Private Market Financing for - Developing Countries - IMF ...

92

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Private Market Financing for - Developing Countries - IMF ...

WORLD ECONOMIC AND FINANCIAL SURVEYS

Private Market Financing for

Developing Countries

Prepared by a Staff Team in thePolicy Development and Review Department

Steven DunawayRobert Rennhack

Brian AitkenGeorge Anayiotos

David AndrewsJahangir Aziz

Juan Jose Fernandez-AnsolaShogo Ishii

Thomas LaursenPaul MylonasSusan Prowse

Alejandro SantosAnne Jansen

Jolanda HeemskerkLouis Pauly

INTERNATIONAL MONETARY FUNDWashington, DC

March 1995

©International Monetary Fund. Not for Redistribution

© 1995 International Monetary Fund

Charts and Cover Design: IMF Graphics Section

ISBN 1-55775-456-XISSN 0258-7440

Price: US$20.00(US$12.00 to full-time faculty members and

students and universities and colleges)

Please send orders to:International Monetary Fund, Publication Services

700 19th Street, N.W., Washington, D.C. 20431, U.S.A.Tel: (202) 623-7430 Telefax: (202) 623-7201

recycled paper

©International Monetary Fund. Not for Redistribution

Contents

Page

Preface vii

I. Overview and Current Issues 1Progress with Commercial Bank Debt Restructuring 1

Recent Experience 1Prospects 2

Private Financial Flows 2Recent Experience 2Durability of Market Re-Entry and Pricing of Risk 2

II. Commercial Bank Debt Restructuring 5Overview 5Recent Bank Packages 5Debt-Conversion Activity 10Secondary Market Developments 11

III. Recent Developments in Private Market Financing 13Bonds 13Bond Pricing 17Equities 21Commercial Bank Lending 25Other Issues 28

IV. Institutional and Regulatory Framework for Developing Country Financing 31Reform of Regulatory Structures 31Expanding the Investor Base 32Regulatory Harmonization 33Regulatory Changes in Creditor Countries 34

Securities Markets 34Provisioning Standards 34

V. Foreign Direct Investment 35Recent Trends in Direct Investment 35Behavior of Foreign Direct Investment Transactions in a Crisis 36

Statistical Appendix 41

Bibliography 81

Tables

II. 1. Commercial Bank Debt- and Debt-Service-Reduction Operations 1987-July 1994 6

2. Bank Menu Choices in Debt-Restructuring Packages 7

©International Monetary Fund. Not for Redistribution

CONTENTS

Page

II. 3. Buy-Back Equivalent Prices in Debt- and Debt-ServiceReduction Operations 8

4. Debt Conversions 11III. 5. International Bond Issues by Developing Countries and Regions 15

6. Credit Ratings of Developing Country Borrowers 187. International Equity Issues by Developing Countries and Regions 248. Terms of Long-Term Bank Credit Commitments 289. Total Returns on Equity in Selected Emerging Market Countries:

Before and After Opening to Foreign Investors 3010. U.S. Net Purchases of Foreign Equity in Selected Countries:

Before and After Opening to Foreign Investors 30

AppendixAl. Chronology of Bank Debt Restructurings and Bank Financial Packages,

1984-July 1994 41A2. Amounts of Medium- and Long-Term Bank Debt Restructured 42A3. Terms and Conditions of Bank Debt Restructurings and Financial

Packages, July 1989-July 1994 43A4. Debt and Debt-Service Reduction in Commercial Bank Agreements

1987-July 1994 50A5. International Bond Issues by Developing Countries and Regions,

by Type of Borrower 60A6. Yield Spread at Launch for Unenhanced Bond Issues by Developing

Countries and Regions 62A7. Maturing Bonds of Developing Countries by Regions 64A8. International Bond Issues by Developing Countries by Currency of

Denomination 65A9. Enhancements of International Bond Issues by Developing Countries 66

A10. Granger Causality Tests on Daily Data of Brady Par Bond Prices 67Al l . Granger Causality Tests on Daily Data of Sovereign Eurobond Prices 68A12. Emerging Markets Mutual Funds 69A13. Net Bond and Equity Purchases by Emerging Markets Mutual Funds 70A14. Issues of Closed End Funds Targeting Emerging Markets in

Developing Countries and Regions 71A15. Bank Credit Commitments by Country or Region of Destination 72A16. Terms on Syndicated Bank Credits for Selected Developing Countries

and Regions 73A17. Correlation Among Total Returns on Bonds for Selected Countries 74A18. Correlation Among Secondary Market Prices of Brady Bonds 75A19. Correlation Among Total Returns on Equity for Selected Countries 77A20. Provisioning Regulations Against Claims on Developing Countries 78A21. Net Foreign Direct Investment Flows to Developing Countries 80

ChartsI. 1

II.III.

2.3.4.5.

Selected Developments in Secondary Market Prices DuringNegotiations of Bank Restructuring Packages 3

Maturing Bonds of Developing Countries 4Secondary Market Prices of Bank Claims on Selected Countries 12Private Market Financing to Developing Countries 13Yield Spreads at Launch for Unenhanced Bond Issues by Developing

Countries 14Secondary Market Yield Spreads on U.S. Dollar Denominated Bonds by

Selected Developing Countries 14

IV

6.

©International Monetary Fund. Not for Redistribution

Contents

Page

7. Comparison of Yields of Sovereign Bonds to Yields on U.S. CorporateBonds 20

8. Comparison of Sovereign Bond Spreads 219. Comparison of Movements in Spreads and Economic Variables for

Mexico and Venezuela 2210. Comparison of Movements in Spreads and Economic Variables for

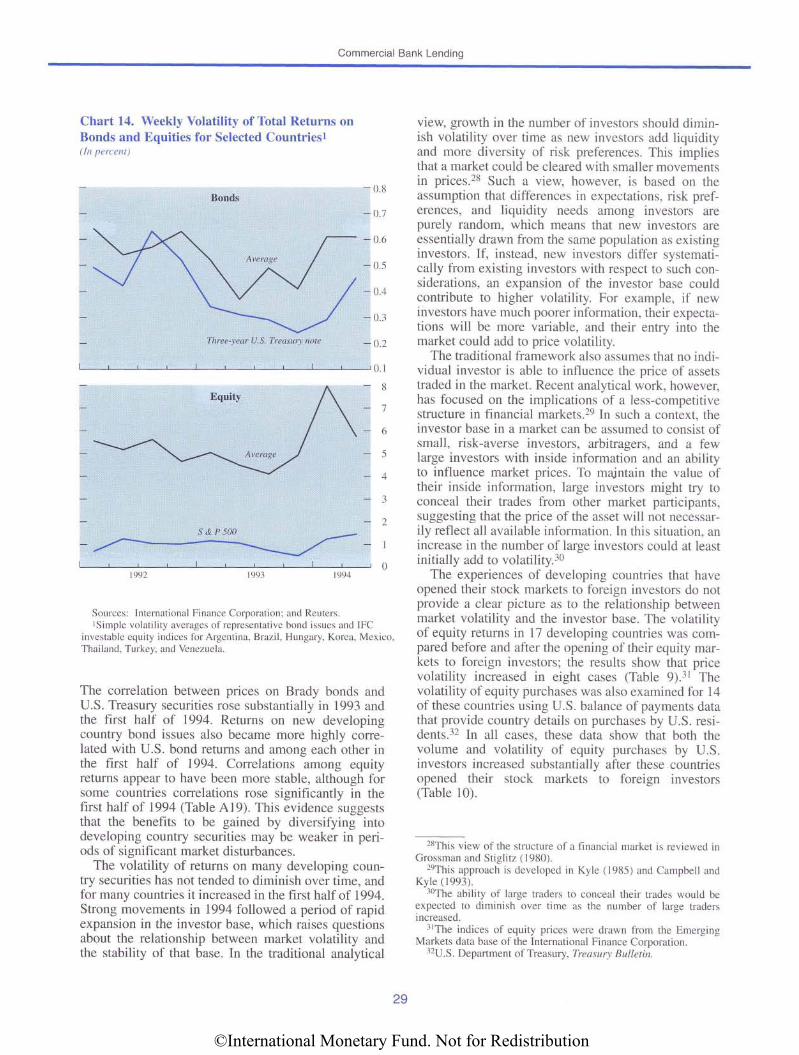

Hungary and Turkey 2311. Emerging Market Mutual Funds 2512. Share Price Indices for Selected Markets in Latin America 2613. Share Price Indices for Selected Markets in Asia 2714. Weekly Volatility of Total Returns on Bonds and Equities for

Selected Countries 29V. 15. Net Foreign Direct Investment to Developing Countries 36

16. Composition of Net Private Capital Flows 37

The following symbols have been used throughout this paper:

. . . to indicate that data are not available.

