Quanzhou Huixin Micro-credit Co., Ltd. 泉州匯鑫小額貸款股份 ...

437

The Stock Exchange of Hong Kong Limited and the Securities and Futures Commission take no responsibility for the contents of this Post Hearing Information Pack, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this Post Hearing Information Pack. POST HEARING INFORMATION PACK OF Quanzhou Huixin Micro-credit Co., Ltd. * 泉州匯鑫小額貸款股份有限公司 (the ‘‘Company’’) (Established in the People’ s Republic of China with limited liability) WARNING The publication of this Post Hearing Information Pack (the ‘‘PHIP’’) is required by The Stock Exchange of Hong Kong Limited (the ‘‘Exchange’’) and the Securities and Futures Commission (the ‘‘Commission’’) solely for the purpose of providing information to the public in Hong Kong. This PHIP is in draft form. The information contained in it is incomplete and is subject to change which can be material. By viewing this document, you acknowledge, accept and agree with the Company, its sponsor, advisers and members of the underwriting syndicate that: (a) this document is only for the purpose of providing information about the Company to the public in Hong Kong and not for any other purposes. No investment decision should be based on the information contained in this document; (b) the publication of this document or supplemental, revised or replacement pages on the Exchange’ s website does not give rise to any obligation of the Company, its sponsor, advisers or members of the underwriting syndicate to proceed with an offering in Hong Kong or any other jurisdiction. There is no assurance that the Company will proceed with the offering; (c) the contents of this document or supplemental, revised or replacement pages may or may not be replicated in full or in part in the actual final listing document; (d) this PHIP is not the final listing document and may be updated or revised by the Company from time to time in accordance with the Rules Governing the Listing of Securities on the Exchange; (e) this document does not constitute a prospectus, offering circular, notice, circular, brochure or advertisement offering to sell any securities to the public in any jurisdiction, nor is it an invitation to the public to make offers to subscribe for or purchase any securities, nor is it calculated to invite offers by the public to subscribe for or purchase any securities; (f) this document must not be regarded as an inducement to subscribe for or purchase any securities, and no such inducement is intended; (g) neither the Company nor any of its affiliates, sponsor, advisers or members of the underwriting syndicate is offering, or is soliciting offers to buy, any securities in any jurisdiction through the publication of this document; (h) no application for the securities mentioned in this document should be made by any person nor would such application be accepted; (i) the Company has not and will not register the securities referred to in this document under the United States Securities Act of 1933, as amended, or any state securities laws of the United States; (j) as there may be legal restrictions on the distribution of this document or dissemination of any information contained in this document, you agree to inform yourself about and observe any such restrictions applicable to you; and (k) the application to which this document relates has not been approved for listing and the Exchange and the Commission may accept, return or reject the application for the subject public offering and/or listing. If an offer or an invitation is made to the public in Hong Kong in due course, prospective investors are reminded to make their investment decisions solely based on the Company’ s prospectus registered with the Registrar of Companies in Hong Kong, copies of which will be distributed to the public during the offer period. * For identification purpose only

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Quanzhou Huixin Micro-credit Co., Ltd. 泉州匯鑫小額貸款股份 ...

The Stock Exchange of Hong Kong Limited and the Securities and Futures Commission take no responsibility forthe contents of this Post Hearing Information Pack, make no representation as to its accuracy or completenessand expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon thewhole or any part of the contents of this Post Hearing Information Pack.

POST HEARING INFORMATION PACK OF

Quanzhou Huixin Micro-credit Co., Ltd.*

泉州匯鑫小額貸款股份有限公司(the ‘‘Company’’)

(Established in the People’s Republic of China with limited liability)

WARNING

The publication of this Post Hearing Information Pack (the ‘‘PHIP’’) is required by The Stock Exchange of HongKong Limited (the ‘‘Exchange’’) and the Securities and Futures Commission (the ‘‘Commission’’) solely for thepurpose of providing information to the public in Hong Kong.

This PHIP is in draft form. The information contained in it is incomplete and is subject to change which can bematerial. By viewing this document, you acknowledge, accept and agree with the Company, its sponsor, advisersand members of the underwriting syndicate that:

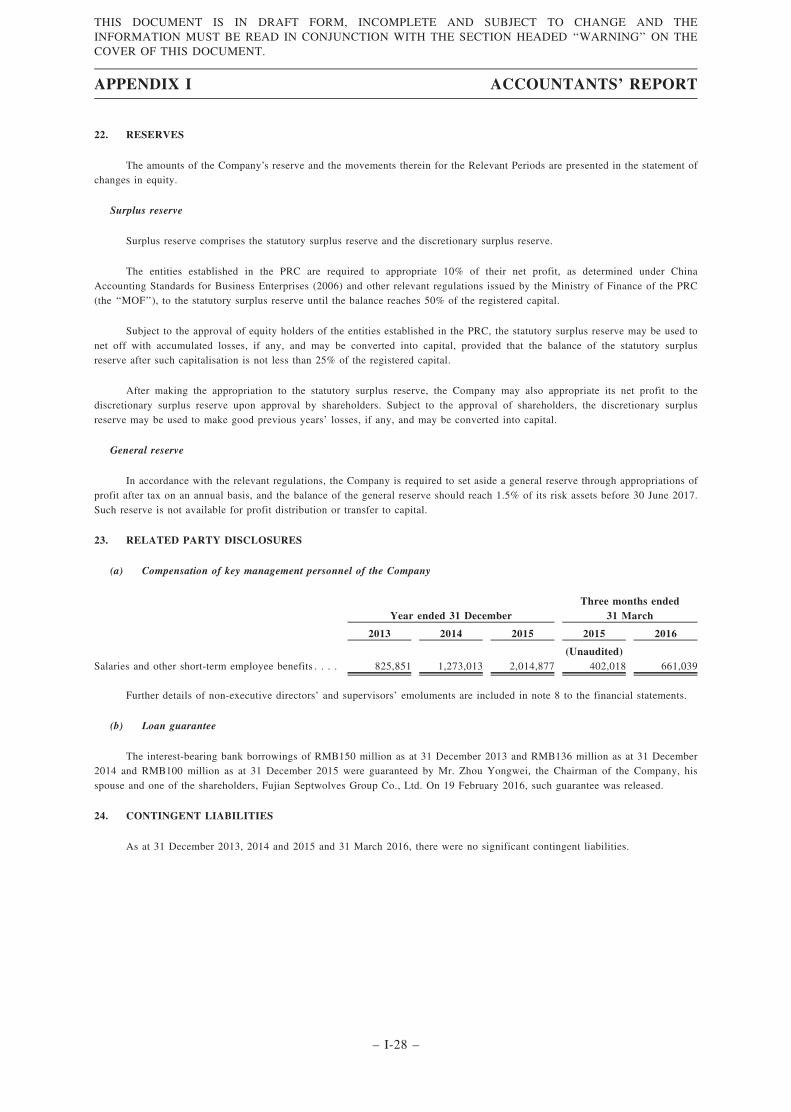

(a) this document is only for the purpose of providing information about the Company to the public in HongKong and not for any other purposes. No investment decision should be based on the information contained inthis document;

(b) the publication of this document or supplemental, revised or replacement pages on the Exchange’s websitedoes not give rise to any obligation of the Company, its sponsor, advisers or members of the underwritingsyndicate to proceed with an offering in Hong Kong or any other jurisdiction. There is no assurance that theCompany will proceed with the offering;

(c) the contents of this document or supplemental, revised or replacement pages may or may not be replicated infull or in part in the actual final listing document;

(d) this PHIP is not the final listing document and may be updated or revised by the Company from time to timein accordance with the Rules Governing the Listing of Securities on the Exchange;

(e) this document does not constitute a prospectus, offering circular, notice, circular, brochure or advertisementoffering to sell any securities to the public in any jurisdiction, nor is it an invitation to the public to makeoffers to subscribe for or purchase any securities, nor is it calculated to invite offers by the public to subscribefor or purchase any securities;

(f) this document must not be regarded as an inducement to subscribe for or purchase any securities, and no suchinducement is intended;

(g) neither the Company nor any of its affiliates, sponsor, advisers or members of the underwriting syndicate isoffering, or is soliciting offers to buy, any securities in any jurisdiction through the publication of thisdocument;

(h) no application for the securities mentioned in this document should be made by any person nor would suchapplication be accepted;

(i) the Company has not and will not register the securities referred to in this document under the United StatesSecurities Act of 1933, as amended, or any state securities laws of the United States;

(j) as there may be legal restrictions on the distribution of this document or dissemination of any informationcontained in this document, you agree to inform yourself about and observe any such restrictions applicable toyou; and

(k) the application to which this document relates has not been approved for listing and the Exchange and theCommission may accept, return or reject the application for the subject public offering and/or listing.

If an offer or an invitation is made to the public in Hong Kong in due course, prospective investors are reminded tomake their investment decisions solely based on the Company’s prospectus registered with the Registrar ofCompanies in Hong Kong, copies of which will be distributed to the public during the offer period.* For identification purpose only

If you are in any doubt about any of the contents of this document, you should seek independent professional advice.

Quanzhou Huixin Micro-credit Co., Ltd.*

泉州匯 鑫小額貸款股份 有限公司(Established in the People’s Republic of China with limited liability)

[REDACTED]

Number of [REDACTED] under the[REDACTED]

: [REDACTED] H Shares (subject to the[REDACTED])

Number of [REDACTED] : [REDACTED] H Shares (subject toadjustment and the [REDACTED])

Number of [REDACTED] : [REDACTED] H Shares (subject to adjustment)Maximum [REDACTED] : HK$[REDACTED] per [REDACTED],

plus brokerage of 1%, [REDACTED]transaction levy of [REDACTED], andHong Kong Stock Exchange trading fee of0.005% (payable in full onapplication in Hong Kong dollars andsubject to refund)

Nominal value : RMB1.00 per H ShareStock code : [REDACTED]

Sole Sponsor

[REDACTED][REDACTED]

Hong Kong Exchanges and Clearing Limited, The Stock Exchange of Hong Kong Limited and Hong Kong Securities Clearing Company Limited take no responsibilityfor the contents of this document, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoeverarising from or in reliance upon the whole or any part of the contents of this document.

A copy of this document, having attached thereto the documents specified in ‘‘Appendix VII — Documents Delivered to the Registrar of Companies in Hong Kong andAvailable for Inspection,’’ has been registered by the Registrar of Companies in Hong Kong as required by Section 342C of the Hong Kong Companies Ordinance. TheSecurities and Futures Commission and the Registrar of Companies in Hong Kong take no responsibility for the contents of this document or any other documentreferred to above.

The [REDACTED] is expected to be fixed by agreement between the [REDACTED] (on behalf of [REDACTED]) and us on [REDACTED]. [REDACTED] is expected tobe on or around [REDACTED], [REDACTED] and, in any event, not later than [REDACTED], [REDACTED]. The [REDACTED] will be not more than [REDACTED]and is currently expected to be not less than [REDACTED]. If, for any reason, the [REDACTED] is not agreed by [REDACTED], [REDACTED] between the[REDACTED] (on behalf of [REDACTED]) and us, [REDACTED] will not proceed and will lapse. Investors applying for [REDACTED] must pay, on application, themaximum [REDACTED] of [REDACTED] per Share, unless otherwise announced, together with brokerage of 1%, SFC transaction levy of [REDACTED] and HongKong Stock Exchange trading fee of 0.005% subject to refund if [REDACTED] finally determined is lower than HK$[REDACTED] per Share.

[REDACTED] (on behalf of [REDACTED]) may, with the consent of the Company, reduce the number of [REDACTED] being offered under [REDACTED] and/or theindicative [REDACTED] range below that stated in this document at any time on or prior to the morning of the last day for lodging applications under [REDACTED]. Insuch a case, an announcement will be published in the [South China Morning Post] (in English) and the [Hong Kong Economic Times] (in Chinese) as well as ourwebsite www.qzhuixin.net not later than the morning of the day which is the last day for lodging applications under [REDACTED]. For further information, see‘‘Structure of [REDACTED].’’

We are incorporated, and substantially all of our businesses are located, in the PRC. Potential investors should be aware of the differences in legal, economic andfinancial systems between the PRC and Hong Kong and that there are different risk factors relating to investments in PRC-incorporated companies. Potential investorsshould also be aware that the regulatory framework in the PRC is different from the regulatory framework in Hong Kong and should take into consideration the differentmarket nature of our H Shares. Such differences and risk factors are set out in ‘‘Risk Factors,’’ ‘‘Appendix IV — Summary of Principal PRC and Hong Kong Legal andRegulatory Provisions’’ and ‘‘Appendix V — Summary of the Articles of Association’’ in this document. Prior to making an investment decision, potential investorsshould consider carefully all of the information set out in this document, including the risk factors set out in ‘‘Risk Factors.’’

The obligations of [REDACTED] under [REDACTED] are subject to termination by [REDACTED] (on behalf of [REDACTED]) if certain grounds arise prior to 8:00a.m. on [REDACTED] commences on the Hong Kong Stock Exchange. See ‘‘[REDACTED] — [REDACTED] — [REDACTED] — Grounds for termination.’’

The [REDACTED] have not been and will not be registered under the U.S. Securities Act or any state securities laws of the United States and may not be offered, sold,pledged or transferred within the United States. The [REDACTED] may be offered, sold or delivered outside the United States in offshore transactions in accordancewith Regulation S under the U.S. Securities Act.

* For identification purposes only

IMPORTANT

[REDACTED]

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THEINFORMATION MUST BE READ IN CONJUNCTION WITH THE SECTION HEADED ‘‘WARNING’’ ON THECOVER OF THIS DOCUMENT.

[REDACTED]

EXPECTED TIMETABLE(1)

– i –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THEINFORMATION MUST BE READ IN CONJUNCTION WITH THE SECTION HEADED ‘‘WARNING’’ ON THECOVER OF THIS DOCUMENT.

[REDACTED]

EXPECTED TIMETABLE(1)

– ii –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THEINFORMATION MUST BE READ IN CONJUNCTION WITH THE SECTION HEADED ‘‘WARNING’’ ON THECOVER OF THIS DOCUMENT.

This document is issued by Quanzhou Huixin Micro-credit Co., Ltd. solely in connection with

[REDACTED] and does not constitute an offer to sell or a solicitation of an offer to buy any security

other than [REDACTED] offered by this document pursuant to [REDACTED]. This document may

not be used for the purpose of, and does not constitute, an offer or invitation in any other

jurisdiction or in any other circumstances. No action has been taken to permit a [REDACTED] of

[REDACTED] or the distribution of this document in any jurisdiction other than Hong Kong.

You should rely only on the information contained in this document and the [REDACTED] to

make your investment decision. The Company has not authorized anyone to provide you with

information that is different from what is contained in this document. Any information or

representation not made in this document must not be relied on by you as having been authorized by

the Company, the Sole Sponsor, [REDACTED], [REDACTED], [REDACTED], [REDACTED], any of

their respective directors, employees, agents or professional advisers or any other person or party

involved in [REDACTED].

