Merchant bank

47

1. Merchant Banking EXECUTIVE SUMMARY Although merchant banking activity was ushered in two decades ago, it was only in 1992 after the formation of Securities and Exchange Board of India that it is defined and a set of rules and regulations in place. Today a merchant banker is who has the ability to merchandise that is, create or expand a need and fulfill capital requirements. I have given an overview about the financial markets and the role of merchant bankers in the growth of these markets. My project covers how the merchant banks works, rules & regulations laid by SEBI & its impact on the merchant banking activities. Their importance in the economy is expected to grow even further in the coming years with an increasing proportion of household savings getting invested in corporate & other securities. Hence, my project covers the challenges and advantages, which India will get and is getting by merchant banking activities. I have covered several services provided by Merchant Bankers & the role of Merchant bankers in providing those services to the business world. Finally, the top players, which exist in merchant banking, are also covered; their services are also been focused. To get the practical knowledge about merchant banking activities I have interviewed visited State bank of India, Kotak mahindra bank and SPA Merchant bankers ltd. 1 2. Merchant Banking INDEX SR.NO. CONTENTS PAGE NO. 1. Introduction 1 2. History 2 3. Definition 4 4. Evolution & Emergence of Merchant Banking 5 5. Merchant Banking in India 6. Merchant banking past and present 7 7. Need & Importance in India 8 8. Role of Merchant Bankers 9 9. Merchant Bankers Commission 11 10. Commercial Banks & Merchant Baks 12 11. Growth of Merchant Banks in India 13 12. Problems of Merchant Bankers 14 13. Current Scenario 15 14. Merchant Banking Indian Scenario 16 15. Merchant Banking International Scenario 17 16. Merchant Banking Organisation 19 17. Qualities of good Merchant Bankers 20 18. Responsibilities of Merchant banker 22 19. Registration of Merchant Banker 24 20. Scope of services 26 21. Services Rendered by Merchant Bankers 27 22. Recent Trends 39 23. Players in Merchant Banking 41 24. Merchant Banking – Future

Transcript of Merchant bank

1. Merchant Banking EXECUTIVE SUMMARY Although merchant banking activity was ushered in two decades ago, it was onlyin 1992 after the formation of Securities and Exchange Boardof India that it is defined and a set of rules and regulations in place. Today a merchant banker is who has theability to merchandise that is, create or expand a need and fulfill capital requirements. I have given an overview aboutthe financial markets and the role of merchant bankers in the growth of these markets. My project covers how the merchant banks works, rules & regulations laid by SEBI & itsimpact on the merchant banking activities. Their importance in the economy is expected to grow even further in the coming years with an increasing proportion of household savings getting invested in corporate & other securities. Hence, my project covers the challenges and advantages, which India will get and is getting by merchant banking activities. I have covered several services provided by Merchant Bankers & the role of Merchant bankers in providingthose services to the business world. Finally, the top players, which exist in merchant banking, are also covered; their services are also been focused. To get the practical knowledge about merchant banking activities I have interviewed visited State bank of India, Kotak mahindra bankand SPA Merchant bankers ltd. 1

2. Merchant Banking INDEX SR.NO. CONTENTS PAGE NO. 1. Introduction 1 2. History 2 3. Definition 4 4. Evolution & Emergence of Merchant Banking 5 5. Merchant Banking in India6. Merchant banking past and present 7 7. Need & Importance in India 8 8. Role of Merchant Bankers 9 9. Merchant BankersCommission 11 10. Commercial Banks & Merchant Baks 12 11. Growth of Merchant Banks in India 13 12. Problems of Merchant Bankers 14 13. Current Scenario 15 14. Merchant Banking Indian Scenario 16 15. Merchant Banking International Scenario 17 16. Merchant Banking Organisation 19 17. Qualities of good Merchant Bankers 20 18. Responsibilities of Merchant banker 22 19. Registration of Merchant Banker 24 20. Scope of services 26 21. Services Rendered by Merchant Bankers 27 22. Recent Trends 39 23. Players in Merchant Banking 41 24. Merchant Banking – Future

Development 48 25. Questionnaire 51 26. Annexure 53 27. Conclussion 62 28. Bibliography 63 2

3. Merchant Banking INTRODUCTION The term Merchant Banking has its origin in the trading methods of countries in the late eighteenth and early nineteenth century when trade-taking place was financed by bill of exchange drawn by merchanting houses. At that time the merchants were 3

4. Merchant Banking merely financing their own activities. As international trade grew and other lesser- known names wanted to import goods from abroad, the established merchants ‘lent their names’ to the newcomers by agreeing toaccept bills of exchange on their behalf. The acceptance houses would charge a commission for this service and thus there grew up the business of accepting bills of finance trade not merely of themselves, but of others. Acceptance business thus became and to a degree always has been hallmark of true Merchant Banks. The second historical of Merchant Banks was the raising of capital for foreign Government. In many cases, the Merchant Banks have been trading in the countries concerned and gained the confidenceof Governments and other authorities in those countries. Thus the second principal ingredient of Merchant Banking became and still is raising of capital through the issue of stocks and bonds. Therefore, Merchant Banks can be acceptinghouses or issuing houses or both. Merchant Banking started in the beginning of 20th century in UK and USA. More recently, the services offered by Merchant Banks have entered into the other areas of operations. Their role is wide ranging and they can now provide most of the financial services required by a company, touching almost all aspects of establishing and running of industrial units on sound financial footing. Dictionary meaning of ‘merchant bank’ refers to an organization that underwrites corporate securities and advises such clients on issues like corporatemergers, etc. involved in the ownership of commercial ventures. This organization may be a bank, corporate body, firm or proprietary concern. HISTORY OF MERCHANT BANKING During the seventeenth and most of the eighteenth century

international finance was centred on Amsterdam. ConsequentlyAmsterdam merchants became the first masters 4

5. Merchant Banking of the various financial techniques and developments which, in the course of time, became identifiedwith the emergent profession of ‘Merchant Bankers’. Commercial Banking and Investment Banking are often confusedwith Merchant Banking. In many ways, there may be similarities in their functions. However, in certain ways, Merchant Banking is distinctly different from commercial Banking and Investment Banking. The primary function of a commercial bank is to receive deposits from the public and lend the same to others. Commercial Banks can undertake someof the merchant banking activities like Issue Management whereas Merchant Banking Units can not undertake commercial banking activities. However, the functions of Merchant Banking may not widely vary from Investment Banking. The Merchant Banker mainly deals with Issue Management, post issue services, corporate adviser services etc. the Investment Banker undertaken trading in securities, Investment advises and Bought out deals which are not the main activities of Merchant Bankers. In todays Scenario the Merchant banker and management consultants undertake advisory services to the corporate sector. The Merchant Banker advices corporation and firms relating to opening of issues, receiving loans etc, which the management consultants also do. The management consultant have a wide area operations like production, Marketing, Personnel Relations, of finance etc. but they lack statutory recognition to undertake capital market related activities which has enabled the merchant banker to cater to the needs of the Corporate Sector. A merchant bank may be considered as an institution which centres its operation on all or mostof the following activities. (1) corporate financial advice,on such diverse matters as new share and bond issues, capital reconstructions, mergers and acquisitions; (2) The taking of deposits and currency, money market operations including foreign exchange dealing; (3) Medium-term lending and syndication of loans; (4) Acceptance credits and all

forms of export finance; (5) The holding and dealing in quoted and unquoted investment; and 5

6. Merchant Banking (6) Fund management on behalf of clients, most typically pension funds, unit trust, investment trusts and wealthy individuals. DEFINITION The first authoritative definition for the term ‘Merchant Banker’ has been given in the Rule 2 (e) of SEBI (Merchant Bankers) Rules, 1922. Accordingly, “A Merchant Banker means any person who is engaged in the business of Issue Management either by making arrangements regarding selling, buying or subscribing to Securities 6

