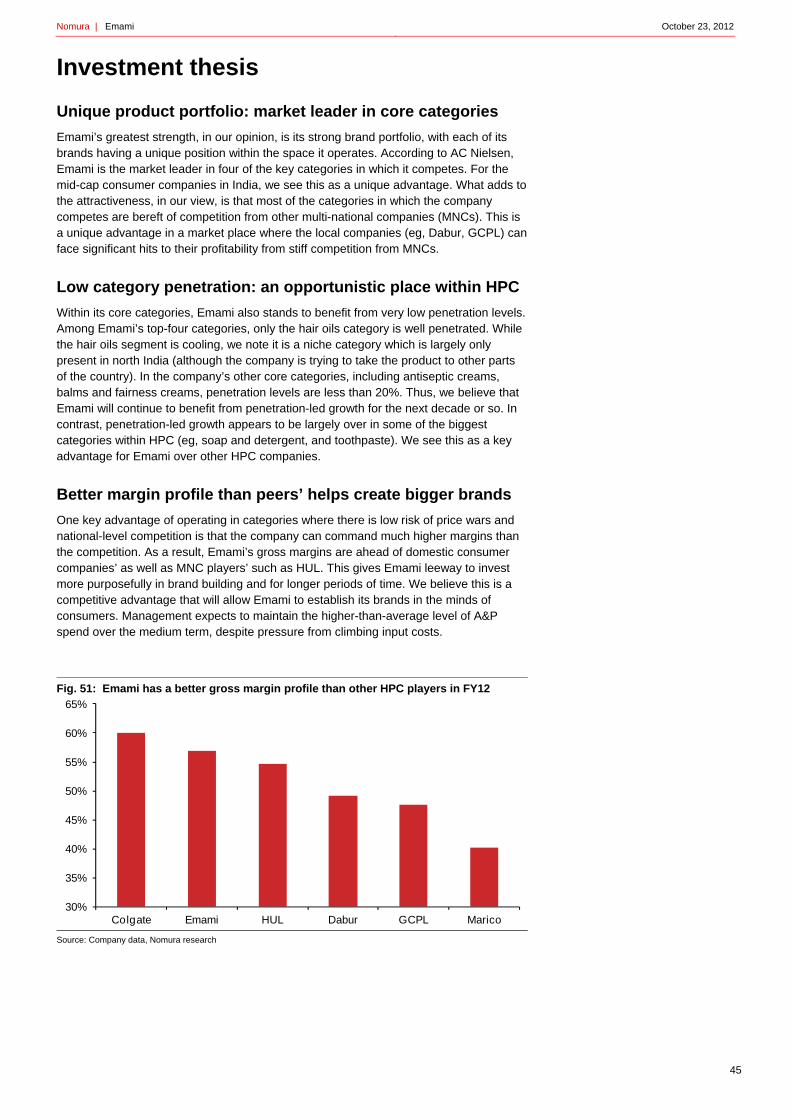

Leveraging the valuation gap to buy emerging market growth ...

86

See Appendix A-1 for analyst certification, important disclosures and the status of non-US analysts. Equity Research ANCHOR REPORT India consumer: Breaking through with global M&A? Leveraging the valuation gap to buy emerging market growth outside India Indian consumer companies are increasingly growing overseas inorganically, rather than relying on domestic organic growth. In the past few years, Marico has acquired firms in S Africa, SE Asia and Vietnam, Dabur in Turkey and the US, Godrej in Argentina, Indonesia and Africa. We see several reasons for this trend: slowing growth opportunities at home now that some categories such as soaps, detergents, hair oils, etc. have matured, availability of attractive targets in emerging markets, ability to build scale, and being rewarded in terms of valuation multiples. In this report, we look at each of these factors in detail and discuss why we like GCPL, which has been leading the inorganic growth push. We initiate on Emami, the top player in cooling oil, antiseptic cream, balm and men’s fairness cream, with a Buy, and upgrade Marico to Neutral. Key analysis in this anchor report includes: Trends in overseas acquisitions done by Indian companies over the past couple of years. Why growing inorganically overseas has been a rewarding exercise. What the future holds in terms of inorganic growth. October 23, 2012 Research analysts India Consumer Related Manish Jain - NFASL [email protected] +91 22 4037 4186 Anup Sudhendranath - NSFSPL [email protected] +91 22 4037 5406

-

Upload

khangminh22 -

Category

Documents

-

view

5 -

download

0

Transcript of Leveraging the valuation gap to buy emerging market growth ...

See Appendix A-1 for analyst certification, important disclosures and the status of non-US analysts.

Equity Research

AN

CH

OR

RE

PO

RT

India consumer: Breaking through with global M&A?

Leveraging the valuation gap to buy emerging market growth outside India

Indian consumer companies are increasingly growing overseas inorganically, rather than relying on domestic organic growth. In the past few years, Marico has acquired firms in S Africa, SE Asia and Vietnam, Dabur in Turkey and the US, Godrej in Argentina, Indonesia and Africa.

We see several reasons for this trend: slowing growth opportunities at home now that some categories such as soaps, detergents, hair oils, etc. have matured, availability of attractive targets in emerging markets, ability to build scale, and being rewarded in terms of valuation multiples.

In this report, we look at each of these factors in detail and discuss why we like GCPL, which has been leading the inorganic growth push.

We initiate on Emami, the top player in cooling oil, antiseptic cream, balm and men’s fairness cream, with a Buy, and upgrade Marico to Neutral.

Key analysis in this anchor report includes:

Trends in overseas acquisitions done by Indian companies over the past couple of years.

Why growing inorganically overseas has been a rewarding exercise.

What the future holds in terms of inorganic growth.

October 23, 2012

Research analysts

India Consumer Related

Manish Jain - NFASL [email protected] +91 22 4037 4186

Anup Sudhendranath - NSFSPL [email protected] +91 22 4037 5406

India consumer

GENERAL CONSUMER

EQUITY RESEARCH

Breaking through with global M&A?

Leveraging the valuation gap to buy emerging market growth outside India

October 23, 2012

Action: Inorganic growth will continue to be a theme Mid-cap consumer companies have been particularly active over the past few years in driving inorganic growth. We see several reasons behind this trend including: a) slowing medium-term growth opportunity in the home market, b) availability of attractive targets outside India, c) ability to build scale, and d) being rewarded by the market with higher valuation multiples.

We look at each of these factors in detail and believe this is a trend which will continue in the medium term. We continue to like Buy-rated GCPL, which has been leading the inorganic growth push and we think will continue to do so in the near to medium term.

We initiate on Emami with a Buy rating and TP of INR648. We believe that along with Emami’s position as a focused operator in niche segments, its willingness to look at inorganic growth opportunities means an ability to drive sector-leading profit growth in the medium term. We also upgrade Marico to Neutral as falling raw material prices and the incorporation of a recent acquisition lead to a significant upgrade to our numbers.

Catalysts: Ability to drive inorganic growth in the medium term Strong delivery in the domestic business will be the key driver of earnings and stock prices in the near term, in our view. However, we expect that over the medium term, a company’s ability and willingness to explore inorganic growth opportunities will also be a key factor. Markets have rewarded companies for successfully integrating acquisitions, which we believe will encourage companies to look more favourably to these opportunities in the future.

Valuation: Sector valuations expensive; prefer to play via mid-caps; Top picks: Emami and GCPL At an average FY14F PE multiple of 28.6x, we see sector valuations expensive relative to the Sensex. However within this context, we prefer companies that offer reasonable visibility on growth and less demanding valuations. We like Emami, where we see potential for upside surprise on earnings, and GCPL, where performance of the international business – both organic and inorganic – could surprise positively. Valuations for each are below the sector, further supporting our view at current levels. Fig. 1: Stocks for action

Source: Bloomberg, Nomura estimates, pricing as of 18 Oct 2012. * initiating

Anchor themes

We believe Indian companies will continue to explore inorganic growth opportunities abroad on account of 1) slowing category growth in India; 2) ability to invest for future growth; and 3) being rewarded by the market by way of higher multiples.

Nomura vs consensus

We believe valuation multiples for consumer companies will remain high in the near term and do not see correction back to long-term averages soon.

Research analysts

India Consumer Related

Manish Jain - NFASL [email protected] +91 22 4037 4186

Anup Sudhendranath - NSFSPL [email protected] +91 22 4037 5406

Company Ticker Rating TP (INR) Current price (INR) Upside (%)

Emami HMN IN Buy* 648 517.0 25.3%

Marico MRCO IN Neutral↑ 220 206.0 6.8%

GCPL GCPL IN Buy 800 685.0 16.8%See Appendix A-1 for analyst certification, important disclosures and the status of non-US analysts.

