Excessive commodity price volatility: Macroeconomic effects ...

Upload

khangminh22Category

view

1download

0

COMMODITY.* MARK<ETSl 3 1XANDTHE DEVELOPING COUNTRIES Vol 5 N' .1

November

Global economic prospects and developing countries

Oil prices expected to weaken

Grains lead declines in food prices

Metals and minerals post small declines

l

,R~~~~'

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CONTENTS AND SUMMARY

SUMMARY PAGE 4 ture of speculative money from coffee mar-

kets. El Nifio affects supplies of IndonesianS 5 SPECIAL FEATURE and Colombian coffee, keeping prices from

6 ZU- _ * GLOBAL ECONOMIC PROSPECTS AND THE falling very far.* . DEVELOPING COUNTRIES PAGE 6 M TEA PAGE 15

* Developing country growth in 1996 was the London prices are 31 % higher than in the

* * * U highest so far this decade. The external envi- third quarter last year in real terms. Tightronment for developing countries is expect- world stocks, uncertain global weather con-

ed to remain broadly favorable over the com- ditions, and seasonal effects are likely to keeping decade. The challenge for policymakers world prices high.

in developing countries is to establish theconditions that attract more global produc- FOODtion and realize more of its benefits. FATS AND OILS

* FATS AND OILS PAGE 1 6ENERGY Although the regional effects of El Niino may

* COAL PAGE 9 be large, world supply of fats and oils is notWeak demand and rising supplies lead to expected to be severely affected. Declines in

lower prices this year. Prices are expected to the Southern hemisphere should be offset bydecline in 1998 with increasing production, increases in North America. EU reforms

greater competition, and growing reliance under Agenda 2000, if implemented, couldon spot markets by purchasers. further depress EU oilseed production.

* NATURAL GAS PAGE 9 * COCONUT OIL PAGE 16

US prices surge on strong demand for stor- Production is expected to increase slightly inage and flat production. Prices are expected 1997/98. The 1998/99 outlook is not asto decline in 1998 on higher production promising because of severe El Ninlo-related

CHANGE IN QUARTERLY from the Gulf of Mexico and rising imports drought in the Philippines.PRICES, 2Q97 TO 3Q97 from Canada later in the year. In Europe * PALM OIL PAGE 17Percent

Energy + 1.0 prices remain indexed to oil, but the intro- El Nifio-related droughts are expected toNonenergy -7.9 duction of UK spot gas into the continent in affect yields from 1998 on. Reduced yieldsTotal agriculture -9 7 late 1998 and ongoing liberalization of the and increased consumption in Indonesia and

Beverages -12.3Total food -7.8 gas sector will lead to lower real prices. Malaysia will push up prices.

Fats and oils -8.8 * PETROLEUM PAGE 10 * SOYBEAN OIL PAGE 17Grains -9 3Other food -5.6 The market balance is much improved from Prices remain unchanged while production

Raw materials -9.1 a year ago because of higher inventories, ris- is expected to rise. Stocks are decliningTimoer -11.5

Fertilizers -3.0 ing production, and renewed exports from sharply. While El Nifno is expected to affectMetals and minerals -1.9 Iraq. Higher production from OPEC and both Argentina and Brazil, favorable weath-

non-OPEC sources is expected to lower prices er in North America should offset any

next year. decline in production.

BEVERAGES GRAINS* COCOA PAGE 14 * GRAINS PAGE 18

The impact of El Ninio is intensifying the Large supplies and currency devaluations inrecent structural deficits in the cocoa mar- Asia cause grain prices to weaken during the

ket. Production is stagnant, and consump- quarter. World grain production is estimatedtion is growing. Prices are up accordingly. to be slightly above last year's level and 8.5%

* COFFEE PAGE 14 above levels in 1995/96. Stocks are expectedArabica prices fall sharply on expectations of to build, but still remain low by historicala large crop in Brazil next year and the depar- standards at 15.4% of total use.

2 COMMODITY MARKETS AND THE DEVELOPING COUNTRIES

CONTENTS AND SUMMARY

* MAIZE PAGE 18 * RUBBER PAGE 23

Prices strengthen from their mid-summer International prices slide, but producerlows. Production is expected to shrink 2.4%, prices improve following devaluations inand stocks are expected to drop 14%, keep- Asia. El Nifio's arrival ushers in drought anding the market tight and prices firm. threatens supplies.* RICE PAGE 19 * TIMBER PAGE 23

Devaluation of the baht reduces the US dol- Sluggish demand in Europe and Japan con-lar price of Thailand's rice exports by 15%. tributes to price declines for tropical timber.World production and stocks are projected Reduced housing starts, a stronger dollar,to rise slightly from last year's levels. The and the substitution of softwood logs forthree largest exporters are expecting good tropical logs are also depressing demand.

harvests and large supplies for export, whichshould keep prices from rising. FERTILIZERS* WHEAT PAGE 1 9 * FERTILIZERS PAGE 24

Prices fall to $146.2/ton for the third quar- Most prices remain strong, with the excep-

ter, from a high of $262/ton in May 1996. tion of urea. However, weak world grainWorld production for 1997/98 is expected to prices may drive fertilizer prices down.reach a record 603 million tons, up 3.4% * POTASSIUM CHLORIDE PAGE 24

from the previous year, putting year-ending Prices remain firm as supplies from Canadastocks up 18%. Prices should remain near have been limited. An increase in second-current levels until the spring of 1998, when half contract prices of $5/ton was sought andnew crop prospects begin to emerge. attained by some exporters. However, most

prices remained at $116.5/ton.OTHER FOOD * TSP PAGE 25

* BANANAS PAGE 20 Producers are operating at near capacity,Prices fall, and El Nifio threatens produc- and production is up 4% for the first half oftion. The WTO rejects the EU's appeal of its 1997. With such rapid production growth,banana export regime. demand is not likely to be strong enough to* SHRIMP PAGE 20 support prices at current levels.

Prices continue to rise, bringing the year's * UREA PAGE 25increase to 15%. Reasons include smaller Prices continue to fall, with the average downharvests in Thailand and increasing demand 11.1% from the second quarter. Furtherin major importing countries. declines will probably be limited in the near* SUGAR PAGE 21 term as demand begins to increase for thePrices remain firm, with world supplies spring plantings. However, supply remains wellexpected to decline. The US and Mexico con- ahead of demand, and more firms are cuttingtinue to quarrel over high-fructose corn production in response to building inventories.syrup.

METALS AND MINERALSAGRICULTURAL RAW * ALUMINUM PAGE 26

MATERIALS Consumption growth in Europe and the US* COTTON PAGE 22 and investment fund buying spur prices.Production and consumption remain in Consumption weakens in Asia, mainly as abalance. Declining Chinese imports may result of the recent currency crisis.offset any increase in prices stemming from * COPPER PAGE 26

El Nifio effects. State-owned textile indus- Increased demand in Western Europe andtries in China and India are undergoing North America is not enough to offset lowerreform. demand from Asia and worldwide growth in

NOVEMBER 1997 3

CONTENTS AND SUMMARY

copper supplies. Prices continue to fall to their IEA projections at the beginning of the year.

lowest levels of the year. OPEC production continued to edge up,

* GOLD PAGE 27 bringing output to 2.3 mb/d above quota.Prices continue to fall on central bank selling There are indications that OPEC may raise

and a loss of speculative interest. Prices aver- quotas at its November meeting, which would

age $323.6/toz for the quarter. At current lead to higher output from the Gulf countries.prices, mine closures are expected. Although a rollover of Iraq's oil-for-food deal in

* IRON ORE AND STEEL PAGE 28 December may be in doubt due to heightened

Despite high levels of production, the global tensions over weapons inspections, continued

iron ore market remains tight. Performance in Iraqi exports plus higher output from the rest

steel markets is more varied. Demand is up in of OPEC would likely tip the balance into sur-

Europe but way down in Southeast Asia plus. Non-OPEC supplies are projected to

because of the recent currency crisis. increase significantly in 1998. Thus oil pricesare projected to decline next year.

COMMODITY PRICES Coffee prices fell sharply as the risk of cold

* COMMODITY PRICE INDICES PAGE 5 weather in Brazil subsided and prospects for

* COMMODITY PRICE OUTLOOK PAGE 29 next year's crop brightened. Nevertheless,

prices for arabica were more than 50% higherSUMMARY than a year ago because of lower supplies.

The World Bank's index of energy prices Estimates for the 1997/98 crop have been low-

rose 1 % in the third quarter on strong ered more than 10% in both Brazil anddemand and lower than expected supplies. Colombia. Robusta prices, which had previ-Nonenergy prices fell nearly 8%, however, ously risen less than arabica prices, fell 12%,

with declines in all the main groups (table 1). reflecting good supply availability. There is

Beverage prices were down 12%, pulled down some nervousness in the market about possibleby an 18% drop in arabica coffee prices as ElNifno effects, but thus far the only large effect

Brazil's frost season ended. Tea and cocoa has been in Indonesia, where drought signifi-prices recorded moderate increases. Food cantly reduced production. Many Central and

prices fell 7.8%, with a 9.3% decrease in grains South American countries worry that recentand moderate declines in most other foods. dry weather will lower the quality of this year's

Metals and minerals prices fell only 2% for the crops and cause production declines next year.group, but there were larger drops in several Grains prices led the decline in foodindividual products. Timber prices fell 11.5% prices, with wheat off 13.8%, maize down

on sluggish demand, while rubber prices 6.8%, and rice down 3.9%.

plunged nearly 20%, in part a consequence of Metals and minerals prices posted thecurrency devaluations, which stimulated pro- smallest decline among the main commodityduction among South east Asian producers. groups, mostly because of a large increase in

Cotton and sugar prices remained firm. zinc prices and a moderate rise in aluminumPetroleum prices rose during the quarter, a prices due to strong demand in the US and

response to the temporary halt in Iraqi supplies Europe. Copper prices fell 9.4% on risingfrom May to August, continued shortfalls in stocks and weak demand. Price declines werenon-OPEC supplies, and strong demand, par- also recorded for nickel (down 8.1%), silver

ticularly for transport fuels in the US. However, (4.7%), and gold (5.7%). Iron ore marketsprices were 20% belowJanuary levels, reflect- remain tight, despite high production,ing the improved market balance. Stocks have because of strong demand. Steel demand

risen, particularly in North America and remains strong in the US construction sectorEurope. Non-OPEC supplies were 1.0 mb/d but is weakening in Asia following the recenthigher than a year earlier, but 0.8 mb/d below currency crises.

