Merchant Operations: Real Option Management of Commodity ...

156

Foundations and Trends R in sample Vol. xx, No xx (2013) 1–151 c 2013 Tepper Working Paper 2013-E3; May 2013; prepared for Foundations and Trends in Technology, Information and Operations Management DOI: xxxxxx Merchant Operations: Real Option Management of Commodity and Energy Conversion Assets Nicola Secomandi 1 and Duane J. Seppi 2 1 Tepper School of Business, Carnegie Mellon University, 5000 Forbes Av- enue, Pittsburgh, PA 15213-3890, USA, [email protected] 2 Tepper School of Business, Carnegie Mellon University, 5000 Forbes Av- enue, Pittsburgh, PA 15213-3890, USA, [email protected] Abstract The value chain for energy and other commodities entails physical con- versions through refineries, power plants, storage facilities, and trans- portation and other capital-intensive infrastructure. When the opera- tion of such commodity conversion assets occurs alongside liquid mar- kets for the input and output commodities, the operating flexibility of conversion assets can be managed as real options on the underlying commodity prices. Merchant operations is an integrated trading and operations approach that (i) buys and sells commodities to support market-value maximizing optimal, or at least near-optimal, operating policies and (ii) values conversion assets, for capital budgeting, based on the cash flows such policies produce. This monograph introduces the concept of merchant operations, presents the basic principles of op- tion valuation, surveys foundational models of commodity and energy

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Merchant Operations: Real Option Management of Commodity ...

Foundations and TrendsR© insampleVol. xx, No xx (2013) 1–151c© 2013 Tepper Working Paper 2013-E3; May2013; prepared for Foundations and Trendsin Technology, Information and OperationsManagementDOI: xxxxxx

Merchant Operations: Real OptionManagement of Commodity and Energy

Conversion Assets

Nicola Secomandi1 and Duane J. Seppi2

1 Tepper School of Business, Carnegie Mellon University, 5000 Forbes Av-enue, Pittsburgh, PA 15213-3890, USA, [email protected]

2 Tepper School of Business, Carnegie Mellon University, 5000 Forbes Av-enue, Pittsburgh, PA 15213-3890, USA, [email protected]

Abstract

The value chain for energy and other commodities entails physical con-versions through refineries, power plants, storage facilities, and trans-portation and other capital-intensive infrastructure. When the opera-tion of such commodity conversion assets occurs alongside liquid mar-kets for the input and output commodities, the operating flexibility ofconversion assets can be managed as real options on the underlyingcommodity prices. Merchant operations is an integrated trading andoperations approach that (i) buys and sells commodities to supportmarket-value maximizing optimal, or at least near-optimal, operatingpolicies and (ii) values conversion assets, for capital budgeting, basedon the cash flows such policies produce. This monograph introducesthe concept of merchant operations, presents the basic principles of op-tion valuation, surveys foundational models of commodity and energy

price evolution, analyzes the structure of optimal operating policies forcommodity conversions (focusing specifically on inventory and otherintertemporal linkages in storage, inventory acquisition and disposal,and swing assets), considers a variety of heuristic storage operatingpolicies, and discusses future trends in this multidisciplinary area ofresearch and business applications.

Contents

1 Aim and Scope 1

2 Commodity Conversion Assets and MerchantOperations 3

2.1 Commodities and Energy Sources 32.2 Physical and Financial Markets 52.3 Conversion Assets and Merchant Operations 72.4 Commodity Conversion Assets as Real Options 92.5 Outline of this Monograph 132.6 Notes 14

3 Real Option Valuation 16

3.1 Statically Complete Markets 193.2 Dynamically Complete Markets 213.3 Dynamically Incomplete Markets 293.4 Calibration 303.5 Summary 31

i

ii Contents

3.6 Notes 32

4 Modeling Commodity and Energy Prices 33

4.1 Spot-price Evolution Models 414.2 Futures Term Structure Models 504.3 Equilibrium Models 564.4 Empirical Research on Commodity Prices 584.5 Summary 594.6 Notes 60

5 Modeling Storage Assets 61

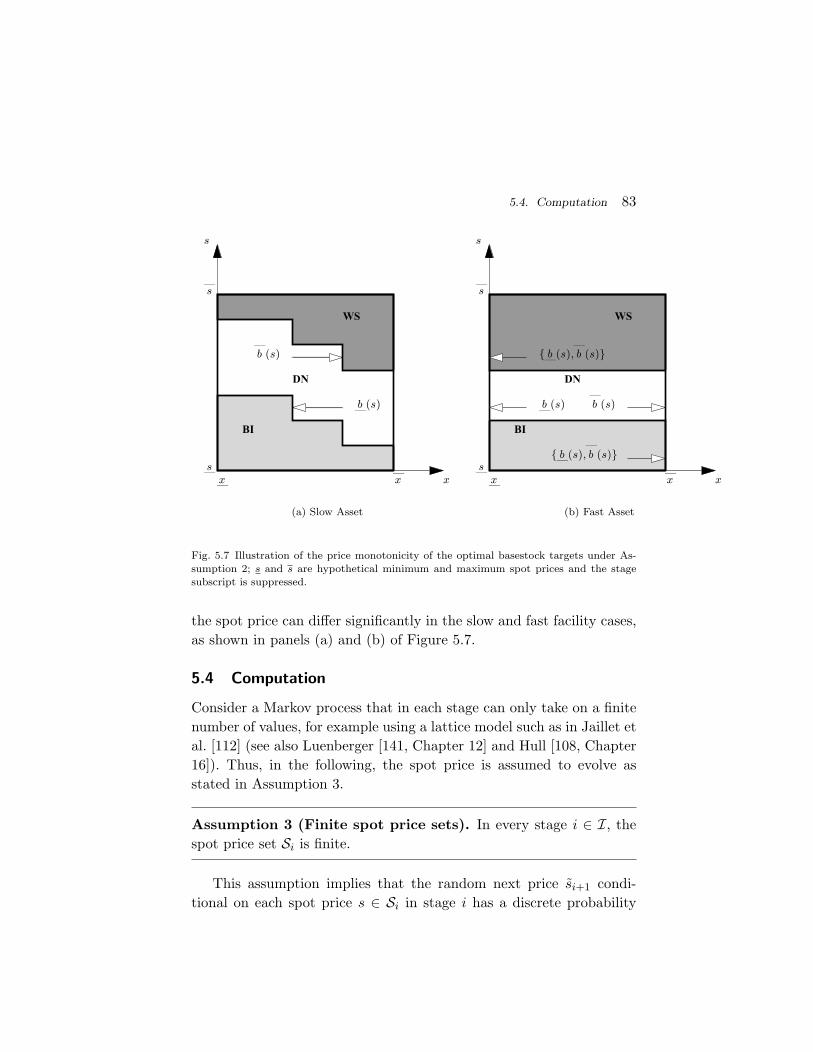

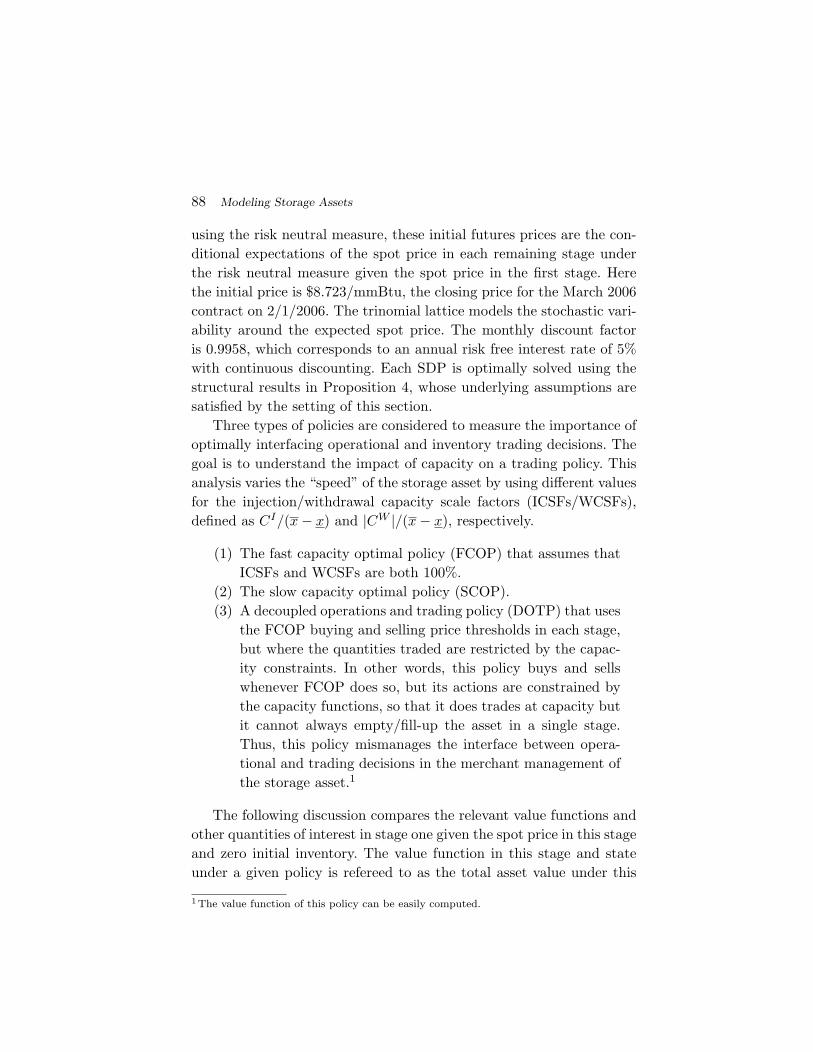

5.1 Model 665.2 Basestock Optimality 715.3 Price Monotonicity of the Optimal Basestock Targets 805.4 Computation 835.5 The Value of Optimally Interfacing Operational and

