winning a deal in private equity: do educational networks ...

Upload

independentCategory

view

1download

0

AN INTRODUCTION TO PRIVATE EQUITY

www.lloydbancaire.com

2

Essen%ally private equity is an alterna%ve way of owning a company

What is private equity?

Private Equity is not necessarily a cure-‐all soluIon to company ownership. It is merely an alternaIve to public company ownership (buying shares in companies through the stock market). But it’s aPracted a lot of interest and a lot of capital in recent years, driven especially by benign market condiIons and accessible and affordable credit.

3

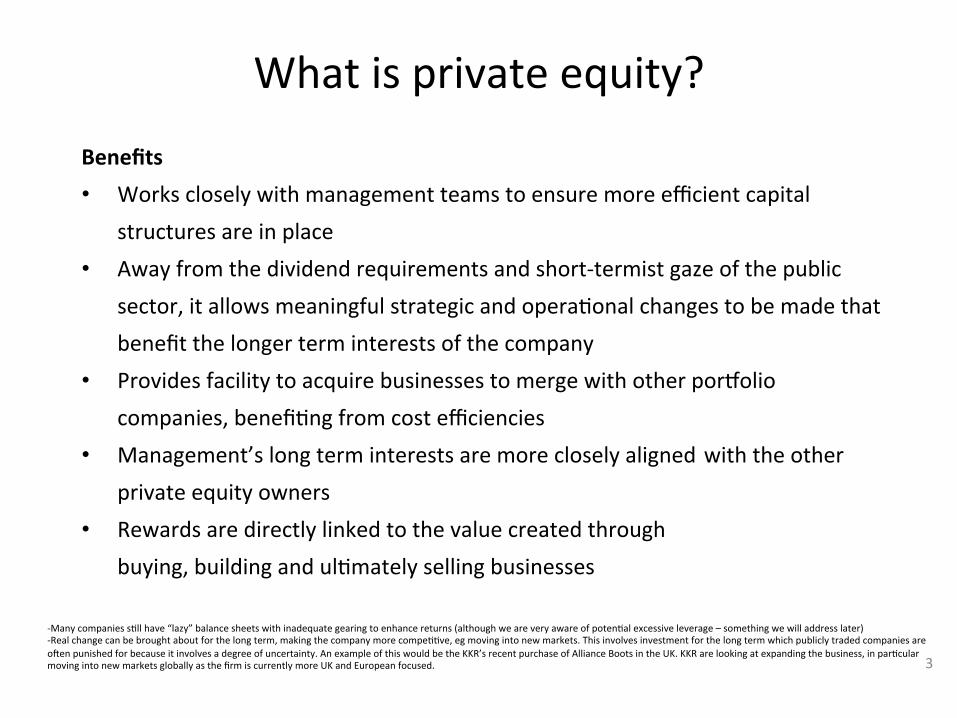

Benefits • Works closely with management teams to ensure more efficient capital

structures are in place • Away from the dividend requirements and short-‐termist gaze of the public

sector, it allows meaningful strategic and operaIonal changes to be made that benefit the longer term interests of the company

• Provides facility to acquire businesses to merge with other porXolio companies, benefiIng from cost efficiencies

• Management’s long term interests are more closely aligned with the other private equity owners

• Rewards are directly linked to the value created through buying, building and ulImately selling businesses

What is private equity?

-‐ Many companies sIll have “lazy” balance sheets with inadequate gearing to enhance returns (although we are very aware of potenIal excessive leverage – something we will address later) -‐ Real change can be brought about for the long term, making the company more compeIIve, eg moving into new markets. This involves investment for the long term which publicly traded companies are o^en punished for because it involves a degree of uncertainty. An example of this would be the KKR’s recent purchase of Alliance Boots in the UK. KKR are looking at expanding the business, in parIcular moving into new markets globally as the firm is currently more UK and European focused.

