Microcredit in reducing Domestic Violence against women in Bangladesh

39

Microcredit in Reducing Domestic Violence against Women: An Analysis of a Die Lichbrücke e.V., Germany Supported Credit Program in Bangladesh Dr. Muhammad Matiur Rahman 1 Abstract: The accompanying research has been carried out to explore the role of microcredit in reducing domestic violence against women particularly among the beneficiaries of a Die Lichtbrücke e.V., Germany supported credit program in Bangladesh. While collecting data and information from field various data collection tools such as survey questionnaire, Focus Group Discussion (FGD) have been used. Simple Random Sampling (SRS) technique has been adapted to select the respondents for the present research. Only those who are in the credit program for more than six years were selected as respondents. In addition, control group comprising women who are not credit recipients from BMTC project was selected as respondents to compare their situation regarding domestic violence. A 60 member and 30 non-member respondents were selected for interview. It has been found that a significant change occurred among the beneficiaries of BMTC credit program in terms of economic condition, empowerment and reduction of domestic violence against women. Microcredit program of BMTC project helped to reduce domestic violence of its members. The types of domestic violence that the members had to face earlier (before joining credit group) have been reduced significantly. Microcredit membership reduced the following acts of violence against women - verbal abuse; battering/physical hurt; tortured for not giving dowry; forced sex; throwing or breaking of household assets to show anger; threatening with weapons; deprivation from food/meal: prevention of doing household work; threat of giving talak (divorce);etc. Inclusion in the credit programme has empowered them and brought economic wellbeing to their household. The credit program helped in reducing domestic violence against the women members through a) Collective action through the membership of a loan- group, b) Women’s’ exposure to the community; c) Rise of the 1 Dr. Muhammad Matiur Rahman is a former Ph.D Fellow of the Institute of Bangladesh Studies (IBS), Rajshahi University and currently working in an International Donor Organization in Dhaka.

-

Upload

independent -

Category

Documents

-

view

1 -

download

0

Transcript of Microcredit in reducing Domestic Violence against women in Bangladesh

Microcredit in Reducing Domestic Violence againstWomen: An Analysis of a Die Lichbrücke e.V., Germany

Supported Credit Program in BangladeshDr. Muhammad Matiur Rahman1

Abstract: The accompanying research has been carried outto explore the role of microcredit in reducing domesticviolence against women particularly among thebeneficiaries of a Die Lichtbrücke e.V., Germany supportedcredit program in Bangladesh. While collecting data andinformation from field various data collection tools suchas survey questionnaire, Focus Group Discussion (FGD) havebeen used. Simple Random Sampling (SRS) technique has beenadapted to select the respondents for the presentresearch. Only those who are in the credit program formore than six years were selected as respondents. Inaddition, control group comprising women who are notcredit recipients from BMTC project was selected asrespondents to compare their situation regarding domesticviolence. A 60 member and 30 non-member respondents wereselected for interview. It has been found that asignificant change occurred among the beneficiaries ofBMTC credit program in terms of economic condition,empowerment and reduction of domestic violence againstwomen. Microcredit program of BMTC project helped toreduce domestic violence of its members. The types ofdomestic violence that the members had to face earlier(before joining credit group) have been reducedsignificantly. Microcredit membership reduced thefollowing acts of violence against women - verbal abuse;battering/physical hurt; tortured for not giving dowry;forced sex; throwing or breaking of household assets toshow anger; threatening with weapons; deprivation fromfood/meal: prevention of doing household work; threat ofgiving talak (divorce);etc. Inclusion in the creditprogramme has empowered them and brought economic wellbeingto their household. The credit program helped in reducingdomestic violence against the women members through a)Collective action through the membership of a loan- group,b) Women’s’ exposure to the community; c) Rise of the

1 Dr. Muhammad Matiur Rahman is a former Ph.D Fellow of the Institute ofBangladesh Studies (IBS), Rajshahi University and currently working in anInternational Donor Organization in Dhaka.

Microcredit in Reducing Domestic Violence against Women: An analysis ofa Die Lichtbrücke e.V., supported Credit Program in Bangladesh: Matiur

Rahman

2

women’s’ self-esteem; d) Women’s’ economic contributiontowards the household.

Key Words: Microcredit, Domestic Violence, Empowerment, Bangladesh

1.1 Introduction

Microcredit for women is as a proven and effective povertyalleviation intervention, with a positive impact on economicgrowth and a number of social development indicators. It iswidely recognized that there is a direct relationship betweenaccess to credit and an increase in the status of women withintheir household and community. Provision of credit is believedto lead to the empowerment of women.

The use of microcredit is becoming increasingly common as apoverty reduction strategy within development agenciesprograms. Studies suggest that it has numerous positiveeffects on health, nutrition, education and other areas. Also,scholars have reported that microcredit can reduce domesticviolence which leads to the psychological, physical and sexualdetriments of women everywhere.

Domestic violence, or violence perpetuated in the home orfamily environment, is a major social problem in Bangladesh.Domestic violence is physical, sexual, economic, orpsychological abuse directed towards one’s spouse, partner, orother family member within the household.

Domestic violence is an epidemic in Bangladesh and has fatalconsequences. The causes of domestic violence are complex:cultural, economical, legal and political factors co-work tomaintain an unequal relationship between the sexes and thesubordination of women.

Microcredit programs' main target is women. There are strongevidences that, microcredit programs contribute to women'sempowerment. It increases self-confidence and self-esteemamong women. It also increases women’s decision making powerin the areas of family planning, children's marriage, buying

Microcredit in Reducing Domestic Violence against Women: An analysis ofa Die Lichtbrücke e.V., supported Credit Program in Bangladesh: Matiur

Rahman

3

and selling of properties and sending daughters to school.There are ample evidences that members of microcredit groupshave been able to stop domestic violence due to personalempowerment and through group action.

In the present research it has been examined whether theparticipation of women in microcredit program of a DieLichtbrücke e.V.,Germany supported project in Bangladesh hasreduced domestic violence against them or not.

1.2 About Die Lichtbrücke e.V., Germany

The Die Lichtbrücke e.V., Germany is a registered charitywhich was founded in 1983 in Engelskirchen, Germany. It is afree organization of development cooperation and humandeprivation that want to convert human deprivation into ahumane development. The organization has a Christianfoundation and works non-denominational and non-partisan, together with all people of good will. The DieLichtbrücke e.V is a non- profit and non-governmentalorganization as part of the umbrella organization Venro. As asign of trust, the Die Lichtbrücke e.V receives the DZI sealsince 2002.

1.3 Die Lichtbrücke e.V., Germany Supported Programs inBangladesh

The Die Lichtbrücke e.V., Germany is supporting the projectsof eight partner-organizations in Bangladesh. The fightagainst poverty through small-credit-programs is an importantfocus among the project supports. A remarkable amount offinancial means has accumulated in the last years withindividual partners in Credit-Revolving-Funds. These creditfunds are administered by the respective partner-organization.The major aim of the credit fund is to reduce poverty andimprove livelihood condition of the targeted rural poor womenin Bangladesh. Poor women receive small loan from the partnerorganization becoming member of samity. They invest the loanmoney in various sectors like agriculture, poultry, small

Microcredit in Reducing Domestic Violence against Women: An analysis ofa Die Lichtbrücke e.V., supported Credit Program in Bangladesh: Matiur

Rahman

4

business, grocery, etc. The credit makes them empower and helpto reduce violence against them.

1.4 Objective of the Study

The broad objective of the accompanying study is to explorewhether domestic violence against women has been reduced ornot among the beneficiaries of a DLB supported credit programin Bangladesh.

1.5 Project Selected for the Study

According to the suggestions of Bridge of Light Germany onecredit programme namely BACE-Mitali Training Center withDemonstration Farm (BMTC) of BACE located at Birgonj, Dinajpurhas been taken for the present study for analysis.

1.6 Brief about BMTC Project

Bangladesh Association for Community Education (BACE) with thefinancial assistance of Die Lichtbrücke, e.V., (DLB) Germanyestablished BACE Mitali Training Centre with DemonstrationFarm Project (BMTC) in Birgonj Upazila of Dinajpur district in1999. The 1st phase of the project having ended on 31 December,2002. Die Lichtbrücke e.V., Germany provided partial financialsupport for the 2nd phase (2003-2005). After successfullycompletion of the 2nd phase (2003-2005) Die Lichtbrücke e.V.Germany approved partial financial support for another 3 years(2006-2008). After the end of this phase it is continuing withpartial financial assistance of DLB to till date.

