Norwegian - Energy Company ASA - Cision

196

(a public limited liability company organized under the laws of the Kingdom of Norway) Organization number: 987 989 297 Subsequent Offering of up to 2,500,000 additional Offer Share with preferred allocation to Eligible Shareholders as of 25 April 2008 at a subscription price of NOK 23.50 per New Share, raising up to NOK 58,750,000 in gross proceeds. Subscription Period from and including 29 May 2008 to and including 13 June 2008 the Private Placement at a subscription price of NOK 23.50 raising gross proceeds of NOK 450,001,500 The new shares have not been and will not be registered under the U.S. Securities act of 1933, as amended. See “risk factors” in section 2 for a discussion of certain matters that should be considered in connection with an investment in the new shares. MANAGED BY Prospectus dated 28 May 2008 Norwegian Energy Company ASA Listing of 19,149,000 New Shares on Oslo Børs ASA, each with a nominal value of NOK 3.10 placed in

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Norwegian - Energy Company ASA - Cision

(a public limited liability company organized under the laws of the Kingdom of Norway)Organization number: 987 989 297

Subsequent Offering of up to 2,500,000 additional Offer Share with preferred allocation to Eligible Shareholders as of 25 April 2008 at a subscription price of NOK 23.50 per New Share, raising up to NOK 58,750,000 in gross proceeds.

Subscription Period from and including 29 May 2008 to and including 13 June 2008

the Private Placement at a subscription price of NOK 23.50 raising gross proceeds of NOK 450,001,500

The new shares have not been and will not be registered under the U.S. Securities act of 1933, as amended. See “risk factors” in section 2 for a discussion of certain matters that should be considered in connection with an investment in the new shares.

MANAGED BY

Prospectus dated 28 May 2008

Norwegian Energy Company ASA

Listing of 19,149,000 New Shares on Oslo Børs ASA, each with a nominal value of NOK 3.10 placed in

i

Important information This Prospectus has been prepared in order to provide information about Norwegian Energy Company ASA (“Noreco” or the “Company”) and its business in connection with (i) the listing of 19,149,000 New Shares issued in the private placement completed in April 2008 (the “Private Placement”) and (ii) the subsequent offering of up to 2,500,000 Offer Shares in Noreco offered to Eligible Shareholders as described in this Prospectus (the “Subsequent Offering”).

For the definitions and capitalized terms used throughout this Prospectus, see Section 17 “Definitions and Glossary of Terms” of this Prospectus, which also applies to the prevailing pages of this Prospectus.

_______________________

The Company has furnished the information in this Prospectus. The Managers make no representation or warranty, expressed or implied, as to the accuracy or completeness of such information, and nothing contained in this Prospectus is, nor shall be relied upon as, a promise or representation by the Managers. This Prospectus has been prepared to comply with the Norwegian Securities Trading Act and the Norwegian Regulation on Contents of Prospectuses, which implements the Prospectus Directive (EC/2003/71), including the Commission Regulation EC/809/2004, in Norwegian law. Oslo Børs has reviewed and approved this Prospectus in accordance with the Norwegian Securities Trading Act section 7-7. This Prospectus has been published in an English version only.

All inquiries relating to this Prospectus should be directed to the Company or the Managers. No other than the Company is authorised to give any information about, or make any representation on behalf of, the Company in connection with the Subsequent Offering, and, if given or made, such other information or representation must not be relied upon as having been authorised by the Company.

The information contained herein is as of the date hereof and subject to change, completion or amendment without notice. There may have been changes affecting the Company or its subsidiaries subsequent to the date of this Prospectus. Any new material information and any material inaccuracy that might have an effect on the assessment of the Shares arising after the publication of this Prospectus and before the listing of the Offer Shares on Oslo Børs and the completion of the Subsequent Offering, will be published and announced promptly as a supplement to this Prospectus in accordance with section 7-15 of the Norwegian Securities Trading Act. Neither the delivery of this Prospectus nor the completion of the Listing or the Subsequent Offering at any time after the date hereof will, under any circumstances, create any implication that there has been no change in the Company’s affairs since the date hereof or that the information set forth in this Prospectus is correct as of any time since its date.

The distribution of this Prospectus and the offering of Offer Shares may in certain jurisdictions be

restricted by law. Persons in possession of this Prospectus are required to inform themselves about and to

observe any such restrictions. This Prospectus does not constitute an offer of, or a solicitation of an offer

to purchase, any of the Offer Shares in any jurisdiction or in any circumstances in which such offer or

solicitation would be unlawful. No one has taken any action that would permit a public offering of Offer

Shares to occur outside of Norway.

The Offer Shares have not been and will not be registered under the U.S. Securities Act of 1933 as amended, or with any securities authority of any state of the United States. The Offer Shares may not be offered or sold in or into the United States, Canada, Japan or Australia.

The contents of this Prospectus shall not to be construed as legal, business or tax advice. Each reader of this Prospectus should consult its own legal, business or tax advisor as to legal, business or tax advice. If you are in any doubt about the contents of this Prospectus, you should consult your stockbroker, bank manager, lawyer, accountant or other professional adviser.

In the ordinary course of their respective businesses, the Managers and certain of its respective affiliates have engaged, and may continue to engage, in investment and commercial banking transactions with the Company and its subsidiaries.

Without limiting the manner in which the Company may choose to make any public announcements, and subject to the Company’s obligations under applicable law, announcements relating to the matters described in this Prospectus will be considered to have been made once they have been received by Oslo Børs and distributed through its information system.

_______________________

Investing in the Company’s Shares involves risks. See Section 2 “Risk Factors” of this Prospectus.

1

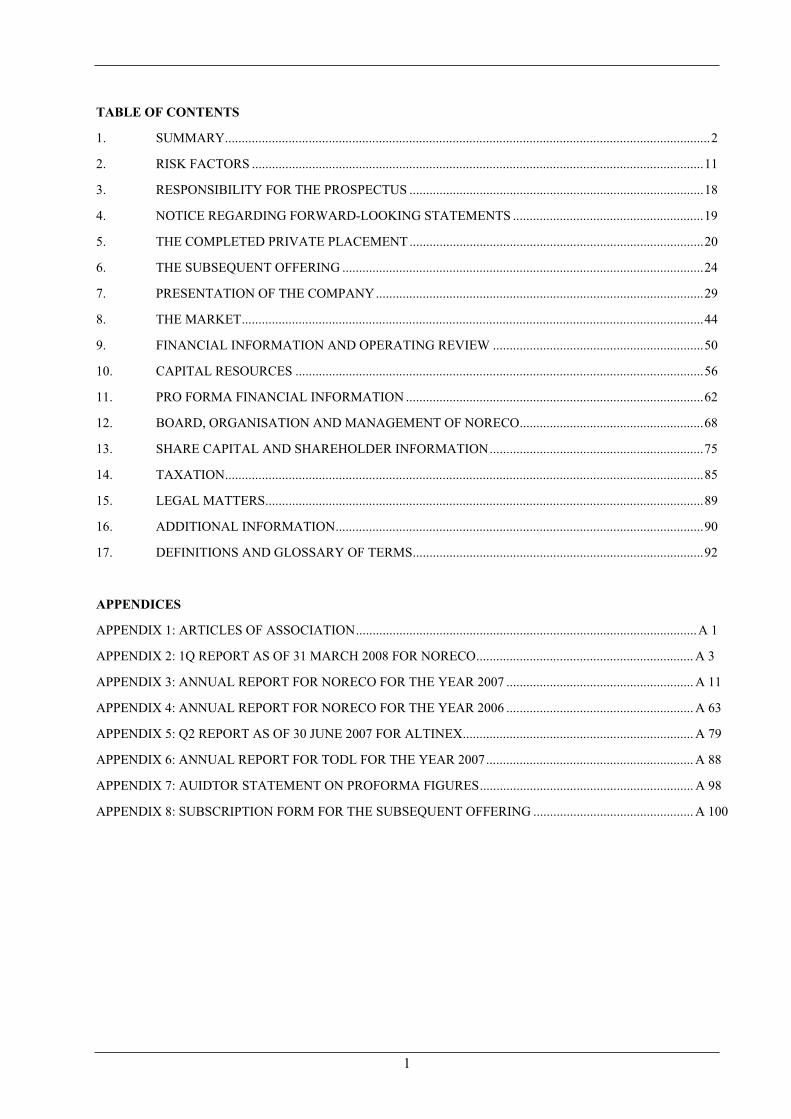

TABLE OF CONTENTS

1. SUMMARY.................................................................................................................................................2

