Publishing Summary of the main report " Baerekraftig biodrivstoff for luftfart " (Available in...

22

Intended for Publishing Document Summary of the main report “Bærekraftig biodrivstoff for luftfart”(Available in Norwegian only) Date 03/2013 SUMMARY SUSTAINABLE AVIATION BIOFUELS

-

Upload

independent -

Category

Documents

-

view

1 -

download

0

Transcript of Publishing Summary of the main report " Baerekraftig biodrivstoff for luftfart " (Available in...

Intended for

Publishing

Document

Summary of the main report “Bærekraftig biodrivstoff for luftfart”(Available in

Norwegian only)

Date

03/2013

SUMMARY

SUSTAINABLE

AVIATION BIOFUELS

2

EXECUTIVE SUMMARY

The report «Sustainable Aviation Biofuel in Norway» has been commissioned by Avinor, SAS,

Norwegian and The Federation of Norwegian Aviation Industries The report sets the stage for a new

knowledge basis for production of sustainable biofuel for aviation in Norway. The goal has been to

assess the possibilities for profitable and sustainable production of Jet A-1 in Norway within 2020-25.

The whole value chain has been considered, from cultivation and harvesting of feedstocks, processing

and refining, to fuel delivered at the airport.

The project scope has been wide and the project has broken new ground thus the analysis contain a

number of uncertainties. It will be necessary with further and detailed investigations to be able to reach

investment decisions and identify ideal locations for multiple production plants.

In addition to renewal of the aircraft fleet, sustainable Jet A-1 biofuel1 is the most important reduction

measure for greenhouse gas emissions (GHG) for the next 10-15 years. It is a precondition that the

fuel is sustainable. The EU sustainability criteria have been used as the basis for how sustainability is

defined. The project does not consider first generation feedstocks or resources for food and feed.

To reach the Norwegian aviation industry own 10-15 % GHG-reduction targets by 2020-25, 190-250

million liters of renewable Jet A-1 is needed. This amount of fuel is equal to biomass with an energy

content of 6-8 TWh.

Currently there are no technological barriers for using renewable Jet A-1. However, large scale

production technologies are immature and not competitive with present fossil Jet A-1 prices and CO2-

taxes. From a number of production processes, Ramboll considers two processes most suitable for a

Norwegian value chain within 2025:

1. Thermochemical processing and gasification of forest biomass (Fischer-Tropsch, FT)

2. Refining of bio-alcohols2 to Jet A-1 (Alcohol-to-Jet, AtJ).

In addition to Jet A-1, byproducts such as biodiesel are produced from the FT-production plants. FT-

based fuels were certified in 20093, while the AtJ-process is expected to be certified within 2014.

The assessment of land based and marine feedstock in Norway shows that forest biomass is the most

important feedstock on a short term basis. Imported feedstocks are competitively available. Norwegian

micro and macroalgae4 resources for energy and fuel purposes will most probably not be available in

large volumes before 2025.

Norwegian timber harvesting volumes towards 2020-25 will most likely remain on today’s level. There

is a 7 TWh increased harvesting potential, mainly from logging residues. If all of this should be

processed, an amount of 230 million liters Jet A-1 could be produced, depending on processing

technology utilized. In comparison, there is an expected demand of 1000 million liters in Norway in

2020. There is a technical potential for increased harvesting when sustainable and biological diversity

criterias are kept.

A production plant with a 50 million liter output has been used for cost calculations. A production plant

with a FT-process is expected to produce up to 50 % paraffinic petroleum, the basis for Jet A-1.

Biodiesel, naphtha and other byproducts will also be produced. 8-10 production plants, or fewer larger

ones, are needed to produce 230 million liters. A feasibility study for suitable production plant locations

has been performed including cost of logistics.

The price of FT-based Jet A-1 can be competitive with fossil and conventional Jet A-1 by 2025, provided

sales income from the byproducts biodiesel and bionaphtha. The estimated production costs in 2012

are 11 NOK/liter for renewable Jet A-1, which is 5 NOK/liter higher than the present market price for

fossil Jet A-1. Based on the theory of learning curves5, the production cost is estimated to be 7

1 Synthesized

2 Bioethanol, bio-butanol etc.

3 HEFA-fuels were certified in 2011, HEFA is Hydroprocessed Esters and Fatty Acids.

4 Seaweed

5 Learning curves and projections are described in further detail in the main report. Investment costs are expected to be drastically reduced for

each new production facility and operation costs will be reduced as the process becomes more efficient and technologically mature.

3

NOK/liter in 2025 and coincide with the market price for Jet A-1. The income from byproducts is

estimated to 141 mill. NOK, based on today’s market prices, which results in a reduction of production

costs of 5 NOK per liter produced Jet A-1 (included above).

AtJ-based Jet A-1 is a more expensive fuel. There is not sufficient information about the quantities of

byproducts from an AtJ-process to estimate the sales income from byproducts. The bioalcohol market

price development is the single most important driver for AtJ profitability. Due to immature technology

and limited available process data, the uncertainty is high, and both processes should include a 50 %

uncertainty on top of the estimates.

The climate effect from the biofuels has been calculated with life cycle assessment procedures (LCA).

The results conclude with an 81 % climate reduction with FT-fuels, while AtJ results in a 65 %

reduction. Both the processes are within the EU 60 % reduction sustainability criteria for biofuels from

new biofuel production plants after 2017. However, the methodologies for calculating environmental

and societal damages are presently widely discussed by experts.

It is technical and economically feasible to facilitate a sustainable and renewable Jet A-1 production by

2020-25 in Norway. Preliminary analysis show that the fuel could be competitive, but it is crucial that

the byproduct sales provide an income. The overall estimates show it is necessary with further

calculations to estimate the profitability more precisely for a specific production plant. Today there is

economic and technological uncertainty related to sustainable biofuel production. Predictable and long

term framework conditions are needed to reduce risk and realize sustainable aviation biofuel as an

environmental alternative for Norwegian aviation.

4

1. INTRODUCTION

Aviation affects the environment locally and globally. Aviation GHG emissions has received more and

more attention the past years.

Norwegian domestic aviation emitted 1.2 Mtons of CO2-eqvivalents in 2011, equal to 2.3 % of the total

Norwegian emissions. Additionally, emissions from international flights from Norway were 1.3 million

CO2-eqvivalents in 2010. The aviation industry expects a high traffic growth towards 2025. Emissions at

higher altitude are expected to lead to increased global warming in a short term.6

The aviation industry acknowledges the climate change challenges and wants to actively contribute to

emission reductions. The most important aviation industry GHG measures are related to new aviation

fleets with more efficient engines and bodies as well as airport operations. With the expected traffic

growth the energy efficiency and operations measures are not sufficient to stabilize the emissions.

Biofuels will be an important measure to reduce the emissions, but sustainable fuels are only available

in small quantities at a high cost. The project investigates and assesses the possibilities for profitable

and sustainable production of Jet A-1 in Norway. Avinor’s goal is to accelerate the production plant

localization and production start-up.