Project Components

The Projects has 5 main components as follows:

1) Education Program2) Training3) Demonstration Farm4) Microcredit, and 5) Cultural activities

Microcredit in Reducing Domestic Violence against Women: An analysis ofa Die Lichtbrücke e.V., supported Credit Program in Bangladesh: Matiur

Rahman

5

Microcredit Program

Credit has been distributed among the targeted poor andlandless people trough forming groups or samity for undertakingincome generation activities. The microcredit program has now106 groups, 1,883 group members, 1822 loanee members (up toJune 2011). Till 30 June, 2011 around taka 103,501,000 hasbeen disbursed among beneficiaries. The total outstanding wastaka 136, 471, 41 for the same period.

Location of the beneficiaries

The project beneficiaries are from 58 villages of 10 Unionsnamely Shibrampur, Polashbari, Sotogram, Nijpara, Mohammadpur,Bhognagar, Satore, Mohanpur, Moricha and Birgonj Pourashava ofBirgonj sub-district under Dinajpur district, Bangladesh.

In terms of economic and educational condition, BirgonjUpazila is relatively disadvantaged in comparison to otherareas. The majorities of the families live below the povertylevel and are not able to meet the basic necessities of life.Around 83% of the inhabitants earn their livelihood byagriculture. Most of them are poor and landless. A majority ofpeople have no land or employment opportunity.

Map 1.1: Map of Dinajpur District indicates Birganj andKaharole Upazila where BMTC project is implementing.

Microcredit in Reducing Domestic Violence against Women: An analysis ofa Die Lichtbrücke e.V., supported Credit Program in Bangladesh: Matiur

Rahman

6

PANCHAGARH

TH A KU R G AO N

DINAJPUR

NILPHAMARI

LALMONIRHAT

RANG PUR KURIGRAM

G A IB A ND H A

JOYPURHAT

BOGRANAOGAON

NAW ABGONJ

RAJSHAHI NATORE SIRAJGONJ

PABNA

KUSHTIA

JHENAIDAHMAGURA

JESSORENARAIL

KHULNAJHALOKATI

BAR G U N A

BAGERHAT

PATUAKHALI

BARISAL

G O P ALG O N J

MADARIPUR

SHARIATPUR

MUNSHIGONJ

FARIDPUR

RAJBARI

JAMALPUR

SHERPUR

TANGAIL

M YMENSING HNETROKON A

SUNAMGANJ SYLHET

MOULAVIBAZAR

HOBIGONJKISHO REGONJ

GAZIPURN AR SIN G D I

DHAKAMANIKGONJ N'GONJ

BRAHMANBARIA

COM ILLACHANDPUR

LAXMIPUR NOAKHALI

FENI

MAYANMA

R

M E H E RP U R

BAY OF BENGAL

KHAGRACHHARI

RANGAMATI

CHITTAGONG

BANDARBAN

COX'SBAZAR

INDIA INDIA

INDIA

SATKHIRA PIROJPUR BHO LA

C H U AD A N G A

K utubdia

S andw ip

H atiya

Birganj

ThakurgaonPanchagarh

Nilphamari

Rangpur

Biral

Phulbari

Birampur

HakimpurJoypurhat

Gaibandha

Ghoraghat

Nawabganj

DinajpurSadarParbatipur

Kaharole

Chirirbandar

BochaganjKhansama

DINAJPUR

2.1 Research Approach

The research has been carried out using both qualitative andquantitative research methods. A survey has been conductedamong the selected credit beneficiaries of the project. A wellstructured short questionnaire was used for this purpose. Thecontents of the questionnaire were determined according to theobjective of the research. Credit beneficiaries’ presentsituation and prior situation (before joining the creditprogram) regarding economic condition, empowerment anddomestic violence were assessed setting proper questions.However, to get an in-depth picture of reduction of domesticviolence some Focus Group Discussion (FGD) and case studieswere also conducted among the credit beneficiaries.

Microcredit in Reducing Domestic Violence against Women: An analysis ofa Die Lichtbrücke e.V., supported Credit Program in Bangladesh: Matiur

Rahman

7

2.2 Sample Design

Till June 2011there were 1,883 group members. Out of themaround 1,200 beneficiaries are within credit program for morethan 6 years. Simple Random Sampling (SRS) method was adaptedto select the respondents for the present research. Only thosewho are in the credit program for more than six years wereselected as respondents for the study. In addition, somecontrol group members (who are not credit recipients from BMTCor similar project) were selected as respondents to comparetheir situation regarding domestic violence with the creditbeneficiaries.

2.3 Sample Size

A 5% of the total credit beneficiaries among 1,200beneficiaries within 6 years involvement in the credit programhave been randomly selected as respondents. So, the number ofrespondents was 60. Beside, to understand the effectiveness ofthe credit program contributing to reduce domestic violence -some women who were not member of any credit group wereselected as respondents. A 30 respondents of such categorywere selected as control respondents. Control grouprespondents have been considered to compare the economic,empowerment and domestic violence situation with the creditbeneficiaries. It is noted here that 60 beneficiaries havebeen selected from 10 villages of 10 Unions under BMTCproject. The control respondents (who are not credit groupmember) have also been selected randomly from 3 villages thatare not under BMTC program. Moreover, 2 Focus GroupDiscussions (FGDs) with women beneficiaries from 3 villagesunder BMTC project area were also conducted.

2.4 Selection of Respondents

From the list of the credit beneficiaries- respondents havebeen chosen randomly using Simple Random Sampling (SRS)procedure. The lottery technique was applied to select therequired number (60) of the respondents. The control grouprespondents (30) have been selected randomly considering same

Microcredit in Reducing Domestic Violence against Women: An analysis ofa Die Lichtbrücke e.V., supported Credit Program in Bangladesh: Matiur

Rahman

8

socioeconomic condition of a credit beneficiary. FGD memberwere selected from 3 samities of 3 villages. The number of FGDparticipants were 7/8 persons in a session.

2.5 Data Collection Tools

Survey QuestionnaireA well structured short questionnaire has been used tocollect necessary information from the creditbeneficiaries. The questionnaire was designed in Bengaliusing familiar words and unequivocal and straightforwardfor easy understanding of the respondents.

Focus Group Discussion (FGD)A checklist was also developed to conduct the FGDsession. A total of 2 FGDs were conducted with creditbeneficiaries.

2.6 Field Data Collection

Field data were collected from the selected respondents ofBMTC microcredit beneficiaries. Four data collectors weredeployed and trained. They helped the researcher to selectappropriate cases and to collect information or data from theselected respondents. Moreover, 1 data editor, 1 data coder, 1data analyst and 1 data entry operator were also recruited inthis regard.

Beside primary data, secondary materials (such as books,journals, documents, survey and evaluation reports andresearch studies) were also reviewed for this study.

2.7 Data Analysis

After having data from the field the first step is theirprocessing as editing, coding, cleaning and entry. To analyzethe data SPSS software was used in this regard. The data waspresented in various tabular, graphical and statisticalprocesses in this report.

Microcredit in Reducing Domestic Violence against Women: An analysis ofa Die Lichtbrücke e.V., supported Credit Program in Bangladesh: Matiur

Rahman

9

3.1 Background Profile of the Respondents

This section portrays the demographic and social conditions,such as the age structure, education, occupation, religion ofthe respondents. Moreover, changes in the economic, livelihoodcondition and empowerment status have also been assessed inthis section.

Profile of Samity Member

Age Structure

Analysis of age structure showsthat majority of the femalerespondents (31.6%) belong to themiddle age group (36-40 years).More than one-fourth (30%) ofthem have been foundcomparatively young (age rangingfrom 31 to 35). About 17% of therespondents belong to young agegroup (26-31 years) and only6.7% of them have found over 45years and over age group (Figure3.1). The mean age of therespondents is 36 years. Themaximum age is 49 and minimumage is 28 years.

Educational Profile

Educational status is considered as one of the primecomponents of human capital. Analysis shows that out of thetotal respondents (60) about one-third of them (31.6%)completed primary level education (Class five). Only around6.7% of them have secondary level education (SSC andequivalent) and a majority of them (61.7%) can sign their nameonly (Figure 3.2).

Occupational Profile

Distribution of occupationalpattern shows that about two-

Microcredit in Reducing Domestic Violence against Women: An analysis ofa Die Lichtbrücke e.V., supported Credit Program in Bangladesh: Matiur

Rahman

10

thirds (65%) of the respondents are housewife. The secondlargest portion of the respondents (32.7%) have found aslaborer. On the other hand, only 3.3% of them reported farmingas their prime occupation (Figure 3.3).

