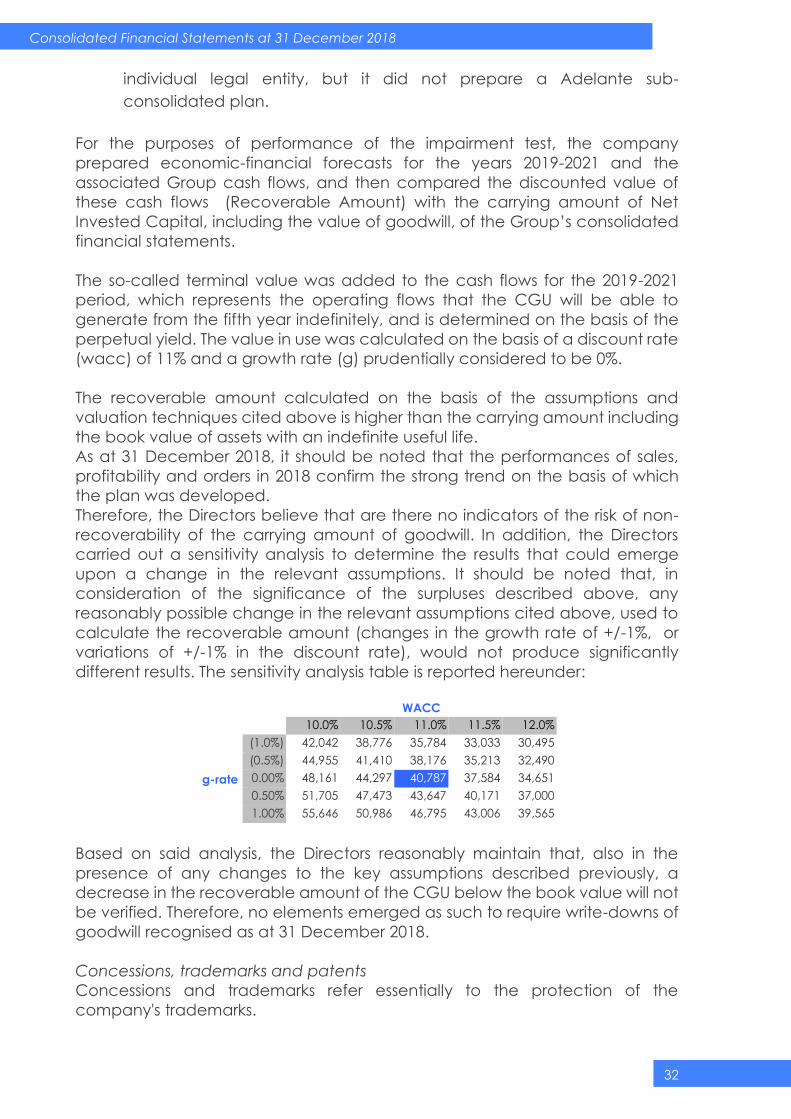

FINANCIAL STATEMENTS - wiit.cloud

139

FINANCIAL STATEMENTS 2018 Report on Operations

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of FINANCIAL STATEMENTS - wiit.cloud

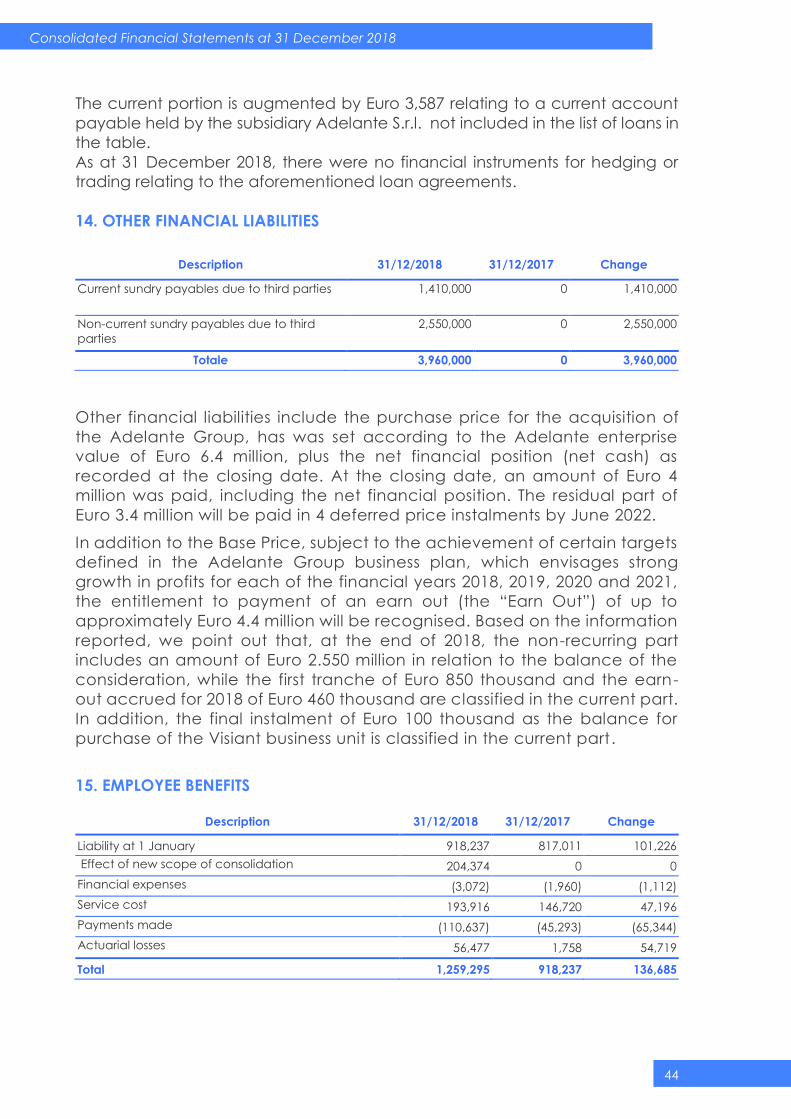

FINANCIAL

STATEMENTS

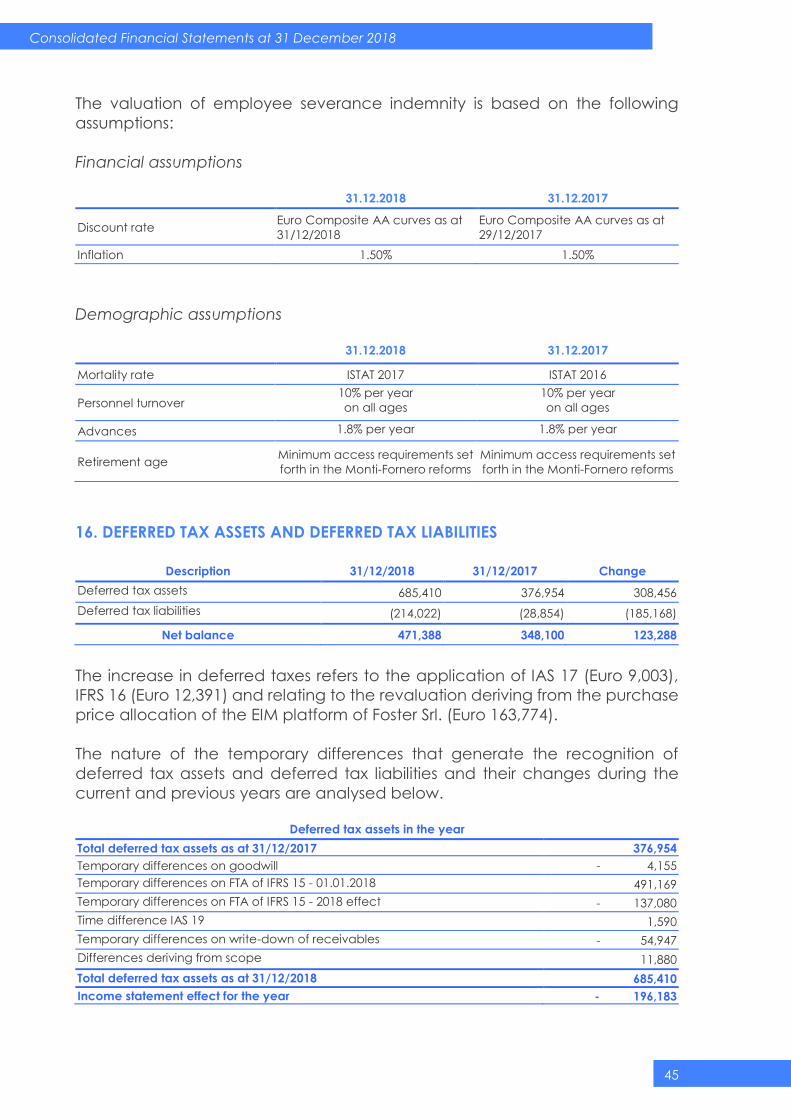

2018

Report on Operations

2

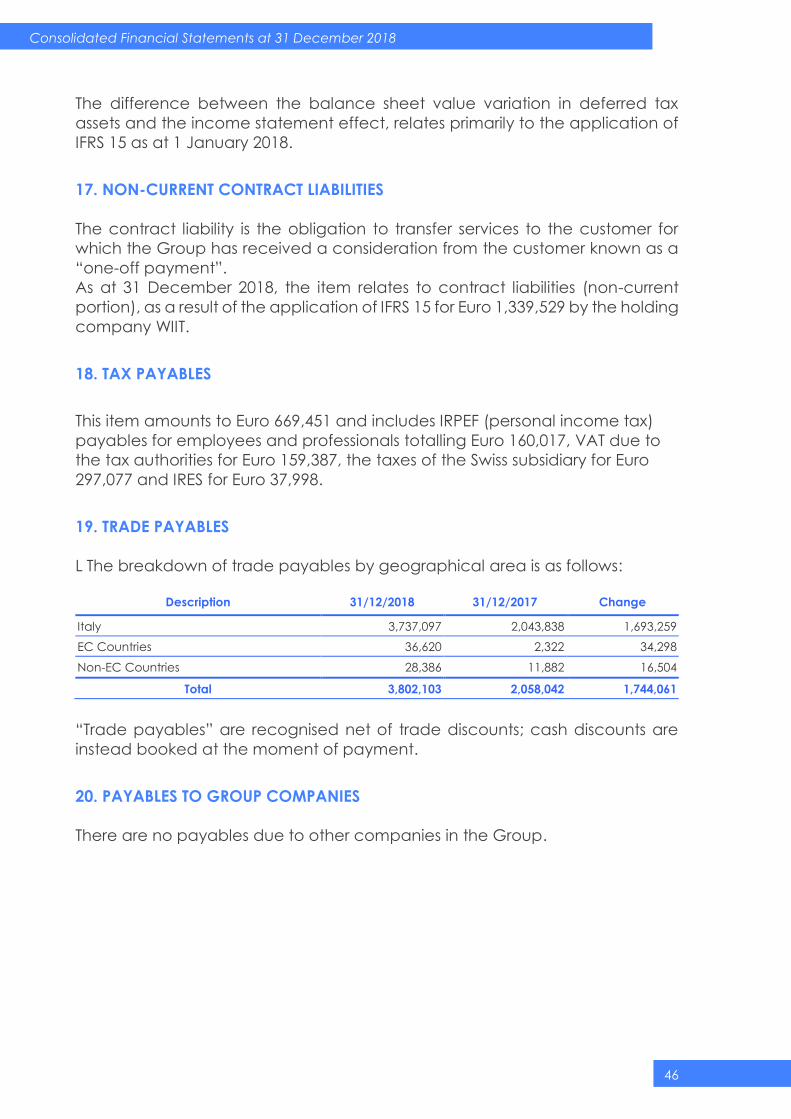

2

Company: Wiit S.p.A.

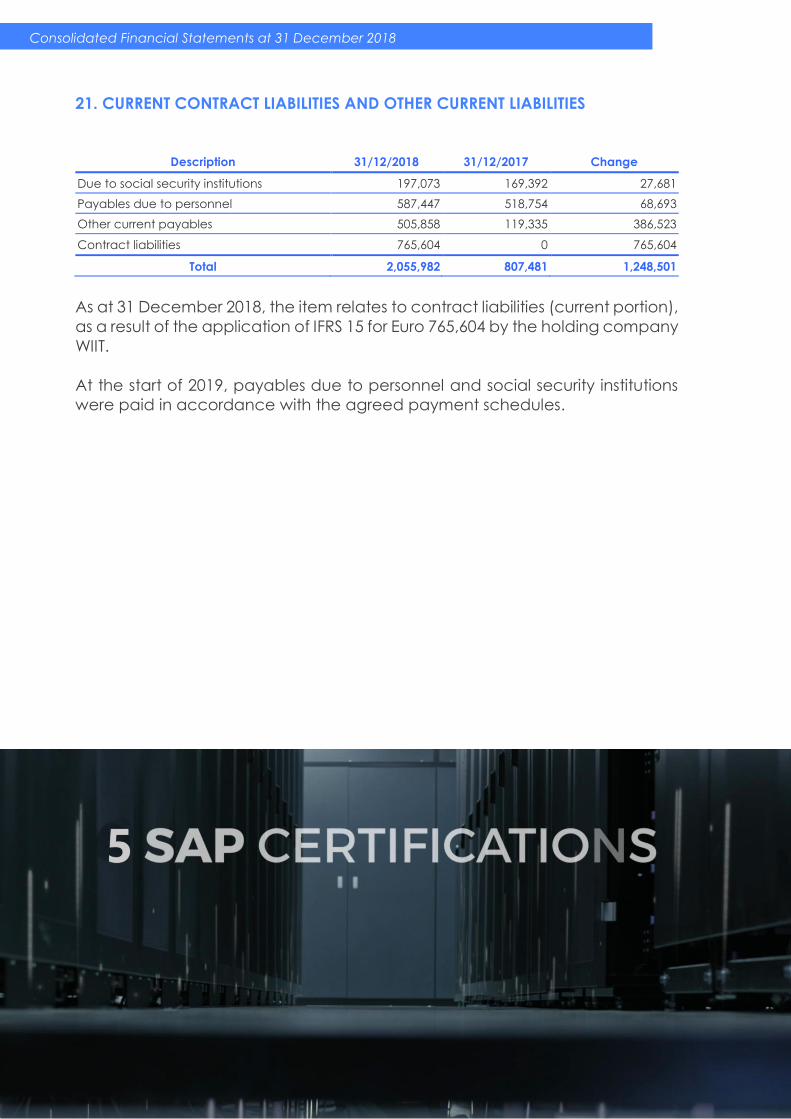

Registered office: Milano, Via Muzio Attendolo detto Sforza n.7

VAT no. and Tax Code: 01615150214

Share Capital: 2,652,066.00 fully paid-in

Milan Register of Companies No. n. 01615150214

R.E.A. (economic and administrative

index) No.

n. 1654427

Number of shares 2.652.066

Wiit Spa is subject to the management and coordination activities of Wiit Fin S.r.l.

Letter to the shareholders

Shareholders,

over the past few years, the harmonization of accounting rules has been one of the

main objectives of the European Community to facilitate the development and

efficiency of European financial markets.

The application of different accounting principles in each member country has in fact

determined a low degree of comparability of the financial statements of European

companies, constituting in fact a brake on the development of these markets. The

European accounting legislation (and in particular the IV and VII directive, respectively

regarding the financial statements and the consolidated financial statements),

differently applied in the individual member countries, was no longer adequate to

guarantee this objective.

We therefore remind you that starting from 2015 the Company has decided to apply

the IAS / IFRS international accounting standards issued by the IASB (International

Accounting Standard Board) and therefore the attached financial statements have

been prepared in compliance with the aforementioned principles.

Chairman & Managing Director

(Riccardo Mazzanti)

4

FINANCIAL STATEMENTS 2018 - REPORT ON OPERATIONS

5

FINANCIAL STATEMENTS 2018 - REPORT ON OPERATIONS

INDEX

Profile ................................................................................................................................ 6

L’offerta ..................................................................... Errore. Il segnalibro non è definito.

Corporate Bodies ............................................... Errore. Il segnalibro non è definito.

Report on Operations ....................................... Errore. Il segnalibro non è definito.

Operating conditions and business developmentErrore. Il segnalibro non è definito.

