Evaluation of Norwegian Space Programs - Regjeringen.no

241

A review of the economi policies for developmen Evaluation of N Space Program Economics policies for developmen capabilities in Norway July 2012 Evaluation commissioned by the Ministry of Trade and Industry ics and public nt of space Norwegian ms nt of space

-

Upload

khangminh22 -

Category

Documents

-

view

5 -

download

0

Transcript of Evaluation of Norwegian Space Programs - Regjeringen.no

A review of the economics and publicpolicies for development of space

Evaluation of NorwegianSpace Programs

Economics

policies for development of spacecapabilities in Norway

July 2012

Evaluationcommissioned by theMinistry of Trade andIndustry

A review of the economics and publicpolicies for development of space

Evaluation of NorwegianSpace Programs

policies for development of space

This material was prepared by PricewaterhouseCoopers AS (PwC) for the specific use of the Ministry of Trade and Industry andrelied upon by any third party without PwC’s prior written consent.

This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advinformation contained in this publication without obtaining specific professional advice. No representation or warranty (expraccuracy or completeness of the information contained in this publication, and, to the extent permitted by law, PwC, its partaccept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refrainiinformation contained in this publication or for any decision based on it.

The information used by PwC in preparing this report has been obtained from a variety of sources as indicated within the repoanalysis of financial information and accounting records, it has not included an audit in accordance with generally acceptedanalysis of financial information and accounting records, it has not included an audit in accordance with generally acceptedor agreed-upon procedure of the Company’s existing business records, not a qualified legal opninion of compliance with applicablforensic investigations of detailed proceedings. Accordingly we assume no responsibility and make no representations with rescompleteness of any information provided to us.

By its very nature, evaluation work cannot be regarded as an exact science, and the conclusions arrived at in many cases willdependent on the exercise of individual judgment. There is, therefore, no indisputable single value and we normally express olikely range. The statements in this report express PwC opinion at the time the evaluation was performed. We reserve the righnotice.

For inquieries please contact team lead: Ivar Strand [email protected]

PwC

This material was prepared by PricewaterhouseCoopers AS (PwC) for the specific use of the Ministry of Trade and Industry and is not to be used, distributed or

This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon theinformation contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to theaccuracy or completeness of the information contained in this publication, and, to the extent permitted by law, PwC, its partners, employees and agents do notaccept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the

The information used by PwC in preparing this report has been obtained from a variety of sources as indicated within the report. While our work has involvedanalysis of financial information and accounting records, it has not included an audit in accordance with generally accepted auditing standards, due diligenceanalysis of financial information and accounting records, it has not included an audit in accordance with generally accepted auditing standards, due diligence

upon procedure of the Company’s existing business records, not a qualified legal opninion of compliance with applicable laws and regulations or aforensic investigations of detailed proceedings. Accordingly we assume no responsibility and make no representations with respect to the accuracy or

By its very nature, evaluation work cannot be regarded as an exact science, and the conclusions arrived at in many cases will of necessity be subjective anddependent on the exercise of individual judgment. There is, therefore, no indisputable single value and we normally express our assessment as falling within alikely range. The statements in this report express PwC opinion at the time the evaluation was performed. We reserve the right to change opinion without

Objective of NorwegianObjective of Norwegianspace activities

To provide substantial and persistentcontributions to:

•wealth creation•innovation•knowledge development•environmental

Objective of NorwegianObjective of Norwegian

To provide substantial and persistent

wealth creation

knowledge developmentenvironmental- and public safety

Executive summary

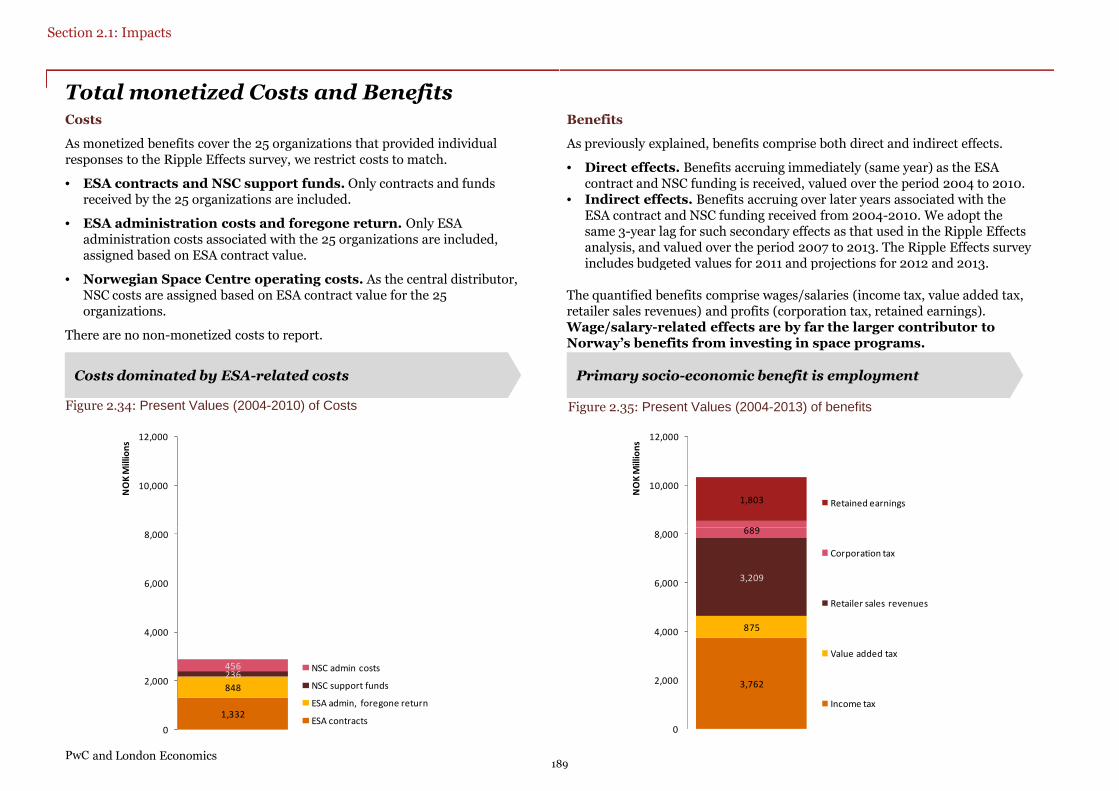

The objective is to evaluate the performance of Norwegian spaceprograms and in particular participation in ESA, the Radarsat agreementand the national support funds. Its focus is on whether the programscontribute to the accomplishments of the space policy objectives;identifies impacts and socioeconomic benefits of the programs, andsuggests areas of improvement. Scientific activities were not part of theassignment. The review is commissioned by the Ministry of Trade andIndustry and delivered in July 2012. The main conclusions can besummarized as follows.

Important aspects of the model for public support work. The nationalservice programs, matched with special initiatives such as Radarsat andAIS satellite deliver cost-efficient capabilities for public sector. There is apositive interaction between the important instruments such as nationalprograms for industrial development and ESA programs. ESAparticipation also enhances capabilities of Norwegian business. There areripple effects, meaning that contracts from ESA results in additional sales.There are differences between segments. Other services results in highestripple effects and this is growing. The space center leadership and expertadvisory capacities are widely appreciated among business andgovernment alike. There are also several other areas of strengths andsuccesses observed including positive contributions from the supportschemes:

a) Considerable global market share in mobile satcom services andearth observation (largely optical and radar images trackingservices).

b) Rapid growth and strength among several companies across all ofthe value chain and especially in the mobile satcom and earthobservation services segments.

c) Growth and gaining share also for some companies in the spacemanufacturing segment. Albeit smaller as share of turnover inNorway and with low overall worldwide market shares. There arehigh levels of public support here.

d) Highly successful public sector programs to enhance marinemonitoring and surveillance capabilities that shows real worldimpacts. Emerging valuable programs for land use and some areinstitutionalized.

4

At the same time, the evaluation points to a number of areas weredevelopments are a concern and warrants rethinking and furtherdeliberations. Adjustments and

a) Overall, sales are not increasing and world wide market sharesare declining. The sector is declining as share of GDP, as shareof service exports and product exports. There are few newentrants to the space segment over the last decade. Amongthose firms supported there is not growth in space relatedlabor. Structural shifts in ownership to foreign conglomerateslabor. Structural shifts in ownership to foreign conglomerateshave uncertain impacts. Ground equipment producers have haslost much sales volume and market share. Public expenditureon space are rising faster than commercial sales.

b) Support is highly concentrated among few repeat actors. It isfurther concentrated in the space segment and for groundequipment producers. This is in accordance with classicaltechnology development strategy to support early stagedevelopment, but is a more questionable match with growthpotential and strength.

c) External political environment including EU/ESA convergenceis likely to be more challenging with impacts both on access todecision making arenas in Europe and market access forbusiness. External market developments showcommercialization and growth of new service conceptsworldwide. Norwegian policies are little adapted to thisenvironment and a rethink of commercialization strategies andenvironment and a rethink of commercialization strategies andthe public role could be helpful.

4

PwC

Summary

Report

This is the short version of the report. Important patterns ofdevelopment, findings, analysis and observations are presentedhere over the next thirty pages.

More in-depth analysis and data work, and a more nuanceddiscussion is presented in a detailed analysis attached to this.Methodologies and appropriate references to data sources arealso found in the detailed analysis.

Table of Contents Summary Report

Summary report

Objective, scope, and methodologies of the review

Overview of developments

The value chain

Section Overview

The value chain

External policy developments

Norwegian policy implementation

ESA participation

Distribution of funds

Industry impacts

Impact on Norwegian economy of ESA participation

Public service programs

Impact of public service programs

Progress against policy objectives

Adjustment of objectives and strategies is recommended

Governance framework and risks

Suggestions

Appendices

1 Detailed analysis

7

8

9

Page

9

14

15

16

17

18

19

20

21

22

2525

27

28

29-240

The objective

The objective is to evaluate the participation in ESA, the Radarsat agreementand the national support funds. The evaluation should also provide a basis forassessing the socio-economic benefits of the programs. The review iscommissioned by the Ministry of Trade and Industry and delivered in July2012. The ministry highlights three themes of particular importance:

-Whether the programs contribute to the accomplishments of the space policyobjectives;

Summary report

Objective, scope, and methodologies of the review

objectives;

-Assess the socioeconomic benefits of participation in the programs, and

-Identify areas of improvement.

The scope

The request from the Ministry outlines a number of areas and detailedquestions, all relevant to evaluate the past performance of the space programs,as well as to point the way ahead. There is a range of policy instruments tosupport space activities in Norway. This work is to focus on the following three:

1. Participation in the ESA. ESA mandatory and the Optional program,

participation in which should reflect the Norwegian priorities.