Page

EXPECTED TIMETABLE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . i

CONTENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . iii

SUMMARY AND HIGHLIGHTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

DEFINITIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

GLOSSARY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

FORWARD-LOOKING STATEMENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34

RISK FACTORS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

WAIVERS FROM STRICT COMPLIANCE WITH THE LISTING RULES . . . . . . . . . . . . . 61

INFORMATION ABOUT THIS DOCUMENT AND [REDACTED] . . . . . . . . . . . . . . . . . . . . . 65

DIRECTORS, SUPERVISORS AND PARTIES INVOLVED IN[REDACTED] . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69

CORPORATE INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 73

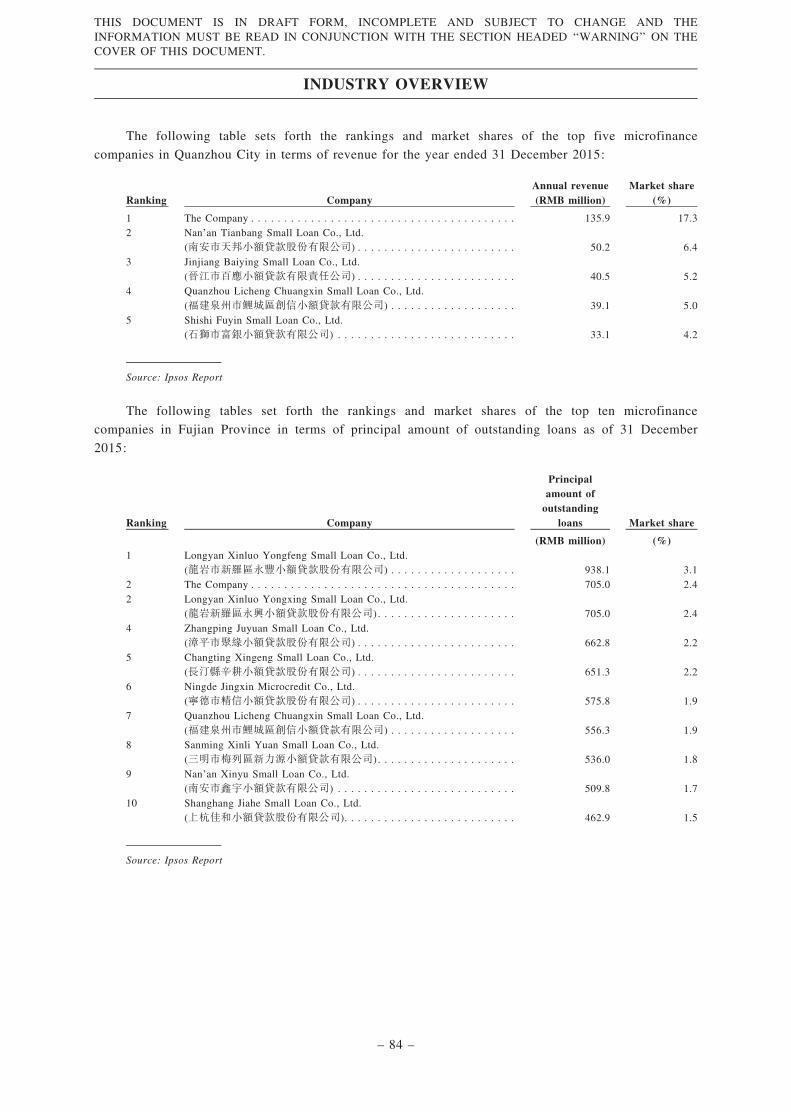

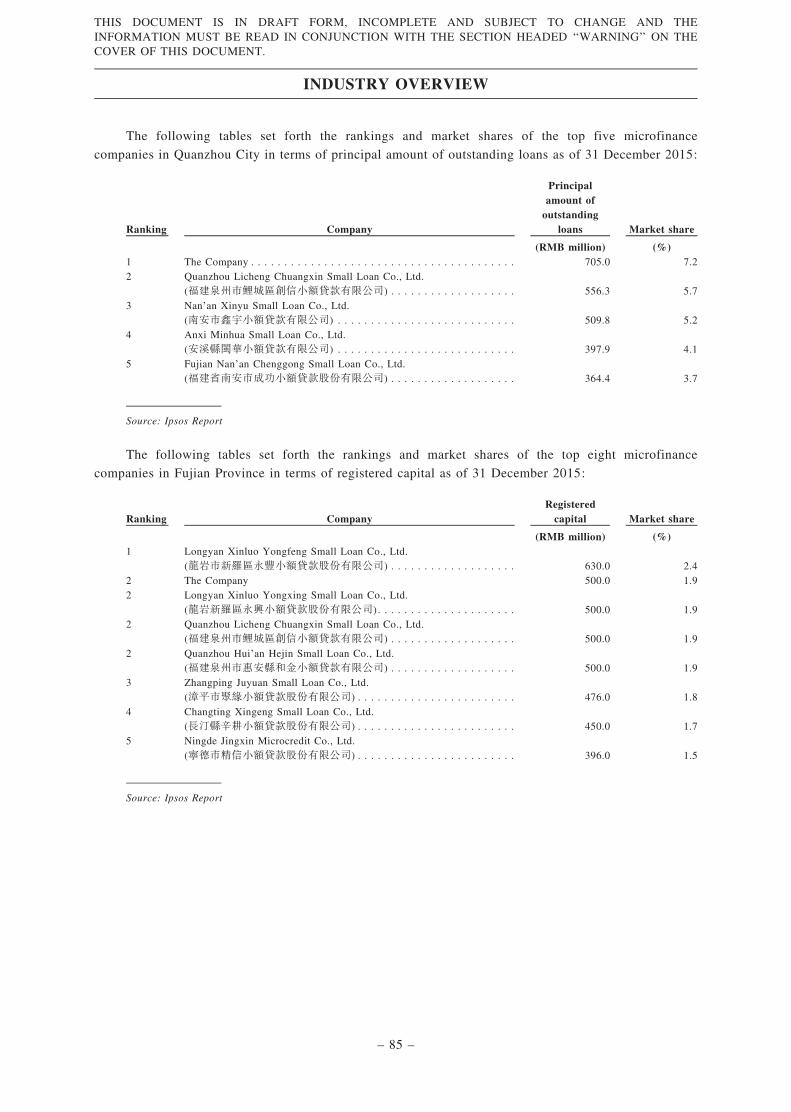

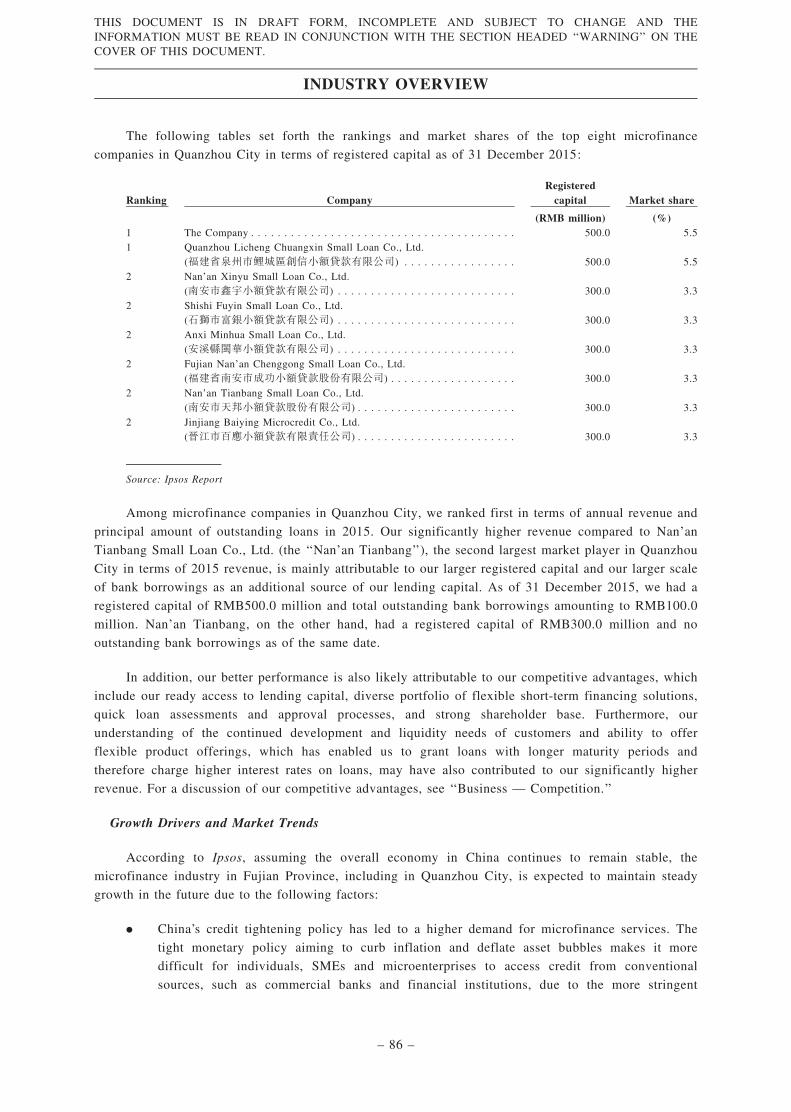

INDUSTRY OVERVIEW . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 76

REGULATORY OVERVIEW . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 89

HISTORY AND DEVELOPMENT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 103

CONTENTS

– iii –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THEINFORMATION MUST BE READ IN CONJUNCTION WITH THE SECTION HEADED ‘‘WARNING’’ ON THECOVER OF THIS DOCUMENT.

Page

BUSINESS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 114

RELATIONSHIP WITH SUBSTANTIAL SHAREHOLDERS . . . . . . . . . . . . . . . . . . . . . . . . . . 178

DIRECTORS, SUPERVISORS AND SENIOR MANAGEMENT . . . . . . . . . . . . . . . . . . . . . . . . 193

PERSONS HAVING NOTIFIABLE INTERESTS UNDER THE SFO . . . . . . . . . . . . . . . . . . . 208

SHARE CAPITAL . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 215

FINANCIAL INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 219

FUTURE PLANS AND [REDACTED] . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 260

UNDERWRITING . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 262

STRUCTURE OF THE [REDACTED] . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 271

HOW TO APPLY FOR [REDACTED] . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 280

APPENDIX I — ACCOUNTANTS’ REPORT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . I-1

APPENDIX II — UNAUDITED PRO FORMA FINANCIAL INFORMATION . . . . . . . II-1

APPENDIX III — TAXATION AND FOREIGN EXCHANGE . . . . . . . . . . . . . . . . . . . . . . . III-1

APPENDIX IV — SUMMARY OF PRINCIPAL PRC AND HONG KONG LEGALAND REGULATORY PROVISIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . IV-1

APPENDIX V — SUMMARY OF THE ARTICLES OF ASSOCIATION . . . . . . . . . . . . V-1

APPENDIX VI — STATUTORY AND GENERAL INFORMATION . . . . . . . . . . . . . . . . . VI-1

APPENDIX VII — DOCUMENTS DELIVERED TO THE REGISTRAR OFCOMPANIES IN HONG KONG AND AVAILABLEFOR INSPECTION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . VII-1

CONTENTS

– iv –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THEINFORMATION MUST BE READ IN CONJUNCTION WITH THE SECTION HEADED ‘‘WARNING’’ ON THECOVER OF THIS DOCUMENT.

This summary aims to give you an overview of the information contained in this document.

Since it is a summary, it does not contain all the information that may be important to you. You

should read this document in its entirety before you decide to invest in [REDACTED].

There are risks associated with any investment. Some of the particular risks in investing in the

[REDACTED] are set out in ‘‘Risk Factors’’ in this document. You should read that section carefully

before you decide to invest in [REDACTED].

OVERVIEW

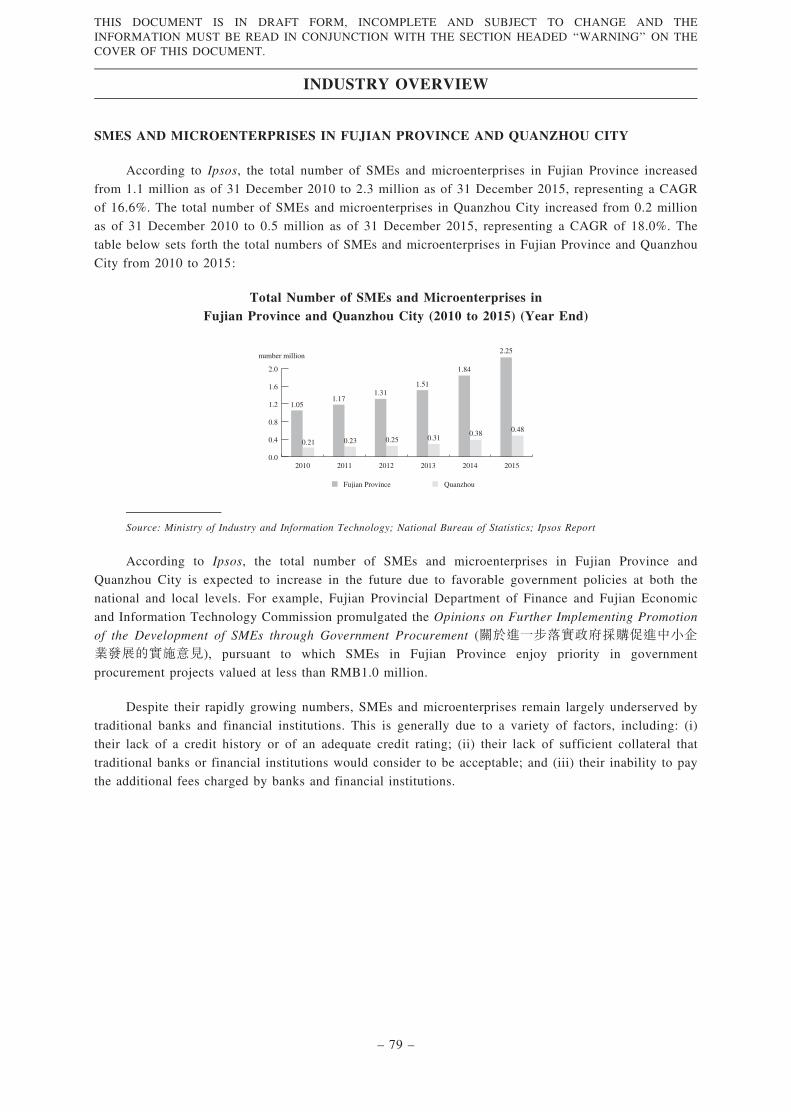

Based in Quanzhou City, we were the largest licensed microfinance company in Fujian Province in

terms of 2015 revenue, according to Ipsos. We are primarily dedicated to providing local entrepreneurial

individuals, SMEs and microenterprises with practical and flexible short-term financing solutions to

support their continued development and address their ongoing liquidity needs. We generate

substantially all of our income by charging interest on the loans extended to our customers. We

primarily offer short-term credit-based loans, which generally had maturity profiles of up to six months

and ranged in size from RMB1.0 million to RMB10.0 million during the Track Record Period. To a

lesser degree, we also provide collateral-backed loans. We provide two types of loans, namely,

revolving loans and term loans, to our customers. As of 31 March 2016, we had a registered capital of

RMB500.0 million. We had a market share of approximately 7.2% in Quanzhou City’s microfinance

market in terms of principal amount of outstanding loans as of 31 December 2015, according to Ipsos.

Our business scale has expanded rapidly since our inception in January 2010, and we have built a solid

customer base in line with the growth in our business scale. During the Track Record Period, we had a

portfolio of over 600 different customers.

Our Revenue and Profit Source

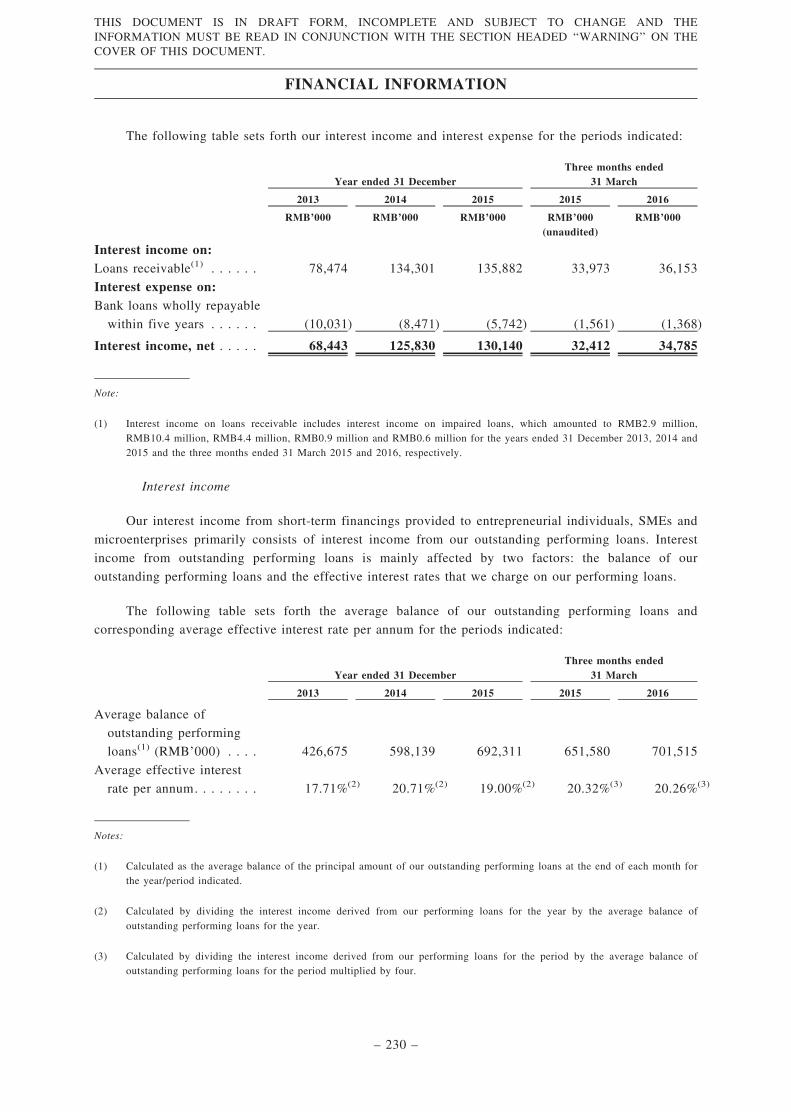

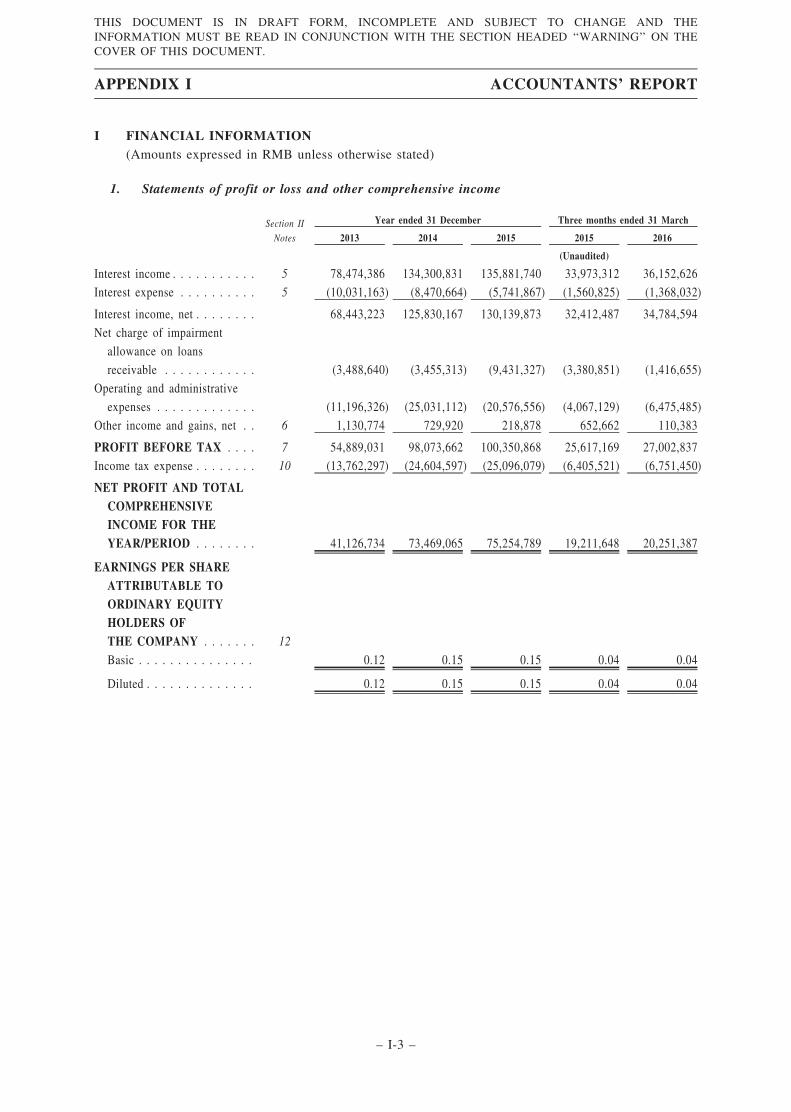

For the years ended 31 December 2013, 2014 and 2015, we generated interest income of RMB78.5

million, RMB134.3 million and RMB135.9 million, respectively. For the three months ended 31 March

2015 and 2016, we generated interest income of RMB34.0 million and RMB36.2 million, respectively.

Our interest income during the Track Record Period primarily consisted of interest income from our

outstanding performing loans, which was affected by two factors: (i) the balance of our outstanding

performing loans, and (ii) the effective interest rates that we charge on our performing loans. The

interest rates we charge on our loans vary depending on the tenure of each loan or drawdown, the credit

profile of the customer, and the prevailing conditions of the lending market. The table below sets forth

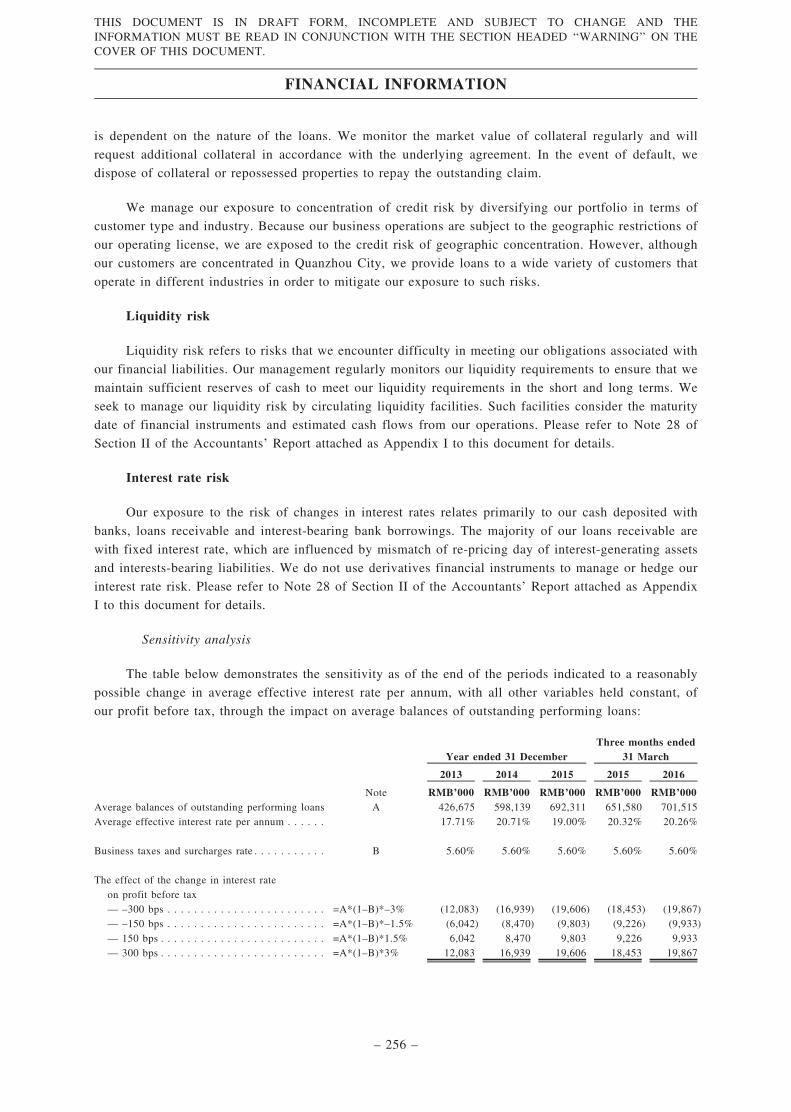

the average balance of our outstanding performing loans and corresponding average effective interest

rate per annum for the periods indicated:

Year ended 31 DecemberThree months ended

31 March

2013 2014 2015 2015 2016

Average balance of outstanding performing

loans(1) (RMB’000) . . . . . . . . . . . . . . . . . . 426,675 598,139 692,311 651,580 701,515

Average effective interest rate per annum . . . . . 17.71%(2) 20.71%(2) 19.00%(2) 20.32%(3) 20.26%(3)

SUMMARY AND HIGHLIGHTS

– 1 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THEINFORMATION MUST BE READ IN CONJUNCTION WITH THE SECTION HEADED ‘‘WARNING’’ ON THECOVER OF THIS DOCUMENT.

Notes:

(1) Calculated as the average balance of the principal amount of our outstanding performing loans at the end of each month forthe year/period indicated.

(2) Calculated by dividing the interest income derived from our performing loans for the year by the average balance ofoutstanding performing loans for the year.

(3) Calculated by dividing the interest income derived from our performing loans for the period by the average balance ofoutstanding performing loans for the period multiplied by four.

