Installation, Operating & Maintenance Instructions - VAT Valves

Upload

khangminh22Category

view

0download

0

BEPSJoy Svas -Salee contemplates a period of unprecedented change for interna onal corporate tax law

Legislation Back to basics:input VATNatasha Siddiqi considers the challenges of input VAT recovery

20 30 36

www.tax.org.uk www.a .org.uk

Patrick King examines how advisers can cope with the complex mountain that is the UK tax code

Excellence in Taxation March 2016www.taxadvisermagazine.com

PLUS Tax policy – Tax at university – Cross-border VAT – STBV – Trust income – Inducement payments

Harriet Brown considers the uncertain es that an HMRC discovery assessment can cause, page 22

Nowhere to hide?

BE FIRST OFF THE

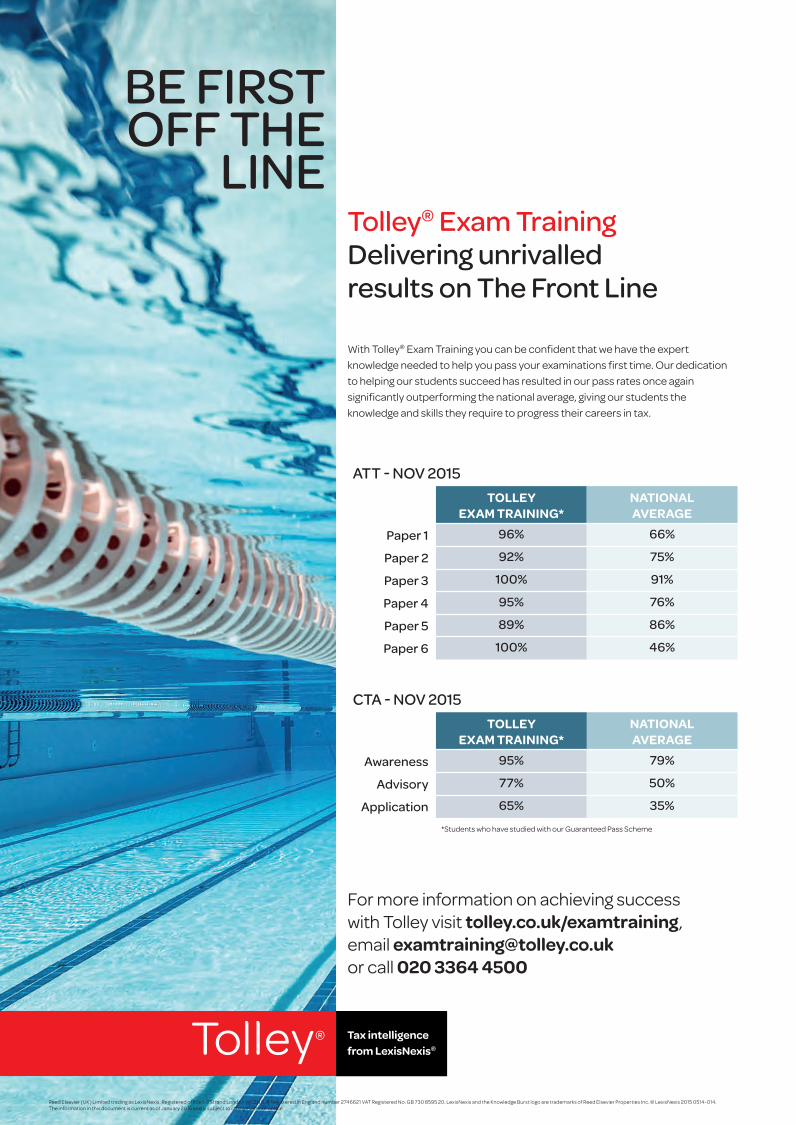

LINETolley® Exam Training Delivering unrivalled results on The Front Line

With Tolley® Exam Training you can be confident that we have the expert knowledge needed to help you pass your examinations first time. Our dedication to helping our students succeed has resulted in our pass rates once again significantly outperforming the national average, giving our students the knowledge and skills they require to progress their careers in tax.

For more information on achieving success with Tolley visit tolley.co.uk/examtraining, email [email protected] or call 020 3364 4500

ATT - NOV 2015TOLLEY

EXAM TRAINING*NATIONAL AVERAGE

Paper 1 96% 66%

Paper 2 92% 75%

Paper 3 100% 91%

Paper 4 95% 76%

Paper 5 89% 86%

Paper 6 100% 46%

CTA - NOV 2015TOLLEY

EXAM TRAINING*NATIONAL AVERAGE

Awareness 95% 79%

Advisory 77% 50%

Application 65% 35%

*Students who have studied with our Guaranteed Pass Scheme

Reed Elsevier (UK) Limited trading as LexisNexis. Registered office 1-3 Strand London WC2N 5JR Registered in England number 2746621 VAT Registered No. GB 730 8595 20. LexisNexis and the Knowledge Burst logo are trademarks of Reed Elsevier Properties Inc. © LexisNexis 2015 0514-014. The information in this document is current as of January 2015 and is subject to change without notice.

MAGNETICNORTH

GUIDING YOU TO THE BEST TAX JOBS IN THE NORTH OF ENGLAND

Tel: 0333 939 0190 Web: www.taxrecruit.co.ukMike Longman FCA CTA: [email protected]; Ian Riley ACA: [email protected]; Alison Riordan: [email protected]

CORPORATE TAX MANAGER HARROGATE £40,000 to £50,000 dep on expLeading national firm seeks an experienced corporate tax manager to provide compliance and advisory services to a portfolio of clients ranging from OMB’s to large groups. REF: A2461

TAX ADVISORY MANAGER LYMM £ dependent on experience Unique opportunity to join a forward thinking firm of tax advisers. You will provide technical support to the directors working on a wide range of clients including SME’s, OMB’s and private clients. Part time considered and flexible working available. REF: A2462

VAT MANAGER MANCHESTER OR LEEDS To £54,000 + benefits Are you an indirect tax specialist? We are handling a number of Big 4 opportunities with work ranging from pure advisory projects to compliance reviews & due diligence. REF: R2442

IN-HOUSE TAX ACCOUNTANT MANCHESTER £38,000 to £45,000 A super in-house opportunity to join the central tax team. Ideal for a first move from practice, you will be responsible for corporation tax compliance and accounting for the UK Group. REF: R2457

HEAD OF TAX REPORTING CHESHIRE £ Generous package on offer A rare, senior in-house tax appointment has arisen with the Head Office tax team of a global FTSE 250 group. Opportunities like this don’t come around often. REF: R2459

PRIVATE CLIENT AND TRUST MANAGER WEST YORKSHIRE To £40,000 You will be responsible for looking after the compliance and advisory affairs of a portfolio of HINWIS and family trusts. Trust experience is essential.

REF: A2463

CORPORATE TAX MANAGER NEWCASTLE £Highly competitive A fantastic opportunity for an ambitious, driven corporate tax manager to join a Top 10 firm. You will manage the department and a portfolio of large multinational clients. This is a key hire that could lead to partnership for the right candidate. REF: A2460

PART TIME TAX SENIOR SOUTH MANCHESTER To £30,000 FTE Growing Independent firm looking for an experienced Tax Senior to work 3 or 4 days per week in a compliance focussed role. Friendly team and great working environment add to the attraction of this position. REF: A2464

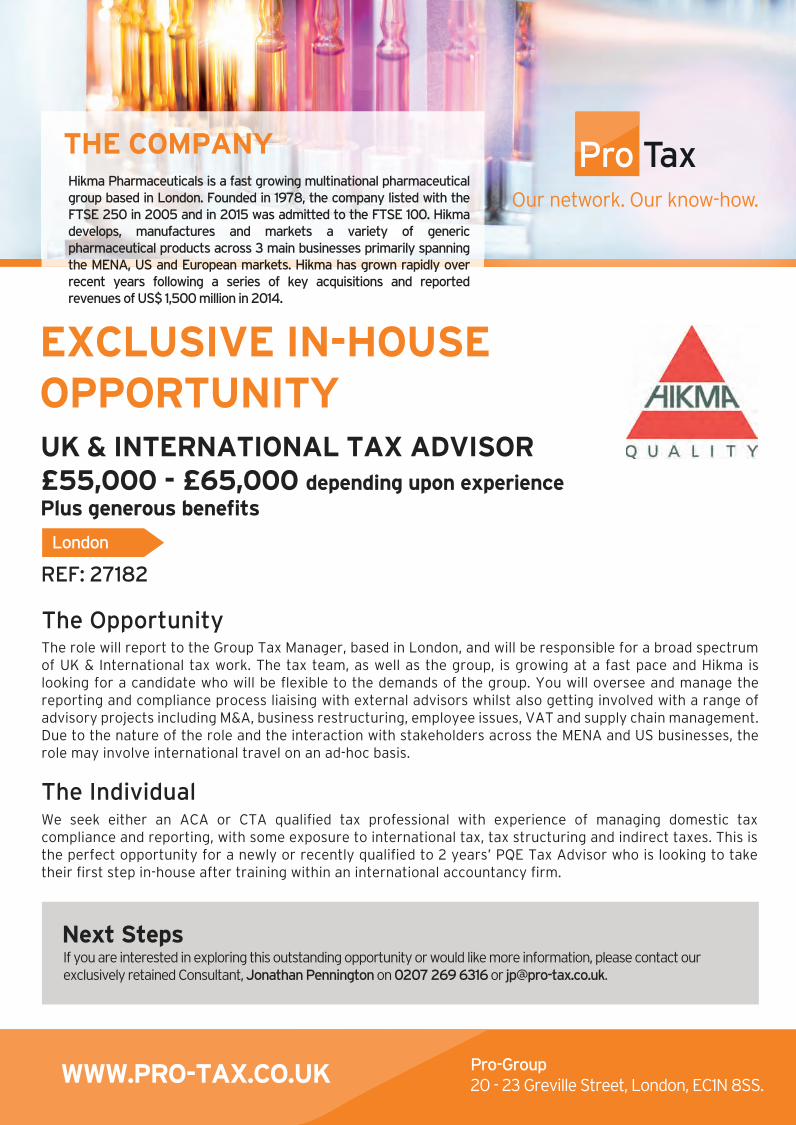

WWW.PRO-TAX.CO.UK Pro-Group20 - 23 Greville Street, London, EC1N 8SS.

