Growth of Micro-Credit

21

GROWTH OF MICRO-CREDIT IN INDIA: AN EVALUATION (90th Conference volume of Indian Economic Association 2007 512 Dr. Md. Tarique * & Ranjan Kumar Thakur † The success of Grameen Bank in Bangladesh has established the fact and several literatures in this regard also acknowledge the fact that poor are bankable in terms of capacity to save and repay the loans provided the same are collected at the doorstep in small amount at frequent intervals. This is the basic principle of micro-finance, which suits the mindset, and capacity of the poor. There are two major models under microfinance, i.e., Self-Help Group (SHG)-Bank Linkages and Micro-Finance Institutions (MFI) - Bank Linkages being operated in the country. SHGs are the real grass root level setups for micro-credit growth. They reach the poorest sections in rural settings as well as are empowering lakhs of women and entrepreneurs all around India. Although the growth of SHGs in India has been phenomenal there are some significant problems faced by them which might hamper their growth in the coming years. For instance politicizing of subsidy allotment among SHGs has become a big problem. With some efforts substantial progress can be made in taking MFIs to the next orbit of significance and sustainability. This needs innovative and forward-looking policies, based on the ground realities of successful MFIs. This, combined with a commercial approach from the MFIs in making Micro Finance Financially Sustainable, will make this Sector vibrant and help achieve its single-minded mission of providing Financial Services to the Rural Poor. I. INTRODUCTION "If you can run a bank, lend money, and get it back, cover all your costs, and make a profit, and people get out of poverty, what else do you want?" Mohammad Yunus, micro-credit pioneer and founder of the Grameen Bank. India has 400 million people who qualify to being very poor, living on less than $1 per day. The Reserve Bank of India (RBI) and the Government of India are acutely conscious of the need to reach bank credit to this section of society, especially in rural India. Micro- financing is an enormous step in this direction. Micro-finance is the provision of a broad range of financial services such as deposits, loans, payment services, money transfers, and insurance to poor and low-income households and, their micro-enterprises. (ADB, Financial Services for the Poor, 2005). It is basically lending small sums of money without collateral, to the poor, who have an entrepreneurial spirit. Microfinance is a * Lecturer, University Deptt. Of Economics, B.R.A.Bihar University, Muzaffarpur. † Research Scholar, University Deptt. Of Economics, B.R.A.Bihar University, Muzaffarpur.

Transcript of Growth of Micro-Credit

GROWTH OF MICRO-CREDIT IN INDIA: AN EVALUATION (90th Conference volume of Indian Economic Association 2007

512

Dr. Md. Tarique* & Ranjan Kumar Thakur†

The success of Grameen Bank in Bangladesh has established the fact and several literatures in this regard also acknowledge the fact that poor are bankable in terms of capacity to save and repay the loans provided the same are collected at the doorstep in small amount at frequent intervals. This is the basic principle of micro-finance, which suits the mindset, and capacity of the poor. There are two major models under microfinance, i.e., Self-Help Group (SHG)-Bank Linkages and Micro-Finance Institutions (MFI) - Bank Linkages being operated in the country. SHGs are the real grass root level setups for micro-credit growth. They reach the poorest sections in rural settings as well as are empowering lakhs of women and entrepreneurs all around India. Although the growth of SHGs in India has been phenomenal there are some significant problems faced by them which might hamper their growth in the coming years. For instance politicizing of subsidy allotment among SHGs has become a big problem. With some efforts substantial progress can be made in taking MFIs to the next orbit of significance and sustainability. This needs innovative and forward-looking policies, based on the ground realities of successful MFIs. This, combined with a commercial approach from the MFIs in making Micro Finance Financially Sustainable, will make this Sector vibrant and help achieve its single-minded mission of providing Financial Services to the Rural Poor.

I. INTRODUCTION

"If you can run a bank, lend money, and get it back, cover all your costs, and make a profit, and people get out of poverty, what else do you want?" Mohammad Yunus, micro-credit pioneer and founder of the Grameen Bank.

India has 400 million people who qualify to being very poor, living on less than $1 per

day. The Reserve Bank of India (RBI) and the Government of India are acutely conscious

of the need to reach bank credit to this section of society, especially in rural India. Micro-

financing is an enormous step in this direction. Micro-finance is the provision of a broad

range of financial services such as deposits, loans, payment services, money transfers,

and insurance to poor and low-income households and, their micro-enterprises. (ADB,

Financial Services for the Poor, 2005). It is basically lending small sums of money

without collateral, to the poor, who have an entrepreneurial spirit. Microfinance is a

* Lecturer, University Deptt. Of Economics, B.R.A.Bihar University, Muzaffarpur. † Research Scholar, University Deptt. Of Economics, B.R.A.Bihar University,

Muzaffarpur.

GROWTH OF MICRO-CREDIT IN INDIA: AN EVALUATION (90th Conference volume of Indian Economic Association 2007

513

bottom-up approach to spread credit among the poorest population whether rural or

urban.

According to a recent report of the RBI, banks and co-operative institutions made serious

efforts in meeting the needs and demands of the rural sector. As a result, the outreach of

Indian banking system has seen rapid growth in rural areas. In so far as all the Scheduled

Commercial Banks (SCBs) including RRBs are concerned, 48 percent of their total

branches (32,303 branches which translates to a population of about 23,000 per branch),

31 percent (13.67 crore) of their deposit accounts and 43 percent (2.55 crore) of their

borrower accounts are in the rural areas. Such an unprecedented expansion of the formal

financial infrastructure has reduced the dependence of the rural populace on the informal

money lending sector from 68.3 percent in 1971 to 36 percent in 1991. (All India Debt

and Investment Survey, 1991).