Our Customers

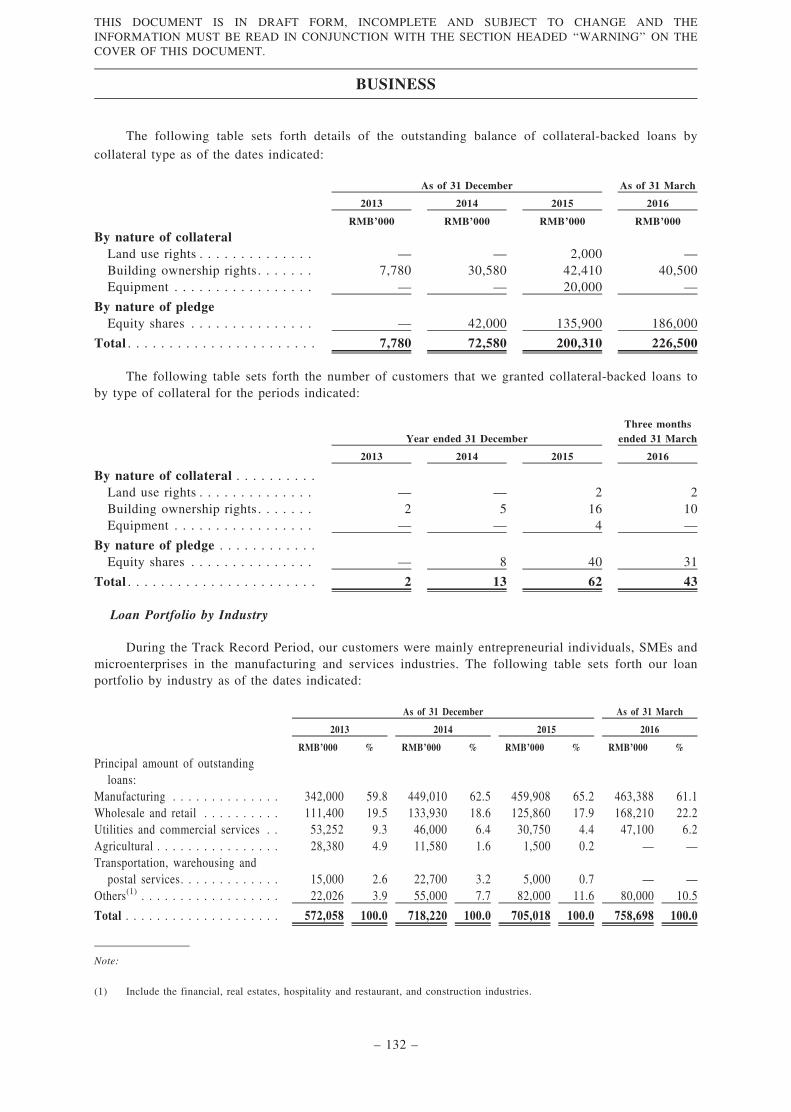

Our customers, which primarily include entrepreneurial individuals, SMEs and microenterprises in

Quanzhou City, mainly operate in the manufacturing and services industries. We focus on providing

financial solutions to such customers because their financial needs have largely been underserved in

China’s banking system, in spite of their rapid growth and their significant contribution to China’s

economic development. We committed to diversify our customer base during the Track Record Period.

As a result, interest income from our largest customer accounted for 4.0%, 3.0%, 2.2% and 1.8% of our

total interest income for the years ended 31 December 2013, 2014 and 2015 and the three months ended

31 March 2016, respectively. Interest income from our top five customers accounted for 15.9%, 11.2%,

8.6% and 8.0% of our total interest income for the years ended 31 December 2013, 2014 and 2015 and

the three months ended 31 March 2016, respectively.

Government Support

From the commencement of our operations on 8 January 2010 until 30 April 2014, we were

licensed to base our operations in Licheng District of Quanzhou City. As one of the first group of pilot

microfinance companies, we were also permitted during this period to provide our loan services to SMEs

and microenterprises with a business presence, as well as individuals who reside, in any area within

Quanzhou City. After the Pilot Measures was promulgated, on 30 April 2014, the Quanzhou Financial

Affairs Bureau expressly defined the areas where we are permitted to operate our businesses and offer

our loan services to be Nan’an City, Jinjiang City, Luojiang District and Licheng District, which are

subordinated administrative districts of Quanzhou City. Accordingly, we have limited our operations to

these licensed geographic areas since 30 April 2014. Our location in Quanzhou City, scale of operations,

in-depth knowledge of the local market and credit environment, and strong reputation as a preferred

provider of credit-based and short-term financing solutions for entrepreneurial individuals, SMEs and

microenterprises in Quanzhou City have enabled us to benefit from certain preferential government

policies. In addition, as Quanzhou City was approved as a pilot financial reform zone for comprehensive

reform of financial service and real economy by the State Council in 2012, the Fujian provincial

government subsequently implemented a series of financial reform policies and measures with the aim of

developing and cultivating the local financial services sector, channeling private capital to support the

financing needs of SMEs and local microenterprises. To promote the development of the local services

industry, the government of Licheng District provided us with a RMB619,300 grant in 2013 to subsidize

our local income tax payment for the year ended 31 December 2011. In addition, in 2015, we recorded a

government grant of RMB500,000 provided by the government of Quanzhou City as a governmental

reward fund, the purpose of which is to support [REDACTED] of local enterprises. Moreover, in April

2014, the NDRC designated Quanzhou City as a pilot zone for the comprehensive reform of the private

economy, initiating reform programs that include improving the financial services sector as well as

SUMMARY AND HIGHLIGHTS

– 2 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THEINFORMATION MUST BE READ IN CONJUNCTION WITH THE SECTION HEADED ‘‘WARNING’’ ON THECOVER OF THIS DOCUMENT.

increasing the financial support of, and the financing resources available to, private enterprises. We

believe that, by taking advantage of these supportive policies, we will be able to achieve successful

business growth and to better serve our existing and new customers.

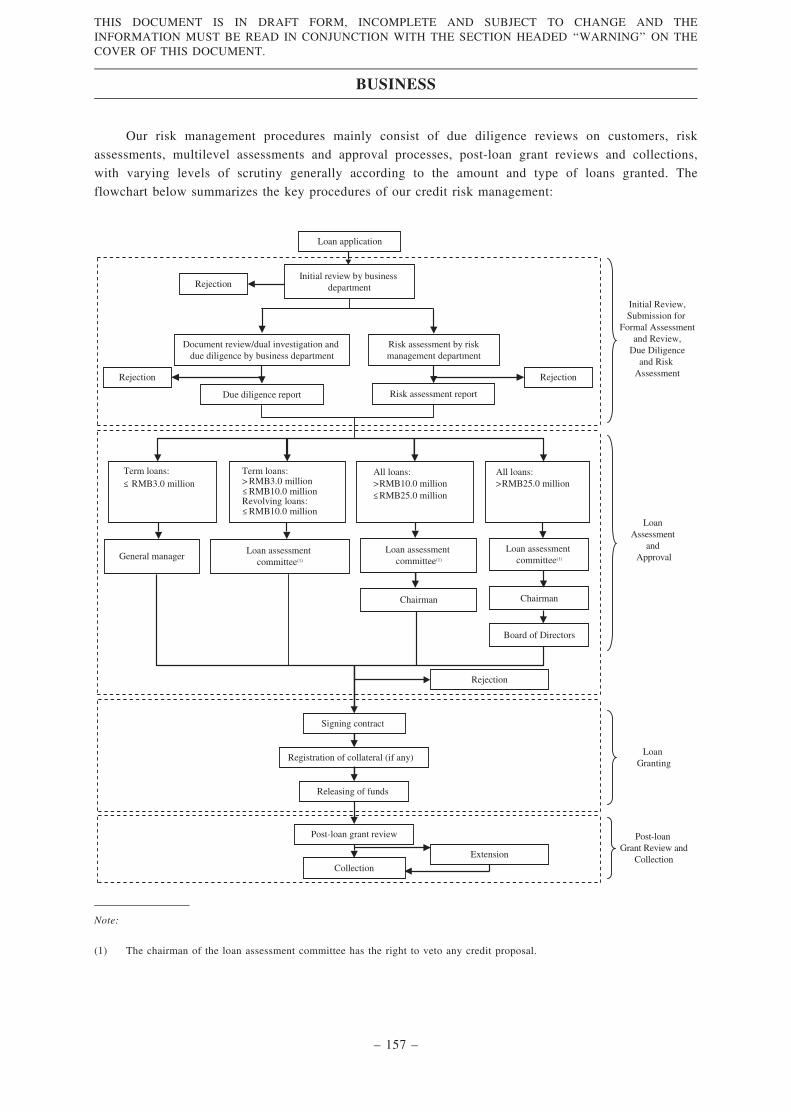

Our Credit Risk Management

Credit risk is the principal risk inherent in our business. We have developed a credit risk

management system in order to effectively identify, manage and minimize credit risks in connection

with each loan we grant. In general, our credit risk management process begins with an initial review

and mainly consists of due diligence reviews on customers, risk assessment reviews, multilevel

assessments and approvals, post-loan grant reviews and collections. Our credit evaluation procedures

enable us to evaluate our customers’ creditworthiness, which provides an important reference for our

credit risk management. While we develop and expand our business operations, we continue to monitor

and improve the performance and function of our risk management system to respond to changes in

market conditions, the regulatory environment and our product portfolio. To address operational and

legal risks, we have adopted and implemented streamlined procedures to ensure our efficient operation

and compliance with applicable laws and regulations. For more details, see ‘‘Business – Risk

Management’’ beginning on page 155 of this document.

Our Track Record

We experienced steady growth during the Track Record Period. Our net loans receivable, being our

gross loans receivable deducting the allowance for impairment losses, was RMB526.3 million,

RMB685.4 million, RMB692.1 million and RMB753.9 million as of 31 December 2013, 2014 and 2015

and 31 March 2016, respectively. Our net interest income was RMB68.4 million, RMB125.8 million and

RMB130.1 million for the years ended 31 December 2013, 2014 and 2015, respectively. Our net interest

income was RMB32.4 million and RMB34.8 million for the three months ended 31 March 2015 and

2016, respectively. Our net profit, being our net profit and total comprehensive income, was RMB41.1

million, RMB73.5 million and RMB75.3 million for the years ended 31 December 2013, 2014 and 2015,

respectively. Our net profit was RMB19.2 million and RMB20.3 million for the three months ended 31

March 2015 and 2016, respectively.

OUR COMPETITIVE STRENGTHS

. We are the largest licensed microfinance company in Fujian Province in terms of 2015

revenue, primarily dedicated to providing entrepreneurial individuals, SMEs and

microenterprises with quick access to short-term financing.

. We have a strong shareholder base, substantial financial strengths and a sound credit rating.

. We are located in a pilot financial reform zone and benefit from preferential government

policies.

. We adopt sound and effective risk management practices and are dedicated to enhancing our

risk control procedures year by year.

. Our experienced management team and experienced personnel have an in-depth industry

knowledge that ensures the successful development of our business.

SUMMARY AND HIGHLIGHTS

– 3 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THEINFORMATION MUST BE READ IN CONJUNCTION WITH THE SECTION HEADED ‘‘WARNING’’ ON THECOVER OF THIS DOCUMENT.

OUR BUSINESS STRATEGIES

. Further enlarge our capital base and diversify our funding sources

. Expand our product offerings and customer base

. Expand the geographical coverage of our business

. Seek opportunities for strategic acquisitions and investments

. Enhance our corporate governance and strengthen our risk management efforts and internalcontrols

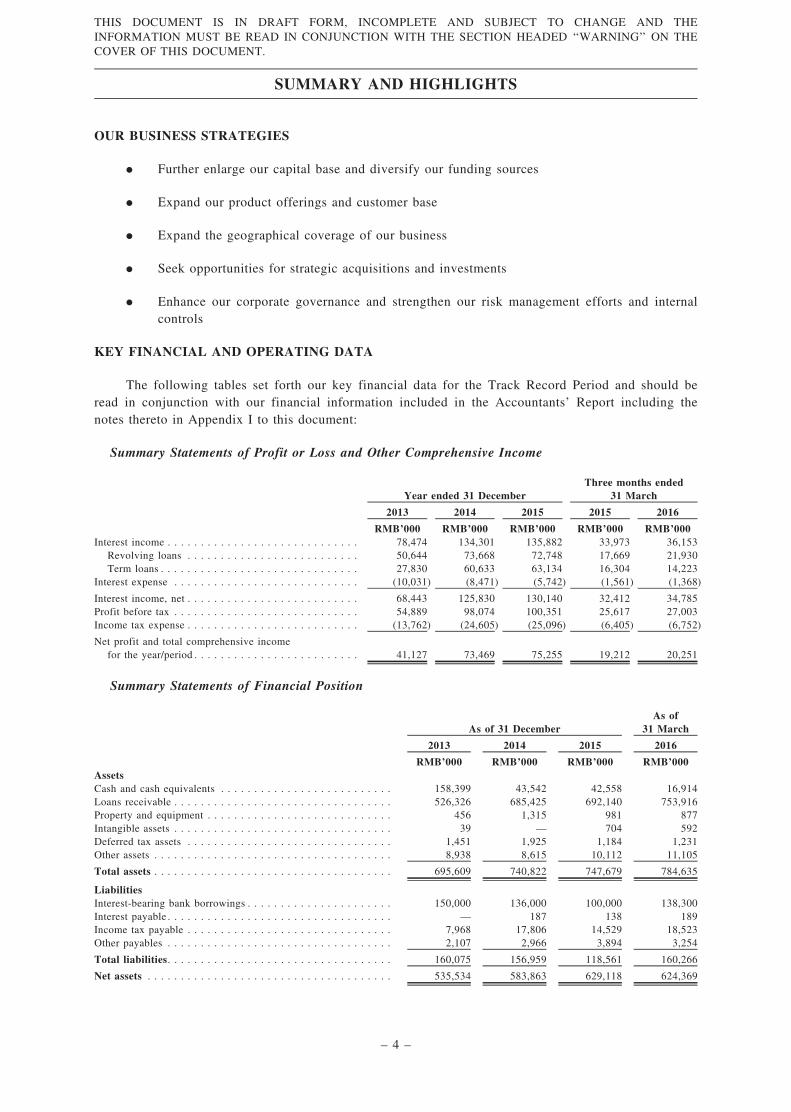

KEY FINANCIAL AND OPERATING DATA

The following tables set forth our key financial data for the Track Record Period and should beread in conjunction with our financial information included in the Accountants’ Report including thenotes thereto in Appendix I to this document:

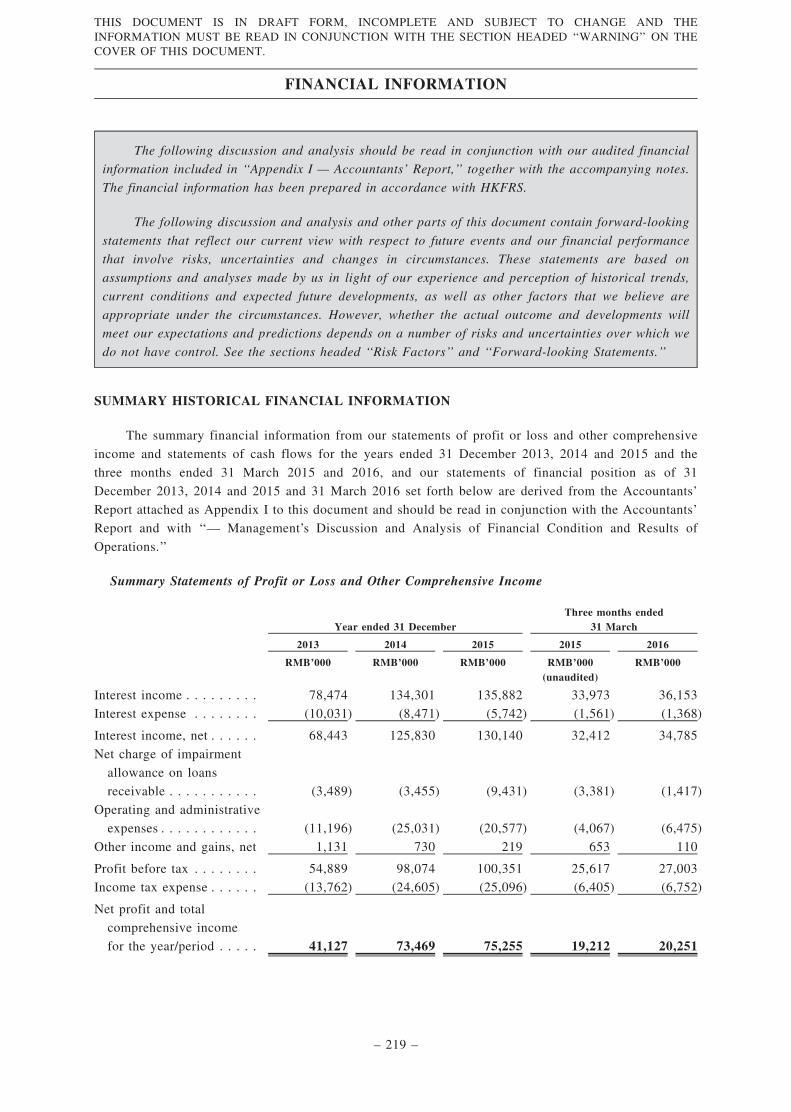

Summary Statements of Profit or Loss and Other Comprehensive Income

Year ended 31 DecemberThree months ended

31 March

2013 2014 2015 2015 2016

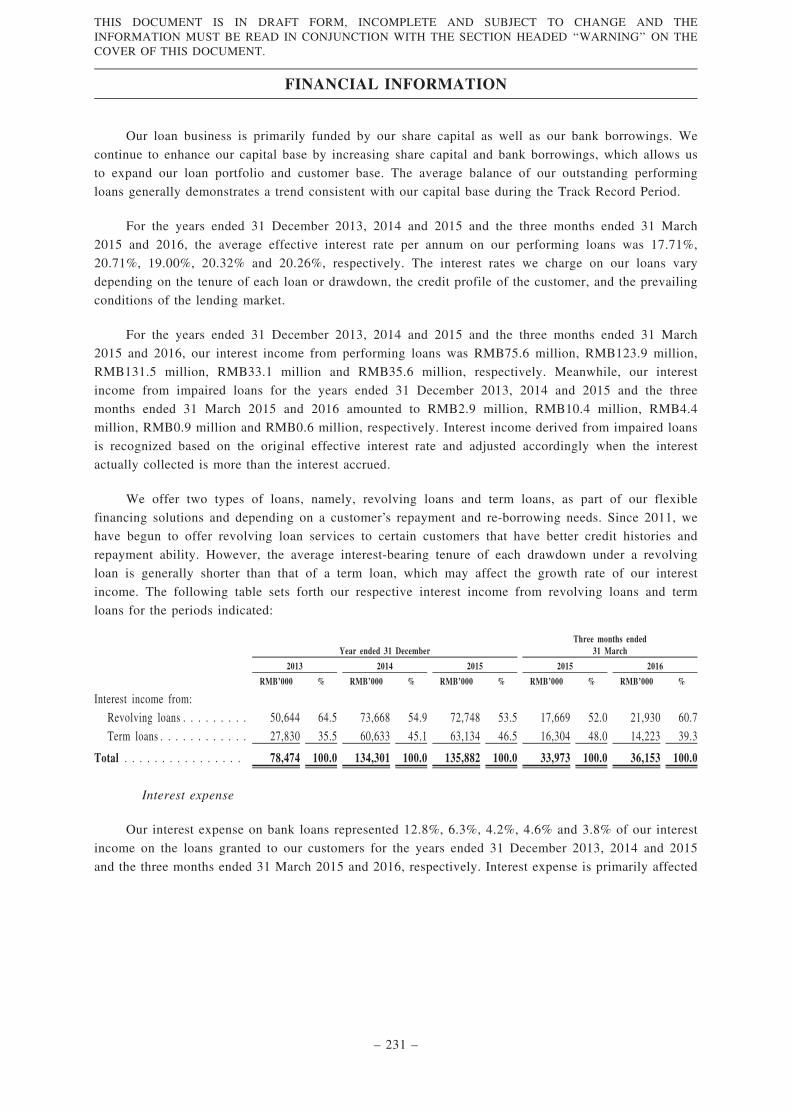

RMB’000 RMB’000 RMB’000 RMB’000 RMB’000Interest income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 78,474 134,301 135,882 33,973 36,153

Revolving loans . . . . . . . . . . . . . . . . . . . . . . . . . . 50,644 73,668 72,748 17,669 21,930Term loans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27,830 60,633 63,134 16,304 14,223

Interest expense . . . . . . . . . . . . . . . . . . . . . . . . . . . . (10,031) (8,471) (5,742) (1,561) (1,368)

Interest income, net . . . . . . . . . . . . . . . . . . . . . . . . . . 68,443 125,830 130,140 32,412 34,785Profit before tax . . . . . . . . . . . . . . . . . . . . . . . . . . . . 54,889 98,074 100,351 25,617 27,003Income tax expense . . . . . . . . . . . . . . . . . . . . . . . . . . (13,762) (24,605) (25,096) (6,405) (6,752)

