May 11, 2022 Ms. Carla Harris EHS & Regulatory, Regulatory ...

Upload

khangminh22Category

view

4download

0

RBI'S PROPOSED REGULATORY FRAMEWORK FOR NBFCS:

Kolkata:1006-1009, Krishna

224 AJC Bose Road

Kolkata – 700 017

Phone: 033 2281 3742/7715

Email: [email protected]

New Delhi:A-467, First Floor,

Defence Colony,

New Delhi-110024

Phone: 011 41315340

Email: [email protected]

Mumbai:403-406, Shreyas Chambers

175, D N Road, Fort

Mumbai

Phone: 022 2261 4021/ 62370959

Email: [email protected]

Website: www.vinodkothari.com

Vinod Kothari Consultants P. Ltd.

Vinod Kothari, Vinod Kothari Consultants P Ltd

COPYRIGHT & DISCLAIMER

The presentation is a property of Vinod Kothari Consultants P. Ltd. No part of it can be copied, reproduced or

distributed in any manner, without explicit prior permission. In case of linking, please do give credit and full link.

This presentation is only for academic purposes; this is not intended to be a professional advice or opinion.

Anyone relying on this does so at one’s own discretion. Please do consult your professional consultant for any

matter covered by this presentation.

No circulation, publication, or unauthorized use of the presentation in any form is allowed, except with our prior

written permission.

No part of this presentation is intended to be solicitation of professional assignment.

Vinod Kothari Consultants P. Ltd.

ABOUT US

Vinod Kothari Consultants P. Ltd is a consultancy company with

over 30 years of vintage

Based out of Kolkata, New Delhi & Mumbai

We are a team of qualified company secretaries, chartered

accountants, CFAs, lawyers and managers.

Our Organization’s Credo:

Focus on capabilities; opportunities follow

Vinod Kothari Consultants P. Ltd.

STATE OF THE INDIAN NBFC SECTOR

Vinod Kothari Consultants P. Ltd.

ROLE OF NON-BANKING FINANCIAL INTERMEDIARIES IN SYSTEMIC INTER-

CONNECTIVITY

World-over, the role of non-banking financial intermediaries in systemic stability of the financial sector has been under focus

FSB’s report on shadow-banking every year focuses on this

Risk arises from inter-connectivity

Banks lend to NBFCs

Mutual funds invest in NBFC securities

NBFCs securitise assets which end up on the balance sheets of banks and mutual funds

Some degree of insurance company exposure on NBFCs too

Regulatory arbitrage: The shadow banking sector substantially serves the same economic function as banks, and yet escapes financial regulation; this provides them a significant regulatory arbitrage

Scalar approach can be deployed to create a balanced regulatory approach

RBI states that “The fundamental premise underlying the NBFC regulatory framework is ‘less rigorous’ regulation”

The statistics show that spill over systemic risk from NBFC sector is rising rapidly

The inflection point in NBFC landscape was default of a leading CIC:

In terms of policy, CIC should be having minimal leverage

Vinod Kothari Consultants P. Ltd.[1] See an article by Vinod Kothari, tilted Shadow Banking in India – Creating an Opportunity out of a Crisis, at http://vinodkothari.com/2020/01/shadow-banking-in-india/

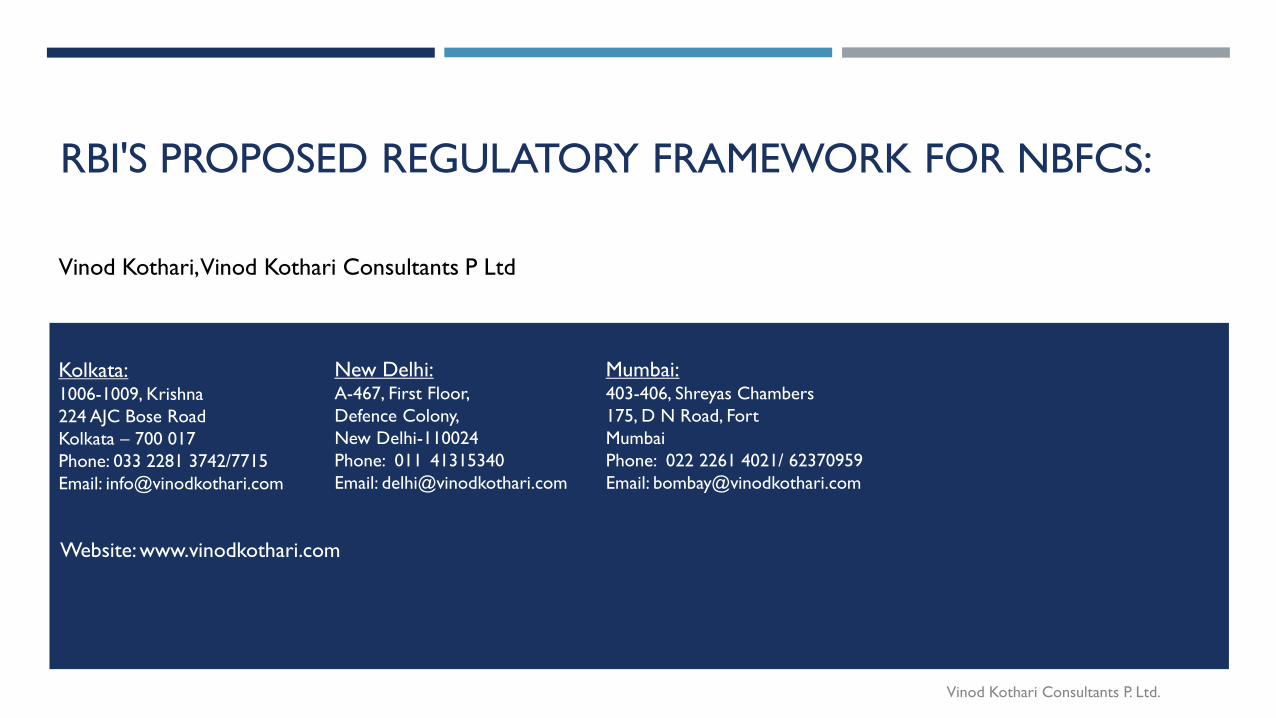

BILATERAL EXPOSURE IN FINANCIAL SECTOR

36.435

35.8 35.834.6

34.7

5.10 4.90 5.01 5.08 5.29 5.31

14.0% 14.0% 14.0%

14.2%

15.3%15.3%

13.0%

13.5%

14.0%

14.5%

15.0%

15.5%

0

5

10

15

20

25

30

35

40

Jun-19 Sep-19 Dec-19 Mar-20 Jun-20 Sep-20

In L

akh C

r

Bilateral Exposure in Financial Sector NBFCs Share NBFCs Share %

7.1

5.9

4.2

1.2

0.1

-0.1-0.5

-3.9

-5.7

-8.4-10

-8

-6

-4

-2

0

2

4

6

8

AM

Cs

Insu

rance

PSB

s

PFs

UC

Bs

FBs

AIF

Is

PV

Bs

HFC

s

NB

FCs

Net recievable (+) / Net Payable (-) to Institutions as on Sept 2020

Vinod Kothari Consultants P. Ltd.Source: Financial Stability Report Jan 2021 I VKC Analysis

STATISTICS ON IMPORTANCE OF NBFCS IN INDIAN FINANCIAL SECTOR

Balance sheet size of NBFCs has increased more than two folds; CAGR of 18.89% over last 5 years

“Public funds” had CAGR of 14.77% over last 5 year

NBFCs were the largest net borrowers of funds from the financial system, with gross payables of ₹9.37 lakh crores and gross receivables of ₹ 0.93 lakh crores as at end-September 2020

HFCs were the second largest borrowers, with gross payables of around ₹6.20 lakh crores and gross receivables of ₹0.53 lakh crores

NBFCs were second largest recipient of funds from MFs as well as insurance companies, followed by HFCs.

7 NBFCs have asset size of more than 1 lakh crore

The NBFC sector has grown from being 12% of bank’s balance sheet to more than 25%.

Vinod Kothari Consultants P. Ltd.Sources: Discussions paper by the RBI, Financial Stability Report-Jan-21 and

VKC Analysis

THE EXISTING & PROPOSED REGULATORY

FRAMEWORK

Vinod Kothari Consultants P. Ltd.

PRESENT REGULATORY FRAMEWORK

NBFCs

CICs

Not-registerable

Not holding “public funds” OR not having assets >

Rs. 100 cr.

Registerable

Systemically imp: asset size >Rs. 100

cr.

Non-systemically Imp

Other NBFCs

Systemically imp [asset size > 500

cr.]

