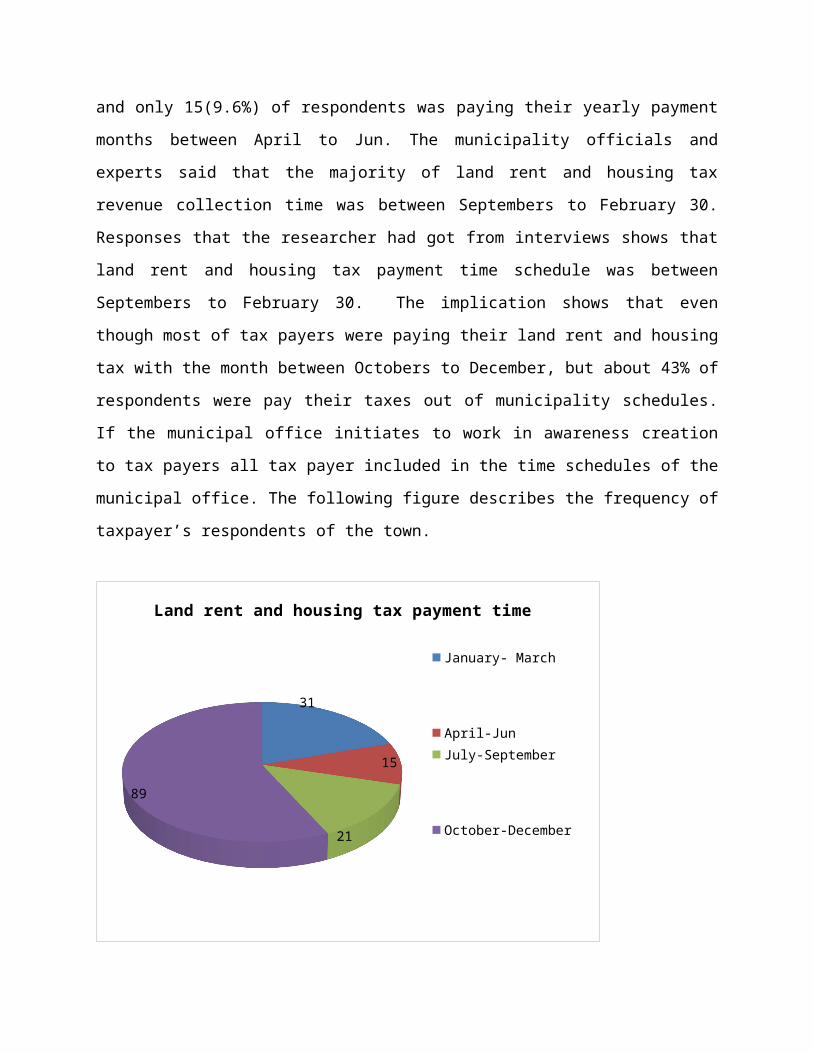

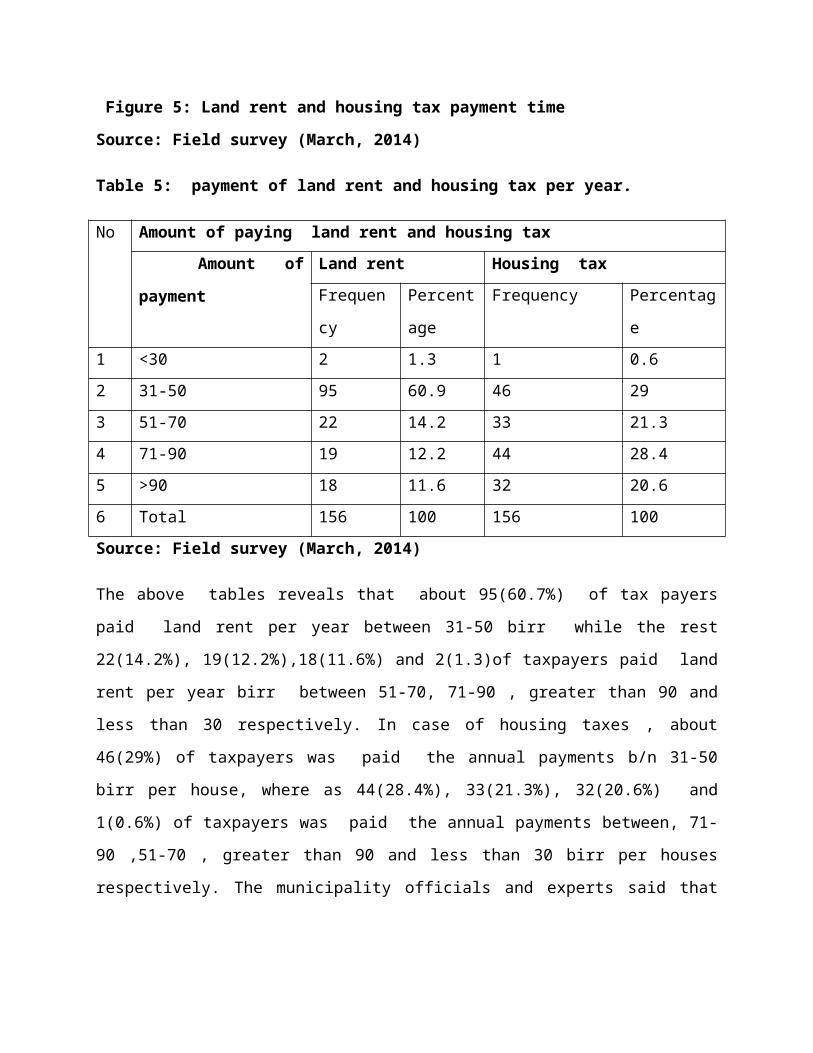

LTP system in Kercha town

98

CHAPTER ONE 1.0. INTRODUCTION Generally land and property taxes are the main source of revenue for towns to improve urban infrastructure. In most countries land and property taxes are related to local public services and infrastructural provision. The efficiency of local governments to tax land and property is linked directly with the quality and quantity of the provision of local public goods. David L. Cameron (1999) stated that the study of property taxation is closely tied to the study of the provision of public goods as any general equilibrium analysis of property taxation must consider the public benefits provided through a system of property taxation. Land and property taxation is a tool that used to improve the quality and quantity of infrastructure through improving revenue of the municipality. Efficiency and effectiveness in land and property taxation can be achieved through improving land and property taxation challenges. The purpose of this research was assessing land and property taxation practices in kercha town. Assessing Land and property tax administrative aspects have received the main attention of the researcher to conduct the study. The study proposal organized in five chapters. These are introduction, Literature review, methodology, Data organization and analysis and conclusion and recommendation.

-

Upload

independent -

Category

Documents

-

view

2 -

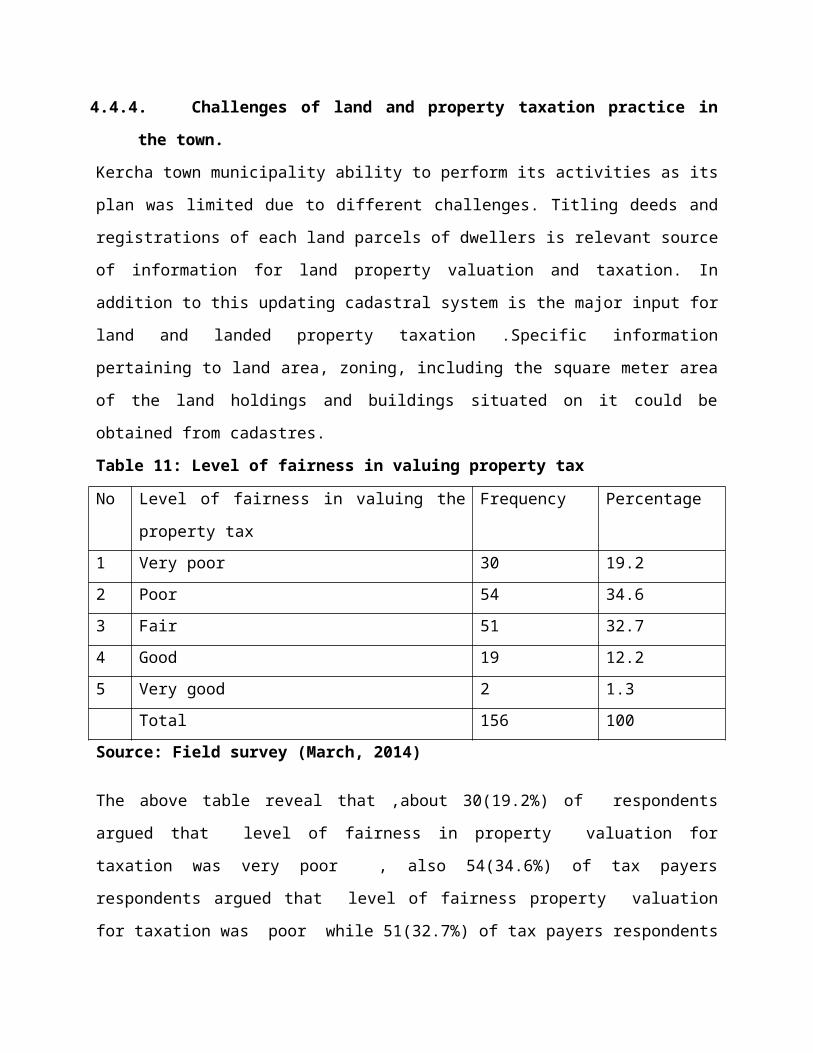

download

0

Transcript of LTP system in Kercha town

CHAPTER ONE

1.0. INTRODUCTION

Generally land and property taxes are the main source of revenue

for towns to improve urban infrastructure. In most countries land

and property taxes are related to local public services and

infrastructural provision. The efficiency of local governments to

tax land and property is linked directly with the quality and

quantity of the provision of local public goods. David L. Cameron

(1999) stated that the study of property taxation is closely tied

to the study of the provision of public goods as any general

equilibrium analysis of property taxation must consider the

public benefits provided through a system of property taxation.

