Part II: Macroeconomic Markets

34

Part II: Macroeconomic Markets ECO2142 Fall 2014 _ Yves TEHOU 3

-

Upload

christianity -

Category

Documents

-

view

0 -

download

0

Transcript of Part II: Macroeconomic Markets

Part II: Macroeconomic Markets

ECO2142 Fall 2014 _ Yves TEHOU 3-‐

Chapter 3 The Goods Market

• Equilibrium in the goods market. • Determina8on of output. • Interac8on among demand, produc8on, and income.

• How fiscal policy can be used to affect output.

ECO2142 Fall 2014 _ Yves TEHOU

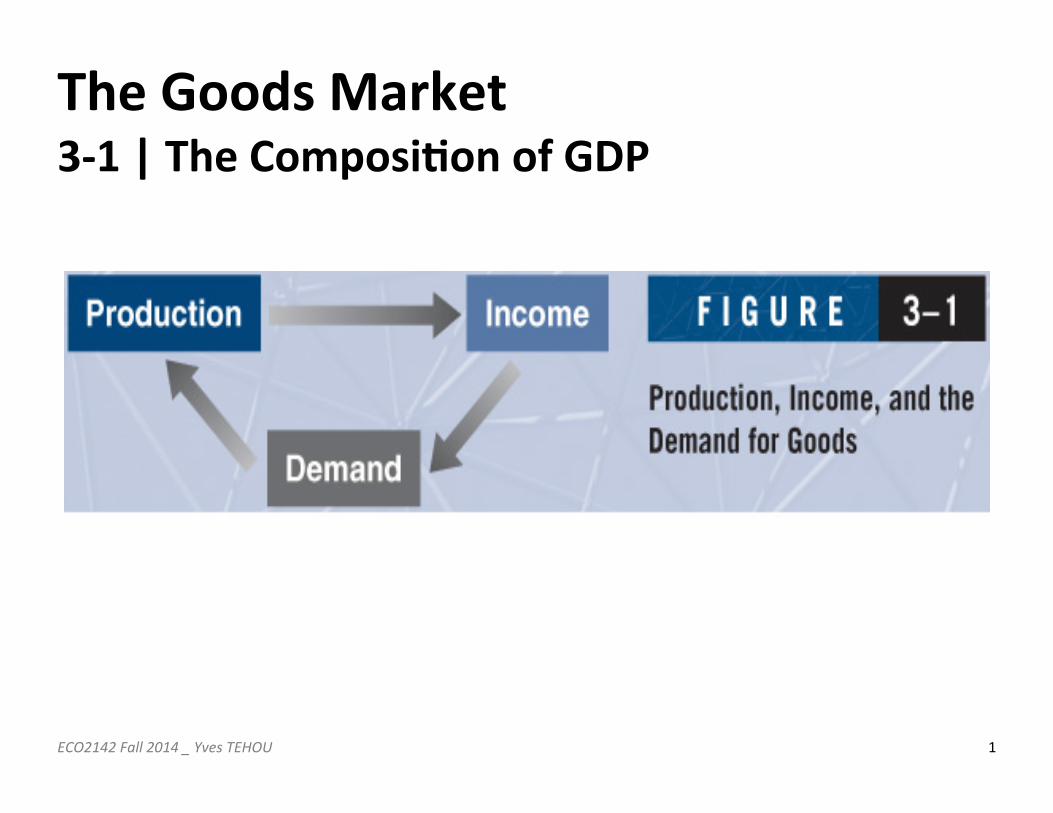

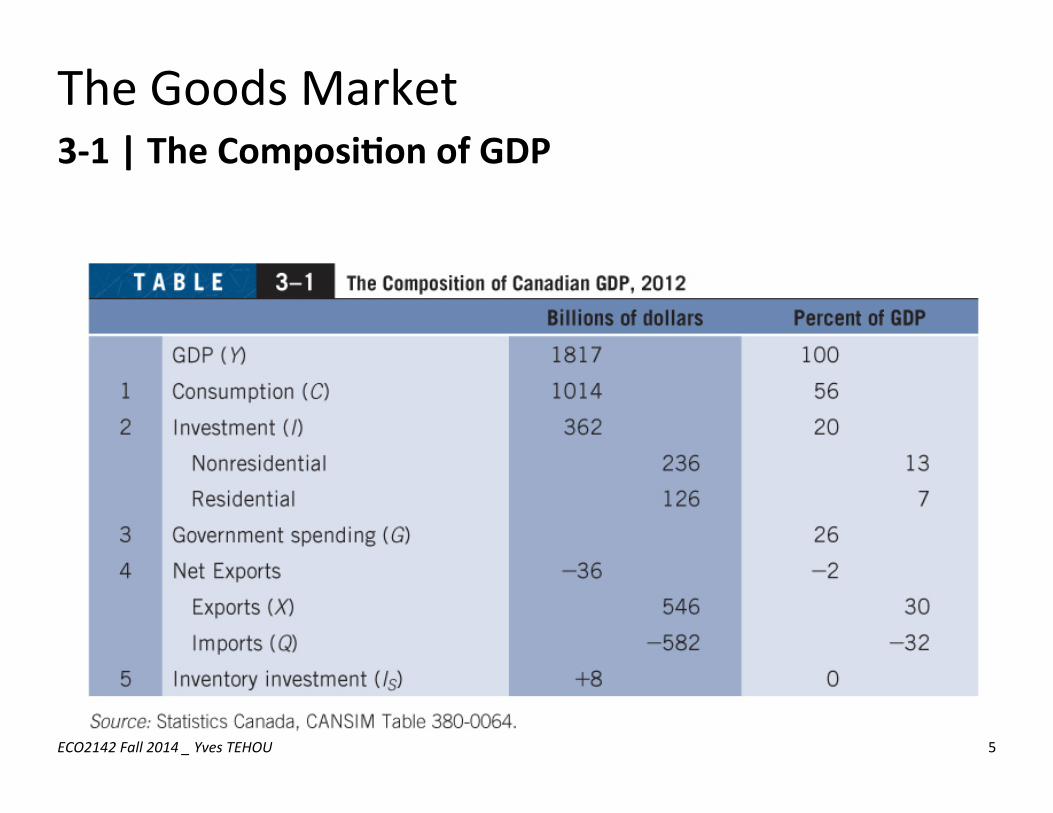

The Goods Market 3-‐1 | The Composi;on of GDP

ECO2142 Fall 2014 _ Yves TEHOU 1

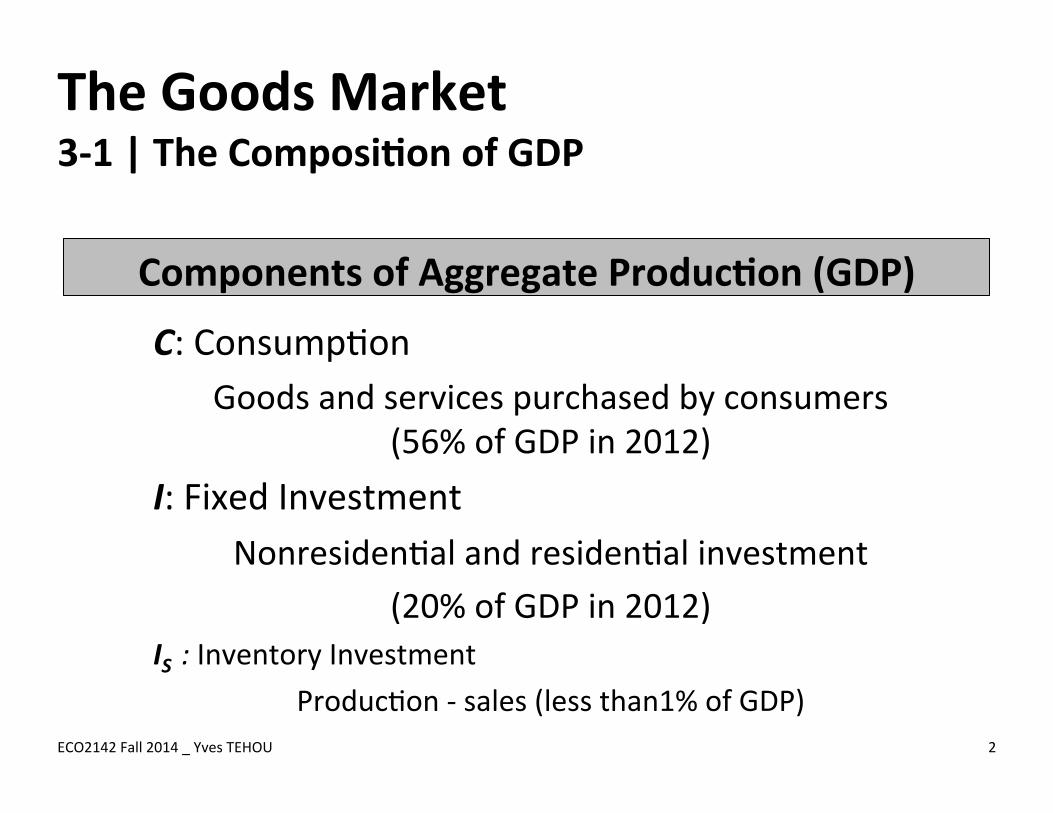

The Goods Market 3-‐1 | The Composi;on of GDP

Components of Aggregate Produc;on (GDP)