Next StepsIf you are interested in exploring this outstanding opportunity or would like more information, please contact our exclusively retained Consultant, Jonathan Pennington on 0207 269 6316 or [email protected].

We seek either an ACA or CTA qualified tax professional with experience of managing domestic tax compliance and reporting, with some exposure to international tax, tax structuring and indirect taxes. This is the perfect opportunity for a newly or recently qualified to 2 years’ PQE Tax Advisor who is looking to take their first step in-house after training within an international accountancy firm.

The Individual

The role will report to the Group Tax Manager, based in London, and will be responsible for a broad spectrum of UK & International tax work. The tax team, as well as the group, is growing at a fast pace and Hikma is looking for a candidate who will be flexible to the demands of the group. You will oversee and manage the reporting and compliance process liaising with external advisors whilst also getting involved with a range of advisory projects including M&A, business restructuring, employee issues, VAT and supply chain management. Due to the nature of the role and the interaction with stakeholders across the MENA and US businesses, the role may involve international travel on an ad-hoc basis.

The Opportunity

London

REF: 27182

UK & INTERNATIONAL TAX ADVISOR£55,000 - £65,000 depending upon experiencePlus generous benefits

Hikma Pharmaceuticals is a fast growing multinational pharmaceutical group based in London. Founded in 1978, the company listed with the FTSE 250 in 2005 and in 2015 was admitted to the FTSE 100. Hikma develops, manufactures and markets a variety of generic pharmaceutical products across 3 main businesses primarily spanning the MENA, US and European markets. Hikma has grown rapidly over recent years following a series of key acquisitions and reported revenues of US$ 1,500 million in 2014.

THE COMPANY

EXCLUSIVE IN-HOUSE OPPORTUNITY

CONTENTS

Welcome3 Editor’s Welcome

Surprise discoveryChris Ma os

4 President’s pageIn praise of technical offi cers and the technical steering groupMichael Steed

5 CIOT Vice-President’s page More educa on in tax?John Preston

6 ATT WelcomeIn pensions we trustRalph Pe engell

Briefi ngsFrom Ar llery House

8 Spotlight on branches – European

9 CIOT President’s Luncheon

10 ATT appoints new execu ve director

Recruitment 56 Looking at the best

industry jobs

Technical From the Technical team

40 Exclusion of some companies from NIC employment allowance

45 Disclosures and HMRC’s KYC ini a ve

46 Re-launch of the CCCTB

47 Engagement with poli cians and parliament

48 Higgs case and s 34(1) me limits – an update

49 Compliance Reform Forum

50 Changes to class 2 NIC

51 Recent submissions

Features

14 Tax policyNo vote? No tax! Helen Thornley refl ects on the extremes that taxpayers went through to try to change tax policyGENERAL FEATURE I

16 Tax at UniversityMastering tax Andy Lymer explains why universi es play an important role in the development of tax professionalsGENERAL FEATURE I

20 Legisla onThe tax mountain Patrick King considers how to cope with the abundance of the UK tax codeGENERAL FEATURE I

22 Discovery assessmentsSurprise discovery Harriet Brown considers the uncertain es that an HMRC discovery assessment can causeMANAGEMENT OF TAXES

25 BEPS – EU digital taskforceVirtual compliance Bill Dodwell looks at the dilemma faced by the new EU digital taskforce in discerning digital services compliance in a global marketplace

INTERNATIONAL TAX

26 Cross-border VATPublished diff erences Chris Lallemand and John Voyez consider cross-border compliance for VAT

INDIRECT TAX

28 Interna onally mobile employeesRelaxed workers Stephanie Symonds-Dye considers a welcome update on short term business visitors

EMPLOYMENT TAX

30 BEPSAround the world in 13 reports Joy Svas -Salee contemplates a period of unprecedented change for interna onal corporate tax law

LARGE CORPORATE TAX OMB

34 Back to basics: trust incomeHandbag secrets Fiona Walker explains the income tax posi on for se lors and benefi ciaries of trusts

INHERITANCE TAX

36 Back to basics: input VAT recoveryVAT’s your purpose? Natasha Siddiqi considers the challenges of input VAT recovery

INDIRECT TAX

38 Inducement paymentsSmiley’s People Keith Gordon discusses the Upper Tribunal’s decision in HMRC v Smith & Williamson Corporate Services Ltd and HMRC v Patrick SmileyEMPLOYMENT TAX

Branch events 54 Dates for your diary

Disciplinary 55 Findings and orders of the

Disciplinary Tribunal

www.taxadvisermagazine.com | March 2016 1

Education December 2015 Exams

11 ADIT Results

Book online at www.tax.org.uk/studenttrainingdays and www.att.org.uk/studenttrainingdays

Training Days run by tutors from BPP, Kaplan Financial and Tolley Tax Training.

These training sessions are intended for students taking the ATT and CTA Fine tune your examination skills for key topics by getting advice from expert tutors

CTA Programme

Saturday 12 March, 10:00 - 17:00

London

Price: £100

CTA Webinar

Saturday 19 March, 9:30 - 14:00

Price: £50

ATT Programme

Saturday 12 March, 10:00 - 17:00

London

Price: £90

Sitting the CTA or ATT examinations

in May 2016?AQ&

“ I feel that the skills I picked up in the session are

the difference between a pass

and a fail”

“ ... for individuals like myself who are self-studying this gives a much better understanding of the style of answers required”

“Fabulous training day,

excellent tutor and venue, very good value for money”

www.taxadvisermagazine.com | March 2016 3

Welcome from the [email protected], Tax Adviser

Details of the editorial advisory board can be found at www.taxadvisermagazine.com/editorialadvisoryboard

Chris Ma osEditor, Tax Adviser

Tax has become too

complex an area for any single individual tax adviser or general practitioner to know it all

Surprise discovery

Recent cases indicate that the discovery provisions do not give HMRC carte blanche to make an assessment and advisers must

consider whether one has been validly made. Harriet Brown considers the uncertain es that an HMRC discovery assessment can cause on page 22.

The tax mountainTax has become too complex an area for any individual adviser or general prac oner to know it all. It is essen al to engage tax specialists and ensure your CPD keeps up with the demands of your clients. Patrick King considers how to cope with the abundance of the UK tax code on page 20.

Mastering taxAs legisla on con nues to change the tax landscape, substan al numbers obtaining a university educa on in taxa on will be key to the evolu on of the tax profession. What can you expect of a university graduate in 2016? Andy Lymer explains on page 16 why universi es play an important role in the development of tax professionals.

VAT’s your purpose?CIOT prize winner Natasha Siddiqi is an example of a university postgraduate who has been a racted to a career in taxa on a er a brief introduc on in the poli cs degree she studied at Cardiff University. On page 36, Natasha provides a back to basics guide to input VAT recovery. She highlights how the process is not always clear cut for any business, large or small.

Around the world in 13 reportsRecommenda ons made in the G20/OECD BEPS project have been ra fi ed, approved and adopted. Most changes will apply regardless of a group’s

size, although the focus (and debate) so far has been on the larger mul na onals. Joy Svas -Salee contemplates a period of unprecedented change for interna onal corporate tax law on page 30.

Smiley’s PeopleKeith Gordon discusses the Upper Tribunal’s decision on the tax treatment of an incen ve payment made to a group of employees on page 38. HMRC considered a goodwill payment to a ract a team of investment managers as cons tu ng employment income. The case confi rms that client rela onships and connec ons are not themselves assets, even if they might in some circumstances be turned to account.

Technical teams: Newsdesk and Tax VoiceThe ATT, CIOT and LITRG technical teams have been busy commen ng on the many dra Finance Bill clauses. You can read all about these responses on page 40. The technical team is an important part of the ins tute’s and associa on’s engagement with parliament and policy-makers and also supports the technical commi ees and sub-commi ees. This month we are promo ng the Tax Voice supplement from our sub-commi ees. Each month features a diff erent area of tax. Issues so far include: Management of Taxes Voice, Indirect Tax Voice, and Property Tax Voice. You can fi nd out more from the adver sement on page 13.