Net profit and total comprehensive incomefor the year/period . . . . . . . . . . . . . . . . . . . . . . . . . 41,127 73,469 75,255 19,212 20,251

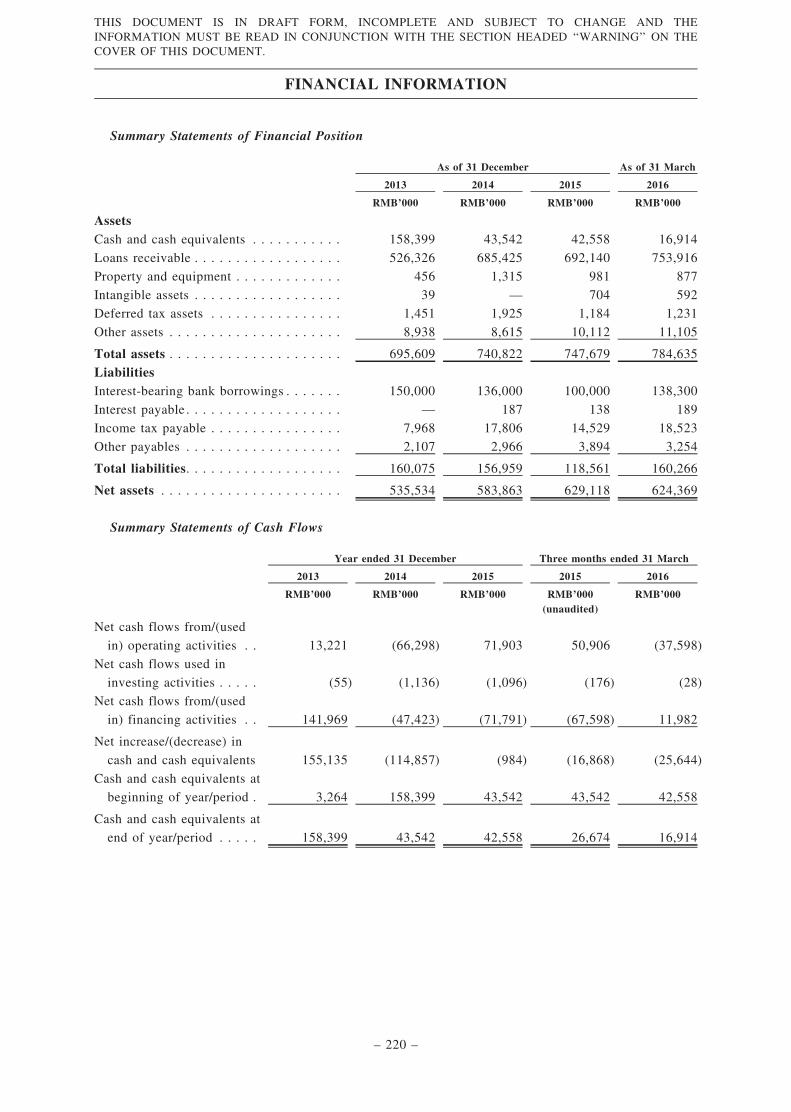

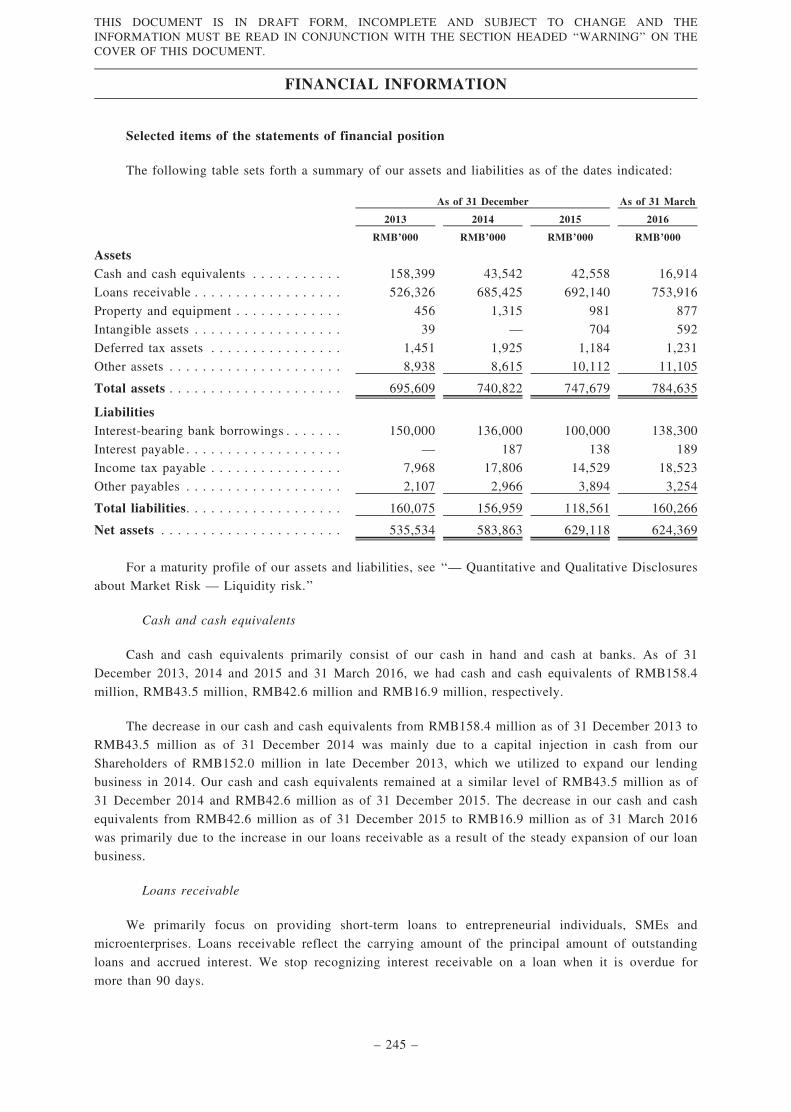

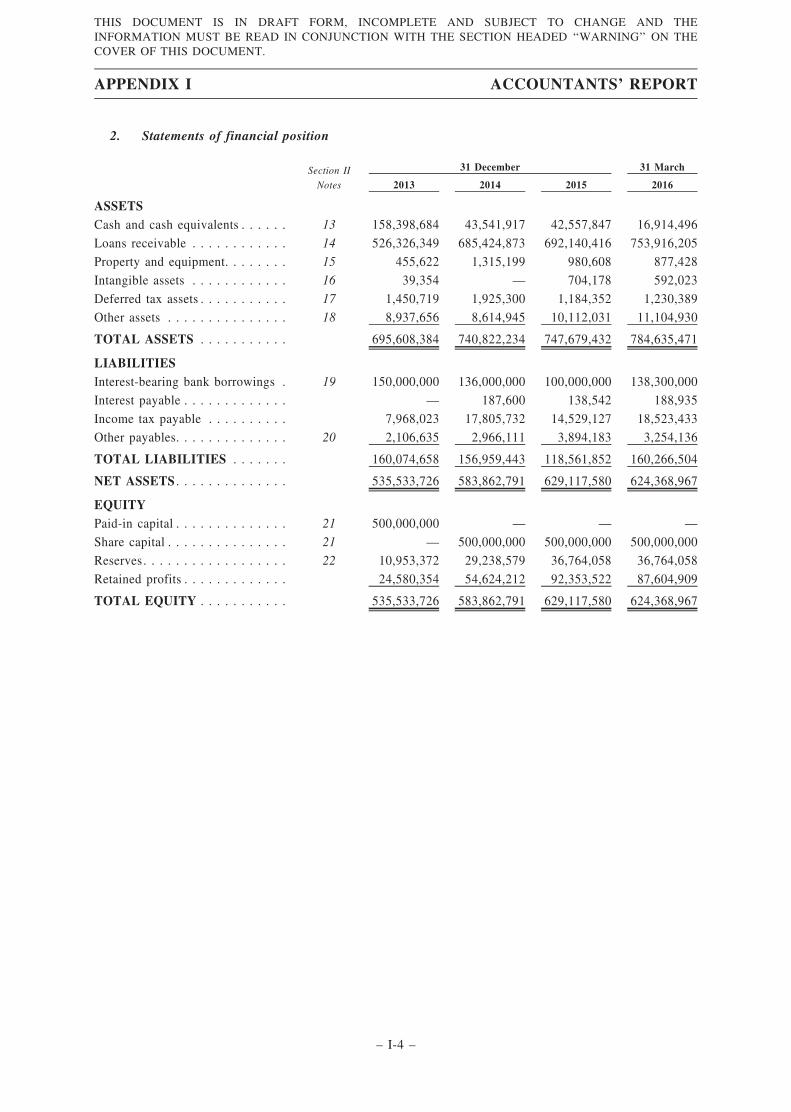

Summary Statements of Financial Position

As of 31 DecemberAs of

31 March

2013 2014 2015 2016

RMB’000 RMB’000 RMB’000 RMB’000AssetsCash and cash equivalents . . . . . . . . . . . . . . . . . . . . . . . . . . 158,399 43,542 42,558 16,914Loans receivable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 526,326 685,425 692,140 753,916Property and equipment . . . . . . . . . . . . . . . . . . . . . . . . . . . . 456 1,315 981 877Intangible assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39 — 704 592Deferred tax assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,451 1,925 1,184 1,231Other assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8,938 8,615 10,112 11,105

Total assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 695,609 740,822 747,679 784,635

LiabilitiesInterest-bearing bank borrowings . . . . . . . . . . . . . . . . . . . . . . 150,000 136,000 100,000 138,300Interest payable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . — 187 138 189Income tax payable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7,968 17,806 14,529 18,523Other payables . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2,107 2,966 3,894 3,254

Total liabilities. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 160,075 156,959 118,561 160,266

Net assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 535,534 583,863 629,118 624,369

SUMMARY AND HIGHLIGHTS

– 4 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THEINFORMATION MUST BE READ IN CONJUNCTION WITH THE SECTION HEADED ‘‘WARNING’’ ON THECOVER OF THIS DOCUMENT.

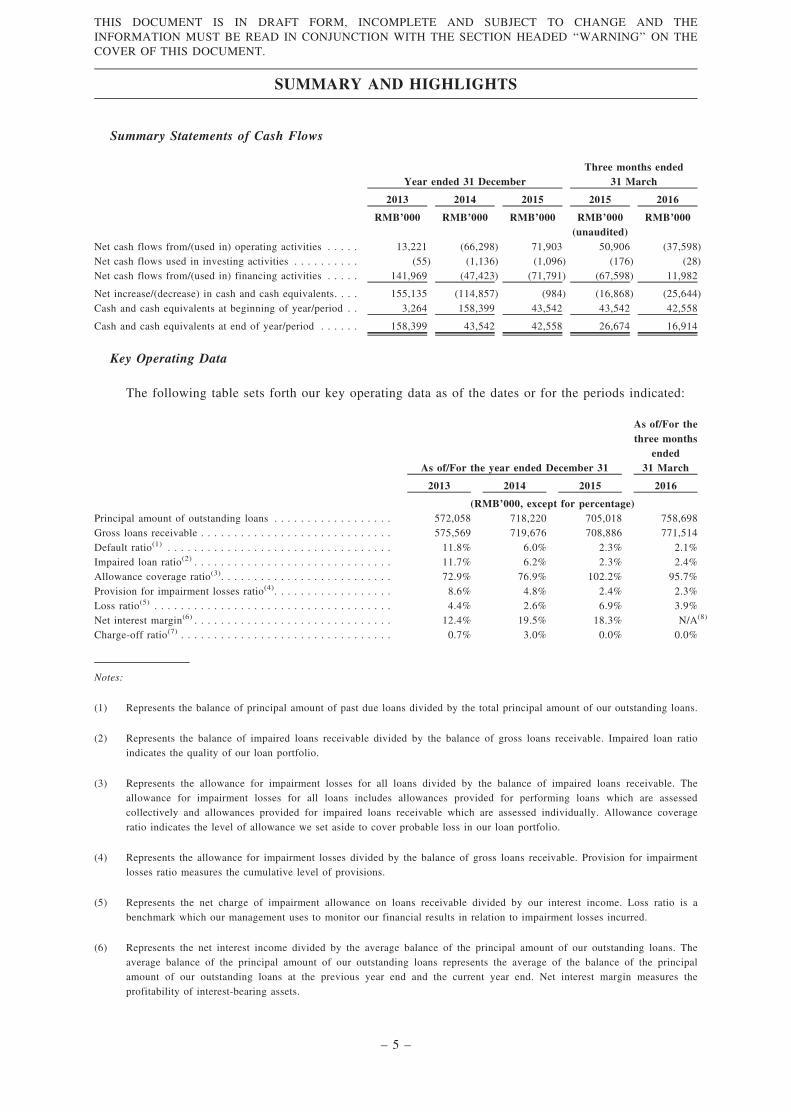

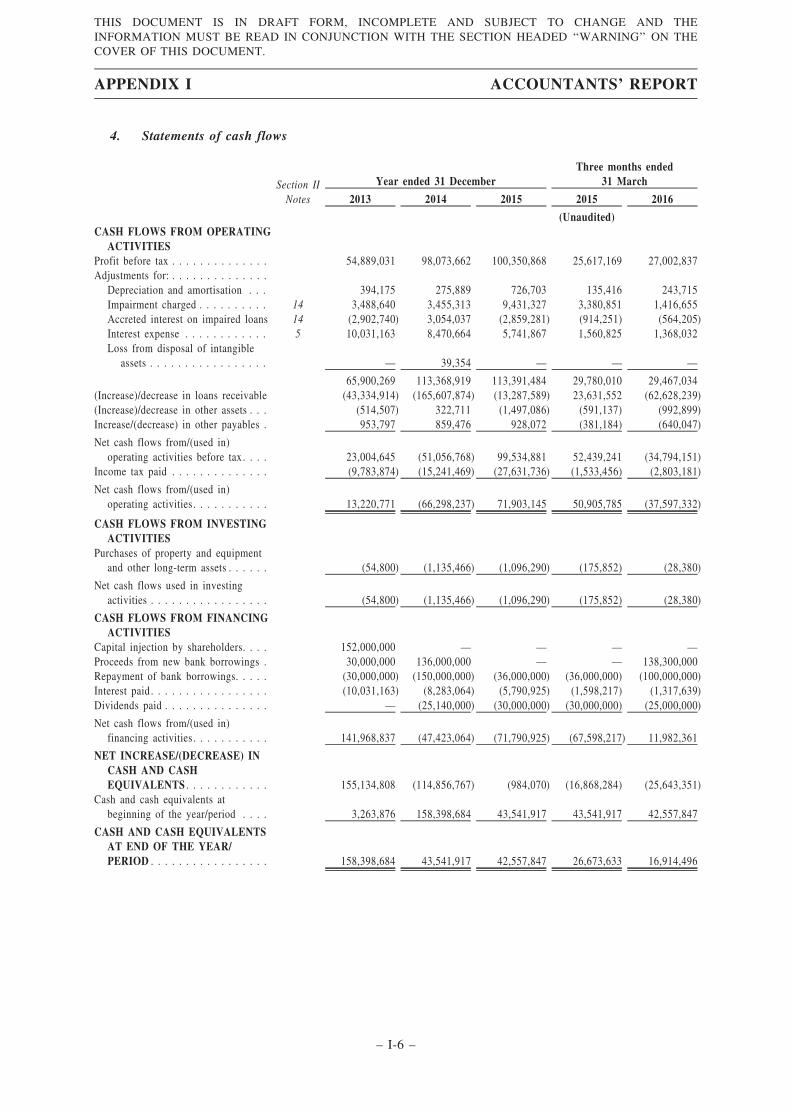

Summary Statements of Cash Flows

Year ended 31 DecemberThree months ended

31 March

2013 2014 2015 2015 2016

RMB’000 RMB’000 RMB’000 RMB’000 RMB’000(unaudited)

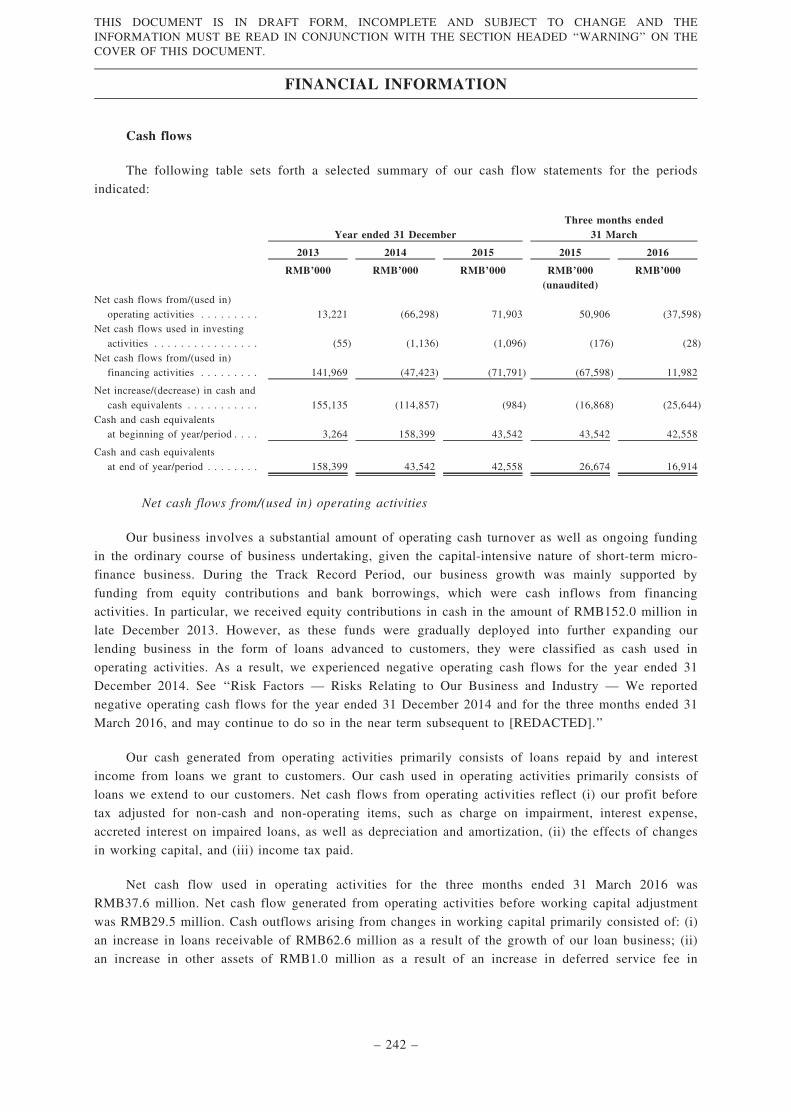

Net cash flows from/(used in) operating activities . . . . . 13,221 (66,298) 71,903 50,906 (37,598)Net cash flows used in investing activities . . . . . . . . . . (55) (1,136) (1,096) (176) (28)Net cash flows from/(used in) financing activities . . . . . 141,969 (47,423) (71,791) (67,598) 11,982

Net increase/(decrease) in cash and cash equivalents. . . . 155,135 (114,857) (984) (16,868) (25,644)

Cash and cash equivalents at beginning of year/period . . 3,264 158,399 43,542 43,542 42,558

Cash and cash equivalents at end of year/period . . . . . . 158,399 43,542 42,558 26,674 16,914

Key Operating Data

The following table sets forth our key operating data as of the dates or for the periods indicated:

As of/For the year ended December 31

As of/For thethree months

ended31 March

2013 2014 2015 2016

(RMB’000, except for percentage)Principal amount of outstanding loans . . . . . . . . . . . . . . . . . . 572,058 718,220 705,018 758,698Gross loans receivable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 575,569 719,676 708,886 771,514

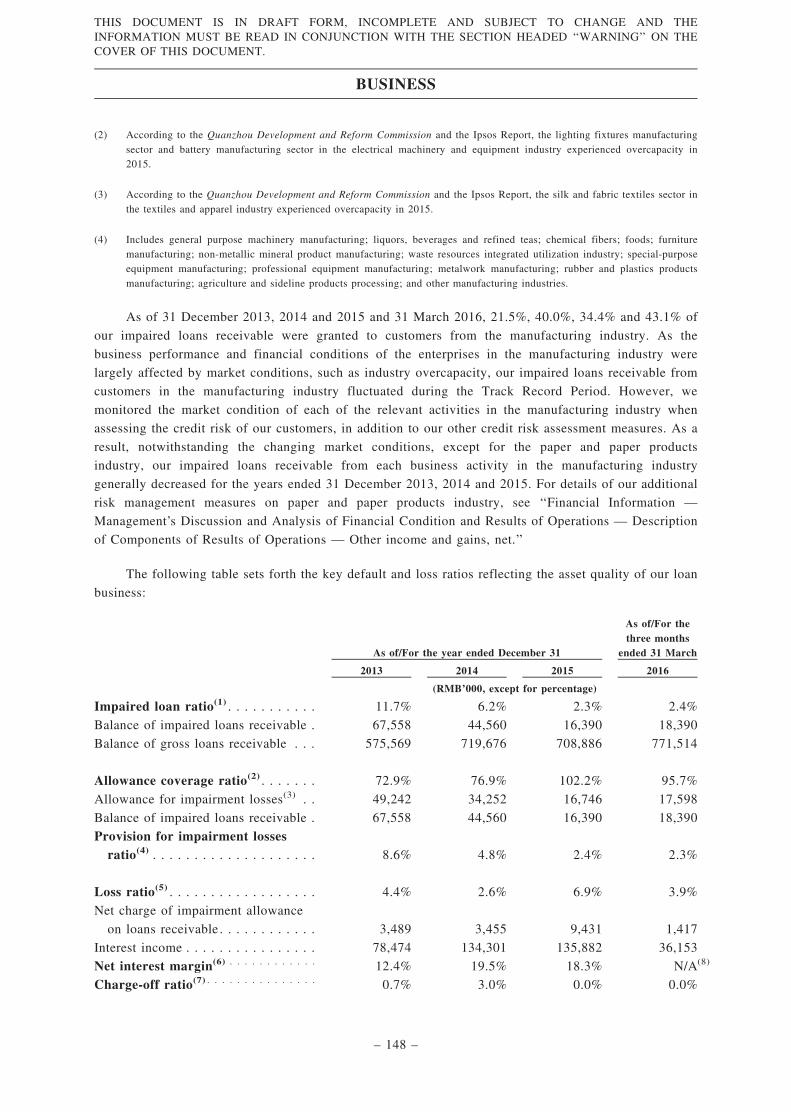

Default ratio(1) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11.8% 6.0% 2.3% 2.1%Impaired loan ratio(2) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11.7% 6.2% 2.3% 2.4%Allowance coverage ratio(3). . . . . . . . . . . . . . . . . . . . . . . . . . 72.9% 76.9% 102.2% 95.7%

Provision for impairment losses ratio(4). . . . . . . . . . . . . . . . . . 8.6% 4.8% 2.4% 2.3%Loss ratio(5) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4.4% 2.6% 6.9% 3.9%Net interest margin(6) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12.4% 19.5% 18.3% N/A(8)

Charge-off ratio(7) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.7% 3.0% 0.0% 0.0%

Notes:

(1) Represents the balance of principal amount of past due loans divided by the total principal amount of our outstanding loans.