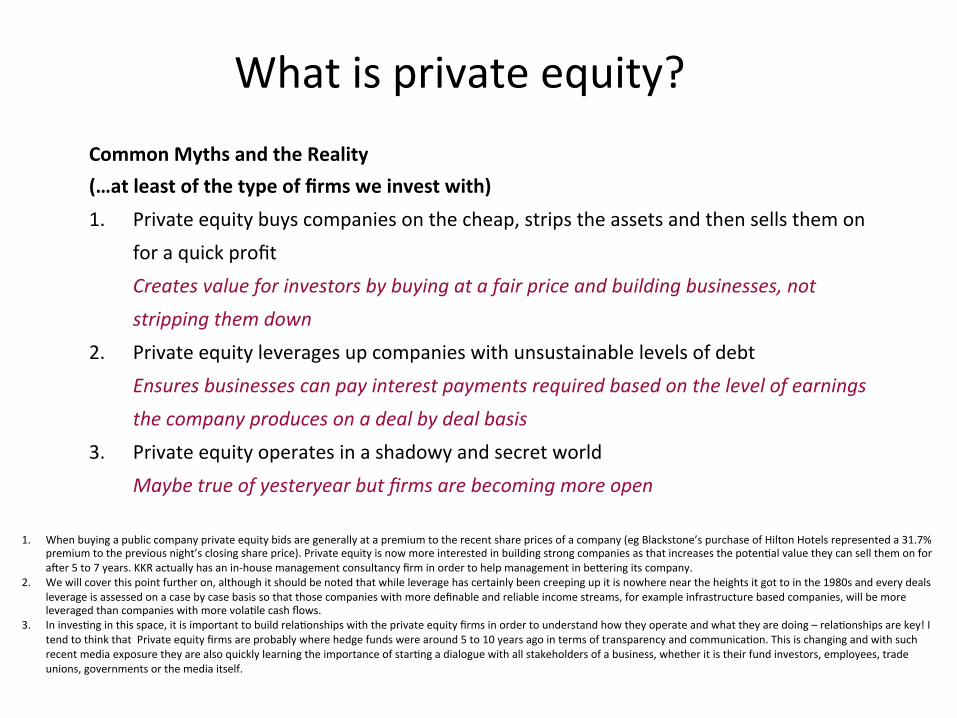

Common Myths and the Reality (…at least of the type of firms we invest with) 1. Private equity buys companies on the cheap, strips the assets and then sells them on

for a quick profit Creates value for investors by buying at a fair price and building businesses, not stripping them down

2. Private equity leverages up companies with unsustainable levels of debt Ensures businesses can pay interest payments required based on the level of earnings the company produces on a deal by deal basis

3. Private equity operates in a shadowy and secret world Maybe true of yesteryear but firms are becoming more open

What is private equity?

1. When buying a public company private equity bids are generally at a premium to the recent share prices of a company (eg Blackstone’s purchase of Hilton Hotels represented a 31.7% premium to the previous night’s closing share price). Private equity is now more interested in building strong companies as that increases the potenIal value they can sell them on for a^er 5 to 7 years. KKR actually has an in-‐house management consultancy firm in order to help management in bePering its company.

2. We will cover this point further on, although it should be noted that while leverage has certainly been creeping up it is nowhere near the heights it got to in the 1980s and every deals leverage is assessed on a case by case basis so that those companies with more definable and reliable income streams, for example infrastructure based companies, will be more leveraged than companies with more volaIle cash flows.

3. In invesIng in this space, it is important to build relaIonships with the private equity firms in order to understand how they operate and what they are doing – relaIonships are key! I tend to think that Private equity firms are probably where hedge funds were around 5 to 10 years ago in terms of transparency and communicaIon. This is changing and with such recent media exposure they are also quickly learning the importance of starIng a dialogue with all stakeholders of a business, whether it is their fund investors, employees, trade unions, governments or the media itself.

5

• Buy Outs/Buy Ins: either providing the capital to enable current operaIng management to acquire an exisIng business or enabling an external manager to buy into a company

• Venture Capital: investments made at an early stage in a company’s life • Development Capital: financing provided for the growth or expansion of a company • Mezzanine Debt: typically debt capital giving the lender rights to convert to an

ownership or equity interest if the loan is not paid back in Ime and in full

What is private equity? Categories of investment

Private equity broadly refers to equity investment in companies that are not traded on public stock markets

• Buyouts o^en take controlling posiIons in companies and work with the management teams to build significant value. These are what we have been hearing so much of in the press over the last few years Other frequently used terms include Leveraged Buyout.

• Venture Capital was on everyone’s lips during the tech and internet boom of the late 1990s. This is the highest risk area as you are backing untried companies and someImes untried managers, but can lead to excepIonal returns if they get it right, a^er all this is how Google and YouTube

started! • Development, Expansion or Growth Capital is an intermediate financing stage enabling a company to conInue to grow, launch new products or expand in to new regions. • Mezzanine Debt is a lower risk form of private financing. It is a hybrid financial instrument o^en employed in buyouts and other private equity transacIons. In a company’s capital structure, mezzanine is subordinated to senior debt, but ranks ahead of equity. It carries a higher rate of interest than senior debt, and may be bundled with an equity parIcipaIon such as warrants or common stock. Mezzanine securiIes can be designed to meet a broad range of financing needs and risk/return targets by combining various structural features. For example, interest payments can be broken down into current coupons, which are paid on a periodic basis, and accrued or “payment-‐in-‐kind” interest, which is added to the principal amount of the loan. ConIngent coupons can link interest payments to the fulfilment of operaIonal milestones or other condiIons.

