Media Corporate IR Net

28

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Media Corporate IR Net

AMETEK is a leading global manufac-turer of electronic instruments andelectric motors.

Our vision is to double the size andprofitability of AMETEK over the nextfive years. Our objective is to achievedouble-digit annual percentage growthin earnings per share over the businesscycle and superior return on total capi-tal. Guiding AMETEK is a CorporateGrowth Plan based on four key strate-gies: Operational Excellence, StrategicAcquisitions & Alliances, Global &Market Expansion, and New Products.

To Our Shareholders | page 2AMETEK At a Glance | page 6Strategies for Growth | page 8Financial Review | page 16Directors and Officers of the Company | page 24Shareholder Information | inside back cover

The product names with TM are trademarks and with ® are registered trademarks of AMETEK, Inc.

Corporate OfficeAMETEK, Inc.37 North Valley RoadBuilding 4P.O. Box 1764Paoli, PA 19301-0801610-647-2121 or 800-473-1286The Corporate Office is located in suburbanPhiladelphia.

Investor CommunicationsInvestors seeking the Form 10-K andadditional information about theCompany may call or write to InvestorRelations at the Corporate Office.AMETEK earnings announcements,press releases, SEC filings, and otherinvestor information are available inthe Investors section of AMETEK’sWeb site: www.ametek.com

Annual MeetingTuesday, May 21, 2002, 3 p.m.

J. P. Morgan Chase & Co.11th Floor Conference Center270 Park AvenueNew York, NY 10017All shareholders are invited to attend.

Stock Exchange ListingsNew York and Pacific; symbol: AME

Shareholder ServicesAmerican Stock Transfer and Trust Co.59 Maiden LaneNew York, NY 10038Attn: Shareholder Services718-921-8200 or 800-937-5449www.amstock.com

AMETEK’s transfer agent responds toinquiries regarding dividend payments,direct deposit of dividends, stock transfers,address changes, and replacement of lostdividend payments and lost stock certificates.

Independent AuditorsErnst & Young LLPPhiladelphia, PA

Corporate CounselStroock & Stroock & Lavan LLPNew York, NY

2001 AMETEK Annual Report | 1

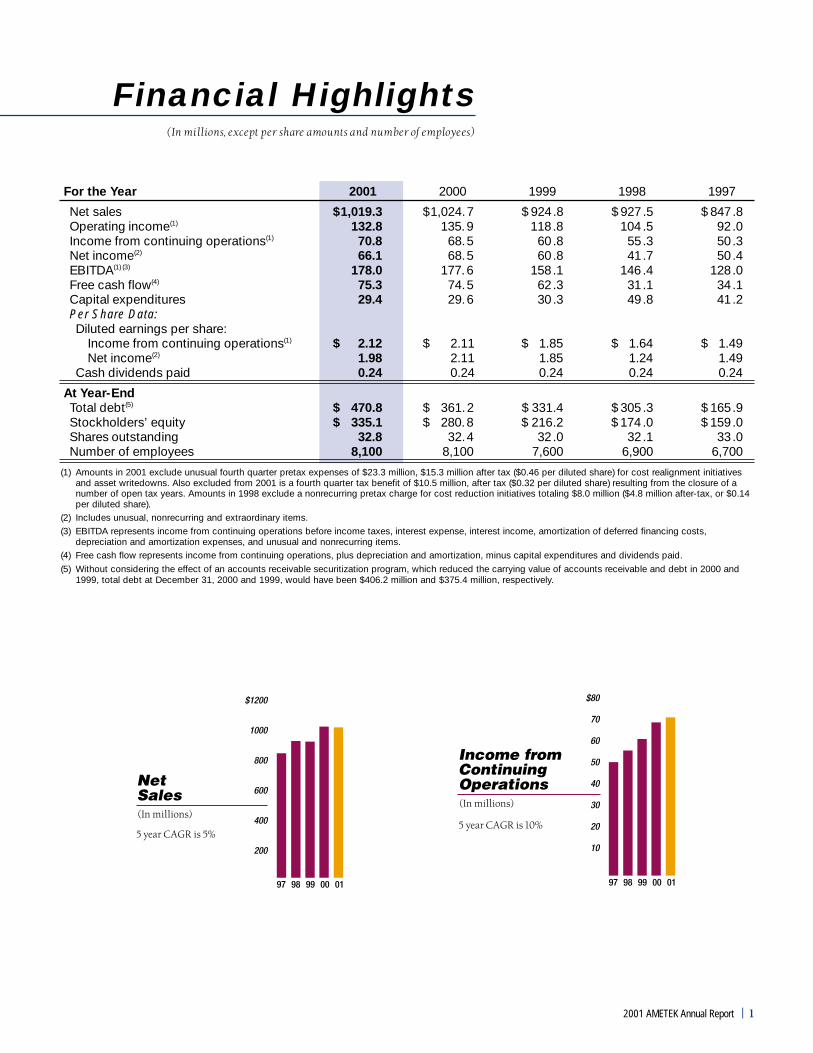

(In millions, except per share amounts and number of employees)

Financial Highlights

For the Year 2001 2000 1999 1998 1997

Net sales $1,019.3 $1,024.7 $ 924.8 $ 927 .5 $ 847.8Operating income(1) 132.8 135.9 118.8 104 .5 92.0Income from continuing operations(1) 70.8 68.5 60.8 55.3 50.3Net income(2) 66.1 68.5 60.8 41.7 50.4EBITDA(1) (3) 178.0 177.6 158.1 146 .4 128.0Free cash flow(4) 75.3 74.5 62.3 31.1 34.1Capital expenditures 29.4 29.6 30.3 49.8 41.2Per Share Data:Diluted earnings per share:

Income from continuing operations(1) $ 2.12 $ 2.11 $ 1.85 $ 1.64 $ 1.49Net income(2) 1.98 2.11 1.85 1.24 1.49

Cash dividends paid 0.24 0.24 0.24 0.24 0.24

At Year-EndTotal debt(5) $ 470.8 $ 361.2 $ 331.4 $ 305 .3 $ 165.9Stockholders’ equity $ 335.1 $ 280.8 $ 216.2 $ 174 .0 $ 159.0Shares outstanding 32.8 32.4 32.0 32.1 33.0Number of employees 8,100 8,100 7,600 6,900 6,700

(1) Amounts in 2001 exclude unusual fourth quarter pretax expenses of $23.3 million, $15.3 million after tax ($0.46 per diluted share) for cost realignment initiativesand asset writedowns. Also excluded from 2001 is a fourth quarter tax benefit of $10.5 million, after tax ($0.32 per diluted share) resulting from the closure of anumber of open tax years. Amounts in 1998 exclude a nonrecurring pretax charge for cost reduction initiatives totaling $8.0 million ($4.8 million after-tax, or $0.14per diluted share).

(2) Includes unusual, nonrecurring and extraordinary items.(3) EBITDA represents income from continuing operations before income taxes, interest expense, interest income, amortization of deferred financing costs,

depreciation and amortization expenses, and unusual and nonrecurring items.(4) Free cash flow represents income from continuing operations, plus depreciation and amortization, minus capital expenditures and dividends paid.

(5) Without considering the effect of an accounts receivable securitization program, which reduced the carrying value of accounts receivable and debt in 2000 and1999, total debt at December 31, 2000 and 1999, would have been $406.2 million and $375.4 million, respectively.

2 | 2001 AMETEK Annual Report

To OurShareholders

Clear Vision • Sound Strategies • Solid Performance

We are pleased with our performance in 2001. While

improve—hopefully a conservativeassumption. When we completed ourinitial planning process, it becameapparent that additional costreduction measures were required.As in the past, we moved quickly toalign our cost structure to the realitiesof the economic environment.

As a result, we recognized expensesin the fourth quarter of 2001 totaling$15.3 million after tax, or 46 cents perdiluted share, associated with thesecost reduction activities. Theseactions will yield significant futurebenefits totaling $25 millionannually. The expenses we incurredwere largely offset by an $11 million,or 32 cents per share, tax benefitresulting from the closure of severalopen tax years.

Clear VisionOur vision is clear—to double the sizeand profitability of AMETEK in fiveyears.

We remain focused on growing andacquiring differentiated businessesthat compete on product capabilities,have high profit margins, and offersuperior returns to our investors.These include our electronic instru-ments businesses, technical motors,specialty metals, and our power andswitch business. They account forabout 70% of our current sales.

We will continue to manage ourcost-driven businesses—primarilyglobal floor care motors—for strongcash generation. We also willselectively pursue growth opportuni-ties through implementation of ourbest-cost strategy to leverage the sizeand scope of these businesses.

many industrial companies sufferedsignificant declines in sales andprofitability due to the difficulteconomic environment, we estab-lished new records for income anddiluted earnings per share, beforeunusual items. We streamlined ourcost structure and are now wellpositioned when the economyimproves.

2001 ResultsOur sales of $1.02 billion wereessentially unchanged from the prioryear. We benefited from the acquisi-tions of GS Electric, EDAX, RochesterInstruments, and Prestolite. Ouraerospace and power instrumentsbusinesses did extremely well,while many of our other businessesencountered weakness due to theeconomic slowdown.

Operating income of $132.8 millionwas down 2%. Income increased 3% to$70.8 million and diluted earnings pershare were $2.12, compared with $2.11in 2000. Including unusual items, netincome for 2001 was $66.1 million, or$1.98 per diluted share.

The economic environmentremains uncertain. Our plans for 2002assume that the economy will not

2001 AMETEK Annual Report | 3

Sound StrategiesGuiding our efforts is a CorporateGrowth Plan based on Four GrowthStrategies: Operational Excellence,Strategic Acquisitions & Alliances,Global & Market Expansion, andNew Products.

We believe the sound executionof these Four Growth Strategies willallow us to realize our vision for thefuture. We made significant stridesduring 2001 in executing thesestrategies:

Operational ExcellenceOperational Excellence is the corner-stone strategy of AMETEK that allowsus to operate our business efficientlyin both good times and bad. It pro-vides the framework for our othergrowth strategies and serves as acatalyst for achieving our long-termgoals.

Our emphasis on OperationalExcellence resulted in cost reductionsthat allowed us to grow incomein 2001 despite one of the mostchallenging economic environmentsin years. This was accomplishedwithout compromising the long-termgrowth potential of our business.

An outcome of our OperationalExcellence efforts is the marginperformance of the ElectromechanicalGroup. Its margins increased year overyear from 15.1% to 15.6%, due largelyto smooth and efficient motor plantconsolidations and expansions.

Strategic Acquisitions & AlliancesWe have enjoyed great success withacquisitions. Our stated objective is forone-half to two-thirds of our revenue

growth to come from acquisitions.That translates into $100 million ormore in acquired revenue annually.Since 1999, we have maintained thatpace, completing nine acquisitionswith annualized revenues totalingmore than $375 million. In 2001, weadded three acquisitions:¤ Instruments for Research and

Applied Science (IRAS), a manufac-turer of highly differentiatedanalytical instruments

¤ EDAX, a leader in advancedinstrumentation for elementaland structural analysis

¤ GS Electric, a leader in seriesuniversal and permanent magnetmotors

IRAS, with about $50 millionin annual sales, was acquired inDecember 2001. Its products are usedin nuclear spectroscopy, electrochem-istry, and electronic signal processing.

EDAX, acquired in July, also is amanufacturer of highly differentiatedinstruments that are used primarilyfor microanalysis in electron micro-scope systems. With annual sales ofabout $35 million, EDAX moves usinto the measurement of solidmaterials.

Both EDAX and IRAS expand ourpresence in laboratory instrumentsand complement our processinstruments businesses, which focuslargely on the measurement of liquidsand gases.

In May, we acquired GS Electricwith about $65 million in annualsales. It is an excellent fit with ourexisting motor businesses. With it,we gain additional share of the floor

Frank S. Hermance, Chairman andChief Executive Officer

4 | 2001 AMETEK Annual Report

care and outdoor power equipmentmotor markets and substantiallyincrease our sales of permanentmagnet motors—a technology thathad not been a large part of ourproduct portfolio.

