53422 - World Bank Documents & Reports

341

• INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT INTERNA TIONAL FINANCE CORPORATION INTERNA TIONAL DEVELOPMENT ASSOCIATION 1986 ANNUAL MEETINGS OF THE BOARDS OF GOVERNORS SUMMARY PROCEEDINGS WASHINGTON, D.C. SEPTEMBER 30-0CTOBER 3, 1986 Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

Upload

khangminh22 -

Category

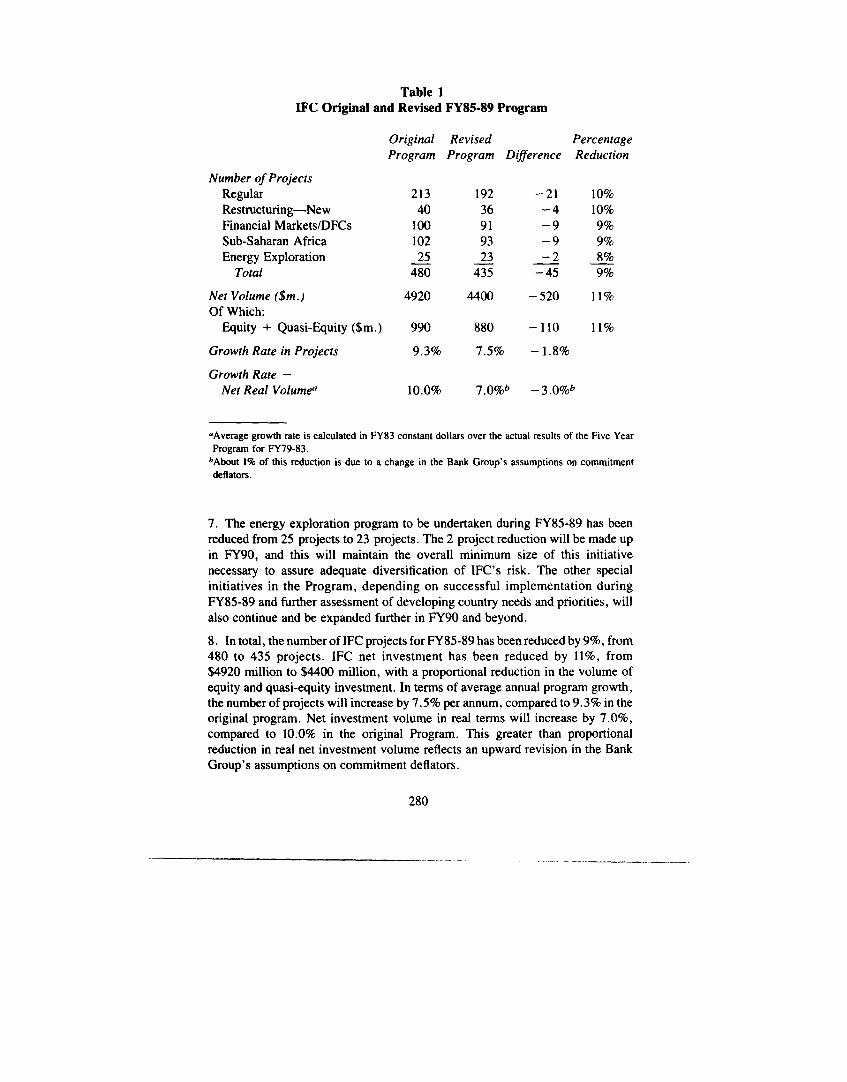

Documents

-

view

0 -

download

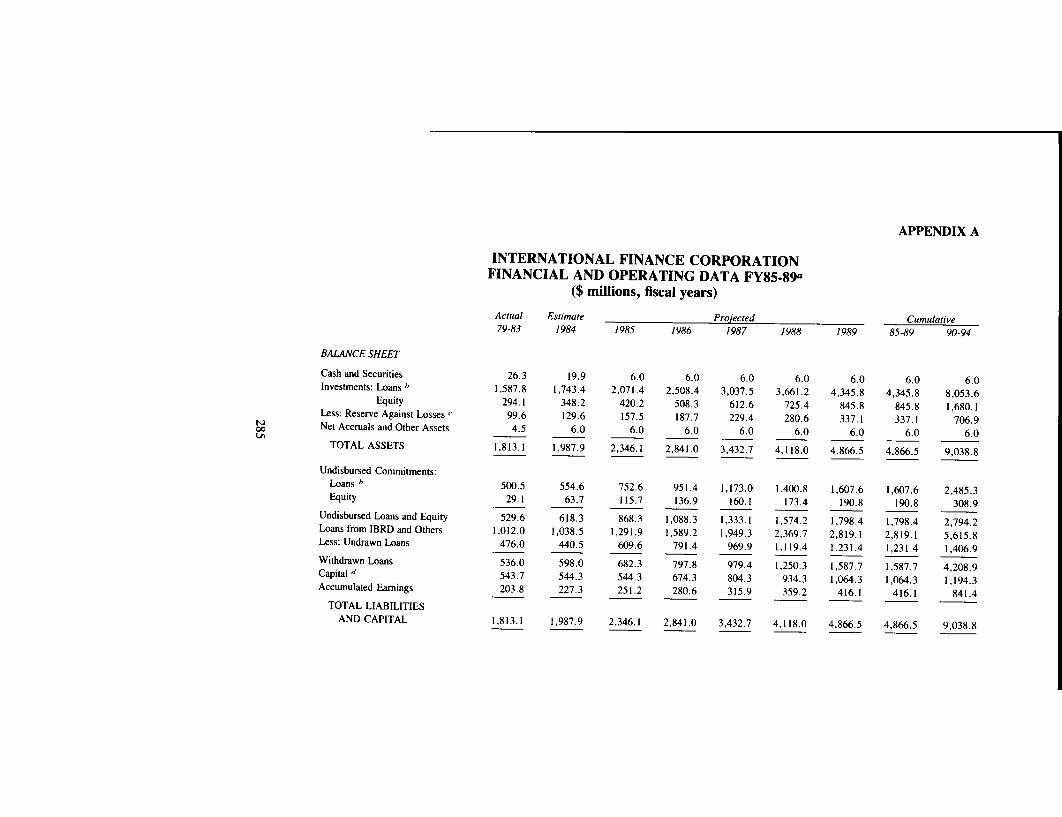

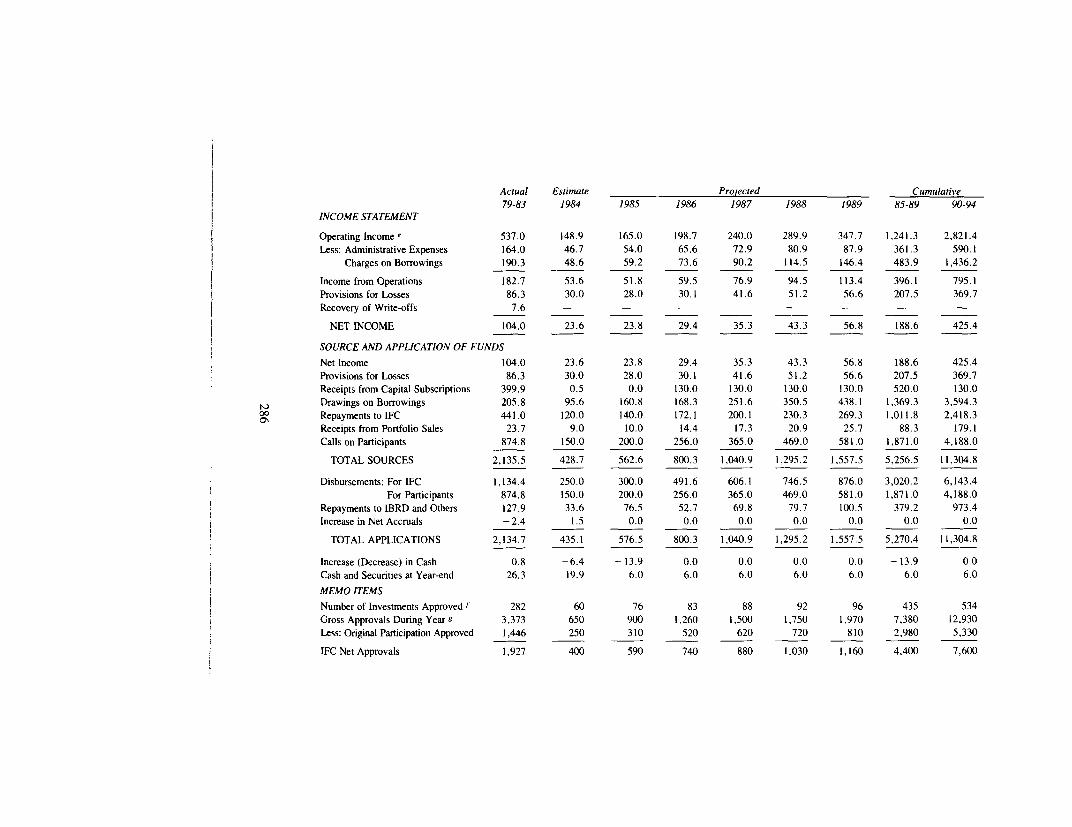

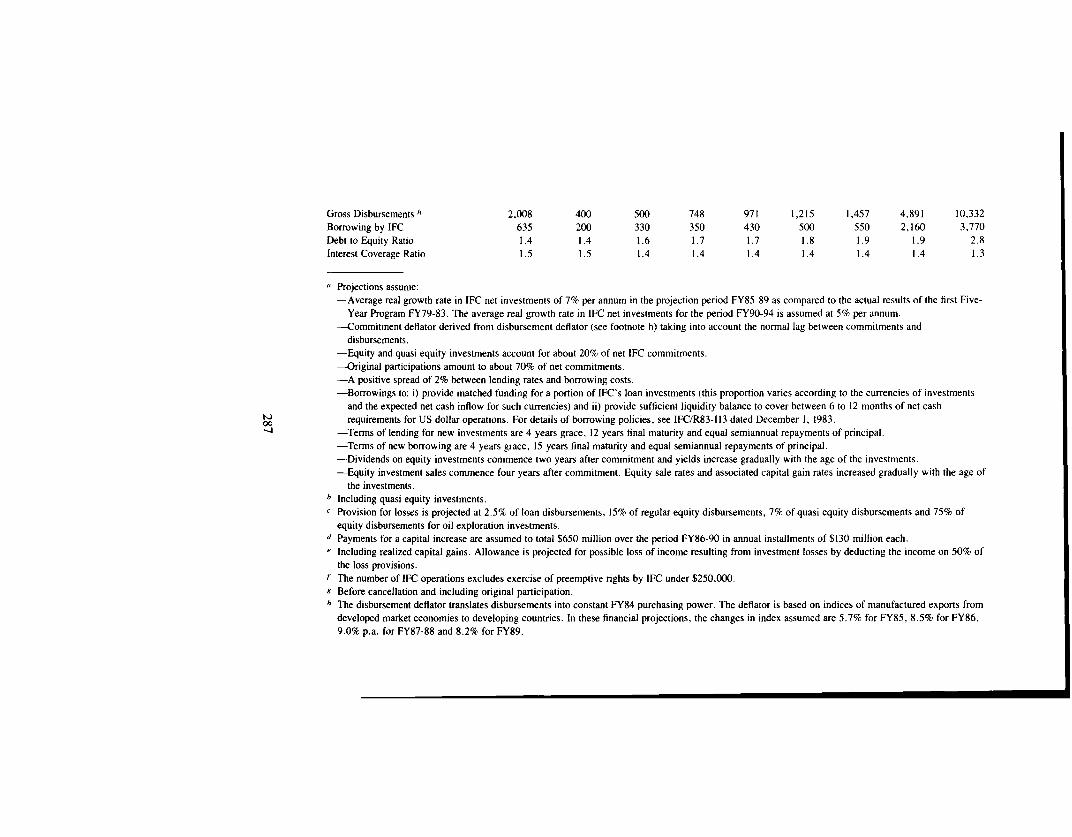

0

Transcript of 53422 - World Bank Documents & Reports

• INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

INTERNA TIONAL FINANCE CORPORATION INTERNA TIONAL DEVELOPMENT ASSOCIATION

1986 ANNUAL MEETINGS OF THE

BOARDS OF GOVERNORS

SUMMARY PROCEEDINGS

WASHINGTON, D.C. SEPTEMBER 30-0CTOBER 3, 1986

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

wb350881

Typewritten Text

53422

INTRODUCTORY NOTE

The 1986 Annual Meeting of the Board of Governors of the International Bank for Reconstruction and Development. held jointly with that of the International Monetary Fund, took place in Washington, D.C., September 3D-October 3 (inclusive). The Honorable Virgilio Barco, President of the Republic of Colombia and Governor of the Bank and Fund for Colombia, served as Chairman at the Opening Session. succeeded by The Honorable Cesar Gaviria Trujillo. Minister of Finance and Public Credit and Governor of the Bank and Fund for Colombia, who served as Chairman for the remaining sessions. The Annual Meetings of the Bank's affiliates. the International Finance Corporation (IFC) and the International Development Association (IDA), were held in conjunction with the Annual Meeting of the Bank.

The Summary Proceedings record in alphabetical order of member countries, the texts of statements by Governors relating to the activities of the Bank. IFC and IDA. The texts of statements concerning the IMF are published separately by the Fund.

