NBFCS DRIVE ON MULTIPLE FRONTS - Banking Frontiers

56

NBFCS DRIVE ON MULTIPLE FRONTS Vol. 20 No. 8 December 2021 `75 Pages 56 www.bankingfrontiers.com www.bankingfrontiers.live Turtlemint pg 6 Indian Bank pg 14 Future Generali pg 24 JM Financial pg 33 NABARD pg 38

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of NBFCS DRIVE ON MULTIPLE FRONTS - Banking Frontiers

DIGITAL TRANSFORMATION

NBFCs DRIVE

ON MULTIPLE FRONTS

Vol. 20 No. 8 December 2021 `75

Pages 56

www.bankingfrontiers.comwww.bankingfrontiers.live

Turtlemint pg 6

Indian Bank pg 14

Future Generali pg 24

JM Financial pg 33

NABARD pg 38

Presents

The Pandemic aftereffects are slowly fading and the economies are rising. There is a new optimism in the air, newer opportunities. Organisations are now stepping up the gas on growth by hiring more, investing more and experimenting more.

One of the most important boon is the quick transformation into the world of digital. The world of remote meetings, remote events, remote customer onboarding, servicing and the acceptance to a world of digital possibilities and innovations.

It is in the midst of these possibilities that Banking Frontiers presents its 11th Finnoviti and 8th Technoviti Awards and Conclave 2022 with the Theme: Innovate to Accelerate.

This is going to be a two-day conference which will be followed by the Technoviti Awards on Day 1 for Financial technology and Fintech innovations and Finnoviti Awards and Conclave for Financial Services and Technology Innovations.

Innovate to Accelerate will cover interesting themes around: Ecosystem building, Global expansions, Digital Acceleration, Investments, Trending technologies and much more.

Join us in Co-creating, Co-innovating and Rediscovring the growth of the financial services which is accelerating itself to newer growth trajectories. Join the Finnoviti & Technoviti 2022 conference, Share your nomination with us, meet up with your potential partners and customers and Engage, en-roll and transact. In short with Finnoviti, Technoviti the twin carnival of innovations, you can Innovate to Accelerate.

For details contact us

ASHISH VERMA +91 - 98332 36943 [email protected]

STALIN SALDHANA +91 - 91677 94513 [email protected]

Call for Nominations!

2022

BANKING FRONTIERS

THEMEINNOVATE TO ACCELERATE

K N O W L E D G E P A R T N E R

Virtual Summit l 6th March 2022

Banking Frontiers December 2021 3

Editor’s BlogManoj AgrawalMobile : 98673 66111Email : [email protected]

December 2021 - Vol. 20 No. 8

Group Publisher : Babu Nair

Group Editor : Manoj Agrawal

Editor : N. Mohan

Editorial Mehul Dani, Ravi Lalwani, Aditya Arya

Research Editors V. Babu, Ratnakar Deole, W.A. Wijewardena, Sanchit Gogia, K.C. Shashidhar, Dr L.S. Subramanian, Ajay Kumar

Advisor-Alliances Ateeq Siddique

Marketing Kailash Purohit, Wilhelm Singh, Dhara Thobani, Rohit Kahar,

Events & Operations Shirish Joshi, Stalin Saldhana, Pramod Jadhav, Ashish Verma, Ramesh Vishwakarma, Sushant Tulapurkar

Design Somnath Roy Choudhury, Sudarshan Herle

Published By Glocal Strategies & Services D-312, Twin Arcade, Military Road, Marol, Andheri (E), Mumbai 400059, India. Tel: +91-22-29250166 / 29255569 Fax: +91-22-29207563

Printed & Published by Babu Nair on behalf of Glocal Strategies & Services and Printed at Indigo Presss (India) Pvt Ltd., Plot No. 1C/716, Off Dadoji Konddeo Cross Road, Between Sussex and Retiwala Indl.Estate, Byculla (E), Mumbai 400027.

Editor: Manoj Agrawal (Responsible for selection of news under PRB Act)

Throughout the year, I have written about business and technology and risk and compliance and more. Since this is the year end, let me look at people in this final edit.

2021 has no doubt been a disaster in many ways for many p e o p l e . W i t h o u t dwelling further, I also observe that it has been a tide that has lifted many people.

The talent demand has grown dramatically during the year, especially in some key areas like cybersecurity, data science, machine learning, payments, open banking, risk management and many others. All these areas have experienced a rapid level of growth and transformation, which is being powered only by human intellect. This tide has lifted those who are already in these areas and those have joined in recently.

Another interesting development is that more and more people are going ahead and doing short term courses to augment their knowledge and advance their careers. I see more and more posts on Linkedin where people post what new course they have done and got certified. This is a good indication that there will not be a situation of an extreme talent crunch in the years ahead. For institutes and organizations offering such courses, this a fertile ground. Banking Frontiers too offered a couple of master classes on AI in Financial Services. We hope to scale up these master classes further in 2022.

One area where most large financial organizations are hiring is at the frontline. Organizations that have a large customer base and are looking to expand further, are boosting their fontline workforce to acquire new customers and to cross-sell to existing customers. Technology helps engage with the tech savvy customers, but for the masses, a first-time purchase of an insurance policy or a mutual funds or a home loan will not be a click-click-click process. Even for the tech savvy, assisted models are growing for complex products.

So, let me end with the thought that 2022 promises to be a year of a variety of positive transformations – for individuals as well as organizations – and we at Banking Frontiers look forward to sharing such developments with all our readers.

2022 could be a

glorious year

N E W S Regulator

4 Banking Frontiers December 2021

Bangladesh to have cybersecurity response teamT h e B a n g l a d e s h Bank is setting up an emergency response team for the financial sector, Fin-Cert, to avert cyberattacks. Bangladesh had faced a major cyberattack 5 years ago when hackers managed to steal $81

million from the central bank’s accounts with the Federal Reserve Bank of New York. A senior official of the central bank said Fin-Cert will exclusively concentrate on the financial industry for emergency security and will take measures to stave off any possible cyberattacks. The measures it will take include malware threats to banks from hackers, which the banks are not able to counter. The banks will then share the issue with the Fin-Cert platform anonymously and also alert other banks and check if anyone else is having similar problems. If any banks have a solution, they will share the information on the platform. Fin-Cert will also monitor the banking sector’s cyber security situation and provide necessary support and advisories to help prevent probable and imminent cyberattacks.

RBI working out details on CBDC implementationThe Reserve Bank of India is working out a phased implementation strategy for introduction of Central Bank Digital Currency (CBDC) by examining use cases to avoid any disruptions, the Government said. The RBI has moved a proposal to this effect to enhance the scope of the definition of ‘bank note’ to include currency in digital form. The government told the country’s Parliament that the purpose of creating a digital currency is to provide significant benefits, such as reduced dependency on cash, higher seigniorage due to lower transaction costs and reduced settlement risk. The new digital currency would also possibly lead to a more robust, efficient, trusted, regulated and legal tender-based payments option.

Indonesia, UAE central banks sign agreementThe central banks of Indonesia and the United Arab Emirates (UAE) have signed an agreement to boost payment system cooperation. The agreement is focused on safer and more efficient transactions, cross-border payment systems and anti-money laundering and anti-terrorism efforts, the 2 central banks said. A statement issued by the UAE’s central bank, the partnership aims to improve collaboration in payment systems and digital financial innovation, including conventional and Islamic finance. The Bank of Indonesia said the agreement shows its commitment to fighting terrorism funding and money laundering, while also helping the country become a member of the Paris-based Financial Action Task Force (FATF).

Saudi Arabia to give more licenses to digital banksSaudi Arabia is giving operating licences to more digital banks. Saudi Central Bank Governor Fahad al-Mubarak said the Kingdom had issued license for its first digital banks - STC Bank and the Saudi Digital Bank this year, after the Council of Ministers approved license for 2 local digital banks. Following this, STC Pay was converted to STC Bank with a capital of SR 2.5 billion and the Saudi Digital Bank came into being with a capital of SR 1.5 billion. Al-Mubarak said Saudi Arabia has a cross-border digital currency scheme with the United Arab Emirates. He also pointed out that there is a unified currency for the clearing system among the banks in the region. This, he added, has given the country the ability, which exceeds the capability of any others in the region, to move to digital currency at the regional level.