Microcredit in Reducing Domestic Violence against Women: An analysis ofa Die Lichtbrücke e.V., supported Credit Program in Bangladesh: Matiur

Rahman

11

Religion

The religion distribution ofthe respondents shows that mostof them are Muslim (46.6%).About one-third (31.7%) of themare Hindu and over one-fifth(21.7%) belong to indigenouslike Santal religion (Figure3.4).

Duration of Samity Membership

The duration of membership ofsamity shows that over one-fifthof the members (21.7%) areinvolved in samity activitiestill around 11 years. Over one-fourth (26.6%) of them havemembership with the Samity foraround 9 years and 25% of themfor 10 years. Only 1.7% of them have found 5 years involvementwith Samity activities. The mean year of Samity membership is9.27 years (Figure 3.5).

Frequencies of Loan taken by Samity Member

It has been found that around 21.7% of the members tookhighest 11 times loan from samity. Around 10 times has takenby 25% members and 9 times by 26.6% members. Around 5 timesloan has taken only by 1.7% members (Table 3.1).

Table 3.1: Percentage distribution of the respondentsaccording to the number of taking loan from Samity.

Frequency/ number of loan Frequency % (Total)5 1 1.77 6 10.0

Microcredit in Reducing Domestic Violence against Women: An analysis ofa Die Lichtbrücke e.V., supported Credit Program in Bangladesh: Matiur

Rahman

12

8 9 15.09 16 26.610 15 25.011 13 21.7

Total 60 100.0

Total Amount of Loan money Taken by Samity Member

It has been found that majority of the respondents (38.3%) hastaken total amount of money within the range of 810, 00 to100,000. Only 1.7% of them have taken loan from the Samitytaka 140,000 and more .And only 5% of them have taken loanwithin the range of taka 1,000 to 20,000. Over one-fifth(21.7%) of them has taken total amount of loan as taka 61,000to 80,000. The mean amount of loan money taken by loaneemembers is taka 78,003.33 (Table 3.2).

Table 3.2: Percentage distribution of the respondentsaccording to their total amount of loan taken

Total amount of loan in taka Frequency % (Total)1,000-20,000 3 5.021,000-40,000 4 6.741,000-60,000 8 13.361,000-80,000 13 21.781,000-1,00,000 23 38.31,01,000-1,20,000 6 10.01,21,000-1,40,000 2 3.31,40,000+ 1 1.7Total 60 100.0

Amount of Last Loan Money

It has also been found that only 3.3% of the respondents havetaken taka 27,000 as last loan money. The highest portion ofthe respondents is 11.7% who has taken 18,000 as the last loanmoney and also the same portion of them have mentioned taka10,000 as their last loan money. Taka 11,000, 12,000 and14,000 have mentioned as last loan money by same portion ofthe respondents (8.3%) (Table 3.3).

Microcredit in Reducing Domestic Violence against Women: An analysis ofa Die Lichtbrücke e.V., supported Credit Program in Bangladesh: Matiur

Rahman

13

Table 3.3: Percentage distribution of the respondentsaccording to their response on last loan money

Amount of last loan money in taka Frequency % (Total)7000 3 5.09000 3 5.010000 7 11.711000 5 8.312000 5 8.313000 4 6.714000 5 8.315000 3 5.016000 2 3.317000 4 6.718000 7 11.719000 2 3.320000 4 6.722000 2 3.325000 1 1.726000 1 1.727000 2 3.3Total 60 100.0

Microcredit in Reducing Domestic Violence against Women: An analysis ofa Die Lichtbrücke e.V., supported Credit Program in Bangladesh: Matiur

Rahman

14

Income Generating Activities (IGA) Sectors Where Loan Money Utilized

It has been found that more than one-third of the memberrespondents utilized their loan money in livestock (cow andgoat raring) sector. On the other hand around 31.6% of themutilized it in cultivation. The others sectors arerickshaw/van purchase and land purchase (Table 3.4).

Table 3.4: Percentage distribution of the respondentsaccording to their response on purpose (IGA) ofspending money

Purpose of spending money Frequency % (Total)Livestock (Cow and goat raring) 21 35.0Cultivation 19 31.6Small business 18 30.0Rickshaw / van purchase 1 1.7Land purchase 1 1.7Total 60 100.0

Person Encouraged Becoming Samity Member

Majority portion of the womenrespondents (75%) reported that‘Credit Supervisor’ of BMTCproject were encouraged them tobecome Samity member. The personor factors are ‘Group Leader’(5%), ‘Social Worker’ (10%) and‘Self Motivation’ (10%) (Figure3.6).

3.2 Profile of Non- Samity Member

Around 30 non-samity members (control group) were also selectedfor the study to know their situation regarding domesticviolence which may help us to understand the importance of

Microcredit in Reducing Domestic Violence against Women: An analysis ofa Die Lichtbrücke e.V., supported Credit Program in Bangladesh: Matiur

Rahman

15

microcredit in reducing domestic violence against women in theprogram areas. Their background profile is also describedhere.

Age Composition

Distribution of the age group of the non-member womenrespondent shows that same portion of them (26.7%) fall in theage group between 26 and 35. Around (20%) of them fall in theage group between 20 to 25. Only 3.3 percent respondents werefound 46 and over aged. The mean age of the respondents is32.53 and minimum and maximum age is 20 and 50 yearsrespectively. So, it can be said that most of the respondentsare young (Table 3.5).

Microcredit in Reducing Domestic Violence against Women: An analysis ofa Die Lichtbrücke e.V., supported Credit Program in Bangladesh: Matiur

Rahman

16

Table 3.5: Percentage distribution of the respondents according to their age structure

Age range Frequency % (Total)20-25 6 20.026-30 8 26.731-35 8 26.736-40 3 10.041-45 4 13.346+ 1 3.3Total 30 100.0

Education

The educational level of the non- member women respondentsshows that more than two-fifth (43.3%) of them have onlyprimary level (Class 1 to 5) education. But around two-fifth(40%) of them can sign only their name. Only 16.7 percent ofthe respondents have only secondary level education (Table3.6).

Table 3.6: Percentage distribution of the respondentsaccording to their Education

Education category Frequency % (Total)Can sign only 12 40.0Primary (Class 1-5) 13 43.3Secondary (Class 6-10) 5 16.7Total 30 100.0

Occupational Profile

Distribution of the occupational pattern of the non-memberwomen respondents shows that majority of them (60%) arehousewife while a good portion of them (40%) mentioned theiroccupation as laborer (Table 3.7).

Table 3.7: Percentage distribution of the respondentsaccording to their main occupation

Occupation Frequency % (Total)Housewife 18 60.0Labor 12 40.0

Microcredit in Reducing Domestic Violence against Women: An analysis ofa Die Lichtbrücke e.V., supported Credit Program in Bangladesh: Matiur

Rahman

17

Total 30 100.0

Religion

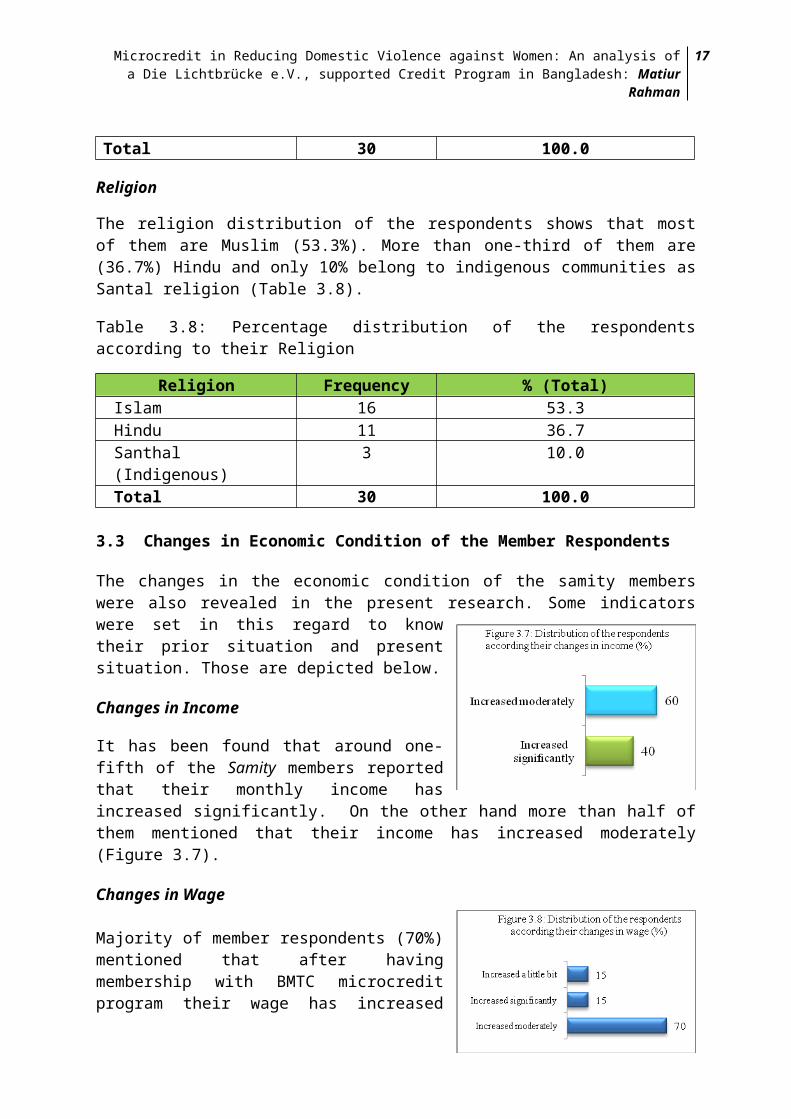

The religion distribution of the respondents shows that mostof them are Muslim (53.3%). More than one-third of them are(36.7%) Hindu and only 10% belong to indigenous communities asSantal religion (Table 3.8).