Not-systemically imp

No public funds, no interface

With public funds or customer

interface

EVOLUTION OF REGULATORY FRAMEWORK FOR NBFCS

Regulatory Framework -1998

New regulatory Framework in Jan-1998 upon newly acquired powers under RBI Act.

Provided for

•1. Categorisation of NBFCs

•2. Defining “Deposit”

•3. Min. credit rating and NOF

•4. Prohibition on loan against own shares

•5.Widen scope for “auditors certificate”

Classification of Systemically Important NBFCs – Usha Thorat report 2011

Classified NBFCs with asset size => Rs. 100 cr. as “Systemically Important”

Prudential Regulations such as CAR and exposure norms made applicable

Revised Regulatory Framework - 2014

Rapid growth of NBFC sector influenced RBI to review the regulatory framework in 2014

Provided for-

1. Min NOF of Rs. 2 cr.

2. Limit for being classified as systematically important was increased to Rs. 500 cr. from Rs. 100 cr.

3. Harmonization of norms

4. Review of corporate governance norms

Vinod Kothari Consultants P. Ltd.

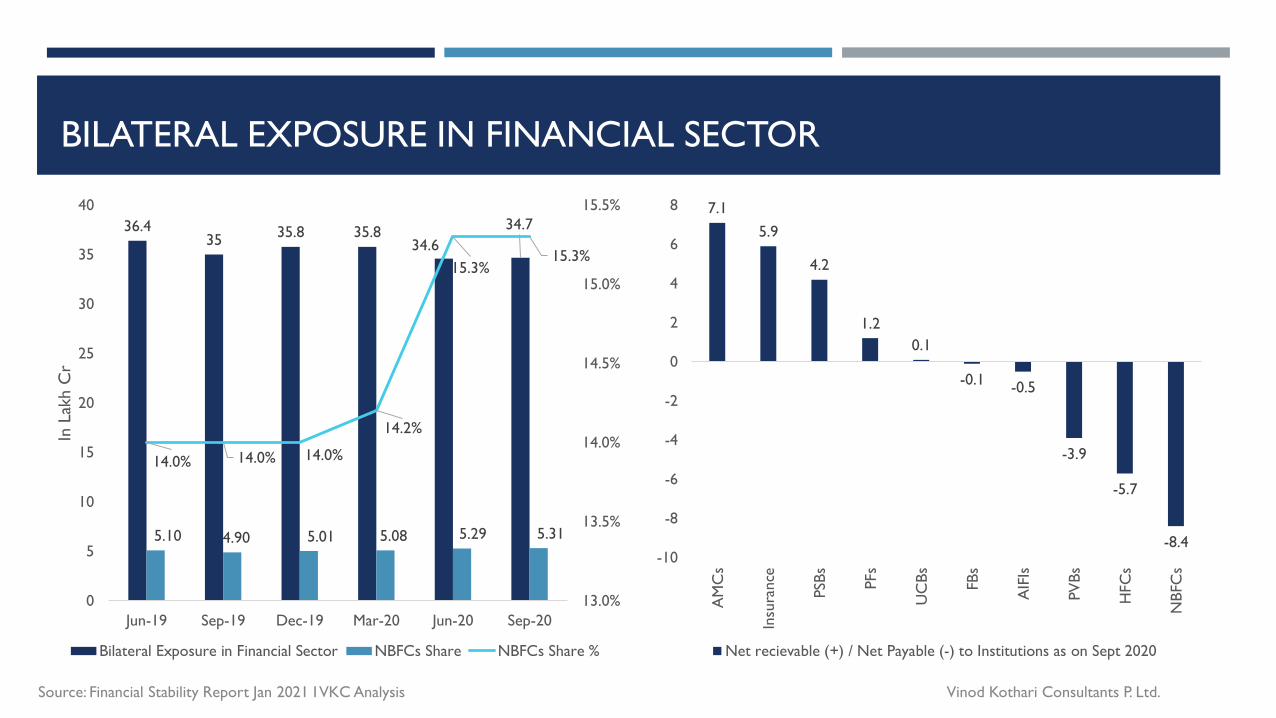

EXISTING REGULATORY FRAMEWORK FOR NBFC-ND-SI

From the viewpoint of volume of NBFC assets, this

category is obviously the most important – hence, the

most important for systemic risks too

Aspects of regulatory framework:

Capital requirements – 15% consisting of 10% tier 1

Provisioning norms -0.40% for standard and 10% for sub-

standard

Corporate governance norms – Fit and proper

requirements, Committees, audit partner rotation, balance

sheet and website disclosures

Fair practices code

Grievance redressal mechanism

Applicable to all NBFCs

Reporting to CICs

Fair practices code

KYC norms

Change of control Directions

Vinod Kothari Consultants P. Ltd.

REGULATORY ARBITRAGE BETWEEN BANKS AND NBFCS

Regulatory arbitrage has been the subject matter of

policy makers’ attention for long time; multilateral

bodies have also been pointing the same out

NBFCs can virtually do everything that banks can;

however, without having similar regulations

Structural arbitrage:

No CRR/SLR

No priority sector lending

No restriction on investments in shares of other

companies

No Shareholding limits – not more than 10% shares in a

banking co

FDI is freely allowed

Prudential arbitrage

Licensing of banks is all time open

Ownership restriction – business houses do not own

banks – proposal currently under examination

Entry point capital requirement is much higher

Provisioning requirements – asset-based provisioning

requirements in case of standard assets

Basel III has leverage

Vinod Kothari Consultants P. Ltd.

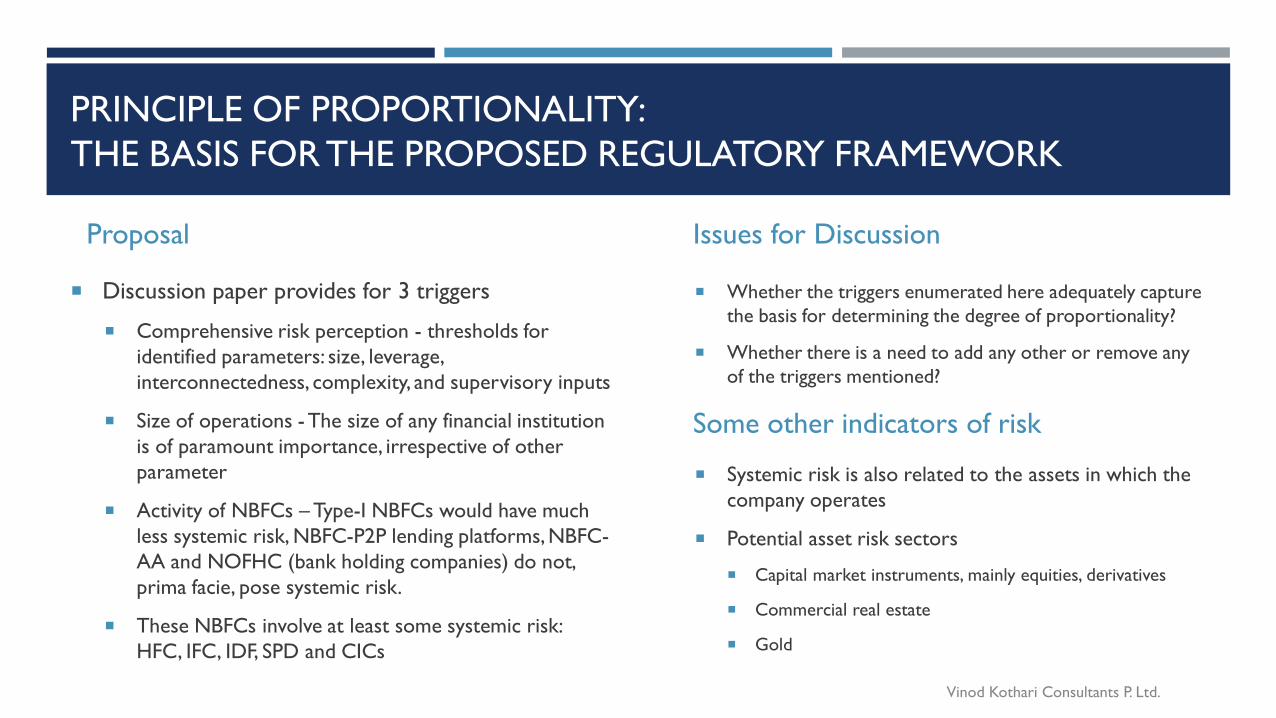

PRINCIPLE OF PROPORTIONALITY:

THE BASIS FOR THE PROPOSED REGULATORY FRAMEWORK

Proposal

Discussion paper provides for 3 triggers

Comprehensive risk perception - thresholds for

identified parameters: size, leverage,

interconnectedness, complexity, and supervisory inputs

Size of operations -The size of any financial institution

is of paramount importance, irrespective of other

parameter

Activity of NBFCs – Type-I NBFCs would have much

less systemic risk, NBFC-P2P lending platforms, NBFC-

AA and NOFHC (bank holding companies) do not,

prima facie, pose systemic risk.

