State of Mineral Finance: - PDAC

40

State of Mineral Finance: 2015 – Déjà Vu Written by: Samad Uddin M.Sc. Director, Capital Markets, PDAC Published on: March 1, 2015 Email: [email protected]

-

Upload

khangminh22 -

Category

Documents

-

view

4 -

download

0

Transcript of State of Mineral Finance: - PDAC

0 State of Mineral Finance 2015

March 1, 2015

State of Mineral Finance: 2015 – Déjà Vu

Written by: Samad Uddin M.Sc.

Director, Capital Markets, PDAC

Published on: March 1, 2015

Email: [email protected]

1 State of Mineral Finance 2015

March 1, 2015

2 State of Mineral Finance 2015

March 1, 2015

Executive Summary

2015 is expected to be another challenging year for the exploration industry. 2014 has been a year

of share consolidations, mergers and acquisitions, delistings from exchanges, weak share prices and

low discovery rates. While the downturn may have bottomed out, the turnaround will likely not

take place until 2016.

The global economy is expected to grow by 3.8% in 2015, 4.0% in 2016 and 4.1% in 2017. Canadian

growth is also expected to be positive - albeit at a slower pace – and is forecasted to grow by 2.4%,

2.4%, and 2.2% respectively. As major economies continue to face uneven growth, metal prices are

expected to face similar prospects driven by anaemic demand. Aluminum is the exception; a robust

17% price increase is expected in the next three years (2015-2017) followed by nickel (up 7.1%), zinc

(up 6.8%) and lead (up 5.5%). Copper prices are projected to remain at their current levels and

uranium is projected to experience a 20% drop over the next three years.

Total financing activity (including debt and equity) across all exchanges in the mining sector has

dropped significantly, falling on average by 13.6% annually since 2007 (for a total decline of over

60% in that period). Majority of the decline was due to a drop in equity financing, which fell by 80%

for the same period. The overall decline in 2014 was not as dramatic, dropping by 1% over 2013

levels, as financing activities start to stabilize. In terms of the number of deals, a total of 2,895

financings were announced globally (2,707 equity, 188 debt). This was a drop from the peak of 3,827

total financings announced in 2007.

On the TSX and TSXV, the share of debt financing came in at 81% (TSX) and 47% (TSXV) respectively

in 2014. As average prices continue to decline – share prices for mining companies on the TSXV

have declined by 83%, from 62 cents in 2007 to 11 cents in 2014 – it is becoming too costly,

restrictive and dilutive to issue equities. Debt issuance is rarely an attractive alternative for most

juniors, as they do not typically have the revenues required.

The largest financings took place during the second quarter of 2014 when a total of $9.7 billion was

raised, $8.9 billion of which was from the TSX and $820 million from the TSXV. In the final quarter of

2014, a total of $5.3 billion was raised for the mining sector (from all Canadian exchanges). The

Venture exchange did manage to improve financing in Q4 2014 compared to Q4 2013, as financing

increased by 14% to $778 million. Despite this improvement, Q4’s result was far lower than the peak

reached in Q2 2007 when a total of $3.2 billion was raised on the TSXV. The corresponding drop in

financings for exploration by issuers listed on Canadian exchanges was far worse, falling off a cliff

from $1.3 billion in Q4 2007 to a low of $150M in Q4 of 2014 (an 88% drop). Looking at yearly

totals, from 2007 to 2014 financing for exploration fell by 91%.

As expected, during this downturn the number of M&A deals increased in 2014 both globally and in

Canada. 62 deals were announced in Canada in 2014 compared to 158 globally. By value, global

M&A activities have fallen since peaking at $64.5 billion in 2012 to $16.7 billion in 2014. The value of

Canadian M&A activities has been steady at around $6 billion between 2012 and 2014.

3 State of Mineral Finance 2015

March 1, 2015

Globally, exploration budgets dropped by 26% in 2014, reflecting weak commodity prices and the

limited prospects for a robust recovery in demand. Canada and Australia continued to be the two

top destinations for exploration, attracting $1.5 billion (13.9%) and $1.3 billion (11.7%) respectively.

Grassroots exploration in Canada fell by 37% between 2013 and 2014, while spending on existing

minesites increased 13.5% and spending on late stage & feasibility fell by 25.5%.

Exploration companies increasingly relied on flow-through shares to raise risk capital, which will

help many companies to hold onto their claims in Canada. The data in this report clearly reveals the

important counter-cyclical role played by flow through during the recent downturn. As overall

financing levels for exploration fell, the proportion of financings using flow-through shares went up.

Flow-through accounted for 72% of all financing raised for exploration stage activities from 2012-

2014, highlighting its importance as an incentive in attracting capital to the riskiest stage of the

mining cycle.

New exemptions along with a cooperative regulatory regime are major changes to the Canadian

regulatory landscape that could have profound impact on the way junior issuers raise capital,

expanding access to a wider pool of investors and potentially reducing the costs of raising capital.

4 State of Mineral Finance 2015

March 1, 2015

Table of Contents

Executive Summary ___________________________________________________________ 2

Table of Contents _____________________________________________________________ 4

Introduction _________________________________________________________________ 6

Sources of Information______________________________________________________________ 6

Assumptions and Limitations _________________________________________________________ 7

SECTION I: The Macroeconomic Environment _______________________________________ 8

Uneven and Feeble Economic Growth _________________________________________________ 8

Weak Commodity Prices ____________________________________________________________ 9

SECTION II: Financing Trends ___________________________________________________ 12

Downturn in Global Financing Trends _________________________________________________ 12

Canadian Financing Levels Bounce at the Bottom _______________________________________ 15

Debt Issuance Increases while Equity Suffers ___________________________________________ 18

Sharp Drop in Canadian Listings _____________________________________________________ 19

Share Prices Reach Bottom _________________________________________________________ 20

Mergers and Acquisitions Increase ___________________________________________________ 21

SECTION III: Exploration Trends _________________________________________________ 23

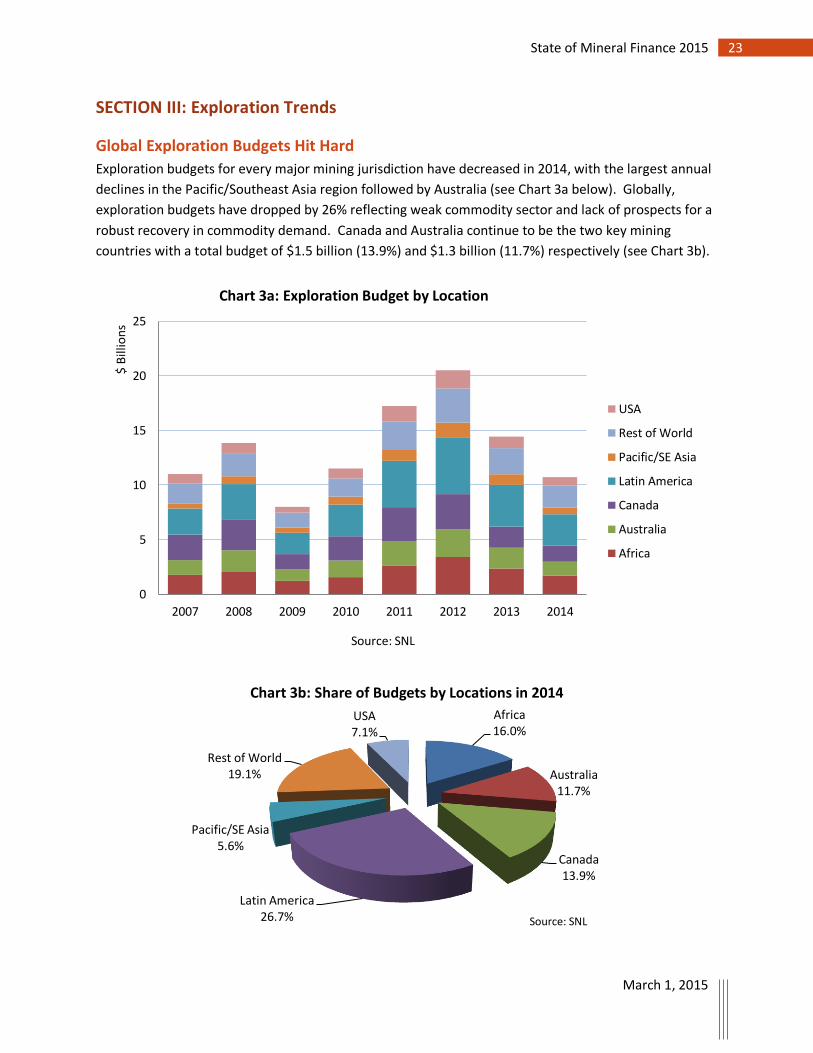

Global Exploration Budgets Hit Hard __________________________________________________ 23

Sharp Drop in Canadian Exploration Budgets ___________________________________________ 25

Capital Raised for Exploration Falls off a Cliff ___________________________________________ 26

Working Capital Turns to Survival Capital ______________________________________________ 27

SECTION IV: Fiscal Support and Capital Market Reform ______________________________ 29

Use of Flow-Through Shares Buffers the fall in Financings _________________________________ 29

Regulatory Developments in Canadian Capital Markets __________________________________ 31

New Exemptions Could Help _______________________________________________________________ 31

Cooperative Capital Market Regulator – A Tool to Harmonize Regulations ___________________________ 33

Looking Ahead ______________________________________________________________ 35

ANNEX A: Supplementary Charts and Tables ______________________________________ 36

5 State of Mineral Finance 2015

March 1, 2015

6 State of Mineral Finance 2015

March 1, 2015

Introduction The Prospectors & Developers Association of Canada (PDAC) has always had a strong interest in the

ability of prospectors and mineral exploration companies (juniors1) to raise capital. In 2012, the PDAC

Board of Directors established a ‘capital crisis committee’ to more closely monitor the financing

activities of publicly listed companies in order to better understand the financing difficulties being faced

by the industry, leading to quarterly reports throughout 2013 and 2014. These reports were prepared

by Michael Doggett of Beach Meadows Resources and can be found on the PDAC website.2

This new report builds on these quarterly reports, and is broken down into five sections:

1) The macroeconomic environment

2) Financing trends

3) Exploration trends

4) Fiscal incentives and capital market reforms

5) Annex

The global macroeconomic focus provides a backdrop of the environment under which the mining

sector is operating in as the health of the macro economy dictates the demand for raw materials driven

by industrial output. This section also includes commodity prices broken down by the major metals, as

prices are a key factor that drives investment into companies specializing in those commodities.

The financing trends and exploration trends are the core of the report. The financing trends section

includes sections on capital raising via debt and equities, number of deals, Canada specific financings,

M&As, market capitalization, trading volumes, listings etc. The exploration trends section includes an

analysis of exploration budgets by region, stages of development and company type, as well as

information on exploration financing. The fourth section provides information on fiscal incentive and

regulatory reforms that have an impact on capital raising. Finally the report provides concluding remarks

about the overall financing environment for juniors with an emphasis on future prospects.

Sources of Information

The report extracts data on mining finance from several standard industry recognized sources. The

definitions used in the report are taken directly from the source and have not been altered by the

1 While there are many factors that, taken together, define a junior exploration company, a key defining

feature is that “it is neither a producing company nor the recipient of significant income from

production or from some other business venture”. See Natural Resources Canada definition here:

http://www.nrcan.gc.ca/mining-materials/statistics/8854.

2 The report can be accessed from the link: http://www.pdac.ca/pdf-viewer?doc=/docs/default-

source/default-document-library/capital-crisis-report-update---q2-report.pdf

7 State of Mineral Finance 2015

March 1, 2015

author. In order to make an unbiased assessment about the sector as a whole the data is not dissected

or adjusted other than computing for exchange rates and indexing. Where such modifications are

made, an explanation with appropriate reference is provided. The report is meant to be as consistent as

possible and, where applicable, further improve the quality of the data and how it is presented.

The data collected in the report is primarily sourced from the following:

- TMX Group’s MiG report

- SNL Metals & Mining

- World Bank’s Commodity Markets Outlook

- International Monetary Fund’s World Economic Outlook

- Gamah International’s Monthly Report on Mining and Exploration Company Financings (MECO)

Additional information is collected from various sources for which the reference is made in the

appropriate text, tables and charts.

Assumptions and Limitations

The time period chosen in this report is meant to show recent trends, in particular, since the 2007-08

financial crisis. This report is not meant to provide a longer term view (prior to 2007) of the financing

trends for the mineral sector or relationships to commodity price cycles. The purpose of the report is to

inform PDAC members on the latest financing developments and to provide a backdrop for policy

advocacy by the PDAC, on behalf of its members.

The data used in the report is considered to be accurate as of February 18, 2015. Assumptions and

estimates used to produce the data are from the sources; any modifications to the data are clearly

outlined in the report. For a full description and explanation of the methodology used to produce this

report, please contact the author, Samad Uddin, at [email protected].

8 State of Mineral Finance 2015

March 1, 2015

SECTION I: The Macroeconomic Environment

Uneven and Feeble Economic Growth

Industrial output is a key factor in determining demand for mineral resources and financing activities.

As economic growth picks up, so does industrial output, which has an impact on commodity prices and

investment in the sector. The commodity growth cycles in the past had a positive correlation with

global economic growth and therefore, keeping the pulse of the economic climate is an important

determinant of future potential for mineral resource development and financing. Countries such as

Canada and Australia that are natural resource endowed benefit as global economic growth picks up;

particularly in countries that are major consumers and net importers of mineral resources.

An important source of information on historical and forecasted economic growth is from the

International Monetary Fund’s (IMF) World Economic Outlook. The IMF in their most recent report3

identified four key areas of development that could impact global economic growth. The first is the low

crude oil price environment, which from a junior exploration company’s perspective, is a positive

development as it reduces operating expenses for remote exploration activities that depend on diesel

generators. However, weak demand for raw materials from major economies, particularly from

emerging economies, is another reason for driving both oil and metal prices lower. Additionally,

countries that depend on investment in the oil and gas sectors lose out on capital spending on major

projects as oil prices drop. For example, integrated oil producer Husky Energy Inc., has announced a cut

to its capital spending by $2 billion for 2015, which will have a direct impact on economic growth in

Western Canada. U.S. now being a major producer of oil will also suffer a similar fate when it comes to

investment in the oil sector.

The second factor is the uneven levels of growth in the major economies. U.S. growth has picked up;

however, other major economies such as Japan are experiencing slowdowns in economic activity.

Without a uniform level of growth amongst major industrialized countries, global growth will not be as

robust as it could have been. The third issue is the appreciation of the U.S. dollar relative to other major

currencies, which could help to offset the impact of lower commodity prices for resource countries

(apart from the U.S.) as most commodities are priced in U.S. dollars. As the U.S. dollar appreciates, the

commodity exporting countries can reduce their losses by benefiting from the stronger U.S. dollar to

buffer their exposure to weak prices. The last factor that could impact economic growth is the increase

in interest rates for many of the emerging economies that are also commodity exporters. Higher

interest rates are not favorable for business as lending costs increase resulting in a slower economic

growth environment than if interest rates were lower.