Table 3.8: Percentage distribution of the respondentsaccording to their Religion

Religion Frequency % (Total)Islam 16 53.3Hindu 11 36.7Santhal (Indigenous)

3 10.0

Total 30 100.0

3.3 Changes in Economic Condition of the Member Respondents

The changes in the economic condition of the samity memberswere also revealed in the present research. Some indicatorswere set in this regard to knowtheir prior situation and presentsituation. Those are depicted below.

Changes in Income

It has been found that around one-fifth of the Samity members reportedthat their monthly income hasincreased significantly. On the other hand more than half ofthem mentioned that their income has increased moderately(Figure 3.7).

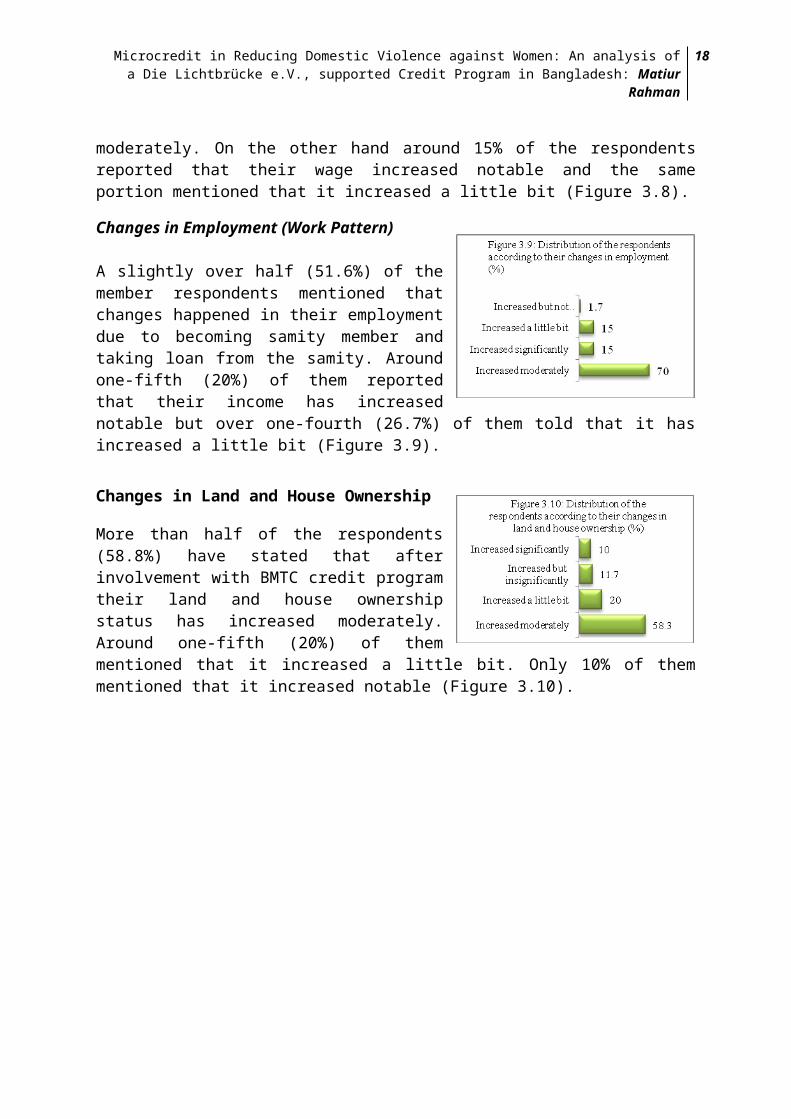

Changes in Wage

Majority of member respondents (70%)mentioned that after havingmembership with BMTC microcreditprogram their wage has increased

Microcredit in Reducing Domestic Violence against Women: An analysis ofa Die Lichtbrücke e.V., supported Credit Program in Bangladesh: Matiur

Rahman

18

moderately. On the other hand around 15% of the respondentsreported that their wage increased notable and the sameportion mentioned that it increased a little bit (Figure 3.8).

Changes in Employment (Work Pattern)

A slightly over half (51.6%) of themember respondents mentioned thatchanges happened in their employmentdue to becoming samity member andtaking loan from the samity. Aroundone-fifth (20%) of them reportedthat their income has increasednotable but over one-fourth (26.7%) of them told that it hasincreased a little bit (Figure 3.9).

Changes in Land and House Ownership

More than half of the respondents(58.8%) have stated that afterinvolvement with BMTC credit programtheir land and house ownershipstatus has increased moderately.Around one-fifth (20%) of themmentioned that it increased a little bit. Only 10% of themmentioned that it increased notable (Figure 3.10).

Microcredit in Reducing Domestic Violence against Women: An analysis ofa Die Lichtbrücke e.V., supported Credit Program in Bangladesh: Matiur

Rahman

19

Changes in Essential HouseholdAssets Ownership

Around 45% of member respondentsmentioned that their ownership inessential household assets hasincreased moderately while around30% of them mentioned it assignificantly increased (Figure 3.11).

Changes in the Ownership of Cow, Goat, Duck and Chicken

Around half of the memberrespondents (50%) mentioned thatafter becoming member in the Samitytheir ownership of cows, goat, duckand chicken has increasedmoderately. On the other hand around43.3% of them reported that their ownership on the same hasincreased significantly (Figure 3.12).

Based on the findings it can be said that there happened asignificant changes in income, wage, employment and ownershipon land, household assets, etc of the member of BACE BMTCproject.

3.4 Changes in Social and Livelihood Condition

The changes in the social livelihood condition of the samitymembers were also revealed in the present research. Someindicators were set in this regard to know their priorsituation and present situation. Those are presented below.

Affordability of taking 3 times nutritious meal in a day

Microcredit in Reducing Domestic Violence against Women: An analysis ofa Die Lichtbrücke e.V., supported Credit Program in Bangladesh: Matiur

Rahman

20

A large majority of the respondents(85%) mentioned that at present theyare capable enough to take 3 timesnutritious food in a day and only 15%of them reported that they can affordit irregularly / sometimes. On theother hand a good portion of them(78.3%) mentioned that beforebecoming Samity member they could notmanage 3 times nutritious food always in a day and over one-fifth of them (21.7%) can never afford it (Figure 3.13). Thus,there is a significant change happened among the Samity memberhaving 3 times meal in a day. A major portion who earliercould afford irregularly or sometimes to manage 3 times mealin a day earlier they now can manage it regularly.

Microcredit in Reducing Domestic Violence against Women: An analysis ofa Die Lichtbrücke e.V., supported Credit Program in Bangladesh: Matiur

Rahman

21

Ability of Sending Children intoSchool

Almost all the member respondents(96.7%) mentioned that at presentthey have the ability to send theirchildren in to school. On the otherhand before becoming member of thesamity more than half (56.7%) ofthem had the ability to send theirchildren irregularly and 43.3% of them could not send theirchildren in to school at all (Figure 3.14).

Affordability of Taking Medical Treatment during Illness

A large majority of the memberrespondents (81.7%) reported thatthey are now capable enough to takemedical treatment for their familymembers during illness. On the otherhand more than half of them (55%)mentioned that before becoming Samitymember they could not affordtreatment regularly during illnessof their family members and 41.7% of them could not take thetreatment at all (Figure 3.15).