Washington, D.C. January, 1987

III

T. T. THAHANE Vice President and Secretary

THE WORLD BANK

CONTENTS

Opening Remarks by Ronald Reagan President of the United States

Page

Opening Address by the Chairman Virgilio Barco Governor of the Fund and Bank for Colombia 8

Annual Address by Barber B. Conable President of The World Bank

Report by Ghulam Ishaq Khan

16

Chairman of the Development Committee 24

Statements by Governors and Alternate Governors .................. 30

Page

Afghanistan ............ 30 *Arab States, League of .. " 32 * Argentina .............. 35

Australia ..... . . . . . . . . .. 39 Austria ................ 44

*Bahamas ............... 46 Bangladesh ............. 50 Belgium ............... 54

*Belize ................. 60 Bolivia ................ 62 Canada ................ 65 China ................. 69

*Ecuador . . . . . . . . . . . . . . .. 71 Egypt ................. 76 Fiji ................... 80 France. . . . . . . . . . . . . . . .. 82 Germany. . . . . . . . . . . . . . . 85 Greece . . . . . . . . . . . . . . . .. 89 India .................. 93 Indonesia .............. 96 Iran. Islamic Rep. of ..... , 10 I Ireland ................ , 106 Israel ................. , 109 Italy ................... 112 Japan ................. , 119 Kiribati ................ 124 Korea ................. 124

* Speakinx on behalf' (If' (/ group of' countries

v

Page

Lao People's Democratic Republic ............ 126

Malaysia ..... . . . . . . . . .. 129 Malta .................. 131 Nepal ................. 133 Netherlands ........... " 135 New Zealand ........... 140

*Norway ... . . . . . . . . . . . .. 143 Pakistan ............... 146 Papua New Guinea ., ... " 150 Paraguay .. . . . . . . . . . . . .. 156 Peru. . . . . . . . . . . . . . . . . .. 158 Philippines ............. 170 Poland. . . . . . . . . . . . . . . .. 174 Romania ............... 176 South Africa ............ 179 Spain. . . . . . . . . . . . . . . . .. 182 Sri Lanka .............. 185

*Sweden ................ 190 Thailand ............... 193 Turkey ................ 195 United Kingdom. . . . . . . .. 199

*United Kingdom. . . . . . . .. 203 United States ........... 207 Viet Nam .............. 214

*Western Samoa .......... 216 Yugoslavia ............. 217

*Zaire .................. 220

Page

Concluding Remarks by Mr. Conable ............................. 226

Concluding Remarks by the Chairman, Cesar Gaviria Trujillo .......... 228

Remarks by Ibrahim Abdul Karim, Governor of the Fund and Bank for Bahrain ................................ 229

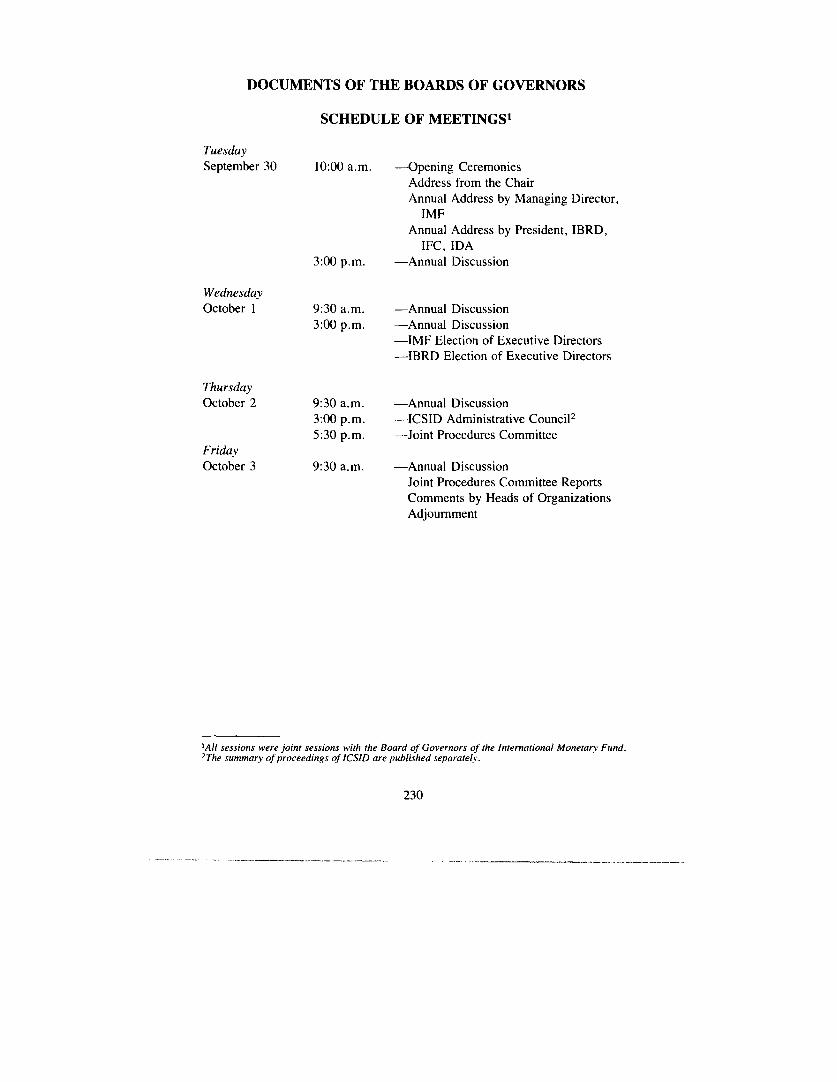

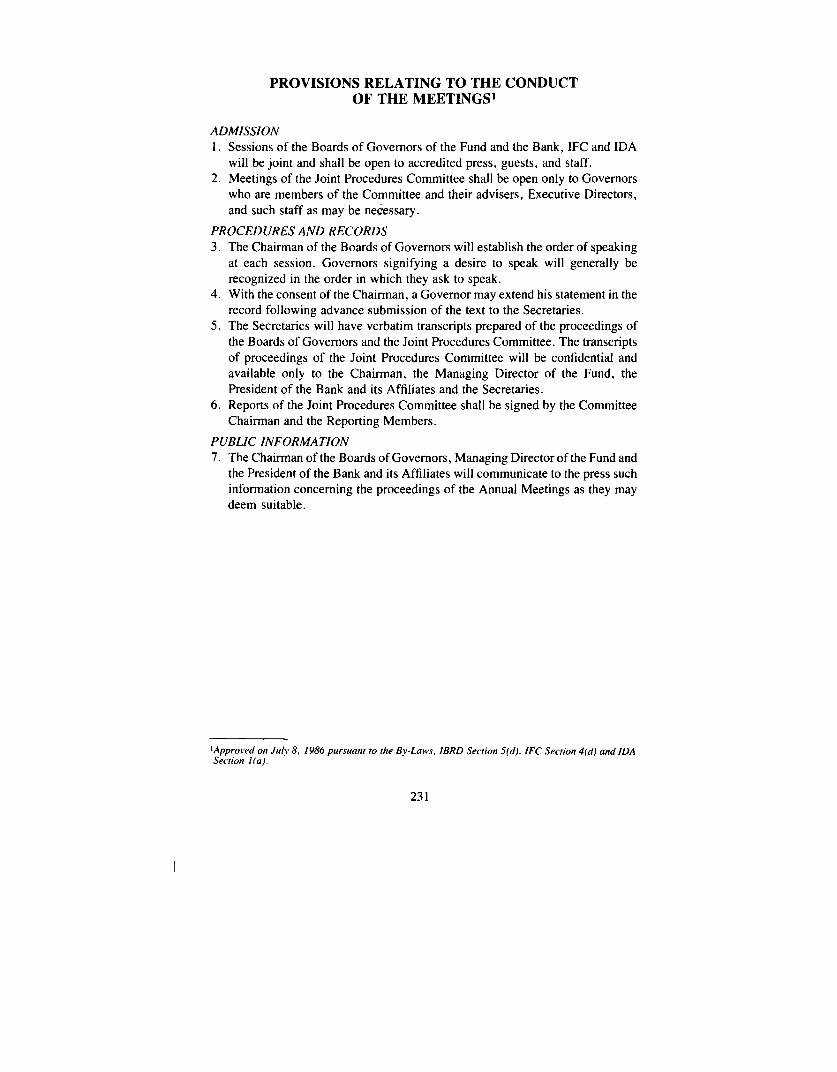

Documents of the Boards of Governors ............................ 230 Schedule of Meetings ........................................ 230 Provisions Relating to the Conduct of the Meetings ................ 231 Agendas ................................................... 232

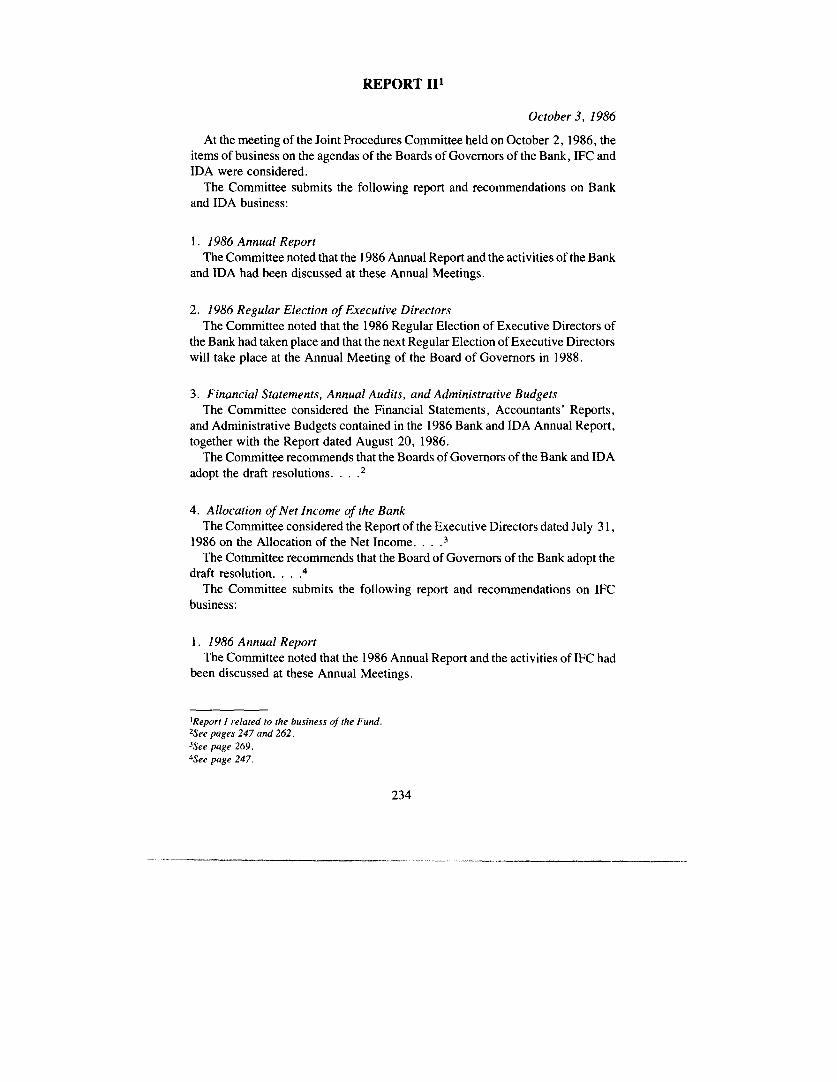

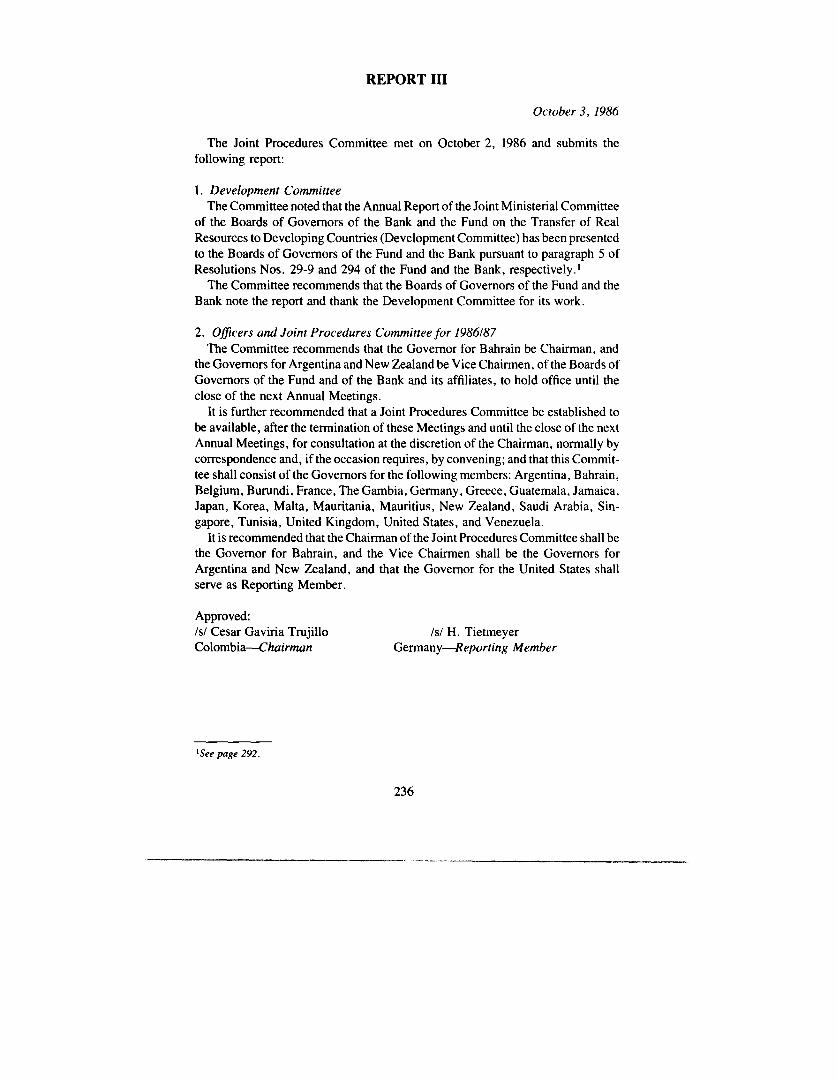

Joint Procedures Committee ..................................... 233 Report II .................................................. 234 Report III .................................................. 236

Resolutions Adopted by the Board of Governors of the Bank Between the 1985 and 1986 Annual Meetings ................. 237

No. 408 ... Salary of the President ............................ 237 No. 409 ... Number of Elected Executive Directors ............... 237 No.410 ... Increase in Certain Subscriptions to