These NBFCs involve at least some systemic risk:

HFC, IFC, IDF, SPD and CICs

Issues for Discussion

Whether the triggers enumerated here adequately capture

the basis for determining the degree of proportionality?

Whether there is a need to add any other or remove any

of the triggers mentioned?

Vinod Kothari Consultants P. Ltd.

Some other indicators of risk

Systemic risk is also related to the assets in which the

company operates

Potential asset risk sectors

Capital market instruments, mainly equities, derivatives

Commercial real estate

Gold

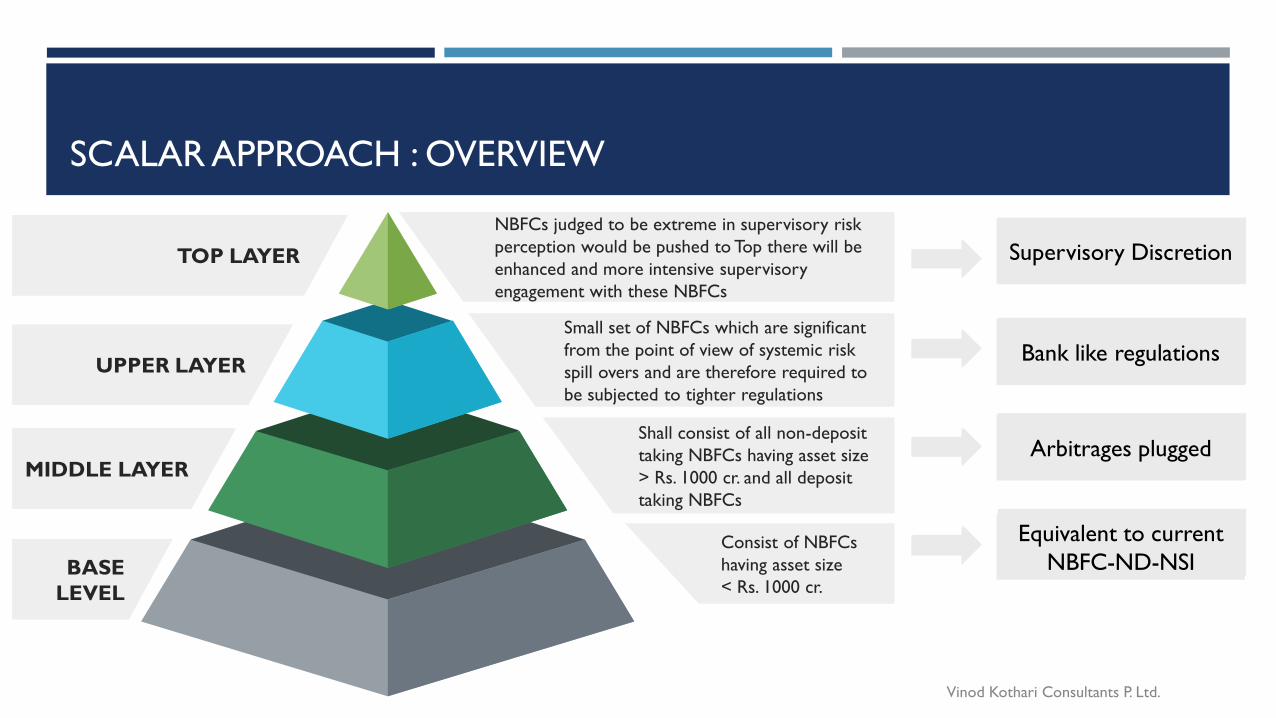

SCALAR APPROACH : OVERVIEW

Vinod Kothari Consultants P. Ltd.

Bank like regulations

Arbitrages plugged

Equivalent to current

NBFC-ND-NSI

Supervisory DiscretionTOP LAYER

UPPER LAYER

MIDDLE LAYER

BASE

LEVEL

NBFCs judged to be extreme in supervisory risk

perception would be pushed to Top there will be

enhanced and more intensive supervisory

engagement with these NBFCs

Small set of NBFCs which are significant

from the point of view of systemic risk

spill overs and are therefore required to

be subjected to tighter regulations

Shall consist of all non-deposit

taking NBFCs having asset size

> Rs. 1000 cr. and all deposit

taking NBFCs

Consist of NBFCs

having asset size

< Rs. 1000 cr.

Bank like regulations

Arbitrages plugged

Equivalent to current

NBFC-ND-NSI

Supervisory Discretion

SCALAR VIEW BY NUMBERS

Vinod Kothari Consultants P. Ltd.

• No company to be there; except exceptionally

Top

• To have about 25-30 cos. Based on parameters; however, top 10 surely

Upper

Layer

• May have about 270 -300 cosMiddle layer

• May have about 9000+ cos

Base layer

SCALAR APPROACH: FILTERING PROCESS (1/2)

Vinod Kothari Consultants P. Ltd.

Size Scale of Significance

Upper Layer

Top 10 NBFCs to be included

Top 50 NBFCs by asset size to go following filters

Size – 35%

Interconnectedness – 25%

Complexity – 10%

Supervisory Inputs – 30%

Activity

Housing Finance

companies

Standalone Primary

Dealers

IFCs

Always NBFC-ML

IDFs

CICs

Middle Layer Base Layer

Type-I NBFCs

Peer to Peer

Account Aggregators

NOFHC

Asset Size upto Rs.

1000 cr

SCALAR APPROACH: FILTERING PROCESS (2/2)

Two-Phase parametric Analysis for UL

Quantitative Factors

Weight – 70%

Qualitative Factors/Supervisory

Inputs

Weight – 30%

Quantitative Measures

Size & Leverage

Inter-connectedness

Complexity

Qualitative Measures

Nature and type of liabilities

Group Structure

Segment penetration

Vinod Kothari Consultants P. Ltd.

QUANTITATIVE MEASURES

Parameters Sub-Para Weights Parameter WeightsCategory

Weight

1. Size & Leverage Total exposure (on- and off-balance sheet) & Leverage - total debt to total equity 20 + 15 35

2. Inter-connectedness (i) Intra-financial system assets

• Lending to financial institutions (including undrawn committed lines);

• Holdings of securities issued by other financial institutions;

• Net mark-to-market reverse repurchase agreements with other financial

institutions;

• Net mark-to-market OTC derivatives with financial institutions.

10 25

(ii) Intra-financial system liabilities

• Borrowings from financial institutions (including undrawn committed lines)

• All marketable securities issued by the finance company to financial institutions;

• Net mark-to-market repurchase agreements with other financial institutions;

• Net mark-to-market OTC derivatives with financial institutions

10

(iii) Securities outstanding with non-financial institutions (issued by the NBFC) 5

3. Complexity (i) Notional Amount of Over-the-Counter (OTC) Derivatives

• OTC derivatives cleared through a central counterparty

• OTC derivatives settled bilaterally

5 10

(ii) Trading and Available-for-Sale Securities 5

Vinod Kothari Consultants P. Ltd.

QUALITATIVE MEASURES

Vinod Kothari Consultants P. Ltd.

Parameters Sub-Para WeightsParameter

Weights

Category

Weight

Nature and type of

liabilities

• The amount and type of liabilities, including the degree of reliance on short-term funding

• Liquid asset ratios, which are intended to indicate a nonbank financial company’s ability

to repay its short-term debt.

• The ratio of unencumbered and highly liquid assets to the net cash outflows that a

nonbank financial company could encounter in a short-term stress scenario.

• Callable debt as a fraction of total debt, which provides one measure of a nonbank

financial company’s ability to manage its funding position in response to changes in

interest rates.

• Asset-backed funding versus other funding, to determine a nonbank financial company’s

susceptibility to distress in particular credit markets.

• Asset-liability duration and gap analysis, which is intended to indicate how well a

nonbank financial company is matching the re-pricing and maturity of the nonbank

financial company’s assets and liabilities.

• A study on the borrowings split by type i.e. Secured debt securities; subordinated debt

securities; preferred shares/CCPS; CPs; unsecured debt; securitisation and any other

10 30

Group Structure • Total Number of entities

• Total number of layers

• Total Intra group exposure

10

Segment

penetration

The importance of the NBFC as a source of credit to a specific segment or area 10

SCALAR APPROACH: DISCUSSION POINTERS 1/2

Whether the 9000 odd companies that constitute

the bottom of pyramid deserves to be painted

with the same brush? If the stance of the new

regulatory framework is differential regulation, is

it appropriate to treat 9000 cos all alike?

