Global Blue

31

INTERNATIONAL SHOPPERS What’s happening in the British & Scottish markets? June 11 th 2019

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Global Blue

INTERNATIONAL SHOPPERSWhat’s happening in the British & Scottish

markets?

June 11th 2019

Methodology

Figures are based on issued and validated Tax Free forms with a valid passport numbers issued by one of Global Blue partner store worldwide.

2

ELITE

Globe shoppers who have spentmore than €40,000 in the last 24 months

FREQUENT

Globe shoppers who have made more than 3 trips in the past 24 months

INFREQUENT

Globe shoppers travelling at least once within a year

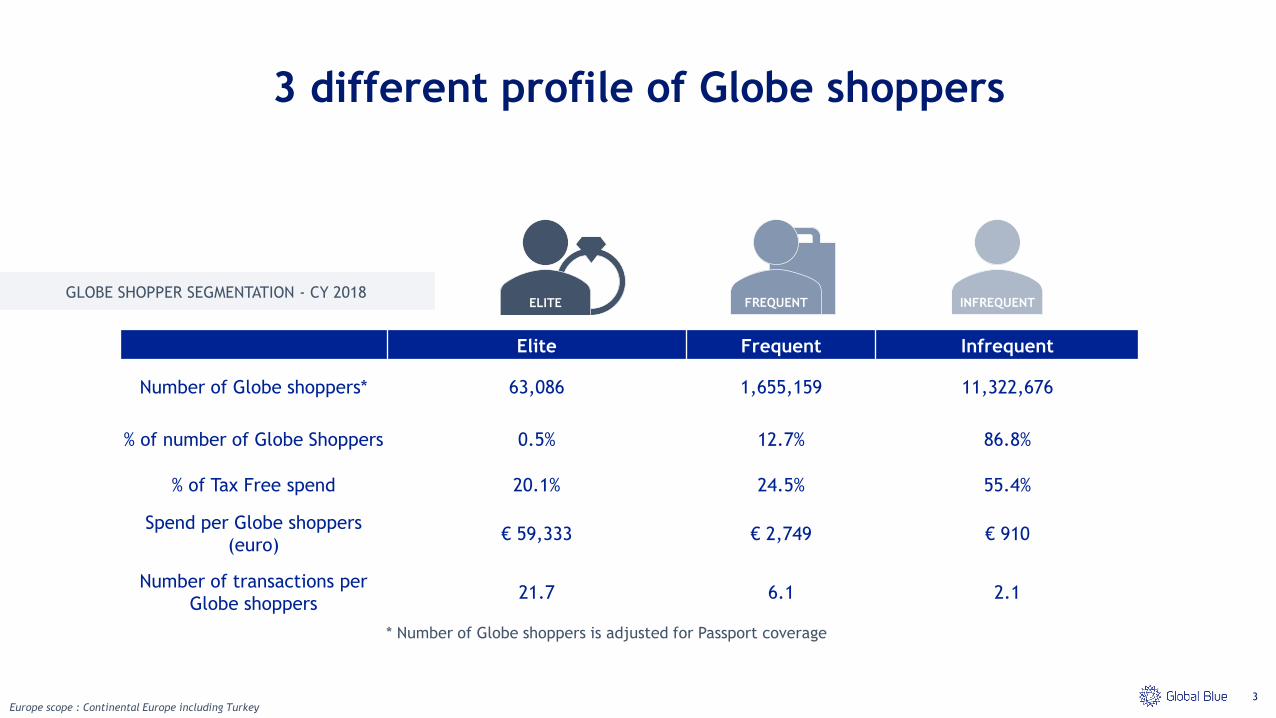

In 2018, Global Blue served 13.2 Million international shoppers for a total of 36 Million transactions

