World Bank Commodity Models Volume 1

573

World Bank Commodity Models Volume 1 Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of World Bank Commodity Models Volume 1

World Bank Commodity ModelsVolume 1

Pub

lic D

iscl

osur

e A

utho

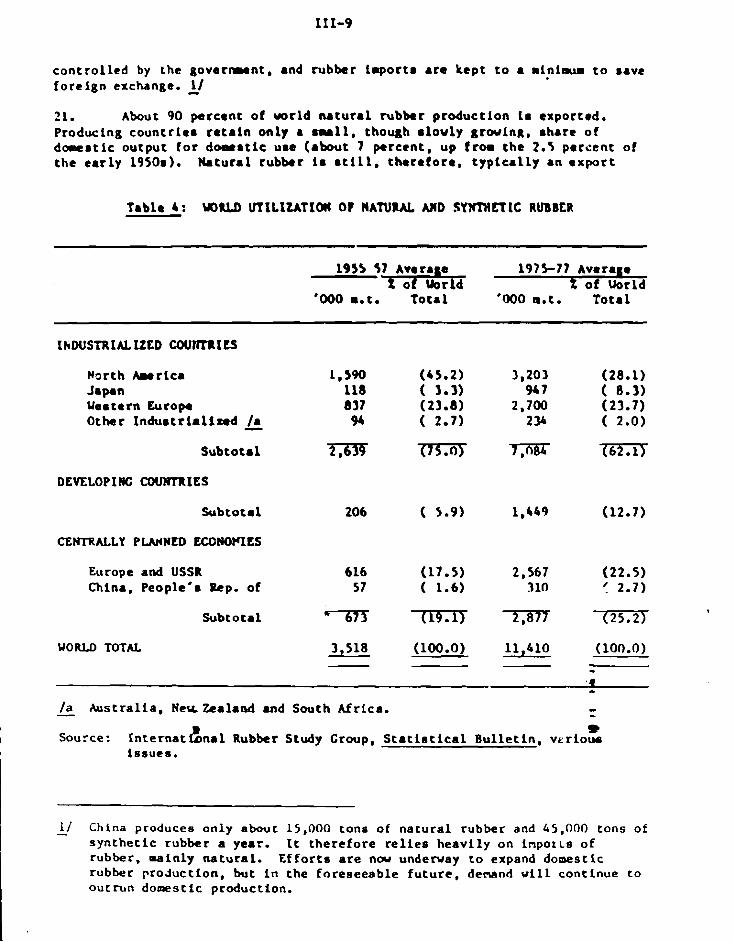

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

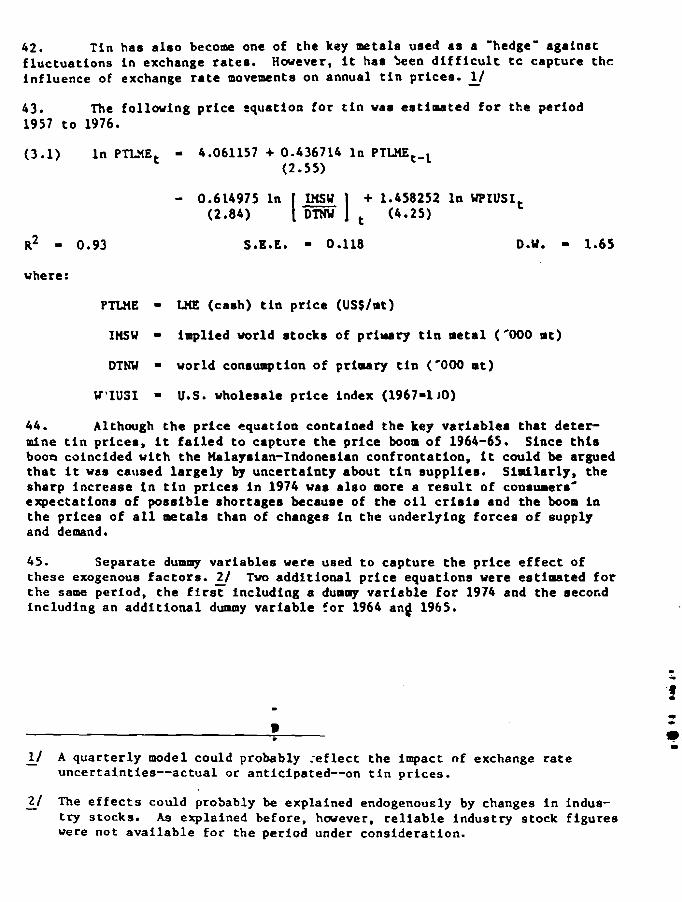

rized

Pub

lic D

iscl

osur

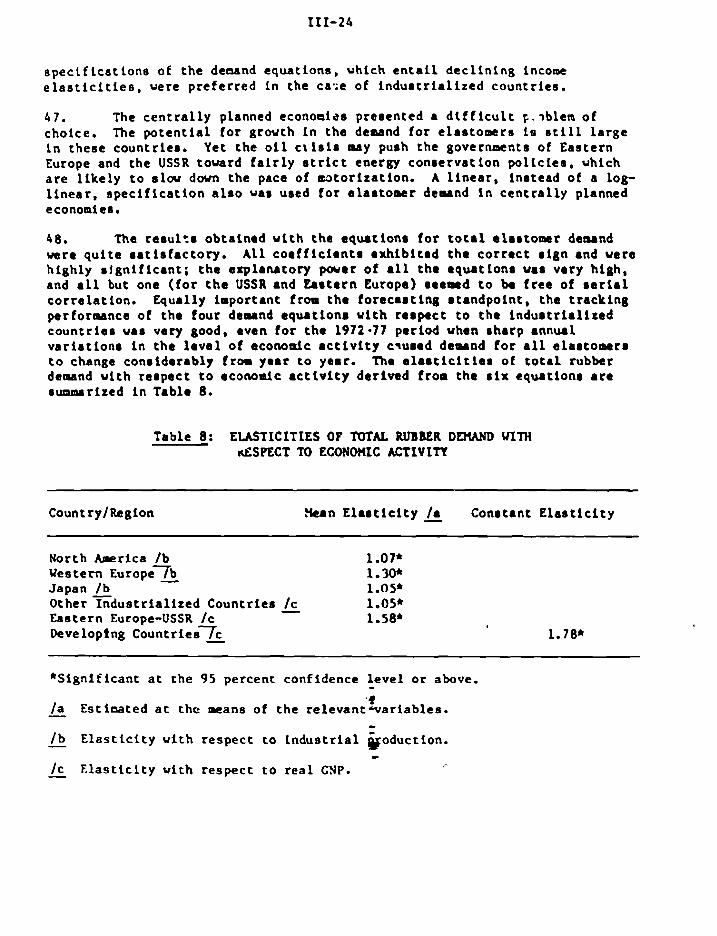

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

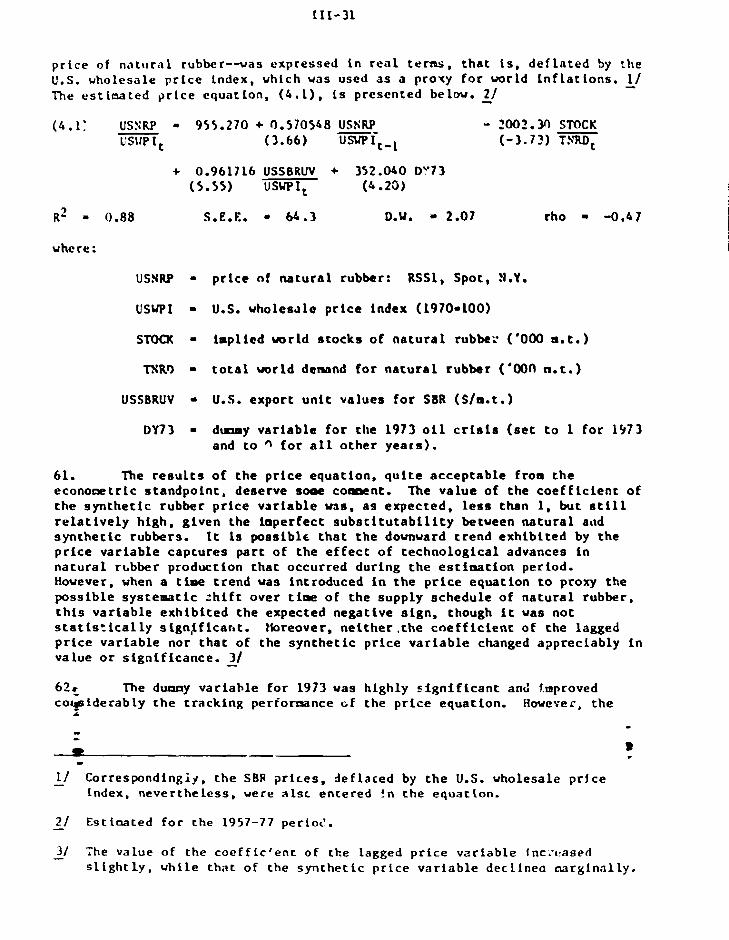

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Papers presented at the Vkbddq on C d i Modek and Pdides

- a

cjpyright O 1981 . The Wmld Bank 181 8 H Street. N.W. Washington. n.C. 20433, USA.

The views and interpretations in this document are those of thr! authors and should not be attributed to the World Bank, to its affiliated organizations. or to any individual acting in their behalf.

The r e r e a r c h m r k presented i n t h e r e t w , volumem goem back r r v e r a l years i n t i r e . 'Ihe s t a f f of t h e Div i r ion h a r incur red n u a t o u r debtm of g r a t i t u d e i n tirlm period. Nr. l h u t e r T i m , former D i r e c t o r of t h e Rconoaic k r a l y s l r and Projectionm Department, gave thim w r k t h e o r i g i n a l i apu l re . Mrs. Helen Hugher, uho rucceeded a s D i r e c t o r , encouraged i t and r t e e r e d i t through i ts var iour phaser. Prof. J. U e l b r o e c k (Free Univers i ty of 6 r u x e l l e r ) , Prof. C. Mpe (Univers i ty of Pennrylvania) and Prof. K. b u r s e n ( U n i v e r s i t y of k r h u s ) f o l l o v d i t c l o r e l y and c o n t r i b u t e d t o t h i s w r k i n v a r i o u s uoys.

The p a r t i c i p a n t s of t h e lh rkshop on Comodi ty Models and P o l i c i e s , h e l d i n Aarhus, Denmark, i n December 1979 deserve a s p e c i a l mention f o r t h e i r r e v i e v s and c o n s t r u c t i v e c r i t i c i s m of t h e models a s doer t h e Danish Research Council f o r the S o c i a l Sciences, rrhich shouldered p a r t of t h e c o s t s of t h e Aarhus Workshop. A l l t hese c o n t r l b u t l o n r a r c g r a t e f u l l y acknovledged.

F i n a l l y , a p a r t i c u l a r thank you is due t o Lenore Beacham, Debbie Kreamer, and Barbara Thoapsoa who typed t h e va r ious d r a f t s of t h i s r epor t and t o Vhitney V a t r i s s rrho e d i t e d t h e va r ious papers.

While t h e r e l a t i v e i s p o r t n n c e o f l r i ~ r y c o m o d i t i e s i n m r l d t r a d e h a s b e e n d e c l i n i n g o v e r t h o yearm, c o t m o d i t y e x p r t s c o n t i n u e t o be a t m j o r s o u r c e o f f o r e i g n e x c h n n p e f o r m n y . !eveloping c o u n t t ies. For t h e r e c o u n t r i e n t h e v o l a t i l i t y o f c o m o d i t y l r a r k e t n a n d t h e c o n a c q u c n t r r n c e r t a i n t i e s a b o u t e x p o r t e a r n i n g @ a n d r e t u r n s t o invcmrtacnts r t i l l c a n n t i t u t e r n c o r r s i d e r n b l c problem.