Land and property taxation is a tool that used to improve the

quality and quantity of infrastructure through improving revenue

of the municipality. Efficiency and effectiveness in land and

property taxation can be achieved through improving land and

property taxation challenges.

The purpose of this research was assessing land and property

taxation practices in kercha town. Assessing Land and property

tax administrative aspects have received the main attention of

the researcher to conduct the study. The study proposal organized

in five chapters. These are introduction, Literature review,

methodology, Data organization and analysis and conclusion and

recommendation.

This introduction part of the study was describing the general

information about the study area. In this part Back ground of the

study, statements of the problem, objectives of the study,

research question of the study, conceptual definition of

variables, and description of the study are, significance of the

study, scope of the study area, and organization of the paper

described.

1.1. Back ground of the study

Urban land has become the base for socio-economic development

serving as the main revenue sources for municipalities. The

revenue collected from such taxes is often an important source of

finance for local governments. The extent to which those

governments have control over property taxes is thus often an

important determinant of the extent to which they are able to

make autonomous expenditure decisions (Richard M. Bird and Enid

Slack, 2002).

Recently, many developing and transitional countries have become

interested in land and property taxes. Latin America, for

example is considering the property tax is the most important

source of own revenues for local governments around the world.

Many fiscally decentralized economies as well as an increasing

number of countries that have embarked upon a decentralization

process look at the property tax as the main source of revenue

autonomy for their sub-national governments (Cristian S. and

Jorge Martinez-Vazquez, 2011). China, too, is considering the

role of land and property taxation in its burgeoning urban areas

(Bird, 2005). For various reasons and with varying degrees of

urgency, property taxation, keeps popping up on the policy

agendas of countries around the world (Gregory. Ingram and yu-

Hung Hong, 2007).

From a purely fiscal perspective, the extent to which real

estate taxes can produce revenue to finance local services is

especially important in country that are decentralizing, which

may emerging economics have been doing in recent years. When such

countries, additional revenues from property taxes are obviously

desirable moreover, at least some countries are beginning to pay

attention to the potentially beneficial a locative effects that

properly structured and implemented land taxes might have in both

rural and urban contexts(In Gram, Gregrag. and Yu-Hung Hong,

2007).

Kercha town was because of different factors the revenue that

generated from land and properly taxation was low. Local property

taxes may play a critical role in helping to develop the town

economy, institutional capacity, improve infrastructure provision

and ensure good governance. The reason that why Kercha town has

low revenue? The question was answered at the end of assessing

land and property taxation experience of the town.

1.2. Statement of the problem

Urban area is one of the current issues that need development. In

the development process financial resource have great functions

to improve urban infrastructure provision of any city or town.

But, to do so, generating revenue play an indispensable role. One

of revenue generating source of any city or town is taxation of

land and property. Land and property taxation is the practice of

creating and using national and/or local revenues from land and

improvements over land. Land and property taxation is a key to

managing local and central governments affairs. The way in which

land-based taxation is used can stimulate land market

development, particularly land market transactions (UN-Habitat,

2011).

In most developing countries the potentials of generating

revenue from land and property taxation was low. Different

research finding in developing countries particularly like

Ethiopia showed that land and property taxation is not exploited

to its full potential. Belayneh, (2008) identified that, the

share of land and property tax to total revenue in the Shone town

was 37.2%.

The study area, kercha town was found in Oromia Region Guji Zone

Kercha woreda.It is highly cash crop area and would have been

gotten revenue from these investment activities. Land and

property taxes are important to increase revenue; controls land

use, redistributes wealth and controlling influence over local

government mercantilism. The improvement of basic amenities and

visible services, such as local roads, garbage collection, street

lighting and cleaning, parks and so on, bring extraordinary

benefits for the poor population (Yiyi Xu, 2011). However, in the

town there is no adequate infrastructure provision such as

inefficient road and water lines, unavailability of solid waste

disposal site, availability of vacant and fenced plots, breakdown

and gorge of road, no sewerage line and the like. This is the

reason why the researcher will be like to do the research on

assessment of land property taxation practice.

Previously, some researchers have been done describe the

knowledge gap on the land and property taxation practices and

challenges. For example two researches were done on South Nations

Nationality and Peoples Republic of Ethiopia such as Belayneh

Bassa (2011) describes the knowledge gap on his research on land

and property taxation practices. Whereas Yonas Debebe 2009,

describe the knowledge gap about land and property taxation

challenges. But the researcher will see the problem with the

land and property taxation practice in relation to why? all plots

and buildings in town is not included in tax base of

municipality to improve the share of revenues generate from

land and property taxation practice by assessing the last five

consecutive years. In addition to this, researches are not done

in Oromia region Guji Zone Kercha town in relation to land and

property taxation practices. If the revenue improve the question

of infrastructure provision and other social services improve.

Because of this, identifying revenue generating sources is

mandatory.

1.3. Research objectives

1.3.1. Main objective

General objective of the study is assessing land and property

taxation practices in Kercha town

1.3.2. Specific objective

1. To assess the total numbers of land and property that

included tax base of the town.

2. To assess the total revenue collected from land and property

taxes in relation to other sources of the town in the past

five consecutive years.

3. To assess land and property tax payers attitudes in the

town.

4. To assess challenges of land and property taxation practice

in the town.

1.4. Research question

On the basis of the research objectives, the following

research questions were formulated.

1. What is the total numbers of plots and buildings in the town &

tax payer included in tax base?

2. How much is the share of land and property tax from the total

revenue collected?

3. What is the attitude of tax payers towards land and property

taxation?

4. What are the challenges affecting land and property taxation

practice in the town?

1.5. Conceptual Definition

Land:-An area that someone owns, often including the building on

it (Macmillan Dictionary)

Taxation is compulsory levy that is most important source of

government revenue.

Revenue -is the amount of money in birr collected from land rent

and building tax

Property – is immovable residential or commercial buildings

built on formal sub divided plot and land process that are

privately owned.

Valuation - has often been defined as the art and/or science of

estimating values

Value-is the estimate of the price that would be achieved if the

property were to be sold in the market.

1.6. Significance of the study

This study, beyond its academic importance, it can help Kercha

town municipality to improve land and property taxation practice.

The major problem of land and property taxation will be

identified by this study. Therefore, Kercha town administration

office can improve its revenue generation from land and property

tax by strongly implementing the solution that will be

recommended by this study. In addition to this decision makers

formulate appropriate policy, rules and regulation based on

findings. Lastly, the study can be used as secondary sources of

data for further investigation in land and properly taxation

system.

1.7. Scope of the study

The study has both thematic and geographical boundaries.

Thematically, the study will focus on the assessment of land and

property taxation system. Only taxation of land and property is

beyond scope of this study. Again land property taxation will be

assessed as a source of revenue not as tools for land use.

Geographically, the study will be bounded to Kercha town

municipality administration from 2001-2005 using land and

property tax payers in the town. 1.8. Description of the study area

Location: The study conducted in Oromia region,Guji zone, Kercha

town. Kercha is found in southern Oromia region at 475km far

from the capital city Addis Ababa and 356km from Nagele town.

Astronomically the town is located between 5o58’24” - 6o22'48”

northing latitudes and 38o57'22” - 41o34'55” easting longitudes.

The area coverage of the town is 538 hectares.

Population: The current total population of the town is 13,233

(Ministry of water and Energy population projection, 2011). Since

the fast growth rate of the population, the total population of

the town become increasing from time to time.

Vegetation :Most of the periphery areas of the town is covered

by Coffee Plant, Eucalyptus tree , Dokima and other trees and

also in the town few private compounds, governmental

organizations like schools, offices and other institutions trees

those are planted and growing well. Although the temperature of

Kercha town has Moderate climatic conditions, it has lacks formal

urban greeneries and open spaces. Areas that have to be covered

by vegetation.

Soil: The major soils of Kercha district are sand soil (2%),

Loom soil (10%), and clay soil (20%), Red soil (67%) and other

type of soil (1%) with high spatial coverage of red soil.

Therefore, it has little agricultural potential other mostly

developed on gentle slopes, Very good base saturation and

fertility are the major important for agricultural production.

Kercha town soil types are red and its slope is mainly gentle.

Climate, Temperature and Rainfall

Climatic condition of the town can be seen with different

elements of climatic conditions.The Annual temperature of Kercha

town is in between 18oc (the minimum value) and 25oC (the maximum

value) the temperature of the town of Kercha is

weynadega(moderate)..

The mean annual rain fall the town is about 1500mm-3000mm. Kercha

town gets rain on the months of July, August, September and

October have high rainfall. Moreover the months of March, April

and May are also rainy months.

Economic activity

Due to geographical position of the town proximity to border of

the country, most of the town peoples engaged in different trade

activity directly or in directly. Retailing, service, owner of

infant industry sectors like, woodwork, metalwork, Coffee

industries, informal traders and others 22% were the indicators

of economic activities of the town.

Land use: According to the master plan of the town, the town

is divided in different land use patterns. Residential, commerce,

industry, institutions, open space, and others are the dominant

land use patterns of the town.

