REI - World Bank Documents & Reports

81

RESTR I CTED REI Report No. PA- 18# This report was prepared for use within the Bank and its affiliated organizations. They do not accept responsibility for its accuracy or completeness. The report may not be published nor may it be quoted as representing their views. INTERNATIONAL BANK FOR RECONSTRUCTION AND. DEVELOPMENT INTERNATIONAL DEVELOPMENT ASSOCIATION SECOND LIVESTOCK DEVELOPMENT PROJECT COLOMBIA September 3, 1969 Agriculture Projects Department Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

Upload

khangminh22 -

Category

Documents

-

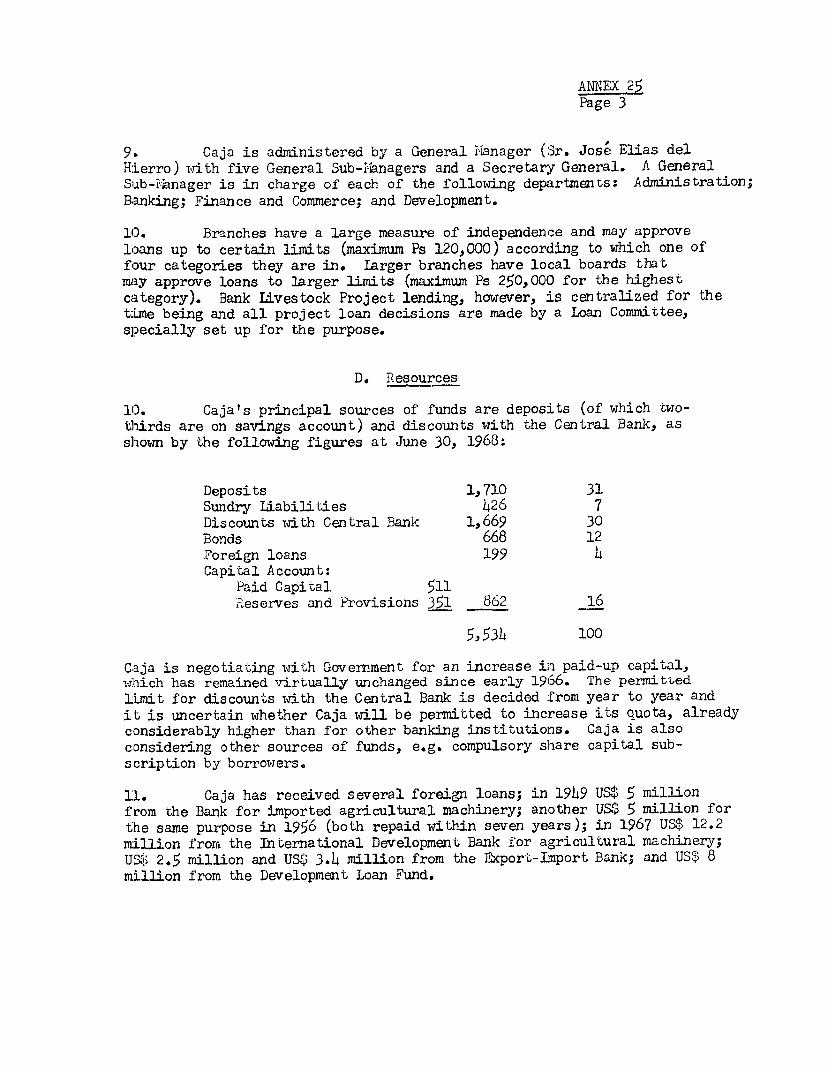

view

1 -

download

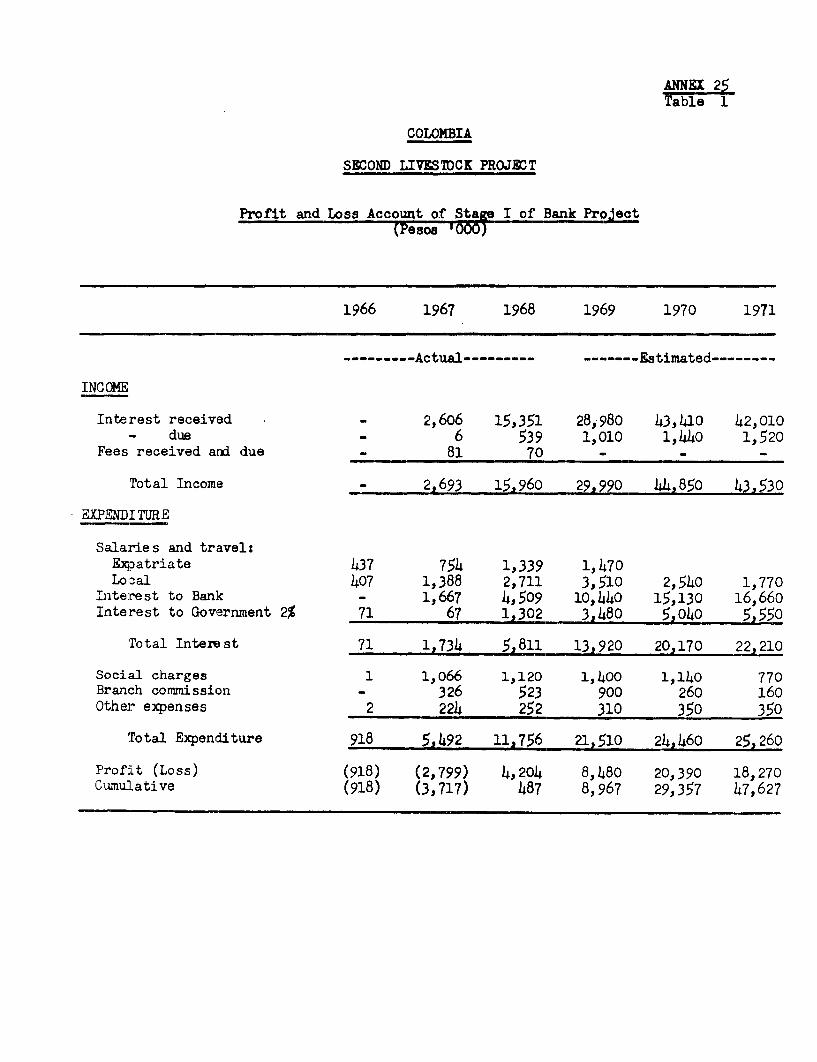

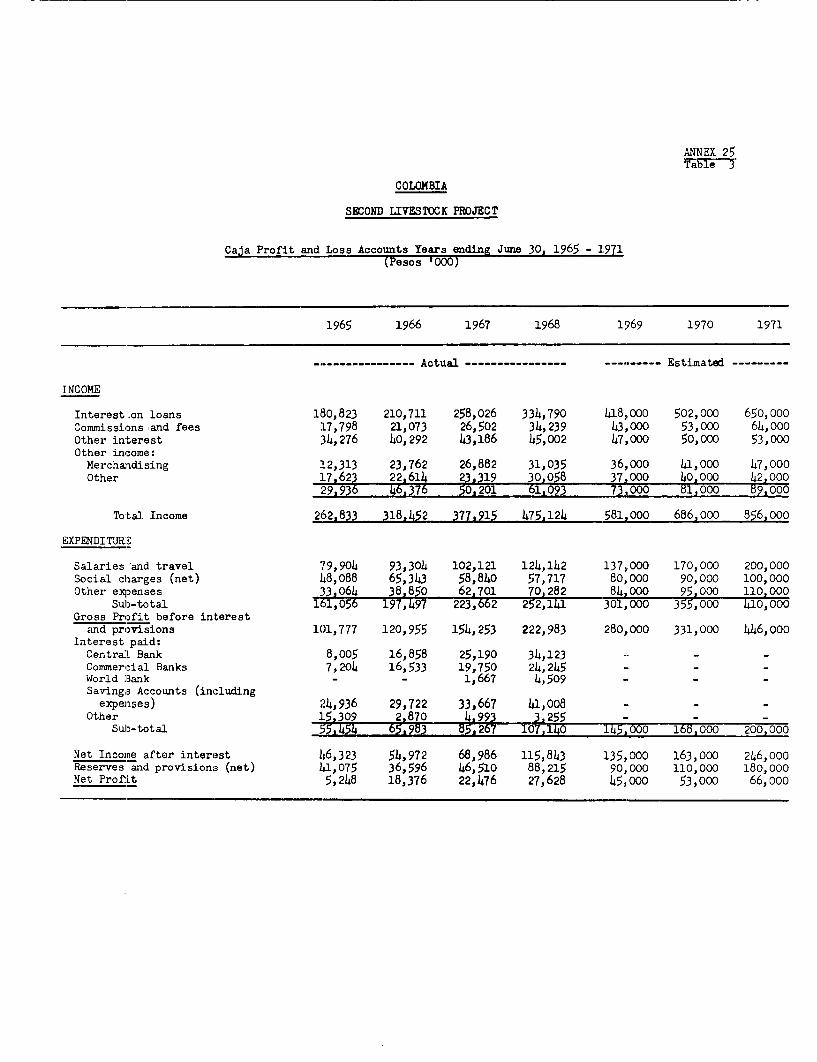

0

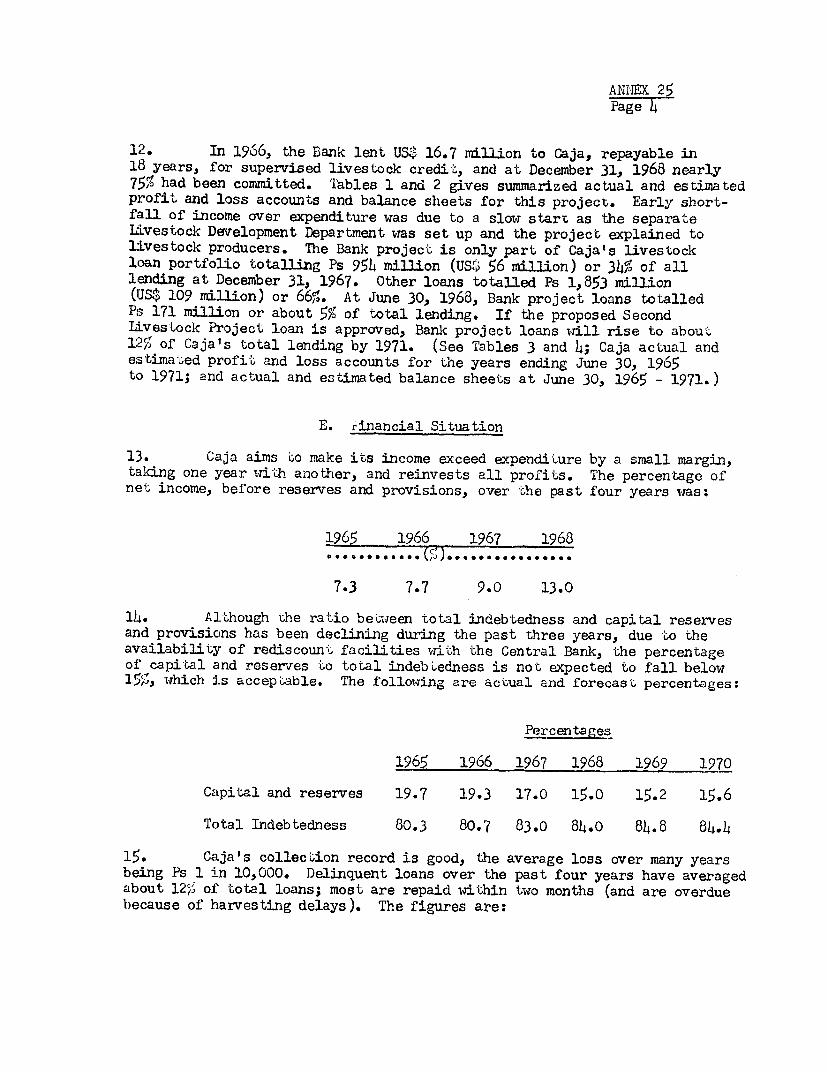

Transcript of REI - World Bank Documents & Reports

RESTR I CTEDREI Report No. PA- 18#

This report was prepared for use within the Bank and its affiliated organizations.They do not accept responsibility for its accuracy or completeness. The report maynot be published nor may it be quoted as representing their views.

INTERNATIONAL BANK FOR RECONSTRUCTION AND. DEVELOPMENT

INTERNATIONAL DEVELOPMENT ASSOCIATION

SECOND LIVESTOCK DEVELOPMENT PROJECT

COLOMBIA

September 3, 1969

Agriculture Projects Department

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVAIENTS

US$ 1 - Colombian Pesos 17.20Colombian Peso 1 = US$ 0.o58Colombian Peso 1,000,000 0 US$ 58,140

WEIGHTS AND MEASURES

Metric System

1 kilogram (kg) m 2.20 pounds1,000 kg - 1 metric ton a 0.98 long ton1 meter (m) - 1.09 yards1 kilometer (k2) = 0.62 mile1 hectare (ha) G 10,000 m2 = 2.47 acres1 squi9re kilometer = 100 ha = 0.39 square mile

- 247.11 acres1 liter = 0.26 gallon

GLOSSARY OF ABBREVIATIONS

AFF - Agricultural Financing FundCaja - Caja de Credito Agrario, Industrial y MineroCOFIAGRO - Corporation for Promotion of Agriculture and Livestock

ExportsFEDEGAN - Federation of Colombian Livestock ProducersFMD - Foot-and-Mouth-DiseaseGDP l Gross Domestic ProductICA - Agriculture and Livestock Institute of ColombiaIDEMA - Agrarian Marketing InstituteLA?TA - Latin American Free Trade AssociationLDD - Livestock Development DepartmentUSAID - United States Agency for International Development

COLOMBIA

SECOND LIVESTOCK DEVELOPMENT PROJECT

TABLE OF CONTENTS

Page No.

SUMMARY AND CONCLUSIONS . . . . . .

I. INTRODUCTION .1... . . . . . . . . . . . . . . . . . . .

II. BACKGROUND .1... . . . . . . . . . . . . . . . . . . . .

A. General .1... . . . . . . . . . . . . . . . . . . . .B. The Livestock Sub-sector . . . . . . . . . . . . . . . 2C. Animal Health . . . . . . . . . . . . . . . . . . . . . 4D. Government Policies and Agricultural Services . . . . . 5E. The First Livestock Development Project Loan 448-Co . 6

III. THE SECOND PROJECT . . . . . . . . . . . . . 8. . . . . . . 8

A. General Description . . . . . . . . . . . 8. . . . . . . 8B. Detailed Features. 9C. Cost Estimates .11D. Proposed Financing .13E. Procurement . . . . . . . . A . . . . . . . . . . . . . 14F. Disbursements and Auditing . . . . . . . . . . . . . . 15G. Organization and Management . . . . . . . . . . . . . . 15H. Lending Operations . . . . . . . . . . . . . . . . . . 17I. Financial Operating Results . . . . . . . . . . . . . . 17

IV. MARKETS, PRICES AND RANCHERS' BENEFITS . . . . . . . . . . 18

A. Markets and Prices .18B. Ranchers' Benefits . . . . . . . . . . . . . . . . . 18

V. ECONOMIC BENEFITS AND JUSTIFICATION . . . . . . . . . . . . 20

VI. RECOMMENDATIONS . . . . . . . . . . . . . . . . . . . . . . 20

This appraisal report is based on the findings of a mission whichvisited Colombia in January/February 1969. The report was prepared by Messrs.J. C. Gerring, P. G. Nelson, C. M. Bell and J. C. Percival.