2. The funds managed by the National Space Center for dedicated programs

for industrial development and public service development including

special initiatives such as AIS and Radarsat to enhance public sector

capabilities.

PwC

capabilities.

3. Purchasing of radar satellite data through a separate agreement with

Canadian firm MDA.

Interactions between these instruments are important and we will explore

those when relevant to inform the analysis. The focus the last ten years and if

data is available, even longer back. There are long lead times in development of

space activities and the fruition of policies may not be seen for decades. The

Ministry mandate focuses on the years 2004-2010. Science is an integral part of

the space activities. There are many space science activities in Norway and

meaningful analysis of this needs to be holistically. That is beyond this work.

7

Objective, scope, and methodologies of the review

Methodology and data

The evaluation combines indepth interviews with considerable quantitative

analysis of the support schemes and the sector in general. This includes:

Administrative and business data: Considerable quantitative data have

been used. The data are collected by the MoTI, NSC and ESA for different

purposes but has some overlaps. As in all administrative datasets there are

certain inconsistencies, broken time series and varying sample sizes. We havecertain inconsistencies, broken time series and varying sample sizes. We have

integrated this as best as possible and supplemented with information from

corporate reports, financial statements and press and investor information. In

total this is robust though there are minor unresolved inconsistencies. The

evaluation also uses company specific information drawn from publically

available sources. We have had access to non-public sensitive information of

single companies and this has been important to calculate certain aggregate

numbers.

Document analysis: Nearly 1500 pages of relevant documents has been

reviewed. Important documents includes annual reports and budget proposals,

company annual reports, international studies, and a range of market analysis.

This also includes information from press releases, investor relation reporting,

financial analysts, as well as quarterly and annual reports.

Interviews. The analysis is further strengthened by interviews of actors across

7

Interviews. The analysis is further strengthened by interviews of actors across

all segments of the value chain, private and public alike.

The value chain for space related activities can be defined in several ways.

We have based the analysis upon prevailing standards in market analysis and

official publications. This is adapted to the Norwegian context where

appropriate.

To utilize international expertise in the area and also to avoid any ties or

conflict of interests with Norwegian space programs, the report has been

develop din English. The report is translated into Norwegian and both versions

made available.

Overview of developments

Activity has declined in real terms but may bereemerging. Turnover declined from 2003 butshown real growth in the last few years. Activitiesincreased strongly prior to 2003 and have sinceleveled off. Total activity in this figure includes bothinstitutional and commercial activities, but excludesconsumer TV i.e.. Canal Digital and Viasat. Theconsumer segments has not been a focus of the

The sector constitutes a little over 0,2 percent ofGDP in 2010, a reduction of about 33 percent from2003. Measured against the less oil dependent GDPMainland numbers we find the same pattern ofdecline albeit with slightly higher numbers.

The export ratio in this sector is quite high, but wefind a decline measured against other Norwegianexports. Measured against other services exports we

Summary report

Figure 1: Turnover space industries in Norway

Turnover declined since 2003

Figure 2: Turnover as share of GDP

Declining share of the economy

consumer segments has not been a focus of theNorwegian space programs.

Activity may have contracted as much as 25 percentbetween 2003 and 2007 if adjusted for producerprice inflation (PPI). The extent of the declinedepends upon how price inflation is adjusted for.

Services constitute the largest segment and hasincreased in significance over time. Productmanufacturing is about 20 percent of total in 2010.

The decline is confirmed when comparing againstother core economic parameters.

exports. Measured against other services exports wealso find a decline of space related exports since2003. Compared against other exports ofmanufactured goods, we find an even moresignificant drop of about 43 percent since 2003.This share has declined since the late nineties and isnow at about 0,3 percent of total product exports.

PwC

7 bn

6 bn

5 bn

4 bn

3 bn

2 bn

1 bn

Nominal

CPI adjusted

PPI adjusted

1997 2010

Sales-25%

1997

GDP

Figure 1: Turnover space industries in Norway Figure 2: Turnover as share of GDP

8

The sector constitutes a little over 0,2 percent ofGDP in 2010, a reduction of about 33 percent from2003. Measured against the less oil dependent GDPMainland numbers we find the same pattern ofdecline albeit with slightly higher numbers.

The export ratio in this sector is quite high, but wefind a decline measured against other Norwegianexports. Measured against other services exports we

Norwegian firms gained global market share duringthe first five years of the decade. This wasparticularly driven by gains in the mobile satcommarkets. Since then the share has declined andcurrently stands at about 2 percent.

The industry remains highly commercial with 75percent of sales to maritime and offshore industries.It is more commercial than its peers in other

2: Turnover as share of GDP

Declining share of the economy

Figure 3: Global market share of Norwegian

Loosing global market share

exports. Measured against other services exports wealso find a decline of space related exports since2003. Compared against other exports ofmanufactured goods, we find an even moresignificant drop of about 43 percent since 2003.This share has declined since the late nineties and isnow at about 0,3 percent of total product exports.

It is more commercial than its peers in othercountries.

In summary, this is a picture of an industrywith declining sales, loosing share of theeconomy, and that looses global marketshare.

0,0 %

0,1 %

0,2 %

0,3 %

0,4 %

0,5 %

2010

-33%

2: Turnover as share of GDP Figure 3: Global market share of Norwegianspace business (excluding consumer markets)

8

0,0 %

0,5 %

1,0 %

1,5 %

2,0 %

2,5 %

3,0 %

2000 2005 2010

Global market share

Details and source information are available on pages 44 to 55 in the main report.

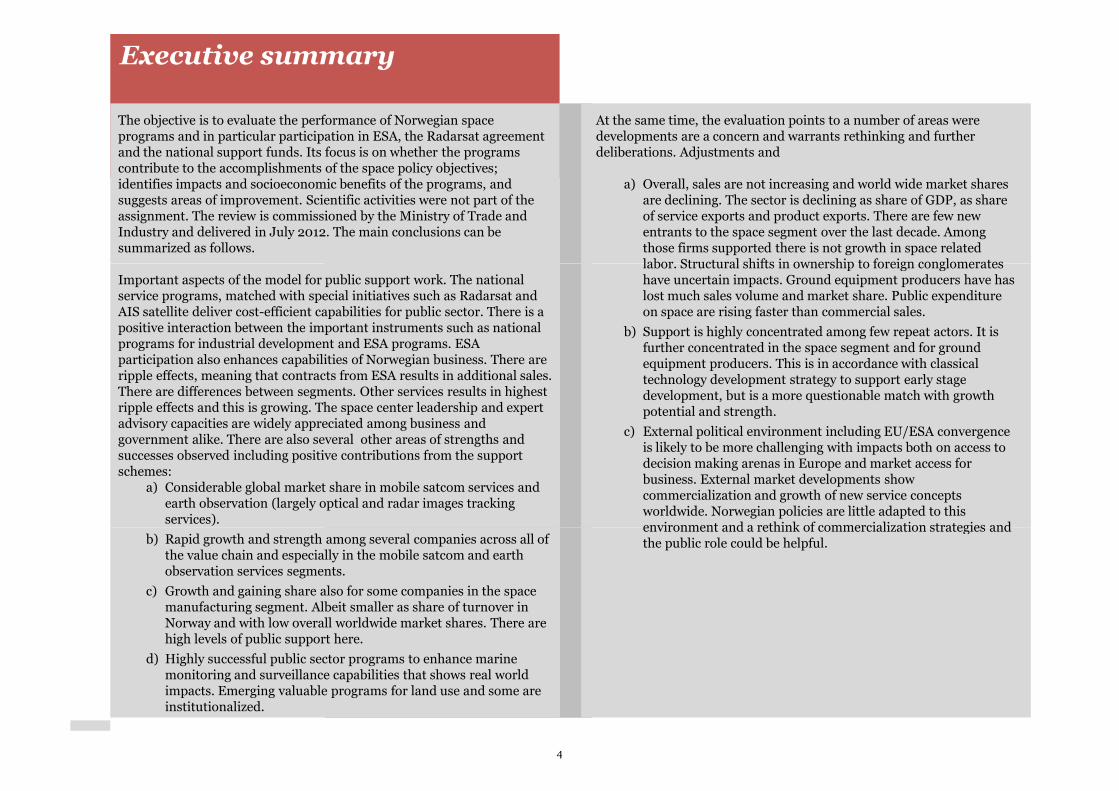

The value chain for space related activities

When assessing how space activities contribute to wealth creation and otherobjectives it is useful to define the scope and range of space activities in theeconomy. We do this by mapping a value chain, that is understanding howactors and stages interact. There are three distinct elements of the space valuechain:

First, there is the institutional segment. Historically, developments havebeen much driven by military needs, i.e. communications and remote sensing

Summary report

been much driven by military needs, i.e. communications and remote sensingneeds. Scientific explorations of space also constitutes a core rationale andother public sector requirements such as environmental monitoring areimportant. These are often requirements for which there exist no privatemarket or suppliers. New developments are necessary and these requiresignificant investments and entails risks that few private enterprises are willingto embark upon alone.

There are also commercial space segments. We can divide this into itsmain value chain activities such as illustrated above. In principle, theinstitutional activities of governments can be grouped along the samedimensions but the commercial activities can be analyzed with moregranularity mostly because of better availability of data and information. Manyof the same private actors are also involved a contractors for developments ofpublic systems and in some cases with mixed public and private financialinvolvement, it is not always possible to distinguish the institutional andcommercial segments entirely.

PwC 9

activities

Much of the commercial value chain is driven by the demand forcommunication services. This creates the demand for satellites, launchers andground equipment. Most important is transmission of TV signals, but also forinternet broadband and other communication services. Of increasingimportance, albeit small yet, is also developments of remote sensingcapabilities such as the images found on Google Earth. These service marketsoperate on pure commercial terms. There are international agreementsgoverning use of frequencies and location of satellites but little other policygoverning use of frequencies and location of satellites but little other policyintervention. Much of the technological base has however been developedunder institutional programs.

The satellite manufacturing and launcher segments are more captive. Most ofthe demand for their products stems from public sources. Nation states (andintergovernmental organizations such as ESA) typically prefer enterprises fromtheir own countries. As such this market segment has more captivecharacteristics than the service segment. i.e. in the U.S government spending isestimated to constitute 85 percent of the demand for space manufacturing inthe U.S. In Europe the ratio is closer to 50 percent. Yet, when a Satellite TVorganization needs to increase their satellite capabilities, the manufacturingand business mechanisms around this are commercial.