With whole lot of discussion on leaving Type 1

NBFCs virtually free, there is intensive regulatory

interface in those cases too

Whether the layers in the regulatory pyramid

capture the calibrated classification of NBFCs

based on their likely systemic impact?

Is the activity-based classification of NBFC-AA,

P2P, NOFHC in Lower Layer and NBFC-HFC,

IFC, IDF, CIC and SPDs in Middle Layer

justified?

Issues for Is the scoring methodology for the

quantitative and qualitative parameters

adequate to identify NBFCs which have

systemic significance?

None of the parameters give importance to the

fragility of the business model, is thatappropriate?

Vinod Kothari Consultants P. Ltd.

SCALAR APPROACH: DISCUSSION POINTERS 2/2

Are there any suggestions on weights assigned to different parameters?

The risk weight assigned to the composition of liabilities is only 10% - given the potential impact of the liabilities profile of a company could have own its stability – do you think 10% weight is sufficient?

Whether the sample of the top 50 NBFCs is appropriate or NBFCs above a certain specified asset size threshold should constitute the sample?

Currently, government-owned NBFCs are sought to be exempted from UL categorisation

Is this appropriate?

The proposal also says entities selected to be in the UL will stay there, unless there is a compelling reason

Is this appropriate??

Currently the scalar matrix for identification of inter-connectedness has weights for lending to financial system and borrowing from financial system

Should it actually be either of these? Because an entity that borrows heavily from financial system but lends nothing to financial system may have the weights evened out

Should issue of debentures/CP/securitisation also be counted for inter-connectivity?

The metrics in nature and type of liabilities are all seemingly covered by the ALM framework

Vinod Kothari Consultants P. Ltd.

IMPLEMENTATION PLAN

When an NBFC is to be classed as UL entity, it will be

given an opportunity to prepare a roadmap to remove

the differential risks

8 weeks for preparing the road map

18 months for implementation

During this period, the NBFC will be under calibrated

increment to business with supervisory engagement

Enhanced regulatory treatment for at least 4 years

In other words, once an NBFC is classified as UL

entity, it stays there for 4 years

Even though it does not meet the parametric criteria in

the subsequent years

Vinod Kothari Consultants P. Ltd.

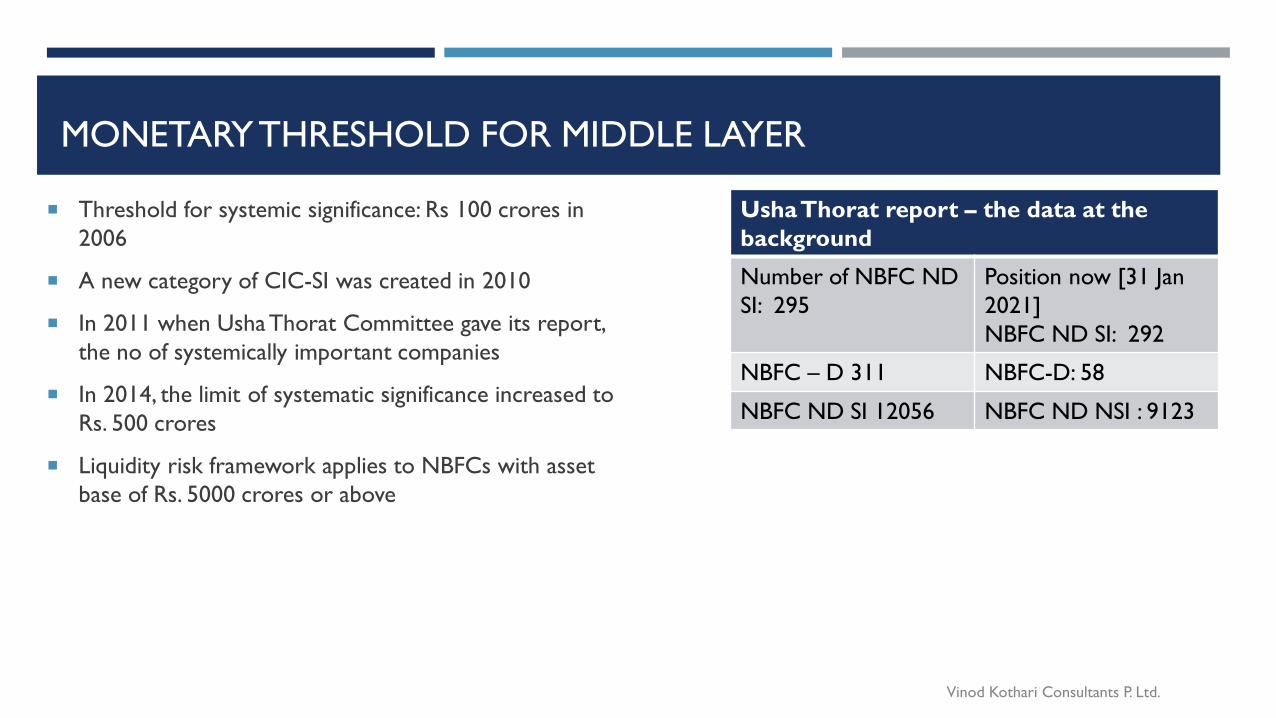

MONETARY THRESHOLD FOR MIDDLE LAYER

Threshold for systemic significance: Rs 100 crores in

2006

A new category of CIC-SI was created in 2010

In 2011 when UshaThorat Committee gave its report,

the no of systemically important companies

In 2014, the limit of systematic significance increased to

Rs. 500 crores

Liquidity risk framework applies to NBFCs with asset

base of Rs. 5000 crores or above

UshaThorat report – the data at the

background

Number of NBFC ND

SI: 295

Position now [31 Jan

2021]

NBFC ND SI: 292

NBFC – D 311 NBFC-D: 58

NBFC ND SI 12056 NBFC ND NSI : 9123

Vinod Kothari Consultants P. Ltd.

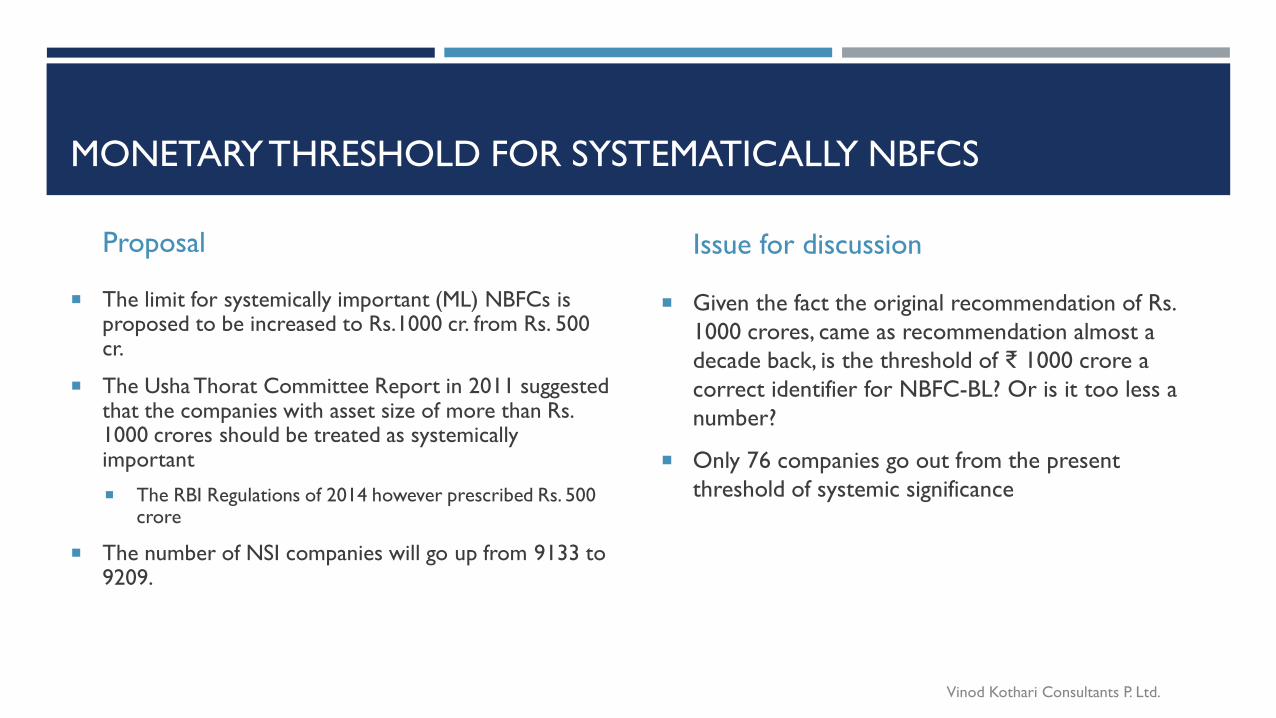

MONETARY THRESHOLD FOR SYSTEMATICALLY NBFCS

Proposal

The limit for systemically important (ML) NBFCs is proposed to be increased to Rs.1000 cr. from Rs. 500 cr.

