PUB-8176 - World Bank Documents

250

A WORLD BANK COUNTRY STUDY PUB-8176 Argentina Provincial Government Finances p,~~~~~~ S2. k~~~ ,.~¿i r ruw Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of PUB-8176 - World Bank Documents

A WORLD BANK COUNTRY STUDY

PUB-8176

ArgentinaProvincial Government Finances

p,~~~~~~ S2.

k~~~~~~~~~~~~~~.,.~¿i r

ruw

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

A WORLD BANK COUNTRY STUDY

ArgentinaProvincial Government Finances

The World BankWashington, D.C

Copyright 0 1990The International Bank for Reconstructionand Development/THE WORLD BANKs1818 H Street, N.W.Washington, D.C. 20433, U.S.A.

AUi nghts reservedManufactured in the United States of AmericaFirst printing August 1990

World Bank Country Studies are aunong the many reports originally prepared for internal useas part of the continuing analysis by the Bank of the economic and related conditions of itsdeveloping member countries and of its dialogues with the govermments. Sorne of the reports arepublished in this series with the least possible delay for the use of governments and theacademic, business and financial, and development comnmunities. The typescript of this papertherefore has not been prepared in accordance with the procedures appropriate to formal printedtextt, and the World Bank accepts no responsíbility for errors.

The World Bank does not guarantee the accuracy of the data induded in thii publication andacceptt no responsibility whatsoever for any consequence of their use. Any naLps that accompanythe text have been prepared solely fCr the convenience of readers; the designations andpresentation of material in them do not imply the expression of any opinion whatsoever on thepart of the World Bank, its affiliates, or its Board or member countries conceming the legal statusof any country, territory, city, or area or of the authorities thereof or concerning the delimitationof its boundaries or its national affiliation.

The material in this publication is copyrighted. Requests for permission to reproduce portionsof it should be sent to Director, Publications Department, at the address shown in the copyrightnotice above. The World Bank encourages dissemination of its work and will normally givepermission promptly and, when the reproduction is for noncommercial purposes, without askinga fee. Permission to photocopy portions for classroom use is not required, though notification ofsuch use having been made will be appreciated.

The complete backlist of publications from the World Bank is shown in the annual Index ofPublications, which contains an alphabetical title list (with full ordering informa.tion) and indexesof subjects, authors, and countries and regions. The latest edition is available free of charge fromthe Publications Sales Unit, Department F, The World Bank, 1818 H Street, N.W., Washington,D.C. 20433, U.S.A., or from Publications, The World Bank, 66, avenue d'Iéna, 75116 Paris, France.

ISSN: 0253-2123

Libray of Congress Cataloging-in-Publication Data

Argentina, provincial covernuent finances.p. cm. -- (A World Bank country study)

ISBN 0-8213-1634-61. Finance, Public--Argentina--Provinces. I. International Bankfor Reconstruction and Development. II. SeriesHJ906.A495 1990 90-42637336'.01382--dc20 CIP

PBEFACE

This report lo based partially on the findings of a missionthat visited Argentina from July 15 (seven days after the inauguration of thenew Government) through August 1, 1989. The mission comprised the followingmembere:

James Hicks (Misesion Leader);David Vetter (Public Finance);Lubomir Ficinski (Expenditure Planning and Execution);Humberto Petrei (Budgeting); andBarbara Nunberg (Personnel Policies and Practices).

Prior to the mission, extensive field work, coordinated byMr. Vetter, wag undertaken by Alfredo Perazzo and Guillermo Diaz. Theseconsultante visited the six case study Provinces (Buenos Aires, Chubut,Cordoba, Salta, Santiago del Estero, and Santa Fe), and collected detailedfinancial data that prevíously had not been available in a central place.Thelr final report (May 1989) provided invaluable support to the miesion.Thlu report, together with the individual reports of the other missionmember., were used by Mesers. Hicks and Vetter in writing the present report.

The July 1989 mission, and subsequent missions in December1989 and Hay 1990, visited the Provinces of Buenos Aires, Cordoba, La Pampa,Mendoza, Neuquen and Santa Fe, primarily for investigation of budgetingprocedures, tax administration, personnel procedures, and expenditure planningand execution. Duríng these latter missions, the substantial progresoachieved In lmplementing (with support from a Project Preparation FacilityAdvance from the World Bank) the Provincial Government Financial ManagementInformation System was reviewed. This progress includes reporting andanalyols of the 1987-89 executed budgets for all provinces. Although the1987-89 budget Lnformation was not available when this study was prepared, asummary of this period's provincial budget performance la presented inSection D of the Executive Summary.

A great debt of gratitude le due the national officiale,that supported the miesions, as well as the authorities and staffs of theProvinces of Buenos Aires, Chubut, Cordoba, La Pampa, Mendoza, Neuquen, Salta,Santa Fe, and Santiago del Estero; without their cooperation and support, thisreport would not have been possible.

lii

currency Equivalente

Due to the extremely high ratee of inflation in Argentina, al:l

monetary units are expressed in US dollare of July 1988. Argentine currency

is transformed into Australes of this date using a weighted average of the

Consumer Price Index for Buenos Aires (50 percent) and the Wholesale Price

Index of INDEC (50 percent) and, then, into dollars using the average exchange

rate of the "mercado financiero" for July 1988 (US$1 = 12.28 Australes>. The

rate of the "mercado financiero" was slightly above that of the "mercado

paralelo" for this month.

Fiscal Year

January 1 - December 31

Gloesary of Abbreviations and Acronyms

CFI Federal Investment Cauncil

(Consejo Federal de Inversiones)

FAP Financial Action Plan

FEDEI Special Fund for Electrification of the Interior

(Fondo Especial para Eletrificacion del Interior)

FIEL Foundation for Latin American Economic Studies

(Fundacion de Investigaciones Economicas Latinoamericanas)

FMIS Financial Management Information System

FONAVI National Housing Fund(Fondo Nacional ¿te la Vivienda)

GDP Gross Domestic Product

GPP Gross Provincial Prodluct

INDEC National Institute of Statistics and Censuses(Instituto Nacional de Estadistica y Censos)

IMF International Monetary Fund

OB Output-Oriented Budgeting

PBS Provincial Planning and Budgeting System

TPI Tranefers for Provincial Investments

iv

TABLE OF CONTENTS

EXECUTIVE SUMARY . . . . . . . . . . . . . . . . . . . . . . . . . . vii

PART 1 - MAIN REPORT

CHAPTER 1: INTRODUCTION . . . . . . . . . . . . . . . . . . . . . . . 1

A. Importance of the Study . . . . . . . . . . . . . . . . . . . 1B. Objectives . . . . . . . . . . . . . . . . . . . . . . . . . 4

C. Interfaces with Other Bank Studies and Limitations . . . . . 5

D. Coverage . . . . . . . . . . . . . . . . . . . . . . . . . . 6

E. Methodology and Sources of Data . . . . . . . . . . . . . . . 8

CHAPTER II: OVERVIEW OF THE PROVINCES IN ARGENTINA'S PUBLIC SECTOR . . 13

A. International Comparisons of Fiscal Decentralization . . . . 13B. Four Types of Transfers from the Central Government . . . . . 13

C. Fiscal Federalism in Argentina . . . . . . . . . . . . . . . . 15

D. The Revenue Sharing Law of 1987 . . . . . . . . . . . . . . . 19

E. Summary and Recommendations . . . . . . . . . . . . . . . . . 28

CHAPTER III: PROVINCIAL REVENUES . . . . . . . . . . . . . . . . . . . 33

A. Provincial Own-Source Revenues . . . . . . . . . . . . . . . 33

B. Comparatíve Performance on Current Revenues . . . . . . . . . 38C. The Efficiency of Revenue Collection . . . . . . . . . . . . 43

D. Recommendations for Increasing Provincial Revenues . . . . . 50

E. Simulation of Total Impact of Improved Tax Collection . . . 54

CHAPTER IV: PROVINCIAL EXPENDITURES . . . . . . . . . . . . . . . . . 57

A. Current Expenditures . . . . . . . . . . . . . . . . . . . . . 57

B. Capital Spending . . . . . . . . . . . . . . . . . . . . . . . 64C. Comparative Evaluation of Expenditures . . . . . . . . . . . . 64

D. The Distribution of Expenditures by Functional Categories . . 65E. Distribution of Benefits from Public Expenditures . . . . . . 67

F. Increasing the Efficiency and Equity of Resource Allocation 67

CHAPTER V: PROVINCIAL DEFICITS AND SOURCES OF CREDIT . . . . . . . . . 72

A. The Rapid Rise of the Provincial Fiscal Deficit . . . . . . . 72

B. Financing the Provincial Deficit . . . . . . . . . . . . . . . 75C. Recommendations . . . . . . . . . . . . . . . . . . . . . . . 79

