INDIA AND ITS TELEVISION: OWNERSHIP, DEMOCRACY AND THE MEDIA BUSINESS, Emerging Economy studies,...

14

NOT FOR COMMERCIAL USE India and Its Television: Ownership, Democracy, and the Media Business Nalin Mehta 1 Abstract With annual revenues of about $17 billion in 2012, India is among the world’s top 15 global media and entertainment markets. While much attention has been focused in recent years on India’s rise as an emerging economy, its great-power potential as the world’s largest democracy and the future trajectory of its growth but the role of India’s burgeoning media industry in this wider story is much less understood. For a country with the world’s largest newspaper market, second largest telecommunications market, third largest television market and second largest Facebook community, the virtual absence of India from most mainstream global communications studies within academia is strange. In revenue terms, India’s share of the global media sector still remains small but within the top 15 media and entertainment economies, only India has had consistent over-15 percent growth rates for years. Yet, outside of India, within the wider ambit of policy and international relations, few understand the crucial role Indian media play in the ebbs and flows of Indian politics and how central it is to India’s boisterous democracy. This article concentrates on Indian television and its future directions. Combined with the rise of the other device that has grown faster than toilets in India—the mobile phone—television has fundamentally reshaped Indian democracy and emerged as a critical social lever. This article outlines ownership patterns in Indian television, the divergences and commonalities across regional languages and what this means for India’s democracy. Keywords India, Indian television, Indian media, ownership patterns, regional languages and media in India, Indian politics and democracy, digital media Article Emerging Economy Studies 1(1) 50–63 © 2015 International Management Institute SAGE Publications sagepub.in/home.nav DOI: 10.1177/2394901514562304 http://emi.sagepub.com 1 Associate Professor, Shiv Nadar University, National Capital Region, Delhi Corresponding author: Nalin Mehta, 1743, ATS Village, Sector 93A, Noida, 201301 Uttar Pradesh, India. E-mail: [email protected] In October 2012, owners, chief executive officers (CEOs), and leaders of some of India’s biggest media groups met in a five-star hotel in Delhi to confabulate for two days on how to shift gears in their business, take advantage of the tectonic shifts in the global economy, and turn India into a major global player in this sector. With annual revenues of $17 billion, India was among the top 15 global media and entertainment markets at the time, but the aim of this elite group was to figure out a roadmap for taking it to the top three in the list, with up to $100 billion in revenues. 2 With India’s media grandees rubbing shoulders with global media CEOs, management gurus, and the leading lights of cultural studies like Arjun Appadurai, this was a rare closed-door business meeting designed for introspection, rather than self-promotion. It was also a rare occasion to think outward for expansion, rather than inward at the million internal struggles which normally 2 CII India-The Big Picture Summit, October 29–30, 2014.

-

Upload

timesofindia -

Category

Documents

-

view

0 -

download

0

Transcript of INDIA AND ITS TELEVISION: OWNERSHIP, DEMOCRACY AND THE MEDIA BUSINESS, Emerging Economy studies,...

NOT FOR COMMERCIA

L USE

India and Its Television: Ownership, Democracy, and the Media Business

Nalin Mehta1

AbstractWith annual revenues of about $17 billion in 2012, India is among the world’s top 15 global media and entertainment markets. While much attention has been focused in recent years on India’s rise as an emerging economy, its great-power potential as the world’s largest democracy and the future trajectory of its growth but the role of India’s burgeoning media industry in this wider story is much less understood. For a country with the world’s largest newspaper market, second largest telecommunications market, third largest television market and second largest Facebook community, the virtual absence of India from most mainstream global communications studies within academia is strange. In revenue terms, India’s share of the global media sector still remains small but within the top 15 media and entertainment economies, only India has had consistent over-15 percent growth rates for years. Yet, outside of India, within the wider ambit of policy and international relations, few understand the crucial role Indian media play in the ebbs and flows of Indian politics and how central it is to India’s boisterous democracy. This article concentrates on Indian television and its future directions. Combined with the rise of the other device that has grown faster than toilets in India—the mobile phone—television has fundamentally reshaped Indian democracy and emerged as a critical social lever. This article outlines ownership patterns in Indian television, the divergences and commonalities across regional languages and what this means for India’s democracy.

KeywordsIndia, Indian television, Indian media, ownership patterns, regional languages and media in India, Indian politics and democracy, digital media

Article

Emerging Economy Studies1(1) 50–63

© 2015 InternationalManagement Institute

SAGE Publicationssagepub.in/home.nav

DOI: 10.1177/2394901514562304 http://emi.sagepub.com

1 Associate Professor, Shiv Nadar University, National Capital Region, Delhi

Corresponding author: Nalin Mehta, 1743, ATS Village, Sector 93A, Noida, 201301 Uttar Pradesh, India. E-mail: [email protected]

In October 2012, owners, chief executive officers (CEOs), and leaders of some of India’s biggest media groups met in a five-star hotel in Delhi to confabulate for two days on how to shift gears in their business, take advantage of the tectonic shifts in the global economy, and turn India into a major global player in this sector. With annual revenues of $17 billion, India was among the top 15 global media and entertainment markets at the time, but the aim of this elite group was to figure out a roadmap for taking it to the top three in the list, with up to $100 billion

in revenues.2 With India’s media grandees rubbing shoulders with global media CEOs, management gurus, and the leading lights of cultural studies like Arjun Appadurai, this was a rare closed-door business meeting designed for introspection, rather than self-promotion. It was also a rare occasion to think outward for expansion, rather than inward at the million internal struggles which normally

2 CII India-The Big Picture Summit, October 29–30, 2014.

NOT FOR COMMERCIA

L USE

Mehta 51

besiege the Indian media sector. This was important not just for those who are interested in media per se or rise and fall of individual companies but because of the larger role media industries play at the center of large economies, as shapers of identity and as levers of social power and democracy.