Fig.1. Administrative map of the study area

Map of Oromia Regional State in Ethiopia Map of Guji Zone

in Oromia Regional State

Map of Kercha town Kercha Woreda

Scale:0 80 160 240 32040

M eters

N

é

Source: Oromia National Regional State Program of Plan on

Adaptation to Climate

Change (February , 2011)

1.9. Organization of the paper

Generally the paper comprises five major parts. The first part

is the introductory part which contains back ground, statement of

the problems, objectives, research question, conceptual

definition, significance of the study, description of the study

area, and organization of the thesis. The second part deals with

the review of literature about the theoretical and empirical

aspects of land and property taxation system. The third part deal

with the methodology of the research has presented. The fourth

part describes analysis interpretation and discussion of the

data and finally conclusion and recommendation was illustrated.

CHAPTER TWO

2.0. REVIEW OF RELATED LITERATURE

2.1. Introduction

The study was used various literatures refer to achieve its

objectives. This review literature part was describes the review

of different literatures in relation to the objectives of the

study. In this part the theoretical and the empirical aspects of

the land and property taxations system was reviewed. Concepts and

theories of land and property taxation, land and property tax

revenue, challenges of land and property taxation and tax payer’s

attitudes was included in the theoretical literature review

aspects. In the empirical review aspects the experience of

Brazil, India and Ethiopia was discussed.

2.2. Theoretical literature reviews

2.2.1. Concepts and Theories of Land and Property taxation

Property taxes are typically defined to encompass those taxes

levied on both real and personal property that are dependent on

the value of the property itself. In the world, the definition of

the concept of land and property taxations is different from one

country to the other countries. United States, the property tax

is the principal source of revenue for county and municipal

governments (David L. Cameron, 1999). In Brazil, Regarding the

city of Porto Alegre, the property tax is the second most

important source of revenue and raising revenue for financing

public services. In this context, property taxes are defined as

an annual tax on land and buildings (Claudia M. De Cesare, 1997).

Significantly across jurisdictions with respect to the types of

property that comprise the tax base as well as the exclusions for

specific types of property, the assessment techniques used to

determine the value of the property subject to the tax, and the

tax rates applicable to the various classes of property.

In theory land and property taxes are the main sources of revenue

for local governments and a tool. In urban development, taxation

is an important conduit to generate revenue and also a tool to

redistribute wealth. The objectives of taxation are many,

including alleviating poverty and sharing societal benefits with

low-income and disadvantaged groups (UN-HABITAT, 2011). Land and

property taxes have effects in the improvement of infrastructural

provision. Richard M. Bird and Enid Slack (2002) stated that

Taxes on land and property have both fiscal and non-fiscal

effects. The revenue collected from such taxes is often an

important source of finance for local governments. The extent to

which those governments have control over property taxes is thus

often an important determinant of the extent to which they are

able to make autonomous expenditure decisions.

There are two different ways in which land property tax can be

explained. These are land value taxation and Land and property

taxation (UN-HABITAT, 2011)

A. Land and property taxation is the practice of creating and

using national and/or local revenues from land and

improvements over land. It is a key to managing local and

central governments affairs. The way in which land-based

taxation is used can stimulate land market development,

particularly land market transactions. It is often a mixture

of revenue streams and collection methods from local to

national levels.

B. Land value taxation could be site value rating, which is a

tax on the value of the land only; excluding the value of

buildings and improvements, or a form of composite rating,

also referred to as the two – rate system(the value of the

land and the value of the buildings or improvements )

In land and property taxation system identification of properties

and tax payers are must. Roy Bahl (n.d) argued that a key

problem in developing countries has been to assemble a complex

tax roll. If the tax base is the value of land and improvements,

the three steps must be identified is all parcels and their

taxable characteristics, the characteristics of any improvements

on the land and identification of the owner of the property.

I. Property Tax base

According to Enid Slack (n.d) argument, the base for the property

tax is “real property,” it is defined as land and improvements to

the land, machinery and equipment that is permanently attached to

real property is included and other characteristics of the

property tax base include exemptions and property valuations.

David L. Cameron (1999) also argues that Market value is the

property tax base of a municipality. He defined tax base as “the

most probable price in terms of money that a property would sell

in a competitive and open market, assuming that seller and buyer

are acting prudently and knowledgeably, without any special

stimulus” . The tax base includes land and immovable improvements

attached to land. The tax covers all property-use classes,

including vacant land, residential and non-residential property.

II. Property tax rate

To set municipal tax rates, a municipality first determines its

expenditure requirements. It then subtracts non-property tax

sources of revenue available (intergovernmental transfers, user

fees, and other revenues) to determine how much it has to rise

from property taxes. The property tax requirements are divided by

the taxable assessment base to determine the tax rate. The

municipality may levy a series of rates that differ by property

class. Variable tax rates are different rates for different

classes of property (residential, commercial, and industrial, for

example) (Ibid).

2.2.2. Land and Property tax revenue

Local revenue generation is based on the decentralization policy

and the accompanying constitutional and other legal provisions

making it operational. The diversity in the list of factors that

have contributed to the interest in fiscal decentralization

reflects institutional differences across countries.

Institutional factors, such as political, social, legal and

economic conditions are important for the analysis of public

finance issues, but they are especially important for the

analysis of fiscal decentralization (Global Institute for

Research and education 2013).

Land and property tax is used as a source of revenue for local

governments of the town or city administration. The revenue

collected from land and improvements will be strongly influenced

by the completeness of the tax roll, the quality of valuation

practices and the adequacy of collection procedures or system.

As M. Bird & Enid Slack (2006) said that ‘the property tax

remains the predominant option for raising revenues at the local

government level in Latin America’ and, it might be added,

elsewhere as well. The potential yield of land and property taxes

is unlikely to be huge, revenues from this source will not be

very elastic, and administrative costs are substantial.

Nonetheless, an expanded property tax is indeed both a logical

and a desirable objective for many countries, particularly those

in which local governments are expected to play an increasing

role in allocating public sector resources.

Taxes on land and property are found everywhere; both in

principle and practice, such taxes may have important fiscal and

non-fiscal effects. The revenue they produce is often an

important source of finance for local governments. The extent to

which local governments have control over property taxes is an

important determinants of the extent to which they are able to

make autonomous expenditure decision and the degree of such

autonomy is, in turn, and important element is improving the

delivery of local public service (Dick,Nezer, 1989).

In urban area revenue that collected from land and property

taxes have a great roll in economic factors of the town or city.

A Nobel Prizewinning economist William Vickrey(n,d) argued that

‘the property tax is, economically speaking, a combination of one

of the worst taxes ,the part that is assessed on real estate

improvements and one of the best taxes that is the tax on land or

site value.

Billing and Collection

In most countries that employ land property taxations, the

billing and collection functions take place at the local level.

Even in cases where the tax is a national rather than a local

tax, billing and collection are generally through local offices.

UN-HABITAT (n.d) said that in tax collection system there are

different steps or procedures. The last step in administering

property tax, collection may present the most difficult problems

because costs are high and collection efficiency often low. The

source of the problem may lie with an adequate collection

procedure, with the structure of the tax itself, with an adequate

set of penalties necessarily to enforce the tax, or with the

inducements necessarily to stimulate collection.

The depressed collection efficiency has been attributed to:

lack of taxpayer’s confidence or understanding in how the

tax is levied, collected and used,

lack of appropriate collection and enforcement mechanisms

and

Lack of political will.

In Latin America, The amount of property tax revenues that

governments are able to collect varies widely across nations and

across jurisdictions within any country, and it depends on a wide

range of institutional, cultural, political and economic factors.

Collection success requires political will, judicial support and

sound administrative practices (UN-HABITAT n.d).

Cristian Sepulveda Jorge Martinez-Vazquez (2011) also suggested

that there are several factors that might create a difference

between potential and actual tax collections. The presence of

centrally imposed exemptions eroding the tax base, or greater

administrative and compliance costs, and the taxpayers

willingness to contribute to the provision of public goods, are

some examples of factors that might truly reduce fiscal

disparities. But historically low tax collections might also be

caused by inefficiency, political favors and corruption. In this

context, it is desirable to have some information about the

determinants of fiscal capacity

2.2.3. Taxpayer’s attitudes

Creating awareness to Taxpayer’s attitudes towards LPT is the

basic responsibilities of the organization where as paying taxes

are the civic duty and obligations of taxpayers. They are aware

how, when, why and where they pay tax. Evaluating the land

property taxation from the taxpayer’s perspective will focus on

the overall tax burden, fairness in the distribution of that

burden across households, and the cost incurred by taxpayers in

complying with the tax. Since the base of the LPT is land and

immovable improvements, fairness is assessed by comparing the

taxes paid on similar properties (Connellan, O. 2004).

Fairness of the tax system and peer influence altering taxpayers’

attitudes and perceptions to tax compliance. It is widely

believed by tax administrators and the taxpayers that growing

dissatisfaction with the fairness of tax system is the major

causes for increasing tax noncompliance. Thus unfairness of the

tax system may reflect taxpayer’s perceptions that they are

overpaying taxes in relation to the value of the services

provided by government or in relation to what other taxpayers

pay. (Muhammad A .U. Rozilah K. and David M, 2012)

Taxpayer

Taxpayer is a person who occupying or having land and property

and pay a taxes. The property is legally liable for rates (the

occupier is rate able in respect of the property occupied). But a

vacant site or derelict building will not be liable to rates

until it can be used for a valuable purpose and therefore capable

of commanding a rent. Certain taxpayers are exempt from paying

rates including: those who occupy agricultural land and

buildings; diplomats and those with diplomatic immunity;

registered charities, which enjoy a combination of mandatory and

discretionary rate relief; and other nonprofit organizations, who

can apply for discretionary rate relief. Ratepayers who suffer

financial hardship can also apply to the billing authority for

rate relief (Ibid).

Claudia M. De Cesare (1997) also argued that the property owner

is primarily responsible for paying the property tax. The

occupier or user, even without legal authorization to use the

property, can be requested to pay the tax. Some properties are

exempted from property tax, such as properties used for

governmental purposes, for defenses and infrastructure purposes

and for public or social interest without profit purposes.