The Usha Thorat Committee Report in 2011 suggested that the companies with asset size of more than Rs. 1000 crores should be treated as systemically important

The RBI Regulations of 2014 however prescribed Rs. 500 crore

The number of NSI companies will go up from 9133 to 9209.

Issue for discussion

Given the fact the original recommendation of Rs.

1000 crores, came as recommendation almost a

decade back, is the threshold of ₹ 1000 crore a

correct identifier for NBFC-BL? Or is it too less a

number?

Only 76 companies go out from the present

threshold of systemic significance

Vinod Kothari Consultants P. Ltd.

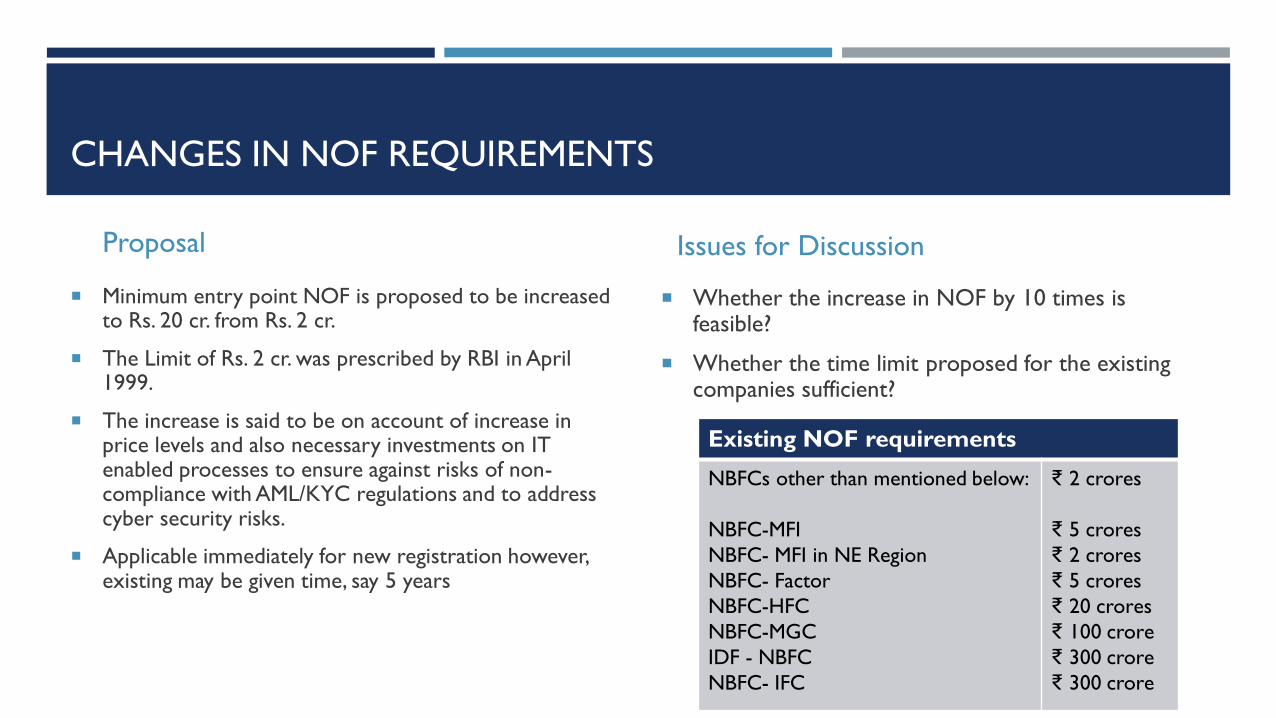

CHANGES IN NOF REQUIREMENTS

Proposal

Minimum entry point NOF is proposed to be increased to Rs. 20 cr. from Rs. 2 cr.

The Limit of Rs. 2 cr. was prescribed by RBI in April 1999.

The increase is said to be on account of increase in price levels and also necessary investments on IT enabled processes to ensure against risks of non-compliance with AML/KYC regulations and to address cyber security risks.

Applicable immediately for new registration however, existing may be given time, say 5 years

Issues for Discussion

Whether the increase in NOF by 10 times is feasible?

Whether the time limit proposed for the existing companies sufficient?

Vinod Kothari Consultants P. Ltd.

Existing NOF requirements

NBFCs other than mentioned below:

NBFC-MFI

NBFC- MFI in NE Region

NBFC- Factor

NBFC-HFC

NBFC-MGC

IDF - NBFC

NBFC- IFC

₹ 2 crores

₹ 5 crores

₹ 2 crores

₹ 5 crores

₹ 20 crores

₹ 100 crore

₹ 300 crore

₹ 300 crore

PROPOSALS FOR NBFCS –BL

Vinod Kothari Consultants P. Ltd.

MAJOR PROPOSALS FOR THE BASE LAYER

The current regulations require NPA classification of the asset having more than 180 DPDs the same is proposed to be reduced to 90 DPDs in order to bring it in sync with the regulatory guidelines for other classes of NBFCs

The board shall be required to have –

Adequate experience and educational qualification

At least one of the directors should have experience in retail lending in a bank/NBFC

For the Risk Management Committee -

Current requirements at asset level of Rs 100 crores

Overall role and responsibilities to be laid out, and

Composition could be Board or Executive level as to be decided by the Board

The regulations for sale of stressed assets shall be made at par with banks once guidelines are finalized

Additional disclosures on type of exposures, related party transactions, customer complaints shall be prescribed Vinod Kothari Consultants P. Ltd.

Issues for discussion

Is the threshold of ₹ 1000 crore a correct identifier for

NBFC-BL?

Are there any suggestions on the disclosure framework

for NBFCs-BL?

Feedback on harmonization of NPA norms

Specific regulatory concessions to Type I NBFC

There are 9000 odd NBFCs covered by this – while

there is tightening of regulations, there is no loosening

at this level. Is this the idea of scale-based regulation?

Is the current definition of “Type 1” a farce? Inter-

corporate borrowings should be a part of “public

funds”?

Proposal

PROPOSAL FOR NBFCS ML

Vinod Kothari Consultants P. Ltd.

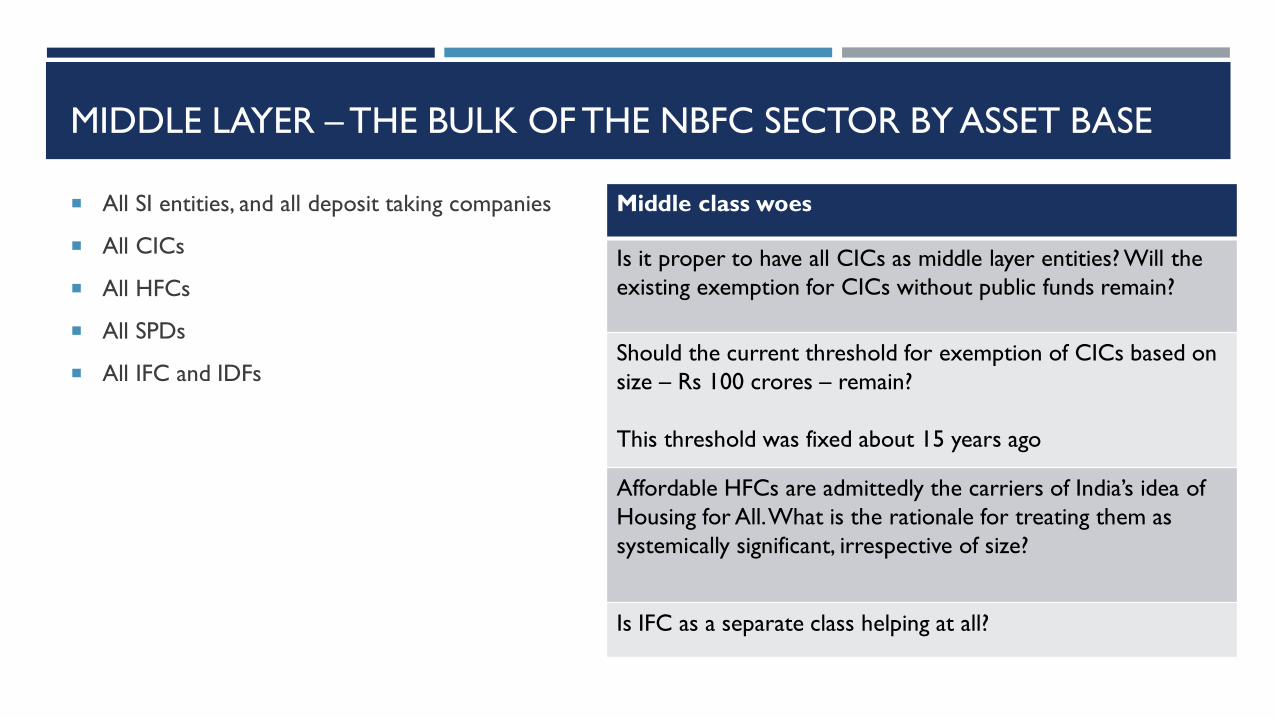

MIDDLE LAYER – THE BULK OF THE NBFC SECTOR BY ASSET BASE

All SI entities, and all deposit taking companies

All CICs

All HFCs

All SPDs

All IFC and IDFs

Middle class woes

Is it proper to have all CICs as middle layer entities? Will the

existing exemption for CICs without public funds remain?