(2) Represents the balance of impaired loans receivable divided by the balance of gross loans receivable. Impaired loan ratioindicates the quality of our loan portfolio.

(3) Represents the allowance for impairment losses for all loans divided by the balance of impaired loans receivable. Theallowance for impairment losses for all loans includes allowances provided for performing loans which are assessedcollectively and allowances provided for impaired loans receivable which are assessed individually. Allowance coverage

ratio indicates the level of allowance we set aside to cover probable loss in our loan portfolio.

(4) Represents the allowance for impairment losses divided by the balance of gross loans receivable. Provision for impairmentlosses ratio measures the cumulative level of provisions.

(5) Represents the net charge of impairment allowance on loans receivable divided by our interest income. Loss ratio is a

benchmark which our management uses to monitor our financial results in relation to impairment losses incurred.

(6) Represents the net interest income divided by the average balance of the principal amount of our outstanding loans. Theaverage balance of the principal amount of our outstanding loans represents the average of the balance of the principalamount of our outstanding loans at the previous year end and the current year end. Net interest margin measures the

profitability of interest-bearing assets.

SUMMARY AND HIGHLIGHTS

– 5 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THEINFORMATION MUST BE READ IN CONJUNCTION WITH THE SECTION HEADED ‘‘WARNING’’ ON THECOVER OF THIS DOCUMENT.

(7) Represents the total write-offs during the period divided by the total principal amount of our outstanding loans at the year/

period end. Charge-off ratio measures the gross credit loss of our loan portfolio.

(8) Such ratio is not meaningful as it is not comparable to annual numbers. The net interest margin for the three months ended31 March 2016 is 19.0%, on an annualized basis, representing the net interest income for the three months ended 31 March

2016 divided by the average balance of the principal amount of our outstanding loans, multiplied by four.

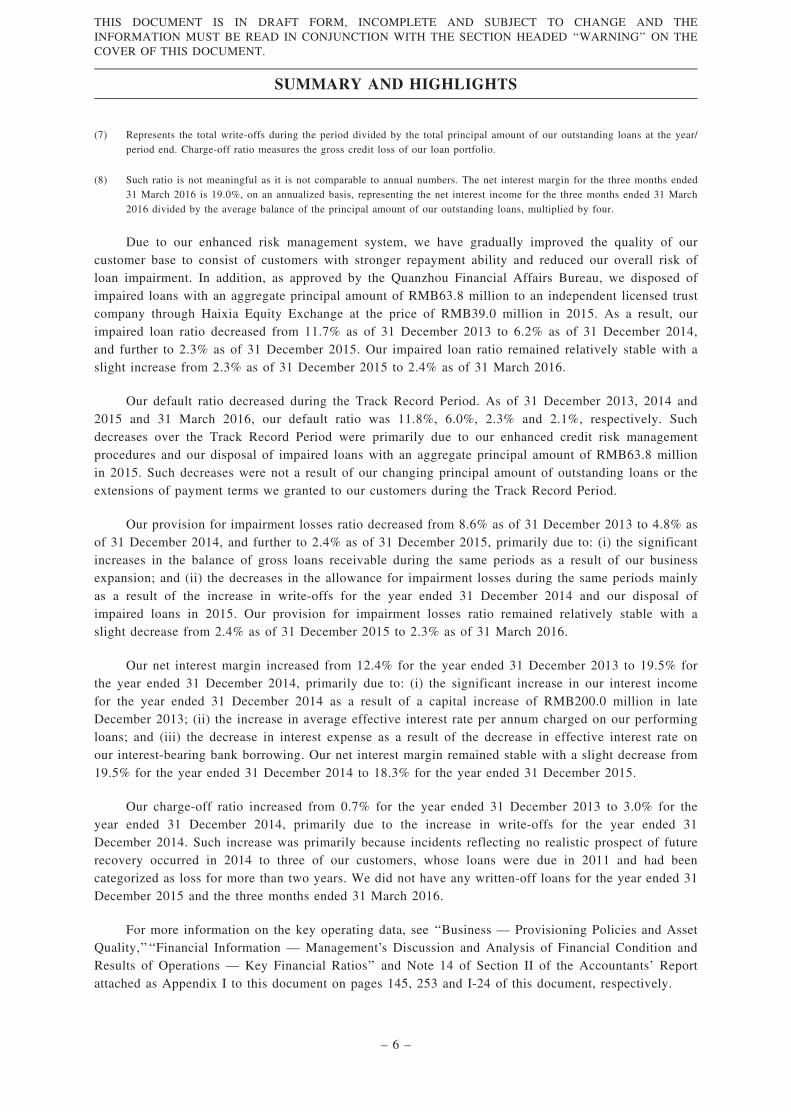

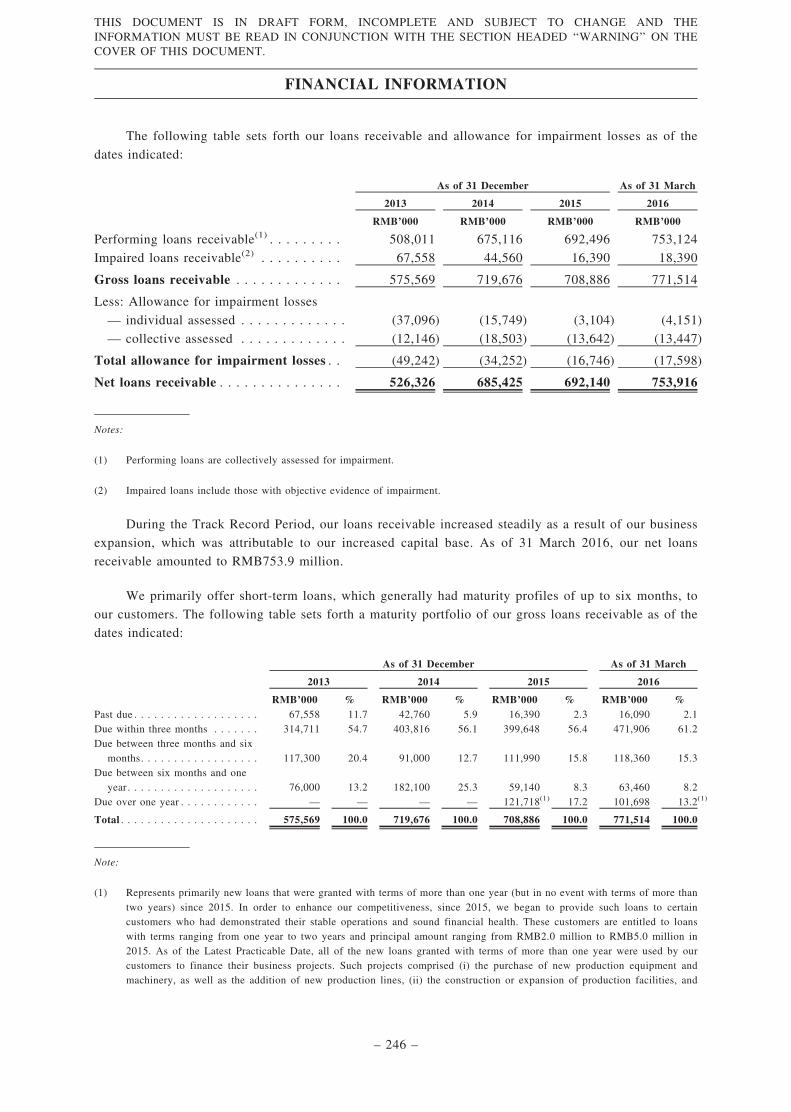

Due to our enhanced risk management system, we have gradually improved the quality of ourcustomer base to consist of customers with stronger repayment ability and reduced our overall risk ofloan impairment. In addition, as approved by the Quanzhou Financial Affairs Bureau, we disposed ofimpaired loans with an aggregate principal amount of RMB63.8 million to an independent licensed trustcompany through Haixia Equity Exchange at the price of RMB39.0 million in 2015. As a result, ourimpaired loan ratio decreased from 11.7% as of 31 December 2013 to 6.2% as of 31 December 2014,and further to 2.3% as of 31 December 2015. Our impaired loan ratio remained relatively stable with aslight increase from 2.3% as of 31 December 2015 to 2.4% as of 31 March 2016.

Our default ratio decreased during the Track Record Period. As of 31 December 2013, 2014 and2015 and 31 March 2016, our default ratio was 11.8%, 6.0%, 2.3% and 2.1%, respectively. Suchdecreases over the Track Record Period were primarily due to our enhanced credit risk managementprocedures and our disposal of impaired loans with an aggregate principal amount of RMB63.8 millionin 2015. Such decreases were not a result of our changing principal amount of outstanding loans or theextensions of payment terms we granted to our customers during the Track Record Period.

Our provision for impairment losses ratio decreased from 8.6% as of 31 December 2013 to 4.8% asof 31 December 2014, and further to 2.4% as of 31 December 2015, primarily due to: (i) the significantincreases in the balance of gross loans receivable during the same periods as a result of our businessexpansion; and (ii) the decreases in the allowance for impairment losses during the same periods mainlyas a result of the increase in write-offs for the year ended 31 December 2014 and our disposal ofimpaired loans in 2015. Our provision for impairment losses ratio remained relatively stable with aslight decrease from 2.4% as of 31 December 2015 to 2.3% as of 31 March 2016.

Our net interest margin increased from 12.4% for the year ended 31 December 2013 to 19.5% forthe year ended 31 December 2014, primarily due to: (i) the significant increase in our interest incomefor the year ended 31 December 2014 as a result of a capital increase of RMB200.0 million in lateDecember 2013; (ii) the increase in average effective interest rate per annum charged on our performingloans; and (iii) the decrease in interest expense as a result of the decrease in effective interest rate onour interest-bearing bank borrowing. Our net interest margin remained stable with a slight decrease from19.5% for the year ended 31 December 2014 to 18.3% for the year ended 31 December 2015.

Our charge-off ratio increased from 0.7% for the year ended 31 December 2013 to 3.0% for theyear ended 31 December 2014, primarily due to the increase in write-offs for the year ended 31December 2014. Such increase was primarily because incidents reflecting no realistic prospect of futurerecovery occurred in 2014 to three of our customers, whose loans were due in 2011 and had beencategorized as loss for more than two years. We did not have any written-off loans for the year ended 31December 2015 and the three months ended 31 March 2016.

For more information on the key operating data, see ‘‘Business — Provisioning Policies and AssetQuality,’’‘‘Financial Information — Management’s Discussion and Analysis of Financial Condition andResults of Operations — Key Financial Ratios’’ and Note 14 of Section II of the Accountants’ Reportattached as Appendix I to this document on pages 145, 253 and I-24 of this document, respectively.

SUMMARY AND HIGHLIGHTS

– 6 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THEINFORMATION MUST BE READ IN CONJUNCTION WITH THE SECTION HEADED ‘‘WARNING’’ ON THECOVER OF THIS DOCUMENT.

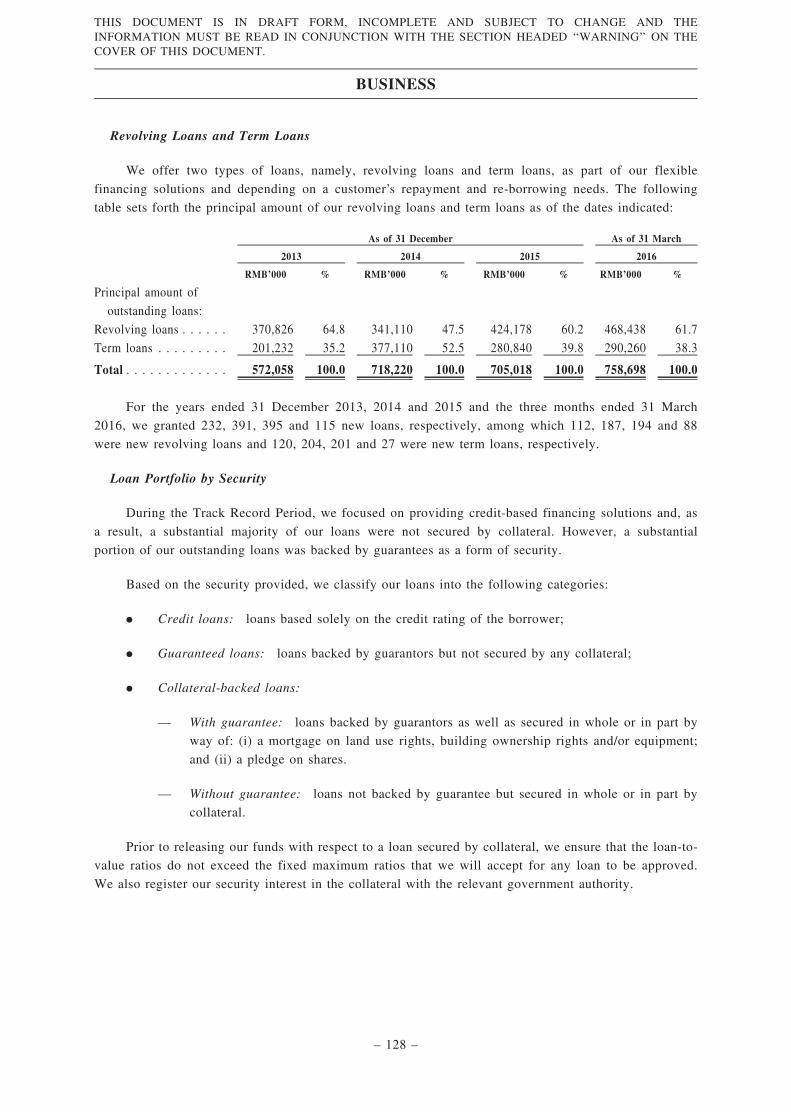

We provide two types of loans, namely, revolving loans and term loans. For our revolving loans,

we generally grant a credit line to our customers with a term of up to one year. For our term loans, we

generally grant loans ranging from RMB1.0 million to RMB10.0 million to our customers with a term

ranging from one to six months. The following table sets forth the principal amount of our outstanding

loans by flexibility as of the dates indicated:

As of 31 December As of 31 March

2013 2014 2015 2016

RMB’000 % RMB’000 % RMB’000 % RMB’000 %Principal amount of outstanding

loans:

Revolving loans . . . . . . . . . . . . . 370,826 64.8 341,110 47.5 424,178 60.2 468,438 61.7Term loans . . . . . . . . . . . . . . . . . 201,232 35.2 377,110 52.5 280,840 39.8 290,260 38.3

Total . . . . . . . . . . . . . . . . . . . . . 572,058 100.0 718,220 100.0 705,018 100.0 758,698 100.0

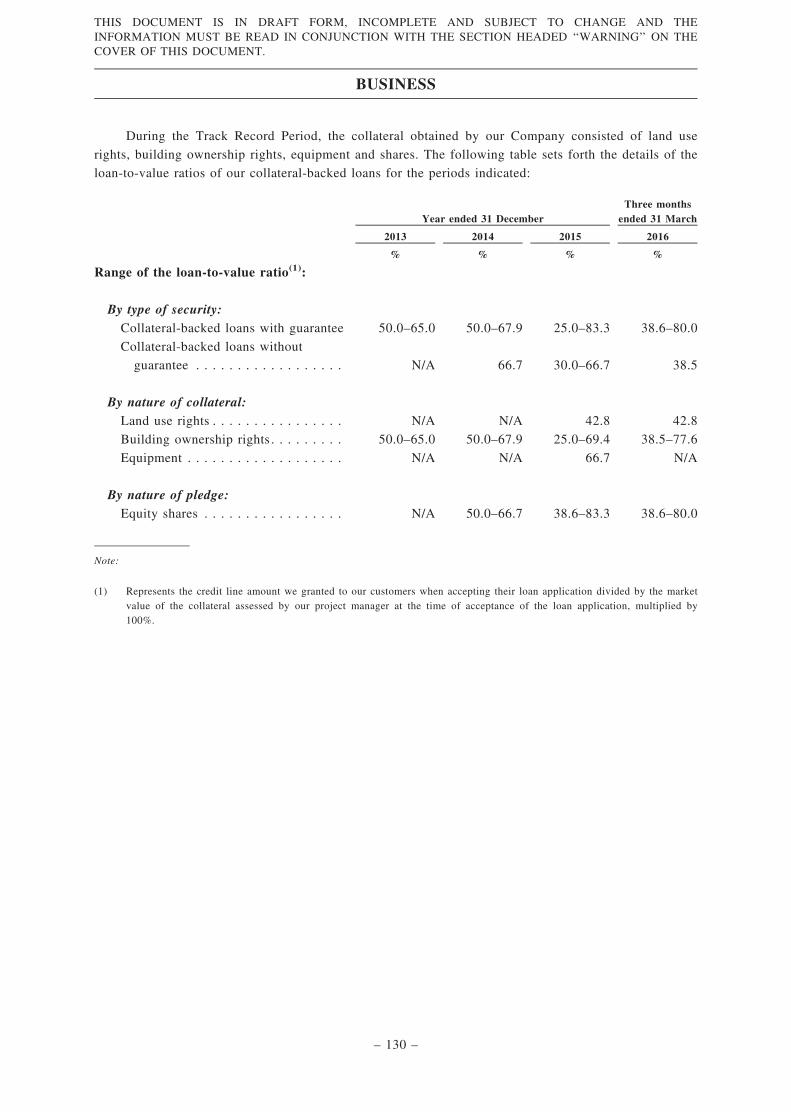

During the Track Record Period, we focused on providing credit-based financing solutions and, as

a result, a substantial majority of our loans were not secured by collateral. However, a substantial

portion of our outstanding loans were backed by guarantees as a form of security. Guarantors of loans

that we extend to our customers are individuals and/or non-financial institutional enterprises. The

following table sets forth the principal amount of our outstanding loans guaranteed by different types of

guarantors as of the dates indicated:

As of 31 December As of 31 March

2013 2014 2015 2016

RMB’000 % RMB’000 % RMB’000 % RMB’000 %Principal amount of

outstanding loansguaranteed by:

Individuals . . . . . . . . . . . 257,832 45.9 289,810 41.0 294,930 44.7 286,850 40.2