Much attention has been focused in recent years on the rise of India as a global economy, its great power potential as the world’s largest democracy, and the future trajectory of its growth. The role of India’s burgeoning media industry in this wider story is much less understood. For a country with the world’s largest newspaper market, second-largest telecommunications market, third-largest television market, and second-largest Facebook community, the virtual absence of India from most mainstream global communication studies within academia is strange (Mehta, in press).

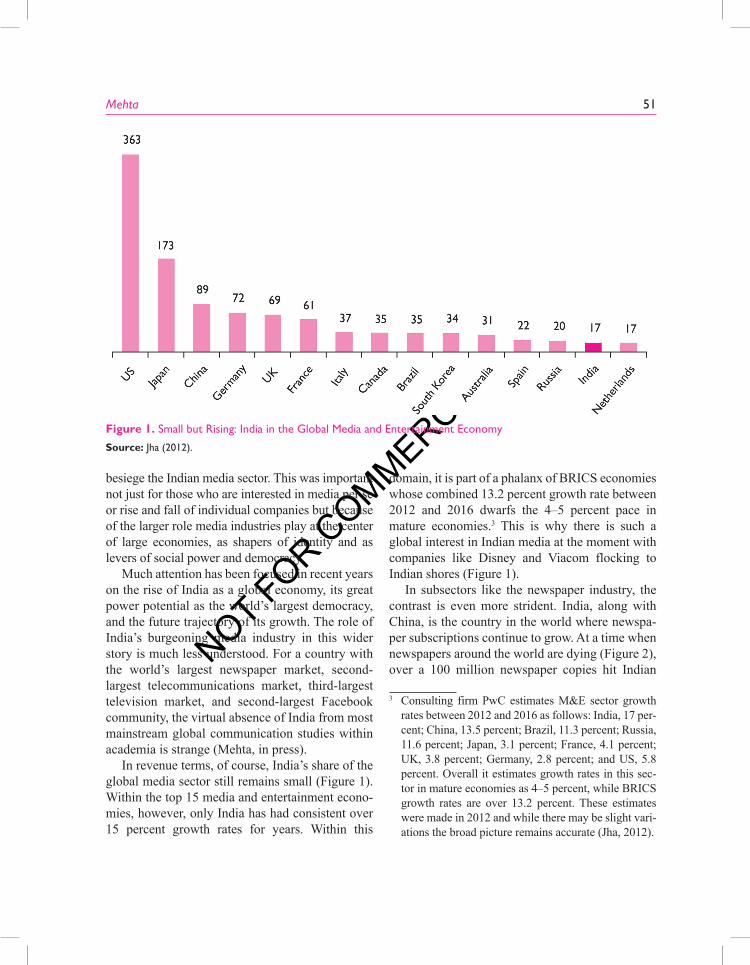

In revenue terms, of course, India’s share of the global media sector still remains small (Figure 1). Within the top 15 media and entertainment econo-mies, however, only India has had consistent over 15 percent growth rates for years. Within this

domain, it is part of a phalanx of BRICS economies whose combined 13.2 percent growth rate between 2012 and 2016 dwarfs the 4–5 percent pace in mature economies.3 This is why there is such a global interest in Indian media at the moment with companies like Disney and Viacom flocking to Indian shores (Figure 1).

In subsectors like the newspaper industry, the contrast is even more strident. India, along with China, is the country in the world where newspa-per subscriptions continue to grow. At a time when newspapers around the world are dying (Figure 2), over a 100 million newspaper copies hit Indian

3 Consulting firm PwC estimates M&E sector growth rates between 2012 and 2016 as follows: India, 17 per-cent; China, 13.5 percent; Brazil, 11.3 percent; Russia, 11.6 percent; Japan, 3.1 percent; France, 4.1 percent; UK, 3.8 percent; Germany, 2.8 percent; and US, 5.8 percent. Overall it estimates growth rates in this sec-tor in mature economies as 4–5 percent, while BRICS growth rates are over 13.2 percent. These estimates were made in 2012 and while there may be slight vari-ations the broad picture remains accurate (Jha, 2012).

Figure 1. Small but Rising: India in the Global Media and Entertainment Economy

Source: Jha (2012).

NOT FOR COMMERCIA

L USE

52 Emerging Economy Studies 1(1)

streets every morning. Regional markets like Oriya, the language of the ‘backward’ eastern state of Odisha, generate 3.5 million newspapers a day, and Marathi and Telugu generate more than 6 mil-lion newspapers each. Such numbers exceed the newspaper subscriptions in countries such as Canada and Australia.4

Numbers like these illustrate the size and scope of India’s media. Yet, outside India, within the wider ambit of policy and international relations, few understand the crucial role Indian media play in the ebbs and flows of Indian politics, and how central it is to public debate in India’s boisterous democracy.

4 Data from Robin Jeffrey, Visiting Research Professor, National University of Singapore. Prof. Jeffrey has since the 1990s maintained the most accurate and up-to-date chart of national and regional newspaper circulations in India combining data from various sources.

This article concentrates on Indian television and its future directions. In September 2009, India’s then prime minister, army chief, and national security advisor launched a coordinated attempt to douse television speculation about alleged Chinese military incursions on the disputed eastern border. All three leaders issued denials after days of intense focus by India’s private TV news networks which had accused the government of hushing up Chinese aggression. Both Indian and Chinese governments denied the incidents (China Foreign Ministry, 2009), but such was the heat created by what one editor called ‘war-mongering TV channels’ (Gupta, 2009) that then National Security Advisor M.K. Narayanan appeared on a television interview on CNN-IBN with a dire warning:

I don’t know what the reason is why there is so much reporting … but I think this is a national security issue … the more you raise people’s con-cerns, the tensions could rise and we would then

Figure 2. Estimated Change in Newspaper Revenues: Year on Year (2007–2009)

Source: Nielsen and Levy (2010).

