Macroeconomic Volatility in General Equilibrium - Global ...

Upload

independentCategory

view

2download

0

UNION BUDGET 2013-14 : A MACROECONOMIC PERSPECTIVE

Every year a budget is prepared where , a certain amount of fundis ascertained for different needs to be fulfilled for thedevelopment and advancement of our nation India. But according tothe Budget displayed during the end of every financial year it isfound the expenditure rises from the estimated budget each yearand every time, though the escalaration of prices of thecommodity does not vary that much as and when the budget is madeor been prepared at the beginning of the financial year. So, afew questions that blow through the minds that , if the money isover spent and work is not yet completed and target for the yearis not fulfilled, then who is falling the Budget of our nation?Is it the Planning Commission? Of the Finance Ministry? Thatevery year a promise of surplus is made but by the end of theyear we end up with a deficit in our revenue.

The Union Budget for FY14 is presented at a time when the Indianeconomy is faced with various challenges posed by domestic andglobal issues. The budget was expected to implement fiscalprudence on one hand and support growth on the other. The Financeminister has articulated a Fiscal Deficit (FD) target of 4.8% ofGDP during FY14 with a commitment to bring down the FD, RevenueDeficit and the Effective Revenue Deficit to 3.0%, 1.5% and zero,respectively by FY17.While fiscal deficit has been targeted to belower than the previous year, total expenditure has been budgetedat Rs.16,652.97 bn, a 16% increase as compared to the revisedestimates (RE) of FY13. Besides, there has been a significanthike in plan expenditure which is likely to boost rural demandand support inclusive growth. Concerns do arise on whether thegovernment would be able to generate the requisite revenue tofinance the total expenditure laid out in the budget. If revenuegeneration falters owing to failure of revival of economic growthor due to difficulties in implementing the revenue generatingmeasures, either fiscal consolidation will have to be foregone orexpenditure will need to be curtailed.

For FY14, total expenditure is budgeted to increase by 16.4% toRs.16,652.97 bn as compared to the revised estimates (RE) of

Rs.14,308.25 bn for FY13. As in the last budget, the planexpenditure received a major boost with an allocation ofRs.5,553.22 bn, an increase of 29.4% over FY13 (RE). Non-planexpenditure is also budgeted to increase by 10.8 % toRs.11,099.75 bn. The subsidy though budgeted to decrease by 10.3%during FY14 from the revised estimates of FY13; is budgeted toincrease by over 21.6% over the budget estimates of FY13.

Though such huge increase in expenditure is made, but how far arewe segregating the money to its actual place to fulfill the yearstarget of development? A proper watch on the money anddistribution of funds in different sectors is needed to be keptso that a proper record of cost incurred could be maintainedaccordingly with the progress of work completed. As the focus ofthe government towards increasing investment in infrastructure,creating a regulatory authority for the road sector, introducinginvestment allowance for attracting new high value investments,creating industrial corridors besides announcement of projects inNational Waterways, Road and Ports sectors, devising a PPP policyframework in the coal sector to some extent would boostinfrastructure activities. Besides, a number of initiatives inthe Oil & Gas sector is also commendable.

SECTORAL IMPACT

Sector Rating

1. Agriculture Positive+2. Infrastructure Positive3. Banking, Financial Services and Insurance (BFSI) Positive+/Marginally

Positive/Positive/Positive4. Real Estate & Construction Marginally Positive5. Oil & Gas Marginally

Positive6. Pharmaceuticals & Healthcare Marginally

Positive

Ratings:

Positive+ Predominantly positive proposalsPositive Positive proposalsMarginally Positive Positive proposals but not upto industry

expectations

Agriculture

• Rs.270.49 bn allocated to the Ministry of Agriculture, anincrease of 22% over the RE of current fiscal year.

• Allocation of Rs.34.15 bn for agricultural research.

• For FY14, target of agricultural credit kept at Rs.7,000 bn.

• Interest subvention scheme for short-term crop loans to becontinued. Scheme extended forcrop loans borrowed from private sector scheduled commercialbanks.

• Rs.10 bn allocated for bringing Green Revolution to easternIndia.

• Rs.5 bn allocated to start a programme of crop diversificationthat would promote technological innovation and encourage farmersto choose crop alternatives.

• Rashtriya Krishi Vikas Yojana and National Food SecurityMission provided Rs.99.54 bn andRs.22.50 bn respectively.

• Allocation for Integrated watershed programme increased fromRs.30.50 bn in FY13 (BE) toRs.53.87 bn in FY14.

• Allocation made for pilot programme on Nutri-Farms forintroducing new crop varieties that

are rich in micro-nutrients.

• The Indian Institute of Agricultural Bio-technology will beestablished at Ranchi, Jharkhand.

• Pilot scheme to replant and rejuvenate coconut gardensimplemented in some districts ofKerala and the Andaman & Nicobar Islands extended to the entirestate of Kerala.

• Matching equity grants to registered Farmer ProducerOrganization (FPO) upto a maximum ofRs.1 mn per FPO to enable them to leverage working capital fromfinancial institutions.

• A Credit Guarantee Fund to be created in the Small Farmers’Agri Business Corporation withan initial corpus of Rs.1 bn.

• National Livestock Mission to be set up and a provision ofRs.3.07 bn made for the Mission.

• Additional provision of Rs.100 bn for National Food SecurityAct.

From the above allocations a sharp increase in prices offood articles, especially proteins, fruits and vegetables and thegrowing foodgrains stocks in public sector, the Government hasmaintained its focus on the agriculture sector through increasedallocations and introducing initiatives for creating efficientagricultural market as our nation has a base source in generatingrevenue from this. The hike in farm credit limit and creation ofa credit guarantee fund for Farmer Producer Organisations (FPOs)would provide some respite to small and marginal farmers. Thishas not only encouraged the farmers but also given them theconfidence in risk taking of agricultural diversification ontheir land seasonally. The programme of crop diversificationwould be an effective measure to alleviate rural poverty andgenerate rural employment. While the measures announced in the

Budget for the agriculture sector are positive, legal impedimentsare also there restricting the entry of big private players tomarketing, storage and processing facilities of agriculturalcommodities also need to be modified.

Infrastructure

Infrastructure Financing

• Infrastructure Debt Fund (IDF) to be encouraged. These fundswill raise resources and provide long-term low-cost debt toinfrastructure projects through take-out finance, creditenhancement and other innovative means.

• India Infrastructure Finance Corporation Ltd (IIFCL) inpartnership with the Asian Development Bank (ADB) will provideaccess to the bond markets for long term funds through creditenhancements to infrastructure companies.

• Allowed some institutions to issue tax free bonds up to Rs.500bn in FY14 strictly on capacity to raise funds from the market.

• With assistance from World Bank and the ADB, to build roads inthe Northern Eastern states and connect them to Myanmar.

• Increased corpus of the Rural Infrastructure Development Fund(RIDF) operated by NABARDto Rs.200 bn in FY14.

• Allocation of Rs.50 bn to NABARD to finance construction ofwarehouses, godowns, silos andcold storage units designed to store agricultural produce.