ECO2142 Fall 2014 _ Yves TEHOU 2

C: Consump8on Goods and services purchased by consumers

(56% of GDP in 2012) I: Fixed Investment

Nonresiden8al and residen8al investment (20% of GDP in 2012)

IS : Inventory Investment Produc8on -‐ sales (less than1% of GDP)

The Goods Market 3-‐1 | The Composi;on of GDP

ECO2142 Fall 2014 _ Yves TEHOU 3

G: Government Spending Purchases by federal, provincial, and local governments. Excludes transfer payments

(26% of GDP in 2012)

The Goods Market 3-‐1 | The Composi;on of GDP

ECO2142 Fall 2014 _ Yves TEHOU 4

X – Q: Net Exports Exports (X) -‐ Imports (Q)

(35% of GDP in 2012) (32% of GDP in 2012)

X > Q: trade surplus X < Q: trade deficit (2% of GDP in 2012)

The Goods Market 3-‐1 | The Composi;on of GDP

ECO2142 Fall 2014 _ Yves TEHOU 5

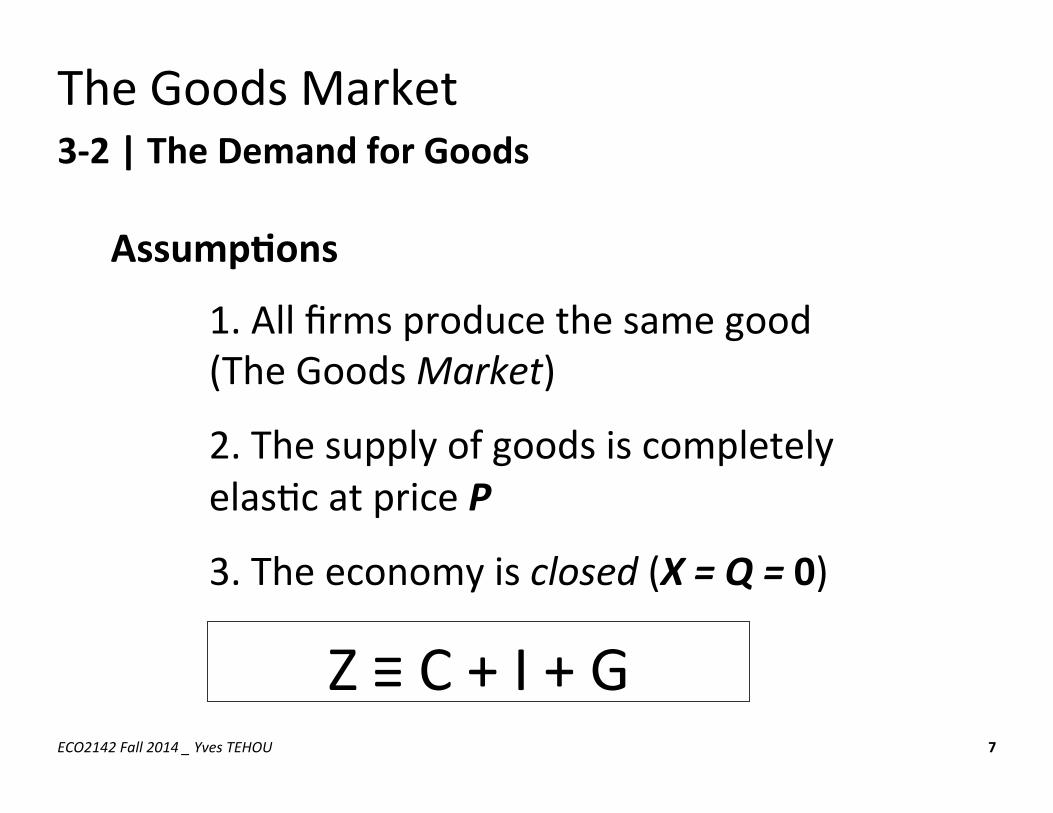

The Goods Market 3-‐2 | The Demand for Goods

Total Demand

ECO2142 Fall 2014 _ Yves TEHOU 6

Z ≡ C + I + G + X -‐ Q

The Goods Market 3-‐2 | The Demand for Goods

Assump;ons

ECO2142 Fall 2014 _ Yves TEHOU 7

1. All firms produce the same good (The Goods Market)

2. The supply of goods is completely elas8c at price P