Journal of The Chartered Ins tute of Taxa on and The Associa on of Taxa on TechniciansAr llery House, 11-19 Ar llery Row, London, SW1P 1RT. tel: 020 7340 0550The CIOT is a registered charity – No. 1037771; The ATT is a registered charity – No. 803480

EDITORIALEditor Chris Ma osDeputy Editor Stefan BlackPublisher Chris Jones

ADVERTISING & MARKETINGHead of Sales Charlo e Sco charlo e.sco @lexisnexis.co.uktel: 020 8212 1980Commercial Marke ng Director Sanjeeta Patel

PRODUCTIONProduc on Manager Angela WatermanProduc on Assistant Nigel HopeDesign Manager Ellio TompkinsDesigner Jo Jamieson

Offi ces LexisNexis, Quadrant House, The Quadrant, Su on, Surrey SM2 5AS.tel: 020 8686 9141

UK subscrip on rate 2016£100.00 for 12 issues

Europe subscrip on rate 2016 £132.00 for 12 issues

O/S subscrip on rate 2016 £206.00 for 12 issues

ATT student rate 2016 £48.00 for 12 issues

For Tax Adviser magazine subscrip on queries contact 0845 370 1234 or email [email protected]

For any queries regarding late deliveries/non-receipt please direct to Julie e Walker, Magazine Distribu on Administratorjulie [email protected]: 020 74002817

Reprints: Any ar cle or issue may be purchased. Details available from Charlo e Sco charlo e.sco @lexisnexis.co.uktel: 020 8212 1980

© 2016 Chartered Ins tute of Taxa on (CIOT).

Printed by Headley Brothers Ltd,Ashford, Kent.

This product comes from sustainable forest sources. Reproduc on, copying or extrac ng by any means of the whole or part of this publica on must not be undertaken without the wri en permission of the publishers.

This publica on is intended to be a general guide and cannot be a subs tute for professional advice. Neither the authors nor the publisher accept any responsibility for loss occasioned to any person ac ng or refraining from ac ng as a result of material contained in this publica on.

ISSN NO: 1472-4502

This, to my eye, is one

of the central tie-beams of the process. Our members operate in practice, largely in the OMB space and experience of that sphere is vital. We need to refl ect what our members do and support them and represent them technically. Our technical offi cers and members of the TSG do this ably

I never cease to be amazed by our technical offi cers. There are only two of them – Will Silsby and Alison Ward – yet they manage a

prodigious output. Over my presiden al year and especially the past few months, I have had many dealings with them.

I was bred and bu ered in technical tax during my training with Coopers & Lybrand (now PwC). It’s an area that I enjoy, so I understand and respect what Alison and Will do.

Their job is to provide the ATT with a solid tax technical base that we can use as an educa onal charity and a members’ organisa on. They carry on a fi ne tradi on that was started when one of our former presidents, John Kimmer, was appointed as the ATT’s fi rst technical offi cer in 2010. It had become clear that the volume of work was too great to be carried by volunteer members alone.

They a end mee ngs – lots of them, mostly with HMRC and also with our own technical steering group (TSG), where they act as co-ordinators.

They reply to consulta ons and not just a few – there was a blizzard of them in 2015 (with two Finance Acts) and the pace has not dropped this year. They sort them, rank them and reply to those that are relevant to our members.

The way this happens is as follows: a consulta on or dra Finance Bill clause will be issued by HMRC and our brave techies will decide whether it is of interest to us and select it accordingly. They will then ask for input from the TSG whose members will contribute to the response. Since 2013, we have expanded the consulta on process to include contributors – mainly ATT members who have expressed an interest in adding their input in par cular areas.

The TSG is an important beast at the ATT. It comprises members (and a few non-members) with good technical experience, who have a sense of public duty and who meet four mes a year in Ar llery House. Their only reward is coff ee and biscuits! They come from all over the realm. The TSG also counts some council members and other former ATT presidents such as Peter Gravestock and Yve e Nunn among its number. We have benefi ted greatly from their experience and knowledge.

This, to my eye, is one of the central e-beams of the process. Our members operate in prac ce, largely in the OMB space and experience of that sphere is vital. We need to refl ect what our members do and support them and represent them technically. Our technical

offi cers and members of the TSG do this ably.Either Alison or Will will dra a response and

members of the TSG will add their views. The duo will peer review each other’s work.

Then comes the ‘three eyes review’. The dra response will go to the TSG chairman for a fi nal review, so three people will have seen it before it goes out of the door (reputa onal ma ers will also be run past the president).

For years, Paul Hill has undertaken the fi nal review but, with his re rement, we have had to deal with this diff erently. So now, the TSG is co-chaired by Yve e and me and we review the technical output between us. Actually, we rather enjoy it! During January (yes, January!) we saw lots of technical consulta ons and dra FB16 clause comments out of the door and much midnight oil was burned with Yve e and I dividing the load. But I return to the central point: we all have extensive OMB experience and it helps us. But it would not be possible without our TSG members and especially our two technical offi cers (who also had to buy in extra supplies of midnight oil).

As a group, we also see press releases out of the door and these go through the same review process before being handed over to the PR and press team at Ar llery House for their comment and review.

There’s another thing. In 2014, I persuaded the techies to a end our ATT members’ conferences and joint tax skills courses with the AAT. This was a bit of a masterstroke; they have been a huge source of extra comment and the members have enjoyed talking to them and listening to them. Long may it last.

One fi nal note: I would encourage members to come onto TSG if they have an interest in technical tax (I mean who wouldn’t?). They can be ‘virtual members’ or contributors if they wish so they don’t have to a end mee ngs in London, so if that grabs you, please talk to Alison or Will.

In praise of technical offi cers and the technical steering group

Michael SteedPresident, ATTpresident@a .org.uk

[email protected] Fairpo

President’s [email protected] Steed

4 March 2016 | www.taxadvisermagazine.com

This lack of understanding

of tax has signifi cant implications

The fi rst me I wrote this column I expected to be drowned in hate mail but now that I am down to just one sack of the stuff a

day I am being let loose again. This me I expect that everyone reading it will simply want to pat me on the head in sympathy for my naivety but here goes!

Unless anyone reading this has been living under a rock for a while, they will agree that tax as a subject currently occupies more topical debate – and certainly more media coverage – than at any me since I’ve been prac sing (which my children assure me must surely predate the Boer war)!

And yet the quality of that debate is appallingly low.

I’m not talking here about the debate on tax avoidance, although that is clearly one part of it: I’m referring to the en re subject. Indeed, a principal reason why it is so diffi cult to have an intelligent debate about tax avoidance is that the level of knowledge and understanding of tax in general is so low. Although one could argue that the level of public debate about many issues is poor, I am focusing on tax since that is the area where we can have the greatest impact.

The CIOT is, of course, an educa onal charity and we do a great deal of work in trying to inform the tax debate (at all levels including working with schools) but perhaps all of us might think what more we can do?

This general lack of understanding on tax has signifi cant implica ons for our society. Some would argue that successive chancellors of all poli cal par es have faced less scru ny over some of their less straigh orward proposals than might have been jus fi ed because most of the electorate didn’t understand the implica ons. Gordon Brown’s aboli on of advance corpora on tax might be the most drama c example but we can all think of others.

At the same me, chancellors have been unable even to raise the possibility of some reforms because they know the resul ng headlines would be of the ‘scandal’ variety. Take VAT.

One way in which its regressive nature has been addressed is by zero-ra ng of par cular items. However, zero-ra ng also gives tax breaks to people who don’t need them. When my kids were growing up I benefi ted from their clothes being zero-rated even though I was fortunate enough to have aff orded the tax. An approach adopted by some countries is to standard-rate everything and address the impact on those on lower incomes through the benefi t system. This would raise an enormous amount of money and could be seen as a ‘fairer system’. I emphasise I am not necessarily advoca ng this approach. I

am merely saying it’s an example of a poten ally interes ng reform that could never be seriously debated because few would be able to look past their knee-jerk reac ons.

I recognise that most eyes glaze over as soon as tax is men oned and only headlines that can be portrayed as a scandal a ract a en on. But there is evidence that, whenever the proverbial person on the Clapham omnibus does spend the me to understand the issues, they see things diff erently. Our president, Chris Jones, gave a great example last month in his ar cle about how he was proud to be a tax adviser. The sub-text was he avoided ge ng beaten up by helping a member of the public understand the complexity of the tax issues involved. So perhaps we all need to do more to educate the public about tax as a form of self-preserva on in more ways than one.

A review of our examsOn the subject of educa on, it is essen al that our exams con nue to meet the needs of all our stakeholders while maintaining the high standards of which we are all so proud. Accordingly, a working party, chaired by former president John Bea e, will be reviewing our exam system, which was introduced in 2009. Any changes will not be introduced before 2018 (and probably not un l 2019).

With very best wishes to all.

More education in tax?

John PrestonVice-President, [email protected]

[email protected] Fairpo

CIOT Vice-President’s page

www.taxadvisermagazine.com | March 2016 5

ATT [email protected] Pettengell

I hope George Osborne doesn’t change the pensions tax rules in his Budget speech. There are many rumours in the press sugges ng

that tax reliefs will be reduced but I feel any change would have a nega ve impact on a fragile pensions industry.

The demographic me bomb, fi rst predicted back in the 1980s, is now on our doorstep and it’s important that the public have as much confi dence as possible in the pensions industry so that they will be encouraged to save for their future and avoid the fi nancial burden being placed on our children.

I have found that the public’s confi dence in pensions has increased since the introduc on of the freedoms and fl exibility set out in the Taxa on of Pensions Act 2014, so fi ngers crossed this confi dence will con nue a er the Budget.

In November, the Finance (No 2) Act 2015 received royal assent and clarifi ed the taxa on of money purchase pensions (defi ned contribu on pensions) le to a trust when the stakeholder dies.

For most money purchase pensions it is now possible to have a choice on death: to leave the pension to a trust, pay out directly to your benefi ciaries, or to cascade the pension down to family or friends, free of inheritance tax, within the framework of the pension scheme wrapper, known as Flexi Access.