• Reduced the rate of tax on interest to non-resident investorsfrom 20% to 5% on long term infrastructure bonds in foreigncurrency and extended the same benefit to investments made

through a designated bank account in rupee-denominated long terminfrastructure bonds.

Roads and Highways

• A regulatory authority for the road sector is proposed to beconstituted to address the unattended challenges includingfinancial stress, enhanced construction risk and contractmanagement issues.

• 3,000 kms of road projects will be awarded in the first sixmonths of FY14.

Rural Infrastructure

• Budgetary allocation of ` 801.94 bn for rural development schemes in FY14, representing an increase of 46% over FY13 (RE). Allocation of ` 330 bn to Mahatma Gandhi National Rural Employment Guarantee Scheme (MGNREGS), ` 217 bn to Pradhan MantriGram Sadak Yojana(PMGSY) and ` 151.84 bn to Indira Awaas Yojana (IAY).

• Allocation of a portion of funds to new programme PMGSY-II which will benefit states whichhave completed PMGSY; other states will continue with PMGSY.

Urban Infrastructure

• Allocation of ` 148.73 bn for the Jawaharlal Nehru National Urban Renewal Mission (JNNURM). A significant portion of this will be used to support the purchase of upto 10,000 buses.

Ports

• Two new major ports will be established in Sagar, West Bengaland in Andhra Pradesh whichwill add 100 mn tonnes of capacity.

• A new outer harbour will be developed at Thoothukkudi, TamilNadu at an estimated cost ofRs.75 bn.

In the present budget Government has taken a number ofmeasures such as encouragement to IDF, credit enhancement forlong term funds, increased corpus of RIDF etc to mobilise fundsin the infrastructure sector through innovative instruments. TheBudget has also allowed some institutions to issue tax free bondsup to Rs.500 bn in FY14. These measures are likely to providesome support to infrastructure financing going forward. Theproposal to constitute a regulatory authority for the road sectorto address some of the challenges faced by the sector is a goodmove. Also, awarding of 3,000 kms of road projects in the firstsix months of FY14 is expected to enhance road connectivity inIndia. Further, a 46% increase in budgetary allocation for ruraldevelopment schemes is expected to improve overall ruralinfrastructure. Further, the new proposals for industrialcorridors are welcome initiatives as they are expected to easecongestion and aid in the rapid development of the industry.Given the increased focus to revive growth in the infrastructuresector by boosting infrastructure financing coupled with themeasures to increase thrust on rural infrastructure and urbaninfrastructure, the Budget is expected to have a positive impacton the infrastructure sector.

But this is the sector where proper cost of work is neededto be watched carefully, as allocation funds is properly beenutilized or not. A cost accountant should be hired by thegovernment to keep a watch on the cost of work completed on thematerials as been said in the tender of the contractors. A propercost efficiency report can help the government to implement newaction and ideas as they could get a clear view on the workprogress by the cost accountants report. The funding of money isprepared on the basis of the demand of the cabinet ministers andthe State Chief Ministers to develop their respective states. Butthe Cost Accountants if been appointed by the Government, they

can picturize/display of the cost occurred according to the fundsdistributed in individual sectors.

Banking, Financial Services and Insurance (BFSI)

Banking –

Agricultural and Rural Finance

• The target for credit flow to farmers raised from Rs.5,750 bn in FY13 to Rs.7,000 bn in FY14.

• The interest subvention scheme for short term crop loans to continue and farm loans repaid on time to get credit at 4% p.a. Scheme extended to crop loans borrowed from private sector Scheduled Commercial Banks (SCBs).

Financial Inclusion

• SCBs and all Regional Rural Banks (RRBs) are on core banking solution (CBS) and electronicpayment systems (NEFT and RTGS). All other banks including some co-operative banks are to be on CBS and e-payment systems by December 31, 2013. All branches of Public Sector Banks(PSBs) to have ATMs by March 31, 2014.

• An IT-based project to modernise the postal network at an expenditure of Rs.49.09 bn has been initiated. Post offices will be on CBS and offer real-time banking services. Provision of Rs.5.32 bn for the project in FY14 is proposed.

Housing Credit

• The provision under Rural Housing Fund enhanced from Rs.40 bn to Rs.60 bn.

• Additional deduction of interest up to Rs.0.1 mn for a person taking first home loan up to Rs.2.5 mn during the period April 1,2013 to March 31, 2014.

Capital Support and Funding

• A sum of Rs.140 bn capital allocated to PSBs for FY14, keepingin view compliance of PSBs with Basel III norms.

• Setting up of India’s first Women’s Bank as a PSB with aprovision of Rs.10 bn as initial capital is proposed. Necessaryapprovals and the banking license expected by October 2013.

• National Housing Bank to set up Urban Housing Fund with aprovision of Rs.20 bn to the fund.

• Infrastructure Debt Funds (IDF) to be encouraged.

• The corpus of the Rural Infrastructure Development Fund (RIDF)will be raised to Rs.200 bn.

• Rs.50 bn will be made available to NABARD to financeconstruction of warehouses andgodowns.

• Issuance of infrastructure tax-free bonds up to Rs.500 bn to beallowed during FY14.

• Enhancing the refinancing capability of SIDBI from the currentlevel of Rs.50 bn to Rs.100 bn per year.

• Additional sum of Rs.1 bn to be provided to India MicrofinanceEquity Fund.

• A corpus of Rs.5 bn to SIDBI to set up a Credit Guarantee Fundfor factoring.

The Budget is expected to have a positive impact on thebanking industry. Some of the growth drivers of the Indian

banking sector include financial inclusion and enhanced paymentsystems which will help the banking sector to achieve its aim ofexpansion and growth. A number of measures have been announcedtowards enabling inclusive growth such as other banks includingsome co-operative banks adopting CBS and e-payment systems, allbranches of PSBs having ATMs, post offices becoming a part of thecore banking solution and offering real-time banking services andsetting up of India’s first Women’s Bank as a PSB. Measures havealso been announced to enable better flow of credit to varioussectors, including agriculture, housing, infrastructure and MSMEswhich is expected to encourage overall credit growth. Inaddition, the Budget has emphasized on the financialstrengthening of PSBs. The allocations made towards capitalinfusion in PSBs are expected to bring more stability to thesector. The Government aims to keep all the PSBs adequatelycapitalized for compliance with Basel III regulation. Overall,the Budget is likely to have a significant positive impact on thebanking industry by focusing on financial inclusion, boostingcredit growth and supporting capital base of banks.

Real Estate and Construction

• National Housing Bank (NHB) to set up Rs.20 bn Urban HousingFund in FY14.

• Proposal to provide Rs.60 bn to the Rural Housing Fund in 2013-14 through National HousingBank for rural housing.

• First housing loan up to Rs.2.5 mn would get additionaldeduction of interest up to Rs.0.1 mn which will enhance thetotal deduction to Rs.0.25 mn in FY14.

• Excise duty on marble slabs increased from Rs.30 per sq. mtr toRs.60 per sq. mtr.

• Reduction in abatement rate on home and flat having a carpetarea of more than 2,000 sq. ft. or costing more than Rs.10 mnfrom 75% to 70%.

• TDS at the rate of 1% to be charged on the transfer ofimmovable property (which excludeagriculture property) where the consideration exceeds Rs.5 mn.