3. The economy is closed (X = Q = 0)

Z ≡ C + I + G

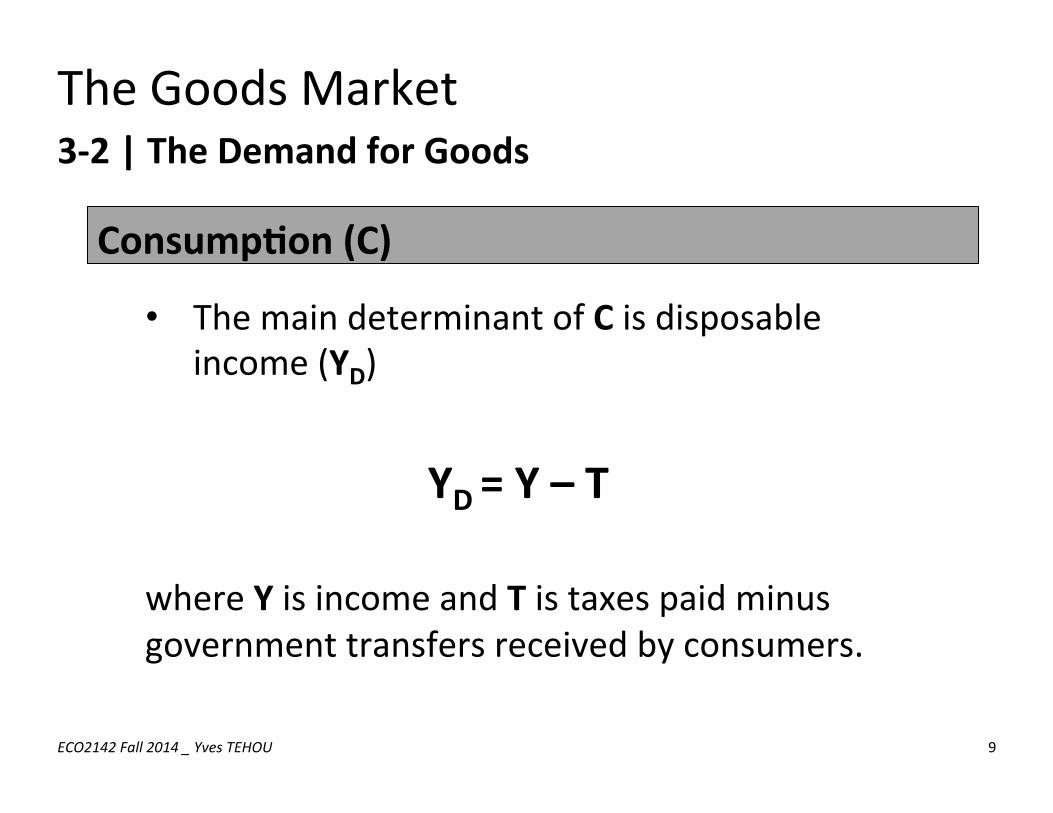

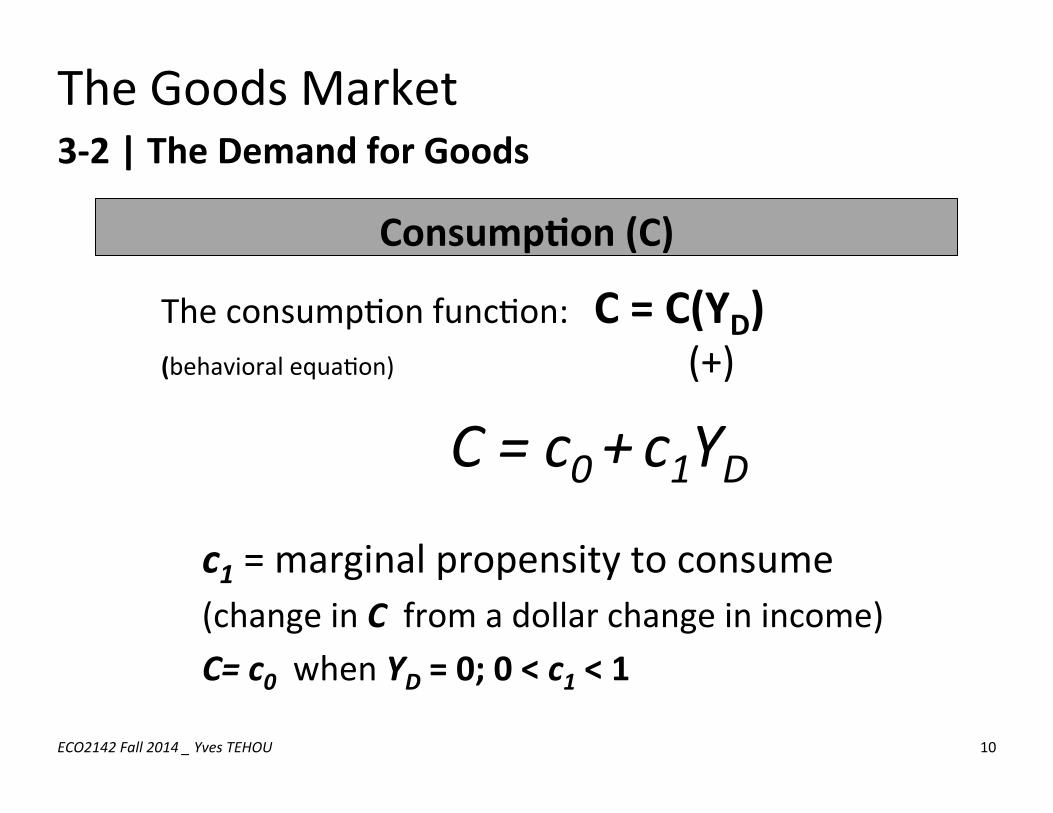

The Goods Market 3-‐2 | The Demand for Goods Consump;on (C)

ECO2142 Fall 2014 _ Yves TEHOU 9

• The main determinant of C is disposable income (YD)

YD = Y – T

where Y is income and T is taxes paid minus government transfers received by consumers.

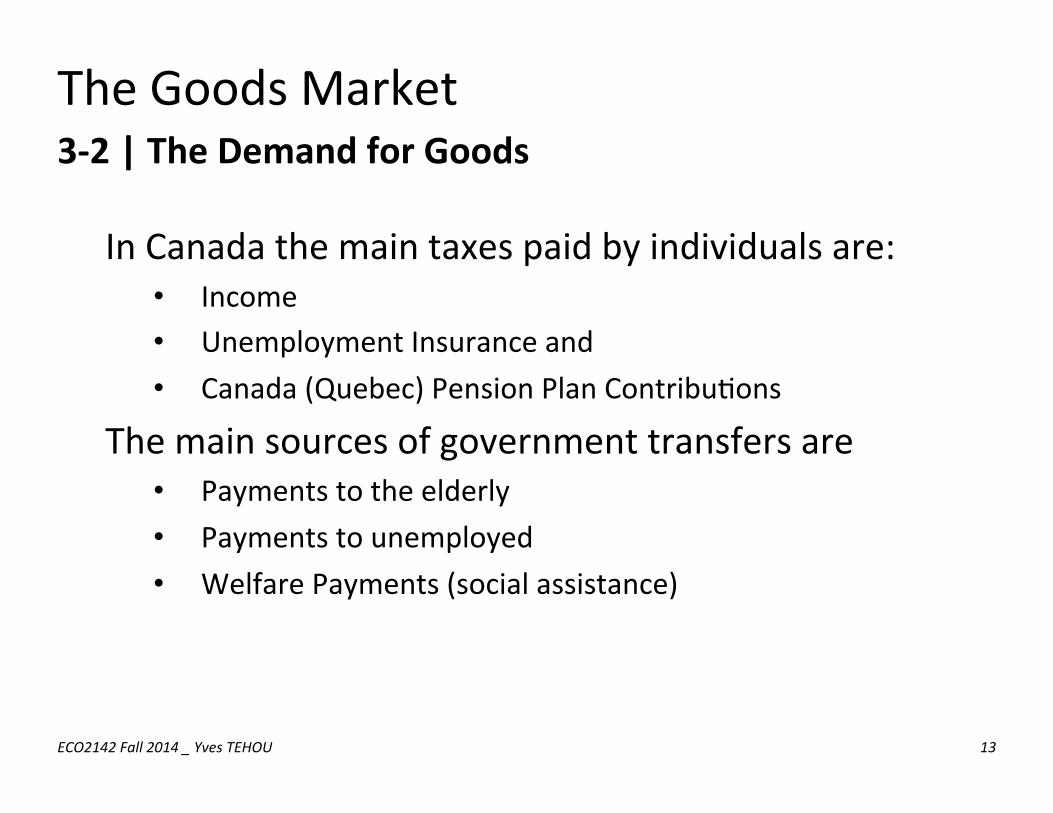

The Goods Market 3-‐2 | The Demand for Goods

ECO2142 Fall 2014 _ Yves TEHOU 13

In Canada the main taxes paid by individuals are: • Income • Unemployment Insurance and • Canada (Quebec) Pension Plan Contribu8ons

The main sources of government transfers are • Payments to the elderly • Payments to unemployed • Welfare Payments (social assistance)

The Goods Market 3-‐2 | The Demand for Goods Consump;on (C)

ECO2142 Fall 2014 _ Yves TEHOU 10

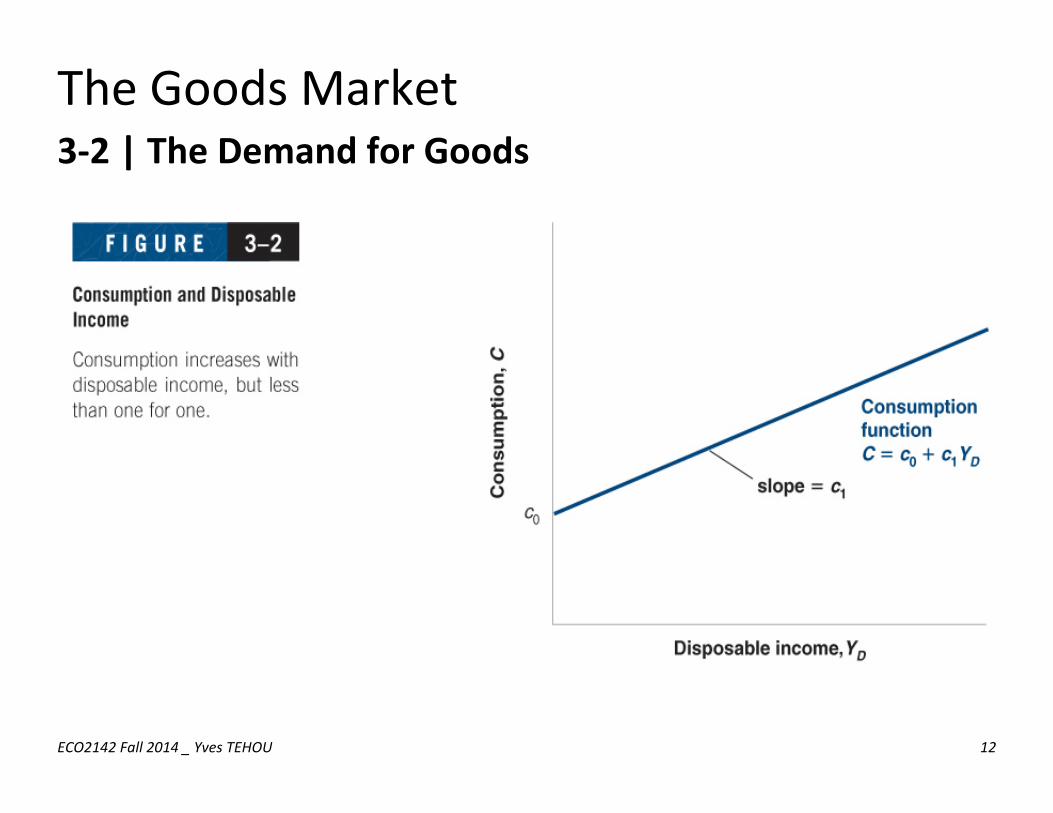

The consump8on func8on: C = C(YD) (behavioral equa8on) (+) C = c0 + c1YD

c1 = marginal propensity to consume (change in C from a dollar change in income) C= c0 when YD = 0; 0 < c1 < 1

