Oil and Gas Fiscal Regime in Tanzania

178

i Petroleum Taxation: A Critical Analysis of Oil and Gas Fiscal Regime in Tanzania September 2014 By Raphael Bahati Tweve Mgaya Dissertation Supervisor: Mr William Craig Submitted in partial completion of the degree of MSc Oil and Gas Law Degree

-

Upload

independent -

Category

Documents

-

view

1 -

download

0

Transcript of Oil and Gas Fiscal Regime in Tanzania

i

Petroleum Taxation:

A Critical Analysis of Oil and Gas Fiscal Regime in Tanzania

September 2014

By Raphael Bahati Tweve Mgaya

Dissertation Supervisor: Mr William Craig

Submitted in partial completion of the degree of MSc Oil and Gas Law Degree

ii

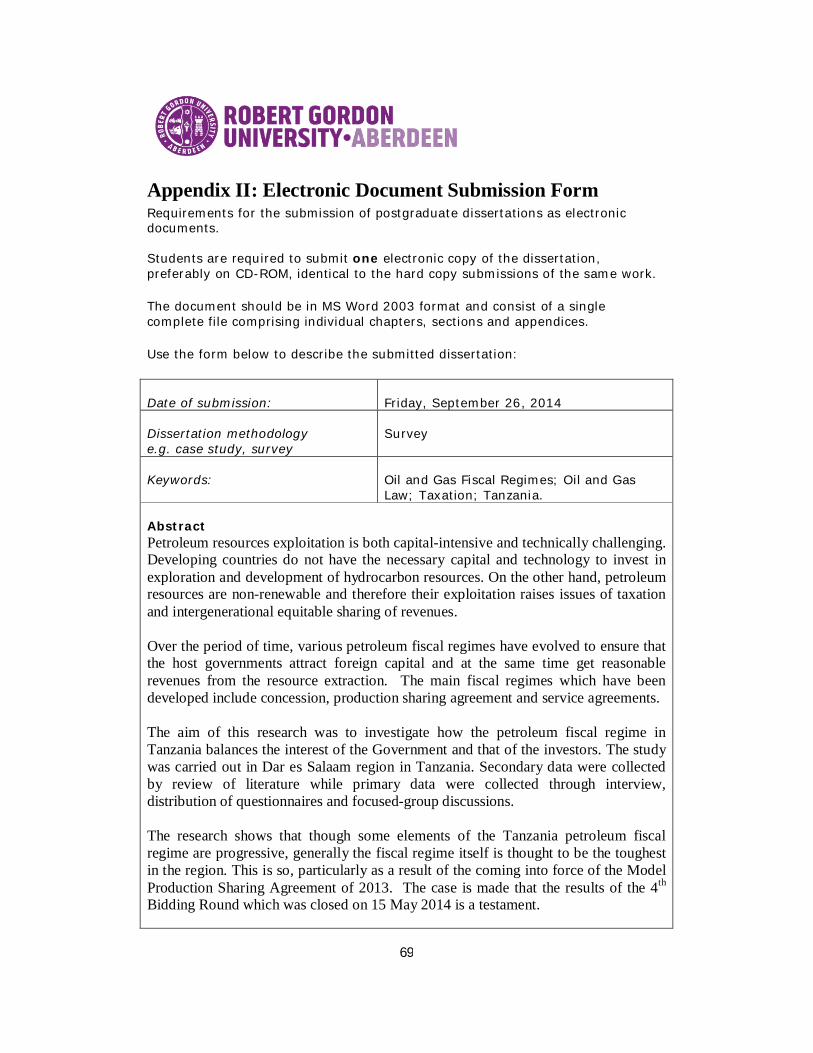

ABSTRACT Petroleum resources exploitation is both capital-intensive and technically challenging.

Developing countries do not have the necessary capital and technology to invest in

exploration and development of hydrocarbon resources. On the other hand, petroleum

resources are non-renewable and therefore their exploitation raises issues of taxation

and intergenerational equitable sharing of revenues.

Over the period of time, various petroleum fiscal regimes have evolved to ensure that

the host governments attract foreign capital and at the same time get reasonable

revenues from the resource extraction. The main fiscal regimes which have been

developed include concession, production sharing agreement and service agreements.

The aim of this research was to investigate how the petroleum fiscal regime in

Tanzania balances the interest of the Government and that of the investors. The study

was carried out in Dar es Salaam region in Tanzania. Secondary data were collected

by review of literature while primary data were collected through interview,

distribution of questionnaires and focused-group discussions.

The research shows that though some elements of the Tanzania petroleum fiscal

regime are progressive, generally the fiscal regime itself is thought to be the toughest

in the region. This is so, particularly as a result of the coming into force of the Model

Production Sharing Agreement of 2013. The case is made that the results of the 4th

Bidding Round which was closed on 15 May 2014 is a testament.

iii

ACKNOWLEDGEMENTS

The author wishes to express thanks to all those who have assisted and advised during

this research, with particular mention of: Mr. William Craig, for his thoughtful

guidance as a dissertation supervisor; the staff of the University of Robert Gordon and

the University of Dar es Salaam for their tireless support particularly in regard to

library services; my employer, the Tanzania Development Corporation for affording

me ample time and financial resources for this work. Appreciation are also due to the

my colleagues Goodluck Shirima, Kelvin Gadi, Burton Mwaka and Pascal Lyimo

through whose support in one way or the other has helped me to accomplish this

research. Any shortcomings in this research are entirely my own.

iv

TABLE OF CONTENTS ABSTRACT ............................................................................................................................. ii

ACKNOWLEDGEMENTS ........................................................................................................ iii

ABBREVIATIONS .................................................................................................................. vii

LIST OF STATUTES .............................................................................................................. viii

LIST OF TABLES ..................................................................................................................... ix

LIST OF FIGURES .................................................................................................................... x

CHAPTER ONE: INTRODUCTION ........................................................................................... 1

1.1 Background 1

1.2 Overview of Tanzania 1

1.2.1 History .................................................................................................................. 1

1.2.2 Economy ............................................................................................................... 2

1.2.3 Petroleum Exploration History .............................................................................. 3

1.3 Statement of the Problem 7

1.4 Research Questions 9

1.4.1 Main Question ...................................................................................................... 9

1.4.1 Specific Questions ................................................................................................. 9

1.5 Objectives of the Research 9

1.5.1 Main Objective ..................................................................................................... 9

1.5.2 Specific Objectives ................................................................................................ 9

1.6 Significance of the Study 10

1.7 Scope of the Study 10

1.8 Limitations to the Study 10

1.8.1 Limited Resources ............................................................................................... 11

1.8.2 Access to Confidential Information..................................................................... 11

1.8.3 Lack of Cooperation from Respondents............................................................... 11

1.8.4 Delimitation of the Research ............................................................................... 11

v

1.9 Methodology 12

1.9.1 Population .......................................................................................................... 12

1.9.2 Sample Size and Sampling Technique .................................................................. 12

1.9.3 Types of Data and Collection Methods ................................................................ 12

1.9.4 Data Processing and Analysis Methods ............................................................... 13

CHAPTER TWO: CRITICAL ANALYSIS OF PETROLEUM FISCAL REGIMES......................... 14

2.1 The Rationale for Special Petroleum Tax Regime 14

2.2Types of Fiscal Regimes 14

2.2.1 Concessionary Systems ....................................................................................... 16

2.2.2 Contractual Systems ........................................................................................... 18

2.3 Fiscal Components of Contractual Systems 22

2.3.1 Royalty ............................................................................................................... 22

2.3.2 Cost Recovery Limit............................................................................................. 25

2.3.3 Profit Oil Split ...................................................................................................... 26