A t t e m p t s to e x p l a i n t h e b e h n v i o r o f commodity m a r k e t s u s i n g q u n n t i t n t i v e t a c h n i q u e s r e n c h b a c k to t h e b e g i n n i n g o f t h i s c e n t u r y . The r e f i n e m e n t o f t h e s e t e c h n i q u e r h a s c o c t i n u e d e v e r n i n c e . An i m p r e s n l v e amount o f q u a n : i t r r t i v e e n * i d e n c e h a s been g a t h e r e d o v e r time o n v . ~ r i o u s a s p e c t n o f c-dity m a r k e t s . Ye t , t h e deve lopment o f c c o n o m t r i c m o d e l s o f commodity m r k e t s h a s b e e n a r e l ~ t l v e l y r e c e n t phenomenon, u h i c h f o l l o r d , r a t h e r t h a n p r e c c c d e d , t h e d e v e l o p a e n t o f m c r o e c o n o m i c m o d e l s .

I t u a s n o t u n t i l t h e 1960s t h a t e c o n o m e t r i c c o m o d i t y a o d e l i n g begnn i n e a r n e s t . The %rid Bank h a s b e e n somewhat i n t h e f o r e f r c n t o f t h e s e enr1.y d e v e l o p e n t s , w i t h i t s c o c o a nnd r u b b e r m o d e l s c o m p l e t e d i n t h e l a t e 1960s - I n c o n n e c t i o n d t h t h e c o m d i t y s t a b i l i z a t i o n s t u d i e s u n d e r t a k e n t o ~ e t h e r w i t h t h e I n t e r n a t i o n a l S o n e t n r y Fund. Co-dity r e l a t e d w r k had by t h e n gone o n (n t h e Bank f o r s e v e r a l y e a r s nnd h n s s i n c e c o n t i n u e d . P r o j e c t e v a l u a t i o n a c d b i l a n c e o f p a y m e n t s n m l y s i s o f d e v e l o p i n g c o u n t r i e s r e q u i r e d r o n t i n u o u ~ a n d s y s t e a a t i c s t u d y o f c o a n o d i t y m a r k e t s a n d v i e w s o n commodity p r i c e d e v e l o p a e n t s . The Coamodit ies and E x p o r t P r o j e c t i o n s D i v i s i o n h a s , o v e r t h e y e a r s , p e r f o m d mst o f t h e s e f u n c t i o n s .

I n 1973 t h e D i v i s i o n embarked o n a m a j o r e f f o r t t o c o n s t r l l c t c o m p l e t e m o d e l s f o r s e v e r a l o f t h e corwnodi t ieu o f s p e c i a l i n t e r e s t to t h e Bank. T h i n w r k is s t i l l continuing.

T h e u a l n p u r p o s e o f t h e s e m o d e l s v a s t o p r o v i d e i n p u t s to t h e p r i c e p r o j e c t i o n w r k o f the D i v i s i o n , e v e n i f some v e r s i o n s o f t h e m o d e l s t h a t were

:developed e r e u s e d a s c o a p o n e n t s o f l a r n e r m o d e l s o f d e v e l o p i n g c o u n t r i e s ' , ~ r o u t h a n d t r a d e s u c h a s t h e SIXLINK model. 1 - - D e v e l o p e d by t h e s t a f f o f t h e b i v i s i o n a s o p e r a t i o n a l t o o l s , i h c s e w d e l s h a d t o c o n f o r m t o some ' b a s i c * c r i t e r i a : t h e y -re t o be r e l a t Q v c l y %na11 i n s i z e , e a s i l y and c h e a p l y m a n a g e a b l e , u p d a t a b l e and m a i n t a i n ' h b l e , g i v e n t h e r e s o u r c e c o n s t r a i n t s o f t h e D i v i s i o n . For t h e s e r e a s o n s , t h e mode l s b u i l t =re l a r g e l y e c o n o m e t r i c t n n a t u r e , t h e y were e s t i m a t e d u s i n g r e l a t i v e l y s i m p l e p r o c e d u r e s - u s u a l 1y OLS--and bir i 1t a r o u n d a common s t r u c t u r e - - t y p i c a l l y a s r rpp lv b l o c k , a demand b l o c k and a n i n v e n t o r y demand c q r i a t f o n n o r m a l i u ? d o n p r t c e .

T h e s e t h e o r e t i c a l a n d e m p i r i c a l s i m p 1 i f i c a t i o n s r e p r e s e n t t h e c o s t , o f t e n r e l r i c t a n t l y p a t d by t h e v a r i o u s a u t h o r s , o f b u i l d i n g and r n ; ~ i n t n i r ~ i n g i n a r e l a t i v e l y r r m i l l l and o p e r a t i o n a l l y o r i e n t e d r e s e a r c h o u t f i t a l a r g e numher o f s t r u c t u r a l m o d e l s o f c o m o d i t y m r k e t s .

Xlttt *.he except lo^., ~ 1 1 e l r [ o r e , 0: L I ~ L - i I S E and, pertraps, the j u t e ~ o d e l r , none o t t h e o t h e r s p r e r e n t e d i n t h i r paper approacher t h e f r o n t i e r 8 of academic knowledge on econometric model b u i l d i n g . Yet , t h e knouledge and c r a f t m a n ~ h i p of t h e v a r i o u r authorr--who a l l have c o n r i d e r a b l e colmodity expert ise-show up c l e a r l y a t v a r i o u r point*. Examples of t h e improvementr on t h e " r t a t e o f t h e a r t r " i n econometric c o a a o d i t y modelr can be found i n t h e r y n t h e t i c p r i c e index of t h e f a t 8 and o i l 8 model, t h e market oha re e q u a t i o n r o f t h e rubber model and t h e p r i c e / c o r t r e l a t i o n r h i p r o f t h e rupp ly equa t ion r of t h e t i n model.

Given t h e main purpore of t h e r e modelr--market p r i c e r i a r l a t i o n r and projectionr--and t h e conrequent r t r u c t u r a l c h a r a c t e r i r t i c r o f moat of them, t h e i r u r e f u l n e r s a 8 i n r t n r a e n t r f o r p o l i c y r i m u l a t i o n r ha8 been r awwha t l imi t ed . T h i r i r a l i m i t a t i o n t h a t rrc hope t o overcome a8 w r k on t h e "next genera t ion" o f modelr proceedr. A. p o l i c y a n a l y s i s w i l l p l ay a n i n c r e a s i n ~ r o l e i n t h e f u t u r e w,rk o f t h e D i v i r i o n , i ts modeling e f f o r t 8 m y have t o be r c o r l e n t e d acco rd ing ly .

We e n v i r a g e t h e deve lop len t of a few more programming type models f o r meta l r r r k e t r , t h e c o n r t r u c t i o n of t r a d e b l o c k s i n t h e e x l r t i n g econometric- models and t h e l i n k i n g o f some of t h e s i n g l e models now being developed o r r e t o o l e d (e.g. foodgrainr-feedgrainr-livestock, and t eve rages ) .

The modelr s o f a r developed by t h e C o ~ o d i t i e r and Export P r o j e c t i o n s Div i s ion a r e h e r e p re sen ted i n tw , v o l m e r . The f i r s t volume c o n t s i n s t hose t h a t -re f o r s s l l y d i s c u s s e d a t t h e Aarhus Workshop on C o m o d i t y Hodels and P o l i c i e s . The second i n c l u d e s models t h a t = r e subsequen t ly developed o r reshaped. T h e i r main purpose i s t o assemble i n a " s i n g l e place" most of t h e c o m d i t y models developed i n t h e Bank i n r e c e n t y e a r s and g i v e the r e a d e r s and u s e r s a f a i r l y complete r e f e r e n c e ins t rument .

I n c l o s i n g t h i s p r e f a c e , I w u l d l i k e t o thank a l l my former c o l l e a g u e s i n t h e Commodities and Export P r o j e c s i o n s Div i s ion who carved o u t t h i s e f f o r t o v e r t h e y e a r s wi th competence, en thus iasm and de t e rmina t ion , wi thout n e g l e c t i n g any of t h e o t h e r t a s k s normal ly performed by them. I t vas a p l e a s u r e and p r i v i l e g e t o s h a r e v i t h them t h i s g r e a t l e a r n i n g exper ience . -

Table of Contents

W D E L I N C THE WORLD COtQK)DIN MRKETS: P E R S P E C N V E S ON THE USE O F C-DITY M E T MODELS FOR FORECASTING AND SIWtATlON.. . . . . . . . . . . . . . . . 1 P. Gerard A k

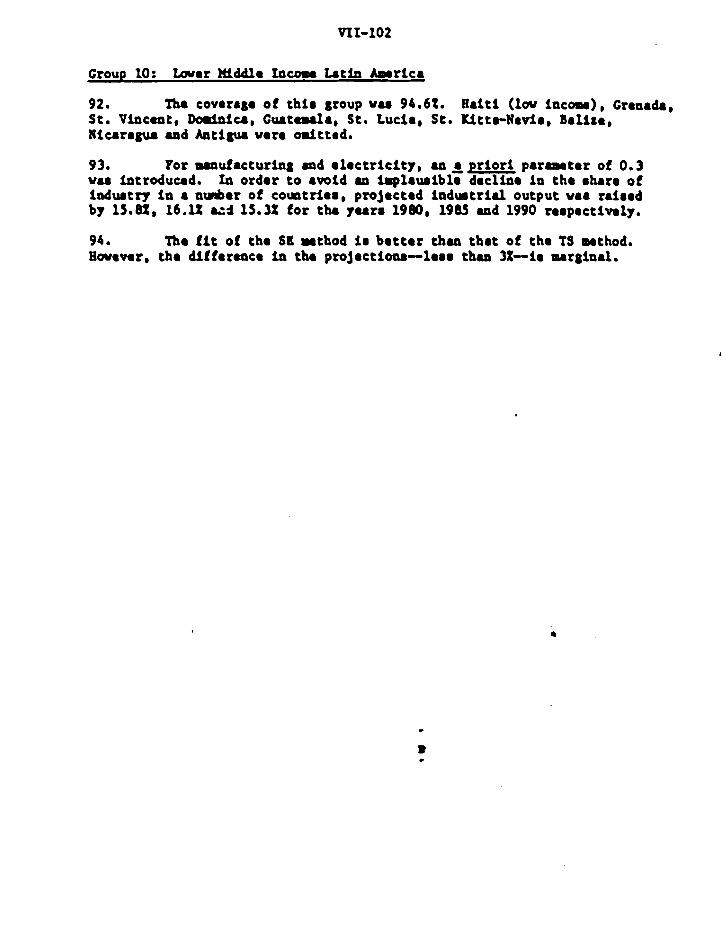

ON THE EVALUATION OF ECONOMIC POReCfiTS..............*.....w..... 27 Svend Hyllsbety

THE UORLD T I N ECONCXY: AN ECONOnerRIC ANALYSIS...................... I- 1 Jaebir Chhabra, kao CriZli, Peter PoZtcrk

C M N T S ON THE U I S E HoDEL DEVELOPED BY H. HASHI~O.......e....e.... I I A - 1 Robert van der Sands

COMMENTS (33 THZ V I S E HODEL DEVELOPED BY H. HASHIHOTO.........e....... IIB-1 Ebbe Yndgaad

AN ECONOMETRIC W D E L OF THE WORLD RUBBER ECONOIff.. ................... I1 1-1 Er,,so Gr i l l i , Rag Rslterline) Peter PoZtak ,

A DYNAXIC S I W L A T L O N XODEL O F THE W R L D JUTE ECONOWY................. IV-1 .Jock Anderson, C k r t e s Blitzer, Tom Cachois, k z o Gri l l i - - THE W R L D TEA ECONOW: AN ECONOMETRIC HODEL O F I T S J * STRUCTURE, PERFOPdWYCE AND PROSPECTS....e..e....e........ee...,...o... V- 1 Soeng-I! Chrolg, Gd. . . 2 2 V F ~ o n g 3

- * I

STRUCLIJRE h~ PROSPECTS O F THE W R L D FATS AND O I L S ECONOMY ........... VI-1 S u m Arcgz~s~o, Peter PoZtak

ENERGY D E W ! IN THE DEVELOPING WORLD: ESTIHATIONS AND PROJECTIONS TO 1990 BY REGION AND C O U m R Y . . . . . . . . . . . . . . . . . . . . . . . . . . . . V I I - 1 Lutz Zo.ffp:ma, Katthias Kors