Ramboll has on the basis of both own studies and procured reports identified the possibilities for

renewable Jet A-1 in Norway. The project has included the following topics:

1. «Sustainable Aviation Biofuel Conversion and

Production Technology Benchmarking», Sintef Energy

2. «Sustainable land based biomass resources»,

The Norwegian University of Life Sciences

3. «Biofuel Production Plant Localization Feasibility Study», Analyse & Strategi

4. «Marine resources for Aviation Biofuels», DNV KEMA

5. «Import of feedstocks for

Sustainable Aviation Biofuels in Norway», LMC International

The main goal has been to estimate a production cost per liter for sustainable Jet A-1 with Norwegian

feedstock towards 2020-25. The whole value chain has been assessed, from growing and harvesting of

feedstock, processing and refining, to fuel delivered at the airport. The figure below illustrates the main

topics investigated.

The project is founded on investigating a production value chain based on Norwegian local and national

resources. Feedstock import has been investigated, but only as a supplement to Norwegian resources.

The project has neither looked into nor compared other aviation industry measures with sustainable

biofuels. Nor does the report assess socioeconomic evaluations of sustainable aviation biofuel

production in Norway.

The work has been carried out in close collaboration with a steering committee led by Avinor, with

committee members from the Federation of Norwegian Aviation Industries, Norwegian and SAS.

6 Avinor, Norwegian, NHO Luftfart, SAS & Widerøe (2008), Aviation in Norway, Sustianability and Social Benefit (Bærekraftig og samfunnsnyttig

luftfart), and (2011) Aviation in Norway, Sustianability and Social Benefit. Report 2 (Bærekraftig og samfunnsnyttig luftfart, Rapport 2).

5

Additionally, external resources have been involved through a reference group, with representatives

from research and development, industry and trade, biomass producers, environmental organizations,

as well as other non-governmental organizations.

The project has mapped the whole value chain from sustainable resources to promising Jet A-1

production technologies suitable for Norway. The project scope has been wide and the project has

broken new ground, but the methods for calculation of climate effect and life cycle analyses (LCA) are

renowned. Some of the results are uncertain due to immature and non-proven full scale production

plant system designs as well as limited available public data. There is also high uncertainty concerning

policies and market development, in addition to scientific disagreements regarding methodology for

calculating climate effects and the definition of sustainable biomass harvesting.

2. BACKGROUND

The Norwegian aviation industry has mapped emissions from flights and helicopter traffic annually for

many years. The main emissions are from jet flights. The most important emission abatement measure

is fleet renewal. A CO2-tax on domestic flights was implemented in 1999, and from 2012 all domestic

and international flights has to conform to the EU emission trade system (ETS). Due to expected traffic

growth, the measures are most likely not sufficient to stabilize the aviation industry emissions7.

New and innovative technological solutions, such as electric powered propulsion based on fuel cells and

batteries demands extensive aircraft design changes and is not a commercial alternative before 2050.

The aviation industry is convinced short to medium term GHG abatement measure solutions have to

rely on biofuel in addition to more efficient engines and aircraft bodies.

Renewable Jet A-1 can be blended 50 % with fossil and conventional Jet A-1. There are no technical

barriers concerning the use of biofuels. Two types of production processes for renewable fuels have

been certified technologically for 50 % blending. Extensive test flight programs have been conducted,

also with commercial flights. However, renewable Jet A-1 is currently produced in small quantities at

high costs, usually as part of research or for test flights.

2.1 Sustainability

A key project precondition has been to only assess sustainable biofuel options. This means the following

topics have to be managed well:

- Nature, environment and climate: Reduction of GHG and local pollution, prevent loss of

biological diversity and ecosystem services, as well as high agricultural standards

- Social issues: human rights, working rights, rights to cultivate land, health and food

security

- Economics: profitability, long term economic development, new jobs, and an optimal

societal resource management

The EU sustainability criterias, as defined in the Renewable Energy Directive (RED), have been chosen

to define sustainability.8 The criterias are valid in Norway and states sustainability requirements which

have to be fulfilled.

Large scale use and production of biofuels is currently in an early development phase, and it is

uncertain how the topics listed above will be affected. Both regulations and methodology is currently

under development. Unresolved questions are, among others, how to deal with direct and indirect land

use change, carbon debt and carbon payback time in addition to albedo effects.9.

Biofuels can be produced sustainably, or unsustainably with negative effects on nature and society. The

whole biomass to biofuel value chain has to be sustainable in every step, and feedstock type is usually

the most significant parameter.

7 Avinor, Norwegian, NHO Luftfart, SAS & Widerøe: Aviation in Norway, Sustianability and Social Benefit. Report 2 (Bærekraftig og

samfunnsnyttig luftfart. Rapport 2) (2011)

8 The European Parliament and the European Council (2009). EU Directive 2009/28/EF, Renewable Energy Directive.

9 The albedo effect explains how the climate is affected when sunlight is reflected less at dark surfaces and more from light surfaces. (SNL).

6

The main goal with biofuels is to reduce GHG emissions from the aviation industry. The biofuel climate

effect is therefore important to identify. The climate effect has been estimated for the proposed value

chains.

2.2 How much renewable Jet A-1 – and how much feedstock?

A sustainable biofuel bottleneck is feedstock accessibility. With current technology it is not possible to

replace all fossil fuels. The Norwegian aviation industry has a 15 % emission reduction target by 2020-

25. The target cannot be fulfilled without sustainable biofuels. To reach this goal, 190 – 250 million

liters is needed.10 This amount requires biomass with an energy content of 6 – 8 TWh 11. Biological

residues can be used for biofuels. If residues from Norwegian forests12 are to be used, this equals 2,7 –

3,6 million cubic meters.

In comparison, all forest biomass based measures from Climate cure 202013, will increase the demand

up to 6,6 million cubic meters, which equals approximately 14 TWh. 17 TWh of biomass was used in

Norway in 2010.14

A production plant with a 50 million liter output has been used for cost calculations. The production has

been optimized for Jet A-1-production, but with byproducts which can be used in other transport

sectors. Such a case has been named «Biojet Norway Inc.». 8-10 plants, or fewer large ones, are

needed to produce enough Jet A-1 to provide a climate effect of 15 % from Norwegian Aviation. In

addition there will be reduced emissions from road transport.

This project seeks to answer the three following questions to establish «Biojet Norway Inc.»:

1. Which technology and feedstock(s) are suitable for a Norwegian production

of renewable Jet A-1 within 2020-25?

2. Can the biofuel be sustainable, regarding nature and environment, social aspects and

economy?

3. Is it possible to establish sustainable and profitable production of Jet A-1 biofuels to enable a

demand from the aviation industry?

3. RENEWABLE JET A-1 PRODUCTION TECHNOLOGY

Sustainable or renewable Jet A-1 can be produced with various technologies and feedstocks. The

pathways are usually divided into three main categories: Biochemical, thermochemical and

chemical, but can also be a combination of these categories.

