International Banking Centers, Geography, and Foreign Banks

32

International Banking Centers, Geography, and Foreign Banks BY ADRIAN E. TSCHOEGL This essay reviews much of the recent literature on international financial centers from both economics and geography and critiques the thesis of an ‘‘end of geography.’’ Banks have dispersed from traditional centers those activities involving frequent routine, standardized, and small-scale transactions. At the same time, the banks have kept in the international financial centers those activities involving innovative, customized, and large-scale transactions. In all of this, place still matters, but different places matter for different activities. Finally, foreign banks make their greatest contribution to their host center when the presence of foreign banks enhances domestic competition and innovation. The innovation that the rivalry between institutions induces makes the environment in international finan- cial centers a turbulent one. I. INTRODUCTION Ž . O’Brien 1992 has argued that deregulation and modern communications have brought about ‘the end of geography’ in banking and finance. O’Brien accepts that ‘everybody has to be somewhere,’ but argues that banks and other financial institutions no longer have to be in financial centers. 1 In this essay I review much of the recent literature on international financial centers with two objectives. My first objective is to critique the ‘‘end of geography’’ thesis. My second objective is to provide an integrative survey that draws the attention of economists to the work of geographers. The ‘‘end of geography’’ thesis has two flaws. The first flaw is the assumption that the homogenization of regulation and the improvement of communica- tions necessarily imply increased decentralization. I argue below that the relevant unit of analysis is not the bank or other financial institution but rather the activity. Improved communications permit decentralization of some activi- ties, but facilitate the centralization of others. Many routine activities appear to be decentralizing, but for activities that require innovation centralization Ž . appears to be persisting and perhaps even intensifying. Walter 1998 refers to these as centrifugal and centripetal forces and argues that the location of 1 O’Brien credits the trenchant observation that everybody has to be somewhere to the comedian Spike Milligan. The remark was Milligan’s response when an acquaintance ex- pressed surprise at meeting Milligan at some untoward place. Financial Markets, Institutions & Instruments, V. 9, No. 1, January 2000. Q 2000 New York University Salomon Center. Published by Blackwell Publishers, 350 Main St., Malden, MA 02148, USA, and 108 Cowley Road, Oxford, OX4 1JF, UK.

Transcript of International Banking Centers, Geography, and Foreign Banks

International Banking Centers, Geography, andForeign Banks

BY ADRIAN E. TSCHOEGL

This essay reviews much of the recent literature on international financialcenters from both economics and geography and critiques the thesis of an ‘‘end ofgeography.’’ Banks have dispersed from traditional centers those activities involvingfrequent routine, standardized, and small-scale transactions. At the same time, thebanks have kept in the international financial centers those activities involvinginnovative, customized, and large-scale transactions. In all of this, place stillmatters, but different places matter for different activities. Finally, foreign banksmake their greatest contribution to their host center when the presence of foreignbanks enhances domestic competition and innovation. The innovation that therivalry between institutions induces makes the environment in international finan-cial centers a turbulent one.

I. INTRODUCTION

Ž .O’Brien 1992 has argued that deregulation and modern communicationshave brought about ‘the end of geography’ in banking and finance. O’Brienaccepts that ‘everybody has to be somewhere,’ but argues that banks and otherfinancial institutions no longer have to be in financial centers.1

In this essay I review much of the recent literature on international financialcenters with two objectives. My first objective is to critique the ‘‘end ofgeography’’ thesis. My second objective is to provide an integrative survey thatdraws the attention of economists to the work of geographers.

The ‘‘end of geography’’ thesis has two flaws. The first flaw is the assumptionthat the homogenization of regulation and the improvement of communica-tions necessarily imply increased decentralization. I argue below that therelevant unit of analysis is not the bank or other financial institution but ratherthe activity. Improved communications permit decentralization of some activi-ties, but facilitate the centralization of others. Many routine activities appearto be decentralizing, but for activities that require innovation centralization

Ž .appears to be persisting and perhaps even intensifying. Walter 1998 refers tothese as centrifugal and centripetal forces and argues that the location of

1 O’Brien credits the trenchant observation that everybody has to be somewhere to thecomedian Spike Milligan. The remark was Milligan’s response when an acquaintance ex-pressed surprise at meeting Milligan at some untoward place.

Financial Markets, Institutions & Instruments, V. 9, No. 1, January 2000. Q 2000 New YorkUniversity Salomon Center. Published by Blackwell Publishers, 350 Main St., Malden, MA 02148,USA, and 108 Cowley Road, Oxford, OX4 1JF, UK.

Adrian E. Tschoegl2

activities in particular places is the outcome of their interplay, which may bedifferent for each activity and which changes over time.

Ž .The first flaw ties directly into the second. As Martin 1994; p. 263 argues,‘ . . . while the speed of information communication has annihilated space . . . it

Žhas by no means undermined the significance of location, of place’ emphasis.in the original . Not all locations are equally attractive for all activities. In the

Ž .terms of Emery and Trist’s 1965 seminal work on causal textures of environ-ments, the banks inhabit several environments. A bank with far-flung domesticbranches may find that most occupy a ‘‘placid, randomized’’ environment inwhich ‘‘goods’’ and ‘‘bads’’ are almost randomly distributed over a ground.However, in any sufficiently large set of environments, there will be pockets oforder, or in their terms, environments of ‘‘clustered’’ goods and bads. As a

Ž .result, banks seek out the good locations and avoid the bad . The presence ofŽmany banks then may enhance the attractiveness of a location i.e., produces

.agglomeration economies . Furthermore, the banks’ strategic interaction witheach other may then create a ‘‘disturbed reactive’’ environment in theselocations. Rivalry between banks for customers generates innovation. Theinnovation introduces a change gradient, which is one source of a ‘‘turbulent’’environment. Cooperation among banks in a location to induce the localgovernment to enhance the attractiveness of that location to customers isanother factor generating turbulence, as the governments themselves becomerivals seeking to cooperate to mute the rivalry.

My second objective in this essay is to provide the non-specialist reader withan annotated bibliography that may function as a guide to further exploration.This means that on occasion this essay may read like a list of authors, forwhich dry listing I apologize. However, there are now large literatures oninternational financial centers in both geography and international finance

Ž .that appear to be developing in some isolation from each other. Martin 1999has criticized the new ‘‘economic geography’’ as being neither new nor geogra-phy. Economic geographers, he argues, long ago abandoned the mathematicaltreatment now coming into vogue among geographical economists because ofthe limits these put on understanding. Instead, economic geographers havechosen discursive theorizing and intensive forms of empirical investigation.Martin makes at least one palpable hit when he notes that although economicgeographers read the work of geographical economists, the reverse is not true.

Ž . Ž .Following Porter 1994 and Dunning 1998 , my aim in this essay is tocontribute to the introduction of issues of location into the study of themultinational enterprise, in this case banks, by at least introducing some of thegeographers’ work.

Before I return to the main thrust of the essay, I would like to list tworecent compendia of published papers on international financial centers. JonesŽ .1992b has collected articles on multinational and international banking, some

Ž .of which deal with centers. Lastly, Roberts’ 1994a, b, c, d four volumes reprintan even more extensive collection of articles.

International Banking Centers, Geography, and Foreign Banks 3

In Section II I examine typologies of international banking centers. I do thisboth to establish some common vocabulary and to disaggregate ‘‘banks’’ intoactivities. What distinguishes financial centers one from another is the activi-ties that take place in them. Section III addresses the question of whyinternational banking centers are where they are. Here I begin to deal with theissue of the clustering of the ‘‘goods’’ that draw banks. Section IV deals withstrategic interaction between the banks themselves and with how the clusteringof banks itself creates favorable locations. Section V then examines thecontribution of foreign banks to their host centers. This introduces thefeedback loop that makes the environment turbulent. Lastly, Section VI is asummary.

II. WHAT TYPES OF INTERNATIONAL BANKING CENTERSARE THERE?

Traditionally, financial centers represent the primary markets where, as Coak-Ž .ley 1992 has put it, finance capital and currency is collected, switched,

disbursed and exchanged. Centers differ though in the scale and scope of theactivities that occur within them and these differences have led such scholars

Ž .as Reed 1981 and the others I discuss below to develop typologies. Thesetypologies try to rank or to classify, using two dimensions, places that exist in acharacteristic space that has at least four dimensions.

Ž .Walter 1988 coined the acronym CAP}Client, Arena and Product}todescribe the space that a financial institution occupies. The description re-quires that one specify the type of client the institution is serving, where inphysical space the clients are or come from, and what product the institution isdelivering to these clients. To these three dimensions I would add a fourth thattakes the value-added chain into account; different parts of the productionprocess for a particular product can take place in different locations. Theunion of the spaces that the firms that make up the center occupy then definesthe center’s region in the characteristic space. The spaces that the firmsoccupy in turn consist of the activities the firms engage in where we define theactivity as the combination of stage in the value added-chain of a productaimed at a client from a particular arena or catchment basin.

