Lecture 9 Relative Valuation - GU

22

-

Upload

khangminh22 -

Category

Documents

-

view

4 -

download

0

Transcript of Lecture 9 Relative Valuation - GU

Relative Valuation

Lecture 9 Relative Valuation

Diem Nguyen

Spring 2020

1 / 22

Relative Valuation

Multiple Basics

Outline

1 Multiple Basics

2 Multiples and Firm Fundamentals

2 / 22

Relative Valuation

Multiple Basics

Relative Valuation

Relative valuation → the value of an asset is derived from themarket pricing of comparable assets.

Price standardized (e.g., by earnings, sales, book value) →multiples

Applying relative valuation:1 Method of comparables:

→ value �rms based on comparable �rms' multiplesSimilar �rms should trade at similar price.Value = Multiple of comparables × Firm-speci�c variable.

2 Screening on multiples:

→ buy/sell recommendations based on relative multiplesFirms with relatively extreme multiples may be mispriced

3 / 22

Relative Valuation

Multiple Basics

The Steps

Method of comparables:1 Identify comparable �rms

Similar risk, growth potential and cash �ows

2 Calculate relevant multiples for the comparable �rms3 Apply these multiples to the corresponding measures for the

target �rm

Screening on multiples:1 Identify a multiple on which to screen stocks2 Rank stocks on that multiple3 Buy stocks with the lowest multiples and short stocks with the

highest ones

4 / 22

Relative Valuation

Multiple Basics

Popularity

Most equity valuations on Wall Street are relative valuations

Almost 85% of equity research reports are based upon amultiple and comparables.More than 50% of all acquisition valuations are based uponmultiples.

Terminal value in discounted cash�ow valuations is quite oftenestimated using a multiple.

5 / 22

Relative Valuation

Multiple Basics

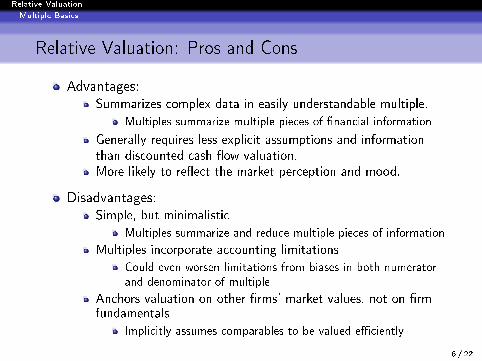

Relative Valuation: Pros and Cons

Advantages:Summarizes complex data in easily understandable multiple.

Multiples summarize multiple pieces of �nancial information

Generally requires less explicit assumptions and informationthan discounted cash �ow valuation.More likely to re�ect the market perception and mood.

Disadvantages:Simple, but minimalistic

Multiples summarize and reduce multiple pieces of information

Multiples incorporate accounting limitations

Could even worsen limitations from biases in both numeratorand denominator of multiple

Anchors valuation on other �rms' market values, not on �rmfundamentals

Implicitly assumes comparables to be valued e�ciently

6 / 22

Relative Valuation

Multiple Basics

Standardized Values and Multiples

7 / 22

Relative Valuation

Multiple Basics

Guidelines

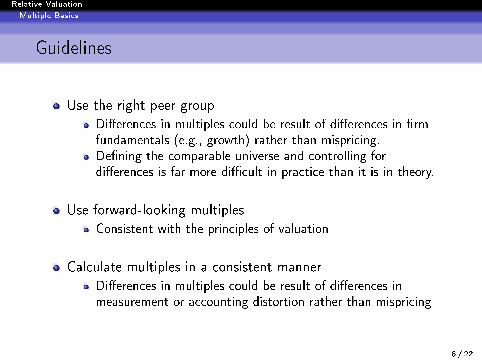

Use the right peer group

Di�erences in multiples could be result of di�erences in �rmfundamentals (e.g., growth) rather than mispricing.De�ning the comparable universe and controlling fordi�erences is far more di�cult in practice than it is in theory.