Russia norms for banks financing eco-friendly projects

New Governor for Qatar Central Bank

Qatar’s ruler, Sheikh Tamim bin Hamad Al Thani has appointed Sheikh Bandar bin Mohammed bin Saoud Al Thani as the Governor of the Qatar Central Bank. Sheikh Bandar has spent most of his professional life in the financial and regulatory sector. Prior to his appointment as the Governor of the Central Bank, he was Head of the State Audit Bureau. He has also held the position of President of the Arab Organization of Supreme Audit Institutions (ARABOSAI) and Chairman of the Executive Council of the Organization. He has also held several senior positions in the Qatar Central Bank, where he started his career in the Credit and Banking Supervision Section, and joined the Investment Department as head of trading and managing the foreign exchange reserves at the central bank. He has an Executive Master of Business Administration (EMBA) from the HEC Paris.

The Bank of Russia proposes to ease capital requirements for banks that lend money to eco-friendly projects and raise them for those giving loans to firms that do not disclose their ecological impact. Russia is the world’s fourth-largest emitter of greenhouse gases and relies heavily on fossil fuel exports. The central bank will take climate risks into account when making regulatory decisions on so-called green and less eco-friendly ‘brown’ projects. It is expected that the proposal should help Russian companies attract extra investment, including from abroad.

Banking Frontiers December 2021 5

Neobanks

US neobank SoFi has members, and not customersSoFi is a unique financial services institution in the US, that mostly finances student loans, but is a successful model for neobanks:

US neobank SoFi, or Social Finance, was originally a student-loan platform, but now it aims to be a

source for everything in personal finance. Headed by Anthony Noto, who was instrumental in Twitter becoming a global platform for information, and had worked with Goldman Sachs as its Managing Director, SoFi today offers personal and home loans, investment services, small-business financing, a credit card and several other financial products. It considers its customers as members and encourages them to avail more than one financial offering, a strategy aimed at cutting down customer acquisition costs. In the process, it is creating for the customers a high-level seamless experience.

In May 2021, SoFi became a publicly traded company, called SoFi Technologies, following a merger with Social Capital Hedospophia Holdings Corp. It is now a leading, publicly traded consumer-focused financial technology platform on Nasdaq. It raised $2.4 billion in cash proceeds from the transaction, which it intends to use for growth, market expansion and development of new product offerings, as well as for geographic expansion and building the first digital one-stop-shop for members to ‘borrow, save, spend, invest and protect’ their money. At present, its offerings mainly constitute student loan refinancing, mortgages, personal loans, credit card, investing and banking through both a mobile app and desktop interfaces. Its target customers are ‘high earners not well-served’, or people who have taken out financial offerings from multiple institutions.

NEWS FEED FOR CUSTOMERSNoto, who has vast understanding of technology and finance, believes that no one in the past had really built a financial services experience on one digital platform and used data to drive great value. Something unique that Noto has designed for SoFi is a feed of financial information like the news feeds on Twitter and

Facebook, and which include daily podcasts and newsletter. It also includes third-party content, using data to determine what is most relevant to a particular user. Its customers can enjoy learning freely from a certified financial planner or avail free estate planning services. The neobank plans to have a customer base of 3 million by the end of 2021.

While SoFi at the moment does not have a banking charter in the US, it is regulated by 50 states for lending, which means it has to comply with 50 different sets of compliance rules. It has in March this year, acquired California-based community bank Golden Pacific Bancorp for $22.3 million and through it hopes to obtain the national bank charter. By being a bank, SoFi will be able to offer more loans and no longer have to limit its number of mortgages. The license will also allow it to determine its own interest rates instead of relying on a sweep partner.

SoFi has partnership with 6 banks, including Metabank, Hills Bank & Trust, EagleBank and Wells Fargo.

The neobank intends to become profitable on a GAAP basis by 2023, projecting $200 million in GAAP net income in that year. While its revenue comes from lending, it expects the business to become more balanced by 2025 with greater revenue from financial services and the company’s technology platform.

BUYING GALILEOSoFi now owns the Galileo platform, which it acquired in April 2020 for $1.2 billion. Salt Lake City-based Galileo is the API standard for card issuing and is the platform that powers world’s leading fintechs, financial services providers and investment firms. The platform uses APIs to enable enterprises build financial services offerings. The APIs enable account setup, funding, direct deposits, money transfers, bill payment and other capabilities. Galileo now provides SoFi’s main technology infrastructure.

One unique thing about SoFi is that it does not use credit scores, or FICO scores, from any of the US’s credit bureaus to determine the creditworthiness of its customers. It has its own AI-based underwriting model that examines free cash flow, professional history and education in addition to a history of responsible bill payment to evaluate its borrowers and to increase customer engagement. It does not take deposits and finances its loans through venture capital, bond issues via securitization and debt financing. It has its own hedge fund to purchase the loans it issues.

STUDENT LOAN REFINANCINGSoFi today is the largest provider of student loan refinancing, with over $5 billion dollars in loans funded. Unlike traditional lenders, its proprietary underwriting approach takes into account merit and employment history to offer unique products that its ‘members’ will not find elsewhere.

SoFi’s key milestones are: u $5B+ total loan originations u Secured $1B in Series E funding in

September 2015, the largest single financing round in the fintech space to date

u First rated P2P securitizationu $2 billion + in securitized products issuedu GAAP profitable

Insurance & Technology

6 Banking Frontiers December 2021

How Turtlemint sells 10,000 insurance policies every dayThe platform provides advisors with digital tools enabling them to sell multiple insurance products of different companies through one single app:

Founded in 2015, India-born insurance platform Turtlemint has a unique online-offline model.

Dhirendra Mahyavanshi, Co-Founder, explains: “Our hybrid model empowers insurance advisors across the country with digital tools to navigate an otherwise cumbersome offline selling process at scale quickly. We have grown significantly since inception via our user-friendly and innovative digital platform.”

MOBILE APP, SEAMLESS SELLOne of the main reasons why Turtlemint has been able to achieve good growth is because it has not lost sight of its overarching goal to improve insurance penetration in the country by leveraging the right technology tools. It currently has a base of approximately 3.5 million clients, which it acquired online in a short span. It sells around 10,000 policies daily. Health insurance is its fastest-growing segment which has grown by 2x in the last year and by 35% y/y in the first half of the current FY.

Turtlemint has been empowering the most important cog in the insurance ecosystem, i.e., the insurance advisor by leveraging the technology. Dhirendra explains: “Our mobile app Mintpro enables advisors to seamlessly sell the right insurance policies to their clients and also to expand their business. The pandemic has accelerated the pace of digital adoption and I am happy to say that we are already ahead of the curve when it comes to creating seamless digital solutions.”

100% of Turtlemint’s business is digitally driven. The app has various facets - firstly, it provides insurance advisors with digital tools that can enable them to sell multiple insurance

products of multiple insurance companies through one single mobile application. Secondly, the app helps insurance advisors to expand their business through better service to existing clients and by expanding the client base. Dhirendra adds: “We have created a groundbreaking multilingual digital solution in the form of the Mintpro app that empowers advisors and enables them to grow their business by selling the right insurance policies, to the right people, and in a seamless manner.”

UPSKILLING ADVISORS ONLINETurtlemint has a vast pool of point-of-sale persons (PoSPs), its insurance advisors. Dhirendra explains: “These PoSPs are trained digitally and equipped

to issue an insurance policy instantly online to our prospective buyer. We have been able to create India’s largest PoSP network of more than 1,25,000 advisors. This indicates a 161% increase in PoSPs over the last year. A majority of our PoSPs - approximately 76.5% - fall in the 22-40 years age group, who are highly tech savvy. From a geographical presence perspective, approximately 9.33% are from tier 1, around 26.4% are from tier 2, and a significant 64.27% are from tier 3 cities.”

The app allows the insurance advisors to upskill by providing access to a comprehensive online skill development program. Dhirendra further says: “The program offers 70+ courses ranging from insurance advisor certification to personality development courses, sales skills, podcasts, etc. We have a dedicated section for advisors that provides several tools that can help them achieve their main goal. The tools can help them get new leads, access posters, videos, curated daily news, product videos, brochures, etc.”

IN-HOUSE TECH TEAM, TOOLSTurtlemint proactively leverages existing and emerging technologies to create efficient and customized solutions for cl ients. Dhirendra explains: “We have a tech team of 150+ developers and all the development and product innovation are done in-house. We use tools like Jira, Slack, Monday & Google Business Solutions for seamless communication between teams. We use Amazon Web Services for hosting, server space, etc.”

People and technology form the very core of Turtlemint’s business strategy. Dhirendra adds: “An unwavering focus

Dhirendra Mahyavanshi points out that Turtlemint has been fairly active on multiple social media channels

Banking Frontiers December 2021 7

Anand Prabhudesai explains that data science and data engineering have become critical focus areas for the next phase of growth

on harnessing the value of these two factors has held us in good stead and enabled it to grow at a strong clip. More specifically, we have been able to double our revenue run rate.”