NOT FOR COMMERCIA

L USE

Mehta 53

be facing a situation of the kind that we wish to avoid [sic.]…. It could create a problem of a kind and I have been through [in] [the] 1962 [war]… then of course we didn’t [then] have the media of this kind….

What we need to be careful of is that we don’t have an unwarranted incident or an accident of some kind, that’s what we are trying to avoid. But there’s always concern that if this thing goes on like this someone somewhere might lose his cool and something might go wrong. (CNN-IBN, 2009)

That this statement came in a television interview was no accident. The government was asking India’s TV networks to tone down. Television was seen to have largely led the debate; print was seen to have followed. Anecdotal evidence certainly supported this view. Among others, B.V. Rao, a former TV news editor and media columnist, noted that the government was asking the media to ‘back off’ because ‘this time the frenzy seemed to have spread even to print [from television]’ (Rao, 2009).

Whether the allegations about border incursions were true or not is outside the scope of this arti-cle. Such shadowboxing between the media and the government on tricky issues is part of every democracy, and India is no exception to that. It is pertinent for our purposes, however, that this was the second time in the year that India’s TV news networks were accused of side tracking bilateral relations with another country.

When a group of Indian students were injured in a racist attack in Melbourne in May 2009, the story was initially virtually ignored in the national newspapers. It was first given prominence when Times Now, one of the most popular 24-hour satellite news channels in the country, ran an emotional campaign around it. The network made the story its first headline and ran a sustained campaign about injured Indian pride. Times Now’s commercial success has been built on an aggressive policy of pursuing stories with a nationalist angle—especially those involving nonresident Indians; a hard line on security, especially on Pakistan and

China; and the notion of a powerful India, an India that is no more a pushover. Television ratings show that its audiences like that tone, and this, in turn, affects its choice and treatment of stories. The Australian racism story fitted its template very well. Once it got traction and the Ministry of External Affairs was forced to react, every other media group, television and print, followed suit. This is the nature of the media—the story had become too big for others to ignore (Wade, 2009).

The intense focus meant that every attack on an Indian thereafter—even ones that were part of general crime patterns and not racist—were framed through the same lens. Once such reports would have been relegated to the inside pages of newspapers or, at best, would have made it to a box item on the front page. Now, they became part of an ongoing media discourse about a resurgent India that would not take things lying down.

At a time when Indo-Australian relations had been on the upswing after years of historical mistrust, the story upset the trajectory of bilat-eral relations, with the Indian Foreign Minister, facing middle class anger in television studios, issuing warnings to Australia. The central role of television in this discourse was best summed up in a tongue-in-cheek account published in the Hindustan Times:

Other countries have think-tanks, India makes do with prime-time chat shows...

To media consumers who got initiated into Australian society this past week, that country must seem formidably scary, almost the fastness of Ming of Mongo. There was discussion on a ‘white Australia’ policy that went out of business 30 years ago. Clips of Australian cricketers sledg-ing or arguing with Indian, West Indian and Sri Lankan cricketers were juxtaposed with report-age of attacks on Indian students, as if one were dealing with a nation of all-purpose bigots.

On one television show, an anchor said Australia had been preceded by attacks on Indians in Germany, the United States and Idi Amin’s Uganda and wondered why the world hated

NOT FOR COMMERCIA

L USE

54 Emerging Economy Studies 1(1)

Indians. This is a happy universe of nuance-free non sequiturs.

Even so, India’s television-propelled middle class opinion is a clear and present reality. It will shape discourse that will hassle and harangue governments, demand instant action and colour-ful rhetoric. In some senses, the drama outside the Delhi airport during the IC-814 hijack was a teaser trailer. This is the new India. Now even Kevin Rudd (then-Australian prime minister) knows that. (Malik, 2009)

For our purposes, it is immaterial whether the tel-evision coverage was right or wrong, nuanced or simplistic, sensationalist or measured. The point is that both the examples cited above underlined the centrality of 24-hour private satellite news as a new factor in the Indian political and social matrix. In both cases, the discourse of Indian television had serious consequences for domestic policy imperatives and an impact beyond India’s bor-ders. A detailed study of Indian news television’s impact on foreign policy is still to be written, but it is important to reiterate how recent the phenom-enon of private TV news is.

This is a country where as late as 1994, a prime minister canceled the launch of a new state TV channel because it promised to show live cur-rent affairs programs. Narasimha Rao’s reason-ing could not have been clearer: ‘We cannot have live broadcasts. It is too dangerous,’ he said, while cancelling the launch of DD 3 in October 1994 (Ghose, 2005). The fear was that there would be no way of controlling anybody from saying anything against the ruling Congress on live programming. Historically, in India, control over television has been central to the state’s self-image—broadcast-ing’s principal objective was to ‘display and enact government control’—and live television threat-ened to break down the edifice on which Indian television had been built.

Despite the best efforts of the Indian state to resist the forces of change in the 1990s, India has gone in two decades from just one state-owned

television network to over 800 licensed private satellite channels. Most Indians, of course, did not have TV sets till the mid-1990s. There were only a grand total of 55 licensed TV sets in India when Nehru died in 1964, about a lakh when Indira Gandhi imposed the Emergency in 1975, and a lit-tle over 2 million connections at the time of the Asian Games in 1982. This is when the needle first began shifting toward a truly national medium and as many as 34 million families owned TV sets by the time Manmohan Singh opened up the economy in 1991 (Mehta, 2008, pp. 31, 42–43). As a percentage of the population, though, this was negligible. By 2014, however, about 65 per-cent of Indian households owned a television set (MPA Asia, 2014) though more than half still did not have access to an indoor toilet.5

Consider this: in 1992, if you divided India’s population (Registrar General of Indai, 2001) by the total number of television sets in the country, the number of people clustering around a set would have been a little over 26.6 By 2014, that ratio had come down substantially to just about 8 people per television set, despite a substantial increase in the population.7 In a little over two decades, the total number of Indian television households jumped almost five times to reach 160 million.8 It made India the world’s third largest television market,

5 In July 2014, over 130 million Indian households did not have indoor toilets, 72 percent of rural Indian still defecated behind bushes and nearly 600 million were living without toilets (The Economist, 2014).