Research and development activities ......................................................................... 26

Relations with subsidiaries, associates, holding companies and sister companies . 27

Information relating to risks and uncertainties pursuant to art. 2428, paragraph 2, point

6-bis, of the Italian Civil Code

................................................................................... Errore. Il segnalibro non è definito.

Business outlook ............................................................................................................... 34

Programmatic Security Document ............................................................................... 35

Proposed allocation of profit for the year ............. Errore. Il segnalibro non è definito.

6

FINANCIAL STATEMENTS 2018 - REPORT ON OPERATIONS

Profile

WIIT S.p.A. is a company that heads up a Group that operates in the Cloud Computing

sector whose core business consists of the preparation and provision of IT infrastructures

designed to cater for specific customer requirements (mainly in Hosted Private Cloud

and Hybrid Cloud mode) and the provision of complementary services for the

configuration, management and control of the infrastructures in order to ensure their

functionality and continuous availability (primarily PaaS or Platform-as-a-Service).

The company provides Cloud solutions for the so-called “critical applications” of its

customers and, that is, the applications which, if they failed to function correctly, could

impact the customer’s “business continuity”, and which must therefore function

correctly and continuously. The main market ERP – Enterprise Resource Planning

applications, such as SAP, Oracle and Microsoft fall under these types of applications,

plus the critical applications developed on an ad hoc basis to meet the customer’s

business needs (so-called “custom” applications).

For the performance of its operating activities, the company makes use of two

proprietary Data Centres, the main one of which, located in Milan, is TIER IV certified

(i.e. maximum level of reliability) by the Uptime Institute.

In order to ensure the “business continuity” of its customers, the company’s services are

provided through several servers and storage devices, a set-up that ensures they are

constantly available in the event one of them malfunctions or stops working. Hence the

company provides its customers with the Business Continuity and Disaster Recovery

service (which allows data processing systems and all critical customer data to be

replicated almost in real time) and saves the data on a daily basis (back-up).

The Offer

WIIT’s offer is focused on the Hosted Private Cloud and Hybrid Cloud sectors, which

involve the creation of custom IT infrastructures for customers. To a lesser extent, the

Group provides Cloud services in the Public Cloud sector, integrating and managing

the solutions - more standardised - offered by the large market operators, in order to

adjust them into line with the needs of its customers.

As part of its activities, the company offers its own services to customers by combining

the different basic component of each service category, in order to construct a custom

Hosted Private Cloud and/or Hybrid Cloud proposal, based on the specific service,

performance and security requirements of each customer.

7

FINANCIAL STATEMENTS 2018 - REPORT ON OPERATIONS

The main categories of services that the Group offers to its customers are reported

below. In particular, a description is provided of the services ranging from the bare

minimum service known as ‘Infrastructure as a Service’ - which forms the basis of the

provision of other services - to the more complex Business Process Outsourcing service.

IaaS (Infrastructure as a Service): consists of providing servers, storage and networks;

PaaS (Platform as a Service): is the main service offered by the Group and includes

not only IaaS services, but also database provision services or ERP solutions in on-

demand mode;

End User Productivity: are customer contact services and contain all those

technologies and methodologies for improving both individual productivity and the

customer-WIIT interface;

Application Management: this relates to application life cycle management services,

which include corrective and evolutionary maintenance and the development of

new functionalities.

SaaS (Software as a Service): this relates to software platforms and applications

provided to the customer as “services”;

Business Process Outsourcing: includes end-to-end services for the management of

entire business processes which form part of the customer’s value chain.

Services are normally provided by the company under a standard type contract,

unique for all the different types of services (IaaS, Paas, End User Productivity,

Application Management, SaaS and Business Process Outsourcing), which are usually

combined within the framework of a single economic and contractual offer.

The contract term is generally between three and five years, usually with automatic

renewal for periods of equal length (except for the possibility of cancellation within 6

months of the expiry date). Contracts normally provide for the initial supply of services

targeted at implementing the so-called “start-up” phase, which serve the provision of

8

FINANCIAL STATEMENTS 2018 - REPORT ON OPERATIONS

the services offered by the Group (“start-up activities”) and subsequent provision of

the specific services requested by the customer.

Certificazions

The company makes use of two proprietary Data Centres, the main one of which, located in Milan, is TIER

IV certified (i.e. maximum level of reliability) by the Uptime Institute. As of today, there are 47 data centres

in the world certified as TIER IV by the Uptime Institute) in the category “Constructed Facility”

(https://uptimeinstitute.com/TierCertification/constructed-facility-certifications.php).

In relation to Data Centres, over time the company has obtained international certifications, in particular

for the security of its own services, such as certifications ISO20000 (Process Compliance), ISO27001

(Information Security), and ISO22301 (Business Continuity) and for the methods of provision of services

compliant with standard ITIL (Infrastructure Library).

The company has also certified the information systems management model of its customers according

to international standard ISO/IEC 20000:2005, as well as its own organisation according to standard ISO

9001 for the development and provision of Business Process Outsourcing services such as: Help Desk IT,

Desktop Management, Server Management, Application Management, Asset Management, System

Housing and Hosting Document Processing System Management.

In order to guarantee the correct management and protection of the data and information managed

through its information systems, in 2012, the company obtained international certification ISO/IEC

27001:2005 (international regulation which sets out the requirements that must be satisfied by a security

management system in information technologies) and has developed a methodology regarding business

continuity based on directive ISO 22301, moving from an approach not based solely on technology, but

able to direct all the processes involved in the restoration of operations.

In addition to these certifications, the company is a top SAP partner and one of the two companies

worldwide to have obtained, as of today, 5 of the 6 SAP operating certifications in the Outsourcing

Operation domain (https://www.sap.com/dmc/exp/2018_Partner_Guide/#/partners).

9

FINANCIAL STATEMENTS 2018 - REPORT ON OPERATIONS

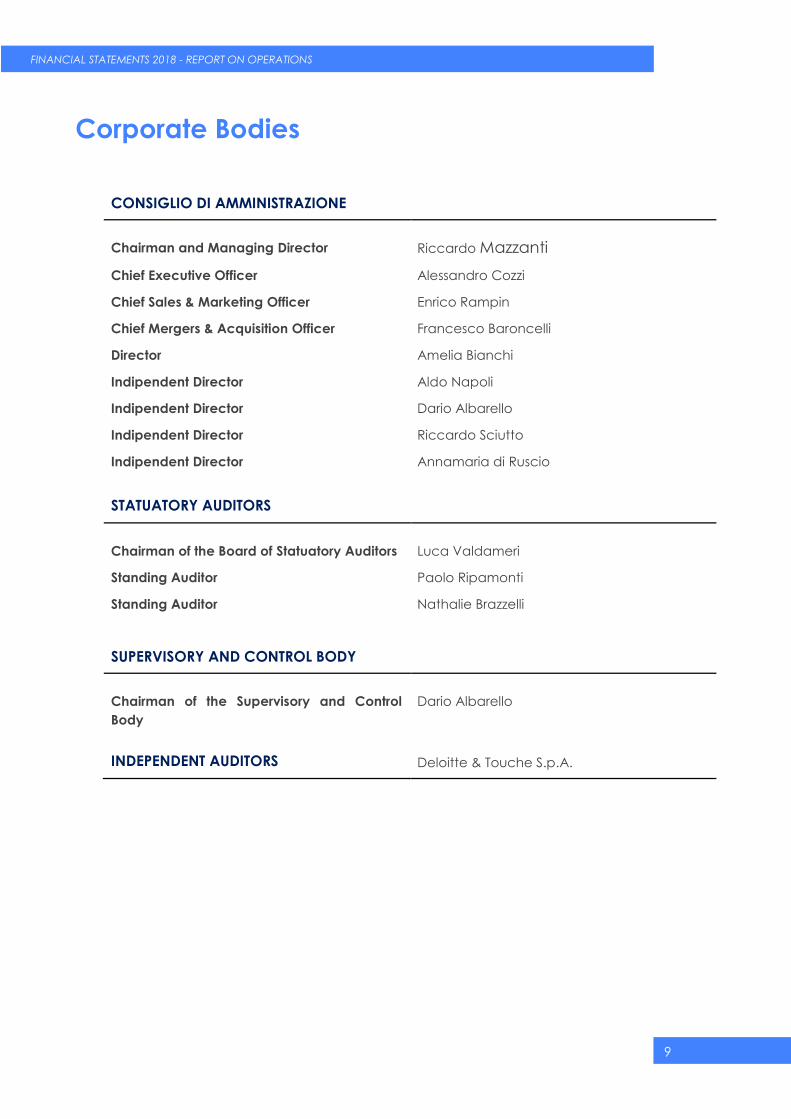

Corporate Bodies

CONSIGLIO DI AMMINISTRAZIONE

Chairman and Managing Director Riccardo Mazzanti

Chief Executive Officer Alessandro Cozzi

Chief Sales & Marketing Officer Enrico Rampin

Chief Mergers & Acquisition Officer Francesco Baroncelli

Director Amelia Bianchi

Indipendent Director Aldo Napoli

Indipendent Director Dario Albarello

Indipendent Director Riccardo Sciutto

Indipendent Director Annamaria di Ruscio

STATUATORY AUDITORS

Chairman of the Board of Statuatory Auditors Luca Valdameri

Standing Auditor Paolo Ripamonti

Standing Auditor Nathalie Brazzelli

SUPERVISORY AND CONTROL BODY

Chairman of the Supervisory and Control

Body

Dario Albarello

INDEPENDENT AUDITORS Deloitte & Touche S.p.A.

10

FINANCIAL STATEMENTS 2018 - REPORT ON OPERATIONS

Governance and significant events in the year.

On 18 July 2018, the deed of acquisition of 100% of the shares representing the share

capital of Adelante Srl was signed. Adelante is a company specialised in the digital

transformation of medium-sized enterprises and operating - also through the Group

companies - in the provision of Cloud Computing services, managed services,

managed security, business process outsourcing and unified communication. The

acquisition comes under the strategy declared during the listing process, which sees

an increase in the market share on the Italian market, also through the consolidation

of Italian operators operating on the cloud. Adelante will be able to reach its full

business potential, both by benefiting from scale economies deriving from its

membership of the group and by expanding its portfolio of services on “mission critical

applications, in which WIIT today expresses its real leadership. The acquisition of

Adelante, based in Florence, will also allow the group to strengthen its presence on

the medium-sized enterprise market of central Italy. This transactions enables us to

better capitalise on the production capacity available in WIIT, but also strengthen our

managerial position, with a view to potential further acquisitions that underpin the

group’s globalisation strategy.

The entrance by the Adelante Group into the WIIT Group represents an important

opportunity for achieving additional, yet more ambitious results.

Both companies involved in the deal are part of the ELITE ecosystem.

The purchase price for the acquisition has been set according to the Adelante

enterprise value of Euro 6.4 million, plus the net financial position (net cash) as

recorded at the closing date. It is specified that the Base Price was determined using

the market multiples method, considering the capacity to generate income and the

forecast prospective cash flow of the Adelante Group.

Description of Adelante's business

Adelante, which is already involved in the Borsa Italiana Elite acceleration route, with

the aim of consolidating development and strengthening the growth pursued, is

specialised in the digital transformation of medium-sized enterprises and operates -

including through the Adelante Group companies - providing cloud computing

services, managed services, managed security, business process outsourcing and

unified communication services.

Adelante owns 100% of the share capital of ICT Watcher Sh.p.k. (an Albanian

company) and 20% of the share capital of Comm.it S.r.l., which in turn owns 100% of

the share capital of Comm.IT Software Sh.p.k. (an Albanian company; jointly the

“Affiliates” and together with Adelante, the “Adelante Group”).

The Adelante Group has a business model and resources that integrate perfectly with

the WIIT strategy and, therefore, it is expected that the Transaction will make it

possible to immediately create notable synergies both in terms of competitive

positioning and the service level offered to medium-sized enterprises in central and

northern Italy, by means of the centralisation of various operations, such as operation

services and the use of WIIT data centre services.

11

FINANCIAL STATEMENTS 2018 - REPORT ON OPERATIONS

On 3 December 2018, the Consolidating company completed the acquisition of

65.03% of the shares representing the share capital of Foster S.r.l., a company that

owns a document management platform through which the Group provides, among

other things, enterprise information management and digital business process

outsourcing services, hence obtaining control of 100% of the shares representing

share capital.

In November 2018, the Board of Directors examined and approved the proposed

listing of ordinary WIIT shares on the MTA (screen-based equities market), organised

and managed by Borsa Italiana S.p.A. and, given the conditions were satisfied, on

the STAR Segment.

By means of the listing, the Group will be able to attract the attention of a broader

and diversified investor base with benefits not only in terms of an increase in value

and visibility, Group positioning with respect to its competitors and strategic partners

but also in relation to greater market liquidity with respect to the liquidity that normally

characterises a multi-lateral trading system. In addition, the listing on the MTA, taking

into account the obligations which companies listed on said market must fulfil, will

further boost the professional growth of the management and, generally speaking,

the Group structure, with the resultant benefits stemming from said growth.

12

FINANCIAL STATEMENTS 2018 - REPORT ON OPERATIONS

Report on Operations

13

FINANCIAL STATEMENTS 2018 - REPORT ON OPERATIONS

Report on Operations Dear Shareholders,

Over the last few years, harmonisation of accounting rules has been one of the main

objectives of the European Community, in order to facilitate the development and

efficiency of the European financial markets.

The application of different accounting standards in each member country has

actually meant that the financial statements of European companies are difficult to

compare, indeed putting the brakes on the development of these markets. The

European accounting regulations (and in particular Directives IV and VII, regarding

the separate financial statements and the consolidated financial statements

respectively), applied differently in the individual member countries, are no longer

suitable for guaranteeing said objective.

Therefore, we should also point out to you that, as of 2015, the Company started to

apply the international accounting standards (IAS/IFRS) issued by the IASB

(International Accounting Standards Board) and, therefore, the attached financial

statements were drafted in compliance with the aforementioned standards.

Operating conditions and business development

The Group offers Cloud and IT Outsourcing for critical applications. The offer is

composed of the following multi-year and ongoing services:

Hosted Private Cloud, for companies that intend to make use of the Cloud services

provided by Outsourced Data Centres; and

Hybrid Cloud, for companies that intend to use a hybrid model of the following types

of infrastructures: Private Cloud (within the company), Hosted Private Cloud (data

centre outside the company with largely dedicated and customised infrastructures)

and Public Cloud (data centre outside the company and standard and shared

infrastructures).

The Group also boasts advanced Cyber Security solutions.

The generally rather high level of efficiency and the long-term contracts in the

portfolio allow WIIT to approach 2019 with a competitive offer and with expectations

of natural growth.

The sector in which the company operates presents indicators of growth which,

together with the consolidated ability to acquire and retain customers, to continue

to seize numerous internal growth opportunities and to evaluate interesting external

growth opportunities, means we have positive expectations for the year 2019.

Pursuant to art. 2428, it should be noted that the activities are carried out in the Milan

office, via Muzio Attendolo detto Sforza 7 and in the secondary offices of Rome in Via

Ercolano Salvi 12, of Castelfranco Veneto (TV) in Piazza della Serenissima 20 as

regards the consolidating company, as well as in the offices of Bagno a Ripoli in Via

14

FINANCIAL STATEMENTS 2018 - REPORT ON OPERATIONS

S.Pertini 7 and Tirana Torre Drin Via Abdi Toptani, respectively for Adelante Srl and

ICTW.

In July 2016, the consolidating company established a subsidiary in Switzerland, which

started to operate continuously in both Switzerland and in the USA (Florida).

General economic trend

Growth of the global economy continued in the last few months, but signs of a

cyclical deterioration in many advanced and emerging economies materialised;

global trade prospects continue to worsen, after the slowdown in the first part of last

year. Uncertainties over the economic situation have had repercussions on the

international financial markets, with a decrease in long-term yields and fall in share

prices. Global prospects were impacted by risks relating to a negative outcome to

commercial negotiations between the United States and China, the possible

heightening of financial tensions in emerging countries and the methods with which

Brexit will be implemented.