Global Blue segments the different globe shoppers across 3 profiles

3

GLOBE SHOPPER SEGMENTATION - CY 2018

Europe scope : Continental Europe including Turkey

3 different profile of Globe shoppers

Elite Frequent Infrequent

Number of Globe shoppers* 63,086 1,655,159 11,322,676

% of number of Globe Shoppers 0.5% 12.7% 86.8%

% of Tax Free spend 20.1% 24.5% 55.4%

Spend per Globe shoppers

(euro)€ 59,333 € 2,749 € 910

Number of transactions per

Globe shoppers21.7 6.1 2.1

ELITE FREQUENT INFREQUENT

* Number of Globe shoppers is adjusted for Passport coverage

4

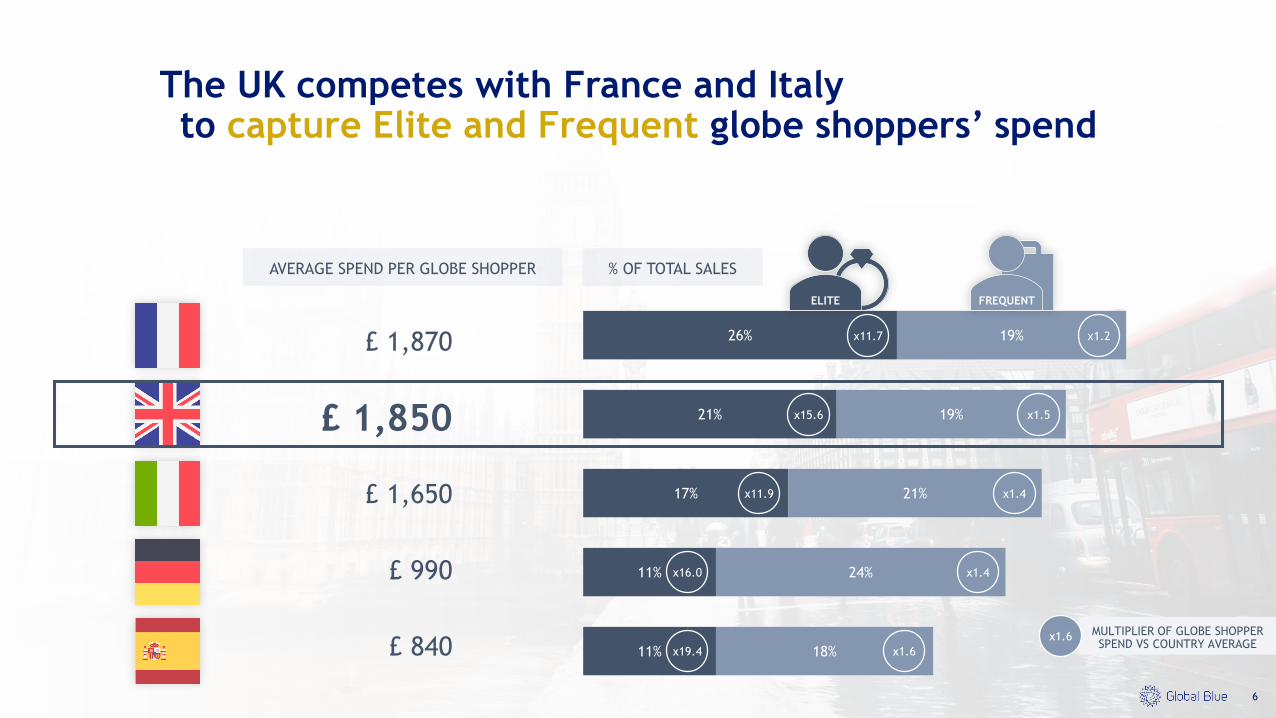

▪ How does the British market perform in Europe?

▪

▪

▪

TAX FREE SALESTOTAL MARKET (GBP)

#2

The UK is the 2nd largest European country in terms of Tax Free Shopping

5

4.8 Billions 3.4 Billions 2.8 Billions 2.1 Billions 1.9 Billions

* Source of Data: Global Blue internal Analysis - Spend and transactions expended to Full market, excluding cross border transactions

The UK competes with France and Italy to capture Elite and Frequent globe shoppers’ spend

6

AVERAGE SPEND PER GLOBE SHOPPER

£ 1,870

£ 1,850

£ 1,650

£ 990

£ 840 11%

11%

17%

21%

26%

18%

24%

21%

19%

19%

% OF TOTAL SALES

ELITE FREQUENT

x11.7

x15.6

x11.9

x16.0

x19.4

x1.2

x1.5

x1.4

x1.4

x1.6

MULTIPLIER OF GLOBE SHOPPER SPEND VS COUNTRY AVERAGE

x1.6

The UK is the preferred destination for GCC globe shoppers

7

% OF TOTAL COUNTRY TAX FREE SPEND

GCC

26% 13% 7%9% 11%

32% 33% 35%42% 37%

SEA

13% 10% 7%GCC

5%GCC

9%

GR. CH. GR. CH. GR. CH. GR. CH. GR. CH.

Globe shoppers are especially looking for British brandswhen visiting the UK

8

INDEX VS EUROPERAN SPEND SHARE FOR INTERNATIONAL BRANDS IN 2018

31 159 57

42 72 178

UK BRANDS

214

FRENCH BRANDS ITALIAN BRANDS

55 94

Tax Free Shopping spend has progressed slightly faster in the UK than Continental Europe since 2015

9

EVOLUTION OF TAX FREE SHOPPING SPEND (BASE 100 – 2013)