ANNEXES

1. Government Policies and Agricultural Services

2. Banking and Credit

3. Loan 448-Co - Details of Investments

4. La Costa - Capital Expenditure and Financing

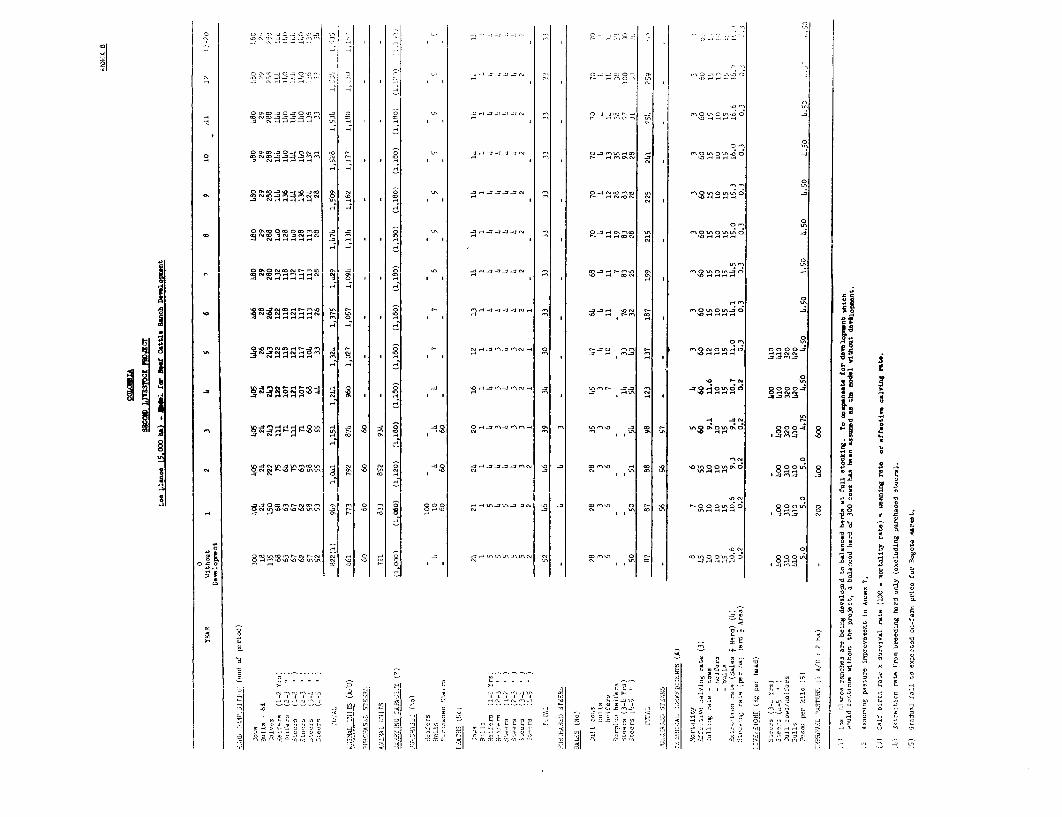

5. - Model for Beef Cattle Ranch Development

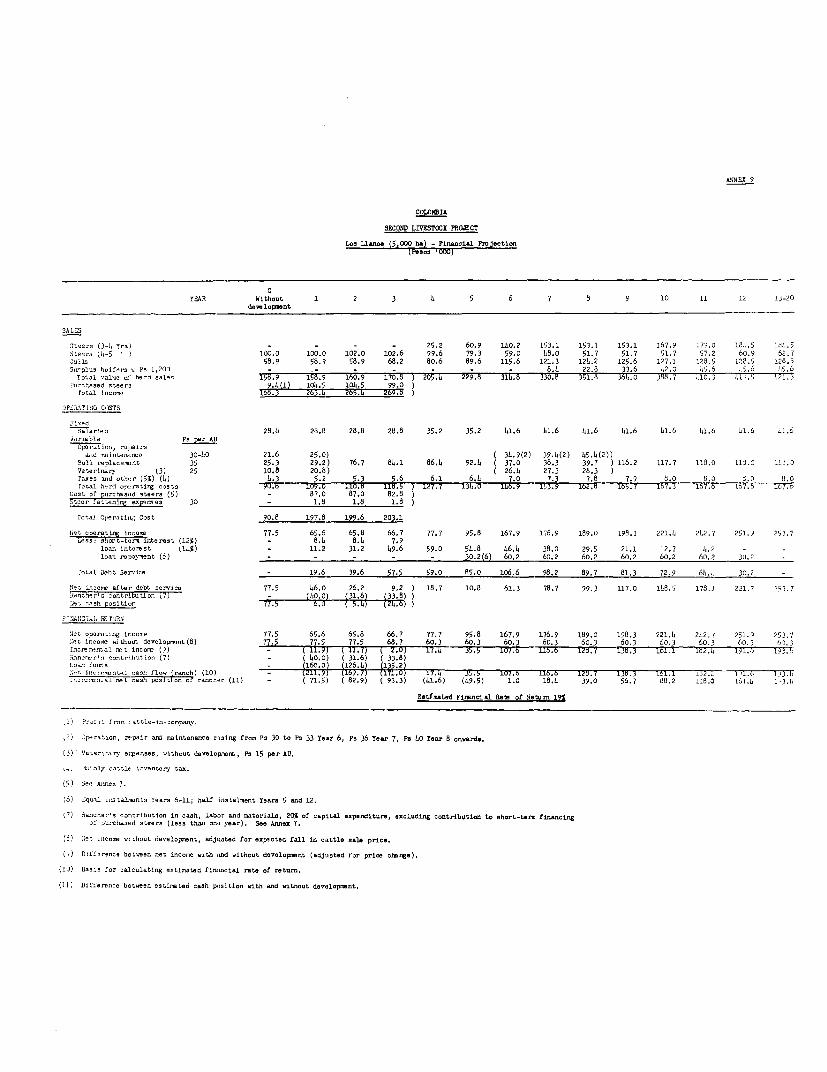

6. - Financial Projections

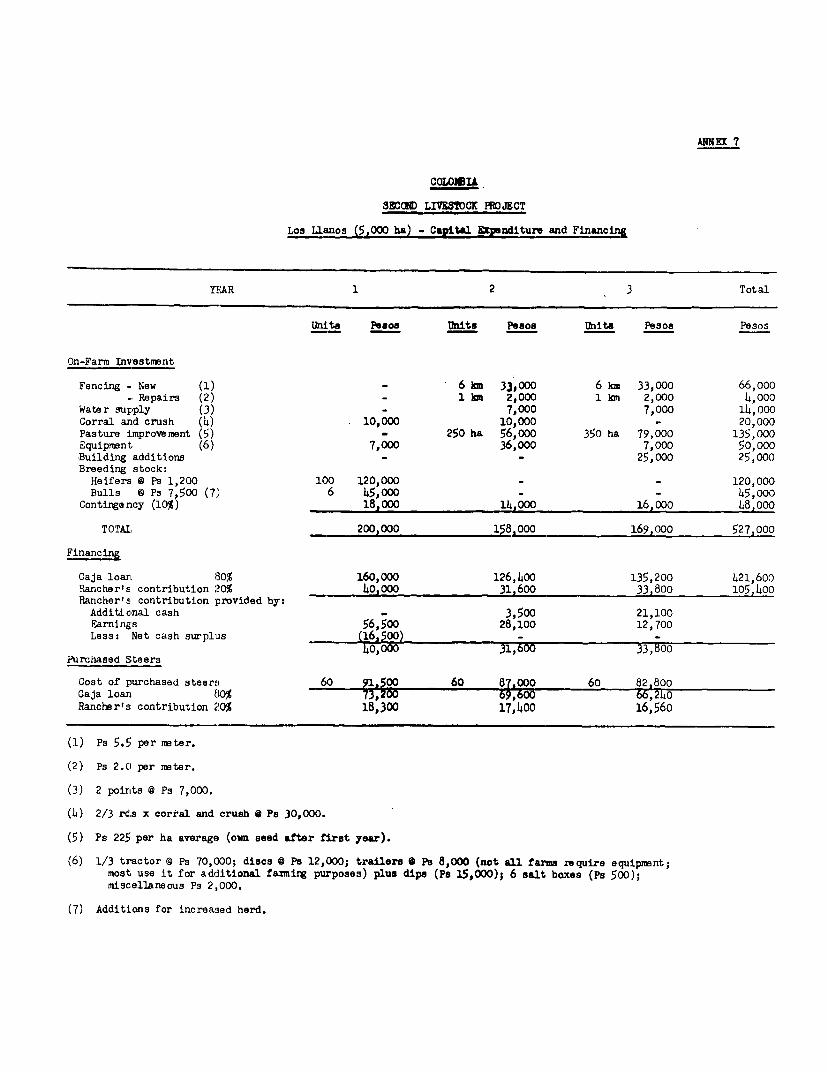

7. Los Llanos - Capital Expenditure and Financing

8. - Model for Development

9. - Financial Projections

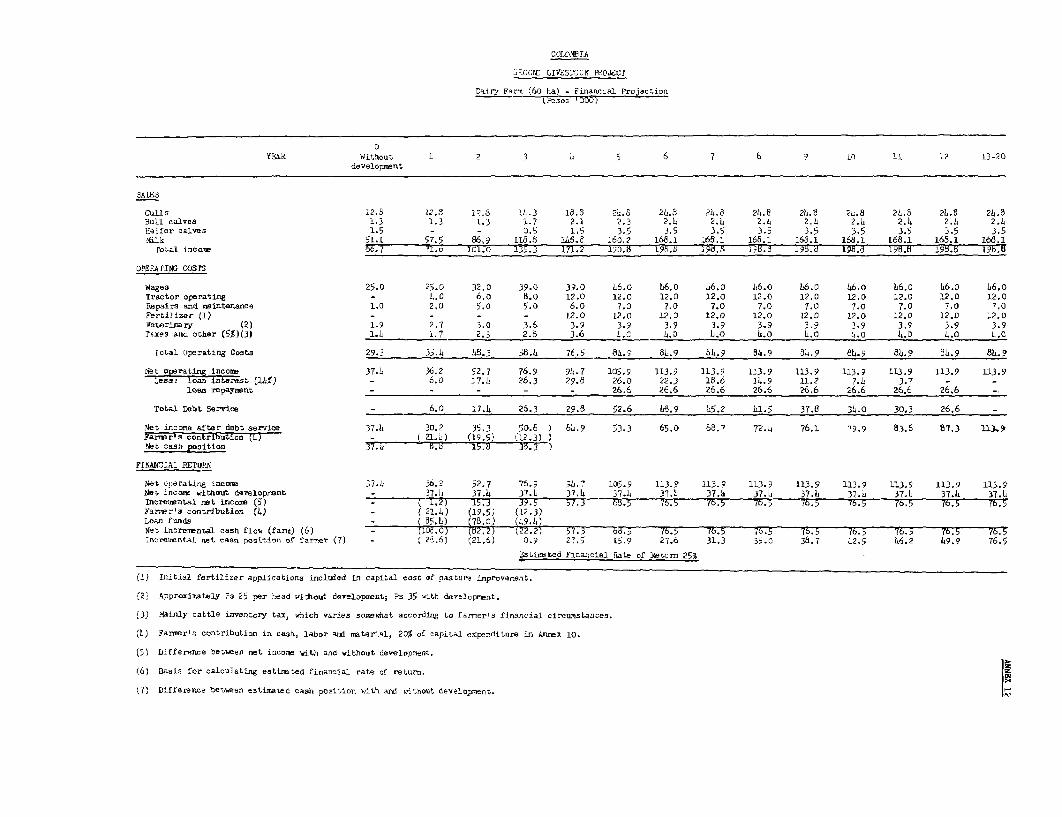

10. Dairy Farms - Capital Expenditure and Financing

11. - Model for Development

12. - Financial Projections

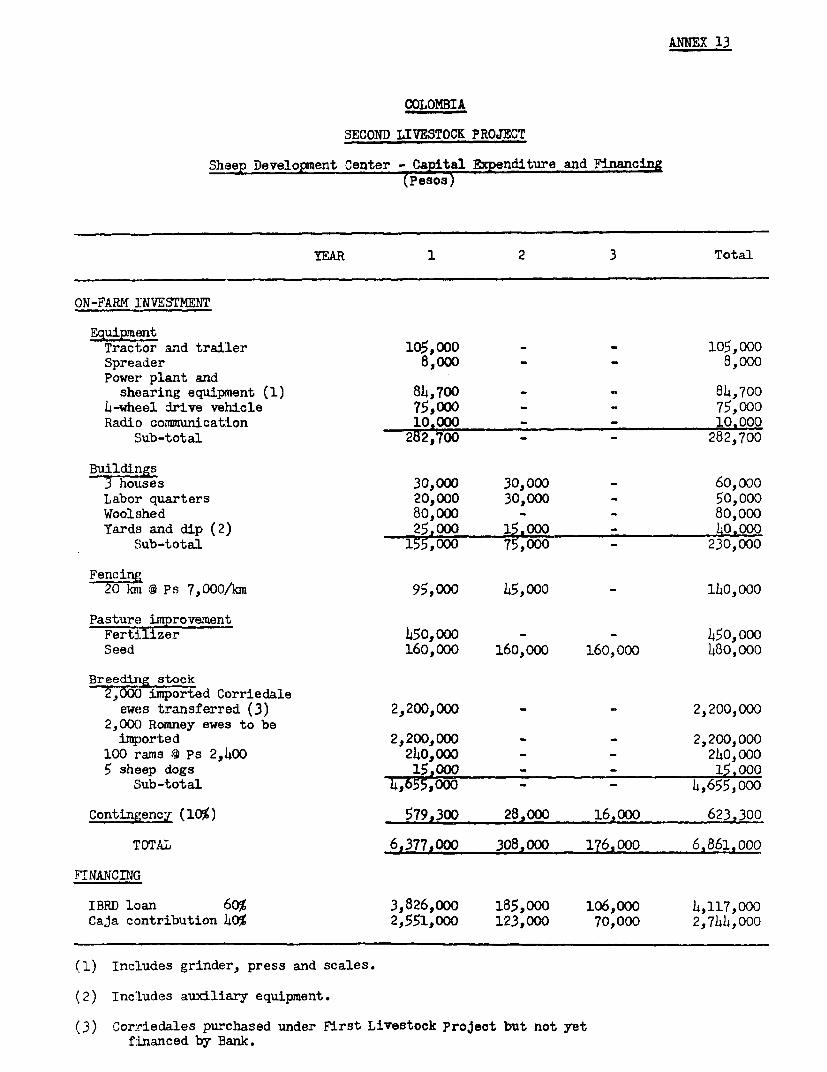

13. Sheep Development Center - Capital Expenditure and Financing

14. - Financial Projections

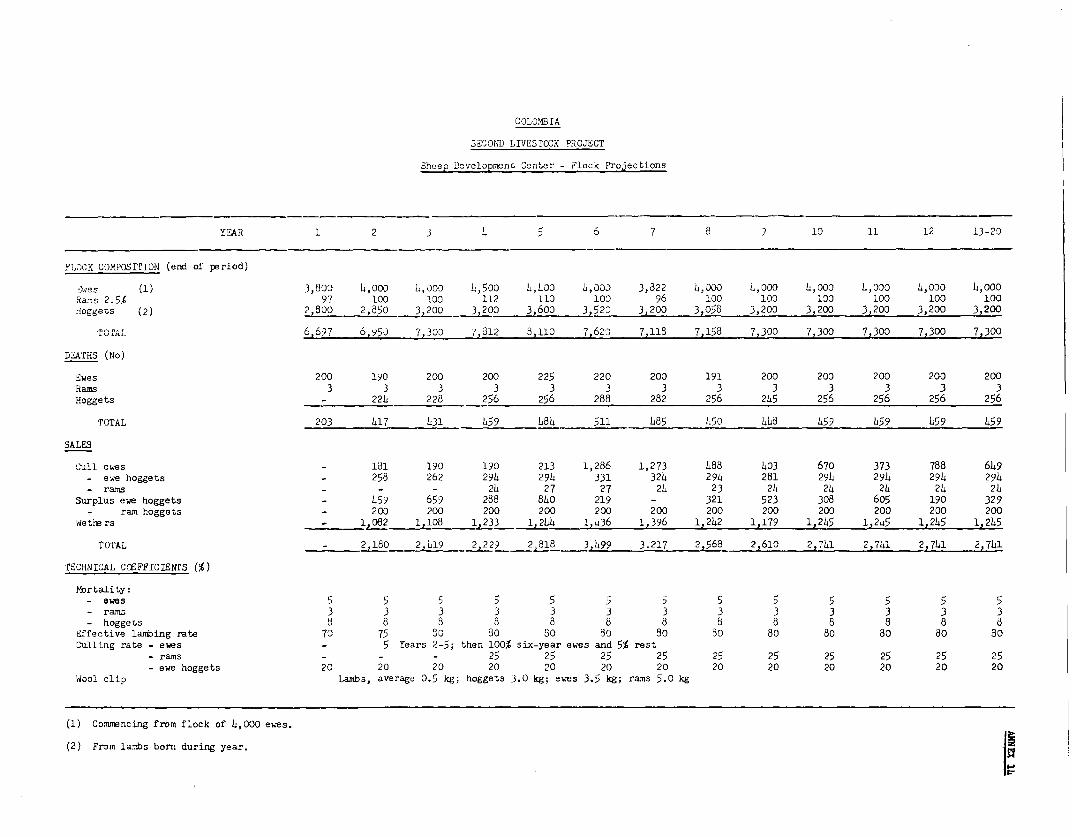

15. - Flock Projections

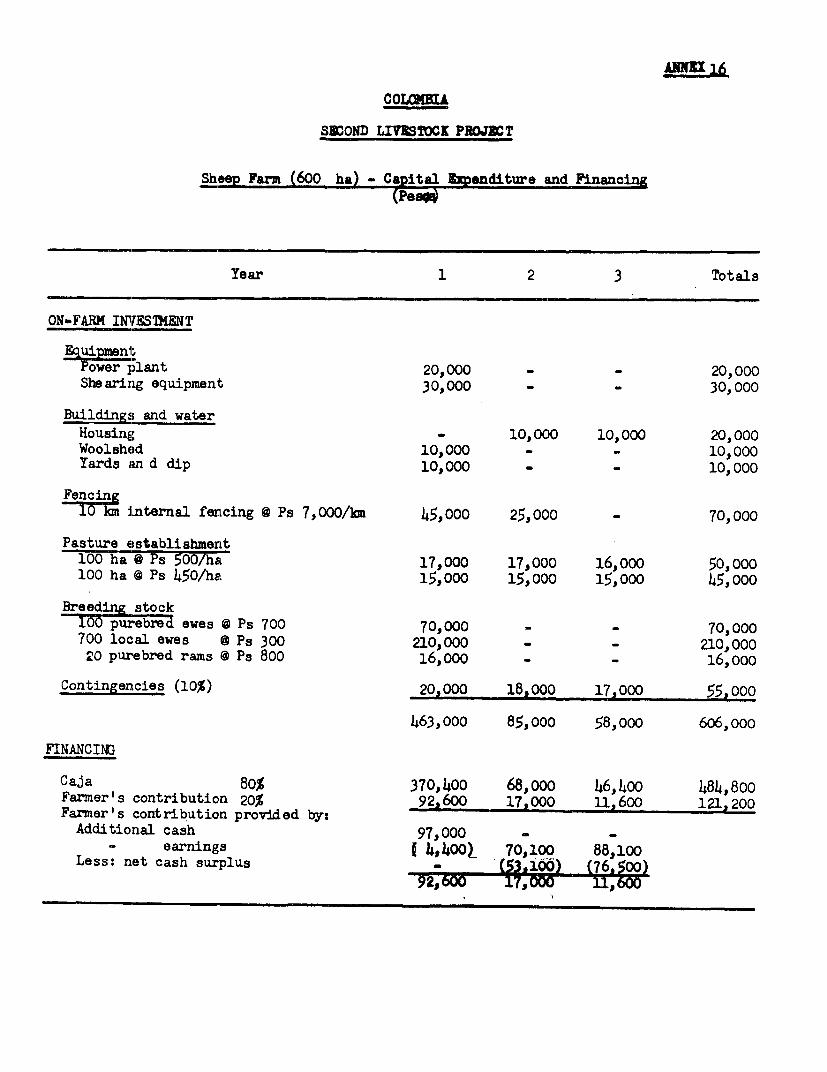

16. Sheep Farms - Capital Expenditure and Financing

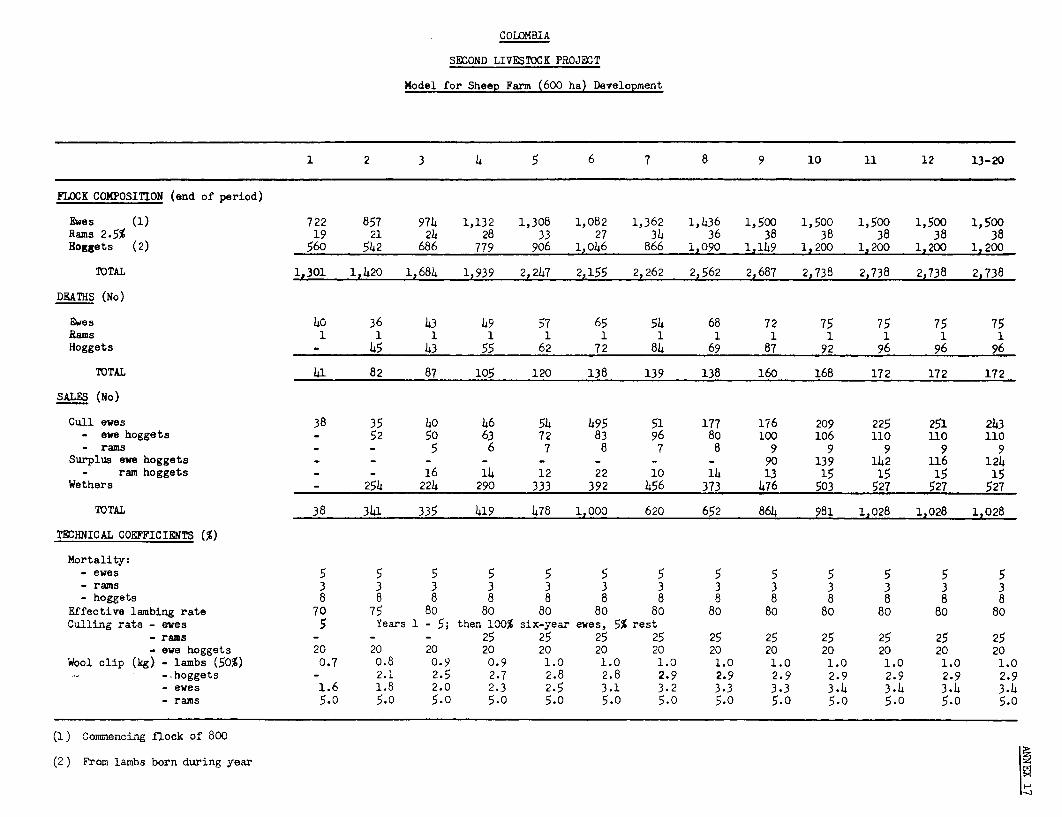

17. - Model for Development

18. - Financial Projections

19. Phasing of Investment and Financing

20. Cost of Technical Services

21. Project Cash Flow

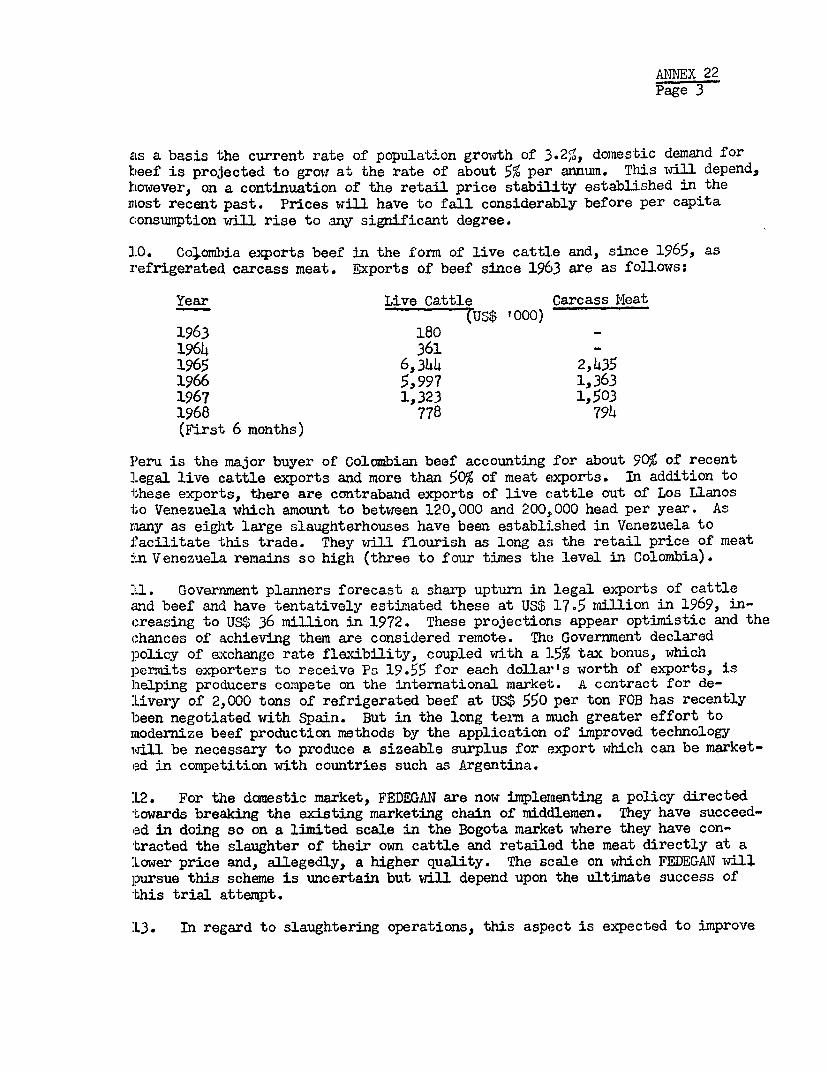

22. Marketing

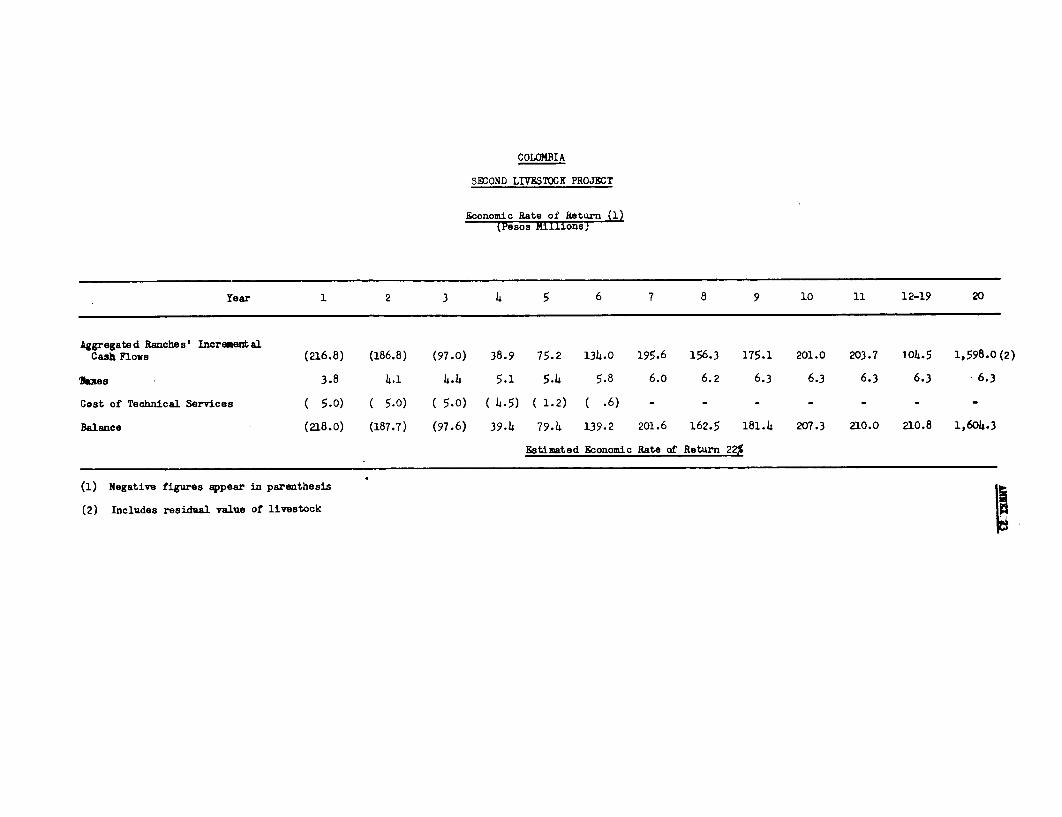

23. Economic Rate of Return

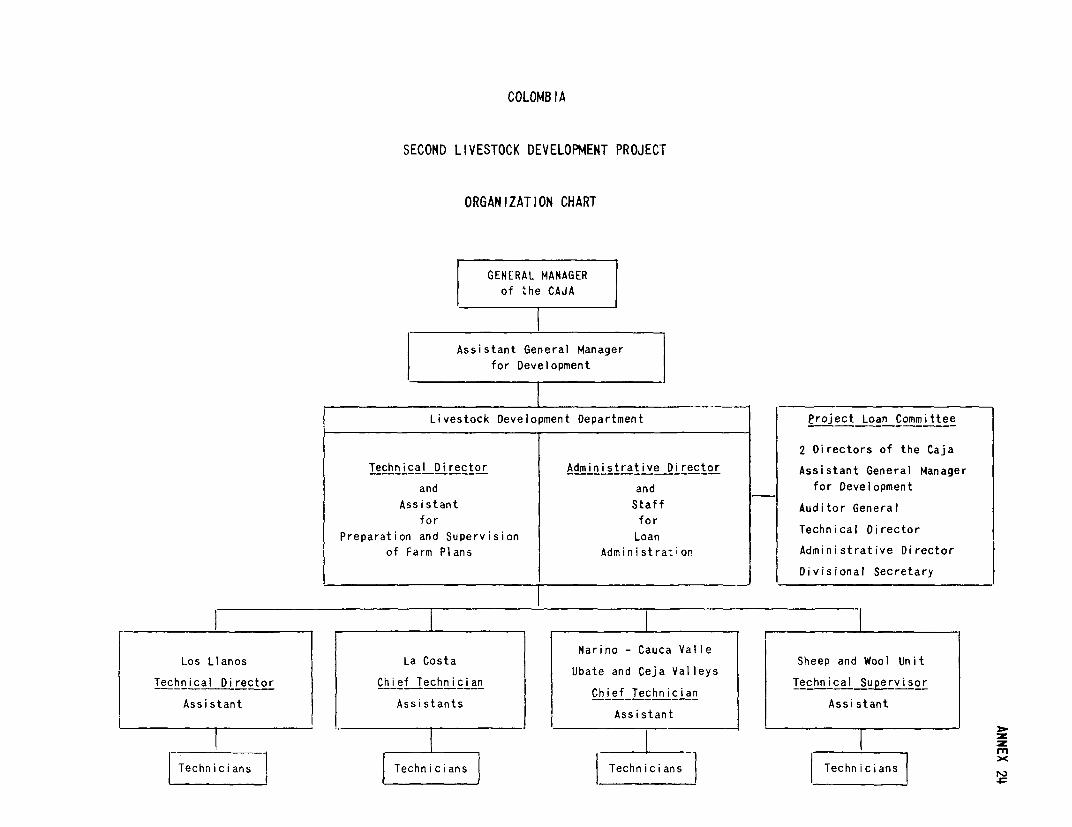