Should the current threshold for exemption of CICs based on

size – Rs 100 crores – remain?

This threshold was fixed about 15 years ago

Affordable HFCs are admittedly the carriers of India’s idea of

Housing for All. What is the rationale for treating them as

systemically significant, irrespective of size?

Is IFC as a separate class helping at all?

CAPITAL REQUIREMENTS

Proposals

At present, NBFCs are on a Basel I type framework (i.e. uniform risk weights for counterparties, no capital for market risk or operational risk)

CRAR of 15% is required with 10% in Tier I

No changes for Capital requirements for NBFC-ML is proposed

Ratings-based risk weights are not applicable –the risk weight still date to Basel I era

Issues for Discussion

Are the existing capital requirements adequate to take care of loss absorbency in the NBFCs?

Should the Basel II risk weights not be applicable?

24.5 24.1

29.7

6.8 6.9 8.4

0

5

10

15

20

25

30

35

Baseline Medium High

CRAR of NBFCs against GNPA levels

CRAR GNPA

Based on above data the current levels of CRAR requirements

looks adequate even for high risk scenarios

Vinod Kothari Consultants P. Ltd.Source: Stress Testing of NBFC sector I Financial Stability Report January 2021

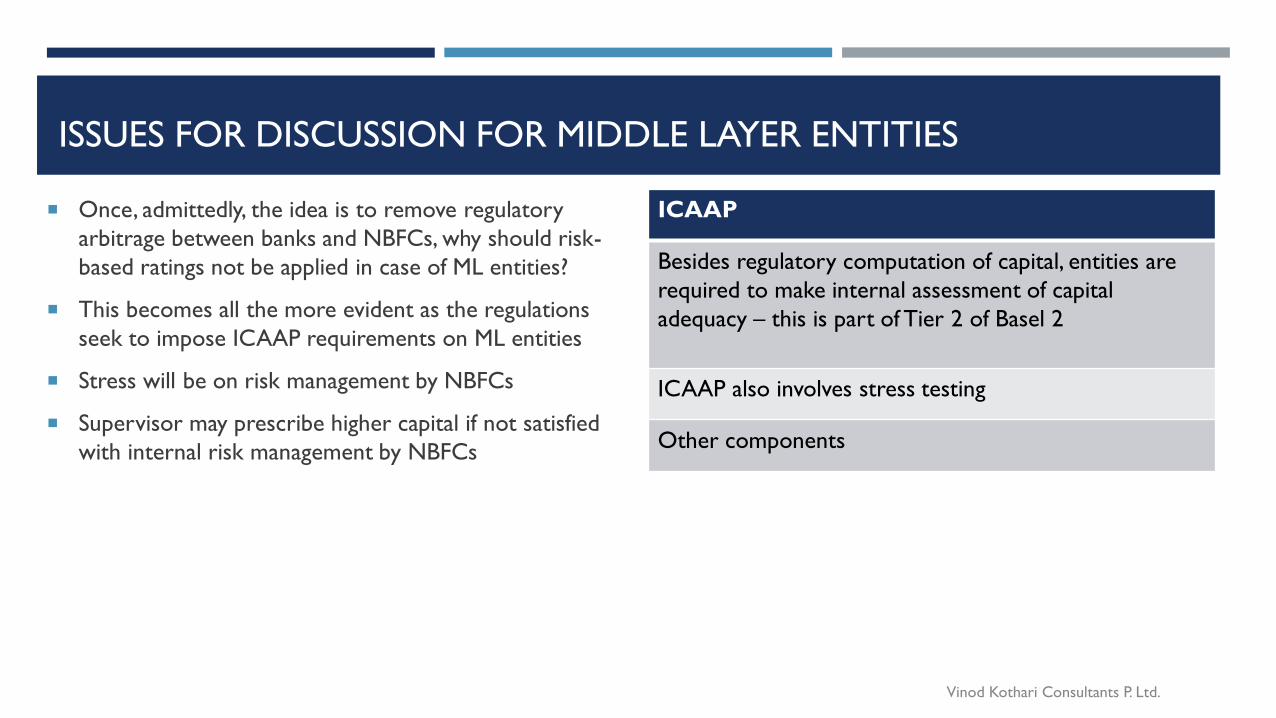

ISSUES FOR DISCUSSION FOR MIDDLE LAYER ENTITIES

Once, admittedly, the idea is to remove regulatory

arbitrage between banks and NBFCs, why should risk-

based ratings not be applied in case of ML entities?

This becomes all the more evident as the regulations

seek to impose ICAAP requirements on ML entities

Stress will be on risk management by NBFCs

Supervisor may prescribe higher capital if not satisfied

with internal risk management by NBFCs

ICAAP

Besides regulatory computation of capital, entities are

required to make internal assessment of capital

adequacy – this is part of Tier 2 of Basel 2

ICAAP also involves stress testing

Other components

Vinod Kothari Consultants P. Ltd.

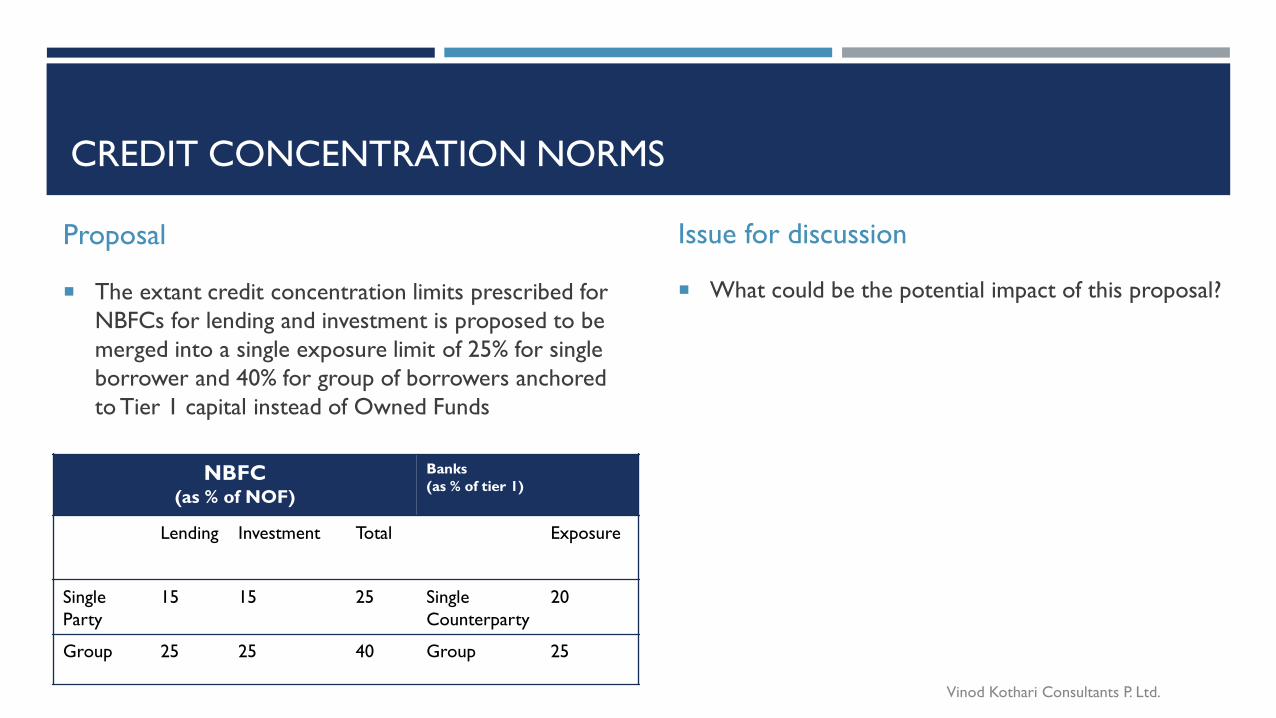

CREDIT CONCENTRATION NORMS

Proposal

The extant credit concentration limits prescribed for

NBFCs for lending and investment is proposed to be

merged into a single exposure limit of 25% for single

borrower and 40% for group of borrowers anchored

to Tier 1 capital instead of Owned Funds

NBFC(as % of NOF)

Banks

(as % of tier 1)

Lending Investment Total Exposure

Single

Party

15 15 25 Single

Counterparty

20

Group 25 25 40 Group 25

Vinod Kothari Consultants P. Ltd.

