Hang Lung Properties: comeback time? - IIS Windows Server

76

See important disclosures, including any required research certifications, beginning on page 75 Hong Kong Real Estate 21 May 2018 Hang Lung Properties: comeback time? Q&A on the prospect of the market reassessing HLP’s ambitious wealth-building effort

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Hang Lung Properties: comeback time? - IIS Windows Server

See important disclosures, including any required research certifications, beginning on page 75

Hong Kong Real Estate

21 May 2018

Hang Lung Properties: comeback time?

Q&A on the prospect of the market reassessing HLP’s ambitious wealth-building effort

2

Hang Lung Properties: comeback time?: 21 May 2018

Table of contents

Page

1 Is there lasting value in malls in this age of e-commerce?

5

2 Are malls in China structurally undermined by oversupply and e-commerce?

17

3 Has HLP found the best way to manage its retail properties?

31

4 Can HLP execute well in tier-2 cities? 49

5 Can HLP make a comeback? 61

Company Section:

Hang Lung Properties 69

3

Hang Lung Properties: comeback time?: 21 May 2018

Contributing Daiwa Analysts:

Jonas Kan, CFA

(852) 2848 4439

Thoughts on the prospect of the market reassessing HLP’s ambitious wealth-building effort

About 13 years ago, Hang Lung Properties (HLP) embarked on an ambitious wealth-

building venture in the property space. The move involved using the over HKD22bn in

profit the company stands to realise from Hong Kong’s residential property sector to

fund a series of investments in China which, if successful, have the potential to

transform the company. If the company can become a leading player in the commercial

property sector in Greater China, it will also be an important stock in global property or

even global equities.

It is clear to us that this effort warrants investors’ attention. But there have been

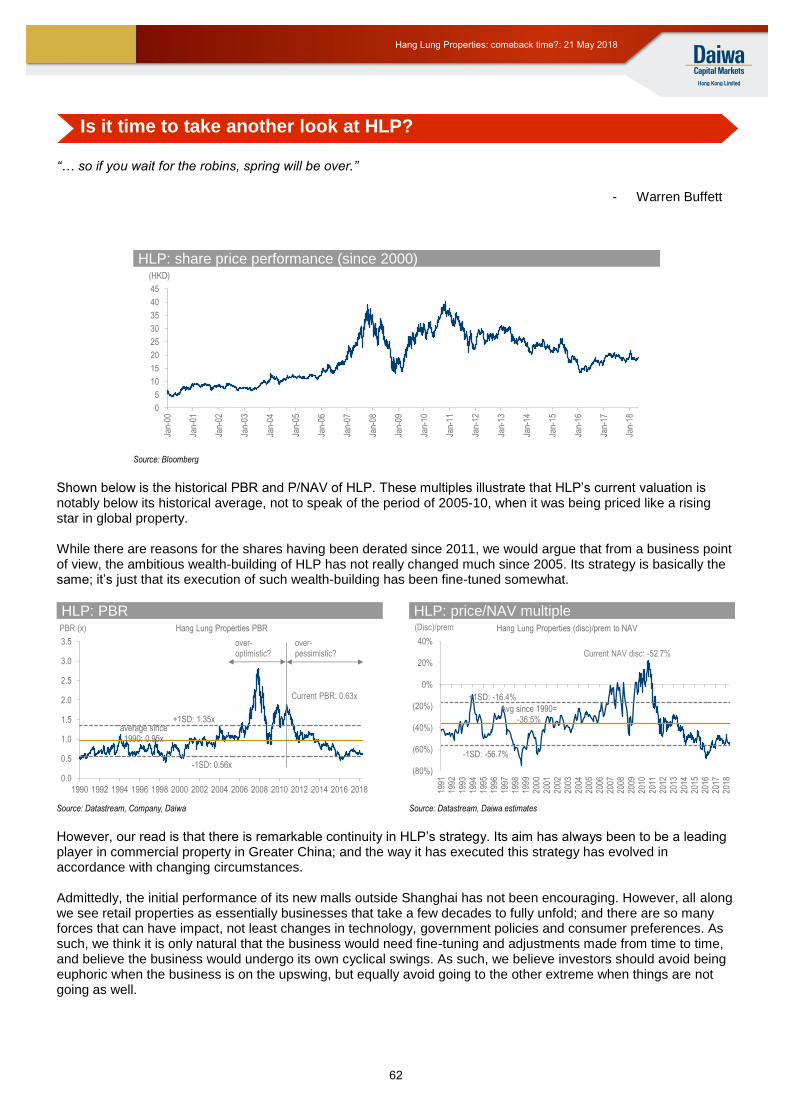

pendulum swings in terms of how this ambition has been priced into HLP shares. From

2005-11, HLP traded like a rising star in global property; since then, its valuation has

been notably derated. Although the company’s gross rentals and BVPS rose at CAGRs

of 7.2% and 4.2%, respectively, from 2011-17, HLP’s current share price of HKD18.58

is down 54% from its 2010 peak of HKD40.30.

Have the fundamentals determining HLP’s earnings and business prospects really

swung so much? Either way, our view is that HLP’s response to the China retail

property downcycle over the past few years has been anything but passive. We believe

it has made considerable efforts to strengthen its platform to execute its ambitious

plans (see Question 3, page 31), which could potentially put it on a much stronger

footing when the industry environment improves. In this regard, we think the retail sales

environment in China started to get under way in Shanghai in 2H16 and has spread to

other cities. Most importantly, we have seen improvement in the results of a number of

its malls.

In this report, we spell out our thoughts on the major issues that we think investors

need to consider in assessing whether HLP shares are still undergoing a structural

derating — or whether now is the time to buy into the turnaround of an ambitious, yet

safe and reliable vehicle through which to play the long-term potential associated with

having a network of prime commercial property assets in major cities across Greater

China.

There are 2 additional issues that we believe are relevant to HLP’s credentials as a

turnaround stock: 1) whether the Hong Kong family-run property companies can

integrate into the global capital market, and 2) whether the global investing world will

regard China stocks, or companies offering solid exposure to China, much more

seriously in the years to come.

In our view, HLP shares now offer global investors a safe and attractive way to play our

highlighted investment themes.

Jonas Kan, CFA, Head of HK/China Property Research

4

Hang Lung Properties: comeback time?: 21 May 2018

5

Hang Lung Properties: comeback time?: 21 May 2018

Question 1

Is there lasting value in malls in this

age of e-commerce?

6

Hang Lung Properties: comeback time?: 21 May 2018

“Market economies are driven by what Professor Joseph Schumpeter, a number of decades ago, called “Creative Destruction”. By this he meant newer ways of doing things, newer products, and novel engineering and architectural insights that induce the continuous obsolescence and retirement of factories and equipment and a reshuffling of workers to new and different activities. Market economies in that sense are continuously renewing themselves... ”

- Alan Greenspan That e-commerce is now a major factor in the world of retailing is beyond dispute. E-commerce has really taken off in China and many other parts of the world. With continuous improvements in Internet technology, payment security and efficiency, logistics support, as well as the rise of consumers born post-2000, e-commerce is only going to grow in importance. Indeed, retail property stocks in the US have been sold down notably in recent years. We note that major internet giants such as Amazon continue to buy offline assets, which could pose a threat to the incumbent owners of bricks-and-mortar assets. At the same time, large retailers in the US have been bargaining hard with landlords on leasing terms, such that the leasing terms that some US retail landlords can realise are far less favourable than before. Conventional wisdom has it that what is happening now in the US is likely to play out in other parts of the world over time. By extension, the argument goes that the world’s retail property stocks should be avoided as this continued derating of retail property assets has the makings of a structural trend.

China: online retail transaction value as % of total retail value

China: e-commerce gross merchandise value (GMV)

Source: iResearch, Daiwa forecasts Source: iResearch, Daiwa forecasts

We can see the logic in this argument, and it is important not to underestimate the impact of the disruption and creative destruction associated with Internet technology on retailing and, by extension, the retail property sector. E-commerce will certainly take a share of the overall retail pie. But history tells us that economic reality often develops in ways more subtle and complex than a linear extrapolation of existing trends might indicate. After all, there are certain things that e-commerce can’t do. One cannot eat online, for example. But service, experience, human touch, “to see and to-be-be-seen”, face-to-face interaction, socialising with friends and peers, among others, are other elements that cannot be provided, or as effectively provided, by an online platform. All of which begs the question: are online and offline necessarily mutually exclusive? Is it too simplistic to divide the retail landscape into merely online and offline?

4.2%

6.3%7.9%

10.7%

13.3%

15.5%

19.5%

21.5%23.6%

25.4%

0%

5%

10%

15%

20%

25%

30%

2011 2012 2013 2014 2015 2016 2017 2018E 2019E 2020E

757 1,311

1,848

2,815

3,877

5,156

7,148

8,654

10,410

12,279

200

2,200

4,200

6,200

8,200

10,200

12,200

14,200

2011 2012 2013 2014 2015 2016 2017 2018E 2019E 2020E

(CNYbn)

E-commerce is set to disrupt the retailing and retail property landscape

But are online and offline mutually exclusive propositions?

7

Hang Lung Properties: comeback time?: 21 May 2018

Ultimately, the fundamentals of the business are that retailers make money from selling products to consumers, and hence retailers must be prepared to pay whomever and whatever can help them generate sales revenue from consumers. There are aspects where the offline platform can have an edge over the online platform. Equally, there are areas where the offline platform is hard to replace.