6

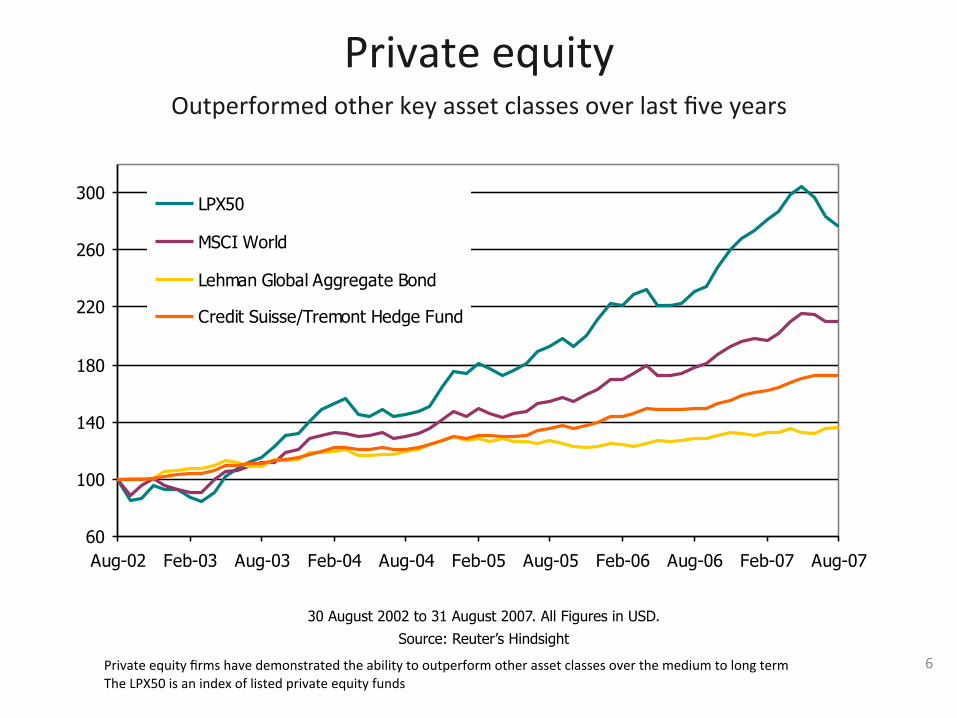

Private equity Outperformed other key asset classes over last five years

30 August 2002 to 31 August 2007. All Figures in USD.

Source: Reuter’s Hindsight

60

100

140

180

220

260

300

Aug-02 Feb-03 Aug-03 Feb-04 Aug-04 Feb-05 Aug-05 Feb-06 Aug-06 Feb-07 Aug-07

LPX50

MSCI World

Lehman Global Aggregate Bond

Credit Suisse/Tremont Hedge Fund

Private equity firms have demonstrated the ability to outperform other asset classes over the medium to long term The LPX50 is an index of listed private equity funds

7

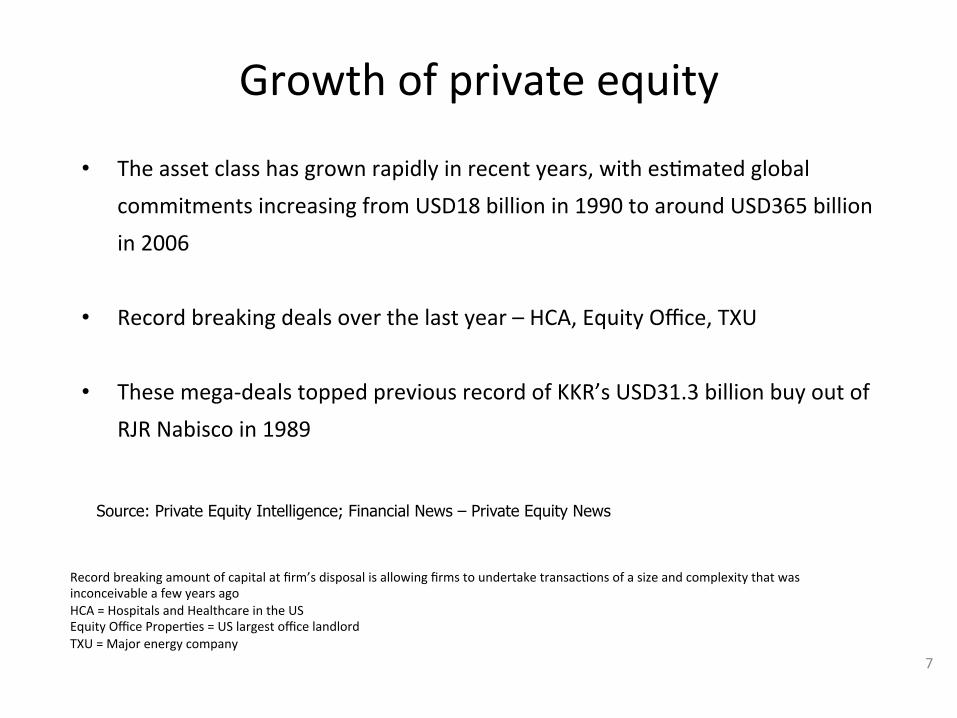

• The asset class has grown rapidly in recent years, with esImated global commitments increasing from USD18 billion in 1990 to around USD365 billion in 2006

• Record breaking deals over the last year – HCA, Equity Office, TXU

• These mega-‐deals topped previous record of KKR’s USD31.3 billion buy out of RJR Nabisco in 1989

Growth of private equity

Source: Private Equity Intelligence; Financial News – Private Equity News

Record breaking amount of capital at firm’s disposal is allowing firms to undertake transacIons of a size and complexity that was inconceivable a few years ago HCA = Hospitals and Healthcare in the US Equity Office ProperIes = US largest office landlord TXU = Major energy company