The success of Grameen Bank in Bangladesh has established the fact and several

literatures in this regard also acknowledge the fact that poor are bankable in terms of

capacity to save and repay the loans provided the same are collected at the doorstep in

small amount at frequent intervals. This is the basic principle of micro-finance, which

suits the mindset, and capacity of the poor. It was defined in 1997, Micro-credit summit

as "Programmes that provide credit for self-employment and other financial and business

services including saving and technical assistance to very poor person". The Grameen

bank experience of Bangadesh has demonstrated that if the poor are supplied with

working capital, they can generate productive self-employment (Hussain 1998).

Types of Organizations and Composition of the Sector:

Microfinance providers in India can be classified under three broad categories: formal,

semiformal, and informal. The formal banking sector constitutes the first category while

the semi-formal group consists of a variety of MFIs and SHGs. Informal providers, on the

other hand, are not legal entities and include moneylenders and various social networks.

Today, semi-formal and informal lenders dominate the sectori.

GROWTH OF MICRO-CREDIT IN INDIA: AN EVALUATION (90th Conference volume of Indian Economic Association 2007

514

Formal :

Despite the large size of the formal financial sector, its outreach to the poor remains

rather limited. The banking sector consists of 105 commercial banks, 196 regional rural

banks (RRB), and 12,128 cooperative banks. Cooperative banks primarily service rural

areas and were the first to provide financial services to the poor. Among the most

prominent is the Self-Employed Women’s Association (SEWA) Bank, which primarily

services urban women. In March 1999, deposits held by cooperative banks totaled Rs.

677 billion, while their loan portfolios stood at Rs. 708 billion. RRBs provide credit for

agriculture and micro-enterprise and generally target the poor. As of March 1999, their

deposits stood at Rs. 268 billion while their advances totaled Rs. 113 billion.ii Within

commercial banks’ priority lending requirements, 18 percent is for agriculture, and 10

percent is for disadvantaged groups. Today, formal banks are increasingly using

microfinance to meet these targets.

Semi-Formal :

The majority of institutional microfinance providers in India are semi-formal

organizations broadly referred to as MFIs. Registered under a variety of legal acts, these

organizations greatly differ in philosophy, size, and capacity.

The least regulated institutions include over 500 non-government organizations (NGOs)

registered as societies, public trusts, or non-profit companies. While NGOs play a crucial

role in the formation and bank linkage of SHGs, microfinance is often but a subset of

their activities. Nonetheless, many NGOs have emerged as successful financial

intermediaries between banks and apex institutions on the one hand, and individuals,

SHGs, and other groups of borrowers on the other.

Other semi-formal providers can be further classified under two groups, mutual benefit

and for-profit institutions, neither of which is constrained to serving only the poor.

Mutual benefit institutions include state credit cooperatives, national credit cooperatives,

MACS may not be able to access government funds, their greater accountability and

relative freedom from government intervention has prompted a majority of state credit

cooperatives to transform into MACS, leading to a total number of 92,000.

GROWTH OF MICRO-CREDIT IN INDIA: AN EVALUATION (90th Conference volume of Indian Economic Association 2007

515

The largest and most profitable MFIs in India are registered as non-banking financial

companies (NBFC). While the vast majority of the 37,000 NBFCs target the rural and

urban middle class, a few such as BASIX focus on providing microfinance services to the

poor. Unlike NGOs, NBFCs, with permission from RBI, are able to mobilize savings and

can thus provide a wider array of services.

Informal :

In addition to friends and family, moneylenders, landlords, and traders constitute the

informal sector. While estimates of their importance vary significantly, it is undeniable

that they continue to play a significant role in the financial lives of the poor. Data from

the 1992 All India Debt and Investment Survey (AIDIS) reveals that households in the

lowest asset ownership category owed 58 percent of their outstanding debt to the

informal sector. Other studies suggest that the informal sector accounts for as much as 84

percent of poor households’ credit usage. While the informal sector charges the highest

interest rates on loans, these are increasingly being driven down by competition from

other microfinance providers (Mahajan and Ramola)iii.

In India, the micro-finance movement is gaining momentum over the past one and half

decade with the active involvement of around 3000 NGOs with the support of apex

institutions such as NABARD, SIDBI, Rashtriya Mahia Kosh etc. Micro-finance

initiatives through SHG-Bank Linkage programme has passed through various phases

since 1992. It is in this backdrop that the present paper tries to analyse the importance

and the growth of micro financing in India. The entire paper is organised into four

segments—Section -1 presents the introductory portion. Section -2 gives a bird’s eye

view on the microfinance model and their growth and performance in India. Section -3 is

assigned to the problems faced by micro-financing in India and finally Section -4

furnishes the concluding observations.

II. GROWTH AND PERFORMANCE

A. Why Micro Credit

The multiplier theory occupies an important place in modern economic theory. The basic

concept of multiplier says that the effect of investment on income, output or employment

is manifold than the original increase in investment. The same can be distinctly

GROWTH OF MICRO-CREDIT IN INDIA: AN EVALUATION (90th Conference volume of Indian Economic Association 2007

516

demonstrated in a credit programme for the rural poor through the continuous expansion

of their economic base. Incomes also rise if borrowings from the banks are being

channelised for productive purposes i.e. invested. The vicious cycle of “low income →

low savings → low investment → low income” can be broken with the injection of credit

in the cycle. “Credit intended for more investment → more income → more savings →

more investment → more income” is the result that is sought through the credit

intervention. It is assumed that those who save and those who borrow are two different

groups of people. Savers put away deposits in banks while borrowers go to the bank and

borrow the savings of others at price. However, a saver can himself be an investor, as is

usual in the case of the poor. His investment is calibrated in very small steps and any

time. The peer pressure, subtle, at times not-so-subtle, keeps the group members in line

and contributes to the collective strength of the groupiv. The impact of micro finance on

the different sectors of the economy can be well understood with the help of following

diagram:

Experiences throughout the globe have proven that microfinance can improve the

livelihoods of poor and low income people in a significant manner. This helps poor

people to have access to savings, credit, insurance and other financial services so that

they are able to cope up with every day demands more resiliently and confidentlyv.