Trading Decisions 855.6 Conclusions 925.7 Notes 92

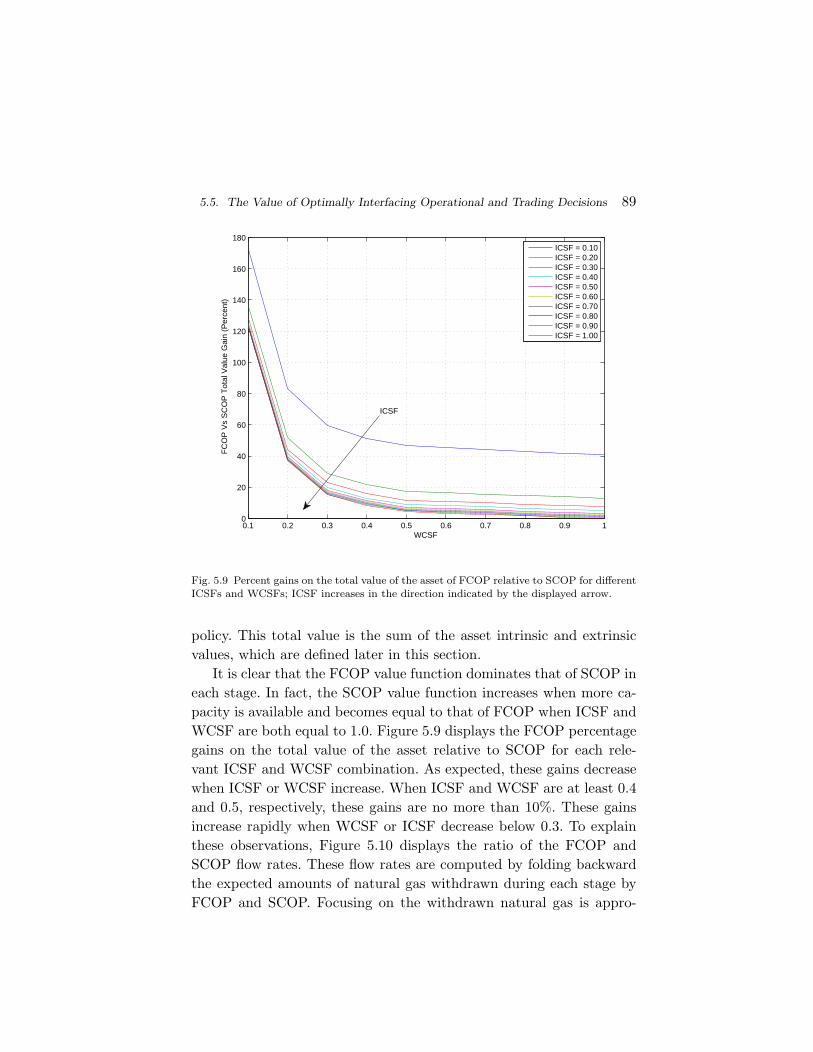

6 Benchmarking the Practice Based Management ofStorage Assets 95

6.1 Valuation Problem and Exact SDP 996.2 Practice-based Heuristics 1026.3 ADP Model 1066.4 Upper Bounds 1106.5 Numerical Results 1116.6 Conclusions 1186.7 Notes 119

7 Modeling Other Conversion Assets 121

7.1 An Inventory Disposal Asset 1227.2 An Inventory Acquisition Asset 125

Contents iii

7.3 Swing Assets 1277.4 Conclusions 1307.5 Notes 130

8 Trends 133

8.1 Financial Hedging 1338.2 Analysis of Other Commodity Conversion Assets 1348.3 Approximate Dynamic Programming 1358.4 Price Model Error 1368.5 Price Impact 1368.6 Equilibrium Asset Pricing 1378.7 Capacity Choice 137

Acknowledgements 139

References 140

1

Aim and Scope

Commodity conversion assets perform various transformation pro-cesses, including the production, refining, industrial and commercialconsumption, and distribution of physical commodities and energysources, such as grains, metals, coal, crude oil, and natural gas. Thismonograph deals with the management and valuation of conversionassets. Commodities and energy are traded on physical markets. It isthus natural to approach the management of commodity conversionassets from the perspective of merchant operations. This approach ad-justs the level of the conversion activities to profit from the dynamicsof commodity prices.

Managing merchant operations to maximize the market value ofcommodity conversion assets is a complex task. It requires both mod-els of the evolution of commodity prices and stochastic optimizationmodels of the conversion activities. The existence of traded contractson commodities and energy sources allows commodity conversion assetsto be interpreted as real options on the prices of the underlying com-modities. This real option interpretation greatly facilitates formulatingthe necessary mathematical models.

The valuation of real options shares the same theoretical founda-

1

2 Aim and Scope

tions as the valuation of financial options. The specific real options val-uation complications that arise in the context of merchant operationsare distinguished from financial options valuation problems by one ormore of the following features: decisions at multiple dates, intertempo-ral linkages across decisions, payoffs determined by operational costsand contractual provisions, engineering-based constraints on operat-ing decisions, and quantity decisions rather than binary exercise/no-exercise decisions. The valuation of Bermudan financial options alsoinvolves decisions at multiple dates and intertemporal linkages acrossdecisions, but the other features in this list are largely unique to mer-chant operations. Moreover, even when the structure of an optimaloperating (exercise) policy can be explicitly characterized, determiningsuch a policy typically involves numerical computation and approxi-mations. Closed-form solutions are thus rare in merchant operations,while they are more widespread in the valuation of financial options.

The aim of this monograph is to present the basic tenets of merchantoperations, that is, the management of commodity conversion assets asreal options on commodity prices. The focus here is on the foundationalprinciples that underlie the valuation of real options, on basic modelsof both the evolution of commodity and energy prices and commodityconversion assets, and on optimal and heuristic operating policies.

In terms of current research, the scope of this monograph is lim-ited to models that represent the foundations of merchant operations.There are many models in the current literature that pass this test.The limited number of pages available to this monograph thus furtherreduces its scope. In addition, this monograph includes a discussion offuture trends in merchant operations research and applications.

2

Commodity Conversion Assets and MerchantOperations

This chapter briefly introduces the basic commodity groups in §2.1,and illustrates the trading of commodities in physical and financialmarkets in §2.2. This discussion provides the necessary elements forintroducing the concepts of commodity conversion assets and merchantoperations in §2.3. This chapter also shows that merchant operationscan be usefully cast in the framework of real options in §2.4, providingsome examples of the real option management of commodity conversionassets. Some of these examples are substantial simplifications of howcommodity conversion assets are operated in practice, but they setthe stage for more realistic models. The discussion of these examplesprovides a point of departure for the rest of this monograph, which isoutlined in §2.5. Section 2.6 offers pointers to the existing literature.

2.1 Commodities and Energy Sources

According to the Webster’s New Universal Unabridged Dictionary[201], a commodity is “any unprocessed or partially processed good.”Commodities can be grouped according to three basic categories: agri-culturals, metals, and energy sources. Each of the groups includes sev-

3

4 Commodity Conversion Assets and Merchant Operations

eral commodity types, for example:

• Agriculturals: grains (corn, oats, rice, and wheat), oil andmeal (soybean, soyoil, and soymeal), livestock (pork andbeef), foodstuff (cocoa, coffee, orange juice, potatoes, andsugar), textiles (cotton), and forest products (lumber andpulp).

• Metals: gold, silver, platinum, palladium, copper, and alu-minum.

• Energy sources: coal, crude oil, heating oil, gasoline, naturalgas, propane gas, and electricity.

Commodity types can be further categorized according to grade andquality. In addition, due to limited transportation and storage capacity,the same commodity type at different locations and/or times effectivelyconstitutes separate commodities. For instance, consider natural gas attwo ends of a pipeline that transports it, or the availability of naturalgas in a storage facility at two different dates. Thus, location and timeare defining attributes of commodity types.

Commodities are basic inputs to production, distribution, and con-sumption activities. They thus play important economic roles. For ex-ample, natural gas is extensively used for heating, e.g., by about 50%of the households in the United States (Casselman [46]), and electricitygeneration, e.g., about 30% of worldwide electricity production is basedon natural gas (Geman [91]); it is also increasingly the fuel of choice fornew electricity generation projects, due in part to the recent shale gasboom (Smith [183]); it is having an impact on the worldwide liquefiednatural gas trade (Davis and Gold [60]) and the planning of new majorpipeline constructions (Chazan [52], Gold [97]); and it is an input toseveral manufacturing processes, including the refining of oil, and theproduction of chemicals, ammonia and methanol, steel and aluminum,and paper (Kaminski and Prevatt [118]).

Although energy is just one commodity group, it is emphasized inthe title of this section and throughout this monograph because thereis a substantial literature that deals with the application of real optionmethods to energy.

2.2. Physical and Financial Markets 5

2.2 Physical and Financial Markets

Commodities are traded in physical and financial markets. In bothcases, transactions can be on a spot or forward basis. Spot transac-tions involve the immediate, or at least very near term (e.g. , nextday), transfer of the physical commodity or financial ownership thereof.With forward transactions this transfer occurs at a specified date in thefuture.

Physical trading eventually leads to the transfer of a commodityfrom one party to another party. For example, the same lot of naturalgas for next day delivery may be purchased and sold several timesduring a given day, but this lot must be transfered from a seller to abuyer on the delivery date.

Financial markets for commodities, such as the Chicago Mercan-tile Exchange (CME), the New York Mercantile Exchange (NYMEX),the IntercontinentalExchange (ICE), and the London Metal Exchange(LME) trade various contracts that specify different commodity own-ership structures. Futures contracts specify obligations to deliver orreceive a given amount of a commodity, at a given price, and at a givenmaturity. (One month maturity futures typically have the highest vol-ume.) Selling and purchasing, respectively, a futures contract entailsthe obligation to deliver and receive a commodity. However, most fu-tures traders typically close out their positions via an offsetting tradebefore maturity. Thus, futures trading need not lead to physical han-dling of a commodity. Futures prices are set for each delivery date tomake the value of the futures contract zero. Hence, there is a singlefutures price for each delivery date.

Options contracts on futures specify the right to purchase or sella given futures contracts at a given price and maturity. Call and putoptions on futures, respectively, given their owners the right to purchaseand sell a futures at a contractually specified strike price. The payoff ofa call option is the positive part of the difference between the futuresprice at the option maturity and the strike price. The payoff of a putoption is the positive part of the difference between the strike price andthe futures price at maturity. Typically, there are options traded withmany strikes and expiries.