126

134

105

136

100

110

120

130

140

150

2013 2014 2015 2016 2017 2018

CAGR5 YEARS +6.3%

CAGR5 YEARS +6.1%

CHINA

GCC x1.5

x1.7

x2.1US

2016, June 23rd

BREXIT REFERENDUM

x1.2SEA

INDEX VS 2013

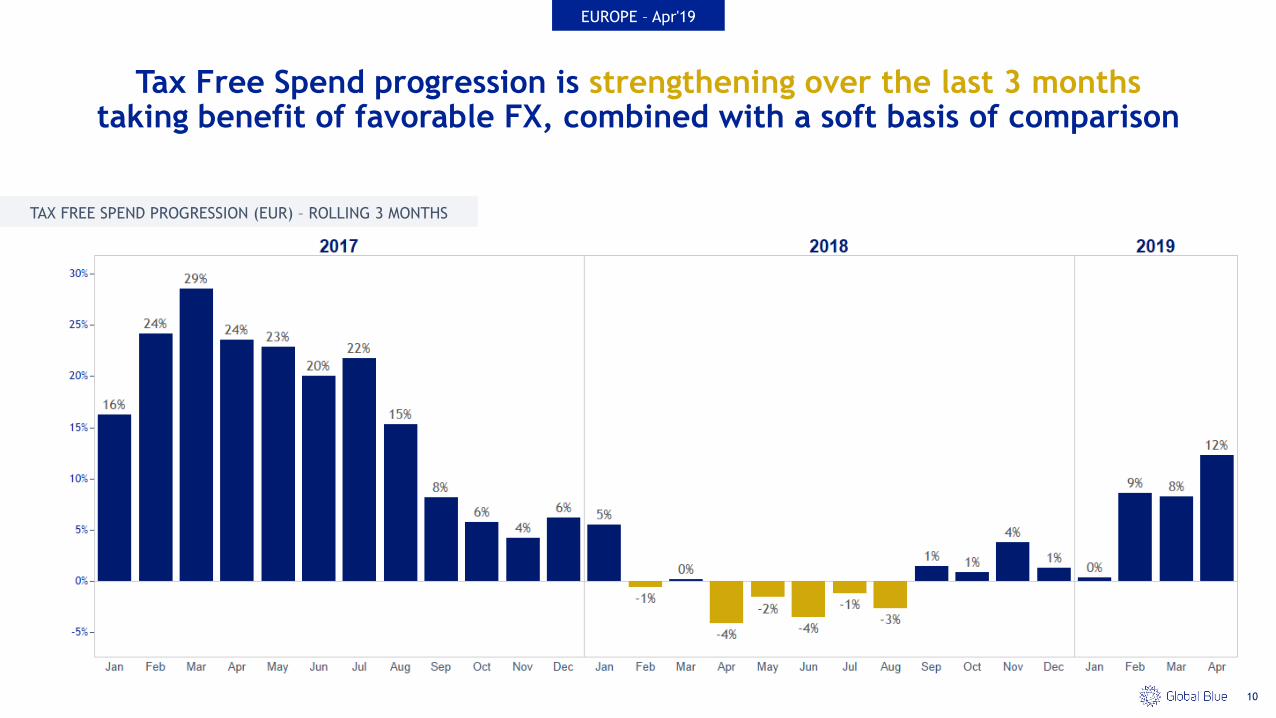

Tax Free Spend progression is strengthening over the last 3 months taking benefit of favorable FX, combined with a soft basis of comparison

10

EUROPE – Apr'19

TAX FREE SPEND PROGRESSION (EUR) – ROLLING 3 MONTHS

11

▪

▪ British Tax Free Shopping market specificities

▪

▪

A MARKET ORIENTED TOWARDS

LUXURY12

13

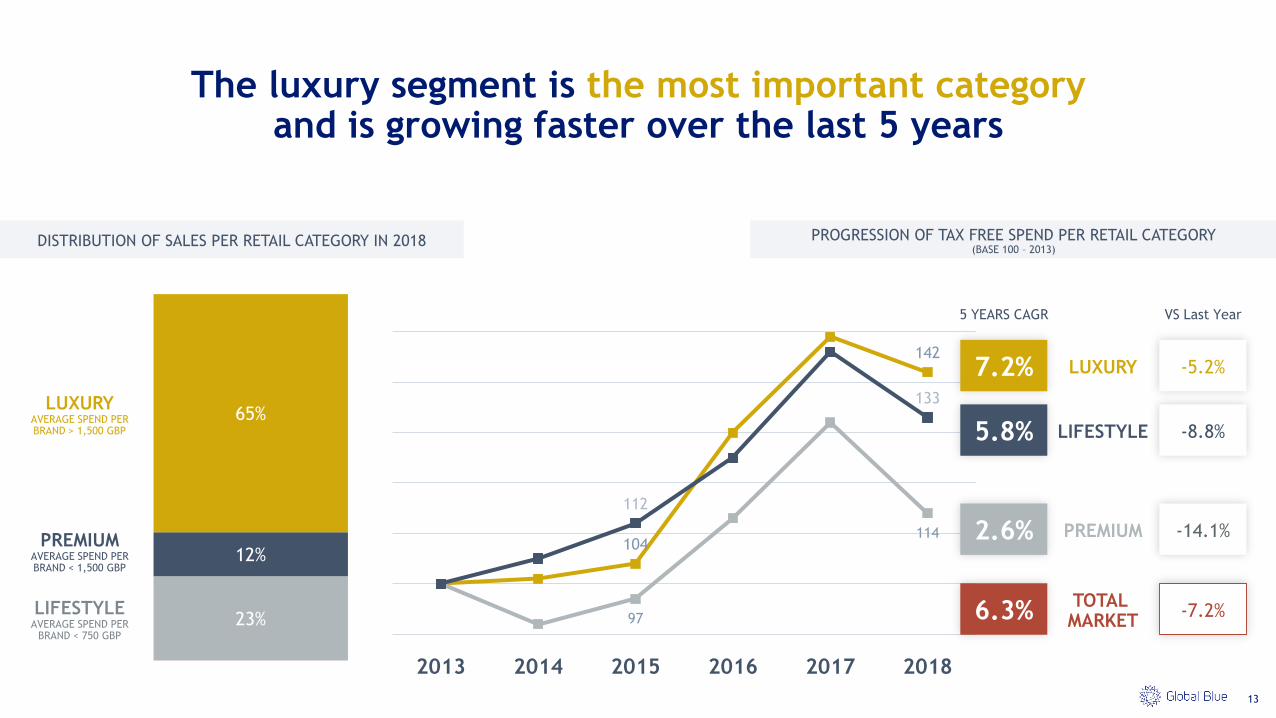

The luxury segment is the most important categoryand is growing faster over the last 5 years

23%

12%

65%

DISTRIBUTION OF SALES PER RETAIL CATEGORY IN 2018

104

142

97

114

112

133

2013 2014 2015 2016 2017 2018

PROGRESSION OF TAX FREE SPEND PER RETAIL CATEGORY (BASE 100 – 2013)

