GRUPO MODELO S.A.B. DE C.V.

36

FINANCE IN A GLOBAL PERSPECTIVE (78-612-01) CASE REPORT: GRUPO MODELO S.A.B. DE C.V. PROFESSOR: DR. KEITH C.K. CHEUNG GROUP MEMBERS HONGRU WANG (103915852) XIAONAN WANG (103698018) KAIDAN LUO (103937294) JIAJIA LI (103932479)

Transcript of GRUPO MODELO S.A.B. DE C.V.

FINANCE IN A GLOBAL PERSPECTIVE

(78-612-01)

CASE REPORT: GRUPO MODELO S.A.B. DE

C.V.

PROFESSOR: DR. KEITH C.K. CHEUNG

GROUP MEMBERS

HONGRU WANG (103915852)

XIAONAN WANG (103698018)

KAIDAN LUO (103937294)

JIAJIA LI (103932479)

XUE FEI (103796040)

CASE SUBMITTED: 04 /09 / 2013

Grupo Modelo S.A.B. de C.V.

Introdution

Grupo Modelo, founded in 1925, is the leader in Mexico in

beer production, distribution and marketing. It has a

total annual installed capacity of 71.5 million

hectoliters. Currently, it brews and distributes 14

brands, including Corona Extra, the number one Mexican

beer sold in the world, Modelo Especial, Victoria,

Pacífico and Negra Modelo. It exports seven brands and is

present in more than 180 countries. It is the importer of

Anheuser-Busch InBev’s products in Mexico, including

Budweiser, Bud Light and O’Doul’s. It also imports the

Chinese Tsingtao brand and the Danish beer Carlsberg.

Through a strategic alliance with Nestlé Waters, it

produces and distributes in Mexico the bottled water

brands Sta. María and Nestlé Pureza Vital, among others.

Grupo Modelo trades in the Mexican Stock Exchange since

1994 with the ticker symbol GMODELOC and in 2011 it was

included in its Sustainability Index. It also quotes as

an ADR under the ticker GPMCY in the OTC markets and in

Latibex in Spain as XGMD.

Grupo Modelo evaluates all business results, including

financing costs, in US dollars. The company needs to

borrow $10000000 or the foreign currency equivalent for

four years. For all issues, interest is payable once per

year, at the end of the year. Available alternatives are

as follows:

1. Sell Japanese yen bonds at par yielding 3% per annum.

The current exchange rate is ¥105/$, and the yen is

expected to strengthen against the dollar by 2% per

annum.

2. Sell euro-denominated bonds at par yielding 7% per

annum. The current exchange rate is $1.1960/€, and the

euro is expected to weaken against the dollar by 2% per

annum.

3. Sell US dollar bonds at par yielding 5% per annum.

Japanese Euro US

dollar

Alternatives yen bonds bonds bonds

Coupon rate 3.000% 7.000% 5.000%

Current spot rate, $/¥or $/€ 0.0095 1.1960

Expected change in the value

of the foreign currency2.000% -2.000% 0.000%

Principal needed by Grupo

Modelo

$10,000,00

0

Calculation of the dollar cost debt alternatives Year 0 Year 1 Year 2 Year 3 Year 4

Japanese yen bonds:Proceeds and principal and interest payments

¥1,050,000,000

(¥31,500,000) (¥31,500,000) (¥31,500,000)(¥1,081,500,000)

Expected exchange rate($/yen) 0.0095 0.0097143 0.0099 0.0101 0.0103

US dollar equivalent in expected cash flows $10,000,000 ($306,000) ($312,120) ($318,362) ($11,149,051)

IRR of US$ cash flow stream (cost of funds) 5.060%

euro-denominated bonds:Proceeds and principal and interest payments €8,361,204 (-€585,284) (-€585,284) (-€585,284)

(-€8,946,488)

Expected exchange rate ($/€) 1.1960 1.1721 1.1486 1.1257 1.1032

US dollar equivalent in expected cash flows $10,000,000 ($686,000) ($672,280) ($658,834) ($9,869,339)