The Goods Market 3-‐2 | The Demand for Goods

ECO2142 Fall 2014 _ Yves TEHOU 12

The Goods Market 3-‐2 | The Demand for Goods

ECO2142 Fall 2014 _ Yves TEHOU 14

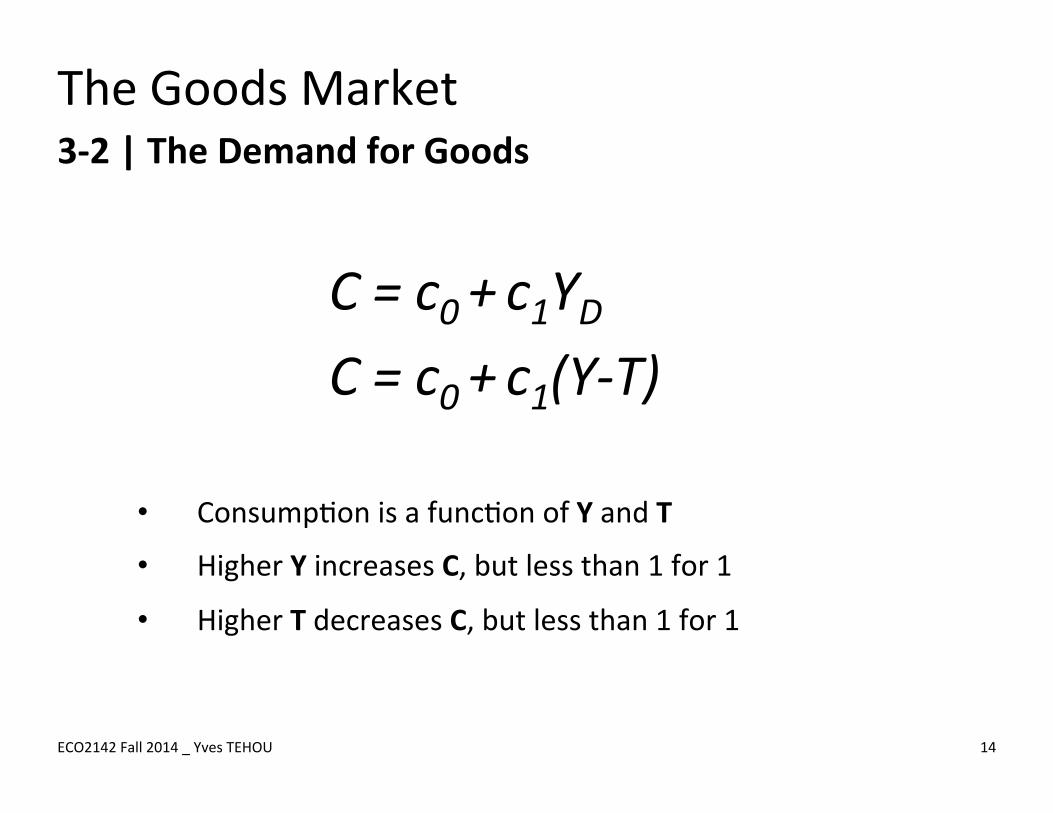

C = c0 + c1YD C = c0 + c1(Y-‐T)

• Consump8on is a func8on of Y and T

• Higher Y increases C, but less than 1 for 1

• Higher T decreases C, but less than 1 for 1

The Goods Market 3-‐2 | The Demand for Goods

Investment (I)

ECO2142 Fall 2014 _ Yves TEHOU 15

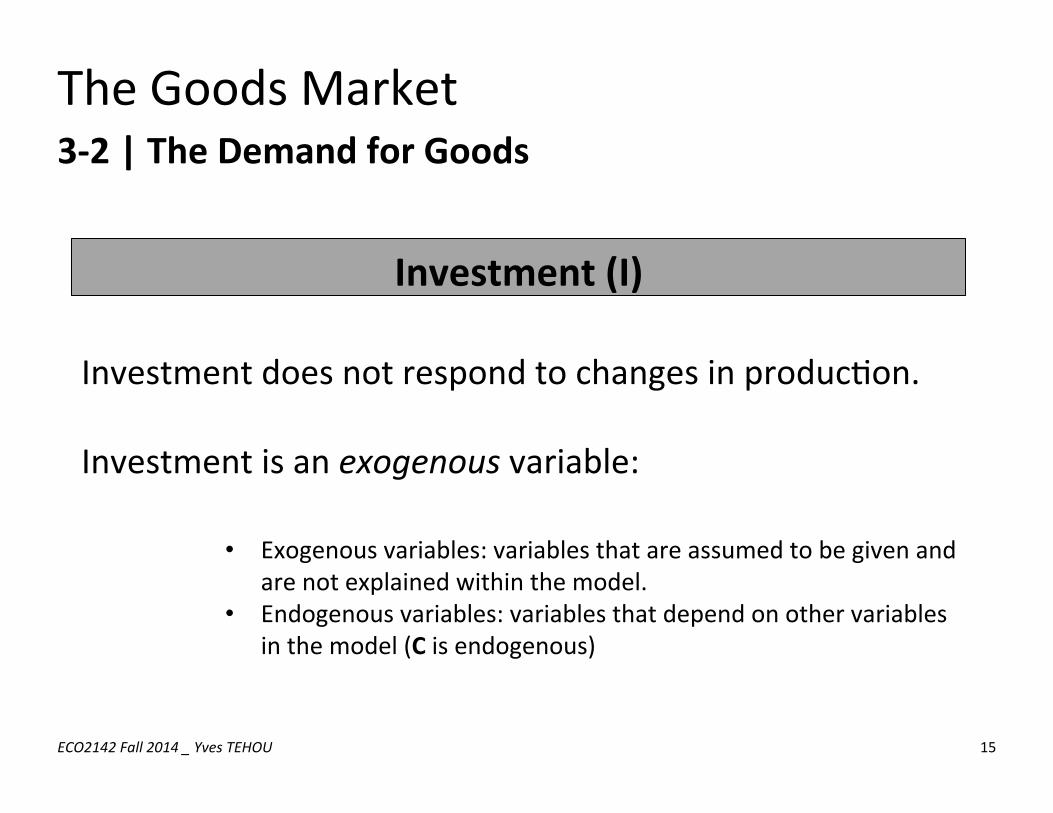

Investment does not respond to changes in produc8on. Investment is an exogenous variable:

• Exogenous variables: variables that are assumed to be given and are not explained within the model.

• Endogenous variables: variables that depend on other variables in the model (C is endogenous)

The Goods Market 3-‐2 | The Demand for Goods Government Spending (G) and Taxes (T)

ECO2142 Fall 2014 _ Yves TEHOU 16

Government Spending and Taxes do not respond to changes in produc8on. Government Spending is an exogenous variable Taxes is an exogenous variable

The Goods Market 3-‐3 | The Determina;on of Equilibrium Output

Total Demand

ECO2142 Fall 2014 _ Yves TEHOU 17

Z ≡ C + I + G • Demand for Goods (Z) depends on income (Y),

taxes (T), investment (I), government spending (G)