With the NHB setting up an Urban Housing Fund and enhancingthe fund allocation to Rural Housing Fund from Rs.40 bn in FY13to Rs.60 bn in FY14, the Government is trying to focus onmitigating acute housing shortage by providing low costaffordable houses. Further, the extension of enhanced interestdeduction granted on housing loan is expected to promote homeownership in tier-II and III cities and towns on one hand andencourage the growth in various other sectors like steel, cement,brick, wood, paint, glass etc. The increased fund allocation forthe construction of urban and rural housing units is likely tohave a multiplier effect on the economy via growth in downstreamsectors and increase in employment. However, the reduction inabatement rate would result in increased service tax outflow andmaking the luxury house more expensive. Also, the hike in exciseduty on marble would increase the development cost of thedeveloper which may be passed on to the end customer. Theintroduction of TDS on transfer of high value immovable propertywhich is generally charged on gross value of the property islikely to have an unfavorable impact on the cash flow of theseller in a situation of distress property sales or on propertysale making minimal gain. The various announcements by theGovernment during the Budget will have direct and indirect impacton the construction and real estate sector. Overall the Budget ismarginally positive for the construction and real estate sector.

Oil & Gas

• Oil and gas exploration policy will be reviewed and newcontracts will be moved from profitsharing to revenue sharing model.

• Natural gas pricing policy will be reviewed.

• Policy to encourage the exploration and production of shale gaswill be announced.

• Revenue sharing policy on shale gas exploration would beannounced.

• Oil and gas blocks awarded under the New Exploration LicensingPolicy (NELP), but which are stalled will be cleared.

• Petroleum subsidy for FY14 is expected to be at Rs.650 bn downfrom Rs.960 bn incurred during FY13.

• 5 million tonne Dhabol LNG terminal will be operational inFY14.

Announcements outlined in the Budget are positive for theoil and gas sector as they are aimed at removing the prevailingambiguity surrounding cost recovery during exploration andnatural gas pricing. Further, the policy announcement surroundingNELP blocks and shale gas exploration is aimed at safeguardingthe energy security of the country by increasing domesticproduction. The existing profit sharing model has delayedapprovals in the oil and gas sector due to the involvement of theGovernment in day-to-day operations so as to monitor the cost ofexploration. Shift from profit sharing to revenue sharing modelwould reduce the involvement of the Government in the day-to-dayoperations and is expected to remove delays in approvals.Proposed review of natural gas pricing would help to address theprevailing uncertainty regarding natural gas pricing. A liberalpricing policy would help in attracting fresh investments intooil and gas exploration from both private and overseas players.Further, clearing of blocks awarded under New ExplorationLicensing policy (NELP) would encourage better participation in

the coming rounds of auctions of oil and gas blocks. Focus onshale gas exploration and production is in line with the growinginterest in shale gas exploration around the world. This type ofpolicy would help improve the domestic energy production.

Pharmaceuticals & Healthcare

• Proposal to allocate Rs.373.3 bn to the Ministry of Health andFamily Welfare (MoHFW). Out of this, Rs.212.39 bn will beallotted to the new National Health Mission (NHM), including therural mission and the proposed urban mission.• To provide Rs.47.27 bn for medical education, training andresearch.

• Proposal to provide Rs.1.5 bn to the national programme for thehealthcare of elderly, which is being implemented in 100 selecteddistricts across 21 Indian states.

• Proposal to allocate Rs.10.69 bn to the department of AYUSH(Ayurveda, Unani, Siddha andHomoeopathy).

• Proposal to earmark Rs.3,000 mn in FY14 for a multi-sectoralprogramme for maternal care and address child malnutritionproblem. This programme will be executed across 100 districts inFY14 and is aimed to be scaled up to include 200 districts in thesubsequent year.

• Provision to offer MRP based assessment in respect of brandedmedicaments of AYUSH andbio-chemic systems of medicine with a reduction of 35%.

• Allocation of Rs.177 bn in FY14 to Integrated Child DevelopmentServices (ICDS) scheme.

The Budget has focused towards improving the welfare andhealth of family. Allocation of Rs. 373.3 bn towards MoHFW andRs.177 bn towards ICDS scheme is expected to have a positive

impact on the sector. Further, to integrate the department ofAYUSH into the healthcare delivery system, Rs.10.69 bn has beenallocated to the same through the National Health Mission (NHM).The measures announced in the Budget are expected to have amarginally positive impact on the sector.After wringing its hands over how rising healthcare costs waspushing 39 million into poverty and promising to stop this fromhappening, the government has increased allocation this year byjust Rs 2,840 crore which is less than the amount that was notreleased last year out of the total allocated amount. Thegovernment on has admitted to low health allocation, which is themajor driver for high infant and maternal mortality rates. Byit's own admission, India has the lowest health spending as aproportion of gross domestic product (GDP), with the overallnumber looking a little better due to the contribution by theprivate sector. According the data in the Economic Survey, India spends around4.1% of GDP on health, while China and Russia, that are among thelow spenders among the 11 countries identified in the governmentdocument, spending at least a percentage point more. OnlyIndonesia has a poorer allocation (2.6%) among the 11 countries,while Brazil and South Africa are neat the 9% range. This makesIndia the worst performer among the BRICS group. In fact theexpenditure in Brazil and South Africa is closer the average inseveral developed countries such Australia, Norway and the UK.Only the United States has a double digit spend, estimated @17.6% of GDP. What adds to the woes is the overlap of government schemes.Several flagship programmes such as Janani Suraksha Yojna (JSY),Janani Shishu Suraksha Karyakram (JSSK) and Indira GandhiMatritva Sahyog Yojna (IGMSY) end up focusing on the samebeneficiaries. For instance, JSY aims to bring down the maternalmortality rate by promoting institutional deliveries. JSSK, a newinitiative, entitles all pregnant women delivering in publichealth institutions to no-expenses delivery and IGMSY is aconditional cash transfer scheme for pregnant and lactatingwomen. The survey said there was a need to identify overlappingschemes and weed out or converge them. "A threshold level could

also be fixed for the schemes as a critical minimum investment oroutlay is needed for any programme to be successful," it said. The survey cited the suggestion made by the committee on'restructuring of centrally sponsored schemes' that such schemesshould have a minimum plan expenditure of Rs 10,000 crore overthe five year plan. As per latest UN figures, India accounts forone-third of deaths of pregnant women, mainly due tocomplications such as severe bleeding after childbirth,infections, high blood pressure during pregnancy and unsafeabortion.CHANGE IN CENTRAL PLAN OUTLAY

(`Rs.inbn)