CHAPTER VI: BUDGETING, EXPENDITURE PLANNING AND IMPLEMENTATION . . . . 81

A. A Normative Introduction . . . . . . . . . . . . . . . . . . . 81B. Assessment of the Current Situation: Budgeting . . . . . . . . 82

v

vi

C. An Aseessment of the Current Situation: Expenditure Planning. 86D. Assessment of Current Situation: Project Execution and

Procurement ... . ....... . . . . 89E. An Agenda for Improving Expenditure Planning and Budgeting . . 92

CRAPTFR VII: A STRATEGY FOR PROVINCIAL FISCAL REFORM AND EXPENDITUREEFFICIBNCY . . . . . . . . . . . . . . . . . . . . . . . 102

A. Design Criteria for the Strategy ... . . . . . . . . . . 103B. Instrumento and Actioris Required for Strategy Implementation 105

PART II: IAiXEKES AND STATISTICAL APPENDIX

INTRODUCTION . . . . . . . . . . . . . . . . . . . . . .. . . . . ;117

ANNfX CHAPTER 1. OVFRVIEW OF THI PUBLIC FINANCE DATA AND REPORTIMIPRCDURES . . . . . . . . . . . . . . . . . . . . . . . . . . 118

A. Government Structure for Provision of Public Servi.ces . . . 118

B. The Availability of Data ... . . . . .. 118C. The Reporting System fo.r Provincial Public Finance Data . . 120D. Transfers from the Central Government ... . .. . . . . . 125E. Rationale for Inter-goverrnmental Traneifers .. . . 127

A~nNX CHAPTER II. SOCIO-ECONOMIC< STRATIFICATION OF THF PROVINCES . . 129

A. The CFI Stratification of Provinces .1.. . . . . . . . . . 129B. Population, Product: and Poverty by Province and CFI Group . 1.30

ANNEX CHAPTER III. FIELD WORK IN THE PROVINCtS . . . . . . . . . . . 132

8TATISTICAL APPENDIX . . . . . . . . . . . . . . . . . . . . . . . . 134

TABLE OF COOTENTS . . . . . . . . . . . . . . . . . . . . . . . . . . 134

Tables 1 - 25 ............. ....... ...... . 137_ 2.18

MAPz IBRD 20474

vii

EXECUTIVE SUNMARY

1. Reducing the public sector deficit is of fundamentalimportance for success of Argentina's medium-term adjustment program,and to address the underlying structural problems and sources ofinstability in ite economy. There have been three major sources of thisdeficit: (a) the Central Government itself, including the officialbanking and finance entities, as well as social security; (b) the publicsector enterprises; and (c) the provincial governments.

2. Successful implementation of the medium-term adjustmentprogram must include, of course, measures to adequately address allthree sources of this deficit. In the past, only the Central Governmentand public enterprises have received priority analysis regarding theirroles in creating excessive public sector deficits. Increasingly,however, it has been recognized by national and provincial authoritiesthat the provincial governments cannot be ignored in the nationaladjustment program, as the provinces have become the largest, andfastest growing, contributors to the consolidated public sector deficit.

3. Thus, despite its fundamental importance to macroeconomicpolicy formulation and implementation, provincial public financegenerally has not received the attention that its importance in nationalfiscal policy requires. This is partly because the provinces aredifficult and costly to study, in that they are numerous (22),institutionally complex, extremely heterogeneous by almost anyindicator, and spatially dispersed. Furthermore, there are not evenadequate up-to-date data on provincial public finance.

4. 1/ While provincial expenditures rose rapidly over the 1970-86period,- reaching over 11.2 percent of GDP in 1986, total own-sourceprovincial revenues actually dropped from a high of 5.6 percent of GDPin 1980 to only 5.0 percent of GDP in 1986. The total fiscal deficit ofthe provinces in 1986 before transfers from the central government was6.2 percent of GDP (about US$4 billion), much higher than the public

1/ For a description of the distribution of service deliveryresponsibilities by level of government, see Annex Chapter I,Section A.

- viii -

sector enterprises and social security combined.2/ After transfers, tlheprovinces showed a slight fiscal surplus, but at the expense of helpingtransform the national administration's before transfer surplus of 5.4percent of GDP into a fiBcal deficit of 4.6 percent of GDP aftertransfers. Preliminary data indicate that the situation hasdeteriorated significantly since 1986.

5. A prime contrilbutor to these skyrocketing prcvincial deficitswas the perverse incentives that prevailed in national/provincialrelationships before the implementation of the Revenue Sharing Law in1988, in which provincial financial mis-management generally wasrewarded by ad hoc transfers from the Central Government or bysubsidized loans from the Central Bank. Before implementation of thisnew Revenue Sharing Law, tranefere predominantly were discretionarygrants from the Secretari.a de Hacienda that were neither transparent norpredictable. Also, the C'entral Bank has provided rediscounts oroverdrafts for the Provincial Banks to meet the liquidity crisis caused'by their deficit financirng to the provincial governmenta. Theseprovincial/national finarncia]. practices have contributed tounsustainable public sector fiscal and quasi-fiscal deficits, and theircontinuation would undermfine national efforts to attain price stabilityand to promote sustainable economic development.

6. Although the necesEity of bringing irresponsible provincialdeficits under control is of utmost and urgent concern, the role of theprovinces in promoting Argentinals economic development must not beneglected. The provinces are increasingly important providers of publicservices, especially for education and health. Expenditures ofArgentina's provincial governments in 1986 amounted to 3.1.2 percent ofGDP (or US$7.8 billion) with investments accounting for 2.6 percent ofGDP (US$l.6 billion). The new Government's strategy of decentralizationshould substantially increase this importance.

7. The primary objective of this sector study is to assist theGovernment of Argentina in identifying and implementing appropriatemeasures that will result in an effective an,d equitable reduction in theProvinces' contribution to excessive, consolidated public sectordeficits. To meet this objective the study seeks to go beyond thedocumentation of how much provincial financial management hasdeteriorated. It also seE!ks:

(a) to identify relationships and incentives that explain why thiscrisis has devel.oped; and

2/ All transfers under the ad hoc revenue sharing agreements during1984-86 are treated as grants to the provinces, as the criteriaused in their distribution were neither predictable nortransparent. See para. 2.04 for a discussion.

- ix -

(b) to recommend to the Government a strategy for provincialfiscal reform and improved expenditure efficiency.

8. Chapters I and II present a description of the study'l acopeand methodology, as well as an overview of the provinces in Argentina,spublic sector. Chapters III-V provide analysis of provincial revenues,expenditures and sources of deficit financing. Chapter VI asaseesprovincial practices regarding budgeting, expenditure planning andimplementation, and Chapter VII recommends a strategy for provincialfiscal reform and improved expenditure efficiency. This Summarypresents the principal conclusions reached in this study, itsrecommended strategy for improvement, and finally an estimate of thepotential pay-off to result from implementation of the proposedstrategy.

A. Principal Conclusions

9. A basic conclusion of this study is that there is a stronggeneral consensus at both the central and provincial government levelson the need for fundamental reforms in the financial relationshipsbetween the Central and Provincial Governments. Reforms inintergovernmental financial relationships are an integral part of thestrategy outlined below, and the key to their succese is politicalcommitment at both provincial and central levels. At the provinciallevel, there ie an enormous potential for improved financial management,and these improvements do not require complicated or technicallydifficult initiatives. Rather, dramatic improvements may be attainedfrom quite simple reforms in provincial revenue and expenditureplanning, budgeting and administration. These reforme were not adoptedin the past due to the perverse incentives in the system ofintergovernmental transfers (para. 5), as well as inadequate controls ofrediscounting by provincial banks. National Government officials haveexpressed a firm commitment to the elimination of these perverseincentives, and provincial government officials have expressed stronglytheir desire for increased financial and political autonomy.Sustainable increases in provincial autonomy will require, however,significant improvements in provincial financial management. Theprimary areas for potential improvement are summarized below.

Increasing Revenues

10. There is a very wide margin for increasing provincial tax andnon-tax revenues by increasing the efficiency of billing and collectionprocedures. Just the most basic improvements in these collection andbilling procedures could increase revenues significantly, as well asreduce the inequities resulting from "free-riding` by those who are notbilled and by evaders.

11. Eventually, tax reform should eliminate the considerableoverlap of provincial taxes with those at the national and municipal

- x -

levels. In the meantime, the three levels should increase cooperationin the administration of these taxes.

