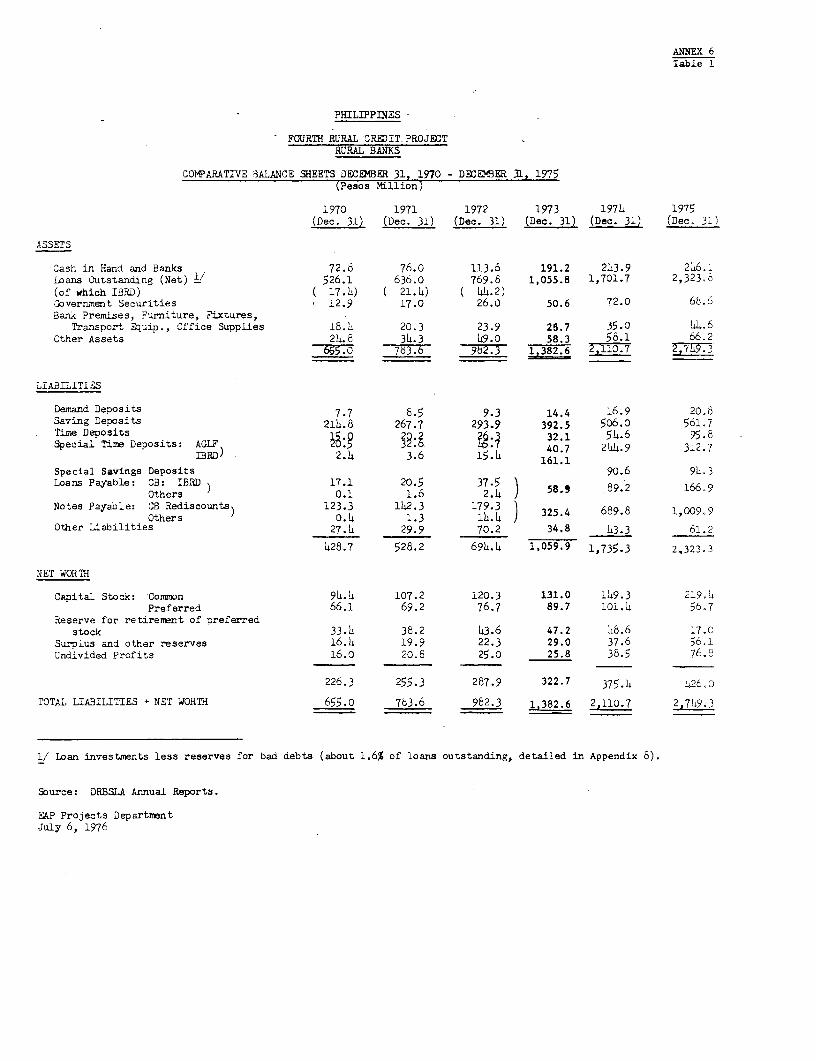

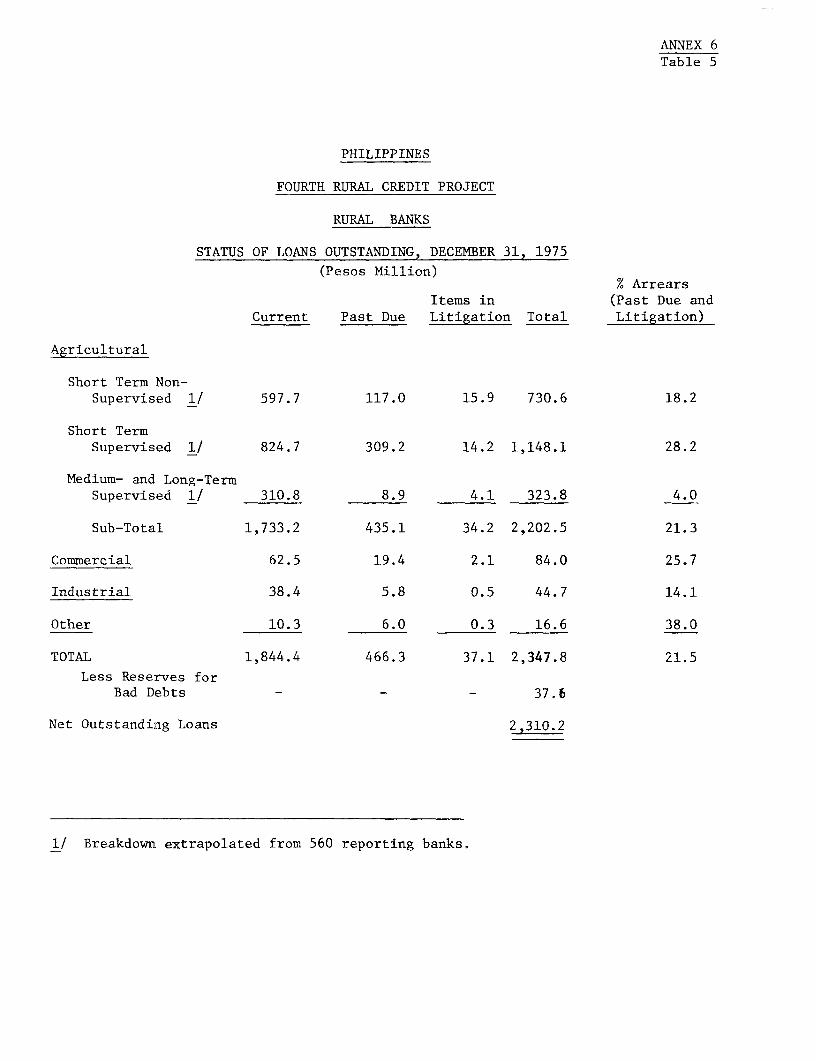

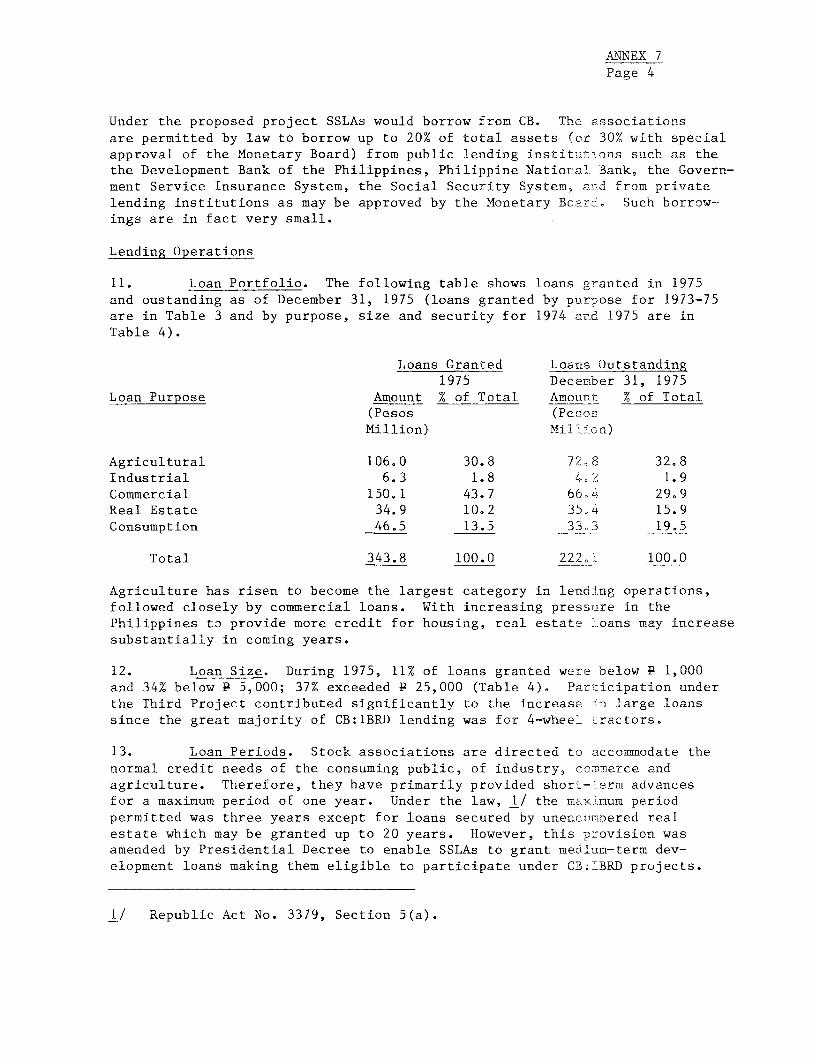

Philippines: Appraisal of - Fourth Rural Credit Project

183

ReportNo. 1415-PH Philippines: Appraisal of P Fourth Rural CreditProject March 7, 1977 RuralCredit and Agro-Business Division East Asia and Pacific Regional Office FOR OFFICIAL USE ONLY U Documentof the World Bank Thisdocument hasa restricted distribution and may be used by recipients only in the performance of their official duties. Its contents maynot otherwisebe disclosed without World Bank authorization. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