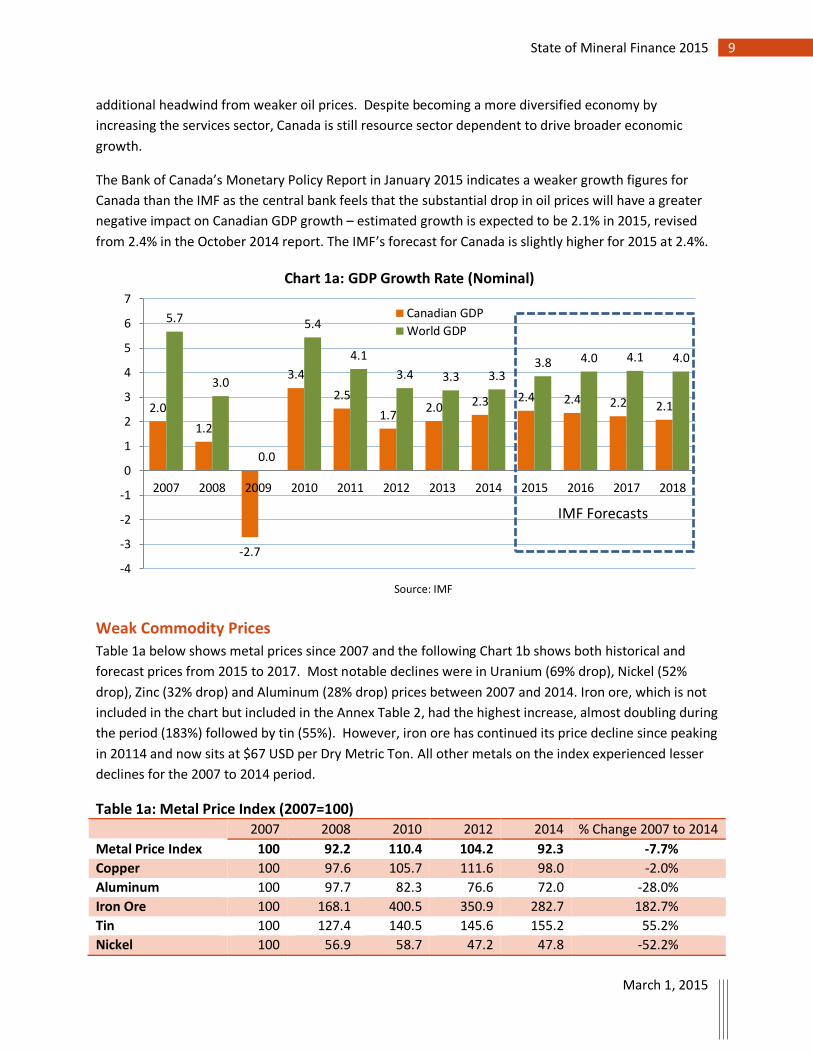

The Chart 1a below provides global GDP forecast and Canada’s growth forecasts. It is not surprising that

Canadian growth is lower than global growth given the weak commodity sector, which is facing

3 IMF World Economic Outlook Update – January 19, 2015

9 State of Mineral Finance 2015

March 1, 2015

additional headwind from weaker oil prices. Despite becoming a more diversified economy by

increasing the services sector, Canada is still resource sector dependent to drive broader economic

growth.

The Bank of Canada’s Monetary Policy Report in January 2015 indicates a weaker growth figures for

Canada than the IMF as the central bank feels that the substantial drop in oil prices will have a greater

negative impact on Canadian GDP growth – estimated growth is expected to be 2.1% in 2015, revised

from 2.4% in the October 2014 report. The IMF’s forecast for Canada is slightly higher for 2015 at 2.4%.

Weak Commodity Prices

Table 1a below shows metal prices since 2007 and the following Chart 1b shows both historical and

forecast prices from 2015 to 2017. Most notable declines were in Uranium (69% drop), Nickel (52%

drop), Zinc (32% drop) and Aluminum (28% drop) prices between 2007 and 2014. Iron ore, which is not

included in the chart but included in the Annex Table 2, had the highest increase, almost doubling during

the period (183%) followed by tin (55%). However, iron ore has continued its price decline since peaking

in 20114 and now sits at $67 USD per Dry Metric Ton. All other metals on the index experienced lesser

declines for the 2007 to 2014 period.

Table 1a: Metal Price Index (2007=100) 2007 2008 2010 2012 2014 % Change 2007 to 2014

Metal Price Index 100 92.2 110.4 104.2 92.3 -7.7%

Copper 100 97.6 105.7 111.6 98.0 -2.0%

Aluminum 100 97.7 82.3 76.6 72.0 -28.0%

Iron Ore 100 168.1 400.5 350.9 282.7 182.7%

Tin 100 127.4 140.5 145.6 155.2 55.2%

Nickel 100 56.9 58.7 47.2 47.8 -52.2%

2.0

1.2

-2.7

3.4

2.5

1.7 2.0 2.3 2.4 2.4 2.2 2.1

5.7

3.0

0.0

5.4

4.1

3.4 3.3 3.3 3.8 4.0 4.1 4.0

-4

-3

-2

-1

0

1

2

3

4

5

6

7

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Source: IMF

Chart 1a: GDP Growth Rate (Nominal)

Canadian GDP

World GDP

IMF Forecasts

10 State of Mineral Finance 2015

March 1, 2015

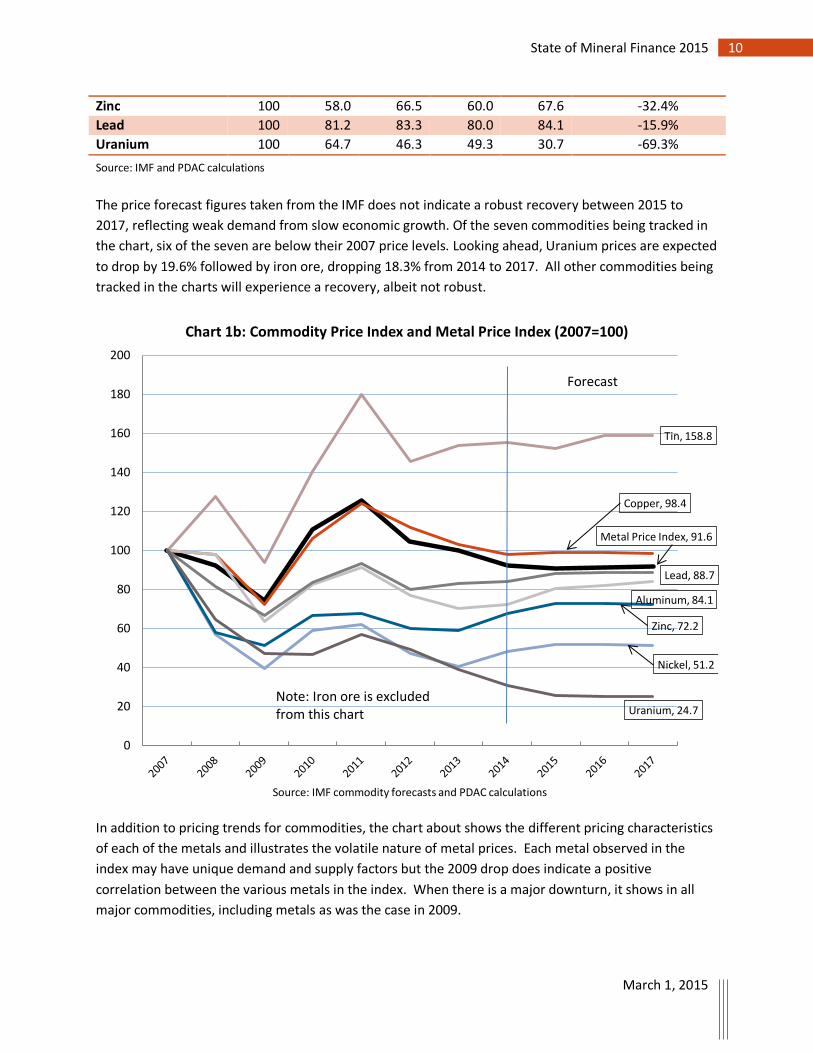

Zinc 100 58.0 66.5 60.0 67.6 -32.4%

Lead 100 81.2 83.3 80.0 84.1 -15.9%

Uranium 100 64.7 46.3 49.3 30.7 -69.3%

Source: IMF and PDAC calculations

The price forecast figures taken from the IMF does not indicate a robust recovery between 2015 to

2017, reflecting weak demand from slow economic growth. Of the seven commodities being tracked in

the chart, six of the seven are below their 2007 price levels. Looking ahead, Uranium prices are expected

to drop by 19.6% followed by iron ore, dropping 18.3% from 2014 to 2017. All other commodities being

tracked in the charts will experience a recovery, albeit not robust.

In addition to pricing trends for commodities, the chart about shows the different pricing characteristics

of each of the metals and illustrates the volatile nature of metal prices. Each metal observed in the

index may have unique demand and supply factors but the 2009 drop does indicate a positive

correlation between the various metals in the index. When there is a major downturn, it shows in all

major commodities, including metals as was the case in 2009.

Metal Price Index, 91.6

Copper, 98.4

Aluminum, 84.1

Tin, 158.8

Nickel, 51.2

Zinc, 72.2

Lead, 88.7

Uranium, 24.7

0

20

40

60

80

100

120

140

160

180

200

Source: IMF commodity forecasts and PDAC calculations

Chart 1b: Commodity Price Index and Metal Price Index (2007=100)

Forecast

Note: Iron ore is excluded from this chart

11 State of Mineral Finance 2015

March 1, 2015

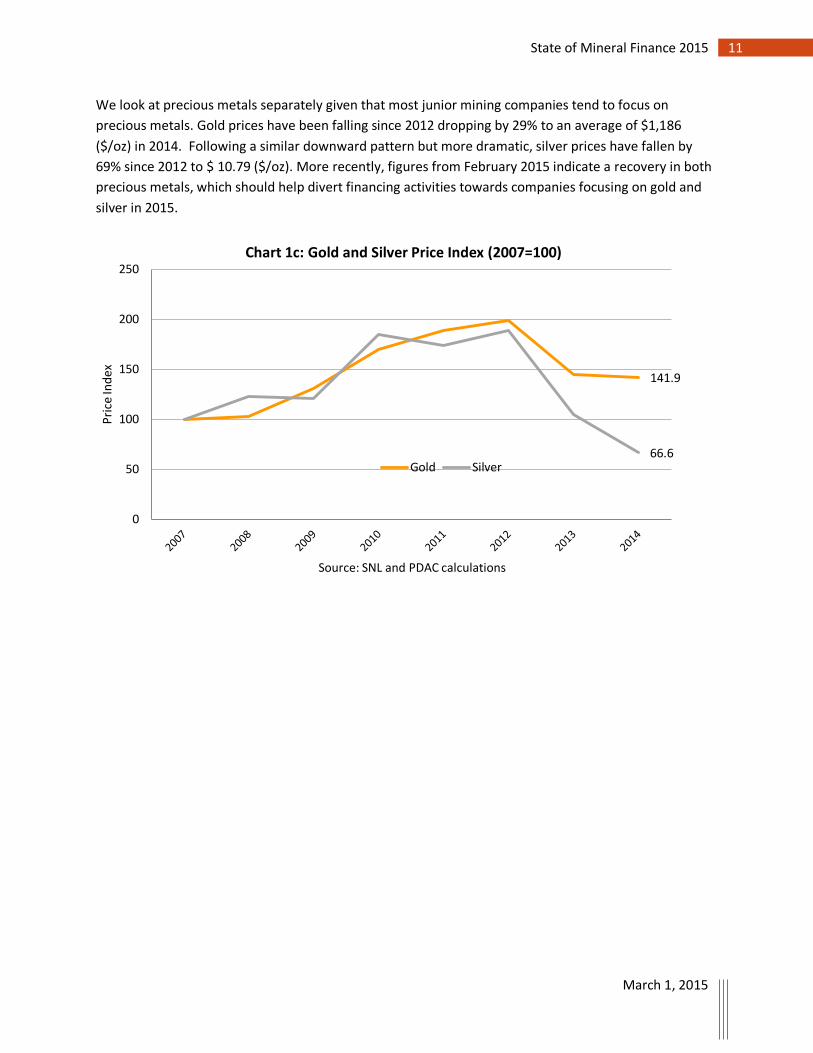

We look at precious metals separately given that most junior mining companies tend to focus on

precious metals. Gold prices have been falling since 2012 dropping by 29% to an average of $1,186

($/oz) in 2014. Following a similar downward pattern but more dramatic, silver prices have fallen by

69% since 2012 to $ 10.79 ($/oz). More recently, figures from February 2015 indicate a recovery in both

precious metals, which should help divert financing activities towards companies focusing on gold and

silver in 2015.

141.9

66.6

0

50

100

150

200

250

Pri

ce In

dex

Source: SNL and PDAC calculations

Chart 1c: Gold and Silver Price Index (2007=100)

Gold Silver

12 State of Mineral Finance 2015

March 1, 2015

SECTION II: Financing Trends

Downturn in Global Financing Trends

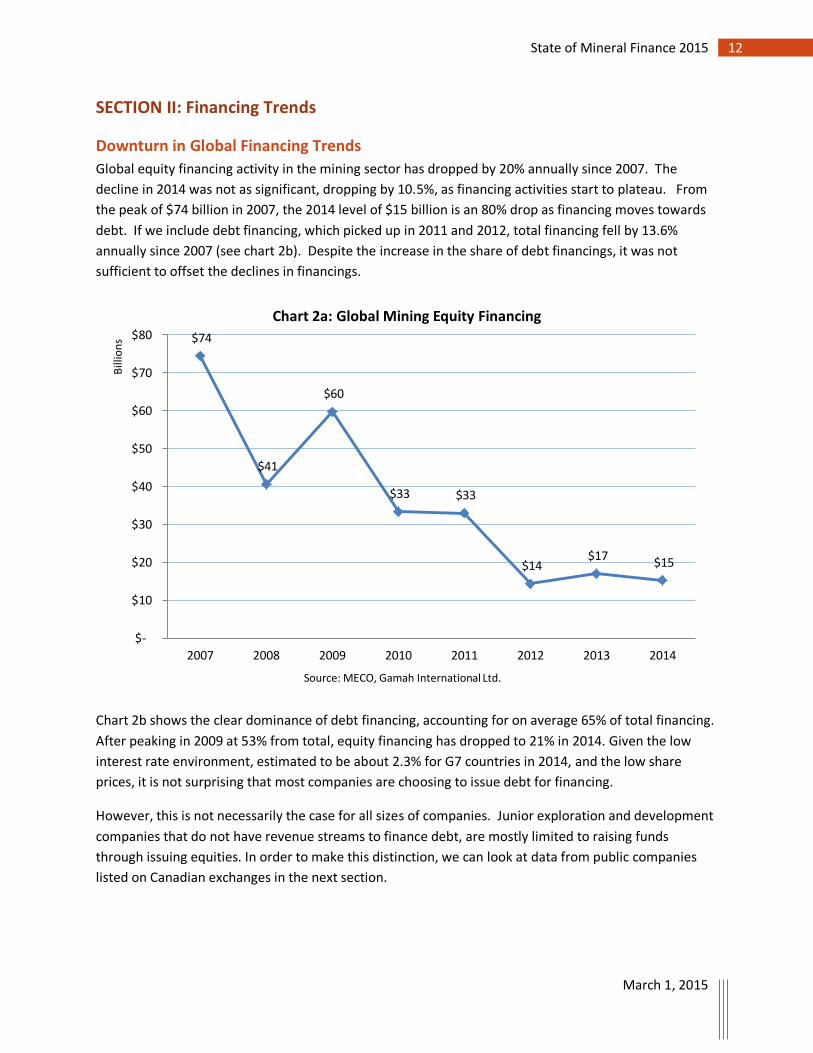

Global equity financing activity in the mining sector has dropped by 20% annually since 2007. The

decline in 2014 was not as significant, dropping by 10.5%, as financing activities start to plateau. From

the peak of $74 billion in 2007, the 2014 level of $15 billion is an 80% drop as financing moves towards

debt. If we include debt financing, which picked up in 2011 and 2012, total financing fell by 13.6%

annually since 2007 (see chart 2b). Despite the increase in the share of debt financings, it was not

sufficient to offset the declines in financings.

Chart 2b shows the clear dominance of debt financing, accounting for on average 65% of total financing.

After peaking in 2009 at 53% from total, equity financing has dropped to 21% in 2014. Given the low

interest rate environment, estimated to be about 2.3% for G7 countries in 2014, and the low share

prices, it is not surprising that most companies are choosing to issue debt for financing.

However, this is not necessarily the case for all sizes of companies. Junior exploration and development

companies that do not have revenue streams to finance debt, are mostly limited to raising funds

through issuing equities. In order to make this distinction, we can look at data from public companies

listed on Canadian exchanges in the next section.

$74

$41

$60

$33 $33

$14 $17

$15

$-

$10

$20

$30

$40

$50

$60

$70

$80

2007 2008 2009 2010 2011 2012 2013 2014

Bill

ion

s

Source: MECO, Gamah International Ltd.