2.3.4 Government Participation ................................................................................... 27

2.3.5 Other Fiscal Instruments ..................................................................................... 29

CHAPTER THREE: CRITICAL ANALYSIS OF PETROLEUM FISCAL REGIME IN TANZANIA........... 32

3.1 The Overview of the Oil and Gas Fiscal Regime of Tanzania 32

3.1.1 Elements of PSA Regime in Tanzania ................................................................... 33

3.2 The Perceptions of the Industry on the Oil and Gas Fiscal Framework 43

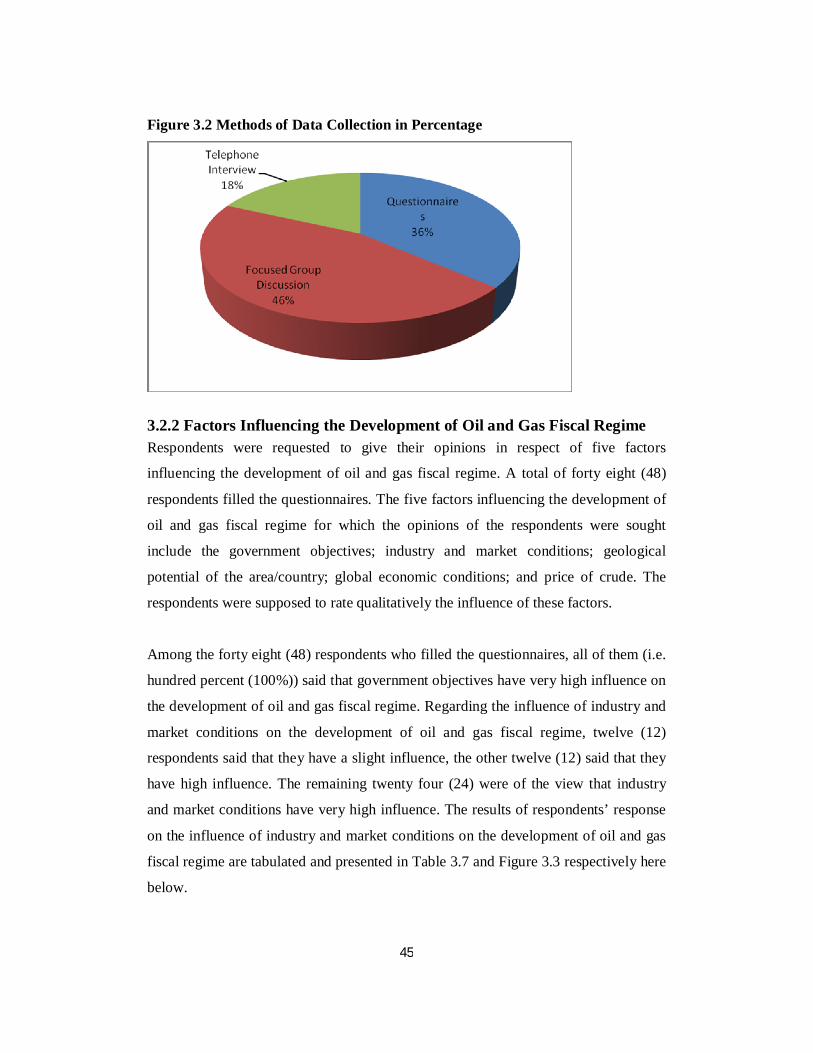

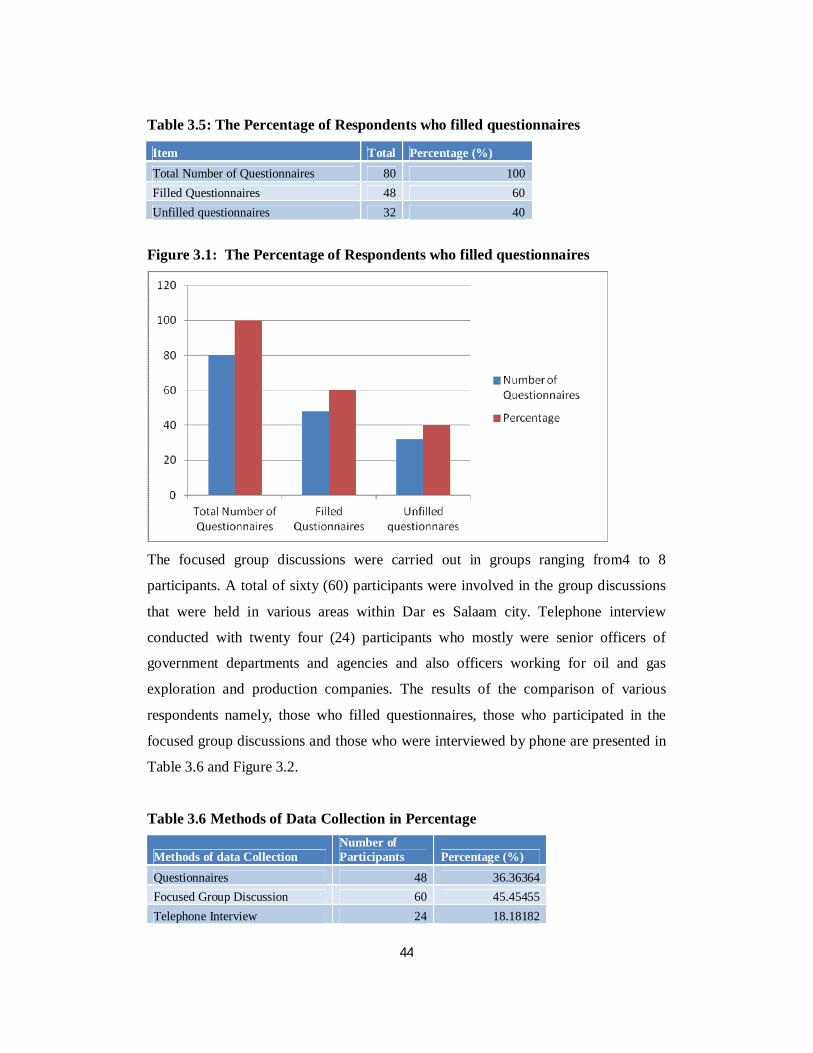

3.2.1 Analysis of Survey Methods ................................................................................ 43

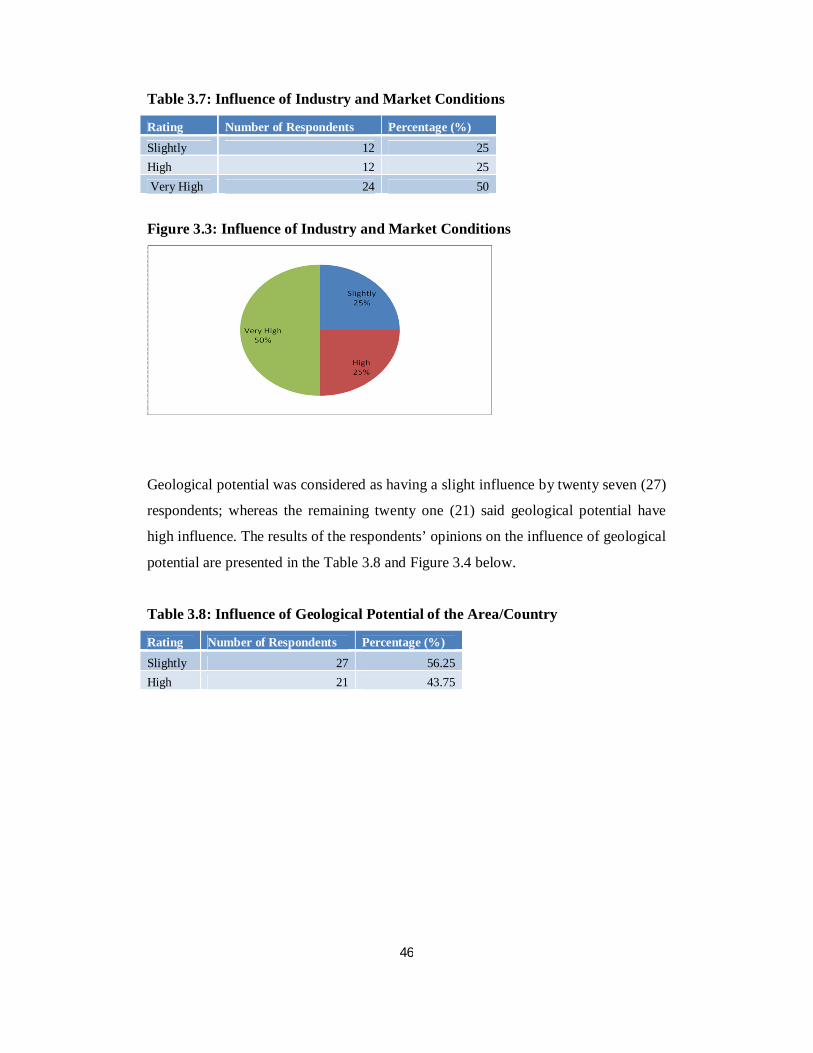

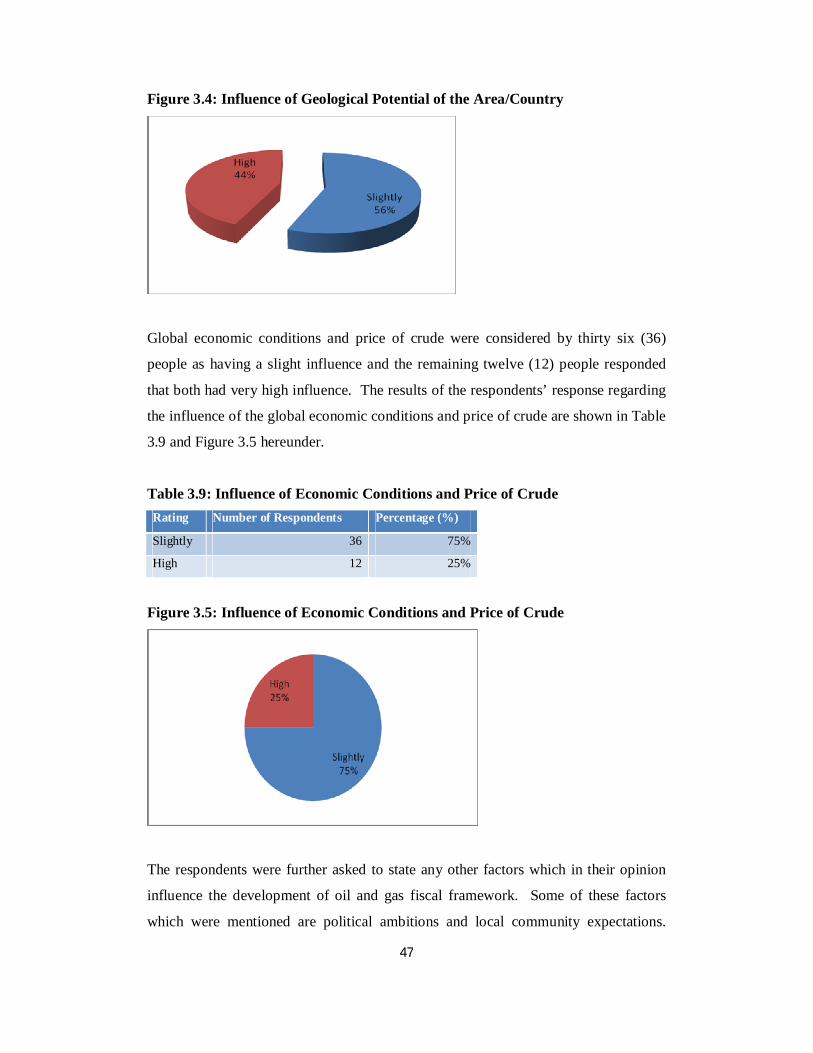

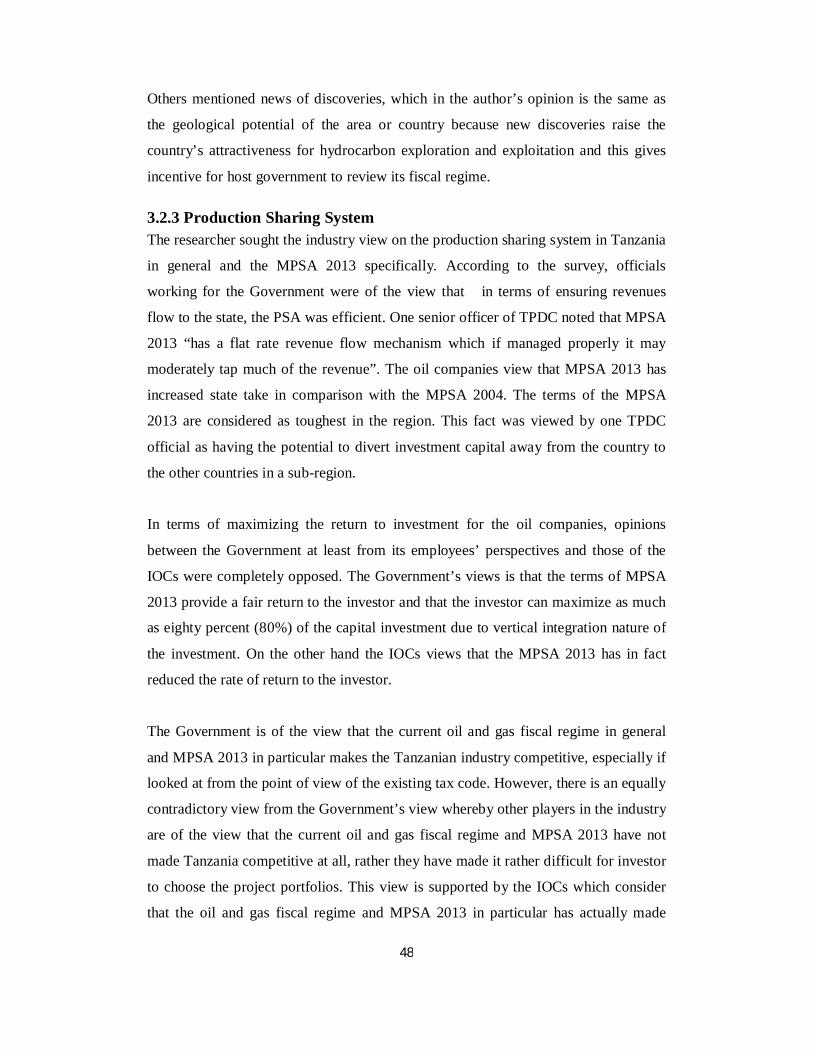

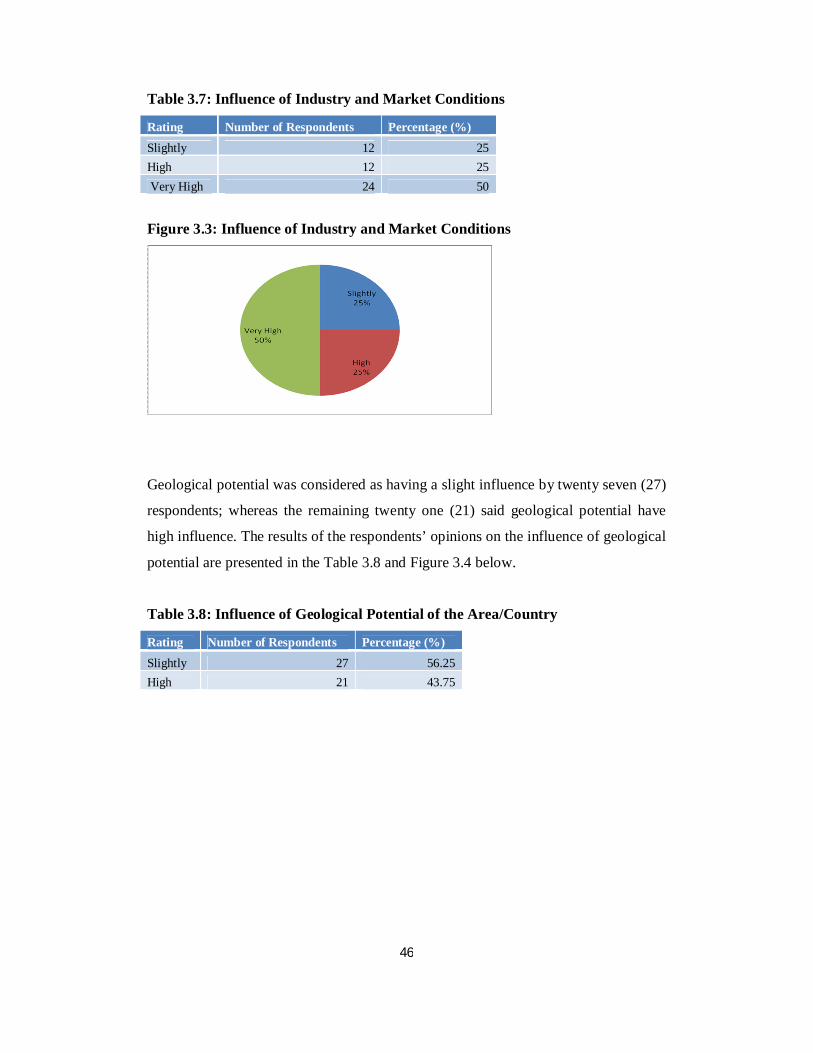

3.2.2 Factors Influencing the Development of Oil and Gas Fiscal Regime ..................... 45

3.2.3 Production Sharing System ................................................................................. 48

CHAPTER FOUR: ASSESSMENT OF THE SUSTAINABILITY OF THE PETROLEUM FISCAL REGIME IN TANZANIA ....................................................................................................................... 50

4.1 Objectives of the Government and the Investors 50

4.2 Measures Sustainability 53

4.2.1 Efficiency ............................................................................................................ 53

vi

4.2.2 Neutrality ........................................................................................................... 53

4.2.3 Equity ................................................................................................................. 54

4.2.4 Risk Sharing ........................................................................................................ 55

4.2.5 Stability............................................................................................................... 56

4.2.6 Clarity and simplicity ........................................................................................... 57

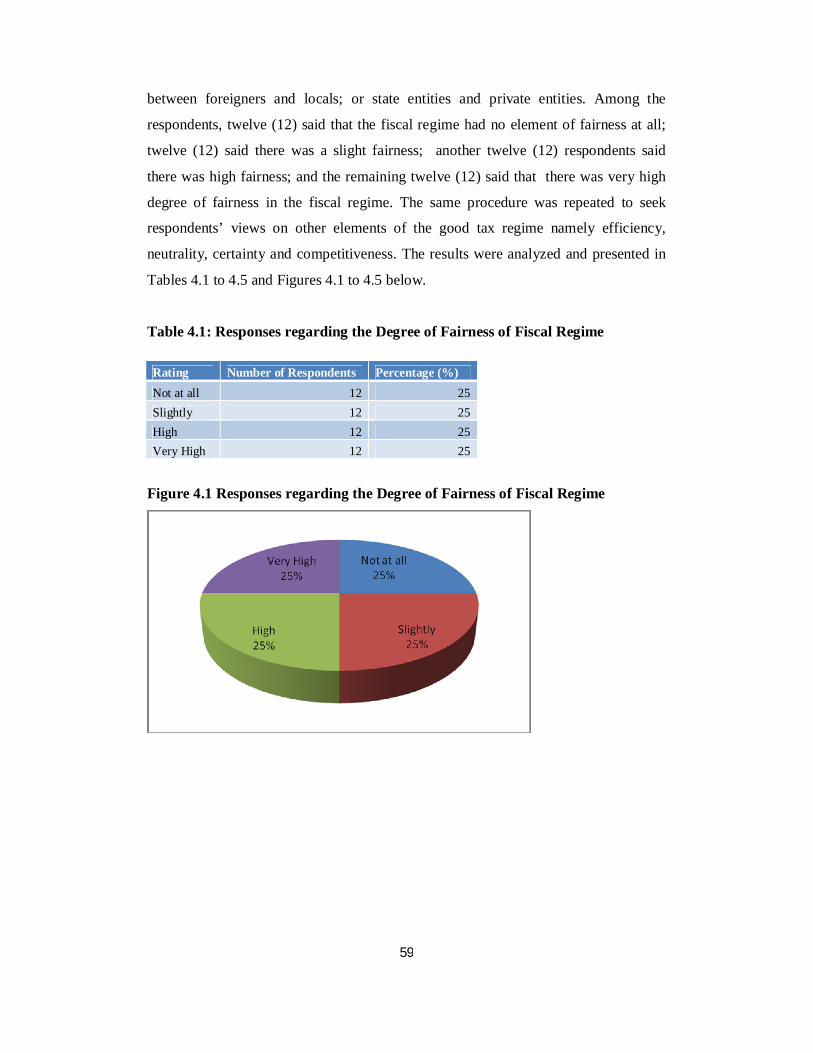

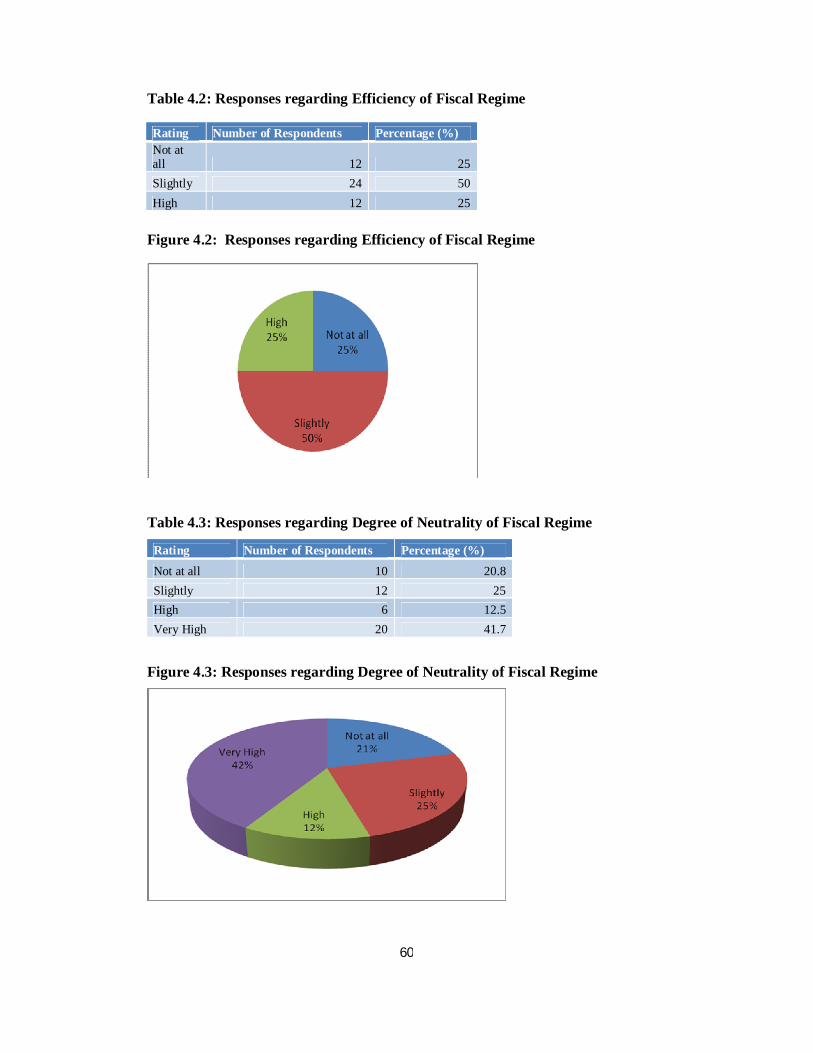

4.3 Perceptions on the Sustainability of the Current Fiscal Regime .............................. 58

CHAPTER FIVE: RECOMMENDATIONS .................................................................................. 62

5.1 Recommendations 62

5.1.1 Royalty ............................................................................................................... 62

5.1. 2 Cost Recovery Limit ............................................................................................ 63

5.1. 3 Additional Profit Tax .......................................................................................... 63

5.1. 4 Income Tax ........................................................................................................ 63

5.1. 5 Government Participation .................................................................................. 63

5.1. 6 Ring Fencing ....................................................................................................... 64

5.1. 7 Transfer Pricing Rules ......................................................................................... 64

5.1. 8 Bonuses ............................................................................................................. 64

5.2 Conclusion 64

Appendix I: Copy Right Declaration Form ............................................................................ 68

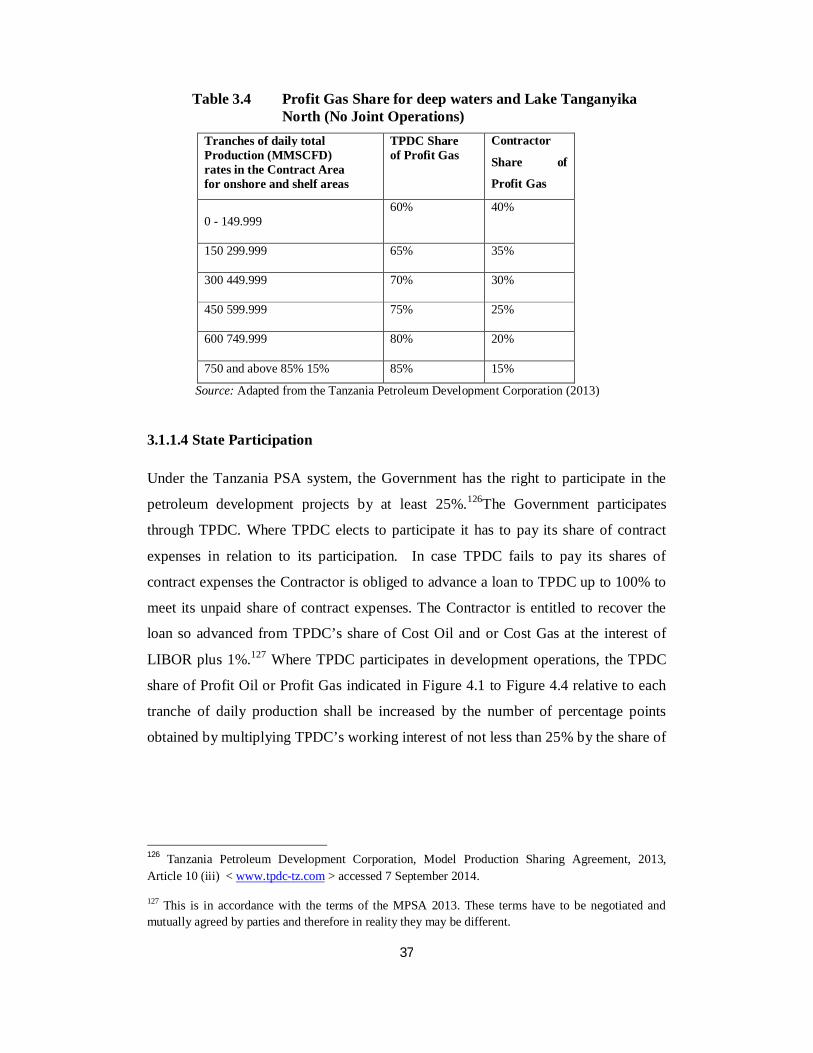

Appendix II: Electronic Document Submission Form ............................................................ 69

Appendix III: Dissertation Supervision Record ...................................................................... 70

BIBLIOGRAPHY .................................................................................................................... 71

vii

ABBREVIATIONS

AMT Alternative Minimum Tax

APT Additional Profit Tax

CIT Corporate Income Tax

DSE Dar es Salaam Stock Exchange

EWURA Energy and Water Utilities Regulatory Authority

FANCP First Accumulated Net Cash Position

GDP Gross Domestic Product

GNI Gross National Income

IOCs International Oil Companies

ITA Income Tax Act

MEM Ministry of Energy and Minerals

MPSA Model Production Sharing Agreement

PE Permanent Establishment

PSA Production Sharing Agreement

SANCP Second Accumulated Net Cash Position

SPSS Social Package for Social Sciences

TPDC Tanzania Petroleum Development Corporation

TRA Tanzania Revenue Authority

VAT Value Added Tax

viii

LIST OF STATUTES Financial laws (Miscellaneous Amendment) Act, 1997 Income Tax Act, 2004