2.2.4. Challenges of land and property taxation practice

There are many challenges that affect land and property taxation

system. But for the purpose of this study the researcher will be

used the following.

I. Absence of a uniform system of Property valuation

Valuation is the process of determining the current worth of an

asset, mostly real Property (Daniel Weldegebriel 2013).It is the

major technical challenge in property tax administration and is

especially difficult in developing and transition countries. A

proper valuation activity requires that a number of preconditions

are in place these are; a clear definition of taxable property

value in tax law, an adequate number of trained valuers either

working in the government sector available to the government

sector on a contract basis and the availability of some reliable

source of data on property values, land values and rental values

(Dick N.2011).

Connellan. O. (2004) also argues that there is no legal

requirement to use any particular method of valuation for rating

purposes, although certain specified operational hereditaments,

normally occupied by providers of utilities such as gas,

electricity and water, are valued using a statutory formula.

Valuation has no similarity between countries to country.

Because of this Valuation has subjective approach. Enid Slack

(n.d) stated that Property tax revenues are low in many

developing and transitional economies in part because of the way

in which the tax is administered different. At the local level

valuation department is responsible for the valuation roll and

issuance of the tax demand notices, the actual revenue collection

activities are administered through in different cases depends

up on the level (rank) of the towns. Some towns collect their

revenues through Districts revenue office and the other with

their revenue offices.

According to (Daniel Weldegebriel 2013) explanation the absence

of uniformity of valuation is because of different factors. These

are absence of modern real property registration and cadastre,

non-transparency of the real property market system, absence of

systematically organized data the qualification and expertise of

professional assessors. Existing experience shows that

professionals who practice valuation are largely ignorant of

basic approaches of valuation, have no special training and have

not even gone through short courses or trainings on property

valuation. Belachew Yirsaw (n.d) stated that gaps and problems in property

valuation are widespread. A contributing factor is the absence of

a uniform system of land valuation in line with Ethiopia’s land

tenure system. This uniformity can best be achieved by creating a

specialized institution to set guidelines for land and property

valuation in urban areas. Such an institution would be most

effective if supported by legislative provisions at the federal

level. Moreover, to the extent that the current infrastructure-

based valuation system is to be maintained in urban areas, the

outdated studies used as the basis for valuation need to be

updated.

II. Informal settlement

Informal settlements are the serious problems in relation to

decreasing land and property taxes revenue that facing whichever

urban centers in both developing and developed country. Dwellings

in illegal settlements generally lack formal legal titles, and

they may show irregular development patterns, lack essential

public services such as sanitation, and occur on environmentally

vulnerable or public land. Whether they are built on private or

public land, informal settlements are developed. It also poses

both high direct costs for local governments when they undertake

upgrading programs and substantial indirect costs when coping

with other impacts of informality, such as public health,

criminal violence, and related social problems (Edesio Fernandes

2011).

Abbay Tsehaye, (2005), also explained that Informal (Illegal)

settlement has its own impacts on land and property taxation

system. Because the illegal settlers have no title, not

construction permits, the place also have no infrastructure

provision and the like .This practice is a bottleneck for the

city/town administration to administer the revenue that

generating from land and property taxes. This has three

challenges for the municipality. The first thing is decreasing

the revenue, the second, it brings economically and social

disaster when the city/town needs to develop the land demolishing

is mandatory. Thirdly, on the other hand regularization to all

with no penalty and disregarding the master plan will encourage

similar actions and damage public interest. Considering this

dilemma a policy direction of regularizing most of the illegal

settlements with penalty but demolishing those violating the

major rules and reserved areas of roads, Parks, and other public

uses has been set already.

Informal settlements are strongly a sever challenges to the town

developments with playing a great roll in reducing land and

property taxes revenue. The magnitude of informal urban land

development has direct relationship with the dynamism of urban

areas: major urban centers and those that are fast growing

experience concerted informal development. This informality has

its own impact on land and property taxation systems and the

expansion of the town infrastructure (Belachew Yirsaw n.d).

III. Cadastral registration Problem

Identifying the tax able property in levy assets tax is the first

component to be collect revenue from land and property. This will

be practiced by cadastral survey that agreed out by professional

land surveyors. The professionals land surveyors who have to be

aware of the legal and fiscal description of the land and

property taxes.

A "cadastre," or official property register, can take a number of

forms. A legal cadastre lists title or ownership to land and

buildings; a fiscal cadastre contains tax information, such as

valuations and assessments; and a physical cadastre deals with

parcel boundaries and building information. Because these

functions are closely related, cadastre is often used to refer

generally to the combined set of records, an integrated or master

cadastre.

According to Stoter,Jantien,ED(2006) arguments cadastres can be

classified in to different types based on different criteria.

Some of them are: Deeds Vs Title Registration, A centralized or

decentralized cadastral registration, Land registration with

separate or integrated cadastre, Fiscal or legal Cadastre,

Financed by Government or Cost recovery and General or fixed

boundaries. But for the purpose of the study from different

type’s cadastre fiscal cadastre is the most important improve the

revenue of the organization of land and property tax system.

IV. Institutional Capacity of the municipality

Institutional capacity refers to the ability to implement and

improve revenue administration focusing on efficiency and

effectiveness Well-developed institutions enjoy an enabling

environment of key players using available resources to generate

revenue (Global Institute For Research and education 2013).

Institutional arrangements’ comprises set of rules, both formal

and informal which govern choices that people can make. It is

define the distribution of choice and incentives faced by

individuals and groups. Institution needs to change as economic

and social circumstance change: emerging problems requires

flexibility and innovation.

Belachew Yirsaw (n.d) stated Global Institute For Research and

education(2013) that there is lack of public awareness on land

policy and negative consequences of informal

developments .Informal developments that comprise construction

without permit on legally occupied land and informal land

occupation is high in major cities. There is no organized land

occupation and informal accesses to land are through gift or

market mechanisms.

According to UN-HABITAT (2011) argument there are various

innovative approaches to land and property taxation policies,

reforms and instruments have been used for a range of purposes

including revenue generation for financing urban infrastructure

and development, supporting decentralization, ensuring affordable

housing, maintaining urban infrastructure and investments. These

innovations in land and property taxation should be documented

for knowledge sharing, with the view to improve urban land and

property management. Building institutional capacity is important

for effective delivery of urban services. Urban land policy

reforms become important if the full value of urban property is

to be captured.

Generally institutional capacity refers to the ability to an

implement and improves revenue administration focusing on

efficiency and effectiveness.

In principle, assignment of responsibilities for policy making

and implementation in unambiguous: the federal level formulates

policies; regional or municipal governments are responsible for

implementation and management of land administration; and the

judiciary resolves disputes that might arise in the process. The

practice is more complex and could give rise to concerns

regarding governance. Well-developed institutions enjoy an

enabling environment of key players using available resources to

generate revenue (Ibid).

V. Organizational Capacity

Organizational capacity has irreplaceable role in any city or

town of the country. It is the ability to enlist all actors

involved and with their help generate new ideas that develop and

implement a policy designed to respond to fundamental

developments and create conditions for a sustainable development.

The organizational capacity have different elements These are

administrative structure, Strategic networks, Vision and

strategy, leader ship political support, societal support and

Spatial-economic conditions. So, organizing capacity is important

for increasing the municipality revenues that gain from land and

property taxation system (Laura Capel-Tatjer&Marisa P.de

Brit,n.d)

Global Institute For Research and education(2013)also stated that

limited expertise (man power) and little transfer of knowledge by

the various stakeholders; lack of appropriate and sustainable

technology; lack of proper planning facilities, equipment and

reliable data and information user fees concept not well

appreciated are organizational capacity challenges of land and

property taxation system.

2.3. Empirical Literature of the study (International

experiences)

2.3.1. Using the Property Tax for Value Capture: A Case Study

from Brazil:

Initiative of the study.

The city of Porto Alegre, Brazil, is using the property tax as an

instrument for capturing land value increments, deterring land

speculation and promoting rational urban development. Porto

Alegre is the capital and largest city of Brazil's southernmost

state; Rio Grande do Sul With a population of 1.5 million

inhabitants and approximately 450,000 real estate units in 1994,

city officials estimated a shortfall of more than 50,000

residential properties (Claudia M. De Cesare, 1999).

In Brazil property taxes has the meaning of an annual tax on

land and buildings.

Factors encouraged Porto Alegre's initiative

Factors encouraged Porto Alegre's initiative to use the property

tax as an instrument for simultaneously capturing increased land

value, deterring land speculation, and promoting social fairness

and economic growth:

Stimulation of urban land occupation and development, since

the private market was not responding positively to the demand

from low- and middle-income residents.

Reduction of the housing shortfall. Provision of assistance to

low-income families, guaranteeing better living and working

opportunities.

Recovery of land value generated by public investment, by

encouraging individuals who had been favored by public

investment to return those benefits to the community.

Avoidance of large additional investments in public

infrastructure and services by applying financial resources

rationally.

Achievements of the Initiatives:

As of October 1997, the initiative has not yet achieved its

desired results. Only five of the 120 vacant sites are being

developed. The land owners of 50 properties are paying the

property tax at the progressive rate. Three of the properties

were removed from the list because they had been incorrectly

included in the first place due to inaccurate records about their

physical characteristics. The development status of the remaining

62 properties has not been defined. Some are owned by wealthy and

politically powerful landowners who appealed to the Supreme Court

against the constitutionality of the measures undertaken by the

city government. Indeed, two landowners (A and B) who hold nearly

44 percent of the vacant land are appealing, and other landowners

seem to be waiting for the judiciary outcome to make their own

decisions.