LUXURYAVERAGE SPEND PER BRAND > 1,500 GBP

PREMIUMAVERAGE SPEND PER BRAND < 1,500 GBP

LIFESTYLEAVERAGE SPEND PER

BRAND < 750 GBP

13

LUXURY7.2% -5.2%

LIFESTYLE5.8% -8.8%

PREMIUM2.6% -14.1%

5 YEARS CAGR VS Last Year

TOTAL MARKET6.3% -7.2%

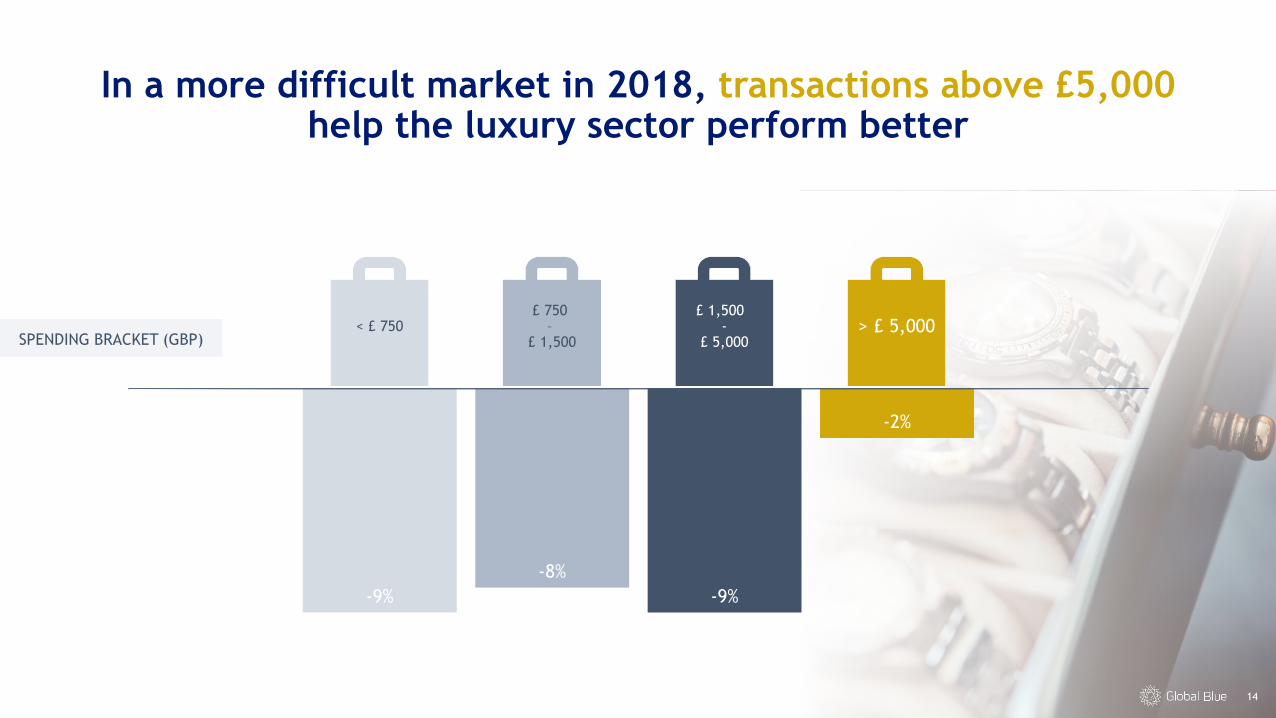

In a more difficult market in 2018, transactions above £5,000 help the luxury sector perform better

14

-9%

-8%

-9%

-2%

< £ 750£ 750

–£ 1,500

£ 1,500 -

£ 5,000> £ 5,000

SPENDING BRACKET (GBP)