24. Organization and Management Organogram

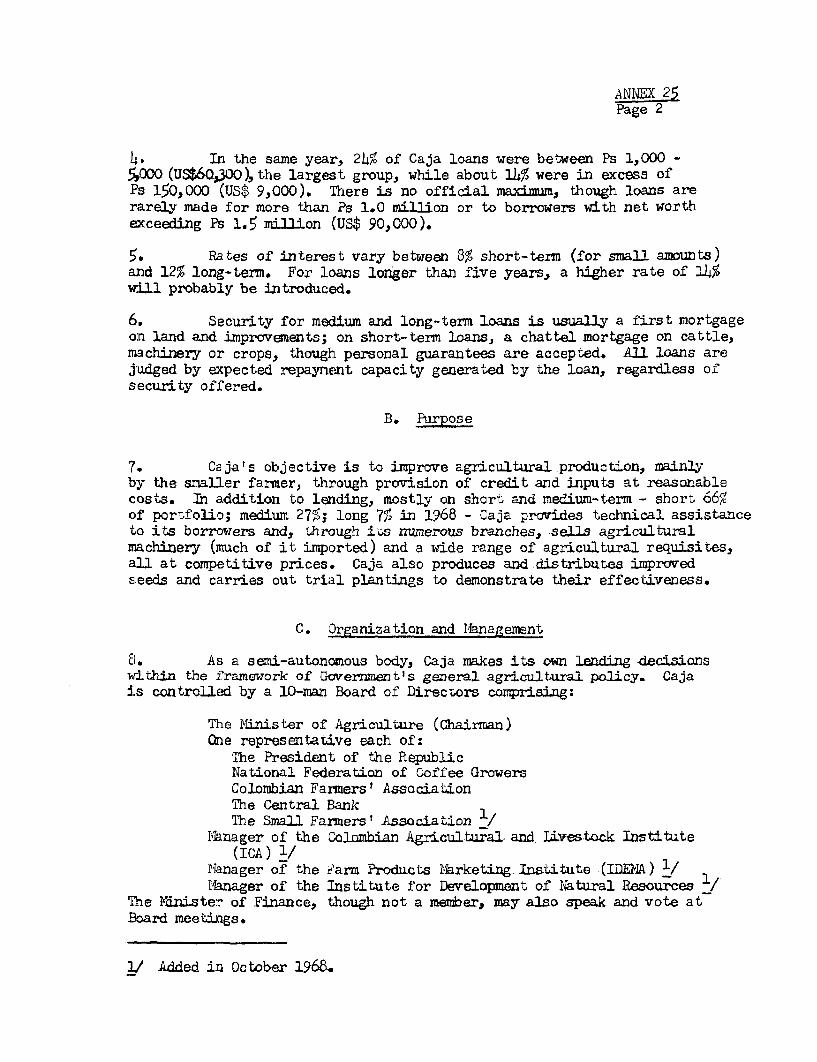

25. The Agrarian Industrial and Mining Credit Bank(Caja de Credito Agrario Industrial y Minero)

MAP

COLOMBIA

SECOND LIVESTOCK DEVELOPMENT PROJECT

SUMMARY AND CONCLUSIONS

i. A livestock project in Colombia is appraised in this report. TheProject is an extension of a development program started in 1966 when BankLoan 448-co of US$ 16.7 million was granted. Although coffee remains themain earner of foreign exchange in the country, livestock accounts for overhalf of agriculture's contribution to the Gross Domestic Product (GDP). TheGovernment recognizes that continued economic growth is to a large degreedependent on modernization of the livestock industry and that livestock pro-ducts could become important export commodities.

ii. Up to September, 1969, loans totalling about US$ 15 million wereapproved under the first project by Caja de Credito Agrario, Industrial yMinero (Caja) - the intermediary credit institution. These were extended toabout 630 operators - 530 beef, 90 dairy and 8 sheep. While the period is tooshort to evaluate a livestock operation, progress has been good and it isevident that the development plans being financed and implemented are soundlybased.