Chart 2a: Global Mining Equity Financing

13 State of Mineral Finance 2015

March 1, 2015

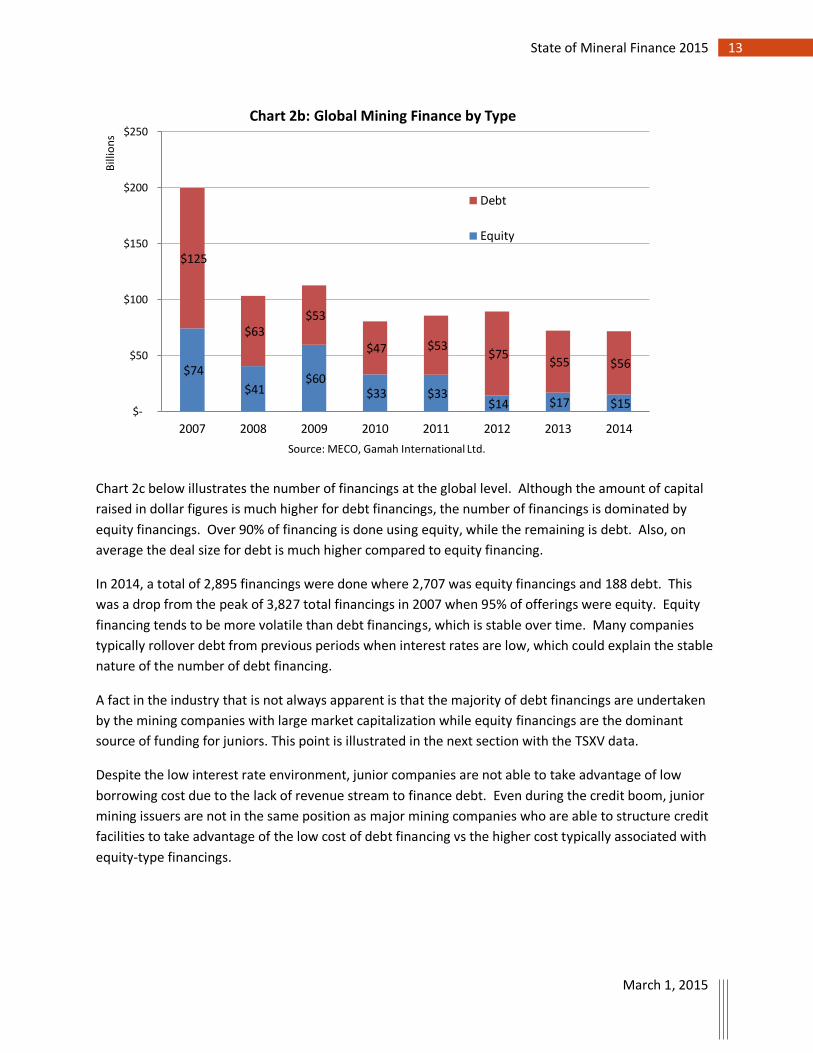

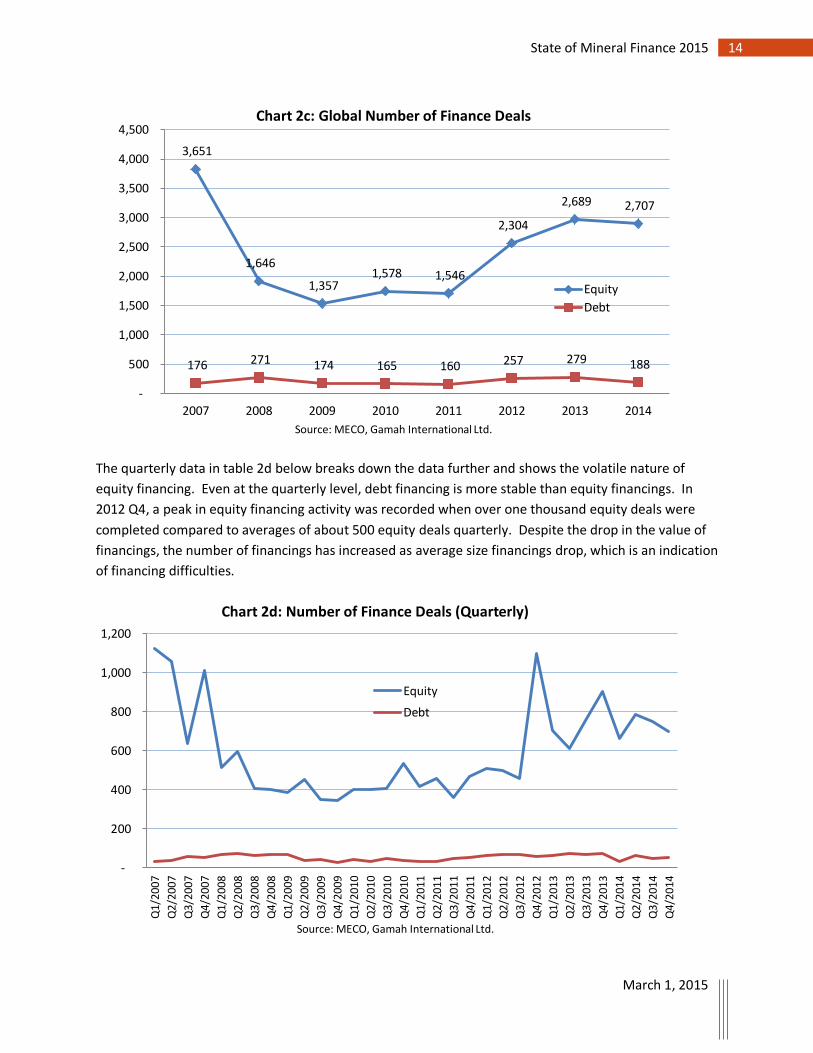

Chart 2c below illustrates the number of financings at the global level. Although the amount of capital

raised in dollar figures is much higher for debt financings, the number of financings is dominated by

equity financings. Over 90% of financing is done using equity, while the remaining is debt. Also, on

average the deal size for debt is much higher compared to equity financing.

In 2014, a total of 2,895 financings were done where 2,707 was equity financings and 188 debt. This

was a drop from the peak of 3,827 total financings in 2007 when 95% of offerings were equity. Equity

financing tends to be more volatile than debt financings, which is stable over time. Many companies

typically rollover debt from previous periods when interest rates are low, which could explain the stable

nature of the number of debt financing.

A fact in the industry that is not always apparent is that the majority of debt financings are undertaken

by the mining companies with large market capitalization while equity financings are the dominant

source of funding for juniors. This point is illustrated in the next section with the TSXV data.

Despite the low interest rate environment, junior companies are not able to take advantage of low

borrowing cost due to the lack of revenue stream to finance debt. Even during the credit boom, junior

mining issuers are not in the same position as major mining companies who are able to structure credit

facilities to take advantage of the low cost of debt financing vs the higher cost typically associated with

equity-type financings.

$74

$41 $60

$33 $33 $14 $17 $15

$125

$63 $53

$47 $53 $75

$55 $56

$-

$50

$100

$150

$200

$250

2007 2008 2009 2010 2011 2012 2013 2014

Bill

ion

s

Source: MECO, Gamah International Ltd.

Chart 2b: Global Mining Finance by Type

Debt

Equity

14 State of Mineral Finance 2015

March 1, 2015

The quarterly data in table 2d below breaks down the data further and shows the volatile nature of

equity financing. Even at the quarterly level, debt financing is more stable than equity financings. In

2012 Q4, a peak in equity financing activity was recorded when over one thousand equity deals were

completed compared to averages of about 500 equity deals quarterly. Despite the drop in the value of

financings, the number of financings has increased as average size financings drop, which is an indication

of financing difficulties.

176 271 174 165 160 257 279 188

3,651

1,646

1,357 1,578 1,546

2,304

2,689 2,707

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

2007 2008 2009 2010 2011 2012 2013 2014

Source: MECO, Gamah International Ltd.

Chart 2c: Global Number of Finance Deals

Equity

Debt

-

200

400

600

800

1,000

1,200

Q1/

2007

Q2/

2007

Q3/

2007

Q4/

2007

Q1/

2008

Q2/

2008

Q3/

2008

Q4/

2008

Q1/

2009

Q2/

2009

Q3/

2009

Q4/

2009

Q1/

2010

Q2/

2010

Q3/

2010

Q4/

2010

Q1/

2011

Q2/

2011

Q3/

2011

Q4/

2011

Q1/

2012

Q2/

2012

Q3/

2012

Q4/

2012

Q1/

2013

Q2/

2013

Q3/

2013

Q4/

2013

Q1/

2014

Q2/

2014

Q3/

2014

Q4/

2014

Source: MECO, Gamah International Ltd.

Chart 2d: Number of Finance Deals (Quarterly)

Equity

Debt

15 State of Mineral Finance 2015

March 1, 2015

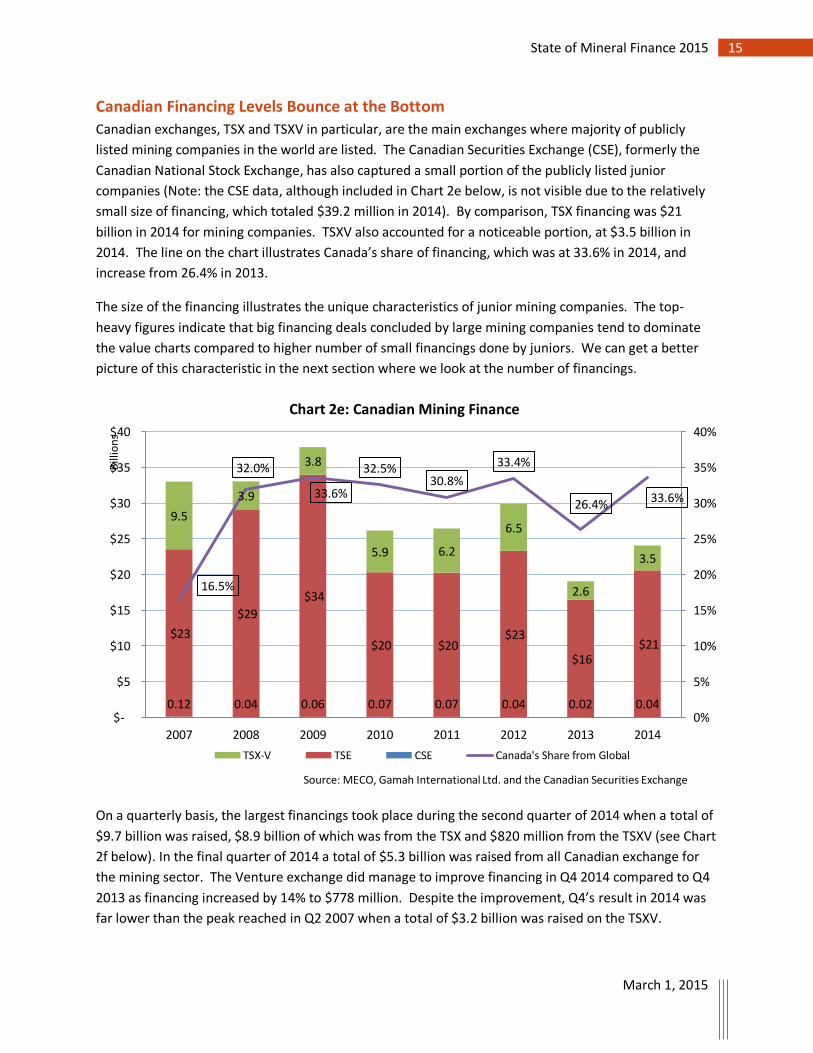

Canadian Financing Levels Bounce at the Bottom

Canadian exchanges, TSX and TSXV in particular, are the main exchanges where majority of publicly

listed mining companies in the world are listed. The Canadian Securities Exchange (CSE), formerly the

Canadian National Stock Exchange, has also captured a small portion of the publicly listed junior

companies (Note: the CSE data, although included in Chart 2e below, is not visible due to the relatively

small size of financing, which totaled $39.2 million in 2014). By comparison, TSX financing was $21

billion in 2014 for mining companies. TSXV also accounted for a noticeable portion, at $3.5 billion in

2014. The line on the chart illustrates Canada’s share of financing, which was at 33.6% in 2014, and

increase from 26.4% in 2013.

The size of the financing illustrates the unique characteristics of junior mining companies. The top-

heavy figures indicate that big financing deals concluded by large mining companies tend to dominate

the value charts compared to higher number of small financings done by juniors. We can get a better

picture of this characteristic in the next section where we look at the number of financings.

On a quarterly basis, the largest financings took place during the second quarter of 2014 when a total of

$9.7 billion was raised, $8.9 billion of which was from the TSX and $820 million from the TSXV (see Chart

2f below). In the final quarter of 2014 a total of $5.3 billion was raised from all Canadian exchange for

the mining sector. The Venture exchange did manage to improve financing in Q4 2014 compared to Q4

2013 as financing increased by 14% to $778 million. Despite the improvement, Q4’s result in 2014 was

far lower than the peak reached in Q2 2007 when a total of $3.2 billion was raised on the TSXV.