4 COMMODITY MARKETS AND THE DEVELOPING COUNTRIES

COMMODITY PRICE INDICES

FIGURE 1. WEIGHTED INDEX OF PRIMARY COMMODITY PRICES FOR LOW- AND MIDDLE-INCOMEECONOMIES

ENERGY (CRUDE OIL) NONENERGY COMMODITIESIndex: current VS dollars (1990=100) Index: current US dollars (1990=100)150 ^}130

25

130 Vs ll 120

110 115

90 105 i

70 ~~~ ~ ~~~~~~~~~~~~100 70 M 95

50 ~~~~~~~~~~~~~~~~~9085

30 8083 84 85 86 87 88 89 90 91 92 93 94 95 96 97 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97

TOTAL FOOD METALS AND MINERALSIndex: current US dollars (I 990=100) Index: current US doilars (i990=100)130 A 140

120 120120

I MON A 1'. 1~~~~~~~~~~~00

90 ~~~~~~~~~~~~~~~~9080

80 70

70 6083 84 85 86 87 88 89 90 91 92 93 94 95 96 97 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97

TABLE 1. WEIGHTED INDEX FOR PRIMARY COMMODITY PRICES FOR Low- AND MIDDLE-INCOMEECONOMIES IN CURRENT DOLLARS(I 990= 1 00)

Nonenergy Metalscommod- Total agri- Total Fats Other Total raw and

Energy ities culture Beverages food and oils Groins food materials Timber Fertilizers minerals(I00)a (100) (69.1) (16.9) (29.4) (i O) (6.9) (12.4) (22.8) (9.3) (2.7) (28.2)

Annual1994 69.4 111.6 123.3 148.8 106.8 125.9 102.1 93.9 125.8 156.6 93.4 84.61995 75.1 122.2 131.3 151.2 1 16.9 136.6 120.4 98.8 135.2 139.5 103.6 101.61996 89.3 1I 5.I 1 25.5 126.5 123.6 147.0 140.6 95.0 127.1 139.5 1 19.8 89.1

Quarterly1996Q3 90.8 1 13.1 124.7 126.6 123.2 147.7 139.6 94.0 125.2 141.1 121.1 83.81996Q4 101.4 1 10.8 120.7 124.0 1 16.8 147.8 118.4 90.5 123.3 139.9 123.0 85.11997Q1 91.8 1 19.3 130.0 150.7 122.5 154.5 122.7 96.3 124.4 140.2 124.2 92.51997Q2 80.4 126.0 139.6 197.8 119.5 151.8 1 16.5 94.8 122.4 140.5 120.0 93.11997Q3 81.1 116.0 126.0 173.6 1 10.2 138.5 105.7 89.5 1 11.3 124.3 116.4 91.3

Monthly1996 Sep 97.3 111.8 123.1 123.7 121.4 152.7 127.4 92.5 124.8 142.3 122.5 82.81996 Oct 103.2 109.9 121.1 126.6 116.1 145.4 120.0 89.9 123.4 142.4 123.0 81.31996 Nov 97.9 111.6 121.3 125.3 116.9 147.8 117.4 91.3 124.2 141.6 123.0 86.61996Dec 103.2 110.7 119.7 120.1 117.4 150.2 117.9 90.3 122.4 135.8 123.0 87.41997jan 101.5 115.0 124.2 129.4 121.4 152.0 123.7 95.1 123.8 139.0 124.5 91.61997 Feb 89.3 1 19.2 130.0 151.3 122.2 153.9 122.6 96.0 124.3 140.2 124.1 92.11997 Mar 84.5 123.7 135.9 171.3 123.9 157.5 121.6 97.7 125.1 141.2 124.1 93.71997Apr 78.2 124.0 137.4 179.8 124.7 158.0 119.4 100.4 122.4 140.0 122.5 91.21997May 84.7 129.8 144.7 219.7 119.3 152.9 118.7 92.2 122.0 140.5 118.8 94.21997Jun 78.3 124.2 136.7 193.8 114.6 144.4 111.4 91.9 123.0 141.0 118.8 94.01997Jul 80.1 117.5 127.6 173.4 110.2 137.7 106.6 89.8 116.1 133.8 117.9 92.61997Aug 81.7 116.2 125.9 173.0 110.0 136.5 106.2 90.6 111.4 123.9 115.7 92.51997Sep 81.6 114.3 124.6 174.2 110.3 141.3 104.2 88.3 106.3 115.2 115.7 88.8

Note: Weighted by average 1987-89 export values for Jov- and middle-income econormes.a. Crude oil index.Source: World Bank, Development Prospects Group.

NOVEMBER 1997 5

SPECIAL FEATURE

GLOBAL ECONOMIC regions where incomes fell in the past 10 years,

PROSPECTS AND THE are expected to achieve positive per capitaDEVELOPING COUNTRIES income growth (though the projected pace of

Developing country growth in 1996 was the about 1 percent would remain below that inhighest so far this decade, an estimated 5.6% high-income countries).

(excluding transition economies), and the In some of these countries basic political andmost rapid rate in 20 years. The integration of macroeconomic conditions for investor confi-

developing countries in the world economy dence are still lacking, and many enterprisesalso gained ground: foreign direct investment remain largely cut off from foreign markets and

in developing countries topped $100 billion competition because ofpolicyweaknesses, insti-

for the first time, approaching 2% of their tutional impediments, and inadequacies in

GDP. Their international trade volumes transport and communication services. Theexpanded at a robust 7%, despite a downturn same is true of some economies in Europe and

in overall world trade growth. Central Asia, although most of the countries in

The external environment for developing the region are expected to recover much of thecountries is expected to remain broadly favor- ground lost during the difficult transition from

able over the coming decade. World output a planned to a market economy.

growth in 1997-2006 is expected to average Developing countries in South Asia will3.4% a year, more than half a percentage point continue to show faster growth in output and

higher than during the past decade, with mod- investment and will further increase their

est inflation of about 2.5% in the Group of 7 share ofworld trade. Though there is still some(G-7) countries and real short-term interest way to go before finns in India are fullyrates of slightly more than 3%. In this setting exposed to international markets, recentdeveloping country growth is expected to aver- reforms there have proved resilient, and

age nearly 5.5%, double its pace in the pre- growth in the South Asia region is expected toceding decade, accompanied by mounting improve on historical trends. Countries in

capital inflows and solid increases in trade of Latin America, which have become consider-

7%-8% a year. ably more integrated into the world economy

Economic growth is expected to increase in over the past decade, should also experienceevery region except East Asia, where it should accelerated growth in the next decade, though

still remain high (table 2). Sub-Saharan Africa in some large countries the risk of macroeco-and the Middle East and North Africa, two nomic instability persists.

TABLE 2. WORLD GROWTH SUMMARYPercentage change per year in real GDP

Estimates Forecasts1 966-73 1974-80 198 1-90 1991-95 1996 1 997-06

World 5.1 3.3 3.1 2.0 2.9 3.4High-income countries 4.8 2.9 3.1 1.9 2.5 2.8OECD countries 4.7 2.8 3 1.8 2.3 2.7Non-OECD countries 9.3 7.7 6.5 6.6 5.8 5.6

Developing countries 6.4 4.7 3 2.3 4.5 5.4EastAsia 7.3 6.4 7.7 10.7 8.6 7.6South Asia 3.7 4 5.7 4.6 6.5 5.9Sub-Saharan Africa 4.5 2.8 1.9 1.3 3.8 4.1Latin America and the Caribbean 6.4 4.9 1.6 3.3 3.5 4.2Europe and Central Asia 6.6 4.8 2.5 -5.9 -0.3 4.5Middle East and North Africa 8.7 4.9 0.8 2.6 4.1 3.6

Memorandum itemsEastern Europe and former Soviet Union 6.7 4.9 2.3 7.6 -1.8 4.6Developing countries excluding

Eastern Europe and former Soviet Union 6.3 4.7 3.2 5 5.6 5.5

Note: GDP nneasured at market prices and expressed in 1 987 prices and exchange rates. Growth rates over historic intervals are computed us ng east squares method.Source: World Bank data and baseline projections, June 1997.