Figure 1 shows an overview of possible feedstocks, how these can be processed before being refined,

processed and treated to different end products. Different technologies with various process designs will

affect the volume and composition of the end products. Some production plants are more flexible with

options to produce more or less of renewable power or vary the production of biofuels following market

demand.

10 The following factors are used: Emission reductions of 60 - 80 % compared to fossil fuels, an expected consumption of 1000 Mliters in 2020.

The conversion rate is assumed to be 14 % by mass. The conversion rate can be up to 25 % which means less feedstock is needed to reach 15

% climate emission reductions.

11 Energy content = 5 kWh/kg.

12 Biomass with approximately 50 % humidity

13 For instance biodiesel and bioethanol for land transport, electrification of cars and trains and so forth

14 Trømborg, E., Bolkesjø, T. F., Bergseng, E., Rørstad, P. K., (2012). Biomassetilgang fra landbaserte ressurser, Universitetet for Miljø- og

Biovitenskap

7

Figure 1 – Biofuel feedstocks, process routes and end products15

The optimal conversion technology suitable for Biojet Norway Inc. depends on the chosen value chain.

There is possible to establish several value chains for sustainable biofuels in Norway.

Sintef Energy has assessed possible sustainable Jet A-1 biofuel production technologies suitable for

Norwegian value chains towards 2020/25. Thermochemical processes (FT), and processes where

bioalcohols are processed and refined to Jet A-1 have been selected as the most probable.

1) Thermochemical processing and gasification of forest industry biomass

(FT Jet A-116).

This process use heat and catalysts to break up the feedstock hydrocarbons, which later can

be rearranged to the desired molecule length and type of biofuel. The process is called

Fischer-Tropsch (FT). Most of the process steps are well known from the oil and gas

industry. Jet A-1 based on coal has been produced with FT-technology since the 1960s. The

main challenge is gasification of biomass and gas cleaning before the FT synthesis gas

production. The process and FT-fuels was certified for Jet A-1 production in 2009. The value

chain is illustrated in Figure 1 with the number 1.

The process can utilize most types of fossil and organic materials as well as biomass and

waste from the forest industry. Byproducts from the FT-process are biodiesel, bionaphtha,

different chemicals in addition to heat.

2) Jet A-1 produced from renewable second generation bioethanol

(Alcohol-to-Jet, AtJ17)

The AtJ process includes refining of bioalcohols to Jet A-1. The AtJ-process does not include

the bioalcohol production, but use alcohols as feedstock. The value chain is shown in Figure

1 with the number 2. The process and AtJ-fuels is not certified for blending with

conventional Jet A-1, but is expected to be certified within 2013-2014. All the AtJ-steps are

well known from the petrochemical industry, but the process is not a competitive process

with bioalcohols at present.

15 Ramboll, Sintef Energy 2012

16 Fischer-Tropsch synthetic paraffinic kerosene (FT-SPK)

17 Alcohol to Jet synthetic paraffinic kerosene (AtJ-SPK)

2

1

8

Alcohols can be produced from various feedstocks, for instance lignocellulose from trees or

energy crops, as well as agricultural waste, but also sugars and starch from edible plants,

microalgae or alginate from seaweed (macroalgae).

The advantage with the AtJ value chain is that various bioalcohols available globally can be

used. The company Borregaard is for instance producing more than 20 million liters per year

of second generation bioethanol from Norwegian forests. Norwegian spruce is a highly

suitable feedstock for second generation bioethanol.

Other production technologies and value chains have been evaluated, but the process is considered less

suitable for Biojet Norway Inc. within the timeframe 2020-25:

Thermochemical (FT) refining of municipal waste, forest industry and other industry residuals with high

temperature gasification is technological feasible and performs well environmentally. Such a production

plant is currently being commissioned in London18. This conversion technology is not assessed as

suitable in Norway because a large share of the waste is recycled and there is recently established

substantial waste-to-energy (WtE) capacity.

On a longer term, after 2025, the AtJ-process based on bioethanol from seaweed (macroalgae) is a

possibility for third generation biofuels. The Norwegian coastline has exceptionally good seaweed

cultivation conditions. Industrial players are currently establishing a value chain for industrial cultivation

and harvesting of macroalgae.

After 2030 is it estimated possible to produce AtJ based on bioethanol from microalgae. With chosen

arctic algae in combination with industrial waste heat and CO2, there may be a foundation for

microalgae-based biofuels in Norway.

Even though the HEFA-process and HEFA-fuels are certified for Jet A-1 blending, it is not considered

suitable for Norwegian value chains. The challenge is access to the resources, either as oil crops or

fatty acids. Both feedstocks are highly limited in Norway, and a Norwegian Jet A-1 production based on

HEFA has to rely on imports. Sustainable HEFA resources are limited (traditional oil crops) and the

resources have high costs (oil rich energy crops).

4. COMPETITIVE SUSTAINABLE FEEDSTOCKS

The biomass and feedstock potential towards 2020/25 in Norway has been mapped. Resources

available today, mainly from forest feedstocks, but also marine feedstocks have been investigated.

Import of biomass has been analyzed to evaluate the possibility of import combined with use of

Norwegian resources.

More or less all biological matter may be converted to some kind of liquid biofuel. Alcohol production

from sugar and starch is a well-known process, while alcohol produced from lignocellulose is a more

recent process. Technological development enables the use of new feedstocks.

Figure 2 shows the main biofuel feedstock categories. Biofuels are usually referred to as first, second or

third generation. First generation biofuels are usually based on traditional agricultural plants. Biofuels

based on lignocellulose from wood is usually named second generation biofuels. In addition, third

generation biofuels is used when the feedstocks do not need fresh water. The project has only

evaluated second and third generation biofuels, and not any resources that may compete with food or

feed.

18 Solena Biofuels

9

Figure 2 – Biofuel feedstock categories19

Feedstocks have to be both sustainable as well as suitable for conversion with existing production

technologies. There must be a long term supply security at an acceptable price. Policies and framework

conditions which may support or limit certain feedstocks are also important.

4.1 Forest feedstocks

The Norwegian University of Life Sciences (UMB) has assessed land-based sustainable feedstock

potentials.20 The biomass resources may originate from forests, other wood based biomass, and

biomass from agriculture or waste. UMB considers forest biomass as the most important biofuel

feedstock, for the timeframe towards 2020/25.

Figure 3 illustrates forest resources by quality and usage. The shaded areas symbolize higher quality

forest feedstocks, which are not considered as energy feedstocks. Potential biofuel resources are

pulpwood and logging residues such as branches, stumps and roots.

Figure 3 – Forest resource categories and use

Currently about half of the forest biomass is harvested when a tree is logged. The rest is roots,

branches and stumps. Some of these resources are used for energy production, but the current usage

is low and increasing. Harvesting of stumps and roots is not done because of high costs and due to

environmental considerations such as nutrient supply.