2012-13 2013-14 % Change

Revised Estimates Budget Estimates

Ministry of Agriculture 137.87 170.95 23.99

Ministry of Commerce and Industry 30.00 37.27 24.23

Ministry of Corporate Affairs 0.28 0.34 21.43

Ministry of External Affairs 16.20 30.00 85.19

Ministry of Finance 178.15 201.32 13.01

Ministry of Health and Family Welfare 248.94 327.45 31.54

Ministry of Heavy Industries and Public Enterprises 18.44 23.89 29.56

Ministry of Labour and Employment 20.33 25.24 24.15

Ministry of Micro, Small and Medium Enterprises 28.83 32.85 13.94

Ministry of Power 546.96 593.29 8.47

Ministry of Road Transport and Highways 289.33 375.00 29.61

Ministry of Rural Development 550.00 801.94 45.81

From the above data we find an increase in expenditure ofdifferent sectoral plan outlay that our government made in thisyears union budget from the previous year. But how the governmentwill measure their work in these individual areas. If measurementof work is done from the statements of the ministers and properdistribution of funds then who is there to report on the workcompleted and the on the work in progress. And here our nationlacks from the developed countries of the world like USA andChina. There, the government keeps professionals to report on thefunding allocated from the government on the work that isplanned in the years budget. The report helps the government intaking managerial decisions to advance the work throughtechnology and man power. But in our nation , no such interest isshown from the government , though we have far more betterfinancial professional bodies than other nations like TheInstitute of Cost Accountants Of India , The Institute ofChartered Accountants and others. A cost accountant canefficiently ascertain the cost required for a particular work andcan help the government in valuating the funds allocation. Thereport of worked being progressed or if the fund allocated isbeen properly utilized in that particular sector effectively isalso needed to be recorded to make an effective budgetaryplanning. The Indian Merchants' Chamber recently invitedexperts to discuss the implications of Budget 2013 at an eventtitled 'Key macro aspects of the Union Budget 2013-14'.Senior Supreme Court advocate Dinesh Vyas welcomed the provisions

for infrastructure development made by finance minister PChidambaram. However, he cautioned, "Considering the massivefiscal deficit the country has, it is a major concern and to keepit under control is a big task. India's rating by internationalfinancial institutions which is trending downwards will have anegative impact on the foreign investment flow into the country."Rajan Vora, chairman of the chamber's direct tax committee, madea pertinent point as he spoke about the implications of directtax proposals in Budget 2013. "Better management and utilisationof taxes is the need of the hour rather than devising better waysto collect them," he said. Vora was explaining the "illogical provisions" in theproposed widening of taxes. He explained key announcements,taxation rates, commodities transaction tax and majorinternational tax proposals and their impact on the businesscommunity."This year's Budget shows the lack of coordination between thefinance ministry and the IT department," said Vikram Nankani,chairman of IMC's indirect taxation committee. Nankani alsopointed out the pros and cons of service tax, CENVAT CreditScheme, Voluntary Compliance Encouragement Scheme, central exciseduty, customs legislative amendments and other technical taxprovisions made in the Budget.

‘Faced with huge fiscal deficit’- Union Finance Minister P. Chidambaram

Union Finance Minister P. Chidambaram shaved off Rs.91,838 crore from the budgeted Plan expenditure of Rs. 5,21,025crore for the current fiscal in the backdrop of a growing fiscaldeficit. The government has also raised the Plan expenditure byjust 6.58 per cent to Rs. 5,55,322 crore (33% of the totalproposed expenditure) from the Budget estimates of Rs. 5,21,025crore for the current fiscal. The Plan expenditure budget

estimates for the current fiscal at Rs 5.21 lakh crore was about18 per cent higher than the budget estimates of such expenditureat Rs 4,41,547 crore in 2011-12. The non-Plan Expenditure for2013-14 is budgeted at Rs 11,09,975 crore which is 14.5 per centhigher than the budget estimate of Rs 9,69,900 crore for thecurrent fiscal. However the total budgeted expenditure for 2013-14 is 16.4 per cent higher than the revised estimate of Rs14,30,825 crore for the current fiscal.

However, the jump in the Plan expenditure for 2013-14 is29.4 per cent when compared to the revised estimates of the samefor the current fiscal at Rs. 4,29,187 crore. The governmentspending on social sector schemes such as Bharat Nirman, theMahatma Gandhi National Rural Employment Guarantee Act and theNational Rural Health Mission. Besides, it includes the Centre’sassistance to States and Union Territories. The Finance Ministerhas pegged the fiscal deficit for the current fiscal at 5.2 percent of the gross domestic product and at 4.8 per cent for 2013-14.

“In the budget for 2012-13, the estimate of Plan expenditurewas too ambitious and the estimate of Non-Plan expenditure wastoo conservative. Faced with huge fiscal deficit, I had no choicebut to rationalize expenditure. We took a dose of bittermedicine. It seems to be working,” Mr. Chidambaram said in hisspeech in the Lok Sabha. "Government is concerned about theproliferation of CSS and Additional Central Assistance (ACA)schemes. They were 173 in number at the end of the 11th Plan. Iam glad to announce that the schemes will be restructured into 70schemes. Each scheme will be reviewed once in two years," theMinister said in the House.

The Economic Survey has warned that by 2020, India could be facedwith up to 16.7 million 'missing jobs'. In other words, withincreasing shift away from agriculture and younger people joiningthe job market, the survey warned that the demographic dividendcould turn into a 'demographic curse' with industry and theservices sector unable to provide jobs for up to 16.7 million job

seekers by 2020. Even under a much more conservative scenario, bythe end of the decade, 2.8 million people could be out huntingfor non-existent jobs. While industry is creating jobs, too manysuch jobs are low productivity non-contractual jobs in theunorganized sector, offering low incomes, little protection, andno benefits.

Growth without employment is a big risk to our nation. Thesurvey said that unlike in China, in India, the value added byindustry and manufacturing to the economy had not kept pace withthe number of people migrating to jobs in the sector. The reason:most of the jobs added in the non-agricultural economy are reallyjust of lowly-paid construction workers and most others are alsoof informal nature - without social security and better terms forthe labour. The service sector, on the other hand, the surveysaid, had added value to the economy but not added jobs inproportion when compared to other Asian economies that are on asimilar economic growth trajectory.

In India, too many small firms stay small and unproductiveand are not allowed to die gracefully. Too many large profitablefirms prefer relying on temporary contract labour and machinesthan on training workers for longer-term jobs. Keepingagricultural labour out of the picture, 95% of all other jobs areinformal in nature. Problems such as lack of resources for micro,small and medium enterprises and lagging infrastructure growthwere also at play. India's high rate of informality is a drag onits economic development and a source of considerable inequityexisted between informality (of jobs) and poverty in India. Keypolicy message is that India has to focus on an agenda to createproductive jobs outside of agriculture.

India Inc gave a thumbs up to the UPA-II's last Union Budgetbefore the general elections next year and said finance ministerP Chidambaram presented a "bold" and "growth-oriented" Budget.Hailing the announcements, industry chamber CII said the Budgetfocuses on growth and attracting more investments. "Manyproposals are development-inclusive. It will add to the country'sGross Domestic Product (GDP) growth. We are particularly glad to

see incentives for agricultural sector, MSME sector,infrastructure and capital market," CII president Adi Godrejsaid.

Union Budget 2013-14 – Policy Initiatives

1. Budgetary measures to support growth, saving andinvestment

While emphasising the need for investment to restart the growthengine, the Union Budget 2013-14 has laid particular focus oninfrastructure investment. It has adopted a multipronged approachto address the divergent constraints facing the infrastructuresector. While on the one hand, it has proposed measures tofacilitate and encourage investment in sectors like roads, ports,coal, power and waterways, it has tried, on the other hand, toaddress various sector-specific bottlenecks, such as,restructuring problems in power sector and pricing issues in coaland oil/ gas sectors. The focus has also been on the financingand regulatory issues.