Affordability of Buying NecessaryClothes for All Members

Around 60% of the member respondentsstated that at present they have theability to buy all necessary clothesfor all members of the family. Onthe other hand, around same portionof them could manage all necessary

Microcredit in Reducing Domestic Violence against Women: An analysis ofa Die Lichtbrücke e.V., supported Credit Program in Bangladesh: Matiur

Rahman

22

clothes for their family members before becoming samitymembers (Figure 3.16).

Thus, it can be inferred that BMTC credit program has broughta significant change of the members of affordability of taking3 times meal, sending children into school, taking medicaltreatment and buying necessary clothes for family members.

3.5 Empowerment

Empowerment of women is a process through which women ingeneral and poor women in particular get the opportunity tojoin the workforce, contribute to family income, and havedignity, recognition and place in family as well as insociety. Education of girls and women is an indispensible toolto empower women.

For the present study to assess the empowerment of womenmember respondents at household level some indicators wereset. Those are analyzed below.

Use of Loan Money Independently

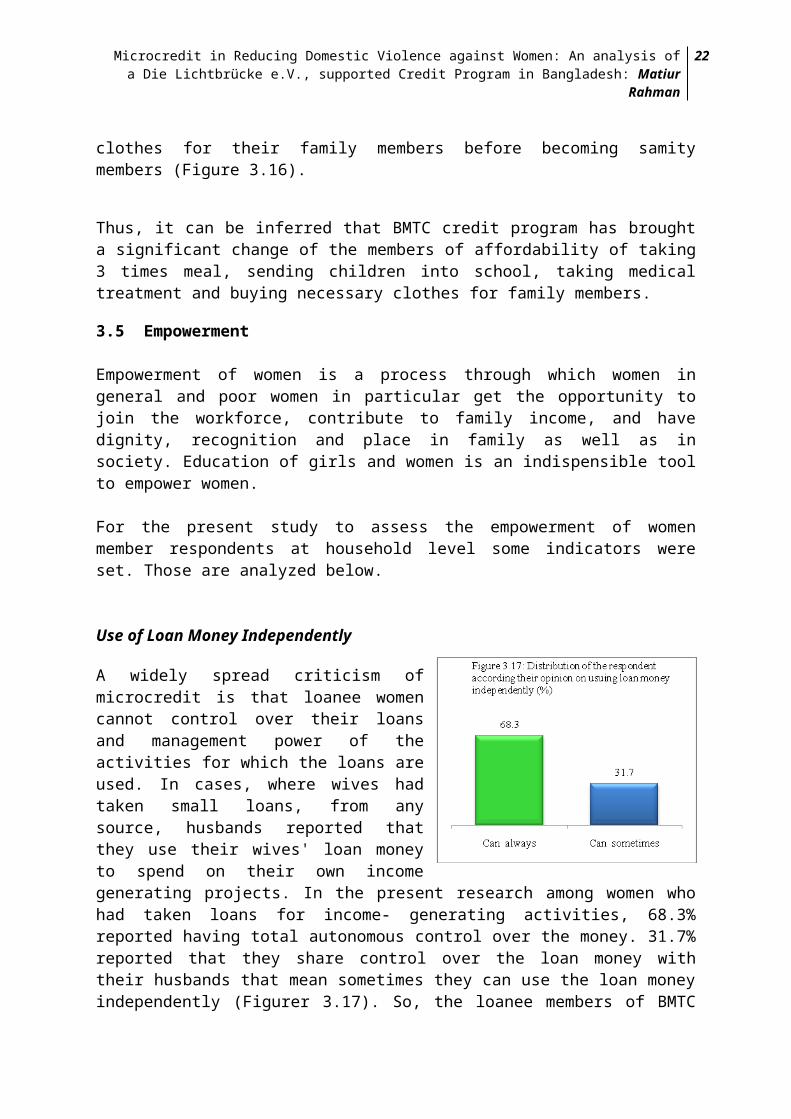

A widely spread criticism ofmicrocredit is that loanee womencannot control over their loansand management power of theactivities for which the loans areused. In cases, where wives hadtaken small loans, from anysource, husbands reported thatthey use their wives' loan moneyto spend on their own incomegenerating projects. In the present research among women whohad taken loans for income- generating activities, 68.3%reported having total autonomous control over the money. 31.7%reported that they share control over the loan money withtheir husbands that mean sometimes they can use the loan moneyindependently (Figurer 3.17). So, the loanee members of BMTC

Microcredit in Reducing Domestic Violence against Women: An analysis ofa Die Lichtbrücke e.V., supported Credit Program in Bangladesh: Matiur

Rahman

23

project are more empowered to usetheir loan money.

Working outside the Home

Although at present women areworking in different sectorsoutside the home but majority ofour society people believe thetraditional view that home is theonly work place for women in oursociety. Only male is fit for workoutside the home. If any womengoes to work outside the homemajority of the society people cannot accept it as a verysimple matter. So, women who go to work outside the home haveto face many awful situations. In the present study this facthas also been explored. According to the data majority of thewomen respondents (68.3%) admitted that before becoming Samitymember they could not work outside the home. But at present30% of them can work outside always and over two-third (66.7%)of them can work sometimes (Figure 3.18). The respondents whostated that they can or could do any work outside home alsomentioned the reasons of it. The reasons that they mentionedare: husband does not like it; others family members do notlike it; they do not consider themselves able/fit;surroundings condition is not favorable, etc.

Participation in Samity Meeting

Now a day many women can participate in the Samity (microcreditgroup) and social activities. But 15 to 20 years ago it wasimpossible to many of Bangladeshi women to participate in theSamity meeting. In the present research about 81.7 percentmember respondents stated that they could not participate inany Samity/CBO/ social activities before becoming Samity member.On the other hand, now a day, almost all of them (93.3%) canparticipate in the Samity meeting and other social activities(Figure 3.19). The reasons for not participating in Samityactivities are: surroundings condition is not favorable;

Microcredit in Reducing Domestic Violence against Women: An analysis ofa Die Lichtbrücke e.V., supported Credit Program in Bangladesh: Matiur

Rahman

24

husband does not like it; others family members do not likeit, etc.

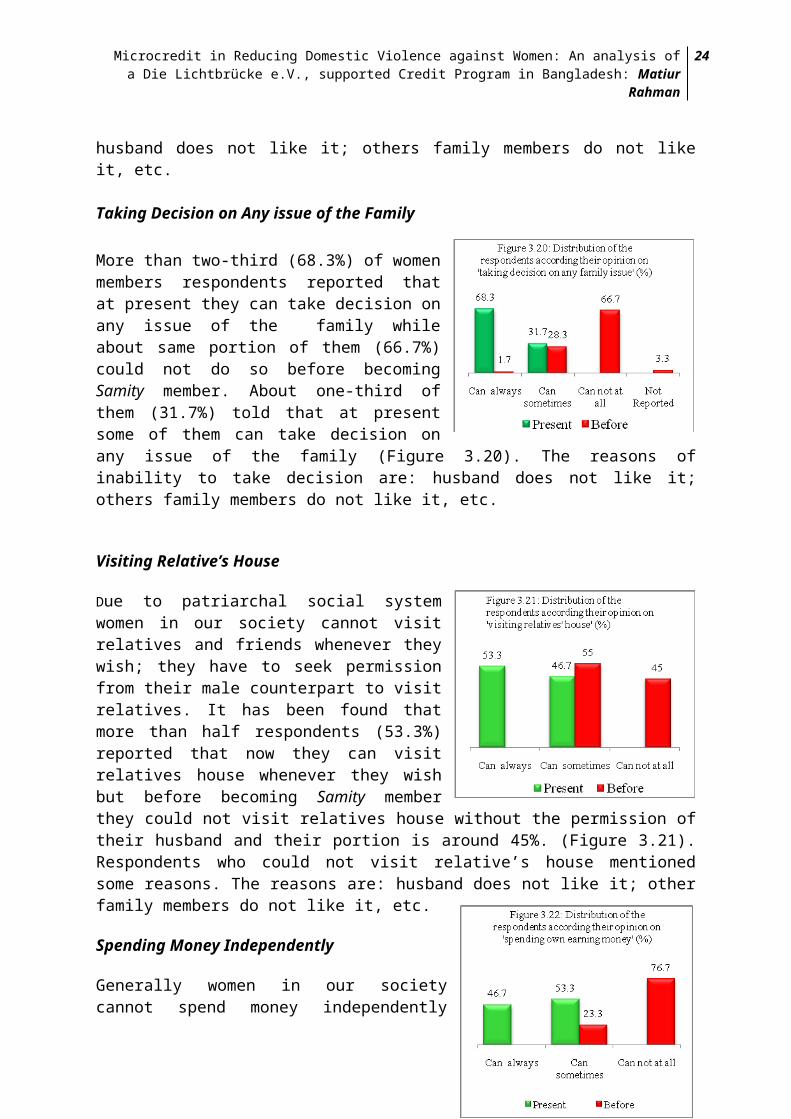

Taking Decision on Any issue of the Family

More than two-third (68.3%) of womenmembers respondents reported thatat present they can take decision onany issue of the family whileabout same portion of them (66.7%)could not do so before becomingSamity member. About one-third ofthem (31.7%) told that at presentsome of them can take decision onany issue of the family (Figure 3.20). The reasons ofinability to take decision are: husband does not like it;others family members do not like it, etc.