— to indicate that the figure is zero or less than half the final digit shown, or that the item does notexist;

between years or months (e.g., 1992-93 or January-June) to indicate the years or months covered,including the beginning and ending years or months;

/ between years (e.g., 1992/93) to indicate a crop or fiscal (financial) year.

"Billion" means a thousand million.

Minor discrepancies between constituent figures and totals are due to rounding.

The term "country," as used in this paper, does not in all cases refer to a territorial entity that is a stateas understood by international law and practice; the term also covers some territorial entities that are notstates, but for which statistical data are maintained and provided internationally on a separate and inde-pendent basis.

V

©International Monetary Fund. Not for Redistribution

This page intentionally left blank

©International Monetary Fund. Not for Redistribution

Preface

This study was prepared in the Policy Development and Review Department of theInternational Monetary Fund, under the direction of Steven Dunaway, Chief of the Debt andProgram Financing Issues Division, with Robert Rennhack, Deputy Chief of the division. Itsauthors are Brian Aitken, George Anayiotos, David Andrews, Jahangir Aziz, Juan Jose Fer-nandez-Ansola, Shogo Ishii, Thomas Laursen, Paul Mylonas, Susan Prowse, and AlejandroSantos, economists in the division; Anne Jansen, research officer in the division; and JolandaHeemskerk, an intern at the IMF during the summer of 1994. The study updates informationand analyses contained in Private Market Financing for Developing Countries, World Eco-nomic and Financial Surveys (Washington: IMF, December 1993).

The work benefited from comments by staff in other departments of the IMF and by mem-bers of the Executive Board. Opinions expressed, however, are those of the authors and donot necessarily represent the view of the IMF or its Executive Directors. The study was com-pleted in October 1994 and reflects developments to that time.

Louis Pauly prepared the text for publication. The authors are also grateful to DelreneAlvis, Lucia Buono, Ida Jenkins, and Anne-Barbara Hyde for their valuable word-processingservices. Juanita Roushdy of the External Relations Department, gave the manuscript a finaledit and coordinated production.

VII

©International Monetary Fund. Not for Redistribution

This page intentionally left blank

©International Monetary Fund. Not for Redistribution

IOverview and Current Issues

ver the period since the end of 1992, steadyprogress has been achieved toward resolving the

commercial bank debt problems of middle-incomecountries.1 By the end of 1994, most of the majordebtor countries in this group will have completedrestructurings of their bank debt. At the same time, anumber of developing countries—including some ofthe former major debtors—have expanded their accessto spontaneous private financing, as investor interest indeveloping country bonds and equities broadened sig-nificantly. The markets for these securities ran intosubstantial turbulence at times during the first half of1994, however, reflecting higher interest rates in inter-national markets prompted by the tightening of mone-tary conditions in the United States and by adversedevelopments in some developing countries.

Progress with Commercial Bank DebtRestructuring

Recent ExperienceOver the past year, Brazil, Bulgaria, the Dominican

Republic, Jordan, Poland, Sao Tome and Principe, andZambia completed bank-debt-restructuring packageswith support from the Fund, the World Bank, and bilat-eral official agencies. Ecuador also is expected to com-plete an arrangement with its bank creditors before theend of 1994. By that time, a total of 21 countries willhave concluded bank debt- and debt-service-reductionoperations. Debt worth approximately $170 billion willhave been restructured, representing roughly 75 per-cent of bank debt outstanding at the end of 1989 for thegroup of heavily indebted developing countries (TableAl). Panama and Peru are the most heavily indebtedmiddle-income countries that have not yet regularizedrelations with their commercial bank creditors; both areengaged in negotiating restructuring agreements.

South Africa continued to address its external debtproblems through a rescheduling of obligations tocommercial banks. Agreement on a fourth and finalarrangement following the 1985 payment "standstill"was reached in September 1993. In the case of Russia,

'For earlier periods, see Collyns and others (1993, 1992, and1991). For information on official financial flows to developingcountries, see Kuhn and others (1994).

talks have focused on rescheduling its stock of bankdebt and capitalizing a declining share of interestarrears. A preliminary agreement was reached in July1993, but its implementation was delayed pending res-olution of issues regarding Russia's waiving sovereignimmunity and designation of the official agency thatwould be the signatory to the agreement. These issueswere resolved in September 1994, and the agreement isto come into effect by the end of the year, after Russiamakes a previously agreed payment of $500 millionwith respect to past due 1993 interest obligations.

A growing number of low-income countries also aremaking efforts to resolve their debt problems, oftenaided by the resources of the debt reduction facility forcountries of the International Development Associa-tion (IDA). Progress for most, however, remains slow.With the backing of IDA resources and assistance fromofficial bilateral sources, debt buy-backs have beenconcluded by Bolivia, Guyana, Mozambique, Niger,Sao Tome and Principe, Uganda, and Zambia. Prelimi-nary discussions on similar operations are under waywith several other countries.

Further innovations in debt operations have occurredover the past year. Bulgaria's discount bond, for exam-ple, involves a much steeper discount than has been thecase in previous debt packages. In addition, Poland'sagreement provided for some debt reduction for inter-est arrears and did not include interest collateral. Pack-ages now generally include limits on the use of certainoptions or explicit rebalancing clauses to providecountries with more certainty as to the up-front costs ofan operation and the profile of debt-service relief ulti-mately provided. The Fund and the World Bank havealso shown increased flexibility in the use of their ownresources by eliminating the segmentation provisionsin their guidelines governing support for bank debtoperations.

Over the past year, bank debt operations for Braziland Jordan were financed entirely by the debtor coun-tries themselves. While not directly involved in thesedeals, the international financial institutions have pro-vided some indirect support. The bank deal with Jor-dan was predicated on the existence of a Fundarrangement with the country. In the case of Brazil, thecountry's stabilization program, which was expected tobe monitored by the Fund, and continuing discussionson a Fund arrangement were considered sufficientassurance to enable completion of negotiations withcreditors.

1

O

©International Monetary Fund. Not for Redistribution

I OVERVIEW AND CURRENT ISSUES

Prospects

Notwithstanding recent progress, certain develop-ments appear likely to make future negotiationsbetween indebted developing countries and the holdersof their commercial bank obligations more complex.Nonbank investors now have purchased significantamounts of bank debt in the secondary market. Diffi-culties in persuading them to accept certain aspects ofthe debt packages negotiated by bank advisory com-mittees have contributed to delays in completing somerecent restructuring operations. Negotiating commit-tees in the future will have to take better account of thediverse interests of these investors.

Another possible complication arises from the mar-ket impact of speculation that a country will concludea debt- and debt-service-reduction operation. Forexample, so-called pre-Brady speculation has con-tributed to the run-up in the secondary market pricesfor the bank debt of Panama and Peru. In recent years,such price run-ups have tended to be earlier and largerthan was the case for countries that concluded debtpackages in 1989 and 1990 (Chart 1). As a conse-quence, secondary market prices may not always fullyreflect a country's medium-term capacity to service itsdebt and the up-front costs of completing a debt-restructuring agreement may be bid up significantly.The potential effects of such speculation will need tobe taken into consideration in negotiating the terms ofbank packages in the remaining cases.

While most of the major baric debt cases have beenresolved, attention still needs to be focused on theproblems of low-income countries. In many of thesecountries, the process of debt restructuring has beendelayed owing to economic and political difficulties.Although the amounts owed by these countries aresmall compared with the debt of the large middle-income debtor countries, individual debt burdens formany are severe. In some cases in the past, commercialbanks have accepted steep discounts on these debts,particularly when they had no significant longer-termbusiness interests and had already made provisions forlosses. Additional flexibility will be needed in thefuture. There will also be a continuing substantial needfor concessional assistance to finance debt operations.For some low-income countries, the total amount ofassistance required to buy back bank debt, even at verysteep discounts, is likely to be relatively large.Resources from the debt reduction facility for IDAcountries and from other official agencies may not besufficient. In such cases, it may not be enough to orga-nize simple buy-backs of commercial bank debt.Instead, more complex operations may have to be con-sidered that reduce up-front costs but still provide debtand debt-service reduction in line with a country's pay-ments capacity over the medium term. Such dealsmight involve options that include larger discounts ondiscount bonds, par bonds bearing lower interest rates,

more favorable treatment of past due interest, and lessthan full collateralization of principal.

Private Financial Flows

Recent ExperienceThe resurgence in private market financing to devel-

oping countries that began in the late 1980s continuedduring 1993 as both portfolio flows and net foreigndirect investment rose sharply.2 The strong expansionin international bond and stock placements was fueledin large part by a broadening of the investor base toinclude a wider group of institutional investors.3

Medium- and long-term commercial bank lending,however, remained limited. Moreover, while total pri-vate market financing for developing countries as agroup increased strongly in 1993, much of these flowscontinued to go to a small number of countries, pri-marily in Asia and Latin America.

