IMPACT_OF_INTERNET_BANKING_ON_THE_ZIMBABWEAN_BANKING_SECTOR-AN_APPLICATION_OF_THE_MULTINOMIAL_LOGIT_MODELLING.pdf...

17

International Journal of Economics, Commerce and Management United Kingdom Vol. II, Issue 8, 2014 Licensed under Creative Common Page 1 http://ijecm.co.uk/ ISSN 2348 0386 IMPACT OF INTERNET BANKING ON THE ZIMBABWEAN BANKING SECTOR AN APPLICATION OF THE MULTINOMIAL LOGIT MODELLING Ndlovu, Ian Department of Banking, National University of Science and Technology, Zimbabwe [email protected], [email protected] Siyavora, Agnes Telone Zimbabwe (Pvt) Ltd., Zimbabwe (Alumnus) Department of Banking, National University of Science and Technology, Zimbabwe [email protected] Abstract In 2011 Internet World Stats, pegs internet use at 11.5 percent in Zimbabwe but actual internet banking users constituted a fraction of the internet users. The adoption of internet banking in Zimbabwe has been sluggish over the past decade owing to the economic recession that Zimbabwe experienced from 2003-2008. The study’s major goal was to assess the impact of internet banking on banks in Zimbabwe. The maintained hypothesis was that internet banking had no impact on the banking sector. A cross sectional survey was used to gather information and views were drawn from fourteen commercial banks and the central bank. Three sets of questionnaires, each for a specific group were distributed. The research findings revealed that the competitive advantage of internet banking lies in cost reduction and consumer satisfaction. The study found out that internet banking improved operational efficiency. The major factors for the efficiency were attributed to the overall decrease in operational cost, total cost of employment and expenses incurred on fixed assets. The overall benefit of internet banking was convenience to customers. The study recommends that banks improve basic functionality of bank websites. Government must increase investments in education, infrastructural development to enable consumers to adopt the innovation. Keywords: Internet banking, efficiency, banking, logit model

Transcript of IMPACT_OF_INTERNET_BANKING_ON_THE_ZIMBABWEAN_BANKING_SECTOR-AN_APPLICATION_OF_THE_MULTINOMIAL_LOGIT_MODELLING.pdf...

International Journal of Economics, Commerce and Management United Kingdom Vol. II, Issue 8, 2014

Licensed under Creative Common Page 1

http://ijecm.co.uk/ ISSN 2348 0386

IMPACT OF INTERNET BANKING ON THE ZIMBABWEAN BANKING SECTOR

AN APPLICATION OF THE MULTINOMIAL LOGIT MODELLING

Ndlovu, Ian

Department of Banking, National University of Science and Technology, Zimbabwe

[email protected], [email protected]

Siyavora, Agnes

Telone Zimbabwe (Pvt) Ltd., Zimbabwe

(Alumnus) Department of Banking, National University of Science and Technology, Zimbabwe

Abstract

In 2011 Internet World Stats, pegs internet use at 11.5 percent in Zimbabwe but actual internet

banking users constituted a fraction of the internet users. The adoption of internet banking in

Zimbabwe has been sluggish over the past decade owing to the economic recession that

Zimbabwe experienced from 2003-2008. The study’s major goal was to assess the impact of

internet banking on banks in Zimbabwe. The maintained hypothesis was that internet banking

had no impact on the banking sector. A cross sectional survey was used to gather information

and views were drawn from fourteen commercial banks and the central bank. Three sets of

questionnaires, each for a specific group were distributed. The research findings revealed that

the competitive advantage of internet banking lies in cost reduction and consumer satisfaction.

The study found out that internet banking improved operational efficiency. The major factors for

the efficiency were attributed to the overall decrease in operational cost, total cost of

employment and expenses incurred on fixed assets. The overall benefit of internet banking was

convenience to customers. The study recommends that banks improve basic functionality of

bank websites. Government must increase investments in education, infrastructural

development to enable consumers to adopt the innovation.

Keywords: Internet banking, efficiency, banking, logit model

© Ndlovu & Siyavora

Licensed under Creative Common Page 2

INTRODUCTION

Globalization, fierce competition and technological developments in Southern Africa have

exerted a lot of pressure on the banking institutions in Southern Africa over the past two

decades. Banks have resorted to finding new avenues of operation so as to provide convenient

banking to their customers. The adoption of internet banking has led to the transformation of the

distribution of the traditional banking practices in economies such as Zimbabwe. Most

commercial banks have augmented their service distribution with websites which allow

customers to check account balances, transfer funds and to receive payment over the internet.

According to the Zimbabwe Internet Blog NMB, FBC, CBZ and CABS introduced internet

banking in 2008 into the country which has allowed customers to transfer funds between

accounts, make payment for certain utilities, checking balance statement and making foreign

exchange transactions.