iii. The proposed loan would extend the on-going first projects over afour year period and would be directed at increasing the production of beef,dairy products, and wool, with major emphasis in the North Coast region. Itis estimated that an additional 700 beef ranchers, 250 dairy farmers and 20wool growers would be involved. Incremental investments would be similar tothose in the first project and would be principally for pasture improvement,breeding stock, fencing, buildings, agricultural equipment and machinery.To facilitate the development of a commercial sheep industry, the projectwould establish a Sheep Development Center with breeding and training func-tions.

iv. Loans for farm development would be made by Caja at 14% interestper annum for terms of 12 years, including grace periods of 4 years for beefand dairy producers and 6 years for wool growers. Investments on each ranchwould be phased over three years.

v. Caja - the Administering Agency - would be responsible for projectorganization and management as was the case with the first loan. The Live-stock Development Department within Caja would be responsible for the prepa-ration and implementation of farm development plans. 'The technical staffwould be headed by a technical director, two regional chief technicians, anda technical supervisor of a sheep and wool unit to be established in theLivestock Development Department. Development plans prepared by the technicalstaff and approved by the technical director would be the basis for loan ap-provals by the Project Loan Committee.

vi. Project costs are estimated at about US$ 44.1 million, of whichabout US$ 29.6 million would be for farm development. The remainder would

be for technical services, incremental operating costs, interest paymentsduring development, and short-term finance for feeder steers. Except fornearly one-half, of the cost of technical services, these items would befinanced by Caja and partcipating farmers. Project costs would be financedapproximately as follows:

Amount Percent(USTM)

IBRD 18.3 42

Caja 9.5 21

Ranchers 16.3 37

44.1 100

vii. Project goods that could be ordered in bulk would be procured byCaja through international competitive bidding. This would be fertilizers,pasture seeds, weedicides, and fencing materials. Manufactured inputs forwhich bulk procurement is not practicable and which are available eitherlocally or do not require import licenses, would be obtained through exist-ing commercial channels in Colombia. The Government would enable all othermanufactured items of the type used as Project inputs to be imported byCaja as promptly as needed. All livestock would be locally supplied exceptsheep which would be imported.

viii. Disbursements of the Loan would be made to the Agricultural Financ-ing Fund (AFF), a special fund managed by the Banco de la Republica. Dis-bursements would be made on the following basis:

- 75% of the amount disbursed by Caja for farm loans;

- 60% of disbursements made by Caja for goods and servicesprocured for the development of the Sheep DevelopmentCenter;

- 100% of the foreign exchange cost of technical services.

For goods purchased through international competitive bidding, payments wouldbe made directly from the AFF special fund to such foreign suppliers.

ix. The ratte of return to the economy would be about 22%. Participat-ing livestock producers would earn about 20% to 25% of their incremental in-vestments and would realize substantial increases in their net earnings be-ginning with Years 7-10 when full farm development would be achieved.

x. The second livestock project is suitable for a Bank loan of US$ 18.3million for a term of 18 years including a grace period of 6 years. Abouttwo-thirds of the Loan would cover the estimated foreign exchange component

- iii -

and the other one-third would be for local costs. The Borrower would be theGovernment which would bear the foreign exchange risk. It would on-lend theLoan proceeds through the Agricultural Financing Fund, Banco de la Republica(Central Bank) to Caja at not more than 10.5% interest on the same amortiza-tion as for the, Bank loan.

COLOMBIA

SECOND LIVESTOCK DEVELOPMENT PROJECT

I. INTRODUCTION

1.01 The Government of Colombia has requested a second loan to helpfinance the continuation of its program of livestock development. This wasinitially supported by the Bank with a loan of US$ 16.7 million (448-co),1966. Results of the first project have been satisfactory and commitmentsare more than a year ahead of schedule.

1.02 In connection with the first loan, a joint Bank/FAO mission visitedColoimbia in March/April 1965. This mission assessed the potential of thelivestock industry and, within the framework of an overall development plan,assisted the Colombian authorities to prepare a project suitable for Bankfinancing. The outcome was a three-year development project, administeredby the Caja de Credito Agrario, Industrial y Minero (Caja) embracing threesegments of the livestock industry; namely, beef cattle, dairy cattle andsheep. This first application was appraised by a joint Bank/FAO mission inOctober/November 1965. Because the proposed loan is a continuation of aBank project, a review of the first project is included in this report.

1.03 This appraisal report is based on the findings of a mission whichvisited Colombia in January/February 1969. The mission was composed ofMessrs. J. C. Gerring (leader), P. G. Nelson, C. M. Bell (Bank) and J. C.Percival (Consultant).

II. BACKGROUND

A. General

22.01 Colombia, with an area of 1.14 million km , is the fourth largestcountry in South America. Though situated within the tropics (latitude 130Nto 4OS), its land surface ranges in altitude and contour from low-lying flatplains to open highland savannahs and mountains which rise steeply to morethan 5,000 meters above sea level. In consequence, there are considerablevariations in climate and a wide range of ecological zones. Virtually anykind of crop or pasture can be grown.

2.02 The population, increasing at around 3.2% per annum, is about 20million. Economic growth (GDP) has fluctuated between 3% and 6% per year,in real terms, during the last five years. At the end of 1968, average percapita income was about US$ 287 equivalent.

2.03 Agriculture accounts for about 30% of GDP, 75% of total exports, 95%of the food supply, and over 50% of the supply of industrial raw materials.The sector employs about 50% of the Colombian work force. Coffee currentlyaccounts for 60% of total commodity exports, but because of market limitations

-2-

under the International Coffee Agreement, the Government places high priorityon diversification. Since 1958, growth of non-coffee agriculture has reacheda level of about 4.3% per year, due mainly to an expansion in acreage. Des-pite this, only about a quarter of the land area is now used for agriculture,including livestock production. While there is still much room for furtherexpansion, the real and most immediate need is to intensify productionmethods through improved technology and credit, with the objective to outpacegrowth in domestic demand and thus produce supplies for export. Moderniza-tion, of the livestock sub-sector, and, in particular, the beef cattle sectorwould make an important contribution towards achieving this objective.

2.04 Colombia's foreign exchange gap and the related problem of infla-tion have been the most persistent barriers to sustained growth of the econ-omy. Government policies aim to arrest the past rate of inflation and pro-vide incentives for the development of non-coffee exports within the con-straint of a tight monetary program. Attesting to a measure of success, pricesincreased in 1968 by 6.4%, as compared to 8% in 1967 and 16% in 1966, and minorexports are increasing at the target rate of about 20% per annum. 1/

B. The Livestock Sub-Sector

2.05 Output from the livestock sub-sector, over 80% of which is beef,contributes about 17% of GDP. The cattle industry, in fact, occupies almost90% of the land now used for the whole of the agricultural sector. This im-pressive pasture resource, approximating some 30 million ha, gives someindication of the potential for increasing production. Further vast areas ofboth tropical lowlands and temperate highlands await development.

Beef Cattle

2.o6 The national herd is estimated at around 18 million head. By roughestimate, about 85% is beef and the remainder dairy cattle; combined beef/dairy operations are common. The tropical regions of the North Coast (LaCosta) including the lower Magdalena and Cauca River Valley, contain most ofthe country's beef cattle. In this area, as well as in the middle MagdalenaValley, ranching is more developed than in other parts of the country. Inthe tropical lowlands of the Eastern Plains (Los Llanos), ranching is stillat a more primitive stage and is based on the use of natural unimprovedpastures.

2.07 Since 1963, around 2 million cattle have been slaughtered annually(these official estimates do not include subsistence killings, or illegal ex-ports 2/). This offtake of approximately 12% reflects the present low level

1/ See the Bank's 1968 Economic Report, "Current Economic Position andProspects of Colombia"

2/ Exports for which the foreign exchange iB not surrendered to the CentralBank.

- 3 -

of productivity, as well as the existing potential for a substantial increase.An of'ftake of 20% would be a reasonable target.

2.08 Beef consumption per capita is around 20 kg per year 1/, and atthis level, Colombia has been consuming most of the beef it produces. Highconsumer prices in relation to incomes have limited the growth in domesticdemand; also, producers' prices, averaging US$ 0.30 equivalent per kg live-weight, are higher than most world market prices, which average aroundUS$ C.27. Thus, it is difficult to export under present conditions. Re-cently, a more f'lexible exchange rate and a 15% export tax bonus 2/ haveimproved the prospects for increasing exports. But for these to besignificantly ernlarged and sustained, a major improvement in the presentstandard of ranch and herd management will be essential.

Dairy Cattle

2.09 About 3.5 million cattle contribute to milk production under a widerange of climatic conditions. Methods of production and levels of outputvary considerably. In the temperate zones, dairying is more intensive withEuropean breeds, Holstein and Brown Swiss, predominating. In the tropicalregions, and particularly in the North Coast, Criollo/Zebu crossbred cattleare used as well as beef cows which, in addition to rearing their calves,are commonly milked once daily.

2.10 The more specialized dairy farms tend to be concentrated aroundurban centers. In such areas, land values are high and competition fromcash cropping is considerable. Under these conditions, milk production usingexisting methods is a high-cost, marginal enterprise. Population increaseshave led to a growing consumer demand, and steadily rising prices have broughtabout a considerable extension of the milk producing areas so that processorsare collecting milk from lower-cost producers over gradually increasing dis-tances. The resulting high cost of transport is a critical factor in somezones.

2.11 Milk production is estimated at around 2 million tons per year orbelow 4 litres per day per cow in milk. This is a low average yield. Abouthalf of the milk is consumed directly, largely in the raw state. Most of theremainder is usedi for on-farm production of cottage cheese and butter, witha small percentage (less than 5%) also going into powdered and condensed milk.There is little, if any, control over quality standards.

1/ I'er capita beef consumption in South America ranges from 8 kg (Bolivia)to 80 kg (Argentina).

2/ Exporters of goods, other than coffee and petroleum, are issued taxexemption certificates equivalent in value to 15% of exports. Thesemay be traded at a discount or used after one year of issuance fortax payments.

2.12 While there are no serious technical barriers to considerable in-creases in production, economic factors until recently have imposed severelimitations to expansion. Alternative use of land for high value cash cropsreduced dairying in some areas. In a few areas, the threat of compulsoryacquisition of farms as part of land reform programs acted as a deterrent.Producer price controls in the face of rising costs gave little or no incen-tive to raise output. In consequence of these forces at work, a criticalsupply situation developed in the main consuming centers of Bogota, Medellinand Cali, where population growth has been 6 to 8% per annum.

2.13 In May 1967, price controls were lifted in the larger centers.This action together with a growing regional demand have provided a suitableclimate for introducing modern low-cost production techniques through anextended credit program. Assurances were obtained during negotiations thatthe Government would maintain policies which would encourage the expansionof milk, beef and wool production.

Sheep

2.14 The sheep population is estimated at around 1.3 million. Abouttwo-thirds of the sheep are "Criollo', a native type upgraded to variouslevels by crossing with Suffolk, Romney and Corriedale breeds. They are keptby peasant farmers mostly in small flocks of up to about 20 head. Around1,000 tons of coarse wool are produced annually and used mainly by the cot-tage industries. The remainder is absorbed by the woollen textile industry,which is mostly based on imported fine wools (7,000 to 8,ooo tons are importedannually). Commercial sheep farming in the modern sense is virtually non-existent, yet there are more than 2 million ha of highlands, currently unusedor only of marginal value for other purposes, which could be exploited.

C. Animal Health

2.15 When agricultural services were reorganized in September of lastyear, responsibility for animal health was delegated to the Agriculture andLivestock Institute (ICA). Supervision of vaccine production standards andquality control is a specific responsibility of ICA, but present testingfacilities are inadequate. The manufacture of vaccines has been relinquishedby Government but production on a commercial basis has not been operatinglong enough for performance to be assessed. Measures are being taken to im-prove both the quality and quantity of vaccines produced as well as the over-all facilities for disease control. Assurances were obtained during negotia-tions that the Government would take measures satisfactory to the Bank toimprove the quality and increase the supply of cattle vaccines, and to improvethe overall facilities for disease control.

2.16 The four major animal health problems are: foot-and-mouth disease(FMD), brucellosis, tick infestation, and numerous internal parasites. On-farm preventive measures against FMD vary considerably, from vaccination offattening cattle only to twice yearly vaccination of the herd. The recom-mended practice of vaccinating every four months is seldom practised. For

-5-

this reason, in the proposed Project, assurances were obtained during nego-tiat:Lons that all cattle on Project ranches would be compulsorily vaccinatedagainst FMD. Vaccination of heifer calves against brucellosis, as well asprophylactic measures to control both ticks and internal parasites, are re-ceiving wider acceptance. However, improved nutrition and herd managementpractices are the priority needs to reduce losses and raise production.

D. Government Policies and Agricultural Services

2.17 The Government recognizes that development of the livestock industrycoul(d play a key role in achieving Colombia's objective of a sustained growthin GI)P of 6% per year, in real terms. To this end, the Government has setout to streamline its agricultural services, increase the volume of directedcrediit, and encourage the development of exports (Annex 1).

2.18 General measures to promote exports are a more flexible exchangerate policy and the 15% tax bonus incentive for all exports, except coffeeand petroleum (para 2.08). More specifically, the Government has begun toactivrely promote meat exports through a semi-government lending institution,Corporacion Financiera de Fomento Agropecuario y de Exportaciones (COFIAGRO).This Corporation provides finance for Indugan, a Colombian cattle companyparti.ally financed by IFC, and for exporters of agricultural products; about80% of COFIAGRO's current portfolio is related to beef operations. Domesticmarketing of beef is also being improved; the Government in cooperation withthe USAID has placed special emphasis on the reorganization of slaughteringfacilities. In addition, livestock industry problems in general are underconstant review by the Federacion Colombiaha de Ganaderos (FEDEGAN), an asso-ciation of livestock producers.

2.19 The abolition of milk price controls (para 2.13) has improved theprospects for further development of the dairy industry. Colombia's member-ship in the Latin American Free Trade Association (LAFTA) affects the woolindustry, since trade within this region is subjected to very low importduties; Colombian producers at present receive no special protection orsupport.

2.20 The taxation system, including the level of taxes, has been underreview by a high-level Government Commission and recommendations are nowbeing presented to the Government. Livestock enterprises are taxed in variousways. While the total burden on the producer is substantial, net returnsprovide a reasonable incentive for investments (paras 4.04 and 4.05).

2.21 The entire credit system, which is complex, is also under review bythe Monetary Board. Agricultural credit policy is being studied by the De-partment of Planning. At present, the Caja and Banco Ganadero are the twomost important sources of credit to livestock producers (Annex 2, Table 2).In adldition, conmercial banks are required by law to lend 15% of their de-posits to agriculture including loans for livestock development. Anotherform of credit commonly used in Colombia, known as "cattle-in-partnership",

-6-

is made available in the form of cattle for which the rancher provides pastureand supervision. Profits are shared when the cattle are sold. This systemoperates through both the public (Fondos Ganaderos) 1/ and the private sectors.Although external finance for livestock development is available to supplementdomestic sources there is still an unsatisfied demand for long-term credit.

E. The First Livestock Development Project - Loan 448-Co

General

2.22 The first project, the loan for which became effective on November16, 1966, had the primary objective of increasing the production of beef tomeet a growing domestic demand and to provide a surplus for export. The majorpart of the project, involving 800 farms, was in the North Coast region. Thispart of the country has the highest potential for increasing production aswell as being a logical outlet for beef exports at the port of Barranquilla,which has slaughtering and shipping facilities. A smaller part of the project,involving 90 farms to test certain low-cost techniques for ranch development,was in a designated area of the Eastern Plains, where an extensive type ofranching is still practiced.

2.23 Dairy sector investments were limited to pilot operations in theDepartment of Narino (150 farms), in the Southwest region, and an area aroundBarranquilla in the North (100 farms). The high altitude area of Narino istechnically suited for the development of low-cost dairy manufacturing whicheventually could concentrate on powdered milk. To this end, the project aimedto introduce improved pasture species coupled with modern management techniques,such as those commonly practiced in New Zealand. A successful development alongthese lines would mesh well with the needs of the major consuming centers,which then could supplement their fluid milk supplies with reconstitutedmilk in the off season. In the tropical zone around Barranquilla, wheremixed dairy/beef operations are common, the aim was to stimulate considerableincreases in output of both milk and beef through planned investments onselected farms.

2.24 To determine the feasibility of establishing commercial-size sheepoperations, the project provided for the development of 35 pilot sheep farms.

2.25 To manage the project, a special Livestock Development Department(LDD) was established within the Caja. This Department provides the bank-ing iservices, assesses the creditworthiness of applicant borrowers, assistsranchers in the preparation of farm development plans, and also supervisestheir implementation. The technical services are under a Technical Directorand three Regional Chief Technicians who were internationally recruited.

1/ Specialized livestock credit agencies established in most Departmentsof Colombia and supported by public funds.