Non-financial institutionalenterprises . . . . . . . . . 49,500 8.8 107,600 15.3 56,570 8.6 97,600 13.7

Individuals and non-

financial institutionalenterprises . . . . . . . . . 254,726 45.3 308,810 43.7 308,518 46.7 329,248 46.1

Total . . . . . . . . . . . . . . . 562,058 100.0 706,220 100.0 660,018 100.0 713,698 100.0

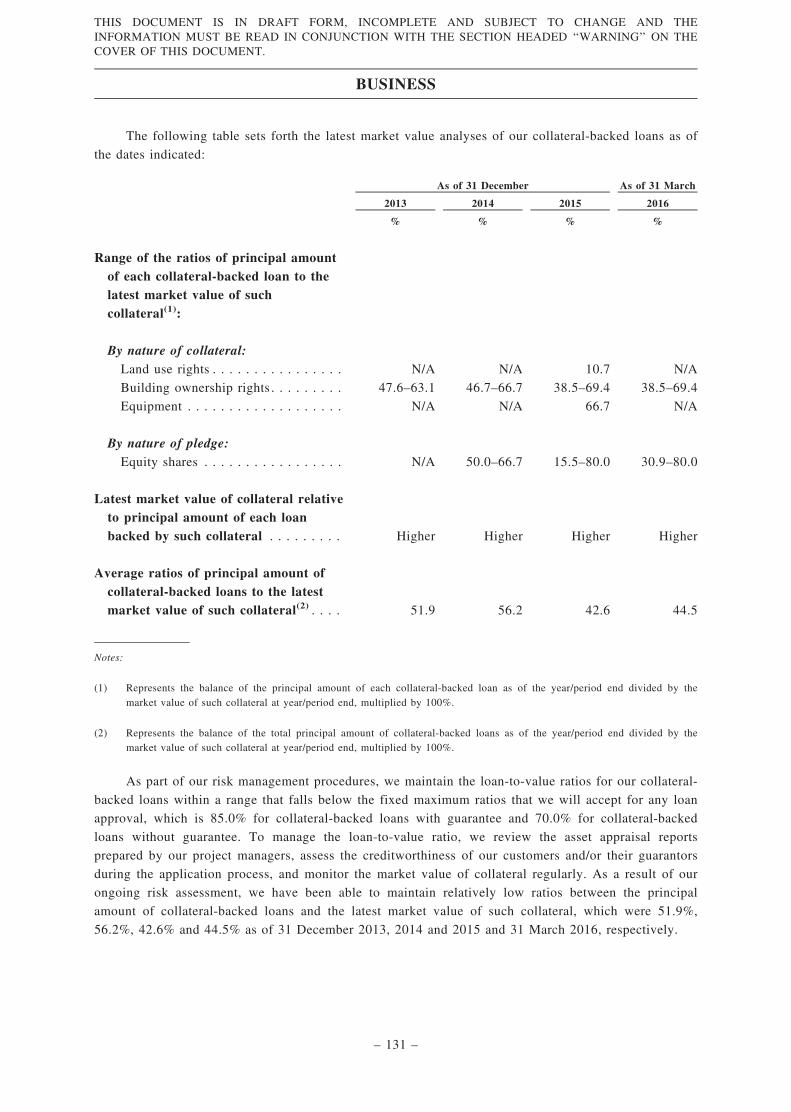

For guaranteed loans, we review the creditworthiness of guarantors using a process that is similar

to our review of a customer’s creditworthiness. For collateral-backed loans, we ensure that the loan-to-

value ratios do not exceed the fixed maximum ratios that we will accept for any loan to be approved.

We also register our security interest in the collateral with the relevant government authority. Where

tangible assets are provided as collateral, we conduct on-site visits to inspect such collateral and monitor

closely the volatility of the value of the collateral, particularly real property, by conducting on-site visits

of the relevant property and performing online research on the general market conditions where such

property is located. For equity rights of non-public companies provided as a pledge, we monitor the

operating conditions of non-public companies by requesting such companies to provide us with their

financial statements periodically and conducting on-site visits or telephone interviews with our

customers. In addition, we refer to the market price and liquidity of similar equities transacted in the

market to assess the value of the pledged equity rights. For more details, see ‘‘Business — Risk

Management — Credit Risk Management — Due diligence and risk assessment’’ on page 158 of this

document.

SUMMARY AND HIGHLIGHTS

– 7 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THEINFORMATION MUST BE READ IN CONJUNCTION WITH THE SECTION HEADED ‘‘WARNING’’ ON THECOVER OF THIS DOCUMENT.

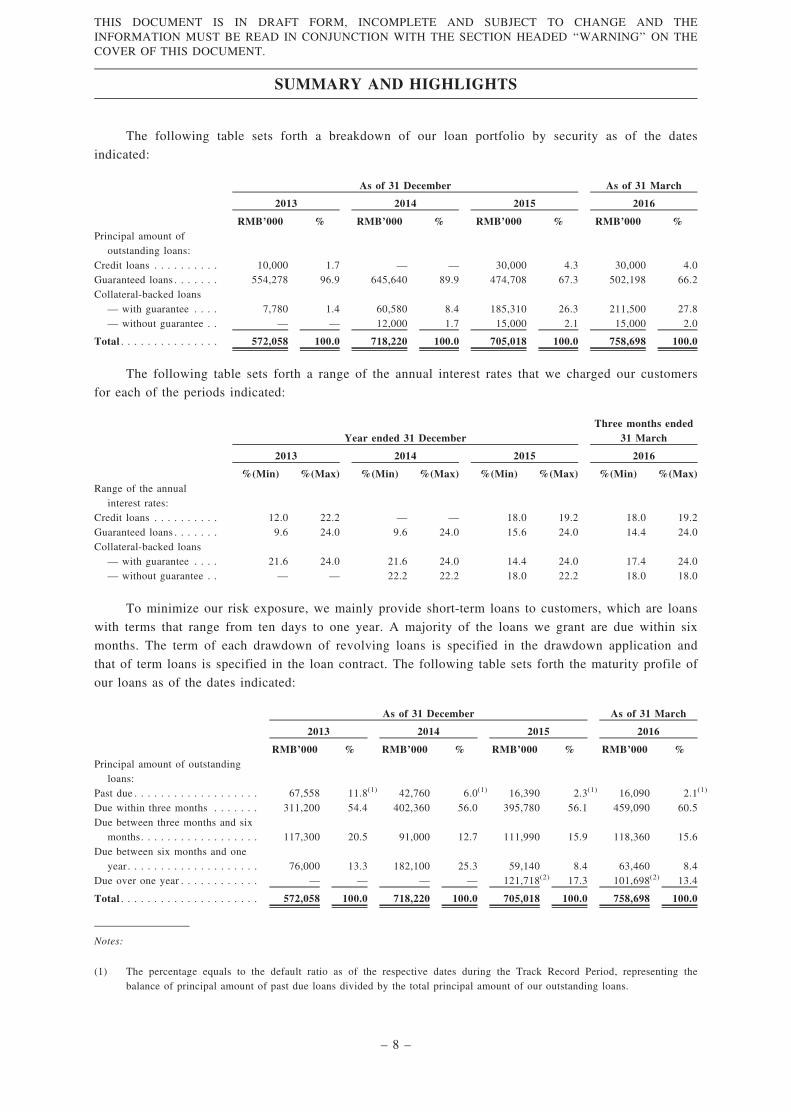

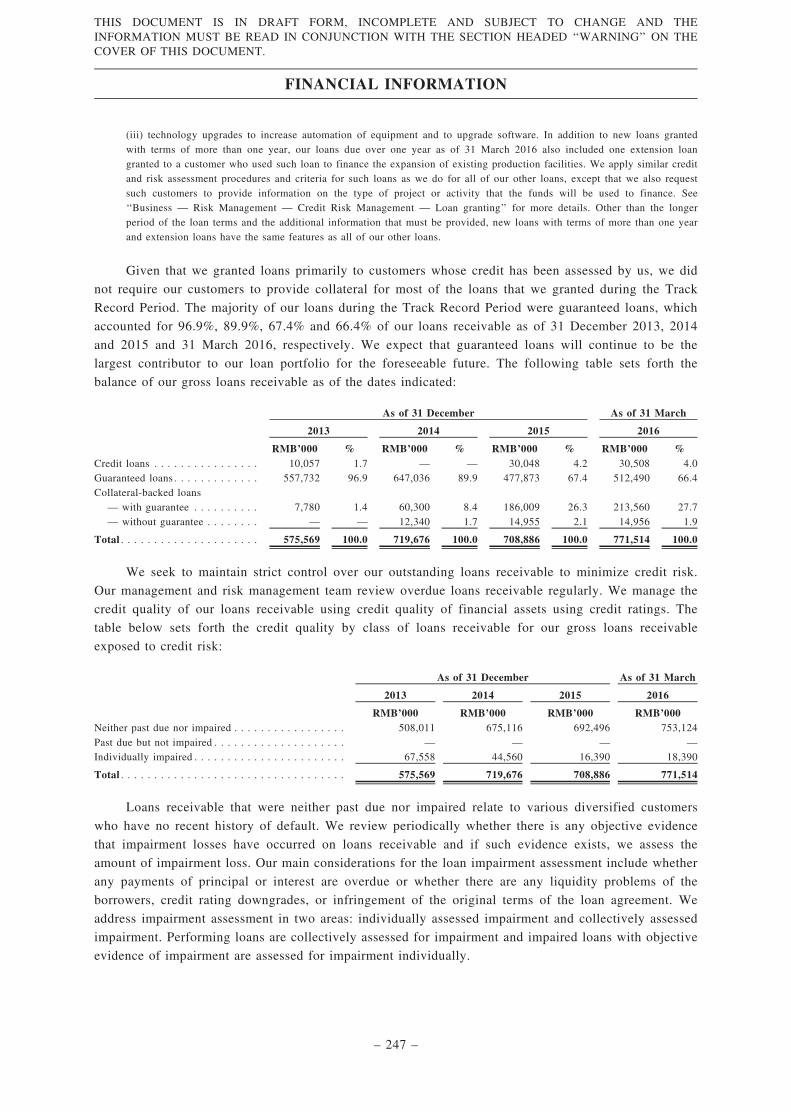

The following table sets forth a breakdown of our loan portfolio by security as of the dates

indicated:

As of 31 December As of 31 March

2013 2014 2015 2016

RMB’000 % RMB’000 % RMB’000 % RMB’000 %Principal amount of

outstanding loans:

Credit loans . . . . . . . . . . 10,000 1.7 — — 30,000 4.3 30,000 4.0Guaranteed loans . . . . . . . 554,278 96.9 645,640 89.9 474,708 67.3 502,198 66.2Collateral-backed loans

— with guarantee . . . . 7,780 1.4 60,580 8.4 185,310 26.3 211,500 27.8— without guarantee . . — — 12,000 1.7 15,000 2.1 15,000 2.0

Total . . . . . . . . . . . . . . . 572,058 100.0 718,220 100.0 705,018 100.0 758,698 100.0

The following table sets forth a range of the annual interest rates that we charged our customers

for each of the periods indicated:

Year ended 31 DecemberThree months ended

31 March

2013 2014 2015 2016

%(Min) %(Max) %(Min) %(Max) %(Min) %(Max) %(Min) %(Max)Range of the annual

interest rates:Credit loans . . . . . . . . . . 12.0 22.2 — — 18.0 19.2 18.0 19.2

Guaranteed loans . . . . . . . 9.6 24.0 9.6 24.0 15.6 24.0 14.4 24.0Collateral-backed loans

— with guarantee . . . . 21.6 24.0 21.6 24.0 14.4 24.0 17.4 24.0— without guarantee . . — — 22.2 22.2 18.0 22.2 18.0 18.0

To minimize our risk exposure, we mainly provide short-term loans to customers, which are loans

with terms that range from ten days to one year. A majority of the loans we grant are due within six

months. The term of each drawdown of revolving loans is specified in the drawdown application and

that of term loans is specified in the loan contract. The following table sets forth the maturity profile of

our loans as of the dates indicated:

As of 31 December As of 31 March

2013 2014 2015 2016

RMB’000 % RMB’000 % RMB’000 % RMB’000 %Principal amount of outstanding

loans:Past due . . . . . . . . . . . . . . . . . . . 67,558 11.8(1) 42,760 6.0(1) 16,390 2.3(1) 16,090 2.1(1)

Due within three months . . . . . . . 311,200 54.4 402,360 56.0 395,780 56.1 459,090 60.5Due between three months and six

months. . . . . . . . . . . . . . . . . . 117,300 20.5 91,000 12.7 111,990 15.9 118,360 15.6

Due between six months and oneyear . . . . . . . . . . . . . . . . . . . . 76,000 13.3 182,100 25.3 59,140 8.4 63,460 8.4

Due over one year . . . . . . . . . . . . — — — — 121,718(2) 17.3 101,698(2) 13.4

Total . . . . . . . . . . . . . . . . . . . . . 572,058 100.0 718,220 100.0 705,018 100.0 758,698 100.0

Notes:

(1) The percentage equals to the default ratio as of the respective dates during the Track Record Period, representing thebalance of principal amount of past due loans divided by the total principal amount of our outstanding loans.

SUMMARY AND HIGHLIGHTS

– 8 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THEINFORMATION MUST BE READ IN CONJUNCTION WITH THE SECTION HEADED ‘‘WARNING’’ ON THECOVER OF THIS DOCUMENT.

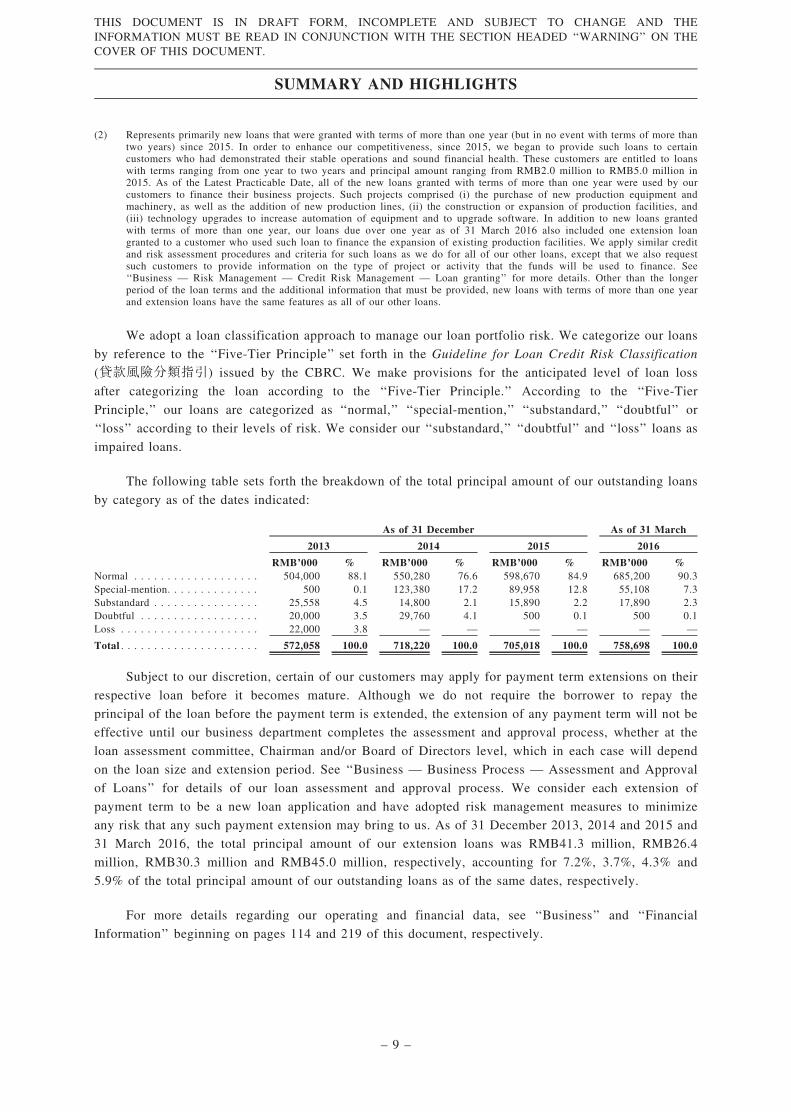

(2) Represents primarily new loans that were granted with terms of more than one year (but in no event with terms of more thantwo years) since 2015. In order to enhance our competitiveness, since 2015, we began to provide such loans to certaincustomers who had demonstrated their stable operations and sound financial health. These customers are entitled to loanswith terms ranging from one year to two years and principal amount ranging from RMB2.0 million to RMB5.0 million in2015. As of the Latest Practicable Date, all of the new loans granted with terms of more than one year were used by ourcustomers to finance their business projects. Such projects comprised (i) the purchase of new production equipment andmachinery, as well as the addition of new production lines, (ii) the construction or expansion of production facilities, and(iii) technology upgrades to increase automation of equipment and to upgrade software. In addition to new loans grantedwith terms of more than one year, our loans due over one year as of 31 March 2016 also included one extension loangranted to a customer who used such loan to finance the expansion of existing production facilities. We apply similar creditand risk assessment procedures and criteria for such loans as we do for all of our other loans, except that we also requestsuch customers to provide information on the type of project or activity that the funds will be used to finance. See‘‘Business — Risk Management — Credit Risk Management — Loan granting’’ for more details. Other than the longerperiod of the loan terms and the additional information that must be provided, new loans with terms of more than one yearand extension loans have the same features as all of our other loans.

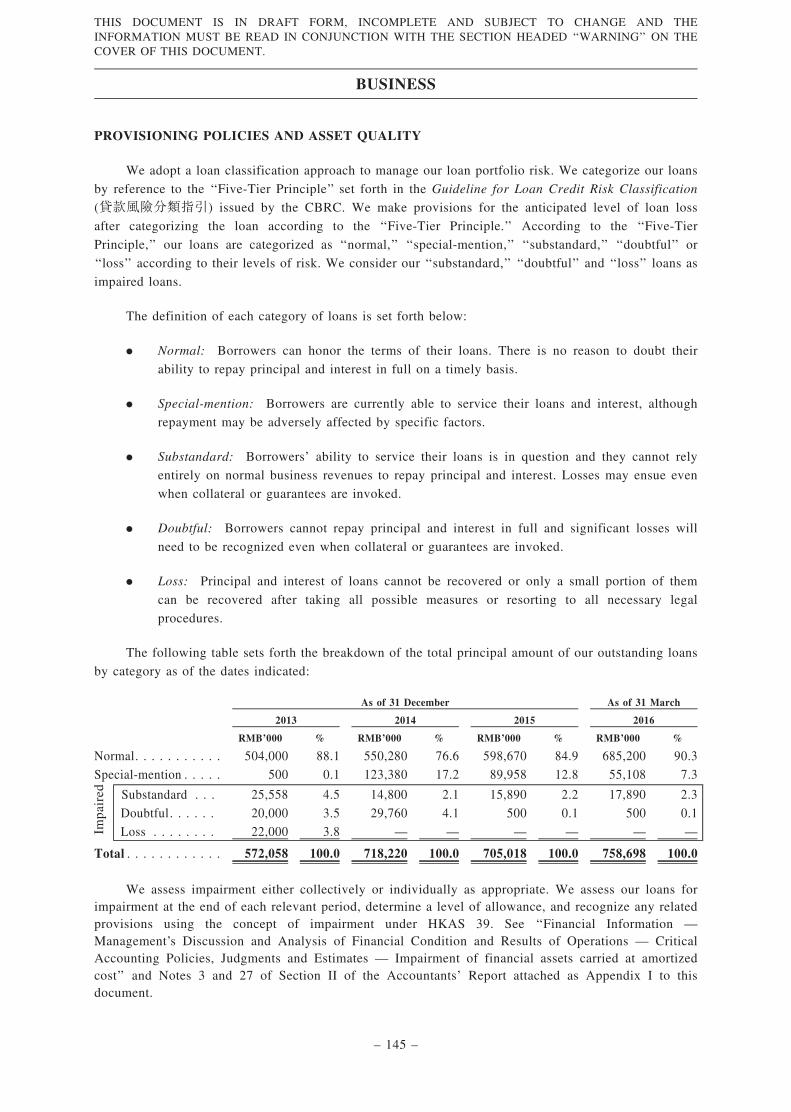

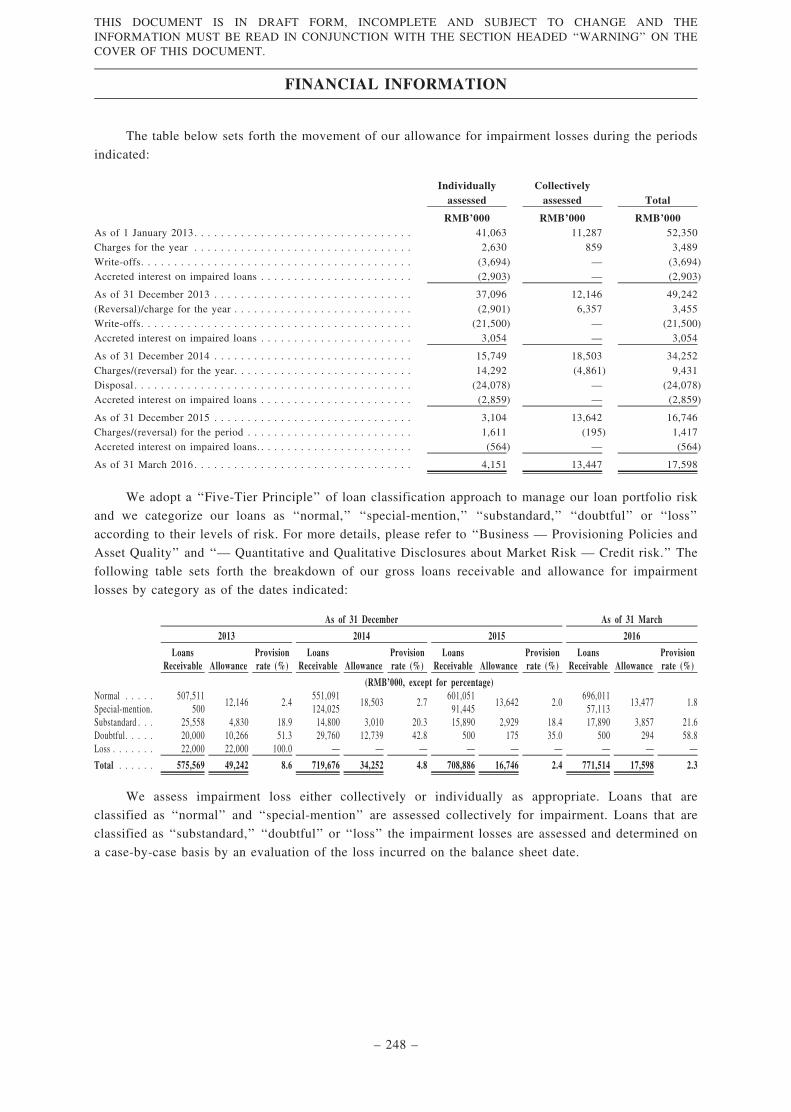

We adopt a loan classification approach to manage our loan portfolio risk. We categorize our loans

by reference to the ‘‘Five-Tier Principle’’ set forth in the Guideline for Loan Credit Risk Classification

