Optimal monetary policy in a model of the credit channel

52

by Fiorella De Fiore and Oreste Tristani OPTIMAL MONETARY POLICY IN A MODEL OF THE CREDIT CHANNEL WORKING PAPER SERIES NO 1043 / APRIL 2009

-

Upload

khangminh22 -

Category

Documents

-

view

4 -

download

0

Transcript of Optimal monetary policy in a model of the credit channel

by Fiorella De Fioreand Oreste Tristani

OPTIMAL MONETARY POLICY IN A MODEL OF THE CREDIT CHANNEL

WORk INg PAPER SER I E SNO 1043 / APR I L 2009

WORKING PAPER SER IESNO 1043 / APR I L 2009

This paper can be downloaded without charge fromhttp://www.ecb.europa.eu or from the Social Science Research Network

electronic library at http://ssrn.com/abstract_id=1383502.

In 2009 all ECB publications

feature a motif taken from the

€200 banknote.

OPTIMAL MONETARY POLICY

IN A MODEL OF

THE CREDIT CHANNEL 1

by Fiorella De Fiore and Oreste Tristani 2

1 We wish to thank Michael Woodford for many interesting discussions and Krzysztof Zalewski for excellent research assistance. We also thank

for useful comments and suggestions Kosuke Aoki, Ester Faia, Giovanni Lombardo, Pedro Teles, Christian Upper, Tony Yates and seminar

participants at the EEA 2008 meetings, CEF 2008, the Norges Bank Workshop on “Optimal Monetary Policy”, the BIS-CEPR-ESI

12th Annual Conference on “The Evolving Financial system and the Transmission Mechanism of Monetary Policy”,

the Swiss National Bank Research Conference 2008 on “Alternative Models for Monetary Policy Analysis”

and seminars at the Bank of England, the University of Aarhus and the Università Cattolica in Milan.

2 European Central Bank, DG Research, Kaiserstrasse 29, D-60311 Frankfurt am Main, Germany;

e-mail: [email protected], [email protected]

© European Central Bank, 2009

Address Kaiserstrasse 29 60311 Frankfurt am Main, Germany

Postal address Postfach 16 03 19 60066 Frankfurt am Main, Germany

Telephone +49 69 1344 0

Website http://www.ecb.europa.eu

Fax +49 69 1344 6000

All rights reserved.

Any reproduction, publication and reprint in the form of a different publication, whether printed or produced electronically, in whole or in part, is permitted only with the explicit written authorisation of the ECB or the author(s).

The views expressed in this paper do not necessarily refl ect those of the European Central Bank.

The statement of purpose for the ECB Working Paper Series is available from the ECB website, http://www.ecb.europa.eu/pub/scientific/wps/date/html/index.en.html

ISSN 1725-2806 (online)

3ECB

Working Paper Series No 1043April 2009

Abstract 4

Non-technical summary 5

1 Introduction 6

2 The environment 9

2.1 Households 10

2.2 Wholesale fi rms 12

2.3 Retail fi rms 16

2.4 Monetary policy 18

2.5 Market clearing 19

3 The linearized equilibrium conditions 20

3.1 Impulse responses 23

4 Second order welfare approximation 26

5 Optimal policy 30

5.1 Discretion 30

5.2 Optimal monetary policy under commitment 30

6 Conclusion 33

Appendices 34

References 42

Figures 44

European Central Bank Working Paper Series 48

CONTENTS

4ECBWorking Paper Series No 1043April 2009

AbstractWe consider a simple extension of the basic new-Keynesian setup in which we relax the assumption of frictionless financial markets. In our economy, asymmetric information and default risk lead banks to optimally charge a lending rate above the risk-free rate. Our contribution is threefold. First, we derive analytically the loglinearised equations which characterise aggregate dynamics in our model and show that they nest those of the new- Keynesian model. A key difference is that marginal costs increase not only with the output gap, but also with the credit spread and the nominal interest rate. Second, we find that financial market imperfections imply that

output and inflation stabilisation. Third, we show that, in our model, an aggressive easing of policy is optimal in response to adverse financial market shocks.

Keywords: optimal monetary policy, financial markets, asymmetric information

JEL Classification: E52, E44

exogenous disturbances, including technology shocks, generate a trade-off between

5ECB

Working Paper Series No 1043April 2009

Non-technical summary We analyse whether and how financial market conditions ought to have a bearing on

monetary policy decisions. More specifically, we ask the following questions: Should

financial market variables matter per se for monetary policy, or should they only be

taken into account to the extent that they affect output and inflation? Can financial

shocks that increase credit spreads generate a large enough economic reaction to justify

aggressive interest rate cuts?