8

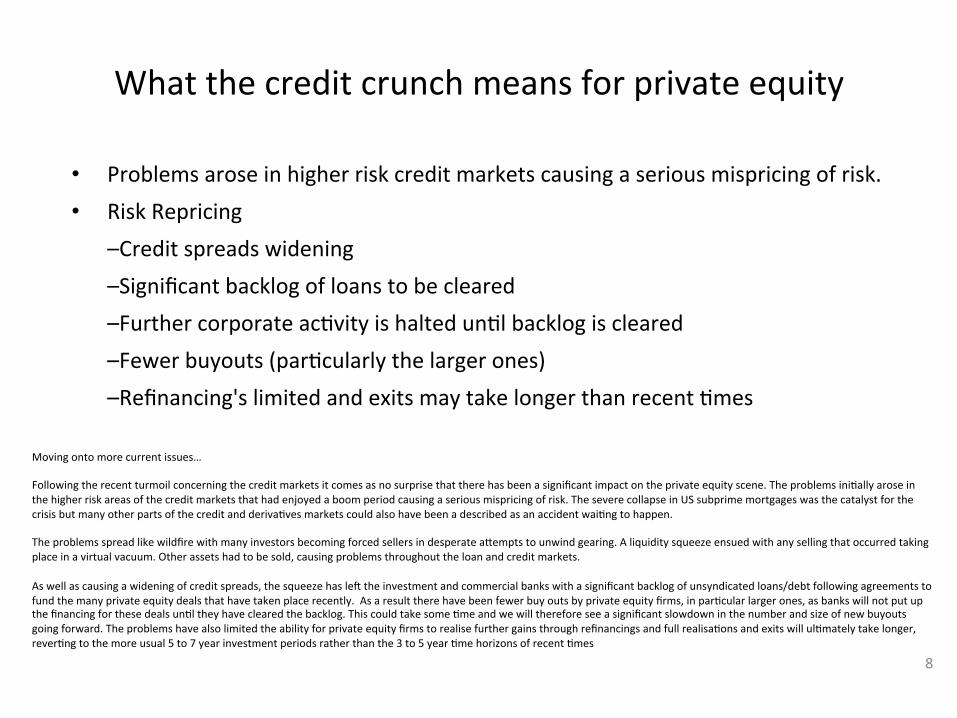

• Problems arose in higher risk credit markets causing a serious mispricing of risk. • Risk Repricing

– Credit spreads widening – Significant backlog of loans to be cleared – Further corporate acIvity is halted unIl backlog is cleared – Fewer buyouts (parIcularly the larger ones) – Refinancing's limited and exits may take longer than recent Imes

What the credit crunch means for private equity

Moving onto more current issues… Following the recent turmoil concerning the credit markets it comes as no surprise that there has been a significant impact on the private equity scene. The problems iniIally arose in the higher risk areas of the credit markets that had enjoyed a boom period causing a serious mispricing of risk. The severe collapse in US subprime mortgages was the catalyst for the crisis but many other parts of the credit and derivaIves markets could also have been a described as an accident waiIng to happen. The problems spread like wildfire with many investors becoming forced sellers in desperate aPempts to unwind gearing. A liquidity squeeze ensued with any selling that occurred taking place in a virtual vacuum. Other assets had to be sold, causing problems throughout the loan and credit markets. As well as causing a widening of credit spreads, the squeeze has le^ the investment and commercial banks with a significant backlog of unsyndicated loans/debt following agreements to fund the many private equity deals that have taken place recently. As a result there have been fewer buy outs by private equity firms, in parIcular larger ones, as banks will not put up the financing for these deals unIl they have cleared the backlog. This could take some Ime and we will therefore see a significant slowdown in the number and size of new buyouts going forward. The problems have also limited the ability for private equity firms to realise further gains through refinancings and full realisaIons and exits will ulImately take longer, reverIng to the more usual 5 to 7 year investment periods rather than the 3 to 5 year Ime horizons of recent Imes

9

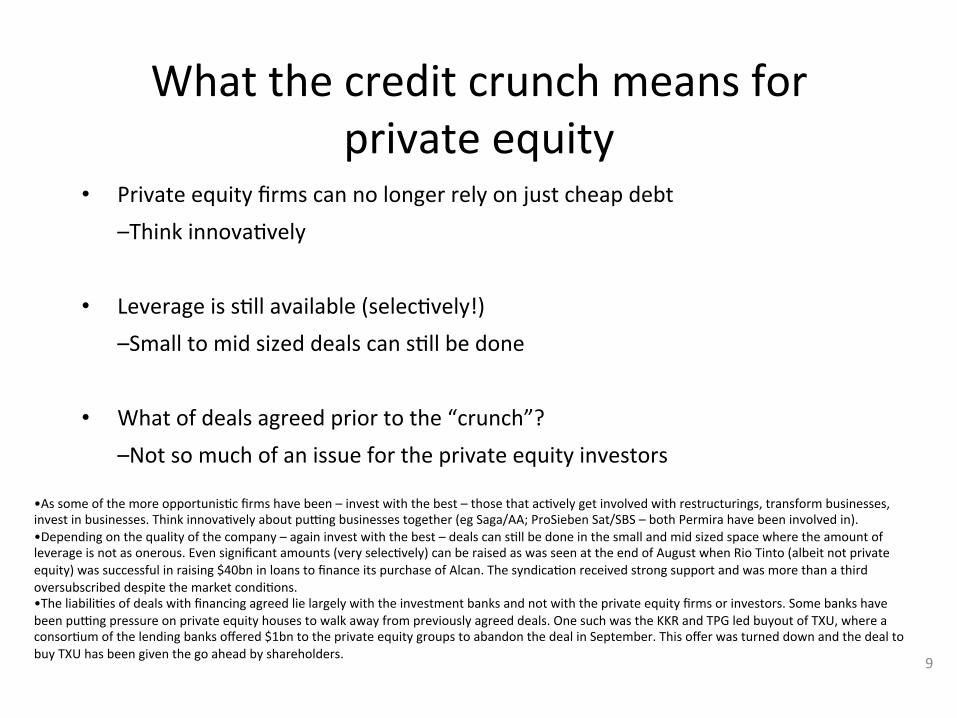

• Private equity firms can no longer rely on just cheap debt – Think innovaIvely

• Leverage is sIll available (selecIvely!)