Fundamentals of the retailing business

Source: Daiwa

It is also instructive to look at how some of the most successful operators of online platforms (eg, Apple and Amazon) have actively moved to secure quality offline platforms. We see these companies’ moves as evidence of our view that offline and online platforms are complementary in certain ways, ie, that the strongest operators of online platforms recognise that they need offline platforms to take their businesses to the next level. Retailers of the future are unlikely to be purely online or offline. To be successful, in sustained fashion, retailers will need to do well online and offline, in our view. As such, we expect the coming years to be characterised by convergence, where offline platforms go more offline, and offline ones take on more online elements.

Against this backdrop, the real question is not whether online will replace offline altogether. As pointed out by Professor Joseph Schumpeter, the capitalist process is driven by a process of “creative destruction.” Some offline assets will be rendered outdated because of the advent of e-commerce. Equally, some online platforms might become outdated, too. At the same time, some offline assets might become stronger after taking on more online elements, and vice-versa. We believe that technology and the Internet are so pervasive that probably every property asset, offline or online, will be affected one way or another. As such, perhaps the more pertinent question is this: which offline assets can constantly reinvent themselves and evolve with the advent of technology? In other words, we believe that property assets need to face up to the fact that the development of technology and use of the Internet will have lasting implications for retailing and consumption habits. It is now a question of who can adapt best to these changing circumstances. Some property assets will be more insulated from the impact than others; those that can leverage the resulting changes might do much better than others; and those that are complacent may gradually lose relevance.

Will malls that can re-invent themselves do even better?

8

Hang Lung Properties: comeback time?: 21 May 2018

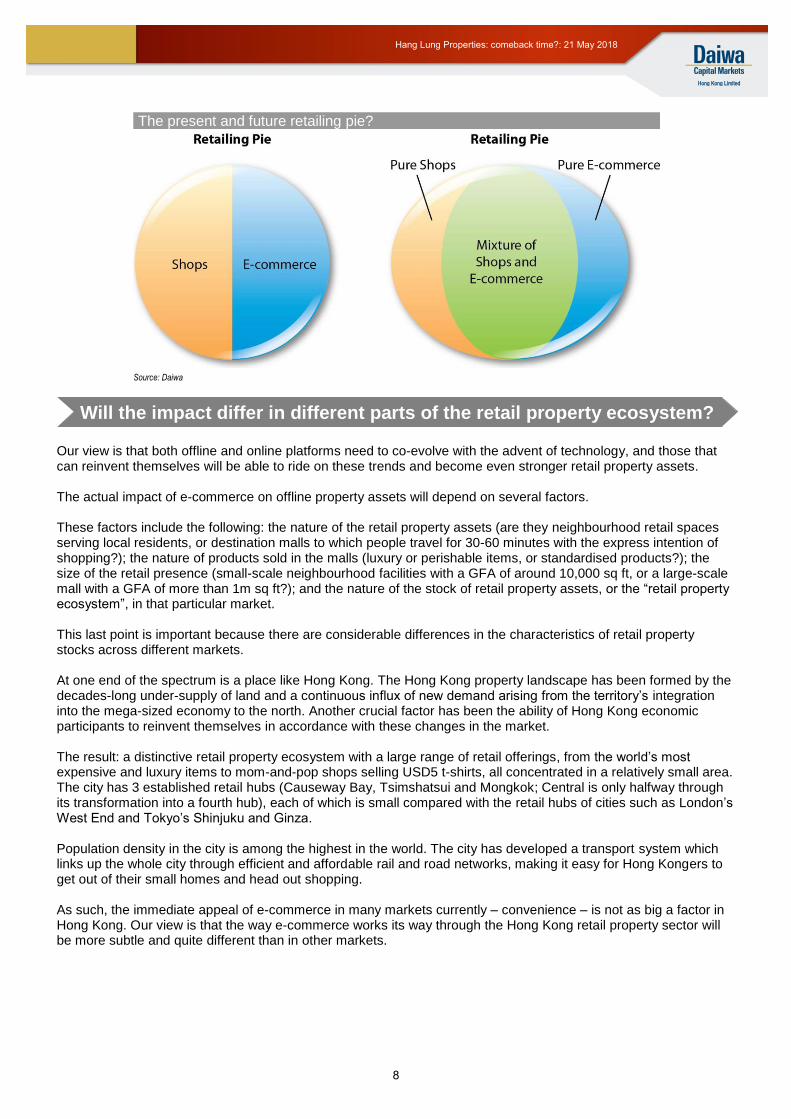

The present and future retailing pie?

Source: Daiwa

Our view is that both offline and online platforms need to co-evolve with the advent of technology, and those that can reinvent themselves will be able to ride on these trends and become even stronger retail property assets. The actual impact of e-commerce on offline property assets will depend on several factors. These factors include the following: the nature of the retail property assets (are they neighbourhood retail spaces serving local residents, or destination malls to which people travel for 30-60 minutes with the express intention of shopping?); the nature of products sold in the malls (luxury or perishable items, or standardised products?); the size of the retail presence (small-scale neighbourhood facilities with a GFA of around 10,000 sq ft, or a large-scale mall with a GFA of more than 1m sq ft?); and the nature of the stock of retail property assets, or the “retail property ecosystem”, in that particular market. This last point is important because there are considerable differences in the characteristics of retail property stocks across different markets. At one end of the spectrum is a place like Hong Kong. The Hong Kong property landscape has been formed by the decades-long under-supply of land and a continuous influx of new demand arising from the territory’s integration into the mega-sized economy to the north. Another crucial factor has been the ability of Hong Kong economic participants to reinvent themselves in accordance with these changes in the market. The result: a distinctive retail property ecosystem with a large range of retail offerings, from the world’s most expensive and luxury items to mom-and-pop shops selling USD5 t-shirts, all concentrated in a relatively small area. The city has 3 established retail hubs (Causeway Bay, Tsimshatsui and Mongkok; Central is only halfway through its transformation into a fourth hub), each of which is small compared with the retail hubs of cities such as London’s West End and Tokyo’s Shinjuku and Ginza. Population density in the city is among the highest in the world. The city has developed a transport system which links up the whole city through efficient and affordable rail and road networks, making it easy for Hong Kongers to get out of their small homes and head out shopping. As such, the immediate appeal of e-commerce in many markets currently – convenience – is not as big a factor in Hong Kong. Our view is that the way e-commerce works its way through the Hong Kong retail property sector will be more subtle and quite different than in other markets.

Will the impact differ in different parts of the retail property ecosystem?

9

Hang Lung Properties: comeback time?: 21 May 2018

The retail property ecosystem in the US is very different. As a result of the abundant availability of land, many US cities are spread out. While Hong Kong might be an extreme example of urbanisation, US cities as a whole are not so urbanised. Apart from cities of the size of New York, San Francisco, Chicago, and Miami, most US cities are spread out and not as urbanised as the likes of Singapore and Tokyo. Hence, while the major malls in Hong Kong are concentrated in a small area within a handful of districts, the US has many large-scale malls, mainly in suburban areas.

Characteristics of different “retail property ecosystems”

Source: Daiwa

Whereas a country such as Japan is linked by rail, the US is all about roads. Most people in the US commute by car rather than use large-scale public transport, and many people are prepared to travel for 60-90 minutes by car to shop at a large-scale suburban mall. Also, the rise of credit cards since the 1960s had a major impact on the development of the US retail sector, as it provided a big boost to retail spending. In other words, the retail property ecosystems of Hong Kong and the US differ in many fundamental ways. As such, it is reasonable to expect the development of e-commerce to have a different impact in each market.

The “retail property ecosystem” in the US today is a result of decades of evolution and adaptations to various factors, some of which may longer apply. Indeed, the US might have been “over-retailed” in some respects for some time. As a market with abundant land, and one where the advent of credit cards spurred retail spending, the US boasts many large-scale malls, many located outside the central parts of cities. At the time these malls were built, shopping alone was thought to be enough to compel consumers to accept the commute times to visit them. In fact, the US ranks very high in terms of retail space per capita. Although there are some variances in the available data, roughly speaking, US retail space per capita stands at over 2 sq m, compared with about 1 sq m in Australia and about 0.3 sq m in China.

Is e-commerce likely to play out differently across different “retail

property ecosystems”?

10

Hang Lung Properties: comeback time?: 21 May 2018

Retail space per capita of major retail markets in the world

Source: Matasii, GGP, Zero Hedge

In any case, many retail facilities in the US are well over 1m sq ft in size. More importantly, many of these malls offer visitors little to do other than shop, and basic F&B (like food courts) and entertainment (like cinemas). This approach was probably fine back in the days when consumers had fewer ways to spend their time (and money), but the world has changed. Today’s consumers have multiple ways to shop, with the Internet offering generally lower prices and e-commerce logistics having improved to the extent that same-day delivery is viable in many cities. Not surprisingly, some consumers prefer to shop online, making a few “clicks” on their smartphones and receiving the items shortly afterwards rather than travelling long distances just to buy something. Another important factor is the position of the retailers relative to the landlords. In our opinion, the relative position of retail landlords in Hong Kong is probably among the highest in the world, if not the highest. Indeed, Hong Kong has many ingredients to be a landlord market in retail property – there are only a handful of major retail landlords in Hong Kong and they generally have strong bargaining over retail tenants. By contrast, large retailers in the US have arguably just as much bargaining power as large landlords. Indeed, many of the large retailers have been leveraging the rise of e-commerce to bargain for lower rents and more flexible leasing terms from landlords. All things considered, the predicament faced by some US retail landlords could be also partly related to the structural characteristics of the US market and we may need to exercise caution while extrapolating from the US situation. Meanwhile, despite the challenges being faced by many malls in the US, some prime retail property assets in the US are holding up and the situation faced by the strongest retail landlords in the US is still notably better than the average. As such, we think it is too early, and probably misguided, to argue that e-commerce will completely replace bricks-and-mortar stores. We believe that the roles of e-commerce and bricks-and-mortar stores will continue to evolve and adapt to each other. In short, we still see lasting value in physical malls, notwithstanding our view that e-commerce is here to stay and is likely to flourish over time.