Mining (Mineral Oil) Ordinance) 1958 Petroleum (Exploration and Production) Act, 1980

ix

LIST OF TABLES Table 2.1 Key Features between Concessionary System and Contractual

System.............................................................................................. 19

Table 2.2 The Differences between Concessionary Systems and Production

Sharing Contracts................................................................................21

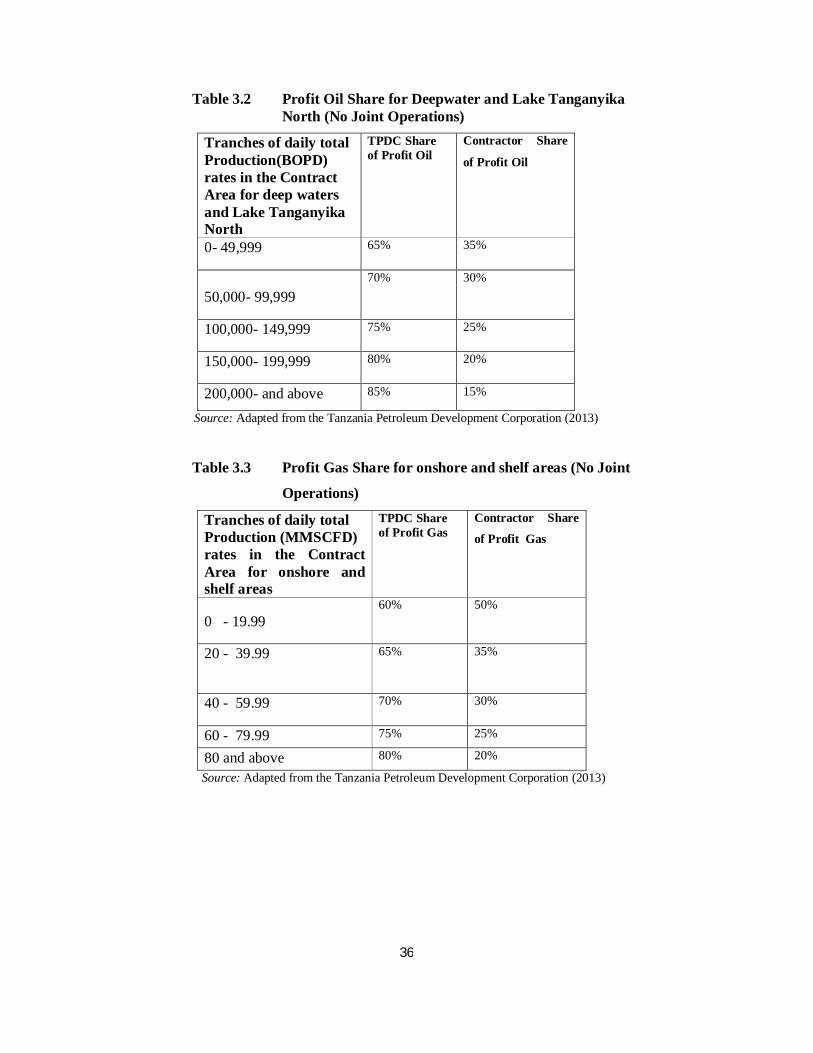

Table 3.1 Profit Oil Share for Onshore and Shelf areas (No Joint Operations)...35

Table 3.2 Profit Oil Share for Deepwater and Lake Tanganyika North (No Joint

Operations) .........................................................................................36

Table 3.3 Profit Gas Share for Onshore and Shelf areas (No Joint Operations)..36

Table 3.4 Profit Gas Share for Deepwater and Lake Tanganyika North (No Joint

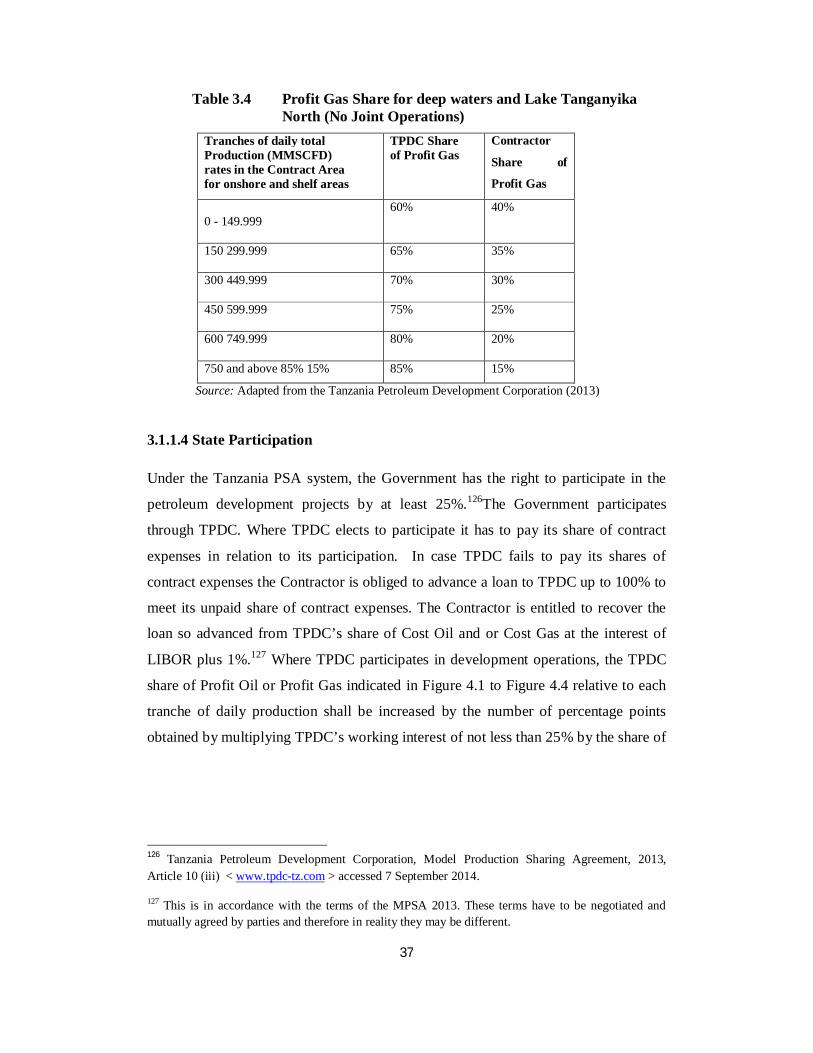

Operations)...........................................................................................37

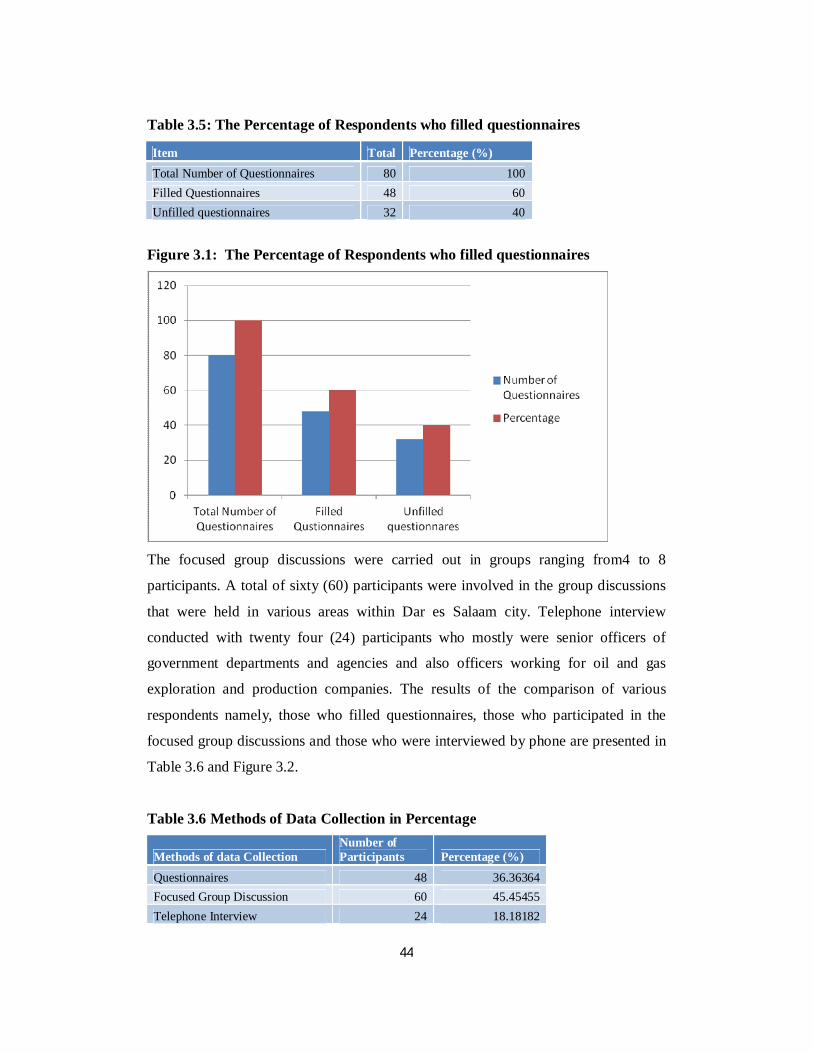

Table 3.5 The Percentage of Respondents who filled Questionnaire.................44

Table 3.6 Methods of Data Collection in Percentage..........................................44

Table 3.7 Influence of Industry and Market Conditions......................................46

Table 3.8 Influence of Geological Potential of the Area/Company....................46

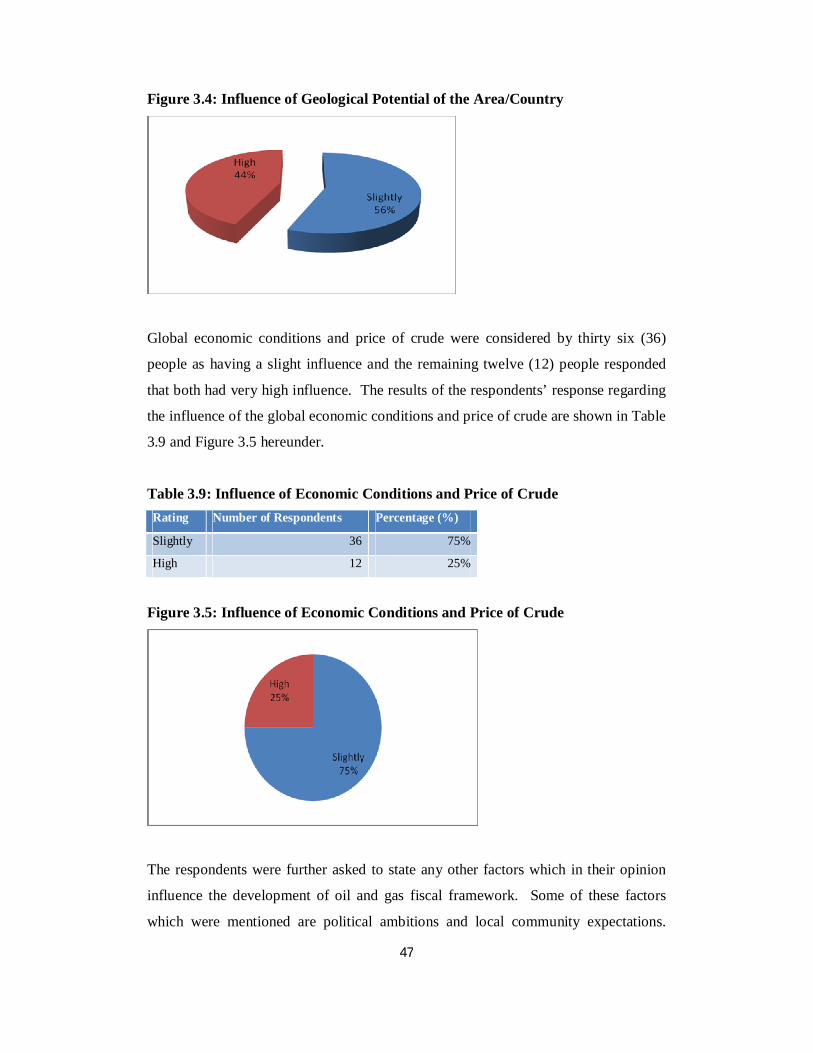

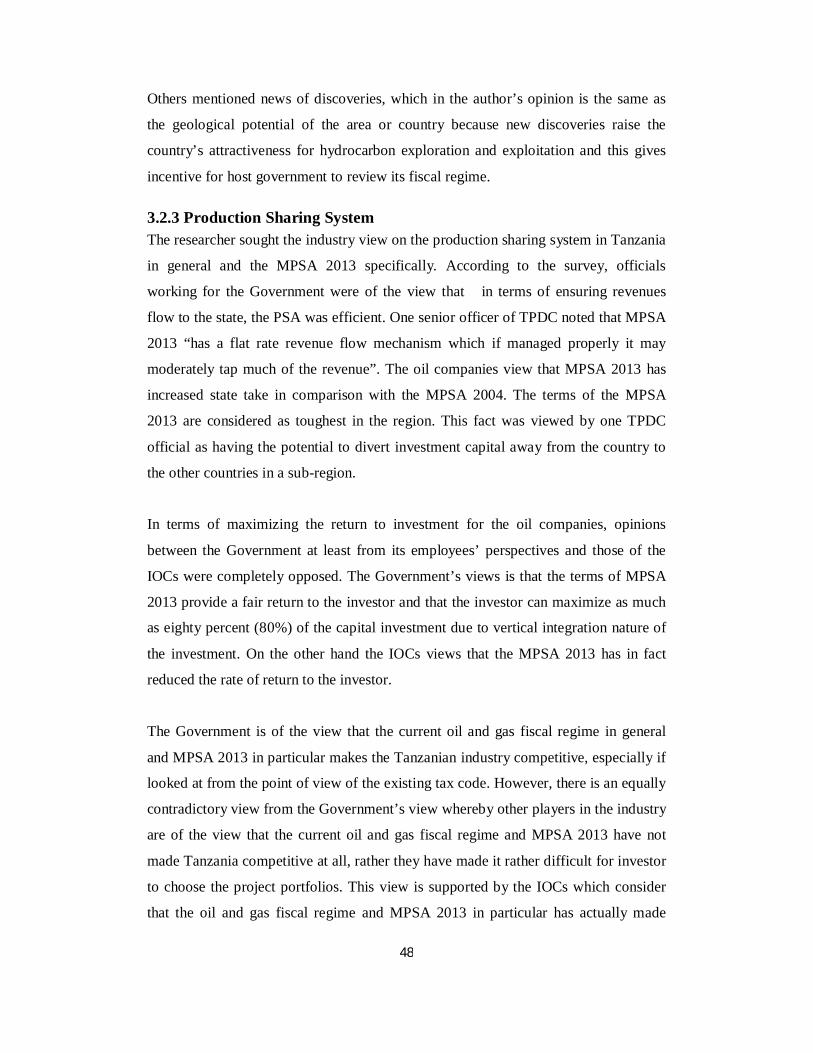

Table 3.9 Influence of Economic Conditions and Price of Crude.......................47

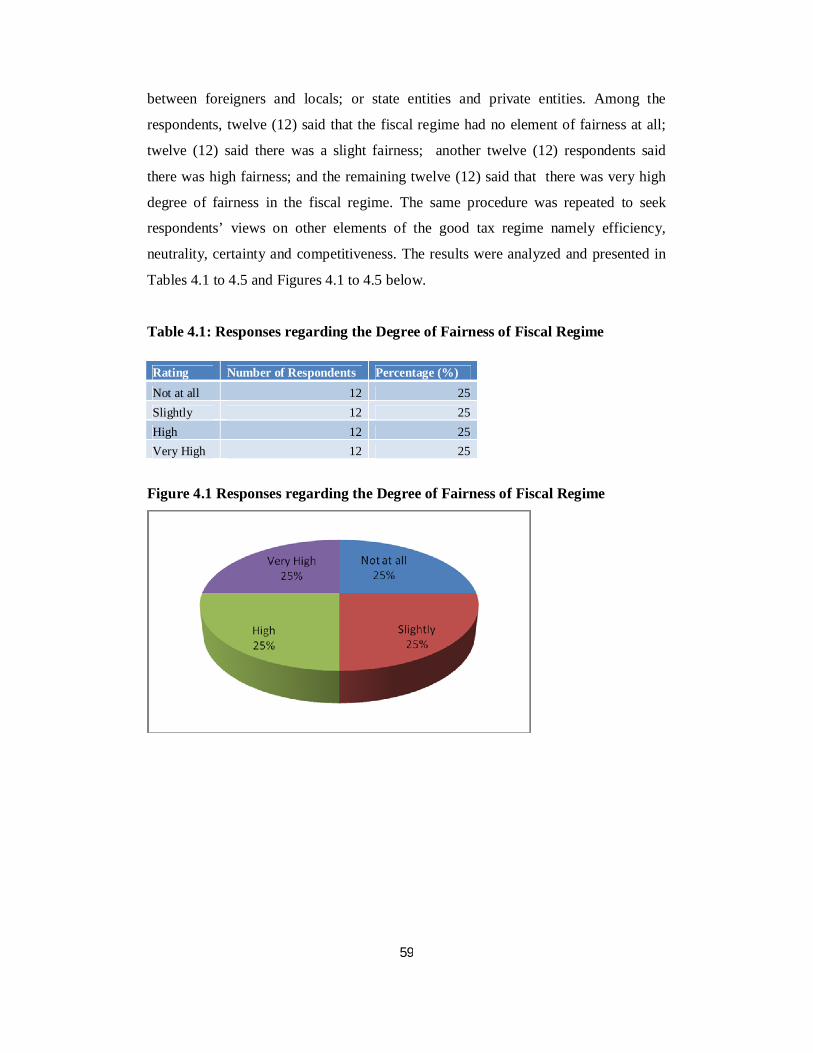

Table 4.1 Responses regarding the Degree of Fairness of Fiscal Regime..........52

