 offshore blocks which cover an area of 220,000 km2 span-ning from the north of Corfu to the south-eastern part of Crete, possibly before the end of 2014.

Although there have been no official statements or documents outlining a comprehensive Greek hydrocar-bons exploration policy, looking at the Greek debate it is possible to present a basic outline:

First, Greece does not wish to test its relations with neighbouring countries. Athens needs stability on the foreign policy front to facilitate recovery from the economic cri-sis. This is not suggest that Greece would not react to a move by an-other side attempting to change the bilateral status quo. Greece will play strictly by the international rules of the law of the sea, and that will in-clude bilateral consultations with other countries with which Greece shares maritime zones. Talks are under way with Egypt, Albania and Libya, although the domestic situa-tion in that country is rather chaotic, leaving very little room for substan-tive negotiations.

It is not clear whether such talks will take place anytime soon with Turkey, despite the fact that there have been more than 60 rounds of high-level consultations between diplomats. Although it appears reasonable to

IT IS THROUGH IGB AND ITS CONNECTION WITH

TAP THAT GREECE CAN ALSO START OFFER ITS

NORTH-EASTERN EUROPEAN NEIGHBOURS THE

TRANSIT SECURITY THAT NABUCCO FAILED TO

DELIVER.

111

CASPIAN REPORT, FALL 2014

assume that all the main ideas, op-tions and scenarios for addressing bilateral issues have been discussed in the context of such deliberations, Turkey has adamantly opposed any discussion of the delimitation of the respective exclusive economic zones of the two countries. Furthermore, both sides currently have other do-mestic and foreign policy priorities (especially in view of the arc of crisis extending from Ukraine to Mashrek and the Persian Gulf). Moreover, the relative stability and predictabil-ity of their bilateral relations allow them to put the resolution of bilat-eral differences on the back burner. It should be noted, though, that Tur-key’s non-recognition of the Repub-lic of Cyprus - whose EEZ borders the respective zones of both Turkey and Greece - seriously complicates the situation.

Second, the importance of potential hydrocarbon deposits for economic recovery and national energy se-curity in the minds of Greek deci-sion-makers cannot be emphasised enough. Greece will claim any sub-stantial deposits in her maritime zones, as defined by the interna-tional law of the sea. No Greek gov-ernment - irrespective of ideological orientation -can afford to neglect that course of action. To achieve that goal, Greece will use a variety of po-litical and diplomatic means, includ-ing cooperation with countries and companies with similar interests. In this context, the concept of common EU maritime policy and maritime zones will also be used, despite its (currently) largely symbolic value.

But Greece will also emphasise the importance of potential hydrocar-bon discoveries for European energy security, along with the existing and possible new discoveries in the EEZs of Cyprus and Israel.

Third, problems with neighbouring countries around the exploration of hydrocarbons may only arise if substantial deposits are discovered in disputed areas. Even then, how-ever, the international law of the sea offers mutually satisfactory solu-tions, and more importantly, allow them to sell such an agreement to their respective publics. A necessary precondition would of course be relevant political will and the adher-ence to UNCLOS. Greece may not, in principle, be opposed to “win-win” solutions, even including joint ex-ploitation of resources, provided, of course, that issues of borders and ownership have been settled in ad-vance.

In addition, Greece will likely try to enlarge its footprint on the energy map through other projects, in ad-dition to the exploitation of poten-tial hydrocarbons deposits in vari-ous parts of the country, notably in Western Greece and the maritime areas south of Crete. In a difficult pe-riod for Greece, such energy projects provide an excellent opportunity for diplomatic and economic gains.

EASTERN MEDITERRANEAN HYDROCARBONS

The discovery of significant natural gas deposits in the exclusive eco-nomic zones of Israel and Cyprus and the prospective deposits of the Levant Basin may provide an ad-ditional energy source outside the former Soviet space and the Middle East proper, thereby contributing to the diversification of Europe’s natural gas supplies. Although the

E N E R GY- R E L AT E D P ROJ E CTS C A N B E

INSTRUMENTAL IN GREECE’S EFFORT TO REPAIR

ITS IMAGE, REGAIN A LEADING ROLE IN THE

REGION, INCREASE ITS INFLUENCE, ACCUMULATE

‘DIPLOMATIC CAPITAL’, AND BOOST ECONOMIC

GROWTH IN THE MEDIUM- TO LONG-TERM.

112

THAN

OS D

OKOS

, TH

EODO

RE T

SAKI

RIS

deposits discovered so far in Cyprus and Israel are not expected to have a transformative effect on Europe’s energy situation, they can hardly be ignored as long as Europe contin-ues to voice concerns about its en-ergy security (and especially given the ongoing crisis in Ukraine). In any case, the picture may change as there are additional exploratory ef-forts under way in Cyprus, Israel and Greece.

Although Greece is not a central player in this energy-focused power game, it is more than just an inter-ested party. Cyprus and especially Israel will, of course, make the key decisions regarding energy mat-ters in the Eastern Mediterranean as they own the resources. Greece, on the other hand, is not a produc-er. Though that may change in due course, there is no certainty. For the time being it can only hope to be a transit country. The economic stakes will be high if the choice for an export route is an LNG plant, as there are several Greek ship owners that have invested heavily in LNG carriers.

In addition, LNG terminals, either the existing one in Revythousa,

near Athens, or the planned ones in Northern Greece may become part of an natural gas network that will link with a number of Balkan and Central European interconnec-tors, thereby making a substantial contribution to the energy security of countries like Bulgaria, Hungary, Slovakia and Austria. Finally, if tech-nological and financial conditions allow and if more reserves are con-firmed, Greece could also benefit through the construction of a pipe-line (East Mediterranean Gas Cor-ridor) to transport natural gas from the Israeli and Cypriot deposits in the Eastern Mediterranean through Greece to Western European mar-kets, especially if combined with prospective Greek hydrocarbons production.

113

CASPIAN REPORT, FALL 2014

![“Yunanistan” [Greece]](https://static.fdokumen.com/doc/165x107/63250e4a85efe380f30680d9/yunanistan-greece.jpg)