For most money purchase pensions, if the stakeholder dies before they turn 75 the payment to a trust is tax-free. This provides the opportunity for succession planning and controlling the value of the assets a er death. The other choices are that the fund can be paid directly to the deceased’s benefi ciaries tax-free, or cascaded down to children, grandchildren, widow or friends free of inheritance tax in most situa ons. The recipients of a fl exi-access pension, known as nominees, can con nue drawing tax-free income and capital out of a tax-privileged regime, where all growth and most of the income generated from investments is also tax-free within the wrapper for the rest of their lives.

Developing a strategy becomes more complicated if a client dies a er the age of 75, but at least Finance (No 2) Act 2015 gives us clarity. I s ll believe that, for clients who want to leave their pension funds on death to a spouse, children, grandchildren or friends, a combina on of bequeathing the death benefi ts to a discre onary trust plus using fl exi-access rules to nominate a range of benefi ciaries within the pension scheme is the best pre-death strategy. However, it is essen al to document clearly what the client’s wishes are in a formal le er of wishes.

The payment to a trust if the client dies a er they have turned 75 is taxed at 45%. But there is an

income tax credit for the benefi ciary, so it may not be as bleak as this may ini ally sound. For example:

Clive dies aged 79. The value of his money purchase pension is £300,000. The pension administrator pays a lump sum to a trust and pays a tax bill of £135,000 (45% of £300,000), leaving £165,000 to be held by the trustees. In the next year, with the fund s ll worth £165,000, the trustees decide to distribute £20,000 to Clive’s son, Chris.

Chris will be treated for tax purposes as receiving £36,363 (£36,363 x 45% = £16,363; £36,363 - £16,363 would leave a net sum of £20,000). Chris will be assessed on £36,363 as income in the year of receipt. However, Chris is a basic rate tax payer and his liability on £36,363 would be £7,272. Since he has a tax credit of £16,363, represen ng the a ributed por on of the 45% paid by the pension administrator on the ini al payment to the trust, not only can he off set this credit against the liability of £7,272 (so he pays no tax on the £20,000 he has received) but he can also receive a further tax credit of £9,090 to set against other income.

If the benefi ts are not paid to a trust if death is a er age 75, the taxa on is straigh orward in that the benefi ciaries are taxed at their marginal rate on receipt of them.

The alterna ve, if the appropriate paperwork is in place before death, is that the pension fund can be passed down to children or grandchildren without a tax charge. But when the benefi ciaries take funds from their new fl exi-access pension, the withdrawals will be taxed on them as income.

The importance of a client planning a strategy during their life me, with their advisers’ help around the new rules, is fundamental to realising the best outcome for their client and their family.

The importance

of a client planning a strategy during their lifetime, with their advisers’ help around the new rules, is absolutely fundamental to getting the best outcome for their client and their family in the event of their death

In pensions we trust

Ralph Pe engellDeputy President, ATTpage@a .org.uk

6 March 2016 | www.taxadvisermagazine.com

@ourATT on

+BETTER TOGETHER

OVER 2,000 CIOT MEMBERS HAVE ALREADY CHOSEN TO BECOME JOINT MEMBERS OF THE ATT.

WWW.ATT.ORG.UK/JOINT

BRIEFINGS

8 March 2016 | www.taxadvisermagazine.com

Chairman: Anne FairpoContact details: [email protected] Branch website: www.tax.org.uk/European CIOT and ATT members and students connected to this branch: 461

FURTHER INFORMATION

The European Branch was founded in 1995 to provide a forum for Chartered Tax Advisers dealing with cross-border issues in Europe.

Regular conferences are held in several in capital ci es to update members and non-members on the interna onal tax developments in the UK and other EU member states –

Forthcoming conferences:

Friday 11 MarchParis ConferenceCMS Bureau Francis Lefevrewww.tax.org.uk/parisconference2016

Friday 23 September 9th Young Interna onal Corporate Tax Prac oners’ ConferenceLondon

Friday (14 or 21) October Milan Conference

Friday 20 November20th Cross-Atlan c & European Tax SymposiumLondon

CIOT/ATT

as well as those involving the OECD and other interna onal organisa ons.

Cases in the Court of Jus ce of the EU and tax ini a ves of the EU Commission are regularly examined at joint conferences in English with corresponding tax professional organisa ons such as the Interna onal Fiscal Associa on and other CFE affi liates facilitates. This

Spotlight on branches – European

BRANCHES gives members and non-members great networking opportuni es with UK and foreign tax prac oners in a s mula ng professional se ng.

Our Cross-Atlantic Symposium held with the International Fiscal Association, British branch, which is now in its 20th year, is a highlight of the international tax calendar in London and reflects our commitment to remaining at the cutting edge of cross-border taxation.

The Young International Corporate Tax Practitioners’ Conference is another successful initiative to enable practitioners in the early years of practice to engage with this challenging area of taxation and we recently held our sixth Indirect Tax Conference – VAT being, of course, the quintessentially European tax.

We look forward to welcoming CIOT and ATT members and students to our conferences, and also ADIT affiliates and students.

CIOT

EVENT

Fellows’ dinnerThe seventh Fellows’ dinner will take place at Haberdashers’ Hall on 13 July 2016. See www.tax.org.uk/fellowsdinner2016 or email Lisa Drakley at [email protected] to sign up for this popular and pres gious event.

Anne Fairpo

CIOT President’s Luncheon

EVENT

Former Chancellor Ken Clarke has become the 27th recipient of a CIOT honorary fellowship. The award was made at the ins tute’s annual President’s Luncheon at the elegant Drapers’ Hall in the City of London.

Making the award, CIOT president Chris Jones described Mr Clarke as one of the foremost poli cal fi gures of the past 30 years. He said the award recognised the structural and long-las ng changes to the tax system made during his four years as chancellor. These included the introduc on of insurance premium tax, airline passenger duty and landfi ll tax. He noted that, refl ec ng more recently on his me as chancellor, Mr Clarke had said: ‘Poli cs was diff erent then – people did not expect budgets always to be popular. They did expect budgets to have things they did not like in them.’

Accep ng the award, Mr

Clarke cheerily observed that the ins tute had ‘taken some me deciding’ to honour him,

given that it was 20 years ago since he had been at the Treasury. He said that being chancellor was the job he had enjoyed most in government, although he had had no exper se in taxa on and so had to draw on the knowledge of his adviser on this area, one Edward Troup, now HMRC’s tax assurance commissioner. He expressed his gra tude to the ins tute for honouring him.

The event was a ended by many leading fi gures from the world of tax, including Troup himself, shadow fi nancial secretary Rob Marris MP, and members of the public accounts commi ee and Treasury commi ee of the House of Commons.

Chris Jones again took the opportunity to promote the Bridge the Gap campaign, encouraging the profession to support the work of the tax advice chari es.

BRIEFINGS

www.taxadvisermagazine.com | March 2016 9

CIOT

More than 250 guests a ended the President’s Luncheon at Drapers’ Hall

CIOT

CIOT AGM

Members may remember that at last year’s annual mee ng a resolu on was passed to make a change to the Ins tute’s royal charter. The change enabled electronic vo ng and it is hoped that this will increase Members’ par cipa on in the AGM.

CIOT is delighted to confi rm that we are working with Electoral Reform Services (ERS) to deliver this.

The April edi on of Tax Adviser will provide informa on for members to vote by proxy electronically.

There will be an individual two-part code on the reverse of the address wrapper enabling members to vote easily on a CIOT pla orm on the ERS website. In addi on, members will receive an email from the ERS (and a reminder email) with

the required codes. Votes may also be cast through a link on that email.

If members prefer to vote by post using a paper proxy vo ng form, as previously, they will s ll be able to do this.The reverse side of the April Tax Adviser wrapper will also act as a paper proxy vo ng form. The only change will be that members are asked to return this to the ERS address shown on the form rather than to the CIOT.

If members have any queries on the vo ng process for 2016 email the secretary, Rosalind Baxter, at [email protected].

Members may vote in the AGM only if they have paid their subscrip on for 2016.

Rt Hon Kenneth Clarke CH QC MP receiving his honorary fellowship cer fi cate from CIOT President Chris Jones

Electronic proxy voting information

BRIEFINGS

10 March 2016 | www.taxadvisermagazine.com

COUNCIL

The CIOT’s council approved a new team of offi cers at its January mee ng. They will begin their new roles on 10 May and hold them for a year.

Bill Dodwell, Deloi e’s head of tax policy, will be the ins tute’s new president. He is currently deputy president and chairs the technical commi ee. Mr Dodwell said: ‘It will be a privilege to succeed Chris Jones as president in May. The CIOT’s role has never been more important in working to

CIOT announces offi cers for 2016–17CIOT

improve public understanding of the tax system and I look forward to con nuing to work with the CIOT offi cers and council in 2016–17.’ Mr Jones remains president un l May.

Vice-president John Preston will advance to deputy president in May. He is a former member of PwC’s global tax leadership team, responsible for external rela ons, regula on and policy. He is current chairman of the ins tute’s examina on commi ee.

He said: ‘Tax has never been more topical an issue than over

the past few years and the CIOT has been a key voice in the na onal debate. I look forward to working with my fellow offi cers in con nuing this.’

Ray McCann, a partner at New Quadrant Partners, will be the new vice-president. A former senior HMRC inspector, Mr McCann is also a former chairman of the joint CIOT/Associa on of Taxa on Technicians professional standards commi ee.