IRR of US$ cash flow stream (cost of funds) 4.860%

US dollar bonds:

Proceeds and principal and interest payments $10,000,000 ($500,000) ($500,000) ($500,000) ($10,500,000)

IRR of US$ cash flow stream (cost of funds) 5.000%

As the article mentioned, the company needs to borrow

$10,000,000 or the foreign currency equivalent for four

years. For all issues, interest is payable once per year,

at the end of the year. That means Grupo Modelo should

pay the interest at end of each year in this four-year-

period, and pay the principal at the end of the fourth

year. However, since the company faces foreign currency

bonds to choose from, foreign exchange rate and inflation

are two key points that we ought to consider. IRR is used

to rank several prospective projects the firm is

considering. Although the coupon rate of Japanese yen

bonds is 3%, lower than both 5%(US dollar bonds) and 7%

(euro-denominated bonds), the yen is expected to

strengthen against the dollar by 2% per annum, the euro

is expected to weaken against the dollar by 2% per annum.

IRR of US$ cash flow stream (cost of fund) of euro-

denominated bonds tends to be the lowest (4.860%).

Consequently, because of the expected exchange rates, the

Euro-denominated bonds have the lowest all-in-cost of

funds for the Mexico-based company, Grupo Modelo. For

this perspective, we recommend the company to accept the

euro-denominated bonds.

Currency Exchange Rate Risk

However it is impossible for the yen and euro to

appreciate or depreciate exactly 2% against the dollar.

Violation of parity can occur for a number of reasons.

They may reflect imbalances either in currency markets,

interest rate market, or derivatives. So, if Grupo Modelo

issues foreign currency debt, its cost of debt (rB)

depends on the foreign cost of debt (rB¿) as well as the

percent change in the value of the foreign currency (s).

rB ¿ (1+rB

¿) × (1+s)

We have collected data about historical rate for US

dollar to yen and US dollar to euro from 2007 to 2012:

Year 2007 2008 2009 2010 2011 2012

$/¥ 0.0085 0.0097 0.0107 0.0114 0.0125 0.0125

s

13.8755% 10.5151% 6.6074% 10.1380%

-

0.1128

%

Year 2007 2008 2009 2010 2011 2012

$/¥ 1.3687 1.4637 1.3908 1.3252 1.3912 1.2852

s

6.9379% -4.9791% -4.7177% 4.9805%

-

7.6211

%

The historical rate of yen and euro indicated that the

average percent change in the value of yen and euro are

8.2046% and -1.0799% respectively. Their standard

deviations are 5.3143% and 6.5620% respectively. Which

means the expected spot rate of euro in the future is

likely to appreciate, and Grupo Modelo will not only pay

more interest but also incurs losses related to repayment

in a stronger currency. In order calculate the

distribution of financing cost, we roughly forecast the

foreign currency fluctuation, then generate scenarios and

associated probabilities.

Scenarios for yen:

Probabi

lity

Percent

Change(s)Cost of Debt(rB

)= (1+rB¿) × (1+s)

10% -1.3820% 1.5765%

30% 4.1262% 7.2500%

20% 8.2046% 11.4508%

30% 12.2831% 15.6515%

10% 17.7913% 21.3250%

Average cost of Debt is 11.4508% with a sigma σ=5.4853%.

Scenarios for euro:

Probabil

ity

Percent

Change(s)Cost of Debt(rΒ

)= (1+rB¿) × (1+s)

10% -12.9174% -6.8217%

30% -6.1159% 0.4560%

20% -1.0799% 5.8445%

30% 3.9561% 11.2330%

10% 10.7576% 18.5107%

Average cost of Debt is 5.8445% with a sigma σ=7.0362%.

Grupo Modelo should use multiple-currency financing to

achieve diversification benefit. By diversifying

financing portfolios, Grupo Modelo can lower financing

cost and currency exchange rate risk.