2. RISK FACTORS .......................................................................................................................................11

3. RESPONSIBILITY FOR THE PROSPECTUS ........................................................................................18

4. NOTICE REGARDING FORWARD-LOOKING STATEMENTS .........................................................19

5. THE COMPLETED PRIVATE PLACEMENT ........................................................................................20

6. THE SUBSEQUENT OFFERING ............................................................................................................24

7. PRESENTATION OF THE COMPANY..................................................................................................29

8. THE MARKET..........................................................................................................................................44

9. FINANCIAL INFORMATION AND OPERATING REVIEW ...............................................................50

10. CAPITAL RESOURCES ..........................................................................................................................56

11. PRO FORMA FINANCIAL INFORMATION .........................................................................................62

12. BOARD, ORGANISATION AND MANAGEMENT OF NORECO.......................................................68

13. SHARE CAPITAL AND SHAREHOLDER INFORMATION................................................................75

14. TAXATION...............................................................................................................................................85

15. LEGAL MATTERS...................................................................................................................................89

16. ADDITIONAL INFORMATION..............................................................................................................90

17. DEFINITIONS AND GLOSSARY OF TERMS.......................................................................................92

APPENDICES

APPENDIX 1: ARTICLES OF ASSOCIATION......................................................................................................A 1

APPENDIX 2: 1Q REPORT AS OF 31 MARCH 2008 FOR NORECO................................................................. A 3

APPENDIX 3: ANNUAL REPORT FOR NORECO FOR THE YEAR 2007 ........................................................ A 11

APPENDIX 4: ANNUAL REPORT FOR NORECO FOR THE YEAR 2006 ........................................................ A 63

APPENDIX 5: Q2 REPORT AS OF 30 JUNE 2007 FOR ALTINEX..................................................................... A 79

APPENDIX 6: ANNUAL REPORT FOR TODL FOR THE YEAR 2007.............................................................. A 88

APPENDIX 7: AUIDTOR STATEMENT ON PROFORMA FIGURES................................................................ A 98

APPENDIX 8: SUBSCRIPTION FORM FOR THE SUBSEQUENT OFFERING ................................................ A 100

2

1. SUMMARY

The following summary should be read as an introduction to this Prospectus, and is qualified in its entirety, by

the more detailed information and the Appendices appearing elsewhere in this Prospectus. Any decision to invest in the Shares should be based on a consideration of the Prospectus as a whole.

In case a claim relating to the information contained in the Prospectus is brought before a court, the plaintiff investor might have to bear the cost of translating the Prospectus before legal proceedings are initiated. Civil

liability attaches to those persons who have tabled the summary including any translation thereof, and applied

for its notification, but only if the summary is misleading, inaccurate or inconsistent when read together with the other parts of the Prospectus.

For definitions and capitalized terms used throughout this Prospectus, please refer to Section 17 “Definitions and Glossary of Terms”.

1.1 DESCRIPTION OF NORECO

1.1.1 Introduction

Noreco is an independent oil and gas exploration, development and production company whose activities are focused on the North Sea (mainly Norway, Denmark and United Kingdom).

1.1.2 History

The Company was founded on 28 January 2005. In October 2005, Lyse Energi, Hitec Vision (HVPE), 3i and Noreco’s founders agreed to raise up to NOK 550 million in new equity in the Company, and they remained the primary owners of the Company until May 2007 when the Company raised NOK 880 million in new capital and NOK 440 million in convertible bonds from Norwegian and international institutional investors and was transformed to a Norwegian public limited liability company.

In May 2007, Noreco started acquiring shares in Altinex ASA (“Altinex”), a Norwegian oil company listed on Oslo Børs. Through acquisitions in the market and a mandatory offer set forth on 23 July 2007 Noreco acquired a total of 192,146,106 shares representing 97.14% of the share capital in Altinex to a price of NOK 22 per share. Due to the high acceptance level, Noreco decided to carry out a compulsory acquisition of the remaining shares in Altinex to the same price as in the mandatory offer. As a consequence, Noreco became the owner of 100% of Altinex on 29 August 2007.

On 13 July 2007 the Company issued a NOK 2,300,000,000 Senior Secured callable bond loan and a NOK 500,000,000 Senior Secured callable bond loan in order to finance the acquisition of Altinex.

On 3 September 2007, the extraordinary general meeting of Altinex resolved to apply for a de-listing from Oslo Børs. The shares were de-listed on 13 October 2007.

On 10 October 2007, the extraordinary general meeting of Noreco resolved, inter alia, to split the face value of the Shares into 4, creating a new face value of NOK 3.10 per Share.

On 19 October 2007, the Company completed a Private Placement of shares totalling approximately NOK 550 million in gross proceeds.

On 26 October 2007 and 31 October 2007, Noreco announced the sales of Altinex Services AS and Altinex Reservoir Technology AS.

On 9 November 2007, Noreco was listed on Oslo Børs ASA with the ticker code “NOR”.

On 25 April 2008, Noreco announced its agreement to acquire all the shares in Talisman Oil Denmark Limited for a consideration of US$ 83 million. In order to partly finance the transaction, Noreco completed on 28 April 2008 a Private Placement by issuing new shares totalling approximately NOK 450 million.

1.1.3 Business description

The Company employs 71 oil and gas professionals in its offices in Stavanger, Oslo and Copenhagen. Noreco currently has 8 wholly owned (directly or indirectly) subsidiaries (jointly referred to as the “Noreco Group” or

3

the “Group”). Noreco has ownership in a total of 52 licenses in Norway, Denmark and UK. The portfolio consists of 7 producing fields, Brage and Enoch in Norway, and South Arne, Siri, Nini, Lulita and Cecilie in Denmark. The net total production from these fields in 1Q 2008 was 9,950 boe/day.

There are a total of 15 discoveries in the portfolio, 10 of which are in Norway, 4 in Denmark and 1 in UK.

1.2 PURPOSE AND BACKGROUND FOR THE OFFERINGS

On 25 April 2008, Noreco announced its share sale agreement entered into with Paladin Resources Limited (whose ultimate parent company is Talisman Energy Inc) to acquire all the shares in Talisman Oil Denmark Limited for a consideration of US$ 83 million. The transaction includes the producing Siri field in the Danish sector of the North Sea, and will increase Noreco's daily production by more than 20% and add 4.35 million barrels of oil to the Company's proven and probable (2P) reserves.

In order to partly provide the funding required for the acquisition and to increase the equity for general corporate purposes, the Board of Directors of Noreco resolved to raise funding in the form of up to NOK 450 million in new equity through the Private Placement and a further NOK 57.8 million through the Subsequent Offering.

1.3 DESCRIPTION OF THE OFFERINGS

1.3.1 The Private Placement

On 25 April 2008, the Board of Directors resolved to conduct a private placement of up to 19,149,000 New Shares to a subscription price of NOK 23.50 per share, constituting approximately NOK 450 million in gross proceeds. The Private Placement was underwritten with a total of NOK 300 million consisting of a consortium of existing and new shareholders.

The notice of allocation was sent to the investors on 28 April 2008 and payment was received on 2 May 2008. The investors in the Private Placement were delivered existing and unencumbered shares in Noreco in accordance with a Share Lending Agreement entered into between a consortium of lenders, Noreco and the Managers. Please see section 5.7 for a description of the settlement procedure in the Private Placement.