2.3.2. Property taxation experience of India

According UN-HABITAT (2011) most of the cities in India are

unable to meet the increasing demand for infrastructure due to

their slow growth in municipal revenue. Municipal Corporation’s

by virtue of their status, derive their fiscal powers from the

state governments. The revenue powers also vary across states and

cities e.g. Octroi levying (Municipal Corporation entire focus is

on octrol collections rather than implementation of property tax

reforms). In view of the poor financial condition of the cities,

it is being recognized that property tax must be made a revenue

productive tax instrument through an appropriate reform strategy.

The last decade, especially the post 74th constitutional

Amendment act phase, has witnessed considerable interest in

property tax reform both from the administrative and the

taxpayers perspectives. Bangalore, Delhi and Pune have all

introduced innovative practices in various area related to the

tax administration, assessment and collection.

Most states in India the deficiency in the system of properly

taxation does not allow for full exploitation of the revenue

potential of this tax. This deficit occurred due to poor

assessment, administrate and information system of property

taxation (UN-HABITAT, 2011).

2.3.3. Land and Property taxation trends in Ethiopia

In Ethiopia land and property taxation begins during Milinik by

the small efforts of ministry of Interior .Daniel T. (2006)

argued that there was little effort by the centrally based

Ministry of Interior, to register land and assess taxes for some

urban centers in the country. Later on this responsibility was

given to the Ministry of Urban Development and Housing. This

sporadic attempt was carried out mainly for the purpose of

assessing and collecting land and building tax. Thus, until

recently registration of land was carried out by some

municipalities, which have the capacity to do so. While, the

Ministry of Works and Urban Development carried out assessment of

building tax, except few urban centers.

Land and property taxes comprise the most common source of

revenue for local authorities. The revenue will be used to

financing towns or cities infrastructure provision and other

basic services including roads, water supply, garbage site

selection, health and educational services. Even if there had

been tax on land in Ethiopia for many years, this does not

indicate the existence of land registration. Emphasizing on this

relationship between tax and ownership in that Ethiopian context,

land tax the payment of the traditional been regarded as

obligation to certify with ‘yerist wereket’ or rist paper. This

paper shows holder of ownership and increase evidence (Ibid).

In urban areas property taxes are essentially concerned with

improvements to land. Therefore, in areas and taxes should

generally be based up on its valuation. However, in Ethiopia, due

to the inefficiency and absence of basic information, valuation

is difficult. The formulation of land valuation method is also

deemed to be difficult until now. Hence land rent in the urban

centers is simply paid based on its area and location or grade of

land. Until recently, land rent urban centers of Ethiopia are

paid in accordance with proclamation No. 80 of 1974.

According to Nega Wolderebreal (2005) considering the lack of

land value appraiser, the city government of Addis Ababa should

review the rent every five years. Currently, there is a need to

develop a value based taxation systems, but first there is a need

to establish a workable real property registration and

information system. Therefore, the process should involve the

public at large.

Yonas Debebe (2011) stated that in Sawla town about 37% of the

residence parcels of land have not title deed and planning map.

This weakness of the town municipality in tenure system

realization made the taxpayers to be irritated for paying their

property tax. Because of weak guaranteed tenure of land owning,

different obstacles facing property tax system of the town. It

persuades informal land market in the town that distorts land

value and restricts land taxation revenue. Without any guidance

and document a agreeing to the transfer the ownership is passed

between the sellers and purchasers, the town could not levying

land transferring service charge. The buyers are not being

voluntary for service charge and paying land rent and building

taxes timely. They preserve the lands for speculative purpose by

holding with any development as observed in the field observation

during the data collection period.

2.4. Knowledge gap

The review of theoretical and empirical literature indicates the

research gap in experience of land and property taxation.

However, there is a research which is conducted before on the

practices of land and property taxation and challenges also. But

the researcher was seen the problem with the land and property

taxation in relation to why? all plots and buildings in the towns

are not included in tax base of municipality to improve the

share of revenues generate from land and property taxation

practice by assessing the last five consecutive years. If the

revenue improve the question of infrastructure provision and

other social services improve. So, identifying each the revenue

generating sources is mandatory. This is the gap between the

theory and principle practice of land and property taxation. In

principle Taxes on land and property have important in fiscal and

non-fiscal effects. The revenue they produce is often an

important source of finance for local governments. This paper

was found out whether or not in practice.

2.5. Conclusion

From the review literature, it is possible to conclude that the

major source of revenue for any municipality is tax from land and

property. But due to many interrelated factors the revenue will

be collected from land and property is still underutilized in

many developing countries as well in Ethiopia. As identified in

the review literature in the case studies weak management of

cadastre information, recording, tilting, and registration of

land owning, absence of uniform valuation and up grading their

value, managerial inefficiencies in land supply and taxation

issues. In addition to the above mention challenges the review

literature also showed that the inability to use all land tax

bases and rates which could be relativist for municipality, the

absence of the integrated sartorial planning and participation of

stalk holders were the weakness of those were hampered land

proper tax revenue generation.

Fig. 2 Conceptual frame work

Total no of plots in

Total no of buildings Trend of

No of plots included inBilling and

Improvement ofinfrustructure

Assessment of Land &

Assessing tax

Identifying no of plots and tax payers

Assessing revenueof land& propertytaxes

Identifying challenges of

t

ax

es

No of buildings

Source: researcher compliance

CHAPTER THREE

3.0. RESEARCH METHODOLOGY3.1. Introduction

This part was describing the procedures that used in conducting

this research. It was describe, the research design such as

research approach, research type, research strategy and research

time dimension, methods of data collection , sampling techniques

Assessing tax Identifying challenges of

such as population or universe, sampling frame, sampling unit

sample size and sample, Source of data such as primarily and

secondary data sources ,Data collection tools(Instruments),Data

analysis and interpretation, Operationalization frame work of

variables , data presentation and limitation of the study.

3.2. Research Design

In this study the researcher was discuss in brief about research

approach, research type, research strategy and, research

dimension in the research design part of the study.

3.2.1. Research approach

In this study the researcher was use both qualitative and

quantitative research approach. Quantitative research approach

used because to analyze the objectives of the study which have

quantitative aspects of land and property taxation such as number

of plots (the taxable and non taxable), revenue generated, number

of buildings and other quantitative aspects. Qualitative research

approach used in order to measure attitudes and satisfactions of

tax payers,

3.2.2. Research type

For this study descriptive research would be used to conduct

this study because descriptive research is an appropriate. since

the study aims at finding or assessing the facts regarding the

land and property taxation system and it describes the state of

relationships as it exists at present (Kothari, 1995).

3.2.3. Research Strategy

The researcher was used Survey research strategy. Because Survey

research is a strategy that canvases social phenomenon or reality

by collecting information from sample or whole population using a

questionnaire and it is efficient to collect information from

large population.

3.2.4. Research Dimension

For This study cross sectional time dimension research design was

appropriate. The researcher was used this design because the

study involves undertook the research only once. The researcher

was observing a sample of a population at one point in time.

3.3. Methods of data collection

For fulfilling the specific objectives of the study the

researcher was using questionnaires, interview and document

review data collection tools in order to address the study

objectives.

3.3.1. Questionnaires

The questionnaires was being used in order to gather information

from household who own pay tax of land and property tax for the

municipality, how much plot they own, how much money they pay,

the service provision that they get from the municipality. The

questionnaires was consists both closed and open ended

questionnaires. It was administered in written form for each

sample households in order to get in depth information from the

respondents.

3.3.2. Interviewing

The interview was administered for collecting information from

the government official workers concerning the land and property

taxation, challenges and availability of residential land and

property taxation information. Personal interview (semi-

structured questions) would be used for collecting information

from each respondent from government offices who will be take

part as a sample purposively in the study.

3.3.3. Document Review

The document review was also administered for collecting written

information from different published documents .These documents

was include reports (monthly, quarterly, half of a year and

yearly), different books, research reports, official report,

government policies, government strategies, local government

programmer and plan and website .The researcher was grasp

further detailed information about the study by reviewed this

documents.

3.4. Sampling Techniques

Samples of the study were drawing through both probability and

non-probability sampling techniques. The probability sampling was

used because it gave the population equal chance of being

selected in the sample. From the probability sampling techniques,

a systematic random sampling method was employed to select sample

house hold from the registration list. The purposive non-

probability sampling method would be used to obtain reliable

information from the municipality office workers, Woreda revenue

office workers, kebele managers, and other key respondents and

made the sample more representatives of the entire population.

Table1. Sampling technique method

Sampling

Techniques

Specific

Technique

s

Variables Instruments

Probabilit

y

Systemati

c

sampling

Households from both 01

and 02 kebeles of the

town.

Survey

Non-

Probabilit

y

Purposive

sampling

Six(6) experts from

municipality office, two

(2) experts from woreda

revenue office and

four(4) persons from the

kebeles administration.

Interview

Source: researcher compliance

3.4.1. Population or universe

The study populations for the research were households of the

town. According to the municipality data, the number of

households with in the town is 2,206 .The samples were drawn

using systematic random probability sampling. The town has two

kebeles (01 and 02). The two kebele administrative body,

municipality officials and experts and district revenue office

experts (tax collectors) considered as the population from which

the samples were selected purposively. The reason was choosing

population purposively was that to increase the reliability of

the data that gathered in relation to land and property tax in

the town.

3.4.2. Sampling frame

The sampling frame of this study about 1,332 households

registered on municipality tax base records that pay tax on land

and property tax recorders and samples that selected purposively.

The samples were selected from the list of this tax base

document.

3.4.3. Sampling unit

The sampling unit of the study was registered tax payer

households, experts from the municipality office, and tax

collectors from the district revenue office and kebeles

administrators.

