THE EXPERIENCE OF GREECE FROM ITS PARTICIPATION IN THE EUROZONE

Upload

independentCategory

view

2download

0

Journal of Banking & Finance 38 (2014) 51–63

Contents lists available at ScienceDirect

Journal of Banking & Finance

journal homepage: www.elsevier .com/locate / jbf

News spillovers from the Greek debt crisis: Impact on the Eurozonefinancial sector

0378-4266/$ - see front matter � 2013 Elsevier B.V. All rights reserved.http://dx.doi.org/10.1016/j.jbankfin.2013.09.015

⇑ Corresponding author. Tel.: +1 210 458 7429.E-mail addresses: [email protected] (K. Bhanot), [email protected]

(N. Burns), [email protected] (D. Hunter), [email protected] (M. Williams).1 Tel.: +1 210 458 7429.2 Tel.: +1 813 974 6319.3 Tel.: +1 708 534 4958.4 See, for example, ‘‘Who’s Next? Spain? Italy?’’, Wall Street Journal, February 4,

2010 by Neil Shah. However, the Managing Director of the International MonetaryFund contended that contagion from Greece to Portugal or Spain was unlikely (see,‘‘Greek Woes ‘Unlikely to Spread’,’’ BBC News March 08, 2010).

5 See, for instance, ‘‘Greek contagion fears spread to other EU banks,’’Times June 15, 2011 by M. Murphy, K. Hope, J. Thompson, and J. Wilsonw w w . f t . c om / i n t l / c m s / s / 0 / a c 9 1 8 9 4 6 - 9 7 5 a - 1 1 e 0 - 9 c 9 d - 0 0 1 4 4 f ehtml#axzz1TR8tvAUu). See also ‘‘Containing Contagion’’, Bloomberg MSeptember 2011 and ‘‘Greece: time for a haircut’’, Financial Times, July 15,

Karan Bhanot a,⇑, Natasha Burns a,1, Delroy Hunter b,2, Michael Williams c,3

a Department of Finance, One UTSA Circle, College of Business, The University of Texas at San Antonio, TX 78249, United Statesb Department of Finance, College of Business, University of South Florida, Tampa, FL, United Statesc Governors State University, 1 University Parkway, University Park, IL, United States

a r t i c l e i n f o a b s t r a c t

Article history:Received 16 October 2012Accepted 20 September 2013Available online 7 October 2013

JEL classification:G1G01G14G15

Keywords:ContagionSpilloversEurozone debt crisis

We examine the impact of changes in Greek sovereign yield spreads on abnormal returns of financial sec-tor stocks for a sample of Eurozone countries, during the Greek debt crisis. We find that increases in yieldspreads are associated with negative abnormal returns on financial stocks in the Portugal, Spain andNetherlands. These abnormal returns are driven in part by ratings downgrades and other unfavorablenews announcements about Greece. We isolate the effects of known transmission channels–impairmentof financial firms’ asset base due to cross-holdings of Greek bonds, from increases in domestic interestrates and higher funding costs. Our analysis indicates that news events lead to spillovers in excess ofwhat can be explained by these channels of transmission.

� 2013 Elsevier B.V. All rights reserved.

1. Introduction tive action. The link between the outcome in Greece and the possible

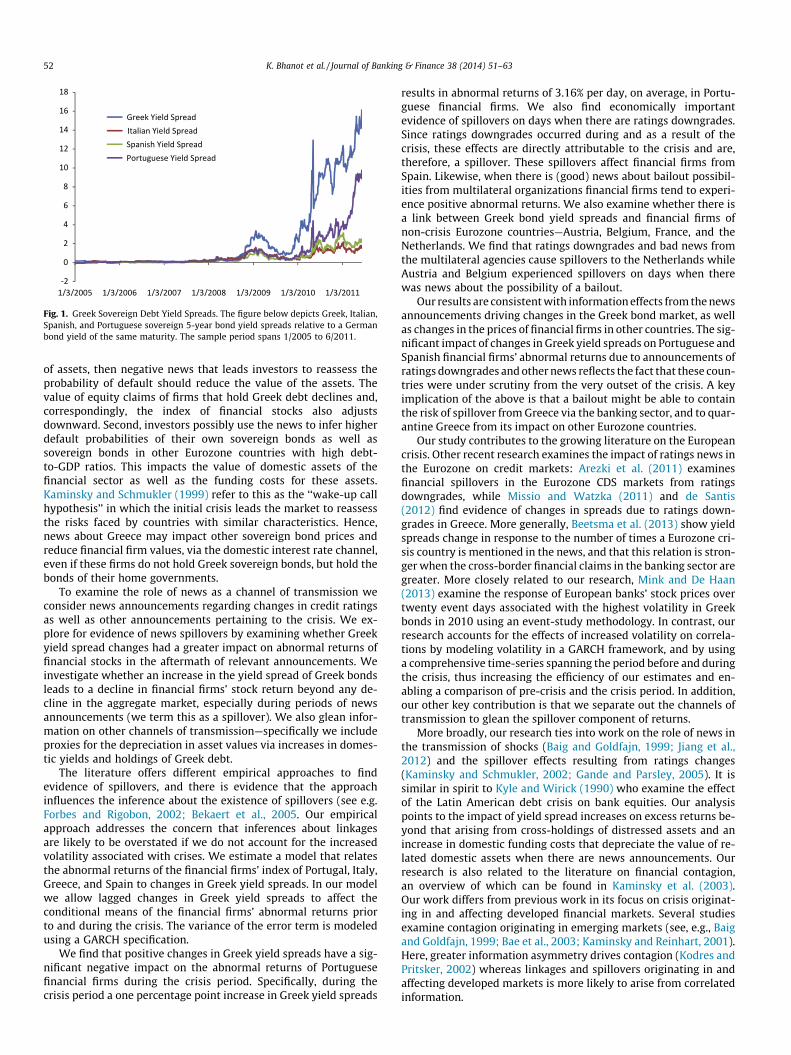

The sharp increase in yield spreads of Greek sovereign bonds rel-ative to German sovereign bonds starting in the latter part of 2009(Fig. 1), was covered extensively by the financial press and dubbed‘‘the Greek debt crisis’’. The crisis started when the Greek govern-ment announced that its debt service relative to receipts was muchlarger than previously acknowledged. Eurozone policymakers andmultilateral organizations raised concerns that the Greek debt crisiscould spread and impact Portugal, Italy, and Spain—countriesviewed by many to have similar underlying weaknesses as Greece.4

The crisis also caught the attention of the rating agencies who re-sponded by adjusting their credit ratings for Greece and other coun-tries, while multilateral organizations, such as the InternationalMonetary Fund (IMF), urged Eurozone member nations to take collec-

impairment of the assets of Europe’s largest banks due to their invest-ment in Greek sovereign bonds was at the fore in many discussions.5

This link between Greek bond yield spreads and financial sector re-turns is the focus of this research.

In this article we investigate whether increases in the yieldspreads of Greek sovereign bonds led to negative abnormal returnsin banks and other financial firms (herein after, financial firms) ofPortugal, Italy, Greece, and Spain in the period after the start of theGreek debt crisis in November 2009. In particular, we focus onGreek yield spread changes around news announcements and theirspillover to financial stocks in the Eurozone. As these newsannouncements occur frequently during this time period we canassess their impact on cross-market linkages.

Even though the Greek economy is a small component of theEurozone (less than 3% of total GDP), news about the ability ofGreece to service its debt possibly impacts domestic financial firmsand firms in other Eurozone countries for a number of reasons.First, if financial firms hold Greek bonds as part of their portfolio

Financial(http://

a b 4 9 a .agazine,

2011.

Fig. 1. Greek Sovereign Debt Yield Spreads. The figure below depicts Greek, Italian,Spanish, and Portuguese sovereign 5-year bond yield spreads relative to a Germanbond yield of the same maturity. The sample period spans 1/2005 to 6/2011.

52 K. Bhanot et al. / Journal of Banking & Finance 38 (2014) 51–63

of assets, then negative news that leads investors to reassess theprobability of default should reduce the value of the assets. Thevalue of equity claims of firms that hold Greek debt declines and,correspondingly, the index of financial stocks also adjustsdownward. Second, investors possibly use the news to infer higherdefault probabilities of their own sovereign bonds as well assovereign bonds in other Eurozone countries with high debt-to-GDP ratios. This impacts the value of domestic assets of thefinancial sector as well as the funding costs for these assets.Kaminsky and Schmukler (1999) refer to this as the ‘‘wake-up callhypothesis’’ in which the initial crisis leads the market to reassessthe risks faced by countries with similar characteristics. Hence,news about Greece may impact other sovereign bond prices andreduce financial firm values, via the domestic interest rate channel,even if these firms do not hold Greek sovereign bonds, but hold thebonds of their home governments.

To examine the role of news as a channel of transmission weconsider news announcements regarding changes in credit ratingsas well as other announcements pertaining to the crisis. We ex-plore for evidence of news spillovers by examining whether Greekyield spread changes had a greater impact on abnormal returns offinancial stocks in the aftermath of relevant announcements. Weinvestigate whether an increase in the yield spread of Greek bondsleads to a decline in financial firms’ stock return beyond any de-cline in the aggregate market, especially during periods of newsannouncements (we term this as a spillover). We also glean infor-mation on other channels of transmission—specifically we includeproxies for the depreciation in asset values via increases in domes-tic yields and holdings of Greek debt.

The literature offers different empirical approaches to findevidence of spillovers, and there is evidence that the approachinfluences the inference about the existence of spillovers (see e.g.Forbes and Rigobon, 2002; Bekaert et al., 2005. Our empiricalapproach addresses the concern that inferences about linkagesare likely to be overstated if we do not account for the increasedvolatility associated with crises. We estimate a model that relatesthe abnormal returns of the financial firms’ index of Portugal, Italy,Greece, and Spain to changes in Greek yield spreads. In our modelwe allow lagged changes in Greek yield spreads to affect theconditional means of the financial firms’ abnormal returns priorto and during the crisis. The variance of the error term is modeledusing a GARCH specification.