The research covers the time from 2003 to 2012 and will be confined to commercial

banks. The research was only based on the information and communication technology

department of the bank, since its service delivery and customer related customers who bank

with the mentioned banks are the main target. It will covered electronic banking services that

have got to do with service delivery and how customers adopt the services. This research also

focused on identifying the benefits derived from using internet banking in the banks themselves

(cost effective) and to the banking environment. The critical success factors were identified to

assess the effectiveness of internet banking in the Banking Sector. The study will attempt to

identify the risks and challenges that banks might have faced during the 2003- 2012 period as

this is the time most Banks introduced E-banking services and to evaluate the risks

management policies that might have been used to reduce the risks associated with Internet

Banking.

The study sought to analyse the benefits and critical success factors of internet-banking

services in Zimbabwe. It was also the goal of the research to assess the impact of internet-

banking services on the performance of banks. The study also sought to identify risks and

challenges that Zimbabwean banks face in using internet-banking to improve service delivery.

LITERATURE REVIEW

Pikkarainen, Karjaluoto, and Pahnila (2004) cited in Ankit (2011) define internet banking as an

‘Internet portal, through which customers can use different kinds of banking services ranging

from bill payment to making investments’. With the exception of cash withdrawals internet

banking is defined as electronic systems that enable bank customers to obtain access to their

accounts and general information on bank products and services through the use of bank’s

website, without the intervention or inconvenience of sending letters, faxes, original signatures

International Journal of Economics, Commerce and Management, United Kingdom

Licensed under Creative Common Page 3

and telephone confirmations. Chang (2003), Sullivan and Wang (2005) are of the view that

internet banking is a process of innovation whereby customers handle their own banking

transactions without visiting brick and mortar bank structures where they interact with bank

personnel. Dube et al (2009) observe that internet banking can be divided into three types, that

is, informational, transactional and communicative.

Informational websites provide customers access to general information about the

financial institution and its products or services. Such websites carry low risk as informational

websites typically have no path between the server and the bank’s internal network. Because of

its simplicity, informational websites can be identified as the first level of internet banking.

Examples include enquiry about master card credit balances (FBC Bank in Zimbabwe) and

enquiry about bank interest rate, currency and exchange rate, news and information, economic

data and information.

Communicative or Simple transactional websites allows some form of interaction

between the banking system and the customer which is limited to emails, account inquiry, loan

application o static file update. Advanced transactional websites provide customers with the

ability to conduct transactions through the financial institution’s website by initiating banking

transactions or buying products and services. Banking transactions can range from something

as basic as a retail account balance inquiry to a large business-to-business funds transfer.

The critical success factors of internet banking are successful internal e-banking

configuration, security, ease of use or user friendliness of the system, synchronization of

existing e-banking tools with internet banking, technological infrastructure, customer service and

customer occupation. Internet banking configuration must start internally for commercial banks

to succeed in adopting this type of e-banking technology. El Sawy et al (1999) observes that

current business designs and organisational models are insufficient to meet the challenges of

doing business in the e-commerce era. This implies that the re-engineering the internal

business processes is a critical issue which also involves transformation of the existing

technology. Internal processes must provide quick and efficient customer service (Orr, 2004).

Security is of paramount importance in setting up an internet banking facility. Enos

(2001), argues that internet banking must offer secure transactions as well as secure front end

and back end systems. In building secure transaction systems factors that have to be

considered are improving customer trust and integrating the current services offered to the

customer into the new system (Enos 2001).

The findings of Ramseook-Munhurrun and Naidoo (2011) reveal that reliability and

security are perceived as the most important dimensions in internet banking transactions that

influences satisfaction and behavioural intentions. The more people feel secure, the more they

will adopt internet banking. Daniel (1999) concurs that the level of security or risk associated

© Ndlovu & Siyavora

Licensed under Creative Common Page 4

with a new technology impact much on its acceptance. An empirical survey by Sathye (1999) of

Australian consumers confirmed the fact that level of risk or security has a great impact on

internet banking adoption. An empirical study by Lockett and Littler (1997) corroborates the

assertion that the use of electronic banking involves risk.

Akbar and Noorjahan (2009) emphasize convenience as one of a critical adoption factor

for internet banking. Mäenpää et al (2008) noted seven dimensions of internet banking services

which are convenience; security; status; auxiliary features; personal finances; investment; and

exploration. In setting up internet banking services commercial banks must make sure that the

systems are well integrated and much convenient to the customer. Kerem (2002) asserts that

there are management aspects that have to be looked into for the success of internet banking.

According to Stamoulis (2000), banks usually feed their websites with corporate profile,

product and pricing information, interest rates and application forms. However they need to look

beyond the usual contents and make their websites far richer in terms of content in order to

attract a large number of visitors. Re-drawing of the internet market maps is a vital prerequisite

for the electronic banking strategy, because the internet requires different marketing methods

compared to other service distribution channels (Stamoulis, 2000, Rockart, 1979). Therefore the

richness of a medium’s content plays a big role and is critical in attracting a large number of

consumers of internet banking services.

Excellent customer service is important in developing successful internet banking

services. Regan and Macaluso (2000) argue that the internet can transfer power from the

supplier to the customer thereby improving customer loyalty. On the other hand Orr (2004) sees

provision of a pleasant experience on the delivery channels as one of the key requirements in

the adoption of successful internet banking services. Franco and Klein (2009) stress the

importance of upgrading technological infrastructure as a measure of synchronising its speed

with that of electronic commerce in general. Bradley and Stewart (2003), Maholtra and Singh

(2007) and Sathye (1999) found that reliability was an important determinant for consumers who

used electronic banking.