Visiting Relative’s House

Due to patriarchal social systemwomen in our society cannot visitrelatives and friends whenever theywish; they have to seek permissionfrom their male counterpart to visitrelatives. It has been found thatmore than half respondents (53.3%)reported that now they can visitrelatives house whenever they wishbut before becoming Samity memberthey could not visit relatives house without the permission oftheir husband and their portion is around 45%. (Figure 3.21).Respondents who could not visit relative’s house mentionedsome reasons. The reasons are: husband does not like it; otherfamily members do not like it, etc.

Spending Money Independently

Generally women in our societycannot spend money independently

Microcredit in Reducing Domestic Violence against Women: An analysis ofa Die Lichtbrücke e.V., supported Credit Program in Bangladesh: Matiur

Rahman

25

rather they need permission from their husband (or other malemembers in the absence of husband). But in the present study,around 46.7% of member respondents reported that they canspend money without the permission of their husband but morethan half (53.3%) of them stated that they can do thissometimes. On the other hand over three-fourth (76.7%) ofthem admitted that before becoming Samity member they could notspend any money independently (Figure 3.22). In most caseshusbands do not permit their wife to spend money independtly.The other prime reasons are: other family members do not likeit; surroundings condition is not favorable, etc.

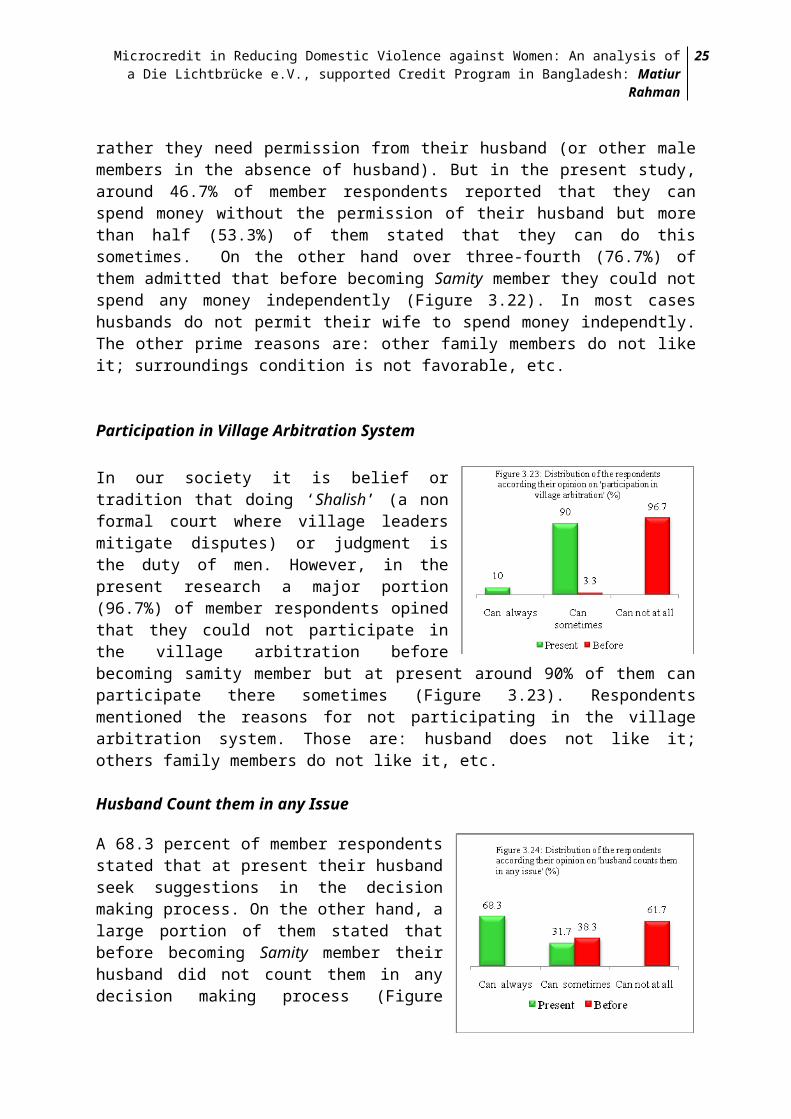

Participation in Village Arbitration System

In our society it is belief ortradition that doing ‘Shalish’ (a nonformal court where village leadersmitigate disputes) or judgment isthe duty of men. However, in thepresent research a major portion(96.7%) of member respondents opinedthat they could not participate inthe village arbitration beforebecoming samity member but at present around 90% of them canparticipate there sometimes (Figure 3.23). Respondentsmentioned the reasons for not participating in the villagearbitration system. Those are: husband does not like it;others family members do not like it, etc.

Husband Count them in any Issue

A 68.3 percent of member respondentsstated that at present their husbandseek suggestions in the decisionmaking process. On the other hand, alarge portion of them stated thatbefore becoming Samity member theirhusband did not count them in anydecision making process (Figure

Microcredit in Reducing Domestic Violence against Women: An analysis ofa Die Lichtbrücke e.V., supported Credit Program in Bangladesh: Matiur

Rahman

26

3.24). Respondents who stated that their husbands do not countthem also mentioned the following reasons. Those are: husbanddoes not like it; others family members do not like it; theydo not consider themselves able/fit; others family members donot like it, etc.

Use of Sanitary Latrine

Use of sanitary latrine (hygienic latrine) is also anindicator of empowerment of microcredit group members. Thedata of the following table shows that before joining BMTCcredit group no one of the selected respondents could usesanitary latrine. But at present almost all of them (98.3%)have installed sanitary latrine in their household and nowthey can use it. It is an indication of empowerment, as wellas results of improvement of their awareness level whichhappened due to receiving training from the BMTC center (Table3.9).

Table 3.9: Percentage distribution of the respondentsaccording to their response on having sanitarylatrine in the household

Having sanitarylatrine

Present BeforeFrequency % (Total) Frequency %

(Total)Yes 59 98.3 - -No 1 1.7 60 100.0Total 60 100.0 60 100.0

Increased Social Acceptance

Microcredit membership enhances the social status andacceptance of poor people. In the present research almost allof the survey respondents (98.3%) admitted that their socialacceptance has been increased after joining BMTC credit group(Table 3.10).

Microcredit in Reducing Domestic Violence against Women: An analysis ofa Die Lichtbrücke e.V., supported Credit Program in Bangladesh: Matiur

Rahman

27

Table 3.10: Percentage distribution of the respondentsaccording to their response on increasing socialacceptance

Increased socialacceptance

Present BeforeFrequency % (Total) Frequency %

(Total)Yes 59 98.3 - -No 1 1.7 - -Total 60 100.0 60 100.0

Based on the above mentioned findings, it is now evident thatBMTC microcredit program has helped women of rural Bangladeshto become self empowered and paved their way for theirinclusion to the greater society.

4.1 Reduction of Domestic Violence

The ultimate aim of the present study was to explore therelation between microcredit membership and reduction ofdomestic violence. In this section nature and reduction ofdomestic violence against women who are member of BMTC projecthas been explored. The opinion of member women respondentshave been analyzed below.

Verbal abuse

Verbal abuse is best describedas an ongoing emotionalenvironment organized by theabuser for the purposes tocontrol. Verbal abuse is a verycommon form of domesticviolence. In the presentresearch a large majority of themember respondents (95%)admitted that after becomingSamity member they do not have toface such type of violence any more. Verbal abuse has beenreduced significantly. But before joining in the Samity a largemajority of them (90%) admitted that they had to face verbal

Microcredit in Reducing Domestic Violence against Women: An analysis ofa Die Lichtbrücke e.V., supported Credit Program in Bangladesh: Matiur

Rahman

28

abuse frequently. On the other hand verbal abuse is a dailymatter to the non-member respondents. A large majority of thenon-samity member (86.7%) admitted that they become victim ofverbal abuse in their daily life. So, it indicates thatmicrocredit membership reduce verbal abuse as a form ofdomestic violence against women (Figure 4.1).