Toward the end of 1993 and in early 1994, spreadson bonds narrowed appreciably, and demand for devel-oping country bonds, as well as equities, began to falldramatically. This coincided with increases in U.S.interest rates and adverse developments in several bor-rowing countries. In addition, highly leveraged'inves-tors were reported to have liquidated their positions indeveloping country securities in an effort to meet mar-gin requirements or to take profits. The slide in demandfor these bonds and equities continued through April1994, before recovering moderately in May and June.

While countries with weaker economic performanceexperienced cutbacks in market access somewhat ear-lier than others, financing flows to all developingcountries, including those in Asia and stronger per-formers in Latin America, fell to very low levels byApril 1994. Both issuers and purchasers pulled backsharply in the wake of overall market uncertainties.Bonds placed after February 1994 tended to be fromonly the better credit risks and to carry floating interestrates and shorter maturities. While highly leveragedinvestors unwound most of their positions, it appearsthat institutional investors generally maintained theirholdings, even if they curtailed their demand for newbond and equity issues.

Durability of Market Re-Entryand Pricing of Risk

The increase in private financing to developingcountries over the past few years and the market's abil-

2International bond and equity flows amounted to $71 billion in1993 ($33 billion in 1992); net foreign direct investment flowsamounted to $58 billion in 1993 ($39 billion in 1992). Direct pur-chases of equity and bonds by nonresidents in local markets are notincluded because of the lack of sufficient data.

3The expansion of the investor base is discussed further in Gold-stein and others (1994).

2

©International Monetary Fund. Not for Redistribution

Private Financial Flows

Chart 1. Selected Developments in Secondary Market Prices DuringNegotiations of Bank Restructuring Packages

Sources: Salomon Brothers; ANZ Grindlays Bank; and IMF staff estimates.'Per unit of claim.

ity to rebound from a moderate correction in 1992engendered optimism about the sustainability of theprocess of market re-entry.4 While the sharp correctionin early 1994 raised fresh doubts, the emergence of a

4The 1992 market correction is described in Goldstein and others(1993).

3

recovery later in the year reinforced that optimism. Asnoted in previous reports in this series, three conditionsappear basic to sustaining private flows to developingcountries: an expanded investor base, appropriate pric-ing and assessment of risk, and continued implementa-tion of sound policies that help match future debt-servicing requirements to payments capacity. Progresscontinues to be made along these lines.

©International Monetary Fund. Not for Redistribution

I OVERVIEW AND CURRENT ISSUES

Chart 2. Maturing Bonds of Developing Countries(In millions of U.S. dollars)

Sources: International Financing Review; EuroWeek; and IMF staffestimates.

The expansion of the investor base in 1993 was partof a trend toward the globalization of portfolios. Rela-tive stability of the investor base in 1994, despite themarket correction, has been encouraging. As newinvestor groups come into the market, flows and pricesof developing country securities could nevertheless besubject to considerable volatility, especially if newinvestors have poorer information and different liquid-ity preferences than existing investors. Although anumber of developing countries have experiencedincreased volatility in security prices following theopening of local stock markets to foreign investors, adiversified and stable investor base can be expectedover time to promote reduced fluctuations in assetprices, particularly as information becomes morewidely disseminated.

The sharp run-up in the prices of developing countrysecurities in late 1993 and early 1994 raises questionsabout the pricing of risk. It appears that the marketranks countries in a manner that is broadly consistentwith their recent economic performance and immedi-ate prospects. It is unclear, however, whether investorsdifferentiate carefully among different borrowers. Ingeneral, and as would be expected, issuers from coun-tries that previously rescheduled their debt tend to payhigher spreads, while those from countries withstronger growth and better inflation performance tendto pay lower ones. Beyond such broad differentiations,however, the market may be slow to make finer dis-tinctions. For example, yield spreads on bonds ofcountries that ran into difficulties in late 1993 wereslow to react to the deterioration in their economic per-formance until it was widely recognized; at that point,the response was quite significant. Investors also havebeen attracted to developing country securities becausereturns historically have not closely tracked pricedevelopments in industrial country financial markets.Under these circumstances, the diversification of port-folios by including developing country securities couldraise the portfolios' expected returns for a given levelof risk. Experience during the market turbulence in1994, however, suggests that asset returns of develop-ing and industrial countries tend to become moreclosely related in turbulent periods.

To maintain market access on reasonable terms,countries need consistently to implement strongmacroeconomic and structural policy programs. Main-tenance of such programs is likely to be particularlyimportant in the period ahead, given the high degree ofuncertainty with regard to interest rate movements inthe industrial countries. Developing countries are alsonow entering a period of rising debt amortization as thebullet repayments on bonds issued earlier this decadeare beginning to fall due (Chart 2). The increasing inte-gration of international financial markets also meansthat interest rates and equity prices in developing coun-

tries will become more sensitive to developments inasset prices in the major industrial countries. A moreopen international environment will have to be takeninto consideration by developing countries in deter-mining the appropriate stances of monetary, fiscal, andexchange rate policies. While at times it might appeartempting to supplement such policies with capital con-trols, such actions would ultimately tend to be counter-productive. To provide a basis for sustained portfoliocapital flows, continued efforts are also needed tostrengthen financial markets in developing countries.Structural reforms to increase market transparency andreduce transaction costs and risks are important in fos-tering investor confidence. Intermediation of capitalflows through the banking system points as well to theneed for adequate banking regulation and supervision.

Developing countries can improve the mix of exter-nal financing by taking steps to remove obstacles tonon-debt-creating capital flows. In recent years, inter-national equity placements and direct purchases ofequities by foreigners in domestic stock markets haverisen sharply. At the same time, there has also been asurge in foreign direct investment inflows. These flowsgenerally entail longer-term commitments on the partof foreign investors. Nevertheless, foreign directinvestment flows, taking into account reinvested andrepatriated earnings, also exhibit some of the samecharacteristics as other flows during periods of domes-tic macroeconomic instability. While investment posi-tions are rarely liquidated rapidly, the totality oftransactions associated with foreign direct investmentmay give rise to net outflows of funds.

4

©International Monetary Fund. Not for Redistribution

IICommercial Bank Debt Restructuring

Overview

rogress has been made by a number of the heavilyindebted middle-income developing countries in

regularizing their relations with commercial bank cred-itors. To many observers, the conclusion of the Brazil-ian debt package in April 1994 is seen as marking theend of the debt crisis that began in August 1982 whenMexico announced its inability to service its externalobligations to commercial creditors. Along with Brazil,Bulgaria, the Dominican Republic, Jordan, Poland,Sao Tome and Principe, and Zambia completed debt-and debt-service-reduction operations or comprehen-sive debt buy-backs over the past year. Ecuador and itsbank creditors also reached agreement, and the restruc-turing package is scheduled to be completed before theend of 1994. By that time, 21 countries will have con-cluded debt- and debt-service-reduction operationsrestructuring $170 billion of original commercial bankclaims (Tables 1 and A2), or 75 percent of commercialbank debt owed by heavily indebted developing coun-tries at the end of 1989.5 Debt reduction achieved willamount to an estimated $76 billion at a cost of about$25 billion.

Allocations to the different options available in bankpackages have varied depending (among other things)on explicit limits imposed by debtor countries, oninterest rate developments following the issuance ofterm sheets, on creditors' perceptions of country credi-tor risks, and on the prospect of capital gains (Tables 2and A3). In general, packages have been cost-effectivein that the cost per unit of debt reduction obtained hasbeen broadly in line with prices prevailing in the sec-ondary market at the time agreements in principle werereached (Tables 3 and A4).

Following the trend of previous years, debt conver-sion activity was less buoyant in 1993. This partlyreflected a shift in emphasis in the privatization pro-gram in Argentina, which accounted for about half ofdebt conversions in 1992, as priority shifted fromreducing foreign commercial bank debt to reducingforeign currency denominated domestic debt instru-

ments. In addition, the decline in debt conversionsreflected the rise in secondary market prices for thedebt of many countries and the reduced scale of privat-izations, owing to countries having substantially com-pleted their schemes.