The tail end of the value chain is the consumer distribution. This includesservice provision such as TV or broadband access, and also equipmentmanufacturing of i.e. GPS hand- or vehicle equipment, chipsets for smartphones or TV set top boxes. These segments are the largest ones in economic

9

phones or TV set top boxes. These segments are the largest ones in economicterms but has not been a focus of Norwegian space programs and are not partof this analysis.

Illustration of the value chain for space

Figure 4a: The value chain concept for space industries

The value chainentertainment to

Institutional

To understand the industry we review the followingfour value chain segments:

I. Satellite components and launchers.This includes all Norwegian manufacturerswho deliver components for launchers or

Public/Scientific/Millitary

Institutionalwho deliver components for launchers orsatellites. Most of these are private enterprisesbut one is affiliated with a university andincluded here.

II. Ground equipment. This includes allproducers of ground equipment. Productofferings vary but all are involved inprofessional markets only. None sell toconsumer markets.

III. Satellite communications services. Thesefirms are service providers only. They may ownan infrastructure, i.e. satellites or groundstations, but they do not manufactureequipment. This is the largest segment inNorway.

PwC 10

Norway.

IV. Other services. These are also pure serviceproviders. The range in offerings quite wide,from offshore surveying, met services andground station operators. These do notproduce hardware, but may own infrastructurei.e. ships or grounds stations.

space activities

value chain concept for space industries

stretches from scientific exploration of space to delivery ofto consumers

Commercial Consumer

Satelliteand

Launchers

Groundequipment

Satelliteservices

Media andequipment

Commercial Consumer

10

Figure 4b: Turnover space value chain global and in Norway ex consumer TV

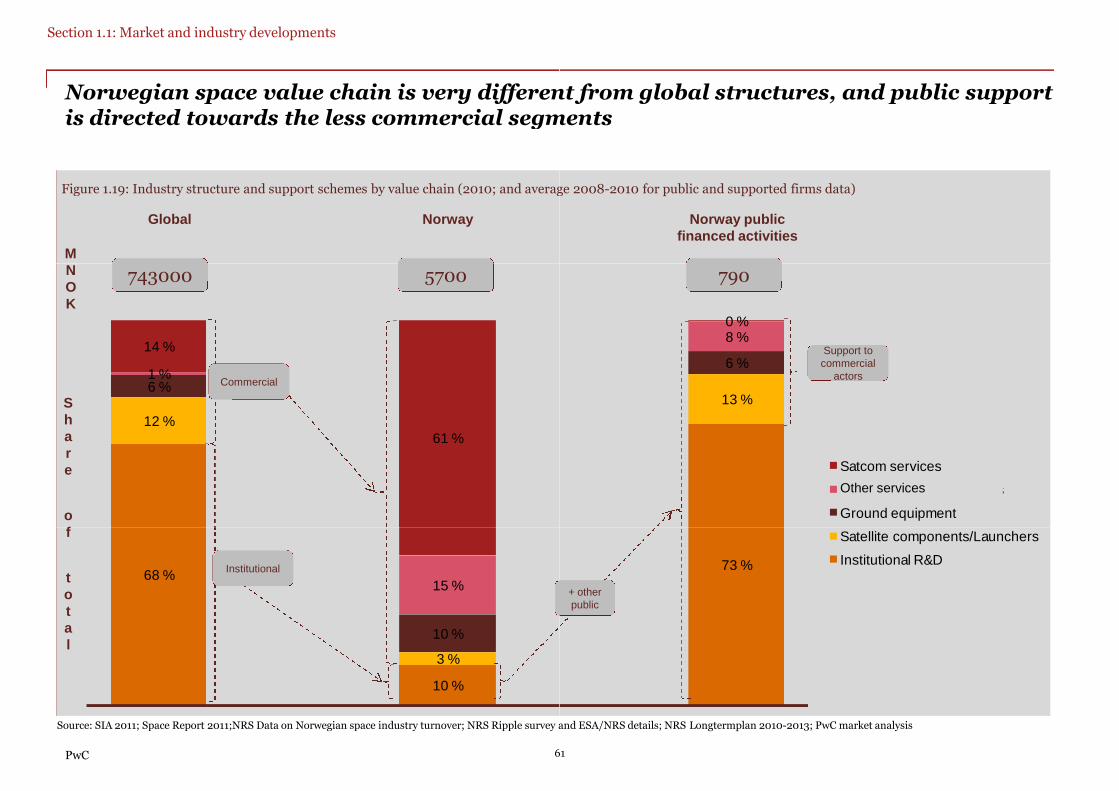

Norwegian space value chain is very different from global structures, and public supportis directed towards the less commercial segments

The value chain and public support

Global

The size and growth rates of different segments varyacross countries and in Norway the services segmentis particularly large. The figure to the right shows thedistribution of institutional and various commercialsegments.

Globally, we find that the institutional segment of thevalue chain is particularly large. This is mostlyvalue chain is particularly large. This is mostlyexplained by the large U.S government expendituresestimated at nearly 65 billion dollars in 2010equivalent to one- third of total turnover globallyincluding consumer satellite TV.

In Norway we find that the institutional side is muchsmaller than the commercial segments. This reflectsthe success of the industry in global commercialmarkets. The commercial value chain ischaracterized by a very large communication servicessegment. There are companies with large global marketshares included in this. There is also a rapidly evolvingearth observation community, as well as a small butspecialized space manufacturing industry.

At the same time, the public support I Norway isfocused on the upstream production of satellite

Satcomservices

Otherservices

Groundequipment

PwC

focused on the upstream production of satellitecomponents and ground equipment. This constitutesabout 80 percent of total support. The differencebetween support and industry size is most marked forthe satellite components segments where 36 percent ofthe total support is allocated yet the segment onlyconstitutes about 3 percent of the space relatedturnover in Norway.

Satellite communications services, which is by far thelargest segment in Norway, receives nearly no supportwith only about 1 percent of total over the last decade.

Satellitecomponents/Launchers

InstitutionalR&D

11

: Turnover space value chain global and in Norway ex consumer TV- and electronics (2010 est.)

Norwegian space value chain is very different from global structures, and public supportis directed towards the less commercial segments

Global Norway Share of public support in Norway

≤1%

19%

20%

≤1%

12 %

6 %1 %

14 %

61 %

24%

36%

68 %

10 %

3 %

10 %

15 %

11

Figure 5: Turnover space manufacturing andlaunchers

Space manufacturing shows growthand commercial sales

Manufacturing recieves most support but is loosing market shares

Launch and satellite manufacturing receives most of theNorwegian support, and is a small growing segment witha fractional global market share. Launcher marketaccess is only through Ariane-5. Arianespace capturesmost of the commercial launch revenues but competitionis escalating. Growth in demand for launchers, but evenmore rapid growth of supply from commercial, U.S. andAsian providers. It is unclear whether support for

Summary report

Ground equipment has much declinein sales and flat growth for survivors

1990 1995 2000

Public

Commercial

Figure 7: Turnover ground equipment prod.

Asian providers. It is unclear whether support forlaunchers is justified in light of the competitivepositioning and the poor potentials for growth and wealthcreation.

Norwegian satellite component manufacturing ismostly financed by public funds but commercial share hasbeen increasing. High entry barriers for satellitecomponents manufacturing but competition escalating.Access to European institutional markets will becomemore difficult in light of more open competition pushedby the EU. With one exception, the position of Norwegianmanufacturers in commercial markets is not strong. Riskthat they will be insufficient in size and scope to competewith integrated global conglomerates. Also in thissegment there is reason to question the sustainability ofthe support schemes.

PwC

2000

All Supportedfirms

Survivors

the support schemes.

The once large ground equipment industry has seenmuch decline. The Norwegian strength is sales tomaritime industries. There is strong growth of worldwideground equipment markets. Norwegian producers havelost global market share. This is sensitive to the collapseof one large company, but remaining firms have notgrown to cover the gap.

Sales have also developed at a much slower rate than theoverall growth of electronics manufacturing in Norway.The overall electronics industry in Norway does well, andit is not evident why space sales are falling.

12Details and source information are available on pages 56 to 87 in the main report.

: Turnover space manufacturing and

Space manufacturing shows growthand commercial sales

300

Sale

s(m

illion

NO

Kn

om

inal)

Figure 6: Estimated global market share 2009-2010

Sat

…and fractional global commercialmarket share but increasing

most support but is loosing market shares

CAGR10%

Ground equipment has much declinein sales and flat growth for survivors

-

100

200

2000 2005 2010S

ale

s(m

illion

NO

Kn

om

inal)

Launchers≈

0,3%

Satmanufacturing≈

0,2 %

…and loss of global market share

: Turnover ground equipment prod. Figure 8: Estimated global market share 2005-2010 exconsumer equipment

0 %

25 %

50 %

75 %

100 %

2005 2010

consumer equipment

0,0 %

1,0 %

2,0 %

3,0 %

2005 2006 2007 2008 2009 2010

-50%

12

Figure 10: Sales Satcom services ex TVDTH

Satcom services growing albeitslowly…

0,7

NOK

Satcom services are leading globally but loosing shares. Othergrowth potential.

SatCom services have lost some global market sharebut still accounts for two-thirds of commercial spacesales in Norway. It operates nearly autonomous fromthe public support schemes. Relatively small publicinvestments here have had big impacts. This segmenthas also seen new entrants with rapid growth. Fixedsatellite operator Telenor goes strongly, but hasdivested most of its other large engagements in space.

Summary report

Other services has rapid growth…

Figure 12: Turnover other services

0

0,1

0,2

0,3

0,4

0,5

0,6

0,7

2005 2007

Sale

s(B

nU

S)

CAGR3%

divested most of its other large engagements in space.Norwegian firms are global market leaders. Firms inthe fast growing mobile maritime segment have beenattractive acquisition targets for global operators. Newentrants may challenge the positions in maritimemobile markets including from Ericsson. Uncertainimpact of foreign acquisitions on satcom serviceindustry. There is a risk of dwindling satcom servicesactivities and policy tools are not suited to redress theissue.