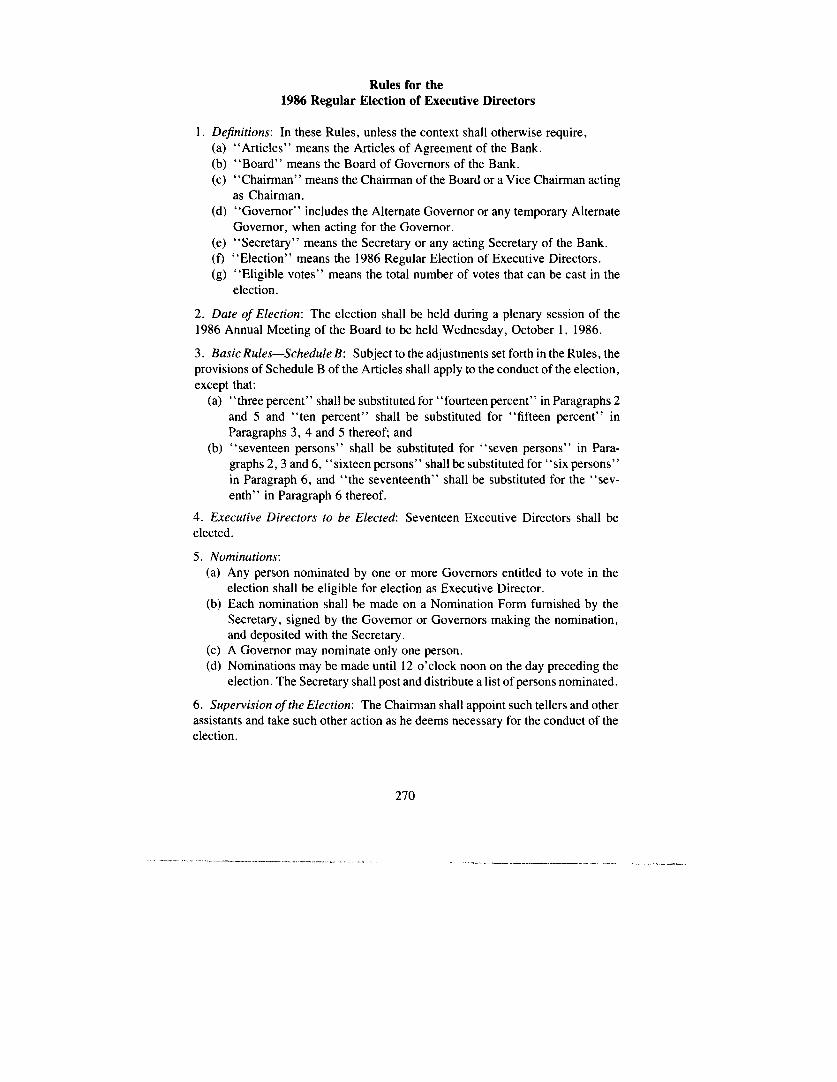

Capital Stock .................................... 237 No.411 ... Membership of the Polish People's Republic ........... 241 No. 412 ... Membership of the Republic of Kiribati ............... 244 No. 413 ... 1986 Regular Election of Executive Directors .......... 246

Resolutions Adopted by the Board of Governors of the Bank at the 1986 Annual Meeting ............................... 247

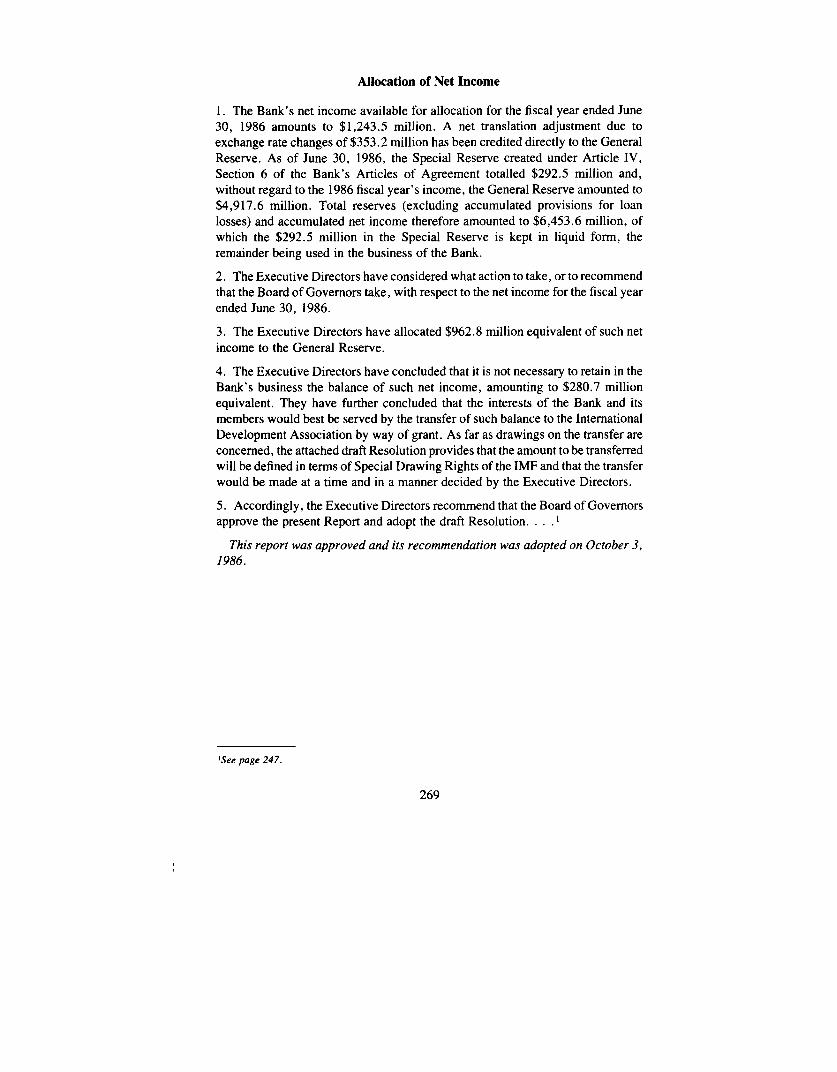

No.414 ... Financial Statements, Accountants' Report and Administrative Budget ......................... 247

No.415 ... Allocation of FY86 Net Income ..................... 247

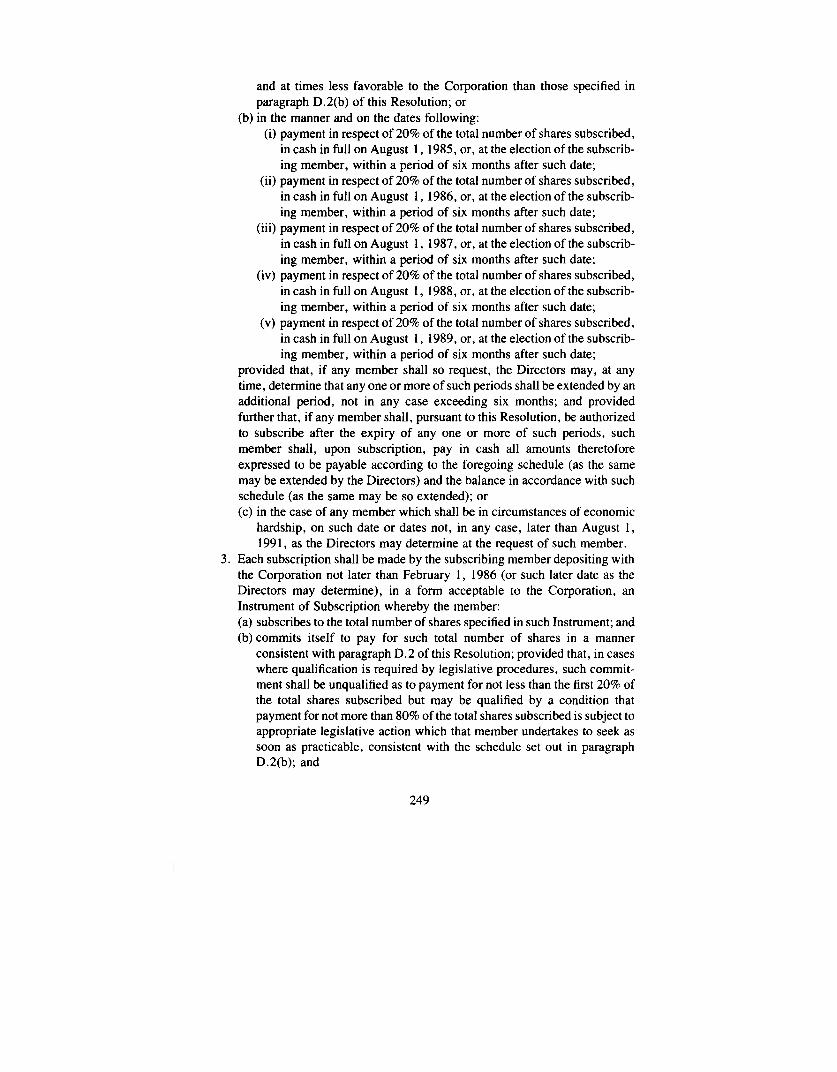

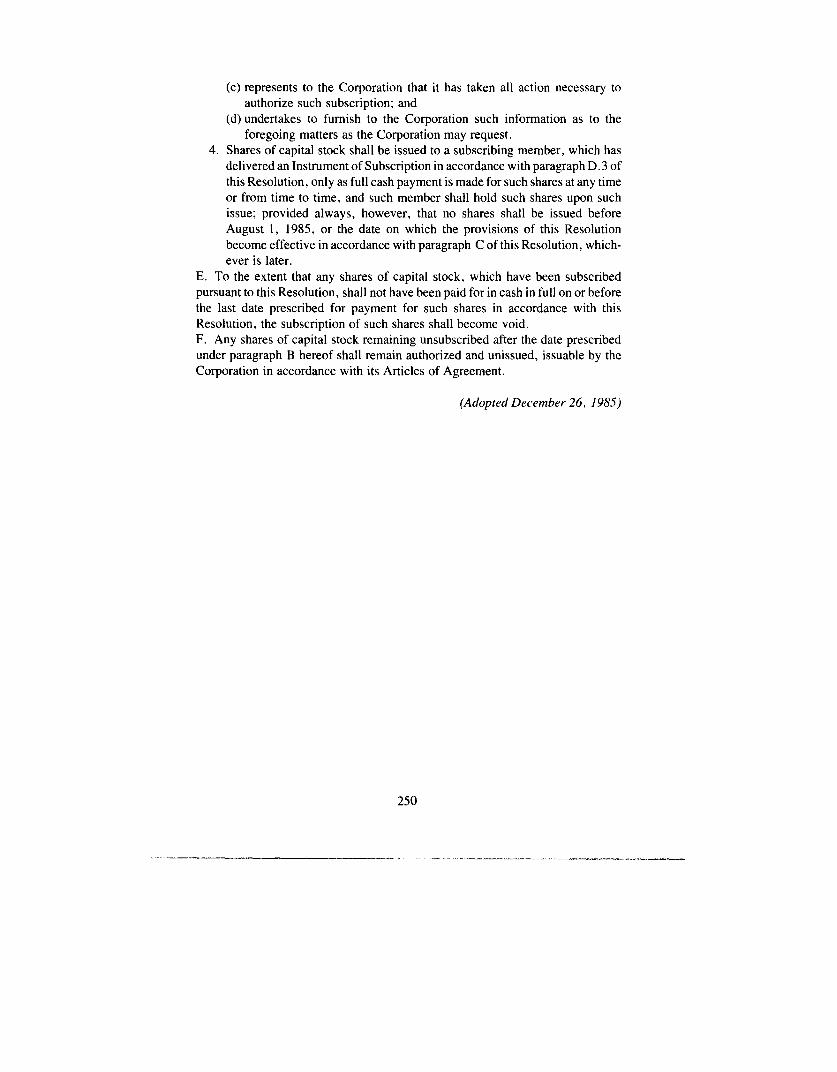

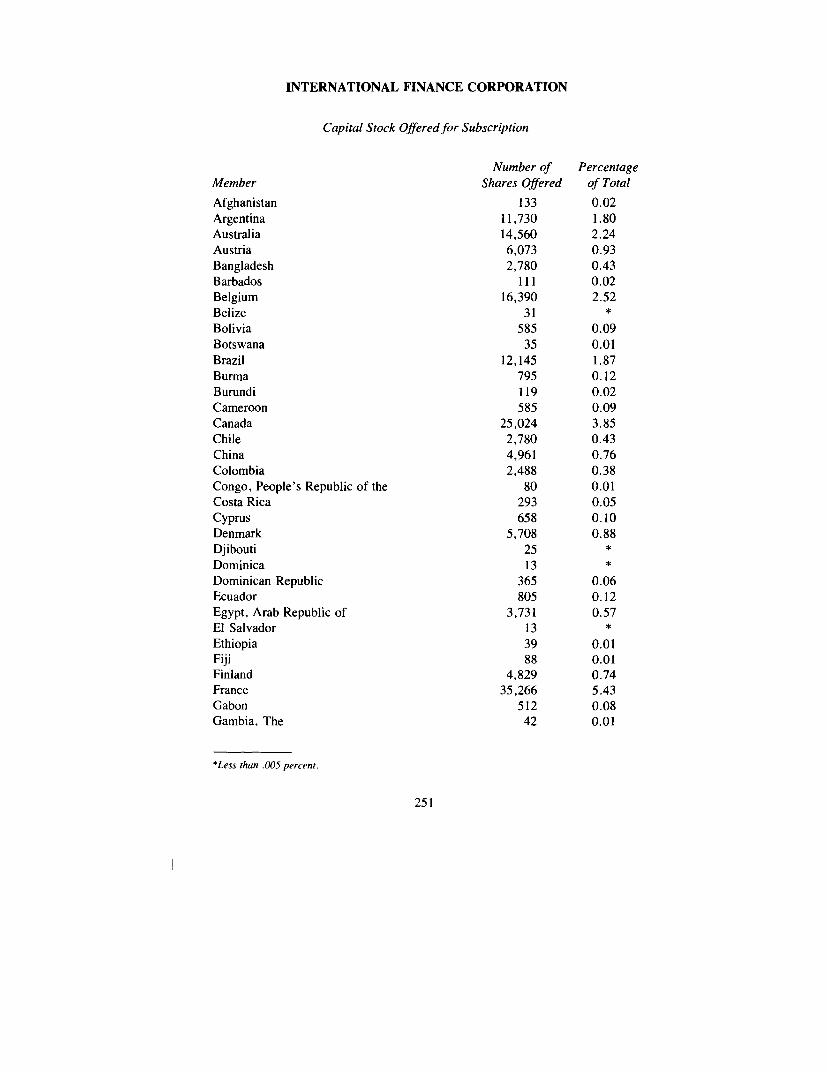

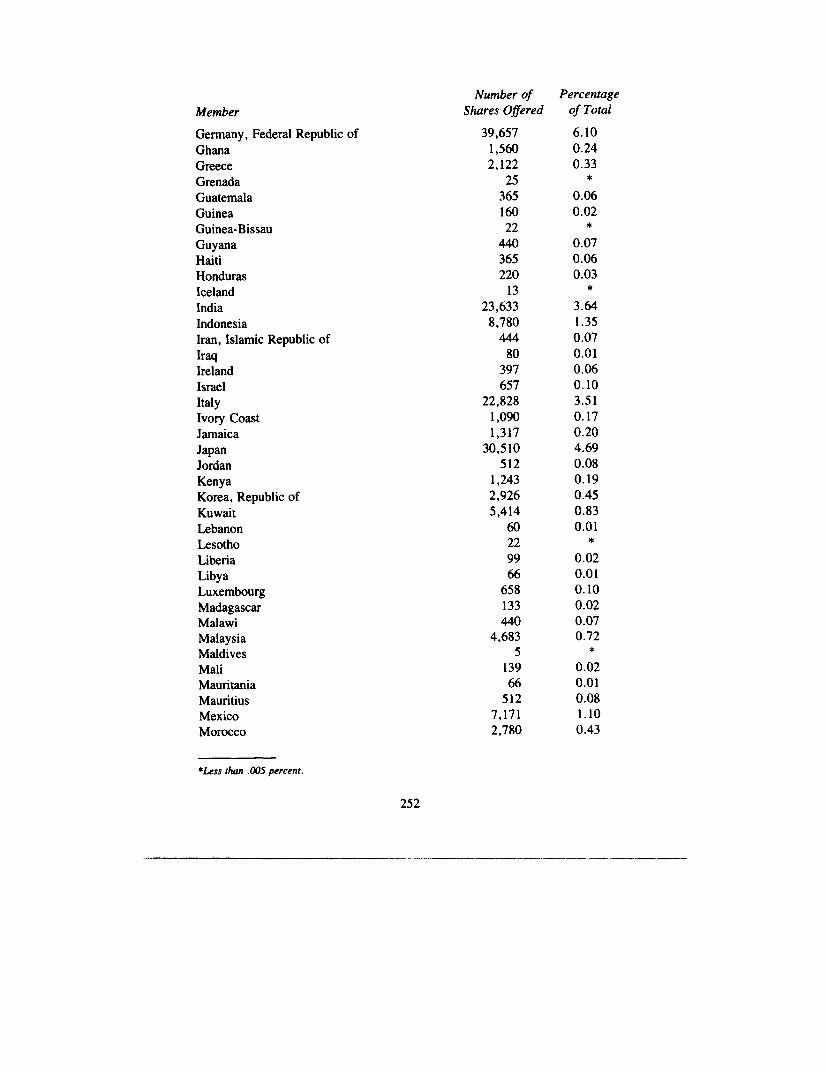

Resolutions Adopted by the Board of Governors of IFC Between the 1985 and 1986 Annual Meetings ................. 248