7. Merchant Banking as Manager, Consultant, Adviser of rendering Corporate Advisory Service in relation to such Issue Management”. Sec/5 (b) of the Banking Regulation Act,1949 defines Banking as “accepting, for the purpose of lending or investment of deposits of money from the public, repayable on demand or otherwise and withdrawable by cheque,draft, order or otherwise”. The Notification of the Ministryof Finance defines a merchant banker as, “any person who is engaged in the business of issue management either by makingarrangements regarding selling, buying or subscribing to thesecurities as manager, consult, adviser or rendering corporate advisory service in relation to such issue management”. EVOLUTION & EMERGENCE OF MERCHANT BANKING Indiahas entered the 21st century as one of the Asia’s most dynamic economies. This is the part of the assessment made by International Financial and Capital Market Institutions based on India’s economic and financial reforms initiated in1991 and brought to fruition in various budget. 7

8. Merchant Banking The progress of any economy mainly depends on the efficient financial system of the country. Indian economy is no exception financial system of the country. The importance of the financial sector reforms affirms an effective means for solving the problems of economic, financial and social in India and elsewhere in thedeveloping nations of the world. The progress of the Securities Industry of any country depends mainly on the flow of funds. In fact, capital generation is the lifeblood of the capital market without which the health and soundness

of the financial system cannot be geared and for which well-developed capital market as well as money market is essential. India’s capital market is among the largest in the developing world. The market is comprised of 24 stock exchanges transacting long-term debt; debentures and equity shares both electronic and physical forms. Derivatives financial instruments are also be added to the market shortly. The number of firms listed on the Indian Stock Exchange is more than the USA. Market Capitalisation of listed firms is 1980s was similar to Brazil, Malaysia, Singapore and Denmark. The capital market of the country, however, underwent dramatic changes since the beginning of 1980s basically because of a progressive realization that the command economy on which the emphasis was placed could not lead to higher levels of economic development and that aslant towards a market-oriented economy is necessary. It is in the context of fast expanding economy and a liberalized and deregulated atmosphere that the growth of the Indian Stock Market activities has to be viewed. No wonder that themarkets have registered a quantum jump judge by any standards. MERCHANT BANKING IN INDIA In India prior to the enactment of Indian Companies Act, 1956,managing agents acted as issue houses for securities, evaluated project reports, planned capital structure and to some extent provided venture capital for new firms. Few share broking firms also functioned as merchant bankers. 8

9. Merchant Banking The need for specialized merchant banking services was felt in India with the rapid growth in the number and size of the issues made in the primary market. The merchant banking services were started by foreign banks, namely the National Grindlays Bank in 1967 and the City Bank in 1970. The Banking Commission in its report in 1972 recommended the setting up of merchant banking institutions. This marked the beginning of specialized merchant banking in India. To begin with, merchant banking services were offered along with other traditional banking services. In the mid-Eighties, the Banking Regulation Act was amended permitting commercial banks to offer a wide range of financial services through

the subsidy rule. The State Bank of India was the first India Bank to set up merchant Banking division in 1972. Later ICICI set up its Merchant Banking division followed byBank of India, Bank of Baroda, Canada Bank, Punjab National Bank and UCO Bank. The merchant banking gained prominence during 1983-84 due to new issue boom. MERCHANT BANKING: PASTAND PRESENT Many banks entered merchant banking in the 1960sto take advantage of the economies of scope produced when private equity investing is added to other bank services, particularly commercial lending. As lenders to small and medium-sized companies, banks become knowledgeable about individual firms’ products and 9

10. Merchant Banking prospects and consequently are natural providers of direct private equity investment to these firms. As mentioned above, commercial banks were the largestproviders of venture capital in the 1960s. In the middle to late 1980s, the decision to enter merchant banking was thrust on other banks and bank holding companies by unforeseen events. In those years, as a result of the LDC (less-developed-country) debt crisis, many banks received private equity from developing nations in return for their defaulted loans. At that time, many of these banks set up merchant banking subsidiaries to try to get some value from this private equity. Also at about that time, most commercial banks began refocusing their private equity investments to middle-market and public companies (often low-tech, already profitable companies) and, rather than providing seed capital, financed expansion or changes in capital structure and ownership. Most particularly, they took equity positions in LBOs, takeovers, or recapitalizations or provided subordinated debt in the form of bridge loans to facilitate the transaction. Often they did both. Commercial banks financed much of the LBO activityof the 1980s.Then, in the mid-1990s, major commercial banks began once again focusing on venture capital, where they hadsubstantial expertise from their previous exposure to this kind of investment. Some of these recent venture-capital investments have been spectacularly successful. For example,the Internet search engine Lycos was a 1998 investment of

Chase Manhattan’s venture-capital arm. Commercial banks are permitted to report either realized or unrealized gains on their merchant-banking portfolios, as long as they are consistent in the reporting. This option makes it difficult for one to compare different entities’ financial results andcould lead to an overly liberal reporting of profits. NEED &IMPORTANCE IN INDIA Important reason for the growth of merchant banking is due to exerting excess demand on the sources of funds forever expanding industry and trade. 10

11. Merchant Banking Corporate sector had the only alternative to avail of the capital market services for meeting their long-term financial requirements through capital issues of equity and debentures. With the growing demand for funds there was pressure on capital market thatenthused the commercial banks, share brokers and financial consultancy firms to enter into the field of merchant banking and share the growing capital market. In India haveopened their merchant banking windows and are competing in this field, and also doing advisory functions as merchant bankers as well as managing public issues in syndication with other merchant bankers. Merchant banks can play highlysignificant role in mobilizing funds of savers to investible channels assuring promising return on investments. activity. With the growth of merchant banking profession corporate enterprises in both public and private, sectors would be able to meet the growing requirements for the funds for establishing new enterprises,undertaking expansion/modernization/diversification of the existing enterprises. Merchant banks have been procuring impressive support from capital market for the corporate sector for financing their projects. In view of multitude of enactments, rules and regulations, guidelines and offshoot press release instructions brought out by the Government from time to time imposing statutory obligations upon the corporate sector to comply with all those requirements prescribed therein, the need of skilled agency existed which could provide counseling. Merchant bankers advise the investors of the incentives available in the formof tax reliefs, other statutory relaxations, good return

on investment and capital appreciation in such investment tomotivate them to invest their savings in securities. Thus, the merchant bankers help industry and trade to raise funds,and the investors to invest their saved money in sound andhealthy concerns with confidence, safety and organizations for higher yields. ROLE OF MERCHANT BANKERS 11

12. Merchant Banking The role of merchant banker is dynamic in the wake of diverse nature of merchant banking services. Merchant banker’s dynamism lies in promptly attending to thecorporate problems and suggests ways and means to solve it. The nature of merchant banking services is development oriented and promotional to help the industry and trade to grow and survive. Merchant banker is, therefore, dedicated to achieve this objective through his dynamism. He is alwaysawake to renew his skills, develop expertise in new areas soas to equip himself with the knowledge and techniques to deal with emerging new problems of corporate business world.He has to keep pace with the changing environment where Government rules, regulations and policies affecting business conditions frequently change; where science and technology create new innovations in production processes ofindustries envisaging immediate renovations, diversification, modernizations or replacements of existing plant and machinery or other equipments putting new demands for finances and necessitating overhauling of the capital structure of the firms. Merchant banker has to think and devise new instruments of financing industrial projects. He has to assume wider responsibilities of saving industrial units from going sick and guiding industries to be set up industrially backward areas to eliminate regional imbalancesin industrial development of the country. He has to guide the wider section of the community possessing surplus money to invest in corporate securities and other productive investment channels. He has to help the industry in different forms to ensure that it runs risk free and devoid of uncertainty by assisting the has to watch the interest and win over the confidence of the Government, its agencies,along with the entrepreneurs, the investors and the whole community. He must bridge the communication gap between

different sections and resolve the problem being faced in different areas concerned with the business world. To discharge the above role, a merchant banker has t be dynamic. For this reason, a merchant banker is sometimes, called M.B i.e. Moving Bottom, i.e., one who never sits at one place, always moving- attending meetings and meeting clients and constituents, doing business and getting business by attending meetings and conferences, imparting knowledge to others and acquiring new knowledge to maintain his supremacy in possession of latest information. His role depicts a personality cult, which is unique and envious to be followed by others. 12