Because yen has a relatively high probability to

appreciate, and the average financing cost in yen is much

larger than the other two currencies, we suggest that the

weight of yen financing should be low (10% out of total).

Weight of euro and dollar are 50% and 40% respectively.

Probabi

lity

rB in

yenrB in euro 10%JPY+50%EUR+40%USD

10%1.5765

%-6.8217% -1.2532%

30%7.2500

%0.4560% 2.9530%

20%11.450

8%5.8445% 6.0673%

30%15.651

5%11.2330% 9.1817%

10%21.325

0%18.5107% 13.3878%

The average cost of portfolio is 6.0673% with a sigma

σ=4.0666%. The low standard deviation of for the

portfolio is a typical consequence of diversification.

Despite diversifying currencies strategies, Grupo Modelo

can also use currency swaps to reduce borrowing cost

through the exchange of interest payments in one currency

for interest payments in another. Payments are based on a

notional principal amount, the value of which is fixed in

exchange rate terms at the swap’s inception. The swap

market is thriving and tends to be more standardized, so

that variance in terms is minimized, and it is easy for

Grupo Modelo to find counterparties.

For Grupo Modelo, it can swap out 1,050,000,000 Japanese

bonds into a Dollar liability. The other institute can be

a Japanese subsidiary located in U.S. It has issued bond

of $10,000,000 US dollar bonds at par with a coupon of

5%. The following chart can help illustrate how currency

swaps work:

At origination:

At each annual settlement date:

At maturity:

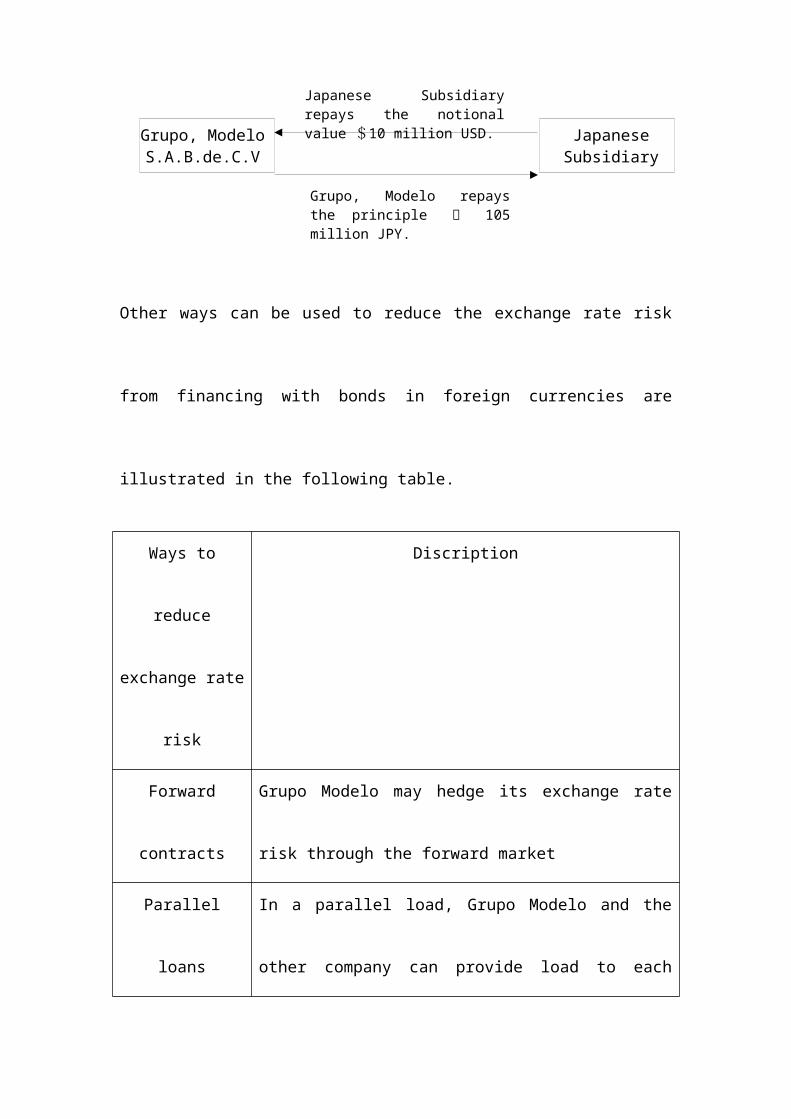

Grupo,Modelo get ¥ 105million Japanese bonds.