6 COMMODITY MARKETS AND THE DEVELOPING COUNTRIES

SPECIAL FEATURE

THE BIG 5 that fast growth in the Big 5 will generate sig-

Increased integration and faster growth in nificant increases in world food and energy

China, India, Indonesia, Brazil, and Russia- prices do not appear to be well founded.five countries that today account for half theworld's labor force but only 8-9% of its GDP OPENNESS AND GROWTH

or international trade-will likely redraw the Several trends in the world today are con-

economic map of the world over the next tributing to the expansion of cross-border

quarter century, although these countries' production by multinational enterprises and

share of world trade is barely one-quarter their networks of closely associated firms.

that of the European Union's today, it could, These include the liberalization of econom-under reasonably conservative assumptions, ic policies in most countries, continuing

be 50 percent larger by 2020. The share in reductions in the costs of transport and com-

world output of both the Big 5 and develop- munications, and the growing importance of

ing countries in general will nearly double, knowledge and other intangible assets inwith developing countries absorbing half the modern production and distribution. These

growth in industrial country exports over the forces are heightening the competitive pres-

next quarter century. sures on firms in both industrial and devel-

Model simulations for the world economy oping countries, while also facilitating theirin 2020 suggest that the emergence of the Big efforts to improve efficiency and gain access

5 will generate significant welfare gains for to new markets by reorganizing productionboth the industrial countries and most other processes on a global basis.

developing countries, resulting from broad- The challenge for policymakers in devel-er opportunities for specialization along oping countries is to establish the conditionslines of comparative advantage and from that help attract more global production and

improved terms of trade. The emergence of realize more of its benefits. These include

the Big 5 is expected to have a beneficial political and macroeconomic stability, openeffect on real wages for both skilled and trade and investment regimes, better trans-

unskilled workers in most countries and port and communication infrastructure, ade-regions. quate protection for property rights, and a

Among developing regions the Middle East predictable institutional environment with-

and North Africa, Sub-Saharan Africa, and out excessive red tape. Ensuring that foreignLatin America and the Caribbean derive the and domestic firms face a high degree oflargest welfare gains from the emergence of competition in host country markets is likelythe Big 5. Trade liberalization and increased to be important in maximizing the spiliover

participation by countries with abundant benefits of global production.unskilled labor, such as China and India, are There is growing evidence that increased

expected to lower relative prices for some openness and faster economic growth golabor-intensive products, generating some together, suggesting that the longer-term

pressure on unskilled wages in a few countries effects of trade liberalization on employ-with closely similar endowment structures. ment, wages, and income are likely to be

These countries will, however, have the strongly positive. To be effective, however,incentive and the ability to offset such pres- trade liberalization requires resources to besures by accelerating their own trade liberal- redeployed between sectors. In the process,ization (a policy tending to benefit their most workers in import-competing industries may

abundant factor of production, unskilled become unemployed for a time. The outputlabor) and by undertaking other reforms to losses suffered by the economy as a result-improve the efficiency of resource allocation the social costs of adjustment-are expected

and use. The analysis also suggests that fears to be temporary, and empirical estimates sug-

NOVEMBER 1997 7

SPECIAL FEATURE

gest that they tend to be small, especially rel- tor weaknesses that increase exposure and vul-

ative to benefits. nerability to external shocks. StrengtheningThe size of adjustment costs will never- the framework of institutions and improving

theless be affected by the policy environ- access to information to allow markets to workment, and there is indeed much that more effectively will be an important consid-

governments can do to minimize them. eration for development strategy in many-

Adjustment costs will be lower if macroeco- countries.' Growing competitive pressures and

nomic stability and other complementary rapid transformation of the world economypolicies strengthen the credibility of reforms along many dimensions will give unprece-

and support a quick and substantial increase dented weight to the ability to handle change.

in new private investment. Adjustment will Careful management of the transitional strains

be delayed and its costs will be higher if labor associated with global integration will be anand other factor markets are distorted and important task for all countries in the coming

inflexible. decades.

Trade reforms are undertaken because As to the risks to the natural environment

they yield large net social gains. By con- from faster growth, in the long run greater

tributing to improved growth in the longer reliance on market forces is likely to be reflect-

term, liberalization is likely to make a sub- ed in many countries in more efficient use ofstantial contribution to the reduction of natural resources such as energy. Demand for

poverty. And where unskilled labor is the rel- a cleaner environment rises with income, andatively abundant factor of production, it is so growth in developing countries will also be

likely to raise returns to this factor. associated with greater incentives for policy-

Nevertheless, the private costs of trade lib- makers to implement strong environmentaleralization for specific groups, such as capital- policies over time. Nevertheless, given the

ists and workers in the previously protected complexity and scope of this issue, it is clear

sectors of the economy, can sometimes be that analysis of the environmental implications

large. Given that these losses are usually more of global integration is an important task forconcentrated among a few groups than are the further research.larger but more widely diffused gains from

trade, the opposition to liberalization will This feature is drawn from World Bank,

often be more focused and better organized Global Economic Prospects and the Developing

politically than is support for it. Countries, Washington D.C., 1997. To pur-chase a copy, contact the World Bank

POVERTY AND THE ENVIRONMENT Bookstore at 202-473-2941 or visit the

Prospects for the global economy are World Bank's publication catalog at

among the most promising for growth and www.worldbank.org.poverty reduction in developing countries in 1. Joseph E. Stiglitz, "Agenda for Development

many decades. However, such encouraging in the Twenty-First Century," in Boris Pleskovic

projections must be qualified by significant and Joseph E. Stiglitz, eds., Annual World Bank

areas of risk for individual countries, including Conference on Development Economics 1997,

macroeconomic imbalances or financial sec- Washington D.C.: World Bank, forthcoming.

8 COMMODITY MARKETS AND THE DEVELOPING COUNTRIES

ENERGY

COAL Y NATURAL GAS Pising crude oilYEARLY (US doliars/mt) ~3.82 3.0 smcrdo

5650 US thermal, fo.b. Hompton DEC1981 Roods, Norfolk. 96 25 producfion and

2A0 stocks improve5 \/, market balance.

48.50 80 85 90 Sptcalpie1984 (US dollars/mmbtu) Spot coal prices

fall, but US gas2U8 prices surge on

43.10 96 strong demand980 °° k / /for storage.

997 2.0

36.17 38.48 97 1990 3 /001.84 ~~~~~~~~.891 987 1 MAR 101.4

96 97 1996Q4

WEAK DEMAND AND GROWING SUPPLIES LEAD TO US PRICES RISE SHARPLY ON STRONG STORAGE

LOWER PRICES DEMAND 91.8/997Spot coal prices fell significantly in the US natural gas prices rose strongly in the I

third quarter, with some shipments selling third quarter on heavy demand for storagefor a few dollars per ton below contract injection and flat domestic production, with

80.4 81.1prices. Modest demand growth, ample end-September prices 45%, or $1 per million 997 1997

stocks, and growing production contributed Btu (mmbtu), higher than end-June levels. Q2 Q3

to the lower prices. Given this weak pricing End-use gas consumption was weak, howev-environment, some buyers in Asia and er, in part because of mild summer weatherEurope are tendering for greater volumes on and fuel switching induced by sharply high-the spot market, hoping that low spot prices er prices. There is increased anxiety aboutwill influence current contract negotiations gas deliverability in the US, with the possibil-for next year. Producers will try to get at least ity of still higher prices during the winter ifa rollover of 1997 prices, but contract prices the weather turns sharply cold.are likely to be lower in 1998. Storage levels are estimated to approach

US coal prices fell as exports declined and 2,900 billion cubic feet (Bcf) at end-mild weather lowered electricity demand. October, some 100 Bcf higher than a yearThe coal industry received a boost in August, ago but well below prior year levels. Thehowever, when Ontario Hydro announced lower inventories reflect improved manage-that it will overhaul its production facilities, ment of storage, technological changes infollowing a critical report from the Nuclear facilities, and a more integrated transporta-Performance Advisory Group. The company tion network. However, higher and morewill idle several nuclear units over the next volatile prices have been associated withthree years, and US coal and oil imports will lower levels of storage, although other fac-fill most of the power generation gap. tors such as weather, deliverability, and

In 1998 US coal demand is expected to transportation bottlenecks also contributedrebound with a recovery in electricity con- to the price swings.sumption and lower hydroelectric output US gas production has been fairly stagnant(assuming normal weather rather than the wet because of delays in the flow of deepwater gasweather experienced in the Pacific Northeast from the Gulf of Mexico and an early pro-this year.) However, production increases and duction decline in the shallow water shelf ofderegulation of the power sector are expected the Gulf. Higher demand in California hasto contribute to lower prices. Productivity diverted supplies that normally would be trav-increases should help to increase producer eling east, and gas exports from Canadamargins hurt by lower prices. remain capped because of pipeline con-

NOVEMBER 1997 9

ENERGY

straints. Combinedwith these short-term sup- PETROLEUMply limitations, the pressure to inject gas into 23.61 (OS dollars/obl)

OCT Spot, oeerage of Brent,storage has led to the recent surge in natural 96 23.23 Duboi, cnd West Texos

JAN Intermnediote.gas prices. 97

Prices are expected to fall in 1998 withincreased production from the deepwaterGulf. Gas-related drilling has been high, and 1

new discoveries have been made in both the 97

shallow and deepwater Gulf. Pipeline expan- 40 \ .6

sions from Canada-Northern Border and 30 97

TransCanada-will be completed in late 1998 20

and will ease supply conditions for the 90

1998/99 winter season. A key element in thesupply equation is the shallow water shelf ofthe Gulf. RISING PRODUCTION AND INVENTORIES IMPROVE

Gas prices slipped in Europe because of MARKET BALANCE

lagged contract price indexingwith petroleum Oil prices were fairly flat for most of the

products. Gas demand has been sluggish this third quarter before rising sharply in late

year compared with last year's strong cold September and early October. The market

weather-induced growth. Despite the cyclical remained evenly balanced during the quar-

changes in demand, the power generation ter, aided by the resumption of Iraqi oilsector continues to grow, particularly in the exports in August and a strong US gasolineUK The conversion of household heating sys- market. Non-OPEC supplies continue totems to gas continues at a rapid rate, and the come in below expectations, which hasshare of gas in new residential and commer- helped put a floor on oil prices in the uppercial buildings remains high. After rising 8% in teens (dollars per barrel). Oil stocks have