We find that positive changes in Greek yield spreads have a sig-nificant negative impact on the abnormal returns of Portuguesefinancial firms during the crisis period. Specifically, during thecrisis period a one percentage point increase in Greek yield spreads

results in abnormal returns of 3.16% per day, on average, in Portu-guese financial firms. We also find economically importantevidence of spillovers on days when there are ratings downgrades.Since ratings downgrades occurred during and as a result of thecrisis, these effects are directly attributable to the crisis and are,therefore, a spillover. These spillovers affect financial firms fromSpain. Likewise, when there is (good) news about bailout possibil-ities from multilateral organizations financial firms tend to experi-ence positive abnormal returns. We also examine whether there isa link between Greek bond yield spreads and financial firms ofnon-crisis Eurozone countries—Austria, Belgium, France, and theNetherlands. We find that ratings downgrades and bad news fromthe multilateral agencies cause spillovers to the Netherlands whileAustria and Belgium experienced spillovers on days when therewas news about the possibility of a bailout.

Our results are consistent with information effects from the newsannouncements driving changes in the Greek bond market, as wellas changes in the prices of financial firms in other countries. The sig-nificant impact of changes in Greek yield spreads on Portuguese andSpanish financial firms’ abnormal returns due to announcements ofratings downgrades and other news reflects the fact that these coun-tries were under scrutiny from the very outset of the crisis. A keyimplication of the above is that a bailout might be able to containthe risk of spillover from Greece via the banking sector, and to quar-antine Greece from its impact on other Eurozone countries.

Our study contributes to the growing literature on the Europeancrisis. Other recent research examines the impact of ratings news inthe Eurozone on credit markets: Arezki et al. (2011) examinesfinancial spillovers in the Eurozone CDS markets from ratingsdowngrades, while Missio and Watzka (2011) and de Santis(2012) find evidence of changes in spreads due to ratings down-grades in Greece. More generally, Beetsma et al. (2013) show yieldspreads change in response to the number of times a Eurozone cri-sis country is mentioned in the news, and that this relation is stron-ger when the cross-border financial claims in the banking sector aregreater. More closely related to our research, Mink and De Haan(2013) examine the response of European banks’ stock prices overtwenty event days associated with the highest volatility in Greekbonds in 2010 using an event-study methodology. In contrast, ourresearch accounts for the effects of increased volatility on correla-tions by modeling volatility in a GARCH framework, and by usinga comprehensive time-series spanning the period before and duringthe crisis, thus increasing the efficiency of our estimates and en-abling a comparison of pre-crisis and the crisis period. In addition,our other key contribution is that we separate out the channels oftransmission to glean the spillover component of returns.

More broadly, our research ties into work on the role of news inthe transmission of shocks (Baig and Goldfajn, 1999; Jiang et al.,2012) and the spillover effects resulting from ratings changes(Kaminsky and Schmukler, 2002; Gande and Parsley, 2005). It issimilar in spirit to Kyle and Wirick (1990) who examine the effectof the Latin American debt crisis on bank equities. Our analysispoints to the impact of yield spread increases on excess returns be-yond that arising from cross-holdings of distressed assets and anincrease in domestic funding costs that depreciate the value of re-lated domestic assets when there are news announcements. Ourresearch is also related to the literature on financial contagion,an overview of which can be found in Kaminsky et al. (2003).Our work differs from previous work in its focus on crisis originat-ing in and affecting developed financial markets. Several studiesexamine contagion originating in emerging markets (see, e.g., Baigand Goldfajn, 1999; Bae et al., 2003; Kaminsky and Reinhart, 2001).Here, greater information asymmetry drives contagion (Kodres andPritsker, 2002) whereas linkages and spillovers originating in andaffecting developed markets is more likely to arise from correlatedinformation.

Changes in Greek yield spread

Fig. 2. Changes in Greek Sovereign Debt Yield Spreads. The figure below depictschanges in Greek sovereign bond yield spreads relative to a German bond yield ofthe same maturity. The sample period spans 1/2005 to 6/2011.

K. Bhanot et al. / Journal of Banking & Finance 38 (2014) 51–63 53

The remainder of this article is organized as follows. Section 2describes the data and Section 3 outlines the methodology.Section 4 presents the results and Section 5 concludes.

2. Data

Our sample spans the period from January 2005 to June 2011.The pre-crisis or base period is 1/2005 to 10/2009, whereas the cri-sis spans the period 11/2009 to 6/2011. The start date for the crisisperiod coincides with investors’ concerns about the quality ofGreek sovereign debt in October 2009, after the Greek governmentrevealed that the government budget deficit for 2009 was 12.7% ofgross domestic product (GDP), much higher than the 6.7% of GDPstated earlier in the year. We obtain daily data on yields of 5-yearsovereign bonds for Germany (the benchmark), Greece, Italy, Por-tugal, and Spain (the crisis countries) and Austria, Belgium, France,and the Netherlands (the non-crisis countries) using Bloomberg.6

Gaps in the data for both the 5-year and 10-year bonds for Irelandprevent us from including Ireland in our analysis. The sample periodcontains 1,600 daily observations.

The yield spread for Greece is computed as the yield on sover-eign debt of Greece minus yield on German debt at time t. Germandebt yields are selected as a reference because of Germany’s relativeeconomic stability during the recent credit crisis and its economiccentrality within the Eurozone. This spread reflects perceptionsabout the incremental sovereign default risk relative to the bench-mark. The corresponding change in yield spread over one time per-iod (denoted YG,t) is computed as the first difference in yieldspreads. Yield spreads are driven by certain state variables andwhen these state variables change so do the spreads. Thus changesin yield spreads convey important information about changes ineconomic conditions that are of interest to market participants.Although yield spreads might capture more than a default pre-mium, e.g., a liquidity premium, this does not raise a substantialconcern for us. This is because the default premium should be thedominant premium in the spreads given that these are among thelargest and most active bond markets in the world, which shouldminimize the liquidity premium. More important, if the changesin yield spreads are driven by other factors this should weakenour results. Hence, our tests can be regarded as conservative.

We also obtain an index of stock prices of the financial firms foreach of the sample of countries (MSCI index of financial stocks) aswell as the aggregate market index for each country. We computedaily returns as 100 times log first difference of the respective in-dicex and define ‘‘abnormal’’ returns as the return on the financialfirms index minus the return on the domestic market index (de-noted Ri,t where i = P, I, G, and S for Portugal, Italy, Greece, andSpain). These data are obtained from Bloomberg. Our objective isto examine the relationship between Ri,t and YG,t during the crisisperiod and especially around news announcements.

We collect news announcements that pertain to Greece (labeledGreek) and the rest of the Eurozone (labeled NonGreek) from theWall Street Journal (see Appendix A for a listing of announcementsand announcement dates).7 The announcements for these twogroups are further separated into three categories: (1) ratings out-looks from the three ratings agencies (denoted Ratings), (2) unfavor-able announcements from ‘‘third party’’ agencies, such as theEuropean Monetary Union and the IMF (denoted Bad) and (3) favor-able announcements by third party agencies (denoted Good). The lat-ter two types include macroeconomic forecasts, austerity plans, andbailout package declarations. We separate ratings agency announce-ments from those by other agencies because the announcements of

6 We choose the 5-year bonds because of data availability and the fact that they arethe most actively traded maturity (Alexopoulou et al. (2009)).

7 See ‘‘A Euro Crisis Deal Emerges’’, Wall Street Journal, December 2, 2011.

ratings agencies may have a more substantial impact on bond yieldspreads than the announcements of other agencies. For example,Kaminsky and Schmukler (1999) examine market reactions duringthe Asian crisis to news announcements on fiscal and monetary pol-icy, credit ratings changes, and agreements with international orga-nizations like the IMF or World Bank. They find that markets reactnegatively to ratings downgrades but positively to agreements withinternational agencies. Further, markets react more strongly to newsby ratings agencies and international agencies than they react topolitical news and news on capital controls or monetary policy.

In addition to news announcements we collect quarterly data onGreek debt held by financial institutions in our sample countries(Greek Debt Holdings) as tabulated by the Bank of International Set-tlements for the period July 2007 to April 2011.8 Following Beetsmaet al. (2013) we use this as a proxy for public debt holdings, and we lin-early interpolate these holdings to match our daily measure of returns.

Fig. 1 plots sovereign yield spreads for Portugal, Italy, Greece,and Spain, while Fig. 2 plots changes in yield spreads for Greeceover the full sample. The figures show that yield spreads andchanges in spreads on Greek sovereign debt increased sharply sub-sequent to October 2009, even though there was already a smallincrease in spreads following the U.S. financial crisis of 2007. Ta-ble 1 contains summary statistics of the changes in Greek sover-eign bond yield spreads (YG,t) and abnormal returns on the indexof financial firms for Greece (RG,t), Portugal (RP,t), Italy (RI,t), andSpain (RS,t). The mean daily change in Greek yield spreads overthe full sample period (Panel A) is positive, 0.013%. On the otherhand, all mean abnormal returns on the financial firms’ indicesare negative, suggesting that these firms underperformed the gen-eral market on average.

During the pre-crisis period (Panel B) the mean change in Greekyield spreads is neither economically nor significantly different fromzero. Likewise, it is not surprising that there is no particular patternin the signs of the abnormal returns in this period. During the crisisperiod (Panel C) the average change in the Greek yield spread andits volatility are large—approximately 5 and 31 basis points perday, respectively. Similarly, the magnitude of the negative abnormalreturns increases substantially, especially in Portugal, where themean abnormal return is statistically significant. The increase inthe volatility of the variables in the crisis period can overstate thecorrelation between yield spreads and abnormal returns and leadto spurious evidence of changes in linkages across markets, a poten-tial problem resolved by our methodology which we discuss next.

8 Unavailability of Greek bond holdings data for Italy restricts the sample to thisperiod, for a total of 930 daily observations. For models not containing bond holdingsdata and for non-crisis countries the sample period starts in January 2005. See http://stats.bis.org/bis-stats-tool/.

Table 1Summary statistics of yield spread changes and financial firms’ excess returns.