3.4.4. Sample size

In this study, the researcher gave emphasis to the sample size in

order to ensure the requirements of efficiency,

representativeness, reliability and flexibility. The total

numbers of population which were included in the tax base of the

town were 1332.From these 705 and 627 peoples were from 01

kebele and kebele 02 respectively.

The study area was including both kebeles to make representative

sample. First, the total sample size was selected from total

population frame by using formula. Second, after total sample

size determination, the sample size for each kebeles was also

selected from total sample size based on population size of each

kebeles.

To calculate sample size, different authors used different

formulas. For the purpose of this study, the researcher was

select to use the formula set by Kothari (1995), calculated as

follows considering the level of acceptable margins of error at

7%. Therefore, the sample size of household respondents was

selected by using the following formulas.

If N is between 1,000 -10,000, then the sample size is calculated

as the formula n¿ z2pqd2 ;

And

n=fn=

n

(1+nN) , where

N = Target population

n = Desired sample size

z = Confidence level (95%= standard value is 1.96)

p = Estimated characteristics of study population (0.5)

q = 1-p

d = level of statistical significance set or margin of error

(standard value is 0.07)

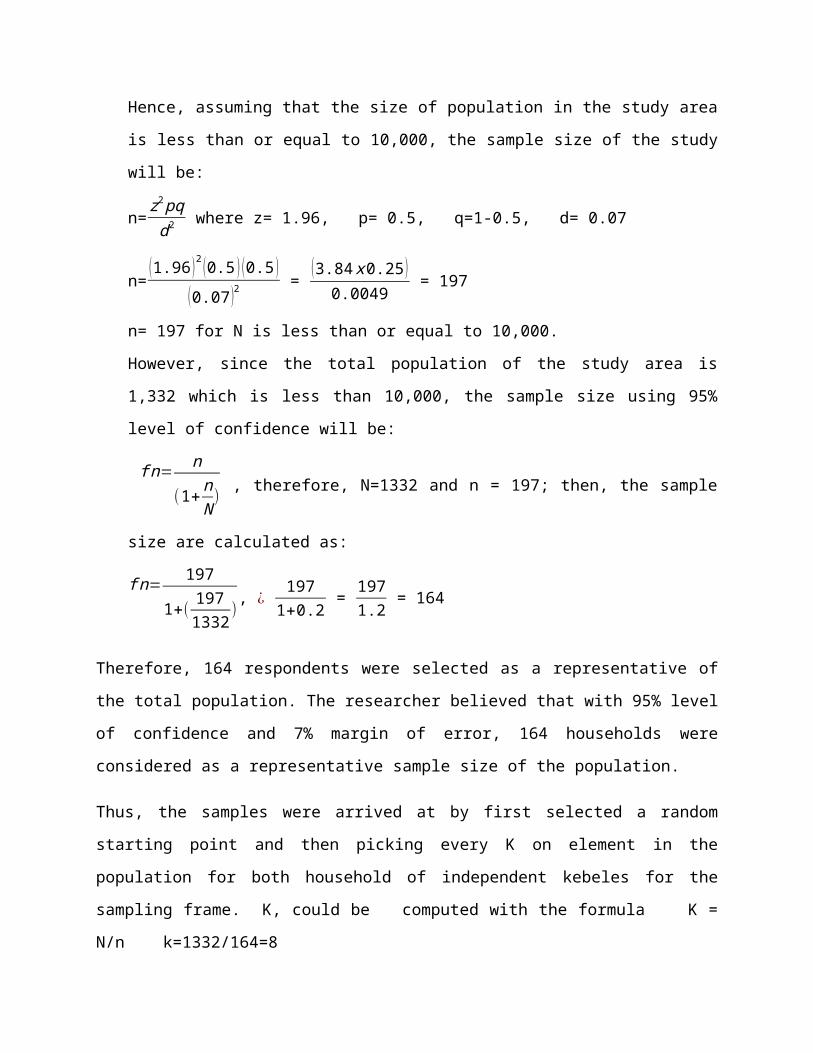

Hence, assuming that the size of population in the study area

is less than or equal to 10,000, the sample size of the study

will be:

n=z2pqd2 where z= 1.96, p= 0.5, q=1-0.5, d= 0.07

n= (1.96)2 (0.5 ) (0.5 )(0.07)2

= (3.84x0.25)0.0049 = 197

n= 197 for N is less than or equal to 10,000.

However, since the total population of the study area is

1,332 which is less than 10,000, the sample size using 95%

level of confidence will be:

fn= n

(1+nN) , therefore, N=1332 and n = 197; then, the sample

size are calculated as:

fn=197

1+(1971332

), ¿ 197

1+0.2 = 1971.2 = 164

Therefore, 164 respondents were selected as a representative of

the total population. The researcher believed that with 95% level

of confidence and 7% margin of error, 164 households were

considered as a representative sample size of the population.

Thus, the samples were arrived at by first selected a random

starting point and then picking every K on element in the

population for both household of independent kebeles for the

sampling frame. K, could be computed with the formula K =

N/n k=1332/164=8

The researcher was choose a number between 1 and 8 randomly and 5

choosed.

This number was the equivalent to the 1st household to survey,

the second sample was 5+8=13 and the other sample was also

calculating until 164 in the same way.

After the total sample size was calculated, respondents from both

kebeles was selected based on their population size.

Table 2: Number of representative respondents from both

kebele

Name of

kebele

Target

population

Share of one kebele from the

total sample sizeKebele 01 705 87Kebele 02 627 77Total 1332 164Source: researcher compliance

To increase the validity of the study and cross check the

responses of households, based on non-probability sampling

method, the researcher was select twelve (12) key informants

purposively. Hence, the Mayor, three (3) experts from land

department, two (2) other core processor owners from the

municipal, two tax collectors from woreda revenue office and two

leaders from each kebele were interviewed. In addition to these

to realize the information the researcher was reviewed document.

Totally the researcher was used be used 174 sample size for the

study.

3.5. Source of data

The researcher was used both primary and secondary data which

conducting this research.

3.5.1. Primary data sources

The primary data was collected from house hold and government

official by questionnaire interview, and Personal or Filed

observation of the researcher.

3.5.2. Secondary data source

The researcher was used secondary data sources of both published

and unpublished documents from document review, different books,

research report, official report, government policies,

strategies, programmers and website.

3.6. Data analysis and Interpretation

For the purpose of data analysis and interpretation the

researcher was used SPSS, Excel, and some related tools. Both

SPSS and Excel tools were used to analyze some of the qualitative

and quantitative data types that were collected through

questionnaire, interview and document reviewing. Latter all of

the basic data was converted into graphs, charts, tables and

descriptions.

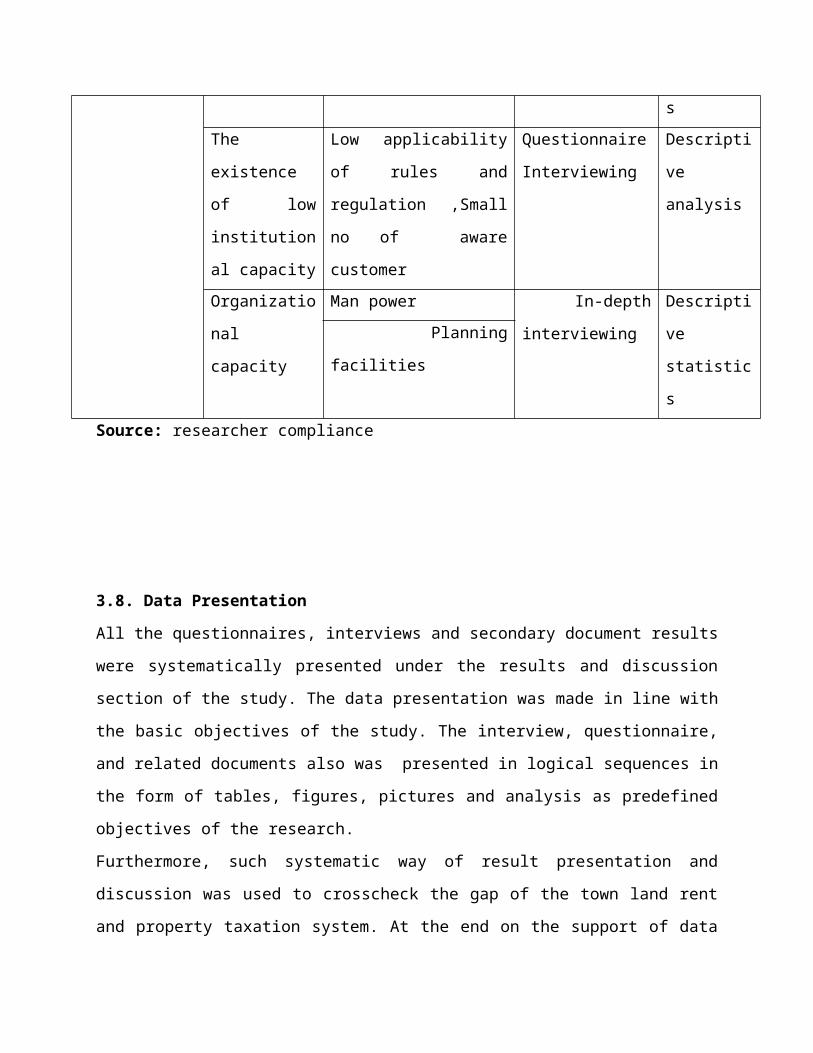

3.7. Operationalization frame work

Research

objectives

Concepts Variables Methods of

data

Methods

of data

collection analysisTo assess

the total

amount of

land plots

and

buildings in

the town and

amount of

taxpayers

included in

tax base.