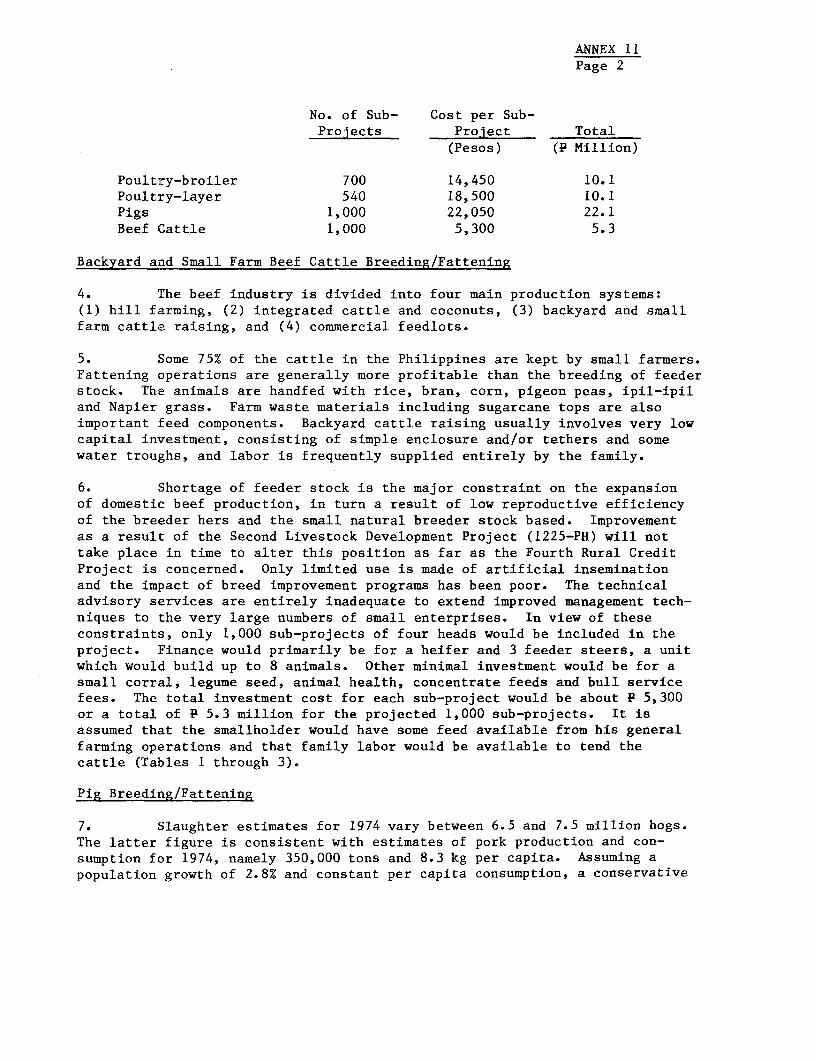

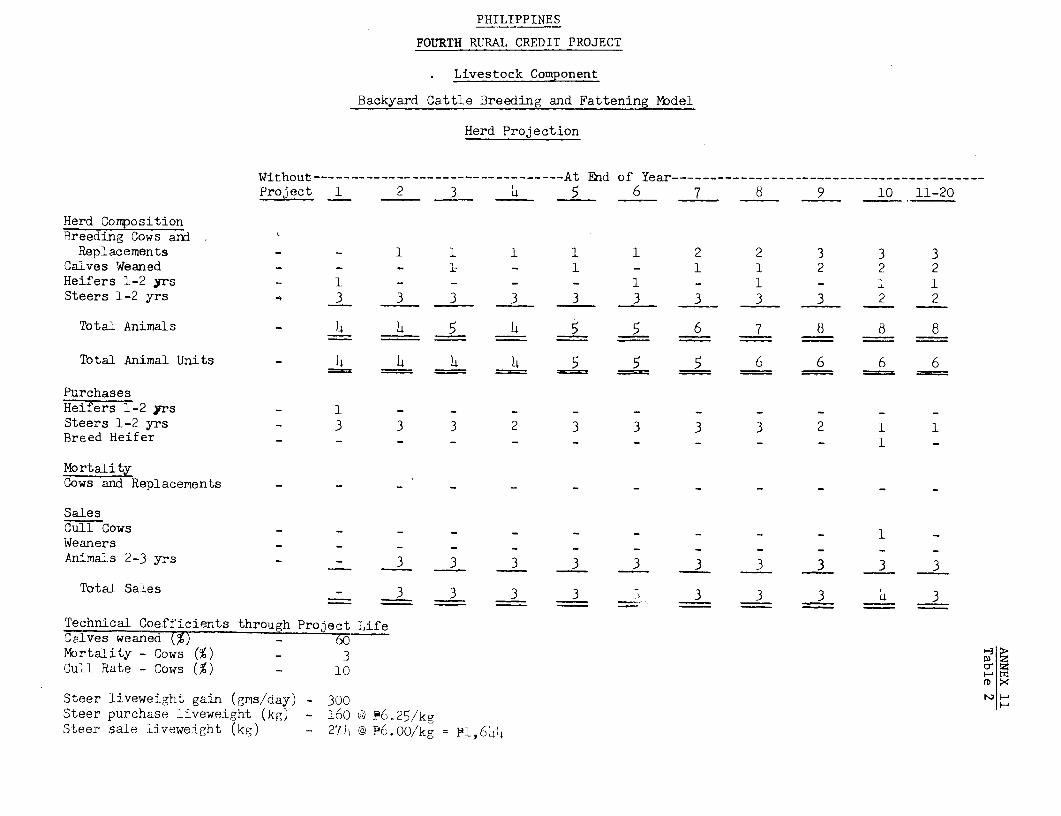

-

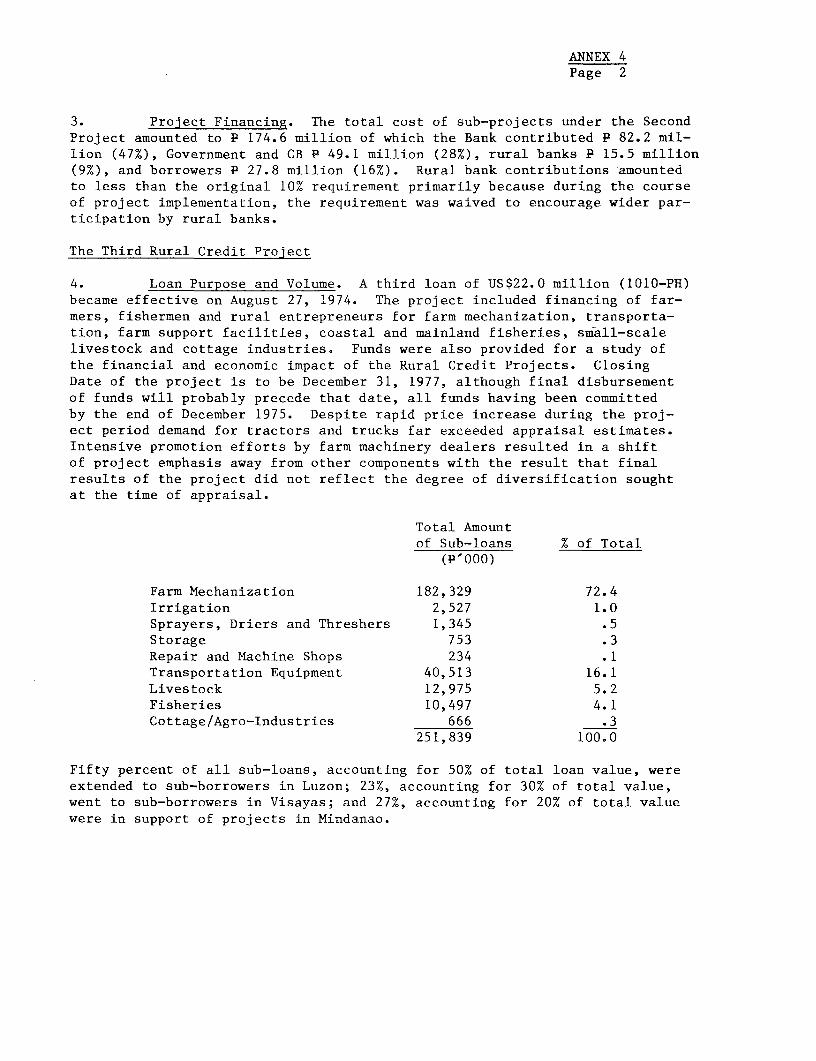

Upload

khangminh22 -

Category

Documents

-

view

4 -

download

0

Transcript of Philippines: Appraisal of - Fourth Rural Credit Project

Report No. 1415-PH

Philippines: Appraisal of PFourth Rural Credit Project

March 7, 1977

Rural Credit and Agro-Business DivisionEast Asia and Pacific Regional Office

FOR OFFICIAL USE ONLY

U

Document of the World Bank

This document has a restricted distribution and may be used by recipientsonly in the performance of their official duties. Its contents may nototherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

US$1.00 = Pesos (P) 7.5P 1.00 = US$0.1333

WEIGHTS AND MEASURES - METRIC SYSTEM

1 hectare (ha) 2.47 acres1 kilometer (km) = 0.62 miles1 kilogram (kg) = 2.2 pounds1 cavan (paddy) = 50 kg [a1 cavan (corn) = 57 kg1 picul (sugar) = 63.5 kg

ABBREVIATIONS

ACA - Agricultural Credit AdministrationAMDA - Agricultural Machinery Dealers AssociationAMTESP - Agricultural Machinery Testing, Evaluation and

Standardization ProjectCB - Central Bank of the PhilippinesDBP - Development Bank of the PhilippinesDRBSLA - Department of Rural Banks and Savings and Loan

Associations, CBIGLF - Industrial Guarantee and Loan FundIRRI - International Rice Research InstituteLBP - Land Bank of the PhilippinesMAU - Management Advisory UnitNFAC - National Food and Agriculture CouncilNIA - National Irrigation AdministrationPCAC - Presidential Committee on Agricultural CreditPNB - Philippine National BankSSLA - Stock Savings and Loan AssociationsTBAC - Technical Board on Agricultural CreditTSEU - Technical Support and Evaluation UnitUPLB - University of the Philippines, Los Banos

FISCAL YEAR

Government: January 1 to December 31CB: January 1 to December 31Rural Banks: January 1 to December 31SSLAs: January 1 to December 31

/a The former weight of 44 kg for cavan is sometimesstill used in the Philippines.

FOR OFFICIAL USE ONLY

PHILIPPINES

FOURTH RURAL CREDIT PROJECT

TABLE OF CONTENTS

Page No.

SUMMARY AND CONCLUSIONS ............................. i- iv

I. INTRODUCTION ........................................ 1

II. BACKGROUND .......................................... 1

General ......................... 1Economy ................................... . 2Agricultural Sector ..... .............. 2Agricultural Credit ............................ 3

III. RURAL BANKING INSTITUTIONS .......................... 6Rural Banks .................................... 6Stock Savings and Loan Associations .... ........ 8

IV. REVIEW OF PREVIOUS RURAL CREDIT PROJECTS ........... . 9Performance Under First, Second andThird Rural Credit Projects .................. 9

Issues Arising From Previous Projects ........ .. 11

V. THE PROJECT ....... .............. .................... 14Detailed Features ............... ............... 14Cost Estimates ......................... 19Financing .................... .................. 20Procurement ................... ................. 21Disbursement ........................... 22

VI. ORGANIZATION AND MANAGEMENT ......................... 22Department of Rural Banks and Savings andLoan Associations ............................ 22

Lending Policies, Terms and Criteria .... ....... 25Organization of Agricultural MachineryTesting, Evaluation and StandardizationProject ...................................... 27

Project Monitoring ............................. 27

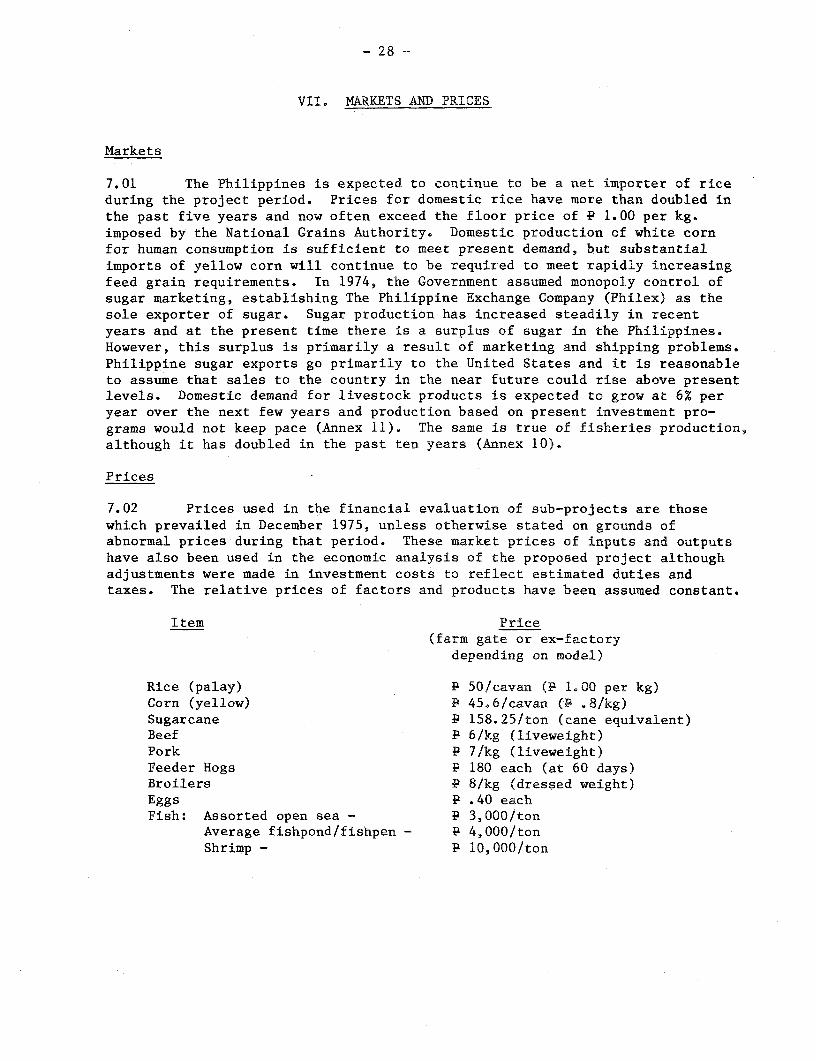

VII. MARKETS AND PRICES .................................. 28Markets ........................................ 28Prices .... 28

VIII. BENEFITS AND JUSTIFICATION .......................... 29

IX. RECOMMENDATIONS ..................................... 31

This document has a restricted distribution and may be used by recipients only in the performance |of their official duties. Its conterts may not otherwise be disclosed without World Bank authorization.