The Budget proposes to carry forward the initiatives to boostinfrastructure investment, including encouraging InfrastructureDebt Funds; credit enhancement via India InfrastructureCorporation-Asian Development Bank partnership to infrastructurecompanies that may access the bond market; increase in theaggregate ceiling of issuance of tax-free bonds to `500 billionin 2013-14; and setting up a regulatory authority for the roadsector to address issues such as financial stress, enhancedconstruction risk and contract management. Further, in order toattract new investment and to quicken the implementation ofprojects, an investment allowance for new high value investmentswould be introduced. A company investing `1 billion or more in

plant and machinery during the period April 1, 2013 to March 31,2015 will be entitled to deduct an investment allowance of 15 percent of the investment. This will be in addition to the currentrates of depreciation. This is expected to provide significantspill-over benefits to small and medium enterprises.

In order to incentivise the household sector to save in financialinstruments rather than purchase gold, the Budget has announced(i) liberalisation of the Rajiv Gandhi Equity Savings Scheme (ii)enhancement of interest exemption limit in respect of loans forthe first home from a bank or a housing finance corporation up toRs.25 lakh during the period April 1, 2013 to March 31, 2014 and(iii) introduction of Inflation Indexed Bonds or InflationIndexed National Security Certificates that will protect savingsfrom inflation, especially the savings of the poor and middleclasses.

2. Initiatives relating to Banking and Financial Sector

A provision of Rs.140 billion for infusing capital in publicsector banks has been made in the Budget for 2013-14, over andabove Rs.125 billion for 13 public sector banks provided in 2012-13 to ensure their compliance with the Basel III regulations. Toaddress gender-related aspects of empowerment and financialinclusion, the Budget has proposed to set up India’s firstWomen’s Bank as a public sector bank and Government shall provideRs.10 billion as initial capital. The policy measures allowingFIIs to use their investments in corporate bonds and governmentsecurities as collateral for margin requirements would help boostpositive sentiment among FIIs.

Key deficits for 2013-14 broadly in linewith the path envisaged by the KelkarCommitteePursuant to the mid-year corrective measures undertaken by theCentral government, the fiscal consolidation process was resumed

in 2012-13, which is expected to continue in 2013-14. Theconsequent improvement in fiscal position is expected to be seenin select fiscal indicators in 2013-14 vis-à-vis their respectiverevised estimates for 2012-13. The rolling targets set out for2014-15 and 2015-16 indicate continuation of this momentum,although slight deviations in revenue and fiscal deficits fromthe path envisaged by the Kelkar Committee would persist (Table1).

The revised estimates for Central government financesfor 2012-13 show that the gross fiscal deficit- GDP ratio wasmarginally higher than the budgeted level. This reflected a sharpincrease of around `408 billion in the revenue deficit and theshortfall of `60 billion in disinvestment proceeds which wasoffset by a reduction of around `390 billion in net capitalexpenditure (capital outlay + loans and advances, net ofrecoveries). There was a slippage in achieving the budgetedrevenue deficit-GDP ratio of 3.4 per cent, reflecting the impactof a sharp rise in non-plan revenue expenditure, particularlysubsidies, coupled with shortfall in revenue receipts (both taxand non-tax) during the year.

Table 1: Select Fiscal Indicators (Per cent of GDP)

2012-13(RE)

2013-14(BE)

RollingTargets

2014-15 2015-16

1 2 3 4 5

Revenue Deficit 3.9

3.3

2.7

2.0

(3.4)

Effective Revenue Deficit#

2.7

1.8

0.9

0.0

(1.8)

Fiscal Deficit 5.2

4.8

4.2

3.6

(5.1)

Gross Tax Revenue 10.4

10.9

11.2

11.5

Total Outstanding Liabilities*

45.9

45.7

44.3

42.3

Memo: Kelkar Committee Recommendations

Revenue Deficit 3.7 2.8 2.0 NA

Fiscal Deficit 5.2 4.6 3.9 NA

Total Outstanding Liabilities 46.1 44.9

42.9 NA

# : Excludes grants for creation of capital assets from the total revenue expenditure* : Includes external debt at current exchange rates and excludes part of NSSF and total MSS liabilities.NA. : Not AvailableNote: Figures in parentheses relate to budget estimates.

During 2013-14, the GFD-GDP ratio is estimated to decline furtherto 4.8 per cent (Statement 1). The envisaged correction isexpected to be achieved through reduction of 0.6 percentagepoints in revenue deficit- GDP ratio. The reduction in revenuedeficit would be brought about by revenue enhancing measures andexpenditure control measures, particularly subsidies. The grossfiscal deficit of the Centre, however, continues to bepredominantly structural in nature (Chart 1).

The proportion of the gross fiscal deficit that would be pre-empted by the revenue deficit is expected to decline to around 70per cent in 2013-14 from 75 per cent in 2012-13, showing somequalitative improvement in the process of fiscal correction

(Chart 2). Adherence to the proposed strategy of fiscalcorrection would be important for the actual outturn of thegrowth process.

Revenue Receipts to improve in 2013-14

Gross tax revenues in the revised estimates for 2012-13 recordeda shortfall of around 3.7 per cent over the budgeted level. Unionexcise duties, customs duties, corporation tax and wealth taxcollections declined, even as income tax and service taxcollections showed an improvement. The decline in non-taxrevenues largely reflected a decline of around `390 billion intelecommunication receipts.

With the expected growth of 19.1 per cent in tax revenues, the gross tax-GDP ratio is estimated to improve by 0.5 percentage points to 10.9 per cent during 2013-14. In similar lines, the nettax revenue of the centre is budgeted to increase to 7.8 per centof GDP in 2013-14 from 7.4 per cent in 2012-13 (RE) (Table 2).

Table 2: Revenue Account of the Central Government(Per cent of GDP)

1 2 3 4 5 6 7

2008-09

2009-10

2010-11

2011-12

2012-13 (RE)

2013-14 (BE)

Revenue Receipts 9.6 8.8 10.1 8.4 8.7 9.3

(i) Tax revenue (Net) 7.9 7.0 7.3 7.0 7.4 7.8

(ii) Non Tax Revenue 1.7 1.8 2.8 1.4 1.3 1.5Revenue 14.1 14.1 13.4 12.8 12.6 12.6Expenditure Revenue Deficit 4.5 5.2 3.2 4.4 3.9 3.3

Memo Item : Effective Revenue - - 2.1 2.9 2.7 1.8

Deficit

Table 3 : Tax Buoyancy*

2004-05 to 2007-08

2008-09 to 2011-12

2012-13 (RE)

2013-14 (BE)(Average)

1 2 3 4 5

Corporation Tax 2.1 0.9 1.0 1.3

Income Tax 1.7 0.8 1.8 1.5Customs Duty 1.4 0.6 0.9 1.0Union Excise Duty 0.5 0.2 1.6 1.1

Service Tax 4.1 1.2 3.1 2.7Gross Tax Revenue 1.6 0.6 1.4 1.4

RE: Revised Estimates BE: Budget Estimates * Calculated as ratios of tax growth to nominal GDP growth.