1.3.2 The Subsequent Offering

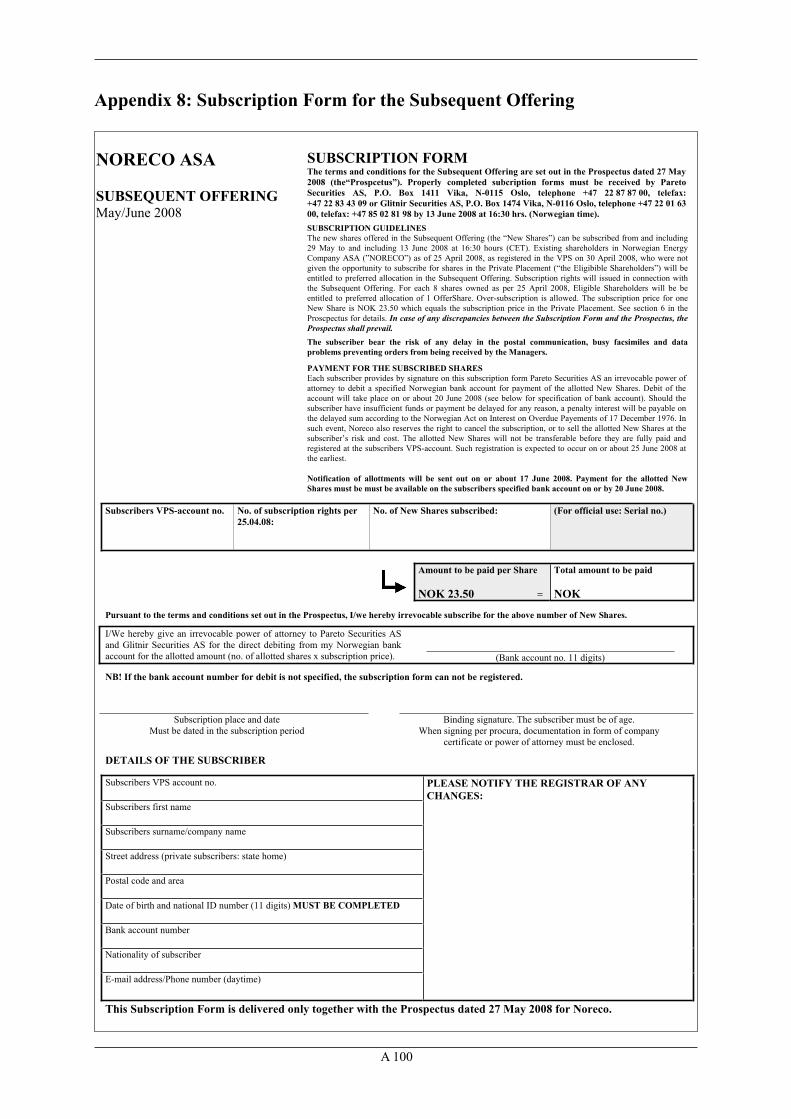

The shareholders of Noreco as of 25 April 2008, as registered in the VPS on 30 April 2008, except for those shareholders who were given the opportunity to subscribe for new Shares in the Private Placement and their respective affiliates, will, to the extent possible, be given preferred allocation in the Subsequent Offering to the extent required to maintain their relative ownership as of 25 April 2008 following the Private Placement. The Eligible Shareholders will be given preferred allocation for 1 Offer Shares for each 8 Shares owned as of 25 April 2008, rounded up to the nearest whole share.

The Subscription Period for the Subsequent Offering will commence on 29 May 2008 and expire at 16:30 hours (CET) on 13June 2008. The Subscription Period may not be extended.

The subscription price in the Subsequent Offering is NOK 23.50 per Offer Share, which is equal to the subscription price in the Private Placement.

Subscriptions for Offer Shares must be made on a Subscription Form attached as Appendix 8 hereto.

1.4 CONDITIONS AND TIME TABLE FOR THE SUBSEQUENT OFFERING

Below is a brief overview of the terms and time table for the Subsequent Offering:

Shares offered............................................................ Up to 2,500,000 Offer Shares

Subscription price per share ...................................... NOK 23.50 per Offer Share equalling the price in the Private Placement.

Record date................................................................ 25 April 2008

Subscription period.................................................... From and including 29 May to and including 16.30 hours (CET) on 13 June 2008.

4

Preferred allocation ................................................... Eligible Shareholders, i.e. shareholders as of 25 April 2008 (appearing in the VPS on 30 April 2008) who were not invited to participate in the Private Placement are eligible for preferred allocation.

Subscription rights..................................................... The Company will not issue any subscription rights. Each share held by Eligible Shareholders as of the Record Date will be given preferred allocation for 1 Offer Share per 8 Shares owned per record date.

Allocation date .......................................................... On or about 17 June 2008.

Payment date ............................................................. On or about 20 June 2008.

Distribution of allocated shares ................................. On or about 25 June 2008.

Listing of the Offer Shares ........................................ On or about 26 June 2008.

Orders for Offer Shares must be made on a Subscription Form as attached as Appendix 8 hereto. The Subscription Form must be received by the Managers by 16:30 hours (CET) on 13 June 2008.

The Board and the Managers may at their sole discretion refuse any improperly completed, delivered or executed Subscription Form or any subscription which may be unlawful. A subscription is irrevocable and may not be withdrawn, cancelled or modified once it has been received by on of the Managers.

Allotment of the Offer Shares is expected to take place on or about 17 June 2008. The Board reserves the right to round off, cancel or reduce any subscription.

The following allocation criteria will be used in the Subsequent Offering:

1. All Eligible Shareholders will be allocated 1 Offer Share per 8 Shares owned as of 25 April 2008 (appearing in the VPS on 30 April 2008).

2. In the event all Eligible Shareholders do not fully utilize their pre-emptive right, those Eligible Shareholders who have over-subscribed, will have a right to be allocated remaining shares not subscribed for on a pro rata basis. In the event a pro rata allocation is not possible due to few remaining shares, the Company will determine the allocation by drawing lots or applying similar mechanisms through the automated procedure applicable through VPS.

3. To the extent the Subsequent Offering is not fully subscribed and allocated in accordance with 1 and 2 above, allocation will be made to other Subscribers not being Eligible Shareholders.

General information on the number of Offer Shares is expected to be published on or about 16 June 2008 in the form of a stock exchange release through the Oslo Børs information system. All Subscribers being allotted Offer Shares will receive a letter from VPS confirming the number of Offer Shares allotted to the Subscriber and the corresponding amount to be paid. This letter is expected to be mailed on or about 17 June 2008.

Each Subscriber must provide a one-time authorization to debit a specified bank account with a Norwegian bank for the amount (in NOK) payable for the Offer Shares allotted to such Subscriber by signing the Subscription Form when subscribing for Offer Shares. The amount will be debited on or about 20 June 2008. Subscribers not having a Norwegian bank account must ensure that payment for their Offer Shares with cleared funds is made on or before 12:00 (CET) on 20 June 2008 and should contact the Managers in this respect.

1.5 THE LISTING AND ADMISSION TO TRADING OF THE NEW SHARES AND THE OFFER

SHARES

Following the publication of this Prospectus, the Shares issued in the Private Placement will be listed and begin trading on Oslo Børs at the date hereof, being on or about 28 May 2008.

The Offer Shares to be issued to subscribers in the Subsequent Offering will also be listed on Oslo Børs. Assuming timely payment by all Subscribers, the Company expects that these shares will be listed on Oslo Børs on or about 26 June 2008.

5

1.6 EXPENSES IN CONNECTION WITH THE OFFERINGS

Costs attributable to the Private Placement and the Subsequent Offering will be borne by the Company. The total costs are expected to amount to approximately NOK 24 million.

1.7 SUMMARY OF RISK FACTORS

A number of risk factors may adversely affect the Company and the Group as a whole. Below is a brief summary of the most relevant risk factors described in Section 2. Please note that the risks mentioned below are not the only risks that may affect the Company’s business or the value of the Shares. Additional risks not presently known to the Board of Directors of the Company or which are currently considered immaterial may also impair its business operations and prospects.

Operational and industry risk: Market and industry risk include risks related to the Group’s ability to find, acquire, develop and produce from oil and gas reserves that are economically recoverable, risk of inaccurate or incorrect reserves and resource information, risk of required substantial investments in the near future, risk relating to the price of oil and gas, political and regulatory risk, environmental and HSE risk, risk for increased competition, risk for third parties to operate its assets, risk of unexpected shutdowns, risk of future decommissioning liabilities, risk for not attracting and retaining personnel, risk of labour disputes, risk related to legal disputes, and risk associated with damaged equipment and the Group’s insurance policies.

Financial risk: Financial risk include the risk that the Company’s debt arrangements may restrict the Group’s business going forward, the risk of not being able to refinance existing debt, the risk of not being able to comply with covenants of a general, financial and technical nature, and risk associated with exchange rate fluctuation.

Risk factors relating to the Shares: The risks related to the Shares include price volatility of publicly traded securities, difficulties for foreign investors to enforce civil liabilities in Norway, significant restrictions on U.S. investors’ ability to transfer or resell their Shares, and the risk that foreign shareholders may be diluted if they are unable to participate in future offerings.