Walter’s first dimension is the Client base of the firms that populate thecenter. Clients may be governments, non-financial corporations, financial cor-

Ž .porations, high net-worth wealthy individuals, and retail customers. In theŽ .major centers see below the clients are primarily firms and governments.

Other centers specialize in private banking; they serve wealthy individualsseeking a safe place to put their money.

Walter’s second dimension is the Arena the center serves. Walter empha-sizes that the arena is not simply a geographic area but encompasses issues ofregulatory and monetary sovereignty. Nevertheless, we can distinguish, inorder of increasing range, between domestic regional, national, international

Adrian E. Tschoegl4

regional and global or world centers. What distinguishes a purely domesticcenter from an international center is where the clients come from. If theclients come only from the region or the nation, the center is domestic even ifsome of the banks in the center are foreign. What makes a center interna-tional is that customers have crossed borders to reach it. We can further

Ž .distinguish between onshore and offshore banking centers OBCs . In anŽ .onshore center, the arena includes the nation or a portion of it and may

include clients from abroad. OBCs serve non-residents; the arena is strictlyexternal to the nation.

Ž .Johns 1994 suggests that there are now four primary clusters of OBCs,each linked to a major onshore center and its time zone. The Caribbean-CentralAmerican centers serve the Americas and operate within New York’s timezone. The European enclave, coastal enclave and island centers serve Europeand operate within London’s time zone or those of Continental Europe. SomeMediterranean and Gulf centers serve the Middle East. Lastly, Hong Kong,and Singapore on the one side, and Vanuatu and Nauru on the other, servethe Asia-Pacific Basin while spanning Tokyo’s time zone.

Some scholars have extended the Arena dimension to include the serviceproviders. Thus a host center is a location in which foreign banks haveestablished offices but which is not the location of headquarters for interna-tionally active banks. Some host centers serve primarily domestic clients. Thepresence of foreign banks that compete with local banks in the local marketdistinguishes, for example, Atlanta from Minneapolis-St. Paul. Both are finan-cial centers for non-financial firms in their regions but only Atlanta is a host

´Ž .center O hUallachain 1994 . OBCs are primarily host centers. Brealey and´Ž .Kaplanis 1996 identify 2561 foreign offices for the world’s 1000 largest banks;

banks with headquarters in OBCs account for 15 foreign offices though theOBCs themselves are host to 232 offices.

Walter’s third dimension, Product, looks at the services that the banksŽ .provide. When Dufey and Giddy 1978 focused on cross-border intermedia-

tion, they based their functional classification of financial centers on products.Banks move funds from one country to another because of their access todepositors or borrowers. In a funding center the banks offer deposit serviceslocally to fund loans abroad; in a lending center banks bring in funds to offerloans locally. However, the range of potential services goes much beyond thesebalance sheet-based activities. Banks also make markets in foreign exchangeŽ .forex and other financial instruments, move payments, issue financial guaran-tees and engage in a host of other fee-based activities. Depending on homeand host-country regulations, banks may also provide insurance, investment

Ž .banking, stockbroking and the like. Lastly, as Abraham et al., 1994 point out,one must also realize that centers are not static; over time what banks do in acenter may change.

The product dimension encompasses more than a simple enumeration ofŽ .the products available in the center. Park and Essayyad 1989 combined the

International Banking Centers, Geography, and Foreign Banks 5

functional approach with some consideration of the volumes involved. Thusone may compare centers in terms of the daily value of forex transactions thatoccur there or the assets on the books of the banks there.

Ž .The fourth dimension we distinguish is the value-added chain. Kogut 1985points out that corporate strategy comprises not only a product-market con-figuration but also a production configuration. For firms, competitive advan-tage concerns what markets the firms should sell to. Comparative advantageconcerns where, across borders, the firm should break the value-added chain.In services, production has traditionally taken place simultaneously and incontact with consumption. However, the notion of the separation of produc-tion and consumption is at the heart of O’Brien’s thesis of ‘‘the end ofgeography.’’

In banking, classifications by stage of the value-added chain have limitedthemselves to distinguishing between functional and booking centers. In afunctional center bankers meet clients or trade in markets from that location.Booking centers simply provide a legal place of record for transactions thatactually take place elsewhere. Booking centers are also known as ‘‘brass plate’’centers after the brass plate with the bank’s name outside a lawyer’s officethat, together with a file of incorporation papers in the lawyer’s office,represents the bank’s only physical presence in the center. The author’srecollection, based on personal experience, is that in the mid-1970s, the

Ž .personnel serving then Security Pacific National Bank’s Nassau Bahamasbranch actually worked on the 35th floor of the bank’s headquarters in LosAngeles.

Onshore centers are always functional; offshore centers may be functionalŽ .or purely booking centers. Johns 1994 reports that many observers expected

regulatory harmonization and the liberalization of the 1980s to undermine therationale and hence continued existence of the OBCs. However, most of thecenters have succeeded in developing functional niche markets.

The OBCs’ niches are of two, not necessarily disjoint, types. One set ofservices, especially private banking, continues to depend on favorable regula-tions, especially with regard to tax treatment and secrecy. For instance, CobbŽ . Ž1998 reports that the Isle of Man targeted wealthy high net worth in the

. Ž .jargon individuals seeking to mitigate UK taxes. Hampton’s 1996 case studyof the emergence of Jersey as an offshore center too identifies an initial role offavorable tax treatment for wealthy UK citizens, though he argues that secrecywas not a major factor in this case. Later the creation of favorable regulationsdrew other activities, broadening the product dimension and the client base.

The centers that specialize in private banking and that are politicallyŽ .independent may be the first stop for flight capital Jain 1988 or money

Ž . Ž .laundering Walter 1989 . Hampton 1995r96 argues that the existence of theoffshore banking centers facilitates and even encourages onshore corruption.

The more benign set of services that OBCs can provide take advantage ofimprovements in telecommunications that permit firms to move back-office

Adrian E. Tschoegl6

Ž .mainly routine and clerical operations to locations where premises and laborare cheaper while continuing to serve distant customers. For example, O’Con-

Ž .nell and Kennedy 1994 report that Dublin’s international financial center hasconcentrated on ‘‘long-distance’’ services: these include funds management,asset financing, treasury management, insurance and reinsurance activity andprovision of administrative and custodial services. The emphasis is on busi-nesses that do not require close physical proximity to customers.

Ž .McKillop and Hutchinson 1991 report that in the UK, not only arefinancial institutions decentralizing their back offices, but there is some evi-dence for a dispersal of head offices as well. Space still matters though.Physical proximity to London explains why Cardiff, with no history as afinancial center, has experienced significant growth in financial sector employ-ment while Edinburgh has not. Furthermore, front offices are less likely thanhead or back offices to move from the central capital markets. Similarly Rosen

Ž .and Murray 1997 attribute part of the decline in New York City’s share ofemployment in the financial sector in the US to the dispersal of back-officefunctions to cities offering lower labor and real estate costs and Walter and

Ž .Saunders 1991 provide a number of examples.An even more recent innovation is the development of calling centers. In a

calling center transactions take place between distant customers who transactover phones lines with the personnel staffing the calling center. Currently,firms can contract with a specialized firm or establish their own in-housecalling centers. These firm-level centers do not interact directly with eachother but there is some tendency for calling centers to agglomerate. Forinstance, Omaha, Nebraska has become an important US center for callingcenters. The seed was the presence of the headquarters for the US Strategic

Ž .Air Command SAC and its communications. After the US stood down thebombers and disbanded SAC, the civilian telephone communications infra-

Ž .structure remained Porter 1998 . In the UK, Leeds has apparently becomeŽ .the center for financial services call centers Tighe 1997 . There, more than 25

Ž .centers including many belonging to banks employ more than 10,000 people.The development dates from 1989 when First Direct set up the UK’s firstall-telephone banking service.

Several authors have gone beyond typologies to produce rankings of centers.Ž .Reed 1980 & 1981 pioneered the use of cluster analysis or other statistical

Ž .methods to rank financial centers. Abraham et al., 1994 apply factor analysisto measures of the importance and magnitude of the activities in various

Ž . Ž .European centers. Scholtens 1992a uses ten criteria that Kindleberger 1974Ž .proposed to rank European centers. Begg 1991 uses a mix of product or

function, client and other characteristics to group European financial centersinto a seven-fold typology that ranges from local retail centers to nodes of theglobal financial system.