He said: ‘As the fi rst former member of HMRC to hold one of the senior offi cer roles in

the CIOT, I hope to con nue to build on the strong rela onship between the CIOT and HMRC as well as encourage more HMRC people to become chartered tax advisers (CTAs).’

It was also confi rmed that Glyn Fullelove will succeed Mr Dodwell as chairman of the CIOT’s technical commi ee. Mr Fullelove is group tax director at Informa plc and chairs the ins tute’s interna onal taxes sub-commi ee, one of the 11 that report to the technical commi ee.

John Preston Ray McCannBill Dodwell

Glyn Fullelove

APPOINTMENT

Jane Ashton, who became a member of the ATT in 1993, has had a career in tax that has spanned more than 30 years. She has served on the ATT council for ten years, the member steering group (previously known as the member and student services commi ee) for more than 18 years, and is a former chairman of its business development steering group.

Jane has had a role in signifi cant change projects, including the introduc on of the fi rst online services for self-assessment and corpora on tax. More recently she was a senior leader in the strategic

design authority team at HMRC.As well as a Fellow of

ATT, she is a member of the Associa on of Project Managers (APM) and an associate member of the Bri sh Computer Society (BCS).

Jane started as execu ve director on 1 March, replacing Andrew Pickering, who re red a er more than 22 years with the ATT. The execu ve director is the senior member of staff , overseeing the associa on’s work and providing strategic guidance to the leadership team.

Jane said: ‘I am looking forward to helping to lead the ATT through the next few years when we will see unprecedented change in the

tax world.‘I will be working with the

president and the council to make sure that we con nue to provide fi rst-class qualifi ca ons for our students and support for our members to enable them to thrive in this me of change.

‘I will be looking for ways in which we can improve knowledge of, and debate about, the tax system so that the ATT con nues to be the leading professional body for those providing UK tax compliance services.’

ATT president Michael Steed said: ‘Jane brings a wealth of relevant experience and understands our organisa on, its aims and its values.

‘I would also like to pay

tribute to Andrew Pickering. The ATT has changed enormously during Andy’s me at the helm – we have fi ve mes as many members as when he arrived and our technical and other ac vity has grown massively.

‘Andy’s steady hand and wise counsel have been real assets guiding us through this me of transforma on. In many

ways he was the ATT and I hope h e can now re re happily, knowing that our organisa on is in such safe hands.’

ATT appoints Jane Ashton as new executive director

Jane Ashton

ATT

ADVANCED DIPLOMA IN INTERNATIONAL TAXATION

Results and prizes December 2015

The Chartered Ins tute of Taxa on (CIOT), the principal body in the United Kingdom concerned solely

with taxa on, announced on 4 February the results of its ADIT (Advanced Diploma in Interna onal Taxa on) examina ons held on 8, 9 and 10 December 2015. There were 237 candidates in total. Candidates sat exams in 36 diff erent countries and territories, using the on-screen method.

169 students passed at least one ADIT exam in December 2015. A total of 42 students (including four with dis nc on) have completed ADIT in the last six months, and can now add the post-nominals ‘ADIT’ a er their name, including the fi rst students to achieve ADIT from

Tanzania and Uganda.The Institute President, Chris Jones,

commenting on the results said:‘I congratulate all candidates who

passed ADIT examinations in December. Achieving ADIT is a challenge, and demonstrates a high standard of knowledge and expertise in the theory and practice of international tax. Candidates who have passed one or more of the exams should feel very proud of their achievement.

‘When combined with the June 2015 exam results, the success of ADIT students si ng in December means that, for the fi rst me, more than 100 students have completed ADIT in the last twelve months.

The success of ADIT students around the world is an extremely posi ve development for the interna onal tax community, as more prac oners than ever before can now put the ‘ADIT’ le ers a er their name and apply the skills learned over the course of their ADIT studies in their day-to-day work.

‘It shows the growing awareness of the qualifi ca on in the business world and the success of innova ons such as on-screen tes ng.

‘We hope that those who have achieved the qualifi ca on will, if they are not already Chartered Tax Advisers (CTAs), choose to become Interna onal Tax Affi liates and thereby con nue their rela onship with the CIOT.’

Awards

The Heather Self Medal for the highest marks in Paper 1 – Principles of Interna onal Taxa onThe medal has been jointly awarded to Anne Margaret Gormley of Dublin, Ireland, who is employed by the Offi ce of the Revenue Commissioners, and Yulia Logunova of Luxembourg, who is employed by Rakuten Europe.

The Raymond Kelly Medal for the highest marks in Paper 2 – Advanced Interna onal Taxa on (Jurisdic on): United Kingdom op onThe medal has been awarded to Robert Bruce Mitchell Black of Cardiff , United Kingdom, who is employed by HMRC in Warrington.

The Worshipful Company of Tax Advisers Medal for the highest marks in Paper 3 – Advanced Interna onal Taxa on (Thema c)The medal has been awarded to Charlo e Bea e of London, United Kingdom, who is employed by Deloi e and sat Paper 3.01: EU Direct Tax op on.

The Wolters Kluwer Prize for the highest marks in Paper 3 – Advanced Interna onal Taxa on (Thema c): Transfer Pricing op onThe prize has been awarded to Yulia Logunova of Luxembourg, who is employed by Rakuten Europe.

Individual paper passes are as follows (for details of awards, distinctions and overall passes, please see the Awards, Distinctions and Overall Passes List, available at www.adit.org.uk/results):

Paper 1 – Principles of International Taxation

Ahabwe, A (Kampala, Uganda)

Ahamed, M F (Leicester, United Kingdom)

Akinola, D (London, United Kingdom)

Ali, I (Bradford, United Kingdom)

Aquilina, A (Gharghur, Malta)

Averyanova, V (Moscow, Russian Federa on)

Aziz, T M (Bangalore, India)

+ = Award Winner* = Dis nc on for overall performance in three examina on papers or two examina on papers and a thesis

Berberausaite, G (Adliswil, Switzerland)

Bha , F (Mumbai, India)

Brown, M B (Slough, United Kingdom)

Cerfontaine, F B J (London, United Kingdom)

Chakraborty, S (Navi Mumbai, India)

Chong, J C J (Uxbridge, United Kingdom)

Ciantar, D (Zebbug, Malta)

Ciurez, L A (Bucharest, Romania)

Clemente Lorente, E (London, United Kingdom)

Comia, V M D (Doha, Qatar)

Delivan, I (Bucharest, Romania)

Dhameja, S (Midrand, South Africa)

Dietz, N J (London, United Kingdom)

Dossani, A A (Karachi, Pakistan)

Drumgoole, H (Dublin, Ireland)

Evans, J P (London, United Kingdom)

Gibbons, E (Dublin, Ireland)

Gilmar n, E (Carlow, Ireland)

Gormley, A M (Dublin, Ireland) +

Hargreaves, V (Twickenham, United Kingdom)

Hibbombo, H (Kampala, Uganda)

Ho, C Y C (Kowloon, Hong Kong)

Hughes, K (Horley, United Kingdom)

Ikpaisong, I J (Abuja, Nigeria)

Ilin, A (Jeleznodorozny City, Russian Federa on)

Jain, T K (Delhi, India)

Kalogirou, Z (Nicosia, Cyprus)

Killilea, S (Clarenbridge, Ireland)

www.taxadvisermagazine.com | March 2016 11

Koteiche, S (Beirut, Lebanon)

Lakshmi Narasimhan, N (Chennai, India)

Lampiris, N (Paris, France)

Lees, F J (Enfi eld, United Kingdom)

Logunova, Y (Senningerberg, Luxembourg) +

Luvuuma, R (Kampala, Uganda)

MacLeod, S (London, United Kingdom) *

Maliko, W H (Maisons-Laffi e, France)

Mar Beso, I (Maidenhead, United Kingdom)

Masoud Ibrahim Mina, W (Cairo, Egypt)

Michaelides, A M (Nicosia, Cyprus)

Nath Varma, P (Vacoas, Mauri us)

Nitoiu, A (Bucharest, Romania)

O’Brien, D (Sheffi eld, United Kingdom)

Orr, J (Glasgow, United Kingdom)

Pavlou, M (Nicosia, Cyprus)

Raman, A K (New Delhi, India)

Romanovs, V (London, United Kingdom)

Ryan, S (Dublin, Ireland)

Scicluna, A (Zabbar, Malta)

Shah, T (Ahmedabad, India)

Simionescu, C (Sfantu Gheorghe, Romania)

Solayen, L (Rose Hill, Mauri us)

Stec, P (Warsaw, Poland)

Storr, A (London, United Kingdom)

Sykes, R (Congleton, United Kingdom)

Timohin, D (Toronto, Canada)

Ti er, P (Balrothery, Ireland)

Tusiime, M (Kampala, Uganda)

Udeci, N (Bucharest, Romania)

Van Lare, M E (London, United Kingdom)

Vongayi, F (Harare, Zimbabwe)

Walters, A I (Salford, United Kingdom)

Wray, M (Purley, United Kingdom)

Yong, N (Hartlebury, United Kingdom)

Zinovyeva, Y (Moscow, Russian Federa on)

Zysk, K (Warsaw, Poland)

Paper 2.09 – Advanced International Taxation (Jurisdiction): United Kingdom option

Baldwin, A L (Christchurch, United Kingdom)

Black, R B M (Cardiff , United Kingdom) + *

Brooks, T D (Warrington, United Kingdom)

Chau, G (London, United Kingdom)