Recent Bank Packages

While Argentina's debt- and debt-service-reductionpackage closed on April 7, 1993, about 6 percent of eli-gible principal (amounting to $19.4 billion) and 100percent of past due interest ($8.6 billion) wereexchanged at a later date because of reconciliationproblems. All collateral and guarantees (totaling $3.1billion), however, were deposited with the collateralagent (the Federal Reserve Bank of New York), and thedownpayment on past due interest ($0.7 billion) andthe bonds related to unreconciled debts were depositedwith the escrow agent (the Bank of England) on theclosing date. Reconciliation of the remaining principalwas completed on September 27, 1993, and the releaseof bonds covering past due interest and the corre-sponding cash payments was made in four tranches:the first on October 29, 1993 (83 percent); the secondon December 29, 1993 (14 percent); the third on Feb-ruary 28, 1994 (3 percent); and the fourth and last onApril 28, 1994 (negligible amounts).

Brazil completed one of the largest and most com-plex debt- and debt-service-reduction operations onApril 15, 1994. Completion of the deal came almosttwo years after the agreement in principle was reached,following four extensions of the closing date. Since anarrangement with the Fund was not likely to be ineffect at closing (this had been a condition in the termsheet), a waiver from bank creditors had to berequested. This waiver was granted on March 24,1994. The process was also delayed because of prob-lems in obtaining full creditor participation.6

The deal restructured $40.6 billion in eligible princi-pal and $6.0 billion in past due interest. Out of a menuof six options, only five were actually used. Creditorsaccepted the May 1993 limits suggested by the author-ities on the amount of debt allocated to the par and new

5 A further 10 percent of the stock of commercial bank debt out-standing in 1989 has been extinguished through debt conversionsand other mechanisms. Of the remaining debt that has not beenrestructured, Peru and Panama account for more than 20 percent,and four low-income countries (Cameroon, Congo, Cote d'lvoire,and Nicaragua) account for another 17 percent.

6In the end, one major creditor, a large nonbank investor holdingroughly $1.4 billion of Brazil's debt, refused to participate in thedeal. That creditor subsequently filed a law suit in the United Statesto force payment of past due interest on Brazil's original debt andto accelerate payments of principal arrears.

5

P

©International Monetary Fund. Not for Redistribution

COMMERCIAL BANK DEBT RESTRUCTURING

Table 1. Commercial Bank Debt- and Debt-Service-Reduction Operations, 1987-July 19941

(In millions of U.S. dollars)

Argentina (1992)Bolivia

(1987)(1993)

Brazil (1992)Bulgaria (1993)Chile (1988)Costa Rica (1989)Dominican Republic (1993)Ecuador(1994)6

Guyana (1992)Jordan (1993)Mexico

(1988)(1989)

Mozambique (1991)Niger(1991)Nigeria (1991)Philippines

(1989)(1992)

Poland (1994)Sao Tome and PrincipeUganda (1993)Uruguay (1991)Venezuela (1990)Zambia (1994)

Total

DebtRestructuredUnder DDSR

Operation3

(1)

19,397643473170

40,6006,186

4391,456

7764,520

69736

51,9023,671

48,231124111

5,8115,8121,3394,4739,918

10152

1,60819,700

200

170,170

Debt

Buy-back(2)

—331253

78—

798439991272

—69——

—124111

3,3902,6021,3391,2632,454

10152633

1,411200

13,986

Debt

reductionDiscountexchange4

(3)

2,35623218250

4,9741,865

—177

1,180—84

7,9531,1156,838

————

—2,401

———

511—

21,733

and Debt-Service

Debt-servicePrincipal

collateralizedpar bond4

(4)

Reduction (DDSR)2

reduction

Otherpar bond4

(5)

Prepaymentsthrough

collateral-ization

(6) 0

(Concluded agreements)

4,29129

293,996

—

——

826—

1116,484

6,484——

651516

516779

——

1602,012

—

19,855

——

337421

__101—————

————

116

11672———

471__

1,519

2,73920

713

3,891443

__3663

595—

1177,777

5557,222

——

352467

467602——95

1,639—

18,835

Totalr)=(2)+. .+(6)

9,386612442170

13,1983,527

4391,128

5112,600

69312

23,1731,670

20,544124111

4,3933,7011,3392,3626,309

10152888

6,043200

75,927

Total Debt andDebt-Service

Reduction/Debt

Restructured(7)/(l)

48.495.293.5

100.032.557.0

100.077.565.857.5

100.042.544.645.542.6

100.0100.075.663.7

100.052.863.6

100.0100.055.230.7

100.0

44.6

Cost ofDebt

Reduction5

3,059613526

3,900652248196149583

10118

7,677555

7,1221223

1,7081,795

6701,1251,866

118

4632,585

22

25,146

Source: IMF staff estimates.'Debt and debt-service reduction are estimated by comparing the present value of the old debt with the present value of the new claim, and adjusting for

prepayments made by the debtor. The methodology is described in detail in Annex I of Private Market Financing for Developing Countries (Washington:International Monetary Fund, December 1992). The amounts of debt reduction contained in this table exclude debt extinguished through debt conversions.

2The figure for debt-service reduction represents the expected present value of the reduction in future interest payments arising from the below-marketfixed interest rate path on the new instruments relative to expected future market rates. The calculation is based on the estimated term structure of interestrates at the time of agreement in principle.

3Includes debt restructured under new money options for Mexico (1989), Uruguay (1991), Venezuela (1989), and the Philippines (1992); the Philippines'(1989) new money option was not tied to a specific value of existing debt.

4Excludes prepayment of principal and interest through guarantees.5Cost at the time of operation's closing. Includes principal and interest guarantees, buy-back costs, and for Venezuela, resources used to provide

comparable collateral for bonds issued prior to 1990. Excludes cash downpayments related to past due interest.6Closing of the operation has been delayed and is expected to take place in the first quarter of 1995.

money options and the minimum allocation for the dis-count bond. The final allocation was (1) 35 percent forthe discount bond; (2) 32 percent for the par bond; (3)22 percent for the capitalization bond with temporaryinterest reduction; (4) 6 percent for the new moneyoption; and (5) 5 percent for the front-loaded interestreduction bond (FLIRB). No allocation was made tothe restructuring option.

The cost of the enhancements required for the oper-ation is estimated at $3.9 billion, of which $2.8 billionin collaterals was delivered at closing, with the rest to

be phased in over a two-year period in four semiannualinstallments. Phase-in bonds and partly collateralizedbonds were issued at closing and were to be exchangedfor fully collateralized instruments over the next twoyears.7 The Bank for International Settlements is ser-ving as the collateral agent. Financing for the operationcomes from $0.4 billion collected in the new money

7These phase-in and partly collateralized bonds apply only to thepar and discount bond options. The FLIRBs were fully collateral-ized at closing, and the other options did not require collateral.

6

©International Monetary Fund. Not for Redistribution

Overview

Table 2. Bank Menu Choices in Debt-Restructuring Packages(In percent of total eligible bank debt)

ArgentinaBoliviaBrazilBulgariaCosta Rica

Dominican RepublicEcuadorJordanMexicoNigeria

Philippines (1989)1

Philippines (1992)PolandUruguayVenezuela

Total2

Debt Reduction

Buy-back

46—1363

35

——62

100282539

7

8

Discountexchange

34353560—

65583343—

—54—

9

34

Debt-Service

Principalcollateralized

parexchanges

661932——

42674738

42183338

39

Reduction

Other parexchanges

52737

——

17

—15

5

NewMoney

—6

——

11—

134

2831

9

OtherNon-Debt- andDebt-Service-

ReductionOptions

_22——

——

—

——

5

Sources: National authorities; and IMF staff estimates.]The agreement included new money but was not tied to a specific amount of eligible debt.2Weighted average.

option and from Brazil's own resources. Zero-couponU.S. Treasury securities used as collateral for the dealwere purchased by Brazil in the secondary market.

In one of the fastest completions of a menu-baseddebt- and debt-service-reduction operation, Jordanconcluded a deal with its banks on December 23, 1993,two weeks after the formal signing of the agreementand less than six months after reaching an agreement inprinciple. The package covered eligible principal of$740 million and past due interest of $120 million.Following considerable official buy-backs in the sec-ondary market before the commitment date (about 12percent of the total bank debt outstanding), the finalallocation of eligible principal was (1) 67 percent forthe par bond; (2) 33 percent for the discount bond; and(3) negligible amounts for the (below-market price)buy-back. The $150 million cost of the operationincluded $29 million for cash payments on past dueinterest. Financing was covered entirely by the coun-try's own resources.

Bulgaria reached an agreement in principle with itscommercial bank creditors on November 24, 1993. Aterm sheet was distributed to banks on March 11, 1994,and the package was completed on July 29, 1994. Eli-gible principal amounted to $6.2 billion, including $1.9billion in short-term debt. The menu consisted of threeoptions: (1) a 50 percent discount exchange; (2) aFLIRB; and (3) a buy-back at 25 3/16 cents on the dollarper unit of claim. Partial interest payments were re-sumed shortly after the agreement in principle was

reached. Retroactive to March 1993, the rate paid was5 percent of amounts due, or roughly $30 million aquarter.