L i s t of . a r t i c i p a n t s . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ANNEX

)IM)ELINC OF M E WRU) COWODIfl MARKETS: PeaSPeCfms ON use OF c m x m WARI;E~ HUDELS

FOR FOBECASruo(; AND SantUTION

MIDELI= THE WRLD COMDITY W E T S : PERSPECTIVES ON THE USE OF CO!4HODITv NARKET HoDELS

FOR FORECASTING AND SIMULATION

1 . The c x t e n s i o a o f e c o n o a e t r i c modeling to t h e i n t e r m t i o n a l primary c o a w d l t y marke t s has come a t a time when t h e r e is i n c r e a s i n g need f o r a f o r e c a s t i n g and s i u l a t i o n tool. Qua t i t a t i v e , f r e q u e n t l y econometr ic , a n a l y s i s of t h e behavior of c o d i t y markets is a n e s s e n t i a l ingredient i n f o r n u l a t l n g t h e c o r o d i t y s t a b i l i z a t i o n agreements which w i l l be a c o r n e r s t o n e i n nor th-south r e l a t i o n s . Hodels a r e -w be ing used to e v a l u a t e t h e p e r f o r m n c e and cost of va r ious s t a b i l i z a t i o n schemes. They a l s o s e r v e t o

I a p p r a i s e t h e impact of f l u c t u a t i o n s i n t h e primary c o m o d l t y markets on t h e economlee of producing and c o n s d n g count t ies , t o f o r e c a s t long-run demand and supply f o r b a s i c c o r r o d l t l e a , t o estimate t h e e a r n i n g p o t e n t i a l s of deve lop ing c o u n t r i e s , t o measure t h e impact of e x p l o i t i n g t h e manganese

I nodu les on t h e ocean f l o o r , e t c .

2. The a o d e l s used f o r t h e s e purposes m e t t a k e i n t o account t h e d i v e r s i t y of t h e c o m o d i t y markets and t h e s p e c i f i c n a t u r e of t h e problems be ing cons idered . Despi te t h i s need f o r f l e x i b i l i t y , t h e e c o n o c ~ e t r l c models o t c o m d i t y markets have tended t o conform t o c e r t a i n p a t t e r n s . Methods of a p p i y i n g t h e models i n a realistic w a y - o o e t h a t t a k e s advantage of t h e structure and c o n s i s t e n c y of t h e w d e l , w i thou t i g n o r i n g t h e r e a l i t i e e of t h e world-have a l s o been developed. Thus t h e r e have been s u b s t a n t i a l advances i n a p p l y i n g economet r i c s t o t h e f i e l d of commodity marke t s , but c l e a r l y t h e r e a r e

I ~ t i l i shortcomings. The f r o n t i e r f o r f u r t h e r deve lopaen t l a broad and a s y e t unexplored.

3. T h i s pape r ' f i r s t c o n s i d e r s t h e "t ypica ' l" a p p l i e d econometric models. It t h e n d i s c u s s e s hov such models a r e used f o r f o r e c a s t f n g itnd s imula t ion . F i n a l l y , it p o i n t s o u t t h e p r i n c i p a l problems.

I - - ME BASIC '~(ARKET NODEL" PATTERN '!

4. , Econometric models of commodity markets have g r e a t promise even - t h o ' h , w i th some g l a r i n b excep t ions , they a r e relative..^ simple. T h i s i s i n 9 8 p a r ,because few economiets a p p r e c i a t e t h e technics.'. and commercial r e a l i t i e s . o f t h e worldwide markets f o r b a s i c commodities--the d i f f e r e n c e s i n q u a l i t y , t h e t e c h n i c a l a s p e c t s of product ion , t h e systems of commercia l iza t ion , t h e

I t r a n s p o r t a t t on and p rocess ing complexes, t h e s u b s t.1 t ~ l t i o n of s y n t h e t i c 1 mate r i a l , p r i c e mechanisms, e t c . I n t u r n , b u s i n e s s s p e c i a l i s t s o f t e n do no t

a p p r e c i ~ t e t h e unde r ly ing economic behavior and t h e a b i l i t y of s t r u c t u r a l models, even i f s imp le , t o provide u s e f u l i n s i g h t s i n t o market o p e r a t i o n s .

5. A g r a d a t i o n of comaodity market nwjdels can be v i s u a l i t e d an scring from t h e s i n p l e s t , h igh ly aggregated mods1 t o i n c r e a s i n g l y complex ryrL9lar. Useful models range from t h e two-equation "mini" models, which e u w m r i t e chc i n t e ~ ~ c t i o n o f v o r l d rupply and demand, t o s o r e complex econometric modela of some one o r two hundred equat ions on up t o t h e p r o g r a a d n g modela which incorpora te thousandr of r e l a t i o n r h i p r .

6 . The focua here in on what can be c a l l e d "market w d e l a , " aa d1rt:nct from "proaramming modela." L/ This d i s t i n c t i o n 1s bared not on ly on :t.e s t r u c t u r e and focur of the m d a l , bur a l r o on i t r purpore and a p p l l c ~ ~ b i l l t y . A marker model is concerned with t h e 6 " c m i n a t i o n of p r icea and wltlr t h e behavior of t h e p a r t i c i p a n t s i n the ma r:. It focure r on the r e c o n c i l i a t i o n of demand and rupply. Prograwahg moder., which g e n e r a l l y draw on highly d e t a i l e d eng ineer ing da ta , focur p r l a u r i l y on o p t l a i t a t i o n with r e r p e c t :o the vo luma c o n r u w d and produced, the l o c a t i o n of product ion and c o n r u q t i o n , o r t h e technologier used. I n a market model, theae q u e r t i o n r a r e i n c i d e n t a l t o t h e o v e r a l l d e r c r i p t i o n of the opera t ion of t h e market.

7. The d i r c u a r i o n here is a l r o l a l t e d t o econometric market models, p r i n c i p a l l y because t h i n type of ayrtem i s moat comonly used f o r f o r e c a r t i n g and s imula t ion of the e f f e c t a of policies.

Simple Hodel Under Competitive Contiitions

R . An example of a simple aa rke t model under competi t ive cond i t ions l a the f r w w o r k of t h e s e r i e s of models constructed by Mama and B t h m n (1976) f o r cocoa, c o f f e e , sugar , wheat and o t h e r food mate r ia l s . There modela were d e l i b e r a t e l y designed t o be slmple s o t h a t they could be i n t e g r a t e d i n t o the COHLIhX world model system (Ada?, 1979b). Never theless , they con ta in the under lying framework of t h e t y p i c a l comaodity model t h a t assumes competi t ive condi t ions .

9. The b a s i c approach on t h e supply s i d e is t o hypothesize p r o f i t maximization under cond i t ions of competi t ion, s u b j e c t t o an assumed production

.function, product and f a c t o r p r i c e s and, i n t h e cape of a g r i c u l t u r a l c o ~ m o d i t i e s , weather condi t ions . These assumptions can be t r a n s l a t e d i n t o a supply func t ion i n terms of the comnodity's own p r i c e , c o s t s of producticn, technology, v e a t 5 e r , e t c . - - where S, = production of commqdity j

s P, = market p r ice of comodi ty j

P,, = c o s t of v a r i a b l e inputs

1/ For a d i s c u s s i o n of the d i f f e r e n t types of models, see AJaas (1973) and - Labys (1978a. 1978b).

Pf - o p p o r t u n i t y c o s t of i n p u t s of f i x e d f a c t o r s

T - tior t r e n d , sometimes r e p r e s e n t i n g tccbnology

U - weather c o n d i t i o n s a f f e c t i n g y i e l d

10. Tuo f a c t o r s need t o be noted. Compet i t ive c o n d i t i o n s may no t app ly s t r i c t l y , a s p roduce r s of mnny a g r i c u l t u r a l p r o d u c t s have l i t t l e v o i c e i n t h e d e t e r m t n a t i o n o f p r i c e , a t l e a s t a t t h e n l c r o l e v e l , and a r e responding t o t h e i r e x p e c t a t i o n s of u r k e t " p r i ce . Sccond, t h e response of supply m y have a long l a g , g i v e n t h e r o l e of e x p e c t a t i o n r , a s well a s t h e f requency of b i o l o g i z a l and t e c h n i c a l de l ays . In t h e c a r e of c o f f e e , f o r example, i t may t a k e f o u r t o s even y e a r s be fo re n u p l a n t i n g # produce , and t h e r e may be l i t t l e o r no s h o r t - t e n f l e x i b i l i t y .

11. On t h e dermnd s i d e , l t is a s s t n e d , a s is customary, t h a t u t i l i t y meximira t ion on t h e p a r t o f consumers w i l l de t e rmine t h e f i n a l demand f o r a commodity. ffouever, i n most i l r s tances , t h e p r i a a r y comnodity is no t c o n a ~ e d d l r e c t l y , b u t r e q u i r e s i n t e r a c d i n t c p rocess ing o r m y o n l y r e p r e s e n t a smal l p a r t of t h e c o a t of a f i n a l p rod tc t . The d.-mand f u n c t i o n f o r primary coamodi t ies may t h u s i n c l u d e e l emen t s of f i n a l demand o r of i n t e m e d i a t e deatand, producing a f u n c t i o n

where Dj - cor.supption of c o c ~ m d i t y j

P, - p r i c e of comaodity j

P + ~ - p r i c e s of com?eting coaoodi t ies

T - a tioe t r end f o r t a s t e o r t e c h n o l o g i c a l chances

Again, i t is necessa ry t o a l l o v L f o r l a g s which may r e f l e c t t h e g radua l a d a p t a t i o n o f t h e c o n s m e r o r t h e t ime r e q u i r e d to develop s u b s t i t u t e s .

12. For most coomodi t ies , a model c o n s i s t i n g o n l y of equat ion? (1 ) and ( 2 ) vould be t o o s imple , s i n c e i n v e n t o r i e s a b s o r b d i s c r e p a n c i e s b e p e e n product ion and c o n s m p t i o n and p r ; r i d e a n impor tant l i n k i n t h e methanism t h a t de t e rmines p r t c e s . T y p i c a l l y , i nven to ry supply 1s determined by t h e i d e n t i t y

where I = a v a i l a b l e i n v e n t o r i e s

S j = product ion of c o m o d i t y j

Dj = consunpt ion of connodi ty j

hs i s noted belov, although t h i s i d e n t i t y d e f i n e s t h e i n v e n t o r i e s , the f a i l u r e o f computed i n v e n t o r i e s t o correspond t o a c t u a l d a t a is a f requent problem.

13. The l a s t func t ion of t h e system is t h e p r i c e e q u a t i o c usua l ly

This equat ion r e a l l y represen t s a demand f o r inven tor iee equation. Renormalized, i t bccomes:

In t h i s form, i t is a demand f o r inven tor ies equat ion, v i t h t h e des i red i n v e n t o r i e r a func t ion of conrumption ( a s o r t of t r a n s a c t i o n requirement f o r inven tor ies ) and a func t ion of pr ice .

14, The p r i c e term r e q u i r c r exp lamt ion . The demand f o r inven tor ies f o r s p e c u l a t i v e purposes i n v o l i e s a procorr of maximizing the expected p r o f i t by holding inventor ies . Invctntorier a r o accumulated u n t i l , a t t h e margin, the d i f f e r e n c e betveerr t h e cxpected p r i c e md t h e a c t u a l p r i c e e q u a l s the c o s t of holding t h e a d d i t i o n a l inventory. Tho func t ion could bo def ined a s

vhere P' - expected p r i c e

C - a mcasure of t h e ca r ry in& c o a t , inc lud ing a component f o r r i s k

IS. Since t h e r e is no i n f o r u t i o n on pa, i t i n customary to introduce a c t u a l p r i c e s a s a proxy f o r t h e p r i c e t e n . The i m p l i c i t a s s m p t i o n is t h a t of r e g r e r s i v e expectations-if tho p r i c e is unusually high, i t is expected t o f a l l ; s i n i l a r l y , i f i t is low, i t is l i k e l y to r i s e . Thur t h e r e l a t i o n between i n v e n t o r i e s and p r i c e i r genera l ly expected t o be negative.