The increase in tax revenues is sought to be achieved throughhigher excise and custom duties on certain products andimposition of additional surcharge on high income individuals.The tax buoyancies of corporation tax and customs duties areestimated to record improvements in 2013-14 (Table 3).

The sharp rise in budgeted non-tax revenues is on account ofhigher dividend receipts from state-owned enterprises (mainly inthe financial sector) and proceeds from telecom spectrum sales.

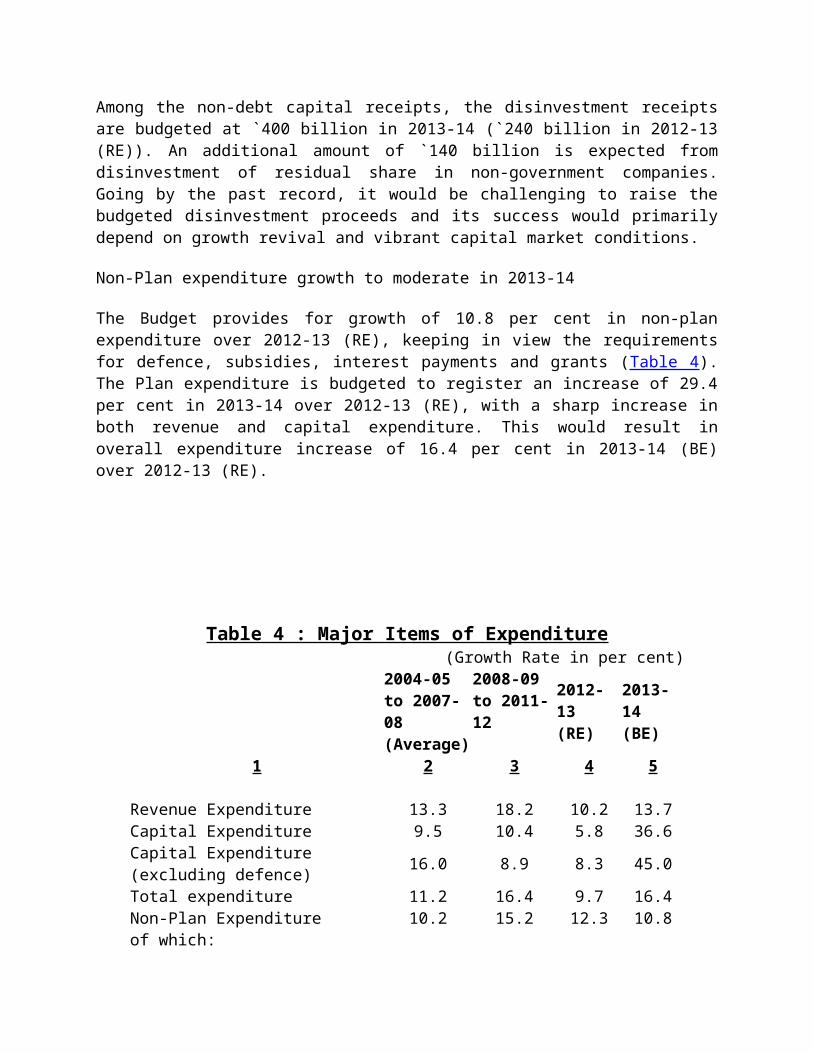

Among the non-debt capital receipts, the disinvestment receiptsare budgeted at `400 billion in 2013-14 (`240 billion in 2012-13(RE)). An additional amount of `140 billion is expected fromdisinvestment of residual share in non-government companies.Going by the past record, it would be challenging to raise thebudgeted disinvestment proceeds and its success would primarilydepend on growth revival and vibrant capital market conditions.

Non-Plan expenditure growth to moderate in 2013-14

The Budget provides for growth of 10.8 per cent in non-planexpenditure over 2012-13 (RE), keeping in view the requirementsfor defence, subsidies, interest payments and grants (Table 4).The Plan expenditure is budgeted to register an increase of 29.4per cent in 2013-14 over 2012-13 (RE), with a sharp increase inboth revenue and capital expenditure. This would result inoverall expenditure increase of 16.4 per cent in 2013-14 (BE)over 2012-13 (RE).

Table 4 : Major Items of Expenditure(Growth Rate in per cent)

2004-05 to 2007-08

2008-09 to 2011-12

2012-13 (RE)

2013-14 (BE)(Average)

1 2 3 4 5

Revenue Expenditure 13.3 18.2 10.2 13.7Capital Expenditure 9.5 10.4 5.8 36.6Capital Expenditure (excluding defence) 16.0 8.9 8.3 45.0

Total expenditure 11.2 16.4 9.7 16.4Non-Plan Expenditure 10.2 15.2 12.3 10.8of which:

Non-Plan Revenue Expenditure 10.4 18.2 13.3 8.0

1. Interest Payments 8.5 12.4 15.9 17.12. Grants to States 32.8 9.7 12.4 33.03. Subsidies 12.9 35.1 18.2 -10.3Non-plan Capital Expenditure 19.9 4.2 2.5 42.9

Plan Expenditure 14.0 19.5 4.1 29.4Plan Revenue Expenditure 22.1 18.3 2.9 29.1Plan Capital Expenditure -5.7 25.8 9.1 30.6RE : Revised Estimates, BE: Budget Estimates

The restraint on non-plan revenue expenditure growth is criticalto ensure that the fiscal consolidation going forward issustainable, and not excessively reliant on revenue augmentation.The growth in non-plan revenue expenditure is budgeted to becontained at 8.0 per cent (13.3 per cent in 2012-13). Theexpenditure on subsidies is budgeted lower at 2.0 per cent of GDPin 2013-14 as against 2.6 per cent of GDP in 2012-13. Thecredibility of the fiscal correction process would depend to alarge extent on meeting these targets.

Resource transfers from the Centre to States toincrease in 2013-14

The Thirteenth Finance Commission had recommended higher share ofcentral taxes to be transferred to the states and an increase ingrants-inaid, in order to minimise the vertical fiscal imbalancesbetween the Centre and the states. Although the Centre hadbudgeted increase in all three forms of transfers (taxdevolution, grants-in-aid and loans to the states) to statesduring 2012-13, the shortfall in Centre’s revenues during 2012-13(RE) is reflected in lower gross and net transfers to the states,both in terms of GDP as well as in absolute terms. During 2013-14, gross and net transfers as ratios to GDP are budgeted toincrease by 0.3 percentage points each to 5.2 per cent and 5.1per cent, respectively.

Disinvestment proceeds to get credited in National Investment Fund

In pursuance of the decision to use disinvestment proceeds from central PSUs only for select capital investment, the disinvestment proceeds from the year 2013-14 will get credited to the public account under the National Investment Fund (NIF) and will be withdrawn for/invested in approved purposes. During 2013-14, out of total disinvestment proceeds, the government proposes to finance recapitalisation of public sector banks (`140 billion) and invest in modernisation and other capital projects of railways (`260 billion). The use of disinvestment proceeds for capital investment would increase resource flowstowards more productive purposes.