Coverage Number plots, and

Buildings

identified

Reviewing

records,

Interviews

Descripti

ve

statistic

sTax base Number of

Taxpayers, taxable

plots & buildings.

Reviewing

records,

Interviews

Descripti

ve

analysisTax rate % of tax per year Reviewing

records,

Interviews

Descripti

ve

analysis

To assess

the total

revenue that

is collected

from land

and property

taxes in

relation to

other

sources of

the town in

the past

five

consecutive

Demand of

collection/

Financial

Municipal office

revenue collected

Interviewing

& documents

reviewing

Descripti

ve

statistic

sSocial

service

aspect

Accessibility of

road , water,

Sewage , electric

po

Questionnaire

s, discussion

Descripti

ve

analysis

Utilization of

the community

Questionnaire

s

D.

analysis

years.To assess

land and

property tax

payers

attitudes in

the town

Awareness

creation

No of award

customers

Questionnaire

s

>>

Finance Revenue increases Review of

records

Descripti

ve

statistic

sAwareness &

satisfactio

n

No of Training

given or

discussion on

meeting

Interviewing

questionnaire

s

Descripti

ve

statistic

sGovernment

action

Correction measure

will take

Questionnaire

s

Descripti

ve

analysisTo assess

the

challenges

of land and

property

taxation

practice in

the town.

Absence of

uniform

valuation

Different taxes

for similar

property.

Questionnaire

,

Interviewing

Descripti

ve

statistic

s the

existence

of informal

settlement

No of informal

settlers InterviewingDescripti

ve

statistic

sCadastral

registratio

n problem

Recorded parcels

of land

Document

review

Interviewing

Descripti

ve

statistic

sThe

existence

of low

institution

al capacity

Low applicability

of rules and

regulation ,Small

no of aware

customer

Questionnaire

Interviewing

Descripti

ve

analysis

Organizatio

nal

capacity

Man power In-depth

interviewing

Descripti

ve

statistic

s

Planning

facilities

Source: researcher compliance

3.8. Data Presentation

All the questionnaires, interviews and secondary document results

were systematically presented under the results and discussion

section of the study. The data presentation was made in line with

the basic objectives of the study. The interview, questionnaire,

and related documents also was presented in logical sequences in

the form of tables, figures, pictures and analysis as predefined

objectives of the research.

Furthermore, such systematic way of result presentation and

discussion was used to crosscheck the gap of the town land rent

and property taxation system. At the end on the support of data

analysis, graphical information and theoretical facts of the

study was summarized by conclusion and recommendation.

3.9. Limitations of the Study

The study was get possible statistical data from available

documents as well as information obtained through questionnaires

from the respondents and interviewing with officials, experts and

kebele managers respondent. However, during data collection the

following problems were faced the researcher. Some of them were:

Lack of skilled man power that gives appropriate data, lack of

well organized data, unwillingness of the respondents,

transportation problem and the likes were serious problems that

were affected the researcher.

CHAPTER FOUR4.0. Data Analysis, Interpretation and Discussion

4.1. Introduction

This chapter presents the analysis of the study. The study

findings were triangulated in order to cross-check the validity

of the data and generate in-depth understanding of the issue

understudy. The chapter was contains five parts. The first part

deals about Response Rate, the second part was about demographic

characteristics of respondents, the third part presents the

analysis, interpretation and discussions of the study on an

assessment of land and property taxation practice in the past

five consecutive years (2001-2005 E.C.) in kercha town. In line

with the study objective, it organized into four sections the

total numbers of land plots and property and land plots and

property included in the tax base of the town, the total revenue

collected from land and property taxes in relation to other

sources of the town, land and property tax payers attitudes and

challenges of land and property taxation practice in the town.

The fourth part deals with the interpretations and discussions of

data gathered from different categories of respondents by using

different techniques.

4.2. Response Rate

The respondents were divided in to tax payers, Officials and

kebele managers. Tax payers were treated using questionnaires

while Officials and kebele managers were treated using

interviews .The total questionnaires being distributed were 164

,the interview questions prepared for 12 key informants,

totally 174 respondents were involved. From total questionnaires

distributed to tax payers, 156 returned on the schedule. The

remaining 8 respondents were not responded and returned properly

on time to use for the study. This indicates that the overall

response rate of the study was 95.12%.

For the purpose of getting reliable data and organize, changing

the questionnaires from English language to regional working

language is mandatory. Because of this both the questionnaires

and interviewing questions were converted in to Afan Oromo.

Finally the data was organized and analyzed in English language.

4.3. Demographic Data

Kebeles of respondents: The findings show that both 01 and 02

taxpayer’s 53, 21% and 46.79% of respondents were included in the

sample respectively. Accordingly the 01 and 02 ratio in the

sample taxpayers respondents were around 1:1.

Sex of respondents: The findings show that 87.2% of male and

12.8% of female taxpayer’s respondents were included in the

sample. Accordingly the male and female ratio in the sample

taxpayers respondents were 7:1.

Age of respondents: The findings show that 46.8% of respondents

found age between 23-34, 38.5% of respondents found age between

35-50, 12.8% of respondents found age greater than 50.and1.92%

of taxpayers respondents were found age between 18-24.

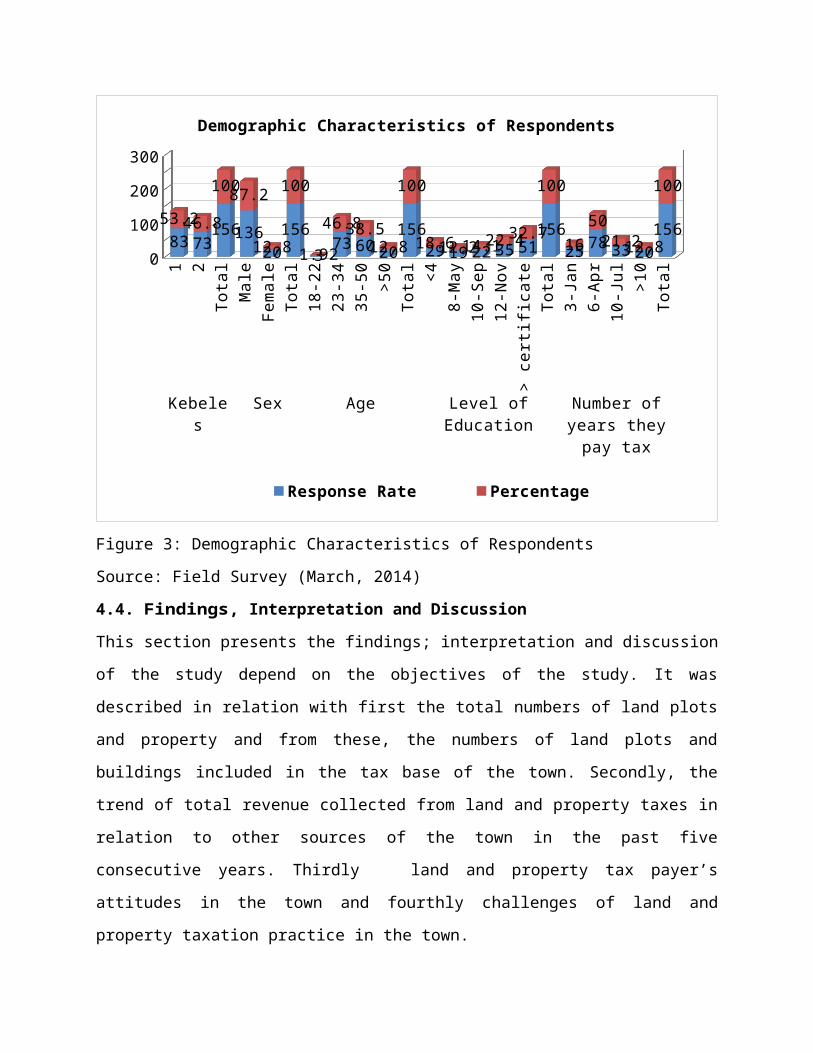

Level of Education: The majority of tax payers respondents head

about 32.7% which had certificate and above ,about 22.4% of

respondents was attend grade 11-12 education, 18.6% of

respondents was attend primary education , 14.1% of

respondents was also attend grade 9-10 and 12.2% of

respondents was reached grade 5-8 in their education.

Number of years they pay tax: Of all tax payer respondents, 50%

of taxpayers respondents were paid tax for 4-6 years , 21.2% of

taxpayers respondents were paid for 7-10 ,16% of taxpayers

respondents were paid for 1-3 years and 12.8% of taxpayers

respondents were also paid for more than 10 years .Demographic

characteristics of the sample tax payers’ respondents by their

living kebels, Sex, Age, level of education and numbers of

taxpayers indicated here under the following figure.

1 2To

tal

Male

Fema

leTo

tal

18-2

223

-34

35-5

0>5

0To

tal <4

8-Ma

y10

-Sep

12-N

ov>

cert

ific

ate

Tota

l3-

Jan

6-Ap

r10

-Jul >10

Tota

l

Kebeles

Sex Age Level of Education

Number of years they pay tax

0

100

200

300

83 73156136

20156

3 73 60 20156

29 19 22 35 51156

25 78 33 2015653.246.8

10087.2

12.8

100

1.9246.838.5

12.8

100

18.612.214.122.432.7

100

165021.212.8

100

Demographic Characteristics of Respondents

Response Rate Percentage

Figure 3: Demographic Characteristics of Respondents

Source: Field Survey (March, 2014)

4.4. Findings, Interpretation and Discussion

This section presents the findings; interpretation and discussion

of the study depend on the objectives of the study. It was

described in relation with first the total numbers of land plots

and property and from these, the numbers of land plots and

buildings included in the tax base of the town. Secondly, the

trend of total revenue collected from land and property taxes in

relation to other sources of the town in the past five

consecutive years. Thirdly land and property tax payer’s

attitudes in the town and fourthly challenges of land and

property taxation practice in the town.