Battering/Physical hurt

Battering or physical hurt isalso a common form of domesticviolence on women. In thepresent research it has beenfound that before becoming Samitymember around two-third (66.7%)of them became victim ofbattering. But at present alarge portion of them (96.7%)mentioned that they do not haveto face such occurrences anymore. Their husbands do not beat them as they can take loanfrom Samity and use it for household income generating purpose.But on the other hand, a large portion of the non-memberrespondents reported that they become victim of batteringfrequently by their husband (Figure 4.2).

Torturing for not Giving Dowry

Dowry practice in Bangladesh isprevailing for many years.Illegal demand for dowrysometimes brings an awfulsituation for a girl inBangladesh society and sometimesit cost death of the girl. In

Microcredit in Reducing Domestic Violence against Women: An analysis ofa Die Lichtbrücke e.V., supported Credit Program in Bangladesh: Matiur

Rahman

29

the present research a large majority (95%) of the respondentsmentioned that now they do not have to face domestic violenceparticularly torture for not giving dowry any more. It becomespossible because they are now financially capable to helptheir husband. They took loan from Samity and give it to theirhusband for income generation activities. But before becomingthe Samity member they had to face such occurrences. Around 40%of them mentioned that earlier their husband and other familymembers used to torture them for not giving dowry. On theother hand over one-third (66.7%) of the non-memberrespondents mentioned that they are tortured by their husbandsand other family members for not giving dowry (Figure 4.3).

Forced Sex by Husband

Forced sex is also a form ofdomestic violence against women.For the present research morethan one-fifth of the women(21.7%) respondents reported thattheir husband forced them to dosex against their will beforejoining the Samity. But at presenta very little of them (3.3%) mentioned about it. On the otherhand, around 30% of the non-member women respondents mentionedthat their husband forced them to do sex against their will(Figure 4.4). Throwing or Breaking of Household Assets to show Anger

Sometimes husbands give threatto their wife to control them bythrowing or breaking downhouseholds essentials. In thepresent research, a largeportion of the respondents(81.7%) mentioned that beforejoining the Samity they had toface such type of domesticviolence. But it has beenreduced gradually whenever they

Microcredit in Reducing Domestic Violence against Women: An analysis ofa Die Lichtbrücke e.V., supported Credit Program in Bangladesh: Matiur

Rahman

30

join the BMTC credit group. On the other hand, over two-thirdsof the non-samity member (66.7%) reported that their husbandsthreat them doing aggressive behavior like breaking orthrowing household assets (Figure 4.5).

Threatening with Weapons

Threaten with weapons is anotherform of domestic violenceagainst women. In the presentresearch, a good majority of therespondents (46.7%) mentionedthat before joining BMTC creditgroup their husband threatenedwith weapons for torturing butafter joining samity thisincident has decreased graduallyand at present only 3.3% of themmentioned about it. But it is prevailing among those who are notBMTC credit group member. It has been found that around 60% ofthe non-samity member mentioned that their husband sometimesthreatened them with weapons as a part of torturing (Figure4.6).

Make Deprived from Food/Meal

Depriving from meal or creatingbarrier to take regular meal isanother form of domesticviolence against women. As apunishment husband and othermembers of the family practiceit to wife or to any femalemember of the household. In thepresent research around 46.7%of the respondents mentionedthat before joining in the Samity they had to experience suchoccurrences but presently they do not have to face it likeearlier. This is due to becoming a member of the credit group.On the contrary, more than half of the non-member respondents

Microcredit in Reducing Domestic Violence against Women: An analysis ofa Die Lichtbrücke e.V., supported Credit Program in Bangladesh: Matiur

Rahman

31

(56.7%) reported that they have to face such incident often(Figure 4.7).

Preventing Doing Household Work

Sometimes husbands or otherfamily members do not allowwomen (especially wife) to dodaily household works. Thishappened mainly when people ofhusband’ house demand dowry.They do it as a punishment ofthe women or wife. In thepresent research about half(48.3%) of the respondentreported that they had to face this form of violence by theirhusband and other family member before joining the Samity. Butit has been reduced gradually after becoming the Samity member.At present only 5% of them agreed that they have to face suchincident sometimes. On the other hand around 43.7% of the non-BMTC credit group member reported that they have to face itstill now (Figure 4.8).

Threat of Giving Talak (Divorce)

Threat of giving divorce byhusband is a major form ofdomestic violence against women.In the survey data reveals thatmore than half of therespondents (51.7%) mentionedthat they had to face suchthreat from their husband beforejoining in the samity. But ithas been reduced significantlyand at present only 3.3 of them reported that sometimes theyhave to face it. On the other hand, around 63.3% of the non-member respondents stated that their husband threat them ofgiving divorce. So, it has seen that membership with

Microcredit in Reducing Domestic Violence against Women: An analysis ofa Die Lichtbrücke e.V., supported Credit Program in Bangladesh: Matiur

Rahman

32

microcredit group help decreasing domestic violence againstwomen like threat of giving divorce (Figure 4.9).

Insulting Inside or Outside the Home

It has been found that a largemajority of the memberrespondents (71.7%) mentionedthat their husband and otherfamily members insulted theminside and outside the homebefore joining the Samity. Only3.3% of them reported that sometimes they have to face suchincident. Conversely, a large number of non-member respondents(73.3%) reported that they experience such incident often(Figure 4.10).

Provoking others to Insult or MakingMisbehave

More than two-fifth of therespondents (41.7%) reportedthat their husband provokedother family members to insulther or misbehaved with herbefore joining Samity. But atpresent it has been reduced andonly 3.3% of them mentioned that they have to face suchoccurrences. On the other hand, more than half (53.3%) of thenon-member reported the same (Figure 4.11).

Blaming of Involving into IllicitRelations

About one-third (31.7%) ofrespondents mentioned thatbefore joining the Samity their

Microcredit in Reducing Domestic Violence against Women: An analysis ofa Die Lichtbrücke e.V., supported Credit Program in Bangladesh: Matiur

Rahman

33

husband and others family member blamed them to involve intoan illicit relation and tortured them over this issue. Butthis type of violence reduced gradually after joining in thecredit group. Now, a very little portion of them mentionedabout such type of harassment or torture. On the contrary,more than two-fifth (43.3%) of the non-samity member reportedthat their husband and other family members blamed ofinvolving illegal relations with someone (Figure 4.12).

Preventing Visiting Parent’s House

About two-third (65%) of therespondents for the presentresearch have reported thattheir husband prevented them tovisit their parent’s housebefore joining the Samity. Butat present they do not facesuch type of problems. Only3.3% of the member respondents mentioned it in the presentresearch. A good portion of non-samity member (73.3%)mentioned the same (Figure 4.13).

Keeping Away Child from Mothers

Keeping away child from motheris a form of domestic violence.In the present research aboutone-third of the memberrespondents (31.7%) mentionedthat before joining the Samitythey had to face such type ofincident frequently. But atpresent only 3.3% of them mentioned about it. On the otherhand, around 30% non-samity members reported the same (Figure4.14).

Provoking to Commit Suicide

Although provoke to commit suicide is a form of domesticviolence against women but for the present research no one

Microcredit in Reducing Domestic Violence against Women: An analysis ofa Die Lichtbrücke e.V., supported Credit Program in Bangladesh: Matiur

Rahman

34

admitted that they had to experience such incident duringbefore or after joining the samity activities.

Stopped Talking

More than half of therespondents (58.3%) in thepresent research reported thattheir husband and some otherfamily members used to stoptalking with them as apunishment before joining inthe Samity. But this situationhas change a lot after becoming member of the Samity. Atpresent only 5% of the member and 76.7% non-member mentionedabout it (Figure 4.15).

Deprivation from Household Assets:Deprivation of women fromhousehold assets is another formof domestic violence againstwomen. Over two-fifth (41.7%) ofthe respondents of the presentstudy admitted that theirhusband deprived them fromhousehold assets before joiningin the Samity. But at present ithas been reduced. Their husband changed a lot. Only 3.3% of themember and 43.3% non-member respondents mentioned that theirhusband practiced it in spite of having membership with creditgroup (Figure 4.16).

Respondents who mentioned about violence on them were alsoasked about their perpetrators. Most of them mentioned thathusband is the main perpetrators. Also they have mentionedtheir father/mother-in-Laws, others male member of the family,sister-in-law/ wife of brother-in-law who are responsible fordomestic violence on women.