19 Ramboll, Sintef Energy (2012)

20 Trømborg, E., Bolkesjø, T. F., Bergseng, E., Rørstad, P. K., (2012). Biomassetilgang fra landbaserte ressurser, Universitetet for Miljø- og

Biovitenskap

Sugar and starch

Traditional agricultural products

Micro and Macroalgae

Cellulosic

crops

Forest

Agricultural waste

Energy crops

Biomass from algae

Waste and residues

Oil-crops

Traditional oil-crops

New oil-crops (non-edible)

Microalgae

10

Harvesting all logging residues is not profitable. Normally, 60 – 80 % of the biomass is harvested. The

sustainable potential is most likely much lower, possibly 50-60 % of the theoretical potential. Roots,

stump and branch-harvesting correlates with the logging volumes, lumber demand and prices.21

Figure 4 illustrates the Norwegian forest annual growth, harvesting, current «equilibrium levels» and

potential. The annual growth in 2012 is 28 million cubic meters. 17 million cubic meters is considered

the maximum allowable quantity to be harvested.22. In comparison, 11 million cubic meters is currently

harvested annually. This implies a possibility to increase the harvest with 6 million cubic meters.

Figure 4 – Annual growth, «equilibrium levels» and theoretical increased potentials (2012)

Forrest resource availability is dependent on timber prices, energy cost levels and the forest operations

costs. UMB has investigated two scenarios including increased forest harvesting for the next two

decades. Both scenarios assume a timber demand at current levels. 23

If the harvesting in 2025 is assumed to remain at today’s level, the increased potential is

equal to 7 TWh/year. The potential consists mainly of residues not used today. If all of this is

used for renewable Jet A-1, this could result in approximately 230 million liters, in addition to

approximately 50 million liters biodiesel and naphtha, which could be used for other means of

transport.

If the harvesting increases up to «equilibrium levels», the total potential will be

approximately 16 TWh/year in 2025. More than a third of this amount will be pulpwood, the

rest will be logging residues. This would result in more than 500 million liters of renewable Jet

A-1 if used to produces biofuels.

Based on the market conditions, the potential is estimated to be between 3.5 TWh, at a chips price of

0.18 NOK/kWh, and 9 TWh, at a chips price of 0.24 NOK/kWh. However, UMB considers that a sharp

increase in harvest is unlikely, and well below the equilibrium levels towards 2025. The most realistic

level, establishing many smaller biofuel plants, is therefore maximum 7 TWh by utilizing logging

residues that are not used from the current harvest today. At larger plants, pulpwood must also be

utilized to avoid high transport costs. A larger biofuel plant will partly compete with the wood

processing industry for pulpwood, or replace the demand from discontinued plants.

The current biomass price of just below 0.2 NOK/kWh is a possible price level for Biojet Norway Inc.,

also towards 2020-2025 if the production is based on a combination of wood types and logging residues

chips.

Forest biomass is the key to more bioenergy and more biofuel for transport. It is a political ambition in

Norway to increase the use of bioenergy, as well as contributions to the development of second

generation biofuel production. Therefore, there is reason to believe that the use of Norwegian forest

21Trømborg, E., Bolkesjø, T. F., Bergseng, E., Rørstad, P. K.,(2012). Biomassetilgang fra landbaserte ressurser, Universitetet for Miljø- og

Biovitenskap

22 This amount includes national environmental restrictions for forest protection and the «Living Forest» standards, which implies considerations

for protected areas and sustainable forest operations concerning biological nutrients. Norwegian: Balansekvantum

23 Wood chips price delivered to production plant is 0.2 NOK/kWh in all scenarios

11

resources for biofuel production will not be restricted, given that the current sustainability criterias are

met. Biomass from forest is a sustainable resource if harvested and used in an efficient manner, as part

of holistic forest management. Increased use of wood as construction materials can both replace more

carbon intensive construction materials as well as be a form of carbon storage in long lived construction

and wood products. Lower qualities and forest resources can be used for energy- and fuel production.

4.2 Marine feedstock

Renewable Jet A-1 and other types of biofuels can be produced from organisms living in freshwater and

saltwater. This includes seaweed (macro algae), micro algae, and waste from fishery and aquaculture.

DNV KEMA and Ramboll have identified the possibility of using marine feedstock for biofuel production.

There is a great interest in algae as feedstock for biofuel production, as algae have characteristics that

enable large production volumes of feedstock, with low risk of adverse effects on environmental and

social issues:

- Algae do not compete with traditional food crops, neither for agricultural land

- Algae convert solar energy and carbon dioxide to biomass rapidly, provided sustainable

access to nutrients

- Algae produce in many instances more biomass per area and volume than land based plants

- Many types of algae can be cultivated in saltwater, brackish water and polluted water and

add in most cases less pressure on freshwater than other biomass resources

- Algae and microorganisms can utilize CO2-emissions from industry

- Products and chemicals from algae can have many uses and are utilized for high value

products, such as protein for animal feed, chemicals such as Omega-3 and pharmaceutical

chemicals

Microalgae can provide high biomass productivity and can be cultivated in open ponds or in closed

systems (photobioreactors). There exist thousands of different types of algae that require different

growing conditions. The types of microalgae used in commercial production today are optimized for

cultivation in areas with mild climate and abundant sunshine. Microalgae are produced both in reactors

and in open systems, but the production is only profitable when algae-oils are produced for further

processing into chemicals with a high selling price. Researchers and entrepreneurs have for decades

sought to realize the great theoretical potential algae hold, but with mixed results for biofuels. There is

however a rapid technological development, with more than 150 companies and 60 laboratories and

research centers internationally developing algae for different purposes. These investments indicate

considerable optimism in the industry, and a number of algae plants are notified to be initiated

internationally in 2013.

Figure 5 – Production of microalgae in open and closed systems, © Sapphire Energy, New Mexico, USA, & Biopharmia, Kjeller

Research is currently identifying suitable microalgae for Norwegian conditions. Climate and the limited

availability of large, flat areas make production in open ponds less suitable in Norway. The use of

photobioreactors is the most relevant production method. One major challenge is the availability of

sufficient nutrients. In Norway, there are plenty of waste heat and CO2-rich flue gas from industrial

plants near the coast, which can be used for microalgae production. In closed plants, added nutrients

can come from sewage and waste water or as waste products from certain types of industry. Extraction

of nutrients from rocks and minerals may also be an opportunity for sustainable supply of nutrients.

12

However, in today’s market the prices for biofuels for aviation are lower than for alternative products

where algae can be utilized. In the project’s report about marine resources, DNV KEMA is of the opinion

that there will be little or no biomass or oil from microalgae for biofuel production in Norway towards

2025-2030.24

Macroalgae (seaweed) also have high biomass productivity and is today harvested for among other

alginate production and food. Macroalgae is an important product from aquaculture globally, especially

in the form of seaweed cultivation in China. The algae biomass can also be utilized for biofuels and a

variety of other purposes. Large scale cultivation of macroalgae in the ocean may have some of the

same sustainability challenges as cultivation of food crops, especially related to biodiversity.