Nomura | India consumer October 23, 2012

2

Contents

3 Executive summary

5 Key figures

7 India consumer has witnessed steady acceleration in growth…

11 What are the common trends that we can identify from recent acquisitions?

13 Six reasons why Indian companies have looked abroad for inorganic growth

31 Key trends we expect to emerge in the medium term

34 Key conclusions

38 Which companies screen well for being potential acquirers?

40 Companies’ views on inorganic growth; a prominent theme

42 Emami

63 Marico Industries

72 Godrej Consumer

81 Appendix A-1

Nomura | India consumer October 23, 2012

3

Executive summary In this report we have looked at why Indian consumer companies are increasingly looking at growing their business outside India by taking the inorganic growth route. We believe it is a reflection of a few factors, including slowing medium-term growth in some HPC categories in India, cheaper valuations for acquisitions done abroad, no sparse availability of potential targets in India (even relatively smaller ones), easy access to capital on account of strong balance sheets, need to look for another avenue for medium- to long-term growth and ambitions to become an emerging market consumer company. The high valuations at which domestic FMCG companies are trading is another incentive for companies to acquire cheaply abroad and achieve higher valuations for the consolidated entity at home.

Underlying growth slowing in the domestic markets across mature HPC categories We find that in many of the mature categories such as soaps, detergents, hair oils etc. the penetration-led growth seen since FY2000 is over. Over the past couple of years, a significant part of the growth which the companies have delivered has been led by distribution expansion and market share gains. We believe that incrementally, growth will be slow from current levels in these categories and the cost of driving growth will likely see a rise. We analyze the growth trajectory in these categories over the past five years and what is the likely growth over the next couple of years. For example, in the laundry segment, sales achieved an 8.4% CAGR over the last five years, which is expected by to slow to 7.1% in 2012 (source: Euromonitor). In bath and shower, the past 5-year CAGR has been 11.7%, with 2012 growth expected to be 8.5%. We expect similar trends across most of the mature HPC categories over the next three years.

Competitive activity in domestic market likely to remain high Competitive activity in mature categories is the best reflection of slowing growth in the categories, in our view, and as they remain at elevated levels. Profitability in these segments has seen a structural decline and will likely remain at these suppressed levels in the medium term. Companies have to spend a significant amount of money to support brands and maintain market share in the mature categories. The high input cost environment in the last year or so has meant a further hit to profitability, although there should be some respite from this in FY13F, we expect, due to falling commodity costs. In emerging HPC categories such as surface cleaners, conditioners, hair gels etc., we still see growth ahead, but the cost of growing the category is significant. Considering the demographics in India and the under-penetration across many consumer segments, we believe the market will remain both attractive and competitive in the medium term.

Ambition to become emerging market consumer company We believe one reason for companies looking at inorganic growth is the ambition to become an emerging market consumer company. We find that even MNCs such as Unilever and P&G have taken this route over the past decade to grow in emerging markets. We believe Indian companies will increasingly look at this route, and in the medium term, we expect that mid-cap consumer companies in India such as Marico, Dabur, and GCPL will have a significant part of their revenues coming from overseas markets in the next 3-5 years.

Markets rewarding inorganic growth There is also a history of markets rewarding companies that have successfully taken inorganic growth opportunities. One best example is GCPL, which has not only been rewarded with similar multiples for its acquisitions, but over the last couple of years, as the company has shown delivery on said targets, its P/E multiple has seen a significant expansion. Marico and Dabur have also been rewarded for inorganic growth; however, the scale has been much smaller compared with GCPL in terms of acquisitions.

Trend of growing inorganically will likely continue Going forward, the trend of Indian companies taking the inorganic growth route is likely to continue, in our view. We find there are certain advantages of growing inorganically:

• wider availability of assets in other emerging markets,

• lower cost of the acquisitions, and

• easy availability of funding.

Nomura | India consumer October 23, 2012

4

Domestic consumer companies such as Dabur, Marico and GCPL have all used this route over the last few years, and we believe they will continue to look at inorganic growth opportunities in the medium term.

We also believe that companies have recognized the need for growing inorganically over the last few years and have put in place management structures which allow them to focus on growing the international business without having any of the pressures of dealing with the issues in the domestic market. We believe that for the companies under our coverage this will significantly enhance the focus internally on growing the international business.

Domestic business growth will be distribution led in the near term Domestic business growth especially for HPC companies is slowing. In that context, we believe one of the common themes that every consumer company has addressed during its investor meetings is to increase its distribution strength. This increase in distribution has come in many forms.

Our discussions with various consumer companies indicates that in the next 2-3 years, management focus will be more on driving increased distribution reach. This is also evident from the actions taken by all the companies in the sector in the last year or so, in our view. Increasingly companies are talking about broadening the direct distribution reach, which should help drive growth in the near term. Also as a result of improved distribution, we note that listed companies have gained share, even as overall category growth has slowed.

Valuations should reflect inorganic growth in the medium term We believe this trend of inorganic growth is likely to continue in the near term. Based on how the market has perceived these acquisitions in the past year or so, we believe that if companies are able to show execution and deliver consistent results, they are rewarded with higher multiples for the consolidated entity. We note this has been clearly reflected in GCPL, where valuation multiples have seen a significant rise over the last couple of years, in conjunction with its acquisitions.

In the case of large caps, we do not see inorganic growth as being as relevant, as their portfolio of products gives them enough opportunity to growth organically. However, we believe segments driving this growth will be different going forward, reflecting the penetration levels across segments. For example, personal products will likely be the key driver of growth for HUVR in the next decade, in our view, versus soaps & detergents which drove growth over the past ten years.

Among the food names in the sector, the inorganic growth theme is less relevant, in our view, as market growth opportunity in India is significant, driven by shifting demographics as well as changing tastes and preferences and increasing incomes. We see limited need or willingness among the food names to explore the inorganic growth route in the near to medium term.

Nomura | India consumer October 23, 2012

5

Key figures Fig. 2: Growth of the Indian FMCG sector (USD mn)

Source: Euromonitor

Fig. 3: Food sub-segment has grown faster

(USDmn) 2005 2011F CAGR (%)

HPC 6,206 12,056 14%

Food 5,902 14,288 19%

Others 2,120 4,073 14%

Total 14,228 30,416 16%

HPC (%) 44% 40%

Food (%) 41% 47%

Others (%) 15% 13%

Total 100% 100%

Source: Euromonitor

Fig. 4: Domestic growth is down from 2006 levels, recent uptick is a result of distribution push across companies; reason to look at inorganic growth

Source: Company, Nomura research

Fig. 5: Domestic acquisition opportunities are more limited and are increasingly getting more expensive; time to look abroad

Date Acquirer Target Transaction Size Deal Multiple

Feb-12 Marico Paras Pharma personal care brands INR~ 7.5bn 5x Sales

Mar-11 Cargill India Sweekar (Marico brand) INR~ 2bn 1.2x Sales

Dec-10 Reckitt Benckiser Paras Pharmaceuticals INR32.6bn 8x Sales

Nov-08 Dabur Fem Care Pharma INR2.84bn 3x Sales

Oct-08 Emami Zandu INR8bn 4x Sales

Jan-05 Dabur Balsara INR1.43bn 0.7x Sales

Source: Company data, Nomura research

0

10,000

20,000

30,000

40,000

50,000

60,000

2005

2006

2007

2008

2009

2010

2011

F

2012

F

2013

F

2014

F

2015

F

0%

5%

10%

15%

20%

25%

30%

2006 2007 2008 2009 2010 2011 2012

GCPL Domestic Marico Domestic Dabur HUL

Nomura | India consumer October 23, 2012

6

Fig. 6: Recent overseas acquisitions by Indian companies – a trend we expect to see continuing over the medium term

Acquirer Acquired Region Date Revenues Areas

Marico ICP Vietnam Vietnam 2011 USD25mn Personal care and men’s grooming products

Marico Derma RX Singapore 2010 USD11mn Skin care solutions

Marico Code 10 Malaysia 2010 USD2.7mn Range of hair creams and hair gels

Marico Ingwe South Africa 2010 USD3.3mn Immuno boosters and the medi pack range

Marico Fiancee Egypt 2006 NA Hair creams and gels

Marico Hair Code Egypt 2006 NA Hair creams and gels

Dabur Hobi Kozmetik Turkey 2010 USD30mn Hair care and skin care products

Dabur Namaste Group USA 2011 USD93mn Ethnic hair care products

Dabur Fem Care India 2007 USD22mn Women’s skin care products

Godrej Consumer Darling Africa 2011 USD222 Ethnic Hair care

Godrej Consumer Tura Nigeria 2010 USD50 Personal care

Godrej Consumer Megasari Indonesia 2010 USD120 Insecticides

Godrej Consumer Issue Argentina 2010 USD33 Hair colours

Godrej Consumer Argencos Argentina 2010 USD12 Hair Care

Source: Company data, Nomura research

Fig. 7: Inorganic growth has helped mid-cap companies grow in scale over the last few years