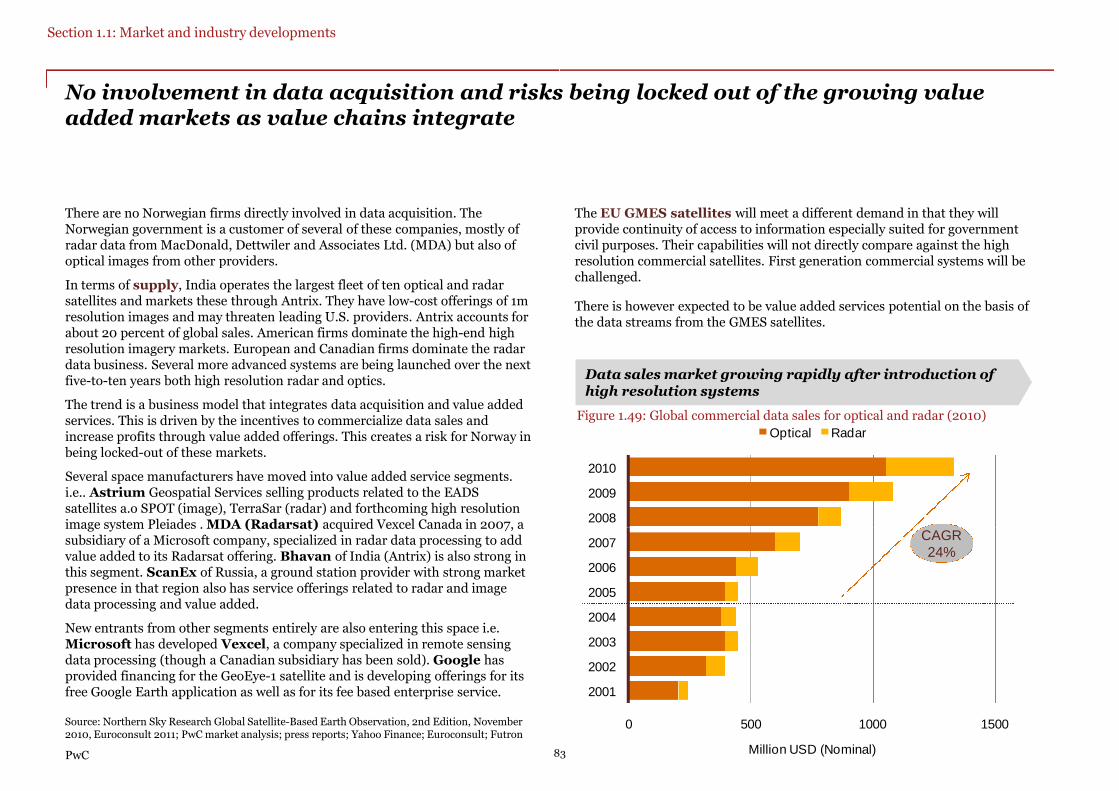

Other services are emerging with strong Norwegiancapabilities and market shares. The supply side of thismarket is commercializing while demand remainsmostly government. Image data sales market isgrowing rapidly after introduction of high resolutionimage and radar. Norway has no involvement in data

PwC

2005 2006 2007 2008

CAGR16%

image and radar. Norway has no involvement in dataacquisition and risks being locked out of the growingvalue added markets as value chains integrate. KSAThas a sweet spot in ground station and data distributionand a basis for expanding value added services. Thereare advanced commercial surveying and met servicesactors in Norway. Surveying off- and onshoreincreasingly using satellite information in addition tonavigation. One of Europe's fastest growingcommercial met services is based in Norway andoperates in six countries. Government support is veryselective and broader support for commercializationcould be considered.

13Details and source information are available on pages 56 to 87 in the main report.

: Sales Satcom services ex TVDTH

Satcom services growing albeit

Figure 11: Estimated global market share 2005-2010

…but loosing ground in globalmarkets

USD 5,0 %

Satcom services are leading globally but loosing shares. Other servcies ahs

Other services has rapid growth……and possible large global marketshares

: Turnover other services Figure 13: Estimated global market share 2010

0

1

2

3

2009S

ale

s(B

nN

OK

)0,0 %

1,0 %

2,0 %

3,0 %

4,0 %

2005 2006 2007 2008 2009 2010

Glo

balm

ark

etsh

are

CAGR3%

0

0,3

0,6

0,9

2008 2009 2010

Sale

s(B

nN

OK

)

13

Note: Robust estimates of total information services marketvolume does not exist. Better estimates exist of the EO andMet services markets and against those the Norwegianmarket share may be in the range of 3-10 percent.

3-10 percent

External developments contributes to loss of competitiveness

Developments in the external institutional andpolitical arena have implications for the relevanceand effectiveness of the national space programs.

Five perspectives are important:

1. The U.S. 2010 space policy could be a gamechanger for commercialization. It is likely to impactmarkets and industry and also create opportunities

Future contract awards will be more competitivebut likely not fully aligned with EU procurementdirectives in all ESA programs. Contracts under EUfunded programs are likely to remain competitive.This will lead to reduces market access forNorwegian firms compared to today's moreprotected regime.

Summary report

markets and industry and also create opportunitiesfor non-american government to acquire new andbetter services. The definition of commercializationimplies capital risk for private actors and goesbeyond previous practices of sub-contractingcommercial vendors. U.S. business will continue tohave anchor tenants in government but will alsohave stronger incentives to further commercializeproducts and services.

2. European issues. This is primarily about thereconfiguration of ESA and EU relationships withthe implications this has for priorities and directionof policies, as well as governance structures, andaccess and opportunities for Norwegian firms andother interests.

This is an ongoing, and slow moving process, but

There is a considerable financing gap for the policy.EU has not provided financing for space activities inthe Medium-term Financing framework therebythreatening the completion and operation of a.o theGMES Sentinel flagship program for earthobservation. EU wants member states to cover.Future challenges for Norway include both access todecision making arenas in Europe and marketaccess for business to institutional markets inEurope.

3. Peer country developmentsSwitzerland and Sweden are discussed. A commonthread is that all are realigning policies due tochanging environments. Canada has embarkedupon a significant policy process, Sweden has calledfor one, while Switzerland completed its new policy

PwC

This is an ongoing, and slow moving process, butcertain emerging patterns can be ascertained. Theimportant ramifications for Norwegian policyinclude: That the Commission wishes to bettercoordinate activities of member states, and spaceinfrastructure is to be explored jointly.

The EU space policy involves continuation of theflagship programs Galileo and GMES, spaceexploration and military ambitions. It might entailrestructuring of the EU/ESA relationship.

for one, while Switzerland completed its new policyin 2008.

4. Commercialization and private risk.Increasingly national programs organized aspartnerships with commercial orientation andprivate capital at risk. Boundaries between publicand private roles are shifting. This is particularlyseen within the earth observation image and radarsegments but also in military communications. Thisis driven by U.S. and European concepts.

14

External developments contributes to loss of competitiveness

Future contract awards will be more competitivebut likely not fully aligned with EU procurementdirectives in all ESA programs. Contracts under EUfunded programs are likely to remain competitive.This will lead to reduces market access forNorwegian firms compared to today's more

5. Emerging market countries expansion andsigns of future of low-cost space, commoditizationand service expansion will threaten Norwegianfirms. Commercial capabilities are still limited.Those relate primarily to operation of SatComservices for domestic or regional markets; Thelauncher industries of Russia and China havesignificant market shares and especially China has

Figure 14: Indicative market prices highresolution, fresh images, per Sq km

Indian low-cost image challenger

There is a considerable financing gap for the policy.EU has not provided financing for space activities in

term Financing framework therebythreatening the completion and operation of a.o theGMES Sentinel flagship program for earthobservation. EU wants member states to cover.Future challenges for Norway include both access todecision making arenas in Europe and marketaccess for business to institutional markets in

3. Peer country developments. Canada,Switzerland and Sweden are discussed. A commonthread is that all are realigning policies due tochanging environments. Canada has embarkedupon a significant policy process, Sweden has calledfor one, while Switzerland completed its new policy

significant market shares and especially China hasbegun to make inroads into the more profitablesegment of launching commercial communicationssatellites directly in competition with a.oArianespace. In India especially the image segmentis semi-commercialized and they have gainedshares in the global image sales markets.

The Asian space race is driving competition andlaunch of military and surveillance satellites.

$9

$17

$19

$25

Cartosat-2 (1m)

Worldview-1 (0,5m+)

Ikonos (1m)

Geoeye-1 (0,5m+)

for one, while Switzerland completed its new policy

4. Commercialization and private risk.Increasingly national programs organized aspartnerships with commercial orientation andprivate capital at risk. Boundaries between publicand private roles are shifting. This is particularlyseen within the earth observation image and radarsegments but also in military communications. Thisis driven by U.S. and European concepts.

14 Details and source information are available on pages 88 to 111 in the main report.

The objective of this analysis is to review how theprograms have been implemented. What has beenthe activities? Where has the monies been spentand to what effect?

There is real growth in public expenditure forspace and 60 percent of it for Space Centermanaged programs. We also find that other

The core rationale for participation in theEuropean Space Agency relates to access to pooledcapabilities and development programs beyondwhat Norway could accomplish on its own. Theability to get access to “costmeets demand and requirements for publicagencies is emphasized in addition to access toscientific programs and instruments for

Norwegian policy implementation is mostly about ESA, but fastest growth fornational programs

Summary report

managed programs. We also find that otherspending, in particular on R&D is quite significantat about 30 percent of total.

The important dedicated space programs for thisreview includes:

•ESA participation which remains the primaryinstrument for developing capabilities; and

•National programs including special initiativessuch as Radarsat and AIS satellite development.

scientific programs and instruments forresearchers. Another rationale is that Norwegianindustry gets access to technology developmentprograms and qualified ESA assistance, andopportunities to deliver into ESA developmentprograms of satellites and other systems. Largesegments of the space industry value chain iscaptive to government programs, and in absence ofESA access, Norwegian industry would not haveaccess to important markets.

Figure 15: All Norwegian expenditure on spaceincluding ESA, Space programs, science andgovernment agencies

Top line growth in all publicexpenditure on space

Figure 16: ESA and Galileo contributions fromNorway

Contributions to ESA growing evenfaster

PwC

-

150

300

450

600

750

900

2005 2006 2007 2008 2009

MIllio

nN

OK

(Cu

rren

t)

2002 2004 2006

Gallileo

ESA

CAGR10%

CAGR11%

15

The core rationale for participation in theEuropean Space Agency relates to access to pooledcapabilities and development programs beyondwhat Norway could accomplish on its own. Theability to get access to “cost-efficient” systems thatmeets demand and requirements for publicagencies is emphasized in addition to access toscientific programs and instruments for

National program financing is increasing fasterthan ESA contributions. Financing has nearlytripled in monetary terms since 2005, and alsomore than doubled as share of ESA contributions.The increase has mostly been for special programsor initiatives. Prominent among these are theRadarsat agreement, The AIS Satellite programand infrastructure developments such as for

Norwegian policy implementation is mostly about ESA, but fastest growth for

scientific programs and instruments forresearchers. Another rationale is that Norwegianindustry gets access to technology developmentprograms and qualified ESA assistance, andopportunities to deliver into ESA developmentprograms of satellites and other systems. Largesegments of the space industry value chain iscaptive to government programs, and in absence ofESA access, Norwegian industry would not haveaccess to important markets.

and infrastructure developments such as formaintenance at Andøya Rocket range, and supportfor the KSAT station in Antarctica.