13. Merchant Banking In the days ahead, merchant bankers have very significant role to play tuning their activities to the requirements of the growth pattern of corporate sector, the industry and the economy as a whole, which is, in it, a challenging task and to meet these challenges merchant bankers will have to be more vigorous and strategicin playing their role. They will have also to adopt new waysand means in discharging their role. ROLE IN THE MARKET The Securities and Exchange Board of India (SEBI) has stated that merchant bankers must be involved more closely in the market making process as share brokers do not have the requisite expertise to evaluate the fundamentals of the scrips before taking over the role of market makers. Further, share brokers generally being partnership; firms donot have the financial clout which is necessary for market making activity. Resultantly, the SEBI has suggested that any member of the stock exchange along with one merchant banker registered with SEBI could act as a market maker. TheSEBI has felt that to ensure liquidity of scrip it was necessary to facilitate greater movement, which could only be achieved through the institution of market makers. Marketmakers would also create a market for the scrips by offeringtwo way quotes to the investors. A minimum of ten scrips hasbeen proposed by SEBI for the market makers. MERCHANT BANKERS COMMISSION 13

14. Merchant Banking As determined by the Finance Ministry, Government of India, Merchant Bankers are eligible to charge

commission / fee from their clients as detailed below : (i) A Merchant Banker can charge 0.5% as the maximum as commission for whole of the issue. (ii) They can charge project appraisal fees. (iii) A lead manager can claim a commission of 0.5% up to Rs.25 crore and 0.2% in excess of Rs.25 crore. (iv) Underwriting Commission. Type of Security On amount Devolving on underwriters On amount subscribed by public 1.Equity shares 2.Preference share/debentures (a) Upto Rs. 5 lakh (b) Excess of Rs. 5 lakh 2.50 2.50 2.00 2.501.50 1.00 (v) Brokerage commission 1.5%. (vi) Other expenseslike advertising, printing, Registrar’s expenses, stamp dutyetc., in connection with the issue can be reimbursed from its clients. COMMERCIAL BANKS AND MERCHANT BANKS There are differences in approach, attitude, and areas of operations between commercial banks and merchant banks. The differencesbetween merchant banks and commercial banks are summarized below: 14

15. Merchant Banking COMMERCIAL BANKS MERCHANT BANKS • Basically deal in debt related finance and their activities are appropriately arrayed around credit proposals, credit appraisal and loan sanctions. • Are asset oriented and theirlending decisions are based on detailed credit analysis of loan proposals and the value of security offered against loans. They generally avoid risks. • They are merely finanaciers. • Basically they deal with mainly funds raised through money market and capital market and the area of activity is ‘equity and equity related finance’. • Are management oriented. They generally are willing to accept risks of business. • There activities include project counseling, corporate counseling in areas of capital restructuring, amalgamations, mergers, takeovers etc., discounting and rediscounting of short term paper in money markets, managing, underwriting and supporting public issuesand new issue market and acting as brokers and advisers on portfolio management in stock exchange. This activities haveimpact on growth, stability and liquidity of money markets. GROWTH OF MERCHANT BANKING IN INDIA Formal merchant banking activity in India was originated in 1969 with Merchant

Banking Division set up by the Grindlays Bank, the largest foreign bank in the 15

16. Merchant Banking country. The main service offered at that time to the corporate enterprises by the merchant banksincluded the management of public issues and some aspects offinancial consultancy. Other foreign banks like Citi Bank, Chartered Bank also assumed the merchant banking activity inIndia. State Bank of India started merchant banking in 1973 followed by ICICI in 1974. Both these Indian merchant bankers emerged as leaders in merchant banking having done significant business during the period of 1974-1987 in comparison to foreign banks. The early and mid-seventies witnessed a boom in the growth of merchant banking organizations in the country with various commercial banks, financial institutions, broker’s firms entering in to the field of merchant banking. The early growth of merchant banking in the country is assigned to the Foreign Exchange Regulation Act, 1973 (FERA) where under large number of foreign companies operating in India were required to dilutetheir foreign holdings in order to continue business in the country. This had caused two-pronged effect viz. firstly, inthe form of spate in ‘Foreign Exchange Regulation Act Issues’ eliciting interest of the investors by creating massive awareness about capital markets amongst the new class of investing public, secondly, merchant banking activity became attractive to banks and the firms of consultants and share brokers who entered into this fields vigorously to reap the advantages of the expanding capital markets. PROBLEMS OF MERCHANT BANKERS 1. SEBI guidelines have authorized merchant bankers to undertake issue related activities only with an exception of portfolio management. These guidelines have made the merchant bankers either to restrict their activities or think of separating 16

17. Merchant Banking these activities from the present one and float new subsidiary and enlarge the scope of its activities. 2. SEBI guidelines stipulate a minimum net worthof Rs.1 crore for authorization of merchant bankers. Small but professional and specialized merchant bankers who do nothave a net worth of Rs.1 crore may have to close down their

business. The entry is denied to young, specialized professionals into merchant banking business. 3. Non co-operation of the issuing companies in timely allotment of securities and refund of application money is another problem of merchant bankers. The guidelines have put the responsibility on the merchant bankers. They have to seek the co- operation of the issuing company to shoulder the responsibility. CURRENT SCENARIO 17

18. Merchant Banking Merchant banking is an area that we need to build and grow in the years to come. As India forms part of the global village, it becomes increasingly necessary for us to look at this business in a more holisticmanner. Obviously, international players with strong domestic partners such as DSP Merrill Lynch, JM Morgan Stanley, Kotak Mahindra Capital, together with experienced organisations like Enam and institutional backed investment bankers such as ICICI Securities, etc., are the ones who have expertise, muscle, and placement power in a greater measure than relatively new entrants. The red hot economy isthe obvious starting point. India is likely to end the year with GDP growth in excess of 7 percent. Companies and private equity investors are sitting on large piles of cash.In 2006 deal activity was largely restricted to the IT and Telecom sectors. Thus, while there is a steady flow of deals, there is now a shortage of talent to do the job. MERCHANT BANKING: INDIAN SCENARIO Merchant Banking activity was formally initiated into the Indian capital markets when Grindlays Bank received the license from Reserve Bank in 1967. Grindlays which 18

19. Merchant Banking started with management of capital issues, recognized the needs of emerging class of entrepreneurs for diverse financial services ranging from production planning and system design to market research. Apart from meeting specially, the needs of small- scale units it provided management constancy services to large andmedium sized companies. Following Grindlays Bank, Citi Bank set-up its Merchant Banking division in 1970. The division took up the task of assisting new entrepreneur and existing units in the evaluation of new projects and raising funds

through borrowing and issue of equity. Management consultantservices were also offered. Consequent to the recommendations of Banking Commission in1972, that Indian bank should start Merchant Banking Division in 1972. In the initial years the SBI’s objective was to render corporate advice and assistance to small and medium entrepreneurs. Theeconomic reforms initiated by the Government since July 1991in the files of industry, trade and financial sector have paved the way for rapid development of the economy. Several projects have been conceived since then and almost all the major groups in the country that have announced their intentions to set-up mega projects in infrastructure sector envisaging investment of thousands of crores. With several large projects been set-up and many more on the drawing board, the demand for a complete range of Merchant Banking services encompassing project advisory services, issue management and financial advisory services for corporate sector has increased considerably. This has led to a sharp growth in the Merchant Banking business in the last 2 years.MERCHANT BANKING: INTERNATIONAL SCENARIO 19

20. Merchant Banking The Merchant Banking scenario in developed countries like USA and UK are different from Indian Merchant Banking activities. The Merchant banker is also called as Investment Bankers. A brief outline of Merchant Banking in USA and UK has shown in the following paragraphs. Merchant Banks in UK In United Kingdom, MerchantBanks came on the scene in the late eighteenth century and early nineteenth century. Industrial revolution made Englandinto a powerful trading nation. Rich merchant houses that made their fortunes in a colonial trade diversified into banking. Their principle activity started with the acceptance of commercial bills pertaining to domestic as well as international trade. The acceptance of the trade bills and their discounting gave rise to acceptance houses, discount houses, and issue houses. Merchant Bankers initially included acceptance houses, discount houses and issue houses. A Merchant Banker was primarily a merchant rather than his customers entrusted banker but him with funds. Merchant Banks in UK: Finance foreign trade,