12. The case studieis done in six provinces show that improvedbilling and collection procedures (e.g., better cadastres, informationsystems and management techniques) could substantially increaseprovincial tax revenues wi.thout raising nominal rates. 'Where feasibleand cost effective, billiriq and collection should be privatized (e.g.,as in the collection of delinquent property taxes in the province ofSanta Fe). After privatizing as much as is desirable and possible, anyadditional qualified staffE nec:essary for adequate tax administrationshould be recruited, if possible through reallocation andl training ofexisting provincial person,nel (thereby not increasing payrollexpenditures), or, as a last resort, by new hiring. Improved fiscalperformance would require not only better billing and more aggressivecollection, but aleo improvements in the quality of services that shouldhelp increase the willingness to pay taxes and fees.

13. Rough estimates based on "reasonable" improvements in taxadministration, without any nominal increases in tax rates or changes inlegislation, would produce a total increase in tax revenues of 38percent (US$461 milllon, or about 0.5 percent of GDP) for five of theprovinces studied.

14. Billing and collection of non-tax revenues tendl to be evenless efficient than for tax revenues. There is a clearly a need forgreater emphasis on cost recovery for public services through user feesand tariffs. This is especially true for the water companies whichoften require constant transfers from the provincial governments. Wateris rarely metered, and botlh billing and collection procedures are oftenmonumentally inefficient. Usera perceive the fees to be unfair, asthey are not based on actuall consumption. Also, consumere may notrespond to increases in tariff s (such as the very high ones of July1989) by reducing consumption. For all of these reasons, the watercompanies often represent a kind of "black hole-' in provincial publicfinance.

Reducing Expenditures and Increaging Their Efficiency

15. Expenditures for the general administrations of all provincesand the Federal Capital rose from 7.5 percent of GDP in 1970 to 11.2percent of GDP (or about US$8 billion) in 1986. The data from the casestudies show that expenditures increased by over seven percent in 1987,even though total revenues declined.

16. The driving force in the increase of current expenditures wasclearly personnel, but transfers to municipalities and other entitieswere also important. Provincial public employment in onlr the generaladministration increased by over 230,000 (34 percent) in all provincesduring the 1983-86 period, to 913,000 in 1986.

- xi -

17. Clearly, provincial personnel policies constitute a priorityarea of reform not only because personnel expenditures represent asizeable portion of total provincial expenditures (an average of 46percent between 1981 and 1986), but also because personneladministration systems in the provinces studied showed seriousdeficiencies in management capacity, resulting in inefficiency anddiminished incentives to performance.

18. A program to improve the management of provincial publicpersonnel systems should include several policy measures. First, thedata base neede to be strengthened. Most fundamental le theimplementation of a public employee census to determine the number andprofile of government personnel. Second, the links between thepersonnel management system and the payroll system should bestrengthened, so that cross-checking between the two systems can be usedto identify ghost workers or double employment. Any gaps between thesetwo systems should be analyzed and closed.

19. Where high employment, low salaries and wage compression areacute, a careful strategy of rationalization should be developed, withcost estimates for ite implementation. Employment reduction and theredistribution of resulting salary savings to decompress the wagestructure and increase incentives to professional levels should be agoal In some cases.

20. Rationalization and control of transfers could produceimportant savinge for provinces. Discretionary grante to municipalitiesshould be reduced and/or replaced with automatic revenue sharingand matchíng grante tied to improved fiscal effort and efficíency.Transfere to public enterprises should be reduced to a minimum byimproving their efficiency and encouraging full coet recovery, as wellas by privatization. Laws regulating pension funde and other transfereto individuals should be reviewed and administrative procedurestightened to discourage abuses.

21. Basic improvements in organization and management ofprovincial governments, direct and indirect administration, could savemuch time and money for both the government and those needing services.

22. Direct subsidies should be transparent and clearly targeted tothe loweet income families. The provinces should emphasize provision ofthose services which tend to go to lower income groups, such as basiceducation.

Improving Fiscal Planning, Budgeting and Execution

23. Most provincial budgets currently are definitely not usefulinstrumento for the programming, management, control and evaluation ofpublic expenditures, because: they lack an adequate strategy forhandling inflation; the budget offices are under-staffed and under-equipped, as well as politically weak; the methodologies are deficient;

- xii -

coverage is incomplete; reporting is slow and not pertinent; and controlis merely legalistic.- The lack of an adequate strategy for dealingwith inflation leads to a number of important distortions in thebudgetary process, inclucling: the approval of the budget during or evenafter the fiscal year, serial budgeting and discontinuities in budgetexecution.

24. There are some changes that should be adopted immediately toimprove the budgeting process. First, a more systemati, way of dealincjwith inflation must be aclopted. Second, the central and decentralizedbudget offices should be strengthened by: giving them greater authorityin budget preparation, improving their information systiems and up-grading their personnel. Firially, the annual budget should be part of amedium term expenditure plan.

25. There are several approaches that may deal eflectively withinflation during budget formulation and execution. The Province ofMendoza employs a very sophisticated strategy (See Box 6.1 at the end ofChapter 6). As the budget is expressed in physical as well as monetaryunits, the Mendoza budget office can continually adjust budgetallotments to current prices, using actual market prices. However, itapproves expenditures only if revenues are sufficient tco cover them.This equilibration of exp,enditures and revenues does not requireapproval of the legislature. The opposite of this strategy could alsobe used: expenditures could be adjusted monthly or quarterly by the risein revenues, but with an option for review by the legislature, if totalreal expenditures rise or decline by a percentage defined in the law.For example, the legislature could specify that it would have the optionto review the budget, if total real expenditures were 20 percent higheror lower than those predicted for the time period. Yet another optionwould be to approve contingency measures for each of these eventualitiesas part of the budget.

26. Investment planning for new projects tends to be haphazard,and there is virtually no planning for preventive maintenance in mostprovinces. Project identification, evaluation and selection should beimproved by adopting more rigorous methodologies and strengthening theresponsible entities. Preventive maintenance plans shouLd be elaboratediand implemented.

27. Improvements in project execution procedures could cut atleast 15 percent in the construction cost of civil works and 10 percentin goods and services expenditures with no loss in qualitV. Thepotential savings for all provinces in 1986 are estimated at aboutUS$230 million in construction and at US$95 million in goods andservices for a total of US$325 million (about 0.5 percent of GDP).These estimates exclude provincial public enterprises.

3/ The Province of Mendoza is a notable exception. See para. 6.59.

- xiii -

28. To lower the cost of new investments, the provinces should:improve procurement procedures, abolish "Buy Argentina" and "Buy

Province" legislation, reduce design errors and changes, improve themethodology for adjusting prices for inflation, and establish aninformation system about projects and costs. For example, simpleimprovements in procurement procedures, such as adopting the lowestevaluated price for bid evaluation, could reduce current and capitalexpenditures by at least 10 percent, or about US$400 million. Also,elimination of "buy Argentina" and "buy province" legislation would notonly lower costs, but also help to modernize industry by stimulatingcompetition. Strategies for maximizing the impact of publicexpenditures on private investment should be developed. Provincesshould analyze their comparative advantages for different kinds of

activities (i.e., those that they could stimulate without subsidies),such as in the primary sector as well as in industry and tourism.Possible forward and backward linkages should also be explored. Forexample, the highest priority might be irrigation, which could in turnproduce demands for processing of the increased production, as well asfor inputs. Ways of informing the private sector of these opportunitiesshould be developed.

B. The Proposed Strategy for Reform

29. The need for fiscal reform in the provincial public sector isevident and fully supported by the officials at the national andprovincial levels. The objectives of this reform should not be just toreduce the deficit (although this is by far the most urgent), but alsoto transform the provinces into agents of development which generatesurpluses that they can invest wisely to increase total provincialproduct, thereby augmenting their future tax revenues.

30. To be successful, a strategy for provincial fiscal reform andimproved expenditure efficiency must encompass two dimensions: nationaland sub-national.

(a) At the national level, there must be in place a system ofintergovernmental transfers (including revenue sharing,matching grants and loans) that are predictable, transparent,financially sustainable, and that provide incentives toprovincial fiscal autonomy. The granting of credit to theprovincial banks by the Central Bank must be rigorouslycontrolled.

(b) The sub-national level of the strategy must include the entiresub-national public sector, not only provincial centraladministrations, but also their indirect administrations,including public enterprises, as well as direct and indirectmunicipal government administrations. A broad approach to theentire sub-national public sector is necessary because inArgentina's federal system, fiscal reform is only as strong as

- xiv -

the weakest link in the system. National public sectordeficit reduction efforts will fail if provincial governmentfinances are not sound, and these, in turn, will not be soundif provincial enterprises and/or municipalitiLes generatedeficite that demand provincial 'bail-outs" that eventuallywork their way up to the Central Bank or the NationalSecretaria de Hacienda.