Z ≡ c0 + c1(Y-‐T) + I + G

The Goods Market 3-‐3 | The Determina;on of Equilibrium Output

Assume

ECO2142 Fall 2014 _ Yves TEHOU 18

• Firms do not hold inventories

• Y = supply of goods

Supply of goods (Y) = Demand for goods (Z) Equilibrium occurs when

The Goods Market 3-‐3 | The Determina;on of Equilibrium Output

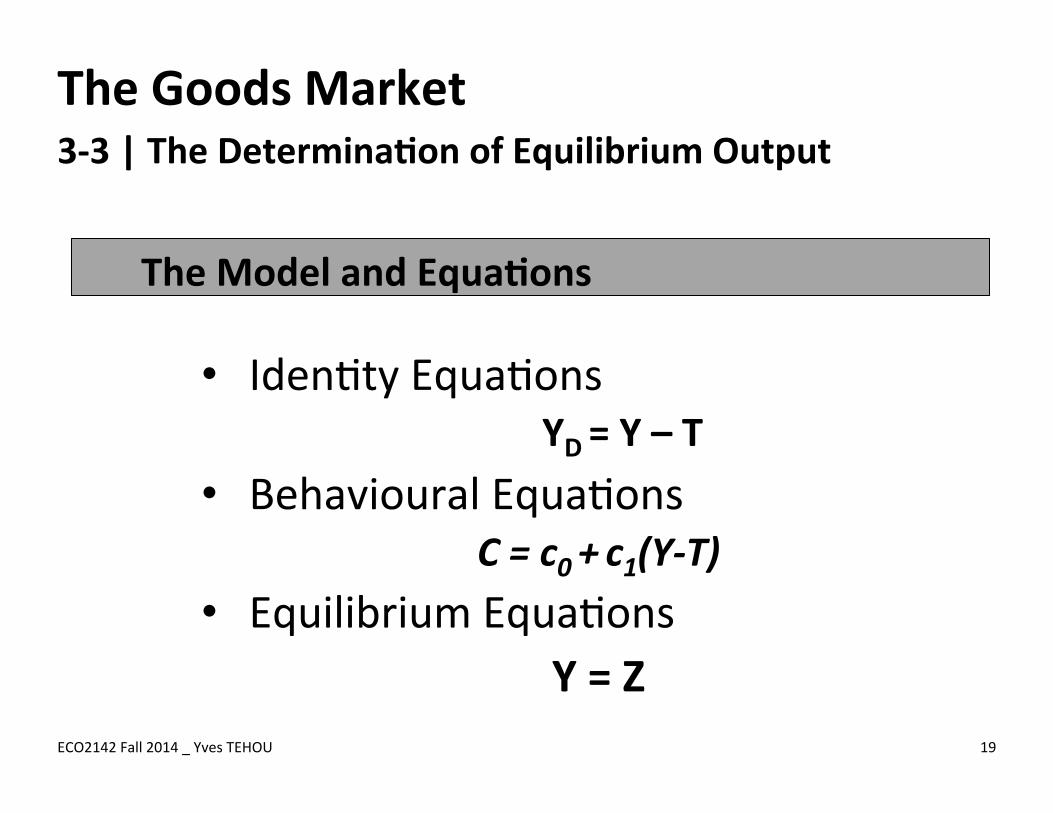

The Model and Equa;ons

ECO2142 Fall 2014 _ Yves TEHOU 19

• Iden8ty Equa8ons YD = Y – T

• Behavioural Equa8ons C = c0 + c1(Y-‐T)

• Equilibrium Equa8ons Y = Z

The Goods Market 3-‐3 | The Determina;on of Equilibrium Output

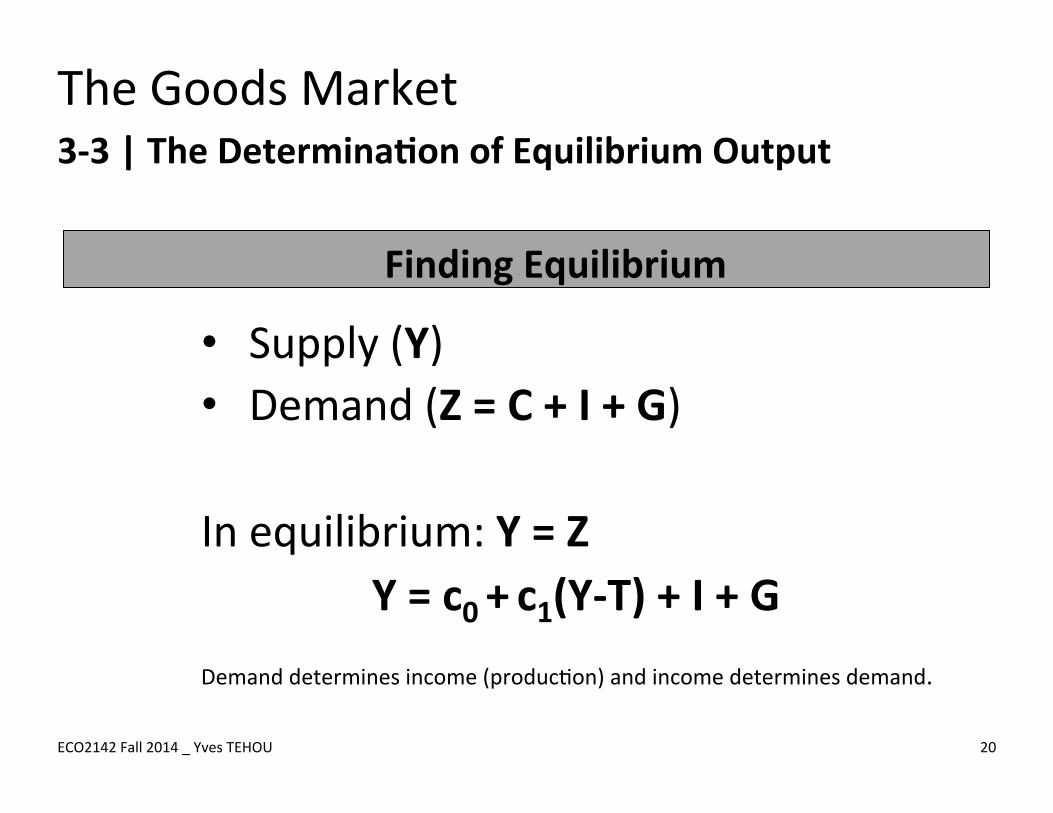

Finding Equilibrium

ECO2142 Fall 2014 _ Yves TEHOU 20

• Supply (Y) • Demand (Z = C + I + G)

In equilibrium: Y = Z

Y = c0 + c1(Y-‐T) + I + G Demand determines income (produc8on) and income determines demand.

The Goods Market 3-‐3 | The Determina;on of Equilibrium Output

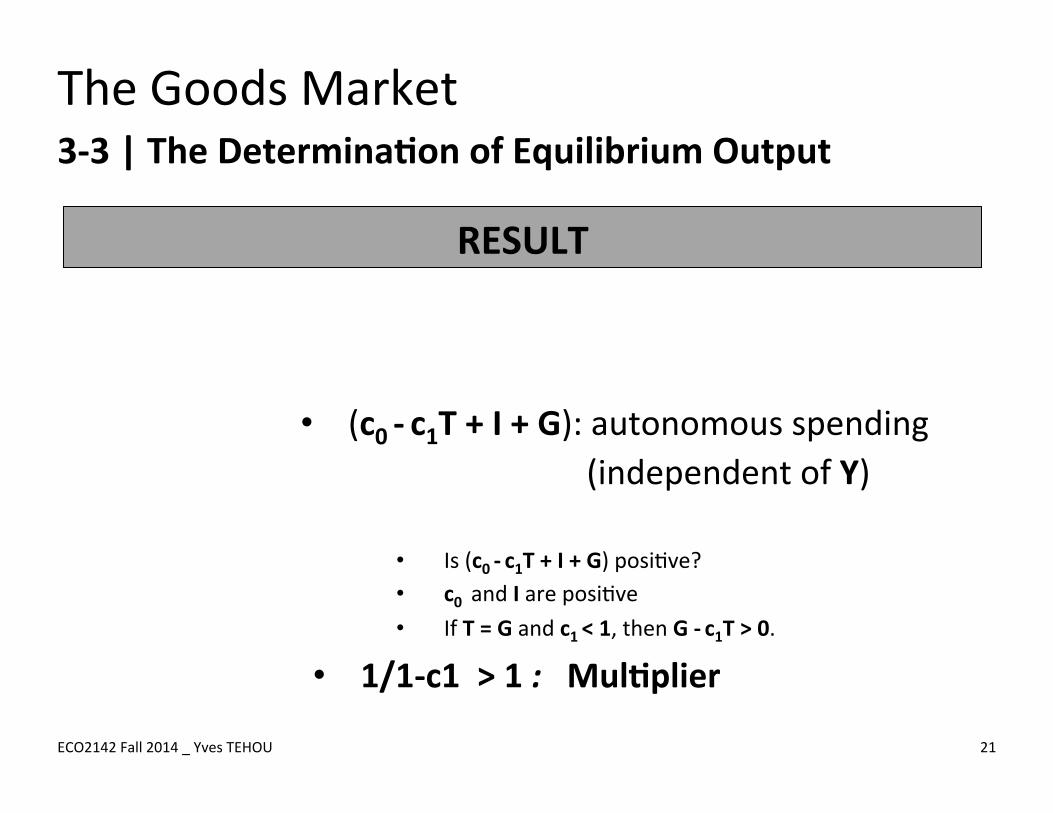

ECO2142 Fall 2014 _ Yves TEHOU 21

• (c0 -‐ c1T + I + G): autonomous spending (independent of Y)

• Is (c0 -‐ c1T + I + G) posi8ve? • c0 and I are posi8ve • If T = G and c1 < 1, then G -‐ c1T > 0.