Variable Obs Mean Std Min Max

Panel A: Full-sample summary statisticsChanges in Greek yield spread (YG,t) 1591 0.013** 0.157 �2.000 1.349Greek financial firms excess returns (RG,t) 1591 �0.008 0.864 �3.669 4.639Portuguese financial firms excess returns (RP,t) 1591 �0.055* 1.148 �5.910 5.958Italian financial firms excess returns (RI,t) 1591 �0.009 0.725 �3.742 5.895Spanish financial firms excess returns (RS,t) 1591 �0.010 0.716 �4.055 5.962

Panel B: Pre-crisis summary statisticsYG,t 1192 0.001 0.037 �0.245 0.359RG,t 1192 0.013 0.759 �3.064 4.411RP,t 1192 �0.026 1.121 �5.910 5.958RI,t 1192 0.008 0.672 �3.742 4.387RS,t 1192 �0.003 0.704 �4.055 5.289

Panel C: Post-crisis summary statisticsYG,t 398 0.051** 0.305 �2.000 1.349RG,t 398 �0.072 1.119 �3.669 4.639RP,t 398 �0.135** 1.221 �3.926 3.981RI,t 398 �0.061 0.862 �3.008 5.895RS,t 398 �0.032 0.749 �2.248 5.962

Pre-crisis Post-crisis

YG,t YG,t-1 YG,t YG,t-1

Panel D: Correlation between greek spread changes and financial firms’ excess returnsRG,t �0.189** �0.053* �0.428** �0.001RP,t �0.111** �0.017 �0.286** �0.018RI,t �0.270** �0.145** �0.375** �0.019RS,t �0.287** �0.067** �0.397** �0.057*

The overall sample period is 1/2005 to 6/2011 and is partitioned into two sub-samples: a pre-crisis period spanning 1/2005 to 10/2009 and a crisis period spanning 11/2009to 6/2011. Greek sovereign bond yield spreads are measured relative to the yields on similar maturity bonds for Germany. Financial sector excess returns are returns on theMSCI index of financial firms minus the returns on the country’s MSCI aggregate stock market index. All data are at the daily interval.* Significance at 10% level.** Significance at 5% level.

54 K. Bhanot et al. / Journal of Banking & Finance 38 (2014) 51–63

3. Methodology

To provide evidence of spillovers from the Greek debt crisis tothe financial and banking stocks of other countries, we estimatethe following system of equations for the conditional mean ofGreek, Italian, Portuguese, and Spanish financial firms’ stock re-turns Eq. (1) and changes in Greek bond yield spreads Eq. (2):

Ri;t ¼ bi0 þX3

L¼1

biLRi;t�L þX

j¼P;I;G;S;j–i

dijRj;t�1 þ biMMont þ biHHolt

þ biCCrisist þ /Yi;t þ kiYþG;t�1 þ ciGðY

þG;t�1 � CrisistÞ

þ giðGreek Debt Holdingsi;tÞ þ ei;t ð1Þ

YG;t ¼ bG0 þX3

L¼1

bGLYG;t�L þX

j¼P;I;G;S

dGjRj;t�1 þ bGMMont þ bGHHolt

þ bGCCrisist þ eY ;t: ð2Þ

In the conditional mean (Eq. (1)) Ri,t, where i = G, I, P, and S, is thedaily abnormal return on the index of the Greek, Italian, Portuguese,and Spanish financial firms, respectively. YG,t represents dailychanges in Greek yield spreads, while YþG;t represents the positivechanges in Greek yield spreads. Yi,t represents changes in countryi’s own bond yield spread. The models of abnormal returns in Eq.(1) are estimated as a function of the first three lags of the abnormalreturn to account for autocorrelation because untreated autocorre-lation can cause misspecification of the conditional variance mod-els. Also included is one lag of each of the other three abnormalreturns to capture any mean spillover between financial firmsacross countries.

Mon is a dummy variable defined as one on Mondays and zerootherwise to account for the fact that more information may be

released over the two-day weekend than on weekdays. Crisis is adummy variable defined as one during the Greek debt crisis, 11/2009 to the end of the sample. It should be noted that if one ofthe markets has a ‘holiday’, i.e., when it is closed for any tradingday other than the weekend, we delete the observations for theother markets. Hence, each market has exactly the same tradingdays. This approach is standard in the literature that uses dailydata in multivariate GARCH models to study volatility spillover(e.g., Karolyi (1995)). We define a dummy variable, Hol, as one aftera market holiday and zero otherwise.

To capture the impact of news spillovers we modify the aboveinteraction term by substituting news that pertains to Greeceand other countries, respectively, for the Crisis dummy variableas follows: biGðYþG;t�1 � Newst�1;NonGreekÞ þ ciGðY

þG;t�1 � Newst�1;GreekÞ

where Newst�1,j = Ratings, Bad, or Good. We conjecture that newsabout the probability of default and other macroeconomic condi-tions of the crisis countries have an effect on the extent of the rela-tionship between spreads and financial stock returns. The indicatorvariable Newst,j is defined as one on the date of an announcement,and zero otherwise. Creating this all-encompassing dummy fornon-Greek countries rather than country-specific dummies reflectsthe fact that while an announcement about a particular countryrepresents information about that country’s fundamentals it alsoserves as a potential source of news for all the other countries.The coefficient k tells us if an increase in Greek yield spreadsimpacts the abnormal returns in the pre-crisis period, while thecoefficient c indicates if the impact during the crisis is differentfrom that in the pre-crisis period after controlling for the impactof increased domestic bond spreads. That is, it is the differential(incremental) effect of a positive change in yield spreads duringthe crisis. Evidence of spillover requires that c < 0; i.e., that higheryield spreads lead to a decline in returns, beyond that of the mar-ket, during the crisis relative to the impact in the pre-crisis period.

Table 2Impact of changes in Greek yield spreads on financial firms’ excess returns.

i = Greece i = Portugal i = Italy i = Spain i = Greece (yield spread)

bi0 0.0608*** bi0 0.0087 bi0 0.0241* bi0 0.0133 bi0 �0.0006bi,1 0.0408* bi,1 0.0333 bi,1 0.0349 bi,1 0.096*** bi,1 0.1911bi,2 �0.0663*** bi,2 �0.03 bi,2 0.0142 bi,2 �0.0152 bi,2 0.004bi,3 �0.0462*** bi,3 �0.0193 bi,3 �0.001 bi,3 0.0102 bi,3 �0.0223dP �0.0022 dG �0.0096 dG �0.0344 dG �0.0287 dG �0.0003dI 0.0675** dI 0.0007 dP �0.0187 dP 0.0052 dP 0.0001dS �0.0027 dS 0.1062** dS 0.0454 dI 0.0427 dI �0.0017**

biC �0.1301*** biC �0.1242** biC �0.0659 biC �0.0567 dS 0.0006biM �0.0989*** biM 0.0384 biM 0.0066 biM �0.047 biC 0.0243***

biH �0.0525 biH �0.184 biH �0.049 biH 0.0533 biM 0.0004/ �1.1432*** / �3.2848*** / �2.2255*** biH 0.0095*

ki �0.1967 ki 3.0497* ki 0.8539 ki 0.7555ciG 0.3109 ciG �3.1631* ciG �0.8792 ciG �0.5317

The table reports parameter estimates of the model:

Ri;t ¼ bi0 þX3

L¼1

biLRi;t�L þX

j¼P;I;G;S;j–i

dijRj;t�1 þ biMMont þ biHHolt þ biC Crisist þ /Yi;t þ kiYþG;t�1 þ ciGðY

þG;t�1 � CrisistÞ þ ei;t

where Ri,t, i=G, I, P, and S, is the daily excess return on the index of the Greek, Italian, Portuguese, and Spanish financial stocks. Yi,t is the change in yield spread of country i;Mon (Hol) is a dummy variable defined as 1 on Mondays (after the reopening of the market after a close for any reason other than the weekend), and zero otherwise; Crisis is adummy variable defined as 1 during the Greek debt crisis 11/2009 to 06/2011, and zero otherwise; YþG;t�1 is 1 lag of positive changes in Greek yield spreads; and YþG;t�1 � Crisist

is an interaction term between the lagged positive changes in Greek yield spreads and the crisis variable. The full sample covers the period 1/2005 to 6/2011 and the crisisperiod is 11/2009 to 6/2011. All data are at the daily interval. The last column reports parameter estimates of the conditional mean of yield spread changes (Eq. 2).* Significance at 10% level.** Significance at 5% level.*** Significance at 1% level.

Table 3Accounting for Greek bond holdings in the impact of greek yield spread changes.

i = Greece i = Portugal i = Italy i = Spain i = Greece (yield spread)

bi0 0.0657** bi0 �0.4539** bi0 �0.0551 bi0 �0.0165 bi0 0.000bi,1 0.0493⁄ bi,1 0.0766*** bi,1 0.0252 bi,1 0.1019*** bi,1 0.2786***

bi,2 �0.0823*** bi,2 �0.0465*** bi,2 0.0047 bi,2 �0.0295* bi,2 �0.0335bi,3 �0.0739*** bi,3 �0.0363** bi,3 �0.0205 bi,3 0.0019 bi,3 �0.046dP 0.0209 dG �0.0429 dG �0.041 dG �0.0179 dG �0.0013dI 0.0351 dI 0.014 dP �0.0231 dP 0.0161 dP �0.0001dS �0.0029 dS 0.1119** dS 0.0829*** dI 0.0414 dI �0.0012biC �0.1337*** biC �0.1681* biC �0.0504 biC �0.0895** dS �0.0009biM �0.1405** biM 0.013 biC 0.0487 biM �0.0335 biC 0.0236***

biH 0.0594 biH �0.1856 biH �0.1557 biH �0.0778 biM 0.0002/ �1.2734*** / �3.2768*** / �1.9926*** biH 0.0191**

ki 0.2613 ki 4.1611*** ki 0.7944 ki 1.1348ciG �0.0546 ciG �4.3536*** ciG �0.7499 ciG �0.8799

gi 0.0001** gi 0.0000 gi 0.0000

The table reports parameter estimates of the model in Table 2 except for accounting for Greek debt holdings by financial firms in country i (Greek Debt Holdings):

Ri;t ¼ bi0 þX3

L¼1

biLRi;t�L þX

j¼P;I;G;S;j–i

dijRj;t�1 þ biMMont þ biHHolt þ biC Crisist þ /Yi;t þ kiYþG;t�1 þ ciGðY

þG;t�1 � CrisistÞ þ giðGreek Debt Holdingsi;tÞ þ ei;t

where Ri,t, i = G, I, P, and S, is the daily excess return on the index of the Greek, Italian, Portuguese, and Spanish financial stocks. Yi,t is the change in yield spread of country i;Mon (Hol) is a dummy variable defined as 1 on Mondays (after the reopening of the market after a close for any reason other than the weekend), and zero otherwise; Crisis is adummy variable defined as 1 during the Greek debt crisis, and zero otherwise; YþG;t�1 is 1 lag of positive changes in Greek yield spreads; and YþG;t�1 � Crisist is an interactionterm between the lagged positive changes in Greek yield spreads and the crisis variable. Due to the availability of Greek debt holdings, the sample covers the period 7/2007 to4/2011 and the crisis period is 11/2009 to 4/2011. All data are at the daily interval. The last column reports parameter estimates of the conditional mean of Greek yield spreadchanges Eq. (2).* Significance at 10% level.** Significance at 5% level.*** Significance at 1% level.