RESEARCH METHODOLOGY

This study adopted a cross sectional survey design in order to assess the maintained

hypothesis that internet banking has an insignificant impact on commercial bank viability against

the alternative hypothesis that internet banking has a significant impact on commercial banking.

The population sample consisted of 14 commercial banks offering internet banking from the 17

commercial banks in Zimbabwe. The list of banks excludes Interfin banking Corporation which is

currently under curatorship. Stanbic Bank and TN Bank (now called Steward Bank) were also

International Journal of Economics, Commerce and Management, United Kingdom

Licensed under Creative Common Page 5

excluded from the study as they had not yet implemented internet banking during the study

period.

The targeted population consisted of operations managers, supervisors and employees

in both the front and back offices. Two questionnaires were administered to each and every

commercial bank under assessment. Service providers were selected because they are the

ones that provide internet services to the commercial banks and customers. The internet service

providers that were used consisted of Econet Wireless, ZOL, and Africom.

Customers were also selected because they are the ones using internet banking. The

customers were drawn from Bulawayo. The researchers mainly focused on self-employed,

professionally employed people as well as students. The Reserve Bank of Zimbabwe was

considered as the part of the population for they perform the role of supervision, regulation and

it has the statistical information as far as bank performance in Zimbabwe is concerned.

The researchers used stratified sampling underpinned by purposive sampling. The

sampling method enabled the researcher to obtain representatives from each subgroup within

the population and helped ensure focus on important subpopulations of the population. The

method has one main weakness which is its non-probabilistic nature, and that elements of the

sampling frame did not have equal chances of being selected. The researcher divided the

population into subgroups and each subgroup had homogeneous characteristics. This was

meant to increase accuracy of results and to reduce chances of bias. Customers were divided

into individual customers and corporate entities. The major advantage of using stratified

sampling coupled with purposive sampling is that comprehensive results were obtained within

the stipulated time frame and cost constraint. Therefore, allocation and use of resources was

efficient as key informants were targeted.

Face to face interviews enabled the researchers to ask probing questions or to make

clearer those questions which seemed ambiguous from the perspective of some interviewees.

This method of data collection proved cheaper as it enabled the respondents to open up and

provide additional information they thought helpful. This was cost effective in terms of both time

and money. Questionnaires allowed the respondents to respond better to sensitive questions

since they felt more anonymous.

Three sets of questionnaires were administered to commercial banks, other

stakeholders (the Reserve Bank of Zimbabwe, internet service providers and telecommunication

companies) and bank customers. The questionnaires were designed so that they elicited

responses that address benefits, risks and viability issues associated with internet banking. All

of questionnaires were directly administered by the researchers. A total of 88 questionnaires

were distributed to the target population. The researchers distributed 60 questionnaires to the

customers; twenty eight questionnaires to the banks, that is, two (2) questionnaires were

© Ndlovu & Siyavora

Licensed under Creative Common Page 6

administered to each bank. The researchers visited local institutions such as the local banks

(NMB, MBCA, Kingdom and Barclays), Bulawayo Polytechnic, NUST and self-employed people

so as to administer customer questionnaires. Questionnaires facilitated uniformity in responses

especially for closed-ended questions, thereby facilitating data analysis and presentation.

The questionnaire was also relevant in the context of this study as both open ended and

closed ended questions were used to obtain data from the targeted population. These data

collection instruments were efficient and provided an easy way to decode and build a platform

for analysis of data to be made. However, due to the fact that questionnaires were standardized

and had to be short and precise, it was not possible to explain and interpret some of the

questions that respondents might have misinterpreted.

Face to face and telephone interviews were used to compliment data acquired from the

questionnaires. Interviews were quite fruitful as they clarified some questions. All interviews

were guided by eight structured questions that were standardized so as to obtain comparable

responses from different respondents. The interviews were conducted on five selected banks

namely Kingdom, CBZ, Ecobank, Standard Chartered, and MBCA. Appointments were made

with respondents from the RBZ and internet service providers. It was however difficult to

schedule appointments with the key informants on the subject under study, as they were often

busy fulfilling demanding duties in their organizations.

Gathered data was analysed using the Statistical Package for Social Sciences (SPSS)

which supports unequal probability and accommodates clustering of the population sample. This

software package was useful in predicting the future outcome, thus it acted as an analytical tool

for manipulating all the data that was gathered for analysis and presentation. The study also

involved estimating a multinomial logit model using SPSS.

The study also adopted logistic regression for multinomial outcomes which is extensively

used in the social sciences including economics, banking and finance (Filmer and Pritchett

2001; Manski and McFadden, 1981 and Maddala, 1988). Selected responses to the individual

customer questionnaire were coded with numbers ranging from 1 to 3, 1 to 4 and 1 to 8 for

different questions whose responses conformed to the Likert Scale. The models that were fitted

to the data are:

Security = 𝛽1education+ 𝛽2conven+ 𝛽3income

Conven= 𝛽1education+ 𝛽2security+ 𝛽3income

Where, security means security of internet banking, education is education level of respondents,

conven is convenience of internet banking transactions and income refers to the income level of

respondents, 𝛽1, 𝛽2 and 𝛽3 are the coefficients of the model. The multinomial logit model was

estimated using SPSS software.