RPA, DEEP LEARNING, OCRExamples of how Turtlemint leverages technology are interesting. Dhirendra describes: “We use intelligent automation with technologies like Robotic Process Automation (RPA) for repetitive, manual and cumbersome tasks like policy database reconciliation, claims and issuance. We deploy Deep Learning models that leverage and analyze the data collected through user interactions, while ensuring that the privacy of users is maintained. These models help us to predict user churn, identify upsell/cross-sell opportunities, enhance the conversion of the leads, etc.”

Chatbots are used for handling user

queries to reduce turnaround time and improve consumer happiness. At Turtlemint, these are used to quickly respond to standard user queries. Dhirendra further states: “We deploy Deep Learning and Optimal Character Recognition (OCR) capabilities for extracting relevant information from digital documents. These are used for generating quotes from the previous year’s policy copy or RC book. The same technology is also used to reduce all the manual efforts to ensure the completeness of the data in MIS.”

GENERATING LEADS, GROWTurtlemint has also introduced multi-channel and multi-platform short story formats for content consumption. Dhirendra says: “A similar approach is also being followed for consumer education and awareness. In addition to creating visibility, this also helps in generating leads for advisors.” The Mintpro app has a GROW section which has a wide range of content. Dhirendra further says: “This content is easily shareable amongst all members of the Mintpro ecosystem.”

SOCIAL MEDIA PRESENCETurtlemint has a strong presence on social media. It has always believed that a subject like insurance and special technology in insurance needs to be accurately communicated and made relatable to the target audience so that its true benefits can be reaped by all ecosystem stakeholders. Thus, Dhirendra points out: “We are fairly active on multiple social media channels and consistently post information related to insurance concepts, educational videos, industry updates, and current affairs. A similar approach is also being followed for consumer education and awareness. In addition to creating visibility, this also helps in generating leads for advisors. For video content, we have Youtube channel www.youtube.com/c/InsuranceGyan. For the other educational and industry updates, we have active LinkedIn, Twitter and Facebook channels.”

Acquiring Startup To Realize Data Engineering Plans

In the post covid- scenario, Turtlemint has set its targets and plans for IT, digital initiatives, for business growth in the foreseeable future. Dhirendra reveals: “Turtlemint strongly believes that the technology will continue to be the main driving force in the insurance ecosystem, orchestrating change and enabling inclusive growth. As we forge ahead, we plan to focus on automating processes and optimally leveraging data science, data engineering, Robotic Process Automation (RPA), and deep learning and OCR capabilities.”

Turtlemint recently acquired Pune based startup IOPhysics Systems. IOPhysics has a highly talented tech team. The startup aims to help data scientists and data engineers derive intelligence from structured or unstructured data in real-time. As part of their highway to a 100 Unicorns program, Microsoft recognised IOPhysics as the ‘Most Innovative & High Potential Startup’ across tier-2 cities in India. As a part of the deal, Turtlemint will also be taking over the IOPhysics IP and product portfolio. Passion Connect, the HR advisory unit incubated by Blume Ventures, one of Turtlemint’s investors, played a crucial role in this acquisition.

Turtlemint co-founder Anand Prabhudesai explains the whole process: “As our company goes into the next phase of growth, data science and data engineering have become critical focus areas. Passion Connect recognized this need, leveraged its strong network in the startup community and connected us to various startup teams across domains. We loved the IOPhysics team, their IP and product since it allows developers to be cloud-agnostic and pick data platforms that suit the best need for the use case.”

IOPhysics’ founder and CEO Ashish Gawali will join the Turtlemint team as their VP, Data Science and Data Engineering, while the rest of the IOPhysics team will join the tech and data science verticals at Turtlemint. Its USP is its flexibility to integrate any data with any public cloud data platform of choice and data visualization tool – all with an easy-to-use interface. Ashish Gawali, founder, IOPhysics, says: “When we were introduced to Turtlemint, we realized that both teams shared the same passion for improving people’s lives, even in remote pockets of the country. In addition, we have immense respect for the intelligence and experience of their leadership team.”

Brokerages

8 Banking Frontiers December 2021

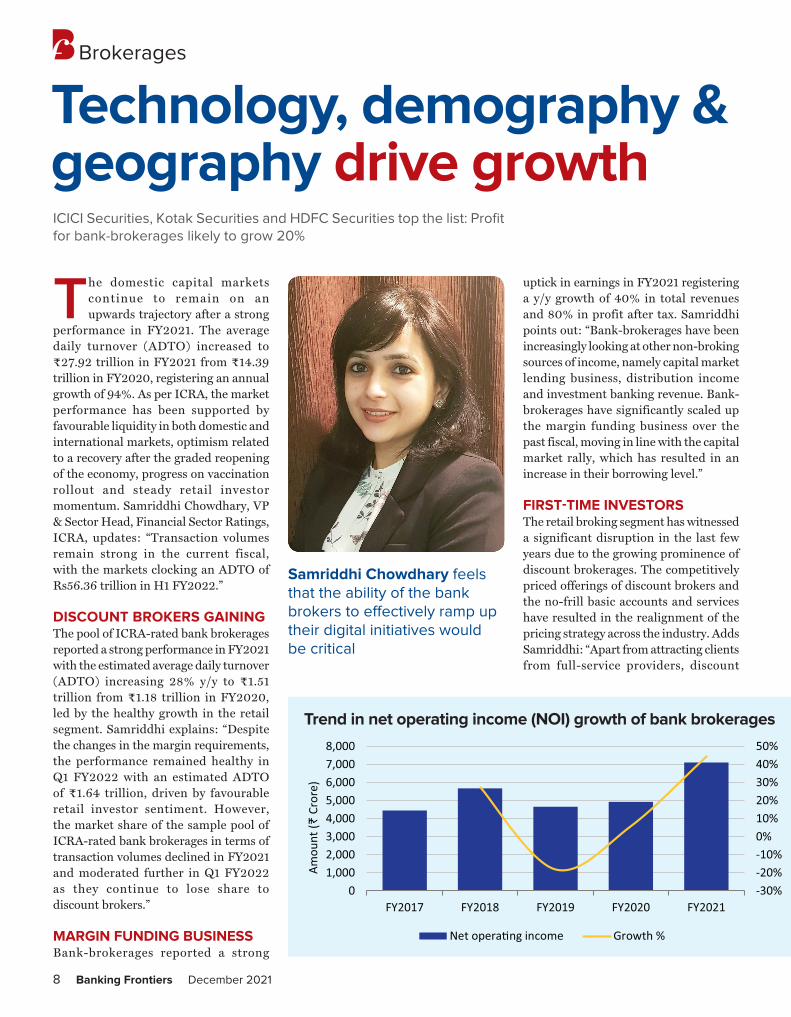

Technology, demography & geography drive growthICICI Securities, Kotak Securities and HDFC Securities top the list: Profit for bank-brokerages likely to grow 20%

The domestic capital markets continue to remain on an upwards trajectory after a strong

performance in FY2021. The average daily turnover (ADTO) increased to `27.92 trillion in FY2021 from `14.39 trillion in FY2020, registering an annual growth of 94%. As per ICRA, the market performance has been supported by favourable liquidity in both domestic and international markets, optimism related to a recovery after the graded reopening of the economy, progress on vaccination rollout and steady retail investor momentum. Samriddhi Chowdhary, VP & Sector Head, Financial Sector Ratings, ICRA, updates: “Transaction volumes remain strong in the current fiscal, with the markets clocking an ADTO of Rs56.36 trillion in H1 FY2022.”

DISCOUNT BROKERS GAININGThe pool of ICRA-rated bank brokerages reported a strong performance in FY2021 with the estimated average daily turnover (ADTO) increasing 28% y/y to `1.51 trillion from `1.18 trillion in FY2020, led by the healthy growth in the retail segment. Samriddhi explains: “Despite the changes in the margin requirements, the performance remained healthy in Q1 FY2022 with an estimated ADTO of `1.64 trillion, driven by favourable retail investor sentiment. However, the market share of the sample pool of ICRA-rated bank brokerages in terms of transaction volumes declined in FY2021 and moderated further in Q1 FY2022 as they continue to lose share to discount brokers.” MARGIN FUNDING BUSINESSBank-brokerages reported a strong

uptick in earnings in FY2021 registering a y/y growth of 40% in total revenues and 80% in profit after tax. Samriddhi points out: “Bank-brokerages have been increasingly looking at other non-broking sources of income, namely capital market lending business, distribution income and investment banking revenue. Bank-brokerages have significantly scaled up the margin funding business over the past fiscal, moving in line with the capital market rally, which has resulted in an increase in their borrowing level.”