1995 and 10% in 1996, gas demand is expect- risen appreciably this year, particularly in theedtoincreasejustl% thisyearand4% in 1998, US and Europe, and inventories headingassuming normal weather. into the peak-demand season are in much

On the supply side, imports from Algeria better shape than a year ago, especially heat-

and Norway have risen strongly, while sup- ing oil. Consequently, price spikes are lessplies from the Netherlands have contracted, likely to occur this winter, barring unfore-in part because mild weather has reduced seen circumstances. But stocks remain low bydemand. Imports from Algeria, Norway, historical standards, so any sudden loss of

and Russia are expected to increase in 1998, supply or surge in demand due to extreme

along with initial UK supplies through the weather could result in much higher prices.Interconnector pipeline, due to open in the Prices remained firm despite higherfourth quarter of 1998. OPEC production because of continued

The UK continues to make rapid progress strong growth in demand and shortfalls inin liberalizing its gas market. Gas prices are non-OPEC supplies. OPEC crude oil pro-

now decoupled from oil prices and are set duction averaged 27.30 million barrels perlargely by the forces of gas competition. The day (mb/d), up 0.47 mb/d from the secondgas futures market on the International quarter (table 3). Part of the increase was due

Petroleum Exchange (IPE) has been strug- to higher output from Iraq, but productiongling to generate sufficient liquidity, and also rose in Saudi Arabia and Venezuela and

trading is still dominated by a few companies. a number of other countries.Many more players are expected to enter the OPEC production was 2.3 mb/d over itsmarket once the contract develops. self-imposed quota, with all countries pro-

10 COMMODITY MARKETS AND THE DEVELOPING COUNTRIES

ENERGY

ducing above their assigned levels. Iraq was Soviet Union (FSU). While quarterly growthonly marginally over quota, while several was modest, production was 1.0 mb/d higherother countries were well above. Venezuela than a year ago. Despite significant growth,continues to have the highest over-quota pro- non-OPEC supplies continued to come in wellduction, with output approaching 0.9 mb/d. below expectations, with third-quarter outputNigeria followed with 0.41 mb/d above 0.8 mb/d less than projected by thequota, Saudi Arabia with 0.28 mb/d (includ- International EnergyAgency at the beginninging its half share of Neutral Zone produc- of the year. Much of the shortfall is the resulttion), and Qatar with 0.27 mb/d. There are of technical problems and delayed start-up ofindications that OPEC may raise quotas at its new fields in the North Sea and elsewhere.semi-annual meeting in November. Many of the new projects that involve new

Iraqi oil exports ceased between May and technologies-such as floating, production,August, providing some support to oil prices. storage and offshore loading (FPSOs)-haveIraq wanted an aid distribution plan to be been fast tracked, and slippages haveapproved by the UN before resuming its oil occurred. These and other projects will be

shipments under the second six-month oil- coming onstream in the near future, and non-for-food arrangement. The second $2 billion OPEC supplies are projected to increase sub-

deal is divided into two 90-day periods and is stantially in the coming year.scheduled to end in early December. Iraq was Oil demand rose an estimated 3% in the

permitted to capture some of the production third quarter, with increases in all the mainlost in the delayed start-up of the first period, regions. Total OECD demand was up an esti-and its output reached nearly 1.7 mb/d in mated 2%, reflecting strong US growth of 3%September. The decision on whether to renew but little growth in the rest of the OECD. Oilthe deal will affect the direction of prices over demand was up 5% in the developing coun-the winter. tries, with strong growth in Latin America and

Non-OPEC production rose 0.3 mb/d Asia. It is uncertain how the recent turmoil in(table 4), with much of the growth occurring Asian currency markets will affect near-termin the UK, Canada, and Latin America (main- oil demand growth, but some slowdown is like-ly Mexico). Norwegian production slowed for ly. The apparent increase in consumption inroutine summer maintenance programs, and the FSU also contributed to the growth inoutput also fell in the countries of the former world oil demand in the third-quarter.

TABLE 3. OPEC CRUDE OIL PRODUCTIONAND QUOTAS TABLE 4. NON-OPEC OIL SUPPLYMillions of barrels per day Millions of barrels per doy

1995 1996 2Q97 3Q97 Quotas Change

Algeria 0.76 0.82 0.85 0.85 0.750 1995 1996 2Q97 3Q97 2Q97 to 3Q97

Indonesia 1.34 1.39 1.38 1.38 .330 Unites States 8.61 8.59 8.64 8.60 -0.04Iran 3.65 3.67 3.62 3.65 3.600 Canada 2.40 2.46 2.37 2.53 0.16Iraq 0.55 0.58 1.05 1.22 1.200 United Kingdom 2.79 2.81 2.51 2.75 0.24Kuwait 1.84 1.81 1.81 1.83 2.000a Norway 2.91 3.23 3.35 3.20 -0.15L bya 1.41 1.39 1.43 1.43 1.390 Other OECD 1.31 1.35 1.40 1.43 0.03Neutral Zone 0.43 0.48 0.52 0.54 Latin America 6.08 6.54 6.81 6.95 0.14Nigeria 1.93 2.15 2.29 2.28 1.865 Africa 2.58 2.68 2.80 2.85 0.05Qatar 0.45 0.49 0.61 0.65 0.378 Middle East 1.87 1.92 1.89 1.85 -0.04Saudi Arabia 7.94 7.91 7.92 8.01 8.000a China 2.99 3.12 3.22 3.19 -0.03UAE 2.20 2.23 2.23 2.25 2.161 OtherAsia 2.14 2.11 2.11 2.11 0.00Venezuela 2.75 2.94 3.16 3.22 2.359 FSU 7.13 7.07 7.20 7.13 -0.07Total Crude 25.23 25.84 26.83 27.30 25.033 Eastern Europe 0.23 0.22 0.22 0.22 0.00NGLsb 2.42 2.61 2.77 2.83 Processing gain 1.46 1.52 1.56 1.56 0.00Total OPEC 27.66 28.45 29.60 30.13 Total non-OPEC 42.50 43.60 44.08 44.36 0.28

a. Quota ncludes half share of Neutra Zone. Note: Includes natural gas liquids (NGLs), nonconventiona, and other supplyb. Natural gas liquids. sources.Source: Internatonal Energy Agency and CPECNA Source International Energy Agency.

NOVEMBER 1997 11

ENERGY

A much improved stock picture is a An important uncertainty in the oil mar-major difference in the market over a year ket is whether Iraq's oil-for-food deal will be

ago. OECD oil stocks rose significantly in renewed by the UN. Escalating conflicts

August and September, particularly in between Iraq and the UN over weapons

Europe and North America and mainly for inspections could bring further UN-sanc-

petroleum products. Higher production of tioned oil exports to a halt and could even

crude and high refinery utilization rates result in renewed hostilities. While such

accounted for the buildup in product political developments are difficult to pre-

stocks. Inventories are above last year's lev- dict, it is becoming increasingly likely that aels in all OECD regions. Stocks are espe- third tranche of UN-sanctioned exports will

cially improved in the US and Europe, with be delayed. That in itself would help to sup-

improvements in the stocks of heating oil port prices.

particularly important entering the winter However, Saudi Arabia has come out inheating season. favor of raising OPEC production quotas at

The market is projected to be adequate- the organization's meeting in November, to

ly balanced for the fourth quarter, assuming move the ceiling closer to actual demand for

normal weather. Non-OPEC supplies are OPEC crude oil. Saudi Arabian Oil Ministerprojected to rise by 1.6 mb/d, but there is a Ibrahim al-Naimi has reportedly indicated

likelihood of further shortfalls that could that the Saudis are looking to increase mar-require a small stock draw, not untypical for ket share and that they would be willing to

the fourth quarter. step in to replace any lost Iraqi volumes if theThe market is in much better shape head- oil-for-food deal is not renewed in

ing into the winter than it was a year ago, December. There was no mention about howwhen extremely low stocks and the failure of new production levels would be set, but theIraqi crude exports to re-enter the market Saudis would want firm commitments to new

caused prices to surge. Only a mild winter quotas by all members. Kuwait has indicatedkept prices from soaring higher in the first that it wants a higher quota if new allocations

quarter of this year. Although improved are set.

inventories make a price spike less likely this While the three Gulf countries with sparewinter, stocks are still low by historical stan- production capacity-Saudi Arabia, Kuwait,

dards. Any disruption to supplies or strong and the United Arab Emirates-have kept

demand could cause prices to jump. production close to their quota levels the past

TABLE 5. OIL CONSUMPTION

Millions of barrels per day Percentage change

FSU and Developing FSU and DevelopingOECD Eastern Europe countries Toral OECD Eastern Europe countries Total

1990 38.3 9.9 18.2 66.3 0.4 -4.4 3.7 0.51991 38.3 9.4 19.0 66.7 0.2 -4.7 4.6 0.71992 39.0 8.2 20.1 67.3 1.7 -13.0 5.8 0.81993 39.2 7.0 21.5 67.7 0.5 -14.6 7.1 0.61994 40.2 6.0 22.5 68.6 2.4 -14.3 4.5 1.31995 40.6 5.9 23.6 70.1 1.0 -1.3 5.0 2.11996 41.3 5.6 24.9 71.8 1.9 -5.9 5.4 2.41 Q96 42.3 5.9 24.9 73.1 2.6 -6.3 5.2 2.7

2Q96 39.8 5.6 24.4 69.8 1.0 -1.8 5.2 2.23Q96 40.8 5.4 24.5 70.7 2.0 -3.6 5.1 2.64Q96 42.4 5.4 25.6 73.4 2.0 -1 1.5 6.1 2.21 Q97 42.0 5.7 26.2 73.9 -0.7 -3.4 5.2 1.1

2Q97 40.9 5.7 25.7 72.3 2.8 1.8 5.2 3.63Q97 41.7 5.6 25.7 73.0 2.1 3.7 5.0 3.3

Source International Energy Agency and World Bank.