In Norway, wild growing macroalgae for alginate production is harvested today. The conditions along

the coast are well suited for cultivation of local species of seaweed. As for microalgae however, several

issues along the production chain must be resolved before macroalgae can be cultivated, harvested and

processed in an industrial scale. The biofuel stakeholders in Norway involved in macroalgae production

are focusing on production of ethanol from sugar-containing macroalgae. Ethanol is therefore the most

likely energy carrier for macroalgae in the first place. According to stakeholders in Norway, ethanol

production based on seaweed is at earliest possible in 2020. Even though a future potential for a

macroalgae industry in Norway, DNV KEMA believes that it is unlikely that macroalgae will be a

feedstock utilized in commercial aviation in 2025-2030.

The development of fish farming in Norway over the past 30-40 years can give an indication of the

development of the macroalgae industry. Besides favorable natural conditions, well-developed

regulations and management expertise related to aquaculture are relevant for large scale macroalgae

cultivation.

Both micro- and macroalgae have been processed to biofuels, and test flights with biofuels from

microalgae are conducted. The algae industry is in the starting block regarding large scale production,

and focuses today on special production in small quantities, compared to the great volumes necessary

for biofuel production. A major challenge for algae biofuel is the energy balance. Currently, several

algae-oil production processes use more energy during processing and refining than the final energy

content of the biofuel.

Waste from fishery and aquaculture industry represents a substantial volume every year, and

amounted to 815.000 tons in 2011. The majority of this (76 % in 2011) will be utilized for other

purposes such as fish food and –oil. The remaining volume is today dumped offshore. About half of this

volume consists of cod bones, which contains minerals and substances making it unsuitable for biofuel.

There is therefore little gain in feedstock from fisheries for biofuel production.

Before algae are produced in a larger volume, biomass from Norwegian forests will be the most

important feedstock for Biojet Norway Inc. In addition, there are various opportunities for

supplementary import of raw materials.

4.3 Import of feedstocks and primary processed goods

LMC International has analyzed sourcing strategies and import prices of sustainable feedstocks.25 LMC

concludes that there will be produced significant amounts of sustainable feedstocks internationally in

2020. The prices will be competitive with Norwegian resources, even with transport costs included.

Availability depends mainly on local logistics chains for gathering and compressing. According to IEA,

the Nordics will be a net importer of biomass, which will be the main energy carrier in the region,

towards 2030 and 2050.26

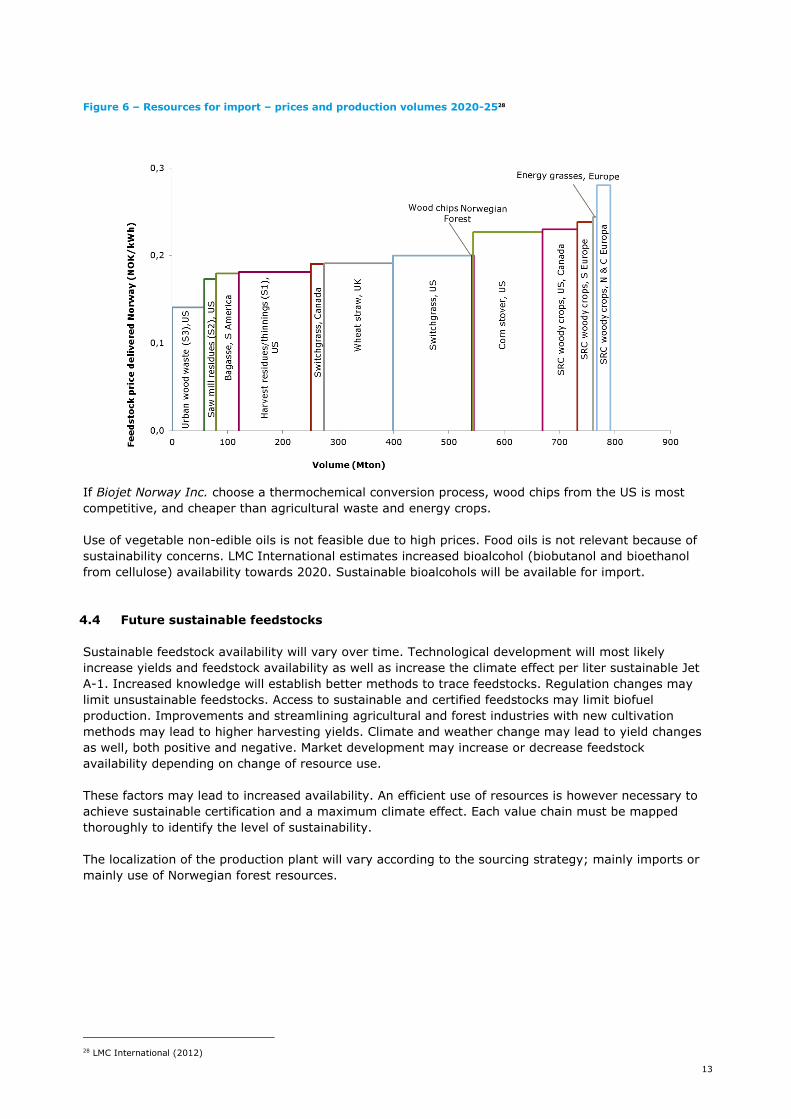

Figure 6 shows estimated prices (NOK/kWh) for certain sustainable feedstocks available for import in

2020-25. Each column represents one type of feedstock, the height represents the price and the width

the volume available for import in 2020/25.27. In comparison, Norwegian wood chips with a volume of

1,2 Mton annually is estimated available at 0,2 NOK/kWh in 2020/25.

24 DNV KEMA (2012), Marine Resources for Biofuel Production

25 LMC International (2012). Sustainable aviation biofuels in Norway

26 IEA, Nordic Energy Technology Perspectives, Pathways to a Carbon Neutral Energy Future (2013)

27 Million tons, dried and compressed, approximately 8 % humidity

13

Figure 6 – Resources for import – prices and production volumes 2020-2528

If Biojet Norway Inc. choose a thermochemical conversion process, wood chips from the US is most

competitive, and cheaper than agricultural waste and energy crops.

Use of vegetable non-edible oils is not feasible due to high prices. Food oils is not relevant because of

sustainability concerns. LMC International estimates increased bioalcohol (biobutanol and bioethanol

from cellulose) availability towards 2020. Sustainable bioalcohols will be available for import.

4.4 Future sustainable feedstocks

Sustainable feedstock availability will vary over time. Technological development will most likely

increase yields and feedstock availability as well as increase the climate effect per liter sustainable Jet

A-1. Increased knowledge will establish better methods to trace feedstocks. Regulation changes may

limit unsustainable feedstocks. Access to sustainable and certified feedstocks may limit biofuel

production. Improvements and streamlining agricultural and forest industries with new cultivation

methods may lead to higher harvesting yields. Climate and weather change may lead to yield changes

as well, both positive and negative. Market development may increase or decrease feedstock

availability depending on change of resource use.

These factors may lead to increased availability. An efficient use of resources is however necessary to

achieve sustainable certification and a maximum climate effect. Each value chain must be mapped

thoroughly to identify the level of sustainability.