The schemes for industry and earth observationservice development have seen some increase inabsolute terms. These programs have decreased insignificance compared to other special programs.

: ESA and Galileo contributions from

Contributions to ESA growing even

Figure 17: All national funds including Radarsat,AIS, industry development, service development

National programs growing fasterthan ESA contributions

-

15

30

45

60

75

2006 2008 2010

MIllio

nE

UR

(Cu

rren

t)

0 %

5 %

10 %

15 %

20 %

-

25

50

75

100

2000 2005 2010

Sh

are

ofE

SA

co

ntr.

Millio

nN

OK

no

min

al

Share of ESA contribution

All national programs

CAGR

15 Details and source information are available on pages 112 to 134 in the main report.

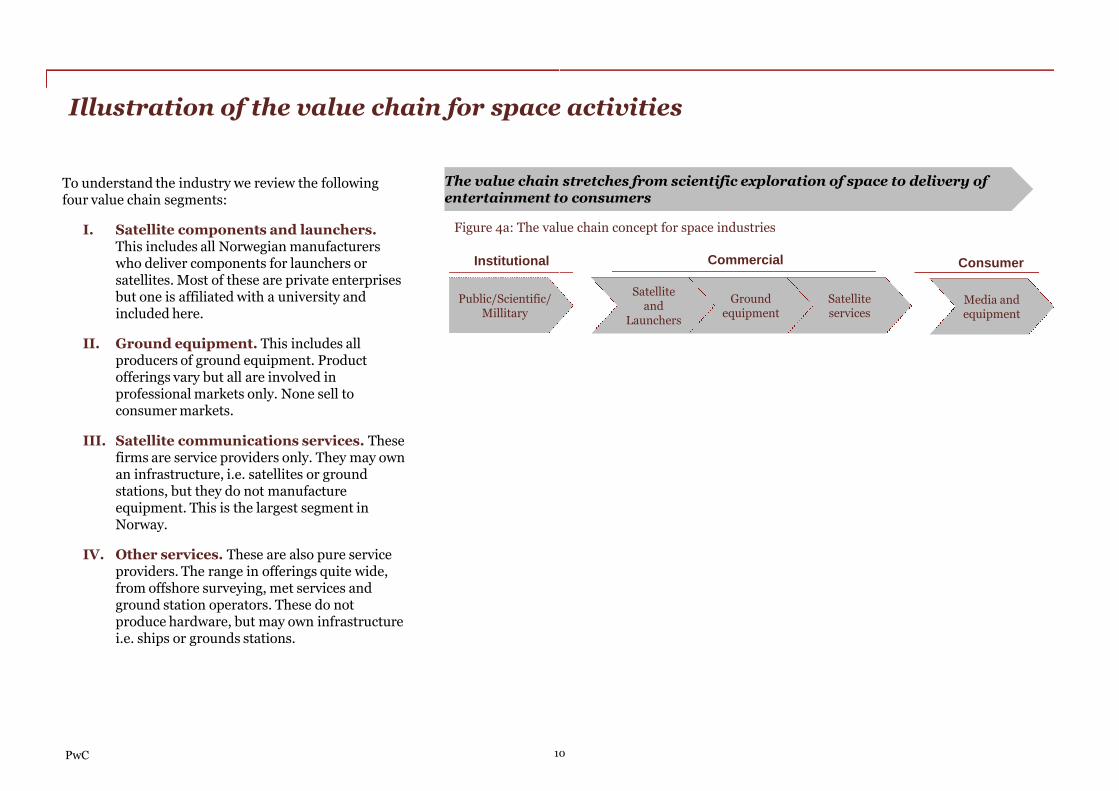

The European Union is now the largest singlecontributor to ESA at about 20 percent of the 2011budget. ESA’s expenditures have generally grownsince 2002 albeit with a significant decline in 2010.Budgets for 2011 are higher but not as high as the2009 record levels. There are some difficulties inmatching incomes and expenditure and ESA hasfor the last two years recorded operational

About two-thirds of contributions have been forOptional programs. There is possibly a trendchange whereby the share is increasing and thelevels of Optional financing in 2010 reached nearlythree-quarters. This seems to be sustained also in2011.The Galileo and GMES programs currently underimplementation are not part of the numbers below

ESA contributions increases and most for the optional programs, butdeclining share returned as contracts to Norwegian firms

Summary report

for the last two years recorded operationalsurpluses of 1 billion Euros.

Norwegian contributions to ESA have increased atan annualized rate of 11 percent between 2002 and2010. In nominal terms this implies more than adoubling. Contributions have risen faster than formany other ESA states and the share of the totalfinancing envelope for ESA is increasing. Thecontribution was equivalent to 2,8 percent ofactual ESA spending in 2010, and about 1,8percent of total income.

implementation are not part of the numbers belowbut could possibly be considered Optionalprograms although the mechanisms are differentgiven the involvement of the EU.Norway is below mid-point in terms of ratiobetween mandatory and Optional programs. Somenations, both small and large have considerablyhigher Optional program weighting.Norway participates in most Optional programs.Some other countries including Sweden,Switzerland and the U.K has a more selectiveparticipation.

Figure 18: Norwegian contribution as share ofESA finance

Gaining share of ESA financing

Figure 19: Mandatory and Optional programshares for Norway 2002-2010

No clear trend, but Optionalincreased significantly in 2010

PwC

ESA finance shares for Norway 2002-2010

0,0 %

0,5 %

1,0 %

1,5 %

2,0 %

2,5 %

3,0 %

2002 2006 2010

Perc

en

tag

esh

are

ESA totalincome

ESA OPEX

Incomecontributionmemberstates

62 %61 %67 %66 %

2002 2004

Optional

Mandatory

ESA overallratio

16

thirds of contributions have been forOptional programs. There is possibly a trendchange whereby the share is increasing and thelevels of Optional financing in 2010 reached nearly

quarters. This seems to be sustained also in

The Galileo and GMES programs currently underimplementation are not part of the numbers below

Norway is an up-and-coming ESA player especiallyin Optional programs where the growth rate hasbeen highest. Longer term, telecom has been themost favored Optional program. This constitutes ofa number of smaller programs most of which aretechnology development programs wherebyindustry gets 50 percent financing and access toqualifies ESA assurance of their work. Earth

ESA contributions increases and most for the optional programs, butdeclining share returned as contracts to Norwegian firms

implementation are not part of the numbers belowbut could possibly be considered Optionalprograms although the mechanisms are differentgiven the involvement of the EU.

point in terms of ratiobetween mandatory and Optional programs. Somenations, both small and large have considerablyhigher Optional program weighting.Norway participates in most Optional programs.Some other countries including Sweden,Switzerland and the U.K has a more selective

qualifies ESA assurance of their work. Earthobservation sees almost as high share at about 16percent of total financing. Much has happenedover time. A shift can be observed from 2007whereby a significant share was allotted to thegeneral technology program. This nowencompasses about 25 percent of total Optionalcontributions.Over the last nine years we observe that thevolume of contracts returned is 58 percent ofaccumulated contributions to ESA. The ratio hasbeen declining.

: Mandatory and Optional program2010

No clear trend, but Optionalincreased significantly in 2010

Figure 20: ESA contribution and contract ratio

Not all funds are returned ascontracts and gap is increasing

2010

66 %53 %70 %69 %65 %74 %

2006 2008 2010

Sh

are

ofto

tal

16

0

10

20

30

40

50

60

2002 2004 2006 2008 2010

Eu

rom

illion

Contribution

Contracts

Details and source information are available on pages 112 to 134 in the main report.

Distribution of funds is highly concentrated: Four firms receives 50 percent;63 organizations share the rest.As many as 67 organizations have been involved ineither the ESA or national space funds programsover the last decade.

Distribution is highly concentrated:

• four firms receiving 50 percent overall; for ESAmandatory programs 80 percent is captured bythree firms;

Regarding distribution of public funds:

Satellite component and launch manufacturersreceive most and more than a third of total. Theshare has declines some but the amounts haveremained about the same. Number of organizationsinvolved have increased over the decade.

Ground equipment captures about twenty

Summary report

Figure 21: Distribution of funds among value chain actors

Most support for space manufacturing, and more R&D organizations participating

Total value of contracts 2000-2010

three firms;

• a further 11 organizations receiving the next 30percent; and

• 52 organizations share the remaining 20 percentand many of these amounts are very small lowerthan 0,1 percent of total.

The ESA system seem in practice favor largerorganizations due to relatively high transactionscosts and risks. Smaller firms have mostly accessedthe technology development programs.

Ground equipment captures about twentypercent.

Other services receive 20 percent butfunding is concentrated to only one or two firms.

Telecom satellite servicesminor amounts distributed across one or two firmsover the decade.

Institutional R&D captures about 24 percent oftotals. Their share has more than doubled over thedecade.

PwC

Satcom services

Earth observation services

Ground equipment

Satellitecomponents/Launchers

Institutional R&D24 %

36 %

19 %

20 %

1 %

0 %

50 %

100 %

All 2000-2010

Total value of contracts 2000-2010

-

5

10

15

20

25

30

35

40

2000

Number of organizations

17

Other services

Distribution of funds is highly concentrated: Four firms receives 50 percent;

Regarding distribution of public funds:

and launch manufacturersreceive most and more than a third of total. Theshare has declines some but the amounts haveremained about the same. Number of organizationsinvolved have increased over the decade.

captures about twenty

Those firm that receive support have a decliningshare of total space sales in Norway. During thistime we have seen an increase in the ESA contractsfor that same group. We should keep in mind thatall this takes place in a context where there hasbeen a real decline in commercial space sales overthe last decade.

Firms that engage with ESA typically target

Most support for space manufacturing, and more R&D organizations participating

Figure 21b: Sales by actor

Sales of those who do not receivesupport grows faster than those thatreceive public support

captures about twenty

ther services receive 20 percent but thefunding is concentrated to only one or two firms.

Telecom satellite services have received onlyminor amounts distributed across one or two firms

captures about 24 percent oftotals. Their share has more than doubled over the

Firms that engage with ESA typically targetdifferent markets segments than those that operateoutside of the institutional markets.

All upstream firms engage with ESA, i.e..manufacturing of launchers and satellitecomponents; while there is much less institutionalactivity from firms that operate in the downstreamsegments i.e.. satellite communications servicesegments. This also reflects the demand structurein the institutional markets which is predominantlyabout science and manufacturing.

2005 2010

Number of organizations

17

1997 2001 2005 2009

Sales non-ESA firms

Sales ESAfirms

ESA sales

Details and source information are available on pages 112 to 134 in the main report.