K. Bhanot et al. / Journal of Banking & Finance 38 (2014) 51–63 55

Eq. (2) specifies the changes in Greek yield spreads similar toabove, with the exception of the interaction terms.

We also include the contemporaneous change in the country’sown bond yield spread (Yi,t), except in the conditional mean forthe returns on Greek financial firms (where we assume that thelagged Greek yield spread is sufficient to control for this effect).9

9 We also estimate the crisis model (Eq. (1)) with the contemporaneous Greek yieldspreads in the Greek excess returns model. Its inclusion made no material differenceto the inferences below.

This captures any direct spillover from the domestic bond marketto the country’s financial sector. The bond market is one importantchannel of transmission of shocks to the financial sector, as we ex-plain in more detail later, which allows us to attribute the effect ofchanges in yield spreads on the financial sector to different channels.The Greek Debt Holdings variable captures the impact on returns viathe domestic holdings of Greek debt.

Eqs (1) and (2) of the above system could be estimated using or-dinary least squares. However, Forbes and Rigobon (2002) demon-strate that this is likely to lead to wrong inferences because it does

Table 4Impact of ratings downgrade announcements on financial stock excess returns.

i = Greece i = Portugal i = Italy i = Spain

bi0 0.0689** bi0 �0.4134** bi0 0.0023 bi0 �0.0374bi,1 0.0453* bi,1 0.0947*** bi,1 0.0253 bi,1 0.1018***

bi,2 �0.0802*** bi,2 �0.0436 bi,2 0.0026 bi,2 �0.0213bi,3 �0.0715*** bi,3 �0.0357 bi,3 �0.0176 bi,3 �0.0021dP 0.0247 dG �0.0434 dG �0.0397 dG �0.0107dI 0.0341 dI 0.0043 dP �0.0067 dP 0.0251dS �0.0083 dS 0.1075** dS 0.0977** dI 0.0323biC �0.1342*** biC �0.2607*** biC �0.0695 biC �0.1115**

biM �0.1389** biM 0.0271 biM 0.0291 biM �0.0427biH 0.0538 biH �0.2772 biH �0.1799 biH �0.0962

/ �1.5968 / 1.0054 / 2.442ki 0.2627 ki �0.0005 ki 0.0343 ki 0.4275biG 0.4698 biG 0.2356 biG �0.5726 biG �0.8105ciG �0.8073 ciG �0.684 ciG �0.4297 ciG �1.3001***

gi 0.0001** gi 0.0000 gi 0.0001

The table reports parameter estimates of the model:

Ri;t ¼ bi0 þX3

L¼1

biLRi;t�L þX

j¼P;I;G;S;j–i

dijRj;t�1 þ biMMont þ biHHolt þ biC Crisist

þ /Yi;t � Ratingt�1;NonGreek þ kiYþG;t�1 þ biGðYþG;t�1 � Ratingt�1;NonGreekÞ

þ ciGðYþG;t�1 � Ratingt�1;GreekÞ þ giðGreek Debt Holdingsi;tÞ þ ei;t

where Ri,t, i = G, I, P, and S, is the daily excess return on the index of the Greek,Italian, Portuguese, and Spanish financial stocks. Yi,t is the change in yield spread ofcountry i; Mon (Hol) is a dummy variable defined as 1 on Mondays (after thereopening of the market after a close for any reason other than the weekend), andzero otherwise; Crisis is a dummy variable defined as 1 during the Greek debt crisis,and zero otherwise; Rating is a dummy variable that is set to 1 if there is anannouncement of a downgrade of Greek debt and any other crisis country’s debt,respectively, and zero otherwise; YþG;t�1 is 1 lag of positive changes in Greek yieldspreads; YþG;t�1 � Ratingt is an interaction term between the lagged positive changesin Greek yield spreads and the particular Rating variable; and Greek Debt Holdings isGreek debt holdings by financial firms in country i. Due to the availability of Greekdebt holdings, the sample covers the period 7/2007 to 4/2011 and the crisis periodis 11/2009 to 4/2011. All data are at the daily interval. The parameter estimates ofthe conditional mean of Greek yield spread changes Eq. (2)) are omitted.* Significance at 10% level.** Significance at 5% level.*** Significance at 1% level.

Table 5Impact of bad news announcements on financial stock returns.

i = Greece i = Portugal i = Italy i = Spain

bi0 0.0690*** bi0 �0.4069*** bi0 0.0100 bi0 �0.0419bi,1 0.0470** bi,1 0.0903*** bi,1 0.0271 bi,1 0.1101***

bi,2 �0.0810*** bi,2 �0.0414* bi,2 0.0047 bi,2 �0.0196bi,3 �0.0736*** bi,3 �0.0331* bi,3 �0.0163 bi,3 �0.0061dP 0.0239 dG �0.0427 dG �0.0358 dG �0.0095dI 0.0330 dI 0.0086 dP �0.0098 dP 0.0238dS �0.0042 dS 0.1094** dS 0.0989*** dI 0.0296biC �0.1282*** biC �0.2471*** biC �0.0706 biC �0.0990**

biM �0.1420** biM 0.0152 biM 0.0225 biM �0.0547biH 0.0562 biH �0.2726⁄ biH �0.1821 biH �0.1038

/ �5.4621*** / �7.173*** / �8.5675***

ki 0.1868 ki �0.1906 ki �0.0107 ki 0.1683biG �2.2983 biG �0.8968 biG 0.3811 biG �2.881⁄ciG 0.2778 ciG 0.4622 ciG �0.2439 ciG 0.1839

gi 0.0001*** gi 0 gi 0.0001

The table reports parameter estimates of the model:

Ri;t ¼ bi0 þX3

L¼1

biLRi;t�L þX

j¼P;I;G;S;j–i

dijRj;t�1 þ biMMont þ biHHolt þ biC Crisist

þ /Yi;t � Badt�1;NonGreek þ kiYþG;t�1 þ biGðYþG;t�1 � Badt�1;NonGreekÞ

þ ciGðYþG;t�1 � Badt�1;GreekÞ þ giðGreek Debt Holdingsi;tÞ þ ei;t

where Ri,t, i = G, I, P, and S, is the daily excess return on the index of the Greek,Italian, Portuguese, and Spanish financial stocks. Yi,t is the change in yield spread ofcountry i; Mon (Hol) is a dummy variable defined as 1 on Mondays (after thereopening of the market after a close for any reason other than the weekend), andzero otherwise; Crisis is a dummy variable defined as 1 during the Greek debt crisis,and zero otherwise; Bad is a dummy variable that is set to 1 if there is anannouncement of bad news by the IMF, ECB, or other similar agencies about Greeceand other crisis countries, respectively, and zero otherwise; YþG;t�1 is 1 lag of positivechanges in Greek yield spreads; YþG;t�1 � Badt is an interaction term between thelagged positive changes in Greek yield spreads and the particular bad news vari-able; and Greek Debt Holdings is Greek debt holdings by financial firms in country i.Due to the availability of Greek debt holdings, the sample covers the period 7/2007to 4/2011 and the crisis period is 11/2009 to 4/2011. All data are at the dailyinterval. The parameter estimates of the conditional mean of Greek yield spreadchanges Eq. (2)) are omitted.* Significance at 10% level.** Significance at 5% level.*** Significance at 1% level.

56 K. Bhanot et al. / Journal of Banking & Finance 38 (2014) 51–63

not account for the change in volatility during the crisis. They notethat estimating the system using a GARCH model adequately ad-dresses this concern. Therefore, we specify the conditional variancefor each abnormal return i, where i = G, I, P, and S, respectively, andthe change in Greek yield spreads as follows:

r2e;i;t ¼ a0;i þ a1;ie2

i;t�1 þ bir2e;i;t�1 þ mi;MMont þ mi;HHolt

þ mi;CCrisist þ wi;1jYG;t�1j þ wi;2jYi;t�1j ð3Þ

rij;t ¼ qij �ffiffiffiffiffiffiffiffiffir2

e;i;t

q ffiffiffiffiffiffiffiffiffir2

e;j;t

qh i: ð4Þ

In Eq. (3) the conditional variance is a function of a constant, thelagged squared errors from the conditional mean model, laggedown variance, the Monday, market holiday, and crisis dummies aspreviously defined. The conditional variance of the abnormal re-turns also includes the Greek and own-country lagged absolutechange in yield spreads to account for exogenous shocks to volatil-ity.10 Finally, the conditional covariance between each pair in thesystem is estimated as a product of a constant correlation, qij, andthe standard deviations in the two markets Eq. (4).

10 All conditional variances for changes in Greek yield spreads were estimated asIGARCH models given concerns of weak-form non-stationarity in some cases. This isnot a major concern because our purpose is simply to account for changing varianceso as not to overstate the evidence of contagion, not to obtain estimates of theconditional variance for forecasting, where non-stationarity is of concern. Moreover,it should be noted that the IGARCH model can be strongly stationary although it is notweakly stationary (Nelson (1990)).

The changes in Greek yield spreads had a large negative outlieron May 10, 2010, the date the EU announced the €750 billion bail-out mechanism and so to ensure it does not overly influence ourresults, we truncate the change in yield spread throughout thesample and set the lowest return equal to -2%.

The above models are estimated using a quasi-maximum likeli-hood (QML) approach (Bollerslev and Woolridge, 1992). Hence thestandard errors are robust to the distribution (e.g., non-normality)of the errors. Additionally, the models are subject to several modeldiagnostics, such as tests for the presence of autocorrelation in themodel residuals, tests for the stationarity of the estimated condi-tional volatilities, and tests of the joint effect of the change inGreek yield spreads on the financial markets. The purpose of thesetests (which are not reported, but are available on request) is to en-sure that the estimated models are not misspecified and that thereis a high probability that the models converged at the globalmaximum.