Table 5: Total Subsidies(Amount in Rs. billion)

2011-12 2012-13 (BE) 2012-13 (RE) 2013-14 (BE)

Amount Per centto GDP Amount Per cent

to GDP Amount Per centto GDP Amount Per cent

to GDP1 2 3 4 5 6 7 8 9

Total Subsidies 2,179.4 2.4 1,900.2 1.9 2,576.5 2.6 2,310.8 2.0i. Food 728.2 0.8 750.0 0.7 850.0 0.8 900.0 0.8ii. Fertiliser 700.1 0.8 609.7 0.6 659.7 0.7 659.7 0.6iii. Petroleum 684.8 0.8 435.8 0.4 968.8 1.0 650.0 0.6iv. Interest subsidy 50.5 0.1 79.7 0.1 74.2 0.1 80.6 0.1

v. Other subsidies 15.7 0.0 24.9 0.0 23.8 0.0 20.5 0.0

RE: Revised Estimates BE: Budget Estimates

Table 6: Major Expenditure Indicators for 2013-14: Budget

Estimates vis-à-vis Kelkar CommitteeRecommendations

(Per cent of GDP)

Items BudgetEstimates

KelkarCommittee

Recommendations

1 2 3Non-Plan Expenditure 9.8 9.1On Revenue Account 8.7 8.2of which: Subsidies 2.0 1.7On Capital Account 1.0 0.9Plan Expenditure 4.9 4.9On Revenue Account 3.9 3.6On Capital Account 1.0 1.3Total Expenditure 14.6 13.9On Revenue Account 12.6 11.7On Capital Account 2.0 2.2

Budgeted market borrowings of government in 2013-14 to impact liquidity

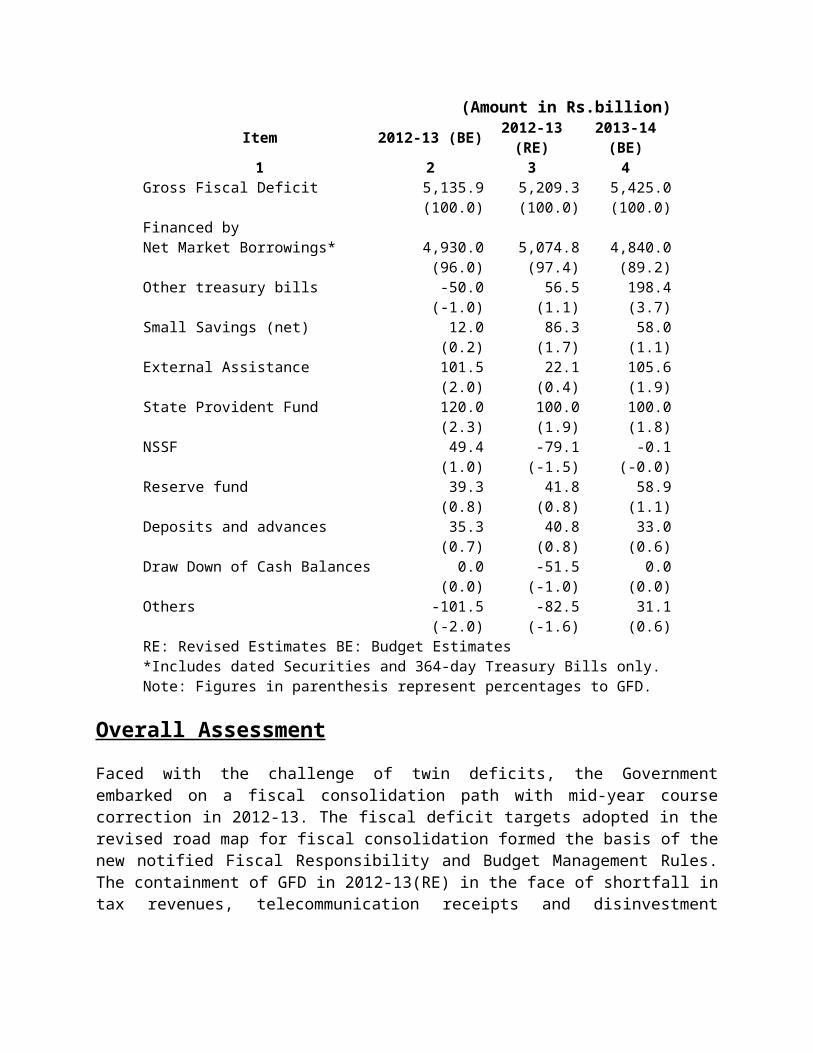

During 2012-13, net market borrowings (through dated securities and364-day treasury bills) financed around 97 per cent of the grossfiscal deficit (Table 8). While the borrowings through datedsecurities were reduced by `120 billion from the budget estimates dueto additional cushion available from higher opening cash balances andsurpluses of state governments invested in Central Government treasurybills, borrowings under 364-day treasury bills increased by `260billion.

Fiscal deficit would continue to be largely financed by marketborrowings during 2013-14. The net market borrowing for 2013-14, asannounced in the Union Budget, is `4,840 billion, which financesaround 89 per cent of the GFD of `5,425 billion. The proposed move tointroduce buy-back/switches of government securities aggregating `500billion in 2013-14, would ease the redemption pressure in the maturitybuckets 2014-15 to 2018-19. This would help in effective debtmanagement.

Given the large size of market borrowings, substantial liquidityinjection by the Reserve Bank may be required. If market borrowingsare contained within the budgeted amount, it could provide somerequired monetary space and enable efficient monetary-fiscalcoordination.

Table 8 : Financing Pattern of Gross Fiscal Deficit

(Amount in Rs.billion)Item 2012-13 (BE) 2012-13

(RE)2013-14(BE)

1 2 3 4Gross Fiscal Deficit 5,135.9 5,209.3 5,425.0 (100.0) (100.0) (100.0)Financed by Net Market Borrowings* 4,930.0 5,074.8 4,840.0 (96.0) (97.4) (89.2)Other treasury bills -50.0 56.5 198.4 (-1.0) (1.1) (3.7)Small Savings (net) 12.0 86.3 58.0 (0.2) (1.7) (1.1)External Assistance 101.5 22.1 105.6 (2.0) (0.4) (1.9)State Provident Fund 120.0 100.0 100.0 (2.3) (1.9) (1.8)NSSF 49.4 -79.1 -0.1 (1.0) (-1.5) (-0.0)Reserve fund 39.3 41.8 58.9 (0.8) (0.8) (1.1)Deposits and advances 35.3 40.8 33.0 (0.7) (0.8) (0.6)Draw Down of Cash Balances 0.0 -51.5 0.0 (0.0) (-1.0) (0.0)Others -101.5 -82.5 31.1 (-2.0) (-1.6) (0.6)RE: Revised Estimates BE: Budget Estimates *Includes dated Securities and 364-day Treasury Bills only. Note: Figures in parenthesis represent percentages to GFD.