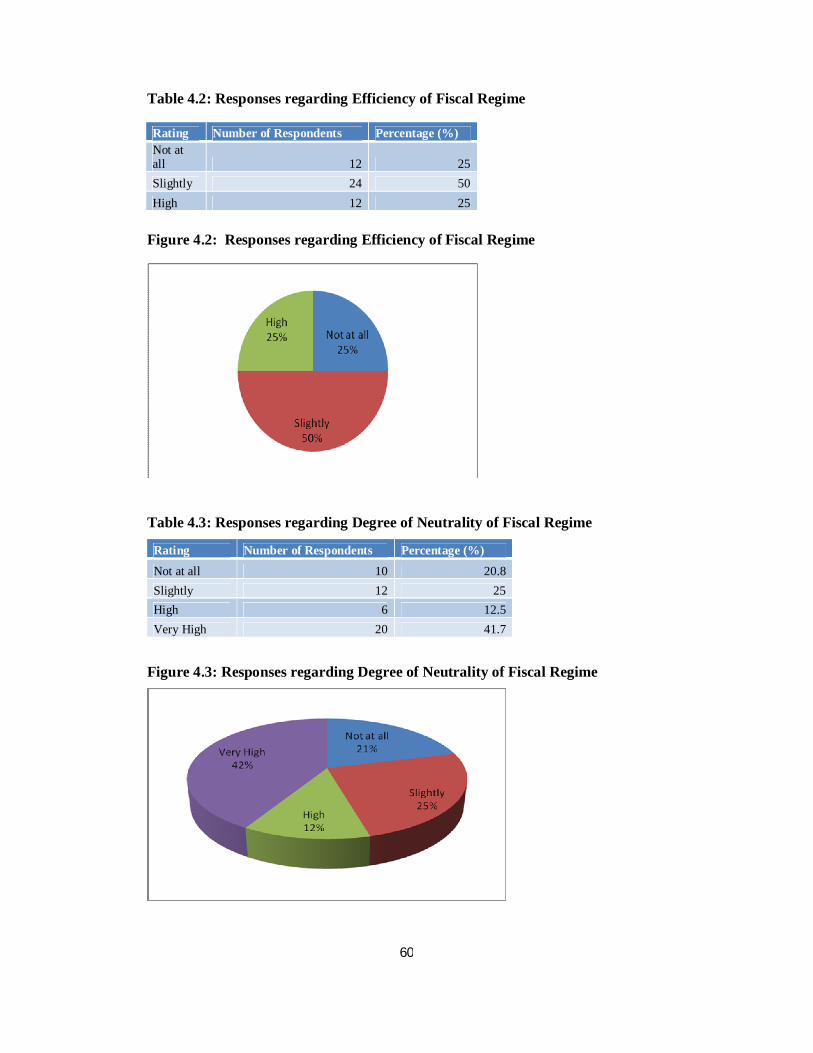

Table 4.2 Responses regarding the Efficiency of Fiscal Regimes......................60

Table 4.3 Responses regarding the Neutrality of Fiscal Regime........................60

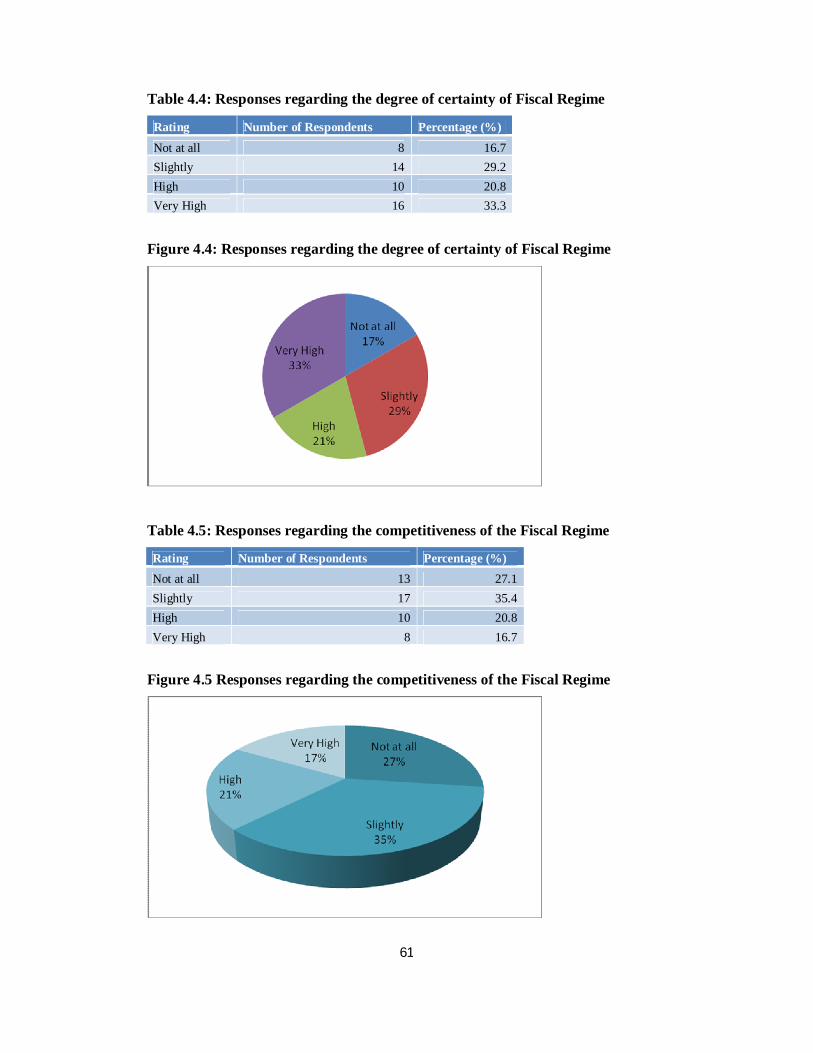

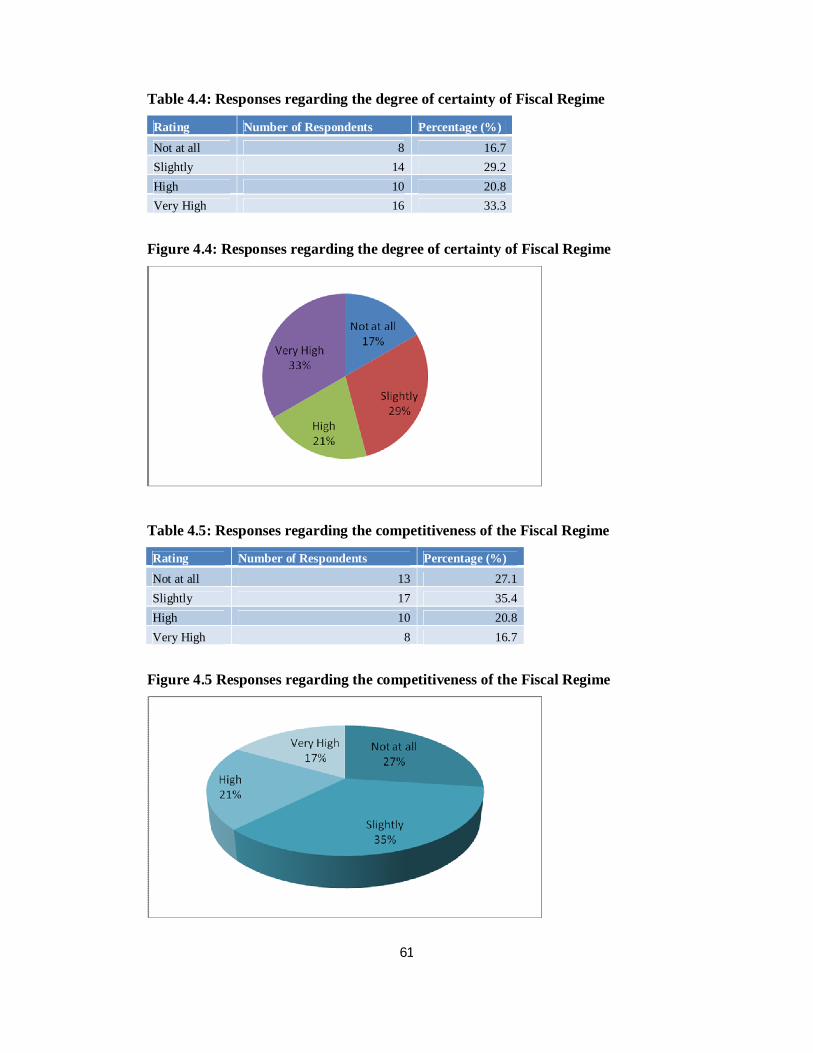

Table 4.4 Responses regarding the Degree of Certainty of Fiscal Regime........61

Table 4.5 Responses regarding the Competitiveness of Fiscal Regime..............61

x

LIST OF FIGURES Figure 1.1 The Map of Tanzania........................................................................2

Figure 2.1 Classifications of Petroleum Fiscal Regimes...................................16

Figure 2.2 Incremental Sliding Scale Royalty...................................................24

Figure 2.3 Slab Sliding Scale Royalty..............................................................25

Figure 3.1 The Percentage of Respondents who filled Questionnaire.................................44

Figure 3.2 Methods of Data Collection in Percentage......................................45

Figure 3.3 Influence of Industry and Market Conditions.................................46

Figure 3.4 Influence of Geological Potential of the Area/Company................47

Figure 3.5 Influence of Economic Conditions and Price of Crude...................47

Figure 4.1 Responses regarding the Degree of Fairness of Fiscal Regime......52

Figure 4.2 Responses regarding the Efficiency of Fiscal Regimes..................60

Figure 4.3 Responses regarding the Neutrality of Fiscal Regime....................60

Figure 4.4 Responses regarding the Degree of Certainty of Fiscal Regime....61

Figure 4.5 Responses regarding the Competitiveness of Fiscal Regime..........61

1

CHAPTER ONE: INTRODUCTION

1.1 Background The oil and gas exploration in Tanzania started in early 1950s1. The exploration

activities have continued in the country since then with the first commercial natural

gas discovery being made at Songo Songo Island in 1973. The second natural gas

discovery was made at Mnazi bay in 1982.2 More gas discoveries were made from

2010 to 2012 especially in the deepwater in the Indian Ocean and up to now a total of

50.5trillion cubic feet of natural gas have been discovered in Tanzania.3 Commercial

gas production in Tanzania started in 2004 at Songo Songo Island and in 2006 at

Mnazi bay gas fields. Despite, the long history of oil and gas exploration in Tanzania

no research has ever been carried out in the field of oil and gas fiscal regime.

Therefore, this study has a special significance in that it is a pioneer study.

This Chapter basically introduces the subject of the study. It is divided into eight main

sections namely: background to the study, statement of the problem and objectives of

the study and research questions. The other sections are the scope of the study, the

rationale or significance of the study; limitations to the study and methodology. At

this juncture, the detailed discussion for the abovementioned is in order.

1.2 Overview of Tanzania

1.2.1 History Tanzania is a United Republic which came into existence on 26th April 1964 as a

result of the Union between the Republic of Tanganyika and the People Republic of

Zanzibar. The Republic of Tanganyika got its independence from Britain on 9th

December 1961 and Zanzibar became independent following a revolution which

overthrew the Oman Sultanate on 12th January 1964.4 Tanzania covers an area of

1 See at< http://www.tpdc-tz.com/exploration_history.htm >accessed 7 September 2014.

2 Ibid.

3 This is in accordance to the recent report of the Tanzania Petroleum Development Corporation.

4 Anthony Clayton, ‘The Zanzibar Revolution and its Aftermath’ (1983) 53(4), Africa: Journal of International African Institute, 98-100.

2

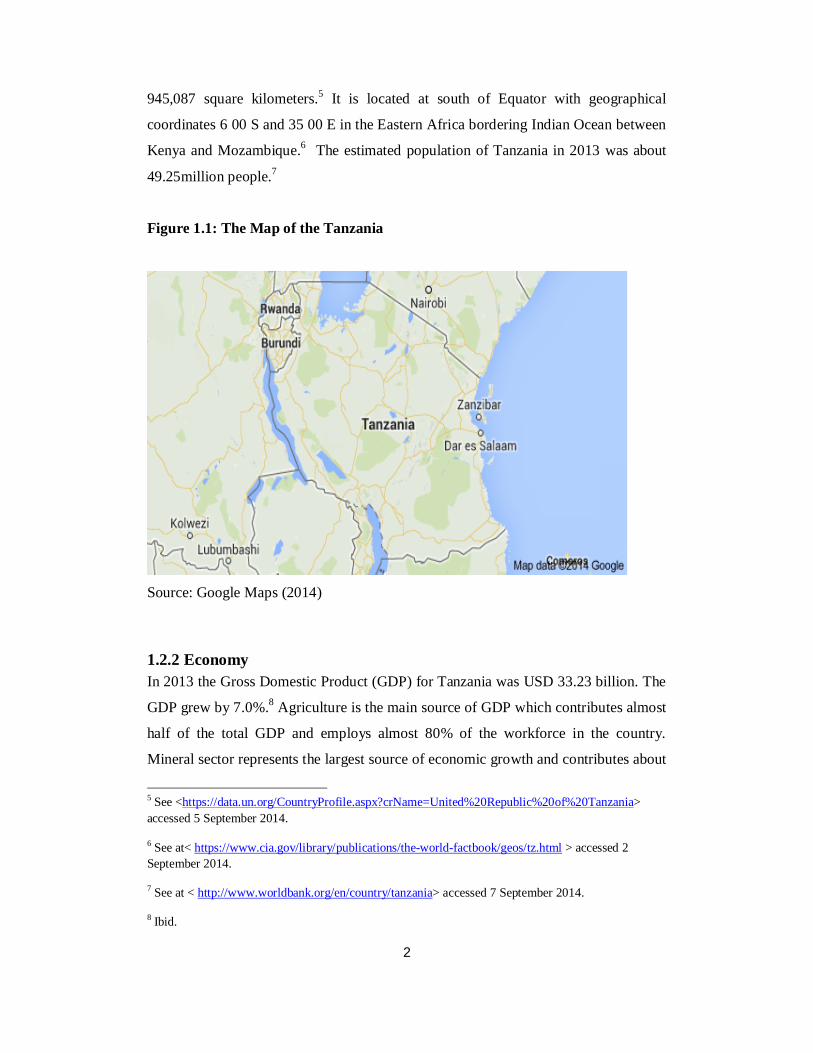

945,087 square kilometers.5 It is located at south of Equator with geographical

coordinates 6 00 S and 35 00 E in the Eastern Africa bordering Indian Ocean between

Kenya and Mozambique.6 The estimated population of Tanzania in 2013 was about

49.25million people.7

Figure 1.1: The Map of the Tanzania

Source: Google Maps (2014)

1.2.2 Economy In 2013 the Gross Domestic Product (GDP) for Tanzania was USD 33.23 billion. The

GDP grew by 7.0%.8 Agriculture is the main source of GDP which contributes almost

half of the total GDP and employs almost 80% of the workforce in the country.

Mineral sector represents the largest source of economic growth and contributes about

5 See <https://data.un.org/CountryProfile.aspx?crName=United%20Republic%20of%20Tanzania> accessed 5 September 2014.

6 See at< https://www.cia.gov/library/publications/the-world-factbook/geos/tz.html > accessed 2 September 2014.

7 See at < http://www.worldbank.org/en/country/tanzania> accessed 7 September 2014.

8 Ibid.

3

3% of the GPD.9 According to the National Bureau of Statistics of Tanzania the

Annual Headline Inflation Rate for the month of July, 2014 increased slightly to 6.5%

from 6.4% in June, 2014.10 The Gross National Income (GNI) per Capital is USD

1,702.12.11

1.2.3 Petroleum Exploration History The oil and gas industry in Tanzania is still emerging12, however following the huge

natural gas discoveries since 2010, there have been rapid developments in the

industry. Currently, it is estimated that the discovered natural gas in place in Tanzania

is 50.5 trillion cubic feet (TCF)13. This has necessitated the existing oil and gas

exploration companies together with the Government of Tanzania to embark on the

construction of a Liquefied Natural Gas (LNG) Project to commercialize the huge gas

discoveries.14

On the other hand, the significant natural gas discoveries have raised concerns among

industry participants with respect to robustness and effectiveness of the oil and gas

legal and regulatory framework vis a vis the rapid developments in the industry. In

response to these concerns, the Government has started to carry out legal and

regulatory reforms which are necessary to cope with the new and rapid development

in the oil and gas industry. In this regard, the Government has promulgated for the

first time the Natural Gas Policy 2013 with the principal objective of providing

guidance for the sustainable development and utilization of the natural gas resource in

9 See at < http://www.tanzaniainvest.com/economy > accessed 6 September 2014.

10 See ‘Tanzania Inflation Increases to 6.5% in July 2014’ <http://www.tanzaniainvest.com/economy/news/1218-tanzania-inflation-increases-to-65-in-july-2014-> accessed 2 August 2014.

11 United Nations Development Programme, Human Development Reports, < http://hdr.undp.org/en/countries/profiles/TZA > accessed 15 September 2014.

12 Ombeni Sefue, ‘Toward a Gas Economy in Tanzania’ < http://naturalresourcecharter.org/sites/default/files/Ombeni%20Sefue_0.pdf > accessed 7 August 2014.

13 See ‘I will be the last to lead an impoverished Tanzania – JK’ The Guardian, 7th August 2014. 14 Brian Cassidy and Steven Fox, ‘East Africa: from niche play to key LNG Suppliers?’ (April 2014), Vol.81, Issue 3, Petroleum Economist.