Global & Market ExpansionWe intend to grow international sales,which now account for about a thirdof our sales, to half of our totalrevenues. We plan to achieve that goalby capitalizing on opportunities innew and emerging markets, expand-ing low-cost operations worldwide,and improving international market-ing and distribution.

We’ve already done an excellentjob adapting our proven technicalcapabilities to serve new marketsegments. We took our core compe-tency in process analyzers fordetecting moisture and modified thetechnology for use by the natural gas

and semiconductor industries.Our latest generation of moistureanalyzers for the semiconductorindustry has established newstandards for accuracy, stability,sensitivity, and speed.

We’ve taken a similar approachwith our power instruments business.Here we applied our leadership insensors and monitors for jet aircraftengines and developed a family ofproducts specifically for electricity-generating turbines. Our sensors andinstruments are now found on nearlyevery major turbine generator in theworld.

Acquisitions have opened newmarket opportunities to us. A fewexamples: IRAS and EDAX, acquiredin 2001, provide new markets for ouranalytical instruments. RochesterInstrument Systems, acquired in 2000,allowed us to enter the attractivemarket for power transmission anddistribution instrumentation.Drexelbrook Engineering and PatriotSensors & Controls, acquired in 1999,provided us with a leading positionin level measurement for the processindustries.

One key to our success in globalfloor care motors is our best-coststrategy, where we are locating moremanufacturing in low-cost locales.During 2001, we moved additionalEuropean motor manufacturing to ouroperations in the Czech Republic andexpanded our capabilities in Reynosa,Mexico; Shanghai, China; and SãoPaulo, Brazil.

That best-cost approach has beenapplied to other businesses as well.

Clockwise, from bottom left: Albert J. Neupaver, President, Electromechanical Group; Thomas F.Mangold, Jr., President, Electronic Instruments; Frank S. Hermance, Chairman and ChiefExecutive Officer; John J. Molinelli, Executive Vice President—Chief Financial Officer; Robert W.Chlebek, President, Electronic Instruments

2001 AMETEK Annual Report | 5

We now manufacture heavy-vehicleproducts, aerospace and powerinstruments, and switch productsin Reynosa.

New ProductsWe’ve made a significant invest-ment in new products. We havedevoted more than $130 millionover the past three years to productinnovation and development.We also are taking new productsinto global markets. Productssuch as the Model 5910 high-accuracy moisture analyzer, theIntelliPoint RFTM process level gauge,the Minijammer® brushless blower,and the ADVANTEKTM floor caremotor were developed with globalmarkets in mind.

We expect the pace of our productdevelopment efforts to continue,especially as we integrate our recentacquisitions and further leverage ourtechnical capabilities.

Solid PerformanceWe are pleased with our 2001performance. We owe much ofthe credit to AMETEK colleaguesworldwide. I want to thank themfor their dedication, hard work, andcommitment to our Company.

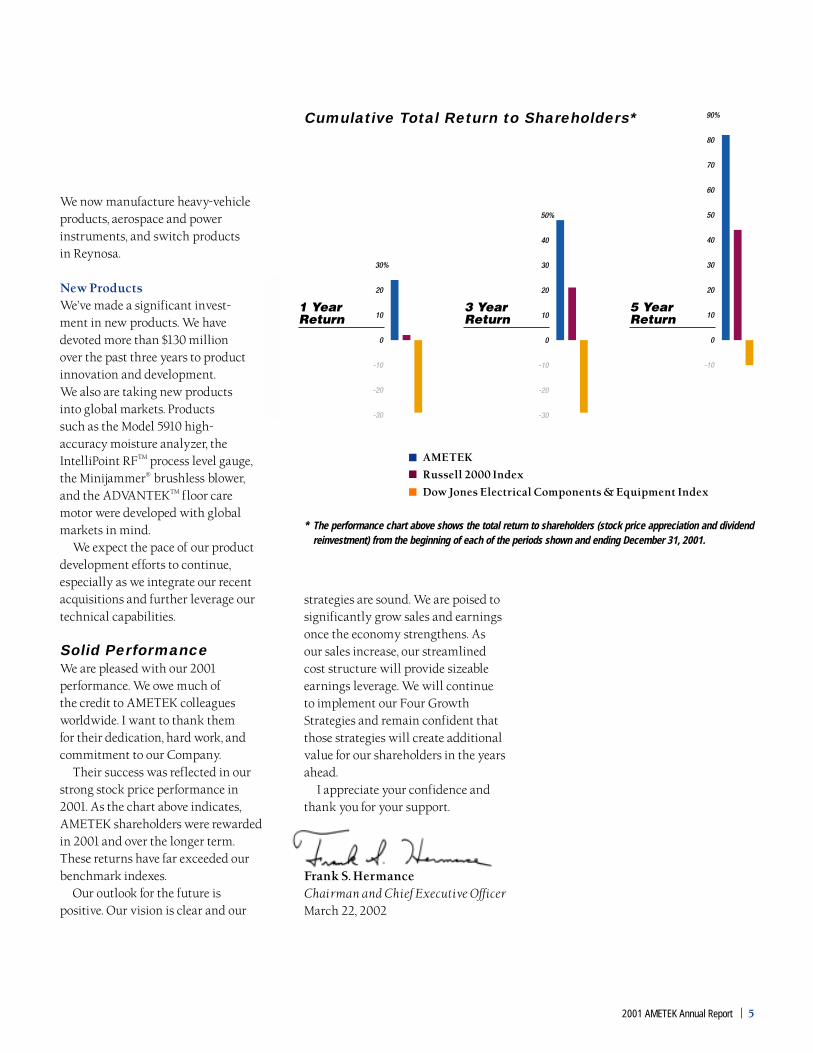

Their success was reflected in ourstrong stock price performance in2001. As the chart above indicates,AMETEK shareholders were rewardedin 2001 and over the longer term.These returns have far exceeded ourbenchmark indexes.

Our outlook for the future ispositive. Our vision is clear and our

strategies are sound. We are poised tosignificantly grow sales and earningsonce the economy strengthens. Asour sales increase, our streamlinedcost structure will provide sizeableearnings leverage. We will continueto implement our Four GrowthStrategies and remain confident thatthose strategies will create additionalvalue for our shareholders in the yearsahead.

I appreciate your confidence andthank you for your support.

Frank S. HermanceChairman and Chief Executive OfficerMarch 22, 2002

Cumulative Total Return to Shareholders*

AMETEK

Russell 2000 Index

Dow Jones Electrical Components & Equipment Index

* The performance chart above shows the total return to shareholders (stock price appreciation and dividendreinvestment) from the beginning of each of the periods shown and ending December 31, 2001.

6 | 2001 AMETEK Annual Report

AMETEK At a GlanceClear Vision • Sound Strategies • Solid Performance

6 | 2001 AMETEK Annual Report

Headquartered in suburban Philadelphia, Company Highlights¤ Posted strong 2001 performance

despite a challenging operatingenvironment

¤ Set records for income and dilutedearnings per share, before unusualitems

¤ Streamlined cost structurethrough emphasis on OperationalExcellence

¤ Completed three strategic acquisi-tions with annualized sales ofnearly $150 million

AMETEK’s sales are evenly dividedbetween two operating groups:

Electronic Instruments Group(EIG)—a leader in advanced monitor-ing, testing, calibrating, measurement,and display instruments sold toprocess, aerospace, power, andindustrial markets worldwide.

Electromechanical Group (EMG)—the world’s largest manufacturer ofair-moving electric motors for thefloor care market and a leader indirect-current air-moving motorsfor aerospace, business machine,mass-transit, medical, and computermarkets.

AMETEK, Inc., is a leading globalmanufacturer of electronic instru-ments and electric motors, withapproximately 8,100 employees.AMETEK has plants and operationsin the United States and 15 othercountries.

2001 AMETEK Annual Report | 72001 AMETEK Annual Report | 7

Group Highlights

Electronic Instruments Group¤ Acquired two highly differentiated

instrument manufacturers:

—EDAX, a leader in advancedinstrumentation for elementaland structural analysis and systemsused with electron microscopes andx-ray fluorescence spectrometers

—Instruments for Research andApplied Science (IRAS), producer ofa broad range of instruments usedin nuclear spectroscopy, electro-chemistry, and electronic signalprocessing

¤ Expanded position in electric powerinstrumentation through acquisi-tion and internal development

¤ Broadened leadership in levelmeasurement and processautomation sensors with innovativeproducts and product lineextensions

¤ Introduced high-accuracy analyzersfor the process, semiconductor, andnatural gas industries

¤ Relocated additional instrumentmanufacturing lines to low-costfacilities

¤ Implemented OperationalExcellence and Six Sigmaprocess improvement initiatives

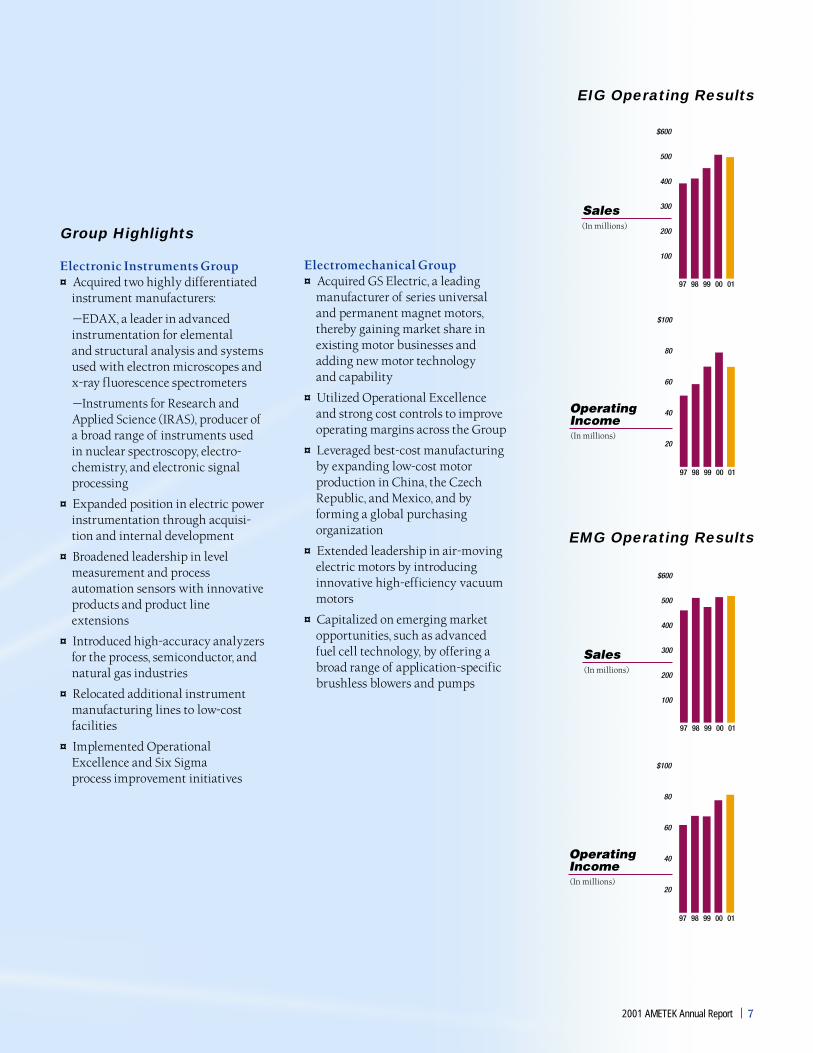

EIG Operating Results

EMG Operating Results

Electromechanical Group¤ Acquired GS Electric, a leading

manufacturer of series universaland permanent magnet motors,thereby gaining market share inexisting motor businesses andadding new motor technologyand capability