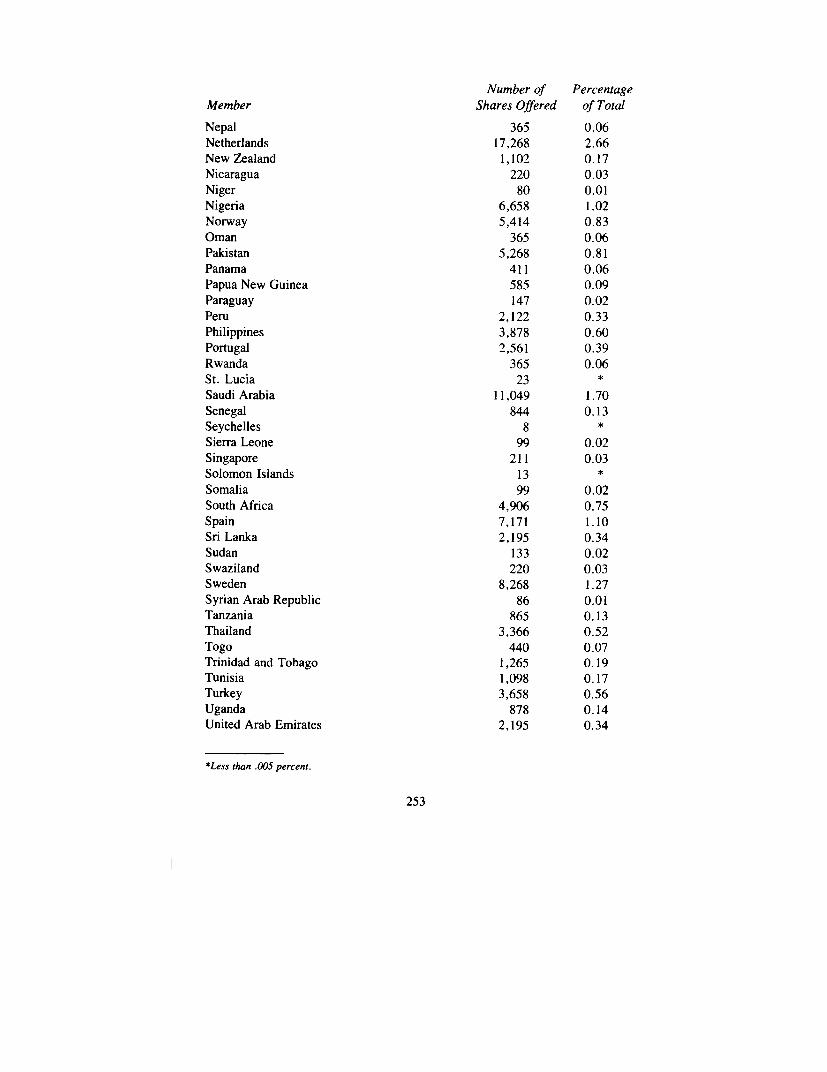

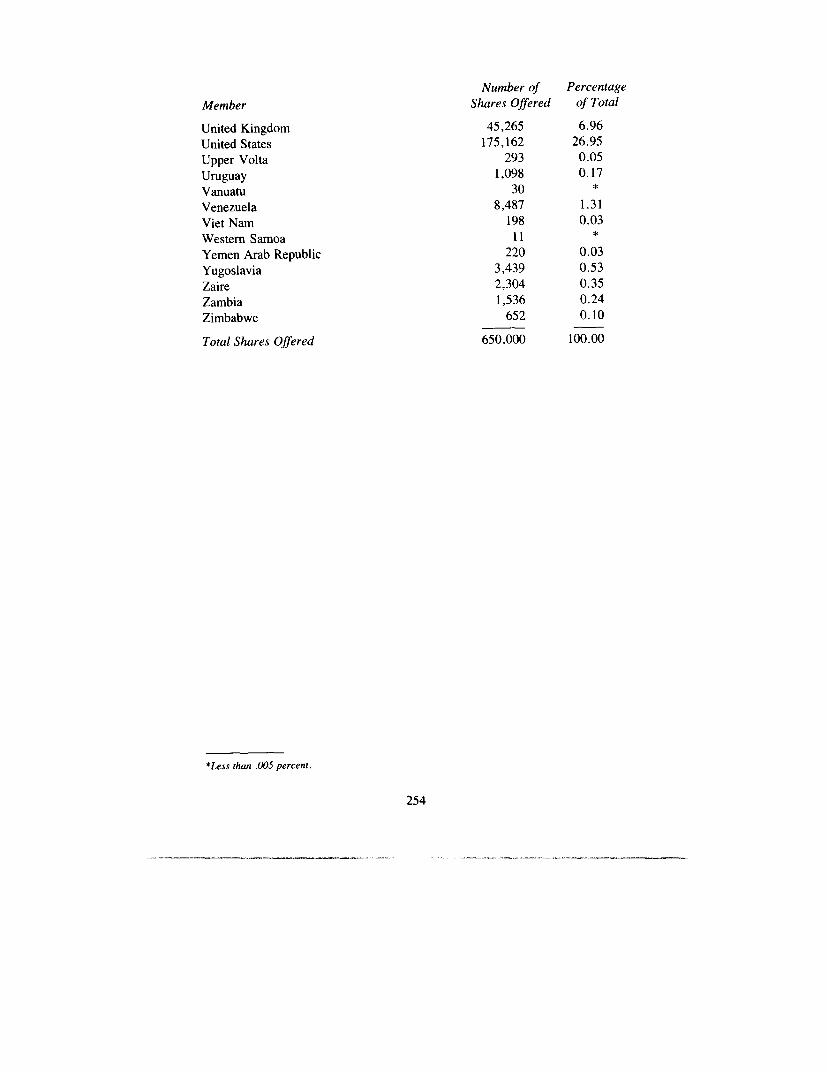

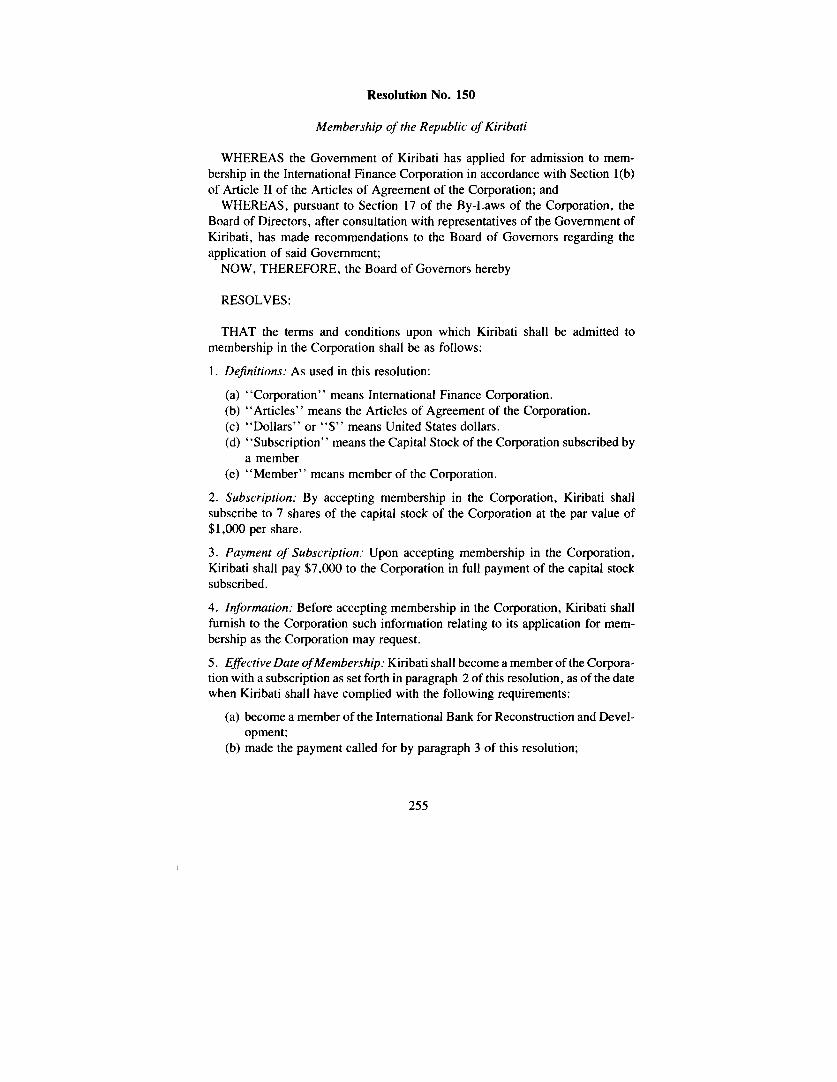

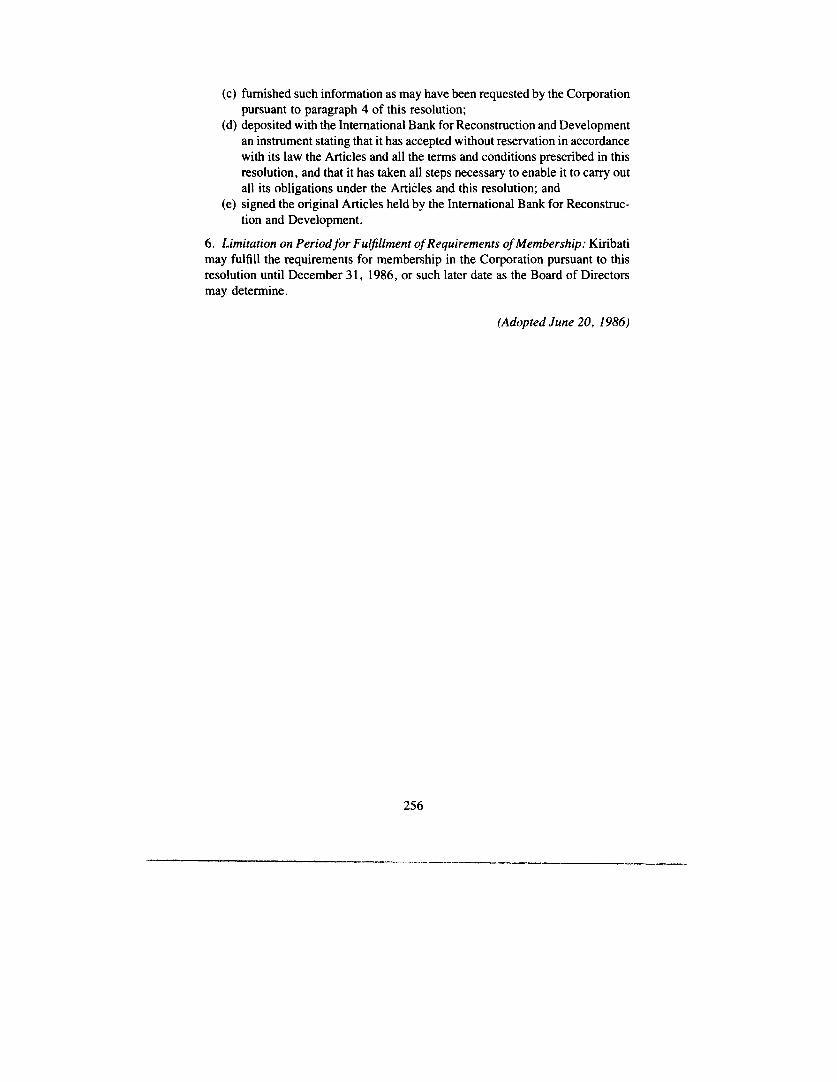

No. 149 ... Increase of Capital ............................... 248 No. 150 ... Membership of the Republic of Kiribati ............... 255

Resolutions Adopted by the Board of Governors of IFC at the 1986 Annual Meeting ............................... 257

No. 151 ... Financial Statements, Accountants' Report and Administrative Budget ......................... 257

VI

Page

Resolutions Adopted by the Board of Governors of IDA Between the 1985 and 1986 Annual Meetings ................. 258

No. 139 '" Membership of St. Christopher and Nevis ........ . . . .. 258 No. 140 '" Membership of the Republic of Kiribati .............. , 260

Resolution Adopted by the Board of Governors of IDA at the 1986 Annual Meeting ............................... 262

No. 141 ... Financial Statements, Accountants' Report and Administrative Budget ......................... 262

Reports of the Executive Directors of the Bank ...... . . . . . . . . . . . . . . .. 263 Number of Elected Executive Directors .......................... 263 Increase in Certain Subscriptions to Capital Stock . . . . . . . . . . . . . . . . .. 265 1986 Regular Election of Executive Directors ..................... 268 Allocation of FY86 Net Income ................................ 269