-2-

ANNEXES

1. Small-Scale Agriculture in the Philippines2. Cottage and Agro-Industries in the Philippines

3. Agricultural Credit4. Summary of Previous Rural Credit Projects5. Central Bank of the Philippines6. Rural Banks7. Stock Savings and Loan Associations8. Farm Mechanization and Transport9. Cottage and Agro-Industries10. Fisheries Development11. Livestock Development12. Monitoring and Evaluation13 Project Cost Estimate

14. Estimated Quarterly Schedule of Disbursements15. Phasing of the Lending Program16. Summary of Financial Rates of Return

17. Economic Evaluation

PHILIPPINES

APPRAISAL OF THE

FOURTH RURAL CREDIT PROJECT

SUMMARY AND CONCLUSIONS

i. The Government of the Philippines has requested a Bank loan toassist in the financing of the medium- and long-term credit program admin-istered by the Central Bank of the Philippines (CB). This would be thefourth loan since 1965 in support of this program, in which funds are on-lentthrough qualified rural banks and stock savings and loans associations (SSLAsito farmers, fishermen, and rural entrepreneurs. On the basis of the findingspresented in this report, a loan of US$36.5 million is recommended.

ii. Seventy percent of the Philippine population of 42.5 million livesin rural areas. Agriculture accounts for 50% of total employment, 70% ofcommodity export earnings, and 35% of GNP. Remarkable growth was achievedin agricultural production in the 1960's (7.7% per year between 1965 and1970), primarily as a result of improved technology and the increased useof cash inputs in rice production. After a period of adverse weather con-ditions in the early 1970's, production has again recovered. However, ade-quate supplies of production and term credit are essential to the continuedgrowth of production and the Government has undertaken a number of specialfinancing programs to augment private sector resources used in agriculturaldevelopment. The Rural Credit Projects supported by the Bank have been themajor component of Government assistance in term credit. Government goalsfor the agriculture sector are self-sufficiency in food grain production,expansion of agricultural exports, implementation of the Agrarian ReformProgram, improvement of income distribution and nutritional level, and con-servation of natural resources. Cottage and agro-industries in rural areasare viewed as a means of diversifying the rural economy and creating pro-ductive employment.

iii. Under the previous Rural Credit Projects, the first of which wasundertaken in 1965, a total of 10,860 sub-loans were made for farm mechani-zation, processing and storage, transportation, minor irrigation, fisheries,livestock and cottage and agro-industries. Bank loans totalling US$40 mil-lion accounted for approximately 50% of total sub-project costs. Approxi-mately 83% of total costs were for farm mechanization sub-projects, althoughthis share was reduced to 72% under the most recent project. The RuralCredit Prcjects have been instrumental in mobilizing domestic funds formedium- and long-term investments in agriculture and related industries.They have contributed to rural productivity and incomes and have generated

- ii -

substantial employment opportunities. However, arising from experience underprevious projects, the proposed project would include specific measures toaffect the following: the channeling of a larger share of project proceedsto smaller farmers and entrepreneurs; a reduction in the share of projectproceeds used for large-scale mechanization; improvements in the procurementpractices and guidelines governing farm machinery financing; greater attentionto the inter-relationship of the project with other rural credit programs; andimprovements in repayment performance among sub-borrowers.

iv. The proposed project would provide medium- and long-term credit(US$89.9 million) through qualified rural banks and stock savings and loanassociations to about 16,000 farmers, fishermen, and rural entreprenuers forinvestment in: farm mechanization (US$55.3 million); light transporation(US$1.5 million); cottage and agro-industries (US$7.0 million), coastal andinland fisheries (US$17.6 million) and small-scale livestock development(US$8.5 million). In addition, funds would be included for: a study toassess the impact of farm mechanization in the Philippines; an AgriculturalMachinery Testing, Evaluation and Standardization Project; training of creditpersonnel; and service vehicles for CB field personnel engaged in the project.

v. Total project costs are estimated to be P 684.4 million (US$91.3million). Foreign exchange costs would be US$29.4 million (32%). The pro-posed Bank loan of US$36.5 million, which would be for a period of 15 yearsincluding a 4-1/2 year grace period, would finance 40% of project costs. CBand the Government would provide 40%, rural banks and SSLAs 10% and sub-borrowers 10%. Terms and conditions for the release of project funds wouldbe set out in the Rules and Regulations governing the project, which wouldbe subject to Bank approval.

vi. As in the Third Project, machinery and equipment, including trucks,irrigation pumps, engines and equipment for fishing boats, and machinery andequipment for cottage and agro-industries would be purchased locally by sub-borrowers under initial supervision of the on-lending institution. Suffi-cient private contractors are available for construction of boats, buildingsand other civil works. The size of individual contracts would be too smallfor international competitive bidding and bulking of contracts would notbe practicable because of their wide dispersal both in location and time.All sub-project contracts would be made through ordinary commercial channels.The purchse of service vehicles by CB would be through local competitivebidding in accordance with procedures acceptable to the Bank. The procurementof four-wheel tractors and imported power tillers would continue to be subjectto ceiling price guidelines although these guidelines would be modified toreduce retail prices from present levels.

vii. Disbursement of loan proceeds to CB would be as follows:

- iii -

(i) 45% of the sub-loans disbursed by rural banks andSSLAs, against certified statement of expenditure;

(ii) 40% of the costs of instruction, materials and rentalof facilities for training and the preparation of acredit handbook, against certified statement ofexpenditure;

(iii) 100% of the c.i.f., ex-factory cost of vehicles, or40% off-the-shelf, against invoice;

(iv) 40% of the cost of the farm mechanization study,against certified statement of expenditure; and

(v) 66% of the cost of civil works and equipment contractsfor the Agriculture Machinery Testing, Evaluation andStandardization Project, against invoice, to be passedon to the Department of Agriculture.

viii. The Director of CB's Department of Rural Banks and Savings andLoan Associations (DRBSLA) would assume overall responsibility for imple-mentation of all aspects of the project except the Agricultural MachineryTesting, Evaluation and Standardization Project, for which funds would bechanneled through the Department of Agriculture to the University of thePhilippines at Los Banos. CB Agricultural Credit Supervisors or members ofCB Loan Teams would assist rural banks and SSLAs to prepare sub-projects.Loan Teams would evaluate sub-projects and, if approved, would recommend toDRBSLA the transfer of Special Time Deposits to an account of the on-lendinginstitution. Disbursement against sub-borrower contracts would be made bythe on-lending institution, direct to suppliers where possible. During theproject period, a gradual transfer of lending authority to qualified on-lend-ing institutions is envisaged, with technical assistance and post-approvalreview by Loan Teams. Monitoring, reporting and technical support would beprovided by the Technical Support and Evaluation Unit of DRBSLA. In addi-tion, a Management Advisory Unit would be established in the Departmentconsisting of a small number of experienced senior officers who would provideassistance to rural banks on managerial problems outside the regular super-vision and regulatory structure.

ix. Project funds for sub-loans would be channeled through rural banks(90%) and stock savings and loan associations (10%). The system of ruralbanks, consisting of 786 individual banks, is the largest network of bank-ing facilities in rural areas. Two hundred and forty five of these banksparticipated in the Third Project. DRBSLA provides rural banks with train-ing, technical assistance, and credit facilities, and supervises all aspectsof their operations. Loans by rural banks, of which 90% go to agriculture,increased over 200% between 1972 and 1975, to P 2,324 million (US$310 million),primarily as a result of Government supported food production credit programssuch as Masagana 99. This rapid expansion has been accompanied by a deteriora-tion in collections; arrears were 21.4% of outstanding portfolio on December 31,1975 compared to 16.7% a year earlier. Measures presently being taken to

- iv -

improve this situation, and implications for the proposed project are dis-cussed in this report. There are 44 SSLAs in the Philippines, of which 13participated in the Third Project. About 31% of total lending in 1975 ofP 77 million (US$10 million) went to agriculture, an increase of 13% fromthe previous year. Collection performance is satisfactory. SSLAs are alsoregulated by DRBSLA and receive the same training and technical assistanceservices as rural banks. They do not, however, participate in special financ-ing programs other than the Rural Credit Projects.

x. At full development, the project is expected to result in incre-mental production of agricultural commodities, small implements, handicraftsand rural services with a total annual value of P 379.4 million (US$50.6 mil-lion). It is expected to create 10,280 man years of employment per year, themajority of which would be unskilled. Fifty seven percent of all sub-projectsother than four-wheel tractors, amounting to US$11 million of loan proceedswould accrue to smaller farmers and entrepreneurs who would derive an averagenet income from sub-projects of P 5,445 per year. Custom hire services wouldalso be used primarily by smaller farmers who occupy the majority of cultivatedlands and do not generally own tractors or tillers. The project would have anet foreign exchange contribution of US$9.2 million per year primarily throughimport substitution. Financial rates of return for sub-projects and an overalleconomic rate of return have been determined and are satisfactory.

xi. The proposed project is recommended for a loan of US$36.5 millionwith a 15 year maturity, including a grace period of 4-1/2 years.

PHILIPPINES

FOURTH RURAL CREDIT PROJECT

I. INTRODUCTION

1.01 The Government of the Philippines has requested a Bank loan toassist in the financing of the medium- and long-term rural credit programadministered by the Central Bank of the Philippines (CB). This would be thefourth loan in support of this program, previous loans having been made in 1965(432-PH, US$5.0 million), 1969 (607-PH, US$12.5 million), and 1974 (1010-PH,US$22.5 million). The third loan was fully committed in December 1975 and isexpected to be fully disbursed by the end of March 1977, 8 months before theClosing Date. The proposed loan would be the eighteenth Bank loan in supportof agricultural and rural development in the Philippines.

1.02 As under the Third Rural Credit Project, the project would providefunds to CB which would on-lend, through qualified rural banks and stocksavings and loan associations, to farmers, fishermen and rural entrepreneurs.However, the project would place less emphasis on farm mechanization andtransportation than did previous projects and focus to a greater extent onthe development of fisheries, livestock, and cottage and agro-industries. TheGovernment has decided to place greater emphasis on the financing of smallerfarmers and a quota would be established for lending to this target group.Additional funds would be provided for training of credit staff both of CBand onlending institutions, and for other project support investments.

1.03 This report is based on a project proposal submitted in March 1976by CB and on the findings of an appraisal mission composed of Messrs.Y. Nakahara, J. Brown, D. Steel, D. Forno (Bank), H. Lapp, R. Jessup andH. Deomampo (Consultants) which visited the Philippines in May-June 1976. 1/

II. BACKGROUND

General

2.01 The Republic of the Philippines, with an area of about 30 millionha, consists of more than 7,000 islands scattered along the archipelago

1/ The mission also examined issues relating to the agricultural creditsector, small-scale agriculture, and credit aspects of the AgrarianReform Program.