Growth weakened in the Euro area; in November, industrial production fell

significantly in Germany, France and Italy. Inflation, although remaining at largely

positive values fell due to the slowdown in the prices of energy products. The

Governing Council of the ECB reiterated its intention to maintain a significant

monetary stimulus for a prolonged period.

In Italy, after a halt in growth in the third quarter, the available economic indicators

suggest that activity could have fallen further in the fourth quarter. The reduction in

domestic demand contributed to the weakening in the summer months, in particular

investments and, to a lesser extent, household spending. According to the customary

economic survey conducted by the Bank of Italy in collaboration with Il Sole 24 Ore,

the investment plans of industrial and services companies will be reduced in scope in

2019 as a result of both political and economic uncertainty and commercial tensions.

The trend in Italian exports was still favourable in the second half of the year; the

slowdown in global trade, however, influenced the prospective valuations of

companies regarding foreign orders. The current account balance remains largely

positive; the country’s net foreign debt position continues to improve, which fell by a

little over 3% of GDP at the end of September.

Overall inflation fell to 1.2% in December, especially due to the deceleration in the

prices of energy products; the trend in the core component remained weak (0.5%).

Company expectations regarding the trend in prices were revised downward slightly.

In addition to the global factors of uncertainty outlined, the downside risks for growth

are connected to a possible fresh increase in sovereign yields, a more rapid

deterioration in private sector financing conditions and a further downturn in

companies’ propensity to invest. A more marked dissipation of tensions on the

Government bond yields could instead promote higher rates of growth.

15

FINANCIAL STATEMENTS 2018 - REPORT ON OPERATIONS

Growth in demand and trends in the macro-markets in which the Company operates

The Group operates primarily in the ICT services market, and more specifically, the

Cloud Computing segment.

In preparing this section, the Parent Company Wiit S.p.A. used the information taken

predominantly from the Assinform Report entitled “Il Digitale in Italia – 2018 Mercati,

Dinamiche, Policy” (The Digital Industry in Italy - 2018 Markets, Trends, Policies). Some

information has been taken from the Observatory of the Polytechnic of October 2018

called “Cloud Transformation Observatory - Cloud Transformation: evolving towards

the agile organisation with clouds”.

The Cloud market is experiencing a period of profound change, supported by the

growing perception of its role as an enabler for emerging technological trends, the

path that business users are taking to develop and migrate their information systems

and the corresponding change in the offer portfolio of the players in the Digital

market.

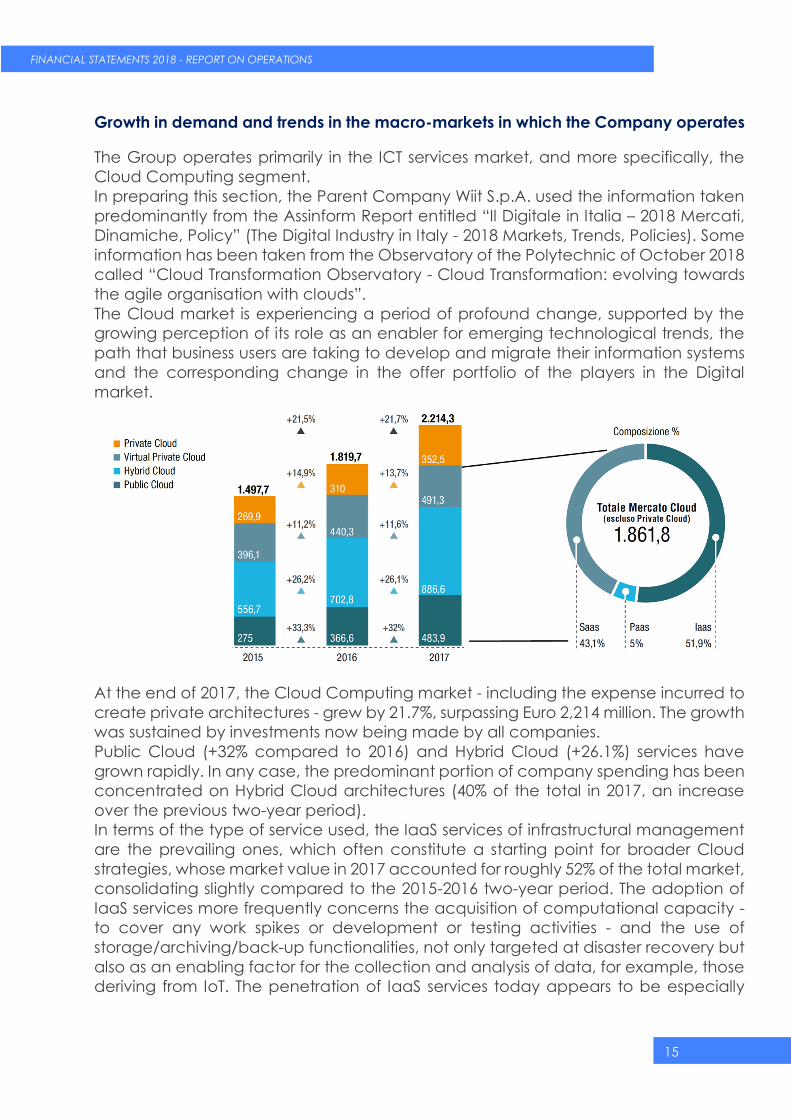

At the end of 2017, the Cloud Computing market - including the expense incurred to

create private architectures - grew by 21.7%, surpassing Euro 2,214 million. The growth

was sustained by investments now being made by all companies.

Public Cloud (+32% compared to 2016) and Hybrid Cloud (+26.1%) services have

grown rapidly. In any case, the predominant portion of company spending has been

concentrated on Hybrid Cloud architectures (40% of the total in 2017, an increase

over the previous two-year period).

In terms of the type of service used, the IaaS services of infrastructural management

are the prevailing ones, which often constitute a starting point for broader Cloud

strategies, whose market value in 2017 accounted for roughly 52% of the total market,

consolidating slightly compared to the 2015-2016 two-year period. The adoption of

IaaS services more frequently concerns the acquisition of computational capacity -

to cover any work spikes or development or testing activities - and the use of

storage/archiving/back-up functionalities, not only targeted at disaster recovery but

also as an enabling factor for the collection and analysis of data, for example, those

deriving from IoT. The penetration of IaaS services today appears to be especially

16

FINANCIAL STATEMENTS 2018 - REPORT ON OPERATIONS

significant in the Utility, Distribution and Services sectors and, looking forward, it is

expected to increase among industrial and financial companies.

These are followed closely by SaaS services, accounting for approximately 43% of the

total market in 2017, a slight increase compared to the previous two-year period. The

incidence of SaaS is significant in all sectors and in relation to tactical application

areas (Office Automation and Collaboration), which represent, without doubt, the

main areas in which application Cloud services are applied. The use of SaaS services

appears to have also registered growth in relation to solutions that satisfy precise

requirements (CRM, Business Intelligence/Business Analytics, HR Management) or,

nonetheless, attributable to the main digital platforms (Mobile, IoT).

In this case, the most active companies are found in the Industry,

Telecommunications, Distribution and Services sectors. In the immediate future, SaaS

will be utilised increasingly more by industrial companies, also for more strategic

business applications such as, for example, ERP and management applications,

given that fears over the need to place management data on external infrastructures

are easing. In addition, the adoption of ERP and management solutions in SaaS

makes it possible, nonetheless, to customise and parametrise them, a requirement

experienced in particular by companies for the front-end components of the

platforms. However, some obstacles remain, including the fact that the broadband

network is not widely distributed, an issue experienced, in particular, by

manufacturing firms in decentralised locations with respect to large urban centres.

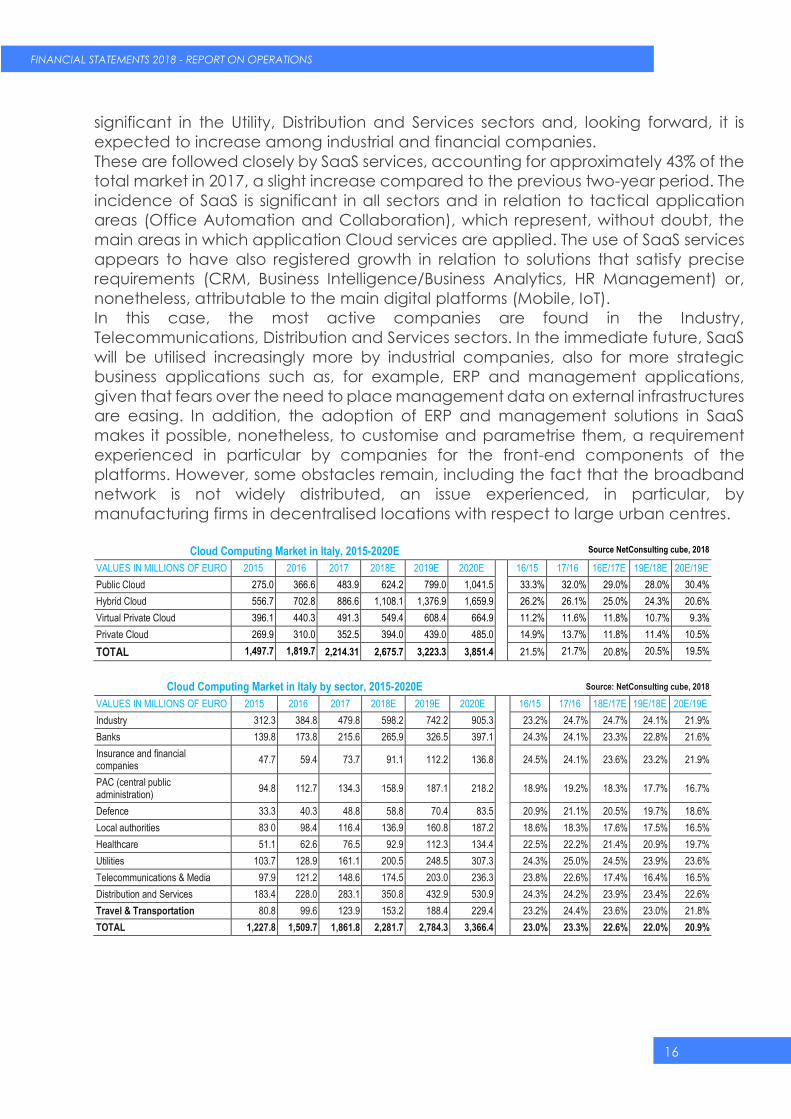

Cloud Computing Market in Italy, 2015-2020E Source NetConsulting cube, 2018

VALUES IN MILLIONS OF EURO 2015 2016 2017 2018E 2019E 2020E 16/15 17/16 16E/17E 19E/18E 20E/19E

Public Cloud 275.0 366.6 483.9 624.2 799.0 1,041.5 33.3% 32.0% 29.0% 28.0% 30.4%

Hybrid Cloud 556.7 702.8 886.6 1,108.1 1,376.9 1,659.9 26.2% 26.1% 25.0% 24.3% 20.6%

Virtual Private Cloud 396.1 440.3 491.3 549.4 608.4 664.9 11.2% 11.6% 11.8% 10.7% 9.3%

Private Cloud 269.9 310.0 352.5 394.0 439.0 485.0 14.9% 13.7% 11.8% 11.4% 10.5%

TOTAL 1,497.7 1,819.7 2,214.31 2,675.7 3,223.3 3,851.4 21.5% 21.7% 20.8% 20.5% 19.5%

Cloud Computing Market in Italy by sector, 2015-2020E Source: NetConsulting cube, 2018

VALUES IN MILLIONS OF EURO 2015 2016 2017 2018E 2019E 2020E 16/15 17/16 18E/17E 19E/18E 20E/19E

Industry 312.3 384.8 479.8 598.2 742.2 905.3 23.2% 24.7% 24.7% 24.1% 21.9%

Banks 139.8 173.8 215.6 265.9 326.5 397.1 24.3% 24.1% 23.3% 22.8% 21.6%

Insurance and financial companies

47.7 59.4 73.7 91.1 112.2 136.8

24.5% 24.1% 23.6% 23.2% 21.9%

PAC (central public administration)

94.8 112.7 134.3 158.9 187.1 218.2

18.9% 19.2% 18.3% 17.7% 16.7%

Defence 33.3 40.3 48.8 58.8 70.4 83.5 20.9% 21.1% 20.5% 19.7% 18.6%

Local authorities 83 0 98.4 116.4 136.9 160.8 187.2 18.6% 18.3% 17.6% 17.5% 16.5%

Healthcare 51.1 62.6 76.5 92.9 112.3 134.4 22.5% 22.2% 21.4% 20.9% 19.7%

Utilities 103.7 128.9 161.1 200.5 248.5 307.3 24.3% 25.0% 24.5% 23.9% 23.6%

Telecommunications & Media 97.9 121.2 148.6 174.5 203.0 236.3 23.8% 22.6% 17.4% 16.4% 16.5%

Distribution and Services 183.4 228.0 283.1 350.8 432.9 530.9 24.3% 24.2% 23.9% 23.4% 22.6%

Travel & Transportation 80.8 99.6 123.9 153.2 188.4 229.4 23.2% 24.4% 23.6% 23.0% 21.8%

TOTAL 1,227.8 1,509.7 1,861.8 2,281.7 2,784.3 3,366.4 23.0% 23.3% 22.6% 22.0% 20.9%

17

FINANCIAL STATEMENTS 2018 - REPORT ON OPERATIONS

According to the figures of the Observatory of the Polytechnic (which interviewed

142 large companies and 285 small and medium companies), the Cloud is viewed as

an ally by three out of four companies, who consider it a key element in introducing

innovations, which would otherwise be too costly to achieve internally in terms of

times, costs and skills. However, it is not just a matter of technological innovation but

also of flexibility to change: in fact, for 74% of companies, the Cloud makes it possible

to enhance the company’s agility. This means guaranteeing that the technological

layer is always updated and in step with market rates, which best supports the

development and rapid release of new services and which makes it possible not to

focus on technical-operational management but on the company’s business

priorities. In fact, in 59% of cases, the Cloud is identified as a tool that allows IT to best

respond to business requirements, and in 57% of responses, a factor that enables the

transformation of the business.

A process of transformation of company IT systems has taken hold in the last few

years, in which businesses have now moved from using the Cloud solely for a few

specific processes, to making it the bedrock of their IT strategy.

Again according to the Observatory of the Polytechnic, Hybrid and Virtual Private

Cloud services are used by one out of two companies.

Marketing Communication & Brand Positioning

The Company’s marketing strategy focuses on activities targeted at raising

awareness of the WIIT brand and the generation of new business opportunities, by

operating on off-line and on-line channels. In relation to brand awareness, the

Company has run multi-channel advertising campaigns with the goal of reaching the

decision-makers of the WIIT customer target. For these purposes, the Company takes

advantage, by way of an example, of its presence on walls in the national and

European departure areas of Milano Linate, as well as on LCD screens throughout the

Milano Linate and Milano Malpensa airports, or the presence and communication

through all the main business-oriented social media like Linkedin, Twitter, Youtube.

Public relations and press office activities have also endorsed brand-related

information with articles and editorials in general interest and specialist newspapers.

Lead generation campaigns (i.e. targeted at identifying users potentially interested

in purchasing services supplied by WIIT), supported by surveys and studies aimed at

chief information officers and chief financial officers of companies who could

become potential customers, have made it possible to improve the management of

customer relations and provide the sales department with support in creating new

opportunities.

An Inbound Marketing project was launched in 2018 which consists of the creation of

digital content in line with the interests of customers (actual or potential) in order to

attract additional customers to the Company’s services. In particular, this project

involves the publication of WIIT Magazine, an integrated section of the company site,

whose contents are also disseminated through company social media. The objective

of the project is to grow and spread the culture and knowledge of the Cloud

18

FINANCIAL STATEMENTS 2018 - REPORT ON OPERATIONS

dedicated to company strategic applications among the management of Italian

companies, through a description of the best practices applied by WIIT.

The visibility of WIIT Magazine and WIIT services is also supported by Google AdWords

campaigns on specific keywords in the Cloud world, as well as landing pages and

banners on portals of interest to customers. All the company marketing activities are

tracked and managed in the company CRM.

In order to improve the visibility of the Cloud services dedicated to critical

applications, every year WIIT takes part in SAP Now, the most important SAP event

targeted at its customers/potential customers.