1.8 DIRECTORS, SENIOR MANAGEMENT AND EMPLOYEES

1.8.1 Board of Directors

The Company’s Board of Directors consists of five members: Lars Takla (Chairman), John Hogan (deputy chairman), Roger O’Neil (member), Therese Log Bergjord (member) and Heidi Marie Petersen (member). For more information, please refer to Section 11 below.

1.8.2 Management

The Group’s executive management comprises: Scott Kerr (CEO), Synnøve Røysland (VP, Southern North Sea), Rune Martinsen (VP, Northern North Sea), Thor Arne Olsen (VP, Commercial), Reinert Seland (VP, Exploration), Jan Nagell (CFO), Birte N. Borrevik (VP, Drilling and Projects), Stig Frøysland (VP, HSE/HR) and Einar Gjelsvik (VP, External Relations). For more information, please refer to Section 11 below.

1.8.3 Employees

As of the date of this Prospectus, the Noreco Group employs 71 oil and gas professionals in its offices in Stavanger, Oslo and Copenhagen. For more information, please refer to Section 11 below.

1.9 ADVISORS AND AUDITORS

1.9.1 Managers

The Managers for the Private Placement were Pareto Securities AS, P.O. Box 1411 Vika, 0115 Oslo, Norway and Glitnir Securities AS, P.O. Box 1474 Vika, 0161 Oslo, Norway. The Managers for the Subsequent Offering are Pareto Securities AS and Glitnir Securities AS.

6

1.9.2 Legal advisor

The legal advisor to the Company is Arntzen de Besche Advokatfirma AS, P.O. Box 2734 Solli, 0204 Oslo, Norway.

1.9.3 Independent Auditor

The Company’s independent auditor is KPMG AS. For further information, please refer to Section 9.5 in this Prospectus.

1.10 SUMMARY OF OPERATING AND FINANCIAL INFORMATION

The selected financial information set forth in this Prospectus should be read in conjunction with the financial statements and the notes to those statements set out in Appendices 2, 3 and 4 in addition to section 9, 10 and 11 in this Prospectus.

1.10.1 Consolidated income statements

Amounts in NOK 000’s As per 31

March 2008

(unaudited)

IFRS

As per 31

March 2007

(unaudited)

IFRS

FY ended 31

Dec 2007

(audited)

IFRS

FY ended 31

Dec 2006

(audited)

IFRS

Operating revenues ........................................ 435,763 - 839,664 - Total operating expenses ................................ 294,284 19,248 790,614 87,235

Operating result ............................................ 141,479 (19,248) 49,051 (87,235)

Financial income ............................................ 26,248 214 149,001 1,374 Financial expenses.......................................... 164,617 1,087 447,212 2,204

Net financial result........................................ (138,368) (873) (298,210) (830)

Ordinary profit/loss before tax.................... 3,110 (20,121) (249,159) (88,064)

Tax 31,469 15,258 50,469 68,205

Profit/loss for the period .............................. (28,359) (4,865) (198,690) (19,859)

1.10.2 Consolidated balance sheet

Amounts in NOK 000’s As per 31

March 2008

(unaudited)

IFRS

As per 31

March 2007

(unaudited)

IFRS

FY ended 31

Dec 2007

(audited)

IFRS

FY ended 31

Dec 2006

(audited)

IFRS

ASSETS

Total fixed assets ............................................ 8,810,011 17,015 8,746,954 15,832 Total current assets ......................................... 1,580,765 155,628 1,583,735 94,276

TOTAL ASSETS .......................................... 10,390,775 172,642 10,330,688 110,108

EQUITY AND LIABILITIES

Equity

Share capital .................................................. 346,390 31,422 345,385 31,422 Other equity .................................................... 1,321,943 24,470 1,332,066 24,302

Total equity ................................................... 1,668,333 55,892 1,677,451 55,724

Total liabilities and obligations ...................... 7,818,048 252 7,712,504 252 Total short term debt....................................... 904,394 116,498 940,733 54,132

Total liabilities .............................................. 8,722,442 116,750 8,653,237 54,384

TOTAL LIABILITIES AND EQUITY ...... 10,390,775 172,642 10,330,688 110,108

7

1.10.3 Cash flow statement

Amounts in NOK 000’s As per 31

March 2008

(unaudited)

IFRS

As per 31

March 2007

(unaudited)

IFRS

FY ended 31

Dec 2007

(audited)

IFRS

FY ended 31

Dec 2006

(audited)

IFRS

Net cash flow from operating activities .......... 38,815 (34,468) 247,406 (80,373)

Net cash flow from investing activities .......... (309,752) (920) (4,522,036) (9,916)

Net cash flow from financing activities .......... (125,926) 68,050 5,257,667 60,643

Net change in cash and cash equivalents. .. (396,863) 32,662 983,037 (29,645)

Cash and cash equivalents at start of the

period ............................................................. 973,402 11,970 11,970 41,616

Effects of changes in exchange rates on

cash and cash equivalents (17,694) (21,605)

Cash and cash equivalents at end of the

period ............................................................. 558,845 44,632 973,402 11,970

1.10.4 Significant changes in the Company’s financial or trading position since 31 March 2008

On 25 April 2008, Noreco entered into a share sale agreement with Paladin Resources Limited (whose ultimate parent company is Talisman Energy Inc) to acquire all the shares in Talisman Oil Denmark Limited for a consideration of US$ 83 million. In order to partly finance the acquisition and to increase the equity for general corporate purposes, Noreco completed a Private Placement raising a total of NOK 450 million.

The Company is not aware of any other significant changes in the financial or trading position of the Noreco Group which has occurred since 31 March 2008.

1.11 PRO FORMA FINANCIAL INFORMATION

On 25 April 2008, Noreco entered into a share sale agreement with Paladin Resources Limited (whose ultimate parent company is Talisman Energy Inc) to acquire all the shares in Talisman Oil Denmark Limited (TODL). Effective date is 1 January, 2008. Completion is expected to take place by June 2008. The pro forma financial information is based on a share of ownership of 100%, corresponding to the share ownership as of the date of this Prospectus.

The unaudited pro forma financial information has been prepared in accordance with EU Regulation No 809/2004, as included in the Norwegian Securities Trading Act section 5-13 and the CESR’s Level 3 guidance. Because of its nature, the pro forma financial information addresses a hypothetical situation and therefore does not represent the Company’s actual financial position or results. The pro forma profit and loss and balance sheet information does not have a continuing impact on Noreco. The pro forma financial information is prepared for illustrative purposes only.

The pro forma financial statements is set out in Sections 11.5 and 11.6 to this Prospectus.

8

1.12 CAPITALISATION AND INDEBTEDNESS

The table below sets forth the Company’s audited and unaudited consolidated cash and equivalents and capitalisation as at 31 March 2008. The table should be read together with the consolidated financial statements and the related notes thereto, as well as the information under Section 9 “Financial Information and operating review”.

Amounts in thousand NOK 31.03.2008

Unaudited

Total current debt .............................................................................. 904,394

Total non-current debt ........................................................................ 7,818,048

Total shareholders’ equity .............................................................. 1,668,333

Liquidity ......................................................................................... 558,845

Current financial receivable1 ......................................................... 115,943

Current financial debt ..................................................................... 387,349

Non-current financial indebtedness ............................................... 4,632,731

Net financial indebtedness ........................................................... 4,345,292

1.13 MAJOR SHAREHOLDERS AND RELATED PARTY TRANSACTIONS

1.13.1 Major shareholders

As of 26 May 2008 the Company had a total of 1,429 shareholders divided into 1,314 Norwegian and 115 foreign owners.

The table below shows the 5 largest shareholders in Noreco as per 26 May 2008:

Shareholder No of shares %

1 LYSE ENERGI AS 2 17,355,940 13.3%

2 NEC INVEST AS C/O HITECVISION PRIV 16,725,396 12.8%

3 NORDEA BANK NORGE AS AVD VERDIPAPIRFINANS 11,525,527 8.8%

4 IKM INVEST AS 3 8,239,216 6.3%

5 VERDIPAPIRFONDET KLP 5,053,787 3.9%

1.13.2 Related party transactions

Since its inception, the Company has been party to the following related party transactions4:

In connection with the raising of the initial funding from 3i Companies, Lyse Energi and HVPE, Noreco entered into an agreement with Melberg Partners, a company partly owned by Tollak Melberg, one of the Noreco founders and then board member, to provide economic support, investment advice and financial modelling. The contract was completed in October 2005 when Noreco raised private equity capital. However, the compensation for this work was to be paid as the equity was drawn and this resulted in payments to Melberg Partners being made in 2005, 2006 and 2007. All payments to Melberg Partners have now been completed and there is no contractual relation between Noreco and Melberg Partners at this time.