FIRST-TIME INVESTORSThe retail broking segment has witnessed a significant disruption in the last few years due to the growing prominence of discount brokerages. The competitively priced offerings of discount brokers and the no-frill basic accounts and services have resulted in the realignment of the pricing strategy across the industry. Adds Samriddhi: “Apart from attracting clients from full-service providers, discount

Samriddhi Chowdhary feels that the ability of the bank brokers to effectively ramp up their digital initiatives would be critical

-30%-20%-10%0%10%20%30%40%50%

01,0002,0003,0004,0005,0006,0007,0008,000

FY2017 FY2018 FY2019 FY2020 FY2021

Amou

nt (`

Cro

re)

Net opera�ng income Growth %

Trend in net operating income (NOI) growth of bank brokerages

Banking Frontiers December 2021 9

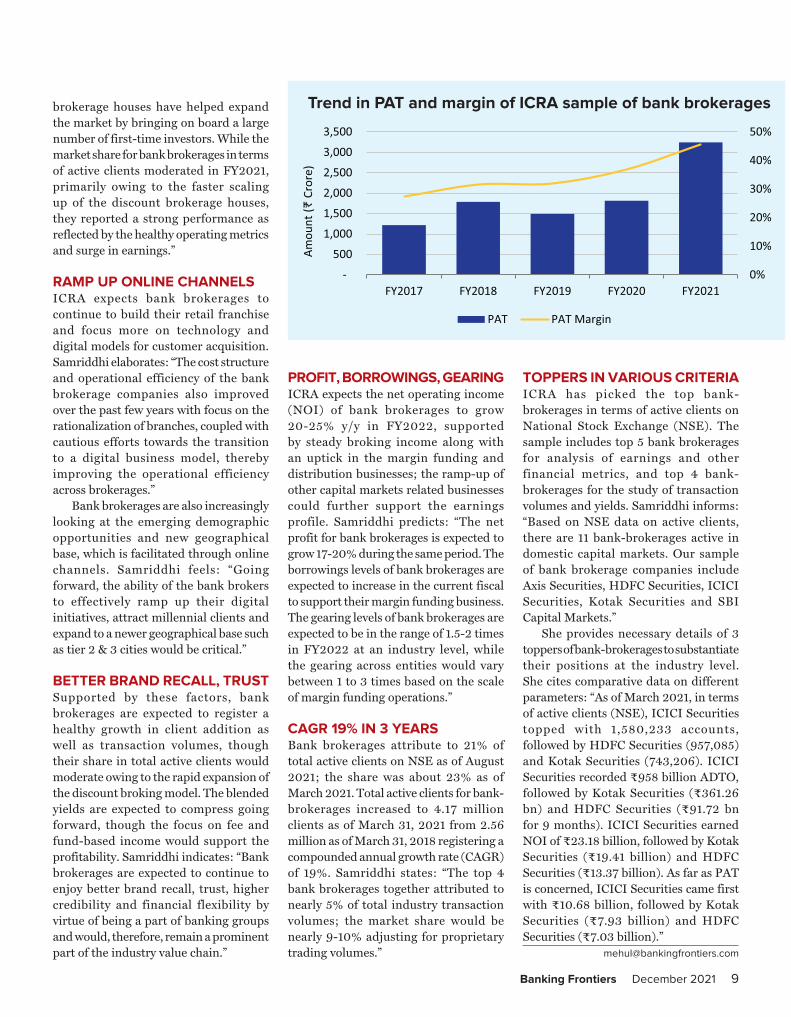

brokerage houses have helped expand the market by bringing on board a large number of first-time investors. While the market share for bank brokerages in terms of active clients moderated in FY2021, primarily owing to the faster scaling up of the discount brokerage houses, they reported a strong performance as reflected by the healthy operating metrics and surge in earnings.”

RAMP UP ONLINE CHANNELS ICRA expects bank brokerages to continue to build their retail franchise and focus more on technology and digital models for customer acquisition. Samriddhi elaborates: “The cost structure and operational efficiency of the bank brokerage companies also improved over the past few years with focus on the rationalization of branches, coupled with cautious efforts towards the transition to a digital business model, thereby improving the operational efficiency across brokerages.”

Bank brokerages are also increasingly looking at the emerging demographic opportunities and new geographical base, which is facilitated through online channels. Samriddhi feels: “Going forward, the ability of the bank brokers to effectively ramp up their digital initiatives, attract millennial clients and expand to a newer geographical base such as tier 2 & 3 cities would be critical.”

BETTER BRAND RECALL, TRUSTSupported by these factors, bank brokerages are expected to register a healthy growth in client addition as well as transaction volumes, though their share in total active clients would moderate owing to the rapid expansion of the discount broking model. The blended yields are expected to compress going forward, though the focus on fee and fund-based income would support the profitability. Samriddhi indicates: “Bank brokerages are expected to continue to enjoy better brand recall, trust, higher credibility and financial flexibility by virtue of being a part of banking groups and would, therefore, remain a prominent part of the industry value chain.”

PROFIT, BORROWINGS, GEARINGICRA expects the net operating income (NOI) of bank brokerages to grow 20-25% y/y in FY2022, supported by steady broking income along with an uptick in the margin funding and distribution businesses; the ramp-up of other capital markets related businesses could further support the earnings profile. Samriddhi predicts: “The net profit for bank brokerages is expected to grow 17-20% during the same period. The borrowings levels of bank brokerages are expected to increase in the current fiscal to support their margin funding business. The gearing levels of bank brokerages are expected to be in the range of 1.5-2 times in FY2022 at an industry level, while the gearing across entities would vary between 1 to 3 times based on the scale of margin funding operations.”

CAGR 19% IN 3 YEARSBank brokerages attribute to 21% of total active clients on NSE as of August 2021; the share was about 23% as of March 2021. Total active clients for bank-brokerages increased to 4.17 million clients as of March 31, 2021 from 2.56 million as of March 31, 2018 registering a compounded annual growth rate (CAGR) of 19%. Samriddhi states: “The top 4 bank brokerages together attributed to nearly 5% of total industry transaction volumes; the market share would be nearly 9-10% adjusting for proprietary trading volumes.”

TOPPERS IN VARIOUS CRITERIAICRA has picked the top bank-brokerages in terms of active clients on National Stock Exchange (NSE). The sample includes top 5 bank brokerages for analysis of earnings and other financial metrics, and top 4 bank-brokerages for the study of transaction volumes and yields. Samriddhi informs: “Based on NSE data on active clients, there are 11 bank-brokerages active in domestic capital markets. Our sample of bank brokerage companies include Axis Securities, HDFC Securities, ICICI Securities, Kotak Securities and SBI Capital Markets.”

She provides necessary details of 3 toppers of bank-brokerages to substantiate their positions at the industry level. She cites comparative data on different parameters: “As of March 2021, in terms of active clients (NSE), ICICI Securities topped with 1,580,233 accounts, followed by HDFC Securities (957,085) and Kotak Securities (743,206). ICICI Securities recorded `958 billion ADTO, followed by Kotak Securities (`361.26 bn) and HDFC Securities (`91.72 bn for 9 months). ICICI Securities earned NOI of `23.18 billion, followed by Kotak Securities (`19.41 billion) and HDFC Securities (`13.37 billion). As far as PAT is concerned, ICICI Securities came first with `10.68 billion, followed by Kotak Securities (`7.93 billion) and HDFC Securities (`7.03 billion).”

0%

10%

20%

30%

40%

50%

- 500

1,000 1,500 2,000 2,500 3,000 3,500

FY2017 FY2018 FY2019 FY2020 FY2021Am

ount

(` C

rore

)PAT PAT Margin

Trend in PAT and margin of ICRA sample of bank brokerages

Business Technology Alignment

10 Banking Frontiers December 2021

Cooperative banks & technological adoption - Keeping pace with the competitionIn an exclusive interaction, Mannu Singh, Vice-President, Tata Teleservices shares the details about the next gen connecting solutions for cooperative banks in India:

Ravi Lalwani: What offerings from Tata

Tele Business Services have become

popular among cooperative banks?

Mannu Singh: Most of the cooperative banks have a core banking setup hosted on their data centre centrally and all branches are required to connect to the setup. The core banking services include mortgages, deposits, loan, and credit processing capabilities, with interfaces to general ledger systems, and reporting tools. Cooperative banks make these services available to their customers across multiple channels like ATMs, internet banking, mobile banking, and branches that are geographically spread across cities and states.

Tata Tele Business Services (TTBS) is a smart connectivity solution that helps bank branches to connect seamlessly. u Secure MPLS network for banks to

prioritize and set up highly efficient routes for customer traffic, get assured of a high QoS, and benefit from any-to-any connectivity.

u Multiple PRI lines facilitate the concurrent transmission of voice as well as data traffic over the dedicated line with the flexibility of using multiple channels at the same time.

u High-speed internet leased line with secured connectivity for business efficiency.