Donaldson, A S (Beckenham, United Kingdom)

Han, P S S (London, United Kingdom)

Lanzoni, C (Onchan, Isle of Man)

MacLeod, S (London, United Kingdom) *

Magee, C L (Leeds, United Kingdom)

Pickering, D M (Birmingham, United Kingdom)

Paper 3.01 – Advanced International Taxation (Thematic): EU Direct Tax option

Bea e, C (London, United Kingdom) + *

Eaton Richards, A (Qormi, Malta)

Giusto, A (Mosta, Malta)

Grehan, J P (Windsor, United Kingdom)

Jouini, T (Croydon, United Kingdom)

Stanica, A (Bucharest, Romania)

Sykes, R (Congleton, United Kingdom)

Paper 3.03 – Advanced International Taxation (Thematic): Transfer Pricing option

Abazadze, K (Tbilisi, Georgia)

Agnew, M (Dublin, Ireland)

Ahtchieva, G V (Sofi a, Bulgaria)

Akiwumi, A L (Bromley, United Kingdom)

Ali, Y A (London, United Kingdom)

Azzopardi, A (Msida, Malta) *

Bajaj, M (Bangalore, India)

Barbu, M I (Birmingham, United Kingdom)

Basikoro, K (Birmingham, United Kingdom)

Berg, T (Sea le, United States of America)

Bhardwaj, N (London, United Kingdom)

Borg Sant, N (Mosta, Malta)

Bostrenghi, P (Galway, Ireland)

Butnaru, I (Bucharest, Romania)

Cahalane, N (Lucan, Ireland)

Campbell, G J (Aberdeen, United Kingdom)

Casey, N (Roundwood, Ireland)

Ceroni, M (Dublin, Ireland)

Chan, S Y (Singapore, Singapore)

Coughlan, D (Cork, Ireland)

De Alba, G (Madrid, Spain)

De Biasio, R (Lausanne, Switzerland)

Dus, Z (Poznan, Poland)

Ene, C (Bucharest, Romania)

Etheridge, J (London, United Kingdom)

Fernandez Guerra Fletes, A (Kingston upon Thames, United Kingdom)

Grennan, D (Dublin, Ireland)

Guthrie, C A (Kingston, Jamaica)

Hawkins, T W (Copenhagen, Denmark)

Invernizzi, B (Cremeno, Italy)

Ion, A A (Bucharest, Romania)

Ionescu, A D (Boulder, United States of America)

Jain, S (Jaipur, India)

Jain, T K (Delhi, India)

Jebena, A B (Addis Ababa, Ethiopia)

Kale, S (Amsterdam, Netherlands)

Karameta, A (London, United Kingdom)

Kaushal, H (Khanna, India)

Kikhonia Febby, C (Jakarta, Indonesia)

Korobova, I (St. Petersburg, Russian Federa on)

Kotwal, A (Houston, United States of America)

Kumar, M (Bangalore, India)

Le Page, M (St. Sampsons, Channel Islands)

Lewis, B R (Plymouth, United Kingdom)

L’Héri er, A (St-Aubin-Sauges, Switzerland)

Logunova, Y (Senningerberg, Luxembourg) +

MacLeod, S (London, United Kingdom) *

Maloney, L (Hyde, United Kingdom)

Milojevic, M (Belgrade, Serbia)

Muraka, G (Kampala, Uganda)

Nagarka , N (Bedford, United Kingdom)

Ngo, M B (Ho Chi Minh City, Vietnam)

Nicholson, E M (Hong Kong, Hong Kong SAR)

Oikonomou, K (Athens, Greece)

Okolonji, P (London, United Kingdom)

O’Toole, P A (Greystones, Ireland)

Parsad, J P D (Curepipe, Mauri us)

Pho ou, A S (Larnaca, Cyprus)

Power, D (Naas, Ireland)

Radi, C (Valcea, Romania)

Rainsford, A (Tunbridge Wells, United Kingdom)

Ramos Floering Junior, E (Cologne, Germany)

Ramtohul, A (Bon Accueil, Mauri us)

Rapo, M P (Helsinki, Finland)

Ricke s, K J (London, United Kingdom)

Scerri, A (Fgura, Malta)

Schubert, A (London, United Kingdom)

Scicluna, L (Sliema, Malta)

Sco , J B (Oxford, United Kingdom)

Seja , U (Jakarta, Indonesia)

Semikore, J (Johannesburg, South Africa)

Smythe, G (Croydon, United Kingdom)

EXAM RESULTS

12 March 2016 | www.taxadvisermagazine.com

Tax Voice is a new supplement from our

sub-committees brought to you by the

Tax Adviser Online team. Recent issues

include; Management of Taxes Voice,

Indirect Tax Voice and Property Tax Voice.

Find out more at www.taxadvisermagazine.com

SPECIALISMFOR YOUREXPERTISETECHNICAL

For informa on:Our goal is to make ADIT a truly interna onal qualifi ca on. As this vision is realised, interna onal tax prac oners moving from one country to another will share an interna onally recognised qualifi ca on that sets a global benchmark in interna onal tax exper se. The ADIT standard is supervised by an Academic Board of dis nguished and highly respected interna onal tax professionals.

ADIT is a modular qualifi ca on with three examina ons, of which Paper 2 or Paper 3 may be subs tuted by a thesis. Those who have completed all the elements to be awarded the qualifi ca on may use the designatory le ers ‘ADIT’. ADIT is a free-standing qualifi ca on which will not give the right to membership of the Chartered Ins tute of Taxa on. However, ADIT holders may apply to become an ‘Interna onal Tax

Affi liate of the Chartered Ins tute of Taxa on’. This ongoing link with the CIOT will en tle the individual to receive a number of benefi ts.

Email: [email protected].

Enquiries regarding these results should be directed to:Rory Clarke (ADIT Examina ons Manager Email: [email protected].

Soberanis Mota, R (San ago, Chile)

Solanki, K (Mumbai, India)

Storr, A (London, United Kingdom)

Stuart, A (Hong Kong, Hong Kong SAR)

Takuro, T (Lagos, Nigeria)

Thomas, B (Dubai, United Arab Emirates)

Tornea, I (Bucharest, Romania)

Travers, M (Dublin, Ireland)

Tucungwirwe, D (Kampala, Uganda)

Tusabe, J J (Kampala, Uganda)

Varfolomeeva, E (Nicosia, Cyprus)

Vartak, S U (Mumbai, India)

Wray, M (Purley, United Kingdom)

Zhang, N (Ashburn, United States of America)

Zuberi, S E (Karachi, Pakistan)

EXAM RESULTS

www.taxadvisermagazine.com | March 2016 13

TAX POLICY

© IS

tock

phot

o/C

SA-

Imag

es

Name Helen ThornleyPosition Senior Tax ConsultantCompany Armstrong WatsonEmail [email protected] le Helen Thornley MA (Cantab) FCA CTA TEP is based in Cumbria and specialises in private client work. She writes, blogs and tweets

on the interes ng aspects of old and new taxes.

PROFILE

14 March 2016 | www.taxadvisermagazine.com

If you want to make your voice heard on the subject of tax these days, there are plenty of ways to go about it. Indeed,

part of the role of the CIOT and ATT is to ensure members’ voices are heard at a na onal level, responding to consulta ons, and providing educated comment on our tax system.

Although we may not always get what we want, we do have the opportunity to make representa on.

But at the start of the 20th century, women had no such opportunity. Subjected to tax on their income, but with no vote and therefore no say over the government that taxed them, some suff ragists resorted to dras c ac on – tax resistance.

One such campaigner was Dora Montefi ore. She fi rst refused to pay her taxes during the Boer War. However, she gained li le a en on. For the issue of female suff rage, she decided to make a more public stand.

On 24 May 1906, having failed to pay the income tax demanded of her, Dora barricaded herself into her home in Hammersmith, west London, accompanied by her maid. Refusing to let in the Revenue bailiff s, a siege began.

Following rules that are not dissimilar today, the bailiff s could not enter by force, during the hours of darkness, nor through anything other than the door. It was six weeks before court permission was granted for a forced entry. During that me Dora kept the gates barred, passed the weekly wash over the back wall and spoke daily to crowds of people from her terrace at the front.

The publicity was huge. In the fi rst full day of the siege, more than 20 reporters arrived to interview Dora and her supporters. They even staged photos showing food being handed over the high walls that surrounded her house. Dora hung a red banner across the front of her home and news of her ac ons spread across the world.

The Women’s Tax Resistance League itself was formally created in 1909 under the mantra ‘No vote, no tax’. They drew inspira on from historical tax resisters such as John Hampden. Using an image of a ship in full sail they were referencing the ‘ship money’ case taken by Hampden against Charles I in 1637. ‘Ship money’

Helen Thornley refl ects on the extremes that taxpayers went through to try to change tax policy

was a tax imposed by Charles without parliamentary approval, which Hampden considered uncons tu onal. Hampden lost his case, but the defeat was so narrow that it encouraged wider resistance and, eventually, the tax was abandoned.

League members who refused to pay o en had their goods seized and sold at public auc on. These sales were used as an opportunity to promote the suff rage cause. In 1913 a scuffl e at one in London was even reported in the New York Times. During the incident, a suff ragist called Beatrice Harraden was hurt. As an author she was liable to income tax on the profi ts of her wri ng. She explained her refusal to pay by saying: ‘It is a culmina on of the government’s injus ce and stupidity to ask that we pay an income tax on income earned by brains, when they are refusing to consider us eligible to vote.’