– Small to mid sized deals can sIll be done • What of deals agreed prior to the “crunch”?

– Not so much of an issue for the private equity investors

What the credit crunch means for private equity

• As some of the more opportunisIc firms have been – invest with the best – those that acIvely get involved with restructurings, transform businesses, invest in businesses. Think innovaIvely about puxng businesses together (eg Saga/AA; ProSieben Sat/SBS – both Permira have been involved in). • Depending on the quality of the company – again invest with the best – deals can sIll be done in the small and mid sized space where the amount of leverage is not as onerous. Even significant amounts (very selecIvely) can be raised as was seen at the end of August when Rio Tinto (albeit not private equity) was successful in raising $40bn in loans to finance its purchase of Alcan. The syndicaIon received strong support and was more than a third oversubscribed despite the market condiIons. • The liabiliIes of deals with financing agreed lie largely with the investment banks and not with the private equity firms or investors. Some banks have been puxng pressure on private equity houses to walk away from previously agreed deals. One such was the KKR and TPG led buyout of TXU, where a consorIum of the lending banks offered $1bn to the private equity groups to abandon the deal in September. This offer was turned down and the deal to buy TXU has been given the go ahead by shareholders.

10

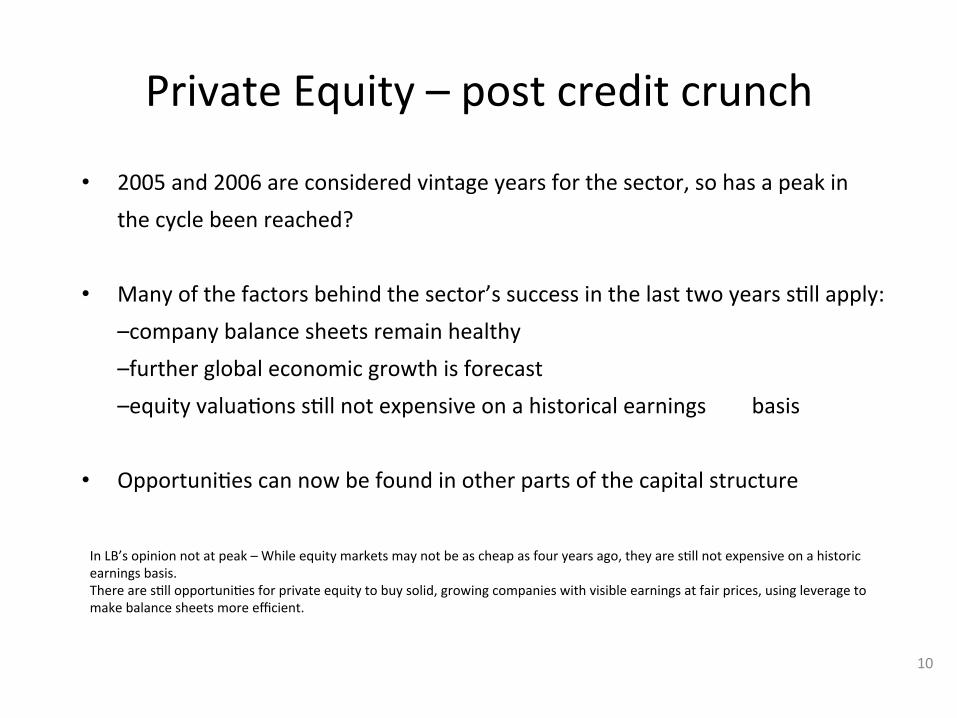

• 2005 and 2006 are considered vintage years for the sector, so has a peak in the cycle been reached?

• Many of the factors behind the sector’s success in the last two years sIll apply:

– company balance sheets remain healthy – further global economic growth is forecast – equity valuaIons sIll not expensive on a historical earnings basis

• OpportuniIes can now be found in other parts of the capital structure

Private Equity – post credit crunch

In LB’s opinion not at peak – While equity markets may not be as cheap as four years ago, they are sIll not expensive on a historic earnings basis. There are sIll opportuniIes for private equity to buy solid, growing companies with visible earnings at fair prices, using leverage to make balance sheets more efficient.