Grupo,Modelo

S.A.B.de.C.V

JapaneseSubsidiary

The Japanese Subsidiaryget $10 million US

dollar bonds.

Grupo, ModeloS.A.B.de.C.V

JapaneseSubsidiary

Japanese Subsidiarypays 3% JPY interest.

Grupo, Modelo pays 5%USD interest.

Other ways can be used to reduce the exchange rate risk

from financing with bonds in foreign currencies are

illustrated in the following table.

Ways to

reduce

exchange rate

risk

Discription

Forward

contracts

Grupo Modelo may hedge its exchange rate

risk through the forward market

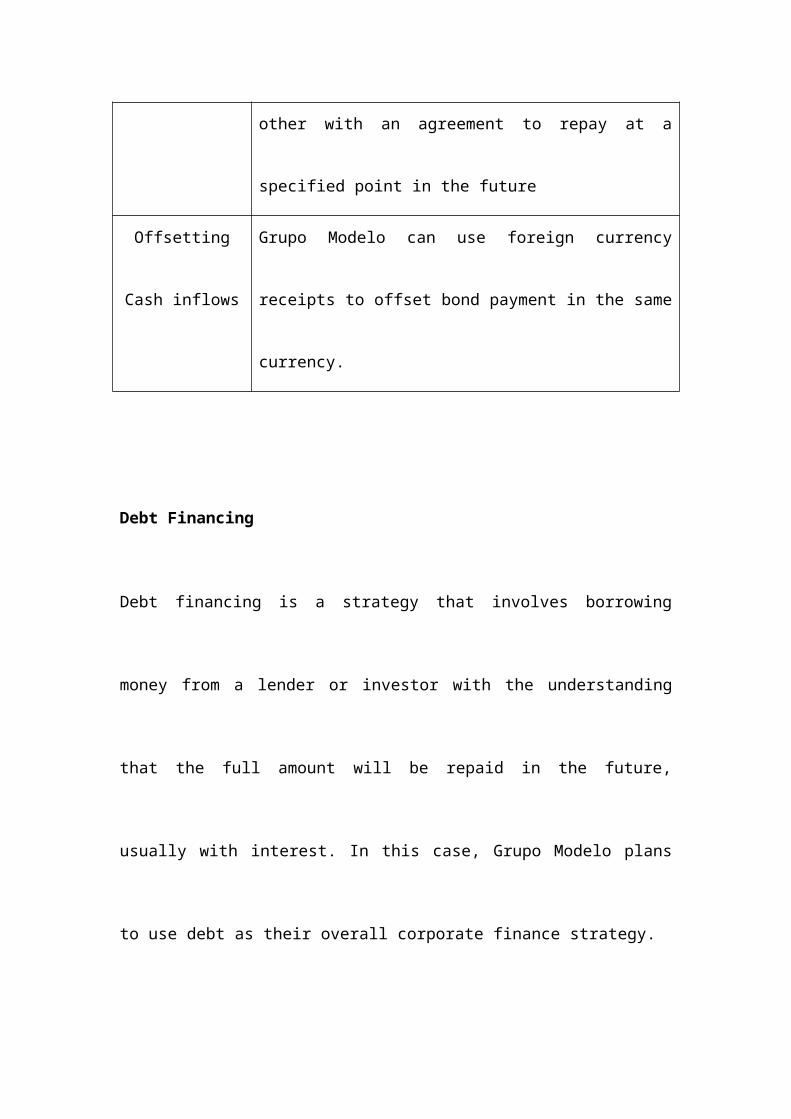

Parallel

loans

In a parallel load, Grupo Modelo and the

other company can provide load to each

Japanese Subsidiaryrepays the notionalvalue $10 million USD.