Ultimately, we believe that the debate between online and offline boils down to the question of what retail property management is really about. Our view is that retail property management is still a relatively young industry. We have seen many different models of retail property management, and it is not yet clear which one will become the industry benchmark — if indeed it is possible to have such a benchmark (also see Question 3, page 31). We like to view the retail property management business as a 3-legged stool, with the retail manager facing consumers on the one hand and retailers on the other. Seen in this light, the role of the retail property manager is about creating 2 virtuous cycles: 1) between consumers and the mall, and 2) between retailers and the mall. Once these virtuous cycles have been established, a third virtuous cycle — one encompassing retailers, the mall, and consumers — can be established, which should result in a growing number of quality consumers and retailers gravitating to the mall. In turn, this third cycle can continue to drive expansion of the overall retail pie in that market, allowing the mall to take market share from other players.

0

1

2

3

US Canada Australia UK China

(sq m)

The roles of online and offline: further thoughts

11

Hang Lung Properties: comeback time?: 21 May 2018

We believe that an important part of the business involves the creation of a virtuous cycle driving consumer spending in malls either directly (through direct spending in the malls) or indirectly (through spending online after visiting the malls or developing trust and confidence about the shop and products after visiting the mall). In our opinion, this virtuous cycle involves 4 major steps and hence requires considerable time and effort to establish. We envisage that in the future, virtually all retailers will need to have both offline and online platforms. In the table on the next page, we summarise what retailers’ online and offline platforms can do.

The virtuous cycle driving consumer spending in a mall

Source: Daiwa

12

Hang Lung Properties: comeback time?: 21 May 2018

The 4 major processes in the virtuous cycle Offline dimension Online dimension

1. Getting potential customers to first try visiting the mall

- The attraction can come from the city and the districts they are in, the ambience inside the malls, as well as the variety and quality of the retailers

- The attraction comes from ease of access and time savings

- Still there are human needs which need to be satisfied by a social setting like malls (eg, dining, eating, friends, seeing and being seen)

- While one can chat and interact online, this is not a substitute for face-to-face meetings. Nor can one eat online

- Can appeal to the 5 senses of human beings - Cannot appeal to the 5 senses of human beings

- Looks a richer platform to offer some new products and experiences to consumers

- Looks inferior in these respects. That said, once the consumer is familiar with the products (say, has tried them before) and has developed sufficient trust in the shops, it would be more convenient to place new orders online than taking the time to go to the physical shop to buy and then line up to pay

- Managers can launch promotional activities (say, performances by celebrities, special shows) to attract potential customers

- Hard to match the physical store in the area of launching promotional events and activities

- Offers many advantages in terms of launching new products - Looks more convenient to buy established and familiar products

2. Getting customers to shop in the mall

- Can make use of the environment, atmosphere and sales techniques of sales staff to stimulate sales

- More difficult to "create" demand. Spending likely to come more from people who already have desires to buy and some specific items to look for

- Can have impulse buying and emotional purchases - Harder to stimulate" impulse buying" and "emotional purchases"

- Can use "sales services" and persuasion to stimulate sales and leverage on sales techniques and customer-sales relationship to stimulate sales

- Hard to use services to stimulate sales

- Assurance of after-sale service and venues where customers can complain and change products are important to stimulate sales

- Online platform can make after-sales service more efficient and effective, but probably cannot completely replace human services

- Offer many ways to help consumers become aware of the product and develop interest in buying that product

- Useful platform for customers to place orders on products they are aware of and want to buy

3. Getting customers to come to the mall repeatedly to shop

- More ways to get consumers to develop sentimental attachment to/positive impression of the mall

- More difficult to get the customers to develop sentimental attachment. That said, the messages and reminders offered by offline platforms can help reinforce such feelings among consumers. If utilised effectively, the mall could become akin to another online friend of customers.

- More ways to get consumers to feel they are being taken care of - More difficult to get customers to develop such feelings. Again, the offline platform can have ways to reinforce such feelings after they have formed (messages, discount coupons, etc).

- More ways to get consumers to feel they can access the most trendy items and get a sense of the trends of the day by visiting the mall

- More difficult for this to be done. However, the offline platform can offer ways to reinforce such feelings.

4. Getting customers to get more of their friends to try visiting the mall

- The physical mall allows customers to meet and socialise with their friends - More difficult for this to be done. That said, messages, coupons and other offers can be forwarded by the offline platform to reinforce the socialising effects resulting from meeting in the mall.

- The mall becomes a place customers are familiar with and have an emotional attachment to

- More difficult for this to be done. That said, there are many ways in which the offline platform can help in facilitating customers to introduce the place to his/her friends.

Source: Daiwa

Meanwhile, we believe that another important part of the retail property management business involves the creation of another virtuous cycle, whereby an increasing number of strong retailers and up-and-coming retailers are compelled to enter the mall. In our opinion, this virtuous cycle also involves 4 major steps and would likewise take time and effort to establish. At this stage, we see the virtuous cycle between the mall and retailers as being mainly about developing a strong partnership so that both parties become long-term stakeholders in each other’s businesses.

13

Hang Lung Properties: comeback time?: 21 May 2018

The virtuous cycle driving retailers’ leasing demand for mall spaces

Source: Daiwa

While we think that retailers will pay increased attention to the importance of offline platforms, our take is that at this stage the creation of this virtuous cycle is driven more by the interaction between mall manager and retailers, as well as the mall manager’s ability to kick-start a virtuous cycle between the mall and the consumers. As we see it, the impact of e-commerce and the advent of Internet technology on this part of retail property management will not be as pronounced on the consumer side. However, the mall manager’s ability to leverage on technology to improve the competitiveness of the mall and develop a virtuous cycle between the mall and consumers would be of great significance in getting retailers to develop a long-term commitment to the mall and partner with the mall to weather challenging times.

The virtuous cycle between the mall, consumers and retailers

Source: Daiwa

Based on the above factors, we believe that the impact of e-commerce on the retail property sector is more multi-dimensional and complex than it may first appear, and that both the online and offline platforms have roles to play in the retail property management process. While the offline platform is powerful and will likely become more powerful over time, we do not think that it will replace the offline dimension completely, on the 4 aspects noted above, any time soon. At the same time, we contend that the mall-retailer relationship will remain an important part of the mall management business — one that may not be directly impacted by e-commerce and Internet technology.

14

Hang Lung Properties: comeback time?: 21 May 2018

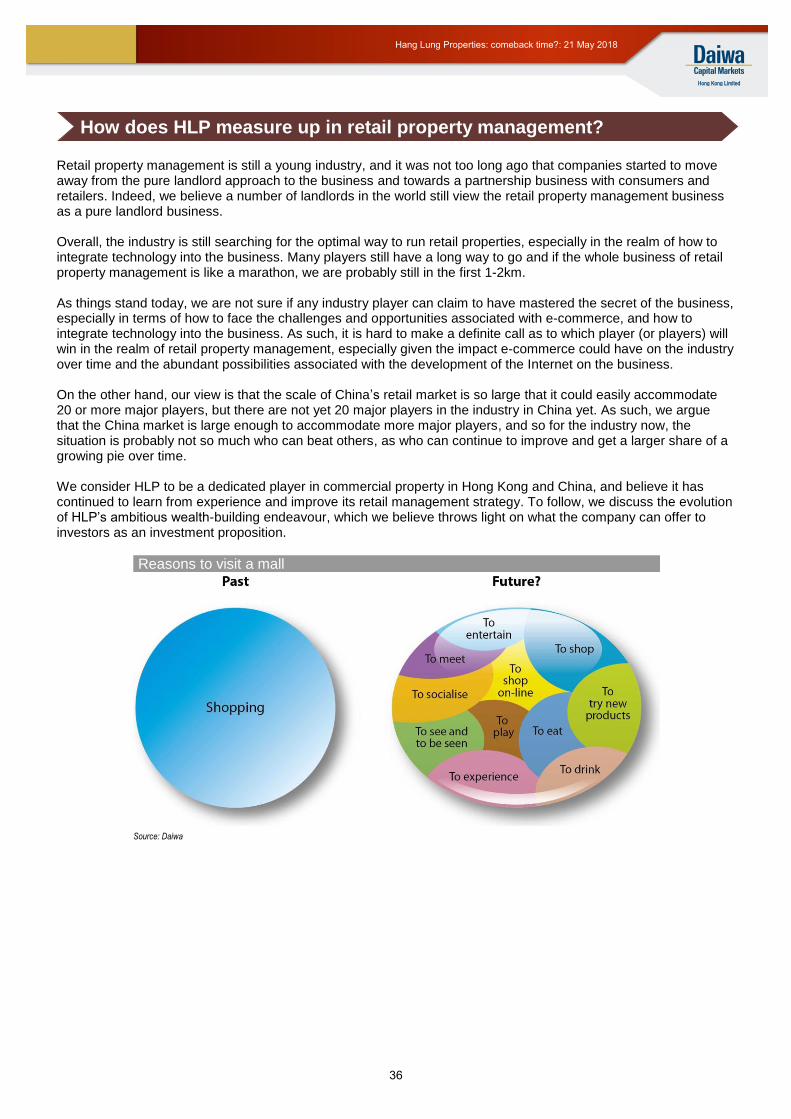

In any case, we foresee the relative roles of online and offline platforms continuing to evolve.