International Journal of Economics, Commerce and Management, United Kingdom

Licensed under Creative Common Page 7

ANALYSIS AND DISCUSSION OF FINDINGS

Preliminary Analysis

This research targeted the commercial banks, services provider and the actual users of internet

banking (customers) in an attempt to identify the impact that internet banking has had on the

Zimbabwean Banking Sector. Seventy eight (78) questionnaires were administered to the

sample and 67 were returned fully completed. Thus the response rate was 76 percent.

Respondents from eleven banks only filled in one out of two questionnaires administered to

them because they were busy. In some banks the target respondents were not available to fill in

the questionnaires. To ensure validity and accuracy of responses, return visits were arranged

on a case by case basis. Ten questionnaires from customers were not fully completed and they

had irrelevant information. The majority of the bank respondents were from the Information

Technology Department with a 35 percent response rate while representatives from corporate

department constituted 23 percent of the population sample. The researchers believed that by

targeting these two groups, different opinions could obtain about internet banking features and

users. The response rates are shown on the table below:

Table 1- Questionnaire Response Rate

Group of respondents No.distributed No. Returned Response Rate

Commercial Banks 28 17 61%

Individual Customers 50 41 82%

Corporate Customers 10 9 90%

Total 88 67 76%

The figure below depicts classification of respondents according to departments. The key

departments captured are retail, information technology (IT), credit, consumer, corporate and

system bank officers.

Figure 1: Occupation of Bank Respondents

12%

35%

18%

23%

6%6%

Credit IT Retailing Corporate Consumer System

© Ndlovu & Siyavora

Licensed under Creative Common Page 8

The Figure 1 shows that the modal class of respondents was that of information technology (IT)

personnel in banks followed by the corporate relations officers and retail banking sections. The

thrust of the investigation of effects of internet banking on commercial banking predisposed the

three classes of bank manpower to be the leading respondents to the survey.

Customer Response Rate

The survey on internet banking customers showed that 78.2 percent of the population

constituted non-internet banking users. Three out of every ten people of the target population

were users of internet banking according to the survey. This showed an increase in the number

of internet banking users with a moderate adoption rate of 58.8 percent. Internet banking

customers were divided into individual customers and corporate clients. Out of the 50 targeted

customers, 9 respondents were corporate entities mainly from the retail industry with 56 percent

response rate as shown on the figure 2 overleaf.

Figure 2: Line of Business of Corporate Respondents

Demographic Profile of Customers using Internet Banking

The study examined the perceptions of 41 account holders of various banks who were active

users of internet banking associated with different demographic characteristics outlined in Table

2 on next page.

0

20

40

60

11.1

55.6

11.111.1

11.1

percent of respondents

International Journal of Economics, Commerce and Management, United Kingdom

Licensed under Creative Common Page 9

Table 2- Demographic Profile of Customers

N= 41

Age 15-25 years 18 44%

26-35years 19 46%

36-45 years 2 5%

46-55years 2 5%

Occupation Professional Employment 26 63%

Self employed 1 2%

Student 14 34%

Income $90-$250 10 24%

$251-$1000 17 41%

$1000-$5000 12 29%

Above $5000 1 2%

Missing 1 2%

The table shows that a greater percentage of the respondents were below 35 years of with a

response rate of 90.2 percent while the remaining 9.8 percent comprised of individual above the

age of 36 years.

Self-employed people, that is, those in the informal sector were part of the target

population. Very few of the self employed were found to be active users of internet that is why

their proportion in the sample is 2.4 percent. This showed that a great magnitude of the parallel

market is unbanked and therefore do not use internet banking. The highest proportion of the

sample was professional employees with 63.4 percent who made use of internet banking at

work. Customers working at the banks had internet bank accounts because it was mandatory to

have an internet banking account.

Approximately 54 percent of the respondents were undergraduates implying that the

level of education has an impact on internet banking adoption rates. Due to the weak

performance of the economy a large fraction of the respondents of 39.4 percent belonged to

income group below $1, 000.