The discount bond involves a 30-year bullet repay-ment and bears an interest rate of % over the Londoninterbank offered rate (LIBOR). The principal is fullycollateralized, and there is a 12-month rolling interestguarantee at 7 percent. The FLIRB carries an 18-yearmaturity with eight years of grace. The interest ratestarts at 2 percent in the first year and increases in stepseach year, reaching 3 percent by year seven; subse-quently, it reverts to a market rate of % over LIBORuntil maturity. There is no principal guarantee, but thebond has a 12-month rolling interest guarantee at 2.6percent (for the seven years of interest reduction), cap-italizing earned income until it reaches 3 percent.Equal amortization payments are due semiannually.Special issues of discount and FLIRB bonds will bemade to cover 30 percent of the short-term debt allo-cated to the different options. These bonds carry aninterest rate 1/2 of 1 percent higher than that on bondsexchanged for medium- and long-term debt. Somedebt reduction on past due interest is achieved througha lowering of the interest rate for capitalization pur-poses. The package also includes a value recoveryclause on the discount bonds linked to the overall per-formance of the Bulgarian economy.

The term sheet limited the allocation for the FLIRBsto 30 percent. Rebalancing was not needed by the com-mitment date (May 18, 1994), since the allocation was

7

©International Monetary Fund. Not for Redistribution

COMMERCIAL BANK DEBT RESTRUCTURING

Table 3. Buy-Back Equivalent Prices in Debt- and Debt-Service-Reduction Operations1

(In percent of face value)

ArgentinaBrazilBulgariaCosta Rica2

Dominican Republic

EcuadorJordanMexico2

Nigeria2

Philippines (1989)

Philippines (1992)PolandUruguay2

Venezuela2

Total4

Debt

Buy-back

251625

39

4050

52415645

41

ReductionDiscountexchange

252618—28

192533——

14—35

27

Debt-Service Reduction

Principalcollateralized

parexchange

3236—

—

29413936—

45224538

36

Other parexchanges

198

2 9 3

—

—

—

28——25

21

Overallpackage

3030181826

2435363950

48255338

33

SecondaryMarket Price

at Time ofAgreementin Principle

3735271923

2339444050

53395446

37

Source: IMF staff estimates.'The buy-back equivalent price for a debt exchange is the total value of enhancements as a proportion of the total reduction in claims

payable to banks, including effective prepayments through collateralization, evaluated at prevailing interest rates at time of agreement inprinciple. This is the price at which the debt reduction achieved through a debt exchange is equivalent to the debt reduction under a buy-backat this price.

2The calculations include estimates of value recovery clauses.3Weighted average of the buy-back equivalent price of the series A par bond (33 cents), the series B par bond (0 cents), and the series A

past due interest bond (119 cents).4Weighted average.

(1) 60 percent for the discount bond; (2) 27 percent forthe FLIRB; and (3) 13 percent for the buy-back. Inter-est arrears estimated at about $1.9 billion wereincluded in the operation. A cash payment of 3 percentwas made, with remaining amounts (other thanamounts purchased in connection with the buy-backoption) rescheduled in the form of a 17-year uncollat-eralized bond bearing a market interest rate of % overLIBOR and a grace period of seven years. Amortiza-tion is in semiannual installments on a back-loadedschedule. The cost of the operation was $716 million,which was initially financed by the country's ownresources. However, after the closing of the operation,Bulgaria requested and received additional financialassistance from the Fund and the World Bank in sup-port of the debt- and debt-service-reduction operation.

On February 14, 1994, the Dominican Republic for-mally signed an agreement to restructure $1.1 billionof its commercial bank debt, including interest arrearsof $320 million. The operation closed on August 31,1994. After an initial allocation failed to provide the 50percent debt reduction included in the term sheet, cred-itors were asked to rebalance their commitments. Thefinal allocation on eligible principal was 65 percent tothe discount exchange, 35 percent to the buy-back, andno allocation to the FLIRB. The up-front cost of the

operation was about $190 million, financed entirely bythe country's own resources.

A highly innovative and somewhat controversialagreement in principle was reached between Polandand its bank advisory committee on March 10, 1994.The larger-than-anticipated debt reduction entailed inthe agreement produced a significant decline in theprice of Polish debt in the secondary market after theannouncement. The agreement restructured $12.7 bil-lion, comprising virtually all of Poland's outstandingcommercial bank debt. A term sheet was distributed tobanks on May 23, 1994, and commitments were dueon June 29, 1994. That date was subsequentlyextended to improve chances that approval of a waiverfor a buy-back would be received from creditors hold-ing 95 percent of the debt. That figure was achieved,and the deal was completed on October 27, 1994. Eli-gible principal amounted to $9.9 billion, of which $1.1billion was short term. The menu for eligible principalincluded six options, four for medium- and long-termdebt and two for short-term debt. The options formedium- and long-term principal were (1) a buy-backat 41 cents on the dollar per unit of claim; (2) a 45 per-cent discount bond exchange; (3) a below-marketinterest rate par exchange; and (4) a new moneyoption, whereby in exchange for 35 percent of new

8

II

©International Monetary Fund. Not for Redistribution

Overview

money, old claims are rescheduled on somewhat morefavorable terms than in the other options. The optionsfor short-term principal were (1) a buy-back at 38 centson the dollar per unit of claim and (2) a below-marketinterest rate par bond exchange, with an interest rateprofile marginally higher than that for the par bondexchange for medium- and long-term principal.

The discount bond in the Polish package involved a30-year bullet repayment bearing a market interest rateof % over LIBOR. Principal was fully collateralized.The par bond also involved a 30-year bullet repaymentcarrying a prearranged interest rate profile starting at2.75 percent in year one, rising in increments to 5 per-cent in year twenty-one, and remaining at that levelthereafter. The interest rate profile on the short-termpar exchange was somewhat higher, in that the interestrate rises at a somewhat faster rate after year one. Bothpar bonds included full principal collateral. The newmoney option involved the exchange at par of up to 5percent of eligible principal for a debt conversionbond, with the creditor providing $35 in new moneyfor each $100 in debt tendered. The 25-year debt con-version bond had no principal collateral and carried asub-market interest rate starting at 4.5 percent in yearone, increasing to 7.5 percent in year eleven and there-after. This was an innovative feature of the package; inthe past, these types of bonds involved no debt- ordebt- service reduction. This bond has a grace periodof 20 years with equal semiannual amortization pay-ments. The 15-year new money bond also has no prin-cipal collateral. It carries a market rate of % overLIBOR, a grace period of ten years, and an even amor-tization schedule. None of the bonds in the package iscovered by interest guarantees.

Bank creditors allocated their medium- and long-term debt as follows: (1) 24.6 percent to the buy-back;(2) 60.8 percent to the discount exchange; (3) 10.3 per-cent to the par exchange; and (4) 4.4 percent to the newmoney option. Allocation of the short-term debt was asfollows: (1) 26.1 percent to the buy-back and (2) 73.9percent to the par exchange.

In the Polish package, past due interest of $3.5 bil-lion was effectively subject to debt and debt-servicereduction. Debt reduction of about 15 percent wasobtained by reducing the capitalization rate on interestarrears. Debt-service reduction was also obtainedthrough a below-market interest rate for the associatedbond. In theory, there were five modalities for dealingwith past due interest, two for interest arrears on short-term principal and three for interest arrears onmedium- and long-term principal. The options forshort-term interest arrears are exactly the same as theoptions for short-term principal. The three options forinterest arrears on medium- and long-term principalincluded (1) a cash payment corresponding to 85 per-cent of interest due in December 1989 to regularizeprevious anomalies and catch up on payments of inter-est due on medium- and long-term principal accruingsince May 1993 (about $160 million); (2) a buy-back

at the same price as medium- and long-term principal;and (3) a bond covering past due interest at below-market rates. The latter bond has a 20-year term and isuncollateralized; it carries an interest rate that starts at3.25 in year one and rises to 7 percent in year nine andthereafter. The amortization schedule on these bondsprovides for eight years grace followed by back-loadedsemiannual payments. Starting in March 1994, partialinterest payments on medium- and long-term principalwere increased to 30 percent of interest due. The finalagreement did not include a rebalancing clause, exceptfor the limit of 5 percent of eligible principal on thenew money option and an undetermined maximum onthe buy-back in the event that insufficient financingwas available. There was no currency option or valuerecovery clause. Implementation of a debt-conversionprogram is expected. The cost of the operation was$2.1 billion, financed with resources from the Fund,the World Bank, the new money option, and Poland'sown contribution.