While suff rage es like Emily Davison broke the windows of the chancellor of the exchequer’s house, tax resistance was generally considered a more ladylike method of direct ac on. In 1913 the then Duchess of Bedford refused to pay income tax and had a silver cup distrained. The daughter of the last, exiled, Maharaja of

the Sikh Empire, Princess Sophia Duleep Singh, was also a member of the tax resistance league. An ardent suff ragist, she lived in a grace-and-favour house of Queen Victoria. She resisted paying her dog, carriage and other licences.

The league had male supporters too, although some were more willing than others. Married women had been able to keep their income from their own work and investments since 1870, but their earnings were s ll added to their husband’s for income tax purposes. One schoolmaster in Clapton, east London, had li le op on over tax resistance when his wealthy wife refused to put him in a posi on to pay the liability generated by her income. He went to prison for her principles.

In 1914, the league members voted to pay their taxes on account of the war and the organisa on fi nally disbanded in 1918 when ini al electoral reforms were achieved.

These days, with HMRC’s new powers for direct recovery of debts, the modern day tax resister would probably struggle to mount such a public and sustained campaign as the league did. Engaging with consulta ons is a much safer op on.

No vote?

No tax!

BROADEN YOURHORIZONS

Essential Tax Handbooks for 2016 from Tolley

Leading tax experts choose Tolley time and time again for easy to use expert guidance, commentary on tax legislation and in-depth reference.

To view our complete collection of essential taxbooks for 2016, please visitwww.lexisnexis.co.uk/tax16.

RELX (UK) Limited, trading as LexisNexis. Registered office 1-3 Strand London WC2N 5JR Registered in England number 2746621 VAT Registered No. GB 730 8595 20. LexisNexis and the Knowledge Burst logo are trademarks of Reed Elsevier Properties Inc. © LexisNexis 2016 SA-1215-054.The information in this document is current as of January 2016 and is subject to change without notice.

TAX AT UNIVERSITY

16 March 2016 | www.taxadvisermagazine.com

H istorically, tax has been one of the traditional graduate professions. However, as the

world is changing, is there still a role for universities to help develop the next generation of tax professionals? Will direct entry schemes provide the bulk of the cohort in the future? Will higher degrees and the probably forthcoming degree apprenticeships in accounting or law, or even tax itself, be key suppliers of future CIOT and ATT members?

I am perhaps not the right person to argue against the proposition that universities should continue to be a key provider of future tax professionals – I

Mastering taxAndy Lymer explains why universi es play an important role in the development of tax professionals

am hardly unbiased! So, assume what follows is the case for universities remaining a key supply channel, albeit changed in key areas.

Universities have been central in developing people who form the basis of most of the UK’s professions, and tax is no different. If we use CIOT and ATT membership pipelines as a proxy of the current trend of graduate mix within the tax profession, in the past six months at least 63% and 70% respectively of new student applicants have been graduates. Meanwhile, 4% of CIOT applications have higher degrees (master’s or PhDs). However, that clearly suggests around

What is the issue?Are universi es likely to con nue to play an important role in developing the next genera on of tax professionals? What does it mean to me?

With mul ple routes into the tax profession, I need to know what I can expect of a university graduate – it may not be what I brought when I joined from a university, if I went to one. Is what they are off ering now what we need? Could a master’s degree be something of value to me and my staff ? What can I take away?

Is there a role I can play in shaping the next genera on of tax professionals studying at a university? Can I off er advice and support to my local university, or one I have a par cular link to perhaps as an alumni? They will probably welcome my contact

KEY POINTS

TAX AT UNIVERSITY

© IS

tock

phot

o/Po

nyW

ang

Other MSc courses with large tax elements are taught at: Bournemouth University (LLM interna onal tax law – linked to CIOT ADIT qualifi ca on): www. nyurl.com/gppdrvc. Bournemouth University (MSc/PGDip interna onal taxa on and fi nance – linked to CIOT ADIT qualifi ca on): www. nyurl.com/z67h23x. Manchester Metropolitan University (tax and fi scal policy): www. nyurl.com/h37egp3. Kings College London (interna onal tax law) (linked with ADIT): www. nyurl.com/h4e7hbf. LSE – (LLM in Tax): www. nyurl.com/gkrfl c6. University of Dundee (petroleum tax and fi nance): www. nyurl.com/hzp56kq. University of Oxford (MSc in taxa on) (specifi cally for those with experience in tax): www. nyurl.com/gr44soe. University of Exeter (MSc accoun ng and tax): www. nyurl.com/zjdu98k. This is suitable for those with some prior study experience of tax or those wishing to convert into tax or accoun ng a er comple ng an undergraduate course in a diff erent area. University of Birmingham (MSc by research (taxa on)) (linked with CIOT ‘fellowship by thesis’ route): www. nyurl.com/o27wogh. CIOT (Fellowship): www. nyurl.com/zchklwt.There are also opportuni es to study for a PhD at most universi es accommoda ng

tax academics.

TABLE – MSC COURSES

Name Andy LymerPosition Professor of Accoun ng and Taxa on, Deputy Dean: Birmingham Business SchoolOrganisation University of BirminghamTel 0121 414 8307Email [email protected] le Professor Lymer teaches and researches UK and interna onal

taxa on. He is co-author of Taxa on: Policy and Prac ce, the 22nd edi on of which was published in August 2015. He is Director of the Research Centre on Household Assets and Savings Management (CHASM) that produces research on the role of assets and their distribu on in people’s lives, from pensions to housing to fi nancial savings.

PROFILE

www.taxadvisermagazine.com | March 2016 17

one-third of new entrants are looking to build careers in tax without having gone through university.

Universities, therefore, are far from providing the only entry route into this profession. There have always been other entry routes into a profession that rewards talent regardless of educational background. However, a university education, whether related to tax or on a different and unrelated subject, has been the main route in.

Universities provide a chance for personal and technical development in the chosen field of study. They allow students to leave home, often for the

first time, into a fairly controlled halfway house to the ‘real world’, to develop their intellectual skills to become freer thinkers, and to explore the theoretical as well as the practical elements of their chosen subject. Good university programmes should provide a foundation that does not merely deliver ‘off the shelf’ technical capability, but also provides breadth of understanding and a grounding in principles and theory that can be applied throughout a subsequent career.

That is the theory anyway. In practice universities do this to varying extents; people experience different mixes of the technical and theoretical elements of their subject based not only on the institution they study at, but also the individual lecturers they are exposed to. What specific mix prospective students can expect has been difficult to judge from the packaging since the convergence of the polytechnics, with their bias towards technical skill development, and universities, which accentuated theory and principles. These days, neither technical skill nor theory-based courses intrinsically offer ‘better’ employment prospects because

all higher education establishments, of whatever type, meticulously plan their programmes and linked activities to benefit their ‘customers’.

The new teaching excellence framework (TEF) assessment, coming to a university near you soon, may well bring institutions closer together yet further, because it will require more information on teaching activities to made available to the market, detailing what happens within any particular ‘ivory tower’.

Universities have had to face up to a changing world as students, being the direct purchasers of services and products the institutions are selling, become customers in the fullest sense of the word. They are now responsible for settling the fees for their courses, give or take their eligibility for government loans, or another lender like the ‘bank of mum and dad’. Since March 2015, according to the Competition and Markets Authority, universities have fallen under consumer rights legislation, giving the buyer of a degree the same rights as if they were sold any other product or service. This makes developing and evolving courses during that period’s study more difficult for

TAX AT UNIVERSITY

18 March 2016 | www.taxadvisermagazine.com

universities.Within this dynamic environment,

what is offered as tax education by UK universities at present? How are tax education offerings affected? Perhaps, a little oddly, there are only two undergraduate degrees containing a substantive amount of the subject to warrant using the ‘tax’ in their course titles. Both degrees are at the University of Bournemouth: BA (hons) accounting and taxation (www.tinyurl.com/hhed3ky); and LLB in law and taxation (www.tinyurl.com/jrpentc). Perhaps it is unrealistic to expect 17-year-olds to opt for a tax-focused degree in significant numbers to make it a more mainstream offering. Degree apprenticeships might change this, with universities eyeing up such an opportunity – more of which later.

Our profession benefits from attracting people who have studied degree courses that span a range of professional disciplines, such as business, law, economics, or even an unrelated degree, before recognising the particular attractions of a career in tax. Many accounting, law and economics degrees will have at least one tax course required of students, with some offering a second.

At my institution, for example, students are lucky enough to be given an introduction to income taxes (UK personal and corporate tax) and consumption taxes (VAT) in a compulsory course on our accounting degrees, and an optional final year in comparative and international tax (with wealth taxes thrown in for good measure). Law students can take a revenue law course and those taking economics-related degrees will have various macro and public economics courses that offer different perspectives on the need for, and role and use of, taxation. We have also taught tax to social policy and politics students. This is typical of many ‘research-led’ universities and others that would not class themselves that way. In many cases, syllabuses of professional accounting bodies are followed closely for bachelor degrees that provide significant exposure to tax for students on those programmes.

It could be argued that such courses provide only limited exposure to tax in the ‘real world’, however, so fail to adequately sell tax as a career of choice. Offers of experience and short-term internships help to address this by becoming common additions within degree courses.

Many undergraduate degrees offer a chance to extend business placements. At Bournemouth University there is a 40-week placement option.