Customer Banking Patterns

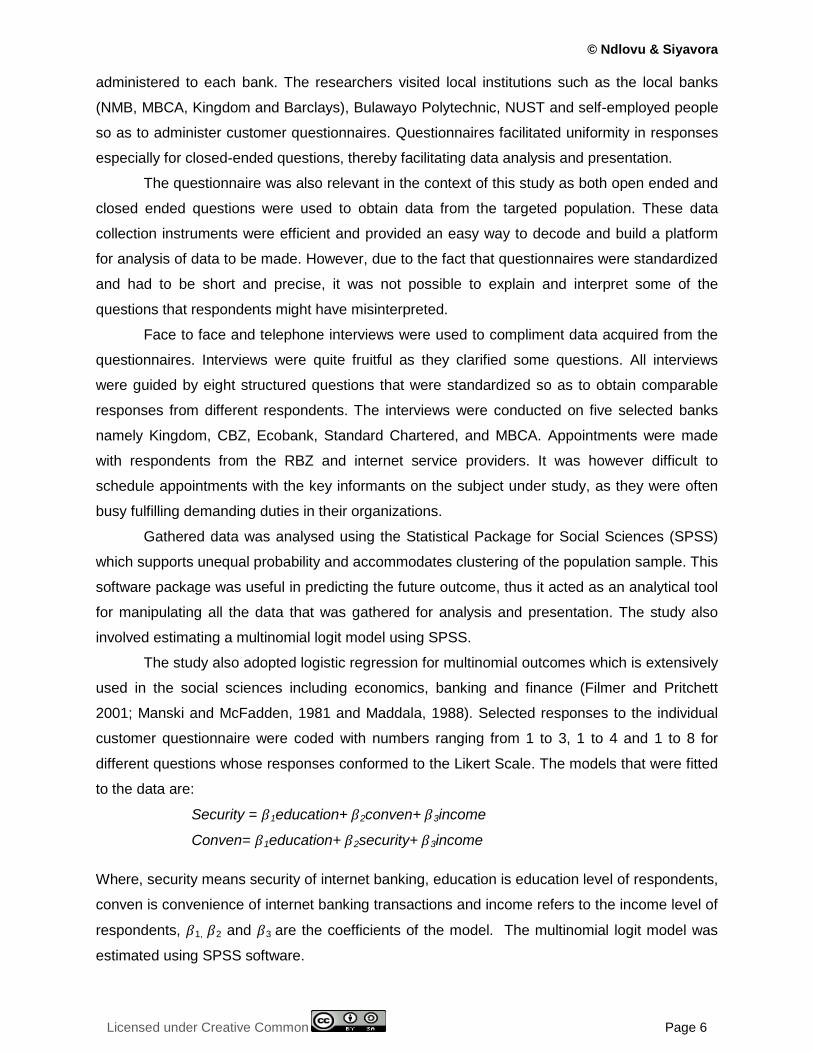

The respondents were asked to indicate the reason why they chose their current banks as their

internet banks. The analysis of the results presented in Figure 3 below shows that most

customers choose a bank where they had an account as their internet bank. Thirty percent were

infuenced by the excellence of services offered in choosing a bank for internet facilitated

transactions.

© Ndlovu & Siyavora

Licensed under Creative Common Page 10

Figure 3 : Choice of Internet Bank

In the category of individual customers, males were the frequent users of internet banking

where most of them transacted from their work place. More females did internet banking

transactions at home. A greater proportion of males save over $10 by using internet banking

compared to 2.14 percent of females who save the same amount of money through E-banking

services.

Figure 4 overleaf show that 42.9 percent of females use internet banking for wire

transfers while 40.7 percent of males use internet banking mostly for bill payments. It was

interesting to observe that corporate clients in retailing mainly used internet banking services for

balance enquiry rather more than bill payments and wire transfers.

Figure 4 – Frequently used Internet Banking Features

The most enjoyed benefit of internet banking was convenience with a response rate of 68.3

percent. Twenty nine (29%) percent of the respondents indicated that internet banking facilities

offered by their banks reduced their trips to the bank to one per month. Corporate customers

likewise also enjoy the convenience banking that internet banking offers.

21.20%

48.50%

30.30%

Well established brand name Already have an existing account excellent services offered