6 India had 34,858,000 television sets in 1992 (Joshi & Trivedi, 1994, p. 16).

7 There were estimated to be 160 million television sets in India by 2014. The population had gone up to 1.26 billion according to Census and World Bank data.

8 The Indian Space Research Organisation estimated 34 million TV sets in 1991, the National Readership Survey in 2006 estimated 112 million television sets in the country, and industry estimates in 2014 placed the number of television sets at 160 million.

NOT FOR COMMERCIA

L USE

Mehta 55

just behind China and the United States (PwC-FICCI, 2008, p. 36).

There has been a simultaneous increase in what people can actually see on these TV sets. In 2000, India had 132 television channels, by 2014 this number had gone up to over 800 licensed channels in various languages.9 The first Indian 24-hour news channel only started broadcasting in 1998, but by 2014, almost half of the 800 or so licensed channels in India were broadcasting news in 15 languages and over 150 (in 11 languages) were 24-hour news channels. Even the staid public broadcaster Doordarshan, which ran only two channels in 1997—DD I and DD II—was operating as many as 35 channels by 2014.10 I have detailed the political, economic, and social reasons behind the remarkable rise of private Indian satellite television in India on Television, but the massive increase in numbers sharply illustrate the massive changes in Indian broadcasting (Mehta, 2008).

The power of television is even more potent now with the rise of the other device that has grown faster than toilets in India: the mobile phone. Almost every Indian had a mobile phone by 2014 and the marriage between the internet

9 2000 estimate is by Uday Shankar, CEO, Star India. 2014 channel data are from Total Number of TV Channels Goes up To 813, 2014; Telecom Regulatory Authority of India,2014’. While TRAI reported 793 channels licensed by Ministry of Information and Broadcasting in July 2014, this number had reached as high as 877 in 2013 but several licenses were canceled by the Ministry in 2013 due to lack of use. At the same time, other sources from Ministry of Information and Broadcasting in the same time period, reported a total of 798 licensed channels. ‘Total number of Permitted TV channels in India as of July is 798, I&B Ministry gave clearance to three New Channels’, August 5, 2014, http://telecomtalk.info/total-number-of-tv-channels-in-india-as-of-july798/120527/ (accessed on August 6, 2014). The numbers keep fluctuating with several applications pending with the Ministry.

10 Figures from Sircar (2014).

and the mobile phone—still very nascent but large enough to be revolutionary in scope—had begun to fundamentally reshape the nature of communications and media businesses. The smarter television executives have already begun redefining some of their leading soap operas—changing plot lines and characters—based on the real-time reactions they get from Twitter chatter driven primarily through mobile phones.11 By 2013, more than 227 million were using mobile phones or tablets to watch television, see films, listen to music, or to see cricket (Kohli Khandekar, 2013). More than half the Google downloads in the country were for videos and this meant that television was becoming much more personalized and reaching much further than ever before.

The figures tell a story of India’s TV boom. But it is only half of the story. Within India, the growth of the medium unleashed new battles over control, over media ownership and over who ultimately controlled the public sphere. These questions are especially important for a profession, whose very existence depends on the rhetoric of public service and probity. Its rise has had significant implica-tions for Indian democracy, and its daily travails as a business, as a cultural commodity, and as a significant lever of society offer an unparalleled view into the daily theater of India.

Television touches virtually everyone in Indian society, but in the din of daily headlines, it is important to delineate some fundamental ques-tions. Who really owns Indian television? What are the patterns of control nationally and across regional languages? Are there any commonalities across languages and regions? Can we discern underlying trends that drive the business and what are the politics? At a time when many believe, on one side, that corporate India is buying up Indian

11 Uday Shankar, CEO Star TV and Sudhanshu Vats, Group CEO Viacom 18 Media in conversation on panel on ‘Engaging a Billion Consumers in the Media and Entertainment Industry’, FICCI Frames March 12, 2013.

NOT FOR COMMERCIA

L USE

56 Emerging Economy Studies 1(1)

television and, on the other, that ownership is irrelevant because digital media have created an information revolution which no one can control, these questions are at the heart of the debate about modern media. These are the questions this essay seeks to answer.

Ownership Patterns in Indian Television Since 2008, India’s television map has changed significantly with a spate of buyouts and moves toward consolidation. This phase has coincided with a greater corporatization of the industry, the availability of greater capital for expansion, and with a realization that it is the regional markets where the primary growth lies.

The first thing that stands out when one looks at the ownership map of India is that five players dominate the TV entertainment business: Star, Zee, Sony, Sun, and Viacom. Between them, by 2012, these five big players ran about 10–12 percent12 of all channels in the country and controlled about 61 percent of the viewing market (see Figure 3).

The second thing that stands out is how little they control. The 61 percent viewing market share of the big five companies might seem like a lot, but not when one knows that this is the lowest when compared with other countries with big television industries.

The top five companies in the United States control as much as 69 percent of the cable TV market (and the top six companies almost 80 percent, if you calculate by revenue share) (Noam, 2009, p. 101); the top five in the United Kingdom and Australia over 80 percent, and the top five in Canada almost 80 percent. In Japan, this is as high as 92 percent, in Brazil, 77 percent, and in Italy and Mexico, the top two companies control almost everything (Figure 4). In international terms, Indian television remained a highly competitive and tough market, despite the trend toward consolidation.