How have these helped banks to

strengthen their business?

TTBS provides advanced bespoke solutions which provide secured connectivity, flexibility and are backed by 24x7 managed support services. These solutions help build operational efficiency, greater customer satisfaction and increased customer base.

Operational efficiency: Bank staff can easily and at a quickly access accurate,

timely, and actionable information about customer relations. A single view between banks and customers at any time helps speed up operations. The bank gets further advantages by easily introducing new financial products and manage changes in existing products. The seamless merging of back-office data and self-service operations brings in a great deal of operational efficiency.

G r e a t e r c u s t o m e r satisfaction: The entire range of banking products including savings, deposit accounts, etc, are available from any location seamlessly through reliable and secure connectivity solutions from TTBS. Easy accessibility and customer operations through multiple channels, including mobile banking and the web, become possible.

Increased customer base: The availability of real-time transactions and the entire portfolio of financial products available through the internet and mobile banking enable reaching out faster to customer and helps in increasing the customer base. The flexibility to scale up solutions helps in easy expansion of services.

How does Tata Tele Business

Services help banks identify the best

technologies and services to achieve

their business goals?

Tata Tele Business Services works as a progressive digital catalyst to enable the banks to adopt the best connectivity and collaboration solutions that significantly boost their customer experience and help them to do big. The most

Banking Frontiers December 2021 11

important challenge in the transition towards ‘digitization’ is the cooperative bank’s preparedness and readiness in terms of technology and innovation. Some of them lack reliable connections that can ensure secure transactions and protection of all customer data. Given the transaction data’s sensitive nature, there is a need for a seamless and secure communication channel that provides the right collaborative tools to make transactions more efficient. They must also make sure that they are equipped with an easy to configure hosted infrastructure that facilitates a distributed working environment.

TTBS has an array of solutions to help co-operative banks leverage digitalization:

Smart VPN: An MPLS-based virtual private network that enables you to share data securely and confidentially over any internet service, from any location.

Smart Internet Leased Line: A dedicated source of secured internet service with uncontended bandwidth and symmetric upload & download for remote users.

Session Initiation Protocol (SIP): A signaling protocol to facilitate interactive communication sessions, including voice, video, and chat over the internet.

Hosted PBX: A feature-rich SIP-based telephony solution for outbound calls from any location.

Cyber Security Solutions: With ever-increasing cyber threats and

data breaches, the importance of cyber security cannot be overlooked. TTBS offers endpoint security, email security, web security, multi-factor authentication, and virtual firewall.

We have recently introduced the industry’s first ‘Customer Experience Platform (CEP)’. CEP provides first-hand experience of our solutions and services to our potential customers, and shows how they can utilize these for improving their business processes, and then make an informed buying decision. Additionally, our solution experts are available for interactive consultative sessions with our customers to guide them to smoothly integrate these solutions within their existing technological framework with minimum disruptions.

What would Tata Tele Business Services

advise banks for improving overall

customer experience?

TTBS helps with evolved connectivity and security solutions for BFSI operational efficiency and improved customer experience. As the cooperative banking sector sets upon its post-covid digital transformation journey, the key imperatives that it must consider include:u Have robust smart internet

connectivity which is highly secured. u Focus on enhancing d ig i ta l

banking experiences as customers are becoming more comfortable with digital modes of banking and transactions.

u Emphasize more on the adoption of cloud solutions which are capex and opex light and provide anywhere, anytime working flexibility to the banking workforce.

u Stress more on cybersecurity and data privacy to provide secured and uninterrupted services. To add further, a better managed

toll-free number can help the bank bring a paradigm shift in its customer experience by enabling customers to conveniently reach out to the bank without any cost - this is also as per RBI’s recommendation.

How is Tata Tele Business Services

helping banks migrate from the capex

model to the opex model? How does it

help - especially when the service loads

fluctuate from minimal to peak?

Being fast and flexible is at the foundation of all digital and network transformation initiatives today. For cooperative banks the cost of building and maintaining their private networks can be high and legacy connectivity solutions (like private WANs using MPLS) can be financially crippling.

This is where TTBS introduced SDWAN-iFLX which brings intelligence and flexibility. Powered by Fortinet, the SD-WAN iFLX solution offers operational simplicity, application-level prioritization, and visibility, integrated security, enhanced overall business application environment as well as much-needed resilience at an affordable price point.

Finally, how can the technology ROI be

justified?

As the businesses of customers expand and grow, their banking needs too are rapidly evolving. Post covid, the quantum of financial transactions over digital modes has increased tremendously. With the penetration of the internet and smartphones, customers are using more digital payment gateways than using cash for transactions. Cooperative Banks need to add more and more products in their kitty and at the same time, increase channels of accessibility to their customers.

With this, the need for robust networking practices has skyrocketed. Connectivity across branch locations that is seamless, break-free, with minimum or no downtime, congestion-free, and with faster speed is quite the necessity today for operational resilience. At the same time, secure connectivity is what most banks today look at. Cyber security is like insurance to prevent great financial, legal, and reputation loss which may directly impact the loss of customer base and business, especially in the competitive scenario today.

Customer View“For a seamless banking experience, we chose to use Tata Tele Business Services’ MPLS solution. With maximum uptime, stable and reliable VPN connectivity, and 24x7 support team, uninterrupted and smooth operations are ensured, increasing our productivity and enhancing our customer experience and digital onboarding.”

- Pragnesh J. Mehta Executive Officer IT, Sardar Bhiladwala

Pardi Peoples (SBPP) Cooperative Bank

Research Report – Data Maturity

12 Banking Frontiers December 2021

Enterprise data strategy boosts profits by 5.97%

Cloudera has announced the findings of a global research report, created in association

with technology market research firm, Vanson Bourne. The report examines the correlation between the maturity of an organization’s enterprise data strategy (defined as an organization-wide, integrated, holistic strategy across all lines of business) and its business performance. It also explores the impact that the ongoing covid-19 pandemic and its uncertainties have on businesses.

The research found that organizations with mature enterprise data strategies in place for at least 12 months report higher profit growth at an average of 5.97%, according to surveyed senior business decision makers (SDMs). 96% of SDMs reported that the way data is handled and managed has positively impacted their organizations’ performance, and close to two-thirds (64%) reported stronger levels of resiliency from the presence of a mature data strategy. Both SDMs and IT decision-makers (ITDMs) share similar views, recognizing data as a strategic business resource, but these groups have differing opinions on operational processes and implementation.

HINDERANCES TO INNOVATIONVisibility remains a key issue for organizations, with 89% reporting secure, centralized governance and compliance over the entire lifecycle as being valuable when handling and managing data. Only 12% of surveyed ITDMs report that their organization interacts with all stages of the data lifecycle process – something immensely helpful in helping organizations achieve an enterprise data strategy. Without complete control and visibility over every aspect of data, organizations will lack key capabilities required to drive innovation.

EFFECTIVE ENTERPRISE DATA STRATEGIES REMAIN KEY Organizations see the value in enterprise data strategies but struggle to make them effective. Organizations utilizing

enterprise data strategies for more than a year reported them to be very effective (63%), along with higher profit growth. Nearly all ITDMs (91%) whose organizations have an enterprise data strategy in place agree that their current strategy is key to their business resiliency. SDMs surveyed report an average of $384,962 lost annually due to missed opportunities involving data, with the telecom industry reporting the highest average annual loss of $6,617,348.

THE FUTURE IS HYBRIDThe report shows an anticipated shift to hybrid cloud in the next 18 months. With both SDMs and ITDMs reporting that 43% of their workforce will continue working remotely in the next year, organizations are investing in infrastructure to support hybrid working environments. A majority (79%) of ITDMs’ organizations are looking to house their data and performance analytics on hybrid architectures. Among cloud options, multi-cloud emerged as a clear favorite, with 44% of ITDMs indicating their preference for multi-cloud architectures in 18 months’ time. With the hybrid data cloud, organizations can access and analyze data fast and with ease to make smarter, data-driven decisions to effectively meet the demands of today’s hyper-competitive business climate.

Accessing and managing data from multiple sources and locations will give organizations the control and flexibility of utilizing a hybrid workforce while still being able to run business as usual. Nearly all SDMs (92%) believe that making sense of all data across hybrid, multi-cloud and on-premises architectures is or would be valuable. This finding mirrors the sentiments of a majority of ITDMs (90%), who report that managing data with at least some cloud capacity is a priority for their organization. A similar majority (89%) believe that organizations implementing a hybrid architecture as part of its data strategy will gain a competitive advantage.