Hodels Under C a r t e l Condit ions

16. The e s s e n t i a l d i f f e r e n c e between c o r p e t i t i v e models and those under c a r t e l (monopoly o r o l igopoly) cond i t ions is t h a t , under competi t ion, producers o r consuaers maximize t h e i r p r o f i t s wi thout recognizing t h a t t h e i r a c t i o n s may a f f e c t pr ices . I n t h e monopolist ic case , market p a r t i c i p a n t s recognize t h a t t h e i r s a l e s a f f e c t p r i c e and, moreover, t h a t they do s o i n a dynamic s e n s e , i.e., a c t i o n s today w i l l a f f e c t the r e s u l t not only today, but

, a l s o i n t h e fu tu re , The s e p l e models of petroleum, bauxi te and copper by. Pindyck (1978) i l l u s t r a t e a type of mnopoly model vhich nay be app l icab le t 3

a number of primary commodity markets. The -in 4i;:inction between the monopoly model and t h e compet i t ive market model is t h e introduction of a ao.iopoly producer and the not ion of a l i m i t pr ice . To incorpora te these f a c t o r s i n t h e monopoly model, supply is divided i n t o tuo components, one o r i g i n a t i n g i n t h e c a r t e l (S,), the o t h e r o r i g i n a t i n g ou t s ide (Snc). - 17. With respect t o t h e non-cartel component, a tra*cional supply func t ion such a s t h a t i n equat ion (2 ) may apply. However, i t i s impartant t c

r e c o g n i z e t h a t t h e s o u r c e s o f s u p p l y o u t s i d e t h e c a r t e l a r e l i k e l y t o p r o v i d e a l t o g e t h e r d i f f e r e n t r a v u a t e r i a l s - - c l a y as a s o u r c e o f a l u n i n l n rii:,ler t h a n b a u x i t e - - o r p e r h a ~ s s y n t h e t i c s u b s t i t u t e s . The s u p p l y f rom t h e s e s o u r c e s m y b e z e r o s o l o n g a s t h e p r o d u c t ? o n c o s t s c a n n o t be net. Once p r i c e 2xceeds c o s t , however , t h e s u p p l y may be v e r y l a r g e . The p r o d u c t i o n c o s t f rom Ion- c a r t e l s o u r c e s b e c o w s t h e l i m i t p r i c e beyond v h i c h t h e c a r t e l p e i c e c a n n o t r ise.

18. Demand f o r t h e c a r t e l s u p p l y is d e f i n e d a s t h e d i f f e r e n c e hetween demand a n d s u p p l y f r , I n o n - c a r t e l s o u r c e s

P r i c e a n d s u p p l y a r e d e t e r . ~ i n e d s i u u l t a n e o u s l y by t h e c a r t e l , a s s u n i n g t h a t i t c h o o s e s a p r i c e t r a j e c t o r y b*Ier time s o a s t o maximize t h e discoun:ed p r e s e n t v a l u e o f t h c f u t u r e n e t r e v t n u e e t ream. Qua t !on (6) i e t h e o b j e c t i v e f u n c t l ~ n of c a r t e l p roducerq

n

where U - p r e s e n t v a l u e o f t h e n e t f o t u r e r e v e n u e e t r e n m

r - t h e d i s c o i ~ n t rate nsairncd

C - t h e p r o d u c t i o n c o s t

Thc s y s t e a c a n be f u r t h e r r e f i n e d by r e c o g n i z i n g t h a t , f o r a n e x h a u s t i 5 l e r e s o u r c e , c o s t s i n c r e n s e as t h e r e s o u r c e b a s e is u s e d up.

19. Such a framework has c o n s i d e r a b l e p o t e n t i a l f o r t a k i : ~ i n t o a c c o u n t t h e changed c h a r a c t e r o f r e l a t i o n s be tween p r o d u c e r a n d c n n s u a e r c , o u t , t r i e s which \as been a p p a r e n t i n r e c e n t y e a r s .

E l a b o r a t i o n o f Coruaoditv Xnrket M d e l s

20. The s i m p l e c o n p e - i t i v e a n d c a r t e l models a r e o n l y t h e f i r s t s t e p i n t h e d e v e l o p a e n t o f more comprehens ive a n d r ea l i s t i c r c p r e s e q t a t i o n s o f the w o r l d cocmodi t y m a r k e t s . C o n s i d e r a b l y n o r e d e t a i l e d are t h e a p p l l e d m o d e l s , which : n v ~ l v e d i s a g g r e g a t i o n . D i s a g g r e g a t i o n s e r v z s n o t o n l y t o g i v e - b e t t e r r e p r e s e n t a t i o n o f m a r k e t b e h a v i o r , b a t a l s o p e r t l i t s m a r k e t deve lopments t o be b e t t e r r e c o g n i z e d .

21. n n t h e d e r n n d ' s i d e , i t is cus tomqry t o b r e a k dermnd down by consuming r e g i o n a n d t y p e o f consumer. Such d i s a g ~ r e g a t i o n is p a r t i c u l a r l y i n p a r t a n t i f d i f f e r 2 n c e s a r e e x p e c t e d i n t h e b e h a v f q r a l r e s p o n s e s , t e c h n o l o g i e s and t a s t e s , a n d f o r e i g n e x c h a n g e c o n s t r a i n t s o f - h e d i f f e r e n t r e g i o n s . - ; 3 6 L . '! On t h e s u p p l y s i d e , breakdowns hy c o u n t r y o r r e g i o n are u s e f u l , par- t i c u l a r _ l y t o r e f l e c t d i f f e r e n c e s i n t h e c n d i t t o n s o f p r o d u c t i o n and t o a d j u s t - f o r the - impac t o f w e a t h e r c o n d i t i o n s o r d i s e a s e o n a g g r e g a t e p r o d u c t i o n . ~ e s o u r d ? a v a i l a b i l i t t e s and p r o d u c t i o n c a p a c i t y can a l s o b e broken o u t . 8 -

23. I t is a l s o important t o recognize t h a t l o c a l r egu la t iona , much aa mininun p r i c e s , product ion quotaa , marketing boarda, expor t t axe r , e t c . , may play a r 3 l e i n d e t e n a i n i n g output. In many c a r e s t h e assumption t h a t producers respond t o t h e world coumodity p r i c e is i n v a l i d , s i n c e t h e p r i c e obta ined hy l o c a l producero dev ia te0 g r e a t l y f r o a t h e p r i c e p r e v a i l i n g i n ~ r l d coamodity marketa. Th i s a100 means t h a t a l o n g with d i saggrega t ion of supply , i t is necessary t o di6aggrega:e p r i c e , t o t r a n s l a t e t h e world market ? r t c e ir.to t h a p r i c e s t h a t apply i n t h e producing a rea .

24. The need t o d e a l wi th nominal p r i cea i n var ioua cur renc ico 10 a complication. One approach hao k e n t o f o r m l a t e t h e commodity p r i c e i n U.S. d o l l a r b , a d j u a t e d f o e t h e change i n p r i c e l eva lo , and then simply t o conver t t o o t h e r c u r r e n c i e s us ing exchange r a t a o ( r o w o f t h e problems r e l a t i n g t o cha r o l e of i n f l a t i o n and I r t a r m t i o n a l exchange r a t e movements a r e noted belw).

25 Another problem 10 t h a t t y p i c a l l y i t has n o t been poss ib le t o o b t a i n a r e a l i s t i c d i saggrega t ion of s t o c k s i n t o those h e l d by consumere and those held by producero, thoae being held f o e opecu la t ive purposes and those held f o r o r d i n a r y t r a n s a c t i o n o , f o r a u m p l e . The d a t a on s t o c k s a r e g e n e r a l l y d e f i c i e n t and lust be computed from the r e c o n c i l i a t i o n of supply and demand. I n sone a o d e l s , i t h a s been h e l p f u l t o d i v i d e t h e world market i n t o major b locks , f o r example, t h e U.S. market and t h e r e s t of t h e world, a s i n t h e copper model of F i s h e r , e t . a l . (1972), wl th t r a d e f l o v s l i n k i n g t h e markets. General ly , though, i t h a s been d i f f i c u l t t o r econc i l e t h e t r a d e ~ t a t i s t l c s o n commodities wi th those aeasur ing product ion and consumption, and t h e r e a r e feu models of c o m o d l t y markets i n which a n a t t empt has been m d e t o e x p l a i n t h e movements of commodities i n i n t e r n a t i o n a l t r a d e i n any d e t a i l .

APPLICATION OF COHHODITY HARKET HODELS

26. %is s e c t i o n cons ide r s t h e use of c o w d i t y market rnccels i n p r a c t i c e , f ~ l l w i n g a note of caut ion. The a p p l i c a t i o n of a c d e l s c a l l s f o r a c a r g f u l balance between a b s t r a c t i o n and r e a l i t y . The ,model bu i lde r and user t r y t o take advantage of t h e p o s s i b i l i t i e s of s i m p l i f y i n g t h e r e a l world which t h e model r e p r e s e n t s . S t i l l , t he m d e l m e t not be s o d i f f e r e n t from t h e r e a l cwrld as t o l o s e re levance. The w d e l is a t o o l ; t o be u s e f u l , i t nus t cap tu re t h e e s s e n t i a l s of r e a l behaviof. Fur ther , t h e user of the model must be aware of i t s correspondence t o r e a l w o r l d cond i t ions . Does i t t ake i n t o account t h e f o r c e s c u r r e n t l y af fect ing ' the market? Does i t take i n t o account t h e l a t e s t s t a t i s t i c s and o t h e r i n f o r ~ t i o n about market cond i t ions? Does i t a l low f o r e x p e c t a t i o n s ? Does i t c o n s i w a c t u a l and p o t e n t i a l p o l i c i e s , f o r example, s t a b i l i z a t i ~ n ,ans, o r t h e a c t i o n s of producer country groups? Even i f a f a i l u r e t o t a k e 11 . . . account what is a c t u a l l y going on i n t h e market does not a f f e c t t h e r e s u l t s of t h e computation, i t nay undermine t h e c r e d i b i l i t y of t h e conclusions.

27. Commodity u a r k e t models have many d j e r s e a p p l i c a t i o n s . Here :he focus is on a p p l i c a t i o n s fo r :

I. Short - tern f o r e c a s t i n g of p r i c e s and t h e earnings uf producing ing c o u ~ ~ t r f es;

11. Long-tern p r o j e c t i o n s o f s u p p l i e s and o f p r i c e s a l o n e ; and

1 . S l m u l a t i o n s of t h e c f f e c t s o f a l t e r n o t i v e s t a b i l i z a t i o n schemes.

28. In t h i s p a p e r , s h o r t - t e r m f o r e c a s t s have been d e l i b t . n l y s e p a r a t e d f r o s long-term o n c s . The i n f o r m t i o n r e q u l r e d t o ~ k e a s h o r t - t e r m f o r e c a s t I s q u i t e d ! f f e r e m : C r o n i h s * f o r a l t - v - t e r n p r o j e c t i o n , and t h t f ~ r c e u n f f c c t i n p . t h e s h o r t - t e r m out l .ook o r e d i f f e r e n t , a s n r e t h e u n c e r t n i n t i c s .

Sho r t -Te rn F o r e c a s t i n & - 29. The s h o r t - r u n f o r e c a s t is u s e f u l a s n way o f e v a l u a t i n g t h e p r o s p e c t s f o r coanodf t y p r i c e s o v e r n one o r two-yenr p e r i o d . I t is a means of a p p r a i s i n g t h e s h o r t - r u n p r o s p e c t s f o r c a r n i n g s i n p roduc ing c o u n t r i e s and f o r measu r ing t h e I ? f l a t i o n a r y and b a l a n c e o f payments p r e s s u r e s which commodity marke t c o n d i t i o n s m y impose on t h e economies o f consuming c o u n t r i e s .