Issue capital, Manage individual funds, Undertake foreign security business, and Foreign loan business. They also used to finance sovereign government through grantof long-term loans. Since the end of Second World War commercial banks in Western Europe have been offering multiple services including Merchant Banking services to their individual and corporate clients. British banks set-updivision or subsidiaries to offer their customers Merchant Banking services. Merchant Banking in USA 20

21. Merchant Banking Merchant banks make the primary marketsin USA, arrange mergers and acquisitions, undertake global, custody, proprietary trading and market making, niche business, fund management and advisory services to governments and firms. The increased regulation and control of domestic operations gave a fillip to large US banks to undertake Merchant Banking functions in international capital markets. The US investments Banks have extended their operations to the international level. They are largely responsible for the development of the Euro-dollar market in the securities and globalisation of capital markets. They have a prominent presence in London and other European financial centers. Merchant Banks have today a strong parent, a strong balance sheet and a strong international network to play a global role. MERCHANT BANKING ORGANISATIONS 21

22. Merchant Banking In India, merchant banks operate in theform of Divisions of Indian and Foreign banks and financial institutions, subsidiary companies established by banks likeSBI Capital Markets Ltd., can Bank Financial Services Ltd., PNB Capital Services Ltd., Indian Bank Merchant Banking services Ltd., etc., the firm organized by the stock brokers, stock exchange dealers, the financial and technicalconsultants and chartered accountants. Securities and Exchange Board of India (SEBI) has divided merchant bankers into four categories, which are as follows: - CATEGORIES ACTIVITIES NETWORTH Category I To carry on the activity of issue management and to act as adviser, consultant, manager,underwriter, portfolio manager. Rs.1crore Category II To actas adviser, consultant, co-manager, underwriter, portfolio

manager. Rs.50 lakhs Category III To act as underwriter, adviser or consultant to an issue. Rs. 20 lakhs Category IV To act only as adviser or consultant to an issue Nil Merchant Bankers are classified into 4 categories as shown in the above table having regard to their nature and range of activities and their responsibilities to SEBI, investors and issuers of securities. The minimum net worth and initialauthorization fee depends on the category. The first category consists of merchant bankers who carry on any activity of issue management, determining financial structure, tie-up of financiers, advisor or consultant to anissue, portfolio manager and underwriter. The second category consists of those authorized to act in the capacityof co- manager/advisor, consultant, and underwriter to an issue or portfolio manager. The third category consists of those authorized to act as underwriter, advisor or consultant to an issue. The fourth category consists of merchant bankers who act as advisor or consultant to an issue. QUALITIES OF GOOD MERCHANT BANKERS 22

23. Merchant Banking Merchant bankers are individual expertswho organize and manage the merchant banks. The operations of merchant banks are, therefore, influenced by the personality trait of these individuals. For the success of merchant bank’s operations, the qualities which merchant bankers should have are discussed below:- LEADERSHIP:– merchant banker should possess all relevant skills, updateknowledge to interact with the clients and effectively communicate. Leadership is synonymous with followers who follow the one who leads. AGGRESSIVE ACTION:- aggressiveness is a personality trait of a good leader butin merchant banking it has a wider connotation. Aggressive merchant bankers are always looking for new business. Once abusiness opportunity has been located, the merchant banker has got to obtain the mandate for the merchant banking assignment from the clients at once which will depend upon his own communication skills, persuasiveness and the background of the organization to which he belongs. A good merchant banker is one who does not allow his client to think anything outside except what has been advised.

COOPERATION AND FRIENDLINESS:- These two characteristics arethe symbols of good leadership but it hardly needs to be stressed that cooperation and friendliness coupled with persuasiveness are the main instruments with which a merchant banker mixes with the people, gathers information, obtains business mandate and renders satisfactory services to the clients. Business of an honest business merchant banker spreads with geometrical propagation when he shares the thoughts of his clients with sympathetic gestures and offers pragmatic suggestions without greed or favours. Very often, rude, intemperate and indifferent disposition or blunt out burst withdrew fortunate business opportunities forever. Friendliness and cooperation must flow as natural traits in the merchant banker to win the trust of the clients. CONTACTS :– success of merchant banker depends upon his sociable nature and the richness of wider contacts. A merchant banker is supposed to be acquainted deeply with all the constituents of merchant banking. The scope of contact encompasses intimate contiguity and acquaintances within his own organization, Central and State23

24. Merchant Banking Government Offices where compliances under various relevant enactments are to be reported, Indianand foreign banks, financial institutions at Central and State levels, promoters/directors/owners and chief executives of the private and public enterprises which wouldbe prospective beneficiaries of merchant banking services, printers, advertising agencies, brokers and stock exchange dealers, advocates and solicitors and members of the press whose services are availed of in executing merchant banking assignments. Merchant bankers should widen contacts and references and continue to maintain them with goodness, honour and humour by meeting people. ATTITUDE TOWARDS PROBLEM SOLVING:– The most important personality trait of a merchant banker is his attitude towards problem solving. Even client coming to him has got to return fully satisfied having consulted a merchant banker. Positive approach to understand the view points of others, their difficulties andtheir adverse circumstances is possible only when a person

is skilled in human relations particularly the inter-personal and intra-personal behavior. Effective communication and proper feedback are the pre-requisite for creating a positive attitude towards problem solving. Many persons are effective in this trait without any training forreasons of cultivating a habit from environment in which they have been brought up at home, in school, college and office. This is so important that it must be treated as a separate objective quality of a good merchant banker. INQUISITINESS FOR ACQUIRING NEW SKILLS, INFORMATION AND KNOLEDGE: – merchant bankers lice on their wits they earn bygiving information to needy clients. Therefore, they should keep abreast with latest information in the area of the service product, they market. This is possible if merchant bankers possess the quality of inquisitiveness. The above qualities of a merchant banker are only illustrative. All good qualities in merchant bankers are difficult to be defined so elaborately. Nevertheless, merchant banker shouldpossess super business acumen, managerial abilities, administrative capacities and salesmanship so as to understand the problems and sell the service product to the needy clients. 24

25. Merchant Banking RESPONSIBILITIES OF MERCHANT BANKER ♦To the Investors Investor protection is fundamental to a healthy growth of the Capital Maerket. Protection is not to be conceived as that of compensating for the losses suffered. The responsibility of the Merchant Banker in ensuring the completeness of the disclosures is of paramountimportance in view of the fact that entire reliance is basedon offer Document either Prospectus or Letter of Offer because an independent agency like a Merchant Banker has done the scrutiny. Capital structuring The Merchant ♦Bankers while designing the capital structure take into account the various factors such as Leverage effect on earnings per share, the project cost and the gestation period, cash flow ability of the company, the cost of capital, the considerations of management control, size of the company, and general economic factors. These exercise are done mainly in order to meet the fund requirement of the

company taking due cognizance of the investor’s preference. Project Evaluation and due Diligence Due diligence and ♦project evaluation is another major responsibility of the Merchant Banker. Where the project has already been appraised by a bank/financial institution, the Merchant Banker relies on the said appraisal before accepting an assignment. However, where the project has not been appraised by as bank/financial instituion, the Merchant Bankundertakes a detailed evaluation of the project before taking up an assignment for issue management. Legal aspect♦The factors that are looked into in case of the legal aspects are: Compliance with the SEBI guidelinesand the various guidelines issued by the Ministry of Finance and Department of CompanyAffairs. Pending litigation’s towards tax liabilities or any criminal/civil prosecution any of the directors for any offenses. Fair and adequate disclosures in the prospectus. 25