Issue for discussion

What could be the potential impact of this proposal?

LENDING RESTRICTION ON ML NBFCS

Proposals Issue for discussion

Is the current view taken by some NBFCs that

lending to individuals is not covered by

concentration limits fair, reasonable?

LAS limits – NBFCs give a secured loan and top it up

with unsecured loan

Implication of the NSE circular for stock exchange

members

Are the suggested changes adequate to contain risks

from SSE?

Vinod Kothari Consultants P. Ltd.Source: RBI Trends and Progress in Banking report 2020

Internal limits on sensitive sector exposures, but it should be supplemented by adequate disclosures

Restrictions on grant of loans and advances for/to the following:

Buy back of shares/ securities

Activities leading to Ozone Depleting Substances

As defined in Ozone Depleting Substances (Regulation and Control)

Directors and relatives of directors

Officers and relatives of Senior Officers

Real Estate – only where project approvals other permissions are in place.

The IPO financing by NBFCs shall be capped at Rs.1 crore.

Is the current view taken by some NBFCs that

lending to individuals is not covered by

concentration limits fair, reasonable?

LAS limits – NBFCs give a secured loan and top it up

with unsecured loan

Implication of the NSE circular for stock exchange

members

Are the suggested changes adequate to contain risks

from SSE?

Proposals

GROWTH IN CREDIT DEPLOYMENT IN REAL STATE SECTOR

Commercial Real Estate

69.3

30.1

21.2

-14.8-20

-10

0

10

20

30

40

50

60

70

80

2016-17 2017-18 2018-19 2019-20

YoY growth rate

Housing Loan

Vinod Kothari Consultants P. Ltd.

-27.9

16.4 18.2

37.1

-40

-30

-20

-10

0

10

20

30

40

50

2016-17 2017-18 2018-19 2019-20

YoY growth rate

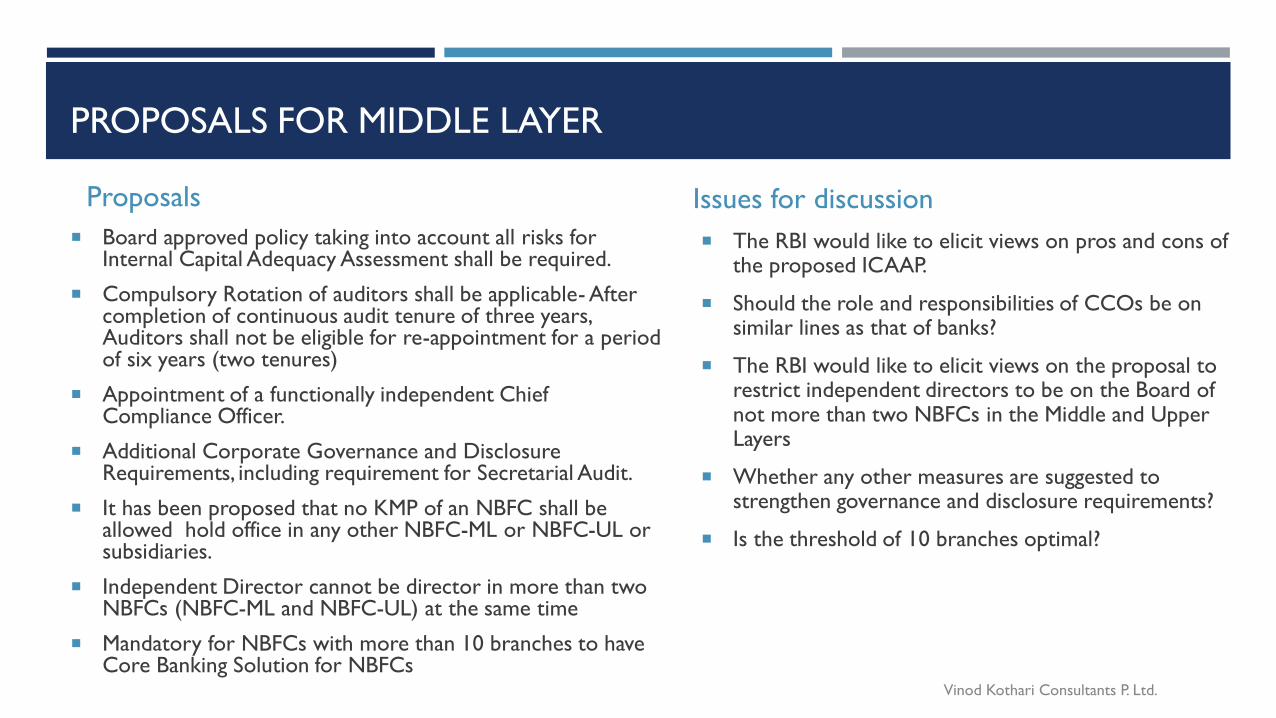

PROPOSALS FOR MIDDLE LAYER

Board approved policy taking into account all risks for Internal Capital Adequacy Assessment shall be required.

Compulsory Rotation of auditors shall be applicable- After completion of continuous audit tenure of three years, Auditors shall not be eligible for re-appointment for a period of six years (two tenures)

Appointment of a functionally independent Chief Compliance Officer.

Additional Corporate Governance and Disclosure Requirements, including requirement for Secretarial Audit.

It has been proposed that no KMP of an NBFC shall be allowed hold office in any other NBFC-ML or NBFC-UL or subsidiaries.

Independent Director cannot be director in more than two NBFCs (NBFC-ML and NBFC-UL) at the same time

Mandatory for NBFCs with more than 10 branches to have Core Banking Solution for NBFCs

Vinod Kothari Consultants P. Ltd.

The RBI would like to elicit views on pros and cons of the proposed ICAAP.

Should the role and responsibilities of CCOs be on similar lines as that of banks?

The RBI would like to elicit views on the proposal to restrict independent directors to be on the Board of not more than two NBFCs in the Middle and Upper Layers

Whether any other measures are suggested to strengthen governance and disclosure requirements?

Is the threshold of 10 branches optimal?

Issues for discussionProposals

REMUNERATION CONTROLS ON ML ENTITIES AND OTHER CORPORATE

GOVERNANCE REQUIREMENTS

Compensation guidelines in line with those in

case of banks may be fixed for NBFCs

To prevent against excessive risk taking due to

misalignment of incentives

Minimum stipulations:

Nomination/remuneration committee

Principles of fixed/variable pay structures

Malus/clawback provisions

Several corporate governance requirements

Requirement of independent director

Other requirements are similar to those in case of

corporate governance norms for banks/listed

entities

Issues

RBI currently stipulates audit committee and NRC

for private companies as well. Given the fact that

there are no independent directors in such

companies, these committees serve no purpose

It will be questionable as to how independent

directors may be required in private limited

companies?

Vinod Kothari Consultants P. Ltd.

OTHER REQUIREMENTS FOR ML ENTITIES

Board approved internal limits for sectoral exposures

Dynamic vulnerability assessment of various sectors

Funding of IPOs

a limit of Rs 1 crore proposed

Sub limit with the internal limit for CRE financing for

land acquisition

Lending restrictions

Restrictions on lending to directors, senior officers and

their relatives

NBFCs not to lend against share buybacks

Issues

Many NBFCs have sectoral focus. They may do

assessment, but how can they move out of their sector?

For example, a factoring entity will be focused on trade

receivables, and gold lending company will be focused

on gold loan

Vinod Kothari Consultants P. Ltd.

PROPOSALS FOR NBFC UL

Vinod Kothari Consultants P. Ltd.

PRUDENTIAL REQUIREMENTS

Proposals

CET 1 may be prescribed at 9% within the Tier I

capital in addition to the CRAR requirements,

NBFCs will also be subjected to a leverage

requirement

NBFCs falling in Upper Layer may use differential

standard asset provisioning on lines of banks.