30. On t h e demand s i d e , t h e dominant e l emen t i n t h e s h o r t - r u n f o r e c a s t is t h e b u s i n e s s c y c l e i n consumi n ~ c o u n t r i e s . Sho r t - t e rm e l a s t i c i t i e s o f demand w i t h r e s p e c t t o p r i c e a r e t y p i c a l l y q u i t e low. Bus ine s s c o n d i t i o n s , which c a u s e s h i f t s i n t h e c o n s u n p t i o n o f many c o u n o d i t i e s , a r e b road ly p r e d i c t a b l e , s o t h a t f o r e c a s t i n g d e ~ a n d f o r consumption o r a s i n p u t s i n t o i n d u s t r i a l a c t i v i t y is n o t d i f f i c u l t . F o r e c a s t i n g s u p p l y and i n v e n t o r i e s p r e s e n t s more d i f f i c u l t problems. The o u t p u t o f a g r i c u l t u ~ a l p r o d u c t s is a f f e c t e d by w e a t h e r c o n d i t i o n s ; y i e l d s a r e n o t a b l y d i f f i c u l t t o p r e d i c t . Supply is a l s o i n f l u e n c e d by s t r i k e s and p o l i t i c a l d i s t u r b a n c e s . I ndeed , t h e s e f a c t o r s , v h i c h a r e a l l b u t u n p r e d i c t a b l e , have been a p r i n c i p a l c a u s e o f t h e sho r t - run f l u c t u a t i o n s i n c o m ~ o d i t y p r i c e s and e a r n i n g s . F i n a l l y , w i t h r e s p e c t t o i n v e n t o r i e s , a b a s i c p r o b l e n w i t h many commodit ies is t h e d i f f i c u l t y o f - z a s u r i n g t\e l e v e l o f i n v e n t o r i e s by r e c o n c i l i n g s t a t i s t i c s on consumption and p r o d u c t i o n w i t h t h o s e on t r a d e . Moreover, i t is t h e a c t u a l l e v e l o f i n v e n t o r i e s , and n o t j u s t t h e change , t h a t is i m p o r t a n t , s i n c e t h e impact o f i n v e n t o r i e s on p r i c e s is no~ . - l i nea r . *When i n v e n t o r i e s a r e low, t h e impact o f a change i n i n v e n t o r y may be g r e a t e r t han when t h e y a r e h i g k . I n v e n t o r i e s a l s o pose problems v i t h r e s p e c t t o e x p e c t a t i o n s , a n i s s u e which is c o n s i d e r e d f u r t h e r below. - - 31. X s h o r t - t e r m f o r e c a s t f o r co -d i t i e s is by n a t u r e s u b j e c t t o '! c o n s i d e r a b l e uncerta- inty. An impor t an t r o l e o f t h e model is t o s e r v e as-a framework f o r makin t h e f o r e c a s t , and a l l o w i n g e x t e r n a l c o n d i t i o n s t o b e t ake , . i n t o account.!The model a l s o s e r v e s a s a n i n s t r m e n t t o r a p p r a l s i % a l t e r n a t i v e s c e n a r i o s o f e x t e r n a l c o n d i t i o n s and a l t e r n a t i v e p o s s i b i l i t i e s w i t h r e s p e c t t o y i e l d s o r supp ly d i s t u r b a n c e s .

Long-Tern P r e d i c t i o n s

32. Long-term p r e d i c t i o n s a r e a n i n p o r t a n t i n g r e d i e n t i n e v a l u a t i n g t h e e a r n i n g s w t e n t i a l o f p roduccr c o u n t r i e s t o be d e r i v e d from e x p o r t s o f p r imary connod i t i e s . T h i s i s a c e n t r a l c o n s i d e r a t i o n when p l a n n i n g a development s t r a c e e v .

33. Even though the sane model MY be used f o r long-run projections a s is used f o r short-term ones, the c r i t i c a l considerations tha t e n t e r i n to the two are very d i f ferent. On the deaand aide, long-run e l a s t i c i t i e s may be higher than short-run e l a s t i c i t i e s , s ince there is more scope fo r adaptation t o higher pr ices i n the long run. Horeover, the deve lopen t and introduction of synthe t ic subs t i t u t e s can tecome a threa t i n the long run.

34. Long-run considerat ions a re a l s o cons iderably d i f fcrent from thc short run on the supply side. Comtra in ts a r i s i n g out of the limits of the na tura l resource base MY apply, par t icu lar ly fo r exhaustible resources. Even i f a par t icu lar commodity is not exhausted, production cos t s may s t i l l r i s e a s the most favorable o r accessible sources a r e used up. On the other hand, the long-run supply e l a s t i c i t y with respect t o pr ice m y be a grea t deal l a r ~ e r than the short-run rasponre. Part icular ly i f the price rises above production coa ts f o r some producers, the long-run oupply response may l\a very large, and the pr ice may quickly be driven back d w n t o equal i ty with cobt. Inventories, which play such an important ro le i n the short-run forecas t , a r t not an important conrideration i n the long-run project ion. While inventories may get out of l i n e v i th requirement8 temporarily, the long-run forecast m e t assume tha t market forccr w i l l cause inventories t o be adjusted i n accordance with aurket requirements. A forccast which assumes tha t inventories w i l l accumulate in the long run without appropriate aarke t adjustments is unrea l i s t ic .

35. This discussion suggests tha t long-run forecaste a r e a l s o subject t o wide bands of e r ror . Past projections of demand over the long-run, such a s those of the Pnley Report, have been very vide of the mark. On the other hand, technological infornation about resource a v a i l a b i l i t i e s and production cos t s can serve a s a useful guide on the accuracy of long-term projections.

Simulation

36. With respect t o s h l a t i o n s tudies , the focus is on those dealing with the s t a b i l i z a t i o n of pr ices in the comnodity markets f o r which models have been widely used. It can be argued tha t simulation t e a t s have someyhat l e s s need f o r realism, t h a t a model can s t i l l serve t o simulate market behavior even i f i t cannot forecasc well. Obviously, t h i s depends on the source of the forecast error . I f the e r r o r i n the forecas t derives from unpredictable exogenous events, the nodel may be useful f o r policy simulation. I f , on the other hand, the e r r o r a r i s e s because the model f a i l s t o describe the underlying economic processes, o r the equations a re poorly o r incompletely specif ied, the w d e l nay not be usefu l f o r simulations even i f i t happens t o f i t i n the sample period. 8

37. The c r i t i c a l i ssue in simulation i s the accuracy of the behavioral responses. However, they may not be enough. I t is important tha t the model be complete and that the c i r c u i t of feedback re la t ionships not be interrupted. Horeover, i t i s important tha t some of the policy responses be t rea ted endogenously. An example would be the recognition tha t the government may recycle tax earnings from comodity production i n t o additior.al i n f r a s t ruc tu re , which may ul t imately fos t e r addi t ional supplies. Similarly, i t i s necessary t o recognize tha t some governments neut ra l ize the operations

of the international markets through the imposition of special exchange rates or domestic producer prices. If these are assumed to be fixed while the market novcrs, the simulations will be incorrect.

38. One of the most iaportant applications of the commodity narket models is for evaluating alternative commodity market stabilization schemes. The broadest efforts in this direction have involved the Caaunon Fund proposal, for example, those by Ekhrman (1978). The custooary procedure has been to specify and to estimate the models assuming that an effective comsodity agreement was not in operation. Some stockpile purchases and sales are included in the sample period, as are some restrictions on production and export sales, but there is typically no explicit or implicit assmption that prices will be held within certain limits or that producers expect prices to be stabilized. N w , then, is such a model used for stabilization simulations?

39. Thia is done by imposing the actions of the stabilization agency on the model. In the case ?f stabilization with a buffer stock, a price ceiling and floor are established. If the =:el yielded a solution calling for a price b e l w the floor, the buffer stock w u l d buy to bring the price to the floor level. If the price obtained through the model solution exceeded the ceiitng, the stockpile agency w u l d draw on its stock to provide additional eupplies until the price uaa reduced to the ceiling level. Typically, a aechaniom is included to keep track of the status of the stockpile agency--it8 stock holdings, financial position and the gains and loasea from ita transactions. Normally, these conputations have been made in a deterministic fashion over the sample period, assuming neither random error in the coefficients or the equations, or in the exogenous variables.

40. The result ia an approximation of "what night have happened if" a stabilization scheme had been applied. Hwever, the calculatlon Is unique and does not a l l w for the probabllistic nature of the real world and, conse- quently, of the costs of a stabilization scheme. Stochastic s h l a t l o n in the exogenous variables, in the errors of the equatlona, and posslbly in the errors of the coefficient8 offers interesting possibilities for evaluating the risks association with stabilization schemes (Ford, 1978).

1

4 1. Relow is 9 iiscussion of a serious speclflcatlon problem, essentially a rational expectatio~s problem, which results &en the market response recog- nizes the imposition of a stabilization scheme. -

8 BRONTIERS OF ECONO!ETRIC CO?MODIfY MARKET MODELING -

4 2 . In tKls section, the frontiers of econometric modeling of commodity markets is coeidere~. It focuses on the gaps, not so much to find the flaws in present procedures as to point to areas where additional research is needed. The concern is particularly with those aspects of comnodity mark#-t modeling that have iumediate ioplications in terns of the applicat1l:ty of models for forecasting and simulation. The following are the principal considerat ions:

1. Commodity modelr and in f l a t ion and exchange rates--the " f l i gh t out of money";

11. The responres of c o m d i t y markets t o s t a b i l i z a t i o n policy; and

ill. Integrat ion of c o ~ w d i t y w d e l s in to other econorzic model cystems a

Iapact of In f l a t ion and Exchange Rates

4 3. The r e l a t ion rh ip between comwdity pr icer , i n f l a t i o n , and exchange r a t e s i s not well underrtood. Evidence from the 19708, when the price rvingr i n the major coamodity marketa were not predicted, r h w r tha t t h i r i r one of the inportant gapr i n current coumdity aodeling work.

44 . There i s no record of the ante forecart ing performance of cocmodity modele such a r the one p r o v i T f o r macroeconomic modele by HcNeer (1979). On the bae i r of '.he ex st record of e r ro r derived from model slmulations for the sumple p e ~ f i n d on the bas is of annual da ta) , average e r r o r s were obtained f o r pricer f o r eight ag r i cu l tu ra l w d e l r (Adam and Behrman, 1976). The range war from 3.2 percent for r i c e t o 11.3 percent for sugar and 13.1 percent for cocoa. These a r e f a i r l y reasonable resu l t s . The e r ro r i s l i ke ly t o be greater fo r ex ante forecasts than fo r s iau la t ionr during the sample period. Yet i n n o r ~ p e r i o d s , the modelr have been found useful fo r forecast ing outr ide the rumple period, though only when adjustments have been made t o l i n e up the forecasts and t o introduce known external 1n:ormation. Unfortunately, the saac cannot be ra id fo r periodr of rapid i n f l a t i o n and exchange r a t e in s t ab i l i t y . Hort modele estimated over a eample period prior t o 1973 have not predicted fu l ly the upsurge in comodity gricer which occurred i n 1973-74. Even modelr which included these years i n the sample period have not performed well over these years. - 11

45. This suggests tha t proper treatment of i n f l a t i o n and exchange r a t e s is a c r i t i c a l problem i n current commodity modeling. The d i f f i c u l t y is probably not one of simply t rans la t ing world prices i n t o appropriate domestic pr ices through exchange rates . I t is one of accounting for expectations conceAing i n f l a t i o n and exchange r a t e s i n the s t ruc tu re ' o f the commodity model. Although expectations a f f ec t both the detaand and the eupply s ides of a model, i t is not c l e a r tha t t h i s i s where the problem of in f l a t ion and exchange r a t e i n s t a b i l i t y has its impactc It is more l i ke ly , tha t expectations a f f e c t the equation fo r theZenand for inventories o r price. In t h i s case, the d i f f i c u l t y l i e s in g e t t i n w a handle on expectations a s to the nominal price of the coarmodity. The n o r w l approach which assumes regressive expectations, i s c l ea r ly inappropriate w en prices o r exchange ra tes a r e 'L

11 The continuous time copper node1 by Denis Richard may Le an exception. - However, the very close f i t of t h i s model, with a consistent lag, is sus- picious, par t icu lar ly since i t does not recognize external forces such a s exchange ra te i n s t a b i l i t y .

u n s t a b l e . A t t h e same t ime, i t is n o t c l e a r t h a t o t h e r conven t iona l approaches t o t h e f o r n a t i o n o f e x p e c t a t i o n s , v h i c h f o r m l a t e t h e expec ted p r i c e a s some form of t h e ve igh ted ave rage of p a s t p r i c e s , a r e b e t t e r . Indeed , one m y v a n t t o v i s u a l i z e t h e h o l d i n g of c o n n o d i t i e s a s p a r t of t h e e n t i r e phenomenon o f a s s e t adjustne:lt--"f 1 i gh t o u t of moneyQ'-which o c c u r s d u r i n g a pe r iod of r a p i d i n f l a t i o n o r exchange r a t e i n s t a b i l i t y .