26. Merchant Banking Pricing of the Issue The Merchant ♦Banker looks into the various factors while pricing the issue. Some of the factors are past financial performance ofthe company, Book value per share, stock market performance of the shares. The Merchant Banker has a vital role to play in pricing of the instrument. Marketing of the Issue ♦Marketing of the issue is a vital responsibility of the Merchant Banker. The first stage is Pre-issue marketing for placement of the issue with the financial institutions, banks, mutual funds, FII’s and NRI’s. The second stage is the marketing of the issue to the general public through various vehicles such as press, brokers, etc. Bought out ♦Deals The concept of wholesale but out of public offerings by the Merchant Bankers started off with over the Counter Exchange of India where a Merchant banker acts also as a sponsor and either takes up the entire issue to be offered wholly of jointly with other co-investors and off-loads the same to the public at a later date by an offer for sale. Major amendments were made to the SEBI regulations regardingMerchant Bankers. The duration of this transaction period has not officially been announced. 26

27. Merchant Banking REGISTRATION OF MERCHANT BANKER The term ‘Merchant Banking’ originated in the 18th and early 19th centuries in the United Kingdom when trade between countries was financed by bills of exchange drawn on the principal merchant houses. With the increase in international trade, the established merchants started the practice of lending their names to the new comers and accepting the bills of exchange on their behalf. They would charge a commission for the purpose and thus acceptance business became the hallmark of Merchant Bankers. Once thesebanks had gained the confidence of the government, they alsoentrusted with the job of issuing bonds in the London market. Although Merchant Banking activity ushered in two decades ago, it was only in 1992, in India, after the formation of SEBI that is defined and a set of rules and regulations governing it are in place. In fact, the origin of Merchant Banking is to be traced to Italy in late medieval times and France during the seventeenth and eighteenth centuries. Merchant Banker invested accumulated profits in all kinds of promising activities. Since they added banking business into the profession of Merchant activities and became a Merchant Banker. A distinction was existed in banking systems between moneychanger and exchanger. Moneychangers concentrate on the mutual exchange of different currencies, operated locally and later accepteddeposits for security reasons. Passage of time money changers evolved into public or deposit banks whereas exchangers, who operated internationally, engaged in bill-broking that raising foreign exchange and provision of long-term capital for public borrowers. The exchanges were remitters and Merchant Bankers. In the seventeenth century, a Merchant Banker was a dealer in bills of exchange who operated with correspondents abroad and speculated on the rate of exchange. Initially, Merchant Bankers were not banksat all and a distinction was drawn between banks, Merchant Banks and other Financial Institutions. Among all these, Institutions it was only banks that accepted deposits from public. No person s allowed carrying out any activity as a Merchant Banker unless he or she holds a certificate grated

by SEBI. Registration with SEBI is mandatory to carry out the business of merchant banking in India. 27

28. Merchant Banking An applicant should comply with the following norms: The applicant should be a body corporateThe applicant should not carry on any business other than those connected with the securities market The applicant should have necessary infrastructure like office space, equipment, manpower etc. The applicant must have at leasttwo employees with prior experience in merchant banking Any associate company, group company, subsidiary or interconnected company of the applicant should not have been a registered merchant banker The applicant should not have been involved in any securities scam or proved guilt for any offence The applicant should have a minimum net worth of Rs.5 crores 28

29. Merchant Banking MERCHANT BANKING SERVICES: SCOPE In thepresent dynamic environment where public money is playing a vital role in financing a large number of projects, both in the public and private sectors, Merchant Banking has a significant role in managing the show and meeting the growing demands for funds by the corporate sector. Merchant Banking includes a whole gamut of activities which meet the needs of both corporate and individual investors and which range from identification, evaluation, promoting and financing of projects (both domestic and overseas) by raising resources in the equity and long-term loans, to organize and participate in international consortia, to raise foreign currency loans and to offer advisory services on various matters related to finance, investment, capital management, structure, mergers, amalgamation, takeovers and acquisitions. They also play a useful role in the portfolio management, money market operations, venture capital, leasing, etc. Merchant bankers act as a guide for the entrepreneurs who are unaware, or have little knowledge or experience, of the complexities involved in the above spheres. In addition to the above, the scope of Merchant Banking services has extended to providing advisory servicesto companies to increase or divest their stakes, public sector undertaking disinvestments, international issues,

etc. With the OTCEI being operation now, Merchant Bankers will have a key role to play in terms of appraising the projects and offering two-way quotes for market making in case of entrepreneur going for listing in the above exchange. Merchant Bankers act as a critical link between the corporate who are intend to raise funds and the investors who are interested to invest in securities Industry. Besides issue management, the Merchant Bankers arealso undertake the activities like underwriting connected with the public issue management business, Managing/advisingon International offerings of Debt/Equity i.e., GDR, ADR, Bonds and other instruments, Private placement securities, Primary or Satellite dealership of government securities, Corporate Advisory services related to securities market (e.g., Takeovers, acquisitions, disengagement), Stock-Broking, Advisory Services for projects, Syndication of rupee term loans and International Financial Advisory Services. The services can be represented as follows: - 29

30. Merchant Banking SERVICES RENDERED BY MERCHANT BANKERS Among the important financial intermediaries are the merchant bankers. The services of Merchant bankers have beenidentified in India with just issue management. It is quite common to come across reference to merchant banking and financial services as though they are distinct categories. The services provided by merchant banks depend on their inclination and resources - technical and financial. Merchant bankers (Category 1) are mandated by SEBI to managepublic issues (as lead managers) and open offers in take-overs. These two activities have major implications for the integrity of the market. They affect investors' interest and, therefore, transparency has to be ensured. These are also areas where compliance can be monitored and enforced. Merchant banks are rendering diverse services and functions,which are as follows: 30

31. Merchant Banking ISSUE MANAGEMENT: The public issue of securities is the core of merchant banking function. At one time it was constructed as the sole function. Merchant bankers were identified as issue houses. It was later perceived that they provide other financial services. When

companies seek to raise resources for implementation of a new project or finance expansion or modernization or diversification of an existing unit or fund long term working capital requirement, they retain the services of a merchant banker. To a large extent the type of issue would vary with the purpose for which funds are raised. Merchant bankers when retained as managers to issue will have to assist the company in all the stages connected with public issue. The merchant bankers help corporate to raise money from the markets through the issue of shares, debentures, bonds etc. They are designated as managers to the issue. Their main business is to attract public money to capital issues. They usually render the following services: Drafting of prospectus and getting it approves from the stock exchanges. Obtaining consent/acknowledgement from SEBI. Appointing bankers, underwriters, brokers, advertisers, printers etc. Obtaining the consent of all the agencies involved in the public issue. Holding road shows, to sell the issue. These shows are held for the analysts, brokers & institutional investors. The purpose of these shows is to answer queries from these people about the company and the project for which the funds are being raised. Deciding the pattern of advertising. Deciding the branches where application money should be collected. Deciding the dates of opening and closing of the issue. Obtaining the daily report of application money collected atvarious branches. Obtaining subscription to the issue. After the close of the issue, obtaining consent of stock exchange for deciding basis of allotment etc. 31

32. Merchant Banking CORPORATE ADVISORY SERVICES RELATING TO THE ISSUE In India, the pricing of issues is now freelydecided by the company, with valuable inputs from the merchant bankers, who have to sell the issue at the decided price. The pricing of the issue especially in a public issueis very important. The pricing has to be such, that the investors will be attracted to invest in the issue at that price, at the same time the company should get the premium that it is looking for. After all, the premium can play a very role in deciding the company’s capital structure, as

larger the premium lesser will be the requirement for borrowed funds. The promoter also needs to decide whether togo in for a fresh issue or to go for a rights issue. Howeverthis will depend mainly on the quantum of funds that the company needs to raise. The success of the issue is dependent on the selection of the right type of security. Inthis matter, the expert advice of merchant bankers is of immense importance. In the issue management the merchant bankers have to coordinate the various agencies to the issue. The success of the issue depends on the cooperation of all the agencies involved. The merchant bankers offer following services during the public issues: Preparing an action plan and budget for the total expenses for the issue. Preparation of application to SEBI and assistance in obtaining the consent from SEBI. Drafting of the prospectus. Selection of underwriters, Brokers etc. Selection of bankers to the issue. Selection of advertising agency for publicity. Obtaining approval of the institutional underwriters and stock exchanges for publication of the prospectus. Companies are free to appointone or more agencies as Managers to an issue. SEBI guidelines insist that all issues should be managed by at least one authorized merchant banker, functioning either as the sole or lead manager to the issue. 32