-7-

2.26 The total cost of this first project was estimated at US$ 28 mil-lion. Of this, US$ 25 million was allocated for farm development to financesuch items as pasture improvement, fencing, water supplies, stock handlingfacilities, farm buildings.and breeding stock. US$ 1.34 million was setaside for technical services and the remaining US$ 1.66 million for financ-ing machinery for contractors and equipment for dairy cooperatives. TheBank loan of US$ 16.7 million covered 60% of the project cost, including allforeign exchange costs (which amounted to about 33% of the total). The re-maining 40% was shared equally by the Caja and participating ranchers.

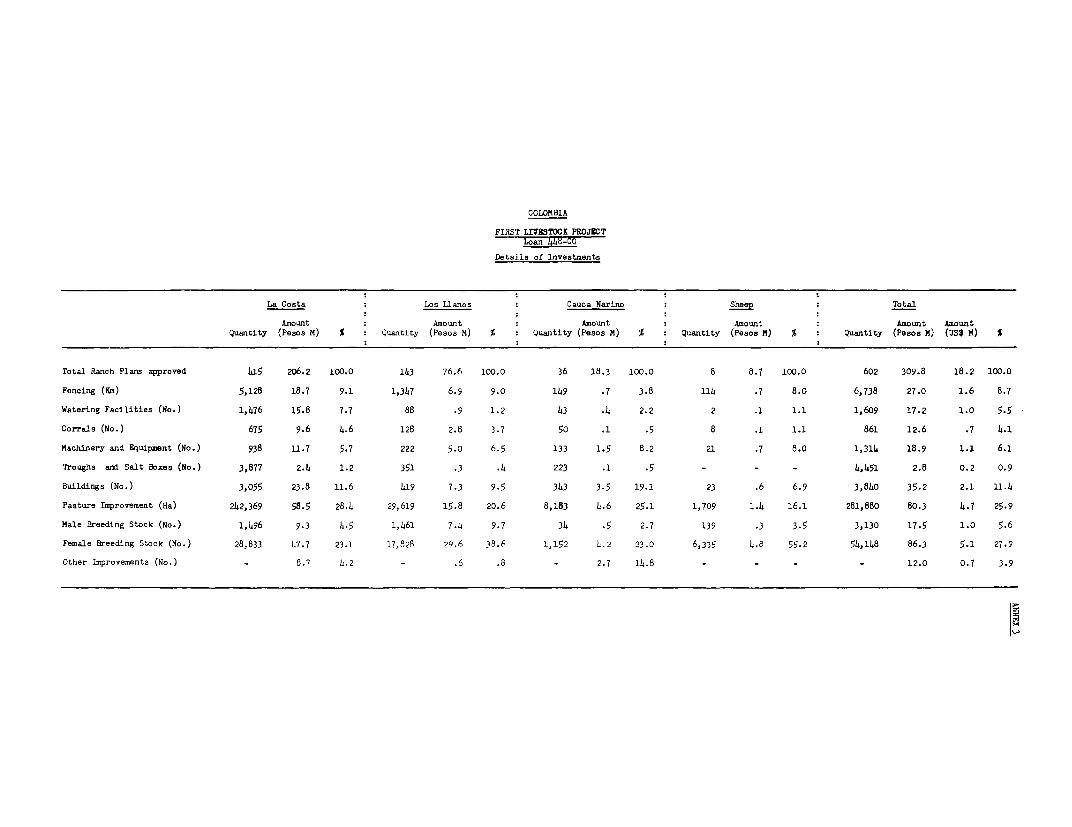

2.27 As of September 30, 1969 a total of 630 loans had been approved,committing loan funds equivalent to about US$ 15 million. This representsabout 75% of the US$ 20 million equivalent allocated for this purpose. De-tails of the kind of investments made are set out in Annex 3. All loan fundsare expected to be disbursed by December 1970, one year ahead of the closingdate.

Lending Procedures

2.28 This project has been Colombia's first experience with such alending program for ranch development, based on loans with a term of 12 years,and the loan amounts assessed on the basis of specific investment programsfor each ranch involved. The loan processing procedure includes an estimateof the expected impact of the plan on herd buildup, on the farmer's income,and on his net cash position after payment of interest and principal for theperiod of the loan. Participating ranchers have responded well to the tech-nical service aspects, which combine on-farm inspection of expenditures withadvisory services and periodic review of development plans and problems. Thesystem has proven to be well conceived in terms of the problems at hand andthe project management has made good progress in implementing the project.

lBeef Cattle

2,29 Of the 602 loan applications approved by the end of 1968, 510 werefor beef production, 84 for dairying and eight for sheep operations. In theNiorth Coast zone, where 367 loans for beef development were made, the ranchesvary widely in size, between 100 and 2,000 ha, and average 700 ha; on average,these ranches carry 600 head of cattle. In the Eastern Plains region, where1143 ranch loans were approved, the average size is 5,000 ha carrying 700head, with EL range from 200 to 30,000 ha. The average size of :Loans grantedfor beef operations has been close to the original estimate of IJS$ 25,600.

2.30 The project has been in operation for a little more than two years.From on-ranch observations, it is evident that the development plans beingfinanced and implemented are soundly based. This is particularly true inthe North Coast region. In the Eastern Plains insufficient progress hasbeen made to determine the feasibility of particular pasture establishmenttechniques. To facilitate supervision in this area, the Bank has recentlyfinanced the purchase of a small plane by Caja.

-8-

Dairy Cattle

2.31 In both the Barranquilla and Narino areas, the demand for dairyloans has been less than expected. Demand for credit was initially weak be-cause of low milk prices. Producer incentives have been restored by higherprices in the Barranquilla area, but development in the Narino district isinhibited by the very limited local demand. However, where loans have beenmade, the results are encouraging; higher per cow production has beenachieved together with improvements in carrying capacity. Furthermore,project management has successfully demonstrated that these improvementscan be achieved without the feeding of concentrates, a practice which,because of the ample pasture resources available, cannot now be economicallyjustified.

Sheea

2.32 The introduction of commercial sheep farming to Colombia, even onthe limited scale originally proposed, has met with some difficulties. Thesedifficulties were expected, considering the small amount of local expertisein relation to the investment program (the eight loans issued averageUS$ 53,400 equivalent as against the original estimate of US$ 43,000 equiva-lent). Demand for loan funds has been low and the effort required from projectmanagement has been considerable. In April 1968, a shipment of 5,000 sheep(Romey-Marsh and Corriedales) was imported under the project from New Zealand.These sheep have proved to be highly adaptable to Colombian conditions. Bythe end of the year, 3,000 of these had been distributed to project ranches.

Other Categories

2.33 Under the first project, provision was made for loans to dairy co-operatives and to contractors for the purchase of heavy machinery. The sizeof loans that could be made to cooperatives under Colombian law were, in fact,too small to be attractive, and the anticipated demand from contractors hasnot eventuated. Consequently, no loans have been made for either category.

III. THE SECOND PROJECT

A. General Description

3.01 The Project would be a further stage of the long-range program ofthe Government of Colombia to develop the livestock industry. It would extendthe existing project over a further four years (into 1973) and would continuethe present emphasis on increasing beef production in the North Coast region.About 700 beef ranchers, 250 dairy farmers, and 20 sheep producers would par-ticipate in the Project. On-farm development would generally be spread overa three-year period.

- 9 -

B. Detailed Features

Beef Cattle

3.02 The Project would cover about 500 farms in the North Coast confinedto the Departments of Atlantico, Bolivar, Cesar, Cordoba, Magdalena and Sucre;and 100 farms in the Departments of Meta and Boyaca in the Eastern Plainsregion. A further 100 beef cattle farms in the Magdalena Valley as far Southas Neiva in the Department of Huila would be brought into the Project oncetechnical services are adequate for this purpose. Investments which haveproved to be necessary in the first stage would continue to be financed inthe second. These include fencing, water supply, stock handling facilities,pasture improvement, machinery and equipment, farm buildings and breedingstock.

Cattle Purchases

3.03 Under the first project, breeding cattle purchases were limited toa percentage of the total cost of individual ranch development plans: theycould not exceed 30% in the North Coast and 50% in the Eastern plains.Ranchers have been pressing for an increase in these percentages and, inpractice, most plans have allocated the maximum allowable. The main concernis to ensure that stock purchases are related to a rancher's surplus feedsituation and indicated managerial skill. Thus, it is proposed in the secondProject to base this allowable percentage on the productivity of the appli-cant borrower's existing herd, with a maximum of 50% of individual ranch de-velopment plans. If a ranch had only average production coefficients (wean-ing rates, weight/age ratios, etc.) no further purchases of breeding heiferswould be financed until a significant improvement in productivity had beenachieved. On the other hand, if production coefficients are already wellabove average, then up to 50% of the investment outlay could be used for thepurchase of additional breeding stock. The Project assumes an average of 30%of total investment going for breeding cattle purchases. Assurances as tothe conditions under which breeding stock would be financed were obtainedduring negotiations. In addition provision has been made for short-termfinance for the purchase of feeder steers for fattening.

Pasture Improvement

3.04 In the North Coast and Magdalena Valley areas cattle are grazedmainly on artificial pastures of guinea, puntero, para and pangola grasses,depending upon the environment. In addition to the application of fertiliz-ers, a variety of techniques would be used to improve such pastures rangingfrom surface cultivation and reseeding to complete renewal. In the EasternPlains region, where natural pastures are grazed, it is proposed to try outalternative low-cost methods of introducing improved pasture plants. Ifsuccessful, such methods would be applicable on a wide scale. Trials ofthese different methods are included in the Project.

- 10 -

Dairy Cattle

3.05 The major milk consuming centers in Colombia are Bogota, Medellin,Cali and the urban complex of Barranquilla and Cartagena on the North Coast.The proposed Project would include specialized dairy farms supplying each ofthese centers (see Map). The existing project area in the Department ofNarino, which has already been enlarged to include the Cauca, would be furtherextended to include the Department of Valle to cover a total of 100 dairyfarms. Cali is the chief consuming center in this region. A further 50 dairyfarms would be included in the North Coast to continue the first project inthat region. Two new areas that would be included in the Project are theUbate Valley, north of Bogota and strategically placed to supply the Bogotamarket, and the Ceja Valley, where milk is produced for sale in Medellin.The development of 50 farms in each region would be financed. Since theProject areas selected are reasonably close to consuming centers, no specialproblems of transportation are envisaged. To permit close Project supervision,the 50 farms to be covered in the Ceja Valley would not be brought into theProject before the second year.

3.06 Specialized dairy farming throughout Colombia is characterized bythe feeding of concentrates and by the use of soilage. 1/ In the more temper-ate regions, despite the natural occurrence on much of the land of such valu-able pasture plants as white clover, Yorkshire fog and cocksfoot, there appearsto be little if any appreciation of the part which grazing pastures would playin suibstantially reducing production costs. More intensive use of pastures bygrazing for milk production would eliminate the need for both concentratesand s3oilage at this stage of development. This has been amply demonstratedin the first project. The objective would be to extend this practice and forthis purpose the Project includes pasture improvement, machinery, fencing,water supply, farm roads, buildings, and breeding stock on a total of 250dairy farms.

Sheep

3.07 It is clear that some modifications in the approach of the firstproject will be necessary. Under conditions where neither the farmer norhis men are familiar with the day-to-day operations of a commercial-sizesheep farm, the difficulty of successfully establishing and supervising suchoperELtions has been evident. More emphasis must be given to the provisionof pIofessional services as well as the training of farm workers. It wouldtake a very long time and be expensive to develop a viable sheep industry,based solely on imported sheep. It is, therefore, proposed to use a selectionof the 880,000 native Criollo sheep population. Of these, it is estimatedthat about 30,000 young breeding ewes, with wool of suitable quality, couldbe selected each year for grading-up with purebred Romney or Corriedale rams.Such ewes could be purchased at from a quarter to a third of the price ofimported ewes.

1/ The growing of fodder to be cut green, chopped and fed to stock in shedsor yards.

3.08 The P'roject includes the establishment by the Caja of a Sheep Develop-

ment; Center, covering approximately 1,500 ha. This Center would be used: (i)

as a breeding unit, of approximately 7,000 sheep, to propagate purebred Romney

and Corriedale rams for grading-up purposes; (ii) to train technicians as wellas iarm workers to help with the Project; and (iii) as a demonstration farm forexisting and potential participants in the Project. Investments in this Center

would include the purchase of imported foundation breeding stock, as well as

fencing, pasture improvement, stock handling facilities, buildings and machin-ery. During negotiations, assurances were obtained that the Caja would ac-

quire the use of a suitable area of land for a period and on terms and con-

ditions satisfactory to the Bank.

3.059 Management of the sheep development program, including the Center,

would be vested in a special Sheep and Wool Unit to be established within

the existing L:Lvestock Development Department of the Caja. As with the first

project, assurances were obtained during negotiations that a qualified techni-cal expert, internationally recruited and acceptable to the Bank, would beemployed as the supervisor of the Sheep and Wool Unit for a period and onterms and conditions satisfactory to the Bank.

3.10 Also,, the Project includes the development of 20 more sheep farms

to consist of :Iocally procured sheep, fencing, pasture improvement, machineryand equipment, water supply, stock handling facilities and buildings.

C. Cost Estimates

3.11 Total Project costs are estimated at about US$ 44.1 million. Ofthis amount, about US$ 29.6 million is for actual on-farm investments based

on current prices. A 10% contingency allowance is included to cover unfore-

seerL costs and possible price increases. Incremental operating costs and

retentions during development amount to US$ 2.0 million and cover additionalexpenses arising from the Project as well as the income foregone by the re-tention of breeding stock, which otherwise would be sold for income. These

costs and investments have been assessed over the initial Project period

during which the ranchers' net operating income would be lower than the pre-development levrel. Interest payments during the same period would amountto about uS$ 7.8 million equivalent. Short-term finance for feeder steersis estimated at US$ 3.6 million equivalent and the cost of technical servicesat US$ 1.2 million equivalent. The direct and indirect foreign exchangecomponent of the proposed Project is estimated to be US$ 12.4 million or 28%

of the total cost. The buildup of total cost for major investment categories

is provided in the following table:

- 12 -

(Ps millions) (US$'000 equivalent) TPC-/ FEC-3/Local Foreign Total Local Foreign Total Per Cent

On-Farm Investment

Fencing 30.5 10.2 40.7 1,794 600 2,394 5.4

Water supply 9.3 9.2 18.5 547 541 1,o88 2.5

Corrals and crushes 14.2 - 14.2 836 - 836 1.9

Pasture improvementand weed control 85.7 70.2 155.9 5,042 4,129 9,171 20.8

Equipment 13.5 25.0 38.5 794 1,470 2,264 5.1

Building improvements 31.7 7.9 39.6 1,864 465 2,329 5.3

Access roads and drain-age 3.6 0.4 4.0 212 24 236 0.5

Breeding stock 144.2 2.5 146.7 8,482 147 8,629 19.6

Subtotal 332,7 125.4 458.1 19,571 7,376 26,947 61.1 27.4

Contingencies 30.4 15.1 45.5 1,788 888 2,676 6.1

Subtotal 363.1 140.5 503.6 21,359 8,264 29,623 67.2 27.9

Incremental Operating Costsand Retentions DuringDevelopment 34.0 - 34.0 2,000 - 2,000 4.5 -

Interest During Developmentl/ 70.7 61.2 131.9 4,157 3,602 7,759 17.6 46.4

Short-Term Finance forFeeder Steers 60.9 - 60.9 3,582 - 3,582 8.1 -

Techntical Services

Technical management - 6.4 6.4 - 376 376 o.9

Local staff and training 8.4 1.7 10.1 494 100 594 1.3

Transportation 0.5 1.1 1.6 29 65 94 0.2

Administration 1.6 - 1.6 94 - 94 0.2

Subtotal 10.5 9.2 19.7 617 541 1,158 2.6 46.7

Total Cost 539.2 210.9 750.1 31,715 12,407 44,122 100.0 28.1

1/ Excluding interest on short-term finance.2 Total Project Cost.3/ Foreign Exchange Component.