DATA DRIVES SUCCESS BEYOND PROFITSUtilizing data and analytics can yield more benefits than simply increasing profit margins or gaining a competitive advantage. Most organizations recognize the vital link between Diversity, Equity, and Inclusion (DEI) initiatives and organizational success. The research found that thoughtful data collection and analytics contribute to the success of DEI initiatives. Nearly all ITDMs (96%) and SDMs (95%) believe that data and analytics are important to ensuring successful and effective DEI initiatives, and 95% of both ITDMs and SDMs agree that DEI initiatives contribute to organizational success. Organizations with effective enterprise data strategies in place are better able to utilize data and analytics to benchmark and evaluate employee diversity programs. With greater visibility over diversity within organizations, comes better decision-making, greater innovation and higher engagement in the workplace.

METHODOLOGYVanson Bourne conducted the survey online and over the phone between July and September 2021, surveying 3150 respondents holding either c-level, senior management or middle management positions from large organizations. Respondents were from 15 markets: Australia, China, France, Germany, India, Indonesia, Italy, Japan, Singapore, South Africa, South Korea, Spain, UAE, UK, and the USA.

Banking Frontiers December 2021 13

Social Transformation

Crime & Intoxication drops where PMJDY flourishes

Sound financial inclusion policies have a multiplier effect on economic growth, reducing poverty

and income inequality, while also being conducive for financial stability. India has stolen a march in financial inclusion with the initiation of PMJDY accounts since 2014, enabled by a robust digital infrastructure and also careful recalibration of bank branches and thereby using the BC model judiciously for furthering financial inclusion. The number of bank branches per 100,000 adults rose to 14.7 in 2020 from 13.6 in 2015, which is higher than Germany, China and South Africa, says Dr. Soumya Kanti Ghosh, Group Chief Economic Adviser, State Bank of India, in a recent research report.

DIGITAL PAYMENT LED FISuch financial inclusion has also been enabled by use of digital payments as between 2015 and 2020, mobile and internet banking transactions per 1,000 adults have increased to 13,615 in 2019 from 183 in 2015.

In the last 7 years of launch of PMJDY scheme, the total number of accounts opened under PMJDY has reached 437 million, with `1.46 trillion of deposits as on October 20, 2021. Of these accounts, nearly 2/3 are operational in rural and semi-urban areas. More than 78% of PMJDY accounts were with PSBs and 18.2% are of RRBs, while non-PSBs’ share is 3%.

SBI’s research also shows that states with higher PMJDY accounts balances have seen a perceptible decline in crime. It has also been observed that there is both statistically significant and economically meaningful drop in consumption of intoxicants such as alcohol and tobacco products in states where more PMJDY accounts are opened.

OUTLETS IN VILLAGES UPThe number of ‘Banking Outlets in Villages - BCs’ has risen from 34,174 in March’10 to 1.24 mn in December’20. Such progress shows an impressive outreach of banking services through

branchless banking. However, the success of financial inclusion depends upon Banking Correspondents (BCs), who are micro-level entrepreneurs. Interoperability of transactions is permitted by RBI at the retail outlets or sub-agents of BCs ( at the point of customer interface), subject to certain conditions. Herein lies the problem.

`7 BN INTERCHANGE FEE The research report from the State Bank of India’s Economic Research Department further notes that it is sometimes observed that there is no uniformity among the BCs across banks regarding adherence to the above guidelines. PSBs mostly follow ‘Branch Led BC Model’, while other banks follow ‘Branch Less/Corporate BC model’. The BCs of PSBs extend basic banking services, including opening of accounts, from a fixed location under the oversight of specific bank branch. The BCs of other banks operate through ‘Micro ATM/Kiosk Application on Mobile’ and primarily provide fee-based financial services, viz. withdrawals and remittance services, using hand-held devices. This also adds to the bottom-line by way of interchange fee from the PSBs or remittance fee from PSB customers.

As a typical example, BCs convert AePS ON-US transactions of one set of bank customers, to AePS OFF-US issuer transactions and also carry out multiple AePS ON-US and AePS OFF-US transactions on the primary bank application/software. Data indicates that

the share of OFF-US transactions in AePS increased from 4% in September’16 to 51% in September’21. Considering these facts, PSBs (that opened around 77% of the PMJDY accounts) are now net payers of interchange fee. It is estimated that the PSBs could be paying around ̀ 6-7 bn per annum as interchange fee.

FINE-TUNE BC MODELSThe following recommendations have been suggested in the report to make the BC model more rigorous and uniform across all banking entities.

Firstly, as AePS works like a Point of Sales (PoS), logically the ‘acquiring bank’ should pay the interchange fee to the ‘issuing bank’. Alternatively, there could be rationalization in interchange fee as there is no level playing field in infrastructure provided by all banks. With requisite savings, banks can further strengthen/upgrade their BC model and promote financial inclusion in a more holistic manner.

Secondly, RBI should disincentivise BCs who are converting the ON US transactions of PSB customers to AePS OFF US transaction in order to earn interchange fee and more commission. For this, a comprehensive database of BC agents be prepared through IBA’s BC registry, JanDhan Dharshak App and RBI’s CISBI portal.

Additionally, the log-in to the AEPS applications of the non-branch BC model must be through Aadhaar authentication. This will prevent anyone from logging and performing unverified transactions. This will also result in BCs and their friends and relatives not being able to game the system by opening accounts with multiple banks and performing round tripping/ withdrawals.

Some minor tweaks in the existing branch less BC model could act as a multiplier for promoting financial inclusion objectives. This is all the more important as 347 million informal labour force is currently being formalized through the E-Shram portal.

Dr. Soumya Kanti Ghosh

Leadership

14 Banking Frontiers December 2021

LDP identifies & grooms future leaders at Indian Bank

Indian Bank commemorated its 115th foundation day on August 15, 2021. The bank has a staff of 24,821 officers, 12,995

clerks, 2769 sub-staff and 311 full time sweepers, totaling to 40,896 staff, as of Q1 FY 22. Females comprise 28% of the staff. Shanti Lal Jain assumed charge as MD & CEO of Indian Bank on 1st September 2021. He is supported by 3 executive directors - Shenoy Vishwanath V., Imran Amin Siddiqui and Ashwani Kumar.

LEADERSHIP: ONLINE TOOLSFor existing employees, the Indian Bank conducts 4 tests in a year to test the knowledge of the employees regarding latest banking updates and policies. Earlier the bank didn’t link these tests to annual performance appraisal report (APAR) score, however, Dhanaraj T, GM, HRM / CDO, (Chief Development Officer), clarifies: “At present these tests carries weightage in the APAR score. The bank conducts Leadership Development Program (LDP) for officers in scale IV to VI and psychometric test is part of LDP. In the current FY, our bank has launched the LDP for 800 officers in scale IV. The objective of this exercise is to identify and groom future leaders of the bank.”

The LDP consists of 3 phases – phase 1 entails the administration of online tools (psychometric assessments, situation judgement test, managerial aptitude and leadership simulation tests). Dhanaraj adds: “The phase 2 entails a set of TBEIs (Targeted Behavioral Event Interviews) and GDs (group discussions) for the top 250 participants. Phase 3 consists of panel interviews conducted by the senior management.”

MAPPING COMPETENCIESThe bank gives score for knowledge test at the end of each training program. For Leadership Development Program, each tool has been mapped to specific competencies. Dhanaraj explains: “Participants are then scored on a scale of 1 (novice) to 5 (expert). After competencies of business acumen and inspirational leadership are being measured by the Psychometric Assessment Tool, the participants score at the sub competency level is averaged, to arrive at

the parent competency score. The parent competency scores are then averaged to arrive at the tool-wise score.”

TECHNICAL SKILLSThe bank finds outcomes of these tests to be satisfactory for over a period of time. The tools are intended to identify participant’s behavioural and technical skills and competencies. Dhanaraj underlines: “These tools are robust and provide a comprehensive analysis of the participant’s behavioural tendencies.”

Indian Bank conducts knowledge tests 4 times in a year. The LDP is conducted on a yearly basis, and the validity of such test is 3 years. Dhanaraj informs: “The content of each of the online tools would be regularly updated to ensure the tools are in line with market best practices.”

ROBUST TECH, INFRAThe bank conducts knowledge tests online and they are created in-house. As the LDP is a large exercise, being administered for 800 officers across various locations in India, robust technology and infrastructure is of paramount importance. Dhanaraj updates: “Phase 1 of the LDC has been conducted online without any technological

hindrances during the ongoing pandemic. All the above listed phase 1 tools have been administered online. The phase 2 tools had been undertaken seamlessly over MS Teams, with participants and assessors joining from various locations.”