4

the country.15 The Government has also prepared a Gas Utilization Master Plan16 with

major use of natural being focused on power generation.17

At the time of writing this report, the Government is developing an Upstream

Petroleum Policy of 2014 whose major objective is to set out legal and regulatory

framework for exploration, production and utilization of the country’s petroleum

resources in an effective and efficient manner.18 Besides, the Government is also

developing the Local Content Policy 2014 in order to promote participation of

Tanzanians into the oil and gas industry, transfer of technology and ensure the oil and

gas industry development benefits other sectors of the economy in the country.19 The

Gas Act Bill has also been drafted and is ready for tabling to the Parliament before

the end of the year 2014 for deliberations and enactment. The amendments of the

upstream petroleum legislation, the Petroleum (Exploration and Production) Act of

1980 (hereinafter called the PEPA) are also in the final stages and interestingly the

author is a member to one of the Government Committee which is tasked with

preparing the amendment proposals.

In October 25, 2013 the Government of the United Republic of Tanzania launched its

4th Licensing round whereby the Model Production Sharing Agreement (MPSA) 2013

15 The United Republic of Tanzania, The National Natural Gas Policy, 2013 < http://www.tanzania.go.tz/egov_uploads/documents/Natural_Gas_Policy_-_Approved_sw.pdf > accessed 7 August 2014.

16 Christopher B. Strong (ed.) (2013), ‘The Oil and Gas Law Review’ Law Business Research Limited p.244.

17 The United Republic of Tanzania, ‘Power System Master Plan 2012 Update’ < http://www.google.co.tz/url?sa=t&rct=j&q=&esrc=s&frm=1&source=web&cd=1&ved=0CBsQFjAA&url=http%3A%2F%2Fwww.tanesco.co.tz%2Findex.php%3Foption%3Dcom_docman%26task%3Ddoc_download%26gid%3D68%26Itemid%3D172&ei=Q4bjU_Z2qaHRBb3sgRA&usg=AFQjCNEg6xTNJJ2b8KSGVWD_itOiUX-Faw&bvm=bv.72676100,d.d2k > accessed 7 August 2014

18 The United Republic of Tanzania, The National Petroleum Policy of Tanzania (Draft 2, April 2014) < http://www.tpdc-tz.com/National%20Petroleum%20Policy.pdf > accessed 7 August 2014.

19 The United republic of Tanzania, Local Content Policy of Tanzania for Oil and Gas Industry 2014 (Draft I)’ < http://www.mem.go.tz/wp-content/uploads/2014/05/07.05.2014local-content-policy-of-tanzania-for-oil-gas-industry.pdf > accessed 21 June 2014.

5

became effective. The terms of MPSA 2013 are considered as tough by the industry20

in comparison with the preceding MPSAs namely MPSA 2004 and MPSA 3008.

However, the Government views that the new MPSA 2013 terms are fair and

equitable because in the Government views they reflect the changed geological

potential of the country. Under the MPSA 2013 the Government aims at maximizing

its revenue and at the same time ensuring that the industry remains competitiveness in

region.21

The current MPSA 2013 is the sixth version22 in Tanzania since the commencement

of the oil and gas exploration in the country in early 1950s.23 BP and Shell started

petroleum exploration in Tanzania (then Tanganyika territory) in 1952 under the

concession agreement with the government based on the Mining (Mineral Oil)

Ordinance, CAP. 39924. BP and Shell held exploration acreage along the Coastal

Basin including the islands of Zanzibar, Pemba and Mafia.25 The licensees carried out

geological and geophysical surveys which however did not lead to any commercial

20 Tanzania outlines new oil and gas production terms, Reuters, Monday 4 November 2013 < http://www.reuters.com/article/2013/11/04/tanzania-energy-idUSL5N0IP37820131104 > accessed 6 August 2014.

21 The East African region, covering Uganda, Kenya, Tanzania and Mozambique in this case is a hotspot for hydrocarbon exploration particularly following significant oil discoveries in Uganda and Kenya and natural gas discoveries in Mozambique and Tanzania / these countries.

22 The previous version of Model Production Agreements (MPSAs) were the 1989, 1995, 2000, 2004 and 2008. The discussion on these Model PSAs is outside the scope of this study.

23Tanzania Petroleum Development Corporation, ‘Exploration History’ < http://www.tpdc-tz.com/exploration_history.htm > accessed 15 August 2014.

24 This Act was repealed by the Petroleum (Exploration and Production) Act, 1980.

25Yona S. M. Killagane, ‘Tanzania’s Model Production Sharing Agreement’

<http://www.google.co.uk/url?sa=t&rct=j&q=&esrc=s&source=web&cd=10&ved=0CGwQFjAJ&url=http%3A%2F%2Fwww.energy.eac.int%2Feapc2005%2Fpdfs%2Fconfrence%2520proceedings%2FCountry%2520Presentations%2FTanzania%2FModel%2520Production%2520Sharing%2520Agreement%2520%2520Mr.%2520Yona%2520Killagane.pdf&ei=vZ0QVJWPH4iXaoT9gegG&usg=AFQjCNEu5ivHTpba-xR40UzzZ_-GKgfWqg&sig2=Y9yHaKjRuQqDa2toL9Dy0Q&bvm=bv.74649129,d.d2s> accessed 2 August 2014.

6

discoveries and as a result the concession was relinquished in 1964.26 AGIP

negotiated a service agreement with the Tanzania Government for the whole area

relinquished by BP/Shell. The service agreement was amended in 1970 to

accommodate TPDC through the first Production Sharing Agreement.27 In 1973,

AGIP SpA made the first natural gas discoveries in Songo Songo Island.28 The

enactment of the PEPA and increase in the oil prices prompted the increased

exploration activity in the country especially in 1980 to 1991 resulting gas discovery

at Mnazi bay.29

The first offshore licensing round was launched in September 2000 whereby six

deepwater blocks were put up for bids. Three companies submitted their bids and after

successful negotiations, block 6 was awarded to Brazil’s Petrobas and a

corresponding PSA was signed with the Government and TPDC in April 2001.30 The

second bid was launched in June 2001 in which eleven blocks were on offer.31

Following the second bidding round, TPDC received two bids and after successfully

negotiations four PSAs for blocks 9, 10, 11 and 12 were all executed with Shell

International in September 2002.32 The third bidding round which was launched in

2004 was more successful that the previous rounds. Between 2005 and 2007, block 5

was awarded to Petrobras, block 2 to Staoil and blocks 1, 3 and 4 were awarded to

Ophir Energy. Besides, block 8 and block 7 were awarded in 2011 and 2007 to

26 David Ledesma, ‘East Africa Gas-Potential for Export’ (March, 2013), The Oxford Institute for Energy Studies p. 12.

27 Yona S.M. Killagane (n 25) 4.

28 Tanzania Petroleum Development Corporation, ‘Exploration History’ < http://www.tpdc-tz.com/tpdc/directorate/exploration/Exploration_History.php > accessed 16 August 2014.

29 David Ledesma (n 26) p. 12.

30 GEO ExPro, ‘New Offshore Licensing Round for Tanzania’ < http://www.geoexpro.com/articles/2012/10/new-offshore-licensing-round-for-tanzania > accessed 15 August 2014.

31 Ibid.

32 David Ledesma (n 26) p. 12.

7

Petrobras and Dominion Petroleum respectively.33 The 4th Offshore Licensing

Round34 was launched on 23rd October 2013 and TPDC received four bids from the

following companies: China National Offshore Oil Corporation (CNOOC) (Block

4/3A); ExxonMobil and Statoil consortium (Block 4/3A); Gazprom (Block 4/3B); and

Mubadala (Block 4/2A); and RAKGas LLC (Lake Tanganyika).35

It is generally argued that there had been a success in the subsequent rounds since the

first offshore round in 2000. Until 2013, Tanzania in particular and the East African

region generally became a hydrocarbon hotspot. Therefore it was expected that the 4th

Licensing Round would attract a lot of interests form IOCs. However, the results

have been disappointing. At the time of writing this Report, the Government

Negotiation Team is meeting with CNOOC and RAGas LLC for the negotiation of

the PSAs in respect of the Blocks for which bids were submitted. Gazprom withdrew

from the bid before the opening a ExxonMobil and Statoil consortium and Mubadala

bids were according to a senior TPDC officer, way below the bidding thresholds and

so they were both disqualified. It is questionable if the current petroleum fiscal regime

is sustainable and thus balances the interests of the Government and the interests of

the investors.

1.3 Statement of the Problem Following huge natural gas discoveries in the country particularly commencing in

2010, the Government of the United Republic of Tanzania has taken various steps to

address the oil and gas legal framework which is thought to be not comprehensive

enough. The Government has also adopted measures to ensure the management and

administration of the discovered natural gas resources for the benefit of the entire 33 GEO ExPro (n 30) p.12.

34 Seven (7) Deep Sea Offshore Blocks and the Lake Tanganyika North Offshore Block have been offered under this bid. These blocks are seven deepsea blocks (Blocks 4/2A, 4/3A, 4/3B, 4/4A, 4/4B, 4/5A, 4/5B) with an average size of 3000 sq. km and with a water depth of between 2000m to 3000m, and the North Lake Tanganyika block. See at < http://www.tz-licensing-round.com > accessed 15 August 2014.

35 Leigh Elston, ‘Five groups bid in Tanzania’s fourth licensing round’ Natural Gas Daily 15 May 2014 < http://interfaxenergy.com/gasdaily/article/8177/five-groups-bid-in-tanzanias-fourth-licensing-round > accessed 22 September 2014.

8

Tanzanian society. These measures include the promulgation of the Natural Gas

Policy 2013, the adoption of the Gas utilization Master Plan and the MPSA 2013.

The terms of the current MPSA 2013 applicable in Tanzania petroleum industry

which can in force on 23rd October 2013 are considered as relatively tough from the

investor’s point of view as compared to previous MPSAs such as MPSA 1995, MPSA

2004, and MPSA 2008. There have been a total of four bids since the launching of the

first licensing round for deepwater in 2000. In contrast with the previous bids, the 4th

Bidding Round has been launched in Tanzania against the backdrop that the country

has been a hotspot for hydrocarbon exploration and productions. This has been largely

due to the huge discoveries of hydrocarbons in the country and in the neighbouring

countries. Therefore, it would be expected that the response of the oil and gas

exploration and production would be significantly higher in the 4th Bidding round

than in the previous bids. However, the reality seems to be quite different and this

study will explain why that is the case.

The efficiency of the new oil and gas fiscal regime is yet to be tested. It remains to be

seen how this fiscal regime will balance, as it should, the interests of the government

and those of the investors. Inefficient tax has distortionary effect to the economy, i.e.

it disincetivizes the development of marginal fields and exploration of new deposits; it

leads to premature abandonment of the fields; changes the depletion rate; and may

encourage oil companies to resort to tax avoidance.36 A good fiscal regime needs to

be simple to understand and to administer otherwise it may induce manipulation.37

The aim of this study was to find out how the current oil and gas fiscal regime

balances the achievement of the government above objectives and interests and the

interests of the investors.

36 Alexander G. Kemp, ‘Economic Consideration in the taxation of petroleum exploitation’ from Kameel I.F. Khan (ed.), Petroleum Resources and development: economic, legal and policy issues for developing countries (Belhaven Press, 1987) 121.

37 A. Ogunlade, ‘How Can Government Best Achieve its Objectives for Petroleum Development: Taxation and Regulation or State Participation?’ (2010) 8(4) OGEL < www.ogel.org > accessed 23 June 2014.

9

1.4 Research Questions

1.4.1 Main Question This main question for this study was to seek an answer for the following main

question:

How the current oil and gas fiscal regime balances the government objectives and

interests and the interests of the investors in the petroleum industry?

1.4.1 Specific Questions The specific research questions of this study were as stated here below:

i) What are the features of the oil and gas fiscal regime?

ii) What are the objectives of the government and the investors in the

petroleum industry?

iii) How does the current oil and gas fiscal regime help the government to

achieve its objectives and promote the interests of the investors in the

petroleum industry?

iv) What are the perceptions of the industry in respect to the current oil and

gas fiscal regime?

1.5 Objectives of the Research

1.5.1 Main Objective The main objective of the research was to find out how the current oil and gas fiscal

regime balances the government objectives and interests in the petroleum industry and

the interests of the investors.

1.5.2 Specific Objectives The research has the following specific objectives:

i) To identify features and discuss the oil and gas fiscal regime in Tanzania.

ii) To identify and discuss the objectives of the government and the investors

in the petroleum industry.

10

iii) To find out how does the current oil and gas fiscal regime helps the

government to achieve its objectives and promote the interests of the

investors in the petroleum industry.

iv) To carry out a survey of and discuss the perceptions of the industry in

respect to the current oil and gas fiscal regime.

1.6 Significance of the Study In this study, an assessment is made on how the current oil and gas fiscal regime

balances the government objectives and interests and the interest of the investors in

the petroleum industry. Besides, the study also describes the features of the current oil

and gas fiscal regime in Tanzania and discusses the perceptions of the industry in

respect with the existing fiscal regimes with the focus on the MPSA 2013. It is hoped

that this study will be useful for both individuals and organizations in the following

ways:

i) It will help policy makers and industry regulators to appreciate weakness

existing in the oil and gas fiscal regime;

ii) It will help future researchers to identify gaps which requires future

research;

iii) Due to very low level of local studies in the subject, it will be used as an

essential empirical reference for future researchers; and

iv) It will enable the researcher to fulfil the requirement for the degree of MSc

Oil and Gas law of the University of Robert Gordon.

1.7 Scope of the Study This study was undertaken in Tanzania. The data for the research were collected in

Dar es Salaam city from the oil and gas industry regulators, tax authorities, national

oil companies and other oil and gas companies. Due to resources limitations, data

were collected from a targeted sample of 132 participants.

1.8 Limitations to the Study Every research is subject to limitations specific to its setting. In course of this study,

the researcher encountered a number of constraints which affected the outcome of the

11

study. These constraints are stated and discussed in the subsequent paragraphs.

Nevertheless, it is the researcher’s belief that such limitations did not affect the

validity and reliability of the findings of the study.

1.8.1 Limited Resources The researcher had little fund necessary for carrying out the study, such as meeting

the costs to reach many respondents physically or through telephone interview. Other

resources constraints were the shortage of time for research. This study had to be

accomplished within the period of not more than four months. However, the

researcher countervailed the time constraints by adhering to the time schedule and by

ensuring the full utilization of the short time available.

1.8.2 Access to Confidential Information It is quite common in the oil and gas industry for participants to enter into

confidentiality agreements to protect commercially sensitive information. In order to

countervail this situation, a researcher had to get official authorizations to be able to

access the data for the research from various entities such as the Tanzania Revenue

Authority (TRA), the Ministry of Energy and Minerals (MEM), TPDC, non-

government organizations and oil and gas companies. For those respondents who

were hesitant to give their opinions on the information which were in the public

domain, the researcher explained to them that such information was not protected by

confidentiality agreements. This enabled the researcher to win the confidence of the

respondents and thus get the access to such information.

1.8.3 Lack of Cooperation from Respondents The researcher encountered difficulties in getting people to agree to participate in the

study. Some turned down the interview on the ground that there were not

knowledgeable enough in the subject. Others received the questionnaire but never

turned up with a filled questionnaire. Other respondents said that since they were not

public relations officers so they would not respond.

1.8.4 Delimitation of the Research This research was restricted to individuals who are working in the oil and gas industry

mainly officers working for the Government and Government agencies, local and

international oil and gas exploration companies. The study also involved employees

12

of oil and gas companies operating in Tanzania upstream sector. The group of people

was targeted because the researcher believes that they have the necessary information

sought for the research. The Dar es Salaam region was chosen as a focus of research

since it is the centre from which all oil and gas exploration and production companies

operate. Besides, Dar es Salaam is also a location where the researcher works and

lives and thus it was thought to be a logistically convenient location for data

collection and report writing.

1.9 Methodology

1.9.1 Population The population of the study comprised of all individuals working in oil and gas

industry based in Dar es Salaam region in Tanzania. In particular, these included

employees of the Ministry of Energy and Minerals (MEM), TPDC, TRA, Energy and

Water Utilities Regulatory Authority (EWURA) and oil and gas exploration

companies.

1.9.2 Sample Size and Sampling Technique The questionnaires were distributed to targeted individuals, telephone interviews were

also carried out and focused group discussions were also held. In case of the focused

group discussion, the group ranged between 4 to 8 participants with the researcher as

a moderator of the discussion. There were a total of 48 respondents who responded to

the by filling a questionnaire. Purposive sampling (i.e. non-probability sampling) was

employed in the collection of data for the study. Individuals with special knowledge

in the subject were targeted for interview. This sampling technique was chosen since

the researcher believed that it was the most appropriate to obtain data which required

specialized knowledge of the industry.

1.9.3 Types of Data and Collection Methods The primary data were collected through interview, focus group discussions and

questionnaires. The data which was collected was firsthand data that no one has

access to it before. This was mainly because the data were given by individuals who

had firsthand experience. Secondary data were collected by the review of various

documents and publications that were reviewed by the researcher. These documents

included books, reports, magazines, journals and empirical reports. These documents

13

were accessed from TPDC, MEM, TRA, EWURA and from the University of Robert

Gordon and the University of Dar es Salaam libraries. Other documents included

reports which were availed to the researcher from oil and gas companies operating in

Tanzania upstream petroleum sector. The researcher also accessed some information

by use of the internet.

1.9.4 Data Processing and Analysis Methods After the collection of raw data, the researcher had to check for errors and

inconsistencies of collected data. This was done by processing data. Initially data

entry was performed and followed by editing and coding. The analysis of quantitative

data was performed by using the Microsoft Statistical Package for Social Sciences

(SPSS). Figures such as pie-chart and bar charts were used to present the findings.

14

CHAPTER TWO: CRITICAL ANALYSIS OF PETROLEUM FISCAL REGIMES

2.1 The Rationale for Special Petroleum Tax Regime The taxation of oil and gas resources is given special treatment in petroleum

producing countries due to a number of reasons. Oil and gas resources are exhaustible

resources i.e. their prices are volatile and their production is unpredictable.38 This

poses challenges in many ways. While exhaustibility raises challenges in terms of

sustainability and intergenerational equity in the allocation of resources, the

uncertainty and volatility of petroleum revenues makes it difficult for fiscal policy

making and macroeconomic management.