¤ Utilized Operational Excellenceand strong cost controls to improveoperating margins across the Group

¤ Leveraged best-cost manufacturingby expanding low-cost motorproduction in China, the CzechRepublic, and Mexico, and byforming a global purchasingorganization

¤ Extended leadership in air-movingelectric motors by introducinginnovative high-efficiency vacuummotors

¤ Capitalized on emerging marketopportunities, such as advancedfuel cell technology, by offering abroad range of application-specificbrushless blowers and pumps

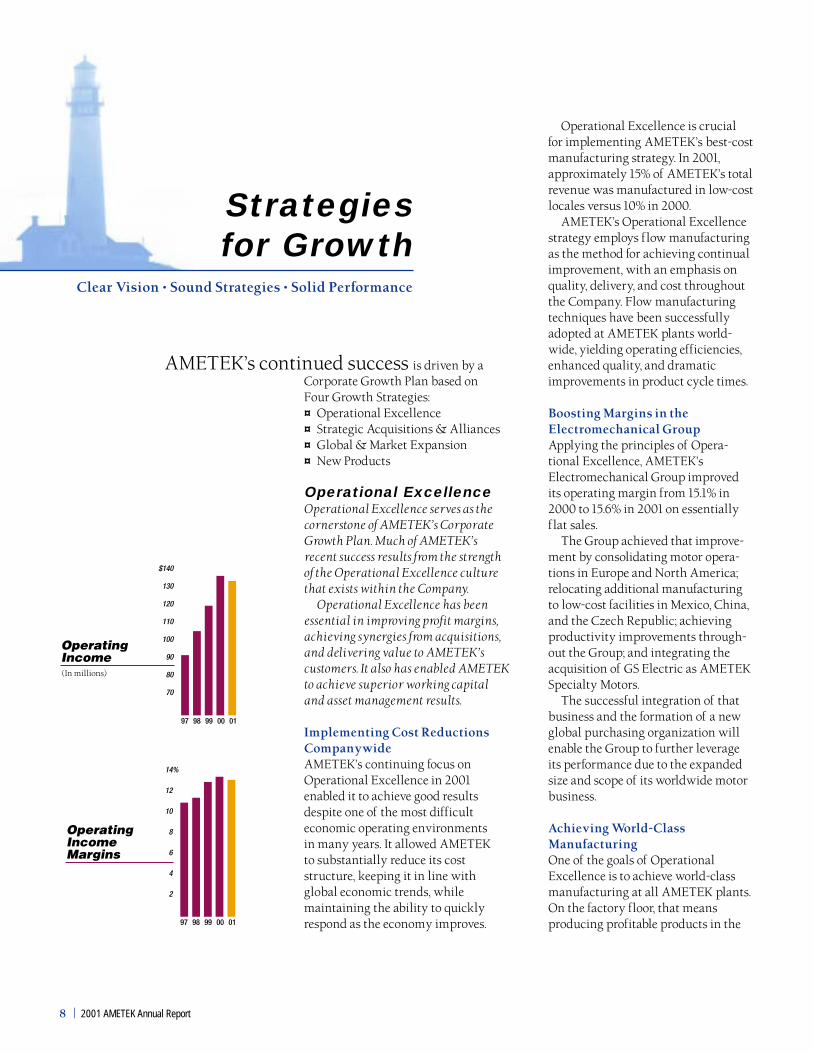

8 | 2001 AMETEK Annual Report

Strategiesfor Growth

Clear Vision • Sound Strategies • Solid Performance

AMETEK’s continued success is driven by a

Operational Excellence is crucialfor implementing AMETEK’s best-costmanufacturing strategy. In 2001,approximately 15% of AMETEK’s totalrevenue was manufactured in low-costlocales versus 10% in 2000.

AMETEK’s Operational Excellencestrategy employs flow manufacturingas the method for achieving continualimprovement, with an emphasis onquality, delivery, and cost throughoutthe Company. Flow manufacturingtechniques have been successfullyadopted at AMETEK plants world-wide, yielding operating efficiencies,enhanced quality, and dramaticimprovements in product cycle times.

Boosting Margins in theElectromechanical GroupApplying the principles of Opera-tional Excellence, AMETEK’sElectromechanical Group improvedits operating margin from 15.1% in2000 to 15.6% in 2001 on essentiallyflat sales.

The Group achieved that improve-ment by consolidating motor opera-tions in Europe and North America;relocating additional manufacturingto low-cost facilities in Mexico, China,and the Czech Republic; achievingproductivity improvements through-out the Group; and integrating theacquisition of GS Electric as AMETEKSpecialty Motors.

The successful integration of thatbusiness and the formation of a newglobal purchasing organization willenable the Group to further leverageits performance due to the expandedsize and scope of its worldwide motorbusiness.

Achieving World-ClassManufacturingOne of the goals of OperationalExcellence is to achieve world-classmanufacturing at all AMETEK plants.On the factory floor, that meansproducing profitable products in the

Corporate Growth Plan based onFour Growth Strategies:¤ Operational Excellence¤ Strategic Acquisitions & Alliances¤ Global & Market Expansion¤ New Products

Operational ExcellenceOperational Excellence serves as thecornerstone of AMETEK’s CorporateGrowth Plan. Much of AMETEK’srecent success results from the strengthof the Operational Excellence culturethat exists within the Company.

Operational Excellence has beenessential in improving profit margins,achieving synergies from acquisitions,and delivering value to AMETEK’scustomers. It also has enabled AMETEKto achieve superior working capitaland asset management results.

Implementing Cost ReductionsCompanywideAMETEK’s continuing focus onOperational Excellence in 2001enabled it to achieve good resultsdespite one of the most difficulteconomic operating environmentsin many years. It allowed AMETEKto substantially reduce its coststructure, keeping it in line withglobal economic trends, whilemaintaining the ability to quicklyrespond as the economy improves.

2001 AMETEK Annual Report | 9

shortest time possible and with thelowest possible level of inventory. Italso means having flexible productioncapabilities that meet customers’delivery requirements while main-taining the highest level of quality.

Across the Company, OperationalExcellence has resulted in a perma-nent change in the way AMETEKdoes business. Following are a fewexamples:¤ Application of flow manufacturing

techniques allowed AMETEK’sReynosa, Mexico, plant to greatlyreduce the amount of scrap, work-in-progress inventory, and floorspace required.

¤ At AMETEK National ControlsCorp. implementation of flowmanufacturing helped reducemanufacturing expenses nearly 5%,improved plant efficiency by 11%,and reduced inventory by 27%.

¤ On-time delivery at AMETEKProcess & Analytical Instrumentsaveraged 98% in 2001. That businessnow produces 9 out of 10 of itsThermox® process analyzers onflow manufacturing lines.

¤ The Six Sigma method of continu-ous improvement has beensuccessfully adopted by many ofAMETEK’s instruments businesses.

Earning Recognitionfor E-ProcurementDuring 2001, AMETEK introduced anInternet-based procurement systemthat is expected to yield significantsavings on goods and services pur-chased. AMETEK’s e-procurementsolution already has attracted indus-try attention, and several leadingbusiness publications prominentlyfeatured the initiative this past year.In addition, the Aberdeen Group—a leading information technologyservices firm—placed AMETEK’sinitiative among the most successfuldeployments of Internet-basede-procurement.

Strategic Acquisitions& AlliancesAcquisitions are key to AMETEK’sCorporate Growth Plan. AMETEK hasdemonstrated the soundness of itsapproach with a string of successfulacquisitions that have enhanced itsexisting strengths, broadened itsproduct capabilities, and extended itsreach into new markets and regionsof the globe.

Acquisitions have added toAMETEK’s positions in laboratoryand research equipment; power,aerospace, and process instruments;electromechanical products; specialtymotors; and food service controls.

AMETEK has continually improvedits ability to successfully acquire andintegrate new businesses and considersthat ability an important corecompetency.

Adding a New Growth PlatformDuring 2001, AMETEK added twohighly differentiated analyticalinstruments businesses to its processinstruments portfolio. The first wasEDAX, Inc., acquired in July, and thesecond was Instruments for Researchand Applied Science, or IRAS, acquiredat year-end.

EDAX manufactures instrumentsused in electron microscope systems

Dr. John H. Lux AwardThe AMETEK Aerospace Transducer DevelopmentProgram Team—winners of the 2001 Dr. John H.Lux Total Quality Accomplishment Award—serves as an outstanding example of OperationalExcellence at AMETEK.

The team was formed to supply GE PowerSystems with a gas-turbine pressure-monitoringsystem. Critical to success was 100% on-timedelivery and quality performance. The team drewupon all aspects of Operational Excellence tooptimize cost, quality, delivery, and inventorymanagement. Since delivering the first productionunit, on-time delivery performance has been ator near 100%.

The team’s success elevated AMETEK’s rolefrom a component supplier to a developer ofvalue-added systems, and it has generatedadditional opportunities for AMETEK.

The team members are Carlos Avon, AbelBaca, Bob Blanchard, Peter Duong, DennisEchternach, John Ginkus, Randy Jorgensen,Sherrill Lane, Kevin McGee, Steven Peterson,Pat Sheridan, and Roland Wheeler.

The Lux Award honors late AMETEK ChairmanDr. John H. Lux for his dedicated leadership andcontributions to the Company.

10 | 2001 AMETEK Annual Report

and x-ray fluorescence spectrometers.EDAX instruments identify andquantify the elemental compositionand structure of solid materials andhave applications in the metallurgy,pharmaceutical, chemical, andsemiconductor industries. They alsoare used in government laboratoriesand academic institutions.

EDAX broadens AMETEK’s techni-cal competency in the measurementof physical properties; adds newtechnologies, applications, and endmarkets to AMETEK’s base businessin industrial and process instruments;and greatly expands AMETEK’spresence in the laboratory instru-ment market.

EDAX has leading positions in several emergingtechnologies. One is crystallography, whichallows the microstructure of a material to beanalyzed and mapped. EDAX instruments areused with advanced electron microscopes tocapture information that can be of criticalimportance to better understand the performanceof metals, minerals, and semiconductors. TheEDAX instrument carries out the analysis oncethe image is formed by the electron microscope,as with the silver chloride crystal shown at right.

IRAS, too, is a highly differentiatedanalytical instruments business. LikeEDAX, IRAS significantly extendsAMETEK’s core competency in themeasurement of physical propertiesand enhances its position in labora-tory and research instruments.

IRAS has three product lines: Thefirst—nuclear spectrometry instru-ments and systems marketed underthe ORTEC® brand name—includeshigh-purity germanium detectors andspectrometers used for the detection,identification, and monitoring ofradioactive materials. These productshave applications in laboratoryresearch and in the increasinglyimportant areas of environmental

2001 AMETEK Annual Report | 11

monitoring and detection of nuclearand chemical weapons.

The second product line—PrincetonApplied Research products—consistsof high-precision, electrochemicalanalysis instruments used in research,life sciences, corrosion, and semicon-ductor applications.

The third product line—SignalRecovery products—includes a varietyof instruments that measure low-levelor noisy electrical signals. Thoseproducts have applications in theelectronics, optics, and researchmarkets.

IRAS operates as a new division—Advanced Measurement Technology,while EDAX became a new unitwithin AMETEK’s Process & Analyti-cal Instruments division. Both are partof AMETEK’s Electronic InstrumentsGroup. They offer AMETEK opportu-nities for expansion into new, fast-growing analytical instrumentmarkets and are expected to serve asfuture growth platforms.

Building Strength in KeyMotor MarketsAcquired in May 2001, GS Electric is anexcellent fit with AMETEK’s existingelectric motor businesses. Togetherthey extend AMETEK’s globalleadership in floor care motors andfurther leverage its extensive manufac-turing and distribution capabilities. Inaddition, the acquisition of GS Electricbrings mass and expertise in perma-nent magnet motors, which enablesAMETEK to participate in a variety ofnew niche markets with a full rangeof motor options.