Source: Company, Nomura research

Fig. 8: Market has rewarded them with high multiples

Source: Company, Nomura research

0

1

2

3

4

5

6

7

8

CLG

T

HU

VR

ITC

Dab

ur

Mar

ico

GC

PL

(x)

10x

15x

20x

25x

30x

35x

Oct

-08

Jan

-09

Ap

r-09

Jul-

09

Oct

-09

Jan

-10

Ap

r-10

Jul-

10

Oct

-10

Jan

-11

Ap

r-11

Jul-

11

Oct

-11

Jan

-12

Ap

r-12

Jul-

12

Oct

-12

GCPL Dabur Marico

Nomura | India consumer October 23, 2012

7

India consumer has witnessed steady acceleration in growth… The FMCG industry, accounting for ~2.2% of the country’s GDP and an estimated size of USD30bn, according to Euromonitor, witnessed steady sales at a 16% CAGR over CY05-CY11. Growth picked up from a CAGR of 12.5% in CY06-09 to 15.6% over the last couple of years. We attribute this to: 1) acceleration in India’s GDP growth and favourable macro-economic conditions; 2) a sharp increase in rural incomes; and 3) rising consumption culture.

Fig. 9: Indian consumer sector has seen robust growth in the last decade (USD mn)

Source: Euromonitor

… But growth has not been even throughout the sector However, within the FCMG industry, the food sector has outgrown the HPC space in the last decade. Our analysis shows that the processed and packaged food sector (~47% of the FMCG market) witnessed 19% sales growth in CY05-11F compared with 14% sales growth in the HPC segment and 16% sales growth in the overall FMCG industry.

Fig. 10: FMCG sector growth led by food sector

2005 2011F CAGR

HPC 6,206 12,056 14%

Food 5,902 14,288 19%

Others 2,120 4,073 14%

Total 14,228 30,416 16%

Source: Euromonitor

Fig. 11: Share of food increasing in FMCG

2005 2011F

HPC (%) 44% 40%

Food (%) 41% 47%

Others (%) 15% 13%

Total 100% 100%

Source: Euromonitor

HPC categories are seeing a slowdown… The growth differential is exaggerated in the mature HPC categories where incremental value growth is slowing into single digits. We identify these categories as bath and shower, dishwashing, insecticides and laundry care. Growth in these categories has been robust in the last decade (source: Euromonitor) led by the under penetration theme, but over the next decade, we see these categories as increasingly mirroring growth rates in globally. Going by Euromonitor estimates, growth in categories such as laundry, insecticides etc, will likely slow to mid- to high-single digits over the next couple of years. As we see from the table below, growth in the laundry segment, which has already trended down to high-single digits in the past five years, is expected to further slow down over the next couple of years. Similarly in the bath and shower segment, value growth reached a 12% CAGR over 2005-10 but will incrementally slowdown over the next couple of years to less than 9%.

0

10,000

20,000

30,000

40,000

50,000

60,000

2005 2006 2007 2008 2009 2010 2011F 2012F 2013F 2014F 2015F

Nomura | India consumer October 23, 2012

8

Fig. 12: Mature HPC categories are seeing a slowdown in India

Household & Personal Care (USDmn) 2005 2010 2012F 2005-10 CAGR (%) 2012F

Laundry detergent 1,644 2,464 2,876 8.4% 7.1%

Insecticides 401 575 664 7.5% 6.6%

Dishwashing 171 315 391 13.0% 10.5%

Surface care 58 101 125 11.8% 10.3%

Total household 2,359 3,591 4,221 8.8% 7.5%

Bath & shower 1,283 2,262 2,698 12.0% 8.5%

Hair care 913 1,723 2,191 13.5% 12.5%

Oral care 627 1,021 1,248 10.2% 9.7%

Skin care 456 884 1,203 14.2% 15.7%

Men's Grooming 268 540 730 15.0% 16.3%

Total personal care 3,847 7,158 9,143 13.2% 12.5%

Source: Euromonitor

… however, this growth is still better relative to other Asian countries HPC markets globally have seen mixed fortunes over the last few years, based on data from Euromonitor. Growth rate across the regions gives a fair indication of the growth markets and which ones are seeing a slowdown. For example, the eastern European market has grown at an average 8.8%, with Russia leading the growth. Western European markets have seen the slowest growth globally at 3.4% for the period FY06-10, with countries such as France, Italy and Spain recording low single-digit growth rates, albeit off a large base. This compares with Asian markets, where growth has been much more robust led by India and China.

However, within the global landscape, India continues to grow solidly. Average value growth in the past 5 years in the personal care category has been close to 13.2%, which is higher than the growth recorded in any other major region in the world. We highlight that for the next few years, we expect that growth will remain robust and Indian companies will continue to rely on certain categories within the HPC space to drive growth. These categories are typically under-penetrated, and hence offer growth opportunities in terms of driving consumption. We identify these categories as skin care, men’s grooming, hair care, body care and surface cleaners etc. which are relatively new categories in India.

Fig. 13: Personal care category value growth (%) by region 2006-10

Source: Euromonitor

13.2

11.5 11.1

8.8

6.05.3

3.8 3.4 3.0 2.8 2.7 2.71.4 1.1

0

2

4

6

8

10

12

14

Ind

ia

Ch

ina

Rus

sia

E E

uro

pe

So

uth

K

ore

a

Po

lan

d

UK

W E

uro

pe

Tai

wan

Hun

gar

y

Ger

man

y

Sp

ain

Italy

Fra

nce

Nomura | India consumer October 23, 2012

9

Mature categories are slowing…per capita consumption theme not working In categories such as toothpaste and soaps, per-capita consumption in India is still well below global averages; thus we see a possibility that those numbers would move up, increasing value growth for the category over the medium term.

However, data from Colgate over the past decade suggests this has not really played out so far, with per-capita consumption of toothpaste at a CAGR of 5% over FY06-FY10. This is not to suggest a change in consumption pattern cannot happen in the medium term, but in the near term, we see no evidence to suggest a change is happening on a wider scale. Consumption habits in HPC categories are also driven by habits. For example, based on studies by Colgate most people in India prefer to brush teeth once a day rather than twice a day. This is despite recommendations from dentists that twice a day is necessity. This habit has started to change in the bigger cities, but in smaller towns, the adage ‘old habits die hard’ remains true to this day.

Fig. 14: Toothpaste penetration in India

Source: Colgate

Fig. 15: Toothpaste per capita consumption (grams per year)

Source: Colgate

Emerging HPC categories offer expensive growth… The ‘emerging’ categories within the HPC space are in niche areas such as surface cleaners, dishwashing, etc. These categories do offer growth domestically, in our view, but it is an expensive exercise to build these categories from scratch and involves a significant amount of investment. Managements have been going slowly on making these investments, given the various challenges already faced in terms of the high level of competition in current categories, as well as pressure to maintain profitability. Fig. 16: HPC category growth in India

Source: Euromonitor, Nomura research

40%

48%

56%

64%

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009 0

75

150

225

300

375

China Malaysia India

2010 2006

0%

2%

4%

6%

8%

10%

12%

14%

16%

Men

's G

room

ing

Ski

n c

are

Hai

r car

e

Dis

hw

ashi

ng

Bat

h &

sh

ow

er

Sur

face

car

e

Ora

l car

e

Laun

dry

d

eter

gen

t

Inse

ctic

ides

Nomura | India consumer October 23, 2012

10

… and small scale makes revenue impact on companies insignificant Looking at the size of some of the emerging HPC categories, we note two key things: first, the categories are very small in terms of revenue contribution. For example, according to data from Euromonitor, the surface cleaning category size is USD114mn, which is ~0.9% of India’s overall HPC segment. Similarly, the dishwashing detergent category is USD354mn which is 2.9% of overall HPC segment. While these categories recorded a 12%-plus CAGR over CY06-11 they are still not very relevant within the HPC segment, in our view. While a category such as shampoo is reasonably well penetrated and large as a percentage of the overall HPC category, a sub-segment within that such as conditioners are still less than 1% of overall HPC sales. Although these emerging categories are growing at much faster pace than both the mature HPC segments and the overall HPC market, we believe it will be at least five years before these segments become more relevant in the larger scheme of things.