International Banking Centers, Geography, and Foreign Banks 7

Ž .Campayne 1992 has produced what is arguably the most sophisticatedanalysis in that he distinguishes between centers and activities, and thenrelates the two. The centers group into the familiar pattern of London, Tokyoand New York at the top, followed by a number of regional centers, followedin turn by host centers in which the foreign banks serve their multinationalcorporate customers. The activities cluster into four groups. The highest order

Ž .activities essentially investment banking take place in only a few centers andŽinvolve only a few banks. The lowest order activities essentially commercial

.banking take place in many locations and involve many banks. As one mightexpect, higher order activities take place only in top centers, and lower orderactivities take place in both higher and lower-ranked centers. Lastly, Liu and

Ž .Strange 1997 use twelve variables to cluster 12 financial centers in theAsia-Pacific region into four clusters. In their analysis, the first cluster consistsof Tokyo alone. They then use factor analysis to generate three explanatoryfactors that they label internationalization of the economy, openness to foreignbanking, and creditworthiness.

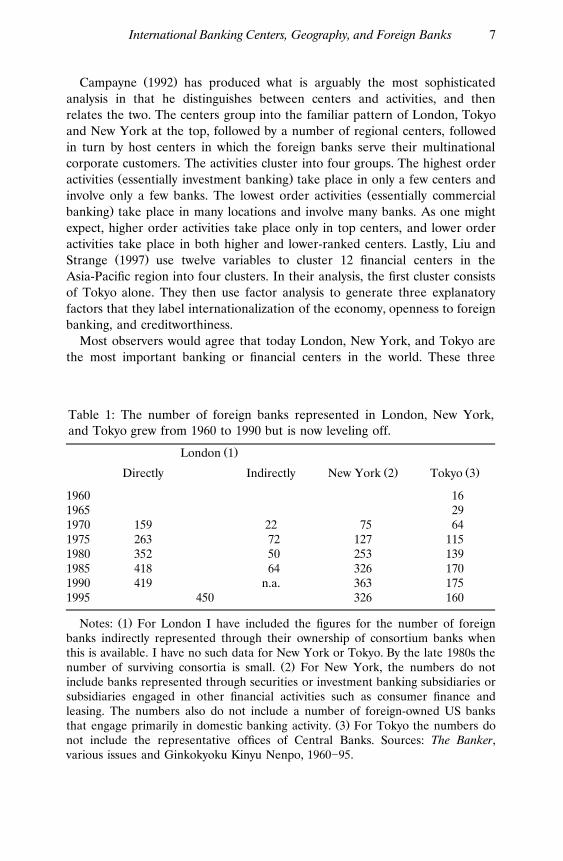

Most observers would agree that today London, New York, and Tokyo arethe most important banking or financial centers in the world. These three

Table 1: The number of foreign banks represented in London, New York,and Tokyo grew from 1960 to 1990 but is now leveling off.

Ž .London 1

Ž . Ž .Directly Indirectly New York 2 Tokyo 3

1960 161965 291970 159 22 75 641975 263 72 127 1151980 352 50 253 1391985 418 64 326 1701990 419 n.a. 363 1751995 450 326 160

Ž .Notes: 1 For London I have included the figures for the number of foreignbanks indirectly represented through their ownership of consortium banks whenthis is available. I have no such data for New York or Tokyo. By the late 1980s the

Ž .number of surviving consortia is small. 2 For New York, the numbers do notinclude banks represented through securities or investment banking subsidiaries orsubsidiaries engaged in other financial activities such as consumer finance andleasing. The numbers also do not include a number of foreign-owned US banks

Ž .that engage primarily in domestic banking activity. 3 For Tokyo the numbers donot include the representative offices of Central Banks. Sources: The Banker,various issues and Ginkokyoku Kinyu Nenpo, 1960]95.

Adrian E. Tschoegl8

cities have more foreign banks operating within their boundaries than otherŽ .major cities Table 1 and were the most central of the 14 centers that Choi et

Ž .al., 1986 & 1996 studied. Banks from all the other centers had offices inLondon, New York and Tokyo, but there were no other cities where banksfrom all other centers, including these three, had offices. The three are the

Ž .sites for many other important financial markets as well. As Callier 1986points out, banks that trade forex from just these three cities can cover 22.5

Ž .hours while operating only during normal business hours. Dufey 1998a addsthat any institution that wishes to offer forex or interest rate derivatives has tobe in all three sites in order to span time zones and to be able to execute thenecessary supporting dynamic hedging strategies. It is therefore not surprisingto see that currently banks are centralizing their forex trading in these threecenters. However, when we speak of a hierarchy of centers, we both rankcenters on one dimension, and perhaps imply that centers of lower rank aresubordinate to centers of higher rank. The terminology of hierarchy then hastwo problems.

The first problem is that one can only unambiguously describe one center asŽ .being larger or more important than another when the ‘characteristic’ space

that one center occupies falls entirely within the space of another. Whencenters do not cover the same region in characteristic space, ranking becomes

Ž .more difficult. As Scholtens 1992a; p. 299 argues, ‘‘the geography of financeis not as strictly tripolar as generally assumed.’’ Banks in different centers dodifferent things and so while London, New York and Tokyo may be theprimary loci for certain products, other centers may be equally or moreimportant loci for others. If one were looking for a metric for an unidimen-sional ranking of centers perhaps value-added in financial services would bemost appropriate, though obviously difficult to estimate.

The second problem with a hierarchical ranking of centers is the frequentlyimplicit or even sometimes explicit implication of a notion of subordination.Many important functional centers are in cities that were the capitals of

Ž .imperial powers e.g., London, Paris, and Tokyo or the financial centers ofŽ .hegemonic powers e.g., New York . In terms of the categories of core and

periphery, the most important centers tend to be in and of the core. This leadsŽ .Meyer 1986 to examine links between headquarters and branch offices and

argue that core metropolises dominate the peripheral metropolises of SouthAmerica. However, location is not function.

Financial centers are highly competitive marketplaces not command bunkers.There is no center, with the exception perhaps of Tokyo, which has theheadquarters of more than a handful of the world’s largest banks. At the sametime, each of the largest centers is a host to branches or subsidiaries of almostall the world’s other major banks or financial firms. Many of these banks come

Ž .from peripheral countries. Consequently, as Tschoegl’s 1982 data shows, theoverall concentration among international banks is low; his data for foreign

Ž .banks in Japan almost all of which are in Tokyo; Tschoegl 1988 shows more

International Banking Centers, Geography, and Foreign Banks 9

concentration but still low levels overall. A center is a central marketplacewhere buyers meet with and choose from amongst many service providers.

III. WHY ARE INTERNATIONAL BANKING CENTERS WHERETHEY ARE?

Ž .Arndt 1988 points out that standard notions of comparative advantage basedon factor costs do not take us far in understanding the location of financialcenters. As Kogut’s argument about comparative advantage makes clear, costsmatter as a component of strategy. However, simple considerations of the costof labor, land and capital tell us little about the location of financial centers.Instead, international politics, domestic regulation, the development oftelecommunications and aviation networks and the location of cities have allcombined to favor some places and disfavor others.

INTERNATIONAL POLITICS

International politics cannot create international financial centers, but it canfacilitate their emergence. A major example is the emergence of London asthe center for the Eurodollar market. Also efforts to encourage countries toopen to foreign banks may facilitate the emergence of national host centers.

The growth of London as the center of the Eurodollar market traces itsorigins in the 1950s to the desire of the USSR to hold US dollar balances tofacilitate its trade. At the same time the USSR wanted to limit its vulnerability

Ž .to US sanctions. Sampson 1981 reports that the solution was for MoscowNarodny Bank, the agent for the USSR, to maintain its US dollar-

Ž .denominated deposits in London. As Dufey and Giddy 1978 point out, thesubsequent growth of the Eurodollar market derived from other factors, but

Ž .the seed had been planted. Goldberg and Saunders 1980 have an early articlethat examines empirically the role of regulation in explaining the growth ofAmerican banks in the UK, that is, in the center of the Eurodollar market.

Since the late 1970s, the government of the United States has worked toincrease openness abroad to the establishment of foreign banks. The UnitedStates is home to many internationally competitive banks and their lobbying isone impetus. As part of their strategy for enhancing the importance of NewYork as a financial center through the importance of the banks headquartered

Ž .there, Rosen and Murray 1997 urge the city and the state to work toencourage national efforts along those lines.