4.2 Key Mechanism of Reducing Domestic Violence

Microcredit in Reducing Domestic Violence against Women: An analysis ofa Die Lichtbrücke e.V., supported Credit Program in Bangladesh: Matiur

Rahman

35

In order for a woman to be empowered, she needs access to thematerial, human, and social resources necessary to makestrategic choices in her life. Not only have women beenhistorically disadvantaged in access to material resourceslike credit, property, and money, but they have also beenexcluded from social resources like education or insiderknowledge of some businesses2.

Based on the above findings, in the present research, keymechanisms of microcredit for reducing domestic violenceagainst women are also analyzed. Through the following waymicrocredit can help reducing domestic violence against women.

i. Group members’ collective actionii. Self exposure of the loanee membersiii. Built in self-esteem of the loanee membersiv. Loanee members’ financial support to household.

i. Group members’ collective action is reported as aneffective way to reduce domestic violence against women.The idea is that there is a force within these women thatdoesn’t realizes until the individuals come together toform a group. The group can pose as a safe haven forabused women or help women morally or economically toleave a violent partner. “We are able to overcome abuse when weare in group because we get support from the women in the groups”mentioned by a women who is an active member of a creditgroup for many years. The group can also intervene in aviolent home to discuss with and convince the husband toend the abuse. Group members could also act as a tool toraise awareness to these issues.

ii. Another category of mechanisms is the women’s selfexposure to the community. With a wage work outside thehome, contact with other women through the loan group andwith the reputation as a provider the woman is morevisible to the community. As a more public person, the

2 Susy Cheston, and Lisa Kuhn (2010), ‘Empowering Women through Microfinance’Research sponsored by the Women’s Opportunity Fund and its funding partners:Elizabeth Foster and Michael Walsh, Gems of Hope USA, and the Morrow CharitableTrust.

Microcredit in Reducing Domestic Violence against Women: An analysis ofa Die Lichtbrücke e.V., supported Credit Program in Bangladesh: Matiur

Rahman

36

husband may avoid abuse his wife, since he has the eyesof the community on him.

iii. Another possible explanation could be the rise of thewoman’s self – esteem, a mechanism often mentioned whenreading about microcredit and domestic violence. In noneed of further elaboration, the thought is that aconfident and secure woman will stand up for herselfagainst abuse.

iv. The loanee members’ financial support to the householdmeans that her role as a wage earner increases herimportance. The money the woman brings home to her familyis significant for their survival and well – being. Butinjured, beaten women may not be able to work andtherefore the family risks losing an income for a shorteror longer period ahead.

Women that have participated in microcredit program alsoreported a greater affection and respect from their spouse dueto being more important for their livelihood. As abreadwinner the women experiences more bargaining power in thehousehold and there’s more room for negotiating and decisionmaking. With her income, the woman is not as economicallydependent on her husband for the support for her and herchildren. Just the fact that she is financially independentcould bring some credibility to the threat of leaving anabusive relationship. Another factor is that the woman’scontribution the household can ease conflicts deriving fromstress and scarcity.

4.3 Summarization of Findings of Focus Group Discussion (FGD)

The opinion and statement of some FGD participants is depictedbelow briefly for better understanding of the importance ofBMTC microcredit component to reduce domestic violence againstwomen.

One BMTC credit group members stated that:

I am married over 17 years. Before joining the BMTC credit group myhusband used to abuse me whenever he got angry. He did not count me as a

Microcredit in Reducing Domestic Violence against Women: An analysis ofa Die Lichtbrücke e.V., supported Credit Program in Bangladesh: Matiur

Rahman

37

human being because I could not give him any money except doing thehousehold works. But while I became member of BACE Samity and got loanfrom the Samity he became very happy. We jointly purchased some chickenfrom the first loan and spent some money for household purpose. By this wayI have taken 8 times loan from the Samity and improved our livelihoodcondition. My husband became happy with me and leaves the habit oftorturing me gradually. Now we are living happily.

Another woman of BMTC credit group also stated that:

My husband tortured me frequently for any mistake before my joining in thecredit group. He demanded me to bring dowry from my parent’s house. Butmy parent was very poor. They did not have the capacity to give him dowryagain and again. Once I came to know about the BMTC Samity of BACEtrough one of my neighbor and became member of this Samity. I receivedtraining on various issues from the BMTC and got credit money. I also cameto know about the bad effect of dowry and violence on women. I told it to myhusband. But at first he did not want to hear about it or change his behavior.He became happy only on my receiving loan money. Then some of my fellowmembers visited him and motivated him. They told him about the bad effectof violence. By this way he gradually changed his attitude towards me. I amwith this Samity more than 9 years. In the mean time I received 9 times loanand invest those loan money in cultivation, cow purchasing, poultry raring,etc. All these have been possible because of my becoming Samity member.After around 2/ 3 years of my membership with the Samity my husbandgradually changed himself and gave up torturing me. Even he visited theBMTC center and meet with high officials of the center. Now he is pleased. Mychildren also go to school and we take 3 times meal in a day. My husbandnever demand dowry now. We are living happily.

Other group member stated that:

Before joining the BMTC Samity I was very afraid. I believed that my husbandis second after the God. So, he has any power to control me and abuse me.He sometimes used to torture me regarding any issue of me. Even if I couldnot cook good meal for him then he threw the meal and started to beat me.My father-in-law and mother-in-law and other members of the family used toverbally abuse me whenever they got chance. At last I came to know aboutthe BMTC Samity through a social worker of the organization. He suggestedme to become member of the Samity. Then I got admitted in a Samity of myvillage. But my husband and other members did not like it. They told me to

Microcredit in Reducing Domestic Violence against Women: An analysis ofa Die Lichtbrücke e.V., supported Credit Program in Bangladesh: Matiur

Rahman

38

leave the Samity membership. But the social worker and other members ofthe Samity took my side and they tried to understand my husband and othermembers. When I got the first loan my husband took all the money and spentit. So, I was in trouble to repay the installments. But other fellow membershelped me to repay the loan money. In the mean time I have received trainingon livestock, kitchen gardening, cow raring, nursery, leadership quality andso on. By the pressure of my fellow member and social worker, manager myhusband malted a bit and started to help me. I have taken 10 times loan fromthe Samity. I have purchased a ‘Tempoo’ for my husband by the loan moneyand he runs the Tempoo now. We have improved our livelihood condition alot. Now my husband or other family member did not dare to do misbehavewith me or tortured me. We are passing our days happily.

So, it can be said that microcredit can contribute to reducedomestic violence against women. And BACE BMTC project isplaying a significant role to reduce domestic violence againstwomen through its microcredit component.

4.4 Conclusion

Microcredit is not only poverty – reducing tool but it hasmany positive effects on women empowerment, health andimproving gender relations. Microcredit also reduces domesticviolence against women and it brings healthy gender relation.The present research would be helpful to understand thesignificant relationship between microcredit program andreduction of domestic violence against women in Bangladesh. Itwill also be helpful for policy makers and organizations toadopt additional proper actions for program intervention toreduce domestic violence against women.

ABBREVIATIONS:

BACE Bangladesh Association for Community EducationBMTC BACE-Mitali Training CenterCBO Community Based OrganizationDLB Die Lichtbrücke e.V.FGD Focus Group DiscussionHDRC Human Development Research CentreSRS Simple Random Sampling

Microcredit in Reducing Domestic Violence against Women: An analysis ofa Die Lichtbrücke e.V., supported Credit Program in Bangladesh: Matiur

Rahman

39

References:

Bhuiya, A. U., Sharmin, T., & Hanifi, M. A. (2003). Nature ofdomestic violence against women in a rural area of Bangladesh:Implication for preventive interventions. Health, Population, andNutrition Journal: ICDDR,B, 21(1), 48 – 54.

Hadi, A. (2005). Women’s Productive role and marital violencein Bangladesh. Journal of Interpersonal Violence, 20(3), 181-189. Naved, R. T. & Persson, L. A. (2005). Factors associated withspousal physical violence against women in Bangladesh. Studies inFamily Planning, 36(4), 289-300.

Rahman, Muhammad Matiur (2012),’Domestic Violence on Women inBangladesh: A Case Study of Jhenaidah’ Unpublished PhD thesis,Institute of Bangladesh Studies, University of Rajshahi,Rajshahi, Bangladesh.

Schuler SR, Hashemi SM, Riley AP, Akhter S (1996). Creditprograms, patriarchy and men’s violence against women in ruralBangladesh. Soc Sci Med, 43(12), 1729–42. Susy Cheston,and Lisa Kuhn (2010), ‘Empowering Women throughMicrofinance’ Research sponsored by the Women’s OpportunityFund and its funding partners: Elizabeth Foster and MichaelWalsh, Gems of Hope USA, and the Morrow Charitable Trust.