Fig. 17: Smaller categories will take a significant time to become relevant in terms of size

(USDmn) CY06 CY11 CAGR (%) % of Total CY06 % of Total CY11

Dishwashing 196 354 13% 2.9% 2.9%

Surface Care 64 114 12% 0.9% 0.9%

Male Grooming 300 628 16% 4.4% 5.2%

Source: Euromonitor

Inorganic growth can provide the next leg of growth For many HPC companies in India, we think the key strategic question is where are the medium-term growth drivers? It is in this context that we believe companies in the HPC space are increasingly looking at the next driver of growth. While HPC categories in India are still attractive in the near term, albeit with their own challenges, we believe the inorganic growth route can provides these companies the next leg of growth. Additionally, it fulfils their ambitions (GCPL, Marico and Dabur have all announced in the past to grow their international businesses) to become an emerging market consumer company.

First steps have already been taken… now time to take it to the next level Increasing overseas exposure through organic growth in the form of exports was the first step. This started about a decade back for our companies under coverage. They now have a sizeable organic presence in countries outside India and have also set up manufacturing facilities in countries outside India.

Over the last five years, companies such as Marico, GCPL and Dabur have also made several acquisitions across various geographies. We believe this is the first step towards recognizing the need to have medium-term growth drivers in place and to diversify away from being a pure domestic business. As we look back at these acquisitions, we have identified that there are various common threads. We identify them below, as we believe there are some key conclusions that can be drawn from the nature of these acquisitions.

Pace of inorganic growth will likely increase over the next few years We also believe that HPC companies that have not yet made acquisitions will increasingly look at taking the inorganic route over the next few years. Emami has been looking aggressively at targets in India, according to management, but apart from the Zandu acquisition, has failed to close any other large deal. Emami has created a niche for itself within the HPC space, with many of its products having only regional competition. The company’s long-term vision is also clear: they will look to grow within India as it is more consistent with their long-term strategy. Emami has been involved in bidding for recent deals including the Paras Pharma deal. It was not successful in the end, despite bidding a higher amount than eventual winning bid. (Source: Emami loses Paras despite highest bid, Business Standard, December 14, 2010). Inorganic growth is part of company’s long-term strategy, but the difference with other HPC players is that Emami will only look to acquire within India.

Nomura | India consumer October 23, 2012

11

What are the common trends that we can identify from recent acquisitions? Looking back at the acquisitions which have happened in the last few years, we find that there are several common threads across these transactions. We these common qualities are not a coincidence and that companies are actively looking for some these threads when evaluating potential targets. We identify what we consider the most important common threads among these acquisitions below:

• Acquisitions are in related businesses

• Family-owned businesses where ability or willingness to scale up is not there

• Most acquired companies in our sample were privately held

• Revenue size is not very large relative to the acquirer, making it easier to assimilate

• Geography has been largely in other emerging markets, with Africa a big driver

Acquisitions are in related businesses One common them we have identified in recent acquisitions is that companies have targeted companies in related businesses. For example, Marico has in the past acquired companies in the hair care segment, where they have number of years of experience with the hair oil brand. Likewise, Godrej Consumer’s acquisitions have been in line with its stated 3x3 strategy. In our view, the idea of going for acquisitions in related areas is that companies have a certain expertise in the category, albeit in another geography, but it gives them the opportunity to more easily integrate the acquisitions as well as looking at potential revenue/cost synergies . We believe this is a deliberate strategy, and one which will continue to be important going forward.

Fig. 18: Recent overseas acquisitions by Indian companies (full list)

Acquirer Acquired Region Date Revenues Areas

Marico ICP Vietnam Vietnam 2011 USD25mn Personal care and mens grooming products

Marico Derma RX Singapore 2010 USD11mn Skin care solutions

Marico Code 10 Malaysia 2010 USD2.7mn Range of hair creams and hair gels

Marico Ingwe South Africa 2010 USD3.3mn Immuno boosters and the medi pack range

Marico Fiancee Egypt 2006 NA Hair creams and gels

Marico Hair Code Egypt 2006 NA Hair creams and gels

Dabur Hobi Kozmetik Turkey 2010 USD30mn Hair care and skin care products

Dabur Namaste Group USA 2011 USD93mn Ethnic hair care products

Godrej Consumer Darling Africa 2011 USD222 Ethnic Hair care

Godrej Consumer Tura Nigeria 2010 USD50 Personal care

Godrej Consumer Megasari Indonesia 2010 USD120 Insecticides

Godrej Consumer Issue Argentina 2010 USD33 Hair colours

Godrej Consumer Argencos Argentina 2010 USD12 Hair Care

Source: Company data, Nomura research

Family-owned businesses where ability or willingness to scale up is absent Again, if we look at acquisitions over the past few years, another common element we found among them that is that the acquired businesses have frequently been owned by families. These family businesses have a strong brand recall and an established presence in the local markets, but the owners may not have had the ability or willingness to scale up the business. This is not uncommon even in India, where our interaction with various companies did suggest there are small niche regional players in the food and

Nomura | India consumer October 23, 2012

12

HPC space which are family-owned businesses but not present at a national level. Additionally, we note that these smaller businesses may need access to capital to scale up their businesses, and that access may or may not be available. Increasing the size of a company also brings in the need to hire more managers to manage it, as it is not possible for the controlling families to manage it on their own.

Most acquired companies in our sample were privately held Another common thread we observed in our sample of acquisitions is that most of them were not listed companies. While inherently it would seem that should not be a consideration, experience of some listed companies in India has not been smooth. For example, when Dabur acquired Fem, it had to undergo a lengthy battle with minority shareholders before getting control of the company. Although laws in each country with regard to takeover of a listed company are different and depend on how much minority interest is to be acquired, we believe it is much tougher to acquire a listed entity. We believe this has been a consideration for the Indian companies when they have looked at potential targets abroad.

Revenue size is not very large relative to the acquirer, making it easier to assimilate When we look at the average size of our sample of acquisitions, we find that on average they are similar to bolt-on acquisition and not a game-changing one for the buyer. For example, Marico’s acquisitions have been in the region of USD3-25mn, where the revenue base for FY12 was in excess of USD771mn. Similarly, when we look at acquisitions made by other mid-cap companies such as Dabur and GCPL, each of their acquisitions was small in revenue terms vs their own size and can be viewed by the market as a bolt-on deal. GCPL ended up making several smaller (in revenue terms) acquisitions over a short period of time, which exaggerated the impact in FY11. The exception to our findings was GCPL’s acquisition of Megasari in Indonesia, where we think GCPL acquired an attractive asset at a reasonable price. Today, the Indonesia business is a key component of the consolidated GCPL. The acquisition was large in terms of absolute revenues, which GCPL broke down into phases to ease the transition. In our view, the idea behind keeping the acquisition size small is that they are easier to assimilate. Dabur CEO Duggal made a similar observation as well in past comments (Source: Smaller buyouts easier to assimilate, Economic Times, July 5, 2010).

Geography has been largely in other emerging markets, with Africa a big driver Another common thread we observe has been the geographic location of where the acquisitions have taken place. GCPL has an established strategy of looking for inorganic growth in South East Asia, Latin America and Africa, according to management. Marico has looked at a variety of geographies including Asia, South Africa, while Dabur has also largely done deals in emerging markets. We believe the bias for these geographies is likely to continue in the medium term.

Nomura | India consumer October 23, 2012

13

Six reasons why Indian companies have looked abroad for inorganic growth

We believe there are six key reasons why Indian companies have started to look outside India for growth. The strategy of growing inorganically seems counter-intuitive given India’s consumption-driven economy likely makes it an attractive market, in our view. However, as we highlight below, we have identified some specific reasons that we believe are driving Indian consumer companies abroad in search of inorganic growth.