RESULT

• 1/1-‐c1 > 1 : Mul;plier

The Goods Market 3-‐3 | The Determina;on of Equilibrium Output

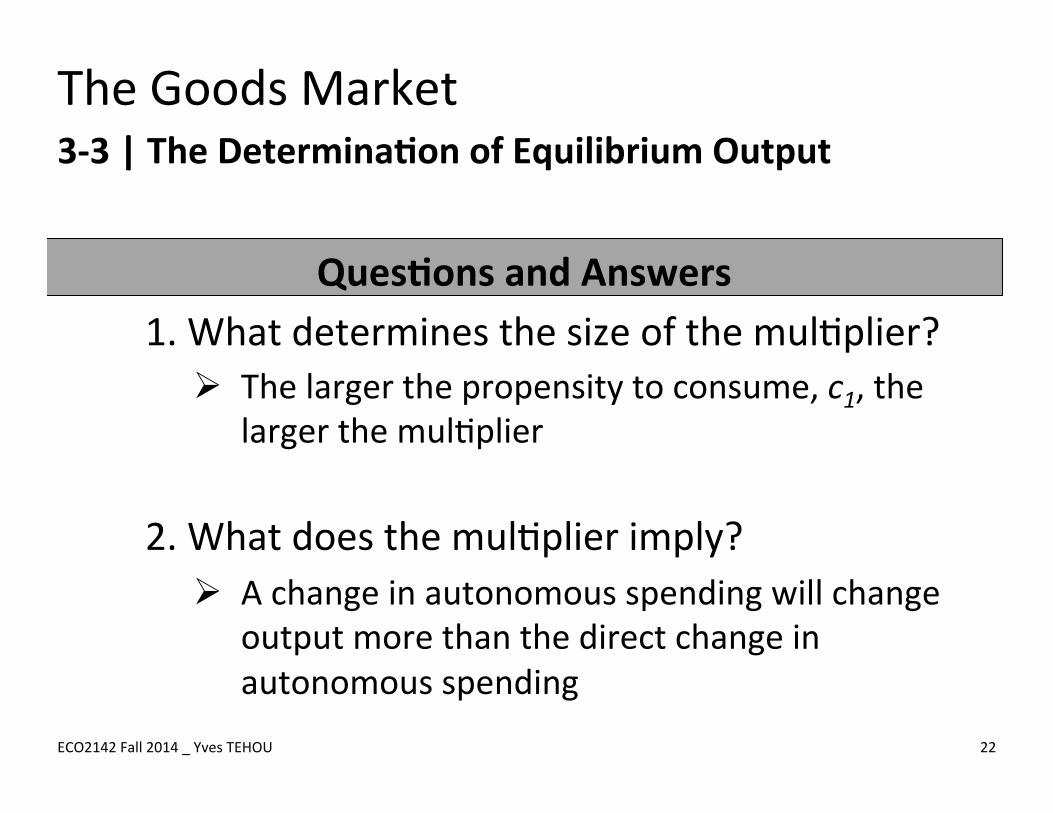

Ques;ons and Answers

ECO2142 Fall 2014 _ Yves TEHOU 22

1. What determines the size of the mul8plier? Ø The larger the propensity to consume, c1, the

larger the mul8plier

2. What does the mul8plier imply? Ø A change in autonomous spending will change

output more than the direct change in autonomous spending

The Goods Market 3-‐3 | The Determina;on of Equilibrium Output

Example

ECO2142 Fall 2014 _ Yves TEHOU 23

• c0 increases by $ 1billion • c1 = 0.6

Change in Y = Change in c0 X Mul8plier = $ 1 billion X = $ 1 billion X 2.5

The Goods Market 3-‐3 | The Determina;on of Equilibrium Output

Ques;ons

ECO2142 Fall 2014 _ Yves TEHOU 3-‐28

1. Would a change in I, G, or T have the same impact on Y?

2. Where does the mul8plier come from?

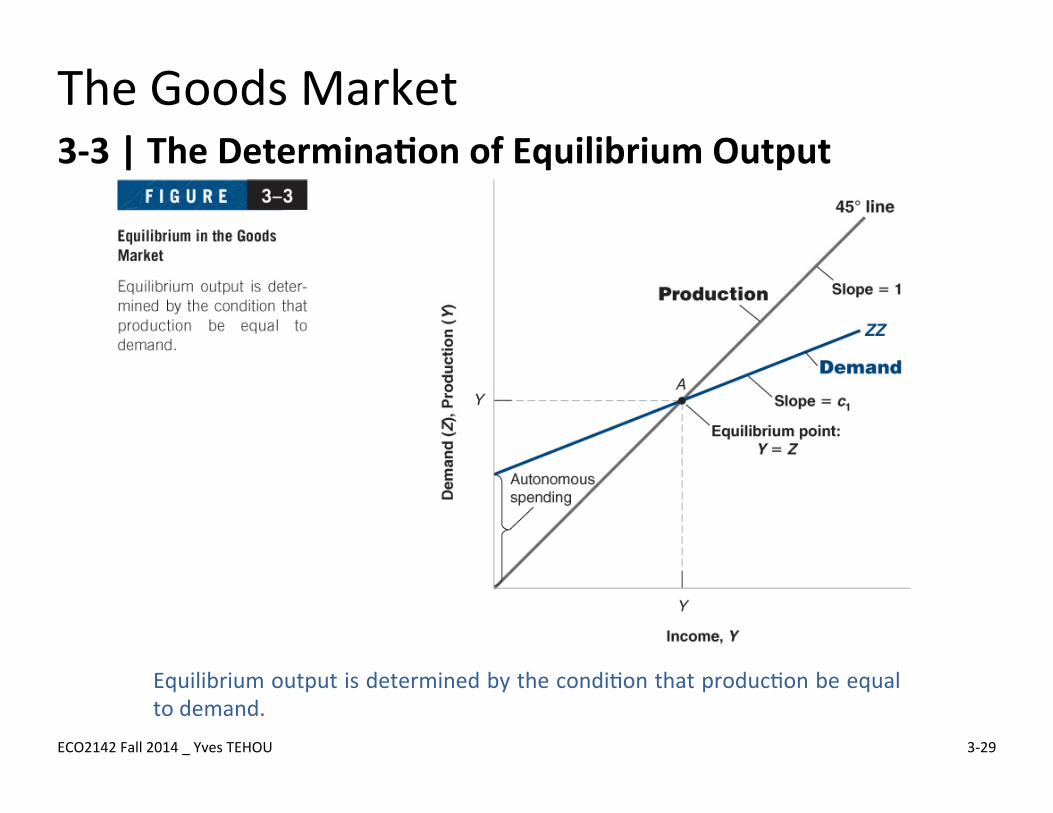

The Goods Market 3-‐3 | The Determina;on of Equilibrium Output

Equilibrium output is determined by the condi8on that produc8on be equal to demand.