The oil and gas industry is inherently risky. The main risks are geological,

commercial and political risks. These risks are particularly complicated for the reason

that the oil and gas projects involves high capital costs, long project life cycles,

volatile prices and unpredictable reserves. Besides, due to non-renewability of

petroleum resources, most governments target at taxing as much economic rent as

possible. Due to the complex nature of the petroleum investment it is pertinent that

any government must ensure that a proper tax regime that balances the interest of the

state and that of the investor is put in place. It is argued that such tax must target an

economic rent39 and must comprise of the features of good fiscal regime discussed in

the following paragraphs.

2.2Types of Fiscal Regimes Petroleum operations are subject to various tax instruments both those that are

specific to the petroleum industry and those that are applicable to all other industries. 38 Steven Barnett and Rolando Osowski, ‘Operational Aspects of Fiscal Policy in Oil-Producing Countries’(International Monetary Fund, 2002) p.13-15 <http://www.google.co.uk/url?sa=t&rct=j&q=&esrc=s&source=web&cd=3&ved=0CDQQFjAC&url=http%3A%2F%2Fwww.mafhoum.com%2Fpress4%2F120E11.pdf&ei=pBkRVNT7IJTUarHGgZgP&usg=AFQjCNGXp2wfXDnS2UPc1lBUy_M_pgddaQ&sig2=oERYaszRWQRA1CfPO4Zmrw&bvm=bv.74894050,d.d2s > accessed 10 September 2014.

39 Peter Mullins, ‘International tax issues for resource sector’ in Philip Daniel and aothers(eds.),The Taxation of Petroleum Minerals (Routledge 2010) p.378.

15

There are other non-tax instruments to which the oil and gas regime is also subject.

The non-tax instruments include bonuses, production sharing and surface rentals.40

Governments need to design tax regimes to achieve particular objectives which

include maximizing the value of revenues from the resource being produced; job

creation; transfer of technology; development of local infrastructure and capacity; and

ensure energy security. The government needs also to design fiscal regime in such a

way as does attract investors and particularly foreign investors in the case petroleum

industry.

Foreign investments in petroleum industry increase petroleum resources development

and reserves; increase access to modern technology; improve management skills and

profit orientation; increase financial resources for development; establish long term

relationships with international oil companies and global oil and gas markets.41 In

order to achieve these objectives, governments need to design fiscal regime which

among others ensures that: tax revenues are predictable and stable; high extraction of

economic rent during the period of high profit; tax instruments do not introduce

distortions to the economy; ensure high revenues in the early period of the life cycle

to increase the net present value of revenues; tax is neutral and thus eliminate negative

impacts on resource allocations.

Different countries in the world have adopted various oil and gas fiscal regimes

depending on many factors including historical backgrounds, prevailing geological

potentials and government objectives, among others. Some jurisdictions have more

than one oil and gas fiscal regimes and others have fiscal regimes which are ‘hybrid’

i.e. comprise of elements of more than one fiscal regime. The main oil and gas fiscal

regimes that exist in the world are concessionary systems and contractual systems

40 Silvana Tordo, ‘Fiscal Systems for Hydrocarbons: Design Issues’ (World Bank Working Paper no.123, 2007) <http://www.google.co.uk/url?sa=t&rct=j&q=&esrc=s&source=web&cd=1&ved=0CCEQFjAA&url=http%3A%2F%2Fsiteresources.worldbank.org%2FINTOGMC%2FResources%2Ffiscal_systems_for_hydrocarbons.pdf&ei=NH__U4D0MPGR0QWpzICgAg&usg=AFQjCNFP4d02s8z8bbH3Tj3mn7WxJAr0QA&sig2=IFdwkUpx2g7Ro_Dc9pEDeg&bvm=bv.74035653,d.ZGU > accessed 12 July 2014.

41 William T. Onorato and J. Jay Park, ‘World Petroleum Legislation: Frameworks that Foster Oil and Gas Development’ (2001) 39 (1) Alberta Law Review, p. 70.

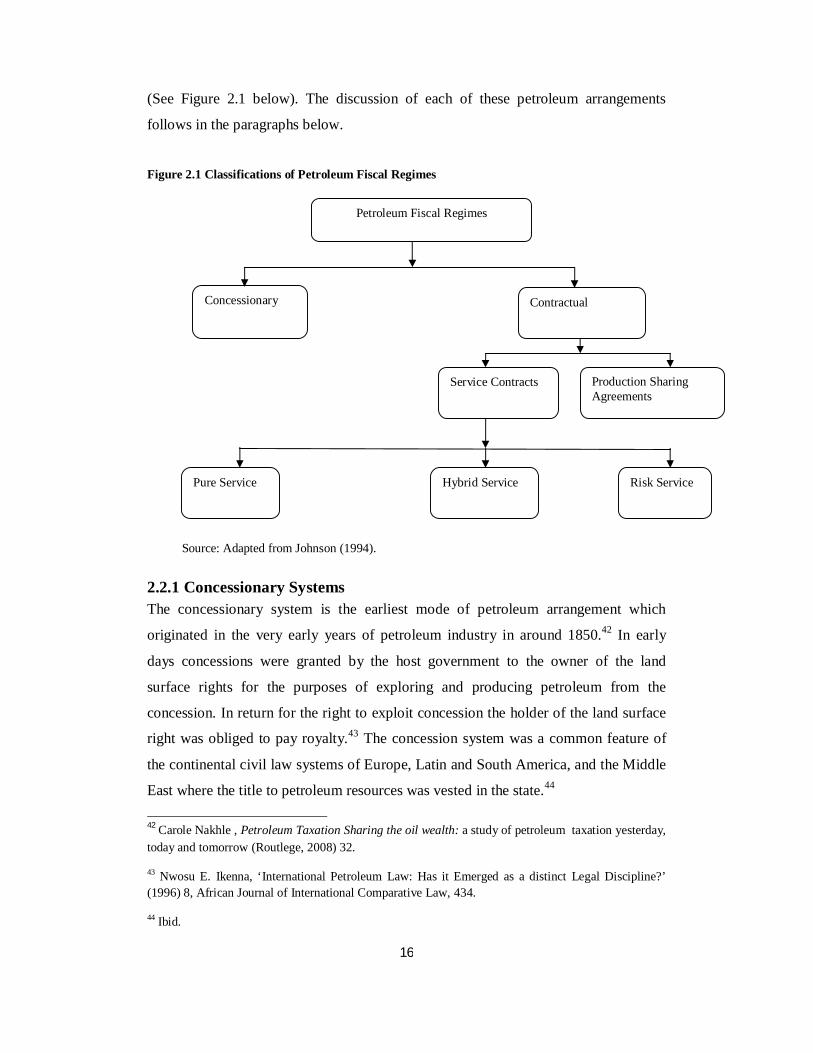

16

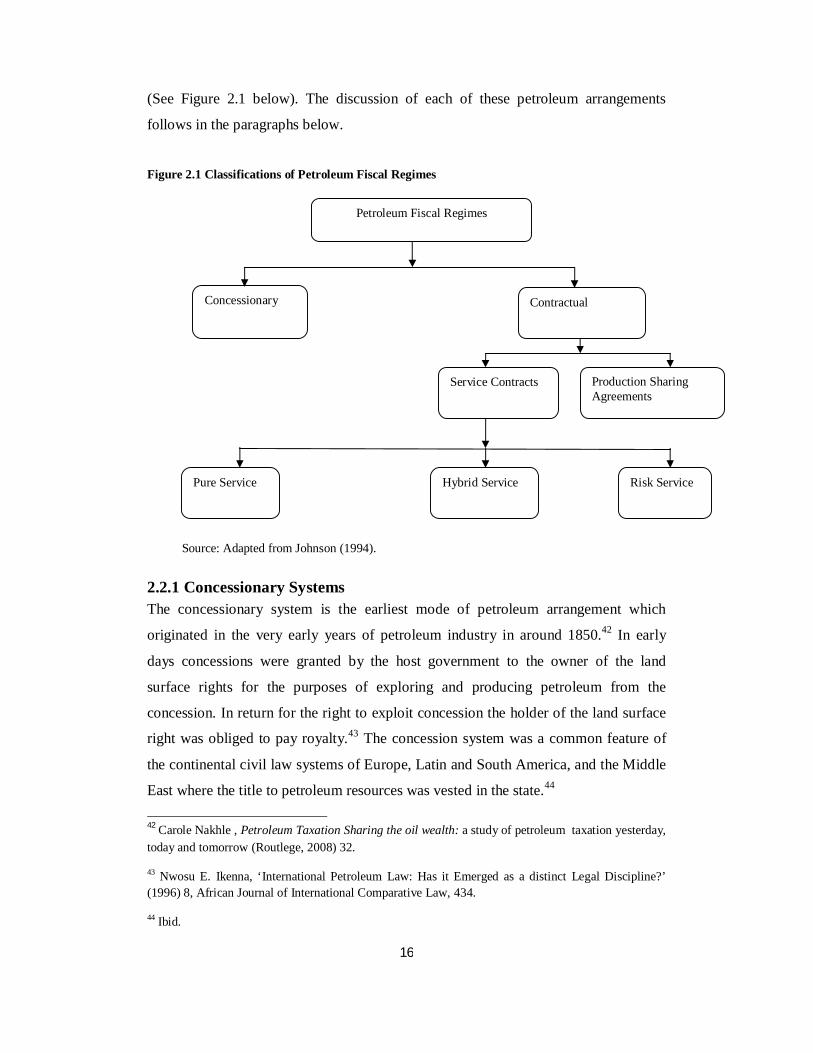

(See Figure 2.1 below). The discussion of each of these petroleum arrangements

follows in the paragraphs below.

Figure 2.1 Classifications of Petroleum Fiscal Regimes

Source: Adapted from Johnson (1994).

2.2.1 Concessionary Systems The concessionary system is the earliest mode of petroleum arrangement which

originated in the very early years of petroleum industry in around 1850.42 In early

days concessions were granted by the host government to the owner of the land

surface rights for the purposes of exploring and producing petroleum from the

concession. In return for the right to exploit concession the holder of the land surface

right was obliged to pay royalty.43 The concession system was a common feature of

the continental civil law systems of Europe, Latin and South America, and the Middle

East where the title to petroleum resources was vested in the state.44 42 Carole Nakhle , Petroleum Taxation Sharing the oil wealth: a study of petroleum taxation yesterday, today and tomorrow (Routlege, 2008) 32.

43 Nwosu E. Ikenna, ‘International Petroleum Law: Has it Emerged as a distinct Legal Discipline?’ (1996) 8, African Journal of International Comparative Law, 434.

44 Ibid.

Petroleum Fiscal Regimes

Contractual

Production Sharing Agreements

Service Contracts

Pure Service Hybrid Service Risk Service

Concessionary

17

Early concessions were characterized by long term periods and lower host

government control of management of resources and conduct of operations by the oil

company.45 The well known concession which was granted on 28th May 1901 by the

Persian government to William Knox D’Arcy to carry out petroleum exploration and

production throughout Persia was valid for the period of sixty years. 46 In return

D’Arcy was obliged to pay bonuses to the government and 16 percent of the

company’s annual profit.47Besides, early concessions gave oil companies wider

freedom to explore and exploit petroleum and host countries did not exercise any

control over the management of resource and conduct of operations by the oil

companies operating within their jurisdictions. Concession contracts were popular

petroleum arrangements between host states and oil companies up until 1950s. In

Tanzania, concession was the first phase of exploration history whereby in 1952-1964

BP and Shell were awarded concessions along the coast of Tanzania (then

Tanganyika) including the islands of Unguja, Pemba and Mafia.48

Around 1960s tension began to build between host countries and oil companies over

the sharing of revenues and control of resources under the concession arrangement.

The conflict between host countries and oil companies was further amplified by the

external factors such as the passing of various United Nations resolution in respect of

ownership of natural resources49; the rise of crude prices in early 1970s; the formation

45 A. Al Faruque, ‘Utility of Flexible Mechanisms and Progressive Tax System Stability in Fiscal Regime of Petroleum Contract: An Appraisal’ (2004) 2 (3) OGEL < www.ogel.org > accessed 28 July 2014.

46 Daniel Yergin, ‘The Prize: The Epic Quest for Oil, Money & Power (Free Press, 2008).

47 Nwosu E. Ikenna (n 43) 434.

48 Emma Msaky, ‘A Presentation to the delegation from Tanzania Private Sector Foundation (TPSF), <http://www.google.co.tz/url?sa=t&rct=j&q=&esrc=s&source=web&cd=2&ved=0CCQQFjAB&url=http%3A%2F%2Fwww.tpdctz.com%2FOIL%2520and%2520GAS%2520EXPLORATION.pdf&ei=bCwCVNH2J6bgyQPx64CICw&usg=AFQjCNFk4kY0_JYxyj5o8f-zusYeqz5ZMw&bvm=bv.74115972,d.d2k> accessed 30 August 2014.

49 Some of these resolutions includes the Permanent Sovereignty over Natural Resources General Assembly resolution 1803 (XVII) passed in New York on 14 December 1962, see at < http://legal.un.org/avl/ha/ga_1803/ga_1803.html > accessed 11 September 2014.

18

of the Organization of Petroleum Exporting Countries (OPEC) in 196050; the expansion of

petroleum industry further to downstream; the emergence of independent oil

companies between 1957 and 1960 and state oil companies which offered more

attractive terms to host countries than the majors.51

Concession system is also referred to as royalty/tax arrangement. Under concession

the oil company acquires title to petroleum produced at the wellhead and the oil

company has to pay royalty and tax only to the host government. The contractor also

owns assets and the government or its agents do not monitor operations and

expenditure unless the oil company defaults payment of taxes.52 The oil company has

the right to own the produced petroleum except that it may be required to supply local

markets.53 Unlike the old concessions, modern concessions consists of short-term

period, the state has a greater control over resource and project management. Modern

concessions also comprise of various taxes including bonuses, royalty, income tax and

additional profit tax.54 It is argued that concessions are less-self enforcing since their

fiscal arrangement are incorporated into legislations instead of the contract itself, thus

they are susceptible to legislative changes.55

2.2.2 Contractual Systems The source of contractual systems is based on the French legal philosophy since the

Napoleonic era which vested ownership of mineral resources in the host government

on behalf of the populace.56 Under the contractual systems, an oil company is engaged

to explore, develop and produce petroleum at its own risks; the state owns the

resources and ownership is transferred to the oil company at the delivery point; and

50 The Organization of Petroleum Exporting Countries, ‘Brief History’ <http://www.opec.org/opec_web/en/about_us/24.htm > accessed 12 June 2014.

51 Ibid 435.

52 Emma Msaky (n 48) 3.

53 Carole Nakhle (n 42) 32.

54 A. Al Faruque (n 45) 14.

55 Ibid.

56 Daniel Johnson, Petroleum Fiscal Systems and Production Sharing Contracts (PennWell Books 1994) p.22.

19

ownership of assets reverts to the host government immediately and thus the host

government is responsible for abandonment unless otherwise expressly agreed.57

Contractual systems are divided into production sharing agreements and risk service

agreements. The key distinctive features between concessionary and contractual

systems are summarized in the Table 2. 1below.

Table 2.1: Key Distinctive Features between Concessionary System

and Contractual System

Concessionary Systems Contractual Systems

In its most basic form, a concessionary system has three components: royalty; deductions (such as operating costs, depreciation, depletion and amortization, intangible drilling costs); and tax.

Under a production sharing contract (PSC) the contractor receives a share of production for services performed. In its most basic form, a PSC has four components: royalty, cost recovery, profit oil, and tax.

The royalty is normally a percentage of the proceeds of the sale of hydrocarbon. It can be determined on a sliding scale, the terms of which may be negotiable or biddable, and paid in cash or in kind. The royalty represents a cost of doing business and is thus tax-deductible.

Similar to concessionary systems. In addition, normally royalties are not cost recoverable.

The definition of fiscal costs is described in the legislation of the country or in the particular concession agreement. Royalties and operating expenditures are normally expensed in the year in which they occur, and depreciation is calculated according to applicable legislation. Some countries allow the deduction of investment credits, interest on financing, and bonuses.

Fiscal costs are defined and rules for amortization and depreciation are established in the legislation of the country or in the particular PSC. After payment of royalties, the contractor is allowed to recover costs in accordance with contractual provisions (a cost recovery limit may apply). The remainder of the production is split between the host government and the oil company at a stipulated (often negotiated) rate.

The taxable income under a concessionary agreement may be taxed at the country’s basic corporate tax rate. Special investment incentive programs and special resource taxes may also apply. Tax losses are normally carried forward until full recovery.

Corporate taxes may apply or may be paid by the host government or its NOC on behalf of the contractor. Income tax is calculated on taxable income (revenue net of royalties, allowable costs, and government share of profit oil). Tax losses are normally carried forward until full recovery. In most countries, when cost recovery limits exist, the company’s share of profit oil in any given accounting period is not the taxable base

Source: Adapted from Silvana Tordo (2007)

57 A. Karembu Njeru, ‘Kenya Oil and Gas Fiscal Regime: An Economic Analysis on Attainment of Government Objectives’ (2009) 7(3) OGEL p.3 < www.ogel.org > accessed 2 August 2014.