33. Merchant Banking Ordinarily, not more than two merchant bankers should be associated as lead managers, advisors and consultants to a public issue. In issues of over Rs. 100 crores, the number could be up to a maximum of four. The responsibilities of merchant bankers in management of publicissues are many. Some of these are: We have seen that many unscrupulous promoters have raised money from the market. This has hurt the investors a lot and has also made investors nervous about stock market investments. This in turn affects the functioning of stock markets both the primary and the secondary markets. It is therefore necessarythat merchant bankers are satisfied with the viability of the project, which they can then sell to the investors with confidence. It is therefore important for the reputation of merchant bankers, to only associate themselves with good

issues. The merchant banker should act as the custodians of the investors money and this puts a lot of responsibility onthem. To discharge this function the merchant bankers have to exercise due diligence independent by verifying the contents of the prospectus and the reasonableness of the views expressed therein. It is the responsibility of the merchant bankers to get the securities listed on all the stock exchanges mentioned in the prospectus. With the introduction of Demat accounts the complaints about allotment have surely gone down. It is the responsibility ofthe merchant bankers to ensure timely refunds and allotment of securities to the investors. The merchant bankers have tocertify that they verified everything and that they believe it to be true. This assures the investing public about the safety of their investment. The precautions by the merchant bankers would ensure that all the fake companies, whose intention is to defraud the investors, don’t have access to the market. UNDERWRITING 33

34. Merchant Banking Underwriting is like insurance against the failure of an issue. It is a guarantee to the issuing the company, that the money that it requires for its projectwill definitely be raised. It means that even if the issue is not fully subscribed to by the public, the underwriters will make up the short fall. Underwriting involves the underwriter agreeing to subscribe directly, or to procure subscription for the unsubscribe portion of the issue, whichis not taken up. For the risk that the underwriter takes, heis paid commission. New companies entering the markets for the first time, always face number of problems in raising funds from the market. One of the biggest problems of coursethat the company is not well known to the investors and manyof them will be unwilling to invest their money in such ventures. Many a times even existing companies may find it difficult to raise money, due to some reasons. Issuing companies therefore approach different underwriters with a request to underwrite the issue. Underwriters on their part need to satisfy themselves about the viability of the project and also about the integrity of the promoters of thecompany. It must be noted that when an issue is under

subscribed, the underwriters will pick the shares and only if the project is good enough, then in future they can sell the shares in the market and get not only their money back, but can also make a decent profit as well. It is obligatory for the merchant bankers to accept a minimum 5% underwritingin the issue subject to a ceiling. By taking underwriting inan issue managed by them, they show their full commitment tothe issue that they are managing. MERGERS AND ACQUISITIONS Mergers and acquisitions (M&A) and corporate restructuring are a big part of the corporate finance world.Every day, Wall Street investment bankers arrange M&A transactions, which bring separate companies together to form larger ones. When they're not creating big companies from smaller ones, corporate finance deals do the reverse and break up companies through spin-offs, carve-outs or tracking stocks. 34

35. Merchant Banking Role of Merchant Banker Mergers & Acquisitions is an area where Merchant Bankers act as intermediaries in negotiating on one with corporate interested in hiving of divisions/companies which are not with in the purview of the long-term business strategy of the group/company, and on the other hand for Corporate interested in non organic growth by acquiring companies/units for reason strategic or non strategic in nature. Mergers can be beneficial for both the entities, as due to competition the companies unable to survive or prosper on their own may like to merge and face competition and achieve growth targets. Takeovers may be hostile or friendly in nature, hostile takeovers are without the consent of the company and company being takeover may work out an anti takeover strategy to counter the threat. Merchant Bankers provide following services in M&A: - Identification of potential takeover targets. Financial & Technical appraisal of the merger/takeover proposal. Negotiation with the parties for arriving at the suitable price or exchange ratio. Assistance in obtaining necessary approval & addressing procedural & legal issues.PROJECT COUNSELLING Project counseling is very important and lucrative merchant banking services which only very few

merchant bankers having advantages of knowledge, skills and experience over others are able to render satisfactorily. The corporate seek advice in respect of identification of profitable investment opportunities in the related business areas (like forward/backward integration) or as part of diversification process. The merchant bankers carry out detailed studies on product demand patterns, cost structures, etc., to enable the corporate in preparation of feasibility study may involve arrangement of a foreign collaboration, advice on technical parameters and also legalissues. Scope of services 35 ♦

36. Merchant Banking Project counseling services are needed by industrial entrepreneurs in India in the following areas:- Preparation of project report Deciding upon the financing pattern to finance the cost of the project. Aspects of project appraisal with financial institutions/banks. Project report Project report consists♦of technical process, location, management profile, means offinancing, reports on market surveys and market explorations. Merchant bankers advise the clients on projectpreparation. Merchant bankers, on behalf of their clients, engage technical consultants specialized in the specific area, and marketing experts to prepare technical feasibilityreport and market survey reports. Merchant bankers maintain the list of such experts approves by financial institutions and assign the work to these experts. Project report ♦purpose Project report about the proposed activity is prepared to obtain government approvals particularly in the following areas: Grant of industrial license to undertake specified industrial activity. Foreign investment and technology tie-up. Grant import license for importing rawmaterial, plant, machinery and equipments. Grant of foreign exchange allocation for import of capital goods or raw materials, etc. Grant of subsidies and other concessions from the government at center or state levels or from government sponsored agencies, etc. LOAN SYNDICATION It refers to assistance rendered by merchant banks to get mainly term loans for projects. Such loans may be obtained from a single development finance institution or

a syndicate or consortium as in the case of large term loans. Merchant banks can also help corporate clients to raise syndicated loans from commercial banks. 36

37. Merchant Banking Scope of service Once the client ♦company has decided about the project proposed to be undertaken, the next step is looking for the sources wherefrom funds could be procured to implement the project. The responsibility of locating the sources of finance, approaching these sources by putting in requisite prescribedapplications and complying with all the formalities involvedin the sanction and disbursal of loan rests with the merchant bankers who provide the service of loan/credit syndication. Loan syndication in the case of domestic borrowing is undertaken with the institutional lenders and the banks. Amongst institutional lenders the following institutions are the main suppliers of the long and medium term funds with which the merchant bankers contact, liaison and arrange loans working for and on behalf of their clients. 1. All India financial institutions i. Industrial Finance Corporation of India (IFCI) ii. Industrial Development Bank of India (IDBI) iii. Industrial Credit & Investment Corporation of India Ltd (ICICI) 2. State level financial bodies i. State Financial Corporations (SFCs) ii. State Industrial Development Corporations (SIDCs) iii. StateIndustrial & Investment Corporations (SIICs) 3. All India level investment institutions i. Life Insurance Corporation of India (LIC) ii. Unit Trust of India (UTI) iii. General Insurance Corporation of India (GIC) & its subsidiary companies. 4. Commercial banks: Commercial banks join in consortium loan being provided by the above institutions. 5.Mutual Funds & Venture Capital Funds: these funds generally invest in equity but mutual funds contribute to the issues of Debentures/Bonds on private placement basis as well as subscribe to public issues. RESTRUCTURING SERVICES 37

38. Merchant Banking Merchant bankers assist the management of the client company to successfully restructure various activities, which include mergers and acquisitions, divestitures, management buyouts, joint venture among others. To help companies achieve the objectives of these

restructuring strategies, the merchant banker participates in different activities at various stages which include understanding the objectives behind the strategy (objectivescould be either to obtain financial, marketing, or production benefits), and help in searching for the right partner in the strategic decision and financial valuation ofthe proposal. CAPITAL ASSISTANCE In providing financial assistance, merchant banks offer a full understanding of allfacets of the capital markets. This includes all types of debt and equity financing available from both the domestic and international markets. It should be understood that interest rates are not the only definition of capital costs.Restrictions on availability, prepayment terms, and operating effectiveness can often outweigh what might appearto be inexpensive capital with low interest rates. Too often, capital includes costs, which force an entrepreneur or a business to undertake undesirable actions. In the short-run, some actions might be necessary, but often in thelong run are detrimental. The traditional merchant banker understands these capital limitations and can structure a transaction, which is beneficial to all sides of the table -- not just the capital source. He also knows how to substitute one type of capital for another, sometimes utilizing internal sources from asset repositioning or cash creation from improvements in working capital. He understands fully the risk versus return elements necessary to complete the capital procurement process. CORPORATE ADVISORY SERVICES Merchant bankers offer customised solutions to solve the financial problems of their clients. Advice is sought in areas of financial structuring (as shownin the Modern Manufacturing case above). Merchant bankers study the working capital 38