12 COMMODITY MARKETS AND THE DEVELOPING COUNTRIES

ENERGY

few years, others like Venezuela, Nigeria, Should Iraqi exports fail to resume, SaudiAlgeria, and Qatar have allowed production to Arabia and others could make up for these

rise and appear to have no intention of letting lost volumes under the guise of higher quo-

this growth subside. While raising the overall tas. Prices would not necessarily weaken sub-OPEC quota by 2.0 mb/d would not neces- stantially if all producers, particularly the

sarily affect prices since output already Gulf countries, maintain production disci-

exceeds this amount, higher ceilings would be pline. However, if the non-OPEC supply pro-

granted to the three Gulf producers. Thus jections are reasonably accurate, higher

total OPEC production next year could rise OPEC production will likely tip the balance

considerably unless all members adhered to into surplus and lower prices.new allocations. This seems unlikely for many The call on OPEC crude next year will be

of the countries that are above quota now. partly determined by the severity of theThe 1998 projections for supply and weather this winter. Extreme conditions

demand leave little room for higher pro- could deplete inventories and necessitateduction from the three Gulf producers, or higher output from OPEC; but this is

from OPEC for that matter, according to unlikely to prevent prices from falling. A

the IEA (table 6). Non-OPEC supplies are new risk to the forecast may be weakerprojected to rise by 2.0 mb/d in 1997, due demand in Asia following the recent cur-

partly to the catch-up in delayed projects rency crises. While it is unclear to whatthis year. British Petroleum has announced extent economic activity and hence oilthat its output alone will increase by 0.4 demand will be affected, Asian oil demandmb/d over the coming 12 months. While is apt to slow next year.

the IEA forecast may again may be opti- The past couple of years have seen dis-mistic, any errors should be considerably appointments in new non-OPEC supplies,less than those for this year and last. necessitating higher output from OPEC

Prices are expected to weaken next year producers. Now OPEC may be set to raise its

due to rising supply, particularly if OPEC quotas just when demand for its crude hasraises quotas and Iraqi exports continue. temporarily stopped growing.

TABLE 6. WORLD PETROLEUM DEMAND AND SUPPLYMillions of barrels per day

1995 1996 IQ97 2Q97 3Q97 4Q97 1997 Q98 2Q98 3Q98 4Q98 / 998

DemandOECD 40.6 41.3 42.0 40.9 41.7 43. 41.9 42.7 40.9 42.0 43.7 42.3FSU 4.8 4.3 4.3 4.4 4.4 4.6 4.4 4.4 4.4 4.4 4.6 4.5Other 24.7 26.2 27.6 27.0 26.9 28.1 27.4 28.7 28.4 28.3 29.5 28.7Total 70.1 71.8 73.9 72.3 73.0 75.8 73.7 75.8 73.7 74.7 77.8 75.5

SupplyOECD 18.0 18.4 18.7 18.3 18.5 19.6 18.8 19.4 19.1 19.6 20.9 19.8FSU 7.1 7.1 7.0 7.2 7.1 7.2 7.1 7.2 7.3 7.3 7.3 7.3Other5 17.4 18.1 18.6 18.6 18.8 19.1 18.8 19.4 19.6 19.7 20.0 19.6OPEC b 27.7 28.5 29.6 29.6 30.1 30.1 29.7 30.2 30.2 30.2 30.2 30.2Tota 70.2 72.1 73.9 73.7 74.5 76.0 74.4 76.2 76.2 76.8 78.4 76.9

Stock chonge and miscellaneousOECD -0.3 -0.1 0.3 0.2 0.3Floating/transit 0.1 -0. i 0.1 0.5 0.4Other/miscellaneous 0.3 0.4 -0.5 0.7 0.8Total 0.1 0.3 0.0 1.4 1.5 0.2 0.7 0.4 2.5 2.1 0.6 1.4

Note: Includes natural gas liquids (NGLs), nonconvent onal, and other supply sources.a. Includes processing gains (1.5 mb/d in 1996).b. Includes NGLs (2.6 mb/d in 1996).Source: Intemational Energy Agency and World Bank.

NOVEMBER 1997 13

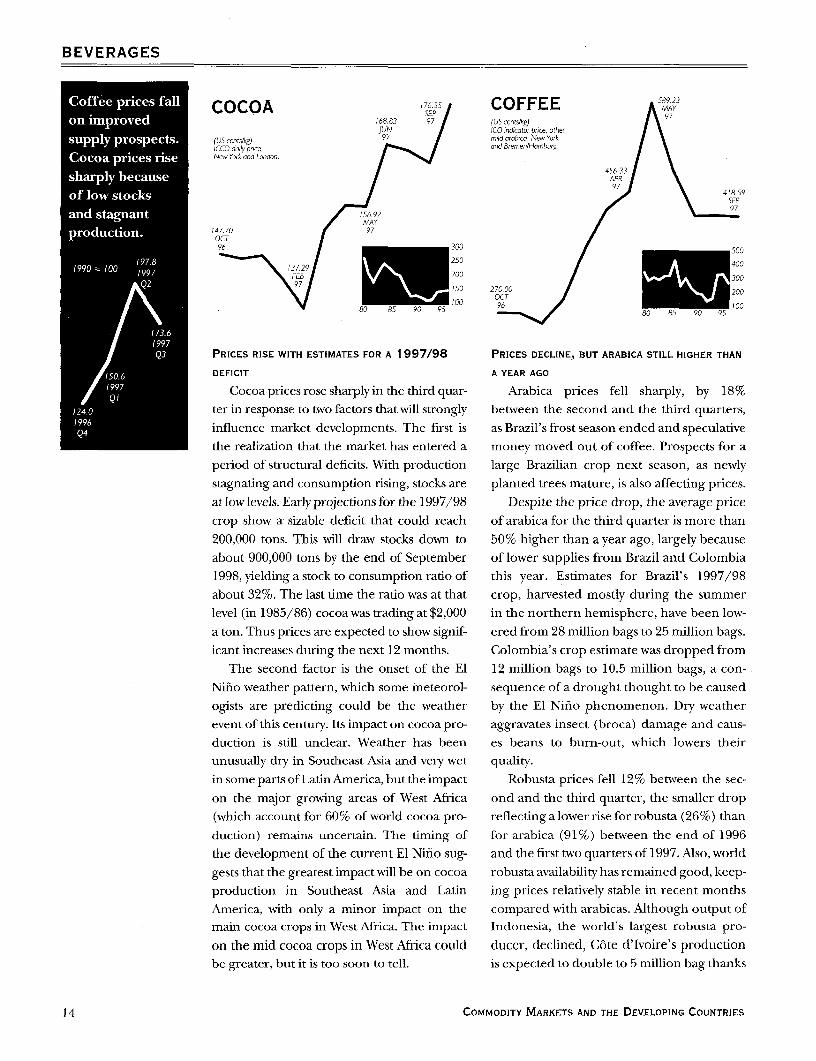

BEVERAGES

s I COCOA 1776 55 COFFEE 5892Y168.83 97 (US cents/kg) 97JUN ICO inJcato price, stneri 5 (US cents4g) 97 mild ctrobic Na, Ykrk

JCCC daily pace, and Bremen/lismburg.; * * * - New Yonk and Lodon.a

456.33APR97

418.59SEP

156.92 97MAY

147.70 97OCT96 300 500

329 - 250 400FE7.29/ p200 30

97 -_/Z 50 270.00 _ 200

80 85 90 95 808 96 0 95 100

PRICES RISE WITH ESTIMATES FOR A 1997/98 PRICES DECLINE, BUT ARABICA STILL HIGHER THAN

DEFICIT A YEAR AGO

Cocoa prices rose sharply in the third quar- Arabica prices fell sharply, by 18%ter in response to two factors that will strongly between the second and the third quarters,

influence market developments. The first is as Brazil's frost season ended and speculativethe realization that the market has entered a money moved out of coffee. Prospects for aperiod of structural deficits. With production large Brazilian crop next season, as newlystagnating and consumption rising, stocks are planted trees mature, is also affecting prices.

at low levels. Early projections for the 1997/98 Despite the price drop, the average price

crop show a sizable deficit that could reach of arabica for the third quarter is more than

200,000 tons. This will draw stocks down to 50% higher than a year ago, largely becauseabout 900,000 tons by the end of September of lower supplies from Brazil and Colombia1998, yielding a stock to consumption ratio of this year. Estimates for Brazil's 1997/98about 32%. The last time the ratio was at that crop, harvested mostly during the summerlevel (in 1985/86) cocoa was trading at $2,000 in the northern hemisphere, have been low-

a ton. Thus prices are expected to show signif- ered from 28 million bags to 25 million bags.icant increases during the next 12 months. Colombia's crop estimate was dropped from