Grupo, Modelo repaysthe principle ¥ 105million JPY.

JapaneseSubsidiary

Grupo, ModeloS.A.B.de.C.V

other with an agreement to repay at a

specified point in the future

Offsetting

Cash inflows

Grupo Modelo can use foreign currency

receipts to offset bond payment in the same

currency.

Debt Financing

Debt financing is a strategy that involves borrowing

money from a lender or investor with the understanding

that the full amount will be repaid in the future,

usually with interest. In this case, Grupo Modelo plans

to use debt as their overall corporate finance strategy.

Grupo Modelo can be beneficial from the debt financing.

The primary advantage of debt financing is that it allows

Grupo Modelo to retain ownership and control of the

company. In contrast to equity financing, Grupo Modelo

are able to make key strategic decisions and also to keep

and reinvest more company profits. Another advantage of

debt financing is that it provides Grupo Modelo with a

greater degree of financial freedom than equity

financing. Debt obligations are limited to the loan

repayment period, after which the lender has no further

claim on the business, whereas equity investors' claim

does not end until their stock is sold. Furthermore, debt

financing is also easy to administer, as it generally

lacks the complex reporting requirements that accompany

some forms of equity financing.

Tax deductibility of interest payments on debt is a huge

attraction for debt financing. Debt financing offers

Grupo Modelo a tax advantage, because the interest paid

on loans is generally deductible. In most cases, the

principal and interest payments on a business loan are

classified as business expenses, and thus can be deducted

from the firm’s business income taxes.

The international debt market offers the borrower a wide

variety of different maturities, repayment structures,

and currencies of denomination. The markets and their

many different instruments vary by source of funding,

pricing structure, maturity, and subordination or linkage

to other debt and equity instruments. The three major

sources of debt funding on the international markets are

International bank loans and syndicated credits

Euronote market

International bond market.

Source: http://zh.scribd.com/doc/13576697/Financial-Structure-and-

International-Debt

International bank loans have traditionally been sourced

in the Eurocurrency markets. And eurocredits are bank

loans denominated in eurocurrencies and extended by banks

in countries other than in whose currency the loan is

denominated. Syndication allows many different investors

to “participate” in the funding of the loan, thereby

allowing them to diversify their risk or exposure to the

individual borrower.

Euronotes and euronote facilities are short to medium in

term and are either underwritten or non-underwritten.

Euro-commercial paper is a short-term debt obligation of

a corporation or bank (usually denominated in US

dollars). And euro medium-term notes is a new entrant to

the world’s debt markets.

All international bonds fall within two generic

classifications, Eurobonds and foreign bonds. The

distinction between categories is based on whether the

borrower is a domestic or a foreign resident, and whether

the issue is denominated in the local currency or a

foreign currency.

Equity Financing

However, debt financing also has its disadvantages. New

businesses sometimes find it difficult to make regular

loan payments when they have irregular cash flow. In this

way, debt financing can leave businesses vulnerable to

economic downturns or interest rate hikes. Most lenders

provide severe penalties for late or missed payments,

which may include charging late fees, taking possession

of collateral, or calling the loan due early. Failure to

make payments on a loan, even temporarily, can adversely

affect a small business's credit rating and its ability

to obtain future financing.

Additionally, carrying too much debt is a problem because

it increases the perceived risk associated with

businesses, making them unattractive to investors and

thus reducing their ability to raise additional capital

in the future. Since lenders primarily seek security for

their funds, it can be difficult for unproven businesses

to obtain loans. Finally, the amount of money small

businesses may be able to obtain via debt financing is

likely to be limited, so they may need to use other

sources of financing as well. So we do not think that the

higher the debt ratio, the better for the company.