(for example: farm credit and SME@ 0.25%, CRE @ 1.00%,

CRE-RH @ 0.75%, and all other loans 0.40 %)

Issues for discussion

In addition to leverage and differential standard asset

provisioning, should any other tool be prescribed?

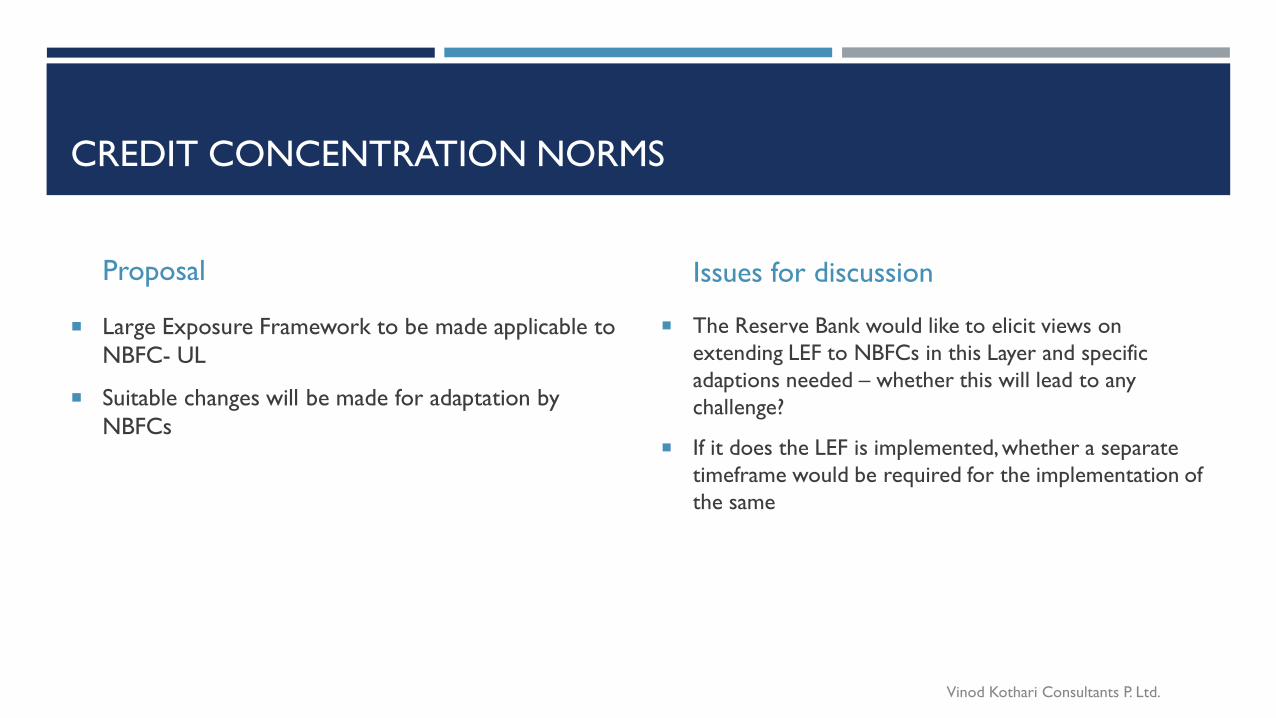

CREDIT CONCENTRATION NORMS

Proposal

Large Exposure Framework to be made applicable to

NBFC- UL

Suitable changes will be made for adaptation by

NBFCs

Vinod Kothari Consultants P. Ltd.

Issues for discussion

The Reserve Bank would like to elicit views on

extending LEF to NBFCs in this Layer and specific

adaptions needed – whether this will lead to any

challenge?

If it does the LEF is implemented, whether a separate

timeframe would be required for the implementation of

the same

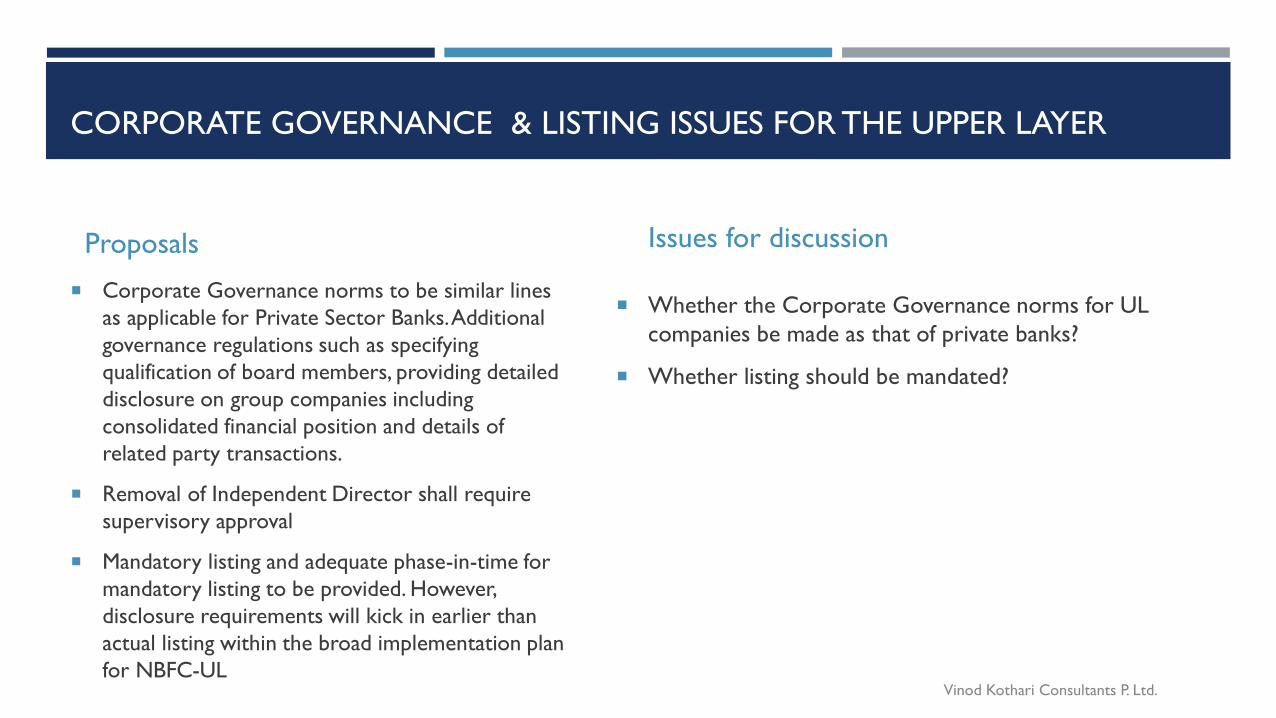

CORPORATE GOVERNANCE & LISTING ISSUES FOR THE UPPER LAYER

Corporate Governance norms to be similar lines

as applicable for Private Sector Banks. Additional

governance regulations such as specifying

qualification of board members, providing detailed

disclosure on group companies including

consolidated financial position and details of

related party transactions.

Removal of Independent Director shall require

supervisory approval

Mandatory listing and adequate phase-in-time for

mandatory listing to be provided. However,

disclosure requirements will kick in earlier than

actual listing within the broad implementation plan

for NBFC-ULVinod Kothari Consultants P. Ltd.

Proposals Issues for discussion

Whether the Corporate Governance norms for UL

companies be made as that of private banks?

Whether listing should be mandated?

ISSUES THAT HAVE NOT BEEN ADDRESSED

CHANGE OF CONTROL DIRECTIONS

Current requirements for change of control are

triggered based on share capital, voting rights or change

of directorships

In lots of cases, boards are quite small and change of

directorship happens autonomously or unconnected

with any change of shareholding

The application of change of control norms in such

cases is completely unwarranted

Change of control as per extant norms

• Change of directorship resulting in change of 1/3rd or

more of the management

• Change in shareholding resulting in acquisition/transfer

of 26% or more of paid up capital

• Any other takeover or change of control

Prior Approval of the RBI required to be taken

Public Notice required to be given

Vinod Kothari Consultants P. Ltd.

REGISTRATION WITH MULTIPLE CICS

Existing CIC requirements:

Every NBFC to register with all CICs (presently 4)

Submit credit information of customers

Update on monthly basis or shorter intervals as decided with the CICs

Vinod Kothari Consultants P. Ltd.

REGULATORY DISAPPROVAL FOR MULTIPLE NBFCS IN A GROUP

Many business groups have multiple NBFCs for variety of reasons:

Their businesses are clearly different

Their shareholdings are different

They have group shareholdings which are subject matter of internal family ownership

If the NBFCs in question do not have public funds, should it at all matter whether there multiple NBFCs in the

group?

Vinod Kothari Consultants P. Ltd.

Copyright © 2022 FDOKUMEN