0.12 0.04 0.06 0.07 0.07 0.04 0.02 0.04

$23

$29

$34

$20 $20 $23

$16 $21

9.5

3.9

3.8

5.9 6.2

6.5

2.6

3.5

16.5%

32.0%

33.6%

32.5% 30.8%

33.4%

26.4% 33.6%

0%

5%

10%

15%

20%

25%

30%

35%

40%

$-

$5

$10

$15

$20

$25

$30

$35

$40

2007 2008 2009 2010 2011 2012 2013 2014

Bill

ion

s

Source: MECO, Gamah International Ltd. and the Canadian Securities Exchange

Chart 2e: Canadian Mining Finance

TSX-V TSE CSE Canada's Share from Global

16 State of Mineral Finance 2015

March 1, 2015

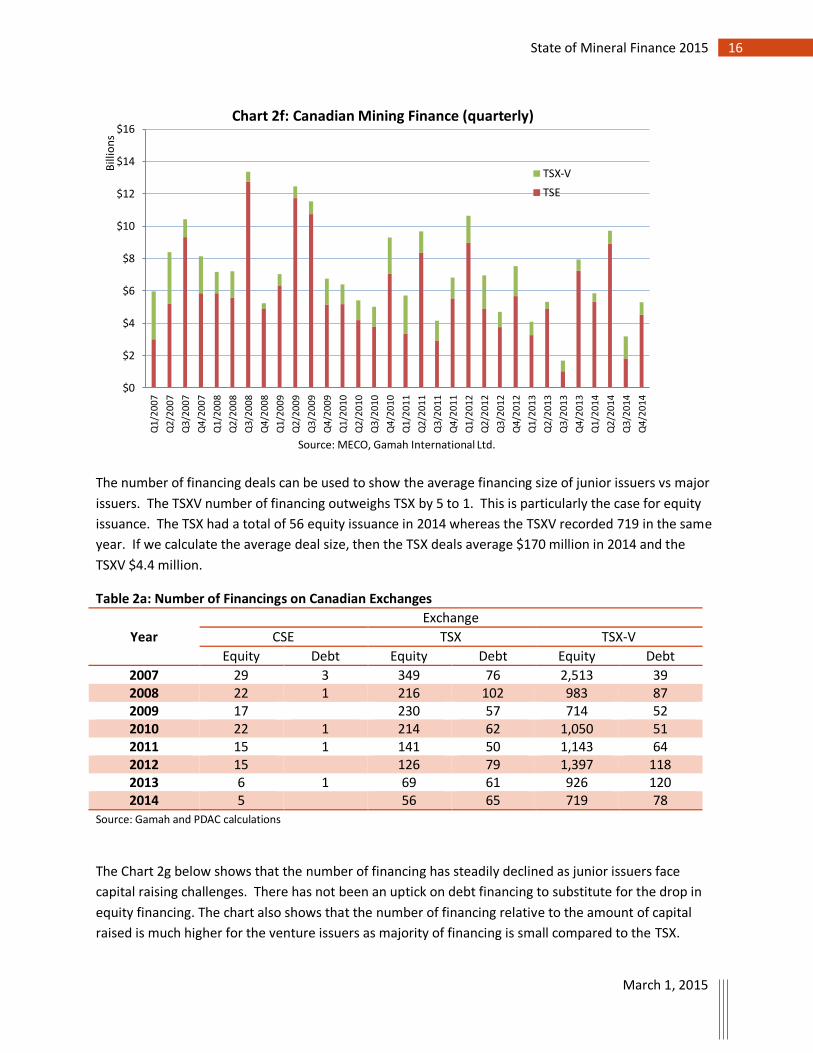

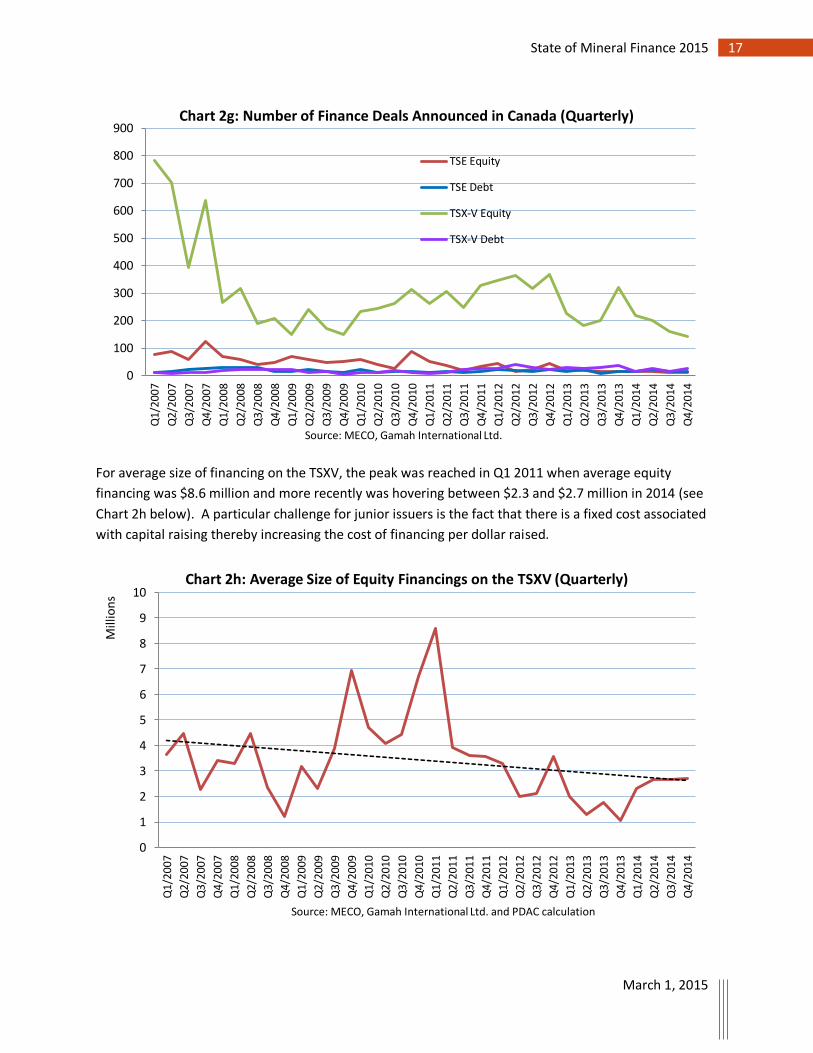

The number of financing deals can be used to show the average financing size of junior issuers vs major

issuers. The TSXV number of financing outweighs TSX by 5 to 1. This is particularly the case for equity

issuance. The TSX had a total of 56 equity issuance in 2014 whereas the TSXV recorded 719 in the same

year. If we calculate the average deal size, then the TSX deals average $170 million in 2014 and the

TSXV $4.4 million.

Table 2a: Number of Financings on Canadian Exchanges

Year

Exchange

CSE TSX TSX-V

Equity Debt Equity Debt Equity Debt

2007 29 3 349 76 2,513 39 2008 22 1 216 102 983 87 2009 17

230 57 714 52

2010 22 1 214 62 1,050 51 2011 15 1 141 50 1,143 64 2012 15

126 79 1,397 118

2013 6 1 69 61 926 120 2014 5

56 65 719 78

Source: Gamah and PDAC calculations

The Chart 2g below shows that the number of financing has steadily declined as junior issuers face

capital raising challenges. There has not been an uptick on debt financing to substitute for the drop in

equity financing. The chart also shows that the number of financing relative to the amount of capital

raised is much higher for the venture issuers as majority of financing is small compared to the TSX.

$0

$2

$4

$6

$8

$10

$12

$14

$16

Q1

/20

07

Q2

/20

07

Q3

/20

07

Q4

/20

07

Q1

/20

08

Q2

/20

08

Q3

/20

08

Q4

/20

08

Q1

/20

09

Q2

/20

09

Q3

/20

09

Q4

/20

09

Q1

/20

10

Q2

/20

10

Q3

/20

10

Q4

/20

10

Q1

/20

11

Q2

/20

11

Q3

/20

11

Q4

/20

11

Q1

/20

12

Q2

/20

12

Q3

/20

12

Q4

/20

12

Q1

/20

13

Q2

/20

13

Q3

/20

13

Q4

/20

13

Q1

/20

14

Q2

/20

14

Q3

/20

14

Q4

/20

14

Bill

ion

s

Source: MECO, Gamah International Ltd.

Chart 2f: Canadian Mining Finance (quarterly)

TSX-V

TSE

17 State of Mineral Finance 2015

March 1, 2015

For average size of financing on the TSXV, the peak was reached in Q1 2011 when average equity

financing was $8.6 million and more recently was hovering between $2.3 and $2.7 million in 2014 (see

Chart 2h below). A particular challenge for junior issuers is the fact that there is a fixed cost associated

with capital raising thereby increasing the cost of financing per dollar raised.

0

100

200

300

400

500

600

700

800

900

Q1/

2007

Q2/

2007

Q3/

2007

Q4/

2007

Q1/

2008

Q2/

2008

Q3/

2008

Q4/

2008

Q1/

2009

Q2/

2009

Q3/

2009

Q4/

2009

Q1/

2010

Q2/

2010

Q3/

2010

Q4/

2010

Q1/

2011

Q2/

2011

Q3/

2011

Q4/

2011

Q1/

2012

Q2/

2012

Q3/

2012

Q4/

2012

Q1/

2013

Q2/

2013

Q3/

2013

Q4/

2013

Q1/

2014

Q2/

2014

Q3/

2014

Q4/

2014

Source: MECO, Gamah International Ltd.

Chart 2g: Number of Finance Deals Announced in Canada (Quarterly)

TSE Equity

TSE Debt

TSX-V Equity

TSX-V Debt

0

1

2

3

4

5

6

7

8

9

10

Q1/

200

7

Q2/

200

7

Q3/

200

7

Q4/

200

7

Q1/

200

8

Q2/

200

8

Q3/

200

8

Q4/

200

8

Q1/

200

9

Q2/

200

9

Q3/

200

9

Q4/

200

9

Q1/

201

0

Q2/

201

0

Q3/

201

0

Q4/

201

0

Q1/

201

1

Q2/

201

1

Q3/

201

1

Q4/

201

1

Q1/

201

2

Q2/

201

2

Q3/

201

2

Q4/

201

2

Q1/

201

3

Q2/

201

3

Q3/

201

3

Q4/

201

3

Q1/

2014

Q2/

2014

Q3/

2014

Q4/

2014

Mill

ion

s

Source: MECO, Gamah International Ltd. and PDAC calculation

Chart 2h: Average Size of Equity Financings on the TSXV (Quarterly)

18 State of Mineral Finance 2015

March 1, 2015

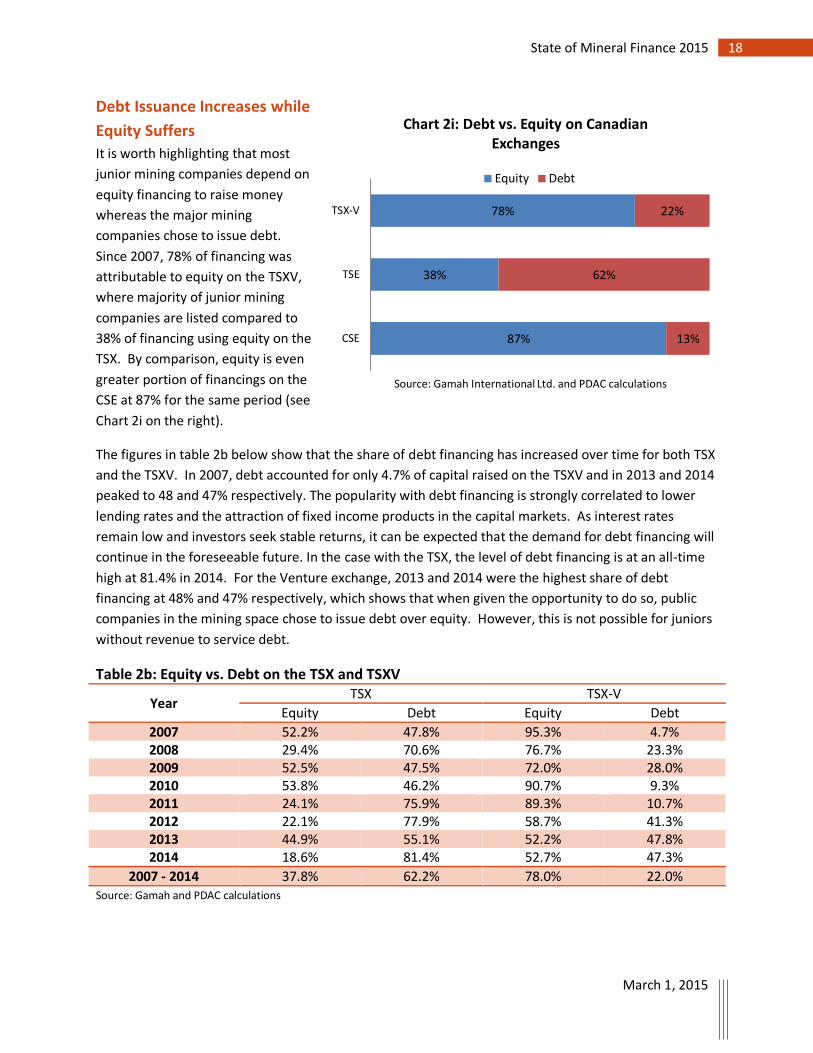

Debt Issuance Increases while

Equity Suffers

It is worth highlighting that most

junior mining companies depend on

equity financing to raise money

whereas the major mining

companies chose to issue debt.

Since 2007, 78% of financing was

attributable to equity on the TSXV,

where majority of junior mining

companies are listed compared to

38% of financing using equity on the

TSX. By comparison, equity is even

greater portion of financings on the

CSE at 87% for the same period (see

Chart 2i on the right).

The figures in table 2b below show that the share of debt financing has increased over time for both TSX

and the TSXV. In 2007, debt accounted for only 4.7% of capital raised on the TSXV and in 2013 and 2014

peaked to 48 and 47% respectively. The popularity with debt financing is strongly correlated to lower

lending rates and the attraction of fixed income products in the capital markets. As interest rates

remain low and investors seek stable returns, it can be expected that the demand for debt financing will

continue in the foreseeable future. In the case with the TSX, the level of debt financing is at an all-time

high at 81.4% in 2014. For the Venture exchange, 2013 and 2014 were the highest share of debt

financing at 48% and 47% respectively, which shows that when given the opportunity to do so, public

companies in the mining space chose to issue debt over equity. However, this is not possible for juniors

without revenue to service debt.

Table 2b: Equity vs. Debt on the TSX and TSXV

Year TSX TSX-V

Equity Debt Equity Debt

2007 52.2% 47.8% 95.3% 4.7% 2008 29.4% 70.6% 76.7% 23.3% 2009 52.5% 47.5% 72.0% 28.0% 2010 53.8% 46.2% 90.7% 9.3% 2011 24.1% 75.9% 89.3% 10.7% 2012 22.1% 77.9% 58.7% 41.3% 2013 44.9% 55.1% 52.2% 47.8% 2014 18.6% 81.4% 52.7% 47.3%

2007 - 2014 37.8% 62.2% 78.0% 22.0% Source: Gamah and PDAC calculations

87%

38%

78%

13%

62%

22%

CSE

TSE

TSX-V

Source: Gamah International Ltd. and PDAC calculations

Chart 2i: Debt vs. Equity on Canadian Exchanges

Equity Debt

19 State of Mineral Finance 2015

March 1, 2015

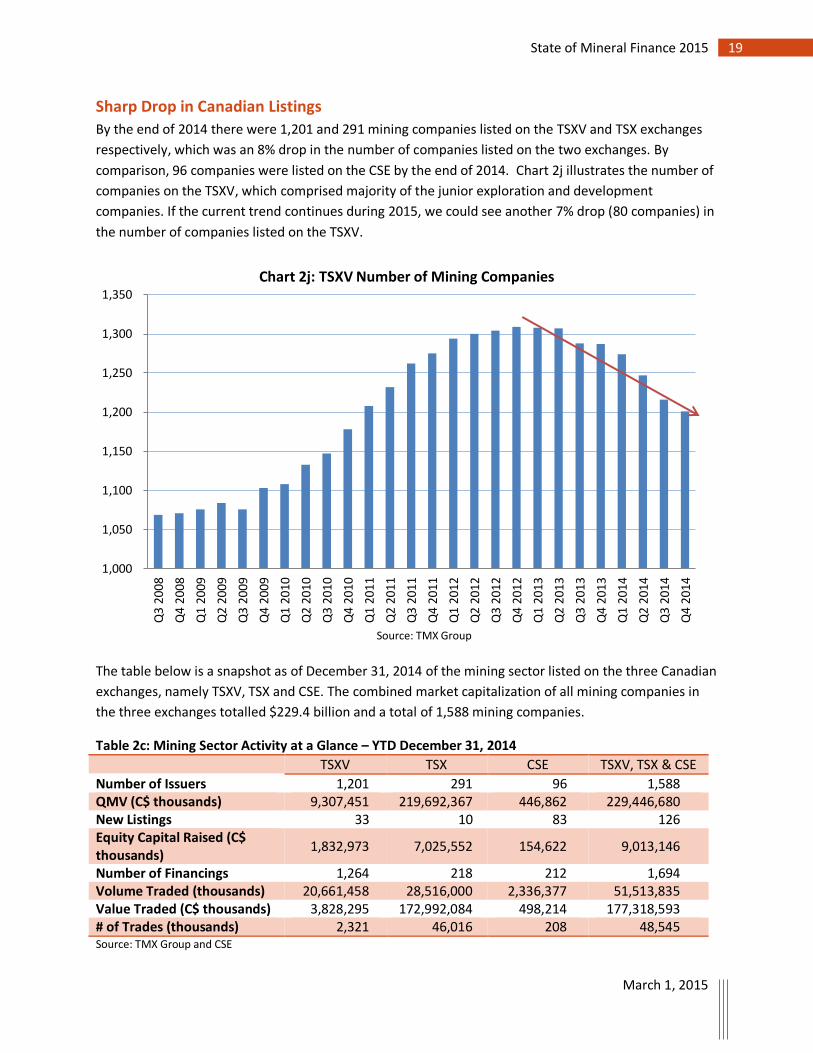

Sharp Drop in Canadian Listings

By the end of 2014 there were 1,201 and 291 mining companies listed on the TSXV and TSX exchanges

respectively, which was an 8% drop in the number of companies listed on the two exchanges. By

comparison, 96 companies were listed on the CSE by the end of 2014. Chart 2j illustrates the number of

companies on the TSXV, which comprised majority of the junior exploration and development

companies. If the current trend continues during 2015, we could see another 7% drop (80 companies) in

the number of companies listed on the TSXV.

The table below is a snapshot as of December 31, 2014 of the mining sector listed on the three Canadian

exchanges, namely TSXV, TSX and CSE. The combined market capitalization of all mining companies in

the three exchanges totalled $229.4 billion and a total of 1,588 mining companies.