Besides, with the help of micro credit, poor people can set up their own micro enterprises.

GROWTH OF MICRO-CREDIT IN INDIA: AN EVALUATION (90th Conference volume of Indian Economic Association 2007

517

Thus, it helps in alleviating poverty by providing a regular source of livelihood, creating

jobs, allowing children to go to school, enabling families to obtain healthcare and

empowering people to make their choices that best serve their needs. Since more than

90% of microfinance beneficiaries are women, empowering the lady of house does more

miracles in uplifting the standard of living of poor and enables them to be integrated with

overall economic development of the nation and this will be one step forward in the

direction of empowerment of women.

Micro-finance initiatives are now recognised as a cost effective and sustainable way of

expanding the banking system to the rural poor. The guiding spirit behind microfinance

initiatives is:

i. To offer cost effective approach to formal institutions for expanding outreach to

poor;

ii. To develop collateral substitutes;

iii. To focus on the rural and the urban poor, especially women;

iv. To pilot test other micro-credit delivery mechanisms as alternative channels to

the formal banks; and

v. To effectively pursue the objectives of macro-economic growth.

There are two major models under microfinance, i.e., Self-Help Group (SHG)-Bank

Linkages and Micro-Finance Institutions (MFI) - Bank Linkages being operated in the

country. The growth of the Microfinance industry in India has been phenomenal. The

SHGs have also managed to create deep roots within the country. However much needs

to be done to see significant change in different parts of the country. NABARD has been

successful in creating the largest network of microfinance in India. If other institutions

have a similar vision and work towards it with similar zeal then the day is not far when

we would have enough employment for the poor, increase in their standard of living,

poverty alleviation, and improvement in literacy rates and thereby empower the nation as

a whole.

B. Self-Help Group (SHG)-Bank Linkage Programme

SHGs are the real grass root level setups for micro-credit growth. They reach the poorest

sections in rural settings as well as are empowering lakhs of women and entrepreneurs all

GROWTH OF MICRO-CREDIT IN INDIA: AN EVALUATION (90th Conference volume of Indian Economic Association 2007

518

around India. The various models like peer group, bank-linked SHGs, NGO-linked SHGs

help in creating a social infrastructure with which the rural population is comfortable,

which helps make in-roads for spread of credit. The SHG-bank linkage programme was

launched in 1992 as a Pilot Project for linking 500 SHGs and supported by the Reserve

Bank through its policy support. The Programme envisaged organisation of the rural poor

into SHGs, building their capacities to manage their own finances and then negotiating

bank credit on commercial terms. The poor were encouraged to voluntarily come together

to save small amounts regularly and extend micro loans among themselves. Once the

group attained the required maturity for handling larger resources, bank credit could

follow. The focus of micro-finance initiatives is largely on those rural poor who have no

access to the formal banking system. The target-group broadly comprises small and

marginal farmers, landless agricultural and nonagricultural labourers, artisans and

craftsmen and other rural poor engaged in small businesses such as vending and hawking.

The SHGs registered or unregistered which are engaged in promoting savings habits

among their members would be eligible to open savings bank accounts with banks. These

SHGs need not necessarily have already availed of credit facilities from banks before

opening savings bank a ccounts. As per operational guidelines of NABARD, SHGs are

sanctioned savings linked loans by banks (varying from a saving to loan ratio of 1:1 to

1:4). Experience showed that group dynamics and peer pressure brought in excellent

recovery from members of the SHGS. Banks were advised that the flexibility allowed to

the banks in respect of margin, security norms, etc. under the pilot project would continue

to be operational under the linkage programme even beyond the pilot phase. Keeping in

view the nature of lending and status of borrowers, the banks prescribe simple

documentation for lending to SHGs. The defaults by a few members of SHGs and/or their

family members to the financing bank do not ordinarily come in the way of financing

SHGs per se by banks provided the SHG is not in default to it. However, the bank loan

may not be utilized by the SHG for financing a defaulter member to the bank.

Historically, there is a concentration of SHGs in Southern States mainly on account of

proactive role played by the State Governments. However, NABARD has taken up

intensification of the SHG bank linkage program in 13 identified priority States which

GROWTH OF MICRO-CREDIT IN INDIA: AN EVALUATION (90th Conference volume of Indian Economic Association 2007

519

account for about 70.0 per cent of the rural poor population, viz., Uttar Pradesh, Orissa,

West Bengal, Madhya Pradesh, Maharashtra, Gujarat, Rajasthan, Chhatisgarh, Jharkhand,

Bihar, Uttaranchal, Assam and Himachal Pradesh. Consequently, the share of cumulative

SHGs credit linked in Southern States declined to 54.0 per cent in March 2006 from 71.0

per cent in March 2001. During 2005-06, the number of SHGs credit linked increased

significantly in some of the major priority States such as Maharashtra (60,324), Orissa

(57,640), West Bengal (43,553), Uttar Pradesh (42,263), Rajasthan (38,165), Assam

(25,215) and Chhattisgarh (12,722) See Table-1. During 2005- 06, the number of SHGs

credit linked in 13 priority States constituted 54.4 per cent of the all India credit linkage

of 6,20,109 SHGs. At present, there are over 2.2 million SHGs credit linked with banks.

Out of this, there are over a million SHGs which are now over three years old. These

SHGs have not only availed of loans but have also gone in for repeat loans. It is being

emphasised that a number of the older SHGs would now be in a position to graduate into

micro enterprises by taking to income generating activities. Though micro enterprises are

not a panacea for the complex problem of chronic unemployment and poverty, yet

promotion of micro enterprises is a viable and effective strategy for achieving significant

gains in incomes and assets of poor and marginalised people.