Rules for the 1986 Regular Election of Executive Directors ............ 270

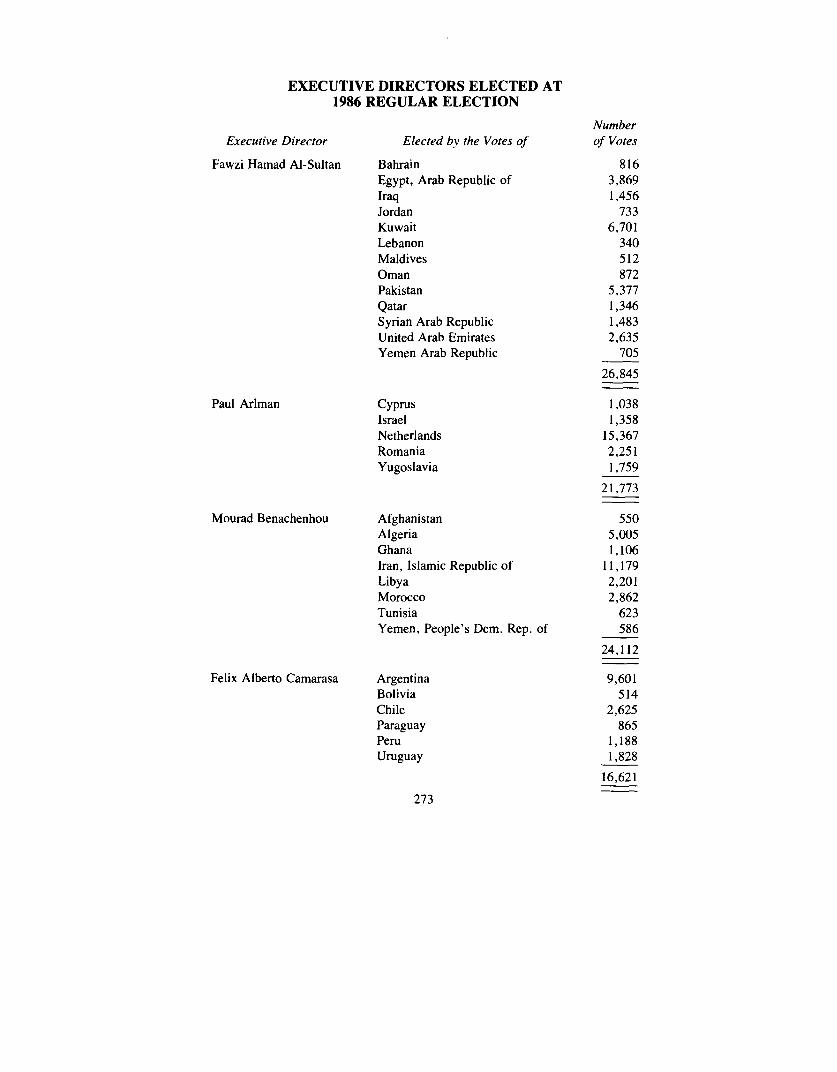

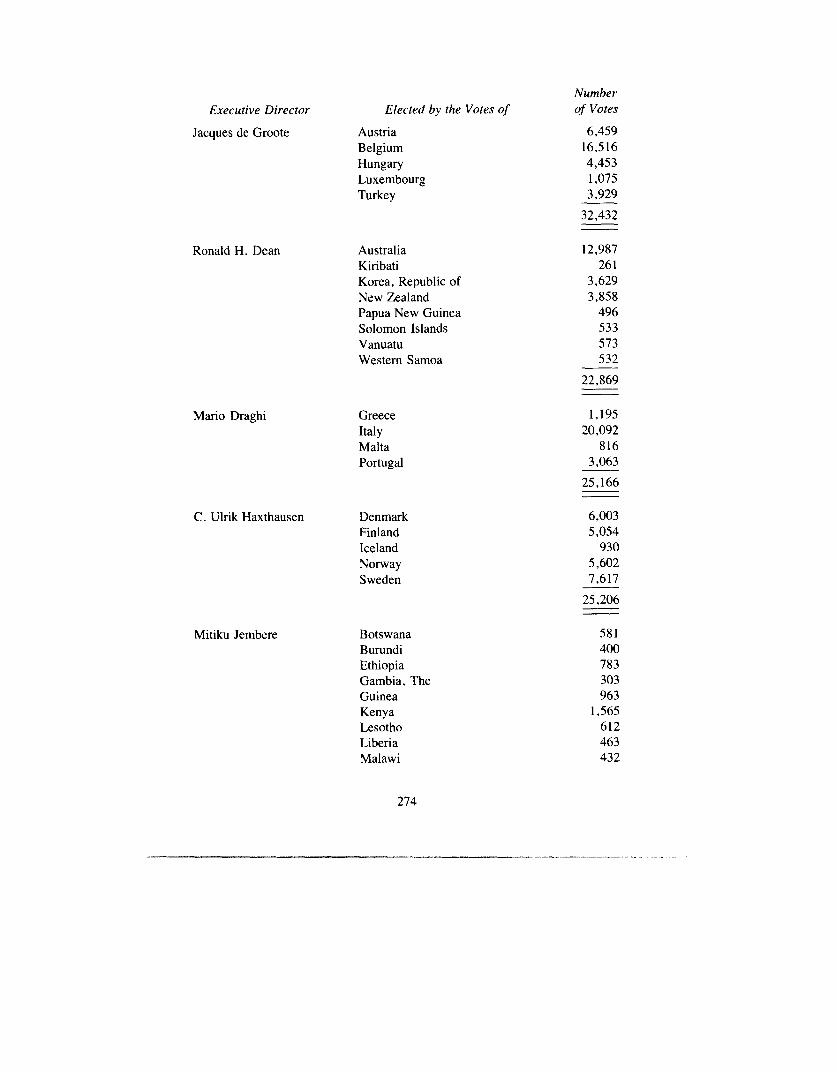

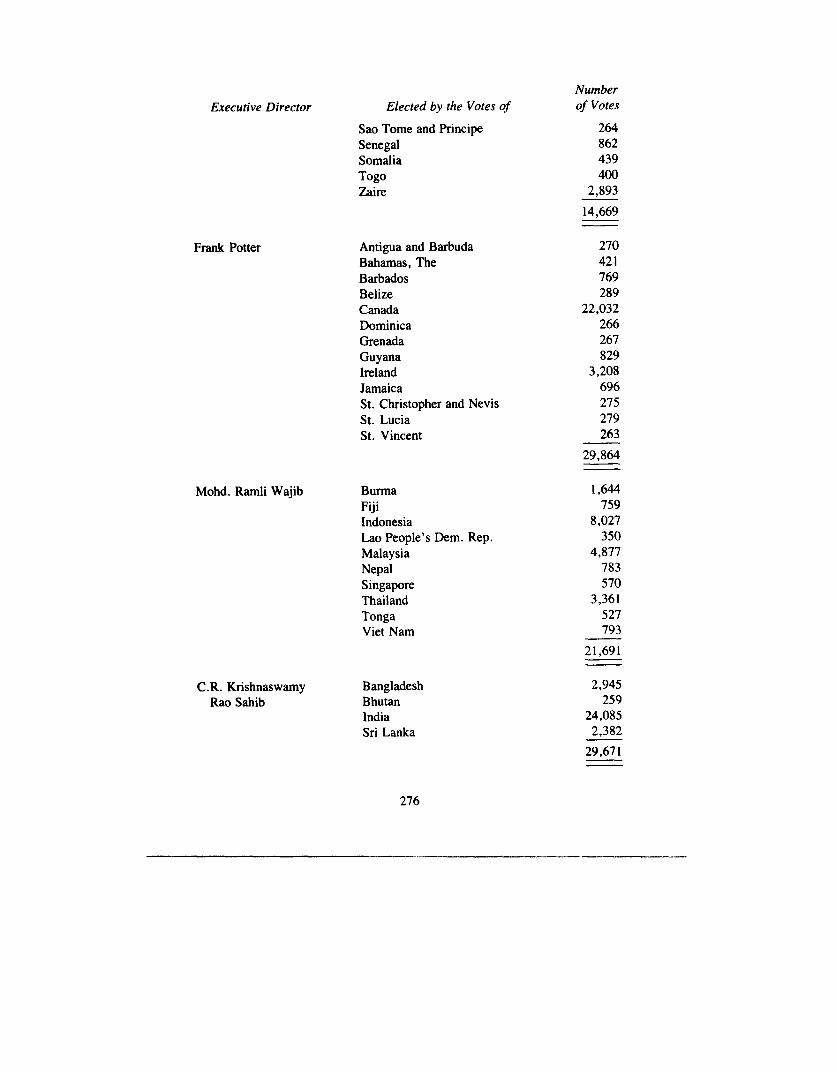

Executive Directors Elected at the 1986 Regular Elections ............. 273

Report of the Board of Directors of IFC . . . . . . . . . . . . . . . . . . . . . . . . . . .. 278 Increase in Authorized Capital of the Corporation and Increase

of Members' Subscriptions Thereto ........................... 278

Report of the Chairman of the Development Committee ............... 291

Annual Report of the Development Committee ...................... 292

Accredited Members of Delegations at 1986 Annual Meetings ... . . . . . .. 293

Observer at 1985 Annual Meetings ............................... 329

Representatives of International Organizations ...................... 329

Executive Directors, Alternates and Advisors ....................... 330

Officers of the Boards of Governors and Joint Procedures Committee for 1986-87 ........................ . 331

Reference List of Principal Topics Discussed ....................... 332

VII

OPENING REMARKS BY THE HON. RONALD REAGAN PRESIDENT OF THE UNITED STATES

Mr. Chairman, Managing Director de Larosiere, President Conable, Governors of the International Monetary Fund and of the World Bank Group, and distinguished guests:

Before I begin. I want to share with you an announcement that I made only an hour ago at the White House. Ten days ago. Soviet General Secretary Gorbachev proposed to me that we hold a preliminary meeting to make concrete preparations for his coming visit to the United States. And now that Nicholas Daniloffhas been released, as we insisted, an important obstacle has been removed. and I have accepted Mr. Gorbachev's proposal. We have agreed to meet in Iceland on October 11 and 12. It will be to prepare the ground for a productive summit covering all the issues on our agenda: arms reductions, human rights, regional conflicts. and bilateral relations.

For all the American people, I am pleased to welcome you once more to the United States for your Forty-First Annual Meetings and honored to address you once again. Let me note at the outset that both the IMF and the World Bank are in a year of changes at the helm.

At the IMF, Managing Director de Larosiere has announced his intention to resign after eight years of service-eight of the most challenging years in the Fund's history. I might add. He has met those challenges with strong leadership, a skillful negotiating style. and complete dedication to the mission of the institution he leads and serves. He has enhanced the prospects of the world economy for all of us. We salute him for his service.

At the World Bank, one of this century's most distinguished members of the U.S. House of Representatives. Barber Conable. has taken the tiller. In the United States. President Conable has been known for his extensive grasp of national finance. He had a profound influence on the development of American economic policy in the last decade. and now those same enormous talents will be guiding the Bank. He is also a good friend. Barber. congratulations.

If this is a time of changes for the Fund and for the Bank. these are even more dramatic times for the world economy. Throughout the world these last five years. we have seen men and women begin to challenge old dogmas and rediscover timeless truths. We have seen that nations that have embraced the enduring principles of economic growth have become more prosperous and secure. And those that have not. have weakened. faltered, and fallen behind.

We have heard many names given to these rediscovered economic insightsnames describing policies of taxation, regulation. government spending. monetary management. and trade. But all these names-and the many theories with which they are associated--come down in the end to one name. one theory. one word. The word is "freedom." in this case economic freedom.

In so many addresses to so many international forums during the past 51/~ years, I have repeated America's vision of the future. It rests on that word: a word that

means trust in the people more than in governments. trust in what the people can achieve when they are able to reach and climb as far as their natural talents and native abilities will take them. And each time I have spoken about this vision I have said that, as with political freedom. economic freedom is not just a question of absolutes-not just a case of an open economy or a totalitarian one-but also of degree.

Even in free market economies. high taxes make people less free to work. save, and invest. Excessive regulation makes them less able to experiment and innovate. Too much government spending can rob those on the receiving end of a reason to labor and those who must pay of their incentive to strive. And restrictions on trade rob every worker of the opportunity to have the markets for his products grow to reach all mankind and rob every consumer of a better way of life.

In the last 5 Y2 years now. we in the United States have done our best to be faithful to this economic creed. When our Administration came into office. we found the American economy on the brink of disaster. A decade of rising inflation and soaring taxes had taken its toll. Our economy was stagnating and threatening to fall. dragging the entire world economy down with it. The sources of our problems weren't hard to find. The noted British historian. Paul Johnson. commented on the various studies of them this way: "The most detailed analysis of this stagnation and decline ... suggested the causes were ... failure to control the money supply. excessive tax burdens and above all government intervention and regulation ...

And so in 1981 America took a new course. We cut all forms of intervention in the economy; we cut the scope of regulation; we brought down tax rates; and we lowered the rate of increase in government spending. By early 1983. we began to see the results as America entered what is now one of our longest-lived expansions in the postwar era. an expansion that has been accompanied by falling inflation and falling interest rates. Today. a greater percentage of our people are at work than at any time in our history. And in the last four days we have just taken another great step on the road to sustained growth with the passage of historic tax reform legislation. We will never forget that our growth has been and remains important not only to Americans but to people everywhere. Our growth has fueled the growth of the entire world economy.

Two years ago, when I last addressed this body. I suggested that the lessons of freedom. the marketplace. and growth were ones that all nations could embrace. I suggested that if the world economy were to grow as all of us hoped it would. we needed to turn away from small-minded calculators in big state bureaus and look instead to large-minded entrepreneurs in small private enterprises-whether industrial. commercial. or agricultural-for these people know secrets more profound than those revealed in all of the charts and analyses produced by all the agencies and bureaus put together.

Again. a statistic from our own situation comes to mind. According to the M.I.T. Program on Neighborhood and Regional Change. between 1981 and 1985 businesses that were less than five years old and businesses that had fewer than 20

2

employees created more jobs than America as a whole. If we had had no entrepreneurs. we in America would have lost more than 3 million jobs in that time instead of the large gains we in fact enjoyed.

All of us here today can take great satisfaction knowing that this message of economic freedom is at last being heard and acted upon in Europe and Africa, in Asia and Latin America. Only a few years ago in Western Europe, for example, capital markets were, to a large extent. closed to entrepreneurs. in part because steep taxation sapped Europe' s risk-takers of any reason to take a chance on a new company or a new idea. And with labor regulations that made it more difficult to lose a job than get divorced, entrepreneurial activity was at a low ebb. Now, however, this is changing. As inflation and interest rates have fallen and new policies have been adopted to encourage growth and entrepreneurship, Europe has begun to put behind it a decade in which not one net new job was created. and once more is seeing new growth. new jobs, new companies. new opportunities-new hope.