Department stores are the preferred destination for luxury shopping

15

42%

50%

8%

DEPARTMENT STORE DOWNTOWN OUTLET

% OF TAX FREE SPEND PER RETAIL CATEGORY

-5%

-8%

4%

DEPARTMENT STORE DOWNTOWN OUTLET

PROGRESSION OF TAX FREE SPEND 2018 VS 2017

£ 3,047

£ 2,004

£ 922

£

Spend per

globe shopper

LUXURY BRANDS

A MARKET WITH A UNIQUE

NATIONALITY MIX16

17

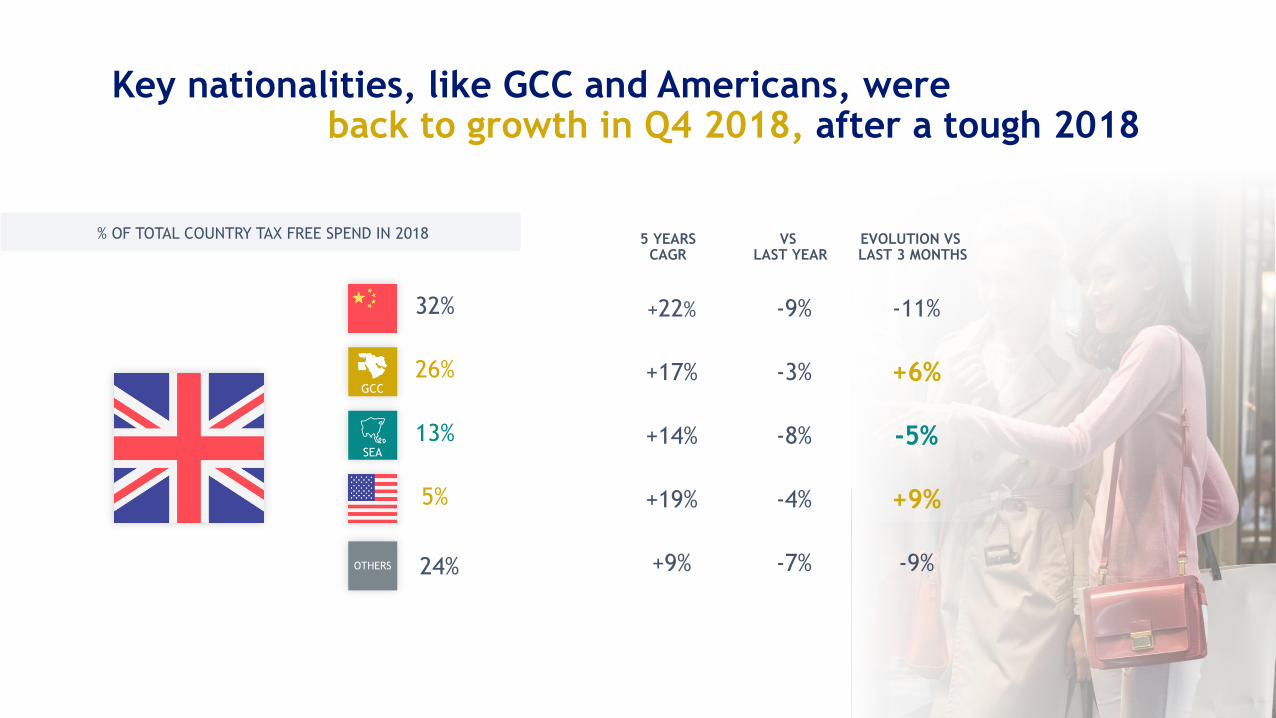

Key nationalities, like GCC and Americans, were back to growth in Q4 2018, after a tough 2018

5 YEARSCAGR

VS LAST YEAR

EVOLUTION VS LAST 3 MONTHS

32%

GCC

26%

SEA

13%

5%

+22% -9% -11%

+17% -3% +6%

+14% -8% -5%

+19% -4% +9%

+9% -7% -9%OTHERS

% OF TOTAL COUNTRY TAX FREE SPEND IN 2018

24%

18

▪

▪

▪ Scottish Tax Free Shopping market specificities

▪

19

A MARKET ORIENTED TOWARDS

LOCAL EXCELLENCE AND PREMIUM QUALITY

20

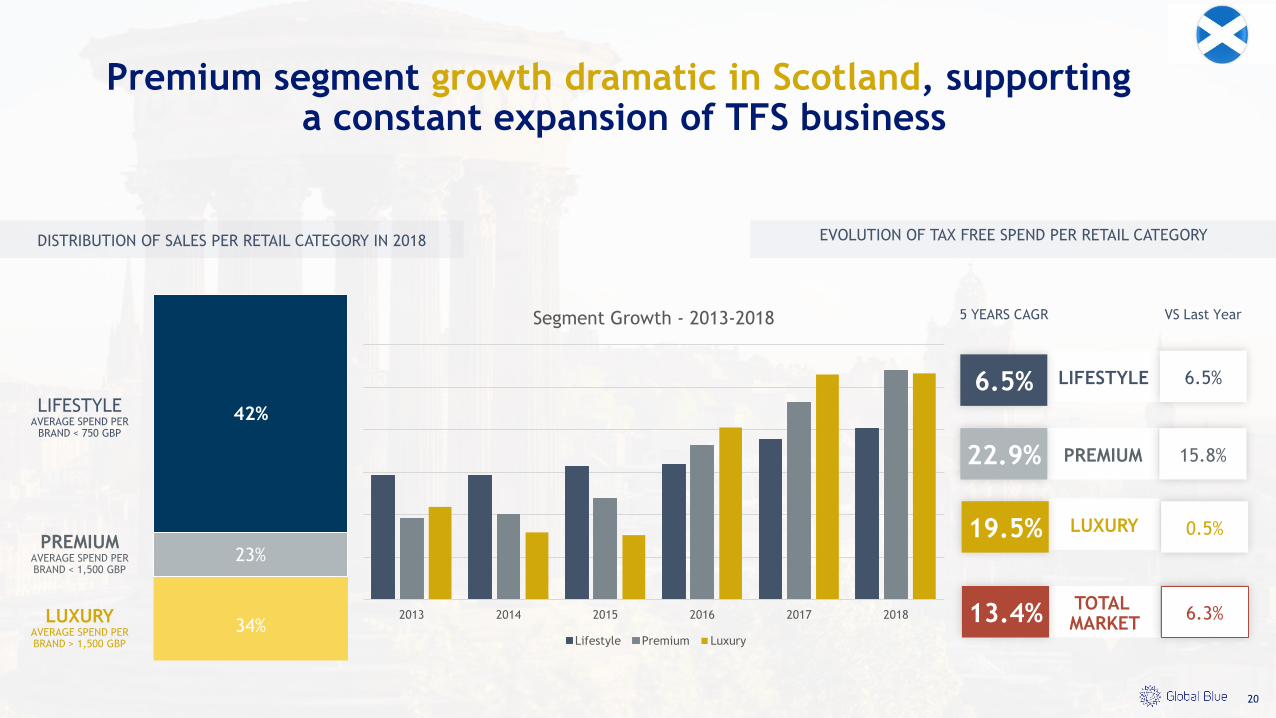

Premium segment growth dramatic in Scotland, supporting a constant expansion of TFS business