Des gn Critería for the Strategy

31. The criteria for design of the strategy may be grouped in twobroad categories: intergovernmental tranefers and provincial financialmanagement. Implementation of an improved system of intergovernmentaltranefers ie the responsibility primarily of the Central Government,while responsibility for improved provincial financial management rests3with the provinces, although the Central Government may provide valuab]Leaseistance to them. A fundamental prerequisite for success informulating and implementing a strategy for provincial fiscal reform arndimproved expenditure effiLciency is a transparent (sanctioned throughlegielation and implemented through the budgetary process) anddieciplined proceso for eaccess to credit by the sub-national publicsector. Therefore, the Central Bank should continue to maintain etrictcontrole on rediscounts by provincial banks, thereby not allowing itefunde to be used by provincial banks to finance their provincialgovernment deficits. Furthermore, prudential regulation le required inmany provinces in order to have adequate discipline and control over theprovincial banke' operations. Without these disciplinary measures, thedetailed proposale presented below will be doomed to fa:ilure.

32. The Central Government and Intermovernmental rransfero. Thesystem for the transfer of revenues from the Central to ProvincialGovernmente (and from Provincial to Municipal Governments) should bebased predominantly on a revenue sharing system that is legally mandatedand formula-driven. This ie based on the normative position that arevenue sharing system should provide sufficient revenues to sub-national governmente so that, when combined with a reasonable revenueeffort by the sub-national governmente, these may at leatst adequatelyoperate and maintain their existing services. The overalí system ofintergovernmental tranefers should provide, therefore, not only areliable source of revenues to provinces, but also stron.g incentives toimproved provincial revenuae performance. Discretionary grants shouldform a emall part of the `pool" of resources flowing from the Central toProvincial Governments, basically limited to providing support inemergencies such as floodLng. New provincial investments should befinanced by provincial savringe in current account and by responsibleborrowing. Given this normative framework, the etrategy for provincialfiscal reform should include an intergovernmiental transfer system that:

(a) is predictable;(b) ¡e transparent;

- xv -

(c) provides transfers in sustainable and equitable quantities;and

(d) provides incentives to provincial fiscal autonomy.

33. Provincial Financial Management. Within the nationalframework described above, the strategy requires that provincialgovernments adopt financial management practices that promote:

(a) provincial financial autonomy;(b) management efficiency;(c) public accountability; and(d) expenditures that support sustainable economic development.

Instrumsnts and Actione Required for Strategy Implementation

34. Following the framework for strategy design, recommendationsfor strategy implementation are presented according to the policyinstrumente and actions to be taken by the Central and Provincial levelsof government. Implementation must be actively pursued by both levelsif the strategy le to be successful.

35. The recommended policies and actions to be taken at theCentral Government level may be summarized in three areas: RevenueSharing System; Special Transfer9 for Provincial Investments; andProvincial Financial Management Information System.

36. Revenue Sharing System. Although the current Revenue SharingSystem (RSS -- sistema de coparticipacion), regulated under the December1987 legislation, may be criticized on several grounds, it is a vastimprovement over the chaotic transfer system prevailing before it wentinto effect. To its merit, the current RSS fully meets two of thecriteria for intergovernmental fiscal relations set out above, in thatít provides shared revenues that are transparent and predictable forboth Central and Provincial Governments. The RSS alzo appears to befiscally sustainable, given reasonable levels of price stability. Inaddition, to the extent that all provinces recognize that nationalrevenue sharing will be the only guaranteed intergovernmental transferto be received from the Central Government, the RSS also providesincentives to provincial fiscal autonomy. However, its equity might becriticized, in that its inter-jurisdictional redistribution of revenuesresults in a flow of potential resources away from provinces with thegreatest number of households with unsatisfied basic needs.

37. lt ¡e recomnmended, therefore, that the basic RSS currently inplace not be changed in the near-term. As part of the continualevaluation of the system, however, it also is recommended that theCentral Government implement a system for monitoring the efficacy of thesystem, taking into account the criteria noted above (predictable,transparent, sustainable, equitable, and promoting provincial fiscalautonomy). Basic inputs for monitoring and evaluation of the RSS couldbe provided by the Provincial Financial Management Information System,

- xvi -

described below. EspeciaLly important is the evaluation of the fiscalimpacts resulting from decentralizing the responsibility for theprovision of public services to sub-national governments, such as therecent transfer of responmibility for secondary education to theprovinces. This continuing evaluation should also cover the relativeefficiency of different levelis of governments in the provision of publicservices, according to their different characteristics (e.g., populatiornsize, per capita product, etc.) It is very important, however, that thecontinual evaluation of the RSS, and eventual changes to improve it, notbe done solely on the bas;is of provincial financial management; rather,it should be made in the broader context of national fiscal policies forstabilization and economic development.

38. Special Transfero for Provincial Investments (TPI). The RSSshould be considered primarily as resources designated to meetprovincial recurrent expenditures. Creation of a new system of matchinggrants, the TPI, is recommrended, and it would be designed to meet threebasic needs: (a) to immediately provide strong national incentives toprovincial fiscal autonomy; (b) to provide financing for capitalimprovements programs in the near-term for those provinces that generatecurrent account savings; and (c) to promote, in the medium- and long-term, the transition of the financing of provincial capit:al investmentsfrom earmarked, segmented sources of funding to competitive, non-segmented financing through domestic financial markets.

39. Several alternatives for providing resources for the TPI maybe considered. First, ending the industrial promotion regime wouldeliminate a national fiscal drain estimated conservatively at 3.5percent of GDP, or close to US$2.5 billion, per year (see Chapter II,Section D). The provinces should develop new strategies for regionaldevelopment that would not require the subsidies of industrialpromotion--that would move with market forces rather than against them.This would involve identif,ying provincial comparative advantages insectors that could attract significant private investment. A part ofthe fiscal gain to be received by ending the industrial promotion regimecould be allocated to the TPI. As an alternative, or complement, to theabove, the TPI could be funded by the "pooling` of appropriate "specialpurpose' funds presently transEferred to provinces as current and capitalgrants (discretionary, earrnarked transfers) such as FEDEI, the nutritionand tobacco funds, etc. Together, these funds (excluding the HousingFund, FONAVI, which is considered a loan fund and reported "below theline") have amounted to alrnost one percent of GDP, or about US$600million per year, and they are transferred to provinces on an ad hocbasis, without regard to their financial performance. An alternativeto combining all of these funds into one new fund via legislation couldbe to allocate their resources as matching grants in accord withimprovements in fiscal efficiency via executive ordere.

40. Initially, the TE'I could be included as a line-item in thenational budget, with clear regulatíons for use of TPI funds.

- xvii -

Strong incentives to promote provincial fiscal autonomy would be

provided through strict criteria for provincial acceso to the TPI.Access to TPI grants would be limited to those provinces that have inplace a Financial Action Plan (see para. 49) that has resulted incurrent account savings (without grants) at least during the precedingquarter. Access to the TPI only after a province has begun to generatecurrent savings would provide not only a strong incentive for thesesavings, but also an incentive for provinces to improve their financialreporting systems.

41. The TPI would provide much-needed resources for capitalexpenditures in those provinces that have demonstrated the financialcapacity to properly operate and maintain their existing servicedelivery facilities and obligatione. This matching capital granttransfer mechanism should not be considered a permanent facility,however. Rather, it should be a transitory mechanism necessary toprovide incentives and support to the necessary structural changes inthe financial relationship between the Central and ProvincialGovernments.-

42. Thus, the TPI should be viewed as an initial step, moving awayfrom supporting provincial expenditures with national deficit financing,and toward the provinces eventually financing their investments withtheir own savings and with borrowing obtained through the nationalfinancial markets. Currently, however, Argentina's financial markets areunstable and segmented, and they are not efficiently mobilizing domesticsavings and allocating resources. Therefore, in the near-term, theTPI's key role would be to provide incentives fór provinces to becomesavers, thereby reducing sub-national government pressures on theconsolidated public sector deficit. Combined with deficit-reducingmeasures by the Central Government and its public enterprises, the TPIwould therefore contribute to the macroeconomic conditions necessary forthe financial sector to perform more efficiently.

43. As Argentinals financial markets attain acceptable levels ofdomestic savinga mobilization and of efficient resource allocation, theTPI could be phased out, with the provinces thereafter competing forfunds in non-segmented financial markets.

44. In summary, the proposed TPI would be guided by four generalprinciples:

(a) acceso to the TPI by provinces would be voluntary;

4/ One example of such a transitory measure was approved by theCongress in December 1989: it defines the sources of revenues andalso clear regulationa for their allocation among provinces,including the exclusion of provinces failing to undertake measuresto reduce their fiscal deficits.

- xviii -

(b) accees to TPI grarits would be competitive, w.Lth thoseprovinces maki.ng greater financial management improvemente(generating greater current account surpluses3) being eligibleto receive more fr-om the TPI;

(c) the quantity of funds allocated to the TPI, ag well as theconditions for transfer of these funds to provinces, would beconsistent with the national strategy for development andstrengthening over time of national financia]. markets; and

(d) TPI grant financing would be available only for expendituresthat are part of a provincial budget that has been accepted 'bya national authority on the basis of its verification that theexpenditures are directed to operations that are economicallyefficient, financially sustainable and institutionallymanageable (see discussion of the Provincial Planning andBudgeting System, PBS, para. 52).