(貸款風險分類指引) issued by the CBRC. We make provisions for the anticipated level of loan loss

after categorizing the loan according to the ‘‘Five-Tier Principle.’’ According to the ‘‘Five-Tier

Principle,’’ our loans are categorized as ‘‘normal,’’ ‘‘special-mention,’’ ‘‘substandard,’’ ‘‘doubtful’’ or

‘‘loss’’ according to their levels of risk. We consider our ‘‘substandard,’’ ‘‘doubtful’’ and ‘‘loss’’ loans as

impaired loans.

The following table sets forth the breakdown of the total principal amount of our outstanding loans

by category as of the dates indicated:

As of 31 December As of 31 March

2013 2014 2015 2016

RMB’000 % RMB’000 % RMB’000 % RMB’000 %Normal . . . . . . . . . . . . . . . . . . . 504,000 88.1 550,280 76.6 598,670 84.9 685,200 90.3Special-mention. . . . . . . . . . . . . . 500 0.1 123,380 17.2 89,958 12.8 55,108 7.3Substandard . . . . . . . . . . . . . . . . 25,558 4.5 14,800 2.1 15,890 2.2 17,890 2.3Doubtful . . . . . . . . . . . . . . . . . . 20,000 3.5 29,760 4.1 500 0.1 500 0.1Loss . . . . . . . . . . . . . . . . . . . . . 22,000 3.8 — — — — — —

Total . . . . . . . . . . . . . . . . . . . . . 572,058 100.0 718,220 100.0 705,018 100.0 758,698 100.0

Subject to our discretion, certain of our customers may apply for payment term extensions on their

respective loan before it becomes mature. Although we do not require the borrower to repay the

principal of the loan before the payment term is extended, the extension of any payment term will not be

effective until our business department completes the assessment and approval process, whether at the

loan assessment committee, Chairman and/or Board of Directors level, which in each case will depend

on the loan size and extension period. See ‘‘Business — Business Process — Assessment and Approval

of Loans’’ for details of our loan assessment and approval process. We consider each extension of

payment term to be a new loan application and have adopted risk management measures to minimize

any risk that any such payment extension may bring to us. As of 31 December 2013, 2014 and 2015 and

31 March 2016, the total principal amount of our extension loans was RMB41.3 million, RMB26.4

million, RMB30.3 million and RMB45.0 million, respectively, accounting for 7.2%, 3.7%, 4.3% and

5.9% of the total principal amount of our outstanding loans as of the same dates, respectively.

For more details regarding our operating and financial data, see ‘‘Business’’ and ‘‘Financial

Information’’ beginning on pages 114 and 219 of this document, respectively.

SUMMARY AND HIGHLIGHTS

– 9 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THEINFORMATION MUST BE READ IN CONJUNCTION WITH THE SECTION HEADED ‘‘WARNING’’ ON THECOVER OF THIS DOCUMENT.

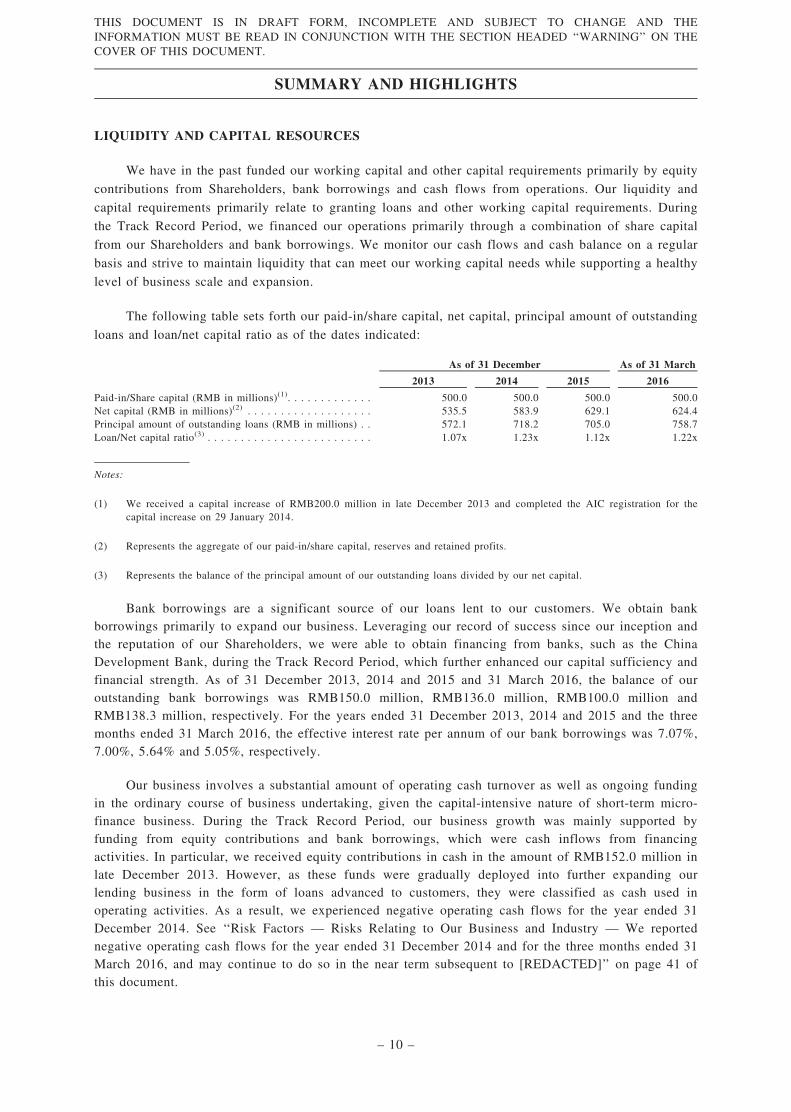

LIQUIDITY AND CAPITAL RESOURCES

We have in the past funded our working capital and other capital requirements primarily by equity

contributions from Shareholders, bank borrowings and cash flows from operations. Our liquidity and

capital requirements primarily relate to granting loans and other working capital requirements. During

the Track Record Period, we financed our operations primarily through a combination of share capital

from our Shareholders and bank borrowings. We monitor our cash flows and cash balance on a regular

basis and strive to maintain liquidity that can meet our working capital needs while supporting a healthy

level of business scale and expansion.

The following table sets forth our paid-in/share capital, net capital, principal amount of outstanding

loans and loan/net capital ratio as of the dates indicated:

As of 31 December As of 31 March

2013 2014 2015 2016

Paid-in/Share capital (RMB in millions)(1). . . . . . . . . . . . . 500.0 500.0 500.0 500.0Net capital (RMB in millions)(2) . . . . . . . . . . . . . . . . . . . 535.5 583.9 629.1 624.4Principal amount of outstanding loans (RMB in millions) . . 572.1 718.2 705.0 758.7Loan/Net capital ratio(3) . . . . . . . . . . . . . . . . . . . . . . . . . 1.07x 1.23x 1.12x 1.22x

Notes:

(1) We received a capital increase of RMB200.0 million in late December 2013 and completed the AIC registration for thecapital increase on 29 January 2014.

(2) Represents the aggregate of our paid-in/share capital, reserves and retained profits.

(3) Represents the balance of the principal amount of our outstanding loans divided by our net capital.

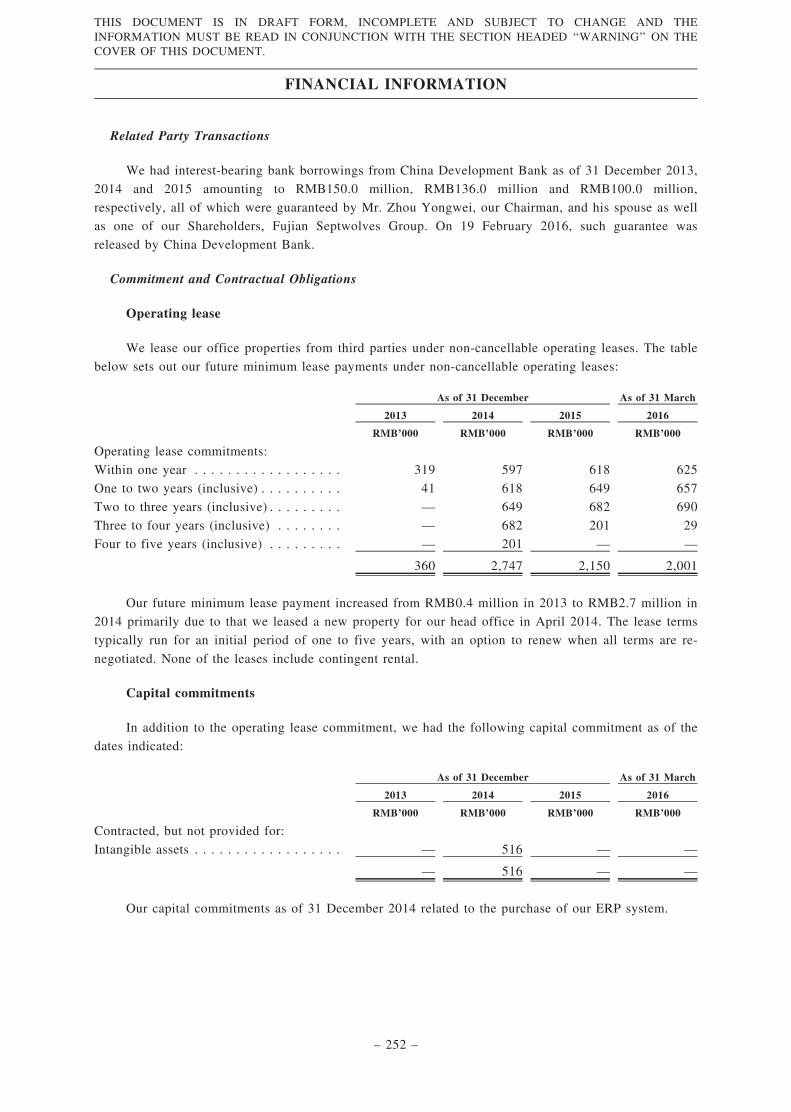

Bank borrowings are a significant source of our loans lent to our customers. We obtain bankborrowings primarily to expand our business. Leveraging our record of success since our inception andthe reputation of our Shareholders, we were able to obtain financing from banks, such as the ChinaDevelopment Bank, during the Track Record Period, which further enhanced our capital sufficiency andfinancial strength. As of 31 December 2013, 2014 and 2015 and 31 March 2016, the balance of ouroutstanding bank borrowings was RMB150.0 million, RMB136.0 million, RMB100.0 million andRMB138.3 million, respectively. For the years ended 31 December 2013, 2014 and 2015 and the threemonths ended 31 March 2016, the effective interest rate per annum of our bank borrowings was 7.07%,7.00%, 5.64% and 5.05%, respectively.

Our business involves a substantial amount of operating cash turnover as well as ongoing fundingin the ordinary course of business undertaking, given the capital-intensive nature of short-term micro-finance business. During the Track Record Period, our business growth was mainly supported byfunding from equity contributions and bank borrowings, which were cash inflows from financingactivities. In particular, we received equity contributions in cash in the amount of RMB152.0 million inlate December 2013. However, as these funds were gradually deployed into further expanding ourlending business in the form of loans advanced to customers, they were classified as cash used inoperating activities. As a result, we experienced negative operating cash flows for the year ended 31December 2014. See ‘‘Risk Factors — Risks Relating to Our Business and Industry — We reportednegative operating cash flows for the year ended 31 December 2014 and for the three months ended 31March 2016, and may continue to do so in the near term subsequent to [REDACTED]’’ on page 41 ofthis document.

SUMMARY AND HIGHLIGHTS

– 10 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THEINFORMATION MUST BE READ IN CONJUNCTION WITH THE SECTION HEADED ‘‘WARNING’’ ON THECOVER OF THIS DOCUMENT.

We plan to use the [REDACTED] from [REDACTED] to further expand our loan business. See‘‘Future Plans and [REDACTED]’’ beginning on page 260 of this document.

OUR SUBSTANTIAL SHAREHOLDERS

As of the Latest Practicable Date, Fujian Septwolves Group directly held approximately

[REDACTED] of our Shares. Immediately following the completion of [REDACTED], Fujian

Septwolves Group will directly hold approximately [REDACTED]% of our then total issued Shares,

assuming [REDACTED] is not exercised (or approximately [REDACTED]% if [REDACTED] is

exercised in full). Fujian Septwolves Group, Mr. Zhou Yongwei and Ms. Chen Pengling are the

Substantial Shareholders within the meaning of the Listing Rules that can exercise or direct the exercise

of 10% or more of voting power in any of our Shareholders’ general meetings, and are expected to

remain as the Substantial Shareholders immediately following the completion of [REDACTED]. For

further details, please refer to the section headed ‘‘Relationship with Substantial Shareholders’’

beginning on page 178 of this document.

As at the Latest Practicable Date, apart from our Company, our Substantial Shareholders and their

respective close associates had interests in certain Finance Businesses, including provision of

microcredit service in Xiamen City, financing guarantee service, finance leasing service and pawn loan

service. A brief summary of the major differences between such Finance Businesses and our current

business which illustrates a clear delineation is set out in the section headed ‘‘Relationship with

Substantial Shareholders — Finance Businesses Engaged by Our Substantial Shareholders —

Delineation of Business’’ beginning on page 181 of this document.

RECENT DEVELOPMENTS

On 18 August 2016, we received a government grant of RMB2.7 million from the government of

Quanzhou City as a governmental reward fund, on the basis that: (i) we were converted into a joint

stock limited liability company for [REDACTED] purpose; and (ii) the amount of EIT we paid increased

each year from 2013 to 2015. Such government grant was a one-off incident and there were no

unfulfilled conditions and other contingencies attached to such government grant.

Our Directors confirm that since 31 March 2016 (being the date as of which the latest audited

financial information of our Company was prepared) and up to the date of this document, there had been

no material adverse change in our business and financial condition, including any material deterioration

in the financial condition and creditworthiness of our customers or their guarantors as a whole and any

material decrease in the valuation of the collateral provided. In addition, since 31 March 2016 and up to

the date of this document, there had been no event which would materially affect the information shown

in our financial information included in the Accountants’ Report attached as Appendix I to this

document.

SUMMARY AND HIGHLIGHTS

– 11 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THEINFORMATION MUST BE READ IN CONJUNCTION WITH THE SECTION HEADED ‘‘WARNING’’ ON THECOVER OF THIS DOCUMENT.

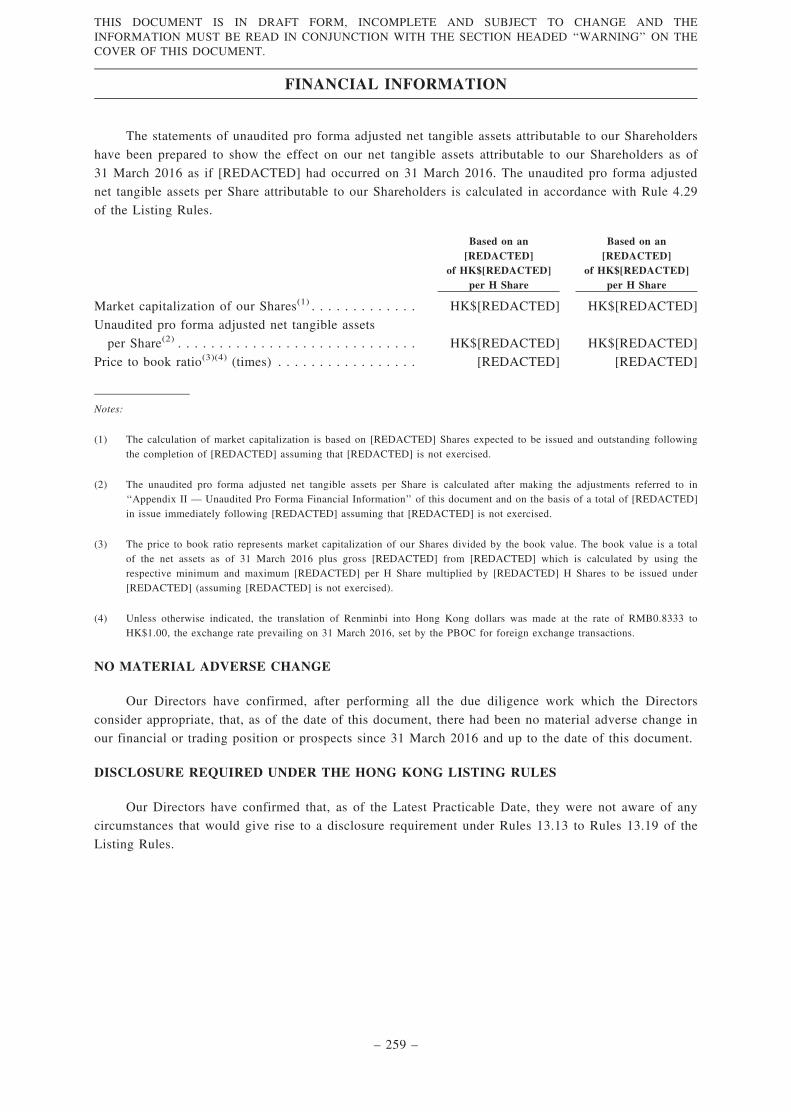

[REDACTED] STATISTICS

Based on an[REDACTED]

of HK$[REDACTED]per H Share

Based on an[REDACTED]

of HK$[REDACTED]per H Share

Market capitalization of our Shares(1) . . . . . . . . . . . . . . HK$[REDACTED] HK$[REDACTED]Unaudited pro forma adjusted net tangible asset

per Share(2) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . HK$[REDACTED] HK$[REDACTED]Price to book ratio(3)(4) (times) . . . . . . . . . . . . . . . . . . [REDACTED] [REDACTED]

Notes:

(1) The calculation of market capitalization is based on [REDACTED] Shares expected to be issued and outstanding followingthe completion of [REDACTED] assuming that [REDACTED] is not exercised.