• Domestic HPC growth still good, but incrementally slowing down

• Domestic acquisition opportunities are limited and relatively expensive compared with overseas acquisitions

• Ambition to become and emerging market consumer company

• Availability of low-cost funding

• Markets have rewarded this growth strategy

• Need for companies to look for newer markets to drive medium-term growth

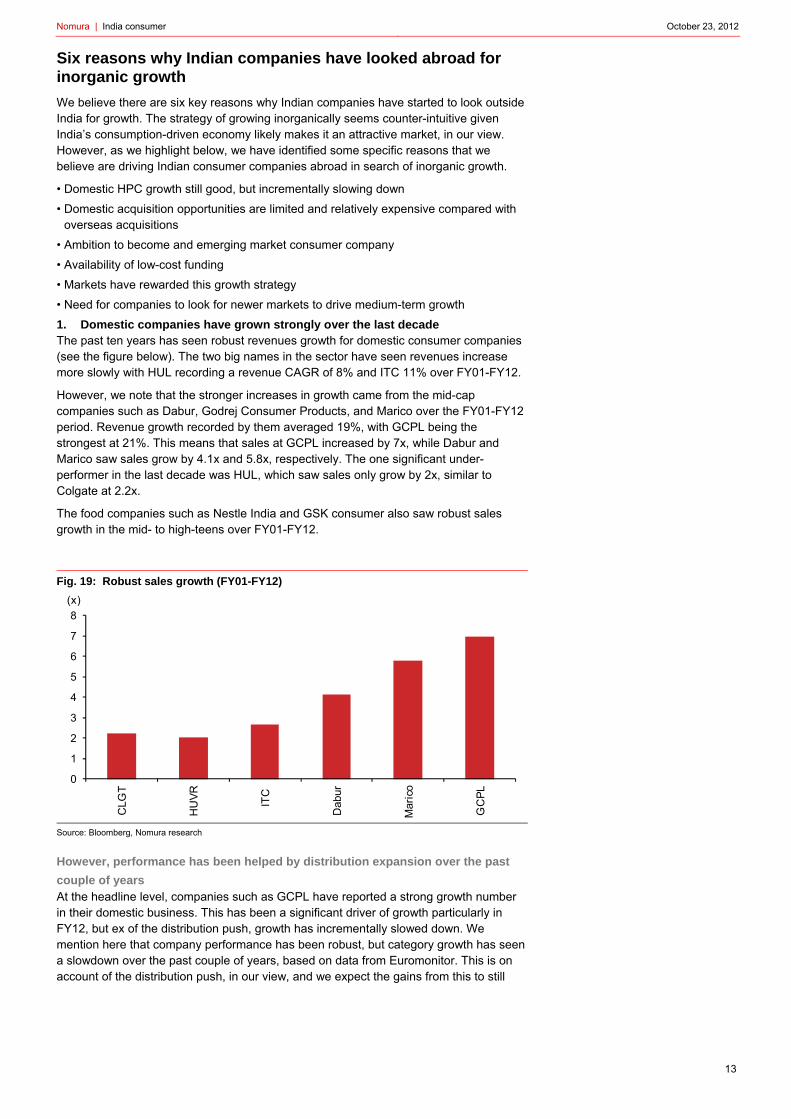

1. Domestic companies have grown strongly over the last decade The past ten years has seen robust revenues growth for domestic consumer companies (see the figure below). The two big names in the sector have seen revenues increase more slowly with HUL recording a revenue CAGR of 8% and ITC 11% over FY01-FY12.

However, we note that the stronger increases in growth came from the mid-cap companies such as Dabur, Godrej Consumer Products, and Marico over the FY01-FY12 period. Revenue growth recorded by them averaged 19%, with GCPL being the strongest at 21%. This means that sales at GCPL increased by 7x, while Dabur and Marico saw sales grow by 4.1x and 5.8x, respectively. The one significant under-performer in the last decade was HUL, which saw sales only grow by 2x, similar to Colgate at 2.2x.

The food companies such as Nestle India and GSK consumer also saw robust sales growth in the mid- to high-teens over FY01-FY12.

Fig. 19: Robust sales growth (FY01-FY12)

Source: Bloomberg, Nomura research

However, performance has been helped by distribution expansion over the past

couple of years At the headline level, companies such as GCPL have reported a strong growth number in their domestic business. This has been a significant driver of growth particularly in FY12, but ex of the distribution push, growth has incrementally slowed down. We mention here that company performance has been robust, but category growth has seen a slowdown over the past couple of years, based on data from Euromonitor. This is on account of the distribution push, in our view, and we expect the gains from this to still

0

1

2

3

4

5

6

7

8

CLG

T

HU

VR

ITC

Dab

ur

Mar

ico

GC

PL

(x)

Nomura | India consumer October 23, 2012

14

accrue for the next couple of years, but overall, given the high penetration level in many of these segments, we believe the medium-term growth trajectory will likely slow.

While we do not expect a significant slowdown in the performance of the domestic HPC companies in the next three years, over the longer term, sales growth performance will likely lag those of food companies where penetration levels in most of the categories are still fairly low. As we highlighted in our report ‘Young and Hungry’ dated 21 February 2011, longer term, we see food companies as much better placed to drive growth organically, which is significantly ahead of HPC companies.

Fig. 20: Domestic business of HPC companies slowing to below long-term average

Source: Company data, Nomura research

The category growth has seen a slowdown driven by certain structural drivers We believe the slowing category growth has been driven by certain key changes in the dynamics of the large HPC categories. We identify them as:

High penetration levels As we have highlighted before, one of the key issues facing the HPC companies is the high penetration levels reached in many of the categories such as toilet, soaps, detergents, hair oil etc. where penetration-led growth is largely behind us. Most consumers already use these products and hence it is incrementally difficult to deliver growth in these categories expect for the “premiumisation” drive. However, these categories are largely commodity plays and hence it is difficult to keep moving consumers to pay more for the same product. This has meant category growth is slowing, which we expect it to further slow over the next decade. In our view, this is the key reason why HUL is increasingly looking at personal products as a growth driver rather than soaps and detergents. Marico recognized this some time back, we believe, and is now looking to grow in other segments such as food, where penetration levels are much lower.

Fig. 21: Penetration-led growth seems to be over

Source: HUL, GCPL

0%

5%

10%

15%

20%

25%

30%

2006 2007 2008 2009 2010 2011 2012

GCPL Domestic Marico Domestic Dabur HUL

Category Urban Rural Urban Rural

Toothpaste 70% 32% 89% 45%

Washing Powder 95% 92%

Hair Wash 40% 16% 62% 46%

Talcum Powder 48% 25% 66% 37%

2002 2010

Nomura | India consumer October 23, 2012

15

High competitive intensity As these mature HPC categories have become increasingly commoditised and penetration levels have peaked, the most likely way for companies to grow within this is to drive market share gains. Thus, competitive intensity has increased significantly in these categories as companies look to maintain growth momentum. However as competitive intensity increases, the cost of driving incremental growth also increases substantially, which has meant profitability has taken a hit in these categories. We believe this high level of competitive intensity is likely to remain in the medium term and possibly even increase from current levels, if larger players try to gain share.

Fig. 22: HUL A&P spend has increased significantly over the medium term

Source: Company data, Nomura research

Profitability on a structural decline As a result of the highly competitive nature of the HPC categories in India and the increasing cost of driving growth, we expect profitability in key segments such as soaps and detergents, toothpaste, hair oils etc will likely decline further from current levels. We have already seen examples of how in many of these categories, profitability has come under pressure in the last few years. We believe an effective way to capture this decline is to see how margins in the soaps and detergents segment have moved within HUL’s portfolio. A decade back soaps and detergents used to be a highly profitable category with margins in the 20%-plus range; structural decline has taken that to low-double digits now, a result of severe competition, which has necessitated large A&P support from companies and thus had an adverse impact on margins.

Fig. 23: HUL soaps and detergents segment margins

Source: Company data, Nomura research

8%

9%

10%

11%

12%

13%

14%

15%

16%

Jun-05 Jun-06 Jun-07 Jun-08 Jun-09 Jun-10 Jun-11 Jun-12

0

5

10

15

20

25

30

35

Mar

-02

Aug

-02

Jan

-03

Jun

-03

No

v-03

Ap

r-04

Sep

-04

Feb

-05

Jul-

05

Dec

-05

May

-06

Oct

-06

Mar

-07

Aug

-07

Jan

-08

Jun

-08

No

v-08

Ap

r-09

Sep

-09

Feb

-10

Jul-

10

Dec

-10

May

-11

Oct

-11

Mar

-12

Aug

-12

Nomura | India consumer October 23, 2012

16

If we look at other companies, where the core domestic business or category is seeing a slowdown, we also see a similar downward trajectory in profitability. For example, coconut oil under the ‘Parachute’ brand continues to be a very important part of Marico’s portfolio. We believe the company’s margins are still significantly impacted by what happens in that category. We see the margin trend moving downwards after having seen a structural upswing in the early part of the decade. In our view, the recent rise is purely on account of a sharp decline in input prices, but over a period of time, we see this trending down as the cost of driving incremental growth in the category increases.

Fig. 24: Marico EBITDA margins

Source: Company data, Nomura research

2. Limited consolidation opportunity in domestic market One of the first questions that we believe bears is considering is why has there been limited consolidation in the domestic market? We believe that in any market when organic growth slows, companies will start to look at consolidating within the local market. We believe the reasons are twofold:

• First, companies understand the market already and it is easier to drive product and marketing strategies if they have knowledge of the consumers in the market

• Second, larger-scale means larger share of profits, more scope for driving efficiencies, which gets reflected in valuations

We see India as a distinct market, where consolidation among local players has not really played out in the last decade on a big scale. There are some specific reasons for this, in our view.