The localization of the production plant will vary according to the sourcing strategy; mainly imports or

mainly use of Norwegian forest resources.

28 LMC International (2012)

14

5. LOCALIZATION OF «BIOJET NORWAY INC.»

A feasibility study on production plant localization has been conducted. A favorable location is important

for profitable and sustainable production. Analyse & Strategi has identified the most promising

localization alternatives with corresponding logistics costs.29

The locations have been chosen based on defined criterias, e.g.:

- Production and conversion technology

- Feedstock and distance to source

- Jet A-1 end use location

- Byproduct markets

- Synergies with established industry

- Area and existing regulations

- Transport infrastructure

Proximity to large wood processing industry facilities is advantageous if a thermochemical process is

chosen. If the production line is based on import, vicinity to a harbor is important. Proximity to railway,

harbor, or areas with large storage facilities are important aspects to secure production. To generate

income from heat sales, the plant needs to be located next to industry or district heating networks

which can utilize waste heat.

An assessment of possible locations resulted in five relevant areas which were analyzed in detail, see

Figure 7. Certain locations were more advantageous than others, especially related to conversion

processes.

Figure 7 – Feasibility of possible production plant locations30

The logistics cost is a minor part of the total production costs31. The localization feasibility study is an

initial study and more detailed assessments are needed to identify the most suitable locations.

Technology and feedstocks are the most important aspects in identifying a suitable location.

29 Analyse & Strategi (2012). «Biofuel Production Plant Localization Feasibility Study»

30 Analyse & Strategi (2012), Ramboll

31 Transport of pulp wood to the production plant and Jet A-1 transport to Gardermoen airport is approximately 5 % of the total production

costs

15

6. PRODUCTION COSTS

Production costs have been estimated to evaluate the feasibility of a profitable Norwegian production

value chain for Biojet Norway Inc. Operating and ivestment costs, with required return on capital, has

been assessed to estimate total production costs per liter renewable Jet A-1 compared to market prices

for fossil Jet A-1. Profitability is defined as when the market price for Jet A-1 exceeds the production

costs of renewable Jet A-1 (NOK/liter).

The conversion technology development is an important factor affecting the profitability. Technological

learning and development is mainly achieved through research and development, up-scaling and

collaboration between different industrial players32.

From the pilot and demonstration plants of today, the production price per liter will decrease when full

scale plants are up and running and accumulated volumes increase (often defined through learning

curves).

External regulations and policies, such as financial support and incentives facilitate lower production

costs and increased security for the investors. Financial risk reduction measures are the most important

aspects of establishing biofuel production. Other factors such as oil price, CO2 and NOx-taxes also affect

the production plant’s profitibality.

The price per liter of renewable Jet A-1 from a thermochemical process (FT) is calculated with and

without the sales income from byproducts. Production cost is defined as investment and operation

costs. To be able to compare production costs with Jet A-1 market prices the production cost is divided

by renewable Jet A-1 volumes. Due to lack of data on byproducts, sales income is not estimated for the

AtJ-process (see Ch. 6.2)

The production costs are estimated based on input from the work packages, such as feedstock prices33,

logistics costs34 and production technologies35 as well literature studies performed by Ramboll36. The

production plant is not positioned in detail, but is assumed to be located within certain areas (Ch. 5).

One of the main challenges when estimating production costs is the technology conversion factors,

either by mass or energy content. Conversion factors show how much of the feedstock that is

converted into different end products and Jet A-1. Ramboll’s analysis show a wide spread in liters

renewable Jet A-1 per kilo of biomass. The cost assumptions also have a high degree of uncertainty.

There are few pilot and demonstration plants for renewable Jet A-1, and only a small amount of data is

public. Assumptions on conversion factors, investments and operations costs are uncertain and have a

significant effect on the financial results. Future Jet A-1 market prices are difficult to predict, even

though it correlates closely to oil prices.

The numbers presented below must be read with an uncertainty factor of 50 % at this stage of the

assessment. The spread of uncertainty is shown in graphs and identified by scenarios, and thus not

included in the estimates.

The calculations use a weighted average cost of capital (WACC) before tax of 7 %. The lifetime of the

production plant is set to 30 years. All numbers are adjusted to 2012-levels. The calculations are in real

numbers to allow for more easily comparison of the cost development, and to directly read the results

in charts and graphs.

32 Intergovernmental Panel on Climate Change (2011). Special Report on Renewable Energy Sources and Climate Change Mitigation

33 Trømborg et al. (2012) og LMC International (2012)

34 Analyse & Strategi (2012)

35 Sintef Energy (2012)

36 Detailed references are listed in the main report

16

6.1 Thermochemical processing and gasification of biomass from forestry and the forest

industry (Fischer Tropsch, FT)

The Biojet Norway Inc. FT-production plant is assumed to produce 50 M liters in total where 27 M liters

Jet A-1 12 M liters biodiesel and 11 M liters naphtha may be produced as byproduct. The plant will also

produce substantial amounts of waste heat.

Table 6.1 lists some input parameters used in the FT-biofuel production cost estimates.

Table 6.1 – FT-biofuel production cost input parameters (2012)

Costs NOK (2012 real terms)

Investment costs 5 NOK per liter Jet A-1

Operation costs 2 NOK per liter Jet A-1

Feedstock costs 1 NOK per kg dry matter

Resource conversion 9 Kg. dry matter per liter Jet A-1

If the FT production plant would have been operative today, the production cost without byproduct

sales would have been 16 NOK/liter. If sales of byproducts are included, the price is estimated to be 11

NOK/liter. Currently the market price of fossil Jet A-1 is approximately 6 NOK/liter.

Byproduct sales incomes are shown in Table 6.2.

Table 6.2 – Byproduct sales input parameters37, (2012)

Product Market

price Volume Income

Biodiesel 9 NOK/l 12 Mliters 108 MNOK

Naphtha 3 NOK/l 11 Mliters 33 MNOK

The investment and feedstock cost constitutes of 90 % of the total production costs. A significant

reduction is necessary to enable profitable production. The business case has an investment cost of

min. 1675 MNOK.

Three scenarios havr been established to estimate the future production costs; baseline, optimistic and

pessimistic. The projections are based on renewable energy and biofuel learning curves. The basis

scenario assumes a 40 % reduction in investment cost in 2030 compared to 2012, while the optimistic

assumes 50 % and the pessimistic 30 %.

The conversion rate is assumed to decrease. The baseline scenario assumes a reduction from 9 to 6

kg/liter, optimistic 5 kg/liter and the pessimistic scenario assumes 7 kg/liter. Sales income from

byproducts is held constant for all scenarios. This gives an estimated production cost for FT of 7

NOK/liter by 2025.

Figure 8 illustrates the three scenarios with an assumed production start in 2012 towards 2030.

Expected fossil Jet A-1 market price is shown with the blue line38. This development follows the IEA

reference oil price scenario. The carbon costs are based on UK Department of Energy & Climate Change

(2010). The green thick line represents the projected renewable Jet A-1 trend line without byproduct

sales income39 (all 2012 NOK in real terms).