Table 2c: Mining Sector Activity at a Glance – YTD December 31, 2014

TSXV TSX CSE TSXV, TSX & CSE

Number of Issuers 1,201 291 96 1,588 QMV (C$ thousands) 9,307,451 219,692,367 446,862 229,446,680 New Listings 33 10 83 126 Equity Capital Raised (C$ thousands)

1,832,973 7,025,552 154,622 9,013,146

Number of Financings 1,264 218 212 1,694 Volume Traded (thousands) 20,661,458 28,516,000 2,336,377 51,513,835 Value Traded (C$ thousands) 3,828,295 172,992,084 498,214 177,318,593 # of Trades (thousands) 2,321 46,016 208 48,545 Source: TMX Group and CSE

1,000

1,050

1,100

1,150

1,200

1,250

1,300

1,350

Q3

2008

Q4

2008

Q1

2009

Q2

2009

Q3

2009

Q4

2009

Q1

2010

Q2

2010

Q3

2010

Q4

2010

Q1

2011

Q2

2011

Q3

2011

Q4

2011

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

Q2

2014

Q3

2014

Q4

2014

Source: TMX Group

Chart 2j: TSXV Number of Mining Companies

20 State of Mineral Finance 2015

March 1, 2015

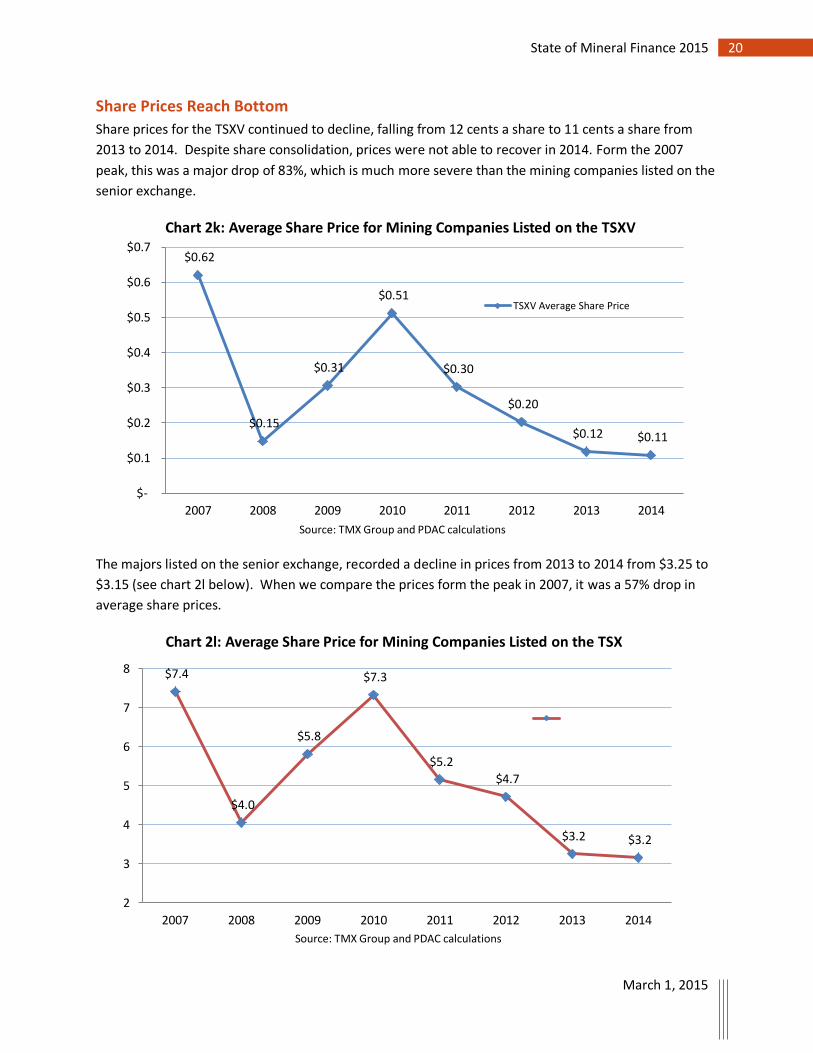

Share Prices Reach Bottom

Share prices for the TSXV continued to decline, falling from 12 cents a share to 11 cents a share from

2013 to 2014. Despite share consolidation, prices were not able to recover in 2014. Form the 2007

peak, this was a major drop of 83%, which is much more severe than the mining companies listed on the

senior exchange.

The majors listed on the senior exchange, recorded a decline in prices from 2013 to 2014 from $3.25 to

$3.15 (see chart 2l below). When we compare the prices form the peak in 2007, it was a 57% drop in

average share prices.

$0.62

$0.15

$0.31

$0.51

$0.30

$0.20

$0.12 $0.11

$-

$0.1

$0.2

$0.3

$0.4

$0.5

$0.6

$0.7

2007 2008 2009 2010 2011 2012 2013 2014

Source: TMX Group and PDAC calculations

Chart 2k: Average Share Price for Mining Companies Listed on the TSXV

TSXV Average Share Price

$7.4

$4.0

$5.8

$7.3

$5.2

$4.7

$3.2 $3.2

2

3

4

5

6

7

8

2007 2008 2009 2010 2011 2012 2013 2014

Source: TMX Group and PDAC calculations

Chart 2l: Average Share Price for Mining Companies Listed on the TSX

21 State of Mineral Finance 2015

March 1, 2015

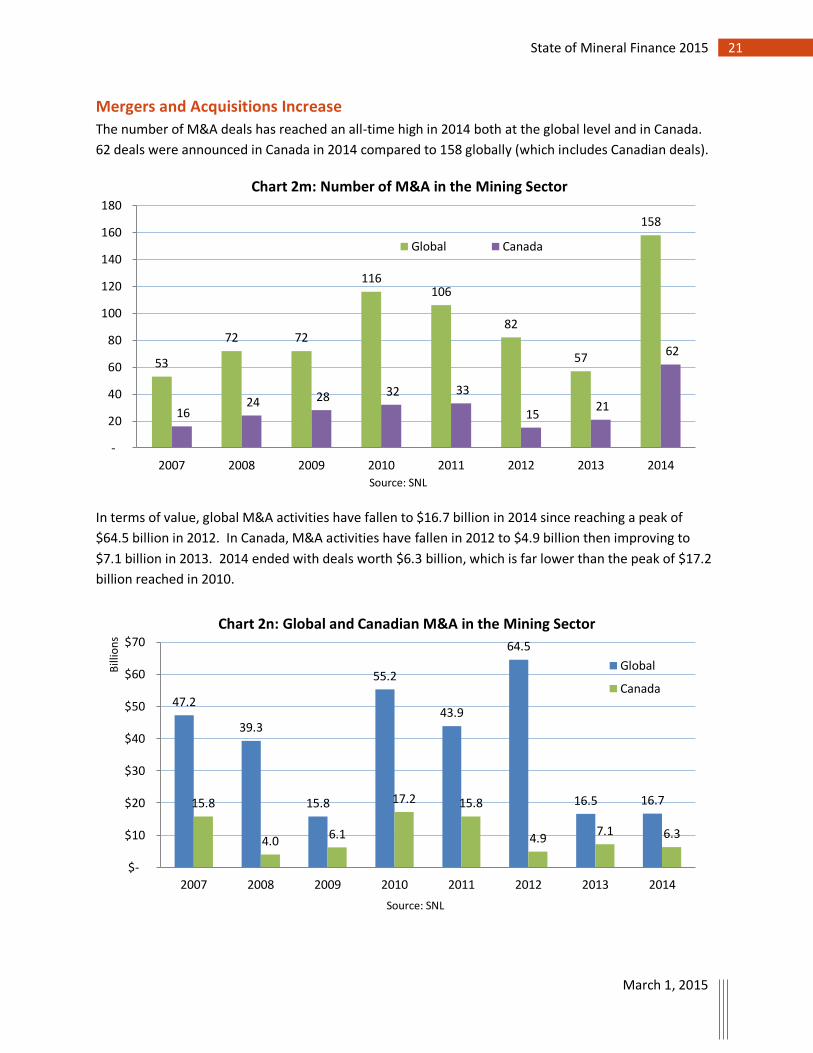

Mergers and Acquisitions Increase

The number of M&A deals has reached an all-time high in 2014 both at the global level and in Canada.

62 deals were announced in Canada in 2014 compared to 158 globally (which includes Canadian deals).

In terms of value, global M&A activities have fallen to $16.7 billion in 2014 since reaching a peak of

$64.5 billion in 2012. In Canada, M&A activities have fallen in 2012 to $4.9 billion then improving to

$7.1 billion in 2013. 2014 ended with deals worth $6.3 billion, which is far lower than the peak of $17.2

billion reached in 2010.

53

72 72

116 106

82

57

158

16 24 28 32 33

15 21

62

-

20

40

60

80

100

120

140

160

180

2007 2008 2009 2010 2011 2012 2013 2014

Source: SNL

Chart 2m: Number of M&A in the Mining Sector

Global Canada

47.2

39.3

15.8

55.2

43.9

64.5

16.5 16.7 15.8

4.0 6.1

17.2 15.8

4.9 7.1 6.3

$-

$10

$20

$30

$40

$50

$60

$70

2007 2008 2009 2010 2011 2012 2013 2014

Bill

ion

s

Source: SNL

Chart 2n: Global and Canadian M&A in the Mining Sector

Global

Canada

22 State of Mineral Finance 2015

March 1, 2015

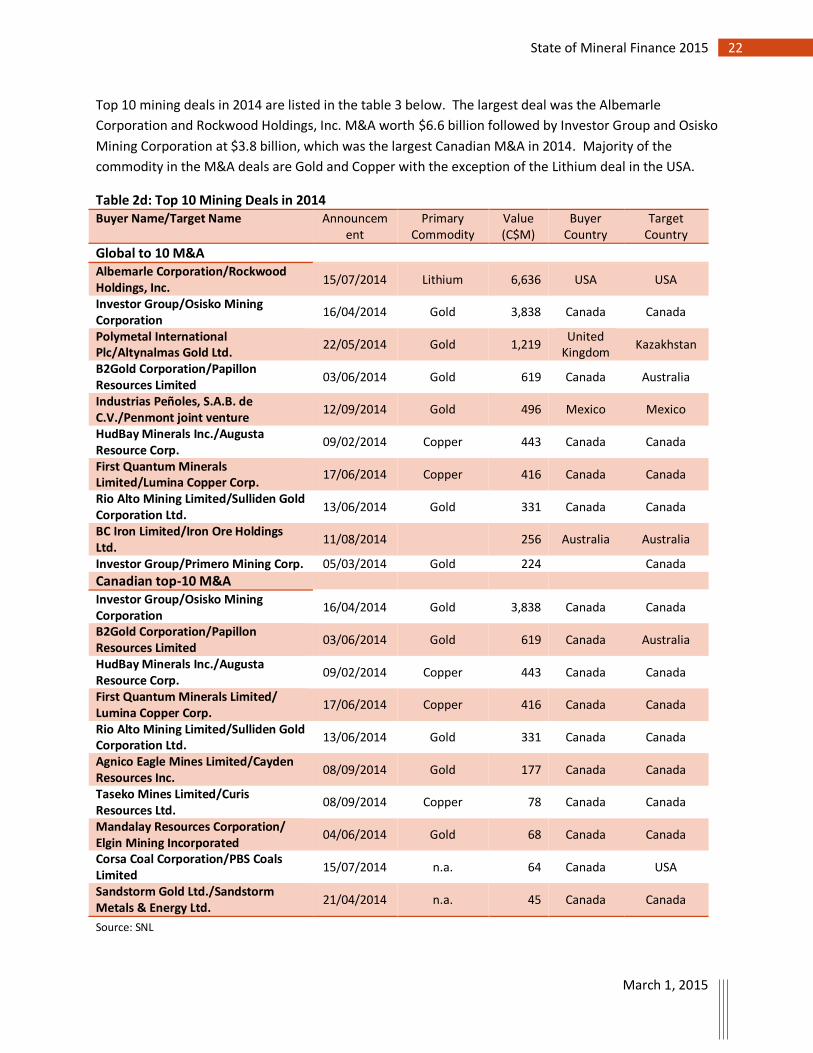

Top 10 mining deals in 2014 are listed in the table 3 below. The largest deal was the Albemarle

Corporation and Rockwood Holdings, Inc. M&A worth $6.6 billion followed by Investor Group and Osisko

Mining Corporation at $3.8 billion, which was the largest Canadian M&A in 2014. Majority of the

commodity in the M&A deals are Gold and Copper with the exception of the Lithium deal in the USA.

Table 2d: Top 10 Mining Deals in 2014

Buyer Name/Target Name Announcement

Primary Commodity

Value (C$M)

Buyer Country

Target Country

Global to 10 M&A

Albemarle Corporation/Rockwood Holdings, Inc.

15/07/2014 Lithium 6,636 USA USA

Investor Group/Osisko Mining Corporation

16/04/2014 Gold 3,838 Canada Canada

Polymetal International Plc/Altynalmas Gold Ltd.

22/05/2014 Gold 1,219 United

Kingdom Kazakhstan

B2Gold Corporation/Papillon Resources Limited

03/06/2014 Gold 619 Canada Australia

Industrias Peñoles, S.A.B. de C.V./Penmont joint venture

12/09/2014 Gold 496 Mexico Mexico

HudBay Minerals Inc./Augusta Resource Corp.

09/02/2014 Copper 443 Canada Canada

First Quantum Minerals Limited/Lumina Copper Corp.

17/06/2014 Copper 416 Canada Canada

Rio Alto Mining Limited/Sulliden Gold Corporation Ltd.

13/06/2014 Gold 331 Canada Canada

BC Iron Limited/Iron Ore Holdings Ltd.

11/08/2014

256 Australia Australia

Investor Group/Primero Mining Corp. 05/03/2014 Gold 224

Canada

Canadian top-10 M&A

Investor Group/Osisko Mining Corporation

16/04/2014 Gold 3,838 Canada Canada

B2Gold Corporation/Papillon Resources Limited

03/06/2014 Gold 619 Canada Australia

HudBay Minerals Inc./Augusta Resource Corp.

09/02/2014 Copper 443 Canada Canada

First Quantum Minerals Limited/ Lumina Copper Corp.

17/06/2014 Copper 416 Canada Canada

Rio Alto Mining Limited/Sulliden Gold Corporation Ltd.

13/06/2014 Gold 331 Canada Canada

Agnico Eagle Mines Limited/Cayden Resources Inc.

08/09/2014 Gold 177 Canada Canada

Taseko Mines Limited/Curis Resources Ltd.

08/09/2014 Copper 78 Canada Canada

Mandalay Resources Corporation/ Elgin Mining Incorporated

04/06/2014 Gold 68 Canada Canada

Corsa Coal Corporation/PBS Coals Limited

15/07/2014 n.a. 64 Canada USA

Sandstorm Gold Ltd./Sandstorm Metals & Energy Ltd.

21/04/2014 n.a. 45 Canada Canada

Source: SNL

23 State of Mineral Finance 2015

March 1, 2015

SECTION III: Exploration Trends

Global Exploration Budgets Hit Hard

Exploration budgets for every major mining jurisdiction have decreased in 2014, with the largest annual

declines in the Pacific/Southeast Asia region followed by Australia (see Chart 3a below). Globally,

exploration budgets have dropped by 26% reflecting weak commodity sector and lack of prospects for a

robust recovery in commodity demand. Canada and Australia continue to be the two key mining

countries with a total budget of $1.5 billion (13.9%) and $1.3 billion (11.7%) respectively (see Chart 3b).

0

5

10

15

20

25

2007 2008 2009 2010 2011 2012 2013 2014

$ B

illio

ns

Source: SNL

Chart 3a: Exploration Budget by Location

USA

Rest of World

Pacific/SE Asia

Latin America

Canada

Australia

Africa

Africa 16.0%

Australia 11.7%

Canada 13.9%

Latin America 26.7%

Pacific/SE Asia 5.6%

Rest of World 19.1%

USA 7.1%

Chart 3b: Share of Budgets by Locations in 2014

Source: SNL

24 State of Mineral Finance 2015

March 1, 2015

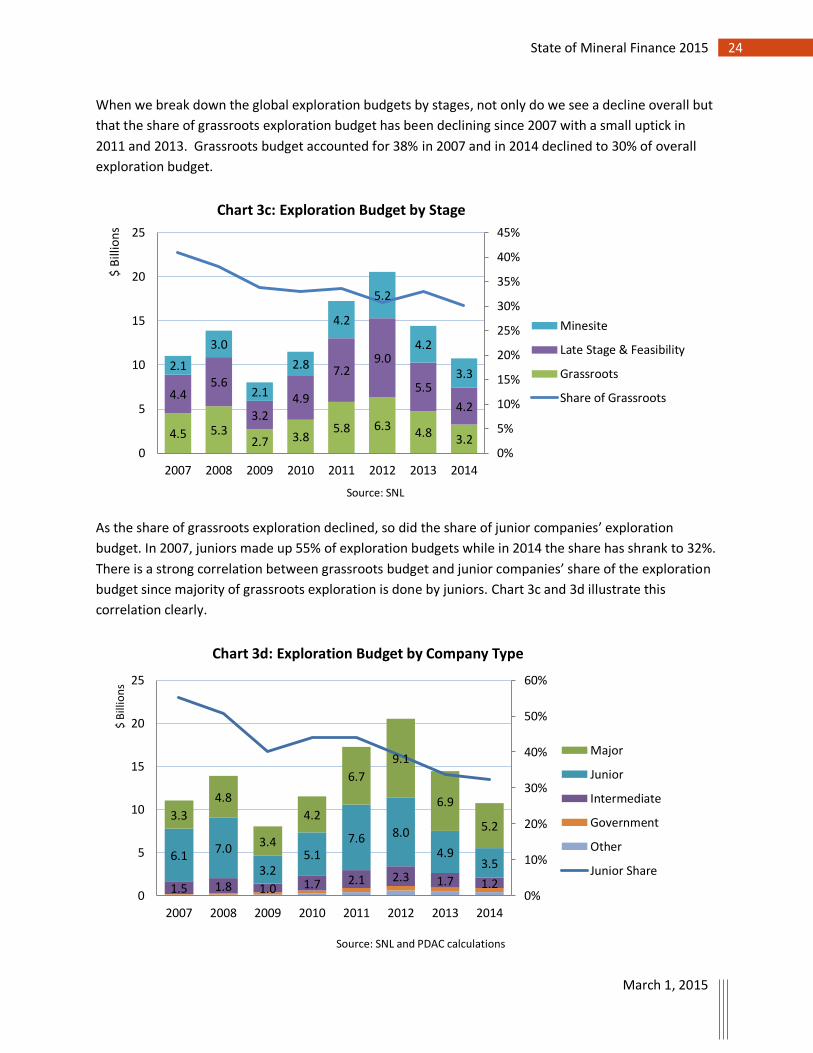

When we break down the global exploration budgets by stages, not only do we see a decline overall but

that the share of grassroots exploration budget has been declining since 2007 with a small uptick in

2011 and 2013. Grassroots budget accounted for 38% in 2007 and in 2014 declined to 30% of overall

exploration budget.