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

Bill paymentsWire transfers

Balance enquiry

21.40%

42.90%

28.60%

40.70%

22.20%29.60%

Female

Male

International Journal of Economics, Commerce and Management, United Kingdom

Licensed under Creative Common Page 11

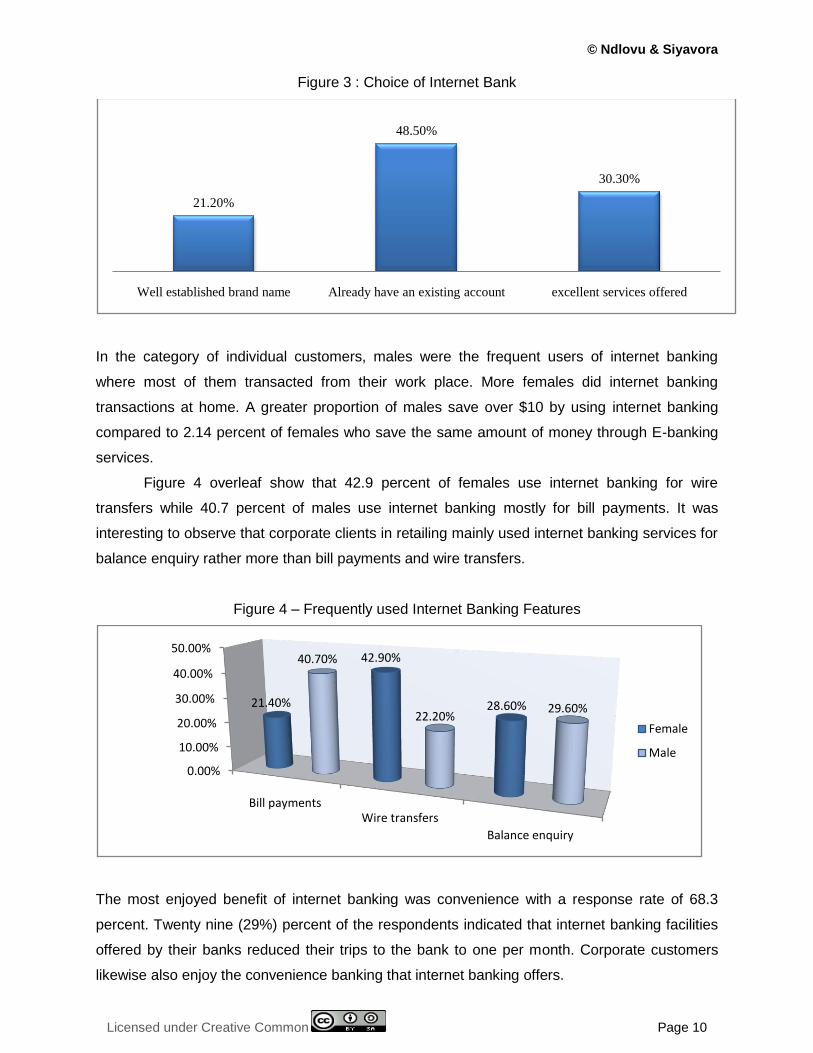

Advantages and challenges of Internet banking

Network failure was a challenge that most respondents faced in the execution of their

transactions with a response rate of 88 percent. This network failure was blamed on power

outages and operational failure of bank systems due to lack of adequate capitalization to

facilitate constant upgrading of telecommunications infrastructure. Some banks such as CBZ

Bank, Standard Chartered Bank and Barclays were found to be having up to date and reliable e-

banking systems that enable customers to access their accounts wherever they are. The figure

below shows the major hindrances to the optimal utilization of internet banking in Zimbabwe.

Figure 5 – Challenges Encountered by Customers

Results showed that most banks have transactional websites with a frequency of 9 out of 17

while 35.3 percent of the banks still have informational website. The survey revealed that

individuals transacted more than corporate clients with 53 percent response rate.

Benefits of Internet banking to Banks

Almost all respondents highlighted that improved service quality and customer retention and

switching were the two major benefits that were enjoyed by the internet banks with a response

rate of 70.6 percent. Only 29.4 percent indicated that internet banking had an added advantage

of reduced cost and higher profit margins. Therefore due to the convenience that customers

enjoy from using internet banking, banks have benefited in terms of improvements in customer

retention and switching. Banks have highlighted that the motive behind E-banking is to provide

convenient banking to the customers and from the response that was obtained, internet banking

has served the purpose that it was intended to serve. Two of the interviewed respondents

observed that the use of the internet has it easier for banks to reach and serve their consumers,

even over long distances. Moreover, internet banking has resulted in cost savings for banks by

offering standardized, low transaction - value added banking services ( bill payments, balance

inquiries, account transfer ) through the online channel, while focusing their resources into

specialized, high-value-added transactions (for example, small business lending, personal trust

services, investment banking) the bank websites.

0%

50%

100%

Security Network failures High transaction costs

corporates

individuals

© Ndlovu & Siyavora

Licensed under Creative Common Page 12

Challenges Encountered by Banks

The most common challenge faced by the banks was lack of expertise and a low uptake of the

E-banking services due to low customer confidence in formal banking systems. Four out of five

respondents highlighted that prior the multi-currency regime dominated by the United States

dollar, the uptake of internet banking was high. Nevertheless, after dollarization internet banking

experienced a downturn due to low disposable income.

It has also been argued that large sums of money are in the informal sector and the

unbanked. The detailed results on bank challenges are depicted on Figure 6 below. Operational

factors were a challenge to approximately 24 percent of the target population.

Figure 6- Challenges Encountered by Banks

Risks associated with Internet Banking

The data obtained reveals that there are risks that have been inherent in the use of internet

banking. According to BCBS (2001), the adoption of fast changing technology has led to the

birth of new risks that are classified as operational risks, business strategic risks and legal and

reputation risks. Internet banking just like any technology used by banks and other financial

intermediaries opens avenues for threats and opportunities as well. The upside linked to the

implementation of internet banking is that carrying out transactions with the bank becomes more

convenient. The downside is that internet banking may open the door for identity theft and other

forms of malfeasant behaviour that sometimes characterise e-banking transactions. Figure 7 on

the next page shows the responses obtained with regards to the class of risk that banks faced

due to internet banking.

23.5

17.6

35.3

23.5 compatibility ,cost of implementation and maintenance

security concerns and inadequate legislation

lack of expertise and low customer confidence

operational problems

International Journal of Economics, Commerce and Management, United Kingdom

Licensed under Creative Common Page 13

Figure 7 – Risks Associated with Internet Banking

A total of 41.2 percent of the respondents felt that the banks were vulnerable to operational risk

followed by 35.3 percent who believed that internet banking posed transactional risk. According

to the BCBS (2001), operational, legal, reputational and transaction risk classes add to the total

risk profile of the bank.