ECO2142 Fall 2014 _ Yves TEHOU 3-‐29

The Goods Market 3-‐3 | The Determina;on of Equilibrium Output

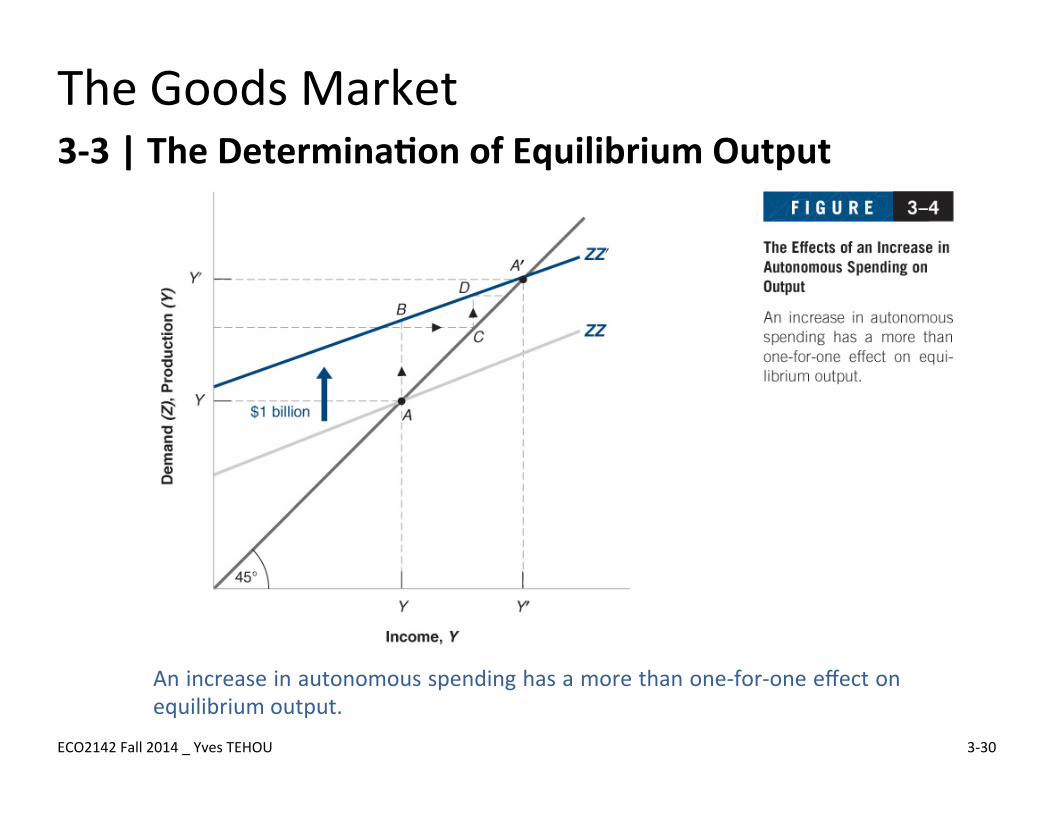

An increase in autonomous spending has a more than one-‐for-‐one effect on equilibrium output.

ECO2142 Fall 2014 _ Yves TEHOU 3-‐30

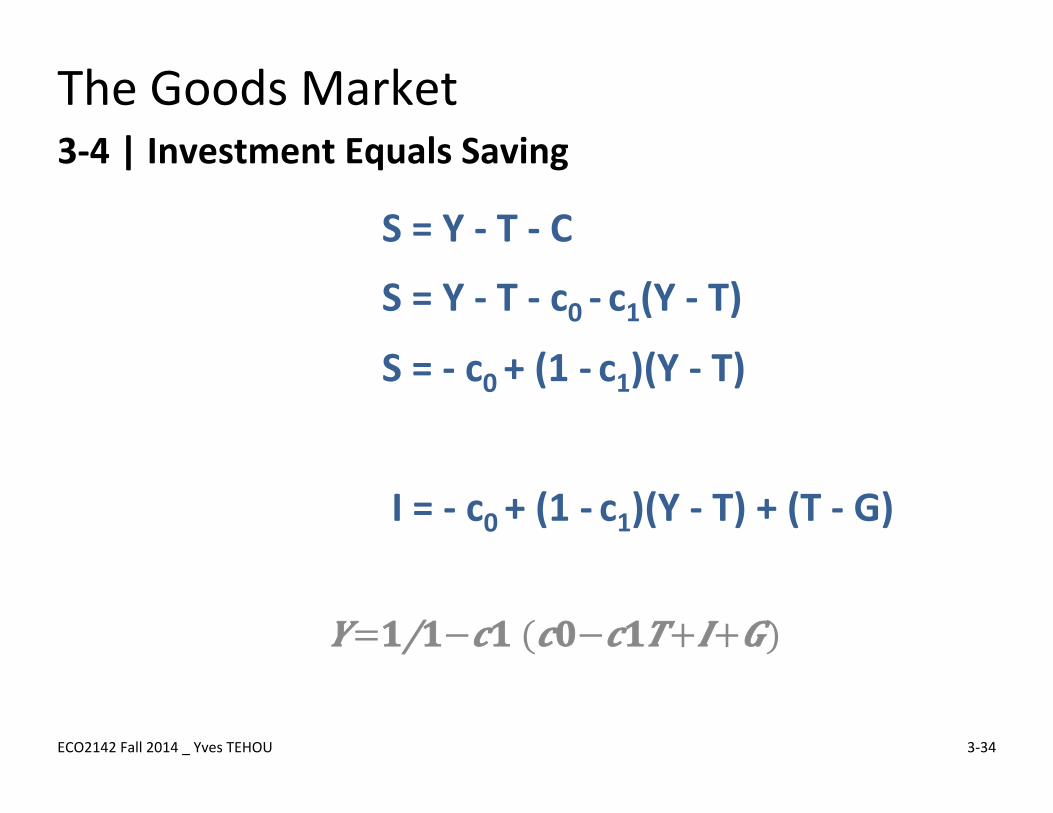

The Goods Market 3-‐4 | Investment Equals Saving

ECO2142 Fall 2014 _ Yves TEHOU 3-‐31

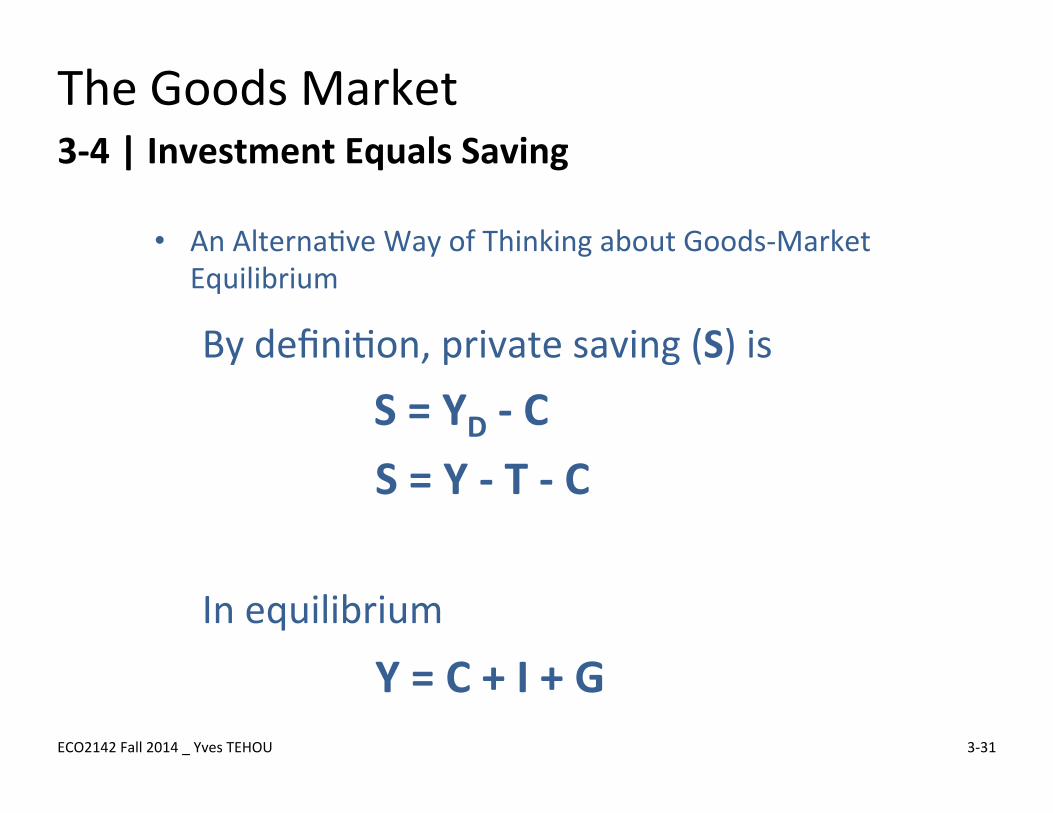

By defini8on, private saving (S) is S = YD -‐ C S = Y -‐ T -‐ C In equilibrium Y = C + I + G