- 2 -

which extends over 1,600 km north and south. It is divided into threemain parts: Luzon in the north, the Visayas and Mindanao in the south.The population is estimated to be some 42.5 million, growing at 2.8%per annum (at the end of 1975), of which about 70% lives in rural areas.Luzon has the largest population (53%), with about 5 million concentratedin the Greater Manila area alone, the balance being evenly distributedbetween the Visayas (25%) and Mindanao (22%).

2.02 The climate is tropical and characterized by high temperature,humidity and rainfall. Mean temperatures range from 21 C in January to190C in May. Rainfall shows a wider range, from 1,000 mm in southwestMindanao to 5,500 mm in the highlands of Luzon. Most areas lave one majorrainy season but the rainfall pattern varies widely across the country.Climatically, the Philippines has high potential for agricultural production.

Economy

2.03 Real gross national product has been growing at 6 percent annuallyin recent years, and in 1976 reached a level of $390 per capita at currentprices and exchange rates. Major assets of the Philippines for economicdevelopment include relatively abundant mineral (with the exception of pet-roleum) and water resources, a climate favorable to large-scale agriculturalproduction, a high level of general education, and a vigorous entrepreneurialclass. Significant liabilities include a high population density in rela-tion to arable land and a high rate of population growth. Poverty and un-equal distribution of income are longstanding problems and a significantcurrent problem is the large current account deficit of about $1 billion in1976, brought about by a deterioration in the external terms of trade since1974. The Government is attacking these problems through increased effortsin rural development, family planning and labor-intensive export-orientednontraditional industries, In 1976, nontraditional exports increased by about50%. The Bank, in its Basic Economic Report, and the Government regard GNPgrowth of 7 percent a year as a feasible objective, and that the externalaccounts situation is and will remain manageable provided that external debtcontinues to be managed carefully and that nontraditional exports continueto grow at a fairly rapid pace.

Agricultural Sector

2.04 Agriculture is the most important sector in terms of employmentand export earnings. It accounts for about 50% of total employment and70% of commodity export earnings, consisting mainly of coconut and sugar-cane products. Agriculture also contributes 35% of GNP consisting of foodcrops (12%), export crops (9%), livestock (6%), fisheries (4%) and others(4%).

2.05 Agricultural output was accelerated during the late 1960's duelargely to increased rice production, a result of introducing a new tech-nological package of irrigation, high yielding varieties, fertilizersand other farm inputs. The annual growth over 1965-70 was 7.7%. From 1971to 1973 crops were seriously affected by adverse weather conditions and cropdiseases but production has since recovered.

2.06 More than half of the total land area of 30 million ha is forest-land and about one-third is cultivated including plantations. An additional2.5 million of fairly level or slightly sloping land is classified as avail-able for cultivation, of which 1.0 million ha is cogun grassland, difficultand expensive to reclaim. With the rate of land expansion for farm landslowing down in recent years, it has been clear that most of the increasedproduction and farm incomes must come from higher yields, intensificationof land use and cultivation of higher value crops.

2.07 The Government goals for the agricultural sector are self-sufficiency in food grain production, expansion of agricultural exports,implementation of the Agrarian Reform Program, improvement of income dis-tribution and nutritional level, and conservation of natural resources.

Agricultural Credit

2.08 Agricultural credit available from both Government and non-Government institutions probably accounts for about one-third of all agri-cultural credit, the remainder being provided by traditional non-institu-tional sources. In nominal terms, institutional credit for agriculture hasincreased continuously. In real terms, it grew rapidly during the first halfof the 1960's, decelerated during the second half and actually started todecline in the early 1970's. With the introduction of supervised food pro-duction programs, real growth has once again been substantial since 1973(Annex 3, Tables 1 and 2). One limitation on the flow of credit to agricul-ture is the inadequate coverage of institutions serving rural areas; anotheris collateral requirements which preclude access to credit by a large numberof small farmers. In efforts to overcome these problems, the Government ispromoting the expansion of the rural banking system and has introduced specialcredit programs such as Masagana 99 to provide production credit to smallfarmers without collateral. The Rural Credit Projects and other Bank-supportedprojects have provided additional investment credit to rural areas.

2.09 Government Institutions. About 20% of the institutional creditto agriculture is provided by the public sector principally through thePhilippines National Bank (PNB), and, to a much lesser degree, the Agricul-tural Credit Administration (ACA). 1/ In addition, the Land Bank of thePhilippines (LBP) has been revitalized and is expected to play an essentialrole in financing land transfer under the Agrarian Reform Program and provid-ing credit, mainly to agrarian reform beneficiaries.

2.10 PNB is the largest bank with about 170 branches and 120 mobileoffices. Its total assets increased from P 6.2 billion in 1973 to P 15 bil-lion (US$2 billion) in 1975. Traditionally, its agricultural lending has beento commercial farms and plantations primarily for seasonal credit for pro-duction inputs, marketing and processing. Now it also finances half of theshort-term credit for food grain production under Masagana 99 and Masaganang

1/ The CB support of agricultural credit is in the form of rediscountingfacilities and Special Time Deposits for other public and privateinstitutions.

-4-

Maisan. As a result, about 30% of its total lending is for agriculture. DBPprovides medium- and long-term credit for a wide range of enterprises in theagricultural sector. In 1975, 23% of its loan approvals, reaching P 2.4billion (US$330 million), was to agriculture. Since 1972, the DevelopmentBank of the Philippines (DBP) has been the credit channel for seven IBRDagricultural projects. 1/ ACA finances production and marketing cooperativesand small farmers but, owing to lack of funds and poor loan recovery, itslending has decreased and its future role is under review.

2.11 Private Institutions. Commercial banks are the most importantprivate institutions providing some 55% of all institutional agriculturalcredit, although this amounts to less than 10% of their portfolios. CB nowrequires that a minimum of 25% of all commercial bank lending go to agri-culture. Instead of making direct loans, many banks purchase CB Certificatesof Indebtedness, the proceeds of which are used by CB to refinance agriculturalloans provided by other credit institutions. About 30 commercial banks servethe agricultural sector directly, mostly in the form of short-term credit formarketing and trade financing in copra and sugarcane.

2.12 The next important private institutions are rural banks (786 inJune 1976) with total assets of some US$470 million. They provide about20% of all institutional agricultural credit, mainly under the Masagana 99and Masaganang Maisan, and are also gradually increasing their term lendingprimarily under the Rural Credit Projects supported by the Bank. Althoughmuch smaller in scale, there are savings and loan associations and privatedevelopment banks which lend about a third of their funds to agriculture.

2.13 Cooperatives have begun to assume an important role in theflow of credit to small farmers, particularly agrarian reform beneficiaries.Membership in a Samahang Nayon (pre-cooperative at the village level) is a pre-requisite of credit for agrarian reform beneficiaries, and is encouraged forall small borrowers. Samahang Nayons in turn become shareholders in market-ing, processing and service cooperatives usually established at the pro-vincial level. Samahang Nayons may acquire up to 40% equity in rural banksand one bank has now been established in Nueva Ecija under full cooperativeownership. Government training courses for members and management aremandatory prerequisites for any financial undertakings by Samahang Nayons.At the end of March 1976, about 17,000 Samahang Nayon had been organizedand 90 cooperatives organized at higher levels. At that time, total sav-ings of Samahang Nayons amounted to P 29 million. It is too early, however,to predict the success of this program but it is evident that assistancein financial management and control will be essential to members' confidencein the success of cooperatives.

1/ Rice Processing and Storage Project, Loan 720-PH, US$14.3 millionFirst Fisheries Project, Loan 891-PH, US$11.6 millionFirst Livestock Development Project, Loan 832-PH, US$7.5 millionFirst Industrial and Small Holder Tree Farmers Project Loan 998-PH,

US$50.9 million (US$2.0 million for tree farming)Second Livestock Development Project, Loan 1225-PH, US$20.0 millionSecond Grain Processing Project, Loan 1269-PH, US$11.5 millionSecond Fisheries Projects, Loan 1270-PH, US$12.0 milli-on

-5-

2.14 Interest Rates. The annual interest rate for credit from Govern-ment sources is normally 12% for loans secured by land, and 14% for others.An exception is the 12% interest rate for supervised credit made availableunder Masagana 99 and other Government food grain production credit programsfor which real estate collateral is not required. Recently the MonetaryBoard has raised the ceiling interest rates to 17% for loans less than twoyears and 19% for loans over two years which is not applicable to ruralbanks 1J. The effective cost of credit from agricultural input suppliers isbetween 15% and 25% per annum; from private moneylenders the cost is muchhigher.

2.15 Development Policies for the Agricultural Credit Sector. InSeptember 1975, the Presidential Committee on Agricultural Credit (PCAC) andits working group, the Technical Board on Agricultural Credit (TBAC) wereestablished. 21 Their establishment and composition attest to the Government'sintention to address carefully and vigorously issues surrounding the futureof this sector. TBAC has its own staff of about 30 persons who conduct studiesof various aspects of the rural credit sector under the direction of the Boardand review studies conducted by CB, Government agencies and special committees.Over the past year a useful dialogue has been established between members ofthese units and representatives of the Bank, and attention is now being givento issues which ought to determine the nature of future Bank support for thesector. Among these are; the identification of target groups with clearlydefined credit needs, determination of the most suitable long-term roles forvarious credit institutions, the coordination of credit and technical assist-ance to borrowers, new sources of funds such as supplier's credit, and thefinancing of marketing and storage facilities.

1/ These ceiling interest rates include commissions, premiums, fees, andother charges of 3%. Loans over two years may not exceed 80% and 100%,respectively, of time deposits and deposit substitutes with a remainingmaturity of more than two yeats.

2/ The members of PCAC are: Governor, Central Bank (Chairman); Secretary,Department of Agriculture (Vice-Chairman); Director-General, NationalEconomic and Development Authority; Secretary, Department of Local Govern-ment and Community Development; Secretary, Department of National Resources;Secretary, Department of Agrarian Reform; President, Philippine NationalBank; Chairman, Development Bank of the Philippines; and President, LandBank of the Philippines.

The members of TBAC are representatives of: Central Bank (Chairman),Department of Agriculture (Vice-Chairman), Department of Local Governmentand Community Development, Department of Natural Resources, NationalEconomic and Development Authority, Philippine National Bank, NationalFood and Agriculture Council, Department of Agrarian Reform, AgriculturalCredit Administration, Development Bank of the Philippines, Land Bank ofthe Philippines and a separate representative from the DRBSLA, CentralBank.

- 6 -

III. RURAL BANKING INSTITUTIONS

3.01 Although commercial banks provide over one half of the insti-tutional credit for agriculture, the rural banking system (presently with786 individual banks) has the largest network of banking facilities serv-ing the rural areas and is capable of financing a large number of mediumand small farmers. In providing medium- and long-term loans for ruraldevelopment, rural banks and SSLAs, which supplement the rural bankingsystem to extend its coverage to rural areas, have proved successful ascredit channels for the three Rural Credit Projects and would continue tobe the credit channels for the proposed Fourth Project.

3.02 Rural banks and SSLAs are private banks, supervised by CB'sDepartment of Rural Banks and Savings and Loan Associations (DRBSLA)OMost are established, capitalized and managed by close family groups,although cooperatives are now entitled to acquire shares of rural banks upto a maximum of 40%. In some cases, banks and SSLAs are owned by thesame group of investors.