The second factor is the onset of the El 12 million bags to 10.5 million bags, a con-Nifo weather pattern, which some meteorol- sequence of a drought thought to be caused

ogists are predicting could be the weather by the El Nino phenomenon. Dry weatherevent of this century. Its impact on cocoa pro- aggravates insect (broca) damage and caus-duction is still unclear. Weather has been es beans to burn-out, which lowers theirunusually dry in Southeast Asia and very wet quality.

in some parts ofLatinAmerica, butthe impact Robusta prices fell 12% between the sec-

on the major growing areas of West Africa ond and the third quarter, the smaller drop(which account for 60% of world cocoa pro- reflecting a lower rise for robusta (26%) than

duction) remains uncertain. The timing of for arabica (91%) between the end of 1996the development of the current El Nifio sug- and the first two quarters of 1997. Also, worldgests that the greatest impact will be on cocoa robusta availability has remained good, keep-production in Southeast Asia and Latin ing prices relatively stable in recent monthsAmerica, with only a minor impact on the compared with arabicas. Although output ofmain cocoa crops in West Africa. The impact Indonesia, the world's largest robusta pro-

on the mid cocoa crops in West Africa could ducer, declined, Cote d'Ivoire's productionbe greater, but it is too soon to tell. is expected to double to 5 million bag thanks

14 COMMODITY MARKETS AND THE DEVELOPING COUNTRIES

BEVERAGES

to higher prices and good weather. Uganda's TEAoutput should remain stable at around 4 mil- (t

(US cents/kg) lion bags. Vietnam's production is expected 23o0.18oras. 230.78

overage for all tea.AP

to be up 7% from the previous year's record 9|

crop. 22.

There is considerable nervousness in the 97

world coffee market because of the possibleeffect of the El Nifio phenomenon on pro- 12 205.74

duction in a number of countries. Although 9 JUL97

the only significant effect so far seems to be 350

a large production reduction in Indonesia, 350

where drought has reduced crop expecta- OCT 200

tions by 30% from last year's bumper harvest 96 80 85 90 95 150

of 7 million bags, and to a lesser extent in

Colombia and Papua New Guinea. However, STRONG GLOBAL DEMAND KEEPS PRICES HIGH

many Central and South American countries Strong global demand and sharply

are concerned that recent dry weather will reduced Kenyan production kept tea prices

lower the quality of the coffee beans pro- high during the third quarter. London prices

duced this year and that next year's crops will averaged 226 ¢/kg for the quarter, 36% above

be substantially smaller. the same quarter last year in real terms. The

Papua New Guinea's crop also appears to rise has been sharpest in Mombassa-up 54%

be affected by the dry weather, but production in real terms in response to the short supplyis expected to decline no more than about 7% following the severe drought in the first quar-over last year. Costa Rica has declared a state ter. Even Colombo prices were up 9% in real

of emergency, but so far there are no reports terms, despite Sri Lanka's record crop.of any significant production declines. World supply has remained tight, mainly

Neighboring El Salvador has reported no dam- because of the 23% drop in production in the

age from El Niiio-related weather patterns. first eight months of this year over the samePrices in the next several months will period last year. Kenya produced a record

depend on prospects for next year's crops in 250,000 tons of black tea last year, making it

Brazil and other Latin American countries. the world's largest black tea exporter. That

One preliminary estimate puts Brazil's position is expected to revert to Sri Lanka this1998/99 crop at 30 million bags, some 20% year. Many parts ofIndonesiawere affected by

higher than the current crop. Uncertainty sur- the drought caused by El Nifno, thoughrounds other Latin American crops for next detailed information on the impact on tea is

year because of El Nifno. not yet available. Good rainfall boosted pro-For the longer-term, the high prices of duction in Malawi and South India.

the past four years are likely to affect pro- World demand has been strong, with con-

duction. Average production costs are esti- sumption up in all major tea consuming coun-

mated at around, 2200/kg for arabicas and, tries except the UK and the US. Consumption1300/kg for robustas, giving coffee growers has grown especially rapidly in Central Asia,in most producing countries large profits India, the Middle East, and Russia.over the past four years. At least some of Global demand is likely to continue to

these profits would have gone into new grow. Uncertain global weather conditionsplantings, which will result in large crops in and low stocks in producing and importing

three to five years' time. Thus, the past four countries are likely to increase concerns aboutyears could be the beginning of another tea availability. Prices should remain high at

boom and bust coffee cycle. least until early next year.

NOVEMBER 1997 15

FOOD

FATS AND OILS COCONUT OIL6. S ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~(US doltor*/t)

PRODUCTION TO INCREASE SLIGHTLY DESPITE 77700 Phdippnes/ndonesion,a 1 EL NINO oalkiDEC buk c.f Rotterdam.

This year's severe El Nifno (with the latestTiT* - .* 6

indicators still alarming, and some meteo-rologists warning that the impact could be OCT 0

l*. E _ even worse than in 1982/83) looms large in 96

any discussion of the commodity outlook.65400 ~~~~6/L00

l K However, its impact on fats and oils prices 1,200 MAY SEP

for the rest of the year and into 1998 are _8 00 \ 97

uncertain. While output is expected to 600400

decline in the Pacific rim, it is expected to 200~~~~~~~~~~~~~~~~~~~~~~~~80 85 90 95increase in North America, so the net effect

on supply is a matter of relative effects. In PRICES CONTINUE TO DECLINE

terms of distribution, however, Southeast Prices suffered a further downturn from

Asian oil producers are expected to incur $667/ton last quarter to $592/ton this quarter,

substantial losses. down almost 21 % from a year ago ($746/ton).

The 1997/98 stocks to use ratio will As with all lauric oils, prices have been heavily

reach 10.4 for oilseeds, the second lowest in influenced by the major oilseed competitors.three decades. Current forecasts are for no World production of coconut oil is expect-more than a 2.3 million ton increase (to ed to increase slightly, from 3.1 million tons in100.8 million tons) in world production of 1996/97 to 3.2 million tons in 1997/98. While

fats and oils in 1997/98. Oil World reports production in the Philippines, the dominant

that once the harvest pressure subsides in coconut oil producer, will increase from 1.22

October, prices are expected to rise until to 1.33 million tons, production fromJanuary, with a possible temporary down- Indonesia (the second largest producer) isward reaction during the holiday season. expected to decline from 0.77 to 0.73 million

Reforms of the EU's Common tons. A small increase is expected in India (theAgricultural Policy, announced by the third largest producer), from 0.35 to 0.37 mil-Commission as Agenda 2000, call for cut- lion tons. The same pattern is reflected inting preferential area aid to oilseed farmers exports: they are expected to increase in the

(as defined in the 1992 EU reform) to the Philippines from 0.91 to 1.02 million tons and

same level as that for cereals. Before the to decline in Indonesia from 0.46 to 0.39 mil-1992 reform, EU farmers were selling their lion tons.oilseeds at what World Commodity Report The US and the EU, the dominant coconut

called "impossibly high prices." If the pro- oil importers, will absorb 0.49 and 0.61 millionposed reform materializes, oilseed produc- tons of coconut oil, more than two-thirds ofers may lose as much as 20% of their world exports (expected to reach 1.62 millionincome. tons in 1997/98). Coconut oil exports account

Now that an estimated 15% of this year's for slightly more than 3% of world trade in theUS soybean crop is of gene-modified origin, 10 major oils.buyers worldwide are increasingly con- Oil World reports that fromJune/July 1998

cerned about the safety of these products. onward, production of copra in theThe legal position of these products is not Philippines is expected to take another down-yet clear in the EU. Given that separation of turn, which is likely to become stronger in theconventional and modified crops would be second half of 1998, as production begins to

costly to maintain and monitor, the situa- show the effects of severe El Nifno-caused

tion is unlikely to be resolved soon. drought conditions in early 1997.

16 COMMODITY MARKETS AND THE DEVELOPING COUNTRIES

FOOD

PALM OIL SOYBEAN OIL 55700 FATSAND OL

580.00 DuSch, crude,/ Coconut andFEB rob. ex-roil]. }

9ob7e541m0 / palm oil pricesMA decline, while soy

/ \ 523 °° .0 8 00 0 V prices remain532 00 \>;7 OCT JUL flat.

96~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~9

(US dollarslmt) \ mMalaysurn, 5% bulk, 498.00 1990 = 100cctf NWEumpe. JUL 1 5

800 97 154.5700 1997 151.6

600 600 QI\ 1997514.00 500 2Z

400 DEC96 400

200 300 80 85 90 95 80 85 90 95 300

1996PRICES HIT NEW LOWS PRODUCTION IS EXPECTED TO RISE Q4

Palm oil prices dropped to a new low of Prices averaged $545/ton in the third

$508/ton from $549/ton last quarter-the quarter, virtually unchanged from last quarter 13851997

previous low was $511/ton in the third quar- but slightly lower than the $561/ton in the Q3

ter of last year. Palm oil, which accounts for same quarter last year. The continued weak-

about 40% of world oil trade, is heavily influ- ness in prices reflects record-level production

enced by its three major competitors: soy, that Oil World predicts will reach 21.9 million

rapeseed, and sunflower. tons in 1997/98, almost 6% higher than theOil World revised its earlier forecast of a 20.7 million tons in 1996/97. This revival in

1.24 million ton increase in palm oil output the supply of soybeans is reflected in Chicagoto a 0.65 million ton increase. This downward soybean futures prices, which declined by as

revision reflects the El Nifio-caused droughts much as 20%, and is the main force behindat the end of 1996 and early 1997 in the fall in the prices of other oils.