We present a simple extension of the basic new-Keynesian setup in which we relax the

assumption of frictionless financial markets. In our model, asymmetric information and

default risk lead banks to charge a lending rate above the risk-free rate. Moreover,

financial contracts are denominated in nominal terms, so that monetary policy affects

firms’ financing costs.

Our contribution is threefold. First, we show that the log-linearised equations which

characterise the aggregate dynamics in our model nest those of the new-Keynesian

model. A key difference is that marginal costs increase not only with the output gap,

but also with the credit spread and the nominal interest rate. Moreover, financial

market imperfections imply that exogenous disturbances, including technology shocks,

Second, we derive a second-order approximation of the welfare function. We show that

welfare is affected by the volatility of inflation and the output gap, as in the benchmark

case with frictionless financial markets. However, it is also affected by the volatility of

the nominal interest rate and of the credit spread. As a result, the target rule which

would characterise optimal policy under discretion ought to include a reaction to credit

spreads and the nominal interest rate.

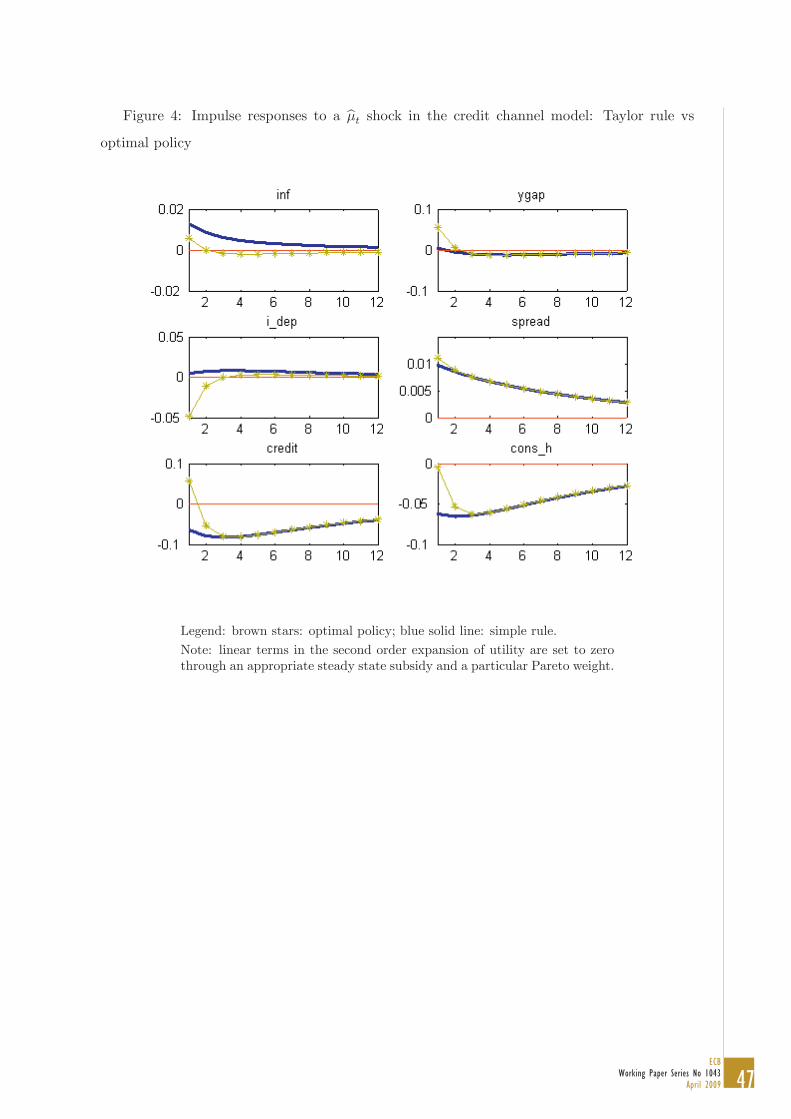

Third, we show that, in our model, an aggressive easing of monetary policy is optimal

in response to an adverse financial market shock that increases the credit spread. The

main reason is that this shock generates an undesirable fall in household consumption.

The marked easing of monetary policy is aimed at smoothing household consumption.

At the same time, the upward pressure on inflation generated by the interest rate cut

through higher aggregate demand is attenuated by the direct negative effect on

marginal costs. Both inflation and household consumption move less than they would

under a Taylor rule.

generate a trade-off between output and inflation stabilisation.