Rural Banks 1/

3.03 Organization. Establishment of rural banks is authorized bythe Monetary Board and the Government may at the time of establishmentassist them by subscribing in the form of preferred shares up to an amountequal to shares subscribed by private individuals. At the end of 1975,shares held by the Government had decreased to 26% of paid-in capital throughacquisition by private shareholders. DRBSLA provides rural banks with train-ing for management and staff, technical assistance in lending and administra-tion, and funds through Special Time Deposits. It also supervises and examinestheir operations. Funds are also provided by CB's Department of Loans andCredits (DLC) through rediscounting facilities. During the first two yearsof a Four-Year Development Program for the rural banking system (1974-77),140 new rural banks were established compared to a target of 100 each yearfor the plan period. This very rapid expansion has placed a heavy bur-den on training and supervision staff of CB. Rural banks are typicallyestablished by prominent financial or professional members of the smallercommunities they serve. Their investment portfolios, which average P 3 mil-lion, consist of loans to borrowers within a small radius, perhaps concentra-ted within 20 km. Staffed by a manager, an accountant, a cashier, one or twotechnicians, and support staff, they rely heavily on an intimate knowledgeof local conditions and borrower reputations to protect the quality of theirportfolios. Types of loans reflect the predominant credit needs of therespective communities, but, in the main, short-term agricultural productionloans constitute the majority of their portfolios.

i/ A more detailed description of rural bank operations appears asAnnex 6.

-7-

3.04 Financial Resources. As of December 30, 1975, rural banks'total resources were P 2,749 million (US$377 million), consisting ofP 276 million (US$38 million) in paid-capital, P 150 million (US$20 million)in surpluses, reserves and undistributed profits, P 678 million (US$93million) in deposits, and P 1,489 million (US$204 million) in borrowing,the bulk from CB. In the past three years, total liabilities more thantripled from P 694 million at the end of 1972 to P 2,323 million at theend of 1975. This increase was primarily due to the introduction of thefood grain production programs (Masagana 99 and Masaganang Maisan) and toincreased disbursements under the Rural Credit Projects.

3.05 A large portion of borrowings is made through CB's rediscountingfacilities. CB rediscounts promissory notes up to 100% of face value undersupervised production schemes (rice, corn and sugar) a: 1% per year and (80%at 5% per year for non-supervised ordinary schemes), with a limit of 500%of the borrowing bank's net worth plus 100% of its average monthly savingdeposits over the preceding four months for supervised ciredit (100% and 50%respectively for non-supervised credit). The terms are up to 180 days forcommercial loans, 270 days for agricultural and industrial loans, and 360days for loans to cooperatives. Another facility provided by CB is theadvancement of funds as Special Time Deposits to finance special programsincluding the Rural Credit Projects. These deposits are secured by promis-sory notes from the recipient banks.

3.06 Deposits are another major source of funds for rural banks auth-orized by the Monetary Board. Annual interest rates as of January 1976vary from 7.5% for savings deposits to 9% and 12.5% for time deposits of90 days and 2 years, respectively. National and regional savings campaignssupported by CB in the past year have been very successful.

3.07 Lending Operations. The loan portfolio of rural banks increasedrapidly in recent years; from P 770 million (US$103 million) at the end of1972 to P 2,324 million (US$310 million) at December 31, 1975; an increaseof over 300%. More than 90% of these loans were to agriculture. The numberof loans exceeded 1,000,000 in both 1974 and 1975 and the average loan sizein 1975 was P 2,220 (US$296). Medium- and long-term financing is limitedalmost entirely to that supported by the Bank through the CB:IBRD programand accounts for less than 10% of rural bank loan portfolios.

3.08 Arrears. The overdues position of rural banks is not satisfactory.As of December 31, 1975, arrears amounted to 21.4% of outstanding portfolio,an increase from 16.7% at December 31, 1974. In absolute terms, arrearsincreased from P 287.0 million at the end of 1974 to p 503.4 million at theend of 1975. During the appraisal of the proposed project a more detailedanalysis was conducted of 268 banks, including those participating in theThird Project as of December 31, 1975. As of March 31, 1976, overdues amongthese banks accounted to 36% of demand. Only 111 were below the 20% criterionwhich was to have been introduced April 1, 1976, had funds not been fullycommitted prior to that date. In the case of 112 banks arrears were found toexceed 40% of demand. Measures presently being taken to improve this situa-tion and implications for the proposed projects are discussed in para 6.09.

- 8 -

3.09 Profits. Although rural banks' income and expenditure both increasedby about three times, net income and return to common stocks have shown someimprovement in 1974 and 1975. However, the profitability of individual banksseems to differ widely, even without considering adequacy of reserves for baddebts. The generally high level of returns to common stock despite seriousarrears problems is a reflection of the very high degree of leverage encour-aged by the present CB financial assistance to the system. Commitments to re-ducing arrears can be expected to increase meaningfully only as CB creditfacilities are more stringently tied to collection performance.

Stock Savings and Loan Associations (SSLAs) 1/

3.10 Organization, SSLAs are registered as stock corporations afterapproval by the Monetary Board and the Securities and Exchange Commission.They can accept deposits from the public and make loans to the public.They are now classified as banking institutions and, unlike rural banks,may open branch offices with approval of the Monetary Board. They do notenjoy exemption from taxes and Government fees and charges and cannotreceive capital assistance from the Government. At the end of December1975, there were 44 SSLAs (compared with 67 non-stock savings and loanassociations), including about 20 in the Greater Manila area.

3.11 Financial Resources. At December 31, 1975, the total paid-upcapital of all SSLAs was P 54.4 million (17% of total resources). Themain source of funds is savings and time deposits collected from stock-holders and the public. Savings contributed about a half of total resourceswhile time deposits contributed 18%. SSLAs insure their savings and de-posits with the Philippine Deposit Insurance Corporation and, in addition,they have organized their own Guaranty Fund to ensure the liquidity ofindividual associations. Borrowings were mainly from CB for participationunder the Rural Credit Projects (11% of total resources).

3.12 Lending Operations. In the past, SSLAs lent prlrLarily forcommercial and housing purposes, but lending to agriculture has graduallyincreased during 1974 and 1975 (13% in 1974; 31% in 1975). About two-thirds of SSLA loans are secured by collateral.

3.13 Collection and Profits. Collection of loans to date is satis-factory. Net income of all SSLAs is improving gradually and in 1975, itwas P 4.5 million or 8% of the paid-up capital compared to P 1.7 million(5% of paid-up capital) in 1972.

1/ A more detailed description of SSLA operations appears as Annex 7.

-9-

IV. REVIEW OF PREVIOUS RURAL CREDIT PROJECTS

a. Performance under First, Second and Third Rural Credit Projects

4.01 First Rural Credit Project (Loan 432-PH). This loan of US$5.0million assisted in establishing for the first time a nationwide system tochannel medium- and long-term credit through the rural banks to farmers andfishermen. Between 1965 and 1969, 148 rural banks participated in theproject and financed about 2,600 farmers for the purchase of farm machineryand irrigation pumps, and for development of fisheries and livestock as inthe following table:

No. of Amount in Amount as AverageCategory Sub-loans Million Pesos % of Total Sub-loan Size

Farm Machinery 2,118 19.1 89.3 9,000Irrigation Pumps 279 1.0 4.6 3,600Fisheries, Livestock 197 1.3 6.1 6,600

Total 2,594 21.4 100.0 8,250

4.02 Second Rural Credit Project (Loan 607-PH) This loan of US$12.5million financed basically the same sub-loan categories as the First Projectbut included, in addition, storage and processing facilities and on-farmtransportation equipment. Because of the low demand for term credit duringthe initial stage of project implementation, caused primarily by the effectof the peso devaluation as well as several natural disasters, final disburse-ment was completed in June 10, 1974, a delay of 18 months. From 1969 to1974, project funds were channeled through 228 rural banks to about 4,000farmers. The breakdown by major components is given in the following table:

No. of Amount in Amount as AverageCategory Sub-loans Million Pesos % of Total Sub-loan Size

Farm Mechanization 2,997 109.1 74.3 35,400Processing & Storage 161 4.7 3.2 29,200Transportation 229 12.8 8.7 55,900Fisheries 265 9.1 6.2 34,350Livestock 413 11.1 7.6 26,900

Total 4,065 146.8 100.0 36,100

4.03 Third Rural Credit Project (Loan 1010-PH). Under this loan ofUS$22.5 million a number of new sub-loan categories were added, the majoradditions being farm machinery repairshops, reconditioned trucks, fishmealplants and woodcraft plants. Other new categories were fishpens and small

- 10 -

dairy farming. Stock savings and loan associations (SSLAs) were includedto provide additicnal channels to project beneficiaries. The strong demandfor tractors, power tillers and trucks continued under the third loan and CBfully committed project funds during December 1975, about 18 months ahead ofschedule. Sub-loans were provided to 4,200 farmers through about 245 ruralbanks and 13 SSLAs as in the following table:

No. of Amount in Amount as AverageCategory Sub-loans Million Pesos % of Total Sub-loan Size

Farm Mechanization 2,930 182.3 72.4 62,200Farm Transportation 566 40.5 16.1 72,700Farm Support Facilities 293 4.9 1.9 16,600Fisheries 184 10.4 4.1 57,000Livestock 213 13.0 5.2 60,900Cottage and Agro-Industries 25 0.7 0,3 26,600

Total 4,211 251.9 100.0 60,000

4.04 Regional Distribution of Proceeds. The flow of funds under thethree projects has been concentrated in Luzon as shown in the following table,although there is a trend toward more even distribution among regions.

First Loan Second Loan Third LoanNo. Amount No. Amount No. Amount

Luzon 66% 66% 61% 66% 50% 50%Visayas 18% 17% 20% 22% 23% 30%Mindanao 16% 17% 19% 12% 27% 20%

4.05 Financing Pattern. Under the First Project, the Bank's share intotal cost of sub-projects was limited to 55%, rural banks were required tocontribute 10% and sub-borrowers, 30%. In the Second and Third Projects, theBank's limit was reduced to 50%, the rural banks' contribution was the same10%, and sub-borrowers' contribution was lowered to 10%. The following tablepresents the actual shares in sub-project financing:

First Loan Second Loan Third Loan

IBRD 55% 47% 47%Central Bank 25% 28% 27%Rural Banks /a 5% 9% 9%Sub-borrowers 15% 16% 17%

/a Rural bank contributions did not reach the required minimum 10% becausethe condition was waived during project implementation (the First andSecond Projects) and because contributions in some cases was mistakenlycalculated on the basis of sub-loans instead of total sub-project costs(the Third Project).

- 11 -

4.06 Participation of On-Lending Institutions. Participation under theRural Credit Projects was constrained primarily by arrears criteria and bythe operating radius of Loan Teams (nine operated under the Third Project)to process sub-loans. Actual participation under the three projects was asfollows:

First Loan Second Loan Third Loan

Rural Banks 148 228 245SSLAs - - 13

b. Issues Arising from Previous Projects

4.07 Overall Assessment. The Rural Credit Projects have been instru-mental in mobilizing domestic funds for medium- and long-term investments inagriculture and related industries. As a result of previous projects, ruralbanks began term lending, and the rules and operations of rural banks generallyhave been improved. Farm mechanization under previous projects has increasedcrop yields and cropping intensity by facilitating the adoption of improvedtechnology and efficient use of irrigation facilities. Farm incomes and ruralemployment opportunities have been increased among the beneficiaries. However,progress in lending to smaller farmers has been disappointing. While large-scale mechanization is an important factor in the growth of the rural economy,the distribution of project proceeds among sub-loans categories has been heav-ily weighted in favor of four-wheel tractors and due attention does not appearto have been given to other categories. The impact of previous projects onparticipating institutions has been positive and there is scope for the use ofthis mechanism to further strengthen the lending capacity and procedures andthe financial control of on-lending institutions. It is difficult to assesswith any precision the extent to which project funds have been additional orsubstitutive. However, in view of the fact that rural banks depended almostentirely on previous projects for term-lending resources and recognizing theshortage of investment credit in rural areas, it is reasonable to assume thatfunds have been additional. Substitution may have occurred in the case ofsome sugarcane tractors, and this category would be reduced under the proposedproject.