39. Merchant Banking practices that exist within the companyand suggest alternative policies. They also advise the company on rehabilitation and turnaround strategies, which would help companies to recover from their current position.FACTORING SERVICE Factoring involves the outright sale of account receivable. By such sale a client (the exporter or manufacturer) transfers his/her ownership of the accounts to

a factor (an organization, firm). The factor buys all the client’s outstanding invoices and takes over all the subsequent dealings with the buyer/importer/customer. It is short-term debt financing. Here three parties are involved 1.The factoring organization /firms 2.The manufacturer/exporter/seller 3.The importer/customer/buyer Role Of Merchant Banker In Factoring The merchant banker mayact as factor organization with a view to earning a great amount of commission. The factor provides the following services: (a) Financing (b) Advisory services if necessary (c) Collection of bills/Account Receivable against sales proceeds. (d) Maintenance of sales ledger (e) Provide further if necessary (f) Covering losses if there are any ASSET SECURITIZATION It is a process through which some inactive assets (mortgage assets) are converted into cash/active assets. It is long-term debt financing. Here assets are converted into long-term bonds. The whole processis done by the Special Purpose Vehicle (SPV). In this approach, the merchant banker for issuance of security bondsagainst the assets with a matching of time and terms betweenmortgage property and security bonds. Here the selection of asset is generally considered on the basis of the following:(I) Quality of assets 39

40. Merchant Banking (ii) Certainty of repayment (iii) Good ranking from the credit rating agency. The process of asset securitization takes place in the following firms: Originating Institutions/Firm Special Purpose Vehicle (SPV) Merchant Banker (MB) FOREX SERVICES This aspect of banking is becoming increasingly important as the forex flow in the country is increasing and the international markets are funding the operations of the corporate in India. The success of any business is measured by the fund management; this makes treasury management as a very critical finance function. Management of treasury profit center requires a wide variety of knowledge in the area of global money markets and financial instruments such as deposit certificates, treasury bills, forecasting, source evaluation and cost of domestic and foreign currency funds. Treasury and risk management ensures cost effectiveness in

planning strategies in this era of deregulation. Role of merchant banker in Forex function The currency values, interest rates, share index and commodities affect the financial derivatives like futures, swaps and other tools ofrisk management. Corporates therefore employ well-trained professionals to manage treasury and forex functions so thatthey can ensure competent management. Thus, this service is provided to Corporates through merchant bankers. Merchant bankers assess various markets to advice Corporates or otherbanks that needs currency. Merchant bankers constantly update about the policies of the regulatory bodies, monitorsthe current prices, makes predictions based on the analysis of trends etc HIRE PURCHASE SERVICE It involves a system under which term loans for purchases of goods and services are advanced to be liquidated in stages through a contractual obligation. The goods whose purchases are thus financed may be consumer goods or producer 40

41. Merchant Banking goods or they may be simply services such as air travel. Hire-purchase credit may be provided by the seller himself or by any financial institution. However,unlike in other countries, the emphasis in India is on the provision of instalment credit for productive goods and services rather than for purely consumer goods. Role of Merchant Banker Merchant Banker undertakes the activity of financing for hire-purchase activities. The merchant banker looks more to the credit-worthiness and business morality ofthe buyer than the value of security LEASE FINANCE COMPANIES Lease finance companies provide finance to acquire the use of assets for a stipulated period of time without owning them. The user of the asset is known as the lessee, and the owner of the asset is known as the Lessor. Leasing is medium- term arrangement for finance. Role of Merchant Banker Merchant Bankers helps in assessing the credit risk of industrial borrowers. The merchant bankers provide help in evaluating lease proposals. He analyse the merits and demerits of lease finance with reference to a given proposal and leave it to their clients to decide on the appropriate source and type of finance, thus enlarging their range of choices and the variety of services available

to them. VENTURE CAPITAL Venture capital is money provided by professionals who invest alongside management inyoung, rapidly growing companies that have the potential to develop into significant economic contributors. Venture capital is an important source of equity for start-up companies. Professionally managed venture capital firms generally are private partnerships or closely-held corporations funded by private and public pension funds, endowment funds, foundations, corporations, wealthy individuals, foreign investors, and the venture capitalists themselves. Role of Merchant Banker 41

42. Merchant Banking Merchant Bankers assist ventures proposals of technocrats, with high technology, which are new, and high risk. To seek assistance from venture capital funds or companies. They also provide technical, financial & managerial services & help the company to set up a track record. The assistance should mainly be for equity support, through loan support to supplement this may be extended. RECENT TRENDS Merger & Acquisition transaction -- Merchant banks' services not taxable The Finance Ministry has excluded services provided by merchant banks and other agencies in a merger and acquisition (M&A) transaction from the scope of taxable services provided by a`management consultant.' The rationale accorded is that the role of such agencies is limited to compliance of any statute or regulation -- such as takeover regulations of theSecurities and Exchange Board of India (SEBI) -- and not governed by any contractual relationship with the advisee company. Merchant banks do not provide any consultancy on anM&A transaction, but merely verify and submit a report to the authorities concerned, according to the Central Board for Excise and Customs (CBEC). Barring the services of merchant banks, any service rendered in relation to an M&A transaction will be covered under the scope of taxable service provided by the management consultant and will be liable to service tax, the Board has ruled. Industry representatives held that services provided in respect of M&A cannot be construed as a management consultancy service,but were in the nature of financial advisory service. 42