The figure indicates that the FT process might be profitable before 2025. The optimistic scenario leads

to profitability by 2021 (7 NOK/liter). The pessimistic scenario results leads to profitability by 2026 (8

NOK/liter).

37 Market price based on World Oil Outlook 2012 (OPEC 2012).

38 Macfarlane, R.; Mazza, P., Allan (2011)

39 The projections are based on an exponential function based on historical learning rates from biofuel production plants

17

Figure 8 – Price development and profitability of FT-biofuel included byproduct sales (2012)40

The FT-production plant profitability assumes byproduct sales income. Waste heat sales income is not

included and could increase the profitability. Without byproduct sales the production plant would not be

profitable until after 2030.

6.2 Jet A-1 produced from renewable second generation bioethanol (Alcohol-to-Jet, AtJ)

It is assumed that an AtJ-refinery will purchase commercially available bioethanol. This estimate also

assumes 27 M liters renewable Jet A-1, in addition to not specified byproducts.

With a conversion rate of 1 liter Jet A-1 per 4 liters of bioethanol, and a bioethanol price of 6 NOK/liter

the resulting Jet A-1 cost from the AtJ-process is 27 NOK/liter in 2012. The feedstock cost is about 90

% of the total production costs and the AtJ-process therefore largely depends on the bioethanol price.

Table 6.3 shows an overview of production costs.

Table 6.3 – Production costs AtJ

Production costs NOK/liter

Investment costs 1

Operation costs 2

Feedstock costs 24

Total 27

There are various AtJ-processes and with a specific AtJ-process a detailed analysis is needed to identify

exact conversion rates and byproducts. The assessment has not been able to identify possible sales

income from AtJ byproducts, and the resulting total renewable Jet A-1 production cost including sales.

Figure 9 illustrates three scenarios for the AtJ production costs; basis, optimistic and pessimistic.

Without byproduct sales income the projected production costs will not reach Jet A-1 market price until

after 2030.

40 Ramboll, Macfarlane, R.; Mazza, P., Allan, (2011), IEA (2012), UK Department of Energy & Climate Change (2010)

18

Figure 9 – AtJ Production costs projections 2012-2030, without byproduct sales (2012)41

With the current learning rates, FT biofuels are expected to be competitive with conventional fossil Jet

A-1 before 2025. Due to lack of data, the AtJ-process competitiveness is more uncertain. However, the

estimates for both processes are at a high level of uncertainty. The production cost assessment has

been based on corporate economics and does not include socioeconomic evaluations.

7. RENEWABLE JET A-1 CLIMATE EFFECT

Life cycle assessments (LCA) are conducted for the comparison of the climate impact of renewable Jet

A-1 with fossil jet A-1. Life cycle assessment42 is the leading methodical tool for calculations of climate-

and other environmental impacts of products, services and systems. The principal of a life cycle

approach is that all inputs and their associated environmental impacts, which are included in the

product’s life cycle, are included in a holistic comparison of alternative products43.

The life cycle assessments are based on a hypothetical plant, Biojet Norway Inc., and are analyzing the

value chain from cultivation and harvest of feedstock to combustion of renewable Jet A-1 in the aircraft

engine. The results are compared to corresponding assessments for fossil Jet A-1. Figure 10 illustrates

the value chain used for FT Jet A-1.

Figure 10 – Value chain for renewable Jet A-1 via a FT plant

41 Ramboll, Macfarlane, R.; Mazza, P., Allan, (2011), IEA (2012), UK Department of Energy & Climate Change (2010)

42 Life Cycle Assessments (LCA).

43 The Simapro software and the database Ecoinvent (v 2.2 May 2012) has been used with Norwegian adaptions

19

The assessment has shown that the most suitable feedstock for Biojet Norway Inc. is Norwegian forest

resources. Norwegian forest feedstock is therefore the basis for all life cycle assessments in the

project44. The amount of raw material that ends up as Jet A-1 (mass conversion factor) is 14 % for both

production routes.

The results are expressed as CO2-equivalents per energy unit45 in the fuel, where the different gases’

global warming potential is expressed by the same unit. The climate impact indicates in this context the

ability to heat the atmosphere. Reduced climate impact is therefore the positive effect achieved by

replacing fossil fuels with biofuels. In life cycle assessment, climate impact is characterized as Global

Warming Potential (GWP). The time horizon in the calculations is 100 year.

The results from the life cycle assessment conducted in this study show that renewable Jet A-1 from

the FT process has a reduction in climate impact of about 81 % compared to fossil Jet A-1, while an

AtJ-process gives a reduction of about 65 %.

Both processes meet the EU sustainability criteria of minimum 60 % reduction for new biofuel plants

after 2017.

Figure 11 shows the results for each of the biofuels and for fossil Jet A-1. The red dotted line shows the

requirement of at least 60 % emissions reduction.

Figure 11 – Life cycle assessments of renewable and fossil Jet A-1, compared to EU’s sustainability criteria

The figure also shows where in the value chain emissions occur. For renewable Jet A-1 the processing

of feedstock to Jet A1- contributes the most to the greenhouse gas emissions. For fossil Jet A-1

combustion dominates.

The analyses are based on current EU guidelines for calculations of climate impact from biofuels46. The

most common approach in such climate calculations is to calculate the greenhouse gas emissions from

biogenic sources, for example combustion of plant material, as climate neutral. It is assumed that the

same amount of CO2 released from the value chain is sequestered in new growth. Critics have argued

that such an approach can be misleading, as the time horizon also plays an important role regarding

actual climate impact. For example, harvest and subsequent combustion of wood today, will lead to

CO2-emissions that will spend several decades in the atmosphere before the same amount of carbon is

sequestered in new forest. Meanwhile, the emissions will contribute to global warming. Performed

sensitivity analysis shows that such an approach to biogenic CO2-emissions potentially can result in

significantly higher climate impact from the analyzed processes for production of biofuel for aviation.

On the other hand, FN’s intergovernmental panel on climate change (IPCC) relates the 2-degree target

to long term stabilization of greenhouse gases in the atmosphere. Temporary emissions from rotation

forestry will, unlike fossil emission, not affect the equilibrium between CO2 in the oceans, on land and in

44 The consumption is 70 % pulp wood and 30 % logging residues

45 Megajoule, MJ

46 As described in the Renewable Energy Directive (RED), Annex V.

0 20 40 60 80 100

Råvare Transport Prosessering Forbrenning i flymotor

Thermo-chemical FT-plant

Reference-case:Fossil Jet A-1

AtJ-process(Bioethanol+AtJ)

60 % GHG reductions compared to fossil Jet A-1

29 g CO2-ekv./MJ

16 g CO2-ekv./MJ

84 g CO2-ekv./MJ

GWP [g CO2-ekv./MJ]

20

the atmosphere when it stabilizes 100-300 years in the future. Life cycle analysis based on a 100-year

perspective will not capture this fundamental difference between fossil emissions and temporary

emissions from harvest. The standard methodology in LCA-analysis, however, has 100 years as time

horizon.