As the share of grassroots exploration declined, so did the share of junior companies’ exploration

budget. In 2007, juniors made up 55% of exploration budgets while in 2014 the share has shrank to 32%.

There is a strong correlation between grassroots budget and junior companies’ share of the exploration

budget since majority of grassroots exploration is done by juniors. Chart 3c and 3d illustrate this

correlation clearly.

4.5 5.3 2.7 3.8

5.8 6.3 4.8

3.2

4.4 5.6

3.2

4.9

7.2 9.0

5.5

4.2

2.1

3.0

2.1

2.8

4.2

5.2

4.2

3.3

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

0

5

10

15

20

25

2007 2008 2009 2010 2011 2012 2013 2014

$ B

illio

ns

Source: SNL

Chart 3c: Exploration Budget by Stage

Minesite

Late Stage & Feasibility

Grassroots

Share of Grassroots

1.5 1.8 1.0 1.7 2.1 2.3 1.7 1.2

6.1 7.0

3.2 5.1

7.6 8.0

4.9 3.5

3.3

4.8

3.4

4.2

6.7

9.1

6.9

5.2

0%

10%

20%

30%

40%

50%

60%

0

5

10

15

20

25

2007 2008 2009 2010 2011 2012 2013 2014

$ B

illio

ns

Source: SNL and PDAC calculations

Chart 3d: Exploration Budget by Company Type

Major

Junior

Intermediate

Government

Other

Junior Share

25 State of Mineral Finance 2015

March 1, 2015

Average corporate exploration budget has declined in 2014 to $138 million from $190 million in the

previous year, which is a 27% drop. As reported by SNL, the number of junior and intermediate

companies with current exploration budgets and revenue fell to 252 in 2014 from 273 in 2013.

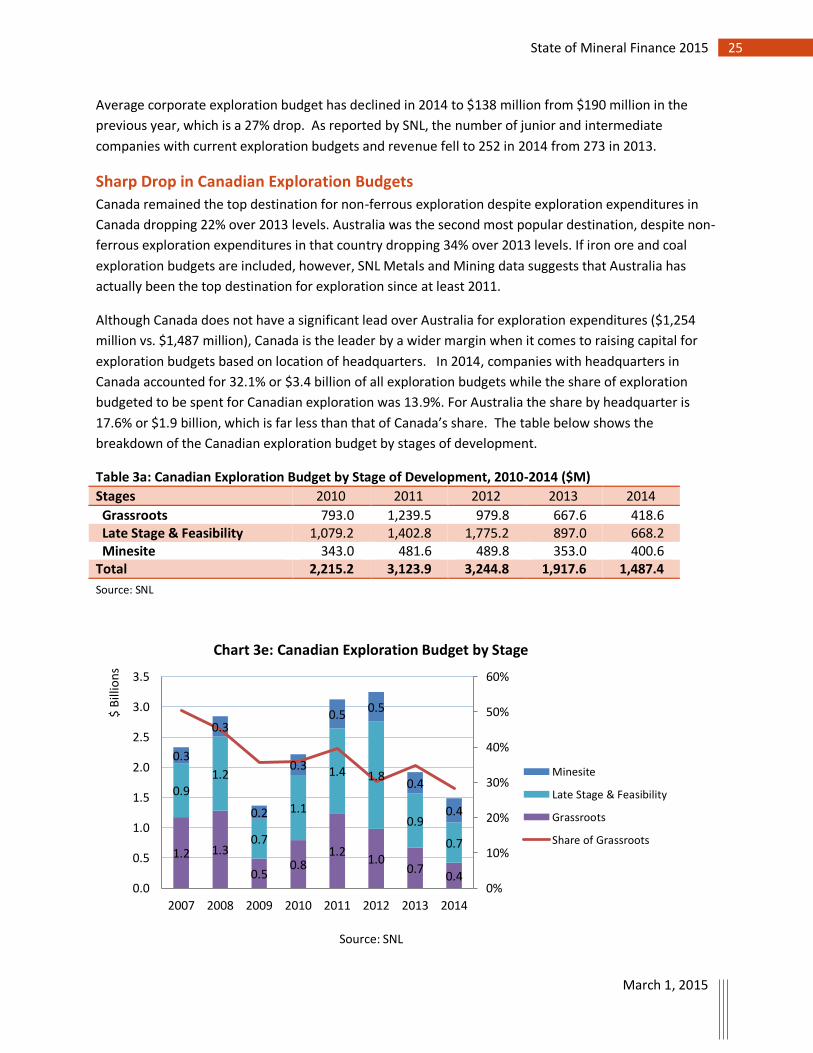

Sharp Drop in Canadian Exploration Budgets

Canada remained the top destination for non-ferrous exploration despite exploration expenditures in

Canada dropping 22% over 2013 levels. Australia was the second most popular destination, despite non-

ferrous exploration expenditures in that country dropping 34% over 2013 levels. If iron ore and coal

exploration budgets are included, however, SNL Metals and Mining data suggests that Australia has

actually been the top destination for exploration since at least 2011.

Although Canada does not have a significant lead over Australia for exploration expenditures ($1,254

million vs. $1,487 million), Canada is the leader by a wider margin when it comes to raising capital for

exploration budgets based on location of headquarters. In 2014, companies with headquarters in

Canada accounted for 32.1% or $3.4 billion of all exploration budgets while the share of exploration

budgeted to be spent for Canadian exploration was 13.9%. For Australia the share by headquarter is

17.6% or $1.9 billion, which is far less than that of Canada’s share. The table below shows the

breakdown of the Canadian exploration budget by stages of development.

Table 3a: Canadian Exploration Budget by Stage of Development, 2010-2014 ($M)

Stages 2010 2011 2012 2013 2014

Grassroots 793.0 1,239.5 979.8 667.6 418.6 Late Stage & Feasibility 1,079.2 1,402.8 1,775.2 897.0 668.2 Minesite 343.0 481.6 489.8 353.0 400.6 Total 2,215.2 3,123.9 3,244.8 1,917.6 1,487.4

Source: SNL

1.2 1.3

0.5 0.8

1.2 1.0

0.7 0.4

0.9 1.2

0.7

1.1

1.4 1.8

0.9

0.7

0.3

0.3

0.2

0.3

0.5 0.5

0.4

0.4

0%

10%

20%

30%

40%

50%

60%

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2007 2008 2009 2010 2011 2012 2013 2014

$ B

illio

ns

Source: SNL

Chart 3e: Canadian Exploration Budget by Stage

Minesite

Late Stage & Feasibility

Grassroots

Share of Grassroots

26 State of Mineral Finance 2015

March 1, 2015

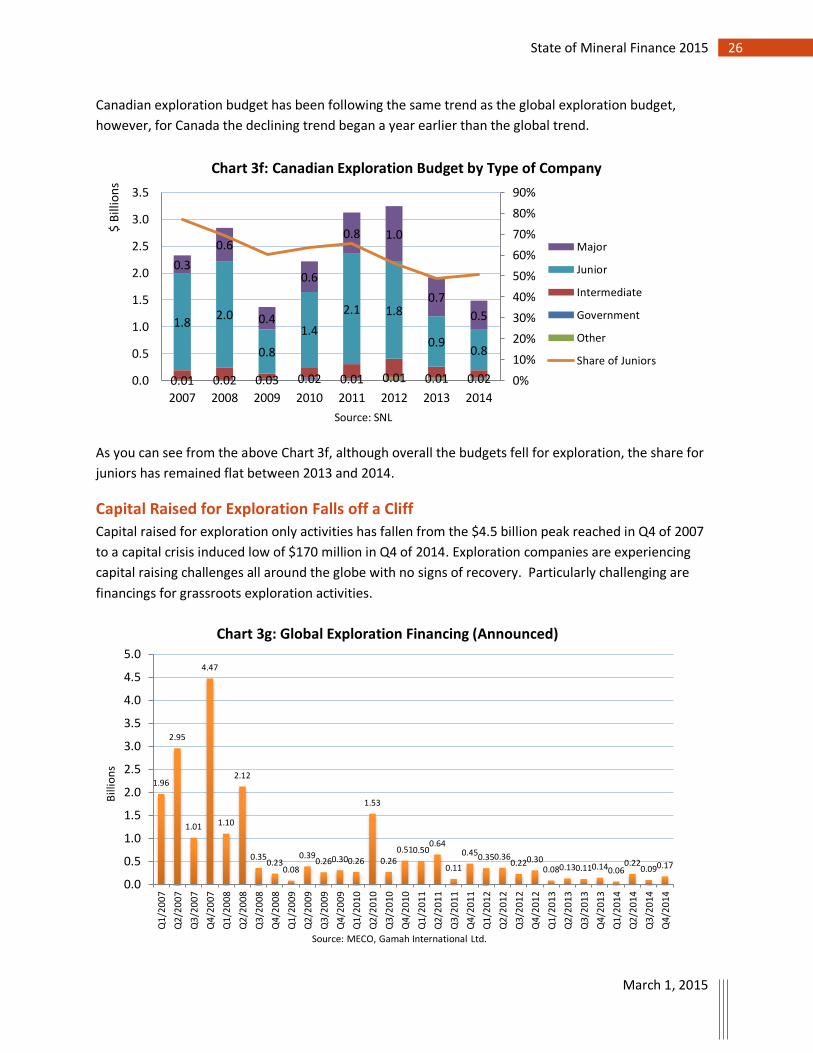

Canadian exploration budget has been following the same trend as the global exploration budget,

however, for Canada the declining trend began a year earlier than the global trend.

As you can see from the above Chart 3f, although overall the budgets fell for exploration, the share for

juniors has remained flat between 2013 and 2014.

Capital Raised for Exploration Falls off a Cliff

Capital raised for exploration only activities has fallen from the $4.5 billion peak reached in Q4 of 2007

to a capital crisis induced low of $170 million in Q4 of 2014. Exploration companies are experiencing

capital raising challenges all around the globe with no signs of recovery. Particularly challenging are

financings for grassroots exploration activities.

0.01 0.02 0.03 0.02 0.01 0.01 0.01 0.02

1.8 2.0

0.8

1.4

2.1 1.8

0.9 0.8

0.3

0.6

0.4

0.6

0.8 1.0

0.7

0.5

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2007 2008 2009 2010 2011 2012 2013 2014

$ B

illio

ns

Source: SNL

Chart 3f: Canadian Exploration Budget by Type of Company

Major

Junior

Intermediate

Government

Other

Share of Juniors

1.96

2.95

1.01

4.47

1.10

2.12

0.35 0.23

0.08

0.39 0.26 0.30 0.26

1.53

0.26 0.51 0.50

0.64

0.11

0.45 0.35 0.36 0.22 0.30

0.08 0.13 0.11 0.14 0.06 0.22

0.09 0.17

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Q1

/20

07

Q2

/20

07

Q3

/20

07

Q4

/20

07

Q1

/20

08

Q2

/20

08

Q3

/20

08

Q4

/20

08

Q1

/20

09

Q2

/20

09

Q3

/20

09

Q4

/20

09

Q1

/20

10

Q2

/20

10

Q3

/20

10

Q4

/20

10

Q1

/20

11

Q2

/20

11

Q3

/20

11

Q4

/20

11

Q1

/20

12

Q2

/20

12

Q3

/20

12

Q4

/20

12

Q1

/20

13

Q2

/20

13

Q3

/20

13

Q4

/20

13

Q1

/20

14

Q2

/20

14

Q3

/20

14

Q4

/20

14

Bill

ion

s

Source: MECO, Gamah International Ltd.

Chart 3g: Global Exploration Financing (Announced)

27 State of Mineral Finance 2015

March 1, 2015

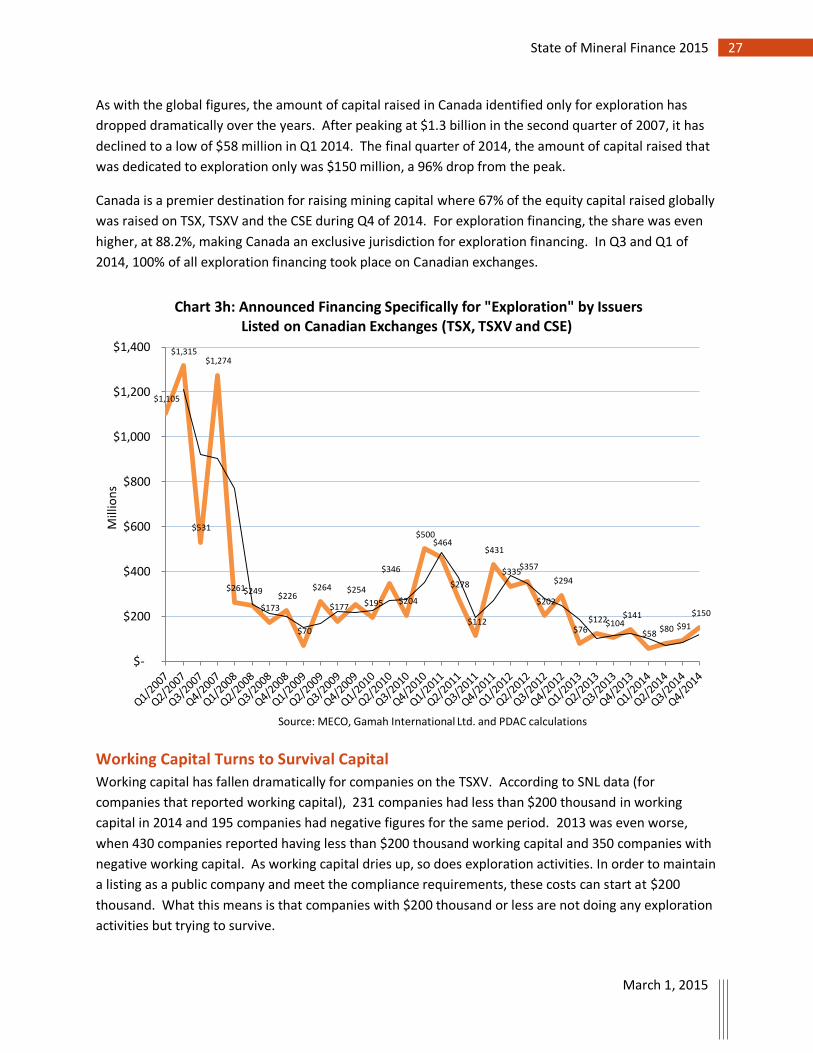

As with the global figures, the amount of capital raised in Canada identified only for exploration has

dropped dramatically over the years. After peaking at $1.3 billion in the second quarter of 2007, it has

declined to a low of $58 million in Q1 2014. The final quarter of 2014, the amount of capital raised that

was dedicated to exploration only was $150 million, a 96% drop from the peak.

Canada is a premier destination for raising mining capital where 67% of the equity capital raised globally

was raised on TSX, TSXV and the CSE during Q4 of 2014. For exploration financing, the share was even

higher, at 88.2%, making Canada an exclusive jurisdiction for exploration financing. In Q3 and Q1 of

2014, 100% of all exploration financing took place on Canadian exchanges.