Graduation of SHG members to take up micro enterprises requires intensive training on

various aspects of management including understanding the market structure, fine-tuning

of skills and entrepreneurship management. During 2005-06, a focussed and location

specific Micro Enterprise Development Programme (MEDP) on skill upgradation and

development for sustainable livelihood for members of matured SHGs was launched. The

MEDP aims at facilitating quick inputs to members of matured SHGs on technical skills

in enterprises, basic entrepreneurial inputs and aspects covering markets. The active

participation of women (90%), and timely loan repayment (95%) continue to be

prominent features of the programme. The programme has enabled an estimated 24.25

million poor households in the country to access to Micro-Finance (MF) from the formal

banking system, as on 31st March 2005, registering a growth of 45 per cent over the

previous year.

GROWTH OF MICRO-CREDIT IN INDIA: AN EVALUATION (90th Conference volume of Indian Economic Association 2007

520

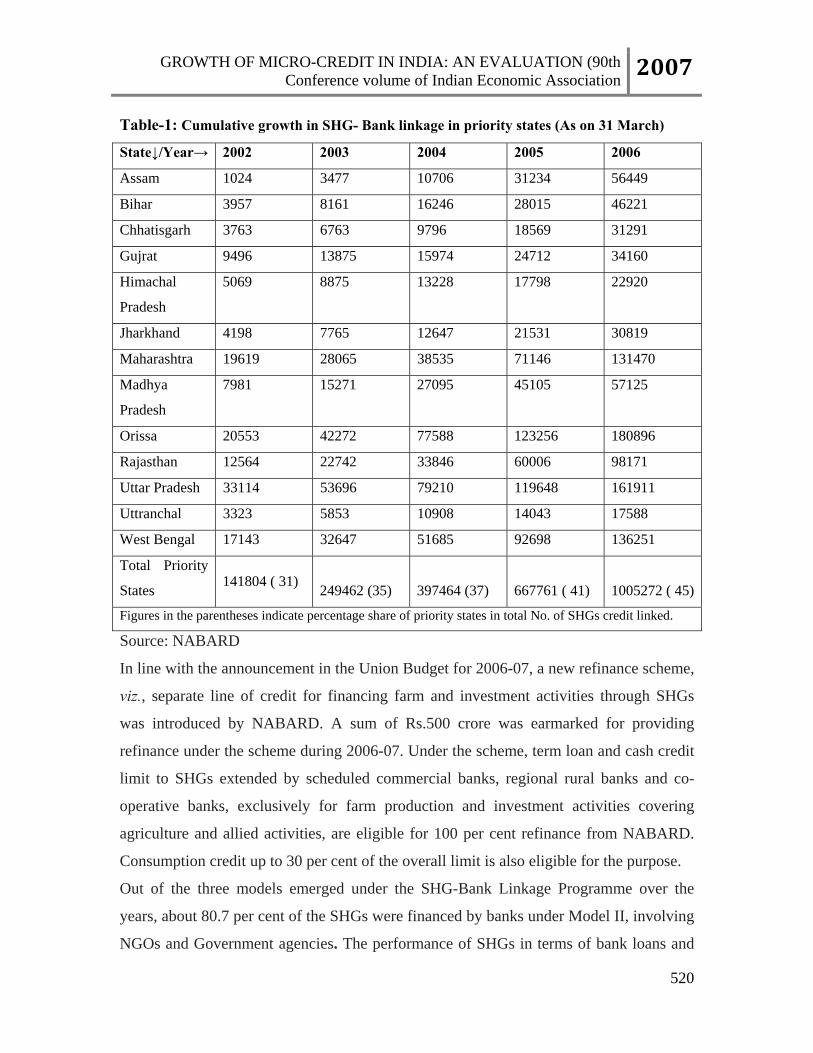

Table-1: Cumulative growth in SHG- Bank linkage in priority states (As on 31 March)

State↓/Year→ 2002 2003 2004 2005 2006

Assam 1024 3477 10706 31234 56449

Bihar 3957 8161 16246 28015 46221

Chhatisgarh 3763 6763 9796 18569 31291

Gujrat 9496 13875 15974 24712 34160

Himachal

Pradesh

5069 8875 13228 17798 22920

Jharkhand 4198 7765 12647 21531 30819

Maharashtra 19619 28065 38535 71146 131470

Madhya

Pradesh

7981 15271 27095 45105 57125

Orissa 20553 42272 77588 123256 180896

Rajasthan 12564 22742 33846 60006 98171

Uttar Pradesh 33114 53696 79210 119648 161911

Uttranchal 3323 5853 10908 14043 17588

West Bengal 17143 32647 51685 92698 136251

Total Priority

States 141804 ( 31)

249462 (35)

397464 (37)

667761 ( 41)

1005272 ( 45)

Figures in the parentheses indicate percentage share of priority states in total No. of SHGs credit linked.

Source: NABARD

In line with the announcement in the Union Budget for 2006-07, a new refinance scheme,

viz., separate line of credit for financing farm and investment activities through SHGs

was introduced by NABARD. A sum of Rs.500 crore was earmarked for providing

refinance under the scheme during 2006-07. Under the scheme, term loan and cash credit

limit to SHGs extended by scheduled commercial banks, regional rural banks and co-

operative banks, exclusively for farm production and investment activities covering

agriculture and allied activities, are eligible for 100 per cent refinance from NABARD.

Consumption credit up to 30 per cent of the overall limit is also eligible for the purpose.