6 Commodity Conversion Assets and Merchant Operations

Additional types of options include calendar spread options on fu-tures contracts. These options give their owners the right to exchangea futures contract with a given maturity for a futures contract witha different maturity at a given strike price. Effectively, these optionsgiven their owners the right to purchase or sell the difference betweentwo futures prices at a given maturity and strike price. The payoff ofa call calendar spread option is the maximum between zero and thedifference between the spread between the two futures prices and thestrike price. The payoff of a put spread option is defined in an analogousmanner.

The options so far described are of the European types, meaningthat contractually they can be exercised only at maturity. American(respectively, Bermudan) versions of these options given their ownersthe right to exercise them at any time (respectively, a set of predeter-mined times) before maturity.

Futures, call and put options, and call and put calendar spread op-tion are traded on organized financial exchanges, such as CME, ICE,LME, and NYMEX, which guarantee the clearing of every trade. Thatis, these trades are insured by the exchange against the risk of counter-party default. These contracts and additional contracts are also tradedon over-the-counter (OTC) markets. Trades on OTC markets are di-rectly exposed to greater counterparty default risk.

Physical trading has an obvious use, as it supports the functioningof production, distribution, and consumption processes. The prices ofcommodities and contracts on commodities are variable and uncertain.They exhibit both seasonality (deterministic variability) and volatility(stochastic variability). Some theories explain the existence of financial(futures) markets based on price-risk aversion/control arguments (see,e.g., Keynes [124], Duffie [75]). Others rely on transaction costs princi-ples (Williams [202, 203]). In the context of this monograph, financialmarkets play a useful role in terms of the management of commod-ity conversion assets in the face of variable and uncertain commodityprices, as explained in §§2.3-2.4.

2.3. Conversion Assets and Merchant Operations 7

2.3 Conversion Assets and Merchant Operations

Commodities are produced and used for further processing, consump-tion, and distribution. In this monograph, the industrial facilities thatperform these transformation processes are called commodity conver-sion assets. Conversion here is used in a broad sense. It refers to

• The production of a commodity, such as the extraction ofnatural gas from underground wells;

• A physical transformation of a commodity, such as the refin-ing of crude oil, into another commodity, such as gasoline,jet fuel, and naphtha; or

• A change in availability of a commodity, such as the trans-portation of this commodity in between different locationsor its storage over time.

Managing commodity conversion assets thus requires performing oneor more operational activities, such as the production, processing, re-fining, transportation, storage, distribution, and physical trading ofcommodities.

Consider, for example, a storage asset, such as a grain or metalwarehouse, or an underground natural gas storage facility. Storage isused to help match the supply and demand of a given commodity overtime. Storage assets feature limited space, and may also exhibit limitson the amount of inventory that can be acquired or disposed of dur-ing a given time period. Managing a commodity storage asset requiresdetermining an inventory trading policy subject to space and possiblycapacity constraints.

As another example, consider a refining asset, such as a crude oilrefinery. A crude oil refinery includes various storage tanks for both theinputs, that is, various grades of crude oil, and the intermediate prod-ucts and outputs. Managing this refinery requires a joint inventory andproduction policy that determines the inventory levels in these tanksand how the inputs are converted and blended into refined products.In addition, shipping and transportation policies support the sourcingof crude oil and the distribution of refined products.

8 Commodity Conversion Assets and Merchant Operations

In practice, the owners of the capacity of a given commodity conver-sion assets often rent all or part of this capacity to third parties, suchas commodity and energy merchants, for given time periods throughcontracts. This occurs in the natural gas industry in the United States,where, by federal regulation, the owners of interstate pipelines and stor-age facilities must make their capacity available to shippers on an openaccess basis. Tolling agreements play a similar role in the power genera-tion industry whereby physical generator owners can sell off generationrevenue to investors. In this monograph, contracts on the capacity ofa commodity conversion assets are themselves considered commodityconversion assets. In addition to determining an optimal operating pol-icy for such assets, the determination of their market value is an impor-tant practical problem, as it forms the basis for contract negotiation.

Commodity conversion assets are embedded in a market environ-ment for the commodities that they convert. Indeed, commodity con-version assets are the building blocks of both physical and financialcommodity markets. Commodity production and storage assets, as wellas transportation assets, such as pipelines, ships, and related loadingand unloading facilities at ports, play a central role in the determina-tion of spot and futures prices (Williams and Wright [204]). Commodityconversion assets can thus be managed taking a merchant perspective,which involves the adjustment of the level of the conversion activities toreflect the dynamics of commodity prices. For example, the decision torefine crude oil into refined products depends on the respective spreadsbetween the prices of these products and the price of crude oil. Thelabel merchants operations refers to this approach to the managementof commodity conversion assets.

The optimal management of merchant operations thus requiresmanaging operational activities in the face of variable and uncertaincommodity prices. The valuation of these operational policies also isimportant. In general, these are difficult tasks. Interpreting conversionassets as real options facilitates the execution of these tasks.

2.4. Commodity Conversion Assets as Real Options 9

2.4 Commodity Conversion Assets as Real Options

Managerial flexibility in projects can be viewed as embedded real op-tions. Managerial flexibility in merchant operations is linked to theuncertain evolution of commodity and energy prices. For example, theability of oil and natural gas producers to drill or shut down wells de-pending on the prevailing oil and natural gas prices can be interpretedas a real option on these prices. Other commodity conversion assetshave analogous interpretations as real options on commodity prices.This means that merchant operations of managing commodity conver-sion assets amounts to optimally exercising specific real options. Tomake this concept more concrete, it is useful to discuss some examples.

Simplified commodity production assets and call options.Consider a natural gas well. Let c be the cost of producing one unit ofgas; st be the spot price of natural gas at time t; and Q the rate of pro-duction. For simplicity, ignore the cost of shutting down and resumingproduction, the time required to do so, and any other intertemporalconsiderations (e.g., the ability of the asset manager to time the sale ofnatural gas). Then, the optimal merchant management policy for thissimplified natural gas production asset is to produce and sell Q unitsof natural gas at time t when the spot price of natural gas st exceedsthe marginal production cost c, and do nothing otherwise. The payoffof this policy at time t is

maxst − c, 0 ·Q, (2.1)

which is also the payoff of a call option on Q units of the time t spotprice of natural gas st with strike price equal to c. This observationjustifies thinking of the simplified natural gas well at time t as a realcall option on the spot price with a strike price equal to the marginalproduction cost and notional amount equal to the production rate (thenotional amount of an option is the “number” of such options ownedby a trader). The merchant operations of this asset thus amounts tothe optimal exercise of this option.

The time t futures price with maturity t, Ft,t, is identical to thetime t spot price, st. The payoff (2.1) is thus also the payoff of Q call

10 Commodity Conversion Assets and Merchant Operations

options on the time t futures price with maturity t and strike pricec. As discussed in §2.2, such options are traded on exchanges, such asNYMEX. Thus, the current market value of this simplified commodityproduction asset, when managed at time t as a merchant operations,can be observed from NYMEX.

Transportation assets and spread options. Consider a pipelinethat transports natural gas from Houston, Texas, to New York City,New York. Suppose that a merchant rents an amount Q of the capacityof this pipeline for a given time period, say one year starting at timet. This merchant can maximize the market value of this capacity byoptimally trading natural gas on the Houston and New York City spotmarkets for natural gas over the year. Namely, at time t this merchantcan optimally purchase an amount of natural gas equal to the rentedpipeline capacity on the Houston spot market, ship this natural to NewYork City using this capacity, and sell the shipped natural gas on theNew York City spot market if the New York City natural gas priceexceeds the Houston natural gas price net of the shipping cost.

Let s1,t and s2,t be the spot prices at time t for the Houston andNew York City markets. Denote by c the marginal shipping cost. Thetime t payoff of the optimal shipping policy is

maxs2,t − s1,t − c, 0 ·Q. (2.2)

This payoff assumes that natural gas is simultaneously injected into thepipeline in Houston and delivered in New York City at time t. This isrealistic because the entire pipeline from Houston to New York City isfilled up with natural gas, but it is clear that the delivered natural gasis not physically the same injected natural gas. In addition, the payoff(2.2) ignores the fuel that is used by the pipeline compressors to shipnatural gas.

The payoff (2.2) corresponds to the payoff of Q call spread optionson the spot prices s1,t and s2,t with strike price c. Different from thepayoff (2.1) for the simplified natural gas production asset, the payoff(2.2) involves two distinct commodities: natural gas in Houston at timet and natural gas in New York City at time t. A contract on naturalgas pipeline capacity is thus a cross-commodity conversion asset, which

2.4. Commodity Conversion Assets as Real Options 11

can be interpreted as a real call spread option on the time t spot pricesin Houston and New York City with strike price equal to the marginalshipping cost and notional amount equal to the rented pipeline capac-ity. The merchant operations of this asset corresponds to the optimalexercise of this option.

Other transportation assets share this feature with natural gaspipelines. Examples include power grids, as well as crude oil tankersand trains that haul coal rail cars. The difference between the latter as-sets and power grids and natural gas pipelines is that tanker and trainpayoffs are defined on commodity prices at both multiple location anddates, due to the longer transportation lead time. Transportation as-sets can also entail multiple sourcing and delivery locations. This aspectcan be characterized as a rainbow option, that is, an option to chooseamong multiple prices.

Exchanges such as NYMEX and ICE trade basis swaps for severallocations in the United States. These contracts are essentially futurescontracts on the difference between the futures price at a given loca-tion and the futures price at Henry Hub, the delivery location for theNYMEX natural gas futures contract. The time t spot prices for Hous-ton and New York City, s1,t and s2,t, should be identical to the sum ofthe Henry Hub futures price and the Houston and New York City basisswaps’ prices, respectively. Denote these sums by F1,t,t and F2,t,t. Thus,the payoff (2.2) is that of a spread option on the difference between thefutures prices F2,t,t and F1,t,t net of the strike price c.