11

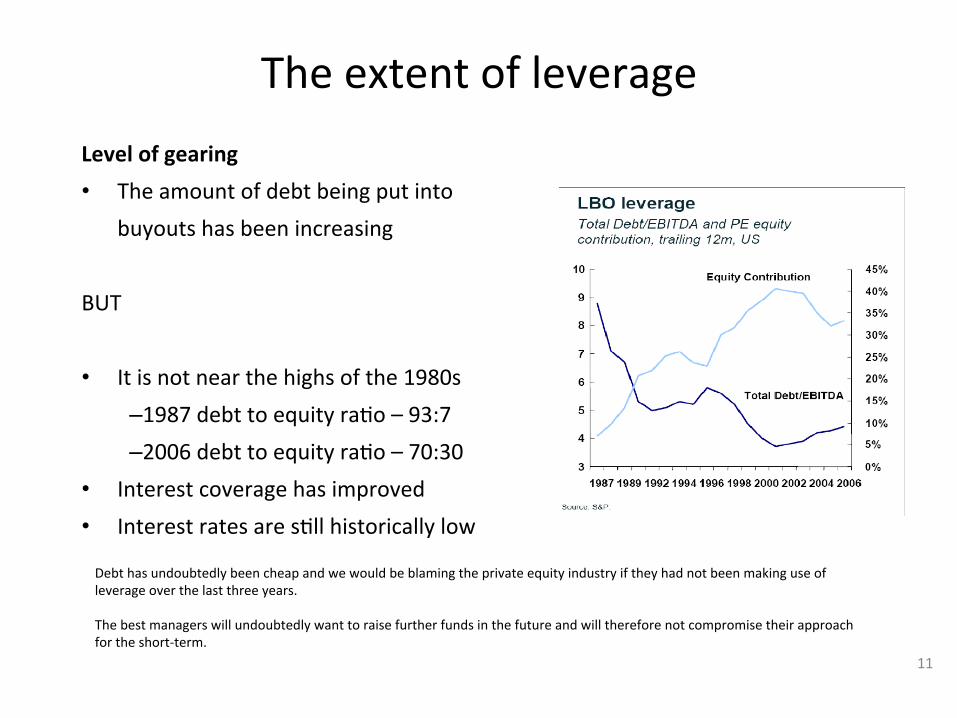

The extent of leverage Level of gearing • The amount of debt being put into

buyouts has been increasing

BUT • It is not near the highs of the 1980s

– 1987 debt to equity raIo – 93:7 – 2006 debt to equity raIo – 70:30

• Interest coverage has improved • Interest rates are sIll historically low

Debt has undoubtedly been cheap and we would be blaming the private equity industry if they had not been making use of leverage over the last three years. The best managers will undoubtedly want to raise further funds in the future and will therefore not compromise their approach for the short-‐term.

12

• Avoid private equity firms involved in over aggressive/unrealisIc leverage and

those paying too much for companies

• Get a greater understanding of the whole market • From the lenders point of view – fixed income fund managers • From sellers point of view – public equity fund managers

• A diversified approach is all important

Invest with the best – and know the market

• It is important to invest with those firms that have solid track records and can exhibit a great understanding of the parIcular market they operate in. They should not be over aggressive in their targets as this increases risk and similarly should not overpay for assets, instead staying disciplined and not afraid of walking away from deals (for example KKR walked from the buyout of US hi fi firm Haman Kardon in September – this was not to do with current markets issues but the company itself). Don’t be too opportunisIc! The solid companies will always have an eye on the next fund raising.

13

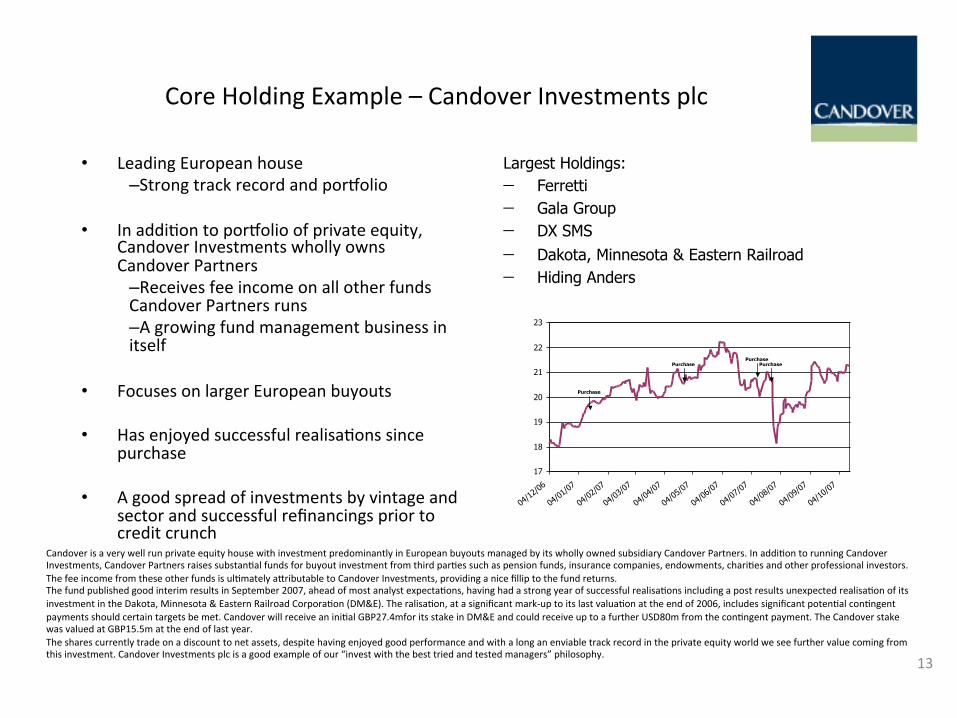

Core Holding Example – Candover Investments plc

• Leading European house – Strong track record and porXolio

• In addiIon to porXolio of private equity, Candover Investments wholly owns Candover Partners – Receives fee income on all other funds Candover Partners runs – A growing fund management business in itself

• Focuses on larger European buyouts

• Has enjoyed successful realisaIons since purchase

• A good spread of investments by vintage and sector and successful refinancings prior to credit crunch