45. Financial Management Information System. In order to providedata essential to macroeconomic policy formulation, as well as tomonitor provincial progreass toward fiscal autonomy, it is recommendedthat the Central Government move immediately to establish a ProvincialFinancial Management Information System (FMIS). Baseline date for theFM!S would be provided by the provinces through their Planning andBudgeting Systems (PBS, para. 52). Initially, the PBS would be theFinancial Action Plan to initiate the process, but a more comprehensiveexpenditure planning and budgeting system would be implemented overtime. The PBS would be the ]sey instrument for the planning, programmirngand control of provincial. revenues and expenditures. It also would bethe primary instrument for analysis of provincial eligi.bility for theTPI resources, in that it: would provide information on the economicefficiency and financial sustainability of the provincial plane.

46. The FMIS would serve two key functions. First, it wouldprovide the Central Government with a necessary input for nationalfiscal policy. Alzo, it wou].d provide the base on which to identifyprovincial neede for technical assistance for improved financialmanagement, and to design such assistance programs. Very usefulexperience in the design and implementation of such information systemscurrently is available in. the five provinces (Buenos Aires, Cordoba, LaPampa, Neuquen and Santa Fe) that are implementing the Bank financedMunicipal Development Prcject (Loan 2920-AR), where municipal financialmanagement information systems are being developed at the provinciallevel. The experience with t.he new budgeting system in the Province ofMendoza is also most interesting, showing how much can be done whenthere is a strong commitment to fiscal reform.

47. A prerequisite for making the FMIS useful, as well as all theother measures recommended for implementation at the Central Governmentlevel, i adequate institutional capacity to manage the overall proceso

- xix -

for restructuring provincial government financial management. There areseveral options for strengthening the Central Government's capacity tooverview the provincial development proceso, with thie proceso including(a) dimensioning and regulating the TPI, (b) development and analysis ofthe FMIS (including monitoring the performance of the RSS), and (c)review of PBSs. One option would be to strengthen the national Ministryof Economy's in-house capacity; another would be to contract with anappropriate technical aseista7ce entity, either a public institution(such as a university or CFI- ), or a private organization(such as FIEL, the Fundacion Mediterranea, or a consulting firm).Because of the transitory nature of the TPI and of national scrutiny ofthe PBSs, sonme contracting of outside support to the Central Governmentmay be the preferred option. In any case, however, a "baseline",permanent strengthening of the Ministry of Economy would be necessary toensure adequate linkages between the proposed FMIS and macroeconomicfiscal policy. Similar institutional support and strengthening would berequired in the provinces in order to implement the recommendations forprovincial government actions described below.

48. At the Provincial Government level, it is recommended that theprovinces undertake the following to implement the strategy for fiscalreform and improved expenditure efficiency: begin immediately toformulate Financial Action Plano; and initiate the design of ProvincialPlanning and Budgeting Systems.

49. FLnancial Action Plano. Provincial FAPe would be the first

step in moving toward provincial financial autonomy. They would becomprised of preliminary annual budgets for a three to five year period.The FAPs would emphasize measures that may be taken immediately toimprove performance, without the need for detailed studies orinformation systems. After the reform proceas is initiated under a FAP,more comprehensive measures could be undertaken through permanentProvincial Planning and Budgeting Systems as the FAP is phased out. Themain objective of the FAP is to identify simple measures that shouldincrease revenues and control expenditures so that the province mayproduce a current account surplus to be used for investments and toamortize loans.

50. on the revenue side, simple improvements in billing andcollection procedures would have considerable pay-offs. On theexpenditure side, the FAP would present the province's plans forreducing expenditures and increasing their efficiency, and it wouldinitiate their implementation. Three general areas appear to beparticularly important: personnel, procurement and investment design

5/ CFI (Consejo Federal de Inversiones) is a rather unique publicinstitution that is financed by a percentage of total provincialrevenue sharing, and ite Board of Governors is comprised of theGovernore of all the provinces. Thus, it is national in scope, butprovincial in focus.

- xx -

and execution. Personnel is by far the largest and fastest growingexpenditure category in most provinces.

51. In summary, the FAP involves implementation of therecommendations presented in the Chaptere I]I-V of this report(revenues, expenditures and deficit financing), and it would be thefiret step in implementing a more effective budgeting process in theprovinces in which the an;nual budget would be a comprehensive one-yearslice of the medium term plan.

52. Provincial Planning and Budgeting System. After an initialperiod (about one year) of implementation of the FAP, provinces couldthen move to implement their PBS. The recommendations of Chapter VIcould serve as guidelines for this, and the experience in Mendoza showsthat such reforms are feasible when political commitment is forthcoming.

53. The PBS would bts a key tool for provincial planning, budgetinqand control. It also would be fundamental for monitoring theeffectiveness of provincial management, not only by provincialauthorities, but also by the Central Government as it formulatesmacroeconomic policy and evaluates whether each province is eligible foraccese to the TPI. Key components of the PBS would include:

(a) planning and control of provincial revenues;

(b) expenditure priorit.es, including

(i) maintenance and rehabilitation

(ii) personnel policies that provide adequate professionalismand perfornmance

(iii) new investments, with projecte costing greater that anamount agreed with the Secretaria de Hacienda subject toa competent. benefit/cost analysis to ensure economicefficiency;

(c) reliable projections of total and incremental (with andwithout a proposed investment) revenues to ensure financialsustainability;

(d) strategies for financing investment costs, incLuding ownsavings and borrowings; and

(e) financial and service delivery relationships withdecentralized provincial agencies and enterprises, as well asmunicipalities.

- xxi -

C. Estimated Pay-Offs of the Strategy

54. 1987 is the latest year for which estimates of executedprovincial budgets are available. The overall performance of allprovinces may be summarized as follows:- current account (withoutgrants) deficit -- US$966 million; capital expenditures -- $2,322

million; and overall need for financing -- $2,762 million. Using the1987 budget estimates for all provinces as a baseline, the lmpact ofdifferent percentage increases in provincial tax and non-tax revenuesand of reductions in expenditures may be estimated. Simulations ofthese improvements provide "orders of magnitude" regarding their resultsin terms of absolute monetary impact, as well as the resultingimprovements (compared to the baseline) on current account savings, withand without grants (i.e., savings and own savings). For example, arelatively modest increase in revenues and decrease in expenditures of15 percent would transform the 1987 current account deficit (withoutgrants) of almost US$ one billion (and a need for financing this deficitand capital expenditures of almost US$ three billion) to a currentaccount surplus of US$ 164 million and an overall need for financing ofUS$l.6 million. Increases of revenues and decreases in currentexpenditures by 25 percent would result in a current account surplus(without grants) of over US$ 900 million, while reducing the overallneed for financing to less than US$900 million.

55. This means that improvement at the 25 percent level wouldenable the provinces to undertake an aggregate capital expenditureprogram on the order of $1.4 billion, fully financed with currentaccount savings combined with modest capital revenues and existing grantfunds. Or, provinces could maintain the 1987 level of capitalexpenditures {$2.3 billion), financed in about equal proportion bycurrent account savings and by long-term borrowings, if available.Improvements of these magnitudes are not unrealistic. They would dependfirst on the political will to undertake the reform strategy recommendedhere, as well on technical assistance in implementing the proposedfinancial management improvements.

D. Updating Po-tecript

56. During the missions that followed the main mission for thisstudy (July 1989), it was noted that some of the key recommendations ofthis report were being implemented. Notable among these measures is theCentral Government's conditioning of significant parts of its granttransfere to provinces that are making demonstrable improvements in themanagement of their finances (see paras. 38-44). The national Ministryof Economy also has made substantial progrese in implementing theProvincial Financial Management Information System as recommended here(paras. 45-46), with close collaboration from the provinces. At the

6/ See paras. 7.31 - 7.32.

- xxii -

time the main body of thíis report was prepared, provincial executed

budget data were available only up to 1986, supplemented by the 1987data from a sample of six provinces collected especially for thisreport. In May 1990, however, the Ministry of Economy assembled the

1987-89 executed budget data for all provinces and the Municipality ofBuenos Aires. A comparison of the mean valu.es for the 1981-86 period

with the 1987-89 data i9 presented below.