6ECBWorking Paper Series No 1043April 2009

7ECB

Working Paper Series No 1043April 2009

8ECBWorking Paper Series No 1043April 2009

9ECB

Working Paper Series No 1043April 2009

10ECBWorking Paper Series No 1043April 2009

11ECB

Working Paper Series No 1043April 2009

12ECBWorking Paper Series No 1043April 2009

13ECB

Working Paper Series No 1043April 2009

14ECBWorking Paper Series No 1043April 2009

15ECB

Working Paper Series No 1043April 2009

16ECBWorking Paper Series No 1043April 2009

17ECB

Working Paper Series No 1043April 2009

18ECBWorking Paper Series No 1043April 2009

19ECB

Working Paper Series No 1043April 2009

20ECBWorking Paper Series No 1043April 2009

21ECB

Working Paper Series No 1043April 2009

22ECBWorking Paper Series No 1043April 2009

23ECB

Working Paper Series No 1043April 2009

24ECBWorking Paper Series No 1043April 2009

25ECB

Working Paper Series No 1043April 2009

26ECBWorking Paper Series No 1043April 2009

27ECB

Working Paper Series No 1043April 2009

28ECBWorking Paper Series No 1043April 2009

29ECB

Working Paper Series No 1043April 2009

30ECBWorking Paper Series No 1043April 2009

31ECB

Working Paper Series No 1043April 2009

32ECBWorking Paper Series No 1043April 2009

33ECB

Working Paper Series No 1043April 2009

34ECBWorking Paper Series No 1043April 2009

35ECB

Working Paper Series No 1043April 2009

36ECBWorking Paper Series No 1043April 2009

37ECB

Working Paper Series No 1043April 2009

38ECBWorking Paper Series No 1043April 2009

39ECB

Working Paper Series No 1043April 2009

40ECBWorking Paper Series No 1043April 2009

41ECB

Working Paper Series No 1043April 2009

42ECBWorking Paper Series No 1043April 2009

43ECB

Working Paper Series No 1043April 2009

44ECBWorking Paper Series No 1043April 2009

45ECB

Working Paper Series No 1043April 2009

46ECBWorking Paper Series No 1043April 2009

47ECB

Working Paper Series No 1043April 2009

48ECBWorking Paper Series No 1043April 2009

European Central Bank Working Paper Series

For a complete list of Working Papers published by the ECB, please visit the ECB’s website

(http://www.ecb.europa.eu).

989 “Modelling loans to non-financial corporations in the euro area” by C. Kok Sørensen, D. Marqués-Ibáñez

and C. Rossi, January 2009

990 “Fiscal policy, housing and stock prices” by A. Afonso and R. M. Sousa, January 2009.

991 “The macroeconomic effects of fiscal policy” by A. Afonso and R. M. Sousa, January 2009.

992 “FDI and productivity convergence in central and eastern Europe: an industry-level investigation”

by M. Bijsterbosch and M. Kolasa, January 2009.

993 “Has emerging Asia decoupled? An analysis of production and trade linkages using the Asian international

input-output table” by G. Pula and T. A. Peltonen, January 2009.

994 “Fiscal sustainability and policy implications for the euro area” by F. Balassone, J. Cunha, G. Langenus,

B. Manzke, J. Pavot, D. Prammer and P. Tommasino, January 2009.

995 “Current account benchmarks for central and eastern Europe: a desperate search?” by M. Ca’ Zorzi,

A. Chudik and A. Dieppe, January 2009.

996 “What drives euro area break-even inflation rates?” by M. Ciccarelli and J. A. García, January 2009.

997 “Financing obstacles and growth: an analysis for euro area non-financial corporations” by C. Coluzzi,

A. Ferrando and C. Martinez-Carrascal, January 2009.

998 “Infinite-dimensional VARs and factor models” by A. Chudik and M. H. Pesaran, January 2009.

999 “Risk-adjusted forecasts of oil prices” by P. Pagano and M. Pisani, January 2009.

1000 “Wealth effects in emerging market economies” by T. A. Peltonen, R. M. Sousa and I. S. Vansteenkiste,

January 2009.

1001 “Identifying the elasticity of substitution with biased technical change” by M. A. León-Ledesma,

P. McAdam and A. Willman, January 2009.

1002 “Assessing portfolio credit risk changes in a sample of EU large and complex banking groups in reaction

to macroeconomic shocks” by O. Castrén, T. Fitzpatrick and M. Sydow, February 2009.

1003 “Real wages over the business cycle: OECD evidence from the time and frequency domains” by

J. Messina, C. Strozzi and J. Turunen, February 2009.

1004 “Characterising the inflation targeting regime in South Korea” by M. Sánchez, February 2009.

1005 “Labor market institutions and macroeconomic volatility in a panel of OECD countries” by F. Rumler

and J. Scharler, February 2009.

1006 “Understanding sectoral differences in downward real wage rigidity: workforce composition, institutions,

technology and competition” by P. Du Caju, C. Fuss and L. Wintr, February 2009.

1007 “Sequential bargaining in a new-Keynesian model with frictional unemployment and staggered wage

negotiation” by G. de Walque, O. Pierrard, H. Sneessens and R. Wouters, February 2009.