34%

23%

42%

DISTRIBUTION OF SALES PER RETAIL CATEGORY IN 2018 EVOLUTION OF TAX FREE SPEND PER RETAIL CATEGORY

LUXURYAVERAGE SPEND PER BRAND > 1,500 GBP

PREMIUMAVERAGE SPEND PER BRAND < 1,500 GBP

LIFESTYLEAVERAGE SPEND PER

BRAND < 750 GBP

20

LUXURY19.5% 0.5%

LIFESTYLE6.5% 6.5%

PREMIUM22.9% 15.8%

5 YEARS CAGR VS Last Year

TOTAL MARKET13.4% 6.3%2013 2014 2015 2016 2017 2018

Segment Growth - 2013-2018

Lifestyle Premium Luxury

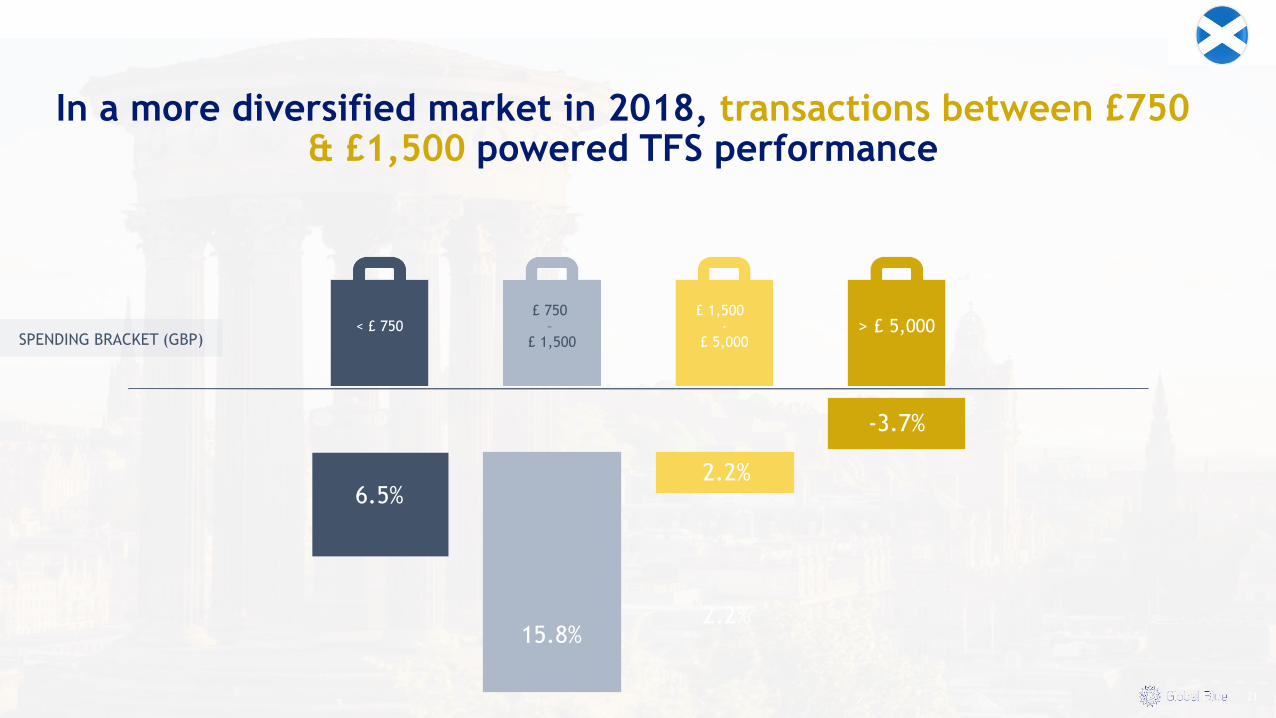

In a more diversified market in 2018, transactions between £750 & £1,500 powered TFS performance

21

< £ 750£ 750

–£ 1,500

£ 1,500 -

£ 5,000> £ 5,000

SPENDING BRACKET (GBP)