Ecuador reached an agreement in principle with itsbank advisory committee on May 2, 1994, to restruc-ture debt amounting to $7.4 billion. A termsheet wascirculated to banks on June 14, 1994. The menu ofoptions for eligible principal, amounting to $4.5 bil-lion, includes (1) a 45 percent discount exchange; and(2) a par exchange at a submarket interest rate. The dis-count bond has a 30-year term with a bullet repayment;it bears a market interest rate of % over LIBOR andincludes full principal collateral and a 12-monthrolling interest guarantee at 7 percent. The par bondalso involves a 30-year bullet repayment; it bears apredetermined below-market interest rate profile start-ing at 3 percent in year one, increasing to 5 percent byyear eleven, and remaining at that rate for the balanceof the bond's maturity. As with the discount bond, theprincipal of the par bond is fully collateralized, but the12-month interest guarantee was fixed at 3.75 percentin year one, with income earnings capitalizing until 5percent is achieved. The termsheet does not includeany mandatory allocation or rebalancing clauses. Italso does not include a currency option or a valuerecovery clause. Creditors have chosen to allocate 58percent of their exposure to the discount exchange and42 percent to the par exchange.

Interest arrears on Ecuador's bank debt is estimatedat $2.9 billion. Implicitly, this estimate involves somedebt forgiveness, because past due interest is calcu-lated from the end of October 1986 to the end ofDecember 1993 at three-month LIBOR plus 13/1instead of the interest rates on the original loan agree-ments.8 From January 1994 through the closing date,interest will accrue at a 4 percent fixed rate. The agree-ment calls for interest arrears to be treated separatelythrough (1) a cash payment of $75 million; (2)issuance of a 10-year uncollateralized interest equal-

8Original contractual interest rates on Ecuador's debt were gen-erally higher, with some loans priced at LIBOR plus 2%.

9

©International Monetary Fund. Not for Redistribution

II COMMERCIAL BANK DEBT RESTRUCTURING

ization bond for $191 million to regularize previousdiscriminatory payments to creditors; and (3) a 20-yearuncollateralized past due interest bond bearing a mar-ket interest rate of % over LIBOR and a ten-year graceperiod. The amortization schedule on the latter bondconsists of back-loaded semiannual payments. ThePDI bond also introduces the innovation of having theoption to capitalize a declining fraction of interest duein the first six years. Partial interest payments wereresumed in May 1994 at a rate of $5 million a month(retroactive to January 1994). The up-front cost of theoperation has been estimated at about $658 million.Financing is expected to come from the Fund, theWorld Bank, official bilateral sources, and the coun-try's own resources. The deal is scheduled to close inDecember 1994.

Sao Tome and Principe concluded a comprehensivebuy-back of commercial bank debt covering $10.1 mil-lion of claims (about 87 percent of eligible debt) at 10cents on the dollar in August 1994. The $1.0 millioncost of the buy-back was entirely financed by the DebtReduction Facility for IDA countries.

Zambia completed a comprehensive buy-back at 11cents per dollar of principal and past due interest intwo transactions, the first on July 26, and the secondon September 14, 1994. Eligible principal coveredamounted to about $200 million (about 79 percent ofeligible debt) and included commercial bank debt, aswell as trade and supplier credits. The cost of the oper-ation thus far has been roughly $25 million, financedby a $13 million grant from the debt reduction facilityfor IDA countries and grants from Germany, theNetherlands, Sweden, and Switzerland. Further buy-backs could take place by the end of 1994, which is theexpiry date for Zambia's grant facility to finance theoperation. An innovation in this buy-back operation isthat, due to initially low levels of creditor participation,the operation has taken place in several tranches,instead of the usual single transaction.

South Africa agreed on a fourth and final reschedul-ing arrangement with its commercial banks at the endof September 1993. The arrangement, which becameeffective at the beginning of 1994, rescheduled thosedebts (some $5 billion) that were still subject to the"standstill" on repayments imposed in 1985. Thearrangement involved a cash payment of 10 percent ofoutstanding debt, with the remainder being resched-uled for eight years on a graduated schedule. Interestmargins were to be negotiated between South Africandebtors and foreign creditors, with margins in excessof 2.5 percent over the relevant base rate requiringapproval by the authorities under exchange controlarrangements.

A rescheduling agreement between Gabon and itscommercial bank creditors was signed on May 26,1994 and became effective on July 1, 1994. The agree-ment covers the principal on debts contracted beforeSeptember 1986 (which amounts to $100 million).These debts are rescheduled for ten years with 2 1/2 years

of grace. Interest arrears accumulated since 1986 (esti-mated at $50 million) were also rescheduled but atshorter maturities. This operation covered most of thecountry's commercial bank debt.

On July 30, 1993, a preliminary rescheduling agree-ment was reached between Russia and its bank credi-tors. This agreement rescheduled the entire stock ofpre-cutoff date debt with a ten-year maturity and afive-year grace period. Russia agreed to pay $500 mil-lion toward interest accrued but unpaid through the endof 1993. Remaining interest arrears were expected tobe rescheduled on the same terms as pre-cutoff dateprincipal. In the event, Russia did not make paymentson interest, and the agreement did not come into effect.Major stumbling blocks included the Russian authori-ties' refusal to waive sovereign immunity and ques-tions regarding which official Russian agency shouldsign the agreement. These issues were finally resolvedin October 1994, and the agreement was scheduled tocome into effect by the end of 1994, following Russianpayment of $500 million on past due interest in 1993,as was previously agreed.

Debt-Conversion ActivityAfter reaching a peak in 1990, debt conversions fell

over the last three years. In 1993, debt conversionswere at their lowest level since the outbreak of the debtcrisis over a decade ago (Table 4). High debt prices inthe secondary market, regularization of relations withcommercial bank creditors, and advances alreadymade in most privatization programs were responsiblefor declining conversion activity.

Argentina, which accounted for two thirds of con-version activity in 1992, shifted its privatization pro-gram to encourage exchanges involving foreigncurrency denominated domestic debt. With buoyantequity markets worldwide, Argentina also elected toprivatize part of the state oil company, YacimientosPetroliferos Fiscales (YPF), through an internationalshare placement, rather than by means of conversionsmade with commercial bank debt. Despite these devel-opments, Argentina still accounted for about one fourthof total bank debt conversions in 1993. While involv-ing only small amounts, debt conversions more thandoubled in Brazil during 1993, reflecting some pickupin interest by foreign investors in the country's privati-zation program. Debt conversion activity in Chile fellby one fourth during 1993, with the high price of com-mercial bank debt in the secondary market continuingto curtail demand for debt conversions under the for-mal mechanisms. All conversion activity took placethrough "informal" schemes, under which residentsretire their debt to the Central Bank by delivery ofChilean debt acquired in the secondary market.

Among other countries, conversions in the Philip-pines declined by about 15 percent as investors' inter-est dropped and debt prices edged up. Activity wasnegligible in Mexico and Nigeria owing to the suspen-

10

©International Monetary Fund. Not for Redistribution

Secondary Market Developments

Table 4. Debt(In millions of U.S.

ArgentinaBrazilChileCosta RicaEcuador

HondurasJamaicaMexicoNigeriaPhilippines

TanzaniaUruguayVenezuelaYugoslavia

Total

Conversions1

dollars)

1987

3361,979

89127

91

1,680

450

__———

4,671

1988

1,1462,0962,940

44261

149

l,0563

40931

_

6050

135

8,782

1989

1,534946

2,76712432

3523

532257630

_

27544

1,369

8,820

1990

6,464283

1,0961745

3322

221217378

114

595681

10,067

1991

13268

8282

20

5236

1,956119489

2144

343631

4,741

1992

2,8252

95385—50

3914

344122379

3334

148

4,468

1993

371219298—

2

_

3—35

349

524887

1,464

First Quarter1994

530

2——

——

—

37

Sources: Central Bank of Argentina; Central Bank of Brazil; Central Bank of Chile; Ministry of Finance of Mexico; Central Bank of thePhilippines; Bank of Jamaica; Central Bank of Venezuela; and IMF staff estimates.

'Face value of debt converted under official ongoing schemes. Figures do not include large-scale, one-off cash buy-backs and debtexchanges.

2Excludes $0.3 billion from the privatization of the state power company deposited in a trust fund for later debt conversion as well as $0.5billion in foreign currency bonds of the Argentine Government (BOCONES) retired with the privatization of the state gas and power companies.

3Does not include an estimated $6-8 billion related to payment at a discount of private-sector debt following the August 1987 signing ofan agreement to restructure debt of the foreign exchange risk coverage trust fund (FICORCA).

sion of conversion programs. In Venezuela, politicaland financial uncertainties were factors behind a fur-ther reduction in conversion activity in 1993.