Reasons to visit the mall

Source: Daiwa

We have established our view that there is lasting value in malls, even in this age of e-commerce. Based on the above analysis, the continued development of e-commerce has the potential to make strong malls even more productive, with the online platform serving to strengthen the appeal of the offline platform which has already built up in the 4 aspects we have outlined. Indeed, one implication of the rise of e-commerce is that the number of physical malls required by the market is likely to shrink considerably. Creating and then maintaining an offline platform is costly. Given that some functions previously performed by a physical mall can now be taken up by the offline platform, and that it is so costly and risky to develop and maintain a mall, we would expect the strong physical malls that have also developed strong online platforms to continue to erode the market share of weaker malls. In other words, while the mall industry is inherently a “winner takes all” business, in that there is a tendency for retail spending to gravitate to the strongest malls, we expect these characteristics to become more pronounced in the age of e-commerce. In this light, strong physical malls that can also develop a strong offline dimension have the potential to become even stronger. As such, we believe that the advent of e-commerce could result in a redistribution of retail spending among different types of mall on the offline platform. Hence, rather than merely thinking in terms of the online platform gaining market share from the offline platform, we might see strong offline malls accelerating their market-share expansion by expanding their online platforms. Below we outline our preliminary thoughts on the future structure of the mall industry.

Could strong malls become much stronger by leveraging on the opportunities provided by e-commerce and offline platforms?

15

Hang Lung Properties: comeback time?: 21 May 2018

Potential future landscape of the mall industry

Source: Daiwa

Seen in this light, we expect that the impact of e-commerce will be multi-dimensional, with the respective roles and importance of online and offline platforms, as well as different types of offline and online platforms, continuing to evolve in accordance with the retail property ecosystems they operate in. As such, one needs to closely examine the retail property ecosystems of the respective markets to gain insight into how the retail property landscape of each market is going to evolve. Investor concerns about the ramifications for China’s retail property sector of an oversupply of commercial property space and the rise of e-commerce prompt us to tackle 2 questions. How does the retail property ecosystem of China look today? And how is China’s retail property sector positioned in the face of the challenges posed by e-commerce?

16

Hang Lung Properties: comeback time?: 21 May 2018

17

Hang Lung Properties: comeback time?: 21 May 2018

Question 2

Are malls in China structurally

undermined by oversupply and

e-commerce?

18

Hang Lung Properties: comeback time?: 21 May 2018

“The future is never clear; you pay a very high price in the stock market for a cheery consensus. Uncertainty actually is the friend of the buyer of long-term values.”

- Warren Buffett It is important to bear in mind when assessing China’s shopping mall sector that this is still a young industry. At this stage, no-one can offer a definitive view of how the sector will end up, in our opinion. Before China adopted its Open Door Policy and Economic Reform in 1978, private consumption beyond daily necessities was nearly non-existent. And in the 2 decades after China embarked on these reforms, income levels were still low and no single Chinese city had attained a critical mass of retailing spending by the middle class or high-income groups. During this period, China’s retail property ecosystem consisted mainly of high-street shops, similar to how Hong Kong was during the 1970s. Looking back, private consumption first became a meaningful commercial industry in China in about 2002, by which time 2 decades of foreign investment and the country’s then-recent accession to the World Trade Organization gave Shanghai a critical mass of retail spending powered by the middle class, expatriates, wealthy individuals, and high-income groups. Department stores (mostly state-owned) were the first retail format to benefit from the take-off of private consumption in China, as at the time they were the dominant format in China as a whole. This dominance still holds, though it has waned as a result of the rise of shopping malls and online platforms. In this light, the shopping mall segment has only a 15- to 20-year history in Shanghai and a shorter history in other cities. The early 2000s saw the first generation of retail malls being established in China. Many of these malls were developed by Hong Kong property companies, including major malls such as Grand Gateway 66, Plaza 66, and Oriental Plaza.

The China retail property sector

Source: Daiwa

The China retail property sector is still a young industry, isn't it?

19

Hang Lung Properties: comeback time?: 21 May 2018

The relatively short history of China’s retail property sector is an important factor, since it takes time for any industry to mature. The formative years of an industry are often characterised by problems and setbacks. But, after a period of consolidation, improvement, and refinement, the strongest industry players come to the fore and then work to consolidate the market and become even stronger over time. Against this backdrop, we hold to our view that China commercial property is a challenging sector to play since it is still in its formative phase. In fact, most cities in China are situated on flat land, which allows them to continue to expand. Indeed, many cities in China now exceed 10,000 sq km in area, or 10x the area of Hong Kong as a whole and over 30x the size of Hong Kong’s urban area. Hence, retail spending in China has to be spread over a much larger territory. Meanwhile, many cities in China appear to view commercial developments as symbols of prosperity, and there seems to be a tendency for them to sell more commercial land and develop more commercial GFA than their stage of development might justify. More fundamentally, we believe that China has yet to develop a proper mechanism to price and allocate capital. At the same time, many developers have come to view commercial developments as a “necessary evil”, one that allows them to get the residential GFA that they need to generate sufficient profits to cover the costs associated with commercial developments. As a result of these factors, excessive capital has been allocated to commercial developments, which explains the widespread over-supply of commercial property in many cities in China. It is beyond dispute that nearly all Chinese cities have faced some degree of oversupply of commercial property space during their development. But the answer to the question of whether Chinese cities face a permanent oversupply of commercial property spaces is more subtle and complex.

China’s 4 autonomous municipalities and provincial capitals Provincial capitals Population (m) City area (sq km)

Shanghai* 24.2 6,340

Beijing* 21.7 16,411

Tianjin* 15.6 11,917

Chongqing* 30.8 82,374

Guangzhou 14.5 7,249

Hangzhou 9.5 16,596

Nanjing 8.3 6,587

Jinan 7.3 7,998

Changsha 7.9 11,816

Chengdu 15.9 14,335

Fuzhou 7.7 12,675

Wuhan 10.9 8,494

Hohhot 3.1 17,200

Zhengzhou 9.9 7,446

Taiyuan 4.4 6,988

Shenyang 8.3 12,860

Shijiazhuang 10.9 13,056

Changchun 7.5 20,594

Nanchang 5.5 7,402

Harbin 10.9 53,076

Guiyang 4.8 8,043

Hefei 8.0 11,445

Xi'an 8.8 10,097

Kunming 6.7 21,013

Haikou 2.2 2,304

Urumqi 3.5 13,788

Lhasa 0.5 29,518

Nanning 7.1 22,112

Yinchuan 2.2 8,875

Lanzhou 3.7 13,086

Xining 2.4 7,660

Source: CEIC Note: *the 4 autonomous municipalities

China retail property is a challenging sector to play

20

Hang Lung Properties: comeback time?: 21 May 2018

Despite the clear evidence of the oversupply of commercial property space in China, the total stock of commercial property space in many Chinese cities does not seem excessive relative to these cities’ likely populations and scale when they reach a mature stage of development. In fact, retail space per capita in the US today is over 7x the equivalent figure for China. In this context, we think the problem may stem as much from the pace at which commercial property space comes out as from the total stock of retail properties and the absolute supply figures. As such, it can be argued that, to a certain extent, the central problem facing China’s commercial property sector is that many players and local governments are trying to accomplish in 5-10 years what it took Western cities 5 decades or more to do. As such, we think the commercial property sector in China has a digestion problem. While oversupply characterised Chaoyang in Beijing, Luijiazui, Nanjing Road and Hu Hai Road in Shanghai, and Futian in Shenzhen at certain times during the past 3 decades, this ceased to be true a few years ago and office rents in these cities have been on the rise for quite some time.

China: retail property stock in major cities

Source: Savills

Of course, not all commercial districts in China can weather the challenges related to oversupply during their formative stages. Our take is that many districts have faced a vicious cycle, whereby quality companies and retailers continue leaving and vacancy rates keep rising. In our view, this is one of the major risks in the China commercial property sector. However, some districts, after navigating this challenging digestion period, have managed to attract a growing number of companies and retailers. Of course, governments can always come up with ambitious plans for new CBDs, whereby construction of a new CBD is commissioned before the existing CBD has been taken up. Given there is so much flat land in Chinese cities, there is a risk that oversupply will exist somewhere in certain cities for years to come.

We are not suggesting that investors should not own China commercial property; rather, we are advocating a selective approach to investing in a sector that can be challenging to play. For example, we do see value in prime commercial property in established central locations in Chinese cities. Among the reasons such property appeals to us are poor city planning and the sheer number of people who want to live in major cities. Generally speaking, cities in China lack robust city planning and highly efficient public transport systems. Moreover, redeveloping existing buildings has become costly and difficult due to the strong bargaining position of the existing inhabitants.

0

2

4

6

8

10

12

Beijing Shanghai Shenyang Chengdu Chongqing Guangzhou Wuhan Tianjin Shenzhen Hangzhou

(m sq m)

To what extent is the oversupply issue a digestion problem?

Is China commercial property worth owning?