In order to promote knowledge in Italy of the main factors of technological

innovation, WIIT is a partner and active member of the Cloud Observatory of the

Milan Polytechnic. The Observatory is, on the one hand, a privileged spectator of the

degree of dissemination of the Cloud as a model in support of business innovation

and, on the other, an advisor for industry operators in proposing suggestions for

consideration and innovation of the offer portfolio, through committees and work

groups that represent opportunities for comparing the customer’s needs with the

potential of Cloud services (supply).

Competition

The company has created and adopted service models that make provision for

direct control of the entire supply chain of technical components and services, with

internal skills and proprietary assets, including, in particular, the primary Data Centre

in Milan, certified at level “Tier IV”, by the Uptime Institute LLC of Seattle (United

States), which represents the highest level of reliability, i.e. business continuity without

incurring interruptions.

The Company’s positioning is a result of the strategy that has, over the years, involved

the construction of a broad offering in the infrastructural domain, and natural growth

thanks to its excellence in providing services.

In the Company’s opinion, the competitors in the domestic Cloud and IT Outsourcing

market can be divided into 3 macro groups:

Very large multi-national companies set up to serve large customers, equipped with

an extensive and clear organisational structure.

National medium-large companies (or that cover several European countries) that

offer a vast range of advisory, system integration, application and hardware sales

services, for which the cloud services are typically not the core business.

National companies that offer a customised niche service for a small number of

customers or that operate on a captive market.

Operating performance in the sectors in which the Company and the Group operate

19

FINANCIAL STATEMENTS 2018 - REPORT ON OPERATIONS

As regards your Company and the Group, the year ended must be viewed in a very

positive light.

The Company also recorded healthy growth in terms of the value of orders (year value)

compared to 2017, in this way guaranteeing the prospect of further growth in the value

of production in 2019.

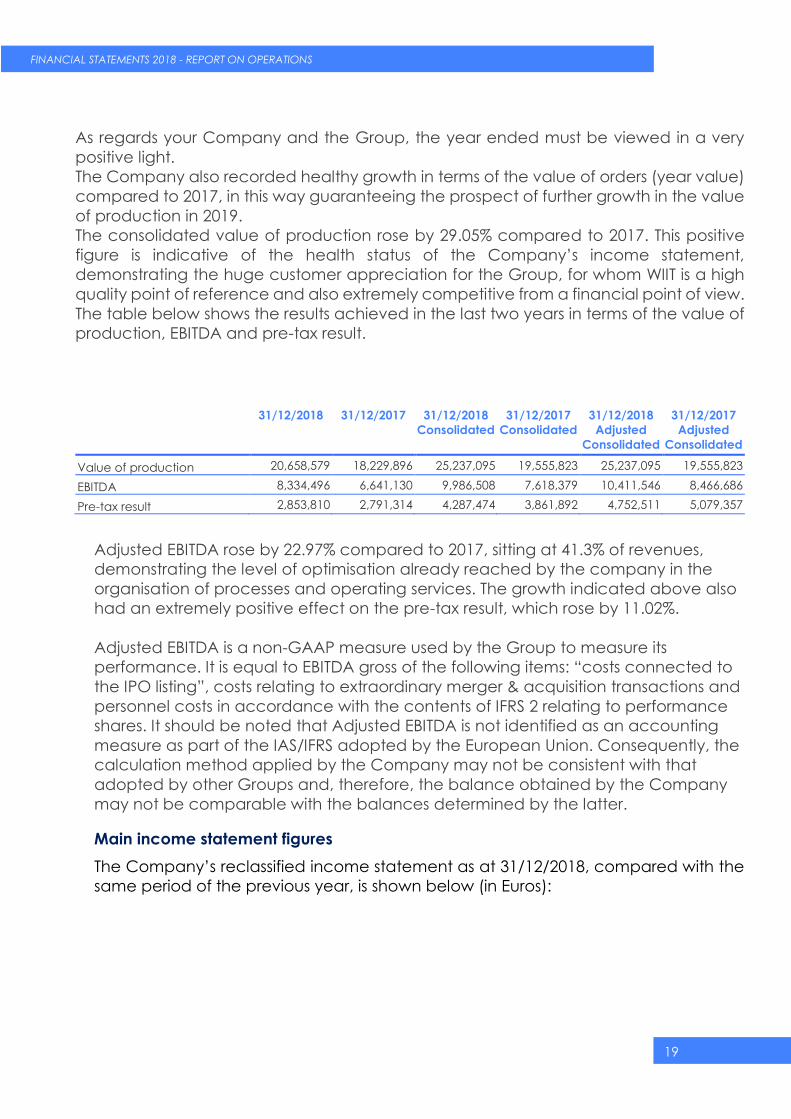

The consolidated value of production rose by 29.05% compared to 2017. This positive

figure is indicative of the health status of the Company’s income statement,

demonstrating the huge customer appreciation for the Group, for whom WIIT is a high

quality point of reference and also extremely competitive from a financial point of view.

The table below shows the results achieved in the last two years in terms of the value of

production, EBITDA and pre-tax result.

31/12/2018 31/12/2017 31/12/2018

Consolidated

31/12/2017

Consolidated

31/12/2018

Adjusted

Consolidated

31/12/2017

Adjusted

Consolidated

Value of production 20,658,579 18,229,896 25,237,095 19,555,823 25,237,095 19,555,823

EBITDA 8,334,496 6,641,130 9,986,508 7,618,379 10,411,546 8,466,686

Pre-tax result 2,853,810 2,791,314 4,287,474 3,861,892 4,752,511 5,079,357

Adjusted EBITDA rose by 22.97% compared to 2017, sitting at 41.3% of revenues,

demonstrating the level of optimisation already reached by the company in the

organisation of processes and operating services. The growth indicated above also

had an extremely positive effect on the pre-tax result, which rose by 11.02%.

Adjusted EBITDA is a non-GAAP measure used by the Group to measure its

performance. It is equal to EBITDA gross of the following items: “costs connected to

the IPO listing”, costs relating to extraordinary merger & acquisition transactions and

personnel costs in accordance with the contents of IFRS 2 relating to performance

shares. It should be noted that Adjusted EBITDA is not identified as an accounting

measure as part of the IAS/IFRS adopted by the European Union. Consequently, the

calculation method applied by the Company may not be consistent with that

adopted by other Groups and, therefore, the balance obtained by the Company

may not be comparable with the balances determined by the latter.

Main income statement figures

The Company’s reclassified income statement as at 31/12/2018, compared with the

same period of the previous year, is shown below (in Euros):

20

FINANCIAL STATEMENTS 2018 - REPORT ON OPERATIONS

31/12/2018 31/12/2017 31/12/2018

Consolidated

31/12/2017

Consolidated

31/12/2018

Adjusted

Consolidated

31/12/2017

Adjusted

Consolidated

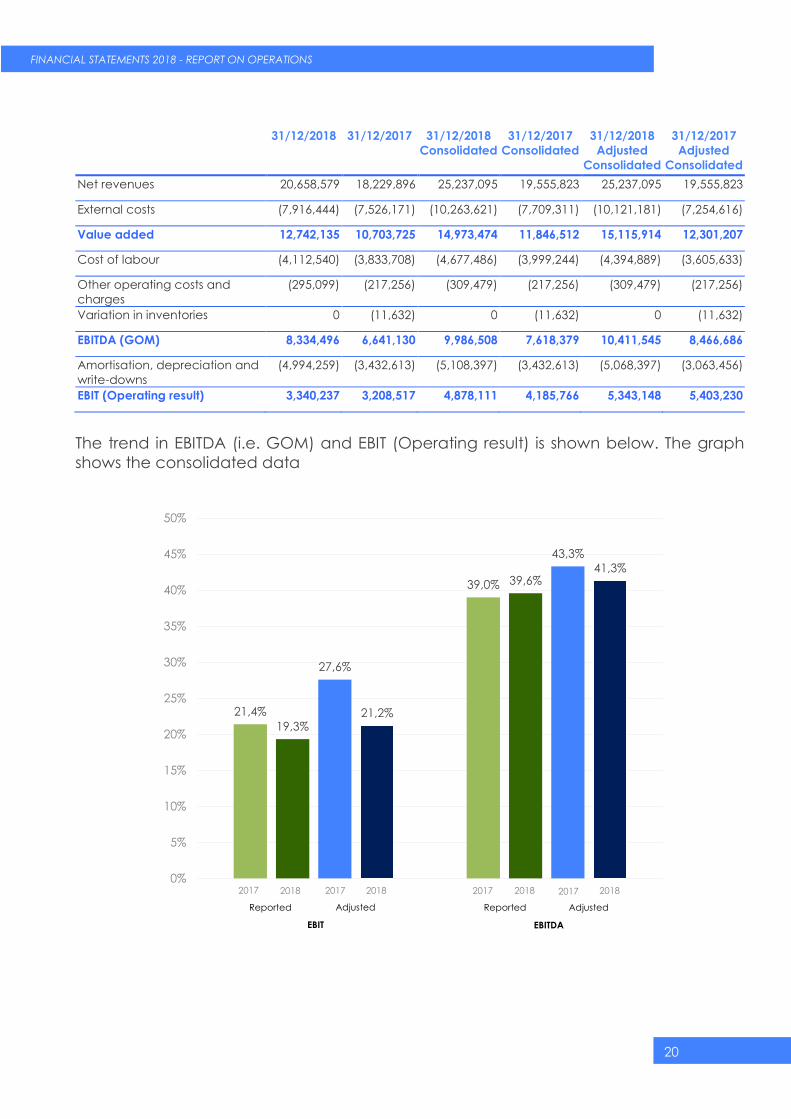

Net revenues 20,658,579 18,229,896 25,237,095 19,555,823 25,237,095 19,555,823

External costs (7,916,444) (7,526,171) (10,263,621) (7,709,311) (10,121,181) (7,254,616)

Value added 12,742,135 10,703,725 14,973,474 11,846,512 15,115,914 12,301,207

Cost of labour (4,112,540) (3,833,708) (4,677,486) (3,999,244) (4,394,889) (3,605,633)

Other operating costs and

charges

(295,099) (217,256) (309,479) (217,256) (309,479) (217,256)

Variation in inventories 0 (11,632) 0 (11,632) 0 (11,632)

EBITDA (GOM) 8,334,496 6,641,130 9,986,508 7,618,379 10,411,545 8,466,686

Amortisation, depreciation and

write-downs

(4,994,259) (3,432,613) (5,108,397) (3,432,613) (5,068,397) (3,063,456)

EBIT (Operating result) 3,340,237 3,208,517 4,878,111 4,185,766 5,343,148 5,403,230

The trend in EBITDA (i.e. GOM) and EBIT (Operating result) is shown below. The graph

shows the consolidated data

21,4%

39,0%

19,3%

39,6%

27,6%

43,3%

21,2%

41,3%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

2017 2018 2017 2018 2017 2017 2018 2018

Adjusted Adjusted Reported Reported

EBITDA EBIT

21

FINANCIAL STATEMENTS 2018 - REPORT ON OPERATIONS

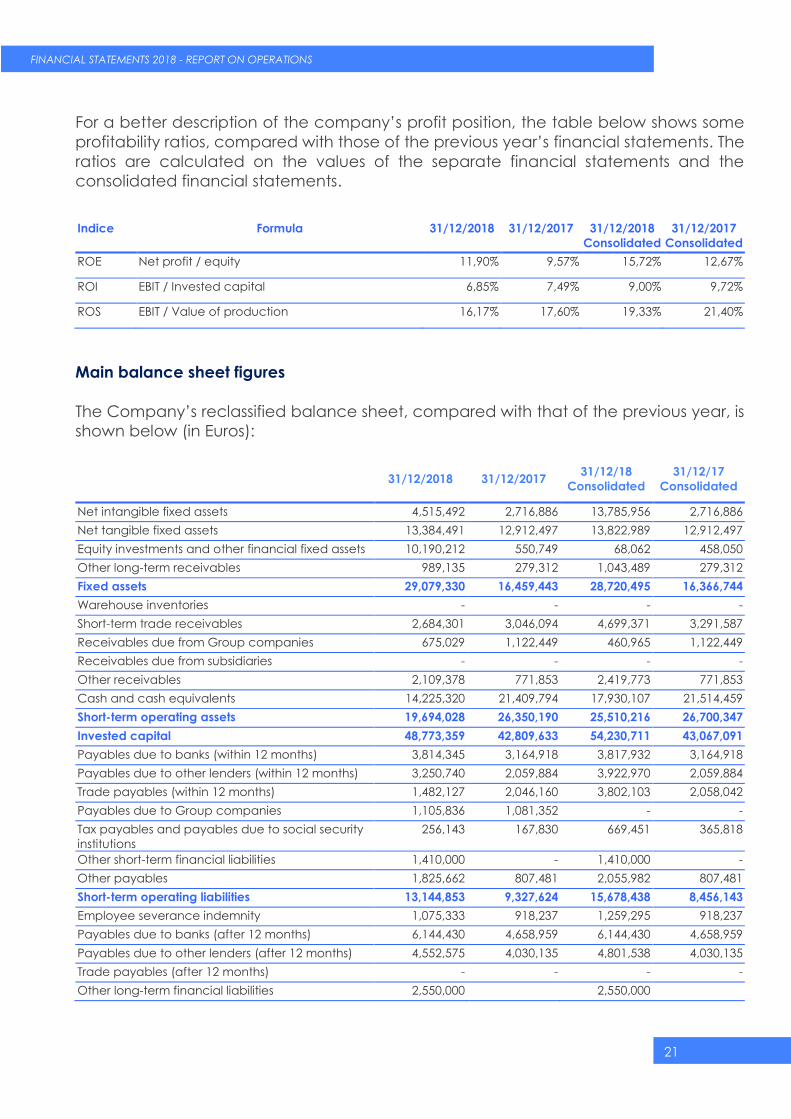

For a better description of the company’s profit position, the table below shows some

profitability ratios, compared with those of the previous year’s financial statements. The

ratios are calculated on the values of the separate financial statements and the

consolidated financial statements.