Largest Holdings: − Ferretti − Gala Group − DX SMS − Dakota, Minnesota & Eastern Railroad − Hiding Anders

17

18

19

20

21

22

23

04/12/06

04/01/07

04/02/07

04/03/07

04/04/07

04/05/07

04/06/07

04/07/07

04/08/07

04/09/07

04/10/07

Purchase

PurchasePurchase

Purchase

Candover is a very well run private equity house with investment predominantly in European buyouts managed by its wholly owned subsidiary Candover Partners. In addiIon to running Candover Investments, Candover Partners raises substanIal funds for buyout investment from third parIes such as pension funds, insurance companies, endowments, chariIes and other professional investors. The fee income from these other funds is ulImately aPributable to Candover Investments, providing a nice fillip to the fund returns. The fund published good interim results in September 2007, ahead of most analyst expectaIons, having had a strong year of successful realisaIons including a post results unexpected realisaIon of its investment in the Dakota, Minnesota & Eastern Railroad CorporaIon (DM&E). The ralisaIon, at a significant mark-‐up to its last valuaIon at the end of 2006, includes significant potenIal conIngent payments should certain targets be met. Candover will receive an iniIal GBP27.4mfor its stake in DM&E and could receive up to a further USD80m from the conIngent payment. The Candover stake was valued at GBP15.5m at the end of last year. The shares currently trade on a discount to net assets, despite having enjoyed good performance and with a long an enviable track record in the private equity world we see further value coming from this investment. Candover Investments plc is a good example of our “invest with the best tried and tested managers” philosophy.

14

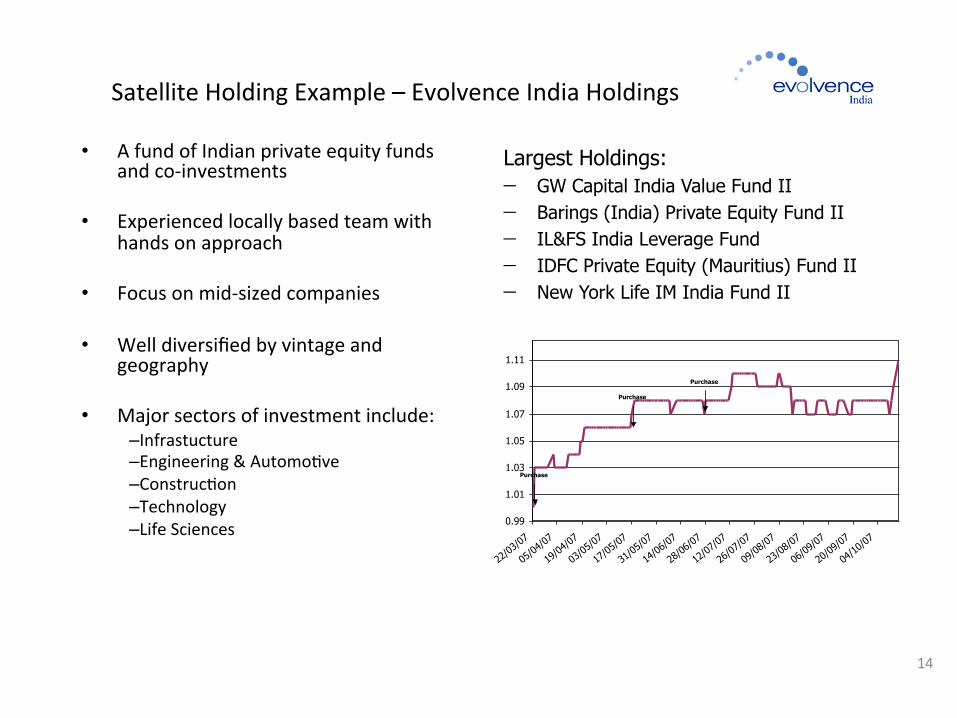

Satellite Holding Example – Evolvence India Holdings

• A fund of Indian private equity funds and co-‐investments

• Experienced locally based team with hands on approach

• Focus on mid-‐sized companies

• Well diversified by vintage and geography

• Major sectors of investment include: – Infrastucture – Engineering & AutomoIve – ConstrucIon – Technology – Life Sciences

Largest Holdings: − GW Capital India Value Fund II − Barings (India) Private Equity Fund II − IL&FS India Leverage Fund − IDFC Private Equity (Mauritius) Fund II − New York Life IM India Fund II

0.99

1.01

1.03

1.05

1.07

1.09

1.11

22/03/07

05/04/07

19/04/07

03/05/07

17/05/07

31/05/07

14/06/07

28/06/07

12/07/07

26/07/07

09/08/07

23/08/07

06/09/07

20/09/07

04/10/07

Purchase

Purchase

Purchase

On the ground presence in New Delhi with an eight member strong team that has vast investment and operaIonal experience in the Indian marketplace.

A hands on approach with representaIon on the Investment CommiPee of three out of the six underlying funds and

Advisory Board seats in two other underlying funds. The Fund believes the “sweet spot” for the Indian Private Equity space over the next couple of years lies with Fund

Managers who target the mid-‐market transacIons, i.e. transacIons in the range of US$ 10 to 30 million.