21

Hang Lung Properties: comeback time?: 21 May 2018

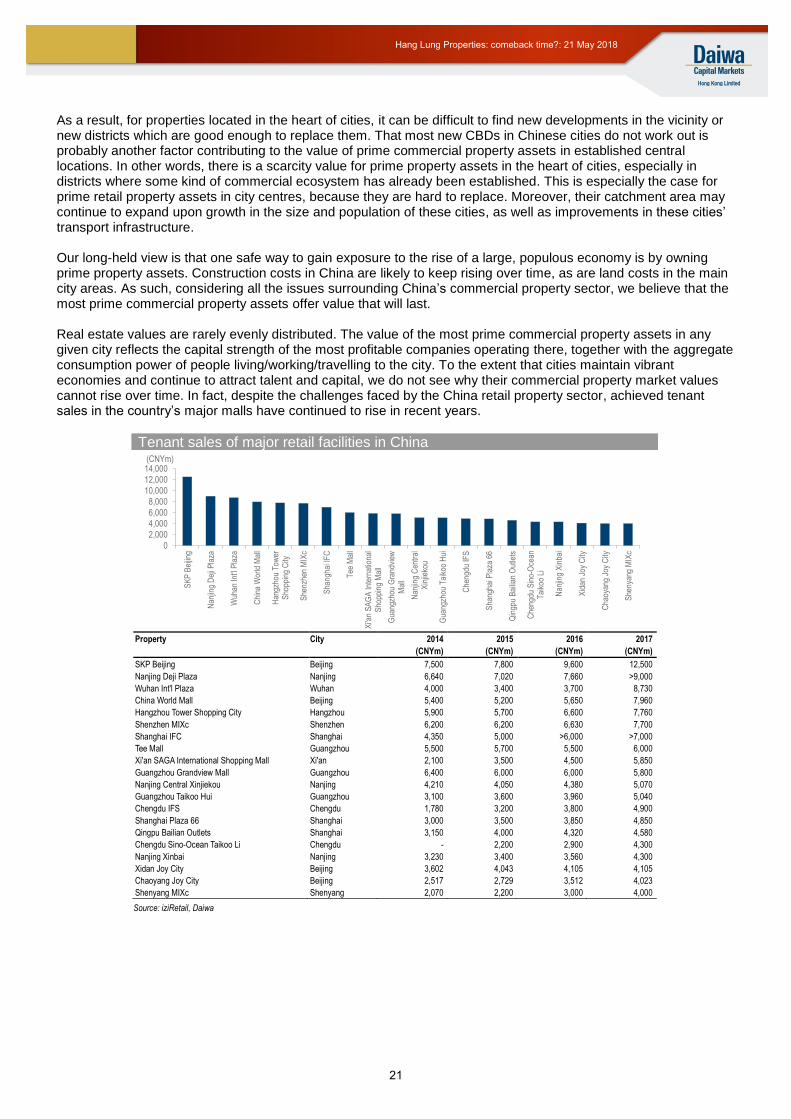

As a result, for properties located in the heart of cities, it can be difficult to find new developments in the vicinity or new districts which are good enough to replace them. That most new CBDs in Chinese cities do not work out is probably another factor contributing to the value of prime commercial property assets in established central locations. In other words, there is a scarcity value for prime property assets in the heart of cities, especially in districts where some kind of commercial ecosystem has already been established. This is especially the case for prime retail property assets in city centres, because they are hard to replace. Moreover, their catchment area may continue to expand upon growth in the size and population of these cities, as well as improvements in these cities’ transport infrastructure. Our long-held view is that one safe way to gain exposure to the rise of a large, populous economy is by owning prime property assets. Construction costs in China are likely to keep rising over time, as are land costs in the main city areas. As such, considering all the issues surrounding China’s commercial property sector, we believe that the most prime commercial property assets offer value that will last. Real estate values are rarely evenly distributed. The value of the most prime commercial property assets in any given city reflects the capital strength of the most profitable companies operating there, together with the aggregate consumption power of people living/working/travelling to the city. To the extent that cities maintain vibrant economies and continue to attract talent and capital, we do not see why their commercial property market values cannot rise over time. In fact, despite the challenges faced by the China retail property sector, achieved tenant sales in the country’s major malls have continued to rise in recent years.

Tenant sales of major retail facilities in China

Property City 2014 2015 2016 2017

(CNYm) (CNYm) (CNYm) (CNYm)

SKP Beijing Beijing 7,500 7,800 9,600 12,500

Nanjing Deji Plaza Nanjing 6,640 7,020 7,660 >9,000

Wuhan Int'l Plaza Wuhan 4,000 3,400 3,700 8,730

China World Mall Beijing 5,400 5,200 5,650 7,960

Hangzhou Tower Shopping City Hangzhou 5,900 5,700 6,600 7,760

Shenzhen MIXc Shenzhen 6,200 6,200 6,630 7,700

Shanghai IFC Shanghai 4,350 5,000 >6,000 >7,000

Tee Mall Guangzhou 5,500 5,700 5,500 6,000

Xi'an SAGA International Shopping Mall Xi'an 2,100 3,500 4,500 5,850

Guangzhou Grandview Mall Guangzhou 6,400 6,000 6,000 5,800

Nanjing Central Xinjiekou Nanjing 4,210 4,050 4,380 5,070

Guangzhou Taikoo Hui Guangzhou 3,100 3,600 3,960 5,040

Chengdu IFS Chengdu 1,780 3,200 3,800 4,900

Shanghai Plaza 66 Shanghai 3,000 3,500 3,850 4,850

Qingpu Bailian Outlets Shanghai 3,150 4,000 4,320 4,580

Chengdu Sino-Ocean Taikoo Li Chengdu - 2,200 2,900 4,300

Nanjing Xinbai Nanjing 3,230 3,400 3,560 4,300

Xidan Joy City Beijing 3,602 4,043 4,105 4,105

Chaoyang Joy City Beijing 2,517 2,729 3,512 4,023

Shenyang MIXc Shenyang 2,070 2,200 3,000 4,000

Source: iziRetail, Daiwa

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

SK

P B

eijin

g

Nan

jing

Dej

i Pla

za

Wuh

an In

t'l P

laza

Chi

na W

orld

Mal

l

Han

gzho

u T

ower

Sho

ppin

g C

ity

She

nzhe

n M

IXc

Sha

ngha

i IF

C

Tee

Mal

l

Xi'a

n S

AG

A In

tern

atio

nal

Sho

ppin

g M

all

Gua

ngzh

ou G

rand

view

Mal

l

Nan

jing

Cen

tral

Xin

jieko

u

Gua

ngzh

ou T

aiko

o H

ui

Che

ngdu

IFS

Sha

ngha

i Pla

za 6

6

Qin

gpu

Bai

lian

Out

lets

Che

ngdu

Sin

o-O

cean

Tai

koo

Li

Nan

jing

Xin

bai

Xid

an J

oy C

ity

Cha

oyan

g Jo

y C

ity

She

nyan

g M

IXc

(CNYm)

22

Hang Lung Properties: comeback time?: 21 May 2018

The threat posed by e-commerce is arguably greater in China than many other parts of the world, since Chinese consumers have led the way in embracing a cashless society. In China, hundreds of millions of people now use their smartphones to manage their daily lives and make payments for purchases using services such as Alipay and WeChat. In these circumstances, it is logical to assume that offline property assets face a genuine threat.

China: market size forecasts of digital payment market transaction volume (2011-20E)

China: digital payment user forecasts (2013-20E)

Source: iResearch, Analysys, Daiwa forecasts Source: iResearch, Analysys, Daiwa forecasts

As a result, we are cautious about the prospects for department stores in China, which run the risk of becoming an outdated format. However, when it comes to shopping malls, we think the situation is more complex. In our opinion, it is fortunate for China’s retail property sector that e-commerce has come to prominence before the total stock of retail property space has become too great. E-commerce has emerged as a force to be reckoned with at a time when China’s retail property ecosystem is still in its formative stages, ie, the ecosystem has time to come to terms with the ramifications of e-commerce before stock within the sector becomes too big to digest. In any case, we take the view that offline and online platforms in China retail are not mutually exclusive. Rather, we believe that the relationship will be multi-dimensional and evolve over time. Although we expect e-commerce to take an increasingly prominent role in the China retail property ecosystem, this does not necessarily mean that the offline components will suffer. Indeed, we believe that some offline property assets could strengthen as a result of e-commerce. One way to assess the impact of e-commerce in China is to determine whether its expansion necessarily spells market-share losses for shopping malls. As argued in Questions 1 and 2, we don’t believe that to be the case. We break the China retail property sector’s development into 5 phases and reiterate that department stores still make up the bulk of the country’s retail space. Shopping malls are a young retail format, and e-commerce is even newer. Against this backdrop, the situation today is not all about e-commerce eating into the market share of shopping malls. Instead, we focus on a scenario where e-commerce and shopping malls together erode the market share of department stores. Rather than viewing e-commerce and shopping malls as head-on competitors, we believe there is scope for them to form alliances in order to win share from department stores.

2,284 3,810 6,593 14,069

24,063

53,851

81,089

105,536

127,040

146,302

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

2011 2012 2013 2014 2015 2016 2017E 2018E 2019E 2020E

CNYbn

260 304

416

475 525

565 599

621

0

100

200

300

400

500

600

700

2013 2014 2015 2016 2017E 2018E 2019E 2020E

in million

Is e-commerce really a threat to China’s mall industry?

23

Hang Lung Properties: comeback time?: 21 May 2018

China still has more retail space than it needs right now, as reflected in the low sales productivity of many retail property assets. But we would point out that it takes time for a new retail format to gain acceptance, and there is also a possibility that the low sales productivity of some malls is a result of immature retail management or the inherent pitfalls of the mall format. In any case, many parties in China — property companies, industry professionals and even the general public —are cognisant of the threat posed by e-commerce to the China mall industry, which we think explains the apparent reluctance of many developers to build large-scale malls in China. In fact, we believe that China’s retail mall industry is now at a stage where the owners and market are seeking to accommodate the rise of e-commerce and digest the retail space that has been built. Relative to consumers’ purchasing power today, China does appear over-built in terms of retail space. It will take time for the country to work through this issue, but we argue that it is too early to conclude that China’s mall industry is in a permanent state of oversupply. One important factor is that China is undergoing urbanisation at a scale that has never been seen before. If we had to summarise Hong Kong property in a single sentence, it would be this: a phenomenon created by the decades-long undersupply of land. If we had to do the same for China property, our sentence would be: a phenomenon centring on the building of metropolitan cities, underpinned by urbanisation at an unprecedented scale. In our opinion, the ongoing construction of the high speed rail system promises to have a transformational impact on the structure of China’s property ecosystem, which the investment world may not yet fully appreciate.