Other factors will have a cooling effect. The forest's ability to take up more carbon can be increased

through good forest management, such as planting, fertilizing, thinning and proper harvesting. New

research suggests that the surface albedo effects, as a result of increased logging, can offset a

significant part of the warming effect resulting from increased (biogenic) CO2-emissions in the short to

medium term47. The albedo effect includes the ratio of incoming radiation and reflection of sunlight from

the Earth's surface. Felling of trees in Norwegian latitudes results in more irradiation, especially from

snow covered logging sites. It is not performed sensitivity analyzes in this project where albedo effects

are included, as methods for calculation and inclusion of surface albedo effects in life cycle assessment

is at an early stage and increases the uncertainty in the figures.

Climate calculation for biofuel is a complex field. There is a considerable uncertainty related to the

methodology and data basis. Changes can be expected as research is providing a better knowledge

base.

Based on current regulations and available knowledge about Biojet Norway Inc.’s production plant, the

life cycle assessments show that there will be a substantial potential for greenhouse gas savings by

replacing fossil Jet A-1 with production processes for sustainable Jet A-1. The saving is greatest for Jet

A-1 from a FT plant. With expected technology development, which will provide more Jet A-1 per unit

feedstock, the climate savings will increase.

8. CO2 ABATEMENT COSTS

The national Climate cure 2020 study on how to reach the Norwegian emission targets was finished in

2010. Several GHG abatement measures were identified and explained, as well as the societal costs.48

The report established a frame of reference to evaluate cross sectorial measures and is still today the

best reference point for Norwegian CO2 abatement costs.

Biofuel introduction was identified as one of the most important transport sector measures. Aviation

biofuel measures were also identified, but based solely on imports. Rough biofuel market price

estimates were used to calculate the aviation CO2 abatement costs.

Climate cure 2020 estimates projected Norwegian GHG emissions by certain identified measures and

policy instruments. A certain methodology was established to estimate socioeconomic consequences

following reduced emissions. The same assumptions are used in this project.49.

The 2020 FT Jet A-1 production cost with byproduct sales income is estimated to be approximately 4

NOK/liter higher than the Jet A-1 market price. The abatement cost is calculated as the extra cost

allocated to the reduced tons of GHG (CO2-equivalents). Estimates show the cost is 1460 NOK/ton with

the use of renewable Jet A-1 in 2020. Towards 2030 the renewable Jet A-1 production cost is expected

to decrease towards the fossil Jet A-1 market price. The CO2 abatement cost is then expected to

decrease to 468 NOK/ton CO2.The Ramboll calculations show somewhat higher costs than Climate cure

for 2020, and about the same levels for 2030.

The figure below shows certain GHG measures with FT-biofuels included. The measure cost is higher

compared to many of the other measures, but with current projections the measure cost may be

negative in 2030 (optimistic scenario), which means a net socioeconomic positive measure.

47 Bright et al. (2012). Climate impacts of bioenergy: Inclusion of carbon cycle and albedo dynamics in life cycle assessment. Environmental

Impact Assessment Review, (doi: 10.1016/j.eiar.2012.01.002.).

48 Klimakur2020, Klif, NVE, Oljedirektoratet, SSB, Statens vegvesen, (2010)

49 «Metode for tiltaks- og virkemiddelanalyser (sektoranalyser) i Klimakur 2020,» Kjernegruppa i Klimakur 2020

21

Figure 12 – Certain Climate cure 2020 measures, with Fischer-Tropsch biofuel estimates

9. CONCLUSIONS

This project seeks to answer the three following questions to establish «Biojet Norway Inc.»:

1. Which technology and feedstocks are suitable for a Norwegian production

of renewable Jet A-1 within 2020-25?

2. How sustainable can the biofuel be, regarding nature and environment, social aspects and

economy?

3. Is it possible to produce sustainable and competitive Jet A-1 biofuels to enable a demand

from the aviation industry?

The most suitable sustainable biofuel production value chains in Norway have been assessed. An overall

assessment has been performed with regards to assumed profitability, feedstock sustainability, mature

conversion technology and production volumes.

Forest feedstocks are the most suitable Norwegian resources for renewable Jet A-1 production towards

2020/25. It is possible to import competitively priced biomass, especially from Northern America.

Two conversion processes are identified as most suitable for Norwegian value chains.

1. Thermochemical processing and gasification of forest biomass (Fischer-Tropsch, FT)

2. Refining of bio-alcohols50 to Jet A-1 (Alcohol-to-Jet, AtJ).

The second generation bioethanol can be produced from Norwegian spruce, imported, or produced from

macro- and microalgae on a longer term. Renewable Jet A-1 based on Fischer-Tropsch synthesis is

certified technologically, while AtJ is expected to be certified by 2013/14.

The biofuels from the two value chains fulfill the EU sustainability criteria, which currently defines

sustainability. The life cycle analysis estimates a GHG reduction, compared to conventional Jet A-1, of

81 % from the FT-process and 65 % from the AtJ-process. The climate effect is considerable by the use

of current methodology. However, the environmental and societal effects of large scale biofuel

production is widely discussed. The effects from land use change and payback times from carbon debt

50 Bioethanol, bio-butanol etc.

22

may lead to less favorable biofuels, but albedo impacts as well as improved forest and agricultural

operations and management may lead to higher GHG reductions.

Renewable Fischer-Tropsch Jet A-1 is expected to be competitive by 2025. The most important

assumption is byproduct sales income. The estimated production costs in 2012 are 11 NOK/liter for

renewable Jet A-1, which is 5 NOK/liter higher than the present market price for fossil Jet A-1..With a

certain technological learning curve the production cost is assumed to be 7 NOK/liter by 2025 and

coincide with the market prices for Jet A-1. The income from byproducts is estimated to 141 mill. NOK,

based on today’s market prices, which results in a reduction of production costs of 5 NOK per liter

produced Jet A-1 (included above).

AtJ-based Jet A-1 is a more expensive fuel, with production costs as high as 27 NOK/liter today without

byproduct sales income. There is however not sufficient information about the quantities of byproducts

from an AtJ-process to estimate byproduct sales income. The bioalcohol market price is the dominating

cost factor. The bioalcohol market price development is the single most important driver for AtJ

profitability.

The conversion rate is one of the most important drivers of renewable profitability. Higher conversion

rates may be reached with increased use of renewable electricity for process heat. Long term policies

and regulation frameworks may lead to lower production costs, accelerate profitability and secure

airline demand.

It is technical and economically feasible to facilitate a Norwegian sustainable and renewable Jet A-1

production by 2020-25. Preliminary analyses show that the fuel could be competitive, but it is crucial

that the byproduct sales provide an income. It is necessary with further calculations to estimate the

profitability more precisely for a specific production plant. Today, there is economic and technological

uncertainty related to sustainable biofuel production. Predictable and long term framework conditions

are needed to reduce risk and realize sustainable aviation biofuel as an environmental alternative for

Norwegian aviation.