Renamed AMETEK SpecialtyMotors, the business is a leader inseries universal and permanentmagnet motors. Roughly two-thirds ofits motor volume is sold to floor care,

outdoor power equipment, and othermarkets AMETEK already serves. Theremaining sales volume comes frompermanent magnet motors used infitness equipment and small house-hold appliances. These markets havehigher growth rates than floor careand outdoor power equipment.

Global & MarketExpansionAMETEK is a global company.Approximately one-third of its salesare to markets outside the UnitedStates. AMETEK has achieved stronginternational sales by positioninglow-cost manufacturing in key globalmarkets and by expanding its salesand distribution presence in Europe,Asia, and Latin America. AMETEKspans the globe with plants and directsales operations in 15 countries outsidethe United States.

Leveraging Opportunitiesin Electric PowerUtility deregulation, increased de-mand for electric power, andinvestment in electric power infra-structure have made the worldwidepower industry an important growthsector for AMETEK. Through acquisi-tions and internal development,AMETEK has expanded its power

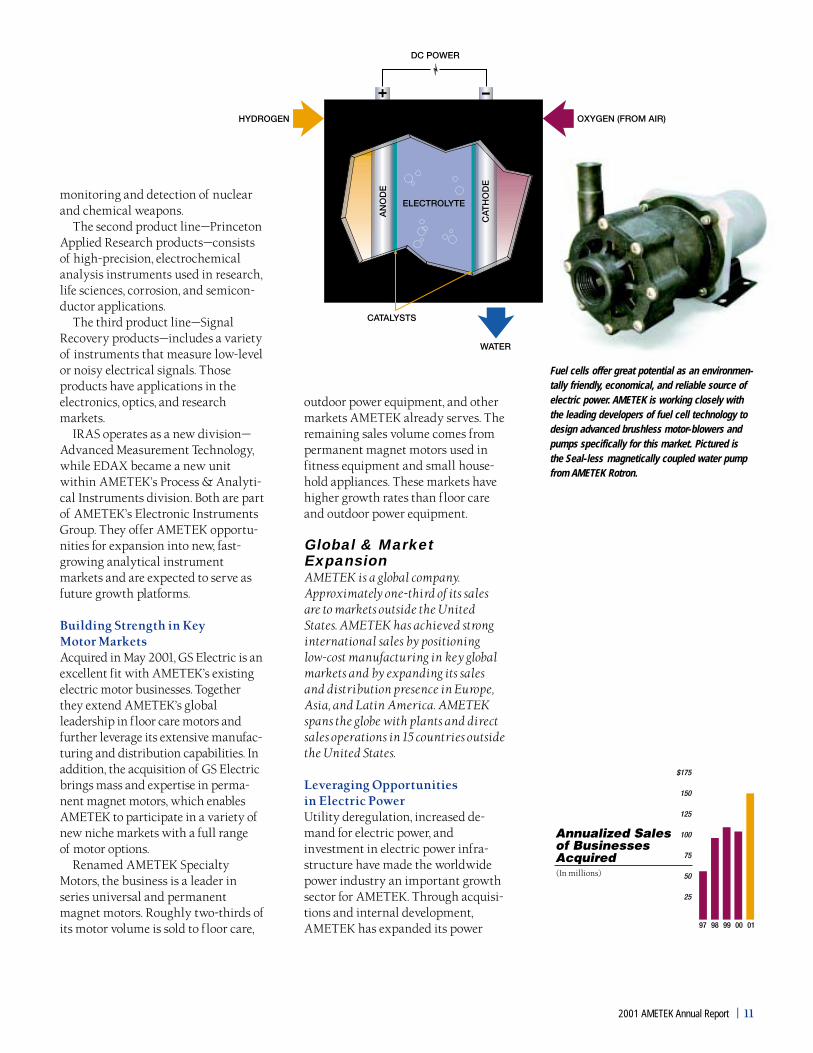

Fuel cells offer great potential as an environmen-tally friendly, economical, and reliable source ofelectric power. AMETEK is working closely withthe leading developers of fuel cell technology todesign advanced brushless motor-blowers andpumps specifically for this market. Pictured isthe Seal-less magnetically coupled water pumpfrom AMETEK Rotron.

12 | 2001 AMETEK Annual Report

At the heart of NASA’s High-Energy SolarSpectroscopic Imager (HESSI) spacecraft,launched in early 2002, are hyperpuregermanium detectors from AMETEK’sAdvanced Measurement Technology business.The detectors are the focal point of thespacecraft’s imaging spectrometer, designedto provide high-resolution images of solarflares during the craft’s two-year orbitalmission.

Pho

to cr

edit

: NA

SA, U

.C. Be

rkel

ey a

nd

HES

SI Te

am

instruments business to serve both theelectric power generation and distri-bution industries worldwide.

AMETEK’s power businessesare proven leaders in each of theirindividual segments. AMETEKsensors and instruments, for example,are sold to most of the world’s turbinegenerator manufacturers. AMETEK’spower quality and metering equip-ment, event recorders, and controlroom annunciators are well recog-nized and used worldwide. All provide

AMETEK with ample opportunitiesfor growth in the expanding electricpower market.

Developing AlternativeEnergy TechnologyFuel cells hold the promise of clean,cheap, and environmentally friendlyenergy. Although the use of fuel cellsis still an emerging technology, recentadvances in design and performancehave made them more attractive as analternative power source. Fuel cellsare expected to play an increasinglyimportant role in providing reliablepower for homes, businesses, andtransportation.

AMETEK is working closely withmajor fuel cell developers in designingadvanced motors, motor-blowers, andpumps specifically for fuel cellapplications. Compact, high-performance Windjammer® brushlessmotor-blowers and Seal-less water

2001 AMETEK Annual Report | 13

pumps from AMETEK Rotron areused for hydrogen purging andcomponent cooling. They offer spark-free and maintenance-free operation,integrated electronic capability, andlong service life.

High-purity metal strip, speciallyformulated metal powders, andprecision wire products fromAMETEK Specialty Metal Productsalso have applications in fuel cells.

Maximizing Global Best-CostMotor ManufacturingAMETEK’s unmatched global motormanufacturing capability is amongthe reasons several leading captivemotor manufacturers chose tooutsource additional motor produc-tion to AMETEK in 2001. AMETEK’sleadership in electric motors is duein large part to its best-cost motormanufacturing capability. AMETEKadded to that strength with recentexpansions in Mexico, China, theCzech Republic, and Brazil.

AMETEK’s motor plant in theCzech Republic now accounts formore than one-third of AMETEK’stotal European motor production—a share that is expected to increasein 2002. Its plant in Shanghai, China,expanded production of householdvacuum motors and began manufac-turing brushless motors in 2001. Inaddition, its plant in São Paulo, Brazil,opened in 1999, initiated vacuummotor production during 2001.

AMETEK’s motor plant in Reynosa,Mexico, now produces more than 70%of AMETEK’s North American outputof household vacuum motors. Openedin 1996, the Reynosa facility is amongthe world’s most advanced motorplants and a pioneer in the use of flowmanufacturing for series universalmotors. In 2000, Reynosa became thefirst motor plant anywhere to produceseries universal motors using acontinuous one-piece process thatsince has been adopted elsewhere

within AMETEK. In 2001, Reynosabegan production of AMETEKPrestolite Power and Switch divisionproducts using flow manufacturingtechniques, thereby greatly reducingcycle time, inventory, and floor space.

New ProductsOne of AMETEK’s great strengths isits ability to develop innovative, newproducts and to market them success-fully. Sales of new products play anincreasingly important role amongAMETEK’s growth strategies.AMETEK’s investment in new productdevelopment—$45 million in 2001—isyielding a large number of innovative,new products.

Providing Sensors forNext-Generation AircraftWhen the first F-35 Joint Strike Fighterfrom Lockheed Martin enters service in2008, engine sensors from AMETEKAerospace will be aboard to provideengine speed, exhaust temperature,oil level, and various other vitalmeasurements.

The F-35 aircraft is expected toserve as the cornerstone of Americanand allied air defense systems wellinto the 21st century. The value toAMETEK of the engine sensor suiteis expected to exceed $80 million overthe life of the program.

AMETEK’s selection to providethe engine sensor suite reflects itsleadership position in aircraft enginesensors, with more than 150 products,including oil level, pressure, enginespeed, and exhaust temperaturesensors; vibration monitors; and fuelflow transmitters.

Troubleshooting Power QualityProblemsThe MERIDIANTM Ultra poweranalyzer—the latest diagnostic toolfrom AMETEK Power Instruments—isable to quickly and accurately identifypower quality problems. The compact,

The Drexelbrook IntelliPoint RFTM level mea-surement instrument introduced by AMETEKSensor Technology represents a technicalbreakthrough for the industry—the first trueno-calibration point level switch using radiofrequency (RF) technology. IntelliPoint userssimply install it in a tank or other vessel andapply the power. The IntelliPoint’s No-Cal TM

technology is able to detect the absence orpresence of, or a change in, material andmake necessary adjustments automaticallywithout the need for calibration.

14 | 2001 AMETEK Annual Report

self-contained unit reduces costlywork stoppages, equipment andcommunications failures, andprocessing and control errors thatresult from poor power quality.The MERIDIAN Ultra analyzer is anessential tool for many continuousmanufacturing processes, industrialhigh-tech production, and users ofsensitive electronic equipment.

Setting the Standard for Ultrahigh-Purity Moisture DetectionThe Model 5910 process analyzer,introduced by AMETEK ProcessInstruments in 2001, establishednew standards for accuracy, stability,and sensitivity in the moistureanalysis of ultrahigh-purity processgases used by the semiconductorindustry. With its ability to rapidlydetect part-per-trillion changes inmoisture concentrations in processgases, the Model 5910 analyzer offersa significant performance enhance-ment at far lower cost than alternativetechnologies.

Improving Motor Designand EfficiencyAs the leader in air-moving motortechnology, AMETEK draws upon itsindustry-leading engineering andmanufacturing experience to developnew and innovative motor products.AMETEK led the way again in 2001

with its ADVANTEKTM family ofhousehold vacuum motors and itsAir-WattTM Series of high-performancecommercial vacuum motors.

The ADVANTEK motor familyincorporates design innovationsthat enhance its manufacturabilitywithout sacrificing performance.Advanced fan and bearing designs,new construction materials, andimproved manufacturing techniquesenable the Air-Watt Series of commer-cial vacuum motors to operate at highspeeds while using less energy.

Offering Breakthrough Solutionsin Sensor TechnologyThe IntelliPoint RF TM level measure-ment instrument, one of several newproducts introduced by AMETEKSensor Technology in 2001, representsa technical breakthrough for theprocess industry. It is the first trueno-calibration point-level instrumentable to detect the presence or absenceof material without manual adjust-ments at both start-up and when thetype of material changes.

Accelerating the Pacein New ProductsOther new products launched in 2001include:¤ AMPHIONTM patented solid-state

power controller from AMETEKAerospace that offers better loadprotection for avionic applications

¤ Food-grade Stik® level sensor fromAMETEK Sensor Technology thatcombines a field-proven position-sensing technology with an innova-tive sensor design in a unique,sanitary level-measuring device

¤ JOFRATM ITC Series of dry-blocktemperature calibrators and LloydInstruments’ LF Plus line ofuniversal material-testing machinesfrom AMETEK Test & CalibrationInstruments

AMETEK’s Reynosa, Mexico, facility was thefirst series universal motor plant anywhereto produce a motor field, armature, and finalproduct using one-piece flow manufacturingtechniques. The Ex-Cell process developedat Reynosa substantially reduces the amountof time, scrap, work-in-process inventory, andfloor space required. AMETEK has transferredthe Ex-Cell process to motor plants in theUnited States, China, and the Czech Republic.

2001 AMETEK Annual Report | 15

A suite of advanced engine sensors from AMETEKwill monitor engine speed, exhaust temperature,oil level, and various other data on the F-35Joint Strike Fighter now under developmentat Lockheed Martin.