China e-commerce: market size forecasts

2011 2012 2013 2014 2015 2016 2017 2018E 2019E 2020E CAGR 17-20E

Total Retail Market Size

China Real GDP Growth % 9.2% 7.8% 7.7% 7.4% 6.9% 6.7% 6.9% 6.5% 6.4% 6.3%

China CPI Change % 5.4% 2.7% 2.6% 2.1% 1.5% 1.3% 4.3% 1.0% 0.9% 0.7%

China Nominal GDP 48,930 54,037 59,524 64,397 68,905 74,413 82,712 88,916 95,406 102,085 7.3%

YoY change % 18.5% 10.4% 10.2% 8.2% 7.0% 8.0% 11.2% 7.5% 7.3% 7.0%

Total Retail Value (CNY bn) 18,123 20,717 23,438 26,239 29,047 33,231 36,626 40,289 44,156 48,263 9.6%

YoY change % 17.3% 14.3% 13.1% 12.0% 10.7% 10.3% 10.3% 10.0% 9.6% 9.3%

Online Shopper Size

Total Population (m) 1,347 1,354 1,361 1,368 1,375 1,383 1,390 1,397 1,404 1,410 0.5%

YoY change % 0.48% 0.50% 0.49% 0.52% 0.50% 0.59% 0.53% 0.50% 0.47% 0.45%

Internet User Penetration % 38.1% 41.7% 45.4% 47.4% 50.1% 52.9% 55.5% 58.3% 61.2% 64.1%

Total Internet Users (m) 513 564 618 649 688 731 772 814 858 904 5.4%

YoY change % 12.2% 9.9% 9.5% 5.0% 6.1% 6.3% 5.6% 5.5% 5.4% 5.3%

Online shopper penetration (%) 37.8% 42.9% 48.9% 55.6% 60.1% 63.8% 69.0% 71.0% 73.0% 74.0%

Total Online Shopper (m) 194 242 302 361 413 467 533 578 627 669 7.9%

YoY change % 20.8% 24.8% 24.7% 19.6% 14.5% 12.9% 14.2% 8.5% 8.4% 6.7%

Average annual spending per online shopper (CNY) 3,901 5,417 6,120 7,798 9,382 11,048 13,411 14,967 16,613 18,357 11.0%

YoY change % 19.7% 38.9% 13.0% 12.5% 12.5% 12.1% 12.1% 11.6% 11.0% 10.5%

Online Retail Market Size

Total Online Retail Value (bn RMB) 757 1,311 1,848 2,815 3,877 5,156 7,148 8,654 10,410 12,279 19.8%

YoY change % 44.6% 73.3% 40.9% 52.4% 37.7% 33.0% 38.6% 21.1% 20.3% 18.0%

Online Penetration % 4.2% 6.3% 7.9% 10.7% 13.3% 15.5% 19.5% 21.5% 23.6% 25.4%

Mobile Online Retail Value (bn RMB) 12 63 170 930 2,016 3,094 5,075 6,491 8,120 9,823 24.6%

YoY change %

425.0% 169.8% 447.1% 116.8% 53.4% 64.1% 27.9% 25.1% 21.0%

Mobile Online Retail Penetration % 1.6% 4.8% 9.2% 33.0% 52.0% 60.0% 71.0% 75.0% 78.0% 80.0%

Total C2C GMV (CNY bn) 589 929 1,203 1,526 1,931 2,269 2,945 3,315 3,748 4,150 12.1%

YoY change %

57.8% 29.4% 26.9% 26.6% 17.5% 29.8% 12.6% 13.1% 10.7%

C2C as % of Online Retail 77.8% 70.9% 65.1% 54.2% 49.8% 44.0% 41.2% 38.3% 36.0% 33.8%

Total B2C GMV (CNY bn) 196 391 648 1,289 1,946 2,887 4,203 5,340 6,663 8,129 24.6%

YoY change %

99.2% 65.6% 99.1% 51.0% 48.3% 45.6% 27.0% 24.8% 22.0%

B2C as % of Online Retail 25.9% 29.8% 35.0% 45.8% 50.2% 56.0% 58.8% 61.7% 64.0% 66.2%

Source: iResearch, CNNIC, Daiwa forecasts

Is retail space in China in a state of permanent over-supply?

24

Hang Lung Properties: comeback time?: 21 May 2018

China’s high-speed railway network

Source: Daiwa

China’s situation may be a difficult to grasp from a US perspective, given the US is linked primarily by roads and planes. For a sense of how China’s property landscape will be in the future, it is worth looking at Japan, a country linked by a rail system that facilitates the movement of people on a very large scale. Many people who work in Tokyo were not born in the city. As a result, Tokyo’s population tends to be much smaller than usual over the New Year holiday as millions of people return to their home towns to celebrate. We believe that it is a similar story in many Chinese cities, though perhaps at even larger scale. On the issue of metropolitanisation, it is illuminating to look at the proportion of a country’s population that lives in its largest city. The development of cities can resemble the development of shopping malls, in that there is a tendency for the largest and strongest to continue to gain market share until it has reached its full potential. This certainly holds true in China, because for people moving from rural areas to cities, every city is new and it is natural to head for the one offering the most opportunities. Hence, as long as the major cities have the necessary land and infrastructure facilities, they can continue to expand. However, while China’s population in tier-1 cities is huge in absolute terms, it does not seem large relative to the overall population. In many countries, the largest city accounts for 10% of the country’s population. Some cities, such as Seoul and Tokyo, account for 20-30% of the population. But in China, the biggest cities (such as Beijing and Shanghai) account for only 2-3% of the country’s population.

25

Hang Lung Properties: comeback time?: 21 May 2018

China: the potential 5 great metropolitan zones

Source: Daiwa

From this perspective, we believe there is considerable room for the populations of major Chinese cities to expand further. Our view is that having a well-established rail system will be conducive to the largest cities gaining population from the rest of the country. However, if Shanghai or Beijing have only 5% of the country’s population, the quantum of population involved would probably put a significant strain on the physical and social infrastructure of the affected cities. In this context, while the existing stock of retail space in many Chinese cities seems large relative to their purchasing power, the balance could be restored as more people migrate to major cities, especially if the income and wealth levels of people continue to rise. Another factor to consider is the threshold effect. As we see it, many people in China are still below the threshold for middle-class retail spending. But they are not that far from the threshold. Once the threshold is passed, the increment could be very substantial, with potentially millions of people entering the bracket for middle-class retail spending. Still another factor to bear in mind is that, when it comes to retail spending, it is never about equalisation. Rather, it is about polarisation, in that the largest and strongest retail assets can always take market share from the smaller ones. As such, even if there is an oversupply of retail space in the industry as a whole, this might be a problem mainly for fringe and under-managed assets. The strongest assets could be quite insulated from this oversupply, in other words. In conclusion, we believe that it is wrong to assume that China’s retail property sector will be in a permanent state of oversupply, and in this regard the challenges faced by the strongest malls are likely to be fairly benign.

26

Hang Lung Properties: comeback time?: 21 May 2018

We have established our view that China retail property has to be seen for what it is: a relatively young industry which has a range of possibilities open to it. E-commerce has taken hold in China, which the market absolutely needs to come to terms with. But we think the impact of e-commerce on China’s retail market could be quite fluid. As discussed in Question 1, the relationship between offline and online platforms may end up being multi-dimensional, as there are certain elements of the offline shopping experience that cannot be duplicated online. More importantly, investors have to recognise that there are many areas where online and offline are complementary. More broadly, we believe that the world is still in the early stages of understanding what drives Chinese consumers. For example, while movies and book stores are regarded in the West as being among the types of trade most impacted by e-commerce, both still look to be flourishing in China. In any case, for all that has been said about Chinese consumers’ willingness to embrace technology, it is hard to imagine them being content to stay at home for hours each day in front of their computers or smartphones. After all, human beings have a fundamental need to go out to see and be seen, and to socialise with friends. While the central role of malls as places to buy goods may be affected by e-commerce, we expect the malls of the future to feature more places to eat, drink, see, play and meet. In short, our take is that China’s retail property ecosystem is in its formative stages and it is not a given that e-commerce will undermine the country’s mall industry. Indeed, based on our analysis (Question 1, page 5), if managers can leverage it well, e-commerce might even enhance the competitiveness of physical malls. Still, with the growing penetration of the Internet and the rise of e-commerce, the world likely won’t need as many malls as it once did. Shown below are our initial thoughts about how the retail property industry as a whole might evolve. We believe that our thesis is likely to hold up for China’s retail property ecosystem as well. Our central argument is that China’s road to having a more stable and sustainable retail property ecosystem may well turn out to be smoother and more pleasant than the US’ road, if only for the reason that China is far from being over-retailed right now (its retail space per sq m is well below 20% of the US equivalent). While many cities in China do face an oversupply of retail space in the near term, we view this primarily as a digestion issue and believe that China’s major cities of the future will still be able to accommodate the construction of many more retail properties.

Reasons to visit a mall

Source: Daiwa

How will China’s retail property ecosystem play out?