Politics can also kill centers and thereby provide an impetus for theemergence of an alternative center in a nearby country. Cases in point includeShanghai vis-a-vis Hong Kong and Beirut vis-a-vis Bahrain.` `

Ž .As Jones 1992 discusses, between the two World Wars, Shanghai was thepremier financial center for Asia, dwarfing Hong Kong and Singapore inimportance. The Communist takeover of China in 1949 resulted in the demise

Adrian E. Tschoegl10

of Shanghai, though the Communists did permit four foreign banks to main-tain branches there, branches which, however, were severely circumscribed interms of the activities the Chinese authorities permitted them. Hong Kong’srise to prominence owes much not only to the choking-off of the dominantcenter, but also to the migration to Hong Kong of many industrialists andbankers displaced by the Revolution.

More usually, politics impedes the development of a center. For instance,the Eastern Mediterranean and the Balkans currently lack a center. The civilwar in Lebanon and consequent chaos undermined Beirut’s role in the regionŽ . ŽJones 1992a . Bahrain has benefited from the vacuum Gerakis and Ronces-

.valles 1983 , but this is because no other satisfactory, proximate locationoffered itself. The difficulty of finding a replacement location is probably duein great part to the enmity between Greece and Turkey, and in part to thelocal pariah state status of Israel. Until recently, no Greek banks had offices inIstanbul and no Turkish banks had offices in Athens. Cyprus provides anoffshore center of sorts, but the foreign banks are dispersed not only betweenthe Republic and the Republic of Northern Cyprus, but also within theRepublic as some foreign banks prefer Famagusta or Limassol to Nicosia.

Lastly, explicit or implicit international ostracism too may prevent a nationalcenter from developing an international dimension. Examples include SouthAfrica and Israel. When the world community declared South Africa a pariahstate, the foreign banks withdrew and no banks from neighboring countriesestablished themselves there. Domestic capital controls to impede capitalflight, itself a consequence of ostracism, further impeded the development ofan international financial center. Now, with the end to apartheid and theconcomitant sanctions, Johannesburg may develop as a center for SouthernAfrica. Similarly many Arab states have explicitly ostracized Israel. Non-Arabbanks have avoided Israel too; currently no major foreign bank has any officein Israel. These banks have had more to lose in terms of the viability of their

Ž .operations elsewhere in the Middle East especially in Saudi Arabia or thecustom of Arab governments than they have to gain from opening a branch inTel Aviv or Jerusalem.

DOMESTIC REGULATION

Ž .Walter 1985 has characterized financial services as ‘one of the most struc-turally complex industries in the world economy’ and as ‘one of the mostheavily regulated.’ The relevant government regulations frequently take the

Ž .form of what Engwall 1992 has called emigration and immigration barriers.Governments impose emigration barriers to keep resources at home, tofacilitate control of the domestic currency, to facilitate prudential supervisionor to impose sanctions on malefactor states. Clearly, if all countries imposedemigration barriers there would be no international financial centers, butgenerally emigration barriers have impeded only the banks subject to them.

International Banking Centers, Geography, and Foreign Banks 11

Immigration barriers are a different story. If a government forbids foreignbanks to enter it is highly unlikely that any city in that country will becomeanything more than a domestic financial center. For reasons that I discusslater, it is unlikely that a center without foreign banks will develop the rangeand depth of services that would attract clients from abroad.

There has been a tendency for much of this century for countries to closeŽ .themselves to foreign banks. Tschoegl 1985 found that many countries that

were open to foreign banks in 1920 closed between 1920 and 1980; nocountries that were closed in 1920 opened. The major correlates of a country’sclosure to foreign banks were hostility to private or to foreign ownership ofbanks. Probably much of this closure occurred after World War II with the

Ž .advent of Communist and Socialist regimes during what Robinson 1964 hascalled the National Era. However, the demise or discrediting of the Commu-nist, Fascist and Statist models has led, since 1980, to many countries openingto foreign banks. Notable examples of opening include Australia, Canada,Mexico, the Nordic countries, Spain and most of the formerly Communistcountries of Eastern Europe. Now Stockholm, for instance, is becoming aregional center for the Nordic and Baltic countries.

Sometimes immigration barriers represent attempts to protect domesticŽ .depositors Tschoegl 1981 . Since the various Basle Accords of the 1970s and

1980s, this has become a less important concern. Today, the main reasongovernments impose immigration barriers is to protect the domestic industry.

A number of countries have tried to have their cake and eat it too byŽ .creating the OBCs that are, as Grubel 1982 points out, the service sector

analog of free trade zones for manufactured goods. The host governmentsdeliberately deregulate a range of economic activities when they are confidentthat they can segregate these activities from the regulated, taxed and protecteddomestic arena. To limit the political costs, the authorities confine the rela-tively unregulated and untaxed Offshore Banking Units to dealing almostexclusively with non-residents.

However, because many countries have offered themselves as sites, mostlarge international banks face redundant options. Nor are banks quick to

Ž .relocate activities. As Rauch 1993 points out, history affects city-industrylocation by creating a first-mover disadvantage that can discourage firms fromrelocating from an old, high cost site to a new, low cost site. O’Connell and

Ž .Kennedy 1994 reveal that the Irish authorities were fully aware of this when,in 1987, they undertook to assist the development of Dublin’s InternationalFinancial Service Center as a functional center.

Lastly, domestic regulation includes the issue of adjudication of contractualdisputes. The character of the legal system is an important determinant of the

Ž .viability of the jurisdiction as a financial system. Rosen and Murray 1997assert that one of New York City’s strengths is that most business transactionsare negotiated under US or British law. This leads to negotiations taking placewhere experts in such law abound, and adjudication taking place in New York

Adrian E. Tschoegl12

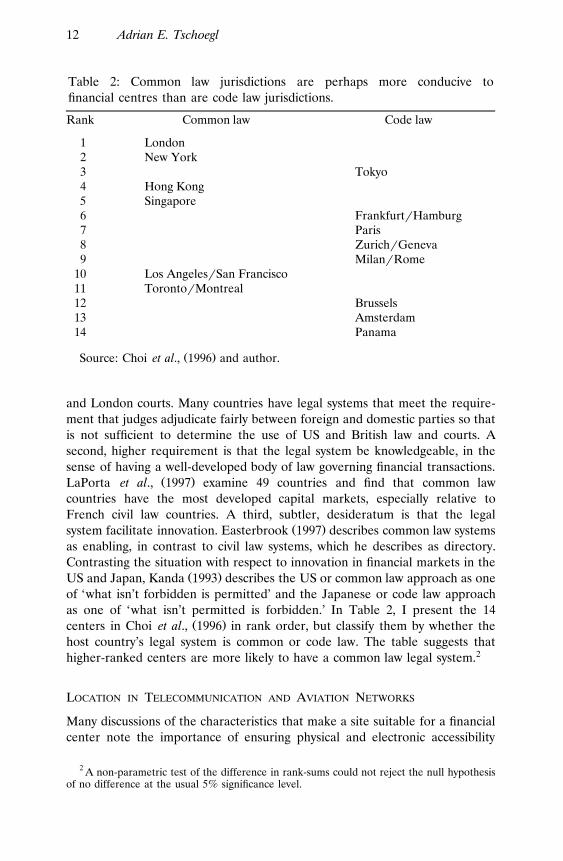

Table 2: Common law jurisdictions are perhaps more conducive tofinancial centres than are code law jurisdictions.

Rank Common law Code law

1 London2 New York3 Tokyo4 Hong Kong5 Singapore6 FrankfurtrHamburg7 Paris8 ZurichrGeneva9 MilanrRome

10 Los AngelesrSan Francisco11 TorontorMontreal12 Brussels13 Amsterdam14 Panama

Ž .Source: Choi et al., 1996 and author.

and London courts. Many countries have legal systems that meet the require-ment that judges adjudicate fairly between foreign and domestic parties so thatis not sufficient to determine the use of US and British law and courts. Asecond, higher requirement is that the legal system be knowledgeable, in thesense of having a well-developed body of law governing financial transactions.

Ž .LaPorta et al., 1997 examine 49 countries and find that common lawcountries have the most developed capital markets, especially relative toFrench civil law countries. A third, subtler, desideratum is that the legal

Ž .system facilitate innovation. Easterbrook 1997 describes common law systemsas enabling, in contrast to civil law systems, which he describes as directory.Contrasting the situation with respect to innovation in financial markets in the

Ž .US and Japan, Kanda 1993 describes the US or common law approach as oneof ‘what isn’t forbidden is permitted’ and the Japanese or code law approachas one of ‘what isn’t permitted is forbidden.’ In Table 2, I present the 14

Ž .centers in Choi et al., 1996 in rank order, but classify them by whether thehost country’s legal system is common or code law. The table suggests thathigher-ranked centers are more likely to have a common law legal system.2

LOCATION IN TELECOMMUNICATION AND AVIATION NETWORKS

Many discussions of the characteristics that make a site suitable for a financialcenter note the importance of ensuring physical and electronic accessibility

2 A non-parametric test of the difference in rank-sums could not reject the null hypothesisof no difference at the usual 5% significance level.