Looking deeper into the Indian figures, no one network controls more than 20 percent of the national market. Only Star approached this mark in 2012, while the other four hovered between 6 and 14 percent (see Figure 3). The share of the big five is distributed across nearly 100 individual

Percentage Viewing Share of TV Market in 2012: Big Five

Network All India

Hindi Andhra Pradesh

Karnataka Kerala Maharashtra West Bengal

Tamil Nadu

Star 19.0 22.5 4.4 13.7 32.8 21.6 25.5 7.6

Zee 14.0 16.7 11.5 9.6 1.3 19.0 21.8 3.2

Sony 12.1 15.8 3.2 3.5 1.7 15.3 10.5 1.6

Sun 10.5 0.2 26.3 36.9 28.5 0.5 0 47.9

Viacom 6.6 8.8 1.6 1.9 0.9 7.6 5.7 0.4

TOTAL 61.0 64.0 47.0 65.6 65.2 64.0 63.5 60.7

Figure 3. Not Quite Masters of the Universe

Source: TAM CS4 data for January–September 2012.13

12 In October 2012, Star TV broadcast 17 channels, Viacom 6, Sony 9, Sun Network 21, and the Zee Network 38. This is a total of 91 which is 31 percent of the 831 channels officially licensed at the time. This figure does not include the news channels controlled by Network 18.

13 Data from TAM, compiled and supplied by R. Padmasri, Star TV.

NOT FOR COMMERCIA

L USE

Mehta 57

channels, and if you drill down by language and by channel, the picture gets much more complicated.

Two distinct models emerge. The first is marked by intense competition and fluctuating fortunes. Four language groups have remained locked in close contests where leads are slim: the Hindi-speaking market, Kerala, West Bengal, and Maharashtra. Star is the leader in these languages, but its next-best competitor in each group is within 5–6 percentage points. This is especially true in Maharashtra where Star has remained neck-and-neck with Zee. The key feature here is that, with the exception of the Asianet channel in Kerala, which alone accounts for one-fifth of the local market for Star, no single channel (as opposed to media group) in any language is so decisively ahead of its rival to be uncatchable. For example, the largest channel in Hindi hovers between 6.5 and 8.5 percent of the

market share, in Marathi between 5 and 7 percent, and in Bengali between 12 and 15 percent.

Leadership in these languages is less about having one big dominant channel and more about building it incrementally by running a diverse line-up of different kinds of programming: general entertainment, music, movies, children-focused channels. This is where conglomerates with diverse offerings and deep pockets have a built-in advantage and this is why standalone channels are difficult to sustain.

The second model is one of complete network dominance. This is the case in Andhra Pradesh, Karnataka, and Tamil Nadu where Sun has held unparalleled sway. It is six times the size of its nearest competitor in Tamil Nadu and more than twice the size of the second-largest networks in Karnataka and Andhra. In contrast to the states with

Country-wise Percentage Viewing Share of Top Five Companies: Select Countries

Figure 4. Why India is Better Off

Source: International figures from Analysis Group, Vertical Integration in TV Broadcasting, and Distribution in G8 Countries and Certain Other Countries (August 7, 2012). http://dwmw.files.wordpress.com/2012/08/analysis-2012-vertical-integration-tv-canada.pdf (accessed on September 30, 2012).

NOT FOR COMMERCIA

L USE

58 Emerging Economy Studies 1(1)

close competition, Sun’s dominance in its three big states is powered by the numero uno status of its flagship channels. In Andhra, Sun’s Gemini TV is nearly twice the size of the next big network Zee Telugu. The same applies in Karnataka, where Uday TV is nearly double its challenger Suvarna TV. And for historical reasons, which go to the heart of how its politics has evolved, Tamil Nadu is a class apart. In 2012, Sun TV’s astounding 31.5 percent share in its original home-ground dwarfed the next best of Vijay TV which stood at a mere 6.5 percent.

Linguistic boundaries and cultural and political nuances give Sun such a leadership in these states, but it is precisely these boundaries and nuances that prevent it from expanding outside its southern bastions and keep its national share where it is.

What does all this amount to and how does Indian ownership diversity match global trends?

This is an important question, and concerns about consolidation are genuine. Yet much of this debate has so far been conducted more with emotion and ideology and less with facts. The data show that with the exception of Tamil news, even the most concentrated language markets in India still remain more diverse than those in most other countries where television is widespread.

To measure owner concentration in industries, policy makers and scholars around the world have, since the early 1980s, used a statistical measure developed by two economists. The Hirfindal–Hirschman index (HH-I) measures owner concentration. Its use became widespread after the US Department of Justice and the Federal Reserve began using it to analyze the competitive effects of mergers. The higher points a market scores on the index, the more concentrated is its ownership, the lower the points, the more diverse the ownership. It

How TV Ownership Concentration in Five Indian Languages Compares Internationally (H-I Index: Less is good)

Figure 5. Problem Yes, But Not so Bad after All

Source: Indian figures from report for Ministry of Information and Broadcasting by Administrative Staff College of India, Study on Cross Media Ownership in India. International figures from Noam, Media Ownership, and Concentration in America, p. 23.

NOT FOR COMMERCIA

L USE

Mehta 59

is not perfect, but it provides a universally accepted method to measure market diversity.

By this measure, ownership concentration in all Hindi news and entertainment channels as well as English news channels in India is moderate and remains among the most diverse in the world. A 2008 study for the Ministry of Information and Broadcasting, which examined five language mar-kets, found that the real problem was in Malayalam, Tamil, and Telugu, which showed very high levels of concentration. The Malayalam TV industry was similar to the situation in Britain, but better than in Sweden, Germany, Italy, and Ireland. Tamil news and Telugu entertainment were undoubtedly among the most concentrated globally, but Tamil entertainment appeared fairly diverse. The Telugu news TV industry is similar to Britain, Sweden, and France—at least by these standards. Data for other Indian languages are not available but see-ing the available Indian figures side by side with international comparisons provides perspective (see data in Figure 5).

Yet statistical analysis of this kind provides at best an incomplete and at worst a misleading picture. To understand this, we must turn to the third key feature of Indian television: news television. The trends in the business of news TV are remarkably different from those in the larger entertainment industry.