And this progress has not been confined to the industrial world alone. Less developed countries have also caught the spirit of freedom and enterprise. In India we have seen-within just a few harvests-a country that imported agricultural products tum into a food exporter. this after incentives were introduced and controls removed. In China. too. we have heard the same story of incentive and bounty. And in famine-stricken Africa. we have seen some countries free their markets and give their farmers incentives to produce. and those countries did not suffer the devastation of their neighbors. Some in fact exported food to those who were starving around them.

As I mentioned in my address to the United Nations of a week ago, we welcome the resolution of the Special Session on Africa that calls for more free market incentives. We in the United States are looking at ways the assistance we provide to African countries can best support development of free markets. especially in agriculture. America hopes other donors will do the same.

All in all. we have made great progress toward a stronger world economy since I last addressed you, and yet problems remain. I would like to turn now to some of these problems and to what we can do to solve them. And let me look at them from three vantage points-that of the United States and the industrial world; that of the developing nations; and finally that of international organizations such as the IMF and the World Bank.

As President of the United States. I am particularly aware of the tasks we in America have before us. Highest among these is curbing the growth of our Government's spending. No nation can survive if government becomes like the man who in winter began to burn the wall boards of his house to keep warm until he had no house left and froze. We have made progress against those who would condemn future generations of Americans to lives of pauperdom; the Gramm-Rudman-Hollings legislation is evidence of this. But, we can and must do more. I pledge to you that I will do all in my power to stop this fiscal death march. And I believe the American people will support me in this effort.

3

We have other items of unfinished business in America-bringing interest rates down even further while keeping inflation under control is one. Reducing our trade imbalances while resisting protectionist pressures at home and abroad is another. We know the role our recovery has played in the world. We know how much rides, not only for ourselves but for much of mankind, in the completion of the work we began 5Y2 years ago.

But while America's expansion is beneficial, other industrial nations must also contribute their fair share to world recovery and adopt more growth-oriented policies. Of course, some dislocations may come in the process, but we must recognize that if we are all to prosper together then we must all work together toward that end. Every nation must contribute to world economic growth. And we must do more than repeat this high-sounding sentiment; we must take practical steps.

We have come a long way since I last spoke to you. The Plaza agreement, concluded last September among five industrial countries, was a beginning toward correcting the excessive volatility in our exchange rates. Since then, we have also coordinated the reduction of interest rates. And at the economic summit in Tokyo earlier this year we agreed to new mechanisms for closer economic cooperation. All of this helps foster world growth, not only for the major nations of the world, but for everyone.

The ·industrial countries have more, much more to do. So, too, do the developing countries. Let me take up now the second great vantage point on the question of world economic growth-that of the developing nations. As I said, many of these nations have adopted policies that promote growth. These include lowering taxes, privatizing public enterprises, liberalizing trade and investment policies, and moving in general to more market-oriented economies. All this is important, not just for the developing countries but for all nations and people who will invest in their businesses, buy their products, sell them goods, and work with them to live in peace and brotherhood on our planet.

As Secretary Baker stressed in presenting the" Program for Sustained Growth" in Seoul last year, growth-oriented reforms are particularly important in the debtor countries. History has shown that when nations have rising popUlations and do not give their people the freedoms that fulfill their aspirations, those nations try to buy peace in their restless and unproductive populations by borrowing themselves into bankruptcy. Either that or they turn to oppression.

So, let us remember that growth is the key to repaying debt while fulfilling the dreams of the people. Several debtor nations have taken long steps up the path to renewed economic strength. Countries like Colombia and Argentina have brought inflation down and opened their markets. Other countries like Senegal and Cote d'Ivoire have made progress in liberalizing their economies. And Mexico and the Philippines both recently agreed to comprehensive, growth-oriented economic programs supported by the IMF and the World Bank. It is important that these programs-as well as the comprehensive programs of other debtor nations-be fully supported by commercial banks.

4

The IMF, of course, plays a central role in the drama of growth in debtor nations. The United States wants to see that role continue. We welcome the increased emphasis in the IMF on growth-oriented reform packages even while continuing the focus on financial stability. For the same reason, we welcome the recent establishment of the Structural Adjustment Facility. And, we urge the IMF to put even more emphasis on market-oriented structural reforms.

The World Bank also has a critical role to play in promoting growth in less developed nations, whether troubled debtor nations or not. We welcome an increase in the practice of lending contingent on countries' turning to more marketoriented policies. We also support the early completion of negotiations for refunding of the International Development Association. And we support the implementation of the convention that establishes the Multilateral Investment Guarantee Agency.

The future of world economic growth depends on choices made all over the world-in industrial countries, in developing countries, in the IMF, and the World Bank. The question is: will we tum toward uplands of freedom and growth, or toward the swamp of state control and stagnation? This is the question every nation and every institution must ask itself. The world's growth depends on our answers, and on something else, closely related to those choices.

This is the last area of problems I wish to discuss with you. This is the one area that can most easily jeopardize all we have achieved and hope to achieve. It might be said that since the end of the Second World War, we-all of the nations represented here-have lived under an economic constitution. In the two decades before the adoption of that constitution, our peoples suffered the horrifying consequences of a collapse in international trade and monetary flows.

Since its adoption, we have had 40 years of a prosperity more widely shared and more generous than the world has ever known. I call the postwar arrangement a constitution, but it has been, in fact, not one constitution but three. I'm speaking of the collection of postwar international economic agreements that created the IMF, the World Bank, and the GAIT (the General Agreement on Tariffs and Trade).

Today, each of those agreements and institutions has come to a turning point. Each is grappling with new challenges, such as debt restructuring, financial instability, trade in new products and new industries, and the rise of worldwide protectionist pressures. Collectively these turning points represent a culmination of the policies that the nations of the free world established right after the war.

Those nations--our nations-saw that the best way to ensure a just and lasting peace was to build an open, growing, and prosperous world economy. The same era that produced the noble proposal of the United Nations also produced the IMF, the World Bank, and the GAIT. These institutions gave us a growing and prosperous world economy. But many of the arrangements originally incorporated into them presumed America's singular strength. And for more than a decade now, Europe and Japan combined have had a role equivalent to that of the United States in world trade and an increasingly important role in finance. Many other coun-

5

tries-those with open markets and low taxes-are growing rapidly, may soon become fully industrialized, and can expect to play more prominent parts, as well.

These have been healthy developments-and ones that reflect the success of our postwar vision. But they have led to strains in the postwar agreements; and these strains have given rise to a new round of significant questions about how the world economy should develop from here----questions such as how can we coordinate our policies to restore stability to exchange rates? How can we resist protectionist pressures as our nations become more nearly equal competitors and world trade grows? How can we manage our financial responsibilities without sacrificing growth? And how should we expand our international constitutions so that the hopes and opportunities of the last generation can also be the hopes and opportunities of the next?

The recent GATT Ministerial was a good first step toward answering some of these questions. The ministers decided on comprehensive negotiations that would include trade in agriculture, services, investment, and intellectual property. But we need more steps. We need, first of all, to resolve that a further opening of the world economy is a goal worth working for.

I know I believe it is. I lived through the Great Depression. I saw what so-called protectionism brought the world-nothing was protected, everything was destroyed back in the 1930s. Today, the stakes are even higher. In my country, for example, up to 10 million jobs are tied to international trade, as is 20 percent of our gross national product, compared to 12 percent in 1929. The choice is simple-we can go forward or backward. I believe that we must move to a more open world economy.

This is why I have vetoed protectionist legislation. It's why I've supported strong and growing roles for the IMF and World Bank. It's why Secretary Baker presented his plan to strengthen our multilateral strategy for dealing with the debt crisis. It's why we've pressed for a new GATT round.

It is also why we have moved and will continue to move aggressively against unfair trading practices in other nations. No trading system among equals can survive if some feel they are being discriminated against and if there are enormous imbalances in trade flows. The only ways to resolve the external imbalances between countries are through increased growth abroad, a greater competitiveness for the U.S. dollar or both, coupled with the opening of markets.

My friends, I believe that the challenge before us is to develop a truly global economy--one that celebrates the diversity of our nations while it opens us to uninhibited trade and investment among our peoples. We have traveled a vast distance toward such a world in the last 40 years. We have come so far and now it is time for stock taking, for planning with open minds the next leg of the journey, and for beginning it.

Let us look with open minds at ways of promoting stable exchange rates and assuring sound money. Let us approach with open minds the next round of trade talks and push them as far as we can to our goal of eliminating all trade barriers.

6

We are, my friends, on a great journey of exploration. And as on all such journeys, from time to time, we tire. But if we are strong and if we continue onward, I believe we will find that a more bountiful land lies before us. Let us all join together on this great journey. Let us reaffirm our commitment to the institutions that have brought us this far. Let us reaffirm our commitment to strengthening them for the adventure that lies ahead.

Thank you, and God bless you all.

7

OPENING ADDRESS BY THE CHAIRMAN, THE HON. VIRGILIO BARCO

Governor of the Fund and Bank for Colombia

I want to welcome you to these Forty-First Annual Meetings ofthe International Monetary Fund and the World Bank. I look forward with much interest to our debates, which will help us to progress beyond the achievements made possible by our last Meetings in Seoul.

On behalf of all those who are gathered here, allow me to express our thanks to President Reagan and, through him, to the people of the United States, and particularly of the city of Washington, for their hospitality.

I take this opportunity to greet the representatives of Poland and Kiribati, whid have recently joined both institutions.

I am also pleased to welcome Mr. Barber Conable, the new President of the World Bank. We are certain that, with his experience and under his leadership, the Bank will be in a position to meet the new challenges that lie ahead.

In my capacity as Chairman of the Boards of Governors allow me to assure you, Mr. Conable, of our cooperation and support, and to wish you the best of success in your new position.

On the eve of these Meetings we were informed of the decision of Mr. Jacques de Larosiere to resign before the end of his second term as Managing Director. Since 1978, when he took office, the international economy has been exposed to the shocks of sharp changes in oil prices, excessive volatility of exchange rates, high interest rates and the problem of the external debt. In these circumstances, the Fund has provided strong support as the focal center of the international monetary system. On behalf of the Governors, may I express to him our appreciation for his achievements in office and wish him equal success in the months during which he remains at the helm of the Fund and in his subsequent activities.

The Fund and the Bank must playa leading role in coping with the difficult situation now confronting the world economy. A substantial part of our deliberations will continue to be devoted to the search for sustained growth of the world economy. By virtue of their responsibility for gathering and channeling financial and technical resources, and as providers of such resources, the two institutions have the mission of assisting developing countries so that they have the support they need to set their economies on the path of sustained growth.

Industrial countries

The crucial importance of the economic performance and of the policies of industrial countries for the developing world was clearly recognized at the last Annual Meetings in Seoul. Unfortunately, developments in the industrial economies have not been overly favorable.

8

The economic recovery set in motion at the end of 1982 showed signs of weakness in 1985, and activity levels in the first half of this year fell far short of expectations.

Thus, the real growth of production in developed countries slowed down from approximately 5 percent in 1984 to about 3 percent in 1985. Reduced momentum in the United States was not offset, as would have been desirable. by higher growth in other industrial countries. In Europe, growth remained at the modest levels of 1984. This caused the economies of the developing countries to weaken further between 1984 and 1985.

This notwithstanding, it should be stressed that some important industrial countries have achieved encouraging progress in the coordination and direction of their economic policies. A positive step was taken at the meeting of the Group of Five, in September 1985. with the decision that their economic strategies should be aimed at achieving balanced growth. while exchange rates should refl~ct equilibrium positions. As a follow-up to this initiative. the seven major industrial countries reached further agreement on coordination of their economic policies at the Tokyo summit in May.

Many of the measures taken by the industrial countries have begun to exert a favorable impact on the international economic environment. Inflation has slowed to the lowest level since 1967. As a result, inflationary expectations have abated even more. facilitating a decline. which to some extent has been coordinated. in nominal interest rates.

Still, the industrial countries have the responsibility of making an even greater effort for creating a favorable and less uncertain external environment that will sustain growth, employment. and political and social stability in the developing countries. In addition, they must provide a dynamic market for exports, allowing free access to their markets and eliminating export subsidies for agricultural products.

What is more, the industrial countries must put into practice their good intentions to fight protectionism by deciding not only to resist protectionist pressures but also to eliminate existing barriers to international trade, particularly those that discriminate against the developing countries.

Further. within the framework of the GATT, they must ensure the success of the new round of multilateral trade negotiations recently initiated at Punta del Este, giving special consideration to the inclusion of agricultural products. The countries meeting at Punta del Este affirmed the purpose of strengthening the links that should exist between world trade and policies promoting domestic growth in order to improve real flows of financing and investment to the developing countries. A major role in this process has been assigned to multilateral credit institutions, particularly the International Monetary Fund and the World Bank.

It is to be hoped that the industrial countries will adopt policies consistent with a further reduction in international interest rates. which continue to be high in real terms compared with historical levels. In this respect, the proposal for a more balanced budget in the United States is very important in that it would contribute to capital formation and economic growth throughout the world.

9

Those industrial countries that have succeeded in controlling inflation and are in a favorable exchange rate situation also have a very special responsibility to adopt economic policies enabling them to make a more positive contribution to world economic growth.

Developing countries

The slower growth of the world economy has had broad negative repercussions in the developing countries, whose export earnings are no longer growing satisfactorily. This explains in part that decrease in the average growth of their aggregate product, which dropped from 4 percent in 1984 to less than 3 percent in 1985. This decline continued in the first half of 1986.

Most developing countries confront a wide range of problems, including particularly the following: high and growing external debt service payments, with the concomitant net outward capital transfers; low saving and investment levels; high inflation rates in some countries; high levels of unemployment and underemployment; widespread extreme poverty; and the political and social instability that usually accompanies such situations.

The debt problem continues to darken the picture for our economies. As I wrote in a letter to Mr. Alden W. Clausen on the occasion of last year's Meetings in Seoul, this problem must be attacked with a medium- and long-term strategy, a strategy based on the necessity of economic growth and acceptance of the fact that the debt burden must be distributed among all parties, not among the borrowers only. It is important to note that, since that time, the validity of this approach has at last been recognized.

The governments of the industrial countries are thus beginning to accept this premise. Under the leadership of the United States, and at the initiative of its Secretary of the Treasury, Mr. James Baker, the United States presented in Seoul a proposal which, besides recognizing the necessity of economic growth as a precondition for solving the debt problem, accepts the principle of the shared responsibility of creditors and debtors.

Although this represents progress and has aroused interest and expectations in the international community, and particularly in the developing countries, a more decisive contribution by this initiative to a solution of the debt problem is still awaited.