These have not always been a formal feature of accounting, economics or law undergraduate degrees at ‘research-led’ universities, with the exception of Aston and Bath. They do, however, appear at Coventry, Derby, De Montfort, Hertfordshire, Leeds Beckett, Manchester Metropolitan, and Westminster to name a few. However, this is changing quickly with more universities embracing the value of extended periods of work combined as formal parts of their programme offerings.

New university-level programmes called degree apprenticeships are being promoted by the Department for Business, Innovation & Skills. These require universities and employers to work together to form undergraduate, and perhaps higher-level, programmes that will create a middle way between conventional three- or four-year degrees and direct entry into work. These schemes are part of the government’s apprenticeships programme overhaul and an extension to the new higher apprenticeships (level 4 and 5 – up to foundation degree level) that cover many business areas, including accountancy and law. The schemes received a significant financial increase after announcement in the autumn statement of the apprenticeship levy/payroll tax that will come in to effect from April 2017, promising ‘three million apprentices by 2020’. Although degree apprenticeships (level 6 and 7 – undergraduate and master’s degree levels) will form only part of this ambitious aim, they are likely to be rolled out in subjects now without them, including accountancy, law and, more specifically, tax. This may significantly affect the ‘sandwich course’ market.

Beyond undergraduate degrees, there is a limited number of taught master’s-level programmes specialising in tax in the UK. This contrasts with continental Europe, the US and Australia where such courses are commonly available.

The full detail of what is taught in undergraduate tax degree offerings has not been examined for more than 15 years and has never been examined at master’s level study. The last study was made by this author and John Craner of the University of Warwick (www.tinyurl.com/gmwxh3r).

As part of the same series of articles, Angharad Miller (Bournemouth University) and Christine Woods published what I believe was the last significant study of UK employer needs of graduates in tax (www.tinyurl.com/jve8stk). Perhaps it is time to revisit both these areas, given all the changes that

have occurred since?Universities are now more open than

ever to engage with employers to think about how, together, they can improve the offering to the next generation of students. The role to which degree apprenticeships may play in this field is yet to be explored. Research into how greater use of internships and longer placements in tax may be of use to all parties is under-developed, despite compelling evidence for their use in other professions.

It may be that a university education is of value to an aspiring tax professional or to one mid-career who is professionally qualified but wishes to study their subject more deeply. However, the evidence for this ought to be reviewed. Although some exciting new opportunities are becoming available, for example with new master’s-level courses coming to the market, further research would help clarify what the right link should be between universities and the tax profession across all levels of study. In the UK we remain some way behind the range and scale of offerings that those in the rest of Europe, in North America and in Australia benefit where better links are in place. This does suggest the UK is missing opportunities others are benefiting from.

UK universities are experiencing significant change and this requires the tax profession – and those advising the next generation of employees – to continually rethink the transition paths. Universities are re-examining their roles in this process and need help to balance the pressures they are under from other directions to develop their offerings. They are now more open to employer advice and suggestions than in the past as they look to reshape their programmes to keep what is good from historical approaches to educating students and develop what is needed for the future.

Read more about PhDs in tax at www. nyurl.com/z9gvod6

FURTHER INFORMATION

www.taxadvisermagazine.com | March 2016 19

Robert Maas will give a résumé of the main points of the budget speechRobert is one of an increasingly rare breed, namely a tax specialist who

Cost: Member – £75Non Member – £85

Thames Valley2016 Budget Conference

Book online at:www.tax.org.uk/thamesvalley

Saturday 9th April 2016

QUALIFIES FOR

CPE/CPDPOINTS

£75for members

Half-Day post-budget conference at:Windsor Racecourse, Maidenhead Road, Windsor SL4 5JJ9:00am for 9:30am start, 12:30 finish

Friday 18 – Sunday 20 March 2016Queens’ College, University of Cambridge

Book online at: www.tax.org.uk/src2016

Conference fee: £695

Spring Residential Conference 2016

Programme topics will include:

The new dividend allowance and dividend tax – is it the end of the world as we know it?

CTA BA (Hons) ACA, RSM

What’s new in IHT? Chris Whitehouse MA BCL CTA (Fellow) TEP Barrister, 5 Stone Buildings

BSc (Hons) MPhil (Oxon) ARICS ATT,

FCA CTA (Fellow) ADIT, Gabelle LLP

MA (Oxon) CTA (Fellow) Solicitor,

Burges Salmon LLP

BA CTA (Fellow) ATT, Tolley

Ask the experts

MA FCA CTA, Thexton Training

Pete Miller CTA (Fellow), The Miller Partnership

DISCOUNTfor three or more from the same

OPENto non

members

LEGISLATION

20 March 2016 | www.taxadvisermagazine.com

Front linesThere have been earlier eff orts to make the tax system easier. In the mid-1990s, poli cians thought the answer lay in the way legisla on was wri en, which gave birth to the Tax Law Rewrite Project. Perhaps, though, a emp ng to clarify the tax code was always doomed to failure. Even Kenneth Clarke, then chancellor, said the work was ‘as ambi ous as transla ng the whole of War and Peace into lucid Swahili’.

Time was called on the project’s work in 2010 when it became clear to many that the intellectual front line should shi to simplifi ca on rather than redra ing parliamentary legalese.

That brought about the founding of the Offi ce of Tax Simplifi ca on (OTS) – to do just that, simplify tax.

The OTS has been illumina ng, especially when trying to clarify the state of the code.

A survey found that since 2009 the code has gone from 11,520 pages (then claimed to be the longest in the world) to 17,795 today. Further digging produced a count of 1,156 tax reliefs. As the OTS wrote, ‘…how can any single taxpayer know them all and so decide which one(s) to go for?’.

The ever-growing size of successive fi nance bills is the killer element. Finance Bill 1965 was about 250 pages long; in 2004 the bill ran to almost 650 pages. Now it averages about 400.

But this is not the whole story for the code. If you take out duplicated and repealed legisla on, according to the OTS, it reduces to 6,960 pages. Smaller, though s ll a daun ng read. The OTS concludes that complexity is not a good thing, but the length of the code is not necessarily the sole measure of complexity. In any case, it rightly says that what advisers seek is clarity.

Whole storySome comfort can be drawn from the OTS’s focus on understanding the scale and composi on of the code, but the truth for advisers is not so simple. Indeed, the

As an entry in the record books Britain’s tax code is not, perhaps, the outstanding achievement we

might want to claim. At an exaspera ng 18,000 pages, the tax code is claimed to be the longest in the world, whereas, say, Hong Kong’s tax compendium is, by comparison, the embodiment of brevity at just under 300 pages.

Indeed, even the mainstream press has taken no ce. Last year, Guardian columnist Marina Hyde wrote: ‘We can crap out tax legisla on like no other na on on earth.’ Not the most elegant appraisal, but no less true for being blunt.

With a code requiring the endurance of a trained athlete to master, advisers are presented with a document that is enormously challenging, if not in mida ng, to work with. Trainee tax advisers might wonder whether they have chosen the right profession. Clients would be forgiven for being reduced to tears.

This does not mean the code is insurmountable. But it does mean, as professionals, that we have to take a ra onal approach; acknowledging the implica ons it has for the way we deliver tax advice, the way we manage our prac ces, and how we tackle the documents themselves.

The tax mountainPatrick King considers how to cope with the abundance of the UK tax code

quan ty of pages is only the star ng point for a tax adviser.

Not only will advisers need to refer to the tax code, but also the statutory instruments, guidance from HMRC and independent providers and case law. A full understanding of a client’s needs involves a poten ally large research eff ort, linking these elements together as well as perhaps more than one act of parliament.

There is no single way of beginning to research a client’s tax ma er. For many, the places to begin are the online sources off ered by LexisNexis and CCH.

These enable one to read around the subject, cross-referencing to guidance and the legisla on. For advisers of a certain genera on (me included) books on the shelf will be the fi rst port of call, but the new genera on of digitally profi cient advisers will feel more at home with online sources.

Whatever the medium, the key to successful research is never to accept the fi rst answer. It will seldom be en rely right and can o en be wrong.

Practicalities of volumeFor those managing prac ces as well as advising clients there is an inevitable

What is the issue?Tax is too complex an area for any single individual tax adviser or general prac oner to know it all What does it mean to me?

You will need to know when to engage tax specialists and ensure your CPD keeps up with the demands of your clients What can I take away?

To paraphrase Donald Rumsfeld, it is important to know what you don’t know. So seek specialist advice if in doubt and make sure you have the appropriate level of CPD for your client base

KEY POINTS

LEGISLATION

Name Patrick KingPosition Partner, Head of TaxCompany MHA MacIntyre Hudson LLPEmail [email protected] le As a member of MacIntyre Hudson’s management board, Patrick is chairman of the fi rm’s tax strategy group, leading a team of

specialists who ensure clients have access to the best tax compliance services and tax mi ga on solu ons. Patrick’s own specialisms are capital tax planning for individuals, corporate restructuring and remunera on planning. He also advises clients on the tax implica ons of buying and selling their business.

PROFILE

A few years ago, MHA MacIntyre Hudson worked on an issue involving a non-UK domiciled individual who was claiming the remi ance basis. It proved an exhaus ng research eff ort to bring together all the elements needed to provide the client with the correct outcome.

The remi ance basis is a known area of complexity, but the client paid tax in the UK only on foreign income that was brought to the UK (remi ed here). The income was from a business source so it was not simply a case of declaring interest from a bank. What we needed to do was determine how much was regarded as remi ed and how much was taxable.

Surely that couldn’t be too hard?We started at the relevant parts of the Income Tax Act 2007 (ITA 2007). This directed