4.08 Project Beneficiaries. Recipients of sub-loans have usually beenowners of 5 ha to 50 ha, the upper limit of farm size for which rural banksare authorized to extend credit. The majority of sub-loans have gone to bor-rowers at the upper end of the size spectrum whose business contacts affordthem the best knowledge of credit opportunities and whose financial positionenables them to provide the most attractive collateral. The major benefit ofprevious projects to small farmers has been the custom hire services, parti-cularly in land preparation, which are offered by the recipients of sub-loans.The credit needs of small farmers are difficult to serve through private,commercially-oriented credit systems such as the networks of rural banks and

- 12 -

SSLAs, and due regard must be given to the financial strength and developmentof the onlending institution. 1/ Nevertheless there are financially viableinvestments which can be tailored to the needs of small entrepreneurs. Thenature and size of most components of the proposed project have been determinedwith this objective in mind and, in addition, it is proposed that a minimumshare of project proceeds be directed to this target group (para 5.02). 2/

4.09 Sub-Loan Components. The financing of four-wheel tractors hasdominated previous projects to a significantly greater degree than projectedduring appraisals, reflecting only in part the financial merits of suchinvestments. Other factors have been the relative ease of processing suchsub-loans, the aggressive promotional activities of the industry, theattractiveness of a chattel mortgage on tractors in terms of ease and valueof resale, and the prominance of typical tractor purchasers in the ruralcommunities. Efforts on the part of the Bank to encourage the promotionof other investments have not succeeded in overcoming these forces and, inorder to provide for the financing in greater numbers of other types ofinvestments, the proposed project would limit the funds available for four-wheal tractors (para 5.03).

4.10 Farm Mechanization. Under certain conditions it has been demon-strated that some types of farm mechanization displace labor, an economicconsideration the more serious by virtue of the fact that it is generallyunskilled labor with few alternative employment opportunities that is effected.Mechanization in the Philippines has been introduced primarily in land prepar-ation and evidence available to date indicates that in fact the result hasbeen to increase labor requirements over the total cropping operation. In-creased yields, cropping intensity and area have been facilitated, therebygenerating additional employment in planting, harvesting and post-harvestoperations. Land preparation and harvesting typically occur at the sametime in multiple cropping areas, and mechanization has to some extent alle-viated labor shortages in land preparation when priority for manual labormust be given to harvesting standing crops. The extent of the labor im-pact of mechanization in the Philippines and the most appropriate typesof mechanization from an employment standpoint have not been adequatelyexamined as a basis for long-term investment policy, however, and theproposed project would include such a study (para 5.10).

4.11 Tractor and Tiller Prices. During appraisal of the proposed proj-ect it was a matter of concern that tractor and tiller prices had risenrapidly in recent years. While this reflects to some extent increases in

1/ OED Report, Agricultural Credit Program, November 1976, ... thefarm development strategy must not succeed at the expense of thechannel's capacity for effective performance", p. 76.

2/ Annex 1 presents a survey of small-scale agriculture in thePhilippines and develops the definition of the proposed targetgroup for the project.

- 13 -

the c.i.f. prices of this imported equipment, CB ceiling price policy andits administrative supervision of machinery procurement for financing underthe CB:IBRD program were found to be unsatisfactory. One detrimental effect ofhigh prices in addition to the impact on sub-borrowers has been the attractioninto the industry of a large number of brands and agencies competing for smallshares of a relatively small, scattered market. The resulting diseconomies, interms of dealer network, for example, are significant. Under the proposed proj-ect ceiling price guidelines for tractors and imported tillers would be modi-fied (para 5.19) and procurement practices improved (para 5.18).

4.12 Interdependence with Other Credit Programs. With the diversific-ation of lending under previous projects and the increased total flow ofcredit to agriculture the interdependence of the CB:IBRD program and othercredit programs, both production and term, has greatly increased in recentyears. Financing under the proposed project must be monitored in the contextof the total impact of credit programs on the financial well-being of on-lending banks and sub-borrowers. Institutional aspects of the project suchas training, CB organization, bank eligibility, and sub-borrower appraisalwould be modified to insure that they complement and take into considerationthe impact of other credit programs on banks and sub-borrowers participatingin the proposed project (Chapter VI).

4.13 Institutional Development. Measures under previous projects suchas the establishment of the Technical Support and Evaluation Unit and LoanTeams and the expansion of Agricultural Credit Supervisors in the field haveresulted in substantial enhancement of CB's capacity to develop and superviseterm credit portfolios in rural banks and SSLAs. However, the expanding numberand diversity of sub-loans placed an increasing burden on CB. With the accu-mulation of experience in term lending on the part of on-lending institutions,it is feasible now to begin a transfer of more responsibility directly tothem. With the Government's desire to promote this development, a numberof training and organizational measures under the proposed project wouldassist in a gradual transfer of lending authority to rural banks and SSLAs(para 5.12 and Chapter VI).

4.14 Repayment Performance. The Government and CB have now acknowledgedthat every effort must be made to reduce high arrearages, and a number ofremedial actions have been taken. The National Commission on CountrysideCredit and Collection (NCCC) chaired by CB's Governor, has been establishedto review the large overdues existing under Government-assisted lendingprograms. Together with its working unit established in CB, it is expectedto assist banks in their collection efforts and to formulate educationalprograms to improve repayment habits in rural areas. CB is implementinga special scheme under which teams of one examiner and one agriculturistwould reside in local areas to strengthen supervision and technical assist-ance to four and eight rural banks, respectively. CB has also decided todeny, as of November 1, 1976, all rediscounting facilities to rural bankswith arrears in excess of 25% of their loan portfolio. 1/ This is not a new

1/ As a result of this action, 257 rural banks were temporarily disqualifiedfrom rediscounting on November 1, 1976.

- 14 -

criterion although it has not been enforced with respect to food productionloans since 1973. It is also proposed that Government undertakes a detailedstudy of the causes of arreazs to assist in the developing measures for theirreduction. Together with improved financial management assistance to banks,it is expected that these measures will reduce present arrears substantially.Arrears criteria for the proposed project are discussed in para 6.09.

V. THE PROJECT

5.01 The project would be a continuation of the Third Rural Credit Proj-ect to provide medium- and long-term credit for another three years. Quali-fied rural banks and SSLAs would lend project funds to about 16,000 farmersand rural entrepreneurs for investment in: (a) farm mechanization; (b) lighttransportation; (c) cottage and agro-industries; (d) coastal and inland fish-eries; and (e) small-scale livestock development. The project would alsoinclude funds for: (f) a study to assess the impact of farm mechanizationin the Philippines; (g) an Agricultural Machinery Testing, Evaluation andStandardization Project to standardize the quality of farm machinery; (h) atraining program to improve the lending capability of CB and rural bank staff;and (i) service vehicles for CB field staff engaged in the project.

5.02 Emphasis would be given to increasing the share of project proceedsaccruing to smaller borrowers above that realized in previous projects. Assur-ances were obtained that a minimum of US$11 million I/ of loan proceeds wouldbe on-lent to small beneficiaries whose total self-earned income per year isless than P 7,500 2/, or whose total self-earned income per year is P 7,500or more and who earn 75% or more of such income from one of the following: aland holding, owned or leased, of not more than seven ha; a fishing enterprise,operated on the basis of ownership or leasehold, consisting of not more thanfive ha of fishponds or fishpens, or not more than one fishing vessel, suchvessel not to exceed five tons; or a cottage or agro-industrial enterpriseowned and operated by them, and consisting of fixed assets of less thanP 100,000, excluding the value of land.

Detailed Features

(a) Farm Mechanization (Annex 8)

5.03 Four-Wheel Tractors. The project would finance about 1,775 tractorsand implement packages for rice, corn and sugarcane farmers. The trend towardthe purchase of larger tractors in the Philippines has resulted in excess

1/ Equivalent to 56.6% of proceeds allocated to sub-projects other than four-wheel tractors or 30.6% of total sub-loan proceeds.

2/ Financing under the project of a small-scale livestock enterprise ofnot more than 10 sows, 200 layers, 400 broilers, or five cattle orcarabaos would usually be for this category of small beneficiaries.

-15 -

power and reduced cost effectiveness of tractor investments, particularly inrice and corn areas (Annex 8, para 18). Under the Third Project a limit of80 hp was placed on tractors to be financed, irrespective of crops cultivated.To further reduce the financing of excess capacity, tractors to be used inrice and corn production, where draft requirements are significantly less,would be limited to a maximum of 68 hp under the proposed project. However,this limitation would be imposed only after a period of 18 months from thedate of the Loan Agreement or after the financing of 1,000 units of tractorsin excess of 68 hp each, whichever should occur first, in order to facilitatethe adjustment of the trade and the reduction of present inventories of largetractors. Assurances were obtained that financing of four-wheel tractors inexcess of 68 hp each would be limited to 1,000 units, of which a maximum of450 units would be financed to be used in sugarcane growing areas, where pur-chasers are typically in a better position to use alternative sources offinancing, 1/ and that loan proceeds used to finance four-wheel tractorsirrespective of horsepower would be limited to US$16.5 million. 2/ One addi-tional limitation would be imposed on tractor financing: for tractors to beeligible for financing under the project, retail prices would not be permittedto exceed ceilings presented in the discussion of procurement (para 5.19).These limitations would be monitored by Loan Teams and the Technical Supportand Evaluation Unit (TSEU).

5.04 Power Tillers. About 7,800 tillers would be financed under theproject. The financial viability of small cultivators is marginal in termsof additional output under normal conditions. However, a major advantage,although difficult to quantify, is the assurance of cultivation capacity incontrast to the uncertainty resulting from the vulnerability of draft animalsto debilitating diseases and their need for prolonged periods of rest. Thisprotection can be afforded by the smaller locally manufactured units and theevaluation of higher cost imported models has been subjected to more stringentfinancial criteria. At present price levels, purchase of imported modelscannot be justified, and financing under the project would be limited to thosewhich conform to ceiling price guidelines presented in procurement paragraph5.19. This limitation would be monitored by Loan Teams and TSEU.

5.05 Other Farm Mechanization. Other items would include about 400small irrigation units, 600 portable threshers of 100-300 cavans per hourcapacity, about 240 implement packages for owners of tractors purchasedoutside of the project, and a small allocation for miscellaneous equipmentsuch as back-pack sprayers. Demand for small-scale irrigation facilitiesis limited at the present time because of uncertainty surrounding waterrights and the absence of detailed groundwater surveys. Some of thislimited demand is now being met by Government agencies such as the NationalIrrigation Authority, the Farm Systems Development Corporation and thePublic Works Department through separate programs offering credit on morelenient, inexpensive terms than can be offered by commercial credit

1/ Under the Third Project, it is estimated that about 600 tractors werefinanced for sugarcane growers.