6.5%

15.8%

2.2%

2.2%

-3.7%

22

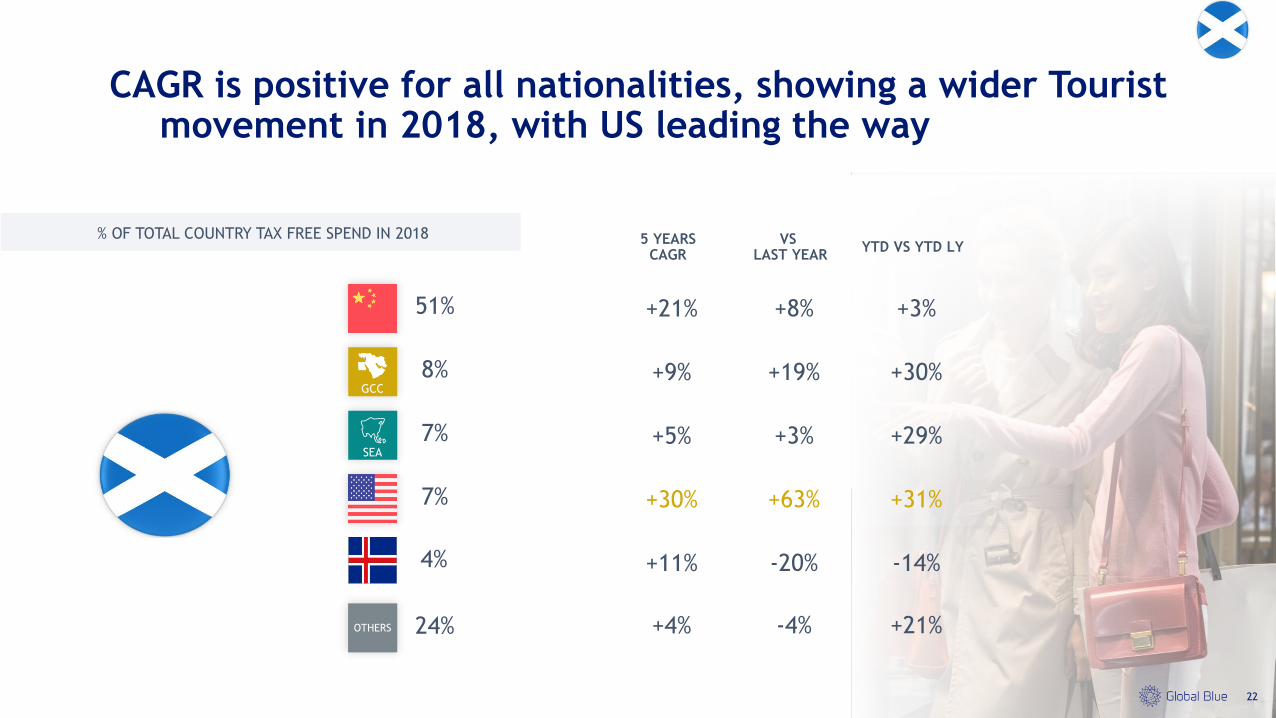

CAGR is positive for all nationalities, showing a wider Tourist movement in 2018, with US leading the way