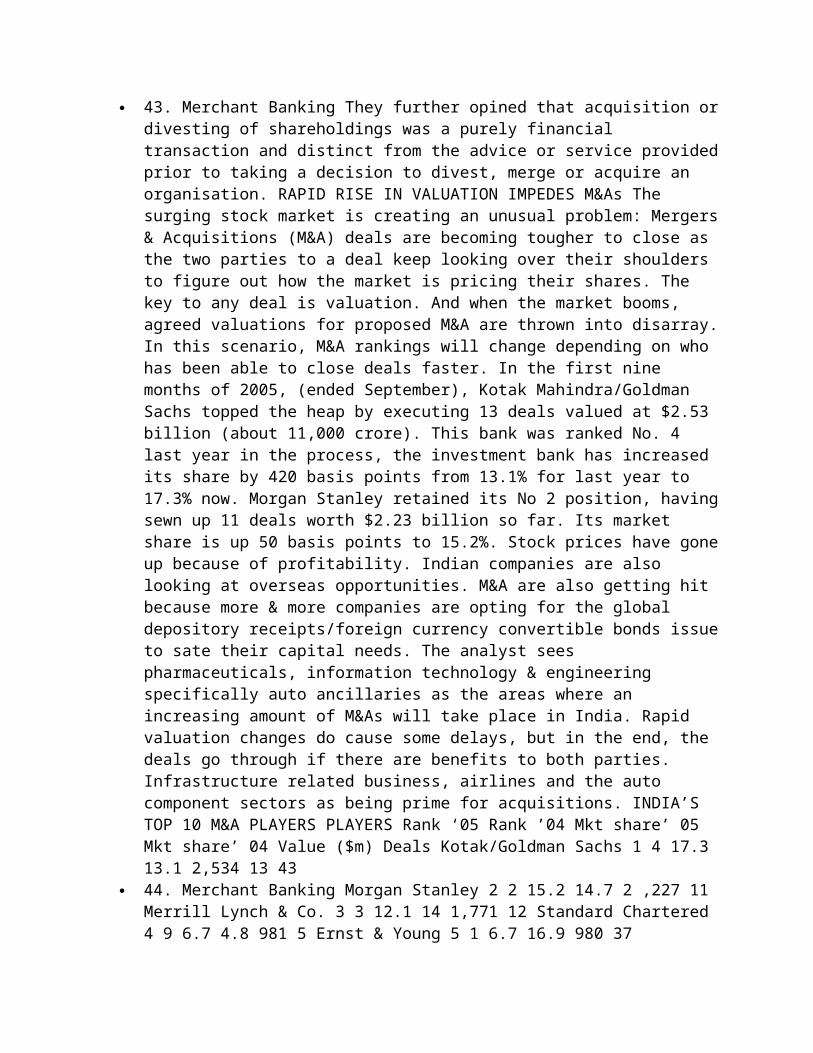

43. Merchant Banking They further opined that acquisition ordivesting of shareholdings was a purely financial transaction and distinct from the advice or service providedprior to taking a decision to divest, merge or acquire an organisation. RAPID RISE IN VALUATION IMPEDES M&As The surging stock market is creating an unusual problem: Mergers& Acquisitions (M&A) deals are becoming tougher to close as the two parties to a deal keep looking over their shoulders to figure out how the market is pricing their shares. The key to any deal is valuation. And when the market booms, agreed valuations for proposed M&A are thrown into disarray.In this scenario, M&A rankings will change depending on who has been able to close deals faster. In the first nine months of 2005, (ended September), Kotak Mahindra/Goldman Sachs topped the heap by executing 13 deals valued at $2.53 billion (about 11,000 crore). This bank was ranked No. 4 last year in the process, the investment bank has increased its share by 420 basis points from 13.1% for last year to 17.3% now. Morgan Stanley retained its No 2 position, havingsewn up 11 deals worth $2.23 billion so far. Its market share is up 50 basis points to 15.2%. Stock prices have goneup because of profitability. Indian companies are also looking at overseas opportunities. M&A are also getting hit because more & more companies are opting for the global depository receipts/foreign currency convertible bonds issueto sate their capital needs. The analyst sees pharmaceuticals, information technology & engineering specifically auto ancillaries as the areas where an increasing amount of M&As will take place in India. Rapid valuation changes do cause some delays, but in the end, the deals go through if there are benefits to both parties. Infrastructure related business, airlines and the auto component sectors as being prime for acquisitions. INDIA’S TOP 10 M&A PLAYERS PLAYERS Rank ‘05 Rank ’04 Mkt share’ 05 Mkt share’ 04 Value ($m) Deals Kotak/Goldman Sachs 1 4 17.3 13.1 2,534 13 43

44. Merchant Banking Morgan Stanley 2 2 15.2 14.7 2 ,227 11 Merrill Lynch & Co. 3 3 12.1 14 1,771 12 Standard Chartered 4 9 6.7 4.8 981 5 Ernst & Young 5 1 6.7 16.9 980 37

Citigroup 6 6 6.6 11 962 8 Ambit Corporate Fin 7 8 6.4 4.9 936 21 DBS Group 8 - 4.8 - 704 1 ICICI Securities 9 5 4.4 12.2 649 10 UBS 10- - 3.8 - 550 3 Rankings based on deals inup to 30th September, 2007 . PLAYERS IN MERCHANT BANKING 1. ENAM ENAM was founded in1984 to provide knowledge-driven financial services at the time when Indian economy investorsfaced a bewildering array of options. ENAM is the one of thelargest underwriters in India. ENAM offers promising & exciting companies the opportunity of assessing the public market equity finances. ENAM’s long-term association with capital markets & primary markets has provided it with deep insights of the functioning of Indian financial institutions. The merchant banking services provided by ENAMare: - Equity debt/syndication: Raising capital through a private placement of a company’s securities is an effective & timely offering to a public offering. ENAM represents the clients in the private placement of debt and equity with institutional & high net worth investors. Corporate Restructuring: - ENAM provides client with strategic and practical solutions to financial challenges.Their restructuring services includes Mergers & Acquisitions, Takeovers, Debt restructuring, Buyers servicesetc. ENAM also provide the seed stage services, value creation services and IPO’s advisory services which are represented below: 44

45. Merchant Banking 2. ICICI SECURITIES ICICI Securities Limited is a leader across the spectrum of Merchant Banking.We are experienced in every aspect of the business from domestic and international capital markets advisory, to M&A advisory, Private Equity syndication, Restructuring and infrastructure advisory. Our investment banking team, based across key cities in India and New York, London, and Singapore consists of professionals with expertise across a range of industries. ICICI SECURITIES provide following services: Mergers and Acquisitions: - ICICI Securities Limited is amongst the first Indian investment Banks to form a dedicated M&A practice and continues to be a leader by providing innovative and unique solutions to achieve varied objectives of the client. They offer a full range of

advisory services, which include joint ventures, mergers, acquisitions, and divestitures. Equity Capital Markets: - ICICI Securities Limited is at the forefront of capital markets advisory having been involved in most major book building and fixed price offerings over the last decade. It is amongst the leading underwriters of Indian equity and equity-linked offerings. Infrastructure Advisory: - ICICI Securities Limited has a dedicated infrastructure verticalfocused on assisting clients in identifying and capitalisingon the 45

46. Merchant Banking opportunities thrown up by the all pervasive boom in the Indian infrastructure sector. Dealingwith Bulls and Bears: - ICICI Securities Limited assists global institutional investors to make the right decisionsthrough insightful research coverage and a client focused Sales and Dealing team. The equity group leverages research and distribution reach to domestic and foreign institutionalinvestors in case of public offerings. Thus the quality of analysis and client servicing standards, are a testimony to the quality of ICICI SECURITIES team. 3. KOTAK SECURITIES LIMITED Kotak Securities Limited, a subsidiary of Kotak Mahindra Bank, is the stock broking and distribution arm of the Kotak Mahindra Group. The company was set up in 1994. Kotak Securities is a corporate member of both The Bombay Stock Exchange and The National Stock Exchange of India Limited. Its operations include stock broking and distribution of various financial products - including private and secondary placement of debt and equity and mutual funds. Currently, Kotak Securities is one of the largest broking houses in India with wide geographical reach. The company has four main areas of business: Kotak Institutional Equities: - Kotak Institutional Equities, among the top institutional brokers in India. It mainly covers secondary market broking and the marketing of equity offerings, including IPOs, to domestic and foreign institutional investors. Structured Finance (Project Finance & Advisory Business): -KMCC has developed expertise in various vertical segments in the infrastructuresector including power, oil, gas, ports, automobiles, steel

& metals and hotels, by offering structured finance solutions. Some of the transactions executed by this team include: Advisor to Ford on financial closure for its Car project in India. Advisor to one of the largest LNG projects on the Western coast of India. 46

47. Merchant Banking Financial advisors and loan syndications to British Gas and GAIL. Mergers & Acquisitions: -In the area of Mergers & Acquisitions, we provide our clients expertise and a comprehensive set of services that help them achieve their strategic and financial objectives. Our spectrum of services include: Divestments Spin-Offs / Restructuring & Joint Ventures /Strategic Alliances 4. CITIGROUP Citigroup Corporate and Investment Banking achieve the extraordinary for our clientsaround the world. No financial institution is more committedto advancing the goals of its clients—our diverse and talented staff in more than 100 countries advises companies,governments and institutions on the best ways to realize their strategic objectives. We create solutions for and provide the broadest possible capital and market access to thousands of issuer and investor clients. And no institutionbetter executes the increasingly complex payment and cash management solutions required in today's global economy. Thefeatures Citigroup are as follows: - Over the years, Citigroup has established a track record of outstanding business milestones such as Cash Management, pioneered by Citigroup in 1986 and utilized by over 900 Corporates with through-puts totaling around $ 35 billion (8% of India's GDP). It is India's largest foreign bank in the FX (foreignexchange) market with a 14 per cent market share. As the leading custodian, Citibank has over $22 billion of custody assets under management. 47

48. Merchant Banking 5. DSP MERRILL LYNCH LTD. DSP Merrill Lynch Limited (DSPML), among India's leading investment banking and brokerage company, is a culmination of a long standing relationship between DSP Financial Consultants Ltd., and Merrill Lynch & Co., the leading international capital raising, financial management and advisory company. DSPML is a full service investment bank and broking company