Cross-commodity spread options are not directly traded onNYMEX or ICE (but they may be traded on OTC markets). However,the time 0 < t market value of these options can be determined usingthe techniques discussed in Chapter 3, based on a stochastic modelof the joint evolution of the prices F1,·,t and F2,·,t during the time in-terval [0, t]. This valuation amounts to the computation of a specificmathematical expectation.

Simplified consumption assets and put options. Commodityconsumption assets play the opposite role of commodity productionassets. Consider a firm that employs a given commodity as its majorinput to its manufacturing process. For example, the input commodity

12 Commodity Conversion Assets and Merchant Operations

could be copper for a company that manufactures pipes. For simplic-ity, suppose that the firm can sell its production at time t at the fixedprice K (this is not entirely realistic, as the firm could adjust its pricingpolicy according to the input price, but represents a situation whereoutput prices are fixed in the short term). This price is net of other(nonrandom) variable manufacturing costs. Suppose that this produc-tion is known with certainty and is equal to Q. Also assume that thefirm does not carry inventory of the input commodity, another simpli-fying assumption.

The manufacturer’s optimal production policy is to purchase thecommodity, produce, and sell its output at time t if the output priceexceeds the input price. The payoff of this policy is

maxK − st, 0 ·Q, (2.3)

The payoff (2.3) is also the payoff of Q European put options on the spotprice at time t. This observation justifies interpreting the commodityconsumption asset as a real put option on the time t spot price of thecommodity with strike price equal to the output price and notionalequal to the manufacturing capacity Q. The merchant operations ofthe manufacturing asset is identical to the optimal exercise of this putoption.

The time t price of a futures contract with maturity at time t is equalto the spot price at this time, that is, Ft,t = st. The time 0 < t marketvalue of the manufacturing asset managed as a merchant operationsis thus the time 0 value of this futures option. Similar to Europeancall options on commodity futures prices, European put options oncommodity futures prices are also traded on exchanges (such as LME).The time 0 value of the commodity conversion asset when managed asa merchant operations at time t can thus be observed from the market,as it amounts to the value of the futures put option multiplied by theproduction capacity for time t.

These examples illustrate that interpreting commodity conversionassets as real options and the merchant operations of such assets as theoptimal exercise of specific real options is useful because it leads to themaximization of the market values of these assets.

2.5. Outline of this Monograph 13

2.5 Outline of this Monograph

In some cases, managing a commodity conversion asset as merchantoperations is simple, such as in the examples discussed in §2.4. However,for most commodity conversion assets this requires the development ofmathematical models that maximize the market value of the merchantoperating policy of such an asset based on a stochastic representationof the evolution of commodity and energy prices, subject to certainmarket pricing consistency criteria. Specifically, the merchant operatingpolicy prescribes how to optimally exercise the managerial flexibilityembedded in the commodity conversion asset, that is, the real optionsthat this asset represents, and the market pricing consistency criteriaensure that this policy maximizes the market value of this asset.

In theory, the development and use of such real option models re-quires the existence of frictionless financial markets for commodity con-tracts. Some commodity and energy industries come close to satisfy-ing these requirements, e.g., grains, soybean, natural gas, and oil allhave fairly liquid financial markets (e.g., CME, ICE, NYMEX). Thereal option modeling approach remains useful in practice even whenthese requirements are not perfectly satisfied, as it provides a consis-tent framework for devising operating policies that strive to maximizethe market value of an asset. Chapter 3 outlines the theory behind thevaluation of real options. Chapter 4 illustrates basic models of the evo-lution of commodity and energy prices that can be used when applyingthis theory.

The transportation assets discussed in §2.4 are fairly realistic repre-sentations of how these assets are operated in practice. In contrast, thecommodity production and consumption assets presented in §2.4 sim-plify many important aspects of how such assets are managed. In par-ticular, these simplified assets neglect a basic aspect that distinguishesmost storable commodity conversion assets: inventory. For commod-ity production assets, inventory represents the reserve of commoditythat can be produced and sold over time. For commodity consump-tion assets, inventory is the input stored in tanks or stockpiles that isavailable for use in the manufacturing process. Refining assets featuresmultiple types of inventory, both for inputs and outputs, but also, pos-

14 Commodity Conversion Assets and Merchant Operations

sibly, for intermediate products; that is, in this case storage is bundledwith cross-commodity transformations. Inventory is important becauseit links decisions across multiple dates and can lead to nontrivial opti-mal quantity decisions, that is, decisions about a commodity conversionasset operating scale. Switching costs incurred to alter the scale of op-erations of a commodity conversion asset can also impose intertemporallinkages across decisions.

From this perspective, storage is a foundational element of com-modity conversion assets. In a simplified model, a single commodity ispurchased from the market at the prevailing spot price, held in stockat a warehouse, and resold back to the spot market at a future date.Chapters 5-6 deal with the structure of the optimal policy for the com-modity storage asset and the benchmarking of policies used to managesuch assets in practice, respectively. Chapter 7 shows that the optimalpolicy structure for a commodity storage asset remains relevant for themerchant operations of other assets, including inventory disposal andacquisition assets and swing assets. In contrast, realistic real optionmodeling of more complicated commodity conversion assets remainsan open area of research and applications. This is one of the trendsdiscussed in Chapter 8.

2.6 Notes

The categorization of commodity groups and types in §2.1 is from Ge-man [91, Table 1, p. 13]. Geman [91] discusses in detail the marketsfor the commodity groups introduced in §2.1. Schofield [166] providesa detailed account of commodity markets and derivatives. Clewlowand Strickland [55], Eydeland and Wolyniec [79], Geman [91], Pilipovic[155], and Burger et al. [36] illustrate various contracts traded in com-modity financial markets, as well as real options models for valuationand risk management of energy derivatives and assets. Hull [110, p. 587]is a comprehensive introduction to derivatives contracts, including fu-tures and options. The collection edited by Ronn [162] includes severalcontributions on the use of real options in energy management. Lep-pard [135] provides a nontechnical introduction to energy derivativesand their role in the risk management of energy assets.

2.6. Notes 15

The real option literature is vast, and no attempt is made hereto provide a comprehensive coverage. Dixit and Pindyck [71] and Tri-georgis [194] provide introductions to real option concepts. Luenberger[141], Clewlow and Strickland [55], Ronn [162], Eydeland and Wolyniec[79], Kaminski [116], Geman [91], and Hull [110] present various com-modity and/or energy applications. Smith and McCardle [182] discusspractical applications of real option concepts in the energy industry.Benth et al. [12] is an advanced treatment of energy price evolutionmodels, a topic discussed in Chapter 4.

The link between the management of commodity conversion assetsas merchant operations and the management of real options is implicitin most of this literature. In practice, the merchant operations approachto managing commodity conversion assets has been embraced by com-mercial banks (see, e.g., Davis [59]) and energy merchants (Ronn [162],Kaminski [116]).

The discussion of the commodity conversion assets considered in§2.4 is based on the work of Brennan and Schwartz [32] on the realoption valuation of natural resource production, the research of Denget al. [67], Eydeland and Wolyniec [79, pp. 59-62], Fleten et al. [86],and Secomandi [170] on the real option valuation of electricity andnatural gas transportation infrastructure, and the paper by McDonaldand Siegel [145] on the real option valuation of manufacturing firms.Secomandi and Wang [176] consider a more realistic model of naturalgas transport assets.

The material at the beginning of §2.5 is based on the chapter bySick [179] and the paper by Smith [180]. Sick [179] emphasizes that theoptimal management of commodity and energy real options often givesrise to stochastic dynamic programs whose formulation must satisfymarket consistency criteria. Such criteria are based on assumptionsthat can be restrictive in applications. Smith [180] points out thateven when these assumptions are not fully satisfied, enforcing thesecriteria provides a consistent framework for informing and supportingmanagerial decision making.

3

Real Option Valuation

Our goal in this chapter is to develop a framework for pricing futurecash flows paid off by real (or financial) commodity options. In partic-ular, the goal is to compute market valuations; that is to say, optionvaluations which are consistent with the market prices of related tradedsecurities.

Option valuation depends, in general, on the probability beliefs andpreferences of the market and on the option payoff function. For com-modity options, the option payoffs are contingent on commodity prices.The evolution of commodity prices can be represented formally as func-tions on a probability space (Ω,F , P ) where Ω is the set of all possiblestates, F = Ft is a filtration which describes the possible evolutionof information about the realized state ω ∈ Ω, and P is a probabilitymeasure over informational states ωt ∈ Ft. Given the probability space,let c∗T denote an option payoff at a future expiration date T where theonly restriction on c∗T is that it must be measurable with respect to FT .In other words, c∗T only depends on commodity price information thatwill be known at date T . For commodity options, the payoffs c∗T aredetermined contractually (as with exchange-traded and OTC call andput options) or operationally (as with real options which must be run

16

17

according to an operating policy which is feasible given physical engi-neering constraints and measurable with respect to information Ft). Inthe absence of arbitrage, a non-negative function ϕ(ωT |ωt) exists suchthat any measurable payoff function c∗T can be valued at date t < T

as1

ct =∫

ωT∈FT

c∗T (ωT )ϕ(ωT |ωt)dωT (3.1)

where ωT is a possible future state given the information FT at dateT , ωt is the state given current information Ft at date t, and ϕ(ωT |ωt)is a state price density giving the market value in state ωt at date t

of a state-contingent dollar in state ωT at date T . The state pricesincorporate everything that matters at date t for valuing future ωT -contingent cash. In particular, state prices depend on the time-value-of-money between dates t and T , the market’s beliefs about the probabilityof state ωT occurring at T given that ωt is the current state at t, andthe market’s preferences in state ωt for state-contingent cash in thefuture state ωT . For example, the market may have a preference forinsurance in some futures states (e.g., down market states in a CAPMworld) but not in others (e.g., up market states). If riskless interestrates are a constant r, the state price valuation equation (3.1) can bemanipulated as

ct =

[∫

ωT∈FT

c∗T (ωT )ϕ(ωT |ωt)∫

ωT∈FTϕ(ωT |ωt)dωT

dωT

][∫

ωT∈FT

ϕ(ωT |ωt)dωT

]

=[∫

ωT∈FT

c∗T (ωT )qRN (ωT |ωt)dωT

]e−r (T−t) (3.2)

to obtain the risk neutral valuation equation2

ct = ERNt [c∗T ]e−r (T−t). (3.3)

The second equality in (3.2) follows from i) the fact that the integral ofthe state prices

∫ωT∈FT

ϕ(ωT |ωt)dωT equals the price of a riskless dis-count bond e−r (T−t) (i.e., of a riskless payoff of $1 in each possible state

1See Harrison and Kreps [104] and Duffie [76] chapters 1 and 6 for more on multi-periodasset pricing and state prices.