1 “Current financial receivable” includes open position asset/open position liability. 2

10,000,000 Shares are registered under ISIN NO 001 0430150 pending automatic transfer to the Company’s existing ISIN

number, being the date hereof.3

4,000,000 Shares are registered under ISIN NO 001 0430150 pending automatic transfer to the Company’s existing ISIN

number, being the date hereof.4

The companies Lyse Energi AS (Lyse), Energivekst AS/Hitec Private Equity AS (HVPE), 3i Companies (3i Group plc, 3i

UK Private Equity 2004/06 LP, 3i Pan European Growth Capital 2005/06 LP) and Norwegian Company Founders DA

(Founders Holding) are shareholders in the Company.

9

Also in connection with the private equity fund raising in October 2005, Noreco agreed to pay legal costs and negotiation costs for the capital providers along with an ongoing monitoring fee to 3i, Lyse Energi, HVPE and Founders Holding. In return Noreco had access to the expertise of these companies including advice on financial questions, the raising of new funds and future funding requirements. The fee was paid quarterly through 2005, 2006 and until June of 2007. In June of 2007 Noreco raised additional capital and the monitoring fee is no longer valid. There is no longer any fee agreement between Noreco and the private equity providers.

The details for payments made to related parties are outlined under Section 13.6.

1.13.3 Trend information

The Company has not experienced any changes or trends outside the ordinary course of business that are significant to the Noreco Group between 31 March 2008 and the date of this Prospectus, other than those described elsewhere in this Prospectus. Please see Section 7 “Presentation of the Company”, Section 8 “The Market”, Section 9 “Consolidated Financial Information” and Section 13 “Share Capital and Shareholder Matters” for more information about significant recent trends in the Group’s business and relevant markets.

1.13.4 Lock-up arrangement

In connection with the listing of the Shares in November 2007, Pareto and SEB Enskilda entered into a lock-up agreement with the management and board members of Noreco, being Scott Kerr, Tor Arne Olsen, Reinert Seland, Einar Gjelsvik, Rune Martinsen, Birte N. Borrevik and Lars Takla. Under the lock-up agreement, these shareholders have agreed not to offer, sell, contract or otherwise dispose of certain number of shares in the Company for a period of 12 months following the first day of trading of the Shares in Oslo Børs (being on 9 November 2007), without the prior written consent of Pareto and SEB Enskilda.

1.14 ADDITIONAL INFORMATION

1.14.1 Share capital and shareholder matters

Noreco is a Norwegian public limited liability company with registration number 987 989 297.

The Company’s registered share capital is NOK 405,752,310.20 consisting of 130,887,8425 Shares each with a nominal value of NOK 3.10 fully paid and issued in accordance with the Norwegian Public Limited Liability Companies Act.

All issued Shares in the Company are vested with equal shareholder rights in all respects. There is only one class of shares and all Shares are freely transferable.

The dilutive effect in connection with the Private Placement and the Subsequent Offering will be approximately 16%, assuming full subscription of the Subsequent Offering.

Prior to the

Private

Placement, and

Subsequent

Offering

Prior to the

Subsequent

Offering

Subsequent

both offerings

No of shares each with a nominal value of NOK 1 ............. 111,738,842 130,887,842 133,387,842 % dilution ...................................................................... 100.00% 85.37% 83.77%

The Shares are registered with VPS under the International Securities Identification Number (ISIN) NO 001 0379266. The New Shares issued in the Private Placement are, until Listing, issued under a separate ISIN number (NO 001 0430150). The registrar for the Shares is Sparebank 1 SR-Bank, Bjergsted Terrasse 1, 4007 Stavanger, Norway.

See Section 12 “Share Capital and Shareholder Information” for a further description of the Company’s share capital.

5A total of 19,149,000 Shares are registered under the separate ISIN number NO 001 0430150. These shares will

automatically assume the Company’s original ISIN number upon publication of this Prospectus, being the date hereof.

10

1.14.2 Articles of Association

The Company’s Articles of Association are included as Appendix 1 to this Prospectus.

According to its Articles of Association, “the business of the company is exploration, production and sale

related to oil and gas activities. The company will obtain participating interests in production licenses by participating in license rounds and through acquisition of participating interests.”

The Company has only one class of shares.

The Board shall consist of three to eight members.

1.14.3 Documents on display

For the life of this Prospectus the following documents may be inspected at www.noreco.com and at the Company’s offices at Haakon VII’s gate 9, 4005 Stavanger, Norway:

• The Company’ Memorandum of Incorporation

• The Articles of Association

• The Company’s historical financial information and auditors report for the 2007, 2006 and 2005 financial years

• The Company’s historical financial information for the three months ended 31 March 2008

• The historical financial information of Altinex for the years 2005-2007

• The prospectus dated 1 November 2007 prepared in connection with the listing of Noreco’s shares on Oslo Børs ASA.

1.14.4 Third party statements

Information contained in this Prospectus which has been sourced from third parties has been accurately reproduced and, as far as the Company is aware and able to ascertain from the information published by that third party, no facts have been omitted that would render the reproduced information inaccurate or misleading.

11

2. RISK FACTORS

2.1 GENERAL

Investing in Noreco involves inherent risks. Prospective investors should consider, among other things, the risk factors set out in this Prospectus before making an investment decision. The risks described below are not the only risks facing the Company and the Group as a whole. Additional risks not presently known to the Company or currently deemed by the Company to be immaterial to the Group’s business may in future impair the Group’s business operations and adversely affect the price of the Company’s Shares. If any of the following risks actually materialize, Noreco’s business, financial position and operating results could be materially adversely affected.

A prospective investor should consider carefully the factors set out below, as well as the information provided elsewhere in the Prospectus, and should consult his or her own expert advisors as to the suitability of an investment in the Shares.

An investment in the Shares is suitable only for investors who understand the risk factors associated with this type of investment and who can afford a loss of all or part of the investment. The information is presented as of the date hereof and is subject to change, completion or amendment without notice.

All forward-looking statements included in this Prospectus are based on information available to the Company on the date hereof and reflect the Company’s present best effort opinions only. The Company assumes no obligation to update any such forward-looking statements unless required by applicable law or regulations. Investors are cautioned that any forward-looking statements are not guarantees of future performance and are subject to risks and uncertainties and that actual results may differ materially from those assumed in the forward-looking statements. Factors that could cause or contribute to such differences include, but are not limited to, those described below and elsewhere in this Prospectus. Reference is also made to Section 4, “Notice regarding forward-looking statements”.

2.2 RISK FACTORS RELATING TO THE GROUP AND THE INDUSTRY IN WHICH IT

OPERATES

2.2.1 The Group is dependent on finding, acquiring, developing and producing oil and gas reserves that

are economically recoverable

The Group is dependent on its ability to appraise, find, acquire, develop and commercially produce oil and gas reserves. The Group must continually locate and develop or acquire new reserves to replace its existing reserves that are being depleted by production. Future increases in the Group's reserves will depend not only on its ability to explore and develop its existing properties but also on its ability to select and acquire suitable additional properties either through awards at licensing rounds or through acquisitions.

Few prospects that are explored are ultimately developed into producing oil and gas fields. Significant expenditure is required to establish the extent of oil and gas reserves through seismic and other surveys and drilling and there can be no certainty that oil and gas reserves will be found.

There are many reasons why the Group may not be able to find or acquire oil and gas reserves or develop them for commercially viable production. For example, the Group may be unable to negotiate commercially reasonable terms for its acquisition, exploration, development or production activities. Further, the Group is dependent on the competence and judgment of third party operators in relation to the development of reserves where it is not itself the operator. The exploration and development of oil and gas assets may be curtailed, delayed or cancelled by unusual or unexpected geological formation pressures, oceanographic conditions, hazardous weather conditions or other factors. There are numerous risks inherent in drilling and operating wells, many of which are beyond the Company’s control. Noreco’s operations may be curtailed, delayed or cancelled as a result of environmental hazards, industrial accidents, occupational and health hazards, technical failures, shortage or delays in the delivery of rigs and/or other equipment, labour disputes and compliance with governmental requirements. Drilling may involve unprofitable efforts, not only with respect to dry wells, but also with respect to wells which, though yielding some petroleum, are not sufficiently productive to justify commercial development or cover operating and other costs. Completion of a well does not assure a profit on the investment or recovery of drilling, completion and operating costs.