2/ US$16.5 million, consisting of $14.0 million base cost estimate plus amaximum share of price contingencies of $2.5 million.

- 16 -

institutions. In the case of portable threshers, technical merit in termsof recovery rates is not reflected in large demand since minimum utilizationrates to assure viability generally require the grouping of farmers or ex-tensive custom work. For both irrigation pumps and portable threshers,our estimates of units to be financed reflect these limitations despitethe potential contribution to increase production.

(b) Light Transportation (Annex 8)

5.06 This category would include about 400 light trucks having a grossvehicle weight of less than 2,500 kg which would be used in rural areas ascargo vehicles for small-scale entrepreneurs and for transportation of mixedcargo and passengers. These multi-purpose vehicles, owned and operated bylocal entrepreneurs, are the traditional means used by small farmers to markettheir produce and to transport production inputs to their farms. No financ-ing of light trucks would be undertaken in the Greater Manila area, to mini-mize the likelihood of project vehicles being used exclusively for passengertransportation. Despite an apparent need for more cargo transportation capa-city in most areas in the Philippines, financing of heavy and medium truckswould be discontinued under the project because of the relatively good finan-cial position of cargo businesses, enabling them to use other sources offinancing.

(c) Cottage and Agro-Industries. (Annex 9)

5.07 This category would include about 225 sub-projects covering awide range of cottage and agro-industries such as rice milling, farm implementmanufacturing, woodworking, handicrafts and manufacturing of concrete pipesand tiles. It would enable rural banks to diversify their lending operationsand serve a wider segment of the rural population. The Bank's Small andMedium Industries Development Project (Loan 1120-PH, US$30.0 million) alsoprovides funds for agro-industries through rural banks but the scale of sub-loan under the proposed project would be smaller. The number of rural banksable to extend and supervise smaller sub-loans would be significantly higherthan those eligible to participate in the Bank's Small and Medium IndustriesDevelopment Project through CB's Industrial Guarantee and Loan Fund (IGLF).

(d) Coastal and Inland Fisheries. (Annex 10)

5.08 Fisheries sub-projects would include about 45 small coastal fishingboats (basnig boats ) and equipment, and about 1,200 inland fishponds andfishpens with a total area of 6,000 ha. Boats of simple traditional designwould be manufactured in small local yards, purchased by local entrepreneurs,and crewed by local fishermen usually on a catch-sharing basis. The maximumsize of a boat financed would be increased from 20 gross tons under the ThirdProject to 40 gross tons in order to permit access to better, more distantfishing grounds. The average size of fishponds and fishpens would be 5 ha.The Bank's Second Fisheries Credit Project (Loan 1270-PH, US$12.0 million)presently administered by DBP would finance larger boats (of 45 gross tonsand above) and fishponds (an average size of 24 ha) and would have no over-lap with the proposed project.

- 17 -

(e) Small-Scale Livestock Development. (Annex 11)

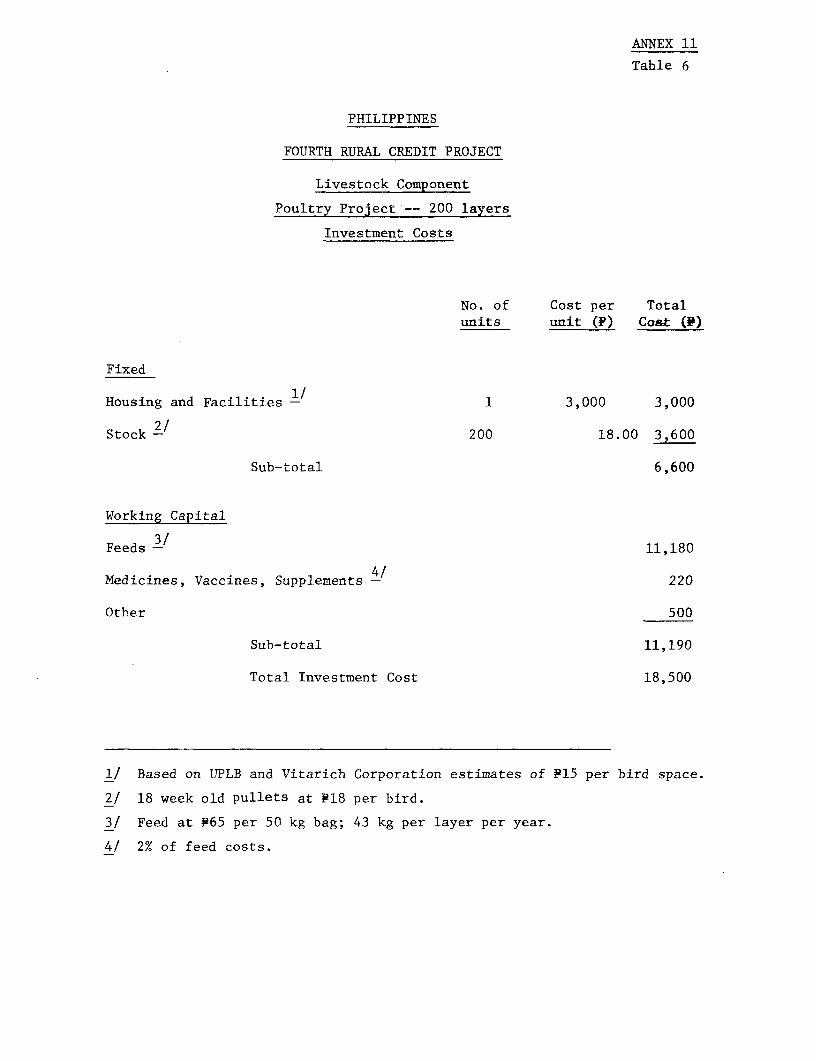

5.09 About 3,240 small-scale livestock sub-projects (1,240 for poultry,1,000 for pig and 1,000 for cattle breeding and fattening) would be includedunder the project to meet the cost of initial stock, pens and shelters,feed and other inputs. Poultry and pig sub-projects financed under theproject would generally be smaller than those to be financed by the Bank'sSecond Livestock Project (Loan 1225-PH, US$20.0 million) administered byDBP. The scale of backyard cattle breeding/fattening farms financed underthe project would be similar to that under the Livestock Project but only200 such sub-loans are included under the latter project, and geographiccoverage by rural banks, being more extensive than that of DBP branches,would permit the proposed project to meet demand not served through theLivestock Project.

(f) Study of Farm Mechanization (Annex 12)

5.10 The benefits of farm mechanization in terms of increased food pro-duction have been demonstrated in some countries to be offset to some extentby detrimental economic and social effects, particularly the displacement ofunskilled labor. Economic and social patterns within the area in questionand the nature of mechanization taking place are key determinants of theseundesirable effects, and evidence that has been acquired for the Philippinessuggests that labor displacement on an annual or area basis is not takingplace. However, a thorough study of the impact of mechanization, both itsadvantages and disadvantages, has not been conducted on a sufficiently largescale to form the basis for long-term Government policy on mechanization.The project would therefore include a study to assess the financial, economicand social impact of farm mechanization. Assurances were obtained that quali-fied consultants would be engaged on terms and conditions acceptable to theBank to conduct this study and that terms of reference for the study would beacceptable to the Bank. Also, a preliminary draft of the study would be sub-mitted to the Bank for its comments.

(g) Agricultural Machinery Testing, Evaluation and Standardization Project(Annex 8)

5.11 With the rapid expansion of farm mechanization in recent years,there has been a proliferation of local manufacturing firms and importers.The proposed project would include an Agricultural Machinery Testing, Evalua-tion and Standardization Project to set quality standards for agriculturalmachinery and to conduct performance testing against such standards. TheProject would be located on the campus of the University of the Philippinesat Los Banos (UPLB) and be directed by a senior member of the Department ofAgricultural Engineering. The following would be the principal objectivesand activities: (i) develop quality and performance standards for Philippinesfarming conditions and types of equipment used in the Philippines; (ii) con-duct field, shop and laboratory testing of equipment to determine capacityand conformity with relevant standards; and (iii) evaluate post-purchase partsand service support. The Project would issue its factual results in bulletinform and would not recommend any products or processes. Assurance were

- 18 -

obtained that the Project would be established at UPLB with organization,staff and facilities acceptable to the Bank, and would thereafter be main-tained beyond the period of the proposed Bank project.

(h) Training

5.12 The project would provide funds to augment the ongoing trainingprograms of CB for its own staff and staff of rural banks and SSLAs.Areas of concentration under the project would include: the evaluationof cottage and agro-industrial sub-projects, for which courses would bedesigned for both CB and on-lending bank staff; and farm budgeting and plan-ning, for the technical staff of on-lending banks. Courses would bedesigned and conducted by CB with the use of non-CB resource staff asappropriate. A handbook would also be prepared for the field staff ofon-lending banks and CB, covering all phases of lending operations. Thepurpose of this handbook would be to standardize the quality and natureof design, appraisal and supervision of production and term credit loans.Assurances were obtained that qualified consultants would be engaged onterms and condition acceptable to the Bank to assist in preparation ofthe handbook and that the outline of the handbook would be acceptable tothe Bank. A preliminary draft of the handbook would also be submitted toBank for its comments.

(i) Service Vehicles

5.13 Under the Second Loan in 1969, 61 service vehicles were financedfor CB field staff. Since that time, field staff have more than doubled,and an additional sixty vehicles would be provided to meet the needs ofthese officers in their bank and sub-project review work.

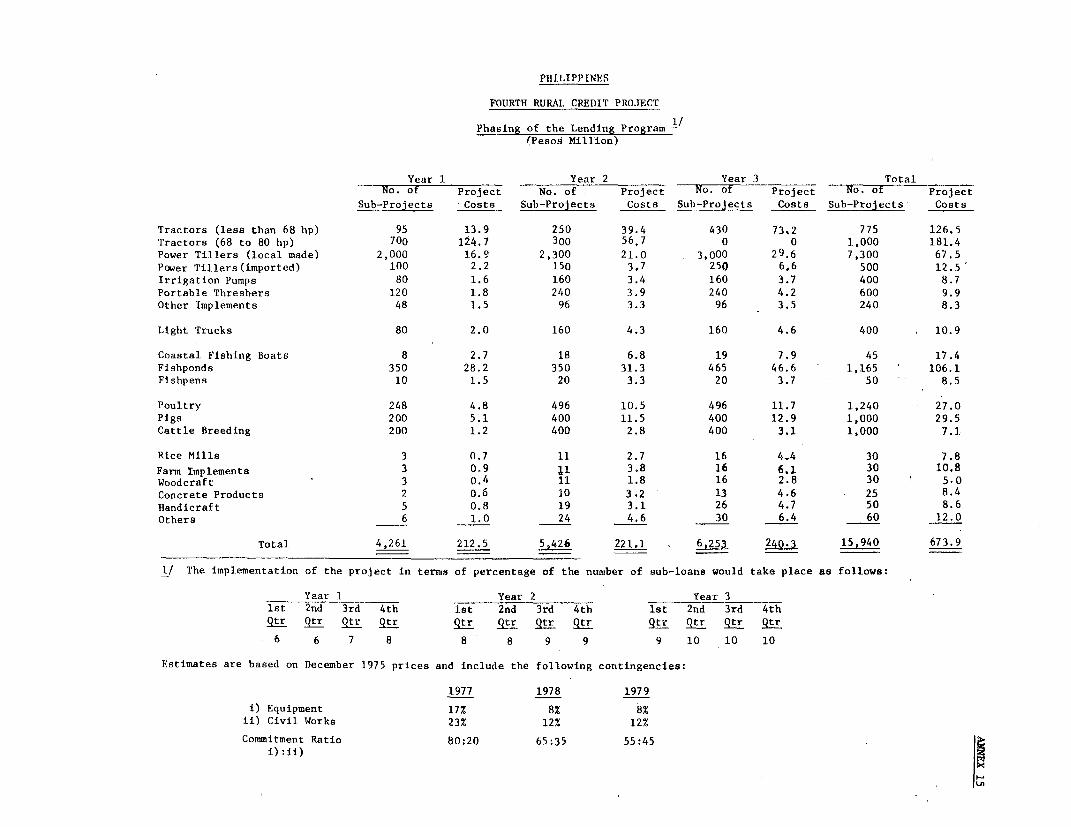

Summary of Sub-Loan Items

5.14 The following summary of sub-loan items is presented in termsof December 1975 prices.

-19 -

Number of ------ Total Cost ----------------Items Units Million Pesos Million US Dollars