2See Schwartz [167], Miltersen and Schwartz [147] and Casassus and Collin-Dufresne [44]for models of commodity option pricing with stochastic interest rates.

18 Real Option Valuation

ωT at T ) and ii) an interpretation of scaled state prices as preference-adjusted risk neutral probabilities qRN (ωT |ωt). The RN probabilitiesare non-negative and integrate to 1 but differ from the objective prob-abilities because the RN probabilities are constructed from state priceswhich depend on market preferences as well as on objective probabili-ties.3

A practical use of RN valuation is that equation (3.3) provides atractable numerical procedure for computing the value of options whenanalytic formulas for option prices are not available. First, N realiza-tions of the underlying state ωT are simulated under the RN probabilitymeasure using Monte Carlo. Second, option payoffs c∗T (i) are computedfor each simulated realization i = 1, . . . , N of the state ωT (i), averaged,and discounted to get an estimated valuation:

ct =∑N

i=1 c∗T (i)N

e−r (T−t). (3.4)

Since averages are unbiased estimators of expected values, the MonteCarlo estimate ct is an unbiased estimate of the option price ct.

Real options often have cash flows, not at just a single date, butrather a stream of cash flows c∗1, c

∗2, . . ., c∗M at a sequence of dates

T1, T2, . . ., TM . Using RN valuation, the value of a sum of cash flows is

ct =M∑

i=1

ERNt [c∗Ti

]e−r (Ti−t). (3.5)

For example, mines generate streams of net profits over time tied tomineral prices. Electric power plants produce streams of operating prof-its tied to the spark spread between power and fuel prices. Natural gasstorage yields a stream of negative cash flows (in months in which gasis purchased and stored) and positive cash flows (in months in whichstored gas is withdrawn and sold).

The purpose of an option pricing model is to specify the risk neu-tral probabilities with which to value future state-contingent cash flows.

3Sometimes RN probabilities are decomposed as qRN (ωT |ωt) = p(ωT |ωt)m(ωT |ωt) wherep(ωT |ωt) is the objective probability and m(ωT |ωt) is called the pricing kernel and rep-resents the equilibrium pricing impact of investor preferences.

3.1. Statically Complete Markets 19

Since existence of state prices – and, hence, of RN probabilities – is en-sured by absence of arbitrage, the focus in this chapter is on two relatedissues: When are RN probabilities unique? And how are RN probabil-ities identified? In particular, this chapter reviews three approachesto identify risk-neutral probabilities. The first approach is possible ina statically complete market. The second is possible in a dynamicallycomplete market. The third requires price-of-risk assumptions when themarket is incomplete. While the discussion here is exposited in termsof commodities, the uniqueness and identification of the RN dynamicsof an option’s underlying variable are generic issues. They arise withoptions on any tradable asset (e.g., stocks, bonds) and on underlyingswhich are not directly tradable (e.g, interest rates, weather, defaultevents).

A key consideration in option pricing is what exactly constitute a“state.” In general, an informational state ωt ∈ Ft in a commodityoption pricing model includes the current spot price st and also anyother factors (i.e., other variables like stochastic volatility) that affectthe dynamics of future spot prices plus the prior history of all statevariables. Equation (3.3) shows that the properties of option pricesfollow directly from the option payoff formula and the RN dynamics ofthe state variables driving the commodity price filtration. This chapterpresents generic approaches to option pricing. Chapter 4 then describesa variety of different commodity option pricing models in terms of theirspecific representations of states, price dynamics, and RN probabilities.

The rest of this chapter proceeds as follows. Section 3.1 explains riskneutral valuation in statically complete markets. Section 3.2 describesrisk neutral valuation in dynamically complete markets based on Blackand Scholes [20] and Black [19]. Section 3.3 discusses the role of Priceof Risk assumption in risk neutral valuation in incomplete markets.Section 3.4 discusses model calibration. Section 3.5 summarizes. Section3.6 includes pointers to the literature.

3.1 Statically Complete Markets

Traded securities are bundles of future state-contingent cash flows invarious future dates and future states. A market is statically complete if

20 Real Option Valuation

any combination of future state-contingent payoffs can be constructedusing buy-and-hold positions in market-traded securities. In particular,a market is statically complete if there are as many traded securitieswith linearly independent cash flows as there are states.

In a statically complete market, state prices can be recovered fromthe prices of traded securities. Let t0 denote the current date and lett1, . . . , tM denote discrete future payment dates. Let Kj denote the to-tal number of discrete (for simplicity) possible states at future paymentdate tj . The total number of future date/state pairs are K =

∑Mj=1 Kj .

Let ϕk denote the state price at date t0 of a state-contingent dollarin the kth possible future state/date pair. Let CFi,k denote the futurecash flow paid off by a particular traded security i in a possible fu-ture date/state k and let Pi,t0 denote the price at date t0 of securityi. State prices equate the values of the future security cash flows withthe current date t0 security prices. If we have N traded securities withlinearly independent future cash flows, then the market prices of thesesecurities imply the system of linear equations

P1,t0 = ϕ1 CF1,1 + ϕ2 CF1,2 + · · ·+ ϕK CF1,K , (3.6)

P2,t0 = ϕ1 CF2,1 + ϕ2 CF2,2 + · · ·+ ϕK CF2,K ,

· · ·PN,t0 = ϕ1 CFN,1 + ϕ2 CFN,2 + · · ·+ ϕK CFN,K .

The solution for the ϕks in (3.6) is unique if the number of tradedsecurities with linearly independent future cash flows, N , equals thenumber of future dates/states K. However, in practice, there are typi-cally many more future states/dates than traded securities, so marketsare rarely statically complete. Hence, state prices cannot be uniquelyidentified algebraically from an under-determined system of N equa-tions in K > N unknowns.

State prices still exist in incomplete markets, in the absence of ar-bitrage, but they are not uniquely identified by traded security prices.There are multiple possible state price vectors which are each con-sistent with the traded security prices. Option pricing models imposeadditional structure on state prices in order to determine state prices inan incomplete market. An option pricing model is correct if its assumed

3.2. Dynamically Complete Markets 21

additional structure on state prices is consistent with the structure infact imposed on state prices by the actual economics of the market

3.2 Dynamically Complete Markets

Markets which are statically incomplete may still be dynamically com-plete if there are dynamic trading strategies with traded securitieswhich can replicate any state-contingent payoff. The link between dy-namic completeness and option pricing was first recognized in Black andScholes [20]. There are two approaches to commodity option pricing indynamically complete markets. The first assumes that the underlyingcommodity is itself a traded asset. This approach applies to commodi-ties like gold which are investable stores of value over time. The secondapproach, due to Black [19], assumes that a traded commodity futurescontract is available.

Commodities which are traded assets: The Black-Scholes ap-proach to identify RN dynamics follows from two key assumptions.First, the underlying commodity is assumed to be an investible asset(e.g., like gold). Second, the objective dynamics of the spot price of thecommodity st are assumed to be the following general Ito process:4

dst = µ(st, t)st dt + v(st, t)st dZt. (3.7)

The assumption of an univariate Ito process for spot prices means thatthe spot price st itself is the only state variable needed to describecommodity price dynamics. Given these two assumptions, generalizedBlack-Scholes RN dynamics can be derived in two steps.

The first step is the derivation of the Black-Scholes partial differ-ential equation. Over time only two things change in a Black-Scholeseconomy – the spot price st and the date t. As a result, option pricesare functions c(st, t) of st and t, where everything else at date t isparametrically fixed by assumption (e.g., interest rates, the forms ofthe local drift and volatility functions µ(·, ·) and v(·, ·)), contractually

4These dynamics generalize the original Black and Scholes [20] derivation for GeometricBrownian Motion prices (i.e., with constant local drifts and volatilities, µ and σ). SeeShreve [178] for more on Ito processes.

22 Real Option Valuation

fixed (e.g., option strike prices and expiration dates), and historicallyfixed (e.g., the path of prior spot prices before date t). However, thevaluation function c(st, t) must be consistent with absence of arbitrage.This no-arbitrage condition imposes restrictions on the types of func-tions c which value commodity price-contingent future cash flows.

Consider a portfolio consisting of a long position in a given optioncombined with a short position of −∆ units of the underlying com-modity. In particular, this is only possible if the commodity is a non-perishable, storable, and, hence, investible asset that can be includedin an investment portfolio. At date t this portfolio is worth ct −∆ st.Since ct is a function c(st, t), Ito’s Lemma tells us how this portfolio’svalue changes in response to the passage of time dt and changes dst inthe underlying spot price:5

dct −∆dst =(

∂c

∂t+

12v2(st, t)s2

t

∂2c

∂s2

)dt +

∂c

∂sdst −∆dst. (3.8)

The portfolio value dynamics have two components: Adeterministic part due to the nonrandom passage of time[∂c/∂t + (1/2)v2(st, t)s2

t ∂2c/∂s2

]dt and a risky part due to ran-

dom changes in the spot price (∂c/∂s−∆) dst. Setting the commodityposition ∆ = ∂c/∂s makes the combined option/commodity portfolioriskless. In particular, the implicit exposure to spot price risk throughthe option, ∂c/∂s, is offset by the direct exposure from the short∆ = ∂c/∂s commodity position. Thus, to avoid arbitrage between thisriskless option/commodity portfolio and riskless t-bills, the functionc(st, t) must satisfy

dct − ∂c

∂sdst =

(ct − ∂c

∂sst

)rdt. (3.9)

In words, the change in the value of the hedged option/commodityportfolio must be the same as would be earned if an equal amount ofmoney, ct − (∂c/∂s)st, were instead invested at the riskless rate. This

5The function c(st, t) is parameterized by everything that is fixed at date t including processparameters, contractual payoff terms, and (for path-dependent options) the history of pastspot prices. For an explanation of Ito’s Lemma, see Shreve [178] or Hull [110].