1981-86

(mean) 1987 1988 1989

Current Revenues 4,972 6,134 5,895 5,634

Current Expenditures 5,344 6,576 6,306 5,626

Grants (Current and Capital) 1,097 622 274 278

Current Account SurplusWithout Grants (Own Saving) (372) (442) (411) 7

Current Account Surplus With

Receipt of Grants (Saving) 725 203 (<.28) 287

Real Investment (Works and Goods) 1,425 1,983 1,523 975

Overall Deficit/Surplus or

Need for Financing (846) (1,847) (1,716) (753)

Net Borrowing 512 1,029 620 295

Net Variation in Short Tern

Assete and Liabilities (334) (818) (1,096) (458)

Gross Fixed Capital Format:Lon 1,420 1,976 1,518 972

Notes: 1981 mean values aret in milliona of US$ of July 1988 (Source:Table 14a of the Statistical Appendix, pp. 174-175).

1987-89 values are ln miLllions of US$ of December 1989 (Source:Argentina, Ministry of Economy, 1990).

57. The above data point to some encouraging trends. Despite 1989being one of the most traumatic years in Argentine history, withhyperinflation during the middle of the year, current revenues increasedby 13 percent as compared to the 1981-1986 average, while currentexpenditures increased only five percent when compared to this average,

- xxiii -

and they decreased by 12 percent from the previous year. This resultedin a small 1989 current account surplus and contributed to a substantialreduction of the overall need for financing. It should be noted,however, that these improvements resulted in a sharp drop In 1989 forgross fixed capital formation and that the net decrease in short termassets and liabilities, although leas than half that of the previousyear, remained high (over 60 percent of the need for financing).

58. A brief indication of how these trende relate to the analysisof this study is presented below.

(a) The new revenue sharing law became effective in 1988, after ahiatus in the revenue sharing system from 1985 to 1987 (eeeSections C and D of Chapter II). This study concludes(Chapter VII, para. 7.10) that the new revenue sharing systemis a significant improvement over the previous, predominantlyad hoc arrangement for intergovernmental fiscal transfers, inthat the new system provides tranefers that are predictableand transparent for both the Central and ProvincialGovernmente. Despite a sharp drop in granto in 1988-89,provincial savings and own savings improved over this period.This indicates that provinces are responding to the improveddiscipline of the revenue sharing system (as well as closercontrol over Provincial Banks, as noted below) and arebeginning to implement current revenue and expenditurereforme, as recommended in Chapters III and IV.

(b) Long term borrowing (greater than one year), as reflected bynet borrowing, as well as short term borrowing, as partiallyreflected by the net variation in short term aseeta andllabilities, have fallen sharply. This indicates that thestrieter controls by the Central Bank on rediscounts andoverdrafts by provincial banks are taking effect. Thesecontrola have limited the capacity of the provincial banks toprovide loans and overdraft facilities to provincialgovernments, as they have done on a significant scale in thepast (see Section B of Chapter V). Alzo, Provinces have notbeen able to obtain substantial credit from commercialfinancial institutiona. As noted in para. 31 above, strictcontrol of the provincial banks by the Central Bank is afundamental prerequisite for implementing the strategy forreform proposed in this study.

(c) Although borrowing has fallen, the most recent data indicatethat there is a substantial potential for provinces toleverage their current account savings to increase theirinvestments and meet their need for financing. In 1989, 12 ofthe 23 provinces (including the Municipality of Buenos Aires)produced current account surpluses (without grante), comparedto only seven in 1987. Summing the 1989 current savings ofthese 12 provinces provides a total own saving of US$ 360

- xxiv -

million, 22 percent greater than the total net borrowing forthat year. Thie indicates that the recommendations of thisreport (paras. 38-44 above, Section C of Chapter V, andSection E of Chapter VI) regarding current account disciplin,eand financing of provincial investment programe are realisticand achievable.

I. INTRODUCTION

A. Importance of the Studv

In the Context of a Country Strategy

1.01 Reducing the public sector deficit is of fundamentalimportance for success of Argentina's medium-term adjustment program,and to address the underlying structural problems and sources ofinstability in its economy. There have been three major sources of thisdeficit: (a) the Central Government itself, including the officialbanking and finance entities, as well as social security; (b) the publicsector enterprises; and (c) the provincial governments.

1.02 The provinces have been responsible for the largest andfastest growing portion of this deficit. While provincial expendituresrose rapidly over the 1970-86 period, reaching over 11.2 percent of GDPin 1986, total own-source provincial revenues actually dropped from ahigh of 5.6 percent of CDP in 1980 to only 5.0 percent of GDP in 1986(Figure 1.1). The total fiscal deficit of the provinces in 1986 beforetransfers from the central government was 6.2 percent of GDP (about US$4billion), much higher than the public sector enterprises and socialsecurity combined (Figure 1.2). The provinces showed a slight fiscalsurplus, but at the expense of helping transform the nationaladministration's before transfer surplus of 5.4 percent of GDP into afiscal deficit of 4.6 percent of GDP after transfers.

1.03 Data from the case studies of six provinces show that theircombined fiscal deficit more than doubled in 1987 to US$1.1 billion (1.8percent of GDP) after transfers, as own-source revenues declined andexpenditures, especially for salaries, continued to rise.y For all 22provinces and the Municipality of Buenos Aires, the total fiscal deficitin 1987 after transfers was estimated at over US$2.8 billion or about 4percent of GDP.' The decline in own-source revenues stems partly fromthe rise of inflation and the resulting Olivera-Tanzi effect, but alsofrom the increasing inefficiency of the provinces in collecting taxes,as well as the reticence of taxpayers to pay taxes and fees for servicesof ever deteriorating quality.

1.04 Despite this importance, provincial public finance has notreceived the attention given to the central government and the publicenterprises. There are not even adequate up-to-date data on provincial

7/ For a description of the case study provinces studied, see para. 1.21.

t./ Estimates of the 1987 total fiscal deficit for all provinces and theMunicipality of Buenos Aires were made through the proportionalexpansion of the data obtained in the six provinces surveyed.

-2-

Figure 1. 1

EXPEMOtTURES ANO OWN4OII0CE REVENUESALL F'ROVINCES ANO THE FEOERAL CAPITAL

s or GOP14

12r

4

2

70 71 72 78 74 75 76 77 78 79 80 81 82 83884 86 U8YEAR

-- WIM-OOURCE REV. -+- TOTAL EXPENO.

*oureg Se Talee S.1 vmd 4.t

Fizure 1.2

PUULIC SECTOR OEPICT UWIEFORE ANO APTER TRANUER8

S OP OO

2

Ml Cm~WAL OVT. 3 PROVINCIALE PuUL.p ENTWEe m OcAL, aECURTY

8e se T~b tt

-3-

Table 1.1: ARGENTINA - PUBLIC SECTOR OEFICIT BYGOVERNMENTAL LEVELS OR ENTITIES, 1986

(Percent of GOP)

Surplus SurplusBefore After

Transfer Transfer

National Administration 5.37 -4.60

Provincial Governments (a) -6.18 0.07

Public Sector Enterprises (PSE) -2.20 0.07

Social Security System -1.29 0.15

Total Non-Financial Public Sector -4.30 -4.30

Quasi-Fiscal -1.00

Total Deficit -5.30

Source: World 9ank, ARGENTINA: REFORMS AND SUSTAINED GROWTH,

Country Economic Memorandum, July 1988.

Note: (a) Following the Ministry of Economy procedure, al]

revenue sharing under the ad hoc agreements was considered tobe grants (ATN) in this table. For the case study data,

transfers made under these ad hoc agreements is considered to

be revenue sharing and, thus, a current revenue from a national

source.

public finance. This is partly because the provinces are difficult andcostly to study, in that they are numerous (22), institutionallycomplex, extremely heterogeneous by almost any indicator, and spatiallydispersed.

1.05 A better understanding of provincial government finance isimportant not only for controlling the fiscal deficit but also forimproving the efficiency of Argentina's public sector, because provincesare increasingly important providers of public services, especially ofhealth and education. The new Government's strategy of decentralizationshould substantially increase this importance. Expenditures ofArgentina's provincial governments in 1986 amounted to 11.2 percent ofGDP (or US$7.8 billion). Investments accounted for US$1.6 billion in1986 (2.6 percent of GDP) of these provincial expenditures, slightlymore than the total investments of all public enterprises and about 60percent more than the central government's investments (including all ofits decentralized entities and special accounts).

- 4 -

1.06 It is clear, therefore, that provincial governments cannot beignored in the efforts to reduce the public sector's fis,cal deficit andto improve its efficiency.

Government's Commnitment to and Cooperation with Study

1.07 The economic team of the new Government has assigned toppriority to the reform of the public sector enterprises and fiscalreform at the sub-national level. The economic teams of' the provincesvisited also showed much interest in the study and in a possible Banklending operation. Thus, at'both the national and provincial levels,officials are quite aware of the need for fiscal reform and increasedprovincial financial autonomy, as they realize that the centralgovernment no longer has the capacity to resolve their revenue problemsvia discretionary transfers. Provincial officials also expressed thedesire for greater political autonomy and freedom from the controls ofthe Central Government.