Indice Formula 31/12/2018 31/12/2017 31/12/2018

Consolidated

31/12/2017

Consolidated

ROE Net profit / equity 11,90% 9,57% 15,72% 12,67%

ROI EBIT / Invested capital 6,85% 7,49% 9,00% 9,72%

ROS EBIT / Value of production 16,17% 17,60% 19,33% 21,40%

Main balance sheet figures

The Company’s reclassified balance sheet, compared with that of the previous year, is

shown below (in Euros):

31/12/2018 31/12/2017 31/12/18

Consolidated

31/12/17

Consolidated

Net intangible fixed assets 4,515,492 2,716,886 13,785,956 2,716,886

Net tangible fixed assets 13,384,491 12,912,497 13,822,989 12,912,497

Equity investments and other financial fixed assets 10,190,212 550,749 68,062 458,050

Other long-term receivables 989,135 279,312 1,043,489 279,312

Fixed assets 29,079,330 16,459,443 28,720,495 16,366,744

Warehouse inventories - - - -

Short-term trade receivables 2,684,301 3,046,094 4,699,371 3,291,587

Receivables due from Group companies 675,029 1,122,449 460,965 1,122,449

Receivables due from subsidiaries - - - -

Other receivables 2,109,378 771,853 2,419,773 771,853

Cash and cash equivalents 14,225,320 21,409,794 17,930,107 21,514,459

Short-term operating assets 19,694,028 26,350,190 25,510,216 26,700,347

Invested capital 48,773,359 42,809,633 54,230,711 43,067,091

Payables due to banks (within 12 months) 3,814,345 3,164,918 3,817,932 3,164,918

Payables due to other lenders (within 12 months) 3,250,740 2,059,884 3,922,970 2,059,884

Trade payables (within 12 months) 1,482,127 2,046,160 3,802,103 2,058,042

Payables due to Group companies 1,105,836 1,081,352 - -

Tax payables and payables due to social security

institutions

256,143 167,830 669,451 365,818

Other short-term financial liabilities 1,410,000 - 1,410,000 -

Other payables 1,825,662 807,481 2,055,982 807,481

Short-term operating liabilities 13,144,853 9,327,624 15,678,438 8,456,143

Employee severance indemnity 1,075,333 918,237 1,259,295 918,237

Payables due to banks (after 12 months) 6,144,430 4,658,959 6,144,430 4,658,959

Payables due to other lenders (after 12 months) 4,552,575 4,030,135 4,801,538 4,030,135

Trade payables (after 12 months) - - - -

Other long-term financial liabilities 2,550,000 2,550,000

22

FINANCIAL STATEMENTS 2018 - REPORT ON OPERATIONS

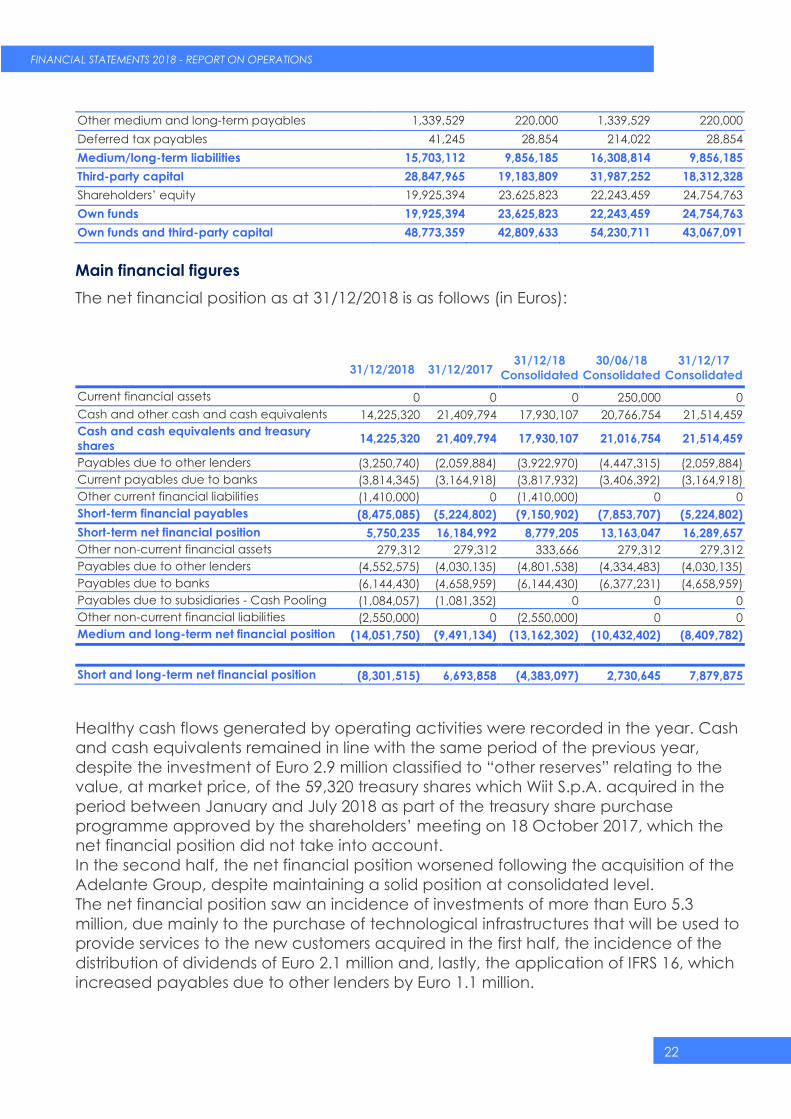

Other medium and long-term payables 1,339,529 220,000 1,339,529 220,000

Deferred tax payables 41,245 28,854 214,022 28,854

Medium/long-term liabilities 15,703,112 9,856,185 16,308,814 9,856,185

Third-party capital 28,847,965 19,183,809 31,987,252 18,312,328

Shareholders’ equity 19,925,394 23,625,823 22,243,459 24,754,763

Own funds 19,925,394 23,625,823 22,243,459 24,754,763

Own funds and third-party capital 48,773,359 42,809,633 54,230,711 43,067,091

Main financial figures

The net financial position as at 31/12/2018 is as follows (in Euros):

31/12/2018 31/12/2017

31/12/18

Consolidated

30/06/18

Consolidated

31/12/17

Consolidated

Current financial assets 0 0 0 250,000 0

Cash and other cash and cash equivalents 14,225,320 21,409,794 17,930,107 20,766,754 21,514,459

Cash and cash equivalents and treasury

shares 14,225,320 21,409,794 17,930,107 21,016,754 21,514,459

Payables due to other lenders (3,250,740) (2,059,884) (3,922,970) (4,447,315) (2,059,884)

Current payables due to banks (3,814,345) (3,164,918) (3,817,932) (3,406,392) (3,164,918)

Other current financial liabilities (1,410,000) 0 (1,410,000) 0 0

Short-term financial payables (8,475,085) (5,224,802) (9,150,902) (7,853,707) (5,224,802)

Short-term net financial position 5,750,235 16,184,992 8,779,205 13,163,047 16,289,657

Other non-current financial assets 279,312 279,312 333,666 279,312 279,312

Payables due to other lenders (4,552,575) (4,030,135) (4,801,538) (4,334,483) (4,030,135)

Payables due to banks (6,144,430) (4,658,959) (6,144,430) (6,377,231) (4,658,959)

Payables due to subsidiaries - Cash Pooling (1,084,057) (1,081,352) 0 0 0

Other non-current financial liabilities (2,550,000) 0 (2,550,000) 0 0

Medium and long-term net financial position (14,051,750) (9,491,134) (13,162,302) (10,432,402) (8,409,782)

Short and long-term net financial position (8,301,515) 6,693,858 (4,383,097) 2,730,645 7,879,875

Healthy cash flows generated by operating activities were recorded in the year. Cash

and cash equivalents remained in line with the same period of the previous year,

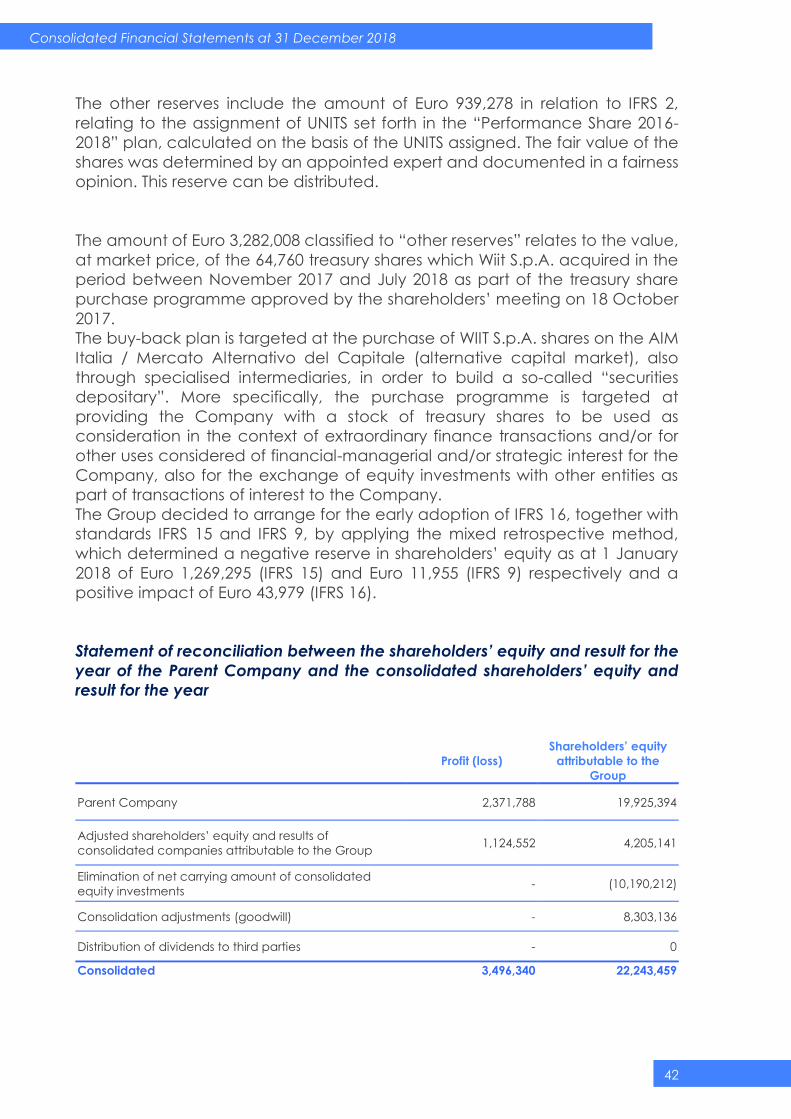

despite the investment of Euro 2.9 million classified to “other reserves” relating to the

value, at market price, of the 59,320 treasury shares which Wiit S.p.A. acquired in the

period between January and July 2018 as part of the treasury share purchase

programme approved by the shareholders’ meeting on 18 October 2017, which the

net financial position did not take into account.

In the second half, the net financial position worsened following the acquisition of the

Adelante Group, despite maintaining a solid position at consolidated level.

The net financial position saw an incidence of investments of more than Euro 5.3

million, due mainly to the purchase of technological infrastructures that will be used to

provide services to the new customers acquired in the first half, the incidence of the

distribution of dividends of Euro 2.1 million and, lastly, the application of IFRS 16, which

increased payables due to other lenders by Euro 1.1 million.

23

FINANCIAL STATEMENTS 2018 - REPORT ON OPERATIONS

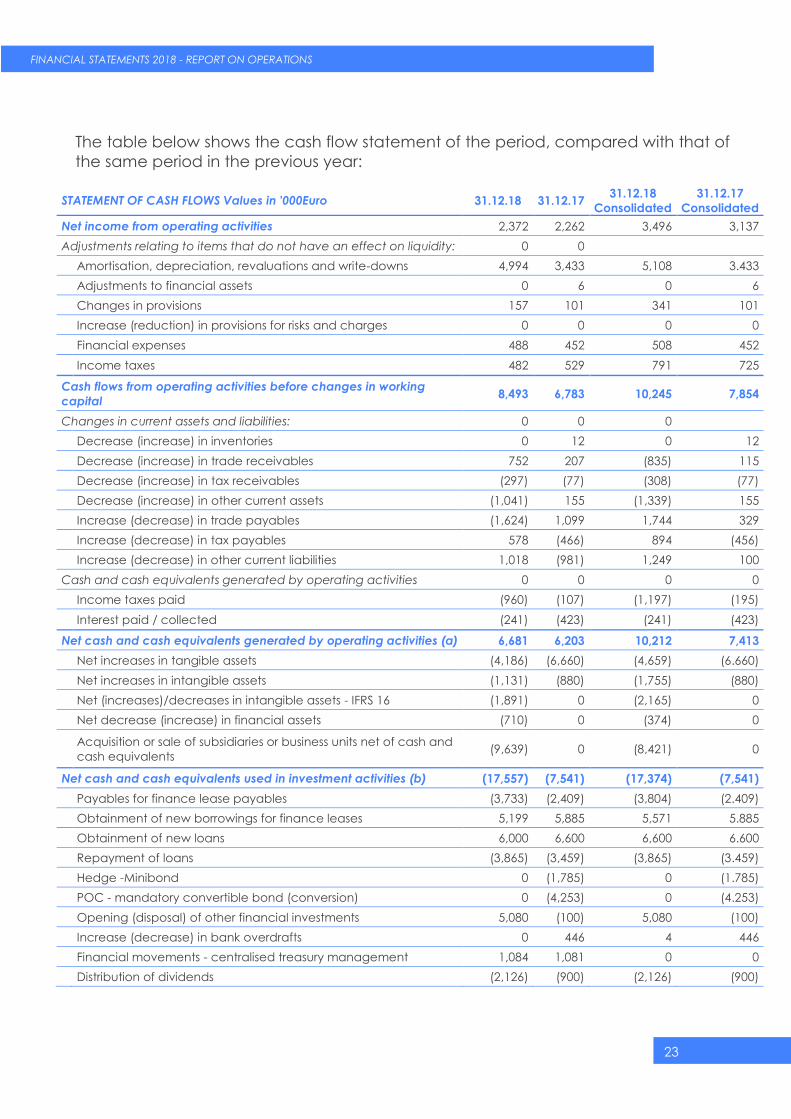

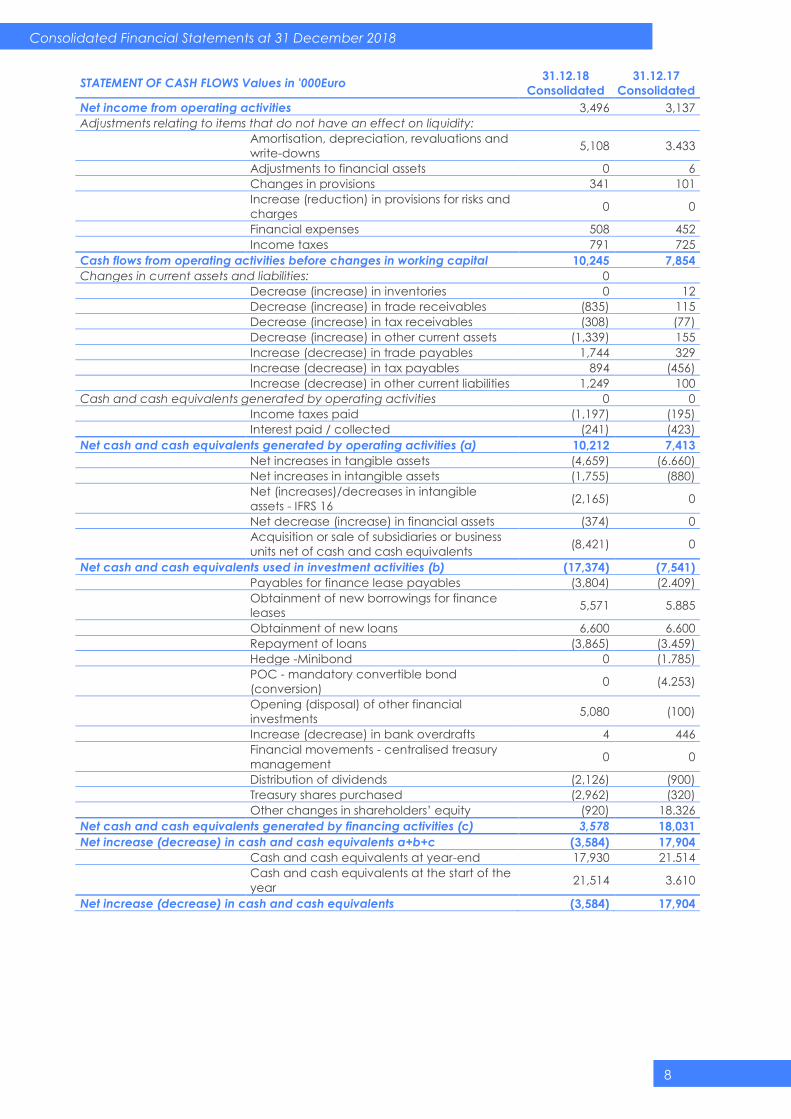

The table below shows the cash flow statement of the period, compared with that of

the same period in the previous year:

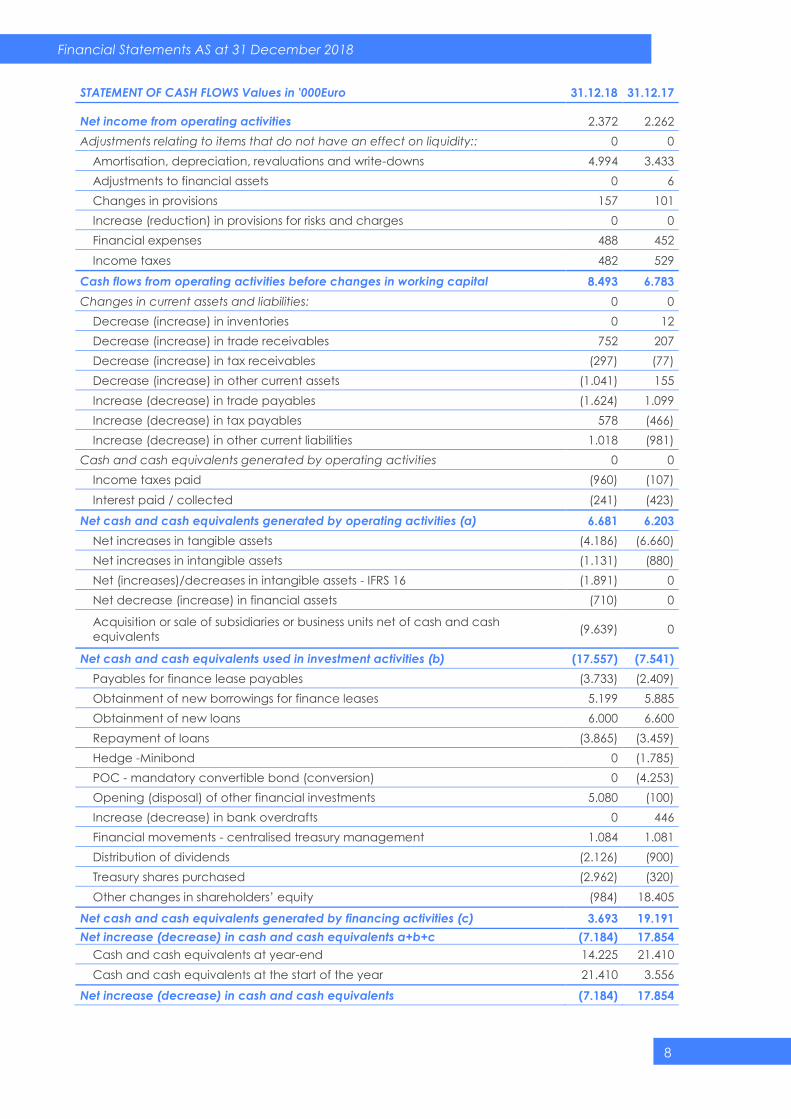

STATEMENT OF CASH FLOWS Values in '000Euro 31.12.18 31.12.17 31.12.18

Consolidated

31.12.17

Consolidated

Net income from operating activities 2,372 2,262 3,496 3,137

Adjustments relating to items that do not have an effect on liquidity: 0 0

Amortisation, depreciation, revaluations and write-downs 4,994 3,433 5,108 3.433

Adjustments to financial assets 0 6 0 6

Changes in provisions 157 101 341 101

Increase (reduction) in provisions for risks and charges 0 0 0 0

Financial expenses 488 452 508 452

Income taxes 482 529 791 725

Cash flows from operating activities before changes in working

capital 8,493 6,783 10,245 7,854

Changes in current assets and liabilities: 0 0 0

Decrease (increase) in inventories 0 12 0 12

Decrease (increase) in trade receivables 752 207 (835) 115

Decrease (increase) in tax receivables (297) (77) (308) (77)

Decrease (increase) in other current assets (1,041) 155 (1,339) 155

Increase (decrease) in trade payables (1,624) 1,099 1,744 329

Increase (decrease) in tax payables 578 (466) 894 (456)

Increase (decrease) in other current liabilities 1,018 (981) 1,249 100

Cash and cash equivalents generated by operating activities 0 0 0 0

Income taxes paid (960) (107) (1,197) (195)

Interest paid / collected (241) (423) (241) (423)

Net cash and cash equivalents generated by operating activities (a) 6,681 6,203 10,212 7,413

Net increases in tangible assets (4,186) (6,660) (4,659) (6.660)

Net increases in intangible assets (1,131) (880) (1,755) (880)

Net (increases)/decreases in intangible assets - IFRS 16 (1,891) 0 (2,165) 0

Net decrease (increase) in financial assets (710) 0 (374) 0

Acquisition or sale of subsidiaries or business units net of cash and

cash equivalents (9,639) 0 (8,421) 0

Net cash and cash equivalents used in investment activities (b) (17,557) (7,541) (17,374) (7,541)

Payables for finance lease payables (3,733) (2,409) (3,804) (2.409)

Obtainment of new borrowings for finance leases 5,199 5,885 5,571 5.885

Obtainment of new loans 6,000 6,600 6,600 6.600

Repayment of loans (3,865) (3,459) (3,865) (3.459)

Hedge -Minibond 0 (1,785) 0 (1.785)

POC - mandatory convertible bond (conversion) 0 (4,253) 0 (4.253)

Opening (disposal) of other financial investments 5,080 (100) 5,080 (100)

Increase (decrease) in bank overdrafts 0 446 4 446

Financial movements - centralised treasury management 1,084 1,081 0 0

Distribution of dividends (2,126) (900) (2,126) (900)

24

FINANCIAL STATEMENTS 2018 - REPORT ON OPERATIONS

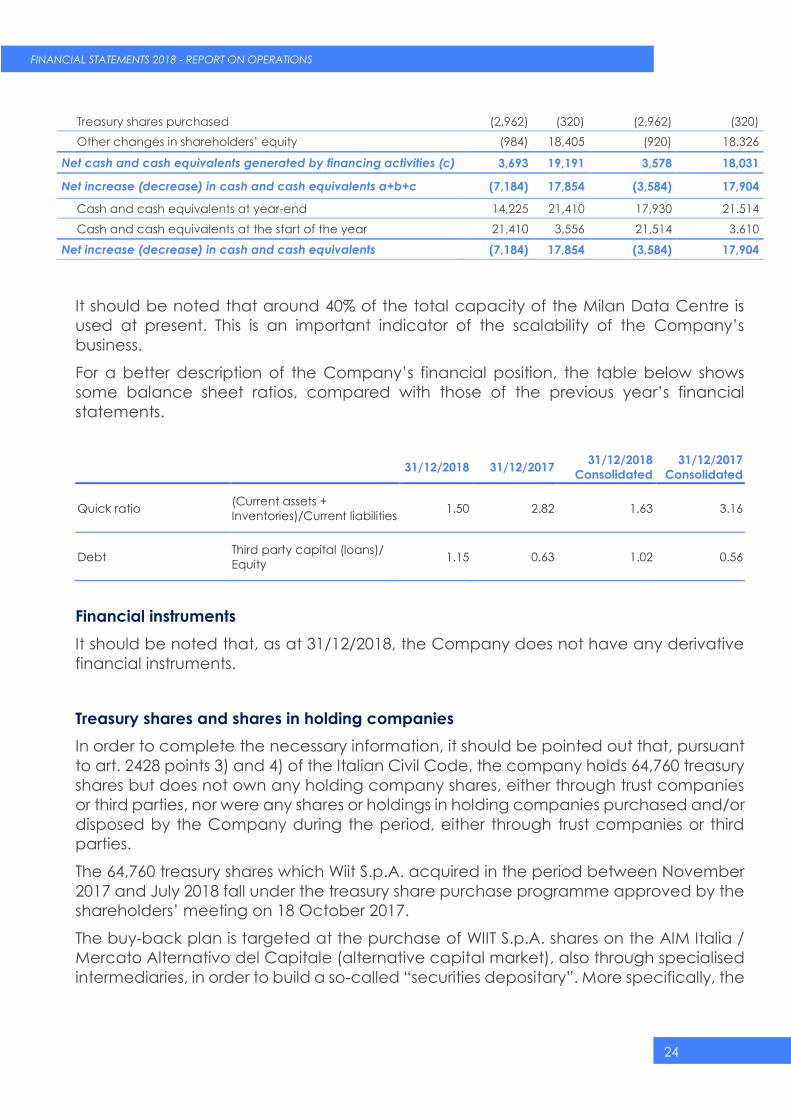

Treasury shares purchased (2,962) (320) (2,962) (320)

Other changes in shareholders’ equity (984) 18,405 (920) 18.326

Net cash and cash equivalents generated by financing activities (c) 3,693 19,191 3,578 18,031

Net increase (decrease) in cash and cash equivalents a+b+c (7,184) 17,854 (3,584) 17,904

Cash and cash equivalents at year-end 14,225 21,410 17,930 21.514

Cash and cash equivalents at the start of the year 21,410 3,556 21,514 3.610

Net increase (decrease) in cash and cash equivalents (7,184) 17,854 (3,584) 17,904

It should be noted that around 40% of the total capacity of the Milan Data Centre is

used at present. This is an important indicator of the scalability of the Company’s

business.

For a better description of the Company’s financial position, the table below shows

some balance sheet ratios, compared with those of the previous year’s financial

statements.

31/12/2018 31/12/2017 31/12/2018

Consolidated

31/12/2017

Consolidated

Quick ratio (Current assets +

Inventories)/Current liabilities 1.50 2.82 1.63 3.16

Debt Third party capital (loans)/

Equity 1.15 0.63 1.02 0.56

Financial instruments

It should be noted that, as at 31/12/2018, the Company does not have any derivative

financial instruments.

Treasury shares and shares in holding companies

In order to complete the necessary information, it should be pointed out that, pursuant

to art. 2428 points 3) and 4) of the Italian Civil Code, the company holds 64,760 treasury

shares but does not own any holding company shares, either through trust companies

or third parties, nor were any shares or holdings in holding companies purchased and/or

disposed by the Company during the period, either through trust companies or third

parties.

The 64,760 treasury shares which Wiit S.p.A. acquired in the period between November

2017 and July 2018 fall under the treasury share purchase programme approved by the

shareholders’ meeting on 18 October 2017.

The buy-back plan is targeted at the purchase of WIIT S.p.A. shares on the AIM Italia /

Mercato Alternativo del Capitale (alternative capital market), also through specialised

intermediaries, in order to build a so-called “securities depositary”. More specifically, the

25

FINANCIAL STATEMENTS 2018 - REPORT ON OPERATIONS

purchase programme is targeted at providing the Company with a stock of treasury

shares to be used as consideration in the context of extraordinary finance transactions

and/or for other uses considered of financial-managerial and/or strategic interest for

the Company, also for the exchange of equity investments with other entities as part of

transactions of interest to the Company.

Information on the environment and personnel

Taking account of the company’s social role, as also highlighted in the report on

operations of the Consiglio Nazionale dei Dottori Commercialisti e degli Esperti Contabili

(National Institute of Chartered Accountants), it is considered appropriate to provide

the following information regarding the environment and personnel.

Personnel

In 2018, there were no workplace fatalities involving personnel listed in the employee

register.

In 2018, there were no serious workplace accidents that involved serious or very serious

injuries to personnel listed in the employee register.

In 2018, no charges were registered against employees or former employees relating to

occupational illnesses and cases of mobbing, for which the company was held to be

definitively liable.

Environment

During 2018, no damages caused to the environment were verified, for which the

company was held to be definitively culpable.

No final sanctions or penalties were imposed on our company in 2018 for

environmental offences or damages.

26

FINANCIAL STATEMENTS 2018 - REPORT ON OPERATIONS

3.2 Research and development activities

Research and development activities include both internal and external costs

incurred, which relate largely to development of the ICT infrastructure. This infrastructure

allows WIIT to provide its services effectively and competitively; we are talking essentially

about the cost of implementing the IT framework through which WIIT interacts with its

customers and is able to provide them with all the services provided for in the contract.

This ICT infrastructure represents, to all intents and purposes, the Company’s strategic

asset, on which the Company’s competitiveness and capacity for market expansion

depend. Capitalised investments of Euro 567,519 were made during the year.

27

FINANCIAL STATEMENTS 2018 - REPORT ON OPERATIONS

Rapporti con imprese controllate, collegate, controllanti e

consorelle

RELATIONS WITH SUBSIDIARIES, ASSOCIATES,

HOLDING COMPANIES AND SISTER

COMPANIES

28

FINANCIAL STATEMENTS 2018 - REPORT ON OPERATIONS

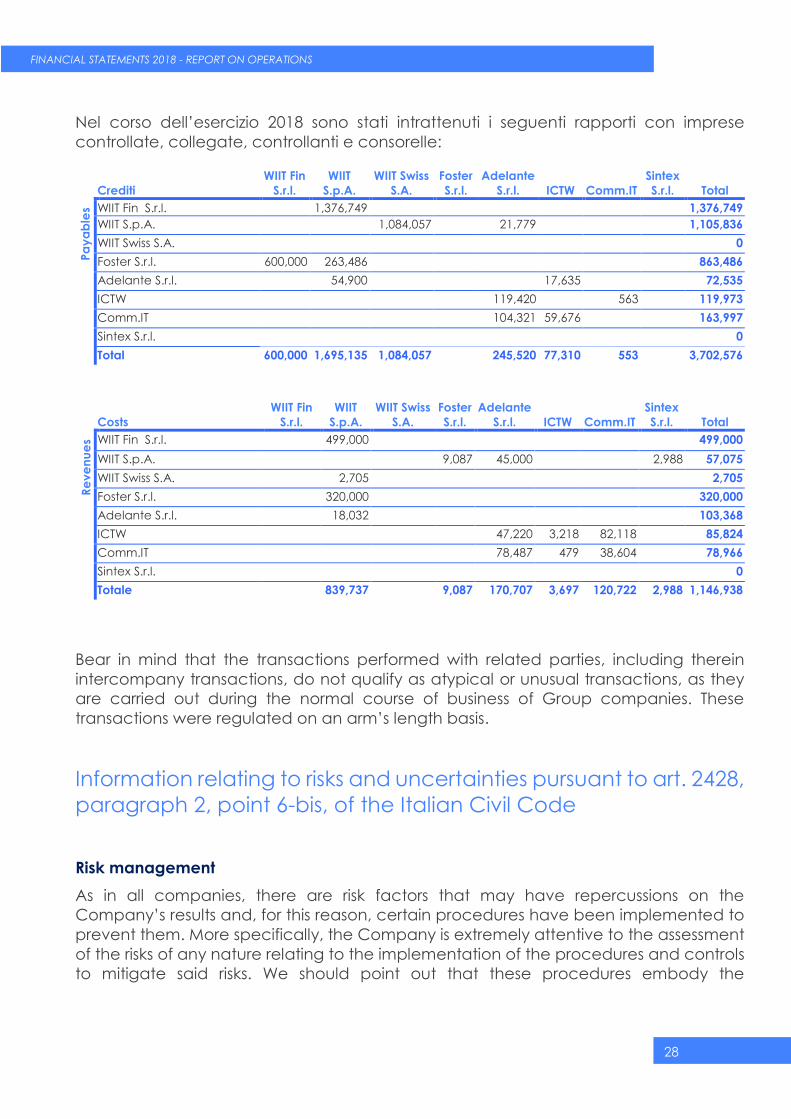

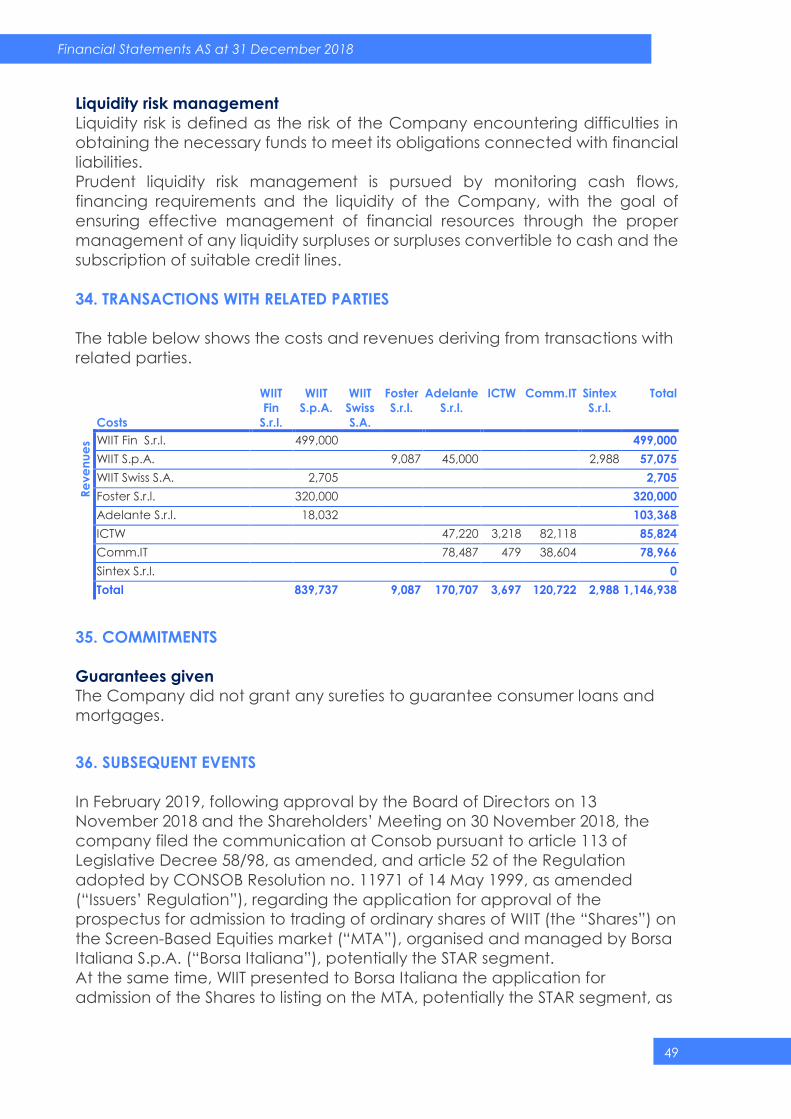

Nel corso dell’esercizio 2018 sono stati intrattenuti i seguenti rapporti con imprese

controllate, collegate, controllanti e consorelle:

Crediti

WIIT Fin

S.r.l.