Out of the three models emerged under the SHG-Bank Linkage Programme over the

years, about 80.7 per cent of the SHGs were financed by banks under Model II, involving

NGOs and Government agencies. The performance of SHGs in terms of bank loans and

GROWTH OF MICRO-CREDIT IN INDIA: AN EVALUATION (90th Conference volume of Indian Economic Association 2007

521

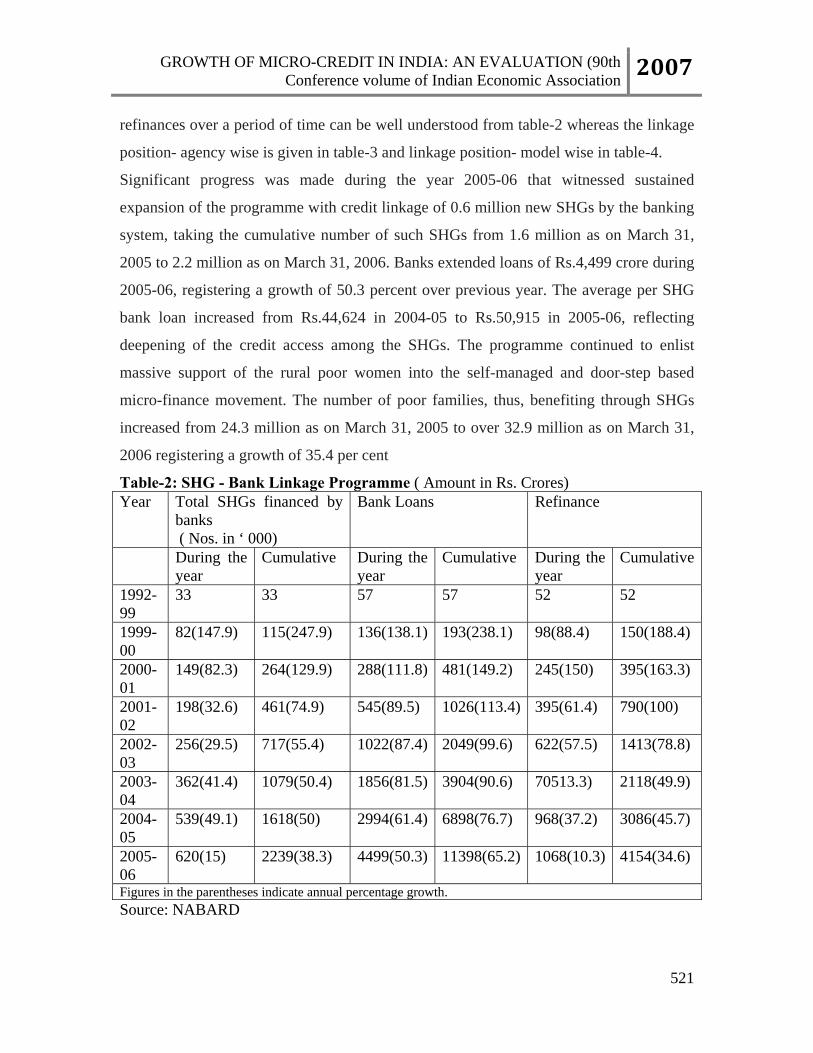

refinances over a period of time can be well understood from table-2 whereas the linkage

position- agency wise is given in table-3 and linkage position- model wise in table-4.

Significant progress was made during the year 2005-06 that witnessed sustained

expansion of the programme with credit linkage of 0.6 million new SHGs by the banking

system, taking the cumulative number of such SHGs from 1.6 million as on March 31,

2005 to 2.2 million as on March 31, 2006. Banks extended loans of Rs.4,499 crore during

2005-06, registering a growth of 50.3 percent over previous year. The average per SHG

bank loan increased from Rs.44,624 in 2004-05 to Rs.50,915 in 2005-06, reflecting

deepening of the credit access among the SHGs. The programme continued to enlist

massive support of the rural poor women into the self-managed and door-step based

micro-finance movement. The number of poor families, thus, benefiting through SHGs

increased from 24.3 million as on March 31, 2005 to over 32.9 million as on March 31,

2006 registering a growth of 35.4 per cent

Table-2: SHG - Bank Linkage Programme ( Amount in Rs. Crores) Year Total SHGs financed by

banks ( Nos. in ‘ 000)

Bank Loans Refinance

During the year

Cumulative During the year

Cumulative During the year

Cumulative

1992-99

33 33 57 57 52 52

1999-00

82(147.9) 115(247.9) 136(138.1) 193(238.1) 98(88.4) 150(188.4)

2000-01

149(82.3) 264(129.9) 288(111.8) 481(149.2) 245(150) 395(163.3)

2001-02

198(32.6) 461(74.9) 545(89.5) 1026(113.4) 395(61.4) 790(100)

2002-03

256(29.5) 717(55.4) 1022(87.4) 2049(99.6) 622(57.5) 1413(78.8)

2003-04

362(41.4) 1079(50.4) 1856(81.5) 3904(90.6) 70513.3) 2118(49.9)

2004-05

539(49.1) 1618(50) 2994(61.4) 6898(76.7) 968(37.2) 3086(45.7)

2005-06

620(15) 2239(38.3) 4499(50.3) 11398(65.2) 1068(10.3) 4154(34.6)

Figures in the parentheses indicate annual percentage growth. Source: NABARD

GROWTH OF MICRO-CREDIT IN INDIA: AN EVALUATION (90th Conference volume of Indian Economic Association 2007

522

The SHG-bank linkage programme is now considered by the banking system as a

commercial proposition, with advantages of lower transaction costs and higher coverage

of rural clientele by the bank branches. Commercial banks have maintained good

progress in financing SHGs as their share increased from 52.1 per cent in 2004-05 to 53.1

per cent in 2005-06 (Table-3). The share of co-operative banks in SHGlinkage increased

marginally from 13.0 per cent to 13.9 per cent over the period, while that of RRBs

declined to 33.1 per cent from 34.8 per cent. Total number of SHGs financed by co-

operative banks increased sharply from 2,11,137 at end- March 2005 to 3,10,230 by end-

March 2006, reflecting significant interest being evinced by many co-operative banks.