¤ Model DCT pressure transducersfrom AMETEK U.S. Gauge, whichincorporate the latest digitalcompensation techniques into anall-purpose industrial pressuretransducer

¤ Next Generation Instrument systemfrom AMETEK Dixson—a fullydigital, multiplexed, heavy-dutyvehicle dashboard instrumentsystem that provides a reliable,expandable, and cost-effectivealternative to analog gaugescurrently found on heavy trucks,agricultural/construction equip-ment, and other vehicles

¤ MAGNA-LATCHTM low-voltagedisconnect contactor fromAMETEK Prestolite Power andSwitch, offering highly reliableperformance for critical telecommu-nications, uninterruptible powersupply, and other applications

¤ Smart Kitchen controller fromAMETEK NCC, which permitswireless communication betweencommercial appliances in quick-service restaurants

Photo

cred

it: Lock

hee

d Mar

tin Co

rpora

tion

16 | 2001 AMETEK Annual Report

FinancialReview

Clear Vision • Sound Strategies • Solid Performance

This 2001 summary annual report containsabbreviated financial data. The completetext of Management’s Discussion andAnalysis and the consolidated financialstatements and footnotes are presented inAMETEK’s 2001 Form 10-K and in anappendix to the Proxy Statement for the2002 Annual Meeting of Shareholders.

OverviewIn 2001, AMETEK had sales of $1 billion ina difficult economic environment. TheCompany also achieved its eighth consecu-tive year of growth in income and earningsper share from continuing operations be-fore unusual items. The primary contribu-tors to this strong performance were costreduction initiatives necessary to size thebusiness to the current economic environ-ment and to continue the Company’sglobal plan of lowering its cost structure,strong growth in its aerospace and powerinstruments business, and the contributionfrom acquired companies.

The Company also set records for in-come and diluted earnings per share in2001 before unusual items. The Companyrecorded unusual pretax expenses totaling$23.3 million ($15.3 million after tax, or$0.46 per diluted share) in the fourth quar-ter of 2001. Those expenses were in re-sponse to weak economic conditions andthe need to realign the Company’s coststructure to the realities of the economy,as well as the effect the economy has hadon AMETEK’s customer base. Also, in thefourth quarter of 2001, the Company recog-nized a tax benefit of $10.5 million after tax($0.32 per diluted share) resulting from theclosure of several open tax years.

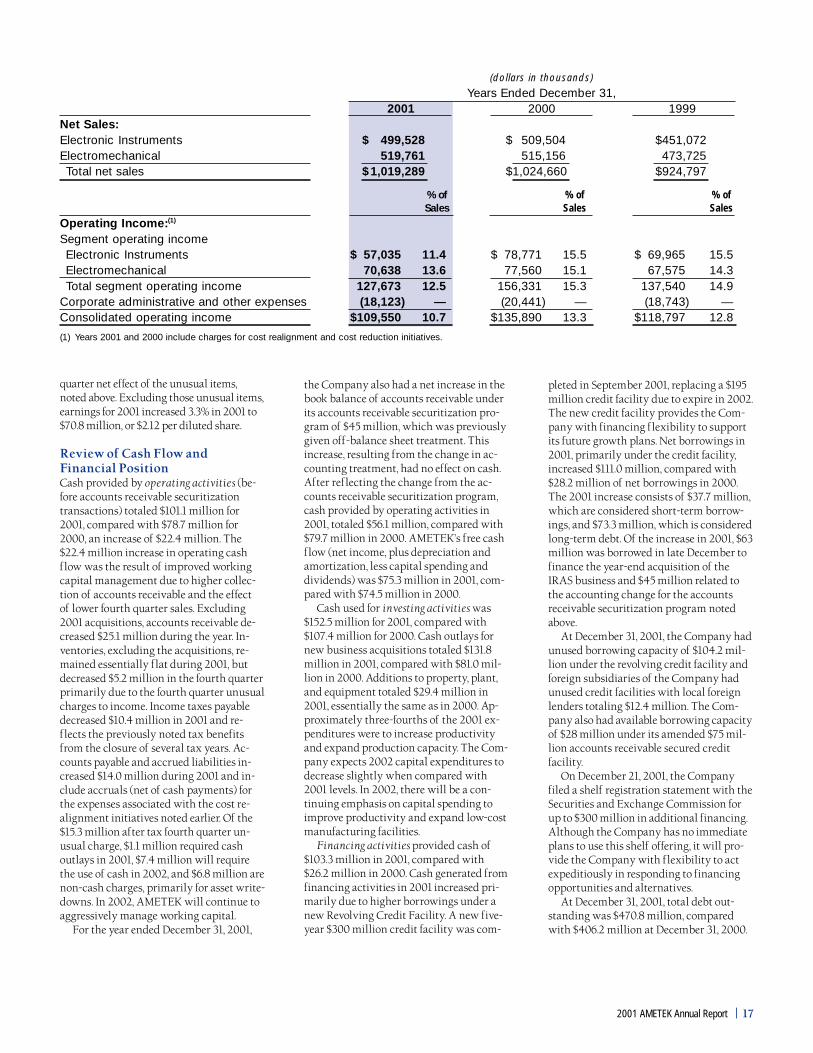

Review of OperationsThe table on the opposite page sets forth netsales and operating income for the Com-pany by business segment and on a consoli-dated basis for the years ended December31, 2001, 2000, and 1999.

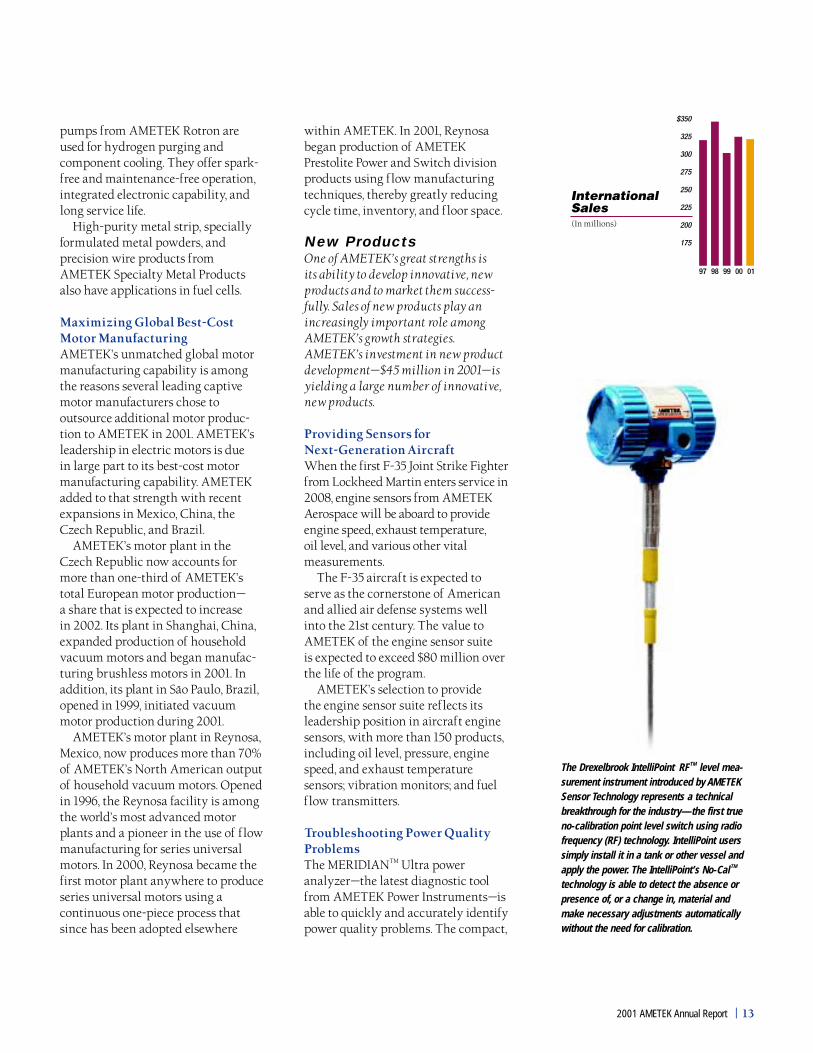

AMETEK reported sales for 2001 of$1,019.3 million, a decrease of 0.5% fromsales of $1,024.7 million in 2000. The de-cline was due to weak economic conditionsthat impacted most of the Company’s busi-nesses. Significantly offsetting those weakeconomic conditions were positive contri-butions from the Company’s recent busi-ness acquisitions and strength in its aero-space and power instruments businesses.Without those recent acquisitions, sales for2001 would have been 10% lower. Sales forthe Electronics Instruments Group’s (EIG)were $499.5 million in 2001, a decrease of2.0% from sales of $509.5 million in 2000.Sales for EIG were lower largely due to adecline in demand from most of its busi-nesses. Recent acquisitions and continuedstrength in the aerospace and power instru-ments businesses offset most of theGroup’s sales decline. Sales for the Electro-mechanical Group (EMG) were $519.8 mil-lion in 2001, an increase of 0.9% from salesof $515.2 million in 2000 due to the salescontribution from acquisitions. OffsettingEMG’s sales increase were adverse eco-nomic conditions and other competitivefactors in the U.S. and European floor caremarkets. Total consolidated internationalsales were $321.2 million in 2001, a decreaseof 1.1% from sales of $324.9 million in2000.

As noted earlier, the Company recordedunusual expenses totaling $23.3 million

(pretax) in the fourth quarter of 2001. Ofthat total, $12.4 million was related to thecosts of employee reductions, facility clo-sures, and the continued migration of pro-duction to low-cost locales and $10.9 mil-lion for asset writedowns. The assetwritedowns were related to receivables($3.3 million), inventory ($6.1 million)and equipment ($1.5 million). The assetwritedowns are primarily the result of thedifficulties the economic environment hashad on a number of AMETEK’s customers.The annualized cost savings resulting fromthe severance and related actions are ex-pected to be approximately $25 million.These cost reduction initiatives are a con-tinuation of programs begun in the fourthquarter of 2000 for which the Companyrecorded a $3.4 million pretax charge inthat quarter and continued during 2001.

Total segment operating income de-clined to $127.7 million in 2001, a decreaseof 18.3%, compared with segment operat-ing income of $156.3 million in 2000. Seg-ment operating margins in 2001 were 12.5%of sales, versus 15.3% of sales in 2000. Theoverall decline in segment operating mar-gins in 2001 was primarily due to the previ-ously noted 2001 fourth quarter unusualcharges. Before the unusual charges, seg-ment operating margins for 2001 were14.8%.

After deducting corporate administra-tive expenses, 2001 consolidated operatingincome was $109.6 million, or 10.7% ofsales, a decrease of $26.3 million, comparedwith 2000 operating income of $135.9 mil-lion, or 13.3 % of sales. Before unusualcharges, 2001 operating income was $132.8million, or 13.1% of sales.

EIG’s 2001 operating income decreased$21.7 million to $57.0 million after unusualexpenses, or 11.4% of sales, down from$78.7 million in 2000, or 15.5% of sales.Without the unusual expenses, EIG’s oper-ating income for 2001 would have been$69.5 million, or 13.9% of sales, a decrease of$9.3 million, compared with 2000. EMG’s2001 operating income decreased $7.0 mil-lion in 2001 to $70.6 million, after unusualexpenses, or 13.6% of sales, down from$77.6 million in 2000, or 15.1% of sales.Without the unusual expenses, EMG’s op-erating income for 2001 would have been$81.3 million, or 15.6% of sales, an increaseof $3.7 million, compared with 2000.

Net income for 2001 was $66.1 million,or $1.98 per diluted share, compared withnet income for 2000 of $68.5 million, or $2.11per diluted share. The 3.5% decrease in netincome was due primarily to the fourth

2001 AMETEK Annual Report | 17

quarter net effect of the unusual items,noted above. Excluding those unusual items,earnings for 2001 increased 3.3% in 2001 to$70.8 million, or $2.12 per diluted share.