WIIT

S.p.A.

WIIT Swiss

S.A.

Foster

S.r.l.

Adelante

S.r.l. ICTW Comm.IT

Sintex

S.r.l. Total

Pa

ya

ble

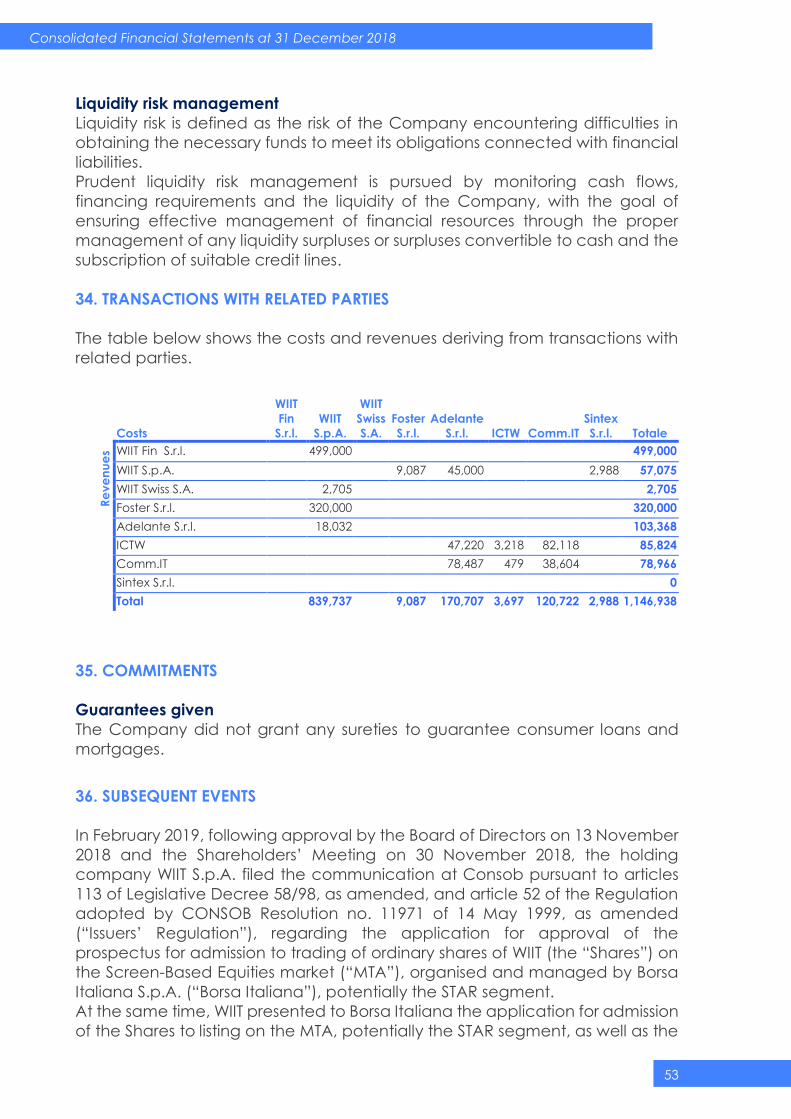

s WIIT Fin S.r.l. 1,376,749 1,376,749

WIIT S.p.A. 1,084,057 21,779 1,105,836

WIIT Swiss S.A. 0

Foster S.r.l. 600,000 263,486 863,486

Adelante S.r.l. 54,900 17,635 72,535

ICTW 119,420 563 119,973

Comm.IT 104,321 59,676 163,997

Sintex S.r.l. 0

Total 600,000 1,695,135 1,084,057 245,520 77,310 553 3,702,576

Costs

WIIT Fin

S.r.l.

WIIT

S.p.A.

WIIT Swiss

S.A.

Foster

S.r.l.

Adelante

S.r.l. ICTW Comm.IT

Sintex

S.r.l. Total

Re

ve

nu

es WIIT Fin S.r.l. 499,000 499,000

WIIT S.p.A. 9,087 45,000 2,988 57,075

WIIT Swiss S.A. 2,705 2,705

Foster S.r.l. 320,000 320,000

Adelante S.r.l. 18,032 103,368

ICTW 47,220 3,218 82,118 85,824

Comm.IT 78,487 479 38,604 78,966

Sintex S.r.l. 0

Totale 839,737 9,087 170,707 3,697 120,722 2,988 1,146,938

Bear in mind that the transactions performed with related parties, including therein

intercompany transactions, do not qualify as atypical or unusual transactions, as they

are carried out during the normal course of business of Group companies. These

transactions were regulated on an arm’s length basis.

Information relating to risks and uncertainties pursuant to art. 2428,

paragraph 2, point 6-bis, of the Italian Civil Code

Risk management

As in all companies, there are risk factors that may have repercussions on the

Company’s results and, for this reason, certain procedures have been implemented to

prevent them. More specifically, the Company is extremely attentive to the assessment

of the risks of any nature relating to the implementation of the procedures and controls

to mitigate said risks. We should point out that these procedures embody the

29

FINANCIAL STATEMENTS 2018 - REPORT ON OPERATIONS

company’s commitments and responsibilities and are based on the utmost

transparency and correctness.

In addition, the Board of Directors, by means of resolution dated 30 July 2013, based on

prior approval of the Organisational and Management Model, including the risk analysis

as set forth in art. 6, paragraph 1, letter a) of Legislative Decree 231/01, also resolved

the appointment of the Supervisory Body, whose task is to monitor the functioning and

observance of the model and oversee its updates.

The risk analysis conducted for the implementation of the Model is incorporated in a

scenario in which the company already possessed an integrated management system,

the DPS and the associated evolution, and already held the certifications relating to

quality (ISO 9001), Management of IT Services (ISO 20000) and security (ISO 27001).

Therefore, as required by art. 2428 of the Italian Civil Code, we summarise the risk factors

below, and the additional general elements, and refer you to the specific

documentation for further details.

EXTERNAL RISKS

Financial risks

The Group is not greatly exposed to financial risks. In fact, as it operates primarily in the

Euro area, the company is only marginally exposed to exchange rate risks due to

transactions in foreign currency; revenues and operating cash flows are not subject to

fluctuations in market interest rates and no significant credit risks are evident given that

the financial counterparties are represented by leading customers considered solvent

by the market.

The financial risks to which the Group is exposed are connected primarily to the

obtainment of funds on the market (liquidity risk) and fluctuations in interest rates

(interest rate risk).

It is certified that, in choosing financing and investment transactions, the Company has

adopted prudence and limited risk criteria and that no speculative transactions were

entered into. The Company covers these financial expenses with cash from operating

activities. In order to monitor the financial risks through an integrated reporting system

and allow analytical planning of future activities, the Company is equipped with a

management control system. The Company also did not make use of derivative

financial instruments to hedge risks linked to the procurement of funding.

However, the main types of financial risk are outlined below, with the relevant

comments on the degree of significance of the exposure to the various risk categories.

Currency risk

Currency risk is defined as the risk of the value of a financial instrument changing as a

result of fluctuations in exchange rates.

30

FINANCIAL STATEMENTS 2018 - REPORT ON OPERATIONS

The WIIT Group is exposed to risk if significant changes in exchange rates occur, taking

into account that, as at the Date of the Prospectus, the Group does not adopt

exchange rate hedging policies.

In particular, the Group is subject (i) to exchange rate risk of a translation nature,

deriving from the fact that the consolidating company Wiit S.p.A., despite preparing its

financial statements in Euro, holds the entire share capital of WIIT Swiss, a Swiss company

that drafts its financial statements in Swiss Francs. Therefore, fluctuations in the exchange

rates used to convert the financial statement figures of WIIT Swiss, originally stated in

Swiss Francs, could influence both the Group’s economic result and its consolidated

shareholders’ equity; and (ii) exchange rate risk of a settlement nature, deriving from

the purchases of services also in non-Euro currencies or US dollars and Albanian Lek (to

a very limited degree).

However, the fact that the core business is performed in the “Euro Area” limits the

Group’s exposure to currency risks deriving from transactions in currencies other than

the functional currency (Euro).

Interest rate risk

Interest rate risk management aims to ensure a balanced debt structure, by minimising

the cost of funding over time.

Interest rate risk is defined as the risk of the value of a financial instrument changing as

a result of fluctuations in market interest rates.

The Group is exposed to the risk of significant fluctuations in interest rates and the risk of

the policies adopted to neutralise these fluctuations being insufficient.

Fluctuations in interest rates influence the market value of the company’s financial

assets and liabilities and the level of net financial expenses, given some of the loans

taken out by the Group are at a variable rate.

Over the years, the Company has taken out almost exclusively medium-term loans with

a variable rate linked to the performance of the 3-month Euribor and at a fixed rate,

and constantly monitors the trend in cash flows.

The details relating to loans in place are reported in the notes to the financial

statements.

Market risk

Market risk is defined as the risk of the value of a financial instrument changing as a

result of fluctuations in market prices.

The Group is exposed to risks connected with the current global economic-financial

situation and, in particular, to the performance of the Italian market as the main market

for the sale of services provided by the Group. More specifically, the instability of the

global political, macroeconomic and financial scenario (in particular in Italy), could

have a major impact on the Group’s productive capacity and growth prospects, with

31

FINANCIAL STATEMENTS 2018 - REPORT ON OPERATIONS

potential negative repercussions on the business, prospects and economic, equity and

financial position of the Parent Company and the Group.

At European level, it should be noted that fears have emerged, on more than one

occasion recently, that the European Union could come to an end or that the individual

member states could abandon the Euro. The UK’s exit from the European Union,

following the referendum on 23 June 2016 (Brexit) is currently the object of international

negotiations to determine the methods that will be used to implement it. In addition,

following the global economic-financial crisis in 2007-2008, the sovereign debt crisis in

Greece, Ireland, Iceland, Portugal, Spain and Cyprus, had a significant impact on the

European financial markets, determining an increase in bond yields and elevated

volatility of the spread on the sovereign debt of many European Union countries,

including Italy. Signs of improvement in the international economic situation have been

observed in more recent periods, to a more significant degree in the US and in China

and in some EU countries, and less marked in other European countries (including Italy).

The Group constantly monitors market risk.

Credit risk

Credit risk is defined as a probable financial loss generated by the non-fulfilment of a

third party payment obligation to the Company.

The WIIT Group is exposed to the risk that its customers may be late or fail to fulfil their

payment obligations according to the agreed terms and methods and the risk of the

internal procedures adopted in relation to the evaluation of the credit rating and

solvency of the customers being insufficient to guarantee successful collections.

Any missed payments, payment delays or other failures to fulfil obligations may be due

to customer insolvency or bankruptcy, to economic events or customer-specific

situations. Late payments could delay cash inflows.

The Company does not have significant concentrations of credit risks, also thanks to the

fact that it does not carry out significant operations in the Public Administration sector,

in line with the Company’s strategic choice.

The Company manages this risk through the selection of counterparties considered

solvent by the market and with a high credit standing, or through the supply of highly

critical and non-interruptible services by its customers.

For commercial purposes, policies are adopted targeted at ensuring the solvency of its

customers, and limiting the exposure to credit risk with respect to an individual customer,

through activities that involve the evaluation of customers and their monitoring.

All receivables are periodically subject to an analytical evaluation per individual

customer, with write-downs effected in the event of impairment.

All details relating to trade receivables are reported in the notes to the financial

statements.

32

FINANCIAL STATEMENTS 2018 - REPORT ON OPERATIONS

Liquidity risk

Liquidity risk is defined as the risk of the Company encountering difficulties in obtaining

the necessary funds to meet its obligations connected with financial liabilities.

Prudent liquidity risk management is pursued by monitoring cash flows, financing

requirements and the liquidity of the Company, with the goal of ensuring effective

management of financial resources through the proper management of any liquidity

surpluses or surpluses convertible to cash and the subscription of suitable credit lines.

Risks deriving from the general conditions of the economy

The Information Technology market is naturally connected to the performance of the

economy. An unfavourable economic phase could slow demand with subsequent

equity, economic and financial effects, especially on subsidiaries.

Risks connected to IT services

The services sector in which the Company operates is characterised by rapid

technological changes and the constant evolution of professional skills and expertise.

The risks connected with the development of the ICT market are mitigated by said

sector in which the company operates and by the internal contractual policies which

make provision for contracts that guarantee a high backlog level and a long-term

business vision.

The phase of contraction in services and IT spending by companies has also promoted

the growth of WIIT, enhancing the offering and the ability of the company to rationalise

and lower the costs of its customers with respect to their competitors.

Risks connected with the evolution of the regulatory framework

In carrying out hosting provider activities, the Group is subject to Directive 2000/31/EC

and Legislative Decree no. 70/2003. Although the aforementioned regulatory provisions

recognise a merely passive role for the hosting provider, limited to an activity of “a mere

technical, automatic and passive nature”, the most recent case law, both Italian and

EU, has also recognised an active role for the provider.

As regards the above, this means that, if said new interpretation should be confirmed,

the provider would also be considered responsible for the content of the information

stored on its servers, given considered the manager. The result is that, in the future, the

Group could therefore be deemed responsible for the contents stored on the Group’s

infrastructures (e.g. information uploaded by customers to its websites) and could,

therefore be involved in the associated disputes (regarding, for example, intellectual

property, civil and/or criminal liability, etc.).

It should be noted that the Group companies are qualified as data controllers pursuant

to Regulation EU 679/2016 on the protection of natural persons with regards to personal

33

FINANCIAL STATEMENTS 2018 - REPORT ON OPERATIONS

data processing and are therefore required to observe the relevant regulation, with the

subsequent costs of compliance (see First Section, Chapter 4, Paragraph 4.1.9. of the

Prospectus).

Lastly, it should be noted that the Parent Company will be required to incur costs and

expenses, including significant, to ensure observance of and compliance with the

legislative and regulatory provisions currently in force, applicable to companies listed

on a regulated market such as the MTA.

INTERNAL RISKS

Risks relating to the dependency on key personnel

The Parent Company and the Group are exposed to the risk of an interruption to

professional collaboration relations with certain top management figures who hold a

key role as well as to the risk of being unable to replace these figures in an adequate

and timely manner. In fact, although the Group has not registered, over the course of

the last few years, turnover of its management and although it believes it is equipped

with an operating structure able to ensure business continuity, it is, nonetheless, exposed

to said risk.

In fact, the Parent Company believes that the success of the WIIT Group depends

largely on some key figures in its top management which, thanks to consolidated

experience in the sector and, as part of their specific responsibilities and competences,

have assumed a key role, over time, in the management of the Group’s business,

making a significant contribution to the development of its activities.

Although, as stated, from an operating and management perspective, the Group

believes it has a structure capable of ensuring business continuity, the loss of the

professional contribution from one or more key figures could have negative

repercussions on the development of activities and on the implementation times of the

Group’s growth strategy. However, the Consolidating company constantly monitors this

risk in order to ensure it is in a position to promptly replace these figures with equally

qualified persons able to guarantee the same operating and professional contribution

and avoid possible negative effects on development activities and on the growth

prospects of the Holding Company and the Group.