3.2. Dynamically Complete Markets 23

leads to the Black-Scholes partial differential equation

∂c

∂t+

12v2(st, t)s2

t

∂2c

∂s2=

(ct − ∂c

∂sst

)r. (3.10)

This equation has infinitely many solutions c. To pick out the specificfunction which prices a given option, a boundary condition is imposedon (3.10) requiring that the function c(sT , T ) equals the payoff functionc∗T on the payoff date T .

As an aside, note that the payoffs of any commodity option canbe exactly replicated, under the Black-Scholes assumptions, by a self-financing dynamic trading strategy. Rearranging (3.9)

dct =∂c

∂sdst +

(ct − ∂c

∂sst

)rdt (3.11)

says that the dollar price change in an option dct over each instant dt

is exactly mirrored by a portfolio consisting of ∂c/∂s units of the com-modity and ct− (∂c/∂s)st dollars in riskless bonds. This demonstratesthat the Black-Scholes market is, indeed, dynamically complete sincethe option payoff c∗T in the PDE boundary condition can be any mea-surable function of ωT since states in Black-Scholes are generated bythe evolution of spot prices. It also means that, in practice, a discretizedversion of (3.11) can be used to hedge options in a Black-Scholes mar-ket.

The second step of the Black-Scholes identification of the RN com-modity price dynamics uses the Black-Scholes PDE to identify so-calledequivalent economies and then makes a convenient choice. In the Black-Scholes model, an economy is described by a collection U , µ, v, r, s0consisting of investor preferences U (i.e., investor utilities), an Ito pro-cess (3.7) for the underlying commodity under the objective measure,a risk-free interest rate r and an initial commodity spot price s0 at abeginning date t0. We know that option prices depend on s0, v(·, ·), andr since they appear explicitly in the Black-Scholes PDE – together withthe strike price, expiration date, etc. and any other contractual termsin the associated boundary condition cT = c∗T – but option prices donot depend directly on either the underlying commodity’s drift µ(·, ·)

24 Real Option Valuation

or on investor risk preferences U . Because the option/commodity ver-sus bonds arbitrage is riskless, neither µ nor U affect the option pricingfunctions c implicitly described by the Black-Scholes PDE.

This last observation leads to a key insight: Option prices in the trueeconomy U , µ, v, r, s0 are unchanged in any alternate (i.e., imaginary)economy Ualt, µalt, v, r, s0 with different investor preferences Ualt andspot price drift µalt(·, ·) but where the local volatility function v(·, ·),interest rate r, and initial spot price s0 are unchanged. This followssince both economies have the same Black-Scholes PDE. Accordingly,we can define a set of equivalent economies with different preferencesUalt and drifts µalt in which all option prices are the same as in thetrue economy.

Options can be priced numerically either by arbitrage (i.e., evalu-ating the replicating portfolio by solving the PDE) or by DiscountedCash Flows (DCF).6 When using DCF to price options, we are free tosearch for a convenient equivalent economy in which the risk-adjusteddiscount rate (unlike in the true economy) is known a priori – thatis, we pick preferences Ualt for which we know how to discount. Sincethe Black-Scholes PDE still holds in this chosen equivalent economy,option prices computed there by DCF are, by construction, identicalto option prices in the true economy.

A convenient choice of an equivalent economy is a risk neutral econ-omy URN , µRN , v, r, s0. With risk neutrality, all expected future cashflows (including those of risky options) are just discounted for time-value-of-money at the risk-free rate. Moreover, the risk-free rate in theequivalent RN economy is the same as in the actual economy by the def-inition of equivalent economies. For the equivalent RN spot commoditymarket to clear (i.e., for supply to equal demand) the RN expected re-turn on investable commodities must equal the risk-free rate, µRN = r.If not, there would be infinite demand either to buy the commodity andborrow (if µRN > r) or short the commodity and lend (if µRN < r).

To summarize, DCF in the equivalent RN economy implies that the

6Discounted Cash Flows values future cash flows as their expected value under the objectivemeasure discounted at the appropriate risk-adjusted discount rate. In contrast, RN valu-ation values future cash flows as their expected value under the RN measure discountedat the risk-free rate. For more on DCF, see any introductory finance textbook.

3.2. Dynamically Complete Markets 25

price of any commodity derivative with a payoff c∗T that is measurablewith respect to date T commodity price information is

ct = cRNt = ERN

t [c∗T ]e−r(T−t) (3.12)

where the underlying spot commodity price follows the equivalent RNprocess

dst = rst dt + v(st, t) st dZt. (3.13)

Later in this chapter we shall see that a so-called price of risk assump-tion is needed to identify the RN dynamics in dynamically incompletemarkets, but no such POR assumption is needed here in the Black-Scholes RN identification. That is part of the appeal of the Black-Scholes approach. However, many commodities – electricity, naturalgas during peak demand times – are not investible assets and, thus,the riskless hedge step in the Black-Scholes identification of the RNdynamics is not possible. Moreover, as will be seen in Chapter 4, thenon-asset nature of many commodities makes the properties of the RNBlack-Scholes spot price process (3.13) inappropriate for valuing op-tions on non-asset commodities.

Commodity futures prices as the underlying variable: A futurescontract with delivery at date τ specifies a futures price which the longinvestor in the futures contract pays to the short investor to buy aunit of a commodity. No money changes hands at initiation, so thefutures price Ft,τ at date t is set to make the date t value of the futurescontract equal to zero. Over the life of the futures contract the futuresprice is reset with payments between the long and short sides equal,in continuous time, to the instantaneous change in the market futuresprice dFt,τ .7 Black [19] developed a riskless hedge argument for pricingoptions whose terminal payoff c∗T at an expiration date T is measurablewith respect to information generated by the futures price Ft,τ for aspecific delivery date τ > T . In other words, the payoff is measurablewith respect to the filtration induced by the futures price Ft,τ alone. Ingeneral, this single-futures price filtration is less informative that thefull commodity spot price filtration Ft.

7 In practice, this settlement/payment process happens daily rather than continuously.

26 Real Option Valuation

The Black argument does not assume that the underlying com-modity is an investible asset – i.e., the commodity can be non-storable/perishable – but it does assume that the futures contract withdate τ delivery is traded and that the objective dynamics of the futuresprice for date τ delivery are8

dFt,τ = µ(Ft,τ , t)Ft,τ dt + v(Ft,τ , t)Ft,τ dZt (3.14)

In the Black model, the futures price Ft,τ is the only underlying statevariable, along with time t, needed to describe its own dynamics. Inthis sense, the information content of a “state” in the Black model isweaker than in Black-Scholes where the filtration fully describes com-modity price dynamics. The Black option price is a function c(Ft,τ , t)of the futures price and time with everything else again parametrically,contractually, or historically fixed. To find valuation functions c whichare consistent with the absence of arbitrage, we consider a portfolioconsisting of a long position in one option combined with a short po-sition −∆ in the date-τ delivery futures contract. Since futures pricesare set on date t to make futures contracts have zero market value, thisportfolio at date t is worth ct −∆0 = ct. Ito’s Lemma and a variationon the Black-Scholes riskless hedge logic imply that, to avoid arbitrage,the Black partial differential equation must hold

∂c

∂t+

12v2(Ft,τ , t)F 2

t,τ

∂2c

∂F 2= ct r. (3.15)

In the Black PDE, there is no analogue to the (∂c/∂s)st term in theBlack-Scholes PDE since futures contracts, by definition, have a marketvalue of 0 at each date t.9

Continuing with the RN identification argument, the Black PDEidentifies a set of equivalent economies Ualt, µalt, v, r, Ft0,τ with po-tentially different investor preferences Ualt and futures price driftµalt(Ft,τ , t) than in the actual economy. Once again, a conve-nient choice of an equivalent economy is a risk neutral economy

8This is a generalization of Black [19] which originally assumed the futures price follows aGeometric Brownian Motion.

9The replicating equation with futures which is analogous to (3.11) is dct = (∂c/∂F )dFt,τ +ctrdt. This says that the change in the option price here is replicated by a position ∂c/∂Fin the futures contract and ct dollars in t-bills.

3.2. Dynamically Complete Markets 27

URN , µRN , v, r, Ft0,τ so that expected option cash flows are just dis-counted for time-value-of-money at the risk-free rate. Since futures havea zero up-front investment cost, the RN expected futures price driftmust be µRN = 0 for markets to clear at the futures price Ft0,τ . Thus,the price of any commodity derivative with a payoff c∗T that is mea-surable with respect to the filtration induced by the futures price Ft,τ

is a discounted RN expectation (i.e, as in (3.3) but where now c∗T isrestricted to functions measurable with respect to the Ft,τ filtration)where the underlying futures price follows the RN process

dFt,τ = v(Ft,τ , t) Ft,τ dZt. (3.16)

An important limitation of the Black approach is the restrictionto valuing option payoffs c∗T which are measurable with respect to thefiltration of one particular futures price. The Black model for a givenfutures price Ft,τ cannot be used – without additional assumptions –to price options on the spot commodity at expiration dates other thandate τ (at which time the instantaneous futures price Fτ,τ equals thespot price sτ ) or to price options whose payoffs depend on informationdefined by the filtration for spot prices generally (e.g., paths of spotprices) or for futures prices Ft,τ ′ for other delivery dates τ ′ 6= τ . Toextend the Black approach to price general payoffs measurable withrespect to commodity spot prices at any date, or futures prices forarbitrary delivery dates, requires a model of the dynamics of the entireterm structure of futures prices (see Section 4.2).