• An Alterna8ve Way of Thinking about Goods-‐Market Equilibrium

The Goods Market 3-‐4 | Investment Equals Saving

ECO2142 Fall 2014 _ Yves TEHOU 3-‐32

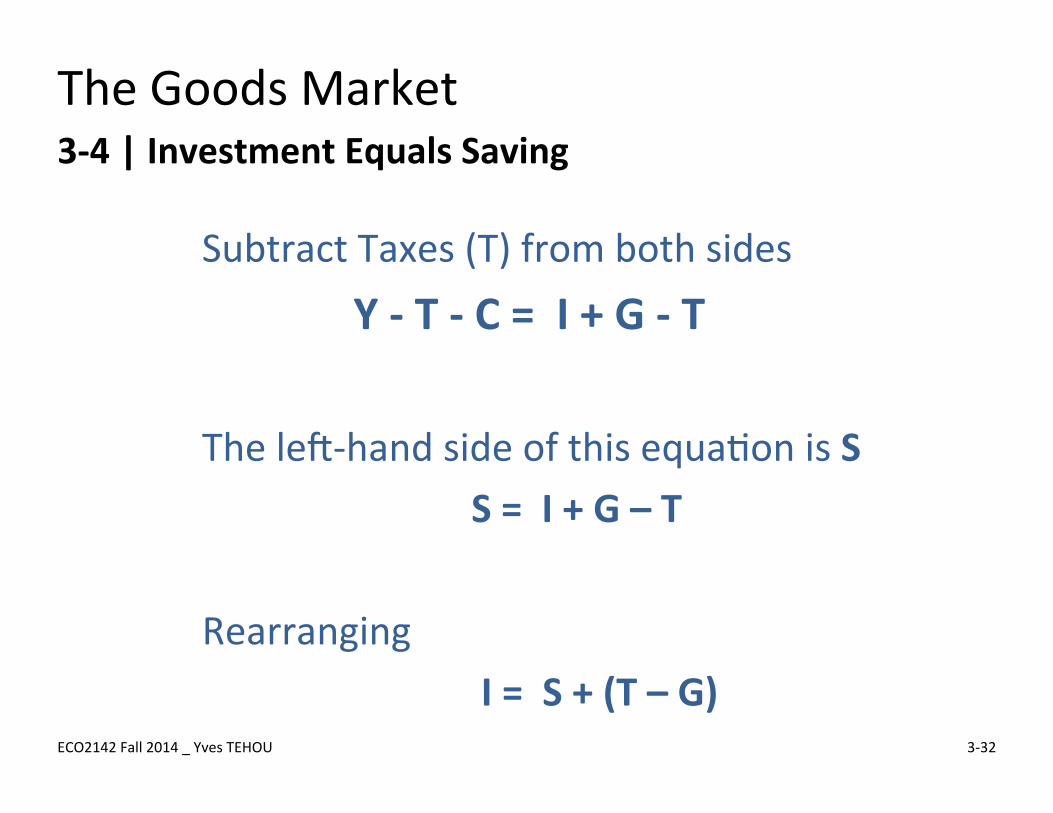

Subtract Taxes (T) from both sides Y -‐ T -‐ C = I + G -‐ T The lej-‐hand side of this equa8on is S S = I + G – T Rearranging I = S + (T – G)

The Goods Market 3-‐4 | Investment Equals Saving

ECO2142 Fall 2014 _ Yves TEHOU 3-‐33

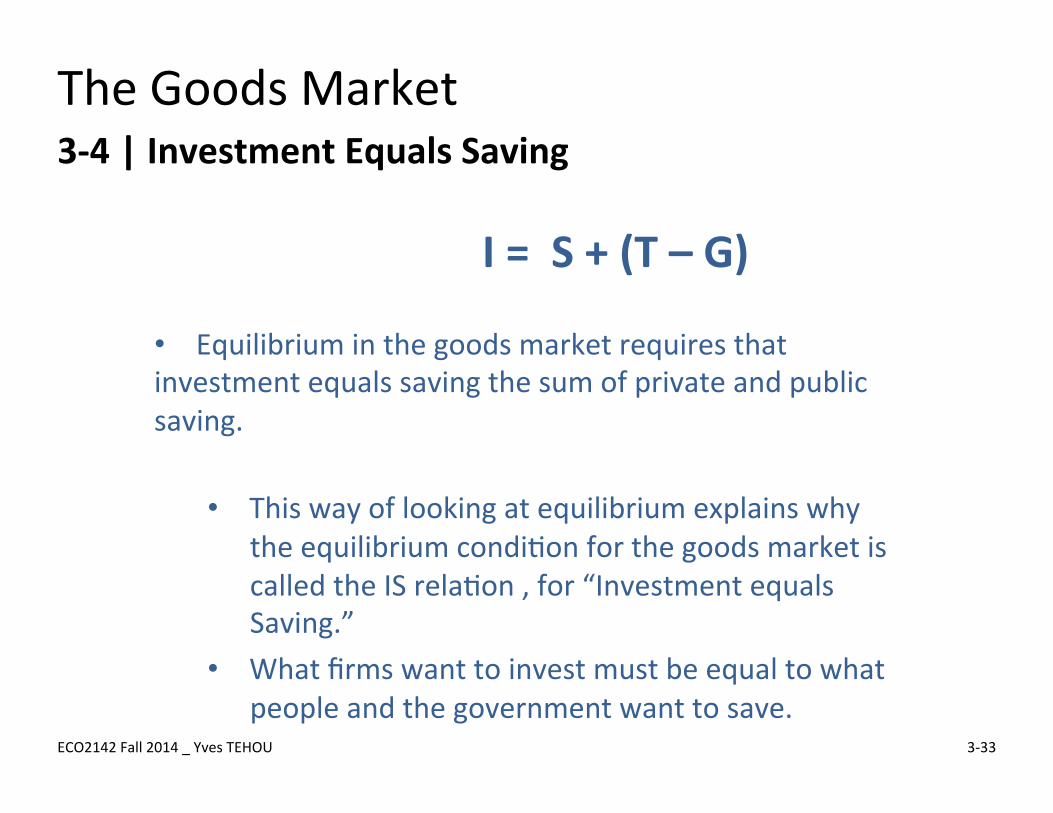

I = S + (T – G)

• Equilibrium in the goods market requires that investment equals saving the sum of private and public saving.

• This way of looking at equilibrium explains why the equilibrium condi8on for the goods market is called the IS rela8on , for “Investment equals Saving.”

• What firms want to invest must be equal to what people and the government want to save.

The Goods Market 3-‐4 | Investment Equals Saving

ECO2142 Fall 2014 _ Yves TEHOU 3-‐34

S = Y -‐ T -‐ C

S = Y -‐ T -‐ c0 -‐ c1(Y -‐ T)

S = -‐ c0 + (1 -‐ c1)(Y -‐ T)

I = -‐ c0 + (1 -‐ c1)(Y -‐ T) + (T -‐ G)

𝒀= 𝟏/𝟏−𝒄𝟏 (𝒄𝟎−𝒄𝟏𝑻+𝑰+𝑮)

The Goods Market 3-‐5 | Is Government Omnipotent? A Warning

Can governments really choose the level of output they want?

ECO2142 Fall 2014 _ Yves TEHOU 3-‐35

• There are many aspects of reality that we have not yet incorporated in our model: • The effects of spending/taxes on demand are much less mechanical than

it appears. They may happen slowly, consumers and firms may be scared of the budget deficit and change their behaviour.

• Maintaining a desired level of output may come with unpleasant side effects. Trying to achieve too high a level of output may, for example, lead to accelera8ng infla8on and may become unsustainable in the medium run.

• Cupng taxes or increasing government spending may lead to large budget deficits and an accumula8on of public debt. Such debt will have adverse implica8ons in the long run.

The Goods Market Summary

Ø GDP is the sum of consump8on, plus investment, plus government spending, plus exports, minus imports, plus inventory investment.

Ø Consump8on (C) is the purchase of goods and services by consumers.

Ø Investment (I) is the sum of nonresiden8al investment -‐ the purchase of new plants and new machines by firms; and of residen8al investment—the purchase of new houses or apartments by people.

Ø Government spending (G) is the purchase of goods and services by federal, provincial, and local governments.

ECO2142 Fall 2014 _ Yves TEHOU 3-‐36

The Goods Market Summary

Ø Exports (X) are purchases of Canadian goods by foreigners. Imports (Q) are purchases of foreign goods by Canadian consumers, Canadian firms, and the Canadian government.

Ø In the short run, demand determines produc8on. Produc8on is equal to income. And income determines demand.

Ø The consump8on func8on shows how consump8on depends on disposable income. The propensity to consume describes how much consump8on increases for a given increase in disposable income.

ECO2142 Fall 2014 _ Yves TEHOU 3-‐37

The Goods Market Summary

Ø Equilibrium output is the point at which supply (produc8on) equals demand. In equilibrium, output equals autonomous spending 8mes the mul8plier.

Ø An alterna8ve way of sta8ng the goods-‐market equilibrium condi8on is that investment must be equal to saving, the sum of private and public saving.

ECO2142 Fall 2014 _ Yves TEHOU 3-‐38