49ECB

Working Paper Series No 1043April 2009

1008 “Liquidity (risk) concepts: definitions and interactions” by K. Nikolaou, February 2009.

1009 “Optimal sticky prices under rational inattention” by B. Maćkowiak and M. Wiederholt, February 2009.

1010 “Business cycles in the euro area” by D. Giannone, M. Lenza and L. Reichlin, February 2009.

1011 “The global dimension of inflation – evidence from factor-augmented Phillips curves” by S. Eickmeier

and K. Moll, February 2009.

1012 “Petrodollars and imports of oil exporting countries” by R. Beck and A. Kamps, February 2009.

1013 “Structural breaks, cointegration and the Fisher effect” by A. Beyer, A. A. Haug and B. Dewald,

February 2009.

1014 “Asset prices and current account fluctuations in G7 economies” by M. Fratzscher and R. Straub,

February 2009.

1015 “Inflation forecasting in the new EU Member States” by O. Arratibel, C. Kamps and N. Leiner-Killinger,

February 2009.

1016 “When does lumpy factor adjustment matter for aggregate dynamics?” by S. Fahr and F. Yao,

March 2009.

1017 “Optimal prediction pools” by J. Geweke and G. Amisano, March 2009.

1018 “Cross-border mergers and acquisitions: financial and institutional forces” by N. Coeurdacier,

R. A. De Santis and A. Aviat, March 2009.

1019 “What drives returns to euro area housing? Evidence from a dynamic dividend-discount model” by

P. Hiebert and M. Sydow, March 2009.

1020 “Opting out of the Great Inflation: German monetary policy after the break down of Bretton Woods”

by A. Beyer, V. Gaspar, C. Gerberding and O. Issing, March 2009.

1021 “Rigid labour compensation and flexible employment? Firm-level evidence with regard to productivity

for Belgium” by C. Fuss and L. Wintr, March 2009.

1022 “Understanding inter-industry wage structures in the euro area” by V. Genre, K. Kohn and

D. Momferatou, March 2009.

1023 “Bank loan announcements and borrower stock returns: does bank origin matter?” by S. Ongena

and V. Roscovan, March 2009.

1024 “Funding liquidity risk: definition and measurement” by M. Drehmann and K. Nikolaou, March 2009.

1025 “Liquidity risk premia in unsecured interbank money markets” by J. Eisenschmidt and J. Tapking,

March 2009.

1026 “Do house price developments spill over across euro area countries? Evidence from a global VAR”

by I. Vansteenkiste and P. Hiebert, March 2009.

1027 “Long run evidence on money growth and inflation” by L. Benati, March 2009.

1028 “Large debt financing: syndicated loans versus corporate bonds” by Y. Altunbaș, A. Kara

and D. Marqués-Ibáñez, March 2009.

50ECBWorking Paper Series No 1043April 2009

1029 “The role of fiscal transfers for regional economic convergence in Europe” by C. Checherita, C. Nickel

and P. Rother, March 2009.

1030 “Forecast evaluation of small nested model sets” by K. Hubrich and K. D. West, March 2009.

1031 “Global roles of currencies” by C. Thimann, March 2009.

1032 “Assessing long-term fiscal developments: a new approach” by A. Afonso, L. Agnello, D. Furceri and R. Sousa,

March 2009.

1033 “Fiscal competition over taxes and public inputs: theory and evidence” by S. Hauptmeier, F. Mittermaier

and J. Rincke, March 2009.

1034 “The role of the United States in the global economy and its evolution over time” by S. Dées

and A. Saint-Guilhem, March 2009.

1035 “The role of labor markets for euro area monetary policy” by K. Christoffel, K. Kuester and T. Linzert,

March 2009.

1036 “Search in the product market and the real business cycle” by T. Y. Mathä and O. Pierrard, March 2009.

1037 “What do asset prices have to say about risk appetite and uncertainty?” by G. Bekaert, M. Hoerova

and M. Scheicher, March 2009.

1038 “Are ‘intrinsic inflation persistence’ models structural in the sense of Lucas (1976)?” by L. Benati, March 2009.

1039 “‘Real Time’ early warning indicators for costly asset price boom/bust cycles: a role for global liquidity”

by L. Alessi and C. Detken, March 2009.

1040 “The external and domestic side of macroeconomic adjustment in China” by R. Straub and C. Thimann,

March 2009.

1041 “An economic capital integrating credit and interest rate risk in the banking book” by P. Alessandri

and M. Drehmann, April 2009.

1042 “The determinants of public deficit volatility” by L. Agnello and R. M. Sousa, April 2009.

1043 “Optimal monetary policy in a model of the credit channel” by F. De Fiore and O. Tristani, April 2009.