Indonesia and Malaysia and other smaller Production in the US, the world's domi-producers. The droughts are expected to nant soybean oil producer, is expected to

lower yields, especially from 1998 on. reach a record 7.6 million tons, followed byStarting October 1, China further Brazil at 3.8 million tons, the EU at 2.9 million

reduced its in-quota tariff on palm oil tons, and Argentina at 2.1 million, all sub-imports from 18% to 9%. The tariffs had stantially higher than their 1996/97 levels.

already been lowered earlier this year, but on The three leading exporters, the US,a temporary basis. Exports of palm oil Brazil, and Argentina, will account for 4.5

increased sharply from Malaysia and million tons, almost three-fourths of worldIndonesia, because of their weakened cur- exports. China's imports are expected to passrencies. the 2 million ton mark, reflecting the increas-

Until last year palm was favored over other ing tightness of vegetable oil supplies.oilseeds because its crushing leaves negligible Current stocks of soybean oil are downmeal for the market. However, as demand for sharply from a year ago in the US, Argentina,

other meals increased, so did competition for and Brazil and in many importing countries,their oil by-products. According to World including China.

Commodity Report, whether palm oil prices con- Drought caused by El Nifio is expected totinue to fall will depend on whether expecta- affect both Argentina and Brazil leading totions of reduced rainfall next year pan out, some anomalies in soybean production.

cutting into supplies, and whether Malaysia, However, favorable weather conditions inthe main supplier, consumes increasingly North America are likely to offset any decline

more of its oil at home. in production.

NOVEMBER 1997 17

FOOD

GRAINS MAIZE 200

PRICES WEAKEN ON LARGE PRODUCTION AND CUR- - 5

RENCY DEVALUATIONS 97

Grain prices fell during the quarter, 80 85 90 95 50

weakened by large supplies and currencydevaluations in Asia. Prices were down

23.5% over the third quarter of 1996 for ,74

wheat, 37.3% for maize, and 14.3% for rice. NOV

Real grain prices, deflated by the manufac-

tures unit value index (MUV), have declined 97

sharply during the past several decades even (USdoIcrs/rt) n06)06

though grain stocks remain tight. Since USno 2yelf-o JUL

1974, when grain prices were at their recenthigh, real wheat prices have fallen 69.9%, STOCKS ARE EXPECTED TO REMAIN TIGHT AND

maize 70.2%, and rice 80.7%. PRICES FIRM

World grain production for 1997/98 Maize prices have strengthened from

* i U(June-July) is estimated at 2.05 billion tons, their mid-summer lows, with the third quar-

slightly above last year's level and 8.5% above ter average export price at $110.4/ton for USthat in 1995/96. Stocks are expected to build No 2. Prices fell to $106/ton duringJuly but

slightly, but at 15.4% of total use, they are still rose to $120/ton in October. World produc-low by historical standards. The lowest stock- tion was below last year's by 2.4%, and stocks

to-use ratio was reached in 1995/96, when are expected to fall 14%. This should keepending-year stocks fell to 14.2% of total use. the market tight and prices firm. Prices couldBefore that, the last time world grain stocks increase quickly, however, if larger than

had fallen that low was in 1972/ 73, when they expected imports emerge.

were 15.1%. World grain trade is expected to Prices have declined sharply from theirreach 208 million tons, about the same as last May 1996 highs of $204/ton, a decline

year, which would be roughly 10.0% of world greater than would be predicted from pro-production. duction increases or stock levels. Stocks are

Currency devaluations in Asia are affect- projected to end the current year at 103 mil-ing world grain markets in two ways. First, the lion tons, up from 95 million tons in mid-

devaluation of the Thai baht lowered the dol- 1996, according to the US Department oflar price of rice exports; since Thailand is the Agriculture (USDA). The difference is small

major rice exporter, this reduced world rice relative to the decline in prices. Trade levelsprices. Second, the currency devaluations in are expected to be nearly the same this yearseveral Asia countries are expected to lower as during the 1995/96 marketing year

grain imports because they will now be more (July-June). The stock to use ratio was 11.3%expensive and because of slower economic in 1995/96 and is projected to be 11.4% atgrowth now projected for these economies. the end of the current year. The recent cur-

Grain yields increased about 1 % over last rency devaluations in several Asian countries

year's and about 6.5% over 1995/96's. After may explain the low price. If the devaluations

stagnating for several years, yields are now result in slower economic growth as well asback to historical levels. Lower fertilizer prices higher import prices, import demand couldmay have contributed to the increase. Urea contract.

fertilizer prices fell sharply in 1997, reversing The largest coarse grain importers overthe trend of the past several years. Prices aver- the past three years have been Japan (22.3%

aged $151.9 a ton for the first three quarters of worldimports),RepublicofKorea (10.1%),

of 1997-well below 1995's $211.5 a ton. Mexico (6.9%), and Taiwan, China (6.7%).

18 COMMODITY MARKETS AND THE DEVELOPING COUNTRIES

FOOD

RICE (USdoDllrs/alt) 500 WHEAT 25 0Thai, 5% broken, white 400 (US dollurs,mt) 20ndicobve market survey 300 US no. I Hord Red Wmter,

pnce fo.b. ngkok. 200 Gulfport prompt pt nt. 183.49 APR

200AP356.00 1 0 0 97 100JAN 80 85 90 95 80 85 90 95

s \ ~~~ ~ ~ ~ ~~~~~~~~~OCT COARSE GRAIN STOCiCS\ \ ~~ ~ ~~~~~~~~~~~~~~96 1 72.35

97\ / FEB \ Market-yejr-ending stocks as %

312.75 \\ofconsumption292OCT 304.50 X \/_ p 1982887

270.60 19.4SEP 136.21 199219397 JUL

97 13.3

17.1 1997/98

THAI RICE PRICES FALL ON CURRENCY DEVALUATION PRICES STABILIZE AFTER DECLINING FROM 1996 /980/8/

Following the devaluation of the baht, the HIGHS 1983184

US dollar price of Thailand's rice exports fell Wheat prices averaged $146.2/ton for the 199S/6

about 15% in recent months. TheJuly export third quarter after falling from a high of

price for Thai 5% broken, white, milled rice, $262/ton in May 1996. World production for

f.o.b. Bangkok, was $320.0/ton. By August 1997/98 (June-July) is expected to reach a Morket-yeor-ending stocks s0%

the price was $285.0/ton and by October it record 603 million tons, up 3.4% from the pre- ofconsumptionwas ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~17.7 18.0

was $265.8/ton. The decline was apparently viousyear. Worldyear-ending stocks are expect- 1980181 1984185

currency related since other market factors ed to be up 18% (to 128 million tons) over the 1990191

showed little change. World rice production recent low of 105 million tons in 1995. Stocks inand stocks are projected to rise slightly from the five largest wheat exporting countries arelast year's levels, as is world trade. The largest expected to increase about 6%. Trade shouldexporters-Thailand, the US, and remain near last year's 97 million tons. With the 14!

Viletnam-are expected to have good har- increase in stocks and trade unchanged, wheat 199219814.0

vests and large supplies for export, which prices should remain near current levels until 198/88 13.5

should keep prices from rising. The increase spring 1998, when information on new plant- 1994/95

in wheat production will also contribute to ings and crop prospects begins to emerge.the supply of foodgrains and buffer any Concern over possible weather disruptions wn 6I

increase in rice prices. because of El Nino remain, although the ofcorupendin

With extremely dry weather in Indonesia, impact on world wheat production has been 34.8

forecasts are for large rice imports in 1998. relatively small so far. Australian production is 1985186

However, USDA production estimates are well below last year's record crop of 23.6 mil-still pointing to a large rice harvest. Malaysia lion tons, but at an estimated 17.5 million tons

26.3and the Philippines could also face produc- it is above the average for 1993-95. India is 1992193

tion problems because of El Nino-induced expecting a record harvest of 69 million tons, 25.6

weather patterns, although just what those 11% above the previous year. China's wheat 2 20.8

impacts will be is not yet clear. India has har- production is up 9.4% over last year's for a 1989/90

vested a record 122 million ton paddy crop record high, and Russia's production is up 1899697

and is expected to export about 1.75 million 26%. The EU has a good, but not record crop, Note Data for 1997/98 are -snated

tons. China is also expected to harvest a and US production is 68.8 million tons. China Source: USDA FAS.

record 195 million tons of paddy rice and to is expected to import only 2 million tons of

export 1 million tons. Bangladesh, which has wheat in 1997/98, far below the 12.5 millionimported as much as 1.5 million tons in tons of 1995/96. Russia, a large importer in

recent years, is expected to be nearly self-suf- some years, is expected to import only 7 million

ficient with imports of about 100,000 tons. tons.

NOVEMBER 1997 19

FOOD

BANANAS 711.54 SHRIMP 557

(US dollars/mt) 97Centrel and SouthAmericon, importer'spnce, free-on-rcil((o.r), US1ports . (US dollars/kg)

1US, Gnifbnoern,heodless, 26-30count per pound,wholesale New York.

493.84JON97

42505 213.88JU6 600 FEB IS

3756397

300 2

96 ~~~~~~~~~~~~~~400 i3.1!

80 85 90 300 96 80 85 90 95

Low INVENTORY AND RISING DEMAND BUOY PRICES

FREE MARKET PRICES SLIP Shrimp prices continued to strengthen in

Free market banana prices continued the third quarter, putting them 15% highertheir seasonal decline during the third quar- than a year ago. Low inventories in the US

ter, falling more than 26% from the second andJapan; small harvests in Bangladesh,

quarter. Banana prices typically peak during India, and Thailand; and seasonally highFebruary and March, and further declines demand in major importing countries con-can be expected during the fourth quarter. tributed to the increase.