- 13 -

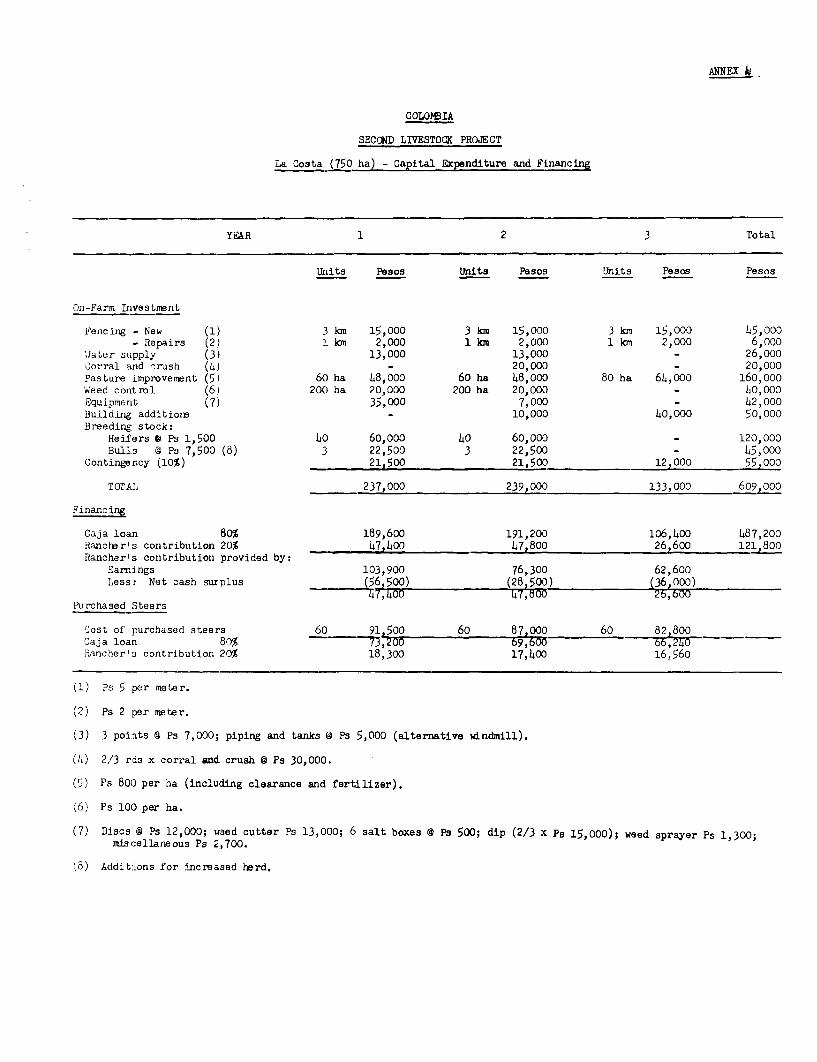

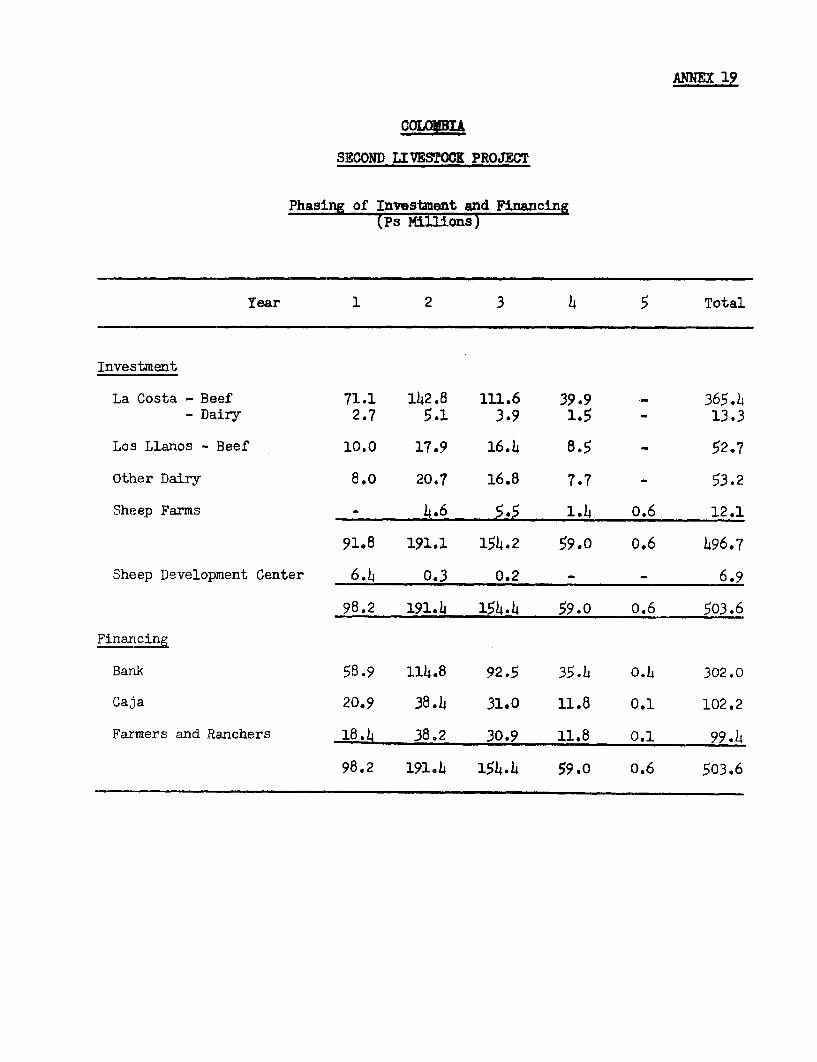

3.12 Based on experience under the first project, representative modelranches have been constructed to estimate costs of on-farm development (An-nexes 4 - 18). The execution of an individual ranch development plan wouldtake about three years and the total investment period over four years. Thedistribution of costs over this period is shown in Annex 19. Details of theestimated cost of technical services are shown in Annex 20.

D. Proposed Financing

3.13 The total Project cost of US$ 44.1 million would be financed asfollows:

(US$ millions)IBRD _aja Rancher Total

(Amt. F(%) ( (A.(%) mt.) (%) Amount

On-Farm Investment 17.77 60 6.01 20 5.84 20 29.62

Incremental OperatingCosts and Retentionsdur:Lng Development - - - - 2.00 100 2.00

Interest during Development - - - - 7.76 l0o 7.76

Short-Term Finance forFeeder Steers - - 2.86 80 0.72 20 3.58

Technical Services 0.54 47 0.62 53 - - 1.16

Total 18.31 42 9.49 21 16.32 37 44.12

3.14 For on-farm investment, the rancher would on average provide, incash, labor or materials, about 20% of the estimated cost. The Caja wouldadvaLnce the balance of 80% of the cost of farm development as loans to ranchers.About 60% of the total cost of on-farm investment would be met from the pro-ceedls of the proposed Bank loan. (This contribution, together with the foreignexchange cost of technical services, has determined the size of the proposedBank loan.) Caja would contribute the remaining 20% from its own resources.In addition, Caja would undertake to make available 80% of ranchers' short-termcapital requirements, which are associated with cattle fattening operations inthe early development period. It is estimated that these needs would amountto about US$ 3,58 million equivalent. During negotiations, assurances wereobtained that the Caja would provide, promptly as necessary, the local curren-cy finds including the short-term capital required for the Project.

3.15' In addition to their contribution to on-farm investments, rancherswould bear in full the incremental operating costs and interest resultingfrom the Project during the development period as defined in para 3.11. Dur-ing this period, they would also contribute the value of stock retained forbreeding which, without the Project, would be sold for income.

- 14 -

3.16 For the Sheep Development Center, the Caja would provide, in cashor naterials, 40% of the estimated cost. The remaining 60% would be madeavailable to Caja from the Bank loan. Appropriate assurances that Caja wouldprovide the local currency funds including the working capital required wereobtained during negotiations. (Annex 13).

E. Procurement

3.17 With the exception of sheep importations, procurement for the on-going project has taken place through normal commercial channels, includinglocEl representatives of international firms. This has not been wholly sat-isfactory and project execution has suffered because items needed to intro-duce, improved techniques have not been made available. During negotiationsassurances were obtained that procurement for the proposed Project would beaccording to international competitive bidding for items suited to bulkordering; namely, fertilizers, pasture seeds, chemicals for weed control,fencing wire and steel fencing posts. These goods would be procured by Caja,in accordance with the Bank's Guidelines for Procurement and on the basis ofprojected demand for Project inputs. 1/ Where local manufacturers are in aposition to bid for these items, they would be protected by a 15% margin, orthe existing level of customs duties, whichever is less. Manufactured in-puts, including machinery and equipment items for which bulk procurementis less suitable, and which are either available locally or do not requireimport licenses, would be procured through normal commercial channels. TheGove-rnment wouLd enable all other manufactured items of the type used asProject inputs to be imported by the Caja promptly as needed.

3.18 Some of the sheep required for the proposed Project are not avail-able locally and would have to be imported. Since the type and quality ofsheep suitable for Colombian conditions can only be obtained from certainareas, international tendering would not be appropriate for livestock pro-curement. All other livestock requirements would be procured locally. Asfor Loan 448-co, assurances were obtained that livestock purchases, with re-gard to quality, source and animal health standards, would be subject to theapproval of the Technical Director.

1/ The Caja is an established distributor of farm inputs and sells a widerange of agricultural requisites (including imports) at competitiveprices, through more than 400 branches.

- 15 -

F. Disbursements and Auditing

3.19 Disbursements of the proceeds of Loan 448-CO have been linked tosub-loans issued by Caja; 75% of sub-loans have been eligJible for reimburse-ment by the Bank covering 60% of total on-farm investments. It is intendedto make the same contribution to on-farm investments in the proposed Project(para 3.14), but the disbursement arrangements would be changed. Bank dis-bursements of the proposed loan proceeds would be made available to theBorrower through the Agricultural Financing Fund (AFF), a special fund managedby the Banco de la Republica. Such disbursements would be made as follows:(a) against payments under agricultural loans made by CaJa to participatingfarmers (75% of payments made under these loans); (b) in respect of the SheepDevelopment Center, for 60% of payments made by Caja fo,r goods and servicesprociured for its development; and (c) for 100% of the foreign exchange costof technical services including transport equipment and training. In orderto comply with the procurement procedures referred to in para 3.17, part ofthe amounts disbursed against agricultural loans would be used by the Borrowerfor payments made to foreign suppliers for imported goods financed under suchloan,s; these payments would be made directly by the AFF to such foreign sup-pliers out of the proceeds deposited by the Bank in a Special Livestock Ac-count opened in the name of the AFF with the Banco de la Republica. Duringnegotiations, assurances were obtained that the Government of Colombia wouldmake the funds credited to the Special Livestock Account freely convertible.

3.20 Each individual farm development loan would normally be disbursedover three years. With some producers being admitted to the program in thesecond year of operation, disbursement of the Bank loan would involve abouta four-year period. The proposed phasing of investments is contained inAnnex 19.

3.21 Caja accounts as well as those of the Banco de Republica are pre-pared semi-annually and are audited by the Government's Superintendent ofBanks annually. During negotiations, assurances were obtained that the Bankwould regularly receive copies of the Special Livestock Account to be kept byAFF, and that all Project Loan Accounts would be audited annually in a mannersatisfactory to the Bank.

G. Organization and Management

3.22 The organization and management of the Project would be carried outby the Caja. The Livestock Development Department (LDD) of the Caja, estab-lished under Loan 448-CO, would be the Project authority controlling the tech-nical and implementation aspects of the Project. A Technical Supervisor of

- 16 -

the Sheep and Wool Unit would be internationally recruited. During negotia-tions, assurances were obtained that the Caja would continue to employ foursenior technical experts 1/, acceptable to the Bank, during the period of dis-bursement, and under terms and conditions satisfactory to the Bank, to assistin carrying out the Project.

3.23 The Technical Director, with the assistance of the Regional ChiefTechnicians and the Supervisor of the Sheep and Wool Unit, would:

a) be responsible for the execution of the Project;

b) assist in the training of the technicians and outline their(luties and responsibilities;

c) report to the General Manager of the Caja through the AssistantGeneral Manager for Development; and

d) be ultimately responsible for promoting the Project, assistingranchers in the preparation of individual development plans,approving and recommending these plans to the Project Committeeas the basis for lending and for supervising the execution ofplans for which loans are made.

In addition the Technical Director would have the authority to approve theagricultural specialists employed by Caja in the Livestock Development Depart-ment as well as the duties and responsibilities assigned to them. LDD wouldestablish and mnaintain farm records for sample farms as needed for Projectevaluation. No loans under the Project would be made except on the recommen-dation of the Technical Director. The Administrative Director of the LDDwould supervise the banking services necessary to maintain Project Loan Ac-couwts, assess the creditworthiness of applicant borrowers, and collect andrecord repayments. Assurances concerning the management of the Project asset out above were obtained during negotiations.

3.24 The Project Loan Committee, established under Loan 448-co, wouldrat:Lfy ranch development plans and would have the authority to approve allloans recommended by the Technical Director (Annex 24). It would disapproveloan applications only on the basis of the prospective borrower's credit-worthiness, which would be provisionally determined prior to preparation ofthe development plan. Financially and administratively, the Caja would pro-cess the approved loans through its regional offices.

1/ The Technical Director, two Regional Chief Technicians and the TechnicalSupervisor of the Sheep and Wool Unit.

- 17 -

H. Lending Operations

3.25 The proposed loan would be made to the Government. The loan wouldbe for 18 years including a six-year grace period. This term would allow forthe complete repayment of all sub-loans including a possible slippage of upto thtree years. The proceeds of the loan would be channelled through a Spe-cial Livestock Account at the Banco de la Republica, the Agricultural Financ-ing Fund (AFF). The Government would on-lend the loan proceeds to Caja at notmore than 10.5% interest but otherwise on the terms of the Bank loan. Themargin between the Bank lending rate and the Government on-lending rate wouldcontribute toward the foreign exchange risk, which would be carried by Govern-ment. During negotiations, assurances were obtained that the Bank loan wouldbe mELde available to Caja on these terms and that the on-lending operationthrough the AFF would be automatic. All creditworthy applicant farmers inthe project areas would be eligible for sub-loans which Caja would make onthe basis of approved farm development plans at an interest rate of 14% fora term of 12 years. A four year grace period would be granted to beef anddairy producers and, to allow for the slower returns from investments insheep farming, a grace period of six years would be granted to wool producers.Assurances were obtained during negotiations that these terms would be availa-ble to sub-borrowers. (In the ongoing project, sub-loans have been issued at12% interest per annum, from which contributions to the foreign exchange riskwas limited to 2% per annum. Also, in some instances, the repayment periodrequired by Caja has been considerably shorter than 12 years.) Individualfarm development loans above US$ 100,000 equivalent would require prior ap-provel by the Bank as would investments in the Sheep Development Center.

I. Financial Operating Results

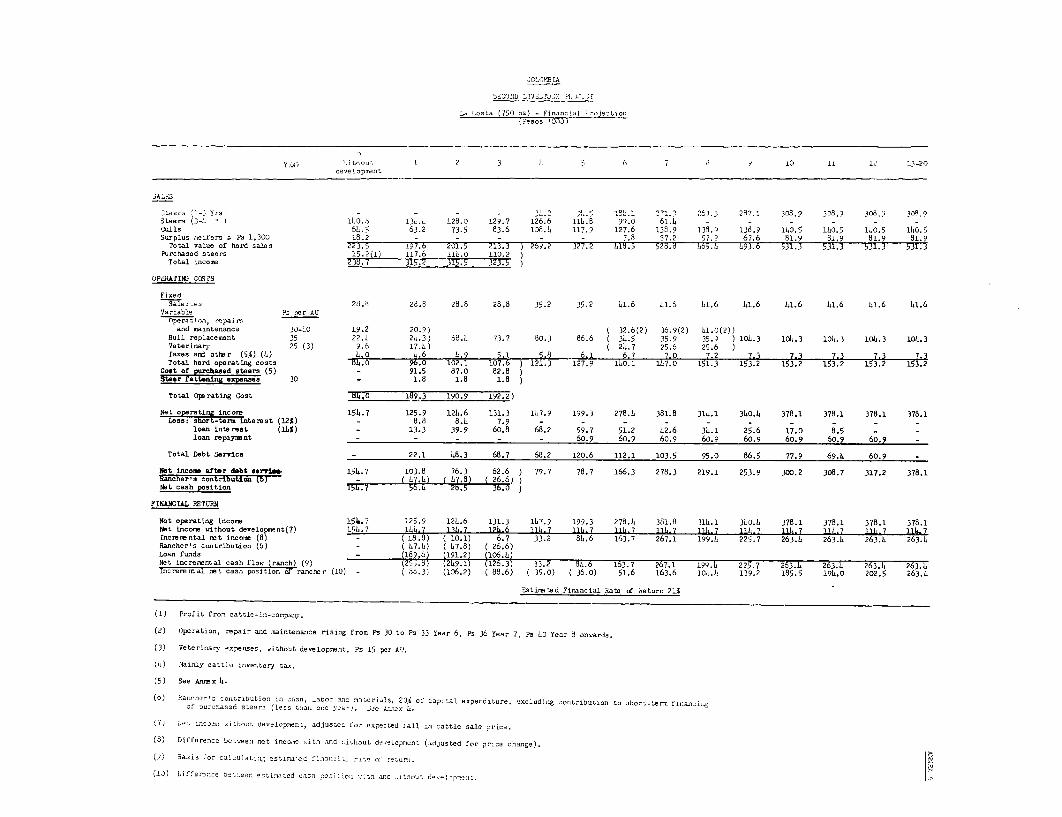

3.26 The excpected cash f:low resulting from the Project is in Annex 21.Incoming loan interest would more than cover Caja expenses in the Projectafter an initial period, and repayments and interest together would coverBank loan debt service. The Caja would also be able to recover its own con-tribution of US.$ 9.5 million with interest. Cash surpluses over and abovethat required for debt service would be used for livestock development loans.