International Banking Centers, Geography, and Foreign Banks 13

Ž .See Langdale 1991, Code 1991, Hepworth 1991 and Daniels 1991 . In theirŽ .survey of bankers in Vancouver and Singapore, Tan and Vertinsky 1987

found that their respondents rated well-developed communication links withthe rest of the world as the most essential attribute for the development of aninternational financial center.

Ž .Warf 1989 argues that telecommunications have not eliminated the impor-tance of location. Instead telecommunications have made place importantbecause of the link between location in space and in time. Location in timematters because of the link with social hours. Banks can and do run 24-hourtrading desks from one location; it is an open question whether this is moreefficient than maintaining three desks, one each in Tokyo, London and NewYork. Warf also points out that communication via satellite links is a two-edgedsword. With satellites, all points on the earth’s surface are equally far apart interms of the monetary cost of communication, but are also equally far apart interms of the time it takes for a message to pass from one location to another.The delay does not matter for data, but does matter for voice.

I am not aware of any article that has explored empirically the role of airlineroutes in the location of financial centers. The nearest example is Keeling’sŽ .1995 analysis of broad trends in global transportation. He focuses on theinternational airline network and calls for further geohistorical analyses oftransport’s role in the evolution of world cities and the world city system. Irwin

Ž .and Kasarda 1991 provide evidence that change in a city’s position in theairline network is a cause rather than a consequence of employment growth.

Ž .Hampton 1994 , in his discussion of Jersey as a model for OBCs, links athriving tourism sector to subsequent success as an OBC. The infrastructure

Ž .that serves tourists air links, hotels, and phone lines can also serve bankersŽ .and lawyers and their clients. Roberts 1995 , in her examination of the

evolution of the Cayman Islands as a financial center, makes the sameobservation.

The impact of aviation on the location of centers may be a fruitful one forexamining the role of changes in technology. The advent of the Boeing 747, animprovement on the 707, has affected the geography of financial centers. The747 does not need to stop to refuel as frequently as some of the planes it hassuperseded. The 747 therefore overflys some cities where the 707 had to stop.Some cities that did not generate much traffic of their own had still benefitedfrom their location on air routes but no longer do so. Also, the increasedpassenger capacity of the 747 has meant that one flight can replace two orthree flights by narrow-bodied jets, further reducing flight density. This has

Žreduced the viability as financial centers of such cities as Anchorage Essayyad. Ž . Ž1989 , Nairobi Grubel 1980, and Simon 1995 , and Panama Lessard &

.Tschoegl 1985 . Although Panama still has the Canal, has favorable legislationand uses the US dollar as its currency, Panama has lost accessibility relative to

Ž .Miami. Grosfoguel 1995 argues that Miami has more advanced facilities incommunications, port, airport, and business services than any country in LatinAmerica and the Caribbean. He conceptualizes Miami as a world city that

Adrian E. Tschoegl14

emerged in the late 1970s to become the core of the Caribbean system of cities´on the basis, in part, of an infrastructure built to serve tourism. O hUallachain´

Ž .1994 argues further that Miami now acts as node for flows of trade andinvestment between the United States, South America and Europe and as aSouth American intraregional center.

LOCATION IN CITIES

Ž .Goldberg and Hanweck 1990 investigated the development of regional bank-ing centers in the United States from 1920 to 1980. They found that bankingcenters tend to develop along with movements in population. Although thegrowth and development of the national economy has dominated the growth ofregional banking, for specific periods local market factors were significant.Still, as centers of population shifted, so did the location of banking centers.

Ž .Daniels 1985 , in his early survey of the geography of services, reports theemergence of corporate complexes that represent an interlocking of headoffice, business and financial service activities. As firms grow, the need forexternal advanced corporate services draws head offices to larger metropolitan

Ž .areas at the expense of smaller cities. Amin and Thrift 1992 posit that citiesthen become localized complexes embedded within ‘‘global production filieres.’’

Ž .Ades and Glaeser 1995 demonstrate that politics may reinforce tendenciesto urban concentration with the result that cities such as London, Tokyo, orParis emerge as primate centers of culture as well as economics and politics.

Ž .Ettlinger and Archer 1987 point out that since 1900 the rank-size distributionof the world’s largest cities has grown increasingly convex. They argue that theconvex distribution reflects dispersed concentrations of economic activity andof population among a number of particularly large centers. These particularly

Ž .large centers are the global cities of Sassen 1991 and Leyshon and ThriftŽ .1997 , and the location of financial centers.

Often the cities that are the home to financial centers are also major ports.ŽOf the 19 cities listed in Table 2, 10 are major ocean ports if one treats Tokyo

.as representing the Tokyo-Yokohama area , as are the top 5 centers. As FujitaŽ .& Mori 1996 point out, port cities are often large cities that have remained

important even after the rise of the service economy has caused access tocheap water transport to lose importance. Being a port features directly in thelocation of financial centers in the case of Amsterdam, London and Piraeusthrough their role in the financing of ships. Being a port features indirectly inthese and other cases through the role of banks in financing trade. As such

Ž . Ž .studies as those of Goldberg et al., 1988 or Heinkel and Levi 1992 , havefound, trade and foreign direct investment in banking go together.

Ž . Ž .Lastly, as Kindleberger 1983 remarked, and Nigh et al., 1986 , GoldbergŽ . Ž .and Johnson 1990 and Yamori 1997 have found, one reason banks go

somewhere is to serve their home country customers that have located in thecountry. At least initially, this will involve the foreign bank establishing one

International Banking Centers, Geography, and Foreign Banks 15

office, generally in the host country’s premier financial center. Frequently thiswill also be the location of the clients’ local head offices, and even if not, willstill provide a central location from which to serve them.

IV. WHY DO BANKS CLUSTER IN CENTERS AND ONCETHERE, HOW DO THEY SURVIVE?

The question of why banks cluster in centers has two answers. As we have seenin the immediately preceding section, the first answer is that banks go wherethe business is. Each bank establishes itself in a center because it expects itspresence to be profitable, whether or not other banks establish themselvesthere also; the scale and diversity of the opportunities may be such that manybanks establish themselves in parallel. The second answer is that banks gowhere there are other banks precisely because there are other banks there.Here we start to address the notion that each bank’s environment includesother banks and that in their location choices the banks react to each other.This is the focus of the present section.

The relative importance of what one might call natural advantage vis-a-vis`agglomeration economies explanations remains an open question, and may

Ž .well be industry and location-specific. Porter 1998 is among the most elo-quent of the advocates for the importance of the role of clusters of firms tounderstanding competitive advantage in an industry. However, Ellison and

Ž .Glaeser 1999 find that a substantial portion of geographic concentrationamong manufacturing industries in the US stems from natural advantages.

Ž .Dumais et al., 1997 find that labor mix is a far more important driver ofindustrial concentration than any of their other explanatory variables, includ-ing those he used to capture transport costs and intellectual spillovers.

GOING WHERE OTHER BANKS ARE

The rubric of ‘‘going where other banks are’’ incorporates three differentmotivations or effects. First, some banks specialize in inter-bank activities suchas correspondent banking or trading in the wholesale financial markets. Thesebanks look to interact with other banks so for them centers are where thebusiness is. Second, there is some evidence for strategic behavior amongmultinational firms, including banks. Strategic behavior may cause severaldifferent geographic patterns. In the ‘oligopolistic reaction’ pattern that

Ž . Ž .Knickerbocker 1973 and Flowers 1976 first identified, a firm matches theŽ .location choices of a rival. In Graham’s 1978, 1990 & 1998 ‘exchange of

threat’ pattern a firm establishes itself in its rival’s home market in order todeny the rival a profit sanctuary. In the ‘mutual forbearance’ pattern a firmavoids markets in which a rival had already established itself and the rival

Ž . Ž .reciprocates. Yu and Ito 1988 and Ito and Rose 1994 find evidence ofŽ .oligopolistic reaction among manufacturing firms. Choi et al., 1986 & 1996

Adrian E. Tschoegl16

found evidence for both exchange of threat and forbearance among large,Ž .international banks and Ball and Tschoegl 1982 found evidence consistent

with oligopolistic reaction for foreign banks establishing themselves in TokyoŽ .and California. Engwall and Wallenstal 1988 argued that Swedish banks in¨

Ž .their internationalization copied each other. Jacobsen and Tschoegl 1999argue that the Nordic consortium banks may have exhibited both oligopolisticreaction and some forbearance depending on the characteristics of the placesinvolved. That is, the banks met in London and New York, and avoided eachother elsewhere.