E-LEARNING PLATFORMIndian Bank has unveiled the IB e-note / e-dak facility, aimed at providing a paperless working environment and to improve the turnaround time considerably. Dhanaraj elaborates: “The bank has customized Microsoft SharePoint. It also unveiled ‘Ind Guru’, an e-learning platform for its employees that offers technology enabled solutions aimed at capacity building. The bank identifies the process automation and digital workflow amongst the other initiatives as a part of its digital transformation.”

CHANGE AGENTSPost covid pandemic, Indian Bank has focused on ensuring flexibility in work and the workplace. Given the ongoing pandemic, WFH (work from home) opportunities are being explored. Dhanaraj clarifies: “A greater emphasis is being placed on employee health and well-being. The bank has appointed several change agents to drive the amalgamated organization’s new vision and mission.”

Indian Bank has been maintaining its database in SAP (systems, applications, and products) through which training data for any period can be fetched. Dhanaraj states: “The details of untrained employees for any period can also be obtained from SAP.”

PERSONALIZED PLANThe details of certification courses completed by the employees is also maintained in SAP by the bank. As part of LDP, all participants receive individual development reports, highlighting their areas of strength and development. Dhanaraj emphasizes: “Each participant will create a personalized development plan, mapped over a 9-month period. The intent of the personalized development plan is for participants to identify various tips and guidelines.”

Dhanaraj T informs that Indian Bank has launched the LDP for 800 officers in scale IV

Banking Frontiers December 2021 15

Human Resources

Covid impacts job satisfaction, but not attritionPraveen Menon, Chief People Officer at IndiaFirst Life Insurance Company updates about changing employee expectations & job satisfaction scenario at his organization

Ravi Lalwani: Has job satisfaction among

employees increased or decreased

during covid times?

Praveen Menon: Work From Home (WFH) has resulted in stretched working hours combined with other issues like household chores, distractions and digital stress. These have impacted the mental wellbeing of many. Social de-stressing had not been possible till now. Our experience suggests that job satisfaction levels during the covid era had relatively gone down as compared to that of pre-covid time.

Is the trend the same for younger, middle

age and older employees? Is it the same

for men and women?

Data crunching to exactly know the demographic trend towards job satisfaction levels remains to be done. However, covid has certainly triggered a thought amongst the working population on a sense of purpose in what they do and a sense of belonging as to who they are affiliated to. This also has got accentuated with other variables of life, such as physical health, emotional wellbeing, loss of dear ones, life expectancy, and much more. So, it will be safe to assume that the job satisfaction trend would be on a lower scale for most.

In which areas have employee

expectations changed the most during

covid?

Based on the external environment and employee feedback, some of the areas that organizations have consciously started rebooting and redefining their philosophies are as follows:u Work-Life Balanceu Organizational Stabilityu Learning & Development opportunities

provided by the organizationu Holistic career growth opportunitiesu Organization values and CARE

approach

u A bigger sense of purpose & belonging

Give examples of how your organization

is increasing job satisfaction among

employees?

Following are some initiatives undertaken by us to increase job satisfaction and engagement levels amongst our employees. u EVP: We have created an Employee

Value Proposition (EVP), which is on the principles of gives & gets. Gives are the expectation from the employee and gets would be what an employee can expect in return from the organization. Gives & gets have been clearly articulated to provide clarity to all employees.

u C a r e e r K u n d a l i : W e h a v e scientifically curated career paths for employees based on their aspirations and competencies. Skillsets, role changes, career pitstops, role

changes, and timelines have been defined clearly.

u CARE: In line with our #EmployeeFirst philosophy we try and moot CARE as our motto towards our employees. Some of the initiatives undertaken include (i) Work from anywhere guidelines rolled out (ii) Additional covid leaves policy introduced (iii) Special covid allowance equivalent to one-month gross salary given to front line employees (iv) Employment opportunity to spouses of deceased employee + Children education reimbursement policy rolled out (v) Additional medical coverage for family members under group Mediclaim policy introduced (vi) Employee Assistance Program like mental counselling and doctor on call (vii) Infrastructure like laptops and telephone lines for employees to seamlessly operate (viii) Increments, bonuses, and promotions rolled out as usual (ix) Continued with recognition platform virtually.

Did the attrition rate at your organization

change during the covid times? What

are the top reasons identified from exit

interviews?

During the covid period, attrition had not increased. However, we saw a marginal spike in attrition in FY22. This trend could be in line with the ‘Great Resignation’ syndrome happening across the world.

Some roles that have opened up big time are Digital, Analytics, Tech, and HR where currently the opportunities are galore with handsome rewards. Some of the reasons cited by exiting employees are better opportunities, better remuneration, getting into start-ups, trying to start something on their own, and also taking a break to pursue other interests.

Praveen Menon says that in his experience, job satisfaction levels during the covid era had relatively gone down as compared to that of pre-covid time

Transformation

16 Banking Frontiers December 2021

Deutsche Bank aims to become a totally tech bankIn a short span of time after it launched its tech upgrade, Deutsche Bank is today aiming to be a high-tech bank:

When Deutsche Bank started its tech upgrade in 2018, one of the focus points has been the use of natural

language processing and the bank has been able to derive extreme benefits. For example, its technology staff has evolved a tool using NLP to read through the bank’s archive of millions of emails exchanged between employees, partners and customers and developed sets of keywords and their relationships to people and other keywords. This offered unprecedented access to data for the bank, which hitherto remained untraced and unused. For example, the technology team analyzed emails for years for insider trading and other compliance uses. It used tools developed using NLP to create open source libraries to mine information hidden in these sources and got an insight across many additional areas in the bank.

UNATTENDED AUTOMATONThe bank had also developed robotic process automation and unattended intelligent automation with the help of specialist software companies. It now has a digital app on the desktop to automate repetitive tasks, using the tool, which it calls unattended intelligent automation. The bank has automated the integration between its systems and third-party systems. It also uses specialized software tools to implement artificial intelligence that will cut in half the time it takes to screen clients for adverse media, part of the bank’s KYC screening processes. The software scans news sentiment and context for negative news, rather than looking for rudimentary word associations.

The bank has also opted for an agile development approach, which teaches employees to think about automating processes, so everyone uses the same project management language and metrics. It has standardized the process with digital tools that do not require the average employee to be a programmer.

AUTOMATING AMLIn earlier days, money laundering regulations required manual screening of every financial

transaction. Now, using RPA, it has streamlined the manual side of the processes and is said to have saved some 210,000 hours of work that employees would typically do by hand. During Brexit, the automation process helped the bank to check over 3.4 million positions, automatically close 380,000 accounts and migrate 80,000 accounts.

The bank believes that the turnaround effort is an ongoing process and it is kept at a constant momentum. So, recently, the bank signed an agreement with Oracle to modernize its data handling software behind key trading, risk management and capital planning so that it can gain a competitive edge.

TIE-UP WITH ORACLEA majority of the bank’s applications - some 40 petabytes - are on Oracle Databases already. It decided to move the databases worldwide to more current versions on Oracle Exadata Cloud@Customer, which provides high-performance database services managed by Oracle in a private cloud. The migration that will take about 3 to 5 years, will help save millions of euros for the bank even while continuing complying with European data protection rules. Compared with software that runs in the public cloud, Oracle Exadata Cloud@Customer service runs in the bank’s own computing centers. This allows the bank keep total control of customer data, while Oracle manages the hardware and nondisruptive software updates. The system also delivers lower network latency compared with public clouds, especially critical for banking applications that require nearly real-time responses to market events.

The bank and Oracle have also agreed to form a joint innovation partnership, bringing together Oracle’s and the bank’s engineering and technology teams to explore potential uses for data security technologies, blockchain, AI and analytics to develop new financial products and services.

The bank now aims to have software engineers constitute more than half of its total number of employees and covert itself

into a totally technology driven organization.

SHOWING RESULTSWith its aim to use technology to simplify its operations, have better controls and reduce expenses, the bank, which has significant operations in investment, retail and corporate banking and asset management, has started showing results of its long-drawn overhaul process set in motion some 2 years ago by its CEO Christian Sewing. It has reported its best quarterly and half-year earnings in July 2021 since 2015, while the combined profit its 4 core divisions rose by 90% from the previous year.

The bank is a founding member of ‘Verimi’, a combination of ‘verify’ and ‘me’, which is a consortium of leading companies from a variety of industries. Its main purpose is to function as a cross-industry digital identification and verification platform to serve the needs of consumers. It provides a single sign-on for customers to access and use potentially limitless services - from banking to airline reservations to telecommunications) and allows them to transact with as many companies as they need to without having to provide their sign-in credentials each time. Using Verimi, companies can recognize users and at the same time its users can remain in control of their data. Each individual decides how much or how little to share. Verimi aims to give German (and, later, European) consumers a single, secure payment platform that can be used for transactions with any company.