Use forward-looking multiples

Consistent with the principles of valuation

Calculate multiples in a consistent manner

Di�erences in multiples could be result of di�erences inmeasurement or accounting distortion rather than mispricing

8 / 22

Relative Valuation

Multiple Basics

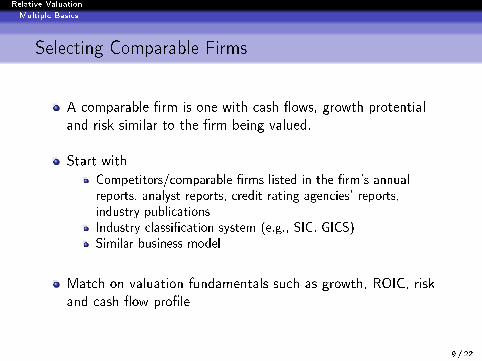

Selecting Comparable Firms

A comparable �rm is one with cash �ows, growth protentialand risk similar to the �rm being valued.

Start with

Competitors/comparable �rms listed in the �rm's annualreports, analyst reports, credit rating agencies' reports,industry publicationsIndustry classi�cation system (e.g., SIC, GICS)Similar business model

Match on valuation fundamentals such as growth, ROIC, riskand cash �ow pro�le

9 / 22

Relative Valuation

Multiple Basics

Selecting Comparable Firms

10 / 22

Relative Valuation

Multiple Basics

Forward Multiples

Forward-looking multiples are consistent with the principles ofvaluation

A company's value equals the present value of future cash�ow, not sunk costs.

Forward-looking earnings are typically normalized → theybetter re�ect long-term cash �ows by avoiding one-time pastcharges.

To build a forward-looking multiple:

Choose a forecast year for earnings that best represents thelong-term prospects of the business.Firms in periods of stable growth and pro�tability → nextyear's estimate.Firms generating extraordinary earnings (either too high or toolow) or for companies whose performance is expected tochange → use projections further out.

11 / 22

Relative Valuation

Multiple Basics

Forward Multiples

Empirical evidence → forward-looking multiples are betterpredictors of value than historical multiples.

Liu et al. (2002), Equity valuation using multiples, Journal ofAccounting Research

Historical earnings-to-price (E/P) ratios had much higherstandard deviation compared to one-year forward E/P ratios(6.0 percent versus 3.7 percent).

Kim & Ritter (1999), Valuing IPOs, Journal of FinancialEconomics

Moving from multiples based on historical earnings tomultiples based on one- and two-year forecasts, the averagepricing error fell from 55.0 percent to 43.7 percent to 28.5percent, respectively, and the percentage of �rms valuedwithin 15 percent of their actual trading multiple increasedfrom 15.4 percent to 18.9 percent to 36.4 percent.

12 / 22

Relative Valuation

Multiple Basics

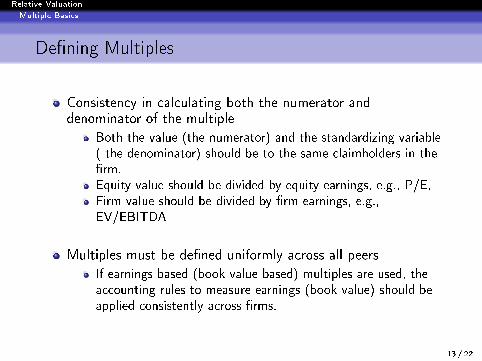

De�ning Multiples

Consistency in calculating both the numerator anddenominator of the multiple

Both the value (the numerator) and the standardizing variable( the denominator) should be to the same claimholders in the�rm.Equity value should be divided by equity earnings, e.g., P/E,Firm value should be divided by �rm earnings, e.g.,EV/EBITDA

Multiples must be de�ned uniformly across all peers

If earnings based (book-value based) multiples are used, theaccounting rules to measure earnings (book value) should beapplied consistently across �rms.

13 / 22

Relative Valuation

Multiples and Firm Fundamentals

Outline

1 Multiple Basics

2 Multiples and Firm Fundamentals

14 / 22

Relative Valuation

Multiples and Firm Fundamentals

Multiples and Firm Fundamentals

Multiples are determined by �rm fundamentals:

variables that drive discounted cash �ow valuation: growth,risk and cash �ow patterns.

How do changes in these fundamentals change the multiple?