Keeping equity ratio appropriately is also important for

the MNC.

Traditionally, Grupo Modelo can use equity financing by

the following ways.

Venture capital and IPO

financing

Internal equity External

equity

Venture capital financing

during start-up stage.

When the start-up

matures, firm seeks to

exit investment by

arranging an IPO.

The use of

operating cash

flow to fund

investments

Low transaction

cost

Could

conduct a

seasoned

offering

and issue

additional

shares

The advantage of equity financing is that equity

financing doesn't have to be repaid. Plus, you share the

risks and liabilities of company ownership with the new

investors. Since you don't have to make debt payments,

you can use the cash flow generated to further grow the

company or to diversify into other areas. Maintaining a

low debt-to-equity ratio also puts you in a better

position to get a loan in the future when needed.

Equity ratio equals one minus debt ratio, so when we

decrease the debt ratio means increasing the equity

ratio. When the debt ratio is low, principal and interest

payments don't command such a large portion of the

company's cash flows, and the company is not as sensitive

to changes in business or interest rates from this

perspective. A low debt ratio may also indicate that the

company has an opportunity to use leverage as a means of

responsibly growing the business that it is not taking

advantage of.

After the analysis above, we conclude that it is

necessary for us to decide a proper debt ratio (equity

ratio) for the company. And like all financial ratios, a

company's debt ratio should be compared with their

industry average or other competing firms. However, it

will vary by industry so it is difficult to establish one

guideline for an acceptable debt level. So we would

suggest a proper proportion by watching the history debt

ratio data in the brewery industry.

Symbo

lCompany Debt Ratio

Total

Assets

SAM Boston Beer Company 0.0003 359.48M

ABVCompanhia de Bebidas das

Americas Ambev0.0951 27.88B

BREW Craft Brew Alliance 0.1079 165.66M

FMX Fomento Economico Mexicano 0.1472 22.52B

CCU United Breweries Company 0.2484 2.786B

TAPMolson Coors Brewing

Company0.3687 16.21B

BUD Anheuser-Busch Inbev 0.4938 122.62B

Source: https://ycharts.com/industries/Beverages%20-%20Brewers/debt_equity_ratio,gross_profit_margin

The above companies are of different range of assets and

debt ratios. According to the chart, we could easily see

Anheuser-Busch Inbev has a relatively high debt ratio

(0.4938) compared with other companies’, because the

substantial amount of money (total asset: 122.62B) enable

the company to keep a balance in cash flow without

default. We suggest that Grupo Modelo could keep its debt

ratio around 0.2088,( the average debt ratio in brewery

industry ) should not be more than 0.5.

Optimal Capital Structure

Grupo Modelo's capital structure is its ratio of long-

term debt to equity. There is an advantage to using debt

rather than equity as capital because the interest

payments on debt are tax deductible. The greater the use

of debt is, however, the greater the interest expense and

the higher the probability that the firm will be unable

to meet its expenses. Consequently, the rate of return

required by potential new shareholders or creditors will

increase to reflect the higher probability of bankruptcy.

The tradeoff between debt’s advantage (tax deductibility

of interest payments) and its disadvantage (increased

probability of bankruptcy) is illustrated in the

following exhibit.

Source:http://academic.cengage.com/resource_uploads/downloads/0538482214_252184.pdf

As the exhibit shows, the firm’s cost of capital

initially decreases as the ratio of debt to total capital

increases. However, after some point (labeled X), the

cost of capital rises as the ratio of debt to total

capital increases. This suggests that the firm should

increase its use of debt financing until the point at

which the bankruptcy probability becomes large enough to

offset the tax advantage of using debt. To go beyond that

point would increase the firm’s overall cost of capital.

Conclusion

Grupo Modelo should use both debt financing and equity

financing, and make an optimal balance between them. Debt

ratio can range from 15% to 30% (around the average level

in the brewery industry). Besides, Grupo Modelo should

issue bonds in several foreign currencies or use currency

swaps to avoid exchange rate risk.