Tractors 1,775 259.9 34.7Power Tillers 7,800 64.8 8.6Portable Threshers 600 8.0 1.1Irrigation Pumps 400 7.0 0.9Other Implements 240 6.8 0.9Light Trucks 400 8.8 1.2Coastal Fishing Boats 45 13.4 1.8Fishponds 1,165 80.0 10.7Fishpens 50 6.3 0.8Poultry 1,240 20.1 2.7Pigs 1,000 22.0 2.9Cattle Breeding/Fattening 1,000 5.3 0.7

Cottage and Agro-Industries 225 39.2 5.2

Total 15,940 541.6 72.2

Project Area

5.15 The project would be country-wide in scope although coverage interms of individual communities would depend on participation by ruralbanks and SSLAs. Only about 100 rural banks are expected to participatein the project during the first six months as a result of the enforcementof arrears criteria. Participation may be expected to increase graduallyas more rural banks reduce arrears to acceptable levels (para 6.09). Thedistribution of on-lending institutions will remain approximately as it wasunder the Third Project: two-thirds in Luzon, and the balance evenly dis-tributed in the Visayas and Mindanao. The expanded coverage of cottage andagro-industries is likely to induce greater participation among SSLAs in thesmall municipal centers of the country.

Cost Estimates

5.16 Total project cost is estimated to be US$91.3 million. Toensure sufficient funds for a steady flow of sub-projects over the pro-posed three year period, a price contingency of 13.7% has been added tothe December 1976 base cost estimates. I/ The estimated foreign exchangecomponent is US$29.4 million (32%).

1/ Financial and economic evaluation has been conducted on the basis ofcost prevailing at the time of project preparation, December 1975. How-ever, for this aggregate cost table, the base cost estimate has beenadjusted to December 1976 levels by adding estimated cost increases of9% for equipment and 11% for civil works. To December 1976 costs, pricecontingencies have been added as follows:

1977 1978 1979

i. Equipment 8% 8% 8%ii. Civil works 11% 12% 12%

Commitment Ratio 80:20 65:35 55:45(i:ii)

- 20 -

Million Pesos Million US$ Foreign

Local Foreign Total Local Foreign Total Exchange

Farm Mechanization 228.8 154.9 377.7 29.7 20.7 50.4 42Light Transportation 5.8 3.8 9.6 0.8 0.5 1.3 40Fisheries Development 94.3 15.4 109.7 12.6 2.0 14.6 14Small-Scale Live-

stock Development 46,7 5.2 51.9 6.2 0.7 6.9 10Cottage and Agro-

Industries 31.7 11.7 43.4 4.2 1.6 5.8 27

Sub-Total 401.3 191.0 592,3 53.5 25.5 79.0 32

Training 1.8 - 1.8 0.2 - 0.2 0Study 0.7 - 0.7 0.1 - 0.1 0Vehicles 1.6 1.7 3.3 0.2 0.3 0.5 50Agricultural

Machinery

Testing, Evaluation 3.1 0.7 3.8 0.4 0.1 0.5 19and Standardization

Project

Sub-Total 7.2 2.4 9.6 0.9 0.4 1.3 24

Base Cost Estimate 408.5 193.4 601.9 54.4 25.9 80.3 32Price Contingency 56.1 26.4 82.5 7.5 3.5 11.0 32

Total Project Cost 464.6 219.8 684.4 61.9 29.4 91.3 32

Financing

5.17 Total project costs of US$91.3 million equivalent would be financed

as follows:

Million US$ Million Pesos Percent

IBRD 36.5 273.8 40CB/Government 36.6 273.8 40Rural Banks/SSLAs 9.1 68.4 10 /a

Beneficiaries 9.1 68.4 10

Total 91.3 684.4 100

/a Average figure. Rural Banks in operation for less than three years

and with a net worth not exceeding P 500,000 may be authorized to

contribute only 5%.

- 21 -

Bank funds would be lent to CB. Together with the Government and CB contri-bution, loan proceeds would be onlent to rural banks and SSLAs in the form ofSpecial Time Deposits. A minimum contribution of 10% would be required ofrural banks and SSLAs except in the case of recently established rural bankswith limited resources (net worth less than P 500,000), in which case theminimum contribution would be 5%. The minimum sub-borrower's contributionwould be 10%. Terms and conditions for the release of project funds wouldbe set out in the Rules and Regulations governing the program, and assuranceswere obtained that the Rules and Regulations, and changes thereto, would besubject to Bank approval. Funds for AMTESP would be transferred from CB tothe Department of Agriculture which would in turn allocate them to AMTESP.

Procurement

5.18 As in the Third Project, machinery and equipment, including trucks,irrigation pumps, engines and equipment for fishing boats, and machinery andequipment for cottage and agro-industries would be purchased locally by sub-borrowers under initial supervision of the on-lending institution. There isadequate representation of major international manufacturers. Sufficientprivate contractors are available for construction of boats, buildings andother civil works. Building materials, including lumber and cement, are pro-duced locally. The size of individual contracts would be too small for inter-national competitive bidding and bulking of contracts would not be practicablebecause of their wide dispersal both in location and time. All sub-projectcontracts would be made through ordinary commercial channels and assuranceswere obtained that at least three price quotations would be required forall sub-project contracts in excess of P 10,000 except in remote areas wheresupplier representation is insufficient, in which case a certified statementto that effect by the financing institution would be required. The purchaseof service vehicles by CB would be through local competitive bidding in accord-ance with the procedures acceptable to the Bank.

5.19 CB would modify its present ceiling price guidelines on four-wheeltractors and imported power tillers so that the maximum retail prices to beconsidered for financing under the project would be 170% of the bodega (ware-houses) cost for four-wheel tractors and 175% for imported power tillers, thebodega cost being defined as the sum of (a) c.i.f. Manila, (b) 30% of c.i.f.Manila (42% for imported power tillers) primarily to cover duties and taxes butalso including miscellaneous costs, and (c) the direct cost of local content 1/,Prices would vary by models. Monitoring of these tractor and tiller priceswould continue to be the responsibility of DRBSLA.

1/ The approximate effect of these price revisions would be to reducetractor prices on average by 11% and imported tiller prices on aver-age by about 15%.

- 22 -

Disbursement

5.20 Disbursement of loan proceeds to CB would be as follows:

(i) 45% of the sub-loans disbursed by rural banks and SSLAs,against certified statements of expenditures;

(ii) 40% of the costs of instruction, materials and rental offacilities for training and the preparation of a credithandbook, against certified statements of expenditures;

(iii) 100% of the c.i.f., ex-factory cost of vehicles, or40% off-the-shelf, against invoice;

(iv) 40% of the cost of the farm mechanization study, againstcertified statements of expenditures; and

(v) 66% of the cost of civil works and equipment contracts forthe Agriculture Machinery Testing, Evaluation and Standardi-zation Project, against invoice, to be passed on to theDepartment of Agriculture.

5.21 In the case of disbursement against certified statements ofexpenditures, supporting documentation would not be submitted for review butwould be retained by CB and available for inspection by the Bank during thecourse of project supervision. An estimated quarterly schedule of disburse-ments appears in Annex 14.

VI. ORGANIZATION AND MANAGEMENT

6.01 The credit component of the project together with related trainingand support facilities would, as with previous Rural Credit Projects, be theresponsibility of CB's DRBSLA. Funds for the Agricultural Machinery Testing,Evaluation and Standardization Project would be channelled through theDepartment of Agriculture to the University of the Philipines at Los Banos(UPLB).

Department of Rural Banks and Savings and Loan Associations.

6.02 Organization. DRBSLA is headed by a Director who is supported inoverall department management by an Associate Director. The Department'seight operating divisions responsible for supervision and sub-loan assistanceunder special schemes are grouped according to geographic jurisdiction and,together with the Accounting and Special Services Division, are placed underone of the three Assistant Directors. DRBSLA is the largest department in CBwith over 700 staff. Its functions are distinguishable broadly into two dis-tinct categories; credit activities, and audit and examination of rural banksand SSLAs. Although present policy within CB limits management of departments

- 23 -

to only one Associate Director, the size and nature of DRBSLA's responsibili-ties appears to warrant positions for two Associate Directors. Field-basedstaff such as Agricultural Credit Supervisors and members of Loan Teams areunder the direct supervision of the Division responsible for the territoryto which they are assigned. Training, legal services, statistical operationsand other required services are separately managed within the Department. TheTechnical Support and Evaluation Unit was established under the Third Projectin the Office of the Director. Members of the Unit have developed good work-ing ties with field staff, particularly Loan Teams, and this organizationalarrangement would continue under the proposed project.

6.03 Project Implementation. The Director, DRBSLA would assume overallresponsibility for implementation of all aspects of the project exceptAMTESP (para 6.12). At the outset, the following cycle and responsibilitieswould apply to sub-loans: a technician of the on-lending institution wouldprepare the sub-project, generally with the assistance of a CB AgriculturalCredit Supervisor or Loan Team member; the on-lending institution wouldconduct credit and collateral checks, assemble the sub-loan application andsupporting documentation, and submit these to the Loan Team; the Loan Teamwould conduct an appraisal of the proposal and, if it is approved, wouldsubmit its recommendation to DRBSLA together with documents of obligation onthe part of the on-lending institution; upon release of Special Time Depositsby the Accounting and Special Services Division, which would be released underthe proposed project by four Loan Teams located at three regional offices andat headquarters, in the name of the on-lending institution, disbursementagainst sub-borrower contracts would be made by the on-lending institution,direct to suppliers where possible. The authorities and responsibilitiesdescribed above would change gradually under the project as the Departmentbegins to introduce more decentralized decision-making and administrativeprocesses.

6.04 Decentralization of DRBSLA Operations. It is the intention of theDepartment to decentralize its operations increasingly to regional offices ofCB in order to expedite the release and recovery of funds and improve thesupervision of financial institutions. In the context of term lending opera-tions and the CB:IBRD program, decentralization would take several specificforms.

(a) Evaluation of sub-loan proposals would be graduallytransferred to selected rural banks from Loan Teams.This transfer must be gradual, establishing in effectfree limits for qualified banks within which they wouldbe authorized to approve specific types of sub-loans,subject to technical support and post-approval audit byLoan Teams. Such authority would be granted and amendedon a bank by bank basis by the Director, DRBSLA, actingon recommendation of the Loan Team of the region. Assur-ances were obtained that steps would be taken to imple-ment this tranfer.

- 24 -