The relationship between a fundamental (like growth) and amultiple (such as P/E) is usually not linear.It is not possible to properly compare �rms on a multiple, if wedo not know how fundamentals and the multiple move.

15 / 22

Relative Valuation

Multiples and Firm Fundamentals

Price-Earnings Ratio

P/E = Market price per share/Earnings per share

Deriving fundamentals:

P0 =Div1rE − g

(DDM)

→ P0

EPS1=Div1/EPS1rE − g

=Payout ratio

rE − g(1)

Determinants of P/E:

Growth → P/E increases with growth rateRisk → P/E decreases with riskPayout ratio → P/E increases with payout ratio

16 / 22

Relative Valuation

Multiples and Firm Fundamentals

Price-Earnings Ratio

P0

EPS1=

Payout ratio

rE − g

g = (1− Payout ratio)ROE → Payout ratio = 1− g/ROE

→ P0

EPS1=

1− g/ROE

rE − g(2)

P/E increases as ROE increases

17 / 22

Relative Valuation

Multiples and Firm Fundamentals

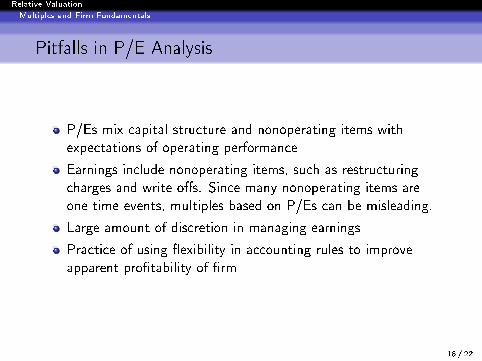

Pitfalls in P/E Analysis

P/Es mix capital structure and nonoperating items withexpectations of operating performance

Earnings include nonoperating items, such as restructuringcharges and write-o�s. Since many nonoperating items areone-time events, multiples based on P/Es can be misleading.

Large amount of discretion in managing earnings

Practice of using �exibility in accounting rules to improveapparent pro�tability of �rm

18 / 22

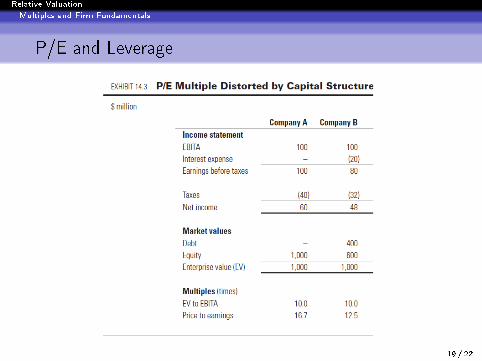

Relative Valuation

Multiples and Firm Fundamentals

P/E and Leverage

19 / 22

Relative Valuation

Multiples and Firm Fundamentals

Price-to-Book

P/B = Market value of equity/Book value of equity

Determinants: ROE, growth rate, rE , payout ratio

P0 =EPS1 × Payout ratio

rE − g

=ROE × BV0 × Payout ratio

rE − g

→ P0

BV0=ROE × Payout ratio

rE − g

=ROE − g

rE − g

20 / 22

Relative Valuation

Multiples and Firm Fundamentals

Enterprise Value to EBITDA

EV/EBITDA = (Market value of equity + Market value ofdebt - Cash)/EBITDA

Deriving fundamentals:

V0 =FCFF1

WACC − g

FCFF =EBIT (1− t)− (CAPEX − DA + ∆Working capital)

=(EBITDA− DA)(1− t)− (CAPEX − DA + ∆Working capital)

=EBITDA(1− t)− DA(1− t)− Reinvestment

→ V0

EBITDA=

(1− t)− DAEBITDA(1− t)− Reinvestment

EBITDA

WACC − g(3)

21 / 22

Relative Valuation

Multiples and Firm Fundamentals

Enterprise Value to EBITDA

V0

EBITDA=

(1− t)− DAEBITDA(1− t)− Reinvestment

EBITDA

WACC − g

Determinants of EV/EBITDA:

Tax rate (t)Depreciation and amortizationReinvestment needWACCExpected growth

22 / 22