Most firms that operate in the ESA market haveother business outside of the space markets. Thereare only a few producers that are entirely spacefocused. The share of space related sales havegenerally fallen over the last decade for theseenterprises. This can indicate a shift in focus andlack of alignment in corporate strategy with spacemarkets, or it can indicate faster growth in other

Employment for space work has not picked upeven for the surviving firms. There is a declinesince the late 1990’s having nearly lost half of theemployees that were involved at the peak. Thesurviving firms show a flat trend over the last 15years. Profits have increased in absolute termsthough margins have stayed at about the samelevels indicating cost increases.

Declining turnover of the supported industry, no job creation, butconciderable spinoff sales are reported

Summary report

markets, or it can indicate faster growth in othersegments.

Space revenues have declined overall in particularduring the last five years for ESA firms. This ismuch due to a few companies.Its encouraging that there is robust growth, both innominal and real terms, for the surviving firms.This growth has been consistent since 1985 at anannualized growth rate of about 16 percent.

levels indicating cost increases.

ESA contracts have increased over the last decadenearly doubling. This growth rate is well above theinflation and thus indicating growth in real terms.It is also faster than the growth of ESA budgetsoverall indicating that Norwegian firms have takena larger share of the ESA market. As share of spacesales for these firms we see that ESA contractspeaked significantly in the midpercent.

Figure 22: Sales for ESA involved firms

Decline for all ESA involved firms,though growth for surviving firms

Figure 23: Employment for space related workamong ESA firms

Lost jobs, and no growth forsurviving firms

PwC

0,0

0,3

0,6

0,9

1,2

1,5

1985 1990 1995 2000 2005 2010

Billio

nN

OK

All supported firms

Surviving supported firms

1985 1990 1995 2000

All supported firms

Surviving supported firms

18

CAGR16%

Employment for space work has not picked upeven for the surviving firms. There is a declinesince the late 1990’s having nearly lost half of theemployees that were involved at the peak. Thesurviving firms show a flat trend over the last 15years. Profits have increased in absolute termsthough margins have stayed at about the samelevels indicating cost increases.

An important rationale for public support toprivate firms through ESA is the access it providesto cutting edge technology development programs.Firms emphasize the highly qualified interactionsat all stages in the process including with theNorwegian space centre. Firms also emphasize theinteraction between the national support schemesfor industrial development that allows early stage

Declining turnover of the supported industry, no job creation, but

levels indicating cost increases.

ESA contracts have increased over the last decadenearly doubling. This growth rate is well above theinflation and thus indicating growth in real terms.It is also faster than the growth of ESA budgetsoverall indicating that Norwegian firms have takena larger share of the ESA market. As share of spacesales for these firms we see that ESA contractspeaked significantly in the mid-nineties. Now 20

for industrial development that allows early stagework before ESA.

An important metric to gauge the success of this isthe multiplier between support and sales generatedfrom this. Firms have reported data since the early1990’s. Considerable impacts are observed. Themultiplier is at 4,3 currently adjusted for inflation.Median firm impact is 3,5. Thus one ESA contractresults in additional sales of about four times theamount indicating an impact.

: Employment for space related work

Lost jobs, and no growth for

Figure 24: Multiplier of ESA support on sales

Considerable multiplier on sales

8

0

200

400

600

800

1000

1200

2000 2005 2010

Peo

ple

All supported firms

Surviving supported firms

0

1

2

3

4

5

6

7

8

1989 1994 1999 2004 2009

Mu

ltiplie

r

Inflationadjusted

Nominal

18 Details and source information are available on pages 157 to 171 in the main report.

Positive impacts on Norwegian economy mostly by firms spinoff salesThe multiplier shows divergence across differentvalue chain segments. There are differences inlevels and shifts over time.

Services how the highest levels (6,8) and anincreasing trend. Ground equipment is lower andhas been sliding for decades. Satellite componentand manufacturing show multiplier of about 3,4and slowly increasing.

A measure of the returns for the Norwegianeconomy is to measure the relationship betweenfinancial inputs and outputs. This is a measuretaking into account all Norwegian funding for ESAand corresponding national industrial funds. Wealso take into account overheads in ESA,distribution of contracts by value chain andvariations in multipliers, including contracts forscientific and public agencies, tax cost and import

Summary report

Sales multiplier differs acrosssegments

Figure 25: Sales multiplier by value chainsegment

and slowly increasing.

R&D multiplier is sliding. These are R&D instituteswho are engaged with much applied researchfunded through public or private sources. Theiradditional income may stem from other publicfinanced programs, i.e.. FP7, or industrial sources.Scientific institutions and public agencies with ESAcontracts do not have ripple effects of this natureand are not included.

scientific and public agencies, tax cost and importcontent.

The net gains for economic activity in Norway isabout 16 percent. There may be additional economywide technological gains not accounted for. Abudget allocation of 100 will result in an increasedactivity level in the economy of 100+16. We shouldalso note that Norway has other objectives with ESAparticipation including access and contribution to acommon European infrastructure. Those benefitswill be additional.

Full money cycle analysis show aboutsixteen percent gain in activity

Figure 26: Flow of funds and impacts of ESAmultiplier

PwC

segment

0

2

4

6

8

10

1991 1996 2001 2006

Mu

ltip

lier

Services

Ground equipment

Satellitecomp./Launchers

R&D/Institutional

19

multiplier

Governmentbudget

ESA/Space centre

Contracts

Multipliers

Tax cost andimport content

Net+economy widetech gains

Positive impacts on Norwegian economy mostly by firms spinoff salesA measure of the returns for the Norwegianeconomy is to measure the relationship betweenfinancial inputs and outputs. This is a measuretaking into account all Norwegian funding for ESAand corresponding national industrial funds. Wealso take into account overheads in ESA,distribution of contracts by value chain andvariations in multipliers, including contracts forscientific and public agencies, tax cost and import

To understand the wealth creation dynamics, thecurrently active successful firms have been studiedin more detail.

This analysis looks at the costs associated with afirm contract and compares these to the benefits itcreates. We focus on a more recent time periodfrom 2004 to 2013 (projected sales). A subset of 25currently active firms have been studied.scientific and public agencies, tax cost and import

The net gains for economic activity in Norway isabout 16 percent. There may be additional economywide technological gains not accounted for. Abudget allocation of 100 will result in an increasedactivity level in the economy of 100+16. We shouldalso note that Norway has other objectives with ESAparticipation including access and contribution to acommon European infrastructure. Those benefits

currently active firms have been studied.Costs include ESA contract and NRC supportvalue, ESA admin and foregone returns. Costs areassigned proportionally by contract value. Thisdiffers from the approach to the left where all costsincluding those not attributable to firms wereincluded. Impacts are seen from salaries andprofits. Wage related effects is by far the largestcontributor to benefits comprising 76 percent.

Full money cycle analysis show aboutsixteen percent gain in activity

: Flow of funds and impacts of ESA12

Costs

12000

Benefits

×3,6

Value creation impacts from firmswith ESA contracts at 3,6 ratio

Figure 27: NPV costs and benefits 2004-2013

19

Government

ESA/Space centre

Tax cost andimport content

Net+economy wide

100

100 + ≥160

2

4

6

8

10

0

2000

4000

6000

8000

10000

2000

4000

6000

8000

10000Income tax

Value addedtax

Retail salesrevenue

Corporatetax

Retainedearnings

Wage

Profits

×3,6

Bill

ion

NO

KDetails and source information are available on pages 170 to 173, and 182 to 197 in the main report.

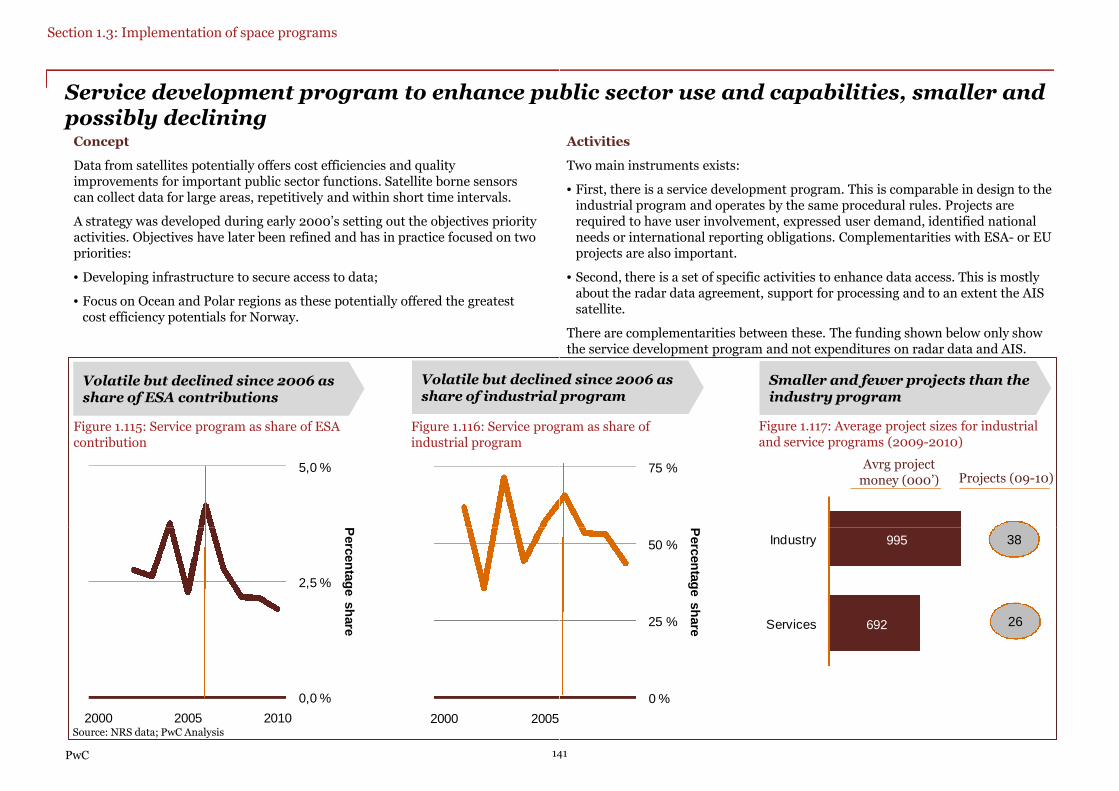

Data from satellites potentially offers cost efficiencies and qualityimprovements for important public sector functions. Satellite borne sensorscan collect data for large areas, repetitively and within short time intervals.A strategy was developed during early 2000’s setting out the objectivespriority activities. Objectives have later been refined and has in practicefocused on two priorities:• Developing infrastructure to secure access to data;• Focus on Ocean and Polar regions as these potentially offered the greatest

Public service programs has enhancedmaritime surveillance capabilities

Summary report

• Focus on Ocean and Polar regions as these potentially offered the greatestcost efficiency potentials for Norway.