Review of Cash Flow andFinancial PositionCash provided by operating activities (be-fore accounts receivable securitizationtransactions) totaled $101.1 million for2001, compared with $78.7 million for2000, an increase of $22.4 million. The$22.4 million increase in operating cashflow was the result of improved workingcapital management due to higher collec-tion of accounts receivable and the effectof lower fourth quarter sales. Excluding2001 acquisitions, accounts receivable de-creased $25.1 million during the year. In-ventories, excluding the acquisitions, re-mained essentially flat during 2001, butdecreased $5.2 million in the fourth quarterprimarily due to the fourth quarter unusualcharges to income. Income taxes payabledecreased $10.4 million in 2001 and re-flects the previously noted tax benefitsfrom the closure of several tax years. Ac-counts payable and accrued liabilities in-creased $14.0 million during 2001 and in-clude accruals (net of cash payments) forthe expenses associated with the cost re-alignment initiatives noted earlier. Of the$15.3 million after tax fourth quarter un-usual charge, $1.1 million required cashoutlays in 2001, $7.4 million will requirethe use of cash in 2002, and $6.8 million arenon-cash charges, primarily for asset write-downs. In 2002, AMETEK will continue toaggressively manage working capital.

For the year ended December 31, 2001,

the Company also had a net increase in thebook balance of accounts receivable underits accounts receivable securitization pro-gram of $45 million, which was previouslygiven off-balance sheet treatment. Thisincrease, resulting from the change in ac-counting treatment, had no effect on cash.After reflecting the change from the ac-counts receivable securitization program,cash provided by operating activities in2001, totaled $56.1 million, compared with$79.7 million in 2000. AMETEK’s free cashflow (net income, plus depreciation andamortization, less capital spending anddividends) was $75.3 million in 2001, com-pared with $74.5 million in 2000.

Cash used for investing activities was$152.5 million for 2001, compared with$107.4 million for 2000. Cash outlays fornew business acquisitions totaled $131.8million in 2001, compared with $81.0 mil-lion in 2000. Additions to property, plant,and equipment totaled $29.4 million in2001, essentially the same as in 2000. Ap-proximately three-fourths of the 2001 ex-penditures were to increase productivityand expand production capacity. The Com-pany expects 2002 capital expenditures todecrease slightly when compared with2001 levels. In 2002, there will be a con-tinuing emphasis on capital spending toimprove productivity and expand low-costmanufacturing facilities.

Financing activities provided cash of$103.3 million in 2001, compared with$26.2 million in 2000. Cash generated fromfinancing activities in 2001 increased pri-marily due to higher borrowings under anew Revolving Credit Facility. A new five-year $300 million credit facility was com-

pleted in September 2001, replacing a $195million credit facility due to expire in 2002.The new credit facility provides the Com-pany with financing flexibility to supportits future growth plans. Net borrowings in2001, primarily under the credit facility,increased $111.0 million, compared with$28.2 million of net borrowings in 2000.The 2001 increase consists of $37.7 million,which are considered short-term borrow-ings, and $73.3 million, which is consideredlong-term debt. Of the increase in 2001, $63million was borrowed in late December tofinance the year-end acquisition of theIRAS business and $45 million related tothe accounting change for the accountsreceivable securitization program notedabove.

At December 31, 2001, the Company hadunused borrowing capacity of $104.2 mil-lion under the revolving credit facility andforeign subsidiaries of the Company hadunused credit facilities with local foreignlenders totaling $12.4 million. The Com-pany also had available borrowing capacityof $28 million under its amended $75 mil-lion accounts receivable secured creditfacility.

On December 21, 2001, the Companyfiled a shelf registration statement with theSecurities and Exchange Commission forup to $300 million in additional financing.Although the Company has no immediateplans to use this shelf offering, it will pro-vide the Company with flexibility to actexpeditiously in responding to financingopportunities and alternatives.

At December 31, 2001, total debt out-standing was $470.8 million, comparedwith $406.2 million at December 31, 2000.

(dollars in thousands)

Years Ended December 31,2001 2000 1999

Net Sales:Electronic Instruments $ 499,528 $ 509,504 $451,072Electromechanical 519,761 515,156 473,725Total net sales $1,019,289 $1,024,660 $924,797

% of % of % ofSales Sales Sales

Operating Income:(1)

Segment operating incomeElectronic Instruments $ 57,035 11.4 $ 78,771 15.5 $ 69,965 15.5Electromechanical 70,638 13.6 77,560 15.1 67,575 14.3Total segment operating income 127,673 12.5 156,331 15.3 137,540 14.9

Corporate administrative and other expenses (18,123) — (20,441) — (18,743) —Consolidated operating income $109,550 10.7 $135,890 13.3 $118,797 12.8

(1) Years 2001 and 2000 include charges for cost realignment and cost reduction initiatives.

18 | 2001 AMETEK Annual Report

The weighted average interest rate on totaldebt outstanding at December 31, 2001, was5.2%, compared with 7.3% at December 31,2000. Debt as a percentage of capitalizationdecreased to 58.4% at December 31, 2001,from 59.1% at December 31, 2000. EBITDAin 2001 was $178.0 million, compared with$177.6 million in 2000. AMETEK’s debt-to-EBITDA ratio (computed in accordancewith the Company’s credit agreement) was2.4 to 1 at December 31, 2001, comparedwith 2.2 to 1 at the prior year-end, and itsEBITDA covered interest expense 6.4 timesin 2001, compared with 6.1 times in 2000.All of the above financial ratios were well

The financial statements in this summaryannual report were derived from the con-solidated financial statements that appearin an appendix to the Proxy Statement forthe 2002 Annual Meeting of Shareholders.

Management has prepared and is re-sponsible for the integrity of the consoli-dated financial statements and related in-formation. The statements are preparedin conformity with accounting principlesgenerally accepted in the United Statesconsistently applied and include certainamounts based on management’s best esti-mates and judgments. Historical financialinformation elsewhere in this summaryannual report is consistent with that inthe financial statements.

In meeting its responsibility for thereliability of the financial information,management maintains a system of inter-

nal accounting controls, including aninternal audit program. A more completedescription of these controls along withmanagement’s opinion as to their overalleffectiveness, is contained in the detailedReport of Management included in anappendix to the Proxy Statement.

The Company’s independent auditors,Ernst & Young LLP, are engaged to renderan opinion as to whether management’sfinancial statements present fairly, in allmaterial respects, the Company’s financialposition and operating results. Their reporton these condensed financial statementsis included below.

The Audit Committee of the Board ofDirectors, which is composed solely ofDirectors who are not employees of theCompany, meets with the independentauditors, the internal auditors, and manage-

ment to satisfy itself that each is properlydischarging its responsibilities. The reportof the Audit Committee is included in theProxy Statement. Both the independentauditors and internal auditors have directaccess to the Audit Committee.

Management recognizes its responsibil-ity for conducting the Company’s activitiesaccording to the highest standards ofpersonal and corporate conduct. Thatresponsibility is characterized andreflected in key policy statementspublicized throughout the Company.

John J. MolinelliExecutive Vice President—Chief Financial OfficerJanuary 29, 2002

Report of Management

To the Board of Directors andShareholders of AMETEK, Inc.We have audited, in accordance with audit-ing standards generally accepted in theUnited States, the consolidated balancesheets of AMETEK, Inc. at December 31,2001 and 2000 and the related consolidatedstatements of income, stockholders’ equity,and cash flows for each of the three years in

the period ended December 31, 2001 (notpresented separately herein) and in ourreport dated January 29, 2002, we ex-pressed an unqualified opinion on thoseconsolidated financial statements. In ouropinion, the information set forth in theaccompanying condensed consolidatedfinancial statements (presented on pages19 through 21) is fairly stated in all material

respects in relation to the consolidated fi-nancial statements from which it has beenderived.

Philadelphia, PAJanuary 29, 2002

Report of Independent Auditors onCondensed Consolidated Financial Statements

within the allowable limits under theCompany’s debt agreements.

During 2001 the Company repurchased440,000 shares of its common stock at acost of $11.6 million, compared with 83,500shares acquired in 2000 at a cost of $1.6million. At December 31, 2001, approxi-mately $16 million of the current $50 mil-lion share repurchase authorization wasunexpended.

Forward-Looking InformationExcept for historical information containedin this summary annual report, certainstatements made herein, which state the

Company’s prediction for the future, areforward-looking statements, which involverisks and uncertainties that exist in theCompany’s operations and business envi-ronment and are subject to change based onvarious important factors. Actual resultsmay differ materially from those expressedin any forward-looking statement made by,or on behalf of, the Company. Additionalinformation concerning factors that couldcause actual results to differ from projec-tions is contained in the Company’s Form10-K for the year ended December 31, 2001,filed with the Securities and ExchangeCommission.

2001 AMETEK Annual Report | 19

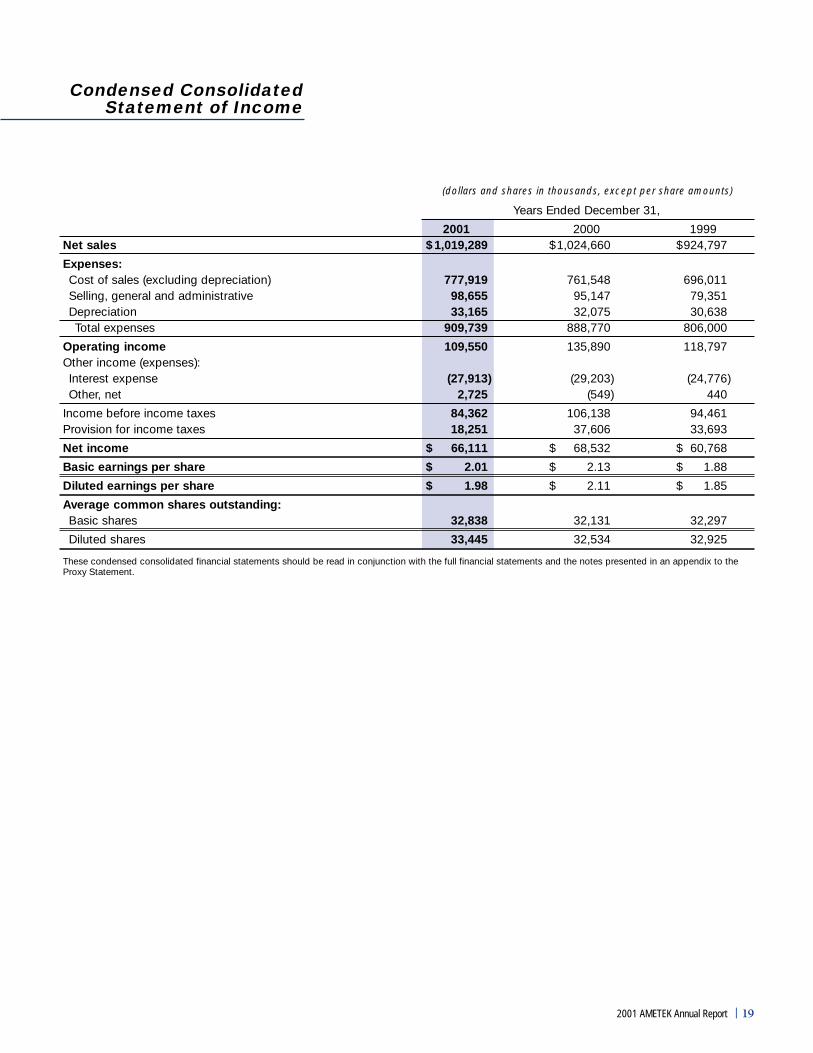

Condensed ConsolidatedStatement of Income

Years Ended December 31,

2001 2000 1999Net sales $ 1,019,289 $1,024,660 $924,797

Expenses:Cost of sales (excluding depreciation) 777,919 761,548 696,011Selling, general and administrative 98,655 95,147 79,351Depreciation 33,165 32,075 30,638Total expenses 909,739 888,770 806,000

Operating income 109,550 135,890 118,797Other income (expenses):Interest expense (27,913) (29,203) (24,776)Other, net 2,725 (549) 440

Income before income taxes 84,362 106,138 94,461Provision for income taxes 18,251 37,606 33,693

Net income $ 66,111 $ 68,532 $ 60,768

Basic earnings per share $ 2.01 $ 2.13 $ 1.88

Diluted earnings per share $ 1.98 $ 2.11 $ 1.85

Average common shares outstanding:Basic shares 32,838 32,131 32,297

Diluted shares 33,445 32,534 32,925

These condensed consolidated financial statements should be read in conjunction with the full financial statements and the notes presented in an appendix to theProxy Statement.