A New Indian Power Elite: Who Owns the News and Why? As a genre, news attracts less than 10 percent of viewership in India and only about 16–17 percent of advertising (FICCI-KPMG, 2010–2011, p. 20). Yet more than half of the over 877 licensed TV

channels in the country are news channels, and one-third of these beam 24-hour news.14 This is a bizarrely high ratio compared to other countries. It is especially so when everyone in the industry agreed that news channels had turned into finan-cial black holes and enjoy a negligible market share. Yet news channels kept getting launched and money pumped into them.

Hardly any news channel in India made money. With the exception of a handful of channels, most news channels had never made money across their whole life-cycles. As film-maker Prakash Jha, who started Maurya TV in Bihar, told an interviewer, ‘I was crazy to have entered the media business. It was the love for my state that inspired me to launch the channel. But I am bleeding right now. My revenues don’t even cover one-third of the cost of running it’ (Shukla, 2012).

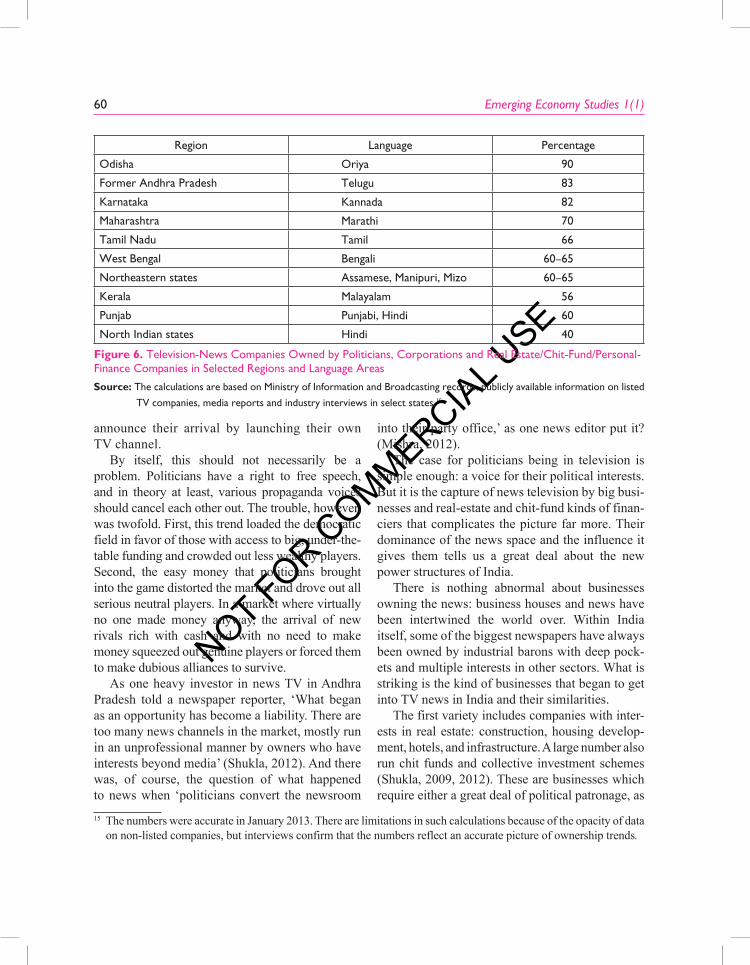

Three kinds of people have been major inves-tors in news television in the past decade: poli-ticians, real estate, chit fund and money market companies, and large corporations. My research shows that between them such companies make up over 80 percent of the news TV business in Andhra, Karnataka, and Orissa and between 60 and 70 percent in Punjab, Maharashtra, West Bengal, Tamil Nadu, and the Northeast (see Figure 6). A decade ago, only a handful of states like Tamil Nadu had channels like Sun TV or Jaya TV, which were set up as propaganda arms of rival political parties. By 2013, this was the norm across India.

Politicians got into the television business for obvious reasons: to gain a platform to relay their messages to voters. In Andhra Pradesh, only 2–3 of the 14 news channels are not controlled by politicians or their proxies. The growth in news was not driven by companies looking to create new platforms for serious coverage but by power players looking to spread their own propaganda and views. From Sakshi TV of Jagan Reddy of the YSR Congress to Captain TV of the Tamil actor Vijaykanth, it was almost an unwritten rule for new entrants on the political stage to

14 Of the 877 channels, licenses were canceled for 61 in 2013 by the Ministry of Information and Broadcasting due to non-fulfillment of license condi-tions. Data on channels from Ministry of Information and Broadcasting. Information on cancelations from Cablequest (June 28, 2013).

NOT FOR COMMERCIA

L USE

60 Emerging Economy Studies 1(1)

announce their arrival by launching their own TV channel.

By itself, this should not necessarily be a problem. Politicians have a right to free speech, and in theory at least, various propaganda voices should cancel each other out. The trouble, however, was twofold. First, this trend loaded the democratic field in favor of those with access to big, under-the-table funding and crowded out less wealthy players. Second, the easy money that politicians brought into the game distorted the market and drove out all serious neutral players. In a market where virtually no one made money anyway, the arrival of new rivals rich with cash and with no need to make money squeezed out genuine players or forced them to make dubious alliances to survive.

As one heavy investor in news TV in Andhra Pradesh told a newspaper reporter, ‘What began as an opportunity has become a liability. There are too many news channels in the market, mostly run in an unprofessional manner by owners who have interests beyond media’ (Shukla, 2012). And there was, of course, the question of what happened to news when ‘politicians convert the newsroom

Region Language Percentage

Odisha Oriya 90

Former Andhra Pradesh Telugu 83

Karnataka Kannada 82

Maharashtra Marathi 70

Tamil Nadu Tamil 66

West Bengal Bengali 60–65

Northeastern states Assamese, Manipuri, Mizo 60–65

Kerala Malayalam 56

Punjab Punjabi, Hindi 60

North Indian states Hindi 40

Figure 6. Television-News Companies Owned by Politicians, Corporations and Real Estate/Chit-Fund/Personal-Finance Companies in Selected Regions and Language Areas

Source: The calculations are based on Ministry of Information and Broadcasting records, publicly available information on listed

TV companies, media reports and industry interviews in select states.15

into their party office,’ as one news editor put it? (Mishra, 2012).