4. Results

4.1. Preliminary evidence

We begin with an examination of the contemporaneous corre-lation between changes in Greek sovereign bond yield spreadsand the abnormal returns on financial stocks in the Eurozone crisiscountries, Greece, Italy, Portugal, and Spain, to determine if theyare different in the pre-crisis and crisis periods. This provides

Table 6Impact of good news announcements on financial stock returns.

i = Greece i = Portugal i = Italy i = Spain

bi0 0.0707** bi0 �0.3985* bi0 �0.0279 bi0 �0.026bi,1 0.0448* bi,1 0.0875*** bi,1 0.0326 bi,1 0.1093***

bi,2 �0.0843*** bi,2 �0.0429* bi,2 �0.0041 bi,2 �0.0274bi,3 �0.0738*** bi,3 �0.0315 bi,3 �0.0166 bi,3 �0.0039dP 0.0238 dG �0.0504 dG �0.0405* dG �0.0161dI 0.0298 dI 0.0205 dP �0.0101 dP 0.0241dS �0.0072 dS 0.1085** dS 0.1022*** dI 0.0315biC �0.1182** biC �0.2557*** biC �0.0785* biC �0.0938**

biM �0.143** biM 0.0229 biM 0.0288 biM �0.0492biH 0.059 biH �0.2854* biH �0.1770 biH �0.1011

/ �4.7296*** / �4.874*** / �8.1516***

ki �0.1165 ki 0.0866 ki 0.1180 ki 0.0142biG 0.1226 biG 7.8532* biG 6.0892*** biG �0.1666ciG 0.7267 ciG �3.4567*** ciG �1.954 ciG �0.9511

gi 0.0001* gi 0.0000 gi 0.0001

The table reports parameter estimates of the model:

Ri;t ¼ bi0 þX3

L¼1

biLRi;t�L þX

j¼P;I;G;S;j–i

dijRj;t�1 þ biMMont þ biHHolt þ biC Crisist

þ /Yi;t�1 � Goodt�1;NonGreek þ kiY�G;t�1 þ biGðY�G;t�1 � Goodt�1;NonGreekÞ

þ ciGðY�G;t�1 � Goodt�1;GreekÞ þ giðGreek Debt Holdingsi;tÞ þ ei;t

where Ri,t, i = G, I, P, and S, is the daily excess return on the index of the Greek,Italian, Portuguese, and Spanish financial stocks. Yi,t is the change in yield spread ofcountry i; Mon (Hol) is a dummy variable defined as 1 on Mondays (after thereopening of the market after a close for any reason other than the weekend), andzero otherwise; Crisis is a dummy variable defined as 1 during the Greek debt crisis,and zero otherwise; Good is a dummy variable that is set to 1 if there is anannouncement of good news by the IMF, ECB, or other similar agencies aboutGreece and other crisis countries, respectively, and zero otherwise; Y�G;t�1 is 1 lag ofnegative changes in Greek yield spreads; Y�G;t�1 � Goodt is an interaction termbetween the lagged negative changes in Greek yield spreads and the particular goodnews variable; and Greek Debt Holdings is Greek debt holdings by financial firms incountry i. Due to the availability of Greek debt holdings, the sample covers theperiod 7/2007 to 4/2011 and the crisis period is 11/2009 to 4/2011. All data are atthe daily interval. The parameter estimates of the conditional mean of Greek yieldspread changes Eq. (2) are omitted.* Significance at 10% level.** Significance at 5% level.*** Significance at 1% level.

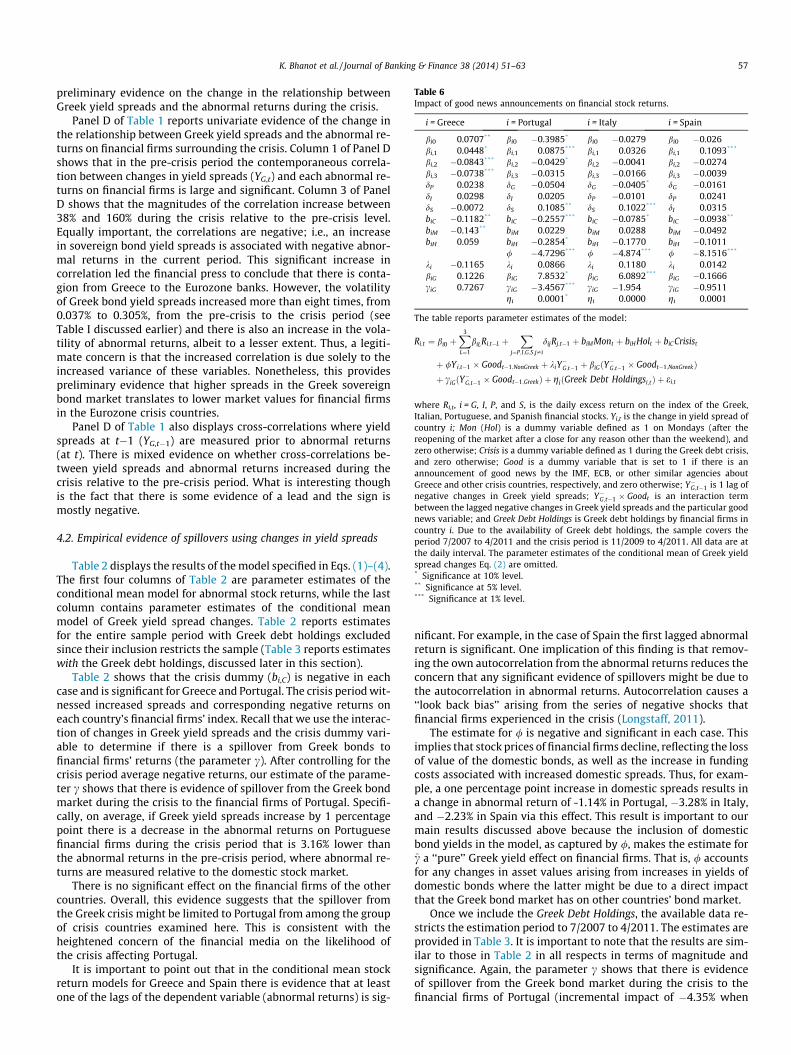

K. Bhanot et al. / Journal of Banking & Finance 38 (2014) 51–63 57

preliminary evidence on the change in the relationship betweenGreek yield spreads and the abnormal returns during the crisis.

Panel D of Table 1 reports univariate evidence of the change inthe relationship between Greek yield spreads and the abnormal re-turns on financial firms surrounding the crisis. Column 1 of Panel Dshows that in the pre-crisis period the contemporaneous correla-tion between changes in yield spreads (YG,t) and each abnormal re-turns on financial firms is large and significant. Column 3 of PanelD shows that the magnitudes of the correlation increase between38% and 160% during the crisis relative to the pre-crisis level.Equally important, the correlations are negative; i.e., an increasein sovereign bond yield spreads is associated with negative abnor-mal returns in the current period. This significant increase incorrelation led the financial press to conclude that there is conta-gion from Greece to the Eurozone banks. However, the volatilityof Greek bond yield spreads increased more than eight times, from0.037% to 0.305%, from the pre-crisis to the crisis period (seeTable I discussed earlier) and there is also an increase in the vola-tility of abnormal returns, albeit to a lesser extent. Thus, a legiti-mate concern is that the increased correlation is due solely to theincreased variance of these variables. Nonetheless, this providespreliminary evidence that higher spreads in the Greek sovereignbond market translates to lower market values for financial firmsin the Eurozone crisis countries.

Panel D of Table 1 also displays cross-correlations where yieldspreads at t�1 (YG,t�1) are measured prior to abnormal returns(at t). There is mixed evidence on whether cross-correlations be-tween yield spreads and abnormal returns increased during thecrisis relative to the pre-crisis period. What is interesting thoughis the fact that there is some evidence of a lead and the sign ismostly negative.

4.2. Empirical evidence of spillovers using changes in yield spreads

Table 2 displays the results of the model specified in Eqs. (1)–(4).The first four columns of Table 2 are parameter estimates of theconditional mean model for abnormal stock returns, while the lastcolumn contains parameter estimates of the conditional meanmodel of Greek yield spread changes. Table 2 reports estimatesfor the entire sample period with Greek debt holdings excludedsince their inclusion restricts the sample (Table 3 reports estimateswith the Greek debt holdings, discussed later in this section).

Table 2 shows that the crisis dummy (bi,C) is negative in eachcase and is significant for Greece and Portugal. The crisis period wit-nessed increased spreads and corresponding negative returns oneach country’s financial firms’ index. Recall that we use the interac-tion of changes in Greek yield spreads and the crisis dummy vari-able to determine if there is a spillover from Greek bonds tofinancial firms’ returns (the parameter c). After controlling for thecrisis period average negative returns, our estimate of the parame-ter c shows that there is evidence of spillover from the Greek bondmarket during the crisis to the financial firms of Portugal. Specifi-cally, on average, if Greek yield spreads increase by 1 percentagepoint there is a decrease in the abnormal returns on Portuguesefinancial firms during the crisis period that is 3.16% lower thanthe abnormal returns in the pre-crisis period, where abnormal re-turns are measured relative to the domestic stock market.

There is no significant effect on the financial firms of the othercountries. Overall, this evidence suggests that the spillover fromthe Greek crisis might be limited to Portugal from among the groupof crisis countries examined here. This is consistent with theheightened concern of the financial media on the likelihood ofthe crisis affecting Portugal.

It is important to point out that in the conditional mean stockreturn models for Greece and Spain there is evidence that at leastone of the lags of the dependent variable (abnormal returns) is sig-

nificant. For example, in the case of Spain the first lagged abnormalreturn is significant. One implication of this finding is that remov-ing the own autocorrelation from the abnormal returns reduces theconcern that any significant evidence of spillovers might be due tothe autocorrelation in abnormal returns. Autocorrelation causes a‘‘look back bias’’ arising from the series of negative shocks thatfinancial firms experienced in the crisis (Longstaff, 2011).

The estimate for / is negative and significant in each case. Thisimplies that stock prices of financial firms decline, reflecting the lossof value of the domestic bonds, as well as the increase in fundingcosts associated with increased domestic spreads. Thus, for exam-ple, a one percentage point increase in domestic spreads results ina change in abnormal return of -1.14% in Portugal, �3.28% in Italy,and �2.23% in Spain via this effect. This result is important to ourmain results discussed above because the inclusion of domesticbond yields in the model, as captured by /, makes the estimate forc a ‘‘pure’’ Greek yield effect on financial firms. That is, / accountsfor any changes in asset values arising from increases in yields ofdomestic bonds where the latter might be due to a direct impactthat the Greek bond market has on other countries’ bond market.

Once we include the Greek Debt Holdings, the available data re-stricts the estimation period to 7/2007 to 4/2011. The estimates areprovided in Table 3. It is important to note that the results are sim-ilar to those in Table 2 in all respects in terms of magnitude andsignificance. Again, the parameter c shows that there is evidenceof spillover from the Greek bond market during the crisis to thefinancial firms of Portugal (incremental impact of �4.35% when

58 K. Bhanot et al. / Journal of Banking & Finance 38 (2014) 51–63

Greek spreads increase by 1 percentage point). The estimate for /is again negative and significant in each case, and the Crisis dummy(bi,C) is significant except for the case of Italy.