12

Without successful exploration or acquisition activities, the Group's reserves, production and revenues will decline. There is no assurance that the Group will discover, acquire or develop further commercial quantities of oil and gas.

2.2.2 Reserves and resources information represents estimates which may be inaccurate or incorrect

The reserves data included in this Prospectus are estimates. In general, estimates of the quantity and value of economically recoverable oil and gas reserves and the possible future net cash flows are based upon a number of variable factors and assumptions, such as historic production rates, ultimate reserves recovery, interpretation of geological and geophysical data, timing and amount of capital expenditures, marketability of oil and gas, royalty rates, continuity of current fiscal policies and regulatory regimes, future oil and gas prices, operating costs, development and production costs and workover and remedial costs, all of which may vary from actual results. Estimates are also to some degree speculative, and classifications of reserves are only attempts to define the degree of speculation involved. Consequently, the nature of reserve quantification studies means that there can be no guarantee that estimates of quantities and quality of oil and gas disclosed will be available for extraction. Therefore, actual production, revenues, cash flows, royalties and development and operating expenditures may vary from these estimates. Such variances may be material and may have a material adverse effect on the Company’s valuation, its ability to raise further financing and its financial position in general.

As regards contingent resources, these may not be considered commercially recoverable by the Group for a variety of reasons, including the high costs involved in recovering the contingent resources, the price of oil at the time, the availability of the Group's resources and other development plans that the Group may have. By contrast, prospective resources are those deposits that are estimated, on a given date, to be potentially recoverable from undiscovered accumulations. The Group's estimates of its contingent and prospective resources are uncertain and can change with time and there can be no guarantee that the Group will be able to develop these resources commercially.

2.2.3 Substantial investment will be necessary in the future

The Group will be required to make substantial capital expenditure for the acquisition, exploration, development and production of oil and gas reserves in the future. Such capital expenditures could be covered by revenues, new equity or by obtaining new debt. If the Group’s revenues decline, or if the Company is unable to attract investors to increase the Company’s equity, or if new debt arrangements are not accessible, or only on unattractive commercial terms, the Group will experience a limited ability to undertake or complete future exploration programs, development investments and acquisitions. The Group’s inability to access sufficient capital for its operations could lead to licenses being revoked, or could lead to a material adverse effect on the Group’s financial conditions, results of operations or prospects in general.

2.2.4 Risks relating to the price of oil and gas

The profitability and cash flow of Noreco’s operations will be dependent upon the market price of oil and gas. This is known to fluctuate. Historically, oil prices have fluctuated widely for many reasons, including global and regional supply and demand, and expectations regarding future supply and demand for oil and petroleum products; geopolitical uncertainty; access to pipelines, tanker ships and other means of transporting oil, gas and petroleum products; prices, availability and government subsidies of alternative fuels; prices and availability of new technologies; the ability of the members of the Organisation of Petroleum Exporting Countries (“OPEC”) and other oil-producing nations to set and maintain specified levels of production and prices; political, economic and military developments in oil producing regions, particularly the Middle East; domestic and foreign governmental regulations and actions, including export restrictions, taxes, repatriations and nationalisations; global and regional economic conditions; and weather conditions and natural disasters.

It is impossible to predict accurately future oil and gas price movements. Accordingly, oil and gas prices may not remain at their current levels. The economics of producing from some of the Group's wells may change as a result of lower prices, which could result in a reduction in the volumes of the Group's reserves if some are no longer economically viable to develop. The Group might also elect not to produce from certain wells at lower prices. All of these factors could result in a material decrease in the Group's net production revenue causing a reduction in its oil and gas acquisition, development and exploration activities and financial condition. In addition, bank borrowings available to the Group currently are and in the future are expected to be in part be determined by the Group's borrowing base. A sustained material decline in prices from historical average prices

13

could reduce the Group's borrowing base, thereby reducing the bank credit available to the Group which could result in the Group having to repay a portion, or all, of its bank debt.

2.2.5 Political and regulatory risk

Changes in the legislative and fiscal framework governing the activities of the companies engaged within the oil and gas sector may have a material impact on exploration and development activity or directly affect the Company’s operations. In particular, changes in political regimes will constitute a material risk factor for the Company’s operations in foreign countries. Further, the Group is faced with increasingly complex tax laws. The amounts of taxes the Group pays could increase substantially as a result of changes in, or new interpretations of, these laws, which could have a material adverse effect on its liquidity and results of operations. During periods of high profitability, there are often calls for increased or windfall taxes on oil and gas revenue. Taxes have increased or been imposed in the past and may increase or be imposed again in the future. In addition, taxing authorities could review and question the Group's tax returns leading to additional taxes and penalties which could be material. Decommissioning (where relevant) could also have a material tax impact for the Group’s financial position and results of operations.

In order to conduct its operations in compliance with applicable laws and regulations, the Group must obtain licenses and permits from various government authorities. The Group may incur substantial costs in order to maintain compliance with these existing laws and regulations and additional costs if these laws are revised or if new laws affecting the Group's operations are passed. Furthermore, there can be no assurance that the Group will be able to obtain all necessary licenses and permits that may be required to carry out exploration, development and production operations on its properties.

2.2.6 Environmental and HSE risks

All phases of the oil business present environmental risks and hazards and are subject to environmental regulation pursuant to a variety of international conventions and state and municipal laws and regulations. Environmental legislation provides for, among other things, restrictions and prohibitions on spills, releases or emissions of various substances produced in association with oil and gas operations. The legislation also requires that wells and facility sites be operated, maintained, abandoned and reclaimed to the satisfaction of applicable regulatory authorities. Compliance with such legislation can require significant expenditures and a breach may result in the imposition of fines and penalties, some of which may be material. Environmental legislation is evolving in a manner expected to result in stricter standards and enforcement, larger fines and liability and potentially increased capital expenditures and operating costs. The discharge of oil, natural gas or other pollutants into the air, soil or water may give rise to liabilities to foreign governments and third parties and may require the Company to incur costs to remedy such discharge. No assurance can be given that environmental laws will not result in a curtailment of production or a material increase in the costs of production, development or exploration activities or otherwise adversely affect the Company’s financial condition, results of operations or prospects.

The Group's operations and assets are affected by numerous international, EU and national laws and regulations concerning health and safety and environmental (“HSE'”) matters including, but not limited to, those relating to the health and safety of employees, discharges of hazardous substances into the environment and the handling and disposal of waste. The technical requirements of these laws and regulations are becoming increasingly complex, stringently enforced and expensive to comply with and this trend is likely to continue. The failure to comply with current HSE laws and regulations has and may in the future result in regulatory action, the imposition of fines or the payment of compensation to third parties which each could in turn have a material adverse effect on the Group's business, financial condition and results of operations.

2.2.7 Competition

The oil and gas industry is highly competitive in all its phases. There is strong competition for the discovery and acquisition of properties considered to have commercial potential. Noreco competes with other exploration and production companies, many of which include major international oil and gas companies which may have greater financial resources, staff and facilities than those of the Group. These companies have strong market power as a result of several factors, including the diversification and reduction of risk, including geological, price and currency risks; increased financial strength facilitating major capital expenditures; greater integration and the exploitation of economies of scale in technology and organization; strong technical experience; increased infrastructure and reserves; and strong brand recognition. Due to this competitive environment, the

14

Group may be unable to acquire attractive suitable properties or prospects on terms that it considers acceptable. As a result, the Group's revenues may decline over time, thereby materially and adversely affecting its results of operations or financial condition.

2.2.8 The Group’s debt arrangements may restrict the Group’s business in various ways

The Group’s debt arrangements contain several restrictive covenants, including but not limited to restrictions on assets sales and acquisitions, investments, the ability to pay dividends or other capital distributions, and the possibility to raise additional financial indebtedness. In addition, several financial covenants are imposed on the Company and the Group. Such covenants restrict the Group in various ways in terms of how the Group conducts its business, and the Group may be restricted in responding to changing market conditions or in pursuing favourable business opportunities. Further, the Group will have to dedicate a substantial portion of its cash flow from operations to service debt, which in turn will reduce the amount of cash flow it will have available for capital investment, working capital and other general corporate purposes.