1.08 The new Governm,ant seems well aware of the fact that fiscalreform at the provincial Level is essential in order to maintain theintegrity of the Revenue Sharing Law. Untíl the implementation of thisLaw in 1988, transfers to the provinces were mostly in the form ofdiscretionary grants. This caused a kind of perverse competition amongthe provinces to "run up" large deficits in order to get a larger shareof the grant "pie". The new revenue sharing law reduces discretionarygrants to only one percent of total shared taxes. Both the national anclprovincial authorities seem quite aware of the importance of maintainingthe integrity of automatic dístribution criteria set in this law, andalso of the impossibility of so doing unless efforts are undertaken toreduce provincial fiscal cLeficits. They also realize th.at this isnecessary to reduce pressures for rediscounts to the provincial banksfrom the Central Bank and the resulting quasi-fiscal deficits.

B. Objectives

1.09 The primary objective of this sector study is to assist theGovernment of Argentina irn identifying and implementing appropriatemeasures that will result in an effective and equitable reduction in theProvinces' contribution te excessive, consolidated public sectordeficits.

1.10 A corollary objective is to identify appropriate areas inwhich the Bank may support imp,roved provincial financial management, sothat provinces can generate surpluses and invest them wisely to increasetheir future economic growth and tax revenues.

1.11 The study's more specific objectives are to identify:

(a) specific ways that provincial revenue performance andexpenditure efficiency may be improved;

(b) effective incentives for implementing the above improvements;

(c) appropriate, standard provincial budgeting and reportingprocedures that may also be used for national financialinformation systems necessary for macroeconomic planning; and

(d) needs for institutional reforms necessary to meet thepreceding objectives.

1.12 In addition, the report provides (Part II) basic data onprovincial public finance in a format similar to that widely used by theBank, as well as information to help in interpreting these data and inunderstanding the institutional structures of the provinces. TheStatistical Appendix will greatly facilitate access to and understandingof these data by those interested in provincial public finance inArgentina.

C. Interfaces with Other World Bank Studies and Limitations

1.13 Provincial governments are highly open sub-systems within boththe public sector and the general economy of Argentina. As such, theyare profoundly affected by most fiscal and sectoral policies of theCentral Government. For example, energy policy must address theroyalties paid by public enterprises to the provinces for extraction ofhydrocarbons and uranium, as well as production of hydroelectric power.Industrial development policy must deal with the fiscal loss engenderedby the Industrial Promotion Program, which has substantially reduced the"mass" of resources to be shared among all provinces. National taxpolicy and the efficiency of tax collection also bear directly on this"mass" of revenue to be shared with the provinces. The fiscal deficitsof the provinces can generate quasi-fiscal ones via losses of theprovincial banks and eventual "bail outs" by the Central Bank.

1.14 This study focuses on the budgets and financial management ofthe provinces per se, treatirng the impacts of national policies asexogenous variables that havei or will be covered by on-going research atthe Bank (e.g., energy, indusitrial development, nationaL tax policy,quasi-fiscal deficits, etc.). In other words, the primary focus is onhow the provinces may improvei their own financial management, ratherthan those aspects which would require changes in the national revenuesharing system, national tax policy, national sectoral policies forindustry and energy, etc. For example, this report will discuss theimplications of recent clh,angeis in Industrial Promotion on provincialpublic finance, but will leave the analysis of this sysl:em and specificrecommendations to the orgoirLg sector work on it.1 Simi.larly, theexisting revenue sharing system will also be taken as a given that mustbe dealt with in the broader context of the national taxr system, as itinvolves the comparative analysis of the efficiency of differentgovernmental levels in tax collection.l2 The same goes for royaltiesand energy policy.LW

1.15 In summary, the focus of this study is on how improvedfinancial management of the provincial public sector might not onlylower provincial fiscal deficits, but also generate surpluses that maybe invested in the econom.ic dlevelopment of the provinces.

D. Coverage

1.16 The study covers all 22 provinces of Argentina and the FederalCapital (Municipality of Buenos Aires), but not the Territory of Tierradel Fuego, as it is small (population in 1985 of 36,O00) and directlysubordinated to the Central Government.

1.17 Special emphasis is given to the years after t:he return toconstitutional government, in, 1983, but data from previous years alsoare sometimes analyzed to provide an historical perspective.

1.18 To the extent possible, the entire non-financiLal provincialpublic sector is covered, including both the centralizecd and

2/ The World Bank, "Industrial Policy,n Annex Chapter VII of Argentina:Reforms for Price Stabil'Lty and Growth, (Washington, D.C.: World BankCountry Study, 1990).

]O/ The World Bank, Argentina: Tax Policy for Stabilization and EconomicRecoverv, (Washington, D.C.: World Bank Country Study, 1990).

il! The World Bank, Argentina: Energy Sector Study, August 10, 1989.

-7 -

decentralized administrations and the provincial public enterprises.YlAlthough both the non-consolidated, decentralized entities and thepublic enterprises should be included, the cost of including all suchprovincial entities would haye been prohibitive. Therefore, it wasdecided to concentrate on those that are by far the most important innumber and total expenditures: the public utilities providing water andelectric energy. In some provinces these utilities are provided by thegeneral administration, either directly by its central administration(e.g., water and energy in La Pampa), or by consolidated decentralizedentities ( e. g., water and energy in Salta). To simply presentation,both the non-consolidated decentralized entities and the provincialpublic enterprises will be called public enterprises, unless thedecentralized entities are specifically referenced. Although there arelegal differences between these two types of entities, they are similarin that they have their own sources of revenue and are not consolidatedin the provincial budget. For all of these reasons, the presentation ofthe results will be simplified by using only two main administrativeunits of analysis:

The general administration, covering the centralized entities andthe consolidated, decentralized entities; and

The public enterDrises, including the non-consolidated,decentralized entities and public enterprises.

Public utility enterprises refer to public enterprises, but not thepublic utilities provided by the general administration.L1

1.19 As these public enterprises include important public utilitycompanies, especially in the larger provinces, excluding them results insignificant underestimations of provincial expenditures and borrowingrequirements. Unfortunately, the data currently collected by theNational Ministry of Economy do in fact exclude them. The total impactof including these enterprises in the non-consolidated provincial publicsector has the following impacts for 1985:'l

Capital expenditures + 27.7 percent or US$423 million

Overall deficit + 61.9 percent or US$263 million

121 For a more detailed discussion of the institutional structure of theprovinces see Annex Chapter I, paras. 1.12-1.18.

IV Of the six provinces studied, only the public utilities of Cordobawere, in fact, provided by a public enterprises.

já/ These estimates are based on the supplementary data tables in: FIEL,El Gasto Publico en la Argentina: 1960-85 (Buenos Aires: FIEL,1987).

Borrowing +121.9 percent or US$26.65 million

Floating debt + 58.7 percent or US$362.9 míllion

Applying these percentages to the 1986 data would increase totalprovincial expenditures by, about 2 percent of GDP, summing to 13 percentof GDP, and investment would i.ncrease to about three percent of GDP.

E. Methodologv and Sources of Data

1.20 The lack of consistent and up-to-date informat:ion onprovincial public finance in Argentina is an important barríer to itsunderstanding. The data from the Secretaria de Hacienda of the Ministryof Economy (hereafter called the Hacienda data) that are used in thisreport are deficient in th.at they: (a) exclude a significant part of theprovincial public sector because they do not cover the provincialenterprises, and (b) are out of date.

1.21 For these reason,s, and to obtain qualitative data, casestudies of six provinces were done to fill in the gaps in the Haciendadata (Buenos Aires, Cordoba, Santa Fe, Salta, Santiago del Estero andChubut), as well as to obtain data for 1987.»' These six provincesaccounted for 68.8 percent of the total population in the provinces in1985, 62.8 percent of households with unsatisfied basic needs in 1980,and 70.9 percent of the gross provincial product in 1980.L2 These sixprovinces represented an average of about half of total provincialexpenditures and 45 percent of the total deficit for the 1981-86 period.In addition to the six provinces of the case studies, two otherprovinces (Neuquen and La Pampa) were visited during the study's mainmission to collect additional data on budgeting, investment planning,personnel policy and general management. Finally, the Province ofMendoza was visited during a mission (December 1989) to ¿Liscuss theprevious version of this report and to see first hand its innovativebudgeting and tax collection systems. Therefore, nine of the 22provinces were visited during the course of the study. These provincesaccounted for over 75 percent of the population of the provinces in1985, for almost 80 percent of their economic product andL for over 68percent of their population with unsatisfied basic needs.

1.22 Although incomplete and out-of-date, the Hacienda data areuseful for analyzing the historical trends for all of the provinces.The case study data are us,ed to complement the Hacienda d.ata and viceversa. For example, the Hacienda data on all of the provinces providean overview of all 22 provinces, and the data from the case studies

5/ For selection criteria, see Annex Chapter III.