20

2.2.2.1 Production Sharing Agreements

Like farm-out agreements, PSAs originated from agricultural arrangements based on

the sharecropping arrangements whereby the owner of land grants a farmer the right

to grow crops and in return the farmer shares the produce with the land owner in the

pre-agreed ratio.58 The Production Sharing Agreement (PSA)59 was developed

initially in Indonesia in 1966 as a result of host governments’ battle for control of

petroleum resources and the desire to extract higher values from the production. This

was due to weaknesses that were identified under the concessionary system which

predated the PSA system. Under PSA system, the investor, usually referred to as the

contractor assumes all the risks before the production starts and recoups costs and

profits out of the production.60In petroleum industry, PSA is a crucial tool which

enables the cooperation between the host government, the national oil company and

the investor. It provides stable risks sharing contractual arrangement between all the

parties involved.61 It is argued that PSA provides “a flexible tool to adjust the fiscal

package to suit a particular project without changing the overarching fiscal

framework”.62 The ability to be flexible has been the defining criteria for the success

of the PSA system in meet the requirements of both the investor and the

government.63It is further argued that the PSA is the most attractive amongst all the

petroleum contracts today in that it balances the interests of the host country and the

investors to the greatest degree possible. This is so because PSA ensures the state

58 Stephen Harwood, ‘Production Sharing Contracts: Analysis of Comparative Practice in certain African Jurisdictions’ (UNCTAD 11th Africa Oil and Gas Trade & Finance Conference, Nairobi, 23-25 May, 2007) p.3. <http://www.google.co.uk/url?sa=t&rct=j&q=&esrc=s&source=web&cd=2&ved=0CE4QFjAB&url=http%3A%2F%2Fwww.unctadxi.org%2FSections%2FDITC%2FFinance_Energy%2Fdocs%2F11thAfrican%2F11thAfrican_Marc%2520Hammerson.pdf&ei=rWoRVNGzCc7haPjIgPAO&usg=AFQjCNFWs9h8AsnZvdEtevp7OpSb8EEJcg&sig2=vrvfqmELMG35wBnFioBX3Q&bvm=bv.74894050,d.ZGU >

59 In some jurisdiction PSA is synonymously known as production sharing contract (PSC).

60 T. Baunsgaard ‘A Primer on Mineral Taxation’ (2004) 2(3) OGEL pp.12 < www.ogel.org > accessed 12 July 2014.

61 Ibid.

62 T. Baunsgaard (n 60) 13.

63 Thomas W. Walde, ‘Renegotiating Acquired rights in the oil and gas industries: Industry and political cycles meet the rule of law’ (2008) 1 (1) Journal of World Energy Law & Business, p.65.

21

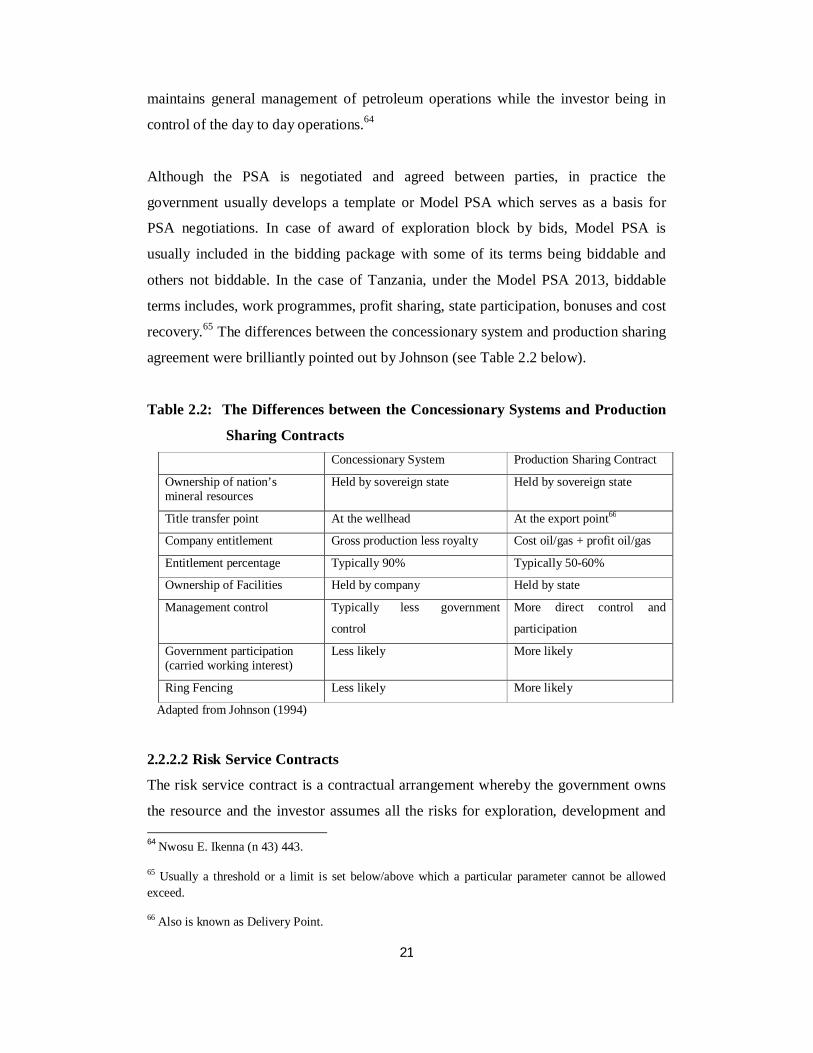

maintains general management of petroleum operations while the investor being in

control of the day to day operations.64

Although the PSA is negotiated and agreed between parties, in practice the

government usually develops a template or Model PSA which serves as a basis for

PSA negotiations. In case of award of exploration block by bids, Model PSA is

usually included in the bidding package with some of its terms being biddable and

others not biddable. In the case of Tanzania, under the Model PSA 2013, biddable

terms includes, work programmes, profit sharing, state participation, bonuses and cost

recovery.65 The differences between the concessionary system and production sharing

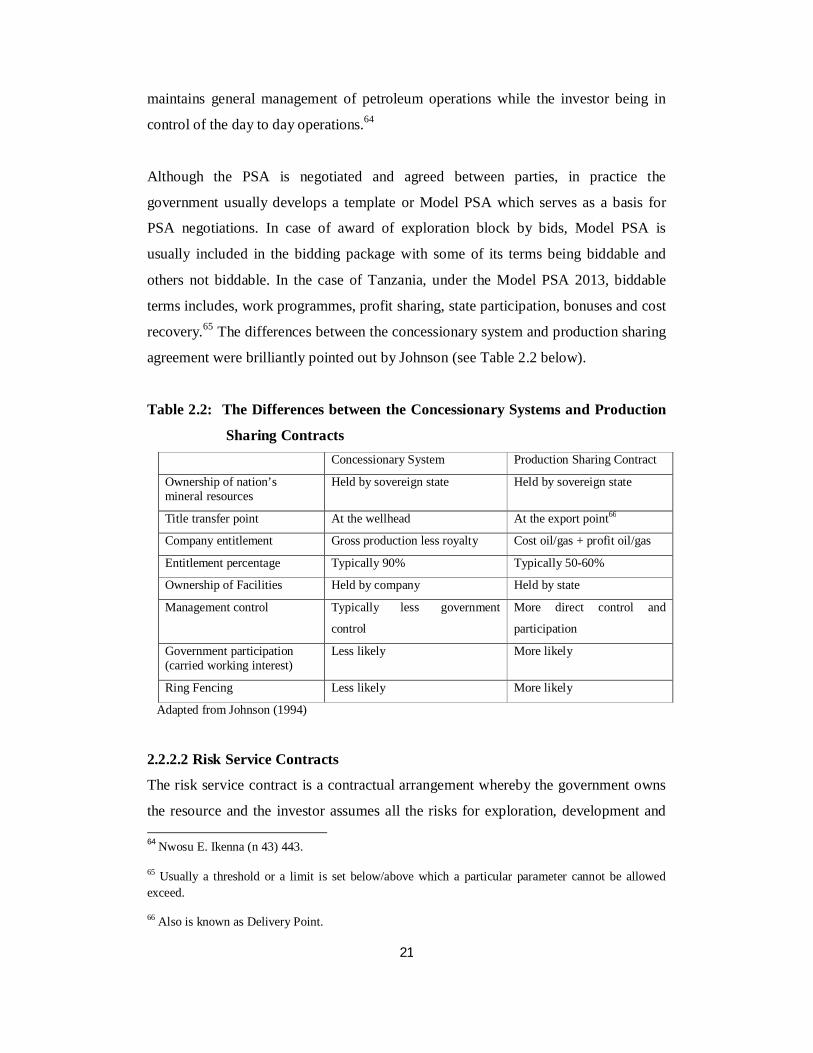

agreement were brilliantly pointed out by Johnson (see Table 2.2 below).

Table 2.2: The Differences between the Concessionary Systems and Production

Sharing Contracts Concessionary System Production Sharing Contract

Ownership of nation’s mineral resources

Held by sovereign state Held by sovereign state

Title transfer point At the wellhead At the export point66

Company entitlement Gross production less royalty Cost oil/gas + profit oil/gas

Entitlement percentage Typically 90% Typically 50-60%

Ownership of Facilities Held by company Held by state

Management control Typically less government

control

More direct control and

participation

Government participation (carried working interest)

Less likely More likely

Ring Fencing Less likely More likely

Adapted from Johnson (1994)

2.2.2.2 Risk Service Contracts

The risk service contract is a contractual arrangement whereby the government owns

the resource and the investor assumes all the risks for exploration, development and 64 Nwosu E. Ikenna (n 43) 443.

65 Usually a threshold or a limit is set below/above which a particular parameter cannot be allowed exceed.

66 Also is known as Delivery Point.

22

production costs. In case the venture is successful, the investor is allowed to recoup its

costs from the petroleum revenues.67 Besides, the investor also in return gets paid a

fixed or a variable fee in cash or in kind.68 The risk service contracts are divided into

pure service contracts and risk service contracts. Under the pure service contract the

investor is paid a fixed fee and all production belongs to the state but under the risk

service contract the investor is paid a fee which is linked to the profit.69

In recent years more countries are adopting service contracts as opposed to production

sharing agreements or concessions in their petroleum development projects.70 This

shift in interest towards service contracts is attributed to two main reasons namely, the

heightened sovereignty concerns and the need by the host countries of capital and

know-how for the development of the petroleum industry. In relation to other forms of

petroleum arrangements, service contracts are quite recent and their application in the

petroleum industry came in late 1980s and early 1990s.71

2.3 Fiscal Components of Contractual Systems Fiscal components of contractual systems are elements which constitute fiscal regime

in contractual systems. These elements include royalty, cost recovery limit, profit oil

split and state or government participation. The discussion on these elements follows

in the following paragraphs.

2.3.1 Royalty Royalty is the most common levy imposed by governments in petroleum resource

extraction. Royalty can either be specific i.e. based on volume or ad valorem i.e. 67 Daniel Johnson (n 56) 87-88.

68 Oscar E. Arrieta, ‘New Petroleum Law of Peru’ (1996) 14(1), Journal of Energy and Natural Resources Law, p. 424.

69 Silvana Tordo (n 40) 8.

70 Abbas Ghandi and C. Y. Cynthia Lin, ‘Oil and Gas Service Contracts around the World: A Review’ p.1 <http://www.google.co.uk/url?sa=t&rct=j&q=&esrc=s&source=web&cd=3&ved=0CDEQFjAC&url=http%3A%2F%2Fwww.des.ucdavis.edu%2Ffaculty%2FLin%2Fservice_contracts_review_paper.pdf&ei=i_ERVM_BN8vH7Ab7o4GoCQ&usg=AFQjCNHuLy_EqmOwCN9BAs-RV6uzY_OIww&sig2=XNc6Bhq2IKrgZ6Ss9Xel3g > accessed 11 September 2014.

71 Ibid 2.

23

based on the value of the petroleum produced. Royalty is said to be a monetary

compensation to the state for the use of state’s property for economic purposes. In

countries like Brazil, royalties are paid on monthly basis relative to each field starting

with the one in which the production commences.72 Royalty is commonly charged as

a percentage of gross revenues from the sale of petroleum resources and it may be

paid either in cash or in kind, i.e. as oil or gas at the existing prices.73 Thus, royalty

can be expressed mathematically as follows:

Royalty = Royalty rate (%) x production (bbl) x oil price ($/bbl)

In terms of administration, specific royalty is said to be easy to administer since the

government is only required to monitor the physical quantity of output. The other

advantage of specific royalty is that from the government perspective, revenues are

not dependent on the price of crude or gas. The shortcoming of specific royalty is that

the government’s revenue does not increase if the real price of the product rises and

the revenues does not keep pace with inflation. In contrast to specific royalty, ad

valorem royalty are preferred since they are sensitive to inflation and to fluctuations

of oil or gas prices.

The governments prefer levying royalty since it ensures early revenues flow to the

state after the commencement of production and that the amount of revenues is easily

predictable.74 However, from the investor’s point of view royalty is a regressive tax

since it is not targeted on profit and it is not sensitive to field sizes, costs and reduces

significantly the net present value (NPV). For these reasons, royalty may have

distortionary effects, including pre-mature abandonment of fields.75

72 Eduardo Pereira (eds.), Brazilian Upstream Oil and Gas: A Practical Guide to the Law and Regulation (Global Business Publishing Ltd, 2012) p.69.

73 Frank Jahn and others, Hydrocarbons Exploration and Production (2nd edition, Elsevier, 2008).

74 T. Baunsgaard (n 60) 10.

75 Greg Gordon and others, Oil and Gas Law: Current Practice and Emerging Trends (2nd edition, Dundee University Press, 2011), p. 138.

24

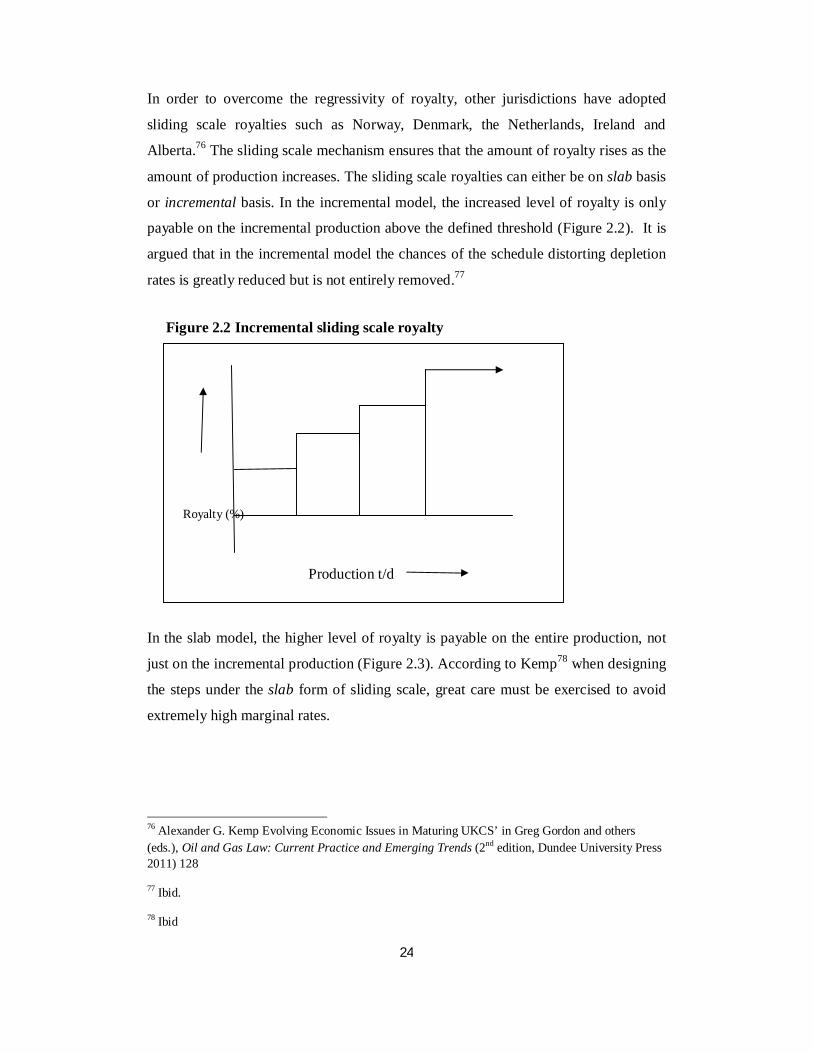

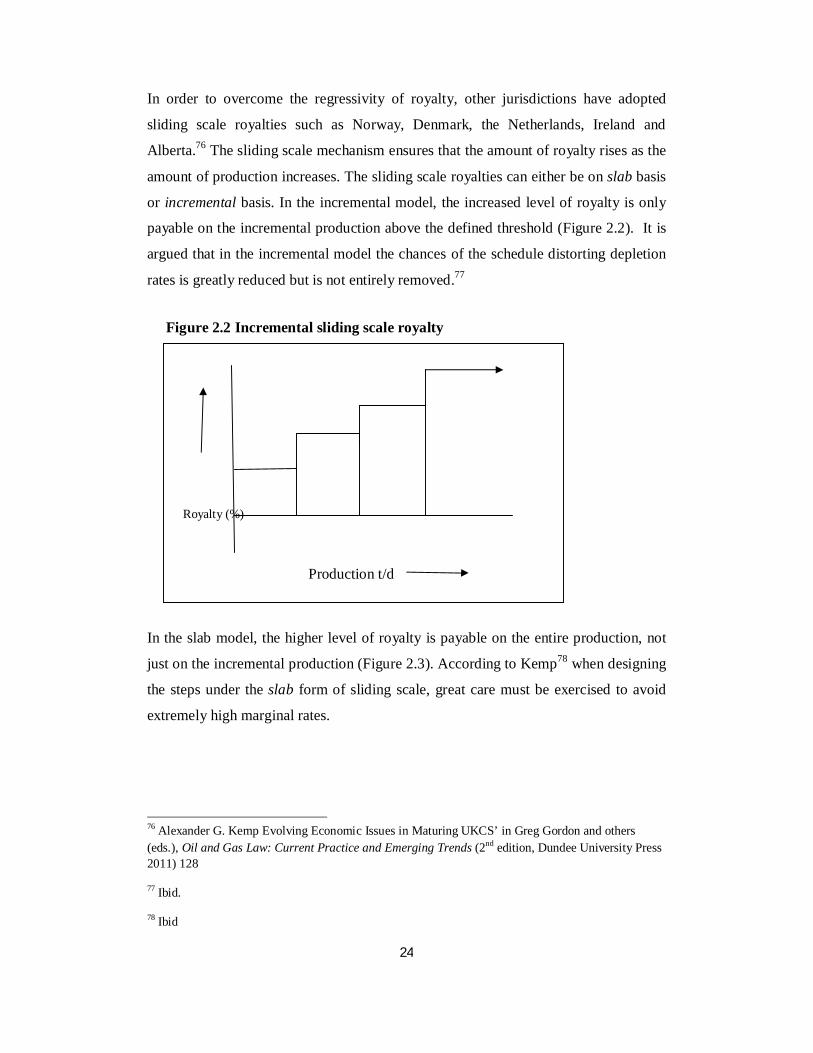

In order to overcome the regressivity of royalty, other jurisdictions have adopted