Lastly, banks agglomerate because of the presence of agglomerationeconomies. What breaks the tautology is the specification of the nature ofthese agglomeration economies, which are of three types. The first type affectsfirms’ revenues; the second type affects firms’ costs, and the third type affectsinnovation.

First, firms can benefit from the proximity of competitors producing similarŽ .but not identical services. Stuart 1975 demonstrates that when negotiation

and purchase require face-to-face contact, the agglomeration of providersreduces buyers’ search costs and thus increases the size of the market thateach seller faces. In banking, face-to-face contact appears to be important incases of initial contact or when customers need unique services. Walter and

Ž .Saunders 1991 argue that as small a move as an investment bank putting itscorporate finance team in Stamford, Connecticut, or Princeton, New Jersey,both only an hour from New York, could severely impair its ability to solicitclients. A client visiting New York to vet several prospective investment bankscould well decide not to bother to make the trip.

Ž . Ž .Daniels 1986 and ter Hart and Piersma 1990 argue that face-to-facecontact is important when banks produce specialized services for corporate

Ž .and other large customers. Thrift 1994 reminds us of the literature on theimportance of face-to-face communication and negotiation in situations involv-

Ž .ing a degree of uncertainty. Pryke and Lee 1995 demonstrate the socialconstruction of production in financial centers using the example of

Ž .mortgage-backed instruments in London. Merton 1995 theorizes that thereason it is generally banks that introduce financial innovations that laterbecome standardized products sold on exchanges is that the contracts initially

Ž .are not well-specified. Rajan 1996 argues that the companies with which abank has relationships provide an ideal testing ground so long as both partiestrust each other and can work out differences. However, working out differ-ences requires personal contact.

Ž .Second, agglomeration may reduce firms’ production costs. As Young 1928pointed out more than 70 years ago, one source of cost reduction is theincrease in specialization that the expansion of a market permits. Young

Ž .focused on specialization within firms, but as Marshall 1890r1961 noted, arelated source of lower costs is the ability of producers to share specialized

International Banking Centers, Geography, and Foreign Banks 17

Žproducers of inputs. Specialized suppliers include law firms, accountants Thrift. Ž .1987 or executive search firms Boyle et al. 1996 .

Marshall also noted the benefit to both workers and employers of thicklabor markets. Thick labor markets free individuals to invest in specializedhuman capital and firms to employ them without fear of holdup costs. Lastly,Marshall emphasized the importance of the presence of tacit productionknowledge. The widespread presence of such knowledge in the center obviatesthe need for some training and hence is a source of lower production costs.

Ž .Porter 1994 , however, proposes that the importance of knowledge that is ‘‘inthe air’’ is due not so much to the effect on costs as to the effects oninformation exchange, the development of working relationships, and thechecks on opportunistic behavior, all of which speed innovation. Earlier,

Ž .Jacobs 1969 suggested that the buildup of knowledge and ideas that growsout of the diversity inherent in cities provides urbanization economies thatfacilitate innovation.

Ž .Henderson et al., 1995 classify the direct and indirect consequences of theexpansion of demand as static externalities. The Marshallian tacit production

Ž .knowledge economies and the Jacobs 1969 urbanization economies theyŽ .classify as dynamic externalities. Henderson et al., 1995 test for static and

dynamic externalities in manufacturing and find evidence for both for highŽ .tech innovative industries but only static externalities for mature industries.

Henderson et al., argue that this is consistent with urban specialization andproduct cycles. Extending the argument to banking, we would expect to findthat the creative part of banking services would prosper in large, diversemetropolitan areas. Mature, more standardized activities would decentralize tosmaller, more specialized cities. This hypothesis appears consistent with theevidence but I am not aware of any formal test.

Ž .Lastly, Malmberg et al., 1996 have a paper in which they focus on the roleof knowledge accumulation in spatial clustering. Their model consists of threeelements. The first element is innovation, which they link to face-to-face andrepeated interaction. This ties in with Henderson et al.’s dynamic externalities.The contribution of Malmberg and his co-authors is in their introduction ofelements pertaining to the transfer of knowledge. The second element isbarriers to diffusion of locally embedded knowledge, of which access to thenetworks for knowledge accumulation and accumulated social capital are mostcritical. The third element is the attraction of knowledge through incumbentsbringing in knowledge from elsewhere and from the locality attracting out-siders with knowledge to contribute.

In the context of banking centers, two hypotheses follow from this model.First, centers that contain the headquarters of multinational banks are morelikely to be centers in which innovation takes place. The operative factorwould be the transfer within the MN bank of ideas from elsewhere via itspersonnel and branches abroad. Second, MN banks would be attracted tocenters where innovation occurs and where they can tap that knowledge, by

Adrian E. Tschoegl18

perhaps, trading it for knowledge that they bring from their home andnetwork. These seem fruitful and untouched areas for research.

COMPETITION WITHIN INTERNATIONAL FINANCIAL CENTERS

Ž .Over the last two decades, foreign direct investment FDI in banking hasdrawn substantial theoretical and empirical attention. Noteworthy early theo-

Ž . Ž . Ž .retical works include Aliber 1976 , Grubel 1977 and Gray and Gray 1981 .Ž . Ž .Scholtens 1992b and Williams 1997 provide recent comprehensive surveys

of the theoretical literature. A major concern in this literature is the liability ofŽ .foreignness. The logic, which traces its origins back to Hymer’s 1976 path

breaking thesis in 1960, is that foreign firms must have offsetting advantagesthat enable them to overcome the liability in their competition with local firms.This liability of foreignness has three aspects.

The first aspect is that the foreign bank is operating at a distance from itsheadquarters and hence may face control and coordination costs that its localcompetitors do not face. However, several studies such as those of Choi et al.,Ž .1986 & 1996 find no effect of distance on the propensity for banks toestablish themselves in banking centers. The second aspect of the liability offoreignness is that the foreign firm must learn the environment of the country

Ž .that it is entering. Caves 1982 has argued that the problems would be mostsevere where the foreign firms are competing with local firms for a share of thehost-country market. Thus the liability of foreignness would be least criticalin financial centers, especially offshore centers, and most critical in retailbanking.

Ž .Zaheer and Mosakowski 1997 studied the entry and survival of banks’forex trading rooms and found that the liability of foreignness changed overtime. In the first two years, the survival rates of host-country and foreign-ownedtrading rooms were similar. For the next fourteen years, trading rooms ownedby foreign banks exited at a higher rate than those owned by host-countrybanks; the exit rate peaked at eight years. Still, foreign banks are present andactive in forex markets in various financial centers.

By contrast, in retail banking foreign banks generally can offer little thatwould act as an advantage to offset the liability of foreignness. Thus TschoeglŽ .1987 argues that one should generally does not see foreign banks entering

Ž .retail markets except in the case of ethnic banking. Dufey and Yeung 1993make the same point with respect to the prognosis for evolution of banking inthe European Union.

The third and last aspect of the liability of foreignness, one that is particu-larly critical in banking, is that the foreign bank must establish relationshipswith clients. When banks follow or lead their customers abroad, the foreignbank is using existing relationships. However, dealing only with home-countrycustomers abroad will limit the foreign bank to a niche in the host country.

Ž .Some banks may be content with that. Tickell 1994 reports that Japanese

International Banking Centers, Geography, and Foreign Banks 19

banks in the UK have not extended their activities beyond lending to thesubsidiaries of Japanese companies. To grow beyond the niche the foreignbanks must establish ties with host-country customers but success here de-

Ž .pends in part on the competitive conditions in the host market. Sagari 1992finds that the more competitive the local environment is, the smaller is the

Ž .presence of foreign banks. Steinherr and Huveneers 1994 provide evidencethat foreign bank penetration of loan markets is lower in countries where asmall number of banks dominate banking. The lack of competitors stunts thedevelopment of an arms-length loan market so domestic firms must formrelationships with the dominant domestic banks. When foreign banks attemptto enter, they will meet resistance from the incumbent banks.