Working Capital Turns to Survival Capital

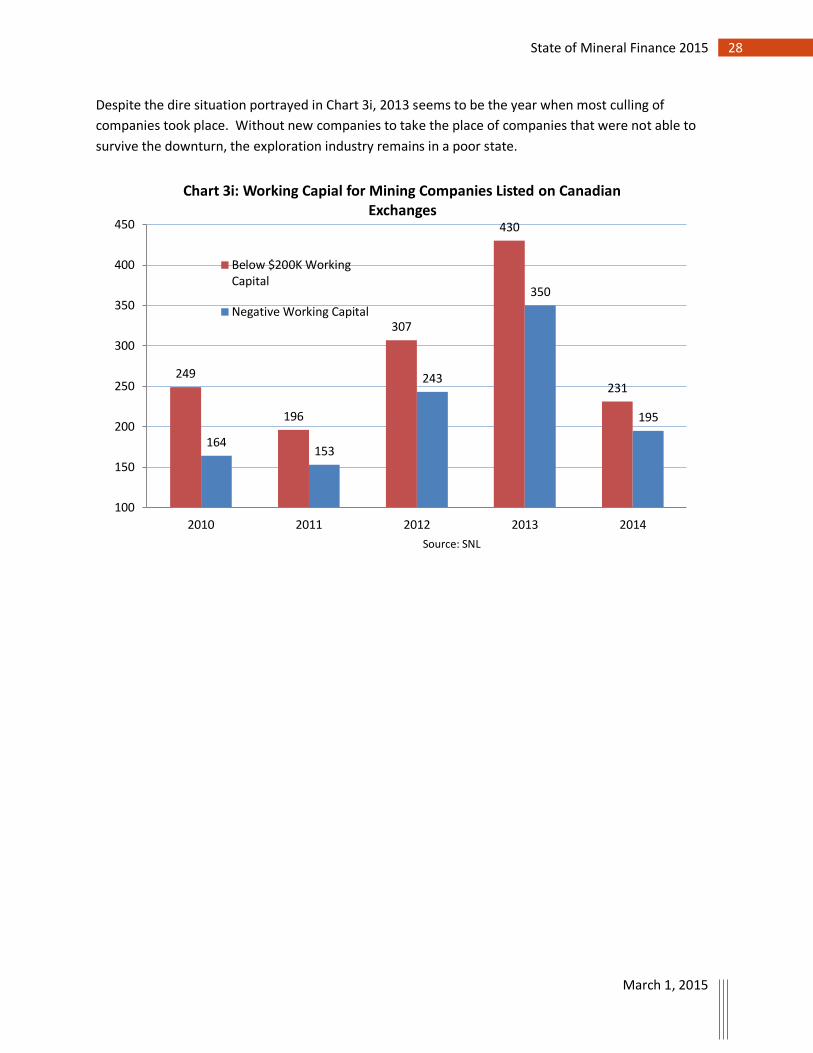

Working capital has fallen dramatically for companies on the TSXV. According to SNL data (for

companies that reported working capital), 231 companies had less than $200 thousand in working

capital in 2014 and 195 companies had negative figures for the same period. 2013 was even worse,

when 430 companies reported having less than $200 thousand working capital and 350 companies with

negative working capital. As working capital dries up, so does exploration activities. In order to maintain

a listing as a public company and meet the compliance requirements, these costs can start at $200

thousand. What this means is that companies with $200 thousand or less are not doing any exploration

activities but trying to survive.

$1,105

$1,315

$531

$1,274

$261 $249

$173

$226

$70

$264

$177

$254

$195

$346

$204

$500 $464

$278

$112

$431

$335 $357

$202

$294

$76 $122 $104

$141

$58 $80 $91

$150

$-

$200

$400

$600

$800

$1,000

$1,200

$1,400

Mill

ion

s

Source: MECO, Gamah International Ltd. and PDAC calculations

Chart 3h: Announced Financing Specifically for "Exploration" by Issuers Listed on Canadian Exchanges (TSX, TSXV and CSE)

28 State of Mineral Finance 2015

March 1, 2015

Despite the dire situation portrayed in Chart 3i, 2013 seems to be the year when most culling of

companies took place. Without new companies to take the place of companies that were not able to

survive the downturn, the exploration industry remains in a poor state.

249

196

307

430

231

164 153

243

350

195

100

150

200

250

300

350

400

450

2010 2011 2012 2013 2014

Source: SNL

Chart 3i: Working Capial for Mining Companies Listed on Canadian Exchanges

Below $200K WorkingCapital

Negative Working Capital

29 State of Mineral Finance 2015

March 1, 2015

SECTION IV: Fiscal Support and Capital Market Reform Canada is a leader for exploration and mineral financing. In order to maintain its leadership, there is a

need to provide an enabling environment for the industry to flourish. In a downturn, such as the one

the industry has been experiencing over the last few years, it is of greater importance to provide the

right fiscal landscape for the industry. Without the right incentives in place, risk capital becomes harder

to access during a downturn and an increasing competitive environment. A good example is the

innovative flow-through system in Canada, which has been l tremendous help to the industry.

Additionally, capital markets play a crucial role in helping the exploration and development companies

to raise risk capital from retail investors. New reform to the capital markets are needed to adapt to the

new structure of capital markets that employ new technology and develop new products. The

traditional model of how exploration companies were financed in the past has changed and capital

market reform is needed to adapt to new ways of raising capital – from both private and public markets.

The Cooperative Capital Market Regulator and new exemptions, if done right, are a step in the right

direction.

Use of Flow-Through Shares Buffers the fall in Financings

Flow-through shares4 are a major source of financing that is targeted specifically to exploration activities

in Canada for companies listed on Canadian exchanges. Flow-through can help attract capital back to

juniors, and back to grassroots exploration because of the ability for investors to benefit from the

Mineral Exploration Tax Credit (METC).5

PDAC was the first organization to recommend the government implement a flow-through program for

the exploration sector and has consistently supported the federal government to keep the METC in

place. The credit was initially implemented in October, 2000 for three years as an interim measure,

extended annually. In the federal government’s Budget 2013 the METC was extended with expiry date

to March 31, 2015.

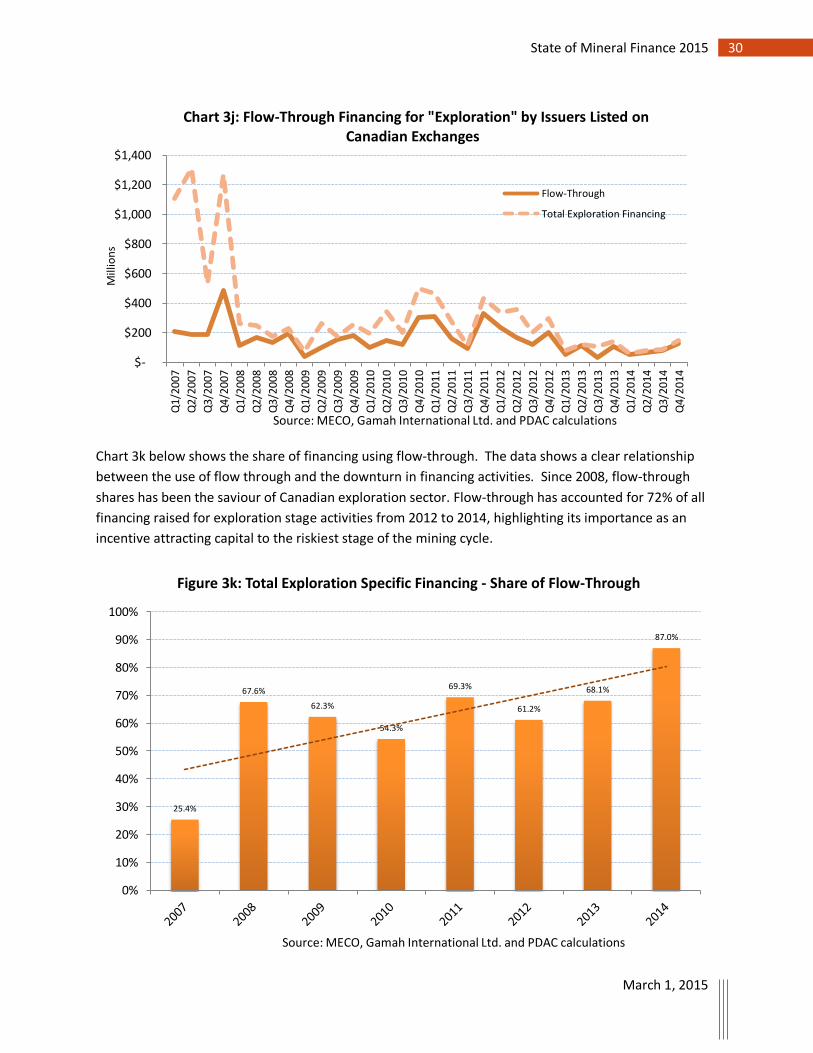

The use of flow-through shares as a share of total capital raised specifically for exploration tend to peak

during time of financing difficulty. Chart 3j shows the total amount of financing for exploration

purposes only from 2007 to 2014, which shows that the amount of financing has fallen from $1.3 billion

during Q4 of 2007 to a low of $150 million in Q4 of 2014. Without an incentive as offered by the flow-

through system, financing would have fallen even further.

4 To understand how the flow-through share works, please see Canada Revenue Agency website:

http://www.cra-arc.gc.ca/tx/bsnss/tpcs/fts-paa/nvstr/hw-eng.html

5 For a description of the METC, see Natural Resource Canada website: http://www.nrcan.gc.ca/mining-

materials/taxation/8874

30 State of Mineral Finance 2015

March 1, 2015

Chart 3k below shows the share of financing using flow-through. The data shows a clear relationship

between the use of flow through and the downturn in financing activities. Since 2008, flow-through

shares has been the saviour of Canadian exploration sector. Flow-through has accounted for 72% of all

financing raised for exploration stage activities from 2012 to 2014, highlighting its importance as an

incentive attracting capital to the riskiest stage of the mining cycle.

$-

$200

$400

$600

$800

$1,000

$1,200

$1,400

Q1/

2007

Q2/

2007

Q3/

2007

Q4/

2007

Q1/

2008

Q2/

2008

Q3/

2008

Q4/

2008

Q1/

2009

Q2/

2009

Q3/

2009

Q4/

2009

Q1/

2010

Q2/

2010

Q3/

2010

Q4/

2010

Q1/

2011

Q2/

2011

Q3/

2011

Q4/

2011

Q1/

2012

Q2/

2012

Q3/

2012

Q4/

2012

Q1/

2013

Q2/

2013

Q3/

2013

Q4/

2013

Q1/

2014

Q2/

2014

Q3/

2014

Q4/

2014

Mill

ion

s

Source: MECO, Gamah International Ltd. and PDAC calculations

Chart 3j: Flow-Through Financing for "Exploration" by Issuers Listed on Canadian Exchanges

Flow-Through

Total Exploration Financing

25.4%

67.6%

62.3%

54.3%

69.3%

61.2%

68.1%

87.0%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Source: MECO, Gamah International Ltd. and PDAC calculations

Figure 3k: Total Exploration Specific Financing - Share of Flow-Through

31 State of Mineral Finance 2015

March 1, 2015

Regulatory Developments in Canadian Capital Markets

The Canadian capital markets have been going through changes both at the provincial level as well as

structural shift in the way regulations are implemented in Canada. New exemptions along with a

cooperative regulatory regime are major changes to the Canadian regulatory landscape in Canada that

could have a profound impact on the way junior issuers raise capital in Canada.

New Exemptions Could Help

Jurisdictions across Canada are responding to the capital crisis by putting forth a range of ‘exempt

market’ proposals (some of which are new; being adopted by a wider range of jurisdictions; and others

being modified).

On June 18, 2014, PDAC made 8 submissions6 related to four types of exemptions: Offering

memorandum exemption (OM); Family, friends and business associates exemption (FFBA); Existing

security holders exemption; and Crowdfunding (and start-up crowd-funding) exemption.

1. OSC - Existing Security Holder (proposed s. 2.9 of OSC Rule 45-501 Ontario Prospectus and

Registration Exemptions) Proposal to introduce a new prospectus exemption that would allow non-

investment fund issuers listed on certain Canadian stock exchanges to distribute securities to

existing security holders in prescribed circumstances. This exemption is in effect starting February

11, 2015 throughout Canada; however it will be subject to different treatment in Ontario.7

2. OSC - Family, Friends and Business Associates (s. 2.5 and proposed s. 2.6.1 of NI 45-106) - Proposal

to introduce a family, friends and business associates prospectus exemption similar to those in

other CSA jurisdictions for non-investment fund issuers. Ontario will be adopting a Family, Friends

and Business Associates Prospectus Exemption effective May 5, 2015, which will be largely

harmonized with the FFBA exemption in the rest of Canada.

6 To see the full submissions by PDAC on the above regulatory proposal, please click on link:

http://www.pdac.ca/policy/securities/policy/2014/06/23/pdac-comments-on-all-of-the-exempt-

market-proposals-from-provincial-securities-regulators

7 In Ontario, it is not available to investment funds; the issuance must not result in an increase of more

than 100% of the outstanding listed securities of the issuer; and the OSC rule provides for Secondary

Market Disclosure Liability, which includes an right of action for damages as compared to the CSA rule

that provides for Contractual Liability, which includes recession rights.

One area of difference that will be harmonized with the CSA rule is that the OSC rule does not require a

pro-rata distribution requirement. Instead the OSC has provided guidance in the companion policy to

OSC Rule 45-501 – i.e. the OSC expects issuers to “fairly allocate investment opportunities among all of

the issuer’s security holders”.

32 State of Mineral Finance 2015

March 1, 2015

3. OM (s. 2.9 of NI 45-106): AB, SK, QC - Proposal to impose new annual caps on the amount that can

be raised from an individual, to address marketing materials and to require annual financial

statements

4. OM: ON - Proposal to introduce an offering memorandum prospectus exemption similar to the

exemption available in certain other CSA jurisdictions (as proposed to be amended) for non-

investment fund issuers.

5. OM: NB - Proposal to adopt an offering memorandum prospectus exemption on the same terms as

in Ontario

6. Crowdfunding and start-up crowdfunding

a. Crowdfunding - (proposed MI 45-108 Crowdfunding) - SK, MB, QC, NB, NS - Proposal to

introduce a new crowdfunding prospectus exemption for non-investment fund issuers and an

associated registration regime for online funding portals.

b. Start-Up Crowdfunding general and blanket orders - MB, QC, NB, NS - Proposal to introduce

new crowdfunding prospectus and registration exemptions for non-reporting issuers similar to

Saskatchewan’s existing regime

7. Crowdfunding – ON – Crowdfunding Prospectus Exemption and Crowdfunding Portal Requirements

8. Start-Up Crowdfunding (BC Notice 2014/03) - BC - introducing new crowdfunding prospectus and

registration exemptions for non-reporting issuers similar to Saskatchewan’s existing regime for

start-ups

For both the OM and the Crowdfunding exemptions, the regulators are going to decide on a final rule or

a second round of comments by summer of 2015. Additionally, two sets of changes to the prospectus

exemptions under National Instrument 45-106 were recently proposed.

With respect to the Accredited Investor and Minimum Investment Amount:

a new risk acknowledgement form for individual accredited investors that describes, in plain

language, the categories of individual accredited investor and identifies the key risks associated

with purchasing securities in the exempt market;

provide expanded guidance on the steps a seller should take to verify the status of purchasers

acquiring securities under prospectus exemptions, including the AI exemption; and

restrict the MA exemption to distributions to non-individual investors.

33 State of Mineral Finance 2015

March 1, 2015

The Minimum Investment Amount will have limited impact on the mining industry. The addition of an

additional risk acknowledgement form is duplicative considering most private placements subscription

agreements usually have an Investor Certificate of some form attached to them.8

Cooperative Capital Market Regulator – A Tool to Harmonize Regulations

The CCMR is a proposed capital markets regulator that has the potential (if all jurisdictions ‘opt-in’) to

harmonize securities regulations across Canada. The new regulator would be a single, operationally

independent, cooperative capital markets regulator that would administer provincial and federal

legislation, and a single set of regulations. It would create uniform provincial and territorial legislation

for each participating jurisdiction. Complementary federal legislation would be in place to address

criminal matters and matters relating to systemic risk in national capital markets and national data

collection.