The program recently adopted for Mexico, which will require substantial financial support from the Fund, the Bank, commercial banks and bilateral sources, illustrates how a concrete program can combine the firm, sovereign decisions of a developing country with the ideas contained in the Baker initiative.

Obviously, it is necessary to bolster this strategy in order to develop an appropriate, equitable solution to the external debt problem. This will require active collaboration on the part of all the parties involved, in a spirit of compromise and commitment accepted by all. As for the debtor countries, they will need to reaffirm their determination to adopt structural reforms on the home front

10

designed to promote exports, saving, domestic as well as foreign investment, and greater economic efficiency, always striving to improve the living standard oftheir peoples.

Admittedly, there is an element of hope in this gloomy picture, thanks to the strong performance of some countries that export manufactured goods and of most of the Asian countries; they have maintained a good rate of growth, though it was lower in 1985.

These developments have yielded substantial progress in the management of the high external debt of some developing countries. It is also clear that these efforts at strengthening their balance of payments position have entailed excessive sacrifices in their investment levels, public as well as private.

But the overall picture is that the export earnings of the developing countries have ceased to grow, as a result of a decline of 2 percent in the terms of trade for basic commodities in 1985, combined with a slowdown in the growth of international trade.

This is largely due to higher protection in the industrial countries and to the increasingly alarming proliferation of nontariff barriers in markets for specific products. An international scenario is thus emerging in which the competitiveness of the developing countries depends less and less on their own efficiency and more and more on political decisions in the industrial countries.

'The developing countries, particularly in Latin America, have been implementing drastic economic reform programs. As a result, there has been an important change in the external current account position particularly for countries that are net importers of capital.

The combined deficit fell from about 18 percent of exports in 1982 to less than 4 percent in 1985, though all countries did not share equally in this achievement. But notwithstanding this success, the trade surplus barely covered net interest payments.

It would therefore be unrealistic to assume that these countries could restructure their economies without additional financial assistance. Yet the behavior of the international commercial banking community does not square with this fact: it has sought to reduce its exposure despite the improving balance of payments of the developing countries. An appropriate response is required to the need for greater flexibility and for the timely rationalization of the regulatory practices applied to commercial banking.

At the same time, the members of the Paris Club, and commercial banks in general. must address themselves more flexibly and appropriately to external debt restructuring and refinancing operations for the developing countries. They should also provide the resources needed to ensure implementation of the program of growth-oriented adjustment proposed at the Seoul Annual Meetings.

Africa's Sub-Saharan countries need special treatment in view of the severe economic and social problems they confront. The main evidence to that effect is that the lowest-income region in Africa is poorer today than it was in 1960. Though some of these countries instituted courageous changes in economic policy in 1985. more generous external support for them has not been forthcoming.

11

In this context it is vital that the Eighth Replenishment of Resources of the International Development Association be of sufficient scope to allow for an improvement of the African countries' growth prospects in coming years.

For their part, the governments of Africa must maintain the political resolve to ensure that domestic as well as external resources are used as efficiently as possible. Donors and lenders to Africa must act effectively to increase the volume of c'oncessional asssistance and so reduce the debt burden of the world's poorest countries.

Africa's development crisis is not solely an African problem; it concerns all of mankind. In view of the scope of Africa's internal and external problems, it needs the support of the entire international community without delay.

Colombia

Colombia has distinguished itself for some decades by the stable, steady economic growth it has achieved. However, it has not been immune to the problems that have affected the world economy, and particularly Latin America, in the last few years.

Although its economy has been beset by difficulties on the external front since the early 1980s, the country, faithful to its historic tradition, has fully respected its debt service commitments and has had no need to restructure its external public debt. As a result, it has been able to maintain its credit standing with foreign commercial banks.

These results must be viewed as part of a long tradition of pragmatic economic policies. Instead of being marked by abrupt changes, our policy-making has sought to keep economic, political and social considerations in balance and to maintain a positive relationship with multilateral agencies.

The role of the International Monetary Fund

The Fund has continued to play a leading role in the international monetary system. In fulfilling its responsibilities, it will be called upon to help formulate programs and policies that are viable in the medium term and promote growth with moderate inflation, high employment, expanding world trade and, above all, a progressive improvement in social conditions.

If stabilization programs are to be effective, apart from taking the special problems of each country into account they must reflect its specific economic structures and political sensitivities. The programs, in tum, will require determined support from governments and public opinion; to that end, when their conditions are being agreed on, care must be taken that the sacrifices they impose do not fall unnecessarily on the poorest segments of the population.

No single policy formula is appropriate. for all countries, particularly developing countries. The Fund must always respond flexibly and expeditiously to changing circumstances in the world economic environment. The formulation and

12

implementation of stabilization programs thus require flexible responses that take into account the frequent changes in the markets for commodities.

The Fund must continue to playa prominent role both in the effort to encourage commercial bank lending to the developing countries and, just as importantly, in promoting and shaping appropriate multi annual agreements for the refinancing and rescheduling of debt payments.

I ask the Governors to support the continuation of a policy of broader access to the Fund's resources and, when the Ninth General Review of Quotas takes place, to decide on a substantial quota increase. This task must be undertaken without delay.

The Fund must playa leading role in improving the coordination of economic policies among industrial countries. Further, the surveillance it regularly exercises under Article IV of its Articles of Agreement can and should be made more effective with regard to the economic policies of industrial countries. In relation to that task, fundamental importance attaches to the leadership the Fund assumes in the management of international monetary and financial problems, giving due consideration to world trade issues.

An allocation of SDRs can provide immediate support to countries facing balance of payments problems. It would be particularly useful given the growing tensions that may well develop in the reserve position of a number of countries in coming years. As a result, I take the liberty of directing a special appeal to the Governors to make known their political will to support a prompt allocation of SDRs.

There is a broad consensus in the Fund's Executive Board in favor of expanding the use of SDRs and possibilities for transferring them, while improving their distribution as part of members' reserves. As regards the latter, it should be noted that the governments of developing countries would view with particular interest the adoption of distribution guidelines that would accord with the needs of our economies.

The role of the World Bank

The World Bank's role has been the subject of major discussion recently. In my opinion, the intensity of the debate and the attention it has attracted are beneficial and fully justified.

The discussion is likely to go on for some time. So far, a relative consensus has been reached on three general areas in which this institution should have broader responsibilities:

In the first place, as suggested by the Development Committee at its April meetings, the Bank should enhance its capacity to support initiatives whose central object is to achieve stable economic growth in member countries. Naturally, this should be in the context of medium-term economic programs.

The Bank has been impro. ing this capability for some years. It has been making more use of various lending instruments, particularly structural and sectoral

13

adjustment loans. In certain circumstances the Bank has accelerated and increased disbursements to the most heavily indebted countries and, in some cases, it has worked with governments on the design and execution of medium-term stabilization programs.

The lessons learned throughout this experience indicate that if medium-term programs of growth with stability are to be given an effective impetus, they must be realistic, planned around specific objectives and appropriate time horizons, and supplemented with adequate and timely contributions of financial resources and technical assistance. These programs must be characterized by high quality and proper control in the planning, implementation and monitoring of economic policy.

The International Development Association will also have to share in this responsibility. As the major source of concessional funds for the poorest countries, IDA exercises the leadership that befits it in assisting these countries to implement economic programs.

In the second place, the Bank must stress its role as coordinator and mobilizer of private and official resources in accordance with the needs of the developing countries. Here again, it bears stating that the Bank has made progress, having innovated and expanded its use of cofinancing as one of its regular tools while enhancing its contribution in the area of technical assistance.

For its part, the International Finance Corporation, having doubled its capital recently, is also playing an innovative role in attracting investment to the private sectors of developing countries.

Finally, a third dimension of the Bank's role, deriving from the other two, has to do with expansion of its program of support lending to meet the challenge arising from the implementation of policies directed toward growth with stability.

The Bank has a lending program of between US$40 billion and US$50 billion for the fiscal years from 1986 to 1988. In the first of these years the Bank has commitments totaling US$13. 2 billion, a 16 percent increase over fiscal year 1985 and near the upper limit of the planning range.

However, as pointed out by the Development Committee early this year, after the 1987 fiscal year the demand for loans from the Bank could easily exceed the level that can be met with its existing capital stock. This emphasizes the need for a positive response on the Governors' part to a new proposal for an increase in the Bank's capital. In addition, the Bank must make better use of its gearing ratio in order to enhance its financing capacity.

It is also important that the Bank carry out an adequate review of the costs of transfers of funds to member countries. Everyone is well aware of the comparatively high level of these costs at the present time.

It is essential that the World Bank Group maintain its commitment to progress and to the eradication of absolute poverty in all countries, particularly in those with the lowest incomes.

The International Development Association has the responsibility of providing, on a world scale, the funds required to accomplish this purpose. Given the

14

importance of that institution, particularly as regards the poorest countriesspecial mention should be made of Sub-Saharan Africa and some regions of Asia and the Pacific-it is our duty to ensure that the Eighth Replenishment provides IDA with adequate funds.

Conclusions

Attainment of economic growth in the developing countries will require a commitment on their part to carry out substantive policy reforms.

The industrial countries, on the other hand, must keep their markets open to developing country exports and assure them of an adequate flow of financial and technical resources. The International Monetary Fund, the World Bank and the Inter-American Development Bank, on a par with other multilateral institutions, will playa crucial role in this process. Above all, close collaboration between the Fund and the World Bank, which has intensified in the past few years, will take on even greater importance in future.

Economic stabilization and restructuring must be pursued simultaneously in order to achieve economic growth with stability, a reduction in unemployment, and eradication of absolute poverty in all of the world's countries.

In turn, the ever-expanding and more dynamic role that we require of institutions such as the Fund and the Bank is intended to secure a more determined and stable contribution on the part of investment and commercial banks to the development process.

Given the guarantees represented by the financial participation of multilateral banks, and thanks to cooperation on the policy and program level with the Fund, the Bank, and the borrowing countries, these banks will have adequate incentive to provide more funds for the developing countries on more favorable financial terms.

The assistance provided by the Fund and the Bank, each in the area of its statutory mandate, must be given in a context of close mutual support. The Bretton Woods institutions must be creative and flexible, and must assume the leadership required to ensure that economic policies are designed for the achievement of lasting solutions-with a social content-to the problems of the international economy.

I must repeat that, if the Fund and the Bank are to meet their obligations successfully, they will need additional financial resources. In addition, their programs must seek the political support of all member countries.

Let us renew our commitment to economic and social progress through international cooperation. Let us see to it that the reordering of our economies is reconciled with higher growth and a better distribution of world economic progress to favor the poorest countries and the most needy popUlation groups.

15

ANNUAL ADDRESS BY

BARBER B. CONABLE President of the World Bank

Mr. Chainnan, Governors, Ladies and Gentlemen: Welcome to these Annual Meetings. Welcome especially to the delegates from our newest member nations: Kiribati and Poland.

I was born in a town named Warsaw. I was educated in Ithaca. I began my legal career in Batavia. For twenty years in the Congress of the United States, I represented the citizens of Lima, Attica, Avon, Castile. Java, and Greece.

Those place names in upstate New York are part of my heritage. These small communities bear witness to the wider world from which America drew its people and culture and to which Americans have turned again for commerce and counsel and collective action. Collective action against global poverty is the common purpose that brings us together today. It brought the World Bank into being four decades ago, and it still defines the goals which I intend to serve with all my energy for the next five years.

By training, I am a lawyer, a negotiator. I know the duties of the public servant who must both lead and respond to constituents. And though I am neither banker nor development technician, I am familiar with the challenges of international economics and trade. Moreover, the discipline of the politics of democracy has educated me not only in conciliating conflicting views and interests but also in seeing the impact of grand designs on individual lives and private aspirations.

I come to you and to this great institution, then, ready both to learn and to lead. Having reti!'ed from public life, I did not expect such an opportunity for public service. But I welcome the challenge with enthusiasm ... as I will welcome your advice and support in meeting it.

I will also, however, genuinely miss the help of two distinguished colleagues, leaders who have contributed much to strengthening international cooperation in the development field.

Ghulam Ishaq Khan is ending his extended term as Chainnan of the Development Committee. He has guided us wisely and finnly, endowing this Committee with lasting influence and significance. We owe him our deep thanks.

And Jacques de Larosiere, what a tribute you gave him this morning, will be leaving the helm of the Fund, where he has served the international community with sensitivity and distinction. He has contributed to intensified IMF-World Bank cooperation, and I personally wish to acknowledge his advice and help to me in recent months. He has been a superbly effective leader of the Fund. We all are grateful for his contribution and regretful of his departure.

* * * *

16

The central challenge to the World Bank is the central concern of our world. It is the same in 1986 as in 1946: to mobilize the will and the resources of the affluent and of the afflicted alike in the global battle against poverty.

We have made real progress in that fight. We have much still to do. We have done well. We must, we can do better. For the Bank to achieve the results of which it is capable, it needs not a new

direction but a renewed drive, a reinvigorated dedication of its original and enduring purpose.

That purpose is development. The Bank's role is to lead in that process, and my priority as President will be to ensure resolute leadership for sustained development.

Ortega y Gasset has written: . 'Nations are formed. are kept alive by the fact that they have a program for tomorrow." The same is true of institutions, and the World Bank family of institutions must have a program for tomorrow not just to live itself. but to lead in making the lives of millions better, fuller. more promising.

The leadership program for sustained development that I wish to present to you today builds on the experience and expertise the Bank has accumulated-the solid, enormous assets of our dedicated and skillful staff. We do not have to reinvent the wheel of development. Its pioneers and past masters are already here and hard at work.

My program also capitalizes on the Bank's physical assets-the financial strength and high liquidity that enable us to move with speed and decisive impact, to lead where private initiatives and investors can confidently follow in implementing strategies of both adjustment and development.

Finally. I intend to use to the maximum the Bank's unique pivotal position in the development process--{)ur central place in the world of private and governmental finance and our broad and deep political support in the developed and the developing world.

Those sources of strength have made the Bank an institution that is larger and more powerful than its parts. We must use this power in a coordinated approach. to take the lead again in the quest for sustained development.

The ingredients of that approach blend the Bank's past accomplishments with its continuing and changing responsibilities. Let me spell out the elements that I believe are basic to leadership for sustained development.

First, let us be clear about our goal. We are a force for development. not primarily an agency for debt management. We will exert our influence

• to shield the development process from the volatility of global financial markets and aid flows,

• to encourage freer world trade, and • to help reduce the relative burden of Third World debt, so that, through a

resumption of growth, borrowing again can become a stimulus to progress. In these ways we can make genuine economic growth the healing antidote wherever poverty is poisoning people's lives and their hopes for the future.

17

These efforts must be both a strategy and a goal. They require that we draw deeply on the reservoir of skills and motivations that the exemplary leadership of the past has built up in the World Bank, and I note here in the audience today the presence of both Tom Clausen and Bob McNamara.