Ž .Steiglitz and Weiss 1981 examine a model in which, to get market share,an entrant has to underprice. Incumbent banks match the price on goodcredits and don’t on bad so the entrant suffers from adverse selection. Engwall

Ž .et al., 1999 find evidence consist with this argument in the case of the growthŽ .of the foreign bank sector in the Nordic countries. Yafeh and Yosha 1995

propose a model in which domestic banks respond to foreign bank entry byincreasing the resources that the domestic banks devote to the formation ofties with firms. The empirical literature on banking relationships is thin, but

Ž .Ongena and Smith 1998a&b provide some useful information on banks’Ž .relationships with companies listed on the Oslo Stock Exchange OSE from

Ž .1979 to 1994. Their data 1998a show that as domestic deregulation pro-gressed the proportion of firms reporting relationships with only one bank rosefrom 65% to over 75% in 1985 when the Norwegian government first permit-ted the entry of foreign banks. Consistent with the Yafeh and Yosha model,foreign banks were hard hit. In 1979, foreign banks accounted for 16% of allrelationships with banks; by 1994, their share had dropped to 5%. With only alimited arms-length market on the one hand and an absence of relationshipswith domestic firms on the other, foreign banks have little scope for lending.To compete for host-country clients, the foreign banks must therefore offerspecial expertise and services. For many banks the sole niche expertise theycan offer is their knowledge of and links to their home country. This shows up

Ž .in the importance of trade financing that Cho et al., 1987 , Goldberg et al.,Ž . Ž .1989 and Grosse and Goldberg 1991 find.

However, banks from some countries may have developed expertise inŽ .services facing a broader demand. Dufey 1998b argues that US banks

dominate investment banking worldwide because of the skill they have devel-Ž .oped in their home markets. Tschoegl 1997 demonstrates that banks from

common law countries with rivalrous domestic markets appear to be strongcompetitors in the forex markets wherever they compete. For 13 OECD

Ž .countries, Moshirian 1994b found that national R&D, physical and humancapital, and banks’ international assets are the factors that account forcompetitiveness in the supply of international financial services. However he

Adrian E. Tschoegl20

uses aggregate data and cannot link specific factors to specific services orfactors or services to specific locations within countries.

V. WHAT DO FOREIGN BANKS CONTRIBUTE TO THEIRHOST CENTERS?

Lastly we come to the issue that the banks affect the environment in whichthey exist. This feedback loop introduces, in Emery and Trist’s term, turbu-lence to the environment.

Offshore and onshore activities of foreign banks differ in the benefits theybring to a country. Offshore banking represents an export of services. TschoeglŽ .1989 and others have argued that the net benefits of hosting offshorebanking are slight but still can be important for small, open economies with

Ž .few alternatives. Moshirian 1994a finds that for some OECD countries tradein financial services is a significant component of current account balances butthe countries he examines have both onshore and offshore banking.

From the point of view of global welfare, the competition among countriesto host offshore banking means the gain to a host center represents little net

Ž .gain overall. Plender 1987 , in his discussion of London’s Big Bang, hasargued that offering reduced regulation and lower taxes to attract footlooseinternational banks may simply shift business and jobs from one location toanother. This may provide little to the world economy beyond a small increasein financial efficiency that is itself subject to decreasing marginal returns.Furthermore, countries may have to give up some of the gain to induce banks

Ž .to move Rauch 1993 , but their loss does not accrue to the countries fromŽ .which the banks move their operations. Similarly, Grubel 1983 has warned

that the costs from trade diversion may exceed the gains from trade creation.Ž .Dufey 1984 has identified one contribution of OBCs to their regions that is

generally overlooked. In situations where domestic financial markets aresubject to bureaucratic-authoritarian regulation, the OBCs can offer an escapevalve for those large domestic firms able to gain access to their services. Thatis, external or offshore markets supplement the highly controlled domesticmarkets.

Permitting the entry of foreign banks and the emergence of an onshore hostcenter may bring benefits that are more general. The first benefit is an

Ž .increase in competition. Semple and Rice 1994 show how Canada’s openinghas resulted in an influx of foreign banks to Toronto, which was already the

Ž .location of the headquarters of Canada’s largest banks. Goldberg 1992 findsforeign commercial banks in the US have had a major competitive impact,

Ž .especially in commercial and industrial loans. Moshirian 1993 estimatesimport and export demand functions for Austria, Belgium Italy, the Nether-lands and the United Kingdom and finds that domestic firms respond to anyincrease in the price of international financial services by domestic financialinstitutions by switching to foreign financial institutions.

International Banking Centers, Geography, and Foreign Banks 21

A second benefit can be a widening of the range of services available todomestic clients and perhaps some pressure on incumbents to innovate. As

Ž .Porter 1990 has argued, the ‘‘presence of strong local rivals is a final, andpowerful, stimulus to the creation and persistence of competitive advantage.’’

When the presence of foreign banks in a center brings about improvementsin the functioning of financial markets in terms of both prices and the range ofservices, this enhances economic growth overall in the region the centerserves. One mechanism is through access to capital and the other is throughefficiency in the use of capital. If financial capital is perfectly mobile, thenfinance can play only a passive role in regional growth. However, Amos and

Ž .Wingender 1993 suggest that capital is not perfectly mobile and link regionalgrowth to credit-induced expenditures. Then if opening to foreign banks bringsincreased access to capital flows this in turn could bring additional economicgrowth. The causal links are ambiguous though. On the one hand, as JainŽ .1986a & b found, there is a link between bank size, trade patterns, and

Ž .lending to developing countries. On the other hand, ter Wengel 1995 foundthat the relaxation of exchange and capital controls by potential host countriesdiminished the incentives of banks to seek direct representation.

The second mechanism through which the presence of foreign banks mayserve growth is through its role in enhancing the development of the financialsystem. As we have already discussed, the presence of foreign banks may

Ž .enhance competition and hence innovation. King and Levine 1993 find strongassociations between measures of the level of financial development and realper capita GDP growth, the rate of physical capital accumulation and improve-ments in the efficiency with which economies employ physical capital.

Ž .As Dufey and Bartram 1997 point out, the desire to draw banks and otherfinancial institutions has led the governments that offer OBCs into competi-tion with each other. Still, the governments also cooperate. In 1980, fifteencenters set up the Offshore Group of Banking Supervisors.3 The purpose of

Žthe Group is to promote greater cooperation i.e., limit competition and the.dissipation of rents and to represent the members’ interests to the Bank for

International Settlements.Governments other than those of OBCs modify regulations to draw business

in a process that sometimes is led and sometimes leads. Thus, Lee andŽ .Schmidt-Marwede 1993 argue that the geography of financial production and

the competitiveness of financial centers are related but distinct processes.Ž .Gleeson 1997 , in her lively history of the foreign banks association in London

Ž .which grew from 14 members in 1947 to 183 members in 1997 , reportsseveral cases of negotiation between the association and the Bank of England

3 The 15 are the Bahamas, Bahrain, Barbados, the Cayman Islands, Cyprus, Gibraltar,Guernsey, Hong Kong, the Isle of Man, Jersey, Lebanon, the Netherlands Antilles, Panama,Singapore, and Vanuatu.

Adrian E. Tschoegl22

Ž .over regulations. More generally, Budd 1995 has shown that major institu-tions in financial centers are becoming incorporated into the formation of

Ž .urban policy. Similarly, Raikes and Newton 1994 report that the variousfinancial exchanges and banks in Europe have lobbied their home govern-ments in an attempt to influence the location of activity. All of this has takenplace in a context of the European Union’s own program of economicliberalization and the creation of a Single Market.

The competition between financial centers is a complex process that actuallyŽ .has drawn relatively little analysis. Walter 1998 has one of the few articles

that explicitly address the issue but even this is only a beginning. One issueworthy of greater exploration is the effect of political autonomy, or rather thelack of it, on policymaking. A city such as New York that is part of a state thatis part of a federal government possesses different degrees of freedom withrespect to policy than a city such as Paris that is part of a highly centralizedcountry that is part of a union of countries. Independent city-states have thegreatest freedom of action, which obviously is one reason why so manyoffshore centers are small island states. Hong Kong’s freedom of action as anEnglish colony remote from the metropole was greater than that after itsaccession to the Peoples Republic of China.

Recapitulating briefly, the entry of foreign banks can bring about a rivalry inan international financial center. This rivalry between disparate financialinstitutions may then result not only in the static benefits of competition, butalso in a tendency to innovation. This innovation in the services and productsthat the institutions offer requires an accommodating change and innovationin domestic laws and regulations. The net result is a turbulent environment inthe center, and because of competition and cooperation between the govern-ments with jurisdiction over the centers, in the entire network of centers.

VI. CONCLUSION

Deregulation and improvements in communications have not meant the end ofgeography as O’Brien has argued. Institutions have not dispersed; instead, thenew developments have freed the banks from the necessity of collocating alltheir activities. Consequently the banks have dispersed from traditional cen-ters activities involving frequent routine, standardized, and small-scale transac-tions. At the same time, the banks have kept in the international financialcenters those activities involving innovative, customized, and large-scale trans-actions. In all of this, place still matters, but different places matter fordifferent activities.