Deutsche Bank branch concept focuses on advisory service

This article has been compiled based on publicly available information on the web, particularly the bank’s own website.

Banking Frontiers December 2021 17

Transformation

Digital strategies help Wells Fargo regain its pre-eminenceA fraud scandal, its severe impact on normal functioning did not deter Wells Fargo. Through new strategies and stress on innovation, the bank is rebuilding its past glory:

Wells Fargo is the fourth-largest bank in the US, with approximately $1.9 trillion in

assets. It offers it various banking services to 1 in 3 US households and more than 10% of small businesses in the country through its Consumer Banking and Lending, Commercial Banking, Corporate and Investment Banking and Wealth & Investment Management.

The bank was in a major fraud scandal controversy where it created millions of fraudulent savings and checking accounts on behalf of its clients without their consent sometime in 2016 and its aftermath had dealt a serious blow to its reputation and operations. It faced several punitive actions - civil and criminal - amounting to $2.7 billion and fine of $185 million by the Consumer Financial Protection Bureau (CFPB). The scandal led to resignations of the bank’s then CEO and several other senior managers and a new management team was installed with reformation of the bank as the prime task.

The bank is now back on a sound footing having almost erased the black chapter and effected operational changes and implemented new strategies, at the same time relying more on technology, especially AI and cloud.

RESTRUCTURING, DIGITAL STRATEGYIt has undertaken a major organizational restructuring and created a new digital strategy. Accordingly, it now has 5 line-of-business CEOs in Consumer and Small Business Banking, Commercial Banking, Corporate & Investment Banking, Wealth & Investment Management and \Consumer Lending. In addition, it has created a new group for Strategy, Digital Platform and Innovation. The department is designed to enhance ‘the company’s focus on planning for the digital future and investing in the customer experience’. The bank also sees AI as a central focus for banking innovation moving forward and has stressed that

digital transformation begins at the line-of-business level, requiring every department to be ‘ideating, redesigning and reimagining the experience’.

However, digital is nothing new at the bank. It has some 30 million digitally active customers, which is 43% of its total customer base.

NEW VIRTUAL ASSISTANTOne recent outcome of this digital stress is the design and development of a virtual assistant to help the bank convert more retail banking customers into digital users. The virtual assistant will be deployed early next year when the bank is proposing to come out with a revamped mobile app and website. Named Fargo, it will be able to execute tasks including paying bills, sending money and offering transaction details and budgeting advice.

CLOUD STRATEGYWells Fargo as part of its digital strategy has also initiated a multi-cloud approach with third-party data centers to drive technological speed, agility and scalability for its customers and employees. It has engaged Microsoft Azure as its primary public cloud provider and Google Cloud as provider of additional business-critical public cloud services. With Microsoft it will use critical data and analytics services to accelerate its digital transformation, including delivering enhanced customer experiences and enabling increased employee collaboration. Google Cloud will drive advanced workloads, and complex AI and data solutions, allowing it to move faster on driving personalized experiences for its customers and clients.

The bank is also readying its mobile app, called Wells Fargo Mobile, hoping to provide its 30 million mobile active customers a new, modern look and feel and a simpler user experience using the app. The app will offer answers to the customers’ everyday banking questions and, rather than self-serving to accomplish a task, customers will be able

to ask Fargo to complete the task for them. The virtual assistant will on its part provide personalized insights and recommendations to help customers better manage their finances.

WELLS FARGO LABSYet another unique thing the bank is initiating is its innovation department, called Wells Fargo Labs. A unique thing about the Labs is a comment box on its website, where any user can offer any suggestions or thoughts on, either the innovations being touted, or fresh ideas they may have. The bank intends to create an idea of community between the innovation team at Wells Fargo, and the users who will ultimately benefit from the initiatives if and when they are implemented.

The bank is now clear that its dark period of scandals and intrusive investigations are over. With the innovations already being put out by the Innovation Labs and those still in development, the bank is clear about its resurgence and getting back to its glorious days. As the Director of Wells Fargo Innovation Group Miranda Hill says, “It is critical for the lab to continually push the boundaries on the future of personal finance and money management. The more we motivate team members to reimagine experiences, the more successful we’ll be as an organization in redefining the future of banking.”

A cardless ATM

This article has been compiled based on publicly available information on the web, particularly the bank’s own website.

Transformation

18 Banking Frontiers December 2021

Banco Santander’s unique thrust on cloudBanco Santander, the Spanish bank with a global footprint, believes its leveraging the cloud is a strategy that can take it to unique levels in terms of products and services and customer experience:

Banco Santander, the Madrid-h e a d q u a r t e r e d S p a n i s h multinational bank that operates

in the whole of Europe and major parts of the Americas, has a unique thrust on cloud. It says this is to facilitate offering innovative products and services, to improve customer experience and to be among the top banks in the world in terms of quality and convenience. The bank is now in the process of delivering one of the fastest cloud adoption projects in the world targeting total implementation by 2023. In doing so, the bank also wants to be a fully digitally-enabled global bank.

At the end of 2020, Banco Santander had more than a trillion euros in total funds, 148 million customers, of which 22.8 million are loyal and 42.4 million are digital, 11,000 branches and 191,000 employees.

The bank had initiated its digital transformation program around 2 years ago and it is well ahead of its plan as more than 60% of its systems worldwide have already migrated to the cloud, making it a leader among European banks in using cloud in its operations. It has said it has been able to move 200 servers to the cloud every working day over the last 2 years, thus moving on its way to become the best open financial services platform. The bank believes the new system will ensure improvement in processes and high level of innovation, thereby improving processes, enabling quick innovation and offering unprecedented service quality.

UNIQUE CLOUD PLATFORMThe bank says the cloud platform, when it becomes fully operational, will host unique technologies that can deliver customer centric and innovative services and applications with better response times. When its ATM system had moved to the cloud, it was possible to offer almost instant response instead of 10 to 20 seconds in the past. Likewise, the bank is able to deliver new capabilities to its

customers in hours rather than days in the past. The platform will also help the bank to reduce its energy consumption for its IT infrastructure by 70%, contributing to its responsible banking targets.

Santander has set up an autonomous cloud-native company, PagoNxt, a fintech that brings together all of Santander’s payments businesses. It is about to develop a unique and disruptive payment services system for the bank.

PagoNxt has recently announced that it is launching its flagship merchant payments business in Europe under the Getnet brand. Getnet is already operational in Brazil, Mexico, Chile, Argentina and Uruguay. In Europe, Getnet will serve foreign and domestic merchants of all sizes in some 30 countries, whether or not they are customers of Santander or not, offering them access to multi-channel, multi-method, multi-country payments.

Santander’s prowess in cloud technology has enabled it to provide its 148 million customers across Europe and the Americas with access to vital financial services during the pandemic. It was able to migrate seamlessly to work from home for more than 100,000 employees in just days.

S a n t a n d e r ’ s c l o u d p l a t f o r m uses in-house and vendor-provided capabilities, giving its 16,500 developers access to the latest technology to enable them to add the functionality the digital-savvy customers seek.

ACCELERATING DIGITIZATIONSantander leverages its scale to invest in digital and technology and the main target is improving customer experience and revenue growth. As part of the digital plan, the bank proposes to invest over €20 billion in technology over the next 4 years. It also hopes that the digital transformation will enable it to remove €1.2 billion in annual costs from its balance sheet, thanks to possible efficiencies brought about by new technology.

USING BIG DATAThe bank’s UK unit, Santander UK, has a unique position in the group as far as use of data is concerned. The bank started a project in 2014 to make use of big data to generate value for customers. In about 9 months, it has created a highly available real-time customer-facing application for customer analytics. The app uses real-time transaction data to help the customers, for example, to understand their card spend across time periods, different categories (travel, food & drink, supermarkets, cash, etc.) and by brand/retailer. The big data platform is also used to power all the new digital applications – customer facing, or on the backend.

Santander has concluded a 5-year $700 million agreement with IBM in 2019, which ensures that its services and applications will have the backing of IBM’s most innovative and disruptive technologies. This includes big data, blockchain and AI technology such as IBM Watson, which Santander will use to incorporate AI capabilities into its operations to improve customer experience, enhance branch advisors’ expertise, and increase employee productivity.

A Banco Santander ATM where the response time is instant rather that a few second

This article has been compiled based on publicly available information on the web, particularly the bank’s own website.

Banking Frontiers December 2021 19