sliding scale royalties such as Norway, Denmark, the Netherlands, Ireland and

Alberta.76 The sliding scale mechanism ensures that the amount of royalty rises as the

amount of production increases. The sliding scale royalties can either be on slab basis

or incremental basis. In the incremental model, the increased level of royalty is only

payable on the incremental production above the defined threshold (Figure 2.2). It is

argued that in the incremental model the chances of the schedule distorting depletion

rates is greatly reduced but is not entirely removed.77

Figure 2.2 Incremental sliding scale royalty

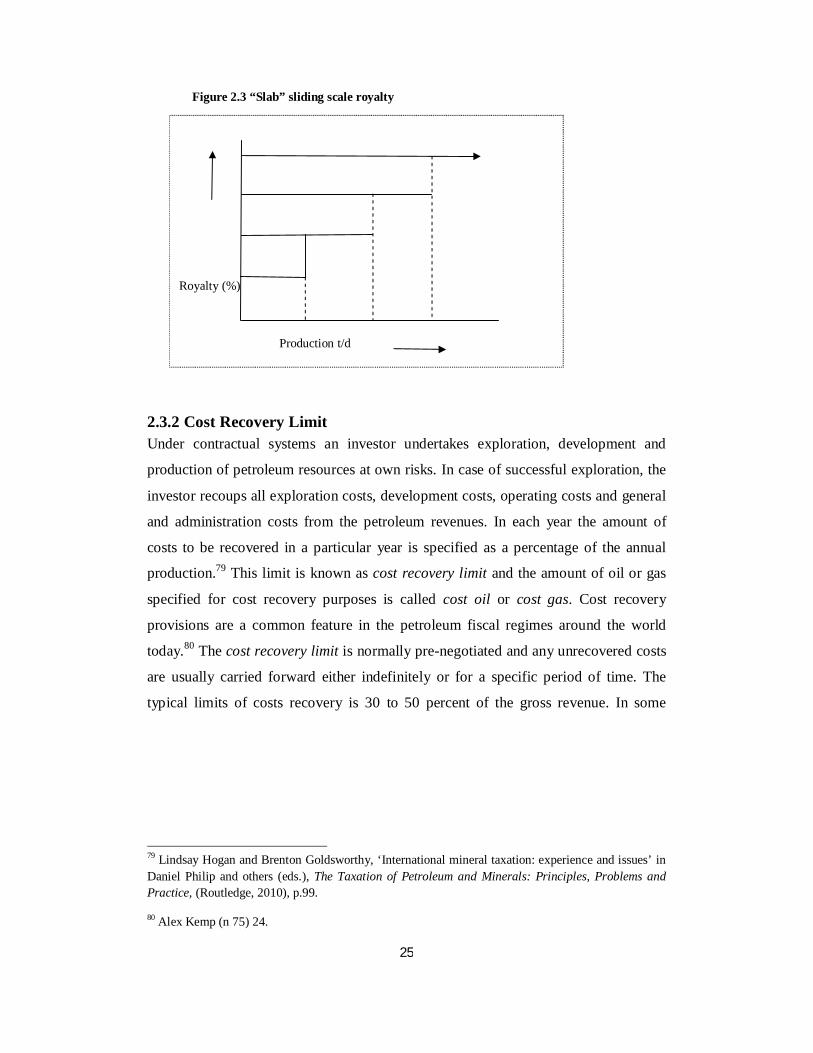

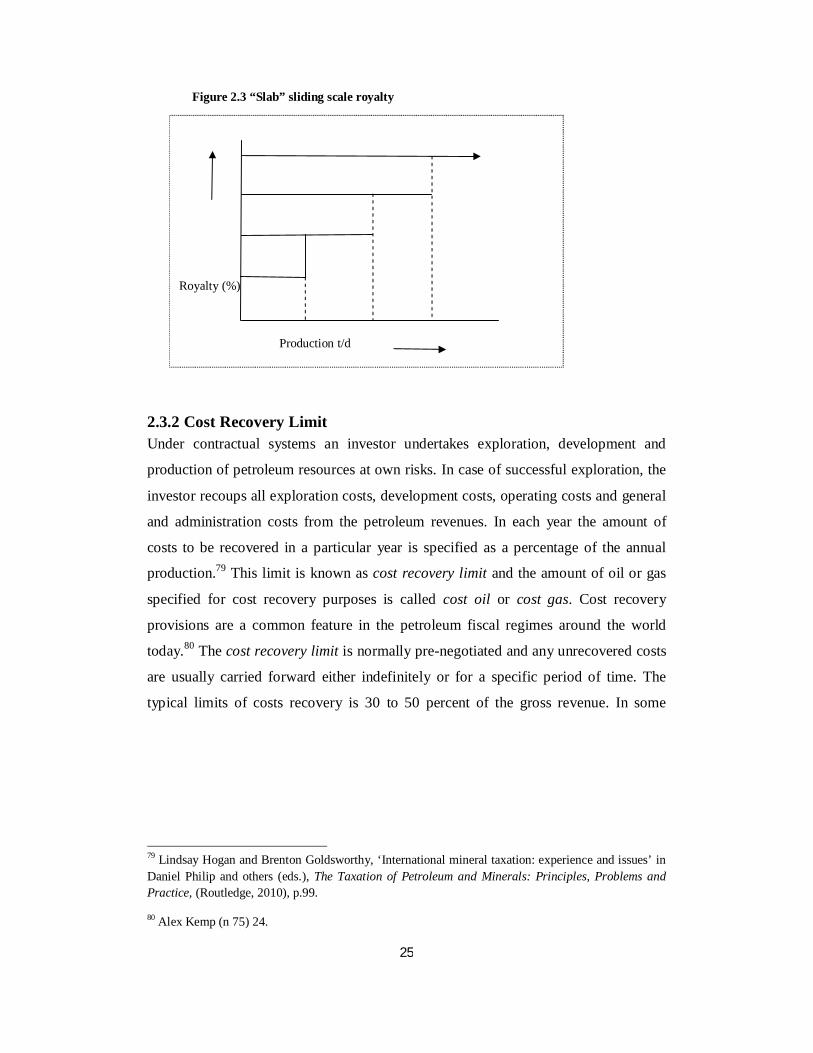

In the slab model, the higher level of royalty is payable on the entire production, not

just on the incremental production (Figure 2.3). According to Kemp78 when designing

the steps under the slab form of sliding scale, great care must be exercised to avoid

extremely high marginal rates.

76 Alexander G. Kemp Evolving Economic Issues in Maturing UKCS’ in Greg Gordon and others (eds.), Oil and Gas Law: Current Practice and Emerging Trends (2nd edition, Dundee University Press 2011) 128

77 Ibid.

78 Ibid

Royalty (%) Production t/d

25

Figure 2.3 “Slab” sliding scale royalty

2.3.2 Cost Recovery Limit Under contractual systems an investor undertakes exploration, development and

production of petroleum resources at own risks. In case of successful exploration, the

investor recoups all exploration costs, development costs, operating costs and general

and administration costs from the petroleum revenues. In each year the amount of

costs to be recovered in a particular year is specified as a percentage of the annual

production.79 This limit is known as cost recovery limit and the amount of oil or gas

specified for cost recovery purposes is called cost oil or cost gas. Cost recovery

provisions are a common feature in the petroleum fiscal regimes around the world

today.80 The cost recovery limit is normally pre-negotiated and any unrecovered costs

are usually carried forward either indefinitely or for a specific period of time. The

typical limits of costs recovery is 30 to 50 percent of the gross revenue. In some

79 Lindsay Hogan and Brenton Goldsworthy, ‘International mineral taxation: experience and issues’ in Daniel Philip and others (eds.), The Taxation of Petroleum and Minerals: Principles, Problems and Practice, (Routledge, 2010), p.99.

80 Alex Kemp (n 75) 24.

Royalty (%) Production t/d

26

jurisdiction, cost recovery can be 100%81 or can vary depending on the location of the

discovery.82

Financing charges are generally not recoverable. In some cases costs which remain

unrecovered at the end of the year of accrual can be carried forward with uplift. The

cost recovery limit is favoured by host governments as it ensures that a state starts to

get part of the revenue from the production right at the commencement of project life

as a profit share.83

2.3.3 Profit Oil Split The amount of oil or gas remaining after the deductions of cost recovery is profit oil

or profit gas. In the case of PSA arrangement, profit oil or profit gas is shared

between the host country and the investor at pre-negotiated ratio and “the investor is

not entitled to its share of production until the oil or gas reaches the export point or an

agreed delivery point.” In general, the contractor is permitted to export its share of

profit oil/gas subject (in some cases) to the meeting of domestic supply

requirements.84

The mechanism of profit oil/gas sharing between the host government and the

investor has changed over the years since the introduction of the first PSA in

Indonesia in 1966. 85 In the early days, production was distributed on a flat basis and

81 Such jurisdictions include Indonesia, Bahrain and Angola. Full cost recovery normally is subject to time limit.

82 In the case of Tanzania, under the MPSA 2004 the cost recovery limit onshore/shelf areas is 50% and in deepwater is 70% of the total production from the Contract Area. The cost recovery limit was changed to 50% of the gross production net of royalty.

83 Lindsay Hogan and Brenton Goldsworthy (n 95) 100.

84 An agreed amount of the contractor’s share must be sold to the government at a heavily discounted rate.

85 M.R. de Oliveira, ‘The Overhaul of the Brazilian Oil and Gas Regime: Does the Adoption of a Production Sharing Agreement bring any Advantage over the current Modern Concession Systems?’ (2010) 8 (4) OGEL, p.60 < www.ogel.org > accessed 2 September 2014. For more on the historical development of PSAs See also Kirsten Bindemann, ‘Production-Sharing Agreements: An Economic Analysis’ ( Oxford Institute for Energy Studies, 1999) <http://www.google.co.uk/url?sa=t&rct=j&q=&esrc=s&source=web&cd=2&ved=0CCkQFjAB&url=http%3A%2F%2Fwww.oxfordenergy.org%2Fwpcms%2Fwp-

27

mutually on contract by contract basis irrespective of the features of the discovery.

For instance, in the first Indonesian PSA the sharing was 65% by 35% in favour of the

government. This was later changed to 85% by 15% in favour of the government in

case of oil in 1976 but remained the same for natural gas. In later years, progressive

sliding scale sharing mechanisms based on daily production rate were incorporated.

For example progressive profit oil increased from 50% by 50% for low production

levels to 85% by 15% for higher levels of production.

In Angola, a progressive scale based on cumulative production from a given field was

introduced in 1979. Thus, the division of profit oil was related to the characteristic of

the field in terms of its location that is onshore, shallow, offshore or deep offshore. In

1983, countries like Liberia, Libya, Equatorial Guinea, Tunisia, India and Azerbaijan

introduced new sharing mechanism based on the rate of return. Generally, the

production sharing between the host country and the Contractor is the function of the

geological potential of the area.86 High costs for exploration and production and less

prospectivity of the block means higher risk to the Contractor/investor in which case

the Contractor will demand favourable terms.

2.3.4 Government Participation State participation is very common practice in the petroleum industry particularly in

the PSA arrangement. State participation allows the government to acquire shares in

the project where there is a commercial discovery. In practice, the level of state

participation is negotiable but it is a function of the geological potential of the area,

the amount of costs involved and the level of maturity of the industry. The state

participation in the petroleum industry emerged mainly due to the following factors:

the decolonization of the Middle Eastern and African countries from the home state of

the international oil companies (IOCs); the formation of OPEC to equalize the

bargaining powers of member states; the promulgation of the UN General Assembly content%2Fuploads%2F2010%2F11%2FWPM25- ProductionSharingAgreementsAnEconomicAnalysis-KBindemann- 1999.pdf&ei=SRMUVIjaL8_caKbtgNAI&usg=AFQjCNFtF9EK9IuN1YF5fNFLjX40NAloCA&sig2=frmmYUxaIxhJKuMcYnU-AQ&bvm=bv.75097201,d.d2s > accessed 12 September 2014.

86 Ibid 61.

28

Resolution on Permanent Sovereignty of states over natural resources; and the

mounting pressure on the need for states to get fair share of returns from petroleum

development and retain control over the resources.87 The rationale for state

participation includes assertion of sovereignty, policy control, technology transfer,

local employment opportunity and higher share of revenue.88

There are several forms of state participation namely, paid up equity on commercial

terms; paid up equity on concessional terms; carried interests with repayment; tax

swapped for equity; free equity; equity in exchange for non-cash contribution such as

state providing infrastructure or project assets; and production sharing consisting of

back-in rights for a state at commerciality.89 It is argued that, when the financial

obligations are taken into account, such as cash calls that the state has to contribute

during development phase, state participation may be a costly option. There are other

disadvantages of state participation which includes the rise of conflict of roles as a

result of the government playing both commercial role as equity holder and regulatory

role. Thus, in this regard Baunsgaard concludes that “the government will be better

off by solely taxing and regulating a project rather than being directly involved as an

equity participant”.90

Furthermore, Ogunlade points out that the state has predominant financial obligations

to its citizens which would be negatively impacted in case the state were to engage in

high capital, high risk ventures like petroleum.91 The state participation has the effect

of reducing the bankable reserves for the investor as such it can potentially affect the

investor’s decision to invest in petroleum. Thus, it is advisable that in order to avoid

87 A. Ogunlade (n 27) 18.

88 H. Abdo, ‘The Story of the UK Oil and Gas Taxation Policy: History and Trends’ (November 2010) 8 (4) OGEL p. 5 < www.ogel.org > accessed 12 July 2014. For more discussion on the rationale for state participation see , Adebola Ogunlade, ‘How Can Government Best Achieve its Objectives for Petroleum Development:Taxation and Regulation or State Participation?’(November 2010) 8 (4) OGEL, p.5 < www.ogel.org > accessed 1 September 2014. 89 A. Ogunlade (n 27) 21.

90 Baunsgaard (n 60) 14.

91 A. Ogunlade (n 27) 22.

29

burdening the state with huge financial commitment in petroleum projects there must

be a minimum level of state participation.92

2.3.5 Other Fiscal Instruments Bonuses: Bonuses are upfront monies paid by oil companies to the government for

signing a PSA; or on discovery of petroleum; or on start of commercial production.93

Bonuses are common and essential element of the petroleum fiscal regimes.94 There

are three types of bonuses namely signature bonuses, discovery bonuses and

production bonuses.95 In principle, bonuses are not recoverable contract expenses but

they are deductible for tax purposes.

Domestic Market Obligation (DMO): DMO is an obligation to Contractor to supply

oil or gas produced in the domestic market, usually at prices much less than the

market price.96 The amount of petroleum for DMO is fixed percent of the production

and it is usually mutually agreed by parties. Most countries have adopted DMO

provisions in their petroleum contracts to ensure the security of energy supply.97 This

arises from the realization that energy sufficiency is the bedrock for economic

9292 Ibid 23.

93 Carole Nakhle, ‘Petroleum Taxation: A Critical Evaluation with Special Application to the UK Continental Shelf’ < http://epubs.surrey.ac.uk/2790/ > accessed 3 September 2014. 94 George Ndi, ’The Contractual and Legal Framework for Petroleum Exploration and Production in Cameroon’ (1992) 10, Journal of Energy and Natural Resources Law, p.275.

95 Signature bonuses are paid during the signing of the PSA, the discovery bonuses are paid on commercial discovery of petroleum and production bonuses are paid when production of petroleum reaches certain predetermined levels.

96 B.C. Land, ‘The Similarities and Differences between Mining and Petroleum Investment: A Comparison of Investment Characteristics, Company Decisions and Host Government Regulation’ (2007) 5(2) OGEL p. 239 < www.ogel.org > accessed 2 September 2014. 97 Theresa O. Okenabirhie, ‘The Domestic Market Supply Obligation: Is this the final Solution to Power Failure in Nigeria? How Can the Government Make the Obligation work?’ (University of Dundee, 2009) <http://www.google.co.uk/url?sa=t&rct=j&q=&esrc=s&source=web&cd=1&ved=0CCEQFjAA&url=http%3A%2F%2Fwww.dundee.ac.uk%2Fcepmlp%2Fgateway%2Ffiles.php%3Ffile%3Dcepmlp_car13_65_266090310.pdf&ei=jxoUVJHhMIfQ7Abk7ID4DQ&usg=AFQjCNEQQuJX5PUogQZZXV4xXjpePjWytQ&sig2=MA6DWgER0Glt6McBeZrYvw&bvm=bv.75097201,d.d2s > accessed 13 September 2014.

30

prosperity, global stability, geopolitical influence and national security.98 It is argued

that DMO petroleum supplied below the market prices to domestic market can have

substantial impact on the project cash flow.99

Income tax: Income tax usually applies to all sectors of the economy. In some

jurisdiction, profit oil or profit gas can be subject to the income tax.100Income tax can

be income tax on employees or corporation income tax. For example, Iran has a

Corporate Income Tax (CIT) on profit101 and Azerbaijan has income tax on

employees.102 Unlike royalties and bonuses, CIT is a progressive tax since it is

targeted at economic rent and thus it is back-loaded. It is therefore argued that CIT