Domestic assets significantly expensive Consumer companies we have met in India over the last couple of years have consistently said their preference is to acquire companies in India. However, there are very few Indian consumer companies which are up for sale, as returns are attractive and reinvestment needs are relatively small. This means very few scalable consumer companies are up for sale in India.

With many of these companies operating in smaller niche segments and/or markets, we have found that they see little reason to sell to established brands. In the few cases where promoters in these businesses are willing to sell out, price demanded is very high. The most recent example of an acquisition in India being very expensive would be the Reckitt Benckiser deal to buy Paras Pharma in December 2010.

Paras Pharma, which had over-the-counter and personal care brands such as ‘Moov’, ‘Krack’, ‘D Cold’, ‘Set Wet’ among others, had sales of close to INR4bn for the year ended March 2010. The deal size was close to INR32.6bn or ~8.2x sales. Paras Pharma had EBITDA of INR1.08bn, which means the deal was done at close to 30x FY10 EBITDA. Paras operated at close to 25-27% EBITDA margins and, according to

8%

9%

10%

11%

12%

13%

14%

15%

16%

Jun

-05

Oct

-05

Feb

-06

Jun

-06

Oct

-06

Feb

-07

Jun

-07

Oct

-07

Feb

-08

Jun

-08

Oct

-08

Feb

-09

Jun

-09

Oct

-09

Feb

-10

Jun

-10

Oct

-10

Feb

-11

Jun

-11

Oct

-11

Feb

-12

Jun

-12

Nomura | India consumer October 23, 2012

17

management, Reckitt Benckiser hopes there is scope to take the margins higher over the medium term.

These valuations are significantly ahead of where domestic companies trade at in India (4-4.5x sales)

Valuations for domestic companies have increased multi-fold over the past ten years and are now at 28.6x FY14F P/E, on our estimate. In the context of high valuations for consumer companies in general, the price paid for Paras Pharma is an indication of how expensive deals are in India.

Emami, which was also said to be in the race to acquire Paras Pharma (source: “Emami loses Paras despite highest bid,” Business Standard, December 2010) said post the announcement of the deal with Reckitt Benckiser that its bid value was much higher at close to INR34bn or 8.5x sales. While there is little to suggest that such valuations can be justified from a shareholder returns perspective, the paucity of targets is what makes the limited numbers of deals that actually go through very expensive, in our view. Marico and Dabur, the two other domestic mid-cap companies, were also in the mix for acquiring Paras Pharma, but eventually opted out of the process (source: “Marico join fray for Paras Pharma,” Reuters, 9 September 2010)

Both companies seemed to have reservations about the valuations that were being asked. Dabur management is quoted in the media as saying they were willing to pay INR25bn for the company, which would still have worked out to 6.25x sales, still expensive even by existing valuations of well established mid cap names such as Dabur itself. Fig. 25: Acquisitions have been getting more expensive

Date Acquirer Target Transaction Size Deal Multiple

Feb-12 Marico Paras Pharma personal care brands

INR~ 7.5bn 5x Sales

Mar-11 Cargill India Sweekar (Marico brand) INR~ 2bn 1.2x Sales

Dec-10 Reckitt Benckiser Paras Pharmaceuticals INR32.6bn 8.2x Sales

Nov-08 Dabur Fem Care Pharma INR2.84bn 3x Sales

Oct-08 Emami Zandu INR8bn 4x Sales

Jan-05 Dabur Balsara INR1.43bn 0.7x Sales

Source: Company data, Nomura research

Marico’s acquisition of some Paras Pharma brands – a case in point Marico acquired the personal care brands of the erstwhile Paras Pharma at the end of FY12, from Reckitt Benckiser for INR7.5bn. The acquisition closed in 1QFY13, so it should have an impact on financials for nine months in the current year. The brands will be transferred from RB to a separate company in which Marico will acquire a 100% stake.

Neutral to negative in the short term, positive long term Overall, while it is a credible move by the company to broaden their product portfolio, in the short term we do not see this as an accretive deal. The multiple paid for the brands was a high 5x sales, which means that the return ratios will only get reflected in the long term. We believe in the short term this deal is neutral for the company, but over the longer term gives it an entry into fast-growing categories such as hair gels and deodorants, which Marico’s management can grow much faster than the erstwhile Paras Pharma group, in our view. This deal again reinforces our view that multiples for domestic acquisition deals will continue to be high.

Family ownership structure prohibits large-scale consolidation One of the other key reasons consolidation among local companies has not played out is the ownership structure of the local companies. Among the listed companies, Dabur, Marico, GCPL, Jyothy Laboratories and Emami all have controlling family ownership, with more than 50% held by the families.

Nomura | India consumer October 23, 2012

18

Most of these companies have a reasonably long history of operation, and family owners continue to see an opportunity to grow the business over the medium term and hence are averse to selling out.

The limited acquisitions that have occurred, such as Emami buying out Zandu, have often happened in somewhat acrimonious circumstances. For example, Emami had to undergo a lengthy court battle to get control of Zandu.

RoE is quite high in the FMCG business in India, and owners of some of the other unlisted companies have been reluctant to sell except when faced with the prospect of exorbitant valuations, as was the case with Paras Pharma.

Another example is the bottled water business in India, where Bisleri has a market leadership position with over 50% of the INR12bn-plus market, despite the entry of multinationals such as Coca Cola and PepsiCo. There were reports in the late 1990s that both these companies were trying to buy out Bisleri, but the family resisted the sale and have gone on to make Bisleri a market-defining brand with a leadership position in the fast-growing bottled water segment. Similarly, the Parle brand of biscuits (privately owned) has continued to define a category of biscuits (Glucose) but has not been sold off to suitors.

A family-owned structure also prevents amalgamation among the players, as there will always be issues with regard to valuation (it is very unlikely that a family will want to give up its full control over a business). We believe these reasons will continue to be relevant even in the medium term, and hence consolidation among the local players looks unlikely.

We believe it is also worth pointing out that multinational companies have a majority shareholding in their listed subsidiaries, so any move on consolidation could well be a decision that needs to be made at the parent-company level. This may also be one of the reasons why decision making on inorganic growth opportunities is a long-drawn process, and hence the smaller number of M&A deals featuring multinationals acquiring local companies in bolt-on deals. In addition, there is the issue of board representation, which makes any deal very complicated.

Fig. 26: Ownership Structure of domestic companies

Company Promoters Ownership (%)

Godrej Consumer Godrej Family 64%

Marico Harsh Mariwala 60%

Dabur Burman Family 69%

Jyothy Labs Ramachandran Family 65%

Emami Agarwal and Goenka Family 73%

Parle Chauhan Family 100%

Britannia Wadia Family 51%

Hindustan Unilever Unilever 52%

Nestle India Nestle SA 63%

Colgate Palmolive Colgate 51%

Source: BSE, Nomura research

Cost of domestic acquisitions has increased with time… With some of the larger domestic acquisitions taking place at sales multiples that could be considered quite expensive, it is easy to extrapolate that all domestic acquisitions have been expensive. However, there have been some deals which have happened at reasonable valuations, but these brands were not growing significantly before being acquired. One example which comes to mind is the acquisition of Fem Care by Dabur in

Nomura | India consumer October 23, 2012

19

2005. This acquisition was done at close to 3x sales, much lower than the Paras Pharma deal multiple.

However, this was done at a time when valuations for consumer companies were not as high as they are today. Deals if done at 3x sales today would be for much less profitable businesses; Fem Care at the time of its acquisition had gross margins in excess of 60%. We estimate the deal, if done today, would have been at close to 6x sales, using the most recent transactions as a guide. Another thing to keep in mind is that Paras Pharma only had a few OTC brands, but some of the domestic FMCG companies have a larger portfolio of brands and hence its valuation multiple would likely be more expensive.

…which means domestic companies have started to look internationally For the reasons we have highlighted above, domestic companies have started to look beyond India in search of acquisition opportunities. This is unsurprising, as the only opportunities that are available for which companies can justify RoCE are all outside the country.

Acquisitions done outside India have been at much cheaper valuations. Additionally, acquisitions done outside India give these companies some amount of geographical diversity in terms of their footprint, which may prove useful over the next few years. Although Indian consumer companies have been acquiring companies outside India for a while now, until recently these acquisitions have been relatively small in size and hence contribution from them has not been significant.

Among the domestic companies, GCPL, Marico and Dabur have been the most active in terms of pursuing inorganic opportunities. We have looked at all the acquisitions done by these companies over the past decade or so. For the purpose of this analysis, we have included all acquisitions, including domestic ones. However, domestic acquisitions have not been a big contributor to overall inorganic acquisitions across these companies, as there have been very few of them over this time period.