Our next objective is to explore if and how news announce-ments affect the impact of changes in Greek yield spreads on finan-cial stock returns in each of these countries.

4.3. News spillovers

We examine how news affects the relationship betweenchanges in Greek yield spreads and financial firm returns – theinformation channel as a mechanism to transmit shocks. We mod-ify Eqs (1)–(4) by replacing the crisis dummy variable in the inter-action term with the news dummies described earlier. For instance,the model of abnormal returns when the news pertains to a creditrating announcement is:

Ri;t ¼ bi0 þX3

L¼1

biLRi;t�L þX

j¼P;I;G;S;j–i

dijRj;t�1 þ biMMont þ biHHolt

þ biCCrisist þ /Yi;t � Ratingt�1;NonGreek þ kiYþG;t�1

þ biGðYþG;t�1 � Ratingt�1;NonGreekÞ þ ciGðYþG;t�1 � Ratingt�1;GreekÞ

þ giðGreek Debt Holdingsi;tÞ þ ei;t ð5Þ

Table 4 reports the estimates of Eq. (5). It should be noted that therewere no upgrades in credit ratings for any of the countries in theEurozone during the crisis period. The results indicate that the crisisdummy (bi,C) is negative and significant in each case except for Italy.However, the parameter estimate for c shows that in Spain there isstrong evidence of spillovers from news about ratings downgrades.The differential effect of a one percentage point increase in Greekbond yield spreads during the crisis is �1.3% in Spain. This resultis both statistically and economically significant. These results indi-cate that, compared to the pre-crisis period, when there is anannouncement of a downgrade higher Greek bond yield spreadslead investors to significantly lower the stock prices of financialfirms from Spain on the following day even after accounting forholdings of Greek debt and increase in domestic funding costs.

Table 7Impact of changes in greek yield spreads on non-crisis countries’ financial firms.

i = Netherlands i = Austria i = Belgium

bi0 �0.0482 bi0 0.0269 bi0 0.04bi,1 �0.0005 bi,1 0.0396 bi,1 0.01bi,2 �0.0343* bi,2 �0.0507** bi,2 �0.01bi,3 �0.063*** bi,3 �0.0465** bi,3 �0.02dA 0.0465** dN �0.0278 dN �0.01dB 0.0130 dB �0.001 dA 0.03dF 0.0300 dF 0.0443 dF 0.00biC 0.1008 biC 0.0242 biC �0.04biM �0.0408 biM �0.0744⁄ biM 0.02biH �0.0714 biH �0.0823 biH �0.02

�0.3912 / �1.3808 / �1.47ki 2.2017 ki �1.5937 ki �0.53ciG �2.1516 ciG 1.6709 ciG 0.07gi 0.0000 gi 0.0000 gi 0.00

The table reports parameter estimates of the model:

Ri;t ¼ bi0 þX3

L¼1

biLRi;t�L þX

j¼P;I;G;S;j–i

dijRj;t�1 þ biMMont þ biHHolt þ biC Crisist þ /Yi;t þ kiYþG;t�1 þ

where i = N, A, B, and F, is the daily excess return on the index of the Netherlands, AustriaMon (Hol) is a dummy variable defined as 1 on Mondays (after the reopening of the markedummy variable defined as 1 during the Greek debt crisis, and zero otherwise; YþG;t�1 is 1term between the lagged positive changes in Greek yield spreads and the crisis variable. D4/2011 and the crisis period is 11/2009 to 4/2011. All data are at the daily interval. The laschanges Eq. (2).* Significance at 10% level.** Significance at 5% level.*** Significance at 1% level.

In Table 5 we report the results when the news announcementsare any type of bad news that emanates from multilateral agenciesor other organizations, using the following model:

Ri;t ¼bi0 þX3

L¼1

biLRi;t�L þX

j¼P;I;G;S;j–i

dijRj;t�1 þ biMMont þ biHHolt

þ biCCrisist þ /Yi;t � Badt�1;NonGreek þ kiYþG;t�1

þ biGðYþG;t�1 � Badt�1;NonGreekÞ þ ciGðYþG;t�1 � Badt�1;GreekÞ

þ giðGreek Debt Holdingsi;tÞ þ ei;t ð6Þ

The crisis dummy (bi,C) is significant in each case except Italy. Theinteraction term parameter estimates (c) however is not significant.Overall, this suggests that even though the general effect of higherGreek bond spreads on other countries’ financial firms during thecrisis is pervasive (crisis dummy is generally significant), therewas no spillover from unfavorable news from multilateral organiza-tions. Most of this negative reaction to negative news announce-ments is captured by the domestic bond market channel via theparameter / that is significant in each case.

Table 6 displays the results for the specification in which goodnews is interacted with negative changes in Greek yield spreads,Y�G;t�1:

Ri;t ¼bi0 þX3

L¼1

biLRi;t�L þX

j¼P;I;G;S;j–i

dijRj;t�1 þ biMMont þ biHHolt

þ biCCrisist þ /Yi;t�1 � Goodt�1;NonGreek þ kiY�G;t�1

þ biGðY�G;t�1 � Goodt�1;NonGreekÞ þ ciGðY�G;t�1 � Goodt�1;GreekÞ

þ giðGreek Debt Holdingsi;tÞ þ ei;t ð7Þ

The good news coefficient is �3.46% for Portugal. The negative coef-ficient implies that good news announcements, such as affirmationof a deal for the bailout of Greece and other such moves by the ECB,are accompanied by a positive abnormal return on financial stocksfor Portugal after controlling for holdings of Greek debt and thedomestic interest rate channel.

i = France i = Greece (yield spread)

19 bi0 0.0592** bi0 �0.001*

59 bi,1 0.0472 bi,1 0.1872***

98 bi,2 �0.0524*** bi,2 0.021292 bi,3 �0.0261 bi,3 �0.032986 dN �0.0179 dN �0.001802** dA 0.0315 dA �0.000376 dB 0.0436 dB 0.000432 biC �0.0313 dF 0.000443 biM �0.0924** biC 0.0247***

44 biH �0.0311 biM 0.000841*** / �1.8983⁄ biH 0.004624 ki 1.039184 ciG �1.042300 gi 0.0000

ciGðYþG;t�1 � CrisistÞ þ giðGreek Debt Holdingsi;tÞ þ ei;t

n, Belgian, and French financial stocks. Yi,t is the change in yield spread of country i;t after a close for any reason other than the weekend), and zero otherwise; Crisis is alag of positive changes in Greek yield spreads; and YþG;t�1 � Crisist is an interaction

ue to the availability of Greek debt holdings, the sample covers the period 1/2005 tot column reports parameter estimates of the conditional mean of Greek yield spread

Table 8Impact of ratings downgrade announcements on non-crisis financial firms.

i = Netherlands i = Austria i = Belgium i = France

bi0 �0.0502 bi0 0.0345 bi0 0.0344 bi0 0.0590**

bi,1 �0.0035 bi,1 0.0419** bi,1 0.0136 bi,1 0.0476bi,2 �0.0367** bi,2 �0.0503*** bi,2 �0.0228* bi,2 �0.0528***

bi,3 �0.0625*** bi,3 �0.0469*** bi,3 �0.0319* bi,3 �0.0254dA 0.0450 dN �0.0256*** dN �0.0185 dN �0.0197dB 0.0104 dB �0.0024 dA 0.0313** dA 0.032dF 0.0296 dF 0.0464** dF 0.0088 dB 0.0443biC 0.0723 biC 0.0281 biC �0.0527 biC �0.0415

K. Bhanot et al. / Journal of Banking & Finance 38 (2014) 51–63 59

In summary, the evidence indicates that financial firms in Por-tugal and Spain experience economically large and statistically sig-nificant incremental negative abnormal returns during the Greekdebt crisis given an increase in Greek yield spreads, especially ondays with unfavorable news announcements related to Greece.On the other hand, good news results in a positive return for Por-tugal. Collectively, the news channel (especially ratings down-grades and good news) is a transmission channel as investors inPortugal and Spain incorporated the impact of the new informationinto their evaluation of domestic financial stock prices.

biM �0.0379 biM �0.0757 biM 0.0232 biM �0.0902**

biH �0.0762 biH �0.0835 biH �0.025 biH �0.0318/ �38.6829** / �1.3863 / �8.8214* / �12.5114ki 0.5117 ki 0.0775 ki �0.2032 ki 0.0814biG �1.434** biG �0.6066 biG �1.6238*** biG �0.2653ciG �1.199** ciG 0.3484* ciG �0.052 ciG �0.2446gi 0.0000 gi 0.0000 gi 0.0000 gi 0.0000

The table reports parameter estimates of the model:

Ri;t ¼ bi0 þX3

L¼1

biLRi;t�L þX

j¼P;I;G;S;j–i

dijRj;t�1 þ biMMont þ biHHolt þ biC Crisist

þ /Yi;t � Ratingt�1;NonGreek þ kiYþG;t�1 þ biGðYþG;t�1 � Ratingt�1;NonGreekÞ

þ ciGðYþG;t�1 � Radingt�1;GreekÞ þ giðGreek Debt Holdingsi;tÞ þ ei;t

where Ri,t, i = N, A, B and F, is the daily excess return on the index of the Netherlands,Austrian, Belgian, and French financial stocks. Yi,t is the change in yield spread ofcountry i; Mon (Hol) is a dummy variable defined as 1 on Mondays (after thereopening of the market after a close for any reason other than the weekend), andzero otherwise; Crisis is a dummy variable defined as 1 during the Greek debt crisis,and zero otherwise; Rating is a dummy variable that is set to 1 if there is anannouncement of a downgrade of Greek debt and any other crisis country’s debt,respectively, and zero otherwise; YþG;t�1 is 1 lag of positive changes in Greek yieldspreads; YþG;t�1 � Ratingt is an interaction term between the lagged positive changesin Greek yield spreads and the particular Rating variable; and Greek Debt Holdings isGreek debt holdings by financial firms in country i. Due to the availability of Greekdebt holdings, the sample covers the period 1/2005 to 4/2011 and the crisis periodis 11/2009 to 4/2011. All data are at the daily interval. The parameter estimates ofthe conditional mean of Greek yield spread changes Eq. (2) are omitted.* Significance at 10% level.** Significance at 5% level.*** Significance at 1% level.