Secondary Market Developments

After remaining stable in the first quarter of 1993,secondary market prices for bank claims and Bradybonds rose sharply later in the year and into early 1994(Chart 3). The weighted average of prices for claims on15 heavily indebted countries peaked in January 1994at about 70 cents on the dollar (compared with 51 centsin December 1992), its highest level in the last sevenyears. The strength in secondary market pricesreflected improving economic situations in majordeveloping countries and greater investor interest inemerging market securities. Subsequently, prices fellsharply in response to higher interest rates in the UnitedStates and market reactions to adverse economic andpolitical developments in some major countries. More-over, during the 1993 run-up in prices, some investorgroups built up some highly leveraged positions; theirsubsequent need to unwind these positions added to thedrop in debt prices during the first half of the year. Bythe end of June 1994, the weighted average price forthe 15 countries had fallen to 58 cents on the dollar.

The stripped price of Argentina's restructured bankclaims rose by 82 percent in 1993, reaching about 80

cents on the dollar by the end of the year.9 Completionof the debt- and debt-service-reduction operation, goodeconomic prospects, the privatization of the largestpublic enterprise (YPF), and Congressional approvalof the social security reform accounted for the solidperformance of Argentine debt prices. By the end ofJune 1994, the price of Argentine claims had declinedin line with overall market developments to 62 centson the dollar.

Following market trends, the price of claims onBrazil also performed well in 1993. Debt pricesclimbed by 62 percent in 1993, reaching about 50 centson the dollar by the end of the year, despite politicaluncertainties and difficulties in completing the debtdeal. By the end of June 1994, the price of Brazilianclaims had fallen back to 41 cents on the dollar. InMexico, while the stripped price of its claims did notchange much over the first three quarters of 1993,prices jumped in the last quarter by about one third fol-lowing the approval of the North American Free TradeAgreement. By year end, Mexican Brady bonds weretrading at almost 90 cents on the dollar. Concernsresulting from an uprising in Chiapas and the assassi-nation of the leading presidential candidate, togetherwith the tightening of monetary policy in the United

9The stripped price is a measure of country risk. It is the ratio ofthe market value of unguaranteed payments to the present value ofsuch payments discounted at a risk-free interest rate.

11

©International Monetary Fund. Not for Redistribution

II COMMERCIAL BANK DEBT RESTRUCTURING

Chart 3. Secondary Market Prices of Bank Claimson Selected Countries(In percent of face value)

Sources: Salomon Brothers; and ANZ Grindlays Bank.

States, led by June 1994 to a decline in the strippedprice of Mexican bonds to 73 cents. The stripped priceson Venezuela's debt increased by about one fourth toreach about 69 cents on the dollar at the end of 1993,despite political uncertainties. Concerns about thehealth of the banking system in the wake of the failureof a major bank and more generally about the country'seconomy, contributed to a sharp decline in Venezuelanclaims in the first half of 1994. By June, they hadfallen to 42 cents on the dollar.

In 1993 and early 1994, considerable price specula-tion accompanied reports that various countries weremaking progress in their discussions with commercial

banks on restructuring agreements. In the case ofEcuador, the price of its debt (including past due inter-est) increased by 84 percent in 1993 to reach a level ofabout 53 cents on the dollar at the end of the year. ForPeru, expectations of a debt-conversion programlinked to privatization ran prices up sharply; the priceof Peruvian claims (including past due interest) rose byabout 250 percent in 1993 and closed the year at 69cents on the dollar. In both cases, prices slid in the firsthalf of 1994, falling to 40 cents and 48 cents, respec-tively, by the end of June.

Price developments on Eastern European countries'debt resembled the behavior of debt prices for otherindebted countries. Prices of claims on Eastern Euro-pean countries increased by about 150 percent to reachalmost 50 cents on the dollar by the end of 1993,before declining by one third in the first half of 1994.The announcement of Bulgaria`s agreement in princi-ple with commercial banks in November 1993 pro-duced a 50 percent increase in the price of its claims toabout 44 cents on the dollar; it fell to 33 cents by theend of June 1994. Expectations of a bank debt agree-ment for Poland contributed to a rise in the price ofPolish debt, which peaked at 51 cents on the dollar inJanuary 1994. It then dropped in line with the generalfall in debt prices; the decline accelerated followingthe announcement of the restructuring agreement inMarch 1994. After falling to 32 cents, it recovered to35 cents by the end of June.

There were indications of significant growth in thevolume of debt instruments trading in the secondarymarket during 1993. These instruments continue to berelatively liquid, as reflected in relatively tight bid-askspreads. Market analysts estimate that trading volumereached nearly $2 trillion in 1993.10 For short periodsof time during the turbulence in bond markets duringthe first half of 1994, however, trading was reported tohave slowed appreciably, with bid-ask spreads widen-ing and dealers at times being reluctant to quote prices.

10The Emerging Markets Traders Association (EMTA) estimatedvolume at $733.7 billion in 1992. EMTA is planning to implementa computerized trade-clearing system to verify bond and loantrades. The system is expected to be in place by January 1995 andwill provide uniform pricing as well as daily volume information,thus reducing transaction costs, contentious trade disputes, and thepossibility of error arising from manual processing.

12

©International Monetary Fund. Not for Redistribution

IllRecent Developments in Private MarketFinancing

rivate market financial flows to developing coun-tries increased significantly in 1992 and 1993

(Chart 4). Bond and equity flows accounted for muchof the increase. The rapid expansion was mirrored in abroadening of the range of developing country borrow-ers attracting international investors, although portfolioflows continued to be concentrated in a few key coun-tries in Asia and Latin America. In contrast, medium-and long-term bank lending to developing countriesremained moderate; banks did demonstrate renewedinterest in such lending, but on a highly selective basis.

In 1994, the situation changed dramatically. Withhigher U.S. interest rates, as well as unfavorable eco-nomic and political developments in some major bor-rowing countries, bond and equity issuance bydeveloping countries plummeted between Februaryand April 1994. A modest recovery came in the follow-ing months, but new flows remained vulnerable, espe-cially because of the uncertain course of U.S. interestrates. Despite the market correction, however, portfo-lio flows to developing countries in the first half of1994 were still significantly higher than levelsrecorded in the early 1990s.

Bonds

country bond placements also increased from $111million in 1992 to $125 million in the first half of1993, and to $135 million in the second half of theyear. In particular, there were a number of sizableissues by borrowers in Latin America.

In the first half of 1994, volatile market conditionsled to a sharp decline in the volume of internationalbond issuance by developing countries. Bonds worth$26.1 billion were issued, most in the beginning of theyear and in June. Beginning in February, as bondyields rose throughout the world, both issuers andinvestors pulled back. For the first half of 1994 as awhole, the developing country share of total interna-tional bond issues fell to 12 percent. The decline wasparticularly notable for countries in Europe and LatinAmerica.

The terms on new issues for many developing coun-try borrowers improved throughout 1993 and into early1994. The average yield spread fell from 288 basispoints in the first quarter of 1993 to a low of 187 basis

Chart 4. Private Market Financing to DevelopingCountries(In millions of U.S. dollars)

Bond placements by developing country borrowersreached $59.4 billion in 1993, more than twice theamount placed in 1992 (Tables 5 and A5).11 There wasa strong acceleration in bond issuance in the final quar-ter of 1993; bonds issued in that quarter amounted to$23.7 billion, almost equal to total issuance activity in1992. This surge reflected a decline in U.S. interestrates combined with relatively high returns in emerg-ing markets. Both factors encouraged a broader rangeof mainstream institutional investors to participatemore actively in these markets. The continued imple-mentation of prudent macroeconomic policies andstructural adjustments in borrowing countries alsoimproved investors' confidence. In relative terms,developing countries continued to increase their shareof total international bond issuance from 7.1 percent in1992 to 12.4 percent in 1993, and to 20.1 percent in thefourth quarter of 1993. The average size of developing

"Includes reported private placements and notes issued underthe Euro-medium-term note programs. The figures differ fromOECD estimates, which have a narrower coverage.

Sources: International Financing Review; OECD; and IMF staffestimates.

1Medium- and long-term bank loan commitments only.