What is important to note is that all these companies have expressed a desire to grow inorganically going forward as well and are on the lookout for new acquisitions across the globe. GCPL has given guidance for a near- to medium-term revenue growth target of 25-30%, of which 20% will come organically and the remaining will be derived inorganically. Dabur management has said that over the next five years, close to 50% of the company’s revenues could come from outside India. Marico has always been an active acquirer, and have stated its desire to increase contribution from the international business to closer to 30% in the medium term.

Wider availability of assets – More assets up for sale in international markets Godrej Consumer has a stated strategy of acquiring companies in line with its 3x3 strategy, i.e., in three continents of Asia, Africa and Latin America in home care, hair care and household insecticides. This gives the company a wider scope to look at potential acquisitions. One of the reasons management said it was looking outside India for acquisitions was the wider availability of assets. Acquisitions outside India are more readily available and at valuations which makes them more attractive.

This sentiment was echoed by Dabur as well as Marico, who have both looked outside India for acquisitions over the past few years. While there will always be an element of risk in overseas acquisitions, the valuations at which these companies are available and the bolt-on nature of these deals continues to attract interest.

Most of the recent acquisitions done by Indian companies have been of niche companies which were privately held by entrepreneurs across markets in Asian, Africa and Latin America. These acquisitions have typically been completed at 1.5-2.0x sales, we estimate – much lower than what the local consumer companies in India trade at (typically 4-5x sales).

One of the key questions investors have been asking is why these investors sell for valuations which are low. We would point out here that the valuation of these businesses takes into account the potential difficulty of growing scale quickly, which can be difficult for those lacking the bargaining power to raise money for organic growth. However, with the resources in the hands of much larger Indian companies that then have the ability to

Nomura | India consumer October 23, 2012

20

leverage these acquisitions in other markets where they already have a presence, the ability to grow scale is much easier. Remember, as we highlight in this report, valuations grow with scale, and this is equally true for Indian companies. At the start of this past decade, when these companies had much smaller scale, valuations were closer to 2x sales; this has now grown to ~6x sales, on our readings.

What are the synergies in these acquisitions? One of the key questions to look at while analyzing the overseas acquisitions is the amount of synergies that are visible over the longer term. We believe synergies will mostly be in the form of revenue synergies, with cost synergies probably more back ended.

GCPL has given some guidance in terms of potential synergies recently, after they have had a chance to look at the acquisitions they did last year closely. Company management have outlined a strategy which they estimate will generate INR15-20bn of revenue synergies from acquisitions made last year over a five-year period from FY11-FY15. During the same period the company expects costs synergies of INR2-2.5bn as investments in more robust supply chain systems and other measures to cut overhead costs flow through to the bottom line.

These synergies will, in our view, be more back ended, with the majority of being realized after the next three years. In the first three years starting FY12, we see revenue synergies as adding close to 3% to sales. This is under the assumption that 10% or so of this targeted INR15bn of revenue synergies materialise in year 1 after the acquisition.

We believe there could be a domestic market for some of the products which companies such as Dabur, GCPL and Marico have acquired in the last few years. For example, GCPL has spoken about getting products from the hair care range in Latin America to India, as well as some of the products from their portfolio in Indonesia to India. Marico has demonstrated certain products such as skin and hair care products can be brought into India from other countries such as Malaysia. Derma RX products could be bought into India at some stage. For Dabur, among their recent acquisitions such as Hobi and Namaste group, only real opportunity is to bring products from Hobi to India, while Namaste’s Hair Extensions is a niche product suited to consumers in a specific geography. Thus, driving revenue synergies could be company specific.

Management bandwidth – critical factor for success of M&A One of the most critical factors in terms of the potential success of an M&A transaction is the availability of management bandwidth. While management focus on key areas of the business is always a good indication of how well the business performs, this is especially true in case of an acquisition, where the number of unknown factors is much higher.

Companies such as Dabur, Marico and GCPL have been very successful over the past decade in terms of growing their businesses in India, but they have considerable less experience working in outside markets.

However, we have seen in many of the recent acquisitions that post closing of the transaction, local management teams have been a key part of new management team. This helps to smooth out transition issues and helps to integrate the acquired businesses within the new company.

We cite the example of two companies which have had different lines of thinking on this subject. GCPL, which has closed several acquisitions across three geographies, has said that the issue of management bandwidth is overplayed. If local management has some key members as part of the new management structure, then GCPL believes the integration of these acquisitions can progress smoothly. Dabur, on the other hand, seems to think it is better to go ahead with smaller acquisitions and at a slower pace, so that current management can give adequate time to integrate the acquisitions. This is one of the reasons why Dabur has proceeded more slowly on acquisitions than GPCL.

While the approach to integrating new acquisitions will continue to be company specific, a decentralised system can potentially mean individual geographies and businesses are run as profit centres. This could give a company the best chance to integrate the acquisitions into the parent successfully.

Nomura | India consumer October 23, 2012

21

3. Ambition to become an emerging market consumer company Godrej Consumer has been at the forefront of the acquisition spree over the past couple of years. The company recognized the issues facing some of the categories in India where it has a large presence, as well as the need to look at other avenues of long-term growth. There are a few roads the company could have taken:

• First, the company could have grown within the HPC space in India by branching out into newer categories, including surface cleaners, talcum powder and toilet fresheners. Some of these categories are small but growing quickly, and others are well established. The issue with this approach is that company would have needed to spend a significant amount of money to grow the newer categories, since there are no established players in the segment and bigger companies such as HUL are trying to establish their presence. This would make competition an expensive proposition.

• The second approach was to enter new categories in the food space, where company has had a limited presence, for example, in the form of a JV with Hershey which is no longer operational. The company also has a JV with Tyson Foods in the packaged meat space, but has no presence outside that in emerging packaged foods such as oats and ready to eat. Packaged Food as a category is underpenetrated and will be a driver of growth for the FMCG industry in the long term, in our opinion. We highlighted the opportunity in the food sector in our 21 February 2011 report, Young and hungry. The company has looked into this opportunity, as can be seen from the JVs into which it has entered, but has not focussed on growing them. We would also highlight the investments would be needed to set up a supply chain, which is very different for food and HPC products.

• The third approach was to grow inorganically. Here, there were two options. The first would be to look at options within India. However, because of the limited sellers in the marketplace, the cost of these acquisitions is very high. We have highlighted some recent acquisitions in India which have been done at very high multiples such as the Paras Pharma deal (8.5x sales). The second option within the organic growth route was to look outside India. This is where Godrej had the best options. The company’s ambition was to become an emerging market consumer company, and acquisitions in other emerging markets were what that was lacking in its portfolio.

As Godrej began to look at its options outside India, management found that not only were there several more options to look at – including markets in South East Asia, Latin America and Africa – but also that valuations outside India were much more supportive.. Additionally because the company was underleveraged at the time (2009), there was significant room for the company to leverage its balance sheet to complete these acquisitions.

If emerging markets are the theme why not look at China? One question which comes to mind is that if Godrej is looking to become an emerging markets consumer company, why has it not made any acquisitions in China, the biggest emerging market in terms of total addressable market.

The company gives two key reasons which we list below.

Scale is vital Scale in the consumer business in China is vital as profitability is dependent on a company’s ability to scale up businesses. Since most mid-cap consumer companies are looking for smaller deals, it is difficult for them to look at large scaled-up businesses. According to Godrej, this is a key entry barrier for companies looking to enter China either organically or inorganically.

Corporate governance issues According to Godrej, Indian companies have not been very satisfied with China’s corporate governance standards, which is a critical issue for them. Language is also another issue, and Indian companies would need a local partner in China.

Nomura | India consumer October 23, 2012

22

Not new; others have taken the path to become an emerging market consumer company Some of the largest consumer companies in the world such as Unilever, Danone, and P&G have in recent years acquired companies in emerging markets of Russia, Brazil, and South East Asia etc, which we attribute to two key reasons.

• To fill a portfolio gap: We understand that a number of small-sized acquisitions made in emerging markets by global consumer companies were to fill their portfolio gaps in the local markets. For example, Unilever in 2008 acquired a Russian ice-cream maker Inmakro, which had a strong brand and product portfolio and a clear market leading position in Central and Eastern Russia, and had a fast-growing business across all regions of the Russian Federation and Kazakhstan. The acquisition further strengthened Unilever’s ice-cream business position.

• Expand business into other geographies: This is more relevant from an Indian company’s perspective. Dabur, Marico, and GPCL have all looked to expand outside India, expanding their footprints in geographies where they have limited or no presence, and acquiring companies in these markets. For example, post the acquisition of Hobi and Namaste, Dabur now has presence in Turkey and the US. Similarly, GPCL now has presence in Indonesia, Argentina, South Africa, etc., following its acquisitions.