4.4. Economic rationale for cross-market linkages

In general, any evidence of spillovers can result from economiclinkages between Greece and the financial firms of other Eurozonecountries. As such, the evidence of spillover needs to be examinedin the context of these fundamental linkages. First, banks in theEurozone crisis countries (Greece, Italy, Portugal, and Spain) mayhave direct holdings of Greek sovereign debt on their books. A neg-ative news announcement impairs the value of Greek bonds and,therefore, bank assets, resulting in a negative return to the residualstock holders. Second, the news has information for other countriesbecause it may imply similar outcomes for other Eurozone countriesthat face fiscal constraints. Thus, news about a ratings downgrade ofGreece implies that, for example, Portugal will be more likely to bedowngraded were it to face similar circumstances. This in turn leadsto an upward spike in interest rates in Portugal and a correspondingdepreciation in asset values of financial institutions. Third, higherrates translate into larger funding costs for the financial institutions.

Our model estimates the impact of these channels. We includequarterly holdings data in the specification via the variable Greekdebt holdings. When included in our models the estimates are notsignificant, except for the case of Portugal (e.g., last line ofTable 5).11 While such aggregate holdings of Greek debt are pub-lished by the ECB, the net exposures are difficult to ascertain becausea part of these holdings are hedged using derivatives or via othermeans.

Our specification also includes the change in the country’s ownbond yield spread—the parameter / captures any direct spilloverfrom the Greek bond market to the country’s stock market via in-creases in the spreads of the domestic bond market. Moreover, wealso allow for own-country (non-Greek) news to affect the domes-tic funding cost. This domestic bond market channel for the trans-mission of shocks to the financial sector is significant in themajority of the tests discussed. For example, Table 5 shows thatan increase in domestic spreads after bad news announcementspartly accounts for the impact on the domestic financial stocks:the parameter estimate / of �5.46, �7.17, and �8.57 for the caseof Portugal, Italy, and Spain are each significant. Thus, we corrobo-rate the transmission channel of domestic funding and interestrates on financial sector returns. The European Banking Authorityconducted stress tests12 from 2009 onwards to assess the abilityof each bank to withstand shocks to yields. Bank-by-bank data showthat the capital ratios for Greece, Italy, Portugal, and Spain are lowerthan those of other Eurozone countries and their asset impairmentwould result in large write-downs in the value of their assets. Ourtests are consistent with these tests.

11 It should be noted that our main goal is to use Greek debt holdings as a controlvariable to ensure that evidence of spillover is not a proxy for the effect of impairedGreek bonds on financial firms’ returns. Hence, for ease of estimation, we do not allowfor the possibility that the coefficient estimate could change sign in the pre-crisis andcrisis periods. The positive coefficient estimate may be because Greek debt holdingshave a positive effect on financial firms’ returns during the pre-crisis period and thisdominates any negative effects during the crisis.

12 See http://www.eba.europa.eu/EU-wide-stress-testing.

Having accounted for the above channels we still find strongevidence of spillover from increasing Greek yield spreads duringthe crisis. This suggests that the spillover effect is greater thancan be justified by these reasons.

4.5. Was there a spillover to the non-crisis countries?

The financial press speculated that the Greek crisis might affectmarkets that are not a part of the crisis countries. For instance, theFinance Minister of Belgium expressed concern that the Greek debtcrisis could spread to Belgium and France. As noted earlier, such ef-fects might arise when either the government-led banks or theirprivate banks are exposed to Greek debt and the capital buffersare not large enough. For instance, France has the largest exposureto Greek debt among all countries; nearly double that of Germany,for instance, as reported on the ECB web site. This exposure is dueto both its private sector banks as well as from the stakes held bygovernment entities. Some of the largest French banks (BNP Pari-bas, Crédit Agricole, and Société Générale) were threatened withratings downgrades as a result of their Greek debt holdings. Banksfrom Austria, Belgium, and the Netherlands were less exposed toGreek debt. When this exposure is coupled with a country’s owndebt burden, it is possible that uncertainty in Greece could causeyields to rise in these other countries.13

13 See http://www.forex-news.co/belgian-finance-minister-greek-debt-crisis-could-spread-to-france.html for the Finance Minister’s comment and ‘‘The countries mostexposed to Greek debt,’’ The Telegraph, 15 Jun 2011.

Table 9Impact of bad news announcements on non-crisis financial firms.

i = Netherlands i = Austria i = Belgium i = France

bi0 �0.0544 bi0 0.0287 bi0 0.0368 bi0 0.0598*

bi,1 0.0027 bi,1 0.0391** bi,1 0.0120 bi,1 0.0428bi,2 �0.0355*** bi,2 �0.049*** bi,2 �0.0202 bi,2 �0.0536����

bi,3 �0.0642*** bi,3 �0.045*** bi,3 �0.0319 bi,3 �0.0257**

dA 0.0445** dN �0.0233 dN �0.0131 dN �0.0147dB 0.0078 dB �0.0075 dA 0.0304 dA 0.0316dF 0.0267 dF 0.0451 dF 0.0056 dB 0.0408biC 0.0943 biC 0.0401 biC �0.0345 biC �0.0392biM �0.0415 biM �0.0788 biM 0.0213 biM �0.0931*

biH �0.0749 biH �0.0898 biH �0.0264 biH �0.0342�119.6834 / �30.1645* / �13.8445*** / �42.5261***

ki 0.3758 ki 0.0444 ki �0.4032 ki 0.1279biG �7.5500*** biG �10.2813*** biG �6.5740** biG �1.4943ciG �1.373 ciG 0.0491 ciG �0.4390 ciG �0.5871gi 0.0000 gi 0.0000 gi 0.0000 gi 0.0000

The table reports parameter estimates of the model:

Ri;t ¼ bi0 þX3

L¼1

biLRi;t�L þX

j¼P;I;G;S;j–i

dijRj;t�1 þ biMMont þ biHHolt þ biC Crisist þ /Yi;t � Badt�1;NonGreek þ kiYþG;t�1 þ biGðYþG;t�1 � Badt�1;NonGreekÞ þ ciGðY

þG;t�1 � Badt�1;GreekÞ

þ giðGreek Debt Holdingsi;tÞ þ ei;t

where Ri,t, i = N, A, B and F, is the daily excess return on the index of the Netherlands, Austrian, Belgian and French financial stocks. Yi,t is the change in yield spread of country i;Mon (Hol) is a dummy variable defined as 1 on Mondays (after the reopening of the market after a close for any reason other than the weekend), and zero otherwise; Crisis is adummy variable defined as 1 during the Greek debt crisis, and zero otherwise; Bad is a dummy variable that is set to 1 if there is an announcement of bad news by the IMF,ECB, or other similar agencies about Greece and other crisis countries, respectively, and zero otherwise; YþG;t�1 is 1 lag of positive changes in Greek yield spreads; YþG;t�1 � Badt

is an interaction term between the lagged positive changes in Greek yield spreads and the particular bad news variable; and Greek Debt Holdings is Greek debt holdings byfinancial firms in country i. Due to the availability of Greek debt holdings, the sample covers the period 1/2005 to 4/2011 and the crisis period is 11/2009 to 4/2011. All dataare at the daily interval. The parameter estimates of the conditional mean of Greek yield spread changes Eq. (2) are omitted.* Significance at 10% level.** Significance at 5% level.*** Significance at 1% level.

Table 10Impact of good news announcements on non-crisis financial firms.

i = Netherlands i = Austria i = Belgium i = France

bi0 �0.0458 bi0 0.0436 bi0 0.0313 bi0 0.0592**

bi,1 �0.0069 bi,1 0.0405* bi,1 0.0159 bi,1 0.0476bi,2 �0.0366*** bi,2 �0.0484*** bi,2 �0.0150 bi,2 �0.0506***

bi,3 �0.0616*** bi,3 �0.0475*** bi,3 �0.0260** bi,3 �0.0232dA 0.0454 dN �0.0268*** dN �0.0163 dN �0.0213dB 0.0088 dB 0.0011 dA 0.0310** dA 0.0332dF 0.0287 dF 0.0475⁄ dB 0.0065 dB 0.0417biC 0.0656 biC 0.0304 biC �0.1258 biC �0.0534biM �0.039 biM �0.0747 biM 0.0226 biM �0.0915**

biH �0.0673 biH �0.0848 biH �0.0238 biH �0.028/ �6.1869 / �29.6157 / �18.2807*** / �15.6899ki �0.5208 ki 0.0821 ki �0.5311* ki �0.2379biG 0.0065 biG 4.6652 biG 3.5246** biG 8.2322***

ciG �1.3784 ciG �1.6335** ciG �2.4133* ciG �1.8098gi 0.0000 gi 0.0000 gi 0.0000 gi 0.0000

The table reports parameter estimates of the model:

Ri;t ¼ bi0 þX3

L¼1

biLRi;t�L þX

j¼P;I;G;S;j–i

dijRj;t�1 þ biMMont þ biHHolt þ biC Crisist þ /Yi;t�1 � Goodt�1;NonGreek þ kiY�G;t�1 þ biGðY�G;t�1 � Goodt�1;NonGreekÞ þ ciGðY

�G;t�1 � Goodt�1;GreekÞ

þ giðGreek Debt Holdingsi;tÞ þ ei;t

where Ri,t, i = N, A, B, and F, is the daily excess return on the index of the Netherlands, Austrian, Belgian, and French financial stocks. Yi,t is the change in yield spread of countryi; Mon (Hol) is a dummy variable defined as 1 on Mondays (after the reopening of the market after a close for any reason other than the weekend), and zero otherwise; Crisis isa dummy variable defined as 1 during the Greek debt crisis, and zero otherwise; Good is a dummy variable that is set to 1 if there is an announcement of good news by theIMF, ECB, or other similar agencies about Greece and other crisis countries, respectively, and zero otherwise; Y�G;t�1 is 1 lag of negative changes in Greek yield spreads;Y�G;t�1 � Goodt is an interaction term between the lagged negative changes in Greek yield spreads and the particular good news variable; and Greek Debt Holdings is Greek debtholdings by financial firms in country i. Due to the availability of Greek debt holdings, the sample covers the period 1/2005 to 4/2011 and the crisis period is 11/2009 to 4/2011. All data are at the daily interval. The parameter estimates of the conditional mean of Greek yield spread changes Eq. (2) are omitted.* Significance at 10% level.** Significance at 5% level.*** Significance at 1% level.