(dollars and shares in thousands, except per share amounts)

20 | 2001 AMETEK Annual Report

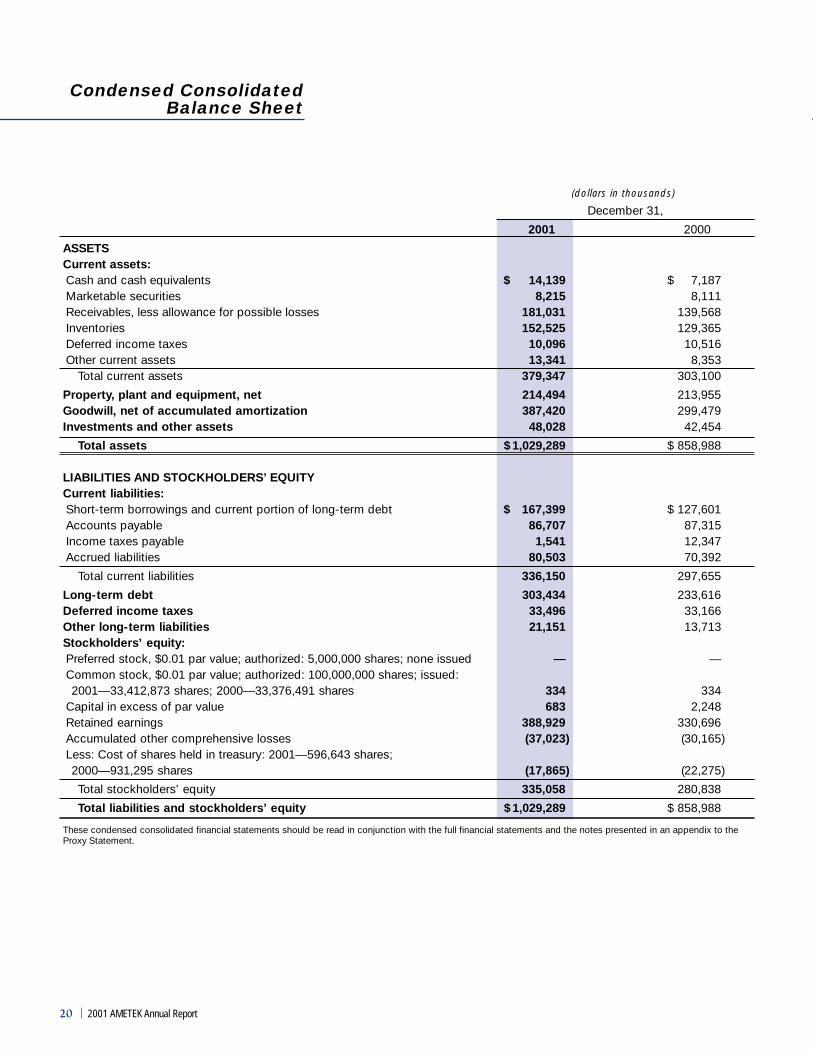

(dollars in thousands)

December 31,

2001 2000

ASSETSCurrent assets:Cash and cash equivalents $ 14,139 $ 7,187Marketable securities 8,215 8,111Receivables, less allowance for possible losses 181,031 139,568Inventories 152,525 129,365Deferred income taxes 10,096 10,516Other current assets 13,341 8,353

Total current assets 379,347 303,100

Property, plant and equipment, net 214,494 213,955Goodwill, net of accumulated amortization 387,420 299,479Investments and other assets 48,028 42,454

Total assets $ 1,029,289 $ 858,988

LIABILITIES AND STOCKHOLDERS’ EQUITYCurrent liabilities:Short-term borrowings and current portion of long-term debt $ 167,399 $ 127,601Accounts payable 86,707 87,315Income taxes payable 1,541 12,347Accrued liabilities 80,503 70,392

Total current liabilities 336,150 297,655

Long-term debt 303,434 233,616Deferred income taxes 33,496 33,166Other long-term liabilities 21,151 13,713Stockholders’ equity:Preferred stock, $0.01 par value; authorized: 5,000,000 shares; none issued — —Common stock, $0.01 par value; authorized: 100,000,000 shares; issued:2001—33,412,873 shares; 2000—33,376,491 shares 334 334

Capital in excess of par value 683 2,248Retained earnings 388,929 330,696Accumulated other comprehensive losses (37,023) (30,165)Less: Cost of shares held in treasury: 2001—596,643 shares;2000—931,295 shares (17,865) (22,275)

Total stockholders’ equity 335,058 280,838

Total liabilities and stockholders’ equity $ 1,029,289 $ 858,988

These condensed consolidated financial statements should be read in conjunction with the full financial statements and the notes presented in an appendix to theProxy Statement.

Condensed ConsolidatedBalance Sheet

2001 AMETEK Annual Report | 21

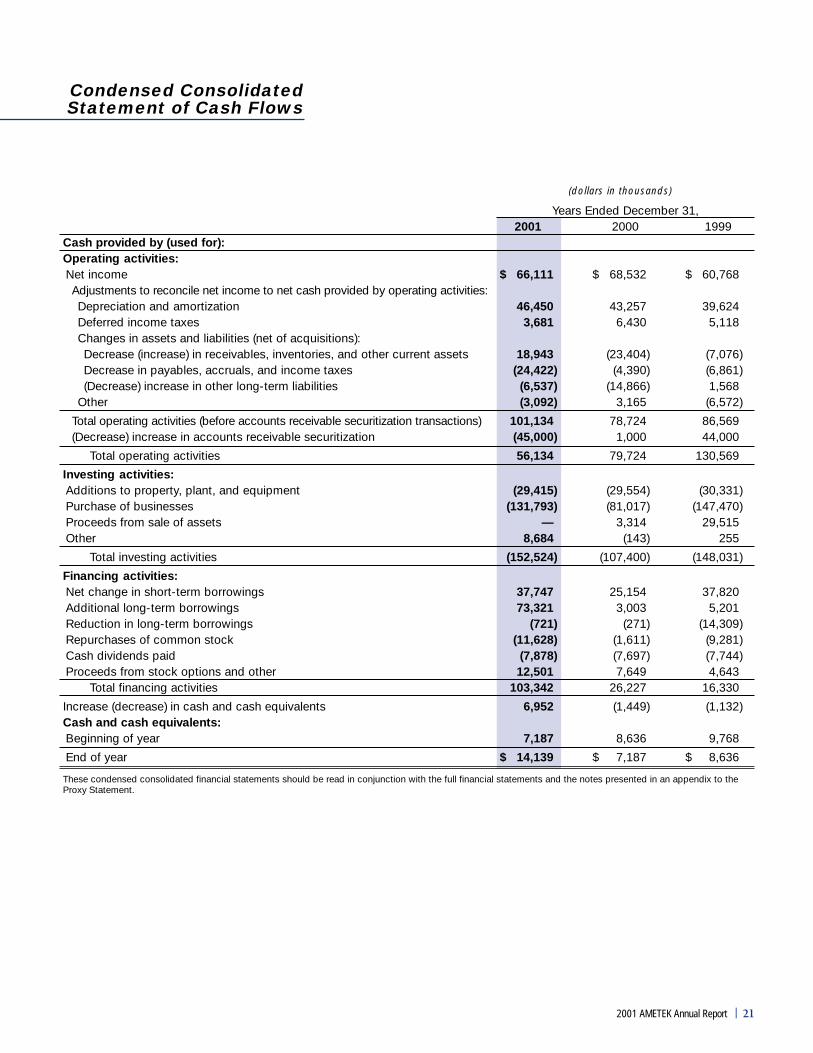

(dollars in thousands)

Years Ended December 31,2001 2000 1999

Cash provided by (used for):Operating activities:Net income $ 66,111 $ 68,532 $ 60,768Adjustments to reconcile net income to net cash provided by operating activities:Depreciation and amortization 46,450 43,257 39,624Deferred income taxes 3,681 6,430 5,118Changes in assets and liabilities (net of acquisitions):Decrease (increase) in receivables, inventories, and other current assets 18,943 (23,404) (7,076)Decrease in payables, accruals, and income taxes (24,422) (4,390) (6,861)(Decrease) increase in other long-term liabilities (6,537) (14,866) 1,568

Other (3,092) 3,165 (6,572)

Total operating activities (before accounts receivable securitization transactions) 101,134 78,724 86,569(Decrease) increase in accounts receivable securitization (45,000) 1,000 44,000

Total operating activities 56,134 79,724 130,569

Investing activities:Additions to property, plant, and equipment (29,415) (29,554) (30,331)Purchase of businesses (131,793) (81,017) (147,470)Proceeds from sale of assets — 3,314 29,515Other 8,684 (143) 255

Total investing activities (152,524) (107,400) (148,031)

Financing activities:Net change in short-term borrowings 37,747 25,154 37,820Additional long-term borrowings 73,321 3,003 5,201Reduction in long-term borrowings (721) (271) (14,309)Repurchases of common stock (11,628) (1,611) (9,281)Cash dividends paid (7,878) (7,697) (7,744)Proceeds from stock options and other 12,501 7,649 4,643

Total financing activities 103,342 26,227 16,330

Increase (decrease) in cash and cash equivalents 6,952 (1,449) (1,132)Cash and cash equivalents:Beginning of year 7,187 8,636 9,768

End of year $ 14,139 $ 7,187 $ 8,636

These condensed consolidated financial statements should be read in conjunction with the full financial statements and the notes presented in an appendix to theProxy Statement.