Still, fresh bananas are not readily storable, Prices were high in Japan and the USand supply disruptions can lead to rapid despite increasing shipments from Bangladeshprice increases. and India. The EU ban on seafood from

Analysts are watching banana producing Bangladesh and India (because their

countries that were most seriouly affected by seafood industries do not meet EU sanitary

earlier El Nifios, including Ecuador, the regulations) resulted in the larger ship-Philippines, and South Africa. Past El Nifios ments to Japan and the US. The ban has

have brought heavy rains and flooding to been in effect since August. The EU'sEcuador and droughts to southern Africa and seafood industry is actively seeking prod-

southeast Asia. Officials are concerned about ucts from other Asian countries to make upthe effects of El Nifio in Ecuador, where flood- for the loss of shrimp from the two coun-ing during the 1982-83 El Nifio wiped out tries. Bangladesh and India, in addition to

roads and transport systems. Producers in the increasing their exports to their traditionalPhilippines have already experienced some markets, are seeking new markets, such as

dryness, although it is too early to asses the China and South Africa.

impact. Producers in South Africa and So far, El Nifio has had a positive effect on

Zimbabwe produce primarily from irrigated world shrimp supply. Supply is increasing infields, and above average rains in the past three Ecuador, one of the largest shrimp producers.seasons have left water reserves high. Wild larvae, preferred by farm operators for

During the quarter the World Trade their high yields, are readily available. A possi-

Organization's (WTO) judges rejected the blenegativeeffectmightbetheinterferenceinEU's appeal of an earlier decision declaring transport caused by heavy rains, especially on

core components of the EU's banana import roads to and from the processors.regime inconsistent with Uruguay Round Given the production problems in many

obligations. No further appeal is available Asian exporting countries and increasingunder WTO rules, and the EU has said it will demand, shrimp prices are expected to stay

accept the ruling. strong for the coming months.

20 COMMODITY MARKETS AND THE DEVELOPING COUNTRIES

FOOD

SUGAR 80 Facing increased pressure from US and

(USAdIy,p,re 40 domestic high-fructose corn syrup produc-mHct ISA dodGrwersyUNCA)cnnoncerow, fo.b., stowd 20 ers, the Mexican National Association of

Cor,bbecn ports. __0 80 85 90 95 Sugarcane Growers (UNPCA) announced a

24.9} / \ verbal agreement between the sugar indus-APR try and the National Association of Soft

2452 A / 2S8 Drink Manufacturers to limit high-fructose

96 / \ / 97 corn syrup use to 350,000 tons a year for the

\4/2w next three years. Mexican domestic sugar\ /JUN prices are insulated from international

prices by NAFTA-based tariffs, but high-fruc-

JAN tose corn syrup imports from the US face

much lower tariffs. To counter the pricePRICES MOVE UP SLIGHTLY advantage of corn syrup over sugar, the

Prices inched upward during the quarter sugar industry will offer preferential priceson mixed news. In its first report on the to soft drink bottlers. Reports suggest dis-

1997/98 crop, the International Sugar Organ- counts as high as 20%. Earlier this year,

ization (ISO) said it expects a deficit of 1.69 Mexico imposed antidumping tariffs on USmillion tons-the first since 1993/94. The exports of high-fructose corn syrup. The US

ISO expects world production to fall slightly announced its intention to take the dispute(0.5%) as consumption continues to grow. to the WTO.

The stocks to consumption ratio is thus In September the Office of the US Trade

expected to drop from 36% to 33%. The ISO Representative released country allocationsreport follows recent upward revisions in esti- for an initial 1.2 million tons of sugar to be

mates of EU and Brazilian crops and a lower- imported under quota arrangements. Another

ing of expectations for India, Poland, and 600,000 tons may be added later. The quotasUkraine. allow countries to export sugar into the pro-

FO Licht reports that some analysts are pre- tected US market, where prices are nearly dou-

dicting production declines of as much as 20% ble world prices. The Dominican Republic,due to El Niiio's effects, though it is unclear Brazil, and the Philippines will receive the

that this will have much of an impact on sugar largest quota allocations.prices. The 1982-83 El Nifio hurt growing con- The Cuban government has agreed to let

ditions in several major sugar producers- foreign investors participate directly in theAustralia, Brazil, Cuba, India, Indonesia, sugar industry through a planned joint ven-Mexico, and Thailand. Production forecasts ture by Cubacol, a government sugar com-

have already been reduced for Indonesia and pany, and Vinumar and Thundergust ofThailand due to dry weather-a signature Spain. The new installation will producecharacteristic of El Nifno in the region. But con- 150,00 hectolitres of high quality alcohol per

ditions in Brazil and the Philippines illustrate year for export. Initial investments arethe type of puzzle analysts face. In Brazil weath- expected to be around $6.5 million.

er patterns will not affect sugar production The Peruvian sugar cooperatives Pomalkauntil the 1998/99 season. Meanwhile, analysts and Casa Grande are looking for strategic part-expect another record crop for 1997/98, help- ners according to the Peruvian Privatizationing to offset the drought-induced reductions Committee. Pomalka is looking for $30-$40

expected in Southeast Asia. In the Philippines million in new capital to upgrade its 7,000

the long dry season induced by El Nifio typi- hectare cane plantation, while Casa Grande

cally falls during the sugar harvesting season, seeks $100 million for its 20,000 hectarefacilitating higher recovery rates. operation.

NOVEMBER 1997 21

AGRICULTURAL RAW MATERIALS

COTTON I79.36 Cotton production is expected to increaseikLt3 ai_ (US cenrs/k) i97Cotton OutlookA 177.72 in Uzbekistan and Pakistan, primarilyIndex cif. Let pooI Aii " i _ xnd Europe.P 97 / \ because of higher yields due to favorable

weather. Production increases are also

175 58 expected in Francophone Africa, where the

97 higher prices received by farmers have appar-

APR /17392ently induced them to expand their cotton1 ~~~~~97

growing area. Substantial increases are also20 /expected in Paraguay and Brazil, partly

200 jbecause of expanded areas induced by the

__i 96 '58 higher prices received by farmers and partly

_ / ~~~~~~~~~~~80 85 90 95 0 because of government decisions to expandcredit and ensure the availability of produc-

tion inputs. Production may decline in

MARKET REMAINS IN BALANCE China, however, by as much as 10% from its

The International Cotton Advisory 1996/97 level, because of reduced areaCommittee (ICAC) estimates that world cot- planted to cotton following disappointment

ton production for 1997/98 will be about 19.7 over prices and buying terms in 1996/97.million tons, while consumption will climb to India may also experience some decline fol-19.4 million tons, keeping the market in rela- lowing the spread of a leaf virus in the north-

tively close balance. ern part of the country. AustralianThis expected balance in world demand production is expected to remain at its

and supply is reflected in the NewYork futures 1996/97 level.

contract, with current quotations for delivery Cotton Outlook reports some uncertaintyin October 1998 and March 1999 virtually the about the Chinese government plans to

same as today's spot prices. The medium sta- reform the state-owned textile sector within anplc cotton indicator price (Cotlook A Index) ambitious three-year time frame. China's fail-averaged 1780/kg, almost unchanged from ure to reform the textile sector could be a

last quarter's 1760/kg and about 5% higher major stumbling block to its membership in

than during the same quarter of 1996. the World Trade Organization. India faces aICAC projections suggest a moderate major challenge in trying to revive a large num-

increase in the A Index for the 1997/98 season ber of loss-making mills within the govern-and a drop to current levels for the 1998/99 sea- ment-run National Textile Corporation. The

son. The extent to which prices actually follow textiles minister indicated last month that

this path will depend largely on two factors: the some units may be transferred on advanta-

El Nifno effect and Chinese stock policies. World geous terms to the governments of the states in

Commodity Report maintains that prices will which the mills are located.remain somewhat higher than previously antic- The textile business in many parts ofipated because of the effects of El Ninlo. Southeast Asia continues to be affected by the

Changes in China's net trade (exports minus recent financial instability and its effect onimports) could have a greater effect on the A exchange rates. The higher increase in the

Index, however. ICAC has estimated that a cost ofimport goods has altered cost structures100,000 ton change in net exports of China in a region accustomed in recent years to

could result in a change in the price of cotton financial stability and currencies that moved inof as much as 2%. Recent domestic policies in concert with the US dollar. However, it is tooChina favor reductions in stocks (and hence in early to tell whether the financial crisis willimports), so this effect could offset any increase result in a structural change in the textile sec-

in prices due to El Nifio. tors of the affected countries.

22 COMMODITY MARKETS AND THE DEVELOPING COUNTRIES

AGRICULTURAL RAW MATERIALS

RUBBER TIMBER 25218

in200 ~~~LOGS 9

25267s G~~~~ OCTA124.12 80 85 90 95 96

\ 1 N.20 \ 242.04J\UN \/\ MA /

7~~~~~~~~~~~~~~9

235.16400 SEP

(US cents/kg) 300Mafaynan, RSS I 86.93 _200 (US dollrs/m3)prompt delivery, SEP Maloys,n, mernti, salesfo.b. Kuala Lumpur. 97 _00 pnce by eaporters, Tokyo.

80 85 90 95

PRICES SLIP ON CURRENCY DEVALUATION PRICES DECLINE ON SLUGGISH DEMAND

Despite a brief two-week rally inJuly, rubber Tropical log prices fell in Japan as hous-prices continue to slide. Policy considerations ing starts slowed and demand for logs for the

have dominated market movements. In July plywood industry was lower as well. At

Thai traders were selling in anticipation of a 113,495 units, housing starts in July were

devalued baht. By September currencies in down 27.8% over the same period in 1996.