P r i c e S t a b i l i z a t i o n P o l i c v S imula t ions

46. Tbe performance of nodc l s t h a t s i m u l a t e t h e e f f e c t s of p o l i c y is d i f f i c u l t t o a p p r a i s e . There Is no o b j e c t i v e s t a n d a r d a g a i n s t v h i c h t o eoapa re a "vhat i f " s i m u l a t i o n . The e r i t i e a l c o n s i d e r a t i o n is v h e t h e r t h e e q u a t i o n s c a t c h f u l l y t h e r e l e v a n t r e l a t i o n s h i p s . Thus s i m u l a t i o n performance c a n be e v a l u a t e d o n l y on t h e b a s i s of v h e t h e r t h e r e sponse d e r i v e d v i t h t h e model c o n f o r m t o a p r i o r i e x p e c t a t i o n s . Does a one-time s t o c k p i l e s a l e a f f e c t t n v e n t o r i e s and p r i c e as i t is supposed t o ? Do supp ly and demand a c t a s one would e x p e c t ? Is t h e r e u l t i m a t e l y a r ead jus tmen t t o e q u i l i b r i u m , p r e f e r a b l y one t h a t is no t Ear from t h e base s o l u t i o n e q u i l i b r i u m ?

47. While i t is h a r d t o g e n e r a l i z e , o v e r a l l , i t a p p e a r s t h a t i t h a s been p o s s i b l e t o b u i l d a o d e l s t h a t can s i m u l a t e behavior o v e r t h e sample pe r iod adequa te ly . T h i s is a n imperfec t test , h w e v e r . Suppose, f o r example, t h a t p o l i c y h a s changed s i n c e t h e time o f e s t i m a t i o n and t h a t t h e p a r t i c i p a n t s i n t h e market a r e a v a r e of t h e p o l i c y change and respond t o i t . T h i s is t h e problem t h a t o c c u r s vhen a s t a b i l i z a t i o n scheme is ;mposed and models a r e used t o e v a l u a t e i ts impact.

48. A c r i t i c a l a s a m p t i o n i n t h e work on s t o c k p i l e s i m u l a t i o n s is t h a t p r i v a t e market behav io r is una f f ec t ed by t h e i m p o s i t i o n o f a s t a b i l i z a t i o n plan. While i t is probably i n a p p r o p r i a t e t o go a s f a r a s t h e t h e o r i e s of r a t i o n a l e x p e c t a t i o n s , v h i c h sugges t t h a t a l l p o l i c y s t e p s a r e f u l l y a n t i c i p a t e d , i t is u n r e a l i s t i c t o assume, on t h e o t h e r hand , t h a t behav io r is unchanged. P a r t i c i p a n t s i n t h e market w i l l acknovledge t h e impact of t h e s t a b i l i z a t i o n p o l i c y i n t h e i r d e c i s i o n making. A s s u m i ~ g t h a t , and g iven t h e v a r i o u s components o f t h e system, v h a t is l i k e l y t o be a l t e r e d by t h e i m p o s i t i o n of a p r i c e s t a b i l i z a t i o n program?

C

49. On t h e demand s i d e , pcf:e s t a b i l i z a t i o n nay be s e e n t o have some, bu t no t a ma jo r , e f f e c t . P r i c e swings a r e l i k e l y t o be moderated and t h e adequacy o f s u p p l y a s su red . On t h e supply s i d e , t h e impact of p r i c e s t a b i l i z a t i o n may be more pronounced. P r i c e e x p e c t a t i o n s p l ay an impor t an t r o l e i n d e t e r m i n i ' o u t p u t . Even i f t h e e x p e c t a t i o n i t s e l f is n o t changed (assuming nc s y s t e m a g c e f f o r t t o a l t e r t h e long-run p r i c e ) , t h e v a r i a n c e o f p r i c e v i l l s u r e l y be - reduced. T h i s l e s s e n s r i s k and should s t i m u l a t e s u p p l y , depending on t h e *

p r i c e . Econone t r i c s t u b i e s by J u s t and o t h e r s shov c l e a r l y t h a t p r i c e * - v a r i a n c e is a f a c t o r i n t h e d e t e r m i n a t i o n of supply . F i n a l l y , t h e most s e r i o u s l y a f f e c t e d p a r t o f t h e m d e l is t h e e q u a t i o n f o r p r i c e o r demand f o r i n v e n t o r i e s ( s e e e q u a t i o n 4). F i r s t , c r ansac t i o n s demand i n c l u d e s a component f o r p r e c a u t i o n a r y r equ i r emen t s , t h a t i s , i t i n c l u d e s s t o c k p i l e s he ld a g a i n s t t h e e v e n t u a l i t y o f supp ly s h o r t a g e s . C l e a r l y , t h e p re sence of an i n t e r n a t i o n a l s t o c k p i l e v i l l reduce t h e need f o r p r e c a u t i o n a r y p r i v a t e s t o c k p i l e s , s u g g e s t i n g t h a t t h e r e is s u b s t i t u t i o n be tveen p r i v a t e and p u b l i c

i n v e n t o r i e s (Cardner , 1977). Second, v i t h r e s p e c t t o expec t ed p r i c e , i f t h e s t a b i l i z a t i o n program i s e f f e c t i v e , t h e v a r i a n c e o f p r i c e shou ld be reduced. his l e s s e n s t h e r i s k , bu t i t a l s o r educes t h e p o s s i b i l i t y of making a k i l l i n g , a s t h e v a r i a n c e o f p r i c e is l i m i t e d t o t h e band be tveen t h e upper and l w e r p r i c e l i m i t . As t h e p r i c e a?proaches t h e upper l i m i t , t h e i n c e n t i v e s t o m a i n t a i n i n v e n t o r y h o l d i n g s a r e reduced--(pe - P) becomes sma l l e r . Indeed , t h e r e may be no s p e c u l a t i v e i n c e n t i v e a t a l l f o r h o l d i n g i n v e n t o r i e s a t t h e upper p r i c e l i m i t . S i m i l a r l y , a s t h e p r i c e a , .)roaches t h e l o v e r bound, i nven to ry -ho lde r s v i l l be v i l l i n g t o a b s o r b la .ge q u n n t i t i e s of i n v e n t o r i e s , s i n c e t h e r e is no r i s k of a f u r t h e r p r i c e d e c l i n e .

50. There is a n o t h e r impor tan t c o n s i d e r a t i o n . What h a s been s a i d above abou t t h e impact of p r i c e s t a b i l i z a t i o n on t h e p a r t i c i p a n t s i n t h e market assumes t h a t t hey b e l i e v e t h e p o l i c y v i l l be e f f e c t i v e . I f t hey doubt i ts e f f e c t i v e n e s s , t h e p i c t u r e is changed. For example, i f t h e p a r t i c i p a n t s i n t h e market l a c k con f idence t h a t t h e p r i c e c e i l i n g and f l o o r c a n be main ta ined , t hey v i l l a c t a s i f t h e r e wre no s t a b i l i z a t i o n a c t i o n . They can be expec t ed t o i g n o r e t h e s i z e of t h e o f f i c i a l s t o c k p i l e and t h e q u a n t i t y of f i n a n c i a l r e s o u r c e s a v a i l a b l e f o r commodity purchases . I f t h e y f e a r t h a t t h e s t o c k p i l e v i l l r un o u t o r t h a t i n s u f f i c i e n t f i n a n c i a l r e s o u r c e s a r e a v a i l a b l e , t hey may s p e c u l a t e a g a i n s t t h e s t a b i l i z a t i o n plan. The h i s t o r y o f t h e I n t e r n a t i o n a l T i n Agreement is an i n t e r e s t i n g i l l u s t r a t i o n o f a c a s e v h e r e t h e a v a i l a b l e s t o c k p i l e van i n s u f f i c i e n t t o ma in t a in t h e p r i c e c e i l i n g .

Commoditv Hodel and Countrv Linkanes

51. Another broad f r o n t i e r a r e a of commodity market modeling is t h e l i n k a g e between c o m o d i t y market models and w d e l s o f t h e o v e r a l l economies of c o u n t r i e s . T h i s is a broad sphere . On t h e one hand, i t i n c l u d e s t h e work on l i n k a g e s be tueen coacmdity w d e l s and , t h o s e of t h e economies of producer c o u n t r i e s . On t h e o t h e r , i t i n c l u d e s t h e impact o f commodity p r i c e s on t h e economies o f consumer c o u n t r i e s . F i n a l l y , i t i n c l u d e s t h e w r l d model s t u d i e s l i k e COHLINK and t h e S h i s h i d o (1977) and t h e World Bank systems.

J2. A g r e a t d e a l o f p r o g r e s s is be ing made i n t h i s a r e a . However, t h e vork is s t i l l i n i ts i n f a n c y , and t h e p o t e n t i a l f o r f u r t h e r a n a l y s i s is v e r y g r e a t . The focus h e r e is o n l y on some l i m i t e d i s s u e s r e l a t i n g t o t h e l i n k a g e s

' bet:een commodity marke t s and t h e models of producing and consuming count r l e s .

53. w i t h r e s p e c t t o producing c o u n t r i e s , t h e i s s u e of t h e e f f e c t o f i n s t a b i l i t y i n t h e c o m m d i t y markets on economic development is c r u c i a l and u n s e t t l e d . 1 1 Recent work a t t h e U n i v e r s i t y o f Pennsylvania (Adams, Behrman and Roldan, 1979, and o t h e r c u r r e n t s t u d i e s ) shov bo th t h e p o t e n t i a l u s e f u l - n e s s of l i n k i n g t h e n o d e l s of commodity marke t s w i t n t h o s e o f producing c o u n t r i e s and t h e s u b s t a n t i a l nunber of i s s u e s vh i ch demyld f u r t h e r s tudy . .

11 For a d i s c u s s i o n , s e e ttanger (1979). The r e s u l t s o f t h e v a r i o u s s t u d i e s - a r e n o t o n l y c o n t r a d i c t o r y , but i n l a r g e p a r t c o u n t e r i n t u i t i v e .

54. I t is a r e l a t i v e l y s t r a i g h t f o n r a r d p a t t e r to b u i l d a model o f a comaodity-producing s e c t o r and t o i n t e g r a t e i t i n t o t h e model of a producing coun t ry . I t t u r n s o u t t o be c o n s i d e r a b l y more d i f f i c u l t t o rhou t h e r e l a t i o n - s h i p r between g r w t h i n t h e producing coun t ry and t h e deve lopaen t o f t h e coamo-dity s e c t o r , p a r t i c u l a r l y w i t h r e s p e c t t o i t s f l u c t u a t i o n r . I t is wel l - knovn t h a t f o r e i g n exchange e a r n i n g s and t a x r e c e i p t r have impor tan t e f t e c t r on domes t i c development and i n f l r t i o n . I t i r n o t g e n e r a l l y a p p r e c i a t e d , however, hou much i n f luence a producer c o u n t r y ' s p o l l c l e r m y have o n a c c e n t u a t i n g or a t t e n u a t i n g t h e impact of c o a a a d i t y marke t f l u c t u a t i o n r . I n any case, s i m u l a t i n g t h e l i nkage be tveen c o m o d i t y marke t s and t h e economies o f producer c o u n t - i t s could thrcw nuch l i g h t on t h e i m p l i c a t i o n s o f a l t e r n a t i v e p r o j e c t i o n s f o r c o m m d i t y marke ts and o f v a r i o u s co-dity s t a b i l i z a t i o n p l a n s on t h e development o f coamodity-producing c o u n t r i e s .