]6/ Excluding the Federal Capital and Tierra del Fuego.

-9 -

provide estimates of how accurate these data portray the situation ofthe provinces, as well as how trends might have shifted in 1987.0i

1.23 The data from these two sources (Hacienda and the casestudies) were analyzed following four basic steps.

(a) The Hacienda data provide a broad overview of general trendsfor the 1970-86 period for all provinces and the FederalCapital.l&

(b) More detailed analysis of budget data for both the direct andindirect administrations is provided by the data obtained inthe six provinces of the original case studies.

(c) Next, using the lessons learned from analysis of the six casestudies, the Hacienda data were restructured to make them moreconsistent over time and across all 22 provinces and theFederal Capital (hereafter called simply provinces), with thedata reported as closely as possible according to IMFguidelines.2l

(d) Finally, executed budget data for all the provinces wereanalyzed, consistently using IMF guidelines, and alsoaccording to the CFI classification of the provinces into fourmain groups:!W

(i) Advanced: large population and high per capitaprovincial product.

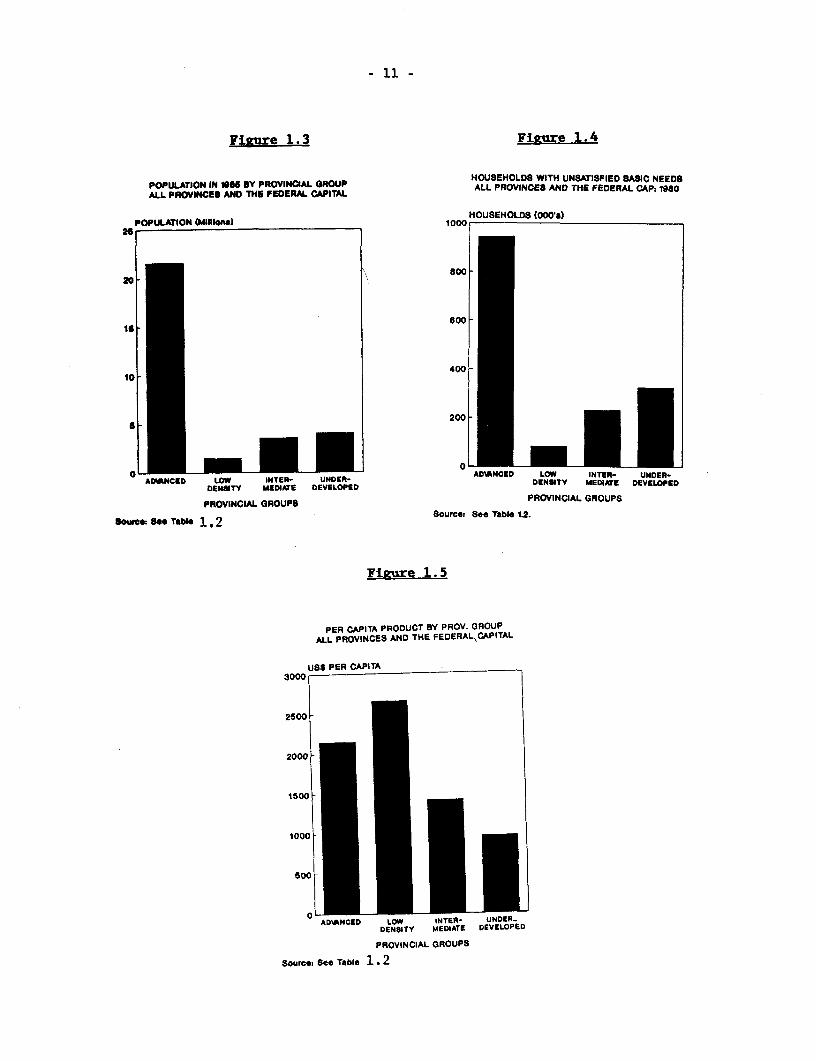

(ii) Low-Density: low demographic density and high percapita product for the "resource frontier".

1i/ For a more detailed discussion of these data, see Annex Chapter II,Sections B and C.

1j8 These data were obtained from the Country Economic Memorandum's timeseries data. See: Argentina: Reforms . , op. cit., StatisticalAppendix.

12/ For further discussion of this methodology and the restructuring ofthe Hacienda data according to the IMF guidelines, see AnnexChapter I.

VQ/ For a more detailed discussion of this classification and of basicindicators of population, product and poverty for each group ofprovinces, see Annex Chapter II.

- 10 -

(iii) Intermediate: intermediate populatoion size and percapita product.

(iv) Underdeveloped: low per capita prodtLCt.

1.24 The diversity of the provinces in terms of almnost anyindicator is impressive and maust be taken ¡ito account when designingstrategies for fiscal reform. See Figures 1.3-1.5 and Box 1.1.

.S.-.-.:'.. -1-$:>.1: TBK eDIVRIT :OF TH 'PKOVINCE';--:--''''-S«<B~~~~~~~~~~~~~~~~~~~~~~~~~~~~~. .. .. . i ...POPUIJ&TIONJ P .OV .` ANDI PEI CAPI-. : PRDUCT

Th 'pro'''i''es'a' reatly tuterms sof popu1at£ in. se er capitp:.-troduc.t--:aud:::. the- :...incidence. of. poverty. yfar: the e:: argest pro ce.by-.any fof these: :crtl:eria la::Buenos ÁAires:witha, ::opulation (2.B*BiLLion)-.abo .-uth :'.same tas tht .ofChile, nivtn n: :an are aru

the. size of Itaíy. Tenof the íeaning' 22 :proVíinces had',popuaisof lesa than 500,00 O tu: 1,985.` Buno irsha ore: than. 3tie

*.R.the populat ion of:-.anyrone -:'of E.E.these. Santa Cruz, t e provincevtth;.-....¿h...t..* ., . -E - --popul-o, ha onl d 1 134,000: inhábiat i t 98 n

La Rioja, he *next argest- ouy1000. Oe 0 rcent ofIArgentina'spOpU atio>n :of :31 ::"Miílitan: in 18 líved u tedac

.::..Group.:whtch la i:comprised of four provincs, and.the .F:deral Capital.'....-.iSe'e 'Figur'e 1...'..44. ....

Although .AlthougE.--thepe ercent:age of hauseholda with unsatisfied basi.::need'.:......'..-tandtb tgher in te provírices f e dlpe Gro uc

as Formosa <(46 8 pret u Santiago: del: Estero. (45A.8 ecn'' -the'..'c'on'cntrationt"'in::.u"absolute term la htghest-i wtu e thret 'argestp'ro svince For' example, of 1:-the 10;.5 ¿miMion: i óiuseholds ittaaunsatisfied bsc 'ees tu 19'89 35 .90 percent. live :Ln 'Buenos- Aires;

a'^''. ftt of 'ht toa of roshod wt Cnai e bab .a'd:

rioad in the 8 provinces of tMe Underdev eloe e Group. See Figre 3

-a.er0--.'io ......... ..... ........Gosa il Product (G is h...-proviucas--. .of- the:::.;: Lo'w.í.r.Density G:;;;Çroup: 9n ::::the w:.0»reanourceroa frontter-sespeciaíly ..... it.hose ijiwiLthi petroleum :i-reserves::................ : Sea0F:igurej 1.5...... 0j---j-'Fo g 'sexample:-i.the -per "lcapita lGPP :of :Santa Cruz:- tuin 1985 v was almost US$3000versiss USS l657 Sin "Buenos' 'Aires tandi leas thau US$900' iLn:the' 0province SR

-. s.^..ofi C.;'>haco, Formosa,- LaRioja, a0isatloned ad Santiag del :Estero..

* f- ,i jE0S EEth -eE a i Uij-f t: ~fEi f hé!4iSE'CUidérevaop rou gu

. - . E . . . -. ............................ i .; . i i 7. - ........................ ........ .... .... '.s -- '.j '.' d .-- '': ''" ''. f f -'S''- ' Si ::.: .':.40 .' .-: :yE: 0 f f E S i j~~~~~~~. .......

.'.,., ~ ~ ft .;,. `í.: Den' ty.i ' t' .

e,. :''" ".s'p'"' e; ¡aft Y h Ç0'!"''' d"tÉ pe'ftrol úm: re er e .0Se,':4:: "!5,0.'';i .......: ....

- 11.

Fiscure 1.3 Figure 1.4

POPULATION IN tOI10 8Y P >VINOAI. GROUP HOUSEHOLDO WITH UNSATISFIED BASIC NEEDO

ALL PROVINCES ANO THE FEDERAL CAPITAL ALL PROVINCE8 ANO THE FEDERAL CAP: 1980