Internet banking has had a positive impact on bank efficiency to a small magnitude as

the magnitude of internet banking users has been relatively low. It has reduced customer

turnaround in banking hall, reduced operational costs through reduced stationery expenses

(bank slips, deposit slips).

Primary data corroborates the fact that the overall benefit of e-banking was convenience

to the customer, as supported by responses obtained from the research with a sixty three

percent response rate. Some of the benefits that were experienced by customers include

efficiency, responsiveness and privacy. These factors have been critical in providing proper

services to the customer thus improving efficiency of commercial banks. The main usage of IB

has been for checking account balances, payment of bills and funds transfers.

The use of Internet Banking was fraught with several challenges such as network failure

and low customer acceptance among others. High operational risks followed by transaction risk

were witnessed due to online banking. A smaller percent (11.8%) of the respondents felt that

the banks were vulnerable to legal risk which had an impact on the banks risk profile.

In view of the extent of IB adoption, a majority of the banks have adopted this technology

and are using the service to reach and serve their clients (corporate and individual customers).

Despite a seemingly good adoption rate, the extent of usage has remained relatively low as not

many consumers are using the facility.

41.20%

11.80%5.90%

35.30%

5.90%

Operational risk - 41.2%

Legal risk-11.8%

Reputation risk-5.9%

Transaction risk-35.3%

any other-5.9%

© Ndlovu & Siyavora

Licensed under Creative Common Page 14

In order to curb the challenges and risk encountered with internet banking, a greater percent of

the respondents advocated for a tight risk management measures. All the respondents did also

state that the use of passwords, security pin codes, firewalls on servers and anti-spyware could

be used to secure electronic banking services.

The Multinomial Logit Modelling

The logit model of convenience of internet banking facilities estimated from selected individual

customer responses is presented on the following table

Table 3: Security of Internet banking model

Variable Coefficient Prob. Stat. significance

Education 0.4112 0.1075 Insignificant

Convenience 0.5156 0.0000 Significant

Income 0.2064 0.1488 Insignificant

Pseudo R-squared 0.1992 LR statistic 23.48172

Log likelihood -52.811 Prob. (LR statistic) 0.000032

The multinomial logit model is:

Security = 0.4112education + 0.5156conven+ 0.2064income

Only convenience of internet banking has a statistically significant relationship with security of

internet banking. This implies that as convenience improves it is highly likely that internet

banking services will also be secure. The Likelihood Ratio statistic is also significant thereby

buttressing the fact that the statistically significant variable of convenience explains security

issues of internet banking.

The logit model of convenience of internet banking facilities estimated from selected

individual customer responses is presented on the following table.

Table 4: Convenience of Internet banking model

Variable Coefficient z-statistic Stat. Significance

Bankloc 0.056061 0.806477 Stat. insignificant

Security 0.354881 4.185289 Stat. Significant

Income 0.305356 1.504150 Stat. insignificant

Pseudo R-squared 0.166771 LR statistic 20.90018

Log likelihood -52.21140 Prob. (LR

statistic)

0.0000110

International Journal of Economics, Commerce and Management, United Kingdom

Licensed under Creative Common Page 15

The multinomial logit model is:

Conven = 0.056061bankloc + 0.354881security + 0.305356income

Results show that bank location and income were found to be insignificantly related to

convenience of internet banking. Nevertheless, security apparently explains convenience in that

as security of internet banking transactions improves there is a higher likelihood that internet

banking becomes more secure for customers.

CONCLUSION

Internet banking has a positive impact on bank efficiency to a smaller extent as the magnitude

of internet banking users in Zimbabwe is relatively low. Internet banking has reduced customer

turnaround in banking hall, reduced operational costs.

It can be said that the overall benefits of e-banking was convenience to the customer, as

supported by responses obtained from the research with a sixty three percent response rate.

Some of the benefits that were experienced by customers include efficiency, responsiveness

and privacy. These factors have been critical in providing proper services to the customer thus

improving efficiency of commercial banks. The main usage of IB has been for checking account

balances, payment of bills and funds transfers.

The operations of the commercial banks can be made effective through e-banking if and

only if the systems that are used are reliable and can perform up to the expectations of users. In

as much as e-banking can be beneficial to commercial banks, its efficiency lies in the bank’s

ability to offer superior financial services. This conclusion is in line with Daniel (1999) who

argues that e-banking includes the systems that enable financial institutions, customers,

individuals or businesses, to access accounts, transact business, or obtain information on

financial products and services through a public or private network, including the internet or

mobile phones.

The following recommendations are made on the basis of the findings of the study:

1. Banks may develop software that integrates the internet banking to mobile banking as a

measure of personalizing banking services thus allowing customers to have all time

(24*7) access and control of their accounts even in areas where internet is scarce.

2. Service providers of e-banking services must offer more responsive security strategies.

3. The commercial banks may engage informative advertising about e-banking products as

well as the merits that come with it. Relevant departments of government could help in

creating awareness of the e-banking services through educational tours and media

campaigns. The implication is that banks need to increase their marketing efforts by

initiating awareness programs to raise customer awareness and interest in internet

© Ndlovu & Siyavora

Licensed under Creative Common Page 16

banking. On the same note banks may also provide adequate education about internet

banking its employees.