The case for politicians being in television is simple enough: a voice for their political interests. But it is the capture of news television by big busi-nesses and real-estate and chit-fund kinds of finan-ciers that complicates the picture far more. Their dominance of the news space and the influence it gives them tells us a great deal about the new power structures of India.

There is nothing abnormal about businesses owning the news: business houses and news have been intertwined the world over. Within India itself, some of the biggest newspapers have always been owned by industrial barons with deep pock-ets and multiple interests in other sectors. What is striking is the kind of businesses that began to get into TV news in India and their similarities.

The first variety includes companies with inter-ests in real estate: construction, housing develop-ment, hotels, and infrastructure. A large number also run chit funds and collective investment schemes (Shukla, 2009, 2012). These are businesses which require either a great deal of political patronage, as

15 The numbers were accurate in January 2013. There are limitations in such calculations because of the opacity of data on non-listed companies, but interviews confirm that the numbers reflect an accurate picture of ownership trends.

NOT FOR COMMERCIA

L USE

Mehta 61

anything do with land in India does, and also gen-erate a great deal of black money. ‘Ab to builder chala rahe hai news channels’ [builders are run-ning news channels now], sums up Arun Jaitley, Union Finance Minister in the Modi government. This has serious implications for what the channels actually show. As Jaitley observed:

The economic model of news channels is still not adequate. Therefore, barring a few channels, or some channels which have a very large regional base, and a handful of national channels, news channels per se are not a profitable business. In fact most of them are making losses. That com-pulsion is pushing the concept of paid news and some recent cases are far more disturbing than even paid news.16

For many of these channels, the boundaries between them and politics are often so porous that they are almost impossible to map. ‘A news chan-nel is a useful asset. It brings influence and access, and opens doors in politics and in government,’ says one senior television manager.17

The second category includes large corporate companies. The most striking example was the deal that gave India’s largest corporate entity, Reliance Industries Limited, ownership of one of the coun-try’s largest regional language news enterprises, Eenadu TV, and Network18—and its subsidiary TV18—the listed entity which controls channels such as CNBC-TV18, CNBC Awaaz, CNN-IBN, IBN7, and IBN-Lokmat. In effect, it initially com-

bined two major media groups to create what many thought was India’s largest media conglomerate.18

Mukesh Ambani’s acquisition of a big share in the TV news market— ostensibly to gain content for Reliance’s mobile phone service Jio—was not the only manifestation of a wider trend. In May 2012, another major Indian conglomerate with deep interests in telecom, the Aditya Birla Group, announced that it was acquiring a 27.5 percent stake in Living Media India Limited (Aditya Birla Group, 2012), the company which runs the India Today Group, including several channels such as Aaj Tak and Headlines Today. In this case, though, full control remained in the hands of India Today chairman Aroon Purie. Similarly, in December 2011, Oswal Green Tech, acquired a 14.17 per-cent shareholding in New Delhi Television in two separate deals from the investment arms of Merrill Lynch and Nomura Capital (Guha Thakurta & Chaturvedi, 2012, p. 12).

In 1956, C. Wright Mills argued in his classic The Power Elite that a small social class of influ-ential people was taking over the key institu-tional ‘command posts’ of American society, the places where the decisions are made and which have the most direct influence on the course of events in society. Arguing that the power of wealth was not nearly as important as the ‘insti-tutional powers of wealth’, Mills showed that a small coalition of big businessmen and ascend-ant military men had come to occupy the levers of power in the American social system with no effective counterweight. The key insight of this argument was that the idea of democracy, where different viewpoints competed in the market-place of ideas and the best argument eventually won, was ‘more a fairy tale than a useful approx-imation’ (Mills, 1958).

India in the twenty-first century is a very different place from the United States of the 1950s, but the example of news television shows us that we may be seeing a similar move on to the strategic command posts of the society. Such a move came from politicians and businesses with

16 Personal interview with Arun Jaitley. At the time of the interview, he was the Leader of Opposition in Rajya Sabha, October 21, 2012.

17 Personal interview with a senior TV consultant who has launched several regional TV networks but declined to be named.

18 In an article in the Economic and Political Weekly, the journalist Paranjoy Guha Thakurta and Subi Chaturvedi (2012) argued that this combined new entity would be larger than the Rupert Murdoch-controlled Star TV and the Bennett and Coleman Company that controls the Times of India Group.

NOT FOR COMMERCIA

L USE

62 Emerging Economy Studies 1(1)

interests in real estate, chit-funds, or personal finance schemes. News TV channels have emerged as vital platforms and crossroads of Indian society and one of its most influential lightning rods in the public sphere. The power elite that emerged in the 1990s understood this and staked a claim to this powerful social lever.

A new media–industrial complex was coming into being, somewhat like the military–industrial complex that emerged in the United States in the 1950s. The structure of the news TV business changed in the first decade of the twenty-first cen-tury. It led to a furious public debate about media ownership, regulation, and content with various bodies like the Telecom Regulatory Authority of India, the Law Commission, and various minis-tries weighing in with their own views on what should be done. Most of these flounder on the question of whether old regulations based on tra-ditional categories of print, television, and internet remain relevant in the age of convergence and the mobile phone. The debate is far from resolved and past experience shows that it is difficult to trust governmental bodies—of any ideological persua-sion—to be neutral arbiters on media matters. One thing though is certain: media plurality remains the best defense against media capture. As Mao said, let a hundred flowers bloom, let a hundred schools of thought contend.

References

Aditya Birla Group (2012, May 18). Aditya Birla Group to invest in Living Media India. Retrieved from http://www.adityabirla.com/media/press_releases/Living-Media-India

Administrative Staff College of India (2009). Study on cross media ownership in India: Draft report. Hyderabad: ASCI.