Table-3: Linkage position (Cumulative) - Agency wise (As at end- March)

(Amount in Rs. Crores)

Number (‘000) of SHGs Bank loan

Percentage

Variation

Percentage

Variation

Agency

2004-

05

2005-

06

2004-

05

2005-

06

2004-

05

2005

-06

2004-

05

2005-

06

Commercial

Banks

843

(52.1)

1188

(53.1)

56.7

(60.3)

40.8

(61.3)

4159 6987 84.4 68.0

Regional Rural

Banks

564

(34.8)

740

(33.1)

38.9

(30.4)

31.2

(29.1)

2100 3322 64.3 58.2

Credit Co-

operative

Banks

211

(13)

310

(13.9)

56.8

(9.3)

46.9 640 1087 72.5 69.9

Total 1618

(100)

2239

(100)

50 38.3 6898

(100)

1139

8

(100)

76.7 65.2

Source: NABARD

Notes: i) Figures in the brackets are percentages to total.

ii) Figures may not add up to their respective total due to rounding off.

GROWTH OF MICRO-CREDIT IN INDIA: AN EVALUATION (90th Conference volume of Indian Economic Association 2007

523

Table-4: Linkage position – Model - Wise

As on March 31,

2005

As on March 31,

2006

Model Type

No. of

SHGs

(‘000)

Bank

Loan

(Rs.

Crore)

No. of

SHGs

(‘000)

Bank

Loan

(Rs.

Crore)

SHGs promoted, guided

and financed by banks

343

(21.2)

1013

(14.7)

449

(20.1)

1637

(14.4)

SHGs promoted by

NGOs / Govt. agencies

and financed by banks

1158

(71.6)

5529

(80.2)

1646

(73.5)

9200

(80.7)

SHGs promoted by NGOs

and financed by banks

using NGOs/formal

agencies as financial

intermediaries

117

(7.2)

356

(5.2)

143

(6.4)

561

(4.9)

Total 1618 6898 2239 11398

Notes: Figures in the brackets are percentage to total.

Source: NABARD

C. MFI – Bank Linkages

Continuous efforts are being made to promote linkages of micro-finance institutions

(MFIs) with banks. With a view to promoting flow of commercial loans from banks to

MFIs, a scheme was launched by NABARD during 2005-06 to provide financial support

to banks towards rating of MFIs. This scheme has since been made more liberal and

extended up to March 31, 2008. A scheme called “Capital/Equity Support to MFIs from

MFDEF” was announced by NABARD. The scheme provides for capital/equity support

to various types of MFIs by NABARD to enable them to leverage capital/equity for

accessing commercial and other funds from banks for providing financial services at an

GROWTH OF MICRO-CREDIT IN INDIA: AN EVALUATION (90th Conference volume of Indian Economic Association 2007

524

affordable cost to the poor and to enable MFIs to achieve sustainability in their credit

operations over a period of three to five years.

In order to examine the issues relating to allowing banks to adopt agency model by using

infrastructure of civil society organisations, appointment of ‘banking correspondents’ to

function as intermediaries between the lending banks and the beneficiaries and

identification of steps to promote MFIs, an in-house Group (Chairman: Shri H.R. Khan)

was set up in the Reserve Bankvi. The Group submitted its final report in July 2005.

Based on the recommendations of the Group and with the objective of ensuring greater

financial inclusion and increasing the outreach of the banking sector, banks have been

permitted to use the services of non-governmental organisations/self-help groups

(NGOs/SHGs), micro-finance institutions (MFIs) and other civil society organisations

(CSOs) as intermediaries in providing financial and banking services through the use of

business facilitator and business correspondent models. MFIs hold significant potential, but they also need to be challenged to make an increasing

contribution to scale consistent with cost sustainability and efficiency of operations.

National Micro Finance information Bureau (NMIB) to gather information on business

correspondents may be established by NABARD. The business facilitators

/correspondents may have the contractual relationship with only one Bank and NMIB

may also facilitate sharing of such information. NABARD may also capture and share

data / information on the MFIs and NGOs associated with SHG Bank Linkage and MFI

Bank Linkage Programme.

With the aim of knowing the appropriate functioning of MFIs, their rating is required.

Basically the rating tools attempt to assess whether the MFI is operating on sound lines

and on sustainable basis. Rating is a pre- requisite for extension of financial

arrangements. Rating can also give a comparative position of the MFI in relation to its

peers. The following non-financial parameters are to be examined while arriving at the

rating of MFIs:

i. Governance – Whether Board members actually participate in the meetings and

take major policy decisions.

ii. Qualification and Competence of Top Management.

GROWTH OF MICRO-CREDIT IN INDIA: AN EVALUATION (90th Conference volume of Indian Economic Association 2007

525

iii. HR Policies – Well laid out recruitment and training system.

iv. Systems and Procedures – Well laid down policies for processing and

authorization.

v. Organizational Structure.

vi. Product Range – In tune with the requirement of client group.

vii. Geographical spread.

With the intention of strengthening the MFI system in the country, the following

proactive measures may be introduced:

i. Introduction of a separate accounting and auditing standards system for MFIs so

that it would establish a uniform accounting system which is less stringent than

the systems applicable to ordinary business firms;

ii. MFIs should be managed by professionals to enable MFIs to maintain a high

degree of professionalism in their operations;

iii. MFIs should make a clearly specified policy statement that includes periodical

voluntary disclosure of operations, activities, financial position for the benefit of

the public;

iv. MFIs should, in their own, consent to having a rating for their business activities,

so that the members of the public would have required information on them.

v. MFIs should strive to build internal reserves out of operational surpluses to enable

them to absorb loan losses, withstand adverse shocks and go through difficult

periods.

III.CHALLENGES BEFORE MICRO-CREDIT AND SOME PROPOSITIONS

International financier George Soros, in his book George Soros on Globalization,

observes that: …The difficulty [of micro-lending] is in scaling it up. Successful micro-

lending operations, although largely self-sustaining, cannot grow out of retained earnings,

nor can they raise capital in financial markets. To turn micro-lending into a big factor in

economic and political progress, it must be scaled up significantly. This would require

general support for the industry as well as capital for individual ventures.