Centers are the locus of the union of the activities of financial institutions,making obsolete typologies of international banking centers that typicallygroup centers along one or two dimensions. The idea that a center representsa union of activities makes it difficult to create meaningful hierarchical

International Banking Centers, Geography, and Foreign Banks 23

rankings. Also, the notion of a hierarchy}in the sense of loci of control}issuspect. Centers are competitive marketplaces. They are locations where manyforeign and domestic financial institutions collaborate and compete for cus-tom. Even in terms of the channeling of information and capital, the metaphorfor the structure of centers is more one of distributed intelligence over anetwork than one of a hierarchy.

The location of international banking centers is not random. They are wherethey are because of a historical process that has resulted in certain placesoffering a cluster of attractions to the banks that have established theiractivities there. International and domestic politics have played a role directly,and indirectly through their effect on the location of non-financial economicactivity. The cities that are the locus of functional centers tend to be ports, andprimate and world cities. To function, the centers must be nodes for telecom-munication and aviation networks but physical infrastructure provides only anecessary and not a sufficient foundation.

The banks cluster certain activities in centers because that is where thebusiness is. The centers are where the clients cluster. The banks also cluster incities because they are reacting to the presence of other banks. Not only dobanks interact with each other in complex patterns of rivalry and cooperation,but they also benefit from static and dynamic agglomeration economies. Thecreative part of banking services prospers in large, diverse metropolitan areas;the mature, more standardized activities decentralize to smaller cities as classic

Ž .factor costs i.e. the cost of land and labor matter more. However, in manycases even the activities that banks are moving out of major centers appear tobe clustering in cities specializing in these activities, thus giving rise to newsatellite or supporting centers.

In and from the centers, the foreign banks compete with each other andwith domestic banks. To compete with domestic banks for domestic clients, theforeign banks must offer greater efficiency or special expertise and services.For many foreign banks the expertise they offer is their knowledge of and linksto their home country. For some foreign banks, the expertise they bring is onebased on products from the home market that represent innovations in thehost. For these banks and others, the expertise may also be one of a capacityfor innovation honed in a rivalrous home market.

Finally, when the foreign banks simply serve their home-country clientsabroad they add only a little value to the host economy. It is when theycompete with domestic banks for host-country clients that the foreign banksmake the greatest contribution. To the degree that their presence enhancesdomestic competition and innovation in financial services, the foreign banksimprove the functioning of the host-country’s financial system. This in turncontributes to real economic growth. The innovation that the rivalry betweeninstitutions induces makes the environment in international financial centers aturbulent one.

Adrian E. Tschoegl24

VII. REFERENCES

Ž .Abraham, J-P., N. Bervaes and A. Guinotte 1994 The Competitiveness of Euro-pean International Financial Centres. In J. Revell, ed. The Changing Face ofEuropean Banks and Securities Markets. London: St. Martin’s Press.

Ž .Ades, A. F. and E. L. Glaeser 1995 Trade and Circuses: Explaining Urban Giants.Quarterly Journal of Economics 62, 195]227.

Ž .Aliber R. 1976 Toward a Theory of International Banking. Economic Re¨iew,Federal Reserve Bank of San Francisco, Spring, 5]8.

Ž .Amin, A., and N. Thrift 1992 Neo-Marshallian nodes in global networks. Interna-tional Journal of Urban Regional Research 16, 571]587.

Ž .Amos, O. M., Jr. and J. R. Wingender 1993 A model of the interaction betweenregional financial markets and regional growth. Regional Science and UrbanGrowth 23, 85]110.

Ž .Arndt, H. W. 1988 Comparative advantage in trade in financial services. BancaNazionale del La¨oro Quarterly Re¨iew 40, 61]78.

Ž .Ball, C. A., and A. E. Tschoegl 1982 The Decision to Establish a Foreign BankBranch or Subsidiary: An Application of Binary Classification Procedures. Jour-

Ž .nal of Financial and Quantitati e Analysis 17 3 , 411]424.Ž .Begg, I. 1991 The spatial impact of completion of the EC internal market for

financial services. Journal of Regional Studies 26, 333]347.Ž .Boyle, M., A. Findlay, E. Lelievre and R. Paddison 1996 World Cities and the

Limits to Global Control: A Case Study of Executive Search Firms in Europe’sLeading Cities. International Journal of Urban and Regional Research 20, 498]516.

Ž .Brealey, R. A. and E. C. Kaplanis 1996 The determination of foreign bankinglocation. Journal of International Money and Finance 15, 577]597.

Ž .Budd, L. 1995 Globalization, Territory and Strategic Alliances in DifferentFinancial Centers. Urban Studies 32, 345]360.

Ž .Callier, P. 1986 ‘‘Professional Trading,’’ Exchange Rate Risk and the Growth ofInternational Banking: A Note. Banca Nazionale del La¨oro Quarterly Re¨iew 38,423]428.

Ž .Campayne, P. 1992 The Impact of Multinational Banks on International Finan-cial Centres. In M. Casson, ed. International Business and Global IntegrationŽ .London: Macmillan .

Ž .Caves, R. E. 1982 Multinational enterprise and economic analysis. New York:Cambridge University Press.

Ž .Cho, K. R., S. Krishnan and D. Nigh 1987 The State of Foreign Banking Presencein the United States. International Journal of Bank Marketing 5, 59]75.

Ž .Choi, S-R., A. E. Tschoegl and C-M. Yu 1986 Banks and the World’s MajorFinancial Centers, 1970-1980. Weltwirtschaftliches Archi 122, 48]64.

Ž .Choi, S-R., D. Park and A. E. Tschoegl 1996 Banks and the World’s MajorBanking Centers, 1990. Weltwirtschaftliches Archi 132, 774]793.

Ž .Coakley, J. 1992 London As An International Financial Centre. In Leslie Buddand Sam Whimster, eds. Global Finance and Urban Li ing. London: Routledge.

International Banking Centers, Geography, and Foreign Banks 25

Cobb, S. C. 1998. Global Finance and the Growth of Offshore Financial Centers:The Manx Experience. Geoforum 29, 7]21.

Ž .Code, W.R. 1991 Information flows and processes of attachment and projection:the case of financial intermediaries. In S. D. Brunn and T. R. Leinbach, eds.Collapsing space and time: Geographic aspects of communication and information.London: Harper and Collins, 111]31.

Ž .Daniels, P. W. 1985 The geography of services. Progress in Human Geography 9,443]451.

Ž .Daniels, P. W. 1986 Foreign Banks and Metropolitan Development: a Compari-son of London and New York. Tidjschrift ¨oor Economische en Sociale Geographie77, 269]287.

Ž .Daniels, P. W. 1991 Internationalization, telecommunications and metropolitandevelopment: the role of producer services. In S. D. Brunn and T.R. Leinbach,eds. Collapsing space and time: Geographic aspects of communication and informa-tion. London: Harper and Collins, pp. 149]169.

Ž .Dufey, G. 1984 Banking in the Asia-Pacific Region. Research in InternationalŽ .Business and Finance 4 Part B , 295]327.

Ž .Dufey, G. 1998a The Changing Role of Financial Intermediation in Europe.Ž .International Journal of Business 3 1 , 49]67.

Ž .Dufey, G. 1998b The Transformation of Banks and Bank Services: Comment.Journal of Institutional and Theoretical Economics 154, 137]143.

Ž .Dufey, G. and S. M. Bartram 1997 The Impact of Offshore Financial Centers onŽ .International Financial Markets. International Executi e 39 3 , 535]579.

Ž .Dufey, G. and I. Giddy 1978 The International Money Market. Englewood Cliffs,New Jersey: Prentice-Hall.

Ž .Dufey, G. and B. Yeung 1993 The Impact of EC 92 on European Banking.Ž .Journal of Financial Management 2 3]4 , 11]31.

Ž .Dumais, G., G. Ellison and E. L. Glaeser 1997 Geographic Concentration as aDynamic Process. NBER Working Paper 6270.

Ž .Dunning, J. H. 1998 Location and the Multinational Enterprise: A NeglectedFactor? Journal of International Business Studies 29, 45]66.

Ž .Easterbrook, F. H. 1997 International Corporate Differences: Markets or Laws.Journal of Applied Corporate Finance 9, 23]29.

Ž .Ellison, G., and E. L. Glaeser 1999 The Geographic Concentration of Industry:Does Natural Advantage Explain Agglomeration. American Economic Re¨iew 89Ž .2; Papers & Proceedings , 311]316.

Ž .Emery, F. E. and Trist, E. L. 1965 The causal textures of organizational environ-ments. Human Relations 18, 21]32.

Ž .Engwall, L. 1992 Barriers in International Banking Networks. In M. Forsgren andJ Johanson, eds. Managing Networks in International Business. Philadelphia:Gordon and Breach, 167]177.