Risks relating to customer dependency

Today, the Holding Company and the Group offer services to companies operating in

the various markets (Finance, Service Provider, Defence, Manufacturing and Utility)

which also have extremely different characteristics.

Company revenues are equally distributed, despite the fact that the exit of some major

customers from the portfolio could impact the Company’s economic, equity and

financial position, without however jeopardising business continuity.

34

FINANCIAL STATEMENTS 2018 - REPORT ON OPERATIONS

Risks connected with contractual commitments

The Company provides outsourced services with a high technology content and high

value and the associated underlying contracts may involve the application of penalties

with regards to observance of the agreed service levels.

At contractual level, maximum penalty amounts are envisaged in relation to the value

of the services provided.

The Company has also taken out insurance policies, deemed adequate, to protect itself

against the risks deriving from civil liability for a total maximum annual amount of Euro 5

million.

In respect of projects of economic/financial importance, extra policies are subscribed,

in addition to the cover referred to above, in order to avoid the negative impacts on

the Company’s economic/equity and financial position.

Business outlook

The year 2019 is another year of significant growth in revenues and profit margins.

The Company continues to strengthen its sales structure for the direct coverage of the

market, also thanks to marketing activities targeted at enhancing the brand and the

analysis of the specific needs of the Company’s target customers.

At the moment of the preparation of this report, there are no events or situations,

including extraordinary or provisional, as such to require significant revisions of the

budget values.

In February 2019, following approval by the Board of Directors on 13 November 2018

and the Shareholders’ Meeting on 30 November 2018, the Parent Company filed the

communication at Consob pursuant to articles 113 of Legislative Decree 58/98, as

amended, and article 52 of the Regulation adopted by CONSOB Resolution no. 11971

of 14 May 1999, as amended (“Issuers’ Regulation”), regarding the application for

approval of the prospectus for admission to trading of ordinary shares of WIIT (the

“Shares”) on the Screen-Based Equities market (“MTA”), organised and managed by

Borsa Italiana S.p.A. (“Borsa Italiana”), potentially the STAR segment.

At the same time, WIIT presented to Borsa Italiana the application for admission of the

Shares to listing on the MTA, potentially the STAR segment, as well as the application for

revocation of its Shares from trading on AIM Italia, subject to their concurrent admission

to trading on the MTA.

35

FINANCIAL STATEMENTS 2018 - REPORT ON OPERATIONS

Programmatic Security Document

Pursuant to annex B, point 26 of Legislative Decree 196/2003, containing the Personal

Data Protection Code, the directors acknowledge that the Parent Company has

adjusted itself into line with the measures governing the protection of personal data, in

light of the provisions introduced by Legislative Decree 196/2003, according to the terms

and methods indicated herein. Following the repeal of the obligation to update the

Programmatic Security Document (DPS) by 31 March of each year (art. 45, letter c) of

Decree Law no. 5 of 9 February 2012, WIIT retained the latest version of the DPS of 30

March 2011 and continued to manage the other security measures, with particular

reference to electronic authentication, the management of authentication credentials,

the authorisation system and the periodic updating of the profile of those responsible,

with the appropriate procedure “Logical accesses and user management” filed at the

Company’s registered office, subject to certification according to the ISO20000 and

ISO27001 standards and which are free to consult at the Company’s registered office.

In 2018, Wiit S.p.A. will become compliant with new European regulation 2016/679 on

privacy (GDPR).

Proposed allocation of profit for the year

In relation to a consolidated profit of Euro 3,496,340, the Parent Company proposes to

allocate its profit of Euro 2,371,788 achieved in the year to the legal reserve (Euro 17,199)

and for the distribution of dividends to shareholders (Euro 2,354,589) for each of the WIIT

shares outstanding excluding treasury shares, for a total of Euro 0.90 per share.

Milan, 15/02/2019 On behalf of the Board of Directors

The Chairman

(Riccardo Mazzanti)

FINANCIAL

STATEMENTS

2018

Financial Statements Wiit S.p.A.

2

Financial Statements AS at 31 December 2018

Company: Wiit S.p.A.

Registered office: Milano, Via Muzio Attendolo detto

Sforza n.7

VAT no. And Tax Code: 01615150214

Share Capital: 2,652,066.00 fully paid-in

Milan Register of Companies

No.

n. 01615150214

R.E.A. (economic and

administrative index) No.

n. 1654427

Number of shares 2,652,066

Wiit Spa is subject to the management and coordination activities of Wiit Fin S.r.l.

sz

<<

3

Financial Statements AS at 31 December 2018

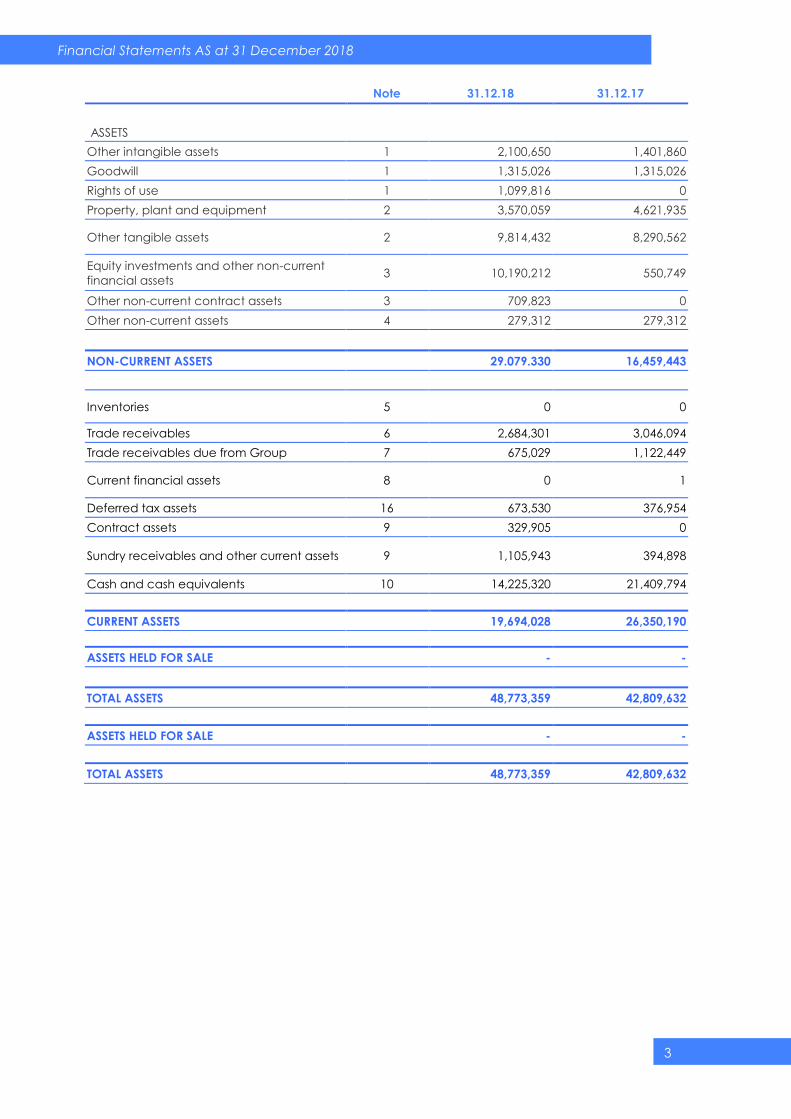

Note 31.12.18 31.12.17

ASSETS

Other intangible assets 1 2,100,650 1,401,860

Goodwill 1 1,315,026 1,315,026

Rights of use 1 1,099,816 0

Property, plant and equipment 2 3,570,059 4,621,935

Other tangible assets 2 9,814,432 8,290,562

Equity investments and other non-current

financial assets 3 10,190,212 550,749

Other non-current contract assets 3 709,823 0

Other non-current assets 4 279,312 279,312

NON-CURRENT ASSETS 29.079.330 16,459,443

Inventories 5 0 0

Trade receivables 6 2,684,301 3,046,094

Trade receivables due from Group 7 675,029 1,122,449

Current financial assets 8 0 1

Deferred tax assets 16 673,530 376,954

Contract assets 9 329,905 0

Sundry receivables and other current assets 9 1,105,943 394,898

Cash and cash equivalents 10 14,225,320 21,409,794

CURRENT ASSETS 19,694,028 26,350,190

ASSETS HELD FOR SALE - -

TOTAL ASSETS 48,773,359 42,809,632

ASSETS HELD FOR SALE - -

TOTAL ASSETS 48,773,359 42,809,632

4

Financial Statements AS at 31 December 2018

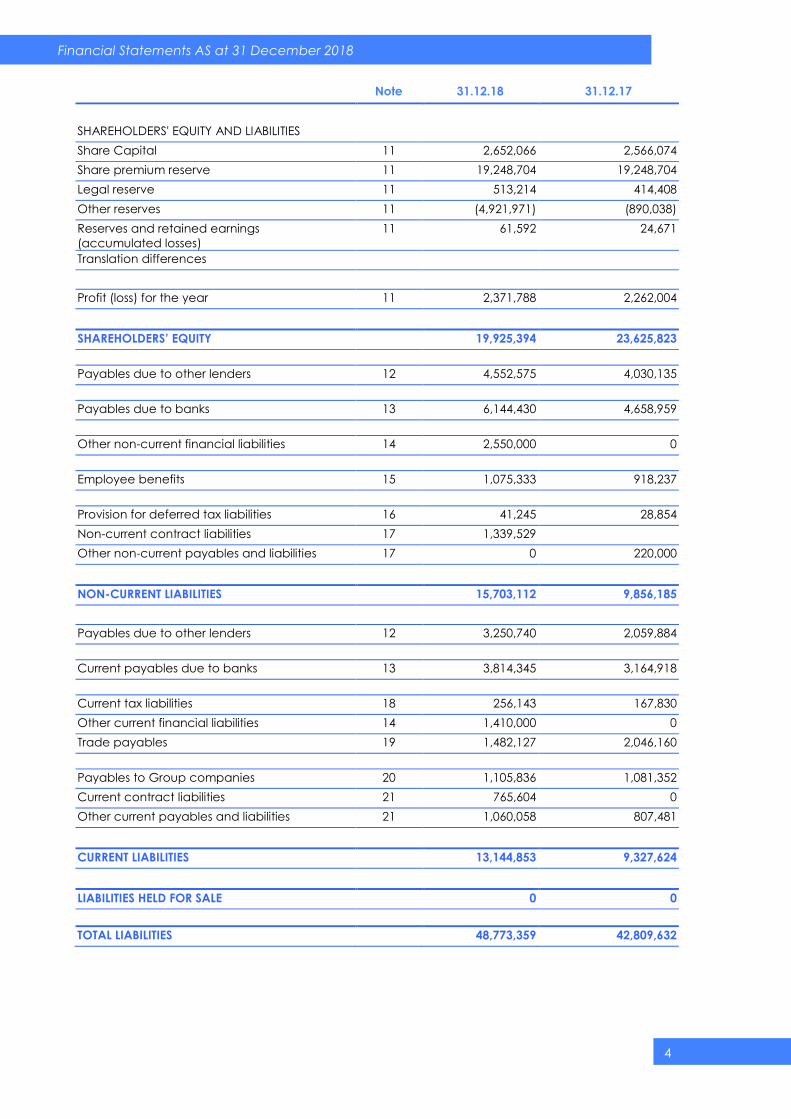

Note 31.12.18 31.12.17

PATRIMONIO NETTO E PASSIVO

SHAREHOLDERS' EQUITY AND LIABILITIES Importi da IVE CEE

Share Capital 11 2,652,066 2,566,074

Share premium reserve 11 19,248,704 19,248,704

Legal reserve 11 513,214 414,408

Other reserves 11 (4,921,971) (890,038)

Reserves and retained earnings

(accumulated losses)

11 61,592 24,671

Translation differences

Profit (loss) for the year 11 2,371,788 2,262,004

SHAREHOLDERS’ EQUITY 19,925,394 23,625,823

Payables due to other lenders 12 4,552,575 4,030,135

Payables due to banks 13 6,144,430 4,658,959

Other non-current financial liabilities 14 2,550,000 0

Employee benefits 15 1,075,333 918,237

Provision for deferred tax liabilities 16 41,245 28,854

Non-current contract liabilities 17 1,339,529

Other non-current payables and liabilities 17 0 220,000

NON-CURRENT LIABILITIES 15,703,112 9,856,185

Payables due to other lenders 12 3,250,740 2,059,884

Current payables due to banks 13 3,814,345 3,164,918

Current tax liabilities 18 256,143 167,830

Other current financial liabilities 14 1,410,000 0

Trade payables 19 1,482,127 2,046,160

Payables to Group companies 20 1,105,836 1,081,352

Current contract liabilities 21 765,604 0

Other current payables and liabilities 21 1,060,058 807,481

CURRENT LIABILITIES 13,144,853 9,327,624

LIABILITIES HELD FOR SALE 0 0

TOTAL LIABILITIES 48,773,359 42,809,632

5

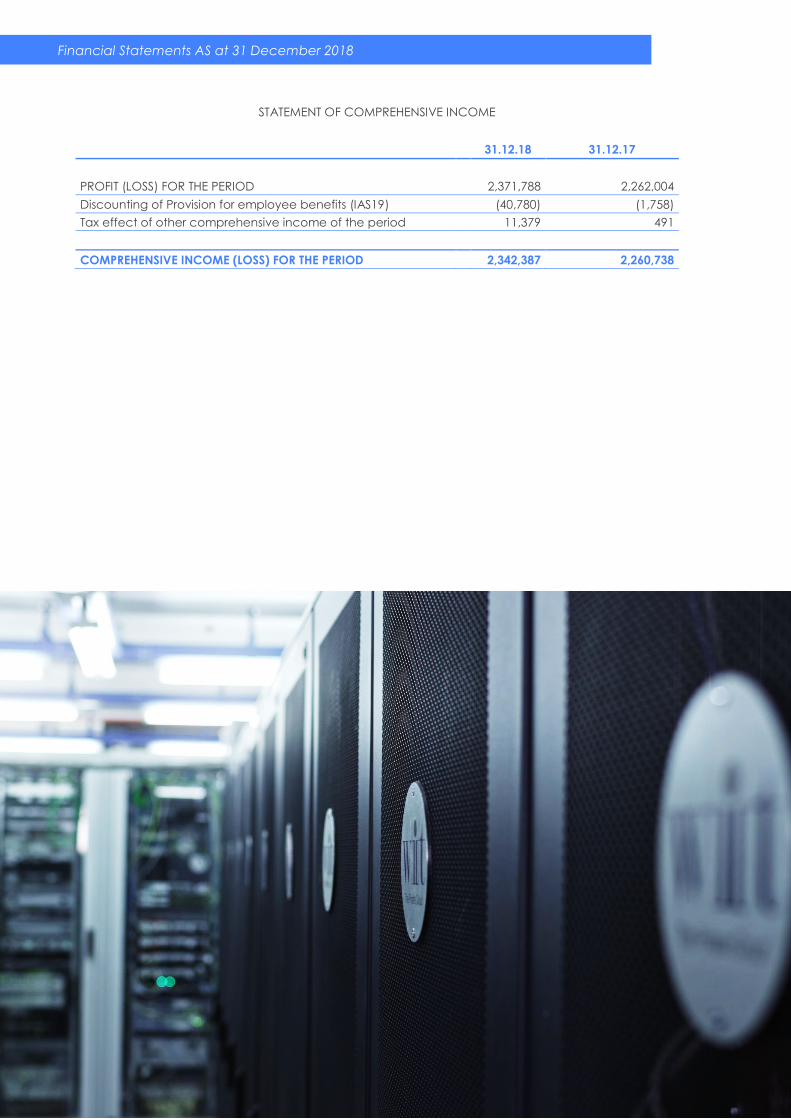

Financial Statements AS at 31 December 2018

INCOME STATEMENT

Note 31.12.18 31.12.17

OPERATING REVENUE AND INCOME

Revenues from sales and services 22 19,988,618 17,482,598

Other revenues and income 23 669,961 747,298

Total operating revenue and income 20,658,579 18,229,896

OPERATING COSTS

Purchases and provision of services 24 (7,916,444) (7,526,171)

Cost of labour 5 (4,112,540) (3,833,708)