Different instruments exists. First, there are special development funds todevelop applications for agencies. Second, there are specialized programssuch as access to radar satellite data and AIS (ship tracking) data. Third, thereare benefits from ESA in terms of access to developments and satelliteinformation.

There are three agencies who operate highly professional and institutionalizedsystems on this basis. Those are the defense, coastal authority and thegeological survey. A fourth, the meteorological institute is a heavy user butoperates mostly on the basis of EUMETSAT specialized data outside of thepurview of this analysis. About ten to fifteen further agencies and R&Dinstitutes have various smaller projects most under implementation.

The flagship program is highly focused on providing maritime operationalservices. This is about surveillance and monitoring of ocean and arctic

PwC 20

services. This is about surveillance and monitoring of ocean and arcticregions, ship traffic, fisheries monitoring, ice coverage and oil spill detection.These services are operating 24/7 integrating the satellite data with othersensors. Land based programs are increasingly important and the geologicalsurvey scans the country to detect surface instabilities and monitors certainhigh risk areas for catastrophic events.

Radar data are purchased to enhance maritime and terrestrial monitoringability. These are much used for defense and security purposes, and wellintegrated into operations. There is also a highly relevant AIS satelliteprogram to enhance maritime surveillance and satellite successfully launchedby government. In total, advanced, integrated and user responsive monitoringsystem, but considerations to cost and governance issues can be addressed.

Figure 28: Snapshot of satellites above Norwegian territories a day inFebruary 2012

Busy above Norwegian waters as ESA satellite Envisatcaptures data enroute north

20 Details and source information are available on pages 135 to 154 in the main report.

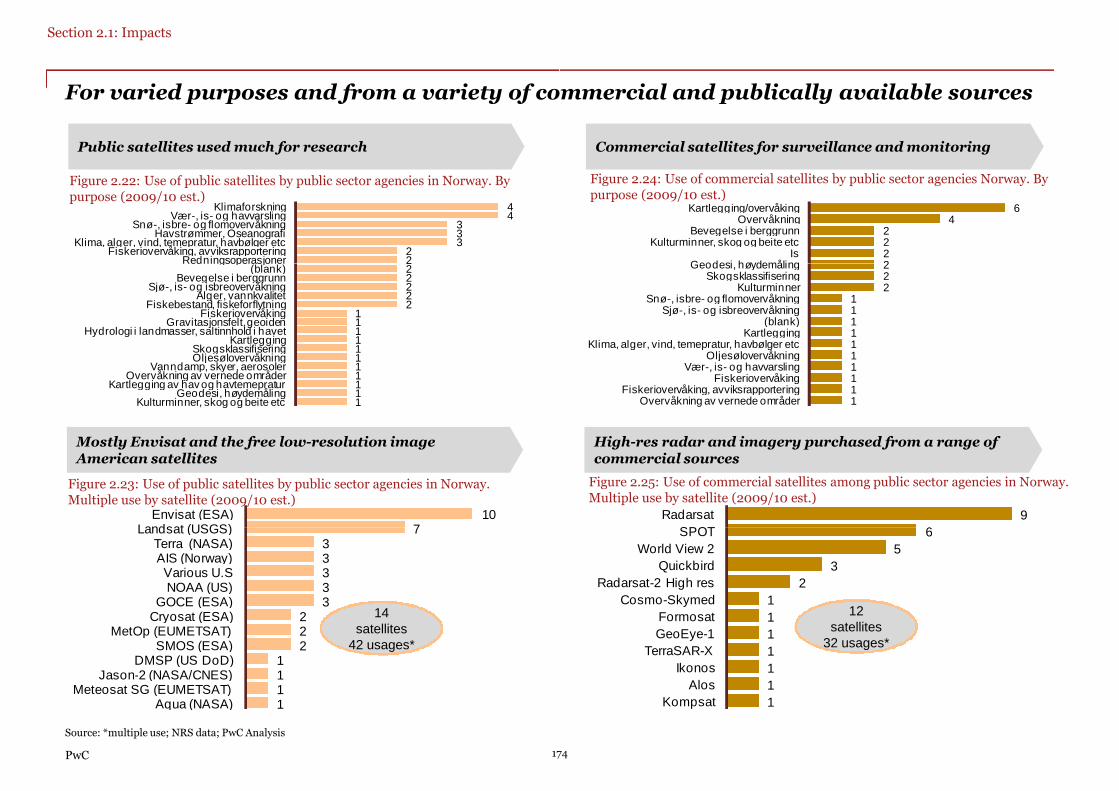

Use of satellite earth observation data is increasing.Agencies may also be using communicationssatellites which is more mainstreamed and notincluded here. Data are mostly used for monitoringand surveillance, but also for a range of otherapplications such as mapping and detecting culturalheritage sites. About 22 agencies have some use withfour big users dominating.

There are no direct benefits stemming fromsatellites. The satellites provide informationthe benefits depend upon how the information isacted upon.

Determining the value of information is complex. Arange of outcomes are likely even in the case offairly closed system contexts like the dedicatedNorwegian used satellite systems (i.e. Radarsat and

Net economic benefits of public service programs, but needs focus on costreduction and benefits realization

Summary report

About half of the satellites used are commercial andprovides high resolution optical images or radar.Public satellites offer free information andgovernment accesses both European and U.Ssatellites.

Norwegian used satellite systems (i.e. Radarsat andAIS).

The value will depend upon perceived risks,effectiveness of response options and theincremental information content value. Economicsciences generally find a value of 1 percent of totaloutput stemming from availability of perfectinformation.

Figure 29: Users of radar data under theagreement 2010

Three professional heavy users ofradar data

Figure 30: Value of satellite information fordetecting illegal fishing (example)

Value of satellite information forillegal fishing between 11

32 %

27 %

23 %

Defence

Geological Survey

Coastal Authorithy

PwC

23 %

3,9 %

3,8 %

2,3 %

2,3 %

1,4 %

1,4 %

1,0 %

0,6 %

0,5 %

0,3 %

0,2 %

Coastal Authorithy

Defence research

NORUT

University of Oslo

Metherological Institute

Geotechnical Institute

Univeristy of Tromsø

Directorate of Fisheries

Nansensenteret

Forest and landscape…

Polarinstitute

Computing Center

- 10 20

Cod

Haddock

Million NOK

21

There are no direct benefits stemming fromsatellites. The satellites provide information – andthe benefits depend upon how the information is

Determining the value of information is complex. Arange of outcomes are likely even in the case offairly closed system contexts like the dedicatedNorwegian used satellite systems (i.e. Radarsat and

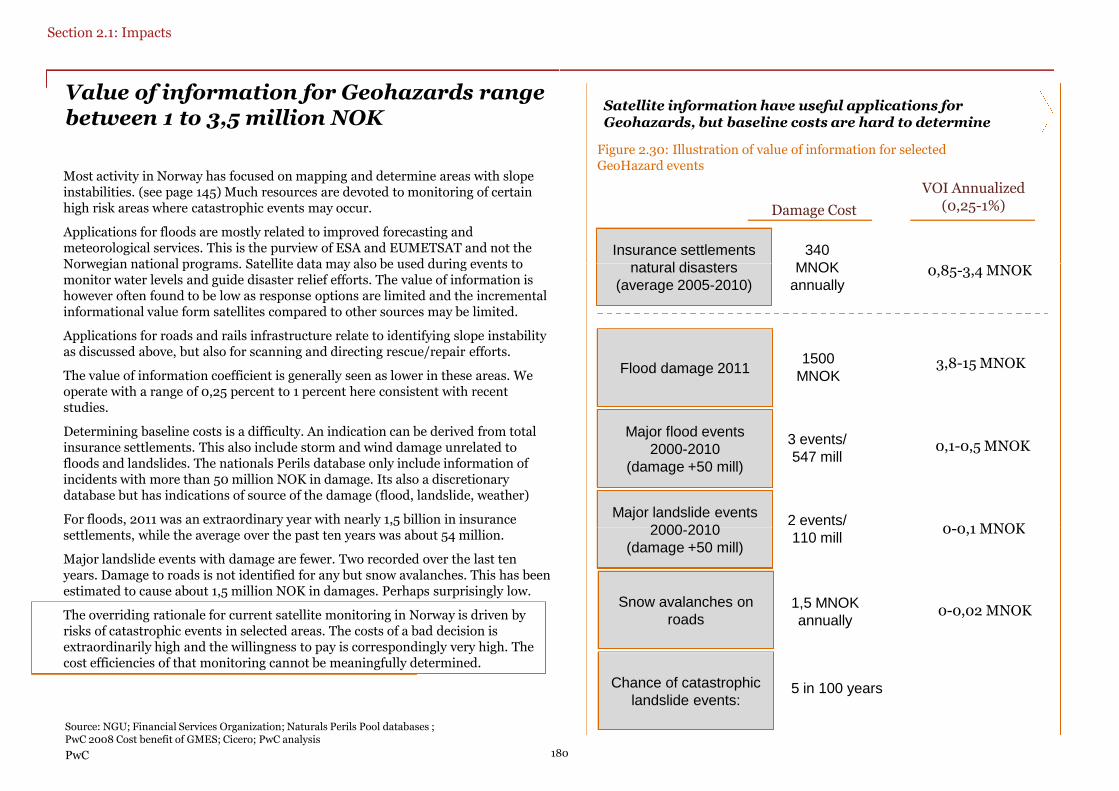

There can be variations. In particular in caseswhere there are deterrence effects such asmonitoring of fisheries and oil spills.

Value of information for oil spills has been found tobe between 1-10 percent across Europe (PwC2008: Booz Co 2011). Value for fisheriesmonitoring have been found to be in the samerange. Value for geohazards is less because the

Net economic benefits of public service programs, but needs focus on cost

Norwegian used satellite systems (i.e. Radarsat and

The value will depend upon perceived risks,effectiveness of response options and theincremental information content value. Economicsciences generally find a value of 1 percent of totaloutput stemming from availability of perfect

range. Value for geohazards is less because theresponse options are more limited.

The value of satellite information in Norway hasbeen quantified across the main usages: Oil spilldetection; fisheries monitoring and geohazards.