Ontario, British Columbia and the federal government initiated the discussion and then Saskatchewan

and New Brunswick joined on July 9, 2014. Prince Edward Island was the last province to join on

September 30, 2014.

PDAC recommends that the participating jurisdictions design the CCMR’s regulations to:

1. Facilitate capital-raising from a broader base of investors to increase global competitiveness. In

order to achieve this recommendation, the PDAC strongly supports modernizing accredited

investor (AI) thresholds and standardizing key prospectus exemptions within the new regulatory

system.

2. Reduce regulatory burden and compliance costs in order to improve efficiency and

competitiveness. PDAC is calling for a simplified, proportional regime for smaller issuers that

eliminate onerous and unnecessary rules for junior exploration companies and other speculative

industries that depend on risk-tolerant capital.

3. Pursue a more effective enforcement regime to increase protection for investors. PDAC strongly

supports effective enforcement as a means to enhance investor confidence in capital markets,

as opposed to just adding more layers of regulation. PDAC is calling for a risk-based approach to

enforcement, with sufficient resources allocated to prosecuting criminals

PDAC has provided detailed comments on the consultation draft of Provincial Capital Markets Act

(PCMA) and the federal Capital Markets Stability Act (CMSA). You can find the submission published on

8 For a revised list of Exempt Market Review, see link

http://www.osc.gov.on.ca/documents/en/News/nr_20150219_family-friends-business-

backgrounder.pdf

Full text of the amendments can be found on link http://www.osc.gov.on.ca/documents/en/Securities-

Category4/ni_20150219_45-106_amendments.pdf

34 State of Mineral Finance 2015

March 1, 2015

the CCMR website: http://ccmr-ocrmc.ca/wp-content/uploads/com_20141208_draft-

legislation_prospectors-developers-association-of-canada.pdf

“The implementation of the Cooperative System will occur in several phases and the parties are working

collaboratively to achieve the agreed upon implementation milestones. These milestones include:

publishing draft initial regulations under the Provincial Capital Markets Act for public comment

by early spring 2015; and

enacting the Provincial Capital Markets Act and the federal Capital Markets Stability Act by June

30, 2015.

The governments are continuing this implementation work with a view to operationalizing the

Cooperative System by the fall of 2015.” Source: CCMR website http://ccmr-ocrmc.ca/

35 State of Mineral Finance 2015

March 1, 2015

Looking Ahead 2014 has come to a close and a new year has already begun. The mining industry, however, continues

to face the same financing challenges that it has faced for the last three years, rooted in macroeconomic

factors such as weak global demand and low commodity prices. Notwithstanding these challenges,

there are signs that the bottom may be near. 2015 may be a pivotal year for the juniors as companies

with low working capital are purchased by, or merge with, companies with high quality assets and

access to capital. In the most optimistic scenario, the industry will see an upward swing in 2016, if

current predictions for global economic growth hold.

As the industry goes through another cyclical downturn, there is also concern that a ‘structural shift’

may be unfolding at the same time that will have significant impacts on the mineral exploration

ecosystem that exists in Canada. This structural shift is a function of an aging retail investor community,

shifts in the broker/dealer landscape that will impact how risk capital flows into juniors, and reforms to

securities regulations that may allow more Canadians to invest in exploration. Industry associations like

the PDAC, along with its provincial and territorial counterparts, will continue work with their members

and stakeholders to navigate these structural and regulatory changes. Survival will require innovation

by both industry and government, from new financing models to securities reforms that facilitate access

to capital and reduce the costs of regulatory compliance.

Fiscal incentives and tax policy will continue to play a key role in attracting risk capital to the exploration

industry. In this regard, the data shows that the flow-through system has been crucial to sustaining

what little financing has taken place in this downturn. This type of innovation in financing has allowed

Canada to become a global mining finance hub, creating economic opportunities in urban centres as

well as the most remote parts of the country. If Canadian jurisdictions continue to support the industry

through sound fiscal policies and reforms to capital markets that have the interests of both investors

and issuers in mind, then the industry will likely be able to survive the current downturn, and witness

better days ahead.

36 State of Mineral Finance 2015

March 1, 2015

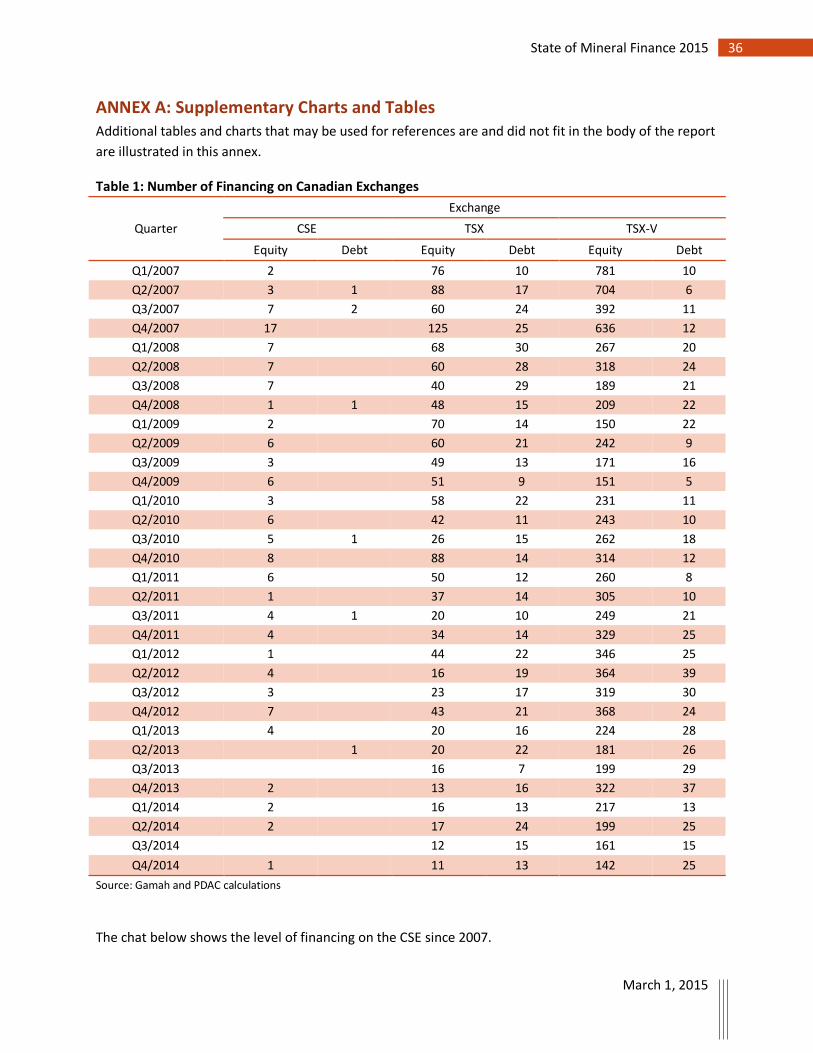

ANNEX A: Supplementary Charts and Tables Additional tables and charts that may be used for references are and did not fit in the body of the report

are illustrated in this annex.

Table 1: Number of Financing on Canadian Exchanges

Quarter

Exchange

CSE TSX TSX-V

Equity Debt Equity Debt Equity Debt

Q1/2007 2

76 10 781 10

Q2/2007 3 1 88 17 704 6

Q3/2007 7 2 60 24 392 11

Q4/2007 17 125 25 636 12

Q1/2008 7

68 30 267 20

Q2/2008 7 60 28 318 24

Q3/2008 7

40 29 189 21

Q4/2008 1 1 48 15 209 22

Q1/2009 2

70 14 150 22

Q2/2009 6 60 21 242 9

Q3/2009 3

49 13 171 16

Q4/2009 6 51 9 151 5

Q1/2010 3

58 22 231 11

Q2/2010 6 42 11 243 10

Q3/2010 5 1 26 15 262 18

Q4/2010 8 88 14 314 12

Q1/2011 6

50 12 260 8

Q2/2011 1 37 14 305 10

Q3/2011 4 1 20 10 249 21

Q4/2011 4 34 14 329 25

Q1/2012 1

44 22 346 25

Q2/2012 4 16 19 364 39

Q3/2012 3

23 17 319 30

Q4/2012 7 43 21 368 24

Q1/2013 4

20 16 224 28

Q2/2013 1 20 22 181 26

Q3/2013

16 7 199 29

Q4/2013 2 13 16 322 37

Q1/2014 2

16 13 217 13

Q2/2014 2 17 24 199 25

Q3/2014

12 15 161 15

Q4/2014 1 11 13 142 25

Source: Gamah and PDAC calculations

The chat below shows the level of financing on the CSE since 2007.

37 State of Mineral Finance 2015

March 1, 2015

Table 2: Metal Price Index (2007=100) Forecasts

Year 2007 2008 2010 2012 2014 % Change from 2007 to 2014

2015 2016 2017

Commodity Price Index

100.0 127.7 112.8 137.7 132.6 32.6% 127.8 126.0 124.2

Crude Oil 100.0 136.4 111.1 147.6 144.5 44.5% 139.7 136.9 134.2

Metal Price Index 100.0 92.2 110.4 104.2 92.3 -7.7% 90.7 91.2 91.6

Copper 100.0 97.6 105.7 111.6 98.0 -2.0% 98.9 98.8 98.4

Aluminum 100.0 97.7 82.3 76.6 72.0 -28.0% 80.2 82.1 84.1

Iron Ore 100.0 168.1 400.5 350.9 282.7 182.7% 230.4 231.0 231.0

Tin 100.0 127.4 140.5 145.6 155.2 55.2% 152.0 158.8 158.8

Nickel 100.0 56.9 58.7 47.2 47.8 -52.2% 51.4 51.5 51.2

Zinc 100.0 58.0 66.5 60.0 67.6 -32.4% 72.9 72.7 72.2

Lead 100.0 81.2 83.3 80.0 84.1 -15.9% 88.1 88.5 88.7

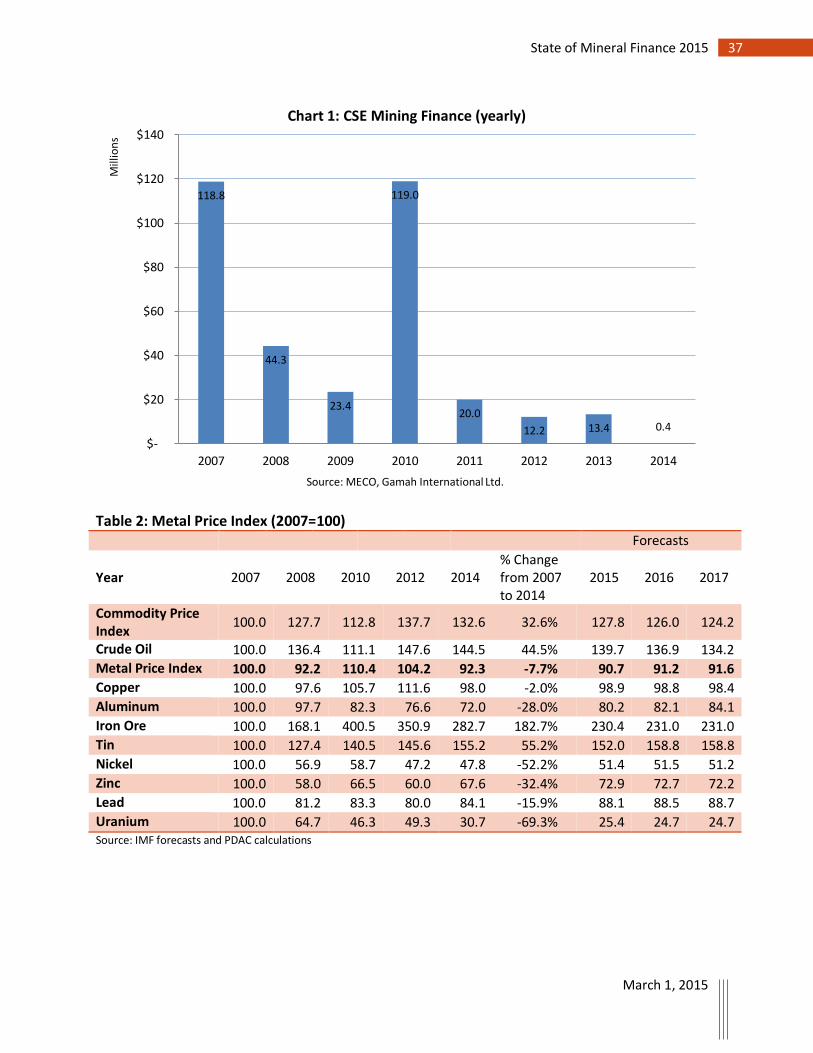

Uranium 100.0 64.7 46.3 49.3 30.7 -69.3% 25.4 24.7 24.7 Source: IMF forecasts and PDAC calculations

118.8

44.3

23.4

119.0

20.0

12.2 13.4 0.4

$-

$20

$40

$60

$80

$100

$120

$140

2007 2008 2009 2010 2011 2012 2013 2014

Mill

ion

s

Source: MECO, Gamah International Ltd.

Chart 1: CSE Mining Finance (yearly)

38 State of Mineral Finance 2015

March 1, 2015

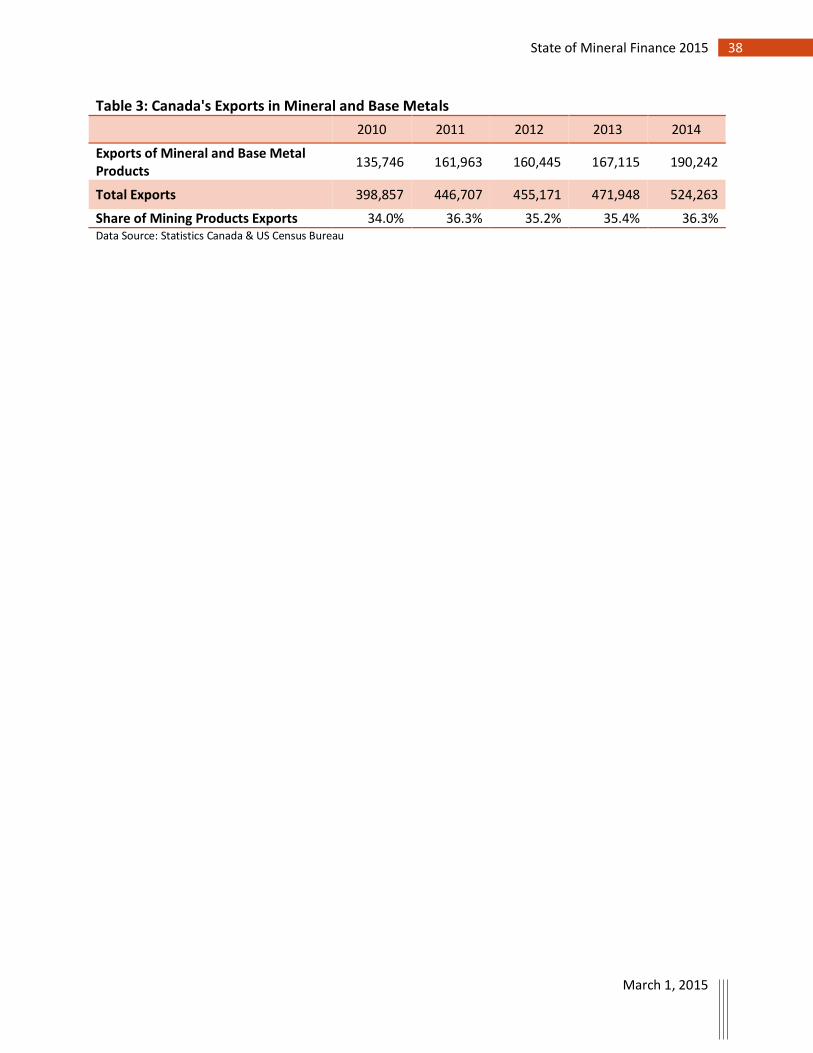

Table 3: Canada's Exports in Mineral and Base Metals

2010 2011 2012 2013 2014

Exports of Mineral and Base Metal Products

135,746 161,963 160,445 167,115 190,242

Total Exports 398,857 446,707 455,171 471,948 524,263

Share of Mining Products Exports 34.0% 36.3% 35.2% 35.4% 36.3% Data Source: Statistics Canada & US Census Bureau

39 State of Mineral Finance 2015

March 1, 2015