Using a commodity option to identify RN dynamics: The limi-tation of option pricing in the single-futures contract Black approach isthat the connection from the futures price (whose RN dynamics dFt,T

are known a priori) back to the more primitive state space inducedby the underlying RN commodity price dynamics is not known. Inother words, the futures price function Ft,τ (st, t) relating Ft,τ and st isnot known. However, if this relation is monotone and known a priori,then we can again uniquely identify the RN commodity price dynam-ics. Moreover, this point is not limited just to futures. It applies toall derivatives subject to a natural monotonicity condition. To see this,suppose that the objective dynamics of the underlying commodity spot

28 Real Option Valuation

price – where the commodity is not an investible asset – are known tobe

dst = µ(st, t)dt + v(st, t)dZt (3.17)

and that there is an option with expiry T with a known pricing functionc(st, t) relating the option valuation and the spot price where ∂c/∂s 6=0. From Ito’s lemma, the dynamics of the known option price are

dct =[∂c

∂t+

12

v2(st, t)∂2c

∂s2+

∂c

∂sµ(st, t)

]dt +

∂c

∂sv(st, t) dZt. (3.18)

Given these assumptions, the question is: what are the RN com-modity spot price dynamics?

dst = µRN (st, t) dt + vRN (st, t) dZt (3.19)

Since the quadratic variation of an Ito process is unchanged under theRN measure, we have vRN (st, t) = v(st, t). Turning to the RN drift,since options are assets, the known option’s RN expected return is therisk-free rate; which implies

∂c

∂t+

12

v2(st, t)∂2c

∂s2+

∂c

∂sµRN (st, t) = r c(st, t) (3.20)

which, when rearranged, gives

µRN (st, t) =rc(st, t)− ∂c/∂t− (1/2) v2(st, t)∂2c/∂s2

∂c/∂s(3.21)

where, since the function c(st, t) is known, all of the partial deriva-tives on the RHS of (3.21) are known, and, thus, the RN commodityprice drift is determined. Given the RN spot price dynamics, we cannow use RN valuation, as in equation (3.5) to value any stream ofcommodity-linked cash flows over time that are measurable with re-spect to the commodity price process. (In addition, the known optioncan be used to hedge dst induced randomness in any other commodity-linked derivative.) Unfortunately, it is rare that the valuation functionc is known a priori for even one option. As a result, this approach andthe RN identification in (3.21) is typically not of practical use.

3.3. Dynamically Incomplete Markets 29

3.3 Dynamically Incomplete Markets

Suppose that spot prices follow a jump-diffusion process

dst = µ(xt− , t)dt + v(xt− , t)dZt + ξ(xt− , t)dJt (3.22)

driven by (continuous) Brownian motion increments dZt and (discon-tinues) Poisson or Compound Poisson jumps dJt where xt is a vectorof state variables (with their own Ito or jump-diffusion dynamics dxt)which affect the spot price drift µ(xt− , t), diffusion volatility v(xt− , t),and the predictable jump magnitudes ξ(xt− , t) and jump probabilityintensities (where the spot price st itself can be one of the state vari-ables).10 Markets are dynamically incomplete when the Brownian mo-tions, jumps, or any of the state variables are not tradable.11 The prob-lem with non-traded randomness in spot price dynamics is that thereare no market prices from which to infer the market preferences whichadjust the objective probabilities into RN probabilities. Equivalently,we cannot construct riskless hedged option/underlying portfolios as inthe Black-Scholes RN identification. In a dynamically incomplete mar-ket, option pricing models therefore impose specific structure on marketrisk preferences in order to compute state prices. These so-called Price-of-Risk (POR) assumptions specify the difference between objectiveand RN probabilities for the underlying commodity price dynamics.Models then assume that the same POR are consistently embedded

10 Jump processes lead to discontinuities in the spot price process and possibly in the statevariables. The t− notation means that local drifts, volatilities and the jump moments donot depend on state variables at date t (which would include any unpredictable jumpsin the state variables occurring at date t) but rather on the limiting values limτ→t xτ ofthe state variables as they approach date t. The realized magnitudes of the jumps dJt

can be either known in advance (e.g., normalized to 1 so that ξ(xt− , t) is the jump size)or they can be i.i.d. random variables (normalized with a mean 1 so that ξ(xt− , t) is theconditional expected jump size). See Chapter 4 and Shreve [178] for more on Poisson andCompound Poisson processes.

11The discussion here is exposited in terms of the physical availability of securities withwhich to trade the state variables and jumps. A market can also be epistemologicallyincomplete if sufficient securities are physically traded, but their dynamics are not knownto the individual wanting an option pricing model. In non-statically complete markets,simply knowing the current prices of traded securities is not sufficient for a market to bedynamically complete. The future dynamics of the traded securities must also be knownin order to recover the implicit underlying RN dynamics. This generalizes the point maderegarding the RN identification in (3.21) in the previous subsection.

30 Real Option Valuation

in all derivative prices. One model of incomplete market option pric-ing differs from another model because of the different particular PORassumptions they make.

Suppose again that the underlying commodity is a non-asset andthat, while there may be observed market prices for some commodityderivatives, there is no traded derivative whose price function is knowna priori. In this case, there is not enough information to pin down theRN spot price dynamics, and derivatives can only be priced given anauxiliary price of risk (POR) assumption. For example, if objective spotprice dynamics are given by (3.17), then a common pricing procedureis to assume RN dynamics

dst = µRN (st, t) dt + v(st, t) dZt, (3.23)

where the RN drift is

µRN (st, t) = µ(st, t) + λ(st, t; θ) (3.24)

where the price-of-risk λ(st, t, θ) is typically assumed to have a func-tional form that makes the RN dynamics qualitatively similar to theobjective dynamics (which can be empirically estimated) and where θ

is a set of parameters which must be calibrated (see §3.4). In contrastto RN asset drifts, non-asset RN drifts have no necessary relation tothe risk-free interest rate.

Although the market in the previous paragraph was not dynamicallycomplete a priori, once we can condition on an assumed POR, themarket may be complete. In particular, given the POR, any optionwith a non-zero sensitivity ∂c/∂s can be used to dynamically synthesizeand price any other measurable commodity state-contingent cash flow.Of course, this only works if the POR assumption is correct. Thus,dynamic replication based on an assumed ad hoc POR is subject toconsiderable potential model risk.

3.4 Calibration

Once the functional form of the RN dynamics has been specified, it stillmust be parametrically calibrated. There are two ways RN dynamicsare calibrated. If parameters are the same under both the objective

3.5. Summary 31

and RN measures, then one approach is to estimate them statisticallyusing historical data. This, of course, assumes that the objective datagenerating process in the future is the same as it was in the past. Statis-tically estimated parameters are also estimated with error. A popularalternative approach is implied calibration. If θ denotes the parametersof the RN dynamics,

dst = µRN (st, t; θ) dt + vRN (st, t; θ) dZt, (3.25)

then the prices of traded commodity-contingent securities depend im-plicitly on θ

ct(θ) = ERNt [c∗T ; θ]e−r (T−t). (3.26)

Implied calibration involves solving numerically for values of θ thatequate one or more model prices ct(θ) with observed market securityprices cMKT

t .

3.5 Summary

This chapter has reviewed how commodity RN price dynamics are iden-tified and the connection with market completeness. A key idea implicitin this discussion was what defines a “state” for commodity price dy-namics. The generalized Black-Scholes model assumes that the date andspot price (st, t) constitute the state variables for describing RN com-modity spot price dynamics. Given this assumption, any Ft-measurablecommodity option payoff can be priced. In contrast, states in the single-futures price Black model are defined based on time and the futuresprice for a particular fixed delivery date T . Given this coarser defini-tion of the driving state variables, (Ft,T , t), the Black model can onlyvalue option payoffs that are measurable with respect to a restrictedfiltration induced just by the particular futures price Ft,T .

When the spot price (or futures price) dynamics depend on factorsother than just the spot price (or futures prices) themselves, then iden-tification of the RN spot price process typically requires price of riskassumptions for the identification of any RN non-asset factor processes.This issue is discussed further in the context of specific multi-factormodels in Chapter 4.

32 Real Option Valuation

3.6 Notes

The existence, uniqueness, and identification of state prices, or equiv-alently RN probabilities, is more general than the application to com-modities. In particular, the same identification issues arise when pricingoptions in incomplete markets for other non-asset underlying variables.This includes option valuation when the underlying variables are inter-est rates, weather, and events such as corporate defaults.

The general theory for dynamic state-contingent claim valuationwas first worked out in Harrison and Kreps [104]. Duffie [76] is a morerecent exposition. Continuous-time models of option pricing rely on themathematics of stochastic calculus. Shreve [178] provides a systematicintroduction to Brownian motions, Ito processes, jump processes, andtheir application to option pricing. When option valuations do not haveanalytic expressions, option price are computed numerically either us-ing tree and lattice methods or via Monte Carlo simulation. Hull [110]gives a description of tree and finite difference methods. Glasserman[94] is a comprehensive reference on Monte Carlo methods in finance.

Our discussion of option pricing in incomplete markets implicitlyassumes that introduction of a new option (which needs to be priced)does not change the fundamental economics of valuation. However,this is a non-trivial assumption. In general, introducing new (non-redundant) securities in an incomplete market increases the span oftradable states which, in turn, can potentially change investor assetsdemands and, thus, can change market-clearing traded securities prices.In this case, the new option needs to be priced to be consistent withthe new post-option-introduction traded security prices, not the pre-introduction prices. A related set of issues has to do with option pricingwhen liquidity is priced. In this case, the state prices implicit in activelytraded securities may include a premium for liquidity which would notcarry over to the valuation of illiquid real options (see Vayanos andWang [197] for a general survey on liquidity and asset pricing). Lastly,it should be noted that Black-Scholes and Black both assume trade oc-curs in frictionless markets (i.e., no bid-ask spreads, transaction costs).Option pricing with frictions is generally difficult.

4

Modeling Commodity and Energy Prices

The valuation of options and derivatives of any type requires specifi-cations for the dynamics of the underlying state variables driving thepayoff cash flows. In the case of real options to physically store andtransform commodities, spot and futures prices at which commoditiescan be bought and sold are natural state variables. Indeed, some realoption pricing models (e.g., Black-Scholes in Chapter 3) just take thespot price as the only state variable. More fundamentally, however,any factor which affects the dynamics of the future supply and demandcurves, and, thus, future prices, is, in principle, a potential state vari-able. Thus, much of this chapter will focus on multi-factor models ofoption pricing.