Second, in development lending, we must maintain on a country-by-country basis a thoughtful mix of investment and adjustment lending. The two must support each other, but in ways appropriate to each country's needs.

Third, as in the past, we will regard agricultural development in the poorest nations as central and critical in the battle against poverty.

Fourth, we will take account of long-term issues in our development activities-the need to stress population concerns, the need to protect the environment as we promote economic advance. and the need to ensure that women are fully integrated in. contribute to and benefit from development programs.

Fifth-the final component that is crucial to the success of all the others-we must maintain flexibility both in the design and the management of the Bank's activities. We have new instruments to use and a talented staff. We must make certain that our structure provides the best match between those resources and our requirements.

As Henry David Thoreau observed long ago. "It is not enough to be busy ... The question is: what are we busy about?" The business of the Bank is development. We are in position to take the lead in that business, to show the way and to set the pace.

That is why the first element of my program is simply a restatement of our fundamental goal. the primacy of sustained development on the Bank's agenda for leadership.

We are all bitterly aware, of course, that development does not proceed automatically and smoothly on its own. In too many nations too many resources meant for development are being diverted into debt service. Stabilization plans, while essential to restore investsor confidence. are also acting in some situations as impediments to growth. Lack of coordination in movements of official capital accentuates the volatile movement of private funds, and one result is to deprive long-term programs of timely access to stable credit. And new threats of protectionism are shrinking the promise of an expanding global marketplace for developed and developing nations alike.

It is not enough to list these problems or acknowledge the obvious linkage between their resolution and our prospects of progress. We must work for a resumption of growth-growth in credit. growth in trade. growth in the official and private resources committed to the fight against poverty. When nations seek the well-springs of economic growth, the Bank must be a guide, not a bystander. in their search.

There is no simple remedy or set of cures for destitution and its companions: disease and despair. But without continuing growth in the economies of the developed and developing nations and in the commerce among them, there is no cure at all.

18

- -._._------------_._----

The World Bank is the most influential intermediary between what Cervantes called the' 'only two families in the world-the Haves and the Have-Nots." In that position, we must both mediate and lead. We must be both advisor and catalytic agent in promoting the coordination and cooperation of creditor and debtor, donor and recipient nation.

The Bank is already exercising that constructive influence. While total IBRD lending in the past fiscal year grew by 16 percent, our loans to ten highly indebted countries that have embarked on adjustment programs increased by 47 percent. And our fast-disbursing adjustment-lending accounted for more than a third of our programs in middle-income nations.

Adjustment lending and investment financing are not mutually exclusive. They need each other. What good can agricultural reforms do if inadequate irrigation leaves farmland parched or inadequate transport leaves farm produce to rot in storage? On the other side of the coin, how can investments bear fruit, how can investors have confidence in a policy environment hostile to change and enterprise?

The Bank's leadership task in the face of such questions is to ensure that adjustment efforts are synchronized with development work. that official capital flows stimulate and draw private investment with them and that the hardest cases get urgent attention.

Where debt and its servicing lie heaviest in the path of growth, where-as in Latin America and Sub-Saharan Africa-falling commodity prices have drastically eroded export earnings, there the Bank must be at the forefront in lending and in spurring other lenders both to reschedule debt and to invest anew.

It is not enough to endorse the proposals U. S. Treasury Secretary Baker made this time last year in Seoul. With regard to the middle-income nations, the private financial community must move from approval in principle to action in practice.

Where the World Bank and IMF are at work in helping debtor nations to mount comprehensive adjustment programs. the commercial banks must be promptly, generously, and imaginatively at our side. A waiting game will be a losing gamefor creditors as much as for debtors.

Only growth will produce the income to ensure debt repayment. And only new capital flows at spreads as low as possible will promote higher growth. And for the very poorest nations. where lack of creditworthiness bars the door to commercial flows. substantial and sustained foreign aid must be available. Here a strong IDA is an imperative.

Equally important is the issue of trade expansion. With growth rates dropping nearly by half in the heavily indebted countries as a group over the last year, it is clear that their economies must generate export surpluses substantial enough to provide for both continued debt service and for new, growth-enhancing investments.

Yet how can they achieve that vital result if export markets shrink or close? Those who wish. as I do. to see the developing countries liberalize their own trade rules must themselves come to court with clean hands. No nations, however strong. can restrict imports and then expect easier entry for their goods and services to the markets of their trading partners.

19

Growth and freer trade go together. The responsibility of the industrial countries to invigorate their own lagging economic growth is matched by their need to open and smooth the road for trade expansion. Such movement is clearly in the selfinterest of the developed world, but it is also vital to the prospects for sustained development among the poorest and those most deeply in debt.

On their behalf, the World bank will do its utmost to ease and accelerate the new round of multinational trade negotiations under GATT auspices. As I did at Punta del Este two weeks ago, I again pledge the Bank's urgent support in the effort to reverse protectionist trends and revive trade expansion.

At the same time that the Bank continues and increases its engagement in improving the climate for developmental progress, we will also continue to expand and refine our investment lending. By giving so much attention to the complex issues addressed in the first point of my leadership program, I do not mean to leave the impression that the second point is in any way secondary.

The Bank has historically developed as a project lender. I intend to see that we go on to do it even better.

We have seen in Asia and Africa, in Latin America and in parts of Europe, how the foundation for growth is laid in the concrete of dams, in the asphalt of roads, in power and communications lines and in the fertile soil of educated minds. We have seen as well how--on such foundations-the countries of the Pacific Rim have built the momentum for export growth, how the world's two most populous nations, India and China, have scored their impressive progress.

Basic investments in development, thus, remain basic to sustained growth. That understanding will continue to direct our lending priorities even as we adjust them to mold new coordinated strategies of investment, a related subject that I will discuss shortly.

Before that, however, let me remind you of the third ingredient of sustained development: food. There is a zero-sum fallacy contending that agricultural trade--especially exports from rich to poor-will shrink as subsistence farmers increase their productivity.

The reverse is true. With development, most of the extra income earned by the poorest farmers goes to improve their families' diet. So investments in farm equipment and techniques, land reform, fertilizer, seeds and crop research can be investments in the long-term growth of international commerce as well as in the immediate improvement of human lives.

The Bank will therefore continue to stress agricultural development, from research to production, as a fundamental of sustained development. But in response to the fourth leadership concern I outlined, we will strengthen our work in all areas, rural and urban, to reflect new attention to the role of population, of the environment and of women in the lives and hopes of the world's poor.

These are not peripheral issues to development work. They are not frills hastily added to our design for growth.

High population growth rates strain both natural and financial resources.

20

Environmental neglect destroys assets vital not just to the quality of life but to life itself.

Women do two-thirds of the world's work. They produce 60 to 80 percent of Africa's and Asia's food, 40 percent of Latin America's. Yet they earn only onetenth of the world's income and own less than I percent of the world's property. They are among the poorest of the world's poor.

We cannot provide leadership for sustained development without providing leadership, as well, to restrain overpopulation, to balance growth with environmental protection, and to match the contributions women make with contributions to their welfare. We must integrate these concerns into our overall development strategy or risk the ultimate failure of our finest work.

Fortunately, the Bank has already accumulated much of the experience necessary to weave population, environmental and women's issues into a tighter fabric of development assistance. Now we must put our knowledge vigorously to work.

We should work on all three fronts at once. It is clear that popUlation pressures are one source of heavy environmental damage, so we must provide training to give women the skills to take charge of their productive and reproductive lives. And it makes little sense to fund agricultural extension services and credit programs in Africa that do not reach the real farmers, the women who work the land.

Similarly, where men and women are closer to the earth than they are in many industrialized nations, we should need little reminder of Francis Bacon's insight: "Nature, to be commanded, must be obeyed." To keep development in harmony with natural forces and resources, we must apply that lesson on the largest scalefrom the planning stage through the execution of every significant project.

We can count on the governments of the developing nations as allies in these endeavors. Many of them have launched efforts of their own to meet these three interlocking concerns. The Bank should build on these beginnings to expand their scale and scope. We can add expertise-whether sophisticated satellite photography to catch the inroads of deforestation or simple, rural health and family clinics-and new funding.

The problems and the paths to their solution are of long standing. It is only our sensitivity to their importance that is new. The time has come to move from that awareness to a concerted, continuing plan of action for sustained development.

In leading that drive-to come now to the final element I have offered for your consideration-the Bank will need a new flexibility, a new impulse to experimentation in many aspects of its work. All institutions-no matter how fresh the challenges they face-grow cautious with age and risk being fettered as well as enriched by tradition.

The World Bank must not become like Eddie Rickenbacker's grandmother who beseeched the would-be aviation pioneer just before he entered pilot training to promise her that he would "always fly slowly and stay close to the ground." Unlike her, we must promise ourselves to be both daring and down to earth, open to innovation in the face of new and familiar challenges. One of the challenges of

21

leadership, which I accept, is to ensure that the Bank's structure is relevant to today's needs and expectations.

I attach particular importance to the IFC and to its role in promoting new, private sector equity investments in developing nations. The IFC has-and can augment-the flexibility to encourage entrepreneurs and innovators to play leadership roles in developing economies. It has-and must expand-the means of channeling the energies of business leaders in industrial countries into the development effort. Strengthened by new capacity to ensure domestic as well as foreign investors through MIGA, we are also acquiring added power to mobilize sources of capital far greater than our own resources.

We will need to develop new techniques to make the most of this promising opportunity and of our central position in the channel of development finance. As an example, we must seek ever-closer partnership with public, private, and voluntary institutions. We have what Archimedes wanted: a place to stand from which to move the earth. At the fulcrum of cooperation, we must be wise and purposeful in moving the levers of coordination.

We must also and always remember that the Bank embodies what Barbara Ward called" a community of moral purpose .. , The program of leadership for sustained development which I have presented to you today is one guide to my priorities. They are to maintain and strengthen the Bank

• as a central force for development, an arsenal of powerful weapons in the struggle against poverty;

• as a major influence for economic adjustment. debt rescheduling and trade liberalization;

• as a steady source of project lending~specially in advancing agriculture beyond subsistence levels;

• as a sensitive advocate of the importance of population. environmental and women's concerns in the developing world and the development process; and

• as a responsive institution, quick to adjust to new needs and to adapt its strength to new challenges.

These are priorities for action in the coming years. But I hope they also suggest a broader goal-to endow the work of the Bank with the sense of urgency that springs from taking sides in a great and righteous cause.

Our cause is the age-old aspiration of mankind, the goal proclaimed by John XXIII in Pacem in Terris: "the common good in human society."

To achieve that good, we must light the darkness of poverty with the sunshine of hope. We must temper prudence with compassion and adjust the self-interest of nation states to the all-encompassing interest of global well-being.

When we read statistics, we must see real people. When we confront problems, we must cast them as opportunities. When we doubt our energy or question our faith in development, we must take fresh resolve from the reality that on our work depends the fate of millions.

* * * *

22

I find, to conclude on a personal note. that it helps me to think of all the members of the World Bank family as developing nations. Relatively advanced as some of us are now, we are still like cyclists; we must go constantly forward to save ourselves from falling.

Coming from a region of America that was wilderness less than two centuries ago, I have profited from an inheritance of development. The earliest settlers, my family among them, benefited from the visionary risk-taking of investors in the Netherlands and from the skills and enterprise of the workers who dug the Erie Canal and thus connected the Commerce of the Great Lakes to the commerce of the Atlantic Ocean.

So as an American and an heir to earlier development, I can look to distant, less fortunate lands and I can see there my forebears and with the right help, the bright future they have yet to build. I can see as well the profound wisdom of an American Indian proverb that declares: "In the beginning God gave to every people a cup of clay. and from that cup they drank their life."

Our common cup is the earth. Let us make from it-for all mankind-a vessel of life. a cornucopia of hope.

As I begin my own work toward that end, I am grateful for the tools and the talents at hand, for the strength of the Bank and the counsel I rely on you to provide.

Our institution is mighty in resources and in experience. But its labors will count for nothing if it cannot look at our world through the eyes of the most underprivileged, if we cannot share their hopes and their fears.

We are here to serve their needs. to help them realize their strength, their potential, their aspirations.

Let us then rededicate ourselves and our institutions to the pursuit of that great and common good. With your support. we can make the dream of sustained development a sustaining reality.

I count on your unstinting help, and for it, I thank you all.

23

REPORT BY GHULAM ISHAQ KHAN Chairman of the Development Committee

I have the honor to present the 1986 Annual Report of the Development Committee. The meeting held on Monday of this week was my last as the Committee's Chairman, and I wish to reiterate my profound appreciation and gratitude to all members of the Committee for the support I consistently received from them in the exercise of my duties. Working together, we have transformed the Committee into an effective forum for a meaningful discussion of global issues.

Recent Developments in the Global Economy

In my statement this morning I shall be covering the two most recent meetings of the Committee, the first held in Washington, D. C. on April to-II, 1986 and the second concluded on September 29. During this time a number of developments in the global economy have given rise to renewed concerned. The period has been marked by sluggish growth in major OECD economies, despite the terms of trade advantage resulting from the sharp drop in oil and commodity prices. The decline in OECD growth is adversely affecting the implementation of adjustment programs and developing countries' growth. The World Bank's most recent estimate for per capita growth in developing countries taken as a group is only about 1.2 percent for 1986.

There has also been a deterioration in the trade picture. The volume of developing countries' exports to all major industrial countries-with the exception of the United States-has either remained stagnant or fallen. Moreover, U. S. exports to developing country markets have been declining in volume as a consequence mainly of the renewed contraction in their economies.

These adverse trends in world trade affecting the developing countries have not been compensated by a"1 enhanced flow of capital to them. On the contrary: there has been a further reduction in the total net inflow of financial resources to developing countries. For the highly indebted countries these flows have actually turned negative. Moreover, flows of official development assistance (ODA), on which the low-income countries are so greatly reliant, have stagnated since 1980.

Issues Facing the Committee

It was against this background that the Committee considered the major issues facing it. These issues have included:

----"evelopments in the highly indebted, middle-income countries and the strategy unveiled by U . S. Treasury Secretary Baker in October 1985 for dealing with the problems of their external indebtedness;

-the economic prospects of both the low-income countries and those middleincome countries which have been able to avoid excessive levels of debt;

24

-the role of the World Bank and its lending program and resource requirements -the role of concessional flows in the restoration of growth and alleviation of

poverty in low-income countries; -the role of the International Development Association (IDA) and the progress

of negotiations for its Eighth Replenishment; -the special problems and needs of sub-Saharan Africa; -and the role of trade in development.

The Highly Indebted, Middle-Income Countries and the Baker Initiative