55. On t h e o t h e r s i d e of t h e market-the l i n k a g e to consuning economier , p r o g r e s s h a s a l s o been a a d e , bu t e i g n i f l c a n t problems remain. P r i c e f l u c t u a t i o n s i n t h e n a r k e t s f o r world c o m o d i t i e s , pe t ro l eum and o t h e r i tem, have had a heavy impact on consu r~ ing c o u n t r i e s . The l i n k a g e s from t h e comr~odity m r k e t s e x t e r n a l t o t h e consuming economies a r e f a i r l y c l e a r , though they a r e not wel l -captured by t h e d a t a on t r a d e volume and p r i ce s . The i s s u e which most macro models over look Is t h e d i r e c t impact o f world commodity marke t s on t h e p r i c e s of pr imary commodities produced i n coneuming economies themselves. For example, t h e rise o f world wheat p r i c e s i n L973.-73 caused a n i n c r e a s e i n t h e c o s t of g r a i n s i n t h e US. The r e s u l t i n g i n ~ r e n ~ e s i n t h e CPI and t h e d i s t o r t i o n s i n t h e d i s t r i b u t i o n of income and i n consumer e x p e n d i t u r e s were s i g n i f i c a n t . Horeover , t h c s i t u a t i o n l e d t o a n t i - i n f l a t i o n a r y monetary and f i s c a l p o l i c y responses . When t h e r e a r e p h y s i c a l supp ly s h o r t a g e s , a s i n t h e c a s e of g a s o l i n e , t h e d i f f i c u l t y of u s i n g t h e models is even g r e a t e r . It is n o t c l e a r t h a t e x i s t i n g macro model s t r u c t u r e s accoun t f o r t h e i rrpact of commodity market f l u c t u a t i o n s on t h e economies of consuming c o u n t r i e s adequa te ly .

56. F i n a l l y , t h e r e Are t h e comprehensive models. They i n c l u d e n o t on ly t h e commodity marke t s , but t h e economies o f producing and consuming c o u n t r i e s a s w e l l . A number of frameworks a r e p o s s i b l e , b u t t h e d i s c u s s i o n h e r e focuses p r imar i l y -on t h a t o f COYLINK, t h e v e r s i o n o f t h e LINK world model sys t em t h a t i n c l u d e s )he conmodity models (Adam, 1979a and b). I n t h e COHLINK sys tem, t h e l i n k a g e s f r o = t h e models o f producing c o u n t r i e s t o t h e models o f consuming c o u n t r i e ~ a r e ach i eved p r i m a r i l y through t h e p r i c e mechanism. To summarize - b r i e f l y , 'ommodity p r i c e s a r e de te rmined i n a s e r i e s o f commodity market % models. e c o m d i t y p r i c e s then e n t e r i n t o t h e world p r i c e mechanism . th rough a t r a n s l a t i o n t o t h e t r a d e p r i c e s o f p roduce r c o u n t r i e s . Tha t is, t h e e x p o r t u n i t v a l u e s o f producing c o u n t r i e s f o r t h e p r i n c i p a l SITC c a t e g o r i e s a r e e x p l a i n e d i n t e r n s of t h e r e l e v a n t commodity p r i c e s . The e x p o r t u n i t v a l u e s of t h e LIhX s y s t e n a r e conve r t ed by a t r a d e m a t r i x procedure i n t o t h e import p r i c e s o f consuming c o u n t r i e s f o r t h e a p p r o p r i a t e SITC c a t e g o r i e s . These p r i c e s t h e n e n t e r i n t o t h e coun t ry models and a f f e c t t h e domest ic p r i c e l e v e l . There is no a t t empt t o show t h e q u a n t i t i e s of t r a d e d commodities n o r t o r e c o n c i l e p r i n a r y c o m o d i t y t r a d e f lows w i t h t h e LINK s y s t e n t r a d e e s t i m a t e s . There i s , however, a c o n p l e t e s i n u l t a n e o u s feedback from t h e economic c o n d i t i o n s p r e v a i l i n g i n t h e i n d u s t r i a l c o u n t r i e s t o t h e commodity n o d e l s , t o t h e producer coun t ry node l s and back t o t h e i n d u s t r i a l c o u n t r i e s .

57. Through t h i s mechanism i t has been p o s s i b l e t o s h w the impact of commodity p r i c e s bn the p r i c e s i n t h e i n d u s t r i a l c o u n t r i e s and on t h e i r expor t p r i ces . For example, a supply shor tage i n a primary c o m o d i t y , ruclr a s is produced by a f r o s t i n t h e cof fee p l a n t a t i o n s o r a s t r i k e i n the copper mines, causes t h e p r i c e of a c o m o d i t y t o be higher ; t h a t p r i c e feeds through the economics of consumer and producer coun t r i e s . S i m i l a r l y , an economic s t imulus i n developed c o u n t r i e s inc reases t h e demand f o r primary cotmmdities, etc.

! 8. An important a spec t of a complete system is t h a t i t accourrt f o r these typee of feedbacks. For r u m p l e , t h e a b i l i t y of producing c o u n t r i e s t o import is inc reased a s e x p o r t s increase . Economic a c t i v i t y i n developed c o u n t r i e s is s t l o u l a t e d by inc reased r e a l d tprnd, but depressed by the need t o pay higher p r i c e s (Adam, 1979a).

59. The focus of LINK has k e n on f o r e c a s t i n g , on business c y c l e develop- rPcnts and on shor t - term policy. While the system works, i t is i n t e r e s t i n g t o no te t h a t i t appears t o a t t e n u a t e p r i c e samewhat. I n soarc respec t s , t h a t r e s u l t r e f l e c t s t h e r e a l w r l d si tuation--st primary commdity t r a d e is c a r r i e d on under c o n t r a c t and does not move with t h e s p o t p r i ces , f o r example. Houevcr, i t a l s o r e f l e c t s t h e na tu re of t h e commdity market models, p a r t i c u l a r l y t h e f a i l u r e of country macro models t o recognize f u l l y t h e r o l e of primary commodity p r i ces . Never theless , d e s p i t e t h e p rob lem wi th t h e p resen t system, a j o i n t country-comodity model is e s s e n t i a l f o r desc r ib ing t h e k inds of f l u c t u a t i o n s now a f f e c t i n g t h e world economy. (It goes almost wi thout saying t h a t such a system mst a l s o inc lude markets f o r fo re ign exchange and i n t e r n a t i o n a l c a p i t a l movements.)

60. The LINK system is being extended t o d e a l w i t h locg-term p r o j e c t i o n s but , a s noted above, long-term f o r e c a s t i n g of t h e commodity markets r equ i res a somevhat d i f f e r e n t eaphasis. It is not c l e a r whether COHLINK a s p resen t ly organized can hand le that kind of task. F a i r l y e l a b o r a t e under ly ing analyses of resource a v a i l a b i l i t i e s and of resource s u b s t i t u t i o n would have t o be c a r r i e d ou t s o that t h e long-term p r o j e c t i o n s f o r t h e commodity markets w i l l be onb t rack ( C o e l l e r and Weinberg, 1978). A long-term-okiented simultaneous system would be a n important t o o l f o r examining t h e k inds of i s s u e s posed by t h e Club of Rome.

- 61. With r e s p e c t t o pol icy s i m u l a t i ns , a country-commodity model system o f f e r s p o s s i b i l i t i e s f o r working ou t f u l ! y t h e impact of proposals c u r r e n t l y being d i scussed i n va r ious North-South fqrups. It is not c l e a r t h a t the b e n e f i t s of s t a b i l i z e d commodity p r i c e s accrue p r i n c i p a l l y t o t h e producing coun t r i e s . I t is a l s o no t c l e a r vhether%igher commodity pr icea se rve a s a mechanism f o r t r a n s f e r r i n g resources from developed t o l e s s developed coun t r i e s . S i a l l a r l y , t h e c o s t and benef i t of commodity market s t a b i l i z a t i o n i n a macro con tex t cannot be appra i sed ye t . These a r e t h e types of i s sues vhich n u s t be seen i n a systems context .

6 2 . The COHLINK approach t s only one of t h e va r ious ways of handling t h e i n t e g r a t i o n of commodity market models i n t o a world system. With o t h e r s , the focus nay be d i f f e r e n t . The l e v e l of aggregat ion can be ma,'? even more

deta i led or , hopefully for many m e n , s h p l e r . The eysttm can lncorporatt input-out-output relations, t t c . This front ier is c l e a r l y one of the most far-reaching of co-di ty .

M a l F. Gerard, "Hurt High C o d i t y P r i c e s Deprese t h e World Economy? An Appl icat ion of a World Hodel System," J o u r n a l o f Po l i cy Hodelin& I (2: 19798).

, " I n t e g r a t i n g C-dity W d e l s i n t o LINK," (1979b). i n Savyer (1979) ( s e e k l v ~ ) .

, "From E c o n o w t r i c m e a l s of t h e Nation t o Hodels of I n d u s t r i e s and Firor ," H u r t o n Quar te r ly , Supplement Summar 1973.

Mama, Fa Gerard and J e r r R. I k h r u n , E c o n m t r i c Hodeling of World Comodi ty Po l i cy (Lexington, W r r t bath-Lexington, 1978).

, E c o n o w t r i c Hodrlr of World A g r i c u l t u r a l C o m d i t y h r k e t s (Cambridge, W r o t I l r l l inger , 1976).

Ma-, Fa Gerard, Jrre R. k h ~ n and R o u u l d o Roldan, " k a s u r i n g t h e Impact of Primary C o a o d i t y F luc tua t ions on E c o n d c Deve lopen t : Coffee aad Brazi l , " b r i a n E C O M ~ C Review 69 (2: 1979).

Behrman, J e r e R., I n t e r n a t i o n a l C o d i t y Agreements: An Evaluat ion of the UNCTAD I n t e g r a t e d C m d i t y Programm (Washington, D.C.: Overseas Development Counsel, 1977).

Fisher , F rank l in et. a l . , "An Econometric Hodel of t h e World Copper Industry," B e l l J o u r n a l (1972).

Ford, Derek J., "Simulation Analyses of S t a b i l i z a t i o r . P o l i c i e s i n t h e I n t e r n a t i o n a l Coffee Market," i a Mama-Behtman (1978) ( see above).

Gardner, Bruce L., "The E f f e c t s of Pub l i c and P r i v a t e Stockpi l ing," Texas 1 A6X, processed, 1977. Q

Coel le r , H.E., aad Alvin H. Weinberg, "The Age of S u b s t i t u t a b i l i t y , " American Econor ic Review 68 (6: 1978).

Labys, Walcer C., "Comodity Markets and nodels: The Range of Experience" (1978a), i n Ma- and Klein (1978). - , "Bibliography of Commodity Xarket H o d a s (1978b) i n Adams and B e h r ~ n (1978) ( see above).

Hanger, John, "A Review of the L i t e r a t u r e on Causes, E f f e c t s , and Other Aspects of Export I n s t a b i l i t y , " Univers i ty o f Pennsylvania, processed, 1979.

Pindyck, Robert S., "Gains t o Producers from t h e C a r t e l i z ~ t i o n of Exhaustible Resources," Review of Economics and S t a t i s t i c s LX (2 : 1978).

Sawyer, John A . , Hodelling the International Transrirrion n t c b n i m (hnr terdaa: Horth-Holland, 1979).

Shishido, S. , e t . a l e , "An Alternat ive World Hodel," Tsultuba Oniverrity, procersed, 1977.

ISSVES M C O ) W I D ~ met anrum SV#URY DISCUSSION

ISSUES IN COXWDITY NDEL BUILDING SWUXY DISCUSSION 11 -

I. INTRODUCTION

1. T h i s s e c t i o n c o n t a i n s a b r i e f r e v i e v of t h e v i e v s o f p a r t i c i p a n t s a t t h e seminar on g e n e r a l i s s u e s r e l a t i n g t o cocapodity models. I n some i n s t a n c e s t h e s e views a r e n o t e n t i r e l y compat ib le , a s v i l l be noted .