Overall AssessmentFaced with the challenge of twin deficits, the Governmentembarked on a fiscal consolidation path with mid-year coursecorrection in 2012-13. The fiscal deficit targets adopted in therevised road map for fiscal consolidation formed the basis of thenew notified Fiscal Responsibility and Budget Management Rules.The containment of GFD in 2012-13(RE) in the face of shortfall intax revenues, telecommunication receipts and disinvestment

proceeds was largely brought about by scaling down planexpenditure and capital expenditure.

The fiscal policy for 2013-14, as enunciated in the Union Budget,has been designed to meet the macroeconomic challenges faced byIndia in an uncertain global environment. The reduction in theGFD-GDP ratio in 2013-14 (BE) is based on higher mobilization ofdisinvestment proceeds, tax revenues, telecommunication receiptsand reduction in expenditure on subsidies. As the Budget relieslargely on revenue-led fiscal consolidation, its success woulddepend on the revival of investment climate and growth. Thereduction in revenue-deficit by 0.6 per cent of GDP during 2013-14 critically hinges upon the success in meeting the projectedtax and non-tax revenues. The government would have to continuewith its efforts towards rationalizing and reducing subsidies inorder to create space for meeting future commitments under theproposed Food Security Act.

The re-prioritization of expenditure in favor of capitalexpenditure would increase capital outlay-GFD ratio from 28.1 percent in 2012-13 to 38.5 per cent in 2013-14. It may be noted thatduring the fiscal consolidation phase the capital outlay-GFDratio, on an average, was as high as 51.4 per cent. The fiscalconsolidation measures announced in the Budget will lay thefoundation for a sustainable rebalancing of Government finances.Fiscal prudence would impart confidence in the economy andsupport domestic and foreign investments. The envisagedelimination of effective revenue deficit by 2015-16 would makeavailable additional resources for financing investment andcapital expenditure (including grants for creation of capitalassets), ensure the use of government borrowing primarily forcapital formation and aid the growth process.

Another change was to stipulate that where a foreign investor'sequity holdings in a firm are over 10%, it would be treated asFDI, while below that threshold it would be FII investment. Thenet effect of the tax changes is estimated to yield an extra Rs13,300 crore in direct taxes and Rs 4,700 crore in indirecttaxes. The total additional resource mobilisation of Rs 18,000crore pales in comparison to the Rs 41,440 crore Pranab Mukherjee

had proposed to raise last year. Despite the relatively modesttax mop-up, the FM has managed to present a budget thatapparently hikes outlays on key areas like education, health andthe social sector by significant amounts — and yet contains thefiscal deficit at 4.8% of GDP. There is a bit of smoke andmirrors in that image, though. Chidambaram constantly referred tohow big the jumps in outlays were relative to the revisedestimates for 2012-13, but chose not to dwell on the fact thatwhen compared with the budget estimates for the same year, theincreases were most often modest. He is also clearly banking onbeing able to cut subsidies by a significant amount - next year'sestimates for combined food, fertilizer and petroleum productsubsidies is almost Rs 27,000 crore less than the revisedestimates for 2012-13. Is that a sign that the government reallymeans it when it says that fuel prices will be periodicallyrevised? We'll have to wait and see.

Statement 1: Budget at a Glance (Amount in Rs. billion)

Items2011-12(Accoun

ts)

2012-13(BudgetEstimat

es)

2012-13(RevisedEstimate

s)

2013-14(BudgetEstimate

s)

Variation in per centCol. 4over

Col. 3

Col. 4over

Col. 2

Col. 5over

Col. 41 2 3 4 5 6 7 8

1. Revenue Receipts (i+ii) 7,514.4 9,356.9 8,718.310,563.3 -6.8 16.0 21.2

i) Tax Revenue (Net to Centre) 6,297.7 7,710.7 7,421.2 8,840.8 -3.8 17.8 19.1

ii) Non-tax Revenue 1,216.7 1,646.1 1,297.1 1,722.5 -21.2 6.6 32.8 of which: Interest Receipts 202.5 192.3 166.0 177.6 -13.7 -18.1 7.02. Capital Receipts 5,529.3 5,552.4 5,590.0 6,089.7 0.7 1.1 8.9 of which: i) Market Borrowings 4,841.1 4,930.0 5,074.8 4,840.0 2.9 4.8 -4.6 ii) Recoveries of Loans 188.5 116.5 140.7 106.5 20.8 -25.3 -24.3

iii) Disinvestment of equity in PSUs 180.9 300.0 240.0 558.1 -20.0 32.7 132.6

3. Total Receipts (1+2) 13,043.714,909.

314,308.316,653.0 -4.0 9.7 16.4

4. Revenue Expenditure (i + ii)

11,457.912,861.

112,630.714,361.7 -1.8 10.2 13.7

i) Non-Plan 8,120.5 8,656.0 9,197.0 9,929.1 6.3 13.3 8.0

ii) Plan 3,337.4 4,205.1 3,433.7 4,432.6 -18.3 2.9 29.1

5. Capital Expenditure (i + ii) 1,585.8 2,048.2 1,677.5 2,291.3 -18.1 5.8 36.6

i) Non-Plan 799.4 1,043.0 819.4 1,170.7 -21.4 2.5 42.9 ii) Plan 786.4 1,005.1 858.1 1,120.6 -14.6 9.1 30.6

6. Total Non-Plan Expenditure (4i + 5i) 8,919.9 9,699.010,016.411,099.8 3.3 12.3 10.8

of which: i) Interest Payments 2,731.5 3,197.6 3,166.7 3,706.8 -1.0 15.9 17.1 ii) Defence 1,709.1 1,934.1 1,785.0 2,036.7 -7.7 4.4 14.1 iii) Subsidies 2,179.4 1,900.2 2,576.5 2,310.8 35.6 18.2 -10.3

7. Total Plan Expenditure (4ii + 5ii) 4,123.8 5,210.3 4,291.9 5,553.2 -17.6 4.1 29.4

8. Total Expenditure (6+7=4+5)

13,043.714,909.

314,308.316,653.0 -4.0 9.7 16.4

9. Revenue Deficit (4-1) 3,943.5 3,504.2 3,912.5 3,798.4 11.6 -0.8 -2.9 (4.4) (3.4) (3.9) (3.3) 10. Effective Revenue Deficit 2,617.7 1,857.5 2,669.7 2,051.8 43.7 2.0 -23.1

(2.9) (1.8) (2.7) (1.8) 11.

Gross Fiscal Deficit (8-(1+2ii+2iii)) 5,159.9 5,135.9 5,209.3 5,425.0 1.4 1.0 4.1

(5.7) (5.1) (5.2) (4.8) 12.

Gross Primary Deficit (11-6i) 2,428.4 1,938.3 2,042.5 1,718.1 5.4 -15.9 -15.9

(2.7) (1.9) (2.0) (1.5)

Notes : 1) Capital Receipts are net of repayments.2) Market borrowings include dated securities and 364 day Treasury Bills.1Assuming real GDP growth of 6.5 per cent and nominal GDP growth of 13.4 per cent.

Source : Budget documents of the Government of India, 2013-14.

* Prepared in the Fiscal Analysis Division of the Department ofEconomic and Policy Research. The previous article on UnionBudget 2012-13 was published in the Reserve Bank of IndiaBulletin, May 2012.

* The Times of India – Union Budget 2013-14.

Copyright © 2022 FDOKUMEN