- 18 -

IV. MARKETS, PRICES AND RANCHERS' BENEFITS

A. Markets and Prices

4.o1 The additional production of beef, dairy products and wool thatwould result from the Project would be marketed through existing channels(par-as 2.08, 2.18 and 2.19). The marketing system would be capable ofhandling the expected increased levels of output (Annex 22).

4.02 The rate of population growth in Colombia is such that substantialincreases in the levels of domestic demand for beef and dairy products canbe expected. With beef, the influence of this factor could be supplementedby the potential for increasing the existing low level of per capita con-sumption. At existing price levels the additional production of beef anddairy products resulting from the Project would be fully absorbed by pro-jected domestic demand increases. Current beef prices paid to producers ofabout 5.50 pesos per kg liveweight provide adequate incentives to expandproduction but are high by international comparisons. Although this situa-tion should improve, the Project justification does not rely on Colombiaachieving increased export business. A price fall to 4.50 pesos per kgliveweight to producers by Year-4 has been assumed.

4.03 The increased production of wool on project farms would be utilizedby the textile industry which currently imports the bulk of its wool require-ments.

B. Ranchers' Benefits

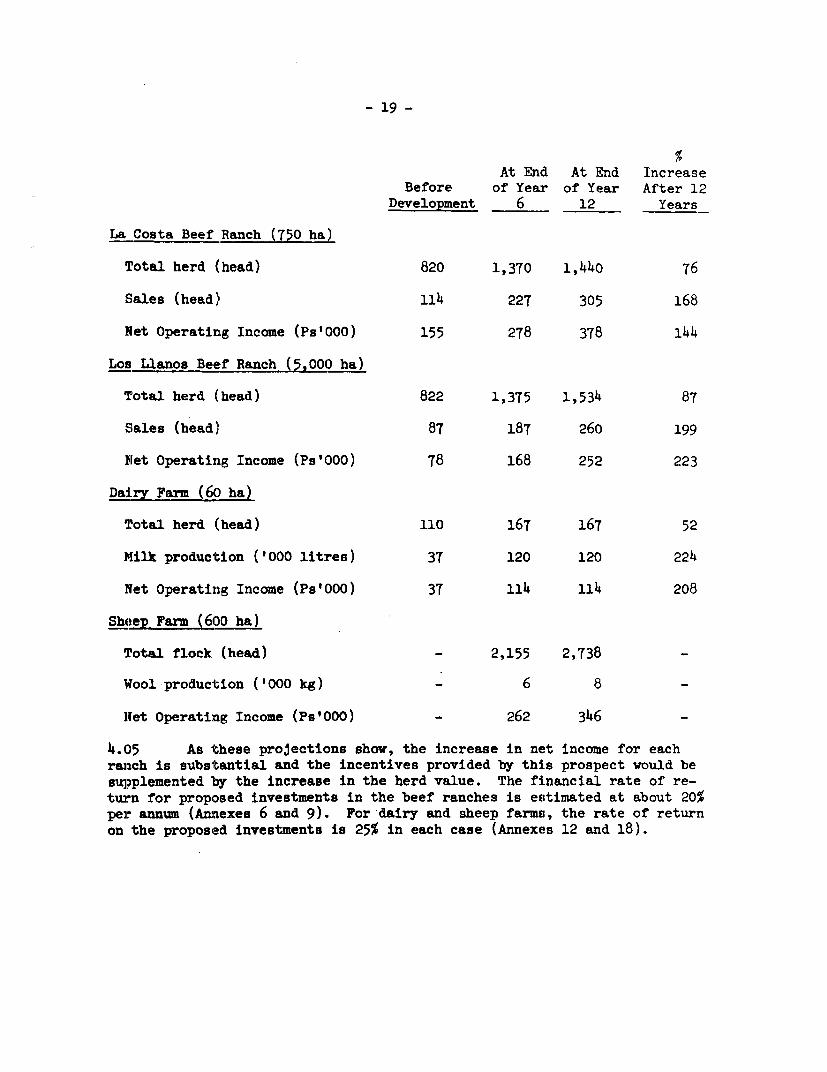

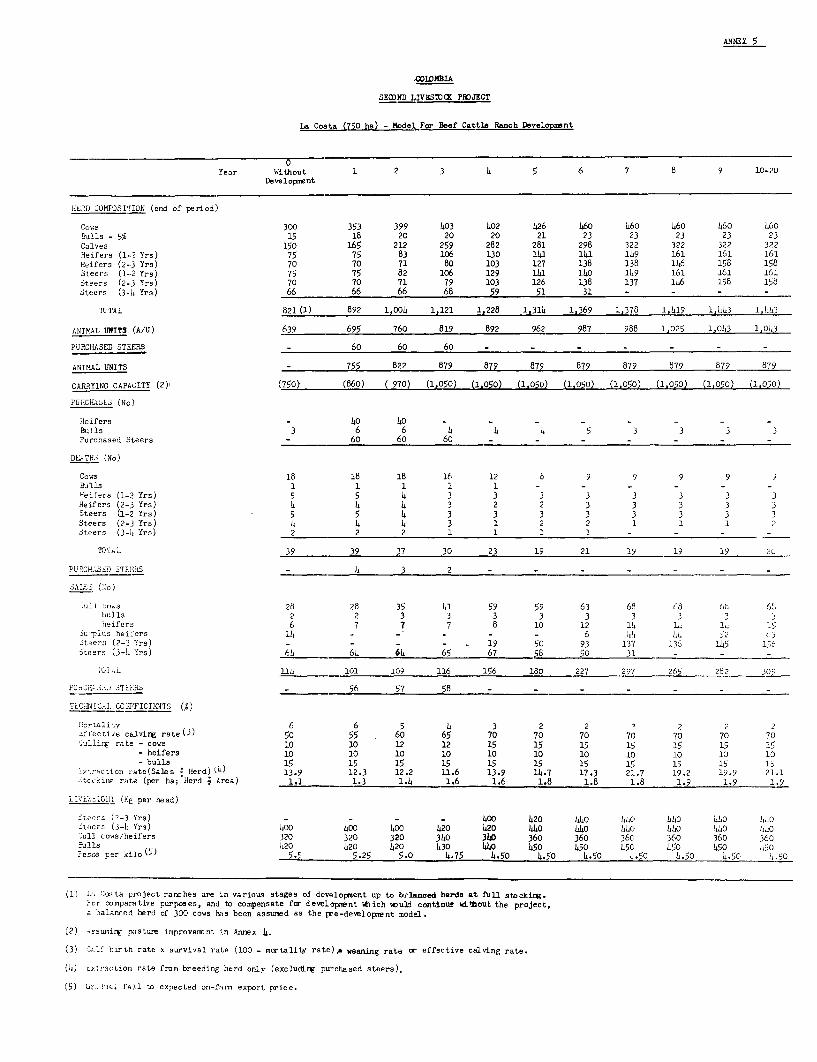

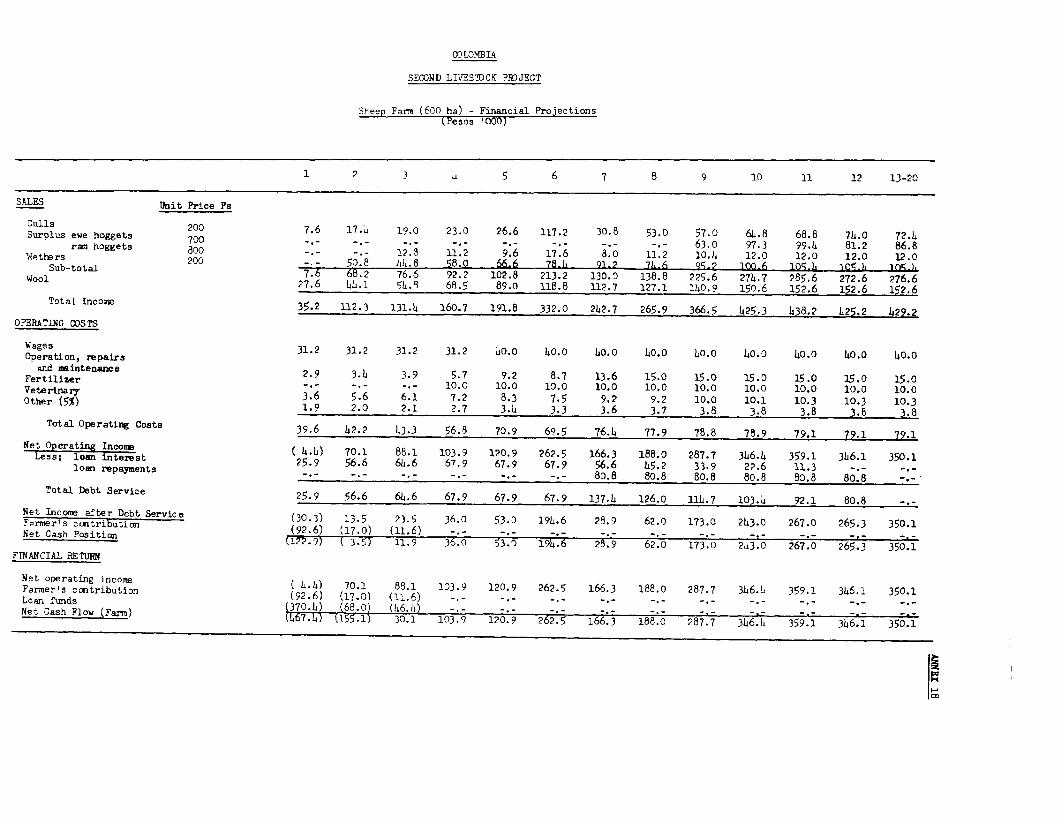

4.04 The benefits to participating ranchers from investments under theProject are projected in Annexes 4 to 18. The estimates are based on modelsof two representative beef ranches, a dairy farm, and a sheep farm. Expectedresults for each ranch at various stages of development are s=mmarized below:

- 19 -

At End At End IncreaseBefore of Year of Year After 12

Development 6 12 Years

La Costa Beef Ranch (750 ha)

Total herd (head) 820 1,370 1,440 76

Sales (head) 114 227 305 168

Bet Operating Income (Ps'000) 155 278 378 144

Los Llanos Beef Ranch (5,000 ha)

Total herd (head) 822 1,375 1,534 87

Sales (head) 87 187 260 199

bNet Operating Income (Ps'000) 78 168 252 223

Dairy Farm (60 ha)

Total herd (head) 110 167 167 52

Milk production ('000 litres) 37 120 120 224

Net Operating Income (Ps'000) 37 114 114 208

Sheep Farm (600 ha)

Total flock (head) - 2,155 2,738 _

Wfool production ('000 kg) 6 8 -

Net Operatinig Income (Ps'000) - 262 346 -

4.05 As these projections show, the increase in net income for eachranch is substantial and the incentives provided by this prospect would be

supplemented by the increase in the herd value. The financial rate of re-

turn for proposed investments in the beef ranches is estimated at about 20%per annum (Annexes 6 and 9). For 'dairy and sheep farms, the rate of returnon the proposed investments is 25% in each case (Annexes 12 and 18).

- 20 -

V. ECONOMIC BENEFITS AND JUSTIFICATION

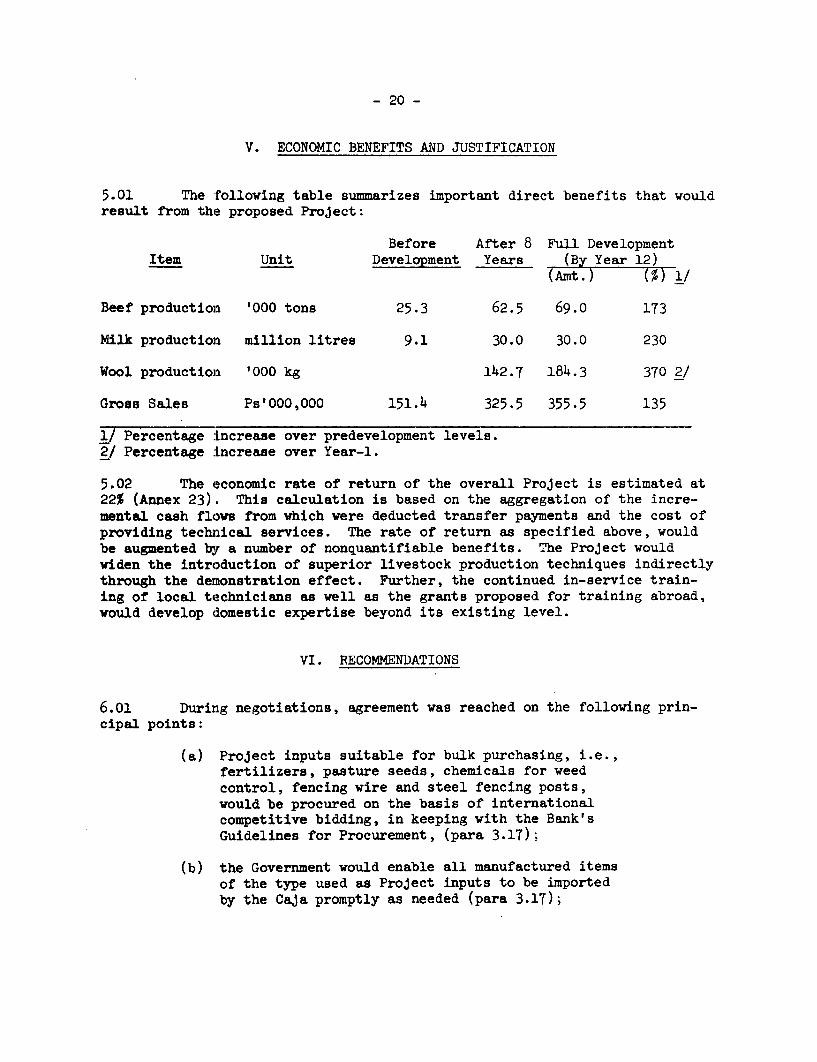

5.0:L The following table summarizes important direct benefits that wouldresult from the proposed Project:

Before After 8 Full DevelopmentItem Unit Development Years (By Year 12)

(Amt.) (% 1/

Beef production '000 tons 25.3 62.5 69.o 173

Milk production million litres 9.1 30.0 30.0 230

Wool production '000 kg 142.7 184.3 370 2/

Gross Sales Ps'000,000 151.4 325.5 355.5 135

1/ Percentage increase over predevelopment levels.2/ Percentage increase over Year-l.

5.02 The economic rate of return of the overall Project is estimated at22% (Annex 23). This calculation is based on the aggregation of the incre-mental cash flows from which were deducted transfer payments and the cost ofproviding technical services. The rate of return as specified above, wouldbe augmented by a number of nonquantifiable benefits. The Project wouldwiden the introduction of superior livestock production techniques indirectlythrough the demonstration effect. Further, the continued in-service train-ing of local technicians as well as the grants proposed for training abroad,would develop domestic expertise beyond its existing level.

VI. RECOMMENDATIONS

6.01 During negotiations, agreement was reached on the following prin-cipal points:

(a) ProJect inputs suitable for bulk purchasing, i.e.,fertilizers, pasture seeds, chemicals for weedcontrol, fencing wire and steel fencing posts,would be procured on the basis of internationalcompetitive bidding, in keeping with the Bank'sGuidelines for Procurement, (para 3.17);

(b) the Government would enable all manufactured itemsof the type used as Project inputs to be importedby the Caja promptly as needed (para 3.17);

- 21 -

(c) the Government would make funds credited to theSpecial Livestock Account freely convertible andavailable promptly as needed for direct paymentsto foreign suppliers of imported goods financedunder the Project (para 3.19).

6.02 No withdrawals on account of agricultural loans to beef producersin the Magdalena Valley would be made until adequate technical services, sat-isfeLctory to the Bank have been made available by the Caja. The Caja agreedfurthermore that technical services would be made available to the MagdalenaValley area only in so far as this would not adversely affect the adequacyof technical services in the.other Project areas (para 3.02).

6.03 No withdrawals on account of the sheep program would be made until(1) Caja has acquired the use of an area of land satisfactory to the Bank andsuitable for the establishment of the Sheep Development Centre (para 3.08)and (2) Caja has established an adequately staffed Sheep and Wool Unit headedby EL Technical Supervisor acceptable to, and upon terms and conditions satis-factory to the Bank (para 3.09).

6.o4 The proposed Project constitutes a suitable basis for a Bank loanof UIS$ 18.3 million, for a term of 18 years including a 6 year grace period.

AI'iUEX I

COLOMBIA

SECOND LIVESTOCK PROJECT

GOVERNMENT POLICIES AND AGRICULTURAL SERVICES

A. Reorganization of the Public Services to Agriculture

1. In September 1968 the Government of Colombia adopted a plan for thereorganization of the public services to agriculture. Previously there hadbeen some 30 institutions serving the agriculture sector with considerableduplication of effort and fragmented responsibility. With the objective ofproviding a sounder basis for further agricultural development, the Governmentadopted a revised structure involving 10 institutions in a three-tieredarrangement. At the top is the Ministry of Agriculture which directs thework of the operating institutions and other supporting agencies. At themiddle level is the Agriculture and Livestock Development Institute (ICA),the Agrarian Marketing Institute (IDEMA), the Agrarian Reform Institute(INCORA) and the Caja de Credito Agrario Industrial y Minero (Caja). Thethird tier comprises the Coffee Bank, the Livestock Bank (Banco Ganadero),the Institute for the Development of Renewable National Resources (INDERENA),a National MeteLology and Hydrology Institute, a Financial Corporation(COFIAGRO) and an 'mr±te*prise for the production of veterinary products(Empresa Zcoprofilatica).