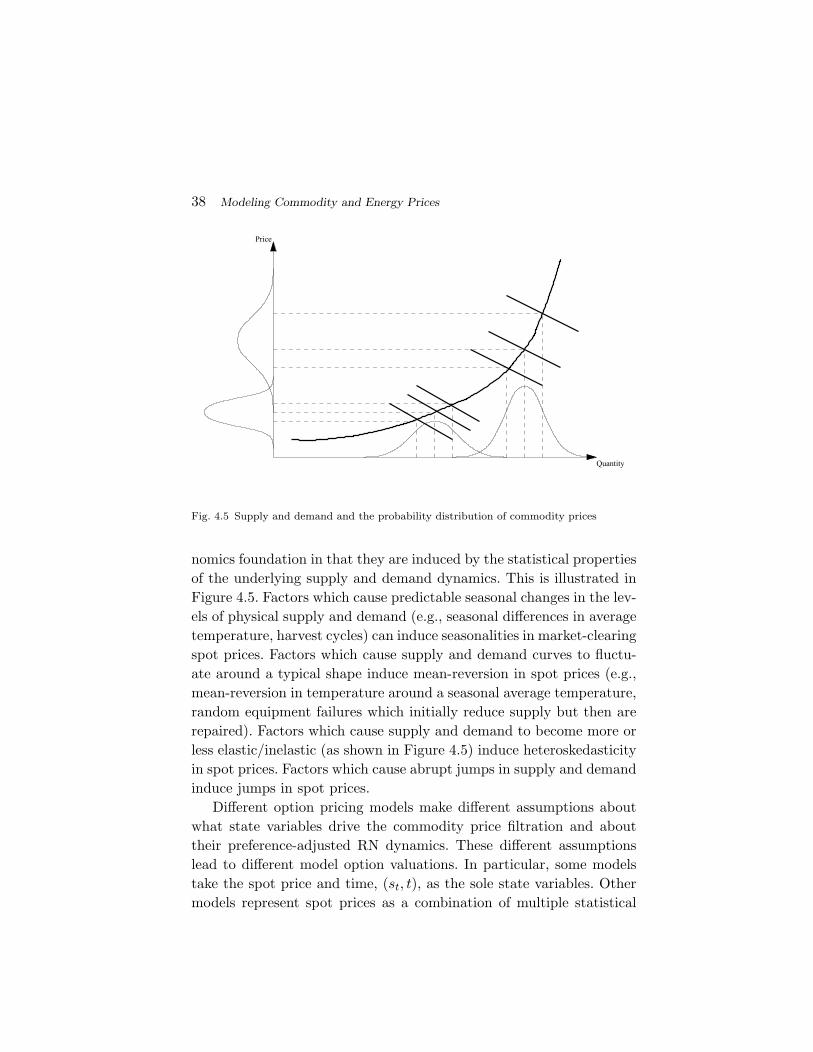

Commodity price processes are defined formally on a probabilityspace (Ω,F , P ) where Ω is the set of all possible states, F = Ft is afiltration which describes the possible evolution of information aboutthe realized state ω ∈ Ω, and P is a probability measure. More con-cretely, the dynamics of commodity prices are induced by the dynamicsof supply and demand. From standard microeconomics, the spot pricest of a commodity at date t is the market-clearing price which equatesphysical supply and demand. This is illustrated in the familiar diagram

33

34 Modeling Commodity and Energy Prices

!

"

Price

Quantity

#

!$!% %"#

&

!$!% %"&

Fig. 4.1 Commodity pricing and supply and demand.

in Figure 4.1. The demand curve D(s, t, xDt ) is the aggregate quantity

of the physical commodity demanded at each possible price s on date t

given the set of factors xDt which affect demand. Demand is the sum of

demands for immediate physical use plus, if the commodity is storable,any speculative inventory demand. The supply schedule S(s, t, xS

t ) isthe aggregate quantity of the physical commodity supplied at each prices on date t given the set of factors xS

t which affect supply. Supply is thesum of current production plus any commodity stocks sold from inven-tories stored in the past. The levels, slopes, and functional forms of thesupply and demand curves can change over time depending on factorssuch as weather, macroeconomic conditions, and the prices of othercommodities which are complements or substitutes in consumption orproduction. In equilibrium, aggregate supply equals aggregate demandat the equilibrium quantity, D(st, t, x

Dt ) = S(st, t, x

St ) = Q(xt, t), at

the market-clearing price

st = s(xt, t), (4.1)

where xt = (xDt , xS

t ) is the combined set of demand and supply factors.The dynamics of market-clearing spot prices dst are induced by theshapes of the supply and demand schedules, as reflected in the pricefunction s(·, ·), and by the dynamics of the supply and demand statevariables dxt.

35

The stochastic processes followed by the state variables xt =(x1,t, . . . , xK,t) are typically represented as a system of stochastic dif-ferential equations like the following:

dxk,t = [mk(xt− , t)− ξk(xt− , t)λ(xt− , t)] dt + vk(xt− , t) dZt

+ξk(xt− , t)dJ t, ∀k = 1, . . . , K, (4.2)

where the instantaneous change dxk,t in the k-th state variable at date t

is driven by potentially three building blocks: The deterministic passageof time dt, the random instantaneous increments of a vector of Brown-ian motions dZt, and the random instantaneous increments of a vectorof Poisson or Compound Poisson jump processes dJ t with possiblystate-dependent jump probability intensities λ(xt− , t) and jump mag-nitudes which are either fixed (and normalized to 1 so that ξ

k(xt− , t) is

the vector of local jump sizes for the k-th state variable) or i.i.d. ran-dom vectors Y t (with mean vector Et[Y t] normalized to the unit vectorso that ξ

k(xt− , t) gives the expected local jump sizes for the k-th state

variable) defined at a discrete set of jump dates (i.e., dates on whichdJ t 6= 0).1 Since Brownian motions are continuous, the Brownian mo-tion increment represents the gradual arrival of incremental news. Thejumps represent the potential arrival of dramatic news which causes dis-continuous changes in the state variables and, thus, in prices. The mag-nitudes of the impacts of these building blocks on dxk,t are determinedby the expressions multiplying them: mk(xt− , t) is the predictable localdrift, vk(xt− , t) is a vector of loadings which scale the local volatili-ties of the Brownian motions, and ξ

k(xt− , t) is a vector which scales

the jump magnitudes. The local drifts, volatility, and jump intensitiesand magnitudes can all depend on the state variables and on time t.Time-dependence in price levels, volatilities, and other dynamics canbe due to predictable seasonalities (e.g., harvests, weather patterns) orpredictable macroeconomic, demographic, or technological trends (e.g.,time to build new power plants, technology adoption dynamics). Thet− notation means that drifts, volatilities and the jump moments donot depend on state variables at exactly date t (which would includeany unpredictable jumps in the state variables occurring at date t) but

1See Shreve [178] for properties of Brownian motions and Poisson processes.

36 Modeling Commodity and Energy Prices

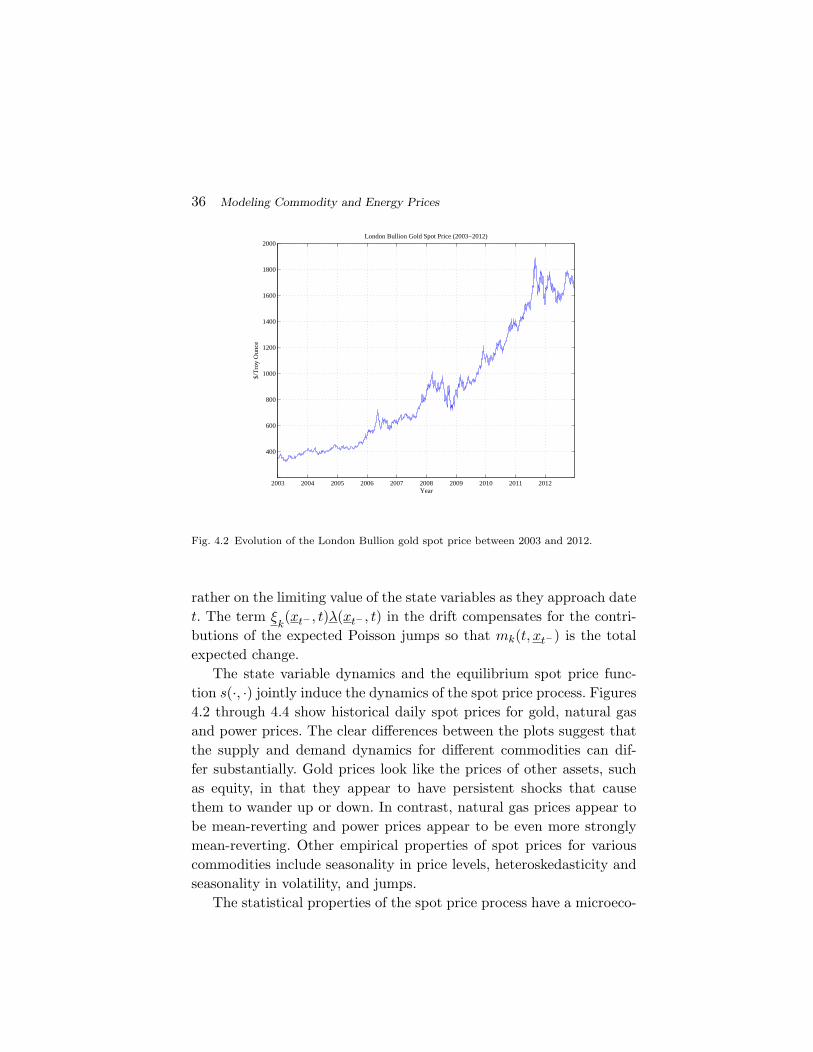

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

400

600

800

1000

1200

1400

1600

1800

2000

$/T

roy

Oun

ce

Year

London Bullion Gold Spot Price (2003−2012)

Fig. 4.2 Evolution of the London Bullion gold spot price between 2003 and 2012.

rather on the limiting value of the state variables as they approach datet. The term ξ

k(xt− , t)λ(xt− , t) in the drift compensates for the contri-

butions of the expected Poisson jumps so that mk(t, xt−) is the totalexpected change.