We apply conservative estimates for value andgenerous estimates of cost. The range of benefits isvalued at between 13-65 million annually. Costs areabout 25 million annually. By far the highestimpact is found from fisheries monitoring. Thereare also important impacts from oil spill detectionand geohazards monitoring. Much resources forthe latter is devoted to monitoring of high riskareas. The cost and loss of life of a major landslidein these areas is extraordinarily high. The

: Value of satellite information fordetecting illegal fishing (example)

Value of satellite information forillegal fishing between 11-56 million

in these areas is extraordinarily high. Theprobabilities are unknown and the cost efficiencyof monitoring cannot be meaningfully ascertained.20 30 40 50

30-35 million 13-65 million

CostsValue of

information

21 Details and source information are available on pages 172 to181 in the main report.

The programs have delivered specific results over time, but declining contribution towealth creation and uncertainty about sustainability

Overall objective

Space activities in Norway shall provide substantial and persistent contributions to wealth creation, innovation,knowledge development, and environmental- and public safety.

The overall goal encompasses different elements. The concepts are not mutuallyexclusive and overlap. i.e.. knowledge development and innovation. The

Summary report

Activities through ESA are less directly relevant for the enhanced public sector

exclusive and overlap. i.e.. knowledge development and innovation. TheMinistry has also defined more specific objectives and a discussion of progresson detailed objectives are found in the main report and the annex.

Specific results, but unclear impact on sustainable growth andwealth creationOverall turnover of the space industries in Norway have declined by between15-25 percent since 2003 depending upon how inflation is adjusted for.Contributions to wealth creation overall in Norway had declined by 33 percentsince 2003 as defined by GDP with or without petroleum included. Employeesinvolved in space activities have declined by nearly 50 percent since late 1990’sthough this measures only captures about 80 percent of companies.

Support for space related activities has provided results, but these are probablydeclining. There has been strong sales growth for those firms that receive mostof the support albeit insufficient to offset the larger decline. There is growth insome segments of the value chain and some firms have seen phenomenal

PwC 22

some segments of the value chain and some firms have seen phenomenalsuccess. These do not necessarily coincide with those that receive support.Ripple effects on sales of the public support are reported and the socio-economic benefits are net positive.

The profile of the support portfolio is increasingly decoupled frommarket developments, business structures and growth potentialover time. As such we question the sustainability of the support overtime. It may also mean that the results are better for the evaluation period as awhole rather than the last few years in isolation.

The programs have delivered specific results over time, but declining contribution towealth creation and uncertainty about sustainability

Space activities in Norway shall provide substantial and persistent contributions to wealth creation, innovation,and public safety.

Substantial and persistent contributions to environmental- and publicsafety are seen.The national programs targeting ocean and polar monitoring capabilities havecontributed towards environmental- and public safety. The systems provideinformation important for environmental safety. The space activities have alsocontributed much to the processing and institutionalizing of the information.Thereby increasing the probability of positive impacts on environmental and publicsafety.

Activities through ESA are less directly relevant for the enhanced public sectorcapabilities. ESA satellites or systems are today largely irrelevant for thesecapacities. There are however other linkages. The knowledge and insights, earlydevelopment of algorithms, and development of the ground station have muchdevelopment of algorithms, and development of the ground station have muchbeen through ESA activities. For the future, the EU GMES holds much potentialalso for Norway. Dedicated access to other sources for a.o radar data is likely to berequired also in the future.

Environmental- and public safety are also concepts which may have differentmeanings depending upon circumstances. They are not defined by the Ministry.

22

Further we discuss the relevance of the policies vis-à-vis the objectives. This is assessing to whatextent the activities are suited to purpose. We willreview the following evaluation questions relatedto relevance:

1. Are the instruments adequate from an overallperspective for achieving the space programs

1. Are the instrumentsoverall perspective for achieving thespace programs goals?

There are differences across segments and we willreview those in turn.

Three observations to note:

Policy and objectives might benefit frombenefits

Summary report

perspective for achieving the space programsgoals?

2. Has the space programs achieved anappropriate balance between the variousinstruments?

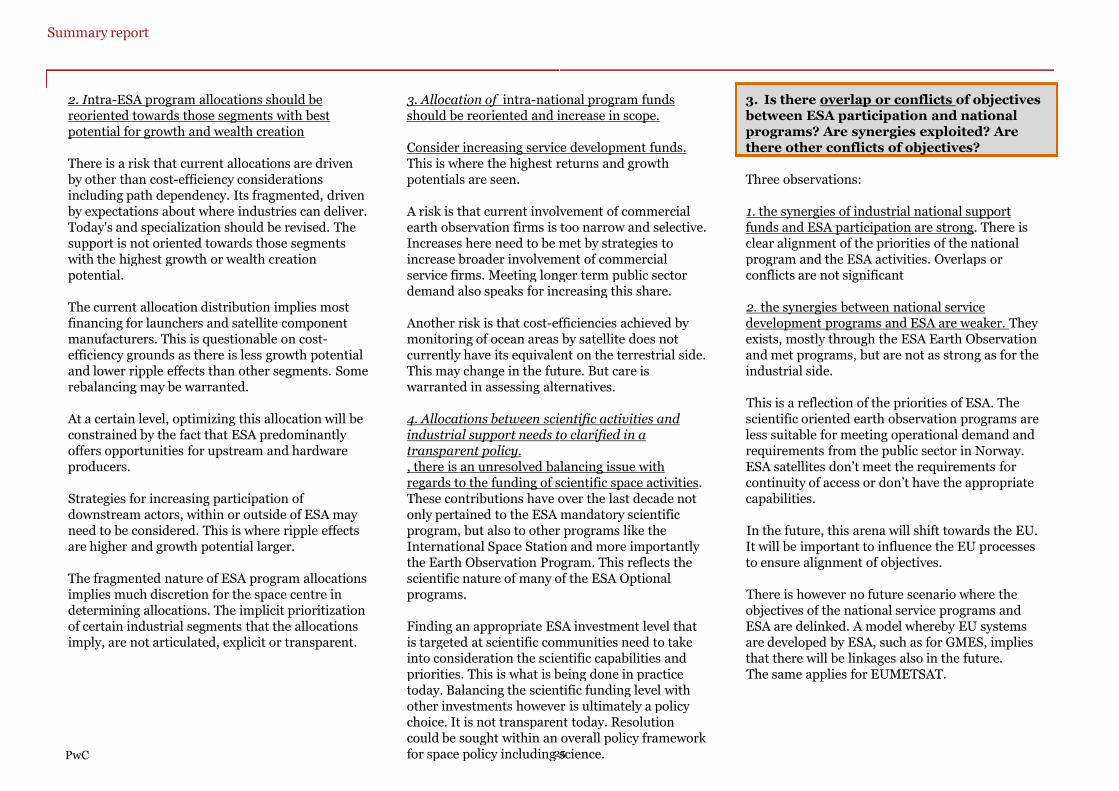

3. Is there overlap or conflicts of objectivesbetween ESA participation and nationalsupport funds? Are synergies exploited?

4. How has the Space programs managed toadapt its instruments and advice to the largercontext in which space activities interacts withother social, market, economic, political andenvironmental processes?

Three observations to note:

1. Limited growth potential in upstreamproduction

There is a mismatch between support for upstreamproduction companies and the potential for growthand wealth creation in this segment. This includesmanufacturers of launchers, satellite componentsand ground equipment.

The support is insufficientgoal would be to build a large and sustainablespace industry. That would require a considerableincrease in Norway’s participation in ESA, which ishardly justifiable in terms of Norway’s overallpolicy for industry.

PwC

Additional issues are discussed in the detailedanalysis.

policy for industry.

The difficulties of attaining competitiveness in ESAand global commercial markets of the upstreamsegments are an indication of this. A sufficientlystrong domestic demand does not exist to createanchor demand for upstream actors. Marketleaders are from larger countries and have sizeabledomestic upstream markets available to them.

23

Are the instruments adequate from anoverall perspective for achieving thespace programs goals?

There are differences across segments and we will

Three observations to note:

These difficulties will only increase driven by fivetrends indicated in the analysis:

- as value chains of global conglomerates convergeacross segments and between system integratorsand component producers;

- as emerging markets gain competitiveness andglobal market shares;

Policy and objectives might benefit from adjustment to ensure

Three observations to note:

1. Limited growth potential in upstream

There is a mismatch between support for upstreamproduction companies and the potential for growthand wealth creation in this segment. This includes

launchers, satellite components

The support is insufficient in size and scope if thegoal would be to build a large and sustainablespace industry. That would require a considerableincrease in Norway’s participation in ESA, which ishardly justifiable in terms of Norway’s overall

global market shares;- as U.S firms are driven onto global markets;- as European countries launch semi-commercial

national programs; and- as access to semi-protected ESA markets become

more difficult due to convergence of EU and ESA.

2. Growth and comparative advantages in theservice sectorsOpposite these constraints in the upstreamsegment stands exceptionally strong domesticdemand from other economic sectors notably frommaritime and offshore industries.These are growth drivers for space groundequipment manufacturers, and providers ofcommunications and earth observation services. In

The difficulties of attaining competitiveness in ESAand global commercial markets of the upstreamsegments are an indication of this. A sufficientlystrong domestic demand does not exist to createanchor demand for upstream actors. Marketleaders are from larger countries and have sizeabledomestic upstream markets available to them.

communications and earth observation services. Inthese segments Norwegian firms are global marketleaders and have considerable market shares inbroadly defined market segments.

The tools seem adequate for satellitecommunications services. Relatively smallinvestments here have had big impacts. Thissegment has also seen new entrants with rapidgrowth. There is no need to match the funding tothe scale of the industrial turnover in the absenceof market failures. Rebalancing could beconsidered to support development of near-market-ready technologies. ESA is ineffective tosupport this segment.23

Tools are also adequate for the ground equipmentindustry. Although the space related turnover hasdropped, there is little evidence of constraints inother segments of electronics and communicationsequipment markets. Those who produce spaceground equipment have also grown more stronglyin other segments. The declining turnover isrelated to collapse of one company. The inability ofother firms to maintain or gain global marketshares seem related to firm level decisions offocusing on other market opportunities.

3. Tools to support environmental and publicsafety objectives are adequate or almost so.

There is a reasonable balance at the moment.Government demand is increasing.For the ocean/polar region services this is abouthaving more refined capabilities. The combinationof national development programs and dedicatedinvestments in a.o radar and AIS are adequate forocean monitoring currently. Emerging difficultieshere are about having flexible access to other

Summary report

focusing on other market opportunities.

Tools are adequate to support earth observationservices firms but may be constrained in the nearfuture. In fact, this is driven by strong demandfrom government for monitoring and surveillancecapabilities. Needs , as in territorial, are at aboutthe same levels as that of Europe combined andthis creates anchor demand for certain services.Norwegian firms also have strong competitivepositions in these segments. The nationaldevelopment programs are especially well suited.There is however a risk that the use of the supportfunds has been selectively targeted at a few actors.A consequence is a narrow base to recruit newservice providers from.

Risks here relate to future developments of EU

here are about having flexible access to othersources of high resolution data to meet moresophisticated demand.