(2) The unaudited pro forma adjusted net tangible assets per Share is calculated after making the adjustments referred to in‘‘Appendix II — Unaudited Pro Forma Financial Information’’ beginning on page II-1 of this document and on the basis ofa total of [REDACTED] Shares in issue immediately following [REDACTED] assuming that [REDACTED] Option is notexercised.

(3) The price to book ratio represents market capitalization of our Shares divided by the book value. The book value is a totalof the net assets as of 31 March 2016 plus gross [REDACTED] from [REDACTED] which is calculated by using therespective minimum and maximum [REDACTED] per H Share multiplied by the [REDACTED] H Shares to be issued under[REDACTED] (assuming [REDACTED] is not exercised).

(4) Unless otherwise indicated, the translation of Renminbi into Hong Kong dollars was made at the rate of RMB0.8333 toHK$1.00, the exchange rate prevailing on 31 March 2016, set by the PBOC for foreign exchange transactions.

DIVIDENDS

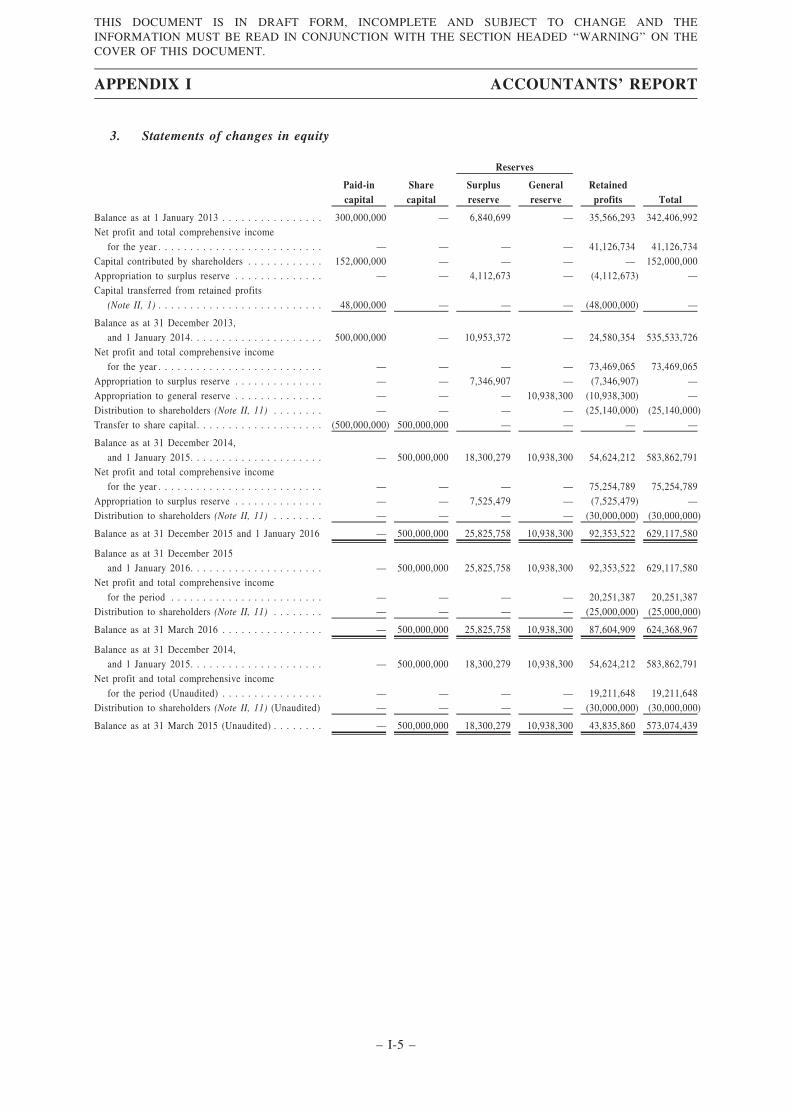

The payment and the amount of any dividends, if paid, will depend on the results of operations,cash flows, financial condition, statutory and regulatory restrictions on the payment of dividends by ourCompany, future prospects and other factors that we may consider relevant. Holders of the Shares willbe entitled to receive such dividends pro rata according to the Shares they hold unless otherwisestipulated in the Articles of Association of our Company. Dividends may be paid only out of ourdistributable profits, as permitted under the relevant laws. The declaration, payment and amount ofdividends will be subject to our discretion. We did not pay any cash dividends for the year ended 31December 2013. We paid cash dividends of RMB25.1 million, RMB30.0 million and RMB25.0 millionfor the years ended 31 December 2014 and 2015 and the three months ended 31 March 2016,respectively.

There can be no assurance that we will be able to declare or distribute any dividend in the amountset out in any plan of the Board or at all. The past dividend distribution record may not be used as areference or basis in determining the level of dividends that may be declared or paid by us in the future.

[REDACTED] EXPENSES

The total estimated [REDACTED] expenses (excluding [REDACTED]) in connection with[REDACTED] was approximately HK$[REDACTED] million, and during the Track Record Period, weincurred [REDACTED] expenses amounting to approximately HK$[REDACTED], among whichapproximately HK$[REDACTED] has been charged to the profit and loss and approximatelyHK$[REDACTED] was capitalized as deferred expenses, which is expected to be charged against equityupon successful [REDACTED] under the relevant accounting standards. We estimate that [REDACTED]expenses to be incurred and charged to the profit and loss in the financial period after 31 March 2016will be approximately HK$[REDACTED].

SUMMARY AND HIGHLIGHTS

– 12 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THEINFORMATION MUST BE READ IN CONJUNCTION WITH THE SECTION HEADED ‘‘WARNING’’ ON THECOVER OF THIS DOCUMENT.

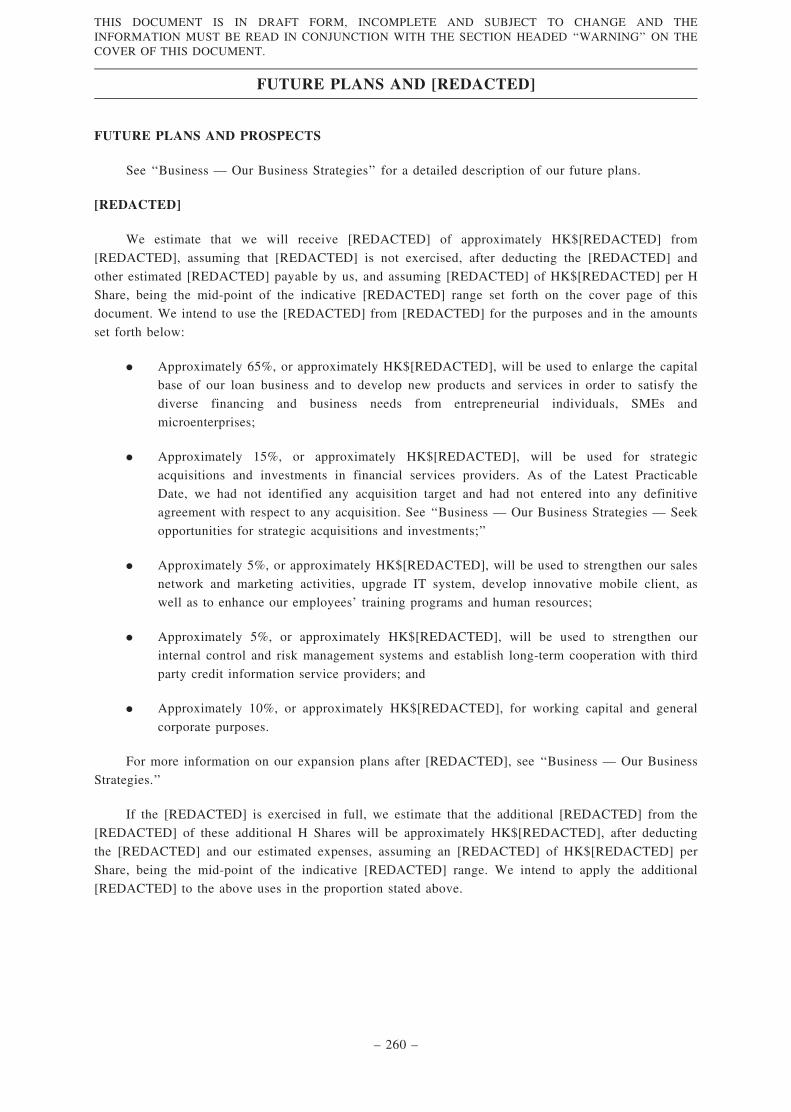

[REDACTED]

We estimate that we will receive [REDACTED] of approximately HK$[REDACTED] from

[REDACTED], assuming that [REDACTED] is not exercised, after deducting the [REDACTED] and

other estimated [REDACTED] payable by us, and assuming [REDACTED] of HK$[REDACTED] per H

Share, being the mid-point of the indicative [REDACTED] range set forth on the cover page of this

document. We intend to use the [REDACTED] from [REDACTED] for the purposes and in the amounts

set forth below:

. Approximately 65%, or approximately HK$[REDACTED], will be used to enlarge the capital

base of our loan business and to develop new products and services in order to satisfy the

diverse financing and business needs from entrepreneurial individuals, SMEs and

microenterprises;

. Approximately 15%, or approximately HK$[REDACTED], will be used for strategic

acquisitions and investments in financial services providers. As of the Latest Practicable

Date, we had not identified any acquisition target and had not entered into any definitive

agreement with respect to any acquisition. See ‘‘Business — Our Business Strategies — Seek

opportunities for strategic acquisitions and investments;’’

. Approximately 5%, or approximately HK$[REDACTED], will be used to strengthen our sales

network and marketing activities, upgrade IT system, develop innovative mobile client, as

well as to enhance our employees’ training programs and human resources;

. Approximately 5%, or approximately HK$[REDACTED], will be used to strengthen our

internal control and risk management systems and establish long-term cooperation with third

party credit information service providers; and

. Approximately 10%, or approximately HK$[REDACTED], for working capital and general

corporate purposes.

If [REDACTED] is exercised in full, we estimate that the additional [REDACTED] from

[REDACTED] of these additional H Shares will be approximately HK$[REDACTED], after deducting

[REDACTED] and our estimated expenses, assuming an [REDACTED] of HK$[REDACTED] per Share,

being the mid-point of the indicative [REDACTED] range. We intend to apply the additional

[REDACTED] to the above uses in the proportion stated above.

For more details, see ‘‘Future Plans and [REDACTED]’’ beginning on page 260 of this document.

REASONS FOR [REDACTED]

Due to the capital intensive nature of the loan business, our operations are largely driven by our

capital base. Consequently, our ability to sustain our operations and expand our business depends, to a

significant extent, on our continued access to funding and ability to expand our capital base. Through

[REDACTED], not only will we be able to raise [REDACTED] from [REDACTED] to execute our

growth strategies, but we will also gain access to the capital markets in future rounds of financing to

fund further growth plans as and when necessary. We believe that raising capital through the issuance of

equity or debt securities as a public company will involve relatively lower financing costs as compared

with bank financing obtained by a private company. By continuing to enlarge our capital base, we will

SUMMARY AND HIGHLIGHTS

– 13 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THEINFORMATION MUST BE READ IN CONJUNCTION WITH THE SECTION HEADED ‘‘WARNING’’ ON THECOVER OF THIS DOCUMENT.

be able to grant more loans to our customers, which in turn will provide us with a more stable flow of

income. We also consider that [REDACTED] will enhance our corporate profile, market reputation and

brand awareness, which we believe will strengthen our customers’ confidence in us, create more

opportunities for us to collaborate with third party credit information companies as well as financial

service providers, and enhance our overall bargaining power in negotiations with banks and other

counterparties.

RISK FACTORS

Our operations involve certain risks, some of which are beyond our control. These risks can bebroadly categorized into: (i) risks relating to our business and industry; (ii) risks relating to doingbusiness in China; and (iii) risks relating to [REDACTED]. Some of the risks generally associated withour business and industry include the followings:

. We operate in a highly regulated industry that is subject to continually evolving laws,regulations and policies, and we may be required to make significant changes to ouroperations from time to time in order to comply with changes in these laws, regulations andpolicies.

. We mainly rely on the creditworthiness of our customers and/or their guarantors, rather thanon collateral, which may limit our ability to recover payments from defaulting customers.

. Our current operations in China are geographically limited to four administrative districts ofQuanzhou City. Any significant deterioration of the economy or business environment ofQuanzhou City could materially adversely affect our financial condition and results ofoperations.

. As our current customers are entrepreneurial individuals, SMEs and microenterprises in fouradministrative districts of Quanzhou City, the credit risks that we are exposed to are greaterthan those faced by larger lenders.

. Our allowance for impairment losses may not be adequate to cover actual losses or prevent amaterial adverse effect on our business, financial condition and results of operations, and anyincreases in our allowance for impairment losses would cause our net profit to decrease.

. We reported negative operating cash flows for the year ended 31 December 2014 and for thethree months ended 31 March 2016, and may continue to do so in the near term subsequentto [REDACTED].

. We may have difficulty sustaining our growth if our access to funding is reduced.

. Changes in interest rates and spread could have a negative impact on our revenue and resultsof operations.

. Competition in the industry in which we operate is growing and could cause us to losemarket share and revenue in the future.

. The evolving PRC legal system has inherent uncertainties that could limit the legal protectionavailable to our Shareholders.

These risks are not the only significant risks that may affect the value of our H Shares. You shouldcarefully consider all of the information set forth in this document and, in particular, should evaluate thespecific risks set forth in ‘‘Risk Factors’’ beginning on page 36 of this document in deciding whether toinvest in our H Shares.

SUMMARY AND HIGHLIGHTS

– 14 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THEINFORMATION MUST BE READ IN CONJUNCTION WITH THE SECTION HEADED ‘‘WARNING’’ ON THECOVER OF THIS DOCUMENT.

In this document, unless the context otherwise requires, the following words and expressions

have the following meanings.

‘‘affiliate(s)’’ any other person(s), directly or indirectly, controlling or

controlled by or under direct or indirect common control with

such specified person(s)

‘‘AIC’’ Administration for Industry & Commerce* (工商行政管理機關)

in the PRC or, where the context so requires, the State

Administration for Industry & Commerce of the PRC (中華人民

共和國工商行政管理總局) or its delegated authority at

provincial, municipal or other local level

‘‘AML Law’’ the Anti-money Laundering Law of the PRC (中華人民共和國反

洗錢法)

[REDACTED] [REDACTED]

‘‘Articles of Association’’ the articles of association of the Company, conditionally adopted

on 25 January 2016 and as amended from time to time, a

summary of which is set out in ‘‘Appendix V — Summary of

Articles of Association’’ in this document

‘‘associate(s)’’ has the meaning ascribed thereto under the Listing Rules

‘‘Baiying Financing Guarantee’’ Fujian Baiying Financing Guarantee Co., Ltd.* (福建百應融資擔

保股份有限公司), previously known as Jinjiang Financing

Guarantee Co., Ltd.* (晉江融資擔保有限責任公司), a company

established in the PRC with limited liability on 25 July 2008,

which is owned as to 58% by Septwolves Group Holding, 22% by

Jinjiang Henglong, and 20% by Jinjiang Baixin

‘‘Baiying Finance Leasing’’ Xiamen Baiying Finance Leasing Co., Ltd.* (廈門市百應融資租

賃有限公司), a company established in the PRC with limited

liability on 9 March 2010, which is owned as to 33.75% by

Septwolves Group Holding, 25% by Hong Kong Septwolves

Group Financial, and three other Independent Third Parties as to

18.75%, 15% and 7.5%, respectively

DEFINITIONS

– 15 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THEINFORMATION MUST BE READ IN CONJUNCTION WITH THE SECTION HEADED ‘‘WARNING’’ ON THECOVER OF THIS DOCUMENT.

‘‘Baiying Microcredit’’ Xiamen Siming Baiying Microcredit Co., Ltd.* (廈門思明百應小

額貸款有限公司), a company established in the PRC with limited

liability on 5 May 2014, which is owned by Septwolves Group

Holding, Xiamen Gaoxinhong, Ms. Wang Jialin (王佳琳)

(daughter in law of Mr. Zhou Yongwei and Ms. Chen Pengling),

Mr. Xie Anju (one of our Shareholders), Mr. Zeng Jianwu (曾建

武) (our former director) and four other Independent Third Parties

as to 49.99%, 15%, 5%, 4.9%, 0.25%, 5%, 5%, 5% and 9.86%,

respectively

‘‘Board’’ or ‘‘Board of Directors’’ the board of directors of the Company

‘‘Business Day(s)’’ any day on which banks in Hong Kong are generally open for

normal banking business to the public and which is not a

Saturday, Sunday or public holiday in Hong Kong

‘‘CAGR’’ compound annual growth rate

‘‘CBRC’’ the China Banking Regulatory Commission (中國銀行業監督管

理委員會)

‘‘CBRC Fujian Bureau’’ the China Banking Regulatory Commission Fujian Bureau (中國

銀行業監督委員會福建監督局 )

‘‘CCASS’’ the Central Clearing and Settlement System established and

operated by HKSCC

‘‘CCASS Clearing Participant’’ a person admitted to participate in CCASS as a direct clearing

participant or general clearing participant

‘‘CCASS Custodian Participant’’ a person admitted to participate in CCASS as a custodian

participant

‘‘CCASS Investor Participant’’ a person admitted to participate in CCASS as an investor

participant who may be an individual or joint individuals or a

corporation

‘‘CCASS Participant’’ a CCASS Clearing Participant, a CCASS Custodian Participant or

a CCASS Investor Participant

‘‘Chairman’’ Mr. Zhou Yongwei, the chairman of the Company

‘‘China’’ or ‘‘PRC’’ the People’s Republic of China, but for the purpose of this

document and for geographical reference only and except where

the context requires, references in this document to ‘‘China’’ and

the ‘‘PRC’’ do not apply to Taiwan, Macau Special

Administrative Region and Hong Kong

DEFINITIONS

– 16 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THEINFORMATION MUST BE READ IN CONJUNCTION WITH THE SECTION HEADED ‘‘WARNING’’ ON THECOVER OF THIS DOCUMENT.

‘‘China Development Bank’’ China Development Bank Co., Ltd. (國家開發銀行股份有限公

司), a company established in the PRC with limited liability,

being an Independent Third Party

‘‘Circular 137’’ the Circular on Relevant Policies for Rural Bank, Loan Company,

Rural Mutual Cooperative and Microfinance Company (關於村鎮

銀行、貸款公司、農村資金互助社、小額貸款公司有關政策的通

知), which was promulgated by the PBOC and the CBRC on

24 April 2008

‘‘close associate(s)’’ has the meaning ascribed thereto under the Listing Rules

‘‘Companies Ordinance’’ or ‘‘Hong

Kong Companies Ordinance’’

the Companies Ordinance, Chapter 622 of the Laws of Hong

Kong, as amended, supplemented or otherwise modified from

time to time

‘‘Companies (Winding Up and

Miscellaneous Provisions)

Ordinance,’’ or ‘‘Hong Kong

Companies (Winding Up and

Miscellaneous Provisions)

Ordinance’’

the Companies (Winding Up and Miscellaneous Provisions)

Ordinance, Chapter 32 of the Laws of Hong Kong, as amended,

supplemented or otherwise modified from time to time

‘‘Company,’’ ‘‘we,’’ ‘‘us’’ or ‘‘our’’ Quanzhou Huixin Micro-credit Co., Ltd.* (泉州匯鑫小額貸款股

份有限公司), a joint stock company established in the PRC with

limited liability on 8 January 2010 converted from our

Predecessor Company on 18 August 2014, and where the context

otherwise requires, our Predecessor Company

‘‘connected person(s)’’ has the meaning ascribed thereto under the Listing Rules

‘‘CSRC’’ the China Securities Regulatory Commission (中國證券監督管理

委員會)

‘‘Deed of Indemnity’’ the deed of indemnity dated 6 September 2016 entered into by

our Substantial Shareholders with and in favor of the Company as

referred to in the section headed ‘‘Appendix VI — Statutory and

General Information — E. Other Information — 1. Indemnities’’

in this document

‘‘Director(s)’’ the director(s) of the Company

‘‘Domestic Share(s)’’ ordinary share in our capital, with a nominal value of RMB1.00

each, which are subscribed for and paid up in Renminbi by PRC

nationals and/or PRC-incorporated entities

‘‘EIT’’ the PRC enterprise income tax

DEFINITIONS

– 17 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THEINFORMATION MUST BE READ IN CONJUNCTION WITH THE SECTION HEADED ‘‘WARNING’’ ON THECOVER OF THIS DOCUMENT.

‘‘EIT Law’’ the PRC Enterprise Income Tax Law (中華人民共和國企業所得

稅法)

‘‘[REDACTED]’’ the application for [REDACTED] to be issued in the applicants

own name, submitted online through the designated website of

the [REDACTED]