We agree – even when MFIs become profitable, accumulated profits will not support the

kind of large-scale growth required to reach large numbers. Until now, many MFIs have

GROWTH OF MICRO-CREDIT IN INDIA: AN EVALUATION (90th Conference volume of Indian Economic Association 2007

526

utilized grants from donors to support their operations both in the early years and as they

scale up. Yet such grants, already limited in size and availability, are becoming harder to

come by as the pool of global MFIs grows. Unfortunately, beyond donors, there really are

no private sources of equity financing available to MFIs around the world, particularly

those working with the poorestvii.

Although the growth of SHGs in India has been phenomenal there are some significant

problems faced by them which might hamper their growth in the coming years. For

instance politicizing of subsidy allotment among SHGs has become a big problem.

Qualification for government subsidy is easily influenced by Panchayat members. Thus,

Panchayats are now competing with NGOs and rural banks in forming SHGs. While the

Panchayat-formed SHGs have the lure of government grants they are often open to

political pressure and misuse of funds by the recommending Panchayats and/or political

parties. Besides, the NGO-formed SHGs have the benefit of honest and expert counseling

from the nursing NGOs. Thus the qualities of NGO-formed groups are usually superior to

those formed by the local government (Panchayats) and villagers are often keen to join

the former. These age-old problems of government initiatives in poverty reduction, unless

stemmed quickly, can actually harm the movement by eroding the fundamental precepts

of self-help and empowerment of the poor. (The Indian Microfinance Experience -

Accomplishments and Challenges Rajesh Chakrabarti, 2005).

The main challenges facing the SHG - Bank linkage model are:

The pace of expansion of the programme.

The limited number of NGOs in regions where the programme has not picked up

The cost of promotion of NGO being high.

The per capita credit outlays are small and not commensurate with the costs

involved in.

bringing the SHGs to the banking main stream.

Overloading of SHG with multiple agenda, particularly Government sponsored

programmes.

GROWTH OF MICRO-CREDIT IN INDIA: AN EVALUATION (90th Conference volume of Indian Economic Association 2007

527

RBI and Government as part of their development role, NABARD, which is spearheading

this programme, and banks who are the main promoters of the programe, may initiate the

following effective steps to overcome these shortcomings:

Promotion of Federation structure: The long term sustainability of the SHG model

may require a federal structure, without severing the linkages that the SHGs have

with the local bank branches. The assumption that the federation structure should

not be supplanted on the SHGs and can be addressed when the demand emerges

needs reconsideration.

Maintenance of National Database on SHGs and MFIs: At present, NABARD is

maintaining the database on SHGs. It publishes annual hand book on micro

finance in India with focus only on SHG Bank linkage programme. It is suggested

that NABARD be assigned the responsibility of collection of data involving the

entire sector, their compilation and dissemination.

Contribution to the MFDEF (Micro Finance Development and Equity Fund) by

Banks: The corpus may be built up on an ongoing basis. A portion of profits of

the bank may be contributed to the fund. The Government may provide tax relief

to Banks for the contributions made.

Role of Corporates in Micro Finance: Corporate India, of late, shown keen

interest in the SHG movement as it provides an alternative business opportunity

for them besides being a means to actualize its corporate social responsibility

objectives. Many corporates have realized that the people at the bottom of

pyramid can be brought into their business model. The group also sees a critical

role of the corporate sector in providing market linkage to the products of the

rural areas on a sustainable basis. The following are the examples

i. ITC (through e-choupal model).

ii. Hindustan Lever Ltd (through Stree sakti project).

iii. Mahindra & Mahindra (through Mahindra Subh labh).

iv. Tata Group (through Tata kisan sansar).

GROWTH OF MICRO-CREDIT IN INDIA: AN EVALUATION (90th Conference volume of Indian Economic Association 2007

528

We further face problems at the level of Micro-finance regulation. A salient feature of

MFIs has been that they have sprung up spontaneously to meet a market demand similar

to the creation of micro businesses. These institutions which have been set-up at first as

small village based voluntary associations to cater to each other's needs have gone

through an evolutionary process to become sometimes national level MFIs. Despite

varying sizes, MFIs handle other people's money and, therefore, the viability and

solvency of these institutions have become a crucial issue in MFI policy frame works.

Given the fact that they function as depositories for the most vulnerable groups at the

bottom of the income pyramid, a failure of an MFI may entail greater social costs from a

welfare point of view than that of a higher level lending institution. The generally agreed

objectives of Prudential Regulation include:

i. Protecting the country's financial system from domino effect preventing the

failure of one institution from leading to a 'run' prompting the failure of others,

and

ii. Protecting small depositors who are not well positioned to monitor the institutions

financial soundness themselves.

The under noted questions indicate the challenges of microfinance regulation:

Currently there are five organisational forms of the MFIs, viz., Trusts;

Societies; Cooperative Societies; Not-for-Profit Companies and Non-

Banking Finance Companies. We will have to weigh the merits and

demerits of recognition of one or more or all the organizational forms

under the formal structured regulatory framework. SHGs are amorphous

entities with no formal organizational structure. We will have to

distinguish micro credit institutions from micro finance institutions. It is

not clear how they will be brought under a formalized frame of regulation.

There are also instances of large corporates undertaking 'micro-credit

activity as a part of their operations. Under their corporate social

responsibilities. The microfinance institutions may invite the overlapping

jurisdiction of several regulatory agencies.

GROWTH OF MICRO-CREDIT IN INDIA: AN EVALUATION (90th Conference volume of Indian Economic Association 2007

529

The latter may need more varied skills and in any case, warrant a policy

view by more than one financial sector regulator?

How do we distinguish micro-finance institution from micro-credit

institution and both these from other financial institutions? Is it by the

ceilings imposed on the size of deposits, lendings and / or by defining

activities? What part or percentage of the activity could be nonfinancial

while the institution continues to be an MFI? Is there merit in

differentiating between not-for-profit MFIs and the profitseeking ones?