27

Hang Lung Properties: comeback time?: 21 May 2018

Potential landscape of the mall industry

Source: Daiwa

If China’s major cities of the future can accommodate many more retail properties, then China’s retail property ecosystem could ultimately be very large and rich, accommodating a large range of retail concepts. Moreover, there could be significant scope for competent retail property managers to exercise their creativity and professional skills, both online and offline. Much depends on the style and quality of China’s retail property managers and developers. If they follow the crowd and build similar developments the length and breadth of the country, we could see many malls in China ending up more like food halls or family entertainment centres. But we contend that the China retail property market is large enough to accommodate at least a handful of top-prime and productive shopping malls. We are of the view that eventually there will be at least 20 of these malls in the country (see our China property sector report of 28 March 2017: Why 20 is the magic number), each with tenant sales in excess of USD1bn. Indeed, China already has at least 7 malls where tenant sales have surpassed USD1bn.

28

Hang Lung Properties: comeback time?: 21 May 2018

Tenant sales of major retail facilities in China

Property City 2014 2015 2016 2017

(CNY m) (CNY m) (CNY m) (CNY m)

SKP Beijing Beijing 7,500 7,800 9,600 12,500

Nanjing Deji Plaza Nanjing 6,640 7,020 7,660 >9,000

Wuhan Int'l Plaza Wuhan 4,000 3,400 3,700 8,730

China World Mall Beijing 5,400 5,200 5,650 7,960

Hangzhou Tower Shopping City Hangzhou 5,900 5,700 6,600 7,760

Shenzhen MIXc Shenzhen 6,200 6,200 6,630 7,700

Shanghai IFC Shanghai 4,350 5,000 >6,000 >7,000

Tee Mall Guangzhou 5,500 5,700 5,500 6,000

Xi'an SAGA International Shopping Mall Xi'an 2,100 3,500 4,500 5,850

Guangzhou Grandview Mall Guangzhou 6,400 6,000 6,000 5,800

Nanjing Central Xinjiekou Nanjing 4,210 4,050 4,380 5,070

Guangzhou Taikoo Hui Guangzhou 3,100 3,600 3,960 5,040

Chengdu IFS Chengdu 1,780 3,200 3,800 4,900

Shanghai Plaza 66 Shanghai 3,000 3,500 3,850 4,850

Qingpu Bailian Outlets Shanghai 3,150 4,000 4,320 4,580

Chengdu Sino-Ocean Taikoo Li Chengdu - 2,200 2,900 4,300

Nanjing Xinbai Nanjing 3,230 3,400 3,560 4,300

Xidan Joy City Beijing 3,602 4,043 4,105 4,105

Chaoyang Joy City Beijing 2,517 2,729 3,512 4,023

Shenyang MIXc Shenyang 2,070 2,200 3,000 4,000

Source: iziRetail, Daiwa

Broadly speaking, we believe that tier-1 cities like Shanghai could accommodate more than 5 major malls over time, while in tier-2 cities there should be room for at least 2 major players, in our view. Hence, players should be safe if they are within these top 2 spots, in our view.

However challenging the situation being faced by malls in China, we think there are mitigating factors to consider. First, land costs in China are not prohibitive; this is especially the case for players which bought land in the early days. The exhibit on the next page shows the cost of land for Hang Lung Properties’ major projects in China, which appear low by most measures. It is very hard to acquire sites with GFAs of multi-million sq ft in the world’s major cities, and the days of being able to do the same in China look to have passed. Second, construction costs in China are not yet prohibitive. While construction costs in China have increased by a great deal in recent years, in the grand scheme of things they do not seem too expensive. For example, a construction cost of CNY10,000/sq m is probably the going rate for prime commercial property assets in China now, while the equivalent figure in Hong Kong is likely to be 5-6x higher. Third, total retail sales in China don’t appear to have reached their limit when considering the population and catchment area of the country’s most prime malls. In fact, the achieved tenant sales of Hong Kong’s major malls are still notably higher than those of China’s major malls. Of course, there are special factors which tend to boost tenant sales in major retail assets in Hong Kong, such as population density and limited stock size. However, given that the populations of many cities in China could end up being many times that of Hong Kong, and that the high-speed rail network should help retail spending gravitate to the strongest mall(s) in major Chinese regions, we think annual sales in the most productive malls in China could ultimately reach USD1-2bn or more.

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

SK

P B

eijin

g

Nan

jing

Dej

i Pla

za

Wuh

an In

t'l P

laza

Chi

na W

orld

Mal

l

Han

gzho

u T

ower

Sho

ppin

g C

ity

She

nzhe

n M

IXc

Sha

ngha

i IF

C

Tee

Mal

l

Xi'a

n S

AG

A In

tern

atio

nal

Sho

ppin

g M

all

Gua

ngzh

ou G

rand

view

Mal

l

Nan

jing

Cen

tral

Xin

jieko

u

Gua

ngzh

ou T

aiko

o H

ui

Che

ngdu

IFS

Sha

ngha

i Pla

za 6

6

Qin

gpu

Bai

lian

Out

lets

Che

ngdu

Sin

o-O

cean

Tai

koo

Li

Nan

jing

Xin

bai

Xid

an J

oy C

ity

Cha

oyan

g Jo

y C

ity

She

nyan

g M

IXc

(CNYm)

Favourable economics for the top malls in China

29

Hang Lung Properties: comeback time?: 21 May 2018

As the following table shows, a mall with 20,000 purchases a day and an average ticket size of HKD200 would generate annual tenant sales of c. HKD1.5bn. Given the population bases of major Chinese cites and the number of wealthy people in these cities, these figures don’t strike us as unattainable. Indeed, SKP Beijing recorded tenant sales of USD1.8bn in 2017, according to IZI Retail. Based on an occupancy cost assumption of about 18%, the annual gross rental generated by these malls could be in a range of USD180-360m.

Annual retail sales sensitivity analysis

Avg. no. of purchases per day

5,000 10,000 15,000 20,000 25,000 30,000 35,000 40,000 45,000 50,000

Avg

. val

ue

per

pu

rch

ase

(HK

D)

200 0.4bn 0.7bn 1.1bn 1.5bn 1.8bn 2.2bn 2.5bn 2.9bn 3.3bn 3.6bn

300 0.5bn 1.1bn 1.6bn 2.2bn 2.7bn 3.3bn 3.8bn 4.4bn 4.9bn 5.4bn

400 0.7bn 1.5bn 2.2bn 2.9bn 3.6bn 4.4bn 5.1bn 5.8bn 6.5bn 7.3bn

500 0.9bn 1.8bn 2.7bn 3.6bn 4.5bn 5.4bn 6.4bn 7.3bn 8.2bn 9.1bn

600 1.1bn 2.2bn 3.3bn 4.4bn 5.4bn 6.5bn 7.6bn 8.7bn 9.8bn 10.9bn

700 1.3bn 2.5bn 3.8bn 5.1bn 6.4bn 7.6bn 8.9bn 10.2bn 11.4bn 12.7bn

800 1.5bn 2.9bn 4.4bn 5.8bn 7.3bn 8.7bn 10.2bn 11.6bn 13.1bn 14.5bn

900 1.6bn 3.3bn 4.9bn 6.5bn 8.2bn 9.8bn 11.4bn 13.1bn 14.7bn 16.3bn

1,000 1.8bn 3.6bn 5.4bn 7.3bn 9.1bn 10.9bn 12.7bn 14.5bn 16.3bn 18.2bn

1,200 2.2bn 4.4bn 6.5bn 8.7bn 10.9bn 13.1bn 15.2bn 17.4bn 19.6bn 21.8bn

1,400 2.5bn 5.1bn 7.6bn 10.2bn 12.7bn 15.2bn 17.8bn 20.3bn 22.9bn 25.4bn

1,600 2.9bn 5.8bn 8.7bn 11.6bn 14.5bn 17.4bn 20.3bn 23.2bn 26.1bn 29.0bn

1,800 3.3bn 6.5bn 9.8bn 13.1bn 16.3bn 19.6bn 22.9bn 26.1bn 29.4bn 32.7bn

2,000 3.6bn 7.3bn 10.9bn 14.5bn 18.2bn 21.8bn 25.4bn 29.0bn 32.7bn 36.3bn

2,200 4.0bn 8.0bn 12.0bn 16.0bn 20.0bn 24.0bn 28.0bn 31.9bn 35.9bn 39.9bn

2,400 4.4bn 8.7bn 13.1bn 17.4bn 21.8bn 26.1bn 30.5bn 34.8bn 39.2bn 43.6bn

2,600 4.7bn 9.4bn 14.2bn 18.9bn 23.6bn 28.3bn 33.0bn 37.8bn 42.5bn 47.2bn

2,800 5.1bn 10.2bn 15.2bn 20.3bn 25.4bn 30.5bn 35.6bn 40.7bn 45.7bn 50.8bn

3,000 5.4bn 10.9bn 16.3bn 21.8bn 27.2bn 32.7bn 38.1bn 43.6bn 49.0bn 54.5bn

Source: Daiwa

Sales value of luxury goods in China

Source: Statista

Chinese consumers like luxury goods. Sales of luxury items to Chinese consumers are believed to account for over one-third of such sales globally, though a large proportion of these transactions are done overseas. However, as and when these sales shift to China, or the number of wealthy and middle-class individuals in China continues to grow, we see considerable room for retail sales of luxury goods in China to rise. Luxury goods are an important part of the story because they tend to carry the highest margins. At the end of the day, we believe that the rents that can be collected by retail landlords will tend towards the sustainable occupancy cost of each particular trade. And we think the sustainable occupancy cost of different trades tends to vary significantly, according to the operating profit per sq ft of each trade. Due to the high operating margins, we believe that luxury items will remain the trade that can pay the highest unit rents. Hence, in terms of sales productivity, the contribution from the luxury trades should not be underestimated. In sum, our view is that the China retail property ecosystem is still evolving and it is too early to pass a definitive judgment on it. We do know that what China is experiencing now, in terms of urbanisation and acceptance of a cashless society, is unprecedented in human history. There are no past examples to draw on in analysing these factors. We think it would be sensible to at least allow for the possibility that China will provide upside surprises, just as it has done before.