LIMITATIONS

The study had the following limitations:

1. The research was conducted within nine months which is a short period of time. This

limited the number of interviews that the researchers were able to conduct.

2. The study was financed by the researchers from their own limited financial resources.

This limited the number of trips that researchers were able to make to the branches of

the banks that formed the population of study.

3. Most banks in Zimbabwe have confidentiality clauses as part of their employment

contracts. This constrained access to relevant but confidential information.

REFERENCES

Akbar, M. M. and Noorjahan, P. (2009). Impact of Service Quality, Trust and customer Satisfaction on Customers Loyalty. ABAC Journal 29 (1), 24-38

Al-Sukkar, A. and Hasan, H. (2005) Toward a Model for the Acceptance of Internet Banking in Developing Countries. Information Technology for Development, 11(4), 384-397

Ankit S. (2011). Factors Influencing Online Banking Customer Satisfaction and Their Importance in Improving Overall Retention Levels: An Indian Banking Perspective. Information and Knowledge Management, 1(1), 45-53

Basel Committee on Banking Supervision (BCBS) (2001). Range of Practice in Banks’ Internal Ratings Systems. Retrieved on April 2, 2010 from: www.bis.org/publ/bcbs66.pdf

Bradley, L. and Stewart, K. (2003). Delphi Study of Internet banking. MCB UP Limited, pp. 272-281

Chang, Y.T. (2003). Dynamics of Banking Technology Adoption: An Application to Internet Banking, Department of Economics. Workshop Presentation

Dube, T., Chitura, T., Chitura, T. and Langton, R. (2009). Adoption and Use of Internet Banking in Zimbabwe: An Exploratory Study. Journal of Internet Banking and Commerce, 14 (1), 1-13

El Sawy, O. A., Malhotra, A., Gosain, S., Young, K. M. (1999). IT-Intensive Value Innovation in the Electronic Economy: Insights from Marshall Industries. MIS Quarterly, 23 (3), 305-335

Enos, L. (2001) Report: Critical Errors in Online Banking’, E-Commerce Times, April 11, Retrieved on May 23, 2013 from http://www.ecommercetimes.com/perl/story/8867.htm

Filmer D., and Pritchett L. H. (2001). Estimating Wealth Effects without Expenditure Data—Or Tears: An Application to Educational Enrollments in States of India, Retrieved on 20 June, 2013 from http://vanneman.umd.edu/socy699J/FilmerP01.pdf

Franco, S. C., and Klein, T. (1999), Online Banking Report,’ Piper J’affray Equity Research, retrieved on 21 June 21, 2012 from www.pjc.com/ec-ie01.asp?team=2

Kerem, K. (2003). Internet Banking in Estonia. PRAXIS Center for Policy Studies, 11(4), 363-379.

Locket A. and Little D. (1997). The adoption of direct banking services. Journal of Marketing Management, 13, 751-771

Maddala, G.S. (1988). Introduction to Econometrics. Macmillan, New York

International Journal of Economics, Commerce and Management, United Kingdom

Licensed under Creative Common Page 17

Malhotra, P. and Singh, B. (2007). Determinants of Internet banking adoption by banks in India. Emerald Internet Research, 17 (3), 323-339,

Mäenpää, K., Kaleb, S.H., Kuuselaa, H., and Mesiranta, N. (2008). Consumer perceptions of internet banking in Finland: the moderating role of familiarity. Journal of Retailing and Consumer Services, 15, 266-276

Manski C. F., and McFadden D. L. (1981). Structural Analysis of Discrete Data and Econometric Applications. The MIT Press, Cambridge

Orr, B. (2004). E-Banking job one: Give customers a good ride. ABA Banking Journal, 96(5), 56-57.

Ramseook-Munhurrun, P. and Naidoo, P. (2011). Customers' perspectives of service quality in Internet banking. Services Marketing Quarterly, 32, 247-264

Regan, K. and Macaluso, N. (2000). Report: Consumers Cool to Net Banking. e-Commerce Times, October 3,’ Retrieved on June 20, 2012 from http://www.ecommercetimes.com/news/articles2000/001003-4.shtml

Rockart, J. (1979). Chief Executives Define Their Own Data Needs. Harvard Business Review, 57(2), 81-93

Sathye, M. (1999). Adoption of Internet Banking by Australian Consumer: An Empirical Investigation. International Journal of Bank Marketing, 21(6), 312-323

Simpson, J. (2002). The Impact of the Internet in Banking: Observations and Evidence from Developed and Emerging Markets. Telematics and Informatics, 19(4), 315–330.

Stamoulis, D. S. (2000). How Banks Fit in an Internet Commerce Business Activities Model. Journal of Internet Banking and Commerce, retrieved on October 20, 2013 from http://www.arraydev.com/commerce/jibc/0001-03.htm

Sullivan, R. and Wang, Z. (2005). Internet Banking: An exploration in Technology Diffusion and Impact. Working Paper No 05-05. Payments Systems Research Department, Federal Reserve Bank of Kansas City