There is also a need to recognise the large regional differences in the

spread of SHGs and the MFIs across the country. While the issue needs

deeper analysis to identify the reasons for such variation and to promote

balanced growth of the MFIs, it, prima facie, appears that the MFIs have

flourished more in the Southern States with well-developed banking

infrastructure and outreach. Thus, the MFIs in our country would seem to

be a supplement rather than a substitute for a developed banking

infrastructure.

The role of foreign capital and venture capital in regard to the MFIs would

have to be carefully considered. It may be necessary to recognise here the

orientation of micro-finance activity given the limitation of size and skills

in the MFIs and then consistency with the risk reward bias of such sources

of commercial capital. As regards external -commercial borrowings, the

imperatives of exchange rate risk and the capacity of the MFIs to

effectively assess and manage this risk would also need to be duly

reckoned.

What could be the scope and effectiveness of a self regulatory

organisation. for the MFIs and how would it mesh with the possible

formalised regulatory framework under contemplation ?

Credit rating is usually assigned for specific instruments issued or for a

defined purpose and often, on a continuing basis. There is merit in

devising rating system for the MFIs, recognising that such exercises are

GROWTH OF MICRO-CREDIT IN INDIA: AN EVALUATION (90th Conference volume of Indian Economic Association 2007

530

seldom for localised views amongst decentralised entities. It will be

instructive to review our experience so far in regard to utility and quality

of rating exercises of MFIs. How to ensure that the rating exercise adds

value to the localised operations of the MFIs?

What are the prospects for expanding the permission accorded by the RBI

to the non-banking financial companies for offering credit and other

financial services to not-for-profit companies? What are the prospects for

creating a separate category of NBFC-MFIs to be regulated by RBI?

Given the need for streamlining micro finance and promoting it as an effective tool for

poverty alleviation, ADB (2000) has made the following proactive recommendations to

be adopted by the Reserve Bank of India (RBI):

i. RBI should promote understanding that higher interest rates provide increased

access to finance for the poor rather than exploiting them;

ii. RBI should initiate action to bring the needed legal framework for MFIs;

iii. RBI should establish prudential regulation and supervision structures for MFIs

which are appropriate to their size;

iv. RBI should develop prudential norms and reporting standards for MFIs.

IV. CONCLUSION In India, Economic Reforms with a human face have been accepted as the guiding

principle of sustainable development. Keeping the Poor at centre stage, the Policies need

to be reoriented so as to develop and optimize the potential of such a large segment of the

Population and enable them to contribute in the growth process significantly in terms of

output, income, employment and consumption. After the pioneering efforts of the last ten

years, the Micro Finance Scene in India has reached a take-off point. With some efforts

substantial progress can be made in taking MFIs to the next orbit of significance and

sustainability. This needs innovative and forward-looking policies, based on the ground

realities of successful MFIs. This, combined with a commercial approach from the MFIs

in making Micro Finance Financially Sustainable, will make this Sector vibrant and help

achieve its single-minded mission of providing Financial Services to the Rural Poor.

GROWTH OF MICRO-CREDIT IN INDIA: AN EVALUATION (90th Conference volume of Indian Economic Association 2007

531

It is necessary to recognize that we, in India, have to focus on extending financial

services in both rural and urban areas for ensuring financial inclusion of all segments of

the population. At the same time, one should avoid the temptation of creating one set of

banking and financial institutions to cater to the poor or the unorganized, and another for

the rest. The medium to long-term objective should be to ensure inclusion of all segments

in the mainstream institutions while taking advantage of the flexibility of multiplicity of

models of delivering a wide range of financial services. In this light, a comprehensive

framework to revive the cooperative credit system, revitalize the Regional Rural Banks

and reorient commercial banking system needs to get a high priority while

simultaneously encouraging and enabling the growth of micro-finance movement in

India, which has been very successful. We need to build on its strengths and extend it to

vast areas, which are inadequately covered by both banking and micro-credit entities.

Micro-finance, broadly defined, needs to be explored in the light of the new paradigm

described. RBI and NABARD recognize the growing importance of micro-finance and

are committed to enable its healthy growth. However, several issues, both in regard to

regulation as well as development of the MFIs need to be considered and must be

comprehensively addressed. While the report of the Khan Committee would provide a

good starting point for taking a view on developmental aspects, in particular, the CGAP's

Guiding Principles on Regulation and Supervision on Micro-finance provide a valuable

and globally relevant framework in regard to the regulatory issues. The proposed forum

for a consultative process on the MFIs would also be useful in evolving an appropriate

framework for development of the MFI sector. No doubt, a very well-crafted balance

between the regulation and growth objectives would be warranted in formulating our

approach to a regulatory regime, keeping in view the big challenge of financial inclusion

of a large segment of the Indian population.

GROWTH OF MICRO-CREDIT IN INDIA: AN EVALUATION (90th Conference volume of Indian Economic Association 2007

532

REFERENCES

i Economic and Political Weekly, “Microfinance: Productive Linkages,” March 6, 2004: http://www.epw.org.in/showArticles.php?root=2004&leaf=03&filename=6907&filetype=html ii PlanetFinance, “Country Study: India,” July 2000: http://www.planetfinance.org. iiiMahajan, Vijay and Bharti Gupta Ramola, “Microfinance in India – Banyan Tree and Bonsai,” BASIX Quarterly Review, October 2004. iv Microfinance India conference and a look at the expanding market by Sukhwinder Singh Aurora,Financial sector team ,policy division ,DFID,United Nations Capital Development Fund (UNCDF ) ,Issue 13 / June 2005 v Micro-Finance : Reserve Bank's Approach - Address by Dr.Y.V.Reddy, Governor, RBI at the Micro- Finance Conference organised by the Indian School of Business, Hyderabad on August 6, 2005. vi Report of the Internal Group to examine issues relating to Rural Credit and Microfinance, RBI, July 2005. vii Micro finance in India: Sectoral issues and challenges(Nov.2004): Y.S.P. Thorat, Managing Director NABARD.