By geography – underlying funds have parIcular strengths in major business locaIons such as New Delhi (North India), Mumbai (West India) and Bangalore (South India)

To take advantage of the opportuniIes in a diversified manner, EIF has selected few Fund Managers with solid track record in that market segment and aligned with them. In addiIon, a well-‐qualified research team provides preliminary market, investment and economic analysis on focus sectors for the Fund.

Also a good example of how we work together within the research and investment team at Lloyd Bancaire Partners as I was able to uIlise our Jack Aldhous, who runs our India OpportuniIes Fund to assist on views and due diligence with her network of contacts in India.

Consolidated ConstrucIon ConsorIum Ltd.

South India’s leading construcIon contractor with a significant corporate porXolio High growth sector, strong track record of growth, technocrat and professional management, high

quality clients and projects, strong order book, aPracIve valuaIons and exit visibility Expected to be listed on the Indian Bourses in a few days at over 3.5 x of invested capital

Zylog Systems Ltd. IT Services company with about 35% of revenues from Value –Added-‐ Reselling High growth sector, strong growth track record , EBITDA expansion possibility, very aPracIve valuaIons

and exit visibility The company was recently listed on the Indian stock exchanges and is currently trading at 1.3x of

invested capital Emaar MGF Land Pvt. Ltd.

Amongst the three largest real estate developers in India. A JV with Emaar properIes-‐ one of the largest real estate developers in the world

Experienced Management and Promoters, aPracIve sector outlook, reputable JV partner Red herring prospectus filed. IPO is expected by Q1, 2008

Koutons Retail India Pvt. Ltd. Amongst the leading value retailers in apparels with a pan-‐India presence Experienced Management and Promoters, aPracIve sector outlook Expected to be listed on the Indian Bourses in a few days at over 1.75 x of invested capital

Shriram EPC Ltd. A leading Engineering, Procurement and ConstrucIon (EPC) company Excellent track record, aPracIve outlook for Infra, Robust order book Red herring prospectus filed. IPO is expected by Q1, 2008.

RSB Group (New Investments) Invested in a leading auto ancillary group with a diversified product porXolio and a blue chip clientele Experienced Management and Promoters, aPracIve sector outlook, Valuable JV alliances

On the ground presence in New Delhi with an eight member strong team that has vast investment and operaIonal experience in the Indian marketplace. A hands on approach with representaIon on the Investment CommiPee of three out of the six underlying funds and Advisory Board seats in two other underlying funds. The Fund believes the “sweet spot” for the Indian Private Equity space over the next couple of years lies with Fund Managers who target the mid-‐market transacIons, i.e.

transacIons in the range of US$ 10 to 30 million.

By geography – underlying funds have parIcular strengths in major business locaIons such as New Delhi (North India), Mumbai (West India) and Bangalore (South India)

To take advantage of the opportuniIes in a diversified manner, EIF has selected few Fund Managers with solid track record in that market segment and aligned with them. In addiIon, a well-‐qualified research team provides preliminary market, investment and economic analysis on focus sectors for the Fund.

Also a good example of how we work together within the research and investment team at Lloyd Bancaire Partners as I was able to uIlise our Jack Aldhous, who runs our India OpportuniIes Fund to assist on views and due diligence with her network of contacts in India.

Consolidated ConstrucIon ConsorIum Ltd.

South India’s leading construcIon contractor with a significant corporate porXolio High growth sector, strong track record of growth, technocrat and professional management, high quality clients and projects, strong order book,

aPracIve valuaIons and exit visibility Expected to be listed on the Indian Bourses in a few days at over 3.5 x of invested capital

Zylog Systems Ltd. IT Services company with about 35% of revenues from Value –Added-‐ Reselling High growth sector, strong growth track record , EBITDA expansion possibility, very aPracIve valuaIons and exit visibility The company was recently listed on the Indian stock exchanges and is currently trading at 1.3x of invested capital

Emaar MGF Land Pvt. Ltd.

Amongst the three largest real estate developers in India. A JV with Emaar properIes-‐ one of the largest real estate developers in the world Experienced Management and Promoters, aPracIve sector outlook, reputable JV partner Red herring prospectus filed. IPO is expected by Q1, 2008

Koutons Retail India Pvt. Ltd. Amongst the leading value retailers in apparels with a pan-‐India presence Experienced Management and Promoters, aPracIve sector outlook Expected to be listed on the Indian Bourses in a few days at over 1.75 x of invested capital

Shriram EPC Ltd. A leading Engineering, Procurement and ConstrucIon (EPC) company Excellent track record, aPracIve outlook for Infra, Robust order book Red herring prospectus filed. IPO is expected by Q1, 2008.

RSB Group (New Investments) Invested in a leading auto ancillary group with a diversified product porXolio and a blue chip clientele Experienced Management and Promoters, aPracIve sector outlook, Valuable JV alliances

16

• Private equity funds are generally difficult to access for the everyday investor

• Like hedge funds, investors face a series of obstacles: lack of access to funds, size of entry, ability to diversify and lack of investment experIse

• Moreover, liquidity is extremely restricIve in this arena with private equity funds commonly implemenIng long lock-‐ins in excess of 3 – 5 years

How to invest in private equity?

• Like hedge funds private equity funds are generally less regulated than ordinary mutual funds and therefore can’t adverIse or promote themselves • They are almost inaccessible for everyday investors • And in our seminar I’ll explain Lloyd Bancaire’s investment approach to private equity

17

Copyright © 2022 FDOKUMEN