2.2.9 Current production is concentrated in a few number of fields

The Group’s current production of oil and gas is concentrated in a small number of offshore fields. If mechanical problems, storms or other events curtail a substantial portion of the Group's production or if the actual reserves associated with any one of the Group's producing fields are less than the Group's estimated reserves, the Group's results of operations and financial condition could be adversely affected.

2.2.10 The Group relies on third parties to operate some of its assets

While the Group operates certain of its assets, it is not the operator of some of its current development and production assets. The operating agreements with third party operators typically provide for a right of consultation or consent in relation to significant matters and generally impose standards and requirements in relation to the operator's activities. Nevertheless, the Group generally has limited control over the day-to-day management or operations of those assets and is therefore dependent upon the activities of the third party operator. A third party operator's mismanagement of an asset may result in delays or increased costs to the Group. While the Group has purposely acquired interests in assets that are operated by operators it believes to be reputable, there can be no assurance that the operator will observe such standards or requirements.

If a party with an interest in the Group's assets elects not to participate in certain activities relating to those assets that require that party's consent, the Group may be unable to undertake such activities alone or together with the other participants at the desired time or at all. Other participants in the Group's assets may default on their obligations to fund capital or other payments in relation to the assets. In such circumstances, the Group may be required under the terms of operating agreements to contribute all or part of any funding shortfall. Any such delay in or inability to undertake activities or fulfil an obligation to provide further funding could adversely affect the Group's business, results of operations or prospects.

2.2.11 The Group holds a number of licenses in their initial terms

The Group holds a number of interests in exploration licenses or in other licenses that are in their initial terms. The early stages or exploration period of a license are commonly the most risky. These phases of the term of a license require high levels of relatively speculative capital expenditure without a commensurate degree of certainty of a return on that investment.

2.2.12 Unexpected shutdowns may occur

Mechanical problems, accidents, oil leaks or other events at the Group's producing fields or its pipelines or subsea infrastructure may cause an unexpected production shutdown at these fields. Any unplanned production shutdown of the Group's facilities could have a material adverse effect on the Group's business, financial condition and results of operations. In June 2007, a water injection pipeline between the Siri and the Nini platform ruptured. Noreco, through its subsidiary Altinex, holds a 30% interest in this pipeline. The conclusion after detailed investigations is that the whole pipeline needs to be replaced. A replacement can probably not be effected before 2009. Dong (the operator) is however working on a solution to maintain production until then. The replacement costs are assessed at DKK 450-500 million. In addition the licensees have suffered a loss of production income, not yet be finally determined. The Group underwriters have been advised of the incident and have had presented the Group’s initial insurance claim is under preparation both in respect of the physical damage and the loss of production income.

15

2.2.13 Risks associated with future decommissioning liabilities

The Group, through its license interests, has in the past assumed certain obligations in respect of the decommissioning of its fields and related infrastructure and is expected to assume additional decommissioning liabilities in respect of its future operations. These liabilities are derived from legislative and regulatory requirements concerning the decommissioning of wells and production facilities and require the Group to make provision for and/or underwrite the liabilities relating to such decommissioning. The oil and gas industry currently has little experience of decommissioning petroleum exploration and production infrastructure in the North Sea as few such structures have been removed in this region. It is, therefore, difficult to forecast accurately the costs that the Group will incur in satisfying its decommissioning obligations. When its decommissioning liabilities crystallize, the Group will be jointly and severally liable for them with other former or current partners in the field. In the event that other partners default on their obligations, the Group will remain liable and its decommissioning liabilities could be magnified significantly through such default. Any significant increase in the actual or estimated decommissioning costs that the Group incurs may adversely affect its financial condition.

2.2.14 The Group is dependent on attracting and retaining personnel

The Group's success depends, to a large extent, on certain of its key personnel. The loss of the services of any key personnel could have a material adverse affect on the Group. The Group does not maintain, nor does it plan to obtain, key person insurance against the loss of any of its key personnel. In addition, the competition for qualified personnel in the oil and gas industry is intense. There can be no assurance that the Group will be able to continue to attract and retain all personnel necessary for the development and operation of its business.

2.2.15 Risks associated with labour disputes

The Group's contractors or service providers may be limited in their flexibility in dealing with their staff due to the presence of trade unions among their staff. If there is a material disagreement between contractors or service providers and their staff belonging to trade unions, the Group's operations could suffer an interruption or shutdown that could have a material adverse effect on its business, results of operations or financial condition.

2.2.16 Risks associated with legal disputes in general

The Group currently is currently involved in disputes as described in Section 15.1 of the Prospectus, and may from time to time be involved in other legal disputes related to the Group’s operations or otherwise. The outcome of existing and any future disputes may adversely affect the Group’s business, results of operations or financial condition.

2.2.17 Risk associated with damaged equipment and the Group’s insurance policies

The Group’s equipment, including equipment owned by the licenses in which the Group holds interests, may be damaged or in need for replacement. For instance, the water injection pipeline between the Nini field and the Siri Field has been damaged due to a certain type of aggressive corrosion and needs to be replaced and production from the field could be ceased during replacement. Although the Group, or the license in which the Group has an interest, in general will have insurance coverage for property damage and, currently, in respect of loss of production income, it is not certain that all incidents will be covered or that the sums insured under such coverage will be sufficient to hold the Group harmless from the loss occurred. Thus, any significant loss or liability for which the Company is not insured or is found not to be covered could have an adverse effect on the Group’s business, financial condition and results of operation. Further, such damages may lead to the Group’s insurance premiums or the applicable deductibles under the relevant policies being increased.

2.3 RISK FACTORS RELATING TO THE GROUP’S FINANCING

2.3.1 Borrowing and leverage

Borrowings create leverage and the Group is highly leveraged. In addition, the current financing structure is rather complex with several bonds having been issued as well as several bank loan facilities currently being in place. The debt arrangements include several covenants and undertakings of a general, financial and technical nature and several of the debt arrangements contain cross-default provisions. Failure by the borrowers or other obligors to meet any of the covenants or undertakings could result in all outstanding amounts under the different debt arrangements becoming immediately due for payment. In addition, security rights granted to the lenders could be enforced. If outstanding debts were declared due for immediate payment, there would be no assurances that the Group would be able to meet its obligations, and there are no assurances that the Group would be able to

16

obtain alternative financing, either on a timely basis or at all. Any breach of existing covenants and undertakings with a subsequent claim for repayment of all debts outstanding would thus have a material adverse effect on the Group’s financial position and is likely to have a material adverse effect on the value of the Company’s shares, the Group’s operations and future success.

As for new borrowings, the Group will seek to borrow only when the directors of the Company believe that such borrowings will benefit the Group after taking into account considerations such as the need to refinance existing debt, the costs of the borrowing, the repayment schedules and the likely returns on the assets financed with the borrowed monies. However, no assurance can be given that the income will exceed the interests and costs associated with the loans, nor be sufficient to repay the loans when due. Further, no assurances can be given that the Group will be able to refinance on economically attractive terms, or at all.

2.3.2 Risk associated with exchange rate fluctuations

The Group has operations which generate significant cash flows in a variety of currencies. The Group also comprises businesses with various functional currencies (US$ and NOK). Although the Group may undertake limited hedging activities in an attempt to reduce certain currency fluctuation risks, these activities provide only limited protection against currency-related losses.

2.4 RISK FACTORS RELATING TO THE SHARES IN NORECO

2.4.1 Volatility of share price

There can be no assurance that an active market can be sustained with respect to the Shares. The market price of the Shares could fluctuate widely to a number of factors, some of which are beyond the Company’s control, in response, including the following:

• actual or anticipated variations in operating results and/or production levels;

• fluctuations in oil prices and reserve levels;

• changes in financial estimates or recommendations by stock market analysts regarding the Company or its competitors;

• announcements by the Company or its competitors of significant acquisitions, strategic partnerships, joint ventures or capital commitments;

• sales or purchases of substantial blocks of stock;

• additions or departures of key personnel;

• future equity or debt offerings by the Company and its announcements of these offerings; and

• general market and economic conditions.

Moreover, in recent years, the stock market in general has experienced large price fluctuations. These broad market fluctuations may adversely affect the Company's stock price, regardless of its operating results.