Cablequest (2013, June 28). Ministry cancels license of 61 channels. Cablequest. Retrieved from http://www.cablequest.org/news/government-news/item/2680-ministry-cancels-license-of-61-tv-channels.html

CNN-IBN (2009). NSA says media hype on Chinese intrusions risky (Unpublished). Retrieved September 19, 2009, from http://ibnlive.in.com/news/nsa-says-media-hype-on-chinese-intrusions-risky/101741-3.html

China Foreign Ministry (2009). Spokesperson Jiang Yu’s Regular Press Conference on September 15. Retrieved September 20, 2009, from http://www.fmprc.gov.cn/eng/xwfw/s2510/t584510.htm

FICCI-KPMG. Hitting the High Notes: FICCI-KPMG Indian Media and Entertainment Industry Report 2010–11. KPMG.

Ghose, B. (2005). Doordarshan days. New Delhi: Penguin/Viking.

Guha Thakurta, Paranjoy, & Chaturvedi, Subi (2012). Corporatisation of the media: Implications of the RILK-Network18-Eenadu Deal. EPW, XLVII(7), 10–13.

Gupta, S. (2009, September 19). Stop fighting the 1962 War. The Indian Express. Retrieved September 20, 2009, from http://www.indianexpress.com/news/stop-fighting-the-1962-war/518975/0

Jha, Smita (2012, October 30). Indian entertainment outlook. Paper presented at CII India-The Big Picture Summit, New Delhi.

Joshi, S. R., & Trivedi, Bela (1994). Mass media and cross-cultural communications: A study of television in India (SRG-94-041). Ahmedabad: ISRO.

Kohli Khandekar, Vanita (2013, September 23). How Telcos lost the media plot. Business Standard.

——— (2013, December 1). Net profits. Caravan. Retrieved June 1, 2014, from http://www.caravanmagazine.in/perspectives/net-profits

Mehta, Nalin (in press). Behind a billion screens: Inside Indian television. New Delhi: HarperCollins.

——— (2008). India on television: How satellite TV channels changed the ways we think and act. New Delhi: HarperCollins.

Mishra, Mahendra (2012, February 16). Let’s differentiate ‘news channels’ from ‘views channels’ to save real journalism. IndianTelevision.com. Retrieved January 1, 2014, from http://www.indiantelevision.com/special/y2k12/Mahendra_Mishra_yearender.htm

MPA Asia (2014, July). India pay-TV and Broadband—Future Trends.

NOT FOR COMMERCIA

L USE

Mehta 63

Noam, Eli (2009). Media ownership and concentration in America. New York: Oxford University Press.

Nielsen, Rasmus Kleis, & Levy, David A.L. (Eds). (2010). The changing, business of journalism and its implications for democracy. Oxford: Reuters Institute of Journalism.

PricewaterhouseCoopers (PwC)-FICCI (2008). The Indian entertainment industry: An unfolding opportunity. New Delhi: FICCI.

Rao, B.V. (2009). Madam minister, please read the NBA’s unwritten code of collective silence. Retrieved January 13, 2014, from http://www.exchange-4media.com/e4m/news/fullstory.asp?news_id=35997§ion_id=6&pict=5&tag=31896

Shukla, Archana (2012, August 19). We also make TV news. The Indian Express.

——— (2009). News, uninterrupted. The Indian Express.The Economist (2014, July 19).The final frontier.

The Economist. Retrieved October 6, 2014, from http://www.economist.com/news/asia/21607837-fixing-dreadful-sanitation-india-requires-not-just-building-lavatories-also-changing

Registrar General of India (2001). Projected and actual population of India, states and union territories, 1991. New Delhi: Office of the Registrar General, India.

Sircar, Jawhar (2013). Prasar Bharti at the crossroads. Yojana, 57, 4.

Mills, C. Wright (1958, March). The structure of power in American Society. The British Journal of Sociology, 9(1).

——— (1956). The power elite. New York: OUP.Telecom Regulatory Authority of India (2014, July

30). Indian telecom services performance indicator Report for the Quarter ending March, 2014’, Information Note to the Press (Press Release No. 48/2014).

Total Number of TV Channels goes up to 813 (2014, September 19). Retrieved October 1, 2014, from http://www.indiantelevision.com/regulators/i-and-b-ministry/total-number-of-tv-channel-goes-up-to-813-140919

Wade, M. (2009, July 4). Serious damage as ‘Racist Australia’ airs in India. Sydney Morning Herald. Retrieved September 39, 2009, from http://www.theage.com.au/world/serious-damage-as-racist-australia-airs-in-india-20090703-d7u4.html

Author’s Biography

Nalin Mehta is Associate Professor, Shiv Nadar University, Consulting Editor, Times of India, and Editor, South Asian History and Culture (Routledge) as well as the Routledge book series by the same name. He has previously been Managing Editor, Headlines Today, Adjunct Professor, Indian Institute of Management, and held senior positions with the UN and Global Fund in Geneva, Switzerland. He is currently on the governing board of the University Grants Commission Consortium for Educational Communication, which coordinates the work of 22 universities centres nationwide. He has held fellowships at National University of Singapore, Australian National University, Canberra, La Trobe University, Melbourne, and the International Olympics Museum, Lausanne.

His books include India on Television: How Satellite Channels Have Changed the Way We Think and Act (HarperCollins: 2008), which was awarded the 2009 Asian Publishing Award for Best Book; Sellotape Legacy: Delhi and the Commonwealth Games (HarperCollins: 2010), with Boria Majumdar; Olympics: The India Story (HarperCollins: 2008, 2012 and republished Routledge: 2008). His edited books include Television in India: Satellites, Politics and Cultural Change (Routledge: 2008, 2010); Gujarat Beyond Gandhi: Identity, Conflict and Society (Routledge: 2010, 2011) with Mona G. Mehta

His forthcoming book Behind a Billion Screens: Inside Indian Television is in press with HarperCollins.