2. Accompanying this reorganization was the creation of an ExecutiveAgricultural Committee for the purpose of making policy recommendations andcoordinating the work of the different regions. This Committee is chairedby the Minister of Agriculture and consists of the heads of ICA, IDEMA, INCORA,Caja, Banco Ganadero, INDERENA and the Coffee Growers Federation.

ICA

3. This Institute has absorbed all agencies operating in the field of tech-nical research and extension as related to non-coffee agriculture. Inaddition to these functions, ICA is to provide the general services of qualitycontrol of agricultural inputs such as seeds, vaccines) fertilizers andpesticides and has been charged with the responsibility of inspection of allforms of meat and milk for the domestic and export markets and, in addition,is responsible for the regional veterinary diagnostic centers. It is ageneral policy of the Government to encourage private enterprise; this ex-tends to agriculture and the provision of extension services by private con-sultants. With respect to the latter, ICA has assumed responsibility forissuing licences to suitably qualified advisory personnel and providing over-all guidance and supervision. The Government is eager to establish ICA asinter alia, a central repository for extension services, but it would bepremature at this stage to attempt to judge their prospects for success.However, there is little doubt that the organization is now faced with con-siderably increased responsibilities. Although several top-level administra-tors have recently been employed to consolidate this reorganized institute,

ANNEX 1Page 2

at the same time it is proposed to withdraw the Rockefeller personnelbeginning this year. At the field level, although well endowed withagricultural technicians, the staff of ICA is essentially researchorientated and have had little or no experience in the use of credit.For sometime ICA will find it difficult to effectively provide and over-see technical supervision on the scale envisaged by the Government.

IDEMA

4. The IDEMA institute is responsible for orderly domestic pricing anddistribution of farm products as well as the general promotion of non-coffee agricultural exports. Up until now IDEMA has focussed attention oncrop products only but is currently in the process of establishing a live-stock committee which will consider all aspects of the beef industry - livecattle as well as refrigerated, frozen and canned beef. In undertakingthis role, IDEMA will work closely with COFIAGRO (para 5) and will make thepolicy recommendations previously made by the Federation of Colombian Live-stock Producers (FEDEGAi). For the last few years, this organization oflivestock producers has been contracted by the Government to organizeexports of meat and cattle, make studies of the industry and provide re-commendations on general lines for development. As much as FEDEGAN wouldlike to continue in this role and even increase its operational effective-ness, the Government, however, sees FEDEGAN's role somewhat differentlyand appears intent on restricting the Federation to conducting studies ofthe industry. FEDEGAN will be represented on the livestock committee set

up by IDENa and only through this medium will it take part in making policydecisions and exercising marketing control. With respect to dairying andsheep production, IDE11A has done nothing so far. On the dairy side, itintends confining its attention to the marketing of fresh milk only.

COFIAGRO

5. COFIAGRO is a public company, created in 1966 for the purpose offinancing exporters of agricultural products and, in particular, exportersof beef. COFIAGRO presently has a paid-up capital of Ps h0 million withownership in the hands of the Government (Ps 13 million), Banco Ganadero(Ps 15 million) and INCORA (Ps 12 million). A 50% increase in paid-upcapital is expected in the near future.

6. Some 80% of COFIAGRO's portfolio is in enterprises engaged in the ex-

port of beef; it is a major shareholder in INGRAL, S.A., a private companywhich owns an abattoir and freezing plant located in Barranquilla and hasmade a loan of Ps 5 million to INDUGAN, a cattle-in-partnership company par-

tially financed by IFC, for the sole purpose of developing that company'sexport operations. In fact, INGRAL and INDUGAN are about to collaborate inthe formation of a beef export company. On a trial basis, the two companies

recently negotiated an export contract with Spain for 2,000 tons of refrigera-ted beef for which shipments commenced in March 1969. In fulfilling its roleas a beef exporter, COFIAGRO has assigned top priority to ensuring that beef

supplies are available to meet the requirements of export contracts. To this

Ai7E5X IPage 3

end the corporation proposes to finance, by loans and equity participationin cattle-in-partnership companies, a herd of some 150,000 head within thenext 1½ to two years to enable contracts entered into by INGRAL to be met.

B. Fiscal Policy

Taxation on Livestock Production

7. A high level commission has recently completed a study of the overalltax system in Colombia and will soon present its recommendations to theGovernment. There have been no indications as to the nature of the proposedreforms, but it is reasonably certain that they will provide for greaterrevenue in the framework of a more equitable and efficient structure.

8. Taxation on livestock enterprises takes many forms and there is a-wide variety of tax exemptions and deductions from income for people en-gaged in stock raising and agriculture (with the exception of coffee,sugar-cane, and bananas). Important income and wealth tax benefits designed toencourage large and medium-scale investments in agriculture lapsed onDecember 31, 1968, having been in effect since 1958. In view of the im-pending tax reform, this situation is not necessarily significant nor areliable indication of present Government thinking.

9. With respect to general income taxes, an important feature of thedetermination of taxable income concerns the calculation of profits derivedfrom the sale of cattle. This is taken to be the increase in value duringthe year of sale only. By excluding any value added in earlier years, thelaw favors longer-term operations rather than short-term fattening withinany one year. Additional incentives accrue to such enterprises throughthe exemption of livestock kept for breeding and raising from the netwealth tax (in effect until 1970). Without these tax advantages the netprofitabiLity of cattle operations would be seriously reduced.

10. Special taxes levied on the livestock producer are:

a) On the consumption and export of cattle, levied at the pointof slaughter or export at the rate of Ps 50 per head formales and Ps 100 per head for females.

b) Selective inventory tax: equivalent to the value of 4 kgliveweight per head of male cattle over one year. For thispurpose the Minister of Agriculture sets an average priceat the end of each tax year.

At the Government's discretion, up to 50% of the two tax revenues referredto above can be directed toward improving the livestock industry, for example,to organize technical assistance, to promote exports, to regulate prices andto enforce international health regulations. For these purposes up to 45% isallocated to Banco Ganadero and up to 5% to FEDEGAN. A conservative estimateof

ANNEX IPage 4

the yields from these two taxes amounts to about Ps 220 million. In 1968 theamiounts received by Banco Ganadero and FEDEGAN were Ps 30 million (less thanUli%) and Ps 6.5 million (about 3%) respectively. Budget allocations for 1969will leave Banco Ganadero's receipts unchanged and will increase the amountgcing to FEDEGAN to Ps 7 million.

11. In addition, 1% of net investment in livestock, when that investment isin excess of Ps 15,000 (effective through 1970) is levied au livestockproducers as a general inventory tax. There are no exemptions from this taxas there are for the net wealth tax. The livestock producer has the alterna-tive of paying the tax in cash or subscribing to shares of Banco Ganadero orFondos Ganaderos (para 2.21 of the main report). The latter alternative isthe one generally followed and these proceeds represent an important sourceof funds for the two institutions. The securities purchased are marketable,but only at a substantial discount.

Incentives for Export Promotion and Import Substitution

12. Since March 1967, tax credit certificates or bonuses have been grantedtc) exporters of all ccmmodities with the excepticn of coffee and petroleum,equal to 15% of the value of exports. Given the existing prices and exportmarketing facilities, this rebate enables export to take place on a limitedsc:ale. Short of increasing this incentive, lower cost production and/or amore favorable exchange rate would be necessary to enable Colombian meatexports to increase to any appreciable extent. Domestic price support for theexport market has been successfully operated for sugar and cotton, but theexisting marketing situation for beef, characterized by a multitude of pro-ducers, middlemen and slaughterhouses would make control of such supportprices impossible. A fund for the promotion of exports, set up by the samedecree that established the 15% tax credit, is authorized to discount billsand other documents on behalf of exporters.

13. The Government's policy with respect to wool imports gives no preferenceor protection to the local producer and is a reflection on the low prioritycurrently being given to the development of this particular infant industry.Imiports of fine wool from the Latin American Free Trade Association (LAFTA)are subject to an ad valorem duty of 9 - 11% without the normal requirementfor a deposit with the Banco de la Republica. Imports from other countriesattract a duty of 15 - 17% and a peso deposit requirement of 70% of the valueof the imports and, as a result, accounted for only 2.7% of total imports in1967.

C. Credit Policies

14. Apart from the institutional problems, the Government is seriously con-cerned with two aspects of credit to the agricultural sector, the operation ofLaw 26 and the low level of interest rates. Law 26 is an important source offunds for agriculture; inter alia the law requires commercial banks, the Caja

ANNEX IPage 5

and Banco Ganadero to lend 15% of their deposits for agricultural development,in.cluding livestock. It is required that this money be made available toproducers at 8% interest for periods varying up to five years. The law hasbeen quite ineffective, however, as the Government has only been able to ens-arethat the funds are lent to landowners/farmers and has not been able to controltheir use. For security reascns, banks have generally offered their resourcesto their best clients, the one group with the least need for cheap short-termcredit and allegedly with the least predilection toward utilizing the funds foragricultural development. The Colombian entrepreneur has, characteristically,multi-interests and as often as not is reputed to have gocd if not better usesthan agriculture for short-term credit.

15. Reform of Law 26 has been proposed by the Executive Agricultural Committeeand accepted by the 1Minister of Agriculture. It is now in the process ofbeing reviewed by the Attorney General's Department to determine how the re-form can be nade effective. It is proposed that the funds, instead of beinglent directly by the banks, be channelled through the Fondo Financiera Agrarioin. the Banco de la Republica from where they will be available for the re-discount of supervised loans made to farmers for purposes approved by theFondo. Rather than the existing 8% rate of interest, the reform if adopted,would increase this rate and provide for periodic reviews by the MonetaryBoard.

16. In general, the Government is concerned about the low interest rates toagriculture and intends to increase these rates to ensure better utilizationof scarce capital resources. For the on-lending of external loans, it isproposed that interest rates be such that the borrower will bear most, if notall, of the foreign exchange risk.

D. Prices

17. There is no control over the price of livestock or meat. In May 1967,price controls of milk in towns of 70,000 or more inhabitants were lifted fora period of three years. However, the Association of Milk Producers (ANALAC),together with the Department of Economic Regulations, agreed on a maximumprice per bottle of raw milk to distributors. There is control on the marginscharged for the processing, distribution and sale of milk and these are setby the Department of Economic Regulation. The maximum margin for pasteuri-zed milk is Ps 0.25 per 750 cc bottle and this covers all costs from pointof collection to factory sale. The maximum margin for distribution isPs 0.05 per bottle and for retail sales Ps 0.04 per bottle.

ANNEX 2

COLOMBIA

SECOND LIVESTOCK PROJECT

BAIKING AND CREDIT

A. Introduction

1. The Colombian banking system is characterized by governmental directionof credit through a ccmplex of official rediscount facilities and reserverequirements. While this has been successful, to an extent, in channellingcredit towards priority agricultural and industrial development, its rigidityhas hampered monetary control. Government is gradually introducing changes tomake the system more effective, both in directing credit to development sectorsand in controlling the monetary system.

B. The Banking System

2. There are 16 commercial banks in Colombia, h semi-official banks, 6foreign comnercial banks, 13 development finance companies and the privatelyoaned, but naw closely controlled, Central Bank, the Banco de la Republica.The Central Bank also has an 80% interest in the Banco Central Hipotecario(Central Mortgage Bank).

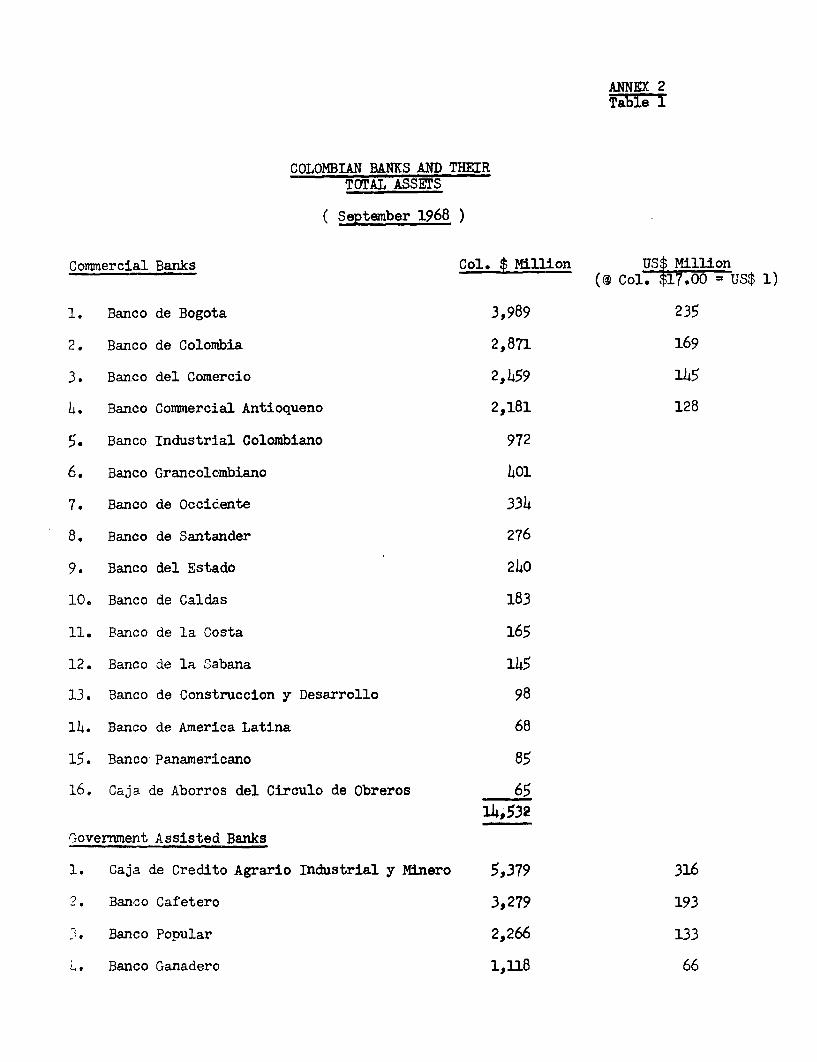

3. A list of banks and their total assets is given in Table I, attached;the Government owned Agrarian Bank (Caja de Credito Agrario Industrial y Minero- Caja) is much the largest, apart from the Central Bank itself.

4. The Central Bank holds the national reserves, is the sole bank of curr-ency issue, and is bancer for Government and for other banks. Its assetsexceed the combined total of the commercial banks. The Central Bank alsoadministers five special Funds, of which the two most important are thePrivate Investment Fund (Fondo Inversiones Privadas), created in 1ebruary 1963as a channel for foreign loans in the private sector (mainly industry andexport promotion); and the Agricultural Financing Fund (Fondo FinancieroAgrario) created in Mkay 1966 to provide supervised short-term credit foragriculture

5. The commercial banks have head offices in principal towns and manybranches; the development finance companies are mostly regional; Caja is basedin Bogota, the capital; and has 638 branches or agencies throughout Colombia.So the country is well provided with banking services and general short-termcredit, though credit may not be easy to get in particular sectors (e.g.cattle fattening) either through deliberate Government policy or the banks'own choosing. Demand for short-term credit is intensified by reluctance ofthose who need short-term financing for their enterprises, to use their own

funds fcr tho purpose. Actual and potential inflation discourages long-termlending, though the development finance companies make long-term loans, mainly

LhNTEX 2Page 2

industrial and sometimes associated with equity participation. Governmenthas slowed inflation somewhat in recent years (see Section F) and hasassisted long-term lending, notably for livestock development, with helpfrom AID, the Inter-American Development Bank and the World Bank. It isgenerally true, however, that long-term money is scarce.

C. Control of the Banking_System

Reserves

6. Since 1963, the Government appointed Monetary Board has had legisla-tive control of the banking system; it has been increasingly effective duringthe last two years. It sets the proportion of bank deposits which must bekept in reserve and not used for lending. This proportion was 33% at thebeginning of 1969, subject to investment of part of a bank's portfolio indevelopment (see para 8(i)) and to certain other requirements. The reserverequirement rose steadily from 24% in 1964 to a peak of 34% between Januaryand May 1968. 1Most banks invest in development, as required for the 33%reserve; without this investment, the reserve proportion is 37%. Of the 33%reserve, 1% of deposits may be invested in Agricultural (and some otherspecified) Bonds, and 3/4% in loans for special purposes (e.g. municipal orreconstruction). All the rest must now be in cash or deposits with theCentral Baxk, in contrast to previous other exceptions. The Central Bankprovides statistical and information services to the M4onetary Board and aGovernment Department, the Superintendency of Banks, ensures compliance andregularly inspects all banks (including Caja).

D. Direction of Credit