2.4.2 Shareholders not participating in future offerings may be diluted and pre-emptive rights may not

be available to US holders of the Company’s Shares

Shareholders in Norwegian public companies such as the Company have pre-emptive rights to subscribe for new shares proportionate to the aggregate amount of the shares they hold. Such pre-emptive rights may be set aside by the shareholders meeting, which could result in existing shareholders being diluted as a result of the share issue.

The Company is not currently subject to the reporting requirements of the US Securities Exchange Act of 1934, as amended, and has no intention to subject itself to such reporting requirements by filing a registration statement under the US Securities Act to register any rights or new Shares. For reasons relating to US securities laws (and the laws in certain other jurisdictions) or other factors, US investors (and investors in such other jurisdictions) may not be able to participate in a new issuance of shares or other securities and may face dilution as a result. If US holders of the Shares (or holders of Shares in other jurisdictions) are not able to receive, trade or exercise pre-emptive rights granted in respect of their Shares in any rights offering by the Company, then they may not receive the economic benefit of such rights. In addition, their proportional ownership interests in the Company will be diluted.

17

2.4.3 It may be difficult for investors based in the United States to enforce civil liabilities predicated on

U.S. securities laws against the Company, its affiliates, directors and officers

The Company is organized under the laws of Norway. The Company’s directors and officers reside outside of the United States, and the Company’s assets are located outside of the United States. As a result, it may be difficult for investors in the United States to effect service of process within the United States upon the Company or the Company’s directors and officers or to enforce judgments obtained in U.S. courts predicated on the civil liability provisions of U.S. Federal securities laws against the Company or the Company’s directors and officers. In addition, punitive damages in actions brought in the United States or elsewhere may be unenforceable in Norway.

2.4.4 Holders of the Company’s Shares that are registered in a nominee account may not be able to

exercise voting rights as readily as shareholders whose shares are registered in their own names

with the VPS

Beneficial owners of the Company’s Shares that are registered in a nominee account may not be able to vote such shares unless their ownership is re-registered in their names with the VPS prior to the Company’s general meetings. The Company cannot guarantee that beneficial owners of the Company’s Shares will receive the notice for a general meeting in time to instruct their nominees to either effect a re-registration of their shares or otherwise vote their shares in the manner desired by such beneficial owners.

2.4.5 The transfer of Shares is subject to restrictions under the securities laws of the United States and

other jurisdictions

The Company has not registered the Shares under the Securities Act or the securities laws of jurisdictions other than Norway and the Company does not expect to do so in the future. The Shares may not be offered or sold in the United States or to U.S. persons (as defined in Regulation S under the Securities Act) nor may they be offered or sold in any other jurisdiction in which the registration of the shares is required but has not taken place, unless an exemption from the applicable registration requirement is available or the offer or sale of the shares occurs in connection with a transaction that is not subject to these provisions.

2.4.6 The ability of shareholders to make claims against the Company following registration of the

share capital increase in the Norwegian Register of Business Enterprises is severely limited under

Norwegian law

Following the registration of the capital increase relating to any Shares of the Company in the Norwegian Register of Business Enterprises, subscribers or purchasers of those Shares have very limited recourse against the Company under Norwegian law.

18

3. RESPONSIBILITY FOR THE PROSPECTUS

The Board of Directors of Norwegian Energy Company ASA accepts responsibility for the information contained in this Prospectus. The Board of Directors hereby declares that, having taken all reasonable care to ensure that such is the case, the information contained in this Prospectus is, to the best of our knowledge, in accordance with the facts and contains no omissions likely to affect its import.

Stavanger, 27 May 2008

The Board of Directors of Norwegian Energy Company ASA

Lars Takla Chairman

John Hogan Roger O'Neil

Therese Log Bergjord Heidi Marie Petersen

19

4. NOTICE REGARDING FORWARD-LOOKING STATEMENTS

This Prospectus includes “forward-looking” statements, including, without limitation, projections and expectations regarding the Group’s future financial position, business strategy, plans and objectives. When used in this document, the words “projects”, “forecasts”, “estimates”, “expects”, “anticipates”, “believes”, “plans”, “intends”, “may”, “might”, “will”, “would”, “can”, “could”, “should”, “seek to” or, in each case, their negative, or other variations or similar expressions, as they relate to the Company, its subsidiaries or its management, are intended to identify forward-looking statements. Such forward-looking statements involve known and unknown risks, uncertainties and other factors, which may cause the actual results, performance or achievements of the Company and its subsidiaries, or, as the case may be, the industry, to materially differ from any future results, performance or achievements expressed or implied by such forward-looking statements. Such forward-looking statements are based on numerous assumptions regarding the Company’s present and future business strategies and the environment in which the Company and its subsidiaries will operate. Factors that could cause the Group’s actual results, performance or achievements to materially differ from those in the forward-looking statements include but are not limited to:

• the competitive nature of the markets in which the Group operates,

• global and regional economic conditions,

• government regulations,

• changes in political events,

• force majeure events

Prospective investors in the Shares are cautioned that forward-looking statements are not guarantees of future performance and that the Group's actual financial position, operating results and liquidity, and the development of the industry in which it operates may differ materially from those made in or suggested by the forward-looking statements contained in this Prospectus. The Group cannot guarantee that the intentions, beliefs or current expectations upon which its forward-looking statements are based will occur. These forward-looking statements are subject to risks, uncertainties and assumptions, including those discussed elsewhere in this Prospectus. Forward-looking statements include statements regarding:

• oil and gas reserves quantities;

• obtaining permits;

• retaining licenses and title to assets;

• the amount and nature of capital expenditure;

• drilling of wells;

• the timing and amount of future production and operating costs;

• availability of equipment;

• business strategies and plans of management; and

• prospect development and property acquisitions.

Some important factors that could cause actual results to differ materially from those in the forward-looking statements are, in certain instances, included with such forward-looking statements and in Section 2 “Risk Factors” in this Prospectus.

The Company undertakes no obligation update or revise any forward-looking statement, whether as a result of new information, future events or otherwise. All subsequent written and oral forward-looking statements attributable to the Group or to persons acting on the Group's behalf are expressly qualified in their entirety by the cautionary statements referred to above and contained elsewhere in this Prospectus.

20

5. THE COMPLETED PRIVATE PLACEMENT

5.1 INTRODUCTION

On 25 April 2008, Noreco announced its share sale agreement entered in with Paladin Resources Limited (whose ultimate parent company is Talisman Energy Inc) to acquire all the shares in Talisman Oil Denmark Limited for a consideration of US$ 83 million. The transaction includes the producing Siri field in the Danish sector of the North Sea, and will increase Noreco's daily production by more than 20% and add 4.35 million barrels of oil to the company's proven and probable (2P) reserves.

Talisman Oil Denmark Limited's interest in the Danish sector of the North Sea includes the entire 30% non-operated interest in License 6/95, which contains the producing Siri field. Noreco owns a 20% interest in the Siri field, and will after the transaction hold a 50% share in the field. The Siri platform is an important hub for other fields and discoveries in the area. Noreco holds significant interests in the area, including the Cecilie, Nini, Nini East and Rau fields, and this transaction will create synergies for Noreco in the area.

The acquisition will continue Noreco’s strategic intent to build a leading independent oil and gas company in the North Sea.

The effective date of the transaction is 1 January 2008, and the completion of the acquisition is expected to take place by June 2008, and will be subject to the fulfilment of usual government consents.

In order to partly provide the funding required for the acquisition and to increase the equity for general corporate purposes, the Board of Directors of Noreco resolved to raise funding in the form of up to NOK 450 million in new equity through the Private Placement and a further NOK 57.8 million through the Subsequent Offering (described in more detail in Section 6 to this Prospectus).

5.2 THE SHARES AND SHARE CAPITAL

5.2.1 Share capital

The Company’s registered share capital is NOK 405,752,310.20 consisting of 130,887,842 Shares each with a nominal value of NOK 3.10 fully paid and issued in accordance with the Norwegian Public Limited Liability Companies Act. All issued Shares in the Company are vested with equal shareholder rights in all respects. There is only one class of shares and all Shares are freely transferable.

5.2.2 VPS registration

The Shares are registered with VPS under the International Securities Identification Number (ISIN) NO 001 03792666. The registrar for the Shares is Sparebank 1 SR-Bank, Bjergsted Terrasse 1, 4007 Stavanger, Norway.

5.2.3 Legislation and rights attached to the Shares