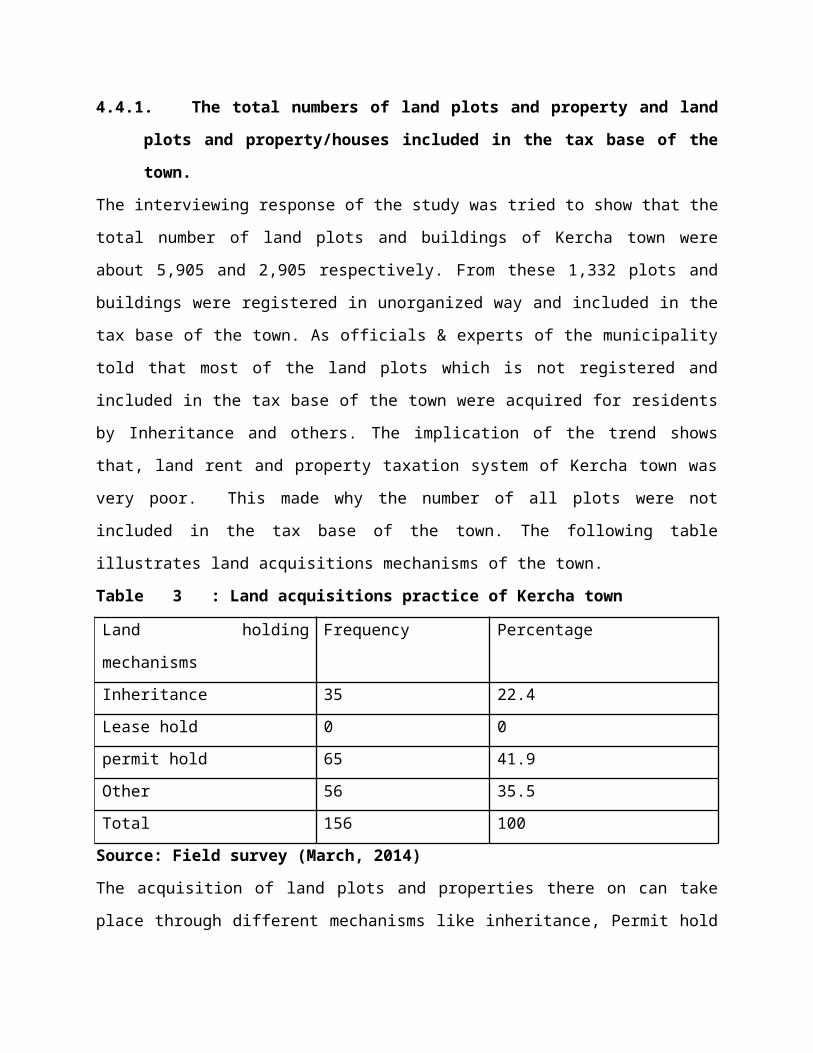

4.4.1. The total numbers of land plots and property and land

plots and property/houses included in the tax base of the

town.

The interviewing response of the study was tried to show that the

total number of land plots and buildings of Kercha town were

about 5,905 and 2,905 respectively. From these 1,332 plots and

buildings were registered in unorganized way and included in the

tax base of the town. As officials & experts of the municipality

told that most of the land plots which is not registered and

included in the tax base of the town were acquired for residents

by Inheritance and others. The implication of the trend shows

that, land rent and property taxation system of Kercha town was

very poor. This made why the number of all plots were not

included in the tax base of the town. The following table

illustrates land acquisitions mechanisms of the town.

Table 3 : Land acquisitions practice of Kercha town

Land holding

mechanisms

Frequency Percentage

Inheritance 35 22.4Lease hold 0 0permit hold 65 41.9Other 56 35.5Total 156 100Source: Field survey (March, 2014)

The acquisition of land plots and properties there on can take

place through different mechanisms like inheritance, Permit hold

and others (buying of properties on plots, gifts). The study

established that only 41.9% of respondents were holding land with

permit hold, 22.6% and 35.5% of respondents were holding land

with inheritance and others respectively. Officials and experts

also agree to the responses of taxpayers because the majority of

land plots of the town acquired through inheritance, buying of

properties on plots, gifts and the like.

The result of the study shows that, only 22.6% of land plots

included in the tax base of the town from the total land plots of

the town. This hinders the town revenue was low. The implication

of the study shows that most of tax payer respondents acquired

their land plots through transferring from one person to another

illegally. In addition, as officials said that the reason why all

land plots was not included in tax base was the municipality has

lack of man power (skilled and in number), financial problems and

the like. Most of land plots were occupied through inheritance,

buying of properties on plots, gifts and the rest up to now a

day, it was occupied by farmers. Land plots that occupied by

farmers were not taxable to the municipality. The document

reviewed shows that, the municipality had not well organized

records of land plots and buildings in the town.

In land and property taxation system identification of properties

and tax payers are must. Roy Bahl (n.d) argued that if the tax

base is the value of land and improvements, the three steps must

be identified is all parcels and their taxable characteristics,

the characteristics of any improvements on the land and

identification of the owner of the property. Enid Slack (n.d)

also argument, land and improvements to the land, machinery and

equipment that are permanently attached to real property are

included and other characteristics of the property tax base

include exemptions and property valuations. But in kercha town

there was no identification of land and property practice.

Moreover, officials said that the reason of identification

problems of land and property which were not included in the tax

base of the municipality was lack of man power and financial

capacity problems were bottleneck of the municipality. These

imply that due to different problems most of land plots and

building were not included in the tax base of the town. In the

different property taxes like building permit tax, house transfer

tax, wall and roof tax and other taxes were collected. The

following table elaborates building permit taxes and tax payer’s

certificates information of the town.

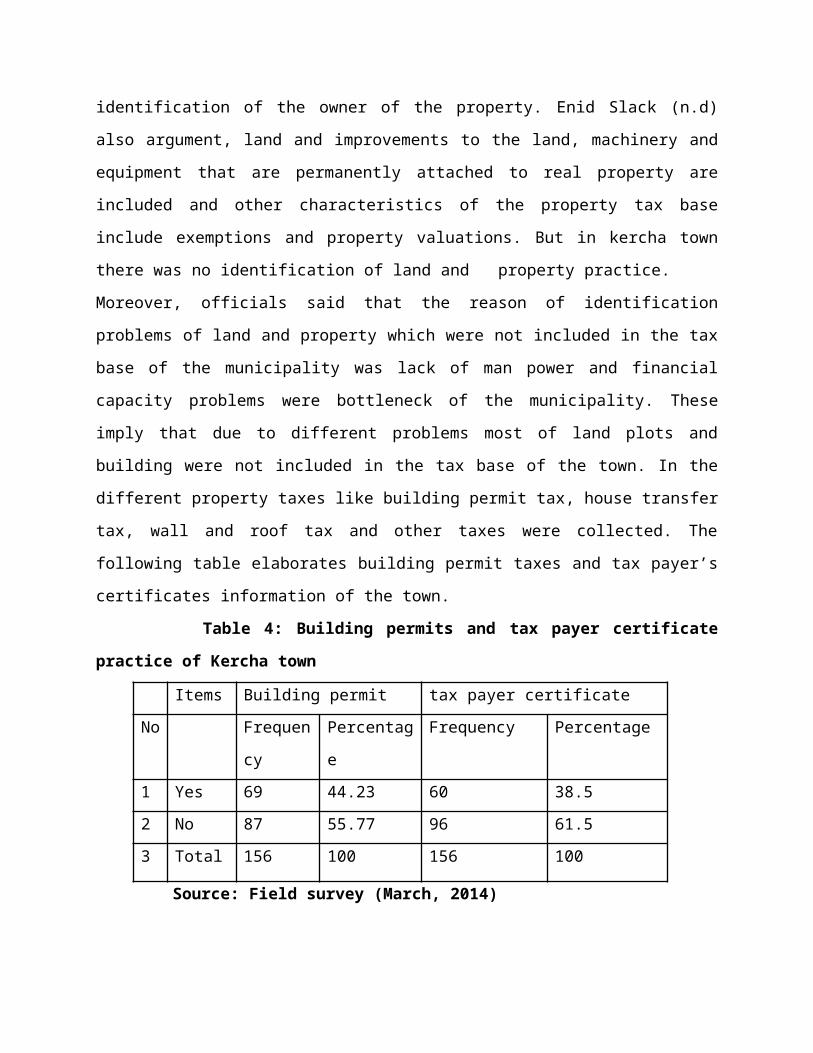

Table 4: Building permits and tax payer certificate

practice of Kercha town

Items Building permit tax payer certificateNo Frequen

cy

Percentag

e

Frequency Percentage

1 Yes 69 44.23 60 38.52 No 87 55.77 96 61.53 Total 156 100 156 100

Source: Field survey (March, 2014)

As we understand from the above table, about 87 (55.77%) of

taxpayer respondents build their house without building permit.

The rest 69(44.23%) of taxpayer respondents build their house

with building permit. Accordingly, 96(61.5%) of taxpayer

respondents had not taxpayer certificate and only 60(38.5%) of

taxpayer respondents had taxpayer certificate. Responses of

interviewing and document analysis also share the responses of

respondents.

The results of the above table shows that not only from the

total number of houses which is found in the town but also from

the taxable houses most of houses was built without building

permit tax. According to the interview informants, in the town

there were about 2,952 houses. From these, the total tax payers

of housing tax of the town municipality record were only

1,332(45%) of houses included in the tax base of the town. As