2 . The o b s e r v a t i o n s can be c a t e g o r i z e d under t h r e e Ireadings:

- Hethodology; - Economic theo ry ; and - O r g a n i t a t i o n

3. ;t was a rgued t h a t t h e model t echn iques be ing used i n t h e flank's commodity uork a r e i n g e n e r a l t o o p r i m i t i v e . As more a p p r o p r i a t e methods f c r mode l l i ng cocmodity marke t s o r e a v a i l a b l e , new ones need n o t ba developed. Rather , t h e problem is t o a d a p t and app ly t h e t e s t o f t h e e x i s t i n g t echn iques .

A. Improvements i n E s t i m a t i o n Techniques 21 - 4. The a p p l i c a t i o n o f s i n g l e e q u a t i o n e s t i m a t i o n s is a common f e a t u r e o f many of t h e Bank's commodity m d e l s . Hweve r , t hey a r e of t e n a n unnecessary s i m p l i f i c a t i o n . Both e f f i c i e n c y and f l e x i b i l i t y may be enhanced by u s i n g sys tems e s t i m a t i o n e i t h e r t o t a k e advantage of t h e s i m i l a r s p e c i f i c a t i o n s o f t h e e q u a t i o n s f o r a number o f u n i t s o r t o impose i ~ r i o r i , c ro s s - equa t ion c o n s t r a i n t s . The former i nvo lves t e s t i n g f o r i d e n t i c a l p a r m e t e r s on c e r t a i n s u b s t c e of v a r i a b l e s and c c p l o i t i n g e r r o r c o t r e l a t i o n e (e.g., Z e l l n e r ' s SIJRE [ s e e d n g l y u n r e l a t e d r e g r e s s i o n e q u a t i o n e l ) . 21 The l a t t e r i n v o l v e s t h e decomposi t ion of pa rame te r s i n t o s e p a r a t e p a r t s (e.g., a r e a 1's income e l a s t i c i t y f o r good j (Si ) might be w r i t t e n Bi = pi + v ), a s w e l l a s t h e J u s e o f a p r i o r i z h e o r e r i c d l r e s t r i c t i o n s l l k e t i e s y m e t r y of t h e s u b s t i t u t i o n m a t r i x T n demand theory . I n a d d i t i o n , t h e r e are t h e n r u demand systems such a e ).(uellbauerO s PTCL ( ~ r l c e - independent h e n e r a l i t e d - l i r e a r i t y ) - k ! and PICUX;

11 T h i s smmary draws on v r i t t e n c o m r r n t s b f r o n s e v e r a l p a r t i c i ) a n t s , n o t a b l y - R. V. Bacon, J. H. P. Pae l inck and A. H i n t e r s , i n a d d i t t o n t o t h e p l e n a r y d i s c u s s i o n a t t h e seminar .

- 21 Z e l l n e r (1979) appea red a t t h e same t ime a s t h e s emina r and c o n t a i n s oa-173 -

views s i m i l a r t o t h o s e expressed a t t h e c o n c l r d i n g summary s e s s i o n . d - .I - 31 Z e l l n e r (1962). - w * .. 41 Ehrellbauer (1975). -

( l r l c e independent &ene=aliord I ~ ~ - ~ d e ~ t y ) L/ o r k a t o ~ * r AIDS ( a l m r t i d e a l d&nd g r t c n r ) ; &/ t h y - p x ~ l d e =ch s o r e f I e x i b l e t h r o r e t i cy1 t o o l s - than d z the o l d LES ( 1 L s t a r f r p a m d i t v e s ~ r t e ~ ) . - - 3/

5. Irr so# c o n t r a s t t o t h e s e =re c h e o = t i d r e c o ~ ~ t n d a t i o n s a r e some i c o n o c l a s t i c r u g g e r t i o u s t h r t mZght 5C =th a m s U e r l n g , a t l e a s t i n :he s h o r t e r run. For example, the u ~ ~ u u l c r L r e r i a a o f regreamion models may be fornulaced r r a q u a d r a t i c f a . ? =*U c, v h e e F is r m i g h t a r t r i x . - - 0

6 . P r r g m t i c a l l y , t h e F b u e r c s s k u l a h v a r i e d a c t o r d i n g t o the p u q o s e of the model under t r t i a u t i a r - Lf, fur Lmrtance, t h e model is t o ba used i o r rhorw- te rn fomccmrtlng, t h e damrod q u a t X o a r ahould k h e a v i l y veighted i n o r d e r t o h - l i e t t ! -11-1 b t h t r k o r of t b ryatem; f o r long- t e r n forecantm, p a r l w u r a &uLd be earr ;nr ta t w f d r th h e l p of heavfly- v e i & t d r u ~ p l y e q u t i o m r . A/ 7 . Becaura t h e w r i e s a r e o f o a caaabiard vtth c r o r n e c t i o a analysim, c o a p s f t e - p r r n m e t e r e r t i a a t b a a shocLd k r y s z m a c l c a l l y used l a o r d e r t o e x t r a c t a s m c h i n f o m z i o n u p l ~ a f L l e f s o a cha &at.. If c i a a country index and t a t ime i a d u , a :yp-l tqurc2oa auld be v r f t t e a as:

'ct - (a + a , + 4 1 % + --•

where a is t h e g e n e r i c coppoocnc. a, che counrcy-rpccific compoaent, and a t the t iu te-speci f ic cap-nt. Tho r r f a W l l t y of V r a P c t e r r is taken i n t o account s o t h a t i n f a c t t h e l i n a r m d e l otanim for a non-linear one, the l i n e a r f t y being only 1-1. 5-/

8. Scme combination of t h e f o n t ?type e s c b a t i o n octbod w i t h the c o a s p o s i t e - p a r a t e r m e b d cam IE e-bagmi, h t u yet tbe re h a s been no exper ience v i t h it.

9. Even though ttre a b o r e m t k m e d airclmveazziot of r h e l i n e a r i z a t i . problem n igh t be a c c e p t a b l e i n same d t u a z r i o n i , thrt p r o c e b r e genera l ly reco-nded is t o apply no p r i o r l i z e a r f t l t i a r a n d t o use some modern couputer ized, poverful mon-5- e s 3 ~ ~ 1 3 c n r l g o r l t h n .

3. S?ecEi d o a a n d f-valmatioo

10. Concerning t h e f u n k t e m r a l %sue of f w to e r a l u a z e r d e l s , it may be argued thac g e n e r a l ( I f s e a r ? dynsanic - M e :

11 h e l l b a s e r (1980). - 21 Deacon and Xuel lbauer (1380a and 5 ) . - 31 e.g., Thei l (1975)- - A / Furcner d e t a i l s nay be f z ~ ; r & i n faelfrnck IL97&, 1?78b),

51 See Pael inck (1977, 1 9 7 h and 15-9). -

ought t o be es t ima ted only by means of systems methods. S ing le equat ion OLS- e s t i m a t i o n v i l l lead t o b iased e s t i m a t e s o f parameters , and t h e usual s t a t i s t i c s ( t , Durbin-Watson) provided by t h e s t endard l i b r a r y program a r e misleading. Modern e s t i m t i o n programs inc lude b e t t e r adapted procedures.

- 1 11. It is recommended t h a t t h e e igenvalues of 3 1 alu_fys be analyzed t o s e e i f t h e model is s t a b l e . F u r t h e m r e , t h e s t r u c t u r e 3 1 can r e v e a l t h e n o n - i d e n t i f i a b i l i t y of c e r t a i n equat ions i n t h e system. A s tudy of t h e r e l a t i v e c o n t r i b u t i o n of the endogenous dynamics (@) and t h e exogcnoue v a r i a b l e s t o t h e explanation of t h e y t ' s a l s o deservee a t t e n t i o n , a s t h i s i e of importance in t - r n of t h e model's c a p a c i t y f o r p r o j e c t i o n s .

12. I t is a l s o d e s i r a b l e t o apply t h e nodern non-nested t e s t e o r d i s c r i m i n a t i n g betvcen models. Fur ther , i t is obviously important t o suppor t t h e s p e c i f i c a t i o n of any model a s s t r o n g l y a s p o s s i b l e no t only by economic theory, but a l s o by includi.rg ext raneous information. Th i s means t h a t t h e a p p r o p r i a t e e s t i n a t i o n procedure w i l l o f t e n be of t h e r e s t r i c t e d l e a s t squares o r t h e Coldberger-Zel1.neres mixed type.

C. Forecast in&

13. Given t h e purpose of t h e Bank's c o m o d i t y models, t h e accuracy of t h e i r f o r e c a s t i n g is of course c r l c i a l . I t should be recognized t h a t t h e f o r e c a s t e r r o r of a model stem; from two sources , v iz . e r r o r s i n t h e e s t i m a t e s of parameters and, ( o f t e n ) more important ly , e r r o r s i n t h e f o r e c a s t of t h e exogenous v a r i n b l c s of t h e nodel. It would be d e s i r a b l e t o s u b j e c t one of t h e e x i s t i n g models t o a s y s t e ~ t i c assessment of t h e r e l a t i v e importance of t h e sources of e r r o r s . 2J

14. Very o f t e n a po in t f o r e c a s t is of l i t t l e i n t e r e s t i f not accompanied by a s t andard e r r o r . I t should , t h e r e f o r e , be common p r a c t i c e t o c a l c u l a t e t h i s e r r o r vhenever a f o r e c a s t is nade. Fur ther , a more sys temat ic use of s t andard e r r o r s might be a nore r e l i a b l e and more widely accep tab le measure of t h e f o r e c a s t range than thd l e s s theoret ica l ly-based methods sometimes app l i ed (e.g., f i t t i n g l i n e s t o extreme d a t a s e t s ) .

15. The ex-post s imula t ion by a model may r e v e a l e s s e n t i a l s p e c i f i c a t i o n e r r o r s i n 15s dynamics. I f s imula t ions based on h i s t o r i c a l lagged endogenous and model-generated laqged ecdogenous v a r i a b l e s d e v i a t e s u b s t a n t i a l l y and s y s t e m a t i c a l l y from each o t h e r , i t vould be an i n d i c a t i o n t h a t t h e dynamics of t h e model &ht have been misspeci f ied . - 16. A t p r e s e n t , f o r e c a s t s a r e used f o r both short/medium and f o r mediumllong-run purposes. There is a tendency t o g e n e r a t e these on t h e b a s i s

11 Pesaran 6 Deacon (1978). - 21 For ~ - ~ t h o d o l o g y , e t c . , s e e Fe lds te in (1971). -

of d i f f e r e n t approaches and then t o l i n k them u s i n g a mechanis t ic br idging approach. Although t h i s procedure may be a t t r i k r t a b l e ta some i n s t i t u t i o n a l c o n s t r a i n t , i t s e e m very u n s a t i s f a c t o r y from a n econometric point of view. A model b u i l t t o c a p t u r e long-run dynamics which m i s s p e c i f i e s shor t - run dynamics (e.g., by i g n o r i n ~ them) is l i k e l y t o m i s s t a t e s e r i o u s l y t h e long-run dynamics a e ~ w e l l (and vice-versa). A p o s s i b l e avenue f o r e x p l o r i n g t h i s ques t ion f u r t h e r would be t o d e r i g n one model t o s e r v e both putposes and t o i n v e s t i g a t e whether I t is p o s s i b l e t o work up t o a series of i n t e g r a t e d short- tenn/long- term f o r e c a s t s . Ll

111. ECONOMIC THEORY

17 A p u r i r t ' s c la im is that be fore any model i r b u i l t , t h e t h e o r e t i c a l p r o p e r t i e s i t h a s t o s a t i s f y should ba c l e a r l y s t a t ed- -espec ia l ly , given t h e use of models, f o r a p p l i c a t i o n i n long-run work. With r e s p e c t t o e s t ima t ions , nothing should be accepted t h a t does n o t match those a p r i o r i requirementr , even i f s i g n i f i c a n t parameters have t o be r e j e c t e d o r 5 r i o r i va lues g, impoced. I f t h e t h e o r e t i c a l model w i l l n o t f i t , r econs i e r t e theory.