0

10

20

30

40

50

60

70

80

2010 2011 2012 2013 2014 2015 2016 2017 2018E 2019E 2020E

(EURbn)

30

Hang Lung Properties: comeback time?: 21 May 2018

In any case, we believe that the malls in the established city centres of major Chinese cities are well protected from the rise of e-commerce and concern about the oversupply of retail space in the country. We see real potential for this market. The question is: who has the vision and capability to navigate the challenges in the sector and get the most from it. Is Hang Lung Properties the way to play the potential of the China retail property sector? And has Hang Lung Properties found the best way to manage its retail properties in China?

31

Hang Lung Properties: comeback time?: 21 May 2018

Question 3

Has HLP found the best way to

manage its retail properties?

32

Hang Lung Properties: comeback time?: 21 May 2018

“Look at stocks as businesses, look for businesses you understand, run by people you trust and are comfortable with, and leave them alone for a long time.”

- Warren Buffett Before we address the question of whether HLP has found a way to manage its retail properties, we first examine the different philosophies of the retail property management business. We believe looking at the philosophies provides the context through which investors can assess how HLP has evolved over the years and how its credentials have strengthened. While it is typical for the stock market to use a conventional demand and supply analysis to analyse the prospects for all property asset classes, we do not think this approach is enough to analyse the retail property sector. While we do not dispute the importance of a conventional demand and supply analysis, we would caution that the way demand and supply factors work for retail properties or shopping malls is more subtle and complex than for other property segments such as offices. In our opinion, one of the most important factors determining the value of retail properties is their management. We see 2 opposing philosophies in the running of retail property business. At one end of the spectrum, retail property management is seen as simply a landlord business, while at the other end, it is seen as more as a partnership (between the owner of the property and its retail tenant clients).

The “landlord business” versus the “partnership business” Landlord business Partnership business

Focus Minimising vacant space Maximising tenant sales

Tenant mix No special strategy, other than maximising the achieved rent

Creating an environment which is most conducive to repeat shoppers and to facilitate the malls becoming more popular and more relevant

Tenant sales No special attention. Caring mainly whether the tenants pay rent on time

Closely monitoring changes in tenant sales, their distribution, etc., to get a pulse on the most current situation of the mall

Positioning No special attention paid to fine-tuning the mall's positioning

Constant fine-tuning to search for an optimal positioning in the prevailing retail environment

Tenant relationship Getting tenants to pay the maximum rent Work as partners with tenants to create a larger pie for all

No special attention paid to the tenant or working team on major retail groups

Dedicated teams to work with major retail groups to facilitate the execution of their retail strategy

Customer traffic Wait passively for shoppers to come Using active promotions to attract its repeat visits by target shoppers

Source: Daiwa

Overall, retail property management is still a relatively young industry, and as such, has required different players to seek and experiment with different models for the business. In general, most property companies (not only in Hong Kong but in other parts of the world as well) tend to start off primarily adopting the “landlord business” approach for ease and simplicity. If an owner of a property sees itself just as a landlord, its priorities are generally just that of minimising vacancy rates and making sure space is leased to the highest bidders, while the operating cost for managing the property is minimised. This way to manage the business is relatively straightforward and simple, though the trade-off is that, if a retail property is managed in such a way, its aggregate tenant sales growth would not be much better than that of the overall market. This management approach allows the asset to ride on the growth of the overall market or the growing importance of the district where it is located, but may not allow the mall to demonstrate exceptional resilience during difficult times – nor outperform peers in the same district in a consistent and sustained manner. By way of contrast, under a partnership business, the priorities and focus of the landlord are very different as its focus is on growing the pie of aggregate tenant sales rather than merely filling up the space. Instead of merely trying to fill up the space, the priority is to ensure the tenant mix is right, that more shoppers prefer to shop in the mall and that they return repeatedly so that they gradually form a habit to shop in the mall instead of going to other malls in other districts or buying online.

What are the different ways to manage retail property?

33

Hang Lung Properties: comeback time?: 21 May 2018

In our view, if a retail property is managed in this way, then considerable importance needs to be placed on: 1) monitoring how consumer behaviour in the mall and the broader retail market changes, 2) the overall positioning of the mall, 3) the appropriate trade mix inside the mall, 4) the store management strategies of the retailers, 5) the changing merchandise and positioning of each of the retailers inside the mall, and most importantly, 6) how to continue to fine-tune and modify the various aspects of the mall so that the mall can stay strong and relevant in terms of being able to attract the most popular retailers and the biggest spenders. In short, instead of being a passive landlord collecting rent determined by the market, a retail property owner can also become an active manager, providing a crucial link between the retailers and shoppers, and bringing its own input (such as promotions, hardware improvements, changes in positioning and tenant mix, etc.) to work to drive up retail sales at the mall to get a larger portion of the city’s overall retail pie. As such, we believe retail property management is a management-intensive business and that landlords play an important and leading role in the development of a mall and the growth of retail sales for tenants in the mall. We believe there are significant differences between the achieved retail sales – and hence retail rental income performance – of malls under these 2 different models. While most property owners/developers tend to adopt the traditional landlord model to run their business, our read is that the strongest players in the industry tend to be those that lean more towards the latter model.

In our opinion, retail property companies need to build an effective and productive partnership with both their tenants and their customers, thus creating what we refer to as the 3 virtuous cycles (between consumers and the mall; between retailers and the mall; and between customers and the tenants of the mall) as explained on page 13. We think this approach constitutes the ideal management style retail property managers should move towards over time. However, as to how this form of management can be executed, we do not think there is a ready formula. As far as we can discern, there are 4 different models under which to achieve an effective and productive partnership with tenants and customers, which we examine below before moving on to look at how HLP has fared in this regard.

1) Systematic and professional management of retail property assets The first model focuses on the systematic and professional management of retail property assets. In our opinion, the value that can be created by systematic and professional management of retail property assets is significant. Retail is essentially a fragmented industry everywhere, with retail sales in a city being spread around easily hundreds, if not thousands, of retail properties; and very often a typical mall’s share of the city’s retail pie tends to be very small, often well under 0.5%. What this means is that there is often substantial room for a popular mall or a network of well-managed malls to continue to take market share from the less-well-managed retail property assets. We think what commercial real-estate companies like the US’s Simon Property (Not rated) and Australia’s Westfield (Not rated) have demonstrated is that retail property can be a scalable business, and that once a company has got a proper system in place (eg, with specialised teams dedicated to leasing, development; effective communication and co-ordination among the different brands, etc.), the number of malls it is capable of running at the same time can be expanded significantly to possibly well over 100. Moreover, through building up a proper and effective system, retail landlords can ensure that each of the malls within a large portfolio can maintain a certain minimum standard and that the time required for nurturing new malls can be shortened. Needless to say, having a large retail mall network and professional team in place is conducive to expanding through M&A. We can see that the building up of a system to manage retail property assets in a systematic and professional way would significantly enhance the potential of a retail landlord. It appears to us that property companies in the US, Europe and Australia appreciate this aspect better than those in smaller markets, probably because their markets are much larger in geographical reach and they can have a large number of malls in their portfolio.

What are the 4 different models for retail property management?

34

Hang Lung Properties: comeback time?: 21 May 2018

2) Maximising sales productivity Another model is to focus on maximising sales productivity. It appears to us that the property companies in Hong Kong, and Asia historically, tend to put less emphasis on the creation and building of a proper and effective system to run their businesses. We think this is understandable because most property companies in Hong Kong and Asia do not generally have many malls to manage. As such, having the right key person in place to manage each major mall can be more important and effective than developing a proper and effective system. In any case, our read is that while Western companies appear to excel more in the scale they can manage, when it comes to the sales productivity of individual malls, the property companies in Hong Kong are more advanced. As a matter of fact, the sales productivity demonstrated by some of the malls in Hong Kong, such as Harbour City, is notably higher than that of their Western counterparts and we believe this mall has placed considerable emphasis on maximising its sales productivity, one main objective a retail mall should aim to achieve, in our view.

Retail sales at Harbour City versus the Hong Kong retail sector since 2003 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Harbour City retail sales (HKDbn) 4.7 6.8 7.8 8.9 11.4 13.5 15.5 20.1 27.1 30.8 33.8 35.0 30.7 27.7 30.2

YoY change (%) 44.7% 14.7% 14.1% 28.1% 18.4% 14.8% 29.7% 34.8% 13.7% 9.7% 3.6% -12.1% -9.7% 9.1%

HK overall retail sales (HKDbn) 172.9 191.5 204.4 219.0 247.0 273.1 274.7 325.0 405.7 445.5 494.4 493.2 475.2 436.6 446.1

YoY change (%) 10.8% 6.7% 7.2% 12.8% 10.6% 0.6% 18.3% 24.9% 9.8% 11.0% -0.2% -3.7% -8.1% 2.2%

Market share (%) 2.7% 3.6% 3.8% 4.1% 4.6% 4.9% 5.6% 6.2% 6.7% 6.9% 6.8% 7.1% 6.5% 6.3% 6.8%

Source: Company, Daiwa

Retail sales per sq ft at Harbour City versus the top players in the US

Source: Wharf REIC

3) Using mixed development to underpin long-term and sustainable growth