Condensed ConsolidatedStatement of Cash Flows

22 | 2001 AMETEK Annual Report

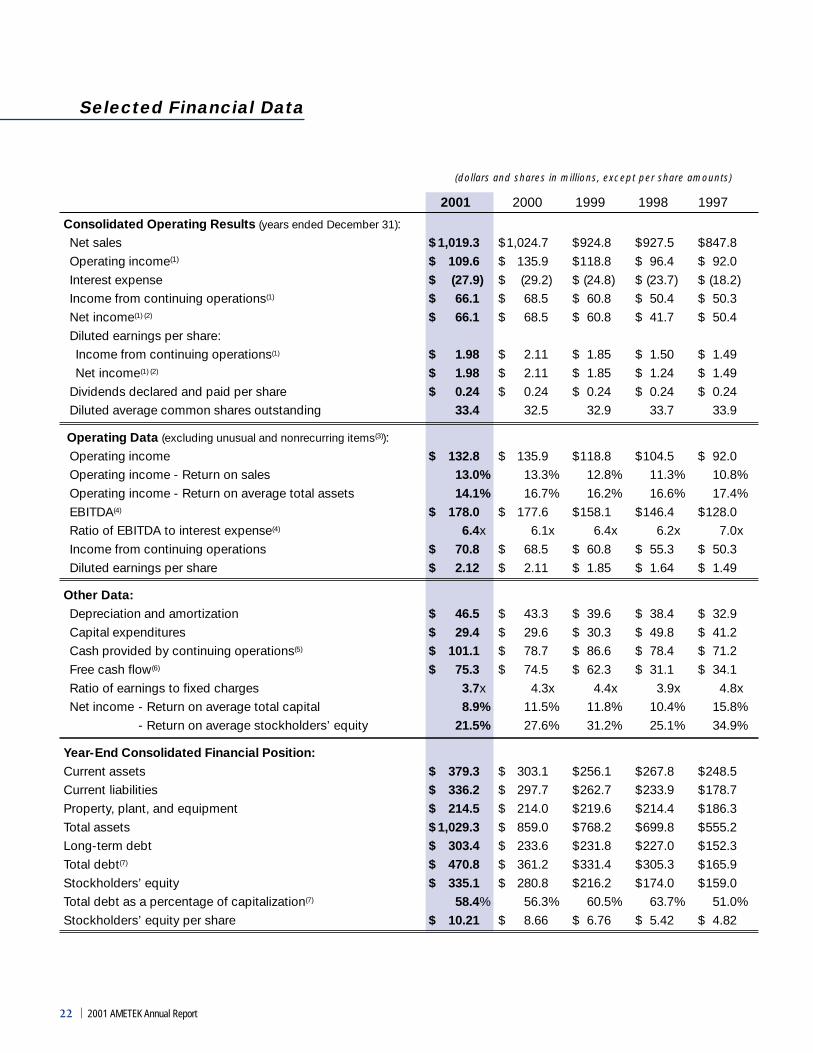

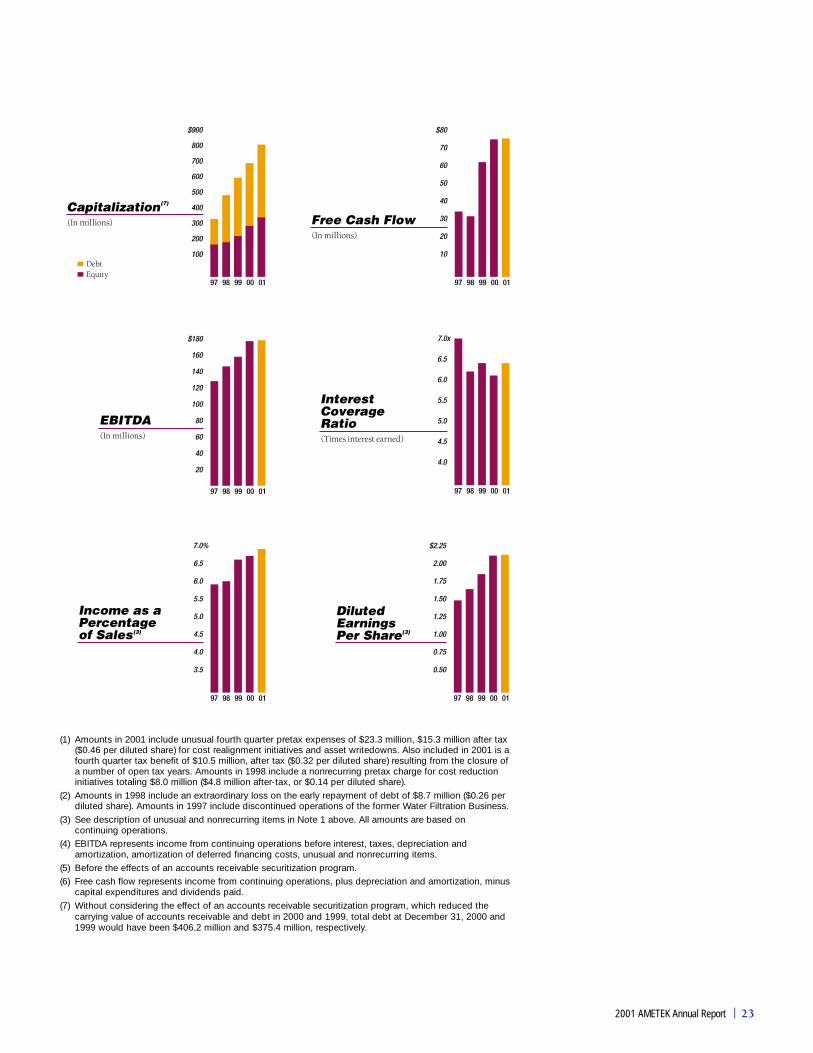

Selected Financial Data

(dollars and shares in millions, except per share amounts)

2001 2000 1999 1998 1997

Consolidated Operating Results (years ended December 31):

Net sales $ 1,019.3 $1,024.7 $924.8 $927.5 $847.8

Operating income(1) $ 109.6 $ 135.9 $118.8 $ 96.4 $ 92.0

Interest expense $ (27.9) $ (29.2) $ (24.8) $ (23.7) $ (18.2)

Income from continuing operations(1) $ 66.1 $ 68.5 $ 60.8 $ 50.4 $ 50.3

Net income(1) (2) $ 66.1 $ 68.5 $ 60.8 $ 41.7 $ 50.4

Diluted earnings per share:

Income from continuing operations(1) $ 1.98 $ 2.11 $ 1.85 $ 1.50 $ 1.49

Net income(1) (2) $ 1.98 $ 2.11 $ 1.85 $ 1.24 $ 1.49

Dividends declared and paid per share $ 0.24 $ 0.24 $ 0.24 $ 0.24 $ 0.24

Diluted average common shares outstanding 33.4 32.5 32.9 33.7 33.9

Operating Data (excluding unusual and nonrecurring items(3)):

Operating income $ 132.8 $ 135.9 $118.8 $104.5 $ 92.0

Operating income - Return on sales 13.0% 13.3% 12.8% 11.3% 10.8%

Operating income - Return on average total assets 14.1% 16.7% 16.2% 16.6% 17.4%

EBITDA(4) $ 178.0 $ 177.6 $158.1 $146.4 $128.0

Ratio of EBITDA to interest expense(4) 6.4x 6.1x 6.4x 6.2x 7.0x

Income from continuing operations $ 70.8 $ 68.5 $ 60.8 $ 55.3 $ 50.3

Diluted earnings per share $ 2.12 $ 2.11 $ 1.85 $ 1.64 $ 1.49

Other Data:Depreciation and amortization $ 46.5 $ 43.3 $ 39.6 $ 38.4 $ 32.9

Capital expenditures $ 29.4 $ 29.6 $ 30.3 $ 49.8 $ 41.2

Cash provided by continuing operations(5) $ 101.1 $ 78.7 $ 86.6 $ 78.4 $ 71.2

Free cash flow(6) $ 75.3 $ 74.5 $ 62.3 $ 31.1 $ 34.1

Ratio of earnings to fixed charges 3.7x 4.3x 4.4x 3.9x 4.8x

Net income - Return on average total capital 8.9% 11.5% 11.8% 10.4% 15.8%

- Return on average stockholders’ equity 21.5% 27.6% 31.2% 25.1% 34.9%

Year-End Consolidated Financial Position:Current assets $ 379.3 $ 303.1 $256.1 $267.8 $248.5

Current liabilities $ 336.2 $ 297.7 $262.7 $233.9 $178.7

Property, plant, and equipment $ 214.5 $ 214.0 $219.6 $214.4 $186.3

Total assets $ 1,029.3 $ 859.0 $768.2 $699.8 $555.2

Long-term debt $ 303.4 $ 233.6 $231.8 $227.0 $152.3

Total debt(7) $ 470.8 $ 361.2 $331.4 $305.3 $165.9

Stockholders’ equity $ 335.1 $ 280.8 $216.2 $174.0 $159.0

Total debt as a percentage of capitalization(7) 58.4% 56.3% 60.5% 63.7% 51.0%

Stockholders’ equity per share $ 10.21 $ 8.66 $ 6.76 $ 5.42 $ 4.82

2001 AMETEK Annual Report | 23

(1) Amounts in 2001 include unusual fourth quarter pretax expenses of $23.3 million, $15.3 million after tax($0.46 per diluted share) for cost realignment initiatives and asset writedowns. Also included in 2001 is afourth quarter tax benefit of $10.5 million, after tax ($0.32 per diluted share) resulting from the closure ofa number of open tax years. Amounts in 1998 include a nonrecurring pretax charge for cost reductioninitiatives totaling $8.0 million ($4.8 million after-tax, or $0.14 per diluted share).

(2) Amounts in 1998 include an extraordinary loss on the early repayment of debt of $8.7 million ($0.26 perdiluted share). Amounts in 1997 include discontinued operations of the former Water Filtration Business.

(3) See description of unusual and nonrecurring items in Note 1 above. All amounts are based oncontinuing operations.

(4) EBITDA represents income from continuing operations before interest, taxes, depreciation andamortization, amortization of deferred financing costs, unusual and nonrecurring items.

(5) Before the effects of an accounts receivable securitization program.(6) Free cash flow represents income from continuing operations, plus depreciation and amortization, minus

capital expenditures and dividends paid.(7) Without considering the effect of an accounts receivable securitization program, which reduced the

carrying value of accounts receivable and debt in 2000 and 1999, total debt at December 31, 2000 and1999 would have been $406.2 million and $375.4 million, respectively.

24 | 2001 AMETEK Annual Report

Board of DirectorsLewis G. ColePartner, Stroock & Stroock & Lavan LLP,Attorneys

Helmut N. FriedlaenderPrivate Investor

Sheldon S. GordonChairman of Union Bancaire PrivéeHoldings, Inc.

Frank S. HermanceChairman and Chief Executive Officer

Charles D. KleinFinancial Adviser; A Managing Directorof American Securities, L.P.

James R. MaloneFounding Partner and Managing Director,Bridge Associates LLC

David P. SteinmannA Managing Director of AmericanSecurities, L.P.

Elizabeth R. VaretPrivate Investor; Chairman of AmericanSecurities, L.P.

Corporate Executive OfficeFrank S. HermanceChairman and Chief Executive Officer

John J. MolinelliExecutive Vice President—Chief Financial Officer

Robert W. ChlebekPresident, Electronic Instruments

Thomas F. Mangold, Jr.President, Electronic Instruments

Albert J. NeupaverPresident, Electromechanical Group

Corporate OfficersWilliam J. BurkeVice President,Investor and Corporate Relations

William D. EgintonVice President, Corporate Development

William P. LawsonVice President and Chief InformationOfficer

Robert R. Mandos, Jr.Vice President and Comptroller

Deirdre D. SaundersVice President and Treasurer

Isaac S. SmallsVice President, Financial Reporting

John J. WeaverVice President, Human Resources

Donna F. WinquistVice President and General Counsel

Operating OfficersTiziano BarniVice President, Vacuum Products Division,Ciaramella Division and AMETEKelectromotory S.R.O.

Donald W. CarlsonVice President, U.S. Gauge

Raymond J. CavanaughVice President, Chemical Products

John Wesley HardinVice President, Dixson

Laurence K. HaywardVice President, Prestolite Powerand Switch

Stephen N. HoilesVice President, Test and CalibrationInstruments

Mark G. JantzenVice President, Global Floor Care

Timothy N. JonesVice President, Process and AnalyticalInstruments

Jon P. KidderVice President, Advanced MeasurementTechnology

Edward G. KramerVice President, Global Specialty Motors

Lim Meng KeeVice President, Asia

John H. Porter*Vice President—Engineering,Electromechanical Group

Joseph H. Ricketts, Jr.Vice President, Specialty Metal Products

Jon SlaybaughVice President, Specialty Motors

Roger A. SmithVice President, Lamb Electric

Peter M. StewartVice President, Rotron

James E. VisnicVice President, Sensor Technology

David A. ZapicoVice President, Aerospace and PowerInstruments

Operating ManagersJürgen GassenGeneral Manager, AMETEK PrecisionInstruments Europe GmbH

Ronald MakGeneral Manager, AMETEK MotorsShanghai

Odair Chieffe MonteiroGeneral Manager, AMETEK do Brasil Ltda.

* Retiring April 30, 2002