60 K. Bhanot et al. / Journal of Banking & Finance 38 (2014) 51–63

Tables 7–10 provide model parameter estimates for each of thefour models estimated above for the non-crisis countries-Austria,Belgium, France, and the Netherlands. While our parameter

estimates for the crisis model (Table 7) indicate that there are nosignificant news spillovers generally during the crisis period, thereis some evidence of spillovers due to ratings downgrades, bad

K. Bhanot et al. / Journal of Banking & Finance 38 (2014) 51–63 61

news, and good news announcements. For example, the crisismodel in Table 7 shows that the crisis dummy (bi,C) is insignificantin each of the four cases (this is also the case for Tables 8–10). Sim-ilarly, the parameter estimates of the change in Greek yieldspreads, c, in Table 7 are also insignificant. However, when thereare announcements of Greek bond downgrades (Table 8) and badnews about the Greek economy from the multilateral agencies (Ta-ble 9) the parameter estimates for c are significant and economi-cally large (�1.20% and �1.37%) in the case of the Netherlands.Likewise, there is evidence of significant spillovers to Austria andBelgium when there is good news about Greece from the multilat-eral agencies.

Overall, there is evidence that the Greek debt crisis spilled overto, and had a negative effect on the abnormal returns of, the finan-cial firms of the non-crisis countries in our sample. These resultscannot be attributed in total to the cross holdings of Greek bondsor higher domestic funding costs, even though there is some indi-cation that own-country bad news increased the impact of positivechanges in Greek yield spreads.

4.6. Other evidence and extensions

During the crisis investors might have become concerned notonly about changes in the probability of default as measured bychanges in the yield spread, but also about the uncertainty withwhich this was evolving. One way that this uncertainty is mani-fested is in the volatility of the changes in Greek yield spreads.Consistent with models of investor uncertainty and stock returns(Veronesi, 1999 and others), if in periods of high uncertainty inves-tors in financial firms frequently revise and update their estimatesof the risk involved in holding these firms, then we should observea negative relationship between the volatility of changes in yieldspreads and the value of financial firms. We replace YþG;t in the crisismodel (Eq. (1) in Table 3) with an estimate of the conditional var-iance of the positive errors from the conditional mean model of thechanges in Greek yield spreads as a proxy for this uncertainty. Thisis consistent with common practice (see, e.g., Elder and Serletis,2010 and references therein). The evidence indicates that theuncertainty about the changes in Greek bond yields has a negativeeffect on the financial firms of the crisis countries. The results indi-cate that all coefficient estimates are negative (we do not includethese tables). However, only the Italian and Portuguese financialfirms display a statistically significant negative abnormal return gi-ven an increase in the variance of Greek bond yield spreads. Specif-ically, a one unit increase in the variance of yield spreads leads toan abnormal return of �8.23 and �14.66% on the index of theItalian and Portuguese financial firms. We do not find statisticallysignificant evidence of spillover for the non-crisis countries.

5. Conclusions

In this paper we examine whether news about the sovereigndebt crisis in Greece led to spillovers in the banking and financialsectors (financial firms) in Greece, Italy, Portugal, and Spain. Wedefine a spillover as an event where increases in Greek yieldspreads lead to negative abnormal returns on an index of financialfirms in another country. The sample period is from 01/2005 to 06/2011, with the crisis being the period 11/2009 to the end of thesample.

Using a multivariate GARCH model containing a conditionalmean model of the returns for each of the index of financial firmsand changes in Greek yield spreads, we find significant evidence ofspillovers. We find that on the days when there areannouncements of Greek ratings downgrades or when there isgenerally good news from the IMF or other multilateral agencies,

there is a substantial increase in the spillover from the Greek bondmarket after we control for other channels of transmission. Thus,news announcements provide additional and unique cues to inves-tors on the future outcomes for the financial sector in theEurozone.

Our analysis also sheds light on the different means by whichnew information about potential default of the Greek debt is incor-porated in the prices of financial firms in the Eurozone countries.We find evidence of direct spillover from the Greek bond marketto other country stock markets via increases in the spreads of thedomestic bond market. Thus, we corroborate the transmissionchannel of domestic funding and interest rates on financial sectorreturns. Collectively, our results help uncover the extent of eco-nomic linkages across the Eurozone countries. Our key finding isthat news events lead to spillover in excess of what can be ex-plained by the other channels of transmission.

Acknowledgements

We thank the anonymous referee, Warren Bailey, Paul Irvine,Andrew Karolyi, and seminar participants at FMA 2011 andEuropean FMA 2012 for helpful comments.

Appendix A. All news announcements

These news announcements are from ‘‘A Euro Crisis DealEmerges’’, Wall Street Journal, December 2, 2011.

Date

Text20091004

The Socialist party, Pasok, wins early elections inGreece. George Papandreou becomes primeminister20091020

Greek government takes office and embarks on anausterity plan to begin to bring its debt burdendown by 201220091022

Rating agency Fitch lowers its rating on Greece toA minus from A20091029

Moody’s considers possible downgrade of Greekcurrency rating20091119

Portugal raises its 2009 budget deficit forecast to8% of GDP from its previous forecast of 5.9% ofGDP20091207

S&P lowers outlook on Portugal’s A plus rating toA minus20091208

Fitch downgrades Greece to BBB+ with a negativeoutlook20091209

S&P lowers its rating on Spain to negative 20091216 S&P cuts Greece’s bond rating to BBB+ from Aminus

20091222 Moody’s Investors Services downgrades Greece’sdebt only one notch down A1 to A2

20090115 Portugal treasury puts statement to reassureinvestors that the government is committed todeficit reduction

20010120

Portugal government said it would freezegovernment wages and reduce payrolls20100126

Greece prepares to sell at least 1.5 billion ($) inglobal bonds due to weak European demand20100126

Portugal reports a higher-than-expected budgetdeficit of 9.4% of GDP20100128

Greek–German 10 year spreads surges to a newrecord of 405 basis points, exceeding 400 basispoints for the first time(continued on next page)

62 K. Bhanot et al. / Journal of Banking & Finance 38 (2014) 51–63

Appendix A. (continued)

Date

Text20100129

Greek finance minister denies involvement in anEmergency EU bailout plan for Greece20100129

Spain says 2009 budget deficit was higher thanexpected at 11.4% of GDP, unveils new deficitreduction measures20100202

The Greek government outlines spending cuts andmeasures to boost tax revenue in a bid to pare thebudget deficit to 3%20100203

The EU endorses Greece’s austerity program 20100203 Spain raises budget deficit forecasts to 9.8% ofGDP in 2010, 7.5% of GDP in 2011, 5.4% in 2012,and 3% in 2013

20100209

Germany considers a plan with its EU partners tooffer Greece and other Euro-zone members loanguarantees20100211

EU president says European leaders have reacheda deal on helping Greece with a debt crisis20100215

Fellow Euro-zone countries will give Greece onemonth to show it can right its unbalanced budget20100217

The Spanish government gets a boost with a new$6.9 billion bond issue that is well received byinvestors20100223

Fitch downgrades the country’s four major banksto BBB. Fitch characterizes its outlook for Greenbanks as ‘‘negative’’20100303

The Greek government announces a new austerityplan that will yield E4.8 billion in savings20100304

ECB president calls for more IMF involvement inGreece20100304

Greece raises some cash with a new bond issuethat was 3 times oversubscribed with $20.5billion nine offers received20100305

German PM avoids giving Greece a commitmentof financial assistance20100307

French President Nicolas Sarkozy says a numberof EU countries are preparing a support packagefor Greece20100308

Portugal’s government announces new budgetcuts, inducing a ramped-up privatization plan20100309

Greek announces that it has not sought help fromAmerica20100311

Greek protests and strikes begin 20100316 Greece avoids a downgrade by S&P – plans toreduce its deficit was supportive of the nationscurrent BBB+ long-term credit rating

20100318

Greece requests EU leaders to agree to a packageof standby loans20100322

Spain reaches a broad agreement on cost-savingmeasures with Spain’s regional governments20100324

Fitch lowers Portugal’s sovereign credit rating onenotch to AA minus20100325

The ECB announces that it will continue to acceptbonds with ratings as low as BBB minus ascollateral next year20100325

Leaders of 16 Euro-zone nations back a deal underwhich they and the IMF would jointly bail outGreece20100331

About 50,000 people take to the streets to protestausterity plans, amid a nationwide general strikeAppendix A. (continued)

Date

Text20100409

Fitch cuts its rating for Greece by two notches toBBB minus from BBB+: outlook remains negative20100411

Finance ministers from the 16-nation Euro-zoneagree that Greece can borrow up to E30 billion20100422

The EU statistical agency says that the Greekbudget deficit in 2009 was wider than thegovernment has estimated20100422

Moody’s lowers Greece’s government bond ratingfrom A2 to A3 and says further downgradespossible20100423

Greece begins announcing aid requests from EUcountries and the IMF20100427

S&P cuts its ratings on Greece into Junk territory 20100427 S&P cuts its rating on Portugal by two notches toA minus

20100428 S&P downgrades Spain’s long-term credit ratingto AA with a negative outlook

20100429 Greece agrees with the IMF and EU to takeadditional austerity measures

20100502 Greece reaches a deal with other Euro-zonecountries and the IMF for a huge bailout

20100505 Moody’s placed Portugal under review for adowngrade due to sovereign-debt fears

20100505 Three people die in violent street protests inAthens

20100507 Germany’s Lower House passes the Greek bailoutbill granting approximately $28.3 billion in loans

20100512 Spain announces that it will cut public-sectorwages by 5% this year (2010) and freeze them fornext year (2011)

20100513

Portugal approves tax increases and salaryreductions for politicians and other publicemployees20100519

Spain raises taxes for high-income earners 20100529 Fitch removes Spain’s triple-A credit rating,dropping it by a notch to double-A-plus

20100614 Moody’s cuts its rating on Greece into junkterritory

20100713 Moody’s downgrades Portugal’s government-bond rating to A1 from Aa2

20100930 Moody’s downgrades Spain’s credit rating by onenotch to Aa1.

20110114 Fitch lowers Greece’s rating to BB+ 20110225 Center-right Fine Gael party wins most seats inParliament but falls short of securing an overallmajority

20110307

Moody’s cuts Greece’s credit rating to B1 from Ba1 20110307 Fine Gael, Labor parties form a coalitiongovernment. Enda Kenny to be voted primeminister

20110310

Moody’s lowers Spain’s rating to Aa2 20110311 EU leaders agree on rules for a permanent, €500billion bailout fund

20110315 Portugal’s government collapses in a fight overausterity measures

20110329 S&P’s cuts Greece’s rating to double-B-minus fromdouble-B-plus

20110329 S&P’s cuts Portugal’s rating to triple-B-minusfrom triple B

K. Bhanot et al. / Journal of Banking & Finance 38 (2014) 51–63 63

Appendix A. (continued)

Date

Text20110401