5 YEARSCAGR

VS LAST YEAR

YTD VS YTD LY

51%

GCC

8%

SEA

7%

7%

+21% +8% +3%

+9% +19% +30%

+5% +3% +29%

+30% +63% +31%

+11% -20% -14%

OTHERS

% OF TOTAL COUNTRY TAX FREE SPEND IN 2018

24%

4%

+4% -4% +21%

2019A year of economic

growth

23

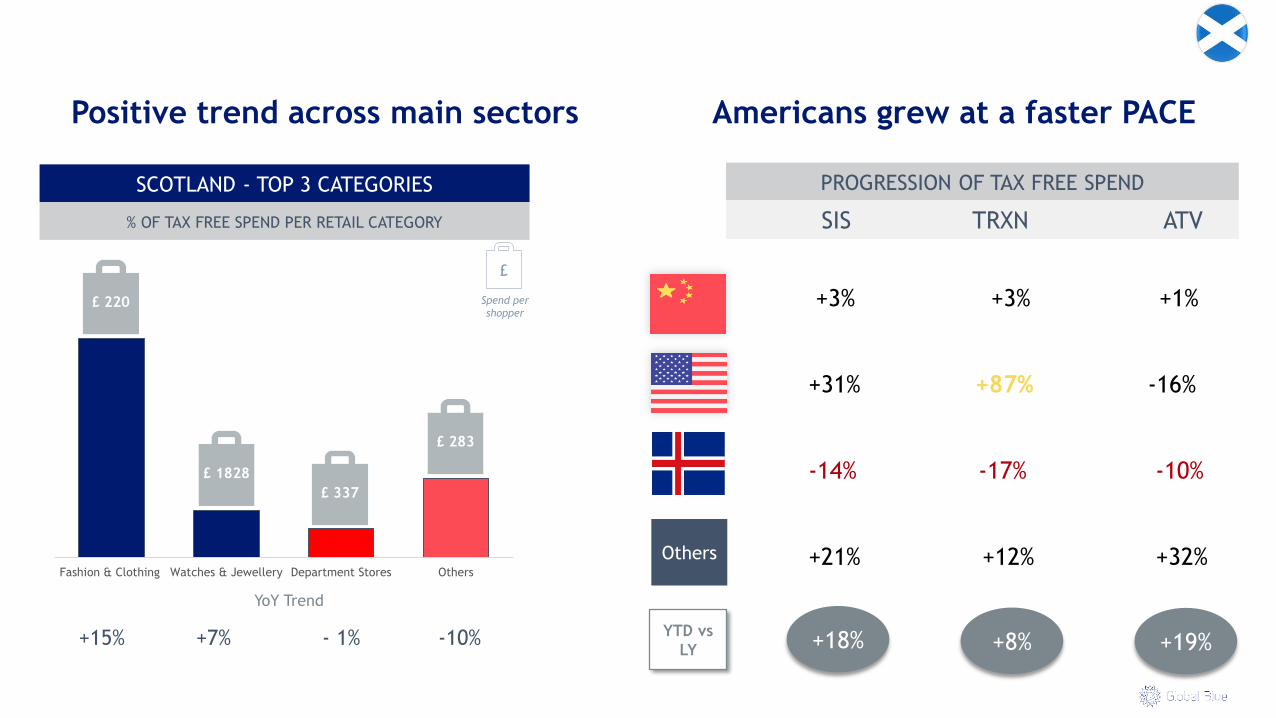

Fashion & Clothing Watches & Jewellery Department Stores Others

£ 220

£ 337

£ 1828

£ 283

Positive trend across main sectors Americans grew at a faster PACE

24

% OF TAX FREE SPEND PER RETAIL CATEGORY

PROGRESSION OF TAX FREE SPENDSCOTLAND - TOP 3 CATEGORIES

+15% +7% - 1% -10%

£

Spend per

shopper

SIS TRXN ATV

+3% +3% +1%

+31% +87% -16%

-14% -17% -10%

+21% +12% +32%

+18% +8%

Others

YoY Trend

+19%YTD vs

LY

OTHER NATIONALITIES

GCCGLOBE SHOPPERS

AMERICANGLOBE SHOPPERS

RUSSIANGLOBE SHOPPERS

CHINESE GLOBE SHOPPERS

-3%

-11%

-21%

13%17%

-2%-6%

3% 3%10%

16%

1%

25

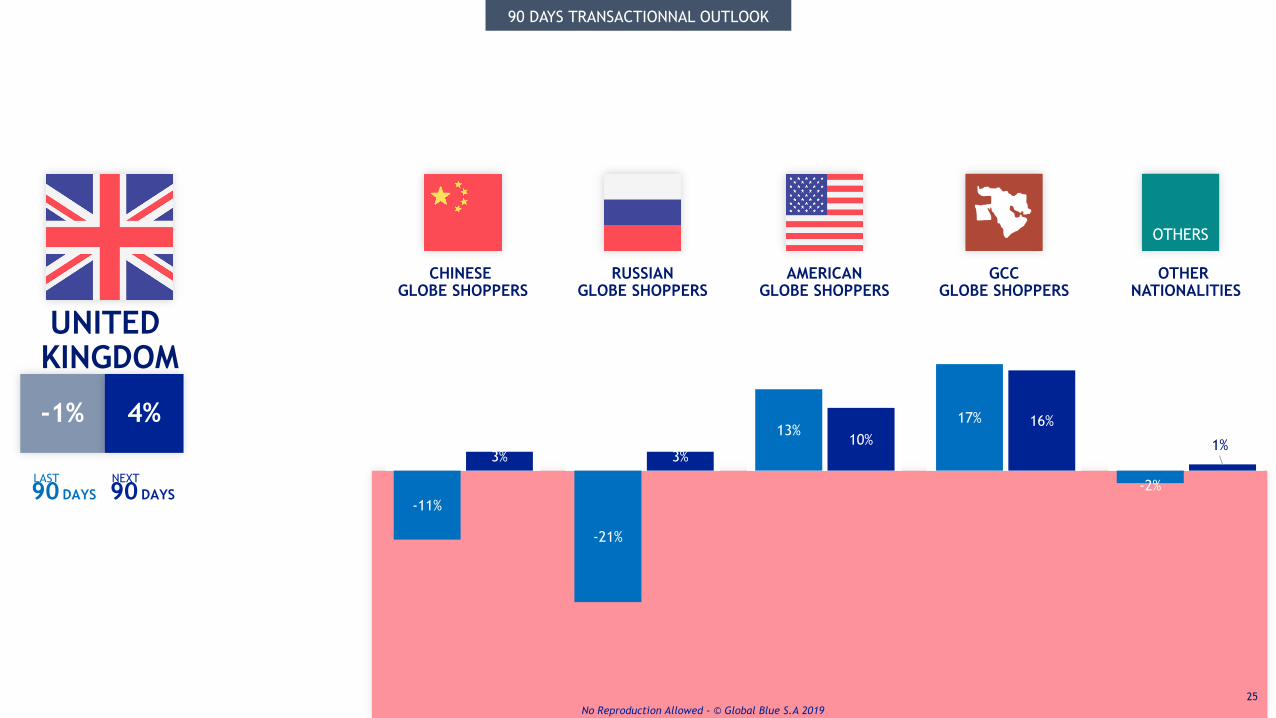

UNITED KINGDOM

90 DAYS

LAST

90 DAYS

NEXT

90 DAYS TRANSACTIONNAL OUTLOOK

OTHERS

-1% 4%

No Reproduction Allowed - © Global Blue S.A 2019

26

▪

▪

▪

▪ How to get ready for tomorrow’s challenges?

27

ANTICIPATE TAX FREE SHOPPING

DIGITISATION

28

DIGITALLY VALIDATED TRANSACTIONPAPER VALIDATED

TRANSACTION

E-validation launched/ implemented (21 countries)

E-validation under study (12 countries)

ITALYLive since

September 1st

2018

PORTUGALLive since July

1st 2018

SPAINMandatory Q1 2019 (January)

IN-STORE1 Issue paper transaction

EXPORT VALIDATION AT AIRPORT 2 Digital self-

service kiosk

90% no queue 10% queue2 Manual rubber stamp

100% queue

AIRPORT REFUND

POINT3 Cash & Card refund

100% queue

1Issue

electronic transaction 3 Card

refund

FOLLOW THE PATH OF EUROPEAN COUNTRIES SMOOTH THE TAX FREE SHOPPING PROCESS

29

ANTICIPATE

BREXIT’S IMPACTS

While only 25% of shoppers visiting the UK will needa 2nd visa to pursue their trip,

70 % Elite & Frequent will need a 2nd one

30

25%35%

81%

75%65%

19%

ELITE FREQUENT INFREQUENT

UK ONLY

UK + OTHERS

75%

25%

UK ONLY

UK + OTHERS

% OF NUMBER OF VISITORS IN THE UK

ENHANCING THE GLOBE SHOPPER

EXPERIENCE TOGETHER