• We believe companies in India such as Marico, Dabur, GCPL and Emami will continue to look for opportunities outside India because they aim to become an emerging-market consumer company. The key reason why these companies will look to take the inorganic growth route is, in our view, the cost involved to take their existing products to those places. As well, if taking the organic growth route, products that have no existing customer base in new geographies will face difficulties in trying to capture audiences. For example, if Dabur were to take its chwanyprash into Indonesia via the organic route, it might be difficult to get consumers into the category. However, as with its acquisitions of Hobi and Namaste, which have already established a customer base, it helps Dabur to establish presence in new markets at lower costs vs via the organic route. We believe small-sized companies and large MNC consumer companies such as Unilever, P&G and Danone will look at the inorganic growth route to further their growth.

As we look back at the acquisitions done by P&G, Unilever and Danone over the last few years, the theme of increasing exposure to emerging markets has clearly played out. This list below identifies the companies and countries in which large MNC players have made bolt on acquisitions. Fig. 27: Emerging markets acquisitions by global MNC consumer companies

Acquirer Target Date Category Country

Unilever EVGA Sep-10 Ice Creams Greece

Unilever Baltimore Holding ZAO Jul-09 Ketchup Russia

Unilever Napoca Feb-09 Ice Cream Romania

Unilever Inmarko Apr-08 Ice Cream Russia

Unilever Kalina Oct-11 Skin Care Russia

Unilever Darko Aug-11 Ice Cream Bulgaria

Danone Unimilk Jun-10 Milk Russia

PepsiCo Wimm-Bill-Dann Jul-11 Dairy and Fruit Juice Russia

Nestle * Progress Oct-11 Baby Food and Juice Russia

Nestle Wyeth's baby formula business April-12 Baby Food Russia

Source: Company

Note: * As per Reuters, Nestle linked with these acquisitions. October 18 2011

4. Availability of Funding Over the last few years, Indian consumer companies have been acquiring overseas companies using a mix of internal accruals as well as foreign-currency denominated funding. For these companies, their cost of debt has been in the range of LIBOR plus

Nomura | India consumer October 23, 2012

23

150-200bps. This cost of debt is a significant deciding factor in acquisitions, on whether it can be EPS accretive from the first year of operation.

We believe Indian consumer companies have strong balance sheets, a result of their strong organic growth over the last decade and minimal re-investment needs, for acquisitions. They have been generating FCF on a consistent basis, and have largely under levered balance sheets, in our view. We believe this should give them access to low-cost debt funding. We believe the low funding cost of GCPL’s past acquisitions in three continents is a key reason that the acquisitions have been EPS accretive.

We estimate that GCPL pays ~3% USD coupon interest for its USD350mn of debt on the balance sheet. Interest payout for FY12 was INR658mn on a consolidated level. Availability of similar funding for all consumer companies that have looked at inorganic growth in the last couple of years implies that most of these acquisitions would have turned largely EPS accretive in Year 1. A decade ago, Indian companies did not have the scale or the balance sheet size to fund acquisitions in the range of USD50-100mn. This has changed dramatically in the last 2-3 years and we believe companies such as GCPL, Dabur and Marico have the means to leverage the size of their balance sheets for acquisitions in the international markets.

Despite the acquisitions in the last few years, mid-cap consumer companies have maintained net debt/EBITDA in the range of less than 1.5:1. We analyse these companies’ “war chest” prior to 2005 and find that most of them have significantly cut back the amount.

Nomura | India consumer October 23, 2012

24

Fig. 28: “War chest” significantly lower

GCPL (INRmn) 2005 2012

EBITDA 1,027 8,777

Debt 61 15,640

Cash 90 6,399

Net Debt (28) 9,242

Net Debt/EBITDA 0.0x 1.1x

Debt/Equity 0.1x 0.6x

Potential Debt (INRmn) 1,081 9,242

Potential Debt (USDmn) 21 178

Dabur (INRmn) 2005 2012

EBITDA 2,133 8,851

Debt 1,509 10,743

Cash 147 4,484

Net Debt 1,361 6,259

Net Debt/EBITDA 0.6x 0.7x

Debt/Equity 0.4x 0.6x

Potential Debt (INRmn) 1,508 6,259

Potential Debt (USDmn) 29 120

Marico (INRmn) 2005 2012

EBITDA 883 4,844

Debt 657 7,623

Cash 338 1,588

Net Debt 319 6,034

Net Debt/EBITDA 0.4x 1.2x

Debt/Equity 0.3x 0.7x

Potential Debt (INRmn) 1,100 6,034

Potential Debt (USDmn) 21 116

Source: Company, Nomura research

Over the past 5-7 years, the Indian consumer companies have grown scale and ability to fund acquisitions. For example, if based on its FY12 net debt/EBITDA level, GCPL would have raised potential debt of USD21mn compared with its current debt size of close to USD178mln, on our estimates. Likewise, at 1.2x net debt/EBITDA, Marico would be able to raise USD116mn vs USD21mn in 2005. Using the same assumption, we estimate Dabur would be able to raise potential “war chest” of USD120mn vs. USD29mn in 2005.

However, as we have seen in the last few years, mid-cap consumer companies have been on an acquisition spree in the last few years, helped by their strong and robust balance sheets and FCF generation potential. GCPL spent close to USD671mn (including full payment for Darling Group), Marico spent close to USD76mn and Dabur spent USD185mn on acquiring companies, on our estimates.

As shown in the table below, the amount of spending by Indian consumer companies on acquisitions have surpassed USD900mn in the past few years. This has been facilitated by their improved scale that have had enabled them to acquire companies of significant size.

Nomura | India consumer October 23, 2012

25

Fig. 29: Recent acquisitions paid for largely by overseas debt

Godrej Consumer Products Est. Deal Size (USDmn)

Tura 50

Megasari 120

Darling 222

Issue 33

Argencos 12

51% stake in GSLL 234

Total 671

Marico Est. Deal Size (USDmn)

ICP Vietnam 50

Derma RX 17

Code 10 4

Ingwe 5

Total 76

Dabur Est. Deal Size (USDmn)

Hobi Kozmetik 45

Namaste Labs 140

Total 185

Source: Company, Nomura research

Equity raising has been limited in the past, but recent deals suggest otherwise While debt funding has been the preferred method of funding acquisitions for the Indian consumer companies, GCPL has raised equity through the Qualified Institutional Placement route in the last few years to fund parts of its acquisitions. In June 2010, GCPL raised USD115mn via QIP, out of the total USD470mn which was raised by debt and equity. GCPL has been the only company among over coverage to have raised equity to pay for these acquisitions, as the size of acquisitions conducted by Marico and Dabur was relatively small and could be funded by debt and internal accruals. In our opinion, as these companies pay lower acquisitions multiples for overseas businesses, usually at less than half of those needed in India, raising equity at the expense of expanded market cap would usually benefit the companies.

Nevertheless, things have changed over the pasts few months with Marico and GCPL raising equity to finance their deals for the Paras brands and Darling Group, respectively. We believe such a trend is likely to become more visible, as companies are likely to be less averse to diluting equity to grow inorganically. In 2012, Marico raised INR5bn via a 4.8% equity sale. Meanwhile, GCPL allotted 16.7mn shares to Temasek to raise INR6.85bn at INR410/- per share to fund its acquisition of Darling Group in January 2012.

How does the Rupee impact the cost of acquisitions We believe one of the most relevant questions is how has the acquisition dynamic changed given the rupee’s increased volatility in the past 12 months. In our view, one of the advantages of using foreign currency debt to acquire companies in the past was the low funding cost.

However, given the recent sharp volatility seen in the rupee, funding now gets more expensive compared with a year ago. Indeed, the rupee has depreciated by 20%-plus since May 2010, suggesting that acquisitions are ~20% more expensive than a year ago, and consequently raises the question of higher cost of debt, etc. We believe in the short term, this is likely to have an impact with companies going slow on overseas acquisitions. If the rupee were to recover to its long-term average of 45 per US dollar, we believe this issue could be resolved.

Nomura | India consumer October 23, 2012

26

As of now, we believe risk management is very important for companies looking to acquire overseas assets in terms of interest payments and principal repayments. GCPL has repayment obligation of USD15mn per quarter, according to management, which we believe will have a significant cash flow impact. Still, we highlight that when companies acquire assets outside India, their revenue base will also expand to include more foreign currencies, which could provide them with a natural hedge against volatility in the INR/USD rate.

Fig. 30: INR/USD rate volatile lately

Source: Bloomberg, Nomura research