13

P

©International Monetary Fund. Not for Redistribution

RECENT DEVELOPMENTS IN PRIVATE MARKET FINANCING

Chart 5. Yield Spreads at Launch for Unenhanced Chart 6. Secondary Market Yield Spreads on U.S.Bond Issues by Developing Countries1 Dollar Denominated Bonds by Selected Developing(In basis points) Countries

(In basis points)

Sources: International Financing Review; and Financial Times.1Reflect weighted averages.

points in the first quarter of 1994 (Chart 5).12 The aver-age spread widened sharply in the second quarter of1994 to 259 basis points. This increase occurreddespite the fact that bonds during this period wereissued primarily by borrowers with higher credit rat-ings and carried shorter maturities. The weighted aver-age maturity of bonds issued shortened to 6.3 years inthe first half of 1994, after lengthening from 5.4 yearsin the first quarter of 1993 to 7.2 years in the finalquarter of the year. Yield spreads in the secondary mar-ket for developing country bonds followed a similarpattern; notable increases were observed for bondsissued by Argentina, Brazil, Hungary, Mexico, Turkey,and Venezuela (Chart 6). A tightening of market condi-tions was also reflected in a sharp decline in secondarymarket prices for Brady bonds.

Yield spreads continued to vary considerably amongcountries. While borrowers without records of debt-servicing difficulties commanded lower spreads, mar-ket re-entrants were typically faced with spreads ofover 200 basis points in 1993 and the first half of 1994.Moreover, the spread for public sector borrowers con-tinued to be substantially lower than that for privatesector borrowers (Table A6). Reflecting the uncertainpath of U.S. interest rates, there was also renewedinterest in new issues bearing floating rates. In the first

12 throughout this chapter, yield spreads refer to the differencebetween the yield on a bond at the time of issuance and the yield onU.S. Treasury securities of comparable maturity or other compara-ble government securities if the bond is issued in other currencies.The U.S. Treasury security and other comparable governmentsecurities are used as a proxy for a risk-free return.

Source: Reuters.

half of 1994, floating rate notes accounted for some 20percent of total new issues, up from 8 percent in 1993.

Most of the recent bond issuance by developingcountries represents net capital inflows. Maturingdeveloping country bonds amounted to only $6.3 bil-lion in the period from 1991 to 1993, compared withtotal bond issues worth $96 billion. As of the end ofJune 1994, the total outstanding stock of internationalbonds issued by developing countries is estimated tostand at $117.5 billion, 42 percent of which wasaccounted for by private sector borrowers. Amortiza-tion payments on this stock of debt will rise sharply inthe next few years from an estimated $7.1 billion in1994 to a peak of $21 billion in 1998, as bullet repay-ments on bonds placed in the early 1990s fall due(Table A7).13 Payments are particularly concentrated ina few Western Hemisphere and Asian countries.

Although the range of borrowers continued to widenin 1993, developing country bond issuers remainedconcentrated in a few countries in Latin America, Asia,

13These estimates can vary somewhat depending upon whetherbondholders decide to take early redemption options for somebonds.

14

III

©International Monetary Fund. Not for Redistribution

Bonds

Table 5. International Bond Issues by Developing Countries and Regions1

(In millions of U.S. dollars)

Developing countries

AfricaCongoSouth AfricaTunisia

AsiaChinaHong KongIndiaIndonesiaKoreaMacaoMalaysiaPakistanPhilippinesSingaporeTaiwan Province of ChinaThailand

EuropeCzech RepublicCzechoslovakia, formerHungarySlovak RepublicTurkey

Middle EastIsrael

Western HemisphereArgentinaBarbadosBoliviaBrazilChileColombiaCosta RicaGuatemalaMexicoPanamaPeruTrinidad and TobagoUruguayVenezuela

Memorandum itemsIssues under EMTN programs

ArgentinaBoliviaBrazilColombiaKoreaMexicoPhilippinesThailandVenezuela

Total bond issues ininternational bond markets

Shares of developing countriesin global issuance

1991

12,838

236—

236—

3,000115100227369

2,012

————

16017

1,960—

2771,186

—497

400400

7,242795

——

1,837200

—3,782

50——

578

375———

375—

—

297,588

4.3

1992

23,780

725—

725—

5,9171,359

185

4943,208

————60

610

4,561—

1291,242

—3,190

—

12,5771,570

——

3,655120

—6,100

100100932

1,21540

110

665—

400

333,694

7.1

1993

59,437

—

—

20,4013,0475,887

546485

5,864

954—

1,293—79

2,247

9,638697

—4,796

2403,9052,0022,002

27,3966,233

——

6,679433566

6010,783

30125140

2,348

3,713930

422100177

1,741150194—

480,997

12.4

I

10,109

—

—

2,230406657

30671

——

170——

296

2,863375—

1,363—

1,1251,0001,0004,017

335——

1,327—

—2,205

———

150

607—

62

545—

—

139,867

7.2

1993II

12,117

—

—

3,200651

—

—1,343

500—

175—36

495

1,257——

279—

978

—

7,559606

——

1,635333325

—4,136

——

140385

39350

110509390—

—

107,050

(In percent)

11.3

III

13,492

—

—

3,4811,209

69265—

725

——

190—43

557

1,988322—

1,280240145

1,0021,0027,0221,852

——

1,583—50

601,851

———

1,626

1,439450

10050

646—

194—

116,253

11.6

IV

23,719

—

—

11,391681

4,538481455

3,125

454—

758——

899

3,530——

1,873—

1,657

—

8,7983,440

• —

—

2,134100191

—2,591

3025—

187

1,274430

—150

84460150

—

117,827

20.1

I

17,668

877600

277

7,6451,5001,305

439699

1,273

230—

154—

3181,728

875——6921

785

1,9581,9586,3131,460

—10

1,095—

25050—

3,307

40—

100—

384—1035

189150———

139,820

12.6

1994II

8,443

_—

—

5,465872550195750580155735

45555

86558384

439250

—189——

—

2,539907

20—

100—83

—1,390

40———

695300

——

—395———

77,881

10.8

Sources: IMF staff estimates based on Euroweek, Financial Times, International Financing Review, Financial Market Trends, FinancialStatistics Monthly, and Organization for Economic Cooperation and Development.

'Including note issues under Euro medium-term notes (EMTN) programs.

15

©International Monetary Fund. Not for Redistribution

RECENT DEVELOPMENTS IN PRIVATE MARKET FINANCING

and Europe. Latin American borrowers had the largestshare until they were surpassed by Asian borrowers inthe final quarter of 1993. Bond issues by Latin Ameri-can borrowers doubled to $27.4 billion in 1993,accounting for 46 percent of total issues by developingcountries. That figure declined in the first half of 1994to $8.9 billion, or 34 percent of total issues by devel-oping countries.

Mexico continued to be the leading borrower, rais-ing $10.8 billion in 1993 and $4.7 billion in the firsthalf of 1994. An increasing number of companiesplaced bonds, including several private and publicbanks. Moreover, a few firms floated quite sizableindividual issues during this period, including $1 bil-lion issues by CEMEX (Mexico's largest cement pro-ducer) in May 1993 and BANCOMEXT in January 1994.Mexican entities also opened up new currency sectors,with Mexico's launching of Latin America's first"Samurai" issue since the debt crisis, BANAMEX issuinga Mexican peso-denominated Eurobond, and NAFINSA(a Mexican development bank) placing a "Dragon"bond, marking the first time that a Latin Americannoninvestment grade borrower has been able to issuein that market.

Borrowers in Argentina quadrupled their bond issuesto $6.2 billion in 1993 and raised $2.4 billion in thefirst half of 1994. There were a number of new devel-opments. A $1 billion global sovereign bond wasissued in December 1993 at a spread of 280 basispoints, the first global bond ever issued by a develop-ing country borrower.14 In addition, the first significantconvertible bond by a private telephone companybased in a developing country was placed in March1994. Brazil also increased its bond issuance signifi-cantly in 1993, notwithstanding continued uncertaintyabout the course of its economic policies. All Brazilianbonds were issued by nonsovereign borrowers andincluded the first Euro-yen issue by a Latin Americanentity at a spread of 416 basis points. Venezuelan enti-ties also increased their borrowing activity in 1993;among others, a $1 billion bond was issued by PDVAmerica (a state oil company) at a spread of 210-218basis points, and the first intraregional bond was issuedsimultaneously in Colombia and Luxembourg. Mainlyreflecting the concerns of investors about the country'seconomic situation; however, no international bondswere placed by Venezuelan borrowers during the firsthalf of 1994.

In general, the range of Latin American borrowers inthe international bond market continued to broaden.Colombia, Guatemala, and Peru, and more recently

14Global bonds are issued simultaneously in several major inter-national markets and allow issuers to tap into broader demand andobtain lower rates than those available in a single market. Somemarket participants estimated that Argentina was able to reduce theinterest rate on the funds raised through the global issue by asmuch as 30 basis points.

Barbados, Bolivia, and Costa Rica, tapped the marketfor the first time in many years. Spreads ranged from215 basis points for Colombia to over 700 basis pointsfor Peru. At the same time, recent market re-entrantssuch as Chile, Trinidad and Tobago, and Uruguaymaintained their presence in the market.